CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number:

(811-05498)

Exact name of registrant as specified in charter:

Putnam Master Intermediate Income Trust

Address of principal executive offices:

One Post Office Square, Boston, Massachusetts 02109

Name and address of agent for service:

Robert T. Burns, Vice President One Post Office Square Boston, Massachusetts 02109

Copy to:

Bryan Chegwidden, Esq. Ropes & Gray LLP 1211 Avenue of the Americas New York, New York 10036

Registrant’s telephone number, including area code:

(617) 292-1000

Date of fiscal year end:

September 30, 2015

Date of reporting period:

October 1, 2014 – March 31, 2015

Item 1. Report to Stockholders:

The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940:

Putnam Master Intermediate Income Trust

Semiannual report 3 | 31 | 15

Message from the Trustees

1

About the fund

2

Performance snapshot

4

Interview with your fund’s portfolio manager

5

Your fund’s performance

12

Terms and definitions

14

Other information for shareholders

15

Summary of dividend reinvestment plans

16

Financial statements

18

Shareholder meeting results

94

Consider these risks before investing: International investing involves currency, economic, and political risks. Emerging-market securities carry illiquidity and volatility risks. Lower-rated bonds may offer higher yields in return for more risk. Bond investments are subject to interest-rate risk (the risk of bond prices falling if interest rates rise) and credit risk (the risk of an issuer defaulting on interest or principal payments). Interest-rate risk is greater for longer-term bonds, and credit risk is greater for below-investment-grade bonds. Unlike bonds, funds that invest in bonds have fees and expenses. The value of bonds in the fund’s portfolio may fall or fail to rise over extended periods of time for a variety of reasons, including general financial market conditions, changing market perceptions of the risk of default, changes in government intervention, and factors related to a specific issuer or industry. These factors may also lead to periods of high volatility and reduced liquidity in the bond markets. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk and the risk that they may increase in value less when interest rates decline and decline in value more when interest rates rise. You can lose money by investing in the fund. The fund’s shares trade on a stock exchange at market prices, which may be lower than the fund’s net asset value.

Message from the Trustees

Dear Fellow Shareholder:

The month of March 2015 marked the six-year milestone of the bull market in U.S. stocks, and this June will be the sixth anniversary of the beginning of the U.S. economic recovery as dated by the National Bureau of Economic Research, which has traced the chronology of U.S. business cycles back to 1854.

While six years is above the historical average on both counts, reaching these milestones does not necessarily indicate anything about the sustainability of the expansion or the market advance. However, we believe it is an unusually long period for the Federal Reserve to have refrained from raising interest rates. The Fed now appears poised to act, and speculation is mounting about where equity and fixed-income markets around the world could go from this point forward. Your portfolio manager provides a perspective in the following pages.

At this juncture of the market cycle, you might consult your financial advisor who can help you review your goals and risk profile, and explain the importance of timely adjustments to keep your portfolio equipped for all seasons.

As you make progress toward your long-term financial goals, markets may move in different directions. With Putnam, you are aligned with a group of portfolio managers and analysts who are experienced in navigating through changing markets with consistent strategies. They are dedicated to active, fundamental research, and to helping you meet your financial needs.

As always, thank you for investing with Putnam.

Respectfully yours,

Robert L. Reynolds President and Chief Executive Officer Putnam Investments

Jameson A. Baxter Chair, Board of Trustees

May 6, 2015

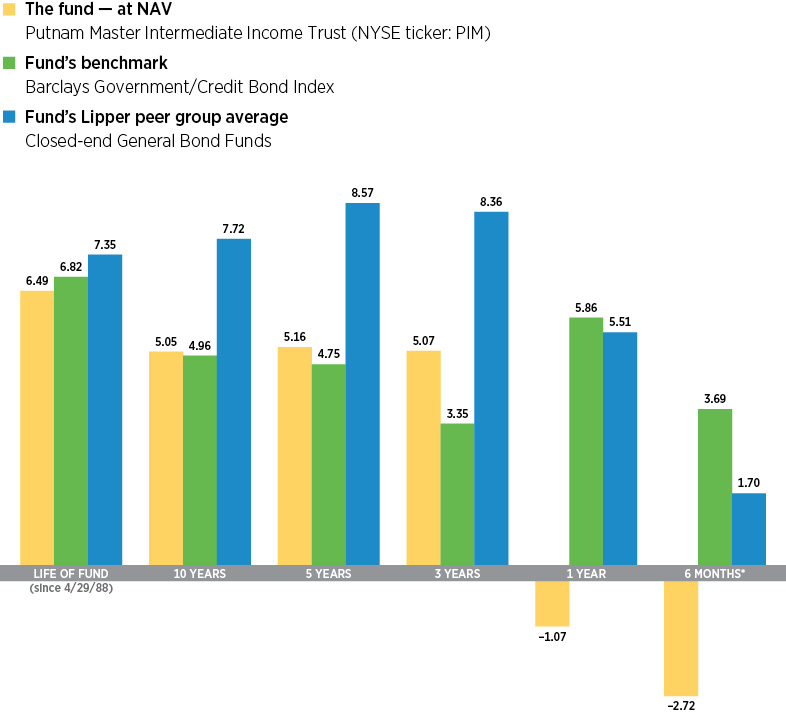

Performance snapshot

Annualized total return (%) comparison as of 3/31/15

Data are historical. Past performance does not guarantee future results. More recent returns may be less or more than those shown. Investment return and net asset value will fluctuate, and you may have a gain or a loss when you sell your shares. Performance assumes reinvestment of distributions and does not account for taxes. Fund returns in the bar chart are at NAV. See pages 5 and 12–13 for additional performance information, including fund returns at market price. Index and Lipper results should be compared with fund performance at NAV. Lipper calculates performance differently than the closed-end funds it ranks, due to varying methods for determining a fund’s monthly reinvestment NAV.

*Returns for the six-month period are not annualized, but cumulative.

4 Master Intermediate Income Trust

Interview with your fund’s portfolio manager

D. William Kohli

Bill, what was the bond market environment like during the six-month reporting period ended March 31, 2015?

The period was punctuated by episodes of interest-rate volatility, but rates generally moved lower. We were not surprised to see some degree of rate volatility, given that the Federal Reserve ended its bond-buying program in October 2014 and the European Central Bank [ECB] officially announced its version of quantitative easing in January. Additionally, with U.S. gross domestic product growing at a 5% annual rate in the third quarter of 2014 — its strongest pace in 11 years — investors sought to fine-tune their forecasts as to when the Fed may begin raising its target for short-term interest rates.

In January, the combination of a stock market pullback, weaker-than-expected U.S. economic data, and continued worries about deflation in Europe fueled investors’ appetite for government bonds. Against this backdrop, the yield on the benchmark 10-year U.S. Treasury fell to 1.64%, its low for the period. In February, concern that the Fed might start raising rates in June hampered Treasuries, causing prices to fall and yields to move higher. During March, however, dovish comments by Fed Chair Janet Yellen reassured investors that the central bank was likely to take a go-slow approach toward raising rates, which helped Treasuries modestly rebound during the final weeks of the period. The 10-year Treasury yield finished

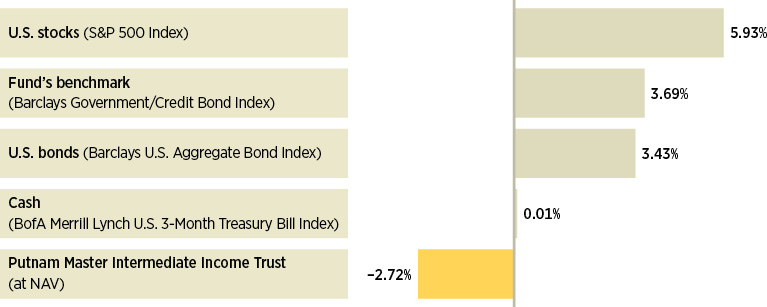

Broad market index and fund performance

This comparison shows your fund’s performance in the context of broad market indexes for the six months ended 3/31/15. See pages 4 and 12–13 for additional fund performance information. Index descriptions can be found on pages 14–15.

