OMB APPROVAL

OMB Number: 3235-0570

Expires: October 31, 2006

Estimated average burden hours per response: 19.3

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-5451

USLICO Series Fund

(Exact name of registrant as specified in charter)

7337 E. Doubletree Ranch Rd., Scottsdale, AZ | | 85258 |

(Address of principal executive offices) | | (Zip code) |

CT Corporation System, 101 Federal Street, Boston, MA 02110

(Name and address of agent for service)

Registrant’s telephone number, including area code: 1-800-992-0180

Date of fiscal year end: | December 31 |

| |

Date of reporting period: | January 1, 2005 to December 31, 2005 |

Item 1. Reports to Stockholders.

The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Act (17 CFR 270.30e-1):

|

|

| |

| Annual Report |

| |

| December 31, 2005 |

| |

| |

| USLICO Series Fund |

| |

| § The Asset Allocation Portfolio |

| |

| § The Bond Portfolio |

| |

| § The Money Market Portfolio |

| |

| § The Stock Portfolio |

|

This report is submitted for general information to shareholders of the ING Funds. It is not authorized for distribution to prospective shareholders unless accompanied or preceded by a prospectus which includes details regarding the funds’ investment objectives, risks, charges, expenses and other information. This information should be read carefully. |

|

| | |

PROXY VOTING INFORMATION

A description of the policies and procedures that the Portfolios use to determine how to vote proxies related to portfolio securities is available (1) without charge, upon request, by calling Shareholder Services toll-free at 1-800-992-0180; (2) on the ING Funds website at www.ingfunds.com and (3) on the Securities and Exchange Commission (“SEC”) website at www.sec.gov. Information regarding how the Portfolios voted proxies related to portfolio securities during the most recent 12-month period ended June 30 is available without charge on the ING Funds website at www.ingfunds.com and on the SEC’s website at www.sec.gov.

QUARTERLY PORTFOLIO HOLDINGS

The Registrant files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. The Registrant’s Forms N-Q are available on the SEC’s website at www.sec.gov. The Registrant’s Forms N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC, and information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330; and is available upon request from the Registrant by calling Shareholder Services toll-free at 1-800-992-0180.

(THIS PAGE INTENTIONALLY LEFT BLANK)

| |

JAMES M. HENNESSY

| Dear Shareholder, |

|

As you may recall, in my last letter I described the enthusiasm that we were experiencing here at ING Funds as we worked to bring more of the world’s investment opportunities to you, the investor. |

|

That enthusiasm, I am happy to report, is continuing to thrive. With the New Year, we have launched a series of new international mutual funds, each created to bring more of the world’s opportunities to you. |

|

Meanwhile, we have also heard you loud and clear. Our research tells us that many investors report that they find investing an intimidating and overly-complex endeavor. That is why ING is committed to helping investors across the country cut through the confusion and clutter. “Your future. Made easier.SM” is more than words; they represent our promise to you. |

Those two objectives — bringing you more of the world’s opportunities and doing it in a way that is easier for you — are behind the development of the new portfolios. |

|

According to a recent finding, 58 percent of the world market capitalization now lies outside of the U.S.1 In other words, the majority of investment opportunities are now beyond our borders and we think that The ING VP Index Plus International Portfolio — a broad-based international portfolio — is an easy, single-step method to gain exposure to many of those opportunities. |

|

Meanwhile, the ING VP Global Real Estate Portfolio was developed as an easy way to bring global — international and domestic — real estate opportunities to the variable portfolio investor. Real Estate Investment Trusts (REITs) are becoming more and more popular around the world, and this new portfolio seeks to capitalize on that popularity. But again, we’ve made it easy. With just one investment, investors bring the diversification of global real estate to their investment strategy. |

|

One of our goals at ING Funds is to find tomorrow’s opportunities today, and we believe these two portfolios are just the latest examples of that plan in action. |

|

On behalf of everyone at ING Funds, I thank you for your continued support and loyalty. We look forward to serving you in the future. |

|

Sincerely, |

James M. Hennessy

President

ING Funds

January 28, 2006

The views expressed in the President’s Letter reflect those of the President as of the date of the letter. Any such views are subject to change at any time based upon market or other conditions and ING Funds disclaims any responsibility to update such views. These views may not be relied on as investment advice and because investment decisions for an ING Fund are based on numerous factors, may not be relied on as an indication of investment intent on behalf of any ING Fund. Reference to specific company securities should not be construed as recommendations or investment advice.

International investing does pose special risks including currency fluctuation, economic and political risks not found in investments that are solely domestic. Investments in issuers that are principally engaged in real estate, including REITs, may subject the Fund to risks similar to those associated with the direct ownership of real estate, including terrorist attacks, war or other acts that destroy real property (in addition to market risks). These companies are sensitive to factors such as changes in real estate values and property taxes, interest rates, cash flow of underlying real estate assets, supply and demand, and the management skill and creditworthiness of the issuer. REITs may also be affected by tax and regulatory requirements.

1 MSCI December, 2005

1

MARKET PERSPECTIVE: YEAR ENDED DECEMBER 31, 2005

In our semi-annual report, we referred to mixed markets in which the U.S. investor lost on both domestic and international stocks, with gains in the latter trumped by the rebounding U.S. dollar. In the second half, global equities registered solid gains, although foreign markets ended the 2005 year more convincingly. The Morgan Stanley Capital International (“MSCI”) World® Index(1) calculated in dollars, including net reinvested dividends rose 10.3% for the six months ended December 31, 2005, and 9.5% for the full year. As for currencies, the dollar extended its first half run for the six months ended December 31, 2005, rising 2.1% against the euro (12.6% for the full year), 6.2% against the yen (14.7% for the full year), and 3.8% against the pound (10.2% for the full year). Commentators explained the U.S. dollar’s unexpected strength by pointing to relatively high U.S. interest rates, the recycling of oil exporters’ burgeoning wealth into dollar securities, the tax-related “repatriation” into dollars of U.S. corporations’ foreign currency balances, and, regarding the yen’s particular weakness, non-Japanese investors pouring money into the stock market but hedging their currency risk. Each dynamic was losing steam by 2005 year-end.

For more than a year, the main issue for US fixed income investors had been the unexpected flattening of the yield curve, i.e. the shrinking difference between short-term and long-term interest rates. From June 2004 through June 2005, the Federal Open Market Committee (“FOMC”) had raised the Federal Funds Rate by 25 basis points nine times, pulling other short-term rates up. However, the yield on the ten-year U.S. Treasury Note had actually fallen by 0.71% over the same thirteen months. This was put down to an apparently growing perception in the market that inflation was a problem solved, due to a vigilant Federal Reserve, cheap goods and labor abroad, consistent productivity growth at home and foreign investors’ hunger for U.S. investments. Occasionally in the second half, for example when Hurricanes Katrina and Rita affected oil prices, having peaked near $70 per barrel at the end of August 2005, there looked to be filtering through to general prices, the trend seemed about to break. Nevertheless, in the end, the forces of the curve flattening prevailed. By December 31, 2005, the FOMC had raised rates four more times, oil prices and the inflation scare had subsided and foreigners were still buying record amounts of U.S. securities. For the six months ended December 31, 2005, the yield on the ten-year Treasury rose by 45 basis points to 4.39% (17 basis points for the full year), and on 13-week U.S. Treasury Bills by 93 basis points (180 basis points for the full year) to 3.98%. The returns on the broad Lehman Brothers Aggregate Bond Index(2) and the Lehman Brothers High Yield Bond Index(3) was - -0.1% and 1.6% for the six months ended December 31, 2005, and 2.4% and 2.7% for the full year, respectively.

The U.S. equities market in the form of the Standard & Poor’s 500 Composite Stock Price (“S&P 500 Index”) Index(4), added 5.8% including dividends in the latter half of 2005 and 4.9% for the full year, thanks to gains of 3.5% in July and November of 2005. Other months were flat to down and by 2005 year-end, the market, trading at a fairly undemanding price-to-earnings level of about 16 times earnings for the current fiscal year, was definitely struggling. Stock investors were initially encouraged by bullish economic reports and even more by second quarter company earnings figures which were, on average up more than 10% year over year. The optimistic mood lasted into early August of 2005, when the S&P 500 Index reached a four-year high, before drifting back as resurgent oil prices made records almost daily. In September and October of 2005 with Hurricanes Katrina and Rita seldom out of the news, two attempted rallies fizzled. High prices at the gas pump were already here. An expensive winter for heating fuel was certain. Sharply rising factory prices started to be found in local Federal Reserve and purchasing managers’ reports and, with consumer confidence slumping, the word “stagflation” was heard more than once. In spite of this, as November approached, an evidently swift recovery from the Hurricanes Katrina and Rita cheered investors and stock prices powered ahead through mid-December 2005, as oil prices fell back below $60 per barrel, inflation moderated, corporate profits remained buoyant and gross domestic product (“GDP”) growth, at 4.1% per annum, was the envy of the developed world. Yet the market gave back nearly 1.6% between Christmas and New Year, when new reports suggested that the end of the bubbling housing market might be at hand. Rising house prices had encouraged the consumer spending that was largely behind robust GDP growth; spending that is, by people who on average were saving little, if anything.

