UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-05309

Nuveen Investment Funds, Inc.

(Exact name of registrant as specified in charter)

Nuveen Investments

333 West Wacker Drive, Chicago, IL 60606

(Address of principal executive offices) (Zip code)

Kevin J. McCarthy

Nuveen Investments

333 West Wacker Drive

Chicago, IL 60606

(Name and address of agent for service)

Registrant’s telephone number, including area code: (312) 917-7700

Date of fiscal year end: June 30

Date of reporting period: June 30, 2014

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policy making roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss.3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

| ||

| Mutual Funds |

| Nuveen Income Funds |

| Annual Report June 30, 2014 |

| Share Class / Ticker Symbol | ||||||||||||||

| Fund Name | Class A | Class C | Class R3 | Class I | ||||||||||

|

| |||||||||||||

Nuveen Core Bond Fund | FAIIX | NTIBX | — | FINIX | ||||||||||

Nuveen Core Plus Bond Fund | FAFIX | FFAIX | FFISX | FFIIX | ||||||||||

Nuveen Inflation Protected Securities Fund | FAIPX | FCIPX | FRIPX | FYIPX | ||||||||||

Nuveen Intermediate Government Bond Fund | FIGAX | FYGCX | FYGRX | FYGYX | ||||||||||

Nuveen Short Term Bond Fund | FALTX | FBSCX | NSSRX | FLTIX | ||||||||||

| ||||||||||||

| ||||||||||||

| NUVEEN INVESTMENTS TO BE ACQUIRED BY TIAA-CREF | ||||||||||||

On April 14, 2014, TIAA-CREF announced that it had entered into an agreement to acquire Nuveen Investments, the parent company of your fund’s investment adviser, Nuveen Fund Advisors, LLC (“NFAL”) and the Nuveen affiliates that act as sub-advisers to the majority of the Nuveen Funds. TIAA-CREF is a national financial services organization with approximately $569 billion in assets under management (as of March 31, 2014) and is a leading provider of retirement services in the academic, research, medical and cultural fields. Nuveen anticipates that it will operate as a separate subsidiary within TIAA-CREF’s asset management business, and that its current leadership and key investment teams will stay in place.

Your fund investment will not change as a result of Nuveen’s change of ownership. You will still own the same fund shares and the underlying value of those shares will not change as a result of the transaction. NFAL and your fund’s sub-adviser(s) will continue to manage your fund according to the same objectives and policies as before, and we do not anticipate any significant changes to your fund’s operations. Under the securities laws, the consummation of the transaction will result in the automatic termination of the investment management agreements between the funds and NFAL and the investment sub-advisory agreements between NFAL and each fund’s sub-adviser(s). The new agreements have been approved by shareholders of your fund.

The transaction is currently expected to close early in the fourth quarter of 2014, but remains subject to customary closing conditions. | ||||||||||||

Must be preceded by or accompanied by a prospectus.

NOT FDIC INSURED MAY LOSE VALUE | ||||||||||||

| ||||||||||||

of Contents

| 4 | ||||

| 5 | ||||

| 14 | ||||

| 17 | ||||

| 28 | ||||

| 29 | ||||

| 34 | ||||

| 37 | ||||

| 38 | ||||

| 89 | ||||

| 91 | ||||

| 92 | ||||

| 96 | ||||

| 106 | ||||

| 129 | ||||

| 130 | ||||

| 132 | ||||

| 142 | ||||

| Nuveen Investments | 3 |

to Shareholders

Dear Shareholders,

After significant growth in 2013, domestic and international equity markets have been less com-pelling during the first part of 2014. Concerns about deflation, political uncertainty in many places and the potential for more fragile economies to impact other countries have produced uncertainty in the markets.

Europe is beginning to emerge slowly from the recession in mid-2013, with improved GDP and employment trends in some countries. However, Japan’s deflationary headwinds have resur-faced; and China shows signs of slowing from credit distress combined with declines in manufacturing and exports. Most recently, tensions between Russia and Ukraine may continue to hold back stocks and support government bonds in the near term.

Despite these headwinds, there are some encouraging signs of forward momentum in the mar-kets. In the U.S., the news is more positive with financial risks slowly receding, positive GDP trends, downward trending unemployment and stronger household finances and corporate spending.

It is in such changeable markets that professional investment management is most important. Investment teams who have experienced challenging markets in the past understand how their asset class can behave in rapidly changing times. Remaining committed to their investment disciplines during these times is a critical component to achieving long-term success. In fact, many strong investment track records are established during challenging periods because experienced investment teams understand that volatile markets place a premium on companies and investment ideas that can weather the short-term volatility. By maintaining appropriate time horizons, diversification and relying on practiced investment teams, we believe that investors can achieve their long-term investment objectives.

As always, I encourage you to communicate with your financial consultant if you have any ques-tions about your investment in a Nuveen Fund. On behalf of the other members of the Nuveen Fund Board, we look forward to continuing to earn your trust in the months and years ahead.

Sincerely,

William J. Schneider

Chairman of the Board

August 25, 2014

| 4 | Nuveen Investments |

Comments

Nuveen Core Bond Fund

Nuveen Core Plus Bond Fund

Nuveen Inflation Protected Securities Fund

Nuveen Intermediate Government Bond Fund

Nuveen Short Term Bond Fund

These Funds feature portfolio management by Nuveen Asset Management, LLC, an affiliate of Nuveen Investments, Inc. In this report, the various portfolio management teams for the Funds discuss economic and fixed income market conditions, key investment strategies and the Funds’ performance for the twelve-month reporting period ended June 30, 2014. These management teams include:

Nuveen Core Bond Fund

Wan-Chong Kung, CFA, has managed the Fund since 2002 and Jeffrey J. Ebert since 2000. Chris J. Neuharth, CFA, joined the Fund as a co-portfolio manager in 2012.

Effective January 10, 2014, the Fund’s investment policies were amended to allow for the investment of up to 20% of its net assets in municipal securities.

Nuveen Core Plus Bond Fund

Chris J. Neuharth, CFA, has managed the Fund since 2006. Timothy A. Palmer, CFA, Wan-Chong Kung, CFA, and Jeffrey J. Ebert have been part of the management team for the Fund since 2003, 2001, and 2005, respectively.

Effective January 10, 2014, the Fund’s investment policies were amended to allow for the investment of up to 20% of its net assets in municipal securities.

Nuveen Inflation Protected Securities Fund

Wan-Chong Kung, CFA, has managed the Fund since its inception in 2004 and Chad W. Kemper joined the Fund as a co-portfolio manager in 2010.

Nuveen Intermediate Government Bond Fund

Wan-Chong Kung, CFA, has managed the Fund since 2002. Chris J. Neuharth, CFA, and Jason J. O’Brien, CFA, have been on the Fund’s management team since 2009.

Nuveen Short Term Bond Fund

Chris J. Neuharth, CFA, has been a co-portfolio manager of the Fund since 2004. Peter L. Agrimson, CFA, joined the Fund as a co-portfolio manager in 2011.

Certain statements in this report are forward-looking statements. Discussions of specific investments are for illustration only and are not intended as recommendations of individual investments. The forward-looking statements and other views expressed herein are those of the portfolio managers as of the date of this report. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements and the views expressed herein are subject to change at any time, due to numerous market and other factors. The Funds disclaim any obligation to update publicly or revise any forward-looking statements or views expressed herein.

Ratings shown are the highest rating given by one of the following national rating agencies: Standard & Poor’s (S&P), Moody’s Investors Service, Inc. (Moody’s) or Fitch, Inc. (Fitch). Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below investment grade ratings. Certain bonds backed by U.S. Government or agency securities are regarded as having an implied rating equal to the rating of such securities. Holdings designated N/R are not rated by these national rating agencies.

| Nuveen Investments | 5 |

Portfolio Managers’ Comments (continued)

What factors affected the U.S. economy and fixed income markets during the twelve-month reporting period ended June 30, 2014?

