UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-5162 |

|

Delaware VIP Trust |

(Exact name of registrant as specified in charter) |

|

2005 Market Street Philadelphia, PA | | 19103 |

(Address of principal executive offices) | | (Zip code) |

|

David F. Connor, Esq. 2005 Market Street Philadelphia, PA 19103 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | (800) 523-1918 | |

|

Date of fiscal year end: | December 31 | |

|

Date of reporting period: | December 31, 2007 | |

| | | | | | | | | |

Item 1. Reports to Stockholders

Delaware VIP Trust — Delaware VIP Balanced Series

For the fiscal year ended Dec. 31, 2007, Delaware VIP Balanced Series returned +0.33% for Standard Class shares with distributions reinvested, and +0.05% for Service Class shares with all distributions reinvested. The Series fell short of its benchmarks: the S&P 500 Index returned +5.49%, and the Lehman Brothers U.S. Aggregate Index returned +6.97% (source: Lipper).

Returns for the portion of assets allocated to equities trailed the equity benchmark, the S&P 500 Index, and detracted from overall performance. In equity investments, the Series’ healthcare investments performed favorably overall. Our investments in telecommunication services also contributed to returns. The fixed income portfolio underperformed the Lehman Brothers U.S. Aggregate Index return.

Overall, the Series seeks a balance of capital appreciation, income, and preservation of capital. During the year 2007, the economic picture was marred by a deepening housing slump and a tumultuous mortgage market. Credit markets, driven by a loss of confidence in the value of many types of debt collateral and the relevance of ratings on that debt, essentially seized up until central banks stepped in to provide sufficient sources of liquidation. By the time the fiscal year ended, the U.S. Federal Reserve had trimmed interest rates at meetings in September, October, and December, for a total of 100 basis points, or one percentage point (to 4.25%).

We had positioned the Series to diminish the effects of private equity take-outs on our corporate bond portfolio. As a result, the Series carried a position in financial hybrid securities that were hurt by the credit crunch early on. The Series also carried an overweight in mortgage and asset-backed investments, which performed poorly during the credit turmoil. Another overweight — in the commercial mortgage-backed sector — also contributed to the performance deficit versus the index. Illiquid markets made it very difficult to adjust the Series’ position as we entered the volatile summer months.

It was a difficult year for the financial sector, as a whole, and several of our financial holdings experienced steep declines, especially Washington Mutual, Discover Financial Services and Huntington Bancshares. At year end, we believed that Washington Mutual could survive the housing market correction and, longer term, offered an attractive risk/reward tradeoff relative to its current price. Despite its decline during the year, we continued to have confidence in Discover’s long-term value. Similarly, we believed Huntington Bancshares, as a traditional bank that profits from spread lending, could meaningfully benefit from an eventual recovery in the economy and credit markets.

The team repositioned the Series to be significantly underweight in the financial sector. Taking into consideration contributions on a duration basis, the Series is now underexposed to corporate bonds in general. In addition, our mortgage investments analysts worked to reduce the asset-backed investment position, and to produce a neutral position versus the benchmark in the structured product area. The Series’ duration was moved to a slightly longer position to capture bond rallies in the weakening economic situation.

The views expressed are current as of the date of this report and are subject to change.

The performance data quoted below represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Please obtain the performance data for the most recent month end by calling the number noted in the introductory section of this report on the page related to this Series.

You should consider the investment objectives, risks, charges, and expenses of the investment company carefully before investing. The Delaware VIP Balanced Series prospectus contains this and other important information about the Series. To obtain a prospectus, contact the company noted on the page related to this Series in the introductory section of this report, either by phone or through the company Web site. We advise you to read the prospectus carefully before you invest.

Delaware VIP Balanced Series

Average annual total returns

For periods ended Dec. 31, 2007 | | 1 year | | 5 years | | 10 years | | Lifetime | |

| | | | | | | | | |

Standard Class shares (commenced operations July 28, 1988) | | +0.33 | % | +8.81 | % | +2.25 | % | +7.75 | % |

| | | | | | | | | |

Service Class shares (commenced operations May 1, 2000) | | +0.05 | % | +8.54 | % | NA | | +2.22 | % |

As disclosed in the Series’ most recent prospectus, expenses for Standard Class and Service Class shares were as follows: The net expense ratios for Standard Class and Service Class shares of the Series were 0.83% and 1.08%, respectively. Total operating expenses for Standard Class and Service Class shares were 0.83% and 1.13%, respectively. Management fees for Standard Class and Service Class shares were 0.65%.

Earnings from a variable annuity or variable life investment compound tax-free until withdrawal and, as a result, no adjustments were made for income taxes.

An expense limitation was in effect for all classes during the periods shown in the Series performance chart above and in the Performance of a $10,000 Investment chart on the next page.

1

Performance of Service Class shares will vary due to different charges and expenses.

Performance data do not reflect insurance fees related to a variable annuity or variable life investment or the deferred sales charge that would apply to certain withdrawals of investments held for fewer than eight years. Performance shown here would have been reduced if such fees were included and the expense limitation removed. For more information about fees, consult your variable annuity or variable life prospectus.

Investments in variable products involve risk. A rise or fall in interest rates can have a significant impact on bond prices and the net asset value (NAV) of the Series. High yielding, noninvestment grade bonds (junk bonds) involve higher risk than investment grade bonds. Adverse conditions may affect the issuer’s ability to pay interest and principal on these securities. The portfolio may have turnover in excess of 100%. High portfolio turnover can increase the Series’ transaction costs and lower returns.

The Series may be invested in foreign high yield corporate bonds, which have special risks that include currency fluctuations, economic and political change, and different accounting standards. Some portfolios offer more risk than others. The Series may utilize futures and swaps for defensive strategy purposes to project or minimize the impact of potential changes.

Please read both the contract and underlying prospectus for specific details regarding the product’s risk profile.

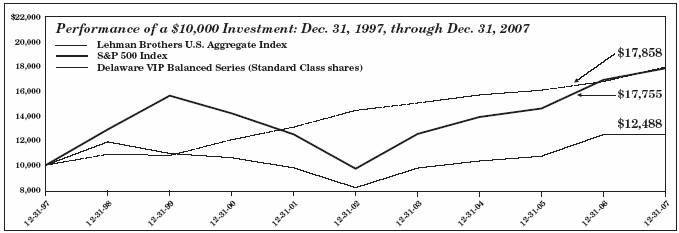

The chart shows a $10,000 investment in the Delaware VIP Balanced Series Standard Class shares for the period from Dec. 31, 1997, through Dec. 31, 2007. Performance of Service Class shares will vary due to different charges and expenses.

The chart also shows $10,000 invested in the S&P 500 Index and Lehman Brothers U.S. Aggregate Index for the period from Dec. 31, 1997, through Dec. 31, 2007. The S&P 500 Index measures the performance of mostly large-capitalization U.S. companies. The Lehman Brothers U.S. Aggregate Index, sometimes also referred to as the Lehman Brothers Aggregate Bond Index, measures the performance of approximately 6,500 publicly issued investment grade (Baa3/BBB- or better) corporate, U.S. government, mortgage- and asset-backed securities with at least one year to maturity and at least $250 million par value outstanding. An index is unmanaged and does not reflect the costs of operating a mutual fund, such as the costs of buying, selling, and holding securities. You cannot invest directly in an index.

2

Delaware VIP Trust — Delaware VIP Balanced Series

Disclosure of Series Expenses

For the Period July 1, 2007 to December 31, 2007

As a shareholder of the Series, you incur ongoing costs, including management fees; distribution and/or service (12b-1) fees; and other Series expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Series and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from July 1, 2007 to December 31, 2007.

Actual Expenses

The first section of the table shown, “Actual Series Return,” provides information about actual account values and actual expenses. You may use the information in this section of the table, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during the period.

Hypothetical Example for Comparison Purposes

The second section of the table shown, “Hypothetical 5% Return,” provides information about hypothetical account values and hypothetical expenses based on the Series’ actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Series’ actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Series and other funds. To do so, compare the 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only. As a shareholder of the Series, you do not incur any transaction costs, such as sales charges (loads), redemption fees or exchange fees, but shareholders of other funds may incur such costs. Also, the fees related to the variable annuity investment or the deferred sales charge that could apply have not been included. Therefore, the second section of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. The Series’ actual expenses shown in the table reflect fee waivers in effect. The expenses shown in the table assume reinvestment of all dividends and distributions.

Expense Analysis of an Investment of $1,000

| | Beginning

Account

Value

7/1/07 | | Ending

Account

Value

12/31/07 | | Annualized

Expense

Ratios | | Expenses

Paid During

Period

7/1/07 to

12/31/07* | |

Actual Series Return | | | | | | | | | |

Standard Class | | $ | 1,000.00 | | $ | 958.60 | | 0.85 | % | $ | 4.20 | |

Service Class | | 1,000.00 | | 957.30 | | 1.10 | % | 5.43 | |

Hypothetical 5% Return (5% return before expenses) | | | | | | | | | |

Standard Class | | $ | 1,000.00 | | $ | 1,020.92 | | 0.85 | % | $ | 4.33 | |

Service Class | | 1,000.00 | | 1,019.66 | | 1.10 | % | 5.60 | |

*“Expenses Paid During Period” are equal to the Series’ annualized expense ratio, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period).

3

Delaware VIP Trust — Delaware VIP Balanced Series

Sector Allocation and Credit Quality Breakdown

As of December 31, 2007

Sector designations may be different than the sector designations presented in other Series materials.

