| |

| SECURITIES AND EXCHANGE COMMISSION |

| |

| CERTIFIED SHAREHOLDER REPORT OF REGISTERED |

| |

| MANAGEMENT INVESTMENT COMPANIES |

| | |

| Investment Company Act file number: | (811-05346) |

| | |

| Exact name of registrant as specified in charter: | Putnam Variable Trust |

| | |

| Address of principal executive offices: | 100 Federal Street, Boston, Massachusetts 02110 |

| | |

| Name and address of agent for service: | Stephen Tate, Vice President |

| | |

| | Boston, Massachusetts 02110 |

| | |

| Copy to: | Bryan Chegwidden, Esq. |

| | |

| | 1211 Avenue of the Americas |

| | |

| | Boston, Massachusetts 02199 |

| | |

| Registrant’s telephone number, including area code: | (617) 292-1000 |

| | |

| Date of fiscal year end: | December 31, 2024 |

| | |

| Date of reporting period: | January 1, 2024 – December 31, 2024 |

| |

| Item 1. Report to Stockholders: |

| |

| The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940: |

| | |

Putnam VT Income Fund | |

Class IA true |

| Annual Shareholder Report | December 31, 2024 |

|

This annual shareholder report contains important information about Putnam VT Income Fund for the period January 1, 2024, to December 31, 2024.

You can find additional information about the Fund at https://www.franklintempleton.com/regulatory-fund-documents. You can also request this information by contacting us at (800) 225-1581.

This report describes changes to the Fund that occurred during the reporting period.

WHAT WERE THE FUND COSTS FOR THE LAST YEAR? (based on a hypothetical $10,000 investment)

| | |

Class Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

Class IA1 | $60 | 0.59% |

| 1 | Does not reflect expenses incurred from investing through variable annuity or variable life insurance products. |

HOW DID THE FUND PERFORM LAST YEAR AND WHAT AFFECTED ITS PERFORMANCE?

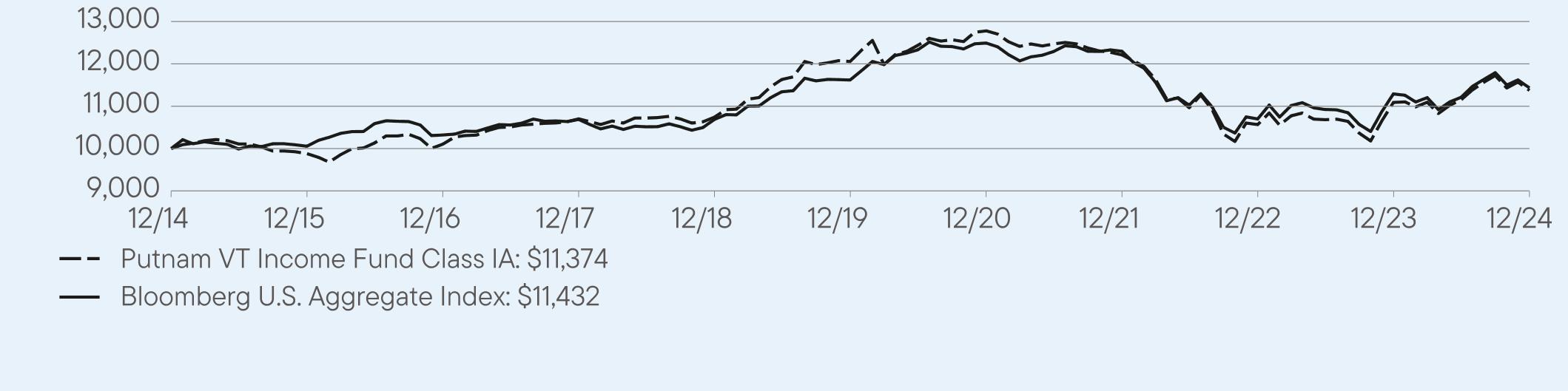

For the twelve months ended December 31, 2024, Class IA shares of Putnam VT Income Fund returned 2.56%. The Fund compares its performance to the Bloomberg U.S. Aggregate Index, which returned 1.25% for the same period.

| |

Top contributors to performance: |

| ↑ | Mortgage credit strategies added value, driven by positioning in both residential (RMBS) and commercial mortgage-backed securities (CMBS). RMBS continued to benefit from U.S. housing market strength, solid borrower fundamentals, and low expectations for a U.S. recession. Additionally, demand for CMBS improved substantially in 2024 despite changes to expectations for the timing and number of rate cuts. |

| ↑ | Corporate credit strategies contributed to returns, as both investment-grade and high yield spreads tightened during the year. |

| ↑ | Prepayment strategies contributed to returns, as seasoned interest-only (IO) and inverse IO bonds are still well “out-of-the-money” and thus benefited from stable prepayment speeds and a strong carry profile. |

| |

Top detractors from performance: |

| ↓ | Term structure strategies were the primary detractor, particularly in the third quarter, as the Fund had a slightly short duration posture in an environment where U.S. Treasury yields rallied across the curve. |

Use of derivatives and the impact on performance:

The Fund utilized futures for hedging treasury term structure risk and for yield curve positioning, which detracted from performance.

| Putnam VT Income Fund | PAGE 1 | 38921-ATSIA-0225 |

HOW DID THE FUND PERFORM OVER THE LAST 10 YEARS?

The Fund’s past performance is not necessarily an indication of how the Fund will perform in the future. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

VALUE OF A $10,000 INVESTMENT – Class IA 12/31/2014 — 12/31/2024

AVERAGE ANNUAL TOTAL RETURNS (%) Period Ended December 31, 2024

| | | |

| | 1 Year | 5 Year | 10 Year |

Class IA | 2.56 | -1.16 | 1.30 |

Bloomberg U.S. Aggregate Index | 1.25 | -0.33 | 1.35 |

Performance does not reflect expenses incurred from investing through variable annuity or variable life insurance products, which if reflected, would reduce performance of the Fund.

Fund performance figures may reflect fee waivers and/or expense reimbursements, without which the performance would have been lower.

Important data provider notices and terms available at www.franklintempletondatasources.com.

KEY FUND STATISTICS (as of December 31, 2024)

| |

Total Net Assets | $138,075,010 |

Total Number of Portfolio Holdings* | 838 |

Total Management Fee Paid | $543,719 |

Portfolio Turnover Rate | 461% |

| * | Includes derivatives, if applicable. |

| Putnam VT Income Fund | PAGE 2 | 38921-ATSIA-0225 |

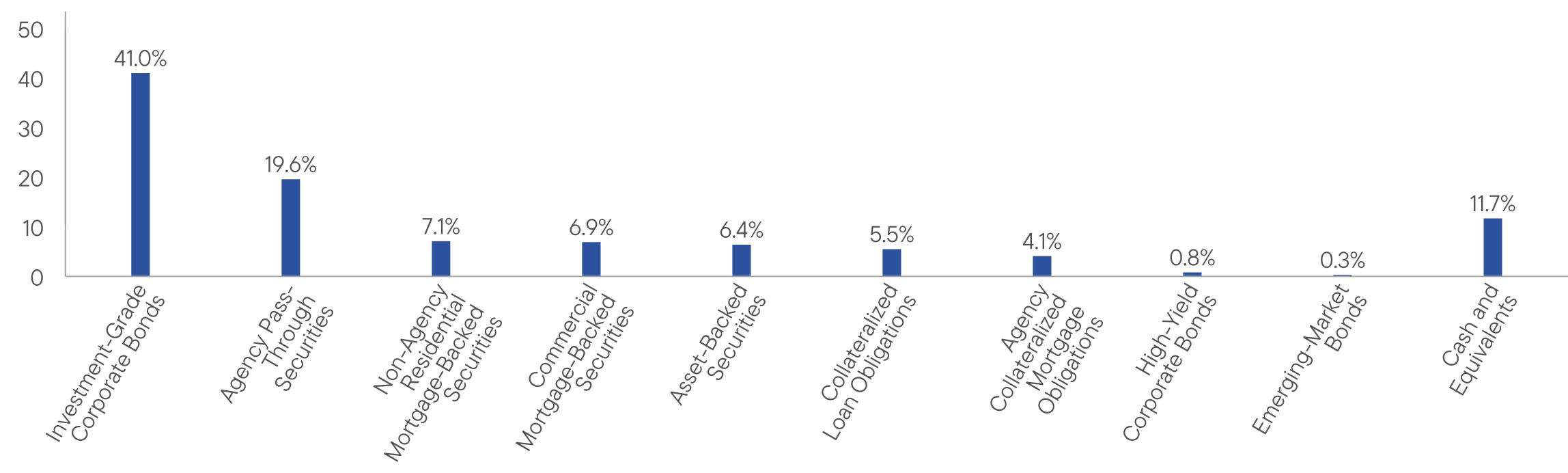

WHAT DID THE FUND INVEST IN? (as of December 31, 2024)

Portfolio Composition (% of Total Net Assets)

| Cash and Equivalents, if any, represent the market value weights of cash, derivatives, short-term securities, and other unclassified assets in the portfolio. Allocations may not total 100% because the chart includes the notional value of certain derivatives (the economic value for purposes of calculating periodic payment obligations), including to-be-announced mortgage security trades, if any, in addition to the market value of securities. Holdings and allocations may vary over time. |

HOW HAS THE FUND CHANGED?

On May 31, 2023, Franklin Resources, Inc. (“Franklin Templeton”) and Great-West Lifeco Inc., the parent company of Putnam U.S. Holdings I, LLC (“Putnam Holdings”), announced that they had entered into a definitive agreement for a subsidiary of Franklin Templeton to acquire Putnam Holdings in a stock and cash transaction (the “Transaction”). The Transaction was completed on January 1, 2024. As part of the Transaction, your Fund’s then-current investment advisor, Putnam Investment Management, LLC (“Putnam Management”), a wholly-owned subsidiary of Putnam Holdings, and your Fund’s then-current sub-advisor, Putnam Investments Limited (“PIL”), an indirect, wholly-owned subsidiary of Putnam Holdings, became indirect, wholly-owned subsidiaries of Franklin Templeton. In connection with the Transaction, shareholders of your Fund approved a new management contract with Putnam Management and a new sub-advisory contract with PIL. The new contracts were identical to the previous contracts, except for the effective dates, initial terms, updates to fund names as necessary to reflect previous name changes, and certain non-substantive changes.

Effective July 15, 2024, Putnam Management transferred its management contract for your Fund to Franklin Advisers, Inc. (“Franklin Advisers”), and Franklin Advisers replaced Putnam Management as the investment advisor to your Fund. In connection with the transfer, your Fund’s portfolio managers, along with supporting research analysts and certain other investment staff of Putnam Management, also became employees of Franklin Advisers. Putnam Management also transferred to Franklin Advisers its sub-management agreement with PIL in respect of your Fund. Franklin Advisers is a direct, wholly-owned subsidiary of Franklin Templeton. In addition, effective July 15, 2024, Franklin Advisers retained Putnam Management as a sub-advisor to your Fund pursuant to a new sub-advisory agreement.

Effective November 1, 2024 (the “Effective Date”), PIL, a sub-advisor of the Fund prior to the Effective Date, merged with and into Franklin Templeton Investment Management Limited (“FTIML”), a wholly-owned subsidiary of Franklin Templeton (the “Merger”). As of the Effective Date, PIL investment professionals became employees of FTIML, and the sub-advisory agreement between Franklin Advisers and PIL with respect to the Fund was terminated. In connection with the Merger, the Fund’s Trustees approved a new sub-advisory agreement between Franklin Advisers and FTIML, pursuant to which FTIML became a sub-advisor of the Fund on the Effective Date.

Effective September 30, 2024, the portfolio managers for the Fund are Albert Chan, Tina Chou, Patrick Klein, Michael Salm and Matthew Walkup.

This is a summary of certain changes to the Fund since January 1, 2024. For more complete information, you may review the Fund’s current prospectus and any applicable supplements and the Fund’s next prospectus, which we expect to be available by May 1, 2025, at https://www.franklintempleton.com/regulatory-fund-documents or upon request at (800) 225-1581 or

funddocuments@putnam.com.

| Putnam VT Income Fund | PAGE 3 | 38921-ATSIA-0225 |

| |

| WHERE CAN I FIND ADDITIONAL INFORMATION ABOUT THE FUND? |

Additional information is available on https://www.franklintempleton.com/regulatory-fund-documents, including its: |

| • prospectus • proxy voting information • financial information • holdings • tax information |

| Putnam VT Income Fund | PAGE 4 | 38921-ATSIA-0225 |

100009881101051070110741120561278012213105661109011374100001005510321106871068811620124921229910699112911143241.019.67.16.96.45.54.10.80.311.7

| | |

Putnam VT Income Fund | |

Class IB true |

| Annual Shareholder Report | December 31, 2024 |

|

This annual shareholder report contains important information about Putnam VT Income Fund for the period January 1, 2024, to December 31, 2024.

