EX-99.(17)(b)

Goldman Sachs Funds

| | | | |

| | |

| Annual Report | | | | October 31, 2014 |

| | |

| | | | Fundamental Emerging Markets

Equity Funds |

| | | | Asia Equity |

| | | | BRIC |

| | | | Emerging Markets Equity |

| | | | N-11 Equity |

Goldman Sachs Fundamental Emerging Markets Equity Funds

| n | | EMERGING MARKETS EQUITY |

| | | | |

TABLE OF CONTENTS | | | | |

| |

Principal Investment Strategies and Risks | | | 3 | |

| |

Investment Process | | | 5 | |

| |

Market Review | | | 6 | |

| |

Portfolio Management Discussions and Performance Summaries | | | 8 | |

| |

Schedules of Investments | | | 35 | |

| |

Financial Statements | | | 46 | |

| |

Financial Highlights | | | 50 | |

| |

Notes to Financial Statements | | | 58 | |

| |

Report of Independent Registered Public Accounting Firm | | | 76 | |

| |

Other Information | | | 77 | |

| | | | |

| | | |

| NOT FDIC-INSURED | | May Lose Value | | No Bank Guarantee |

GOLDMAN SACHS FUNDAMENTAL EMERGING MARKETS EQUITY FUNDS

Principal Investment Strategies and Risks

This is not a complete list of risks that may affect the Funds. For additional information concerning the risks applicable to the Funds, please see the Funds’ Prospectuses.

The Goldman Sachs Asia Equity Fund invests primarily in a diversified portfolio of equity investments in Asian issuers (excluding Japanese issuers). The Fund is subject to market risk, which means that the value of the securities in which it invests may go up or down in response to the prospects of individual companies, particular sectors and/or general economic conditions. Foreign and emerging markets investments may be more volatile than investments in U.S. securities and are subject to the risks of currency fluctuations and adverse economic or political developments. Because of its exposure to Asian issuers, the Fund is subject to greater risk of loss as a result of adverse securities markets, exchange rates and social, political, regulatory or economic events that may occur in Asian countries. The securities of mid- and small-capitalization companies involve greater risks than those associated with larger, more established companies and may be subject to more abrupt or erratic price movements. At times, the Fund may be unable to sell certain of its illiquid investments without a substantial drop in price, if at all.

The Goldman Sachs BRIC Fund invests primarily in a portfolio of equity investments in Brazil, Russia, India and China (“BRIC countries”) or in issuers that participate in the markets of the BRIC countries. The Fund is subject to market risk, which means that the value of the securities in which it invests may go up or down in response to the prospects of individual companies, particular sectors and/ or general economic conditions. Foreign and emerging markets investments may be more volatile than investments in U.S. securities and are subject to the risks of currency fluctuations and adverse economic or political developments. Because of its exposure to the BRIC countries, the Fund is subject to greater risk of loss as a result of adverse securities markets, exchange rates and social, political, regulatory or economic events that may occur in those countries. Because the Fund may invest heavily in specific sectors, the Fund is subject to greater risk of loss as a result of adverse economic, business or other developments affecting such sectors. At times, the Fund may be unable to sell certain of its illiquid investments without a substantial drop in price, if at all. The Fund is “non-diversified” and may invest a larger percentage of its assets in fewer issuers than “diversified” mutual funds. Accordingly, the Fund may be more susceptible to adverse developments affecting any single issuer held in its portfolio and to greater losses resulting from these developments.

The Goldman Sachs Emerging Markets Equity Fund invests primarily in a diversified portfolio of equity investments in emerging country issuers. The Fund is subject to market risk, which means that the value of the securities in which it invests may go up or down in response to the prospects of individual companies, particular sectors and/or general economic conditions. Foreign and emerging markets investments may be more volatile than investments in U.S. securities and are subject to the risks of currency fluctuations and adverse economic or political developments. The securities markets of emerging countries have less government regulation and are subject to less extensive accounting and financial reporting requirements than the markets of more developed countries. Because the Fund may invest heavily in specific sectors, the Fund is subject to greater risk of loss as a result of adverse economic, business or other developments affecting such sectors. At times, the Fund may be unable to sell certain of its illiquid investments without a substantial drop in price, if at all.

The Goldman Sachs N-11 Equity Fund invests primarily in a portfolio of equity investments that are tied economically to the “N-11 countries” or in issuers that participate in the markets of the following N-11 countries: Bangladesh, Egypt, Indonesia, Mexico, Nigeria, Pakistan, Philippines, South Korea, Turkey and Vietnam. While Iran is among the N-11 countries, the Fund will not invest in issuers

3

GOLDMAN SACHS FUNDAMENTAL EMERGING MARKETS EQUITY FUNDS

organized under the laws of Iran, or domiciled in Iran, or in certain other issuers as necessary to comply with U.S. economic sanctions against Iran. The Fund is subject to market risk, which means that the value of the securities in which it invests may go up or down in response to the prospects of individual companies, particular sectors and/or general economic conditions. Foreign and emerging markets investments may be more volatile than investments in U.S. securities and are subject to the risks of currency fluctuations and adverse economic or political developments. Such securities are also subject to foreign custody risk. Because of its exposure to the N-11 countries, the Fund is subject to greater risk of loss as a result of adverse securities markets, exchange rates and social, political, regulatory or economic events that may occur in those countries. The N-11 countries generally have smaller economies or less developed capital markets than traditional emerging markets countries, and, as a result, the risks of investing in these countries are magnified. Because the Fund may invest heavily in specific sectors, the Fund is subject to greater risk of loss as a result of adverse economic, business or other developments affecting such sectors. The Fund may concentrate its investments in a specific industry (only in the event that that industry represents 20% or more of the Fund’s benchmark index at the time of investment), subjecting it to greater risk of loss as a result of adverse economic, business or other developments affecting that industry. At times, the Fund may be unable to sell certain of its illiquid investments without a substantial drop in price, if at all. The Fund is “non-diversified” and may invest a larger percentage of its assets in fewer issuers than “diversified” mutual funds. Accordingly, the Fund may be more susceptible to adverse developments affecting any single issuer held in its portfolio and to greater losses resulting from these developments.

4

GOLDMAN SACHS FUNDAMENTAL EMERGING MARKETS EQUITY FUNDS

What Differentiates Goldman Sachs’ Fundamental Emerging Markets Equity Investment Process?

Goldman Sachs’ Fundamental Emerging Markets Equity investment process is based on the belief that strong, consistent results are best achieved through expert stock selection, performed by our dedicated Emerging Markets Team that works together on a global scale. Our deep, diverse and experienced team of research analysts and portfolio managers combines local insights with global, industry-specific expertise to identify its best investment ideas.

| n | | The Emerging Markets Equity research team, based in the United States, United Kingdom, Japan, China, Korea, Singapore, Brazil, India and Australia, focuses on long-term business and management quality |

| n | | Proprietary, bottom-up research is the key driver of our investment process |

| n | | Analysts collaborate regularly to leverage regional and industry-specific research and insights |

| n | | Members of each local investment team are aligned by sector and are responsible for finding ideas with the best risk-adjusted upside in their respective areas of coverage |

| n | | The decision-making process includes active participation in frequent and regular research meetings |

| n | | The Emerging Markets Equity team benefits from the country and currency expertise of our Global Emerging Markets Debt and Currency teams |

| n | | Security selections are aligned with levels of investment conviction and risk-adjusted upside |

| n | | Continual risk monitoring identifies various risks at the stock and portfolio level and assesses whether they are intended and justified |

| n | | Dedicated portfolio construction team assists in ongoing monitoring and adjustment of the Funds |

Emerging markets equity portfolios that strive to offer:

| | n | | Access to markets across emerging markets | |

| | n | | Disciplined approach to stock selection | |

| | n | | Optimal risk/return profiles | |

5

MARKET REVIEW

Goldman Sachs Fundamental Emerging Markets Equity Funds

Market Review

Emerging markets equities advanced, albeit only modestly, during the 12-month period ended October 31, 2014 (the “Reporting Period”). The Morgan Stanley Capital International (MSCI) Emerging Markets Index (Gross, USD, Unhedged) (the “MSCI® EM Index”) posted a return of 0.64%.* Emerging markets equities edged out developed markets equities, as measured by the MSCI® Europe Australasia and Far East (EAFE) Index, but concerns about slowing economic growth, high inflation and election uncertainty, among others, subdued the overall performance of many of the growth and emerging markets during the Reporting Period. Notably, however, equity market returns varied dramatically by region and by country.

