OMB APPROVAL

OMB Number:

3235-0570

Expires: August

31, 2020

Estimated average

burden hours per

response: 20.6

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number: 811-05371

Russell Investment Funds

(Exact name of registrant as specified in charter)

1301 2nd Avenue 18th Floor, Seattle Washington 98101

(Address of principal executive offices) (Zip code)

Mary Beth R. Albaneze, Secretary and Chief Legal Officer

1301 2nd Avenue

18th Floor

Seattle, Washington 98101

206-505-4846

______________________________________________

(Name and address of agent for service)

Registrant's telephone number, including area code: 800-787-7354

Date of fiscal year end: December 31

Date of reporting period: January 1, 2017 to December 31, 2017

Item 1. Reports to Stockholders

Russell Investment Funds

Russell Investment Funds is

a series investment company

with nine different investment

portfolios referred to as Funds.

These financial statements report

on five of these Funds.

Russell Investment Funds

Annual Report

December 31, 2017

Table of Contents

|

| Page |

| To Our Shareholders | 3 |

| Market Summary | 4 |

| U. S. Strategic Equity Fund | 9 |

| U. S. Small Cap Equity Fund | 27 |

| International Developed Markets Fund | 49 |

| Strategic Bond Fund | 77 |

| Global Real Estate Securities Fund | 129 |

| Notes to Schedules of Investments | 151 |

| Notes to Financial Highlights | 154 |

| Notes to Financial Statements | 155 |

| Report of Independent Registered Public Accounting Firm | 174 |

| Tax Information | 175 |

| Affiliated Brokerage Transactions | 176 |

| Basis for Approval of Investment Advisory Contracts | 177 |

| Shareholder Requests for Additional Information | 178 |

| Disclosure of Information about Fund Trustees and Officers | 179 |

| Adviser, Money Managers and Service Providers | 184 |

Russell Investment Funds

Copyright © Russell Investments 2018. All rights reserved.

Russell Investments’ ownership is composed of a majority stake held by funds managed by TA Associates with

minority stakes held by funds managed by Reverence Capital Partners and Russell Investments’ management.

Frank Russell Company is the owner of the Russell trademark contained in this material and all trademark rights

related to the Russell trademarks, which the members of the Russell Investment group of companies are permitted

to use under license from Frank Russell Company. The members of the Russell Investments group of companies

are not affiliated in any manner with Frank Russell Company or any entity operation under the “FTSE RUSSELL”

brand.

Fund objectives, risks, charges and expenses should be carefully considered before in-

vesting. A prospectus containing this and other important information must precede or

accompany this material. Please read the prospectus carefully before investing.

Securities distributed through Russell Investments Financial Services, LLC, member FINRA and part

of Russell Investments.

Indices and benchmarks are unmanaged and cannot be invested in directly. Returns represent past performance,

are not a guarantee of future performance, and are not indicative of any specific investment. Index return

information is provided by vendors and although deemed reliable, is not guaranteed by Russell Investments or its

affiliates.

Performance quoted represents past performance and does not guarantee future results. The investment return and

principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their

original cost. Current performance may be lower or higher than the performance data quoted.

To Our Shareholders

Fellow Investors,

Being an investor isn’t always easy. A long-term view, consistency and commitment can be vitally important to wealth

creation. Daily headlines and speculation move markets on a short-term basis. While seemingly amplified today, this

type of noise has been, and always will be, present. Consequently, it remains critical to have a thoughtful financial plan,

realistic goals and timelines, and regular check-ins with your financial advisor.

That said, the past 12 months ending December 31, 2017 have arguably been a relatively tame period in which to be a

patient and resolute investor. We don’t get to say that often so please consider some of these facts:

• All major asset classes were positive from January 1, 2017 to December 31, 2017. Global equity markets were up

double digits, fixed income shareholders were rewarded with price appreciation across the spectrum, and diversifying

real assets contributed, too.

• Volatility, as measured by the CBOE VIX, has been very low relative to historical averages. The calendar year-to-

date as of December 31 has seen the fewest number of 1% daily moves in the S&P500® Index in 30 years.

• Global growth has been steady.

At Russell Investments, we expect a return of market volatility to levels more consistent with historical norms. After all,

the current U.S. stock market rally became the second longest and third strongest on record since 1936 on December 31,

2017. This has led U.S. stocks to become more fully valued. The Cyclically Adjusted Price to Earnings Ratio (CAPE)

stood at 33.2 as of December 2017, putting the U.S. stock market among the most expensive markets since this data

started being tracked in 1926. As the saying goes, “History doesn’t repeat itself, but often it does rhyme.” In past

periods of expensive U.S. equity markets, prices had very little upward potential left—low single digit returns. The

Federal Reserve has begun the process of raising interest rates and unwinding its balance sheet—reversing the years of

accommodative monetary policy instituted in response to the Global Financial Crisis. Even though fixed income markets

have remained resilient so far, the simple math of fixed income suggests that bond prices will come under pressure as

yields continue to rise.

Of course, it’s important to remember that markets and geopolitical events will test investors’ resolve every single year.

The past 12 months’ uncertainty surrounding important elections in France, the United Kingdom, South Korea, and

mounting geopolitical tensions between North Korea and the U.S. were no exception. Exceptional investors, however, are

those who look past the short-term uncertainties and have the commitment to stick with their long-term plan.

In this type of environment, we believe that investors who work with a trusted financial advisor to develop—and stick

with—a financial plan, realistic goals and timelines, will be most resilient. In addition, although diversification can’t

guarantee a profit or avoid losses, experience suggests that globally-diversified multi-asset portfolios further help

investors stay the course when markets get choppy. The following pages provide additional insights on the markets and

the performance of Russell Investments Funds (RIF) for the fiscal year ending December 31, 2017.

Russell Investments has an extensive, proud heritage of providing multi-asset solutions to help investors like you reach

your financial goals, whether you’re saving for retirement, already there or building a college fund. Thank you for the trust

you have placed in our firm. All of us at Russell Investments appreciate the opportunity to help you achieve financial

security.

President and Chief Executive Officer, Russell Investment Funds

1 Represented by Russell 1000® Index up 21.69%, MSCI EAFE Index up 25.03%, MSCI Emerging Markets Index up 37.28% (as of 12/31/2017)

2 Represented by Bloomberg Barclays U.S. Aggregate Bond Index up 3.54%, ICE BofA Merill Lynch Global High Yield Index up 10.20%, Bloomberg

Barclays 1-10 Year Municipal Blend Index up 3.49% (as of 12/31/2017)

3 Represented by Bloomberg Commodity Index up 1.70%, S&P Global Infrastructure Index up 19.07%, FTSE EPRA/NAREIT Developed Index up

10.36%(as of 12/31/2017)

To Our Shareholders 3

Russell Investment Funds

Market Summary as of December 31, 2017 (Unaudited)

U.S. Equity Markets

Broadly measured by the Russell 3000® Index, U.S. stocks returned 21.13% for the one-year period, which is the ninth

straight fiscal year ending December 31st that the Russell 3000® Index has finished with a positive absolute return. The

Russell 3000® Index finished with a positive absolute return in each of the fiscal year’s twelve months.

Within U.S. large capitalization stocks, factors that were rewarded during the fiscal year included high beta (beta is a

measure of a stock’s sensitivity to the direction of the market), high historical earnings growth, and the largest capitalization

stocks. Factors that trailed the market included high dividend yield, low price-to-book ratios, and high earnings variability.

Additionally, dynamic stocks outperformed defensive stocks and growth stocks outperformed value stocks across all

market capitalization tiers excluding mid cap. From a sector perspective, information technology, materials, and consumer

discretionary outperformed the Russell 1000® Index by 16.83%, 2.02%, and 1.69%, respectively. Sectors that failed to find

traction during the one-year period were energy, telecommunication services, and real estate, trailing by 23.25%, 23.20%,

and 11.76%, respectively.

The U.S. large cap equity market started off 2017 very strong with the Russell 3000® Index gaining 5.74% from January

through March. The Fed raised its benchmark interest rate by another 25 basis points in March on the back of positive

economic data. However, the interest rate hike was accompanied by dovish language from the Fed which put into question

how many additional rate hikes there might be in 2017. Additionally, the post-Trump risk rally lost some steam in the

latter stages of the period after the new health care bill failed to repeal and replace Obama Care. Retail sales slowed down

in February, however inflation ticked upward to 2.7% year-over-year. In addition, the February non-farm payrolls figure

beat expectations yet again and pushed the unemployment rate down to 4.7%. The U.S. GDP growth rate was also revised

slightly higher to 2.1% for the fourth quarter of 2016.

The Russell 3000® Index increased 3.02% from April through June. While U.S. economic data came in slightly softer

than expected over the period, it was enough for the Fed to raise its short-term interest rate in June. Over the period,

oil prices trended lower and the U.S. dollar was weak compared to most major currencies. Retail sales slowed down in

May, while inflation also slipped lower to 1.9%, moderately under the Fed’s 2.0% target rate. Meanwhile, May non-farm

payrolls grew less then consensus and the unemployment rate fell to 4.3%. Additionally, the U.S. economy expanded faster

than initially reported during the first quarter (1.4% quarter-over-quarter), following an upward revision to secondary

estimates of 1.2%. The Fed raised short-term interest rates by a further 25 basis points to 1.25% as widely expected

and maintained its forecast for one more rate hike in 2017. Fed Chair Janet Yellen also added that the bank would start

unwinding its $4.5 trillion balance sheet later in the year by reducing reinvestment of maturing bonds.

The Russell 3000® Index climbed 4.57% from July through September. U.S. political uncertainty, escalating geopolitical

tension in the Korean peninsula and tropical hurricanes rattled investors. However, a strengthening economic backdrop

influenced a risk-on market environment which also contributed to the Fed developing a slightly more hawkish outlook.