During this reporting period, the U.S. economy continued its bumpy advance toward recovery from recession. The Federal Reserve (Fed) maintained efforts to bolster growth and promote progress toward its mandates of maximum employment and price stability by holding the benchmark fed funds rate at the record low level of zero to 0.25% that it established in December 2008. Based on its view that the underlying strength in the broader economy was enough to support ongoing improvement in the labor market, the Fed began to reduce or taper, its monthly asset purchases in $10 billion increments over the course of five consecutive meetings (December 2013 through June 2014). As of July 2014, the Fed’s monthly purchases comprise $15 billion in mortgage-backed securities (versus the original $40 billion per month) and $20 billion in longer-term Treasury securities (versus $45 billion). Following its June 2014 meeting (subsequent to the close of this reporting period), the Fed reiterated that it would continue to look at a wide range of factors, including labor market conditions, indicators of inflationary pressures and readings on financial developments, in determining future actions, saying that it would likely maintain the current target range for the fed funds rate for a considerable time after the asset purchase program ends, especially if projected inflation continues to run below the Fed’s 2% longer-run goal.

In the second quarter of 2014, the U.S. economy, as measured by the U.S. gross domestic product (GDP), grew 4%. In the previous quarter, GDP contracted at an annualized rate of 2.1%, the economy’s weakest quarter since the recession officially ended in June 2009. The decline during this period was attributed in part to the severe weather of the past winter, which deterred consumer spending and disrupted construction, production and shipping. The Consumer Price Index (CPI) rose 2.1% year-over-year as of June 2014, while the core CPI (which excludes food and energy) increased 1.9% during the same period, in line with the Fed’s unofficial longer-term objective of 2.0% for this inflation measure. As of June 2014, the national unemployment rate was 6.2%, down from the 7.3% reported in July 2013, but still higher than levels that would provide consistent support for optimal GDP growth. The 113,000 net new jobs added in May 2014 meant that the economy finally had regained all of the 8.7 million jobs lost during the recent recession. The housing market continued to post gains, as the average home price in the S&P/Case-Shiller Index of 20 major metropolitan areas rose 9.3% for the twelve months ended May 2014 (most recent data available at the time this report was prepared).

Several events touched off increased volatility in the financial markets. First, in May 2013, then-Fed Chairman Ben Bernanke’s remarks about tapering the Fed’s asset purchase program triggered widespread uncertainty about the next step for the Fed’s quantitative easing program and its impact on the markets as well as the overall economy. This uncertainty was compounded by headline credit stories involving Detroit’s bankruptcy filing in July 2013, the largest municipal bankruptcy in history and the disappointing news that continued to come out of Puerto Rico, where a struggling economy and years of deficit spending and borrowing led to multiple downgrades on the commonwealth’s bonds. Meanwhile, political debate over federal spending continued, as Congress failed to reach an agreement on the federal budget for fiscal 2014. On October 1, 2013, the start date for Fiscal 2014, the federal government shut down for 16 days until an interim appropriations bill was signed into law. (Consensus on a $1.1 trillion federal spending bill was ultimately reached in January 2014, and in February 2014, members of Congress agreed to suspend the $16.7 trillion debt ceiling until March 2015.)

During the reporting period, fixed income spread sectors produced favorable results as investors worked through a high degree of uncertainty surrounding Fed monetary policy, uneven economic growth and the direction of interest rates. At the beginning of the reporting period, fixed income markets were stressed by the Fed’s discussions surrounding the tapering of its monthly security purchases as a step toward slowly normalizing U.S. monetary policy. The uncertainty roiled fixed income investors, leading to increased risk aversion and significant investor flows out of the bond market, which resulted in sharply higher interest rates, declines in risk assets and economic stress among emerging markets (EM). For calendar year 2013, investors withdrew more money out of bond funds than they put in for the first time in nearly a decade. After months of “taper talk,” the Fed finally made it official in December, announcing it would begin reducing asset purchases by $10 billion a month starting in January 2014. Policymakers cited improving economic numbers, particularly lower unemployment figures, as the impetus behind the move. At the same time, the Central Bank calmed market fears by reiterating that tapering did not equate to tightening, making a clear commitment to keep short-term interest rates at their current very low levels until at least 2015.

| 6 | Nuveen Investments |

Fixed income markets showed stabilization as 2014 got under way, even as concerns were raised about economic slowdowns in the U.S. due mostly to weather related issues and in China due to policy shifts to slow the country’s credit growth. Demand for domestic fixed income assets resumed in part due to geopolitical concerns stemming from Russia’s military action in Ukraine and concerns about emerging market growth and stability. The second half of the reporting period largely saw improvements in fundamental and market conditions as investor inflows continued into fixed income markets, yields were generally lower and spreads tightened for risk assets. Markets were further supported by actions taken by policymakers around the globe including various emerging market countries, the Chinese government and the European Central Bank (ECB). The period ended with U.S. economic growth rebounding nicely from its extremely weak first quarter as employment numbers steadily improved, consumer spending picked up and manufacturing increased. With the backdrop of improved U.S. data and reduced policy uncertainty, fixed income markets ended the fiscal year with market volatility declining to historically low levels, prompting some concern from market analysts and policymakers who believed that investors may be growing overly complacent.

Global rates moved lower and yield curves flattened across developed markets against the backdrop of moderate economic growth, accommodative monetary policy and subdued inflation. German rates moved toward historic lows during the period, in some cases reaching fifteen-year lows in spread versus the U.S., while European sovereign bond spreads moved to their lowest post-crisis rates. European investment grade credit marginally outperformed U.S. corporates due to the ECB’s actions and investor demand. In Japan, the market awaited additional structural reforms from President Abe’s government. The Bank of Japan provided no additional stimulus despite the drag from its new sales taxes that went into effect in April; however, the country’s investment fund announced increased allocation to equities and foreign assets. New Zealand and Brazil bucked the trend of looser monetary policy and tightened during the reporting period.

After a difficult start during this reporting period, EM debt ended up posting strong results. Domestic political friction in countries such as Turkey and Venezuela provided local market headline risk, but improved global risk appetite and attractive relative valuations later in the period supported the EM sector. Across these markets, rates generally fell based on reduced inflationary pressures, better external demand and traction on tightening policies implemented last year and in early 2014. Export growth improved across these markets with global purchasing managers indexes turning up marginally. A new government in India brought hope for structural reform, while economic data and policy actions in China indicated stabilization. EM domestic conditions were further underpinned by the ECB’s accommodation, the Fed’s steady hand and renewed positive investor inflows.

Currency performance was mixed with the U.S. dollar giving back some gains amid the Fed’s continued dovish stance. The euro remained stubbornly strong, agitating policymakers. Within the developed markets, the New Zealand dollar and British pound were the strongest performing currencies, while the Japanese yen and Canadian dollar lagged. The best performing EM currencies included the Korean won and the Polish zloty, while the weakest currencies were the Indonesian rupiah and the Chilean peso.

How did the Funds perform during the twelve-month reporting period ended June 30, 2014?

The tables in the Fund Performance and Expense Ratios section of this report provide total return performance information for the one-year, five-year, ten-year and/or since inception periods ended June 30, 2014. Each Fund’s Class A Share total returns at net asset value (NAV) are compared with the performance of the appropriate Barclays Index and Lipper classification average.

What strategies were used to manage the Funds during the twelve-month reporting period and how did these strategies influence performance?

All of the Funds continued to employ the same fundamental investment strategies and tactics used previously, although implementation of those strategies depended on the individual characteristics of the portfolios, as well as market conditions. The Funds’ management teams use a highly collaborative, research-driven approach that we believe offers the best opportunity to achieve consistent, superior long-term performance on a risk-adjusted basis across the full range of market environments. During the reporting period, the Funds were generally positioned for an environment of continued moderate economic growth and improving financial conditions, a posture we remained committed to during the period. Nonetheless, during the period we made smaller scaled

| Nuveen Investments | 7 |

Portfolio Managers’ Comments (continued)

shifts on an ongoing basis that were geared toward improving each Fund’s profile in response to changing conditions and valuations. These strategic moves are discussed in more detail within each Fund’s section of this report.

