Exhibit (e)

Group management report

KfW Financial Report 2020 Group management report | 2

Basic information on KfW Group

Overview

KfW Group consists of KfW and five consolidated subsidiaries. KfW is a promotional bank of the Federal Republic of Germany – which owns 80% of KfW while the German Federal States own 20%. The institutional framework for the promotional mandate, including the Federal Republic of Germany’s liability for KfW’s obligations, is defined in the Law Concerning KfW (KfW Law).

KfW promotes sustainable improvement of economic, social and environmental conditions around the world, with an emphasis on the German economy. The focus of KfW’s promotional activities is on the megatrends anchored in KfW’s strategic objectives. A variety of different financing products and services address in particular the areas of climate change and environment, globalisation, social change, digitalisation and innovation, and small and medium-sized enterprises (SMEs). The domestic promotional lending business with enterprises and private individuals is characterised by the on-lending strategy, in which KfW extends loans to commercial banks, which, in turn, lend the funds to the ultimate borrowers. KfW thus does not have its own network of branch offices. It funds its business activities via the national and international money and capital markets. In addition to KfW, the group’s main operating subsidiaries are (i) KfW IPEX-Bank, which provides export and project finance, and (ii) DEG, which is active in promoting the private sector in developing countries and emerging economies. KfW Capital invests in German and European venture capital and venture debt funds in order to strengthen venture and early growth financing in Germany.

In accordance with the business sector structure for KfW Group, the sectors and their main products and services can be presented as follows:

| | |

Mittelstandsbank & Private Kunden (SME Bank & Private Clients) | | – Start-up financing |

| | – Financing of general corporate investments and investments in innovation, |

| | energy and environmental protection |

| | – Education financing |

| | – Financing for housing construction, conversion and refurbishment |

Individualfinanzierung & Öffentliche Kunden (Customised Finance & Public Clients) | | – Financing of municipal and social infrastructure |

| | – Customised corporate financing with equity and debt capital |

| | – Customised financing of banks and promotional institutions |

| | of the federal states |

KfW Capital | | – Investments in German and European venture capital and venture debt funds |

| Export and project finance | | – Financing of German and European export activities |

| | – Financing of projects and investments which |

| | are of special interest for Germany and Europe |

| | – Promotion of developing countries and emerging economies on behalf |

| | of the Federal Government with budget funds and complementary |

| Promotion of developing countries and emerging economies | | market funds raised by KfW |

| | – Financing provided by DEG – Deutsche Investitions- und |

| | Entwicklungsgesellschaft mbH (private sector promotion) |

| Financial markets | | – Securities and money market investments |

| | – Holding arrangements for the Federal Republic of Germany |

| | – Transactions mandated by the Federal Government, loan granted to Greece |

| | – Funding |

| Head office | | – Central interest rate and currency management |

| | – Strategic equity investments |

3 | KfW Financial Report 2020 Group management report | Basic information on KfW Group

Composition of the KfW Group Total assets (IFRS, before consolidation)

| | | | | | | | | | | | | | | | | | |

| | | | | | | 31 Dec. 2020 | | | | | | | | | | 31 Dec. 2019 | | |

| | | | | | | EUR in millions | | | | | | | | | | EUR in millions | | |

| | | | | | | |

| KfW, Frankfurt am Main, Germany | | | | | | 543,099 | | | | | | | | | | 502,495 | | |

| Subsidiaries | | | | | | | | | | | | | | | | | | |

| KfW IPEX-Bank GmbH, Frankfurt am Main (KfW IPEX-Bank), Germany | | | | | | 29,617 | | | | | | | | | | 27,029 | | |

| DEG – Deutsche Investitions- und Entwicklungsgesellschaft mbH, Cologne (DEG), Germany | | | | | | 6,286 | | | | | | | | | | 6,885 | | |

| KfW Beteiligungsholding GmbH, Bonn, Germany | | | | | | 3,209 | | | | | | | | | | 3,307 | | |

| KfW Capital GmbH & Co. KG, Frankfurt am Main, Germany | | | | | | 413 | | | | | | | | | | 254 | | |

| Interkonnektor GmbH, Frankfurt am Main, Germany | | | | | | 376 | | | | | | | | | | 376 | | |

| Investments accounted for using the equity method | | | | | | | | | | | | | | | | | | |

| Microfinance Enhancement Facility S.A., Luxembourg (20.3%), Luxembourg | | | | | | 575 | | | | | | | | | | 614 | | |

| DC Nordseekabel GmbH & Co. KG, Bayreuth (50.0%), Germany | | | | | | 996 | | | | | | | | | | 888 | | |

| Green for Growth Fund, Southeast Europe S.A., Luxembourg (10.0%), Luxembourg | | | | | | 639 | | | | | | | | | | 525 | | |

| AF Eigenkapitalfonds für deutschen Mittelstand GmbH & Co KG, Munich (47.5%), Germany1) | | | | | | 0 | | | | | | | | | | 90 | | |

coparion GmbH & Co. KG, Cologne (16.4%), Germany | | | | | | 126 | | | | | | | | | | 84 | | |

| 1) | KfW’s shares in AF Eigenkapitalfonds für deutschen Mittelstand GmbH & Co. KG were sold in financial year 2020. |

The development of the group’s operating income is determined by KfW.

Strategic objectives 2025

KfW Group has a set of strategic objectives in place that define KfW’s targeted medium-term positioning. This framework encompasses top-level objectives at the overall bank level and serves as a central, binding reference for the strategic orientation of all business sectors, with a five-year horizon. The strategic objectives for 2025 were adopted in 2020.

KfW’s primary objective is sustainable promotion. It aims to transform the economy and society to improve economic, environmental and social living conditions around the world. This primary objective is supported by the two promotional principles of subsidiarity and sustainability.

Subsidiarity means that KfW focuses on eliminating market weaknesses. Putting this principle into practice, KfW strives to consistently maintain high-quality promotional activities. KfW also aims to increase in the volume of new commitments in line with the nominal growth of Germany’s gross domestic product (“GDP”). However, this principle may be overridden in exceptional situations such as the current COVID-19 pandemic, to allow KfW as a promotional bank to take countercyclical action.

With regard to the principle of sustainability, KfW aims to achieve a ranking among the top five national and international promotional banks in the relevant sustainability ratings (Sustainalytics, imug, ISS ESG). In addition, the contributions of KfW’s financing activities to compatibility with the UN’s Sustainable Development Goals (“SDGs”) and the Paris climate agreement are monitored as a part of achieving the climate goals.

Within the framework of these promotional principles, KfW finances projects relating to the following megatrends of our time: climate change and the environment (target environment quota > 38%), globalisation, social change, as well as digitalisation and innovation. In domestic promotion, KfW aims to achieve an SME ratio of > 40% in financing small and medium-sized German enterprises.

KfW Financial Report 2020 Group management report | Basic information on KfW Group | 4

The primary objective is complemented by secondary objectives in the areas of profitability and efficiency, risk and capital, regulation, digitalisation and process efficiency, as well as customer and employee centricity. Agility is considered a fundamental prerequisite for achieving these objectives.

Internal management system

KfW has an integrated strategy and planning process. Conceived as a group-wide strategy process, group business sector planning is KfW Group’s central planning and management tool. Group business sector planning consists of three consecutive sub-processes performed every year: defining objectives, implementation and quality assurance, and finalisation. The overall strategy and planning process includes the collaboration of staff responsible for planning in all areas.

The group-wide strategic objectives set by the Executive Board form the basis for the group’s planning (defining objectives). This system of objectives serves KfW Group as a roadmap, indicating the direction in which KfW would like to develop over the next five years. It defines KfW Group’s medium-term targeted positioning and sets top-level objectives for the entire bank. The strategic objectives are reviewed annually for relevance, completeness and aspiration level and adjusted where necessary – for example, due to changed parameters or newly determined focus areas. Efforts are made, however, to maintain a high degree of consistency to ensure that there are no fundamental changes made to the strategic road map in the course of the annual review. Within this strategic framework, major medium-term strategic initiatives are developed in a base case scenario by the business sectors and subsidiaries, taking into account their statutory requirements. Promised benefits (such as project efficiencies and cost reduction measures) are also considered in business sector planning. Assumptions regarding the future development of determinant factors are made based on a risks and opportunities assessment. This analysis takes into account both external factors (including market development, regulatory requirements, the competitive situation and customer behaviour) and internal factors and resources (including human and technical and organisational resources, promotional expense, primary cost planning and tied-up capital) as well as targeted earnings levels. It involves evaluation of the key business and revenue drivers for the business sectors and the group. The business sectors are also called upon to address the environmental, social and governance risks (“ESG” risks) resulting from their business model and new (strategic) initiatives. The central departments (e.g. information technology, human resources and central services) play important roles in achieving the strategic objectives. By involving these departments, their own strategies are aligned with the strategic objectives. The first regular capital budget in the base case is prepared on a multi-year horizon. This enables identification of any capital bottlenecks arising from strategic considerations or changed parameters, in response to which measures can be agreed on to mitigate such capital shortages. The Executive Board defines top-down objectives for all departments or subsidiaries (with regard to promotion, risk and finances) for the entire planning period based on the assessment and prioritisation of all strategic initiatives from a group perspective. Strategic group-level planning will be expanded to include business strategy scenario analysis. Scenario analysis is a “what if” analysis of a specific, plausible scenario, looking at the interaction of exogenous influencing factors and translating the results of the analysis into management-relevant parameters in new business, earnings and risk / capital. Such scenarios assist in the process of identifying potential risks and opportunities for promotional targets and KfW’s profitability and risk-bearing capacity and enable these factors to be considered in the further planning process if necessary.

