Exhibit 99

1

* One minority owned

What We Do

•

Skilled Nursing Facility-Based Rehabilitation Programs

•

1,197 programs – 6.4 million patient visits annually

•

Hospital-Based Rehabilitation Programs– 172 Total Units

•

Acute Rehabilitation Units

•

115 programs –46,000 discharges annually

•

Subacute/Transitional Care Units

•

18 units –134,000 patient days annually

•

Outpatient Rehabilitation Programs

•

39 units –1.1 million visits annually

•

Freestanding Hospitals

•

6 Inpatient Rehabilitation Hospitals*

•

256 Beds –2500 discharges annually

•

3 Long-Term Acute Care Hospitals

•

186 Beds – 1400 discharges annually

•

Other Healthcare Services

•

Phase 2 – consulting services for acute care hospitals

•

Polaris Group - consulting services for long-term care facilities

•

VTA Management Services – therapist staffing for healthcare facilities and schools in

New York

3

Hospital-based

Skilled-based

Free Standing

Other Healthcare Services

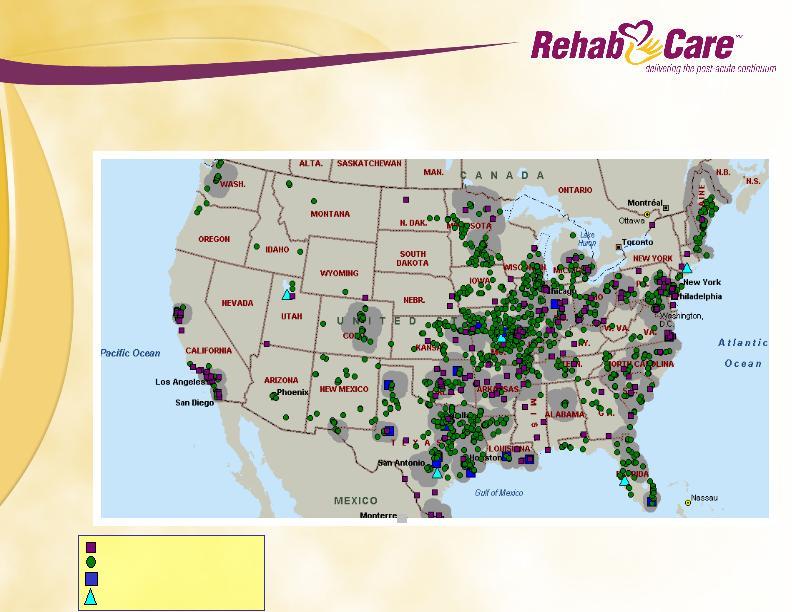

Where We Are

Nearly 1,400 locations servicing approximately 24,000 patient visits each day

4

Medicare Reimbursement for

Post-Acute Services

Post-Acute Services

Medicare reimbursement for post-acute services:

•

Totaled $42 billion in 2005, an increase of 68% since 1999

•

Projected $97 billion by 2014

•

Represents 13% of Medicare’s total spending

CMS contains costs by its PPS adjustments and regulations

5

Our Revenues Follow Patient Care

Trends

Trends

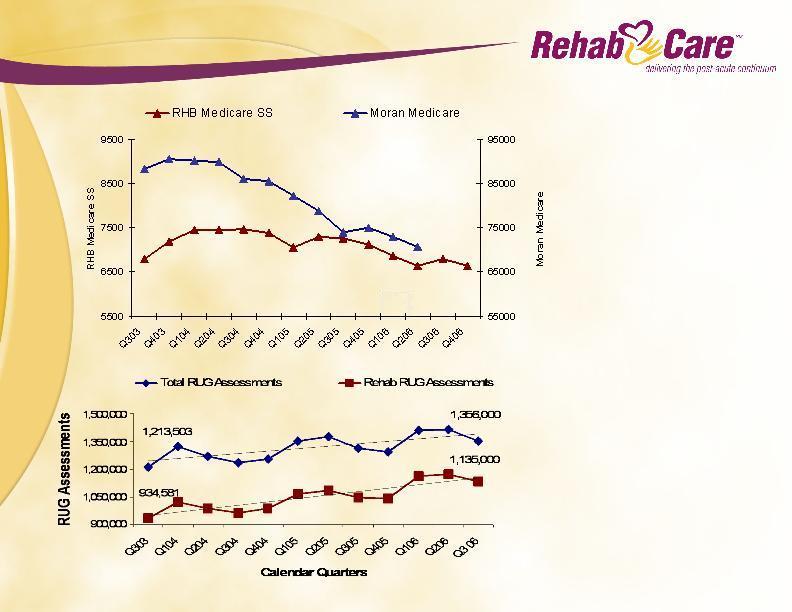

In the time period studied by Moran Report, September 2006:

•

Moran facilities declined 18.4%

•

RehabCare facilities decreased

3.5%

3.5%

•

Since Q3/03, RUG assessments

nationally increased 12%

nationally increased 12%

•

Rehab RUG assessments in that period

increased 21%

increased 21%

•

During the same period, the number of

skilled facilities nationally remained

relatively stable

skilled facilities nationally remained

relatively stable

•

The number of rehabilitation assessments

outpaced the overall increase in total

assessments

outpaced the overall increase in total

assessments

6

Hospital-Based

Rehabilitation Programs

(HRS Division)