Over the period, commodity prices stabilized while a sluggish U.S. dollar lifted a basket of global currencies. In the U.S.,

the latest non-farm payrolls figure continued to point towards a healthy jobs market, although the unemployment rate

ticked higher to 4.4%. Retail sales slowed to 3.2% year-over-year, but inflation edged higher to 1.9% year-over-year, still

under the Fed’s 2.0% target rate. However, the second quarter U.S. economic growth rate was finalized at a strong 3.1%

quarter-over-quarter. Toward the end of the quarter, initial details were released on a potential tax reform plan which was

viewed favorably by market participants.

The Russell 3000® Index continued its upward trend ending the October through December time period up 6.34%.

Investors gravitated toward larger market capitalization growth stocks which outpaced most other groups as the third

quarter reporting season surprised to the upside in terms of earnings growth, sales growth, and profit margins. In the

beginning of December, the Fed raised short-term interest rates by a further 25 basis points to 1.50% as widely expected

and maintained its forecast of three additional rate hikes in 2018. Toward the end of the December, the approval of the

much-anticipated tax package also added to the positive sentiment within equity markets. Additionally, incentives to

4 Market Summary

Russell Investment Funds

Market Summary as of December 31, 2017, continued — (Unaudited)

invest and repatriate overseas profits included in the broader tax legislation were viewed as allowing U.S. companies to

more easily pursue growth strategies.

Non-U.S. Developed Equity Markets

For the fiscal year ended December 31, 2017, developed non-U.S. equity markets, as measured by the Russell Developed

ex-U.S. Large Cap® Index (the “Index”), were up 25.46%. Key drivers of market performance were the U.S. presidential

election, improving global growth, especially in emerging markets and the Eurozone, increases in government bond yields

and the Trump administration’s tax reform bill.

Amid the improving global growth outlook, momentum, growth and quality factors had the strongest outperformance during

the fiscal year followed by a modest outperformance of value factor as investors chased cheaper, cyclical stocks and stocks

with high earnings expectations. Sectors with high growth expectations such as technology, industrials and materials were

rewarded during the period while the more defensive sectors such as consumer staples, utilities and health care suffered.

Energy stocks also underperformed as commodity prices continued to face pressure from excess supply.

In the first quarter of the fiscal year, the Fed met expectations and raised its benchmark rate by another 25 basis points in

light of further positive economic data, following a similar rate increase in December 2016. Additionally, a post-Trump risk

rally lost some steam in the latter stages of the period, after President Trump lost support from his own Republican party for

his health care bill. In Europe, UK Prime Minister Theresa May triggered Article 50 to officially start “Brexit” negotiations,

while investors held caution over electoral developments in the Netherlands, France and Germany. Over the period, oil

prices trended lower while a weaker U.S. dollar lifted emerging market currencies. While markets ground higher during

this period, investor sentiment became more cautionary, avoiding areas like energy and materials.

In the second quarter of the fiscal year, U.S. economic data came in slightly softer than expected. However, it was enough

for the Fed to raise its benchmark rate for the second time in 2017. In Europe, Emmanuel Macron became France’s new

President while the general election in the UK resulted in a challenging “hung Parliament”. Over the period, oil prices

continued their trend lower along with a weakening U.S. dollar against a basket of currencies. The easing political tension

in Europe rewarded the value factor and financial companies in particular.

In the third quarter of the fiscal year, U.S. federal political dysfunction, escalating geopolitical tension in the Korean

peninsula and tropical hurricanes rattled investors. However, a strengthening economic backdrop engendered a risk-on

market environment, and informed developed central banks who became more comfortable with a more hawkish outlook.

Over the period, commodity prices stabilized, rewarding energy stocks. The technology sector continued a strong run as

evidence of disruption in traditional sectors such as retail drove investor sentiment.

In the fourth quarter of the fiscal year, U.S. President Donald Trump experienced his first major legislative victory with

a tax reform deal. Furthermore, strong economic growth in the third quarter paved the way for the Fed to raise its key

interest rate for a third time in December from 1.25% to 1.50%. A combination of strong economic growth and positive

expectations from tax reform led the U.S. markets higher during the quarter. Across the Atlantic, British Prime Minister

Theresa May struck a last-minute deal with the EU to move Brexit talks forward and in November the Bank of England

also raised interest rates for the first time in a decade whilst inflation hit 3.1%. Europe ex-UK and the UK were the biggest

underperformers during the quarter.

Emerging markets and Asia ex-Japan were the stand out non-U.S. markets over the fiscal year, as improving economic

fundamentals along with a weaker U.S. dollar were tailwinds. Conversely, the UK, Europe ex-UK and Canada were the

biggest laggards.

Emerging Markets

The Russell Emerging Markets® Index, as measured in U.S. dollar terms (the “Index”), gained 36.3% over the fiscal year

ended December 31, 2017. The asset class remained buoyant in a period where global growth forecasts were upgraded and

Market Summary 5

Russell Investment Funds

Market Summary as of December 31, 2017, continued — (Unaudited)

inflation remained low. Many emerging countries started to see green shoots as they rebounded from their cyclical lows,

benefiting from lower interest rates and improving economic growth. The U.S. dollar weakened against most emerging

market currencies, despite increasing U.S. interest rates. The U.S. Federal Reserve’s approach was more dovish than

expected by the market which benefited emerging market currencies.

The Index surged 11.7% in the first quarter of 2017, outperforming developed markets as investor appetite for perceived

riskier investments returned. India (19.3%) was the strongest-performing country as Prime Minister Modi’s Party won

key state elections, with the victories demonstrating strong domestic support for Modi’s free-market reform programs.

Mexico (16.4%) rebounded where the peso was among the best-performing currencies against the U.S. dollar as the Trump

administration softened its rhetoric towards the country. South Africa (4.4%) underperformed as speculation surrounding

the independence of the Treasury following the removal of respected finance minister Pravin Gordhan and replacement of

nine other cabinet ministers by President Zuma weighed on sentiment and the value of the rand. After its 2016 rally, Russia

(-2.5%) returned some of its strong performance as hopes of potentially warmer relations and easing of sanctions with the

U.S. following Trump’s election victory partially dissipated.

The Index continued its 2017 rally in the second quarter with a 5.6% climb as sentiment towards the asset class remained

buoyant. A weaker U.S. dollar was a further tailwind, although it was another negative and volatile period for the price

of oil. Emerging Europe (ex-Russia) was the best performing region in emerging markets, following the market-friendly

French Presidential election result. This included Hungary (18.9%), Poland (13.5%) and the Czech Republic (13.1%).

Greece was the strongest-performing country after a 31.9% surge. This came as a deal with its creditors on economic

reforms was agreed after protracted negotiations, which enabled the release of the next bailout tranche. Asian countries

also outperformed over the period. Both India (3.3%) and South Africa (2.6%) lagged the overall benchmark return. In

India, first quarter GDP growth was the weakest in two years at 6.1% year-over-year, as the full impact of Prime Minister

Modi’s demonetisation policy began to come through. The government withdrew the 500 and 1000 rupee notes overnight to

crack down on the black market. South Africa underperformed in a period where President Zuma survived his ANC party

vote of no confidence. Natural resource and energy-driven markets were the weakest performing for the quarter as these

sectors underperformed the market, particularly Russia (-9.7%) and Brazil (-6.7%).

The Index increased 7.4% in the third quarter of 2017. Sentiment towards the asset class remained buoyant amid a tepid

global inflation environment. A weaker U.S. dollar and stable oil prices underpinned investor confidence. However, the

market edged lower in September amid a more hawkish outlook from the U.S. Federal Reserve and increased geopolitical

tensions within the Korean peninsula. Brazil (23.5%) rebounded from a weak second quarter driven by the improved

political environment where congress’ lower house voted down corruption charges against President Temer to keep him in

power. China (13.7%) outperformed, driven by Internet stocks, the strongest-performing sector. Russia climbed 15.5% in

a strong period for the energy sector. Elsewhere, Eastern European countries continued their healthy 2017 performance,

including the Czech Republic (11.3%), Hungary (9.7%) and Poland (8.8%) on robust macro numbers. South Korea (1.6%)

was hampered by heightened political tensions between North Korea and the U.S. Mexico (0.8%) underperformed as

NAFTA renegotiations remained strained. The country was also hit by a series of earthquakes which weighed on investor

confidence. Overall, Greece was the worst-performing country ahead of November’s bailout review with its creditors. The

market slipped 8.8% as banking stocks slumped on possible new European Central Bank and International Monetary Fund

stress tests.

The Index increased 7.7% in the final quarter of 2017. South Africa was the standout performer over the period, as

the market surged 21.4% in reaction to political developments. The South African rand strengthened over the period,

boosted by Moody’s maintaining the country’s Baa3 investment-grade rating. India also surged (13.8%) as the government

announced plans to inject $32 billion into state controlled banks. In Korea (13.1%), the government announced plans to

increase spending and raise the minimum wage, which helped to increase consumer confidence to its highest level since

2010. The market was further buoyed by news that South Korea and China agreed to normalize relations following an

6 Market Summary

Russell Investment Funds

Market Summary as of December 31, 2017, continued — (Unaudited)

earlier fallout over the installation of the U.S. anti-missile system in South Korea. Greece (10.6%) recovered from a weak

third quarter, as the government agreed to additional reforms in the latest bailout review with its creditors, which allowed

the release of the next tranche of funds. Mexico (-8.4%) was the worst-performing country, as it continued to suffer from

peso weakness driven by strained discussions on the future of the North American Free Trade Agreement. Brazil (-2.4%)

suffered from weakness in the real. Investors appeared disappointed that the much-anticipated pension reform bill was

watered down and delayed until February 2018.