You can find additional information about the Fund at https://www.franklintempleton.com/regulatory-fund-documents. You can also request this information by contacting us at (800) 225-1581.

This report describes changes to the Fund that occurred during the reporting period.

WHAT WERE THE FUND COSTS FOR THE LAST YEAR? (based on a hypothetical $10,000 investment)

| | |

Class Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

Class IB1 | $85 | 0.84% |

| 1 | Does not reflect expenses incurred from investing through variable annuity or variable life insurance products. |

HOW DID THE FUND PERFORM LAST YEAR AND WHAT AFFECTED ITS PERFORMANCE?

For the twelve months ended December 31, 2024, Class IB shares of Putnam VT Income Fund returned 2.32%. The Fund compares its performance to the Bloomberg U.S. Aggregate Index, which returned 1.25% for the same period.

| |

Top contributors to performance: |

| ↑ | Mortgage credit strategies added value, driven by positioning in both residential (RMBS) and commercial mortgage-backed securities (CMBS). RMBS continued to benefit from U.S. housing market strength, solid borrower fundamentals, and low expectations for a U.S. recession. Additionally, demand for CMBS improved substantially in 2024 despite changes to expectations for the timing and number of rate cuts. |

| ↑ | Corporate credit strategies contributed to returns, as both investment-grade and high yield spreads tightened during the year. |

| ↑ | Prepayment strategies contributed to returns, as seasoned interest-only (IO) and inverse IO bonds are still well “out-of-the-money” and thus benefited from stable prepayment speeds and a strong carry profile. |

| |

Top detractors from performance: |

| ↓ | Term structure strategies were the primary detractor, particularly in the third quarter, as the Fund had a slightly short duration posture in an environment where U.S. Treasury yields rallied across the curve. |

Use of derivatives and the impact on performance:

The Fund utilized futures for hedging treasury term structure risk and for yield curve positioning, which detracted from performance.

| Putnam VT Income Fund | PAGE 1 | 38921-ATSIB-0225 |

HOW DID THE FUND PERFORM OVER THE LAST 10 YEARS?

The Fund’s past performance is not necessarily an indication of how the Fund will perform in the future. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares.

VALUE OF A $10,000 INVESTMENT – Class IB 12/31/2014 — 12/31/2024

AVERAGE ANNUAL TOTAL RETURNS (%) Period Ended December 31, 2024

| | | |

| | 1 Year | 5 Year | 10 Year |

Class IB | 2.32 | -1.41 | 1.03 |

Bloomberg U.S. Aggregate Index | 1.25 | -0.33 | 1.35 |

Performance does not reflect expenses incurred from investing through variable annuity or variable life insurance products, which if reflected, would reduce performance of the Fund.

Fund performance figures may reflect fee waivers and/or expense reimbursements, without which the performance would have been lower.

Important data provider notices and terms available at www.franklintempletondatasources.com.

KEY FUND STATISTICS (as of December 31, 2024)

| |

Total Net Assets | $138,075,010 |

Total Number of Portfolio Holdings* | 838 |

Total Management Fee Paid | $543,719 |

Portfolio Turnover Rate | 461% |

| * | Includes derivatives, if applicable. |

| Putnam VT Income Fund | PAGE 2 | 38921-ATSIB-0225 |

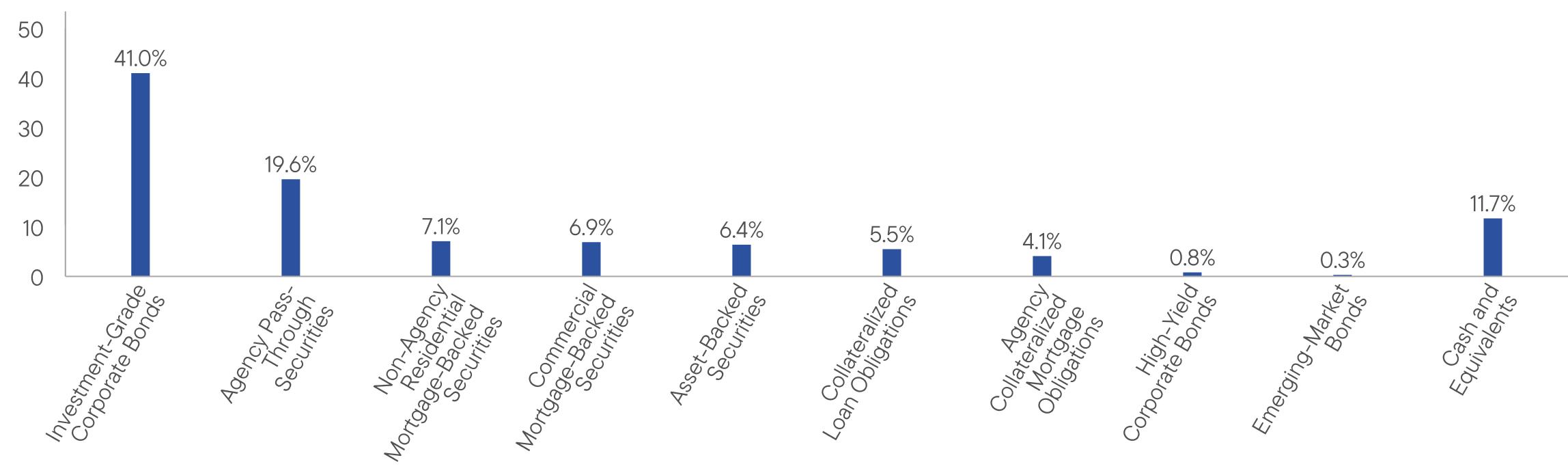

WHAT DID THE FUND INVEST IN? (as of December 31, 2024)

Portfolio Composition (% of Total Net Assets)

| Cash and Equivalents, if any, represent the market value weights of cash, derivatives, short-term securities, and other unclassified assets in the portfolio. Allocations may not total 100% because the chart includes the notional value of certain derivatives (the economic value for purposes of calculating periodic payment obligations), including to-be-announced mortgage security trades, if any, in addition to the market value of securities. Holdings and allocations may vary over time. |

HOW HAS THE FUND CHANGED?

On May 31, 2023, Franklin Resources, Inc. (“Franklin Templeton”) and Great-West Lifeco Inc., the parent company of Putnam U.S. Holdings I, LLC (“Putnam Holdings”), announced that they had entered into a definitive agreement for a subsidiary of Franklin Templeton to acquire Putnam Holdings in a stock and cash transaction (the “Transaction”). The Transaction was completed on January 1, 2024. As part of the Transaction, your Fund’s then-current investment advisor, Putnam Investment Management, LLC (“Putnam Management”), a wholly-owned subsidiary of Putnam Holdings, and your Fund’s then-current sub-advisor, Putnam Investments Limited (“PIL”), an indirect, wholly-owned subsidiary of Putnam Holdings, became indirect, wholly-owned subsidiaries of Franklin Templeton. In connection with the Transaction, shareholders of your Fund approved a new management contract with Putnam Management and a new sub-advisory contract with PIL. The new contracts were identical to the previous contracts, except for the effective dates, initial terms, updates to fund names as necessary to reflect previous name changes, and certain non-substantive changes.

Effective July 15, 2024, Putnam Management transferred its management contract for your Fund to Franklin Advisers, Inc. (“Franklin Advisers”), and Franklin Advisers replaced Putnam Management as the investment advisor to your Fund. In connection with the transfer, your Fund’s portfolio managers, along with supporting research analysts and certain other investment staff of Putnam Management, also became employees of Franklin Advisers. Putnam Management also transferred to Franklin Advisers its sub-management agreement with PIL in respect of your Fund. Franklin Advisers is a direct, wholly-owned subsidiary of Franklin Templeton. In addition, effective July 15, 2024, Franklin Advisers retained Putnam Management as a sub-advisor to your Fund pursuant to a new sub-advisory agreement.

Effective November 1, 2024 (the “Effective Date”), PIL, a sub-advisor of the Fund prior to the Effective Date, merged with and into Franklin Templeton Investment Management Limited (“FTIML”), a wholly-owned subsidiary of Franklin Templeton (the “Merger”). As of the Effective Date, PIL investment professionals became employees of FTIML, and the sub-advisory agreement between Franklin Advisers and PIL with respect to the Fund was terminated. In connection with the Merger, the Fund’s Trustees approved a new sub-advisory agreement between Franklin Advisers and FTIML, pursuant to which FTIML became a sub-advisor of the Fund on the Effective Date.

Effective September 30, 2024, the portfolio managers for the Fund are Albert Chan, Tina Chou, Patrick Klein, Michael Salm and Matthew Walkup.

This is a summary of certain changes to the Fund since January 1, 2024. For more complete information, you may review the Fund’s current prospectus and any applicable supplements and the Fund’s next prospectus, which we expect to be available by May 1, 2025, at https://www.franklintempleton.com/regulatory-fund-documents or upon request at (800) 225-1581 or

funddocuments@putnam.com.

| Putnam VT Income Fund | PAGE 3 | 38921-ATSIB-0225 |

| |

| WHERE CAN I FIND ADDITIONAL INFORMATION ABOUT THE FUND? |

Additional information is available on https://www.franklintempleton.com/regulatory-fund-documents, including its: |

| • prospectus • proxy voting information • financial information • holdings • tax information |

| Putnam VT Income Fund | PAGE 4 | 38921-ATSIB-0225 |

100009854100511061310635118991258112004103461083211083100001005510321106871068811620124921229910699112911143241.019.67.16.96.45.54.10.80.311.7

| |

| (a) The fund’s principal executive, financial and accounting officers are employees of Putnam Investment Management, LLC, the Fund’s investment manager, or Franklin Templeton. As such they are subject to a comprehensive Code of Ethics adopted and administered by Putnam Investment Management, LLC and Franklin Templeton which is designed to protect the interests of the firm and its clients. The Fund has adopted a Code of Ethics which incorporates the Code of Ethics of Franklin Templeton with respect to all of its officers and Trustees who are employees of Putnam Investment Management, LLC and Franklin Templeton. For this reason, the Fund has not adopted a separate code of ethics governing its principal executive, financial and accounting officers. |

| |

| (c) In connection with the acquisition of Putnam Investments by Franklin Templeton, the Putnam Investments Code of Ethics was amended effective January 1, 2024 to reflect revised compliance processes, including: (i) Compliance with the Putnam Investments Code of Ethics will be viewed as compliance with the Franklin Templeton Code for certain Putnam employees who are dual-hatted in Franklin Templeton advisory entities (ii) Certain Franklin Templeton employees are required to hold shares of Putnam mutual funds at Putnam Investor Services, Inc. and (iii) Certain provisions of the Putnam Investments Code of Ethics are amended that are no longer needed due to organizational changes. Effective March 4, 2024, the majority of legacy Putnam employees transitioned to Franklin Templeton policies outlined in the Franklin Templeton Code. |

| |

| Item 3. Audit Committee Financial Expert: |

| |

| The Funds’ Audit, Compliance and Risk Committee is comprised solely of Trustees who are “independent” (as such term has been defined by the Securities and Exchange Commission (“SEC”) in regulations implementing Section 407 of the Sarbanes-Oxley Act (the “Regulations”)). The Trustees believe that each member of the Audit, Compliance and Risk Committee also possesses a combination of knowledge and experience with respect to financial accounting matters, as well as other attributes, that qualifies him or her for service on the Committee. In addition, the Trustees have determined that each of Mr. McGreevey and Mr. Singh qualifies as an “audit committee financial expert” (as such term has been defined by the Regulations) based on their review of his or her pertinent experience and education.The SEC has stated, and the funds’ amended and restated agreement and Declaration of Trust provides, that the designation or identification of a person as an audit committee financial expert pursuant to this Item 3 of Form N-CSR does not impose on such person any duties, obligations or liability that are greater than the duties, obligations and liability imposed on such person as a member of the Audit, Compliance and Risk Committee and the Board of Trustees in the absence of such designation or identification. |

| |

| Item 4. Principal Accountant Fees and Services: |

| |

| The following table presents fees billed in each of the last two fiscal years for services rendered to the fund by the fund’s independent auditor: |

Fiscal year ended | Audit Fees | Audit-Related Fees | Tax Fees | All Other Fees |