Nuveen Core Bond Fund

The Fund’s Class A Shares at NAV outperformed the Barclays Aggregate Bond Index and the Lipper Core Bond Classification Average for the twelve-month reporting period. Virtually all of the Fund’s strategic investment themes were beneficial during the reporting period, helping it to outpace both of these benchmarks. Our sector strategy contributed the most toward its relative performance as we experienced continued success from our focus on underweighting government securities such as Treasuries and agencies and broadly overweighting various spread sectors including investment grade corporates and non-government securitized securities. This strategy added value as excess returns over Treasuries were positive for all major market segments during the reporting period. The most significant driver of the Fund’s results was its overweight position and security selection in the investment grade corporate sector, as spreads between corporates and Treasuries generally tightened during the reporting period. The Fund’s investment grade corporate bond exposure was higher than the benchmark’s corporate weight during the reporting period. Security selection within the corporate market was also broadly successful. We significantly emphasized financials, which proved beneficial given the strong performance of these securities. The yield spread between financials and Treasuries is now tighter than industrials for the first time since before the financial crisis began due to lower overall risk in the global financial system, coupled with higher capital levels and improving asset quality at the banks. Also, Fund results were aided by our emphasis on BBB-rated industrials throughout the reporting period. Our downward bias in credit quality among industrials proved beneficial as lower rated investment grade securities outperformed higher rated investment grade securities during this reporting period.

To a lesser degree, the Fund’s performance was also enhanced by exposure to the various non-government securitized sectors, including commercial mortgage-backed securities (CMBS) and asset-backed securities (ABS). Strengthening economic data resulted in higher demand for these risk assets, while credit fundamentals continued to improve for this asset class due to a recovery in commercial and residential real estate markets. The robust investor demand for CMBS outstripped supply, which was particularly constrained later in the period as portfolio lenders expanded their loan books and crowded CMBS issuers out of the market. This led to strong performance for CMBS across the capital structure.

Meanwhile, an underweight to agency MBS (issued by government agencies such as Fannie Mae, Ginnie Mae and Freddie Mac) did not have a meaningful impact on Fund results during this reporting period. The Fund’s underweight was predicated on our view that the risk/reward profile of this sector is not attractive given an approaching end to Fed purchases and our outlook for higher rates. However, the agency MBS segment continued to be supported by a lack of loan origination due to tepid prepayment activity and a slowdown in home purchase activity, while Fed purchase activity absorbed most new supply. The market was also boosted by range bound rates and low levels of implied volatility.

We also took advantage of a short term opportunity in the municipal market early in the Fund’s reporting period that benefited performance. We added to high quality, long-duration tax-exempt municipals after prices fell dramatically due to large mutual fund redemptions. Partway through the reporting period, we were able to profitably close out this tactical position when prices rebounded back to early 2013 levels. The municipal market recovered in the second half of the Fund’s reporting period, ending the reporting period with significant excess returns over Treasuries.

Given our view that short rates would rise more than long rates as the Fed normalized policy, we maintained the Fund’s more defensive positioning in terms of its interest rate sensitivity. This entailed a shorter duration stance for the Fund versus the benchmark throughout the reporting period. For the same reason, we positioned the Fund with a bias to benefit from a flatter yield curve with an overweight to longer maturity securities and a significant underweight to short/intermediate maturities. In a flattening yield curve environment, yields on shorter maturities will rise more or fall less than yields on longer maturity securities. Both the Fund’s duration and yield curve strategies proved modestly beneficial during the reporting period.

| 8 | Nuveen Investments |

While our key portfolio sector themes of emphasizing income producing sectors, underweighting Treasuries and maintaining a defensive duration bias continued to be supported by the macro environment, we made marginal changes to the Fund’s positioning based on valuations. As spreads tightened, we saw less upside in non-Treasury sectors and scaled back the Fund’s risk levels accordingly. We reduced the Fund’s exposure to investment grade credit toward the end of the reporting period as spreads continued to tighten and spread targets on certain issues were achieved. We also pared the Fund’s MBS, CMBS and ABS weightings for the same reason and used the proceeds from these sales to boost Treasury and cash holdings.

In addition, we continued to utilize various derivative instruments in the Fund during the reporting period. We used Treasury note and bond futures to manage the Fund’s duration and yield curve exposure. To decrease the duration of the Fund’s portfolio, we established short Treasury bond or Treasury note futures positions. These derivative positions detracted from performance during the reporting period. We also used interest rate swaps as part of our portfolio construction strategy to manage the Fund’s duration and overall portfolio yield curve exposure. The interest rate swap positions also detracted from performance during the reporting period.

Nuveen Core Plus Bond Fund

The Fund’s Class A Shares at NAV outperformed both the Barclays Aggregate Bond Index and the Lipper Core Bond Plus Classification Average for the twelve-month reporting period. Virtually all of the Fund’s strategic investment themes were beneficial during the reporting period, helping it to outpace both of these benchmarks. The improvement in credit spreads and the strong performance of high yield credit were two of the key drivers of the Fund’s outperformance, given its ongoing substantial weights to credit and other non-government sectors. The Fund’s positioning in high yield corporates was the largest single contributor as security selection and tactical repositioning within the segment added favorably to results. The high yield bond segment of the market far outpaced the returns of other fixed income asset classes during the reporting period.

Exposure to investment grade credit also aided returns during this reporting period, driven largely by individual credit/security selection and a focus on BBB-rated issues. The investment grade corporate sector of the market advanced over 7 % during the reporting period, according to the Barclays U.S. Corporate Investment-Grade Index. Credit selection within investment grade was strong, notably the Fund’s positioning within the financial, metals/mining, communications and energy industries. Our downward bias in credit quality proved beneficial as lower rated investment grade securities outperformed higher rated investment grade securities during the reporting period.

To a lesser degree, the Fund’s performance was also enhanced in the commercial mortgage-backed securities (CMBS) sector. Strengthening economic data resulted in higher demand for these securities, while credit fundamentals continued to improve for the CMBS asset class due to a recovery in commercial and residential real estate markets. The robust investor demand for CMBS outstripped supply, which was particularly constrained later in the reporting period as portfolio lenders expanded their loan books and crowded CMBS issuers out of the market. This led to strong performance for CMBS across the capital structure. Foreign exposure also made a small positive contribution to performance, given minimal positions within this sector for most of the reporting period.

Meanwhile, an underweight to agency MBS (mortgage-backed securities issued by government agencies such as Fannie Mae, Ginnie Mae and Freddie Mac) was a small drag on relative performance; however, we generally used this underweight to allocate to other better-performing non-government sectors. The Fund’s underweight was predicated on our view that the risk/reward profile of this sector is not attractive given an approaching end to Fed purchases and our outlook for higher rates. However, the agency MBS segment continued to be supported by a lack of loan origination due to tepid prepayment activity and a slowdown in home purchase activity, while Fed purchase activity absorbed most new supply. The market was also boosted by range bound rates and low levels of implied volatility.

Given our view that short rates would rise more than long rates as the Fed normalized policy, we maintained the Fund’s more defensive positioning in terms of its interest rate sensitivity. This entailed a shorter duration stance for the Fund versus the benchmark during the reporting period. For the same reason, we positioned the Fund with a bias to benefit from a flatter yield curve with a

| Nuveen Investments | 9 |

Portfolio Managers’ Comments (continued)

relative underweight in shorter to intermediate maturities. In a flattening yield curve environment, yields on shorter maturities will rise more or fall less than yields on longer maturity securities. The impact from the Fund’s duration and yield curve strategies was negligible during reporting period.

The Fund’s key themes continued to include our positioning in favor of credit sectors with corresponding underweights to MBS and government securities and a defensive interest rate posture. In addition, we continued to find opportunities in individual corporate issues, both newly issued and in the secondary market, which we invested in to help improve the profile of the Fund’s credit exposure. Given the strength in credit fundamentals, we have looked for relative value opportunities on a tactical level both lower in quality and down the capital structure. We retained the Fund’s industry focus on financials as well as cyclically sensitive industries within corporates. We actively managed the level and curve exposure of the Fund’s duration, while remaining defensive overall. The Fund ended the reporting period at the lower end of its interest rate exposure range and with a bias for a flatter yield curve.

During the reporting period, we also continued to utilize various derivative instruments. We used Treasury note and bond futures as part of an overall construction strategy to manage the Fund’s duration and yield curve exposure and used selected foreign bond futures to actively manage exposure to those markets. The effect of these activities detracted from performance during the reporting period. We also utilized interest rate swaps to manage portfolio duration and yield curve exposure, and these positions also detracted from performance.

