UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-05309

Nuveen Investment Funds, Inc.

(Exact name of registrant as specified in charter)

Nuveen Investments

333 West Wacker Drive, Chicago, IL 60606

(Address of principal executive offices) (Zip code)

Mark J. Czarniecki

Vice President and Secretary

333 West Wacker Drive,

Chicago, IL 60606

(Name and address of agent for service)

Registrant’s telephone number, including area code: (312) 917-7700

Date of fiscal year end: December 31

Date of reporting period: December 31, 2020

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policy making roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss.3507.

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

Mutual Funds

31 December

2020

Nuveen Equity Funds

| | | | | | | | | | |

| Fund Name | | Class A | | Class C | | Class R3 | | Class R6 | | Class I |

| Nuveen Global Infrastructure Fund | | FGIAX | | FGNCX | | FGNRX | | FGIWX | | FGIYX |

| Nuveen Global Real Estate Securities Fund | | NGJAX | | NGJCX | | — | | NGJFX | | NGJIX |

| Nuveen Real Asset Income Fund | | NRIAX | | NRICX | | — | | NRIFX | | NRIIX |

| Nuveen Real Estate Securities Fund | | FREAX | | FRLCX | | FRSSX | | FREGX | | FARCX |

As permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Funds’ annual and semi-annual shareholder reports will not be sent to you by mail unless you specifically request paper copies of the reports. Instead, the reports will be made available on the Funds’ website (www.nuveen.com), and you will be notified by mail each time a report is posted and provided with a website link to access the report.

You may elect to receive shareholder reports and other communications from the Funds electronically at any time by contacting the financial intermediary (such as a broker-dealer or bank) through which you hold your Fund shares or, if you are a direct investor, by enrolling at www.nuveen.com/e-reports.

You may elect to receive all future shareholder reports in paper free of charge at any time by contacting your financial intermediary or, if you are a direct investor, by calling 800-257-8787 and selecting option #1. Your election to receive reports in paper will apply to all funds held in your account with your financial intermediary or, if you are a direct investor, to all your directly held Nuveen Funds and any other directly held funds within the same group of related investment companies.

Annual Report

Life is Complex.

Nuveen makes things e-simple.

It only takes a minute to sign up for e-Reports. Once enrolled, you’ll receive an e-mail as soon as your Nuveen Fund information is ready. No more waiting for delivery by regular mail. Just click on the link within the e-mail to see the report and save it on your computer if you wish.

Free e-Reports right to your email!

www.investordelivery.com

If you receive your Nuveen Fund distributions and statements from your financial professional or brokerage account.

or

www.nuveen.com/client-access

If you receive your Nuveen Fund distributions and statements directly from Nuveen.

Must be preceded by or accompanied by a prospectus.

NOT FDIC INSURED MAY LOSE VALUE NO BANK GUARANTEE

Table

of Contents

3

Chair’s Letter to Shareholders

Dear Shareholders,

The rollout of COVID-19 vaccines has kindled the promise of a more normal economy in 2021. Until then, the economic shortfall is expected to be bridged by a combination of fiscal relief measures and easier financial conditions aimed at supporting individuals, businesses and state and local governments. The measures taken to date have already helped the U.S. economy make a significant, although incomplete, turnaround from the depths of a historic recession. In late December 2020, the U.S. government enacted another $900 billion in aid to individuals and businesses, extending some of the programs enacted earlier in the COVID-19 crisis, and more stimulus is anticipated. The U.S. Federal Reserve, along with other central banks around the world, have pledged to keep monetary conditions accommodative for as long as necessary.

While the markets’ longer-term outlook has brightened, we expect intermittent bouts of volatility to continue. COVID-19 cases are still alarmingly high in some regions, and recent economic indicators have shown the dampening effect of renewed restrictions on social and business activity in the latter months of 2020. The pandemic’s course can still be unpredictable, and achieving sufficient inoculation of the population depends on many variables, including logistics, public confidence, real-world efficacy and the emergence of variant virus strains. Additionally, the Biden administration’s full policy agenda and the potential for Congressional gridlock remain to be seen, which could cause investment outlooks to shift. Nevertheless, short-term market fluctuations can provide opportunities to invest in new ideas as well as upgrade existing positioning, within our goal of providing long-term value for our shareholders. For more than 120 years, the careful consideration of risk and reward has guided Nuveen’s focus on delivering long-term results to our shareholders.

The beginning of the year can be an opportune time to assess your portfolio’s resilience and readiness for what may come next. We encourage you to review your time horizon, risk tolerance and investment goals with your financial professional. On behalf of the other members of the Nuveen Fund Board, we look forward to continuing to earn your trust in the months and years ahead.

Sincerely,

Terence J. Toth

Chair of the Board

February 22, 2021

4

Portfolio Managers’ Comments

Nuveen Global Infrastructure Fund

Nuveen Global Real Estate Securities Fund

Nuveen Real Asset Income Fund

Nuveen Real Estate Securities Fund

These Funds feature portfolio management by Nuveen Asset Management, LLC, an affiliate of Nuveen Fund Advisors, LLC, the Funds’ investment adviser. For the Nuveen Global Infrastructure Fund, Jay L. Rosenberg has been a portfolio manager since its inception in 2007 and Tryg T. Sarsland has been a portfolio manager since 2012, and Jagdeep S. Ghuman joined in 2019. For the Nuveen Global Real Estate Securities Fund, Jay L. Rosenberg along with Scott C. Sedlak have been portfolio managers since its inception in 2018. Benjamin T. Kerl and Jagdeep S. Ghuman joined the Nuveen Global Real Estate Securities Fund as portfolio managers in 2019. For the Nuveen Real Asset Income Fund, Jay L. Rosenberg has been portfolio manager since the Fund’s inception in 2011. Brenda A. Langenfeld, CFA, and Tryg T. Sarsland were added as portfolio managers in 2015 and Jean C. Lin, CFA joined in 2019. For the Nuveen Real Estate Securities Fund, Jay L. Rosenberg has served as a portfolio manager since he joined the Fund’s management team in 2005, while Scott C. Sedlak and Sarah Wade joined the team as portfolio managers in 2011 and 2017, respectively.

On the following pages, the portfolio management teams for the Funds discuss the economy and financial markets, key investment strategies and the Funds’ performance for the twelve-month reporting period ended December 31, 2020.

What factors affected the U.S. economy and financial markets during the twelve-month reporting period ended December 31, 2020?

The U.S. economy rebounded more quickly than expected from the deep downturn caused by the COVID-19 crisis and containment measures, but it was not fully recovered by the year’s end. U.S. gross domestic product (GDP) grew 4.0% on an annualized basis in the fourth quarter of 2020 and 33.1% (annualized) in the third quarter, but remained down 3.5% in 2020 overall (from the 2019 annual level to the 2020 annual level) as measured by the Bureau of Economic Analysis “advance” estimate. GDP measures the value of goods and services produced by the nation’s economy less the value of the goods and services used up in production, adjusted for price changes. The economy fell into a deep recession in February 2020 due to the restrictions on business and social activity to mitigate the COVID-19 spread. In the first and second quarters of 2020, annualized GDP shrank 5% and 31.4%, respectively. Government relief programs provided significant aid to individuals and businesses as the economy began reopening in May 2020, which helped the economy bounce back strongly over the second half of the year.

