| | |

| UNITED STATES

SECURITIES AND EXCHANGE COMMISSION |

| | |

| CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

|

| | |

| Investment Company Act file number: | (811-00653) |

| | |

| Exact name of registrant as specified in charter: | Putnam Income Fund |

| | |

| Address of principal executive offices: | 100 Federal Street, Boston, Massachusetts 02110 |

| | |

| Name and address of agent for service: | Stephen Tate, Vice President

100 Federal Street

Boston, Massachusetts 02110 |

| | |

| Copy to: | Bryan Chegwidden, Esq.

Ropes & Gray LLP

1211 Avenue of the Americas

New York, New York 10036 |

| | |

| | James E. Thomas, Esq.

Ropes & Gray LLP

800 Boylston Street

Boston, Massachusetts 02199 |

| | |

| Registrant’s telephone number, including area code: | (617) 292-1000 |

| | |

| Date of fiscal year end: | October 31, 2023 |

| | |

| Date of reporting period: | November 1 , 2022 – October 31, 2023 |

| | |

|

Item 1. Report to Stockholders: | |

| | |

| The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940: | |

Putnam

Income

Fund

Annual report

10 | 31 | 23

Message from the Trustees

December 7, 2023

Dear Fellow Shareholder:

The U.S. economy has defied expectations of a recession year to date, with the pace of growth picking up speed in the third quarter. At the same time, volatility in financial markets has increased. Stock prices fell in late summer and early fall. Bond prices also declined during this time, while yields, which move in the opposite direction, rose. In October 2023, the 10-year U.S. Treasury yield, a key benchmark for setting mortgage rates, briefly rose above 5% for the first time since 2007.

Markets have been pressured by inflation, which has moderated but remains above the U.S. Federal Reserve’s target rate of 2%. In its continuing effort to bring down inflation, the Fed has indicated short-term interest rates will remain high heading into next year. This restrictive policy may keep the risk of recession alive in 2024 unless the U.S. economy slows without contracting.

Your investment team is analyzing shifting market conditions, actively navigating risks, and identifying attractive opportunities for your fund. An update on your fund is in the report that follows.

Thank you for investing with Putnam.

Current performance may be lower or higher than the quoted past performance, which cannot guarantee future results. Share price, principal value, and return will fluctuate, and you may have a gain or a loss when you sell your shares. Performance of class A shares assumes reinvestment of distributions and does not account for taxes. Fund returns in the bar chart do not reflect a sales charge of 4.00%; had they, returns would have been lower. See below and pages 8–11 for additional performance information. For a portion of the periods, the fund had expense limitations, without which returns would have been lower. To obtain the most recent month-end performance, visit putnam.com.

All Bloomberg indices are provided by Bloomberg Index Services Limited.

Lipper peer group median is provided by Lipper, an LSEG company.

* The fund’s benchmark, the Bloomberg U.S. Aggregate Bond Index, was introduced on 12/31/75, and the fund’s Lipper category was introduced on 12/31/59. Both post-date the inception of the fund’s class A shares.

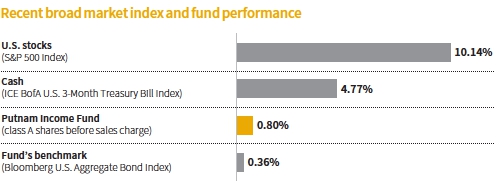

This comparison shows your fund’s performance in the context of broad market indexes for the 12 months ended 10/31/23. See above and pages 8–11 for additional fund performance information. Index descriptions can be found on page 14.

All Bloomberg indices are provided by Bloomberg Index Services Limited.

Brett, please describe investing conditions during the reporting period.

Bond markets faced several headwinds over the period. Stubborn inflation, rising interest rates, banking turmoil, and a U.S. debt ceiling crisis weighed on investor sentiment. The U.S. Federal Reserve continued to raise short-term interest rates to counter high inflation, which remained above its 2% target rate.

In December 2022, as inflation gradually declined, the Fed began to reduce the size and pace of its interest-rate hikes. The U.S. economy, buoyed by a strong labor market, remained in expansion. Company fundamentals were positive, with quarterly earnings reports largely better than expected. Concerns that the Fed’s monetary tightening would tip the U.S. economy into a recession began to subside.

In calendar 2023, new risks emerged. Sticky inflation caused the Fed to keep interest rates higher for longer than anticipated. The failure of several U.S. regional banks in March and concern over the large federal deficit also cautioned investors. In May, U.S. Treasury yields moved higher following a resolution to the months-long U.S. debt ceiling debate. After skipping a rate hike in June, the Fed lifted rates

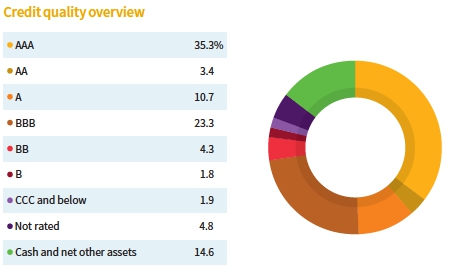

Credit qualities are shown as a percentage of the fund’s net assets as of 10/31/23. A bond rated BBB or higher (A-3 or higher, for short-term debt) is considered investment grade. This chart reflects the highest security rating provided by one or more of Standard & Poor’s, Moody’s, and Fitch. Ratings and portfolio credit quality will vary over time. Due to rounding, percentages may not equal 100%.

Cash and net other assets, if any, represent the market value weights of cash, derivatives, and short-term securities in the portfolio. The fund itself has not been rated by an independent rating agency.

in July. This brought the federal funds rate to a 22-year high of 5.25%–5.50%. The Fed held rates steady thereafter, but indicated another rate hike was possible before year-end calendar 2023.

Against this backdrop, credit spreads largely tightened over the period. [Credit spreads are the yield advantage credit-sensitive bonds offer over comparable-maturity U.S. Treasuries. Bond prices rise as yield spreads tighten and decline as spreads widen.] The yield on the benchmark 10-year U.S. Treasury fluctuated during the period. It began the period at 4.10%, declined to a low of 3.30% in April 2023, and ended the period at 4.88%.

How did the fund perform for the 12 months ended October 31, 2023?

The fund returned 0.80%, outperforming its benchmark, the Bloomberg U.S. Aggregate Bond Index, which returned 0.36%.

Which holdings and strategies detracted from the fund’s performance relative to the benchmark for the reporting period?

The fund’s interest-rate and yield curve positioning were the primary detractors for the reporting period. In January 2023, Treasury rates rallied significantly across most of the curve, with the 10-year Treasury declining 37 basis points by month’s end. As rates rallied, interest-rate volatility fell, which weighed on our term structure positioning. Interest-rate volatility picked up after January 2023 as Treasury rates sold off. However, this was not enough to offset earlier losses.

Our exposure to commercial mortgage-backed securities [CMBS] also weighed on returns. Negative headlines surrounding office properties, along with regional U.S. banking stress, contributed to a broad decline in the CMBS market in the first quarter of 2023. The CMBS market stabilized thereafter but remained challenged by an uncertain economic outlook and weakening liquidity through period-end.

Can you discuss some contributors to fund performance relative to the benchmark for the reporting period?

Prepayment risk strategies, led by our agency interest-only [IO] securities, were notable contributors to relative performance during the period. Prepayment speeds fell over the period, benefiting our agency IO securities. Our tactical mortgage basis positioning also helped results. During the period, we maintained a long mortgage basis, but remained tactical. Our tactical decisions benefited the fund as the basis tightened in the first half of the period and minimized the impact of the basis widening in the second half of the period. [Our long mortgage basis positioning is a strategy that capitalizes on the difference between longer-term U.S. Treasury yields and the interest rates on 30-year home mortgages.]

