UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_________________________

FORM 10-K

(Mark One)

| þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended December 31, 2012 |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the transition period from ______ to ______ |

Commission file number 1-14279

_______________________

ORBITAL SCIENCES CORPORATION

(Exact name of registrant as specified in its charter)

| Delaware | 06-1209561 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| |

45101 Warp Drive Dulles, Virginia 20166 (Address of principal executive offices) (703) 406-5000 (Registrant's telephone number, including area code) |

| |

| Securities registered pursuant to Section 12(b) of the Act: |

| |

Title of each class Common Stock, par value $.01 per share | Name of each exchange on which registered The New York Stock Exchange |

| |

Securities registered pursuant to Section 12(g) of the Act: None |

_______________________

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer þ | Accelerated filer o | Non-accelerated filer o | Smaller reporting company o |

| (Do not check if a smaller reporting company) |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No þ

The aggregate market value of the registrant's Common Stock held by non-affiliates of the registrant based on the closing sales price of the registrant's Common Stock as reported on The New York Stock Exchange on June 29, 2012 was approximately $750,700,000.

As of February 19, 2013, 59,797,541 shares of the registrant's Common Stock were outstanding.

Portions of the registrant's definitive proxy statement to be filed on or about March 8, 2013 are incorporated by reference in Part III of this report.

|

| Item | | Page |

| PART I | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| PART II | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| PART III | |

| | |

| | |

| | |

| | |

| | |

| | |

| PART IV | |

| | |

| | |

| | |

| Pegasus is a registered trademark and service mark of Orbital Sciences Corporation; Taurus is a registered trademark of Orbital Sciences Corporation; Orbital, Minotaur, Antares and Cygnus are trademarks of Orbital Sciences Corporation. |

PART I

General

We develop and manufacture small- and medium-class rockets and space systems for commercial, military and civil government customers, including the U.S. Department of Defense ("DoD"), the National Aeronautics and Space Administration ("NASA") and other U.S. Government agencies. Our products and services are grouped into three reportable business segments: launch vehicles, satellites and space systems, and advanced space programs, which are described below.

| · | Launch Vehicles - Rockets that are used as small- and medium-class space launch vehicles that place satellites into Earth orbit and escape trajectories, interceptor and target vehicles for missile defense systems, and suborbital launch vehicles that place payloads into a variety of high-altitude trajectories. |

| · | Satellites and Space Systems - Small- and medium-class satellites that are used to enable global and regional communications and broadcasting, conduct space-related scientific research, collect imagery and other remotely-sensed data about the Earth, carry out interplanetary and other deep-space exploration missions, and demonstrate new space technologies. |

| · | Advanced Space Programs - Human-rated space systems for Earth-orbit and deep-space exploration, and small- and medium-class satellites primarily used for national security space programs and to demonstrate new space technologies. |

Our general strategy is to develop and expand a core integrated business of space and launch systems technologies and products, focusing on the design and manufacture of affordable rockets, satellites and other space systems in order to establish and expand positions in niche markets that have not typically been emphasized by our larger competitors. Another part of our strategy is to seek customer contracts that will fund new product development and enhancements to our existing launch vehicle and space systems product lines. As a result of our capabilities and experience in designing, developing, manufacturing and operating a broad range of small- and medium-class rockets and space systems, we believe we are well positioned to capitalize on the demand for more affordable space-technology systems in commercial satellite communications, space-based military and intelligence operations, and missile defense programs, and to take advantage of government-sponsored initiatives in human space exploration, space-based scientific research and interplanetary exploration.

Orbital was incorporated in Delaware in 1987 to consolidate the assets, liabilities and operations of two predecessor entities established in 1982 and 1983. Our corporate headquarters are located at 45101 Warp Drive, Dulles, Virginia 20166, our telephone number is (703) 406-5000 and our website is www.orbital.com.

Description of Orbital's Products and Services

Launch Vehicles

Our launch vehicles segment develops and produces space launch vehicles, interceptor launch vehicles and target launch vehicles.

Space Launch Vehicles - We develop and produce small-class launch vehicles that place satellites weighing up to 4,000 lbs. into low-Earth orbit, including the Pegasus, Taurus and Minotaur space launch vehicles that are used by commercial, civil government and military customers. Our Pegasus launch vehicle is launched from our L-1011 carrier aircraft to deploy relatively lightweight satellites into low-Earth orbit. The Taurus launch vehicle is a ground-launched derivative of the Pegasus vehicle that can carry heavier payloads into orbit. The ground-launched Minotaur launch vehicle family combines Minuteman II and Peacekeeper ballistic missile rocket motors with our Pegasus and Taurus technology. In 2012, we conducted one successful Pegasus launch, which deployed the Orbital-built Nuclear Spectroscopic Array Telescope satellite for NASA.

We are nearing completion of a major product development effort to create a medium-capacity rocket, Antares, that we expect will increase the payload capacity of our space launch vehicles to approximately 14,000 lbs. for launches to low-Earth orbit. Antares will be used on our Commercial Orbital Transportation Services ("COTS") test flight and demonstration mission for NASA and under our Commercial Resupply Services ("CRS") contract with NASA to deliver cargo to the International Space Station ("ISS"). We also are marketing the vehicle to other U.S. Government and commercial customers.

Interceptor Launch Vehicles - We develop and produce rockets that are used as interceptor launch vehicles for missile defense systems, including interceptor boosters that carry "kill vehicles" designed to defend against ballistic missile attacks. Pursuant to a contract with The Boeing Company ("Boeing"), we have been the sole supplier of operational and test interceptor boosters for the U.S. Missile Defense Agency's ("MDA") Ground-based Midcourse Defense ("GMD") program, for which our interceptor boost vehicle, a modified version of our Pegasus rocket, is being used as a major operational element in the U.S. national missile defense system. There were two deliveries of this launch vehicle during 2012. In January 2013, one of these vehicles was successfully launched as part of a test of the GMD program. With the award of the follow-on GMD development and sustainment contract in 2011, Orbital will continue to provide booster vehicles in support of the GMD program through 2018.

Target Launch Vehicles - We design and produce target launch vehicles used in the development and testing of missile defense systems. Our target launch vehicles include suborbital rockets and their principal subsystems, as well as payloads carried by such vehicles. Various branches and agencies of the U.S. military, including MDA, use our target launch vehicles as targets for defense-related applications such as ballistic missile interceptor testing and related experiments. These rockets are programmed to simulate incoming enemy missiles, offering an affordable and reliable means to test advanced missile defense systems. Our family of target vehicles extends from long-range ballistic target launch vehicles, which include targets

for testing MDA's GMD system, to medium- and short-range target vehicles designed to simulate threats to U.S. and allied military forces deployed in overseas theaters. We have also developed a short-range supersonic sea-skimming target ("SSST") that flies just above the ocean's surface and is currently being used by the U.S. Navy. In 2012, we performed a total of three successful target missions, including a medium-range target vehicle launched in support of the MDA Aegis Ballistic Missile Defense test program and a target mission for the U.S. Army's Patriot missile defense system. We also delivered 15 SSST vehicles to the U.S. Navy in 2012.

Satellites and Space Systems

Our satellites and space systems segment is involved in developing and producing communications satellites, science and remote sensing satellites, and related subsystems, and we also provide space technical services primarily related to scientific satellite and suborbital research rocket missions.

Communications Satellites - We design and manufacture small geosynchronous-Earth orbit ("GEO") satellites that provide cable and direct-to-home television distribution, business data network connectivity, regional mobile telephony and other space-based communications services.