We utilized foreign exchange forwards to manage the Fund’s foreign currency exposure. For example, the Fund may reduce unwanted currency exposure from the Fund’s portfolio, or may take long forward positions in select currencies in an attempt to benefit from the potential price appreciation. These positions had a positive impact on performance during the reporting period.

We utilized credit default swaps (CDX) during the period. We used CDX high yield swaps to manage exposure to the high yield segment of the market. For example, to hedge a portion of the Fund’s credit exposure to the high yield bond segment of the market, a short CDX N.A. High Yield Index swap would be acquired. The swap positions had a negative impact on performance during the period.

Nuveen Inflation Protected Securities Fund

The Fund’s Class A Shares at NAV performed in line with the Barclays U.S. TIPS Index and outperformed the Lipper Inflation-Protected Bond Funds Classification Average for the twelve-month reporting period. While inflation remained fairly subdued throughout the reporting period, levels did pick up slightly in the final months as economic growth appeared to be improving. As of June 2014, the core Consumer Price Index (CPI) increased at a rate of 1.9% over the past twelve months. Although the Fed continued its steady pull-back on asset purchases, it reaffirmed the need for continued overall accommodative monetary policies. After experiencing heavy outflows in the first half of the reporting period, which drove yields higher, the Treasury inflation protected securities (TIPS) market saw flows turn positive in the final months of the Fund’s reporting period as investors returned to the space. This backdrop resulted in rates falling and prices rising across the TIPS yield curve during the second half of the reporting period. Yields on 10-year TIPS, for example, rose from 0.48% at the beginning of the reporting period to 0.77% in late December before falling back to 0.27% by the end of the reporting period. Meanwhile, the breakeven spread (the difference between the yields of 10-year nominal Treasuries and 10-year TIPS) stayed locked in a fairly narrow range throughout the reporting period, which was likely indicative of investors’ low conviction on inflation. During the reporting period, TIPS outperformed nominal Treasury securities with the benchmark Barclays U.S. TIPS Index gaining 4.44%.

Our sector strategy contributed the most toward the Fund’s relative performance during the reporting period as we continued to experience success from our various out-of-index allocations. The most significant positive contributor was the Fund’s exposure to high yield credit. The high yield corporate sector performed exceptionally well with the backdrop of muted volatility and well-contained Treasury rates. During the reporting period, high yield spreads tightened by 155 basis points versus Treasuries on the strength of improved technicals (renewed investor inflows into the asset class and a market friendly outlook postured by the Fed) and the continued low default environment. The segment outpaced the returns of nearly all other fixed income asset classes, advancing 11.73% as measured by the Barclays High Yield Index.

| 10 | Nuveen Investments |

To a lesser extent, but still positive, the Fund benefited from its modest allocation to commercial mortgage-backed securities (CMBS) as the segment also delivered excess returns over TIPS. Strengthening economic data resulted in higher demand for CMBS, while credit fundamentals continued to improve for the asset class due to a recovery in commercial and residential real estate markets. The robust investor demand for CMBS outstripped supply, which was particularly constrained later in the reporting period as portfolio lenders expanded their loan books and crowded CMBS issuers out of the market. This led to strong performance for CMBS across the capital structure.

Although the Fund’s exposure to emerging markets (EM) debt was minimal, it still modestly benefited results during the reporting period. Emerging markets started out the reporting period underperforming, dragged down by weak currencies, capital outflows, increased geopolitical tensions and slowing growth in China and other emerging markets. However, the tide turned in the final months of the reporting period as EM credits rebounded strongly from their period of underperformance, supported by improvements in fundamentals and investor sentiment. EM debt ended up being one of the best-performing segments of the fixed income market over the reporting period, advancing 10 % in U.S. dollar terms according to Barclays Emerging Markets Index.

The Fund experienced no meaningful detractors during the reporting period. Although our tactical duration moves (which alter the Fund’s sensitivity to changing interest rates) and bias toward a shorter duration met with mixed results throughout the reporting period, these were offset by our successful yield curve positioning, particularly within the Fund’s TIPS portfolio.

With the significant underperformance of the TIPS sector in 2013, we believe reasonable value has been restored in the market. TIPS price action will likely increasingly key off expectations for Fed actions, both on its buybacks as well as the expected timing and pace of fed funds rate normalization, in the context of modestly higher inflation. We have a bias toward increasing the Fund’s TIPS exposure at higher yield levels, while still remaining underweight to TIPS versus the Barclays index. Given our view that short rates will rise more than long rates as the Fed normalizes policy, we are maintaining the Fund’s strategically short duration versus its benchmark and its positioning for a flatter yield curve by underweighting shorter maturity securities out to five years. We continue to opportunistically add to the Fund’s out-of-index exposures, particularly in high yield corporates, with a focus on issue and credit selection.

We also used Treasury note and bond futures as part of an overall portfolio construction strategy to manage the Fund’s duration and yield curve exposure. To decrease the duration of the Fund’s portfolio, we acquired short Treasury bond or Treasury note futures positions. The overall effect on performance during the reporting period was positive. We also used interest rate swaps to manage portfolio duration and yield curve exposure and these positions detracted from performance.

We utilized foreign exchange forwards to manage the Fund’s foreign currency exposure. For example, the Fund may reduce unwanted currency exposure from the Fund’s bond portfolio, or may take long forward positions in select currencies in an attempt to benefit from the potential price appreciation. The positions had a modestly positive impact on performance during the period.

Nuveen Intermediate Government Bond Fund

The Fund’s Class A Shares at NAV performed in line with the Barclays Intermediate Government Bond Index and underperformed the Lipper Intermediate U.S. Government Funds Classification Average for the twelve-month reporting period. The Fund’s results primarily benefited from our sector strategy during this reporting period, including an underweight to U.S. Treasuries and overweight positions in several securitized sectors. These securitized asset classes, which include mortgage-backed securities (MBS), commercial mortgage-backed securities (CMBS) and asset-backed securities (ABS), all produced returns in excess of intermediate maturity Treasuries over the twelve-month reporting period. The Fund’s agency MBS (mortgage-backed securities issued by government agencies such as Fannie Mae, Ginnie Mae and Freddie Mac) exposure proved most beneficial as this segment represented our greatest overweight versus the benchmark and had strong excess returns during this reporting period. The agency MBS segment continued to be supported by a lack of loan origination due to tepid prepayment activity and a slowdown in home purchase activity, while Fed purchase activity absorbed most new supply. The market was also boosted by range bound rates and low levels of implied volatility. While we had positioned some of the Fund’s MBS exposure in seasoned higher coupon paper, we had an even greater allocation to shorter maturity mortgage paper during this reporting period. Both of these sub-sectors of the MBS market performed relatively well.

| Nuveen Investments | 11 |

Portfolio Managers’ Comments (continued)

To a lesser degree, the Fund’s performance was also enhanced by overweight positions in the CMBS and ABS sectors. In the case of the CMBS sector, strengthening economic data resulted in higher demand for these risk assets, while credit fundamentals continued to improve for this asset class due to a recovery in commercial real estate markets. The robust investor demand for CMBS outstripped supply, which was particularly constrained later in the reporting period as portfolio lenders expanded their loan books and crowded CMBS issuers out of the market. This led to strong performance for CMBS across the capital structure. In terms of ABS exposure, Fund results were aided by our positions in higher quality, shorter duration paper, as investors’ search for yield drove increased demand for securities that offer a yield advantage over Treasuries and agencies. Overall, the Fund experienced no meaningful detractors during the reporting period.

Given our view that short rates would rise more than long rates as the Fed normalized policy, we maintained the Fund’s more defensive positioning in terms of its interest rate sensitivity. This entailed a shorter duration stance for the Fund versus the benchmark throughout the reporting period. We also positioned the Fund with an overweight to five- to ten-year maturities in varying degrees, and a corresponding underweight to securities at the short and long end of the yield curve. The Fund’s duration stance proved beneficial, while our yield curve strategy modestly detracted from results during the reporting period.