Consumer spending, the largest driver of the economy, remained resilient despite the disruption caused by the health and economic crisis. Consumer spending declined significantly and unemployment rose sharply starting in March 2020. These measures rebounded markedly in the second half of the year, although the momentum slowed toward year end amid a resurgence of coronavirus infections. The Bureau of Labor Statistics said the unemployment rate rose to 6.7% in December 2020 from 3.6% in December 2019. As of December 2020, slightly more than half of the 22 million jobs lost in March and April 2020 have been recovered. The average

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell or hold a security or an investment strategy and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her advisors.

Certain statements in this report are forward-looking statements. Discussions of specific investments are for illustration only and are not intended as recommendations of individual investments. The forward-looking statements and other views expressed herein are those of the portfolio managers as of the date of this report. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements and the views expressed herein are subject to change at any time, due to numerous market and other factors. The Funds disclaim any obligation to update publicly or revise any forward-looking statements or views expressed herein.

For financial reporting purposes, the ratings disclosed are the highest rating given by one of the following national rating agencies: Standard & Poor’s (S&P), Moody’s Investors Service, Inc. (Moody’s) or Fitch, Inc. (Fitch). This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

Refer to the Glossary of Terms Used in this report for further definition of the terms used within this section.

5

Portfolio Managers’ Comments (continued)

hourly earnings rate appeared to increase, growing at an annualized rate of 5.1% in December 2020, despite the spike in unemployment. Earnings data was skewed by the concentration of job losses in lower-wage work, which effectively eliminated most of the low-wage data, resulting in an average of mostly higher numbers. The overall trend of inflation remained muted, as decreases in gasoline, apparel and transportation prices offset an increase in food prices. The Bureau of Labor Statistics said the Consumer Price Index (CPI) increased 1.4% over the twelve-month reporting period ended December 31, 2020 before seasonal adjustment.

Prior to the COVID-19 crisis recession, the U.S. Federal Reserve (the Fed) had reduced its benchmark interest rate to support the economy’s slowing growth. The Fed also stopped shrinking its bond portfolio sooner than scheduled and began buying short-term Treasury bills to help money markets operate smoothly and maintain short-term borrowing rates at low levels. As the health and economic crisis deepened, the Fed enacted an array of emergency measures in March 2020 to stabilize the financial system and support the markets, including cutting its main interest rate to near zero, offering lending programs to aid small and large companies and allowing unlimited bond purchases, known as quantitative easing. In August 2020, the Fed announced a change in inflation policy to average inflation targeting. Under this regime, the Fed will tolerate the inflation rate temporarily overshooting the target rate to offset periods of below-target inflation, so that inflation averages a 2% rate over time. Fed officials remained cautious, acknowledging the economy’s improvement but concerned about near-term weakness, and left policy unchanged over the remainder of their meetings in 2020.

In March and April 2020, the U.S. government approved three aid packages. These included $2 trillion allocated across direct payments to Americans, an expansion of unemployment insurance, loans to large and small businesses, funding to hospitals and health agencies and support to state and local governments, and more than $100 billion in funding to health agencies and employers offering paid leave. In December 2020, the government enacted a $900 billion relief package extending some of these programs. With Joe Biden winning the U.S. presidential election in November 2020, more fiscal stimulus is anticipated in 2021.

The COVID-19 crisis rapidly dwarfed all other market concerns starting in late February 2020. Equity and commodity markets sold off and safe-haven assets rallied in March 2020 as China, other countries and then the United States initiated quarantines, restricted travel and shuttered factories and businesses. The potential economic shock was particularly difficult to assess, which amplified market volatility. An ill-timed oil price war between the Organization of the Petroleum Exporting Countries (OPEC) and non-OPEC member Russia, which caused oil prices to plunge in March 2020, exacerbated the market sell-off. At year end, the announcement of high efficacy rates in several COVID-19 vaccine trials, followed by regulatory authorizations and public vaccination drives across Western countries, improved the outlook for 2021 and led to risk-on sentiment in the markets.

Geopolitical uncertainty remained elevated during 2020 in anticipation of the U.S. presidential election in November 2020 and the Brexit transition period set to expire in December 2020. Political risks eased somewhat toward the end of the reporting period, as markets ultimately viewed a Biden administration positively and the European Union (EU) and United Kingdom (U.K.) finalized a trade deal in the final days of the transition period. Although China and the U.S. signed a “phase one” trade deal in January 2020, tensions continued to flare over other trade and technology/security issues, Hong Kong’s sovereignty and the management of the COVID-19 crisis.

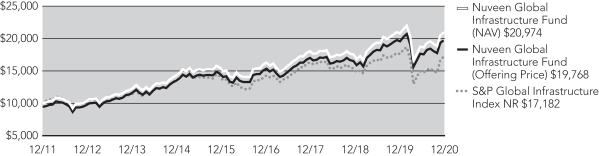

Nuveen Global Infrastructure Fund

How did the Fund perform during the twelve-month reporting period ended December 31, 2020?

The table in the Performance Overview and Holding Summaries section of this report provides total returns at net asset value (NAV) for the period ended December 31, 2020. The Fund’s total returns on NAV are compared with the performance of a corresponding market index.

The Fund’s Class A Shares at NAV outperformed the S&P Global Infrastructure Index NR (Net Return) but underperformed the Lipper classification average during the twelve-month reporting period.

What strategies were used to manage the Fund during the reporting period and how did these strategies influence performance?

The Fund seeks to provide long-term growth of capital and income by investing primarily in equity securities issued by U.S. and non-U.S. companies that typically derive the majority of their value from owned or operated infrastructure assets. During the reporting period, our strategy for managing the Fund remained consistent as we focused on buying global infrastructure companies that

6

own and operate long life assets that have visible cash flows, strong balance sheets, manageable amounts of leverage and inelastic demand characteristics. We believe these types of companies will have ongoing access to capital and the best chances for producing sustainable and growing cash flow. The Fund is structured using a number of core infrastructure companies that we believe should provide long-term outperformance versus the market, combined with more opportunistic holdings that we believe are undervalued by the market in the short term. We have exposure around the globe to a mixture of holdings that represent significant value, as well as positions in companies that may prove to be more stable in a slowly growing global economy.

During the first three months of the reporting period, the health and financial crisis brought about by the COVID-19 crisis clearly impacted markets and caused a sharp sell-off in the global infrastructure sector. As COVID-19 spread, investor confidence was shattered after global output collapsed due to wide swaths of the economy being shut down and entire countries finding themselves locked down in an attempt to blunt the spread of the infection. Within the infrastructure universe, we saw significant divergences in returns between businesses that were most impacted by economic closures and social distancing and those whose businesses were less sensitive to the crisis.

Following the initial crisis, markets shifted sharply again as a result of the massive amounts of global monetary and fiscal stimulus coupled with a significant improvement on the health front as economies that had been affected by the COVID-19 crisis the earliest made headway in its containment. As a result, investor sentiment began to improve dramatically and markets looked forward to recovery as economies started to reopen. However, while broader equity markets showed strength, especially large technology companies, the infrastructure segment remained quite bifurcated because some business models continued to be much more negatively impacted by the ongoing health crisis. Although the unprecedented amounts of global monetary and fiscal certainly benefited the infrastructure group, the most challenged sectors continued to languish in the absence of a marked improvement on the health front and the corresponding lack of global mobility and utilization of the assets.