Early in the Reporting Period, the U.S. Federal Reserve (the “Fed”) announced it would begin tapering its asset purchases in January 2014. The announcement ended seven months of speculation about the beginning of the end of the easy monetary policy that had fueled many emerging market economies in recent years. News of Argentina’s currency devaluation in January 2014 also rippled through emerging market currency and equity markets, forcing many central banks to hike interest rates, which further pressured equity markets.

From a regional perspective, Asia was the best performing region during the Reporting Period as a whole, as India’s equity market soared. India elected a new government by a large majority, raising hopes for bold reforms. Chinese equities struggled early in the Reporting Period amidst renewed concerns about China’s shadow banking system, credit quality and decelerating growth. However, Chinese equities rebounded during the second half of the Reporting Period to outperform the MSCI® EM Index. Central and Eastern Europe was the worst performing region, as the Russian equity market plunged during the Reporting Period due to the rapidly escalating geopolitical situation in Ukraine, economic sanctions from western countries and a sharp decline in the price of oil. Weakness in Latin American equity markets persisted into early 2014, though the region began to rebound toward the middle of the Reporting Period, only to experience weakness again during the second half of the Reporting Period due in part to declines in the energy and materials sectors. Brazilian equities also reflected the effects of slowing economic growth and a heated presidential election in Brazil.

For the Reporting Period overall, the energy sector declined most sharply, as the Brent Crude benchmark oil price sank throughout the second half of the Reporting Period to less than $85 per barrel, the lowest level since 2010. The materials sector also declined significantly due to weak commodity prices. Conversely, the health care and information technology sectors significantly outperformed the MSCI® EM Index during the Reporting Period amidst strong global merger and acquisition activity.

| * | | All index returns are expressed in U.S. dollar terms. |

6

MARKET REVIEW

Looking Ahead

While emerging markets equities edged out the returns of developed markets equities during the Reporting Period, many developing markets continued to face macroeconomic headwinds, negative headlines and country-specific challenges. We fully acknowledge these medium-term factors — including the end of Chinese double-digit economic growth, the impact of the end of quantitative easing on broader equity markets, currency volatility and persistent geopolitical unrest — and incorporate them in our bottom-up fundamental analysis.

The macro concerns that pressured emerging markets equities during the Reporting Period have not changed our longer-term positive view of emerging markets equity fundamentals. We believe the structural story is still intact and the domestically-focused growth of the emerging markets should continue to drive strong returns in their equity markets over the long term. Finally, we believe the recent weakness in emerging markets equities, which, at the end of the Reporting Period, were trading at a significant discount to developed markets on a forward-looking price/earnings ratio basis, may form an attractive entry point for long-term investors.

As bottom-up fundamental investors, we constantly look across a broad range of sectors, countries and market capitalizations to identify what we believe are the most compelling investment opportunities trading at attractive valuations and that may outperform over the market cycle. In particular, we look for companies with strong or improving cash flows and sustainable competitive advantages that should be able to withstand inflationary pressures on their margins while seeking to take advantage of secular growth themes in the growth and emerging markets. Finally, we seek to invest in companies with strong corporate governance track records, especially with respect to their treatment of minority shareholders. While we anticipate the uncertainty of the markets to continue, we believe our focus on companies with strong or improving fundamentals and secular growth opportunities should serve our shareholders well.

As always, we maintain our focus on seeking high-quality equity investments trading at what we believe to be compelling valuations and intend to stay true to our long-term discipline as we seek to navigate potentially volatile markets ahead.

7

PORTFOLIO RESULTS

Goldman Sachs Asia Equity Fund

Investment Objective

The Fund seeks long-term capital appreciation.

Portfolio Management Discussion and Analysis

Effective as of the close of business on April 25, 2014, the Goldman Sachs China Equity Fund was merged into the Goldman Sachs Asia Equity Fund. The reorganization was recommended by Goldman Sachs Asset Management International in connection with an effort to optimize the Goldman Sachs Funds and eliminate overlapping products. The Goldman Sachs Asia Equity Fund (the “Fund”) acquired all of the assets of the Goldman Sachs China Equity Fund — which totaled approximately $25.1 million as of April 25, 2014 — and the Goldman Sachs China Equity Fund was subsequently liquidated and shareholders of the Goldman Sachs China Equity Fund became shareholders of the Fund. Below, the Goldman Sachs Fundamental Asia ex-Japan Equity Portfolio Management Team discusses the Fund’s performance and positioning for the 12-month period ended October 31, 2014 (the “Reporting Period”).

| Q | | How did the Fund perform during the Reporting Period? |

| A | | During the Reporting Period, the Fund’s Class A, B, C, and Institutional Shares generated average annual total returns, without sales charges, of 4.75%, 3.95%, 4.00% and 5.15%, respectively. These returns compare to the 5.73% average annual total return of the Fund’s benchmark, the MSCI® All Country Asia ex-Japan Index (Net, USD, Unhedged) (the “Index”), during the same time period. During the period since their inception on February 28, 2014 through October 31, 2014, the Fund’s Class IR Shares generated a cumulative total return, without sales charges, of 1.30% compared to the 8.59% cumulative total return of the Index. |

| Q | | What key factors were responsible for the Fund’s performance during the Reporting Period? |

| A | | The Fund produced solid absolute returns but its underperformance relative to the Index during the Reporting Period can be primarily attributed to individual stock selection. From a country perspective, stock selection in Indonesia, Hong Kong and Thailand detracted. Having an underweighted allocation to the strongly performing Hong Kong equity market also hurt. Effective stock selection in India, South Korea and Taiwan contributed most positively. |

| Q | | Which stocks detracted significantly from the Fund’s performance during the Reporting Period? |

| A | | Detracting most from the Fund’s results relative to the Index were positions in distressed asset management company China Cinda Asset Management (“Cinda”), South Korean electric home appliance manufacturer LiHom Cuchen and Chinese wastewater and water supply business operator SIIC Environment. |

| | A position in Cinda detracted most from the Fund’s results. The stock’s pullback during the Reporting Period was due primarily to concerns about property price weakness impacting the value of its assets. We believe the negative sentiment may have been overdone given that Cinda’s acquisition costs of these assets were attractive, in our view, leaving substantial room for profit realization. Indeed, we maintained the Fund’s position in Cinda because we believe the company has a strong growth opportunity in the coming years, as banks and non-financial companies in China are expected to increase the securitization and sales of their non-performing loans and receivables in order to strengthen their balance sheets. We believe this provides a robust business opportunity for distressed asset managers such as Cinda. |

| | LiHom Cuchen’s stock, a new purchase for the Fund during the Reporting Period, detracted from the Fund’s results on the back of concerns about potentially weaker than expected third quarter 2014 earnings and risk-averse market sentiment toward small cap names amidst volatility. At the end of the |

8

PORTFOLIO RESULTS

| | Reporting Period, we had put this holding under review pending its earnings announcement. |

| | SIIC Environment, a company operating a wastewater and water supply business in China through its “Build-Operate-Transfer” and “Transfer-Operate-Transfer” business models and another new purchase for the Fund during the Reporting Period, underperformed the Index. We believe the underperformance primarily stemmed from market concerns about the company’s ability to execute its plan to add one million tons of new water projects per day. |

| Q | | What were some of the Fund’s best-performing individual stocks? |

| A | | The Fund benefited most relative to the Index from holdings in Canadian Solar, Hanssem and Bajaj Finance. |

| | The top individual stock contributor to the Fund’s results during the Reporting Period was Canadian Solar, which designs, manufactures and sells solar module products that convert sunlight into electricity for a variety of uses. Canadian Solar outperformed the Index, as the company reported better than expected second quarter 2014 results and delivered an upbeat guidance for the third quarter of 2014. At the end of the Reporting Period, we remained positive on the stock and continued to hold this out-of-Index position, as the company’s strong results and management guidance appear to have dissipated much of the consensus concerns about softer than expected demand from China and a weakening average selling price. |

| | Another significant contributor was Hanssem, which manufactures kitchen and interior furniture and is the industry share leader in a fragmented South Korean furniture market. Its shares rose, as the company reported better than expected top-line growth on an increase in remodeling demand from an improved housing transaction volume. At the end of the Reporting Period, Hanssem led its industry in terms of earnings growth, return on equity and valuation. |