We made some changes to the Fund’s sector positioning during the reporting period based on valuations. As spreads tightened, we saw less upside in non-Treasury sectors and scaled back the Fund’s levels accordingly. We reduced the Fund’s exposure primarily to agency debt, plus a modest reduction in agency MBS, and used the proceeds from these sales to boost its Treasury weighting. Treasuries made up the largest percentage of the Fund’s portfolio followed by MBS at the end of the reporting period.

In addition, we used Treasury note and bond futures as part of an overall portfolio construction strategy to manage the Fund’s portfolio duration and yield curve exposure. To decrease the duration of the Fund’s portfolio, we acquired short Treasury bond or Treasury note futures positions. The overall effect on performance during the reporting period was positive.

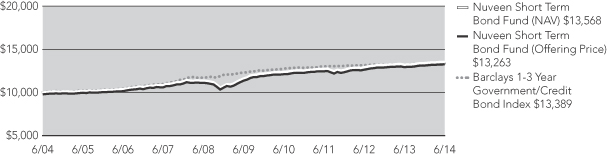

Nuveen Short Term Bond Fund

The Fund’s Class A Shares at NAV outperformed the Barclays 1-3 Year Government/Credit Bond Index and the Lipper Short Investment Grade Debt Funds Classification Average for the twelve-month reporting period. Virtually all of the Fund’s strategic investment themes were beneficial during the reporting period, helping it to outpace both of these benchmarks. Our sector allocations and security selection were broadly successful as we continued to focus on segments of the fixed income market that generate attractive levels of income. We continued to position the Fund with an emphasis on a diversified core portfolio of short duration investment grade corporate debt and securitized debt, which included consumer asset-backed securities (ABS) and commercial mortgage-backed securities (CMBS). We also maintained smaller allocations to non-agency/sub-prime mortgage-backed securities (MBS) and higher-quality (BB-rated), high yield corporates. At the same time, the Fund held a significant underweight to the Treasury and agency segments of the market.

Given our ongoing constructive views on U.S. credit fundamentals, we maintained the Fund’s overweights to both investment grade and high yield corporate bonds. These overweights were strong drivers of the Fund’s outperformance due to the favorable results of the two sectors relative to Treasuries during the reporting period. Within the corporate areas, we also successfully emphasized financials and BBB-rated industrials, both of which outperformed the broader corporate market.

Our focus on opportunities in the non-government mortgage-related sectors also paid off during the reporting period as the broad CMBS and non-agency MBS sectors continued to outperform Treasuries. More specifically, the Fund’s exposure to new security types, such as government-sponsored enterprise (GSE) risk transfer and single-family rental deals (privately held corporations with public purposes created by the U.S. Congress to reduce the cost of capital for certain borrowing sectors of the economy and in which private investors bear some of the credit risk), was particularly beneficial as these securities came to market with attractive risk premiums. Also, the Fund’s exposure to short duration residential mortgage products, both agency and non-agency, performed well as these market sectors were supported by strong housing fundamentals and investor demand for high quality short duration paper. Our more recent ABS purchases, which were mainly floating rate paper, also aided the Fund’s results while helping to reduce the interest rate sensitivity of the portfolio.

| 12 | Nuveen Investments |

Along those lines, we maintained the Fund’s more defensive positioning in terms of its interest rate sensitivity throughout this reporting period, given our view that short rates would rise as the Fed normalized policy. This entailed managing the Fund’s duration to the short end of its one- to three-year range. However, with short-term rates little changed during the reporting period, our duration strategy did not impact the Fund’s results. The Fund had no meaningful detractors to its performance during the twelve-month reporting period.

While our primary portfolio sector theme of being overweight income producing assets in the credit and securitized sectors remained intact during the reporting period, we marginally reduced the Fund’s weightings to the credit sectors as valuations continued to compress. We also continued to add to the Fund’s positions in floating rate and adjustable rate securities, primarily in the securitized sectors. These securities helped us to maintain the Fund’s duration between 1.25 and 1.50 years over the course of the reporting period.

During the reporting period, we also continued to utilize various derivative instruments. For example, we utilized Treasury note futures as part of an overall portfolio construction strategy to manage the Fund’s duration and yield curve exposure. To decrease the duration of the Fund’s portfolio, we established short Treasury bond or Treasury note futures positions. The overall effect on the Fund’s performance during the reporting period was negative. We also used interest rate swaps to manage Fund duration and yield curve exposure; these positions also detracted from performance during the reporting period.

We utilized foreign exchange forwards to manage the Fund’s foreign currency exposure. For example, the Fund may reduce unwanted currency exposure from the Fund’s bond portfolio, or may take long forward positions in select currencies in an attempt to benefit from the potential price appreciation. The positions had a modestly positive impact on performance in the period.

We utilized credit default swaps during the period to manage exposure to a broad segment of the credit markets, or to express a view on credit as part of an overall portfolio sector management strategy. For example, to increase the Fund’s credit exposure to the high yield bond segment of the market, a long CDX High Yield Index swap would be acquired. These activities contributed to performance during the period.

| Nuveen Investments | 13 |

and Dividend Information

Risk Considerations

Nuveen Core Bond Fund

Mutual fund investing involves risk; principal loss is possible. Debt or fixed income securities such as those held by the Fund, are subject to market risk, credit risk, interest rate risk, call risk, derivatives risk, dollar roll transaction risk, and income risk. As interest rates rise, bond prices fall. Foreign investments involve additional risks, including currency fluctuation, political and economic instability, lack of liquidity, and differing legal and accounting standards. Asset-backed and mortgage-backed securities are subject to additional risks such as prepayment risk, liquidity risk, default risk and adverse economic developments.

Nuveen Core Plus Bond Fund

Mutual fund investing involves risk; principal loss is possible. Debt or fixed income securities such as those held by the Fund, are subject to market risk, credit risk, interest rate risk, call risk, derivatives risk, dollar roll transaction risk, and income risk. As interest rates rise, bond prices fall. Below investment grade or high yield debt securities are subject to liquidity risk and heightened credit risk. Foreign investments involve additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. Asset-backed and mortgage-backed securities are subject to additional risks such as prepayment risk, liquidity risk, default risk and adverse economic developments.

Nuveen Inflation Protected Securities Fund

Mutual fund investing involves risk; principal loss is possible. Debt or fixed income securities such as those held by the Fund, are subject to market risk, credit risk, interest rate risk, call risk, derivatives risk, income risk, and index methodology risk. As interest rates rise, bond prices fall. Below investment grade or high yield debt securities are subject to liquidity risk and heightened credit risk. The guarantee provided by the U.S. government to treasury inflation protected securities (TIPS) relates only to the prompt payment of principal and interest and does not remove the market risks of investing in the Fund shares. Foreign investments involve additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. Asset-backed and mortgage-backed securities are subject to additional risks such as prepayment risk, liquidity risk, default risk, and adverse economic developments. The Fund’s investment in inflation protected securities has tax consequences that may result in income distributions to shareholders.

Nuveen Intermediate Government Bond Fund

Mutual fund investing involves risk; principal loss is possible. Debt or fixed income securities such as those held by the Fund, are subject to market risk, credit risk, interest rate risk, call risk, derivatives risk, dollar roll transaction risk, and income risk. As interest rates rise, bond prices fall. Asset-backed and mortgage-backed securities are subject to additional risks such as prepayment risk, liquidity risk, default risk and adverse economic developments.

Nuveen Short Term Bond Fund

Mutual fund investing involves risk; principal loss is possible. Debt or fixed income securities such as those held by the Fund, are subject to market risk, credit risk, interest rate risk, call risk, derivatives risk, and income risk. As interest rates rise, bond prices fall. Below investment grade or high yield debt securities are subject to liquidity risk and heightened credit risk. Foreign investments involve additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. Asset-backed and mortgage-backed securities are subject to additional risks such as prepayment risk, liquidity risk, default risk and adverse economic developments.

| 14 | Nuveen Investments |

Dividend Information

Each Fund seeks to pay dividends at a rate that reflects the past and projected performance of the Fund. To permit a Fund to maintain a more stable monthly dividend, the Fund may pay dividends at a rate that may be more or less than the amount of net investment income actually earned by the Fund during the period. If the Fund has cumulatively earned more than it has paid in dividends, it will hold the excess in reserve as undistributed net investment income (UNII) as part of the Fund’s NAV. Conversely, if the Fund has cumulatively paid in dividends more than it has earned, the excess will constitute negative UNII that will likewise be reflected in the Fund’s NAV. Each Fund will, over time, pay all its net investment income as dividends to shareholders.