Sector | | Percentage

of Net Assets | |

Common Stock | | 59.61 | % |

Consumer Discretionary | | 5.54 | % |

Consumer Staples | | 7.43 | % |

Energy | | 4.10 | % |

Financials | | 13.62 | % |

Health Care | | 10.60 | % |

Industrials | | 3.45 | % |

Information Technology | | 7.44 | % |

Materials | | 1.81 | % |

Media | | 0.00 | % |

Telecommunications | | 3.78 | % |

Utilities | | 1.84 | % |

Convertible Preferred Stock | | 0.08 | % |

Preferred Stock | | 0.09 | % |

Agency Asset-Backed Security | | 0.01 | % |

Agency Collateralized Mortgage Obligations | | 2.48 | % |

Agency Mortgage-Backed Securities | | 5.34 | % |

Agency Obligations | | 2.10 | % |

Commercial Mortgage-Backed Securities | | 3.56 | % |

Convertible Bonds | | 0.21 | % |

Corporate Bonds | | 8.11 | % |

Banking | | 0.68 | % |

Basic Industry | | 0.33 | % |

Brokerage | | 0.43 | % |

Capital Goods | | 0.12 | % |

Communications | | 1.35 | % |

Consumer Cyclical | | 0.43 | % |

Consumer Non-Cyclical | | 1.67 | % |

Electric | | 0.53 | % |

Energy | | 0.56 | % |

Finance Companies | | 0.66 | % |

Insurance | | 0.30 | % |

Natural Gas | | 0.72 | % |

Real Estate | | 0.16 | % |

Technology | | 0.04 | % |

Transportation | | 0.13 | % |

Municipal Bonds | | 1.10 | % |

Non-Agency Asset-Backed Securities | | 4.02 | % |

Non-Agency Collateralized Mortgage Obligations | | 8.28 | % |

U.S. Treasury Obligations | | 6.28 | % |

Discount Note | | 1.94 | % |

Securities Lending Collateral | | 5.79 | % |

Total Value of Securities | | 109.00 | % |

Obligation to Return Securities Lending Collateral | | (5.79 | )% |

Liabilities Net of Receivables and Other Assets | | (3.21 | )% |

Total Net Assets | | 100.00 | % |

Credit Quality Breakdown

(as a % of fixed income investments) | | | |

AAA | | 72.03 | % |

AA | | 7.73 | % |

A | | 8.67 | % |

BBB | | 10.47 | % |

BB | | 0.57 | % |

B | | 0.53 | % |

Total | | 100.00 | % |

4

Delaware VIP Trust — Delaware VIP Balanced Series

Statement of Net Assets

December 31, 2007

| | Number of

Shares | | Value

(U.S. $) | |

| | | | | | |

| COMMON STOCK–59.61% | | | | | |

| Consumer Discretionary–5.54% | | | | | |

| Gap | | 25,800 | | $ | 549,024 | |

| Limited Brands | | 24,400 | | 461,892 | |

| Mattel | | 25,500 | | 485,520 | |

| | | | | 1,496,436 | |

| Consumer Staples–7.43% | | | | | |

| Heinz (H.J.) | | 11,200 | | 522,816 | |

* | Kimberly-Clark | | 7,400 | | 513,116 | |

| Kraft Foods Class A | | 15,300 | | 499,239 | |

| Safeway | | 13,800 | | 472,098 | |

| | | | | 2,007,269 | |

| Energy–4.10% | | | | | |

| Chevron | | 5,900 | | 550,647 | |

| ConocoPhillips | | 6,300 | | 556,290 | |

| | | | | 1,106,937 | |

| Financials–13.62% | | | | | |

| Allstate | | 10,200 | | 532,746 | |

| Chubb | | 9,700 | | 529,426 | |

| Discover Financial Services | | 28,750 | | 433,550 | |

| Hartford Financial Services Group | | 5,600 | | 488,264 | |

| Huntington Bancshares | | 31,300 | | 461,988 | |

| Morgan Stanley | | 8,900 | | 472,679 | |

| Wachovia | | 12,200 | | 463,966 | |

| Washington Mutual | | 22,000 | | 299,420 | |

| | | | | 3,682,039 | |

| Health Care–10.60% | | | | | |

| Abbott Laboratories | | 8,500 | | 477,275 | |

| Baxter International | | 8,300 | | 481,815 | |

| Bristol-Myers Squibb | | 17,500 | | 464,100 | |

| Johnson & Johnson | | 7,200 | | 480,240 | |

| Pfizer | | 21,300 | | 484,149 | |

| Wyeth | | 10,800 | | 477,252 | |

| | | | | 2,864,831 | |

| Industrials–3.45% | | | | | |

| Donnelley (R.R.) & Sons | | 13,000 | | 490,620 | |

| Waste Management | | 13,500 | | 441,045 | |

| | | | | 931,665 | |

| Information Technology–7.44% | | | | | |

| Intel | | 19,500 | | 519,870 | |

* | International Business Machines | | 4,700 | | 508,070 | |

| Motorola | | 29,100 | | 466,764 | |

| Xerox | | 31,800 | | 514,842 | |

| | | | | 2,009,546 | |

| Materials–1.81% | | | | | |

| duPont (E.I.) deNemours | | 11,100 | | 489,399 | |

| | | | | 489,399 | |

| Media–0.00% | | | | | |

† | Century Communications | | 5,000 | | 4 | |

| | | | | 4 | |

| Telecommunications–3.78% | | | | | |

| AT&T | | 12,400 | | 515,344 | |

| Verizon Communications | | 11,600 | | 506,804 | |

| | | | | 1,022,148 | |

| Utilities–1.84% | | | | | |

| Progress Energy | | 10,300 | | $ | 498,829 | |

| | | | | 498,829 | |

| Total Common Stock

(cost $15,005,953) | | | | 16,109,103 | |

| | | | | | |

| CONVERTIBLE PREFERRED STOCK–0.08% | | | | | |

· | Citigroup Funding 4.943% exercise price $29.50, expiration date 9/27/08 | | 900 | | 22,599 | |

| Total Convertible Preferred Stock

(cost $28,488) | | | | 22,599 | |

| | | | | | |

| PREFERRED STOCK–0.09% | | | | | |

| Fannie Mae 8.25% | | 900 | | 23,175 | |

| Total Preferred Stock

(cost $22,500) | | | | 23,175 | |

| | Principal

Amount

(U.S. $) | | | |

| | | | | | |

| AGENCY ASSET-BACKED SECURITY–0.01% | | | | | |

· | Fannie Mae Whole Loan | | | | | |

| Series 2002-W11 AV1 5.205% 11/25/32 | | $ | 1,800 | | 1,800 | |

| Total Agency Asset-Backed Security (cost $1,801) | | | | 1,800 | |

| | | | | | |

| AGENCY COLLATERALIZED MORTGAGE OBLIGATIONS–2.48% | | | | | |

| Fannie Mae | | | | | |

| Series 1996-46 ZA 7.50% 11/25/26 | | 16,716 | | 17,550 | |

| Series 2003-122 AJ 4.50% 2/25/28 | | 16,017 | | 15,785 | |

| Series 2005-67 EY 5.50% 8/25/25 | | 15,000 | | 15,094 | |

· | Series 2006-M2 A2F 5.259% 5/25/20 | | 60,000 | | 59,405 | |

| Fannie Mae Grantor Trust | | | | | |

| Series 2001-T8 A2 9.50% 7/25/41 | | 14,001 | | 15,286 | |

| Fannie Mae Whole Loan | | | | | |

| Series 2004-W9 2A1 6.50% 2/25/44 | | 24,260 | | 25,317 | |

| Series 2004-W11 1A2 6.50% 5/25/44 | | 24,795 | | 26,129 | |

| Freddie Mac | | | | | |

| Series 1730 Z 7.00% 5/15/24 | | 14,361 | | 15,264 | |

| Series 2326 ZQ 6.50% 6/15/31 | | 66,818 | | 70,882 | |

| Series 2557 WE 5.00% 1/15/18 | | 25,000 | | 25,081 | |

| Series 2662 MA 4.50% 10/15/31 | | 30,751 | | 30,467 | |

| Series 2694 QG 4.50% 1/15/29 | | 30,000 | | 29,634 | |

| Series 2872 GC 5.00% 11/15/29 | | 40,000 | | 39,964 | |

| Series 3005 ED 5.00% 7/15/25 | | 40,000 | | 38,965 | |

| Series 3022 MB 5.00% 12/15/28 | | 30,000 | | 30,164 | |

| Series 3063 PC 5.00% 2/15/29 | | 60,000 | | 60,520 | |

| Series 3113 QA 5.00% 11/15/25 | | 36,005 | | 36,129 | |

| Series 3173 PE 6.00% 4/15/35 | | 70,000 | | 71,256 | |

| Series 3337 PB 5.50% 7/15/30 | | 20,000 | | 20,285 | |

t | Freddie Mac Structured Pass Through Securities | | | | | |

| Series T-58 2A 6.50% 9/25/43 | | 26,511 | | 27,690 | |

| Total Agency Collateralized Mortgage Obligations (cost $665,790) | | | | 670,867 | |

| | | | | | | |

5

| | Principal

Amount

(U.S. $) | | Value

(U.S. $) | |

| | | | | | |

| AGENCY MORTGAGE-BACKED SECURITIES–5.34% | | | | | |

| Fannie Mae 6.50% 8/1/17 | | $ | 19,148 | | $ | 19,714 | |

· | Fannie Mae ARM 5.968% 8/1/37 | | 53,198 | | 53,722 | |

| Fannie Mae Relocation 30 yr 5.00% 11/1/34 | | 30,919 | | 30,404 | |

| Fannie Mae S.F. 15 yr TBA | | | | | |

| 4.50% 1/1/23 | | 70,000 | | 68,906 | |

| 5.00% 1/1/23 | | 150,000 | | 150,164 | |

| 5.50% 1/1/23 | | 60,000 | | 60,778 | |

| 6.00% 1/1/23 | | 110,000 | | 112,561 | |

| Fannie Mae S.F. 30 yr | | | | | |

| 5.50% 3/1/29 | | 63,538 | | 63,773 | |

| 5.50% 4/1/29 | | 70,041 | | 70,300 | |

| 5.50% 8/1/37 | | 134,987 | | 134,835 | |

| 6.50% 2/1/37 | | 99,321 | | 102,107 | |

| 6.50% 11/1/37 | | 54,630 | | 56,156 | |

| 7.50% 6/1/31 | | 21,219 | | 22,649 | |

| 9.50% 6/1/19 | | 3,138 | | 3,330 | |

· | Freddie Mac ARM | | | | | |

| 5.683% 7/1/36 | | 20,653 | | 20,930 | |

| 6.335% 4/1/34 | | 8,964 | | 9,057 | |

| Freddie Mac S.F. 15 yr | | | | | |

| 4.00% 2/1/14 | | 46,265 | | 45,921 | |

| 5.00% 6/1/18 | | 17,305 | | 17,348 | |

| Freddie Mac S.F. 30 yr | | | | | |

| 6.00% 6/1/37 | | 35,000 | | 35,526 | |

| 7.00% 11/1/33 | | 11,905 | | 12,490 | |

| Freddie Mac S.F. 30 yr TBA 5.00% 1/1/38 | | 210,000 | | 204,882 | |

| GNMA S.F. 30 yr 7.50% 1/15/32 | | 4,929 | | 5,259 | |

| GNMA S.F. 30 yr TBA | | | | | |

| 5.50% 1/1/38 | | 70,000 | | 70,514 | |

| 6.00% 1/1/38 | | 70,000 | | 71,663 | |

| Total Agency Mortgage-Backed Securities (cost $1,434,608) | | | | 1,442,989 | |

