UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number 811-5344

William Blair Funds

(Exact name of registrant as specified in charter)

| 150 North Riverside Plaza, Chicago, IL | | 60606 |

| (Address of principal executive offices) | | (Zip Code) |

Stephanie G. Braming, Principal Executive Officer

William Blair Funds

150 North Riverside Plaza, Chicago, IL 60606

(Name and address of agent for service)

Registrant’s telephone number, including area code: 312-236-1600

Date of fiscal year end: December 31

Date of reporting period: June 30, 2018

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A Registrant is not required to respond to the collection of information contained in Form N-CSR unless the form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimates and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. (ss) 3507.

Item 1. June 30, 2018 Semiannual Reports transmitted to shareholders.

| | June 30, 2018 |

William Blair Funds Semiannual Report | |

Table of Contents

| June 30, 2018 | William Blair Funds | 1 |

The views expressed in the commentary for each Fund reflect those of the portfolio management team only through the end of the period of the report as stated on the cover. The portfolio management team’s views are subject to change at any time based on market and other conditions and should not be construed as a recommendation. Statements involving predictions, assessments, analyses, or outlook for individual securities, industries, market sectors, and/or markets involve risks and uncertainties, and there is no guarantee they will come to pass.

This report is submitted for the general information of the shareholders of William Blair Funds. It is not authorized for distribution to prospective Fund investors unless accompanied or preceded by the Fund’s prospectus. Please carefully consider a Fund’s investment objectives, risks, charges, and expenses before investing. This and other information is contained in the Fund’s prospectus, which you may obtain by calling 1-800-742-7272. Read it carefully before you invest or send money.

| 2 | Semiannual Report | June 30, 2018 |

Performance as of June 30, 2018—Class N Shares (Unaudited)

| | | | | | | | | | | | | | | 10 yr | | | | Overall |

| | | Year | | | | | | | | | | | (or since | | Inception | | Morningstar |

| | | to Date | | 1 yr | | 3 yr | | 5 yr | | inception) | | Date | | Rating |

| Growth Fund | | | | | | | | | | | | | | | | | | | |

| Class N | | 12.76 | | | 26.06 | | | 12.38 | | | 13.53 | | | 9.77 | | | 3/20/1946 | | ««« |

| Morningstar Large Growth | | 7.51 | | | 20.58 | | | 12.21 | | | 14.37 | | | 10.23 | | | | | Among 1,265 |

| Russell 3000® Growth Index | | 7.44 | | | 22.47 | | | 14.63 | | | 16.14 | | | 11.78 | | | | | Large Growth Funds |

| S&P 500® Index | | 2.65 | | | 14.37 | | | 11.93 | | | 13.42 | | | 10.17 | | | | | |

| | | | | | | | | | | | | | | | | | | | |

| Large Cap Growth Fund | | | | | | | | | | | | | | | | | | | |

| Class N | | 12.28 | | | 30.77 | | | 14.90 | | | 17.40 | | | 11.18 | | | 12/27/1999 | | «««« |

| Morningstar Large Growth | | 7.51 | | | 20.58 | | | 12.21 | | | 14.37 | | | 10.23 | | | | | Among 1,265 |

| Russell 1000® Growth Index | | 7.25 | | | 22.51 | | | 14.98 | | | 16.36 | | | 11.83 | | | | | Large Growth Funds |

| | | | | | | | | | | | | | | | | | | | |

| Mid Cap Growth Fund | | | | | | | | | | | | | | | | | | | |

| Class N | | 11.63 | | | 22.45 | | | 8.85 | | | 10.69 | | | 9.63 | | | 2/1/2006 | | ««« |

| Morningstar Mid-Cap Growth | | 6.39 | | | 18.06 | | | 9.68 | | | 12.31 | | | 9.45 | | | | | Among 541 |

| Russell Midcap® Growth Index | | 5.40 | | | 18.52 | | | 10.73 | | | 13.37 | | | 10.45 | | | | | Mid-Cap Growth Funds |

| | | | | | | | | | | | | | | | | | | | |

| Small-Mid Cap Growth Fund | | | | | | | | | | | | | | | | | | | |

| Class N | | 10.74 | | | 22.81 | | | 13.28 | | | 15.31 | | | 13.04 | | | 12/29/2003 | | ««««« |

| Morningstar Mid-Cap Growth | | 6.39 | | | 18.06 | | | 9.68 | | | 12.31 | | | 9.45 | | | | | Among 541 |

| Russell 2500TM Growth Index | | 8.04 | | | 21.53 | | | 10.86 | | | 13.87 | | | 11.38 | | | | | Mid-Cap Growth Funds |

| | | | | | | | | | | | | | | | | | | | |

| Small-Mid Cap Value Fund | | | | | | | | | | | | | | | | | | | |

| Class N | | 0.84 | | | 10.21 | | | 8.23 | | | 9.56 | | | 12.46 | | | 12/15/2011 | | «« |

| Morningstar Small Blend | | 5.26 | | | 14.67 | | | 9.41 | | | 11.02 | | | — | | | | | Among 639 |

| Russell 2500TM Value Index | | 3.00 | | | 11.49 | | | 9.76 | | | 10.78 | | | 14.21 | | | | | Small Blend Funds |

| | | | | | | | | | | | | | | | | | | | |

| Small Cap Growth Fund | | | | | | | | | | | | | | | | | | | |

| Class N | | 15.41 | | | 26.65 | | | 17.16 | | | 16.06 | | | 12.81 | | | 12/27/1999 | | ««««« |

| Morningstar Small Growth | | 11.05 | | | 22.70 | | | 11.04 | | | 12.76 | | | 10.85 | | | | | Among 606 |

| Russell 2000® Growth Index | | 9.70 | | | 21.86 | | | 10.60 | | | 13.65 | | | 11.24 | | | | | Small Growth Funds |

| | | | | | | | | | | | | | | | | | | | |

| Small Cap Value Fund | | | | | | | | | | | | | | | | | | | |

| Class N | | 1.09 | | | 9.40 | | | 8.68 | | | 9.80 | | | 9.82 | | | 12/23/1996 | | ««« |

| Morningstar Small Blend | | 5.26 | | | 14.67 | | | 9.41 | | | 11.02 | | | 9.73 | | | | | Among 639 |

| Russell 2000® Value Index | | 5.44 | | | 13.10 | | | 11.22 | | | 11.18 | | | 9.88 | | | | | Small Blend Funds |

| | | | | | | | | | | | | | | | | | | | |

| Global Leaders Fund | | | | | | | | | | | | | | | | | | | |

| Class N | | 6.33 | | | 21.58 | | | 10.88 | | | 11.36 | | | 6.52 | | | 10/15/2007 | | «««« |

| Morningstar World Stock | | 0.18 | | | 10.28 | | | 7.91 | | | 9.21 | | | 6.18 | | | | | Among 721 |

| MSCI ACW IMI (net) | | (0.18 | ) | | 11.14 | | | 8.34 | | | 9.60 | | | 6.14 | | | | | World Large Stock Funds |

| | | | | | | | | | | | | | | | | | | | |

| International Leaders Fund | | | | | | | | | | | | | | | | | | | |

| Class N | | 1.04 | | | 13.69 | | | 9.17 | | | 9.58 | | | 10.01 | | | 8/16/2012 | | «««« |

| Morningstar Foreign Large Growth | | (0.43 | ) | | 10.53 | | | 6.62 | | | 7.72 | | | — | | | | | Among 344 |

| MSCI ACW Ex-U.S. IMI (net) | | (3.65 | ) | | 7.75 | | | 5.46 | | | 6.39 | | | 6.96 | | | | | Foreign Large Growth Funds |

| June 30, 2018 | William Blair Funds | 3 |

Performance as of June 30, 2018—Class N Shares (Unaudited)—continued

| | | Year

to Date | | 1 yr | | 3 yr | | 5 yr | | 10 yr

(or since

inception) | | Inception

Date | | Overall

Morningstar

Rating |

| International Developed Plus Fund | | | | | | | | | | | | | | | | | | | |

| Class N | | (2.59 | ) | | 7.50 | | | 4.62 | | | 6.50 | | | 2.04 | | | 5/24/2004 | | «« |

| Morningstar Foreign Large Growth | | (0.43 | ) | | 10.53 | | | 6.62 | | | 7.72 | | | 3.92 | | | | | Among 344 |

| MSCI World Ex-U.S. Index (net) | | (2.77 | ) | | 7.04 | | | 4.87 | | | 6.23 | | | 2.63 | | | | | Foreign Large Growth Funds |

| | | | | | | | | | | | | | | | | | | | |

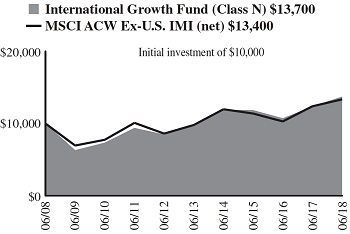

| International Growth Fund | | | | | | | | | | | | | | | | | | | |

| Class N | | (1.78 | ) | | 10.92 | | | 5.03 | | | 6.70 | | | 3.23 | | | 10/1/1992 | | «« |

| Morningstar Foreign Large Growth | | (0.43 | ) | | 10.53 | | | 6.62 | | | 7.72 | | | 3.92 | | | | | Among 344 |

| MSCI ACW Ex-U.S. IMI (net) | | (3.65 | ) | | 7.75 | | | 5.46 | | | 6.39 | | | 2.93 | | | | | Foreign Large Growth Funds |

| | | | | | | | | | | | | | | | | | | | |

| International Small Cap Growth Fund | | | | | | | | | | | | | | | | | | | |

| Class N | | (4.26 | ) | | 8.49 | | | 7.38 | | | 7.36 | | | 5.21 | | | 11/1/2005 | | «« |

| Morningstar Foreign Small/Mid Growth | | 0.51 | | | 15.26 | | | 9.30 | | | 10.19 | | | 6.71 | | | | | Among 108 |

| MSCI ACW Ex-U.S. Small Cap Index (net) | | (2.94 | ) | | 10.57 | | | 7.94 | | | 8.98 | | | 5.77 | | | | | Foreign Small/Mid Growth Funds |

| | | | | | | | | | | | | | | | | | | | |

| Emerging Markets Leaders Fund | | | | | | | | | | | | | | | | | | | |

| Class N | | (6.96 | ) | | 9.71 | | | 4.19 | | | 4.60 | | | 3.54 | | | 5/3/2010 | | ««« |

| Morningstar Diversified Emerging Markets | | (7.05 | ) | | 6.09 | | | 4.76 | | | 4.05 | | | — | | | | | Among 688 |

