UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

__________________________________

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 OR 15(d) of the Securities Exchange Act of 1934

Date of Report (date of earliest event reported): January 10, 2008

REHABCARE GROUP, INC.

(Exact name of Company as specified in its charter)

| Delaware | 0-19294 | 51-0265872 | |

| (State or other jurisdiction | (Commission | (I.R.S. Employer | |

| of incorporation) | File Number) | Identification No.) |

| | | | | | | | | | | |

| 7733 Forsyth Boulevard | |

| Suite 2300 | |

| St. Louis, Missouri | 63105 | |

(Address of principal executive offices) | (Zip Code) |

| | | | | | | | |

(314) 863-7422

(Company's telephone number, including area code)

Not applicable

(Former name or former address if changed since last report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the Company under any of the following provisions:

o Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425)

o Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12)

o Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b))

o Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c))

Item 7.01 | Regulation FD Disclosure |

Beginning on January 10, 2008, RehabCare executives will make presentations at investor conferences to analysts and in other forums using the slides as included in this Form 8-K as Exhibit 99. Presentations will be made using these slides, or modifications thereof, in connection with other presentations in the foreseeable future.

Information contained in this presentation is an overview and intended to be considered in the context of RehabCare's SEC filings and all other publicly disclosed information. We undertake no duty or obligation to update or revise this information. However, we may update the presentation periodically in a Form 8-K filing.

Forward-looking statements have been provided pursuant to the safe harbor provisions of the Private

Securities Litigation Reform Act of 1995. Forward-looking statements involve known and unknown risks

and uncertainties that may cause our actual results in future periods to differ materially from forecasted

results. These risks and uncertainties may include but are not limited to, our ability to consummate

acquisitions and other partnering relationships at reasonable valuations; our ability to integrate

acquisitions and partnering relationships within the expected timeframes and to achieve the revenue,

cost savings and earnings levels from such acquisitions and relationships at or above the levels

projected; our ability to comply with the terms of our borrowing agreements; changes in governmental

reimbursement rates and other regulations or policies affecting reimbursement for the services

provided by us to clients and/or patients; the operational, administrative and financial effect of our

compliance with other governmental regulations and applicable licensing and certification

requirements; our ability to attract new client relationships or to retain and grow existing client

relationships through expansion of our service offerings and the development of alternative product

offerings; the future financial results of any unconsolidated affiliates; our ability to attract and the

additional costs of attracting and retaining administrative, operational and professional employees;

shortages of qualified therapists and other healthcare personnel; significant increases in health,

workers compensation and professional and general liability costs; litigation risks of our past and future

business, including our ability to predict the ultimate costs and liabilities or the disruption of our

operations; competitive and regulatory effects on pricing and margins; our ability to effectively respond

to fluctuations in our census levels and number of patient visits; the adequacy and effectiveness of our

information systems; natural disasters and other unexpected events which could severely damage or

interrupt our systems and operations; changes in federal and state income tax laws and regulations,

the effectiveness of our tax planning strategies and the sustainability of our tax positions; and general

and economic conditions, including efforts by governmental reimbursement programs, insurers,

healthcare providers and others to contain healthcare costs.

Item 9.01 | Financial Statements and Exhibits. |

| (d) | Exhibits - See exhibit index |

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the company has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

Dated: January 10, 2008

By: /s/ Jay W. Shreiner

Name: Jay W. Shreiner

Title: Senior Vice President and

Chief Financial Officer

EXHIBIT INDEX

99 | Investor Relations Presentation in use beginning January 10, 2008. |

Exhibit 99

Investor Presentation, Third Quarter 2007

0

About Us

RehabCare is a leading national provider of

physical rehabilitation services in conjunction with

nearly 1,250 hospitals and skilled nursing facilities

in 43 states and the District of Columbia. We also

own and/or operate 10 freestanding rehabilitation

and long-term acute care hospitals.