As of June 30, 2014, the Nuveen Intermediate Government Bond Fund and Nuveen Short Term Bond Fund had a zero UNII balance while the remaining three Funds had a positive UNII balance for tax purposes. The Nuveen Core Bond Fund and Nuveen Inflation Protected Securities Fund had a positive UNII balance while the remaining three Funds had a negative UNII balance for financial reporting purposes.

In certain instances, a portion of each Fund’s monthly distributions may be paid from sources or comprised of elements other than ordinary income, including capital gains and/or a return of capital. The composition and per share amounts of each Fund’s monthly distributions for the fiscal year ended June 30, 2014, are presented in the Statement of Changes in Net Assets and Financial Highlights, respectively (for reporting purposes) and in Note 6 – Income Tax Information within the accompany Notes to Financial Statements (for income tax purposes), later in this report.

During the fiscal year ended June 30, 2014, a portion of the distributions for the Nuveen Intermediate Government Bond Fund, originally characterized as net investment income, has now been re-characterized as a return of capital, as set forth on the following table. Distributions throughout the fiscal year included the full coupon payment received from the portfolio’s investments in mortgage securities. Adjustments for the portion of the coupon payment attributable to principal paydowns resulted in a portion of the distributions being characterized as a return of capital. The final determination of the source and characteristics of all distributions made by the Fund during calendar year 2014 will be made in early 2015 and reported to shareholders on Form 1099-DIV at that time.

Nuveen Intermediate Government Bond Fund

As of June 30, 2014 | Class A Shares | Class C Shares | Class R3 Shares | Class I Shares | ||||||||||||

Inception date | 10/25/02 | 10/28/09 | 10/28/09 | 10/25/02 | ||||||||||||

Fiscal year ended June 30, 2014: | ||||||||||||||||

Per share distribution: | ||||||||||||||||

From net investment income | $ | 0.11 | $ | 0.05 | $ | 0.09 | $ | 0.14 | ||||||||

From net realized capital gains | — | — | — | — | ||||||||||||

Return of capital | 0.01 | 0.01 | 0.01 | 0.01 | ||||||||||||

Total per share distribution | $ | 0.12 | $ | 0.06 | $ | 0.10 | $ | 0.15 | ||||||||

NAV | $ | 8.81 | $ | 8.83 | $ | 8.81 | $ | 8.82 | ||||||||

Distribution rate on NAV | 2.72% | 1.36% | 2.27% | 3.40% | ||||||||||||

Average annual total returns: | ||||||||||||||||

1-Year on NAV | 1.65% | 0.98% | 1.49% | 1.90% | ||||||||||||

5-Year on NAV | 2.73% | 1.72%* | 2.21%* | 2.93% | ||||||||||||

10-Year on NAV | 3.56% | — | — | 3.74% |

| * | Represents the since inception (cumulative) total return on NAV. |

| Nuveen Investments | 15 |

THIS PAGE INTENTIONALLY LEFT BLANK

| 16 | Nuveen Investments |

and Expense Ratios

The Fund Performance and Expense Ratios for each Fund are shown within this section of the report.

Returns quoted represent past performance, which is no guarantee of future results. Current performance may be higher or lower than the performance shown. Investment returns and principal value will fluctuate so that when shares are redeemed, they may be worth more or less than their original cost. Returns without sales charges would be lower if the sales charge were included. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Returns may reflect a contractual agreement between certain Funds and the investment adviser to waive certain fees and expenses; see Notes to Financial Statements, Note 7—Management Fees and Other Transactions with Affiliates for more information. In addition, returns may reflect a voluntary expense limitation by the Funds’ investment adviser that may be modified or discontinued at any time without notice. For the most recent month-end performance visit www.nuveen.com or call (800) 257-8787.

Returns reflect differences in sales charges and expenses, which are primarily differences in distribution and service fees. Fund returns assume reinvestment of dividends and capital gains.

Comparative index and Lipper return information is provided for the Funds’ Class A Shares at net asset value (NAV) only.

The expense ratios shown reflect the Funds’ total operating expenses (before fee waivers and/or expense reimbursements, if any) as shown in the Funds’ most recent prospectus. The expense ratios include management fees and other fees and expenses.

| Nuveen Investments | 17 |

Fund Performance and Expense Ratios (continued)

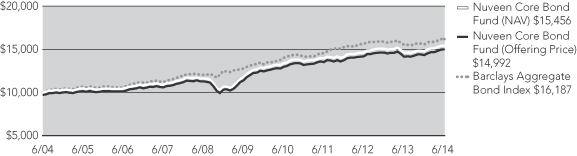

Nuveen Core Bond Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this section. Refer to the Glossary of Terms Used in this Report for definitions.

Fund Performance

Average Annual Total Returns as of June 30, 2014

| Average Annual | ||||||||||||

| 1-Year | 5-Year | 10-Year | ||||||||||

Class A Shares at NAV | 5.94% | 5.67% | 4.45% | |||||||||

Class A Shares at maximum Offering Price | 2.79% | 5.04% | 4.13% | |||||||||

Barclays Aggregate Bond Index | 4.37% | 4.85% | 4.93% | |||||||||

Lipper Core Bond Classification Average | 4.93% | 5.85% | 4.56% | |||||||||

Class I Shares | 6.21% | 5.88% | 4.62% | |||||||||

| Average Annual | ||||||||

| 1-Year | Since Inception* | |||||||

Class C Shares | 5.24% | 2.81% | ||||||

Indexes and Lipper averages are not available for direct investment.

Class A Shares have a maximum 3.00% sales charge (Offering Price). Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within eighteen months of purchase. Class C Shares have a 1% CDSC for redemptions within less than twelve months, which is not reflected in the one-year total return. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| Share Class | ||||||||||||

| Class A | Class C | Class I | ||||||||||

Gross Expense Ratios | 0.80% | 1.55% | 0.55% | |||||||||

Net Expense Ratios | 0.79% | 1.54% | 0.54% | |||||||||

The Fund’s investment adviser has contractually agreed to waive fees and/or reimburse other Fund expenses through October 31, 2014 so that total annual Fund operating expenses, after fee waivers and/or expense reimbursements and excluding acquired fund fees and expenses, do not exceed 0.78%, 1.53% and 0.53% for Class A, Class C and Class I Shares, respectively. Fee waivers and/or expense reimbursements will not be terminated prior to that time without the approval of the Fund’s Board of Directors.

| * | Since inception return for Class C Shares is from 1/18/11. |

| 18 | Nuveen Investments |

Growth of an Assumed $10,000 Investment as of June 30, 2014 – Class A Shares

The graphs do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of Fund shares.

| Nuveen Investments | 19 |

Fund Performance and Expense Ratios (continued)

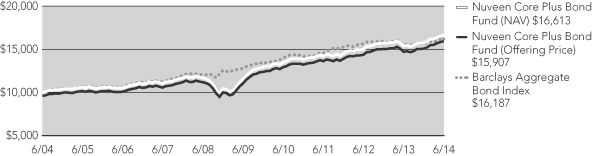

Nuveen Core Plus Bond Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this section. Refer to the Glossary of Terms Used in this Report for definitions.

Fund Performance

Average Annual Total Returns as of June 30, 2014

| Average Annual | ||||||||||||

| 1-Year | 5-Year | 10-Year | ||||||||||

Class A Shares at NAV | 8.23% | 7.69% | 5.21% | |||||||||

Class A Shares at maximum Offering Price | 3.62% | 6.75% | 4.75% | |||||||||

Barclays Aggregate Bond Index | 4.37% | 4.85% | 4.93% | |||||||||

Lipper Core Bond Plus Classification Average | 5.80% | 6.61% | 5.32% | |||||||||

Class C Shares | 7.43% | 6.89% | 4.41% | |||||||||

Class R3 Shares | 7.97% | 7.42% | 4.98% | |||||||||

Class I Shares | 8.64% | 7.98% | 5.47% | |||||||||

Indexes and Lipper averages are not available for direct investment.

