UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-05201

Thornburg Investment Trust

(Exact name of registrant as specified in charter)

c/o Thornburg Investment Management, Inc.

2300 North Ridgetop Road, Santa Fe, New Mexico 87506

(Address of principal executive offices) (Zip code)

Garrett Thornburg, 2300 North Ridgetop Road, Santa Fe, New Mexico 87506

(Name and address of agent for service)

Registrant’s telephone number, including area code: 505-984-0200

Date of fiscal year end: September 30, 2016

Date of reporting period: September 30, 2016

Item 1. Reports to Stockholders

The following annual reports are attached hereto, in order:

Thornburg Low Duration Municipal Fund

Thornburg Limited Term Municipal Fund

Thornburg Intermediate Municipal Fund

Thornburg Strategic Municipal Income Fund

Thornburg California Limited Term Municipal Fund

Thornburg New Mexico Intermediate Municipal Fund

Thornburg New York Intermediate Municipal Fund

Thornburg Limited Term U.S. Government Fund

Thornburg Limited Term Income Fund

Thornburg Low Duration Income Fund

Thornburg Strategic Income Fund

Thornburg Value Fund

Thornburg International Value Fund

Thornburg Core Growth Fund

Thornburg International Growth Fund

Thornburg Investment Income Builder Fund

Thornburg Global Opportunities Fund

Thornburg Developing World Fund

Thornburg Better World International Fund

Thornburg Capital Management Fund

Annual Report

September 30, 2016

THORNBURG

LOW DURATION

MUNICIPAL

FUND

About Thornburg Investment Management

It’s more than what we do.

It’s how we do it.

At Thornburg, we are very different in how we think, invest, and are structured We believe this difference is

what makes us successful in helping individuals reach their long-term financial goals

How we

How we How we’re

Flexible Perspective Our perspective on investment opportunities is more flexible than most, viewing a wide range of opportunities beyond conventional boundaries to find hidden value.

Collaboration Collectively, we hone ideas via borderless cross-pollination for better judgment and better results.

Portfolio Construction Disciplined construction guided more by our convictions than convention.

CONVICTION Thorough analysis and our relative-value framework lead to conviction in our securities selection.

UNCONVENTIONAL Active management means we seek the best value for our clients rather than using conventional benchmarks as our starting point.

Structured for Excellence How we think and how we invest is made possible by how we’re structured.

TEAM APPROACH FAR FROM THE HERD ACCESS & TRANSPARENCY

2 Annual Report

Annual Report

Thornburg Low Duration Municipal Fund

September 30, 2016

| | | | |

Share Class | | NASDAQ Symbol | | CUSIP |

Class A | | TLMAX | | 885-216-788 |

Class I | | TLMIX | | 885-216-770 |

Minimum investments for Class I shares may be higher than those for Class A shares. Class I shares may not be available to all investors.

Investments carry risks, including possible loss of principal. Portfolios investing in bonds have the same interest rate, inflation, and credit risks that are associated with the underlying bonds. The value of bonds will fluctuate relative to changes in interest rates, decreasing when interest rates rise. Unlike bonds, bond funds have ongoing fees and expenses. Please see the Fund’s prospectus for a discussion of the risks associated with an investment in the Fund. Investments in the Fund are not FDIC insured, nor are they bank deposits or guaranteed by a bank or any other entity.

The laddering strategy does not assure or guarantee better performance and cannot eliminate the risk of investment losses.

Diversification does not assure or guarantee better performance and cannot eliminate the risk of investment losses.

Annual Report 3

| | |

| LETTER TO SHAREHOLDERS | | |

| |

Thornburg Low Duration Municipal Fund | | September 30, 2016 (Unaudited) |

October 13, 2016

Dear Fellow Shareholder:

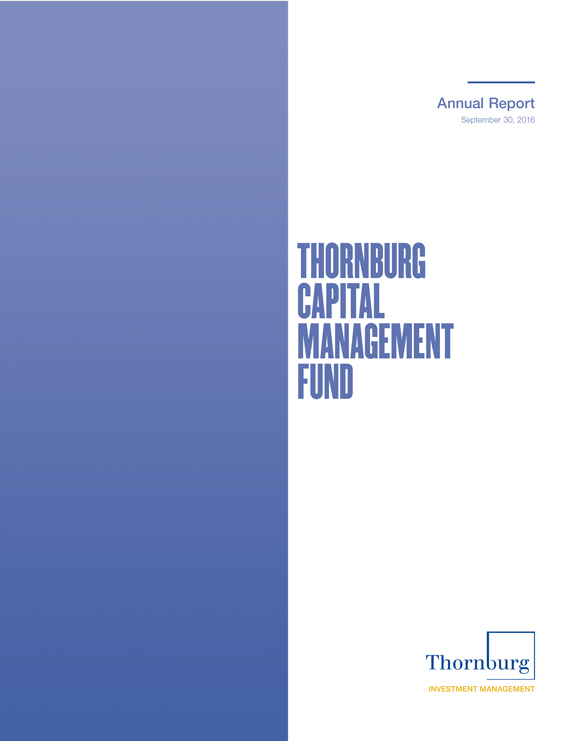

We are pleased to present the annual report for Thornburg Low Duration Municipal Fund. The net asset value (NAV) of the Class A shares decreased by 1 cent to $12.34 per share during the fiscal year ended September 30, 2016. If you were with us for the entire period, you received dividends of 2.889 cents per share. If you reinvested your dividends, you received 2.892 cents per share. Dividends were higher for Class I shares to account for varying class-specific expenses. The Class A shares of your Fund underperformed the index with a 0.15% total return (without sales charge) for the fiscal year ended September 30, 2016, compared to the 0.71% total return for the BofA Merrill Lynch 1-3 Year U.S. Municipal Securities Index. The Fund generated 1.18% more price return and 1.74% less income than the index after accounting for the different treatment of bonds priced above and below par by the index versus the Fund.

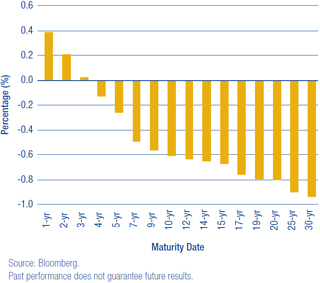

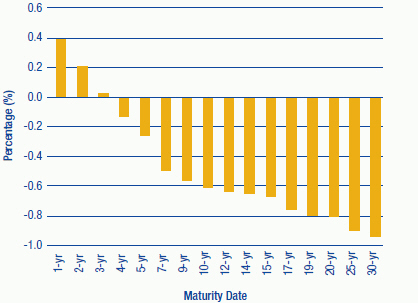

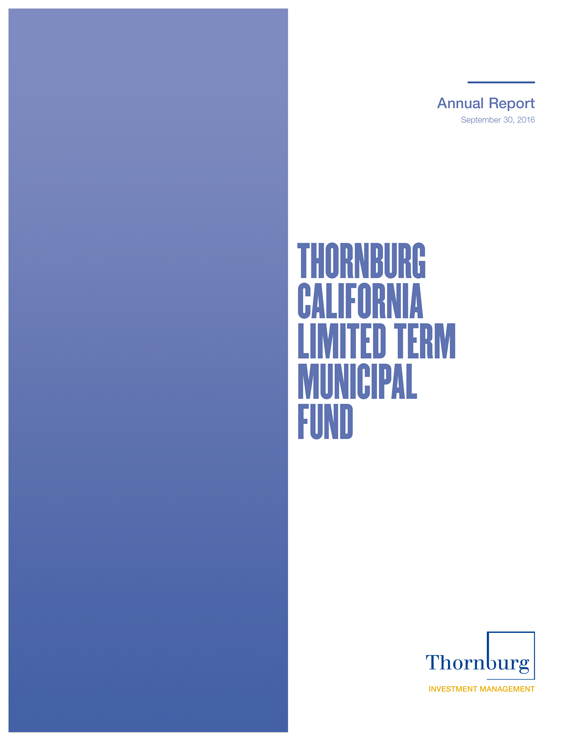

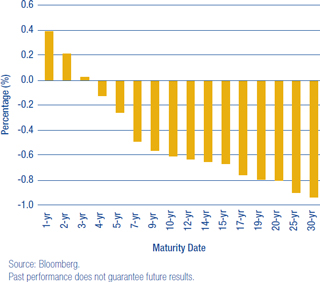

The market’s returns were a result of increasing short-term rates and decreasing long-term rates, shown in Figure 1.

U.S. Economy, Fed Policy, and the Election

The U.S. economy grew at a paltry average rate of 1%, as measured by nominal gross domestic product, for the first three quarters of 2016, much lower than the almost 3% average rate for 2015.

On the employment front, the economy added approximately 200,000 jobs per month for the Fund’s 2016 fiscal year. The May jobs number was a little scary, adding only 24,000 that month. The unemployment rate ticked up to 5.0% in September of 2016 from 4.9% in August, as more previously non-participating workers returned to the labor market.

Inflation has held stable, although it did move up slightly. The Core Personal Consumption Expenditure Index (Core PCE) for August moved up to 1.7% from 1.6% in July, although well below the U.S. Federal Reserve Board’s (the Fed) 2.0% target.

So, all in all, the economy is still growing, jobs are being added and inflation is well behaved. This isn’t a bad scenario for municipal bond investors, except that, at current valuations and 10-year AAA municipal general obligation bonds yielding 1.64%, municipal bond investors are generally not keeping up with inflation.

Elsewhere, the Fed increased the federal funds rate 0.25% in December of 2015. Although many pundits want to blame the credit markets rout on that event, they would be wrong. Oil prices, as measured by WTI crude futures, hit a low of $34.54 on January 20, 2016. Energy producers are a highly leveraged segment of the market, whether through bank loans or other forms of debt. As market participants began to question their ability to service these loans or debt, credit spreads began to widen and the impact of these loans on the financial stability of some banks came into question. The municipal market avoided this distress because bond issuance from energy-producing states was a small fraction of the $3.8 trillion municipal bond market.

