National Medical Health Card Systems (NMHC) Inactive

Filed: 19 Feb 04, 12:00am

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of

the Securities Exchange Act of 1934 (Amendment No. 3)

| Filed by the Registrantý | ||

Filed by a Party other than the Registranto | ||

Check the appropriate box: | ||

o | Preliminary Proxy Statement | |

o | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |

ý | Definitive Proxy Statement | |

o | Definitive Additional Materials | |

o | Soliciting Material Under Rule 14a-12 | |

National Medical Health Card Systems, Inc. | ||||

(Name of Registrant as Specified In Its Charter) | ||||

(Name of Person(s) Filing Proxy Statement, if Other Than the Registrant) | ||||

| Payment of Filing Fee (Check the appropriate box): | ||||

ý | No fee required | |||

o | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | |||

(1) | Title of each class of securities to which transaction applies: | |||

| (2) | Aggregate number of securities to which transaction applies: | |||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): | |||

| (4) | Proposed maximum aggregate value of transaction: | |||

| (5) | Total fee paid: | |||

o | Fee paid previously with preliminary materials: | |||

o | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the form or schedule and the date of its filing. | |||

(1) | Amount previously paid: | |||

| (2) | Form, Schedule or Registration Statement No.: | |||

| (3) | Filing Party: | |||

| (4) | Date Filed: | |||

NATIONAL MEDICAL HEALTH CARD SYSTEMS, INC.

26 HARBOR PARK DRIVE

PORT WASHINGTON, NEW YORK 11050

To our Stockholders:

We are writing to inform you of an important event in the development and growth of our company. On October 30, 2003, New Mountain Partners, L.P. agreed to invest approximately $80 million in National Medical Health Card Systems, Inc. The investment, which will be in the form of a new class of series A convertible preferred stock, is subject to various conditions described in the accompanying proxy statement. We intend to use approximately $50 million of the investment to complete a tender offer for up to 4,545,455 shares of our common stock at a price of $11.00 per share.

The contemplated transactions have the unanimous support of our board of directors. Our board of directors has determined that the issuance of the series A convertible preferred stock and the completion of the tender offer are advisable to, and in the best interests of, our company.

At the annual meeting you will be asked to:

Our board of directors recommends that all stockholders vote "FOR" the approval of the matters on which you are being asked to vote.

The accompanying proxy statement explains the contemplated transactions and other matters and provides specific information concerning the annual meeting. Please read these materials carefully.

We are extremely pleased with our new relationship with New Mountain Partners, L.P., a private equity fund managed by New Mountain Capital, LLC. The contemplated transactions address important issues facing our company today, including the need for new capital to accelerate growth.

Your vote is important. We will not complete the contemplated transactions under our purchase agreement with New Mountain Partners, L.P. unless the conditions to the closing of the contemplated transactions are satisfied or waived, including the approval of the issuance of the series A preferred stock and the amendment to our certificate of incorporation.

We believe this is a very important step forward for our company. As always, we thank you for your continuing support. We look forward to seeing you at the annual meeting of stockholders at our executive offices located at 26 Harbor Park Drive, Port Washington, New York, on March 18, 2004, at 9:30 a.m., local time.

| | | | ||

|---|---|---|---|---|

| Sincerely, | ||||

| ||||

| James J. Bigl President and Chief Executive Officer |

February 19, 2004

The accompanying proxy statement is dated February 19, 2004 and is first being mailed to stockholders on or about February 19, 2004.

NATIONAL MEDICAL HEALTH CARD SYSTEMS, INC.

26 HARBOR PARK DRIVE

PORT WASHINGTON, NEW YORK 11050

NOTICE OF ANNUAL MEETING OF STOCKHOLDERS

TO BE HELD ON MARCH 18, 2004

To the Stockholders of

National Medical Health Card Systems, Inc.:

NOTICE IS HEREBY GIVEN that an Annual Meeting of Stockholders ofNATIONAL MEDICAL HEALTH CARD SYSTEMS, INC., a Delaware corporation, will be held at our executive offices located at 26 Harbor Park Drive, Port Washington, New York, on March 18, 2004, at 9:30 a.m., local time, for the following purposes:

which amendments will be implemented only if the contemplated transactions with New Mountain Partners, L.P. ("New Mountain Partners") are consummated.

We direct your attention to the accompanying proxy statement, which more fully describes the foregoing proposals.

Our board of directors believes that the contemplated transactions involving New Mountain Partners are in our best interests and unanimously recommends that you vote "FOR" the sale of the series A preferred stock and the amendment to our certificate of incorporation. Our board of directors also unanimously recommends that you vote "FOR" the election of each of our nominees for Class II director and the approval of the amendment to the Plan.

Our board of directors has fixed the close of business on February 6, 2004 as the record date for determining stockholders entitled to notice of and to vote at the annual meeting or any adjournments or postponements of the annual meeting. A list of stockholders entitled to vote at the annual meeting will be available for examination at our headquarters, during ordinary business hours, from the date of the proxy statement until the annual meeting. Information concerning the matters to be acted upon at the meeting is set forth in the accompanying proxy statement.

Whether or not you expect to attend the annual meeting, we urge you to complete, date and sign the enclosed proxy card and mail it promptly in the enclosed return envelope. Even if you have given your proxy, you may still vote in person if you attend the annual meeting. However, if your shares are held of record by a broker, bank or other nominee and you wish to vote at the annual meeting, you must obtain from the record holder a proxy issued in your name.

By order of the National Medical Health Card Systems, Inc. Board of Directors,

| | | | ||

|---|---|---|---|---|

| ||||

| Gerald Shapiro Secretary |

Port Washington, New York

February 19, 2004

NATIONAL MEDICAL HEALTH CARD SYSTEMS, INC.

PROXY STATEMENT

| | Page | ||

|---|---|---|---|

| SUMMARY | 1 | ||

| Information About National Medical Health Card Systems, Inc | 1 | ||

| Information About the Annual Meeting of the Stockholders | 1 | ||

| Information About this Proxy Statement | 1 | ||

| Information About Voting | 2 | ||

| Board Recommendation | 2 | ||

| Quorum and Voting Requirements | 2 | ||

| Interests of Management and Directors in the Contemplated Transactions | 3 | ||

| Cost and Method of Soliciting Proxies | 5 | ||

| Opinion of the Financial Advisor to the Special Committee of Our Board of Directors | 5 | ||

| Regulatory Approvals | 5 | ||

| Other Matters | 5 | ||

| SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT | 6 | ||

| PROPOSAL 1—APPROVAL OF THE ISSUANCE AND SALE OF OUR SERIES A PREFERRED STOCK | 8 | ||

| Summary of the Contemplated Transactions | 8 | ||

| Background of the Contemplated Transactions | 9 | ||

| Reasons for the Contemplated Transactions; Recommendation of the Special Committee and Our Board of Directors | 13 | ||

| Impact of the Issuance and Sale of the Series A Preferred Stock on Our Existing Stockholders | 16 | ||

| Opinion of Southwest Securities, Inc. | 17 | ||

| Summary of Southwest Securities' Valuation Approach | 19 | ||

| Certain Financial Projections | 24 | ||

| Reason for Request for Approval | 25 | ||

| Interests of Management and Directors in the Contemplated Transactions | 26 | ||

| Composition of our Board of Directors Following the Contemplated Transactions | 29 | ||

| Terms of the Purchase Agreement | 30 | ||

| Terms of the Series A Preferred Stock | 40 | ||

| Corporate Governance | 43 | ||

| Terms of the Support Agreement | 45 | ||

| Terms of the Registration Rights Agreement | 49 | ||

| Other Terms of the Contemplated Transactions | 51 | ||

| No Appraisal Rights | 52 | ||

| Delaware Anti-Takeover Law and Certain Provisions of Our Certificate of Incorporation | 52 | ||

