UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-05309

Nuveen Investment Funds, Inc.

(Exact name of registrant as specified in charter)

Nuveen Investments

333 West Wacker Drive, Chicago, IL 60606

(Address of principal executive offices) (Zip code)

Christopher M. Rohrbacher

Vice President and Secretary

333 West Wacker Drive,

Chicago, IL 60606

(Name and address of agent for service)

Registrant’s telephone number, including area code: (312) 917-7700

Date of fiscal year end: June 30

Date of reporting period: June 30, 2020

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policy making roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss.3507.

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

Nuveen Income Funds

| | | | | | | | | | |

| Fund Name | | Class A | | Class C | | Class R3 | | Class R6 | | Class I |

| Nuveen Credit Income Fund (formerly known as Nuveen High Income Bond Fund) | | FJSIX | | FCSIX | | FANSX | | — | | FJSYX |

| Nuveen Strategic Income Fund | | FCDDX | | FCBCX | | FABSX | | FSFRX | | FCBYX |

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Funds’ annual and semi-annual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports. Instead, the reports will be made available on the Funds’ website (www.nuveen.com), and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you have already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Funds electronically anytime by contacting the financial intermediary (such as a broker-dealer or bank) through which you hold your Fund shares or, if you are a direct investor, by enrolling at www.nuveen.com/e-reports.

You may elect to receive all future shareholder reports in paper free of charge at any time by contacting your financial intermediary or, if you are a direct investor, by calling 800-257-8787 and selecting option #1. Your election to receive reports in paper will apply to all funds held in your account with your financial intermediary or, if you are a direct investor, to all your directly held Nuveen Funds and any other directly held funds within the same group of related investment companies.

Annual Report

Life is Complex.

Nuveen makes things e-simple.

It only takes a minute to sign up for e-Reports. Once enrolled, you’ll receive an e-mail as soon as your Nuveen Fund information is ready. No more waiting for delivery by regular mail. Just click on the link within the e-mail to see the report and save it on your computer if you wish.

Free e-Reports right to your email!

www.investordelivery.com

If you receive your Nuveen Fund distributions and statements from your financial professional or brokerage account.

or

www.nuveen.com/client-access

If you receive your Nuveen Fund distributions and statements directly from Nuveen.

Must be preceded by or accompanied by a prospectus.

NOT FDIC INSURED MAY LOSE VALUE NO BANK GUARANTEE

Table

of Contents

3

Chair’s Letter to Shareholders

Dear Shareholders,

The COVID-19 crisis is taking an unprecedented toll on our health, societies, economies and financial markets. Our thoughts are with you during this time of significant disruption caused by the disease and its economic fallout. With many regions of the world suppressing the initial spread of the virus, governments and public health officials face the extraordinary challenge of balancing the resumption of economic activity with public safety. New clusters of infection emerged in the U.S. and other countries following their reopening this summer and a new school year and Northern Hemisphere flu season add new variables. Markets have turned their focus to the potential for an economic recovery, although the timing and magnitude are highly uncertain. Elevated market volatility is likely to continue, with economic data, coronavirus infection rates and the upcoming U.S. presidential election under scrutiny.

While we do not want to understate the dampening effect on the global economy, it is important to differentiate short-term interruptions from the longer-lasting implications to the economy. Prior to the COVID-19 crisis, some areas of the global economy were showing signs of improvement after trade tensions had weighed on economic activity for much of 2019. More recently, countries that have reopened have seen marked improvement in some near-term economic indicators. Central banks and governments around the world have announced economic stimulus measures and pledged to continue doing what it takes to support their economies. In the U.S., the Federal Reserve has cut its benchmark interest rate to near zero and introduced similar programs that helped revive the U.S. economy after the 2008 financial crisis. The U.S. Government has approved three relief packages, including a $2 trillion-dollar package directly supporting businesses and individuals. The Coronavirus Aid, Relief and Economic Security Act, called the CARES Act, provides direct payments and expanded unemployment benefits to individuals, loans and grants to small businesses, loans and other money to large corporations and funding for hospitals, public health, education and state and local governments. In the European Union, the European Central Bank recently increased the size of its Pandemic Emergency Purchase Program, known as PEPP, to €1.35 trillion from €750 billion and extended its duration to June 2021.

In the meantime, patience and a long-term perspective are key for investors. When market fluctuations are the leading headlines day after day, it���s tempting to “do something.” However, your long-term goals can’t be met with short-term thinking. We encourage you to talk to your financial professional, who can review your time horizon, risk tolerance and investment goals. On behalf of the other members of the Nuveen Fund Board, we look forward to continuing to earn your trust in the months and years ahead.

Sincerely,

Terence J. Toth

Chair of the Board

August 24, 2020

4

Portfolio Managers’ Comments

Nuveen Credit Income Fund (formerly known as Nuveen High Income Bond Fund)

Nuveen Strategic Income Fund

These Funds feature portfolio management by Nuveen Asset Management, LLC (NAM), an affiliate of Nuveen Fund Advisors, LLC, the Funds’ investment adviser. Kevin Lorenz, CFA and Jean C. Lin, CFA, are portfolio managers for the Nuveen Credit Income Bond Fund. Portfolio managers for the Nuveen Strategic Income Fund include Douglas M. Baker, CFA, Bill Martin, Kevin Lorenz, CFA, Katherine Renfrew and Nicholas Travaglino.

Effective July 7, 2020 (subsequent to the close of the reporting period), the Nuveen High Income Bond Fund’s name was changed to Nuveen Credit Income Fund.

Effective July 7, 2020 (subsequent to the close of the reporting period), the Nuveen Credit Income Fund’s investment objective changed to provide total return with an emphasis on a high level of current income.

Effective July 7, 2020 (subsequent to the close of the reporting period), Anders S. Persson, CFA, Bill Martin, Karina L. Bubeck, CFA and Aashh K. Parekh, CFA, were named as portfolio managers of the Nuveen Credit Income Fund.

Effective August 17, 2020 (subsequent to the close of the reporting period), Brenda A. Langenfeld, CFA, was named as portfolio manager of the Nuveen Credit Income Fund.

Subsequent to the reporting period, management announced that effective December 31, 2020, William Martin will no longer serve as a portfolio manager of the Funds.

Here the Funds’ portfolio management team discusses economic and market conditions, key investment strategies and the Funds’ performance for the twelve-month reporting period June 30, 2020.

What factors affected the U.S. economy and the global stock markets during the twelve-month annual reporting period ended June 30, 2020?

The longest economic expansion in U.S. history came to an abrupt halt in early 2020 amid the COVID-19 coronavirus pandemic. To slow the spread of the virus, large portions of the economy were shut down, with companies closing either temporarily or permanently and most of the U.S. population under stay-at-home orders during March and April 2020. A phased reopening began toward the end of May, but the disruption to the economy has been swift and severe. In June 2020, the National Bureau of Economic Research announced that the economic expansion that began in June 2009 officially ended in February 2020, marking the start of a recession (a several months’ long contraction across the broad economy). As expected, the U.S. economy suffered a sharp contraction in the second quarter of 2020, with gross domestic product (GDP) down 32.9% on an annualized basis according to the

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell or hold a security or an investment strategy and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her advisors.

Certain statements in this report are forward-looking statements. Discussions of specific investments are for illustration only and are not intended as recommendations of individual investments. The forward-looking statements and other views expressed herein are those of the portfolio managers as of the date of this report. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements and the views expressed herein are subject to change at any time, due to numerous market and other factors. The Funds disclaim any obligation to update publicly or revise any forward-looking statements or views expressed herein.

For financial reporting purposes, the ratings disclosed are the highest rating given by one of the following national rating agencies: Standard & Poor’s (S&P), Moody’s Investors Service, Inc. (Moody’s) or Fitch, Inc. (Fitch). This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section.