This early-2016 market turbulence, followed by the May jobs report and the “Brexit” vote in Great Britain, gave the Fed enough pause not to follow their December rate increase with another. So far through 2016, the central bank has insisted that they may increase rates again and again. Last year we said, “Regardless, waiting for the Fed to raise short-term interest rates is akin to Waiting for Godot.” Well, we are still waiting. Meanwhile, the Fed is assuring the markets that the next meeting is “live” and they may raise short-term interest rates again!

The 2016 U.S. presidential race featured two major party candidates with unprecedented high unfavorable ratings with the electorate. At the time of this writing, the election’s result is weeks away. Regardless of the winner, however, the president historically has had very little impact on the course of the economy. Although there is a pattern that if the economy is doing well, the current administration likes

Figure I | 12-Month Change in Rates for AAA Rated General Obligation Municipal Bonds

(as of September 30, 2016)

4 Annual Report

LETTER TO SHAREHOLDERS,

CONTINUED

| | |

| |

Thornburg Low Duration Municipal Fund | | September 30, 2016 (Unaudited) |

to take all the credit; if the economy is not doing well, the current administration blames the previous one. A victory for either candidate could still benefit the municipal bond market, however, as both stumped for large increases in infrastructure spending—with one particularly calling for higher taxes which would lend support to the municipal bond market. If this gets through Congress, it could mean a higher level of municipal bond issuance and ultimately high growth rates for the economy; both occurrences would put upward pressure on municipal bond yields.

The Municipal Bond Market

The value metrics we use at Thornburg all suggest that the municipal bond market is pricing-in the rosiest of scenarios going forward. The main reason for this is that global central banks, with their overly accommodative monetary policies, have pushed investors further out on the risk spectrum in search of yield. That is why, depending on the fund, we have our portfolios positioned in the lower end of their respective risk spectrums. This means that durations (a measure of price sensitivity to changes in interest rates) are low and credit quality is higher than in the past. We continually ask ourselves: are investors getting paid to take risk? The answer we come up with is no!

Inside the Risk Metrics

Let’s first look at real yields, which is how much yield over inflation investors are being paid to own municipal bonds. As mentioned earlier, 10-year AAA general obligation bonds are yielding 1.64% and Core PCE is running at 1.70%, so investors are earning less than inflation. Over the last 20 years, investors have earned an average of 2% over inflation for the opportunity to invest in a 10-year AAA general obligation municipal bond.

The second thing to consider is credit spreads, which reflect the incremental yield an investor earns from owning a lower-rated credit versus a higher-rated credit, and which are now very narrow. As of September 30, 2016, an investor earned about 1% more for owning a 10-year BBB revenue bond versus a 10-year AAA general obligation bond. That is slightly higher than the average 0.75% an investor earned between 1994 and 2007. In 2007, approximately 50% of the new issue municipal bond market was insured by AAA/AAA municipal bond insurers. Today, there are no AAA/AAA municipal bond insurers, and insurance coverage generally accounts for only 6% to 8% of the new issue municipal bond market. On top of that, the security covenants of some current lower-quality investment grade securities are the most lax in years. This is a great time to be an issuer of lower-quality investment grade municipal bonds but not a great time to be an investor in them.

Finally, the slope of the yield curve, which tracks how much incremental yield an investor earns by owning securities with longer maturities, is also quite flat. Currently, investors are earning 0.78% more for owning a 10-year AAA general obligation municipal bond, versus a 1-year AAA general obligation municipal bond. Since 1994, an investor earned on average almost 1.6% to extend maturities from one to 10 years. The stretch for income is causing investors to absorb more risk at lower and lower relative yields.

Aside from valuations, the credit picture for the majority of the U.S. is pretty bright. Except for energy producing states, most regions are showing positive trends along such measures as:

Pensions are still a troubling issue. That is, 35 states reported a pension funding ratio of under 80% in 2014—the Mendoza line between a well-funded state pension and the “other kind.” As the worst career hitter in major league baseball history (.200 batting average), Mario Mendoza Aizpuru’s name ubiquitously symbolizes futility.

Liquidity

Market liquidity is still a concern. The latest example of this is what is happening to yields on Variable Rate Demand Notes (VRDNs). These are securities that are normally held in money market funds and bond fund reserve positions. They can be put back to an intermediary on a daily basis and are relatively secure. Leading up to the finalization of the Securities and Exchange Commisson’s money market fund reform in October of 2016, money market funds were and are repositioning themselves to be compliant with the new regulations. As such, they have had to divest themselves of VRDNs. Intermediaries do not want to hold them on their balance sheets (very expensive), so they raise the yields to clear the market. What used to yield 0.01% in March now yields, as of the time of this writing, 0.90%, or more than a 3-year AA security. This is serendipity for managers like Thornburg holding higher reserves because of concern over market liquidity; for issuers in the VRDN market, it’s not so much.

Main Reason to Own Municipal Bonds

One of the best risk-mitigating tools an investor has is diversification. By splitting a portfolio into several asset classes, an investor may reduce the volatility of the resulting portfolio’s returns. This is because the returns of various asset classes are not always correlated. There are times when this is not the

Annual Report 5

LETTER TO SHAREHOLDERS,

CONTINUED

| | |

| |

Thornburg Low Duration Municipal Fund | | September 30, 2016 (Unaudited) |

case, such as the 2008 financial crisis when all correlations went to one. For the long-term investor, however, we believe the benefits of diversification stand firm. When added to a portfolio of stocks, municipal bonds tend to reduce the volatility of that combined portfolio. Funds such as Thornburg Low Duration Municipal Fund may be a viable choice in a total diversified portfolio of stocks and bonds.

Conclusion

We continue to run this portfolio as an actively managed laddered portfolio. Laddering a portfolio is a simple way to diversify its investment along its entire investment universe. While past performance does not guarantee future results, our study showed that this structure outperformed other structures around 60% of the time and added 0.15% to 0.25% of total return annually.* Our view is that the current investment environment is not compensating investors enough to take on extra risk, so we have positioned our portfolios at the lower end of their risk spectrums. Know that the co-managers of this Fund are invested alongside you.

Thank you for your continued trust in us.

Sincerely,

| | | | |

| |  | | |

| | |

| Christopher Ryon,CFA | | Nicholos Venditti,CFA | | |

Portfolio Manager Managing Director | | Portfolio Manager Managing Director | | |

| * | We examined three hypothetical portfolios of bonds from December 1997 to December 2015. One using a laddering strategy, one using a barbell strategy, and a third using a bullet strategy. For the laddering strategy, the BofA Merrill Lynch 1–12 Year Municipal Index was used as a proxy, since, similar to a ladder, it contains bonds relatively evenly spread across all maturities within the index. The barbell strategy is a duration management technique wherein bonds are clustered at the two extremes of a maturity range. For the barbell strategy, the BofA Merrill Lynch 1–3 Year Municipal Index and BofA Merrill Lynch 8–12 Year Municipal Index were combined. The two indices were weighted in such a way as to give them the same duration as the broader 1–12 Year Index, and each year the portfolio was re-weighted back to the original index weights. This was done to make the two portfolios duration-neutral so that the impact of the strategy chosen could be isolated. The bullet strategy invests at the duration midpoint of the portfolio, therefore the BofA Merrill Lynch 6–8 Year Index was used to represent the bullet strategy. For additional information, see www.thornburg.com/whyladder. Past performance does not guarantee future results. |

The matters discussed in this report may constitute forward-looking statements made pursuant to the safe harbor provisions of the Securities Litigation Reform Act of 1995. These include any advisor or portfolio manager prediction, assessment, analysis or outlook for individual securities, industries, investment styles, market sectors and/or markets. These statements involve risks and uncertainties. In addition to the general risks described for each fund in its current prospectus, other factors bearing on these reports include the accuracy of the advisor’s or portfolio manager’s forecasts and predictions, the appropriateness of the investment strategies designed by the advisor or portfolio manager and the ability of the advisor or portfolio manager to implement their strategies efficiently and successfully. Any one or more of these factors, as well as other risks affecting the securities markets generally, could cause the actual results of any fund to differ materially as compared to its benchmarks.

The views expressed by the portfolio managers reflect their professional opinions and are subject to change. Under no circumstances does the information contained within represent a recommendation to buy or sell any security.

6 Annual Report

| | |

| PERFORMANCE SUMMARY | | |

| |

Thornburg Low Duration Municipal Fund | | September 30, 2016 (Unaudited) |

Average Annual Total Returns

| | | | | | | | |

| | | 1-Yr | | | Since

Incep. | |

A Shares (Incep: 12/30/13) | | | | | | | | |

Without sales charge | | | 0.15 | % | | | 0.28 | % |

With sales charge | | | -1.36 | % | | | -0.28 | % |

I Shares (Incep: 12/30/13) | | | 0.36 | % | | | 0.48 | % |

30-day Yields, A Shares

(with sales charge)

| | | | |

Annualized Distribution Yield | | | 0.30 | % |

| |

SEC Yield | | | 0.60 | % |

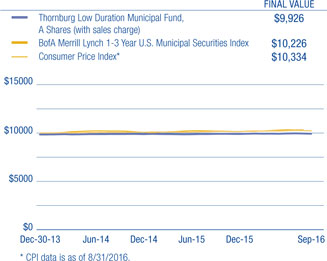

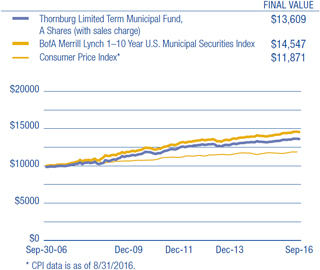

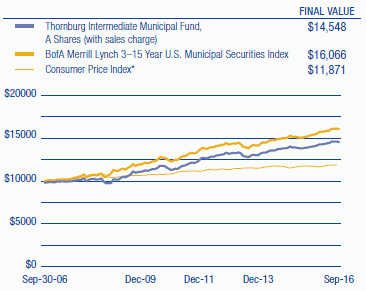

Growth of A Hypothetical $10,000 Investment

Performance data shown represents past performance and is no guarantee of future results. Investment return and principal value will fluctuate so shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than quoted. For performance current to the most recent month end, visit thornburg.com or call 800-847-0200. The performance information does not reflect the deduction of taxes that a shareholder would pay on distributions or the redemption of Fund shares. Returns reflect the reinvestment of dividends and capital gains. Class A shares are sold with a maximum sales charge of 1.50%. There is no sales charge for Class I shares.