Master Intermediate Income Trust 5

the period at 1.92%, down from 2.49% at the beginning of the period.

The U.S. dollar continued to strengthen, rising more than 14% on an absolute basis during the reporting period and outpacing every other major currency, according to the WSJ Dollar Index, which represents multiple currencies. Versus the euro, the dollar’s surge was driven by the ECB’s launch of a larger-than-expected monetary easing program at the same time that the U.S. central bank was preparing to raise interest rates.

After declining since midsummer 2014, oil prices settled into a trading range in February and March. Prices fluctuated in the low- to mid-$50-per-barrel range on signs that U.S. production may be peaking and global demand may be rising.

The fund lagged its benchmark by a significant margin during the period. What factors hampered its relative performance?

It’s important to point out that the fund’s benchmark comprises U.S. Treasuries, government-agency securities, and investment-grade corporate bonds, and

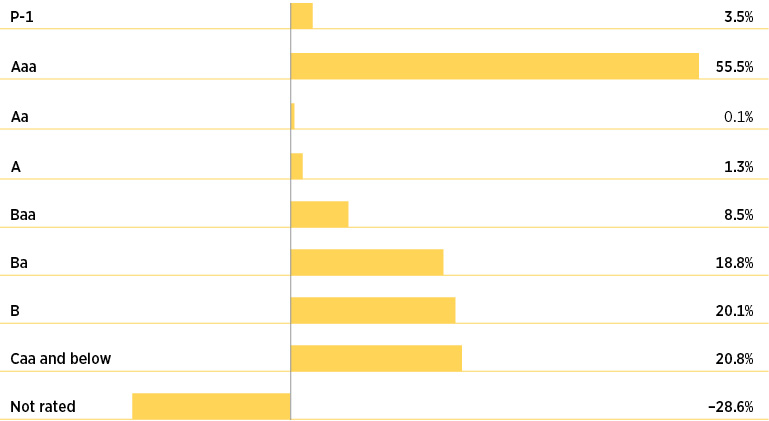

Credit quality overview

Credit qualities are shown as a percentage of the fund’s net assets as of 3/31/15. A bond rated Baa or higher (Prime-3 or higher, for short-term debt) is considered investment grade. The chart reflects Moody’s ratings; percentages may include bonds or derivatives not rated by Moody’s but rated by Standard & Poor’s (S&P) or, if unrated by S&P, by Fitch ratings, and then included in the closest equivalent Moody’s rating based on analysis of these agencies’ respective ratings criteria. Moody’s ratings are used in recognition of its prominence among rating agencies and breadth of coverage of rated securities. To be announced (TBA) mortgage commitments, if any, are included based on their issuer ratings. Ratings may vary over time.

Derivative instruments, including forward currency contracts, are only included to the extent of any unrealized gain or loss on such instruments and are shown in the not-rated category. Cash is also shown in the not-rated category. Derivative offset values are included in the not-rated category and may result in negative weights. The fund itself has not been rated by an independent rating agency.

6 Master Intermediate Income Trust

“Globally, economies are in one of the most disparate growth cycles since the mid-to-late 1990s.”

Bill Kohli

these sectors performed well during the past six months. Our strategy of investing in a variety of out-of-benchmark sectors, which has served the fund well over the long term, was largely unrewarded during the period. However, our biggest overall detractor was the fund’s interest-rate and yield-curve positioning in the United States. The portfolio was defensively positioned for a rising-rate environment, resulting in an overall duration — a key measure of interest-rate sensitivity — that was moderately negative on a net basis. Unfortunately, because rates trended lower during the period, this positioning worked against the fund’s performance.

Elsewhere, our prepayment strategies, which we implemented with securities such as agency interest-only collateralized mortgage obligations [IO CMOs], also detracted. In January, the Obama administration announced that the Federal Housing Administration [FHA]

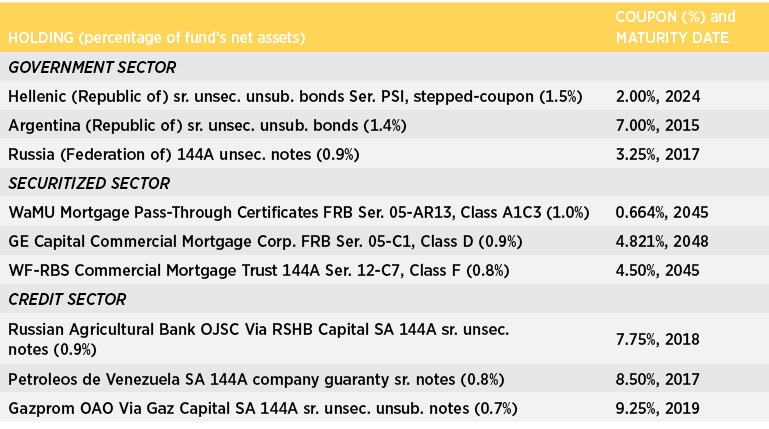

Top holdings

This table shows the fund’s top holdings across three key sectors and the percentage of the fund’s net assets that each represented as of 3/31/15. Short-term holdings, TBA commitments, and derivatives, if any, are excluded. Holdings may vary over time.

Master Intermediate Income Trust 7

would reduce the annual mortgage insurance premiums it charges to borrowers making small down payments. Investors reacted to this development by pricing in the possibility of faster mortgage prepayment speeds, which dampened the returns of existing prepayment-sensitive mortgage-backed securities. What’s more, this announcement came when Treasury yields were sharply declining, compounding the negatives for IO CMOs. The asset class rebounded in February, but did not fully overcome January’s significant downturn.

Our investments in emerging-market [EM] debt, specifically U.S. dollar-denominated holdings in Venezuela and Russia, modestly hampered the fund’s performance. During the first half of the period, declining oil prices soured investor sentiment toward the bonds of these oil-exporting countries. Continued uncertainty regarding Ukraine also weighed on Russia’s bonds.

Within foreign sovereign debt, our exposure to Greece detracted as Greek yields rose sharply. Increasing uncertainty about Greece’s prospects for accessing new financing and its ability to remain within the European Union weighed on the country’s bonds.

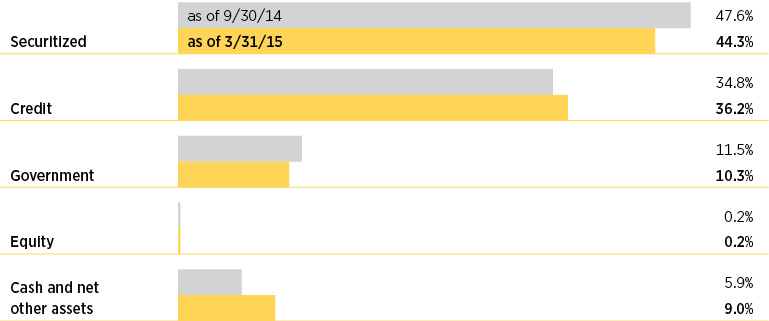

Comparison of top sector weightings

This chart shows how the fund’s top weightings have changed over the past six months. Allocations are shown as a percentage of the fund’s net assets. Cash and net other assets, if any, represent the market value weights of cash, derivatives, short-term securities, and other unclassified assets in the portfolio. Current period summary information may differ from the portfolio schedule included in the financial statements due to the inclusion of derivative securities, any interest accruals, and the use of different classifications of securities for presentation purposes. Holdings and allocations may vary over time.

Cash positions may represent collateral used to cover certain derivative contracts.

8 Master Intermediate Income Trust

Positions in high-yield bonds had a neutral impact on the fund’s return. Following a volatile period during 2014’s fourth quarter, high-yield bonds rallied in late January and February, fueled by oil prices settling into a trading range.