December 31, 2024 | $101,381 | $ — | $8,640 | $ — |

December 31, 2023 | $117,403 | $ — | $9,640 | $ — |

| |

| For the fiscal years ended December 31, 2024 and December 31, 2023, the fund’s independent auditor billed aggregate non-audit fees in the amounts of $872,876 and $369,772 respectively, to the fund, the fund’s investment manager and any entity controlling, controlled by or under common control with the fund’s investment manager that provides ongoing services to the fund. |

| |

| Audit Fees represent fees billed for the fund’s last two fiscal years relating to the audit and review of the financial statements included in annual reports and registration statements, and other services that are normally provided in connection with statutory and regulatory filings or engagements. |

| |

| Audit-Related Fees represent fees billed in the fund’s last two fiscal years for services traditionally performed by the fund’s auditor, including accounting consultation for proposed transactions or concerning financial accounting and reporting standards and other audit or attest services not required by statute or regulation. |

| |

| Tax Fees represent fees billed in the fund’s last two fiscal years for tax compliance, tax planning and tax advice services. Tax planning and tax advice services include assistance with tax audits, employee benefit plans and requests for rulings or technical advice from taxing authorities. |

| |

| Pre-Approval Policies of the Audit, Compliance and Risk Committee. The Audit, Compliance and Risk Committee of the Putnam funds has determined that, as a matter of policy, all work performed for the funds by the funds’ independent auditors will be pre-approved by the Committee itself and thus will generally not be subject to pre-approval procedures. |

| |

| The Audit, Compliance and Risk Committee also has adopted a policy to pre-approve the engagement by the fund’s investment manager and certain of its affiliates of the funds’ independent auditors, even in circumstances where pre-approval is not required by applicable law. Any such requests by the fund’s investment manager or certain of its affiliates are typically submitted in writing to the Committee and explain, among other things, the nature of the proposed engagement, the estimated fees, and why this work should be performed by that particular audit firm as opposed to another one. In reviewing such requests, the Committee considers, among other things, whether the provision of such services by the audit firm are compatible with the independence of the audit firm. |

| |

| The following table presents fees billed by the fund’s independent auditor for services required to be approved pursuant to paragraph (c)(7)(ii) of Rule 2–01 of Regulation S-X. |

Fiscal year ended | Audit-Related Fees | Tax Fees | All Other Fees | Total Non-Audit Fees |

December 31, 2024 | $ — | $791,963 | $72,273 | $864,236 |

December 31, 2023 | $ — | $360,132 | $ — | $360,132 |

| |

| Item 5. Audit Committee of Listed Registrants |

| |

| The registrant’s schedule of investments in unaffiliated issuers is included in the Financial Statements and Other Important Information in Item 7 below. |

| |

| Item 7. Financial Statements and Financial Highlights for Open-End Management Investment Companies. |

Putnam

VT Income

Fund

Financial Statements and Other Important Information

Annual | December 31, 2024

Table of Contents

| | Financial Statements and Other Important Information—Annual | franklintempleton.com |

Report of Independent Registered Public Accounting Firm

To the Board of Trustees of Putnam Variable Trust and Shareholders of

Putnam VT Income Fund:

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities, including the fund's portfolio, of Putnam VT Income Fund (one of the funds constituting Putnam Variable Trust, referred to hereafter as the “Fund”) as of December 31, 2024, the related statement of operations for the year ended December 31, 2024, the statement of changes in net assets for each of the two years in the period ended December 31, 2024, including the related notes, and the financial highlights for each of the five years in the period ended December 31, 2024 (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund as of December 31, 2024, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period ended December 31, 2024 and the financial highlights for each of the five years in the period ended December 31, 2024 in conformity with accounting principles generally accepted in the United States of America.

Basis for Opinion

These financial statements are the responsibility of the Fund's management. Our responsibility is to express an opinion on the Fund's financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits of these financial statements in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. Our procedures included confirmation of securities owned as of December 31, 2024 by correspondence with the custodian, transfer agent and brokers; when replies were not received from brokers, we performed other auditing procedures. We believe that our audits provide a reasonable basis for our opinion.

PricewaterhouseCoopers LLP

Boston, Massachusetts

February 18, 2025

We have served as the auditor of one or more investment companies in the Putnam Funds family of funds since at least 1957. We have not been able to determine the specific year we began serving as auditor.

| The fund’s portfolio 12/31/24 |

| | CORPORATE BONDS AND NOTES (41.5%)* | Principal amount | Value |

| | Banking (8.4%) | | | |

| | ABN AMRO Bank NV 144A unsec. sub. notes 4.75%, 7/28/25 (Netherlands) | | $200,000 | $199,400 |

| | Australia and New Zealand Banking Group, Ltd./United Kingdom 144A jr. unsec. sub. FRB 6.75%, perpetual maturity | | 200,000 | 203,207 |

| | Banco Santander SA jr. unsec. sub. FRB 9.625%, 11/21/53 (Spain) | | 200,000 | 231,027 |

| | Banco Santander SA sr. unsec. unsub. notes 4.379%, 4/12/28 (Spain) | | 200,000 | 195,245 |

| | Banco Santander SA unsec. sub. bonds 6.921%, 8/8/33 (Spain) | | 200,000 | 210,026 |

| | Bank of America Corp. jr. unsec. sub. FRN Ser. AA, 6.10%, perpetual maturity | | 245,000 | 244,960 |

| | Bank of America Corp. sr. unsec. bonds 5.468%, 1/23/35 | | 50,000 | 50,077 |

| | Bank of America Corp. sr. unsec. FRN Ser. MTN, 2.496%, 2/13/31 | | 195,000 | 171,529 |

| | Bank of America Corp. sr. unsec. notes 6.204%, 11/10/28 | | 100,000 | 103,546 |

| | Bank of America Corp. unsec. sub. FRB 3.846%, 3/8/37 | | 550,000 | 487,533 |

| | Bank of America Corp. unsec. sub. FRN (CME Term SOFR 3 Month + 1.02%), 5.38%, 9/15/26 | | 100,000 | 100,166 |

| | Bank of America Corp. unsec. sub. notes 6.11%, 1/29/37 | | 300,000 | 311,025 |

| | Bank of America Corp. unsec. sub. notes Ser. MTN, 5.425%, 8/15/35 | | 100,000 | 97,381 |

| | BPCE SA 144A unsec. sub. notes 4.50%, 3/15/25 (France) | | 317,000 | 316,445 |

| | CaixaBank SA 144A sr. unsec. notes 5.673%, 3/15/30 (Spain) | | 200,000 | 202,027 |

| | Citigroup, Inc. jr. unsec. sub. bonds Ser. CC, 7.125%, 5/29/74 | | 70,000 | 71,475 |

| | Citigroup, Inc. jr. unsec. sub. FRN 3.875%, perpetual maturity | | 90,000 | 87,608 |

| | Citigroup, Inc. sr. unsec. FRN 5.61%, 9/29/26 | | 105,000 | 105,598 |

| | Citigroup, Inc. sr. unsec. FRN 3.106%, 4/8/26 | | 21,000 | 20,901 |

| | Citigroup, Inc. sr. unsec. unsub. FRB 3.887%, 1/10/28 | | 64,000 | 62,751 |

| | Citigroup, Inc. sub. unsec. bonds 6.174%, 5/25/34 | | 76,000 | 77,456 |

| | Citigroup, Inc. unsec. sub. bonds 4.45%, 9/29/27 | | 500,000 | 493,400 |

| | Citizens Bank NA sr. unsec. unsub. FRN 5.284%, 1/26/26 | | 250,000 | 249,988 |

| | Commonwealth Bank of Australia 144A unsec. sub. notes 5.837%, 3/13/34 (Australia) | | 200,000 | 202,319 |

| | Credit Agricole SA 144A jr. unsec. sub. notes 8.125%, 12/23/25 (France) | | 200,000 | 204,265 |

| | Credit Agricole SA 144A unsec. sub. FRN 4.00%, 1/10/33 (France) | | 250,000 | 235,880 |

| | Danske Bank A/S 144A sr. unsec. FRN 6.466%, 1/9/26 (Denmark) | | 200,000 | 200,044 |

| | Deutsche Bank AG unsec. sub. notes 4.50%, 4/1/25 (Germany) | | 200,000 | 199,726 |

| | Fifth Third Bancorp sr. unsec. notes 4.895%, 9/6/30 | | 60,000 | 59,201 |

| | Fifth Third Bancorp sr. unsec. unsub. FRN 6.339%, 7/27/29 | | 115,000 | 119,348 |

| | First-Citizens Bank & Trust Co. unsec. sub. notes 6.125%, 3/9/28 | | 107,000 | 110,171 |

| | ING Groep NV sr. unsec. unsub. FRN 6.083%, 9/11/27 (Netherlands) | | 200,000 | 203,950 |

| | Intesa Sanpaolo SpA 144A unsec. sub. bonds 4.198%, 6/1/32 (Italy) | | 210,000 | 182,797 |

| | JPMorgan Chase & Co. jr. unsec. sub. FRB Ser. HH, 4.60%, perpetual maturity | | 429,000 | 428,158 |

| | JPMorgan Chase & Co. jr. unsec. sub. FRB Ser. W, (CME Term SOFR 3 Month + 1.26%), 5.785%, 5/15/47 | | 63,000 | 59,912 |

| | JPMorgan Chase & Co. jr. unsec. sub. FRN 3.65%, perpetual maturity | | 87,000 | 84,615 |

| | JPMorgan Chase & Co. sr. unsec. unsub. bonds 5.294%, 7/22/35 | | 125,000 | 123,729 |

| | JPMorgan Chase & Co. sr. unsec. unsub. notes 6.07%, 10/22/27 | | 155,000 | 158,671 |

| | JPMorgan Chase & Co. unsec. sub. FRB 5.717%, 9/14/33 | | 380,000 | 388,260 |

| | JPMorgan Chase & Co. unsec. sub. FRB 2.956%, 5/13/31 | | 300,000 | 268,463 |

| | Lloyds Banking Group PLC unsec. sub. FRB 3.369%, 12/14/46 (United Kingdom) | | 305,000 | 211,115 |

| | NatWest Group PLC sr. unsec. unsub. FRN 5.847%, 3/2/27 (United Kingdom) | | 200,000 | 202,012 |

| | PNC Financial Services Group, Inc. (The) unsec. sub. FRB 4.626%, 6/6/33 | | 350,000 | 329,681 |

| | Royal Bank of Canada sr. unsec. notes Ser. GMTN, 5.20%, 8/1/28 (Canada) | | 140,000 | 141,198 |

| | Royal Bank of Canada unsec. sub. notes Ser. GMTN, 4.65%, 1/27/26 (Canada) | | 140,000 | 139,898 |

| | Societe Generale SA 144A jr. unsec. sub. FRB 10.00%, 11/14/73 (France) | | 200,000 | 213,723 |

| | Toronto-Dominion Bank (The) jr. sub. unsec. FRB 8.125%, 10/31/82 (Canada) | | 200,000 | 208,964 |

| | Toronto-Dominion Bank (The) unsec. sub. FRB 3.625%, 9/15/31 (Canada) | | 180,000 | 175,013 |

| | Truist Financial Corp. sr. unsec. unsub. bonds Ser. MTN, 5.711%, 1/24/35 | | 120,000 | 120,975 |

| | Truist Financial Corp. sr. unsec. unsub. FRN Ser. MTN, 4.26%, 7/28/26 | | 105,000 | 104,616 |

| | UBS Group AG jr. unsec. sub. FRN Ser. REGS, 6.875%, perpetual maturity | | 247,000 | 247,646 |

| | UBS Group AG 144A jr. unsec. sub. bonds 6.85%, 9/10/54 (Switzerland) | | 200,000 | 198,315 |

| | UBS Group AG 144A sr. unsec. FRB 9.016%, 11/15/33 (Switzerland) | | 370,000 | 447,013 |

| | UBS Group AG 144A sr. unsec. FRN 2.193%, 6/5/26 (Switzerland) | | 250,000 | 247,066 |

| | US Bancorp unsec. sub. FRB 2.491%, 11/3/36 | | 260,000 | 210,651 |

| | Wells Fargo & Co. jr. unsec. sub. FRN 3.90%, perpetual maturity | | 50,000 | 48,612 |

| | Wells Fargo & Co. sr. unsec. unsub. FRN Ser. MTN, 5.574%, 7/25/29 | | 125,000 | 126,945 |

| | | | |

| | CORPORATE BONDS AND NOTES (41.5%)* cont. | Principal amount | Value |

| | Banking cont. | | | |

| | Wells Fargo Bank, NA unsec. sub. notes Ser. BKNT, 6.60%, 1/15/38 | | $495,000 | $540,289 |