| Required Vote | 52 | ||

| Recommendation of Our Board of Directors | 52 | ||

| UNAUDITED PRO FORMA CONDENSED CONSOLIDATED FINANCIAL INFORMATION | 53 | ||

i

| PROPOSAL 2—AMENDMENTS TO OUR CERTIFICATE OF INCORPORATION | 58 | ||

| Our Current Preferred Stock | 58 | ||

| Purpose and Effect of the Amendments | 58 | ||

| Potential Effects of the Proposed Amendments to the Certificate of Incorporation on Holders of Our Common Stock | 59 | ||

| Implementing the Proposed Amendments to Our Certificate of Incorporation | 60 | ||

| No Appraisal Rights | 61 | ||

| Required Vote | 61 | ||

| Recommendation of Our Board of Directors | 61 | ||

| PROPOSAL 3—ELECTION OF CLASS II DIRECTORS | 62 | ||

| Nomination of Class II Directors | 62 | ||

| Incumbent Directors | 63 | ||

| Required Vote | 64 | ||

| Recommendation of Our Board of Directors | 64 | ||

| Executive Officers | 64 | ||

| Familial Relationships | �� | 65 | |

| Compensation of Directors | 65 | ||

| Meetings and Committees of Our Board of Directors | 65 | ||

| The Audit Committee | 66 | ||

| The Compensation Committee | 66 | ||

| AUDIT COMMITTEE REPORT | 66 | ||

| COMPENSATION COMMITTEE'S REPORT ON EXECUTIVE COMPENSATION | 68 | ||

| SUMMARY COMPENSATION TABLE | 70 | ||

| Option Grants in Last Fiscal Year Table | 73 | ||

| Aggregated Option Exercises in Last Fiscal Year and Fiscal Year-End Option Value Table | 73 | ||

| Employee Contracts, Termination of Employment and Change-in-Control Arrangements | 73 | ||

| Legal Proceedings | 78 | ||

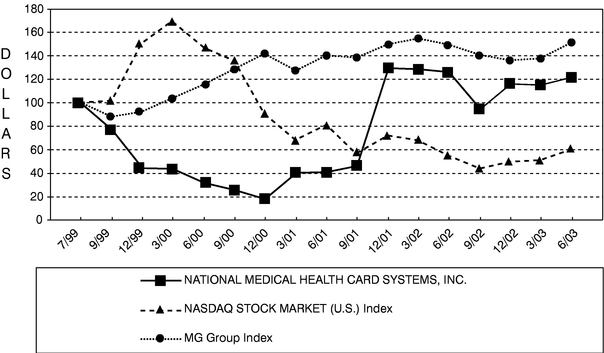

| COMPARATIVE STOCK PERFORMANCE | 79 | ||

| CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS | 80 | ||

| PROPOSAL 4—APPROVAL OF AMENDMENT TO OUR 1999 STOCK OPTION PLAN | 83 | ||

| Summary of the Plan | 83 | ||

| Amended Plan Benefits | 85 | ||

| Equity Compensation Plan Information | 86 | ||

| United States Federal Income Tax Consequences | 87 | ||

| Required Vote | 87 | ||

| Recommendation of Our Board of Directors | 87 | ||

| RELATIONSHIP WITH INDEPENDENT AUDITORS | 88 | ||

| Audit Fees | 88 | ||

| All Other Fees | 88 | ||

| CAUTIONARY STATEMENT CONCERNING FORWARD-LOOKING STATEMENTS | 88 | ||

| DEADLINE FOR RECEIPT OF STOCKHOLDER PROPOSALS | 89 | ||

| SECTION 16(A) BENEFICIAL OWNERSHIP REPORTING COMPLIANCE | 89 | ||

| FINANCIAL STATEMENTS | 89 | ||

| WHERE YOU CAN FIND MORE INFORMATION | 90 | ||

| HOUSEHOLDING OF ANNUAL MEETING MATERIALS | 90 | ||

| OTHER INFORMATION | 91 | ||

ii

| ANNEX A—OPINION OF SOUTHWEST SECURITIES | A-1 | |

| ANNEX B—AMENDED AND RESTATED PREFERRED STOCK PURCHASE AGREEMENT | B-1 | |

| ANNEX C—FORM OF CERTIFICATE OF DESIGNATIONS | C-1 | |

| ANNEX D—FORM OF REGISTRATION RIGHTS AGREEMENT | D-1 | |

| ANNEX E—SUPPORT AGREEMENT | E-1 | |

| ANNEX F—FORM OF AMENDMENT TO CERTIFICATE OF INCORPORATION | F-1 | |

| ANNEX G—1999 STOCK OPTION PLAN | G-1 |

iii

This summary highlights selected information from this proxy statement deemed most material by us. It does not contain all of the detailed information that may be important to you. To understand the contemplated transactions fully and for a more complete description of the legal terms of the transactions, you should read carefully this entire document and the other documents to which we refer. Unless otherwise provided, references to "Health Card," "we," "us" and "our" refer to National Medical Health Card Systems, Inc. and references to "series A preferred stock" refer to our Series A 7% Convertible Preferred Stock, par value $0.10 per share, that we propose to issue to New Mountain Partners.

Information About National Medical Health Card Systems, Inc.

We provide comprehensive pharmacy benefit management services under the name NMHCRX. In addition, we operate a health information company through our wholly owned subsidiary, Integrail, Inc., a mail service pharmacy through our wholly owned subsidiary, NMHCRX Mail Order, Inc., and a specialty pharmacy through our wholly owned subsidiary, Ascend Specialty Pharmacy Services, Inc. Our mission is to improve our clients' members' health through the timely delivery of effective pharmaceutical care and health information management systems.

We were incorporated in New York in 1981 and reincorporated in Delaware in February 2002. Our executive offices are in Port Washington, New York.

Information About the Annual Meeting of the Stockholders

The annual meeting of the stockholders will be held on March 18, 2004 at 9:30 a.m., local time, at our executive offices located at 26 Harbor Park Drive, Port Washington, New York. At the annual meeting, we will ask you to vote to approve:

You can vote at the annual meeting of stockholders if you owned our common stock at the close of business on February 6, 2004.

Information About this Proxy Statement

You are receiving this proxy statement and the enclosed proxy card because our board of directors is soliciting your proxy to vote your shares at the annual meeting. We began mailing this proxy statement on or about February 19, 2004 to all stockholders of record as of February 6, 2004. This proxy statement contains the information we are required to provide to you under the rules of the Securities and Exchange Commission (the "SEC"). It is designed to assist you in voting your shares.

1

Information About Voting

You can vote on the matters to be presented at the annual meeting in two ways:

If you do not indicate instructions on your properly executed proxy card, your shares will be voted"FOR" all of the aforementioned proposals.

You may revoke your proxy at any time before it is exercised at the annual meeting by sending a written notice of revocation to our corporate secretary, Gerald Shapiro, by providing a fully executed proxy bearing a later date, or by voting in person while in attendance at the meeting.

Each share of our common stock is entitled to one vote and is entitled to vote at the annual meeting. As of February 6, 2004, there were 7,965,327 shares of common stock outstanding and entitled to vote at the annual meeting. Each outstanding share of common stock is entitled to one vote on each of the matters to be presented at the meeting. Neither our bylaws nor our certificate of incorporation provide holders of shares of our common stock cumulative voting rights.

Board Recommendation

Our board of directors formed a special committee comprised entirely of non-management, independent directors to review and negotiate the terms of the Contemplated Transactions (as defined below). The members of the special committee are Paul J. Konigsberg (chairman), Gerald Angowitz, Kenneth J. Daley and Ronald L. Fish. The special committee, after completion of its review and deliberations regarding the contemplated transactions, unanimously recommended the issuance of the series A preferred stock, the completion of the tender offer by us and the other transactions contemplated by the purchase agreement (collectively, the "Contemplated Transactions").

In accordance with the unanimous vote of the special committee, our board of directors has determined that the Contemplated Transactions, which are described in this proxy statement, are advisable and in our best interests, and recommends that all stockholders vote "FOR" all of the proposals at the annual meeting.

