| UNITED STATES SECURITIES AND EXCHANGE COMMISSION | ||

| Washington, D.C. 20549 | ||

FORM N-CSR | ||

| CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES | ||

| Investment Company Act file number: | (811-02608) |

| Exact name of registrant as specified in charter: | Putnam Money Market Fund |

| Address of principal executive offices: | One Post Office Square, Boston, Massachusetts 02109 |

| Name and address of agent for service: | Robert T. Burns, Vice President One Post Office Square Boston, Massachusetts 02109 |

| Copy to: | John W. Gerstmayr, Esq. Ropes & Gray LLP 800 Boylston Street Boston, Massachusetts 02199-3600 |

| Registrant’s telephone number, including area code: | (617) 292-1000 |

| Date of fiscal year end: | September 30, 2012 |

| Date of reporting period: | October 1, 2011 — March 31, 2012 |

Item 1. Report to Stockholders: |

| The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940: | |||

Putnam

Money Market

Fund

Semiannual report

3 | 31 | 12

| Message from the Trustees | 1 | ||

| About the fund | 2 | ||

| Performance snapshot | 4 | ||

| Interview with your fund’s portfolio managers | 5 | ||

| Your fund’s performance | 10 | ||

| Your fund’s expenses | 11 | ||

| Terms and definitions | 13 | ||

| Other information for shareholders | 14 | ||

| Financial statements | 15 | ||

Consider these risks before investing: Money market funds are not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other governmental agency. Although the fund seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in this fund.

Message from the Trustees

Dear Fellow Shareholder:

After a quarter century of trending lower, U.S. Treasury rates have shown some upward movement on signs of an improving economy during the past few months. Greece’s successful debt restructuring and some better-than-expected economic data in the United States have helped to coax investors off the sidelines and back into the markets. While we believe the historic bull market in government debt is likely near its close, fixed-income markets today continue to offer myriad investing opportunities.

Investing in fixed-income markets, however, requires particular expertise and the capacity for deep security-level research. We believe Putnam’s veteran fixed-income team is well suited to that task, and offers a long-term track record of uncovering attractive opportunities across all sectors of the bond markets.

In other news, please join us in welcoming the return of Elizabeth T. Kennan to the Board of Trustees. Dr. Kennan, who served as a Trustee from 1992 until 2010, has rejoined the Board, effective January 1, 2012. Dr. Kennan is a Partner of Cambus-Kenneth Farm (thoroughbred horse breeding and general farming), and is also President Emeritus of Mount Holyoke College.

We would also like to take this opportunity to welcome new shareholders to the fund and to thank all of our investors for your continued confidence in Putnam.

About the fund

Seeking to offer accessibility and current income with relatively low risk

For most people, keeping part of their savings in an easily accessible place is an essential part of an investment plan. Putnam Money Market Fund can play a valuable role in many investors’ portfolios because it seeks to provide stability of principal and liquidity to meet short-term needs. In addition, the fund aims to provide investors with current income at short-term rates.

Because it invests in high-quality short-term money market instruments, the fund’s risk of losing principal may be lower than that of other funds. It typically invests in securities that are rated in the highest or second-highest category of at least one nationally recognized rating service. The fund seeks as high a rate of current income as Putnam Management believes is consistent with preservation of capital and maintenance of liquidity. Money market fund yields typically rise and fall along with short-term interest rates. Money market funds may not track rates exactly, however, as securities in these funds mature and are replaced with newer instruments earning the most current interest rates.

Whether you want to earmark money for near-term expenses or future investment opportunities, or just stow away cash for an unforeseen “rainy day,” this fund can be an appropriate choice.

Types of money market securities

Money market securities are issued by governments, government agencies, financial institutions, and established non-financial companies. Securities your fund invests in include:

Commercial paper Short-term unsecured loans issued by large corporations, typically for financing accounts receivable and inventories

Bank certificates of deposit Direct obligations of the issuing commercial bank or savings and loan association

Repurchase agreements (repos) Contracts in which one party sells a security to another party and agrees to buy it back later at a specified price; acts in economic terms as a secured loan

Government securities Direct short-term obligations of governments or government agencies; for example, U.S. Treasury bills

Variable-rate demand notes (VRDNs) Floating-rate securities with a long-term maturity, usually 20 or 30 years, that carry a coupon that resets every one or seven days, making them eligible for purchase by money market mutual funds.

| 2 | 3 |

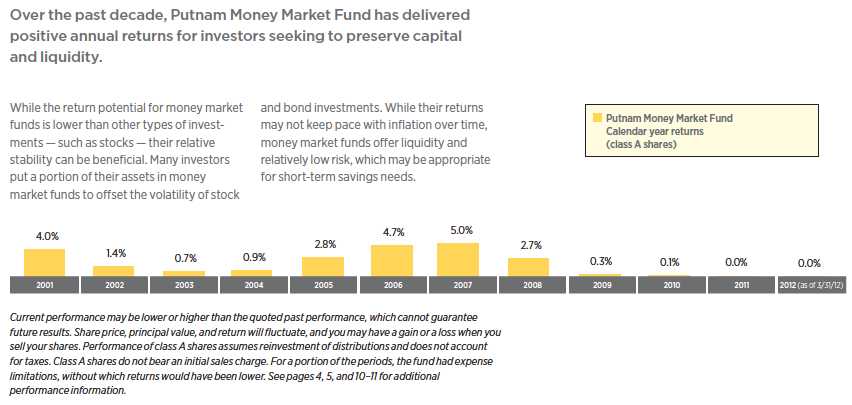

Current performance may be lower or higher than the quoted past performance, which cannot guarantee future results. Share price, principal value, and return will fluctuate, and you may have a gain or a loss when you sell your shares. Performance of class A shares assumes reinvestment of distributions and does not account for taxes. Class A shares do not bear an initial sales charge. Yield reflects current performance more closely than total return. See pages 5 and 10–11 for additional performance information. For a portion of the periods, the fund had expense limitations, without which returns would have been lower. Due to market volatility, current performance may be higher or lower than performance shown. To obtain the most recent month-end performance, visit putnam.com.

* Returns for the six-month period are not annualized, but cumulative.

4

Interview with your fund’s portfolio managers

What was the investment backdrop like during the six months ended March 31, 2012?

Joanne: The six months was a tale of two halves, with investors gaining confidence as the reporting period progressed. Uncertainty remained high in the early months as the large macroeconomic challenges that dominated headlines throughout 2011 continued to weigh on investor confidence. Treasury rates in the United States declined slightly amid solid demand from risk-averse investors, while discussions over reducing the size of the federal deficit continued to take center stage heading into an election year. Outside the United States, little progress was made in the European sovereign debt situation despite ongoing negotiations.

By the first quarter of 2012, however, the U.S. economy had surprised on the upside. Economic data including housing, jobs, consumer confidence, and spending were either stable or slowly improving — suggesting that the U.S. economy, and the global economic outlook for that matter, might not be as bleak as first thought. Signs of a U.S. recovery were welcome news amid Europe’s clear economic deceleration and China’s more measured slowdown. The positive U.S. economic reports were enough to tempt cautious investors who had waited out the uncertainty in lower-risk investments to shift assets into higher-risk strategies, such as equities and high-yield bonds. Treasury rates rose during the risk rally to attract interest amid the stronger economic results.

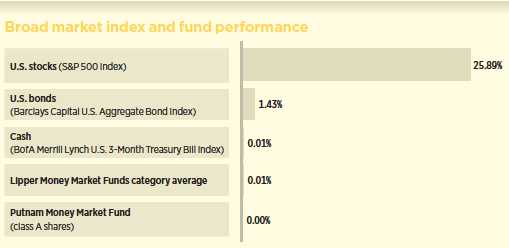

This comparison shows your fund’s performance in the context of broad market indexes for the six months ended 3/31/12. See pages 4 and 10–11 for additional fund performance information. Index descriptions can be found on page 13.

5

How did Putnam Money Market Fund perform in this environment?

Jonathan: The reporting period was a challenging time for investors focused on the short end of the yield curve. The Federal Reserve [Fed] remained firm in its resolve to hold its benchmark federal funds rate steady in the 0%-to-0.25% range to promote growth and maintain liquidity in the financial system. The near-zero rates have hovered at this level for over three years, resulting in historically low returns and yields on money market securities. With its conservative, high-quality focus, the fund delivered performance that was in line with this interest-rate environment.

What were the biggest concerns weighing on the money markets during the reporting period?

Joanne: Low interest rates, the eurozone debt crisis, and further reforms to money market funds preoccupied money-market investors during the period.

Commentary contained in the Fed minutes indicated that the Board of Governors intends to maintain interest rates at their present levels well into 2014 and that it is unlikely to embark on another round of asset purchases [known as QE1 and QE2] unless growth stalls or inflation is less than its 2.0% target. Persistently low rates offer little opportunity for income, but money markets have proven resilient over the past several years as they continue to be a stable and liquid investment alternative with over $2.4 trillion in assets.

During the fourth quarter of 2011, concerns over economic issues in Europe continued to weigh on investor’s minds. Greece remained the focal point as the country sought legislative reforms to control its spending in order to receive further funding from the European Central Bank [ECB]. Many banks hold billions in the sovereign debt of Greece, Spain, Portugal, and other struggling countries, which poses a risk should those countries be faced with default. To ease the pressure from

Allocations are represented as a percentage of portfolio value. Summary information may differ from the portfolio schedule included in the financial statements due to the inclusion of derivative securities and the exclusion of as-of trades, if any,and the use of different classifications of securities for presentation purposes. Holdings and allocations may vary over time.