| | Westpac Banking Corp. unsec. sub. bonds 4.421%, 7/24/39 (Australia) | | 185,000 | 163,843 |

| | | | | 11,599,855 |

| | Basic materials (1.0%) | | | |

| | Celanese US Holdings, LLC company guaranty sr. unsec. bonds 6.379%, 7/15/32 (Germany) | | 90,000 | 91,461 |

| | Celanese US Holdings, LLC company guaranty sr. unsec. notes 6.80%, 11/15/30 (Germany) | | 5,000 | 5,178 |

| | Celanese US Holdings, LLC company guaranty sr. unsec. notes 6.33%, 7/15/29 (Germany) | | 14,000 | 14,294 |

| | Celanese US Holdings, LLC company guaranty sr. unsec. notes 6.165%, 7/15/27 (Germany) | | 73,000 | 74,112 |

| | Celanese US Holdings, LLC company guaranty sr. unsec. notes 1.40%, 8/5/26 (Germany) | | 65,000 | 60,846 |

| | CF Industries, Inc. company guaranty sr. unsec. bonds 4.95%, 6/1/43 | | 227,000 | 200,347 |

| | FMC Corp. sr. unsec. unsub. notes 5.65%, 5/18/33 | | 135,000 | 133,615 |

| | Glencore Funding, LLC 144A company guaranty sr. unsec. bonds 5.634%, 4/4/34 | | 20,000 | 19,923 |

| | Glencore Funding, LLC 144A company guaranty sr. unsec. notes 6.375%, 10/6/30 | | 70,000 | 73,548 |

| | Glencore Funding, LLC 144A company guaranty sr. unsec. notes 4.00%, 3/27/27 | | 124,000 | 121,632 |

| | Huntsman International, LLC sr. unsec. bonds 5.70%, 10/15/34 | | 15,000 | 14,309 |

| | Huntsman International, LLC sr. unsec. notes 4.50%, 5/1/29 | | 150,000 | 143,181 |

| | International Flavors & Fragrances, Inc. sr. unsec. notes 4.45%, 9/26/28 | | 75,000 | 73,395 |

| | International Flavors & Fragrances, Inc. 144A company guaranty sr. unsec. bonds 3.468%, 12/1/50 | | 20,000 | 13,115 |

| | International Flavors & Fragrances, Inc. 144A sr. unsec. notes 2.30%, 11/1/30 | | 35,000 | 29,740 |

| | Nutrien, Ltd. sr. unsec. bonds 5.25%, 1/15/45 (Canada) | | 44,000 | 40,608 |

| | Nutrien, Ltd. sr. unsec. notes 2.95%, 5/13/30 (Canada) | | 25,000 | 22,508 |

| | Nutrien, Ltd. sr. unsec. sub. bonds 4.20%, 4/1/29 (Canada) | | 95,000 | 92,215 |

| | Sherwin-Williams Co. (The) sr. unsec. unsub. bonds 3.30%, 5/15/50 | | 50,000 | 33,125 |

| | WestRock MWV, LLC company guaranty sr. unsec. unsub. notes 8.20%, 1/15/30 | | 105,000 | 119,223 |

| | WestRock MWV, LLC company guaranty sr. unsec. unsub. notes 7.95%, 2/15/31 | | 39,000 | 44,031 |

| | Weyerhaeuser Co. sr. unsec. unsub. notes 7.375%, 3/15/32 R | | 32,000 | 35,653 |

| | | | | 1,456,059 |

| | Capital goods (2.6%) | | | |

| | BAE Systems PLC 144A sr. unsec. bonds 5.50%, 3/26/54 (United Kingdom) | | 200,000 | 194,924 |

| | Berry Global, Inc. company guaranty sr. notes 5.50%, 4/15/28 | | 13,000 | 13,131 |

| | Berry Global, Inc. 144A company guaranty sr. notes 4.875%, 7/15/26 | | 3,000 | 2,990 |

| | Berry Global, Inc. 144A company guaranty sr. notes 1.65%, 1/15/27 | | 155,000 | 145,186 |

| | Berry Global, Inc. 144A company guaranty sr. notes 1.57%, 1/15/26 | | 104,000 | 100,411 |

| | Boeing Co. (The) sr. unsec. bonds 3.95%, 8/1/59 | | 70,000 | 46,287 |

| | Boeing Co. (The) sr. unsec. bonds 5.805%, 5/1/50 | | 45,000 | 41,924 |

| | Boeing Co. (The) sr. unsec. notes 2.95%, 2/1/30 | | 25,000 | 22,342 |

| | Boeing Co. (The) sr. unsec. notes 2.196%, 2/4/26 | | 357,000 | 346,419 |

| | Boeing Co. (The) sr. unsec. unsub. bonds 3.375%, 6/15/46 | | 205,000 | 132,142 |

| | Boeing Co. (The) sr. unsec. unsub. bonds 6.858%, 5/1/54 | | 80,000 | 85,109 |

| | Boeing Co. (The) sr. unsec. unsub. notes 6.528%, 5/1/34 | | 30,000 | 31,444 |

| | Boeing Co. (The) sr. unsec. unsub. notes 6.298%, 5/1/29 | | 30,000 | 31,112 |

| | Boeing Co. (The) sr. unsec. unsub. notes 6.259%, 5/1/27 | | 20,000 | 20,481 |

| | Boeing Co. (The) sr. unsec. unsub. notes 6.125%, 2/15/33 | | 55,000 | 56,891 |

| | Daimler Trucks Finance North America, LLC 144A company guaranty sr. unsec. notes 5.125%, 9/25/27 | | 355,000 | 357,170 |

| | Howmet Aerospace, Inc. sr. unsec. unsub. bonds 5.95%, 2/1/37 | | 16,000 | 16,617 |

| | Howmet Aerospace, Inc. sr. unsec. unsub. notes 6.75%, 1/15/28 | | 135,000 | 141,253 |

| | Howmet Aerospace, Inc. sr. unsec. unsub. notes 3.00%, 1/15/29 | | 142,000 | 132,114 |

| | Johnson Controls International PLC sr. unsec. notes 3.90%, 2/14/26 | | 138,000 | 136,723 |

| | MasTec, Inc. company guaranty sr. unsec. unsub. notes 5.90%, 6/15/29 | | 320,000 | 325,993 |

| | Northrop Grumman Corp. sr. unsec. bonds 5.25%, 5/1/50 | | 45,000 | 42,215 |

| | Oshkosh Corp. sr. unsec. sub. notes 4.60%, 5/15/28 | | 125,000 | 123,458 |

| | Oshkosh Corp. sr. unsec. unsub. notes 3.10%, 3/1/30 | | 15,000 | 13,749 |

| | Republic Services, Inc. sr. unsec. unsub. notes 5.00%, 11/15/29 | | 335,000 | 336,996 |

| | RTX Corp. sr. unsec. notes 5.15%, 2/27/33 | | 30,000 | 29,761 |

| | RTX Corp. sr. unsec. unsub. bonds 6.40%, 3/15/54 | | 50,000 | 54,434 |

| | RTX Corp. sr. unsec. unsub. notes 4.125%, 11/16/28 | | 370,000 | 360,337 |

| | Waste Connections, Inc. sr. unsec. bonds 5.00%, 3/1/34 | | 40,000 | 39,062 |

| | Waste Connections, Inc. sr. unsec. bonds 3.20%, 6/1/32 | | 22,000 | 19,265 |

| | Waste Connections, Inc. sr. unsec. sub. bonds 3.50%, 5/1/29 | | 110,000 | 104,138 |

| | Waste Management, Inc. company guaranty sr. unsec. notes 4.875%, 2/15/29 | | 93,000 | 93,480 |

| | | | | 3,597,558 |

| | | | |

| | CORPORATE BONDS AND NOTES (41.5%)* cont. | Principal amount | Value |

| | Communication services (2.7%) | | | |

| | American Tower Corp. sr. unsec. bonds 5.55%, 7/15/33 R | | $250,000 | $252,275 |

| | American Tower Corp. sr. unsec. bonds 2.70%, 4/15/31 R | | 195,000 | 168,470 |

| | American Tower Corp. sr. unsec. notes 2.90%, 1/15/30 R | | 48,000 | 43,253 |

| | American Tower Corp. sr. unsec. unsub. notes 3.55%, 7/15/27 R | | 118,000 | 114,440 |

| | AT&T, Inc. sr. unsec. unsub. bonds 2.55%, 12/1/33 | | 162,000 | 130,551 |

| | AT&T, Inc. sr. unsec. unsub. notes 4.75%, 5/15/46 | | 335,000 | 291,193 |

| | Charter Communications Operating, LLC/Charter Communications Operating Capital Corp. company guaranty sr. notes 2.25%, 1/15/29 | | 83,000 | 73,223 |

| | Charter Communications Operating, LLC/Charter Communications Operating Capital Corp. company guaranty sr. sub. notes 4.908%, 7/23/25 | | 57,000 | 56,952 |

| | Comcast Corp. company guaranty sr. unsec. notes 3.45%, 2/1/50 | | 135,000 | 92,513 |

| | Comcast Corp. company guaranty sr. unsec. unsub. bonds 2.35%, 1/15/27 | | 172,000 | 164,462 |

| | Crown Castle, Inc. sr. unsec. bonds 3.65%, 9/1/27 R | | 130,000 | 126,103 |

| | Crown Castle, Inc. sr. unsec. notes 4.90%, 9/1/29 R | | 230,000 | 227,584 |

| | Crown Castle, Inc. sr. unsec. notes 4.75%, 5/15/47 R | | 25,000 | 21,289 |

| | Equinix, Inc. sr. unsec. sub. notes 3.20%, 11/18/29 R | | 193,000 | 177,557 |

| | Equinix, Inc. sr. unsec. sub. notes 2.50%, 5/15/31 R | | 70,000 | 59,867 |

| | Rogers Communications, Inc. company guaranty sr. unsec. notes 5.00%, 2/15/29 (Canada) | | 90,000 | 89,463 |

| | Rogers Communications, Inc. company guaranty sr. unsec. unsub. bonds 4.30%, 2/15/48 (Canada) | | 100,000 | 78,280 |

| | Rogers Communications, Inc. company guaranty sr. unsec. unsub. notes Ser. REGS, 3.80%, 3/15/32 (Canada) | | 38,000 | 34,190 |

| | Sprint Capital Corp. company guaranty sr. unsec. unsub. notes 6.875%, 11/15/28 | | 149,000 | 158,276 |

| | T-Mobile USA, Inc. company guaranty sr. bonds 4.50%, 4/15/50 | | 261,000 | 214,269 |

| | T-Mobile USA, Inc. company guaranty sr. notes 3.875%, 4/15/30 | | 7,000 | 6,590 |

| | T-Mobile USA, Inc. company guaranty sr. unsec. bonds 5.75%, 1/15/54 | | 115,000 | 112,290 |

| | T-Mobile USA, Inc. company guaranty sr. unsec. bonds 5.05%, 7/15/33 | | 255,000 | 249,787 |

| | Time Warner Cable Enterprises, LLC company guaranty sr. unsub. notes 8.375%, 7/15/33 | | 155,000 | 174,630 |

| | Verizon Communications, Inc. sr. unsec. unsub. bonds 4.272%, 1/15/36 | | 150,000 | 134,987 |

| | Verizon Communications, Inc. sr. unsec. unsub. notes 4.40%, 11/1/34 | | 85,000 | 78,794 |

| | Verizon Communications, Inc. sr. unsec. unsub. notes 4.329%, 9/21/28 | | 117,000 | 114,647 |

| | Verizon Communications, Inc. sr. unsec. unsub. notes 2.10%, 3/22/28 | | 250,000 | 229,965 |

| | | | | 3,675,900 |

| | Consumer cyclicals (3.1%) | | | |

| | Alimentation Couche-Tard, Inc. 144A company guaranty sr. unsec. notes 3.55%, 7/26/27 (Canada) | | 260,000 | 251,345 |

| | Alimentation Couche-Tard, Inc. 144A sr. unsec. notes 2.95%, 1/25/30 (Canada) | | 134,000 | 120,863 |

| | Amazon.com, Inc. sr. unsec. unsub. bonds 2.70%, 6/3/60 | | 453,000 | 260,130 |

| | Amazon.com, Inc. sr. unsec. unsub. notes 2.10%, 5/12/31 | | 101,000 | 86,302 |

| | Autonation, Inc. company guaranty sr. unsec. notes 4.50%, 10/1/25 | | 16,000 | 15,945 |

| | BMW US Capital, LLC 144A company guaranty sr. unsec. notes 3.95%, 8/14/28 | | 104,000 | 100,517 |