In international markets Japan was the shining star of the second half, soaring 33.3%, based on the MSCI Japan® Index(5) in dollars plus net dividends for the six months ended December 31, 2005, and 25.5% for the full year, as the market repeatedly broke five-year

2

MARKET PERSPECTIVE: YEAR ENDED DECEMBER 31, 2005

records amid new optimism. Investors, albeit mainly foreign ones, came to the belief that Japan is re-emerging as a balanced economy and less dependent on exports. Corporations and the banks have repaired their balance sheets at last. Rising wages are supporting domestic demand, in addition to an expected end to deflation, seems at hand. European ex UK markets leaped 11.8%, according to the MSCI Europe ex UK® Index(6) in dollars including net dividends for the six months ended December 31, 2005 (10.5% for the full year) and 14.7% in local currencies (27.7% for the full year) to the best levels in over four years, despite the first interest rate increase, to 2.5%, in over five years. Mounting evidence of a recovery in local demand, resilient profits and an upsurge of merger and acquisition activity boosted markets that are not particularly expensive. UK equities advanced 6.4% in the six months ended December 31, 2005 (7.4% for the full year) based on the MSCI UK® Index(7) in dollars including net dividends, concealing a more impressive 11.1% increase in pounds (20.1% for the full year), to the highest in four years. The period was dominated by the effect of five interest rate increases to restrain over-stretched consumers and soaring real estate prices. Yet, in the face of mostly miserable economic reports, and despite terrorist attacks in London over two days in July of 2005, investors, encouraged by merger and acquisition activity, supported an inexpensive market yielding over 3%.

(1) The MSCI World® Index is an unmanaged index that measures the performance of over 1,400 securities listed on exchanges in the U.S., Europe, Canada, Australia, New Zealand and the Far East.

(2) The Lehman Brothers Aggregate Bond Index is a widely recognized, unmanaged index of publicly issued investment grade U.S. Government, mortgage-backed, asset-backed and corporate debt securities.

(3) The Lehman Brothers High Yield Bond Index is an unmanaged index that measures the performance of fixed-income securities generally representative of corporate bonds rated below investment-grade.

(4) The Standard & Poor’s 500 Composite Stock Price Index is an unmanaged index that measures the performance of securities of approximately 500 of the largest companies in the U.S.

(5) The MSCI Japan® Index is a free float-adjusted market capitalization index that is designed to measure developed market equity performance in Japan.

(6) The MSCI Europe ex UK® Index is a free float-adjusted market capitalization index that is designed to measure developed market equity performance in Europe, excluding the UK.

(7) The MSCI UK® Index is a free float-adjusted market capitalization index that is designed to measure developed market equity performance in the UK.

All indices are unmanaged and investors cannot invest directly in an index.

Past performance does not guarantee future results. The performance quoted represents past performance. Investment return and principal value of an investment will fluctuate, and shares, when redeemed, may be worth more or less than their original cost. The Funds’ performance is subject to change since the period’s end and may be lower or higher than the performance data shown. Please call (800) 992-0180 or log on to www.ingfunds.com to obtain performance data current to the most recent month end.

Market Perspective reflects the views of the Chief Investment Risk Officer only through the end of the period, and is subject to change based on market and other conditions.

3

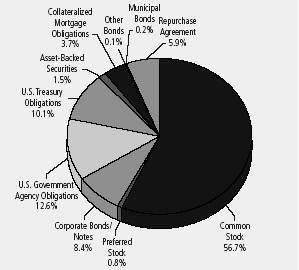

THE USLICO ASSET ALLOCATION PORTFOLIO | PORTFOLIO MANAGERS’ REPORT |

Investment Types

as of December 31, 2005

(as a percent of total investments)

Portfolio holdings are subject to change daily.

The ING USLICO Asset Allocation Portfolio (the “Portfolio” or “Asset Allocation Portfolio”) seeks to obtain high total return with reduced risk over the long-term by allocating its assets among stocks, bonds, and short-term instruments. The equity portion of the Portfolio is managed by Mary Ann Fernandez, Senior Vice President and Portfolio Manager and Shiv Mehta, Portfolio Manager, the money market portion of the Portfolio is managed by David S. Yealy, Portfolio Manager, and the bond portion of the Portfolio is managed by James Kauffmann, Portfolio Manager, ING Investment Management Co. — the Sub-Adviser.

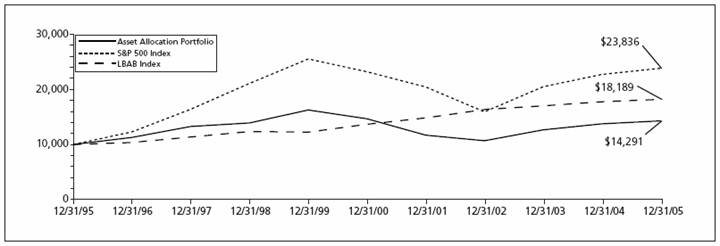

Performance: For the year ended December 31, 2005, the Portfolio provided a total return of 3.91% compared to 4.91% for the Standard & Poor’s 500 Composite Stock Price (“S&P”) Index and 2.43% for the Lehman Brothers Aggregate Bond (“LBAB”) Index.

Portfolio Specifics: Broad based strength in stock selection, especially within industrials and consumer discretionary sectors drove relative performance. Stock selection was unfavorable in the information technology sector however, and modest value was detracted by our holdings (and lack thereof) in utilities as well as in financials.

Within information technology, the Portfolio benefited from stocks such as Jabil Circuit, Taiwan Semiconductor (TSM), Business Objects, and Activision. Jabil and TSM are benefiting from the continuing industry trend towards outsourced manufacturing. Activision introduced a series of new video games consistent with the replacement cycle in the video game console arena. The major detractors from performance were a zero weighting in Apple Computer, which performed extremely well, and an overweight in circuit maker Maxim Integrated Products, which had disappointing results.

The Portfolio’s energy holdings performed well and confirmed our belief that the more attractive business models, the more attractive valuations, and the strongest links to the strength in commodity prices were to be found in the equipment and services companies rather than in the large integrated companies like Exxon and Chevron. The other type of company we emphasized was the independent exploration and production companies.

Within financials, Countrywide and E-Trade were the biggest drags on performance. The Portfolio was underweight utilities throughout the year as companies in the sector traded at all-time high valuations.

The Portfolio’s underweight to longer-dated corporates was beneficial, as later-dated maturities showed great weakness over the year. An overexposure to asset-backed securities and commercial mortgage-backed securities, at the expense of corporates, was beneficial as both sectors produced excess returns (excess returns means the excess over the return from Treasury Securities of comparable term). Lack of adequate compensation for credit risk led to an underweight of riskier sectors, industries and issuers. Positions in bank and insurance names, particularly floating rate preferreds, and lack of exposure in the automotive sectors was a source of positive security selection. As the mortgage sector appeared richly priced, we were largely underweight and our team focused on securities likely to outperform in a rising rate environment and/or an increase in volatility.

Current Strategy and Outlook: Our current strategy is focused on companies with superior capital allocation, strong competitive position, and operations in industries with very attractive outlooks. Key holdings, such as Jabil Circuit, ENSCO International and Halliburton, exhibit strong fundamentals, clear catalysts and attractive valuations.

Our technology holdings reflect our belief that the industry is in a maturation cycle and companies are looking to outsource low return-on-capital endeavors such as production and manufacturing. Contract manufacturers like Jabil and Taiwan Semiconductor continue to benefit from the growth in outsourcing and are well positioned to increase their already dominant market shares.

We have positioned the Portfolio for the possibility that sentiment will reverse and higher risk premiums will be required by the market. ING credit team continues to avoid companies with depressed stock prices and underutilized assets on the books. However, we continue to seek out companies that may weaken in sympathy, but have a lower probability of event risk. Moreover, the maturities of the corporate portfolio are shorter, on balance, than those of the corporate bonds in the benchmark. Our mortgage team has constructed a portfolio designed to offset an increase in volatility and a change in prepayments.