| | Bajaj Finance, an Indian non-banking finance company engaged in consumer finance, small and medium enterprise finance and commercial lending, was a strong contributor to the Fund’s relative results. The company performed well as measured by loan growth, margins and asset quality relative to its peers. Improving consumer sentiment and a strong outlook on consumer durable sales provided a positive backdrop to Bajaj Finance’s consumer lending business. At the end of the Reporting Period, we maintained the position in the Fund based on what we considered to be its healthy return ratios and attractive valuations. |

| Q | | Which equity market sectors most significantly affected Fund performance during the Reporting Period? |

| A | | The biggest detractors from the Fund’s relative results during the Reporting Period were the utilities, energy and telecommunication services sectors. Weak stock selection drove lagging performance in the utilities and energy sectors. Having an underweighted allocation to telecommunication services, which outpaced the Index during the Reporting Period, also hurt. In utilities, a position in SIIC Environment, already mentioned, detracted most. In energy, the Fund’s position in PACC Offshore Services, Singapore’s largest owner and operator of offshore support vessels, was the largest detractor from relative returns. In telecommunication services, a position in KT Corporation, a South Korean-based mobile, broadband and Internet Protocol (“IP”) television provider, disappointed most. |

| | The sectors that contributed most positively to the Fund’s performance relative to the Index were information technology, industrials and materials, where stock selection in each boosted relative results. In information technology, the Fund’s holding in Canadian Solar, mentioned earlier, was the strongest positive contributor. In industrials, a holding in Siemens India, which provides engineering solutions in automation and control, power, transportation and medical, boosted results most. In materials, a position in Monsanto India, the listed subsidiary of the global agricultural company Monsanto, was an outstanding performer. |

| Q | | How did the Fund use derivatives and similar instruments during the Reporting Period? |

| A | | During the Reporting Period, we did not use derivatives to hedge positions or as part of an active management strategy, but we used index futures on an opportunistic basis to ensure the Fund remained almost fully exposed to equities following cash inflows or stock sales. |

| Q | | Did the Fund make any significant purchases or sales during the Reporting Period? |

| A | | In addition to those new purchases already mentioned, within the consumer staples sector in South Korea, we initiated a Fund position in CJ Cheihjedang (“CJCJ”), a company that primarily engages in the production and marketing of processed foods. In our view, the company’s earnings should increase substantially by 2015, as we expect all of its three major businesses — namely, biotechnology, processed foods and raw materials — to enter into a full-fledged turnaround |

9

PORTFOLIO RESULTS

| | mode. CJCJ’s biotechnology business has suffered from competition with Chinese companies. However, we have recently seen some structural change. In its processed food segment, given CJCJ’s dominant market position and research and development capability, we believe it is able to cater to changing consumer needs, thereby improving the segment’s overall growth, margin and stability. Finally, we believe a strong Korean won, weak soft commodity prices and better control of its selling price could lead to a prolonged turnaround in CJCJ’s raw materials business. |

| | We established a Fund position in China Mobile during the Reporting Period in an effort to increase the Fund’s exposure to China’s telecommunication services sector overall. We expect the cost savings from reduced marketing expenses and handset subsidy cuts to improve the company’s profitability in the foreseeable future. |

| | We exited the Fund’s position in Hyundai Mipo Dockyard, one of the world’s top five shipbuilders specializing in mid-sized product carriers and chemical tankers. Consensus expectations on the ship building industry had long been quite low, but a rise in orders drove an increase in Hyundai Mipo Dockyard’s share price during the Reporting Period. As we believe our investment thesis had played out, we opted to eliminate the position and take profits. |

| | We sold the Fund’s position in OCI, a leading producer of poly-silicon, which is the basic material for photovoltaic cells, and a manufacturer of carbon chemicals and fine chemicals. We decided to exit the position because we expected the pace of its earnings growth to be slower than consensus expectations due to weaker than expected poly-silicon price movement and muted demand for its carbon chemicals business. |

| Q | | Were there any notable changes in the Fund’s weightings during the Reporting Period? |

| A | | Most sector weights are usually established within a relatively narrow range from the Index, as our team prefers to make decisions at the individual stock level, where we believe we can generate more added value. That said, during the Reporting Period, the Fund’s exposure to consumer discretionary, health care and materials increased, and its allocations to information technology, industrials and utilities decreased. |

| | Similarly, allocations to countries are directly the result of various stock selection decisions. During the Reporting Period, the Fund’s allocations to China, India and Taiwan increased, and its exposure to South Korea, Singapore and Indonesia decreased. |

| Q | | How was the Fund positioned relative to the Index at the end of the Reporting Period? |

| A | | At the end of the Reporting Period, the Fund had overweighted exposure to China, India, the Philippines, South Korea and Thailand compared to the Index. On the same date, the Fund had underweighted exposure relative to the Index to Hong Kong, Singapore, Taiwan and Malaysia and had rather neutral exposure relative to the Index in Indonesia. |

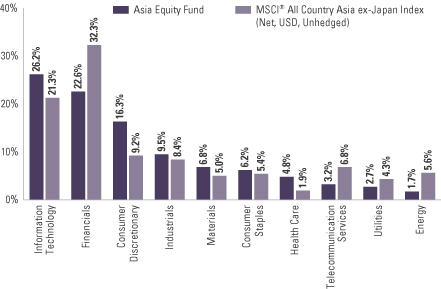

| | From a sector allocation perspective, the Fund had overweighted positions relative to the Index in the consumer discretionary, information technology, health care and materials sectors at the end of the Reporting Period. On the same date, the Fund had underweighted positions compared to the Index in the financials, energy, telecommunication services and utilities sectors and was relatively neutrally weighted compared to the Index in consumer staples and industrials. |

| | As always, we remained focused on individual stock selection, with sector and country positioning being a secondary, closely-monitored effect. |

10

FUND BASICS

Asia Equity Fund

as of October 31, 2014

| | | | | | | | | | |

| | PERFORMANCE REVIEW | |

| | | November 1, 2013–October 31, 2014 | | Fund Total Return

(based on NAV)1 | | | MSCI® All Country Asia ex-Japan Index

(Net, USD, Unhedged)2 | |

| | Class A | | | 4.75 | % | | | 5.73 | % |

| | Class B | | | 3.95 | | | | 5.73 | |

| | Class C | | | 4.00 | | | | 5.73 | |

| | Institutional | | | 5.15 | | | | 5.73 | |

| | | |

| | | February 28, 2014–October 31, 2014 | | | | | | |

| | | Class IR | | | 1.30 | % | | | 8.59 | % |

| | 1 | | The net asset value (“NAV”) represents the net assets of the class of the Fund (ex-dividend) divided by the total number of shares of the class outstanding. The Fund’s performance assumes the reinvestment of dividends and other distributions. The Fund’s performance does not reflect the deduction of any applicable sales charges. |

| | 2 | | The MSCI® All Country Asia ex-Japan Index (Net, USD, Unhedged) is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of Asia, excluding Japan. The MSCI AC Asia ex-Japan Index consists of the following 10 developed and emerging market country indices: China, Hong Kong, India, Indonesia, Korea, Malaysia, Philippines, Singapore, Taiwan, and Thailand. This index is net of dividends re-invested after deduction of withholding taxes, using a tax rate applicable to non-resident institutional investors who do not benefit from double taxation treaties. This series approximates the minimum possible dividend reinvestment. The dividend is reinvested after deduction of withholding tax, applying the rate to nonresident individuals who do not benefit from double taxation treaties. MSCI Barra uses withholding tax rates applicable to Luxembourg holding companies, as Luxembourg applies the highest rates. It is not possible to invest directly in an index. |

| | | | | | | | | | | | | | | | | | | | | | |

| | STANDARDIZED TOTAL RETURNS3 | |

| | | For the period ended 9/30/14 | | One Year | | | Five Years | | | Ten Years | | | Since Inception | | | Inception Date | |

| | Class A | | | 2.84 | % | | | 4.40 | % | | | 7.00 | % | | | 2.23 | % | | | 7/08/94 | |

| | Class B | | | 3.03 | | | | 4.47 | | | | 6.94 | | | | 1.29 | | | | 5/01/96 | |

| | Class C | | | 7.01 | | | | 4.78 | | | | 6.78 | | | | 1.45 | | | | 8/15/97 | |

| | Institutional | | | 9.23 | | | | 6.01 | | | | 8.03 | | | | 2.26 | | | | 2/02/96 | |

| | | Class IR | | | N/A | | | | N/A | | | | N/A | | | | 0.58 | | | | 2/28/14 | |

| | 3 | | The Standardized Total Returns are average annual total returns as of the most recent calendar quarter-end. They assume reinvestment of all distributions at NAV. These returns reflect a maximum initial sales charge of 5.5% for Class A Shares, the assumed contingent deferred sales charge for Class B Shares (5% maximum declining to 0% after six years) and the assumed contingent deferred sales charge for Class C Shares (1% if redeemed within 12 months of purchase). Class B Shares convert automatically to Class A Shares on or about the fifteenth day of the last month of the calendar quarter that is eight years after purchase. Returns for Class B Shares for the period after conversion reflect the performance of Class A Shares. Because Institutional and Class IR Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. The Fund’s Class B Shares are no longer available for purchase by new or existing shareholders. |