| | Brunswick Corp./DE sr. unsec. bonds 5.10%, 4/1/52 | | 85,000 | 66,160 |

| | Brunswick Corp/DE sr. unsec. notes 5.85%, 3/18/29 | | 50,000 | 50,806 |

| | Carnival Corp. 144A company guaranty sr. sub. notes 4.00%, 8/1/28 | | 192,000 | 182,106 |

| | D.R. Horton, Inc. company guaranty sr. unsec. bonds 5.00%, 10/15/34 | | 225,000 | 217,381 |

| | Dick’s Sporting Goods, Inc. sr. unsec. bonds 4.10%, 1/15/52 | | 60,000 | 43,875 |

| | Discovery Communications, LLC company guaranty sr. unsec. unsub. notes 3.625%, 5/15/30 | | 18,000 | 16,020 |

| | Global Payments, Inc. sr. unsec. notes 2.15%, 1/15/27 | | 60,000 | 56,903 |

| | Home Depot, Inc. (The) sr. unsec. unsub. bonds 5.30%, 6/25/54 | | 92,000 | 88,217 |

| | Home Depot, Inc. (The) sr. unsec. unsub. notes 4.95%, 6/25/34 | | 92,000 | 90,812 |

| | Hyatt Hotels Corp. sr. unsec. notes 5.75%, 1/30/27 | | 22,000 | 22,344 |

| | Hyatt Hotels Corp. sr. unsec. notes 5.375%, 12/15/31 | | 75,000 | 74,687 |

| | Hyatt Hotels Corp. sr. unsec. notes 5.25%, 6/30/29 | | 105,000 | 105,126 |

| | Hyundai Capital America 144A sr. unsec. notes 6.375%, 4/8/30 (South Korea) | | 8,000 | 8,363 |

| | Hyundai Capital America 144A sr. unsec. notes 5.40%, 1/8/31 (South Korea) | | 20,000 | 20,004 |

| | Hyundai Capital America 144A sr. unsec. notes 4.55%, 9/26/29 (South Korea) | | 50,000 | 48,560 |

| | Hyundai Capital America 144A sr. unsec. notes 6.50%, 1/16/29 (South Korea) | | 295,000 | 308,038 |

| | Hyundai Capital America 144A sr. unsec. notes 5.35%, 3/19/29 (South Korea) | | 41,000 | 41,246 |

| | Interpublic Group of Cos., Inc. (The) sr. unsec. sub. bonds 4.65%, 10/1/28 | | 150,000 | 148,912 |

| | Moody’s Corp. sr. unsec. bonds 5.25%, 7/15/44 | | 108,000 | 102,762 |

| | Netflix, Inc. sr. unsec. bonds 5.40%, 8/15/54 | | 20,000 | 19,473 |

| | Netflix, Inc. sr. unsec. bonds 4.90%, 8/15/34 | | 15,000 | 14,698 |

| | Netflix, Inc. 144A sr. unsec. bonds 5.375%, 11/15/29 | | 310,000 | 316,183 |

| | Paramount Global sr. unsec. unsub. FRB 4.375%, 3/15/43 | | 20,000 | 14,574 |

| | | | |

| | CORPORATE BONDS AND NOTES (41.5%)* cont. | Principal amount | Value |

| | Consumer cyclicals cont. | | | |

| | Paramount Global sr. unsec. unsub. notes 4.20%, 6/1/29 | | $230,000 | $217,255 |

| | Paramount Global sr. unsec. unsub. notes 3.70%, 6/1/28 | | 55,000 | 51,829 |

| | Paramount Global sr. unsec. unsub. notes 2.90%, 1/15/27 | | 31,000 | 29,677 |

| | PulteGroup, Inc. company guaranty sr. unsec. unsub. notes 6.375%, 5/15/33 | | 95,000 | 100,221 |

| | S&P Global, Inc. company guaranty sr. unsec. bonds 2.50%, 12/1/29 | | 70,000 | 62,936 |

| | S&P Global, Inc. company guaranty sr. unsec. notes 4.75%, 8/1/28 | | 65,000 | 65,111 |

| | S&P Global, Inc. company guaranty sr. unsec. notes 1.25%, 8/15/30 | | 41,000 | 33,935 |

| | Stellantis Finance US, Inc. 144A company guaranty sr. unsec. notes 1.711%, 1/29/27 | | 200,000 | 186,594 |

| | Tapestry, Inc. sr. unsec. bonds 5.50%, 3/11/35 | | 113,000 | 109,970 |

| | Tapestry, Inc. sr. unsec. notes 5.10%, 3/11/30 | | 92,000 | 91,026 |

| | Toll Brothers Finance Corp. company guaranty sr. unsec. notes 3.80%, 11/1/29 | | 145,000 | 136,637 |

| | Toll Brothers Finance Corp. company guaranty sr. unsec. unsub. notes 4.35%, 2/15/28 | | 73,000 | 71,347 |

| | Warnermedia Holdings, Inc. company guaranty sr. unsec. notes 4.279%, 3/15/32 | | 274,000 | 241,523 |

| | | | | 4,290,413 |

| | Consumer finance (1.4%) | | | |

| | AerCap Ireland Capital DAC/AerCap Global Aviation Trust company guaranty sr. unsec. bonds 3.30%, 1/30/32 (Ireland) | | 245,000 | 213,561 |

| | AerCap Ireland Capital DAC/AerCap Global Aviation Trust company guaranty sr. unsec. notes 5.10%, 1/19/29 (Ireland) | | 150,000 | 149,954 |

| | Air Lease Corp. sr. unsec. sub. bonds 4.625%, 10/1/28 | | 40,000 | 39,355 |

| | Air Lease Corp. sr. unsec. sub. notes 3.25%, 10/1/29 | | 260,000 | 240,216 |

| | Aircastle, Ltd. 144A sr. unsec. notes 6.50%, 7/18/28 | | 75,000 | 77,551 |

| | American Express Co. sr. unsec. unsub. notes 5.098%, 2/16/28 | | 50,000 | 50,297 |

| | Aviation Capital Group, LLC 144A sr. unsec. notes 5.375%, 7/15/29 | | 210,000 | 210,255 |

| | Capital One Financial Corp. sr. unsec. unsub. FRN 7.624%, 10/30/31 | | 132,000 | 145,788 |

| | Capital One Financial Corp. unsec. sub. FRB 2.359%, 7/29/32 | | 225,000 | 181,782 |

| | Ford Motor Co. sr. unsec. unsub. notes 5.80%, 3/5/27 | | 305,000 | 307,953 |

| | General Motors Financial Co., Inc. sr. sub. notes 5.80%, 1/7/29 | | 140,000 | 142,887 |

| | General Motors Financial Co., Inc. sr. unsec. notes 4.90%, 10/6/29 | | 91,000 | 89,690 |

| | Macquarie Airfinance Holdings, Ltd. 144A sr. unsec. notes 5.15%, 3/17/30 (United Kingdom) | | 100,000 | 97,994 |

| | | | | 1,947,283 |

| | Consumer staples (1.4%) | | | |

| | Ashtead Capital, Inc. 144A company guaranty sr. unsec. bonds 5.95%, 10/15/33 | | 200,000 | 202,392 |

| | Ashtead Capital, Inc. 144A notes 4.375%, 8/15/27 | | 200,000 | 196,644 |

| | Conagra Brands, Inc. sr. unsec. bonds 5.30%, 11/1/38 | | 65,000 | 61,142 |

| | ERAC USA Finance, LLC 144A company guaranty sr. unsec. bonds 4.20%, 11/1/46 | | 88,000 | 71,808 |

| | ERAC USA Finance, LLC 144A company guaranty sr. unsec. notes 7.00%, 10/15/37 | | 83,000 | 93,929 |

| | ERAC USA Finance, LLC 144A company guaranty sr. unsec. unsub. notes 3.30%, 12/1/26 | | 40,000 | 38,988 |

| | Haleon US Capital, LLC company guaranty sr. unsec. unsub. notes 3.375%, 3/24/29 | | 250,000 | 235,305 |

| | JBS USA LUX SA/JBS USA Food Co./JBS Luxembourg SARL company guaranty sr. unsec. notes 6.75%, 3/15/34 (Luxembourg) | | 65,000 | 68,769 |

| | JBS USA LUX SA/JBS USA Food Co./JBS USA Finance, Inc. company guaranty sr. unsec. notes 5.75%, 4/1/33 (Luxembourg) | | 19,000 | 18,926 |

| | JBS USA LUX SA/JBS USA Food Co./JBS USA Finance, Inc. company guaranty sr. unsec. notes 3.00%, 2/2/29 (Luxembourg) | | 157,000 | 143,336 |

| | Kenvue, Inc. company guaranty sr. unsec. notes Ser. REGS, 4.90%, 3/22/33 | | 315,000 | 309,985 |

| | Kenvue, Inc. company guaranty sr. unsec. unsub. notes Ser. REGS, 5.05%, 3/22/53 | | 24,000 | 22,267 |

| | Mars, Inc. 144A sr. unsec. unsub. notes 4.65%, 4/20/31 | | 46,000 | 44,904 |

| | Philip Morris International, Inc. sr. unsec. unsub. notes 5.125%, 2/15/30 | | 296,000 | 297,654 |

| | Philip Morris International, Inc. sr. unsec. unsub. notes 4.75%, 11/1/31 | | 110,000 | 107,629 |

| | | | | 1,913,678 |

| | Energy (2.4%) | | | |

| | 6297782 LLC 144A company guaranty sr. unsec. bonds 5.584%, 10/1/34 | | 35,000 | 34,064 |

| | 6297782 LLC 144A company guaranty sr. unsec. notes 5.026%, 10/1/29 | | 180,000 | 176,949 |

| | Aker BP ASA 144A sr. unsec. bonds 5.80%, 10/1/54 (Norway) | | 75,000 | 68,009 |

| | Canadian Natural Resources, Ltd. sr. unsec. unsub. notes 7.20%, 1/15/32 (Canada) | | 110,000 | 120,252 |

| | Canadian Natural Resources, Ltd. 144A sr. unsec. notes 5.00%, 12/15/29 (Canada) | | 124,000 | 122,676 |

| | Cheniere Energy Partners LP company guaranty sr. unsec. notes 4.50%, 10/1/29 | | 195,000 | 188,928 |

| | Cheniere Energy Partners LP company guaranty sr. unsec. unsub. notes 3.25%, 1/31/32 | | 89,000 | 77,252 |

| | Columbia Pipelines Operating Co., LLC 144A sr. unsec. bonds 6.544%, 11/15/53 | | 45,000 | 47,202 |

| | Columbia Pipelines Operating Co., LLC 144A sr. unsec. notes 5.927%, 8/15/30 | | 50,000 | 51,485 |

| | | | |

| | CORPORATE BONDS AND NOTES (41.5%)* cont. | Principal amount | Value |

| | Energy cont. | | | |

| | DCP Midstream Operating LP company guaranty sr. unsec. notes 8.125%, 8/16/30 | | $85,000 | $96,691 |

| | Diamondback Energy, Inc. company guaranty sr. unsec. notes 6.25%, 3/15/33 | | 75,000 | 77,998 |

| | DT Midstream, Inc. 144A sr. bonds 5.80%, 12/15/34 | | 200,000 | 201,537 |

| | EQT Corp. sr. unsec. notes 7.00%, 2/1/30 | | 210,000 | 223,553 |

| | Occidental Petroleum Corp. sr. unsec. sub. notes 8.50%, 7/15/27 | | 109,000 | 116,736 |

| | Occidental Petroleum Corp. sr. unsec. sub. notes 7.50%, 5/1/31 | | 235,000 | 257,087 |

| | Occidental Petroleum Corp. sr. unsec. unsub. bonds 5.55%, 10/1/34 | | 30,000 | 29,200 |

| | Occidental Petroleum Corp. sr. unsec. unsub. notes 5.20%, 8/1/29 | | 65,000 | 64,535 |

| | ONEOK, Inc. company guaranty sr. unsec. notes 4.75%, 10/15/31 | | 15,000 | 14,516 |

| | ONEOK, Inc. company guaranty sr. unsec. unsub. notes 6.10%, 11/15/32 | | 205,000 | 212,255 |

| | Ovintiv, Inc. company guaranty sr. unsec. bonds 6.25%, 7/15/33 | | 93,000 | 95,306 |

| | Ovintiv, Inc. company guaranty sr. unsec. notes 5.65%, 5/15/28 | | 29,000 | 29,416 |

| | Ovintiv, Inc. company guaranty sr. unsec. notes 5.65%, 5/15/25 | | 23,000 | 23,058 |

| | Spectra Energy Partners LP sr. unsec. notes 3.375%, 10/15/26 | | 145,000 | 141,689 |

