| | |

| UNITED STATES |

| SECURITIES AND EXCHANGE COMMISSION |

| Washington, D.C. 20549 |

| |

| FORM N-CSR |

| |

| CERTIFIED SHAREHOLDER REPORT OF REGISTERED |

| MANAGEMENT INVESTMENT COMPANIES |

| | |

| Investment Company Act file number: (811- 01561) | |

| | |

| Exact name of registrant as specified in charter: | Putnam Vista Fund |

| |

| Address of principal executive offices: One Post Office Square, Boston, Massachusetts 02109 |

| | |

| Name and address of agent for service: | Beth S. Mazor, Vice President |

| | One Post Office Square |

| | Boston, Massachusetts 02109 |

| | |

| Copy to: | John W. Gerstmayr, Esq. |

| | Ropes & Gray LLP |

| | One International Place |

| | Boston, Massachusetts 02110 |

| | |

| Registrant’s telephone number, including area code: | (617) 292-1000 |

| | | |

| Date of fiscal year end: July 31, 2008 | | |

| |

| Date of reporting period: August 1, 2007 — January 31, 2008 |

Item 1. Report to Stockholders:

The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940:

What makes Putnam different?

In 1830, Massachusetts Supreme Judicial Court Justice Samuel Putnam established The Prudent Man Rule, a legal foundation for responsible money management.

THE PRUDENT MAN RULE

All that can be required of a trustee to invest is that he shall conduct himself faithfully and exercise a sound discretion. He is to observe how men of prudence, discretion, and intelligence manage their own affairs, not in regard to speculation, but in regard to the permanent disposition of their funds, considering the probable income, as well as the probable safety of the capital to be invested.

A time-honored tradition in money management

Since 1937, our values have been rooted in a profound sense of responsibility for the money entrusted to us.

A prudent approach to investing

We use a research-driven team approach to seek consistent, dependable, superior investment results over time, although there is no guarantee a fund will meet its objectives.

Funds for every investment goal

We offer a broad range of mutual funds and other financial products so investors and their financial representatives can build diversified portfolios.

A commitment to doing what’s right for investors

With a focus on investment performance, below-average expenses, and in-depth information about our funds, we put the interests of investors first and seek to set the standard for integrity and service.

Industry-leading service

We help investors, along with their financial representatives, make informed investment decisions with confidence.

Putnam

Vista

Fund

1| 31| 08

Semiannual Report

| |

| Message from the Trustees | 2 |

| About the fund | 4 |

| Performance snapshot | 6 |

| Interview with your fund’s Portfolio Leader | 7 |

| Performance in depth | 13 |

| Expenses | 16 |

| Portfolio turnover | 18 |

| Risk | 19 |

| Your fund’s management | 20 |

| Terms and definitions | 21 |

| Trustee approval of management contract | 23 |

| Other information for shareholders | 28 |

| Financial statements | 29 |

| Brokerage commissions | 51 |

Cover photograph: Vineyard, Napa County, California © Charles O’Rear

Message from the Trustees

Dear Fellow Shareholder:

In early 2008, financial markets face clear challenges. What began as a rise in defaults for a limited segment of the U.S. mortgage market has spread across the global financial sector and produced a significant tightening of credit conditions. Forecasts for global growth have been reduced as a result, and markets have reacted by sending stock prices lower. In the United States, the economy weakened sharply in late 2007, raising the chance of a recession this year. Fortunately, policymakers have taken action to stimulate growth: The Federal Reserve Board cut interest rates, and federal lawmakers, working with the president, approved a $168 billion fiscal stimulus plan.

As investors, it is natural to feel discouraged by disappointing short-term results. During these challenging times, it is important to remember the value of a long-term perspective and the counsel of your financial representative. The normal condition of the economy and corporate earnings is one of growth, albeit with occasional interruptions. As in the past, after a period of weakness the economy is likely to regain its momentum and produce the growth and corporate earnings that investors expect.

Starting this month, we have changed the portfolio manager’s commentary in this report to a question-and-answer format. We feel that this makes the information more readable and accessible, and we hope you think so as well.

2

Lastly, we note that Putnam Investments celebrated its 70th anniversary in November. From modest beginnings in Boston, Massachusetts, the company has grown into a global asset manager that serves millions of investors worldwide. Although the mutual fund industry has undergone many changes since George Putnam introduced his innovative balanced fund in 1937, Putnam’s guiding principles have not. As we celebrate this 70-year milestone, we look forward to Putnam continuing its long tradition of prudent money management. Thank you for your support of the Putnam funds.

Respectfully yours,

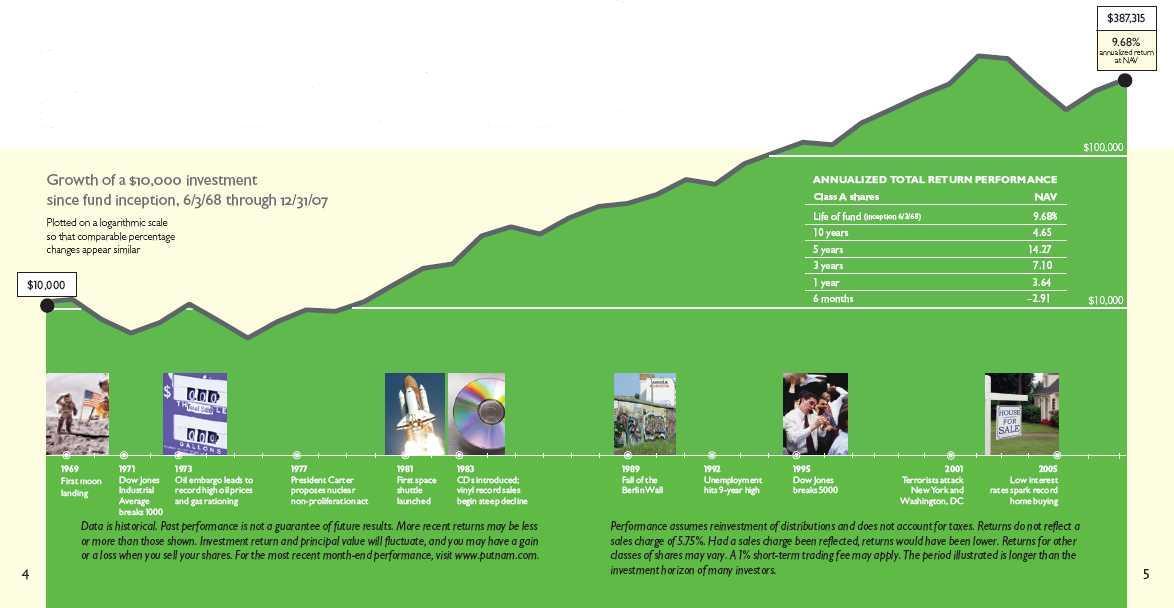

Putnam Vista Fund: Midsize growth companies

have offered investors compelling opportunities

Despite enduring its share of challenges throughout nearly 40 years, over time Putnam Vista Fund has rewarded long-term investors for their persistence, as illustrated in the growth chart below.

There are several key reasons why midsize growth stocks may continue to offer investors compelling opportunities:

First, stocks of midsize companies — also called mid-capitalization or mid-cap stocks —are generally more stable than small-cap stocks. By the time a company’s capitalization qualifies it as mid cap, it is generally large enough to have developed a solid infrastructure, including professional management, a comprehensive business plan, and a mature sales and marketing structure. It has also typically weathered a full economic cycle. These characteristics generally enable midsize companies to offer investors a greater degree of stability than that offered by smaller, less mature companies.

Second, mid-cap stocks generally have greater price inefficiencies than large-cap stocks. While midsize companies may have many of the same business characteristics as large companies, fewer analysts generally follow their stocks. This makes mid-cap stocks less efficiently priced and means that extensive research capabilities, such as those employed by your fund’s management team, can help identify promising midsize companies before the market recognizes their potential.

Third, midsize companies are frequently candidates for acquisition, which could have a positive impact on their stock prices. Buyers find the established business models and well-defined market niches of some midsize companies appealing.

The fund invests some or all of its assets in small and/or midsize companies. Such investments increase the risk of greater price fluctuations. Stocks with above-average earnings growth may be more volatile, especially if earnings do not continue to grow.

Relative stability, inefficient

pricing, and acquisition

potential are a few reasons

to consider mid-cap

growth stocks.

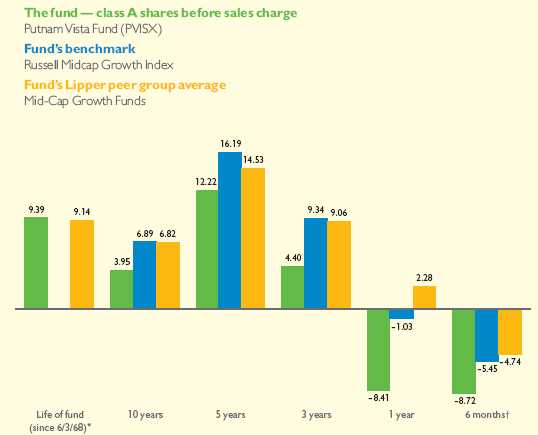

Performance snapshot

Putnam Vista Fund

Average annual total return (%) comparison as of 1/31/08

Current performance may be lower or higher than the quoted past performance, which cannot guarantee future results. Share price, principal value, and return will fluctuate, and you may have a gain or a loss when you sell your shares. Performance of class A shares assumes reinvestment of distributions and does not account for taxes. Fund returns in the bar chart do not reflect a sales charge of 5.75%; had they, returns would have been lower. See pages 13–15 for additional performance information. For a portion of the periods, this fund may have limited expenses, without which returns would have been lower. A 1% short-term trading fee may apply. To obtain the most recent month-end performance, visit www.putnam.com.