Mortgage credit investments, led by our residential MBS, added to fund returns. Despite higher mortgage rates, the U.S. housing market proved to be resilient given constrained supply. Corporate credit holdings, led by our high-grade collateralized loan obligations [CLOs], also was additive. Loan prices recovered in calendar 2023 and CLO spreads tightened, which provided a tailwind for our holdings rated AAA and AA.

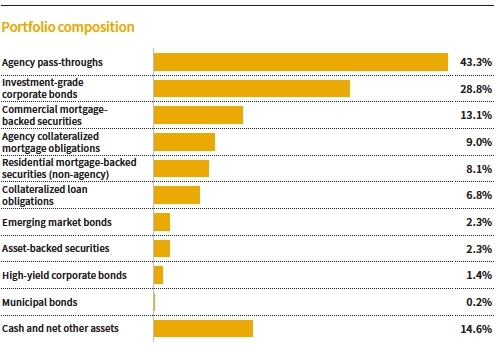

Allocations are shown as a percentage of the fund’s net assets as of 10/31/23. Cash and net other assets, if any, represent the market value weights of cash, derivatives, short-term securities, and other unclassified assets in the portfolio. Summary information may differ from the portfolio schedule included in the financial statements due to the inclusion of derivative securities, any interest accruals, the use of different classifications of securities for presentation purposes, and rounding. Allocations may not total 100% because the chart includes the notional value of certain derivatives (the economic value for purposes of calculating periodic payment obligations), in addition to the market value of securities. Holdings and allocations may vary over time.

How did you use derivatives during the reporting period?

We used futures for yield curve positioning and to hedge Treasury term structure risk. Interest-rate swaps were used to hedge term structure risk and for yield curve positioning. Options known as swaptions were used for hedging duration and convexity and for managing downside risks. Credit default swaps were used to hedge credit and market risks, to gain liquid exposure to individual names, and to gain exposure to specific sectors.

What is the team’s near-term outlook?

Our base-case scenario is that the rate of inflation will settle around 3.0%–3.5% and the U.S. will avoid a recession, in our view. In this case, we believe the Fed will have to keep rates higher for longer while quantitative tightening continues in the background. We expect fixed income spreads to stay flat to slightly tighter. Our alternate scenario is that the U.S. will experience a recession in late 2024, when the Fed’s tightening fully impacts the economy. If a recession does not arrive in calendar 2024, the Fed may not cut interest rates at all, in our view. As liquidity continues to be withdrawn, we expect financial market risks to increase.

What are your current views on the sectors in which the fund invests?

U.S. Treasury rates have traded higher since the resolution of the debt ceiling debate in May 2023. More recently, Treasury rates have rallied significantly on market expectations that point to a pause in the Fed’s rate hikes. Despite the Treasury rally, we believe the Fed will continue to keep interest rates higher for longer on the back of a strengthening U.S. economy and heavy Treasury issuance.

Healthy market technicals [supply/demand metrics] and positive macroeconomic data have kept investment-grade spread volatility low, in our view. These conditions were supportive of high-yield bonds, along with other risk assets. Year to date, corporate fundamentals have been resilient; most quarterly earnings reports surpassed expectations. Technicals also improved with a pickup in inflows in recent months. Low new issuance in high yield, coupled with an increased number of rising stars [companies that show the potential to improve their credit quality], also supported technicals, in our view. We believe valuations are modestly attractive. Credit spreads are pricing in a continued increase in defaults along with slower growth. However, these conditions do not indicate a harsh recession, in our view. Low U.S. dollar prices remain attractive with spreads at their long-term median. We believe risks to our outlook include increased banking volatility, policy missteps from global central banks, a more severe slowdown or recession than anticipated, and heightened geopolitical tensions.

We believe commercial real estate is facing meaningful headwinds and risks from a shift in office demand and rising costs of capital. Property values will likely face pressure over the medium term, with prices varying significantly by geography and property type, in our view. We believe much of the risk has been priced into the market based on substantial spread widening over the past 12 months. The most attractive relative value opportunities require detailed loan-level analysis and security selection, in our view.

U.S. homeowner balance sheets remain well positioned, supported by locked-in, ultra-low mortgage rates and substantial home price appreciation in recent years. We expect changes in home prices to be relatively flat through year-end calendar 2023. However, certain geographies that became overheated during the pandemic may begin to retract, in our view. At current levels, we believe attractive risk-adjusted return opportunities can be found across the capital stack.

We have a cautious intermediate outlook for emerging market [EM] credit. EM sovereigns appear overvalued across the quality spectrum.

We see the risks of recession and inflation in EM economies declining, which may be supportive of EM credit in the near term. We expect slightly more downside within the next three to nine months. We prefer to stay beta neutral [where portfolio risk is not correlated to broader market volatility] and seek relative value opportunities. We remain very selective when adding high-yield risk exposure.

We currently maintain a neutral to slightly long position to the mortgage basis but remain tactical. The systemic risk posed by regional bank failures appears to be behind us, and market supply should taper down in the near term. However, the future of bank demand remains uncertain and may hinge upon regulatory changes.

We expect mortgage prepayment speeds will be stable going forward. We believe our prepayment strategies can offer good protection against a recession that negatively impacts home prices or employment. In our view, many prepayment-sensitive assets now offer an attractive risk-adjusted return at current price levels, and significant upside potential if rates stabilize and volatility declines.

Thank you for your time and for bringing us up to date, Brett.

The views expressed in this report are exclusively those of Putnam Management and are subject to change. They are not meant as investment advice.

Please note that the holdings discussed in this report may not have been held by the fund for the entire period. Portfolio composition is subject to review in accordance with the fund’s investment strategy and may vary in the future. Current and future portfolio holdings are subject to risk.

Of special interest

The fund’s monthly dividend rate for class A shares increased from $0.017 to $0.021 per share in February 2023. This adjustment reflects Putnam Management’s expectations for fund earnings in the current fixed income environment. Similar increases were made to other share classes of the fund.

Your fund’s performance

This section shows your fund’s performance, price, and distribution information for periods ended October 31, 2023, the end of its most recent fiscal year. In accordance with regulatory requirements for mutual funds, we also include performance information as of the most recent calendar quarter-end and expense information taken from the fund’s current prospectus. Performance should always be considered in light of a fund’s investment strategy. Data represent past performance. Past performance does not guarantee future results. More recent returns may be less or more than those shown. Investment return and principal value will fluctuate, and you may have a gain or a loss when you sell your shares. Performance information does not reflect any deduction for taxes a shareholder may owe on fund distributions or on the redemption of fund shares. For the most recent month-end performance, please visit the Individual Investors section at putnam.com or call Putnam at 1-800-225-1581. Class M, R, R5, R6, and Y shares are not available to all investors.