Turning to the positive side, which investments helped the fund’s performance?

Active currency positioning was the biggest contributor, as a long position in the U.S. dollar combined with short positions in most other major market currencies bolstered the fund’s performance. One exception to this strategy was a long position in the British pound sterling, which weakened relative to the U.S. dollar and slightly dampened the overall positive effect of our currency positioning.

Our mortgage credit investments, specifically positions in subordinated mezzanine commercial mortgage-backed securities [CMBS] and non-agency residential mortgage-backed securities [RMBS], also helped performance. Mezzanine CMBS benefited from supportive commercial real estate fundamentals, an improving U.S. economy, and persistent investor demand for higher-yielding bonds. Within non-agency RMBS, our holdings of Alternative-A [Alt-A] securities were helped by a strengthening housing market, coupled with solid investor demand amid shrinking supply. Alt-A securities are created from mortgage pools that occupy the space between riskier subprime mortgages and less risky prime mortgages.

How did you use derivatives during the period?

We used bond futures and interest-rate swaps to take tactical positions at various points along the yield curve, and to hedge the risk associated with the fund’s curve positioning. In addition, we employed interest-rate swaps and “swaptions” — the latter of which give us the option to enter into a swap contract — seeking to offset the

ABOUT DERIVATIVES

Derivatives are an increasingly common type of investment instrument, the performance of which is derived from an underlying security, index, currency, or other area of the capital markets. Derivatives employed by the fund’s managers generally serve one of two main purposes: to implement a strategy that may be difficult or more expensive to invest in through traditional securities, or to hedge unwanted risk associated with a particular position.

For example, the fund’s managers might use currency forward contracts to capitalize on an anticipated change in exchange rates between two currencies. This approach would require a significantly smaller outlay of capital than purchasing traditional bonds denominated in the underlying currencies. In another example, the managers may identify a bond that they believe is undervalued relative to its risk of default, but may seek to reduce the interest-rate risk of that bond by using interest-rate swaps, a derivative through which two parties “swap” payments based on the movement of certain rates.

Like any other investment, derivatives may not appreciate in value and may lose money. Derivatives may amplify traditional investment risks through the creation of leverage and may be less liquid than traditional securities. And because derivatives typically represent contractual agreements between two financial institutions, derivatives entail “counterparty risk,” which is the risk that the other party is unable or unwilling to pay. Putnam monitors the counterparty risks we assume. For example, Putnam often enters into collateral agreements that require the counterparties to post collateral on a regular basis to cover their obligations to the fund. Counterparty risk for exchange-traded futures and centrally cleared swaps is mitigated by the daily exchange of margin and other safeguards against default through their respective clearinghouses.

Master Intermediate Income Trust 9

interest-rate and prepayment risks associated with our CMO holdings, and to help manage overall downside risk. We also utilized total return swaps as a hedging tool and to help manage the portfolio’s sector exposure, as well as its inflation risk. Lastly, we utilized currency forward contracts to hedge the foreign exchange risk associated with non-U.S. bonds and to efficiently gain exposure to foreign currencies.

What is your outlook for the coming months, and how are you positioning the fund?

We remain positive on U.S. economic growth, but the recovery has reverted to a moderate pace after surging in the middle of last year. We believe this slowdown is partly because consumption hasn’t increased as much as was expected. During the past year, rising hourly wages and lower gasoline prices benefited lower-wage workers, which we thought would bolster personal consumption expenditures. However, rather than spending more, these consumers increased their savings. According to the Commerce Department, personal spending increased slightly in February, but was down in December and January. At the same time, the personal savings rate continued to climb, reaching 5.8% in February, its highest level since the end of 2012. As the effects of an unseasonably cold winter in the East and Midwest dissipate, we think consumption will improve.

We believe the Fed is likely to begin raising rates during 2015, possibly in September. Many investors believe the Fed will wait until later in 2015, or even into 2016, before it begins hiking rates. Consequently, there appears to be a considerable disconnect between what the market is forecasting and the Fed’s own outlook, which could spark some volatility. In our view, however, once the central bank begins to raise the federal funds rate, it will make every effort to do so in an orderly, well-communicated fashion in an effort to avoid major financial-market disruption.

Globally, economies are in one of the most disparate growth cycles since the mid-to-late 1990s. Capital is flowing from the eurozone and elsewhere into the United States, seeking to capitalize on opportunities in stocks, high-yield bonds, mortgage-backed securities, and government debt. As a result, developing markets are under pressure since many of those economies require capital inflows to maintain their fiscal and monetary programs. As a result, we’re not enthusiastic about near-term prospects in emerging markets overall, although we continue to find what we believe are attractive country-specific investment opportunities.

Within this environment, we plan to maintain our diversified mortgage, corporate, and sovereign credit exposure primarily through allocations to mezzanine CMBS, high-yield bonds, and peripheral European sovereign bonds, respectively. As for prepayment risk, we expect to maintain our holdings of IO CMOs. We do not believe the new FHA policy is likely to have a major impact on the overall pace of residential refinancing. Moreover, we continue to find prepayment risk attractive, given the potential for higher interest rates as the U.S. economic recovery matures. We’re also excited about ongoing opportunities we see in the foreign-exchange market. Many of the fundamental drivers of currency performance, such as divergent trends in U.S. and foreign economic growth and monetary policies, appear to be gaining momentum.

Thanks for your time and for bringing us up to date, Bill.

The views expressed in this report are exclusively those of Putnam Management and are subject to change. They are not meant as investment advice.

10 Master Intermediate Income Trust

Please note that the holdings discussed in this report may not have been held by the fund for the entire period. Portfolio composition is subject to review in accordance with the fund’s investment strategy and may vary in the future. Current and future portfolio holdings are subject to risk.

Portfolio Manager D. William Kohli is Co-Head of Fixed Income at Putnam. He has an M.B.A. from the Haas School of Business at the University of California, Berkeley, and a B.A. from the University of California, San Diego. Bill joined Putnam in 1994 and has been in the investment industry since 1986.

In addition to Bill, your fund’s portfolio managers are Michael J. Atkin, Kevin F. Murphy, Michael V. Salm, and Paul D. Scanlon, CFA.

How closed-end funds differ from open-end funds

Closed-end funds and open-end funds share many common characteristics but also have some key differences that you should understand as you consider your portfolio strategies.

More assets at work Open-end funds are subject to ongoing sales and redemptions that can generate transaction costs for long-term shareholders. Closed-end funds, however, are typically fixed pools of capital that do not need to hold cash in connection with sales and redemptions, allowing the funds to keep more assets actively invested.

Traded like stocks Closed-end fund shares are traded on stock exchanges and, as a result, their prices fluctuate because of the influence of several factors.

They have a market price Like an open-end fund, a closed-end fund has a per-share net asset value (NAV). However, closed-end funds also have a “market price” for their shares — which is how much you pay when you buy shares of the fund, and how much you receive when you sell them.

When looking at a closed-end fund’s performance, you will usually see that the NAV and the market price differ. The market price can be influenced by several factors that cause it to vary from the NAV, including fund distributions, changes in supply and demand for the fund’s shares, changing market conditions, and investor perceptions of the fund or its investment manager. A fund’s performance at market price typically differs from its results at NAV.

Putnam Master Intermediate Income Trust

Master Intermediate Income Trust 11

Your fund’s performance

This section shows your fund’s performance, price, and distribution information for periods ended March 31, 2015, the end of the first half of its current fiscal year. Performance should always be considered in light of a fund’s investment strategy. Data represent past performance. Past performance does not guarantee future results. More recent returns may be less or more than those shown. Investment return, net asset value, and market price will fluctuate, and you may have a gain or a loss when you sell your shares.