5

Portfolio Managers’ Comments (continued)

Bureau of Economic Analysis “advance” estimate. GDP measures the value of goods and services produced by the nation’s economy less the value of the goods and services used up in production, adjusted for price changes. In the second quarter, steep declines in consumer spending, business investment and exports weighed on economic activity, offsetting increased government spending. By comparison, the annualized GDP growth rate shrank 5% in the first quarter of 2020, after expanding 2.4% in the fourth quarter of 2019 and 2.2% in 2019 overall.

Consumer spending, the largest driver of the economy, was well supported earlier in this reporting period by low unemployment, wage gains and tax cuts. However, the COVID-19 crisis containment measures drove a significant drop in consumer spending and a sharp rise in unemployment starting in March 2020. The Bureau of Labor Statistics said the unemployment rate rose to 11.1% in June 2020 from 3.7% in June 2019. The economy added 4.8 million jobs in June 2020, following the addition of 2.7 million jobs in May 2020. However, the combined job losses in March and April 2020 exceeded 22 million. The average hourly earnings rate appeared to soar, growing at an annualized rate of 5% in June 2020, despite the spike in unemployment. Earnings data were skewed by the concentration of job losses in lower-wage work, which effectively eliminated most of the low data, resulting in an average of mostly higher numbers. The overall trend of inflation weakened considerably, which was attributed to large decreases in gasoline, apparel, air travel and lodging prices offsetting an increase in food prices. The Bureau of Labor Statistics said the Consumer Price Index (CPI) increased 0.6% over the twelve-month reporting period ended June 30, 2020 before seasonal adjustment.

Low mortgage rates and low inventory drove home prices moderately higher in this reporting period, although the period measured only partially reflects the shutdown. The S&P CoreLogic Case-Shiller U.S. National Home Price Index, which covers all nine U.S. census divisions, was up 4.5% year-over-year in May 2020 (most recent data available at the time this report was prepared). The 10-City and 20-City Composites reported year-over-year increases of 3.1% and 3.7%, respectively.

With economic momentum slowing in 2019 from 2018’s stronger pace, the U.S. Federal Reserve (Fed) cut its benchmark interest rate by 0.25% at each of the July 2019, September 2019 and October 2019 policy committee meetings. Markets registered disappointment with the Fed’s explanation that the rate cuts were a “mid-cycle adjustment,” rather than a prolonged easing period, and its signal that there would be no additional rate cuts in 2019. Also in the latter half of 2019, the Fed announced it would stop shrinking its bond portfolio sooner than scheduled, as well as began buying short-term Treasury bills to help money markets operate smoothly and maintain short-term borrowing rates at low levels. Fed Chairman Powell emphasized that the Treasury bill purchases were not a form of quantitative easing. The Fed continued its Treasury bill buying in January 2020, as well as left its benchmark interest rate unchanged, while noting the emerging COVID-19 risks.

As the outbreak spread to the U.S. and significant restrictions on social and economic activity were imposed starting in March 2020, the Fed enacted an array of emergency measures to stabilize the financial system and support the markets, including cutting its main interest rate to near zero, offering lending programs to aid small and large companies and allowing unlimited bond purchases, known as quantitative easing. There were no policy changes at the Fed’s April and June 2020 meetings, where Chairman Powell reiterated a commitment to keep rates near zero until the economy recovers and continued to issue a cautious outlook for the U.S. economy. (Subsequent to the close of the reporting period, there were no policy changes at the Fed’s July 2020 meeting.)

Meanwhile, the U.S. government approved three aid packages, totaling more than $100 billion in funding to health agencies and employers offering paid leave and $2 trillion allocated across direct payments to Americans, an expansion of unemployment insurance, loans to large and small businesses, funding to hospitals and health agencies and support to state and local governments.

While trade and tariff policy drove market sentiment for most of the twelve-month reporting period, the outbreak of the novel coronavirus and its associated disease COVID-19 rapidly dwarfed all other market concerns starting in late February 2020. Equity and commodity markets sold-off and safe-haven assets rallied in March 2020 as China, other countries and then the United States initiated quarantines, restricted travel and shuttered factories and businesses. The potential economic shock was particularly difficult to assess, which amplified market volatility. An ill-timed oil price war between the Organization of the Petroleum Exporting Countries (OPEC) and non-OPEC member Russia, which caused oil prices to plunge in March 2020, exacerbated the market sell-off.

Outside the U.S., many countries implemented lockdowns and restrictions on business activity to reduce infection rates, with a deep impact to their economies. Pandemic responses included central bank monetary easing and quantitative easing, fiscal relief programs, the loosening of fiscal rules and, in the case of emerging markets, emergency financing and debt relief from bilateral

6

creditors and international organizations such as the International Monetary Fund and World Bank. The U.K. formally exited the European Union (EU) at the end of January 2020, triggering the one-year transition period, but Brexit talks were temporarily paused during the virus lockdown. When negotiations resumed, the U.K. continued to indicate it would not seek an extension. Italy’s prime minister unexpectedly resigned in August 2019, and the newly formed coalition government appeared to take a less antagonistic stance towards the EU. To help relieve the coronavirus impact on Italy and other more indebted Southern European countries, the European Commission proposed a €750 billion aid program to be funded by all member states, which was unanimously approved in July 2020 after the close of the reporting period. In Asia, northern countries were among the first to successfully reduce infection rates and relax coronavirus restrictions, but pockets of the disease re-emerged. The widespread anti-government protests roiling Hong Kong throughout 2019 had dissipated amid the lockdown, but tensions flared in late May 2020 when China unexpectedly announced a national security law perceived as a threat to Hong Kong’s sovereignty. India took stringent lockdown steps in March 2020 but still saw a rapid increase in cases. Latin American countries entered the health crisis in already weakened positions, with high government debt and widespread civil unrest. Venezuela’s economic and political crisis continued to deepen. Argentina surprised the market with the return of a less market-friendly administration but continued to pursue a restructuring of its debt. Brazil’s Bolsonaro administration achieved a legislative win on pension reform but had not fully delivered on reviving economic growth. As the pandemic spread to Latin America, the inconsistent government responses, reduced testing capabilities, weaker health care systems, food shortages and public protests contributed to accelerating infection and death rates, while the Southern Hemisphere winter is set to begin.

Prior to the COVID-19 crisis, global markets had become more bullish on the outlook for 2020 as trade policy and Brexit appeared to make progress at the end of 2019. The U.S. and China agreed on a partial trade deal, which included rolling back some tariffs, increasing China’s purchases of U.S. agriculture products and the consideration of intellectual property, technology and financial services rights. The “phase one” deal was signed on January 15, 2020. While much of the focus remained on the U.S.-China relationship, trade spats between the U.S. and Mexico, the EU, Brazil and Argentina also arose throughout the reporting period. In January 2020, the U.S. Congress fully approved the U.S., Mexico and Canada Agreement (USMCA), which replaces the North American Free Trade Agreement. With more clarity on trade deals, the trade-related deterioration in global manufacturing and export data was expected to improve. However, the COVID-19 crisis has since upended those assumptions. Furthermore, tensions between the U.S. and China escalated amid the pandemic, with both sides stoking resentment about the management of the health crisis, Hong Kong’s political protests and trade policy.

How did the Funds perform during the twelve-month reporting period ended June 30, 2020?

The tables in the Fund Performance and Expense Ratios section of this report provide total returns for the Funds for the one-year, five-year, ten-year and/or since inception periods ended June 30, 2020. Each Funds’ Class A Share total returns at net asset value (NAV) are compared with the performance of their corresponding market index and Lipper classification average. The Nuveen Credit Income Fund’s Class A Shares at NAV underperformed both the Bloomberg Barclays High Yield 2% Issuer Capped Index and the Lipper Global High Yield Funds Classification Average for the twelve-month reporting period. The Nuveen Strategic Income Fund’s Class A Shares at net asset value (NAV) underperformed the Bloomberg Barclays Aggregate Bond Index and outperformed the Lipper Multi-Sector Income Funds Classification Average for the twelve-month reporting period. A more detailed account of each Fund’s performance is provided later in this report.