The returns set forth in the tables above represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

11

FUND BASICS

| | | | | | | | | | |

| | EXPENSE RATIOS4 | |

| | | | | Net Expense Ratio (Current) | | | Gross Expense Ratio (Before Waivers) | |

| | Class A | | | 1.69 | % | | | 2.19 | % |

| | Class B | | | 2.45 | | | | 2.95 | |

| | Class C | | | 2.45 | | | | 2.95 | |

| | Institutional | | | 1.29 | | | | 1.79 | |

| | | Class IR | | | 1.44 | | | | 1.94 | |

| | 4 | | The expense ratios of the Fund, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations) are as set forth above according to the most recent publicly available Prospectus for the Fund and may differ from the expense ratios disclosed in the Financial Highlights in this report. Pursuant to a contractual arrangement, the Fund’s waivers and/or expense limitations will remain in place through at least February 28, 2015, and prior to such date the Investment Adviser may not terminate the arrangements without the approval of the Fund’s Board of Trustees. If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. |

| | | | | | | | | | |

| | TOP TEN HOLDINGS AS OF 10/31/145 |

| | | Holding | | % of

Net Assets | | | Line of Business | | Country |

| | Taiwan Semiconductor | | | 3.6 | % | | Semiconductors & | | Taiwan |

| | Manufacturing Co. Ltd. | | | | | | Semiconductor Equipment | | |

| | China Mobile Ltd. | | | 3.1 | | | Telecommunication Services | | Hong Kong |

| | Tencent Holdings Ltd. | | | 3.1 | | | Software & Services | | China |

| | CJ CheilJedang Corp. | | | 2.9 | | | Food, Beverage & Tobacco | | South Korea |

| | Sino Biopharmaceutical Ltd. | | | 2.7 | | | Pharmaceuticals,

Biotechnology & Life

Sciences | | Hong Kong |

| | Industrial & Commercial Bank of China Ltd. Class H | | | 2.7 | | | Banks | | China |

| | SK Hynix, Inc. | | | 2.3 | | | Semiconductors &

Semiconductor Equipment | | South Korea |

| | China Cinda Asset Management Co. Ltd. Class H | | | 2.2 | | | Diversified Financials | | China |

| | PICC Property & Casualty Co. Ltd. Class H | | | 2.2 | | | Insurance | | China |

| | | Galaxy Entertainment Group Ltd. | | | 2.2 | | | Consumer Services | | Hong Kong |

| | 5 | | The top 10 holdings may not be representative of the Fund’s future investments. |

12

FUND BASICS

| | |

| FUND VS. BENCHMARK SECTOR ALLOCATIONS6 |

| As of October 31, 2014 |

| | 6 | | The Fund is actively managed and, as such, its composition may differ over time. Consequently, the Fund’s overall sector allocations may differ from percentages contained in the graph above. The graph categorizes investments using Global Industry Classification Standard (“GICS”), however, the sector classifications used by the portfolio management team may differ from GICS. Underlying sector allocations of exchange traded funds or investment companies held by the Fund are not reflected in the graph above. The percentage shown for each investment category reflects the value of investments in that category as a percentage of market value. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

13

GOLDMAN SACHS ASIA EQUITY FUND

Performance Summary

October 31, 2014

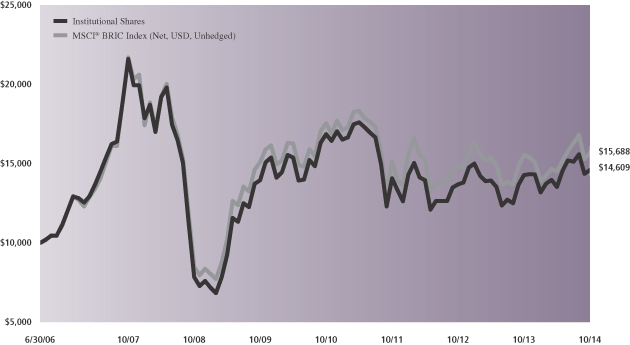

The following graph shows the value, as of October 31, 2014, of a $10,000 investment made on November 1, 2004 in Institutional Shares (at NAV). For comparative purposes, the performance of the Fund’s benchmark, the MSCI® All Country Asia ex-Japan Index (Net, USD, Unhedged) is shown. This performance data represents past performance and should not be considered indicative of future performance, which will fluctuate with changes in market conditions. These performance fluctuations will cause an investor’s shares, when redeemed, to be worth more or less than their original cost. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown and in their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Performance of Class A, Class B, Class C and Class IR Shares will vary from that of Institutional Shares due to differences in class specific fees and any applicable sales charges. In addition to the Investment Adviser’s decisions regarding issuer/industry/country investment selection and allocation, other factors may affect Fund performance. These factors include, but are not limited to, Fund operating fees and expenses, portfolio turnover and subscription and redemption cash flows affecting the Fund.

|

| Asia Equity Fund’s 10 Year Performance |

Performance of a $10,000 Investment, with distributions reinvested, from November 1, 2004 through October 31, 2014.

| | | | | | | | | | | | | | |

| Average Annual Total Return through October 31, 2014 | | | One Year | | | | Five Years | | | | Ten Years | | | Since Inception |

Class A (Commenced July 8, 1994) | | | | | | | | | | | | | | |

Excluding sales charges | | | 4.75% | | | | 6.20% | | | | 7.58% | | | 2.54% |

Including sales charges | | | -1.02% | | | | 5.00% | | | | 6.97% | | | 2.25% |

|

Class B (Commenced May 1, 1996)* | | | | | | | | | | | | | | |

Excluding contingent deferred sales charges | | | 3.95% | | | | 5.42% | | | | 6.91% | | | 1.32% |

Including contingent deferred sales charges | | | -1.05% | | | | 5.09% | | | | 6.91% | | | 1.32% |

|

Class C (Commenced August 15, 1997) | | | | | | | | | | | | | | |

Excluding contingent deferred sales charges | | | 4.00% | | | | 5.40% | | | | 6.76% | | | 1.48% |

Including contingent deferred sales charges | | | 3.00% | | | | 5.40% | | | | 6.76% | | | 1.48% |

|

Institutional (Commenced February 2, 1996) | | | 5.15% | | | | 6.63% | | | | 8.01% | | | 2.29% |

|

Class IR (Commenced February 28, 2014) | | | N/A | | | | N/A | | | | N/A | | | 1.30% |

|

| | * | | Effective at the close of business on November 14, 2014, Class B Shares of the Fund have converted to Class A Shares of the Fund. In addition, effective October 15, 2014, all redemptions of Class B Shares have not been subject to a contingent deferred sales charge. Average annual total returns for Class B Shares through October 31, 2014 have not been adjusted to reflect this change. |

14

PORTFOLIO RESULTS

Goldman Sachs BRIC Fund

Investment Objective

The Fund seeks long-term capital appreciation.