1

Service Lines

$720 million consolidated

revenues(1)

Contract Therapy Division

$405 million revenue - 57% of revenue (1)

1,085 skilled nursing facility programs

39 states

7.5 million annual patient visits

Hospital Rehabilitation Services Division

$169 million revenue - 23% of revenue (1)

154 hospital-based programs

31 states & DC

47,000 inpatient and skilled nursing unit discharges/year

1.0 million annual outpatient visits

$101 million revenue - 14% of revenue (1)

Freestanding Hospitals Division

6 rehabilitation hospitals, 3 LTACHs

1 rehabilitation hospital minority owned (2)

5 states (3)

462 beds (3)

6,100 annualized patient discharges (3)

Other Healthcare Services Division

$45 million revenue - 6% of revenue (1)

Phase 2 Consulting – consulting and care management for hospitals and health systems

Polaris Group – consulting for long-term care facilities

VTA Management Services – therapy and nurse staffing for New York

(1)

For twelve months ended 9/30/07

(2)

Not included in consolidated

revenues

(3)

These statistics include the

minority-owned rehab hospital

2

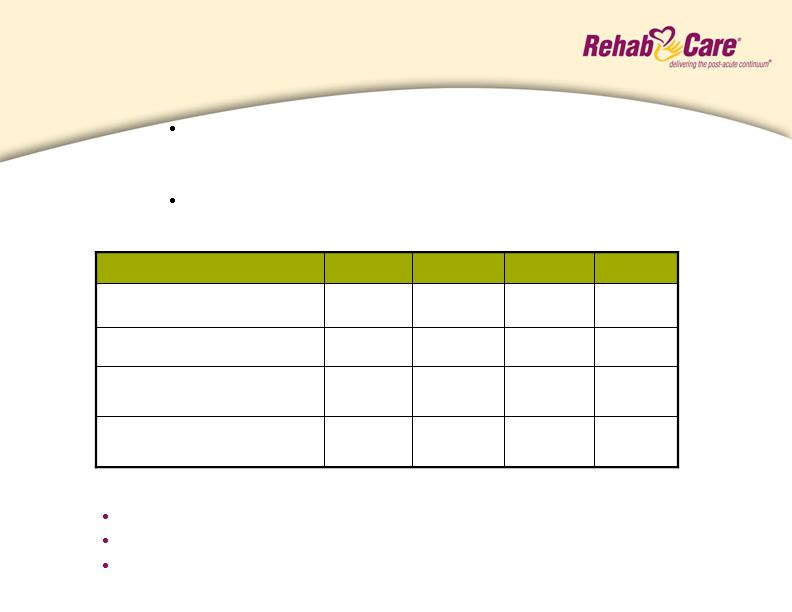

Financial Summary

$0.22

3.9

8.2

$172.9

3Q 07

$0.12(1)

2.1(1)

4.7(1)

$182.2

4Q 06

$0.12

$0.09(2)

Diluted Earnings Per

Share

2.0

1.7(2)

Net Earnings

5.5

4.2(2)

Operating Earnings

$184.0

$181.1

Operating Revenues

1Q 07

2Q 07

(dollars in millions except per

share)

(1) Includes a pretax software development impairment charge of $2.4 million, or $0.09 per diluted

share after tax

(2) Includes a pretax intangible asset impairment charge of $4.9 million ($2.9 million after tax), or $0.17