| | Targa Resources Partners LP/Targa Resources Partners Finance Corp. company guaranty sr. unsec. unsub. notes 5.00%, 1/15/28 | | 220,000 | 217,753 |

| | Targa Resources Partners LP/Targa Resources Partners Finance Corp. company guaranty sr. unsec. unsub. notes 4.875%, 2/1/31 | | 205,000 | 198,083 |

| | Venture Global Calcasieu Pass, LLC 144A company guaranty sr. notes 6.25%, 1/15/30 | | 365,000 | 368,661 |

| | | | | 3,254,891 |

| | Financial (0.7%) | | | |

| | Ally Financial, Inc. company guaranty sr. unsec. notes 8.00%, 11/1/31 | | 145,000 | 160,501 |

| | Ally Financial, Inc. sr. unsec. notes 4.75%, 6/9/27 | | 20,000 | 19,870 |

| | Berkshire Hathaway Finance Corp. company guaranty sr. unsec. notes 4.30%, 5/15/43 | | 210,000 | 181,932 |

| | Intercontinental Exchange, Inc. sr. unsec. bonds 1.85%, 9/15/32 | | 118,000 | 93,483 |

| | Intercontinental Exchange, Inc. sr. unsec. notes 4.35%, 6/15/29 | | 49,000 | 48,002 |

| | Intercontinental Exchange, Inc. sr. unsec. notes 4.00%, 9/15/27 | | 200,000 | 196,864 |

| | Intercontinental Exchange, Inc. sr. unsec. notes 3.65%, 5/23/25 | | 20,000 | 19,920 |

| | Jefferies Financial Group, Inc. sr. unsec. notes Ser. MTN, 5.15%, 9/15/25 | | 55,000 | 55,027 |

| | Jefferies Financial Group, Inc. sr. unsec. notes 6.20%, 4/14/34 | | 75,000 | 77,336 |

| | KKR Group Finance Co. VI, LLC 144A company guaranty sr. unsec. bonds 3.75%, 7/1/29 | | 110,000 | 104,218 |

| | LPL Holdings, Inc. company guaranty sr. unsec. notes 6.75%, 11/17/28 | | 41,000 | 43,079 |

| | Nasdaq, Inc. sr. unsec. sub. bonds 5.55%, 2/15/34 | | 21,000 | 21,197 |

| | | | | 1,021,429 |

| | Health care (4.0%) | | | |

| | AbbVie, Inc. sr. unsec. bonds 5.05%, 3/15/34 | | 61,000 | 60,291 |

| | AbbVie, Inc. sr. unsec. notes 4.95%, 3/15/31 | | 212,000 | 212,013 |

| | Amgen, Inc. sr. unsec. sub. notes 3.20%, 11/2/27 | | 218,000 | 209,742 |

| | Amgen, Inc. sr. unsec. unsub. bonds 5.75%, 3/2/63 | | 75,000 | 71,992 |

| | Amgen, Inc. sr. unsec. unsub. bonds 5.65%, 3/2/53 | | 98,000 | 94,423 |

| | Amgen, Inc. sr. unsec. unsub. notes 5.25%, 3/2/30 | | 273,000 | 275,607 |

| | Becton, Dickinson and Co. sr. unsec. notes 2.823%, 5/20/30 | | 45,000 | 40,378 |

| | Biogen, Inc. sr. unsec. bonds 3.25%, 2/15/51 | | 105,000 | 67,465 |

| | Biogen, Inc. sr. unsec. sub. notes 2.25%, 5/1/30 | | 145,000 | 125,404 |

| | Centene Corp. sr. unsec. sub. notes 2.625%, 8/1/31 | | 180,000 | 148,349 |

| | CVS Health Corp. jr. unsec. sub. bonds 7.00%, 3/10/55 | | 45,000 | 45,263 |

| | CVS Health Corp. sr. unsec. unsub. notes 4.78%, 3/25/38 | | 292,000 | 252,733 |

| | CVS Pass-Through Trust sr. notes 6.036%, 12/10/28 | | 11,338 | 11,403 |

| | CVS Pass-Through Trust 144A sr. mtge. notes 4.704%, 1/10/36 | | 85,040 | 78,896 |

| | DH Europe Finance II SARL company guaranty sr. unsec. notes 2.60%, 11/15/29 (Luxembourg) | | 335,000 | 303,115 |

| | Elevance Health, Inc. sr. unsec. unsub. bonds 5.125%, 2/15/53 | | 65,000 | 57,874 |

| | Elevance Health, Inc. sr. unsec. unsub. notes 2.25%, 5/15/30 | | 215,000 | 186,857 |

| | Eli Lilly and Co. sr. unsec. unsub. bonds 4.875%, 2/27/53 | | 70,000 | 63,417 |

| | GE HealthCare Technologies, Inc. sr. unsec. notes 4.80%, 8/14/29 | | 225,000 | 222,978 |

| | HCA, Inc. company guaranty sr. bonds 5.25%, 6/15/26 | | 35,000 | 35,103 |

| | HCA, Inc. company guaranty sr. notes 4.50%, 2/15/27 | | 66,000 | 65,400 |

| | HCA, Inc. company guaranty sr. notes 4.125%, 6/15/29 | | 30,000 | 28,633 |

| | HCA, Inc. company guaranty sr. unsec. bonds 6.00%, 4/1/54 | | 54,000 | 51,485 |

| | HCA, Inc. company guaranty sr. unsec. bonds 5.60%, 4/1/34 | | 41,000 | 40,409 |

| | HCA, Inc. company guaranty sr. unsec. sub. notes 3.625%, 3/15/32 | | 50,000 | 44,082 |

| | HCA, Inc. company guaranty sr. unsec. unsub. notes 5.375%, 2/1/25 | | 95,000 | 95,022 |

| | | | |

| | CORPORATE BONDS AND NOTES (41.5%)* cont. | Principal amount | Value |

| | Health care cont. | | | |

| | Humana, Inc. sr. unsec. unsub. notes 5.75%, 3/1/28 | | $165,000 | $168,210 |

| | Icon Investments Six DAC company guaranty sr. notes 5.849%, 5/8/29 (Ireland) | | 200,000 | 203,884 |

| | Illumina, Inc. sr. unsec. sub. notes 4.65%, 9/9/26 | | 105,000 | 104,674 |

| | Merck & Co., Inc. sr. unsec. unsub. notes 3.70%, 2/10/45 | | 205,000 | 158,905 |

| | Novartis Capital Corp. company guaranty sr. unsec. unsub. bonds 4.00%, 11/20/45 | | 265,000 | 217,655 |

| | Pfizer Investment Enterprises PTE, Ltd. company guaranty sr. unsec. notes 5.30%, 5/19/53 (Singapore) | | 120,000 | 112,452 |

| | Pfizer Investment Enterprises PTE, Ltd. company guaranty sr. unsec. notes 4.75%, 5/19/33 (Singapore) | | 240,000 | 233,298 |

| | Pfizer Investment Enterprises PTE, Ltd. company guaranty sr. unsec. notes 4.45%, 5/19/28 (Singapore) | | 57,000 | 56,511 |

| | Pharmacia, LLC company guaranty sr. unsec. notes 6.60%, 12/1/28 | | 120,000 | 127,603 |

| | Royalty Pharma PLC company guaranty sr. unsec. bonds 5.40%, 9/2/34 | | 103,000 | 100,286 |

| | Royalty Pharma PLC company guaranty sr. unsec. notes 5.15%, 9/2/29 | | 82,000 | 81,861 |

| | Service Corp. International sr. unsec. notes 3.375%, 8/15/30 | | 15,000 | 13,135 |

| | Thermo Fisher Scientific, Inc. sr. unsec. notes 2.60%, 10/1/29 | | 135,000 | 122,874 |

| | UnitedHealth Group, Inc. sr. unsec. unsub. bonds 4.75%, 7/15/45 | | 50,000 | 44,107 |

| | UnitedHealth Group, Inc. sr. unsec. unsub. bonds 2.90%, 5/15/50 | | 160,000 | 99,283 |

| | UnitedHealth Group, Inc. sr. unsec. unsub. notes 3.85%, 6/15/28 | | 370,000 | 359,782 |

| | Viatris, Inc. company guaranty sr. unsec. notes 2.30%, 6/22/27 | | 110,000 | 103,174 |

| | Wyeth, LLC company guaranty sr. unsec. bonds 5.95%, 4/1/37 | | 225,000 | 235,089 |

| | Zoetis, Inc. sr. unsec. sub. notes 2.00%, 5/15/30 | | 74,000 | 63,705 |

| | | | | 5,494,822 |

| | Insurance (1.6%) | | | |

| | Arthur J Gallagher & Co. sr. unsec. notes 4.85%, 12/15/29 | | 95,000 | 94,607 |

| | Athene Global Funding 144A notes 5.526%, 7/11/31 | | 80,000 | 80,232 |

| | Athene Global Funding 144A notes 5.322%, 11/13/31 | | 74,000 | 72,821 |

| | Athene Holding, Ltd. sr. unsec. bonds 6.25%, 4/1/54 | | 35,000 | 35,096 |

| | Athene Holding, Ltd. sr. unsec. bonds 5.875%, 1/15/34 | | 40,000 | 40,569 |

| | CNA Financial Corp. sr. unsec. notes 5.125%, 2/15/34 | | 65,000 | 63,837 |

| | CNO Financial Group, Inc. sr. unsec. bonds 6.45%, 6/15/34 | | 125,000 | 129,283 |

| | CNO Financial Group, Inc. sr. unsec. unsub. notes 5.25%, 5/30/25 | | 70,000 | 70,011 |

| | CNO Global Funding 144A notes 4.95%, 9/9/29 | | 175,000 | 173,553 |

| | Corebridge Financial, Inc. sr. unsec. notes 3.85%, 4/5/29 | | 100,000 | 95,520 |

| | Corebridge Global Funding 144A sr. unsec. unsub. notes 5.20%, 6/24/29 | | 305,000 | 306,884 |

| | F&G Annuities & Life, Inc. company guaranty sr. unsec. notes 6.50%, 6/4/29 | | 60,000 | 61,300 |

| | Fairfax Financial Holdings, Ltd. sr. unsec. notes 4.85%, 4/17/28 (Canada) | | 220,000 | 218,598 |

| | Fidelity National Financial, Inc. sr. unsec. bonds 3.20%, 9/17/51 | | 89,000 | 54,900 |

| | Liberty Mutual Group, Inc. 144A company guaranty sr. unsec. bonds 5.50%, 6/15/52 | | 200,000 | 184,889 |

| | Marsh & McLennan Cos., Inc. sr. unsec. sub. notes 4.375%, 3/15/29 | | 194,000 | 190,660 |

| | Massachusetts Mutual Life Insurance Co. 144A unsec. sub. bonds 3.729%, 10/15/70 | | 29,000 | 18,754 |

| | Mutual of Omaha Cos. Global Funding 144A notes 5.80%, 7/27/26 | | 125,000 | 126,647 |

| | Teachers Insurance & Annuity Association of America 144A unsec. sub. notes 6.85%, 12/16/39 | | 170,000 | 188,788 |

| | | | | 2,206,949 |

| | Investment banking/Brokerage (1.5%) | | | |

| | Ares Capital Corp. sr. unsec. notes 5.95%, 7/15/29 | | 58,000 | 58,672 |

| | Ares Capital Corp. sr. unsec. sub. notes 7.00%, 1/15/27 | | 35,000 | 36,285 |

| | Ares Capital Corp. sr. unsec. sub. notes 3.875%, 1/15/26 | | 175,000 | 173,097 |

| | Blackstone Private Credit Fund sr. unsec. unsub. notes 3.25%, 3/15/27 | | 112,000 | 107,253 |

| | Deutsche Bank AG/New York, NY sr. unsec. unsub. FRN 2.311%, 11/16/27 (Germany) | | 150,000 | 142,624 |

| | Goldman Sachs Group, Inc. (The) sr. unsec. FRB 4.223%, 5/1/29 | | 353,000 | 343,659 |

| | Morgan Stanley sr. unsec. notes 5.123%, 2/1/29 | | 35,000 | 35,103 |

| | Morgan Stanley sr. unsec. sub. bonds 5.942%, 2/7/39 | | 60,000 | 60,229 |

| | Morgan Stanley unsec. unsub. notes 3.95%, 4/23/27 | | 760,000 | 745,027 |

| | Morgan Stanley unsec. sub. notes 5.297%, 4/20/37 | | 314,000 | 305,257 |

| | Neuberger Berman Group, LLC/Neuberger Berman Finance Corp. 144A sr. unsec. notes 4.875%, 4/15/45 | | 75,000 | 62,105 |

