UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-05349

Goldman Sachs Trust

(Exact name of registrant as specified in charter)

71 South Wacker Drive, Chicago, Illinois 60606

(Address of principal executive offices) (Zip code)

| | |

| Caroline Kraus, Esq. | | Copies to: |

| Goldman Sachs & Co. LLC | | Geoffrey R.T. Kenyon, Esq. |

| 200 West Street | | Dechert LLP |

| New York, New York 10282 | | 100 Oliver Street |

| | 40th Floor |

| | Boston, MA 02110-2605 |

(Name and address of agents for service)

Registrant’s telephone number, including area code: (312) 655-4400

Date of fiscal year end: March 31

Date of reporting period: September 30, 2017

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

| | The Semi-Annual Report to Shareholders is filed herewith. |

Goldman Sachs Funds

| | | | |

| | |

| Semi-Annual Report | | | | September 30, 2017 |

| | |

| | | | Fixed Income Alternatives Funds |

| | | | Long Short Credit Strategies |

| | | | Strategic Macro* |

*Effective June 20, 2017, the Goldman Sachs Fixed Income Macro Strategies Fund was renamed the Goldman Sachs Strategic Macro Fund.

Goldman Sachs Fixed Income Alternatives Funds

| ∎ | | LONG SHORT CREDIT STRATEGIES FUND |

| | | | |

| | | |

| NOT FDIC-INSURED | | May Lose Value | | No Bank Guarantee |

GOLDMAN SACHS LONG SHORT CREDIT STRATEGIES FUND

What Differentiates Goldman Sachs Long Short Credit Strategies Fund’s Investment Process?

The Goldman Sachs Long Short Credit Strategies Fund (the “Fund”) seeks an absolute return comprised of income and capital appreciation.

The Fund uses a bottom-up, fundamental approach with a focus on high conviction ideas across the corporate credit spectrum. Inefficiencies in the credit markets may provide attractive opportunities for investors. The Fund seeks to capitalize on these through an unconstrained approach, security selection and providing active downside management.

| ∎ | | The Fund is not limited by the traditional constraints of a benchmark strategy. |

| ∎ | | The Fund uses a flexible and dynamic strategy that allows it to invest across the spectrum of corporate credit while seeking what we believe are the most attractive risk- adjusted return opportunities. |

| ∎ | | The Fund invests across the spectrum of corporate credit including high yield, investment grade, bank loans, convertibles and preferred equity. |

| ∎ | | The Fund seeks to identify issuers that offer compelling value through bottom-up security selection, with a focus on capital preservation. |

| ∎ | | The Fund’s investment approach allows for flexibility in security selection, irrespective of industry, ratings and maturity constraints. |

| ∎ | | The Fund manages long and short exposures to potentially generate absolute returns. A hedged approach allows the Fund to deploy tactical portfolio tilts via high yield index shorts. |

| ∎ | | Dynamic portfolio management may enhance downside mitigation while providing investors access to security selection expertise. |

1

PORTFOLIO RESULTS

Goldman Sachs Long Short Credit Strategies Fund

Investment Objective

The Fund seeks an absolute return comprised of income and capital appreciation.

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs Asset Management Credit Alternatives Portfolio Management Team discusses the Goldman Sachs Long Short Credit Strategies Fund’s (the “Fund”) performance and positioning for the six-month period ended September 30, 2017 (the “Reporting Period”).

| Q | | How did the Fund perform during the Reporting Period? |

| A | | During the Reporting Period, the Fund’s Class A, C, Institutional, Investor and R Shares generated cumulative total returns, without sales charges, of 1.65%, 1.27%, 1.82%, 1.78% and 1.52%, respectively. These returns compare to the 0.59% cumulative total return of the Fund’s benchmark, the Bank of America Merrill Lynch U.S. Dollar Three-Month LIBOR Constant Maturity Index (the “Index”), during the same time period. |

| | Because the composition of the Index (e.g. short-term securities) is not comparable to the range of instruments in which the Fund may transact (e.g., various credit-related instruments), references to the Index are for informational purposes only and not an indication of how the Fund is managed. |

| Q | | What economic and market factors most influenced the corporate credit markets as a whole during the Reporting Period? |

| A | | During the Reporting Period, moderate economic growth, low inflation and accommodative central bank policy at home and abroad provided a generally favorable backdrop for U.S. corporate credit and also led to notably muted volatility in both the equity and credit markets. |

| | U.S. credit markets, especially U.S. high yield bonds, rallied, as credit spreads, or yield differentials to U.S. Treasuries, tightened during the Reporting Period to near historic low levels. Supporting the markets was steady global economic growth, led by the developed markets. Despite the moderate rate of economic growth and unemployment levels not seen since early 2001, U.S. inflation remained historically low. The U.S. Federal Reserve (the “Fed”) maintained its accommodative approach to raising the targeted federal funds rate. Still, improved economic data led the Fed to raise interest rates by 25 basis points in June 2017 — only the second increase in 2017 to date and only the fourth increase since December 2015. (A basis point is 1/100th of a percentage point.) The Fed indicated it intends to maintain its accommodative monetary stance for the time being, as it expects its rate increases to be gradual. The Fed also unveiled a plan to gradually shrink its balance sheet beginning in October 2017. The Fed’s balance sheet had expanded dramatically in its quantitative easing strategy designed to help the economy recover from the 2007-2008 financial crisis. The European Central Bank similarly flagged a possible tapering of its asset purchases beginning in early 2018. |

| | Further supporting the U.S. credit markets during the Reporting Period were generally healthy credit fundamentals, including strong first quarter 2017 corporate earnings, reported in April 2017. Still, as of September 30, 2017, high yield mutual funds and exchange-traded funds (“ETFs”) experienced year-to-date outflows of more than $11 billion, with $5 billion of outflows seen during the Reporting Period. Despite healthy high yield credit fundamentals, investor uncertainty surrounding compressed high yield spreads — as well as broader macro concerns, including heightened geopolitical tensions, interest rate hikes and global economic growth — contributed to a widespread cautious view toward the high yield market and drove outflows. |

| | The one major interruption to the U.S. corporate credit rally during the Reporting Period was seen in August 2017. While volatility was quite low for the Reporting Period as a whole, we saw some volatility in August 2017 on the back of global political headlines concerning strained tensions with North Korea. The market experienced a quick sell-off early in the |

2

PORTFOLIO RESULTS

| | month, but the market rebounded almost completely by the end of the month. |

| Q | | What key factors were responsible for the Fund’s performance during the Reporting Period? |

| A | | As a part of our investment philosophy, we apply a value-oriented approach to credit market investing, with a focus on capital preservation via high conviction ideas. Consistent with the cornerstone of our fundamentally-based investment process focused on bottom-up security selection, the Fund’s performance during the Reporting Period was attributable to individual security selection. |

| | We maintained our focus on corporate fundamentals and earnings during the Reporting Period. The Fund’s positive performance during the Reporting Period was broad-based, attributable to long positioning in consumer cyclicals, energy and capital goods credits. The largest individual contributors during the Reporting Period included long positions in Jack Cooper Holdings, Transocean and Adient Global Holdings. |

| | Within the Fund’s long positioning, there were no sectors that materially detracted from performance. That said, the three largest individual detractors during the Reporting Period were the Fund’s positions in PetSmart, Uniti Group and Prairie Provident Resources. The Fund’s tactical short position in a high yield credit default swap index, a position taken in an effort to mitigate risk and serve as a portfolio market hedge, detracted from its results during the Reporting Period as spreads tightened. The Fund’s interest rate swaps, which are used to hedge duration, also detracted modestly from performance as spreads tightened. |

| | Importantly, since the Fund’s portfolio is constructed through bottom-up, fundamental research and not relative to a benchmark, there is no requirement to hold issues from any single company or sector. |

| Q | | Which segments of the corporate credit sector most significantly affected Fund performance? |

| A | | The corporate credit markets, as mentioned earlier, broadly rallied during the Reporting Period, driven largely, in our view, by technicals and generally healthy fundamentals. U.S. high yield corporate bonds were one of the strongest performers during the Reporting Period, as spreads narrowed to near historic low levels. Gains were broad-based across virtually all segments of the corporate credit sector. As such, our ability to identify select issuers within the corporate credit sector contributed positively to the Fund’s performance during the Reporting Period. |

| Q | | Did the Fund’s duration and yield curve positioning strategy help or hurt its results during the Reporting Period? |

| A | | The Fund does not use duration and yield curve positioning as active management strategies within its investment process. However, the Fund does implement interest rate swaps to hedge the interest rate risk of certain bonds, thereby limiting the Fund’s exposure to changes in interest rates. The Fund’s interest rate swap positions modestly detracted from its performance, as rates tightened during the Reporting Period. |

| Q | | How did the Fund use derivatives and similar instruments during the Reporting Period? |

| A | | The Fund used credit default swaps via a short position in a credit default swap high yield index to tactically hedge market risk, which detracted from performance. The Fund used interest rate swaps to hedge the interest rate risk of certain bonds, thereby limiting the Fund’s exposure to changes in interest rates. Interest rate swaps modestly detracted from Fund performance during the Reporting Period. The Fund used foreign currency exchange forward contracts to hedge the currency risk in non-U.S. dollar-denominated issues to U.S. dollars. This had a rather neutral impact on the Fund’s performance during the Reporting Period. |

| Q | | Were there any notable changes in the Fund’s weightings during the Reporting Period? |

| A | | During the Reporting Period, we continued to pursue investment opportunities based on fundamental, bottom-up research, which, in our view, offered compelling risk-adjusted return potential. |

| | We increased the Fund’s allocation to secured indebtedness, including high yield and bank loans, during the Reporting Period. We continued to identify opportunities in bank loans given the anticipated rising interest rate environment for the remainder of 2017 and into 2018. |

| | We also found what we considered to be compelling opportunities amongst short duration bonds, especially toward the very short-term end of the yield curve, or spectrum of maturities. We maintained our favor toward short-dated high yield credit securities, which, in our view, offer attractive risk-adjusted yields and some insulation from a potential increase in interest rates. We believe these securities are attractive for maintaining yield while limiting overall interest rate exposure, particularly given Fed interest |