Science and Remote Sensing Satellites - Our small- and medium-class low-Earth orbit satellites and other spacecraft are used to conduct space-related scientific research, collect imagery and other remotely-sensed data about the Earth, carry out interplanetary and other deep-space exploration missions, and demonstrate new space technologies.

During 2012, we delivered five GEO communications satellites to commercial customers and two scientific satellites to NASA; five of these satellites were launched and placed into service in 2012, while the other two were launched in early 2013.

Space Technical Services - We provide advanced space systems and subsystems, including satellite command and data handling, attitude control and structural subsystems and a broad range of space-related technical services, including analytical, engineering and manufacturing services for space-related science and defense programs. We also design, build and integrate a variety of small scientific research rockets and support field operations and launch activities for such vehicles.

Advanced Space Programs

Our advanced space programs segment is involved in developing and producing human-rated space systems and satellites and related systems primarily used for national security space programs.

Human-Rated Space Systems - We design and manufacture advanced human-rated spacecraft to be used in Earth orbit, planetary exploration and other space missions. In 2008, under the COTS research and development program, we entered into an agreement with NASA to design, build and demonstrate a new space transportation system that has the capability to deliver cargo

and other supplies to the ISS. This system will include a new advanced maneuvering spacecraft called Cygnus that will be launched on our Antares launch vehicle and will autonomously rendezvous with the ISS to deliver cargo to the astronauts on board. We expect the COTS demonstration mission will occur in mid-2013. Also in 2008, under the CRS program, NASA entered into a contract with us to perform eight cargo transportation missions to the ISS using the Antares/Cygnus space transportation system we are developing under our COTS program. We expect these missions to be carried out over the next four years.

National Security Space Systems - We develop and produce small- and medium-class satellites and related systems used primarily for national security space missions and related technology demonstration programs.

Customers

Customers that accounted for 10% or more of our consolidated revenues in 2012 were DoD and NASA. Customers that accounted for 10% or more of our consolidated revenues in 2011 were DoD, NASA and Boeing. Customers that accounted for 10% or more of our consolidated revenues in 2010 were DoD and NASA.

Competition

We believe that competition for sales of our products and services is based primarily on performance and technical features, reliability, price, delivery schedule and our ability to customize our products to meet particular customer needs, and we believe that we compete favorably on the basis of these factors. The table below identifies the entities we believe to be our primary competitors for each major product line.

Product Line | Competitors |

| Space launch vehicles | United Launch Alliance (a joint venture between Lockheed Martin Corporation and The Boeing Company) Space Exploration Technologies Corp. Alliant Techsystems Inc. Lockheed Martin Corporation Russian, Indian and Chinese launch vehicles could represent competition for commercial, as opposed to U.S. Government, launches |

| Interceptor launch vehicles | Lockheed Martin Corporation Raytheon Company |

| Target launch vehicles | Lockheed Martin Corporation L-3 Communications, Inc. Alliant Techsystems Inc. Kratos Defense & Security Solutions, Inc. |

Product Line | Competitors |

| Communications satellites | EADS Astrium The Boeing Company Lockheed Martin Corporation Space Systems/Loral, Inc., a subsidiary of MacDonald, Dettwiler and Associates Ltd. |

| Reshetnev Company - Information Satellite Systems Thales Alenia Space Mitsubishi Electric Corp. |

| Science and remote sensing satellites and national security space systems | Ball Aerospace and Technologies Corp. Lockheed Martin Corporation Northrop Grumman Corporation The Boeing Company Alliant Techsystems Inc. Sierra Nevada Corporation Surrey Satellite Technology Limited, a subsidiary of EADS Astrium |

| Space technical services | Our space technical services compete with many companies, from large defense contractors to small niche competitors |

| Human-rated space systems | Space Exploration Technologies Corp. European Space Agency Japan Aerospace Exploration Agency Russian Federal Space Agency |

Many of our competitors are larger and have substantially greater resources than we do. Further, it is possible that other domestic or foreign companies or governments, some with greater experience in the space and defense industry and many with greater financial resources than we possess, will seek to provide products or services that compete with ours in the future. Any such foreign competitor could benefit from subsidies from, or other protective measures by, its home country.

Research and Development

We invest in product-related research and development to conceive and develop new products and to enhance existing products. Our research and development expenses totaled approximately $114.2 million, $102.8 million and $122.3 million for the years ended December 31, 2012, 2011 and 2010, respectively. We believe our research and development expenses will decline in 2013 as we are nearing completion of our Antares and COTS development programs.

Under certain arrangements, such as the COTS program, our customers share in product development costs. For a further discussion of the research and development expenses being funded by our government customer with respect to our COTS program, please see "Consolidated Results of Operations for the Years Ended December 31, 2012, 2011 and 2010 – Research and Development Expenses" in "Item 7 – Management's Discussion and Analysis of Financial Condition and Results of Operations."

Patents and Proprietary Rights

We rely in part on patents, trade secrets and know-how to develop and maintain our competitive position and technological advantage, particularly with respect to our launch vehicle and satellite products. While our intellectual property rights in the aggregate are important to the operation of our business, we do not believe that any single existing patent or other intellectual property right is of such importance that its loss or termination would have a material adverse effect on our business, taken as a whole.

Components and Raw Materials; Seasonality

We purchase a significant percentage of our subassemblies and instruments from domestic and foreign suppliers. We also obtain from the U.S. Government parts and equipment that are used in the production of our products or in the provision of our services. Generally, we have not experienced material difficulty in obtaining product components or necessary parts and equipment and we believe that alternatives to our existing sources of supply are available in most cases, although we could incur increased costs and possible delays in securing alternative sources of supply.

We rely upon sole-source suppliers for most solid-propellant rocket motors and liquid-propellant rocket engines used on our launch vehicles. For example, our Antares launch vehicle uses liquid-propellant AJ-26 engines, which are modified Russian rocket engines, for its first stage that is available solely from one supplier. These engines are no longer in production, and while there is sufficient quantity of these engines to complete the CRS and COTS programs, there is a limited supply available for other potential missions. While we believe that alternative sources for rocket motors and engines would be available, the inability of our current suppliers to provide us with rocket motors and engines, such as the AJ-26, could result in significant contract delays, cost increases and loss of revenues due to the time, resources and effort that would be required to develop or adapt other engines or motors for use in our products.

Our business is not seasonal.

U.S. Government Contracts

During 2012, 2011 and 2010, approximately 79%, 71% and 74%, respectively, of our total annual revenues were derived from contracts with the U.S. Government and its agencies or from subcontracts with other U.S. Government contractors. Most of our U.S. Government contracts are funded incrementally on a year-to-year basis.

Our major contracts with the U.S. Government primarily fall into two categories: cost-reimbursable contracts and fixed-price contracts. Approximately 58% and 42% of our revenues from U.S. Government contracts in 2012 were derived from cost-reimbursable contracts and fixed-price contracts, respectively. Under cost-reimbursable contracts, we recover our actual allowable costs incurred, allocable indirect costs and a fee consisting of (i) a base amount that is fixed at the inception of the contract and/or (ii) an award amount that is based on the customer's evaluation of our performance in terms of the criteria stated in the contract. Our fixed-price contracts include firm fixed-price and fixed-price incentive fee contracts. Under firm fixed-price contracts, work performed and products shipped are paid for at a fixed price without adjustment for actual costs incurred in connection with the contract. Therefore, we bear the risk of loss if costs increase, although some of this risk may be passed on to subcontractors. Fixed-price incentive fee contracts provide for sharing by us and the customer of unexpected costs incurred or savings realized within specified limits, and may provide for adjustments in price depending on actual contract performance other than costs. Costs in excess of the negotiated maximum (ceiling) price and the risk of loss by reason of such excess costs are borne by us, although some of this risk may be passed on to subcontractors.