The business sectors plan their new business, risks and earnings, and each department its budgets and full time equivalents (“FTEs”) as regards implementation and quality assurance based on the top-down objectives defined by the Executive Board, taking into account any changes in external or internal factors and in close collaboration with Accounting. These plans are checked for consistency with the group’s and business sectors’ objectives. The interest rate forecast plays a key role in shaping KfW’s earnings position. Thus, a high and a low interest rate scenario are also examined in addition to the anticipated base case. The plans are also assessed for future risk-bearing capacity in a second round of regular capital budgeting in a base and stress case over a multi-year horizon. The Executive Board approves the resulting budget or has plans fine-tuned in a revision round if necessary (finalisation). Any changes to the business strategy are subject to consultation with the Risk Controlling department in order to ensure consistency between the business and risk strategy. The group business sector planning process ends when the Executive Board has adopted a final budget for the entire planning period, including the future capital requirement.

The key conclusions from the planning process are incorporated into the business and risk strategies. The management has overall responsibility for formulating and adopting both strategies. The business strategy comprises the group’s strategic objectives for its main business activities as well as important internal and external factors, which

5 | KfW Financial Report 2020 Group management report | Basic information on KfW Group

are included in the strategy process. It also contains the business sectors’ contribution to the strategic objectives and the measures for achieving each objective. Moreover, the business strategy combines the budget at the group and business sector levels. The Executive Board sets out KfW Group’s risk policies in its risk strategy, which is consistent with the business strategy. KfW Group has defined strategic risk objectives for factors including risk-bearing capacity and liquidity. The main risk management approaches and risk tolerance are also incorporated into the risk strategy as a basis for operational risk management. The Executive Board draws up the operating budget for the entire planning period, including any future capital requirement as well as the business and risk strategy. The budget is then presented to the supervisory body (Board of Supervisory Directors) for approval, along with the business and risk strategy for discussion. After the Board of Supervisory Directors has decided on the business and risk strategy, it is appropriately communicated to the staff.

The adoption of the business sector planning serves as a foundation for the group’s qualitative and quantitative objectives. The Executive Board reviews target achievement both on a regular and on an ad hoc basis during the current financial year. The assumptions concerning external and internal factors made when determining the business strategy are also subject to regular checks. The development of relevant control variables, their attainment, and the reasons for any shortfalls are analysed as part of strategic management. Strategic assumptions are reviewed, and a systematic variance analysis of early objectives and forecasts is performed at the beginning of every year. Findings gained from this comparison are incorporated into the next planning process. At mid-year, the integrated forecasting process serves as a comprehensive basis for interim management input on quantitative group variables of strategic importance in line with the strategic objectives (new business, risk and earnings in respect of funding opportunities), while providing a well-founded guide to achieving planned objectives. Ad hoc issues of strategic relevance are also addressed in consultation with the group’s departments. Recommendations for action concerning potential strategy adjustments or optimising the use of resources are made as necessary to the Executive Board by means of the strategic performance report. The results of the analysis are included in further strategy discussions and strategic planning processes. The achievement of objectives is regularly monitored by the Board of Supervisory Directors based on reports submitted under the KfW Bylaws. The commentary in these reports outlines analyses of causes and any potential plans for action. Detailed reports are prepared on a monthly or quarterly basis as part of operational controlling. These comprehensive detailed analyses at group, business sector and/or control portfolio level comprise earnings, cost and FTE developments and are reported to specific departments. Additionally, analyses of significant relevance to overall group performance are also presented directly to the Executive Board. The risk controlling function has been implemented alongside strategic and operational controlling. Early warning systems have been established and mitigation measures defined for all material risk types in line with the risk management requirements set out in the risk strategy. All controlling and monitoring approaches are integrated into risk reporting. The Board of Supervisory Directors receives a risk report quarterly.

Alternative key financial figures used

The KfW Group Management Report contains key financial figures that are not defined in the IFRS. In its strategic objectives, KfW uses key indicators prescribed by accounting standards and supervisory regulations as well as key figures that are geared toward promotion as the core business activity. It also uses key figures in which the temporary effects on results determined and reported in the consolidated financial statements in accordance with IFRS and which KfW does not consider representative, are adjusted.

KfW has defined the following alternative key financial figures:

Promotional business volume

Promotional business volume refers to the commitments of each business sector during the reporting period. In addition to the lending commitments shown in the statement of financial position, promotional business volume comprises loans from Federal Government funds for promotion of developing countries and emerging economies – which are accounted for as trust activities – financial guarantees, equity financing and securities purchases in certain asset classes (green bonds until 2019, SME loan securitisation). Promotional business volume also includes grants committed as part of development aid and in domestic promotional programmes. Allocation to the promotional business volume for the current financial year is generally based on the commitment date of each loan, financial guarantee and grant, and the transaction date of the equity finance and securities transactions. On the other hand, allocation of global loans to the promotional institutions of the federal states (Landesförderinstitute – “LFI”) and BAföG government loans is based on individual drawdown volume and date, instead of the total volume of the contract at the time

KfW Financial Report 2020 Group management report | Basic information on KfW Group | 6

of commitment. In the lending business, financing amounts denominated in foreign currency are converted into euros at the exchange rate on the commitment date, whereas in the securities and equity finance business, the conversion generally occurs at the rate on the transaction date.

See the “Development of KfW Group” economic report or segment reports for a breakdown of promotional business volume by individual segment.

Promotional expense

Promotional expense is understood to mean certain expenses from the two business sectors Mittelstandsbank & Privatkunden (SME Bank & Private Clients) and Individualfinanzierung & Offentliche Kunden (Customised Finance & Public Clients) to achieve KfW’s promotional objectives.

Interest rate reductions accounted for at present value are the key component of KfW’s promotional expenses. KfW grants these reductions for certain domestic promotional loans for new business during the first fixed interest rate period in addition to passing on KfW’s favourable funding conditions (obtained on the strength of its triple-A rating). The difference between the fair value of these promotional loans and the transaction value during the first fixed interest rate period, due to the interest rate being below the market rate, is recognised in profit or loss as an interest expense and accounted for as an adjustment to the carrying amount under the item Financial assets at amortised cost. In addition, the accumulated interest rate reductions over the fixed interest rate period are recognised in Net interest income through profit or loss (see the relevant Notes on KfW’s promotional lending business, financial assets at amortised cost, and provisions).

An additional promotional component (in commission expense) comprises the expense paid in the form of upfront fees to sales partners for processing microloans. Promotional expense also contains disposable and product-related marketing and sales expenses (administrative expense), expenses for innovative digital promotional approaches (commission and administrative expense), and, as of the beginning of 2020, promotional grants awarded as a supplement to the lending business (other operating expense).

Cost/income ratio (before promotional expense)

The cost/income ratio (before promotional expense) comprises administrative expense (excluding promotional expense) in relation to net interest income and net commission income before promotional expense.

The cost/income ratio (“CIR”) shows costs in relation to income and is thus a measure of efficiency. To enable comparison of the CIR with other (non-promotional) institutions, an adjustment for promotional expense is made to the numerator (administrative expense) and denominator (net interest income and net commission income).

Consolidated profit before IFRS effects

Consolidated profit before IFRS effects from hedging is another key financial figure based on Consolidated profit in accordance with IFRS. Derivative financial instruments are entered into for hedging purposes. Under IFRS, the requirements for the recognition and valuation of derivatives and hedges give rise to temporary net gains or losses that are offset over the term as a whole. In KfW’s opinion, such temporary effects on results are not representative as they are caused solely by economically effective hedging relationships.

Consequently, the following reconciliations are performed by eliminating temporary contributions to profit and loss as follows:

| – | Valuation results from micro and macro hedge accounting. |

| – | Net gains or losses from the use of the fair value option to avoid an accounting mismatch in the case of funding including related hedging derivatives. |

| – | Net gains or losses from the fair value accounting of hedges with high economic effectiveness but not qualifying for hedge accounting. |

| – | Net gains or losses from foreign currency translation of foreign currency positions, in accordance with recognition and valuation requirements for derivatives and hedging relationships. |

7 | KfW Financial Report 2020 Group management report | Basic information on KfW Group

Economic report

General economic environment

Due to the coronavirus pandemic, global real domestic product (“GDP”) declined by 3.5% year on year in 2020 according to estimates by the International Monetary Fund (“IMF”) (see table on gross domestic product at constant prices). According to the World Bank’s Global Economic Prospects of January 2021, this is the worst global recession since World War II, with more than 90% of developing countries and emerging economies expected to report a per capita decline in GDP. The lowest volume of the year for both global industrial production and global exports was recorded in Q2, followed by a recovery in Q3 (see table on industrial production). In contrast to past recessions, the service sectors reliant on personal contact have been harder hit than the manufacturing sector, based on an analysis in the IMF’s October 2020 World Economic Outlook.