Fund performance Total return for periods ended 3/31/15

NAV

Market price

Annual average

Life of fund (since 4/29/88)

6.49%

6.39%

10 years

63.60

73.47

Annual average

5.05

5.66

5 years

28.62

11.78

Annual average

5.16

2.25

3 years

15.99

14.55

Annual average

5.07

4.63

1 year

–1.07

1.23

6 months

–2.72

0.54

Performance assumes reinvestment of distributions and does not account for taxes.

Comparative index returns For periods ended 3/31/15

Barclays Government/Credit Bond Index

Citigroup Non-U.S. World Government Bond Index

JPMorgan Global High Yield Index†

Lipper Closed-end General Bond Funds category average*

Annual average

Life of fund (since 4/29/88)

6.82%

5.50%

—

7.35%

10 years

62.28

28.09

119.86%

116.04

Annual average

4.96

2.51

8.20

7.72

5 years

26.12

1.92

51.03

53.17

Annual average

4.75

0.38

8.60

8.57

3 years

10.41

–9.63

22.82

27.83

Annual average

3.35

–3.32

7.09

8.36

1 year

5.86

–9.82

1.16

5.51

6 months

3.69

–7.14

0.34

1.70

Index and Lipper results should be compared with fund performance at net asset value. Lipper calculates performance differently than the closed-end funds it ranks, due to varying methods for determining a fund’s monthly reinvestment net asset value.

*Over the 6-month, 1-year, 3-year, 5-year, 10-year, and life-of-fund periods ended 3/31/15, there were 29, 28, 23, 18, 17, and 4 funds, respectively, in this Lipper category.

†The JPMorgan Global High Yield Index was introduced on 12/31/93, which post-dates the fund’s inception.

12 Master Intermediate Income Trust

Fund price and distribution information For the six-month period ended 3/31/15

Distributions

Number

6

Income

$0.156000

Capital gains

—

Total

$0.156000

Share value

NAV

Market price

9/30/14

$5.65

$5.03

3/31/15

5.34

4.90

Current rate (end of period)

NAV

Market price

Current dividend rate*

5.84%

6.37%

The classification of distributions, if any, is an estimate. Final distribution information will appear on your year-end tax forms.

*Most recent distribution, including any return of capital and excluding capital gains, annualized and divided by NAV or market price at end of period.

Master Intermediate Income Trust 13

Terms and definitions

Important terms

Total return shows how the value of the fund’s shares changed over time, assuming you held the shares through the entire period and reinvested all distributions in the fund.

Net asset value (NAV) is the value of all your fund’s assets, minus any liabilities, divided by the number of outstanding shares.

Market price is the current trading price of one share of the fund. Market prices are set by transactions between buyers and sellers on exchanges such as the New York Stock Exchange.

Fixed-income terms

Current rate is the annual rate of return earned from dividends or interest of an investment. Current rate is expressed as a percentage of the price of a security, fund share, or principal investment.

Mortgage-backed security (MBS), also known as a mortgage “pass-through,” is a type of asset-backed security that is secured by a mortgage or collection of mortgages. The following are types of MBSs:

• Agency “pass-through” has its principal and interest backed by a U.S. government agency, such as the Federal National Mortgage Association (Fannie Mae), Government National Mortgage Association (Ginnie Mae), and Federal Home Loan Mortgage Corporation (Freddie Mac).

• Collateralized mortgage obligation (CMO) represents claims to specific cash flows from pools of home mortgages. The streams of principal and interest payments on the mortgages are distributed to the different classes of CMO interests in “tranches.” Each tranche may have different principal balances, coupon rates, prepayment risks, and maturity dates. A CMO is highly sensitive to changes in interest rates and any resulting change in the rate at which homeowners sell their properties, refinance, or otherwise prepay loans. CMOs are subject to prepayment, market, and liquidity risks.

• Interest-only (IO) security is a type of CMO in which the underlying asset is the interest portion of mortgage, Treasury, or bond payments.

• Non-agency residential mortgage-backed security (RMBS) is an MBS not backed by Fannie Mae, Ginnie Mae, or Freddie Mac. One type of RMBS is an Alt-A mortgage-backed security.

• Commercial mortgage-backed security (CMBS) is secured by the loan on a commercial property.

Yield curve is a graph that plots the yields of bonds with equal credit quality against their differing maturity dates, ranging from shortest to longest. It is used as a benchmark for other debt, such as mortgage or bank lending rates.

Comparative indexes

Barclays Government/Credit Bond Index is an unmanaged index of U.S. Treasuries, agency securities, and investment-grade corporate bonds.

Barclays U.S. Aggregate Bond Index is an unmanaged index of U.S. investment-grade fixed-income securities.

BofA Merrill Lynch U.S. 3-Month Treasury Bill Index is an unmanaged index that seeks to measure the performance of U.S. Treasury bills available in the marketplace.

Citigroup Non-U.S. World Government Bond Index is an unmanaged index generally considered to be representative of the world bond market excluding the United States.

JPMorgan Global High Yield Index is an unmanaged index that is designed to mirror the investable universe of the U.S. dollar global high-yield corporate debt market, including domestic (U.S.) and international (non-U.S.) issues. International issues comprise both developed and emerging markets.

14 Master Intermediate Income Trust

S&P 500 Index is an unmanaged index of common stock performance.

Indexes assume reinvestment of all distributions and do not account for fees. Securities and performance of a fund and an index will differ. You cannot invest directly in an index.

Lipper is a third-party industry-ranking entity that ranks mutual funds. Its rankings do not reflect sales charges. Lipper rankings are based on total return at net asset value relative to other funds that have similar current investment styles or objectives as determined by Lipper. Lipper may change a fund’s category assignment at its discretion. Lipper category averages reflect performance trends for funds within a category.

Other information for shareholders

Important notice regarding share repurchase program

In September 2014, the Trustees of your fund approved the renewal of a share repurchase program that had been in effect since 2005. This renewal allows your fund to repurchase, in the 12 months beginning October 8, 2014, up to 10% of the fund’s common shares outstanding as of October 7, 2014.

Important notice regarding delivery of shareholder documents

In accordance with Securities and Exchange Commission (SEC) regulations, Putnam sends a single copy of annual and semiannual shareholder reports, prospectuses, and proxy statements to Putnam shareholders who share the same address, unless a shareholder requests otherwise. If you prefer to receive your own copy of these documents, please call Putnam at 1-800-225-1581, and Putnam will begin sending individual copies within 30 days.

Proxy voting

Putnam is committed to managing our mutual funds in the best interests of our shareholders. The Putnam funds’ proxy voting guidelines and procedures, as well as information regarding how your fund voted proxies relating to portfolio securities during the 12-month period ended June 30, 2014, are available in the Individual Investors section of putnam.com, and on the SEC’s website, www.sec.gov. If you have questions about finding forms on the SEC’s website, you may call the SEC at 1-800-SEC-0330. You may also obtain the Putnam funds’ proxy voting guidelines and procedures at no charge by calling Putnam’s Shareholder Services at 1-800-225-1581.

Fund portfolio holdings

The fund will file a complete schedule of its portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. Shareholders may obtain the fund’s Form N-Q on the SEC’s website at www.sec.gov. In addition, the fund’s Form N-Q may be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C. You may call the SEC at 1-800-SEC-0330 for information about the SEC’s website or the operation of the Public Reference Room.

Trustee and employee fund ownership

Putnam employees and members of the Board of Trustees place their faith, confidence, and, most importantly, investment dollars in Putnam mutual funds. As of March 31, 2015, Putnam employees had approximately $494,000,000 and the Trustees had approximately $141,000,000 invested in Putnam mutual funds. These amounts include investments by the Trustees’ and employees’ immediate family members as well as investments through retirement and deferred compensation plans.