3

PORTFOLIO RESULTS

| | rate hikes thus far and potential additional interest rate increases in the fourth quarter of 2017 and into 2018. |

| | We took a cautious view in the Fund given the rally in the corporate credit markets seen in the Fund’s prior fiscal year and during much of the Reporting Period. Our view was driven by the potential for volatility related to both geopolitical events and macroeconomic uncertainty, including further interest rate hikes, the reduction of the Fed’s balance sheet and the pace of global economic growth. We expressed this view by increasing the Fund’s exposure to a high yield credit default swap index. One of the key tenets of our investment philosophy is capital preservation, which leads us to take a more defensive, cautious position given certain market conditions. We also believe our hedged approach may provide for active downside management for investors seeking to mitigate market risk and volatility. |

| Q | | How was the Fund positioned at the end of the Reporting Period? |

| A | | At the end of the Reporting Period, the Fund was defensively positioned based on our cautious view of the market at the end of September 2017. The Fund remained focused on higher quality issuers in the capital structure and companies with what we considered to be strong cash flow. |

| | Reflecting our modestly defensive Fund positioning, as of September 30, 2017, approximately 46% of the Fund’s total net assets was invested in unsecured debt obligations, 15% in secured debt obligations, 24% in bank loans, 10% in investment grade corporate bonds, less than 1% in preferred and other equity securities and 14% in cash and cash equivalents. The Fund’s notional derivative exposure, calculated as a percentage of total net assets, was -53% in a credit default swap high yield index. (The Fund had a total of 143 holdings from 117 issuers at September 30, 2017, with the Fund’s top long corporate issuers, as measured by a percentage of total net assets invested, being Weatherford International, Frontier Communications and Rite Aid.) |

| Q | | What is the Fund’s tactical view and strategy for the months ahead? |

| A | | At the end of the Reporting Period, we believed the economic backdrop of moderate growth, low inflation and accommodative central bank policy was positive. However, while we believed we may see muted volatility for the remainder of 2017, we also felt we may still see bouts of volatility ahead given broad macro uncertainties, including geopolitics, interest rate increases, reductions in the Fed’s balance sheet and global economic growth. We further believed we may also see a slight uptick in defaults if interest rates rise with increased velocity, especially in 2018, though some of the default risk may be mitigated by economic growth and modestly improved, relatively stable oil prices. |

| | Given this view, we believe a sound approach, grounded in fundamentals with a focus on capital preservation, may offer a compelling means to navigate the current and anticipated market environment in the months ahead. We believe heightened volatility may lead to periods of technical dislocations in the market, which may provide for attractive single-name investing opportunities. While we continued to see value in the credit markets at the end of the Reporting Period, we believe that security selection and a focus on fundamentals will be increasingly important if interest rates continue to rise and should the Fed indeed begin to take a more hawkish, less accommodative approach. (Hawkish tends to suggest higher interest rates; opposite of dovish.) |

| | We intend to remain disciplined in our approach focused on credit selection. Our investment team has been identifying what we view as several investment opportunities in the new issue debt market, as we have seen what we consider to be attractive price entry points. Overall, we believe the Fund’s ability to be flexible across the corporate credit spectrum —high yield, loans, bank loans and investment grade credit —enables the Fund to step in and seek to take advantage of market opportunities when inefficiencies arise as well as to capitalize on changing market conditions. |

4

FUND BASICS

Long Short Credit Strategies Fund

as of September 30, 2017

| | | | | | | | | | | | | | | | | | |

| | PERFORMANCE REVIEW | |

| | | April 1, 2017–September 30, 2017 | | Fund Total

Return

(based on NAV)1 | | | Bank of America Merrill

Lynch U.S. Dollar Three-

Month LIBOR Constant

Maturity Index2 | | | 30-Day

Standardized

Subsidized

Yield3 | | | 30-Day

Standardized

Unsubsidized

Yield3 | |

| | Class A | | | 1.65 | % | | | 0.59 | % | | | 3.09 | % | | | 2.98 | % |

| | Class C | | | 1.27 | | | | 0.59 | | | | 2.46 | | | | 2.35 | |

| | Institutional | | | 1.82 | | | | 0.59 | | | | 3.56 | | | | 3.44 | |

| | Investor | | | 1.78 | | | | 0.59 | | | | 3.46 | | | | 3.35 | |

| | | Class R | | | 1.52 | | | | 0.59 | | | | 2.98 | | | | 2.83 | |

| | 1 | | The net asset value (“NAV”) represents the net assets of the Fund (ex-dividend) divided by the total number of shares outstanding. The Fund’s performance assumes the reinvestment of dividends and other distributions. The Fund’s performance does not reflect the deduction of any applicable sales charges. |

| | 2 | | The Bank of America Merrill Lynch U.S. Dollar Three-Month LIBOR Constant Maturity Index (the “Index”) tracks the performance of a synthetic asset paying LIBOR to a stated maturity. The Index is based on the assumed purchase at par of a synthetic instrument having exactly its stated maturity and with a coupon equal to that day’s fixing rate. That issue is assumed to be sold the following business day (priced at a yield equal to the current day fixing rate) and rolled into a new instrument. |

| | 3 | | The method of calculation of the 30-Day Standardized Subsidized Yield is mandated by the Securities and Exchange Commission and is determined by dividing the net investment income per share earned during the last 30 days of the period by the maximum public offering price (“POP”) per share on the last day of the period. This number is then annualized. The 30-Day Standardized Subsidized Yield reflects fee waivers and/or expense reimbursements recorded by the Fund during the period. Without waivers and/or reimbursements, yields would be reduced. This yield does not necessarily reflect income actually earned and distributed by the Fund and, therefore, may not be correlated with the dividends or other distributions paid to shareholders. The 30-Day Standardized Unsubsidized Yield does not adjust for any fee waivers and/ or expense reimbursements in effect. If the Fund does not incur any fee waivers and/or expense reimbursements during the period, the 30-Day Standardized Subsidized Yield and 30-Day Standardized Unsubsidized Yield will be identical. |

The returns set forth in the table above represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown, except with respect to the 30-day Standardized Unsubsidized Yield. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

5

FUND BASICS

| | | | | | | | | | | | | | | | | | |

| | STANDARDIZED TOTAL RETURNS4 | |

| | | For the period ended 9/30/17 | | One Year | | | Five Years | | | Since Inception | | | Inception Date | |

| | Class A | | | -1.94 | % | | | N/A | | | | -0.64 | % | | | 4/30/14 | |

| | Class C | | | 0.16 | | | | N/A | | | | -0.27 | | | | 4/30/14 | |

| | Institutional5 | | | 2.27 | | | | 2.35 | % | | | 5.26 | | | | 6/15/09 | |

| | Investor | | | 2.18 | | | | N/A | | | | 0.73 | | | | 4/30/14 | |

| | | Class R | | | 1.67 | | | | N/A | | | | 0.24 | | | | 4/30/14 | |

| | 4 | | The Standardized Total Returns are average annual total returns or cumulative total returns (only if the performance period is one year or less) as of the most recent calendar quarter-end. They assume reinvestment of all distributions at NAV. These returns reflect the maximum initial sales charge of 3.75% for Class A Shares and the assumed contingent deferred sales charge for Class C Shares (1.00% if redeemed within 12 months of purchase). Because Institutional, Investor and Class R Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. |

| | 5 | | The average annual total return figures for the Fund’s Institutional Shares, which do not impose an initial sales charge, do not reflect an initial sales charge for the periods shown. Prior to March 24, 2014 (the effective date of the reorganization of the Goldman Sachs Credit Strategies Fund (the “Predecessor Fund”) into the Fund), the maximum initial sales charge applicable to sales of Common Shares of the Predecessor Fund was 2.50%, which is not reflected in the average annual total return figures shown. The Predecessor Fund commenced operations on June 15, 2009. |

The returns set forth in the tables above represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns. Performance reflects applicable fee waivers and/or expense limitations in effect during the period shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Effective at the close of business on March 21, 2014, the Goldman Sachs Credit Strategies Fund (the “Predecessor Fund”), a closed-end management investment company that was operated as an “interval fund,” was reorganized with and into the Fund, with shareholders of the Predecessor Fund receiving Institutional Shares of the Fund upon consummation of the reorganization. Because the Predecessor Fund was the accounting survivor, the Fund has assumed the Predecessor Fund’s historical performance. The performance information for the Fund’s Institutional Shares shown in this report is for the Predecessor Fund for the period prior to March 24, 2014, and reflects the Predecessor Fund’s investment strategies and policies. However, the Fund’s current investment strategies and policies, including the ability to implement short positions, are different from those of the Predecessor Fund. As a result, the Fund’s performance may differ substantially from what is shown for periods prior to March 24, 2014.