Quorum and Voting Requirements

To hold a valid meeting, a quorum of stockholders is necessary. If stockholders entitled to cast at least a majority of all the votes entitled to be cast at the meeting are present in person or by proxy, a quorum will exist. Abstentions and broker non-votes are counted as present for establishing a quorum. A broker non-vote occurs when a broker votes on some matters on the proxy card but not on others because the broker does not have the authority to vote on the other matters.

2

Issuance and Sale of Series A Preferred Stock. The affirmative vote of the holders of a majority of the shares in person or represented by proxy and entitled to vote at the annual meeting is required for the approval of the issuance and sale of the series A preferred stock.

Amendments to Our Certificate of Incorporation. The affirmative vote of the holders of a majority of the outstanding shares of our common stock is required to approve each amendment to our certificate of incorporation. As a result, failures to vote, abstentions and broker non-votes will have the effect of a negative vote. None of the amendments to our certificate of incorporation will be implemented unless all of the amendments receive the required vote for approval.

�� Election of Class II Directors. The nominees receiving the highest number of affirmative votes of the votes cast at the annual meeting either in person or by proxy will be elected as Class II directors. A properly executed proxy card marked "WITHHOLD AUTHORITY" and broker non-votes with respect to the election of one or more Class II directors will not be voted with respect to the director or directors indicated, although it will be counted for purposes of determining whether there is a quorum. Broker non-votes, if any, will not affect the outcome of voting on directors.

Amendment to the Plan. The affirmative vote of the holders of a majority of the shares in person or represented by proxy and entitled to vote at the annual meeting is required for the approval of the amendment to the Plan.

With respect to these proposals, other than the proposal relating to the election of Class II directors, a properly executed proxy marked "ABSTAIN" with respect to such proposal will have the same legal effect as a vote "against" the proposal as it represents a share present or represented at the annual meeting and entitled to vote, but is not considered an affirmative vote for the proposal.

Bert E. Brodsky, the chairman of our board of directors, and certain stockholders related to Mr. Brodsky, who in the aggregate hold 4,943,219 shares of common stock (assuming the exercise of 330,000 options and warrants held by Mr. Brodsky), or approximately 60% of our outstanding common stock, have agreed, pursuant to the support agreement described herein, to vote their shares in favor of the issuance of the series A preferred stock and the amendment to our certificate of incorporation. As long as the purchase agreement between us and New Mountain Partners remains in effect, Mr. Brodsky and the stockholders related to Mr. Brodsky are obligated to vote their shares in favor of these matters, unless our board of directors ceases to recommend approval of these proposals under circumstances permitted by the purchase agreement. Accordingly, adoption of these proposals is assured, absent the occurrence of certain events described elsewhere in this proxy statement.

Interests of Management and Directors in the Contemplated Transactions

Mr. Brodsky and certain stockholders related to Mr. Brodsky have also agreed, pursuant to the support agreement, to tender 4,448,900 shares of our common stock that they hold into the tender offer. Upon the closing of the Contemplated Transactions, options covering 100,000 shares of our common stock will accelerate and become exercisable by Mr. Brodsky at a price of $1.84 per share under his existing stock option agreement. Mr. Brodsky would also be entitled to a severance payment from us of $857,500 upon his resignation as chairman of our board of directors upon the closing of the Contemplated Transactions. However, in connection with the Contemplated Transactions, Mr. Brodsky has agreed to amend his employment agreement to reduce his severance payment to $357,500 and to defer our obligation to pay him that amount until the later of July 1, 2004 or the closing date of the Contemplated Transactions. This amendment would cease to be effective if the closing of the Contemplated Transactions does not occur by July 1, 2004. In addition, we have agreed to indemnify and hold Mr. Brodsky harmless from any "golden parachute" taxes (and any additional federal, state and local taxes incurred by Mr. Brodsky as a result of such indemnification) that he may incur as a result of any payments to Mr. Brodsky from us (including his severance payment and the accelerated vesting of his stock options).

3

We also agreed, pursuant to a side letter agreement dated October 30, 2003, with Mr. Brodsky, that the non-competition covenant contained in the support agreement would be effective in lieu of the non-competition covenant contained in Mr. Brodsky's existing employment agreement with us.

James J. Bigl, a director, our president and chief executive officer, David Gershen, our executive vice president of financial services and treasurer, Tery Baskin, our chief marketing officer, and Agnes Hall, our chief information officer, are each entitled to a transaction bonus upon the closing of the Contemplated Transactions. In connection with the Contemplated Transactions, Messrs. Bigl, Gershen and Baskin and Ms. Hall have agreed to use a portion of their bonuses to purchase additional shares of our common stock after the closing of the Contemplated Transactions. Please see the section "Interests of Management and Directors in the Contemplated Transactions" in Proposal 1 for a more detailed description of the transaction bonuses payable to our executive officers.

In addition, as part of the Contemplated Transactions, Mr. Bigl's employment agreement has been amended to provide that upon a termination of his employment with us for any reason prior to the eighteen-month anniversary of the closing date of the Contemplated Transactions, in addition to any other severance payments that he is otherwise entitled to, Mr. Bigl will become entitled to a lump-sum payment equal to $624,000; provided, however, that if such termination is either by us without cause or by Mr. Bigl for good reason, the lump sum payment will be increased to $874,000.

Upon the closing of the Contemplated Transactions, options granted to Mr. Bigl covering 473,665 shares of common stock will accelerate and become fully vested. Mr. Bigl however, has agreed that with respect to these and other vested options covering 527,330 shares of common stock, he will not exercise (1) options covering more than 93,330 shares before April 30, 2004, (2) options covering more than an additional 34,000 shares before June 12, 2004, (3) options covering more than an additional 133,334 shares before on June 12, 2005, and (4) options covering more than an additional 133,333 shares before June 12, 2006. After June 12, 2006, options covering all of the 527,330 shares will be fully exercisable; provided that, all of these options will become fully exercisable upon either (x) a change in control of us following the closing of the Contemplated Transactions or (y) a termination of Mr. Bigl's employment with us for any reason following the closing of the Contemplated Transactions.

Furthermore, we have agreed to hold Mr. Bigl harmless from any "golden parachute" taxes (and any additional federal, state and local taxes incurred by Mr. Bigl as a result of such indemnification) that he may incur as a result of any payments to Mr. Bigl from us (including his transaction bonus and the accelerated vesting of his stock options).

Upon the closing of the Contemplated Transactions, options granted to Messrs. Gershen and Baskin and Ms. Hall covering 19,985, 58,331, and 47,330 shares of common stock, respectively, will accelerate and become fully vested and immediately exercisable. Also, upon the closing of the Contemplated Transactions, options granted to Patrick McLaughlin, the president of our pharmacy benefit management division, covering 15,000 shares of common stock will accelerate and become fully vested and immediately exercisable.

Upon the closing of the Contemplated Transactions, Kenneth J. Daley, Ronald L. Fish and Gerald Shapiro will resign from our board of directors so that our board may be reconstituted as required under the purchase agreement. When Messrs. Daley and Fish resign upon the closing of the Contemplated Transactions, we will fully vest the 22,000 unvested options to purchase common stock held by each of them so that they become immediately exercisable upon their resignation. To the extent such vesting occurs, we will recognize a one-time charge to our statement of income in the fiscal quarter in which such vesting occurs equal to the difference between the fair market value of our common stock on the date such vesting occurs less the exercise price multiplied by the number of options whose vesting was accelerated. Using an estimated fair market value of $28.43, which represents the closing price of our common stock on February 18, 2004, this will result in a charge

4

against net income of approximately $257,000. See the section titled "Unaudited Pro Forma Condensed Consolidated Financial Information" beginning on page 53 of this proxy statement.

We have entered into indemnification agreements with each of our directors. The agreements provide that we will indemnify each director against any judgments, penalties, fines, amounts paid in settlement and expenses incurred in connection with any actual or threatened proceeding against us or our affiliates. In addition, we agreed to pay in advance certain expenses, including attorneys' fees, incurred by any director prior to the final disposition of such proceedings, except that the director must repay such amounts if it is ultimately determined that the director is not entitled to be indemnified by us.