In the final two months of the reporting period, the infrastructure segment rebounded following favorable vaccine announcements from Pfizer and Moderna, which immediately changed the investment landscape and reversed nearly all the trends within infrastructure that had developed over the past ten months. All of the sectors that had previously been most negatively impacted by the COVID-19 crisis, economic closures and lack of global mobility rallied significantly as investors anticipated a worldwide return to more normalized economic activity in 2021, given the efficacy of the vaccines. However, despite the rally in the infrastructure sector in the final months of the reporting period, it was not enough to make up for the segment’s earlier shortfall. During the reporting period, the infrastructure segment returned -5.76%, as measured by the S&P Global Infrastructure Index NR, significantly underperforming the broader domestic equity market, which returned 18.40%, as measured by the S&P 500® Index, and global equities, which returned 16.25%, as measured by the MSCI All Country World Index. As a result of these dynamics, the various sectors within infrastructure posted quite divergent returns during the reporting period. The Fund’s out-of-index sector exposures in renewable energy, waste and technology infrastructure showed strong gains. More defensive areas like electric utilities and water utilities also posted relatively solid advances. However, sectors with more exposure to the economic cycle, such as pipelines, airports and seaports, sold off sharply.

From a broad perspective, the Fund benefited on a relative basis versus its benchmark from a tilt toward less economically sensitive areas of infrastructure. This shift led to significant outperformance for the Fund relative to the benchmark during the market sell-off in March 2020, and for the reporting period as a whole. Early in the COVID-19 crisis, we believed it would be critically important to reduce exposures to businesses most impacted, while overweighting businesses that would suffer the least. This positioning was successful during the extreme market turmoil. Specifically, we made notable reductions in the pipeline, airport and rail sectors, which funded substantial increases in exposure to technology infrastructure, regulated electric utilities and water utilities. However this same defensive bias, which was further increased during the sell-off, led to some relative underperformance during a portion of the remaining reporting period after many of the most negatively impacted groups recovered sharply.

While the Fund significantly outperformed its benchmark during the reporting period, it still produced negative absolute returns. Compared to the index, the Fund experienced its strongest relative results in the renewable energy, technology infrastructure, electric transmission and waste sectors. The Fund had relatively few noteworthy laggards versus the benchmark during the reporting period, although the airport segment did detract. The Fund underperformed the Lipper average because some of its peers have more exposure to the technology infrastructure sector.

7

Portfolio Managers’ Comments (continued)

The Fund experienced its most favorable relative results in the renewable energy sector, a group that has no exposure in the benchmark. Pure-play renewable companies continued to benefit as the power generation mix moves away from fossil fuels and toward more sustainable sources. Regulators and politicians continued to support capital expenditures to provide the grid with electricity from wind, solar and other renewable, more carbon friendly options. These companies earn a regulated return on that capital expenditure and have a long runway for continued growth. They have also been supported by technicals in the marketplace as investor capital, particularly from institutions, has been supporting the stock prices. Late in fall 2020, shares of these companies advanced strongly after the Biden campaign gained ground and Wall Street began to price in a possible Democratic sweep of the presidency and Senate. That momentum continued into the end of the reporting period following the election results, while all of the fundamental and technical tailwinds for the sector remained firmly in place.

Technology infrastructure exhibited the second strongest area of performance for the Fund during the reporting period. The sector, which primarily consists of cellular tower and data center companies, also has no representation in the benchmark. Tech infrastructure is arguably the sector least affected by the COVID-19 crisis because social distancing measures don’t impact these companies, given that they earn revenue by leasing space to equipment rather than people. Additionally, demand for their assets held steady throughout the reporting period and may have actually increased as people were forced to work and attend school from home. Leading up to the COVID-19 vaccine announcements, tech infrastructure companies had performed very strongly in 2020 as investors looked for defensive areas that had attractive growth prospects. After the announcements, however, this segment served as a source of funds as investors rebalanced their portfolios to get more exposure to value, which had been largely ignored. That said, the Fund benefited from its broad exposure to this sector throughout the reporting period as its holdings posted a collective gain of 22% over the reporting period, led by positions in Cellnex Telecom S.A. and Equinix Inc.

The Fund’s security selection and overweight in the electric transmission sector also contributed favorably to results versus the benchmark. This more defensive area offered substantial insulation from the massive declines experienced by some of the more economically sensitive areas within the Fund’s opportunity set during the March 2020 sell-off. While electricity demand certainly fell among industrial and commercial users due to stay-at-home orders during the COVID-19 crisis, increases in residential demand offset that disruption to some extent. Therefore, although the transmission sector was not able to completely avoid stock price declines during the sell-off, they were much less severe. The Fund’s performance also benefited from our greater diversification within the sector.

The Fund’s waste sector exposure also contributed, which is another area that is not represented in its benchmark. Waste is a group that is more exposed to broader economic activity, especially construction, which has improved dramatically after the relaxation of stay-at-home orders and broad economic closures worldwide. The group as a whole has benefited from these reopening dynamics and all but one of our holdings in the sector posted solid double-digit returns over the reporting period. The Fund’s positions in Waste Management Inc. and French waste company SUEZ SA were standout performers. During the reporting period, Waste Management’s shares advanced strongly after the company finally got approval from the Department of Justice to acquire Advanced Disposal Services following a lengthy delay and some required dispositions. Because of market conditions at the time, Advanced Disposal agreed to a lower purchase price than the previous agreement. Also due to the delay, Waste Management was able to buy back bonds it had previously issued for the acquisition and refinance them at a more attractive rate. In addition, investors were encouraged that the company was able to control costs and actually slightly expand margins during the reporting period, despite the drop in revenues from the COVID-19 crisis. In the case of SUEZ, shares advanced strongly after another French waste and water company, Veolia, made bid for a significant portion of its shares and subsequently raised its offer. Investors were enthused about the potential merger of the two companies. Because the benchmark has no exposure to these two names, their strong returns resulted in significant outperformance.

The Fund’s main detractor resulted from its underweight position in the airport sector. The Fund began the reporting period with an underweight, which was increased further as the COVID-19 crisis burst on the scene and fundamentals in the segment were quite challenged. The segment suffered significantly earlier in 2020 due to the COVID-19 crisis lockdowns, which caused a sharp sell-off among airport stocks. However, as the reporting period progressed, investors began to look for valuation opportunities in areas like airports that had been beaten up earlier in the reporting period. Optimism began to increase regarding the COVID-19 health situation, especially outside the U.S., and passenger traffic showed a slight improvement. However, it was the vaccine announcements in early November 2020 that were the major impetus for a sharp turnaround in the sector.

8

Before the COVID-19 vaccine announcements, we had been modestly rebalancing the Fund back into various areas that had suffered the most during the reporting period, narrowing some of the portfolio’s wide and persistent underweights. However, the COVID-19 vaccine news accelerated these changes as it became clear the worst case scenario was eliminated and vaccine efficacy was better than even the most optimistic expectations. We reduced the Fund’s largest relative overweight in technology infrastructure, and made an even greater reduction to electric utilities. Geographically, we continued to keep the Fund’s portfolio well diversified with broad exposure to well over 20 different countries. Spreading the Fund’s holdings out over many geographies and regulatory jurisdictions to mitigate risk.