| MSCI Emerging Markets Index (net) | | (6.66 | ) | | 8.20 | | | 5.60 | | | 5.01 | | | 3.19 | | | | | Diversified Emerging Markets Funds |

| | | | | | | | | | | | | | | | | | | | |

| Emerging Markets Growth Fund | | | | | | | | | | | | | | | | | | | |

| Class N | | (7.35 | ) | | 10.96 | | | 5.04 | | | 5.76 | | | 1.87 | | | 6/6/2005 | | ««« |

| Morningstar Diversified Emerging Markets | | (7.05 | ) | | 6.09 | | | 4.76 | | | 4.05 | | | 2.09 | | | | | Among 688 |

| MSCI Emerging Markets IMI (net) | | (6.86 | ) | | 7.90 | | | 5.19 | | | 4.93 | | | 2.52 | | | | | Diversified Emerging Markets Funds |

| | | | | | | | | | | | | | | | | | | | |

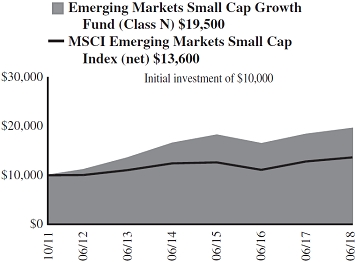

| Emerging Markets Small Cap Growth Fund | | | | | | | | | | | | | | | | | | | |

| Class N | | (9.49 | ) | | 6.22 | | | 2.10 | | | 7.03 | | | 10.54 | | | 10/24/2011 | | «««« |

| Morningstar Diversified Emerging Markets | | (7.05 | ) | | 6.09 | | | 4.76 | | | 4.05 | | | — | | | | | Among 688 |

| MSCI Emerging Markets Small Cap Index (net) | | (8.45 | ) | | 5.64 | | | 2.55 | | | 4.32 | | | 4.75 | | | | | Diversified Emerging Markets Funds |

| | | | | | | | | | | | | | | | | | | | |

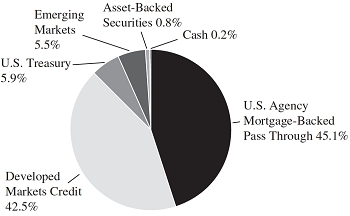

| Bond Fund | | | | | | | | | | | | | | | | | | | |

| Class N | | (2.28 | ) | | (0.62 | ) | | 1.74 | | | 2.54 | | | 4.41 | | | 5/1/2007 | | «««« |

| Morningstar Intermediate-Term Bond | | (1.55 | ) | | (0.36 | ) | | 1.68 | | | 2.20 | | | 3.89 | | | | | Among 878 |

| Bloomberg Barclays U.S. Aggregate Index | | (1.62 | ) | | (0.40 | ) | | 1.72 | | | 2.27 | | | 3.72 | | | | | Intermediate-Term Bond Funds |

| | | | | | | | | | | | | | | | | | | | |

| Income Fund | | | | | | | | | | | | | | | | | | | |

| Class N | | (1.12 | ) | | (0.61 | ) | | 0.83 | | | 1.41 | | | 2.88 | | | 10/1/1990 | | ««« |

| Morningstar Short-Term Bond | | (0.06 | ) | | 0.44 | | | 1.18 | | | 1.27 | | | 2.29 | | | | | Among 447 |

| Bloomberg Barclays Intermediate Government/Credit Bond Index | | (0.97 | ) | | (0.58 | ) | | 1.16 | | | 1.60 | | | 3.08 | | | | | Short-Term Bond Funds |

| 4 | Semiannual Report | June 30, 2018 |

Performance as of June 30, 2018—Class N Shares (Unaudited)—continued

| | | Year

to Date | | 1 yr | | 3 yr | | 5 yr | | 10 yr

(or since

inception) | | Inception

Date | | Overall

Morningstar

Rating |

| Low Duration Fund | | | | | | | | | | | | | | | | | | | |

| Class N | | 0.30 | | | 0.87 | | | 0.75 | | | 0.83 | | | 1.01 | | | 12/1/2009 | | ««« |

| Morningstar Ultrashort Bond | | 0.74 | | | 1.41 | | | 1.14 | | | 0.92 | | | — | | | | | Among 139 |

| Bank of America Merrill Lynch 1-Year U.S. Treasury Note Index | | 0.65 | | | 0.92 | | | 0.64 | | | 0.49 | | | 0.47 | | | | | Ultrashort Bond Funds |

| | | | | | | | | | | | | | | | | | | | |

| Macro Allocation Fund | | | | | | | | | | | | | | | | | | | |

| Class N | | (1.60 | ) | | 0.63 | | | (1.68 | ) | | 2.00 | | | 4.60 | | | 11/29/2011 | | ««« |

| Morningstar Multialternative | | (1.19 | ) | | 2.00 | | | 1.09 | | | 2.02 | | | — | | | | | Among 288 |

| Bank of America Merrill Lynch 3-Month U.S. Treasury Bill Index | | 0.81 | | | 1.36 | | | 0.68 | | | 0.42 | | | 0.34 | | | | | Multialternative Funds |

Performance cited represents past performance. Past performance does not guarantee future results and current performance may be lower or higher than the data quoted. Results shown are average annual total returns, which assume reinvestment of dividends and capital gains. Investment returns and principal will fluctuate and you may have a gain or a loss when you sell shares. For the most current month-end performance information, please call 1-800-742-7272, or visit our Web site at www.williamblairfunds.com. From time to time, the investment adviser may waive fees or reimburse expenses for the Fund. Without these waivers, performance would be lower. Investing in smaller companies involves special risks, including higher volatility and lower liquidity. International and emerging markets investing involves special risk considerations, including currency fluctuations, lower liquidity, economic and political risk. As interest rates rise, bond prices will typically fall and bond funds may become more volatile. Class N shares are available to the general public without a sales load.

Morningstar RatingsTM are as of 06/30/2018 and are subject to change every month. The ratings are based on a risk-adjusted return measure that accounts for variation in a fund’s monthly performance, placing more emphasis on downward variations and rewarding consistent performance. The top 10% of funds in each Category receive 5 stars, the next 22.5% receive 4 stars, the middle 35% receive 3 stars, the next 22.5% receive 2 stars, and the bottom 10% receive 1 star. The Overall Morningstar Rating for a fund is derived from a weighted-average of the performance figures associated with its three-, five- and ten-year (if applicable) Morningstar Rating metrics. The 3/5/10 year Morningstar ratings were as follows: Growth Fund «««/«««/««« and Large Cap Growth Fund ««««/«««««/«««« out of 1,265/1,141/825 large growth funds; Mid Cap Growth Fund «««/««/««« and Small-Mid Cap Growth Fund «««««/«««««/««««« out of 541/480/344 mid-cap growth funds; Small Cap Growth Fund «««««/«««««/««««, out of 606/534/404 small growth funds; Small-Mid Cap Value Fund «««/««/NA and Small Cap Value Fund «««/««/««« out of 639/539/393 small blend funds; Global Leaders Fund ««««/««««/««« out of 721/596/343 world large stock funds; International Developed Plus Fund ««/««/««, International Growth Fund ««/««/««, and International Leaders Fund ««««/««««/NA out of 344/304/218 foreign large growth funds; International Small Cap Growth Fund ««/««/«« out of 108/103/63 foreign small/mid growth funds; Emerging Markets Leaders Fund «««/«««/«««, Emerging Markets Growth Fund «««/««««/«««, and Emerging Markets Small Cap Growth Fund ««/«««««/NA out of 688/489/203 diversified emerging markets funds; Bond Fund «««/««««/«««« out of 878/778/563 intermediate-term bond funds; Income Fund ««/«««/«««« out of 447/378/250 short-term bond funds; Low Duration Fund ««/«««/ NA out of 139/109/NA ultrashort bond funds; and Macro Allocation Fund ««/«««/NA out of 288/148/NA multialternative funds.

Please carefully consider a Fund’s investment objectives, risks, charges, and expenses before investing. This and other information is contained in the Fund’s prospectus, which you may obtain by calling 1-800-742-7272. Read it carefully before you invest or send money.

| June 30, 2018 | William Blair Funds | 5 |

U.S. Growth Market Review and Outlook

Strong second quarter performance across U.S. growth equity benchmarks placed them among the strongest performing investment styles year-to-date. In contrast, first quarter returns were more muted. After robust market performance in January, inflationary fears arose causing market volatility to spike and most major equity benchmarks to retreat in February. While companies generally reported strong financial results for the prior quarter and economic data was mostly positive, trade tensions and building inflationary pressures weighed on returns for the duration of the first quarter.

In the second quarter, growth style indices were broadly positive and volatility moderated from elevated first quarter levels. Higher stock prices and declining volatility were supported by a healthy U.S. economy. Retail spending rebounded, housing starts increased and manufacturing activity remained robust despite an appreciating U.S. dollar. In addition, consumer and business confidence remained elevated. With unemployment reaching 3.8%, its lowest level since 2000, and core inflation just over 2%, in June the Federal Reserve (“Fed”) announced its second rate increase of 2018 and communicated expectations for two more rate increases before year end.

With a strong fundamental backdrop and a positive tax impact, U.S. corporations generally posted robust earnings growth. As a gauge, corporations in the S&P 500 Index reported first quarter earnings growth of approximately 25%, as compared to the same period in the prior year, with over 80% of companies in the Index topping investor expectations. However, aggregate forward P/E ratios contracted as investors appeared to be mindful of risks on the horizon. Notably, trade tensions between the U.S. and China were a focus for investors over the course of the second quarter, and as more countries became involved, anxiety grew that tariffs could potentially escalate into a trade war.

Despite the Fed pursuing monetary tightening and the potential for a global trade war, optimism still persists across consumers, businesses and investors as we enter the tenth year of the current economic expansion. While interest rates remain low relative to history, the Fed has telegraphed a path of rate increases, and its ability to navigate the economy in the face of inflationary pressures from a potential trade war remains a risk. Further, continued uncertainty around the ultimate outcome of proposed tariffs could disrupt business planning and dampen overall productivity. However, the impact of fiscal stimulus in the form of lower corporate tax rates has largely overwhelmed trade concerns thus far. One early benefit of corporate tax reform in the U.S. has been an increase in capital expenditures, which in turn has the potential to boost productivity and create jobs longer-term. In addition, the current administration has been aggressive in reducing regulation on businesses, which could be a continued tailwind for companies.