Cost and Method of Soliciting Proxies

This proxy is being solicited by our board of directors. We will bear the entire cost of the solicitation of proxies, including the charges and expenses of brokerage firms and other custodians, nominees and fiduciaries for forwarding proxy materials to beneficial owners of our shares of common stock. Solicitations will be made primarily by mail, but some of our directors, officers or employees may solicit proxies in person or by telephone, for which such persons will receive no additional compensation.

Opinion of the Financial Advisor to the Special Committee of Our Board of Directors

In deciding to approve the issuance of the series A preferred stock and the amendment to our certificate of incorporation, our board of directors considered a number of factors, including the opinion of the financial advisor to the special committee of our board of directors, Southwest Securities, Inc. On October 29, 2003, Southwest Securities, Inc. delivered its oral opinion to the special committee and our board of directors, which opinion was subsequently confirmed by a written opinion to the special committee dated October 30, 2003, to the effect that, as of that date, the issuance of the series A preferred stock and use of the proceeds from the issuance of the series A preferred stock to effect the tender offer was fair from a financial point of view to non-affiliated holders of our common stock.

The full text of the written opinion of Southwest Securities, Inc., dated October 30, 2003, is attached to this proxy statement as Annex A. We urge you to read this opinion carefully for a description of the assumptions made, matters considered and limitations on the review undertaken in connection with the opinion. The written opinion of Southwest Securities, Inc. is directed to the special committee of our board of directors and does not constitute a recommendation to any stockholder with respect to any matter relating to the Transactions (as defined therein). The written opinion of Southwest Securities, Inc. speaks only as of the date issued.

Regulatory Approvals

In order to complete the Contemplated Transactions, we and the persons ultimately controlling New Mountain Partners (for purposes of the Hart-Scott-Rodino Antitrust Improvements Act of 1976, as amended), if any, are required under the Hart-Scott-Rodino Act, to make filings with the United States Department of Justice and the Federal Trade Commission and wait for the expiration or early termination of the required waiting period. These filings were made on December 31, 2003.

Other Matters

Our board of directors does not know of any other matter that will be presented at the annual meeting other than the proposals discussed in this proxy statement. Generally, no business other than the items discussed in this proxy statement may be transacted at the meeting.

5

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND

MANAGEMENT

The following table sets forth certain information, as of February 6, 2004, concerning the persons or entities known to us to be the beneficial owner of more than 5% of the shares of our common stock as well as the number of shares of common stock that our directors and certain executive officers beneficially own, and that our directors and executive officers own as a group. Except as otherwise indicated below, each of the entities or persons named in the table has sole voting and investment power with respect to all shares of common stock beneficially owned. Unless otherwise indicated, the business address of each stockholder listed below is c/o National Medical Health Card Systems, Inc., 26 Harbor Park Drive, Port Washington, New York 11050.

| Name of Beneficial Owner | Number of Shares Beneficially Owned(1) | Percentage Owned | |||

|---|---|---|---|---|---|

| Bert E. Brodsky | 3,365,374 | (2) | 41.1 | % | |

| Gerald Shapiro | 294,534 | 3.7 | % | ||

| James J. Bigl | 159,335 | (3) | 2.0 | % | |

| Tery Baskin | 121,286 | (4) | 1.5 | % | |

| David Gershen | 60,015 | (5) | * | ||

| Agnes Hall | 24,670 | (6) | * | ||

| Patrick McLaughlin | 41,666 | (7) | * | ||

| Kenneth J. Daley | 24,667 | (8) | * | ||

| Ronald L. Fish | 24,667 | (8) | * | ||

| Gerald Angowitz | 24,667 | (8) | * | ||

| Paul Konigsberg | 14,667 | (8) | * | ||

| Stuart F. Fleischer | — | (9) | * | ||

| All executive officers and directors as a group (12 persons) | 4,155,548 | (10) | 49.3 | % |

6

fully vested and immediately exercisable. Mr. Bigl has agreed that, with respect to those and other options covering 505,804 shares of common stock, he will not exercise (1) options covering more than 93,330 shares before April 30, 2004, (2) options covering more than an additional 34,000 shares before June 12, 2004, (3) options covering more than an additional 133,334 shares before June 12, 2005 and (4) options covering more than an additional 133,333 shares before June 12, 2006. After June 12, 2006, options covering all of the 505,804 shares will be fully exercisable; provided, that, all of these options will become fully exercisable upon either (x) a change in control of us following the closing of the Contemplated Transactions or (y) a termination of Mr. Bigl's employment with us for any reason following the closing of the Contemplated Transactions.

7

PROPOSAL 1—APPROVAL OF THE ISSUANCE AND SALE OF OUR SERIES A

PREFERRED STOCK

We are seeking stockholder approval for the issuance and sale of the series A preferred stock (the "Series A Preferred Stock Proposal") under (1) NASD rule 4350(i)(1)(D)(ii), which is applicable because the shares of the series A preferred stock are convertible into shares of our common stock at a price below the market value of the common stock and are convertible into more than 20% of our common stock and more than 20% of our voting power outstanding before the issuance of the series A preferred stock and (2) NASD rule 4350(i)(1)(B), which is applicable because the issuance and sale of the series A preferred stock will result in a change of control of us.

The following is a summary of the provisions of: (1) the amended and restated preferred stock purchase agreement, dated as of November 26, 2003, between us and New Mountain Partners, L.P. (the "purchase agreement"); (2) the form of certificate of designations governing the series A preferred stock; (3) the form of registration rights agreement between us and New Mountain Partners, L.P.; and (4) the support agreement, dated as of October 30, 2003, between us, New Mountain Partners, L.P., and Bert E. Brodsky and certain stockholders related to Mr. Brodsky (the "support agreement"). New Mountain Partners, L.P. has assigned a portion of its rights and obligations under the purchase agreement and support agreement to New Mountain Affiliated Investors, L.P., a partnership related to New Mountain Partners, L.P. (together with New Mountain Partners, L.P., "New Mountain Partners"). Because this section is a summary, it does not describe every term of the documents. This summary is qualified in its entirety by reference to, and should be read in conjunction with, those documents.

We have attached hereto copies of the purchase agreement, the form of certificate of designations, the form of registration rights agreement, and the support agreement as Annexes B, C, D and E, respectively. We urge all of our stockholders to read these documents carefully.

Summary of the Contemplated Transactions

Pursuant to the purchase agreement, we agreed, subject to various conditions, to issue to New Mountain Partners, and New Mountain Partners agreed to purchase from us, a total of 6,956,522 shares of series A preferred stock at a purchase price of $11.50 per share, for aggregate proceeds of $80,000,003. Once certain conditions described in more detail below have been met or waived, including receipt of certain stockholder approvals sought by this proxy statement, we are obligated to complete the sale of the series A preferred stock to New Mountain Partners and to use approximately $50 million of the proceeds of the sale of the series A preferred stock to fund the purchase price for a tender offer for up to 4,545,455 shares of our outstanding common stock at $11.00 per share. Mr. Brodsky, the chairman of our board, and certain stockholders related to him (assuming the exercise of 330,000 options and warrants held by Mr. Brodsky), currently hold, in the aggregate, approximately 60% of our outstanding common stock and have agreed to tender 4,448,900 shares, or approximately 54% of our outstanding common stock, held by them into the tender offer. If the tender offer is oversubscribed by our stockholders, we will repurchase the shares of common stock on apro rata basis. If the tender offer is fully subscribed by our stockholders and assuming the exercise of 330,000 options and warrants held by Mr. Brodsky, after the tender offer is completed, New Mountain Partners will own securities that are initially convertible into approximately 65% of our issued and outstanding common stock and prior to conversion of the series A preferred stock will be entitled to cast that number of votes that is equal to approximately 61% of our aggregate voting power. Following the closing of the Contemplated Transactions, New Mountain Partners will initially be entitled to nominate and elect 60% of the members of our board of directors. On October 29, 2003, our board of directors approved the terms of the Contemplated Transactions. The Series A Preferred Stock Proposal is subject to the approval of our stockholders as required by the NASD 20% Rule and NASD Control Rule (each as defined below in "Reason for Request for Approval"), as well as the satisfaction or waiver of certain other conditions described below. On October 30, 2003, the last full trading day before the public

8

announcement of the execution of the purchase agreement, the last reported sale price of our common stock, as reported on The Nasdaq National Market (the "Nasdaq Market"), was $13.75 per share. On February 18, 2004, the last reported sale price of our common stock, as reported on the Nasdaq Market, was $28.43 per share.