6

these situations, the ECB enacted the Long Term Refinancing Operation [LTRO], which has helped inject liquidity into the European banking system and, in turn, helped to boost investor confidence.

There has been increased discussion in recent months about the Securities and Exchange Commission [SEC] proposing additional regulations to reduce the susceptibility of money market funds to liquidity runs. These new proposals include requirements for capital buffers, redemption restrictions, and possibly variable-rate net asset values. Although there has been much debate over what form these potential new regulations will take, the SEC has yet to announce any formal action, but is expected to do so over the next several months.

With interest rates pinned down at such low levels for the period, where did you find your best investment opportunities?

Jonathan: Over the course of the period, we found opportunities further out on the money market yield curve, allowing us to extend maturities in the portfolio to take advantage of attractive rates for longer periods of time. The ECB’s massive LTRO has added much needed liquidity to the eurozone banking system and bolstered market sentiment. Given the improving credit picture for certain issuers, we felt more comfortable selectively adding to the fund’s credit exposure by investing in securities issued in Canada, Australia, and the more economically viable Nordic countries in northern Europe. As always, we remained diligent in our fundamental credit research process to avoid exposure to securities that might pose a risk to the fund.

Also, in late February and early March, the U.S. Treasury issued new supply, and rates backed up across the Treasury yield curve. At this time, we opportunistically added to the fund’s position in Treasury bills and notes. We have maintained significant allocations — although lower than in the beginning of the period — to high-quality money market securities, such as repurchase agreements that are collateralized by government securities.

On March 31, 2012, the 7-day yield [with the fund’s expense limitation] was 0.01%, and the portfolio’s WAM [weighted average maturity] was 52 days.

Which fund holdings exemplified your strategy during the period?

Joanne: During the period, the fund was exposed to large, creditworthy banks, such as JPMorgan Chase, Bank of Nova Scotia, and National Australia Bank. Looking at underlying bank fundamentals, we believe we see a relatively improving picture. Asset-quality measures are showing improving trends. Profits are being retained and are helping to build capital. These positive developments are somewhat offset by the banks’ underlying revenue weakness with soft loan demand, pressured interest margins, lower capital markets volume, and ongoing regulatory pressure on fee business. The European sovereign debt stress remains an influence on our overall bank positioning, and we have limited these exposures.

7

U.S. growth appears to be improving but the Fed remains committed to its accommodative monetary policy for the foreseeable future. What are the implications of this policy for money market investors?

Jonathan: We believe the U.S. economy is growing at about a 2.0% pace, although there is considerable month-to-month volatility. Certainly, the labor market is continuing to improve slowly and steadily, and consumer confidence has risen with this better data and declining headline inflation. It is our belief that the economy will maintain this pace of growth in 2012, but we remain concerned about several risks to this outlook. As has been the case for the past two years, macroeconomic concerns — whether they are a hard landing in China, a spike in oil prices, or economic deterioration in Europe — could reassert themselves at any time.

These risk variables have put the Fed in an accommodative stance, which means challenging conditions for money market funds will continue until short-term interest rates begin to rise. When the economic environment starts to solidly improve, we believe interest-rate normalization in the United States will likely occur. Meanwhile, we will continue to focus on safety and liquidity, while looking for competitive yields further out on the money market maturity spectrum when investment opportunities arise.

Thank you, Joanne and Jonathan, for bringing us up to date.

The views expressed in this report are exclusively those of Putnam Management and are subject to change. They are not meant as investment advice.

Please note that the holdings discussed in this report may not have been held by the fund for the entire period. Portfolio composition is subject to review in accordance with the fund’s investment strategy and may vary in the future. Current and future portfolio holdings are subject to risk.

This chart shows how the fund’s top weightings have changed over the past six months. Weightings are shown as a percentage of portfolio value. Summary information may differ from the portfolio schedule included in the financial statements due to the inclusion of derivative securities and the exclusion of as-of trades, if any, and the use of different classifications of securities for presentation purposes. Holdings will vary over time.

8

Portfolio Manager Joanne M. Driscoll has an M.B.A. from the Northeastern College of Business Administration and a B.S. from Westfield State College. A CFA charterholder, Joanne joined Putnam in 1995 and has been in the investment industry since 1992.

Portfolio Manager Jonathan M. Topper is a Portfolio Analyst at Putnam. He has a B.A. from Northeastern University. Jonathan has been in the investment industry since he joined Putnam in 1990.

IN THE NEWS

Thirteen years after the 17-member eurozone adopted a single currency, Greece became the first member country to officially default. All three major ratings agencies — Standard & Poor’s, Moody’s Investors Service, and Fitch Ratings — have declared Greece to be in default on its sovereign debt. The majority of private holders of Greek bonds have agreed to exchange their existing bonds for new, longer-dated ones with lower interest rates and substantially lower face values. In addition to the country’s debt restructuring, sellers of credit-default swaps — a form of private insurance against default — have agreed to pay approximately $2.5 billion to settle their contracts. Both the debt restructuring and the credit-default swap settlement were completed without triggering a wave of deleveraging or a liquidity crisis within the European banking sector, thus avoiding the long-feared worst-case scenario for investors. Nonetheless, Europe’s structural imbalances likely will remain with us for some time.

9

Your fund’s performance

This section shows your fund’s performance, price, and distribution information for periods ended March 31, 2012, the end of the first half of its current fiscal year. In accordance with regulatory requirements for mutual funds, we also include expense information taken from the fund’s current prospectus. Performance should always be considered in light of a fund’s investment strategy. Data represent past performance. Past performance does not guarantee future results. More recent returns may be less or more than those shown. Investment return and principal value will fluctuate, and you may have a gain or a loss when you sell your shares. Performance information does not reflect any deduction for taxes a shareholder may owe on fund distributions or on the redemption of fund shares. For the most recent month-end performance, please visit the Individual Investors section at putnam.com or call Putnam at 1-800-225-1581. Class R shares are not available to all investors. See the Terms and Definitions section in this report for definitions of the share classes offered by your fund.

Fund performance Total return for periods ended 3/31/12

| Class A | Class B | Class C | Class M | Class R | Class T | |||

| (inception dates) | (10/1/76) | (4/27/92) | (2/1/99) | (12/8/94) | (1/21/03) | (12/31/01) | ||

| Net | Net | Net | Net | |||||

| asset | Before | After | Before | After | asset | asset | asset | |

| value | CDSC | CDSC | CDSC | CDSC | value | value | value | |

| Annual average | ||||||||

| (life of fund) | 5.53% | 5.05% | 5.05% | 5.06% | 5.06% | 5.39% | 5.04% | 5.29% |

| 10 years | 19.58 | 15.40 | 15.40 | 15.40 | 15.40 | 18.29 | 15.61 | 17.43 |

| Annual average | 1.80 | 1.44 | 1.44 | 1.44 | 1.44 | 1.69 | 1.46 | 1.62 |

| 5 years | 6.89 | 5.76 | 3.76 | 5.76 | 5.76 | 6.53 | 5.76 | 6.30 |

| Annual average | 1.34 | 1.13 | 0.74 | 1.13 | 1.13 | 1.27 | 1.13 | 1.23 |

| 3 years | 0.16 | 0.09 | –2.91 | 0.09 | 0.09 | 0.12 | 0.09 | 0.10 |

| Annual average | 0.05 | 0.03 | –0.98 | 0.03 | 0.03 | 0.04 | 0.03 | 0.03 |

| 1 year | 0.01 | 0.01 | –5.00 | 0.01 | –1.00 | 0.01 | 0.01 | 0.01 |

| 6 months | 0.00 | 0.00 | –5.00 | 0.00 | –1.00 | 0.00 | 0.00 | 0.00 |

| Net | Net | Net | Net | |||||

| Current yield | asset | Before | After | Before | After | asset | asset | asset |

| (end of period)* | value | CDSC | CDSC | CDSC | CDSC | value | value | value |

| Current 7-day yield | ||||||||

| (with expense limitation) | 0.01% | 0.01% | — | 0.01% | — | 0.01% | 0.01% | 0.01% |

| Current 7-day yield | ||||||||

| (without expense limitation) | –0.27 | –0.77 | — | –0.77 | — | –0.42 | –0.77 | –0.52 |

Current performance may be lower or higher than the quoted past performance, which cannot guarantee future results. None of the share classes carry an initial sales charge. Class B share returns reflect the applicable contingent deferred sales charge (CDSC), which is 5% in the first year, declining over time to 1% in the sixth year, and is eliminated thereafter. Class C share returns reflect a 1% CDSC for the first year that is eliminated thereafter. Class A, M, R, and T shares generally have no CDSC. Performance for class B, C, M, R, and T shares before their inception is derived from the historical performance of class A shares, adjusted for the applicable sales charge (or CDSC) and the higher operating expenses for such shares.

* The 7-day yield is one of the most common gauges for measuring money market mutual fund performance. Yield reflects current performance more closely than total return.

For a portion of the periods, the fund had expense limitations, without which returns and yields would have been lower.

Class B share performance does not reflect conversion to class A shares.

10

Comparative Lipper returns For periods ended 3/31/12

| Lipper Money Market Funds category average* | |

| Annual average (life of fund) | 5.65% |

| 10 years | 16.40 |

| Annual average | 1.53 |

| 5 years | 5.83 |

| Annual average | 1.14 |

| 3 years | 0.12 |

| Annual average | 0.04 |

| 1 year | 0.02 |

| 6 months | 0.01 |

Lipper results should be compared to fund performance at net asset value.