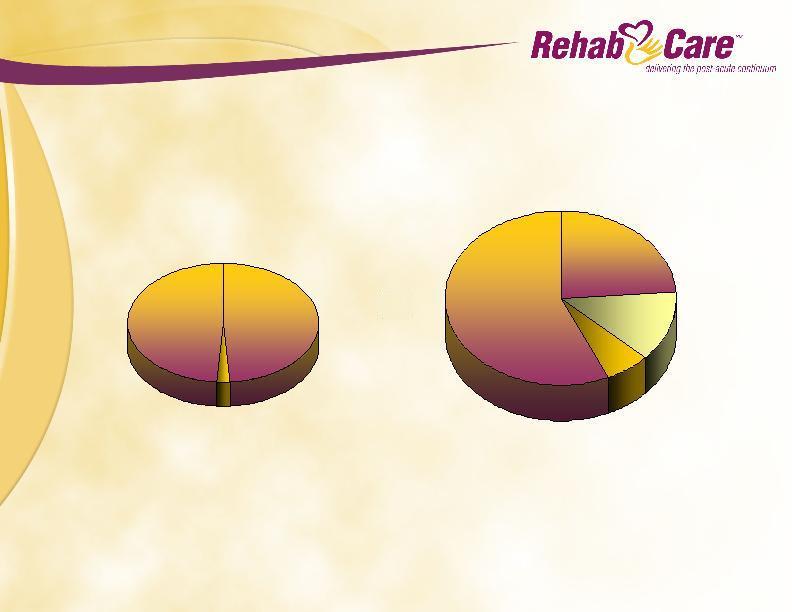

$43.8M

SNF-Based

Rehabilitation Programs

(Contract Therapy Division)

$103.4M

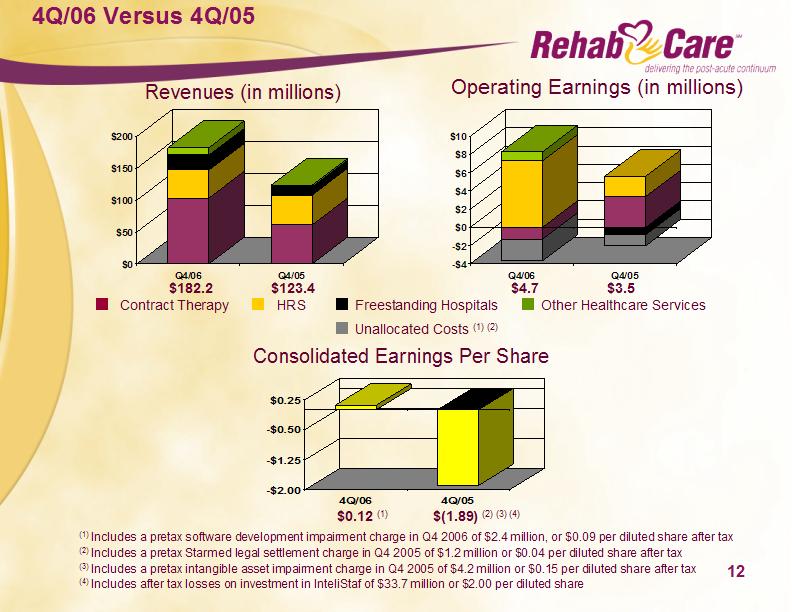

4Q/06

Total Revenue $182.2 million

Other Healthcare

Services

Services

$11.3M

6%

24%

57%

Freestanding

Hospitals

(IRFs and LTACHs)

$23.7M

13%

Our Revenue Trends

Hospital-Based

Rehabilitation Programs

(HRS Division)

$46.7M

SNF-Based

Rehabilitation Programs

(Contract Therapy Division)