U.S./Global Fixed Income Markets

The fiscal year ended December 31, 2017 was characterized by a risk on rally that saw both U.S. and European credit

spreads tighten, global growth improve and conducive monetary policies from central banks. Overall, this proved positive

for fixed income sectors around the globe. The U.S. yield curve saw interest rates rise for the fiscal year with the short end

of the curve rising 88 basis points on a 3-month treasury bill, while the 10-year treasury bond interest rate was flat. The

German Bund saw a parallel shift upwards in interest rates during 2017 and the British Gilt saw interest rates rise on the

short end of the curve and fall on the longer end. The U.S. experienced the largest interest rate moves as the U.S. Federal

Reserve (the “Fed”) raised interest rates three times during the year. Europe had historically low interest rates during the

fiscal year as the European Central Bank (“ECB”) kept rates low and continued with their quantitative easing program,

although it was cut in half to 30 billion euros per month in October. Corporate and high yield spreads grinded tighter on

the back of strong demand and the positive global growth backdrop. A key indicator of global fixed income performance,

the Bloomberg Barclays Global Aggregate Bond Index, returned 7.39% for the fiscal year, in U.S. dollar-hedged terms. The

index had a strong year due to increasing demand, monetary policy remaining accommodative, and the lack of geopolitical

fears being realized.

The Bloomberg Barclays Pan-European Aggregate Bond Index returned 14.21% during the period in U.S. dollar-hedged

terms, but most of that return was due to the euro appreciating 14.15% against the U.S. dollar. The U.S., in comparison,

returned 3.54% during the fiscal year as measured by the Bloomberg Barclays U.S. Aggregate Bond Index. In Europe,

treasuries underperformed the aggregate while financials in the corporate sector was a leading segment. In the U.S.,

the corporate market performed strongly led by lower quality bonds and strong demand from oversees. The U.S. dollar

depreciated against most European currencies, due to improving growth across Europe and the victory of political

candidates that support the European Union.

In the U.S., economic data remained broadly positive, with solid nonfarm payroll gains and a steady decline in the

unemployment rate to decade lows of 4.1%. Gross domestic product (“GDP”) growth had readings over 3.0% for both the

second and third quarter 2017, after it had dipped below 1.5% in the first quarter of 2017. The Consumer Price Index

(“CPI”) started the fiscal year strong at above 2.0% and was a contributing factor as the Fed raised rates, but as the CPI

fell during the year below the Fed’s long-term target of 2.0%, it becomes the Fed’s largest concern.

In Europe, the concerns about a “hard Brexit” diminished over the period, while most of Europe welcomed Emmanuel

Macron’s victory in the French presidential elections. The Bloomberg Barclays Euro Aggregate Corporate Index returned

3.5% over equivalent duration government bonds during the period as financials improved and GDP rose from 1.4% to

2.3% during the fiscal year. The European banking sector had a setback in 2nd quarter 2017 as three banks declared

bankruptcy.

Emerging markets were one of the strongest sectors in 2017 as the U.S. dollar depreciated, global growth was above-

trend and major central bank monetary policy settings were accommodative. Emerging market (“EM”) debt outperformed

developed markets (the Bloomberg Barclays EM Hard Currency Aggregate Bond Index returned 9.61%) as there was

high demand for yield. Local currency EM bonds (those issued in the issuing country’s own currency) were extremely

strong (the Bloomberg Barclays EM Local Currency Government Bond Index returned 14.27%) due to the depreciation of

the U.S. dollar versus a basket of emerging market currencies. The Czech koruna and Polish zloty both appreciated over

Market Summary 7

Russell Investment Funds

Market Summary as of December 31, 2017, continued — (Unaudited)

20% during the year as the koruna was unpegged from the euro and the zloty appreciated on the back of the strong Polish

economy and the appreciation in the euro.

Strong global corporate new issuance volumes continued in the fiscal year along with seemingly endless demand from

overseas buyers. Overall, corporate credit was up globally (the Bloomberg Barclays Global Aggregate Corporate Bond

Index returned 9.09%), with particularly strong performance out of the utilities sector of the market. The best performers

in the index were lower quality issues (BBB cohorts and below), longer maturities (7+ years) and higher beta countries

(Austria and Italy).

High yield corporate credit was among the best-performing segments of the global market (the Bloomberg Barclays Global

High Yield Bond Index returned 10.43%). High yield spreads tightened over the fiscal year due to the strong global

economy and investors searching for the slightest advantage in yields. The interest coverage ratio improved over the year

while the default rate for high yield securities fell, which were both positive factors.

8 Market Summary

Russell Investment Funds

U.S. Strategic Equity Fund

Portfolio Management Discussion and Analysis — December 31, 2017 (Unaudited)

| | | | | | | |

| U. S. Strategic Equity Fund | | | | Russell 1000® Index** | | | |

| | | Total | | | | Total | |

| | | Return | | | | Return | |

| 1 Year | | 20.80 | % | 1 Year | | 21.69 | % |

| 5 Years | | 14.94 | %§ | 5 Years | | 15.71 | %§ |

| 10 Years | | 7.59 | %§ | 10 Years | | 8.59 | %§ |

U.S. Strategic Equity Fund 9

Russell Investment Funds

U.S. Strategic Equity Fund

Portfolio Management Discussion and Analysis, continued — December 31, 2017

(Unaudited)

| |

| The U. S. Strategic Equity Fund (the “Fund”) employs a multi- | value stocks across all market capitalization tiers excluding mid |

| manager approach whereby portions of the Fund are allocated | cap. From a sector perspective, information technology, materials, |

| to different money manager strategies. Fund assets not allocated | and consumer discretionary outperformed the Russell 1000® |

| to money managers are managed by Russell Investment | Index by 16.83%, 2.02%, and 1.69%, respectively. Sectors that |

| Management, LLC (“RIM”), the Fund’s advisor. RIM may change | failed to find traction during the one-year period were energy, |

| the allocation of the Fund’s assets among money managers at | telecommunication services, and real estate, trailing by 23.25%, |

| any time. An exemptive order from the Securities and Exchange | 23.20%, and 11.76%, respectively. |

| Commission (“SEC”) permits RIM to engage or terminate a money | |

| manager at any time, subject to approval by the Fund’s Board, | How did the investment strategies and techniques employed |

| without a shareholder vote. Pursuant to the terms of the exemptive | by the Fund and its money managers affect its benchmark- |

| order, the Fund is required to notify its shareholders within 90 | relative performance? |

| days of when a money manager begins providing services. As of | The Fund’s factor exposures detracted from benchmark-relative |

| December 31, 2017, the Fund had five money managers. | performance over the period, including tilts away from stocks with |

| | high valuations (high price-to-book ratios) and the largest market |

| What is the Fund’s investment objective? | capitalization stocks. However, a tilt away from stocks with high |

| The Fund seeks to provide long term capital growth. | financial leverage (high debt-to-capital ratios) was beneficial and |

| |

| How did the Fund perform relative to its benchmark for the | helped to mitigate some of the underperformance. Industry group |

| fiscal year ended December 31, 2017? | allocation decisions also detracted, including an overweight |

| | to insurance and an underweight to technology hardware & |

| For the fiscal year ended December 31, 2017, the Fund gained | equipment. Stock selection within the industrials, real estate, and |

| 20.80%. This is compared to the Fund’s benchmark, the Russell | consumer staples sectors contributed positively to performance |

| 1000® Index, which gained 21.69% during the same period. The | over the one-year period. |

| Fund’s performance includes operating expenses, whereas index | |

| returns are unmanaged and do not include expenses of any kind. | The Fund employs discretionary and non-discretionary money |

| | managers. The Fund’s discretionary money managers select the |

| For the fiscal year ended December 31, 2017, the Morningstar® | individual portfolio securities for the assets assigned to them. |

| Insurance Large Blend Category, a group of funds that Morningstar | The Fund’s non-discretionary money managers provide a model |

| considers to have investment strategies similar to those of the | portfolio to RIM representing their investment recommendations, |

| Fund, gained 21.28%. This result serves as a peer comparison | based upon which RIM purchases and sells securities for the |

| and is expressed net of operating expenses. | Fund. Fund assets not allocated to discretionary money managers |

| RIM may assign a money manager a specific style or | include assets managed by RIM based upon model portfolios |

| capitalization benchmark other than the Fund’s index. However, | provided by non-discretionary money managers, the Fund’s cash |

| the Fund’s primary index remains the benchmark for the Fund | balances and assets which may be managed directly by RIM to |

| and is representative of the aggregate of each money manager’s | effect the Fund’s investment strategies and/or to actively manage |

| benchmark index. | the Fund’s overall exposures by investing in securities or other |

| | instruments that RIM believes will achieve the desired risk/ |

| How did the market conditions described in the Market | return profile for the Fund. |

| Summary report affect the Fund’s performance? | |

| Broadly measured by the Russell 3000® Index, U. S. stocks | With respect to certain of the Fund’s money managers, William |

| returned 21.13% for the one-year period, which is the ninth | Blair Investment Management, LLC was the best performing |

| straight calendar year that the Russell 3000® Index has finished | manager for the period and outperformed the Russell 1000® |

| with a positive absolute return. The Russell 3000® Index finished | Growth Index. Factor exposures were rewarded, including a tilt |

| with a positive absolute return in each of the calendar year’s | toward high forecasted growth and a tilt away from high financial |

| twelve months. | leverage (high debt-to-capital ratios) . Stock selection within the |

| | information technology, real estate, and health care sectors was |

| Within U. S. large capitalization stocks, factors that were rewarded | notably beneficial. |

| during the calendar year included high beta (beta is a measure of | |

| a stock’s sensitivity to the direction of the market), high historical | Jacobs Levy Equity Management, Inc. had the lowest absolute |

| earnings growth, and the largest capitalization stocks. Factors that | return for the period, although they still outperformed the |

| trailed the market included high dividend yield, low price-to-book | Russell 1000® Value Index. Factor exposures were rewarded, |

| ratios, and high earnings variability. Additionally, dynamic stocks | including a tilt toward high beta stocks and a tilt away from the |

| outperformed defensive stocks and growth stocks outperformed | highest dividend yield stocks. An overweight to the information |