* Over the 6-month, 1-year, 3-year, 5-year, 10-year, and life-of-fund periods ended 3/31/12, there were 259, 258, 244, 232, 185, and 15 funds, respectively, in this Lipper category.

Fund distribution information For the six-month period ended 3/31/12

| Distributions | Class A | Class B | Class C | Class M | Class R | Class T |

| Number | 6 | 6 | 6 | 6 | 6 | 6 |

| Income | $0.000050 | $0.000050 | $0.000050 | $0.000050 | $0.000050 | $0.000050 |

| Capital gains | — | — | — | — | — | — |

| Total | $0.000050 | $0.000050 | $0.000050 | $0.000050 | $0.000050 | $0.000050 |

The classification of distributions, if any, is an estimate. Final distribution information will appear on your year-end tax forms.

Your fund’s expenses

As a mutual fund investor, you pay ongoing expenses, such as management fees, distribution fees (12b-1 fees), and other expenses. In the most recent six-month period, your fund’s expenses were limited; had expenses not been limited, they would have been higher. Using the following information, you can estimate how these expenses affect your investment and compare them with the expenses of other funds. You may also pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial representative.

Expense ratios

| Class A | Class B | Class C | Class M | Class R | Class T | |

| Total annual operating expenses for the fiscal year | ||||||

| ended 9/30/11 | 0.50% | 1.00% | 1.00% | 0.65% | 1.00% | 0.75% |

| Annualized expense ratio for the six-month period | ||||||

| ended 3/31/12* | 0.20% | 0.20% | 0.20% | 0.20% | 0.20% | 0.20% |

Fiscal-year expense information in this table is taken from the most recent prospectus, is subject to change, and may differ from that shown for the annualized expense ratio and in the financial highlights of this report. Expenses are shown as a percentage of average net assets.

* Reflects a voluntary waiver of certain fund expenses.

11

Expenses per $1,000

The following table shows the expenses you would have paid on a $1,000 investment in the fund from October 1, 2011, to March 31, 2012. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

| Class A | Class B | Class C | Class M | Class R | Class T | |

| Expenses paid per $1,000*† | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 |

| Ending value (after expenses) | $1,000.03 | $1,000.03 | $1,000.03 | $1,000.03 | $1,000.03 | $1,000.03 |

* Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of average net assets for the six months ended 3/31/12. The expense ratio may differ for each share class.

† Expenses are calculated by multiplying the expense ratio by the average account value for the period; then multiplying the result by the number of days in the period; and then dividing that result by the number of days in the year.

Estimate the expenses you paid

To estimate the ongoing expenses you paid for the six months ended March 31, 2012, use the following calculation method. To find the value of your investment on October 1, 2011, call Putnam at 1-800-225-1581.

Compare expenses using the SEC’s method

The Securities and Exchange Commission (SEC) has established guidelines to help investors assess fund expenses. Per these guidelines, the following table shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total costs) of investing in the fund with those of other funds. All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

| Class A | Class B | Class C | Class M | Class R | Class T | |

| Expenses paid per $1,000*† | $1.01 | $1.01 | $1.01 | $1.01 | $1.01 | $1.01 |

| Ending value (after expenses) | $1,024.00 | $1,024.00 | $1,024.00 | $1,024.00 | $1,024.00 | $1,024.00 |

* Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of average net assets for the six months ended 3/31/12. The expense ratio may differ for each share class.

† Expenses are calculated by multiplying the expense ratio by the average account value for the period; then multiplying the result by the number of days in the period; and then dividing that result by the number of days in the year.

12

Terms and definitions

Important terms

Total return shows how the value of the fund’s shares changed over time, assuming you held the shares through the entire period and reinvested all distributions in the fund.

Net asset value (NAV) is the price, or value, of one share of a mutual fund, without a sales charge. Net asset values fluctuate with market conditions, and are calculated by dividing the net assets of each class of shares by the number of outstanding shares in the class.

Contingent deferred sales charge (CDSC) is generally a charge applied at the time of the redemption of class B or C shares and assumes redemption at the end of the period. Your fund’s class B CDSC declines over time from a 5% maximum during the first year to 1% during the sixth year. After the sixth year, the CDSC no longer applies. The CDSC for class C shares is 1% for one year after purchase.

Current yield is the annual rate of return earned from dividends or interest of an investment. Current yield is expressed as a percentage of the price of a security, fund share, or principal investment.

Share classes

Class A shares generally are fund shares purchased with an initial sales charge. In the case of your fund, which has no sales charge, the reference is to shares purchased or acquired through the exchange of class A shares from another Putnam fund. Exchange of your fund’s class A shares into another fund may involve a sales charge, however.

Class B shares are not subject to an initial sales charge. They may be subject to a CDSC.

Class C shares are not subject to an initial sales charge and are subject to a CDSC only if the shares are redeemed during the first year.

Class M shares generally are fund shares that have a lower initial sales charge and a higher 12b-1 fee than class A shares and no CDSC. In the case of your fund, which has no sales charge, the reference is to shares purchased or acquired through the exchange of class M shares from another Putnam fund. Exchange of your fund’s class M shares into another fund may involve a sales charge, however.

Class R shares are not subject to an initial sales charge or CDSC and are available only to certain defined contribution plans.

Class T shares are not subject to an initial sales charge or a CDSC (except on certain redemptions of shares acquired by exchange of shares of another Putnam fund bought without an initial sales charge); however, they are subject to a 12b-1 fee.

Comparative indexes

Barclays Capital U.S. Aggregate Bond Index is an unmanaged index of U.S. investment-grade fixed-income securities.

BofA (Bank of America) Merrill Lynch U.S. 3-Month Treasury Bill Index is an unmanaged index that seeks to measure the performance of U.S. Treasury bills available in the marketplace.

Lipper Money Market Funds category average is an arithmetic average of the total return of all money market mutual funds tracked by Lipper.

S&P 500 Index is an unmanaged index of common stock performance.

Indexes assume reinvestment of all distributions and do not account for fees. Securities and performance of a fund and an index will differ. You cannot invest directly in an index.

Lipper is a third-party industry-ranking entity that ranks mutual funds. Its rankings do not reflect sales charges. Lipper rankings are based on total return at net asset value relative to other funds that have similar current investment styles or objectives as determined by Lipper. Lipper may change a fund’s category assignment at its discretion. Lipper category averages reflect performance trends for funds within a category.

13

Other information for shareholders

Important notice regarding delivery of shareholder documents

In accordance with Securities and Exchange Commission (SEC) regulations, Putnam sends a single copy of annual and semiannual shareholder reports, prospectuses, and proxy statements to Putnam shareholders who share the same address, unless a shareholder requests otherwise. If you prefer to receive your own copy of these documents, please call Putnam at 1-800-225-1581, and Putnam will begin sending individual copies within 30 days.

Proxy voting

Putnam is committed to managing our mutual funds in the best interests of our shareholders. The Putnam funds’ proxy voting guidelines and procedures, as well as information regarding how your fund voted proxies relating to portfolio securities during the 12-month period ended June 30, 2011, are available in the Individual Investors section of putnam.com, and on the SEC’s website, www.sec.gov. If you have questions about finding forms on the SEC’s website, you may call the SEC at 1-800-SEC-0330. You may also obtain the Putnam funds’ proxy voting guidelines and procedures at no charge by calling Putnam’s Shareholder Services at 1-800-225-1581.

Fund portfolio holdings

The fund will file a complete schedule of its portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. Shareholders may obtain the fund’s Forms N-Q on the SEC’s website at www.sec.gov. In addition, the fund’s Forms N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C. You may call the SEC at 1-800-SEC-0330 for information about the SEC’s website or the operation of the Public Reference Room.

Trustee and employee fund ownership

Putnam employees and members of the Board of Trustees place their faith, confidence, and, most importantly, investment dollars in Putnam mutual funds. As of March 31, 2012, Putnam employees had approximately $353,000,000 and the Trustees had approximately $81,000,000 invested in Putnam mutual funds. These amounts include investments by the Trustees’ and employees’ immediate family members as well as investments through retirement and deferred compensation plans.

14

Financial statements

A guide to financial statements

These sections of the report, as well as the accompanying Notes, constitute the fund’s financial statements.

The fund’s portfolio lists all the fund’s investments and their values as of the last day of the reporting period. Holdings are organized by asset type and industry sector, country, or state to show areas of concentration and diversification.

Statement of assets and liabilities shows how the fund’s net assets and share price are determined. All investment and non-investment assets are added together. Any unpaid expenses and other liabilities are subtracted from this total. The result is divided by the number of shares to determine the net asset value per share, which is calculated separately for each class of shares. (For funds with preferred shares, the amount subtracted from total assets includes the liquidation preference of preferred shares.)

Statement of operations shows the fund’s net investment gain or loss. This is done by first adding up all the fund’s earnings — from dividends and interest income — and subtracting its operating expenses to determine net investment income (or loss). Then, any net gain or loss the fund realized on the sales of its holdings — as well as any unrealized gains or losses over the period — is added to or subtracted from the net investment result to determine the fund’s net gain or loss for the fiscal period.

Statement of changes in net assets shows how the fund’s net assets were affected by the fund’s net investment gain or loss, by distributions to shareholders, and by changes in the number of the fund’s shares. It lists distributions and their sources (net investment income or realized capital gains) over the current reporting period and the most recent fiscal year-end. The distributions listed here may not match the sources listed in the Statement of operations because the distributions are determined on a tax basis and may be paid in a different period from the one in which they were earned. Dividend sources are estimated at the time of declaration. Actual results may vary. Any non-taxable return of capital cannot be determined until final tax calculations are completed after the end of the fund’s fiscal year.