As noted above, we derive a significant portion of our revenues from U.S. Government contracts, which are dependent on continued political support and funding. All our U.S. Government contracts and, in general, our subcontracts with other U.S. Government prime contractors provide that such contracts may be terminated for convenience at any time by the U.S. Government or the prime contractor, respectively. Furthermore, any of these contracts may become subject to a government-issued stop work order under which we would be required to suspend production. In the event of a termination for convenience, contractors generally are entitled to receive the purchase price for delivered items, reimbursement for allowable costs for work in process and an allowance for reasonable profit thereon or adjustment for loss if completion of performance would have resulted in a loss. For a more detailed description of risks relating to the U.S. Government contract industry, see "Item 1A – Risk Factors."

A portion of our business is classified for national security purposes by the U.S. Government and cannot be specifically described. The operating results of these classified programs are included in our consolidated financial statements. The business risks associated with classified programs, as a general matter, do not differ materially from those of our other U.S. Government contracts, and are subject to the same operational, compliance and financial reporting controls.

Regulation

Our ability to pursue our business activities is regulated by various agencies and departments of the U.S. Government and, in certain circumstances, the governments of other countries. Commercial space launches require licenses from the U.S. Department of Transportation ("DoT") and the reentry of our Cygnus maneuvering spacecraft during the COTS demonstration mission and the operation of our L-1011 aircraft require licenses from certain agencies of the DoT, including the Federal Aviation Administration ("FAA"). The use of the AJ-26 engine, which is a modified Russian rocket engine, on our Antares rocket requires a Russian government license, which we have obtained for our missions currently under contract. The Federal Communications Commission ("FCC") also requires licenses for radio communications during our rocket launches. Our classified programs require that we and certain of our employees maintain appropriate security clearances. We also require export licenses from the U.S. Department of State ("DoS"), the U.S. Department of Commerce ("DoC") and, occasionally, the governments of other countries with respect to transactions we have with foreign customers or foreign subcontractors.

Contract Backlog

Our firm backlog was approximately $2.20 billion at December 31, 2012 and approximately $2.39 billion at December 31, 2011. While there can be no assurance, we expect to convert approximately $940 million of the 2012 year-end firm backlog into revenues during 2013. Our firm backlog as of December 31, 2012 included approximately $2.0 billion of contracts with the U.S. Government and its agencies or from subcontracts with prime contractors of the U.S. Government. Most of our U.S. Government contracts are funded incrementally on a year-to-year basis. Firm backlog from U.S. Government contracts at December 31, 2012 included total funded orders of about $670 million and orders not yet funded of about $1.33 billion. Changes in government policies, priorities or funding levels through agency or program budget reductions by the U.S. Congress or executive agencies could materially adversely affect our financial condition and results of operations. Furthermore, contracts with the U.S. Government may be terminated or suspended by the U.S. Government at any time, with or without cause, which could result in a reduction in backlog.

Total backlog was approximately $5.03 billion at December 31, 2012. Total backlog includes firm backlog in addition to unexercised options, indefinite-quantity contracts and undefinitized orders and contract award selections.

Employees

As of February 19, 2013, Orbital had approximately 3,500 employees. Our employees are not subject to collective bargaining agreements. We believe our employee relations are good.

Executive Officers of the Registrant

The following table sets forth the name, age and position of each of the executive officers of Orbital as of February 19, 2013. All executive officers are appointed annually and serve at the discretion of the Board of Directors.

Name | Age | Position |

David W. Thompson | 58 | Chairman of the Board, President and Chief Executive Officer |

| | |

Garrett E. Pierce | 68 | Vice Chairman and Chief Financial Officer, Director |

Antonio L. Elias | 63 | Executive Vice President and Chief Technical Officer |

| | |

Ronald J. Grabe | 67 | Executive Vice President and General Manager, Launch Systems Group |

| | |

Michael E. Larkin | 57 | Executive Vice President and General Manager, Space Systems Group |

| | |

Frank L. Culbertson, Jr. | 63 | Executive Vice President and General Manager, Advanced Programs Group |

| | |

| Susan Herlick | 48 | Senior Vice President, General Counsel and Corporate Secretary |

David W. Thompson is a co-founder of Orbital and has been Chairman of the Board and Chief Executive Officer of Orbital since 1982. From 1982 until October 1999, he also served as our President, a role he resumed in 2011 following the retirement of James R. Thompson from this position. Prior to founding Orbital, Mr. Thompson was employed by Hughes Electronics Corporation as special assistant to the President of its Missile Systems Group and by NASA at the Marshall Space Flight Center as a project manager and engineer, and also worked on the Space Shuttle's autopilot design at the Charles Stark Draper Laboratory. Mr. Thompson is a Fellow of the American Institute of Aeronautics and Astronautics, the American Astronautical Society and the Royal Aeronautical Society, and is a member of the U.S. National Academy of Engineering.

Garrett E. Pierce has been Vice Chairman and Chief Financial Officer since April 2002, and was Executive Vice President and Chief Financial Officer since August 2000. He has been a director of the Company since August 2000. From 1996 until August 2000, he was Executive Vice President and Chief Financial Officer of Sensormatic Electronics Corp., a supplier of electronic security systems, where he was also named Chief Administrative Officer in July 1998. Prior to joining Sensormatic, Mr. Pierce was the Executive Vice President and Chief Financial Officer of California Microwave, Inc., a supplier of microwave, radio frequency and satellite systems and products for communications and wireless networks. From 1980 to 1993, Mr. Pierce was with Materials Research Corporation, a provider of thin film equipment and high purity materials to the semiconductor, telecommunications and media storage industries, where he progressed from Chief Financial Officer to President and Chief Executive Officer. Materials Research Corporation was acquired by Sony Corporation as a wholly owned subsidiary in 1989. From 1972 to 1980, Mr. Pierce held various management positions with The Signal Companies. Mr. Pierce is a director of Kulicke and Soffa Industries, Inc.

Antonio L. Elias has been Executive Vice President and Chief Technical Officer since September 2012. From October 2001 to September 2012, he served as Executive Vice President and General Manager, Advanced Programs Group, and was Senior Vice President and General Manager, Advanced Programs Group since August 1997. From January 1996 until August 1997, Dr. Elias served as Senior Vice President and Chief Technical Officer of Orbital. From May 1993 through December 1995, he was Senior Vice President for Advanced Projects, and was Senior Vice President, Space Systems Division from 1990 to April 1993. He was Vice President, Engineering of Orbital from 1989 to 1990 and was Chief Engineer from 1986 to 1989. From 1980 to 1986, Dr. Elias was an Assistant Professor of Aeronautics and Astronautics at Massachusetts Institute of Technology. He was elected to the National Academy of Engineering in 2001.

Ronald J. Grabe has been Executive Vice President and General Manager, Launch Systems Group since 1999. From 1996 to 1999, he was Senior Vice President and Assistant General Manager of the Launch Systems Group and Senior Vice President of the Launch Systems Group since 1995. From 1994 to 1995, Mr. Grabe served as Vice President for Business Development in the Launch Systems Group. From 1980 to 1993, Mr. Grabe was a NASA astronaut during which time he flew four Space Shuttle missions and was lead astronaut for development of the International Space Station.