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Fundamental Emerging Markets Equity Portfolio Management Team discusses the Goldman Sachs BRIC Fund’s (the “Fund”) performance and positioning for the 12-month period ended October 31, 2014 (the “Reporting Period”).

| Q | | How did the Fund perform during the Reporting Period? |

| A | | During the Reporting Period, the Fund’s Class A, C, Institutional and IR Shares generated average annual total returns, without sales charges, of 1.89%, 1.13%, 2.29% and 2.07%, respectively. These returns compare to the 0.80% average annual total return of the Fund’s benchmark, the MSCI® BRIC Index (Net, USD, Unhedged) (the “Index”), during the same period. |

| Q | | What key factors were responsible for the Fund’s performance during the Reporting Period? |

| A | | The Fund outperformed the Index on a relative basis during the Reporting Period. Effective stock selection in India and China and an overweighted allocation to the strongly-performing Indian equity market contributed most positively. Russia was the only detractor, due both to the Fund’s overweighted allocation and weak stock selection. |

| Q | | What were some of the Fund’s best-performing individual stocks? |

| A | | The strongest contributors to the Fund’s performance during the Reporting Period were Chinese Internet service company Tencent Holdings, Indian non-banking finance company Bajaj Finance and Brazilian insurance and brokerage holding company BB Seguridade. |

| | Tencent Holdings is an Internet service company in China engaged in social networks, web portals, e-commerce and multiplayer online games. Tencent Holdings’ stock performed well during the Reporting Period, as its introduction of a new version of WeChat — its proprietary social messaging platform, saw the monetization of its mobile platform in 2013. Also, subscriber growth for WeChat was strong in both its domestic and overseas markets. |

| | Bajaj Finance, an Indian non-banking finance company engaged in consumer finance, small and medium enterprise finance and commercial lending, was a strong contributor to the Fund’s relative results. The company performed well as measured by loan growth, margins and asset quality relative to its peers. Improving consumer sentiment and a strong outlook on consumer durable sales provided a positive backdrop to Bajaj Finance’s consumer lending business. At the end of the Reporting Period, we maintained the position in the Fund based on what we considered to be its healthy return ratios and attractive valuations. |

| | Against a backdrop of a difficult macro environment, BB Seguridade performed well, reporting sound results and reiterating its 2014 return on equity guidance. The company was able to increase its market share in new pension contribution and insurance premiums by leveraging the existing client base of Banco do Brasil, its parent company. |

| Q | | Which stocks detracted significantly from the Fund’s performance during the Reporting Period? |

| A | | Detracting most from the Fund’s results relative to the Index were positions in Chinese telecommunication services giant China Mobile, Chinese automobile manufacturer Great Wall Motor and Russian bank Sberbank. |

| | Not holding a position in the strongly-performing stock of China Mobile detracted significantly from the Fund’s relative results. China Mobile’s share price gain was mainly driven by three factors — 1) the Ministry of Industry and Information Technology’s request to reduce marketing expenses; 2) strong fourth generation (4G) subscriber growth; and 3) average revenue per unit improvement. In our view, the marketing expense and handset subsidy cuts could help to offset the negative earnings impact from the implementation of the value-added tax. We noted the short-term benefits on the cost reduction to China Mobile and |

15

PORTFOLIO RESULTS

| | added the stock to the Fund’s portfolio just after the close of the Reporting Period. |

| | Great Wall Motor specializes in the niche sport utility vehicles (“SUV”) segment of the Chinese automobile manufacturing industry. Its auto sales underperformed the industry during the Reporting Period, largely due to a gap in its product cycle, with launches of new SUV models and facelifts of aging small sedan models expected to come in late 2014. The repeated launch delays of high-end SUV model H8 also had a negative effect on investor sentiment. |

| | Sberbank, Russia’s largest bank, was a significant detractor from the Fund’s results during the Reporting Period. The U.S. and Europe imposed new sanctions on Russia in response to the continued conflict in eastern Ukraine. Russian equities experienced a broad-based decline, led by its financials sector. |

| Q | | Which equity market sectors most significantly affected Fund performance during the Reporting Period? |

| A | | Having an overweight to the strongly performing information technology sector and an underweight to the weaker materials sector boosted the Fund’s results significantly during the Reporting Period. Effective stock selection in information technology, financials and materials also contributed positively to the Fund’s performance. In information technology, the Fund’s position in Tencent Holdings, mentioned earlier, was the strongest contributor to relative performance within the sector. In materials, the Fund’s holding in Vale, the third-largest mining company in the world, was the largest contributor. In financials, the Fund’s position in Bajaj Finance, already mentioned, was a particularly strong performer. |

| | Conversely, weak stock selection in the health care, energy and utilities sectors detracted most from the Fund’s performance relative to the Index during the Reporting Period. At an individual stock level, the Fund’s position in OdontoPrev, a dental benefits company in Brazil, was the largest detractor within the health care sector. Within energy, the Fund’s position in Lukoil, Russia’s second-largest oil company, detracted most from performance during the Reporting Period. In utilities, the Fund’s holding in KSK Energy Ventures, an Indian mid-cap power generation company, detracted most from returns. |

| Q | | How did the Fund use derivatives and similar instruments during the Reporting Period? |

| A | | During the Reporting Period, the Fund gained exposure to select stocks through equity-linked notes and participatory notes. We used index futures on an opportunistic basis to ensure the Fund remained almost fully exposed to equities following cash inflows or stock sales. |

| Q | | Did the Fund make any significant purchases or sales during the Reporting Period? |

| A | | During the Reporting Period, we added to the Fund’s position in Sino Biopharmaceutical within the health care sector in China. The company develops drugs for the treatment of ophthalmia, hepatitis and modernized Chinese medicine. |

| | We initiated a Fund position in TCS, India’s largest information technology services company. TCS delivered double-digit growth in U.S. dollar terms in fiscal year 2014 with its new service lines growing ahead of estimates, led by digital, consulting and engineering services. Continued growth momentum as measured by both revenues and profits, with an even better fiscal year 2015 outlook, gives us confidence in the sustainability of the company’s outperformance over key competitors and the industry. |

| | We exited the Fund’s position in Vale, mentioned earlier. We believe the long-awaited iron ore price correction may well be underway and do not see this correction as short-lived. |

| | We trimmed the Fund’s position in ICBC, the world’s largest bank by market capitalization and one of the largest commercial banks in China. We like the bank for its liquid balance sheet and strong management track record. However, we reduced the Fund position in ICBC to lessen exposure to banks overall given headwinds such as slower economic growth and heightened competition from Internet finance. |

| Q | | Were there any notable changes in the Fund’s weightings during the Reporting Period? |

| A | | Most sector weights are usually established within a narrow range from the Index, as our team prefers to make decisions at the individual stock level, where we believe we can generate more added value. That said, during the Reporting Period, the Fund’s exposure relative to the Index in information technology, health care and consumer discretionary increased, and its allocations relative to the |

16

PORTFOLIO RESULTS

| | Index to financials, telecommunication services, materials, energy and utilities decreased. |

| | Resulting from various stock selection decisions, the Fund’s exposure relative to the Index to India increased, and its allocation relative to the Index to China decreased. |

| Q | | How was the Fund positioned relative to the Index at the end of the Reporting Period? |

| A | | At the end of the Reporting Period, the Fund had overweighted exposure to India and Russia and underweighted exposure to Brazil and China relative to the Index. |

| | From a sector perspective, the Fund had overweighted allocations to information technology, health care, consumer staples and consumer discretionary compared to the Index at the end of the Reporting Period. On the same date, the Fund had underweighted exposure to the energy, telecommunication services, materials, utilities, financials and industrials sectors. |

| | As always, we remained focused on individual stock selection, with sector and country positioning being a secondary, closely-monitored effect. |

17

FUND BASICS

BRIC Fund

as of October 31, 2014

| | | | | | | | | | |

| | PERFORMANCE REVIEW | |

| | | November 1, 2013–October 31, 2014 | | Fund Total Return

(based on NAV)1 | | | MSCI® BRIC Index2 | |

| | Class A | | | 1.89 | % | | | 0.80 | % |

| | Class C | | | 1.13 | | | | 0.80 | |

| | Institutional | | | 2.29 | | | | 0.80 | |

| | | Class IR | | | 2.07 | | | | 0.80 | |

| | 1 | | The net asset value (“NAV”) represents the net assets of the class of the Fund (ex-dividend) divided by the total number of shares of the class outstanding. The Fund’s performance assumes the reinvestment of dividends and other distributions. The Fund’s performance does not reflect the deduction of any applicable sales charges. |

| | 2 | | The MSCI® BRIC Index (Net, USD, Unhedged) is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of the following four emerging market country indices: Brazil, Russia, India and China. This series approximates the minimum possible dividend reinvestment. The dividend is reinvested after deduction of withholding tax, applying the rate to non-resident individuals who do not benefit from double taxation treaties. MSCI Barra uses withholding tax rates applicable to Luxembourg holding companies, as Luxembourg applies the highest rates. It is not possible to invest directly in an index. |

| | | | | | | | | | | | | | | | |

| | STANDARDIZED TOTAL RETURNS3 |

| | | For the period ended 9/30/14 | | One Year | | | Five Years | | | Since Inception | | | Inception Date |

| | Class A | | | -1.24 | % | | | -0.66 | % | | | 3.35 | % | | 6/30/06 |

| | Class C | | | 2.68 | | | | -0.30 | | | | 3.28 | | | 6/30/06 |

| | Institutional | | | 4.93 | | | | 0.87 | | | | 4.48 | | | 6/30/06 |

| | | Class IR | | | 4.69 | | | | N/A | | | | -0.76 | | | 8/31/10 |

| | 3 | | The Standardized Total Returns are average annual total returns as of the most recent calendar quarter-end. They assume reinvestment of all distributions at NAV. These returns reflect a maximum initial sales charge of 5.5% for Class A Shares and the assumed contingent deferred sales charge for Class C Shares (1% if redeemed within 12 months of purchase). Because Institutional and Class IR Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. |