We will primarily use the remaining proceeds from the issuance and sale of the series A preferred stock of approximately $22 million, excluding expenses related to the closing of the Contemplated Transactions, for acquisitions and working capital purposes. However, except under certain circumstances, we will be prohibited from using such proceeds to pay any outstanding amounts due under our outstanding credit facility for six months following the closing of the Contemplated Transactions. We regularly review potential acquisitions and engage in discussions with third parties regarding acquisitions, but there can be no assurance that our efforts will result in completed acquisitions. At the time of this proxy statement, we have not entered into any acquisition agreements with any potential acquisition candidate.

Background of the Contemplated Transactions

In April 2002, we entered into an engagement letter with an investment banking firm to act as our financial and capital markets advisor in connection with potential financial and strategic transactions. We engaged the financial advisor following a determination by our board of directors and management that continued growth through acquisitions was critical to support our long-term outlook given our relatively small size compared to our industry peers.

In September 2002, we received an unsolicited non-binding indication of interest from a third party ("Party 1") to acquire us at a price of $11.00 per share for all of our outstanding equity. On November 11, 2002, Party 1 revised its non-binding indication of interest in writing to $13.00 per share for all of our outstanding equity. On November 13, 2002, at a meeting of our board of directors, our board of directors considered the revised unsolicited indication of interest from Party 1. Our board of directors recommended and approved our continued discussions with Party 1 and instructed management to continue to apprise our board of directors of the status of those discussions. We then entered into a confidentiality agreement with Party 1, who then commenced financial and legal diligence. On November 25, 2002, Party 1 verbally increased its non-binding indication of interest to $13.50 per share for all of our outstanding equity.

In early December 2002, Party 1 continued to communicate through our financial advisor that it was still interested in acquiring us for approximately $13.00 to $13.50 per share for all of our outstanding equity. Our board of directors then met with its financial and legal advisors to review the financial and legal aspects of the proposal. Our board of directors authorized management to continue its negotiations with Party 1 and to pursue other potential acquisition partners if negotiations with Party 1 did not progress within a short period of time.

In the first week of January 2003, we instructed our financial advisor to solicit additional indications of interest to acquire us through a targeted auction process. Over the course of the following two weeks, we received several other preliminary non-binding indications of interest from other parties interested in acquiring us for between $11.00 and $15.00 per share for all of our outstanding equity. All of these indications of interest were subject to various conditions, including satisfactory completion of due diligence investigations of us. Three of those parties ultimately commenced due diligence investigations of us.

On January 30, 2003, we received a written non-binding offer from Party 1 informing us it had completed its due diligence and proposed to acquire us for $10.00 per share for all of our outstanding equity. As a result, our discussions with Party 1 slowed. Subsequently, in February 2003, another party ("Party 2") sent us a written offer to acquire us for $12.00 per share, but in March 2003 it informed our financial advisor that its proposal was withdrawn. Following Party 2's withdrawal, Party 1's proposal

9

was the only proposal remaining from the auction process that began in January 2003, and we therefore recommenced active negotiations with Party 1. Our management team and our representatives continued to negotiate a definitive merger agreement with Party 1 through March 2003. As a result of our negotiations with Party 1, on March 10, 2003, Party 1 subsequently increased its non-binding offer to $11.75 per share for all of our outstanding equity. At the beginning of April 2003, however, Party 1 notified us that it was no longer interested in pursuing a transaction with us.

At a meeting of our board of directors on April 18, 2003, Mr. Brodsky, the chairman of our board of directors, advised our board of directors that a private equity firm had submitted a non-binding proposal to acquire us for a purchase price of $10.50 per share in a going-private transaction in which Mr. Brodsky would retain an interest in the acquired company. At the conclusion of the meeting, our board of directors established a special committee comprised entirely of non-management, independent directors (Paul J. Konigsberg (chairman), Gerald Angowitz, Kenneth J. Daley and Ronald L. Fish) for the purpose of evaluating a possible transaction with the private equity firm. The special committee also retained Fulbright & Jaworski L.L.P. to act as its legal advisor and started to consider several investment banks to act as its financial adviser. Following several weeks of discussions with the private equity firm, however, the private equity firm decided to discontinue their discussions with us without providing us any specific reasons for its decision.

In the course of discussions with several other investment banking firms regarding our options to increase our stockholder value, in late July 2003 we were approached by Southwest Securities, Inc. ("Southwest Securities") about a possible equity investment in us by a private equity fund, New Mountain Partners, coupled with a tender offer for shares of our common stock. On July 24, 2003, we entered into a confidentiality agreement with New Mountain Partners to facilitate discussions. We then proceeded to have preliminary discussions with New Mountain Partners with respect to the structure of a proposed investment in us. On August 26, 2003, New Mountain Partners submitted a preliminary non-binding term sheet proposing an investment in us, with a substantial portion of the proceeds to be used to repurchase shares of our common stock held by Mr. Brodsky and certain stockholders related to Mr. Brodsky. On August 27, 2003, we entered into an exclusivity agreement with New Mountain Partners.

We engaged Southwest Securities on July 22, 2003 to serve as our financial advisor for the proposed transaction with New Mountain Partners. In August 2003 our board of directors determined that the special committee would have the authority to negotiate and approve a transaction with New Mountain Partners, and the special committee interviewed several financial advisor candidates, including Southwest Securities. Following the interview process, the special committee, which was composed of the same individuals as the special committee formed on April 18, 2003, formally engaged Southwest Securities as of August 29, 2003 to serve as its financial advisor for the transaction and the engagement agreement, dated July 22, 2003, between us and Southwest Securities was terminated. Our board of directors determined that it did not require a separate financial advisor in light of the special committee's mandate, and our engagement letter with Southwest Securities was terminated concurrently with Southwest Securities' retention by the special committee. Prior to the engagement, Southwest Securities advised the special committee that it had no previous relationship or agreements with New Mountain Partners, was not acting as an advisor to New Mountain Partners with respect to the proposed transactions and had not acted as an advisor to New Mountain Partners with respect to any other transaction and did not receive any, and did not anticipate receiving any, compensation from New Mountain Partners or its affiliates with respect to the proposed transactions.

Our board of directors and special committee also retained Fulbright & Jaworkski L.L.P. to act as their legal advisor in connection with the proposed transaction. Following its engagement, Southwest Securities communicated to New Mountain Partners the special committee's instructions that any use of the proceeds of an investment in us to repurchase outstanding common stock would have to be made to all of our stockholders on apro rata basis.

10

From late August 2003 through the end of October 2003, New Mountain Partners and Deloitte & Touche LLP, its accounting advisor, and Fried, Frank, Harris, Shriver & Jacobson LLP, its legal advisor, conducted an accounting, financial and legal due diligence investigation of us.

On September 11, 2003, New Mountain Partners' legal advisor provided us with an initial draft of a preferred stock purchase agreement providing for an aggregate preferred stock investment of $70 million. On September 17, 2003, New Mountain Partners' legal advisor provided us with an initial draft of the certificate of designations for an 8% participating convertible preferred stock, with a conversion price of $11.00 per share.

On September 18, 2003, the members of the special committee held a telephonic meeting with its legal and financial advisors and representatives of our auditors to discuss the proposed terms and the anticipated impact of the proposed transactions on our reported financial results.