Master Intermediate Income Trust 15

Summary of Putnam Closed-End Funds’ Amended and Restated Dividend Reinvestment Plans

Putnam High Income Securities Fund, Putnam Managed Municipal Income Trust, Putnam Master Intermediate Income Trust, Putnam Municipal Opportunities Trust and Putnam Premier Income Trust (each, a “Fund” and collectively, the “Funds”) each offer a dividend reinvestment plan (each, a “Plan” and collectively, the “Plans”). If you participate in a Plan, all income dividends and capital gain distributions are automatically reinvested in Fund shares by the Fund’s agent, Putnam Investor Services, Inc. (the “Agent”). If you are not participating in a Plan, every month you will receive all dividends and other distributions in cash, paid by check and mailed directly to you.

Upon a purchase (or, where applicable, upon registration of transfer on the shareholder records of a Fund) of shares of a Fund by a registered shareholder, each such shareholder will be deemed to have elected to participate in that Fund’s Plan. Each such shareholder will have all distributions by a Fund automatically reinvested in additional shares, unless such shareholder elects to terminate participation in a Plan by instructing the Agent to pay future distributions in cash. Shareholders who were not participants in a Plan as of January 31, 2010, will continue to receive distributions in cash but may enroll in a Plan at any time by contacting the Agent.

If you participate in a Fund’s Plan, the Agent will automatically reinvest subsequent distributions, and the Agent will send you a confirmation in the mail telling you how many additional shares were issued to your account.

To change your enrollment status or to request additional information about the Plans, you may contact the Agent either in writing, at P.O. Box 8383, Boston, MA 02266-8383, or by telephone at 1-800-225-1581 during normal East Coast business hours.

How you acquire additional shares through a Plan If the market price per share for your Fund’s shares (plus estimated brokerage commissions) is greater than or equal to their net asset value per share on the payment date for a distribution, you will be issued shares of the Fund at a value equal to the higher of the net asset value per share on that date or 95% of the market price per share on that date.

If the market price per share for your Fund’s shares (plus estimated brokerage commissions) is less than their net asset value per share on the payment date for a distribution, the Agent will buy Fund shares for participating accounts in the open market. The Agent will aggregate open-market purchases on behalf of all participants, and the average price (including brokerage commissions) of all shares purchased by the Agent will be the price per share allocable to each participant. The Agent will generally complete these open-market purchases within five business days following the payment date. If, before the Agent has completed open-market purchases, the market price per share (plus estimated brokerage commissions) rises to exceed the net asset value per share on the payment date, then the purchase price may exceed the net asset value per share, potentially resulting in the acquisition of fewer shares than if the distribution had been paid in newly issued shares.

How to withdraw from a Plan Participants may withdraw from a Fund’s Plan at any time by notifying the Agent, either in writing or by telephone. Such withdrawal will be effective immediately if notice is received by the Agent with sufficient time prior to any distribution record date; otherwise, such withdrawal will be effective with respect to any subsequent

16 Master Intermediate Income Trust

distribution following notice of withdrawal. There is no penalty for withdrawing from or not participating in a Plan.

Plan administration The Agent will credit all shares acquired for a participant under a Plan to the account in which the participant’s common shares are held. Each participant will be sent reasonably promptly a confirmation by the Agent of each acquisition made for his or her account.

About brokerage fees Each participant pays a proportionate share of any brokerage commissions incurred if the Agent purchases additional shares on the open market, in accordance with the Plans. There are no brokerage charges applied to shares issued directly by the Funds under the Plans.

About taxes and Plan amendments Reinvesting dividend and capital gain distributions in shares of the Funds does not relieve you of tax obligations, which are the same as if you had received cash distributions. The Agent supplies tax information to you and to the IRS annually. Each Fund reserves the right to amend or terminate its Plan upon 30 days’ written notice. However, the Agent may assign its rights, and delegate its duties, to a successor agent with the prior consent of a Fund and without prior notice to Plan participants.

If your shares are held in a broker or nominee name If your shares are held in the name of a broker or nominee offering a dividend reinvestment service, consult your broker or nominee to ensure that an appropriate election is made on your behalf. If the broker or nominee holding your shares does not provide a reinvestment service, you may need to register your shares in your own name in order to participate in a Plan.

In the case of record shareholders such as banks, brokers or nominees that hold shares for others who are the beneficial owners of such shares, the Agent will administer the Plan on the basis of the number of shares certified by the record shareholder as representing the total amount registered in such shareholder’s name and held for the account of beneficial owners who are to participate in the Plan.

Master Intermediate Income Trust 17

Financial statements

A guide to financial statements

These sections of the report, as well as the accompanying Notes, constitute the fund’s financial statements.

The fund’s portfolio lists all the fund’s investments and their values as of the last day of the reporting period. Holdings are organized by asset type and industry sector, country, or state to show areas of concentration and diversification.

Statement of assets and liabilities shows how the fund’s net assets and share price are determined. All investment and non-investment assets are added together. Any unpaid expenses and other liabilities are subtracted from this total. The result is divided by the number of shares to determine the net asset value per share. (For funds with preferred shares, the amount subtracted from total assets includes the liquidation preference of preferred shares.)

Statement of operations shows the fund’s net investment gain or loss. This is done by first adding up all the fund’s earnings — from dividends and interest income — and subtracting its operating expenses to determine net investment income (or loss). Then, any net gain or loss the fund realized on the sales of its holdings — as well as any unrealized gains or losses over the period — is added to or subtracted from the net investment result to determine the fund’s net gain or loss for the fiscal period.

Statement of changes in net assets shows how the fund’s net assets were affected by the fund’s net investment gain or loss, by distributions to shareholders, and by changes in the number of the fund’s shares. It lists distributions and their sources (net investment income or realized capital gains) over the current reporting period and the most recent fiscal year-end. The distributions listed here may not match the sources listed in the Statement of operations because the distributions are determined on a tax basis and may be paid in a different period from the one in which they were earned. Dividend sources are estimated at the time of declaration. Actual results may vary. Any non-taxable return of capital cannot be determined until final tax calculations are completed after the end of the fund’s fiscal year.

Financial highlights provide an overview of the fund’s investment results, per-share distributions, expense ratios, net investment income ratios, and portfolio turnover in one summary table, reflecting the five most recent reporting periods. In a semiannual report, the highlights table also includes the current reporting period.

18 Master Intermediate Income Trust

The fund’s portfolio 3/31/15 (Unaudited)

U.S. GOVERNMENT AND AGENCY MORTGAGE OBLIGATIONS (55.1%)*

Principal amount

Value

U.S. Government Agency Mortgage Obligations (55.1%)

Federal National Mortgage Association Pass-Through Certificates

5 1/2s, TBA, April 1, 2045

$3,000,000

$3,378,750

5 1/2s, TBA, March 1, 2045

1,000,000

1,128,125

4 1/2s, TBA, May 1, 2045

14,000,000

15,233,750

4 1/2s, TBA, April 1, 2045

19,000,000

20,727,813

4s, TBA, April 1, 2045

17,000,000

18,178,047

3 1/2s, TBA, May 1, 2045

22,000,000

23,056,172

3 1/2s, TBA, April 1, 2045

25,000,000

26,263,673

3s, TBA, April 1, 2045

58,000,000

59,305,000

167,271,330

Total U.S. government and agency mortgage obligations (cost $166,137,540)

Total foreign government and agency bonds and notes (cost $37,239,554)

$30,689,320

Master Intermediate Income Trust 45

SENIOR LOANS (2.3%)* c

Principal amount

Value

Basic materials (0.1%)

Atkore International, Inc. bank term loan FRN 4 1/2s, 2021

$104,213

$102,910

Ineos US Finance, LLC bank term loan FRN 3 3/4s, 2018

70,937

70,507

WR Grace & Co. bank term loan FRN 2 3/4s, 2021

105,774

105,679

WR Grace & Co. bank term loan FRN Ser. DD, 2 3/4s, 2021

38,063

38,029

317,125

Capital goods (—%)

Gates Global, LLC/Gates Global Co. bank term loan FRN 4 1/4s, 2021

141,290

140,672

140,672

Communication services (0.2%)