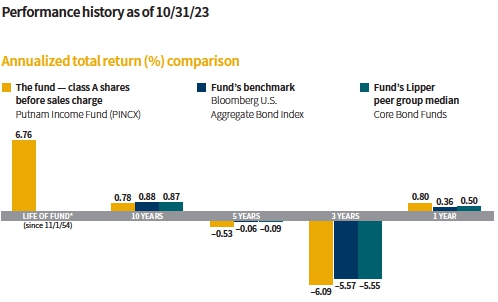

Annualized fund performance Total return for periods ended 10/31/23

| | | | | |

| | Life of fund | 10 years | 5 years | 3 years | 1 year |

| Class A (11/1/54) | | | | | |

| Before sales charge | 6.76% | 0.78% | –0.53% | –6.09% | 0.80% |

| After sales charge | 6.70 | 0.37 | –1.34 | –7.36 | –3.23 |

| Class B (3/1/93) | | | | | |

| Before CDSC | 6.63 | 0.18 | –1.27 | –6.76 | 0.18 |

| After CDSC | 6.63 | 0.18 | –1.59 | –7.56 | –4.44 |

| Class C (7/26/99) | | | | | |

| Before CDSC | 6.67 | 0.18 | –1.28 | –6.77 | 0.04 |

| After CDSC | 6.67 | 0.18 | –1.28 | –6.77 | –0.88 |

| Class M (12/14/94) | | | | | |

| Before sales charge | 6.35 | 0.51 | –0.80 | –6.34 | 0.59 |

| After sales charge | 6.30 | 0.18 | –1.45 | –7.37 | –2.68 |

| Class R (1/21/03) | | | | | |

| Net asset value | 6.49 | 0.52 | –0.77 | –6.32 | 0.58 |

| Class R5 (7/2/12) | | | | | |

| Net asset value | 6.88 | 1.06 | –0.25 | –5.79 | 1.05 |

| Class R6 (7/2/12) | | | | | |

| Net asset value | 6.89 | 1.14 | –0.17 | –5.73 | 1.20 |

| Class Y (6/16/94) | | | | | |

| Net asset value | 6.87 | 1.03 | –0.27 | –5.82 | 1.19 |

Current performance may be lower or higher than the quoted past performance, which cannot guarantee future results. After-sales-charge returns for class A and M shares reflect the deduction of the maximum 4.00% and 3.25% sales charge, respectively, levied at the time of purchase. Class B share returns after contingent deferred sales charge (CDSC) reflect the applicable CDSC, which is 5% in the first year, declining over time to 1% in the sixth year, and is eliminated thereafter. Class C share returns after CDSC reflect a 1% CDSC for the first year that is eliminated thereafter. Class R, R5, R6, and Y shares have no initial sales charge or CDSC. Performance for class B, C, M, R, and Y shares before their inception is derived from the historical performance of class A shares, adjusted for the applicable sales charge (or CDSC) and the higher operating expenses for such shares, except for class Y shares, for which 12b-1 fees are not applicable. Performance for class R5 and R6 shares prior to their inception is derived from the historical performance of class Y shares and has not been adjusted for the lower investor servicing fees applicable to class R5 and R6 shares; had it, returns would have been higher.

For a portion of the periods, the fund had expense limitations, without which returns would have been lower.

Class B and C share performance reflects conversion to class A shares after eight years.

Comparative annualized index returns For periods ended 10/31/23

| | | | | |

| | Life of fund | 10 years | 5 years | 3 years | 1 year |

| Bloomberg U. S. Aggregate | | | | | |

| Bond Index | —* | 0.88% | –0.06% | –5.57% | 0.36% |

| Lipper Core Bond Funds | | | | | |

| category median† | —* | 0.87 | –0.09 | –5.55 | 0.50 |

Index and Lipper results should be compared with fund performance before sales charge, before CDSC, or at net asset value.

All Bloomberg indices are provided by Bloomberg Index Services Limited.

Lipper peer group median is provided by Lipper, an LSEG company.

* The fund’s benchmark, the Bloomberg U.S. Aggregate Bond Index, was introduced on 12/31/75, and the fund’s Lipper category was introduced on 12/31/59. Both post-date the inception of the fund’s class A shares.

† Over the 1-year, 3-year, 5-year, and 10-year periods ended 10/31/23, there were 520, 490, 464, and 339 funds, respectively, in this Lipper category.

Past performance does not indicate future results. At the end of the same time period, a $10,000 investment in the fund’s class B and C shares would have been valued at $10,177 and $10,178, respectively, and no contingent deferred sales charges would apply. A $10,000 investment in the fund’s class M shares ($9,675 after sales charge) would have been valued at $10,183. A $10,000 investment in the fund’s class R, R5, R6, and Y shares would have been valued at $10,531, $11,114, $11,205, and $11,080, respectively.

All Bloomberg indices are provided by Bloomberg Index Services Limited.

Fund price and distribution information For the 12-month period ended 10/31/23

| | | | | | | | | | |

| Distributions | Class A | Class B | Class C | Class M | Class R | Class R5 | Class R6 | Class Y |

| Number | 12 | 12 | 12 | 12 | 12 | 12 | 12 | 12 |

| Income | $0.483 | $0.439 | $0.442 | $0.471 | $0.471 | $0.497 | $0.506 | $0.495 |

| Capital gains | — | — | — | — | — | — | — | — |

| Total | $0.483 | $0.439 | $0.442 | $0.471 | $0.471 | $0.497 | $0.506 | $0.495 |

| | Before | After | Net | Net | Before | After | Net | Net | Net | Net |

| | sales | sales | asset | asset | sales | sales | asset | asset | asset | asset |

| Share value | charge | charge | value | value | charge | charge | value | value | value | value |

| 10/31/22 | $5.47 | $5.70 | $5.39 | $5.41 | $5.27 | $5.45 | $5.40 | $5.54 | $5.58 | $5.58 |

| 10/31/23 | 5.05 | 5.26 | 4.98 | 4.99 | 4.85 | 5.01 | 4.98 | 5.12 | 5.16 | 5.17 |

| Current rate | Before | After | Net | Net | Before | After | Net | Net | Net | Net |

| (end of | sales | sales | asset | asset | sales | sales | asset | asset | asset | asset |

| period) | charge | charge | value | value | charge | charge | value | value | value | value |

| Current | | | | | | | | | | |

| dividend rate1 | 4.99% | 4.79% | 4.34% | 4.33% | 4.95% | 4.79% | 4.82% | 5.16% | 5.35% | 5.11% |

| Current | | | | | | | | | | |

| 30-day | | | | | | | | | | |

| SEC yield | | | | | | | | | | |

| (with expense | | | | | | | | | | |

| limitation)2,3 | N/A | 5.61 | 5.09 | 5.09 | N/A | 5.42 | 5.60 | 6.15 | 6.22 | 6.10 |

| Current | | | | | | | | | | |

| 30-day | | | | | | | | | | |

| SEC yield | | | | | | | | | | |

| (without | | | | | | | | | | |

| expense | | | | | | | | | | |

| limitation)3 | N/A | 5.47 | 4.94 | 4.94 | N/A | 5.28 | 5.45 | 6.00 | 6.07 | 5.95 |

The classification of distributions, if any, is an estimate. Before-sales-charge share value and current dividend rate for class A and M shares, if applicable, do not take into account any sales charge levied at the time of purchase. After-sales-charge share value, current dividend rate, and current 30-day SEC yield, if applicable, are calculated assuming that the maximum sales charge (4.00% for class A shares and 3.25% for class M shares) was levied at the time of purchase. Final distribution information will appear on your year-end tax forms.

1 Most recent distribution, including any return of capital and excluding capital gains, annualized and divided by share price before or after sales charge at period-end.

2 For a portion of the period, the fund had expense limitations, without which yields would have been lower.

3 Based only on investment income and calculated using the maximum offering price for each share class, in accordance with SEC guidelines.

Annualized fund performance as of most recent calendar quarter

Total return for periods ended 9/30/23

| | | | | |

| | Life of fund | 10 years | 5 years | 3 years | 1 year |

| Class A (11/1/54) | | | | | |

| Before sales charge | 6.79% | 1.07% | –0.44% | –5.70% | 0.84% |

| After sales charge | 6.73 | 0.66 | –1.25 | –6.97 | –3.20 |

| Class B (3/1/93) | | | | | |

| Before CDSC | 6.66 | 0.47 | –1.14 | –6.35 | 0.23 |

| After CDSC | 6.66 | 0.47 | –1.46 | –7.16 | –4.39 |

| Class C (7/26/99) | | | | | |

| Before CDSC | 6.69 | 0.47 | –1.15 | –6.36 | 0.28 |

| After CDSC | 6.69 | 0.47 | –1.15 | –6.36 | –0.65 |

| Class M (12/14/94) | | | | | |

| Before sales charge | 6.38 | 0.83 | –0.66 | –5.87 | 0.65 |

| After sales charge | 6.33 | 0.50 | –1.31 | –6.90 | –2.62 |

| Class R (1/21/03) | | | | | |

| Net asset value | 6.53 | 0.83 | –0.66 | –5.90 | 0.64 |

| Class R5 (7/2/12) | | | | | |

| Net asset value | 6.91 | 1.37 | –0.12 | –5.39 | 1.28 |

| Class R6 (7/2/12) | | | | | |

| Net asset value | 6.92 | 1.45 | –0.07 | –5.33 | 1.25 |

| Class Y (6/16/94) | | | | | |

| Net asset value | 6.90 | 1.34 | –0.18 | –5.42 | 1.23 |

See the discussion following the fund performance table on page 8 for information about the calculation of fund performance.