Top Ten Industries*

as of December 31, 2005

(as a percent of net assets) |

| | | |

U.S. Treasury Note | | 8.7 | % |

| | | |

Diversified Financial Services | | 8.2 | % |

| | | |

Federal National Mortgage Association | | 7.8 | % |

| | | |

Banks | | 5.6 | % |

| | | |

Oil & Gas | | 5.3 | % |

| | | |

Federal Home Loan Mortgage Corporation | | 4.5 | % |

| | | |

Semiconductors | | 3.9 | % |

| | | |

Miscellaneous Manufacturing | | 3.7 | % |

| | | |

Insurance | | 3.5 | % |

| | | |

Pharmaceuticals | | 3.3 | % |

* Excludes short-term investments related to repurchase agreements.

Portfolio holdings subject to change daily

4

PORTFOLIO MANAGERS’ REPORT | THE USLICO ASSET ALLOCATION PORTFOLIO |

| | | |

| Average Annual Total Returns for the Periods Ended December 31, 2005 | | |

| | | 1 Year | | 5 Year | | 10 Year | | |

| Asset Allocation Portfolio | | 3.91% | | (0.51)% | | 3.63% | | |

| S&P 500 Index(1) | | 4.91% | | 0.54% | | 9.07% | | |

| LBAB Index(2) | | 2.43% | | 5.87% | | 6.16% | | |

| | | | | | | | | |

Based on a $10,000 initial investment, the graph and table illustrate the total return of Asset Allocation Portfolio against the S&P 500 Index and the LBAB Index. The Indices are unmanaged and have no cash in their portfolios, impose no sales charges and incur no operating expenses. An investor cannot invest directly in an index. The Portfolio’s performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on Portfolio distributions or the redemption of Portfolio shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Manager and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

The performance update illustrates performance for a variable investment option available through a variable annuity contract. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. Please call (800) 922-0180 to get performance through the most recent month end.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The managers’ views are subject to change at any time based on market and other conditions.

Portfolio holdings are subject to change daily.

(1) The S&P 500 Index is an unmanaged index that measures the performance of securities of approximately 500 of the largest companies in the U.S.

(2) The LBAB Index is a widely recognized, unmanaged index of publicly issued investment grade U.S. Government, mortgage-backed, asset-backed and corporate debt securities.

5

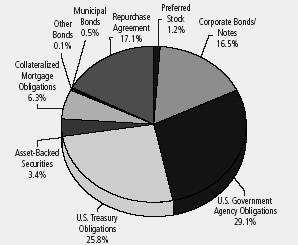

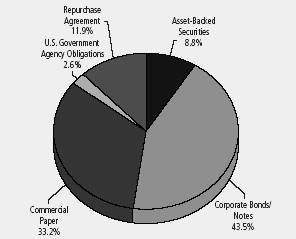

THE USLICO BOND PORTFOLIO | PORTFOLIO MANAGERS’ REPORT |

Investment Types

as of December 31, 2005

(as a percent of total investments)

Portfolio holdings are subject to change daily.

The ING USLICO Bond Portfolio (the “Portfolio” or “Bond Portfolio”) seeks to obtain a high level of income consistent with prudent risk and the preservation of capital. As a secondary objective, the Portfolio seeks capital appreciation when consistent with its principal objective. The Portfolio is managed by James Kauffmann, Portfolio Manager, ING Investment Management Co. — the Sub-Adviser.

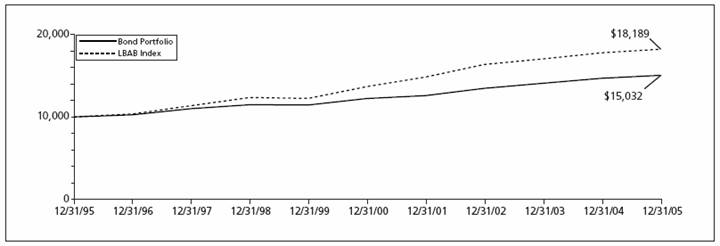

Performance: For the year ended December 31, 2005, the Portfolio provided a total return of 2.42% compared to 2.43% for the Lehman Brothers Aggregate Bond (“LBAB”) Index.

Portfolio Specifics: Evidently accommodation has been removed without hobbling the economy; however, whether the terminal rate on Federal Funds Rate is 4.75% or 5.00% is still open to vigorous debate. The yield curve — which represents the yield on U. S. Treasuries from zero to thirty years — is now very flat. The bellwether ten-year note closed at 4.39% nearly matching the two-year note at 4.40%. The largest rise in yields occurred with shorter maturities; however, the yield on the 30-year bond actually declined.

Our major investment themes remained effectively constant throughout the year, and we positioned the Portfolio accordingly. Rising short-term rates with a tightening Federal Reserve indicated a shorter duration posture with an underweight to shorter maturities, which helped performance through most of the year. Lack of adequate compensation for credit risk led to an underweight of riskier sectors, industries, and issuers coupled with an overweight to the higher quality asset-backed securities and commercial mortgage-backed securities. The mortgage sector also appeared richly priced and/or technically weak. Consequently, we were largely underweight the sector and our mortgage team focused on securities likely to outperform in a rising rate environment and/or an increase in volatility.

Security selection in the mortgage-backed securities sector was particularly positive for performance as we moved up to a 12% exposure to hybrid adjustable rate mortgages instead of traditional pass-throughs by year-end. Our continued underweight to longer-dated corporates was beneficial for most months of 2005. Corporates, overall, gave up 1.15% of excess return (excess return means the excess over the return from Treasury Securities of comparable term), but the most damage occurred in the longer maturities. Over-exposure to asset-backed securities and commercial mortgage-backed securities at the expense of corporate bonds also proved beneficial to results as both sectors produced positive excess returns. Positions in bank and insurance names, particularly floating rate preferreds, and lack of exposure in the automotive sectors were sources of positive security selection, which led to our good competitive performance.

Current Strategy and Outlook: Our outlook did not change during the period, with the exception that the end of the tightening phase is now on the horizon, in our opinion. While the debate on Wall Street about the relationship of inverted yield curves and recessions is lively, we believe that any inversion will likely be brief and will have fewer implications for the domestic economy than in the past. We agree with Federal Reserve officials that “global savings gluts” have better explanatory power for the comparatively low yields on 10- and 30-year U.S. Treasuries than a signal that the economy might soon sputter.

We have positioned the Portfolio for the potentiality that sentiment will reverse and higher risk premiums will be required by the market with “an attendant fall in the price of risky assets.” Indeed, we are keenly aware that preserving capital and receiving adequate compensation for risk are essential elements of successful bond management. Specifically, the ING credit team continues to avoid companies with depressed stock prices and under-utilized assets on the books. However, we continue to look to take advantage of companies that weaken in sympathy but have a lower probability of such event risk. Moreover, the maturities of the corporate portfolio are shorter, on balance, than those of the corporate bonds in the benchmark. Our mortgage team has constructed a portfolio designed to offset an increase in volatility and a change in prepayments. Finally, duration is shorter than the LBAB Index.

Top Ten Industries*

as of December 31, 2005

(as a percent of net assets) | |

| | | |

Federal National Mortgage Association | | 23.6 | % |

| | | |

U.S. Treasury Notes | | 22.2 | % |

| | | |

Federal Home Loan Mortgage Corporation | | 9.6 | % |

| | | |

U.S. Treasury Bonds | | 8.6 | % |

| | | |

Diversified Financial Services | | 5.5 | % |

| | | |

Commercial Mortgage Backed Securities | | 5.1 | % |

| | | |

Banks | | 4.1 | % |

| | | |

Electric | | 2.7 | % |

| | | |

Whole Loan Collateral CMO | | 2.1 | % |

| | | |

Insurance | | 1.5 | % |

* Excludes short-term investments related to repurchase agreements.

Portfolio holdings subject to change daily

6

PORTFOLIO MANAGERS’ REPORT | THE USLICO BOND PORTFOLIO |

| | | |

| Average Annual Total Returns for the Years Ended December 31, 2005 | | |

| | | 1 Year | | 5 Year | | 10 Year | | |

| Bond Portfolio | | 2.42% | | 4.21% | | 4.16% | | |

| LBAB Index(1) | | 2.43% | | 5.84% | | 6.16% | | |

| | | | | | | | | |

Based on a $10,000 initial investment, the graph and table above illustrate the total return of Bond Portfolio against the LBAB Index. The Index is unmanaged and has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Portfolio’s performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on Portfolio distributions or the redemption of Portfolio shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Manager and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

The performance update illustrates performance for a variable investment option available through a variable annuity contract. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. Please call (800) 922-0180 to get performance through the most recent month end.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

The views expressed in this report reflect those of the portfolio manager, only through the end of the period as stated on the cover. The manager’s views are subject to change at any time based on market and other conditions.