| | | | | | |

| AGENCY OBLIGATIONS–2.10% | | | | | |

| Fannie Mae | | | | | |

* | 4.75% 3/12/10 | | 60,000 | | 61,486 | |

* | 4.75% 11/19/12 | | 200,000 | | 207,198 | |

| 4.875% 5/18/12 | | 25,000 | | 26,001 | |

^ | 5.377% 10/9/19 | | 230,000 | | 129,044 | |

| Federal Home Loan Bank 4.50% 10/9/09 | | 25,000 | | 25,397 | |

^ | Resolution Funding Interest Strip 5.24% 10/15/25 | | 275,000 | | 117,862 | |

| Total Agency Obligations

(cost $544,606) | | | | 566,988 | |

| | | | | | |

| COMMERCIAL MORTGAGE-BACKED SECURITIES–3.56% | | | | | |

| Bank of America Commercial Mortgage | | | | | |

· | Series 2004-3 A5 5.316% 6/10/39 | | 30,000 | | 30,861 | |

· | Series 2005-6 AM 5.181% 9/10/47 | | 15,000 | | 14,589 | |

· | Series 2006-3 A4 5.889% 7/10/44 | | 30,000 | | 31,170 | |

| Series 2006-4 A4 5.634% 7/10/46 | | 10,000 | | 10,211 | |

| Bear Stearns Commercial Mortgage Securities | | | | | |

# | Series 2004-ESA E 144A 5.064% 5/14/16 | | $ | 40,000 | | $ | 40,600 | |

· | Series 2007-T28 A4 5.742% 9/11/42 | | 30,000 | | 30,732 | |

t | Commercial Mortgage Pass Through Certificates | | | | | |

#· | Series 2001-J1A A2 144A 6.457% 2/14/34 | | 27,337 | | 28,450 | |

| Series 2006-C7 A2 5.69% 6/10/46 | | 25,000 | | 25,388 | |

· | Credit Suisse Mortgage Capital Certificates Series 2006-C1 AAB 5.555% 2/15/39 | | 15,000 | | 15,215 | |

# | Crown Castle Towers Series 2005-1A C 144A 5.074% 6/15/35 | | 25,000 | | 24,458 | |

| First Union National Bank-Bank of America Commercial Mortgage Trust

Series 2001-C1 C 6.403% 3/15/33 | | 10,000 | | 10,459 | |

| First Union-Lehman Brothers-Bank of America Series 1998-C2 A2 6.56% 11/18/35 | | 19,659 | | 19,645 | |

| General Electric Capital Commercial Mortgage Series 2002-1A A3 6.269% 12/10/35 | | 50,000 | | 52,647 | |

| Goldman Sachs Mortgage Securities II | | | | | |

| Series 2004-GG2 A3 4.602% 8/10/38 | | 20,000 | | 19,965 | |

| Series 2006-GG8 A4 5.56% 11/10/39 | | 40,000 | | 40,624 | |

| Greenwich Capital Commercial Funding Series 2007-GG9 A4 5.444% 3/10/39 | | 25,000 | | 25,148 | |

| JPMorgan Chase Commercial Mortgage Securities | | | | | |

| Series 2002-C1 A3 5.376% 7/12/37 | | 35,000 | | 35,701 | |

| Series 2003-C1 A2 4.985% 1/12/37 | | 68,000 | | 68,228 | |

#· | Series 2006-RR1A A1 144A 5.455% 10/18/52 | | 25,000 | | 21,723 | |

| Lehman Brothers-UBS Commercial Mortgage Trust | | | | | |

| Series 2001-C2 A1 6.27% 6/15/20 | | 4,069 | | 4,099 | |

| Series 2002-C1 A4 6.462% 3/15/31 | | 55,000 | | 58,308 | |

· | Merrill Lynch Mortgage Trust Series 2006-C1 ASB 5.659% 5/12/39 | | 35,000 | | 35,799 | |

| Merrill Lynch/Countrywide Commercial Mortgage Trust Series 2007-5 A1 4.275% 8/12/48 | | 44,688 | | 44,055 | |

· | Morgan Stanley Capital I Series 2007-IQ14 A4 5.692% 4/15/49 | | 25,000 | | 25,482 | |

# | SBA Commercial Mortgage Securities Trust Series 2006-1A B 144A 5.451% 11/15/36 | | 60,000 | | 59,469 | |

6

| | Principal

Amount

(U.S. $) | | Value

(U.S. $) | |

| | | | | | |

| COMMERCIAL MORTGAGE-BACKED SECURITIES (continued) | | | | | |

# | Tower 144A | | | | | | | |

| Series 2004-2A A 4.232% 12/15/14 | | $ | 45,000 | | $ | 44,141 | |

| Series 2006-1 B 5.588% 2/15/36 | | 25,000 | | 24,811 | |

| Series 2006-1 C 5.707% 2/15/36 | | 25,000 | | 24,991 | |

| Wachovia Bank Commercial Mortgage Trust | | | | | |

· | Series 2005-C20 A5 5.087% 7/15/42 | | 15,000 | | 14,936 | |

| Series 2006-C28 A2 5.50% 10/15/48 | | 40,000 | | 40,356 | |

| Series 2007-C30 A3 5.246% 12/15/43 | | 40,000 | | 39,928 | |

| Total Commercial Mortgage-Backed Securities (cost $970,944) | | | | 962,189 | |

| | | | | | |

| CONVERTIBLE BONDS–0.21% | | | | | |

· | U.S. Bancorp 3.176% 9/20/36 exercise price $38.28, expiration date 9/20/36 | | 35,000 | | 34,968 | |

*· | Wyeth 4.886% 1/15/24 exercise price $60.09, expiration date 1/15/24 | | 20,000 | | 21,201 | |