* The inception date of the Russell Midcap Growth Index was December 31, 1985.

† Returns for the six-month period are not annualized, but cumulative.

6

The period in review

How did the fund perform for the period, Kevin?

During the six months ended January 31, 2008, the market generally rewarded stocks that exhibited earnings and price momentum. However, in addition to momentum considerations, the fund’s strategy incorporates quality and valuation measures. Unfortunately, the fund’s strategy wasn’t rewarded during the period. And that’s because, until the final month of the period, market participants were mainly interested in stocks that exhibited earnings and price momentum, with little regard for quality or valuation. As a result, performance was disappointing for the period, with the fund lagging both its benchmark — the Russell Midcap Growth Index — and the average return for its Lipper peer group.

What factors affected the fund’s performance during the period?

The fund was positioned defensively, meaning that we maintained lower-than-benchmark weightings

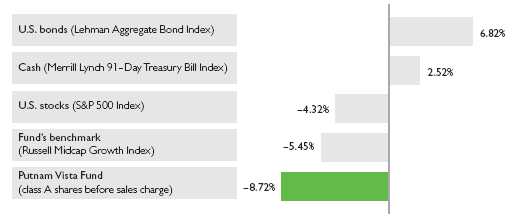

Broad market index and fund performance

This comparison shows your fund’s performance in the context of broad market indexes for the six months ended 1/31/08. See page 6 and pages 13–15 for additional fund performance information. Index descriptions can be found on page 22.

7

in sectors that had not performed well throughout most of the period, particularly consumer cyclicals and financials. However, during January, the Federal Reserve Board took dramatic steps to try to keep the U.S. economy from sliding into a recession by reducing the federal funds target rate from 4.25% to 3.00% . The market reacted positively to this reduction, and economically sensitive sectors, such as consumer cyclicals, and beaten-down financial stocks rebounded strongly. Because the fund was underweighted in these sectors, it did not realize the full benefit of this rebound.

Also during January, French banking giant Societe Generale announced that it sustained more than $7 billion in losses because of unauthorized trades by one of its employees. This announcement caused global markets to sell off sharply, which exacerbated the largely negative sentiment already present in equity markets, both in the United States and abroad.

Overall, the fund’s sector positioning contributed positively to performance. This positive contribution, however, was more than offset by being underweighted in consumer-related and financial stocks late in the period and by subpar stock selection in several sectors.

Top 10 holdings

This table shows the fund’s top 10 holdings and the percentage of the fund’s net assets that each represented as of 1/31/08. Also shown is each holding’s market sector and the specific industry within that sector. Holdings will vary over time.

| | |

| HOLDING (percentage of fund’s net assets) | SECTOR | INDUSTRY |

|

| Autodesk, Inc. (1.7%) | Technology | Software |

|

| Cameron International Corp. (1.7%) | Energy | Energy |

|

| L-3 Communications Holdings, Inc. (1.6%) | Capital goods | Aerospace and defense |

|

| McDermott International, Inc. (1.5%) | Capital goods | Engineering and construction |

|

| C.R. Bard, Inc. (1.4%) | Health care | Medical technology |

|

| Noble Corp. (1.4%) | Energy | Energy |

|

| NVIDIA Corp. (1.4%) | Technology | Electronics |

|

| Genzyme Corp. (1.4%) | Health care | Biotechnology |

|

| AGCO Corp. (1.4%) | Capital goods | Machinery |

|

| Laboratory Corp. of America Holdings (1.4%) | Health care | Health-care services |

|

8

How would you describe your strategy during this period, especially in an environment of increased market volatility?

As I mentioned, given the significant levels of volatility and uncertainty in the market, we positioned the portfolio somewhat more defensively. On the whole, however, we continued to maintain our consistent approach of seeking what we believe to be the most attractive opportunities within the universe of mid-cap growth stocks. We invest in a limited number of stocks, and we look for high-quality growth companies whose stocks are trading at what we consider to be favorable valuations. Our stock selection strategy is based on three fundamental criteria: the quality of the company, its near-term growth prospects, and a valuation forecast that meets our parameters. The ability to rotate among these criteria gives the fund the advantage of potentially favorable positioning whether the market is rewarding one, two, or all three of these factors.

We strongly believe that over the long term our approach offers investors the potential for attractive capital appreciation while managing the downside risk inherent in growth investing.

Which holdings were the top contributors to the fund’s performance?

Stocks in the basic materials sector were the top contributors to results

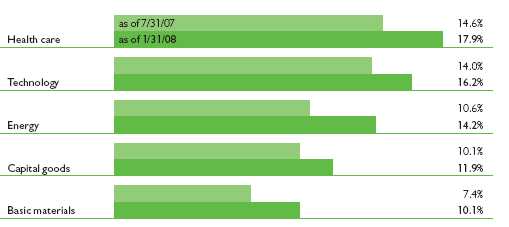

Comparison of top sector weightings

This chart shows how the fund’s top weightings have changed over the past six months. Weightings are shown as a percentage of net assets. Holdings will vary over time.

9

during the period. Specifically, holdings such as CF Industries, a maker of fertilizer products, and Cleveland-Cliffs, a manufacturer of iron ore pellets, were among the leading performers. These companies are benefiting from the rapid development taking place in emerging economies such as China and India. CF Industries is capitalizing on the growing demand for agricultural products and services that will enable farms to increase their productivity. Cleveland-Cliffs’ primary customers are integrated steel companies in the United States and Canada. Steel makers, and Cleveland-Cliffs by association, are helping to fuel the infrastructure building boom that is currently under way in developing countries.

Another top performer was Brazilian bank Unibanco-Uniao de Bancos Brasilieros (Unibanco). Unibanco is a leading credit-card issuer in Brazil and is growing along with the country’s expanding middle class. Compared with the United States, big-ticket items, such as cars, are more expensive in Brazil because of the tariffs that are added to the purchase price. At the same time, Brazilian consumers don’t have as many financing options as we do in the United States. Therefore, while it might sound a bit dubious to us, the Brazilian consumer will often finance a portion of a car or other big-ticket purchase with a credit card. We took profits on Unibanco and sold out of the position prior to the end of the period.

The fund was also helped by our investment in biotechnology firm Genzyme. The stock performed well as the company posted better-than-expected earnings. Genzyme is one of the most diversified biotech companies, with solid growth in its core product offerings, a promising and sizable late-stage pipeline, and a strong financial position.

Now that we’ve heard about the holdings that worked for the fund, which ones detracted from performance?

The number-one detractor was managed-care provider WellCare Health Plans. The stock’s price declined precipitously in late October when word surfaced about an FBI investigation regarding the company’s Medicare billing practices. We eliminated the position prior to the end of the period.

After performing well during the first half of calendar 2007, Ceradyne saw its stock price fall sharply during October and November. With growth stocks, the market typically tries to price the stock based on its collective assessment of a company’s near-term growth prospects. Ceradyne makes advanced technical ceramic products for military and industrial applications, and benefited from increased military spending to finance the Iraq war and military operations in Afghanistan. However, during the period,

10

a consensus emerged that defense spending had reached peak levels, a development that would create a head-wind against future earnings growth for a company such as Ceradyne.

Credit-rating agency Moody’s Corporation also weighed on results because of its exposure to the subprime mortgage loan crisis and weakness in global credit markets. Also, stock in Teradyne — which makes automatic test equipment for the semiconductor and telecommunications industries —fell as the market concluded that a slowing economy will mean lower demand for the firm’s products going forward. Lastly, RadioShack rounded out the major detractors as the company appears to be failing in its turnaround effort, and the stock declined steadily during the period. We eliminated the positions in Moody’s, Teradyne, and RadioShack prior to period-end.

Given the increasing negative sentiment regarding the economy and the continued troubles spawned by the subprime mortgage crisis, what is your outlook, Kevin? And how will it affect your positioning of Putnam Vista Fund?

Evidence is mounting that the U.S. economy is decelerating. Shortly after the period ended, the Institute for Supply Management (ISM) reported that its ISM index, which measures the activity in the economy’s service sector, had fallen to 41.9% . Readings below 50% indicate that most firms are contracting. What’s more, this was the first sub-50% measurement since

I N V E S T M E N T I N S I G H T

How has the U.S. stock market performed during recessions?