Nuveen Credit Income Fund (formerly known as Nuveen High Income Bond Fund)

What strategies were used to manage the Fund during the twelve-month reporting period ended June 30, 2020 and how did these strategies influence performance?

The Fund has an objective of providing high income strategy that blends below investment grade bonds from U.S. and non-U.S. issuers with other income-producing investments to expand return opportunities and increase diversification while seeking a high level of current income.

Interest rates fell sharply resulting in a steepening of the Treasury yield curve. Driven by the five Fed rate cuts, three-month T-bills ended the reporting period 196 basis points lower at 0.16%. The 10-year Treasury yield hit an all-time low well below 1% during the reporting period and ended at 0.66%, which was 134 basis points lower than where it started. As a result, U.S. Treasuries were the best performing asset class during the reporting period, handily outperforming all other fixed income sectors.

7

Portfolio Managers’ Comments (continued)

The high yield market started the reporting period supported by dovish central banks and stable credit fundamentals, which kept recession at bay, while capital from around the globe continued to flow into the asset class in the hunt for yield. Although earnings momentum had moderated by the end of 2019, the supportive macro backdrop and more favorable business sentiment going into 2020 provided a strong tailwind for valuations in the high yield market. However, the sudden onset of COVID-19 led to a near complete shutdown of the capital markets in March 2020, which was exacerbated by the sharp drop in crude oil prices. Together these forces drove a spike in risk premiums and dramatic high yield outflows. High yield spreads peaked at 1,100 basis points before sharply retracing to end the reporting period at 630 basis points over Treasuries after drastic policy measures were enacted, companies tapped credit facilities and more clarity emerged regarding the differentiation between sectors, credit factors and resiliency going into recession. High yield performed well in the final three months of the reporting period as policymakers continued to support healthy market and economic functioning while portions of the country gradually reopened. As a result, high yield experienced sizable inflows back into the market, which were met with one of the largest rounds of quarterly net new issuance ($59 billion) as companies aimed to optimize their capital structure. During the reporting period, high yield significantly underperformed higher quality sectors.

The Fund outperformed during the first half of the reporting period, but significantly underperformed during the COVID-19 crisis volatility in the second half of the reporting period, leading to an overall shortfall versus the benchmark. The most notable cause of the Fund’s underperformance relative to the benchmark was its underweight position in higher quality BB rated credits since this was the best performing ratings category. In March 2020, the market saw a flight to quality that drove the outperformance of BB relative to lower quality credits as the COVID-19 crisis spread and shutdowns took effect. Higher quality was further aided by the Fed’s support of the investment grade corporate market and “fallen angels” (investment grade bonds downgraded to high yield). Despite the underperformance of lower-quality high yield during the reporting period, the Fund’s positive security selection of CCC rated securities contributed favorably, along with an underweight to that segment.

Another significant factor in the Fund’s underperformance was its overweight to the energy sector throughout the reporting period. As noted, oil prices suffered massive declines in the first part of 2020 following the price war between Saudi Arabia and Russia at the same time that demand was quickly dropping following the onset of virus-induced lockdowns. The energy market did stabilize later in the reporting period after OPEC and other oil-producing nations agreed to production cuts and the acute demand shock passed as economies gradually reopened; however, crude oil only recovered about half of the losses experienced earlier in 2020. This did lead higher quality, high yield energy and fallen angels to perform in the final three months of the reporting period, while lower rated high yield exploration and production (E&P) names remained challenged with a handful of bankruptcy filings in that segment.

At the industry level, the Fund’s underweight exposure in capital goods detracted. The segment performed in line with the index as demand for manufactured goods and durables remained intact and consumer confidence began to improve. In addition to the detrimental underweight, the Fund’s positions in aircraft manufacturer Bombardier Inc. and aircraft component maker TransDigm Inc. detracted in this environment. Also, an underweight to packaging companies hindered performance as well. The Fund continued to hold bonds from both Bombardier and TransDigm at the end of the reporting period.

On the positive side, the Fund’s underweight to the highly impacted transportation sector contributed the most to relative performance. The Fund’s exposures were focused on shipping, travel services and less volatile secured airline debt of domestic carriers, which received stimulus support. Because we expect air travel to remain depressed beyond the end of 2020, our exposure in the area had an up-in-quality bias.

Also, the Fund’s underweight to the broader consumer cyclical sector aided performance on a relative basis versus the index. Following elevated volatility, cyclicals in the index ended up rallying back to almost flat for the reporting period based on stronger sentiment driven by supportive stimulus measures, followed by a wave of secured debt issuance in the sector to alleviate solvency risk. The Fund benefited from exposure to retailers with healthy balance sheets and strong online presence (Lithia Motors Inc. and PetSmart Inc.), and underweights among destination-based gaming properties and operators in Las Vegas and Atlantic City. The Fund continued to hold bonds from both Lithia Motors and PetSmart at the end of the reporting period.

Performance was also helped by a slight overweight versus the index in the basic materials sector. An improvement in the macroeconomic backdrop increased the demand for basic materials. However, we remained somewhat cautious given questions surrounding the pace of recovery and the volatility that the sector could experience going forward. As a result, we kept the Fund only modestly

8

overweight in basic materials and with a higher quality bias among our holdings. Naturally, miners and materials producers are heavily correlated with an improvement in industrial and manufacturing activity and infrastructure spending. Although lower supply in the space has reduced concerns of near-term surplus, we will need to see continued growth in demand for the sector to outperform.

Due to the uncertainty surrounding the COVID-19 crisis, we anticipate elevated stress in the energy and consumer discretionary sectors as well as lower quality tiers. In line with that narrative, we continued to position the Fund with a cautious tone and modestly expanded the portfolio’s underweights in more volatile CCC rated securities and in the energy, consumer cyclical and real estate sectors. We believe CCC rated bonds offer poor risk-adjusted returns as they are susceptible to any deterioration in market fundamentals. We anticipate elevated defaults to last through the remainder of 2020. In energy, we decreased exposure to mainly midstream and refining because we expect the sector will continue to be weighed down by softness in demand, shifts in consumer behavior and increased bankruptcy filings in E&P. These factors will have an associated negative impact on the revenues of midstream/gathering and processing companies because production stoppages will result in less volume being processed.

We continue to position the Fund across sectors in defensive credits characterized by strong liquidity profiles, consistent cash flow generation, inelastic demand and/or long-term contracts. During the reporting period, we increased exposure to communications (cable and satellite) and technology because we believed that work-from-home mandates and at-home entertainment demands would bode well for the sectors. We also increased the Fund’s overweight exposure to utilities and increased consumer non-cyclical exposure (food and beverage, health care) in an effort to position more defensively. We maintained slight overweights in bank and non-bank financials, including money-center banks, health insurers, insurance brokers and consumer lenders that have much stronger capital reserves than they did during the 2008 recession. We also trimmed the Fund’s overweight position in the basic industry sector.

During the reporting period, we used high yield CDX swaps to increase the Fund’s high yield credit risk exposure. This had a negligible impact on performance during the reporting period.

Nuveen Strategic Income Fund

What strategies were used to manage the Fund during the twelve-month reporting period ended June 30, 2020 and how did these strategies influence performance?

The Fund seeks to provide investors with total return as a broadly flexible, multi-sector bond Fund. The team actively manages a diversified portfolio of investment grade and high yield debt securities from U.S. and non-U.S. issuers.

Interest rates fell sharply resulting in a steepening of the Treasury yield curve. Driven by the five Fed rate cuts, three-month T-bills ended the reporting period 196 basis points lower at 0.16%. The 10-year Treasury yield hit an all-time low well below 1% during the reporting period and ended at 0.66%, which was 134 basis points lower than where it started. As a result, U.S. Treasuries were the best-performing asset class during the reporting period, handily outperforming all other fixed income sectors.