The returns set forth in the tables above represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

18

FUND BASICS

| | | | | | | | | | |

| | EXPENSE RATIOS4 | |

| | | | | Net Expense Ratio (Current) | | | Gross Expense Ratio (Before Waivers) | |

| | Class A | | | 1.71 | % | | | 1.97 | % |

| | Class C | | | 2.45 | | | | 2.71 | |

| | Institutional | | | 1.31 | | | | 1.57 | |

| | | Class IR | | | 1.46 | | | | 1.72 | |

| | 4 | | The expense ratios of the Fund, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations) are as set forth above according to the most recent publicly available Prospectus for the Fund and may differ from the expense ratios disclosed in the Financial Highlights in this report. Pursuant to a contractual arrangement, the Fund’s waivers and/or expense limitations will remain in place through at least February 28, 2015, and prior to such date the Investment Adviser may not terminate the arrangements without the approval of the Fund’s Board of Trustees. If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. |

| | | | | | | | | | |

| | TOP TEN HOLDINGS AS OF 10/31/145 |

| | | Holding | | % of

Net Assets | | | Line of Business | | Country |

| | Tencent Holdings Ltd. | | | 8.3 | % | | Software & Services | | China |

| | iShares China Large-Cap ETF | | | 5.5 | | | Exchange Traded

Fund | | United States |

| | BB Seguridade Participacoes SA | | | 5.0 | | | Insurance | | Brazil |

| | Banco Bradesco SA | | | 3.4 | | | Banks | | Brazil |

| | AMBEV SA | | | 3.1 | | | Food, Beverage &

Tobacco | | Brazil |

| | OJSC Magnit | | | 3.0 | | | Food & Staples

Retailing | | Russia |

| | Agricultural Bank of China Ltd. Class H | | | 2.9 | | | Banks | | China |

| | Odontoprev SA | | | 2.8 | | | Health Care

Equipment &

Services | | Brazil |

| | OAO Lukoil ADR | | | 2.7 | | | Energy | | Russia |

| | | Hollysys Automation Technologies Ltd. | | | 2.5 | | | Technology

Hardware &

Equipment | | China |

| | 5 | | The top 10 holdings may not be representative of the Fund’s future investments. |

19

FUND BASICS

|

| FUND VS. BENCHMARK SECTOR ALLOCATIONS6 |

| As of October 31, 2014 |

| | 6 | | The Fund is actively managed and, as such, its composition may differ over time. Consequently, the Fund’s overall sector allocations may differ from percentages contained in the graph above. The graph categorizes investments using Global Industry Classification Standard (“GICS”), however, the sector classifications used by the portfolio management team may differ from GICS. Underlying sector allocations of exchange traded funds held by the Fund are not reflected in the graph above. The percentage shown for each investment category reflects the value of investments in that category as a percentage of market value. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

20

GOLDMAN SACHS BRIC FUND

Performance Summary

October 31, 2014

The following graph shows the value, as of October 31, 2014, of a $10,000 investment made on June 30, 2006 (commencement of operations) in Institutional Shares (at NAV). For comparative purposes, the performance of the Fund’s benchmark, the MSCI® BRIC Index (Net, USD, Unhedged), is shown. This performance data represents past performance and should not be considered indicative of future performance, which will fluctuate with changes in market conditions. These performance fluctuations will cause an investor’s shares, when redeemed, to be worth more or less than their original cost. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown and in their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Performance of Class A, Class C and Class IR Shares will vary from that of Institutional Shares due to differences in class specific fees and any applicable sales charges. In addition to the Investment Adviser’s decisions regarding issuer/industry/country investment selection and allocation, other factors may affect Fund performance. These factors include, but are not limited to, Fund operating fees and expenses, portfolio turnover and subscription and redemption cash flows affecting the Fund.

|

| BRIC Fund’s Lifetime Performance |

Performance of a $10,000 Investment, with distributions reinvested, from June 30, 2006 through October 31, 2014.

| | | | | | | | | | |

| Average Annual Total Return through October 31, 2014 | | | One Year | | | | Five Years | | | Since Inception |

Class A (Commenced June 30, 2006) | | | | | | | | | | |

Excluding sales charges | | | 1.89% | | | | 0.49% | | | 4.23% |

Including sales charges | | | -3.70% | | | | -0.63% | | | 3.52% |

|

Class C (Commenced June 30, 2006) | | | | | | | | | | |

Excluding contingent deferred sales charges | | | 1.13% | | | | -0.26% | | | 3.44% |

Including contingent deferred sales charges | | | 0.13% | | | | -0.26% | | | 3.44% |

|

Institutional (Commenced June 30, 2006) | | | 2.29% | | | | 0.90% | | | 4.65% |

|

Class IR (Commenced August 31, 2010) | | | 2.07% | | | | N/A | | | -0.34% |

|

21

PORTFOLIO RESULTS

Goldman Sachs Emerging Markets Equity Fund

Investment Objective

The Fund seeks long-term capital appreciation.

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Fundamental Emerging Markets Equity Portfolio Management Team discusses the Goldman Sachs Emerging Markets Equity Fund’s (the “Fund”) performance and positioning for the 12-month period ended October 31, 2014 (the “Reporting Period”).

| Q | | How did the Fund perform during the Reporting Period? |

| A | | During the Reporting Period, the Fund’s Class A, B, C, Institutional, Service and IR Shares generated average annual total returns, without sales charges, of 5.67%, 4.94%, 4.90%, 6.17%, 5.55% and 5.93%, respectively. These returns compare to the 0.64% average annual total return of the Fund’s benchmark, the MSCI® Emerging Markets Index (Gross, USD, Unhedged) (the “Index”), during the same period. |

| Q | | What key factors were responsible for the Fund’s performance during the Reporting Period? |

| A | | The Fund outperformed the Index on a relative basis during the Reporting Period. Effective stock selection in India, South Korea and Taiwan benefited the Fund’s performance most. Having an overweighted allocation to India, which significantly outpaced the Index during the Reporting Period, also boosted the Fund’s results. Such positive contributors were only partially offset by the detracting effect of weak stock selection in South Africa and allocation positioning in Russia, South Africa and Nigeria. |

| Q | | What were some of the Fund’s best-performing individual stocks? |

| A | | The strongest contributors to the Fund’s performance during the Reporting Period were Hanssem, Bajaj Finance and PCHome Online. |

| | Hanssem, which manufactures kitchen and interior furniture and is the main consolidator of a fragmented South Korean furniture market, was the top individual stock contributor to the Fund’s relative results during the Reporting Period. Its shares rose, as the company reported better than expected top-line growth on an increase in remodeling demand from an improved housing transaction volume. At the end of the Reporting Period, Hanssem led its industry in terms of earnings growth, return on equity and valuation. |

| | Bajaj Finance, an Indian non-banking finance company engaged in consumer finance, small and medium enterprise finance and commercial lending, was another strong contributor to the Fund’s relative results. The company performed well as measured by loan growth, margins and asset quality relative to its peers. Improving consumer sentiment and a strong outlook on consumer durable sales provided a positive backdrop to Bajaj Finance’s consumer lending business. At the end of the Reporting Period, we maintained the position in the Fund based on what we considered to be its healthy return ratios and attractive valuations. |

| | PCHome Online, a leading e-commerce service provider in Taiwan, was a key positive contributor to the Fund’s results during the Reporting Period. The company beat consensus estimates in successive quarters, evidence to the market at large that the third-party payment story remains intact. As e-commerce appears to be entering a positive cycle, PCHome Online also performed well due to its strong earnings growth outlook. |

| Q | | Which stocks detracted significantly from the Fund’s performance during the Reporting Period? |

| A | | Detracting most from the Fund’s results relative to the Index were positions in Great Wall Motor, LiHom-Cuchen and China Mobile. |

| | | Great Wall Motor specializes in the niche sport utility vehicles (“SUV”) segment of the Chinese automobile manufacturing industry. Its auto sales underperformed the industry during the Reporting Period, largely due to a gap in its product cycle, with launches of new SUV models and facelifts of aging small sedan models expected to come in |