It remains to be seen how long the expansion can persist given the unprecedented fiscal stimulus at this point of the economic cycle. Broadly speaking, corporate earnings trends and forward-looking guidance are reflective of the strong economy. But to the extent that rising wages, raw materials prices and freight costs begin to compress margins for the average company, we believe our portfolio companies, which generally offer strong value propositions to their customers and have more pricing flexibility, are better positioned to withstand these pressures. Our focus remains on identifying companies with durable growth drivers, independent of the economic backdrop, whose stocks present compelling risk/reward opportunities.

| 6 | Semiannual Report | June 30, 2018 |

U.S. Value Market Review and Outlook

After a strong start to the year, a spike in market volatility in February, stemming from investor anxiety over higher inflation, wiped out solid market returns in January. While volatility quickly retreated, inflationary concerns continued. The combination of investor concerns about higher inflation and heightened fears of a trade war seemed to overshadow positive economic data and generally strong corporate earnings results, even excluding the positive impact from tax reform.

In contrast to the more muted returns during the first quarter, robust corporate earnings growth and solid domestic economic data contributed to the strong second quarter performance across the domestic equity indices, pushing virtually all into positive territory for the year. Higher stock prices and more moderate volatility were supported by a generally strong U.S. economy, which is expected to grow about 3% this year. Some of the more notable economic data points included a rebound in retail spending, increased housing starts, and strong manufacturing activity, despite appreciation in the U.S. dollar. Consumer, corporate, and investor confidence remained elevated, contributing to higher U.S. Treasury yields. Supported by continued strong domestic economic data, an unemployment rate that dropped to 3.8%, and inflation that was slightly above 2%, the Federal Reserve (Fed) announced its second rate increase for the year and telegraphed expectations for another two rate increases before the end of the year.

Increased trade concerns seemed to motivate investors to rapidly move into smaller cap stocks, as small cap ETFs experienced an inflow of over $9 billion during the second quarter, contributing to the outperformance of this asset class during the period. Smaller cap stocks can be viewed as a safe haven and somewhat insulated in a trade war due to less revenue generation exposure overseas.

As the current bull market enters its tenth year, the U.S. markets have been resilient despite the increased risks posed by the potential for a global trade war, geopolitical tensions, emerging market turmoil, and a possible slowdown in global growth. While the Fed has laid the groundwork for future rate increases, current interest rates remain low relative to history. While global trade tensions continue to fluctuate, an escalation into a full-blown trade war would negatively impact global market activity and may disrupt business planning and dampen overall productivity. To date, the positive impact from lower corporate tax rates has largely overshadowed these trade concerns. In addition, the current administration has been aggressive in reducing regulation on businesses, which could continue to provide a tailwind for companies.

We continue to be mindful about the increased debt levels that companies face, and believe investors should place more of an emphasis on corporate balance sheets. Small cap companies have taken on a considerable amount of debt over the years as a result of a perpetually low interest rate environment. However, with the Fed tightening monetary policy and the potential for higher interest rates on the horizon, this will become a concern at some point. We believe those lower quality companies that are either more highly levered or lack the cash flow necessary to service their debt in a higher interest rate environment should struggle, and the stocks of higher quality companies with solid cash flow should outperform.

From our bottom up perspective, we remain constructive on corporate earnings. Although many companies may face increasing margin pressure from higher wages, raw materials, and freight, some of this year’s pressure will be offset by the lower corporate tax rate. We are also mindful and concerned about rising input costs and are focused on owning companies that have pricing power and are able to mitigate inflationary pressures via new products and price increases. As always, our focus remains on identifying quality companies at discount prices and corporate transformation opportunities, and we continue to find good ideas across sectors. Given our investment approach, we believe our portfolios are well-suited to withstand a variety of market scenarios and add value over the long-term.

| June 30, 2018 | William Blair Funds | 7 |

| | | Growth Fund |

| | | |

| | | The Growth Fund seeks long-term capital appreciation. |

| | | |

| | | AN OVERVIEW FROM THE PORTFOLIO MANAGERS |

| | | |

David C. Fording

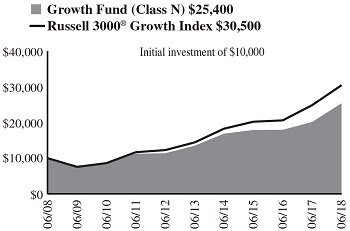

John F. Jostrand | | The William Blair Growth Fund (Class N shares) posted a 12.76% increase, net of fees, for the six months ended June 30, 2018. By comparison, the Fund’s benchmark index, the Russell 3000® Growth Index (the “Index”), increased 7.44%. For the year-to-date period ended June 30, 2018, the Fund outperformed the Index, driven by both positive stock selection and a style tailwind. Stock selection was positive across many sectors, most notably Industrials, Health Care, and Consumer Discretionary. The top contributor to the Fund’s performance was global payments company Mastercard, Inc. (Information Technology), which reported strong financial results amid strong underlying business momentum. Amazon.com, Inc. (Consumer Discretionary) was also a top contributor to the Fund’s performance. Amazon reported strong financial results which reflected accelerating trends across many of its business segments. Other top contributors to the Fund’s performance were CoStar Group, Inc. (Industrials), Domino’s Pizza, Inc. (Consumer Discretionary), and Red Hat, Inc. (Information Technology). Conversely, top detractors from the Fund’s performance were MaxLinear, Inc. (Information Technology) and Monster Beverage Corporation (Consumer Staples). MaxLinear, which produces mixed-signal radio frequency semiconductors used in broadband communications, experienced slowing growth in several of its more mature products, while newer and higher-growth products have yet to offset the slowing growth in some mature products. Energy drink company Monster Beverage reported early in the year that sales growth and earnings missed expectations, as its international distributors reduced inventory. Other top detractors were Newell Brands Inc. (Consumer Discretionary), The Middleby Corporation (Industrials), and Starbucks Corporation (Consumer Discretionary). Additionally, not owning Netflix, Inc. (Consumer Discretionary), a strong relative performer year-to-date, detracted from the Fund’s performance. From a style perspective, as investors became more focused on the potential implications of inflation-related cost pressures on businesses, our higher and more sustainable growth bias, which leads us to companies with value-added products and services and flexible pricing, was a tailwind. Please refer to the U.S. Growth Market Review and Outlook relating to the Fund on page 6 for additional information. |

| 8 | Semiannual Report | June 30, 2018 |

| Performance Highlights (Unaudited) |

Average Annual Total Return through 6/30/2018

| | | Year

to Date | | 1 Year | | 3 Year | | 5 Year | | 10 Year |

| Class N | | | 12.76 | % | | | 26.06 | % | | | 12.38 | % | | | 13.53 | % | | | 9.77 | % |

| Class I | | | 12.95 | | | | 26.39 | | | | 12.71 | | | | 13.88 | | | | 10.12 | |

| Russell 3000® Growth Index | | | 7.44 | | | | 22.47 | | | | 14.63 | | | | 16.14 | | | | 11.78 | |

| S&P 500® Index | | | 2.65 | | | | 14.37 | | | | 11.93 | | | | 13.42 | | | | 10.17 | |

Performance cited represents past performance. Past performance does not guarantee future results and current performance may be lower or higher than the data quoted. Results shown are average annual returns, which assume reinvestment of dividends and capital gains. Investment returns and principal will fluctuate and you may have a gain or loss when you sell shares. For the most current month-end performance information, please call 1-800-742-7272, or visit our Web site at www.williamblairfunds.com. From time to time, the investment adviser may waive fees or reimburse expenses for the Fund. Without these waivers/reimbursements, performance would be lower. Class N shares are available to the general public without a sales load. Class I shares are available to certain institutional investors, and advisory clients of William Blair & Company, L.L.C., without a sales load or distribution (12b-1) or service fees.

The performance highlights and graph presented above do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

The Russell 3000® Growth Index consists of large, medium, and small capitalization companies with above average price-to-book ratios and forecasted growth rates. The index is weighted by market capitalization and large/medium/small companies make up approximately 80%/15%/5% of the index.

The S&P 500® Index indicates broad larger capitalization equity market performance.

This report identifies the Fund’s investments on June 30, 2018. These holdings are subject to change. Not all stocks in the Fund performed the same, nor is there any guarantee that these stocks will perform as well in the future. Market forecasts provided in this report may not necessarily come to pass.

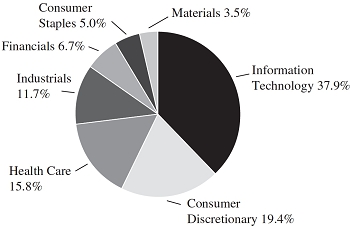

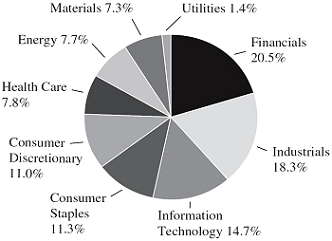

| Sector Diversification (Unaudited) |

The sector diversification shown is based on the total long-term securities.

| June 30, 2018 | William Blair Funds | 9 |

Portfolio of Investments, June 30, 2018 (all dollar amounts in thousands) (unaudited)

| | | | | | | | |

| | | | | | | | |

| | Issuer | | Shares | | | Value | |

| | |

| | Common Stocks | | | | | | | | |

| | | | | | | | | | |

| | Information Technology—37.6% | | | | | | | | |

| * | Adobe Systems, Inc. | | | 20,303 | | | $ | 4,950 | |

| * | Akamai Technologies, Inc. | | | 69,344 | | | | 5,078 | |

| * | Alphabet, Inc. Class “A” | | | 20,989 | | | | 23,701 | |

| | Booz Allen Hamilton Holding Corporation | | | 85,892 | | | | 3,756 | |

| * | Carbon Black, Inc. | | | 84,270 | | | | 2,191 | |

| * | Cars.com, Inc. | | | 66,656 | | | | 1,893 | |

| * | Facebook, Inc. Class “A” | | | 52,935 | | | | 10,286 | |

| * | Guidewire Software, Inc. | | | 25,786 | | | | 2,289 | |

| | Mastercard, Inc. Class “A” | | | 77,317 | | | | 15,194 | |

| * | MaxLinear, Inc. | | | 96,044 | | | | 1,497 | |

| | Microsoft Corporation | | | 243,354 | | | | 23,997 | |

| | National Instruments Corporation | | | 67,277 | | | | 2,824 | |

| * | Pure Storage, Inc. | | | 166,241 | | | | 3,970 | |

| * | Red Hat, Inc. | | | 37,310 | | | | 5,013 | |

| * | Rogers Corporation | | | 15,297 | | | | 1,705 | |

| | Sabre Corporation | | | 142,675 | | | | 3,516 | |

| | Texas Instruments, Inc. | | | 57,478 | | | | 6,337 | |

| * | Ultimate Software Group, Inc. | | | 13,442 | | | | 3,459 | |

| * | Worldpay, Inc. | | | 89,545 | | | | 7,323 | |

| | | | | | | | | 128,979 | |

| | Consumer Discretionary—19.2% | | | | | | | | |

| * | Amazon.com, Inc. | | | 13,359 | | | | 22,708 | |

| | Domino’s Pizza, Inc. | | | 18,819 | | | | 5,310 | |

| * | Grand Canyon Education, Inc. | | | 36,619 | | | | 4,087 | |

| * | Hilton Grand Vacations, Inc. | | | 120,668 | | | | 4,187 | |

| * | Laureate Education, Inc. | | | 157,471 | | | | 2,256 | |

| * | Live Nation Entertainment, Inc. | | | 89,554 | | | | 4,350 | |

| | Six Flags Entertainment Corporation | | | 68,232 | | | | 4,780 | |

| | Starbucks Corporation | | | 98,640 | | | | 4,819 | |

| | Steven Madden, Ltd. | | | 55,828 | | | | 2,964 | |

| * | Ulta Salon Cosmetics & Fragrance, Inc. | | | 27,534 | | | | 6,428 | |

| | Vail Resorts, Inc. | | | 14,277 | | | | 3,915 | |

| | | | | | | | | 65,804 | |

| | Health Care—15.6% | | | | | | | | |

| | Agilent Technologies, Inc. | | | 71,847 | | | | 4,443 | |

| * | Charles River Laboratories International, Inc. | | | 30,964 | | | | 3,476 | |