10 U.S. Strategic Equity Fund

Russell Investment Funds

U.S. Strategic Equity Fund

Portfolio Management Discussion and Analysis, continued — December 31, 2017

(Unaudited)

| | |

| technology sector and an underweight to the consumer staples | | |

| sector contributed positively to performance. Stock selection | There were no changes to the Fund’s structure or the money |

| within the financials, health care, and consumer staples sectors | manager line up during the calendar year. |

| detracted. | | |

| | Money Managers as of December 31, |

| RIM manages a 14% (effective December 31, 2017) strategic | 2017 | Styles |

| allocation to a positioning strategy to seek to achieve the desired | | |

| | Barrow, Hanley, Mewhinney & Strauss, LLC Value |

| risk/return profile for the Fund. The positioning strategy utilizes | Jacobs Levy Equity Management, Inc. | Value |

| the output from a quantitative model to seek to position the portfolio | Mar Vista Investment Partners, LLC | Market-Oriented |

| to meet RIM’s overall preferred positioning. The positioning | Suffolk Capital Management LLC | Market-Oriented |

| strategy underperformed the Russell 1000® Index during the | William Blair Investment Management, LLC Growth |

| one-year period. Factor exposures were mixed, as a tilt toward | The views expressed in this report reflect those of the |

| the largest market capitalization stocks was rewarded while a tilt | portfolio managers only through the end of the period |

| away from the highest beta stocks detracted. Overweights to the | covered by the report. These views do not necessarily |

| telecommunication services and consumer staples sectors notably | represent the views of RIM, or any other person in RIM or |

| detracted during the year. | any other affiliated organization. These views are subject to |

| During the period, RIM used index futures contracts to equitize | change at any time based upon market conditions or other |

| the Fund’s cash. The decision to equitize the Fund’s cash was | events, and RIM disclaims any responsibility to update the |

| beneficial to the Fund’s absolute performance for the calendar | views contained herein. These views should not be relied |

| year as the market had a positive absolute return. | on as investment advice and, because investment decisions |

| | for a Russell Investment Funds (“RIF”) Fund are based on |

| Describe any changes to the Fund’s structure or the money | numerous factors, should not be relied on as an indication |

| manager line-up. | of investment decisions of any RIF Fund. |

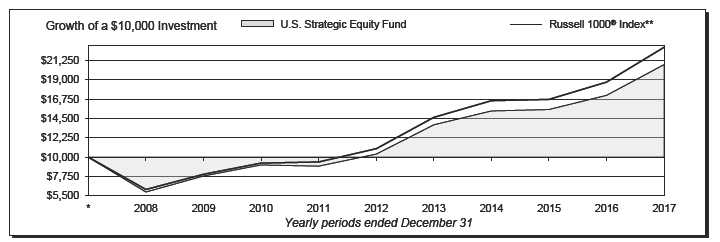

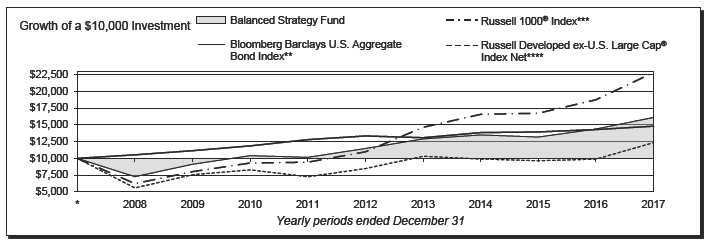

* Assumes initial investment on January 1, 2008.

** The Russell 1000® Index includes the 1,000 largest companies in the Russell 3000® Index. The Russell 1000® Index represents the universe of stocks from

which most active money managers typically select. The Russell 1000® Index return reflects adjustments from income dividends and capital gain distributions

reinvested as of the ex-dividend dates.

§ Annualized.

The performance shown in this section does not reflect any Insurance Company Separate Account or Policy Charges. Performance is historical and assumes

reinvestment of all dividends and capital gains. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more

or less than when purchased. Past performance is not indicative of future results. Additionally, the returns presented herein may differ from the performance reported

in the Financial Highlights as the returns herein are calculated in a manner consistent with standardized performance in accordance with Securities and Exchange

Commission rules, while the performance in the Financial Highlights has been calculated in accordance with U.S. Generally Accepted Accounting Principles (“U.S.

GAAP”).

U.S. Strategic Equity Fund 11

Russell Investment Funds

U.S. Strategic Equity Fund

Shareholder Expense Example — December 31, 2017 (Unaudited)

| | | | | | | |

| Fund Expenses | Please note that the expenses shown in the table are meant |

| The following disclosure provides important information | to highlight your ongoing costs only and do not reflect any |

| regarding the Fund’s Shareholder Expense Example | transactional costs. Therefore, the information under the heading |

| (“Example”) . | “Hypothetical Performance (5% return before expenses)” is |

| | useful in comparing ongoing costs only, and will not help you |

| Example | determine the relative total costs of owning different funds. In |

| As a shareholder of the Fund, you incur two types of costs: (1) | addition, if these transactional costs were included, your costs |

| transaction costs, and (2) ongoing costs, including advisory and | would have been higher. The fees and expenses shown in this |

| administrative fees and other Fund expenses. The Example is | section do not reflect any Insurance Company Separate Account |

| intended to help you understand your ongoing costs (in dollars) | Policy Charges. | | | | | | |

| of investing in the Fund and to compare these costs with the | | | | | | Hypothetical |

| ongoing costs of investing in other mutual funds. The Example | | | | | | Performance (5% |

| is based on an investment of $1,000 invested at the beginning of | | | | Actual | | return before |

| the period and held for the entire period indicated, which for this | | | Performance | | | expenses) |

| | Beginning Account Value | | | | | | |

| Fund is from July 1, 2017 to December 31, 2017. | July 1, 2017 | | $ | 1,000.00 | | $ | 1,000.00 |

| | Ending Account Value | | | | | | |

| Actual Expenses | December 31, 2017 | | $ | 1,108.30 | | $ | 1,020.97 |

| The information in the table under the heading “Actual | Expenses Paid During Period* | | $ | 4.46 | | $ | 4.28 |

| Performance” provides information about actual account values | | | | | | | |

| and actual expenses. You may use the information in this column, | * Expenses are equal to the Fund's annualized expense ratio of 0.84% |

| | (representing the six month period annualized), multiplied by the average |

| together with the amount you invested, to estimate the expenses | account value over the period, multiplied by 184/365 (to reflect the one-half |

| that you paid over the period. Simply divide your account value by | year period) . | | | | | | |

| $1,000 (for example, an $8,600 account value divided by $1,000 | | | | | | | |

| = 8.6), then multiply the result by the number in the first column | | | | | | | |

| in the row entitled “Expenses Paid During Period” to estimate | | | | | | | |

| the expenses you paid on your account during this period. | | | | | | | |

| |

| Hypothetical Example for Comparison Purposes | | | | | | | |

| The information in the table under the heading “Hypothetical | | | | | | | |

| Performance (5% return before expenses)” provides information | | | | | | | |

| about hypothetical account values and hypothetical expenses | | | | | | | |

| based on the Fund’s actual expense ratio and an assumed rate of | | | | | | | |

| return of 5% per year before expenses, which is not the Fund’s | | | | | | | |

| actual return. The hypothetical account values and expenses | | | | | | | |

| may not be used to estimate the actual ending account balance or | | | | | | | |

| expenses you paid for the period. You may use this information | | | | | | | |

| to compare the ongoing costs of investing in the Fund and other | | | | | | | |

| funds. To do so, compare this 5% hypothetical example with the | | | | | | | |

| 5% hypothetical examples that appear in the shareholder reports | | | | | | | |

| of other funds. | | | | | | | |

12 U.S. Strategic Equity Fund

Russell Investment Funds

U.S. Strategic Equity Fund

Schedule of Investments — December 31, 2017

| | | | | | | |

| Amounts in thousands (except share amounts) | | Amounts in thousands (except share amounts) | |

| | | Principal | Fair | | | Principal | Fair |

| | Amount ($) or | Value | | Amount ($) or | Value |

| | | Shares | $ | | | Shares | $ |

| Common Stocks - 93.8% | | | | Molson Coors Brewing Co. Class B | | 2,827 | 232 |

| Consumer Discretionary - 9.6% | | | | Mondelez International, Inc. Class A | | 70,423 | 3,014 |

| Amazon. com, Inc. (Æ) | | 6,380 | 7,461 | Monster Beverage Corp. (Æ) | | 36,026 | 2,280 |

| Aramark | | 3,161 | 135 | PepsiCo, Inc. | | 26,997 | 3,238 |

| Arconic, Inc. | | 9,900 | 270 | Philip Morris International, Inc. | | 51,187 | 5,408 |

| Brunswick Corp. | | 2,400 | 133 | Procter & Gamble Co. (The) | | 2,500 | 230 |

| Carnival Corp. | | 8,393 | 557 | Tyson Foods, Inc. Class A | | 12,634 | 1,024 |

| Carter's, Inc. | | 315 | 37 | Unilever NV | | 48,476 | 2,729 |

| CBS Corp. Class B | | 20,826 | 1,229 | | | | |

| Cooper-Standard Holdings, Inc. (Æ) | | 3,030 | 371 | | | | 24,311 |

| Dollar Tree, Inc. (Æ) | | 33,020 | 3,543 | | | | |

| DR Horton, Inc. | | 26,561 | 1,357 | Energy - 7.2% | | | |

| | | | | Anadarko Petroleum Corp. | | 10,300 | 552 |

| eBay, Inc. (Æ) | | 13,784 | 520 | Andeavor(Æ) | | 2,041 | 233 |

| Estee Lauder Cos. , Inc. (The) Class A | | 13,187 | 1,678 | Arch Coal, Inc. (Æ) | | 6,000 | 559 |

| Ford Motor Co. | | 104,200 | 1,301 | BP PLC - ADR | | 58,018 | 2,438 |

| Fortune Brands Home & Security, Inc. | | 463 | 32 | Chevron Corp. | | 47,479 | 5,945 |