per diluted share after tax

Q3/07 operating earnings of $8.2 million and EPS of $0.22 per

diluted share, are at the highest level in the last 8 quarters

Lower operating revenues reflect elimination of programs that

don’t meet profit and credit objectives

3

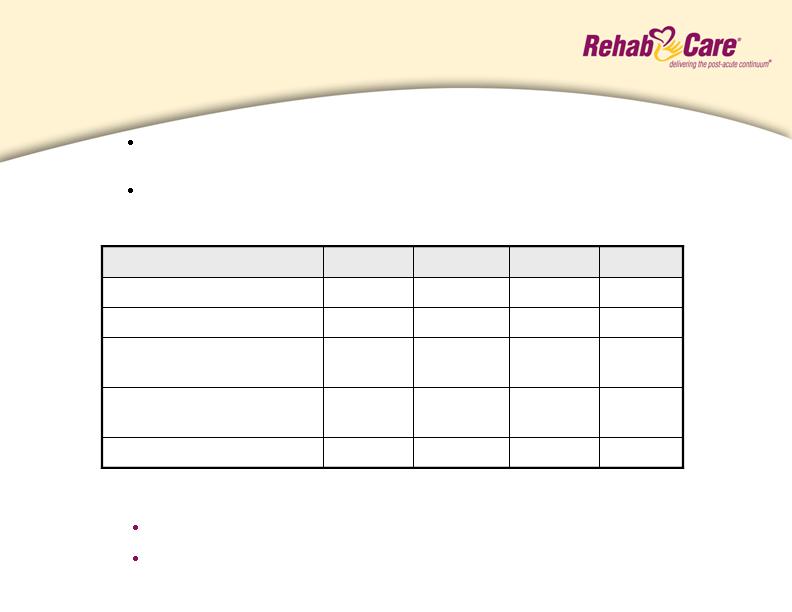

Consolidated Balance Sheet

(Dollars in thousands)

Cash and Cash Equivalents

Total Assets

Total Debt

Stockholders’ Equity

Percent of Debt to Total Capital

12/31/06

9/30/07

$ 9,430

428,296

120,559

$210,779

36%

$ 14,203

425,331

100,600

$235,142

30%

Cash flow from operations totaled $30.9 million for nine

months ended September 30, 2007; $20 million debt

repaid during this period

Cash flow from operations in the fourth quarter of 2007 enabled

additional debt repayment during the quarter.

4

Contract Therapy

Market Overview

The Contract Therapy division manages skilled nursing facility rehab programs that are

designed to provide therapy intervention to both short-stay patients and long-term residents

with a wide range of conditions, including neurological, orthopedic and other conditions

common to the geriatric patient.

Market Size

10,000 Medicare certified skilled nursing facilities

Competitive Landscape

Owned

Self-Operation

Aegis (333)

Kindred - Peoplefirst (332)

Genesis (220)

Sundance (103)

Skilled Healthcare (74)

Managed

RehabCare (1,085)

Aegis (667)

Genesis (480)

Select Medical (400)

Sundance (309)

Kindred - Peoplefirst (286)

EnduraCare (270)

Skilled Healthcare (122)

Source: Information available from public filings or from company websites

5

Contract Therapy

Performance

Q4 06

Q1 07

Q2 07

Q3 07

Dollars in millions

1,085

3.2%

$3.2

$98.3

1,197

(1.2)%

$(1.3)

$103.4

1,146

1,110

Number of Locations End

of Period

(2.2)%

1.1%

Operating Earnings

Margin

$(2.2)

$1.1

Operating Earnings (loss)

$102.8

$100.3

Operating Revenues

Outlook (assumes Part B therapy cap exception remains in place for 2008)

Quarterly sequential improvement in operating earnings

4.5 - 5.5% operating earnings margins during 2008

Return to net additions in locations in 2008

Operating earnings have improved sequentially

each quarter since Q1/07 with a cumulative

improvement of $5.4 million over that time period

Lower operating revenues reflect elimination of programs

that don’t meet profit and credit objectives

6

Contract Therapy

Legislative/Regulatory Environment

Part B Therapy Caps & Physician Fee Schedule (PFS)

The President signed into law the Medicare, Medicaid and SCHIP

Extension Act of 2007 (Extension Act) which includes:

A six-month extension of the exception process which

essentially eliminates the annual limit on therapies for Part B

Medicare beneficiaries

A 0.5% increase in the PFS, which serves as the charge

master for reimbursement for Part B therapy services, for the

next six-month period rather than the 10.1% scheduled

reduction

7

Hospital Rehabilitation Services

Market Overview

Acute care hospital-based inpatient rehabilitation facilities in RehabCare’s Hospital

Rehabilitation Services (HRS) division are for patients who require early, intensive therapies (at

least 3 hours/day 5 days/week) for recovery from stroke, brain injury, neurological disorders,

amputation and other disabling injuries and illnesses. Outpatient therapy programs provide

proactive, exercise-oriented therapy with hands-on treatment for individuals of all ages.