Gross domestic product at constant prices (year-on-year change in %)

| | | | | | | | | | |

| | | |

| | | | | | 2020 estimate | | | | 2019 | |

| | | | | | in % | | | | in % | |

Global economy* | | | | | –3.5 | | | | 2.8 | |

| * | The IMF aggregates the annual growth rates of GDP at constant prices of each country on the basis of the shares of country-specific GDP at purchasing power parities in the corresponding global aggregate to the growth rate of global real GDP. |

Industrial production and trade (Q4 2019 index = 100)

| | | | | | | | | | | | | | | | |

| | Q1 2020 | | | Q2 2020 | | | Q3 2020 | | | October/

November 2020 | |

Volume of global industrial production* | | | 96 | | | | 89 | | | | 98 | | | | 101 | |

Volume of global manufacturing* | | | 99 | | | | 86 | | | | 98 | | | | 100 | |

| * | In constant USD (2020); seasonally adjusted |

Economic development in the member states of the European Economic and Monetary Union (“EMU”) was also affected by the coronavirus pandemic and the steps taken to contain it. Economic output in the EMU countries measured by price-adjusted GDP fell by 6.8% year on year in 2020, following a 1.3% increase in price-adjusted GDP in 2019. This is the largest decline in price-adjusted GDP since the EMU was formed in 1999 (see table on gross domestic product at constant prices). However, the scale of the recession varied between the member states. For instance, price-adjusted GDP fell further in France, Italy and Spain than in Germany. The European Commission attributes these differences to the national containment measures, economic assistance and the significance of the sectors particularly affected, such as tourism.

Gross domestic product at constant prices, year-on-year change

| | | | | | | | | | | | | | | | | | | | |

| | | | | | 2020 | | | 2019 | | | 2011–2019

average | | | Minimum

since 1999 | |

| | | | | | in % | | | in % | | | in % | | | | |

Euro area | | | | | | | –6.8 | | | | 1.3 | | | | 1.4 | | | | –4.5% (2009) | |

Germany | | | | | | | –5.0 | | | | 0.6 | | | | 1.9 | | | | –5.7% (2009) | |

KfW Financial Report 2020 Group management report | Economic report | 8

Against the backdrop of the coronavirus pandemic, price-adjusted GDP in Germany fell by 5.0% in 2020 compared with the previous year, after growing by 0.6% in 2019 and by 1.9% per year on average for the previous ten years (2010 to 2019 inclusive) (see table on gross domestic product at constant prices). Positive impetus for the rates of change in price-adjusted GDP was only provided by price-adjusted government final consumption expenditure (+3.4%) and price-adjusted gross fixed capital formation in construction (+1.5%) in 2020. In contrast, price-adjusted final consumption expenditure declined (–6.0%), as the number of people in employment located in Germany also fell (–1.1%), along with price-adjusted gross fixed capital formation in machinery and equipment (–12.5%) and price-adjusted gross capital formation in other products (–1.1%). Price-adjusted domestic use declined overall by 4.1% in 2020. Net exports slowed the rate of change of price-adjusted GDP by 1.1 percentage points in 2020, with price-adjusted exports falling further (–9.9%) than price-adjusted imports (–8.6%). From a production perspective, the rate of change of price-adjusted GDP was curbed in particular in 2020 by the decline in price-adjusted gross value added in the manufacturing industry (excluding construction) (–9.7%), the retail, transport and hospitality sector (–6.3%), the business services sector (–7.9%) and other services (–11.3%).

Development in the financial markets was dominated by the coronavirus pandemic in 2020. In response to the emerging economic crisis, the US Federal Reserve lowered its key rate range from 1.50%–1.75% to just 0.00%–0.25% in March 2020. It also injected liquidity into the markets via repos (repurchase agreement operations) and greatly expanded its asset purchases. The European Central Bank (“ECB”) introduced several targeted measures starting in March and gradually increased them over the course of the year, without lowering key interest rates any further (the deposit rate remained at –0.5% throughout 2020). The most important instruments include an expansion of asset purchases, primarily via the newly launched ‘Pandemic Emergency Purchase Programme’ (PEPP), which has provided funds of up to EUR 1.850 billion for asset purchases. The programme involves both government and corporate bonds, which can be purchased very flexibly in terms of maturity, asset class and country of origin. Banks were motivated to lend by improved terms for the ECB’s targeted longer-term refinancing operations (“TLTRO III”). For banks that maintain at least their eligible net lending for a certain period, the interest rate applied to all TLTRO III transactions will be 50 basis points lower than the average deposit facility rate over the same period and in no case above –1%.

In light of these monetary policy measures, the situation on the financial markets eased following its volatile development in the spring of 2020. Money-market interest rates, swap rates and government bond yields declined in the euro area and in the US compared to the previous year. For instance, the 3-month EURIBOR averaged –0.43% in 2020 (2019: –0.36%); the 5-year EUR swap rate averaged –0.35% (2019: –0.14%); and the yield of the 10-year German government bond was –0.47% (2019: –0.21%). In the US, the 3-month LIBOR in 2020 was 0.65% on average for the year, compared with 2.33% in the previous year. The 5-year USD swap rate averaged 0.59% in 2020 compared with 1.94% the previous year, and the yield on 10-year US Treasuries was 0.89% compared with 2.14% the previous year. The yield curves for the EUR and the USD moved in opposite directions as measured by the difference between the yields of 10 and 2-year government bonds. On average in 2020, the curve steepness for German government bonds was 22 bp (2019: 46 bp), whereas US government bonds climbed to 50 bp (2019: 17 bp).

The first quarter initially saw major price losses on the stock markets, but a recovery began after a trough in March. The US S&P 500 index actually reached new highs at the end of 2020, and recorded an annual average of 3,218 points, which was 10% above the prior-year average. At the end of 2020, the German DAX 30 was roughly at the year-end level of 2019. Its 2020 average of 12,339 points was around two points above the prior-year average. The trade-weighted euro gained on average around 2% (against the currencies of the 18 most important trading partners outside the euro area) in 2020, but appreciated somewhat less against the US dollar. The EUR/USD exchange rate (measured in USD per EUR) averaged 1.12 in 2019, but was 1.14 in 2020, representing an increase of 2.0%.

9 | KfW Financial Report 2020 Group management report | Economic report

Development of KfW Group

KfW’s business development in 2020 was characterised by the global coronavirus pandemic, which had a significant impact on the group’s net assets, financial position and results of operations. At the same time, KfW recorded its historically strongest promotional year in terms of volume due to the coronavirus aid programmes, with a promotional business volume of EUR 135.3 billion (2019: EUR 77.3 billion).

As a result of pandemic-related effects in 2020, the earnings position, with a consolidated profit of EUR 0.5 billion, was down significantly on the previous year (EUR 1.4 billion), and therefore below expectations (EUR 0.8 billion). The operating result before valuation (before promotional expense) increased from EUR 1.7 billion to EUR 1.9 billion. This is also reflected in the cost-income ratio (before promotional expense), which declined to 41.8% (2019: 44.0%) as a result of increased income from interest and commissions and a slight increase in administrative expense. The valuation result, which was impacted by valuation effects from the coronavirus pandemic, lowered consolidated profit by EUR 1.2 billion (2019: EUR –0.2 billion).

Consolidated total assets rose by EUR 40.4 billion to EUR 546.4 billion in 2020.

The increase was largely attributable to the rise of EUR 33.9 billion in Net loans and advances to EUR 423.7 billion, which in turn was attributable in the amount of EUR 30 billion to disbursements under the KfW Special Programme 2020. The volume of own issues reported under Certificated liabilities amounted to EUR 425.3 billion (31 Dec. 2019: EUR 436.2 billion). The EUR 0.4 billion increase in equity to EUR 31.8 billion was due especially to consolidated comprehensive income.

Business performance in 2020 was largely characterised by the following developments:

A. High demand for the KfW coronavirus aid programmes

The group reached a historic high in 2020 with a promotional business volume of EUR 135.3 billion (+75%). The main drivers of the strong growth were the measures to absorb the economic consequences of the coronavirus pandemic in Germany and abroad, which accounted for a volume of EUR 50.9 billion.

A key component of the coronavirus assistance is the KfW Special Programme 2020 launched by KfW as part of the government stabilisation measures for the coronavirus pandemic. KfW has provided extensive liquidity support for businesses under this programme, and assumes up to 100% of the risk. The KfW Special Programme 2020 was launched in March 2020 based on existing promotional products such as the KfW corporate loan and the ERP Start-up Loan – Universal. A new product offering additional support to businesses was added in April 2020 on behalf of the Federal Government, the KfW Instant Loan with 100% of the risk assumed by KfW. The new ‘Direct participation for syndicate financing’ programme offers flexible financing to commercial companies for their operating equipment and investments. At the end of 2020, the Federal Government and KfW extended the KfW Special Programme 2020, including the KfW Instant Loan, until 30 June 2021.

KfW also set up funding opportunities to secure the liquidity of start-ups, in order to safeguard jobs and innovation in Germany. Students are receiving temporary support during the COVID-19 pandemic in the form of a reduced interest rate of 0% for their KfW Student Loan. KfW is being compensated by the Federal Government for the loss of interest. The KfW Student Loan has also been opened up to all foreign students. The support measures are mandated transactions in accordance with Article 2 (4) of the Law Concerning KfW (KfW-Gesetz – “KfW Law”) with a full federal guarantee, meaning that KfW is released from all risks and charges associated with granting the loan. Cost-based remuneration was agreed with the Federal Government for the KfW Special Programme 2020, including a processing margin for specific large-volume financings within the programme.