Michael E. Larkin has been Executive Vice President and General Manager, Space Systems Group since February 2008 and was Senior Vice President and Deputy General Manager of the Space Systems Group since 2006. From 2004 to 2006, he served as Senior Vice President of Finance of the Space Systems Group. From 1996 to 2004, he was Vice President of the Space Systems Group, and was Director of Finance of the Space Systems Group from 1994 to 1996. Prior to that, he held a variety of program and financial management positions at Fairchild Space and Defense Corporation, a space and military electronics company, until its acquisition by Orbital in 1994.

Frank L. Culbertson, Jr. has been Executive Vice President and General Manager, Advanced Programs Group, since September 2012. From 2008 to 2012, he served as Senior Vice President in the Advanced Program Group where he headed our human space systems efforts. Prior to joining Orbital, Mr. Culbertson was a Senior Vice President at Science Applications International Corporation from 2002 to 2008. Before entering the private sector, Mr. Culbertson served as a NASA astronaut for 18 years, flying three Space Shuttle missions, and began his career as a pilot in the United States Navy.

Susan Herlick has been Senior Vice President, General Counsel and Corporate Secretary since January 2006 and served as Vice President and Deputy General Counsel from 2003 to 2005. From 1997 to 2002, she was Vice President and Assistant General Counsel. She joined Orbital as Assistant General Counsel in 1995. Prior to that, she was an attorney at the law firm of Hogan & Hartson LLP, now Hogan Lovells US LLP.

Available Information

We maintain an Internet website at www.orbital.com. In addition to news and other information about our company, we make available on or through the Investor Relations section of our website our Annual Report on Form 10-K, our Quarterly Reports on Form 10-Q, our current reports on Form 8-K and all amendments to these reports as soon as reasonably practicable after we electronically file this material with, or furnish it to, the U.S. Securities and Exchange Commission ("SEC").

At the Investor Relations section of our website, we have a Corporate Governance page that includes, among other things, copies of our Code of Business Conduct and Ethics, our Corporate Governance Guidelines and the charters for each standing committee of our Board of Directors, including the Audit and Finance Committee, the Corporate Governance and Nominating Committee and the Human Resources and Compensation Committee.

Printed copies of all of the above-referenced reports and documents may be requested by contacting our Investor Relations Department either by mail at our corporate headquarters, by telephone at (703) 406-5543 or by e-mail at investor.relations@orbital.com. All of the above-referenced reports and documents are available from us free of charge.

* * *

Financial information about our products and services, business segments, domestic and foreign operations and export sales is included in "Management's Discussion and Analysis of Financial Condition and Results of Operations" and the notes to our consolidated financial statements, and is incorporated herein by reference.

Special Note Regarding Forward-Looking Statements

Certain statements contained in this Annual Report on Form 10-K are forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 and Section 21E of the Securities Exchange Act of 1934. These forward-looking statements include, but are not limited to, those related to our financial outlook, liquidity, goals, business strategy, projected plans and objectives of management for future operating results, and forecasts of future events. These statements can be identified by the fact that they do not relate strictly to historical or current facts. Forward-looking statements often include the words "anticipate," "forecast," "expect," "believe," "should," "will," "intend," "plan" and words of similar substance. Such forward-looking statements are subject to risks, trends and uncertainties that could cause the actual results or performance of the company to be materially different from the forward-looking statement. Uncertainty surrounding factors such as continued government support and funding for key space and defense programs, including the impact of potential sequestration under the Budget Control Act of 2011, new product development programs, the availability of key product components, product performance and market acceptance of products and technologies, achievement of contractual milestones, government contract procurement and termination risks, and income tax rates may materially impact Orbital's actual financial and operational results. We are under no obligation to, and expressly disclaim any obligation or undertaking to update or alter any forward-looking statement, whether as a result of new information, subsequent events or otherwise, except as required by law.

Investors should carefully consider, among other factors, the risks listed below.

We derive a significant portion of our revenues from U.S. Government contracts, which are dependent on continued political support and funding and are subject to termination by the U.S. Government at any time.

The majority of our total annual revenues and our firm backlog at December 31, 2012 were derived from U.S. Government contracts. Most of our U.S. Government contracts are funded incrementally on a year-to-year basis and are subject to uncertain future funding levels. Our direct and indirect contracts with the U.S. Government may be terminated or suspended by the U.S. Government or its prime contractors at any time, with or without cause. Termination or suspension of any of our significant U.S. Government contracts could result in the loss of future revenues and unreimbursable expenses or charges that could have a materially adverse effect on our financial condition and results of operations. Furthermore, key human space initiatives, missile defense programs, and other space programs must compete with other programs for consideration during the federal budgeting and appropriation process, and support and funding for any U.S. Government program may be influenced by general economic conditions, political considerations and other factors. A decline in U.S. Government support and funding for programs in which we participate could result in contract terminations, delays in contract awards, the failure to exercise contract options, the cancellation of planned procurements and fewer new

business opportunities, any of which could have a material adverse effect on our financial condition and results of operations.

In particular, the Budget Control Act of 2011 commits the U.S. Government to significantly reduce the federal deficit over ten years through caps on discretionary spending and other measures, including automatic across-the-board spending cuts through the sequestration process, if necessary. Such spending cuts would be split equally between defense and non-defense programs over a ten-year period. Although the American Taxpayer Relief Act of 2012 has delayed sequestration temporarily, without further action, it will take effect on March 1, 2013. It remains uncertain whether the contemplated sequester will take place or if it will be delayed, modified or averted. Any automatic across-the-board cuts required by sequestration would affect Orbital's U.S. Government customers, in particular, DoD and NASA. While the impact of sequestration on our individual U.S. Government programs is unclear, funding for programs in which we participate or new contract awards that we seek to win could be reduced, delayed or cancelled. As a result, our business, financial condition and results of operations could be materially adversely affected. Even if sequestration does not occur, our U.S. Government customers could face some level of spending cuts, which could adversely impact our business, financial condition and results of operation.

We are subject to a number of domestic and international laws, regulations and restrictions, the non-compliance with which may expose us to adverse consequences.

As a government contractor, we are subject to extensive and complex U.S. Government procurement laws and regulations, including the Procurement Integrity Act and the False Claims Act. Failure to comply with these laws and regulations could result in contract termination, price or fee reductions, civil or criminal penalties, injunctions and/or administrative sanctions such as suspension or debarment from contracting with the U.S. Government.

In addition, our international business subjects us to numerous U.S. and foreign laws and regulations, including the Foreign Corrupt Practices Act and regulations relating to import-export control. Our failure to comply with these laws and regulations could result in administrative, civil or criminal penalties and administrative sanctions such as suspension or debarment from contracting with the U.S. Government or suspension of our export privileges, which could result in the termination of existing U.S. Government contracts, affect our ability to win new U.S. Government contracts, and impair our ability to serve foreign customers.

Our business could be adversely affected by adverse audit findings by the U.S. Government.

U.S. Government agencies, including the Defense Contract Audit Agency and various agency Inspectors General, routinely audit and investigate government contractors. These agencies review a contractor's performance under its contracts, cost structure and compliance with applicable laws, regulations and standards. Charging practices relating to labor, research and development, and other costs that may be charged directly or indirectly to U.S. Government contracts are often scrutinized to determine that such costs are allowable under U.S. Government contracts and furthermore that such costs are reasonable. Any costs determined to be unallowable or unreasonable may not be reimbursed, and such costs already reimbursed may be

subject to repayment. If the amount of such costs were significant, our results of operations and financial condition could be materially adversely affected. For example, we expect to recover a significant portion of our research and development expenses, including those related to the Antares and COTS development programs, through billings under certain of our U.S. Government contracts in accordance with applicable regulations, but such billings could be reversed or rejected by the U.S. Goverment. Our inability to recover a significant portion of such expenses could materially adversely affect our financial condition and results of operations.