Asurion, LLC bank term loan FRN 8 1/2s, 2021

139,000

139,550

Asurion, LLC bank term loan FRN Ser. B1, 5s, 2019

143,797

144,182

Level 3 Financing, Inc. bank term loan FRN Ser. B1, 4s, 2020

75,000

75,109

Level 3 Financing, Inc. bank term loan FRN Ser. B5, 4 1/2s, 2022

130,000

130,580

489,421

Consumer cyclicals (1.2%)

Caesars Entertainment Operating Co., Inc. bank term loan FRN Ser. B6, 9.005s, 2017

851,175

777,229

Caesars Entertainment Operating Co., Inc. bank term loan FRN Ser. B7, 11 3/4s, 2017

69,650

63,294

Caesars Growth Properties Holdings, LLC bank term loan FRN 6 1/4s, 2021

258,050

228,116

CCM Merger, Inc. bank term loan FRN Ser. B, 4 1/2s, 2021

164,293

164,704

Dollar Tree Stores, Inc. bank term loan FRN Ser. B, 4 1/4s, 2022

60,000

60,609

Getty Images, Inc. bank term loan FRN Ser. B, 4 3/4s, 2019

210,852

177,327

Hilton Worldwide Finance, LLC bank term loan FRN Ser. B, 3 1/2s, 2020

191,447

191,618

iHeartCommunications, Inc. bank term loan FRN Ser. D, 6.922s, 2019

323,000

306,769

JC Penney Corp., Inc. bank term loan FRN 5s, 2019

428,673

421,528

Navistar, Inc. bank term loan FRN Ser. B, 5 3/4s, 2017

111,606

112,071

Neiman Marcus Group, Ltd., Inc. bank term loan FRN 4 1/4s, 2020

286,256

285,019

PetSmart, Inc. bank term loan FRN Ser. B, 5s, 2022

235,000

236,656

ROC Finance, LLC bank term loan FRN 5s, 2019

128,371

123,878

Univision Communications, Inc. bank term loan FRN 4s, 2020

304,313

303,648

Visteon Corp. bank term loan FRN Class B, 3 1/2s, 2021

94,288

94,081

3,546,547

Consumer staples (0.2%)

BC ULC bank term loan FRN Ser. B, 4 1/2s, 2021 (Canada)

153,631

155,058

CEC Entertainment, Inc. bank term loan FRN Ser. B, 4s, 2021

147,510

145,519

H.J. Heinz Co. bank term loan FRN Ser. B2, 3 1/4s, 2020

98,269

98,257

Libbey Glass, Inc. bank term loan FRN Ser. B, 3 3/4s, 2021

84,363

83,835

Revlon Consumer Products Corp. bank term loan FRN Ser. B, 4s, 2019

164,953

164,799

647,468

Health care (0.2%)

Grifols Worldwide Operations USA, Inc. bank term loan FRN 3.172s, 2021

222,750

222,444

Ortho-Clinical Diagnostics, Inc. bank term loan FRN Ser. B, 4 3/4s, 2021

79,400

78,594

46 Master Intermediate Income Trust

SENIOR LOANS (2.3%)* c cont.

Principal amount

Value

Health care cont.

Par Pharmaceutical Cos., Inc. bank term loan FRN Class B2, 4s, 2019

$84,442

$84,266

Patheon, Inc. bank term loan FRN Ser. B, 4 1/4s, 2021 (Netherlands)

119,100

118,405

Valeant Pharmaceuticals International, Inc. bank term loan FRN Ser. E, 3 1/2s, 2020

104,487

104,438

608,147

Technology (0.2%)

Avaya, Inc. bank term loan FRN Ser. B3, 4.676s, 2017

103,771

102,097

Avaya, Inc. bank term loan FRN Ser. B6, 6 1/2s, 2018

206,936

206,275

Dell International, LLC bank term loan FRN Ser. B, 4 1/2s, 2020

64,348

64,688

Freescale Semiconductor, Inc. bank term loan FRN Ser. B5, 5s, 2021

290,575

291,924

664,984

Transportation (0.1%)

Air Medical Group Holdings, Inc. bank term loan FRN 7 5/8s, 2018 ‡‡

205,000

206,025

206,025

Utilities and power (0.1%)

Texas Competitive Electric Holdings Co., LLC bank term loan FRN 4.662s, 2017

496,516

296,757

Texas Competitive Electric Holdings Co., LLC bank term loan FRN 4.662s, 2017

5,096

3,046

299,803

Total senior loans (cost $7,222,072)

$6,920,192

PURCHASED SWAP OPTIONS OUTSTANDING (1.1%)* Counterparty Fixed right % to receive or (pay)/ Floating rate index/Maturity date

Expiration date/strike

Contract amount

Value

Bank of America N.A.

2.175/3 month USD-LIBOR-BBA/Apr-25

Apr-15/2.175

$20,170,400

$276,334

(2.0875)/3 month USD-LIBOR-BBA/Jul-25

Jul-15/2.0875

10,085,200

177,096

(2.685)/3 month USD-LIBOR-BBA/Sep-25

Sep-15/2.685

20,151,100

116,675

1.816/3 month USD-LIBOR-BBA/Apr-25

Apr-15/1.816

20,151,100

24,987

Barclays Bank PLC

(2.1625)/3 month USD-LIBOR-BBA/May-25

May-15/2.1625

20,151,100

168,665

(2.31)/3 month USD-LIBOR-BBA/Apr-45

Apr-15/2.31

4,030,220

133,521

2.31/3 month USD-LIBOR-BBA/Apr-45

Apr-15/2.31

4,030,220

47,355

Citibank, N.A.

2.20/3 month USD-LIBOR-BBA/May-25

May-15/2.20

21,333,200

382,718

2.172/3 month USD-LIBOR-BBA/Apr-25

Apr-15/2.172

10,085,200

137,663

2.043/3 month USD-LIBOR-BBA/May-25

May-15/2.043

10,075,550

105,088

1.4015/3 month USD-LIBOR-BBA/May-20

May-15/1.4015

40,302,200

104,786

(2.13)/3 month USD-LIBOR-BBA/Apr-25

Apr-15/2.13

20,151,100

80,806

1.294/3 month USD-LIBOR-BBA/May-20

May-15/1.294

40,302,200

59,244

1.3735/3 month USD-LIBOR-BBA/May-20

May-15/1.3735

20,151,100

45,541

1.266/3 month USD-LIBOR-BBA/May-20

May-15/1.266

20,151,100

25,390

1.802/3 month USD-LIBOR-BBA/Apr-25

Apr-15/1.802

20,151,100

21,965

Master Intermediate Income Trust 47

PURCHASED SWAP OPTIONS OUTSTANDING (1.1%)* Counterparty Fixed right % to receive or (pay)/ Floating rate index/Maturity date cont.

Expiration date/strike

Contract amount

Value

Credit Suisse International

2.25/3 month USD-LIBOR-BBA/May-25

May-15/2.25

$33,114,000

$702,679

2.09125/3 month USD-LIBOR-BBA/Apr-25

Apr-15/2.09125

20,180,000

167,494

2.09/3 month USD-LIBOR-BBA/Apr-25

Apr-15/2.09

20,180,000

165,880

1.795/3 month USD-LIBOR-BBA/Apr-25

Apr-15/1.795

20,202,300

20,606

Goldman Sachs International

2.655/3 month USD-LIBOR-BBA/May-45

May-15/2.655

5,037,775

316,473

(2.82)/3 month USD-LIBOR-BBA/Jan-46

Jan-16/2.82

3,681,050

138,960

1.84/3 month USD-LIBOR-BBA/Apr-25

Apr-15/1.84

15,113,300

32,494

1.76/3 month USD-LIBOR-BBA/Apr-25

Apr-15/1.76

15,113,300

17,834

Total purchased swap options outstanding (cost $3,081,972)

$3,470,254

PURCHASED OPTIONS OUTSTANDING (0.1%)*

Expiration date/strike price

Contract amount

Value

Federal National Mortgage Association 30 yr 3.0s TBA commitments (Put)

May-15/$102.57

$11,000,000

$99,154

Federal National Mortgage Association 30 yr 3.0s TBA commitments (Put)

Apr-15/103.07

11,000,000

84,964

Total purchased options outstanding (cost $350,626)

$184,118

PREFERRED STOCKS (0.2%)*

Shares

Value

Ally Financial, Inc. 144A 7.00% cum. pfd.