The commitment volume of the KfW Special Programme launched by KfW as part of the government stabilisation measures for the coronavirus pandemic amounted to EUR 44.5 billion by 31 December 2020. Of this, EUR 35.6 billion is attributable to the business sector Mittelstandsbank & Private Kunden (SME Bank & Private Clients) with the KfW Entrepreneur Loan (EUR 28.3 billion), the KfW Instant Loan (EUR 5.8 billion) and the ERP Start-Up Loan (EUR 1.4 billion).

KfW Financial Report 2020 Group management report | Economic report | 10

Commitments under the coronavirus special programme ‘Direct participation for syndicate financing’ reached a volume of EUR 8.4 billion, and commitments under the other coronavirus assistance for domestic business amounted to EUR 1.3 billion for measures for start-ups. A total of EUR 1.1 billion has been committed in student loans since the interest rate was cut. Including coronavirus aid, financing of EUR 106.4 billion (2019: EUR 43.4 billion) was committed in domestic promotional business. In addition to coronavirus aid, the promotional programmes in the area of Energy-efficient Construction and Refurbishment made a particular contribution to growth in promotional business volume in Germany, increasing their volume by 140% to EUR 26.8 billion. Commitments by the subsidiary KfW Capital reached EUR 0.9 billion in 2020, including coronavirus aid under the KfW Special Programme 2020.

International business decreased by 11% to a promotional business volume of EUR 29.0 billion (2019: EUR 32.7 billion). In Export and project finance, the impact of the COVID-19 pandemic on global trade and large areas of the global economy as a whole was reflected in new business, as expected. As a result, commitments of EUR 16.6 billion were below the record amount of the previous year (EUR 22.1 billion), but were maintained at the same level as in the preceding years. At EUR 12.4 billion, the promotion of developing countries and emerging economies was higher than in the previous year (EUR 10.6 billion), with commitments under the Emergency COVID-19 Support Programme for the partner countries of German development cooperation of EUR 4 billion more than offsetting the negative impact of the coronavirus pandemic on new commitments by Financial Cooperation and DEG.

KfW raised EUR 66.4 billion in the capital markets to fund its business activities (2019: EUR 80.6 billion). As part of the KfW Special Programme 2020, KfW accessed new funding sources by participating in federal auctions via the government-owned Economic Stabilisation Fund (Wirtschaftsstabilisierungsfonds – “WSF”) and in the targeted longer-term funding of the Eurosystem via TLTRO III, thereby raising funds in the amount of EUR 39.0 billion (WSF) and EUR 13.4 billion (TLTRO III).

Promotional business volume of KfW Group

| | | | | | | | | | | | | | | | | | |

| | | | | | | |

| | | | | | | 2020 | | | | | | | | | | 2019 | | |

| | | | | | | EUR in billions | | | | | | | | | | EUR in billions | | |

| | | | | | | |

| Domestic business | | | | | | 106.4 | | | | | | | | | | 43.4 | | |

| Mittelstandsbank & Private Kunden (SME Bank & Private Clients) | | | | | | 86.3 | | | | | | | | | | 36.0 | | |

| Individualfinanzierung & Öffentliche Kunden (Customised Finance & Public Clients) | | | | | | 19.2 | | | | | | | | | | 7.2 | | |

| KfW Capital | | | | | | 0.9 | | | | | | | | | | 0.2 | | |

| Financial markets | | | | | | 0.4 | | | | | | | | | | 1.4 | | |

| International business | | | | | | 29.0 | | | | | | | | | | 32.7 | | |

| Export and project finance | | | | | | 16.6 | | | | | | | | | | 22.1 | | |

| Promotion of developing countries and emerging economies | | | | | | 12.4 | | | | | | | | | | 10.6 | | |

| | |

Volume of new commitments1) | | | | | | 135.3 | | | | | | | | | | 77.3 | | |

| 1) | Adjusted for export and project financing refinanced through KfW programme loans. |

B. Impact of the coronavirus pandemic on KfW’s earnings position

The COVID-19 crisis had a major tangible effect on KfW’s earnings position in financial year 2020. The operating result before valuation (before promotional expense) benefited slightly from additional income from the implementation of the KfW Special Programme, while the valuation adjustments resulting from the coronavirus pandemic had a significant adverse effect on the valuation result.

11 | KfW Financial Report 2020 Group management report | Economic report

At EUR 1,855 million (2019: EUR 1,677 million), the Operating result before valuation (before promotional expense) was 11% above the prior-year level and exceeded the target by 19%. This was due to the increase by EUR 117 million to EUR 2,601 million in net interest income (before promotional expense) and by EUR 72 million to EUR 584 million in net commission income (before promotional expense). The increase in net commission income (before promotional expense) is primarily due to the cost-based remuneration for implementing the KfW Special Programme (EUR 79 million) and the processing margins collected for specific financings under the KfW Special Programme 2020 (EUR 20 million). Administrative expense (before promotion expense) rose by EUR 10 million to EUR 1,330 million and was lower than projected (EUR 1,409 million).

The coronavirus pandemic had a significant impact on earnings as regards risk provisions for lending business and the valuation of the equity investment portfolio. For instance, risk provisions for lending business resulted in a negative impact on earnings in 2020 of EUR 777 million, which was above the projected standard risk costs (EUR 466 million) and greater than the prior-year figure (2019: EUR –174 million). The provisions created were primarily general risk provisions in stages 1 and 2 with a net addition of EUR 412 million (2019: EUR 40 million) and the provision for imminent risks in stage 3 of EUR 403 million (2019: EUR 201 million). In order to appropriately reflect the effects of the coronavirus pandemic in the measurement of risk provisions, the risk parameters on which the calculation is based are adjusted by taking macroeconomic factors into account. The main reasons for the increased risk provisions are the sector expectations for aviation and shipping as well as for SMEs and start-ups, which are included in the adjustment of default probabilities. Given the current economic environment, this led to higher probabilities of default and therefore to increased stage transfers. Combined with the effects of rating downgrades and the first coronavirus-induced defaults, the total pandemic-related expenses resulting from risk provisions amounted to EUR 499 million in 2020. The COVID-19 effect was calculated as the deviation of risk provisions for 2020 from the average risk provisions of the last seven years adjusted for non-recurring effects.

In addition, markdowns in the equity investment portfolio fully measured at fair value led to adverse effects on the valuation result. As of 31 March 2020, when the global economic impact from the spread of the coronavirus was not yet appropriately reflected in the valuation techniques used as a standard, a markdown of EUR 645 million was determined based on historical market developments in crisis situations. The markdown was replaced by individual valuations during the second half of the year, as it was possible to reliably estimate the effects of the pandemic in full on the individual investments. As part of the transition to the standard valuation techniques and individual valuations of the investments by the end of the year, the coronavirus-related charges to earnings from the valuation of the entire equity investment portfolio were reduced to EUR 348 million. Taking into account the 2020 valuation effects unrelated to the coronavirus in the amount of EUR 67 million, the 2020 valuation result for the equity investment portfolio is EUR –281 million.

Overall, COVID-19 effects on KfW’s consolidated profit in 2020 amounted to EUR 801 million.

C. Further decreased promotional expense in the low interest rate environment

KfW’s domestic promotional expense, which has a negative impact on KfW Group’s earnings position, was EUR 88 million in financial year 2020 (2019: EUR 159 million), and thus significantly lower than projected (EUR 341 million). This was primarily the result of a decline in interest rate reductions (EUR 54 million; 2019: EUR 137 million), due in particular to the limited need in the low-interest environment for interest rate reductions to achieve our promotional business volume target.

KfW Financial Report 2020 Group management report | Economic report | 12

The following key figures provide an overview of key financial figure development in 2020:

Key financial figures of KfW Group

| | | | | | | | | | | | | | | | | | |

| | | | | | | 2020 | | | | | | | | | | 2019 | | |

| Key figures of the income statement | | | | | | EUR in millions | | | | | | | | | | EUR in millions | | |

| | | | | | | |

| Operating result before valuation (before promotional expense) | | | | | | 1,855 | | | | | | | | | | 1,677 | | |

| Operating result after valuation (before promotional expense) | | | | | | 691 | | | | | | | | | | 1,503 | | |

| Promotional expense | | | | | | 88 | | | | | | | | | | 159 | | |

| Consolidated profit | | | | | | 525 | | | | | | | | | | 1,367 | | |

| Cost-income ratio (before promotional expense)1) | | | | | | 41.8% | | | | | | | | | | 44.0% | | |

| | | | | | | |

| | | | | | | 2020 | | | | | | | | | | 2019 | | |

| Key economic figures | | | | | | EUR in millions | | | | | | | | | | EUR in millions | | |

| | | | | | | |

| Consolidated profit before IFRS effects | | | | | | 633 | | | | | | | | | | 1,447 | | |

| | | | | | | |

| | | | | | | 31. Dec. 2020 | | | | | | | | | | 31. Dec. 2019 | | |

| Key figures of the statement of financial position | | | | | | EUR in billions | | | | | | | | | | EUR in billions | | |

| | | | | | | |

| Total assets | | | | | | 546.4 | | | | | | | | | | 506.0 | | |

| Volume of lending | | | | | | 543.1 | | | | | | | | | | 486.2 | | |

| Volume of business | | | | | | 673.8 | | | | | | | | | | 610.7 | | |

| Equity | | | | | | 31.8 | | | | | | | | | | 31.4 | | |

Equity ratio | | | | | | 5.8% | | | | | | | | | | 6.2% | | |

| 1) | Administrative expense (before promotional expense) in relation to adjusted income. |

| | Adjusted income is calculated from net interest income and net commission income (in each case before promotional expense). |