Portfolio holdings are subject to change daily.

(1) The LBAB Index is a widely recognized, unmanaged index of publicly issued investment grade U.S. Government, mortgage-backed, asset-backed and corporate debt securities.

7

THE USLICO MONEY MARKET PORTFOLIO | PORTFOLIO MANAGERS’ REPORT |

Investment Types

as of December 31, 2005

(as a percent of total investments)

* Excludes other assets and liabilities of -0.2% of net assets.

Portfolio holdings are subject to change daily.

The ING USLICO Money Market Portfolio (the “Portfolio” or “Money Market Portfolio”) seeks maximum current income consistent with preservation of capital and liquidity. The Portfolio is managed by David S. Yealy, Portfolio Manager, ING Investment Management Co. — the Sub-Adviser.

Portfolio Specifics: The year 2005 was one in which the Federal Open Market Committee (“FOMC”) continued its “measured” pace of removing monetary accommodation by raising the Federal Funds Rate 25 basis points at each of its eight FOMC Meetings. The Federal Funds Rate ended the year at 4.25%, a full 2.00% higher that the previous year-end and 3.25% higher than when the FOMC started tightening in June of 2004. Rising short-term interest rates was the primary driver of investment performance for money market funds and investors. Another key event in 2005, for short-term investors, was the nomination of Dr. Ben S. Bernanke in October to replace Alan Greenspan as chairman of the Federal Reserve in January of 2006. Dr. Bernanke is an advocate of explicit inflation targeting and therefore the FOMC is not expected to diverge significantly from the current FOMC as far as inflation fighting is concerned.

The Portfolio was well positioned to take advantage of the rising rate environment. The Portfolio’s primary strategy, which was in place throughout the year, of maintaining a high concentration in interest sensitive floating rate securities and focusing new purchases on very short-term maturities which typically matured prior to or just after the next fed meeting added to the relative performance of the Portfolio. Within the floating rate security sector, we overweighed floaters that reset either weekly or monthly as opposed to quarterly, thereby capturing the rate increases sooner. The Portfolio had purchased a limited amount of longer-term maturity securities in mid-2004 which originally added to performance in 2004 but were a small drag on performance this year as the FOMC increased rates higher than was priced in at the time of purchase. Those securities matured in April and May and the proceeds were reinvested in better performing floating rate securities and very short-term securities.

Current Strategy and Outlook: Despite the change in the FOMC language in December, we continue to anticipate additional FOMC tightenings in 2006 in response to inflationary pressures due to tightening labor conditions and the effect of higher energy prices post Hurricanes Katrina and Rita. Current inflation, as measured by the core personal consumption expenditure (“PCE”), is at the high end of what we believe to be the FOMC’s comfort range and could rise further with the unemployment rate moving below 5.0%. In the near-term, we plan on maintaining our current strategy of focusing new purchases to the next FOMC meeting, maintaining a high exposure to floating rate securities, and making selective purchases in the three-month and under maturity sector where yield levels fully price in 25 basis point increases at each of the Federal Reserve meetings in between. We anticipate having to change our strategy to one focusing more on longer-term fixed rate securities at some point in 2006 as we reach the final stage of the FOMC tightening cycle.

8

PORTFOLIO MANAGERS’ REPORT | ING USLICO MONEY MARKET PORTFOLIO |

Principal Risk Factor(s): An investment in the Portfolio is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Although the Portfolio seeks to preserve the value of your investment, it is possible to lose money by investing in the Portfolio.

The views expressed in this report reflect those of the portfolio managers only through the end of the period as stated on the cover. The portfolio managers’ views are subject to change at any time based on market and other conditions.

Portfolio holdings are subject to change daily. This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

9

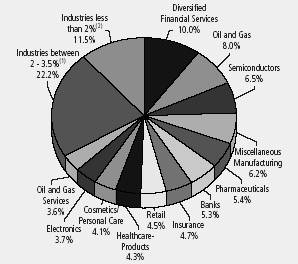

THE USLICO STOCK PORTFOLIO | PORTFOLIO MANAGERS’ REPORT |

Industry Allocation*

as of December 31, 2005

(as a percent of total investments)

* Excludes other assets and liabilities of 0.1% of net assets.

(1) Includes eight industries, which each represent 2 - 3.5% of

total investments.

(2) Includes ten industries, which each represent 1 - 2% of

total investments.

Portfolio holdings are subject to change daily.

The ING USLICO Stock Portfolio (the “Portfolio” or “Stock Portfolio”) seeks intermediate and long-term growth of capital. The Portfolio’s secondary objective is to receive a reasonable level of income. The Portfolio is managed by Christopher F. Corapi, Portfolio Manager and Director of Fundamental Equity Research, ING Investment Management Co. — the Sub-Adviser.

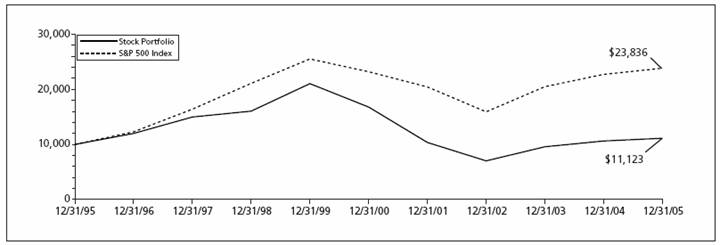

Performance: For the year ended December 31, 2005, the Portfolio provided a total return of 4.67% compared to 4.91% for the Standard & Poor’s Composite Stock Price (“S&P 500”) 500 Index.

Portfolio Specifics: Broad based strength in stock selection, especially within the industrials and consumer discretionary sectors drove relative performance. Stock selection was unfavorable in the information technology sector however, and modest value was detracted by our holdings (and lack thereof) in utilities as well as in financials.

Within information technology, the Portfolio benefited from stocks such as Jabil Circuit, Taiwan Semiconductor (TSM) and Activision. Jabil and TSM are benefiting from the continuing industry trend towards outsourced manufacturing. Product designers, such as chip companies and packaged product makers Hewlett-Packard and Cisco, are increasingly outsourcing their end product manufacturing to foundries and contract manufacturers like these two companies. Activision introduced a series of new video games consistent with the replacement cycle in the video game console arena. The major detractors from performance were a zero weighting in Apple Computer, which performed extremely well, and an overweight in circuit maker Maxim Integrated Products, which had disappointing results.

The Portfolio’s energy holdings performed well and confirmed our belief that the more attractive business models, the more attractive valuations, and the strongest links to the strength in commodity prices were to be found in the equipment and services companies rather than in the large integrated companies like Exxon and Chevron. Halliburton, Schlumberger and ENSCO International provide services and equipment to exploration and production companies and are benefiting from the upswing in capital spending in the sector. The other type of company we emphasized were the independent exploration and production companies, such as EOG Resources, XTO Energy and Plains Exploration & Production. These companies are more focused and niche-like, and more likely to find oil and gas that they can sell at market prices vis-a-vis their larger competitors.

Within financials, Countrywide and E-Trade were the biggest drags on performance. The Portfolio was underweight utilities throughout the year as companies in the sector traded at all-time high valuations.

Current Strategy and Outlook: Our current strategy is focused on companies with superior capital allocation, strong competitive position, and operations in industries with very attractive outlooks. Key holdings, such as Jabil Circuit, ENSCO International and Halliburton, exhibit strong fundamentals, clear catalysts and attractive valuations.

Halliburton continues to offer upside potential in the energy services space, even after performing strongly in 2005. We believe the stock may benefit greatly in 2006 if management spins off their engineering and construction subsidiary Kellogg, Brown & Root. More broadly, we like other energy services stocks based on our forecast for continued robust spending by producers and refiners on creating new production capacity to meet global demand. This bodes well for drillers like ENSCO, who provide contract drilling services to the oil and gas industry. ENSCO enjoys a strong competitive position due to its state of the art fleet of offshore drilling rigs.

Our technology holdings reflect our belief that the industry is in a maturation cycle and companies are looking to outsource low return-on-capital endeavors such as production and manufacturing. Contract manufacturers like Jabil and Taiwan Semiconductor continue to benefit from the growth in outsourcing and are well positioned to increase their already dominant market shares.

Top Ten Holdings

as of December 31, 2005

(as a percent of net assets) | |

| | | |

Exxon Mobil Corp. | | 3.4 | % |

| | | |

Citigroup, Inc. | | 3.3 | % |

| | | |

General Electric Co. | | 3.0 | % |

| | | |

Altria Group, Inc. | | 2.5 | % |

| | | |

Johnson & Johnson | | 2.5 | % |

| | | |

Wells Fargo & Co. | | 2.1 | % |

| | | |

Procter & Gamble Co. | | 2.1 | % |

| | | |

Jabil Circuit, Inc. | | 2.1 | % |

| | | |

Bank of America Corp. | | 2.1 | % |

| | | |

Oracle Corp. | | 2.0 | % |

Portfolio holdings are subject to change daily.