As disclosed in the most recent prospectus, the total annual fund operating expenses are as follows: A shares, 2.85%; I shares, 0.82%. Thornburg Investment Management and/or Thornburg Securities Corporation have contractually agreed to waive fees and reimburse expenses through at least February 1, 2017, for some of the share classes, resulting in net expense ratios of the following: A shares, 0.70%; I shares, 0.50%. For more detailed information on fund expenses and waivers/reimbursements, please see the Fund’s prospectus. Without fee waivers and expense reimbursements, the Annualized Distribution yield would have been negative 1.10%, and the SEC yield would have been negative 0.81%. Unsubsidized yields may be disproportionately negative due to the size of net assets and fixed expenses.

Glossary

BofA Merrill Lynch 1-3 Year Municipal Securities Index – A subset of the BofA Merrill Lynch U.S. Municipal Securities Index including all securities with a remaining term to final maturity less than 3 years.

The BofA Merrill Lynch indices used in the Ladder vs Barbell & Bullet study are model portfolios of municipal obligations throughout the United States, with maturities ranging either from one to three years, six to eight years, eight to twelve years, or one to twelve years. These indices are subsets of the BofA Merrill Lynch U.S. Municipal Securities Index, which is comprised of U.S. dollar denominated investment grade tax-exempt debt publicly issued by U.S. states and territories, and their political subdivisions, in the U.S. domestic market. Qualifying securities must have at least a one-year remaining term to final maturity, a fixed coupon schedule and an investment grade rating.

Unless otherwise noted, index returns reflect the reinvestment of income dividends and capital gains, if any, but do not reflect fees, brokerage commissions or other expenses of investing. Investors may not make direct investments into any index. The performance of any index is not indicative of the performance of any particular investment.

Annualized Distribution Yield – The distribution yield reflects actual distributions made to shareholders. The annualized distribution yield is calculated by summing the last 30 days of income at a given month end and annualizing to a 360-day year. The result is divided by the ending maximum offering price.

Bond Credit Ratings (Credit Quality) – A bond credit rating assesses the financial ability of a debt issuer to make timely payments of principal and interest. Ratings of AAA (the highest), AA, A, and BBB are investment-grade quality. Ratings of BB, B, CCC, CC, C and D (the lowest) are considered below investment grade, speculative grade, or junk bonds.

Core Personal Consumption Expenditure Index (Core PCE) – A measure of the Personal Consumption Expenditure Index that excludes the more volatile and seasonal food and energy prices.

Credit Spread/Quality Spread – The difference between the yields of securities with different credit qualities.

Duration – A bond’s sensitivity to interest rates. Effective duration incorporates the embedded option features, such as call provisions. Bonds with longer durations experience greater price volatility than bonds with shorter durations.

General Obligation Bond (GO) – A municipal bond backed by the credit and “taxing power” of the issuing jurisdiction rather than the revenue from a given project.

Gross Domestic Product (GDP) – A country’s income minus foreign investments: the total value of all goods and services produced within a country in a year, minus net income from investments in other countries.

Laddering – Involves building a portfolio of bonds with staggered maturities so that a portion matures each year. Money that comes in from maturing bonds is typically invested in bonds with longer maturities at the far end of the portfolio.

Revenue Bond – A bond on which the debt service is payable solely from the revenue generated from the operation of the project being financed or a category of facilities, or from other non-tax sources.

SEC Yield – SEC yield is computed in accordance with SEC standards measuring the net investment income per share over a specified 30-day period expressed as a percentage of the maximum offering price of the Fund’s shares at the end of the period.

Variable Rate Demand Note (VRDN) – VRDNs are long-term, floating-rate municipal securities. These highly liquid securities are payable on demand, typically either daily or weekly, meaning the investor can request repayment of the entire debt amount. The coupon rate will adjust on a periodic basis, either daily or weekly.

West Texas Intermediate (WTI) – A grade of crude oil used as a benchmark in oil pricing.

Yield Curve – A line that plots the interest rates, at a set point in time, of bonds having equal credit quality, but differing maturity dates.

Annual Report 7

| | |

| FUND SUMMARY | | |

| |

Thornburg Low Duration Municipal Fund | | September 30, 2016 (Unaudited) |

Objectives And Strategies

The Fund seeks current income exempt from federal income tax, consistent with preservation of capital (may be subject to Alternative Minimum Tax).

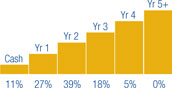

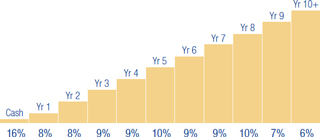

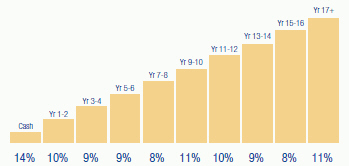

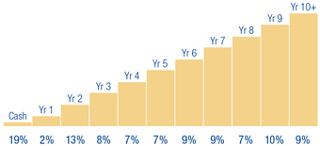

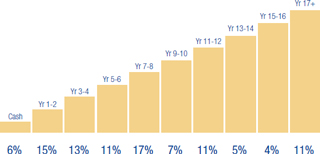

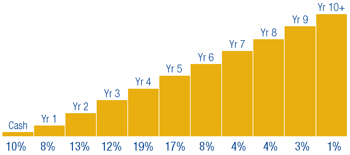

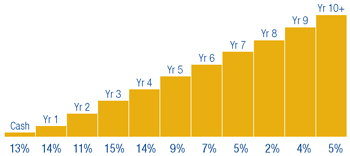

This Fund invests principally in a laddered portfolio of municipal bonds with a dollar-weighted average duration of normally no more than three years. Laddering involves building a portfolio of bonds with staggered maturities so that a portion of the portfolio matures each year. Cash from maturing bonds, if not needed for other purposes, is typically invested in bonds with longer maturities at the far end of the ladder. We regard the strategy as a good compromise for managing different types of risk.

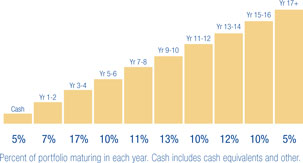

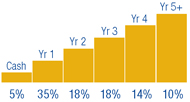

Portfolio Ladder

Percent of portfolio maturing in each year. Cash includes cash equivalents and other.

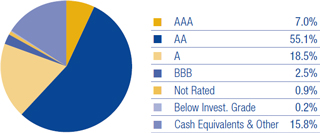

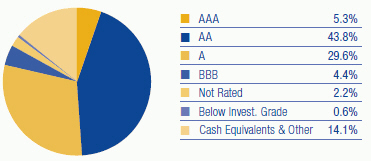

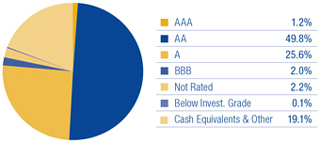

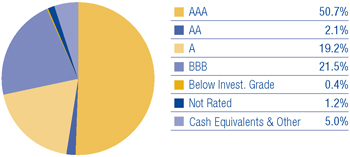

Security Credit Ratings†

A bond credit rating assesses the financial ability of a debt issuer to make timely payments of principal and interest. Ratings of AAA (the highest), AA, A, and BBB are investment-grade quality. Ratings of BB, B, CCC, CC, C and D (the lowest) are considered below investment grade, speculative grade, or junk bonds. Credit quality ratings for Thornburg’s municipal portfolios used the highest rating available from either Standard & Poor’s or Moody’s Investors Service.

Key Portfolio Attributes

| | | | |

Number of Bonds | | | 85 | |

| |

Effective Duration | | | 1.2 Yrs | |

| |

Average Maturity | | | 1.3 Yrs | |

There is no guarantee that the Fund will meet its investment objectives.

All data is subject to change. Charts may not add up to 100% due to rounding.

8 Annual Report

| | |

| SCHEDULE OF INVESTMENTS | | |

| |

Thornburg Low Duration Municipal Fund | | September 30, 2016 |

| | | | | | | | | | | | |

Issuer-Description | | Credit Rating†

S&P/ Moody’s | | | Principal

Amount | | | Value | |

ARIZONA — 1.12% | | | | | | | | | | | | |

Arizona HFA, 3.00% due 12/1/2016 (Scottsdale Lincoln Hospitals) | | | NR/A2 | | | $ | 480,000 | | | $ | 481,680 | |

| | | |

ARKANSAS — 0.73% | | | | | | | | | | | | |

Board of Trustees of the University of Arkansas, 4.00% due 11/1/2018 (Fayetteville Campus) | | | NR/Aa2 | | | | 295,000 | | | | 313,750 | |

| | | |

CALIFORNIA — 10.73% | | | | | | | | | | | | |

Bay Area Toll Authority, 1.00% due 4/1/2047 put 7/1/2017 (San Francisco Bay Area Toll Bridge) | | | AA/Aa3 | | | | 250,000 | | | | 250,050 | |

California Statewide Communities Development Authority, 5.25% due 7/1/2017 (St. Joseph Health System; Insured: AGM) (ETM) | | | AA/A1 | | | | 100,000 | | | | 103,363 | |

City of Chula Vista, 1.65% due 7/1/2018 (San Diego Gas & Electric Co.) | | | A+/Aa2 | | | | 1,000,000 | | | | 1,000,760 | |

City of Los Angeles GO, 3.00% due 6/29/2017 (Cash Flow Management) | | | SP-1+/Mig1 | | | | 500,000 | | | | 508,795 | |