Your fund’s expenses

As a mutual fund investor, you pay ongoing expenses, such as management fees, distribution fees (12b-1 fees), and other expenses. In the most recent six-month period, your fund’s expenses were limited; had expenses not been limited, they would have been higher. Using the following information, you can estimate how these expenses affect your investment and compare them with the expenses of other funds. You may also pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial representative.

Expense ratios

| | | | | | | | |

| | Class A | Class B | Class C | Class M | Class R | Class R5 | Class R6 | Class Y |

| Net expenses for the fiscal | | | | | | | | |

| year ended 10/31/22* | 0.75% | 1.50% | 1.50% | 1.00% | 1.00% | 0.45% | 0.38% | 0.50% |

| Total annual operating | | | | | | | | |

| expenses for the fiscal year | | | | | | | | |

| ended 10/31/22* | 0.85% | 1.60% | 1.60% | 1.10% | 1.10% | 0.55% | 0.48% | 0.60% |

| Annualized expense ratio | | | | | | | | |

| for the six-month period | | | | | | | | |

| ended 10/31/23† | 0.75% | 1.50% | 1.50% | 1.00% | 1.00% | 0.45% | 0.38% | 0.50% |

Fiscal year expense information in this table is taken from the most recent prospectus, is subject to change, and may differ from that shown for the annualized expense ratio and in the financial highlights of this report.

Expenses are shown as a percentage of average net assets.

* Restated to reflect current fees.

† Expense ratios for each class are for the fund’s most recent fiscal half year. As a result of this, ratios may differ from expense ratios based on one-year data in the financial highlights.

Expenses per $1,000

The following table shows the expenses you would have paid on a $1,000 investment in each class of the fund from 5/1/23 to 10/31/23. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

| | | | | | | | |

| | Class A | Class B | Class C | Class M | Class R | Class R5 | Class R6 | Class Y |

| Expenses paid per $1,000*† | $3.67 | $7.34 | $7.33 | $4.90 | $4.89 | $2.21 | $1.86 | $2.45 |

| Ending value (after expenses) | $943.80 | $941.10 | $939.60 | $942.40 | $942.00 | $945.60 | $945.30 | $944.40 |

* Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of average net assets for the six months ended 10/31/23. The expense ratio may differ for each share class.

† Expenses are calculated by multiplying the expense ratio by the average account value for the period; then multiplying the result by the number of days in the period (184); and then dividing that result by the number of days in the year (365).

Estimate the expenses you paid

To estimate the ongoing expenses you paid for the six months ended 10/31/23, use the following calculation method. To find the value of your investment on 5/1/23, call Putnam at 1-800-225-1581.

Compare expenses using the SEC’s method

The Securities and Exchange Commission (SEC) has established guidelines to help investors assess fund expenses. Per these guidelines, the following table shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total costs) of investing in the fund with those of other funds. All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

| | | | | | | | |

| | Class A | Class B | Class C | Class M | Class R | Class R5 | Class R6 | Class Y |

| Expenses paid per $1,000*† | $3.82 | $7.63 | $7.63 | $5.09 | $5.09 | $2.29 | $1.94 | $2.55 |

| Ending value (after expenses) | $1,021.42 | $1,017.64 | $1,017.64 | $1,020.16 | $1,020.16 | $1,022.94 | $1,023.29 | $1,022.68 |

* Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of average net assets for the six months ended 10/31/23. The expense ratio may differ for each share class.

† Expenses are calculated by multiplying the expense ratio by the average account value for the six-month period; then multiplying the result by the number of days in the six-month period (184); and then dividing that result by the number of days in the year (365).

Comparative index definitions

Bloomberg U.S. Aggregate Bond Index is an unmanaged index of U.S. investment-grade fixed income securities.

ICE BofA (Intercontinental Exchange Bank of America) U.S. 3-Month Treasury Bill Index is an unmanaged index that seeks to measure the performance of U.S. Treasury bills available in the marketplace.

S&P 500® Index is an unmanaged index of common stock performance.

Indexes assume reinvestment of all distributions and do not account for fees. Securities and performance of a fund and an index will differ. You cannot invest directly in an index.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg’s licensors approve or endorse this material, or guarantee the accuracy or completeness of any information herein, or make any warranty, express or implied, as to the results to be obtained therefrom, and to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

ICE Data Indices, LLC (“ICE BofA”), used with permission. ICE BofA permits use of the ICE BofA indices and related data on an “as is” basis; makes no warranties regarding same; does not guarantee the suitability, quality, accuracy, timeliness, and/or completeness of the ICE BofA indices or any data included in, related to, or derived therefrom; assumes no liability in connection with the use of the foregoing; and does not sponsor, endorse, or recommend Putnam Investments, or any of its products or services.

Lipper, an LSEG company, is a third-party industry-ranking entity that ranks funds. Its rankings do not reflect sales charges. Lipper rankings are based on total return at net asset value relative to other funds that have similar current investment styles or objectives as determined by Lipper. Lipper may change a fund’s category assignment at its discretion. Lipper category medians reflect performance trends for funds within a category.

Other information for shareholders

Important notice regarding delivery of shareholder documents

In accordance with Securities and Exchange Commission (SEC) regulations, Putnam sends a single notice of internet availability, or a single printed copy, of annual and semiannual shareholder reports, prospectuses, and proxy statements to Putnam shareholders who share the same address, unless a shareholder requests otherwise. If you prefer to receive your own copy of these documents, please call Putnam at 1-800-225-1581 or, for exchange-traded funds only, 1-833-228-5577. We will begin sending individual copies within 30 days.

Proxy voting

Putnam is committed to managing our funds in the best interests of our shareholders. The Putnam funds’ proxy voting guidelines and procedures, as well as information regarding how your fund voted proxies relating to portfolio securities during the 12-month period ended June 30, 2023, are available in the Individual Investors section of putnam.com and on the SEC’s website, www.sec.gov. If you have questions about finding forms on the SEC’s website, you may call the SEC at 1-800-SEC-0330. You may also obtain the Putnam funds’ proxy voting guidelines and procedures at no charge by calling Putnam’s Shareholder Services at 1-800-225-1581 or, for exchange-traded funds only, 1-833-228-5577.

Fund portfolio holdings

The fund will file a complete schedule of its portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-PORT within 60 days of the end of such fiscal quarter. Shareholders may obtain the fund’s Form N-PORT on the SEC’s website at www.sec.gov.

Trustee and employee fund ownership

Putnam employees and members of the Board of Trustees place their faith, confidence, and, most importantly, investment dollars in Putnam funds. As of October 31, 2023, Putnam employees had approximately $466,000,000 and the Trustees had approximately $64,000,000 invested in Putnam funds. These amounts include investments by the Trustees’ and employees’ immediate family members as well as investments through retirement and deferred compensation plans.

Liquidity risk management program

Putnam, as the administrator of the fund’s liquidity risk management program (appointed by the Board of Trustees), presented the most recent annual report on the program to the Trustees in May 2023. The report covered the structure of the program, including the program documents and related policies and procedures adopted to comply with Rule 22e-4 under the Investment Company Act of 1940, and reviewed the operation of the program from January 2022 through December 2022. The report included a description of the annual liquidity assessment of the fund that Putnam performed in November 2022. The report noted that there were no material compliance exceptions identified under Rule 22e-4 during the period. The report included a review of the governance of the program and the methodology for classification of the fund’s investments. Putnam concluded that the program has been operating effectively and adequately to ensure compliance with Rule 22e-4.

