UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-5225

Oppenheimer Quest for Value Funds

(Exact name of registrant as specified in charter)

6803 South Tucson Way, Centennial, Colorado 80112-3924

(Address of principal executive offices) (Zip code)

Arthur S. Gabinet

OFI Global Asset Management, Inc.

Two World Financial Center, New York, New York 10281-1008

(Name and address of agent for service)

Registrant’s telephone number, including area code: (303) 768-3200

Date of fiscal year end: October 31

Date of reporting period: 4/30/2014

Item 1. Reports to Stockholders.

Table of Contents

Class A Shares

AVERAGE ANNUAL TOTAL RETURNS AT 4/30/14

| | | | | | | | | | | | | | | | |

| | | 6-Month | | | 1-Year | | | 5-Year | | | 10-Year | |

Class A Shares of the Fund without Sales Charge | | | 1.91% | | | | 8.84% | | | | 12.21% | | | | 3.87% | |

Class A Shares of the Fund with Sales Charge | | | -3.95 | | | | 2.58 | | | | 10.89 | | | | 3.26 | |

S&P 500 Index | | | 8.36 | | | | 20.44 | | | | 19.14 | | | | 7.67 | |

Russell 1000 Index | | | 8.25 | | | | 20.81 | | | | 19.52 | | | | 8.05 | |

MSCI All Country World Index (ex-U.S.) | | | 2.91 | | | | 9.76 | | | | 12.90 | | | | 7.61 | |

Barclays U.S. Aggregate Bond Index | | | 1.74 | | | | -0.26 | | | | 4.88 | | | | 4.83 | |

Barclays Multiverse Index (ex-U.S.) | | | 2.26 | | | | 1.89 | | | | 5.52 | | | | 5.14 | |

Reference Index | | | 4.27 | | | | 9.73 | | | | 12.16 | | | | 7.43 | |

Performance data quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Fund returns include changes in share price, reinvested distributions, and a 5.75% maximum applicable sales charge except where “without sales charge” is indicated. Current performance may be lower or higher than the performance quoted. Returns do not consider capital gains or income taxes on an individual’s investment. Returns for periods of less than one year are cumulative and not annualized. For performance data current to the most recent month-end, visit oppenheimerfunds.com or call 1.800.CALL OPP (225.5677).

2 OPPENHEIMER GLOBAL ALLOCATION FUND

Fund Performance Discussion

The Fund’s Class A shares (without sales charge) produced a return of 1.91% during the reporting period. The Fund underperformed its Reference Index (the “Index”), a customized weighted index currently comprised of 30% of the Russell 1000 Index, 30% of the MSCI All Country World Index (ex-U.S.), 20% of the Barclays U.S. Aggregate Bond Index, and 20% of the Barclays Multiverse Index (ex-U.S.), which returned 4.27%. The largest detractor was security selection within the portfolio’s underlying investment strategies. Return shaping or hedging strategies, which are primarily used to provide a degree of downside protection in periods of extreme market volatility, also detracted from relative performance. However, like insurance, we expect these strategies to have an associated cost. This was partially offset by asset allocation decisions, which were a slight positive to relative performance.

MARKET OVERVIEW

Markets were volatile this reporting period against the backdrop of a complex market environment. Through December 2013, improvement in the U.S. labor market, consumer spending and retail sales pointed toward a slow but persistent economic recovery. Interest rates climbed higher at a measured rate as investors anticipated that a gradual unwinding of quantitative easing – the so-called tapering – would have a benign impact on interest rates and economic growth. This attitude was bolstered by the Federal Reserve’s (the “Fed’s”) decision in mid-September to delay the onset of tapering. The marketplace interpreted this as a sign that the Fed’s approach to tapering would not be aggressive. Encouraged by this perception, investors showed an aggressive appetite for risk, bidding up equity prices to new highs. Prices for fixed income securities and hard assets commonly used to hedge against a weak economy (e.g., gold) came

under pressure. Emerging market currencies pegged to the U.S. dollar lost ground as well, with emerging markets remaining under pressure due to concerns that the benefits of low developed market interest rates were largely behind them.

The Fed announced its decision to begin tapering in December, affirming its commitment to wean the U.S. economy off easy money. The move persuaded investors that after years of interest rates near all-time lows, the Fed may finally be headed down the path to interest-rate normalization. Prices for bonds and hard assets rose, while equity-market volatility increased as investors considered the potential impact of higher domestic interest rates. The high valuations of stocks, a dip in U.S. retail sales data and a slight uptick in U.S. unemployment in February also colored the market’s mood. So, too, did the less-robust pace of economic

3 OPPENHEIMER GLOBAL ALLOCATION FUND

growth in China and escalating civil unrest in Ukraine. Towards the end of the reporting period, estimates of first quarter 2014 U.S. Gross Domestic Product indicated a slowdown in growth, but the market pushed forward recognizing the difficult winter.

FUND REVIEW

With respect to asset allocation, the portfolio had a modest overweight to equity focused strategies and credit centric fixed income strategies this reporting period. In particular, we currently have a tilt to growth equities and are light on duration in comparison to the blended benchmark. The Fund currently also runs no exposure in international government debt. We are also generally underweight U.S. Treasury securities and investment-grade fixed income. Given natural impediments to Treasury bond price response from such low yields, we favor sourcing downside protection from our return shaping (hedging) strategies. We also favor income alternatives like event-linked bonds that act as an effective diversifier because of their floating rate structure and lack of correlation with traditional financial assets.

The Fund’s asset allocation positioning benefited from its lack of exposure to international (emerging and developed market) sovereign debt. In our view, despite the rise in credit spreads last summer, emerging and developed market sovereign bonds do not offer a sufficient yield cushion in the context of deteriorating trade and fiscal conditions. There may be additional currency

depreciation required to restore balance to some of these markets. Additionally, a less accommodative Fed may be positive for the U.S. dollar, leading to a headwind for foreign currency denominated bonds. This allocation decision added value as international debt markets underperformed the Index.

Some of the Fund’s asset allocation decisions detracted from relative performance. Our cash allocation, which serves to collateralize our upside hedges detracted. However, our tactical upside positioning, often implemented in our return shaping overlays, helped offset some of this (see return shaping section).

During the period, the security selection component of the Fund’s investment process detracted from relative performance. Stock selection within our domestic equity strategies detracted from relative performance. This was partially offset by the international developed market growth strategy, and emerging market equity strategy, which added positive excess returns to the Fund. The international developed market growth strategy outperformed the MSCI All Country World Index (ex-U.S.) by roughly 4.3%, and the emerging market equity strategy outperformed the MSCI Emerging Markets Index by roughly 1.8%.

We currently use derivatives to cheaply mitigate downside risk and efficiently access market upside, techniques we call “return shaping.” Because the Fund’s return shaping

4 OPPENHEIMER GLOBAL ALLOCATION FUND

strategies are designed to improve the overall risk profile of the Fund by dampening volatility, we expect them to come with a cost, like any insurance policy. Although we maintained hedges against many of our downside risk exposures in a rallying market, we financed some of the protection via upside capture strategies, which are intended to capture gains from sustained market appreciation. Our upside capture strategies benefited as equity markets rallied during the period. Specifically, our S&P 500 Index and Euro Stoxx 50 call options were accretive to returns and offset some of the downside hedging cost.

A significant portion of our downside protection strategy entailed owning and selling Chicago Board Options Exchange Market Volatility Index (the “CBOE VIX Index”) futures contracts to protect against market volatility.1 We managed this position by owning near-dated futures and selling longer-dated futures. This strategy, which provides relatively cheap downside protection, detracted from performance. Again, under normal circumstances we expect return shaping strategies to cost money and commensurately enhance returns or partially protect principal in environments of extreme market volatility.

1. The CBOE VIX Index is a measure of market expectations of

near-term volatility conveyed by S&P 500 stock index option prices.

STRATEGY & OUTLOOK

Overall, we remain cautious and are slightly overweight equities in the portfolio relative to the Reference Index, but with defensive hedges built in for downside protection and upside in case of a continued rally. Volatility within the Reference Index is very low, so the carrying cost of hedges is fairly modest. Much of this is due to measures taken by central bankers, which have significantly lifted global equity markets back at least to fair value territory. We believe current zero short-term rates will be left largely unchanged for some time given the Fed’s more dovish stance, and we will continue to see reductions in large scale asset purchases in the U.S. Given this accommodative monetary environment, contained inflation, and positive global growth, we believe equities remain somewhat attractive versus bonds although much less so than at this time last year. Among fixed-income investments, we currently favor floating rate securities and higher yielding corporate bonds, as the corporate sector globally has gone to great lengths to term out debt, improve balance sheet quality, and bolster profit margins. We are currently maintaining very limited exposure to U.S. Treasuries with a view toward eventual rate and borrowing cost increases. Any normalization in monetary policy, such as increased reduction in the pace of asset purchases, could have adverse effects on the Treasury market. At period end, we remain focused on establishing downside protection via derivative strategies, which we have been

5 OPPENHEIMER GLOBAL ALLOCATION FUND

able to purchase at lower costs due to low volatility.

At the end of the day, reduced Fed “intervention” is inevitable. In this environment, we expect correlation among assets to continue to decline as investors focus more on company fundamentals rather than macro events. This may enhance the opportunity for our security selection teams to add value. At the same time, less Fed activity

| | |

| |

Mark Hamilton Portfolio Manager |

in terms of providing market support only enhances the importance of seeking cost-efficient hedges in the event of a downturn. Finally, it is worth noting that most asset classes have returned to at least normal valuation levels as investors gradually returned to the market. Of course, this implies fewer opportunities, but that is one of the advantages of the Fund’s wide ranging mandate.

| | |

| |

Benjamin Rockmuller, CFA Portfolio Manager |

6 OPPENHEIMER GLOBAL ALLOCATION FUND

Top Holdings and Allocations

TOP TEN COMMON STOCK HOLDINGS

| | | | |

Walt Disney Co. (The) | | | 1.0 | % |

Apple, Inc. | | | 0.9 | |

Telefonaktiebolaget LM Ericsson, Cl. B | | | 0.8 | |

SAP AG | | | 0.7 | |

LVMH Moet Hennessy Louis Vuitton SA | | | 0.7 | |

Citigroup, Inc. | | | 0.6 | |

UBS AG | | | 0.6 | |

Microsoft Corp. | | | 0.6 | |

Prudential plc | | | 0.6 | |

Gilead Sciences, Inc. | | | 0.6 | |

Portfolio holdings and allocations are subject to change. Percentages are as of April 30, 2014, and are based on net assets. For more current Fund holdings, please visit oppenheimerfunds.com.