The above-mentioned agencies also review the adequacy of, and a contractor's compliance with, its internal control systems and policies, including the contractor's purchasing, property, estimating, compensation, accounting and information systems. Adverse findings relating to our systems could result in the U.S. Government customer withholding a percentage of payments and also could impact our ability to win new U.S. Government contract awards or option exercises.

Responding to government audits, inquiries or investigations may involve significant expense and divert management attention. Also, if an audit or investigation were to uncover improper or illegal activities, we could be subject to civil and criminal penalties and administrative sanctions, including termination of contracts, forfeiture of profits, suspension of payments, fines and suspension or prohibition from doing business with the U.S. Government. In addition, we could suffer serious reputational harm if allegations of impropriety were to be made against us.

Termination of our contracts could materially adversely affect our backlog and our future financial results.

Approximately 79% of our 2012 revenues were derived from direct or indirect contracts with the U.S. Government. All of our direct and indirect contracts with the U.S. Government or its prime contractors may be terminated or suspended at any time, with or without cause, for the convenience of the government. U.S. Government contract awards also may be subject to bid protests, which may result in a contract award being rescinded or subject to reprocurement. In addition, our commercial satellite contracts also give the customer the right to unilaterally terminate the contract. For these reasons, we cannot assure you that all of our backlog will ultimately be recognized in revenues. The loss of future revenues, incurrence of unreimbursed costs, or liability to the U.S. Government or our commercial customers in connection with other cancelled or rescinded contracts could have a material adverse effect on our financial condition and results of operations. Furthermore, the termination of any contracts for default could also have a material adverse effect on our ability to obtain new business in the future.

We are dependent on a single U.S. Government contract for a large percentage of our revenues and backlog.

Our CRS contract to deliver cargo to the ISS accounted for approximately 24% of our revenues in 2012, and we expect it to continue to account for a material percentage of our revenues in 2013. Given the uncertainty surrounding future government spending and the right of U.S. Government customers to terminate our contracts for convenience, there can be no assurance that the current backlog for this contract ultimately will be recognized in revenues. The cancellation of our CRS contract for any reason, including as a result of reductions in appropriations or our failure to achieve milestones due to technical issues or delays, would likely have a material adverse effect on our financial condition and results of operations. In addition, our failure to achieve certain milestones related to the successful launch of our Antares rocket and the successful delivery of cargo to the ISS could result in a material reduction of future revenues and profit.

We use estimates in accounting for our contracts. Changes in our estimates could materially adversely affect our financial results.

Contract accounting requires judgments in assessing risks, estimating contract revenues and costs and making assumptions related to schedule and technical issues. Due to the nature of many of our contracts, the estimation of total revenues and costs at completion may be complex and is subject to many variables. For example, we make assumptions regarding our performance under contracts, the labor hours, labor rates and costs of materials and subcontracts. Our assumptions regarding the timing and amounts of incentives, penalties, award fees and milestones related to performance on contracts involve a high degree of judgment and estimates by our management. These assumptions are important factors that impact the revenues and profits that we recognize. In the event of a change in total estimated contract revenue, cost or profit, the cumulative effect of such change is recorded in the period the change in estimate occurs.

Because of the significance of the judgments and estimates inherent in our accounting processes described above, it is possible that material adjustments to our financial results could be required if we determine, based on current facts and circumstances known to us, that our prior assumptions are no longer reasonable and need to be revised.

We may not receive full payment for our satellites or launch services and we could incur penalties in the event of a failure or malfunction or if our satellites are not delivered or our rockets are not launched on schedule.

Some of our satellite contracts provide for performance-based payments to be made to us after the satellite is in orbit over periods that may be as long as 15 years. Additionally, some satellite contracts require us to refund a portion of the contract price to the customer if performance criteria, which cover periods of up to 15 years, are not satisfied. Certain contracts include payment milestones that are contingent upon a successful launch. For example, approximately 25% of the contract value of our CRS contract is billable and collectible only upon the completion of launch and delivery milestones for each of eight CRS contract missions.

As of December 31, 2012, we have recognized a total of $974 million of revenues on this contract which has a total contract value of approximately $1.9 billion. If we do not successfully complete these launch and delivery milestones, we may be required to record significant revenue and profit reductions.

While our practice is generally to procure insurance policies that we believe would indemnify us for satellite and launch success incentive fees or contract milestones that are not earned and for performance refund obligations, insurance may not be available on economical terms, if at all, for each of our satellite and launch programs. Further, in some cases, we may elect not to procure insurance. In addition, some of our satellite and launch contracts require us to pay penalties in the event that satellites are not delivered or a launch does not occur, on a timely basis, or to refund cash receipts to the customer if a contract is terminated for default. Our failure to earn performance-based contract milestones, or a requirement that we refund cash to the customer or pay delay penalties, could materially adversely affect our financial condition and results of operations.

Contract cost overruns could materially adversely impact our financial results.

We provide our products and services primarily through cost-reimbursable and fixed-price contracts. Cost overruns, if significant, could materially adversely impact our financial results:

| · | Under cost-reimbursable contracts, we are reimbursed for allowable incurred costs plus a fee, which may be fixed or variable (based, entirely or in part, on the customer's evaluation of our performance under the contract). There is no guarantee as to the amount of fee, if any, that we will be awarded under a cost-reimbursable contract with a variable fee. In addition, the price on a cost-reimbursable contract is based on allowable costs incurred, but generally is subject to customer funding limitations. If we incur costs in excess of the amount funded, we may not be able to recover such costs. |

| · | Under fixed-price contracts, our customers pay us for work performed and products shipped based on an agreed-upon price, without adjustment for any cost overruns. Therefore, we generally bear all of the financial risk as a result of increased costs on these contracts, although some of this risk may be passed on to subcontractors. Some of our fixed-price contracts provide for sharing of unexpected cost increases or savings realized within specified limits and may provide for adjustments in price depending on actual contract performance. We bear the entire risk of cost overruns in excess of the negotiated maximum amount of unexpected costs to be shared. Our commercial contracts are generally fixed-price agreements. In addition, a significant percentage of our revenues from U.S. Government contracts over the last three years was derived from fixed-price agreements, and we believe this trend will continue in future years. |

Our growth strategy depends on major new product development initiatives involving significant technical challenges.

The development of new or enhanced products is a complex and uncertain process that requires the accurate anticipation of technological and market trends and can require a significant

amount of time and expense to complete. New product development programs often experience schedule delays and cost overruns. Our inability to successfully complete our new product development initiatives on schedule and within budget, or to obtain market acceptance, could have a material adverse effect on our financial condition and results of operations.

We are making a substantial investment in the design and development of the Antares launch vehicle and the Cygnus advanced maneuvering spacecraft, and we are considering other product enhancements. As often occurs on major development programs, we have experienced delays in the Antares launch vehicle program due to technical challenges associated primarily with the launch site infrastructure and the AJ-26 engines used in the first stage of the Antares launch vehicle. Continued delays or a launch failure could impact the achievement of performance milestones, result in the cancellation of existing contracts or affect our ability to win new business in the medium-class launch services market, any of which could have a material adverse effect on our financial condition and results of operation.