Financial highlights provide an overview of the fund’s investment results, per-share distributions, expense ratios, net investment income ratios, and portfolio turnover in one summary table, reflecting the five most recent reporting periods. In a semiannual report, the highlights table also includes the current reporting period.

15

The fund’s portfolio 3/31/12 (Unaudited)

| REPURCHASE AGREEMENTS (25.7%)* | Principal amount | Value |

| Interest in $336,173,000 joint tri-party repurchase agreement dated | ||

| 3/30/12 with Citigroup Global Markets, Inc. due 4/2/12 — maturity | ||

| value of $74,000,925 for an effective yield of 0.15% (collateralized by | ||

| various mortgage-backed securities with coupon rates ranging from | ||

| zero % to 5.50% and due dates ranging from 7/1/19 to 3/1/42, | ||

| valued at $342,896,460) | $74,000,000 | $74,000,000 |

| Interest in $83,000,000 joint tri-party repurchase agreement dated | ||

| 3/30/12 with Deutsche Bank Securities, Inc. due 4/2/12 — maturity | ||

| value of $74,000,925 for an effective yield of 0.15% (collateralized by | ||

| a mortgage-backed security with a coupon rate of 4.50% and a due | ||

| date of 5/1/41, valued at $84,660,001) | 74,000,000 | 74,000,000 |

| Interest in $287,000,000 joint tri-party repurchase agreement dated | ||

| 3/30/12 with Goldman Sach & Co. due 4/2/12 — maturity value | ||

| of $74,000,925 for an effective yield of 0.15% (collateralized by various | ||

| mortgage-backed securities with coupon rates ranging from 2.50% | ||

| to 4.50% and due dates ranging from 3/1/27 to 11/1/41, valued | ||

| at $292,740,000) | 74,000,000 | 74,000,000 |

| Interest in $82,300,000 joint tri-party repurchase agreement dated | ||

| 3/30/12 with JPMorgan Securities, Inc. due 4/2/12 — maturity value | ||

| of $33,750,563 for an effective yield of 0.20% (collateralized by various | ||

| corporate bonds and notes with coupon rates ranging from 2.95% | ||

| to 9.375% and due dates ranging from 2/1/14 to 9/30/39, valued | ||

| at $86,420,263) | 33,750,000 | 33,750,000 |

| Interest in $375,000,000 joint tri-party repurchase agreement dated | ||

| 3/30/12 with JPMorgan Securities, Inc. due 4/2/12 — maturity value | ||

| of $73,856,862 for an effective yield of 0.14% (collateralized by various | ||

| mortgage-backed securities with coupon rates ranging from 2.50% | ||

| to 7.50% and due dates ranging from 1/1/13 to 4/1/42, valued | ||

| at $382,500,252) | 73,856,000 | 73,856,000 |

| Interest in $300,800,000 joint tri-party term repurchase agreement | ||

| dated 3/27/12 with Citigroup Global Markets, Inc. due 4/3/12, 0.18% | ||

| (collateralized by various mortgage-backed securities with coupon | ||

| rates ranging from 3.30% to 4.50% and due dates ranging from 12/1/20 | ||

| to 3/1/42, valued at $306,816,796) TR | 34,000,000 | 34,000,000 |

| Interest in $160,000,000 joint tri-party term repurchase agreement | ||

| dated 3/28/12 with Deutsche Bank Securities, Inc. due 4/4/12, 0.14% | ||

| (collateralized by various mortgage-backed securities with coupon | ||

| rates ranging from 3.50% to 4.50% and due dates ranging from 12/1/26 | ||

| to 11/1/41, valued at $163,454,988) TR | 17,500,000 | 17,500,000 |

| Interest in $48,750,000 joint tri-party term repurchase agreement | ||

| dated 3/23/12 with JPMorgan Securities, Inc. due 4/23/12, 0.27% | ||

| (collateralized by various corporate bonds and notes with coupon | ||

| rates ranging from 5.75% to 8.25% and due dates ranging from 4/15/12 | ||

| to 10/15/39, valued at $51,190,659) TR | 13,350,000 | 13,350,000 |

| Interest in $34,000,000 tri-party term repurchase agreement dated | ||

| 3/27/12 with Barclays Capital, Inc. due 4/3/12, 0.15% (collateralized | ||

| by various mortgage-backed securities with coupon rates ranging | ||

| from 2.50% to 4.50% and due dates ranging from 3/1/22 to 1/1/42, | ||

| valued at $34,680,001) TR | 34,000,000 | 34,000,000 |

| Total repurchase agreements (cost $428,456,000) | $428,456,000 | |

16

| ASSET-BACKED COMMERCIAL PAPER (17.3%)* | Yield (%) | Maturity date | Principal amount | Value |

| Alpine Securitization Corp. (Switzerland) | 0.180 | 4/18/12 | $8,400,000 | $8,399,286 |

| Bryant Park Funding, LLC | 0.270 | 6/15/12 | 15,000,000 | 14,991,563 |

| Bryant Park Funding, LLC | 0.240 | 6/27/12 | 1,770,000 | 1,768,973 |

| CAFCO, LLC | 0.300 | 4/9/12 | 5,700,000 | 5,699,620 |

| CAFCO, LLC | 0.220 | 4/11/12 | 2,700,000 | 2,699,835 |

| Chariot Funding, LLC | 0.190 | 5/29/12 | 8,561,000 | 8,558,379 |

| Chariot Funding, LLC | 0.190 | 5/16/12 | 8,000,000 | 7,998,100 |

| CHARTA, LLC | 0.280 | 4/2/12 | 8,400,000 | 8,399,935 |

| CIESCO-LP | 0.270 | 4/4/12 | 8,400,000 | 8,399,811 |

| CRC Funding, LLC | 0.220 | 4/10/12 | 8,400,000 | 8,399,538 |

| Fairway Finance, LLC (Canada) | 0.160 | 6/5/12 | 7,660,000 | 7,657,787 |

| Fairway Finance, LLC 144A (Canada) | 0.282 | 8/16/12 | 12,000,000 | 12,000,000 |

| Fairway Finance, LLC 144A (Canada) | 0.250 | 6/4/12 | 5,500,000 | 5,497,556 |

| Govco, LLC | 0.270 | 4/2/12 | 8,400,000 | 8,399,937 |

| Jupiter Securitization Co., LLC | 0.190 | 6/7/12 | 10,800,000 | 10,796,181 |

| Jupiter Securitization Co., LLC | 0.190 | 5/8/12 | 6,000,000 | 5,998,828 |

| Liberty Street Funding, LLC (Canada) | 0.210 | 4/17/12 | 7,800,000 | 7,799,272 |

| Manhattan Asset Funding Co., LLC (Japan) | 0.280 | 5/16/12 | 2,100,000 | 2,099,265 |

| Manhattan Asset Funding Co., LLC (Japan) | 0.260 | 4/16/12 | 3,100,000 | 3,099,664 |

| Manhattan Asset Funding Co., LLC (Japan) | 0.230 | 4/18/12 | 6,300,000 | 6,299,316 |

| Old Line Funding, LLC | 0.240 | 6/22/12 | 8,500,000 | 8,495,353 |

| Old Line Funding, LLC | 0.200 | 5/15/12 | 14,000,000 | 13,996,578 |

| Old Line Funding, LLC 144A | 0.200 | 4/16/12 | 3,000,000 | 2,999,750 |

| Straight-A Funding, LLC | 0.180 | 5/14/12 | 5,000,000 | 4,998,925 |

| Straight-A Funding, LLC | 0.180 | 5/1/12 | 17,000,000 | 16,997,450 |

| Straight-A Funding, LLC 144A, Ser. 1 | 0.190 | 4/17/12 | 9,000,000 | 8,999,240 |

| Straight-A Funding, LLC 144A, Ser. 1 | 0.180 | 6/15/12 | 18,000,000 | 17,993,250 |

| Straight-A Funding, LLC 144A, Ser. 1 | 0.180 | 5/17/12 | 1,400,000 | 1,399,678 |

| Thunder Bay Funding, LLC | 0.210 | 5/1/12 | 8,800,000 | 8,798,460 |

| Variable Funding Capital Co., LLC 144A | ||||

| (Wachovia Bank NA (LOC)) | 0.180 | 4/26/12 | 10,700,000 | 10,698,663 |

| Variable Funding Capital Co., LLC 144A | ||||

| (Wachovia Bank NA (LOC)) | 0.170 | 4/27/12 | 15,250,000 | 15,248,128 |

| Victory Receivables Corp. (Japan) | 0.290 | 5/7/12 | 15,500,000 | 15,495,505 |

| Victory Receivables Corp. (Japan) | 0.280 | 6/15/12 | 10,000,000 | 9,994,167 |

| Working Capital Management Co. (Japan) | 0.230 | 4/3/12 | 8,434,000 | 8,433,892 |

| Total asset-backed commercial paper (cost $289,511,885) | $289,511,885 | |||

| COMMERCIAL PAPER (14.2%)* | Yield (%) | Maturity date | Principal amount | Value |

| Australia & New Zealand Banking Group, Ltd. | ||||

| (Australia) | 0.541 | 6/29/12 | $5,500,000 | $5,492,658 |

| Australia & New Zealand Banking Group, Ltd. | ||||

| (Australia) | 0.351 | 8/8/12 | 9,800,000 | 9,787,709 |

| Australia & New Zealand Banking Group, Ltd. | ||||

| 144A (Australia) | 0.648 | 1/10/13 | 10,400,000 | 10,400,000 |

| Axis Bank, Ltd. (India) | 0.500 | 4/12/12 | 8,400,000 | 8,398,717 |

| COFCO Capital Corp. | 0.405 | 4/3/12 | 17,000,000 | 16,999,617 |

17

| COMMERCIAL PAPER (14.2%)* cont. | Yield (%) | Maturity date | Principal amount | Value |