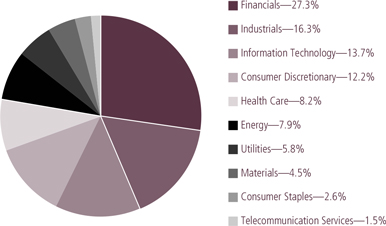

TOP TEN COMMON STOCK INDUSTRIES

| | | | |

Pharmaceuticals | | | 3.8 | % |

Internet Software & Services | | | 3.7 | |

Commercial Banks | | | 3.6 | |

Software | | | 3.6 | |

Oil, Gas & Consumable Fuels | | | 3.0 | |

Capital Markets | | | 2.8 | |

Media | | | 2.6 | |

Biotechnology | | | 2.5 | |

Insurance | | | 2.5 | |

Textiles, Apparel & Luxury Goods | | | 2.5 | |

Portfolio holdings and allocations are subject to change. Percentages are as of April 30, 2014, and are based on net assets.

PORTFOLIO ALLOCATION

| | | | |

Common Stocks | | | 72.0 | % |

Investment Companies Oppenheimer Master Loan Fund, LLC | | | 10.2 | |

Oppenheimer Master Event-Linked Bond Fund, LLC | | | 7.5 | |

Oppenheimer Institutional Money Market Fund | | | 1.0 | |

Non-Convertible Corporate Bonds and Notes | | | 7.5 | |

Corporate Loans | | | 1.0 | |

Exchange-Traded Options Purchased | | | 0.6 | |

Preferred Stocks | | | 0.1 | |

Over-the-Counter Options Purchased | | | 0.1 | |

Rights, Warrants and Certificates | | | — | * |

* Represents a value of less than 0.005%.

Portfolio holdings and allocations are subject to change. Percentages are as of April 30, 2014, and are based on the total market value of investments.

7 OPPENHEIMER GLOBAL ALLOCATION FUND

TOP TEN GEOGRAPHICAL HOLDINGS

| | | | |

United States | | | 64.7 | % |

United Kingdom | | | 4.6 | |

Germany | | | 3.5 | |

Switzerland | | | 3.4 | |

France | | | 3.3 | |

Japan | | | 2.8 | |

Brazil | | | 2.0 | |

India | | | 1.7 | |

Netherlands | | | 1.6 | |

Spain | | | 1.5 | |

Portfolio holdings and allocation are subject to change. Percentages are as of April 30, 2014, and are based on total market value of investments.

REGIONAL ALLOCATION

| | | | |

U.S./Canada | | | 65.8 | % |

Europe | | | 21.9 | |

Asia | | | 7.4 | |

Latin America | | | 3.4 | |

Emerging Europe | | | 0.8 | |

Middle East/Africa | | | 0.7 | |

Portfolio holdings and allocations are subject to change. Percentages are as of April 30, 2014, and are based on the total market value of investments.

8 OPPENHEIMER GLOBAL ALLOCATION FUND

Share Class Performance

AVERAGE ANNUAL TOTAL RETURNS WITHOUT SALES CHARGE AS OF 4/30/14

| | | | | | | | | | | | | | | | | | | | |

| | | Inception Date | | | 6-Month | | | 1-Year | | | 5-Year | | | 10-Year | |

Class A (QVGIX) | | | 11/1/91 | | | | 1.91% | | | | 8.84% | | | | 12.21% | | | | 3.87% | |

Class B (QGRBX) | | | 9/1/93 | | | | 1.50% | | | | 7.90% | | | | 11.27% | | | | 3.40% | |

Class C (QGRCX) | | | 9/1/93 | | | | 1.54% | | | | 8.08% | | | | 11.41% | | | | 3.13% | |

Class I (QGRIX) | | | 2/28/12 | | | | 2.09% | | | | 9.31% | | | | 9.00% * | | | | N/A | |

Class N (QGRNX) | | | 3/1/01 | | | | 1.71% | | | | 8.54% | | | | 11.93% | | | | 3.60% | |

Class Y (QGRYX) | | | 5/1/00 | | | | 2.02% | | | | 9.23% | | | | 12.62% | | | | 4.24% | |

AVERAGE ANNUAL TOTAL RETURNS WITH SALES CHARGE AS OF 4/30/14

| | | | | | | | | | | | | | | | | | | | |

| | | Inception Date | | | 6-Month | | | 1-Year | | | 5-Year | | | 10-Year | |

| Class A (QVGIX) | | | 11/1/91 | | | | -3.95% | | | | 2.58% | | | | 10.89% | | | | 3.26% | |

| Class B (QGRBX) | | | 9/1/93 | | | | -3.50% | | | | 2.90% | | | | 11.00% | | | | 3.40% | |

| Class C (QGRCX) | | | 9/1/93 | | | | 0.54% | | | | 7.08% | | | | 11.41% | | | | 3.13% | |

| Class I (QGRIX) | | | 2/28/12 | | | | 2.09% | | | | 9.31% | | | | 9.00% * | | | | N/A | |

| Class N (QGRNX) | | | 3/1/01 | | | | 0.71% | | | | 7.54% | | | | 11.93% | | | | 3.60% | |

| Class Y (QGRYX) | | | 5/1/00 | | | | 2.02% | | | | 9.23% | | | | 12.62% | | | | 4.24% | |

* Shows performance since inception.

Performance data quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted. Returns do not consider capital gains or income taxes on an individual’s investment. For performance data current to the most recent month-end, visit oppenheimerfunds.com or call 1.800.CALL OPP (225.5677). Fund returns include changes in share price, reinvested distributions, and the applicable sales charge: for Class A shares, the current maximum initial sales charge of 5.75%; for Class B shares, the contingent deferred sales charge of 5% (1-year) and 2% (5-year); and for Class C and N shares, the contingent deferred sales charge of 1% for the 1-year period. There is no sales charge for Class I and Y shares. Because Class B shares convert to Class A shares 72 months after purchase, the 10-year return for Class B shares uses Class A performance for the period after conversion. Returns for periods of less than one year are cumulative and not annualized.

The Fund’s performance is compared to the performance of the S&P 500 Index, the Russell 1000 Index, the MSCI All Country World Index (ex-U.S.), the Barclays U.S. Aggregate Bond Index, the Barclays Multiverse Index (ex-U.S.) and the Fund’s Reference Index. The S&P 500 Index is a capitalization-weighted index of 500 stocks intended to be a representative sample of leading companies in leading industries within the U.S. economy. The Russell 1000 Index

9 OPPENHEIMER GLOBAL ALLOCATION FUND

measures the performance of the large-cap segment of the U.S. equity universe. The MSCI All Country World Index (ex U.S.) is designed to measure global developed and emerging equity market performance excluding the United States. The Barclays U.S. Aggregate Bond Index is an index of U.S dollar-denominated, investment-grade U.S. corporate government and mortgage-backed securities. The Barclays Multiverse Index (ex-U.S.) provides a broad-based measure of the global fixed-income bond market. The Fund’s Reference Index is a customized weighted index currently comprised of 30% of the Russell 1000 Index, 30% of the MSCI All Country World Index (ex-U.S.), 20% of the Barclays U.S. Aggregate Bond Index, and 20% of the Barclays Multiverse Index (ex-U.S.). The Indices are unmanaged and cannot be purchased directly by investors. While index comparisons may be useful to provide a benchmark for the Fund’s performance, it must be noted that the Fund’s investments are not limited to the investments comprising the Index. Index performance includes reinvestment of income, but does not reflect transaction costs, fees, expenses or taxes. Index performance is shown for illustrative purposes only as a benchmark for the Fund’s performance, and does not predict or depict performance of the Fund. The Fund’s performance reflects the effects of the Fund’s business and operating expenses.

The Fund’s investment strategy and focus can change over time. The mention of specific fund holdings does not constitute a recommendation by OppenheimerFunds, Inc. or its affiliates.

Before investing in any of the Oppenheimer funds, investors should carefully consider a fund’s investment objectives, risks, charges and expenses. Fund prospectuses and summary prospectuses contain this and other information about the funds, and may be obtained by asking your financial advisor, visiting oppenheimerfunds.com, or calling 1.800.CALL OPP (225.5677). Read prospectuses and summary prospectuses carefully before investing.

Shares of Oppenheimer funds are not deposits or obligations of any bank, are not guaranteed by any bank, are not insured by the FDIC or any other agency, and involve investment risks, including the possible loss of the principal amount invested.

10 OPPENHEIMER GLOBAL ALLOCATION FUND

Fund Expenses

Fund Expenses. As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, which may include sales charges (loads) on purchase payments, contingent deferred sales charges on redemptions; and (2) ongoing costs, including management fees; distribution and service fees; and other Fund expenses. These examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The examples are based on an investment of $1,000.00 invested at the beginning of the period and held for the entire

6-month period ended April 30, 2014.

Actual Expenses. The first section of the table provides information about actual account values and actual expenses. You may use the information in this section for the class of shares you hold, together with the amount you invested, to estimate the expense that you paid over the period. Simply divide your account value by $1,000.00 (for example, an $8,600.00 account value divided by $1,000.00 = 8.60), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes. The second section of the table provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio for each class of shares, and an assumed rate of return of 5% per year for each class before expenses, which is not the actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example for the class of shares you hold with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as front-end or contingent deferred sales charges (loads). Therefore, the “hypothetical” section of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

11 OPPENHEIMER GLOBAL ALLOCATION FUND

| | | | | | | | | | | | | | |

| Actual | | Beginning

Account Value

November 1, 2013 | | | Ending Account Value

April 30, 2014 | | | Expenses

Paid During

6 Months Ended

April 30, 2014 | | | |

Class A | | $ | 1,000.00 | | | $ | 1,019.10 | | | $ | 6.53 | | | |

Class B | | | 1,000.00 | | | | 1,015.00 | | | | 10.55 | | | |

Class C | | | 1,000.00 | | | | 1,015.40 | | | | 10.19 | | | |

Class I | | | 1,000.00 | | | | 1,020.90 | | | | 4.22 | | | |

Class N | | | 1,000.00 | | | | 1,017.10 | | | | 7.78 | | | |

Class Y | | | 1,000.00 | | | | 1,020.20 | | | | 4.92 | | | |

| | | | |

Hypothetical (5% return before expenses) | | | | | | | | | | | | | | |

Class A | | | 1,000.00 | | | | 1,018.35 | | | | 6.53 | | | |

Class B | | | 1,000.00 | | | | 1,014.38 | | | | 10.54 | | | |

Class C | | | 1,000.00 | | | | 1,014.73 | | | | 10.19 | | | |

Class I | | | 1,000.00 | | | | 1,020.63 | | | | 4.22 | | | |

Class N | | | 1,000.00 | | | | 1,017.11 | | | | 7.78 | | | |

Class Y | | | 1,000.00 | | | | 1,019.93 | | | | 4.92 | | | |

Expenses are equal to the Fund’s annualized expense ratio for that class, multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period). Those annualized expense ratios, excluding indirect expenses from affiliated funds, based on the 6-month period ended April 30, 2014 are as follows:

| | | | | | |

| Class | | Expense Ratios | | | |

Class A | | | 1.30 | % | | |

Class B | | | 2.10 | | | |

Class C | | | 2.03 | | | |

Class I | | | 0.84 | | | |

Class N | | | 1.55 | | | |

Class Y | | | 0.98 | | | |

The expense ratios reflect voluntary and/or contractual waivers and/or reimbursements of expenses by the Fund’s Manager and Transfer Agent. Some of these undertakings may be modified or terminated at any time, as indicated in the Fund’s prospectus. The “Consolidated Financial Highlights” tables in the Fund’s consolidated financial statements, included in this report, also show the gross expense ratios, without such waivers or reimbursements and reduction to custodian expenses, if applicable.