Class A Shares have a maximum 4.25% sales charge (Offering Price). Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within eighteen months of purchase. Class C Shares have a 1% CDSC for redemptions within less than twelve months, which is not reflected in the one-year total return. Class R3 Shares have no sales charge and are only available for purchase by eligible retirement plans. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| Share Class | ||||||||||||||||

| Class A | Class C | Class R3 | Class I | |||||||||||||

Gross Expense Ratios | 0.81% | 1.56% | 1.06% | 0.56% | ||||||||||||

Net Expense Ratios | 0.77% | 1.52% | 1.02% | 0.52% | ||||||||||||

The Fund’s investment adviser has contractually agreed to waive fees and/or reimburse other Fund expenses through October 31, 2014 so that total annual Fund operating expenses, after fee waivers and/or expense reimbursements and excluding acquired fund fees and expenses, do not exceed 0.77%, 1.52%, 1.02% and 0.52% for Class A, Class C, Class R3 and Class I Shares, respectively. Fee waivers and/or expense reimbursements will not be terminated prior to that time without the approval of the Fund’s Board of Directors.

| 20 | Nuveen Investments |

Growth of an Assumed $10,000 Investment as of June 30, 2014 – Class A Shares

The graphs do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of Fund shares.

| Nuveen Investments | 21 |

Fund Performance and Expense Ratios (continued)

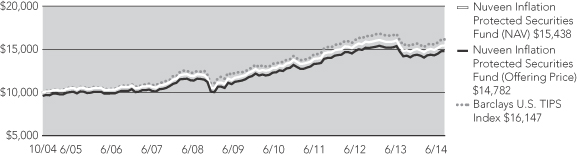

Nuveen Inflation Protected Securities Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this section. Refer to the Glossary of Terms Used in this Report for definitions.

Fund Performance

Average Annual Total Returns as of June 30, 2014

| Average Annual | ||||||||||||

| 1-Year | 5-Year | Since Inception* | ||||||||||

Class A Shares at NAV | 4.35% | 5.55% | 4.56% | |||||||||

Class A Shares at maximum Offering Price | (0.07)% | 4.63% | 4.10% | |||||||||

Barclays U.S. TIPS Index | 4.44% | 5.55% | 5.04% | |||||||||

Lipper Inflation-Protected Bond Funds Classification Average | 3.96% | 4.95% | 4.51% | |||||||||

Class C Shares | 3.76% | 4.90% | 3.83% | |||||||||

Class R3 Shares | 3.97% | 5.19% | 4.25% | |||||||||

Class I Shares | 4.82% | 5.94% | 4.86% | |||||||||

Indexes and Lipper averages are not available for direct investment.

Class A Shares have a maximum 4.25% sales charge (Offering Price). Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within eighteen months of purchase. Class C Shares have a 1% CDSC for redemptions within less than twelve months, which is not reflected in the one-year total return. Class R3 Shares have no sales charge and are only available for purchase by eligible retirement plans. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| Share Class | ||||||||||||||||

| Class A | Class C | Class R3 | Class I | |||||||||||||

Expense Ratios | 0.81% | 1.56% | 1.06% | 0.56% | ||||||||||||

| * | Since inception returns are from 10/01/04. |

| 22 | Nuveen Investments |

Growth of an Assumed $10,000 Investment as of June 30, 2014 – Class A Shares

The graphs do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of Fund shares.

| Nuveen Investments | 23 |

Fund Performance and Expense Ratios (continued)

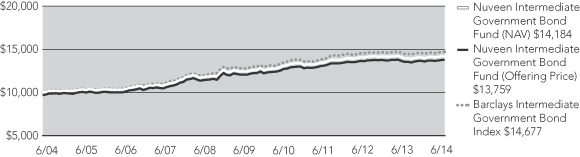

Nuveen Intermediate Government Bond Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this section. Refer to the Glossary of Terms Used in this Report for definitions.

Fund Performance

Average Annual Total Returns as of June 30, 2014

| Average Annual | ||||||||||||

| 1-Year | 5-Year | 10-Year | ||||||||||

Class A Shares at NAV | 1.65% | 2.73% | 3.56% | |||||||||

Class A Shares at maximum Offering Price | (1.38)% | 2.10% | 3.24% | |||||||||

Barclays Intermediate Government Bond Index | 1.53% | 2.83% | 3.91% | |||||||||

Lipper Intermediate U.S. Government Funds Classification Average | 2.17% | 3.02% | 3.73% | |||||||||

Class I Shares | 1.90% | 2.93% | 3.74% | |||||||||

| Average Annual | ||||||||

| 1-Year | Since Inception* | |||||||

Class C Shares | 0.98% | 1.72% | ||||||

Class R3 Shares | 1.49% | 2.21% | ||||||

Indexes and Lipper averages are not available for direct investment.

Class A Shares have a maximum 3.00% sales charge (Offering Price). Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within eighteen months of purchase. Class C Shares have a 1% CDSC for redemptions within less than twelve months, which is not reflected in the one-year total return. Class R3 Shares have no sales charge and are only available for purchase by eligible retirement plans. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| Share Class | ||||||||||||||||

| Class A | Class C | Class R3 | Class I | |||||||||||||

Gross Expense Ratios | 1.01% | 1.76% | 1.26% | 0.76% | ||||||||||||

Net Expense Ratios | 0.85% | 1.60% | 1.10% | 0.60% | ||||||||||||

The Fund’s investment adviser has contractually agreed to waive fees and/or reimburse other Fund expenses through October 31, 2014, so that total annual Fund operating expenses, after fee waivers and/or expense reimbursements and excluding acquired fund fees and expenses, do not exceed 0.85%, 1.60%, 1.10% and 0.60% for Class A, Class C, Class R3 and Class I Shares, respectively. Fee waivers and/or expense reimbursements will not be terminated prior to that time without the approval of the Fund’s Board of Directors.

| * | Since inception returns for Class C and Class R3 Shares are from 10/28/09. |

| 24 | Nuveen Investments |

Growth of an Assumed $10,000 Investment as of June 30, 2014 – Class A Shares

The graphs do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of Fund shares.

| Nuveen Investments | 25 |

Fund Performance and Expense Ratios (continued)

Nuveen Short Term Bond Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this section. Refer to the Glossary of Terms Used in this Report for definitions.

Fund Performance

Average Annual Total Returns as of June 30, 2014

| Average Annual | ||||||||||||

| 1-Year | 5-Year | 10-Year | ||||||||||

Class A Shares at NAV | 2.69% | 3.22% | 3.10% | |||||||||

Class A Shares at maximum Offering Price | 0.37% | 2.75% | 2.87% | |||||||||

Barclays 1-3 Year Government/Credit Bond Index | 1.14% | 1.73% | 2.96% | |||||||||

Lipper Short Investment Grade Debt Funds Classification Average | 1.87% | 2.85% | 2.81% | |||||||||

Class I Shares | 2.93% | 3.42% | 3.29% | |||||||||

| Average Annual | ||||||||

| 1-Year | Since Inception* | |||||||

Class C Shares | 1.89% | 1.74% | ||||||

Class R3 Shares | 2.38% | 2.67% | ||||||

Indexes and Lipper averages are not available for direct investment.

Class A Shares have a maximum 2.25% sales charge (Offering Price). Class A Share purchases of $250,000 or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within eighteen months of purchase. Class C Shares have a 1% CDSC for redemptions within less than twelve months, which is not reflected in the one-year total return. Class R3 Shares have no sales charge and are only available for purchase by eligible retirement plans. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| Share Class | ||||||||||||||||

| Class A | Class C | Class R3 | Class I | |||||||||||||

Gross Expense Ratios | 0.73% | 1.48% | 0.98% | 0.48% | ||||||||||||

Net Expense Ratios | 0.71% | 1.46% | 0.96% | 0.46% | ||||||||||||

The Fund’s investment adviser has contractually agreed to waive fees and/or reimburse other Fund expenses through October 31, 2014 so that total annual Fund operating expenses, after fee waivers and/or expense reimbursements and excluding acquired fund fees and expenses, do not exceed 0.72%, 1.47%, 0.97% and 0.47% for Class A, Class C, Class R3 and Class I Shares, respectively. Fee waivers and/or expense reimbursements will not be terminated prior to that time without the approval of the Fund’s Board of Directors.

| * | Since inception return for Class C Shares is from 10/28/09. Since inception return for Class R3 Shares is from 9/23/11. |

| 26 | Nuveen Investments |

Growth of an Assumed $10,000 Investment as of June 30, 2014 – Class A Shares

The graphs do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of Fund shares.

| Nuveen Investments | 27 |

Dividend Yield is the most recent dividend per share (annualized) divided by the offering price per share.