353

$360,556

M/I Homes, Inc. Ser. A, $2.438 pfd.

4,100

104,960

Total preferred stocks (cost $302,913)

$465,516

CONVERTIBLE BONDS AND NOTES (—%)*

Principal amount

Value

iStar Financial, Inc. cv. sr. unsec. unsub. notes 3s, 2016 R

$100,000

$118,438

Total convertible bonds and notes (cost $104,643)

$118,438

COMMON STOCKS (—%)*

Shares

Value

Lone Pine Resources Canada, Ltd. (Canada) † F

9,978

$399

Lone Pine Resources, Inc. Class A (Canada) † F

9,978

399

Tribune Co. Class 1C F

40,066

10,017

Total common stocks (cost $65,186)

$10,815

SHORT-TERM INVESTMENTS (10.4%)*

Principal amount/shares

Value

Putnam Short Term Investment Fund 0.09% L

Shares 18,639,521

$18,639,521

SSgA Prime Money Market Fund Class N 0.02% P

Shares 2,346,000

2,346,000

U.S. Treasury Bills with effective yields ranging from 0.03% to 0.04%, April 2, 2015 Δ §

$1,067,000

1,066,999

U.S. Treasury Bills with an effective yield of 0.02%, April 23, 2015 Δ §

700,000

699,991

U.S. Treasury Bills with an effective yield of 0.02%, July 2, 2015 Δ

40,000

39,997

U.S. Treasury Bills with an effective yield of 0.10%, July 23, 2015 # Δ §

3,253,000

3,252,590

48 Master Intermediate Income Trust

SHORT-TERM INVESTMENTS (10.4%)* cont.

Principal amount/shares

Value

U.S. Treasury Bills with an effective yield of 0.01%, May 14, 2015 §

$200,000

$199,998

U.S. Treasury Bills with an effective yield of 0.01%, May 21, 2015 # §

1,450,000

1,449,977

U.S. Treasury Bills with an effective yield of 0.01%, May 7, 2015 Δ §

4,000,000

3,999,940

Total short-term investments (cost $31,694,367)

$31,695,013

TOTAL INVESTMENTS

Total investments (cost $477,765,643)

$475,257,574

Key to holding’s currency abbreviations

AUD

Australian Dollar

BRL

Brazilian Real

CAD

Canadian Dollar

CHF

Swiss Franc

CLP

Chilean Peso

EUR

Euro

GBP

British Pound

JPY

Japanese Yen

KRW

South Korean Won

NOK

Norwegian Krone

NZD

New Zealand Dollar

PLN

Polish Zloty

SEK

Swedish Krona

ZAR

South African Rand

Key to holding’s abbreviations

FRB

Floating Rate Bonds: the rate shown is the current interest rate at the close of the reporting period

FRN

Floating Rate Notes: the rate shown is the current interest rate or yield at the close of the reporting period

IFB

Inverse Floating Rate Bonds, which are securities that pay interest rates that vary inversely to changes in the market interest rates. As interest rates rise, inverse floaters produce less current income. The rate shown is the current interest rate at the close of the reporting period.

IO

Interest Only

OAO

Open Joint Stock Company

OJSC

Open Joint Stock Company

PO

Principal Only

REGS

Securities sold under Regulation S may not be offered, sold or delivered within the United States except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the Securities Act of 1933.

TBA

To Be Announced Commitments

Notes to the fund’s portfolio

Unless noted otherwise, the notes to the fund’s portfolio are for the close of the fund’s reporting period, which ran from October 1, 2014 through March 31, 2015 (the reporting period). Within the following notes to the portfolio, references to “ASC 820” represent Accounting Standards Codification 820 Fair Value Measurements and Disclosures and references to “OTC”, if any, represent over-the-counter.

*

Percentages indicated are based on net assets of $303,553,270.

†

This security is non-income-producing.

††

The interest or dividend rate and date shown parenthetically represent the new interest or dividend rate to be paid and the date the fund will begin accruing interest or dividend income at this rate.

Master Intermediate Income Trust 49

‡‡

Income may be received in cash or additional securities at the discretion of the issuer.

#

This security, in part or in entirety, was pledged and segregated with the broker to cover margin requirements for futures contracts at the close of the reporting period.

Δ

This security, in part or in entirety, was pledged and segregated with the custodian for collateral on certain derivative contracts at the close of the reporting period.

§

This security, in part or in entirety, was pledged and segregated with the custodian for collateral on the initial margin on certain centrally cleared derivative contracts at the close of the reporting period.

c

Senior loans are exempt from registration under the Securities Act of 1933, as amended, but contain certain restrictions on resale and cannot be sold publicly. These loans pay interest at rates which adjust periodically. The interest rates shown for senior loans are the current interest rates at the close of the reporting period. Senior loans are also subject to mandatory and/or optional prepayment which cannot be predicted. As a result, the remaining maturity may be substantially less than the stated maturity shown (Notes 1 and 6).

##

Forward commitment, in part or in entirety (Note 1).

F

This security is valued at fair value following procedures approved by the Trustees. Securities may be classified as Level 2 or Level 3 for ASC 820 based on the securities’ valuation inputs (Note 1).

i

This security was pledged, or purchased with cash that was pledged, to the fund for collateral on certain derivative contracts (Note 1).

L

Affiliated company (Note 5). The rate quoted in the security description is the annualized 7-day yield of the fund at the close of the reporting period.

P

This security was pledged, or purchased with cash that was pledged, to the fund for collateral on certain derivative contracts. The rate quoted in the security description is the annualized 7-day yield of the fund at the close of the reporting period (Note 1).

R

Real Estate Investment Trust.

At the close of the reporting period, the fund maintained liquid assets totaling $199,837,681 to cover certain derivative contracts, delayed delivery securities and the settlement of certain securities.

Debt obligations are considered secured unless otherwise indicated.

144A after the name of an issuer represents securities exempt from registration under Rule 144A under the Securities Act of 1933, as amended. These securities may be resold in transactions exempt from registration, normally to qualified institutional buyers.

See Note 1 to the financial statements regarding TBA commitments.

The dates shown on debt obligations are the original maturity dates.

DIVERSIFICATION BY COUNTRY

Distribution of investments by country of risk at the close of the reporting period, excluding collateral received, if any (as a percentage of Portfolio Value):

United States

86.0%

Russia

2.4

Argentina

2.0

Greece

1.9

Venezuela

1.0

Canada

1.0

Brazil

0.8

Luxembourg

0.7

United Kingdom

0.7

Mexico

0.6

Indonesia

0.6

Other

2.3

Total

100.0%

50 Master Intermediate Income Trust

FORWARD CURRENCY CONTRACTS at 3/31/15 (aggregate face value $126,528,888) (Unaudited)

Counterparty

Currency

Contract type

Delivery date

Value

Aggregate face value

Unrealized appreciation/ (depreciation)

Bank of America N.A.