| Total Convertible Bonds

(cost $56,330) | | | | 56,169 | |

| | | | | | |

| CORPORATE BONDS–8.11% | | | | | |

| Banking–0.68% | | | | | |

| JPMorgan Chase 5.75% 1/2/13 | | 30,000 | | 30,605 | |

| JPMorgan Chase Capital XXV 6.80% 10/1/37 | | 25,000 | | 24,111 | |

| Popular North America | | | | | |

| 4.25% 4/1/08 | | 55,000 | | 54,886 | |

· | 5.643% 4/6/09 | | 25,000 | | 25,091 | |

| Popular North America Capital Trust I 6.564% 9/15/34 | | 10,000 | | 8,939 | |

| U.S. Bank North America 4.80% 4/15/15 | | 15,000 | | 14,425 | |

| Wachovia Bank North America 6.60% 1/15/38 | | 10,000 | | 10,083 | |

| Wells Fargo 5.625% 12/11/17 | | 15,000 | | 15,037 | |

| | | | | 183,177 | |

| Basic Industry–0.33% | | | | | |

| duPont (E.I.) deNemours 5.00% 1/15/13 | | 20,000 | | 20,148 | |

| Georgia-Pacific 8.875% 5/15/31 | | 1,000 | | 970 | |

| Lubrizol 4.625% 10/1/09 | | 30,000 | | 30,140 | |

| Potlatch 13.00% 12/1/09 | | 5,000 | | 5,674 | |

| Rohm & Haas 5.60% 3/15/13 | | 31,000 | | 32,249 | |

| | | | | 89,181 | |

| Brokerage–0.43% | | | | | |

| AMVESCAP 4.50% 12/15/09 | | 55,000 | | 54,293 | |

| Goldman Sachs Group 6.75% 10/1/37 | | 33,000 | | 32,435 | |

| Jefferies Group 6.45% 6/8/27 | | 20,000 | | 18,630 | |

| LaBranche 11.00% 5/15/12 | | 1,000 | | 984 | |

| Lazard Group 6.85% 6/15/17 | | 10,000 | | 9,894 | |

| | | | | 116,236 | |

| Capital Goods–0.12% | | | | | |

| L-3 Communications 7.625% 6/15/12 | | $ | 2,000 | | $ | 2,058 | |

· | Masco 5.433% 3/12/10 | | 20,000 | | 19,328 | |

| Textron 6.50% 6/1/12 | | 10,000 | | 10,620 | |

| | | | | 32,006 | |

| Communications–1.35% | | | | | |

| American Tower 7.125% 10/15/12 | | 5,000 | | 5,163 | |

| AT&T 5.10% 9/15/14 | | 5,000 | | 4,955 | |

| AT&T Wireless 8.125% 5/1/12 | | 50,000 | | 55,647 | |

| Citizens Communications 7.125% 3/15/19 | | 5,000 | | 4,775 | |

| Comcast | | | | | |

· | 5.543% 7/14/09 | | 15,000 | | 14,951 | |

| 6.30% 11/15/17 | | 50,000 | | 51,972 | |

# | Donnelley (R.H.) 144A 8.875% 10/15/17 | | 5,000 | | 4,650 | |

| Hughes Network Systems/Finance 9.50% 4/15/14 | | 2,000 | | 2,035 | |

| Rural Cellular 9.875% 2/1/10 | | 5,000 | | 5,213 | |

· | Sprint Nextel 5.243% 6/28/10 | | 15,000 | | 14,422 | |

| Telecom Italia Capital 4.00% 1/15/10 | | 30,000 | | 29,397 | |

| Telefonica Emisiones 5.984% 6/20/11 | | 75,000 | | 77,211 | |

| THOMSON 5.70% 10/1/14 | | 30,000 | | 30,165 | |

| Time Warner Cable 5.40% 7/2/12 | | 45,000 | | 45,135 | |

| Viacom | | | | | |

· | 5.341% 6/16/09 | | 10,000 | | 9,884 | |

| 5.75% 4/30/11 | | 10,000 | | 10,133 | |

| | | | | 365,708 | |

| Consumer Cyclical–0.43% | | | | | |

| CVS Caremark | | | | | |

| 4.875% 9/15/14 | | 10,000 | | 9,672 | |

| 5.75% 6/1/17 | | 15,000 | | 15,124 | |

· | DaimlerChrysler Holding 5.328% 8/3/09 | | 30,000 | | 29,806 | |

| GMAC 6.875% 9/15/11 | | 32,000 | | 27,397 | |

| Host Marriott 7.125% 11/1/13 | | 2,000 | | 2,025 | |

| Majestic Star Casino 9.50% 10/15/10 | | 5,000 | | 4,750 | |

| McDonald’s 6.30% 10/15/37 | | 25,000 | | 26,015 | |

| MGM MIRAGE 7.625% 1/15/17 | | 2,000 | | 1,985 | |

| | | | | 116,774 | |

| Consumer Non-Cyclical–1.67% | | | | | |

| Abbott Laboratories | | | | | |

| 5.15% 11/30/12 | | 30,000 | | 30,694 | |

| 5.60% 11/30/17 | | 40,000 | | 41,175 | |

# | Amgen 144A | | | | | |

| 5.85% 6/1/17 | | 15,000 | | 15,254 | |

| 6.375% 6/1/37 | | 21,000 | | 21,364 | |

| Anheuser Busch 5.50% 1/15/18 | | 20,000 | | 20,457 | |

| Aramark Services 8.50% 2/1/15 | | 2,000 | | 2,035 | |

| AstraZeneca 5.90% 9/15/17 | | 35,000 | | 36,820 | |

| Clorox 5.45% 10/15/12 | | 10,000 | | 10,093 | |

# | Covidien International Finance 144A | | | | | |

| 6.00% 10/15/17 | | 10,000 | | 10,366 | |

| 6.55% 10/15/37 | | 15,000 | | 15,630 | |

7

| | Principal

Amount

(U.S. $) | | Value

(U.S. $) | |

| | | | | | |

| CORPORATE BONDS (continued) | | | | | |

| Consumer Non-Cyclical (continued) | | | | | |

| Diageo Capital | | | | | |

| 5.20% 1/30/13 | | $ | 4,000 | | $ | 4,023 | |

| 5.75% 10/23/17 | | 18,000 | | 18,136 | |

| HCA PIK 9.625% 11/15/16 | | 2,000 | | 2,120 | |

| Kellogg 5.125% 12/3/12 | | 15,000 | | 15,142 | |

| Kraft Foods | | | | | |

| 4.125% 11/12/09 | | 15,000 | | 14,877 | |

| 6.125% 2/1/18 | | 40,000 | | 40,381 | |

| PepsiCo 4.65% 2/15/13 | | 15,000 | | 15,118 | |

| Safeway 6.35% 8/15/17 | | 15,000 | | 15,662 | |

# | UnitedHealth Group 144A | | | | | |

| 5.50% 11/15/12 | | 30,000 | | 30,477 | |

| 6.00% 11/15/17 | | 40,000 | | 40,607 | |

| Wyeth 5.50% 2/1/14 | | 50,000 | | 50,848 | |

| | | | | 451,279 | |

| Electric–0.53% | | | | | |

| AES 7.75% 3/1/14 | | 5,000 | | 5,063 | |

‡# | Calpine 144A 8.496% 7/15/09 | | 196 | | 207 | |

| Commonwealth Edison 6.15% 9/15/17 | | 15,000 | | 15,486 | |

| # Illinois Power 144A 6.125% 11/15/17 | | 10,000 | | 10,122 | |

| Orion Power Holdings 12.00% 5/1/10 | | 5,000 | | 5,475 | |

| Pacific Gas & Electric 5.625% 11/30/17 | | 15,000 | | 15,074 | |

| Pepco Holdings 6.125% 6/1/17 | | 10,000 | | 10,190 | |

# | Power Contract Financing 144A 6.256% 2/1/10 | | 11,083 | | 11,324 | |

| PSEG Power 5.50% 12/1/15 | | 10,000 | | 9,806 | |

| Southwestern Electric Power 5.875% 3/1/18 | | 20,000 | | 19,767 | |

| Virginia Electric & Power 5.10% 11/30/12 | | 30,000 | | 30,160 | |

# | West Penn Power 144A 5.95% 12/15/17 | | 10,000 | | 10,067 | |

| | | | | 142,741 | |

| Energy–0.56% | | | | | |

| Apache 5.25% 4/15/13 | | 15,000 | | 15,371 | |

| CenterPoint Energy Resource 6.125% 11/1/17 | | 10,000 | | 10,196 | |

| Chesapeake Energy 6.625% 1/15/16 | | 2,000 | | 1,965 | |

| Devon Energy 7.95% 4/15/32 | | 5,000 | | 6,137 | |

| EnCana 5.90% 12/1/17 | | 15,000 | | 15,373 | |

| Husky Energy 6.80% 9/15/37 | | 10,000 | | 10,545 | |

| ONEOK Partners 6.15% 10/1/16 | | 5,000 | | 5,088 | |

# | Ras Laffan Liquefied Natural Gas III 144A 5.832% 9/30/16 | | 25,000 | | 25,449 | |

| Suncor Energy 6.50% 6/15/38 | | 15,000 | | 16,093 | |

| TransCanada Pipelines 6.20% 10/15/37 | | 20,000 | | 19,925 | |

| Transocean 6.00% 3/15/18 | | 10,000 | | 9,992 | |

| Whiting Petroleum 7.25% 5/1/13 | | 5,000 | | 4,950 | |

| Williams 7.50% 1/15/31 | | 1,000 | | 1,080 | |

| XTO Energy 6.25% 8/1/17 | | 10,000 | | 10,510 | |

| | | | | 152,674 | |

| Finance Companies–0.66% | | | | | |

· | American Express 6.80% 9/1/66 | | $ | 30,000 | | $ | 30,468 | |

# | Capmark Financial Group 144A 6.30% 5/10/17 | | 17,000 | | 12,693 | |

| FTI Consulting 7.625% 6/15/13 | | 5,000 | | 5,150 | |

| General Electric Capital 5.625% 9/15/17 | | 20,000 | | 20,558 | |

| International Lease Finance | | | | | |

| 5.35% 3/1/12 | | 15,000 | | 15,024 | |

| 5.875% 5/1/13 | | 10,000 | | 10,177 | |

| SLM 5.40% 10/25/11 | | 64,000 | | 58,378 | |

| Washington Mutual | | | | | |

| 5.25% 9/15/17 | | 15,000 | | 12,533 | |

| 5.50% 8/24/11 | | 15,000 | | 13,390 | |

| | | | | 178,371 | |

| Insurance–0.30% | | | | | |

| Berkshire Hathaway Finance 4.85% 1/15/15 | | 15,000 | | 15,044 | |

| Montpelier Re Holdings 6.125% 8/15/13 | | 5,000 | | 4,848 | |

| Unitrin 6.00% 5/15/17 | | 25,000 | | 23,950 | |

| WellPoint | | | | | |

| 5.00% 1/15/11 | | 20,000 | | 20,043 | |

| 5.00% 12/15/14 | | 18,000 | | 17,267 | |

| | | | | 81,152 | |

| Natural Gas–0.72% | | | | | |

| Dynergy Holdings 7.75% 6/1/19 | | 2,000 | | 1,855 | |

| Enterprise Products Operating 5.60% 10/15/14 | | 20,000 | | 19,988 | |

| Inergy Finance 6.875% 12/15/14 | | 5,000 | | 4,888 | |

| Kinder Morgan Energy Partners 5.125% 11/15/14 | | 15,000 | | 14,636 | |

| Southern Union 6.15% 8/16/08 | | 50,000 | | 50,179 | |

| Valero Energy | | | | | |

| 6.125% 6/15/17 | | 10,000 | | 10,181 | |

| 6.625% 6/15/37 | | 10,000 | | 10,103 | |

| Valero Logistics Operations 6.05% 3/15/13 | | 80,000 | | 81,865 | |

| | | | | 193,695 | |

| Real Estate–0.16% | | | | | |

| iStar Financial | | | | | |

| 5.15% 3/1/12 | | 10,000 | | 8,650 | |

| 5.875% 3/15/16 | | 20,000 | | 16,352 | |

| Regency Centers 5.875% 6/15/17 | | 20,000 | | 19,361 | |

| | | | | 44,363 | |

| Technology–0.04% | | | | | |

| Xerox 5.50% 5/15/12 | | 10,000 | | 10,176 | |

| | | | | 10,176 | |

| Transportation–0.13% | | | | | |

# | Erac USA Finance 144A 7.00% 10/15/37 | | 25,000 | | 22,772 | |

| Hertz 8.875% 1/1/14 | | 10,000 | | 10,188 | |

8

| | Principal

Amount

(U.S. $) | | Value

(U.S. $) | |

| | | | | | |

| CORPORATE BONDS (continued) | | | | | |

| Transportation (continued) | | | | | |

| Kansas City Southern Railway 9.50% 10/1/08 | | $ | 1,000 | | $ | 1,025 | |

| | | | | 33,985 | |

| Total Corporate Bonds

(cost $2,193,184) | | | | 2,191,518 | |

| | | | | | |

| MUNICIPAL BONDS–1.10% | | | | | |

| Augusta, Georgia Water & Sewer Revenue 5.25% 10/1/39 (FSA) | | 55,000 | | 57,999 | |

| Buckeye Ohio Tobacco Settlement Financing Authority 5.875% 6/1/47 | | 15,000 | | 14,401 | |

| California State 5.00% 2/1/33 | | 20,000 | | 20,130 | |

| California State University Systemwide Revenue 5.00% 11/1/30 (AMBAC) | | 20,000 | | 20,763 | |

| Illinois State Taxable Pension 5.10% 6/1/33 | | 30,000 | | 28,955 | |

| New Jersey Economic Development Authority Revenue Cigarette Tax 5.75% 6/15/29 | | 40,000 | | 39,250 | |

| New York State Urban Development Series A-1 5.25% 3/15/34 (FGIC) | | 35,000 | | 36,728 | |

| Oregon State Taxable Pension 5.892% 6/1/27 | | 35,000 | | 36,911 | |

| West Virginia Economic Development Authority 5.37% 7/1/20 (MBIA) | | 15,000 | | 15,206 | |

| West Virginia Tobacco Settlement Finance Authority 7.467% 6/1/47 | | 30,000 | | 28,062 | |

| Total Municipal Bonds

(cost $297,348) | | | | 298,405 | |

| | | | | | |

| NON-AGENCY ASSET-BACKED SECURITIES–4.02% | | | | | |

· | Bank of America Credit Card Trust Series 2006-A10 A10 5.008% 2/15/12 | | 380,000 | | 378,363 | |

| Capital Auto Receivables Asset Trust Series 2007-3 A3A 5.02% 9/15/11 | | 25,000 | | 25,186 | |

| Capital One Multi-Asset Execution Trust Series 2007-A7 A7 5.75% 7/15/20 | | 25,000 | | 25,155 | |

| Caterpillar Financial Asset Trust Series 2007-A A3A 5.34% 6/25/12 | | 10,000 | | 10,151 | |

· | Citibank Credit Card Issuance Trust Series 2007-A6 A6 5.238% 7/12/12 | | 300,000 | | 298,043 | |

| CNH Equipment Trust Series 2007-B A3A 5.40% 10/17/11 | | 30,000 | | 30,393 | |

· | Countrywide Asset-Backed Certificates Series 2006-S7 A3 5.712% 11/25/35 | | 25,000 | | 21,633 | |

· | GMAC Mortgage Loan Trust Series 2006-HE3 A2 5.75% 10/25/36 | | 25,000 | | 22,585 | |

| Harley-Davidson Motorcycle Trust Series 2005-2 A2 4.07% 2/15/12 | | 24,389 | | 24,269 | |

| Hyundai Auto Receivables Trust Series 2007-A A3A 5.04% 1/17/12 | | 10,000 | | 10,047 | |