Our success depends on our ability to penetrate and retain markets for our existing products and to continue to conceive, design, manufacture and market new products on a cost-effective and timely basis.

We may experience design, manufacturing, marketing and other difficulties that could delay or prevent the development, introduction or acceptance of new products and enhancements. There can be no assurance that we will be able to achieve the technological advances necessary to remain competitive and profitable, that new products will be developed and manufactured on schedule or on a cost-effective basis or that our existing products will not become technologically obsolete. Our failure to predict accurately the needs of our customers and prospective customers and to develop products or product enhancements that address those needs, may result in the loss of current customers or the inability to secure new customers.

As a result of technical issues with the AJ-26 rocket engines and the limited inventory of such engines, which are no longer being manufactured, it is uncertain whether the AJ-26 engine is a viable long-term option for our Antares launch vehicle. Therefore, while we believe we have an adequate supply of such engines to satisfy our current Antares contracts and a limited number of additional missions, we have been exploring the feasibility of alternative propulsion systems. Any transition to such an alternative would entail a material investment of time and financial resources. If we are unable to identify a viable alternative propulsion system and modify the Antares launch vehicle in a timely and economical manner, it could limit our long-term ability to compete in the medium-class launch services market.

There can be no assurance that our products will be successfully developed or manufactured or that they will perform as intended.

Most of the products we develop and manufacture are technologically advanced and sometimes include novel systems that must function under highly demanding operating conditions. From time to time, we experience product failures, cost overruns in developing and manufacturing our products, delays in delivery and other operational problems. We have experienced product and service failures, schedule delays and other problems in connection with certain of our launch vehicles, satellites, advanced space systems and other products, and may have similar occurrences in the future. Some of our satellite and launch services contracts impose monetary penalties on us for delays and for performance failures, which penalties could be significant. In addition to any costs resulting from product warranties or required remedial action, product failures or significant delays may result in increased costs or loss of revenues due to the postponement or cancellation of subsequently scheduled operations or product deliveries and may have a material adverse effect on our financial condition and results of operations. Negative publicity from a product failure could damage our reputation and impair our ability to win new contracts.

We rely on sole source suppliers for a number of key components.

We rely on sole source suppliers for a number of key components, including most of the rocket motors and engines we use on our launch vehicles. If we were unable to obtain such components in the future, due to supplier's financial difficulties or a supplier's failure to perform as expected, we could have difficulty procuring such components in a timely or cost effective manner. A disruption in the procurement of key components could result in substantial cost increases to us, significant delays in the execution of certain contracts or our inability to complete certain contracts, any of which could result in a materially adverse impact on our financial results. Our inability to execute contracts in a timely manner could also result in the termination of our contracts for default and could impair or damage our customer relationships. In addition, negative publicity from any failure of one of our products as a result of a failure by a key supplier could damage our reputation and could limit our ability to win new contracts.

Our international business is subject to risks that may have a material adverse effect on our financial results.

We sell certain of our communications satellites and other products to non-U.S. customers. We also procure certain key product components from non-U.S. vendors. International contracts are subject to numerous risks, including:

| · | political and economic instability in foreign markets; |

| · | restrictive trade policies of the U.S. Government and foreign governments; |

| · | inconsistent product regulation by foreign agencies or governments; |

| · | the imposition of product tariffs and burdens; |

| · | the cost of complying with a variety of U.S. and international laws and regulations, including regulations relating to import-export control, and the risk of non-compliance; |

| · | the complexity and necessity of using non-U.S. representatives and consultants; |

| · | the inability to obtain required U.S. or foreign country export licenses; and |

| · | foreign currency exposure. |

Such risks could have a material adverse effect on our financial results by increasing our costs, causing material delays or subjecting us to penalties.

We operate in a regulated industry, and our inability to secure or maintain the licenses, clearances or approvals necessary to operate our business could have a material adverse effect on our financial results.

Our ability to pursue our business activities is regulated by various agencies and departments of the U.S. Government and, in certain circumstances, the governments of other countries. Commercial space launches, the reentry of our Cygnus maneuvering spacecraft during the COTS demonstration and CRS operational missions, and operation of our L-1011 aircraft require licenses from certain agencies of the DoT, including the FAA. The use of modified Russian rocket engines on our Antares rocket requires a Russian government license, which we have obtained for our missions currently under contract. The FCC also requires licenses for radio communications during our rocket launches. Our classified programs require that certain of our facilities and certain of our employees maintain appropriate security clearances.

Exports of our products, services and technical information generally require licenses from the DoS or the DoC. In addition, exports of products from our international suppliers may require export licenses from the governments of other countries. We have a number of international customers and suppliers. Our inability to secure or maintain any necessary licenses or approvals or significant delays in obtaining such licenses or approvals could negatively impact our ability to compete successfully in international markets, and could result in an event of default under certain of our international contracts.

There can be no assurance that we will be successful in our future efforts to secure and maintain necessary licenses, clearances or other U.S. or foreign government regulatory approvals. Our failure to do so could prevent or delay the launch of our rockets or delivery of

our other products, which could have a material adverse effect on our financial condition and results of operations.

We face significant competition in each of our lines of business and many of our competitors possess substantially more resources than we do.

Many of our competitors are larger and have substantially greater resources than we do. Furthermore, it is possible that other domestic or foreign companies or governments, some with greater experience in the space and defense industry and many with greater financial resources than we possess, could seek to produce products or services that compete with our products or services, including new launch vehicles using new technology which could render our launch vehicles less competitively viable. Some of our domestic and foreign competitors currently benefit from, and others may benefit in the future from, subsidies from or other protective measures by their home countries.

Our financial covenants may restrict our operating activities.

Our credit facility contains certain financial and operating covenants, including, among other things, certain coverage ratios, as well as limitations on our ability to incur debt, make dividend payments, make investments, sell all or substantially all of our assets and engage in mergers and consolidations and certain acquisitions. These covenants may restrict our ability to pursue certain business initiatives or certain acquisition transactions. In addition, failure to meet any of the financial covenants in our credit facility could cause an event of default under and/or accelerate some or all of our indebtedness, which would have a material adverse effect on our financial condition and results of operations.

The loss of our executive officers or a failure to retain other key personnel could materially adversely affect our operations.

The departure of any of our executive officers or a failure to retain other key employees could have a material adverse effect on our operations. We require experienced and highly skilled engineers and scientists, and personnel with security clearances to perform our contracts and further our business objectives. The competition and demand for such skilled and experienced employees is great, and there can be no assurance that we will continue to attract and retain key personnel. Our failure to do so could have a material adverse effect on our operations by hindering our ability to execute our contracts in a timely and satisfactory manner and to obtain new business.

The anticipated benefits of future acquisitions may not be realized.

From time to time we may evaluate potential acquisitions that we believe would enhance our business. The anticipated benefits of completed business acquisitions may not be fully realized if we are unable to successfully integrate the acquired operations, technologies and personnel into our organization.

We are subject to environmental regulation.

We are subject to various federal, state and local environmental laws and regulations relating to the operation of our business, including those governing pollution, the handling, storage, disposal and transportation of hazardous substances and the ownership and operation of real property. Such laws and regulations may result in significant liabilities and costs and the loss of permits required to conduct certain operations. There can be no assurance that a failure to comply with such laws and regulations would not have a material adverse effect on our business in the future.

Our restated certificate of incorporation, our amended and restated bylaws, and Delaware law contain anti-takeover provisions that may adversely affect the rights of our stockholders.