On September 25, 2003, the members of the special committee met in person with representatives of New Mountain Partners and its legal advisor, as well as the special committee's legal and financial advisors, to negotiate the principal terms of the proposed investment in us. Following discussion of the key terms, the parties agreed, among other things, that the investment amount would be increased from $70 million to $80 million; the conversion price for the series A preferred stock would be increased from $11.00 to $11.50 per share; the dividend on the series A preferred stock would be lowered from 8% to 7% for the first five years and thereafter to 3.5%; and the offer price in the tender offer would be $11.00 per share. The parties also discussed whether all or a portion of the dividends would be payable in-kind rather than in cash.

From the middle of September 2003 to the end of October 2003, our management, representatives of New Mountain Partners and each of their respective advisors spoke on numerous occasions regarding our business and financial condition. During this period, representatives of the special committee, New Mountain Partners and their respective advisors spoke on numerous occassions regarding the terms of the transaction, including the amount of the investment by New Mountain Partners, the closing amount payable to New Mountain Partners, the required tender offer amount, the dividend rate on the series A preferred stock, the special voting rights of the holders of series A preferred stock, the no solicitation covenant, our ability to terminate the transaction to accept a financially superior transaction, the termination fee trigger events, the amount of New Mountain Partners' expenses that we would be required to reimburse, the definition of material adverse effect, and other related provisions and documents. During this period, members of the special committee, Southwest Securities and our auditors discussed the impact of the proposed transactions on our reported financial results. During this period, Mr. Brodsky engaged separate legal counsel and Mr. Brodsky and his legal advisors participated in negotiations with the special committee and New Mountain Partners with respect to the terms of the proposed transactions, including the terms of the support agreement that New Mountain Partners stated was a condition to its participation in any transaction with us.

On October 8, 2003, members of our management and the special committee's legal and financial advisors met with representatives of New Mountain Partners and its legal advisors to discuss the key provisions of the purchase agreement and certificate of designations, focusing on the corporate governance provisions and the obligation to reimburse New Mountain Partners for its out-of-pocket expenses.

On October 9, 2003, the special committee held a meeting with members of management and its legal and financial advisors to discuss the status of the negotiations with New Mountain Partners. The special committee's financial advisor gave an overview of the financial terms of the proposed transactions, including our related expenses and the anticipated impact of the proposed transactions on our reported financial results. A detailed description of the estimated related expenses and the anticipated impact of the proposed transactions on our reported financial results are discussed under

11

the section "Unaudited Pro Forma Condensed Consolidated Financial Information" on page 53 and are summarized below:

The special committee's legal advisor then gave an overview of the transaction documents and the remaining open issues. A lengthy discussion followed the presentations. The special committee authorized its advisors to continue to negotiate the terms of the transaction documents, including a limit on the amount of New Mountain Partners' out-of-pocket expenses that we would be required to pay upon the closing of the proposed transactions and if the transactions were not completed.

During the next two weeks, members of the special committee, our management, the special committee's legal and financial advisors and representatives of New Mountain Partners and its legal advisors continued to negotiate the terms of the key agreements relating to the proposed transactions.

The special committee held a meeting on October 23, 2003 to review with our management and the special committee's legal and financial advisors the status of the negotiations and the proposed terms and conditions of the proposed transactions with New Mountain Partners. During this meeting, the special committee's legal advisor updated the committee on changes to the material terms and conditions of the purchase agreement previously discussed and reviewed the legal duties and responsibilities of our special committee and board of directors in connection with the proposed transactions. Southwest Securities presented a comprehensive analysis of the proposed series A preferred stock financing and tender offer, including a review of the valuation methods it used, and expressed its view that, subject to a review of the final agreements, Southwest Securities should be able to deliver a written opinion that the preferred stock investment and tender offer were fair to our non-affiliated stockholders from a financial point of view. The special committee carefully considered the presentations made and the terms of the proposed transactions. The special committee also negotiated (1) a reduction in the transaction fee payable to its financial advisor, Southwest Securities, from $2.8 million to $2.5 million and (2) a reduction in the severance payments owed Mr. Brodsky in light of the substantial benefits that Mr. Brodsky would realize as a result of the closing of the proposed transactions. Following a thorough discussion, the special committee approved the proposed transactions, subject to the satisfactory negotiation of the final terms of the purchase agreement, support agreement and other related documents.

12

On October 24, 2003, the special committee's legal counsel discussed the remaining issues with Mr. Brodsky's legal counsel, which focused on the no solicitation and termination provisions contained in the purchase agreement and the support agreement. Mr. Konigsberg and the special committee's legal advisor then met with representatives of New Mountain Partners and its legal advisor to discuss those remaining issues.

Negotiation of the transaction agreements continued and the purchase agreement and the other documents contemplated by the purchase agreement were substantially finalized in the late evening of October 28, 2003.

At a meeting of the special committee held on October 29, 2003, the committee members considered the terms of the proposed financing that had been negotiated with New Mountain Partners. The other members of our board of directors joined the meeting as observers and Southwest Securities presented an updated, comprehensive analysis of the proposed series A preferred stock financing and tender offer, including a review of the valuation methods it used, and orally advised the special committee and our board of directors that the transaction was fair to our non-affiliated stockholders from a financial point of view. The oral opinion was subsequently confirmed in writing on October 30, 2003. Our legal advisor reviewed with the special committee and our board of directors the principal terms of the proposed series A preferred stock financing and the tender offer, as well as a discussion of the fiduciary duties of the directors with respect to the proposed transactions. Following thorough discussions, the directors who were not members of the special committee left the meeting and the committee unanimously agreed to approve the proposed transactions and to recommend to the full board that it also approve the proposed transactions. Shortly thereafter, our board of directors approved the proposed transactions.

Late in the evening of October 30, 2003, the purchase agreement and certain other agreements were executed by our appropriate officers, New Mountain Partners and the stockholders executing the support agreement, and the Contemplated Transactions were publicly announced the morning of October 31, 2003.

During the first week of November 2003, we were contacted by representatives of The Nasdaq Stock Market, Inc. ("Nasdaq"), who requested that we modify the manner in which voting rights of holders of the series A preferred stock are calculated in certain circumstances. Following discussion between our and New Mountain Partners' legal advisors, our board of directors met on November 19, 2003 and approved the modification to the terms of the series A preferred stock. The amended and restated purchase agreement reflecting the modification was executed on November 26, 2003.

Reasons for the Contemplated Transactions; Recommendation of the Special Committee and Our Board of Directors

In determining that the Contemplated Transactions are advisable, fair and in our best interests and our stockholders' best interests, the special committee and our board of directors consulted with our management and our board of directors' and the special committee's financial advisor and legal counsel, and considered numerous factors discussed below that supported their recommendations.

In deciding to approve the Contemplated Transactions, our board of directors considered the following factors which were generally viewed as advantages of the Contemplated Transactions:

13

institutional holders of shares of our common stock; the lack of coverage by equity research analysts of our common stock; the low daily trading volume in the shares of our common stock and the lack of liquidity as a result thereof; and the desire on the part of Mr. Brodsky, our largest stockholder, to sell a significant amount of shares of his common stock and the possible negative effect on our common stock resulting from such sales;

14

with several companies interested in acquiring us, but that none of those transactions were completed.

Our board of directors also considered the following factors which were viewed generally as disadvantages of the Contemplated Transactions:

Our board of directors concluded, however, that the potential disadvantages associated with the Contemplated Transactions were outweighed by the advantages of the Contemplated Transactions.

Our board of directors also considered the potential benefits to certain directors, officers and employees discussed in the section below entitled "Interests of Management and Directors in the Contemplated Transactions." Our board of directors did not believe that these interests should affect its decision to approve the Contemplated Transactions since these interests are primarily based on contractual arrangements that were in place before the negotiation of the purchase agreement and our

15

board of directors' view that the judgment and performance of the directors and executive officers would not be impaired by these interests. In considering the Contemplated Transactions, our board of directors considered the impact of these factors and the other factors described below on our stockholders.