Investment grade credit spreads ended 2019 as the tightest levels of the year versus Treasuries as macroeconomic tail risks receded throughout the first half of the reporting period. By March 2020, investment grade credit spreads widened the most we’ve seen since October 2008. By the end of March 2020, spreads started to rally again due to global central bank easing, the approval of the massive U.S. relief package, and the announcement of several liquidity facilities specifically designed to support U.S. investment grade corporate issuers. In the final months of the reporting period, the unprecedented stimulus, Fed support of credit markets and signs of an economic recovery as lockdowns eased helped investment grade credit rebound. In second quarter of 2020, the sector experienced its largest quarterly new issuance on record, which was easily absorbed as the segment saw record inflows. Investment grade credit underperformed Treasuries during the reporting period, but outperformed all other fixed income sectors, particularly high yield credit.

The high yield market started the reporting period supported by dovish central banks and stable credit fundamentals, which kept recession at bay, while capital from around the globe continued to flow into the asset class in the hunt for yield. Although earnings momentum had moderated by the end of 2019, the supportive macro backdrop and more favorable business sentiment going into 2020 provided a strong tailwind for valuations in the high yield market. However, the sudden onset of COVID-19 led to a near complete shutdown of the capital markets in March 2020, which was exacerbated by the sharp drop in crude oil prices. Together these forces drove a spike in risk premiums and dramatic high yield outflows. High yield spreads peaked at 1,100 basis points before

9

Portfolio Managers’ Comments (continued)

sharply retracing to end the reporting period at 630 basis points over Treasuries after drastic policy measures were enacted, companies tapped credit facilities and more clarity emerged regarding the differentiation between sectors, credit factors and resiliency going into recession. High yield performed well in the final three months of the reporting period as policymakers continued to support healthy market and economic functioning while portions of the country gradually reopened. As a result, high yield experienced sizable inflows back into the market, which were met with one of the largest rounds of quarterly net new issuance ($59 billion) as companies aimed to optimize their capital structure. During the reporting period, high yield significantly underperformed higher quality sectors.

In the securitized sectors, both commercial mortgage-backed securities (CMBS) and asset-backed securities (ABS) displayed lower volatility and modest outperformance of Treasuries in the first half of 2020. The CMBS asset class benefited from light new supply and increased demand for this longer duration sector as rates fell. The majority of consumer oriented ABS assets also performed well as the economic environment continued to support consumer credit. However, both segments experienced heavy selling pressure and severely dislocated markets in March 2020 after rates moved lower and credit spreads moved wider amid forced selling driven by mutual fund redemptions. Some of the hardest hit ABS sectors were those most heavily impacted by the COVID-19 crisis such as aircrafts and consumer discretionary, and likewise retail and hotel properties in CMBS. In the final months of the reporting period, ABS and CMBS spreads retraced some lost ground following monetary and fiscal stimulus actions and government intervention in the capital markets, led by higher quality securities. However, during the reporting period, CMBS and ABS underperformed Treasuries and also lagged well behind investment grade corporates.

The Fund outperformed the Bloomberg Barclays Aggregate Bond Index during the first half of the reporting period, but underperformed during the COVID-19 crisis volatility in the second half of the reporting period, leading to an overall shortfall versus the benchmark. The Fund was able to outpace the median return of its Lipper peer group due to our conservative positioning going into the COVID-19 crisis. In the second half of 2019, we had increased the Fund’s exposure in the high quality U.S. Treasury and agency MBS sectors to approximately 15% of the portfolio as valuations in the credit segment, in particular, become expensive. As a result, we were able to meaningfully capitalize on the market’s major dislocation during March 2020, using that liquidity to add back to the Fund’s credit exposure following the sell-off. As a result, the Fund had strong performance relative to its peers.

The most notable detractor from the Fund’s performance was its sector allocations, particularly its out-of-index exposure in high yield bonds, which underperformed the benchmark substantially with a flat return for the reporting period. Also, an underweight position in Treasuries proved detrimental because this segment outperformed all other fixed income sectors by a wide margin with a 10.45% return during the reporting period. The Fund does not have much Treasury exposure due to its broad multi-sector mandate, which favors spread sectors.

Security selection also detracted within the securitized sectors, including the ABS and CMBS segments. Generally speaking, our bias toward the U.S. consumer reflected in the Fund’s consumer-oriented ABS positions did not fare well. For example, selection detracted in ABS segments such as timeshares, restaurants and airline leases. In the CMBS sector, subordinate positions did not perform well during the COVID-19 crisis sell-off.

Interest rate positioning was also an overall drag on results given the move lower in rates. (Bond prices move in the opposite direction of rates.) We consistently positioned the Fund with a shorter duration relative to its benchmark during the reporting period, which lessened its interest rate sensitivity. However, rates fell across the curve with the most pronounced move lower taking place in March 2020 when policymakers made two emergency cuts to the fed funds rate to help combat the impact of the COVID-19 crisis on the economy.

A healthy allocation in preferred and contingent capital (CoCo) securities also hindered results, but was offset by strong security selection in the segment. Despite strong fundamentals and further policy support for the bank sector, fears of another 2008, when banks struggled meaningfully, weighing heavily on preferred and CoCo valuations. However, the Fund’s positions in mostly larger U.S. banks offered value given their historically strong capital positions before the crisis.

Allocations to the investment grade credit and MBS sectors modestly benefited the Fund’s performance. Investment grade credit was the second best performing segment during the reporting period behind Treasuries gaining just over 9%, while the MBS sector was up 5.7%. Both asset classes benefited from the Fed’s buying programs designed to stabilize the financial markets later in the reporting period.

10

Yield curve positioning was also modestly additive during the reporting period, but not enough to offset the drag from the Fund’s short duration stance versus its benchmark. We positioned the Fund to benefit from a steeper yield curve with an overweight in the intermediate portion of the curve and an underweight at the long end, which proved helpful.

The Fund ended the reporting period positioned with an above-average risk profile but we will look for opportunities to get more defensive as the recovery cycle progresses. We believe risk appetites may be stronger than warranted by economic conditions at the end of the reporting period. Therefore, we anticipate we may see buying opportunities toward the later part of 2020 as valuations in risk assets, including the credit sector, may correct as the COVID-19 crisis continues to weigh on the economy.

We ended the reporting period with overweight positions in credit, including hefty allocations in high yield bonds, leveraged loans and preferred/CoCo securities, and more moderate exposure in the ABS and CMBS sectors. Although we increased exposure to the high quality U.S. Treasury and MBS sectors in the second half of 2019 after valuations in the market become expensive, we used these more liquid segments to add back to credit positions following the sell-off caused by the COVID-19 crisis in late March 2020. Therefore, at the end of the reporting period, the Fund had no exposure to U.S. Treasuries and a significant underweight to MBS versus the index.

Toward the end of the reporting period, we shortened the Fund’s duration further in light of well-executed monetary policy and a shifting focus to further government stimulus. We are maintaining that stance because we believe it’s more likely that rates will rise from here. However, we don’t believe significant duration bets are compelling in the current environment given the heavy involvement of the Fed in the Treasury market. The portfolio also remained positioned to benefit from a steeper yield curve with a continued underweight at the long end of the Treasury curve.

During the reporting period, we also continued to use various derivative instruments. We used foreign currency exchange forward contracts to hedge a Euro denominated board position back to U.S. Dollars. This had a negligible impact on performance during the reporting period.

We used U.S. Treasury futures and Eurodollar futures as part of an overall portfolio construction strategy to manage portfolio duration and yield curve exposure and selected foreign bond futures to actively manage exposure to those markets. These positions had a positive impact on performance during the reporting period.

In addition, we used high yield CDX swaps to hedge a portion of the Fund’s high yield credit risk exposure. The effect of these activities on performance was negligible during the reporting period.