12 OPPENHEIMER GLOBAL ALLOCATION FUND

| | |

| |

CONSOLIDATED STATEMENTOF INVESTMENTS April 30, 2014 Unaudited | | |

| | | | | | | | |

| | | Shares | | | Value | |

| |

Common Stocks—70.8% | |

| |

Consumer Discretionary—10.6% | |

| |

Auto Components—0.4% | |

| |

Delphi Automotive plc | | | 27,320 | | | $ | 1,826,069 | |

| |

Dorman Products, Inc.1 | | | 18,320 | | | | 1,054,316 | |

| |

Gentherm, Inc.1 | | | 19,970 | | | | 725,909 | |

| |

Johnson Controls, Inc. | | | 46,260 | | | | 2,088,176 | |

| |

Magna International, Inc. | | | 7,650 | | | | 749,624 | |

| | | | | | | | |

| | | | | | | 6,444,094 | |

|

| |

Automobiles—0.8% | | | | | | | | |

| |

Astra International Tbk PT | | | 3,276,500 | | | | 2,105,245 | |

| |

Bayerische Motoren Werke (BMW) AG | | | 14,193 | | | | 1,777,146 | |

| |

Bayerische Motoren Werke (BMW) AG, Preference | | | 88,159 | | | | 8,682,242 | |

| |

Daimler AG, Sponsored ADR | | | 14,710 | | | | 1,361,337 | |

| | | | | | | | |

| | | | | | | 13,925,970 | |

|

| |

Diversified Consumer Services—0.5% | | | | | | | | |

| |

Apollo Education Group, Inc.1 | | | 30,990 | | | | 894,371 | |

| |

Benesse Holdings, Inc. | | | 31,200 | | | | 1,185,591 | |

| |

Dignity plc | | | 63,038 | | | | 1,525,349 | |

| |

Estacio Participacoes SA | | | 166,800 | | | | 1,786,381 | |

| |

Grand Canyon Education, Inc.1 | | | 12,980 | | | | 559,698 | |

| |

Kroton Educacional SA | | | 42,759 | | | | 915,874 | |

| |

LifeLock, Inc.1 | | | 42,370 | | | | 665,209 | |

| |

New Oriental Education & Technology Group, Inc., Sponsored ADR | | | 55,910 | | | | 1,353,022 | |

| | | | | | | | |

| | | | | | | 8,885,495 | |

|

| |

Hotels, Restaurants & Leisure—1.5% | | | | | | | | |

| |

Buffalo Wild Wings, Inc.1 | | | 15,470 | | | | 2,260,476 | |

| |

Carnival Corp. | | | 54,870 | | | | 2,156,940 | |

| |

Chipotle Mexican Grill, Inc.1 | | | 2,250 | | | | 1,121,625 | |

| |

Chuy’s Holdings, Inc.1 | | | 25,090 | | | | 901,985 | |

| |

Domino’s Pizza Group plc | | | 180,150 | | | | 1,565,400 | |

| |

Fiesta Restaurant Group, Inc.1 | | | 30,070 | | | | 1,100,863 | |

| |

Genting Bhd | | | 520,000 | | | | 1,560,830 | |

| |

Gtech Spa | | | 46,753 | | | | 1,373,360 | |

| |

Home Inns & Hotels Management, Inc., ADR1 | | | 19,680 | | | | 559,306 | |

| |

Jollibee Foods Corp. | | | 243,130 | | | | 938,232 | |

| |

McDonald’s Corp. | | | 43,730 | | | | 4,433,347 | |

| |

MGM Resorts International1 | | | 56,750 | | | | 1,431,803 | |

| |

Red Robin Gourmet Burgers, Inc.1 | | | 19,790 | | | | 1,345,324 | |

| |

Revel Entertainment, Inc.1 | | | 5,092 | | | | — | |

| |

Royal Caribbean Cruises Ltd. | | | 30,460 | | | | 1,618,340 | |

| |

William Hill plc | | | 334,469 | | | | 2,007,838 | |

| |

Wynn Resorts Ltd. | | | 8,990 | | | | 1,832,971 | |

| | | | | | | | |

| | | | | | | 26,208,640 | |

|

| |

Household Durables—0.4% | | | | | | | | |

| |

Cyrela Brazil Realty SA Empreendimentos e Participacoes | | | 67,400 | | | | 408,677 | |

| |

Harman International Industries, Inc. | | | 30,190 | | | | 3,309,126 | |

| |

La-Z-Boy, Inc. | | | 32,460 | | | | 786,506 | |

| |

Newell Rubbermaid, Inc. | | | 29,890 | | | | 899,988 | |

13 OPPENHEIMER GLOBAL ALLOCATION FUND

| | |

| |

CONSOLIDATED STATEMENTOF INVESTMENTS Unaudited / Continued | | |

| | | | | | | | |

| | | Shares | | | Value | |

| |

Household Durables (Continued) | |

| |

SEB SA | | | 18,250 | | | $ | 1,688,282 | |

| | | | | | | | |

| | | | 7,092,579 | |

|

| |

Internet & Catalog Retail—0.4% | | | | | | | | |

| |

Amazon.com, Inc.1 | | | 2,426 | | | | 737,819 | |

| |

B2W Cia Digital1 | | | 31,117 | | | | 345,814 | |

| |

Coupons.com, Inc.1 | | | 5,140 | | | | 86,455 | |

| |

Ctrip.com International Ltd., ADR1 | | | 40,720 | | | | 1,903,253 | |

| |

Priceline.com, Inc. (The)1 | | | 490 | | | | 567,298 | |

| |

RetailMeNot, Inc.1 | | | 18,090 | | | | 539,263 | |

| |

TripAdvisor, Inc.1 | | | 14,100 | | | | 1,138,434 | |

| |

Yoox SpA1 | | | 47,773 | | | | 1,720,979 | |

| |

zulily, Inc., Cl. A1 | | | 6,710 | | | | 285,309 | |

| | | | | | | | |

| | | | 7,324,624 | |

|

| |

Media—2.6% | | | | | | | | |

| |

British Sky Broadcasting Group plc | | | 115,802 | | | | 1,723,865 | |

| |

Cinemark Holdings, Inc. | | | 25,850 | | | | 765,677 | |

| |

Comcast Corp., Cl. A | | | 25,470 | | | | 1,318,327 | |

| |

Grupo Televisa SAB, Sponsored ADR | | | 174,873 | | | | 5,737,583 | |

| |

Liberty Global plc, Cl. A1 | | | 6,979 | | | | 277,904 | |

| |

Liberty Global plc, Series C1 | | | 17,401 | | | | 668,721 | |

| |

Lions Gate Entertainment Corp. | | | 35,910 | | | | 952,692 | |

| |

MDC Partners, Inc., Cl. A | | | 45,160 | | | | 1,102,807 | |

| |

Naspers Ltd., Cl. N | | | 3,822 | | | | 361,838 | |

| |

SES SA | | | 56,200 | | | | 2,117,137 | |

| |

Time Warner, Inc. | | | 34,030 | | | | 2,261,634 | |

| |

Twenty-First Century Fox, Inc., Cl. A2 | | | 57,350 | | | | 1,836,347 | |

| |

Twenty-First Century Fox, Inc., Cl. B | | | 69,520 | | | | 2,177,366 | |

| |

Viacom, Inc., Cl. B | | | 21,610 | | | | 1,836,418 | |

| |

Walt Disney Co. (The) | | | 220,206 | | | | 17,471,144 | |

| |

World Wrestling Entertainment, Inc., Cl. A | | | 21,560 | | | | 420,420 | |

| |

Zee Entertainment Enterprises Ltd. | | | 976,856 | | | | 4,251,772 | |

| | | | | | | | |

| | | | 45,281,652 | |

|

| |

Multiline Retail—0.2% | | | | | | | | |

| |

Dollarama, Inc. | | | 22,545 | | | | 1,875,099 | |

| |

Lojas Americanas SA, Preference | | | 244,490 | | | | 1,851,973 | |

| |

Shinsegae Co. Ltd. | | | 3,481 | | | | 754,460 | |

| | | | | | | | |

| | | | 4,481,532 | |

|

| |

Specialty Retail—1.3% | | | | | | | | |

| |

Gap, Inc. (The) | | | 20,420 | | | | 802,506 | |

| |

Home Depot, Inc. (The) | | | 20,490 | | | | 1,629,160 | |

| |

Industria de Diseno Textil SA (Inditex) | | | 62,630 | | | | 9,420,138 | |

| |

Lithia Motors, Inc., Cl. A | | | 14,130 | | | | 1,049,576 | |

| |

Lowe’s Cos., Inc. | | | 14,530 | | | | 667,072 | |

| |

Tiffany & Co. | | | 103,503 | | | | 9,055,478 | |

| |

TJX Cos., Inc. (The) | | | 21,426 | | | | 1,246,565 | |

| | | | | | | | |

| | | | 23,870,495 | |

14 OPPENHEIMER GLOBAL ALLOCATION FUND

| | | | | | | | |

| | | Shares | | | Value | |

| |

Textiles, Apparel & Luxury Goods—2.5% | |

| |

Brunello Cucinelli SpA | | | 11,590 | | | $ | 334,259 | |

| |

Burberry Group plc | | | 77,567 | | | | 1,950,778 | |

| |

Cie Financiere Richemont SA | | | 35,021 | | | | 3,565,901 | |

| |

G-III Apparel Group Ltd.1 | | | 9,770 | | | | 701,193 | |

| |

Kering | | | 40,230 | | | | 8,906,046 | |

| |

lululemon athletica, Inc.1 | | | 44,630 | | | | 2,049,856 | |

| |

Luxottica Group SpA | | | 17,827 | | | | 1,024,303 | |

| |

LVMH Moet Hennessy Louis Vuitton SA | | | 59,220 | | | | 11,656,990 | |

| |

Nike, Inc., Cl. B | | | 32,572 | | | | 2,376,127 | |

| |

Prada SpA | | | 517,800 | | | | 4,149,057 | |

| |

Salvatore Ferragamo SpA | | | 6,405 | | | | 203,509 | |

| |

Swatch Group AG (The) | | | 2,663 | | | | 1,714,509 | |

| |

Tod’s SpA | | | 23,344 | | | | 3,280,250 | |

| |

VF Corp. | | | 24,380 | | | | 1,489,374 | |

| | | | | | | | |

| | | | 43,402,152 | |

|

| |

Consumer Staples—5.9% | | | | | | | | |

| |

Beverages—2.0% | | | | | | | | |

| |

AMBEV SA, ADR | | | 483,000 | | | | 3,501,750 | |

| |

Anadolu Efes Biracilik Ve Malt Sanayii AS | | | 73,650 | | | | 881,067 | |

| |

Boston Beer Co., Inc. (The), Cl. A1 | | | 1,490 | | | | 366,600 | |

| |

Brown-Forman Corp., Cl. B | | | 47,670 | | | | 4,276,952 | |

| |

C&C Group plc | | | 18,520 | | | | 110,284 | |

| |

Carlsberg AS, Cl. B | | | 28,446 | | | | 2,851,755 | |

| |

Coca-Cola Enterprises, Inc. | | | 65,100 | | | | 2,958,144 | |

| |

Diageo plc | | | 99,865 | | | | 3,061,778 | |

| |

Fomento Economico Mexicano SAB de CV, Sponsored ADR | | | 43,546 | | | | 3,952,670 | |