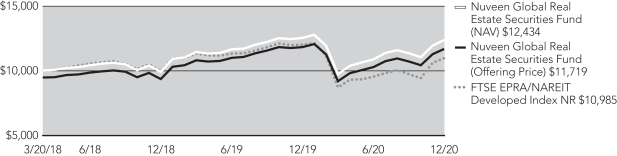

Nuveen Global Real Estate Securities Fund

How did the Fund perform during the twelve-month reporting period ended December 31, 2020?

The table in the Performance Overview and Holding Summaries section of this report provides total returns at net asset value (NAV) for the period ended December 31, 2020. The Fund’s total returns on NAV are compared with the performance of a corresponding market index.

The Fund’s Class A Shares at NAV outperformed the FTSE EPRA/Nareit Developed Index NR (Net Return) and the Lipper classification average during the twelve-month reporting period.

What strategies were used to manage the Fund during the reporting period and how did these strategies influence performance?

The Fund seeks long-term capital appreciation with a secondary objective to provide current income. The Fund invests in income producing equities of companies engaged in the real estate industry. Applying a fundamentally based, relative value process, the investment team diversifies across geographies and sectors of listed global commercial real estate by investing at least 80% of the sum of its net assets and the amount of any borrowings for investment purposes in common stocks, preferred securities and other equity securities issued by U.S. and non-U.S. companies in the real estate industry, including real estate investment trusts (REITs) and similar REIT-like entities. REITs are types of real estate companies that pool investors’ funds for investment in real estate or in real estate related loans or other interests. REITs in the U.S. are generally not taxed on income distributed to shareholders as long as they meet certain requirements of the Internal Revenue Code. Foreign REITs and REIT-like entities are organized outside of the U.S. and generally have operations and receive tax treatment in their respective countries similar to that of U.S. REITs, though some countries may have REIT-like structures that are significantly different from U.S. REITs or may not have adopted a REIT-like structure at all. Equity securities in which the Fund may invest may be of any market capitalization, including small- and mid-capitalization companies.

The Fund may invest at least 40% of its net assets in securities of non-U.S. issuers and, in any case, will invest at least 30% of its net assets in such issuers. The Fund will invest in securities of issuers in at least three different countries and may invest up to 25% of its total assets in securities of emerging market issuers.

The Fund may utilize derivatives, including options, futures contracts, options on futures contracts, and forward foreign currency exchange contracts. The Fund may use these derivatives to manage market or business risk, enhance the Fund’s return, or hedge against adverse movements in currency exchange rates.

During the first three months of the reporting period, the health and financial crisis brought about by the COVID-19 crisis clearly had a devastating impact on financial markets. Although many defensive areas of the markets outperformed broader equities, the traditionally defensive global real estate group did not. The sector experienced a massive sell-off in March 2020 that exceeded even the swiftness of the broader equity market declines. Many global REITs suffered disproportionately at the hands of the COVID-19 crisis because most property types are comprised of physical assets that are meant to facilitate the gathering of people. However, over half of the world’s population was either mandated or strongly encouraged to do precisely the opposite. As a result, some tenants were not able to pay rent to property owners, which affected profitability and cash flow for REITs.

Following the initial crisis, markets shifted sharply again as a result of the massive amounts of global monetary and fiscal stimulus coupled with a significant improvement on the health front as economies that had been affected by the virus the earliest made headway in its containment. As a result, investor sentiment began to improve dramatically and markets looked forward to recovery as

9

Portfolio Managers’ Comments (continued)

economies started to reopen. However, while broader equity markets showed strength, especially large technology-focused companies, global real estate continued to underperform because the segment will likely take longer to recover from the lingering effects of the shutdowns related to the health crisis. The slow pace of reopenings and the difficulty countries had in containing the virus continued to be overhangs for this segment. Retail shopping centers, hotels, restaurants and theaters saw improvements in activity and sales, but at a gradual and uneven pace. The good news, however, was that fundamentals remained solid for several property types that didn’t experience a drop off in demand like data centers, cellular tower companies, industrial facilities and self-storage.

In the final two months of the reporting period, the global real estate segment rebounded following favorable COVID-19 vaccine announcements from several companies, which immediately changed the investment landscape. Investors rotated back into areas of the equity market that had underperformed for most of the reporting period and stand to benefit more from an anticipated return to stronger economic growth in the second half of 2021. As a result, the areas that most significantly underperformed previously within global real estate dramatically reversed course with various retail shopping centers, hotels and some areas of office posting strong gains following the COVID-19 vaccine announcement. The reporting period’s previous winners such as data centers, cellular tower companies, industrial facilities and self-storage were targeted as a source of funds for portfolio rebalancings throughout the industry, including the Fund’s portfolio. While the underlying fundamentals within these categories remained strong, their defensive characteristics and substantial relative outperformance dampened their short-term prospects as the market looked forward to some semblance of normalcy later in 2021. Despite the rally in global real estate in the final months of the reporting period, however, it was not enough to make up for the segment’s earlier shortfall. During the reporting period, the sector returned -8.18%, as measured by the FTSE EPRA/Nareit Developed Index, underperforming the broader domestic equity market by nearly 25%, as measured by the MSCI World Index return of 15.90%. Regionally within the global listed REIT markets, the U.S. return of -7.57%, as measured by the MSCI U.S. REIT Index underperformed Europe’s return of -2.70%.

The Fund significantly outperformed the FTSE EPRA/Nareit Developed Index benchmark and Lipper peer group during the reporting period but still produced slightly negative absolute returns. Generally speaking, the Fund benefited in relative terms by being defensively positioned for the first ten months of the reporting period. We emphasized companies that were less economically sensitive with business models that could function better during the COVID-19 crisis and underweighted areas we felt would be most disproportionately affected by the health crisis such as retail and lodging. From a relative performance standpoint, the Fund experienced positive results primarily from the industrial, technology infrastructure, office and mall sectors, while the specialty and self-storage segments detracted from performance.

The Fund’s overweight and positive selection effect in industrial real estate contributed strongly to relative outperformance and led all other sectors as the drivers affecting the group remained intact throughout the reporting period. The industrial sector continued to directly benefit from the same dynamics in the marketplace that weigh on the regional mall/retail real estate sector from a fundamental point-of-view, which is the disruption from ecommerce. This secular trend was only accentuated by the COVID-19 crisis as many retail stores closed to try to slow the spread. However, industrial facilities remained open and became even more important as much more commerce was executed from people’s homes. Additionally, it was easier for industrial facilities to practice social distancing while remaining operational, which was nearly impossible for several other property types. The industrial group continued to demonstrate some of the strongest fundamentals with ever-increasing demand for logistics and fulfillment facilities outstripping what has been a rather contained supply situation. As the reporting period drew to a close, it appeared this trend was continuing irrespective of the COVID-19 crisis as the group continued to outpace many other categories. The industrial sector trailed only the technology infrastructure sector in terms of absolute returns over the reporting period, and represented the Fund’s largest overweight versus the benchmark.

The technology infrastructure sector, which primarily consists of global data center and cell phone tower companies, also contributed strongly to the Fund’s relative outperformance during the reporting period. Many of the companies within the group posted the strongest absolute returns within the global real estate investable universe. The Fund’s overweight and broad exposure to the group, especially in many companies that don’t have benchmark representation, drove the bulk of the relative gains. Technology infrastructure businesses derive their revenues from leases, which unlike many other real assets, are unaffected by social distancing because the structures possess only equipment and require very little to no human occupancy or interaction. Additionally, demand for the services these companies provide has been much less impacted by lower global mobility and the slowdown in overall economic activity. The sector did experience selling pressure toward the end of the reporting period as money managers repositioned

10

their portfolios toward companies that stand to benefit the most from a more normalized economic environment once the COVID-19 crisis loses steam. Although we trimmed exposure slightly, technology infrastructure still represented the Fund’s second largest overweight at the end of the reporting period versus the index.