Comparison with the previous year’s forecast

| | | | | | | | | | | | | | |

| | | | | | | 2019 Forecast for 2020 | | | | | | 2020 Actual | | |

| | | | | | | | | | | | | | |

| New business | | | | | | | | | | | | | | |

| Promotional business volume | | | | | | EUR 77.0 billion | | | | | | EUR 135.3 billion | | |

| | | | | | | |

| Funding | | | | | | approx. EUR 75 billion | | | | | | EUR 118.8 billion | | |

| | | | | | | |

| Result | | | | | | | | | | | | | | |

| Consolidated profit before IFRS effects | | | | | | EUR 0.8 billion | | | | | | EUR 0.6 billion | | |

| Strategic target consolidated profit | | | | | | EUR 1.0 billion | | | | | | EUR 0.5 billion | | |

| Net interest income (before promotional expense) | | | | | | at 2019 level | | | | | | +5% | | |

| Low interest environment | | | | | | detrimental | | | | | | detrimental | | |

| Net commission income (before promotional expense) | | | | | | at 2019 level | | | | | | +14% | | |

| Administrative expense (before promotional expense) | | | | | | approx. EUR 1.4 billion | | | | | | EUR 1,330 million | | |

| CIR (before promotional expense) | | | | | | 48.0% | | | | | | 41.8% | | |

| Risk provisions for lending business | | | | | | < standard risk costs higher than 2019 | | | | | | EUR – 777 million | | |

Promotional expense | | | | | | EUR 0.3 billion | | | | | | EUR 0.1 billion | | |

The main differences between the forecasts from the Financial Report 2019 and the actual business development in 2020 are presented in the Economic report.

13 | KfW Financial Report 2020 Group management report | Economic report

Development of earnings position

The earnings position in 2020 was characterised by a year-on-year increase in the operating result combined with a decline in the valuation result due to the coronavirus pandemic. This resulted in a consolidated profit of EUR 0.5 billion, which is below both the prior-year figure (EUR 1.4 billion) and the target (EUR 0.8 billion).

Reconciliation of internal earnings position (before promotional expense)

with external earnings position (after promotional expense) for financial year 2020

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | Reconciliation | | | | | | | | | | | | | | | | | |

| | | | | | | | | EUR in millions | | | | | | | | EUR in millions | | | | | | | | EUR in millions | | | | | | | | | |

| | | | | | | | | | | | | |

| Net interest income (before promotional expense) | | | | | | | | | | 2,601 | | | | | | | | | | –54 | | | | | | | | | | 2,547 | | | | | | | | Net interest income | | |

| | | | | | | | | | | | | |

| Net commission income (before promotional expense) | | | | | | | | | | 584 | | | | | | | | | | –11 | | | | | | | | | | 573 | | | | | | | | Net commission income | | |

| | | | | | | | | | | | | |

| Administrative expense (before promotional expense) | | | | | | | | | | 1,330 | | | | | | | | | | 12 | | | | | | | | | | 1,342 | | | | | | | | Administrative expense | | |

| | | | | | | | | | | | | |

| Operating result before valuation (before promotional expense) | | | | | | | | | | 1,855 | | | | | | | | | | –76 | | | | | | | | | | 1,778 | | | | | | | | Operating result before valuation | | |

| | | | | | | | | | | | | |

| Risk provisions for lending business | | | | | | | | | | –777 | | | | | | | | | | –5 | | | | | | | | | | –781 | | | | | | | | Net gains/losses from risk provisions | | |

| | | | | | | | | | | | | |

| Net gains/losses from hedge accounting | | | | | | | | | | 16 | | | | | | | | | | | | | | | | | | | | 16 | | | | | | | | Net gains/losses from hedge accounting | | |

| | | | | | | | | | | | | |

| Other financial instruments at fair value through profit or loss | | | | | | | | | | –428 | | | | | | | | | | | | | | | | | | | | –428 | | | | | | | | Net gains/losses from other financial instruments at fair value through profit or loss | | |

| | | | | | | | | | | | | |

| Securities and investments | | | | | | | | | | –6 | | | | | | | | | | 5 | | | | | | | | | | –1 | | | | | | | | Net gains/losses from disposal of financial assets at amortised cost | | |

| | | | | | | | | | | | | |

| Net gains/losses from investments accounted for using the equity method | | | | | | | | | | 31 | | | | | | | | | | | | | | | | | | | | 31 | | | | | | | | Net gains/losses from investments accounted for using the equity method | | |

| | | | | | | | | | | | | |

| Operating result after valuation (before promotional expense) | | | | | | | | | | 691 | | | | | | | | | | –76 | | | | | | | | | | 614 | | | | | | | | Operating result after valuation | | |

| | | | | | | | | | | | | |

| Net other operating income or loss (before promotional expense) | | | | | | | | | | –2 | | | | | | | | | | –12 | | | | | | | | | | –14 | | | | | | | | Net other operating income or loss | | |

| | | | | | | | | | | | | |

| Profit/loss from operating activities (before promotional expense) | | | | | | | | | | 688 | | | | | | | | | | –88 | | | | | | | | | | 600 | | | | | | | | Profit/loss from operating activities | | |

| | | | | | | | | | | | | |

| Promotional expense | | | | | | | | | | 88 | | | | | | | | | | –88 | | | | | | | | | | 0 | | | | | | | | – | | |

| | | | | | | | | | | | | |

| Taxes on income | | | | | | | | | | 76 | | | | | | | | | | | | | | | | | | | | 76 | | | | | | | | Taxes on income | | |

| | | | | | | | | | | | | |

| Consolidated profit | | | | | | | | | | 525 | | | | | | | | | | | | | | | | | | | | 525 | | | | | | | | Consolidated profit | | |

| | | | | | | | | | | | | |

| Temporary net gains/losses from hedge accounting | | | | | | | | | | –109 | | | | | | | | | | | | | | | | | | | | –109 | | | | | | | | Temporary net gains/losses from hedge accounting | | |

| Consolidated profit before IFRS effects | | | | | | | | | | 633 | | | | | | | | | | | | | | | | | | | | 633 | | | | | | | | Consolidated profit before IFRS effects | | |

KfW Financial Report 2020 Group management report | Economic report | 14

Reconciliation of internal earnings position (before promotional expense)

with external earnings position (after promotional expense) for financial year 2019

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | Reconciliation | | | | | | | | | | | | | | | | | |

| | | | | | | | | EUR in millions | | | | | | | | EUR in millions | | | | | | | | EUR in millions | | | | | | | | | |

| | | | | | | | | | | | | |

| Net interest income (before promotional expense) | | | | | | | | | | 2,484 | | | | | | | | | | –137 | | | | | | | | | | 2,347 | | | | | | | | Net interest income | | |

| | | | | | | | | | | | | |

| Net commission income (before promotional expense) | | | | | | | | | | 512 | | | | | | | | | | –13 | | | | | | | | | | 499 | | | | | | | | Net commission income | | |

| | | | | | | | | | | | | |

| Administrative expense (before promotional expense) | | | | | | | | | | 1,320 | | | | | | | | | | 9 | | | | | | | | | | 1,328 | | | | | | | | Administrative expense | | |

| | | | | | | | | | | | | |

| Operating result before valuation (before promotional expense) | | | | | | | | | | 1,677 | | | | | | | | | | –159 | | | | | | | | | | 1,518 | | | | | | | | Operating result before valuation | | |

| | | | | | | | | | | | | |

| Risk provisions for lending business | | | | | | | | | | –174 | | | | | | | | | | 1 | | | | | | | | | | –173 | | | | | | | | Net gains/losses from risk provisions | | |

| Net gains/losses from hedge accounting | | | | | | | | | | –1 | | | | | | | | | | | | | | | | | | | | –1 | | | | | | | | Net gains/losses from hedge accounting | | |

| | | | | | | | | | | | | |

| Other financial instruments at fair value through profit or loss | | | | | | | | | | –9 | | | | | | | | | | | | | | | | | | | | –9 | | | | | | | | Net gains/losses from other financial instruments at fair value through profit or loss | | |

| | | | | | | | | | | | | |

| Securities and investments | | | | | | | | | | –5 | | | | | | | | | | –1 | | | | | | | | | | –6 | | | | | | | | Net gains/losses from disposal of financial assets at amortised cost | | |

| | | | | | | | | | | | | |

| Net gains/losses from investments accounted for using the equity method | | | | | | | | | | 15 | | | | | | | | | | | | | | | | | | | | 15 | | | | | | | | Net gains/losses from investments accounted for using the equity method | | |

| | | | | | | | | | | | | |

| Operating result after valuation (before promotional expense) | | | | | | | | | | 1,503 | | | | | | | | | | –159 | | | | | | | | | | 1,344 | | | | | | | | Operating result after valuation | | |

| | | | | | | | | | | | | |

| Net other operating income or loss | | | | | | | | | | 46 | | | | | | | | | | | | | | | | | | | | 46 | | | | | | | | Net other operating income or loss | | |

| | | | | | | | | | | | | |

| Profit/loss from operating activities (before promotional expense) | | | | | | | | | | 1,549 | | | | | | | | | | –159 | | | | | | | | | | 1,391 | | | | | | | | Profit/loss from operating activities | | |

| | | | | | | | | | | | | |

| Promotional expense | | | | | | | | | | 159 | | | | | | | | | | –159 | | | | | | | | | | 0 | | | | | | | | – | | |

| | | | | | | | | | | | | |

| Taxes on income | | | | | | | | | | 23 | | | | | | | | | | | | | | | | | | | | 23 | | | | | | | | Taxes on income | | |

| | | | | | | | | | | | | |

| Consolidated profit | | | | | | | | | | 1,367 | | | | | | | | | | | | | | | | | | | | 1,367 | | | | | | | | Consolidated profit | | |

| | | | | | | | | | | | | |

| Temporary net gains/losses from hedge accounting | | | | | | | | | | –80 | | | | | | | | | | | | | | | | | | | | –80 | | | | | | | | Temporary net gains/losses from hedge accounting | | |

| Consolidated profit before IFRS effects | | | | | | | | | | 1,447 | | | | | | | | | | | | | | | | | | | | 1,447 | | | | | | | | Consolidated profit before IFRS effects | | |

At EUR 1,855 million (2019: EUR 1,677 million), the Operating result before valuation (before promotional expense) was above the prior-year level and the target (EUR 1,556 million).