10

PORTFOLIO MANAGERS’ REPORT | THE USLICO STOCK PORTFOLIO |

| | | |

| Average Annual Total Returns for the Years Ended December 31, 2004 | | |

| | | 1 Year | | 5 Year | | 10 Year | | |

| Stock Portfolio | | 4.67% | | (7.91)% | | 1.07% | | |

| S&P 500 Index(1) | | 4.91% | | 0.54% | | 9.07% | | |

| | | | | | | | | |

Based on a $10,000 initial investment, the graph and table above illustrate the total return of Stock Portfolio against the S&P 500 Index. The Index is unmanaged and has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Portfolio’s performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on Portfolio distributions or the redemption of Portfolio shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Manager and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

The performance update illustrates performance for a variable investment option available through a variable annuity contract. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. Please call (800) 922-0180 to get performance through the most recent month end.

This report contains statements that may be “forward-looking” statements. Actual results may differ materially from those projected in the “forward-looking” statements.

The views expressed in this report reflect those of the portfolio manager, only through the end of the period as stated on the cover. The manager’s views are subject to change at any time based on market and other conditions.

Portfolio holdings are subject to change daily.

(1) The S&P 500 Index is an unmanaged index that measures the performance of securities of approximately 500 of the largest companies in the U.S.

11

SHAREHOLDER EXPENSE EXAMPLES (UNAUDITED) |

As a shareholder of a Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution [and/or service] (12b-1) fees; and other Fund expenses. These Examples are intended to help you understand your ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Examples are based on an investment of $1,000 invested at the beginning of the period and held for the entire period from July 1, 2005 to December 31, 2005.

Actual Expenses

The first section of the table shown, “Actual Fund Return”, provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second section of the table shown, “Hypothetical 5% Return”, provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the hypothetical lines of the table are useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | Beginning

Account

Value

July 1, 2005 | | Ending

Account

Value

December 31, 2005 | | Annualized

Expense

Ratio | | Expenses Paid

During the Six

Months Ended

December 31, 2005* | |

| | | | | | | | | | | | |

USLICO Series Fund | | | | | | | | | | | | |

Actual Fund Return | | | | | | | | | | | | |

Asset Allocation Portfolio | | $ | 1,000.00 | | | $ | 1,034.90 | | | 0.90 | % | | $ | 4.62 | | |

Bond Portfolio | | 1,000.00 | | | 997.90 | | | 0.90 | | | 4.53 | | |

Money Market Portfolio | | 1,000.00 | | | 1,015.60 | | | 0.70 | | | 3.56 | | |

Stock Portfolio | | 1,000.00 | | | 1,060.90 | | | 0.81 | | | 4.21 | | |

Hypothetical (5% return before expenses) | | | | | | | | | | | | | |

Asset Allocation Portfolio | | $ | 1,000.00 | | | $ | 1,020.67 | | | 0.90 | % | | $ | 4.58 | | |

Bond Portfolio | | 1,000.00 | | | 1,020.67 | | | 0.90 | | | 4.58 | | |

Money Market Portfolio | | 1,000.00 | | | 1,021.68 | | | 0.70 | | | 3.57 | | |

Stock Portfolio | | 1,000.00 | | | 1,021.12 | | | 0.81 | | | 4.13 | | |

* Expenses are equal to each Portfolio’s respective annualized expense ratios multiplied by the average account value over the period, multiplied by 184/365 to reflect the most recent fiscal half-year.

12

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM |

The Board of Trustees and Shareholders

USLICO Series Fund

We have audited the accompanying statements of assets and liabilities, including the portfolios of investments, of Stock Portfolio, Money Market Portfolio, Bond Portfolio, and Asset Allocation Portfolio, each a series of USLICO Series Fund as of December 31, 2005, and the related statements of operations for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years in the five-year period then ended. These financial statements and financial highlights are the responsibility of management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of December 31, 2005 by correspondence with the custodian and brokers, or by other appropriate auditing procedures when replies from brokers were not received. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of the aforementioned portfolios as of December 31, 2005, the results of their operations, the changes in their net assets, and the financial highlights for the periods specified in the first paragraph above, in conformity with U.S. generally accepted accounting principles.

Boston, Massachusetts

February 24, 2006

13

STATEMENTS OF ASSETS AND LIABILITIES AS OF DECEMBER 31, 2005

| | The

Asset Allocation

Portfolio | | The

Bond

Portfolio | | The

Money Market

Portfolio | | The

Stock

Portfolio | |

ASSETS: | | | | | | | | | |

Investments in securities at value* | | $ | 13,124,611 | | $ | 2,881,328 | | $ | — | | $ | 16,791,897 | |

Short-term investments at amortized cost | | — | | — | | 5,033,872 | | — | |

Repurchase agreement | | 822,000 | | 596,000 | | 678,000 | | 76,000 | |

Cash | | 3,022 | | 1,039 | | 973 | | 378 | |

Receivables: | | | | | | | | | |

Investment securities sold | | 136,004 | | — | | — | | — | |

Interest purchased | | 1,544 | | 1,336 | | — | | — | |

Fund shares sold | | — | | — | | 17,640 | | — | |

Dividends and interest | | 41,016 | | 18,412 | | 10,030 | | 17,511 | |

Prepaid expenses | | 279 | | 81 | | 123 | | 348 | |

Reimbursement due from manager | | 2,921 | | 2,091 | | 361 | | 5,607 | |

Total assets | | 14,131,397 | | 3,500,287 | | 5,740,999 | | 16,891,741 | |

LIABILITIES: | | | | | | | | | |

Payable for investment securities purchased | | 856,820 | | 567,842 | | — | | — | |

Income distribution payable | | — | | — | | 17,640 | | — | |

Payable for interest purchased | | 1,544 | | 1,336 | | — | | — | |

Payable to affiliates | | 3,993 | | 854 | | 1,715 | | 5,137 | |

Payable for trustee fees | | 579 | | 851 | | 2,949 | | 2,280 | |

Other accrued expenses and liabilities | | 49,885 | | 10,714 | | 23,309 | | 43,141 | |

Total liabilities | | 912,821 | | 581,597 | | 45,613 | | 50,558 | |

NET ASSETS | | $ | 13,218,576 | | $ | 2,918,690 | | $ | 5,695,386 | | $ | 16,841,183 | |

NET ASSETS WERE COMPRISED OF: | | | | | | | | | |

Paid-in capital | | $ | 16,516,052 | | $ | 3,017,316 | | $ | 5,695,746 | | $ | 28,897,165 | |

Undistributed net investment income | | 11,253 | | 4,187 | | — | | 6,322 | |

Accumulated net realized loss on investments | | (3,725,809 | ) | (89,040 | ) | (360 | ) | (12,856,057 | ) |

Net unrealized appreciation or depreciation on investments | | 417,080 | | (13,773 | ) | — | | 793,753 | |

NET ASSETS | | $ | 13,218,576 | | $ | 2,918,690 | | $ | 5,695,386 | | $ | 16,841,183 | |

| | | | | | | | | |

|

* Cost of investments in securities | | $ | 12,707,531 | | $ | 2,895,101 | | $ | — | | $ | 15,998,144 | |

| | | | | | | | | |

Net Assets | | $ | 13,218,576 | | $ | 2,918,690 | | $ | 5,695,386 | | $ | 16,841,183 | |

Shares authorized | | unlimited | | unlimited | | unlimited | | unlimited | |

Par value | | $ | 0.001 | | $ | 0.001 | | $ | 0.001 | | $ | 0.001 | |

Shares outstanding | | 1,362,795 | | 297,053 | | 5,695,815 | | 2,166,841 | |

Net asset value and redemption price per share | | $ | 9.70 | | $ | 9.83 | | $ | 1.00 | | $ | 7.77 | |

| | | | | | | | | | | | | | | | | |

See Accompanying Notes to Financial Statements

14

STATEMENTS OF OPERATIONS FOR THE YEAR ENDED DECEMBER 31, 2005

| | The

Asset Allocation

Portfolio | | The

Bond

Portfolio | | The

Money Market

Portfolio | | The

Stock

Portfolio | |

INVESTMENT INCOME: | | | | | | | | | |

Dividends, net of foreign taxes withheld* | | $ | 110,989 | | $ | 1,857 | | $ | — | | $ | 215,741 | |