Market Size

5,000 acute care hospitals (approximately 1,000 hospital-based IRFs)

Competitive Landscape (Acute care hospital-based IRFs)

Self-Operation

RehabCare (108)

Horizon Health (Specialty Rehab Mgmt) (23)

HealthSouth (11)

Milestone(1)

TherEx (formerly National Rehab Partners)(1)

(1) Private company or a subsidiary of a public company; number of locations is not available

Source: Information available from public filings or from company websites

8

Hospital Rehab Services

Performance

Q4 06

Q1 07

Q2 07

Q3 07

Dollars in millions

10,173

154

15.7%

$6.3

$40.3

11,337

11,093

10,786

IRF Discharges

172

16.7%

$7.3

$43.8

164

161

Number of Locations End

of Period

12.0%

12.9%

Operating Earnings

Margin

$5.2

$5.4

Operating Earnings

$43.3

$41.8

Operating Revenues

Outlook

Modest increase in IRF units during 2008

Resumption of 3 – 5% growth in same store discharges during

2008

Continued strong operating earnings performance through

focus on controlling costs

Lower operating revenues reflect impact of the 75% Rule and

reduction in units that don’t meet profit and credit objectives

9

Hospital Rehab Services

Legislative/Regulatory Environment

IRF 75% Rule

The Extension Act:

Permanently freezes the compliance threshold at 60%

for cost reporting periods starting July 1, 2006

Continues the use of comorbid conditions to qualify

patients and averts a planned cut in reimbursement rates

for lower extremity joint procedures

Requires HHS to conduct a study on patient access and

eligibility for rehabilitation services

Eliminates market basket updates through 2009

10

Inpatient rehabilitation facilities (IRFs) are equipped to treat patients with a wide range of

debilitating injuries and illnesses, offering inpatient and outpatient services in a home-like

environment. Long-term acute care hospitals (LTACHs) are specialty care hospitals

designed for extended stay patients with complex and chronic conditions.