| Commonwealth Bank of Australia 144A | ||||

| (Australia) | 0.190 | 6/8/12 | $14,000,000 | $14,000,000 |

| Commonwealth Bank of Australia 144A | ||||

| (Australia) | 0.180 | 10/18/12 | 3,100,000 | 3,099,944 |

| Danske Corp. (Denmark) | 0.210 | 4/4/12�� | 8,400,000 | 8,399,853 |

| DnB Bank ASA (Norway) | 0.411 | 6/29/12 | 14,500,000 | 14,485,303 |

| DnB Bank ASA 144A (Norway) | 0.422 | 4/25/12 | 10,600,000 | 10,600,000 |

| General Electric Capital Corp. | 0.190 | 5/23/12 | 9,000,000 | 8,997,530 |

| General Electric Capital Services | 0.120 | 4/30/12 | 3,100,000 | 3,099,700 |

| HSBC Bank USA, NA | 0.300 | 7/26/12 | 7,000,000 | 6,993,233 |

| HSBC USA, Inc. (United Kingdom) | 0.290 | 6/26/12 | 9,500,000 | 9,493,419 |

| ING (US) Funding, LLC | 0.180 | 4/9/12 | 8,400,000 | 8,399,664 |

| Louis Dreyfus Commodities, LLC, Ser. BARC | ||||

| (Barclays Bank PLC (LOC)) | 0.500 | 4/5/12 | 8,400,000 | 8,399,533 |

| Nordea North America Inc./DE (Sweden) | 0.542 | 9/7/12 | 8,950,000 | 8,928,654 |

| Standard Chartered Bank/New York | 0.531 | 8/20/12 | 8,000,000 | 7,983,393 |

| Standard Chartered Bank/New York | 0.501 | 7/9/12 | 7,900,000 | 7,889,138 |

| State Street Corp. | 0.240 | 7/5/12 | 10,000,000 | 9,993,667 |

| State Street Corp. | 0.230 | 7/19/12 | 7,000,000 | 6,995,125 |

| Sumitomo Mitsui Banking Corp. (Japan) | 0.300 | 4/18/12 | 4,670,000 | 4,669,338 |

| Toyota Credit Canada, Inc. (Canada) | 0.180 | 5/29/12 | 8,450,000 | 8,447,550 |

| Toyota Motor Credit Corp. | 0.160 | 5/15/12 | 8,000,000 | 7,998,436 |

| Westpac Banking Corp. 144A (Australia) | 0.744 | 8/24/12 | 9,300,000 | 9,272,281 |

| Westpac Banking Corp. 144A (Australia) | 0.230 | 7/5/12 | 18,000,000 | 18,000,000 |

| Total commercial paper (cost $237,224,462) | $237,224,462 | |||

| MUNICIPAL BONDS | Maturity | Principal | |||

| AND NOTES (12.7%)* | Yield (%) | date | Rating** | amount | Value |

| California (1.5%) | |||||

| Board of Trustees of the Leland Stanford | |||||

| Junior University Commercial Paper | 0.130 | 4/5/12 | P-1 | $18,200,000 | $18,199,737 |

| California Educational Facilities Authority | |||||

| Commercial Paper (Stanford University), | |||||

| Ser. STAN | 0.120 | 4/20/12 | P-1 | 7,000,000 | 7,000,000 |

| 25,199,737 | |||||

| Connecticut (1.6%) | |||||

| Yale University Commercial Paper | 0.120 | 4/2/12 | P-1 | 26,300,000 | 26,299,912 |

| 26,299,912 | |||||

| District of Columbia (0.2%) | |||||

| American University Commercial Paper, | |||||

| Ser. A | 0.200 | 6/19/12 | A-1 | 3,500,000 | 3,498,464 |

| 3,498,464 | |||||

| Florida (0.7%) | |||||

| Highlands County, Health Facilities | |||||

| Authority VRDN (Adventist Health), | |||||

| Ser. H (U.S. Bank, N.A. (LOC)) M | 0.160 | 11/15/35 | VMIG1 | 11,750,000 | 11,750,000 |

| 11,750,000 | |||||

18

| MUNICIPAL BONDS | Maturity | Principal | |||

| AND NOTES (12.7%)* cont. | Yield (%) | date | Rating** | amount | Value |

| Indiana (1.2%) | |||||

| Saint Joseph County Commercial Paper | |||||

| (University of Notre Dame Du Lac) | 0.150 | 5/3/12 | P-1 | $12,000,000 | $11,998,400 |

| Saint Joseph County Commercial Paper | |||||

| (University of Notre Dame Du Lac) | 0.140 | 4/4/12 | P-1 | 7,276,000 | 7,275,915 |

| 19,274,315 | |||||

| Kentucky (1.1%) | |||||

| Catholic Health Initiatives Commercial | |||||

| Paper, Ser. A | 0.120 | 4/2/12 | P-1 | 6,870,000 | 6,870,000 |

| Kentucky State Economic Development | |||||

| Finance Authority VRDN (Catholic Health | |||||

| Initiatives), Ser. C M | 0.180 | 5/1/34 | VMIG1 | 11,000,000 | 11,000,000 |

| 17,870,000 | |||||

| Maryland (1.2%) | |||||

| Johns Hopkins University Commercial | |||||

| Paper, Ser. A | 0.160 | 5/15/12 | P-1 | 3,250,000 | 3,250,000 |

| Johns Hopkins University Commercial | |||||

| Paper, Ser. A | 0.150 | 6/21/12 | P-1 | 12,367,000 | 12,367,000 |

| Johns Hopkins University Commercial | |||||

| Paper, Ser. C | 0.180 | 6/11/12 | P-1 | 5,000,000 | 5,000,000 |

| 20,617,000 | |||||

| Massachusetts (1.1%) | |||||

| Harvard University Commercial Paper | 0.130 | 5/15/12 | P-1 | 18,802,000 | 18,799,013 |

| 18,799,013 | |||||

| Michigan (0.5%) | |||||

| Trinity Health Corporation Commercial | |||||

| Paper | 0.150 | 4/2/12 | P-1 | 8,200,000 | 8,199,966 |

| 8,199,966 | |||||

| Nevada (0.4%) | |||||

| Truckee Meadows, Water Authority | |||||

| Revenue Commercial Paper, | |||||

| Ser. 06-B (Lloyds TSB Bank PLC/ | |||||

| New York, NY (LOC)) | 0.180 | 4/11/12 | P-1 | 7,000,000 | 7,000,000 |

| 7,000,000 | |||||

| North Carolina (1.0%) | |||||

| Duke University Commercial Paper, | |||||

| Ser. B-98 | 0.180 | 6/19/12 | P-1 | 15,810,000 | 15,803,755 |

| Wake County VRDN, Ser. B M | 0.170 | 3/1/24 | VMIG1 | 1,500,000 | 1,500,000 |

| 17,303,755 | |||||

| Texas (1.9%) | |||||

| Harris County, Health Facilities | |||||

| Development Authority VRDN (Texas | |||||

| Childrens Hospital), Ser. B-1 M | 0.200 | 10/1/29 | VMIG1 | 3,795,000 | 3,795,000 |

| University of Texas Permanent University | |||||

| Fund Commercial Paper | 0.120 | 4/2/12 | P-1 | 28,000,000 | 28,000,000 |

| 31,795,000 | |||||

| Wisconsin (0.3%) | |||||

| Wisconsin State Health & Educational | |||||

| Facilities Authority VRDN (Wheaton | |||||

| Franciscan Services), Ser. B | |||||

| (U.S. Bank, N.A. (LOC)) M | 0.190 | 8/15/33 | VMIG1 | 4,100,000 | 4,100,000 |

| 4,100,000 | |||||

| Total municipal bonds and notes (cost $211,707,162) | $211,707,162 | ||||

19

| U.S. TREASURY OBLIGATIONS (10.0%)* | Yield (%) | Maturity date | Principal amount | Value |

| U.S. Treasury Bills | 0.151 | 10/18/12 | $20,000,000 | $19,983,056 |

| U.S. Treasury Bills | 0.138 | 10/18/12 | 15,000,000 | 14,988,333 |

| U.S. Treasury Bills | 0.099 | 7/19/12 | 15,000,000 | 14,995,458 |

| U.S. Treasury Bills | 0.099 | 7/12/12 | 20,000,000 | 19,994,333 |

| U.S. Treasury Notes k | 1.500 | 7/15/12 | 25,000,000 | 25,101,111 |

| U.S. Treasury Notes k | 1.375 | 10/15/12 | 33,300,000 | 33,517,115 |

| U.S. Treasury Notes k | 0.625 | 1/31/13 | 18,000,000 | 18,063,909 |

| U.S. Treasury Notes k | 0.625 | 7/31/12 | 19,500,000 | 19,533,855 |

| Total U.S. treasury obligations (cost $166,177,170) | $166,177,170 | |||

| U.S. GOVERNMENT AGENCY OBLIGATIONS (8.9%)* | Yield (%) | Maturity date | Principal amount | Value |

| Federal Farm Credit Bank FRB, Ser. 1 | 0.230 | 1/14/13 | $24,300,000 | $24,300,000 |

| Federal Home Loan Bank unsec. discount notes | 0.115 | 8/3/12 | 6,500,000 | 6,497,425 |