Interest | | 246,244 | | 123,607 | | 194,215 | | 28,197 | |

Total investment income | | 357,233 | | 125,464 | | 194,215 | | 243,938 | |

EXPENSES: | | | | | | | | | |

Investment management fees | | 65,308 | | 14,322 | | 29,452 | | 81,868 | |

Transfer agent fees | | 113 | | 216 | | 567 | | 113 | |

Administrative service fees | | 13,062 | | 2,864 | | 5,890 | | 16,373 | |

Shareholder reporting expense | | 22,775 | | 4,595 | | 9,633 | | 21,163 | |

Professional fees | | 30,942 | | 9,162 | | 14,633 | | 33,820 | |

Custody and accounting expense | | 23,725 | | 13,343 | | 9,280 | | 9,235 | |

Trustee fees | | 1,081 | | 730 | | 2,003 | | 698 | |

Miscellaneous expense | | 2,773 | | 1,199 | | 543 | | 1,592 | |

Total expenses | | 159,779 | | 46,431 | | 72,001 | | 164,862 | |

Net waived and reimbursed fees | | (42,125 | ) | (20,631 | ) | (30,732 | ) | (31,987 | ) |

Net expenses | | 117,654 | | 25,800 | | 41,269 | | 132,875 | |

Net investment income | | 239,579 | | 99,664 | | 152,946 | | 111,063 | |

REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS AND INCREASE FROM PAYMENTS BY AFFILIATES AND NET LOSSES REALIZED ON DISPOSAL OF INVESTMENTS IN VIOLATION OF RESTRICTIONS | | | | | | | | | |

Net realized gain (loss) on investments | | 1,027,580 | | (15,369 | ) | 284 | | 1,983,711 | |

Increase from payments by affiliates | | 2,656 | | — | | — | | 5,607 | |

Net gains/losses realized on disposal of investments in violation of restrictions | | 21,757 | | — | | — | | 45,459 | |

Net increase from payments by affiliate and net gains/losses realized on the disposal of investments in violation of securities | | 24,413 | | — | | — | | 51,066 | |

Net change in unrealized appreciation or depreciation on investments | | (781,642 | ) | (17,818 | ) | — | | (1,375,179 | ) |

Net realized and unrealized gain (loss) on investments and net increase from payments by affiliates and net gains/losses realized on disposal of investments in violation of restrictions | | 270,351 | | (33,187 | ) | 284 | | 659,598 | |

Increase in net assets resulting from operations | | $509,930 | | $66,477 | | $153,230 | | $770,661 | |

| | | | | | | | | |

| |

* Foreign taxes withheld | | $ | 142 | | $ | — | | $ | — | | $ | 361 | |

| | | | | | | | | | | | | | | | | | | | | |

See Accompanying Notes to Financial Statements

15

STATEMENTS OF CHANGES IN NET ASSETS

| | The Asset Allocation Portfolio | | The Bond Portfolio | |

| | Year

Ended

December 31,

2005 | | Year

Ended

December 31,

2004 | | Year

Ended

December 31,

2005 | | Year

Ended

December 31,

2004 | |

FROM OPERATIONS: | | | | | | | | | |

Net investment income | | $ | 239,579 | | $ | 206,897 | | $ | 99,664 | | $ | 88,744 | |

Net realized gain (loss) on investments, | | 1,051,993 | | 1,107,793 | | (15,369 | ) | 65,226 | |

Net change in unrealized appreciation or depreciation on investments and net increase from payments by affiliates and net gains/losses realized on disposal of investments in violation of restrictions | | (781,642 | ) | (256,489 | ) | (17,818 | ) | (32,155 | ) |

Net increase in net assets resulting from operations | | 509,930 | | 1,058,201 | | 66,477 | | 121,815 | |

FROM DISTRIBUTIONS TO SHAREHOLDERS: | | | | | | | | | |

Net investment income | | (231,706 | ) | (221,813 | ) | (97,575 | ) | (95,495 | ) |

Total distributions | | (231,706 | ) | (221,813 | ) | (97,575 | ) | (95,495 | ) |

FROM CAPITAL SHARE TRANSACTIONS: | | | | | | | | | |

Net proceeds from sale of shares | | 102,260 | | 57,686 | | 54,323 | | — | |

Dividends reinvested | | 231,706 | | 221,813 | | 97,575 | | 95,495 | |

| | 333,966 | | 279,499 | | 151,898 | | 95,495 | |

Cost of shares redeemed | | (421,956 | ) | (1,238,181 | ) | (68,676 | ) | (246,394 | ) |

Net increase (decrease) in net assets resulting from capital share transactions | | (87,990 | ) | (958,682 | ) | 83,222 | | (150,899 | ) |

Net increase (decrease) in net assets | | 190,234 | | (122,294 | ) | 52,124 | | (124,579 | ) |

NET ASSETS: | | | | | | | | | |

Beginning of year | | 13,028,342 | | 13,150,636 | | 2,866,566 | | 2,991,145 | |

End of year | | $ | 13,218,576 | | $ | 13,028,342 | | $ | 2,918,690 | | $ | 2,866,566 | |

Undistributed net investment income at end of year | | $ | 11,253 | | $ | — | | $ | 4,187 | | $ | 293 | |

| | | | | | | | | | | | | | | |

See Accompanying Notes to Financial Statements

16

STATEMENTS OF CHANGES IN NET ASSETS

| | The Money Market Portfolio | | The Stock Portfolio | |

| | Year

Ended

December 31,

2005 | | Year

Ended

December 31,

2004 | | Year

Ended

December 31,

2005 | | Year

Ended

December 31,

2004 | |

FROM OPERATIONS: | | | | | | | | | |

Net investment income | | $ | 152,946 | | $ | 34,108 | | $ | 111,063 | | $ | 46,861 | |

Net realized gain (loss) on investments | | 284 | | (644 | ) | 2,034,777 | | 2,198,605 | |

Net change in unrealized appreciation or depreciation on investments | | — | | — | | (1,375,179 | ) | (675,185 | ) |

Net increase in net assets resulting from operations | | 153,230 | | 33,464 | | 770,661 | | 1,570,281 | |

FROM DISTRIBUTIONS TO SHAREHOLDERS: | | | | | | | | | |

Net investment income | | (152,954 | ) | (34,100 | ) | (104,741 | ) | (46,861 | ) |

Return of capital | | — | | — | | — | | (33,220 | ) |

Total distributions | | (152,954 | ) | (34,100 | ) | (104,741 | ) | (80,081 | ) |

FROM CAPITAL SHARE TRANSACTIONS: | | | | | | | | | |

Net proceeds from sale of shares | | 183,141 | | 17,915 | | 129,462 | | 536,541 | |

Dividends reinvested | | 152,954 | | 28,447 | | 104,741 | | 80,081 | |

| | 336,095 | | 46,362 | | 234,203 | | 616,622 | |

Cost of shares redeemed | | (484,010 | ) | (387,653 | ) | (377,788 | ) | (70,495 | ) |

Net increase (decrease) in net assets resulting from capital share transactions | | (147,915 | ) | (341,291 | ) | (143,585 | ) | 546,127 | |

Net increase (decrease) in net assets | | (147,639 | ) | (341,927 | ) | 522,335 | | 2,036,327 | |

NET ASSETS: | | | | | | | | | |

Beginning of year | | 5,843,025 | | 6,184,952 | | 16,318,848 | | 14,282,521 | |

End of year | | $ | 5,695,386 | | $ | 5,843,025 | | $ | 16,841,183 | | $ | 16,318,848 | |

Undistributed net investment income at end of year | | $ | — | | $ | 8 | | $ | 6,322 | | $ | — | |

| | | | | | | | | | | | | | | |

See Accompanying Notes to Financial Statements

17

THE USLICO ASSET ALLOCATION PORTFOLIO | FINANCIAL HIGHLIGHTS |

Selected data for a share of beneficial interest outstanding throughout each period.

| | Year Ended December 31, | |

| | 2005 | | 2004 | | 2003 | | 2002 | | 2001(1) | |

Per Share Operating Performance: | | | | | | | | | | | |

Net asset value, beginning of year | $ | 9.50 | | 8.90 | | 7.64 | | 8.64 | | 11.04 | |

Income (loss) from investment operations: | | | | | | | | | | | |

Net investment income | $ | 0.17 | | 0.15 | | 0.15 | | 0.19 | | 0.22 | |

Net realized and unrealized gain (loss) on investments | $ | 0.20 | | 0.61 | | 1.25 | | (0.94 | ) | (2.43 | ) |

Total from investment operations | $ | 0.37 | | 0.76 | | 1.40 | | (0.75 | ) | (2.21 | ) |