11

Risk Considerations and Dividend Information

Risk Considerations

Nuveen Credit Income Fund

Mutual fund investing involves risk; principal loss is possible. There is no guarantee the Fund’s investment objectives will be achieved. Credit risk arises from an issuer’s ability to make interest and principal payments when due, as well as the prices of bonds declining when an issuer’s credit quality is expected to deteriorate. The Fund’s income could decline during periods of falling interest rates. Investments in below investment grade or high yield securities are subject to liquidity risk and heightened credit risk. This Fund is subject to the risks of investing in loans, including senior loans and secured and unsecured junior loans. Unsecured loans are not backed by a security interest in collateral and involve a higher degree of risk than secured loans. Loans are also subject to settlement risk due to the lack of established settlement standards or remedies for failure to settle, and may have limited restrictive covenants on borrowers, which may weaken the Fund’s ability to access collateral securing the loan and enforce its rights as a lender. The Fund may also invest in a pool of loans through collateralized loan obligations (CLOs). In addition to the risks associated with loans and high yield securities, CLOs are subject to the risk that distributions from the collateral may not be adequate to make interest or other payments owed to the Fund. Asset-backed and mortgage-backed securities are subject to additional risks such as prepayment risk, liquidity risk, default risk and adverse economic developments. Preferred securities are subordinate to bonds and other debt instruments in a company’s capital structure and therefore are subject to greater credit risk. Certain types of preferred, hybrid or debt securities with special loss absorption provisions, such as contingent capital securities (CoCos), may be or become so subordinated that they present risks equivalent to, or in some cases even greater than, the same company’s common stock. Non-U.S. investments involve risks such as currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. These and other risk considerations, such as call, derivatives, illiquid investments, interest rate, market, and valuation risks, are described in detail in the Fund’s prospectus.

Nuveen Strategic Income Fund

Mutual fund investing involves risk; principal loss is possible. Debt or fixed income securities such as those held by the Fund, are subject to market risk, credit risk, interest rate risk, call risk, derivatives risk, dollar roll transaction risk, and income risk. As interest rates rise, bond prices fall. Below investment grade or high yield debt securities are subject to liquidity risk and heightened credit risk. Foreign investments involve additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. The Fund gains additional exposure to currency rates, and therefore to the risk of currency fluctuation, through investment in foreign currency contracts. The risks of foreign investments are magnified in emerging markets. Asset-backed and mortgage-backed securities are subject to additional risks such as prepayment risk, liquidity risk, default risk and adverse economic developments.

Dividend Information

Each Fund seeks to pay regular monthly dividends out of its net investment income at a rate that reflects its past and projected net income performance. To permit each Fund to maintain a more stable monthly dividend, the Fund may pay dividends at a rate that may be more or less than the amount of net income actually earned by the Fund during the period. Distributions to shareholders are determined on a tax basis, which may differ from amounts recorded in the accounting records. In instances where the monthly dividend exceeds the earned net investment income, the Fund would report a negative undistributed net ordinary income. Refer to Note 6 – Income Tax Information for additional information regarding the amounts of undistributed net ordinary income and undistributed net long-term capital gains and the character of the actual distributions paid by the Fund during the period.

All monthly dividends paid by each Fund during the current reporting period were paid from net investment income. If a portion of the Fund’s monthly distributions is sourced or comprised of elements other than net investment income, including capital gains and/or a return of capital, shareholders will be notified of those sources. For financial reporting purposes, the per share amounts of each Fund’s distributions for the reporting period are presented in this report’s Financial Highlights. For income tax purposes, distribution information for each Fund as of its most recent tax year end is presented in Note 6 – Income Tax Information within the Notes to Financial Statements of this report.

12

Special Dividend Information for Nuveen Credit Income Fund

The Nuveen Credit Income Fund seeks to pay regular monthly distributions at a level rate that reflects past and projected net income of the Fund. Because the Fund may utilize credit default swaps and invests in non-U.S. debt and fixed-income securities, in certain periods it can experience derivative losses and currency exchange losses on those holdings. Under applicable tax rules, foreign currency exchange gains or losses and certain gains or losses on credit default swap transactions are treated as ordinary income items. Consequently, if a Fund experiences a foreign currency exchange loss in a given fiscal period, that loss may offset and reduce net income which may result in the Fund’s distributions exceeding the amount of its net income for tax purposes, resulting in any over-distribution being reported on the Fund’s Form 1099 as a return of capital. For the fiscal year ended June 30, 2020, the Fund recognized prior year deferred losses related to foreign currency and credit default swap transactions, resulting in a portion of the Fund’s dividends being characterized as a return of capital for tax purposes at fiscal year-end, which is identified in the tables below.

Nuveen Credit Income Fund – Data as of June 30, 2020

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Fiscal Year 2020 | |

| | | | | Percentage of the Distribution | | | | | | Per Share Amounts | |

| Share Class | | Ticker Symbol | | Net

Investment

Income | | | Realized

Gains | | | Return of

Capital | | | Distributions | | | Net

Investment

Income | | | Realized

Gains | | | Return of

Capital | |

Class A | | FJSIX | | | 92.60% | | | | 0.00% | | | | 7.40% | | | $ | 0.3810 | | | $ | 0.3528 | | | $ | 0.0000 | | | $ | 0.0282 | |

Class C | | FCSIX | | | 91.36% | | | | 0.00% | | | | 8.64% | | | $ | 0.3265 | | | $ | 0.2983 | | | $ | 0.0000 | | | $ | 0.0282 | |

Class R3 | | FANSX | | | 92.36% | | | | 0.00% | | | | 7.64% | | | $ | 0.3690 | | | $ | 0.3408 | | | $ | 0.0000 | | | $ | 0.0282 | |

Class I | | FJSYX | | | 92.93% | | | | 0.00% | | | | 7.07% | | | $ | 0.3990 | | | $ | 0.3708 | | | $ | 0.0000 | | | $ | 0.0282 | |

13

THIS PAGE INTENTIONALLY LEFT BLANK

14

Fund Performance

and Expense Ratios

The Fund Performance and Expense Ratios for each Fund are shown within this section of the report.

Fund Performance

Returns quoted represent past performance, which is no guarantee of future results. Investment returns and principal value will fluctuate so that when shares are redeemed, they may be worth more or less than their original cost. Current performance may be higher or lower than the performance shown.

Total returns for a period of less than one year are not annualized (i.e. cumulative returns). Since inception returns are shown for share classes that have less than 10-years of performance. Returns at net asset value (NAV) would be lower if the sales charge were included. Returns assume reinvestment of dividends and capital gains. For performance current to the most recent month-end visit nuveen.com or call (800) 257-8787.

Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Returns may reflect fee waivers and/or expense reimbursements by the investment adviser during the periods presented. If any such waivers and/or reimbursements had not been in place, returns would have been reduced. See Notes to Financial Statements, Note 7 – Management Fees and Other Transactions with Affiliates for more information.

Returns reflect differences in sales charges and expenses, which are primarily differences in distribution and service fees, and assume reinvestment of dividends and capital gains.

Comparative index and Lipper return information is provided for Class A Shares at NAV only.

Expense Ratios

The expense ratios shown are as of the Fund’s most recent prospectus. The expense ratios shown reflect total operating expenses (before fee waivers and/or expense reimbursements, if any). The expense ratios include management fees and other fees and expenses.

15

Fund Performance and Expense Ratios (continued)

Nuveen Credit Income Fund (formerly known as Nuveen High Income Bond Fund)

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this section. Refer to the Glossary of Terms Used in this Report for definitions of terms used within this section.