The SEC 30-Day Yield is a standardized measure of a Fund’s yield that accounts for the future amortization of premiums or discounts of bonds held in the Fund’s portfolio. The SEC 30-Day Yield is computed under an SEC standardized formula and is based on the maximum offer price per share. Dividend Yield may differ from the SEC 30-Day Yield because the Fund may be paying out more or less than it is earning and it may not include the effect of amortization of bond premium.

Nuveen Core Bond Fund

| Share Class | ||||||||||||

| Class A1 | Class C | Class I | ||||||||||

Dividend Yield | 2.25% | 1.57% | 2.56% | |||||||||

SEC 30-Day Yield | 2.27% | 1.62% | 2.59% | |||||||||

Nuveen Core Plus Bond Fund

| Share Class | ||||||||||||||||

| Class A1 | Class C | Class R3 | Class I | |||||||||||||

Dividend Yield | 3.57% | 2.98% | 3.51% | 3.99% | ||||||||||||

SEC 30-Day Yield | 3.32% | 2.72% | 3.21% | 3.71% | ||||||||||||

Nuveen Inflation Protected Securities Fund

| Share Class | ||||||||||||||||

| Class A1 | Class C | Class R3 | Class I | |||||||||||||

Dividend Yield | 1.02% | 0.32% | 0.80% | 1.32% | ||||||||||||

SEC 30-Day Yield | 3.10% | 2.51% | 3.02% | 3.51% | ||||||||||||

Nuveen Intermediate Government Bond Fund

| Share Class | ||||||||||||||||

| Class A1 | Class C | Class R3 | Class I | |||||||||||||

Dividend Yield | 1.06% | 0.34% | 0.82% | 1.36% | ||||||||||||

SEC 30-Day Yield | 0.94% | 0.23% | 0.72% | 1.22% | ||||||||||||

Nuveen Short Term Bond Fund

| Share Class | ||||||||||||||||

| Class A1 | Class C | Class R3 | Class I | |||||||||||||

Dividend Yield | 1.81% | 1.07% | 1.55% | 2.09% | ||||||||||||

SEC 30-Day Yield | 1.24% | 0.53% | 1.02% | 1.52% | ||||||||||||

| 1 | The SEC Yield for Class A Shares quoted in the table reflects the maximum sales load. Investors paying a reduced load because of volume discounts, investors paying no load because they qualify for one of the several exclusions from the load, and existing shareholders who previously paid a load but would like to know the SEC Yield applicable to their shares on a going-forward basis, should understand that the SEC Yield effectively applicable to them would be higher than the figure quoted in the table. |

| 28 | Nuveen Investments |

Summaries as of June 30, 2014

This data relates to the securities held in each Fund’s portfolio of investments as of the end of this reporting period. It should not be construed as a measure of performance for the Fund itself. Holdings are subject to change

Ratings shown are the highest rating given by one of the following national rating agencies: Standard & Poor’s, Moody’s Investors Service, Inc. or Fitch, Inc. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below investment grade ratings. Certain bonds backed by U.S. Government or agency securities are regarded as having an implied rating equal to the rating of such securities. Holdings designated N/R are not rated by these national rating agencies.

Refer to the Glossary of Terms Used in this Report for definitions of terms used within this section.

Nuveen Core Bond Fund

Fund Allocation

(% of net assets)

Corporate Bonds | 42.6% | |||

$1,000 Par (or similar) Institutional Preferred | 1.9% | |||

Municipal Bonds | 1.3% | |||

U.S. Government and Agency Obligations | 11.0% | |||

Asset-Backed and Mortgage-Backed Securities | 39.5% | |||

Sovereign Debt | 0.5% | |||

Investments Purchased with Collateral from Securities Lending | 14.7% | |||

Short-Term Investments | 1.8% | |||

Other Assets Less Liabilities | (13.3)% |

Industries1

(% of total corporate debt holdings)

Banks | 18.6% | |||

Oil, Gas & Consumable Fuels | 10.5% | |||

Metals & Mining | 10.2% | |||

Capital Markets | 8.3% | |||

Media | 6.9% | |||

Diversified Telecommunication Services | 6.3% | |||

Real Estate Investment Trust | 5.6% | |||

Insurance | 5.0% | |||

Health Care Providers & Services | 4.0% | |||

Energy Equipment & Services | 3.7% | |||

Tobacco | 2.3% | |||

Other Industries | 18.6% |

Portfolio Credit Quality2

(% of total long-term investments)

AAA/U.S. Guaranteed | 48.1% | |||

AA | 3.9% | |||

A | 22.2% | |||

BBB | 23.8% | |||

BB or Lower | 1.0% | |||

N/R (not rated) | 1.0% |

| 1 | Corporate debt holdings include corporate bonds (high-yield and investment grade rated), convertible bonds, and any other debt instruments issued by a corporation (or that references a corporation) held by the Fund. |

| 2 | Excluding investments in derivatives. |

| Nuveen Investments | 29 |

Holding Summaries as of June 30, 2014 (continued)

Nuveen Core Plus Bond Fund

Fund Allocation

(% of net assets)

$25 Par (or similar) Retail Preferred | 2.2% | |||

Corporate Bonds | 60.6% | |||

$1,000 Par (or similar) Institutional Preferred | 4.7% | |||

Municipal Bonds | 1.1% | |||

Asset-Backed and Mortgage-Backed Securities | 26.5% | |||

Sovereign Debt | 3.4% | |||

Investments Purchased with Collateral from Securities Lending | 11.0% | |||

Short-Term Investments | 2.2% | |||

Other Assets Less Liabilities | (11.7)% |

Industries1

(% of total corporate debt holdings)

Banks | 13.6% | |||

Oil, Gas & Consumable Fuels | 11.9% | |||

Metals & Mining | 9.3% | |||

Media | 7.5% | |||

Capital Markets | 6.2% | |||

Insurance | 5.6% | |||

Real Estate Investment Trust | 5.6% | |||

Diversified Telecommunication Services | 4.9% | |||

Energy Equipment & Services | 4.1% | |||

Chemicals | 2.8% | |||

Electric Utilities | 2.4% | |||

Wireless Telecommunication Services | 2.2% | |||

Consumer Finance | 2.1% | |||

Health Care Providers & Services | 2.0% | |||

Other Industries | 19.8% |

Portfolio Credit Quality2

(% of total long-term investments)

AAA/U.S. Guaranteed | 19.8% | |||

AA | 4.0% | |||

A | 21.5% | |||

BBB | 40.4% | |||

BB or Lower | 13.9% | |||

N/R (not rated) | 0.4% |

| 1 | Corporate debt holdings include corporate bonds (high-yield and investment grade rated), convertible bonds, and any other debt instruments issued by a corporation (or that references a corporation) held by the Fund. |

| 2 | Excluding investments in derivatives. |

| 30 | Nuveen Investments |

Nuveen Inflation Protected Securities Fund

Fund Allocation

(% of net assets)

Exchange-Traded Funds | 0.1% | |||

Convertible Preferred Securities | 0.1% | |||

$25 Par (or similar) Retail Preferred | 0.1% | |||

Corporate Bonds | 6.7% | |||

$1,000 Par (or similar) Institutional Preferred | 0.1% | |||

Municipal Bonds | 1.1% | |||

U.S. Government and Agency Obligations | 82.3% | |||

Asset-Backed and Mortgage-Backed Securities | 6.4% | |||

Investment Companies | 0.2% | |||

Sovereign Debt | 0.6% | |||