At EUR 2,601 million, Net interest income (before promotional expense) increased compared to the 2019 figure (EUR 2,484 million). The increase was due to interest rate and spread management as well as interest margin income in the lending business. In contrast, return on equity declined.

Net commission income (before promotional expense) amounted to EUR 584 million, which is higher than the 2019 figure (EUR 512 million) and higher than expected (EUR 508 million). This was largely attributable to the cost-based remuneration for the implementation of the KfW Special Programme (EUR 79 million) and the processing margins collected for specific financings under this programme (EUR 20 million). The remuneration from the Federal Government was offset by related administrative expense.

Administrative expense (before promotional expense) increased slightly from EUR 1,320 million to EUR 1,330 million, but was lower than expected (EUR 1,409 million). Personnel expense amounted to EUR 770 million, which is above the previous year’s figure of EUR 749 million. Non-personnel expense (before promotional expense) declined to EUR 560 million (2019: EUR 571 million). The savings of EUR 79 million in administrative expense against budget resulted from a lower-than-projected increase in FTEs and lower costs for external capacity support.

15 | KfW Financial Report 2020 Group management report | Economic report

The cost-income ratio before promotional expense decreased to 41.8% (2019: 44.0%), mainly due to the overall increase in operating income and only slightly increased expenditure. Adjusted for income and expenses from products for which cost-based remuneration has been agreed with the Federal Government, the cost-income ratio for 2020 amounts to 30.0% (2019: 36.0%).

KfW Group’s risk provisions for lending business resulted in a negative impact on earnings in 2020 of EUR 777 million, which was greater than in the previous year (2019: EUR 174 million), and above the projected standard risk costs (EUR 466 million) due to the economic effects of the coronavirus pandemic. Expenses resulting from risk provisions for lending business largely related to the subsidiary DEG in the business sector Promotion of developing countries and emerging economies, and to the business sector Export and project finance.

Net additions to the provision for imminent credit risks (stage 3) including direct write-offs increased by EUR 201 million year on year (2019: EUR 202 million) to EUR 403 million, and primarily related to the business sector Export and project finance with additions of EUR 212 million (2019: reversals of EUR 17 million) and to DEG with additions of EUR 95 million (2019: EUR 109 million). The business sector SME Bank & Private Clients required an addition of EUR 80 million (2019: EUR 114 million). Of this figure, EUR 67 million was attributable to education financing (2019: EUR 86 million).

Net additions to risk provisions of EUR 34 million (2019: EUR –32 million) in stage 1 and EUR 378 million (2019: EUR 72 million) in stage 2 in particular reflect the economic effects of the coronavirus pandemic. In the first quarter of 2020, these effects resulted from the inclusion of the changed macroeconomic environment due to the pandemic in the measurement of risk provisions. In the second quarter of 2020, these effects were due to rating downgrades.

At EUR 60 million, income from recoveries of loans previously written off was below that of the previous year (2019: EUR 77 million). Of this amount, EUR 41 million was attributable to the business sector SME Bank & Private Clients and EUR 16 million to the business sector Promotion of developing countries and emerging economies.

Risk provisions increased to EUR 2.3 billion in financial year 2020 (2019: EUR 1.7 billion), of which EUR 1.3 billion related to provisions for imminent risks in stage 3 (2019: EUR 1.2 billion). Provisions for individual risks in stage 2 that cannot be allocated increased from EUR 0.2 billion to EUR 0.5 billion, and in stage 1 from EUR 0.3 billion to EUR 0.4 billion.

The net losses from hedge accounting and other financial instruments at fair value through profit or loss amounted to EUR 412 million (2019: EUR 10 million) and in financial year 2020 were primarily driven by negative coronavirus-related valuation effects from the equity investment portfolio and purely IFRS-related effects from the measurement of derivatives used for hedging purposes.

The equity investment portfolio measured at fair value through profit or loss was influenced by both the negative coronavirus-related performance of investments and exchange rate-induced reductions in value, particularly due to the depreciation of the US dollar. Overall, it generated expenditure of EUR 312 million (2019: income of EUR 79 million). This development is primarily due to the activities in the business sector Promotion of developing countries and emerging economies, with negative valuation effects of EUR 380 million (2019: EUR +44 million). Of DEG’s negative contribution of EUR 334 million, EUR 150 million was attributable to exchange rate-induced reductions in value.

Net income offset net expenses in foreign currency translation (2019: net expenses of EUR 6 million).

Hedge accounting and borrowings recognised at fair value, including derivatives used for hedging purposes, resulted in net expenses of EUR 109 million (2019: EUR 80 million). The mark-to-market derivatives are part of economically hedged positions. However, if the other part of the hedging relationship cannot be carried at fair value or different valuation methods and parameters have to be applied, this inevitably results in temporary fluctuations in income that are fully offset over the term of the transactions.

The result from the valuation of securities at fair value declined to EUR –5 million (2019: EUR 0 million).

In the case of securities not carried at fair value, developments in the financial markets resulted in a net positive difference of EUR 48 million between the carrying amount and the fair value (2019: EUR 42 million). This development is partly attributable to increases in the value of covered bonds.

KfW Financial Report 2020 Group management report | Economic report | 16

There were net gains of EUR 30 million (2019: EUR 10 million) from securities and investments as well as from investments accounted for using the equity method. Investments accounted for using the equity method contributed EUR 31 million to the result. This was attributable in particular to the performance of the business sector Export and project finance and the business sector Promotion of developing countries and emerging economies, which was offset by the negative performance of the business sector Individualfinanzierung & Öffentliche Kunden (Customised Finance & Public Clients).

Net other operating income (before promotional expense) was EUR –2 million, which was down on the previous year’s figure (2019: EUR 46 million).

At EUR 88 million in 2020, KfW’s domestic promotional expense, which has a negative impact on KfW Group’s earnings position, was below both the prior-year level (2019: EUR 159 million) and projections (EUR 341 million).

Interest rate reductions are the key component of KfW’s promotional expense. KfW grants these for certain domestic promotional loans during the first fixed-interest-rate period, which has a negative effect on its earnings position, in addition to passing on its funding conditions which are influenced by its triple-A rating. The volume of interest rate reductions was EUR 54 million in 2020, which was below both the prior-year figure (2019: EUR 137 million) and the projected figure (EUR 311 million). This was partly due to the low demand for interest rate-reduced promotional loans. Also, due to the persistently low level of interest rates, no additional stimulus in the promotional business was necessary in order to achieve the promotional objectives.

In addition to its lending business, KfW provided promotional grants, in particular for the ERP Digitalisation and Innovation programme, totalling EUR 12 million in financial year 2020, which was recognised as promotional expense in Net other operating income.

Moreover, promotional expenses reported in net commission income and administrative expense were incurred in the amount of EUR 23 million (2019: EUR 22 million). This spending was aimed, among other things, at the sale of KfW’s promotional products.

Accounting for the net income tax result of EUR –76 million (EUR 2019: EUR –23 million), which was largely attributable to impairment of deferred tax assets, the consolidated profit of EUR 525 million was lower than in the previous year (EUR 1,367 million) and below expectations of EUR 839 million.

Consolidated profit before IFRS effects from hedging is another key financial figure based on Consolidated profit in accordance with IFRS to reflect the fact that KfW uses derivative financial instruments solely for hedging purposes. Under IFRS, the requirements for the recognition and valuation of derivatives and hedges give rise to temporary net gains or losses that are offset over the term as a whole. Against this backdrop, the IFRS effects from hedging relationships amounting to EUR –109 million (2019: EUR –80 million) are eliminated.

The reconciled earnings position amounted to a profit of EUR 633 million (2019: EUR 1,447 million). The marked decline in consolidated comprehensive income is primarily due to the effects of the coronavirus pandemic. The result is therefore below the sustainable earnings potential of EUR 1.0 billion.

17 | KfW Financial Report 2020 Group management report | Economic report

Development of net assets

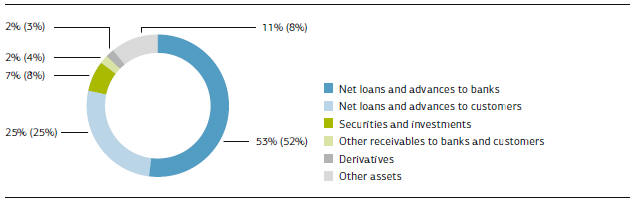

Lending to banks and customers accounted for 78% of the group’s assets as of 31 December 2020 (2019: 77%).