| * | Codexis, Inc. | | | 163,098 | | | | 2,349 | |

| * | Ligand Pharmaceuticals, Inc. | | | 12,793 | | | | 2,650 | |

| | Stryker Corporation | | | 40,791 | | | | 6,888 | |

| | Teleflex, Inc. | | | 12,237 | | | | 3,282 | |

| | UnitedHealth Group, Inc. | | | 55,160 | | | | 13,533 | |

| * | Veeva Systems, Inc. | | | 36,640 | | | | 2,816 | |

| | West Pharmaceutical Services, Inc. | | | 37,324 | | | | 3,706 | |

| | Zoetis, Inc. | | | 121,909 | | | | 10,386 | |

| | | | | | | | | 53,529 | |

| | Industrials—11.5% | | | | | | | | |

| | BWX Technologies, Inc. | | | 102,580 | | | | 6,393 | |

| * | Copart, Inc. | | | 75,092 | | | | 4,247 | |

| * | CoStar Group, Inc. | | | 13,002 | | | | 5,365 | |

| | Healthcare Services Group, Inc. | | | 88,998 | | | | 3,844 | |

| | Raytheon Co. | | | 33,374 | | | | 6,447 | |

| * | The Middleby Corporation | | | 19,839 | | | | 2,072 | |

| * | Verisk Analytics, Inc. | | | 72,190 | | | | 7,771 | |

| | Wabtec Corporation | | | 34,950 | | | | 3,445 | |

| | | | | | | | | 39,584 | |

| | Issuer | | Shares or

Principal

Amount | | | Value | |

| | |

| | Common Stocks—(continued) | | | | | | | | |

| | | | | | | | | | |

| | Financials—6.6% | | | | | | | | |

| | East West Bancorp, Inc. | | | 48,764 | | | $ | 3,179 | |

| * | Encore Capital Group, Inc. | | | 64,894 | | | | 2,375 | |

| | Intercontinental Exchange, Inc. | | | 133,312 | | | | 9,805 | |

| | The Progressive Corporation | | | 125,524 | | | | 7,425 | |

| | | | | | | | | 22,784 | |

| | Consumer Staples—5.0% | | | | | | | | |

| | Costco Wholesale Corporation | | | 31,706 | | | | 6,626 | |

| * | Monster Beverage Corporation | | | 98,547 | | | | 5,647 | |

| | The Estee Lauder Cos., Inc. | | | 33,189 | | | | 4,735 | |

| | | | | | | | | 17,008 | |

| | Materials—3.5% | | | | | | | | |

| | Ball Corporation | | | 136,742 | | | | 4,861 | |

| | Praxair, Inc. | | | 44,499 | | | | 7,037 | |

| | | | | | | | | 11,898 | |

| | Total Common Stocks—99.0%

(cost $224,778) | | | | | | | 339,586 | |

| | | | | | | | | | |

| | Repurchase Agreement | | | | | | | | |

| | Fixed Income Clearing Corporation, 0.350% dated 6/29/18, due 7/2/18, repurchase price $2,559, collateralized by U.S. Treasury Note, 2.000%, due 4/30/24 | | | $2,559 | | | | 2,559 | |

| | Total Repurchase Agreement—0.8%

(cost $2,559) | | | | | | | 2,559 | |

| | Total Investments—99.8%

(cost $227,337) | | | | | | | 342,145 | |

| | Cash and other assets, less liabilities—0.2% | | | | | | | 758 | |

| | Net assets—100.0% | | | | | | $ | 342,903 | |

* = Non-income producing security

See accompanying Notes to Financial Statements.

| 10 | Semiannual Report | June 30, 2018 |

| | | Large Cap Growth Fund |

| | | |

| | | The Large Cap Growth Fund seeks long-term capital appreciation. |

| | | |

| | | AN OVERVIEW FROM THE PORTFOLIO MANAGERS |

| | | |

James S. Golan

David P. Ricci | | The William Blair Large Cap Growth Fund (Class N shares) posted a 12.28% increase, net of fees, for the six months ended June 30, 2018. By comparison, the Fund’s benchmark index, the Russell 1000® Growth Index (the “Index”), increased 7.25%. For the year-to-date period ended June 30, 2018, the Fund outperformed the Index, driven by both positive stock selection and a style tailwind. Stock selection was positive across many sectors, most notably Industrials, Information Technology and Consumer Discretionary. The top contributor to the Fund’s performance for the period was online retailer Amazon.com, Inc. (Consumer Discretionary), which reported strong financial results that reflected accelerating trends across many of its business segments. Digital marketing and media solutions provider Adobe Systems, Inc. (Information Technology) was also a top contributor. Adobe Systems reported earnings and revenue growth that exceeded expectations in the first and second quarter and the stock outperformed. Other top contributors to the Fund’s performance were Mastercard, Inc. (Information Technology), Netflix, Inc. (Consumer Discretionary), and Intuit, Inc. (Information Technology). Conversely, top detractors were Monster Beverage Corporation (Consumer Staples) and Starbucks Corporation (Consumer Discretionary). Energy drink company Monster Beverage reported sales growth and earnings in the first quarter that missed expectations, as its international distributors reduced inventory. Shares of Starbucks underperformed in part due to sluggish same-store sales growth in the U.S., but also in reaction to the company’s pre-announcement of weaker-than-expected second quarter comparable sales which were partially due to weakness in China. Other top detractors were Affiliated Managers Group, Inc. (Financials), Biogen, Inc. (Health Care), and PPG Industries, Inc. (Materials). From a style perspective, as investors became more focused on the potential implications of inflation-related cost pressures on businesses, our higher and more sustainable growth bias, which leads us to companies with value-added products and services and flexible pricing, was a tailwind. Please refer to the U.S. Growth Market Review and Outlook relating to the Fund on page 6 for additional information. |

| June 30, 2018 | William Blair Funds | 11 |

| Performance Highlights (Unaudited) |

Average Annual Total Return through 6/30/2018

| | | Year

to Date | | 1 Year | | 3 Year | | 5 Year | | 10 Year |

| Class N | | | 12.28 | % | | | 30.77 | % | | | 14.90 | % | | | 17.40 | % | | | 11.18 | % |

| Class I | | | 12.38 | | | | 31.02 | | | | 15.17 | | | | 17.69 | | | | 11.46 | |

| Russell 1000® Growth Index | | | 7.25 | | | | 22.51 | | | | 14.98 | | | | 16.36 | | | | 11.83 | |

Performance cited represents past performance. Past performance does not guarantee future results and current performance may be lower or higher than the data quoted. Results shown are average annual total returns, which assume reinvestment of dividends and capital gains. Investment returns and principal will fluctuate and you may have a gain or loss when you sell shares. For the most current month-end performance information, please call 1-800-742-7272, or visit our Web site at www.williamblairfunds.com. From time to time, the investment adviser may waive fees or reimburse expenses for the Fund. Without these waivers/reimbursements, performance would be lower. Class N shares are available to the general public without a sales load. Class I shares are available to certain institutional investors, and advisory clients of William Blair & Company, L.L.C., without a sales load or distribution (12b-1) or service fees.

The performance highlights and graph presented above do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

The Russell 1000® Growth Index consists of large capitalization companies with above average price-to-book ratios and forecasted growth rates.

This report identifies the Fund’s investments on June 30, 2018. These holdings are subject to change. Not all stocks in the Fund performed the same, nor is there any guarantee that these stocks will perform as well in the future. Market forecasts provided in this report may not necessarily come to pass.

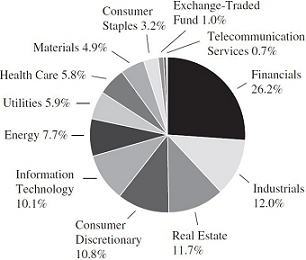

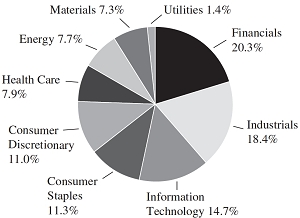

| Sector Diversification (Unaudited) |

The sector diversification shown is based on the total long-term securities.