| |

Fomento Economico Mexicano SAB de CV, UBD | | | 200,050 | | | | 1,817,504 | |

| |

Heineken NV | | | 32,962 | | | | 2,288,001 | |

| |

Nigerian Breweries plc | | | 611,085 | | | | 570,574 | |

| |

PepsiCo, Inc. | | | 19,360 | | | | 1,662,830 | |

| |

Pernod-Ricard SA | | | 30,940 | | | | 3,714,923 | |

| |

SABMiller plc | | | 41,520 | | | | 2,265,102 | |

| |

Tsingtao Brewery Co. Ltd., Cl. H | | | 70,000 | | | | 508,484 | |

| | | | | | | | |

| | | | 34,788,418 | |

|

| |

Food & Staples Retailing—1.0% | | | | | | | | |

| |

Almacenes Exito SA | | | 43,892 | | | | 668,610 | |

| |

Almacenes Exito SA, GDR3 | | | 57,600 | | | | 868,107 | |

| |

BIM Birlesik Magazalar AS | | | 31,202 | | | | 720,596 | |

| |

Cencosud SA | | | 420,359 | | | | 1,400,564 | |

| |

Costco Wholesale Corp. | | | 13,685 | | | | 1,583,081 | |

| |

CP ALL PCL | | | 2,240,300 | | | | 2,911,289 | |

| |

CVS Caremark Corp. | | | 71,510 | | | | 5,200,207 | |

| |

InRetail Peru Corp.1,3 | | | 18,800 | | | | 282,367 | |

| |

Magnit | | | 12,756 | | | | 2,536,054 | |

| |

Walgreen Co. | | | 27,600 | | | | 1,874,040 | |

| |

Whole Foods Market, Inc. | | | 6,800 | | | | 337,960 | |

| | | | | | | | |

| | | | 18,382,875 | |

|

| |

Food Products—1.8% | | | | | | | | |

| |

Aryzta AG1 | | | 34,114 | | | | 3,150,906 | |

15 OPPENHEIMER GLOBAL ALLOCATION FUND

| | |

| |

CONSOLIDATED STATEMENTOF INVESTMENTS Unaudited / Continued | | |

| | | | | | | | |

| | | Shares | | | Value | |

| |

Food Products (Continued) | | | | | | | | |

| |

Barry Callebaut AG1 | | | 1,636 | | | $ | 2,224,384 | |

| |

Boulder Brands, Inc.1 | | | 66,950 | | | | 988,182 | |

| |

ConAgra Foods, Inc. | | | 35,840 | | | | 1,093,478 | |

| |

DANONE SA | | | 21,470 | | | | 1,586,612 | |

| |

Hershey Co. (The) | | | 29,360 | | | | 2,825,606 | |

| |

J&J Snack Foods Corp. | | | 7,222 | | | | 675,979 | |

| |

Kraft Foods Group, Inc. | | | 26,480 | | | | 1,505,653 | |

| |

Nestle SA | | | 64,291 | | | | 4,971,984 | |

| |

Tingyi Cayman Islands Holding Corp. | | | 738,000 | | | | 2,048,952 | |

| |

Ulker Biskuvi Sanayi AS | | | 47,551 | | | | 363,192 | |

| |

Unilever plc | | | 211,574 | | | | 9,473,622 | |

| |

Want Want China Holdings Ltd. | | | 1,220,000 | �� | | | 1,907,538 | |

| | | | | | | | |

| | | | | | | 32,816,088 | |

|

| |

Household Products—0.7% | | | | | | | | |

| |

Colgate-Palmolive Co. | | | 121,810 | | | | 8,197,813 | |

| |

Hindustan Unilever Ltd. | | | 26,093 | | | | 246,497 | |

| |

Reckitt Benckiser Group plc | | | 22,037 | | | | 1,781,858 | |

| |

Reckitt Benckiser Group plc, Sponsored ADR | | | 79,660 | | | | 1,302,441 | |

| |

Unilever Indonesia Tbk PT | | | 121,000 | | | | 307,176 | |

| | | | | | | | |

| | | | | | | 11,835,785 | |

|

| |

Personal Products—0.2% | | | | | | | | |

| |

Colgate-Palmolive India Ltd. | | | 34,752 | | | | 831,517 | |

| |

L’Oreal SA | | | 2,760 | | | | 475,105 | |

| |

Marico Ltd. | | | 120,272 | | | | 411,293 | |

| |

Natura Cosmeticos SA | | | 89,500 | | | | 1,532,910 | |

| | | | | | | | |

| | | | | | | 3,250,825 | |

|

| |

Tobacco—0.2% | | | | | | | | |

| |

Lorillard, Inc. | | | 32,740 | | | | 1,945,411 | |

| |

Swedish Match AB1 | | | 32,061 | | | | 1,101,398 | |

| | | | | | | | |

| | | | | | | 3,046,809 | |

|

| |

Energy—4.6% | | | | | | | | |

| |

Energy Equipment & Services—1.6% | | | | | | | | |

| |

C&J Energy Services, Inc.1 | | | 37,800 | | | | 1,136,268 | |

| |

China Oilfield Services Ltd., Cl. H | | | 246,000 | | | | 585,272 | |

| |

Dril-Quip, Inc.1 | | | 7,190 | | | | 813,333 | |

| |

Eurasia Drilling Co. Ltd., GDR | | | 18,190 | | | | 448,075 | |

| |

Halliburton Co. | | | 41,670 | | | | 2,628,127 | |

| |

Hunting plc | | | 14,380 | | | | 206,144 | |

| |

Matrix Service Co.1 | | | 12,650 | | | | 391,770 | |

| |

National Oilwell Varco, Inc. | | | 19,630 | | | | 1,541,544 | |

| |

Oceaneering International, Inc. | | | 9,050 | | | | 663,184 | |

| |

Saipem SpA | | | 53,447 | | | | 1,433,772 | |

| |

Schlumberger Ltd. | | | 32,448 | | | | 3,295,094 | |

| |

Schoeller-Bleckmann Oilfield Equipment AG | | | 11,677 | | | | 1,487,926 | |

| |

Technip SA | | | 83,850 | | | | 9,444,920 | |

| |

Tenaris SA, ADR | | | 47,420 | | | | 2,088,851 | |

16 OPPENHEIMER GLOBAL ALLOCATION FUND

| | | | | | | | |

| | | Shares | | | Value | |

| |

Energy Equipment & Services (Continued) | |

| |

Transocean Ltd. | | | 67,270 | | | $ | 2,897,319 | |

| | | | | | | | |

| | | | 29,061,599 | |

|

| |

Oil, Gas & Consumable Fuels—3.0% | | | | | | | | |

| |

Anadarko Petroleum Corp. | | | 26,300 | | | | 2,604,226 | |

| |

Antero Resources Corp.1 | | | 9,970 | | | | 654,730 | |

| |

Athlon Energy, Inc.1 | | | 29,120 | | | | 1,176,739 | |

| |

BP plc, Sponsored ADR | | | 43,780 | | | | 2,216,144 | |

| |

Cabot Oil & Gas Corp. | | | 18,280 | | | | 718,038 | |

| |

Chevron Corp. | | | 13,222 | | | | 1,659,625 | |

| |

Cimarex Energy Co. | | | 5,140 | | | | 612,277 | |

| |

CNOOC Ltd. | | | 742,000 | | | | 1,220,047 | |

| |

ConocoPhillips | | | 39,990 | | | | 2,971,657 | |

| |

Diamondback Energy, Inc.1 | | | 25,260 | | | | 1,817,204 | |

| |

Enbridge, Inc. | | | 42,880 | | | | 2,070,675 | |

| |

EOG Resources, Inc. | | | 49,030 | | | | 4,804,940 | |

| |

Gazprom OAO, Sponsored ADR | | | 139,110 | | | | 1,009,364 | |

| |

Genel Energy plc1 | | | 34,960 | | | | 572,770 | |

| |

Koninklijke Vopak NV | | | 27,644 | | | | 1,379,096 | |

| |

Matador Resources Co.1 | | | 27,410 | | | | 787,215 | |

| |

Noble Energy, Inc. | | | 25,520 | | | | 1,831,826 | |

| |

NovaTek OAO, Sponsored GDR | | | 28,000 | | | | 2,913,659 | |

| |

Oasis Petroleum, Inc.1 | | | 16,810 | | | | 781,833 | |

| |

Occidental Petroleum Corp. | | | 45,500 | | | | 4,356,625 | |

| |

Petroleo Brasileiro SA, Cl. A, Sponsored ADR | | | 197,400 | | | | 2,921,520 | |

| |

Phillips 66 | | | 19,620 | | | | 1,632,776 | |

| |

Pioneer Natural Resources Co. | | | 4,900 | | | | 947,023 | |

| |

Repsol SA | | | 118,829 | | | | 3,207,317 | |

| |

Suncor Energy, Inc. | | | 129,590 | | | | 5,002,174 | |

| |

Tullow Oil plc | | | 155,430 | | | | 2,315,249 | |

| | | | | | | | |

| | | | 52,184,749 | |

|

| |

Financials—11.3% | | | | | | | | |

| |

Capital Markets—2.8% | | | | | | | | |

| |

Ameriprise Financial, Inc. | | | 25,650 | | | | 2,863,309 | |

| |

Artisan Partners Asset Management, Inc., Cl. A | | | 16,450 | | | | 955,251 | |

| |

BinckBank NV | | | 5,683 | | | | 64,267 | |

| |

Charles Schwab Corp. (The) | | | 149,600 | | | | 3,971,880 | |

| |

Credit Suisse Group AG1 | | | 138,271 | | | | 4,383,831 | |

| |

Deutsche Bank AG | | | 138,920 | | | | 6,123,770 | |

| |

Evercore Partners, Inc., Cl. A | | | 20,860 | | | | 1,114,550 | |

| |

Financial Engines, Inc. | | | 15,310 | | | | 677,467 | |

| |

Goldman Sachs Group, Inc. (The) | | | 51,810 | | | | 8,280,274 | |

| |

ICAP plc | | | 347,263 | | | | 2,433,832 | |

| |

Invesco Ltd. | | | 80,750 | | | | 2,843,208 | |

| |

Morgan Stanley | | | 105,720 | | | | 3,269,920 | |

| |

Northern Trust Corp. | | | 20,670 | | | | 1,245,368 | |

| |

Tullett Prebon plc | | | 157,630 | | | | 847,653 | |

| |

UBS AG1 | | | 523,314 | | | | 10,952,834 | |

| | | | | | | | |

| | | | 50,027,414 | |

17 OPPENHEIMER GLOBAL ALLOCATION FUND