Fund Performance and Expense Ratios

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | Total Return as of June 30, 2020* | | | | | | | |

| | | Inception Date | | | Average Annual | | | Expense Ratios** | |

| | | 1-Year | | | 5-Year | | | 10-Year | | | Gross | | | Net | |

| Class A Shares at NAV | |

| 8/30/01

|

| | | (5.15)% | | | | 2.53% | | | | 5.22% | | | | 1.04% | | | | 1.03% | |

| Class A Shares at maximum Offering Price | | | 8/30/01 | | | | (9.65)% | | | | 1.54% | | | | 4.72% | | | | — | | | | — | |

| Bloomberg Barclays High Yield 2% Issuer Capped Index | | | — | | | | (0.00)% | | | | 4.79% | | | | 6.67% | | | | — | | | | — | |

| Lipper Global High Yield Funds Classification Average | | | — | | | | (2.53)% | | | | 3.19% | | | | 5.43% | | | | — | | | | — | |

| | | | | | |

| Class C Shares | | | 8/30/01 | | | | (5.75)% | | | | 1.77% | | | | 4.47% | | | | 1.80% | | | | 1.78% | |

| Class R3 Shares | | | 9/24/01 | | | | (5.33)% | | | | 2.28% | | | | 4.97% | | | | 1.29% | | | | 1.28% | |

| Class I Shares | | | 8/30/01 | | | | (5.03)% | | | | 2.78% | | | | 5.49% | | | | 0.79% | | | | 0.78% | |

| * | Class A Shares have a maximum 4.75% sales charge (Offering Price). Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC) of 1%, if redeemed within eighteen months of purchase. Class C Shares have a 1% CDSC for redemptions within less than twelve months, which is not reflected in the total returns. Class C Shares automatically convert to Class A Shares ten years after purchase. Class R3 Shares have no sales charge and are only available for purchase by eligible retirement plans. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors. |

| ** | The Fund’s investment adviser has contractually agreed to waive fees and/or reimburse expenses through July 31, 2022 so that total annual Fund operating expenses (excluding 12b-1 distribution and/or service fees, interest expenses, taxes, acquired fund fees and expenses, fees incurred in acquiring and disposing of portfolio securities (including prime broker fees and charges on short sales), dividend expense on securities sold short and extraordinary expenses) do not exceed 0.75% of the average daily net assets of any class of Fund shares. The expense limitation may be terminated or modified prior to that date only with the approval of the Board of Directors of the Fund. |

16

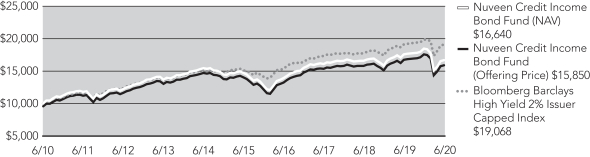

Growth of an Assumed $10,000 Investment as of June 30, 2020 – Class A Shares

The graphs do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of Fund shares.

17

Fund Performance and Expense Ratios (continued)

Nuveen Strategic Income Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this section. Refer to the Glossary of Terms Used in this Report for definitions of terms used within this section.

Fund Performance and Expense Ratios

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | Total Return as of June 30, 2020* | | | | | | | |

| | | | | | Average Annual | | | Expense Ratios** | |

| | | Inception Date | | | 1-Year | | | 5-Year | | | 10-Year | | | Gross | | | Net | |

| Class A Shares at NAV | | | 2/01/00 | | | | 4.63% | | | | 3.79% | | | | 4.83% | | | | 0.97% | | | | 0.85% | |

| Class A Shares at maximum Offering Price | | | 2/01/00 | | | | 0.19% | | | | 2.88% | | | | 4.37% | | | | — | | | | — | |

| Bloomberg Barclays U.S. Aggregate Bond Index | | | — | | | | 8.74% | | | | 4.30% | | | | 3.82% | | | | — | | | | — | |

| Lipper Multi-Sector Income Funds Classification Average | | | — | | | | 1.42% | | | | 3.48% | | | | 4.62% | | | | — | | | | — | |

| | | | | | |

| Class C Shares | | | 2/01/00 | | | | 3.84% | | | | 3.03% | | | | 4.05% | | | | 1.72% | | | | 1.60% | |

| Class R3 Shares | | | 9/24/01 | | | | 4.38% | | | | 3.54% | | | | 4.56% | | | | 1.21% | | | | 1.10% | |

| Class I Shares | | | 2/01/00 | | | | 4.86% | | | | 4.05% | | | | 5.08% | | | | 0.72% | | | | 0.60% | |

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | Total Return as of June 30, 2020* | | | | | | | |

| | | | | | Average Annual | | | Expense Ratios** | |

| | | Inception

Date | | | 1-Year | | | 5-Year | | | Since

Inception | | | Gross | | | Net | |

Class R6 Shares | | | 1/20/15 | | | | 4.96% | | | | 4.14% | | | | 3.78% | | | | 0.63% | | | | 0.51% | |

| * | Class A Shares have a maximum 4.25% sales charge (Offering Price). Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC) of 1%, if redeemed within eighteen months of purchase. Class C Shares have a 1% CDSC for redemptions within less than twelve months, which is not reflected in the total returns. Class C Shares automatically convert to Class A Shares ten years after purchase. Class R3 Shares have no sales charge and are only available for purchase by eligible retirement plans. Class R6 Shares have no sales charge and are available only to certain limited categories of investors as described in the prospectus. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors. |

| ** | The Fund’s investment adviser has contractually agreed to waive fees and/or reimburse expenses through July 31, 2021 so that total annual Fund operating expenses (excluding 12b-1 distribution and/or service fees, interest expenses, taxes, acquired fund fees and expenses, fees incurred in acquiring and disposing of portfolio securities (including prime broker fees and charges on short sales), dividend expense on securities sold short and extraordinary expenses) do not exceed 0.59% of the average daily net assets of any class of Fund shares. However, because Class R6 shares are not subject to sub-transfer agent and similar fees, total annual operating expenses for the Class R6 shares will be less than the expense limitation. The expense limitation may be terminated or modified prior to that date only with the approval of the Board of Directors of the Fund. |

18

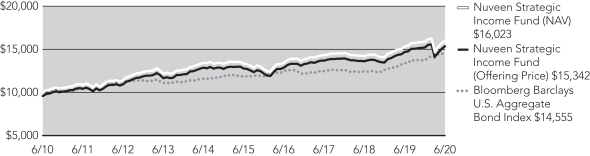

Growth of an Assumed $10,000 Investment as of June 30, 2020 – Class A Shares

The graphs do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or the redemption of Fund shares.

19

Yields as of June 30, 2020

Dividend Yield is the most recent dividend per share (annualized) divided by the offering price per share.

The SEC 30-Day Yield is a standardized measure of a fund’s yield that accounts for the future amortization of premiums or discounts of bonds held in the fund’s portfolio. The SEC 30-Day Yield is computed under an SEC standardized formula and is based on the maximum offer price per share. Subsidized yields reflect fee waivers and/or expense reimbursements from the investment adviser during the period. If any such waivers and/or reimbursements had not been in place, yields would have been reduced. Unsubsidized yields do not reflect waivers and/or reimbursements from the investment adviser during the period. If the fund did not receive a fee waiver/expense reimbursement during the period under its most recent agreement, subsidized and unsubsidized yields will be equal. Refer to the Notes to Financial Statements, Note 7 – Management Fees and Other Transactions with Affiliates for further details on the investment adviser’s most recent agreement with the Fund to waive fees and/or reimburse expenses, where applicable. Dividend Yield may differ from the SEC 30-Day Yield because the fund may be paying out more or less than it is earning and it may not include the effect of amortization of bond premium.

Nuveen Credit Income Fund

| | | | | | | | | | | | | | | | |

| | | Share Class | |

| | | Class A1 | | | Class C | | | Class R3 | | | Class I | |

Dividend Yield | | | 4.62% | | | | 4.13% | | | | 4.56% | | | | 5.10% | |

SEC 30-Day Yield-Subsidized | | | 4.83% | | | | 4.33% | | | | 4.84% | | | | 5.33% | |

SEC 30-Day Yield-Unsubsidized | | | 4.83% | | | | 4.33% | | | | 4.83% | | | | 5.33% | |

Nuveen Strategic Income Fund

| | | | | | | | | | | | | | | | | | | | |

| | | Share Class | |

| | | Class A1 | | | Class C | | | Class R3 | | | Class R6 | | | Class I | |

Dividend Yield | | | 3.55% | | | | 2.99% | | | | 3.47% | | | | 4.03% | | | | 3.93% | |

SEC 30-Day Yield-Subsidized | | | 3.46% | | | | 2.87% | | | | 3.37% | | | | 3.94% | | | | 3.87% | |

SEC 30-Day Yield-Unsubsidized | | | 3.46% | | | | 2.87% | | | | 3.37% | | | | 3.94% | | | | 3.87% | |

| 1 | The SEC Yield for Class A Shares quoted in the table reflects the maximum sales load. Investors paying a reduced load because of volume discounts, investors paying no load because they qualify for one of the several exclusions from the load, and existing shareholders who previously paid a load but would like to know the SEC Yield applicable to their shares on a going-forward basis, should understand that the SEC Yield effectively applicable to them would be higher than the figure quoted in the table. |

20

Holding Summaries as of June 30, 2020

This data relates to the securities held in each Fund’s portfolio of investments as of the end of this reporting period. It should not be construed as a measure of performance for the Fund itself. Holdings are subject to change.