Our charter documents contain provisions which could have an anti-takeover effect, including:

| · | our charter provides for a staggered Board of Directors as a result of which only one of the three classes of directors is elected each year; |

| · | any merger, acquisition or other business combination that is not approved by our Board of Directors must be approved by 66 2/3% of voting stockholders; |

| · | stockholders holding less than 10% of our outstanding voting stock cannot call a special meeting of stockholders; and |

| · | stockholders must give advance notice to nominate directors or submit proposals for consideration at stockholder meetings. |

In addition, we are subject to the anti-takeover provisions of Section 203 of the Delaware General Corporation Law, which restrict the ability of current stockholders holding more than 15% of our voting shares to acquire us without the approval of 66 2/3% of the other stockholders. These provisions could discourage potential acquisition proposals and could delay or prevent a change in control transaction. They could also have the effect of discouraging others from making tender offers for our common stock. As a result, these provisions may prevent our stock price from increasing substantially in response to actual or rumored takeover attempts. These provisions may also prevent changes in our management.

Item 1B.

Unresolved Staff Comments

Not applicable.

Our business operations use approximately 1.6 million square feet of office, engineering and manufacturing space in various locations in the United States, as summarized in the table below.

| Business Unit | Principal Location(s) |

| Corporate Headquarters | Dulles, Virginia |

| Launch Vehicles | Chandler, Arizona; Dulles, Virginia; Vandenberg Air Force Base, California; Wallops Island, Virginia; Huntsville, Alabama |

| Satellites and Space Systems | Dulles, Virginia; Gilbert, Arizona; Greenbelt, Maryland; Wallops Island, Virginia |

| Advanced Space Programs | Dulles, Virginia; Gilbert, Arizona |

Approximately 1.3 million square feet of our property, consisting primarily of office space, is leased and 270,000 square feet is owned. Our owned property consists of our two 135,000 square foot state-of-the-art space systems manufacturing facilities that primarily house our satellite manufacturing, assembly and testing activities in Dulles, Virginia and Gilbert, Arizona. Our manufacturing facility for our launch vehicles in Chandler, Arizona, consisting of approximately 370,000 square feet, is leased.

We believe that our existing facilities are adequate for our immediate requirements.

Item 3.

Legal Proceedings

From time to time we are party to certain litigation or other legal proceedings arising in the ordinary course of business. Because of the uncertainties inherent in litigation, we cannot predict whether the outcome of such litigation or other legal proceedings will have a material adverse effect on our results of operations or financial condition; however, we do not believe that any of these matters will have a material adverse effect on our results of operations or financial condition.

Item 4.

Mine Safety Disclosures

Not applicable.

PART II

Item 5.

Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

On February 19, 2013, there were 2,195 Orbital common stockholders of record.

Our common stock trades on The New York Stock Exchange ("NYSE") under the symbol ORB. The range of high and low sales prices of Orbital common stock, as reported on the NYSE, was as follows:

| 2012 | | High | | | Low | |

4th Quarter | | $ | 15.18 | | | $ | 11.90 | |

3rd Quarter | | | 15.12 | | | | 12.26 | |

2nd Quarter | | | 13.50 | | | | 10.59 | |

1st Quarter | | | 15.23 | | | | 12.96 | |

| | | | | | | | |

| | | | | | | | |

| 2011 | | High | | | Low | |

4th Quarter | | $ | 15.96 | | | $ | 11.80 | |

3rd Quarter | | | 18.48 | | | | 12.19 | |

2nd Quarter | | | 19.33 | | | | 16.33 | |

1st Quarter | | | 19.38 | | | | 16.62 | |

We have never paid any cash dividends on our common stock, nor do we anticipate paying cash dividends on our common stock at any time in the foreseeable future. Moreover, our credit facility contains covenants limiting our ability to pay cash dividends. For a discussion of these limitations, see "Item 7 – Management's Discussion and Analysis of Financial Condition and Results of Operations - Liquidity and Capital Resources."

We did not repurchase any of our equity securities during the fourth quarter of 2012. We did not issue any equity securities on an unregistered basis during 2012.

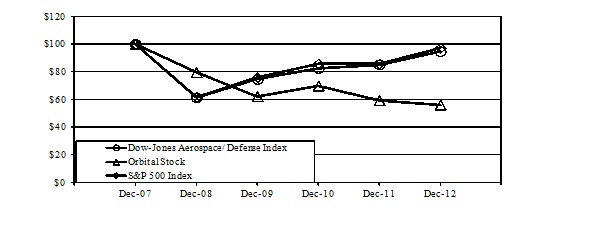

The following graph compares the yearly cumulative total return on the company's common stock against the cumulative total return on the S&P 500 Index and the Dow-Jones Aerospace/Defense Index for the five-year period commencing on December 31, 2007 and ending on December 31, 2012.

| Date | Dec-07 | Dec-08 | Dec-09 | Dec-10 | Dec-11 | Dec-12 |

| S&P 500 Index | 100.000 | 61.514 | 75.942 | 85.649 | 85.647 | 97.128 |

| Dow-Jones Aerospace/Defense Index | 100.000 | 61.340 | 74.610 | 82.495 | 85.152 | 94.729 |

| Orbital Stock $100 Value | 100.000 | 79.649 | 62.235 | 69.861 | 59.258 | 56.158 |

Item 6.

Selected Financial Data

Selected Consolidated Financial Data

The selected consolidated financial data presented below for the years ended December 31, 2012, 2011, 2010, 2009 and 2008 are derived from our audited consolidated financial statements. The selected consolidated financial data should be read in conjunction with Management's Discussion and Analysis of Financial Condition and Results of Operations and our consolidated financial statements and the related notes included elsewhere in this Form 10-K.

| | Years Ended December 31, | |

| | | 2012 | | | 2011 | | | 2010 | | | 2009 | | | 2008 | |

| | (In thousands, except per share data) | |

| Operating Data: | | | | | | | | | | | | | | | |

| Revenues | | $ | 1,436,769 | | | $ | 1,345,923 | | | $ | 1,294,577 | | | $ | 1,125,295 | | | $ | 1,168,635 | |

| Cost of revenues | | | 1,097,190 | | | | 1,074,389 | | | | 1,007,668 | | | | 890,313 | | | | 955,754 | |

| Operating expenses | | | 227,008 | | | | 191,740 | | | | 213,895 | | | | 182,689 | | | | 128,599 | |

| Income from operations | | | 112,571 | | | | 79,794 | | | | 73,014 | | | | 52,293 | | | | 84,282 | |

| Interest income and other | | | 749 | | | | 19,335 | | | | 1,848 | | | | 7,130 | | | | 6,982 | |

| Interest expense | | | (11,275 | ) | | | (11,096 | ) | | | (9,778 | ) | | | (9,039 | ) | | | (8,770 | ) |

| Debt extinguishment expense | | | (10,261 | ) | | | — | | | | — | | | | — | | | | — | |

| Investment losses, net | | | — | | | | — | | | | — | | | | (2,162 | ) | | | (17,800 | ) |

| Income from continuing operations before taxes | | | 91,784 | | | | 88,033 | | | | 65,084 | | | | 48,222 | | | | 64,694 | |

| Income tax provision | | | (30,778 | ) | | | (20,639 | ) | | | (17,615 | ) | | | (11,615 | ) | | | (22,078 | ) |

| Income from continuing operations | | | 61,006 | | | | 67,394 | | | | 47,469 | | | | 36,607 | | | | 42,616 | |

| Income from discontinued operations, net of taxes | | | — | | | | — | | | | — | | | | — | | | | 15,918 | |