County of Los Angeles GO, 3.00% due 6/30/2017 (Cash Management Program) | | | SP-1+/Mig1 | | | | 500,000 | | | | 508,410 | |

County of Los Angeles Redevelopment Refunding Authority, 3.00% due 12/15/2016 (Covina Revitalization-Redevelopment Project) | | | A-/NR | | | | 575,000 | | | | 577,346 | |

Jurupa Public Financing Authority, 4.00% due 9/1/2017 | | | BBB+/NR | | | | 100,000 | | | | 102,474 | |

Riverside County Public Financing Authority, 4.00% due 9/1/2017 (Hemet Project) | | | A+/NR | | | | 485,000 | | | | 498,629 | |

Successor Agency to the Redevelopment Agency of Carson, 4.00% due 10/1/2016 (Carson Merged and Amended Project Area) | | | AA-/NR | | | | 425,000 | | | | 425,038 | |

Successor Agency to the Redevelopment Agency of the City of Chino, 5.00% due 9/1/2017 (Merged Chino Areas 2001 and 2003 and Central City Redevelopment Projects; Insured: BAM) | | | AA/NR | | | | 300,000 | | | | 311,253 | |

Successor Agency to the Redevelopment Agency of the Richmond Community, 4.00% due 9/1/2017 (Harbour and Merged Area Redevelopment Projects; Insured: BAM) | | | AA/NR | | | | 300,000 | | | | 308,475 | |

| | | |

COLORADO — 2.91% | | | | | | | | | | | | |

City of Aurora COP, 3.00% due 12/1/2016 (Aurora Municipal Center) | | | AA-/Aa2 | | | | 530,000 | | | | 531,818 | |

City of Aurora COP, 5.00% due 12/1/2019 (Sports Park and E-911 Projects) | | | AA-/Aa2 | | | | 365,000 | | | | 408,041 | |

Regional Transportation District COP, 5.00% due 6/1/2017 (FasTracks Transportation System) | | | A/Aa3 | | | | 300,000 | | | | 308,013 | |

| | | |

CONNECTICUT — 2.35% | | | | | | | | | | | | |

State of Connecticut GO Floating Rate Note, 1.59% due 6/15/2018 (Various Capital Projects) | | | AA-/Aa3 | | | | 1,000,000 | | | | 1,004,790 | |

| | | |

FLORIDA — 6.69% | | | | | | | | | | | | |

County of Osceola, 5.00% due 10/1/2017 (Transportation Capital Improvements; Insured: AMBAC) | | | A+/A1 | | | | 150,000 | | | | 155,772 | |

Florida Municipal Power Agency, 5.25% due 10/1/2018 (Stanton Project) | | | NR/A1 | | | | 1,000,000 | | | | 1,083,440 | |

Hillsborough County IDA, 5.65% due 5/15/2018 (Tampa Electric Co.) | | | BBB+/A3 | | | | 200,000 | | | | 213,974 | |

Orange County School Board COP, 5.00% due 8/1/2018 (Educational Facilities) | | | NR/Aa2 | | | | 1,000,000 | | | | 1,074,540 | |

Volusia County Educational Facilities Authority, 2.00% due 10/15/2016 (Embry-Riddle Aeronautical University, Inc.) | | | NR/Baa1 | | | | 105,000 | | | | 105,052 | |

Volusia County Educational Facilities Authority, 3.00% due 10/15/2017 (Embry-Riddle Aeronautical University, Inc.) | | | NR/Baa1 | | | | 105,000 | | | | 107,124 | |

Volusia County Educational Facilities Authority, 3.00% due 10/15/2018 (Embry-Riddle Aeronautical University, Inc.) | | | NR/Baa1 | | | | 120,000 | | | | 124,547 | |

| | | |

GEORGIA — 0.47% | | | | | | | | | | | | |

City of Atlanta, 5.25% due 12/1/2016 (Atlantic Station; Insured: AGM) | | | AA/A3 | | | | 200,000 | | | | 201,356 | |

| | | |

GUAM — 1.39% | | | | | | | | | | | | |

Government of Guam, 3.00% due 11/15/2017 (Various Capital Projects) | | | A/NR | | | | 300,000 | | | | 304,839 | |

Government of Guam, 4.00% due 11/15/2018 (Economic Development) | | | A/NR | | | | 275,000 | | | | 288,805 | |

| | | |

IDAHO — 1.18% | | | | | | | | | | | | |

State of Idaho GO, 2.00% due 6/30/2017 | | | SP-1+/Mig1 | | | | 500,000 | | | | 504,155 | |

| | | |

ILLINOIS — 8.66% | | | | | | | | | | | | |

Chicago Park District GO, 5.00% due 1/1/2020 (Capital Improvement Plan) | | | AA+/Ba1 | | | | 500,000 | | | | 551,650 | |

City of Rockford GO, 3.00% due 12/15/2016 (New Fire Station Construction; Insured: AGM) | | | AA/A1 | | | | 250,000 | | | | 251,127 | |

Illinois Educational Facilities Authority, 4.75% due 11/1/2036 put 11/1/2016 (Field Museum of Natural History) | | | A/A2 | | | | 100,000 | | | | 100,281 | |

Illinois Finance Authority, 5.00% due 11/15/2017 (Rush University Medical Center) | | | A+/A1 | | | | 1,000,000 | | | | 1,043,530 | |

Illinois Finance Authority, 5.00% due 8/15/2018 (Silver Cross Hospital and Medical Centers) | | | NR/Baa1 | | | | 500,000 | | | | 531,750 | |

Illinois Finance Authority, 5.00% due 11/15/2018 (Rush University Medical Center) | | | A+/A1 | | | | 500,000 | | | | 540,235 | |

State of Illinois, 4.00% due 6/15/2019 (Build Illinois Program) | | | AAA/Baa2 | | | | 520,000 | | | | 560,004 | |

Town of Cicero GO, 5.00% due 1/1/2018 (Cicero and Laramie Development Areas; Insured: AGM) | | | AA/A2 | | | | 125,000 | | | | 130,743 | |

Annual Report 9

| | |

| SCHEDULE OF INVESTMENTS, CONTINUED | | |

| |

Thornburg Low Duration Municipal Fund | | September 30, 2016 |

| | | | | | | | | | | | |

Issuer-Description | | Credit Rating†

S&P/ Moody’s | | | Principal

Amount | | | Value | |

INDIANA — 2.70% | | | | | | | | | | | | |

City of Evansville, 5.00% due 1/1/2018 (Waterworks District; Insured: BAM) | | | AA/NR | | | $ | 810,000 | | | $ | 848,767 | |

Hammond Multi-School Building Corp., 4.00% due 7/15/2017 (Educational Facilities) (State Aid Withholding) | | | AA+/NR | | | | 300,000 | | | | 306,930 | |

| | | |

KANSAS — 6.57% | | | | | | | | | | | | |

Kansas DFA, 5.00% due 12/1/2016 (Department of Commerce Impact Program) | | | A+/A3 | | | | 400,000 | | | | 402,744 | |

Kansas DFA, 5.00% due 12/1/2018 (Department of Commerce Impact Program) | | | A+/A3 | | | | 1,250,000 | | | | 1,345,237 | |

Topeka Public Building Commission, 5.00% due 6/1/2018 (10th and Jackson Projects; Insured: Natl-Re) | | | AA-/A3 | | | | 1,000,000 | | | | 1,065,530 | |

| | | |

KENTUCKY — 2.60% | | | | | | | | | | | | |

Commonwealth of Kentucky State Property and Buildings Commission, 5.00% due 11/1/2019 (Project No. 112) | | | A/Aa3 | | | | 1,000,000 | | | | 1,114,350 | |

| | | |

LOUISIANA — 2.59% | | | | | | | | | | | | |

City of New Orleans, 5.00% due 12/1/2017 (Water System Facilities Capital Improvement Program) | | | A-/NR | | | | 100,000 | | | | 104,434 | |

City of New Orleans GO, 4.00% due 12/1/2016 (Public Improvements) | | | AA-/A3 | | | | 1,000,000 | | | | 1,005,510 | |

| | | |

MASSACHUSETTS — 1.83% | | | | | | | | | | | | |

City of Quincy GO, 2.00% due 6/16/2017 (Capital Improvements) | | | SP-1+/NR | | | | 500,000 | | | | 503,950 | |

Massachusetts Educational Financing Authority, 5.50% due 1/1/2017 | | | AA/NR | | | | 275,000 | | | | 278,061 | |

| | | |

MICHIGAN — 6.34% | | | | | | | | | | | | |

Berkley School District GO, 4.00% due 5/1/2018 (Educational Facilities; Insured: Q-SBLF) | | | AA-/NR | | | | 1,000,000 | | | | 1,046,600 | |

Charles Stewart Mott Community College GO, 5.00% due 5/1/2018 (Higher Education Facilities) | | | A+/NR | | | | 750,000 | | | | 794,715 | |

Michigan Finance Authority, 4.00% due 11/15/2016 (Sparrow Clinton Hospital Cancer Center and Sparrow Ionia Hospital) | | | A+/A1 | | | | 150,000 | | | | 150,581 | |

Michigan Finance Authority, 5.00% due 5/1/2018 (School District of the City of Detroit; Insured: Q-SBLF) | | | AA-/NR | | | | 250,000 | | | | 264,675 | |

Michigan State Hospital Finance Authority, 5.00% due 11/15/2016 (Ascension Health) | | | AA+/Aa2 | | | | 200,000 | | | | 201,054 | |

Northville Public Schools GO, 5.00% due 5/1/2017 (Educational Facilities; Insured: Q-SBLF) | | | NR/Aa1 | | | | 250,000 | | | | 256,007 | |

| | | |

NEVADA — 0.84% | | | | | | | | | | | | |

City of Reno GO, 5.00% due 6/1/2017 (Fire Protection Projects) | | | A-/A1 | | | | 200,000 | | | | 205,424 | |