6

FUND BASICS

| | | | | | | | | | |

| | EXPENSE RATIOS6 | |

| | | | | Net Expense Ratio (Current) | | | Gross Expense Ratio (Before Waivers) | |

| | Class A | | | 1.47 | % | | | 1.61 | % |

| | Class C | | | 2.22 | | | | 2.36 | |

| | Institutional Shares | | | 1.13 | | | | 1.27 | |

| | Investor | | | 1.22 | | | | 1.36 | |

| | | Class R | | | 1.72 | | | | 1.86 | |

| | 6 | | The expense ratios of the Fund, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations) are as set forth above according to the most recent publicly available Prospectus for the Fund and may differ from the expense ratios disclosed in the Financial Highlights in this report. Pursuant to a contractual arrangement, the Fund’s waivers and/or expense limitations will remain in place through at least July 28, 2018, and prior to such date the Investment Adviser may not terminate the arrangements without the approval of the Fund’s Board of Trustees. If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. |

| | |

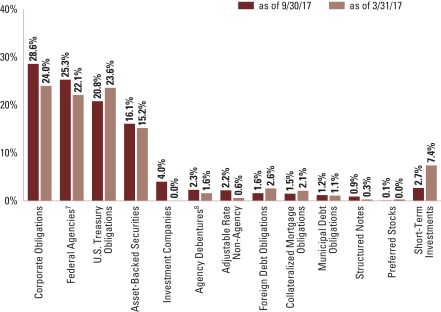

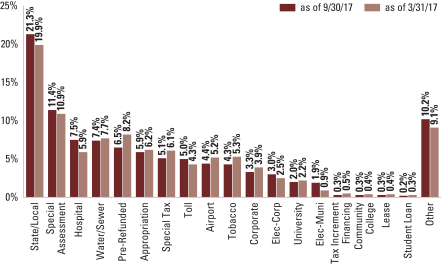

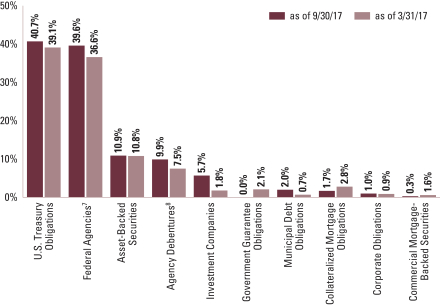

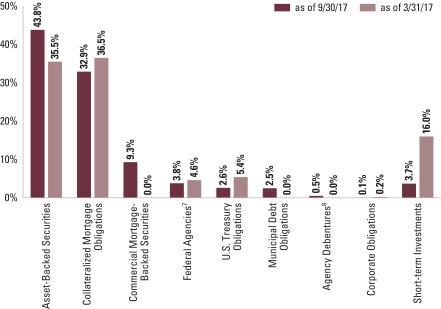

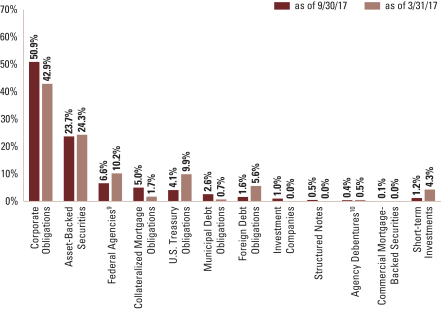

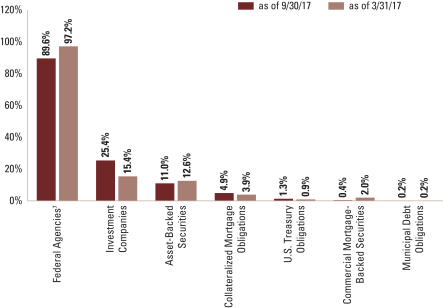

| | SECTOR ALLOCATIONS7 |

| | | Percentage of Net Assets |

| | 7 | | The percentage shown for each investment category reflects the value of investments in that category as a percentage of net assets. Figures in the graph may not sum to 100% due to the exclusion of other assets and liabilities. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

7

FUND BASICS

| | | | | | |

| | TOP TEN INDUSTRY ALLOCATIONS8 | | | | |

| | | As of September 30, 2017 | | Percentage of Net Assets | |

| | Automotive | | | 8.8 | |

| | Health Care – Services | | | 5.1 | |

| | Pipelines | | | 4.7 | |

| | Oil & Gas Services | | | 4.6 | |

| | Oil & Gas | | | 4.4 | |

| | Media – Cable | | | 3.9 | |

| | Telecommunications – Wirelines | | | 3.6 | |

| | Media | | | 3.6 | |

| | Telecommunication Services | | | 3.5 | |

| | | Diversified Financial Services | | | 3.4 | |

| | 8 | | The percentage shown for each investment category reflects the value of investments in that category as a percentage of net assets. The above table depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

8

GOLDMAN SACHS FIXED INCOME ALTERNATIVES FUNDS

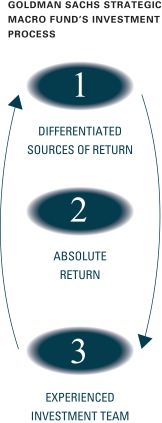

What Differentiates Goldman Sachs Strategic Macro Fund’s Investment Process?

The Goldman Sachs Strategic Macro Fund (the “Fund”) seeks to generate long-term absolute return. Changes in global fixed income and currency markets have created opportunities for generating attractive returns through fixed income alternative and unconstrained investment strategies.

Our investment process seeks to create excess returns by:

| ∎ | | Adopting a global perspective to compare and contrast investment opportunities around the world |

| ∎ | | Employing eight specialist strategy teams that each conduct very detailed fundamental and quantitative research in their search for attractive investments |

| ∎ | | Capturing the value in the inherent diversification benefits among the different investment strategies |

| ∎ | | Using a disciplined risk-management approach to implement the strategy |

We believe the following characteristics drive the implementation and execution of the Fund’s investment process:

| ∎ | | The Fund invests in a portfolio of fixed income, currency, and commodities in an attempt to generate returns different from traditional asset classes. |

| ∎ | | Alternative investments do not necessarily move in tandem with traditional asset classes, such as stocks, bonds and credit. By adding them to the portfolio the Fund seeks to enhance its overall risk/return profile. |

| ∎ | | The Fund seeks to generate returns in up and down markets when asset classes are in or out of favor. |

| ∎ | | The Fund employs alternative investment techniques — such as hedging, leverage and shorting that may provide an opportunity for the Fund to achieve its goal of absolute returns. |

| ∎ | | We have over 300 investment professionals covering multiple sectors of the global fixed income market who are focused on finding investment ideas for our portfolio. |

| ∎ | | The senior professionals on the team have an average of over 20 years of investment experience through multiple market cycles. |

9

PORTFOLIO RESULTS

Goldman Sachs Strategic Macro Fund

Investment Objective

The Fund seeks to generate long-term absolute return.

Portfolio Management Discussion and Analysis

Effective June 20, 2017, the Goldman Sachs Fixed Income Macro Strategies Fund was renamed the Goldman Sachs Strategic Macro Fund (the “Fund”). There was no change to the Fund’s investment philosophy or strategy in connection with this name change. Below, the Goldman Sachs Fixed Income Investment Management Team discusses the Fund’s performance and positioning for the six-month period ended September 30, 2017 (the “Reporting Period”).

| Q | | How did the Fund perform during the Reporting Period? |

| A | | During the Reporting Period, the Fund’s Class A, C, Institutional, Investor and R Shares generated cumulative total returns, without sales charges, of -1.58%, -1.91%, -1.35%, -1.35% and -1.58%, respectively. These returns compare to the 0.59% cumulative total return of the Fund’s benchmark, the Bank of America Merrill Lynch U.S. Dollar Three-Month LIBOR Constant Maturity Index (“the Index”) during the same time period. |

| | Because the composition of the Index (e.g., short-term securities) is not comparable to the range of instruments in which the Fund may transact (e.g., various fixed income, currency and commodities instruments), references to the Index are for informational purposes only and are not an indication of how the Fund is managed. |

| Q | | What economic and market factors most influenced the fixed income market as a whole during the Reporting Period? |

| A | | The performance of the fixed income markets as a whole was primarily driven by geopolitical events, improving economic growth around the world and changing market expectations about central monetary policy. |

| | When the Reporting Period began with the second quarter of 2017, spread, or non-government bond sectors, generally recorded positive returns, though with mixed results relative to U.S. Treasury securities. Political developments led to temporary bouts of volatility early in the quarter, driving weakness in Brazilian, U.S. and U.K. fixed income assets as well as a credit rating downgrade of South Africa’s sovereign debt. Political risks receded in May 2017 on the centrist candidate’s victory in the French presidential election, which was supportive of French and European peripheral bonds broadly. On the economic front, U.S. core inflation weakened for the third consecutive month in May 2017, casting uncertainty over the pace of Federal Reserve (“Fed”) monetary tightening. Nonetheless, comments included in minutes from the Fed’s May and June 2017 policy meetings suggested an announcement about how and when the Fed would begin reducing the size of its balance sheet would be made sooner than the markets had previously anticipated. In Europe, economic data continued to surprise to the upside. At its June 2017 policy meeting, the European Central Bank (“ECB”) provided an optimistic assessment of the risks to growth, but revised downward its medium-term inflation forecasts. The ECB, Bank of Japan (“BoJ”) and Bank of England (“BoE”) left their respective monetary policies unchanged during the second calendar quarter, while the Fed raised interest rates for the second time in 2017 and the fourth time in a decade at its June 2017 policy meeting. As the quarter came to an end, a string of comments from global central bankers triggered a hawkish market reaction. (Hawkish suggests higher interest rates; opposite of dovish.) Global interest rates rose as the market anticipated a faster than expected pace of monetary policy tightening by the BoE, ECB and Bank of Canada (“BoC”). During the second quarter of 2017, the U.S. dollar weakened versus many global currencies. |

| | During the third quarter of 2017, spread sectors broadly advanced, outperforming U.S. Treasury securities. The Fed kept its monetary policy unchanged but unveiled its plans for balance sheet normalization. (Balance sheet normalization refers to the steps the Fed will take to reverse quantitative easing and remove the substantial monetary accommodation it has provided to the economy since the financial crisis began |