Assets as of 31 December 2020 (31 Dec. 2019)

The volume of lending increased significantly compared to the previous year, amounting to EUR 543.1 billion.

Volume of lending

| | | | | | | | | | | | | | |

| | | | | | | |

| | | | | | | 31 Dec. 2020 | | | | | | 31 Dec. 2019 | | |

| | | | | | | EUR in millions | | | | | | EUR in millions | | |

| | | | | | | |

| Loans and advances | | | | | | 425,880 | | | | | | 391,550 | | |

| Risk provisions for lending business | | | | | | –2,130 | | | | | | –1,670 | | |

| Net loans and advances | | | | | | 423,749 | | | | | | 389,881 | | |

| Contingent liabilities from financial guarantees | | | | | | 2,808 | | | | | | 2,636 | | |

| Irrevocable loan commitments | | | | | | 105,282 | | | | | | 82,052 | | |

| Loans and advances held in trust | | | | | | 11,239 | | | | | | 11,679 | | |

Total | | | | | | 543,078 | | | | | | 486,248 | | |

Loans and advances increased by EUR 33.9 billion in 2020, of which around EUR 30 billion was attributable to the KfW Special Programme 2020, with the KfW Entrepreneur Loan and KfW Instant Loan programmes and the KfW Direct participation programme contributing a total of around EUR 29 billion. Overall, disbursements in new lending business more than compensated for unscheduled repayments (EUR 11.5 billion; 2019: EUR 11.6 billion) and scheduled repayments. At EUR 423.7 billion, Net loans and advances accounted for 78% of lending volume.

Contingent liabilities from financial guarantees were EUR 2.8 billion, up EUR 0.2 billion on the prior-year figure (2019: EUR 2.6 billion). Irrevocable loan commitments rose by EUR 23.2 billion to EUR 105.3 billion largely as a result of the KfW Special Programme 2020 with EUR 15.0 billion. The main drivers here too were the KfW Entrepreneur Loan, the Direct participation programme and the KfW Instant Loan, with a total of EUR 13.3 billion. Within assets held in trust, the volume of loans and advances held in trust, which primarily comprised loans to promote developing countries financed by budget funds provided by the Federal Republic of Germany, decreased by EUR 0.4 billion to EUR 11.2 billion.

At EUR 10.7 billion, other loans and advances to banks and customers were EUR 9.0 billion below the previous year’s amount of EUR 19.8 billion. This includes, in particular, short-term secured and unsecured investments held for general liquidity management purposes and in connection with collateral management in the derivatives business. The decline mainly affected short-term, uncollateralised investments.

The total amount of securities and investments, at EUR 38.8 billion, was 3% above the previous year’s level.

KfW Financial Report 2020 Group management report | Economic report | 18

Securities and investments

| | | | | | | | | | | | | | |

| | | | | | | 31 Dec. 2020 | | | | | | 31 Dec. 2019 | | |

| | | | | | | EUR in millions | | | | | | EUR in millions | | |

| | | | | | | |

| Bonds and other fixed-income securities | | | | | | 35,779 | | | | | | 34,511 | | |

| Shares and other non-fixed income securities | | | | | | 0 | | | | | | 0 | | |

| Equity investments | | | | | | 3,016 | | | | | | 3,242 | | |

| Shares in non-consolidated subsidiaries | | | | | | 48 | | | | | | 43 | | |

Total | | | | | | 38,844 | | | | | | 37,795 | | |

The securities portfolio, which increased by 4% in financial year 2020, accounted for a significant portion of securities and investments. Of the increase in the portfolio, EUR 0.9 billion was due to the increase in money-market securities to EUR 2.7 billion, and EUR 0.4 billion to the increase in bonds and other fixed-income securities to EUR 33.1 billion. Equity investments, in contrast, fell by EUR 0.2 billion to EUR 3.0 billion.

Derivatives with positive fair values, which are primarily used to hedge refinancing transactions, declined from EUR 16.2 billion in 2019 to EUR 13.3 billion. This was a result of value adjustments from micro hedging decreasing from EUR 10.9 billion to EUR 8.0 billion.

KfW increased its balances with central banks by EUR 16 billion to EUR 44.2 billion as a precautionary measure, to ensure the expected servicing of coronavirus aid measures and to be able to react on short notice. There were only minor changes in the other asset line items in the statement of financial position.

Development of financial position

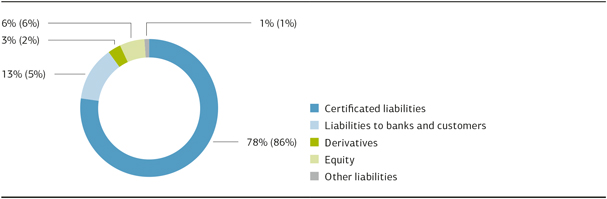

KfW Group’s funding strategy in the national and international capital markets is based on three pillars: “benchmark bonds in euros and US dollars”, “other public bonds” and “private placements”. As part of the KfW Special Programme 2020, KfW accessed new funding sources in the reporting year by participating in federal auctions via the government-owned WSF and in the targeted longer-term funding of the Eurosystem via TLTRO III. The share of total assets accounted for by funding in the form of certificated liabilities therefore declined to 78% (previous year: 86%).

Financial position as of 31 December 2020 (31 Dec. 2019)

Borrowings increased by EUR 35.1 billion to EUR 496.4 billion.

19 | KfW Financial Report 2020 Group management report | Economic report

Borrowings

| | | | | | | | | | | | | | |

| | | | | | | |

| | | | | | | 31 Dec. 2020 | | | | | | 31 Dec. 2019 | | |

| | | | | | | EUR in millions | | | | | | EUR in millions | | |

| | | | | | | |

| Short-term funds | | | | | | 43,988 | | | | | | 44,000 | | |

Bonds and notes | | | | | | 383,975 | | | | | | 395,557 | | |

Other funding | | | | | | 68,394 | | | | | | 21,663 | | |

Total | | | | | | 496,357 | | | | | | 461,221 | | |

Funds raised in the form of certificated liabilities declined by EUR 10.9 billion to EUR 425.3 billion. Of this decline, EUR 11.6 billion was a result of the low volume of medium and long-term bonds and notes issued, which nevertheless remain the group’s principal source of funding. At year-end 2020, such funds amounted to EUR 384.0 billion (31 Dec. 2019: EUR 395.6 billion) and accounted for 77% of borrowings. Short-term issues of commercial paper increased by EUR 0.7 billion to EUR 41.3 billion. Total short-term funds, including demand deposits and term deposits, amounted to EUR 44.0 billion. The new funding sources tapped in connection with the KfW Special Programme 2020 were the main drivers of an increase of EUR 46.7 billion in Other funding to EUR 68.4 billion. In addition to promissory note loans (Schuldscheindarlehen) from banks and customers, which increased by EUR 38.9 billion to EUR 44.4 billion year on year (largely WSF funding), this consisted mainly of repurchase agreements of EUR 13.3 billion (largely TLTRO funding) (2019: EUR 0.2 billion) and cash collateral received of EUR 4.9 billion (31 Dec. 2019: EUR 9.9 billion), primarily to reduce counterparty risk from the derivatives business and liabilities to the Federal Republic of Germany.

The carrying amounts of derivatives with negative fair values, which were primarily used to hedge loans, increased by EUR 4.5 billion, from EUR 9.1 billion at year-end 2019, primarily due to changes in market parameters, and amounted to EUR 13.7 billion at year-end 2020.

There were only minor changes in the other liability line items in the statement of financial position.

At EUR 31.8 billion, equity was EUR 0.4 billion above the level of 31 December 2019 of EUR 31.4 billion. The increase resulted in particular from consolidated profit (EUR 0.5 billion). The equity ratio decreased year on year from 6.2% to 5.8% as of 31 December 2020.

Equity

| | | | | | | | | | | | | | |

| | | | | | | |

| | | | | | | 31 Dec. 2020 | | | | | | 31 Dec. 2019 | | |

| | | | | | | EUR in millions | | | | | | EUR in millions | | |

| | | | | | | |

Paid-in subscribed capital | | | | | | 3,300 | | | | | | 3,300 | | |

Capital reserve | | | | | | 8,447 | | | | | | 8,447 | | |

Reserve from the ERP Special Fund | | | | | | 1,191 | | | | | | 1,191 | | |

Retained earnings | | | | | | 19,411 | | | | | | 18,742 | | |

Fund for general banking risks | | | | | | 600 | | | | | | 600 | | |

Revaluation reserves | | | | | | –1,151 | | | | | | –918 | | |

Total | | | | | | 31,797 | | | | | | 31,362 | | |

The consolidated profit was allocated to retained earnings.