There has been no official declaration that the U.S. economy is in recession. In fact, recessions —defined as two consecutive quarters of negative GDP growth — are confirmed after they are under way. Still, it might be somewhat reassuring to investors to learn that the U.S. stock market, as measured by the broad Standard & Poor’s 500 Index, has performed comparatively well during past recessions. Starting right after World War II, the average performance of the S&P 500 during recessions has been almost exactly the same as its average performance during periods of economic expansion. During recessions, the average return was 12.1% and during expansions, the average return was 12.7% . The average postwar recession lasted 10 months, and by the time it got under way, the market had priced in the bad news. Historically, the market typically bottomed about halfway into the average postwar recession, followed by a median gain of 23% over the next six months.

11

March 2003. Additionally, there was no job growth in January. In fact, the Labor Department reported that employment actually declined by 17,000 jobs in January, which was the first decline since August 2003. And credit-card delinquencies are on the rise. All told, if employment levels continue to decline, the result could be a sharp pullback in consumer spending that would further weaken the economy.

Against this backdrop, we’re keeping the fund defensively positioned. We have increased the fund’s exposure to companies in the consumer staples sector. These companies, and their stocks, tend to hold up better in a slowing economy because they make products that consumers will continue to buy, such as food, beverages, and various household items. In addition, we currently plan to maintain the fund’s lower-than-benchmark weighting in financial company stocks. We believe many banks and brokerages still have a way to go to work through the problems that resulted from the subprime meltdown. We expect to see lower earnings and more layoffs as this corrective process is carried out. Lastly, given the slowing U.S. economy, we plan to add to the fund’s non-U.S. holdings by investing in companies that we believe have healthy business fundamentals in sectors and industry groups that we currently find most attractive, including materials, capital goods, and con sumer staples.

The views expressed in this report are exclusively those of Putnam Management. They are not meant as investment advice.

The fund invests some or all of its assets in small and/or midsize companies. Such investments increase the risk of fluctuations in the value of your investment. Stocks with above-average earnings growth may be more volatile, especially if earnings do not continue to grow.

Please note that the holdings discussed in this report may not have been held by the fund for the entire period. Portfolio composition is subject to review in accordance with the fund’s investment strategy and may vary in the future.

12

Your fund’s performance

This section shows your fund’s performance, price, and distribution information for periods ended January 31, 2008, the end of the first half of its current fiscal year. In accordance with regulatory requirements for mutual funds, we also include performance as of the most recent calendar quarter-end and expense information taken from the fund’s current prospectus. Performance should always be considered in light of a fund’s investment strategy. Data represents past performance. Past performance does not guarantee future results. More recent returns may be less or more than those shown. Investment return and principal value will fluctuate, and you may have a gain or a loss when you sell your shares. Performance information does not reflect any deduction for taxes a shareholder may owe on fund distributions or on the redemption of fund shares. For the most recent month-end performance, please visit the Individual Investors section of www.putnam.com or call Putnam at 1-800-225-1581. Class Y shares are generally only available to corporate and institutional clients and clients in other approved programs. See the Terms and Definitions section in this report for definitions of the share classes offered by your fund.

Fund performance

Total return for periods ended 1/31/08

| | | | | | | | | | |

| | Class A | | Class B | | Class C | | Class M | | Class R | Class Y |

| (inception dates) | (6/3/68) | | (3/1/93) | | (7/26/99) | | (12/8/94) | | (1/21/03) | (3/28/95) |

|

| | NAV | POP | NAV | CDSC | NAV | CDSC | NAV | POP | NAV | NAV |

| Annual average | | | | | | | | | | |

| (life of fund) | 9.39% | 9.22% | 8.41% | 8.41% | 8.56% | 8.56% | 8.68% | 8.59% | 9.12% | 9.48% |

|

| 10 years | 47.32 | 38.87 | 36.58 | 36.58 | 36.62 | 36.62 | 40.04 | 35.14 | 43.93 | 51.04 |

| Annual average | 3.95 | 3.34 | 3.17 | 3.17 | 3.17 | 3.17 | 3.42 | 3.06 | 3.71 | 4.21 |

|

| 5 years | 77.95 | 67.78 | 71.27 | 69.27 | 71.23 | 71.23 | 73.52 | 67.53 | 75.93 | 79.97 |

| Annual average | 12.22 | 10.90 | 11.36 | 11.10 | 11.36 | 11.36 | 11.65 | 10.87 | 11.96 | 12.47 |

|

| 3 years | 13.78 | 7.20 | 11.17 | 8.17 | 11.14 | 11.14 | 12.01 | 8.14 | 12.85 | 14.63 |

| Annual average | 4.40 | 2.34 | 3.59 | 2.65 | 3.58 | 3.58 | 3.85 | 2.64 | 4.11 | 4.66 |

|

| 1 year | –8.41 | –13.64 | –9.13 | –13.67 | –9.19 | –10.10 | –8.92 | –12.14 | –8.65 | –8.22 |

|

| 6 months | –8.72 | –14.00 | –9.13 | –13.67 | –9.11 | –10.02 | –9.01 | –12.22 | –8.89 | –8.60 |

|

Current performance may be lower or higher than the quoted past performance, which cannot guarantee future results. After sales charge returns (public offering price, or POP) for class A and M shares reflect a maximum 5.75% and 3.50% load, respectively, as of 1/2/08. Class B share returns reflect the applicable contingent deferred sales charge (CDSC), which is 5% in the first year, declining to 1% in the sixth year, and is eliminated thereafter. Class C shares reflect a 1% CDSC for the first year and is eliminated thereafter. Class R and Y shares have no initial sales charge or CDSC. Performance for class B, C, M, R, and Y shares before their inception is derived from the historical performance of class A shares, adjusted for the applicable sales charge (or CDSC) and, except for class Y shares, the higher operating expenses for such shares.

For a portion of the periods, this fund may have limited expenses, without which returns would have been lower.

A 1% short-term trading fee may be applied to shares exchanged or sold within 7 days of purchase.

13

Comparative index returns

For periods ended 1/31/08

| | |

| | | Lipper Mid-Cap |

| | Russell Midcap | Growth Funds |

| | Growth Index | category average† |

| Annual average | | |

| (life of fund) | —* | 9.14% |

|

| 10 years | 94.79% | 102.26 |

| Annual average | 6.89 | 6.82 |

|

| 5 years | 111.77 | 98.50 |

| Annual average | 16.19 | 14.53 |

|

| 3 years | 30.74 | 30.18 |

| Annual average | 9.34 | 9.06 |

|

| 1 year | –1.03 | 2.28 |

|

| 6 months | –5.45 | –4.74 |

|

Index and Lipper results should be compared to fund performance at net asset value.

* The inception date of the Russell Midcap Growth Index was December 31, 1985.

† Over the 6-month, 1-year, 3-year, 5-year, 10-year, and life-of-fund periods ended 1/31/08, there were 624, 604, 491, 407, 176, and 10 funds, respectively, in this Lipper category.

Fund price and distribution* information

For the six-month period ended 1/31/08

| | | | | | | | |

| | Class A | | Class B | Class C | Class M | | Class R | Class Y |

| Share value: | NAV | POP† | NAV | NAV | NAV | POP† | NAV | NAV |

|

| 7/31/07 | $11.58 | $12.29 | $9.97 | $10.87 | $10.66 | $11.05 | $11.47 | $12.09 |

|

| 1/31/08 | 10.57 | 11.21 | 9.06 | 9.88 | 9.70 | 10.05 | 10.45 | 11.05 |

|

The classification of distributions, if any, is an estimate. Final distribution information will appear on your year-end tax forms.

* The fund made no distributions during the period.

† Reflects an increase in sales charges that took effect on 1/2/08.

14

Fund performance as of most recent calendar quarter

Total return for periods ended 12/31/07

| | | | | | | | | | | |

| | Class A | | Class B | | Class C | | Class M | | Class R | Class Y |

| (inception dates) | (6/3/68) | | (3/1/93) | | (7/26/99) | | (12/8/94) | | (1/21/03) | (3/28/95) |

| | NAV | POP | NAV | CDSC | NAV | CDSC | NAV | POP | NAV | NAV |

|

| Annual average | | | | | | | | | | |

| (life of fund) | 9.68% | 9.52% | 8.70% | 8.70% | 8.86% | 8.86% | 8.98% | 8.88% | 9.41% | 9.77% |

|

| 10 years | 57.58 | 48.57 | 46.28 | 46.28 | 46.37 | 46.37 | 49.99 | 44.78 | 54.01 | 61.74 |

| Annual average | 4.65 | 4.04 | 3.88 | 3.88 | 3.88 | 3.88 | 4.14 | 3.77 | 4.41 | 4.93 |

|

| 5 years | 94.83 | 83.49 | 87.64 | 85.64 | 87.80 | 87.80 | 89.73 | 83.25 | 92.82 | 97.09 |

| Annual average | 14.27 | 12.91 | 13.41 | 13.17 | 13.43 | 13.43 | 13.67 | 12.88 | 14.03 | 14.53 |

|

| 3 years | 22.84 | 15.77 | 20.14 | 17.14 | 20.11 | 20.11 | 20.99 | 16.78 | 21.97 | 23.73 |

| Annual average | 7.10 | 5.00 | 6.31 | 5.41 | 6.30 | 6.30 | 6.56 | 5.31 | 6.84 | 7.36 |

|

| 1 year | 3.64 | –2.34 | 2.87 | –2.13 | 2.92 | 1.92 | 3.08 | –0.56 | 3.40 | 3.92 |

|

| 6 months | –2.91 | –8.47 | –3.28 | –8.12 | –3.19 | –4.16 | –3.16 | –6.54 | –3.02 | –2.79 |

|

Fund’s annual operating expenses

For the fiscal year ended 7/31/07

| | | | | | |

| | Class A | Class B | Class C | Class M | Class R | Class Y |

|

| Total annual fund | | | | | | |

| operating expenses | 1.11% | 1.86% | 1.86% | 1.61% | 1.36% | 0.86% |

|

Expense information in this table is taken from the most recent prospectus, is subject to change, and may differ from that shown in the next section and in the financial highlights of this report. Expenses are shown as a percentage of average net assets.