10

PORTFOLIO RESULTS

| | in 2007.) This prompted a hawkish market reaction, with the U.S. dollar appreciating and yields on U.S. government bonds rising. However, the U.S. Treasury yield curve, or spectrum of maturities, only steepened modestly due to geopolitical uncertainty and mixed U.S. economic data, including weak inflation readings. (A steepening yield curve is one wherein the differential in yields between longer-term and shorter-term maturities widens.) The central banks of other developed countries also set the stage for less accommodative monetary policy. The BoE noted “a majority” of its policymakers were in favor of tightening policy “over the coming months,” while the BoC surprised the markets with two consecutive rate hikes. The market’s expectations for a BoE rate hike in November 2017, along with a constructive tone for Brexit negotiations, also drove the British pound higher versus the U.S. dollar. (Brexit refers to the U.K.’s efforts to exit the European Union.) Overall, the U.S. dollar continued to weaken relative to many global currencies during the third calendar quarter. |

| | For the Reporting Period as a whole, spread sectors outperformed U.S. Treasury securities, led by high yield corporate bonds, sovereign emerging markets debt and investment grade corporate bonds. Commercial mortgage-backed securities, agency securities, asset-backed securities and mortgage-backed securities also outperformed U.S. Treasuries, albeit to a lesser extent. The U.S. Treasury yield curve flattened slightly during the Reporting Period, as yields on shorter-term maturities generally rose and yields on intermediate- and longer-term maturities fell. The yield on the bellwether 10-year U.S. Treasury declined approximately seven basis points to end the Reporting Period at 2.33%. (A flattening yield curve is one wherein the differential in yields between longer-term and shorter-term maturities narrows.) |

| Q | | What key factors were responsible for the Fund’s performance during the Reporting Period? |

| A | | The Fund seeks long-term absolute return through the implementation of relative value, long/short, macro and other strategies that aim to exploit disparities or inefficiencies in the global fixed income, currency and commodities markets. Absolute return is the return of an investment and is not relative to a benchmark. We believe absolute return performance may be uncorrelated to fixed income and equity markets over the long-term. Relative value strategy means to simultaneously take long and short positions within an investment portfolio. A long/short strategy seeks to produce returns with risk and volatility that are uncorrelated with general global market risk and volatility by simultaneously taking long and short exposures in approximately equal amounts. A macro hedge may be employed as we seek to mitigate the risk of market movements (either up or down), potentially enabling the Fund to pursue returns in a variety of market cycles. In addition, the Fund may use derivatives instead of buying and selling bonds to manage duration, to gain exposure to or to short individual securities, or to gain exposure to an index. Duration is a measure of the Fund’s sensitivity to changes in interest rates. |

| | Investment ideas for the Fund are generated through our specialized top-down and bottom-up strategy teams, in the following areas: Tactical Duration; Country Relative Value; Fundamental Currency; Commodities; Government and Swaps; Liquid Mortgages; Emerging Markets Debt; and Cross Macro. Near the end of 2016, Cross Macro was added as a specific strategy within the Fund. The Cross Macro strategy focuses on relative value investment opportunities across interest rate, currency, commodity and credit markets in combination. It seeks to take advantage of increased market linkages, where one factor can potentially influence many different markets (e.g., crude oil prices). Derivatives are used in combination with cash securities to implement our views in the Fund. |

| | During the Reporting Period, the Fund underperformed the Index due primarily to its Tactical Duration, Country Relative Value and Commodities strategies. Within the Tactical Duration strategy, the Fund was positioned for tightening Fed monetary policy. More specifically, it held a short duration position on the U.S. Treasury yield curve throughout the Reporting Period, which detracted from performance. Short-term U.S. Treasury yields rose in response to Fed rate hikes, but intermediate- and longer-term yields fell on political uncertainty, increased geopolitical risks and a decline in positive economic data surprise. In addition, soft inflation data during the first nine months of 2017 weighed on market expectations for further Fed rate hikes. We maintained the Fund’s short duration position because we believed global economic growth would remain strong and that tightness in the labor market and easy financial conditions in the U.S. would warrant further monetary tightening by the Fed. We also expected U.S. inflation to rebound should wage growth begin to emerge. The Tactical Duration strategy is implemented via interest rate futures. Within the Country Relative Value strategy, performance was hampered by the Fund’s positioning for easier Canadian and European financial conditions relative to those in the U.S., expressed through a long position in Canadian interest rates versus a short position in U.S. interest rates. In response to stronger economic indicators, the BoC |

11

PORTFOLIO RESULTS

| | was surprisingly hawkish, raising rates twice during the summer of 2017. Europe also showed signs of stronger economic growth, and European interest rates rose as markets anticipated the ECB might start tapering its quantitative easing and otherwise reduce its accommodative monetary policy. The Country Relative Value strategy is actively implemented via interest rate swaps and/or futures. Within the Commodities strategy, the Fund’s long positions in crude oil and natural gas detracted from performance. The crude oil markets were pressured by growing inventories, which were particularly elevated in the U.S. Natural gas prices fell on cooler than expected summer weather, which depressed demand, along with higher production. The Commodities strategy uses a blend of commodity futures and options. |

| | The Government/Swaps, Fundamental Currency and Emerging Markets Debt strategies contributed positively to the Fund’s results. Within the Government/Swaps strategy, the Fund benefited from its steepening positions on the U.S. Treasury and European government bond yield curves. Curve steepening positions were implemented through interest rate swaps. In addition, the Fund’s short position in U.K. inflation-linked bonds added to returns. The Government and Swaps strategy is actively implemented via interest rate swaps and/ or futures. Within the Fundamental Currency strategy, the Fund was helped by its long positions in emerging markets currencies, including the Polish zloty, Czech koruna and Mexican peso. The Fund also gained from its long positions in the Swedish krona and Norwegian krone. These results were offset somewhat by the Fund’s short position in the euro, which detracted. The Fundamental Currency strategy employs a mix of non-deliverable currency forwards, forward foreign currency exchange contracts and/or currency options. Within the Emerging Markets Debt strategy, the Fund benefited from its long positions in Mexican, Hungarian and Russian local debt as well as from a short position in Czech local debt. These gains were slightly offset by the Fund’s short position in Hong Kong local debt, which detracted. The Emerging Markets Debt strategy is implemented using cross currency swaps. |

| | The Fund’s Liquid Mortgages and Cross Macro strategies did not have a meaningful impact on performance during the Reporting Period. |

| Q | | How did the Fund use derivatives and similar instruments during the Reporting Period? |

| A | | During the Reporting Period, the Fund invested in interest rate futures, interest rate swaps, total return swaps, swaptions, options on futures, credit default swaps, equity index futures and options, non-deliverable forwards, forward foreign currency exchange contracts, currency options and cross currency swaps. The Fund used interest rate futures to hedge interest rate exposure, i.e., to manage exposure to fluctuations in interest rates, and to facilitate specific duration and yield curve strategies. Interest rate swaps were used to express our views on the direction of interest rates. Total return swaps were employed to manage the Fund’s yield curve exposures across various strategies. Swaptions (or options on interest rate swap contracts) were used to hedge interest rate exposure and manage the Fund’s exposure to potential market volatility. Options on futures were used within the Government and Swaps strategy to allow the Fund the right to enter into futures contracts. Credit default swaps were employed to implement specific credit-related investment strategies. Equity index futures and options were used as a means of reducing Fund volatility. Within the Fundamental Currency strategy, the Fund used non-deliverable currency forwards to gain exposure to a particular country and also to take advantage of relative value opportunities. The Fund also utilized forward foreign currency exchange contracts and currency options within the Fundamental Currency strategy to take long or short positions. Within the Emerging Markets Debt strategy, the Fund employed cross currency swaps to express relative views on given currencies as well as our views on the direction of a country’s interest rates. Derivatives and similar instruments allow us to manage interest rate, credit and currency risks more effectively by allowing us both to apply active investment views with greater versatility and to afford greater risk management precision than we would otherwise be able to implement. Within the Liquid Mortgages strategy, the Fund used mortgage-backed securities forward agreements (known as “TBAs”) in addition to interest only and principal only strips. (Strips are a type of security for which the holder is only entitled to receive regular cash flows derived from incoming interest payments or principal repayments on an underlying loan pool.) During the Reporting Period, the use of derivatives and similar instruments had a negative impact on the Fund’s performance. |

| Q | | Were there any notable changes in the Fund’s weightings during the Reporting Period? |

| A | | Within the Tactical Duration strategy, we moved the Fund to a modestly short duration position on the Japanese government yield curve. Throughout the Reporting Period, the Fund held a short duration on the U.S. Treasury yield |

12

PORTFOLIO RESULTS

| | curve and a neutral duration position on the European government bond yield curve. Within the Country Relative Value strategy, we reduced the Fund’s long position in European interest rates and its short position in U.S. interest rates, as European government bonds outperformed U.S. government bonds during September 2017. Within the Fundamental Currency strategy, we continued to add exposure to a number of emerging markets currencies, such as the Swedish krona, South African rand and Brazilian real, versus the U.S. dollar during the Reporting Period. Within the Commodities strategy, we added a modestly short position in crude oil. The Fund continued to hold a short position in natural gas versus crude oil. Within the Cross Macro strategy, we sought to benefit from tighter financial conditions in the U.S. relative to Asia, Canada and Europe by implementing long positions in Asian interest rates versus short positions in U.S. interest rates. |

| Q | | How was the Fund positioned at the end of the Reporting Period? |

| A | | At the end of the Reporting Period, within the Tactical Duration strategy, the Fund held a short duration position on the U.S. Treasury yield curve, a modestly short duration on the Japanese government bond curve and a neutral duration position on the European government bond yield curve. Within the Country Relative Value strategy, the Fund had long positions in European and Canadian interest rates versus short positions in U.S. and U.K. interest rates. The Fund maintained a short position in U.K. inflation-linked securities. In addition, at the end of Reporting Period, the Fund had a long position in Mexican interest rates and a short position in Czech Republic interest rates. Within the Fundamental Currency strategy, the Fund had short positions in select developed markets currencies, such as the euro and Australian dollar. Within the Commodities strategy, the Fund held a modestly short position in crude oil as well as a short position in natural gas versus crude oil. Within the Emerging Markets Debt strategy, the Fund held long positions in a number of Latin American countries that import oil and rely on American tourism. It also had a short position in Chinese local emerging markets debt. Within the macro hedge, the Fund was positioned for tighter financial conditions in the U.S. relative to Asia, Canada and Europe at the end of the Reporting Period. |