KfW Financial Report 2020 Group management report | Economic report | 20

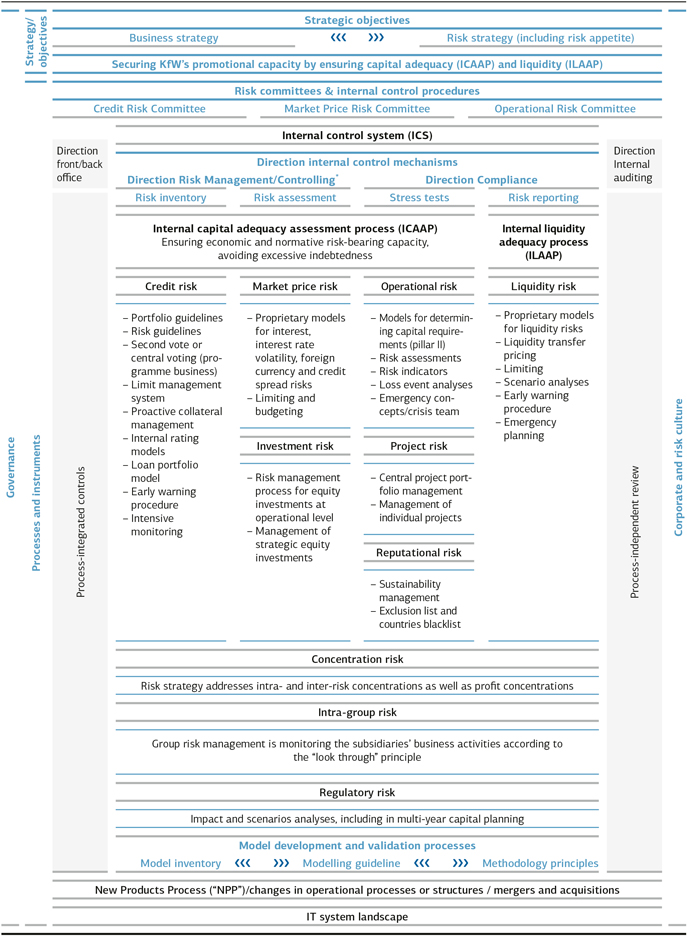

Risk report

Overview of key indicators

Risks are reported on a group level in accordance with KfW Group’s internal risk management. The key risk indicators are presented below:

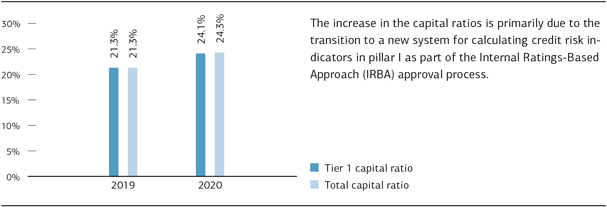

Regulatory capital ratios:

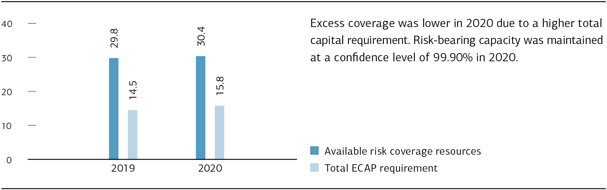

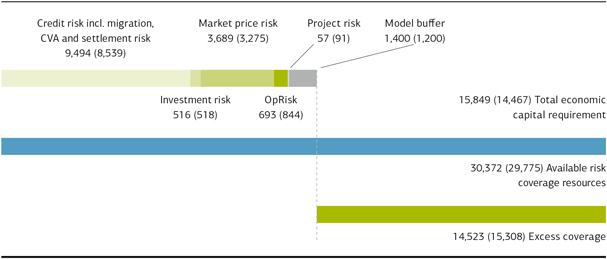

Economic risk-bearing capacity:

(EUR in billions)

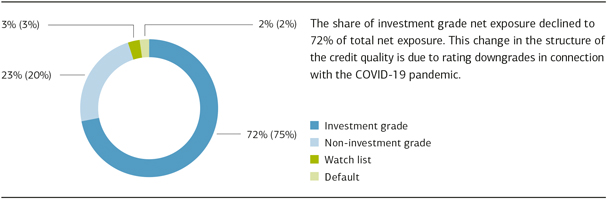

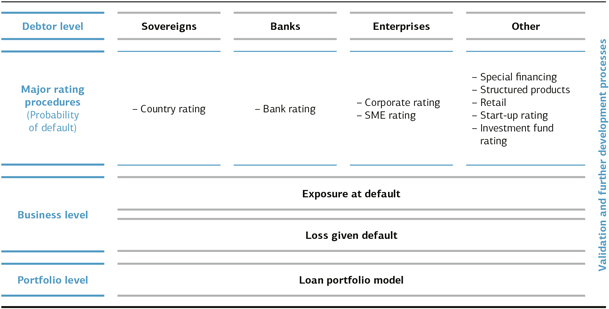

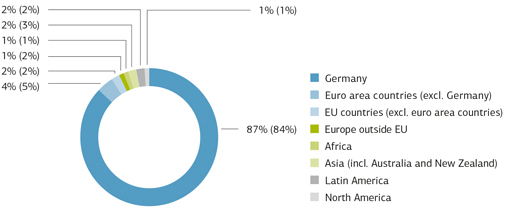

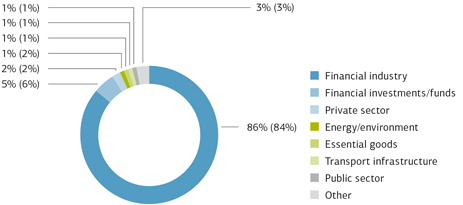

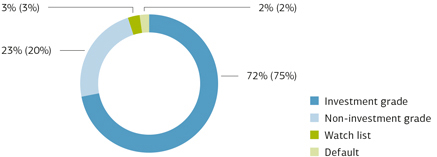

Credit risk:

2020 (2019), Net exposure breakdown

21 | KfW Financial Report 2020 Group management report | Risk report

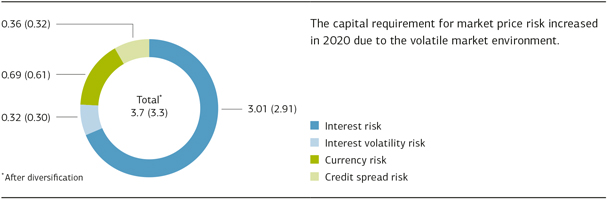

Market price risk:

2020 (2019), ECAP (EUR in billions)

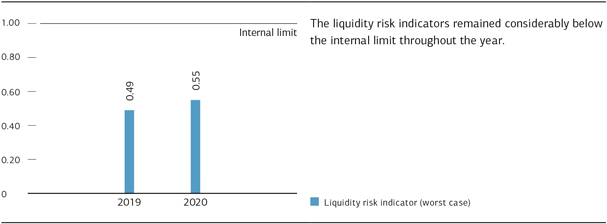

Liquidity risk:

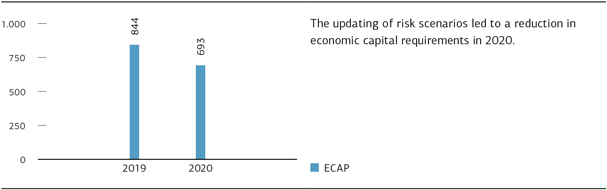

Operational risk:

ECAP (EUR in millions)

KfW Financial Report 2020 Group management report | Risk report | 22

In financial year 2020, as in previous years, KfW Group refined the processes and instruments of its risk management and controlling, taking into account current banking supervisory requirements. This involved, in particular, further developing the credit risk methods for calculating the risk indicators for loss given default (LGD) and exposure at default (EAD) as part of a major project. Following approval by the relevant supervisory authority, these changes were implemented by means of a transition to a new system. The rating (PD – probability of default) procedures were also developed further in line with new supervisory requirements, including with regard to the assignment of default status and safety margins. As part of the enhancement of its credit risk measurement system, the bank also further developed its credit risk reporting systems in order to meet the requirements set out in the BCBS 239 standard on risk data aggregation and risk reporting using a future-viable architecture.

Basic principles and objectives of risk management

KfW Group has a statutory promotional mandate. Sustainable promotion is KfW Group’s overarching purpose. The aim of risk management is for the group to take risks only to the extent that they appear manageable in the context of its current and anticipated earnings position and capital resources. KfW Group’s risk/return management takes into account the business model of a promotional bank without the primary intention of generating a profit and without a trading book, with adherence to supervisory requirements constituting a fundamental prerequisite to the group’s business activities.

The promotional bank business model determines the group’s risk culture with its four regulatory-based elements: leadership culture, responsibilities, communication and incentives. Incentive structures for employees and their responsibilities are designed accordingly. Senior management specifies the desired code of conduct and sets an example in practising it, with the desired dialogue established by means of communication with and through the relevant bodies.

Current developments

The outbreak of the COVID-19 pandemic triggered a drastic and synchronous slump in economic output across the globe and significantly increased uncertainty regarding the future economic outlook. KfW considers the countries that are heavily reliant on tourism or exports of raw materials or that are especially vulnerable in terms of foreign trade to have been greatly affected, particularly if their credit rating was already weak before the crisis. KfW has taken account of this situation since the beginning of the pandemic and has taken steps to counteract it. The collateral requirements for new business in the public sector were increased – in some cases significantly – in many particularly hard-hit countries from March 2020 onwards. Rating committees met more frequently to ensure that the latest risk information was reflected in credit ratings as soon as possible. Rating changes were made primarily for countries in Sub-Saharan Africa, the Middle East and North Africa, and Latin America. These rating downgrades mean that the applicable country limits will potentially be reduced, and changes made to the parameters used to price loans extended to these borrowers. This deterioration in credit quality is also having an impact on the corporate and bank ratings of counterparties in the countries concerned. In addition, a stress test was performed for countries, banks and companies to simulate the effects of a prolonged pandemic.