15

Your fund’s expenses

As a mutual fund investor, you pay ongoing expenses, such as management fees, distribution fees (12b-1 fees), and other expenses. In the most recent six-month period, your fund limited these expenses; had it not done so, expenses would have been higher. Using the information below, you can estimate how these expenses affect your investment and compare them with the expenses of other funds. You may also pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial representative.

Review your fund’s expenses

The table below shows the expenses you would have paid on a $1,000 investment in Putnam Vista Fund from August 1, 2007, to January 31, 2008. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

| | | | | | | |

| | Class A | Class B | Class C | Class M | Class R | Class Y |

|

| Expenses paid per $1,000* | $ 5.48 | $ 9.07 | $ 9.07 | $ 7.87 | $ 6.68 | $ 4.28 |

|

| Ending value (after expenses) | $912.80 | $908.70 | $908.90 | $909.90 | $911.10 | $914.00 |

|

* Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of average net assets for the six months ended 1/31/08. The expense ratio may differ for each share class (see the last table in this section). Expenses are calculated by multiplying the expense ratio by the average account value for the period; then multiplying the result by the number of days in the period; and then dividing that result by the number of days in the year.

Estimate the expenses you paid

To estimate the ongoing expenses you paid for the six months ended January 31, 2008, use the calculation method below. To find the value of your investment on August 1, 2007, call Putnam at 1-800-225-1581.

16

Compare expenses using the SEC’s method

The Securities and Exchange Commission (SEC) has established guidelines to help investors assess fund expenses. Per these guidelines, the table below shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total costs) of investing in the fund with those of other funds. All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

| | | | | | |

| | Class A | Class B | Class C | Class M | Class R | Class Y |

|

| Expenses paid per $1,000* | $ 5.79 | $ 9.58 | $ 9.58 | $ 8.31 | $ 7.05 | $ 4.52 |

|

| Ending value (after expenses) | $1,019.41 | $1,015.63 | $1,015.63 | $1,016.89 | $1,018.15 | $1,020.66 |

|

* Expenses for each share class are calculated using the fund’s annualized expense ratio for each class, which represents the ongoing expenses as a percentage of average net assets for the six months ended 1/31/08. The expense ratio may differ for each share class (see the last table in this section). Expenses are calculated by multiplying the expense ratio by the average account value for the period; then multiplying the result by the number of days in the period; and then dividing that result by the number of days in the year.

Compare expenses using industry averages

You can also compare your fund’s expenses with the average of its peer group, as defined by Lipper, an independent fund-rating agency that ranks funds relative to others that Lipper considers to have similar investment styles or objectives. The expense ratio for each share class shown below indicates how much of your fund’s average net assets have been used to pay ongoing expenses during the period.

| | | | | | |

| | Class A | Class B | Class C | Class M | Class R | Class Y |

|

| Your fund’s annualized | | | | | | |

| expense ratio | 1.14% | 1.89% | 1.89% | 1.64% | 1.39% | 0.89% |

|

| Average annualized expense | | | | | | |

| ratio for Lipper peer group* | 1.44% | 2.19% | 2.19% | 1.94% | 1.69% | 1.19% |

|

* Putnam is committed to keeping fund expenses below the Lipper peer group average expense ratio and will limit fund expenses if they exceed the Lipper average. The Lipper average is a simple average of front-end load funds in the peer group that excludes 12b-1 fees as well as any expense offset and brokerage service arrangements that may reduce fund expenses. To facilitate the comparison in this presentation, Putnam has adjusted the Lipper average to reflect the 12b-1 fees carried by each class of shares other than class Y shares, which do not incur 12b-1 fees. Investors should note that the other funds in the peer group may be significantly smaller or larger than the fund, and that an asset-weighted average would likely be lower than the simple average. Also, the fund and Lipper report expense data at different times and for different periods. The fund’s expense ratio shown here is annualized data for the most rec ent six-month period, while the quarterly updated Lipper average is based on the most recent fiscal year-end data available for the peer group funds as of 12/31/07.

17

Your fund’s

portfolio turnover

Putnam funds are actively managed by teams of experts who buy and sell securities based on intensive analysis of companies, industries, economies, and markets. Portfolio turnover is a measure of how often a fund’s managers buy and sell securities for your fund. A portfolio turnover of 100%, for example, means that the managers sold and replaced securities valued at 100% of a fund’s average portfolio value within a given period. Funds with high turnover may be more likely to generate capital gains that must be distributed to shareholders as taxable income. High turnover may also cause a fund to pay more brokerage commissions and other transaction costs, which may detract from performance.

Funds that invest in bonds or other fixed-income instruments may have higher turnover than funds that invest only in stocks. Short-term bond funds tend to have higher turnover than longer-term bond funds, because shorter-term bonds will mature or be sold more frequently than longer-term bonds. You can use the table below to compare your fund’s turnover with the average turnover for funds in its Lipper category.

Turnover comparisons

Percentage of holdings that change every year

| | | | | |

| | 2007 | 2006 | 2005 | 2004 | 2003 |

|

| Putnam Vista Fund | 111% | 111% | 74% | 78% | 65% |

|

| Lipper Mid-Cap Growth Funds | | | | | |

| category average | 108% | 110% | 115% | 130% | 140% |

|

Turnover data for the fund is calculated based on the fund’s fiscal-year period, which ends on July 31. Turnover data for the fund’s Lipper category is calculated based on the average of the turnover of each fund in the category for its fiscal year ended during the indicated year. Fiscal years vary across funds in the Lipper category, which may limit the comparability of the fund’s portfolio turnover rate to the Lipper average. Comparative data for 2007 is based on information available as of 12/31/07.

18

Your fund’s risk

This risk comparison is designed to help you understand how your fund compares with other funds. The comparison utilizes a risk measure developed by Morningstar, an independent fund-rating agency. This risk measure is referred to as the fund’s Morningstar Risk.

Your fund’s Morningstar® Risk

Your fund’s Morningstar Risk is shown alongside that of the average fund in its Morningstar category. The risk bar broadens the comparison by translating the fund’s Morningstar Risk into a percentile, which is based on the fund’s ranking among all funds rated by Morningstar as of December 31, 2007. A higher Morningstar Risk generally indicates that a fund’s monthly returns have varied more widely.

Morningstar determines a fund’s Morningstar Risk by assessing variations in the fund’s monthly returns — with an emphasis on downside variations — over a 3-year period, if available. Those measures are weighted and averaged to produce the fund’s Morningstar Risk. The information shown is provided for the fund’s class A shares only; information for other classes may vary. Morningstar Risk is based on historical data and does not indicate future results. Morningstar does not purport to measure the risk associated with a current investment in a fund, either on an absolute basis or on a relative basis. Low Morningstar Risk does not mean that you cannot lose money on an investment in a fund. Copyright 2007 Morningstar, Inc. All Rights Reserved. The information contained herein (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete, or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information.

19

Your fund’s management

Your fund is managed by the members of the Putnam Mid-Cap Growth Team. Kevin Divney and Raymond Haddad are the Portfolio Leaders and Brian DeChristopher is a Portfolio Member of your fund. The Portfolio Leaders and Portfolio Member coordinate the team’s management of the fund.

For a complete listing of the members of the Putnam Mid-Cap Growth Team, including those who are not Portfolio Leaders or Portfolio Members of your fund, visit Putnam’s Individual Investors Web site at www.putnam.com.

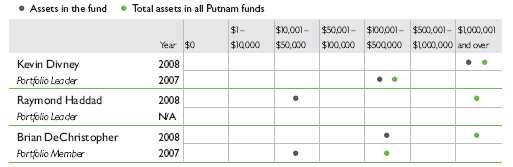

Investment team fund ownership

The table below shows how much the fund’s current Portfolio Leaders and Portfolio Member have invested in the fund and in all Putnam mutual funds (in dollar ranges). Information shown is as of January 31, 2008, and January 31, 2007.

N/A indicates the individual was not a Portfolio Leader or Portfolio Member as of 1/31/07.