·# | MASTR Specialized Loan Trust Series 2005-2 A2 144A 5.006% 7/25/35 | | $ | 20,759 | | $ | 18,871 | |

· | Merrill Lynch Mortgage Investors Series 2006-AR1 A2C 5.025% 3/25/37 | | 25,000 | | 23,293 | |

| Mid-State Trust | | | | | |

| Series 11 A1 4.864% 7/15/38 | | 17,117 | | 16,837 | |

| Series 2004-1 A 6.005% 8/15/37 | | 8,856 | | 8,645 | |

# | Series 2006-1 A 144A 5.787% 10/15/40 | | 21,035 | | 20,055 | |

| Renaissance Home Equity Loan Trust | | | | | |

| Series 2005-4 A2 5.399% 2/25/36 | | 5,324 | | 5,305 | |

| Series 2007-2 AF2 5.675% 6/25/37 | | 25,000 | | 23,820 | |

| Residential Asset Securities Series 2003-KS9 AI6 4.71% 11/25/33 | | 22,092 | | 21,171 | |

·# | SLM Student Loan Trust Series 2003-4 A5C 144A 5.151% 3/15/33 | | 35,000 | | 34,650 | |

| Structured Asset Securities | | | | | |

| Series 2001-SB1 A2 3.375% 8/25/31 | | 27,774 | | 24,055 | |

| Series 2004-16XS A2 4.91% 8/25/34 | | 4,992 | | 4,977 | |

| Triad Auto Receivables Owner Trust Series 2006-C A4 5.31% 5/13/13 | | 40,000 | | 40,222 | |

| Total Non-Agency Asset-Backed Securities

(cost $1,104,331) | | | | 1,087,726 | |

| | | | | | |

| NON-AGENCY COLLATERALIZED MORTGAGE OBLIGATIONS–8.28% | | | | | |

· | Adjustable Rate Mortgage Trust Series 2005-10 3A11 5.416% 1/25/36 | | 33,005 | | 31,908 | |

| American Home Mortgage Investment Trust Series 2005-2 5A1 5.064% 9/25/35 | | 35,000 | | 34,751 | |

| Bank of America Alternative Loan Trust | | | | | |

| Series 2003-10 2A1 6.00% 12/25/33 | | 57,278 | | 57,421 | |

| Series 2004-2 1A1 6.00% 3/25/34 | | 32,721 | | 32,803 | |

| Series 2005-3 2A1 5.50% 4/25/20 | | 32,902 | | 33,097 | |

| Series 2005-5 2CB1 6.00% 6/25/35 | | 34,267 | | 34,353 | |

| Series 2005-9 5A1 5.50% 10/25/20 | | 22,044 | | 22,175 | |

· | Bank of America Funding Securities Series 2006-F 1A2 5.175% 7/20/36 | | 39,659 | | 38,985 | |

| Bank of America Mortgage Securities | | | | | |

· | Series 2003-D 1A2 7.281% 5/25/33 | | 238 | | 239 | |

| Series 2005-9 2A1 4.75% 10/25/20 | | 37,193 | | 36,670 | |

| Chase Mortgage Finance Series 2003-S8 A2 5.00% 9/25/18 | | 70,100 | | 68,646 | |

| Citicorp Mortgage Securities Series 2006-3 1A4 6.00% 6/25/36 | | 35,000 | | 34,609 | |

| Countrywide Alternative Loan Trust Series 2004-28CB 6A1 6.00% 1/25/35 | | 15,987 | | 16,027 | |

· | Series 2004-J7 1A2 4.673% 8/25/34 | | 6,896 | | 6,862 | |

· | Series 2005-63 3A1 5.891% 11/25/35 | | 43,634 | | 42,366 | |

| Series 2006-2CB A3 5.50% 3/25/36 | | 32,060 | | 31,877 | |

t | Countrywide Home Loan Mortgage Pass Through Trust | | | | | |

· | Series 2004-12 1M 5.096% 8/25/34 | | 25,974 | | 25,426 | |

| Series 2005-23 A1 5.50% 11/25/35 | | 20,611 | | 20,269 | |

9

| | Principal

Amount

(U.S. $) | | Value

(U.S. $) | |

| | | | | | |

| NON-AGENCY COLLATERALIZED MORTGAGE OBLIGATIONS (continued) | | | | | |

| Series 2006-1 A2 6.00% 3/25/36 | | $ | 35,248 | | $ | 35,358 | |

| Series 2006-17 A5 6.00% 12/25/36 | | 22,314 | | 22,579 | |

· | Series 2006-HYB3 3A1A 6.095% 5/20/36 | | 43,116 | | 44,661 | |

· | Series 2006-HYB4 1A2 5.627% 6/20/36 | | 27,144 | | 26,837 | |

| Credit Suisse First Boston Mortgage Securities | | | | | |

| Series 2003-29 5A1 7.00% 12/25/33 | | 10,391 | | 10,388 | |

| Series 2004-1 3A1 7.00% 2/25/34 | | 7,395 | | 7,634 | |

| First Horizon Asset Securities | | | | | |

| Series 2003-5 1A17 8.00% 7/25/33 | | 15,065 | | 16,022 | |

· | Series 2004-AR5 4A1 5.70% 10/25/34 | | 30,761 | | 30,680 | |

· | Series 2007-AR2 1A1 5.855% 8/25/37 | | 18,858 | | 18,882 | |

· | Series 2007-AR3 2A2 6.315% 11/25/37 | | 58,051 | | 58,356 | |

· | GMAC Mortgage Loan Trust Series 2005-AR2 4A 5.183% 5/25/35 | | 37,380 | | 36,785 | |

# | GSMPS Mortgage Loan Trust 144A | | | | | |

| Series 1998-3 A 7.75% 9/19/27 | | 26,514 | | 28,600 | |

| Series 2005-RP1 1A3 8.00% 1/25/35 | | 20,020 | | 21,655 | |

| Series 2005-RP1 1A4 8.50% 1/25/35 | | 11,171 | | 12,175 | |

| GSR Mortgage Loan Trust Series 2006-1F 5A2 6.00% 2/25/36 | | 37,087 | | 36,924 | |

· | JPMorgan Mortgage Trust | | | | | |

| Series 2005-A1 4A1 4.779% 2/25/35 | | 38,259 | | 37,411 | |

| Series 2005-A4 1A1 5.401% 7/25/35 | | 45,469 | | 45,002 | |

| Series 2005-A6 1A2 5.138% 9/25/35 | | 60,000 | | 58,682 | |

| Lehman Mortgage Trust | | | | | |

| Series 2005-2 2A3 5.50% 12/25/35 | | 31,960 | | 31,895 | |

| Series 2006-1 3A3 5.50% 2/25/36 | | 37,439 | | 37,180 | |

· | MASTR Adjustable Rate Mortgages Trust | | | | | |

| Series 2003-6 1A2 6.739% 12/25/33 | | 11,992 | | 12,375 | |

| Series 2005-1 B1 5.561% 3/25/35 | | 39,324 | | 38,397 | |

| Series 2005-6 7A1 5.326% 6/25/35 | | 26,751 | | 26,435 | |

| MASTR Alternative Loans Trust Series 2003-6 3A1 8.00% 9/25/33 | | 5,655 | | 5,853 | |

# | MASTR Reperforming Loan Trust 144A | | | | | |

| Series 2005-1 1A5 8.00% 8/25/34 | | 31,677 | | 34,159 | |

| Series 2005-2 1A4 8.00% 5/25/35 | | 13,922 | | 15,039 | |

| Morgan Stanley Mortgage Loan Trust Series 2006-2 6A 6.50% 2/25/36 | | 20,857 | | 20,915 | |

| Nomura Asset Acceptance | | | | | |

| Series 2005-WF1 2A2 4.786% 3/25/35 | | 65,000 | | 61,214 | |

| Series 2006-AF1 1A2 6.159% 5/25/36 | | 60,000 | | 57,385 | |

| Prime Mortgage Trust Series 2004-CL1 1A1 6.00% 2/25/34 | | 15,273 | | 15,512 | |

| Residential Asset Mortgage Products | | | | | |

| Series 2004-SL1 A3 7.00% 11/25/31 | | 6,444 | | 6,584 | |

| Series 2004-SL4 A3 6.50% 7/25/32 | | 22,947 | | 22,782 | |

| Series 2005-SL1 A2 6.00% 5/25/32 | | 26,093 | | 26,320 | |

· | Residential Funding Mortgage Securities I Series 2006-SA3 3A1 6.038% 9/25/36 | | 39,349 | | 39,349 | |