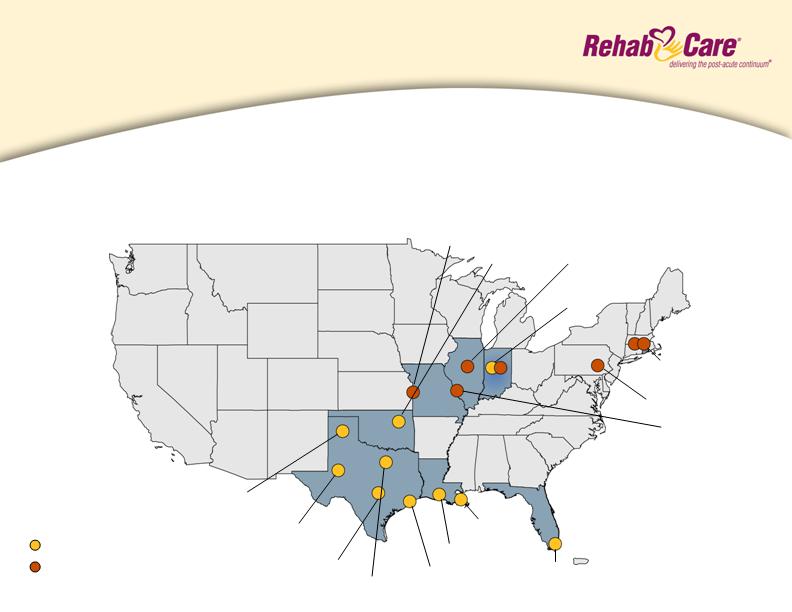

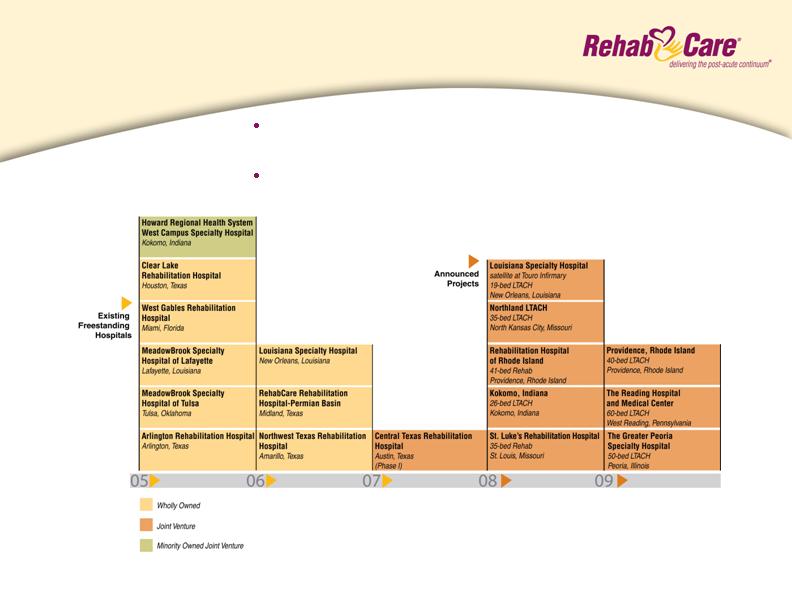

Freestanding Hospitals

Description and Locations

Tulsa, OK

Miami, FL

Arlington, TX

Houston, TX

New Orleans, LA

Amarillo, TX

Midland, TX

Austin, TX

Kokomo, IN

Lafayette, LA

Providence, RI

Peoria, IL

St. Louis, MO

N. Kansas City, MO

Reading, PA

10 current locations

7 future locations

11

Freestanding Hospitals

Market Overview

Competitive Landscape

HealthSouth (94)

RehabCare (7)

Ernest Health (5)

Select Medical (4)

Vibra Healthcare (4)

Centerre (2)

Market Size:

240+ IRFs

Competitive Landscape

Select Medical (87)

Kindred (83)

Regency Hospital (23)

Triumph Healthcare (21)

LifeCare (20)

Vibra Healthcare (9)

HealthSouth (6)

Ernest Health (6)

RehabCare (3)

Market Size:

460+ LTACHs

Freestanding IRFs

LTACHs

Source: Information available from public filings or from company websites

12

Freestanding Hospitals

Performance

(1)

Includes a pretax impairment charge on Louisiana Specialty Hospital intangible asset of $4.9 million

(2)

Includes Central Texas Rehabilitation Hospital, which was in its Medicare demonstration period at 9/30/07. First paying patients were

admitted on November 30, 2007.

Outlook

13-15% EBITDA margins before corporate overhead in 2008 for hospitals in

operation more than one year

$4.5 - $5.5 million of net EBITDA drag in 2008 for hospitals in operation less than

one year

Q4 06

Q1 07

Q2 07

Q3 07

(6.7)%

$(1.6)

$24.4

0.1%

$0.0

$23.7

7.3%

(11.6)%

Operating Earnings Margin (loss)

$1.9

$(3.1)(1)

Operating Earnings (loss)

$26.0

$27.0

Operating Revenues

1,060

6(2)

857

972

1,006

IRF Patient Discharges

5

5

5

Number of IRFs End of Period

386

398

403

380

LTACH Patient Discharges

3

3

3

3

Number of LTACHs End of Period

Q3/07 operating revenues and operating loss impacted by $1.4 million

additional contractual reserve adjustment

Q3/07 operating results also impacted by $700,000 start-up costs

at Central Texas Rehabilitation Hospital

Dollars in millions

13

Freestanding Hospitals

Development Timeline

Division established in 2005 with the acquisition of

MeadowBrook Healthcare

10 existing hospitals, 6 in development, 1 awaiting State

Attorney General approval

Anticipated 4-6 new projects/year

14

Freestanding Hospitals

Legislative/Regulatory Environment

LTACH 25% Rule

The Extension Act:

Eliminates application of the 25% Rule for freestanding LTACHs and

grandfathered LTACHs for next three years

Freezes the 25% Rule for hospital-in-a-hospital (HIH) LTACHs at 50% for

urban and up to 75% for rural and MSA dominant HIH LTACHs for a three

year period

Eliminates the recent payment reductions for very short stay outlier cases for

a three-year period

Imposes a three-year moratorium on new LTACHs and new LTACH beds

with some exceptions

Requires a study by HHS to establish facility and patient criteria.