| 12 | Semiannual Report | June 30, 2018 |

Portfolio of Investments, June 30, 2018 (all dollar amounts in thousands) (unaudited)

| | | | | | | | |

| | | | | | | | |

| | Issuer | | Shares | | | Value | |

| | | | | | | | | | |

| | Common Stocks | | | | | | | | |

| | | | | | | | | | |

| | Information Technology—38.2% | | | | | | | | |

| | Accenture plc† | | | 53,100 | | | $ | 8,687 | |

| * | Adobe Systems, Inc. | | | 28,070 | | | | 6,844 | |

| * | Alphabet, Inc. Class “A” | | | 9,910 | | | | 11,190 | |

| * | Alphabet, Inc. Class “C” | | | 5,026 | | | | 5,607 | |

| * | Facebook, Inc. | | | 53,310 | | | | 10,359 | |

| | Intuit, Inc. | | | 28,300 | | | | 5,782 | |

| | Mastercard, Inc. | | | 43,200 | | | | 8,490 | |

| | Microsoft Corporation | | | 184,960 | | | | 18,239 | |

| * | PayPal Holdings, Inc. | | | 59,870 | | | | 4,985 | |

| * | Red Hat, Inc. | | | 38,010 | | | | 5,107 | |

| | Texas Instruments, Inc. | | | 62,110 | | | | 6,848 | |

| | | | | | | | | 92,138 | |

| | Consumer Discretionary—16.5% | | | | | | | | |

| * | Amazon.com, Inc. | | | 10,440 | | | | 17,746 | |

| * | Live Nation Entertainment, Inc. | | | 130,590 | | | | 6,343 | |

| | McDonald’s Corporation | | | 36,330 | | | | 5,693 | |

| * | Netflix, Inc. | | | 12,680 | | | | 4,963 | |

| | Starbucks Corporation | | | 105,250 | | | | 5,141 | |

| | | | | | | | | 39,886 | |

| | Health Care—15.1% | | | | | | | | |

| * | ABIOMED, Inc. | | | 9,590 | | | | 3,923 | |

| * | Biogen, Inc. | | | 11,500 | | | | 3,338 | |

| | Danaher Corporation | | | 25,300 | | | | 2,496 | |

| | Stryker Corporation | | | 38,370 | | | | 6,479 | |

| | UnitedHealth Group, Inc. | | | 45,630 | | | | 11,195 | |

| | Zoetis, Inc. | | | 104,440 | | | | 8,897 | |

| | | | | | | | | 36,328 | |

| | Industrials—10.2% | | | | | | | | |

| * | Copart, Inc. | | | 84,410 | | | | 4,774 | |

| | Fortive Corporation | | | 58,900 | | | | 4,542 | |

| | Raytheon Co. | | | 29,300 | | | | 5,660 | |

| | TransDigm Group, Inc. | | | 10,800 | | | | 3,727 | |

| * | Verisk Analytics, Inc. | | | 55,600 | | | | 5,985 | |

| | | | | | | | | 24,688 | |

| | Consumer Staples—6.6% | | | | | | | | |

| * | Monster Beverage Corporation | | | 115,740 | | | | 6,632 | |

| | The Coca-Cola Co. | | | 106,600 | | | | 4,676 | |

| | The Estee Lauder Cos., Inc. | | | 32,540 | | | | 4,643 | |

| | | | | | | | | 15,951 | |

| | Financials—5.3% | | | | | | | | |

| | Intercontinental Exchange, Inc. | | | 80,400 | | | | 5,914 | |

| | The Progressive Corporation | | | 115,120 | | | | 6,809 | |

| | | | | | | | | 12,723 | |

| | Materials—3.6% | | | | | | | | |

| | PPG Industries, Inc. | | | 23,460 | | | | 2,433 | |

| | Praxair, Inc. | | | 40,010 | | | | 6,328 | |

| | | | | | | | | 8,761 | |

| | | | Shares or | | | | |

| | | | Principal | | | | |

| | Issuer | | Amount | | | Value | |

| | | | | | | | |

| | Common Stocks—(continued) | | | | | | | | |

| | | | | | | | | | |

| | Real Estate—1.9% | | | | | | | | |

| * | SBA Communications Corporation | | | 27,130 | | | $ | 4,480 | |

| | Energy—1.6% | | | | | | | | |

| | EOG Resources, Inc. | | | 31,240 | | | | 3,887 | |

| | Total Common Stocks—99.0%

(cost $170,213) | | | | | | | 238,842 | |

| | | | | | | | | | |

| | Repurchase Agreement | | | | | | | | |

| | Fixed Income Clearing Corporation, 0.350% dated 6/29/18, due 7/2/18, repurchase price $1,883, collateralized by U.S. Treasury Note, 2.000%, due 4/30/24 | | | $1,883 | | | | 1,883 | |

| | Total Repurchase Agreement—0.8%

(cost $1,883) | | | | | | | 1,883 | |

| | Total Investments—99.8%

(cost $172,096) | | | | | | | 240,725 | |

| | Cash and other assets, less liabilities—0.2% | | | | | | | 486 | |

| | Net assets—100.0% | | | | | | $ | 241,211 | |

† = U.S. listed foreign security

* = Non-income producing security

See accompanying Notes to Financial Statements.

| June 30, 2018 | William Blair Funds | 13 |

| | | Mid Cap Growth Fund |

| | | |

| | | The Mid Cap Growth Fund seeks long-term capital appreciation. |

| | | |

| | | AN OVERVIEW FROM THE PORTFOLIO MANAGERS |

| | | |

Daniel Crowe

Robert C. Lanphier, IV

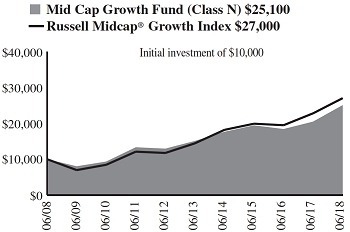

David P. Ricci | | The William Blair Mid Cap Growth Fund (Class N shares) posted a 11.63% increase, net of fees, for the six months ended June 30, 2018. By comparison, the Fund’s benchmark index, the Russell Midcap® Growth Index (the “Index”), increased 5.40%. For the year-to-date period ended June 30, 2018, the Fund outperformed the Index, driven by both positive stock selection and a style tailwind. Stock selection was positive across many sectors, most notably Industrials, including positions in Copart, Inc. and CoStar Group, Inc., and Health Care, including our positions in ABIOMED, Inc. and Encompass Health Corporation. The top individual contributors to the Fund’s performance were ABIOMED and CoStar. ABIOMED develops, manufactures, and markets advanced medical technologies designed to assist or replace the pumping function of a failing heart. The company reported strong results as its Impella heart pump is increasingly becoming the standard of care for acute heart failure patients. Real estate information provider CoStar outperformed due to accelerating growth in both the commercial real estate and multifamily housing segments of its businesses. Another top contributor was Domino’s Pizza, Inc. (Consumer Discretionary). The Middleby Corporation (Industrials) was the top detractor from the Fund’s performance for the year-to-date period. Middleby Corporation reported revenue and earnings that were below expectations primarily due to weakness in its commercial foodservice segment. Coherent, Inc. (Information Technology), which designs and manufactures lasers used to manufacture OLED displays, was also a top detractor. Coherent’s stock came under pressure due to questions surrounding how quickly and to what extent smartphone manufacturers will adopt OLED screens going forward. Other top detractors were Newell Brands Inc. (Consumer Discretionary), Mohawk Industries, Inc. (Consumer Discretionary), and Ball Corporation (Materials). From a style perspective, as investors became more focused on the potential implications of inflation-related cost pressures on businesses, our higher and more sustainable growth bias, which leads us to companies with value-added products and services and flexible pricing, was a tailwind. Please refer to the U.S. Growth Market Review and Outlook relating to the Fund on page 6 for additional information. |

| 14 | Semiannual Report | June 30, 2018 |

| Performance Highlights (Unaudited) |

Average Annual Total Return through 6/30/2018

| | | Year

to Date | | 1 Year | | 3 Year | | 5 Year | | 10 Year |

| Class N | | | 11.63 | % | | | 22.45 | % | | | 8.85 | % | | | 10.69 | % | | | 9.63 | % |

| Class I | | | 11.75 | | | | 22.72 | | | | 9.13 | | | | 10.96 | | | | 9.91 | |

| Russell Midcap® Growth Index | | | 5.40 | | | | 18.52 | | | | 10.73 | | | | 13.37 | | | | 10.45 | |

Performance cited represents past performance. Past performance does not guarantee future results and current performance may be lower or higher than the data quoted. Results shown are average annual total returns, which assume reinvestment of dividends and capital gains. Investment returns and principal will fluctuate and you may have a gain or loss when you sell shares. For the most current month-end performance information, please call 1-800-742-7272, or visit our Web site at www.williamblairfunds.com. Investing in medium capitalization companies involves special risks, including higher volatility and lower liquidity. Medium capitalization stocks are also more sensitive to purchase/sale transactions and changes in the issuer’s financial condition. From time to time, the investment adviser may waive fees or reimburse expenses for the Fund. Without these waivers/reimbursements, performance would be lower. Class N shares are available to the general public without a sales load. Class I shares are available to certain institutional investors, and advisory clients of William Blair & Company, L.L.C., without a sales load or distribution (12b-1) or service fees.

The performance highlights and graph presented above do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

The Russell Midcap® Growth Index is an index that is constructed to provide a comprehensive and unbiased barometer of the mid-cap growth market.

This report identifies the Fund’s investments on June 30, 2018. These holdings are subject to change. Not all stocks in the Fund performed the same, nor is there any guarantee that these stocks will perform as well in the future. Market forecasts provided in this report may not necessarily come to pass.

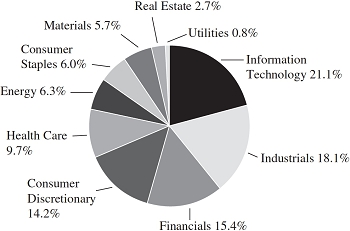

| Sector Diversification (Unaudited) |

The sector diversification shown is based on the total long-term securities.