| GameStop Corp. Class A | | 2,573 | 46 | Cimarex Energy Co. | | 3,130 | 382 |

| Garmin, Ltd. | | 1,124 | 67 | ConocoPhillips | | 17,298 | 949 |

| General Motors Co. | | 38,178 | 1,565 | Core Laboratories NV | | 16,779 | 1,838 |

| Goodyear Tire & Rubber Co. (The) | | 1,155 | 37 | EOG Resources, Inc. | | 12,293 | 1,327 |

| Graham Holdings Co. Class B | | 565 | 315 | Exxon Mobil Corp. | | 57,602 | 4,819 |

| Home Depot, Inc. (The) | | 5,713 | 1,083 | First Solar, Inc. (Æ) | | 9,232 | 623 |

| Hyatt Hotels Corp. Class A(Æ) | | 1,392 | 102 | Kosmos Energy, Ltd. (Æ) | | 10,300 | 71 |

| International Game Technology PLC | | 4,100 | 109 | Marathon Petroleum Corp. | | 20,439 | 1,348 |

| Lear Corp. | | 942 | 166 | National Oilwell Varco, Inc. | | 27,900 | 1,005 |

| Madison Square Garden Co. (The) Class A(Æ) | 4,240 | 894 | Occidental Petroleum Corp. | | 39,685 | 2,924 |

| McDonald's Corp. | | 7,352 | 1,266 | Peabody Energy Corp. (Æ) | | 5,100 | 201 |

| MGM Resorts International | | 36,081 | 1,205 | Phillips 66 | | 26,001 | 2,630 |

| Michael Kors Holdings, Ltd. (Æ) | | 8,800 | 554 | Royal Dutch Shell PLC Class A - ADR | | 18,760 | 1,251 |

| Netflix, Inc. (Æ) | | 4,101 | 787 | Schlumberger, Ltd. | | 26,825 | 1,808 |

| NVR, Inc. (Æ) | | 12 | 42 | Transocean, Ltd. (Æ) | | 16,052 | 171 |

| O'Reilly Automotive, Inc. (Æ) | | 5,492 | 1,321 | Valero Energy Corp. | | 18,246 | 1,677 |

| PulteGroup, Inc. | | 5,088 | 169 | World Fuel Services Corp. | | 11,673 | 328 |

| PVH Corp. | | 1,741 | 239 | | | | |

| Service Corp. International | | 4,222 | 158 | | | | 33,079 |

| Sirius XM Holdings, Inc. | | 76,900 | 412 | | | | |

| Starbucks Corp. | | 74,327 | 4,269 | Financial Services - 21.2% | | | |

| Tapestry, Inc. | | 24,468 | 1,082 | Affiliated Managers Group, Inc. | | 7,564 | 1,553 |

| Target Corp. | | 18,576 | 1,212 | Aflac, Inc. | | 1,759 | 154 |

| Time Warner, Inc. | | 6,729 | 616 | Allstate Corp. (The) | | 12,055 | 1,262 |

| Vail Resorts, Inc. | | 4,377 | 930 | Ally Financial, Inc. | | 7,074 | 206 |

| Wal-Mart Stores, Inc. | | 33,222 | 3,281 | American Express Co. | | 27,138 | 2,695 |

| Walt Disney Co. (The) | | 28,725 | 3,088 | American International Group, Inc. | | 22,200 | 1,323 |

| Whirlpool Corp. | | 3,221 | 543 | American National Insurance Co. | | 1,044 | 134 |

| Yum China Holdings, Inc. | | 7,774 | 311 | American Tower Corp. (ö) | | 27,755 | 3,960 |

| | | | | Aspen Insurance Holdings, Ltd. | | 13,100 | 532 |

| | | | 44,493 | Assured Guaranty, Ltd. | | 3,619 | 123 |

| | | | | Athene Holding, Ltd. Class A(Æ) | | 8,410 | 435 |

| Consumer Staples - 5.3% | | | | Axis Capital Holdings, Ltd. | | 10,980 | 552 |

| Altria Group, Inc. | | 25,163 | 1,797 | Bank of America Corp. | | 187,858 | 5,545 |

| Archer-Daniels-Midland Co. | | 31,532 | 1,264 | Bank of New York Mellon Corp. (The) | | 12,949 | 697 |

| Bunge, Ltd. | | 15,537 | 1,042 | BB&T Corp. | | 823 | 41 |

| Coca-Cola Co. (The) | | 3,242 | 149 | Berkshire Hathaway, Inc. Class B(Æ) | | 31,846 | 6,313 |

| Colgate-Palmolive Co. | | 7,100 | 536 | Broadridge Financial Solutions, Inc. | | 3,297 | 299 |

| Constellation Brands, Inc. Class A | | 3,458 | 790 | Capital One Financial Corp. | | 22,983 | 2,288 |

| Hershey Co. (The) | | 293 | 33 | Cboe Global Markets, Inc. | | 3,020 | 376 |

| Ingredion, Inc. | | 1,485 | 208 | CBRE Group, Inc. Class A(Æ) | | 5,700 | 247 |

| JM Smucker Co. (The) | | 836 | 104 | Citigroup, Inc. | | 30,530 | 2,271 |

| Kraft Heinz Co. (The) | | 2,990 | 233 | Citizens Financial Group, Inc. | | 18,330 | 769 |

See accompanying notes which are an integral part of the financial statements.

U.S. Strategic Equity Fund 13

Russell Investment Funds

U.S. Strategic Equity Fund

Schedule of Investments, continued — December 31, 2017

| | | | | | | |

| Amounts in thousands (except share amounts) | | Amounts in thousands (except share amounts) | |

| | | Principal | Fair | | | Principal | Fair |

| | Amount ($) or | Value | | Amount ($) or | Value |

| | | Shares | $ | | | Shares | $ |

| Comerica, Inc. | | 9,800 | 851 | Align Technology, Inc. (Æ) | | 463 | 103 |

| Discover Financial Services | | 14,200 | 1,092 | Allergan PLC(Æ) | | 13,726 | 2,246 |

| Duke Realty Corp. (ö) | | 16,800 | 457 | Allscripts Healthcare Solutions, Inc. (Æ) | | 27,228 | 396 |

| Dun & Bradstreet Corp. (The) | | 2,290 | 271 | Amgen, Inc. | | 1,385 | 241 |

| E*Trade Financial Corp. (Æ) | | 18,798 | 931 | Anthem, Inc. (Æ) | | 7,903 | 1,778 |

| Equity Residential(ö) | | 15,000 | 957 | Baxter International, Inc. | | 21,144 | 1,367 |

| Essex Property Trust, Inc. (ö) | | 2,810 | 678 | Becton Dickinson and Co. | | 796 | 170 |

| Fidelity National Information Services, Inc. | | 3,151 | 296 | Biogen, Inc. (Æ) | | 3,857 | 1,229 |

| First Republic Bank | | 12,433 | 1,077 | Bio-Rad Laboratories, Inc. Class A(Æ) | | 1,077 | 257 |

| Fiserv, Inc. (Æ) | | 1,154 | 151 | Bio-Techne Corp. (Æ) | | 2,190 | 284 |

| Global Payments, Inc. | | 301 | 30 | Bristol-Myers Squibb Co. | | 17,000 | 1,042 |

| Goldman Sachs Group, Inc. (The) | | 6,024 | 1,535 | Bruker Corp. | | 7,764 | 266 |

| Hartford Financial Services Group, Inc. | | 38,365 | 2,159 | Cardinal Health, Inc. | | 28,250 | 1,731 |

| HCP, Inc. (ö) | | 44,856 | 1,170 | Celgene Corp. (Æ) | | 11,930 | 1,245 |

| Intercontinental Exchange, Inc. | | 23,605 | 1,666 | Centene Corp. (Æ) | | 3,074 | 310 |

| Jack Henry & Associates, Inc. | | 2,035 | 238 | Cerner Corp. (Æ) | | 461 | 31 |

| JPMorgan Chase & Co. | | 73,364 | 7,845 | Charles River Laboratories International, | | | |

| KeyCorp | | 96,386 | 1,944 | Inc. (Æ) | | 440 | 48 |

| Lazard, Ltd. Class A | | 1,027 | 54 | Cigna Corp. | | 2,043 | 415 |

| Leucadia National Corp. | | 2,750 | 73 | Eli Lilly & Co. | | 3,086 | 261 |

| Loews Corp. | | 33,441 | 1,673 | Endo International PLC(Æ) | | 17,300 | 134 |

| M&T Bank Corp. | | 6,996 | 1,196 | Envision Healthcare Corp. (Æ) | | 1,995 | 69 |

| Markel Corp. (Æ) | | 3,724 | 4,241 | Express Scripts Holding Co. (Æ) | | 20,655 | 1,542 |

| MasterCard, Inc. Class A | | 18,140 | 2,745 | Gilead Sciences, Inc. | | 2,536 | 182 |

| MetLife, Inc. | | 7,600 | 384 | Henry Schein, Inc. (Æ) | | 866 | 61 |

| Moody's Corp. | | 15,854 | 2,340 | Humana, Inc. | | 3,008 | 747 |

| Morgan Stanley | | 20,371 | 1,069 | Illumina, Inc. (Æ) | | 388 | 85 |

| Morningstar, Inc. | | 959 | 93 | Intuitive Surgical, Inc. (Æ) | | 525 | 192 |

| Nasdaq, Inc. | | 1,319 | 101 | Johnson & Johnson | | 52,684 | 7,359 |

| New York Community Bancorp, Inc. | | 30,744 | 400 | Laboratory Corp. of America Holdings(Æ) | | 1,642 | 262 |

| Northern Trust Corp. | | 11,300 | 1,129 | LifePoint Health, Inc. (Æ) | | 2,447 | 122 |

| PayPal Holdings, Inc. (Æ) | | 3,501 | 258 | Mallinckrodt PLC(Æ) | | 6,400 | 144 |

| PNC Financial Services Group, Inc. (The) | | 15,219 | 2,196 | McKesson Corp. | | 8,974 | 1,400 |