Trustee and Putnam employee fund ownership

As of January 31, 2008, all of the Trustees of the Putnam funds owned fund shares. The table below shows the approximate value of investments in the fund and all Putnam funds as of that date by the Trustees and Putnam employees. These amounts include investments by the Trustees’ and employees’ immediate family members and investments through retirement and deferred compensation plans.

| | |

| | | Total assets in |

| | Assets in the fund | all Putnam funds |

|

| Trustees | $ 722,000 | $ 90,000,000 |

|

| Putnam employees | $12,118,000 | $669,000,000 |

|

20

Other Putnam funds managed by the Portfolio Leaders and Portfolio Member

Kevin Divney is also a Portfolio Leader of Putnam New Opportunities Fund.

Raymond Haddad is also a Portfolio Leader of Putnam New Opportunities Fund and Putnam OTC & Emerging Growth Fund, and a Portfolio Member of Putnam Discovery Growth Fund.

Brian DeChristopher is also a Portfolio Member of Putnam New Opportunities Fund.

Kevin Divney, Raymond Haddad, and Brian DeChristopher may also manage other accounts and variable trust funds advised by Putnam Management or an affiliate.

Changes in your fund’s Portfolio Leaders and Portfolio Member

During the reporting period ended January 31, 2008, Raymond Haddad became a Portfolio Leader of the fund.

Terms and definitions

Important terms

Total return shows how the value of the fund’s shares changed over time, assuming you held the shares through the entire period and reinvested all distributions in the fund.

Net asset value (NAV) is the price, or value, of one share of a mutual fund, without a sales charge. NAVs fluctuate with market conditions. NAV is calculated by dividing the net assets of each class of shares by the number of outstanding shares in the class.

Public offering price (POP) is the price of a mutual fund share plus the maximum sales charge levied at the time of purchase. POP performance figures shown here assume the 5.75% maximum sales charge for class A shares and 3.50% for class M shares.

Contingent deferred sales charge (CDSC) is generally a charge applied at the time of the redemption of class B or C shares and assumes redemption at the end of the period. Your fund’s class B CDSC declines from a 5% maximum during the first year to 1% during the sixth year. After the sixth year, the CDSC no longer applies. The CDSC for class C shares is 1% for one year after purchase.

21

Share classes

Class A shares are generally subject to an initial sales charge and no CDSC (except on certain redemptions of shares bought without an initial sales charge).

Class B shares are not subject to an initial sales charge. They may be subject to a CDSC.

Class C shares are not subject to an initial sales charge and are subject to a CDSC only if the shares are redeemed during the first year.

Class M shares have a lower initial sales charge and a higher 12b-1 fee than class A shares and no CDSC (except on certain redemptions of shares bought without an initial sales charge).

Class R shares are not subject to an initial sales charge or CDSC and are available only to certain defined contribution plans.

Class Y shares are not subject to an initial sales charge or CDSC, and carry no 12b-1 fee. They are generally only available to corporate and institutional clients and clients in other approved programs.

Comparative indexes

Lehman Aggregate Bond Index is an unmanaged index of U.S. investment-grade fixed-income securities.

Merrill Lynch 91-Day Treasury Bill Index is an unmanaged index that seeks to measure the performance of U.S. Treasury bills available in the marketplace.

Russell Midcap Growth Index is an unmanaged index of those companies in the Russell Midcap Index chosen for their growth orientation.

S&P 500 Index is an unmanaged index of common stock performance.

Indexes assume reinvestment of all distributions and do not account for fees. Securities and performance of a fund and an index will differ. You cannot invest directly in an index.

Lipper is a third-party industry-ranking entity that ranks mutual funds. Its rankings do not reflect sales charges. Lipper rankings are based on total return at net asset value relative to other funds that have similar current investment styles or objectives as determined by Lipper. Lipper may change a fund’s category assignment at its discretion. Lipper category averages reflect performance trends for funds within a category.

22

Trustee approval of

management contract

General conclusions

The Board of Trustees of the Putnam funds oversees the management of each fund and, as required by law, determines annually whether to approve the continuance of your fund’s management contract with Putnam Investment Management (“Putnam Management”). In this regard, the Board of Trustees, with the assistance of its Contract Committee consisting solely of Trustees who are not “interested persons” (as such term is defined in the Investment Company Act of 1940, as amended) of the Putnam funds (the “Independent Trustees”), requests and evaluates all information it deems reasonably necessary under the circumstances. Over the course of several months ending in June 2007, the Contract Committee met several times to consider the information provided by Putnam Management and other information developed with the assistance of the Board’s independent counsel and independent staff. The Contract Committee reviewed and discussed key aspects of this information with all of the Independent Trustees. The Contract Committee recommended, and the Independent Trustees approved, the continuance of your fund’s management contract, effective July 1, 2007.

In addition, in anticipation of the sale of Putnam Investments to Great-West Lifeco, at a series of meetings ending in March 2007, the Trustees reviewed and approved new management and distribution arrangements to take effect upon the change of control. Shareholders of all funds approved the management contracts in May 2007, and the change of control transaction was completed on August 3, 2007. Upon the change of control, the management contracts that were approved by the Trustees in June 2007 automatically terminated and were replaced by new contracts that had been approved by shareholders. In connection with their review for the June 2007 continuance of the Putnam funds’ management contracts, the Trustees did not identify any facts or circumstances that would alter the substance of the conclusions and recommendations they made in their review of the contracts to take effect upon the change of control.

The Independent Trustees’ approval was based on the following conclusions:

• That the fee schedule in effect for your fund represented reasonable compensation in light of the nature and quality of the services being provided to the fund, the fees paid by competitive funds and the costs incurred by Putnam Management in providing such services, and

• That this fee schedule represented an appropriate sharing between fund shareholders and Putnam Management of such economies of scale as may exist in the management of the fund at current asset levels.

These conclusions were based on a comprehensive consideration of all information provided to the Trustees and were not the result of any single factor. Some of the factors that figured particularly in the Trustees’ deliberations and how the Trustees considered these factors are described below, although individual Trustees may have evaluated the information presented differently, giving different weights to various factors. It is also important to recognize that the fee arrangements for your fund and the other Putnam funds are the result of many years of review and discussion between the Independent Trustees and Putnam Management, that certain aspects of

23

such arrangements may receive greater scrutiny in some years than others, and that the Trustees’ conclusions may be based, in part, on their consideration of these same arrangements in prior years.

Management fee schedules and categories; total expenses

The Trustees reviewed the management fee schedules in effect for all Putnam funds, including fee levels and breakpoints, and the assignment of funds to particular fee categories. In reviewing fees and expenses, the Trustees generally focused their attention on material changes in circumstances — for example, changes in a fund’s size or investment style, changes in Putnam Management’s operating costs or responsibilities, or changes in competitive practices in the mutual fund industry — that suggest that consideration of fee changes might be warranted. The Trustees concluded that the circumstances did not warrant changes to the management fee structure of your fund, which had been carefully developed over the years, re-examined on many occasions and adjusted where appropriate. The Trustees focused on two areas of particular interest, as discussed further below:

• Competitiveness. The Trustees reviewed comparative fee and expense information for competitive funds, which indicated that, in a custom peer group of competitive funds selected by Lipper Inc., your fund ranked in the 14th percentile in management fees and in the 10th percentile in total expenses (less any applicable 12b-1 fees) as of December 31, 2006 (the first percentile being the least expensive funds and the 100th percentile being the most expensive funds). (Because the fund’s custom peer group is smaller than the fund’s broad Lipper Inc. peer group, this expense information may differ from the Lipper peer expense information found elsewhere in this report.) The Trustees noted that expense ratios for a number of Putnam funds, which show the percentage of fund assets used to pay for management and administrative services, distribution (12b-1) fees and other expenses, had been increasing recently as a result of declining net assets and the natural operation of fee breakpoints.

The Trustees noted that the expense ratio increases described above were currently being controlled by expense limitations implemented in January 2004 and which Putnam Management had committed to maintain at least through 2007. In anticipation of the change of control of Putnam Investments, the Trustees requested, and received a commitment from Putnam Management and Great-West Lifeco, to extend this program through at least June 30, 2009. These expense limitations give effect to a commitment by Putnam Management that the expense ratio of each open-end fund would be no higher than the average expense ratio of the competitive funds included in the fund’s relevant Lipper universe (exclusive of any applicable 12b-1 charges in each case). The Trustees observed that this commitment to limit fund expenses has served shareholders well since its inception.

In order to ensure that the expenses of the Putnam funds continue to meet evolving competitive standards, the Trustees requested, and Putnam Management agreed, to extend for the twelve months beginning July 1, 2007, an additional expense limitation for certain funds at an

24

amount equal to the average expense ratio (exclusive of 12b-1 charges) of a custom peer group of competitive funds selected by Lipper to correspond to the size of the fund. This additional expense limitation will be applied to those open-end funds that had above-average expense ratios (exclusive of 12b-1 charges) based on the custom peer group data for the period ended December 31, 2006. This additional expense limitation will not be applied to your fund because it had a below-average expense ratio relative to its custom peer group.