| | |

| |

CONSOLIDATED STATEMENTOF INVESTMENTS Unaudited / Continued | | |

| | | | | | | | |

| | | Shares | | | Value | |

| |

Commercial Banks—3.6% | |

| |

Banco Bilbao Vizcaya Argentaria SA | | | 482,549 | | | $ | 5,942,516 | |

| |

Banco Bradesco SA, ADR | | | 75,760 | | | | 1,126,551 | |

| |

Banco Davivienda SA, Preference | | | 55,678 | | | | 792,946 | |

| |

Bancolombia SA, Preference | | | 7,619 | | | | 107,799 | |

| |

Bancolombia SA, Sponsored ADR | | | 12,490 | | | | 711,056 | |

| |

Bank of America Corp. | | | 73,850 | | | | 1,118,089 | |

| |

Bank of the Ozarks, Inc. | | | 16,330 | | | | 978,167 | |

| |

CIT Group, Inc. | | | 28,820 | | | | 1,240,701 | |

| |

Citigroup, Inc. | | | 232,230 | | | | 11,126,139 | |

| |

Commercial International Bank Egypt SAE | | | 136,564 | | | | 726,082 | |

| |

First Financial Holdings, Inc. | | | 11,370 | | | | 653,434 | |

| |

Grupo Financiero Banorte SAB de CV, Cl. O | | | 143,999 | | | | 956,379 | |

| |

Grupo Financiero Inbursa SAB de CV, Cl. O | | | 313,127 | | | | 802,040 | |

| |

Guaranty Trust Bank plc | | | 2,866,834 | | | | 467,902 | |

| |

Home BancShares, Inc. | | | 20,800 | | | | 659,568 | |

| |

ICICI Bank Ltd., Sponsored ADR | | | 195,470 | | | | 8,340,705 | |

| |

Itau Unibanco Holding SA, Preference, ADR | | | 253,774 | | | | 4,151,743 | |

| |

JPMorgan Chase & Co. | | | 47,172 | | | | 2,640,688 | |

| |

KeyCorp | | | 73,150 | | | | 997,766 | |

| |

PNC Financial Services Group, Inc. | | | 22,220 | | | | 1,867,369 | |

| |

Signature Bank1 | | | 19,110 | | | | 2,270,650 | |

| |

Societe Generale SA | | | 57,940 | | | | 3,607,888 | |

| |

Square 1 Financial, Inc., Cl. A1 | | | 3,340 | | | | 62,959 | |

| |

Sumitomo Mitsui Financial Group, Inc. | | | 88,000 | | | | 3,471,307 | |

| |

Turkiye Garanti Bankasi AS | | | 272,477 | | | | 997,934 | |

| |

U.S. Bancorp | | | 48,100 | | | | 1,961,518 | |

| |

Wells Fargo & Co. | | | 76,404 | | | | 3,792,695 | |

| |

Western Alliance Bancorp1 | | | 58,200 | | | | 1,342,674 | |

| |

Zenith Bank plc | | | 3,525,007 | | | | 498,087 | |

| | | | | | | | |

| | | | 63,413,352 | |

|

| |

Consumer Finance—0.4% | | | | | | | | |

| |

American Express Co. | | | 21,406 | | | | 1,871,526 | |

| |

Capital One Financial Corp. | | | 36,920 | | | | 2,728,388 | |

| |

Discover Financial Services | | | 37,930 | | | | 2,120,287 | |

| |

SLM Corp. | | | 40,720 | | | | 1,048,540 | |

| | | | | | | | |

| | | | 7,768,741 | |

|

| |

Diversified Financial Services—1.2% | | | | | | | | |

| |

BM&FBovespa SA | | | 1,133,000 | | | | 5,792,667 | |

| |

CME Group, Inc. | | | 14,670 | | | | 1,032,621 | |

| |

Grupo de Inversiones Suramericana SA | | | 12,219 | | | | 238,377 | |

| |

Haci Omer Sabanci Holding AS | | | 394,688 | | | | 1,667,706 | |

| |

Hong Kong Exchanges & Clearing Ltd. | | | 61,245 | | | | 1,103,839 | |

| |

Marico Kaya Enterprises Ltd.1 | | | 2,405 | | | | 152 | |

| |

McGraw Hill Financial, Inc. | | | 116,130 | | | | 8,585,491 | |

| |

Moscow Exchange (The) | | | 1,322,277 | | | | 1,959,382 | |

| | | | | | | | |

| | | | 20,380,235 | |

|

| |

Insurance—2.5% | | | | | | | | |

| |

Aflac, Inc. | | | 24,960 | | | | 1,565,491 | |

| |

AIA Group Ltd. | | | 379,200 | | | | 1,839,214 | |

18 OPPENHEIMER GLOBAL ALLOCATION FUND

| | | | | | | | |

| | | Shares | | | Value | |

| |

Insurance (Continued) | |

| |

Allianz SE | | | 42,566 | | | $ | 7,376,431 | |

| |

Allstate Corp. (The) | | | 32,650 | | | | 1,859,417 | |

| |

American International Group, Inc. | | | 49,400 | | | | 2,624,622 | |

| |

Aon plc | | | 57,430 | | | | 4,874,658 | |

| |

China Life Insurance Co. Ltd., Cl. H | | | 2,000 | | | | 5,194 | |

| |

Dai-ichi Life Insurance Co. Ltd. (The) | | | 305,400 | | | | 4,223,228 | |

| |

Fidelity National Financial, Inc., Cl. A | | | 87,700 | | | | 2,822,186 | |

| |

Marsh & McLennan Cos., Inc. | | | 41,320 | | | | 2,037,489 | |

| |

MetLife, Inc. | | | 45,830 | | | | 2,399,201 | |

| |

Old Mutual plc | | | 304,254 | | | | 1,030,231 | |

| |

Prudential plc | | | 430,282 | | | | 9,897,143 | |

| |

Sul America SA | | | 100,060 | | | | 733,706 | |

| |

Sun Life Financial, Inc. | | | 18,350 | | | | 620,964 | |

| | | | | | | | |

| | | | 43,909,175 | |

|

| |

Real Estate Investment Trusts (REITs)—0.2% | | | | | | | | |

| |

American Tower Corp. | | | 18,730 | | | | 1,564,330 | |

| |

Public Storage | | | 10,240 | | | | 1,797,222 | |

| | | | | | | | |

| | | | 3,361,552 | |

|

| |

Real Estate Management & Development—0.4% | | | | | | | | |

| |

DLF Ltd. | | | 1,220,788 | | | | 2,830,603 | |

| |

Hang Lung Group Ltd. | | | 129,500 | | | | 703,050 | |

| |

Hang Lung Properties Ltd. | | | 684,570 | | | | 2,045,411 | |

| |

Multiplan Empreendimentos Imobiliarios SA | | | 3,300 | | | | 72,934 | |

| |

SM Prime Holdings, Inc. | | | 2,819,103 | | | | 1,032,250 | |

| |

Soho China Ltd. | | | 926,500 | | | | 734,905 | |

| |

Wallace Theater Holdings, Inc.1,4 | | | 430 | | | | 3,324 | |

| | | | | | | | |

| | | | 7,422,477 | |

|

| |

Thrifts & Mortgage Finance—0.2% | | | | | | | | |

| |

Housing Development Finance Corp. Ltd. | | | 230,967 | | | | 3,451,860 | |

|

| |

Health Care—10.2% | | | | | | | | |

| |

Biotechnology—2.5% | | | | | | | | |

| |

Amgen, Inc. | | | 40,140 | | | | 4,485,645 | |

| |

Biogen Idec, Inc.1 | | | 24,280 | | | | 6,971,274 | |

| |

Celgene Corp.1 | | | 11,963 | | | | 1,758,681 | |

| |

Celldex Therapeutics, Inc.1 | | | 124,160 | | | | 1,862,400 | |

| |

Cepheid, Inc.1 | | | 22,910 | | | | 996,127 | |

| |

Circassia Pharmaceuticals plc1 | | | 249,310 | | | | 1,302,752 | |

| |

Clovis Oncology, Inc.1 | | | 25,380 | | | | 1,372,297 | |

| |

CSL Ltd. | | | 30,100 | | | | 1,919,295 | |

| |

Cubist Pharmaceuticals, Inc.1 | | | 17,870 | | | | 1,251,972 | |

| |

Gilead Sciences, Inc.1 | | | 125,780 | | | | 9,872,472 | |

| |

Grifols SA | | | 57,848 | | | | 3,101,127 | |

| |

InterMune, Inc.1 | | | 20,330 | | | | 652,186 | |

| |

Medivation, Inc.1 | | | 20,320 | | | | 1,223,467 | |

| |

NPS Pharmaceuticals, Inc.1 | | | 27,970 | | | | 744,561 | |

| |

Theravance, Inc.1 | | | 85,550 | | | | 2,303,006 | |

19 OPPENHEIMER GLOBAL ALLOCATION FUND

| | | | |

CONSOLIDATED STATEMENTOF INVESTMENTS Unaudited / Continued | | |

| | | | | | | | |

| | | Shares | | | Value | |

| |

Biotechnology (Continued) | |

| |

Vertex Pharmaceuticals, Inc.1 | | | 72,360 | | | $ | 4,898,772 | |

| | | | | | | | |

| | | | 44,716,034 | |

| | | | | | | | |

| |

Health Care Equipment & Supplies—1.4% | | | | | | | | |

| |

Baxter International, Inc. | | | 25,530 | | | | 1,858,329 | |

| |

Cantel Medical Corp. | | | 15,520 | | | | 514,643 | |

| |

Cardiovascular Systems, Inc.1 | | | 17,130 | | | | 492,487 | |

| |

DexCom, Inc.1 | | | 46,061 | | | | 1,494,219 | |

| |

DiaSorin SpA | | | 34,844 | | | | 1,438,975 | |

| |

Essilor International SA | | | 15,680 | | | | 1,677,893 | |

| |

Globus Medical, Inc., Cl. A1 | | | 58,800 | | | | 1,435,896 | |

| |

Insulet Corp.1 | | | 37,200 | | | | 1,399,836 | |

| |

Mindray Medical International Ltd., ADR | | | 17,790 | | | | 588,137 | |

| |

Novadaq Technologies, Inc.1 | | | 15,810 | | | | 247,426 | |

| |

Shandong Weigao Group Medical Polymer Co. Ltd., Cl. H | | | 650,000 | | | | 657,279 | |