Washoe County School District GO, 5.25% due 6/1/2017 (Educational Facilities; Insured: AGM) | | | AA/Aa3 | | | | 150,000 | | | | 154,389 | |

| | | |

NEW JERSEY — 1.68% | | | | | | | | | | | | |

Essex County Improvement Authority GO, 4.00% due 10/1/2017 (County Correctional Facility) | | | NR/Aa2 | | | | 545,000 | | | | 560,413 | |

New Jersey Health Care Facilities Financing Authority, 5.00% due 1/1/2018 (Hackensack University Medical Center; Insured: AGM) | | | AA/A2 | | | | 150,000 | | | | 157,198 | |

| | | |

NEW YORK — 5.91% | | | | | | | | | | | | |

City of New York GO, 5.00% due 8/1/2017 (Capital Projects) | | | AA/Aa2 | | | | 500,000 | | | | 517,340 | |

City of New York GO, 5.00% due 8/1/2019 (Capital Projects) | | | AA/Aa2 | | | | 450,000 | | | | 500,022 | |

Lake Placid Central School District GO, 5.00% due 6/15/2017 (Educational Facilities; Insured: Natl-Re) (State Aid Withholding) | | | NR/Aa3 | | | | 200,000 | | | | 205,618 | |

Monroe County Industrial Development Corp., 4.00% due 1/15/2018 (Monroe Community College Association; Insured: AGM) | | | AA/A2 | | | | 200,000 | | | | 206,426 | |

New York City Municipal Water Finance Authority, 0.75% due 6/15/2048 put 10/3/2016 (Water & Sewer System; SPA: | | | | | | | | | | | | |

Mizuho Bank, Ltd.) (daily demand notes) | | | AA+/Aa1 | | | | 600,000 | | | | 600,000 | |

New York State Housing Finance Agency, 0.74% due 11/1/2046 put 10/3/2016 (160 Madison Avenue Housing; LOC: PNC Bank, N.A.) (daily demand notes) | | | NR/A1 | | | | 500,000 | | | | 500,000 | |

| | | |

NORTH DAKOTA — 1.75% | | | | | | | | | | | | |

North Dakota Housing Finance Agency, 0.85% due 1/1/2017 (Housing Mortgage Finance Program) | | | NR/Aa1 | | | | 750,000 | | | | 749,693 | |

| | | |

OHIO — 0.47% | | | | | | | | | | | | |

City of Cleveland, 3.00% due 10/1/2016 (Public Facilities) | | | AA/A1 | | | | 200,000 | | | | 200,012 | |

| | | |

OKLAHOMA — 3.21% | | | | | | | | | | | | |

Oklahoma DFA, 5.00% due 8/15/2018 (INTEGRIS Health) | | | AA-/Aa3 | | | | 270,000 | | | | 290,798 | |

Tulsa County Industrial Authority, 5.50% due 9/1/2018 (Jenks Public Schools) | | | AA-/NR | | | | 1,000,000 | | | | 1,083,060 | |

| | | |

OREGON — 1.18% | | | | | | | | | | | | |

State of Oregon GO, 2.00% due 6/30/2017 (Cash Management) | | | SP-1+/Mig1 | | | | 500,000 | | | | 504,460 | |

10 Annual Report

| | |

| SCHEDULE OF INVESTMENTS, CONTINUED | | |

| |

Thornburg Low Duration Municipal Fund | | September 30, 2016 |

| | | | | | | | | | | | |

Issuer-Description | | Credit Rating†

S&P/ Moody’s | | | Principal

Amount | | | Value | |

PENNSYLVANIA — 9.82% | | | | | | | | | | | | |

City of Philadelphia, 5.00% due 10/1/2017 (Pennsylvania Gas Works) | | | A/Baa1 | | | $ | 200,000 | | | $ | 207,880 | |

City of Philadelphia, 5.00% due 7/1/2018 (Pennsylvania Gas Works) | | | AA/A2 | | | | 350,000 | | | | 373,943 | |

Cumberland County Municipal Authority, 3.00% due 1/1/2017 (Diakon Lutheran Social Ministries) | | | NR/NR | | | | 500,000 | | | | 502,370 | |

East Allegheny School District GO, 2.00% due 4/1/2017 (Insured: BAM) (State Aid Withholding) | | | AA/Ba1 | | | | 300,000 | | | | 301,365 | |

Lancaster County Hospital Authority, 5.00% due 11/1/2018 (Masonic Villages) | | | A/NR | | | | 1,500,000 | | | | 1,618,035 | |

Lehigh County IDA, 0.90% due 2/15/2027 put 8/15/2017 (PPL Electric Utilities Corp.) | | | A/A1 | | | | 1,000,000 | | | | 999,040 | |

Wilson School District GO, 3.00% due 6/1/2017 (State Aid Withholding) | | | AA/NR | | | | 200,000 | | | | 202,816 | |

| | | |

SOUTH CAROLINA — 2.67% | | | | | | | | | | | | |

City of North Charleston Public Facilities Corp. COP, 5.00% due 10/1/2017 (Convention Center Complex) | | | AA-/NR | | | | 300,000 | | | | 310,779 | |

Kershaw County Public Schools Foundation, 4.00% due 12/1/2017 (Kershaw County School District) | | | A-/A1 | | | | 500,000 | | | | 516,220 | |

Piedmont Municipal Power Agency, 5.00% due 1/1/2018 (Catawba Project) | | | AA/A3 | | | | 300,000 | | | | 314,706 | |

| | | |

TEXAS — 6.77% | | | | | | | | | | | | |

City of Houston, 4.00% due 9/1/2017 (Convention & Entertainment Facilities Department) | | | A-/A2 | | | | 200,000 | | | | 205,396 | |

City of Houston, 4.00% due 9/1/2018 (Convention & Entertainment Facilities Department) | | | A-/A2 | | | | 675,000 | | | | 712,024 | |

City of Houston Higher Education Finance Corp., 5.00% due 8/15/2018 (KIPP Program; Guaranty: PSF) | | | AAA/NR | | | | 970,000 | | | | 1,042,401 | |

Coastal Water Authority, 4.00% due 12/15/2017 (City of Houston Projects) | | | AA/NR | | | | 905,000 | | | | 938,575 | |

| | | |

WASHINGTON — 2.84% | | | | | | | | | | | | |

King County Public Hospital District No. 2 GO, 5.00% due 12/1/2018 (Evergreen Health) | | | NR/Aa3 | | | | 835,000 | | | | 907,745 | |

Ocean Beach School District No. 101 GO, 4.00% due 12/1/2017 (Educational Facilities) | | | NR/A2 | | | | 300,000 | | | | 310,398 | |

| | | |

WEST VIRGINIA — 0.47% | | | | | | | | | | | | |

Mason County, 1.625% due 10/1/2022 put 10/1/2018 (Appalachian Power Company) | | | BBB+/Baa1 | | | | 200,000 | | | | 201,042 | |

| | | |

WISCONSIN — 0.47% | | | | | | | | | | | | |

Wisconsin Health & Educational Facilities Authority, 1.25% due 8/15/2025 put 8/15/2017 (Aurora Health Care, Inc.) | | | NR/A2 | | | | 200,000 | | | | 200,112 | |

| | | | | | | | | | | | |

TOTAL INVESTMENTS — 96.94% (Cost $41,463,027) | | | | | | | | | | $ | 41,504,454 | |

OTHER ASSETS LESS LIABILITIES — 3.06% | | | | | | | | | | | 1,309,022 | |

| | | | | | | | | | | | |

NET ASSETS — 100.00% | | | | | | | | | | $ | 42,813,476 | |

| | | | | | | | | | | | |

Footnote Legend

| † | Credit ratings are unaudited. Rating changes may have occurred subsequent to the reporting period end. Bonds issued with a maturity of one year or less are assigned Moody’s ratings from MIG-1 to MIG-4 and Standard and Poor’s ratings from SP-1+ to SP-3 with MIG-1 and SP-1+ being the strongest ratings. |

Portfolio Abbreviations

To simplify the listings of securities, abbreviations are used per the table below:

| | |

| AGM | | Insured by Assured Guaranty Municipal Corp. |

| AMBAC | | Insured by American Municipal Bond Assurance Corp. |

| BAM | | Insured by Build America Mutual Insurance Co. |

| COP | | Certificates of Participation |

| DFA | | Development Finance Authority |

| ETM | | Escrowed to Maturity |

| | |

| GO | | General Obligation |

| HFA | | Health Facilities Authority |

| IDA | | Industrial Development Authority |

| Natl-Re | | Insured by National Public Finance Guarantee Corp. |

| PSF | | Guaranteed by Permanent School Fund |

| Q-SBLF | | Insured by Qualified School Bond Loan Fund |

Annual Report 11

| | |

| STATEMENT OF ASSETS AND LIABILITIES | | |

| |

Thornburg Low Duration Municipal Fund | | September 30, 2016 |

| | | | |

ASSETS | | | | |

Investments at value (cost $41,463,027) (Note 3) | | $ | 41,504,454 | |

Cash | | | 105,371 | |

Receivable for investments sold | | | 800,034 | |

Interest receivable | | | 451,901 | |

Prepaid expenses and other assets | | | 13,546 | |

| | | | |

Total Assets | | | 42,875,306 | |

| | | | |

| |

LIABILITIES | | | | |

Payable for fund shares redeemed | | | 932 | |

Payable to investment advisor and other affiliates (Note 4) | | | 4,705 | |

Accounts payable and accrued expenses | | | 55,667 | |

Dividends payable | | | 526 | |

| | | | |

Total Liabilities | | | 61,830 | |

| | | | |

| |

NET ASSETS | | $ | 42,813,476 | |

| | | | |

NET ASSETS CONSIST OF | | | | |

Net unrealized appreciation on investments | | $ | 41,427 | |

Accumulated net realized gain (loss) | | | (23,333 | ) |

Net capital paid in on shares of beneficial interest | | | 42,795,382 | |

| | | | |

| | $ | 42,813,476 | |

| | | | |

| |

NET ASSET VALUE | | | | |

Class A Shares: | | | | |

Net asset value and redemption price per share ($4,241,042 applicable to 343,625 shares of beneficial interest outstanding - Note 5) | | $ | 12.34 | |

Maximum sales charge, 1.50% of offering price | | | 0.19 | |

| | | | |

Maximum offering price per share | | $ | 12.53 | |

| | | | |

| |

Class I Shares: | | | | |

Net asset value, offering and redemption price per share ($38,572,434 applicable to 3,125,633 shares of beneficial interest outstanding - Note 5) | | $ | 12.34 | |

| | | | |

| * | Redemption price per share is equal to net asset value less any applicable contingent deferred sales charge. |

See notes to financial statements.