Important notice regarding Putnam’s privacy policy

In order to conduct business with our shareholders, we must obtain certain personal information such as account holders’ names, addresses, Social Security numbers, and dates of birth. Using this information, we are able to maintain accurate records of accounts and transactions.

It is our policy to protect the confidentiality of our shareholder information, whether or not a shareholder currently owns shares of our funds. In particular, it is our policy not to sell information about you or your accounts to outside marketing firms. We have safeguards in place designed to prevent unauthorized access to our computer systems and procedures to protect personal information from unauthorized use.

Under certain circumstances, we must share account information with outside vendors who provide services to us, such as mailings and proxy solicitations. In these cases, the service providers enter into confidentiality agreements with us, and we provide only the information necessary to process transactions and perform other services related to your account. Finally, it is our policy to share account information with your financial representative, if you’ve listed one on your Putnam account.

Trustee approval of management contracts

Consideration of your fund’s new and interim management and sub-management contracts

At their meeting on June 23, 2023, the Board of Trustees of your fund, including all of the Trustees who are not “interested persons” (as this term is defined in the Investment Company Act of 1940, as amended (the “1940 Act”)) of the Putnam mutual funds, closed-end funds and exchange-traded funds (collectively, the “funds”) (the “Independent Trustees”) approved, subject to approval by your fund’s shareholders, a new management contract with Putnam Investment Management (“Putnam Management”) and a new sub-management contract between Putnam Management and its affiliate, Putnam Investments Limited (“PIL”) (collectively, the “New Management Contracts”). The Trustees considered the proposed New Management Contracts in connection with the planned acquisition of Putnam U.S. Holdings I, LLC (“Putnam Holdings”) by a subsidiary of Franklin Resources, Inc. (“Franklin Templeton”). The Trustees considered that, on May 31, 2023, Franklin Templeton and Great-West Lifeco Inc., the parent company of Putnam Holdings, announced that they had entered into a definitive agreement for a subsidiary of Franklin Templeton to acquire Putnam Holdings in a stock and cash transaction (the “Transaction”). The Trustees noted that Putnam Holdings was the parent company of Putnam Management and PIL. The Trustees were advised that the Transaction would result in a “change of control” of Putnam Management and PIL and would cause your fund’s current Management Contract with Putnam Management and Sub-Management Contract with PIL (collectively, the “Current Management Contracts”) to terminate in accordance with the 1940 Act. The Trustees considered that the New Management Contracts would take effect upon the closing of the Transaction, which was expected to occur in the fourth quarter of 2023.

In addition to the New Management Contracts, the Trustees also approved interim management and sub-management contracts with Putnam Management and PIL, respectively (the “Interim Management Contracts”), which would take effect in the event that for any reason shareholder approval of a New Management Contract was not received by the time of the Transaction closing. The Trustees considered that each Interim Management Contract that became effective would remain in effect until shareholders approved the proposed New Management Contract, or until 150 days elapse after the closing of the Transaction, whichever occurred first. The considerations and conclusions discussed in connection with the Trustees’ consideration of the New Management Contracts and the continuance of your fund’s Current Management Contracts also apply to the Trustees’ consideration of the Interim Management Contracts, supplemented by consideration of the terms, nature and reason for any Interim Management Contract.

The Independent Trustees met with their independent legal counsel, as defined in Rule 0–1(a)(6) under the 1940 Act (their “independent legal counsel”), and representatives of Putnam Management and its parent company, Power Corporation of Canada, to discuss the potential Transaction, including the timing and structure of the Transaction and its implications for Putnam Management and the funds, during their regular meeting on November 18, 2022, and the full Board of Trustees further discussed these matters with representatives of Putnam Management at its regular meeting on December 15, 2022. At a special meeting on December 20, 2022, the full Board of Trustees met with representatives of Putnam Management, Power Corporation of Canada and Franklin Templeton to further discuss the potential Transaction, including Franklin Templeton’s strategic plans for Putnam Management’s asset management business and the funds, potential sources of synergy between Franklin Templeton and Putnam Management, potential areas of partnership between Power Corporation of Canada and Franklin Templeton, Franklin Templeton’s distribution capabilities, Franklin Templeton’s existing service provider relationships and Franklin Templeton’s recent acquisitions of other asset management firms.

In order to assist the Independent Trustees in their consideration of the New Management Contracts and other anticipated impacts of the Transaction on the funds and their shareholders, independent legal counsel for the Independent Trustees furnished an initial information request to Franklin Templeton (the “Initial Franklin Request”). At a special meeting of the full Board of Trustees held on January 25, 2023, representatives of Franklin Templeton addressed the firm’s responses to the Initial Franklin Request. At the meeting, representatives of Franklin Templeton

discussed, among other things, the business and financial condition of Franklin Templeton and its affiliates, Franklin Templeton’s U.S. registered fund operations, its recent acquisition history, Franklin Templeton’s intentions regarding the operation of Putnam Management and the funds following the completion of the potential Transaction and expected benefits to the funds and Putnam Management that might result from the Transaction.

The Board of Trustees actively monitored developments with respect to the potential Transaction throughout the period leading up to the public announcement of a final sale agreement on May 31, 2023. The Independent Trustees met to discuss these matters at their regular meetings on January 27, April 20 and May 19, 2023. The full Board of Trustees also discussed developments at their regular meeting on February 23, 2023. Following the public announcement of the Transaction on May 31, 2023, independent legal counsel for the Independent Trustees furnished a supplemental information request (the “Supplemental Franklin Request”) to Franklin Templeton. At the Board of Trustees’ regular in-person meeting held on June 22–23, 2023, representatives of Putnam Management and Power Corporation of Canada provided further information regarding, among other matters, the final terms of the Transaction and efforts undertaken to retain Putnam employees. The Contract Committee of the Board of Trustees also met on June 22, 2023 to discuss Franklin Templeton’s responses to the Supplemental Franklin Request. Mr. Reynolds, the only Trustee affiliated with Putnam Management, participated in portions of these meetings to provide the perspective of the Putnam organization, but did not otherwise participate in the deliberations of the Independent Trustees or the Contract Committee regarding the potential Transaction.

After the presentations and after reviewing the written materials provided, the Independent Trustees met at their in-person meeting on June 23, 2023 to consider the New Management Contracts for each fund, proposed to become effective upon the closing of the Transaction, and the filing of a preliminary proxy statement. At this meeting and throughout the process, the Independent Trustees also received advice from their independent legal counsel regarding their responsibilities in evaluating the potential Transaction and the New Management Contracts. The Independent Trustees reviewed the terms of the proposed New Management Contracts and the differences between the New Management Contracts and the Current Management Contracts. They noted that the terms of the proposed New Management Contracts were substantially identical to the Current Management Contracts, except for certain changes designed largely to address differences among various of the existing contracts, which had been developed and implemented at different times in the past.