| |

Sonova Holding AG1 | | | 13,572 | | | | 1,963,072 | |

| |

Spectranetics Corp.1 | | | 43,160 | | | | 917,582 | |

| |

St. Jude Medical, Inc. | | | 41,440 | | | | 2,630,197 | |

| |

West Pharmaceutical Services, Inc. | | | 21,920 | | | | 950,890 | |

| |

William Demant Holding1 | | | 15,136 | | | | 1,359,100 | |

| |

Zeltiq Aesthetics, Inc.1 | | | 35,920 | | | | 656,977 | |

| |

Zimmer Holdings, Inc. | | | 42,880 | | | | 4,150,784 | |

| | | | | | | | |

| | | | 24,433,722 | |

| | | | | | | | |

| |

Health Care Providers & Services—1.8% | | | | | | | | |

| |

Acadia Healthcare Co., Inc.1 | | | 32,800 | | | | 1,378,256 | |

| |

Aetna, Inc. | | | 83,930 | | | | 5,996,799 | |

| |

Apollo Hospitals Enterprise Ltd. | | | 43,579 | | | | 646,023 | |

| |

Bangkok Dusit Medical Services PCL, Cl. F | | | 25,000 | | | | 11,433 | |

| |

Cardinal Health, Inc. | | | 87,030 | | | | 6,049,455 | |

| |

Centene Corp.1 | | | 18,320 | | | | 1,216,448 | |

| |

Diagnosticos da America SA | | | 102,900 | | | | 610,086 | |

| |

ExamWorks Group, Inc.1 | | | 39,690 | | | | 1,460,592 | |

| |

HCA Holdings, Inc.1 | | | 13,980 | | | | 726,960 | |

| |

MWI Veterinary Supply, Inc.1 | | | 8,810 | | | | 1,379,998 | |

| |

Sinopharm Group Co. Ltd., Cl. H4 | | | 347,400 | | | | 909,735 | |

| |

Sonic Healthcare Ltd. | | | 118,200 | | | | 1,949,095 | |

| |

Team Health Holdings, Inc.1 | | | 33,430 | | | | 1,620,686 | |

| |

UnitedHealth Group, Inc. | | | 22,860 | | | | 1,715,414 | |

| |

WellPoint, Inc. | | | 66,640 | | | | 6,709,315 | |

| | | | | | | | |

| | | | 32,380,295 | |

| | | | | | | | |

| |

Health Care Technology—0.1% | | | | | | | | |

| |

Cerner Corp.1 | | | 17,890 | | | | 917,757 | |

| |

CompuGroup Medical AG | | | 21,881 | | | | 583,169 | |

| | | | | | | | |

| | | | 1,500,926 | |

| | | | | | | | |

| |

Life Sciences Tools & Services—0.6% | | | | | | | | |

| |

Agilent Technologies, Inc. | | | 36,920 | | | | 1,995,157 | |

| |

Fluidigm Corp.1 | | | 16,850 | | | | 632,886 | |

| |

ICON plc1 | | | 37,220 | | | | 1,443,019 | |

20 OPPENHEIMER GLOBAL ALLOCATION FUND

| | | | | | | | |

| | | Shares | | | Value | |

| |

Life Sciences Tools & Services (Continued) | |

| |

Thermo Fisher Scientific, Inc. | | | 55,710 | | | $ | 6,350,940 | |

| | | | | | | | |

| | | | 10,422,002 | |

| | | | | | | | |

| |

Pharmaceuticals—3.8% | | | | | | | | |

| |

AbbVie, Inc. | | | 51,050 | | | | 2,658,684 | |

| |

Actavis plc1 | | | 8,040 | | | | 1,642,813 | |

| |

Akorn, Inc.1 | | | 50,430 | | | | 1,271,845 | |

| |

Allergan, Inc. | | | 55,320 | | | | 9,174,269 | |

| |

Bayer AG | | | 47,371 | | | | 6,574,106 | |

| |

Bristol-Myers Squibb Co. | | | 89,487 | | | | 4,482,404 | |

| |

Cipla Ltd. | | | 111,107 | | | | 730,467 | |

| |

Galenica AG | | | 1,444 | | | | 1,470,740 | |

| |

Jazz Pharmaceuticals plc1 | | | 4,760 | | | | 642,124 | |

| |

Johnson & Johnson | | | 25,097 | | | | 2,542,075 | |

| |

Merck & Co., Inc. | | | 52,330 | | | | 3,064,445 | |

| |

Novo Nordisk AS, Cl. B | | | 42,648 | | | | 1,935,002 | |

| |

Pacira Pharmaceuticals, Inc.1 | | | 13,850 | | | | 948,586 | |

| |

Perrigo Co. PLC | | | 20,340 | | | | 2,946,452 | |

| |

Pfizer, Inc. | | | 160,684 | | | | 5,026,196 | |

| |

Roche Holding AG | | | 30,180 | | | | 8,872,569 | |

| |

Roche Holding AG, Sponsored ADR | | | 72,860 | | | | 2,670,319 | |

| |

Sanofi, ADR | | | 58,340 | | | | 3,138,692 | |

| |

Shire plc | | | 76,260 | | | | 4,360,194 | |

| |

Teva Pharmaceutical Industries Ltd., Sponsored ADR | | | 26,150 | | | | 1,277,689 | |