IRF 75% Rule

Freestanding Hospitals are subject to the same 75% Rule provisions as

previously discussed. The division had been operating at or above the 60%

compliance threshold for calendar year 2007.

15

Continuous Improvement

Initiatives

Intermediate

Long-Term

Open 4-6 joint ventures

annually

Standardize care

management processes

across Hospitals and

ARUs

Implement IT roadmap for

improved clinical,

revenue cycle, and data

warehouse systems

Standardize and integrate

back office processes and

information systems

Implement centralized

support infrastructure

for Hospitals division

Build out continuum of

care delivery model

around key market

relationships

Implement electronic

medical record system

Continue to address

therapist supply issue

through innovation

programs like Allied

Health Research Institute

and partnerships with

the Universities of

Kansas and Missouri

2008 Initiatives

CT operating earnings

margins to 4.5% - 5.5%

HRS modest increase in

IRF units and resumption of

3-5% growth in same store

discharges

HRS product development

to better match long-term

client needs

Hospitals EBITDA margin to

13-15% target for mature

hospitals

Roll out Patient Plus

compensation program in

CT division

16

Investment Considerations

Why RehabCare?

Increasing market demand

Unique continuum of care model

Demonstrated ability to grow revenue

organically and through acquisitions

Proven ability to adapt to market

and regulatory changes

Expenditures for post-acute services:

Increase of 239% since 1998

Projected increase of 150% by 2016

Represents 12% of Medicare spending

75% rule, Part B therapy caps, LTACH

25% rule, physician fee schedule

(Annualized)

Celebrating 25 years as one of the longest tenured post-acute providers

of service in the industry

17

Safe Harbor

Forward-looking statements have been provided pursuant to the safe harbor provisions of the Private

Securities Litigation Reform Act of 1995. Forward-looking statements involve known and unknown risks

and uncertainties that may cause our actual results in future periods to differ materially from forecasted

results. These risks and uncertainties may include but are not limited to, our ability to consummate

acquisitions and other partnering relationships at reasonable valuations; our ability to integrate

acquisitions and partnering relationships within the expected timeframes and to achieve the revenue,

cost savings and earnings levels from such acquisitions and relationships at or above the levels

projected; our ability to comply with the terms of our borrowing agreements; changes in governmental

reimbursement rates and other regulations or policies affecting reimbursement for the services

provided by us to clients and/or patients; the operational, administrative and financial effect of our

compliance with other governmental regulations and applicable licensing and certification

requirements; our ability to attract new client relationships or to retain and grow existing client

relationships through expansion of our service offerings and the development of alternative product

offerings; the future financial results of any unconsolidated affiliates; our ability to attract and the

additional costs of attracting and retaining administrative, operational and professional employees;

shortages of qualified therapists and other healthcare personnel; significant increases in health,

workers compensation and professional and general liability costs; litigation risks of our past and future

business, including our ability to predict the ultimate costs and liabilities or the disruption of our

operations; competitive and regulatory effects on pricing and margins; our ability to effectively respond

to fluctuations in our census levels and number of patient visits; the adequacy and effectiveness of our

information systems; natural disasters and other unexpected events which could severely damage or

interrupt our systems and operations; changes in federal and state income tax laws and regulations,

the effectiveness of our tax planning strategies and the sustainability of our tax positions; and general

and economic conditions, including efforts by governmental reimbursement programs, insurers,

healthcare providers and others to contain healthcare costs.

18