| Federal Home Loan Bank unsec. discount notes | 0.080 | 6/1/12 | 3,590,000 | 3,589,513 |

| Federal Home Loan Bank unsec. discount notes | 0.070 | 5/30/12 | 5,000,000 | 4,999,426 |

| Federal Home Loan Mortgage Corp. unsec. | ||||

| discount notes | 0.085 | 6/25/12 | 8,300,000 | 8,298,334 |

| Federal Home Loan Mortgage Corp. unsec. | ||||

| discount notes | 0.075 | 5/21/12 | 1,100,000 | 1,099,885 |

| Federal Home Loan Mortgage Corp. unsec. | ||||

| discount notes, Ser. RB | 0.170 | 10/23/12 | 20,000,000 | 19,980,639 |

| Federal National Mortgage Association unsec. | ||||

| discount notes | 0.140 | 8/15/12 | 25,000,000 | 24,986,778 |

| Federal National Mortgage Association unsec. | ||||

| discount notes | 0.110 | 6/25/12 | 3,300,000 | 3,299,143 |

| Federal National Mortgage Association unsec. | ||||

| discount notes | 0.080 | 5/16/12 | 13,350,000 | 13,348,665 |

| Federal National Mortgage Association unsec. | ||||

| discount notes | 0.065 | 5/9/12 | 13,000,000 | 12,999,108 |

| General Electric Capital Corp. FDIC guaranteed | ||||

| notes, MTN, Ser. G k | 2.200 | 6/8/12 | 25,188,000 | 25,285,990 |

| Total U.S. government agency obligations (cost $148,684,906) | $148,684,906 | |||

| CORPORATE BONDS AND NOTES (6.4%)* | Interest | Maturity | Principal | |

| rate (%) | date | amount | Value | |

| Commonwealth Bank of Australia 144A | ||||

| sr. unsec. notes FRN (Australia) | 1.024 | 3/19/13 | $7,850,000 | $7,885,231 |

| General Electric Capital Corp. sr. unsec. | ||||

| notes FRN, EMTN | 0.579 | 5/29/12 | 2,900,000 | 2,901,028 |

| HSBC Bank PLC 144A sr. unsec. unsub. notes | ||||

| FRN (United Kingdom) | 0.965 | 1/18/13 | 8,650,000 | 8,667,939 |

| JPMorgan Chase & Co. sr. unsec. unsub. notes | ||||

| FRN, MTN | 1.141 | 2/26/13 | 7,000,000 | 7,041,760 |

| National Australia Bank, Ltd. 144A sr. unsec. | ||||

| unsub. notes (Australia) | 2.350 | 11/16/12 | 15,275,000 | 15,440,934 |

| Royal Bank of Canada 144A sr. unsec. notes | ||||

| FRN (Canada) M | 0.702 | 5/15/14 | 29,425,000 | 29,427,879 |

| Svenska Handelsbanken AB 144A sr. unsec. | ||||

| unsub. notes FRN (Sweden) | 1.474 | 9/14/12 | 2,000,000 | 2,008,217 |

20

| CORPORATE BONDS AND NOTES (6.4%)* cont. | Interest | Maturity | Principal | |

| rate (%) | date | amount | Value | |

| Svenska Handelsbanken/New York, NY | ||||

| 144A notes FRN (Sweden) | 0.515 | 1/7/13 | $23,500,000 | $23,500,000 |

| Wal-Mart Stores, Inc. sr. unsec. unsub | ||||

| notes stepped-coupon (zero %, 6/1/12) †† M | 5.226 | 6/1/18 | 10,500,000 | 10,589,218 |

| Total corporate bonds and notes (cost $107,462,206) | $107,462,206 | |||

| CERTIFICATES OF DEPOSIT (5.4%)* | Interest | Maturity | Principal | |

| rate (%) | date | amount | Value | |

| Bank of Nova Scotia/Houston | 0.560 | 6/21/12 | $10,500,000 | $10,500,000 |

| Bank of Nova Scotia/Houston FRN | 0.322 | 7/26/12 | 9,000,000 | 9,000,000 |

| Canadian Imperial Bank of Commerce/ | ||||

| New York, NY FRN (Canada) | 0.432 | 10/15/12 | 8,500,000 | 8,500,000 |

| National Australia Bank, Ltd. (Australia) | 0.490 | 4/11/12 | 10,000,000 | 10,000,028 |

| Nordea Bank Finland PLC/New York | 0.874 | 9/13/12 | 17,150,000 | 17,142,420 |

| Standard Chartered Bank/New York | 0.675 | 9/10/12 | 9,200,000 | 9,200,000 |

| Toronto-Dominion Bank/NY (Canada) | 0.582 | 10/19/12 | 14,500,000 | 14,500,000 |

| Toronto-Dominion Bank/NY (Canada) | 0.210 | 5/8/12 | 3,000,000 | 3,000,062 |

| Toronto-Dominion Bank/NY FRN (Canada) | 0.312 | 9/20/12 | 8,370,000 | 8,370,875 |

| Total certificates of deposit (cost $90,213,385) | $90,213,385 | |||

| TOTAL INVESTMENTS | ||||

| Total investments (cost $1,679,437,176) | $1,679,437,176 | |||

Key to holding’s abbreviations

| EMTN | Euro Medium Term Notes |

| FDIC Guaranteed | Federal Deposit Insurance Corp. Guaranteed |

| FRB | Floating Rate Bonds: the rate shown is the current interest rate at the close of the reporting period |

| FRN | Floating Rate Notes: the rate shown is the current interest rate at the close of the reporting period |

| LOC | Letter of Credit |

| MTN | Medium Term Notes |

| VRDN | Variable Rate Demand Notes, which are floating-rate securities with long-term maturities, that |

| carry coupons that reset every one or seven days. The rate shown is the current interest rate at | |

| the close of the reporting period. |

Notes to the fund’s portfolio

Unless noted otherwise, the notes to the fund’s portfolio are for the close of the fund’s reporting period, which ran from October 1, 2011 through March 31, 2012 (the reporting period). Within the following notes to the portfolio, references to “ASC 820” represent Accounting Standards Codification ASC 820 Fair Value Measurements and Disclosures.

* Percentages indicated are based on net assets of $1,669,361,079.

** The Moody’s, Standard & Poor’s or Fitch ratings indicated are believed to be the most recent ratings available at the close of the reporting period for the securities listed. Ratings are generally ascribed to securities at the time of issuance. While the agencies may from time to time revise such ratings, they undertake no obligation to do so, and the ratings do not necessarily represent what the agencies would ascribe to these securities at the close of the reporting period. The rating of an insured security represents what is believed to be the most recent rating of the insurer’s claims-paying ability available at the close of the reporting period and does not reflect any subsequent changes. Security ratings are defined in the Statement of Additional Information.

†† The interest rate and date shown parenthetically represent the new interest rate to be paid and the date the fund will begin accruing interest at this rate.

k The rates shown are the current interest rates at the close of the reporting period.

21

M The security’s effective maturity date is less than one year.

TR Maturity value of a term repurchase agreement will equal the principal amount of the repurchase agreement plus interest.

Debt obligations are considered secured unless otherwise indicated.

144A after the name of an issuer represents securities exempt from registration under Rule 144A under the Securities Act of 1933, as amended. These securities may be resold in transactions exempt from registration, normally to qualified institutional buyers.

The dates shown on debt obligations are the original maturity dates.

| DIVERSIFICATION BY COUNTRY | ||||

| Distribution of investments by country of risk at the close of the reporting period, excluding collateral received, if any (as a percentage of Portfolio Value): | ||||

| United States | 78.5% | United Kingdom | 1.1% | |

| Canada | 6.3 | Denmark | 0.5 | |

| Australia | 6.1 | Switzerland | 0.5 | |

| Japan | 3.0 | India | 0.5 | |

| Sweden | 2.0 | Total | 100.0% | |

| Norway | 1.5 | |||

ASC 820 establishes a three-level hierarchy for disclosure of fair value measurements. The valuation hierarchy is based upon the transparency of inputs to the valuation of the fund’s investments. The three levels are defined as follows:

Level 1: Valuations based on quoted prices for identical securities in active markets.

Level 2: Valuations based on quoted prices in markets that are not active or for which all significant inputs are observable, either directly or indirectly.

Level 3: Valuations based on inputs that are unobservable and significant to the fair value measurement.

The following is a summary of the inputs used to value the fund’s net assets as of the close of the reporting period:

| Valuation inputs | ||||

| Investments in securities: | Level 1 | Level 2 | Level 3 | |

| Asset-backed commercial paper | $— | $289,511,885 | $— | |

| Certificates of deposit | — | 90,213,385 | — | |

| Commercial paper | — | 237,224,462 | — | |

| Corporate bonds and notes | — | 107,462,206 | — | |

| Municipal bonds and notes | — | 211,707,162 | — | |

| Repurchase agreements | — | 428,456,000 | — | |

| U.S. government agency obligations | — | 148,684,906 | — | |

| U.S. treasury obligations | — | 166,177,170 | — | |

| Totals by level | $— | $1,679,437,176 | $— | |

The accompanying notes are an integral part of these financial statements.