The foregoing discussion describes the material factors considered by the special committee of our board of directors and our board of directors in their consideration of the Contemplated Transactions. In view of the wide variety of factors considered by the special committee and our board of directors, the special committee and our board of directors did not find it practicable to, and did not, quantify or otherwise attempt to assign relative weights to the specific factors considered. The special committee and our board of directors viewed their positions and recommendations as being based on the totality of the information presented to, and considered by, them. In addition, individual members of the special committee and our board of directors may have given different weights to different factors. After taking into consideration all the factors set forth above, the special committee and our board of directors determined that the potential benefits of the Contemplated Transactions outweighed the potential disadvantages associated with the Contemplated Transactions.

Impact of the Issuance and Sale of the Series A Preferred Stock on Our Existing Stockholders

The holders of the series A preferred stock will have certain rights that are senior to those of the holders of our common stock. You should consider the following factors in determining whether to vote for this proposal:

16

Opinion of Southwest Securities, Inc.

Introduction

Southwest Securities, Inc. acted as the financial advisor to the special committee of our board of directors in connection with the special committee's analyses and evaluation of the Transactions (as defined below). The special committee of our board of directors requested that Southwest Securities provide the special committee with an opinion as to the fairness, from a financial point of view, to our non-affiliated common stockholders of the issuance of the series A preferred stock and the tender offer, collectively referred to in this section as the "Transactions." In requesting Southwest Securities' opinion, the special committee of our board of directors did not give any special instructions to Southwest Securities or impose any limitation upon the scope of investigation that Southwest Securities deemed necessary to enable it to deliver its opinion.

At the October 29, 2003 meeting of our board of directors, Southwest Securities delivered its oral opinion to the special committee and our board of directors that, based on and subject to the assumptions and conditions set forth therein, each of the proposed issuance of the series A preferred stock and the tender offer is fair to our non-affiliated common stockholders from a financial point of view. On October 30, 2003, at the request of the special committee of our board of directors, Southwest Securities delivered its written opinion, stating that, based on and subject to the assumptions and conditions set forth therein, as of October 30, 2003, each of the proposed issuance of the series A preferred stock and the tender offer is fair to our non-affiliated common stockholders from a financial point of view (the "Southwest Securities Opinion").

A copy of the Southwest Securities Opinion is attached to this proxy statement as Annex A, and Southwest Securities has consented to its attachment hereto. We urge you to read the Southwest Securities Opinion carefully and in its entirety. The Southwest Securities Opinion is directed only to the fairness, from a financial point of view, to our non-affiliated common stockholders of the issuance of the series A preferred stock and the tender offer. The Southwest Securities Opinion does not constitute a recommendation to any stockholder as to how you should vote in respect of the Transactions or whether to tender all or any of your common stock pursuant to the proposed tender offer.

17

In arriving at the Southwest Securities Opinion, Southwest Securities has, among other things:

In connection with its review, Southwest Securities assumed and relied upon the accuracy and completeness of all financial and other information supplied to Southwest Securities by our management, and all publicly available information concerning us, and did not independently verify such information. Southwest Securities also relied upon our management as to the reasonableness and achievability of the financial projections (and the assumptions and bases therein) that we provided to Southwest Securities and Southwest Securities assumed that the projections were reasonably prepared on bases reflecting the best currently available estimates and judgments of our management as to our future operating performance. In arriving at the Southwest Securities Opinion, Southwest Securities relied upon the projected financial data for fiscal 2004 through 2007. The projected financial data for 2004 through 2007 were our latest available projections provided to Southwest Securities by our management as of the date of the Southwest Securities Opinion. We do not publicly disclose internal management projections of the type provided to Southwest Securities in connection with Southwest Securities' review of the Transactions. These projections were not prepared with the expectation of public disclosure. The projections were based on numerous variables and assumptions that are inherently uncertain, including factors related to general economic and competitive conditions. Accordingly, actual results could vary significantly from those set forth in the projections.

The Southwest Securities Opinion does not constitute a recommendation of the Transactions over any alternative transaction (including the alternative not to effect the Transactions) that may be available to us or the effect of any transaction in which we might engage and does not address the underlying business decision of our board of directors to proceed with the Transactions. Furthermore, Southwest Securities was not requested to make, and did not make, an independent appraisal or evaluation of our assets, properties, facilities or liabilities, and Southwest Securities has not been furnished with any such appraisals or evaluations. In addition, Southwest Securities did not assume any obligation to conduct, nor did they conduct, any physical inspection of our properties or facilities. Estimates of values of us and our assets do not purport to be appraisals or necessarily reflect the prices at which we or our assets may actually be sold.

18

The Southwest Securities Opinion is necessarily based on share prices and economic and other conditions and circumstances as they existed or were in effect on, and the information made available to it as of, October 30, 2003. Southwest Securities expressed no opinion as to what the value of our common stock actually would be when the Transactions are consummated or as to the price or trading range at which our common stock may trade at any time following the Transactions.

In connection with rendering the Southwest Securities Opinion, Southwest Securities performed a variety of financial and comparative analyses, including those described below. Although all of the material analyses performed are summarized below, the summary does not purport to be a complete description of the analyses performed and factors considered by Southwest Securities in arriving at the Southwest Securities Opinion. Southwest Securities believes that its analyses must be considered as a whole and that selecting portions of Southwest Securities' analyses and of the factors considered by it, without considering all analyses and factors, could create a misleading view of the processes underlying the Southwest Securities Opinion. The preparation of a fairness opinion is a complex process and is not necessarily susceptible to a partial analysis or summary description. Southwest Securities assumed that the Transactions will be consummated according to the terms and conditions described in the forms of the definitive agreements relating to the Transactions that were reviewed by Southwest Securities, without any waiver or modification of material terms or conditions by any party thereto, including us and New Mountain Partners.

The following is a summary of the principal financial and comparative analyses performed by Southwest Securities in connection with the preparation of the Southwest Securities Opinion. These analyses were presented to the special committee of our board of directors at its meeting on October 29, 2003.

Summary of Southwest Securities' Valuation Approach

Valuation Methodologies. Southwest Securities completed a series of valuation methodologies to determine an estimated value for us before giving effect to the Transactions. The valuation methodologies that Southwest Securities utilized included:

In each analysis, Southwest Securities calculated a range of implied equity values per share of our common stock.

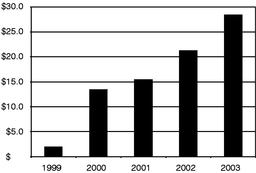

Historical Market Price Analysis. Southwest Securities analyzed the performance of the price of our common stock over the last 18 months, a time period that Southwest Securities determined to be sufficient for its analysis and within the typical range for such an analysis. Eighteen months is also the approximate period of time since we began to explore our strategic alternatives. This 18-month period included 380 trading days, and this analysis concluded that over this period of time, the closing price of our common stock was less than or equal to $11.50 on 327 of the 380 trading days, or 86% of such trading days. Southwest Securities also analyzed the closing stock prices over the last 18 months and the number of shares that traded on each trading day and concluded that during this period of time, 77% of the shares traded on days that the closing price of our common stock was below $11.50. The closing prices of our common stock for the 18 month period that Southwest Securities analyzed ranged from $6.65 to $13.60 and the mean and median were $9.57 and $9.00, respectively. The closing price of our common stock on October 30, 2003, the day prior to the announcement of the Contemplated Transactions, was $13.75 per share.

Selected Comparable Companies Analysis. Southwest Securities compared our relevant historical, current and projected financial and operating results with the financial and operating results of publicly

19

traded companies that operate in the pharmacy benefit management industry (collectively the "Comparable Companies"). The Comparable Companies were chosen by Southwest Securities based on general business, operating and financial characteristics representative of companies in the industry in which we operate. No company or business used in the Comparable Companies analysis is identical or substantially identical to us.