In considering the approval of the proposed New Management Contracts, the Board of Trustees took into account a number of factors, including:1

(i) Franklin Templeton’s and Putnam Management’s belief that the Transaction would not adversely affect the funds or their shareholders and their belief that the Transaction was likely to result in certain benefits (described below) for the funds and their shareholders;

(ii) That Franklin Templeton did not intend to make any material change in Putnam Management’s senior investment professionals (other than certain changes related to reporting structure and organization of personnel discussed below), including the portfolio managers of the funds, or to the firm’s operating locations as a result of the Transaction;

(iii) That Franklin Templeton intended for Putnam Management’s equity investment professionals to continue to operate largely independently from Franklin Templeton, reporting to Franklin Templeton’s Head of Public Markets following the Transaction;

(iv) That, while Putnam Management’s organizational structure was not expected to change immediately following the Transaction, Franklin Templeton intended to revise Putnam Management’s reporting structure in order to include Putnam Management’s fixed income investment professionals in Franklin Templeton’s fixed income group and to include Putnam Management’s Global Asset Allocation (“GAA”) investment professionals in Franklin Templeton’s investment solutions group, with both Franklin Templeton

1All subsequent references to Putnam Management describing the Board of Trustees’ considerations should be deemed to include references to PIL as necessary or appropriate in the context.

groups reporting to Franklin Templeton’s Head of Public Markets;

(v) Franklin Templeton’s expectation that there would not be any changes in the investment objectives, strategies or portfolio holdings of the funds as a result of the Transaction;

(vi) That neither Franklin Templeton nor Putnam Management had any current plans to propose changes to the funds’ existing management fees or expense limitations, or current plans to make changes to the funds’ existing distribution arrangements;

(vii) Franklin Templeton’s and Putnam Management’s representations that, following the Transaction, there was not expected to be any diminution in the nature, quality and extent of services provided to the funds and their shareholders by Putnam Management and PIL, including compliance and other non-advisory services;

(viii) That Franklin Templeton did not currently plan to change the branding of the funds or to change the lineup of funds in connection with the Transaction but would continue to evaluate how best to position the funds in the market;

(ix) The possible benefits accruing to the funds and their shareholders as a result of the Transaction, including:

a. That the scale of Franklin Templeton’s investment operations platform would increase the investment and operational resources available to the funds;

b. That the Putnam open-end funds would benefit from Franklin Templeton’s large retail and institutional global distribution capabilities and significant network of intermediary relationships, which may provide additional opportunities for the funds to increase assets and reduce expenses by spreading expenses over a larger asset base; and

c. Potential benefits to shareholders of the Putnam open-end funds that could result from the alignment of certain fund features and shareholder benefits with those of other funds sponsored by Franklin Templeton and its affiliates and access to a broader array of investment opportunities;

(x) The financial strength, reputation, experience and resources of Franklin Templeton and its investment advisory subsidiaries;

(xi) Franklin Templeton’s expectation that the Transaction would not impact the capabilities or responsibilities of Putnam Management’s Investment Division (other than any impact related to reporting structure changes for Putnam Management’s equity, fixed income and GAA investment groups and to including Putnam Management’s fixed income and GAA investment professionals in existing Franklin Templeton investment groups, as discussed above) and that any changes to the Investment Division over the longer term would be made in order to achieve perceived operational efficiencies or improvements to the portfolio management process;

(xii) Franklin Templeton’s commitment to maintaining competitive compensation arrangements to allow Putnam Management to continue to attract and retain highly qualified personnel and Putnam Management’s and Franklin Templeton’s efforts to retain personnel, including efforts implemented since the Transaction was announced;

(xiii) That the current senior management teams at Putnam Management and Power Corporation of Canada had indicated their strong support of the Transaction and that Putnam Management had recommended that the Board of Trustees approve the New Management Contracts; and

(xiv) Putnam Management’s and Great-West Lifeco Inc.’s commitment to bear all expenses incurred by the funds in connection with the Transaction, including all costs associated with the proxy solicitation in connection with seeking shareholder approval of the New Management Contracts.

Finally, in considering the proposed New Management Contracts, the Board of Trustees also took into account their concurrent deliberations and conclusions, as described below, in connection with their annual review of the funds’ Current Management Contracts and the approval of their continuance, effective July 1, 2023, and the extensive materials that they had reviewed in connection with that review process.

Based upon the foregoing considerations, on June 23, 2023, the Board of Trustees, including all of the Independent Trustees, unanimously approved the proposed New Management Contracts and determined to recommend their approval to the shareholders of the funds.

General conclusions — Current Management Contracts

The Board of Trustees oversees the management of each fund and, as required by law, determines annually whether to approve the continuance of your fund’s management contract with Putnam Management and the sub-management contract with respect to your fund between Putnam Management and PIL. (Because PIL is an affiliate of Putnam Management and Putnam Management remains fully responsible for all services provided by PIL, the Trustees did not attempt to evaluate PIL as a separate entity.) The Board of Trustees, with the assistance of its Contract Committee, requests and evaluates all information it deems reasonably necessary under the circumstances in connection with its annual contract review. The Contract Committee consists solely of Independent Trustees.

At the outset of the review process, members of the Board of Trustees’ independent staff and independent legal counsel considered any possible changes to the annual contract review materials furnished to the Contract Committee during the course of the previous year’s review and, as applicable, identified those changes to Putnam Management. Following these discussions and in consultation with the Contract Committee, the Independent Trustees’ independent legal counsel requested that Putnam Management and its affiliates furnish specified information, together with any additional information that Putnam Management considered relevant, to the Contract Committee. Over the course of several months ending in June 2023, the Contract Committee met on a number of occasions with representatives of Putnam Management, and separately in executive session, to consider the information that Putnam Management provided. Throughout this process, the Contract Committee was assisted by the members of the Board of Trustees’ independent staff and by independent legal counsel for the funds and the Independent Trustees.

At the Board of Trustees’ June 2023 meeting, the Contract Committee met in executive session to discuss and consider its recommendations with respect to the continuance of the contracts. At that meeting, the Contract Committee also met in executive session with the other Independent Trustees to review a summary of the key financial, performance and other data that the Contract Committee considered in the course of its review. The Contract Committee recommended, and the Independent Trustees approved, the continuance of your fund’s Current Management Contracts, effective July 1, 2023, and the approval of your fund’s New Management Contracts and Interim Management Contracts, as discussed above.

The Independent Trustees’ approvals were based on the following conclusions:

• That the fee schedule in effect for your fund represented reasonable compensation in light of the nature and quality of the services being provided to the fund, the fees paid by competitive funds, the costs incurred by Putnam Management in providing services to the fund and the application of certain reductions and waivers noted below; and

• That the fee schedule in effect for your fund represented an appropriate sharing between fund shareholders and Putnam Management of any economies of scale as may exist in the management of the fund at current asset levels.

These conclusions were based on a comprehensive consideration of all information provided to the Trustees and were not the result of any single factor. Some of the factors that figured particularly in the Trustees’ deliberations and how the Trustees considered these factors are described below, although individual Trustees may have evaluated the information presented differently, giving different weights to various factors. It is also important to recognize that the management arrangements for your fund and the other Putnam mutual funds and closed-end funds are the result of many years of review and discussion between the Independent Trustees and Putnam Management, that some aspects of the arrangements may receive greater scrutiny in some years than others and that the Trustees’ conclusions may be based, in part, on their consideration of fee arrangements in previous years. For example, with certain exceptions primarily involving newer funds (including the exchange-traded funds) or repositioned funds, the current fee arrangements under the vast majority of the funds’ management contracts were first implemented at the beginning of 2010 following extensive review by the Contract Committee and discussions with representatives of Putnam Management, as well as approval by shareholders. The Trustees also took into account their concurrent deliberations and conclusions, and the materials that they had reviewed, in connection with their approval on June 23, 2023 of the Interim Management Contracts and the New Management Contracts, which had been proposed in light of the Transaction (which would

cause the fund’s Current Management Contracts to terminate in accordance with applicable law or the terms of each contract).

Management fee schedules and total expenses

The Trustees reviewed the management fee schedules in effect for all funds, including fee levels and any breakpoints. Under its management contract, your fund has the benefit of breakpoints in its management fee schedule that provide shareholders with reduced fee levels as assets under management in the Putnam family of funds increase. The Trustees also reviewed the total expenses of each Putnam fund, recognizing that in most cases management fees represented the major, but not the sole, determinant of total costs to fund shareholders. (Two mutual funds and each of the exchange-traded funds have implemented so-called “all-in” or unitary management fees covering substantially all routine fund operating costs.)

In reviewing fees and expenses, the Trustees generally focus their attention on material changes in circumstances — for example, changes in assets under management, changes in a fund’s investment strategy, changes in Putnam Management’s operating costs or profitability, or changes in competitive practices in the fund industry — that suggest that consideration of fee changes might be warranted. The Trustees concluded that the circumstances did not indicate that changes to the management fee schedule for your fund would be appropriate at this time.