| Popular, Inc. | | 10,200 | 362 | Medtronic PLC | | 11,354 | 916 |

| Progressive Corp. (The) | | 39,356 | 2,217 | Merck & Co. , Inc. | | 77,999 | 4,387 |

| Prudential Financial, Inc. | | 11,400 | 1,311 | PerkinElmer, Inc. | | 3,848 | 281 |

| Reinsurance Group of America, Inc. Class A | 5,320 | 830 | Pfizer, Inc. | | 71,691 | 2,596 |

| Santander Consumer USA Holdings, Inc. | | 5,900 | 110 | Qiagen NV(Æ) | | 5,854 | 181 |

| SBA Communications Corp. (Æ)(ö) | | 7,655 | 1,251 | Quest Diagnostics, Inc. | | 2,546 | 251 |

| SL Green Realty Corp. (ö) | | 8,500 | 858 | Sage Therapeutics, Inc. (Æ) | | 3,064 | 505 |

| State Street Corp. | | 37,062 | 3,617 | Sanofi - ADR | | 23,603 | 1,015 |

| SunTrust Banks, Inc. | | 18,916 | 1,222 | Steris PLC | | 967 | 85 |

| Total System Services, Inc. | | 1,968 | 156 | Stryker Corp. | | 5,794 | 898 |

| US Bancorp | | 49,974 | 2,678 | Teleflex, Inc. | | 204 | 51 |

| Vantiv, Inc. Class A(Æ) | | 841 | 62 | Thermo Fisher Scientific, Inc. | | 1,442 | 274 |

| Visa, Inc. Class A | | 21,138 | 2,411 | United Therapeutics Corp. (Æ) | | 355 | 53 |

| Voya Financial, Inc. | | 18,600 | 920 | UnitedHealth Group, Inc. | | 21,024 | 4,634 |

| Wells Fargo & Co. | | 84,986 | 5,157 | Universal Health Services, Inc. Class B | | 1,799 | 204 |

| XL Group, Ltd. | | 51,040 | 1,795 | Varian Medical Systems, Inc. (Æ) | | 296 | 33 |

| | | | 98,032 | WellCare Health Plans, Inc. (Æ) | | 2,728 | 549 |

| | | | | West Pharmaceutical Services, Inc. | | 302 | 30 |

| Health Care - 10.6% | | | | Zoetis, Inc. Class A | | 38,184 | 2,750 |

| Abbott Laboratories | | 20,470 | 1,168 | | | | 48,738 |

| AbbVie, Inc. | | 1,025 | 99 | | | | |

| Aerie Pharmaceuticals, Inc. (Æ) | | 20,514 | 1,226 | Materials and Processing - 3.0% | | | |

| Aetna, Inc. | | 1,047 | 189 | Ashland Global Holdings, Inc. | | 11,909 | 848 |

| Agilent Technologies, Inc. | | 3,391 | 227 | Ball Corp. (Æ) | | 1,475 | 56 |

| Akorn, Inc. (Æ) | | 12,929 | 417 | Berry Plastics Group, Inc. (Æ) | | 2,443 | 143 |

See accompanying notes which are an integral part of the financial statements.

14 U.S. Strategic Equity Fund

Russell Investment Funds

U.S. Strategic Equity Fund

Schedule of Investments, continued — December 31, 2017

| | | | | | | |

| Amounts in thousands (except share amounts) | | Amounts in thousands (except share amounts) | |

| | | Principal | Fair | | | Principal | Fair |

| | Amount ($) or | Value | | Amount ($) or | Value |

| | | Shares | $ | | | Shares | $ |

| Celanese Corp. Class A | | 9,350 | 1,001 | IHS Markit, Ltd. (Æ) | | 4,998 | 226 |

| Crown Holdings, Inc. (Æ) | | 1,009 | 57 | Jacobs Engineering Group, Inc. | | 12,500 | 825 |

| Domtar Corp. | | 5,152 | 255 | JB Hunt Transport Services, Inc. | | 291 | 33 |

| DowDuPont, Inc. | | 32,919 | 2,345 | Johnson Controls International PLC(Æ) | | 52,258 | 1,992 |

| Ecolab, Inc. | | 18,173 | 2,439 | Kansas City Southern | | 13,122 | 1,381 |

| Hexcel Corp. | | 14,344 | 887 | Kirby Corp. (Æ) | | 989 | 66 |

| Huntsman Corp. | | 3,100 | 103 | Korn/Ferry International | | 1,600 | 66 |

| International Flavors & Fragrances, Inc. | | 1,272 | 194 | L3 Technologies, Inc. | | 1,795 | 355 |

| LyondellBasell Industries NV Class A | | 652 | 72 | Landstar System, Inc. | | 311 | 32 |

| Monsanto Co. | | 3,476 | 406 | Lockheed Martin Corp. | | 2,452 | 787 |

| NewMarket Corp. | | 76 | 30 | ManpowerGroup, Inc. | | 8,466 | 1,067 |

| Owens Corning | | 11,871 | 1,091 | Mettler-Toledo International, Inc. (Æ) | | 3,217 | 1,993 |

| Packaging Corp. of America | | 266 | 32 | Navistar International Corp. (Æ) | | 1,300 | 56 |

| PPG Industries, Inc. | | 9,970 | 1,165 | Norfolk Southern Corp. | | 14,873 | 2,155 |

| Praxair, Inc. | | 16,479 | 2,549 | Northrop Grumman Corp. | | 1,763 | 541 |

| Sonoco Products Co. | | 1,238 | 66 | Old Dominion Freight Line, Inc. | | 828 | 109 |

| Tahoe Resources, Inc. | | 60,615 | 290 | Orbital ATK, Inc. | | 1,927 | 253 |

| | | | 14,029 | Paychex, Inc. | | 2,275 | 155 |

| | | | | Quanta Services, Inc. (Æ) | | 40,053 | 1,567 |

| Producer Durables - 16.7% | | | | Raytheon Co. | | 28,893 | 5,428 |

| 3M Co. | | 1,561 | 367 | Republic Services, Inc. Class A | | 1,807 | 122 |

| Accenture PLC Class A | | 15,138 | 2,318 | Rockwell Automation, Inc. | | 6,471 | 1,271 |

| Adient PLC | | 11,619 | 914 | Rockwell Collins, Inc. | | 4,166 | 565 |

| AECOM(Æ) | | 32,632 | 1,212 | Roper Technologies, Inc. | | 10,766 | 2,788 |

| AGCO Corp. | | 13,400 | 957 | Rush Enterprises, Inc. Class A(Æ) | | 3,100 | 158 |

| Ametek, Inc. | | 3,201 | 232 | Ryder System, Inc. | | 5,300 | 446 |

| Automatic Data Processing, Inc. | | 1,136 | 133 | Sensata Technologies Holding NV(Æ) | | 48,164 | 2,462 |

| Avery Dennison Corp. | | 2,564 | 295 | Southwest Airlines Co. | | 25,342 | 1,659 |

| Babcock & Wilcox Co. (The) Class W(Æ) | | 3,708 | 224 | Spirit AeroSystems Holdings, Inc. Class A | | 2,829 | 247 |

| Boeing Co. (The) | | 5,182 | 1,529 | Square, Inc. Class A(Æ) | | 2,189 | 76 |

| Booz Allen Hamilton Holding Corp. Class A | | 1,868 | 71 | Stanley Black & Decker, Inc. | | 11,728 | 1,990 |

| Carlisle Cos. , Inc. | | 277 | 31 | Teledyne Technologies, Inc. (Æ) | | 256 | 46 |

| Caterpillar, Inc. | | 4,310 | 679 | Textron, Inc. | | 20,165 | 1,141 |

| Copa Holdings SA Class A | | 1,430 | 192 | TransDigm Group, Inc. | | 12,541 | 3,444 |

| Copart, Inc. (Æ) | | 17,502 | 756 | Union Pacific Corp. | | 18,531 | 2,485 |

| CoStar Group, Inc. (Æ) | | 775 | 230 | United Technologies Corp. | | 19,202 | 2,450 |

| CSX Corp. | | 860 | 47 | Verisk Analytics, Inc. Class A(Æ) | | 17,643 | 1,694 |

| Cummins, Inc. | | 3,885 | 686 | Waters Corp. (Æ) | | 908 | 175 |

| Danaher Corp. | | 16,153 | 1,499 | Werner Enterprises, Inc. | | 800 | 31 |

| Delta Air Lines, Inc. | | 22,483 | 1,259 | Xerox Corp. | | 17,400 | 507 |

| Dover Corp. | | 320 | 32 | XPO Logistics, Inc. (Æ) | | 45,452 | 4,163 |

| Eaton Corp. PLC | | 3,243 | 256 | Xylem, Inc. | | 15,326 | 1,045 |

| EMCOR Group, Inc. | | 7,700 | 629 | | | | 77,041 |

| Evoqua Water Technologies Corp. (Æ) | | 712 | 17 | | | | |

| Expeditors International of Washington, Inc. | | 2,546 | 165 | Technology - 17.3% | | | |

| FedEx Corp. | | 6,282 | 1,568 | Adobe Systems, Inc. (Æ) | | 20,436 | 3,581 |

| Fluor Corp. | | 17,900 | 925 | Alibaba Group Holding, Ltd. - ADR(Æ) | | 6,314 | 1,089 |

| Fortive Corp. | | 44,424 | 3,214 | Alphabet, Inc. Class A(Æ) | | 3,731 | 3,930 |

| General Dynamics Corp. | | 2,105 | 428 | Alphabet, Inc. Class C(Æ) | | 6,757 | 7,070 |

| General Electric Co. | | 54,165 | 945 | Amdocs, Ltd. | | 9,214 | 603 |

| Genpact, Ltd. | | 18,050 | 573 | Amphenol Corp. Class A | | 2,969 | 261 |

| Graco, Inc. | | 1,455 | 66 | Analog Devices, Inc. | | 336 | 30 |

| Heico Corp. Class A | | 2,216 | 175 | Apple, Inc. | | 42,826 | 7,248 |

| HEICO Corp. | | 2,343 | 221 | Applied Materials, Inc. | | 2,883 | 147 |

| Honeywell International, Inc. | | 38,589 | 5,919 | Arista Networks, Inc. (Æ) | | 1,174 | 277 |

| Hubbell, Inc. Class B | | 516 | 70 | ARRIS International PLC(Æ) | | 14,200 | 365 |

| Huntington Ingalls Industries, Inc. | | 300 | 71 | Arrow Electronics, Inc. (Æ) | | 2,556 | 206 |

| IDEX Corp. | | 638 | 84 | Benchmark Electronics, Inc. (Æ) | | 800 | 23 |

See accompanying notes which are an integral part of the financial statements.