12 Annual Report

| | |

| STATEMENT OF OPERATIONS | | |

| |

Thornburg Low Duration Municipal Fund | | Year Ended September 30, 2016 |

| | | | |

INVESTMENT INCOME | | | | |

Interest income (net of premium amortized of $1,084,389) | | $ | 423,239 | |

| | | | |

| |

EXPENSES | | | | |

Investment advisory fees (Note 4) | | | 181,950 | |

Administration fees (Note 4) | | | | |

Class A Shares | | | 5,233 | |

Class I Shares | | | 20,650 | |

Distribution and service fees (Note 4) | | | | |

Class A Shares | | | 8,415 | |

Transfer agent fees | | | | |

Class A Shares | | | 27,871 | |

Class I Shares | | | 15,686 | |

Registration and filing fees | | | | |

Class A Shares | | | 26,224 | |

Class I Shares | | | 26,445 | |

Custodian fees (Note 2) | | | 21,861 | |

Professional fees | | | 47,064 | |

Accounting fees (Note 4) | | | 2,075 | |

Trustee fees | | | 2,137 | |

Other expenses | | | 5,580 | |

| | | | |

Total Expenses | | | 391,191 | |

Less: | | | | |

Fees waived by investment advisor (Note 4) | | | (34,946 | ) |

Expenses reimbursed by investment advisor (Note 4) | | | (122,082 | ) |

| | | | |

Net Expenses | | | 234,163 | |

| | | | |

Net Investment Income | | | 189,076 | |

| | | | |

REALIZED AND UNREALIZED GAIN (LOSS) | | | | |

Net realized gain (loss) on investments | | | (18,130 | ) |

Net change in unrealized appreciation (depreciation) on investments | | | (17,236 | ) |

| | | | |

Net Realized and Unrealized Loss | | | (35,366 | ) |

| | | | |

Net Increase in Net Assets Resulting from Operations | | $ | 153,710 | |

| | | | |

See notes to financial statements.

Annual Report 13

| | |

| STATEMENTS OF CHANGES IN NET ASSETS | | |

| |

Thornburg Low Duration Municipal Fund | | |

| | | | | | | | |

| | | Year Ended

September 30, 2016 | | | Year Ended

September 30, 2015 | |

INCREASE (DECREASE) IN NET ASSETS FROM | | | | | | | | |

| | |

OPERATIONS | | | | | | | | |

Net investment income | | $ | 189,076 | | | $ | 112,321 | |

Net realized gain (loss) on investments | | | (18,130 | ) | | | (5,203 | ) |

Net unrealized appreciation (depreciation) on investments | | | (17,236 | ) | | | 24,676 | |

| | | | | | | | |

| | |

Net Increase (Decrease) in Net Assets Resulting from Operations | | | 153,710 | | | | 131,794 | |

| | |

DIVIDENDS TO SHAREHOLDERS | | | | | | | | |

From net investment income | | | | | | | | |

Class A Shares | | | (9,876 | ) | | | (4,414 | ) |

Class I Shares | | | (179,200 | ) | | | (107,907 | ) |

| | |

FUND SHARE TRANSACTIONS (NOTE 5) | | | | | | | | |

Class A Shares | | | 971,622 | | | | 519,307 | |

Class I Shares | | | (3,150,597 | ) | | | 29,065,721 | |

| | | | | | | | |

Net Increase (Decrease) in Net Assets | | | (2,214,341 | ) | | | 29,604,501 | |

| | |

NET ASSETS | | | | | | | | |

Beginning of Year | | | 45,027,817 | | | | 15,423,316 | |

| | | | | | | | |

| | |

End of Year | | $ | 42,813,476 | | | $ | 45,027,817 | |

| | | | | | | | |

See notes to financial statements.

14 Annual Report

| | |

| NOTES TO FINANCIAL STATEMENTS | | |

| |

Thornburg Low Duration Municipal Fund | | September 30, 2016 |

NOTE 1 – ORGANIZATION

Thornburg Low Duration Municipal Fund (the “Fund”) is a diversified series of Thornburg Investment Trust (the “Trust”). The Trust is organized as a Massachusetts business trust under a Declaration of Trust dated June 3, 1987 and is registered as a diversified, open-end management investment company under the Investment Company Act of 1940, as amended. The Fund is currently one of twenty separate series of the Trust. Each series is considered to be a separate entity for financial reporting and tax purposes and bears expenses directly attributable to it. The Fund’s investment objective is to seek current income exempt from federal income tax, as is consistent, in the view of Thornburg Investment Management, Inc., the Trust’s investment advisor (the “Advisor”).

The Fund currently offers two classes of shares of beneficial interest: Class A and Institutional Class (“Class I”). Each class of shares of the Fund represents an interest in the same portfolio of investments, except that (i) Class A shares are sold subject to a front-end sales charge collected at the time the shares are purchased and bear a service fee, (ii) Class I shares are sold at net asset value without a sales charge at the time of purchase and may be subject to a service fee, and (iii) the respective classes may have different reinvestment privileges and conversion rights. Additionally, the Fund may allocate among its classes certain expenses, to the extent allocable to specific classes, including transfer agent fees, government registration fees, certain printing and postage costs, and administrative and legal expenses. Currently, class specific expenses of the Fund are limited to service and distribution fees, administration fees, and certain registration and transfer agent expenses.

The following is a summary of significant accounting policies followed by the Fund in the preparation of its financial statements. The Fund prepares its financial statements in conformity with United States generally accepted accounting principles (“GAAP”), including investment company accounting and reporting guidance in the Financial Accounting Standards Board (the “FASB”) Accounting Standard Codification Topic 946.

NOTE 2 – SIGNIFICANT ACCOUNTING POLICIES

Security Valuation: All investments in securities held by the Fund are valued as described in Note 3.

Allocation of Income, Gains, Losses and Expenses: Net investment income (other than class specific expenses) and realized and unrealized gains and losses are allocated daily to each class of shares based upon the relative net asset value of outstanding shares (or the value of the dividend-eligible shares, as appropriate) of each class of shares at the beginning of the day (after adjusting for the current capital shares activity of the respective class). Expenses common to all Funds are allocated among the Funds comprising the Trust based upon their relative net asset values or other appropriate allocation methods. Operating expenses directly attributable to a specific class are charged against the operating income of that class.

Dividends and Distributions to Shareholders: Dividends and distributions to shareholders, which are determined in accordance with federal income tax regulations and may differ from GAAP, are recorded on the ex-dividend date. Ordinary income distributions, if any, are declared daily and paid monthly. Capital gain distributions, if any, are declared and paid annually and more often if deemed necessary by the Advisor. Dividends are paid and are reinvested in additional shares of the Fund at net asset value per share at the close of business on the ex-dividend date, or at the shareholder’s option, paid in cash.

Investment Income: Interest income is accrued as earned. Premiums and discounts are amortized and accreted, respectively, to call dates or maturity dates using the effective yield method of the respective investments, which is included in interest income on the Statement of Operations.

Custodian Fees: Custodian fees disclosed in the Statement of Operations may include interest expenses incurred by the Fund on any cash overdrafts of its custodian account during the period. Such cash overdrafts may result from the effects of failed trades in portfolio securities and from cash outflows resulting from unanticipated shareholder redemption activity. The Fund pays interest to its custodian on any such cash overdraft at a rate equal to 2.50% of the overdraft amount in excess of $50,000.

Investment Transactions: Investment transactions are accounted for on a trade date basis. Realized gains and losses from the sale of investments are recorded on an identified cost basis.

When-Issued and Delayed Delivery Transactions: The Fund may engage in when-issued or delayed delivery transactions. To the extent the Fund engages in such transactions, it will do so for the purpose of acquiring portfolio investments consistent with the Fund’s investment objectives and not for the purpose of investment leverage or to speculate on interest rate or market changes. At the time the Fund makes a commitment to purchase an investment on a when-issued or delayed delivery basis, the Fund will record the transaction and reflect the value in determining its net asset value. When effecting such transactions, assets of an amount sufficient to make payment for the portfolio investments to be purchased will be segregated on the Fund’s records on the trade date. Investments purchased on a when-issued or delayed delivery basis do not earn interest until the settlement date.

Annual Report 15

| | |

| NOTES TO FINANCIAL STATEMENTS, CONTINUED | | |

| |

Thornburg Low Duration Municipal Fund | | September 30, 2016 |

Guarantees and Indemnifications: Under the Trust’s organizational documents (and under separate agreements with the independent Trustees), its officers and Trustees are provided with an indemnification against certain liabilities arising out of the performance of their duties to the Fund. In the normal course of business the Trust may also enter into contracts with service providers that contain general indemnifications. The Trust’s maximum exposure under these arrangements is unknown. However, based on experience, the Trust expects the risk of loss to be remote.

Use of Estimates: The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases (decreases) in net assets from operations during the reporting period. Actual results could differ from those estimates.

Federal Income Taxes: It is the policy of the Trust to comply with the provisions of the Internal Revenue Code applicable to regulated investment companies and to distribute to shareholders substantially all investment company taxable income including net realized gains on investments (if any), and tax exempt income of the Fund. Therefore, no provision for federal income or excise tax is required.