| Net income | | $ | 61,006 | | | $ | 67,394 | | | $ | 47,469 | | | $ | 36,607 | | | $ | 58,534 | |

| Basic income per share: | | | | | | | | | | | | | | | | | | | | |

| Income from continuing operations | | $ | 1.03 | | | $ | 1.14 | | | $ | 0.81 | | | $ | 0.64 | | | $ | 0.71 | |

| Income from discontinued operations | | | — | | | | — | | | | — | | | | — | | | | 0.27 | |

| Net income | | | 1.03 | | | | 1.14 | | | | 0.81 | | | | 0.64 | | | | 0.98 | |

| Diluted income per share: | | | | | | | | | | | | | | | | | | | | |

| Income from continuing operations | | $ | 1.02 | | | $ | 1.13 | | | $ | 0.81 | | | $ | 0.63 | | | $ | 0.70 | |

| Income from discontinued operations | | | — | | | | — | | | | — | | | | — | | | | 0.26 | |

| Net income | | | 1.02 | | | | 1.13 | | | | 0.81 | | | | 0.63 | | | | 0.96 | |

| Basic weighted-average shares outstanding | | | 59,165 | | | | 58,531 | | | | 57,683 | | | | 56,787 | | | | 58,569 | |

| Diluted weighted-average shares outstanding | | | 59,457 | | | | 59,127 | | | | 58,335 | | | | 57,496 | | | | 59,725 | |

| Cash Flow Data: | | | | | | | | | | | | | | | | | | | | |

| Cash flow from operating activities | | $ | (7,666 | ) | | $ | 65,136 | | | $ | (479 | ) | | $ | 102,783 | | | $ | 108,823 | |

| Cash flow from investing activities | | | (26,586 | ) | | | (59,815 | ) | | | (134,452 | ) | | | (44,105 | ) | | | 17,253 | |

| Cash flow from financing activities | | | 7,357 | | | | 1,483 | | | | 14,360 | | | | (13,999 | ) | | | (33,591 | ) |

| Balance Sheet Data: | | | | | | | | | | | | | | | | | | | | |

| Cash and cash equivalents | | $ | 232,324 | | | $ | 259,219 | | | $ | 252,415 | | | $ | 372,986 | | | $ | 328,307 | |

| Net working capital | | | 522,112 | | | | 416,050 | | | | 316,617 | | | | 364,429 | | | | 349,454 | |

| Total assets | | | 1,211,454 | | | | 1,130,800 | | | | 1,062,536 | | | | 929,481 | | | | 853,895 | |

| Long-term obligations, net | | | 143,236 | | | | 131,182 | | | | 125,535 | | | | 120,274 | | | | 115,372 | |

| Stockholders' equity | | | 713,546 | | | | 643,279 | | | | 568,617 | | | | 502,460 | | | | 473,106 | |

Item 7.

Management's Discussion and Analysis of Financial Condition and Results of Operations

With the exception of historical information, the matters discussed within this Item 7 and elsewhere in this Form 10-K include forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 and Section 21E of the Securities Exchange Act of 1934, as amended, that involve risks and uncertainties, many of which are beyond our control. Readers should be cautioned that a number of important factors, including those identified above in "Item 1 – Special Note Regarding Forward-Looking Statements" and "Item 1A – Risk Factors," may affect actual results and may cause our actual results to differ materially from those anticipated or expected in any forward-looking statement. Our historical results of operations may not be indicative of our future operating results.

Overview

Introduction

Orbital Sciences Corporation develops and manufactures small- and medium-class rockets and space systems for commercial, military and civil government customers. Our primary products and services include the following:

| · | Launch Vehicles - Rockets that are used as small- and medium-class space launch vehicles that place satellites into Earth orbit and escape trajectories, interceptor and target vehicles for missile defense systems and suborbital launch vehicles that place payloads into a variety of high-altitude trajectories. |

| · | Satellites and Space Systems - Small- and medium-class satellites that are used to enable global and regional communications and broadcasting, conduct space-related scientific research, collect imagery and other remotely-sensed data about the Earth, carry out interplanetary and other deep-space exploration missions, and demonstrate new space technologies. |

| · | Advanced Space Programs - Human-rated space systems for Earth-orbit and deep-space exploration, and small- and medium-class satellites primarily used for national security space programs and to demonstrate new space technologies. |

Our general strategy is to develop and expand a core integrated business of space and launch system technologies and products, focusing on the design and manufacture of affordable rockets, satellites and other space systems in order to establish and expand positions in niche markets that have not typically been emphasized by our larger competitors. Another part of our strategy is to seek customer contracts that will fund new product development and enhancements to our existing launch vehicle and space systems product lines. As a result of our capabilities and experience in designing, developing, manufacturing and operating a broad range of small- and medium-class rockets and space systems, we believe we are well positioned to capitalize on the demand for more affordable space-technology systems in commercial satellite communications, space-based military and intelligence operations and military defense programs, and to take

advantage of government-sponsored initiatives in human space exploration, space-based scientific research and interplanetary exploration.

Business and Industry Considerations

U.S. Government Business - During 2012, 2011 and 2010, approximately 79%, 71% and 74%, respectively, of our consolidated revenues were derived from contracts with the U.S. Government and its agencies or from subcontracts with other U.S. Government contractors. Most of our U.S. Government contracts are funded incrementally on a year-to-year basis. As a result, our operations and our financial results in any period could be impacted substantially by trends in U.S. Government spending, shifting priorities in DoD (including MDA), NASA and other agency budgets, the types of contracts and payment terms mandated by the U.S. Government and changes in the Executive Branch and Congress. These factors, which are largely beyond our control, could have a significant impact on our business.

The Budget Control Act of 2011 commits the U.S. Government to significantly reduce the federal deficit over ten years through caps on discretionary spending and other measures, including automatic across-the-board spending cuts through the sequestration process, if necessary. Although Congress has delayed sequestration temporarily, without further action, it will take effect on March 1, 2013. It remains uncertain whether the contemplated sequester will take place, or if it will be delayed, modified or averted. In general, we expect that our U.S. Government customers will experience reductions in their budgets compared to recent levels. Such reductions could occur even if a compromise is reached on U.S. Government spending and sequestration is averted.

NASA continues to prioritize funding for development of U.S. commercial cargo and crew services for the International Space Station. Accordingly, funding for our COTS demonstration mission, including an Antares test launch, and our CRS contract currently remains unaffected by budget cuts. Priorities with respect to Earth and space science investigations are less clear, but we believe the NASA budget for these programs could be reduced as a result of a focus on other programs, which could have a negative impact on certain of our current programs or potential future pursuits.

The majority of Orbital's missile defense interceptor and target launch vehicle revenues comes from programs sponsored by MDA. The Budget Control Act of 2011 provides for a significant reduction in defense budgets over a ten-year period, with further reductions possible in the event of sequestration. Consequently, we expect federal spending on space and missile defense programs to be lower compared to historical levels over the next couple of years. Due to uncertainties regarding funding and federal budgets, we believe certain MDA programs could be delayed or reduced in scope.

We believe that federal budget constraints may impact national security space programs, possibly resulting in program delays, cancellations or scope reductions. DoD and the intelligence community have for some missions historically relied on large multi-mission space systems that are very expensive and require a decade or longer to be built and deployed. We believe that DOD and the intelligence community are considering ways to address their

operational requirements on more limited budgets by considering smaller and more affordable space systems that we believe are within our addressable market; however, it is uncertain whether we will achieve any competitive advantages as a result.