• Economies of scale. Your fund currently has the benefit of breakpoints in its management fee that provide shareholders with significant economies of scale, which means that the effective management fee rate of a fund (as a percentage of fund assets) declines as a fund grows in size and crosses specified asset thresholds. Conversely, as a fund shrinks in size — as has been the case for many Putnam funds in recent years — these breakpoints result in increasing fee levels. In recent years, the Trustees have examined the operation of the existing breakpoint structure during periods of both growth and decline in asset levels. The Trustees concluded that the fee schedules in effect for the funds represented an appropriate sharing of economies of scale at current asset levels. In reaching this conclusion, the Trustees considered the Contract C ommittee’s stated intent to continue to work with Putnam Management to plan for an eventual resumption in the growth of assets, and to consider the potential economies that might be produced under various growth assumptions.

In connection with their review of the management fees and total expenses of the Putnam funds, the Trustees also reviewed the costs of the services to be provided and profits to be realized by Putnam Management and its affiliates from the relationship with the funds. This information included trends in revenues, expenses and profitability of Putnam Management and its affiliates relating to the investment management and distribution services provided to the funds. In this regard, the Trustees also reviewed an analysis of Putnam Management’s revenues, expenses and profitability with respect to the funds’ management contracts, allocated on a fund-by-fund basis.

Investment performance

The quality of the investment process provided by Putnam Management represented a major factor in the Trustees’ evaluation of the quality of services provided by Putnam Management under your fund’s management contract. The Trustees were assisted in their review of the Putnam funds’ investment process and performance by the work of the Investment Process Committee of the Trustees and the Investment Oversight Committees of the Trustees, which had met on a regular monthly basis with the funds’ portfolio teams throughout the year. The Trustees concluded that Putnam Management generally provides a high-quality investment process — as measured by the experience and skills of the individuals assigned to the management of fund portfolios, the resources made available to such personnel, and in general the ability of Putnam Management to attract and retain high-quality personnel — but also recognized that this does not guarantee favorable investm ent results for every fund in every time period. The Trustees considered the investment performance of each fund over multiple time

25

periods and considered information comparing each fund’s performance with various benchmarks and with the performance of competitive funds.

The Trustees noted the satisfactory investment performance of many Putnam funds. They also noted the disappointing investment performance of certain funds in recent years and discussed with senior management of Putnam Management the factors contributing to such underperfor-mance and actions being taken to improve performance. The Trustees recognized that, in recent years, Putnam Management has made significant changes in its investment personnel and processes and in the fund product line to address areas of underperformance. In particular, they noted the important contributions of Putnam Management’s leadership in attracting, retaining and supporting high-quality investment professionals and in systematically implementing an investment process that seeks to merge the best features of fundamental and quantitative analysis. The Trustees indicated their intention to continue to monitor performance trends to assess the effectiveness of these changes and to evaluate whether additional changes to address areas of underperformance are warranted.

In the case of your fund, the Trustees considered that your fund’s class A share cumulative total return performance at net asset value was in the following percentiles of its Lipper Inc. peer group (Lipper Mid-Cap Growth Funds) for the one-, three-, and five-year periods ended March 31, 2007 (the first percentile being the best-performing funds and the 100th percentile being the worst-performing funds):

| | |

| One-year period | Three-year period | Five-year period |

|

| 87th | 42nd | 61st |

(Because of the passage of time, these performance results may differ from the performance results for more recent periods shown elsewhere in this report. Over the one-, three-, and five-year periods ended March 31, 2007, there were 622, 497, and 394 funds, respectively, in your fund’s Lipper peer group.* Past performance is no guarantee of future returns.)

The Trustees noted the disappointing performance for your fund for the one-year period ended March 31, 2007. In this regard, the Trustees considered the efforts of the fund’s investment team in reviewing comprehensively the fund’s investment process.

As a general matter, the Trustees concluded that cooperative efforts between the Trustees and Putnam Management represent the most effective way to address investment performance problems. The Trustees noted that investors in the Putnam funds have, in effect, placed their trust in the Putnam organization, under the oversight of the funds’ Trustees, to make appropriate

* The percentile rankings for your fund’s class A share annualized total return performance in the Lipper Mid-Cap Growth Funds category for the one-, five-, and ten-year periods ended December 31, 2007, were 94%, 76%, and 81%, respectively. Over the one-, five-, and ten-year periods ended December 31, 2007, the fund ranked 564 out of 601, 305 out of 404, and 137 out of 170 funds, respectively. Note that this more recent information was not available when the Trustees approved the continuance of your fund’s management contract.

26

decisions regarding the management of the funds. Based on the responsiveness of Putnam Management in the recent past to Trustee concerns about investment performance, the Trustees concluded that it is preferable to seek change within Putnam Management to address performance shortcomings. In the Trustees’ view, the alternative of terminating a management contract and engaging a new investment adviser for an underperforming fund would entail significant disruptions and would not provide any greater assurance of improved investment performance.

Brokerage and soft-dollar allocations; other benefits

The Trustees considered various potential benefits that Putnam Management may receive in connection with the services it provides under the management contract with your fund. These include benefits related to brokerage and soft-dollar allocations, whereby a portion of the commissions paid by a fund for brokerage may be used to acquire research services that may be useful to Putnam Management in managing the assets of the fund and of other clients. The Trustees indicated their continued intent to monitor the potential benefits associated with the allocation of fund brokerage to ensure that the principle of seeking “best price and execution” remains paramount in the portfolio trading process.

The Trustees’ annual review of your fund’s management contract also included the review of its distributor’s contract and distribution plan with Putnam Retail Management Limited Partnership and the custodian agreement and investor servicing agreement with Putnam Fiduciary Trust Company (“PFTC”), each of which provides benefits to affiliates of Putnam Management. In the case of the custodian agreement, the Trustees considered that, effective January 1, 2007, the Putnam funds had engaged State Street Bank and Trust Company as custodian and began to transition the responsibility for providing custody services away from PFTC.

Comparison of retail and institutional fee schedules

The information examined by the Trustees as part of their annual contract review has included for many years information regarding fees charged by Putnam Management and its affiliates to institutional clients such as defined benefit pension plans, college endowments, etc. This information included comparison of such fees with fees charged to the funds, as well as a detailed assessment of the differences in the services provided to these two types of clients. The Trustees observed, in this regard, that the differences in fee rates between institutional clients and the funds are by no means uniform when examined by individual asset sectors, suggesting that differences in the pricing of investment management services to these types of clients reflect to a substantial degree historical competitive forces operating in separate market places. The Trustees considered the fact that fee rates across all asset sectors are higher on average for funds than for institutional clients, as well as the differences between the services that Putnam Management provides to the Putnam funds and those that it provides to institutional clients of the firm, but did not rely on such comparisons to any significant extent in concluding that the management fees paid by your fund are reasonable.

27

Other information

for shareholders

Important notice regarding delivery of shareholder documents

In accordance with SEC regulations, Putnam sends a single copy of annual and semiannual shareholder reports, prospectuses, and proxy statements to Putnam shareholders who share the same address, unless a shareholder requests otherwise. If you prefer to receive your own copy of these documents, please call Putnam at 1-800-225-1581, and Putnam will begin sending individual copies within 30 days.

Proxy voting

Putnam is committed to managing our mutual funds in the best interests of our shareholders. The Putnam funds’ proxy voting guidelines and procedures, as well as information regarding how your fund voted proxies relating to portfolio securities during the 12-month period ended June 30, 2007, are available on the Putnam Individual Investor Web site, www.putnam.com/individual, and on the SEC’s Web site, www.sec.gov. If you have questions about finding forms on the SEC’s Web site, you may call the SEC at 1-800-SEC-0330. You may also obtain the Putnam funds’ proxy voting guidelines and procedures at no charge by calling Putnam’s Shareholder Services at 1-800-225-1581.

Fund portfolio holdings

The fund will file a complete schedule of its portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. Shareholders may obtain the fund’s Forms N-Q on the SEC’s Web site at www.sec.gov. In addition, the fund’s Forms N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C. You may call the SEC at 1-800-SEC-0330 for information about the SEC’s Web site or the operation of the Public Reference Room.

28

Financial statements

A guide to financial statements

These sections of the report, as well as the accompanying Notes, constitute the fund’s financial statements.

The fund’s portfolio lists all the fund’s investments and their values as of the last day of the reporting period. Holdings are organized by asset type and industry sector, country, or state to show areas of concentration and diversification.

Statement of assets and liabilities shows how the fund’s net assets and share price are determined. All investment and noninvestment assets are added together. Any unpaid expenses and other liabilities are subtracted from this total. The result is divided by the number of shares to determine the net asset value per share, which is calculated separately for each class of shares. (For funds with preferred shares, the amount subtracted from total assets includes the liquidation preference of preferred shares.)

Statement of operations shows the fund’s net investment gain or loss. This is done by first adding up all the fund’s earnings — from dividends and interest income — and subtracting its operating expenses to determine net investment income (or loss). Then, any net gain or loss the fund realized on the sales of its holdings — as well as any unrealized gains or losses over the period — is added to or subtracted from the net investment result to determine the fund’s net gain or loss for the fiscal period.

Statement of changes in net assets shows how the fund’s net assets were affected by the fund’s net investment gain or loss, by distributions to shareholders, and by changes in the number of the fund’s shares. It lists distributions and their sources (net investment income or realized capital gains) over the current reporting period and the most recent fiscal year-end. The distributions listed here may not match the sources listed in the Statement of operations because the distributions are determined on a tax basis and may be paid in a different period from the one in which they were earned. Dividend sources are estimated at the time of declaration. Actual results may vary. Any non-taxable return of capital cannot be determined until final tax calculations are completed after the end of the fund’s fiscal year.