22

Statement of assets and liabilities 3/31/12 (Unaudited)

| ASSETS | |

| Investment in securities, at value (Note 1): | |

| Unaffiliated issuers (at amortized cost) | $1,250,981,176 |

| Repurchase agreements (identified cost $428,456,000) | 428,456,000 |

| Cash | 1,916 |

| Interest and other receivables | 1,508,550 |

| Receivable for shares of the fund sold | 4,346,304 |

| Total assets | 1,685,293,946 |

| LIABILITIES | |

| Distributions payable to shareholders | 6,293 |

| Payable for investments purchased | 2,902,405 |

| Payable for shares of the fund repurchased | 12,113,885 |

| Payable for compensation of Manager (Note 2) | 57,770 |

| Payable for investor servicing fees (Note 2) | 233,763 |

| Payable for custodian fees (Note 2) | 20,559 |

| Payable for Trustee compensation and expenses (Note 2) | 408,600 |

| Payable for administrative services (Note 2) | 7,000 |

| Other accrued expenses | 182,592 |

| Total liabilities | 15,932,867 |

| Net assets | $1,669,361,079 |

| REPRESENTED BY | |

| Paid-in capital (Unlimited shares authorized) (Notes 1 and 4) | $1,670,671,882 |

| Undistributed net investment income (Note 1) | 81 |

| Accumulated net realized loss on investments (Note 1) | (1,310,884) |

| Total — Representing net assets applicable to capital shares outstanding | $1,669,361,079 |

| COMPUTATION OF NET ASSET VALUE AND OFFERING PRICE | |

| Net asset value, offering price and redemption price per class A share | |

| ($1,543,588,915 divided by 1,546,452,358 shares) | $1.00 |

| Net asset value and offering price per class B share ($21,298,600 divided by 21,339,460 shares)* | $1.00 |

| Net asset value and offering price per class C share ($27,044,641 divided by 27,094,133 shares)* | $1.00 |

| Net asset value, offering price and redemption price per class M share | |

| ($27,714,001 divided by 27,765,479 shares) | $1.00 |

| Net asset value, offering price and redemption price per class R share | |

| ($19,848,257 divided by 19,881,526 shares) | $1.00 |

| Net asset value, offering price and redemption price per class T share | |

| ($29,866,665 divided by 29,918,256 shares) | $1.00 |

* Redemption price per share is equal to net asset value less any applicable contingent deferred sales charge.

The accompanying notes are an integral part of these financial statements.

23

Statement of operations Six months ended 3/31/12 (Unaudited)

| INVESTMENT INCOME | |

| Interest (including interest income of $14,112 from investments in affiliated issuers) (Note 5) | $1,888,252 |

| EXPENSES | |

| Compensation of Manager (Note 2) | 2,622,836 |

| Investor servicing fees (Note 2) | 1,503,727 |

| Custodian fees (Note 2) | 18,929 |

| Trustee compensation and expenses (Note 2) | 80,538 |

| Administrative services (Note 2) | 23,099 |

| Distribution fees — Class B (Note 2) | 60,449 |

| Distribution fees — Class C (Note 2) | 72,571 |

| Distribution fees — Class M (Note 2) | 22,195 |

| Distribution fees — Class R (Note 2) | 47,408 |

| Distribution fees — Class T (Note 2) | 39,464 |

| Other | 334,159 |

| Fees waived and reimbursed by Manager (Note 2) | (3,020,303) |

| Total expenses | 1,805,072 |

| Expense reduction (Note 2) | (7,663) |

| Net expenses | 1,797,409 |

| Net investment income | 90,843 |

| Net realized gain on investments (Notes 1 and 3) | 70,745 |

| Net gain on investments | 70,745 |

| Net increase in net assets resulting from operations | $161,588 |

The accompanying notes are an integral part of these financial statements.

24

Statement of changes in net assets

| DECREASE IN NET ASSETS | Six months ended 3/31/12* | Year ended 9/30/11 |

| Operations: | ||

| Net investment income | $90,843 | $244,962 |

| Net realized gain on investments | 70,745 | 224,432 |

| Net increase in net assets resulting from operations | 161,588 | 469,394 |

| Distributions to shareholders (Note 1): | ||

| From ordinary income | ||

| Net investment income | ||

| Class A | (82,478) | (246,692) |

| Class B | (1,208) | (4,169) |

| Class C | (1,454) | (3,340) |

| Class M | (1,482) | (4,478) |

| Class R | (950) | (2,342) |

| Class T | (1,581) | (4,633) |

| Decrease from capital share transactions (Note 4) | (212,656,531) | (392,018,220) |

| Total decrease in net assets | (212,584,096) | (391,814,480) |

| NET ASSETS | ||

| Beginning of period | 1,881,945,175 | 2,273,759,655 |

| End of period (including undistributed net investment | ||

| income of $81 and distributions in excess of net investment | ||

| income of $1,609, respectively) | $1,669,361,079 | $1,881,945,175 |

* Unaudited

The accompanying notes are an integral part of these financial statements.

25

Financial highlights (For a common share outstanding throughout the period)

| INVESTMENT OPERATIONS: | LESS DISTRIBUTIONS: | RATIOS AND SUPPLEMENTAL DATA: | ||||||||||

| Ratio of net | ||||||||||||

| investment | ||||||||||||

| income | ||||||||||||

| Net asset | Ratio | (loss) | ||||||||||

| value, | Net realized | Total from | From | Total return | Net assets, | of expenses | to average | |||||

| beginning | Net investment | gain (loss) | investment | net investment | From | Total | Net asset value, | at net asset | end of period | to average | net assets | |

| Period ended | of period | income (loss) | on investments | operations | income | return of capital | distributions | end of period | value (%) a | (in thousands) | net assets (%) b | (%) |

| Class A | ||||||||||||

| March 31, 2012 ** | $1.00 | .0001 | — c | .0001 | (.0001) | — | (.0001) | $1.00 | — *d | $1,543,589 | .10 *e | .01 *e |

| September 30, 2011 | 1.00 | .0001 | .0001 | .0002 | (.0001) | — | (.0001) | 1.00 | .01 | 1,739,458 | .22 e | .01 e |

| September 30, 2010 | 1.00 | .0001 | (.0003) | (.0002) | (.0005) | — | (.0005) | 1.00 | .06 | 2,131,331 | .32 e | — e,f |

| September 30, 2009 | 1.00 | .0091 | (.0001) | .0090 | (.0086) | — | (.0086) | 1.00 | .86 | 2,482,270 | .56 e,g | .98 e,g |

| September 30, 2008 | 1.00 | .0327 | (.0002) | .0325 | (.0325) | (.0004) | (.0329) | 1.00 | 3.35 | 3,212,674 | .56 g | 3.28 g |

| September 30, 2007 | 1.00 | .0486 h | — c | .0486 | (.0489) | — | (.0489) | 1.00 | 5.01 | 3,394,996 | .54 g | 4.84 g,h |

| Class B | ||||||||||||

| March 31, 2012 ** | $1.00 | .0001 | — c | .0001 | (.0001) | — | (.0001) | $1.00 | — *d | $21,299 | .10 *e | .01 *e |

| September 30, 2011 | 1.00 | .0001 | .0001 | .0002 | (.0001) | — | (.0001) | 1.00 | .01 | 27,668 | .22 e | .01 e |

| September 30, 2010 | 1.00 | .0001 | (.0003) | (.0002) | (.0005) | — | (.0005) | 1.00 | .06 | 37,121 | .32 e | .01 e |

| September 30, 2009 | 1.00 | .0060 | (.0001) | .0059 | (.0054) | — | (.0054) | 1.00 | .54 | 66,020 | .91 e,g | .68 e,g |

| September 30, 2008 | 1.00 | .0277 | (.0002) | .0275 | (.0276) | (.0003) | (.0279) | 1.00 | 2.83 | 99,244 | 1.06 g | 2.83 g |

| September 30, 2007 | 1.00 | .0436 h | — c | .0436 | (.0439) | — | (.0439) | 1.00 | 4.49 | 117,474 | 1.04 g | 4.34 g,h |

| Class C | ||||||||||||

| March 31, 2012 ** | $1.00 | .0001 | — c | .0001 | (.0001) | — | (.0001) | $1.00 | — *d | $27,045 | .10 *e | .01 *e |

| September 30, 2011 | 1.00 | .0001 | .0001 | .0002 | (.0001) | — | (.0001) | 1.00 | .01 | 31,073 | .22 e | .01 e |

| September 30, 2010 | 1.00 | .0001 | (.0003) | (.0002) | (.0005) | — | (.0005) | 1.00 | .06 | 21,991 | .32 e | — e,f |

| September 30, 2009 | 1.00 | .0060 | (.0001) | .0059 | (.0054) | — | (.0054) | 1.00 | .54 | 27,757 | .89 e,g | .62 e,g |

| September 30, 2008 | 1.00 | .0277 | (.0002) | .0275 | (.0276) | (.0003) | (.0279) | 1.00 | 2.83 | 30,609 | 1.06 g | 2.66 g |

| September 30, 2007 | 1.00 | .0436 h | — c | .0436 | (.0439) | — | (.0439) | 1.00 | 4.49 | 19,456 | 1.04 g | 4.34 g,h |

| Class M | ||||||||||||

| March 31, 2012 ** | $1.00 | .0001 | — c | .0001 | (.0001) | — | (.0001) | $1.00 | — *d | $27,714 | .10 *e | .01 *e |

| September 30, 2011 | 1.00 | .0001 | .0001 | .0002 | (.0001) | — | (.0001) | 1.00 | .01 | 31,296 | .22 e | .01 e |

| September 30, 2010 | 1.00 | .0001 | (.0003) | (.0002) | (.0005) | — | (.0005) | 1.00 | .06 | 35,999 | .32 e | — e,f |

| September 30, 2009 | 1.00 | .0080 | (.0001) | .0079 | (.0074) | — | (.0074) | 1.00 | .74 | 46,293 | .68 e,g | .83 e,g |