Less distributions from: | | | | | | | | | | | |

Net investment income | $ | 0.17 | | 0.16 | | 0.14 | | 0.25 | | 0.19 | |

Total distributions | $ | 0.17 | | 0.16 | | 0.14 | | 0.25 | | 0.19 | |

Net asset value, end of year | $ | 9.70 | | 9.50 | | 8.90 | | 7.64 | | 8.64 | |

Total Return(2) | % | 3.93 | † | 8.61 | | 18.54 | | (8.72 | ) | (20.09 | ) |

| | | | | | | | | | | |

Ratios and Supplemental Data: | | | | | | | | | | | |

Net assets, end of year (000’s) | $ | 13,219 | | 13,028 | | 13,151 | | 11,603 | | 12,752 | |

Ratios to average net assets: | | | | | | | | | | | |

Net expenses after expense reimbursement(3) | % | 0.90 | | 0.90 | | 0.91 | | 0.90 | | 0.90 | |

Gross expenses prior to expense reimbursement(3) | % | 1.22 | | 1.09 | | 1.07 | | 1.34 | | 1.76 | |

Net investment income after expense reimbursement(3) | % | 1.83 | | 1.60 | | 1.81 | | 2.42 | | 2.37 | * |

Portfolio turnover rate | % | 308 | | 252 | | 210 | | 258 | | 354 | |

(1) Effective May 11, 2001, ING Investments, LLC ceased serving as the Sub-Adviser to the Portfolio and began serving as Investment Manager to the Portfolio.

(2) Total return is calculated assuming reinvestment of all dividends and capital gain distributions at net asset value.

(3) The Investment Manager has agreed to limit expenses, (excluding interest, taxes, brokerage and extraordinary expenses) subject to possible recoupment by ING Investments, LLC within three years of being incurred.

* Had the Portfolio not amortized premiums and accreted discounts the ratio of net investment income to average net assets would have been 2.09%.

† In 2005, there was no impact on total return due to payment by affiliate.

See Accompanying Notes to Financial Statements

18

THE USLICO BOND PORTFOLIO | FINANCIAL HIGHLIGHTS |

Selected data for a share of beneficial interest outstanding throughout each period.

| | Year Ended December 31, | |

| | 2005 | | 2004 | | 2003 | | 2002 | | 2001(1) | |

Per Share Operating Performance: | | | | | | | | | | | |

Net asset value, beginning of year | $ | 9.93 | | 9.84 | | 9.75 | | 9.41 | | 9.21 | |

Income from investment operations: | | | | | | | | | | | |

Net investment income | $ | 0.35 | | 0.30 | | 0.36 | | 0.39 | | 0.48 | |

Net realized and unrealized gain (loss) on investments | $ | (0.11 | ) | 0.12 | | 0.08 | | 0.35 | | 0.11 | |

Total from investment operations | $ | 0.24 | | 0.42 | | 0.44 | | 0.74 | | 0.59 | |

Less distributions from: | | | | | | | | | | | |

Net investment income | $ | 0.34 | | 0.33 | | 0.35 | | 0.40 | | 0.39 | |

Total distributions | $ | 0.34 | | 0.33 | | 0.35 | | 0.40 | | 0.39 | |

Net asset value, end of year | $ | 9.83 | | 9.93 | | 9.84 | | 9.75 | | 9.41 | |

Total Return(2) | % | 2.45 | | 4.29 | | 4.57 | | 8.07 | | 6.47 | |

| | | | | | | | | | | |

Ratios and Supplemental Data: | | | | | | | | | | | |

Net assets, end of year (000’s) | $ | 2,919 | | 2,867 | | 2,991 | | 3,086 | | 2,846 | |

Ratios to average net assets: | | | | | | | | | | | |

Net expenses after expense reimbursement(3) | % | 0.90 | | 0.90 | | 0.91 | | 0.89 | | 0.90 | |

Gross expenses prior to expense reimbursement(3) | % | 1.62 | | 1.25 | | 1.52 | | 1.37 | | 2.15 | |

Net investment income after expense reimbursement(3) | % | 3.48 | | 3.01 | | 3.65 | | 4.20 | | 5.02 | * |

Portfolio turnover rate | % | 572 | | 463 | | 368 | | 159 | | 215 | |

(1) Effective May 11, 2001, ING Investments, LLC ceased serving as the Sub-Adviser to the Portfolio and began serving as Investment Manager to the Portfolio.

(2) Total return is calculated assuming reinvestment of all dividends and capital gain distributions at net asset value.

(3) The Investment Manager has agreed to limit expenses, (excluding interest, taxes, brokerage and extraordinary expenses) subject to possible recoupment by ING Investments, LLC within three years of being incurred.

* Had the Portfolio not amortized premiums and accreted discounts the ratio of net investment income to average net assets would have been 4.56%.

See Accompanying Notes to Financial Statements

19

THE USLICO MONEY MARKET PORTFOLIO | FINANCIAL HIGHLIGHTS |

Selected data for a share of beneficial interest outstanding throughout each period.

| | Year Ended December 31, | |

| | 2005 | | 2004 | | 2003 | | 2002 | | 2001(1) | |

Per Share Operating Performance: | | | | | | | | | | | |

Net asset value, beginning of year | $ | 1.00 | | 1.00 | | 1.00 | | 1.00 | | 1.00 | |

Income from investment operations: | | | | | | | | | | | |

Net investment income | $ | 0.03 | | 0.01 | | 0.00 | * | 0.01 | | 0.03 | |

Total from investment operations | $ | 0.03 | | 0.01 | | 0.00 | * | 0.01 | | 0.03 | |

Less distributions from: | | | | | | | | | | | |

Net investment income | $ | 0.03 | | 0.01 | | 0.00 | * | 0.01 | | 0.03 | |

Total distributions | $ | 0.03 | | 0.01 | | 0.00 | * | 0.01 | | 0.03 | |

Net asset value, end of year | $ | 1.00 | | 1.00 | | 1.00 | | 1.00 | | 1.00 | |

Total Return(2) | % | 2.63 | | 0.57 | | 0.28 | | 0.88 | | 3.14 | |

| | | | | | | | | | | |

Ratios and Supplemental Data: | | | | | | | | | | | |

Net assets, end of year (000’s) | $ | 5,695 | | 5,843 | | 6,185 | | 6,450 | | 6,400 | |

Ratios to average net assets: | | | | | | | | | | | |

Net expenses after expense reimbursement(3) | % | 0.70 | | 0.88 | | 0.90 | | 0.78 | | 0.90 | |

Gross expenses prior to expense reimbursement(3) | % | 1.22 | | 1.22 | | 1.11 | | 1.03 | | 1.63 | |

Net investment income after expense reimbursement(3) | % | 2.60 | | 0.57 | | 0.28 | | 0.97 | | 3.13 | |

(1) Effective May 11, 2001, ING Investments, LLC ceased serving as the Sub-Adviser to the Portfolio and began serving as Investment Manager to the Portfolio.

(2) Total return is calculated assuming reinvestment of all dividends and capital gain distributions at net asset value.

(3) The Investment Manager has agreed to limit expenses, (excluding interest, taxes, brokerage and extraordinary expenses) subject to possible recoupment by ING Investments, LLC within three years of being incurred.

* Amount is less than $0.005 per share.

See Accompanying Notes to Financial Statements

20

THE USLICO STOCK PORTFOLIO | FINANCIAL HIGHLIGHTS |

Selected data for a share of beneficial interest outstanding throughout each period.

| | Year Ended December 31, | |

| | 2005 | | 2004 | | 2003 | | 2002 | | 2001(1) | |

Per Share Operating Performance: | | | | | | | | | | | |

Net asset value, beginning of year | $ | 7.47 | | 6.77 | | 4.96 | | 7.32 | | 12.42 | |

Income (loss) from investment operations: | | | | | | | | | | | |

Net investment income (loss) | $ | 0.05 | | 0.02 | | (0.01 | ) | (0.04 | ) | (0.05 | ) |

Net realized and unrealized gain (loss) on investments | $ | 0.30 | | 0.72 | | 1.82 | | (2.32 | ) | (5.05 | ) |

Total from investment operations | $ | 0.35 | | 0.74 | | 1.81 | | (2.36 | ) | (5.10 | ) |

Less distributions from: | | | | | | | | | | | |

Net investment income | $ | 0.05 | | 0.02 | | — | | — | | — | |

Net realized gain on investments | $ | — | | — | | — | | — | | — | |

Return of capital | $ | — | | 0.02 | | — | | — | | — | |

Total distributions | $ | 0.05 | | 0.04 | | — | | — | | — | |

Net asset value, end of year | $ | 7.77 | | 7.47 | | 6.77 | | 4.96 | | 7.32 | |

Total Return(2) | % | 4.68 | † | 10.90 | | 36.49 | | (32.24 | ) | (41.06 | ) |

| | | | | | | | | | | |

Ratios and Supplemental Data: | | | | | | | | | | | |

Net assets, end of year (000’s) | $ | 16,841 | | 16,319 | | 14,283 | | 10,140 | | 14,972 | |

Ratios to average net assets: | | | | | | | | | | | |

Net expenses after expense reimbursement/recoupment(3) | % | 0.81 | | 0.90 | | 0.90 | | 0.90 | | 0.90 | |

Gross expenses prior to expense reimbursement/recoupment(3) | % | 1.01 | | 0.81 | | 1.08 | | 1.47 | | 1.42 | |

Net investment income (loss) after expense reimbursement/recoupment(3) | % | 0.68 | | 0.31 | | (0.24 | ) | (0.59 | ) | (0.61 | ) |

Portfolio turnover rate | % | 132 | | 110 | | 189 | | 418 | | 510 | |

(1) Effective May 11, 2001, ING Investments, LLC began serving as Investment Manager to the Portfolio.