· | Structured Adjustable Rate Mortgage Loan Trust | | | | | |

| Series 2004-18 5A 5.50% 12/25/34 | | 33,673 | | 33,171 | |

| Series 2006-5 5A4 5.545% 6/25/36 | | 26,736 | | 25,695 | |

| Structured Asset Securities | | | | | |

· | Series 2002-22H 1A 6.965% 11/25/32 | | $ | 9,414 | | $ | 9,457 | |

| Series 2004-12H 1A 6.00% 5/25/34 | | 32,355 | | 32,709 | |

t | Washington Mutual Alternative Mortgage Pass Through Certificates | | | | | |

| Series 2005-9 3CB 5.50% 10/25/20 | | 46,933 | | 47,212 | |

| Series 2006-5 2CB3 6.00% 7/25/36 | | 41,316 | | 41,156 | |

·t | Washington Mutual Mortgage Pass Through Certificates | | | | | |

| Series 2006-AR8 2A3 6.132% 8/25/36 | | 17,862 | | 17,900 | |

| Series 2006-AR10 1A1 5.942% 9/25/36 | | 37,404 | | 37,795 | |

| Series 2006-AR14 1A4 5.647% 11/25/36 | | 27,473 | | 27,406 | |

| Series 2007-HY3 4A1 5.35% 3/25/37 | | 76,826 | | 76,472 | |

| Wells Fargo Mortgage Backed Securities Trust | | | | | |

· | Series 2004-T A1 6.18% 9/25/34 | | 12,202 | | 12,232 | |

| Series 2005-11 1A3 5.50% 11/25/35 | | 87,884 | | 86,869 | |

| Series 2006-7 2A1 6.00% 6/25/36 | | 78,620 | | 78,276 | |

· | Series 2006-AR6 7A1 5.11% 3/25/36 | | 73,256 | | 71,296 | |

· | Series 2006-AR10 5A1 5.597% 7/25/36 | | 35,995 | | 36,263 | |

| Series 2007-13 A7 6.00% 9/25/37 | | 34,245 | | 34,138 | |

| Total Non-Agency Collateralized Mortgage Obligations

(cost $2,246,508) | | | | 2,236,556 | |

| | | | | | |

| U.S. TREASURY OBLIGATIONS–6.28% | | | | | |

* | U.S. Treasury Bonds 4.75% 2/15/37 | | 323,000 | | 338,140 | |

| U.S. Treasury Inflation Index Notes | | | | | |

¥ | 2.00% 1/15/14 | | 50,881 | | 52,571 | |

| 3.875% 1/15/09 | | 25,478 | | 26,239 | |

| U.S. Treasury Notes | | | | | |

* | 3.125% 11/30/09 | | 186,000 | | 186,262 | |

| 3.625% 12/31/12 | | 775,000 | | 781,054 | |

* | 4.25% 11/15/17 | | 272,000 | | 276,824 | |

^ | U.S. Treasury Strip 4.296% 11/15/13 | | 45,000 | | 36,452 | |

| Total U.S. Treasury Obligations

(cost $1,660,784) | | | | 1,697,542 | |

| | | | | | |

¹ | DISCOUNT NOTE–1.94% | | | | | |

| Federal Home Loan Bank 3.25% 1/2/08 | | 523,094 | | 523,048 | |

| Total Discount Note

(cost $523,048) | | | | 523,048 | |

| Total Value of Securities Before Securities Lending Collateral–103.21%

(cost $26,756,223) | | | | 27,890,674 | |

| | Number of

Shares | | | |

| | | | | | |

| SECURITIES LENDING COLLATERAL**–5.79% | | | | | |

| Investment Companies | | | | | |

| Mellon GSL DBT II Collateral Fund | | 1,565,050 | | 1,565,050 | |

| Total Securities Lending Collateral

(cost $1,565,050) | | | | 1,565,050 | |

10

TOTAL VALUE OF SECURITIES–109.00% (cost $28,321,273) | | $ | 29,455,724 | © |

OBLIGATION TO RETURN SECURITIES LENDING COLLATERAL**–(5.79%) | | (1,565,050 | ) |

LIABILITIES NET OF RECEIVABLES AND OTHER ASSETS–(3.21%) | | (866,715 | ) |

NET ASSETS APPLICABLE TO 1,825,861.1 SHARES OUTSTANDING–100.00% | | $ | 27,023,959 | |

NET ASSET VALUE-DELAWARE VIP BALANCED SERIES STANDARD CLASS ($27,018,048 / 1,825,461 Shares) | | $ | 14.80 | |

NET ASSET VALUE-DELAWARE VIP BALANCED SERIES SERVICE CLASS ($5,911 / 400.1 Shares) | | $ | 14.77 | |

COMPONENTS OF NET ASSETS AT DECEMBER 31, 2007: | | | |

Shares of beneficial interest (unlimited authorization–no par) | | $ | 42,694,049 | |

Undistributed net investment income | | 935,008 | |

Accumulated net realized loss on investments | | (17,759,051 | ) |

Net unrealized appreciation of investments | | 1,153,953 | |

Total net assets | | $ | 27,023,959 | |

* | Fully or partially on loan. |

** | See Note 10 in “Notes to Financial Statements.” |

© | Includes $2,130,472 of securities loaned. |

† | Non-income producing security for the year ended December 31, 2007. |

· | Variable rate security. The rate shown is the rate as of December 31, 2007. |

t | Pass Through Agreement. Security represents the contractual right to receive a proportionate amount of underlying payments due to the counterparty pursuant to various agreements related to the rescheduling of obligations and the exchange of certain notes. |

^ | Zero coupon security. The rate shown is the yield at the time of purchase. |

‡ | Non-income producing security. Security is currently in default. |

¥ | Fully or partially pledged as collateral for financial futures contracts. |

# | Security exempt from registration under Rule 144A of the Securities Act of 1933, as amended. At December 31, 2007, the aggregate amount of Rule 144A securities was $684,829, which represented 2.53% of the Series’ net assets. See Note 11 in “Notes to Financial Statements.” |

¹ | The rate shown is the effective yield at the time of purchase. |

Summary of Abbreviations:

AMBAC – Insured by the AMBAC Assurance Corporation

ARM – Adjustable Rate Mortgage

FGIC – Insured by the Financial Guaranty Insurance Company

FSA – Insured by Financial Security Assurance

GNMA – Government National Mortgage Association

MBIA – Insured by the Municipal Bond Insurance Association

PIK – Pay-In-Kind

S.F. – Single Family

TBA – To be announced

yr – Year

The following futures contracts and swap contracts were outstanding at December 31, 2007:

Futures Contracts(1)

Contracts

to Buy | | Notional

Cost | | Notional

Value | | Expiration Date | | Unrealized

Appreciation | |

5 U.S. Treasury 5 year Notes | | $ | 548,174 | | $ | 551,406 | | 3/31/08 | | $ | 3,232 | |

| | | | | | | | | | | | |

11

Swap Contracts(2)

Credit Default Swap Contracts

Swap Counterparty &

Referenced Obligation | | Notional

Amount | | Annual Protection

Payments | | Termination Date | | Unrealized

Appreciation

(Depreciation) | |

Protection Purchased: | | | | | | | | | |

Goldman Sachs | | | | | | | | | |

Bank of America 5 yr CDS | | $ | 30,000 | | 0.48 | % | 12/20/12 | | $ | (5 | ) |

Best Buy | | | | | | | | | |

5 yr CDS | | 38,000 | | 0.60 | % | 9/20/12 | | 269 | |

10 yr CDS | | 20,000 | | 0.98 | % | 9/20/17 | | 113 | |

Kraft Foods 10 yr CDS | | 40,000 | | 0.77 | % | 12/20/17 | | (72 | ) |

Rohm & Haas 5.5 yr CDS | | 31,000 | | 0.37 | % | 3/20/13 | | 103 | |

JPMorgan Chase Bank | | | | | | | | | |

Embarq 7 yr CDS | | 10,000 | | 0.77 | % | 9/20/14 | | 245 | |

Merrill Lynch 5 yr CDS | | 20,000 | | 0.58 | % | 12/20/12 | | 591 | |

Lehman Brothers | | | | | | | | | |

Capmark Financial 5 yr CDS | | 15,000 | | 1.65 | % | 9/20/12 | | 2,793 | |

Gannet 7 yr CDS | | 30,000 | | 0.88 | % | 9/20/14 | | 167 | |

Home Depot 5 yr CDS | | 45,000 | | 0.50 | % | 9/20/12 | | 722 | |

New York Times 7 yr CDS | | 30,000 | | 0.75 | % | 9/20/14 | | 189 | |

Sara Lee 7 yr CDS | | 30,000 | | 0.60 | % | 9/20/14 | | (347 | ) |

Target 5 yr CDS | | 40,000 | | 0.57 | % | 12/20/12 | | (40 | ) |

V.F. 5 yr CDS | | 22,500 | | 0.40 | % | 9/20/12 | | (10 | ) |

Washington Mutual | | | | | | | | | |

4 yr CDS | | 10,300 | | 0.85 | % | 9/20/11 | | 1,117 | |

10 yr CDS | | 15,000 | | 3.15 | % | 12/20/17 | | 90 | |

| | | | | | | | 5,925 | |

Protection Sold: | | | | | | | | | |

Lehman Brothers | | | | | | | | | |

ABX Home Equity Index 06-2 AA | | (20,000 | ) | 0.17 | % | 5/25/46 | | (2,100 | ) |

ABX Home Equity Index 07-1 AA | | (30,000 | ) | 0.15 | % | 8/25/37 | | (2,950 | ) |

Best Buy | | | | | | | | | |

5 yr CDS | | (19,000 | ) | 0.61 | % | 9/20/12 | | (129 | ) |

10 yr CDS | | (10,000 | ) | 0.99 | % | 9/20/17 | | (49 | ) |

Reynolds American 5 yr CDS | | (60,000 | ) | 1.00 | % | 9/20/12 | | 815 | |

| | | | | | | | (4,413 | ) |

TOTAL | | | | | | | | $ | 1,512 | |

| | | | | | | | | | | |

Interest Rate Swap Contract

Notional Amount | | Expiration Date | | Description | | Unrealized Appreciation | |

$ | 415,000 | | 5/2/12 | | Agreement with Goldman Sachs to receive the notional amount multiplied by the fixed rate of 4.987 and to pay the notional amount multiplied by the 3 month LIBOR % | | $ | 14,758 | |

| | | | | | | | | |

The use of futures contracts and swap contracts involves elements of market risk and risks in excess of the amount recognized in the financial statements. The notional value presented above represent the Series’ total exposure in such contracts, whereas only the net unrealized appreciation (depreciation) is reflected in the Series’ net assets.

(1)See Note 8 in “Notes to Financial Statements.”

(2)See Note 9 in “Notes to Financial Statements.”

See accompanying notes

12

Delaware VIP Trust — Delaware VIP Balanced Series

Statement of Operations

Year Ended December 31, 2007

INVESTMENT INCOME: | | | |

Interest | | $ | 640,818 | |

Dividends | | 531,871 | |

Securities lending income | | 8,089 | |

| | 1,180,778 | |

EXPENSES: | | | |

Management fees | | 205,999 | |

Accounting and administration expenses | | 12,675 | |

Audit and tax | | 12,471 | |

Pricing fees | | 9,758 | |

Dividend disbursing and transfer agent fees and expenses | | 7,971 | |

Reports and statements to shareholders | | 7,549 | |

Custodian fees | | 6,889 | |

Legal fees | | 5,846 | |

Trustees’ fees | | 1,524 | |

Dues and services | | 788 | |

Insurance fees | | 700 | |

Consulting fees | | 605 | |

Trustees’ expenses | | 180 | |

Registration fees | | 39 | |

Distribution expenses – Service Class | | 18 | |

| | 273,012 | |

Less expenses absorbed or waived | | (6,971 | ) |

Less waiver of distribution expenses – Service Class | | (3 | ) |

Less expense paid indirectly | | (1,618 | ) |

Total operating expenses | | 264,420 | |

| | | |

NET INVESTMENT INCOME | | 916,358 | |

| | | |

NET REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS: | | | |

Net realized gain (loss) on: | | | |

Investments | | 2,127,402 | |

Futures contracts | | (14,242 | ) |

Swap contracts | | 20,390 | |

Net realized gain | | 2,133,550 | |

Net change in unrealized appreciation/depreciation of investments | | (2,788,302 | ) |

| | | |

NET REALIZED AND UNREALIZED LOSS ON INVESTMENTS | | (654,752 | ) |

| | | |

NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | | $ | 261,606 | |

See accompanying notes

Delaware VIP Trust — Delaware VIP Balanced Series

Statements of Changes in Net Assets

| | Year Ended | |

| | 12/31/07 | | 12/31/06 | |

INCREASE (DECREASE) IN NET ASSETS FROM OPERATIONS: | | | | | |

Net investment income | | $ | 916,358 | | $ | 1,045,074 | |

Net realized gain on investments | | 2,133,550 | | 1,186,084 | |

Net change in unrealized appreciation/depreciation of investments | | (2,788,302 | ) | 3,149,987 | |