| |

Valeant Pharmaceuticals International, Inc.1 | | | 6,603 | | | | 882,887 | |

| | | | | | | | |

| | | | 66,312,558 | |

| | | | | | | | |

| |

Industrials—10.1% | | | | | | | | |

| |

Aerospace & Defense—2.0% | | | | | | | | |

| |

Airbus Group NV | | | 139,280 | | | | 9,590,222 | |

| |

B/E Aerospace, Inc.1 | | | 11,230 | | | | 985,657 | |

| |

Curtiss-Wright Corp. | | | 11,510 | | | | 735,949 | |

| |

Embraer SA | | | 197,700 | | | | 1,709,454 | |

| |

Embraer SA, ADR | | | 147,440 | | | | 5,071,936 | |

| |

General Dynamics Corp. | | | 6,800 | | | | 744,260 | |

| |

HEICO Corp. | | | 27,080 | | | | 1,498,066 | |

| |

Hexcel Corp.1 | | | 54,090 | | | | 2,255,012 | |

| |

Lockheed Martin Corp. | | | 9,400 | | | | 1,542,916 | |

| |

Precision Castparts Corp. | | | 11,320 | | | | 2,864,979 | |

| |

Rolls-Royce Holdings plc1 | | | 99,470 | | | | 1,767,050 | |

| |

United Technologies Corp. | | | 51,670 | | | | 6,114,111 | |

| | | | | | | | |

| | | | 34,879,612 | |

| | | | | | | | |

| |

Air Freight & Couriers—0.3% | | | | | | | | |

| |

Royal Mail plc1 | | | 117,780 | | | | 1,055,083 | |

| |

United Parcel Service, Inc., Cl. B | | | 48,220 | | | | 4,749,670 | |

| | | | | | | | |

| | | | 5,804,753 | |

| | | | | | | | |

| |

Airlines—0.2% | |

| |

Delta Air Lines, Inc. | | | 106,200 | | | | 3,911,346 | |

21 OPPENHEIMER GLOBAL ALLOCATION FUND

| | | | |

| |

CONSOLIDATED STATEMENTOF INVESTMENTS Unaudited / Continued | | |

| | | | | | | | |

| | | Shares | | | Value | |

| |

Building Products—0.6% | |

| |

A.O. Smith Corp. | | | 23,020 | | | $ | 1,076,415 | |

| |

Allegion plc | | | 39,860 | | | | 1,967,091 | |

| |

Assa Abloy AB, Cl. B1 | | | 121,111 | | | | 6,442,865 | |

| |

Fortune Brands Home & Security, Inc. | | | 35,010 | | | | 1,395,149 | |

| |

Nortek, Inc.1 | | | 5,864 | | | | 481,786 | |

| | | | | | | | |

| | | | 11,363,306 | |

| | | | | | | | |

| |

Commercial Services & Supplies—0.7% | | | | | | | | |

| |

Aggreko plc | | | 62,489 | | | | 1,666,881 | |

| |

Edenred | | | 44,970 | | | | 1,517,509 | |

| |

Mobile Mini, Inc. | | | 57,980 | | | | 2,561,557 | |

| |

Prosegur Compania de Seguridad SA | | | 289,135 | | | | 1,941,547 | |

| |

Tyco International Ltd. | | | 62,030 | | | | 2,537,027 | |

| |

Waste Management, Inc. | | | 29,280 | | | | 1,301,496 | |

| | | | | | | | |

| | | | 11,526,017 | |

| | | | | | | | |

| |

Construction & Engineering—0.5% | | | | | | | | |

| |

Chicago Bridge & Iron Co. NV | | | 12,440 | | | | 996,071 | |

| |

FLSmidth & Co. AS | | | 40,899 | | | | 2,191,073 | |

| |

Koninklijke Boskalis Westminster NV | | | 41,111 | | | | 2,330,358 | |

| |

Leighton Holdings Ltd. | | | 72,400 | | | | 1,285,429 | |

| |

Trevi Finanziaria Industriale SpA | | | 129,332 | | | | 1,489,826 | |

| | | | | | | | |

| | | | 8,292,757 | |

| | | | | | | | |

| |

Electrical Equipment—1.4% | | | | | | | | |

| |

ABB Ltd.1 | | | 63,765 | | | | 1,536,504 | |

| |

ABB Ltd., Sponsored ADR1 | | | 24,910 | | | | 595,847 | |

| |

AMETEK, Inc. | | | 17,270 | | | | 910,474 | |

| |

Eaton Corp. plc | | | 40,760 | | | | 2,960,806 | |

| |

Emerson Electric Co. | | | 61,570 | | | | 4,197,843 | |

| |

Generac Holdings, Inc. | | | 27,030 | | | | 1,591,526 | |

| |

Legrand SA | | | 32,160 | | | | 2,077,873 | |

| |

Nidec Corp. | | | 111,400 | | | | 6,337,143 | |

| |

Prysmian SpA | | | 78,491 | | | | 2,045,093 | |

| |

Schneider Electric SA | | | 19,220 | | | | 1,806,376 | |

| |

Schneider Electric SA, ADR1 | | | 42,920 | | | | 804,321 | |

| | | | | | | | |

| | | | 24,863,806 | |

| | | | | | | | |

| |

Industrial Conglomerates—1.0% | | | | | | | | |

| |

3M Co. | | | 40,070 | | | | 5,573,336 | |

| |

General Electric Co.2 | | | 85,210 | | | | 2,291,297 | |

| |

Jardine Strategic Holdings Ltd. | | | 31,512 | | | | 1,125,368 | |

| |

Seibu Holdings, Inc. | | | 69,700 | | | | 1,274,896 | |

| |

Siemens AG | | | 43,464 | | | | 5,730,043 | |

| |

Siemens AG, Sponsored ADR | | | 6,930 | | | | 913,582 | |

| |

SM Investments Corp. | | | 80,573 | | | | 1,313,604 | |

| | | | | | | | |

| | | | 18,222,126 | |

| | | | | | | | |

| |

Machinery—1.9% | | | | | | | | |

| |

Aalberts Industries NV | | | 103,165 | | | | 3,441,829 | |

| |

Atlas Copco AB, Cl. A | | | 60,877 | | | | 1,771,845 | |

| |

Caterpillar, Inc. | | | 45,070 | | | | 4,750,378 | |

22 OPPENHEIMER GLOBAL ALLOCATION FUND

| | | | | | | | |

| | | Shares | | | Value | |

| |

Machinery (Continued) | |

| |

FANUC Corp. | | | 21,100 | | | $ | 3,796,971 | |

| |

Flowserve Corp. | | | 20,050 | | | | 1,464,652 | |

| |

Middleby Corp. (The)1 | | | 10,440 | | | | 2,635,891 | |

| |

Pall Corp. | | | 10,420 | | | | 876,843 | |

| |

Parker Hannifin Corp. | | | 42,140 | | | | 5,346,723 | |

| |

Pentair Ltd. | | | 37,140 | | | | 2,759,131 | |

| |

Proto Labs, Inc.1 | | | 18,740 | | | | 1,134,520 | |

| |

Timken Co. | | | 11,050 | | | | 697,034 | |

| |

Wabtec Corp. | | | 23,520 | | | | 1,753,416 | |

| |

Weir Group plc (The) | | | 49,526 | | | | 2,253,925 | |

| | | | | | | | |

| | | | 32,683,158 | |

| | | | | | | | |

| |

Professional Services—0.6% | | | | | | | | |

| |

Experian plc | | | 95,346 | | | | 1,832,421 | |

| |

Huron Consulting Group, Inc.1 | | | 18,890 | | | | 1,344,968 | |

| |

Intertek Group plc | | | 37,560 | | | | 1,846,469 | |

| |

Korn/Ferry International1 | | | 23,570 | | | | 684,708 | |

| |

On Assignment, Inc.1 | | | 75,090 | | | | 2,628,150 | |

| |

Paylocity Holding Corp.1 | | | 2,820 | | | | 53,326 | |

| |

SGS SA | | | 691 | | | | 1,726,956 | |

| |

WageWorks, Inc.1 | | | 15,770 | | | | 668,175 | |

| | | | | | | | |

| | | | 10,785,173 | |

| | | | | | | | |

| |

Road & Rail—0.2% | | | | | | | | |

| |

CSX Corp. | | | 46,840 | | | | 1,321,825 | |

| |

Genesee & Wyoming, Inc., Cl. A1 | | | 13,670 | | | | 1,353,467 | |

| |

Localiza Rent a Car SA | | | 2,700 | | | | 40,323 | |

| |

Union Pacific Corp. | | | 8,020 | | | | 1,527,248 | |

| | | | | | | | |

| | | | 4,242,863 | |

| | | | | | | | |

| |

Trading Companies & Distributors—0.6% | | | | | | | | |

| |

Brenntag AG | | | 11,954 | | | | 2,163,013 | |

| |

Bunzl plc | | | 115,038 | | | | 3,273,126 | |

| |

H&E Equipment Services, Inc.1 | | | 75,550 | | | | 2,912,453 | |

| |

United Rentals, Inc.1 | | | 3,470 | | | | 325,590 | |

| |

Wolseley plc | | | 32,040 | | | | 1,855,484 | |

| | | | | | | | |

| | | | 10,529,666 | |

| | | | | | | | |

| |

Transportation Infrastructure—0.1% | | | | | | | | |

| |

Airports of Thailand PCL | | | 26,100 | | | | 157,278 | |

| |

DP World Ltd.5 | | | 17,946 | | | | 332,001 | |

| |

DP World Ltd.5 | | | 62,902 | | | | 1,180,287 | |

| |

Grupo Aeroportuario del Sureste SAB de CV, Cl. B | | | 5,898 | | | | 72,181 | |

| |

International Container Terminal Services, Inc. | | | 57,570 | | | | 139,688 | |

| | | | | | | | |

| | | | 1,881,435 | |

| | | | | | | | |

| |

Information Technology—14.0% | | | | | | | | |

| |

Communications Equipment—1.2% | | | | | | | | |

| |

Cisco Systems, Inc. | | | 152,640 | | | | 3,527,510 | |

| |

Juniper Networks, Inc.1 | | | 143,820 | | | | 3,550,916 | |

| |

QUALCOMM, Inc. | | | 15,220 | | | | 1,197,966 | |

23 OPPENHEIMER GLOBAL ALLOCATION FUND

| | | | |

| |

CONSOLIDATED STATEMENTOF INVESTMENTS Unaudited / Continued | | |

| | | | | | | | |

| | | Shares | | | Value | |

| |

Communications Equipment (Continued) | |

| |

Telefonaktiebolaget LM Ericsson, Cl. B | | | 1,110,418 | | | $ | 13,335,528 | |

| | | | | | | | |

| | | | 21,611,920 | |

| | | | | | | | |

| |

Electronic Equipment, Instruments, & Components—1.3% | | | | | | | | |

| |

Hoya Corp. | | | 84,900 | | | | 2,502,857 | |

| |

Keyence Corp. | | | 19,050 | | | | 7,338,475 | |

| |

Kyocera Corp. | | | 89,100 | | | | 4,188,872 | |

| |

Methode Electronics, Inc. | | | 34,390 | | | | 953,979 | |

| |

Murata Manufacturing Co. Ltd. | | | 69,800 | | | | 5,803,058 | |

| |

Omron Corp. | | | 19,100 | | | | 674,402 | |

| |

TE Connectivity Ltd. | | | 29,070 | | | | 1,714,549 | |

| | | | | | | | |

| | | | 23,176,192 | |

| | | | | | | | |

| |

Internet Software & Services—3.7% | | | | | | | | |

| |

Baidu, Inc., Sponsored ADR1 | | | 37,950 | | | | 5,838,607 | |

| |

Benefitfocus, Inc.1 | | | 6,650 | | | | 215,460 | |

| |

ChannelAdvisor Corp.1 | | | 32,990 | | | | 865,658 | |

| |

Cornerstone OnDemand, Inc.1 | | | 49,590 | | | | 1,822,928 | |

| |

CoStar Group, Inc.1 | | | 13,760 | | | | 2,213,846 | |

| |

Demandware, Inc.1 | | | 19,560 | | | | 970,763 | |

| |

eBay, Inc.1 | | | 161,850 | | | | 8,388,685 | |

| |

Envestnet, Inc.1 | | | 24,770 | | | | 912,774 | |

| |

Facebook, Inc., Cl. A1,2 | | | 157,740 | | | | 9,429,697 | |

| |

Google, Inc., Cl. A1 | | | 13,799 | | | | 7,380,809 | |

| |

Google, Inc., Cl. C1,2 | | | 13,549 | | | | 7,135,716 | |

| |

GrubHub, Inc.1 | | | 1,270 | | | | 39,307 | |

| |

LinkedIn Corp., Cl. A1 | | | 10,950 | | | | 1,680,497 | |

| |

MercadoLibre, Inc. | | | 11,640 | | | | 1,085,663 | |

| |

NAVER Corp. | | | 1,729 | | | | 1,245,030 | |

| |

Pandora Media, Inc.1 | | | 51,840 | | | | 1,214,093 | |

| |

Q2 Holdings, Inc.1 | | | 6,040 | | | | 74,171 | |

| |

Shutterstock, Inc.1 | | | 21,780 | | | | 1,579,268 | |

| |

SPS Commerce, Inc.1 | | | 12,160 | | | | 629,888 | |

| |

Telecity Group plc | | | 99,170 | | | | 1,202,718 | |

| |

Tencent Holdings Ltd. | | | 44,800 | | | | 2,819,077 | |

| |

United Internet AG | | | 41,187 | | | | 1,768,431 | |

| |

Web.com Group, Inc.1 | | | 54,270 | | | | 1,666,632 | |

| |

Yahoo Japan Corp. | | | 307,400 | | | | 1,346,714 | |

| |

Yandex NV, Cl. A1 | | | 98,620 | | | | 2,613,430 | |

| |