| September 30, 2008 | 1.00 | .0312 | (.0002) | .0310 | (.0310) | (.0004) | (.0314) | 1.00 | 3.19 | 53,452 | .71 g | 3.07 g |

| September 30, 2007 | 1.00 | .0471 h | — c | .0471 | (.0474) | — | (.0474) | 1.00 | 4.86 | 42,641 | .69 g | 4.69 g,h |

| Class R | ||||||||||||

| March 31, 2012 ** | $1.00 | .0001 | — c | .0001 | (.0001) | — | (.0001) | $1.00 | — *d | $19,848 | .10 *e | .01 *e |

| September 30, 2011 | 1.00 | .0001 | .0001 | .0002 | (.0001) | — | (.0001) | 1.00 | .01 | 18,508 | .22 e | .01 e |

| September 30, 2010 | 1.00 | .0001 | (.0003) | (.0002) | (.0005) | — | (.0005) | 1.00 | .06 | 16,283 | .32 e | — e,f |

| September 30, 2009 | 1.00 | .0060 | (.0001) | .0059 | (.0054) | — | (.0054) | 1.00 | .54 | 12,589 | .84 e,g | .43 e,g |

| September 30, 2008 | 1.00 | .0277 | (.0002) | .0275 | (.0276) | (.0003) | (.0279) | 1.00 | 2.83 | 5,564 | 1.06 g | 2.54 g |

| September 30, 2007 | 1.00 | .0436 h | — c | .0436 | (.0439) | — | (.0439) | 1.00 | 4.49 | 3,974 | 1.04 g | 4.32 g, h |

| Class T | ||||||||||||

| March 31, 2012 ** | $1.00 | .0001 | — c | .0001 | (.0001) | — | (.0001) | $1.00 | — *d | $29,867 | .10 *e | .01 *e |

| September 30, 2011 | 1.00 | .0001 | .0001 | .0002 | (.0001) | — | (.0001) | 1.00 | .01 | 33,941 | .22 e | .01 e |

| September 30, 2010 | 1.00 | .0001 | (.0003) | (.0002) | (.0005) | — | (.0005) | 1.00 | .06 | 31,034 | .32 e | — e,f |

| September 30, 2009 | 1.00 | .0073 | (.0001) | .0072 | (.0067) | — | (.0067) | 1.00 | .67 | 39,088 | .74 e,g | .64 e,g |

| September 30, 2008 | 1.00 | .0302 | (.0002) | .0300 | (.0300) | (.0004) | (.0304) | 1.00 | 3.08 | 20,037 | .81 g | 2.93 g |

| September 30, 2007 | 1.00 | .0461 h | — c | .0461 | (.0464) | — | (.0464) | 1.00 | 4.75 | 14,743 | .79 g | 4.59 g, h |

See notes to financial highlights at the end of this section.

The accompanying notes are an integral part of these financial statements.

| 26 | 27 |

Financial highlights (Continued)

* Not annualized.

** Unaudited.

a Total return assumes dividend reinvestment and does not reflect the effect of sales charges.

b Includes amounts paid through expense offset arrangements (Note 2).

c Amount represents less than $0.0001 per share.

d Amount represents less than 0.01%.

e Reflects a voluntary waiver of certain fund expenses in effect during the period relating to the enhancement of certain annualized net yields of the fund. As a result of such waivers, the expenses of each class reflect a reduction of the following amounts as a percentage of average net assets (Note 2):

| 3/31/12 | 9/30/11 | 9/30/10 | 9/30/09 | |

| Class A | 0.16% | 0.28% | 0.20% | 0.02% |

| Class B | 0.41 | 0.78 | 0.70 | 0.17 |

| Class C | 0.41 | 0.78 | 0.70 | 0.19 |

| Class M | 0.23 | 0.43 | 0.35 | 0.05 |

| Class R | 0.41 | 0.78 | 0.70 | 0.24 |

| Class T | 0.28 | 0.53 | 0.45 | 0.09 |

f Amount represents less than 0.01% of average net assets.

g Reflects an involuntary contractual expense limitation in effect during the period. For periods prior to September 30, 2009, certain fund expenses were waived in connection with the fund’s investment in Putnam Prime Money Market Fund. As a result of such limitation and/or waivers, the expenses of each class reflect a reduction of the following amounts:

| Percentage of | |

| average net assets | |

| September 30, 2009 | 0.03% |

| September 30, 2008 | <0.01 |

| September 30, 2007 | <0.01 |

h Reflects a non-recurring reallocation of balance credits which amounted to $0.0003 per share and 0.03% of average net assets.

The accompanying notes are an integral part of these financial statements.

28

Notes to financial statements 3/31/12 (Unaudited)

Within the following Notes to financial statements, references to “State Street” represent State Street Bank and Trust Company, references to “the SEC” represent the Securities and Exchange Commission and references to “Putnam Management” represent Putnam Investment Management, LLC, the fund’s manager, an indirect wholly-owned subsidiary of Putnam Investments, LLC.

Putnam Money Market Fund (the fund) is a Massachusetts business trust, which is registered under the Investment Company Act of 1940, as amended, as a diversified open-end management investment company. The investment objective of the fund is to seek as high a rate of current income as Putnam Management believes is consistent with preservation of capital and maintenance of liquidity. The fund invests mainly in money market instruments that are high quality and have short-term maturities. The fund invests significantly in certificates of deposit, commercial paper (including asset-backed commercial paper), U.S. government debt and repurchase agreements, corporate obligations and bank acceptances. The fund may also invest in U.S. dollar denominated foreign securities of these types. Putnam Management may consider, among other factors, credit and interest rate risks, as well as general market conditions, when deciding whether to buy or sell investments.

The fund offers class A, class B, class C, class M, class R and class T shares. Each class of shares is sold without a front-end sales charge. Class A, class M, class R and class T shares also are generally not subject to a contingent deferred sales charge. In addition to the standard offering of class A shares, they are also sold to certain college savings plans and other Putnam funds. Class B shares convert to class A shares after approximately eight years and are subject to a contingent deferred sales charge on certain redemptions. Class C shares have a one-year 1.00% contingent deferred sales charge on certain redemptions and do not convert to class A shares. Class R shares are not available to all investors. The expenses for class A, class B, class C, class M, class R and class T shares may differ based on each class’ distribution fee, which is identified in Note 2.

In the normal course of business, the fund enters into contracts that may include agreements to indemnify another party under given circumstances. The fund’s maximum exposure under these arrangements is unknown as this would involve future claims that may be, but have not yet been, made against the fund. However, the fund’s management team expects the risk of material loss to be remote.

Note 1: Significant accounting policies

Investment income, realized gains and losses and expenses of the fund are borne pro-rata based on the relative net assets of each class to the total net assets of the fund, except that each class bears expenses unique to that class (including the distribution fees applicable to such classes). Each class votes as a class only with respect to its own distribution plan or other matters on which a class vote is required by law or determined by the Trustees. Shares of each class would receive their pro-rata share of the net assets of the fund, if the fund were liquidated. In addition, the Trustees declare separate dividends on each class of shares.

The following is a summary of significant accounting policies consistently followed by the fund in the preparation of its financial statements. The preparation of financial statements is in conformity with accounting principles generally accepted in the United States of America and requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities in the financial statements and the reported amounts of increases and decreases in net assets from operations. Actual results could differ from those estimates. Subsequent events after the Statement of assets and liabilities date through the date that the financial statements were issued have been evaluated in the preparation of the financial statements. Unless otherwise noted, the “reporting period” represents the period from October 1, 2011 through March 31, 2012.

Security valuation The valuation of the fund’s portfolio instruments is determined by means of the amortized cost method (which approximates market value) as set forth in Rule 2a–7 under the Investment Company Act of 1940. The amortized cost of an instrument is determined by valuing it at its original cost and thereafter amortizing any discount or premium from its face value at a constant rate until maturity and is generally categorized as a Level 2 security.

Investments in other open-end investment companies (excluding exchange traded funds), which are classified as Level 1 securities, are based on their net asset value. The net asset value of an investment company equals the total value of its assets less its liabilities and divided by the number of its outstanding shares. Shares are only valued as of the close of regular trading on the New York Stock Exchange each day that the exchange is open.

29

Joint trading account Pursuant to an exemptive order from the SEC, the fund may transfer uninvested cash balances into a joint trading account along with the cash of other registered investment companies and certain other accounts managed by Putnam Management. These balances may be invested in issues of short-term investments having maturities of up to 90 days.

Repurchase agreements The fund, or any joint trading account, through its custodian, receives delivery of the underlying securities, the market value of which at the time of purchase is required to be in an amount at least equal to the resale price, including accrued interest. Collateral for certain tri-party repurchase agreements is held at the counterparty’s custodian in a segregated account for the benefit of the fund and the counterparty. Putnam Management is responsible for determining that the value of these underlying securities is at all times at least equal to the resale price, including accrued interest. In the event of default or bankruptcy by the other party to the agreement, retention of the collateral may be subject to legal proceedings.

Security transactions and related investment income Security transactions are recorded on the trade date (the date the order to buy or sell is executed). Interest income is recorded on the accrual basis. Premiums and discounts from purchases of short-term investments are amortized/accreted at a constant rate until maturity. Gains or losses on securities sold are determined on the identified cost basis.

Interfund lending The fund, along with other Putnam funds, may participate in an interfund lending program pursuant to an exemptive order issued by the SEC. This program allows the fund to lend to other Putnam funds that permit such transactions. Interfund lending transactions are subject to each fund’s investment policies and borrowing and lending limits. Interest earned or paid on the interfund lending transaction will be based on the average of certain current market rates. During the reporting period, the fund did not utilize the program.