The Fund also experienced outperformance from security selection in the office sector, led by an overweight position in Sirius Real Estate Limited, a German firm focused on suburban office parks. Our outlook has been constructive toward German commercial real estate relative to other European countries for some time. Shares were rewarded after investors recognized the company’s attractive valuation relative to European peers, which drove the stock higher at the same time the outlook for the office sector was improving because of the COVID-19 vaccine announcements. Performance within the office segment also benefited from the Fund’s overweight to Norwegian office specialist Entra ASA. Relative to much of the world, the fundamentals in Norway were above average and Entra’s shares were trading at an attractive valuation. Downward pressure on sovereign yields in the country suggested likely tailwinds for the company as well. Toward the end of the reporting period, the stock rallied after its property portfolio was assigned a higher underlying value and Entra received multiple takeover bids.

The mall sector was also a contributor to the Fund’s relative performance due to the Fund’s underweight position. Retail store closures were already near or at peak historical levels in 2018 and 2019 in the U.S. before the COVID-19 crisis hit. While the situation across the rest of the world wasn’t quite as dire because supply wasn’t as elevated on a per capita basis, the impact from ecommerce was still clearly being felt. The COVID-19 crisis only served to make the situation much more severe and the market has significant concerns about tenants’ ability or willingness to pay rent to mall owners. The Fund benefited from its nearly 4% underweight in the mall group. The global mall group still declined by more than 30% in 2020.

The specialty sector, which rebounded after substantial first quarter 2020 weakness, was a modest detractor during the reporting period. Within the benchmark, gaming companies comprise a significant weight within the specialty sector. The gaming segment performed strongly later in the reporting period based on reopening news and the prospect that people would return to casinos following favorable COVID-19 vaccine news. The Fund’s underweight positions in the two of the largest gaming companies in the index, Gaming & Leisure Properties and VICI Properties Inc., led to the relative underperformance within the segment.

The self-storage sector also detracted from the Fund’s relative performance during the reporting period. Heading into the reporting period, we were concerned about modest market oversupply and growing expenses, which somewhat muted the group’s growth prospects. However, the defensive properties of self-storage garnered investor attention during the COVID-19 crisis. As a result, the group provided returns that were substantially better than many areas that experienced massive business disruptions. While we added self-storage exposure to the Fund during the reporting period, a slight underweight persisted resulting in relative underperformance.

The Fund maintained a bias toward higher quality companies and assets within the REIT sector in general because asset type and balance sheet strength remained important considerations for investment. The Fund remained defensively positioned based on our preference for companies with business models that are better able to function well in the current COVID-19 crisis environment. However, the COVID-19 vaccine news late in the reporting period provided a light at the end of the tunnel for most of the more maligned areas of real estate and was the catalyst for rebalancing the Fund’s portfolio. The Fund reduced exposure in sectors that had worked the best prior to the COVID-19 vaccine announcements, namely industrial and technology infrastructure, using the proceeds to fund purchases in areas that had been the most challenged such as retail and net lease. As a result, the Fund’s sector weights showed less deviation versus the index at the end of the reporting period.

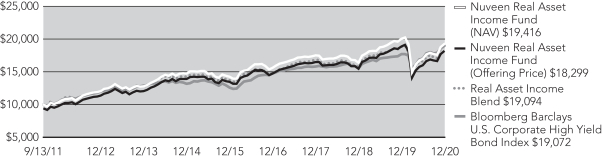

Nuveen Real Asset Income Fund

How did the Fund perform during the twelve-month reporting period ended December 31, 2020?

The table in the Performance Overview and Holding Summaries section of this report provides total returns at net asset value (NAV) for the period ended December 31, 2020. The Fund’s total returns on NAV are compared with the performance of a corresponding market index.

The Fund’s Class A Shares at NAV underperformed the Real Asset Income Blend benchmark, the Bloomberg Barclays U.S. Corporate High Yield Bond Index and the Lipper classification average during the twelve-month reporting period.

11

Portfolio Managers’ Comments (continued)

What strategies were used to manage the Fund during the reporting period and how did these strategies influence performance?

The Fund seeks a high level of current income with a secondary objective of capital appreciation by investing in a global portfolio of infrastructure and commercial real estate related securities (i.e. real assets) across the capital structure. These securities include a combination of infrastructure and real estate common stock, infrastructure and real estate preferred stock, and infrastructure and real estate related debt. Our goal is to combine these securities into a portfolio that provides investors with an attractive level of income and dampens levels of risk versus the broader equity market. We continued to select securities using an investment process that screens for companies and assets across the real assets market that provide higher yields. From the group of securities providing significant yields, we focus on owning those companies and securities with the highest total return potential in the Fund. Our process places a premium on finding securities whose revenues come from tangible assets with long-term concessions, contracts or leases and are therefore capable of producing steady, predictable and recurring cash flows. The Fund’s management team employs a bottom-up, fundamental approach to security selection and portfolio construction. We look for stable companies that demonstrate consistent and growing cash flow, strong balance sheets and histories of being good stewards of shareholder capital.

During the reporting period, the returns among the five “real asset” categories within the Real Asset Income Blend benchmark were quite divergent with an almost 20% spread between the top and bottoming performing categories. The equity market experienced a dramatic sell-off in March 2020 that more significantly impacted the typically defensive real estate and global infrastructure sectors. Although these two segments were able to recover some of the losses later in the reporting period, they still sharply underperformed the broader U.S. and global equity markets. Global real estate was the worst performing segment within the Real Asset Income Blend, ending the reporting period with a -8.18% return, as measured by the FTSE EPRA/NAREIT Developed Index and underperforming the U.S. real estate market. The global infrastructure segment outpaced global real estate, but also ended lower with a return of -5.76%, as measured by the S&P Global Infrastructure Index Net Return (NR). For comparison purposes, U.S. equities gained 18.40% during the reporting period as measure by the S&P 500® Index.

The reason for the substantial underperformance of real estate and global infrastructure was because both segments were more directly impacted by the COVID-19 crisis and the resulting shutdowns. In real estate, most property types are comprised of physical assets that are meant to facilitate the gathering of people, but over half of the world’s population was either mandated or strongly encouraged to do precisely the opposite. Retail shopping centers were closed, hotel occupancy cratered and restaurants and theaters were empty. As the reporting period progressed, the slow and uneven pace of reopenings and the resurgence of the COVID-19 virus in some more populated states of the U.S. and overseas continued to be an overhang for this segment. As a result, some tenants were not able to pay rent to property owners, which affected profitability and cash flow for real estate investment trusts (REITs). In November 2020, however, the real estate segment rebounded following favorable COVID-19 vaccine announcements from Pfizer and Moderna. Investors rotated back into areas of the equity market that had underperformed for most of the reporting period and stand to benefit more from an anticipated return to stronger economic growth in the second half of 2021. Within real estate, retail shopping centers, hotels and some areas of office posted strong gains following the COVID-19 vaccine announcement, while the reporting period’s previous winners such as data centers, cellular tower companies, industrial facilities and self-storage were targeted as a source of funds for portfolio rebalancings throughout the industry.