22

PORTFOLIO RESULTS

| | late 2014. The repeated launch delays of high-end SUV model H8 also had a negative effect on investor sentiment. |

| | South Korean electric home appliance manufacturer LiHom Cuchen’s stock, a new purchase for the Fund during the Reporting Period, detracted from the Fund’s results on the back of concerns about potentially weaker than expected third quarter 2014 earnings and risk-averse market sentiment toward small cap names amidst volatility. At the end of the Reporting Period, we had put this holding under review pending its earnings announcement. |

| | Not holding a position in the strongly-performing stock of China Mobile detracted significantly from the Fund’s relative results. China Mobile’s share price gain was mainly driven by three factors — 1) the Ministry of Industry and Information Technology’s request to reduce marketing expenses; 2) strong fourth generation (4G) subscriber growth; and 3) average revenue per unit improvement. We believe the marketing expense and handset subsidy cuts could help to offset the negative earnings impact from the implementation of the value-added tax. We noted the short-term benefits on the cost reduction to China Mobile and added the stock to the Fund’s portfolio just after the close of the Reporting Period. |

| Q | | Which equity market sectors most significantly affected Fund performance during the Reporting Period? |

| A | | Relative to the Index, strong stock selection within the information technology, financials and materials sectors contributed most positively to the Fund’s performance. Having an overweighted allocation to the information technology sector, which significantly outpaced the Index during the Reporting Period, and an underweighted allocation to the materials sector, which significantly lagged the Index during the Reporting Period, also boosted the Fund’s results. In information technology, the Fund’s holding in PCHome Online, mentioned earlier, was the strongest contributor. In financials, the Fund’s position in Bajaj Finance, already mentioned, was an outstanding performer. In materials, the Fund’s holding in Monsanto India, the listed subsidiary of the global agricultural company Monsanto, boosted Fund results most. |

| | Conversely, weak stock selection and allocation positioning in telecommunication services, consumer staples and utilities detracted most from the Fund’s relative results during the Reporting Period. In telecommunication services, the Fund’s position in Mobile Telesystems, Russia’s largest mobile phone carrier, was the largest detractor from relative returns. In consumer staples, the Fund’s position in Hengan International, the largest producer of sanitary napkins and baby diapers in China, was the biggest disappointment. In utilities, the Fund’s position in KSK Energy Ventures, an Indian mid-capitalization power generation company, detracted most from returns. |

| Q | | How did the Fund use derivatives and similar instruments during the Reporting Period? |

| A | During the Reporting Period, the Fund used equity-linked notes and participatory notes to gain exposure to select stocks. We used index futures on an opportunistic basis to ensure the Fund remained almost fully exposed to equities following cash inflows or stock sales. |

| Q | | Did the Fund make any significant purchases or sales during the Reporting Period? |

| A | Within the consumer discretionary sector in South Africa, we initiated a Fund position in Naspers, a multinational media group. Naspers is a global platform operator with principal operations in Internet services, pay television and print media. The company appears to us to be pushing hard to consolidate its number one position in classified ads in many regions. Also, under its new chief executive officer, the company appears focused on e-commerce upside. Tencent Holdings, of which Naspers is the largest shareholder, offers exposure to the largest and fastest growing mobile market globally. |

| | Within the industrials sector in South Korea, we initiated a Fund position in Hanjin Kal, a holding company with subsidiaries in the South Korean travel industry. We believe the company may be a direct beneficiary of strong tourism in South Korea and that its recent restructuring should improve transparency of the company and crystalize its value. It is a major shareholder of South Korea’s number two low cost carrier, Jin Air. Jin Air has been a beneficiary of increasing overseas travel demand, especially lucrative short-haul routes under the backdrop of a strong Korean won. Given that its subsidiaries are unlisted companies, we believe Hanjin Kal deserves a higher valuation than it had at the end of the Reporting Period. |

| | We exited the Fund’s position in Vale, the third-largest mining company in the world. We believe the long-awaited iron ore price correction may well be underway and do not see this correction as short-lived. |

| | Within the consumer staples sector in Brazil, we eliminated the Fund’s position in beverage company Ambev during the Reporting Period due to the persistent weakness in purchasing power of the Brazilian consumer. |

23

PORTFOLIO RESULTS

| Q | | Were there any notable changes in the Fund’s weightings during the Reporting Period? |

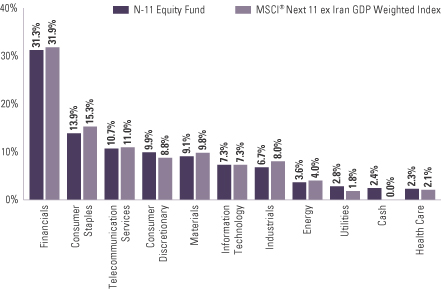

| A | | Most sector weights are usually established within a narrow range from the Index, as our team prefers to make decisions at the individual stock level, where we believe we can generate more added value. That said, during the Reporting Period, the Fund’s exposure relative to the Index to financials, consumer discretionary and health care increased, and its allocations relative to the Index to energy, consumer staples and telecommunication services decreased. |

| | Similarly, allocations to countries are directly the result of various stock selection decisions. As such, the Fund’s exposure relative to the Index in India, Colombia, Thailand and Peru increased, and its allocations relative to the Index to Russia, China, South Korea, Nigeria and Taiwan decreased. |

| Q | | How was the Fund positioned relative to the Index at the end of the Reporting Period? |

| A | | At the end of the Reporting Period, the Fund had overweighted exposures to India, Peru, Georgia, Indonesia and Thailand and underweighted exposures to China, South Africa, South Korea and Malaysia relative to the Index. On the same date, the Fund was relatively neutrally weighted to the Index in the remaining components of the Index. |

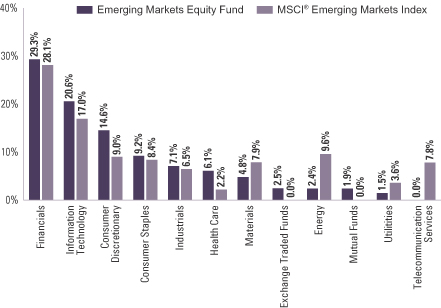

| | From a sector allocation perspective, the Fund had overweighted positions relative to the Index in consumer discretionary, health care, information technology and financials at the end of the Reporting Period. The Fund had underweighted positions compared to the Index in the energy, materials and utilities sectors at the end of the Reporting Period. The Fund had rather neutral positions relative to the Index in the consumer staples and industrials sectors and had no position at all in telecommunication services at the end the Reporting Period. |

| | As always, we remained focused on individual stock selection, with sector and country positioning being a secondary, closely-monitored effect. |