Financial highlights provide an overview of the fund’s investment results, per-share distributions, expense ratios, net investment income ratios, and portfolio turnover in one summary table, reflecting the five most recent reporting periods. In a semiannual report, the highlight table also includes the current reporting period.

29

The fund’s portfolio 1/31/08 (Unaudited)

| | | |

| COMMON STOCKS (98.7%)* | | | |

|

| | Shares | | Value |

|

| Aerospace and Defense (4.0%) | | | |

| Alliant Techsystems, Inc. † (S) | 102,200 | $ | 10,817,870 |

| Goodrich Corp. | 161,700 | | 10,114,335 |

| L-3 Communications Holdings, Inc. | 233,428 | | 25,870,825 |

| Precision Castparts Corp. | 156,600 | | 17,821,080 |

| | | | 64,624,110 |

|

| |

| Automotive (0.8%) | | | |

| AutoZone, Inc. † | 100,800 | | 12,184,704 |

|

| |

| Basic Materials (0.3%) | | | |

| Ceradyne, Inc. † | 98,270 | | 4,731,701 |

|

| |

| Biotechnology (2.2%) | | | |

| Applera Corp. — Applied Biosystems Group | 427,300 | | 13,472,769 |

| Genzyme Corp. † (S) | 288,500 | | 22,540,505 |

| | | | 36,013,274 |

|

| |

| Broadcasting (0.9%) | | | |

| Discovery Holding Co. Class A † | 653,900 | | 15,183,558 |

|

| |

| Building Materials (0.6%) | | | |

| Sherwin-Williams Co. (The) (S) | 158,800 | | 9,084,948 |

|

| |

| Cable Television (1.6%) | | | |

| DISH Network Corp. Class A † | 279,000 | | 7,878,960 |

| Liberty Global, Inc. Class A † (S) | 463,500 | | 18,730,035 |

| | | | 26,608,995 |

|

| |

| Chemicals (5.1%) | | | |

| Albemarle Corp. (S) | 589,100 | | 21,360,766 |

| Celanese Corp. Ser. A | 322,900 | | 12,005,422 |

| CF Industries Holdings, Inc. (S) | 199,700 | | 21,353,921 |

| Mosaic Co. (The) † (S) | 189,800 | | 17,273,698 |

| Sigma-Adrich Corp. | 222,300 | | 11,039,418 |

| | | | 83,033,225 |

|

| |

| Coal (0.9%) | | | |

| Massey Energy Co. (S) | 396,725 | | 14,750,236 |

|

| |

| Commercial and Consumer Services (2.7%) | | | |

| Dun & Bradstreet Corp. (The) | 214,700 | | 19,748,106 |

| Equifax, Inc. | 425,800 | | 15,792,922 |

| Paychex, Inc. (S) | 262,800 | | 8,598,816 |

| | | | 44,139,844 |

30

| | | |

| COMMON STOCKS (98.7%)* continued | | | |

|

| | Shares | | Value |

|

| Communications Equipment (2.2%) | | | |

| F5 Networks, Inc. † | 550,200 | $ | 12,946,206 |

| Harris Corp. | 260,800 | | 14,263,152 |

| Juniper Networks, Inc. † (S) | 303,900 | | 8,250,885 |

| | | | 35,460,243 |

|

| |

| Computers (2.1%) | | | |

| NCR Corp. † | 721,800 | | 15,504,264 |

| Seagate Technology (Cayman Islands) | 341,000 | | 6,912,070 |

| Teradata Corp. † | 497,349 | | 11,846,853 |

| | | | 34,263,187 |

|

| |

| Conglomerates (0.8%) | | | |

| Textron, Inc. | 237,200 | | 13,295,060 |

|

| |

| Consumer Finance (1.0%) | | | |

| Mastercard, Inc. Class A | 77,100 | | 15,959,700 |

|

| |

| Consumer Goods (1.6%) | | | |

| Clorox Co. (S) | 174,997 | | 10,730,816 |

| Newell Rubbermaid, Inc. | 605,300 | | 14,599,836 |

| | | | 25,330,652 |

|

| |

| Electric Utilities (1.0%) | | | |

| Edison International (S) | 310,200 | | 16,180,032 |

|

| |

| Electronics (6.8%) | | | |

| Agilent Technologies, Inc. † (S) | 403,400 | | 13,679,294 |

| Altera Corp. | 909,700 | | 15,364,833 |

| Amphenol Corp. Class A | 460,100 | | 18,376,394 |

| Avnet, Inc. † (S) | 324,700 | | 11,562,567 |

| International Rectifier Corp. † (S) | 140,500 | | 3,910,115 |

| MEMC Electronic Materials, Inc. † | 120,200 | | 8,589,492 |

| NVIDIA Corp. † (S) | 929,050 | | 22,845,340 |

| SanDisk Corp. † (S) | 248,100 | | 6,314,145 |

| Trimble Navigation, Ltd. † | 374,800 | | 9,913,460 |

| | | | 110,555,640 |

|

| |

| Energy (6.0%) | | | |

| Cameron International Corp. † (S) | 689,800 | | 27,771,348 |

| Global Industries, Ltd. † | 306,703 | | 5,416,375 |

| National-Oilwell Varco, Inc. † (S) | 269,600 | | 16,238,008 |

| Noble Corp. | 526,200 | | 23,031,774 |

| Smith International, Inc. | 306,500 | | 16,615,365 |

| Weatherford International, Ltd. † (S) | 154,700 | | 9,562,007 |

| | | | 98,634,877 |

|

| |

| Energy (Other) (1.5%) | | | |

| Compagnie Generale de Geophysique-Veritas SA ADR | | | |

| (France) † | 249,300 | | 11,637,324 |

| First Solar, Inc. † (S) | 8,900 | | 1,617,753 |

31

| | | |

| COMMON STOCKS (98.7%)* continued | | | |

|

| | Shares | | Value |

|

| Energy (Other) continued | | | |

| JA Solar Holdings Co., Ltd. ADR (China) † | 71,800 | $ | 3,649,594 |

| Suntech Power Holdings Co., Ltd. ADR (China) † (S) | 136,700 | | 7,481,591 |

| | | | 24,386,262 |

|

| |

| Engineering & Construction (2.7%) | | | |

| Fluor Corp. (S) | 154,200 | | 18,761,514 |

| McDermott International, Inc. † | 529,100 | | 24,962,938 |

| | | | 43,724,452 |

|

| |

| Environmental (0.9%) | | | |

| Foster Wheeler, Ltd. † | 225,200 | | 15,419,444 |

|

| |

| Financial (2.5%) | | | |

| Assurant, Inc. | 198,600 | | 12,887,154 |

| Intercontinental Exchange, Inc. † | 127,400 | | 17,830,904 |

| Nymex Holdings, Inc. (S) | 89,100 | | 10,246,500 |

| | | | 40,964,558 |

|

| |

| Health Care Services (7.2%) | | | |

| AMERIGROUP Corp. † (S) | 356,375 | | 13,371,190 |

| Charles River Laboratories International, Inc. † (S) | 229,400 | | 14,245,740 |

| Coventry Health Care, Inc. † | 321,200 | | 18,173,496 |

| Health Net, Inc. † | 254,600 | | 11,836,354 |

| Henry Schein, Inc. † (S) | 172,000 | | 9,998,360 |

| Humana, Inc. † (S) | 218,580 | | 17,551,974 |

| Laboratory Corp. of America Holdings † (S) | 298,600 | | 22,060,568 |

| Lincare Holdings, Inc. † (S) | 248,600 | | 8,305,726 |

| Pediatrix Medical Group, Inc. † | 31,800 | | 2,165,262 |

| | | | 117,708,670 |

|

| |

| Investment Banking/Brokerage (2.3%) | | | |

| Affiliated Managers Group † | 105,800 | | 10,401,198 |

| BlackRock, Inc. | 49,100 | | 10,856,010 |

| MF Global, Ltd. (Bermuda) † | 315,200 | | 9,471,760 |

| T. Rowe Price Group, Inc. | 149,700 | | 7,573,323 |

| | | | 38,302,291 |

|

| |

| Lodging/Tourism (0.4%) | | | |

| Choice Hotels International, Inc. | 194,992 | | 6,512,733 |

|

| |

| Machinery (1.4%) | | | |

| AGCO Corp. † (S) | 369,100 | | 22,227,202 |

|

| |

| Manufacturing (2.2%) | | | |

| Cooper Industries, Ltd. Class A (S) | 187,000 | | 8,328,980 |

| ITT Corp. | 145,400 | | 8,641,122 |

| Roper Industries, Inc. | 94,100 | | 5,262,072 |

| Teleflex, Inc. | 97,100 | | 5,740,552 |

| Thomas & Betts Corp. † | 185,000 | | 8,371,250 |

| | | | 36,343,976 |

32

| | | |

| COMMON STOCKS (98.7%)* continued | | | |

|

| | Shares | | Value |

|

| Medical Technology (5.5%) | | | |

| C.R. Bard, Inc. (S) | 239,300 | $ | 23,109,201 |

| DENTSPLY International, Inc. | 356,100 | | 14,710,491 |

| Edwards Lifesciences Corp. † | 147,800 | | 6,838,706 |

| Hologic, Inc. † | 131,600 | | 8,469,776 |

| Kinetic Concepts, Inc. † (S) | 261,176 | | 13,001,341 |

| Varian Medical Systems, Inc. † | 179,100 | | 9,311,409 |

| Waters Corp. † | 260,200 | | 14,948,490 |

| | | | 90,389,414 |

|

| |

| Metals (4.7%) | | | |

| Cleveland-Cliffs, Inc. (S) | 129,861 | | 13,225,044 |

| Kinross Gold Corp. (Canada) † | 444,700 | | 9,841,211 |

| Market Vectors Gold Miners ETF (Exchange-traded fund) | 336,200 | | 16,927,670 |