| | | | | 2,069,311 |

| | Real estate (0.8%) | | | |

| | EPR Properties company guaranty sr. unsec. unsub. notes 4.50%, 6/1/27 R | | 24,000 | 23,601 |

| | Extra Space Storage LP company guaranty sr. unsec. notes 5.90%, 1/15/31 R | | 130,000 | 134,156 |

| | GLP Capital LP/GLP Financing II, Inc. company guaranty sr. unsec. sub. notes 6.75%, 12/1/33 R | | 60,000 | 63,560 |

| | GLP Capital LP/GLP Financing II, Inc. company guaranty sr. unsec. unsub. notes 5.375%, 4/15/26 R | | 88,000 | 88,061 |

| | Prologis LP sr. unsec. unsub. bonds 5.00%, 3/15/34 R | | 110,000 | 107,481 |

| | Prologis LP sr. unsec. unsub. notes 2.25%, 4/15/30 R | | 54,000 | 47,252 |

| | | | |

| | CORPORATE BONDS AND NOTES (41.5%)* cont. | Principal amount | Value |

| | Real estate cont. | | | |

| | VICI Properties LP sr. unsec. unsub. bonds 5.75%, 4/1/34 R | | $70,000 | $70,692 |

| | VICI Properties LP sr. unsec. unsub. notes 4.75%, 2/15/28 R | | 58,000 | 57,553 |

| | VICI Properties LP/VICI Note Co., Inc. 144A company guaranty sr. unsec. notes 4.50%, 9/1/26 R | | 145,000 | 143,808 |

| | VICI Properties LP/VICI Note Co., Inc. 144A company guaranty sr. unsec. notes 3.875%, 2/15/29 R | | 410,000 | 386,637 |

| | VICI Properties LP/VICI Note Co., Inc. 144A company guaranty sr. unsec. notes 3.75%, 2/15/27 R | | 22,000 | 21,361 |

| | | | | 1,144,162 |

| | Technology (3.4%) | | | |

| | Analog Devices, Inc. sr. unsec. notes 5.05%, 4/1/34 | | 95,000 | 94,954 |

| | Apple, Inc. sr. unsec. unsub. notes 4.375%, 5/13/45 | | 468,000 | 413,487 |

| | AppLovin Corp. sr. unsec. sub. bonds 5.95%, 12/1/54 | | 13,000 | 12,818 |

| | AppLovin Corp. sr. unsec. sub. notes 5.375%, 12/1/31 | | 133,000 | 133,098 |

| | AppLovin Corp. sr. unsec. sub. notes 5.125%, 12/1/29 | | 29,000 | 28,940 |

| | Atlassian Corp. sr. unsec. bonds 5.50%, 5/15/34 | | 18,000 | 18,088 |

| | Atlassian Corp. sr. unsec. notes 5.25%, 5/15/29 | | 27,000 | 27,213 |

| | Broadcom Corp./Broadcom Cayman Finance, Ltd. company guaranty sr. unsec. unsub. notes 3.875%, 1/15/27 | | 122,000 | 120,124 |

| | Broadcom, Inc. company guaranty sr. unsec. bonds 4.15%, 11/15/30 | | 158,000 | 151,248 |

| | Broadcom, Inc. sr. unsec. notes 5.05%, 7/12/29 | | 240,000 | 240,990 |

| | Broadcom, Inc. 144A sr. unsec. bonds 4.926%, 5/15/37 | | 400,000 | 380,701 |

| | Cisco Systems, Inc. sr. unsec. bonds 5.30%, 2/26/54 | | 75,000 | 72,957 |

| | Cisco Systems, Inc. sr. unsec. notes 5.05%, 2/26/34 | | 105,000 | 104,664 |

| | Dell International, LLC/EMC Corp. company guaranty sr. bonds 8.35%, 7/15/46 | | 5,000 | 6,367 |

| | Flex, Ltd. sr. unsec. notes 5.25%, 1/15/32 | | 80,000 | 78,698 |

| | Gartner, Inc. 144A company guaranty sr. unsec. bonds 3.75%, 10/1/30 | | 49,000 | 44,766 |

| | Gartner, Inc. 144A company guaranty sr. unsec. notes 3.625%, 6/15/29 | | 80,000 | 74,380 |

| | Hewlett Packard Enterprise Co. sr. unsec. bonds 5.60%, 10/15/54 | | 55,000 | 51,811 |

| | Hewlett Packard Enterprise Co. sr. unsec. bonds 5.00%, 10/15/34 | | 28,000 | 26,928 |

| | Hewlett Packard Enterprise Co. sr. unsec. notes 4.85%, 10/15/31 | | 55,000 | 53,664 |

| | Hewlett Packard Enterprise Co. sr. unsec. notes 4.55%, 10/15/29 | | 101,000 | 98,490 |

| | Marvell Technology, Inc. sr. unsec. notes 5.95%, 9/15/33 | | 67,000 | 69,591 |

| | Marvell Technology, Inc. sr. unsec. notes 5.75%, 2/15/29 | | 68,000 | 69,727 |

| | Meta Platforms, Inc. sr. unsec. bonds 5.75%, 5/15/63 | | 60,000 | 60,636 |

| | Meta Platforms, Inc. sr. unsec. bonds 5.40%, 8/15/54 | | 297,000 | 287,873 |

| | Meta Platforms, Inc. sr. unsec. bonds 5.55%, 8/15/64 | | 30,000 | 29,271 |

| | Meta Platforms, Inc. sr. unsec. notes 4.95%, 5/15/33 | | 242,000 | 242,422 |

| | Meta Platforms, Inc. sr. unsec. notes 4.75%, 8/15/34 | | 30,000 | 29,218 |

| | MSCI, Inc. 144A company guaranty sr. unsec. bonds 3.25%, 8/15/33 | | 250,000 | 211,393 |

| | MSCI, Inc. 144A company guaranty sr. unsec. notes 3.625%, 9/1/30 | | 109,000 | 99,635 |

| | Oracle Corp. sr. unsec. bonds 3.95%, 3/25/51 | | 55,000 | 40,784 |

| | Oracle Corp. sr. unsec. bonds 3.65%, 3/25/41 | | 475,000 | 370,667 |

| | Oracle Corp. sr. unsec. notes 2.875%, 3/25/31 | | 45,000 | 39,618 |

| | Oracle Corp. sr. unsec. notes 1.65%, 3/25/26 | | 130,000 | 125,391 |

| | Oracle Corp. sr. unsec. unsub. bonds 6.50%, 4/15/38 | | 55,000 | 59,160 |

| | Oracle Corp. sr. unsec. unsub. bonds 4.30%, 7/8/34 | | 80,000 | 73,594 |

| | Oracle Corp. sr. unsec. unsub. bonds 4.00%, 11/15/47 | | 110,000 | 83,924 |

| | Sensata Technologies, Inc. 144A company guaranty sr. unsec. notes 3.75%, 2/15/31 | | 84,000 | 73,528 |

| | ServiceNow, Inc. sr. unsec. notes 1.40%, 9/1/30 | | 240,000 | 199,531 |

| | Xilinx, Inc. company guaranty sr. unsec. sub. notes 2.375%, 6/1/30 | | 320,000 | 282,152 |

| | | | | 4,682,501 |

| | Transportation (0.6%) | | | |

| | AS Mileage Plan IP, Ltd. 144A sr. notes 5.021%, 10/20/29 (Cayman Islands) | | 230,000 | 224,269 |

| | Penske Truck Leasing Co. LP/PTL Finance Corp. 144A sr. unsec. bonds 3.40%, 11/15/26 | | 133,000 | 129,525 |

| | Penske Truck Leasing Co. LP/PTL Finance Corp. 144A sr. unsec. notes 4.40%, 7/1/27 | | 110,000 | 108,607 |

| | Ryder System, Inc. sr. unsec. unsub. notes 4.95%, 9/1/29 | | 200,000 | 199,399 |

| | Westinghouse Air Brake Technologies Corp. company guaranty sr. unsec. unsub. bonds 5.611%, 3/11/34 | | 130,000 | 131,790 |

| | | | | 793,590 |

| | Utilities and power (5.9%) | | | |

| | AES Corp. (The) sr. unsec. notes 1.375%, 1/15/26 | | 140,000 | 134,911 |

| | Alexander Funding Trust II 144A sr. notes 7.467%, 7/31/28 | | 100,000 | 105,699 |

| | Ameren Corp. sr. unsec. unsub. notes 5.00%, 1/15/29 | | 75,000 | 75,148 |

| | American Electric Power Co., Inc. sr. unsec. unsub. bonds 5.625%, 3/1/33 | | 45,000 | 45,484 |

| | | | |

| | CORPORATE BONDS AND NOTES (41.5%)* cont. | Principal amount | Value |

| | Utilities and power cont. | | | |

| | American Electric Power Co., Inc. sr. unsec. unsub. bonds 3.25%, 3/1/50 | | $100,000 | $64,307 |

| | American Electric Power Co., Inc. sr. unsec. unsub. notes Ser. J, 4.30%, 12/1/28 | | 210,000 | 205,288 |

| | American Transmission Systems, Inc. 144A sr. unsec. bonds 2.65%, 1/15/32 | | 65,000 | 55,210 |

| | Berkshire Hathaway Energy Co. sr. unsec. bonds 4.25%, 10/15/50 | | 100,000 | 79,066 |

| | CenterPoint Energy Resources Corp. sr. unsec. unsub. bonds 5.40%, 7/1/34 | | 115,000 | 114,779 |

| | Consolidated Edison Co. of New York, Inc. sr. unsec. unsub. notes 4.20%, 3/15/42 | | 85,000 | 71,185 |

| | Constellation Energy Generation, LLC sr. unsec. bonds 6.50%, 10/1/53 | | 106,000 | 112,418 |

| | Constellation Energy Generation, LLC sr. unsec. bonds 6.125%, 1/15/34 | | 44,000 | 46,086 |

| | Constellation Energy Generation, LLC sr. unsec. bonds 5.75%, 3/15/54 | | 43,000 | 41,859 |

| | Constellation Energy Generation, LLC sr. unsec. notes 5.60%, 3/1/28 | | 545,000 | 556,024 |

| | Dominion Energy, Inc. sr. unsec. unsub. bonds 4.90%, 8/1/41 | | 135,000 | 121,048 |

| | DTE Energy Co. sr. unsec. unsub. notes 4.95%, 7/1/27 | | 145,000 | 145,579 |

| | Duke Energy Carolinas, LLC sr. notes 4.95%, 1/15/33 | | 90,000 | 88,549 |

| | Duke Energy Corp. sr. unsec. bonds 5.80%, 6/15/54 | | 21,000 | 20,486 |

| | Duke Energy Corp. sr. unsec. bonds 4.20%, 6/15/49 | | 65,000 | 50,473 |

| | Duke Energy Corp. sr. unsec. notes 5.45%, 6/15/34 | | 29,000 | 28,981 |

| | Duke Energy Corp. sr. unsec. notes 4.85%, 1/5/29 | | 25,000 | 24,895 |

| | Duke Energy Corp. sr. unsec. notes 3.15%, 8/15/27 | | 180,000 | 172,920 |

| | Duke Energy Ohio, Inc. sr. bonds 5.25%, 4/1/33 | | 65,000 | 64,909 |

| | Duke Energy Ohio, Inc. sr. bonds 3.65%, 2/1/29 | | 97,000 | 92,706 |

| | El Paso Natural Gas Co., LLC company guaranty sr. unsec. unsub. notes 8.375%, 6/15/32 | | 200,000 | 235,628 |

| | Electricite De France SA 144A sr. unsec. unsub. bonds 4.75%, 10/13/35 (France) | | 95,000 | 87,514 |

| | Enbridge, Inc. company guaranty sr. unsec. unsub. bonds 4.50%, 6/10/44 (Canada) | | 90,000 | 74,582 |

| | Enbridge, Inc. sr. unsec. unsub. bonds 4.25%, 12/1/26 (Canada) | | 95,000 | 94,147 |

| | Enel Finance International NV 144A company guaranty sr. unsec. unsub. notes 7.50%, 10/14/32 (Netherlands) | | 200,000 | 222,976 |

| | Energy Transfer LP company guaranty sr. unsec. notes 5.50%, 6/1/27 | | 182,000 | 184,397 |

| | Energy Transfer LP company guaranty sr. unsec. notes 2.90%, 5/15/25 | | 37,000 | 36,722 |

| | Energy Transfer LP jr. unsec. sub. FRN 6.625%, perpetual maturity | | 125,000 | 123,403 |