(2) Total return is calculated assuming reinvestment of all dividends and capital gain distributions at net asset value.

(3) The Investment Manager has agreed to limit expenses, (excluding interest, taxes, brokerage and extraordinary expenses) subject to possible recoupment by ING Investments, LLC within three years of being incurred.

† In 2005, 0.01% of the total return consists of a payment by affiliate. Excluding this item, total return would have been 4.66%.

See Accompanying Notes to Financial Statements

21

NOTES TO FINANCIAL STATEMENTS AS OF DECEMBER 31, 2005

NOTE 1 — ORGANIZATION

Organization. USLICO Series Fund (the “Fund”) is an open-end, diversified management investment company registered under the Investment Company Act of 1940 and consists of four separate portfolios. The four portfolios of the Fund are as follows: The Asset Allocation Portfolio (“Asset Allocation Portfolio”), The Bond Portfolio (“Bond Portfolio”), The Money Market Portfolio (“Money Market Portfolio”) and The Stock Portfolio (“Stock Portfolio”). Each Portfolio has its own investment objectives and policies which are detailed in the Prospectus.

The following is a brief description of each Portfolio’s investment objective:

• Asset Allocation Portfolio seeks to obtain high total return with reduced risk over the long term by allocating its assets among stocks, bonds, and short-term instruments;

• Bond Portfolio seeks a high level of income consistent with prudent risk and the preservation of capital and as a secondary objective, the Portfolio seeks capital appreciation when consistent with its principal objective;

• Money Market Portfolio seeks maximum current income consistent with preservation of capital and maintenance of liquidity; and

• Stock Portfolio seeks intermediate and long-term growth of capital and as a secondary objective seeks to receive a reasonable level of income.

The Fund was organized as a business trust under the laws of Massachusetts on January 19, 1988. Shares of the Portfolio are sold only to separate accounts of ReliaStar Life Insurance Company (ReliaStar Life) and ReliaStar Life Insurance Company of New York (ReliaStar Life of New York, a wholly-owned subsidiary of ReliaStar Life) to serve as the investment medium for variable life insurance policies issued by these companies. The separate accounts invest in shares of one or more of the Portfolios, in accordance with allocation instructions received from policyowners. Each Portfolio share outstanding represents a beneficial interest in the respective Portfolio.

On November 10, 2005, the Board of Trustees of USLICO Series Fund approved a proposal to reorganize the following “Disappearing Funds” into the following “Surviving Funds” (the “Reorganization”):

Disappearing Funds | | Surviving Funds |

The Asset Allocation Portfolio | | ING VP Balanced Portfolio |

Bond Portfolio | | ING VP Intermediate Bond Portfolio |

Money Market Portfolio | | ING Liquid Assets Portfolio |

Stock Portfolio | | ING Fundamental Research Portfolio |

The proposed Reorganization is subject to approval by shareholders of the Disappearing Funds. If shareholder approval is obtained, it is expected that the Reorganization would take place during the first quarter of 2006.

ING Investments, LLC (“ING Investments”), an Arizona limited liability company, serves as the Investment Manager to the Portfolios. ING Investments has engaged ING Investment Management Co. (“ING IM”), a Connecticut corporation, to serve as the Sub-Adviser to the Portfolios. ING Funds Distributor, LLC (the “Distributor”) is the principal underwriter of the Portfolios. ING Funds Services, LLC serves as the administrator to each Portfolio. ING Investments, ING IM, the Distributor and ING Funds Services, LLC are indirect, wholly-owned subsidiaries of ING Groep N.V. (“ING Groep”). ING Groep is one of the largest financial services organizations in the world, and offers an array of banking, insurance and asset management services to both individuals and institutional investors.

NOTE 2 — SIGNIFICANT ACCOUNTING POLICIES

The following significant accounting policies are consistently followed by the Portfolios in the preparation of their financial statements. Such policies are in conformity with U.S. generally accepted accounting principles for investment companies.

A. Security Valuation. Investments in equity securities traded on a national securities exchange are valued at the last reported sale price. Securities reported by NASDAQ are valued at the NASDAQ official closing prices. Securities traded on an exchange or NASDAQ for which there has been no sale and securities traded in the over-the-counter-market are valued at the mean between the last reported bid and ask prices. All investments quoted in foreign currencies will be valued daily in U.S. dollars on the basis of the foreign currency exchange rates prevailing at that time. Debt securities are valued at prices obtained from independent services or from one or more dealers making markets in the securities and may be adjusted based on the Portfolios’ valuation procedures. U.S. Government obligations are valued by using market quotations or independent pricing services that use prices provided by market-makers or estimates of market values obtained from yield data relating to instruments or securities with similar characteristics.

Securities and assets for which market quotations are not readily available (which may include certain restricted securities which are subject to limitations as to their sale) are valued at their fair values as determined in good faith by or under the supervision of the Board of Trustees (“Board”), in accordance with methods that are specifically authorized by the Board. Securities traded on exchanges, including foreign exchanges, which

22

NOTES TO FINANCIAL STATEMENTS AS OF DECEMBER 31, 2005 (CONTINUED)

NOTE 2 — SIGNIFICANT ACCOUNTING POLICIES (continued)

close earlier than the time that a Portfolio calculates its net asset value may also be valued at their fair values as determined in good faith by or under the supervision of the Board, in accordance with methods that are specifically authorized by the Board. If an event occurs after the time at which the market for foreign securities held by the Portfolio closes but before the time that the Portfolio’s NAV is calculated, such event may cause the closing price on the foreign exchange to not represent a readily available reliable market value quotation for such securities at the time the Portfolio determines its NAV. In such a case, the Portfolio will use the fair value of such securities as determined under the Portfolio’s valuation procedures. Events after the close of trading on a foreign market that could require the Portfolio to fair value some or all of its foreign securities include, among others, securities trading in the U.S. and other markets, corporate announcements, natural and other disasters, and political and other events. Among other elements of analysis in the determination of a security’s fair value, the Board has authorized the use of one or more independent research services to assist with such determinations. An independent research service may use statistical analyses and quantitative models to help determine fair value as of the time a Portfolio calculates its NAV. There can be no assurance that such models accurately reflect the behavior of the applicable markets or the effect of the behavior of such markets on the fair value of securities, or that such markets will continue to behave in a fashion that is consistent with such models. Unlike the closing price of a security on an exchange, fair value determinations employ elements of judgment. Consequently, the fair value assigned to a security may not represent the actual value that the Portfolio could obtain if it were to sell the security at the time of the close of the NYSE. Pursuant to procedures adopted by the Board, the Portfolio is not obligated to use the fair valuations suggested by any research service, and valuation recommendations provided by such research services may be overridden if other events have occurred or if other fair valuations are determined in good faith to be more accurate. Unless an event is such that it causes the Portfolio to determine that the closing prices for one or more securities do not represent readily available reliable market value quotations at the time the Portfolio determines its NAV, events that occur between the time of the close of the foreign market on which they are traded and the close of regular trading on the NYSE will not be reflected in the Portfolio’s NAV. Investments in securities maturing in 60 days or less, as well as all securities in the Money Market Portfolio, are valued at amortized cost, which, when combined with accrued interest, approximates market value.

B. Security Transactions and Revenue Recognition. Securities transactions are accounted for on the trade date. Realized gains and losses are reported on the basis of identified cost of securities sold. Interest income is recorded on an accrual basis. Dividend income is recorded on the ex-dividend date, or for certain foreign securities, when the information becomes available to the Portfolios. Premium amortization and discount accretion are determined by the effective yield method.

C. Purchases and Sales. Purchases and sales of Portfolio shares are made on the basis of the net asset value per share prevailing at the close of business on the preceding business day.