For infrastructure, two of its largest segments were similarly impacted. Transportation infrastructure, which includes airports, toll roads and passenger rail lines, operated at a fraction of capacity due to lockdowns, border closures, social distancing and general fear of the coronavirus. Although their usage began to increase as the reporting period progressed, restrictions remained. For the same reasons, energy infrastructure was significantly impacted by reduced demand, which came at a time when supply was already elevated. The price war between Saudi Arabia and Russia exacerbated the imbalance and pushed oil prices to an 18-year low in March 2020, which further reduced the need for pipeline infrastructure to move the commodity as production slowed. Energy infrastructure saw some improvement as the reporting period progressed as demand increased after many economies came back online, while OPEC and other oil-producing nations agreed to stem production. However, it was the COVID-19 vaccine announcements in the final two months of the reporting period that buoyed the price of crude oil, as well as the whole energy sector, because of the likely economic reopenings that will eventually result.

In the high yield market, the COVID-19 crisis led to a near complete shutdown of the capital markets in March 2020, which was exacerbated by the sharp drop in crude oil prices. Together these forces drove a spike in risk premiums and high yield outflows, with

12

high yield spreads peaking at 1,100 basis points over Treasuries at the reporting period’s widest point in March 2020. However, policymakers immediately implemented a number of tools at their disposal to support healthy market and economic functioning and companies tapped credit facilities. Investors took courage from these steps resulting in sizable inflows back into the high yield market for the remainder of the reporting period, which were met with the largest net new issuance on record in 2020 as companies aimed to optimize their capital structure. Over the remainder of the reporting period, the high yield market continued to be supported by accommodative policies, gradual reopenings and falling unemployment. After the sharp underperformance in March 2020, high yield spreads retraced to 361 basis points by year end and the market ended the reporting period with a surprisingly strong 7.11% return, as measured by the Bloomberg Barclays U.S. Corporate High Yield Index. Meanwhile, returns between the two preferred indices within the Real Asset Income Blend Index varied more than normal, highlighting the disproportionate impact the COVID-19 crisis has had on real estate. The Bloomberg Barclays Global Capital Securities Index advanced 10.67%, while the return of the Wells Fargo Hybrid & Preferred Securities REIT Index was much more muted at 2.82%.

Throughout the reporting period, the Fund generated a consistent gross yield that remained above our overall yield hurdle, which served as a source of stability for the Fund as it has during previous market declines. However, the Fund underperformed relative to its blended benchmark mainly because of its specific mandate to own only real asset companies, which ended up being disproportionately affected by social distancing and the closure of economies worldwide. Areas that the Fund is unable to own because of its real asset mandate generally held up better. The Fund’s shortfall versus its Lipper group was primarily due to its greater focus on yield compared to its peers because of its income objective. For much of the reporting period, investors remained focused on companies with superior growth expectations over more value-oriented or higher yielding securities. The Fund underperformed the Bloomberg Barclays U.S. Corporate High Yield Bond Index because of its exposures to the real estate and infrastructure equity segments, which significantly underperformed high yield bonds during the reporting period.

The Fund attempted to add value versus the Real Asset Income Blend benchmark in two ways, by re-allocating money among five main security types, finding pockets of value at differing times and, more importantly, through individual security selection. The Fund’s performance was hindered in varying degrees by four of the five segments (real estate preferred, high yield debt, infrastructure preferreds and real estate common equity), while its exposure in the infrastructure equity segment benefited performance results.

The real estate preferred segment was the most significant drag on performance, primarily due to the Fund’s overweight to hotel REIT preferreds and underweight to the self-storage area. Certain sub-property types were much less affected by social distancing, primarily due to the fact that their tenants, in large part, are not people. Self-storage was an area that provided defensive characteristics and garnered investor attention because it is a rather low cost expense for most households and requires no human interaction. As a result, self-storage REIT preferred securities provided positive returns that were substantially better than many areas that experienced massive business disruptions from the COVID-19 crisis. On the other hand, hotel demand cratered as country borders were closed to international air traffic and domestic travel was largely halted from stay-at-home orders and general health concerns.

In the debt area, results were hurt by the Fund’s lack of industrial exposure, which represents almost 15% of the high yield index. The Fund typically has an underweight to industrials because most of the companies within that space don’t meet our definition of infrastructure or real estate. However, much of the industrial category that the Fund is precluded from owning outperformed during the reporting period, leading to its shortfall in the debt portfolio.

While an overweight allocation to the infrastructure preferred segment was positive during the reporting period, security selection detracted primarily due to energy holdings. This segment is a disproportionately large part of the Fund’s investable universe given its real asset mandate. Energy infrastructure, as previously mentioned, was significantly impacted earlier in the reporting period by reduced demand for oil as travel restrictions and shelter-in-place/work-from-home policies greatly reduced both air and automobile traffic. Elevated supply, cratering demand and dramatic price declines for crude oil reduced the need for infrastructure assets as drillers and exploration and production cut activity and expenditures. The Fund’s investments focused on higher quality midstream companies, which performed much better than lower quality upstream, which were not immune to the significant price depreciation. Later in the reporting period, the price of crude oil and the energy sector was buoyed by significant strides made around the world in containing COVID-19, economic reopenings and the COVID-19 vaccine announcements. The Fund’s reduced its energy exposure early in the downturn, and remained committed to its high quality positions within midstream, especially within the preferred group.

13

Portfolio Managers’ Comments (continued)

The Fund was positioned with a modest overweight in real estate common equity relative to the benchmark heading into the reporting period, which proved detrimental given the weakness in the segment. Within the segment, an overweight to the net lease sector detracted the most. Net lease is typically a more defensive group because lease structures are usually longer term in nature, which has historically provided some consistency to earnings in an economic decline. These companies also pay higher dividends than many other sectors, which makes them more appropriate for an income-focused portfolio versus other property types that may not produce high enough dividends. However, many property types were subject to forced closures, which caused considerable fears about future earnings and potential dividend cuts due to the possible inability for tenants to pay rent.

The infrastructure common equity sector aided the Fund’s performance results during the reporting period, mostly due to its out-of-index exposure in alternative energy, by far the strongest performing area within the sector. An overweight in electric transmission and significant underweight within airports also proved beneficial. Besides the energy sector, no group suffered more for most of the reporting period than airports due to the collapse of passenger traffic amidst the COVID-19 crisis. Conversely, no group benefited more from the COVID-19 vaccine announcements, even though airline and airport CEOs remained tempered regarding their projected timelines for a return to pre-COVID activity. Due to the income objective of the Fund, few of the publicly traded airport companies are viable investment opportunities given their low dividend yields. However, because airports are a significant portion of the benchmark, the Fund’s underweight was beneficial.

We continued to actively manage the Fund’s allocations among the five investment categories to reflect what we believed to be the best opportunities in our investment universe. Toward the end of the reporting period following the COVID-19 vaccine announcements, we made substantial portfolio shifts. The Fund narrowed its underweight in equities by the end of the reporting period, adding to areas such as pipelines and renewable energy in infrastructure, along with additions to REIT equities, while reducing U.S. utility equity exposure. We also made small additions to many other equity sectors funded by a decrease in preferred holdings as spreads continued to narrow and yield characteristics in the equity universe became more attractive in relative terms. We reduced debt exposure and also redirected those proceeds into equities, ending the reporting period with a slight underweight in high yield debt relative to the benchmark. Preferred securities continued to represent an overweight, although narrower than at the beginning of the reporting period.