The Fund files income tax returns in United States federal and applicable state jurisdictions. The statute of limitations on the Fund’s tax return filings generally remains open for the three years following a return’s filing date. The Fund has analyzed each uncertain tax position believed to be material in the preparation of the Fund’s financial statements for the fiscal year ended September 30, 2016, including open tax years, to assess whether it is more likely than not that the position would be sustained upon examination, based on the technical merits of the position. The Fund has not identified any such position for which an asset or liability must be reflected in the Statement of Assets and Liabilities.

At September 30, 2016, information on the tax components of capital was as follows:

| | | | |

Cost of investments for tax purposes | | $ | 41,463,027 | |

| | | | |

Gross unrealized appreciation on a tax basis | | $ | 66,634 | |

Gross unrealized depreciation on a tax basis | | | (25,207 | ) |

| | | | |

Net unrealized appreciation (depreciation) on investments (tax basis) | | $ | 41,427 | |

| | | | |

At September 30, 2016, the Fund had deferred tax basis capital losses occurring subsequent to October 31, 2015 through September 30, 2016 of $1,645. For tax purposes, such losses will be recognized in the year ending September 30, 2017.

At September 30, 2016, the Fund had cumulative tax basis capital losses of $21,688, (of which $1,073 are short-term and $20,615 are long-term) generated after September 30, 2011, which may be carried forward to offset future capital gains. To the extent such carryforwards are used, capital gain distributions may be reduced to the extent provided by regulations. Such capital loss carryforwards do not expire.

At September 30, 2016, the Fund had $526 of undistributed net tax basis tax-exempt income, no undistributed tax basis net ordinary income and no undistributed tax basis capital gains.

Distributions from tax exempt income paid by the Fund for the years ended September 30, 2016 and September 30, 2015 are excludable by shareholders from gross income for Federal income tax purposes.

The tax character of distributions paid during the years ended September 30, 2016, and September 30, 2015, was as follows:

| | | | | | | | |

| | | 2016 | | | 2015 | |

Distributions from: | | | | | | | | |

Tax exempt income | | $ | 189,076 | | | $ | 112,321 | |

Ordinary income | | | — | | | | — | |

| | | | | | | | |

Total | | $ | 189,076 | | | $ | 112,321 | |

| | | | | | | | |

NOTE 3 – SECURITY VALUATION

Valuation of the Fund’s portfolio investment securities is performed in accordance with policies and procedures adopted by and under the oversight of the Trustees.

The Trustees of the Trust have appointed the Advisor to assist the Trustees in obtaining market values for portfolio investments, evaluate and monitor professional pricing service providers appointed by the Trustees’ Audit Committee (the “Audit Committee”) to assist in determining fair values for portfolio investments, assist in calculating fair values for portfolio investments in certain circumstances, and to perform other functions in connection with the valuation of investments. The Advisor acts through its Valuation and Pricing Committee

16 Annual Report

| | |

| NOTES TO FINANCIAL STATEMENTS, CONTINUED | | |

| |

Thornburg Low Duration Municipal Fund | | September 30, 2016 |

(the “Committee”) and other employees of the Advisor. The Committee regularly reviews its own valuation calculations, as well as the valuations, valuation techniques and services furnished by pricing service providers, considers circumstances which may require valuation calculations by the Committee, and reviews previous valuation calculations. The Committee reports to the Audit Committee on the Committee’s activities, the performance of pricing service providers, and other matters relating to valuation of portfolio investments.

In those instances when the Committee assists in calculating a fair value for a portfolio investment, the Committee seeks to determine the price that the Fund would reasonably expect to receive upon a sale of the investment in an orderly transaction between market participants on the valuation date. The Committee customarily utilizes quotations from securities broker dealers in calculating valuations, but also may utilize prices obtained from pricing service providers or other methods approved by the Audit Committee. Because fair values calculated by the Committee are estimates, the calculation of a value for an investment may differ from the price that would be realized by the Fund upon a sale of the investment, and the difference could be material to the Fund’s financial statements. The Committee’s calculation of a fair value for an investment may also differ from the prices obtained by other persons (including other mutual funds) for the investment.

Valuation of Securities: Debt obligations held by the Fund which are not listed or traded on exchanges or for which no reported market exists are ordinarily valued at the valuation obtained from a pricing service provider approved by the Audit Committee.

In any case when a pricing service provider fails to provide a valuation for a debt obligation held by the Fund, the Committee calculates a fair value for the obligation using alternative methods under procedures approved by the Audit Committee. Additionally, in cases when management believes that a valuation obtained from a pricing service provider merits review for significant reasons, the Committee decides whether or not to use the valuation calculated by the pricing service provider or to use an alternative method approved by the Audit Committee to calculate a fair value for the obligation.

Valuation Hierarchy: The Fund categorizes its investments based upon the inputs used in valuing those investments, according to a three-level hierarchy established in guidance from FASB. Categorization of investments using this hierarchy is intended by the FASB to maximize the use of observable inputs in valuing investments and minimize the use of unobservable inputs by requiring that the most observable inputs be used when available. Observable inputs are those that market participants would use in valuing an investment based on available market information. Unobservable inputs are those that reflect assumptions about the information market participants would use in valuing an investment. An investment’s level within the hierarchy is based on the lowest level input that is deemed significant to the valuation. The methodologies and inputs used to value investments are not necessarily indications of the risk or liquidity associated with those investments.

Various inputs are used in calculating valuations for the Fund’s investments. These inputs are generally summarized according to the three-level hierarchy below:

Level 1: Quoted prices in active markets for identical investments.

Level 2: Other direct or indirect significant observable inputs (including quoted prices for similar investments in active markets and other observable inputs, such as interest rates, prepayment rates, credit risk, etc.).

Level 3: Significant unobservable inputs (including the Committee’s own assumptions in calculating the fair values of investments).

Valuations for debt obligations held by the Fund are typically calculated by pricing service providers approved by the Audit Committee and are characterized as Level 2 within the valuation hierarchy.

In a limited number of cases the Committee calculates a fair value for investments using broker quotations or other methods approved by the Audit Committee. When the Committee uses a single broker quotation to calculate a fair value for an investment without other significant observable inputs, or if a fair value is calculated using other significant inputs that are considered unobservable, the investment is characterized as Level 3 within the hierarchy. Other significant unobservable inputs used to calculate a fair value in these instances might include an income-based valuation approach which considers discounted anticipated future cash flows from the investment, and application of discounts due to the nature or duration of any restrictions on the disposition of the investment.

Valuations based upon the use of inputs from Levels 1, 2 or 3 may not represent the actual price received upon the disposition of an investment, and the Fund may receive a price that is lower than the valuation based upon these inputs when it sells the investment.

Annual Report 17

| | |

| NOTES TO FINANCIAL STATEMENTS, CONTINUED | | |

| |

Thornburg Low Duration Municipal Fund | | September 30, 2016 |

The following table displays a summary of the fair value hierarchy measurements of the Fund’s investments as of September 30, 2016. In any instance when valuation inputs from more than one level are used to determine the fair value of a specific investment, the investment is placed in the level of the table based upon the lowest level input that is significant in determining the fair value of the investment:

| | | | | | | | | | | | | | | | |

| | | Fair Value Measurements at September 30, 2016 | |

| | | Total | | | Level 1 | | | Level 2 | | | Level 3 | |

Assets | | | | | | | | | | | | | | | | |

Investments in Securities | | | | | | | | | | | | | | | | |

Municipal Bonds | | $ | 41,504,454 | | | $ | — | | | $ | 41,504,454 | | | $ | — | |

| | | | | | | | | | | | | | | | |

Total Investments in Securities | | $ | 41,504,454 | | | $ | — | | | $ | 41,504,454 | | | $ | — | |

In accordance with the guidance prescribed in Accounting Standards Update No. 2011-04, it is the policy of the Fund to recognize transfers between levels and the underlying events which caused the movement. The Fund recognized no transfers between levels for the year ended September 30, 2016.

NOTE 4 – INVESTMENT ADVISORY FEE AND OTHER TRANSACTIONS WITH AFFILIATES

Pursuant to an investment advisory agreement, the Advisor serves as the investment advisor and performs services for the Fund for which the fees are payable at the end of each month. Under the investment advisory agreement, the Fund pays the Advisor a management fee based on the daily net assets of the Fund at an annual rate as shown in the following table:

| | | | |

Daily Net Assets | | Fee Rate | |

Up to $1 billion | | | 0.400 | % |

Next $500 million | | | 0.300 | |

Next $500 million | | | 0.250 | |

Over $2 billion | | | 0.225 | |

The Fund’s effective management fee for the year ended September 30, 2016 was 0.40% of the Fund’s average dividend assets (before applicable management fee waiver of $34,496).

The Fund pays to the Advisor the costs of personnel who perform certain accounting services for the Fund. For the year ended September 30, 2016 the Fund paid $2,075 to the Advisor for these accounting services. The Trust has also entered into administrative service agreements with the Advisor, whereby the Advisor will perform certain administrative services for the shareholders of each class of the Fund’s shares, and for which fees will be payable at an annual rate of up to .125 of 1% per annum of the average daily net assets attributable to each class of shares. Total administrative service fees incurred by each class of shares of the Fund for the year ended September 30, 2016, are set forth in the Statement of Operations.

The Trust has an underwriting agreement with Thornburg Securities Corporation (the “Distributor”), an affiliate of the Advisor, which acts as the distributor of the Fund’s shares. For the year ended September 30, 2016, the Distributor has advised the Fund that it earned net commissions aggregating $41 from the sale of Class A shares of the Fund.

Pursuant to a service plan under Rule 12b-1 of the Investment Company Act of 1940, the Fund may pay to the Advisor or securities dealers and other financial institutions at the Advisor’s request an amount not to exceed .25 of 1% per annum of the average daily net assets attributable to Class A shares of the Fund to obtain various shareholder and distribution related services. For the year ended September 30, 2016, there were no 12b-1 service plan fees charged for Class I shares. The Advisor may pay out of its own resources additional expenses for distribution of the Fund’s shares and shareholder services.