Net increase in net assets resulting from operations | | 261,606 | | 5,381,145 | |

| | | | | |

DIVIDENDS AND DISTRIBUTIONS TO SHAREHOLDERS FROM: | | | | | |

Net investment income: | | | | | |

Standard Class | | (1,095,621 | ) | (1,122,023 | ) |

Service Class | | (180 | ) | (144 | ) |

| | (1,095,801 | ) | (1,122,167 | ) |

| | | | | |

CAPITAL SHARE TRANSACTIONS: | | | | | |

Proceeds from shares sold: | | | | | |

Standard Class | | 1,304,963 | | 35,103,629 | |

Net asset value of shares issued upon reinvestment of dividends and distributions: | | | | | |

Standard Class | | 1,095,621 | | 1,122,023 | |

Service Class | | 180 | | 144 | |

Cost of shares repurchased: | | 2,400,764 | | 36,225,796 | |

Standard Class | | (10,175,063 | ) | (43,084,571 | ) |

Decrease in net assets derived from capital share transactions | | (7,774,299 | ) | (6,858,775 | ) |

| | | | | |

NET DECREASE IN NET ASSETS | | (8,608,494 | ) | (2,599,797 | ) |

| | | | | |

NET ASSETS: | | | | | |

Beginning of year | | 35,632,453 | | 38,232,250 | |

End of year (including undistributed net investment income of $935,008 and $1,093,355,

respectively) | | $ | 27,023,959 | | $ | 35,632,453 | |

See accompanying notes

13

Delaware VIP Trust — Delaware VIP Balanced Series

Financial Highlights

Selected data for each share of the Series outstanding throughout each period were as follows:

| | Delaware VIP Balanced Series Standard Class | |

| | Year Ended | |

| | 12/31/07 | | 12/31/06 | | 12/31/05 | | 12/31/04 | | 12/31/03 | |

| | | | | | | | | | | |

Net asset value, beginning of period | | $ | 15.260 | | $ | 13.530 | | $ | 13.360 | | $ | 12.890 | | $ | 11.170 | |

| | | | | | | | | | | |

Income (loss) from investment operations: | | | | | | | | | | | |

Net investment income(1) | | 0.441 | | 0.405 | | 0.341 | | 0.245 | | 0.211 | |

Net realized and unrealized gain (loss) on investments and foreign currencies | | (0.404 | ) | 1.739 | | 0.135 | | 0.493 | | 1.872 | |

Total from investment operations | | 0.037 | | 2.144 | | 0.476 | | 0.738 | | 2.083 | |

| | | | | | | | | | | |

Less dividends and distributions from: | | | | | | | | | | | |

Net investment income | | (0.497 | ) | (0.414 | ) | (0.306 | ) | (0.268 | ) | (0.363 | ) |

Total dividends and distributions | | (0.497 | ) | (0.414 | ) | (0.306 | ) | (0.268 | ) | (0.363 | ) |

| | | | | | | | | | | |

Net asset value, end of period | | $ | 14.800 | | $ | 15.260 | | $ | 13.530 | | $ | 13.360 | | $ | 12.890 | |

| | | | | | | | | | | |

Total return(2) | | 0.33 | % | 16.20 | % | 3.68 | % | 5.84 | % | 19.21 | % |

| | | | | | | | | | | |

Ratios and supplemental data: | | | | | | | | | | | |

Net assets, end of period (000 omitted) | | $ | 27,018 | | $ | 35,626 | | $ | 38,227 | | $ | 45,407 | | $ | 53,233 | |

Ratio of expenses to average net assets | | 0.83 | % | 0.81 | % | 0.80 | % | 0.77 | % | 0.77 | % |

Ratio of expenses to average net assets prior to expense limitation and expenses paid indirectly | | 0.86 | % | 0.84 | % | 0.85 | % | 0.77 | % | 0.77 | % |

Ratio of net investment income to average net assets | | 2.89 | % | 2.88 | % | 2.57 | % | 1.91 | % | 1.80 | % |

Ratio of net investment income to average net assets prior to expense limitation and expenses paid indirectly | | 2.86 | % | 2.85 | % | 2.52 | % | 1.91 | % | 1.80 | % |

Portfolio turnover | | 134 | % | 131 | % | 200 | % | 247 | % | 231 | % |

(1)The average shares outstanding method has been applied for per share information.

(2)Total investment return is based on the change in net asset value of a share during the period and assumes reinvestment of dividends and distributions at net asset value. Total investment return reflects a waiver by the manager, as applicable. Performance would have been lower had the waiver not been in effect.

See accompanying notes

14

Selected data for each share of the Series outstanding throughout each period were as follows:

| | Delaware VIP Balanced Series Service Class | |

| | Year Ended | |

| | 12/31/07 | | 12/31/06 | | 12/31/05 | | 12/31/04 | | 12/31/03 | |

| | | | | | | | | | | |

Net asset value, beginning of period | | $ | 15.240 | | $ | 13.520 | | $ | 13.340 | | $ | 12.880 | | $ | 11.170 | |

| | | | | | | | | | | |

Income (loss) from investment operations: | | | | | | | | | | | |

Net investment income(1) | | 0.403 | | 0.371 | | 0.310 | | 0.214 | | 0.186 | |

Net realized and unrealized gain (loss) on investments and foreign currencies | | (0.409 | ) | 1.732 | | 0.145 | | 0.488 | | 1.867 | |

Total from investment operations | | (0.006 | ) | 2.103 | | 0.455 | | 0.702 | | 2.053 | |

| | | | | | | | | | | |

Less dividends and distributions from: | | | | | | | | | | | |

Net investment income | | (0.464 | ) | (0.383 | ) | (0.275 | ) | (0.242 | ) | (0.343 | ) |

Total dividends and distributions | | (0.464 | ) | (0.383 | ) | (0.275 | ) | (0.242 | ) | (0.343 | ) |

| | | | | | | | | | | |

Net asset value, end of period | | $ | 14.770 | | $ | 15.240 | | $ | 13.520 | | $ | 13.340 | | $ | 12.880 | |

| | | | | | | | | | | |

Total return(2) | | 0.05 | % | 15.88 | % | 3.51 | % | 5.55 | % | 18.90 | % |

| | | | | | | | | | | |

Ratios and supplemental data: | | | | | | | | | | | |

Net assets, end of period (000 omitted) | | $ | 6 | | $ | 6 | | $ | 5 | | $ | 5 | | $ | 5 | |

Ratio of expenses to average net assets | | 1.08 | % | 1.06 | % | 1.05 | % | 1.02 | % | 0.99 | % |

Ratio of expenses to average net assets prior to expense limitation and expenses paid indirectly | | 1.16 | % | 1.14 | % | 1.15 | % | 1.07 | % | 1.02 | % |

Ratio of net investment income to average net assets | | 2.64 | % | 2.63 | % | 2.32 | % | 1.66 | % | 1.58 | % |

Ratio of net investment income to average net assets prior to expense limitation and expenses paid indirectly | | 2.56 | % | 2.55 | % | 2.22 | % | 1.61 | % | 1.55 | % |

Portfolio turnover | | 134 | % | 131 | % | 200 | % | 247 | % | 231 | % |

(1)The average shares outstanding method has been applied for per share information.

(2)Total investment return is based on the change in net asset value of a share during the period and assumes reinvestment of dividends and distributions at net asset value. Total investment return reflects a waiver by the manager and distributor, as applicable. Performance would have been lower had the waiver not been in effect.

See accompanying notes

15

Delaware VIP Trust — Delaware VIP Balanced Series

Notes to Financial Statements

December 31, 2007

Delaware VIP Trust (Trust) is organized as a Delaware statutory trust and offers 14 series: Delaware VIP Balanced Series, Delaware VIP Capital Reserves Series, Delaware VIP Cash Reserve Series, Delaware VIP Diversified Income Series, Delaware VIP Emerging Markets Series, Delaware VIP Growth Opportunities Series, Delaware VIP High Yield Series, Delaware VIP International Value Equity Series, Delaware VIP REIT Series, Delaware VIP Select Growth Series, Delaware VIP Small Cap Value Series, Delaware VIP Trend Series, Delaware VIP U.S. Growth Series and Delaware VIP Value Series. These financial statements and the related notes pertain to Delaware VIP Balanced Series (Series). The Trust is an open-end investment company. The Series is considered diversified under the Investment Company Act of 1940, as amended, and offers Standard Class and Service Class shares. The Standard Class shares do not carry a 12b-1 fee and the Service Class shares carry a 12b-1 fee. The shares of the Series are sold only to separate accounts of life insurance companies.

The investment objective of the Series is to seek a balance of capital appreciation, income and preservation of capital.

1. Significant Accounting Policies

The following accounting policies are in accordance with U.S. generally accepted accounting principles and are consistently followed by the Series.

Security Valuation—Equity securities, except those traded on the Nasdaq Stock Market, Inc. (Nasdaq), are valued at the last quoted sales price as of the time of the regular close of the New York Stock Exchange (NYSE) on the valuation date. Securities traded on the Nasdaq are valued in accordance with the Nasdaq Official Closing Price, which may not be the last sales price. If on a particular day an equity security does not trade, then the mean between the bid and asked prices will be used. U.S. government and agency securities are valued at the mean between the bid and asked prices. Other long-term debt securities, credit default swap contracts and interest rate swap contracts are valued by an independent pricing service or broker and such prices are believed to reflect the fair value of such securities. Short-term debt securities having less than 60 days to maturity are valued at amortized cost, which approximates market value. Securities lending collateral, which is invested in a collective investment vehicle, is valued at unit value per share. Futures contracts and options on futures contracts are valued at the daily quoted settlement prices. Exchange-traded options are valued at the last reported sale price or, if no sales are reported, at the mean between the last reported bid and asked prices. Generally, index swap contracts and other securities and assets for which market quotations are not readily available are valued at fair value as determined in good faith under the direction of the Series’ Board of Trustees. In determining whether market quotations are readily available or fair valuation will be used, various factors will be taken into consideration, such as market closures, or with respect to foreign securities, aftermarket trading, or significant events after local market trading (e.g., government actions or pronouncements, trading volume or volatility on markets, exchanges among dealers, or news events).

In September 2006, the Financial Accounting Standards Board (FASB) issued FASB Statement No. 157 “Fair Value Measurements” (Statement 157). Statement 157 establishes a framework for measuring fair value in U.S. generally accepted accounting principles, clarifies the definition of fair value within that framework, and expands disclosures about the use of fair value measurements. Statement 157 is intended to increase consistency and comparability among fair value estimates used in financial reporting. Statement 157 is effective for fiscal years beginning after November 15, 2007. Management does not expect the adoption of Statement 157 to have a material impact on the amounts reported in the financial statements.