For the purposes of this analysis, the Comparable Companies selected by Southwest Securities were five companies that operate in the pharmacy benefit management industry as listed below:

In performing its analysis, Southwest Securities calculated multiples of, among other things, each Comparable Company's latest twelve months ("LTM"), projected calendar year 2003 ("CY 2003") and projected calendar year 2004 ("CY 2004") net income (collectively, the "Equity Value Multiples"). Southwest Securities also calculated multiples of each Comparable Company's LTM, CY 2003 and CY 2004 earnings before interest, taxes, depreciation and amortization ("EBITDA") and earnings before interest and taxes ("EBIT") (collectively, the "Enterprise Value Multiples").

Using the above-referenced information, Southwest Securities derived a range of estimated equity and enterprise values for us by applying the above-referenced mean, median, low and high Enterprise Value Multiples and Equity Value Multiples of the Comparable Companies to our appropriate financial statistics. Southwest Securities ultimately derived a range of equity values per share of our common stock for each multiple after taking into account our net debt of $11.5 million as of June 30, 2003 and the number of shares of our common stock outstanding, using the treasury stock method, as of September 30, 2003. In addition to the aforementioned Comparable Companies, Southwest Securities also performed an analysis of HealthExtras, Inc., which is also engaged in the pharmacy benefit management business, and determined that the analysis was not meaningful because of its limited operating history as a pharmacy benefit management company and the absence of publicly available projections.

Southwest Securities applied the Comparable Companies' multiples to our appropriate financial statistics and calculated a range of implied equity values per share of our common stock based on the Comparable Companies' low, mean, median and high multiples. The closing price of our common stock on October 30, 2003, the day prior to the announcement of the Contemplated Transactions, was $13.75 per share. In reviewing the results of its analysis, Southwest Securities noted that the price per share to be received for the series A preferred stock and to be paid in the tender offer, as well as the closing price per share of our common stock on October 29, 2003, two days prior to the announcement of the Contemplated Transactions, were in all cases lower than the values implied by the Comparable Companies' mean, median and high multiples and in some cases lower than the value implied by the

20

Comparable Companies' low multiple. This analysis resulted in the following implied equity values per share of our common stock:

| | Implied Equity Value Per Share of Our Common Stock | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Financial Statistic | ||||||||||||

| Low | Mean | Median | High | |||||||||

| LTM EBITDA | $ | 9.33 | $ | 18.33 | $ | 17.67 | $ | 25.20 | ||||

| LTM EBIT | $ | 8.27 | $ | 15.53 | $ | 16.02 | $ | 19.57 | ||||

| LTM net income | $ | 9.39 | $ | 15.92 | $ | 16.39 | $ | 19.71 | ||||

| CY 2003 EBITDA | $ | 13.22 | $ | 18.60 | $ | 17.59 | $ | 23.33 | ||||

| CY 2003 EBIT | $ | 9.61 | $ | 14.68 | $ | 14.99 | $ | 18.19 | ||||

| CY 2003 net income | $ | 10.68 | $ | 14.98 | $ | 16.11 | $ | 17.86 | ||||

| CY 2004 EBITDA | $ | 25.54 | $ | 35.24 | $ | 33.75 | $ | 44.18 | ||||

| CY 2004 EBIT | $ | 21.58 | $ | 32.05 | $ | 33.79 | $ | 39.76 | ||||

| CY 2004 net income | $ | 22.60 | $ | 32.62 | $ | 35.28 | $ | 38.76 | ||||

Selected Mergers and Acquisitions Analysis. Southwest Securities conducted an analysis of merger and acquisition transactions involving pharmacy benefit management and/or specialty pharmaceutical distribution companies as a method of valuing us. A mergers and acquisitions analysis reviews and analyzes transactions, and the resulting implied multiples, involving companies in the same or similar industries as ours ("Selected Transactions"). No acquired company or business used in the mergers and acquisitions analysis is identical or substantially identical to us, and none of the transactions were identical or substantially identical to the proposed Transactions.

In performing this analysis, Southwest Securities analyzed the acquisition of publicly traded and privately held companies. Southwest Securities then calculated the acquisition multiples paid for these companies. The range of multiples of these transactions was then applied to our financial results. The analysis focused on transactions where the target company's LTM EBITDA was disclosed and calculated the ratio of enterprise value (based on disclosed transaction value) to LTM EBITDA. For the purposes of this analysis, Southwest Securities reviewed more than 60 merger and acquisition transactions since 1998. Southwest Securities then reviewed each of these transactions to determine which transactions involved pharmacy benefit management and/or specialty pharmaceutical distribution companies and selected the transactions that disclosed the information necessary to be included in the analysis. Southwest Securities selected the 14 transactions that met the industry criteria and for which the information that was necessary to calculate the enterprise value and LTM EBITDA was publicly available. Southwest Securities calculated the low, mean, median and high multiples based on these 14 Selected Transactions. In reviewing the results of its analysis, Southwest Securities noted that the price per share to be received for the series A preferred stock and to be paid in the tender offer, as well as the closing market price per share of our common stock on October 29, 2003, two days prior to the announcement of the Contemplated Transaction, were lower than the values implied by the Selected Transactions' mean, median and high multiples. The transactions that Southwest Securities used in this analysis include the following:

21

Using the above-mentioned information, Southwest Securities derived a range of estimated values for us, based upon the implied enterprise values for us, derived by applying the Enterprise Value Multiples of the Selected Transactions to our LTM EBITDA. Southwest Securities ultimately derived a range of equity values per share of our common stock for each multiple after taking into account our net debt of $11.5 million as of June 30, 2003 and our number of shares outstanding, using the treasury stock method, as of September 30, 2003.

Southwest Securities applied the Selected Transactions' multiples to our LTM EBITDA and calculated a range of implied equity values per share of our common stock based on the Selected Transactions' low, mean, median and high multiples. This analysis resulted in the following implied equity values per share of our common stock:

| | Implied Equity Value Per Share of Our Common Stock | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Financial Statistic | ||||||||||||

| Low | Mean | Median | High | |||||||||

| LTM EBITDA | $ | 7.98 | $ | 14.51 | $ | 13.87 | $ | 25.76 | ||||

Discounted Cash Flow Analysis. Southwest Securities performed a discounted cash flow analysis to determine a range of implied present values per share of our common stock premised upon the assumptions summarized below. The discounted cash flow analysis was based upon financial and operating information relating to our business, operations and prospects supplied by our management and covering fiscal years 2004 through 2007.

In order to perform this analysis, Southwest Securities selected discount rates ranging from 25% to 35%, which it determined to be representative of an investor's return on equity expectations for a small market cap growth company. Using these discount rates, Southwest Securities calculated a range of present values of our projected stream of Net Unlevered Cash Flows (as defined below) for fiscal years 2004 through 2007 and a range of present cash values of our terminal value (the "Terminal Value") at June 30, 2007. "Net Unlevered Cash Flows," as used in the analysis, is defined, for each period, as projected EBIT, less taxes at an estimated rate of 41.0%, plus projected depreciation and amortization, plus or minus projected changes in non-cash working capital, less projected capital expenditures. The Terminal Value was computed by multiplying our projected fiscal year 2007 EBITDA by terminal multiples ranging from 5.0x to 9.0x. Southwest Securities determined these multiples to be representative of the multiples applicable to us, which are calculated by dividing potential enterprise value by EBITDA. Southwest Securities also compared this multiple range to the multiples it calculated in the Selected Mergers and Acquisitions Analysis and determined that the range captured more than 70% of the Selected Transactions, and included the mean and median of the Selected Transactions. Southwest Securities calculated present values of the Net Unlevered Cash Flows and Terminal Value and subtracted our net debt of $11.5 million as of June 30, 2003, in order to calculate a range of implied equity values for us. Southwest Securities then calculated a range of implied equity values per share of our common stock by dividing the equity values by the number of shares of our common stock outstanding, using the treasury stock method, as of September 30, 2003, to calculate a range of implied equity values per share of our common stock.

Based on the range of discount rates and terminal multiples referred to above, Southwest Securities calculated a range of implied equity values per share of our common stock between $19.41 and $41.54. The closing price of our common stock on October 30, 2003, the day prior to the announcement of the Contemplated Transactions, was $13.75 per share. In reviewing the results of its

22