| June 30, 2018 | William Blair Funds | 15 |

Portfolio of Investments, June 30, 2018 (all dollar amounts in thousands) (unaudited)

| | | | | | | | |

| | | | | | | | |

| | Issuer | | Shares | | | Value | |

| | |

| | Common Stocks | | | | | | | | |

| | | | | | | | | | |

| | Information Technology—23.6% | | | | | | | | |

| * | Akamai Technologies, Inc. | | | 15,445 | | | $ | 1,131 | |

| | Analog Devices, Inc. | | | 7,575 | | | | 727 | |

| | Booz Allen Hamilton Holding Corporation | | | 35,424 | | | | 1,549 | |

| | Global Payments, Inc. | | | 12,450 | | | | 1,388 | |

| * | GoDaddy, Inc. | | | 15,640 | | | | 1,104 | |

| * | Guidewire Software, Inc. | | | 9,536 | | | | 847 | |

| | j2 Global, Inc. | | | 7,605 | | | | 659 | |

| | Microchip Technology, Inc. | | | 9,585 | | | | 872 | |

| * | Red Hat, Inc. | | | 6,685 | | | | 898 | |

| | Sabre Corporation | | | 27,809 | | | | 690 | |

| * | Tyler Technologies, Inc. | | | 3,770 | | | | 837 | |

| * | Ultimate Software Group, Inc. | | | 5,835 | | | | 1,501 | |

| * | WEX, Inc. | | | 6,240 | | | | 1,189 | |

| * | Worldpay, Inc. | | | 17,659 | | | | 1,444 | |

| | | | | | | | | 14,836 | |

| | Industrials—21.7% | | | | | | | | |

| | BWX Technologies, Inc. | | | 26,714 | | | | 1,665 | |

| * | Copart, Inc. | | | 37,650 | | | | 2,130 | |

| * | CoStar Group, Inc. | | | 5,269 | | | | 2,174 | |

| | Equifax, Inc. | | | 10,975 | | | | 1,373 | |

| | Fortive Corporation | | | 15,330 | | | | 1,182 | |

| * | The Middleby Corporation | | | 10,490 | | | | 1,095 | |

| * | Verisk Analytics, Inc. | | | 18,815 | | | | 2,025 | |

| | Wabtec Corporation | | | 11,045 | | | | 1,089 | |

| | Xylem, Inc. | | | 13,630 | | | | 919 | |

| | | | | | | | | 13,652 | |

| | Consumer Discretionary—18.6% | | | | | | | | |

| | Aptiv plc† | | | 9,990 | | | | 915 | |

| * | CarMax, Inc. | | | 10,480 | | | | 764 | |

| | Domino’s Pizza, Inc. | | | 5,385 | | | | 1,520 | |

| * | Live Nation Entertainment, Inc. | | | 28,965 | | | | 1,407 | |

| * | Mohawk Industries, Inc. | | | 3,670 | | | | 786 | |

| | Ross Stores, Inc. | | | 23,100 | | | | 1,958 | |

| | Six Flags Entertainment Corporation | | | 22,260 | | | | 1,559 | |

| * | Ulta Salon Cosmetics & Fragrance, Inc. | | | 6,340 | | | | 1,480 | |

| | Vail Resorts, Inc. | | | 4,790 | | | | 1,313 | |

| | | | | | | | | 11,702 | |

| | Health Care—16.7% | | | | | | | | |

| * | ABIOMED, Inc. | | | 2,185 | | | | 894 | |

| | Agilent Technologies, Inc. | | | 16,150 | | | | 999 | |

| * | Centene Corporation | | | 9,778 | | | | 1,205 | |

| * | Charles River Laboratories International, Inc. | | | 7,585 | | | | 851 | |

| * | DexCom, Inc. | | | 8,020 | | | | 762 | |

| | Encompass Health Corporation | | | 20,750 | | | | 1,405 | |

| * | IDEXX Laboratories, Inc. | | | 3,025 | | | | 659 | |

| * | Mettler-Toledo International, Inc. | | | 2,170 | | | | 1,256 | |

| | Teleflex, Inc. | | | 3,180 | | | | 853 | |

| * | Veeva Systems, Inc. | | | 11,076 | | | | 851 | |

| | West Pharmaceutical Services, Inc. | | | 7,830 | | | | 777 | |

| | | | | | | | | 10,512 | |

| | | | Shares or | | | | |

| | | | Principal | | | | |

| | Issuer | | Amount | | | Value | |

| | |

| | Common Stocks—(continued) | | | | | | | | |

| | | | | | | | | | |

| | Materials—7.0% | | | | | | | | |

| * | Axalta Coating Systems, Ltd.† | | | 18,815 | | | $ | 570 | |

| | Ball Corporation | | | 47,460 | | | | 1,687 | |

| | Celanese Corporation | | | 5,825 | | | | 647 | |

| | Vulcan Materials Co. | | | 11,390 | | | | 1,470 | |

| | | | | | | | | 4,374 | |

| | Financials—5.9% | | | | | | | | |

| | Cboe Global Markets, Inc. | | | 7,715 | | | | 803 | |

| | East West Bancorp, Inc. | | | 17,585 | | | | 1,146 | |

| | The Progressive Corporation | | | 29,280 | | | | 1,732 | |

| | | | | | | | | 3,681 | |

| | Real Estate—1.9% | | | | | | | | |

| * | SBA Communications Corporation | | | 7,400 | | | | 1,222 | |

| | Energy—1.7% | | | | | | | | |

| * | Parsley Energy, Inc. | | | 34,760 | | | | 1,053 | |

| | Consumer Staples—1.2% | | | | | | | | |

| | Conagra Brands, Inc. | | | 20,205 | | | | 723 | |

| | Total Common Stocks—98.3%

(cost $48,340) | | | | | | | 61,755 | |

| | | | | | | | | | |

| | Repurchase Agreement | | | | | | | | |

| | Fixed Income Clearing Corporation, 0.350% dated 6/29/18, due 7/2/18, repurchase price $1,406, collateralized by U.S. Treasury Note, 2.000%, due 4/30/24 | | | $1,406 | | | | 1,406 | |

| | Total Repurchase Agreement—2.3%

(cost $1,406) | | | | | | | 1,406 | |

| | Total Investments—100.6%

(cost $49,746) | | | | | | | 63,161 | |

| | Liabilities, plus cash and other assets—(0.6)% | | | | | | | (361 | ) |

| | Net assets—100.0% | | | | | | $ | 62,800 | |

* = Non-income producing security

† = U.S. listed foreign security

See accompanying Notes to Financial Statements.

| 16 | Semiannual Report | June 30, 2018 |

| | | Small-Mid Cap Growth Fund |

| | | |

| | | The Small-Mid Cap Growth Fund seeks long-term capital appreciation. |

| | | |

| | | AN OVERVIEW FROM THE PORTFOLIO MANAGERS |

| | | |

Daniel Crowe

Robert C. Lanphier, IV | | The William Blair Small-Mid Cap Growth Fund (Class N shares) posted a 10.74% increase, net of fees, for the six months ended June 30, 2018. By comparison, the Fund’s benchmark index, the Russell 2500™ Growth Index (the “Index”), increased 8.04%.

The Fund’s outperformance for the year-to-date period was driven by a combination of positive stock selection and a tailwind for our investment style. From a style perspective, our higher and more sustainable growth bias, which leads us to companies with value-added products and services and flexible pricing, provided a tailwind. This dynamic was most evident in the first quarter as investors digested the potential for inflation-related cost pressures on businesses. On a stock specific basis, selection was strong across several sectors, most notably in Health Care and Industrials. The top two individual contributors to the Fund’s performance were Health Care holdings ABIOMED, Inc. and Ligand Pharmaceuticals, Inc. ABIOMED develops, manufactures and markets advanced medical technologies designed to assist or replace the pumping function of a failing heart. The stock outperformed as the company reported two quarters of strong patient utilization results in support of our thesis that ABIOMED’s product Impella, the world’s smallest heart pump, will become the standard of care in the markets it serves. Ligand Pharmaceuticals, a biotechnology company focused on the acquisition and development of a portfolio of royalty generating assets, outperformed on strong revenue trends. Other top performing holdings were Copart, Inc. and CoStar Group, Inc. (Industrials) and Domino’s Pizza (Consumer Discretionary). Conversely, Information Technology stock selection detracted from performance, including the Fund’s positions in Rogers Corporation, MaxLinear, Inc. and Coherent, Inc. Shares of advanced materials company Rogers Corporation declined on disappointing results and near term forward looking guidance, as operational challenges, strong product demand against limited manufacturing capacity and rising raw material costs dampened margins. Other notable laggards included LendingTree in Financials and The Middleby Corporation in Industrials. LendingTree, Inc. provides targeted online marketing that generates qualified leads for loan originators and underperformed on decreased optimism for its mortgage business.

Please refer to the U.S. Growth Market Review and Outlook relating to the Fund on page 6 for additional information. |

| June 30, 2018 | William Blair Funds | 17 |

| Small-Mid Cap Growth Fund |

| Performance Highlights (Unaudited) |

Average Annual Total Return through 6/30/2018

| | | Year

to Date | | 1 Year | | 3 Year | | 5 Year | | 10 Year |

| Class N | | | 10.74 | % | | | 22.81 | % | | | 13.28 | % | | | 15.31 | % | | | 13.04 | % |

| Class I | | | 10.91 | | | | 23.10 | | | | 13.59 | | | | 15.61 | | | | 13.33 | |

| Russell 2500TM Growth Index | | | 8.04 | | | | 21.53 | | | | 10.86 | | | | 13.87 | | | | 11.38 | |

Performance cited represents past performance. Past performance does not guarantee future results and current performance may be lower or higher than the data quoted. Results shown are average annual total returns, which assume reinvestment of dividends and capital gains. Investment returns and principal will fluctuate and you may have a gain or loss when you sell shares. For the most current month-end performance information, please call 1-800-742-7272, or visit our Web site at www.williamblairfunds.com. Investing in smaller and medium capitalization companies involves special risks, including higher volatility and lower liquidity. Smaller and medium capitalization stocks are also more sensitive to purchase/sale transactions and changes in the issuer’s financial condition. From time to time, the investment adviser may waive fees or reimburse expenses for the Fund. Without these waivers/reimbursements, performance would be lower. Class N shares are available to the general public without a sales load. Class I shares are available to certain institutional investors, and advisory clients of William Blair & Company, L.L.C., without a sales load or distribution (12b-1) or service fees.

The performance highlights and graph presented above do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

The Russell 2500TM Growth Index measures the performance of those Russell 2500 companies with above average price-to-book ratios and forecasted growth rates.

This report identifies the Fund’s investments on June 30, 2018. These holdings are subject to change. Not all stocks in the Fund performed the same, nor is there any guarantee that these stocks will perform as well in the future. Market forecasts provided in this report may not necessarily come to pass.