| Q | | What is the Fund’s tactical view and strategy for the months ahead? |

| A | | At the end of the Reporting Period, we expected one more Fed rate hike during 2017, and we believed the market was underpricing the pace of future interest rate hikes. As for Europe, we thought that by the end of 2017, the ECB may communicate its plans to reduce asset purchases through its quantitative easing program with tapered purchases likely to continue, we believe, through 2018. In the U.K., we saw scope for a BoE rate hike in November 2017 given policymakers’ communications. Meanwhile, the BoC has commenced a rate hiking cycle, though we expect the trajectory for its future rate hikes to be shallower than in the U.S. In Japan, the BoJ’s monetary policy is likely to remain unchanged in the near term, in our view. However, we note that based on market prices at the end of the Reporting Period, investors appear to believe BoJ monetary policy might fluctuate around the country’s general election and the end of BoJ Governor Haruhiko Kuroda’s term, which is scheduled to occur in April 2018. |

| | In terms of the Fund’s positioning at the end of the Reporting Period, we were continuing to add exposure to emerging markets currencies versus the U.S. dollar because of what we considered a supportive global economic growth environment and improvements in commodity prices. In our opinion, emerging markets assets overall are more resilient now than they were during the 2013 taper tantrum, as evidenced by improved fundamentals, such as healthier account balances in many countries. (Taper tantrum refers to the way markets reacted negatively in 2013 when the Fed suggested it might begin tapering its quantitative easing program.) That said, at the end of the Reporting Period, we were cautious about valuations in emerging markets asset classes, though we acknowledged support from ongoing strength in global and Chinese economic growth, the gradual pace of monetary tightening in developed markets, and higher commodity prices that have buttressed the terms of trade for emerging markets countries. (Terms of trade is a ratio representing the prices of a country’s exports relative to the prices of its imports.) In addition, while China’s economic growth has decelerated in recent years, the pace of the slowing appeared to have moderated during the Reporting Period. We plan to be watchful for any sharp downturn in China’s business cycle, which could be a headwind for the emerging markets. |

13

FUND BASICS

Strategic Macro Fund

as of September 30, 2017

| | | | | | | | | | |

| | PERFORMANCE REVIEW | |

| | | April 1, 2017–September 30, 2017 | | Fund Total Return

(based on NAV)1 | | | Bank of America Merrill Lynch

U.S. Dollar Three-Month LIBOR

Constant Maturity Index2 | |

| | Class A | | | -1.58 | % | | | 0.59 | % |

| | Class C | | | -1.91 | | | | 0.59 | |

| | Institutional | | | -1.35 | | | | 0.59 | |

| | Investor | | | -1.35 | | | | 0.59 | |

| | | Class R | | | -1.58 | | | | 0.59 | |

| | 1 | | The net asset value (“NAV”) represents the net assets of the class of the Fund (ex-dividend) divided by the total number of shares of the class outstanding. The Fund’s performance reflects the reinvestment of dividends and other distributions. The Fund’s performance does not reflect the deduction of any applicable sales charges. |

| | 2 | | The Bank of America Merrill Lynch U.S. Dollar Three-Month LIBOR Constant Maturity Index (the “Index”) tracks the performance of a synthetic asset paying LIBOR to a stated maturity. The Index is based on the assumed purchase at par of a synthetic instrument having exactly its stated maturity and with a coupon equal to that day’s fixing rate. That issue is assumed to be sold the following business day (priced at yield equal to the current day Fixing rate) and rolled into a new instrument. |

| | | | | | | | | | | | |

| | STANDARDIZED TOTAL RETURNS3 |

| | | For the period ended 9/30/17 | | One Year | | | Since Inception | | | Inception Date |

| | Class A | | | -3.41 | % | | | -2.63 | % | | 12/16/13 |

| | Class C | | | -1.45 | | | | -2.13 | | | 12/16/13 |

| | Institutional | | | 0.70 | | | | -1.34 | | | 12/16/13 |

| | Investor | | | 0.70 | | | | -1.46 | | | 12/16/13 |

| | | Class R | | | 0.11 | | | | -1.80 | | | 12/16/13 |

| | 3 | | The Standardized Total Returns are average annual total returns or cumulative total returns (only if the performance period is one year or less) as of the most recent calendar quarter-end. They assume reinvestment of all distributions at NAV or cumulative total returns (only if the performance period is one year or less). These returns reflect a maximum initial sales charge of 3.75% for Class A Shares and the assumed contingent deferred sales charge for Class C Shares (1.00% if redeemed within 12 months of purchase). Because Institutional, Investor and Class R Shares do not involve a sales charge, such a charge is not applied to their Standardized Total Returns. |

The returns set forth in the tables above represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted above. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown. In their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

14

FUND BASICS

| | | | | | | | | | |

| | EXPENSE RATIOS4 | |

| | | | | Net Expense Ratio (Current) | | | Gross Expense Ratio (Before Waivers) | |

| | Class A | | | 1.34 | % | | | 2.69 | % |

| | Class C | | | 2.09 | | | | 3.44 | |

| | Institutional | | | 1.06 | | | | 2.35 | |

| | Investor | | | 1.09 | | | | 2.44 | |

| | | Class R | | | 1.59 | | | | 2.94 | |

| | 4 | | The expense ratios of the Fund, both current (net of applicable fee waivers and/or expense limitations) and before waivers (gross of applicable fee waivers and/or expense limitations) are as set forth above according to the most recent publicly available Prospectus for the Fund and may differ from the expense ratios disclosed in the Financial Highlights in this report. Pursuant to a contractual arrangement, the Fund’s waivers and/or expense limitations will remain in place through at least July 28, 2018, and prior to such date the Investment Adviser may not terminate the arrangements without the approval of the Fund’s Board of Trustees. However, the management fee waiver arrangement with respect to the fee paid by Cayman Commodity-FIMS, Ltd., a wholly-owned subsidiary through which the Fund gains exposure to the commodities markets (the “Subsidiary”), may not be discontinued by the Investment Adviser as long as the contract with the Subsidiary remains in place. If these arrangements are discontinued in the future, the expense ratios may change without shareholder approval. |

15

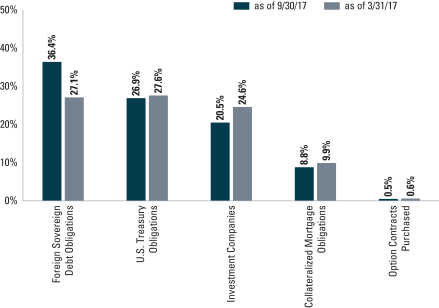

FUND BASICS

Strategic Macro Fund

as of September 30, 2017

|

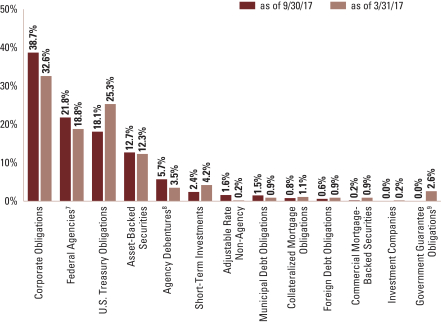

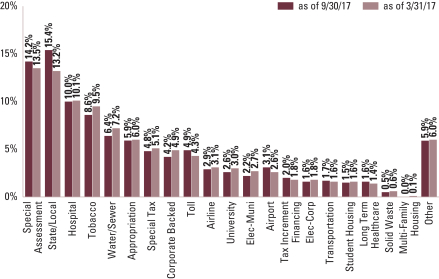

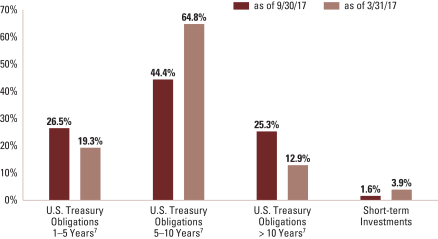

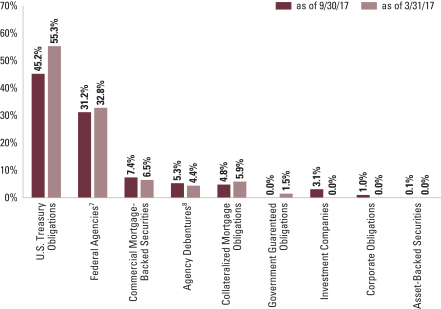

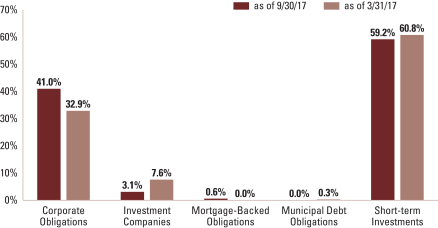

| FUND COMPOSITION5 (%) |

| Percentage of Net Assets |

| | 5 | | The percentage shown for each investment category reflects the value of investments in that category as a percentage of net assets. Figures in the graph may not sum to 100% due to the exclusion of other assets and liabilities. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. |

16

GOLDMAN SACHS LONG SHORT CREDIT STRATEGIES FUND

Schedule of Investments

September 30, 2017 (Unaudited)

| | | | | | | | | | | | | | |

Principal

Amount | | | Interest

Rate | | | Maturity

Date | | | Value | |

| Secured Debt Obligations – 38.9% | |

| Bank Loans(a) – 23.5% | |

| Automotive – 1.1% | |

| American Axle & Manufacturing, Inc. (BB/Ba2) (1M LIBOR +

2.250%)(b) |

|

| $ | 2,357,804 | | | | 3.490 | % | | | 04/06/24 | | | $ | 2,350,448 | |

| | |

| Building Materials – 0.7% | |

| | Builders FirstSource, Inc. (B+/B3) (3M LIBOR + 3.000%)(b) | |

| | 1,360,825 | | | | 4.333 | | | | 02/29/24 | | | | 1,364,009 | |

| | |

| Chemicals – 0.9% | |

| | Kraton Polymers LLC (BB-/Ba3) (1M LIBOR + 3.000%)(b) | |

| | 206,573 | | | | 4.235 | | | | 01/06/22 | | | | 209,039 | |

| New Arclin U.S. Holding Corp. (B+/B2) (3M LIBOR +

4.250%)(b) |

|

| | 691,268 | | | | 5.583 | | | | 02/14/24 | | | | 696,024 | |

| | OXEA Finance & Cy S.C.A. (NR/NR) | |

| | 489,000 | | | | 3.500 | | | | 09/27/24 | | | | 487,778 | |

| | Tronox Blocked Borrower LLC (NR/NR) | |

| | 153,581 | | | | 3.000 | | | | 09/22/24 | | | | 154,125 | |

| | Tronox Finance LLC (BB-/Ba3) | |

| | 354,419 | | | | 3.000 | | | | 09/22/24 | | | | 355,673 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 1,902,639 | |