The Fund began using interest rate futures to partially hedge the portfolio against movements in interest rates. The futures contracts’ impact on performance was negligible during the reporting period.

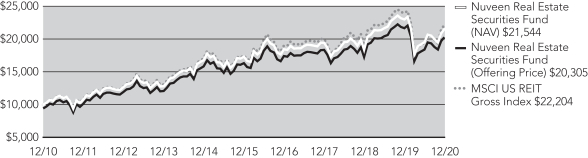

Nuveen Real Estate Securities Fund

How did the Fund perform during the twelve-month reporting period ended December 31, 2020?

The table in the Performance Overview and Holding Summaries section of this report provides total returns at net asset value (NAV) for the period ended December 31, 2020. The Fund’s total returns on NAV are compared with the performance of a corresponding market index.

The Fund’s Class A Shares at NAV outperformed the MSCI U.S. REIT Index but underperformed the Lipper classification average during the twelve-month reporting period.

What strategies were used to manage the Fund during the reporting period and how did these strategies influence performance?

The Fund seeks to provide above average current income and long-term capital appreciation by investing in income producing common stocks of publicly traded companies engaged in the real estate industry. During the reporting period, we continued to implement the Fund’s strategy of investing on a relative value basis. However, the COVID-19 crisis caused significant bifurcation in performance between sectors that were able to continue to operate well during the crisis versus those that were much more negatively impacted. As a result, we made larger-than-normal deviations at the sector level relative to the benchmark, focusing even more on areas like data centers, cell towers and industrial because fundamentals in those sectors were much less impacted by social distancing. We avoided sectors such as retail and lodging, which we believed were most at risk. In the final months of the reporting period, the encouraging news about several COVID-19 vaccines caused us to begin shifting the Fund’s sector weights back toward a more neutral positioning.

14

During the first three months of the reporting period, the health and financial crisis brought about by the COVID-19 crisis clearly had a devastating impact on financial markets. Although many defensive areas of the markets outperformed broader equities, the traditionally defensive real estate group did not. The sector experienced a massive sell-off in March 2020 that exceeded even the swiftness of the broader equity market declines. Many real estate investment trusts (REITs) suffered disproportionately at the hands of the COVID-19 crisis because most property types are comprised of physical assets that are meant to facilitate the gathering of people. However, over half of the world’s population was either mandated or strongly encouraged to do precisely the opposite. As a result, some tenants were not able to pay rent to property owners, which affected profitability and cash flow for REITs.

Following the initial crisis, markets shifted sharply again as a result of the massive amounts of global monetary and fiscal stimulus coupled with a significant improvement on the health front as economies that had been affected by COVID-19 the earliest made headway in its containment. As a result, investor sentiment began to improve dramatically and markets looked forward to recovery as economies started to reopen. However, while broader equity markets showed strength, especially large technology-focused companies, real estate continued to underperform because the segment will likely take longer to recover from the lingering effects of the shutdowns related to the health crisis. The slow pace of reopenings and the difficulty the U.S. had in containing COVID-19 continued to be overhangs for this segment. Retail shopping centers, hotels, restaurants and theaters saw improvements in activity and sales, but at a very gradual and uneven pace. The good news, however, was that fundamentals remained solid for several property types that didn’t experience a drop off in demand like data centers, cellular tower companies, industrial facilities and self-storage.

In the final two months of the reporting period, the real estate segment rebounded following favorable COVID-19 vaccine announcements from Pfizer and Moderna, which immediately changed the investment landscape. Investors rotated back into areas of the equity market that had underperformed for most of the reporting period and stand to benefit more from an anticipated return to stronger economic growth in the second half of 2021. As a result, the areas that most significantly underperformed previously within the real estate sector dramatically reversed course with various retail shopping centers, hotels and some areas of office posting strong gains following the COVID-19 vaccine announcement. The reporting period’s previous winners such as data centers, cellular tower companies, industrial facilities and self-storage were targeted as a source of funds for portfolio rebalancings throughout the industry, including the Fund’s portfolio. While the underlying fundamentals within these categories remained strong, their defensive characteristics and substantial relative outperformance dampened their short-term prospects as the market looked forward to some semblance of normalcy later in 2021. However, despite the rally in real estate in the final months of the reporting period, it was not enough to make up for the segment’s earlier shortfall. During the reporting period, the sector returned -7.57%, as measured by the MSCI U.S. REIT Total Return Index, significantly underperforming the broader domestic equity market, which returned 18.40%, as measured by the S&P 500® Index.

The Fund outperformed the MSCI U.S. REIT benchmark but still produced negative absolute returns during the reporting period. From a relative performance standpoint, the Fund saw positive results primarily from the industrial, multi-family/apartment, community centers and health care REIT sectors. On the negative side, the self-storage, specialty and technology infrastructure segments detracted from performance.

The Fund’s leading contribution came from an overweight allocation to industrial real estate. As we entered the reporting period, the industrial sector was directly benefiting from the same dynamic in the marketplace that was weighing on the regional mall/retail real estate sector, which was the disruption from ecommerce. This secular trend was only accentuated by the COVID-19 crisis as many retail stores were closed to try to slow the spread of COVID-19. However, industrial facilities remained open and became even more important as much more commerce was executed from people’s homes. While warehouses and distribution facilities certainly have people present, they are able to easily practice social distancing. Many of these sites also served businesses that were deemed essential and fulfilled ecommerce orders, while brick-and-mortar retail facilities were closed. The industrial group continued to demonstrate some of the strongest fundamentals with ever-increasing demand for these logistics and fulfillment facilities outstripping what has been a rather contained supply situation. These underlying fundamentals, along with being less affected by social distancing, led to significant outperformance of the group relative to the broader benchmark.

The Fund also benefited from favorable stock selection and allocation effect within the multi-family/apartment sector. The impact from COVID-19 on rents has been dramatic, especially in urban centers of gateway markets like New York City and San Francisco. Unemployment due to the health crisis has disproportionately impacted urban centers relative to suburban areas, including much of

15

Portfolio Managers’ Comments (continued)

the workforce that rents rather than owns property. Demand for apartment space has fallen as renters look for alternative living arrangements, causing rents to decline to stem the outflow. The combination of lower occupancy with lower rents portends more difficult economics for the multi-family sector going forward and the group’s performance suffered as a result. The return for the property type in the index fell more than 15%. The Fund’s underweight position in several large benchmark constituents, as well as more muted losses for its holdings, led to outperformance in the segment.

Community centers, another underweighted sector, contributed to the Fund’s performance. We reduced the Fund’s overall allocation to the group because the underlying fundamentals for retail businesses remained low, especially in light of increasing domestic COVID-19 infections. Of all the business models within the real estate universe, we believed retail would likely remain the most challenged as ecommerce trends showed no signs of slowing their already significant pace of market share gains in terms of overall sales. The market drew the same conclusion as the reporting period progressed. The sector was one of the worst performers in the index during the reporting period in absolute terms.

The health care REIT sector also contributed favorably to the Fund’s relative performance, driven entirely by stock selection. We continued to favor the life science area (lab space for research), as well as medical office space within the group. The Fund’s overweight positions in companies whose businesses are more focused in these areas generated the most outperformance. Demand for and utilization of life science space only grew during the reporting period as testing and research were key to finding a path forward for dealing with COVID-19. Specifically within the life science area, the Fund’s overweight position in Alexandria Real Estate Equities Inc. was the largest contributor. In the medical office space, demand did fall precipitously earlier in the reporting period because patients chose to stay home and put off visits and elective surgeries. However, in relative terms, the segment remained in a favored position due to financial strength and the likelihood that rents would be less impacted than other areas.