$46.7M

4Q/04

Total Revenue $95.1 million

49%

49%

2%

Other Healthcare Services

$1.7M

7

Skilled Nursing Facility-Based

Rehabilitation

Rehabilitation

•

Largest Medicare post acute reimbursement setting

•

Growing care setting, in part due to 75% Rule

•

Lower operating margins require scale for better economies and

improve profitability

•

Acquisition of Symphony

•

Adds critical mass for selective markets; entry into other

markets

•

Adds significant therapist resources and client

relationships

relationships

•

Provides $10-14 million projected annualized cost savings

and operating efficiencies over 18 months – Q4 2006 exit

run rate of $8.5 million cost savings annualized

8

Hospital-Based Rehabilitation

•

Provides 3-5 year contractual relationships with host hospitals

and health systems with existing market share and flow of

patients

•

Remains highest margin business with cash flows to fund other businesses

•

Expect 3-5% historical growth to return after full implementation

of 75% Rule

9

Freestanding Hospitals

•

Provides anchor operations in continuum markets

•

Continues strategy of working with host hospitals and health

systems with existing market share and flow of patients

•

Establishes ownership position and reduces risk of contract

loss

•

Provides a vehicle for expansion of bed capacity

•

Enhances control over quality and competency in clinical and

medical matters

10

Freestanding Hospitals

Joint Venture Strategy

Joint Venture Strategy

Definitive Agreements – Previously Announced

•

Austin -

•

Phase 1 - 20-bed IRF – open mid-2007

•

Phase 2 - replace 20-bed IRF with 36-bed IRF and

40-bed LTACH – projected open 2009

40-bed LTACH – projected open 2009

•

North Kansas City – 35-bed LTACH – open early 2008

•

St. Louis - 35-bed IRF – open early 2009

Other Development Projects

•

Howard Regional – 26-bed LTACH – open late 2007

•

Peoria – 50-bed LTACH – subject to certificate of need

•

In addition to these 5, there are 6 joint venture projects in various stages of development

11

Current Key Initiatives

Improve margins in all businesses

•

Pricing

•

Productivity

Integration of Symphony and synergy realization

•

Roll out handheld technology and train new personnel

Grow freestanding hospital business

•

Joint ventures and acquisitions

Labor resource management

•

Attract and deploy therapists

•

Expand staffing coordination

•

Grow campus recruiting

•

Reduce contract labor

More fully develop continuum market strategy

•

Better manage scarce resources

•

Focus business development efforts

Client retention

•

Develop closer partnerships using technology and clinical resources

Impact of regulation

•

75% Rule, Part B Therapy Caps, Physician Fee Schedule, 25% Rule for LTACHs, Fiscal Intermediary activism

14

Medicare Reimbursement Initiatives

Impacting Rehabilitation Services

Impacting Rehabilitation Services

•

75% Rule

•

Limits the type and number of rehabilitation patients that can be cared for in an acute hospital setting

•

Part B Therapy Caps

•

Limits the amount of therapy services which can be provided to Part B patients in skilled nursing facilities

•

Physician Fee Schedule

•

Establishes reimbursement for Part B

services, including therapy. Adjusted

annually by CMS and Congress

services, including therapy. Adjusted

annually by CMS and Congress

•

25% Rule for LTACHs

•

Restricts HIH LTACHs from accepting more than 25% of their admissions from host acute care hospital

•

Currently operating at 65% compliance in the 60%

compliance requirement

compliance requirement

•

Goes to 65% and 75% beginning July 2007 and

2008, respectively

2008, respectively

•

Proposed legislation calls for freezing threshold

at 60%

at 60%

•

Exception process extended to Jan 1, 2008

Congressional action required for

changes/extension

Congressional action required for

changes/extension

•

Congress eliminated proposed 5% rate reduction

planned for Jan 1, 2007

planned for Jan 1, 2007

•

Part B revenues represent about 35% of our

skilled nursing revenues

skilled nursing revenues

•

Proposed rule issued on January 25, 2007 by CMS

extends 25% admission restriction to all LTACHs

(including freestanding and grandfathered)

extends 25% admission restriction to all LTACHs

(including freestanding and grandfathered)

•

If adopted in its current form, it may have some

negative operating impact on our New Orleans

LTACH and an impairment charge

negative operating impact on our New Orleans

LTACH and an impairment charge

15

What Sets RehabCare Apart

•

25-year expertise in providing post-acute services

•

Unique continuum of care business model

•

Growth orientation with demonstrated ability to grow revenue organically and through acquisitions

•

Proven ability to adapt to market and regulatory changes

17

Safe Harbor

Forward-looking statements have been provided pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Forward-looking statements involve known and unknown risks and uncertainties that may cause our actual results in future periods to differ materially from forecasted results. These risks and uncertainties may include but are not limited to, our ability to consummate acquisitions and other partnering relationships at reasonable valuations; our ability to integrate acquisitions and partnering relationships within the expected timeframes and to achieve the revenue, cost savings and earnings levels from such acquisitions and relationships at or above the levels projected; our ability to comply with the terms of our borrowing agreements; changes in governmental reimbursement rates and other regulations or policies affecting reimbursement for the services provided by us to clients and/or patients; the operational, administrative and financial effect of our compliance with other governmental regulations and applicable licensing and certification requirements; our ability to attract new client relationships or to retain and grow existing client relationships through expansion of our service offerings and the development of alternative product offerings; the future financial results of any unconsolidated affiliates; the adequacy and effectiveness of our operating and administrative systems; our ability to attract and the additional costs of attracting and retaining administrative, operational and professional employees; shortages of qualified therapists and other healthcare personnel; significant increases in health, workers compensation and professional and general liability costs; litigation risks of our past and future business, including our ability to predict the ultimate costs and liabilities or the disruption of our operations; competitive and regulatory effects on pricing and margins; our ability to effectively respond to fluctuations in our census levels and number of patient visits; the proper functioning of our information systems; natural disasters and other unexpected events which could severely damage or interrupt our systems and operations; and general and economic conditions, including efforts by governmental reimbursement programs, insurers, healthcare providers and others to contain healthcare costs.

18

Investor Presentation

Fourth Quarter, 2006