| United States Steel Corp. | 208,000 | | 21,238,880 |

| Yamana Gold, Inc. (Canada) | 978,000 | | 16,117,440 |

| | | | 77,350,245 |

|

| |

| Natural Gas Utilities (1.2%) | | | |

| ONEOK, Inc. | 178,800 | | 8,403,600 |

| Sempra Energy | 40,800 | | 2,280,720 |

| Williams Cos., Inc. (The) | 291,500 | | 9,319,255 |

| | | | 20,003,575 |

|

| |

| Oil & Gas (5.8%) | | | |

| Chesapeake Energy Corp. (S) | 391,700 | | 14,582,991 |

| Frontier Oil Corp. | 532,900 | | 18,795,383 |

| Holly Corp. | 192,500 | | 9,320,850 |

| Noble Energy, Inc. | 245,100 | | 17,789,358 |

| Southwestern Energy Co. † | 242,200 | | 13,541,402 |

| Tesoro Corp. (S) | 341,200 | | 13,323,860 |

| Ultra Petroleum Corp. † | 99,500 | | 6,845,600 |

| | | | 94,199,444 |

|

| |

| Pharmaceuticals (2.9%) | | | |

| Cephalon, Inc. † | 182,100 | | 11,951,223 |

| Endo Pharmaceuticals Holdings, Inc. † | 224,599 | | 5,871,018 |

| Sepracor, Inc. † (S) | 402,100 | | 11,355,304 |

| Watson Pharmaceuticals, Inc. † | 685,200 | | 17,890,572 |

| | | | 47,068,117 |

|

| |

| Power Producers (0.5%) | | | |

| AES Corp. (The) † | 221,000 | | 4,216,680 |

| Reliant Resources, Inc. † (S) | 151,300 | | 3,218,151 |

| | | | 7,434,831 |

|

| |

| Restaurants (1.6%) | | | |

| Darden Restaurants, Inc. | 373,000 | | 10,563,360 |

| Yum! Brands, Inc. | 457,700 | | 15,635,032 |

| | | | 26,198,392 |

33

| | | |

| COMMON STOCKS (98.7%)* continued | | | |

|

| | Shares | | Value |

|

| Retail (2.6%) | | | |

| Aeropostale, Inc. † (S) | 311,050 | $ | 8,762,279 |

| BJ’s Wholesale Club, Inc. † | 300,900 | | 9,761,196 |

| Herbalife, Ltd. (Cayman Islands) (S) | 288,700 | | 11,455,616 |

| TJX Cos., Inc. (The) (S) | 389,000 | | 12,276,840 |

| | | | 42,255,931 |

|

| |

| Schools (2.0%) | | | |

| Apollo Group, Inc. Class A † | 170,300 | | 13,579,722 |

| ITT Educational Services, Inc. † | 206,711 | | 18,883,050 |

| | | | 32,462,772 |

|

| |

| Semiconductor (0.8%) | | | |

| Linear Technology Corp. (S) | 464,800 | | 12,861,016 |

|

| |

| Shipping (0.6%) | | | |

| Overseas Shipholding Group (S) | 149,500 | | 9,750,390 |

|

| |

| Software (3.6%) | | | |

| Autodesk, Inc. † | 679,300 | | 27,953,195 |

| BMC Software, Inc. † # | 522,762 | | 16,749,294 |

| Cadence Design Systems, Inc. † (S) | 233,700 | | 2,372,055 |

| Red Hat, Inc. † (S) | 630,500 | | 11,777,740 |

| | | | 58,852,284 |

|

| |

| Technology Services (0.8%) | | | |

| Fiserv, Inc. † | 250,400 | | 12,863,048 |

|

| |

| Telecommunications (1.8%) | | | |

| Crown Castle International Corp. † (S) | 443,300 | | 16,043,027 |

| NeuStar, Inc. Class A † (S) | 437,300 | | 12,992,183 |

| | | | 29,035,210 |

|

| |

| Telephone (0.6%) | | | |

| Telephone and Data Systems, Inc. | 194,800 | | 10,273,752 |

|

| |

| Tobacco (1.2%) | | | |

| Loews Corp. — Carolina Group | 242,500 | | 19,916,525 |

|

| |

| Waste Management (0.8%) | | | |

| Republic Services, Inc. | 91,100 | | 2,733,000 |

| Stericycle, Inc. † | 163,700 | | 9,700,861 |

| | | | 12,433,861 |

|

| |

| Total common stocks (cost $1,672,037,945) | | $ | 1,608,972,381 |

| | |

| | | | | |

| WARRANTS (0.5%)* † (cost $8,227,399) | | | | |

|

| | Expiration date | Strike Price | Warrants | | Value |

| Genting Berhad 144A (Malaysia) | 1/20/10 | — | 3,594,257 | $ | 8,113,316 |

34

| | | |

| SHORT-TERM INVESTMENTS (21.6%)* | | | |

|

| | Principal amount/shares | | Value |

|

| Putnam Prime Money Market Fund (e) | 25,916,652 | $ | 25,916,652 |

| Short-term investments held as collateral for loaned | | | |

| securities with yields ranging from 2.60% to 5.25% | | | |

| and due dates ranging from February 1, 2008 | | | |

| to March 24, 2008 (d) | $326,269,086 | | 325,798,620 |

|

| Total short-term investments (cost $351,715,272) | | $ | 351,715,272 |

|

| TOTAL INVESTMENTS | | | |

|

| Total investments (cost $2,031,980,616) | | $ | 1,968,800,969 |

* Percentages indicated are based on net assets of $1,630,757,570.

† Non-income-producing security.

# A portion of this security was pledged and segregated with the custodian to cover margin requirements for futures contracts at January 31, 2008.

(d) See Note 1 to the financial statements.

(e) See Note 5 to the financial statements regarding investments in Putnam Prime Money Market Fund.

(S) Securities on loan, in part or in entirety, at January 31, 2008.

At January 31, 2008, liquid assets totaling $8,113,316 have been designated as collateral for open forward commitments.

144A after the name of an issuer represents securities exempt from registration under Rule 144A under the Securities Act of 1933, as amended. These securities may be resold in transactions exempt from registration, normally to qualified institutional buyers.

ADR after the name of a foreign holding stands for American Depository Receipts, representing ownership of foreign securities on deposit with a custodian bank.

| | | | | |

| FUTURES CONTRACTS OUTSTANDING at 1/31/08 (Unaudited) | | | | |

|

| | | | | | Unrealized |

| | Number of | | | Expiration | appreciation/ |

| | contracts | Value | | date | (depreciation) |

|

| NASDAQ 100 Index E-Mini (Long) | 22 | $813,010 | | Mar-08 | $(37,444) |

| Russell 2000 Index Mini (Long) | 26 | 1,859,000 | | Mar-08 | 14,768 |

| S&P 500 Index (Long) | 4 | 1,379,600 | | Mar-08 | (42,115) |

| S&P Mid Cap 400 Index E-Mini (Long) | 17 | 1,370,880 | | Mar-08 | 6,936 |

|

| Total | | | | | $(57,855) |

The accompanying notes are an integral part of these financial statements.

35

Statement of assets and liabilities 1/31/08 (Unaudited)

| |

| ASSETS | |

|

| Investment in securities, at value, including $317,267,058 | |

| of securities on loan (Note 1): | |

| Unaffiliated issuers (identified cost $2,006,063,964) | $ 1,942,884,317 |

| Affiliated issuers (identified cost $25,916,652) (Note 5) | 25,916,652 |

|

| Cash | 4,110,931 |

|

| Dividends, interest and other receivables | 1,384,749 |

|

| Receivable for shares of the fund sold | 1,150,276 |

|

| Receivable for securities sold | 6,932,824 |

|

| Receivable for variation margin (Note 1) | 141,810 |

|

| Total assets | 1,982,521,559 |

|

| |

| LIABILITIES | |

|

| Payable for securities purchased | 15,508,470 |

|

| Payable for shares of the fund repurchased | 6,240,636 |

|

| Payable for compensation of Manager (Notes 2 and 5) | 2,519,293 |

|

| Payable for investor servicing (Note 2) | 427,897 |

|

| Payable for custodian fees (Note 2) | 28,828 |