For financial reporting purposes, the ratings disclosed are the highest rating given by one of the following national rating agencies: Standard & Poor’s, Moody’s Investors Service, Inc. or Fitch, Inc. This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section.

Nuveen Credit Income Fund

Fund Allocation

(% of net assets)

| | | | |

| Corporate Bonds | | | 88.5% | |

| Exchange-Traded Funds | | | 4.4% | |

| Variable Rate Senior Loan Interests | | | 1.5% | |

| Contingent Capital Securities | | | 0.8% | |

| $25 Par (or similar) Retail Preferred | | | 0.4% | |

| $1,000 Par (or similar) Institutional Preferred | | | 0.2% | |

| Common Stocks | | | 0.0% | |

| Investments Purchased with Collateral from Securities Lending | | | 1.1% | |

| Money Market Funds | | | 7.3% | |

| Other Assets Less Liabilities | | | (4.2)% | |

Net Assets | | | 100% | |

Corporate Bonds: Industries

(% of total corporate bonds)

| | | | |

| Media | | | 9.6% | |

| |

Oil, Gas & Consumable Fuels | | | 8.7% | |

| |

Health Care Providers & Services | | | 8.1% | |

| |

Diversified Telecommunication Services | | | 7.1% | |

| |

Chemicals | | | 5.7% | |

| |

Electrical Utilities | | | 4.9% | |

| |

Specialty Retail | | | 4.4% | |

| |

Consumer Finance | | | 4.0% | |

| |

Auto Components | | | 3.2% | |

| |

Metals & Mining | | | 2.9% | |

| |

Diversified Financial Services | | | 2.8% | |

| |

Pharmaceuticals | | | 2.6% | |

| |

Commercial Services & Supplies | | | 2.6% | |

| |

Equity Real Estate Investment Trust | | | 2.4% | |

| |

Trading Companies & Distributors | | | 2.3% | |

| |

Automobiles | | | 2.2% | |

| |

Insurance | | | 2.0% | |

| |

Food Products | | | 2.0% | |

| |

Communications Equipment | | | 2.0% | |

| |

Household Durables | | | 1.7% | |

| |

Other | | | 18.8% | |

Total | | | 100% | |

Portfolio Credit Quality

(% of total long-term fixed-income investments)

| | | | |

| BBB | | | 12.5% | |

| |

BB or Lower | | | 87.0% | |

| |

N/R (not rated) | | | 0.5% | |

Total | | | 100% | |

21

Holding Summaries as of June 30, 2020 (continued)

Nuveen Strategic Income Fund

Fund Allocation

(% of net assets)

| | | | |

| Corporate Bonds | | | 41.3% | |

| Asset-Backed and Mortgage-Backed Securities | | | 31.6% | |

| Variable Rate Senior Loan Interests | | | 9.5% | |

| $1,000 Par (or similar) Institutional Preferred | | | 6.9% | |

| Contingent Capital Securities | | | 4.0% | |

| Sovereign Debt | | | 2.6% | |

| Municipal Bonds | | | 1.9% | |

| $25 Par (or similar) Retail Preferred | | | 0.6% | |

| Investments Purchased with Collateral from Securities Lending | | | 0.3% | |

| Money Market Funds | | | 1.8% | |

| Other Assets Less Liabilities | | | (0.5)% | |

| |

Net Assets | | | 100% | |

Corporate Bonds: Industries

(% of total corporate bonds)

| | | | |

| Banks | | | 17.4% | |

| Oil, Gas & Consumable Fuels | | | 12.5% | |

| Diversified Telecommunication Services | | | 4.7% | |

| Capital Markets | | | 4.6% | |

| Insurance | | | 4.1% | |

| Media | | | 4.1% | |

| Equity Real Estate Investment Trust | | | 3.8% | |

| Chemicals | | | 3.8% | |

| Electric Utilities | | | 3.6% | |

| Consumer Finance | | | 3.5% | |

| Diversified Financial Services | | | 3.1% | |

| Specialty Retail | | | 2.3% | |

| Wireless Telecommunication Services | | | 2.2% | |

| Road & Rail | | | 2.1% | |

| Health Care Providers & Services | | | 1.8% | |

| Aerospace & Defense | | | 1.8% | |

| Automobiles | | | 1.7% | |

| Pharmaceuticals | | | 1.6% | |

| Metals & Mining | | | 1.2% | |

| Trading Companies & Distributors | | | 1.2% | |

| Other | | | 18.9% | |

Total | | | 100% | |

Portfolio Credit Quality

(% of total long-term fixed-income investments)

| | | | |

| AAA | | | 13.6% | |

| AA | | | 3.8% | |

| A | | | 14.5% | |

| BBB | | | 32.7% | |

| BB or Lower | | | 29.4% | |

| N/R (not rated) | | | 6.0% | |

Total | | | 100% | |

22

Expense Examples

As a shareholder of one or more of the Funds, you incur two types of costs: (1) transaction costs, including up-front and back-end sales charges (loads) or redemption fees, where applicable; and (2) ongoing costs, including management fees; distribution and service (12b-1) fees, where applicable; and other Fund expenses. The Examples below are intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds.

The Examples below are based on an investment of $1,000 invested at the beginning of the period and held through the period ended June 30, 2020.

The beginning of the period for the funds is January 1, 2020.

The information under “Actual Performance,” together with the amount you invested, allows you to estimate actual expenses incurred over the reporting period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.60) and multiply the result by the cost shown for your share class, in the row entitled “Expenses Incurred During Period” to estimate the expenses incurred on your account during this period.

The information under “Hypothetical Performance,” provides information about hypothetical account values and hypothetical expenses based on each Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expense you incurred for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the tables are meant to highlight your ongoing costs only and do not reflect any transaction costs. Therefore, the hypothetical information is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds or share classes. In addition, if these transaction costs were included, your costs would have been higher.

Nuveen Credit Income Fund

| | | | | | | | | | | | | | | | |

| | | Share Class | |

| | | A Shares | | | C Shares | | | R3 Shares | | | I Shares | |

Actual Performance | | | | | | | | | | | | | | | | |

Beginning Account Value | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | |

Ending Account Value | | $ | 902.83 | | | $ | 900.37 | | | $ | 902.77 | | | $ | 904.28 | |

Expenses Incurred During the Period | | $ | 4.73 | | | $ | 8.27 | | | $ | 5.91 | | | $ | 3.55 | |

Hypothetical Performance (5% annualized return before expenses) | | | | | | | | | | | | | | | | |

Beginning Account Value | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | |

Ending Account Value | | $ | 1,019.89 | | | $ | 1,016.16 | | | $ | 1,018.65 | | | $ | 1,021.13 | |

Expenses Incurred During the Period | | $ | 5.02 | | | $ | 8.77 | | | $ | 6.27 | | | $ | 3.77 | |

For each class of the Fund, expenses are equal to the Fund’s annualized net expense ratio of 1.00%, 1.75%, 1.25% and 0.75% for Classes A, C, R3 and I, respectively, multiplied by the average account value over the period, multiplied by 182/366 (to reflect the one-half year period).