| | Energy Transfer LP sr. unsec. notes 5.25%, 7/1/29 | | 30,000 | 30,162 |

| | Energy Transfer LP sr. unsec. unsub. notes 6.50%, 2/1/42 | | 20,000 | 20,737 |

| | Evergy Kansas Central, Inc. sr. bonds 5.70%, 3/15/53 | | 60,000 | 59,160 |

| | Evergy Missouri West, Inc. 144A sr. notes 5.15%, 12/15/27 | | 165,000 | 166,330 |

| | Eversource Energy sr. unsec. unsub. notes 5.45%, 3/1/28 | | 165,000 | 167,196 |

| | Eversource Energy sr. unsec. unsub. notes 5.125%, 5/15/33 | | 90,000 | 87,488 |

| | Exelon Corp. sr. unsec. unsub. bonds 5.45%, 3/15/34 | | 225,000 | 224,657 |

| | Exelon Corp. sr. unsec. unsub. notes 5.15%, 3/15/29 | | 280,000 | 281,538 |

| | FirstEnergy Transmission, LLC 144A sr. unsec. notes 4.55%, 1/15/30 | | 45,000 | 43,829 |

| | Florida Power & Light Co. sr. bonds 4.125%, 2/1/42 | | 203,000 | 169,494 |

| | Georgia Power Co. sr. unsec. unsub. bonds 5.25%, 3/15/34 | | 10,000 | 9,928 |

| | Georgia Power Co. sr. unsec. unsub. notes 4.95%, 5/17/33 | | 270,000 | 264,534 |

| | IPALCO Enterprises, Inc. sr. notes 4.25%, 5/1/30 | | 105,000 | 99,055 |

| | Kinder Morgan Energy Partners LP company guaranty sr. unsec. notes 5.40%, 9/1/44 | | 86,000 | 78,607 |

| | NextEra Energy Capital Holdings, Inc. company guaranty sr. unsec. unsub. notes 6.051%, 3/1/25 | | 70,000 | 70,130 |

| | NextEra Energy Capital Holdings, Inc. company guaranty sr. unsec. unsub. notes 3.55%, 5/1/27 | | 100,000 | 97,480 |

| | NiSource, Inc. sr. unsec. unsub. notes 5.20%, 7/1/29 | | 230,000 | 231,972 |

| | NRG Energy, Inc. 144A sr. notes 2.00%, 12/2/25 | | 191,000 | 185,556 |

| | Oncor Electric Delivery Co., LLC sr. bonds 4.95%, 9/15/52 | | 95,000 | 84,937 |

| | Oncor Electric Delivery Co., LLC sr. notes 5.75%, 3/15/29 | | 161,000 | 166,928 |

| | Oncor Electric Delivery Co., LLC sr. notes 3.70%, 11/15/28 | | 90,000 | 86,598 |

| | Pacific Gas and Electric Co. notes 2.10%, 8/1/27 | | 100,000 | 93,319 |

| | Pacific Gas and Electric Co. sr. bonds 6.75%, 1/15/53 | | 75,000 | 81,807 |

| | Pacific Gas and Electric Co. sr. bonds 5.90%, 6/15/32 | | 64,000 | 65,737 |

| | Pacific Gas and Electric Co. sr. bonds 4.95%, 7/1/50 | | 145,000 | 126,085 |

| | Pacific Gas and Electric Co. sr. notes 6.10%, 1/15/29 | | 45,000 | 46,600 |

| | Pacific Gas and Electric Co. sr. notes 3.30%, 12/1/27 | | 190,000 | 181,597 |

| | PacifiCorp sr. bonds 2.70%, 9/15/30 | | 133,000 | 117,577 |

| | Puget Sound Energy, Inc. sr. bonds 5.448%, 6/1/53 | | 160,000 | 152,909 |

| | Sempra Energy sr. unsec. unsub. bonds 5.50%, 8/1/33 | | 50,000 | 50,142 |

| | Southern Co. (The) sr. unsec. bonds 5.70%, 3/15/34 | | 85,000 | 86,803 |

| | Southern Co. (The) sr. unsec. notes 5.50%, 3/15/29 | | 10,000 | 10,206 |

| | Southern Co. Gas Capital Corp. company guaranty sr. unsec. unsub. notes 4.95%, 9/15/34 | | 45,000 | 43,583 |

| | | | |

| | CORPORATE BONDS AND NOTES (41.5%)* cont. | Principal amount | Value |

| | Utilities and power cont. | | | |

| | Virginia Electric and Power Co. sr. unsec. unsub. notes 5.05%, 8/15/34 | | $120,000 | $117,107 |

| | Vistra Operations Co., LLC 144A company guaranty sr. notes 6.00%, 4/15/34 | | 80,000 | 81,118 |

| | Vistra Operations Co., LLC 144A company guaranty sr. notes 4.30%, 7/15/29 | | 82,000 | 78,366 |

| | Vistra Operations Co., LLC 144A company guaranty sr. notes 3.70%, 1/30/27 | | 465,000 | 453,024 |

| | Xcel Energy, Inc. sr. unsec. bonds 5.45%, 8/15/33 | | 170,000 | 168,730 |

| | | | | 8,158,405 |

| | Total corporate bonds and notes (cost $59,364,276) | $57,306,806 |

| | U.S. GOVERNMENT AND AGENCY MORTGAGE OBLIGATIONS (25.7%)* | Principal amount | Value |

| | U.S. Government Guaranteed Mortgage Obligations (12.8%) | | |

| | Government National Mortgage Association Pass-Through Certificates | | |

| | 6.00%, 11/20/53 | $1,028,104 | $1,053,424 |

| | 5.50%, with due dates from 6/20/53 to 4/20/54 | 1,689,734 | 1,689,020 |

| | 5.00%, TBA, 1/1/55 | 3,000,000 | 2,910,586 |

| | 5.00%, with due dates from 5/20/48 to 6/20/48 | 246,264 | 242,696 |

| | 4.50%, TBA, 1/1/55 | 3,000,000 | 2,835,938 |

| | 4.50%, with due dates from 7/20/47 to 5/20/48 | 997,762 | 958,180 |

| | 4.00%, TBA, 1/1/55 | 2,000,000 | 1,842,276 |

| | 4.00%, with due dates from 2/20/48 to 5/20/48 | 646,538 | 591,860 |

| | 3.50%, with due dates from 11/15/47 to 11/20/49 | 678,802 | 613,807 |

| | 3.00%, 2/20/53 | 1,009,703 | 879,759 |

| | 2.50%, with due dates from 9/20/52 to 2/20/53 | 4,801,274 | 4,018,652 |

| | | | 17,636,198 |

| | U.S. Government Agency Mortgage Obligations (12.9%) | | |

| | Federal Home Loan Mortgage Corporation Pass-Through Certificates | | |

| | 6.00%, 9/1/53 | 372,504 | 377,003 |

| | 5.50%, with due dates from 9/1/53 to 11/1/53 | 1,742,483 | 1,734,404 |

| | 4.50%, with due dates from 8/1/44 to 3/1/45 | 196,594 | 189,754 |

| | 4.00%, 9/1/45 | 279,661 | 262,557 |

| | 3.50%, with due dates from 8/1/43 to 2/1/47 | 1,010,235 | 917,166 |

| | 3.00%, with due dates from 3/1/43 to 6/1/46 | 562,217 | 491,493 |

| | Federal National Mortgage Association Pass-Through Certificates | | |

| | 5.50%, with due dates from 9/1/53 to 11/1/53 | 991,053 | 984,814 |

| | 5.28%, 12/1/28 | 226,000 | 230,302 |

| | 5.00%, 3/1/38 | 3,358 | 3,348 |

| | 4.50%, with due dates from 7/1/44 to 5/1/45 | 461,137 | 443,654 |

| | 4.00%, with due dates from 9/1/45 to 6/1/46 | 452,189 | 419,655 |

| | 3.50%, with due dates from 6/1/56 to 9/1/57 | 1,911,600 | 1,691,417 |

| | 3.50%, 7/1/43 | 186,315 | 169,166 |

| | 3.00%, with due dates from 9/1/42 to 4/1/52 | 2,944,655 | 2,557,991 |

| | 2.00%, 1/1/51 | 1,161,960 | 912,294 |

| | 2.00%, 2/1/37 | 879,837 | 782,539 |

| | Uniform Mortgage-Backed Securities | | |

| | 5.00%, TBA, 1/1/55 | 1,000,000 | 965,231 |

| | 2.00%, TBA, 1/1/55 | 5,000,000 | 3,891,016 |

| | 1.50%, TBA, 1/1/40 | 1,000,000 | 857,398 |

| | | | 17,881,202 |

| | Total U.S. government and agency mortgage obligations (cost $36,974,039) | $35,517,400 |

| | U.S. TREASURY OBLIGATIONS (0.1%)* | Principal amount | Value |

| | U.S. Treasury Notes 2.375%, 5/15/27 i | $113,000 | $108,585 |

| | Total U.S. treasury obligations (cost $108,585) | $108,585 |

| | MORTGAGE-BACKED SECURITIES (18.0%)* | Principal amount | Value |

| | Agency collateralized mortgage obligations (4.0%) | | | |

| | Federal Home Loan Mortgage Corporation | | | |

| | REMICs IFB Ser. 3408, Class EK, ((-4.024 x US 30 Day Average SOFR) + 25.33%), 6.832%, 4/15/37 | | $60,709 | $66,039 |

| | REMICs IFB Ser. 3065, Class DC, ((-3 x US 30 Day Average SOFR) + 19.52%), 5.724%, 3/15/35 | | 74,470 | 74,928 |

| | Strips FRB Ser. 406, Class F30, (US 30 Day Average SOFR + 1.15%), 5.719%, 10/25/53 | | 167,488 | 168,722 |

| | | | |

| | MORTGAGE-BACKED SECURITIES (18.0%)* cont. | Principal amount | Value |

| | Agency collateralized mortgage obligations cont. | | | |

| | Federal Home Loan Mortgage Corporation | | | |

| | REMICs Ser. 4132, Class IP, IO, 4.50%, 11/15/42 | | $130,512 | $10,718 |

| | REMICs Ser. 4018, Class DI, IO, 4.50%, 7/15/41 | | 34,881 | 924 |

| | REMICs Ser. 23-5349, Class IB, IO, 4.00%, 12/15/46 | | 442,907 | 89,870 |

| | REMICs Ser. 5050, Class IM, IO, 3.50%, 10/25/50 | | 3,596,118 | 712,917 |

| | REMICs IFB Ser. 4945, Class SL, IO, ((-1 x US 30 Day Average SOFR) + 5.94%), 1.367%, 1/25/50 | | 3,512,247 | 367,493 |

| | REMICs Ser. 3369, Class BO, PO, zero %, 9/15/37 | | 1,148 | 947 |

| | REMICs Ser. 3391, PO, zero %, 4/15/37 | | 10,403 | 8,814 |

| | REMICs FRB Ser. 3117, Class AF, zero %, 2/15/36 | | 3,554 | 3,043 |

| | Federal National Mortgage Association | | | |

| | REMICs Ser. 15-33, Class AI, IO, 5.00%, 6/25/45 | | 631,928 | 86,425 |

| | REMICs Ser. 23-49, Class IB, IO, 3.50%, 3/25/47 | | 267,585 | 42,577 |

| | REMICs Ser. 23-49, Class IA, IO, 3.00%, 8/25/46 | | 744,504 | 94,552 |

| | REMICs Ser. 21-12, Class NI, IO, 2.50%, 3/25/51 | | 3,474,037 | 574,465 |

| | REMICs IFB Ser. 10-35, Class SG, IO, ((-1 x US 30 Day Average SOFR) + 6.29%), 1.717%, 4/25/40 | | 216,414 | 22,318 |

| | Interest Strip Ser. 372, Class 1, PO, zero %, 8/25/36 | | 6,566 | 5,276 |

| | Government National Mortgage Association | | | |

| | Ser. 09-79, Class IC, IO, 6.00%, 8/20/39 | | 246,920 | 31,512 |

| | FRB Ser. 23-152, Class FB, IO, 5.755%, 4/20/51 W | | 228,222 | 233,085 |

| | Ser. 14-180, IO, 5.00%, 12/20/44 | | 754,665 | 153,791 |

| | Ser. 14-76, IO, 5.00%, 5/20/44 | | 218,093 | 46,830 |

| | Ser. 20-46, Class MI, IO, 4.00%, 4/20/50 | | 675,096 | 137,995 |

| | Ser. 15-53, Class MI, IO, 4.00%, 4/16/45 | | 605,587 | 113,864 |

| | Ser. 12-38, Class MI, IO, 4.00%, 3/20/42 | | 1,331,344 | 236,635 |