As in the past, the Trustees also focused on the competitiveness of each fund’s total expense ratio. The Trustees, Putnam Management and the funds’ investor servicing agent, Putnam Investor Services, Inc. (“PSERV”), have implemented expense limitations that were in effect during your fund’s fiscal year ending in 2022. These expense limitations were: (i) a contractual expense limitation applicable to specified mutual funds, including your fund, of 25 basis points on investor servicing fees and expenses and (ii) a contractual expense limitation applicable to specified mutual funds, including your fund, of 20 basis points on so-called “other expenses” (i.e., all expenses exclusive of management fees, distribution fees, investor servicing fees, investment-related expenses, interest, taxes, brokerage commissions, acquired fund fees and expenses and extraordinary expenses). These expense limitations attempt to maintain competitive expense levels for the funds. Most funds, including your fund, had sufficiently low expenses that these expense limitations were not operative during their fiscal years ending in 2022. Putnam Management and PSERV have agreed to maintain these expense limitations until at least February 28, 2025. In addition, Putnam Management contractually agreed to waive fees and/or reimburse expenses of your fund to the extent that expenses of the fund (excluding payments under the fund’s distribution plans, investor servicing fees, brokerage, interest, taxes, investment-related expenses, extraordinary expenses and acquired fund fees and expenses) would exceed an annual rate of 0.33% of its average net assets through at least February 28, 2025. Putnam Management and PSERV’s commitment to these expense limitation arrangements, which were intended to support an effort to have the mutual fund expenses meet competitive standards, was an important factor in the Trustees’ decision to approve your fund’s New Management Contracts and Interim Management Contracts and the continuance of your fund’s Current Management Contracts.

The Trustees reviewed comparative fee and expense information for a custom group of competitive funds selected by Broadridge Financial Solutions, Inc. (“Broadridge”). This comparative information included your fund’s percentile ranking for effective management fees and total expenses (excluding any applicable 12b-1 fees), which provides a general indication of your fund’s relative standing. In the custom peer group, your fund ranked in the third quintile in effective management fees (determined for your fund and the other funds in the custom peer group based on fund asset size and the applicable contractual management fee schedule) and in the fourth quintile in total expenses (excluding any applicable 12b-1 fees) as of December 31, 2022. The first quintile represents the least expensive funds and the fifth quintile the most expensive funds. The fee and expense data reported by Broadridge as of December 31, 2022 reflected the most recent fiscal year-end data available in Broadridge’s database at that time.

In connection with their review of fund management fees and total expenses, the Trustees also reviewed the costs of the services provided and the profits realized by Putnam Management and its affiliates from their contractual relationships with the funds. This information included trends in revenues, expenses and profitability of Putnam Management and its affiliates relating to

the investment management, investor servicing and distribution services provided to the funds, as applicable. In this regard, the Trustees also reviewed an analysis of the revenues, expenses and profitability of Putnam Management and its affiliates, allocated on a fund-by-fund basis, with respect to (as applicable) the funds’ management, distribution and investor servicing contracts. For each fund, the analysis presented information about revenues, expenses and profitability in 2022 for each of the applicable agreements separately and for the agreements taken together on a combined basis. The Trustees concluded that, at current asset levels, the fee schedules in place for each of the funds, including the fee schedule for your fund, represented reasonable compensation for the services being provided and represented an appropriate sharing between fund shareholders and Putnam Management of any economies of scale as may exist in the management of the funds at that time.

The information examined by the Trustees in connection with their annual contract review for the funds included information regarding services provided and fees charged by Putnam Management and its affiliates to other clients, including collective investment trusts offered in the defined contribution and defined benefit retirement plan markets, sub-advised mutual funds, private funds sponsored by affiliates of Putnam Management, model-only separately managed accounts and Putnam Management’s manager-traded separately managed account programs. This information included, in cases where a product’s investment strategy corresponds with a fund’s strategy, comparisons of those fees with fees charged to the funds, as well as an assessment of the differences in the services provided to these clients as compared to the services provided to the funds. The Trustees observed that the differences in fee rates between these clients and the funds are by no means uniform when examined by individual asset sectors, suggesting that differences in the pricing of investment management services to these types of clients may reflect, among other things, historical competitive forces operating in separate marketplaces. The Trustees considered the fact that in many cases fee rates across different asset classes are higher on average for 1940 Act-registered funds than for other clients, and the Trustees also considered the differences between the services that Putnam Management provides to the funds and those that it provides to its other clients. The Trustees did not rely on these comparisons to any significant extent in concluding that the management fees paid by your fund are reasonable.

Investment performance

The quality of the investment process provided by Putnam Management represented a major factor in the Trustees’ evaluation of the quality of services provided by Putnam Management under your fund’s management contract. The Trustees were assisted in their review of Putnam Management’s investment process and performance by the work of the investment oversight committees of the Trustees and the full Board of Trustees, which meet on a regular basis with individual portfolio managers and with senior management of Putnam Management’s Investment Division throughout the year. The Trustees concluded that Putnam Management generally provides a high-quality investment process — based on the experience and skills of the individuals assigned to the management of fund portfolios, the resources made available to them and in general Putnam Management’s ability to attract and retain high-quality personnel — but also recognized that this does not guarantee favorable investment results for every fund in every time period.

The Trustees considered that, in the aggregate, peer-relative and benchmark-relative Putnam fund performance was generally encouraging in 2022 against a backdrop of volatile equity and fixed income markets, driven by factors such as Russia’s invasion of Ukraine, increased tensions with China, disruptions in energy markets and broader supply chains, rising inflation and the significant tightening of monetary policy by the Board of Governors of the Federal Reserve in an effort to combat inflation. The Trustees further noted that, in the face of these numerous economic headwinds, corporate earnings and employment data had been generally robust throughout 2022. For the one-year period ended December 31, 2022, the Trustees noted that the Putnam funds, on an asset-weighted basis, ranked in the 41st percentile of their peers as determined by Lipper Inc. (“Lipper”) and, on an asset-weighted-basis, outperformed their benchmarks by 1.3% gross of fees over the one-year period. The Committee also noted that the funds’ aggregate performance over longer-term periods continued to be strong, with the funds, on an asset-weighted basis, ranking in the 34th, 27th and 22nd percentiles of their Lipper peers over the three-year, five-year and ten-year periods ended

December 31, 2022, respectively. The Trustees further noted that the funds, in the aggregate, outperformed their benchmarks on a gross basis for each of the three-year, five-year and ten-year periods. The Trustees also considered the Morningstar Inc. ratings assigned to the funds and that 40 funds were rated four or five stars at the end of 2022, which represented an increase of 15 funds year-over-year. The Trustees also considered that seven funds were five-star rated at the end of 2022, which was a year-over-year decrease of two funds, and that 83% of the funds’ aggregate assets were in four- or five-star rated funds at year end.

In addition to the performance of the individual Putnam funds, the Trustees considered, as they had in prior years, the performance of The Putnam Fund complex versus competitor fund complexes, as reported in the Barron’s/Lipper Fund Families survey (the “Survey”). The Trustees noted that the Survey ranks mutual fund companies based on their performance across a variety of asset types, and that The Putnam Fund complex had performed exceptionally well in 2022. In this regard, the Trustees considered that the funds had ranked 9th out of 49 fund companies, 3rd out of 49 fund companies and 2nd out of 47 fund companies for the one-year, five-year and ten-year periods, respectively. The Trustees also noted that The Putnam Fund complex had been the only fund family to rank in the top ten in all three time periods. They also noted, however, the disappointing investment performance of some Putnam funds for periods ended December 31, 2022 and considered information provided by Putnam Management regarding the factors contributing to the underperformance and, where relevant, actions being taken to improve the performance of these particular funds. The Trustees indicated their intention to continue to monitor the performance of those funds.