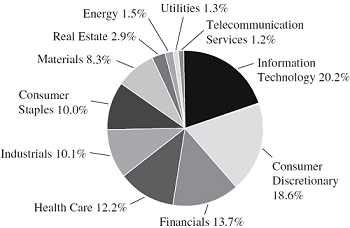

| Sector Diversification (Unaudited) |

The sector diversification shown is based on the total long-term securities.

| 18 | Semiannual Report | June 30, 2018 |

| Small-Mid Cap Growth Fund |

Portfolio of Investments, June 30, 2018 (all dollar amounts in thousands) (unaudited)

| | | | | | | | |

| | | | | | | | |

| | Issuer | | Shares | | | Value | |

| | |

| | Common Stocks | | | | | | | | |

| | | | | | | | | | |

| | Industrials—23.6% | | | | | | | | |

| | BWX Technologies, Inc. | | | 1,035,736 | | | $ | 64,547 | |

| * | Copart, Inc. | | | 1,311,115 | | | | 74,157 | |

| * | CoStar Group, Inc. | | | 186,216 | | | | 76,838 | |

| | Donaldson Co., Inc. | | | 379,300 | | | | 17,114 | |

| * | Genesee & Wyoming, Inc. | | | 323,900 | | | | 26,339 | |

| | Healthcare Services Group, Inc. | | | 864,020 | | | | 37,317 | |

| | HEICO Corporation | | | 669,089 | | | | 40,781 | |

| | Hexcel Corporation | | | 692,162 | | | | 45,946 | |

| | Ritchie Bros Auctioneers, Inc.† | | | 745,913 | | | | 25,451 | |

| * | SiteOne Landscape Supply, Inc. | | | 332,463 | | | | 27,917 | |

| * | Teledyne Technologies, Inc. | | | 193,909 | | | | 38,599 | |

| * | The Middleby Corporation | | | 319,805 | | | | 33,394 | |

| | Toro Co. | | | 253,224 | | | | 15,257 | |

| | TransUnion | | | 798,740 | | | | 57,222 | |

| | | | | | | | | 580,879 | |

| | Health Care—19.7% | | | | | | | | |

| * | Cambrex Corporation | | | 507,126 | | | | 26,523 | |

| * | Catalent, Inc. | | | 814,969 | | | | 34,139 | |

| * | Charles River Laboratories International, Inc. | | | 312,854 | | | | 35,121 | |

| * | DexCom, Inc. | | | 421,951 | | | | 40,077 | |

| | Encompass Health Corporation | | | 838,727 | | | | 56,798 | |

| * | Exact Sciences Corporation | | | 474,824 | | | | 28,390 | |

| * | Glaukos Corporation | | | 642,198 | | | | 26,099 | |

| * | Horizon Pharma plc† | | | 2,268,765 | | | | 37,571 | |

| * | Insulet Corporation | | | 311,100 | | | | 26,661 | |

| * | Ligand Pharmaceuticals, Inc. | | | 268,018 | | | | 55,525 | |

| * | Repligen Corporation | | | 427,341 | | | | 20,102 | |

| | Teleflex, Inc. | | | 113,425 | | | | 30,422 | |

| * | Veeva Systems, Inc. | | | 497,873 | | | | 38,266 | |

| | West Pharmaceutical Services, Inc. | | | 300,664 | | | | 29,853 | |

| | | | | | | | | 485,547 | |

| | Information Technology—19.3% | | | | | | | | |

| * | 2U, Inc. | | | 247,345 | | | | 20,668 | |

| * | Aspen Technology, Inc. | | | 256,600 | | | | 23,797 | |

| | Booz Allen Hamilton Holding Corporation | | | 1,180,443 | | | | 51,621 | |

| * | Coherent, Inc. | | | 113,487 | | | | 17,752 | |

| * | Euronet Worldwide, Inc. | | | 313,698 | | | | 26,278 | |

| * | Fortinet, Inc. | | | 311,400 | | | | 19,441 | |

| * | GoDaddy, Inc. | | | 512,720 | | | | 36,198 | |

| * | Guidewire Software, Inc. | | | 421,326 | | | | 37,405 | |

| | j2 Global, Inc. | | | 377,083 | | | | 32,659 | |

| * | MaxLinear, Inc. | | | 626,863 | | | | 9,773 | |

| | National Instruments Corporation | | | 567,545 | | | | 23,826 | |

| * | Nice, Ltd.—ADR | | | 214,803 | | | | 22,290 | |

| * | Novanta, Inc.† | | | 224,226 | | | | 13,969 | |

| * | Pure Storage, Inc. | | | 1,821,381 | | | | 43,495 | |

| * | Rogers Corporation | | | 320,538 | | | | 35,727 | |

| * | Tyler Technologies, Inc. | | | 109,927 | | | | 24,415 | |

| * | WEX, Inc. | | | 179,053 | | | | 34,106 | |

| | | | | | | | | 473,420 | |

| | Consumer Discretionary—15.6% | | | | | | | | |

| * | Adtalem Global Education, Inc. | | | 976,035 | | | | 46,947 | |

| * | Burlington Stores, Inc. | | | 162,000 | | | | 24,386 | |

| | Cable One, Inc. | | | 17,922 | | | | 13,142 | |

| | Domino’s Pizza, Inc. | | | 161,980 | | | | 45,706 | |

| * | Floor & Decor Holdings, Inc. | | | 631,321 | | | | 31,143 | |

| * | Grand Canyon Education, Inc. | | | 366,535 | | | | 40,909 | |

| | | | Shares or | | | | |

| | | | Principal | | | | |

| | Issuer | | Amount | | | Value | |

| | | | | | | | |

| | Common Stocks—(continued) | | | | | | | | |

| | | | | | | | | | |

| | Consumer Discretionary—(continued) | | | | | | | | |

| * | Hilton Grand Vacations, Inc. | | | 904,488 | | | $ | 31,386 | |

| * | Live Nation Entertainment, Inc. | | | 940,285 | | | | 45,670 | |

| | Six Flags Entertainment Corporation | | | 775,177 | | | | 54,301 | |

| * | Universal Electronics, Inc. | | | 402,400 | | | | 13,299 | |

| | Vail Resorts, Inc. | | | 132,996 | | | | 36,466 | |

| | | | | | | | | 383,355 | |

| | Financials—7.9% | | | | | | | | |

| | Bank of the Ozarks, Inc. | | | 594,302 | | | | 26,767 | |

| | BrightSphere Investment Group plc† | | | 936,476 | | | | 13,354 | |

| | Cboe Global Markets, Inc. | | | 300,956 | | | | 31,321 | |

| | East West Bancorp, Inc. | | | 276,221 | | | | 18,010 | |

| * | Encore Capital Group, Inc. | | | 637,827 | | | | 23,344 | |

| | FirstCash, Inc. | | | 450,527 | | | | 40,480 | |

| * | LendingTree, Inc. | | | 79,288 | | | | 16,952 | |

| | Virtu Financial, Inc. | | | 863,537 | | | | 22,927 | |

| | | | | | | | | 193,155 | |

| | Materials—6.5% | | | | | | | | |

| * | Axalta Coating Systems, Ltd.† | | | 734,811 | | | | 22,272 | |

| | Ball Corporation | | | 1,175,559 | | | | 41,791 | |

| | Celanese Corporation | | | 349,458 | | | | 38,811 | |

| | Martin Marietta Materials, Inc. | | | 253,219 | | | | 56,551 | |

| | | | | | | | | 159,425 | |

| | Real Estate—2.9% | | | | | | | | |

| | Colliers International Group, Inc.† | | | 249,545 | | | | 18,891 | |

| | FirstService Corporation†§ | | | 313,098 | | | | 23,808 | |

| | Jones Lang LaSalle, Inc. | | | 169,481 | | | | 28,132 | |

| | | | | | | | | 70,831 | |

| | Energy—1.7% | | | | | | | | |

| | Diamondback Energy, Inc. | | | 130,460 | | | | 17,165 | |

| * | Parsley Energy, Inc. | | | 797,936 | | | | 24,161 | |

| | | | | | | | | 41,326 | |

| | Consumer Staples—0.8% | | | | | | | | |

| | Nu Skin Enterprises, Inc. | | | 266,722 | | | | 20,855 | |

| | Total Common Stocks—98.0%

(cost $2,010,049) | | | | | | | 2,408,793 | |

| | | | | | | | | | |

| | Repurchase Agreement | | | | | | | | |

| | Fixed Income Clearing Corporation, 0.350% dated 6/29/18, due 7/2/18, repurchase price $17,258, collateralized by U.S. Treasury Note, 2.000%, due 4/30/24 | | | $17,257 | | | | 17,257 | |

| | Total Repurchase Agreement—0.7%

(cost $17,257) | | | | | | | 17,257 | |

| | Total Investments—98.7%

(cost $2,027,306) | | | | | | | 2,426,050 | |

| | Cash and other assets, less liabilities—1.3% | | | | | | | 32,217 | |

| | Net assets—100.0% | | | | | | $ | 2,458,267 | |

ADR = American Depository Receipt * = Non-income producing security

† = U.S. listed foreign security

§ = Deemed illiquid pursuant to Liquidity Procedures approved by the Board of Trustees. This holding represents 0.97% of the Fund’s net assets at June 30, 2018.

See accompanying Notes to Financial Statements.

| June 30, 2018 | William Blair Funds | 19 |

| | | Small-Mid Cap Value Fund |

| | | |

| | | The Small-Mid Cap Value Fund seeks long-term capital appreciation. |

| | | |

| | | AN OVERVIEW FROM THE PORTFOLIO MANAGERS |

| | | |

Chad M. Kilmer

Mark T. Leslie

David S. Mitchell | | The William Blair Small-Mid Cap Value Fund (Class N shares) posted a 0.84% increase, net of fees, for the six months ended June 30, 2018. By comparison, the Fund’s benchmark index, the Russell 2500™ Value Index (the “Index”), increased 3.00%. The Fund’s underperformance relative to the Index was driven by the combination of stock selection and a negative style headwind given the strategy’s larger market cap bias. At the sector level, the most significant detractor from relative performance was Energy, the best performing sector of the market during the period, due to stock selection and the Fund’s lack of exposure to the Oil & Gas Drilling and the Oil & Gas Refining & Marketing sub-industries. The Fund’s relative underperformance within the Industrials sector was due to stock selection within Machinery, as market cycle concerns generally overshadowed positive corporate earnings for the Fund’s more cyclical portfolio holdings. Within Financials, the relative underperformance within the sector was driven by stock selection within Insurance and Banks; pressured by declining interest rates and a flattening yield curve late in the second quarter. The Fund’s relative outperformance within Consumer Discretionary was the result of strong stock selection within the Leisure Facilities, Education Services and Apparel, Accessories & Luxury Goods sub-industries. Within Information Technology, the relative outperformance was driven by stock selection within IT Services and benefitted from General Dynamics’ acquisition of portfolio holding CSRA, Inc. Looking specifically at stock selection, the Fund’s largest detractors from relative performance were Crane Co. (Industrials), Commscope Holding Co., Inc. (Information Technology), and Acuity Brands, Inc. (Industrials). Offsetting these detractors were the Fund’s investments in lululemon athletica (Consumer Discretionary), CSRA (Information Technology), and Vail Resorts, Inc. (Consumer Discretionary). Please refer to the U.S. Value Market Review and Outlook relating to the Fund on page 7 for additional information. |

| 20 | Semiannual Report | June 30, 2018 |

| Performance Highlights (Unaudited) |

Average Annual Total Return through 6/30/2018

| | | Year

to Date | | 1 Year | | 3 Year | | 5 Year | | Since

Inception(a) |

| Class N | | | 0.84 | % | | | 10.21 | % | | | 8.23 | % | | | 9.56 | % | | | 12.46 | % |

| Class I | | | 0.98 | | | | 10.46 | | | | 8.51 | | | | 9.85 | | | | 12.75 | |

| Russell 2500TM Value Index | | | 3.00 | | | | 11.49 | | | | 9.76 | | | | 10.78 | | | | 14.21 | |

| (a) | Since inception is for the period from December 15, 2011 (Commencement of Operations) to June 30, 2018. |

Performance cited represents past performance. Past performance does not guarantee future results and current performance may be lower or higher than the data quoted. Results shown are average annual total returns, which assume reinvestment of dividends and capital gains. Investment returns and principal will fluctuate and you may have a gain or loss when you sell shares. For the most current month-end performance information, please call 1-800-742-7272, or visit our Web site at www.williamblairfunds.com. Investing in smaller and medium capitalization companies involves special risks, including higher volatility and lower liquidity. Smaller and medium capitalization stocks are also more sensitive to purchase/sale transactions and changes in the issuer’s financial condition. From time to time, the investment adviser may waive fees or reimburse expenses for the Fund. Without these waivers/reimbursements, performance would be lower. Class N shares are available to the general public without a sales load. Class I shares are available to certain institutional investors, and advisory clients of William Blair & Company, L.L.C., without a sales load or distribution (12b-1) or service fees.