U.S. Strategic Equity Fund 15

Russell Investment Funds

U.S. Strategic Equity Fund

Schedule of Investments, continued — December 31, 2017

| | | | | | | | | |

| Amounts in thousands (except share amounts) | | Amounts in thousands (except share amounts) | | |

| | | Principal | Fair | | | | Principal | | Fair |

| | Amount ($) or | Value | | | Amount ($) or | | Value |

| | | Shares | $ | | | | Shares | | $ |

| Broadcom, Ltd. | | 3,587 | 922 | Centennial Resource Development, Inc. Class | | | | | |

| CA, Inc. | | 5,291 | 176 | A(Æ) | | | 17,564 | | 348 |

| Cars. com, Inc. (Æ) | | 8,354 | 241 | CenterPoint Energy, Inc. | | | 2,357 | | 67 |

| Cisco Systems, Inc. | | 51,852 | 1,986 | Consolidated Edison, Inc. | | | 3,518 | | 299 |

| Cognizant Technology Solutions Corp. Class | | | | Edison International | | | 13,889 | | 878 |

| A | | 4,843 | 344 | Entergy Corp. | | | 21,107 | | 1,718 |

| CommScope Holding Co. , Inc. (Æ) | | 28,605 | 1,082 | Exelon Corp. | | | 8,669 | | 342 |

| Conduent, Inc. (Æ) | | 5,500 | 89 | Great Plains Energy, Inc. | | | 8,389 | | 270 |

| Corning, Inc. | | 11,477 | 367 | Hawaiian Electric Industries, Inc. | | | 10,452 | | 378 |

| DST Systems, Inc. | | 525 | 33 | NiSource, Inc. | | | 22,500 | | 578 |

| DXC Technology Co. | | 15,463 | 1,467 | PG&E Corp. | | | 14,600 | | 655 |

| EchoStar Corp. Class A(Æ) | | 4,001 | 240 | Pinnacle West Capital Corp. | | | 3,000 | | 256 |

| Electronic Arts, Inc. (Æ) | | 1,544 | 162 | Southern Co. (The) | | | 4,638 | | 223 |

| F5 Networks, Inc. (Æ) | | 1,012 | 133 | Sprint Corp. (Æ) | | | 21,100 | | 124 |

| Facebook, Inc. Class A(Æ) | | 38,094 | 6,722 | T-Mobile US, Inc. (Æ) | | | 12,703 | | 807 |

| FireEye, Inc. (Æ) | | 4,900 | 70 | US Cellular Corp. (Æ) | | | 6,100 | | 230 |

| Gartner, Inc. (Æ) | | 1,235 | 152 | Verizon Communications, Inc. | | | 35,824 | | 1,895 |

| Hewlett Packard Enterprise Co. | | 87,337 | 1,254 | Vistra Energy Corp. (Æ) | | | 8,000 | | 147 |

| HP, Inc. (Æ) | | 62,763 | 1,318 | | | | | | 13,224 |

| Intel Corp. | | 28,754 | 1,328 | | | | | | |

| |

| International Business Machines Corp. | | 8,493 | 1,303 | Total Common Stocks | | | | | |

| Intuit, Inc. | | 25,708 | 4,056 | | | | | | |

| IPG Photonics Corp. (Æ) | | 1,018 | 218 | (cost $335,466) | | | | | 432,951 |

| Jabil Circuit, Inc. | | 6,700 | 176 | | | | | | |

| Juniper Networks, Inc. | | 37,825 | 1,078 | Short-Term Investments - 6.0% | | | | | |

| Lam Research Corp. | | 817 | 150 | U. S. Cash Management Fund(@) | | | 27,698,287 | (8) | 27,698 |

| Leidos Holdings, Inc. | | 5,210 | 336 | Total Short-Term Investments | | | | | |

| Liberty Expedia Holdings, Inc. Class A(Æ) | | 5,351 | 237 | (cost $27,699) | | | | | 27,698 |

| LogMeIn, Inc. | | 849 | 97 | | | | | | |

| Marvell Technology Group, Ltd. | | 95,567 | 2,051 | Total Investments 99.8% | | | | | |

| Maxim Integrated Products, Inc. | | 3,453 | 181 | | | | | | |

| Micron Technology, Inc. (Æ) | | 11,528 | 474 | (identified cost $363,165) | | | | | 460,649 |

| Microsoft Corp. | | 86,612 | 7,409 | Other Assets and Liabilities, Net | | | | | |

| NetApp, Inc. | | 10,046 | 555 | - 0.2% | | | | | 1,078 |

| Nuance Communications, Inc. (Æ) | | 10,800 | 177 | | | | | | |

| NVIDIA Corp. | | 751 | 145 | Net Assets - 100.0% | | | | | 461,727 |

| Oracle Corp. | | 108,938 | 5,150 | | | | | | |

| Progress Software Corp. | | 4,900 | 209 | | | | | | |

| Qorvo, Inc. (Æ) | | 1,249 | 83 | | | | | | |

| QUALCOMM, Inc. | | 48,782 | 3,123 | | | | | | |

| Red Hat, Inc. (Æ) | | 15,043 | 1,807 | | | | | | |

| Salesforce. com, Inc. (Æ) | | 5,759 | 589 | | | | | | |

| Skyworks Solutions, Inc. | | 1,417 | 135 | | | | | | |

| Synopsys, Inc. (Æ) | | 13,746 | 1,172 | | | | | | |

| Take-Two Interactive Software, Inc. (Æ) | | 1,209 | 133 | | | | | | |

| Tech Data Corp. (Æ) | | 7,260 | 711 | | | | | | |

| Texas Instruments, Inc. | | 20,609 | 2,152 | | | | | | |

| Twitter, Inc. (Æ) | | 31,100 | 747 | | | | | | |

| Tyler Technologies, Inc. (Æ) | | 455 | 81 | | | | | | |

| Viavi Solutions, Inc. Class W(Æ) | | 100,600 | 879 | | | | | | |

| VMware, Inc. Class A(Æ) | | 1,125 | 141 | | | | | | |

| Western Digital Corp. | | 9,700 | 771 | | | | | | |

| Xilinx, Inc. | | 2,259 | 152 | | | | | | |

| Zynga, Inc. Class A(Æ) | | 102,400 | 410 | | | | | | |

| | | | 80,004 | | | | | | |

| |

| Utilities - 2.9% | | | | | | | | | |

| AT&T, Inc. | | 103,149 | 4,009 | | | | | | |

See accompanying notes which are an integral part of the financial statements.

16 U.S. Strategic Equity Fund

Russell Investment Funds

U.S. Strategic Equity Fund

Schedule of Investments, continued — December 31, 2017

| | | | | | | | | | | | | | | |

| Futures Contracts | | | | | | | | | | | | | | | |

| Amounts in thousands (except contract amounts) | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | Value and | |

| | | | | | | | | | | | | | | Unrealized | |

| | | | | | | | | | | | | | Appreciation | |

| | | | | | | Number of | Notional | Expiration | | (Depreciation) | |

| | | | | | | Contracts | Amount | | Date | | | $ | |

| Long Positions | | | | | | | | | | | | | | | |

| S&P 500 E-Mini Index Futures | | | | | | | 138 | USD | 18,464 | | 03/18 | | | (57 | ) |

| Total Value and Unrealized Appreciation (Depreciation) on Open Futures Contracts (å) | | | | | | | | (57 | ) |

| |

| |

| Presentation of Portfolio Holdings | | | | | | | | | | | | | |

| Amounts in thousands | | | | | | | | | | | | | | | |

| | | | | | | | Fair Value | | | | | | | | |

| | | | | | | | | Practical | | | | | | |

| Portfolio Summary | | Level 1 | | | Level 2 | | Level 3 | Expedient (a) | | Total | | % of Net Assets | |

| Common Stocks | | | | | | | | | | | | | | | |

| Consumer Discretionary | $ | 44,493 | | $ | — | $ | — | $ | — | $ | 44,493 | | | 9.6 | |

| Consumer Staples | | 24,311 | | | — | | — | | — | | 24,311 | | | 5.3 | |

| Energy | | 33,079 | | | — | | — | | — | | 33,079 | | | 7.2 | |

| Financial Services | | 98,032 | | | — | | — | | — | | 98,032 | | | 21.2 | |

| Health Care | | 48,738 | | | — | | — | | — | | 48,738 | | | 10.6 | |

| Materials and Processing | | 14,029 | | | — | | — | | — | | 14,029 | | | 3.0 | |

| Producer Durables | | 77,041 | | | — | | — | | — | | 77,041 | | | 16.7 | |

| Technology | | 80,004 | | | — | | — | | — | | 80,004 | | | 17.3 | |

| Utilities | | 13,224 | | | — | | — | | — | | 13,224 | | | 2.9 | |

| Short-Term Investments | | — | | | — | | — | | 27,698 | | 27,698 | | | 6.0 | |

| Total Investments | | 432,951 | | | — | | — | | 27,698 | | 460,649 | | | 99.8 | |

| Other Assets and Liabilities, Net | | | | | | | | | | | | | | 0.2 | |

| | | | | | | | | | | | | | | 100.0 | |

| Other Financial Instruments | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| Liabilities | | | | | | | | | | | | | | | |

| Futures Contracts | | (57 | ) | | — | | — | | — | | (57 | ) | | (—)* | |

| Total Other Financial Instruments** | $ | (57 | ) | $ | — | $ | — | $ | — | $ | (57 | ) | | | |

* Less than 0.05% of net assets.