For purposes of the Trustees’ evaluation of the Putnam funds’ investment performance, the Trustees generally focus on a competitive industry ranking of each fund’s total net return over a one-year, three-year and five-year period. For a number of Putnam funds with relatively unique investment mandates for which Putnam Management informed the Trustees that meaningful competitive performance rankings are not considered to be available, the Trustees evaluated performance based on their total gross and net returns and comparisons of those returns to the returns of selected investment benchmarks. In the case of your fund, the Trustees considered that its class A share cumulative total return performance at net asset value was in the following quartiles of its Lipper peer group (Lipper Core Bond Funds) for the one-year, three-year and five-year periods ended December 31, 2022 (the first quartile representing the best-performing funds and the fourth quartile the worst-performing funds):

| |

| One-year period | 1st |

| Three-year period | 4th |

| Five-year period | 2nd |

Over the one-year, three-year and five-year periods ended December 31, 2022, there were 509, 476 and 445 funds, respectively, in your fund’s Lipper peer group. (When considering performance information, shareholders should be mindful that past performance is not a guarantee of future results.)

The Trustees expressed concern about your fund’s fourth quartile performance over the three-year period ended December 31, 2022 and considered the circumstances that may have contributed to this disappointing performance. The Trustees considered Putnam Management’s observation that the fund’s underperformance over those periods was driven by disappointing performance in 2020 and 2021. The Trustees observed that significant underperformance in the securitized products sector in 2021 had contributed to the fund’s disappointing results, noting that prepayment strategies had suffered as a result of significantly elevated refinancing (given strong home price appreciation and low interest rates) relative to expectations. The Trustees considered that the fund’s underperformance was also driven by significant underperformance in the securitized products sector in 2020, which resulted from the outsized impact of the COVID-19 pandemic on the commercial mortgage sector. In addition, the Trustees considered the negative impact that the fund’s term structure strategies had on performance in 2021.

The Trustees noted Putnam Management’s observation that term structure strategies positively contributed to the fund’s performance over the three-year period ended December 31, 2022. The Trustees considered Putnam Management’s discussion regarding the ways in which the fund’s investment approach was evolving. The Trustees also considered that the fund had top quintile performance relative to its peers in 2022, partly due to the solid performance of the commercial mortgage sector. The Trustees noted that Putnam

Management remained confident in the fund’s portfolio managers. The Trustees also considered Putnam Management’s continued efforts to support fund performance through certain initiatives, including structuring compensation for portfolio managers to enhance accountability for fund performance, emphasizing accountability in the portfolio management process and affirming its commitment to a fundamental-driven approach to investing.

As a general matter, the Trustees believe that cooperative efforts between the Trustees and Putnam Management represent the most effective way to address investment performance concerns that may arise from time to time. The Trustees noted that investors in the Putnam funds have, in effect, placed their trust in the Putnam organization, under the oversight of the funds’ Trustees, to make appropriate decisions regarding the management of the funds. The Trustees also considered that Putnam Management has made changes in light of subpar investment performance when warranted. Based on Putnam Management’s willingness to take appropriate measures to address fund performance issues, the Trustees concluded that it continued to be advisable to seek change within Putnam Management to address performance shortcomings. In the Trustees’ view, the alternative of engaging a new investment adviser for an underperforming fund, with all the attendant risks and disruptions, would not likely provide any greater assurance of improved investment performance.

Brokerage and soft-dollar allocations; distribution and investor servicing

The Trustees considered various potential benefits that Putnam Management may receive in connection with the services it provides under the management contract with your fund. These include benefits related to brokerage allocation and the use of soft dollars, whereby a portion of the commissions paid by a fund for brokerage may be used to acquire research services that are expected to be useful to Putnam Management in managing the assets of the fund and of other clients. Subject to policies established by the Trustees, soft dollars generated by these means are used predominantly to acquire brokerage and research services (including third-party research and market data) that enhance Putnam Management’s investment capabilities and supplement Putnam Management’s internal research efforts. The Trustees indicated their continued intent to monitor regulatory and industry developments in this area with the assistance of their Brokerage Committee. In addition, with the assistance of their Brokerage Committee, the Trustees indicated their continued intent to monitor the allocation of the funds’ brokerage in order to ensure that the principle of seeking best price and execution remains paramount in the portfolio trading process.

Putnam Management may also receive benefits from payments made to Putnam Management’s affiliates by the mutual funds for distribution services and investor services. In conjunction with the review of your fund’s management and sub-management contracts, the Trustees reviewed your fund’s investor servicing agreement with PSERV and its distributor’s contract and distribution plans with Putnam Retail Management Limited Partnership (“PRM”), both of which are affiliates of Putnam Management. The Trustees concluded that the fees payable by the mutual funds to PSERV and PRM for such services were fair and reasonable in relation to the nature and quality of such services, the fees paid by competitive funds and the costs incurred by PSERV and PRM in providing such services. Furthermore, the Trustees were of the view that the investor services provided by PSERV were required for the operation of the mutual funds, and that they were of a quality at least equal to those provided by other providers.

Audited financial statements

These sections of the report, as well as the accompanying Notes, preceded by the Report of Independent Registered Public Accounting Firm, constitute the fund’s audited financial statements.

The fund’s portfolio lists all the fund’s investments and their values as of the last day of the reporting period. Holdings are organized by asset type and industry sector, country, or state to show areas of concentration and diversification.

Statement of assets and liabilities shows how the fund’s net assets and share price are determined. All investment and non-investment assets are added together. Any unpaid expenses and other liabilities are subtracted from this total. The result is divided by the number of shares to determine the net asset value per share, which is calculated separately for each class of shares. (For funds with preferred shares, the amount subtracted from total assets includes the liquidation preference of preferred shares.)

Statement of operations shows the fund’s net investment gain or loss. This is done by first adding up all the fund’s earnings — from dividends and interest income — and subtracting its operating expenses to determine net investment income (or loss). Then, any net gain or loss the fund realized on the sales of its holdings — as well as any unrealized gains or losses over the period — is added to or subtracted from the net investment result to determine the fund’s net gain or loss for the fiscal period.

Statement of changes in net assets shows how the fund’s net assets were affected by the fund’s net investment gain or loss, by distributions to shareholders, and by changes in the number of the fund’s shares. It lists distributions and their sources (net investment income or realized capital gains) over the current reporting period and the most recent fiscal year-end. The distributions listed here may not match the sources listed in the Statement of operations because the distributions are determined on a tax basis and may be paid in a different period from the one in which they were earned.

Financial highlights provide an overview of the fund’s investment results, per-share distributions, expense ratios, net investment income ratios, and portfolio turnover (not required for money market funds) in one summary table, reflecting the five most recent reporting periods. In a semiannual report, the highlights table also includes the current reporting period.

Report of Independent Registered Public Accounting Firm

To the Board of Trustees and Shareholders of

Putnam Income Fund:

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities, including the fund’s portfolio, of Putnam Income Fund (the “Fund”) as of October 31, 2023, the related statement of operations for the year ended October 31, 2023, the statement of changes in net assets for each of the two years in the period ended October 31, 2023, including the related notes, and the financial highlights for each of the four years in the period ended October 31, 2023 (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund as of October 31, 2023, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period ended October 31, 2023 and the financial highlights for each of the four years in the period ended October 31, 2023 in conformity with accounting principles generally accepted in the United States of America.

The financial statements of the Fund as of and for the year ended October 31, 2019 and the financial highlights for the period ended on October 31, 2019 (not presented herein, other than the financial highlights) were audited by other auditors whose report dated December 11, 2019 expressed an unqualified opinion on those financial statements and financial highlights.

Basis for Opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits of these financial statements in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. Our procedures included confirmation of securities owned as of October 31, 2023 by correspondence with the custodian, transfer agent, agent banks and brokers; when replies were not received from brokers, we performed other auditing procedures. We believe that our audits provide a reasonable basis for our opinion.