Federal Income Taxes—The Series intends to continue to qualify for federal income tax purposes as a regulated investment company under Subchapter M of the Internal Revenue Code of 1986, as amended, and make the requisite distributions to shareholders. Accordingly, no provision for federal income taxes has been made in the financial statements.

Effective June 29, 2007, the Series adopted FASB Interpretation No. 48 “Accounting for Uncertainty in Income Taxes” (FIN 48). FIN 48 provides guidance for how uncertain tax positions should be recognized, measured, presented and disclosed in the financial statements. FIN 48 requires the evaluation of tax positions taken or expected to be taken in the course of preparing the Series’ tax returns to determine whether the tax positions are “more-likely-than-not” of being sustained by the applicable tax authority. Tax positions not deemed to meet the more-likely-than-not threshold are recorded as a tax benefit or expense in the current year. The adoption of FIN 48 did not result in the recording of any tax benefit or expense in the current period.

Class Accounting—Investment income, common expenses and realized and unrealized gain (loss) on investments are allocated to the classes of the Series on the basis of daily net assets of each class. Distribution expenses relating to a specific class are charged directly to that class.

Repurchase Agreements—The Series may invest in a pooled cash account along with members of the Delaware Investments® Family of Funds pursuant to an exemptive order issued by the Securities and Exchange Commission. The aggregate daily balance of the pooled cash account is invested in repurchase agreements secured by obligations of the U.S. government. The respective collateral is held by the Series’ custodian bank until the maturity of the respective repurchase agreements. Each repurchase agreement is at least 102% collateralized. However, in the event of default or bankruptcy by the counterparty to the agreement, realization of the collateral may be subject to legal proceedings. At December 31, 2007, the Series held no investments in repurchase agreements.

Use of Estimates—The preparation of financial statements in conformity with U.S. generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

16

Delaware VIP Balanced Series

Notes to Financial Statements (continued)

Other—Expenses directly attributable to the Series are charged directly to the Series. Other expenses common to various funds within the Delaware Investments® Family of Funds are generally allocated amongst such funds on the basis of average net assets. Management fees and some other expenses are paid monthly. Security transactions are recorded on the date the securities are purchased or sold (trade date) for financial reporting purposes. Costs used in calculating realized gains and losses on the sale of investment securities are those of the specific securities sold. Dividend income is recorded on the ex-dividend date and interest income is recorded on the accrual basis. Discounts and premiums are amortized to interest income over the lives of the respective securities. Realized gains (losses) on paydowns of mortgage- and asset-backed securities are classified as interest income.

The Series declares and pays dividends from net investment income and distributions from net realized gain on investments, if any, following the close of the fiscal year.

Subject to seeking best execution, the Series may direct certain security trades to brokers who have agreed to rebate a portion of the related brokerage commission to the Series in cash. There were no commission rebates during the year ended December 31, 2007. In general, best execution refers to many factors, including the price paid or received for a security, the commission charged, the promptness and reliability of execution, the confidentiality and placement accorded the order, and other factors affecting the overall benefit obtained by the Series on the transaction.

The Series receives earnings credits from its custodian when positive cash balances are maintained, which are used to offset custody fees. The expense paid under this arrangement is included in custodian fees on the Statement of Operations with the corresponding expense offset shown as “expense paid indirectly.”

2. Investment Management, Administration Agreements and Other Transactions with Affiliates

In accordance with the terms of its investment management agreement, the Series pays Delaware Management Company (DMC), a series of Delaware Management Business Trust and the investment manager, an annual fee which is calculated daily at the rate of 0.65% on the first $500 million of average daily net assets of the Series, 0.60% on the next $500 million, 0.55% on the next $1.5 billion, and 0.50% on average daily net assets in excess of $2.5 billion.

Prior to May 1, 2007, DMC had contractually agreed to waive that portion, if any, of its management fee and reimburse the Series to the extent necessary to ensure that total annual operating expenses, exclusive of taxes, interest, brokerage fees, inverse floater program expenses, 12b-1 plan expenses, certain insurance costs and non-routine expenses or costs including, but not limited to, those relating to reorganizations, litigation, conducting shareholder meetings, and liquidations, did not exceed 0.80% of average daily net assets of the Series.

Effective October 1, 2007, Delaware Service Company, Inc. (DSC), an affiliate of DMC, provides fund accounting and financial administration oversight services to the Series. For these services, the Series pays DSC fees based on the aggregate daily net assets of the Delaware Investments® Family of Funds at the following annual rate: 0.0050% of the first $30 billion; 0.0045% of the next $10 billion; 0.0040% of the next $10 billion; and 0.0025% of aggregate average daily net assets in excess of $50 billion. The fees payable to DSC under the service agreement described above are allocated among all funds in the Delaware Investments® Family of Funds on a relative net asset value basis. Prior to October 1, 2007, DSC provided fund accounting and administrative services to the Series and received a fee at an annual rate of 0.04% of average daily net assets. For the year ended December 31, 2007, the Series was charged $10,178 for these services.

DSC also provides dividend disbursing and transfer agency services. The Series pays DSC a monthly fee based on the number of shareholder accounts for dividend disbursing and transfer agent services.

Pursuant to a distribution agreement and distribution plan, the Series pays Delaware Distributors, L.P. (DDLP), the distributor and an affiliate of DMC, an annual distribution and service fee not to exceed 0.30% of the average daily net assets of the Service Class shares. DDLP has contracted to waive distribution and service fees through April 30, 2008 in order to prevent distribution and service fees of the Service Class shares from exceeding 0.25% of average daily net assets. Standard Class shares pay no distribution and service expenses.

At December 31, 2007, the Series had liabilities payable to affiliates as follows:

Investment

Management

Fee Payable to

DMC | | Dividend Disbursing,

Transfer Agent Fees

and Other Expenses

Payable to DSC | | Distribution

Fee Payable

To DDLP | | Other

Expenses

Payable

to DMC

and Affiliates* | |

$ | 15,196 | | $ | 1,120 | | $ | 1 | | $ | 2,883 | |

| | | | | | | | | | | |

*DMC, as part of its administrative services, pays operating expenses on behalf of the Series and is reimbursed on a periodic basis. Such expenses include items such as printing of shareholder reports, fees for audit, legal and tax services, custodian fees and trustees’ fees.

As provided in the investment management agreement, the Series bears the cost of certain legal and tax services, including internal legal and tax services provided to the Series by DMC and/or its affiliates’ employees. For the year ended December 31, 2007, the Series was charged $1,658 for internal legal and tax services provided by DMC and/or its affiliates’ employees.

Trustees’ fees include expenses accrued by the Series for each Trustee’s retainer and per meeting fees. Certain officers of DMC, DSC and DDLP are officers and/or Trustees of the Trust. These officers and Trustees are paid no compensation by the Series.

17

Delaware VIP Balanced Series

Notes to Financial Statements (continued)

3. Investments

For the year ended December 31, 2007, the Series made purchases and sales of investment securities other than short-term investments as follows:

Purchases other than U.S. government securities | | $ | 30,665,379 | |

Purchases of U.S. government securities | | 11,695,964 | |

Sales other than U.S. government securities | | 38,602,711 | |

Sales of U.S. government securities | | 11,231,647 | |

At December 31, 2007, the cost of investments for federal income tax purposes and unrealized appreciation (depreciation) for the Series were as follows:

Cost of

Investments | | Aggregate

Unrealized

Appreciation | | Aggregate

Unrealized

Depreciation | | Net Unrealized

Appreciation | |

$ | 28,352,958 | | $ | 2,675,086 | | $ | (1,572,320 | ) | $ | 1,102,766 | |

| | | | | | | | | | | |

4. Dividend and Distribution Information

Income and long-term capital gain distributions are determined in accordance with federal income tax regulations, which may differ from U.S. generally accepted accounting principles. Additionally, net short-term gains on sales of investment securities are treated as ordinary income for federal income tax purposes. The tax character of dividends and distributions paid during the years ended December 31, 2007 and 2006 was as follows:

| | Year

Ended

12/31/07 | | Year

Ended

12/31/06 | |

Ordinary income | | $ | 1,095,801 | | $ | 1,122,167 | |

| | | | | | | |

5. Components of Net Assets on a Tax Basis

As of December 31, 2007, the components of net assets on a tax basis were as follows:

Shares of beneficial interest | | $ | 42,694,049 | |

Undistributed ordinary income | | 935,650 | |

Capital loss carryforwards | | (17,689,162 | ) |

Other temporary differences | | (34,101 | ) |

Unrealized appreciation of investments and swap contracts | | 1,117,523 | |

Net assets | | $ | 27,023,959 | |

The differences between book basis and tax basis components of net assets are primarily attributable to tax deferral of losses on wash sales, mark-to-market of futures contracts, tax treatment of credit default and interest rate swap contracts, market discount and premium on debt instruments, straddle deferrals, and tax treatment of contingent payment debt instruments.

For financial reporting purposes, capital accounts are adjusted to reflect the tax character of permanent book/tax differences. Reclassifications are primarily due to tax treatment of gain (loss) on paydowns of mortgage- and asset-backed securities, contingent payment debt instruments, credit default and interest rate swap contracts and market discount and premium on certain debt instruments. Results of operations and net assets were not affected by these reclassifications. For the year ended December 31, 2007, the Series recorded the following reclassifications:

Undistributed

Net

Investment Income | | Accumulated

Net Realized

(Loss) | |

$ | 21,096 | | $ | (21,096 | ) |

| | | | | |

For federal income tax purposes, capital loss carryforwards may be carried forward and applied against future capital gains. $2,137,896 was utilized in 2007. Capital loss carryforwards remaining at December 31, 2007 will expire as follows: $7,639,801 expires in 2009; $9,576,012 expires in 2010; and $473,349 expires in 2011.

18

Delaware VIP Balanced Series

Notes to Financial Statements (continued)

6. Capital Shares

Transactions in capital shares were as follows:

| | Year

Ended

12/31/07 | | Year

Ended

12/31/06 | |

Shares sold: | | | | | |

Standard Class | | 84,727 | | 2,599,584 | |

| | | | | |

Shares issued upon reinvestment of dividends and distributions: | | | | | |

Standard Class | | 72,993 | | 82,019 | |

Service Class | | 12 | | 10 | |

| | 157,732 | | 2,681,613 | |

| | | | | |

Shares repurchased: | | | | | |

Standard Class | | (667,221 | ) | (3,171,452 | ) |

Net decrease | | (509,489 | ) | (489,839 | ) |

7. Line of Credit