| | |

| Commercial Services – 0.6% | |

| | Garda World Security Corp. (B/B1) (PRIME + 3.000%)(b) | |

| | 316,061 | | | | 5.316 | | | | 05/24/24 | | | | 318,826 | |

| | Monitronics International, Inc. (B-/B2) (3M LIBOR + 5.500%)(b) | |

| | 907,152 | | | | 6.833 | | | | 09/30/22 | | | | 899,215 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 1,218,041 | |

| | |

| Communications – Cable & Satellite – 0.2% | |

| Radiate Holdco LLC/Radiate Finance, Inc. (B/B1) (1M LIBOR +

3.000%)(b) |

|

| | 456,852 | | | | 4.235 | | | | 02/01/24 | | | | 450,333 | |

| | |

| Communications – Entertainment – 0.5% | |

| Univision Communications, Inc. (BB-/B2) (1M LIBOR +

2.750%)(b) |

|

| | 1,054,150 | | | | 3.985 | | | | 03/15/24 | | | | 1,044,273 | |

| | |

| Consumer Cyclical Services – 0.9% | |

| | TKC Holdings, Inc. (B/B2) (2M LIBOR + 4.250%)(b) | |

| | 1,936,915 | | | | 5.522 | | | | 02/01/23 | | | | 1,953,050 | |

| | |

| Consumer Durables – 0.3% | |

| | Comfort Holding LLC (CCC+/B2) (1M LIBOR + 4.750%)(b) | |

| | 635,738 | | | | 5.981 | | | | 02/05/24 | | | | 568,191 | |

| | |

| Diversified Financial Services – 0.5% | |

| | Tecomet, Inc. (NR/NR) (3M LIBOR + 3.750%)(b) | |

| | 510,720 | | | | 5.061 | | | | 05/02/24 | | | | 513,595 | |

| | VFH Parent LLC (NR/NR) (3M LIBOR + 3.750%)(b) | |

| | 460,132 | | | | 5.061 | | | | 12/30/21 | | | | 464,734 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 978,329 | |

| | |

| Diversified Telecommunication – 0.9% | |

| | Telesat Canada (BB-/Ba3) (1M LIBOR + 3.000%)(b) | |

| | 1,865,602 | | | | 4.240 | | | | 11/17/23 | | | | 1,878,437 | |

| | |

| Electric – 1.4% | |

| | Talen Energy Supply LLC (NR/NR) (1M LIBOR + 4.000%)(b) | |

| | 2,982,000 | | | | 5.235 | | | | 04/15/24 | | | | 2,903,723 | |

| | |

| Secured Debt Obligations – (continued) | |

| Food & Beverage – 0.8% | |

| | Dole Food Co., Inc. (NR/NR) (PRIME + 1.750%)(b) | |

| 1,723,458 | | | | 4.018 | | | | 04/06/24 | | | | 1,727,491 | |

| | |

| Food & Drug Retailers – 0.7% | |

| | BJ’s Wholesale Club, Inc. (B-/B3) (1M LIBOR + 3.750%)(b) | |

| | 1,424,043 | | | | 4.982 | | | | 02/03/24 | | | | 1,363,008 | |

| | |

| Health Care – Services – 2.2% | |

| | ATI Holdings Acquisition, Inc. (B/B1) (1M LIBOR + 3.500%)(c) | |

| | 318,963 | | | | 4.801 | | | | 05/10/23 | | | | 322,152 | |

| Change Healthcare Holdings, Inc. (B+/Ba3) (1M LIBOR +

2.750%)(b) |

|

| | 924,355 | | | | 3.985 | | | | 03/01/24 | | | | 926,435 | |

| | Envision Healthcare Corp. (BB-/Ba3) (3M LIBOR + 3.000%)(b) | |

| | 1,236,305 | | | | 4.240 | | | | 12/01/23 | | | | 1,238,629 | |

| | Greenway Health LLC (B-/B3) (3M LIBOR + 4.250%)(b) | |

| | 1,028,297 | | | | 5.580 | | | | 02/14/24 | | | | 1,030,868 | |

| | Kindred Healthcare, Inc. (BB-/Ba3) (3M LIBOR + 3.500%)(b) | |

| | 688,886 | | | | 4.813 | | | | 04/09/21 | | | | 689,175 | |

| | Team Health Holdings, Inc. (NR/NR) (1M LIBOR + 2.750%)(b) | |

| | 414,627 | | | | 3.985 | | | | 02/06/24 | | | | 406,596 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 4,613,855 | |

| | |

| Household Products(b) – 0.2% | |

| | AI Aqua Merger Sub, Inc. (NR/NR) (1M LIBOR + 3.500%) | |

| | 409,000 | | | | 4.735 | | | | 12/13/23 | | | | 410,023 | |

| | |

| Life Insurance – 0.2% | |

| | Acrisure LLC (NR/NR) (2M LIBOR + 5.000%)(b) | |

| | 385,065 | | | | 6.272 | | | | 11/22/23 | | | | 389,235 | |

| | |

| Media – Cable – 0.7% | |

| | Atlantic Broadband Finance LLC (NR/NR) | |

| | 1,005,000 | | | | 2.750 | | | | 08/11/24 | | | | 998,246 | |

| | Cable One, Inc. (NR/NR) (3M LIBOR + 2.250%)(b)(c) | |

| | 368,078 | | | | 3.570 | | | | 05/01/24 | | | | 369,918 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 1,368,164 | |

| | |

| Media – Non Cable – 0.6% | |

| | CBS Radio, Inc. (BB-/Ba3) (1M LIBOR + 3.500%)(b) | |

| | 1,338,259 | | | | 4.737 | | | | 10/17/23 | | | | 1,347,466 | |

| | |

| Media-Entertainment – 0.4% | |

| Lions Gate Entertainment Corp. (NR/NR) (1M LIBOR +

3.000%)(b) |

|

| | 838,513 | | | | 4.235 | | | | 12/08/23 | | | | 844,801 | |

| | |

| Packaging – 1.3% | |

| | BWAY Holding Co. (B-/B2) (1M LIBOR + 3.250%)(b) | |

| | 2,644,348 | | | | 4.481 | | | | 04/03/24 | | | | 2,650,482 | |

| | |

| Restaurant – 1.7% | |

| 1011778 B.C. Unlimited Liability Co. (B+/Ba3) (3M LIBOR +

2.250%)(b) |

|

| | 3,475,005 | | | | 3.583 | | | | 02/16/24 | | | | 3,468,923 | |

| | |

| Retailers – 0.6% | |

| | JC Penney Corp., Inc. (BB-/Ba2) (3M LIBOR + 4.250%)(b) | |

| | 1,186,046 | | | | 5.568 | | | | 06/23/23 | | | | 1,151,947 | |

| | |

| Technology – Software – 1.1% | |

| | Kronos, Inc. (B/B2) (3M LIBOR + 3.500%)(b) | |

| | 697,736 | | | | 4.811 | | | | 11/01/23 | | | | 701,413 | |

| | |

| | |

| The accompanying notes are an integral part of these financial statements. | | 17 |

GOLDMAN SACHS LONG SHORT CREDIT STRATEGIES FUND

Schedule of Investments (continued)

September 30, 2017 (Unaudited)

| | | | | | | | | | | | | | |

Principal

Amount | | | Interest

Rate | | | Maturity

Date | | | Value | |

| Secured Debt Obligations – (continued) | |

| Technology – Software – (continued) | |

| | Optiv Security, Inc. (B-/B2) (3M LIBOR + 3.250%)(b) | |

| $ | 500,348 | | | | 4.563 | % | | | 02/01/24 | | | $ | 469,076 | |

| | Peak 10, Inc. (NR/NR) (3M LIBOR + 3.500%)(b) | |

| | 1,036,000 | | | | 4.811 | | | | 08/01/24 | | | | 1,036,000 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 2,206,489 | |

| | |

| Telecommunications – Wireless – 1.0% | |

| | Sprint Communications, Inc. (BB-/Ba2) (1M LIBOR + 2.500%)(b) | |

| | 2,150,133 | | | | 3.750 | | | | 02/02/24 | | | | 2,151,488 | |

| | |

| Telecommunications – Wirelines – 3.4% | |

| | CenturyLink, Inc. (BBB-/Ba3) | |

| | 2,000,000 | | | | 2.750 | | | | 01/31/25 | | | | 1,937,000 | |

| Frontier Communications Corp. (NR/NR) (1M LIBOR +

3.750%)(b) |

|

| | 4,527,653 | | | | 4.990 | | | | 06/15/24 | | | | 4,292,803 | |

| | Windstream Corp. (BB-/B1) (1M LIBOR + 4.000%)(b) | |

| | 857,570 | | | | 5.240 | | | | 03/29/21 | | | | 763,237 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 6,993,040 | |

| | |

| Trading Companies & Distributors(b) – 0.6% | |

| | HD Supply Waterworks Ltd. (NR/NR) (6M LIBOR + 3.000%) | |

| | 1,250,000 | | | | 4.455 | | | | 08/01/24 | | | | 1,251,562 | |

| | |

| | TOTAL BANK LOANS | | | $ | 48,549,447 | |

| | |

| Other Secured Debt Obligations – 15.4% | |

| Auto Components(d)(e) – 0.4% | |

| | Mclaren Finance PLC (B/(P)B2) | |

| | 809,000 | | | | 5.750 | | | | 08/01/22 | | | | 830,899 | |

| | |

| Chemicals(d)(e) – 0.3% | |

| | Cornerstone Chemical Co. (B/B2) | |

| | 605,000 | | | | 6.750 | | | | 08/15/24 | | | | 600,463 | |

| | |

| Commercial Services(d)(e) – 0.8% | |

| | The Hertz Corp. (BB-/B1) | |

| | 1,567,000 | | | | 7.625 | | | | 06/01/22 | | | | 1,614,010 | |

| | |

| Consumer Cyclical Services(d) – 0.9% | |

| | APX Group, Inc. (B-/B1) | |

| | 1,782,000 | | | | 7.875 | | | | 12/01/22 | | | | 1,931,242 | |

| | |

| Containers & Packaging(d)(e) – 0.2% | |

| Ardagh Packaging Finance PLC/Ardagh Holdings USA, Inc.