The performance highlights and graph presented above do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

The Russell 2500TM Value Index consists of small to mid-capitalization companies with below average price-to-book ratios and forecasted growth rates.

This report identifies the Fund’s investments on June 30, 2018. These holdings are subject to change. Not all stocks in the Fund performed the same, nor is there any guarantee that these stocks will perform as well in the future. Market forecasts provided in this report may not necessarily come to pass.

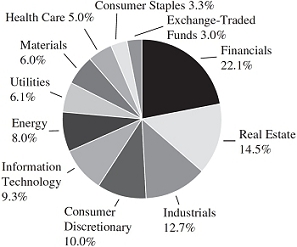

| Sector Diversification (Unaudited) |

The sector diversification shown is based on the total long-term securities.

| June 30, 2018 | William Blair Funds | 21 |

Portfolio of Investments, June 30, 2018 (all dollar amounts in thousands) (unaudited)

| | | | | | | | |

| | | | | | | | |

| | Issuer | | Shares | | | Value | |

| | |

| | Common Stocks | | | | | | | | |

| | | | | | | | | | |

| | Financials—22.0% | | | | | | | | |

| | American Financial Group, Inc. | | | 186 | | | $ | 20 | |

| | CNO Financial Group, Inc. | | | 812 | | | | 16 | |

| * | E*TRADE Financial Corporation | | | 549 | | | | 34 | |

| | East West Bancorp, Inc. | | | 445 | | | | 29 | |

| | First American Financial Corporation | | | 311 | | | | 16 | |

| | FNB Corporation | | | 1,594 | | | | 21 | |

| | Hancock Whitney Corporation | | | 412 | | | | 19 | |

| | Hanover Insurance Group, Inc. | | | 196 | | | | 23 | |

| | Home BancShares, Inc. | | | 999 | | | | 23 | |

| | Iberiabank Corporation | | | 320 | | | | 24 | |

| | PacWest Bancorp | | | 541 | | | | 27 | |

| | Radian Group, Inc. | | | 1,262 | | | | 21 | |

| | Selective Insurance Group, Inc. | | | 367 | | | | 20 | |

| | Sterling Bancorp | | | 1,198 | | | | 28 | |

| * | SVB Financial Group | | | 104 | | | | 30 | |

| | Umpqua Holdings Corporation | | | 921 | | | | 21 | |

| | Voya Financial, Inc. | | | 465 | | | | 22 | |

| * | Western Alliance Bancorp | | | 379 | | | | 21 | |

| | WSFS Financial Corporation | | | 470 | | | | 25 | |

| | Zions Bancorporation | | | 254 | | | | 13 | |

| | | | | | | | | 453 | |

| | Real Estate—14.5% | | | | | | | | |

| | Acadia Realty Trust | | | 1,007 | | | | 28 | |

| | American Assets Trust, Inc. | | | 633 | | | | 24 | |

| | American Campus Communities, Inc. | | | 677 | | | | 29 | |

| | Camden Property Trust | | | 241 | | | | 22 | |

| | Columbia Property Trust, Inc. | | | 1,172 | | | | 27 | |

| | Douglas Emmett, Inc. | | | 494 | | | | 20 | |

| | EPR Properties | | | 452 | | | | 29 | |

| * | Equity Commonwealth | | | 696 | | | | 22 | |

| | Equity LifeStyle Properties, Inc. | | | 230 | | | | 21 | |

| | Healthcare Realty Trust, Inc. | | | 914 | | | | 27 | |

| | Pebblebrook Hotel Trust | | | 736 | | | | 28 | |

| | Terreno Realty Corporation | | | 613 | | | | 23 | |

| | | | | | | | | 300 | |

| | Industrials—12.7% | | | | | | | | |

| | Acuity Brands, Inc. | | | 220 | | | | 25 | |

| | Crane Co. | | | 300 | | | | 24 | |

| * | Gardner Denver Holdings, Inc. | | | 878 | | | | 26 | |

| | GrafTech International, Ltd. | | | 1,759 | | | | 32 | |

| | IDEX Corporation | | | 203 | | | | 28 | |

| | Lennox International, Inc. | | | 145 | | | | 29 | |

| | Old Dominion Freight Line, Inc. | | | 179 | | | | 27 | |

| | Toro Co. | | | 437 | | | | 26 | |

| | UniFirst Corporation | | | 149 | | | | 26 | |

| * | WABCO Holdings, Inc. | | | 170 | | | | 20 | |

| | | | | | | | | 263 | |

| | Consumer Discretionary—10.0% | | | | | | | | |

| | Churchill Downs, Inc. | | | 86 | | | | 25 | |

| | Dunkin’ Brands Group, Inc. | | | 644 | | | | 44 | |

| | Gentex Corporation | | | 1,290 | | | | 30 | |

| * | Michael Kors Holdings, Ltd.† | | | 414 | | | | 28 | |

| | Six Flags Entertainment Corporation | | | 511 | | | | 36 | |

| | Vail Resorts, Inc. | | | 156 | | | | 43 | |

| | | | | | | | | 206 | |

| | | | | | | | |

| | | | | | | | |

| | Issuer | | Shares | | | Value | |

| | |

| | Common Stocks—(continued) | | | | | | | | |

| | | | | | | | | | |

| | Information Technology—9.3% | | | | | | | | |

| * | Acxiom Corporation | | | 791 | | | $ | 24 | |

| | Avnet, Inc. | | | 507 | | | | 22 | |

| | Belden, Inc. | | | 456 | | | | 28 | |

| | Booz Allen Hamilton Holding Corporation | | | 782 | | | | 34 | |

| * | Cadence Design Systems, Inc. | | | 679 | | | | 30 | |

| | j2 Global, Inc. | | | 362 | | | | 31 | |

| | MAXIMUS, Inc. | | | 375 | | | | 23 | |

| | | | | | | | | 192 | |

| | Energy—8.0% | | | | | | | | |

| * | Forum Energy Technologies, Inc. | | | 1,727 | | | | 21 | |

| * | Parsley Energy, Inc. | | | 990 | | | | 30 | |

| | Patterson-UTI Energy, Inc. | | | 1,251 | | | | 23 | |

| | Range Resources Corporation | | | 1,679 | | | | 28 | |

| | Targa Resources Corporation | | | 637 | | | | 32 | |

| * | WPX Energy, Inc. | | | 1,799 | | | | 32 | |

| | | | | | | | | 166 | |

| | Utilities—6.1% | | | | | | | | |

| | Alliant Energy Corporation | | | 625 | | | | 26 | |

| | Atmos Energy Corporation | | | 339 | | | | 31 | |

| | IDACORP, Inc. | | | 250 | | | | 23 | |

| | NiSource, Inc. | | | 957 | | | | 25 | |

| * | Vistra Energy Corporation | | | 885 | | | | 21 | |

| | | | | | | | | 126 | |

| | Materials—6.0% | | | | | | | | |

| | Carpenter Technology Corporation | | | 482 | | | | 25 | |

| | FMC Corporation | | | 223 | | | | 20 | |

| | Minerals Technologies, Inc. | | | 234 | | | | 17 | |

| | PolyOne Corporation | | | 527 | | | | 23 | |

| | Sensient Technologies Corporation | | | 209 | | | | 15 | |

| | Steel Dynamics, Inc. | | | 521 | | | | 24 | |

| | | | | | | | | 124 | |

| | Health Care—5.1% | | | | | | | | |

| | CONMED Corporation | | | 192 | | | | 14 | |

| | Encompass Health Corporation | | | 393 | | | | 27 | |

| * | Hologic, Inc. | | | 583 | | | | 23 | |

| * | Magellan Health, Inc. | | | 183 | | | | 17 | |

| | PerkinElmer, Inc. | | | 311 | | | | 23 | |

| | | | | | | | | 104 | |

| | Consumer Staples—3.3% | | | | | | | | |

| | Ingredion, Inc. | | | 186 | | | | 20 | |

| | J&J Snack Foods Corporation | | | 122 | | | | 19 | |

| | Lamb Weston Holdings, Inc. | | | 411 | | | | 28 | |

| | | | | | | | | 67 | |

| | Total Common Stocks—97.0%

(cost $1,658) | | | | | | | 2,001 | |

See accompanying Notes to Financial Statements.

| 22 | Semiannual Report | June 30, 2018 |

Portfolio of Investments, June 30, 2018 (all dollar amounts in thousands) (unaudited)

| | | | | | | | |

| | | | | | | | |

| | Issuer | | Shares | | | Value | |

| | | | | | | | |

| | Exchange-Traded Fund | | | | | | | | |

| | iShares Russell 2000 Value ETF | | | 471 | | | $ | 62 | |

| | Total Exchange-Traded Fund—3.0%

(cost $62) | | | | | | | 62 | |

| | Total Investments—100.0%

(cost $1,720) | | | | | | | 2,063 | |

| | Cash and other assets, less liabilities—0.0% | | | | | | | — | |

| | Net assets—100.0% | | | | | | $ | 2,063 | |

* = Non-income producing security

† = U.S. listed foreign security

See accompanying Notes to Financial Statements.

| June 30, 2018 | William Blair Funds | 23 |

| | | Small Cap Growth Fund |

| | | |

| | | The Small Cap Growth Fund seeks long-term capital appreciation. |

| | | |

| | | AN OVERVIEW FROM THE PORTFOLIO MANAGERS |

| | | |

Michael P. Balkin