Yelp, Inc.1 | | | 12,680 | | | | 739,498 | |

| |

Youku Tudou, Inc., ADR1 | | | 22,730 | | | | 506,652 | |

| | | | | | | | |

| | | | 65,386,012 | |

| | | | | | | | |

| |

IT Services—0.9% | | | | | | | | |

| |

Acxiom Corp.1 | | | 24,890 | | | | 702,894 | |

| |

Alliance Data Systems Corp.1 | | | 380 | | | | 91,922 | |

| |

Amadeus IT Holding SA, Cl. A | | | 57,082 | | | | 2,376,699 | |

| |

FleetCor Technologies, Inc.1 | | | 7,070 | | | | 806,899 | |

| |

Infosys Ltd. | | | 53,279 | | | | 2,844,991 | |

| |

MasterCard, Inc., Cl. A | | | 56,770 | | | | 4,175,433 | |

| |

MAXIMUS, Inc. | | | 24,050 | | | | 1,023,808 | |

| |

Tata Consultancy Services Ltd. | | | 33,411 | | | | 1,213,659 | |

24 OPPENHEIMER GLOBAL ALLOCATION FUND

| | | | | | | | |

| | | Shares | | | Value | |

| |

IT Services (Continued) | |

| |

Visa, Inc., Cl. A | | | 15,808 | | | $ | 3,202,859 | |

| | | | | | | | |

| | | | 16,439,164 | |

| | | | | | | | |

| |

Semiconductors & Semiconductor Equipment—1.6% | | | | | | | | |

| |

Altera Corp. | | | 207,710 | | | | 6,754,729 | |

| |

ARM Holdings plc | | | 107,520 | | | | 1,624,165 | |

| |

Avago Technologies Ltd. | | | 8,560 | | | | 543,560 | |

| |

Broadcom Corp., Cl. A | | | 23,930 | | | | 737,283 | |

| |

Intel Corp. | | | 74,660 | | | | 1,992,676 | |

| |

Maxim Integrated Products, Inc. | | | 223,110 | | | | 7,237,688 | |

| |

Microchip Technology, Inc. | | | 11,570 | | | | 550,038 | |

| |

Monolithic Power Systems, Inc.1 | | | 48,180 | | | | 1,787,478 | |

| |

Taiwan Semiconductor Manufacturing Co. Ltd. | | | 656,000 | | | | 2,585,964 | |

| |

Texas Instruments, Inc. | | | 66,988 | | | | 3,044,605 | |

| |

Xilinx, Inc. | | | 42,310 | | | | 1,996,609 | |

| | | | | | | | |

| | | | 28,854,795 | |

| | | | | | | | |

| |

Software—3.6% | | | | | | | | |

| |

Adobe Systems, Inc.1 | | | 103,890 | | | | 6,408,974 | |

| |

Aspen Technology, Inc.1 | | | 54,470 | | | | 2,341,665 | |

| |

Autodesk, Inc.1 | | | 36,860 | | | | 1,770,017 | |

| |

Aveva Group plc | | | 31,500 | | | | 1,123,572 | |

| |

CA, Inc. | | | 35,400 | | | | 1,066,956 | |

| |

Citrix Systems, Inc.1 | | | 11,450 | | | | 679,100 | |

| |

Dassault Systemes SA | | | 13,590 | | | | 1,671,609 | |

| |

Gemalto NV | | | 18,642 | | | | 2,089,887 | |

| |

Guidewire Software, Inc.1 | | | 51,420 | | | | 1,941,619 | |

| |

Imperva, Inc.1 | | | 14,810 | | | | 338,853 | |

| |

Interactive Intelligence Group, Inc.1 | | | 22,900 | | | | 1,432,853 | |

| |

Intuit, Inc. | | | 80,180 | | | | 6,073,635 | |

| |

Microsoft Corp. | | | 251,721 | | | | 10,169,529 | |

| |

Oracle Corp. | | | 68,450 | | | | 2,798,236 | |

| |

Proofpoint, Inc.1 | | | 28,200 | | | | 717,408 | |

| |

Sage Group plc (The) | | | 192,419 | | | | 1,386,954 | |

| |

SAP AG | | | 150,195 | | | | 12,090,512 | |

| |

ServiceNow, Inc.1 | | | 18,320 | | | | 910,870 | |

| |

Splunk, Inc.1 | | | 11,890 | | | | 648,837 | |

| |

Synopsys, Inc.1 | | | 21,910 | | | | 824,254 | |

| |

Tableau Software, Inc., Cl. A1 | | | 19,290 | | | | 1,066,158 | |

| |

Temenos Group AG | | | 36,964 | | | | 1,324,877 | |

| |

Tyler Technologies, Inc.1 | | | 20,110 | | | | 1,641,982 | |

| |

Ultimate Software Group, Inc. (The)1 | | | 18,110 | | | | 2,166,499 | |

| |

Workday, Inc., Cl. A1 | | | 6,310 | | | | 461,072 | |

| | | | | | | | |

| | | | 63,145,928 | |

| | | | | | | | |

| |

Technology Hardware, Storage & Peripherals—1.7% | | | | | | | | |

| |

Apple, Inc.2 | | | 25,913 | | | | 15,291,002 | |

| |

EMC Corp.2 | | | 251,440 | | | | 6,487,152 | |

| |

Fusion-io, Inc.1 | | | 157,550 | | | | 1,359,656 | |

| |

NCR Corp.1 | | | 15,680 | | | | 478,397 | |

| |

SanDisk Corp. | | | 19,970 | | | | 1,696,851 | |

| |

Stratasys Ltd.1 | | | 12,950 | | | | 1,254,467 | |

25 OPPENHEIMER GLOBAL ALLOCATION FUND

| | |

| |

CONSOLIDATED STATEMENTOF INVESTMENTS Unaudited / Continued | | |

| | | | | | | | |

| | | Shares | | | Value | |

| |

Technology Hardware, Storage & Peripherals (Continued) | |

| |

Western Digital Corp. | | | 33,970 | | | $ | 2,993,776 | |

| | | | | | | | |

| | | | 29,561,301 | |

| | | | | | | | |

| |

Materials—2.5% | | | | | | | | |

| |

Chemicals—1.5% | | | | | | | | |

| |

Asian Paints Ltd. | | | 77,874 | | | | 652,658 | |

| |

Dow Chemical Co. (The) | | | 52,280 | | | | 2,608,772 | |

| |

Essentra plc | | | 205,412 | | | | 2,780,123 | |

| |

Linde AG | | | 21,507 | | | | 4,460,240 | |

| |

LyondellBasell Industries NV, Cl. A | | | 32,807 | | | | 3,034,647 | |

| |

Methanex Corp. | | | 33,680 | | | | 2,088,160 | |

| |

PolyOne Corp. | | | 42,350 | | | | 1,586,854 | |

| |

Potash Corp. of Saskatchewan, Inc. | | | 32,160 | | | | 1,162,906 | |

| |

PPG Industries, Inc. | | | 21,980 | | | | 4,255,768 | |

| |

Sika AG | | | 571 | | | | 2,314,513 | |

| |

Syngenta AG1 | | | 5,843 | | | | 2,320,057 | |

| | | | | | | | |

| | | | 27,264,698 | |

| | | | | | | | |

| |

Construction Materials—0.5% | | | | | | | | |

| |

Ambuja Cements Ltd. | | | 205,461 | | | | 679,697 | |

| |

Caesarstone Sdot-Yam Ltd. | | | 16,990 | | | | 886,538 | |

| |

Cementos Argos SA, Preference | | | 64,546 | | | | 353,298 | |

| |

Eagle Materials, Inc. | | | 15,990 | | | | 1,332,447 | |

| |

Indocement Tunggal Prakarsa Tbk PT | | | 302,000 | | | | 580,358 | |

| |

James Hardie Industries plc | | | 227,800 | | | | 2,915,401 | |

| |

Semen Indonesia (Persero) Tbk PT | | | 477,000 | | | | 619,764 | |

| |

Ultratech Cement Ltd. | | | 30,473 | | | | 1,029,467 | |

| | | | | | | | |

| | | | 8,396,970 | |

| | | | | | | | |

| |

Metals & Mining—0.4% | | | | | | | | |

| |

Alrosa AO | | | 1,810,382 | | | | 1,870,702 | |

| |

Carpenter Technology Corp. | | | 19,000 | | | | 1,193,200 | |

| |

Glencore Xstrata plc1 | | | 435,420 | | | | 2,350,174 | |

| |

Real Gold Mining Ltd.1 | | | 273,000 | | | | 352 | |

| |

Vale SA, Cl. B, Sponsored ADR | | | 138,340 | | | | 1,828,855 | |

| | | | | | | | |

| | | | 7,243,283 | |

| | | | | | | | |

| |

Paper & Forest Products—0.1% | | | | | | | | |

| |

Louisiana-Pacific Corp.1 | | | 68,630 | | | | 1,124,846 | |

| | | | | | | | |

| |

Telecommunication Services—1.2% | | | | | | | | |

| |

Diversified Telecommunication Services—0.7% | | | | | | | | |

| |

BT Group plc, Cl. A | | | 557,220 | | | | 3,484,913 | |

| |

Iliad SA | | | 3,870 | | | | 1,047,003 | |

| |

Inmarsat plc | | | 143,030 | | | | 1,761,236 | |

| |

Telefonica Brasil SA, ADR | | | 55,600 | | | | 1,178,720 | |

| |

Telefonica Brasil SA, Preference | | | 100 | | | | 2,101 | |

| |

Telefonica SA, Sponsored ADR | | | 32,010 | | | | 536,167 | |

| |

Verizon Communications, Inc. | | | 65,923 | | | | 3,080,582 | |

| |

Ziggo NV | | | 27,046 | | | | 1,174,279 | |

| | | | | | | | |

| | | | 12,265,001 | |

26 OPPENHEIMER GLOBAL ALLOCATION FUND

| | | | | | | | |

| | | Shares | | | Value | |

| |

Wireless Telecommunication Services—0.5% | |

| |

America Movil SAB de CV, Series L, ADR | | | 54,880 | | | $ | 1,101,990 | |

| |

KDDI Corp. | | | 113,500 | | | | 6,041,434 | |

| |

MTN Group Ltd. | | | 82,699 | | | | 1,658,856 | |

| | | | | | | | |

| | | | 8,802,280 | |

| | | | | | | | |

| |

Utilities—0.4% | | | | | | | | |

| |

Electric Utilities—0.3% | | | | | | | | |

| |

Edison International | | | 53,030 | | | | 2,999,377 | |

| |

Entergy Corp. | | | 15,460 | | | | 1,120,850 | |

| |

NextEra Energy, Inc. | | | 20,487 | | | | 2,045,627 | |

| | | | | | | | |

| | | | 6,165,854 | |

| | | | | | | | |

| |

Independent Power and Renewable Electricity Producers—0.1% | | | | | | | | |

| |

APR Energy plc | | | 82,430 | | | | 1,109,640 | |

| | | | | | | | |

| |

Multi-Utilities—0.0% | | | | | | | | |

| |

Sempra Energy | | | 9,140 | | | | 901,295 | |

| | | | | | | | |

Total Common Stocks (Cost $1,011,107,354) | | | | 1,252,219,921 | |

| | | | | | | | |

| | | | | | | | |

| |

Preferred Stocks—0.0% | | | | | | | | |

| |

Ally Financial, Inc., 7% Cum., Series G, Non-Vtg.3 | | | 656 | | | | 652,966 | |

| |

Zee Entertainment Enterprises Ltd., 6% Cum. Non-Cv. | | | INR 21,135,219 | | | | 269,819 | |

| | | | | | | | |

Total Preferred Stocks (Cost $778,848) | | | | 922,785 | |

| | |

| | | Units | | | | |

| |

Rights, Warrants and Certificates—0.0% | | | | | | | | |

| |

Genting Bhd Wts., Strike Price 7.96MYR, 12/18/181 (Cost $77,776) | | | 123,800 | | | | 109,564 | |

| | |

| | | Principal Amount | | | | |

| |

Non-Convertible Corporate Bonds and Notes—7.4% | | | | | | | | |

| |

Access Midstream Partners LP/ACMP Finance Corp., 6.125% Sr. Unsec. Nts., 7/15/22 | | | $ 335,000 | | | | 363,894 | |

| |

Actuant Corp., 5.625% Sr. Unsec. Nts., 6/15/22 | | | 340,000 | | | | 360,400 | |

| |

ADS Waste Holdings, Inc., 8.25% Sr. Unsec. Nts., 10/1/20 | | | 265,000 | | | | 288,519 | |

| |

AES Corp., 7.375% Sr. Unsec. Nts., 7/1/21 | | | 205,000 | | | | 235,750 | |

| |

Affinia Group, Inc., 7.75% Sr. Unsec. Nts., 5/1/21 | | | 510,000 | | | | 548,250 | |

| |

Affinion Group, Inc., 7.875% Sr. Unsec. Nts., 12/15/18 | | | 880,000 | | | | 827,200 | |

| |

Ahern Rentals, Inc., 9.50% Sec. Nts., 6/15/183 | | | 405,000 | | | | 452,587 | |

| |

Air Canada, 6.75% Sr. Sec. Nts., 10/1/193 | | | 320,000 | | | | 345,200 | |

| |

AK Steel Corp., 7.625% Sr. Unsec. Nts., 5/15/20 | | | 400,000 | | | | 403,000 | |

| |

Alcatel-Lucent USA, Inc., 6.75% Sr. Unsec. Nts., 11/15/203 | | | 360,000 | | | | 379,800 | |

| |

Alere, Inc., 6.50% Sr. Sub. Nts., 6/15/20 | | | 305,000 | | | | 321,775 | |

| |

Aleris International, Inc.: | | | | | | | | |

7.625% Sr. Unsec. Nts., 2/15/18 | | | 655,000 | | | | 672,194 | |

7.875% Sr. Unsec. Nts., 11/1/20 | | | 680,000 | | | | 688,500 | |

| |