23

Expense Examples (continued)

Nuveen Strategic Income Fund

| | | | | | | | | | | | | | | | | | | | |

| | | Share Class | |

| | | A Shares | | | C Shares | | | R3 Shares | | | R6 Shares | | | I Shares | |

Actual Performance | | | | | | | | | | | | | | | | | | | | |

Beginning Account Value | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | |

Ending Account Value | | $ | 1,009.50 | | | $ | 1,005.62 | | | $ | 1,008.34 | | | $ | 1,010.24 | | | $ | 1,010.65 | |

Expenses Incurred During the Period | | $ | 4.20 | | | $ | 7.93 | | | $ | 5.44 | | | $ | 2.45 | | | $ | 2.95 | |

Hypothetical Performance (5% annualized return before expenses) | | | | | | | | | | | | | | | | | | | | |

Beginning Account Value | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | |

Ending Account Value | | $ | 1,020.69 | | | $ | 1,016.96 | | | $ | 1,019.44 | | | $ | 1,022.43 | | | $ | 1,021.93 | |

Expenses Incurred During the Period | | $ | 4.22 | | | $ | 7.97 | | | $ | 5.47 | | | $ | 2.46 | | | $ | 2.97 | |

For each class of the Fund, expenses are equal to the Fund’s annualized net expense ratio of 0.84%, 1.59%, 1.09%, 0.49%, 0.59% for Classes A, C, R3, R6 and I, respectively, multiplied by the average account value over the period, multiplied by 182/366 (to reflect the one-half year period).

24

Report of Independent Registered Public Accounting Firm

To the Board of Directors of Nuveen Investment Funds, Inc. and Shareholders of

Nuveen Credit Income Fund (formerly known as Nuveen High Income Bond Fund)

Nuveen Strategic Income Fund

Opinions on the Financial Statements

We have audited the accompanying statements of assets and liabilities, including the portfolios of investments, of Nuveen Credit Income Fund (formerly known as Nuveen High Income Bond Fund) and Nuveen Strategic Income Fund (two of the Funds constituting Nuveen Investment Funds, Inc., hereafter collectively referred to as the “Funds”) as of June 30, 2020, the related statements of operations for the year ended June 30, 2020, the statements of changes in net assets for each of the two years in the period ended June 30, 2020, including the related notes, and the financial highlights for each of the five years in the period ended June 30, 2020 (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of each of the Funds as of June 30, 2020, the results of each of their operations for the year then ended, the changes in each of their net assets for each of the two years in the period ended June 30, 2020 and each of the financial highlights for each of the five years in the period ended June 30, 2020, in conformity with accounting principles generally accepted in the United States of America.

Basis for Opinions

These financial statements are the responsibility of the Funds’ management. Our responsibility is to express an opinion on the Funds’ financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Funds in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits of these financial statements in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. Our procedures included confirmation of securities owned as of June 30, 2020 by correspondence with the custodians and brokers; when replies were not received from brokers, we performed other auditing procedures. We believe that our audits provide a reasonable basis for our opinions.

PricewaterhouseCoopers LLP

Chicago, Illinois

August 27, 2020

We have served as the auditor of one or more investment companies in Nuveen Funds since 2002.

25

Nuveen Credit Income Fund

(formerly known as Nuveen High Income Bond Fund)

Portfolio of Investments June 30, 2020

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Principal

Amount (000) | | | Description (1) | | | | | | | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | | | | | | |

| | | | LONG-TERM INVESTMENTS – 95.8% | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| | | | CORPORATE BONDS – 88.5% | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| | | | Aerospace & Defense – 0.8% | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| $ | 1,350 | | | Bombardier Inc, 144A | | | | | | | | | | | 7.875% | | | | 4/15/27 | | | | B | | | $ | 884,250 | |

| | | | | | | |

| | 275 | | | Howmet Aerospace Inc | | | | | | | | | | | 6.875% | | | | 5/01/25 | | | | BBB– | | | | 298,683 | |

| | | | | | | |

| | 250 | | | TransDigm Inc, 144A | | | | | | | | | | | 8.000% | | | | 12/15/25 | | | | Ba3 | | | | 262,748 | |

| | 1,875 | | | Total Aerospace & Defense | | | | | | | | | | | | | | | | | | | | | | | 1,445,681 | |

| | | | | | | |

| | | | Airlines – 1.3% | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| | 900 | | | Delta Air Lines Inc, 144A | | | | | | | | | | | 7.000% | | | | 5/01/25 | | | | Baa2 | | | | 929,041 | |

| | | | | |

| | 1,400 | | | Mileage Plus Holdings LLC / Mileage Plus Intellectual Property Assets Ltd, 144A | | | | 6.500% | | | | 6/20/27 | | | | Baa3 | | | | 1,403,500 | |

| | 2,300 | | | Total Airlines | | | | | | | | | | | | | | | | | | | | | | | 2,332,541 | |

| | | | | | | |

| | | | Auto Components – 2.9% | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| | 1,000 | | | Adient Global Holdings Ltd, 144A | | | | | | | | | | | 4.875% | | | | 8/15/26 | | | | B | | | | 825,000 | |

| | | | | | | |

| | 200 | | | Adient US LLC, 144A | | | | | | | | | | | 9.000% | | | | 4/15/25 | | | | Ba3 | | | | 215,440 | |

| | | | | | | |

| | 150 | | | Clarios Global LP, 144A | | | | | | | | | | | 6.750% | | | | 5/15/25 | | | | B1 | | | | 156,000 | |

| | | | | | |

| | 1,500 | | | Panther BF Aggregator 2 LP / Panther Finance Co Inc, 144A | | | | | | | | 8.500% | | | | 5/15/27 | | | | CCC+ | | | | 1,507,425 | |

| | | | | | | |

| | 175 | | | Dana Inc | | | | | | | | | | | 5.375% | | | | 11/15/27 | | | | BB+ | | | | 173,688 | |

| | | | | | | |

| | 225 | | | Dana Inc | | | | | | | | | | | 5.625% | | | | 6/15/28 | | | | BB+ | | | | 223,355 | |

| | | | | | | |

| | 700 | | | Goodyear Tire & Rubber Co | | | | | | | | | | | 9.500% | | | | 5/31/25 | | | | BB– | | | | 749,875 | |

| | | | | |

| | 1,475 | | | IHO Verwaltungs GmbH, 144A, (cash 4.750%, PIK 5.500%) | | | | 4.750% | | | | 9/15/26 | | | | BB+ | | | | 1,445,500 | |

| | 5,425 | | | Total Auto Components | | | | | | | | | | | | | | | | | | | | | | | 5,296,283 | |

| | | | | | | |

| | | | Automobiles – 2.0% | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| | 375 | | | Ford Motor Co | | | | | | | | | | | 8.500% | | | | 4/21/23 | | | | BB+ | | | | 396,562 | |

| | | | | | | |

| | 375 | | | Ford Motor Co | | | | | | | | | | | 9.000% | | | | 4/22/25 | | | | BB+ | | | | 405,469 | |

| | | | | | | |

| | 225 | | | Ford Motor Co, (3) | | | | | | | | | | | 9.625% | | | | 4/22/30 | | | | BB+ | | | | 266,468 | |

| | | | | | | |

| | 1,000 | | | Ford Motor Credit Co LLC | | | | | | | | | | | 5.875% | | | | 8/02/21 | | | | BB+ | | | | 1,009,700 | |

| | | | | | | |

| | 700 | | | Ford Motor Credit Co LLC | | | | | | | | | | | 3.219% | | | | 1/09/22 | | | | BB+ | | | | 680,897 | |

| | | | | | | |

| | 1,000 | | | Ford Motor Credit Co LLC | | | | | | | | | | | 4.063% | | | | 11/01/24 | | | | BB+ | | | | 953,550 | |

| | 3,675 | | | Total Automobiles | | | | | | | | | | | | | | | | | | | | | | | 3,712,646 | |

| | | | | | | |