24

FUND BASICS

Emerging Markets Equity Fund

as of October 31, 2014

| | | | | | | | | | |

| | PERFORMANCE REVIEW | |

| | | November 1, 2013–October 31, 2014 | | Fund Total Return

(based on NAV)1 | | | MSCI® Emerging Markets Index

(Gross, USD, Unhedged)2 | |

| | Class A | | | 5.67 | % | | | 0.64 | % |

| | Class B | | | 4.94 | | | | 0.64 | |

| | Class C | | | 4.90 | | | | 0.64 | |

| | Institutional | | | 6.17 | | | | 0.64 | |

| | Service | | | 5.55 | | | | 0.64 | |

| | | Class IR | | | 5.93 | | | | 0.64 | |

| | 1 | | The net asset value (“NAV”) represents the net assets of the class of the Fund (ex-dividend) divided by the total number of shares of the class outstanding. The Fund’s performance assumes the reinvestment of dividends and other distributions. The Fund’s performance does not reflect the deduction of any applicable sales charges. |

| | 2 | | The MSCI® Emerging Markets Index (Gross, USD, Unhedged) is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets. As of June 2, 2014 the MSCI® Emerging Markets Index consists of the following 23 emerging market country indexes: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Peru, Philippines, Poland, Qatar, Russia, South Africa, Taiwan, Thailand, Turkey and United Arab Emirates. It is not possible to invest directly in an index. |

| | | | | | | | | | | | | | | | | | | | |

| | STANDARDIZED TOTAL RETURNS3 |

| | | For the period ended 9/30/14 | | One Year | | | Five Years | | | Ten Years | | | Since Inception | | | Inception Date |

| | Class A | | | 4.05 | % | | | 2.25 | % | | | 8.52 | % | | | 6.17 | % | | 12/15/97 |

| | Class B | | | 4.27 | | | | 2.27 | | | | 8.49 | | | | 6.28 | | | 12/15/97 |

| | Class C | | | 8.20 | | | | 2.63 | | | | 8.30 | | | | 5.85 | | | 12/15/97 |

| | Institutional | | | 10.52 | | | | 3.85 | | | | 9.56 | | | | 7.07 | | | 12/15/97 |

| | Service | | | 10.00 | | | | 3.32 | | | | 9.02 | | | | 6.42 | | | 12/15/97 |

| | | Class IR | | | 10.35 | | | | N/A | | | | N/A | | | | 3.20 | | | 8/31/10 |

| | 3 | | The Standardized Total Returns are average annual total returns as of the most recent calendar quarter-end. They assume reinvestment of all distributions at NAV. These returns reflect a maximum initial sales charge of 5.5% for Class A Shares, the assumed contingent deferred sales charge for Class B Shares (5% maximum declining to 0% after six years) and the assumed contingent deferred sales charge for Class C Shares (1% if redeemed within 12 months of purchase). Class B Shares convert automatically to Class A Shares on or about the fifteenth day of the last month of the calendar quarter that is eight years after purchase. Returns for Class B Shares for the period after conversion reflect the performance of Class A Shares. Because Institutional, Service and Class IR Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. The Fund’s Class B Shares are no longer available for purchase by new or existing shareholders. |

The returns set forth in the tables above represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

25

FUND BASICS

| | | | | | | | | | |

| | EXPENSE RATIOS4 | |

| | | | | Net Expense Ratio (Current) | | | Gross Expense Ratio (Before Waivers) | |

| | Class A | | | 1.72 | % | | | 1.90 | % |

| | Class B | | | 2.47 | | | | 2.65 | |

| | Class C | | | 2.47 | | | | 2.65 | |

| | Institutional | | | 1.32 | | | | 1.50 | |

| | Service | | | 1.82 | | | | 2.00 | |

| | | Class IR | | | 1.47 | | | | 1.65 | |

| | 4 | | The expense ratios of the Fund, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations) are as set forth above according to the most recent publicly available Prospectus for the Fund and may differ from the expense ratios disclosed in the Financial Highlights in this report. Pursuant to a contractual arrangement, the Fund’s waivers and/or expense limitations will remain in place through at least February 28, 2015, and prior to such date the Investment Adviser may not terminate the arrangements without the approval of the Fund’s Board of Trustees If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. |

| | | | | | | | | | |

| | TOP TEN HOLDINGS AS OF 10/31/145 |

| | | Holding | | % of

Net Assets | | | Line of Business | | Country |

| | Tencent Holdings Ltd. | | | 3.0 | % | | Software & Services | | China |

| | Taiwan Semiconductor Manufacturing Co. Ltd. | | | 2.8 | | | Semiconductors &

Semiconductor Equipment | | Taiwan |

| | iShares MSCI South Korea Capped | | | 2.5 | | | Exchange Traded Fund | | United States |

| | iShares China Large-Cap ETF | | | 1.9 | | | Exchange Traded Fund | | United States |

| | Airports of Thailand PCL | | | 1.8 | | | Transportation | | Thailand |

| | BB Seguridade Participacoes SA | | | 1.8 | | | Insurance | | Brazil |

| | SK Hynix, Inc. | | | 1.5 | | | Semiconductors &

Semiconductor Equipment | | South Korea |

| | Banco Bradesco SA | | | 1.5 | | | Banks | | Brazil |

| | Credicorp Ltd. | | | 1.4 | | | Banks | | Peru |

| | | Naspers Ltd. Class N | | | 1.4 | | | Media | | South Africa |

| | 5 | | The top 10 holdings may not be representative of the Fund’s future investments. |

26

FUND BASICS

|

| FUND VS . BENCHMARK SECTOR ALLOCATIONS6 |

| As of October 31, 2014 |

| | 6 | | The Fund is actively managed and, as such, its composition may differ over time. Consequently, the Fund’s overall sector allocations may differ from percentages contained in the graph above. The graph categorizes investments using Global Industry Classification Standard (“GICS”), however, the sector classifications used by the portfolio management team may differ from GICS. Underlying sector allocations of exchange traded funds held by the Fund are not reflected in the graph above. The percentage shown for each investment category reflects the value of investments in that category as a percentage of market value. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

27

GOLDMAN SACHS EMERGING MARKETS EQUITY FUND

Performance Summary

October 31, 2014

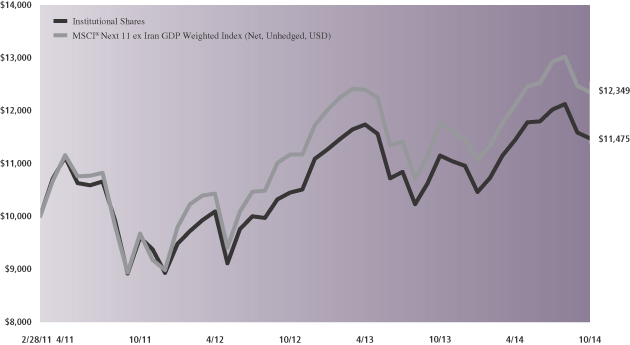

The following graph shows the value, as of October 31, 2014, of a $10,000 investment made on November 1, 2004 in Institutional Shares (at NAV). For comparative purposes, the performance of the Fund’s benchmark, the MSCI® Emerging Markets Index (Gross, USD, Unhedged), is shown. This performance data represents past performance and should not be considered indicative of future performance, which will fluctuate with changes in market conditions. These performance fluctuations will cause an investor’s shares, when redeemed, to be worth more or less than their original cost. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown and in their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Performance of Class A, Class B, Class C, Service and Class IR Shares will vary from that of Institutional Shares due to differences in class specific fees and any applicable sales charges. In addition to the Investment Adviser’s decisions regarding issuer/industry/country investment selection and allocation, other factors may affect Fund performance. These factors include, but are not limited to, Fund operating fees and expenses, portfolio turnover and subscription and redemption cash flows affecting the Fund.

|

| Emerging Markets Equity Fund’s 10 Year Performance |

Performance of a $10,000 Investment, with distributions reinvested, from November 1, 2004 through October 31, 2014.

| | | | | | | | | | | | | | |

| Average Annual Total Return through October 31, 2014 | | | One Year | | | | Five Years | | | | Ten Years | | | Since Inception |

Class A (Commenced December 15, 1997) | | | | | | | | | | | | | | |

Excluding sales charges | | | 5.67% | | | | 3.87% | | | | 8.82% | | | 6.52% |

Including sales charges | | | -0.11% | | | | 2.70% | | | | 8.20% | | | 6.17% |

|

Class B (Commenced December 15, 1997)* | | | | | | | | | | | | | | |

Excluding contingent deferred sales charges | | | 4.94% | | | | 3.10% | | | | 8.17% | | | 6.27% |

Including contingent deferred sales charges | | | -0.06% | | | | 2.74% | | | | 8.17% | | | 6.27% |

|

Class C (Commenced December 15, 1997) | | | | | | | | | | | | | | |

Excluding contingent deferred sales charges | | | 4.90% | | | | 3.11% | | | | 8.01% | | | 5.85% |

Including contingent deferred sales charges | | | 3.90% | | | | 3.11% | | | | 8.01% | | | 5.85% |

|

Institutional (Commenced December 15, 1997) | | | 6.17% | | | | 4.30% | | | | 9.26% | | | 7.07% |

|

Service (Commenced December 15, 1997) | | | 5.55% | | | | 3.78% | | | | 8.71% | | | 6.41% |

|

Class IR (Commenced August 31, 2010) | | | 5.93% | | | | N/A | | | | N/A | | | 3.25% |

|