(BB/Ba3) |

|

| | 391,000 | | | | 4.625 | | | | 05/15/23 | | | | 401,753 | |

| | |

| Health Care – Services(d) – 2.9% | |

| | CHS/Community Health Systems, Inc. (B+/Ba3) | |

| | 2,725,000 | | | | 6.250 | | | | 03/31/23 | | | | 2,690,937 | |

| | HCA, Inc. (BBB-/Ba1) | |

| | 1,411,000 | | | | 5.250 | | | | 06/15/26 | | | | 1,520,353 | |

| | Tenet Healthcare Corp. (BB-/Ba3)(e) | |

| | 1,815,000 | | | | 4.625 | | | | 07/15/24 | | | | 1,796,850 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 6,008,140 | |

| | |

| Media – Cable(d)(e) – 3.2% | |

| | Altice Financing SA (BB-/B1) | |

| | 1,382,000 | | | | 6.625 | | | | 02/15/23 | | | | 1,464,920 | |

| | |

| Secured Debt Obligations – (continued) | |

| Media – Cable(d)(e) – (continued) | |

| | Altice US Finance I Corp. (BB/Ba3) | |

| 1,635,000 | | | | 5.500 | | | | 05/15/26 | | | | 1,720,837 | |

| | Ziggo Secured Finance BV (BB-/Ba3) | |

| | 3,472,000 | | | | 5.500 | | | | 01/15/27 | | | | 3,541,440 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 6,727,197 | |

| | |

| Media – Non Cable(d)(e) – 0.9% | |

| | Univision Communications, Inc. (BB-/B2) | |

| | 602,000 | | | | 5.125 | | | | 05/15/23 | | | | 613,287 | |

| | 1,273,000 | | | | 5.125 | | | | 02/15/25 | | | | 1,284,139 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 1,897,426 | |

| | |

| Oil Field Service(d)(e) – 0.7% | |

| | Transocean Proteus Ltd. (BB-/NR) | |

| | 1,335,700 | | | | 6.250 | | | | 12/01/24 | | | | 1,402,485 | |

| | |

| Pipelines(d)(e) – 3.2% | |

| | Cheniere Corpus Christi Holdings LLC (BB-/Ba3) | |

| | 2,459,000 | | | | 5.125 | | | | 06/30/27 | | | | 2,532,770 | |

| | Cheniere Energy Partners LP (BB/Ba2) | |

| | 3,914,000 | | | | 5.250 | | | | 10/01/25 | | | | 4,002,065 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 6,534,835 | |

| | |

| Real Estate Investment Trust(d)(e) – 0.2% | |

| Uniti Group LP/Uniti Group Finance, Inc./CSL Capital LLC

(B+/B1) |

|

| | 364,000 | | | | 6.000 | | | | 04/15/23 | | | | 347,620 | |

| | |

| Retailing(d)(e) – 1.0% | |

| | PetSmart, Inc. (B/Ba3)(e) | |

| | 2,284,000 | | | | 5.875 | | | | 06/01/25 | | | | 1,992,790 | |

| | |

| Telecommunications – Wireless – 0.7% | |

| | Hughes Satellite Systems Corp. (BBB-/Ba2) | |

| | 1,353,000 | | | | 5.250 | | | | 08/01/26 | | | | 1,407,120 | |

| | |

| TOTAL OTHER SECURED DEBT

OBLIGATIONS |

| | $ | 31,695,980 | |

| | |

| | TOTAL SECURED DEBT OBLIGATIONS | |

| | (Cost $80,613,374) | | | $ | 80,245,427 | |

| | |

| | | | | | | | | | | | | | |

| Unsecured Debt Obligations – 46.2% | |

| Aerospace & Defense – 3.5% | |

| | Bombardier, Inc. (B-/B3)(e) | |

| $ | 614,000 | | | | 6.000 | %(d) | | | 10/15/22 | | | $ | 595,580 | |

| | 1,935,000 | | | | 6.125 | | | | 01/15/23 | | | | 1,862,437 | |

| | 578,000 | | | | 7.500 | (d) | | | 03/15/25 | | | | 577,278 | |

| | TransDigm, Inc. (B-/B3)(d) | |

| | 359,000 | | | | 6.500 | | | | 05/15/25 | | | | 369,321 | |

| | 806,000 | | | | 6.375 | | | | 06/15/26 | | | | 826,150 | |

| | Triumph Group, Inc. (B-/B3)(d) | |

| | 844,000 | | | | 4.875 | | | | 04/01/21 | | | | 823,955 | |

| | 226,000 | | | | 5.250 | | | | 06/01/22 | | | | 220,350 | |

| | 1,758,000 | | | | 7.750 | (e) | | | 08/15/25 | | | | 1,845,900 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 7,120,971 | |

| | |

| | |

| 18 | | The accompanying notes are an integral part of these financial statements. |

GOLDMAN SACHS LONG SHORT CREDIT STRATEGIES FUND

| | | | | | | | | | | | | | |

Principal

Amount | | | Interest

Rate | | | Maturity

Date | | | Value | |

| Unsecured Debt Obligations – (continued) | |

| Automotive – 7.7% | |

| | Adient Global Holdings Ltd. (BB/Ba3)(d)(e) | |

| $ | 2,866,000 | | | | 4.875 | % | | | 08/15/26 | | | $ | 2,930,485 | |

| | Allison Transmission, Inc. (NR/NR)(d)(e) | |

| | 561,000 | | | | 4.750 | | | | 10/01/27 | | | | 565,208 | |

| | Cooper-Standard Automotive, Inc. (B+/B2)(d)(e) | |

| | 2,655,000 | | | | 5.625 | | | | 11/15/26 | | | | 2,711,419 | |

| | Dana, Inc. (BB/B1) | |

| | 434,000 | | | | 6.000 | | | | 09/15/23 | | | | 455,700 | |

| | Delphi Jersey Technologies PLC (BB/B1)(e) | |

| | 451,000 | | | | 5.000 | | | | 10/01/25 | | | | 457,711 | |

| | General Motors Financial Co., Inc. (BBB/Baa3)(d) | |

| | 471,000 | | | | 5.250 | | | | 03/01/26 | | | | 511,297 | |

| | Navistar International Corp. (CCC+/Caa1)(d) | |

| | 3,985,000 | | | | 8.250 | | | | 11/01/21 | | | | 3,999,944 | |

| | Tenneco, Inc. (BB/Ba2)(d) | |

| | 765,000 | | | | 5.000 | | | | 07/15/26 | | | | 781,256 | |

| | Tesla, Inc. (B-/B3)(d)(e) | |

| | 3,482,000 | | | | 5.300 | | | | 08/15/25 | | | | 3,403,655 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 15,816,675 | |

| | |

| Casino & Gaming(e) – 1.0% | |

| | CRC Escrow Issuer LLC Co. (B-/NR) | |

| | 2,122,000 | | | | 5.250 | | | | 10/15/25 | | | | 2,124,639 | |

| | |

| Chemicals(d)(e) – 0.6% | |

| | NOVA Chemicals Corp. (BB+/Ba2) | |

| | 1,185,000 | | | | 5.250 | | | | 08/01/23 | | | | 1,222,031 | |

| | |

| Commercial Services(d) – 1.4% | |

| | Booz Allen Hamilton, Inc. (B+/B1)(e) | |

| | 665,000 | | | | 5.125 | | | | 05/01/25 | | | | 670,819 | |

| | The Hertz Corp. (B-/B3) | |

| | 741,000 | | | | 5.875 | | | | 10/15/20 | | | | 731,737 | |

| | 1,478,000 | | | | 7.375 | | | | 01/15/21 | | | | 1,481,695 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 2,884,251 | |

| | |

| Computer Hardware(d) – 0.9% | |

| | Seagate HDD Cayman (BB+/Baa3) | |

| | 2,023,000 | | | | 4.875 | | | | 06/01/27 | | | | 1,907,524 | |

| | |

| Diversified Financial Services – 2.6% | |

| | DAE Funding LLC (BB/Ba3)(d)(e) | |

| | 2,598,000 | | | | 5.000 | | | | 08/01/24 | | | | 2,662,950 | |

| | Jefferies Finance LLC/JFIN Co-Issuer Corp. (B/B1)(d)(e) | |

| | 227,000 | | | | 6.875 | | | | 04/15/22 | | | | 227,567 | |

| | 1,078,000 | | | | 7.250 | | | | 08/15/24 | | | | 1,079,347 | |

| | Navient Corp. (B+/Ba3) | |

| | 485,000 | | | | 8.000 | | | | 03/25/20 | | | | 535,791 | |

| | 182,000 | | | | 5.000 | | | | 10/26/20 | | | | 187,188 | |

| | 662,000 | | | | 6.625 | | | | 07/26/21 | | | | 709,630 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 5,402,473 | |

| | |

| Electrical(d)(e) – 0.4% | |

| | Talen Energy Supply LLC (B+/B1) | |

| | 944,000 | | | | 9.500 | | | | 07/15/22 | | | | 873,200 | |

| | |

| Entertainment(d) – 0.4% | |

| | Cinemark USA, Inc. (BB/B2) | |

| | 406,000 | | | | 4.875 | | | | 06/01/23 | | | | 410,060 | |

| | |

| Unsecured Debt Obligations – (continued) | |

| Entertainment(d) – (continued) | |

| | Lions Gate Entertainment Corp. (B-/B2)(e) | |

| 493,000 | | | | 5.875 | | | | 11/01/24 | | | | 516,418 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 926,478 | |

| | |

| Food & Drug Retailing(d)(e) – 4.8% | |

| | Dean Foods Co. (BB/B2) | |

| | 2,254,000 | | | | 6.500 | | | | 03/15/23 | | | | 2,287,810 | |

| FAGE International SA/FAGE USA Dairy Industry, Inc.