The self-storage sector was the leading detractor from the Fund’s relative performance. Heading into the reporting period, we were concerned about modest market oversupply and growing expenses, which somewhat muted the group’s growth prospects. However, the world quickly changed and the defensive properties of self-storage garnered investor attention during the COVID-19 crisis. As a result, the group provided returns that were substantially better than many areas that experienced massive business disruptions. While the Fund added self-storage exposure during the reporting period, a slight underweight persisted resulting in relative underperformance.

The specialty sector, which rebounded after substantial first quarter 2020 weakness, was a modest detractor during the reporting period. Within the benchmark, gaming companies comprise a significant weight within the specialty sector. The gaming segment performed strongly later in the reporting period based on reopening news and the prospect that people would return to casinos following favorable vaccine news. Our Fund’s underweight positions in the two of the largest gaming companies in the index, Gaming & Leisure Properties and VICI Properties Inc., led to the relative underperformance within the segment.

The technology infrastructure sector also modestly detracted from relative performance during the reporting period after enjoying the strongest returns in the first half of the reporting period. This sector saw selling pressure toward the end of the reporting period as money managers repositioned their portfolios toward companies that stand to benefit the most from a more normalized economic environment once the COVID-19 crisis loses steam. The primary detractor was the Fund’s small underweight to one of the larger holdings in the benchmark index, Digital Realty Trust Inc., which was mainly due to its elevated valuation versus its peers.

The Fund maintained a bias toward higher quality companies and assets within the REIT sector in general because asset type and balance sheet strength remained important considerations for investment. The Fund remained defensively positioned based on our preference for companies with business models that are better able to function well in the current COVID-19 crisis environment. However, the COVID-19 vaccine news late in the reporting period provided a light at the end of the tunnel for most of the more maligned areas of real estate and was the catalyst for rebalancing the Fund’s portfolio. The Fund reduced its exposure in sectors that had worked the best prior to the COVID-19 vaccine announcements, namely industrial and technology infrastructure, using the proceeds to fund purchases in areas that had been the most challenged such as retail, net lease, apartments and office.

16

Risk Considerations and Dividend Information

Risk Considerations

Nuveen Global Infrastructure Fund

Mutual fund investing involves risk; principal loss is possible. Concentration in infrastructure-related securities involves sector risk and concentration risk, particularly greater exposure to adverse economic, regulatory, political, legal, liquidity, and tax risks associated with master limited partnerships (MLPs) and real estate investment trusts (REITS). Foreign investments involve additional risks including currency fluctuations and economic and political instability. These risks are magnified in emerging markets. Common stocks are subject to market risk or the risk of decline. Small- and mid-cap stocks are subject to greater price volatility. The use of derivatives involves substantial financial risks and transaction costs. The Fund’s potential investment in other investment companies means shareholders bear their proportionate share of fund expenses and indirectly, the expenses of other investment companies. Fund investments in exchange trade funds (ETFs) may involve tracking error. Preferred securities may involve greater credit risk than other debt instruments.

Nuveen Global Real Estate Securities Fund

Mutual fund investing involves risk; principal loss is possible. There is no guarantee the Fund’s investment objectives will be achieved. The real estate industry is greatly affected by economic downturns or by changes in real estate values, rents, property taxes, interest rates, tax treatment, regulations, or the legal structure of the REIT. Prices of equity securities may decline significantly over short or extended periods of time. Non-U.S. investments involve risks such as currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. These and other risk considerations, such as active management, derivatives, preferred security, and, small and mid-cap risks, are described in detail in the Fund’s prospectus.

Nuveen Real Asset Income Fund

Mutual fund investing involves risk; principal loss is possible. Equity investments such as those held by the Fund are subject to market risk, call risk, derivatives risk, other investment companies risk, common stock risk, and tax risks associated with master limited partnerships (MLPs). Concentration in specific sectors may involve greater risk and volatility than more diversified investments: real estate sector involves the risk of exposure to economic downturns and changes in real estate values, rents, property taxes, interest rates and tax laws; infrastructure-related securities may involve greater exposure to adverse economic, regulatory, political, legal, and other changes affecting such securities. Foreign investments involve additional risks, including currency fluctuation, political and economic instability, lack of liquidity, and differing legal and accounting standards. These risks are magnified in emerging markets. Investments in small- and mid-cap companies are subject to greater volatility. In addition, the Fund will bear its proportionate share of any fees and expenses paid by the exchange trade funds (ETFs) in which it invests.

Debt or fixed income securities such as those held by the Fund are subject to market risk, credit risk, interest rate risk and income risk. As interest rates rise, bond prices fall. Below investment grade or high yield debt securities are subject to liquidity risk and heightened credit risk. Preferred securities are subordinated to bonds and other debt instruments in a company’s capital structure and therefore are subject to greater credit risk. Asset-backed and mortgage-backed securities are subject to additional risks such as prepayment risk, liquidity risk, default risk and adverse economic developments.

Nuveen Real Estate Securities Fund

Mutual fund investing involves risk; principal loss is possible. Common stocks and REITs such as those held in the Fund involve market risk, concentration risk, sector risk, and non-diversification risk. The real estate industry is greatly affected by economic downturns that may persist as well as changes in property values, taxes, and regulatory developments. Foreign investments involve additional risks including currency fluctuations, and economic or political instability. These risks are magnified in emerging markets. The use of derivatives involves substantial financial risks and transaction costs. Small cap stocks may experience more volatility than large cap stocks.

17

Risk Considerations and Dividend Information (continued)

Dividend Information

Regular dividends are declared and distributed annually for Nuveen Global Infrastructure Fund, declared daily and distributed monthly for Nuveen Real Asset Income Fund and declared and distributed quarterly for Nuveen Global Real Estate Securities Fund and Nuveen Real Estate Securities Fund. To permit a Fund to maintain a more stable dividend, the Fund may pay dividends at a rate that may be more or less than the amount of net investment income it actually earned during the period.

In certain instances, a portion of each Fund’s distributions may be paid from sources or comprised of elements other than ordinary income, including capital gains and/or a return of capital. This is generally due to the fact that the tax character of Fund distributions for a fiscal year is dependent upon the amount and tax character of distributions received from securities held in the Fund’s portfolio. Distributions received from certain securities in which the Fund invests, most notably real estate investment trust (REIT) securities, may be characterized for tax purposes as ordinary income, long-term capital gain and/or a return of capital. The issuer of a security typically reports the tax character of its distributions only once per year, generally during the first two months of the following calendar year. The full amount of the distributions received from such securities is included in the Fund’s ordinary income during the course of the year until such time the Fund is notified by the issuer of the actual tax character. To the extent that at the time of a particular distribution the Fund estimates that a portion of that distribution is attributable to a source or sources other than ordinary income, the Fund would send shareholders a notice to that effect. The final determination of the sources and tax character of all distributions for the fiscal year is made after the end of the fiscal year.

Additional Dividend Information for Nuveen Global Real Estate Securities Fund, Nuveen Real Asset Income Fund and Nuveen Real Estate Securities Fund