The Advisor and Distributor have contractually agreed to waive fees and reimburse expenses incurred by the Fund so that actual expenses of certain share classes do not exceed levels as specified in the Fund’s most recent prospectus. The agreement may be terminated by the Fund at any time, but may not be terminated by the Advisor or Distributor before February 1, 2017, unless the Advisor ceases to be the investment advisor to the Trust or the Distributor ceases to be the distributor of the Fund prior to that date. The Advisor and Distributor retain the right to be repaid by the Fund for fee waivers and expense reimbursements if expenses fall below the contractual limit prior to the end of the fiscal year.

For the year ended September 30, 2016, the Advisor voluntarily waived Fund level investment advisory fees of $34,946. The Advisor contractually reimbursed certain class specific expenses, administrative fees, and distribution fees of $59,214 for Class A shares and $62,868 for Class I shares.

18 Annual Report

| | |

| NOTES TO FINANCIAL STATEMENTS, CONTINUED | | |

| |

Thornburg Low Duration Municipal Fund | | September 30, 2016 |

Certain officers and Trustees of the Trust are also officers or directors of the Advisor and Distributor. The compensation of independent Trustees is borne by the Trust.

The percentage of direct investments in the Fund held by appointed Trustees, Officers and the Advisor is approximately 75.65%.

The Fund may sell securities to an affiliated fund, or the Fund may purchase securities held by an affiliated fund, provided the affiliation is due solely to having a common investment advisor, common officers, or common trustees, and provided that all such transactions will comply with Rule 17a-7 under the 1940 Act. For the year ended September 30, 2016, the Fund had transactions with affiliated funds of $5,300,754 in sales.

NOTE 5 – SHARES OF BENEFICIAL INTEREST

At September 30, 2016, there were an unlimited number of shares with no par value of beneficial interest authorized. Transactions in shares of beneficial interest were as follows:

| | | | | | | | | | | | | | | | |

| | | Year Ended

September 30, 2016 | | | Year Ended

September 30, 2015 | |

| | | Shares | | | Amount | | | Shares | | | Amount | |

Class A Shares | | | | | | | | | | | | | | | | |

Shares sold | | | 179,515 | | | $ | 2,217,348 | | | | 172,222 | | | $ | 2,123,915 | |

Shares issued to shareholders in reinvestment of dividends | | | 796 | | | | 9,845 | | | | 350 | | | | 4,315 | |

Shares repurchased | | | (101,677 | ) | | | (1,255,571 | ) | | | (130,474 | ) | | | (1,608,923 | ) |

| | | | | | | | | | | | | | | | |

| | | | |

Net increase (decrease) | | | 78,634 | | | $ | 971,622 | | | | 42,098 | | | $ | 519,307 | |

| | | | | | | | | | | | | | | | |

| | | | |

Class I Shares | | | | | | | | | | | | | | | | |

Shares sold | | | 1,018,022 | | | $ | 12,579,199 | | | | 3,405,347 | | | $ | 42,016,558 | |

Shares issued to shareholders in reinvestment of dividends | | | 14,105 | | | | 174,307 | | | | 8,471 | | | | 104,442 | |

Shares repurchased | | | (1,287,521 | ) | | | (15,904,103 | ) | | | (1,059,361 | ) | | | (13,055,279 | ) |

| | | | | | | | | | | | | | | | |

| | | | |

Net increase (decrease) | | | (255,394 | ) | | $ | (3,150,597 | ) | | | 2,354,457 | | | $ | 29,065,721 | |

| | | | | | | | | | | | | | | | |

NOTE 6 – INVESTMENT TRANSACTIONS

For the year ended September 30, 2016, the Fund had purchase and sale transactions of investments (excluding short-term investments) of $12,291,626 and $8,333,000, respectively.

OTHER NOTES

Risks: The Fund’s investments subject it to risks including, but not limited to, management risk, interest rate risk, credit risk, market and economic risk, and liquidity risk. Please see the Fund’s prospectus for a discussion of the risks associated with an investment in the Fund.

Subsequent Events: Fund management believes no events have occurred between September 30, 2016 and the date of issuance of the financial statements that require adjustment to or disclosure in the accompanying financial statements.

Annual Report 19

FINANCIAL HIGHLIGHTS

Thornburg Low Duration Municipal Fund

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | PER SHARE PERFORMANCE (for a share outstanding throughout the Year) | | RATIOS TO AVERAGE NET ASSETS | | | SUPPLEMENTAL DATA | |

Unless Otherwise Noted, Periods are

Fiscal Years Ended Sept. 30, | | Net Asset

Value

Beginning

of Year | | | Net

Investment

Income

(Loss)+ | | Net

Realized

&

Unrealized

Gain (loss)

on

Investments | | | Total from

Investment

Operations | | Dividends

from Net

Investment

Income | | | Dividends

from Net

Realized

Gains | | Total

Dividends | | | Net

Asset

Value

End of

Year | | Net

Investment

Income

(Loss)

(%) | | | Expenses,

After

Expense

Reductions

(%) | | | Expenses,

After

Expense

Reductions

and

Net of

Custody

Credits

(%) | | | Expenses,

Before

Expense

Reductions

(%) | | | Total

Return

(%)(a) | | Portfolio

Turnover

Rate

(%)(a) | | Net

Assets

at End

of

Year

(Thousands) | |

CLASS A SHARES | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

2016(b) | | $ | 12.35 | | | 0.03 | | | (0.01 | ) | | 0.02 | | | (0.03 | ) | | — | | | (0.03 | ) | | $12.34 | | | 0.24 | | | | 0.70 | | | | 0.70 | | | | 2.19 | | | 0.15 | | 21.17 | | $ | 4,241 | |

2015(b) | | $ | 12.34 | | | 0.02 | | | 0.01 | | | 0.03 | | | (0.02 | ) | | — | | | (0.02 | ) | | $12.35 | | | 0.15 | | | | 0.67 | | | | 0.67 | | | | 2.85 | | | 0.22 | | 20.53 | | $ | 3,273 | |

2014(b)(c) | | $ | 12.31 | | | 0.02 | | | 0.03 | | | 0.05 | | | (0.02 | ) | | — | | | (0.02 | ) | | $12.34 | | | 0.20 | (d) | | | 0.66 | (d) | | | 0.65 | (d) | | | 3.14 | (d) | | 0.40 | | 4.54 | | $ | 2,751 | |

CLASS I SHARES | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

2016 | | $ | 12.35 | | | 0.05 | | | (0.01 | ) | | 0.04 | | | (0.05 | ) | | — | | | (0.05 | ) | | $12.34 | | | 0.43 | | | | 0.50 | | | | 0.50 | | | | 0.72 | | | 0.36 | | 21.17 | | $ | 38,572 | |

2015 | | $ | 12.34 | | | 0.04 | | | 0.01 | | | 0.05 | | | (0.04 | ) | | — | | | (0.04 | ) | | $12.35 | | | 0.32 | | | | 0.50 | | | | 0.50 | | | | 0.82 | | | 0.40 | | 20.53 | | $ | 41,755 | |

2014(c) | | $ | 12.31 | | | 0.04 | | | 0.03 | | | 0.07 | | | (0.04 | ) | | — | | | (0.04 | ) | | $12.34 | | | 0.42 | (d) | | | 0.44 | (d) | | | 0.44 | (d) | | | 1.77 | (d) | | 0.56 | | 4.54 | | $ | 12,672 | |

| (a) | Not annualized for periods less than one year. |

| (b) | Sales loads are not reflected in computing total return. |

| (c) | Fund commenced operations on December 30, 2013. |

| + | Based on weighted average shares outstanding. |

See notes to financial statements.

| | | | |

| 20 Annual Report | | | | Annual Report 21 |

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

Thornburg Low Duration Municipal Fund

To the Trustees and Shareholders of

Thornburg Low Duration Municipal Fund

In our opinion, the accompanying statement of assets and liabilities, including the schedule of investments in securities, and the related statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of the Thornburg Low Duration Municipal Fund (the “Fund”) at September 30, 2016, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended and the financial highlights for each of the periods presented, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities at September 30, 2016 by correspondence with the custodian, brokers, transfer agent, and the application of alternative procedures where securities purchased had not been received, provide a reasonable basis for our opinion.

PricewaterhouseCoopers LLP

New York, New York

November 18, 2016

22 Annual Report

| | |

| EXPENSE EXAMPLE | | |

| |

Thornburg Low Duration Municipal Fund | | September 30, 2016 (Unaudited) |

As a shareholder of the Fund, you incur two types of costs:

| | (1) | transaction costs, including |

(a) sales charges (loads) on purchase payments, for Class A shares;

(b) a deferred sales charge on redemptions of any part or all of a purchase of $1 million of Class A shares within 12 months of purchase;

| | (2) | ongoing costs, including management fees; distribution and/or service (12b-1) fees; and other Fund expenses. |

This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on a $1,000 investment beginning on April 1, 2016, and held until September 30, 2016.

| | | | | | | | | | | | |

| | | Beginning

Account Value

4/1/16 | | | Ending

Account Value

9/30/16 | | | Expenses paid

During period†

4/1/16–9/30/16 | |

CLASS A SHARES | | | | | | | | | | | | |

Actual | | $ | 1,000.00 | | | $ | 999.90 | | | $ | 3.50 | |

Hypothetical* | | $ | 1,000.00 | | | $ | 1,021.50 | | | $ | 3.54 | |

CLASS I SHARES | | | | | | | | | | | | |

Actual | | $ | 1,000.00 | | | $ | 1,001.70 | | | $ | 2.46 | |

Hypothetical* | | $ | 1,000.00 | | | $ | 1,022.54 | | | $ | 2.49 | |

| † | Expenses are equal to the annualized expense ratio for each class (A: 0.70%; I: 0.49%) multiplied by the average account value over the period, multiplied by 183/366 to reflect the one-half year period. |

| * | Hypothetical assumes a rate of return of 5% per year before expenses. |

ACTUAL EXPENSES