(BB-/B1) |

|

| | 2,357,000 | | | | 5.625 | | | | 08/15/26 | | | | 2,445,387 | |

| | Pilgrim’s Pride Corp. (NR/B1) | |

| | 441,000 | | | | 5.875 | | | | 09/30/27 | | | | 450,923 | |

| | Pilgrim’s Pride Corp. (BB-/B1) | |

| | 264,000 | | | | 5.750 | | | | 03/15/25 | | | | 272,250 | |

| | Rite Aid Corp. (B-/B3) | |

| | 4,515,000 | | | | 6.125 | | | | 04/01/23 | | | | 4,390,837 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 9,847,207 | |

| | |

| Home Builders(d) – 1.2% | |

| Ashton Woods USA LLC/Ashton Woods Finance Co.

(B-/Caa1)(e) |

|

| | 626,000 | | | | 6.750 | | | | 08/01/25 | | | | 616,610 | |

| | AV Homes, Inc. (B-/B3) | |

| | 927,000 | | | | 6.625 | | | | 05/15/22 | | | | 950,175 | |

| | M/I Homes, Inc. (BB-/B1)(e) | |

| | 348,000 | | | | 5.625 | | | | 08/01/25 | | | | 354,960 | |

| | The New Home Co., Inc. (B-/B3) | |

| | 494,000 | | | | 7.250 | | | | 04/01/22 | | | | 510,055 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 2,431,800 | |

| | |

| Machinery – Construction & Mining(d)(e) – 0.6% | |

| | Terex Corp. (BB/B2) | |

| | 1,172,000 | | | | 5.625 | | | | 02/01/25 | | | | 1,229,135 | |

| | |

| Media(d) – 3.6% | |

| | AMC Networks, Inc. (BB/Ba3) | |

| | 1,594,000 | | | | 4.750 | | | | 08/01/25 | | | | 1,603,963 | |

| | CBS Radio, Inc. (B-/B3)(e) | |

| | 460,000 | | | | 7.250 | | | | 11/01/24 | | | | 489,900 | |

| | CCO Holdings LLC/CCO Holdings Capital Corp. (BB/B1)(e) | |

| | 3,414,000 | | | | 5.750 | | | | 02/15/26 | | | | 3,580,432 | |

| | Cengage Learning, Inc. (CCC+/Caa2)(e) | |

| | 370,000 | | | | 9.500 | | | | 06/15/24 | | | | 319,125 | |

| | Sirius XM Radio, Inc. (BB/Ba3)(e) | |

| | 900,000 | | | | 5.375 | | | | 04/15/25 | | | | 951,750 | |

| | Videotron Ltd. (BB/Ba2)(e) | |

| | 377,000 | | | | 5.125 | | | | 04/15/27 | | | | 392,080 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 7,337,250 | |

| | |

| Oil & Gas(d) – 3.8% | |

| | Covey Park Energy LLC/Covey Park Finance Corp. (B/B3)(e) | |

| | 471,000 | | | | 7.500 | | | | 05/15/25 | | | | 492,784 | |

| | CrownRock LP/CrownRock Finance, Inc. (B+/B3)(e) | |

| | 1,826,000 | | | | 7.125 | | | | 04/15/21 | | | | 1,885,345 | |

| | Extraction Oil & Gas, Inc. (B/B3)(e) | |

| | 763,000 | | | | 7.375 | | | | 05/15/24 | | | | 795,427 | |

| | |

| | |

| The accompanying notes are an integral part of these financial statements. | | 19 |

GOLDMAN SACHS LONG SHORT CREDIT STRATEGIES FUND

Schedule of Investments (continued)

September 30, 2017 (Unaudited)

| | | | | | | | | | | | | | |

Principal

Amount | | | Interest

Rate | | | Maturity

Date | | | Value | |

| Unsecured Debt Obligations – (continued) | |

| Oil & Gas(d) – (continued) | |

| | Gulfport Energy Corp. (B+/B2) | |

| $ | 2,158,000 | | | | 6.625 | % | | | 05/01/23 | | | $ | 2,201,160 | |

| | 862,000 | | | | 6.375 | | | | 05/15/25 | | | | 872,775 | |

| | QEP Resources, Inc. (BB+/Ba3) | |

| | 467,000 | | | | 5.250 | | | | 05/01/23 | | | | 454,158 | |

| | Seven Generations Energy Ltd. (B+/Ba3)(e) | |

| | 1,270,000 | | | | 5.375 | | | | 09/30/25 | | | | 1,279,525 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 7,981,174 | |

| | |

| Oil & Gas Services(d) – 5.2% | |

| | Rowan Cos., Inc. (B+/B2) | |

| | 435,000 | | | | 4.875 | | | | 06/01/22 | | | | 406,725 | |

| | SESI LLC (BB-/B3) | |

| | 1,406,000 | | | | 7.125 | | | | 12/15/21 | | | | 1,437,635 | |

| | 1,313,000 | | | | 7.750 | (e) | | | 09/15/24 | | | | 1,368,803 | |

| | Transocean, Inc. (B/Caa1) | |

| | 819,000 | | | | 5.800 | | | | 10/15/22 | | | | 804,667 | |

| | Trinidad Drilling Ltd. (BB-/Caa1)(e) | |

| | 415,000 | | | | 6.625 | | | | 02/15/25 | | | | 388,544 | |

| | Weatherford International Ltd. (B/Caa1) | |

| | 3,861,000 | | | | 7.750 | | | | 06/15/21 | | | | 4,015,440 | |

| | 1,899,000 | | | | 4.500 | | | | 04/15/22 | | | | 1,761,322 | |

| | 545,000 | | | | 8.250 | | | | 06/15/23 | | | | 561,350 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 10,744,486 | |

| | |

| Pharmaceuticals(d)(e) – 0.8% | |

| | Concordia International Corp. (C/Ca) | |

| | 955,000 | | | | 7.000 | | | | 04/15/23 | | | | 162,350 | |

| | Valeant Pharmaceuticals International, Inc. (B-/Caa1) | |

| | 1,388,000 | | | | 6.375 | | | | 10/15/20 | | | | 1,391,470 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 1,553,820 | |

| | |

| Pipelines(d)(e) – 1.5% | |

| Tallgrass Energy Partners LP/Tallgrass Energy Finance Corp.

(BB+/Ba3) |

|

| | 1,843,000 | | | | 5.500 | | | | 09/15/24 | | | | 1,893,683 | |

| Tallgrass Energy Partners LP/Tallgrass Energy Finance Corp.

(BB+/Ba3) |

|

| | 1,290,000 | | | | 5.500 | | | | 01/15/28 | | | | 1,309,350 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 3,203,033 | |

| | |

| Real Estate Investment Trust – 1.6% | |

| | iStar, Inc. (BB-/B1)(d) | |

| | 834,000 | | | | 5.250 | | | | 09/15/22 | | | | 845,467 | |

| | SBA Communications Corp. (B+/NR)(e) | |

| | 435,000 | | | | 4.000 | | | | 10/01/22 | | | | 437,175 | |

| Uniti Group LP/Uniti Fiber Holdings, Inc./CSL Capital LLC

(CCC+/Caa1)(d)(e) |

|

| | 2,326,000 | | | | 7.125 | | | | 12/15/24 | | | | 1,977,100 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 3,259,742 | |

| | |

| Retailing(d) – 0.4% | |

| | PetSmart, Inc. (CCC+/B3)(e) | |

| | 1,032,000 | | | | 8.875 | | | | 06/01/25 | | | | 820,440 | |

| | |

| Unsecured Debt Obligations – (continued) | |

| Software(d) – 0.5% | |

| | Donnelley Financial Solutions, Inc. (B/B3) | |

| 896,000 | | | | 8.250 | | | | 10/15/24 | | | | 959,840 | |

| | |

| Telecommunication Services – 3.5% | |

| | Frontier Communications Corp. (B/B2) | |

| | 830,000 | | | | 8.500 | | | | 04/15/20 | | | | 805,100 | |

| | Inmarsat Finance PLC (BB+/Ba2)(d)(e) | |

| | 1,404,000 | | | | 4.875 | | | | 05/15/22 | | | | 1,434,011 | |

| | 604,000 | | | | 6.500 | | | | 10/01/24 | | | | 651,741 | |

| | Intelsat Jackson Holdings SA (CCC+/Caa2)(d)(e) | |

| | 611,000 | | | | 9.750 | | | | 07/15/25 | | | | 620,165 | |

| | ViaSat, Inc. (BB-/NR)(d)(e) | |

| | 3,669,000 | | | | 5.625 | | | | 09/15/25 | | | | 3,691,931 | |

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | 7,202,948 | |

| | |

| Utilities(d) – 0.2% | |

| Suburban Propane Partners LP/Suburban Energy Finance Corp.

(BB-/B1) |

|

| | 488,000 | | | | 5.500 | | | | 06/01/24 | | | | 486,780 | |

| | |

| | TOTAL UNSECURED DEBT OBLIGATIONS | |

| | (Cost $95,937,526) | | | $ | 95,335,897 | |

| | |

| | | | | | | | | | | | | | |

| | U.S. Treasury Obligation(f) – 2.4% | | | | | |

| | United States Treasury Bill | |

| $ | 5,000,000 | | | | 0.000 | % | | | 11/02/17 | | | $ | 4,995,800 | |

| | (Cost $4,996,530) | | | | | | | | | |

| | |

| | | | | | | | |

| Shares | | | Description | | Value | |

| | Common Stock* – 0.2% | | | | |

| Oil, Gas & Consumable Fuels – 0.2% | | | |

| | 1,141,924 | | | Prairie Provident Resources, Inc. | | $ | 360,860 | |

| | (Cost $2,946,424) | | | | |

| | |

| | |

| Units | | | Expiration