** Futures and foreign currency exchange contract values reflect the unrealized appreciation (depreciation) on the investments.

(a) Certain investments that are measured at fair value using the net asset value per share (or its equivalent) practical expedient have not been classified

in the fair value levels. The fair value amounts presented in the table are intended to permit reconciliation to the amounts presented in the Schedule of

Investments.

For a description of the Levels, see note 2 in the Notes to Financial Statements.

For a disclosure on transfers between Levels 1, 2 and 3 during the period ended December 31, 2017, see note 2 in the Notes to

Financial Statements.

See accompanying notes which are an integral part of the financial statements.

U.S. Strategic Equity Fund 17

Russell Investment Funds

U.S. Strategic Equity Fund

Fair Value of Derivative Instruments — December 31, 2017

Amounts in thousands

| | | |

| | | Equity |

| Derivatives not accounted for as hedging instruments | Contracts |

| |

| Location: Statement of Assets and Liabilities - Liabilities | | |

| Variation margin on futures contracts* | | $ | 57 |

| |

| | | Equity |

| Derivatives not accounted for as hedging instruments | Contracts |

| |

| Location: Statement of Operations - Net realized gain (loss) | | |

| Futures contracts | | $ | 2,697 |

| |

| |

| Location: Statement of Operations - Net change in unrealized appreciation (depreciation) | | |

| Futures contracts | | $ | 132 |

* Includes cumulative appreciation/depreciation of futures contracts as reported in the Schedule of Investments. Only variation margin is reported within the

Statement of Assets and Liabilities.

For further disclosure on derivatives see note 2 in the Notes to Financial Statements.

See accompanying notes which are an integral part of the financial statements.

18 U.S. Strategic Equity Fund

Russell Investment Funds

U.S. Strategic Equity Fund

Balance Sheet Offsetting of Financial and Derivative Instruments —

December 31, 2017

| | | | | | | | | |

| Amounts in thousands | | | | | | | | | |

| |

| Offsetting of Financial Liabilities and Derivative Liabilities | | | | | | | | |

| | | | | Gross | Net Amounts | |

| | | | | Amounts | of Liabilities | |

| | | Gross | Offset in the | Presented in | |

| | | Amounts of | Statement of | the Statement | |

| | | Recognized | Assets and | of Assets and | |

| Description | Location: Statement of Assets and Liabilities - Liabilities | Liabilities | Liabilities | | Liabilities | |

| Futures Contracts | Variation margin on futures contracts | $ | 67 | | $ | — $ | 67 | |

| Total Financial and Derivative Liabilities | | | 67 | | | — | 67 | |

| Financial and Derivative Liabilities not subject to a netting agreement | | (67 | ) | | — | (67 | ) |

| Total Financial and Derivative Liabilities subject to a netting agreement | $ | — | | $ | — $ | — | |

For further disclosure on derivatives and counterparty risk see note 2 in the Notes to Financial Statements.

See accompanying notes which are an integral part of the financial statements.

U.S. Strategic Equity Fund 19

Russell Investment Funds

U.S. Strategic Equity Fund

Statement of Assets and Liabilities — December 31, 2017

| | | |

| Amounts in thousands | | | |

| Assets | | | |

| Investments, at identified cost | $ | 363,165 | |

| Investments, at fair value(>) | | 460,649 | |

| Cash (restricted)(a) | | 720 | |

| Receivables: | | | |

| Dividends and interest | | 502 | |

| Dividends from affiliated funds | | 21 | |

| Investments sold | | 1,224 | |

| Fund shares sold | | 2 | |

| Total assets | | 463,118 | |

| |

| Liabilities | | | |

| Payables: | | | |

| Investments purchased | | 919 | |

| Fund shares redeemed | | 11 | |

| Accrued fees to affiliates | | 308 | |

| Other accrued expenses | | 86 | |

| Variation margin on futures contracts | | 67 | |

| Total liabilities | | 1,391 | |

| |

| |

| Net Assets | $ | 461,727 | |

| | | |

| |

| |

| |

| Net Assets Consist of: | | | |

| Undistributed (overdistributed) net investment income | $ | 999 | |

| Accumulated net realized gain (loss) | | 12,839 | |

| Unrealized appreciation (depreciation) on: | | | |

| Investments | | 97,484 | |

| Futures contracts | | (57 | ) |

| Shares of beneficial interest | | 249 | |

| Additional paid-in capital | | 350,213 | |

| Net Assets | $ | 461,727 | |

| |

| Net Asset Value, offering and redemption price per share: | | | |

| Net asset value per share: (#) | $ | 18.53 | |

| Net assets | $ | 461,727,292 | |

| Shares outstanding ($. 01 par value) | | 24,917,264 | |

| Amounts in thousands | | | |

| (>) Investments in affiliates, U. S. Cash Management Fund | $ | 27,698 | |

| |

| (a) Cash Collateral for Futures | $ | 720 | |

| (#) Net asset value per share equals net assets divided by shares of beneficial interest outstanding. | | | |

See accompanying notes which are an integral part of the financial statements.

20 U.S. Strategic Equity Fund

Russell Investment Funds

U.S. Strategic Equity Fund

Statement of Operations — For the Period Ended December 31, 2017

| | | |

| Amounts in thousands | | | |

| Investment Income | | | |

| Dividends | $ | 7,967 | |

| Dividends from affiliated funds | | 222 | |

| Total investment income | | 8,189 | |

| |

| Expenses | | | |

| Advisory fees | | 3,372 | |

| Administrative fees | | 231 | |

| Custodian fees | | 58 | |

| Transfer agent fees . | | 20 | |

| Professional fees | | 78 | |

| Trustees’ fees | | 12 | |

| Printing fees | | 61 | |

| Miscellaneous | | 25 | |

| Total expenses | | 3,857 | |

| Net investment income (loss) | | 4,332 | |

| |

| Net Realized and Unrealized Gain (Loss) | | | |

| Net realized gain (loss) on: | | | |

| Investments | | 42,951 | |

| Futures contracts | | 2,697 | |

| Net realized gain (loss) | | 45,648 | |

| Net change in unrealized appreciation (depreciation) on: | | | |

| Investments | | 36,833 | |

| Investments in affiliated funds | | (2 | ) |

| Futures contracts | | 132 | |

| Net change in unrealized appreciation (depreciation) | | 36,963 | |

| Net realized and unrealized gain (loss) | | 82,611 | |

| Net Increase (Decrease) in Net Assets from Operations | $ | 86,943 | |

See accompanying notes which are an integral part of the financial statements.

U.S. Strategic Equity Fund 21

Russell Investment Funds

U.S. Strategic Equity Fund

Statements of Changes in Net Assets

| | | | | | |

| | For the Periods Ended December 31, | |

| Amounts in thousands | | 2017 | | | 2016 | |

| Increase (Decrease) in Net Assets | | | | | | |

| Operations | | | | | | |

| Net investment income (loss) | $ | 4,332 | | $ | 5,039 | |

| Net realized gain (loss) | | 45,648 | | | 35,950 | |

| Net change in unrealized appreciation (depreciation) | | 36,963 | | | 3,237 | |

| Net increase (decrease) in net assets from operations | | 86,943 | | | 44,226 | |

| |

| Distributions | | | | | | |

| From net investments income | | (4,792 | ) | | (4,595 | ) |

| From net realized gain | | (44,141 | ) | | (27,937 | ) |

| Net decrease in net assets from distributions | | (48,933 | ) | | (32,532 | ) |

| |

| Share Transactions* | | | | | | |

| Net increase (decrease) in net assets from share transactions | | (19,336 | ) | | (22,982 | ) |

| Total Net Increase (Decrease) in Net Assets | | 18,674 | | | (11,288 | ) |

| |

| Net Assets | | | | | | |

| Beginning of period | | 443,053 | | | 454,341 | |

| End of period | $ | 461,727 | | $ | 443,053 | |

| Undistributed (overdistributed) net investment income included in net assets | $ | 999 | | $ | 1,460 | |

* Share transaction amounts (in thousands) for the periods ended December 31, 2017 and December 31, 2016 were as follows:

| | | | | | | | | | | | |

| | | 2017 | | | | 2016 | | |

| | | Shares | | | Dollars | | | Shares | | | Dollars | |

| |

| Proceeds from shares sold | | 1,301 | | $ | 22,933 | | | 439 | | $ | 7,344 | |

| Proceeds from reinvestment of distributions | | 2,691 | | | 48,933 | | | 1,943 | | | 32,532 | |

| Payments for shares redeemed | | (5,019 | ) | | (91,202 | ) | | (3,735 | ) | | (62,858 | ) |

| Total increase (decrease) | | (1,027 | ) | $ | (19,336 | ) | | (1,353 | ) | $ | (22,982 | ) |

See accompanying notes which are an integral part of the financial statements.

22 U.S. Strategic Equity Fund

(This page intentionally left blank)

Russell Investment Funds

U.S. Strategic Equity Fund

Financial Highlights — For the Periods Ended

For a Share Outstanding Throughout Each Period.

| | | | | | | | | | | | | | |

| | | $ | | $ | | $ | | $ | | $ | | | $ | |

| | Net Asset Value, | | Net | | Net Realized | | Total from | | Distributions | | | Distributions | |

| | Beginning of | Investment | | and Unrealized | | Investment | | from Net | | | from Net | |

| | | Period | Income (Loss)(a)(b) | | Gain (Loss) | | Operations | | Investment Income | | | Realized Gain | |

| December 31, 2017 | | 17.08 | | . 17 | | 3.29 | | 3.46 | | (. 19 | ) | | (1.82 | ) |

| December 31, 2016 | | 16.64 | | . 19 | | 1.53 | | 1.72 | | (. 17 | ) | | (1.11 | ) |