Australian Dollar

Buy

4/15/15

$617,146

$623,897

$(6,751)

British Pound

Buy

6/17/15

885,427

925,144

(39,717)

Canadian Dollar

Sell

4/15/15

2,175,029

2,295,937

120,908

Chilean Peso

Sell

4/15/15

370,711

$371,692

981

Euro

Sell

6/17/15

323,986

422,835

98,849

Norwegian Krone

Buy

6/17/15

149,579

$133,335

16,244

Barclays Bank PLC

Australian Dollar

Buy

4/15/15

697,818

700,610

(2,792)

British Pound

Buy

6/17/15

768,744

764,414

4,330

Canadian Dollar

Sell

4/15/15

2,873,119

3,062,228

189,109

Euro

Sell

6/17/15

362,197

402,660

40,463

Japanese Yen

Sell

5/20/15

722,407

736,813

14,406

Mexican Peso

Buy

4/15/15

1,476,487

1,518,085

(41,598)

New Zealand Dollar

Sell

4/15/15

717,087

698,933

(18,154)

Singapore Dollar

Sell

5/20/15

1,546,398

1,535,709

(10,689)

Swedish Krona

Buy

6/17/15

665,371

717,854

(52,483)

Swiss Franc

Sell

6/17/15

201,595

204,874

3,279

Citibank, N.A.

Australian Dollar

Buy

4/15/15

637,999

624,531

13,468

Brazilian Real

Buy

4/2/15

203,725

202,681

1,044

Brazilian Real

Sell

4/2/15

401,969

435,587

33,618

British Pound

Buy

6/17/15

745,318

772,663

(27,345)

Canadian Dollar

Sell

4/15/15

1,887,362

1,907,039

19,677

Chilean Peso

Buy

4/15/15

1,537,631

1,531,677

5,954

Danish Krone

Sell

6/17/15

1,458,759

1,525,259

66,500

Euro

Buy

6/17/15

571,442

596,701

(25,259)

Japanese Yen

Sell

5/20/15

1,014,965

1,035,958

20,993

Mexican Peso

Buy

4/15/15

1,479,789

1,465,684

14,105

New Zealand Dollar

Sell

4/15/15

1,161,944

1,179,587

17,643

Norwegian Krone

Buy

6/17/15

789,586

761,497

28,089

Norwegian Krone

Sell

6/17/15

788,372

823,897

35,525

Philippine Peso

Buy

5/20/15

746,907

758,754

(11,847)

Swiss Franc

Sell

6/17/15

1,517,174

1,543,762

26,588

Credit Suisse International

Australian Dollar

Sell

4/15/15

734,578

771,148

36,570

British Pound

Buy

6/17/15

230,104

288,957

(58,853)

Canadian Dollar

Sell

4/15/15

3,408,193

3,476,919

68,726

Euro

Buy

6/17/15

102,900

115,272

(12,372)

Indian Rupee

Buy

5/20/15

3,121,194

3,138,390

(17,196)

Japanese Yen

Sell

5/20/15

54

54

—

New Zealand Dollar

Buy

4/15/15

811,016

825,912

(14,896)

Norwegian Krone

Sell

6/17/15

401,397

419,414

18,017

Master Intermediate Income Trust 51

FORWARD CURRENCY CONTRACTS at 3/31/15 (aggregate face value $126,528,888) (Unaudited) cont.

Counterparty

Currency

Contract type

Delivery date

Value

Aggregate face value

Unrealized appreciation/ (depreciation)

Credit Suisse International cont.

Swedish Krona

Sell

6/17/15

$750,341

$773,529

$23,188

Swiss Franc

Sell

6/17/15

698,408

710,382

11,974

Deutsche Bank AG

Australian Dollar

Buy

4/15/15

134,860

120,351

14,509

British Pound

Buy

6/17/15

1,261,718

1,308,111

(46,393)

Canadian Dollar

Sell

4/15/15

2,913,301

3,014,432

101,131

Euro

Buy

6/17/15

1,717,233

1,725,526

(8,293)

New Zealand Dollar

Buy

4/15/15

2,270,950

2,265,359

5,591

Norwegian Krone

Sell

6/17/15

469,886

491,010

21,124

Polish Zloty

Sell

6/17/15

803,697

812,529

8,832

Swedish Krona

Sell

6/17/15

14,892

15,357

465

Swiss Franc

Sell

6/17/15

149,674

152,191

2,517

Turkish Lira

Buy

6/17/15

227,221

259,330

(32,109)

Goldman Sachs International

Australian Dollar

Buy

4/15/15

747,363

759,400

(12,037)

British Pound

Buy

6/17/15

738,795

765,987

(27,192)

Canadian Dollar

Sell

4/15/15

2,030,090

2,106,319

76,229

Euro

Sell

6/17/15

1,124,479

1,174,295

49,816

New Zealand Dollar

Buy

4/15/15

1,498,685

1,531,128

(32,443)

Norwegian Krone

Sell

6/17/15

1,249,759

1,305,135

55,376

Swedish Krona

Buy

6/17/15

8,173

8,426

(253)

HSBC Bank USA, National Association

Australian Dollar

Buy

4/15/15

53,427

23,200

30,227

British Pound

Buy

6/17/15

736,274

763,398

(27,124)

Canadian Dollar

Sell

4/15/15

2,105,480

2,185,744

80,264

Chinese Yuan

Buy

5/20/15

1,564,080

1,570,048

(5,968)

Euro

Sell

6/17/15

2,540,437

2,726,890

186,453

New Taiwan Dollar

Sell

5/20/15

1,560,210

1,544,338

(15,872)

New Zealand Dollar

Buy

4/15/15

745,385

761,049

(15,664)

Swedish Krona

Sell

6/17/15

144,981

149,534

4,553

JPMorgan Chase Bank N.A.

Australian Dollar

Buy

4/15/15

812,358

831,421

(19,063)

British Pound

Buy

6/17/15

461,691

474,813

(13,122)

Canadian Dollar

Sell

4/15/15

1,622,272

1,719,196

96,924

Euro

Sell

6/17/15

1,803,127

1,934,320

131,193

Indian Rupee

Buy

5/20/15

1,594,685

1,604,246

(9,561)

Japanese Yen

Sell

5/20/15

730,930

745,768

14,838

Malaysian Ringgit

Buy

5/20/15

74,212

62,074

12,138

Mexican Peso

Buy

4/15/15

1,454,243

1,466,597

(12,354)

New Zealand Dollar

Sell

4/15/15

1,295,744

1,295,999

255

Norwegian Krone

Buy

6/17/15

285,405

297,948

(12,543)

Philippine Peso

Buy

5/20/15

746,905

758,923

(12,018)

52 Master Intermediate Income Trust

FORWARD CURRENCY CONTRACTS at 3/31/15 (aggregate face value $126,528,888) (Unaudited) cont.

Counterparty

Currency

Contract type

Delivery date

Value

Aggregate face value

Unrealized appreciation/ (depreciation)

JPMorgan Chase Bank N.A. cont.

Singapore Dollar

Sell

5/20/15

$1,499,163

$1,526,875

$27,712

South African Rand

Buy

4/15/15

407,424

401,315

6,109

South Korean Won

Sell

5/20/15

1,536,067

1,531,435

(4,632)

Swedish Krona

Buy

6/17/15

186,287

225,333

(39,046)

Swiss Franc

Buy

6/17/15

181,157

166,704

14,453

Royal Bank of Scotland PLC (The)

Australian Dollar

Buy

4/15/15

1,196,619

1,248,458

(51,839)

British Pound

Buy

6/17/15

249,675

294,858

(45,183)

Canadian Dollar

Sell

4/15/15

2,178,660

2,286,405

107,745

Euro

Sell

6/17/15

1,530,376

1,594,698

64,322

New Zealand Dollar

Sell

4/15/15

802,653

761,324

(41,329)

Norwegian Krone

Buy

6/17/15

921,176

898,978

22,198

Singapore Dollar

Sell

5/20/15

2,980,785

3,035,908

55,123

Swedish Krona

Buy

6/17/15

22,681

43,954

(21,273)

State Street Bank and Trust Co.

Australian Dollar

Sell

4/15/15

311,274

344,514

33,240

British Pound

Buy

6/17/15

141,443

192,159

(50,716)

Canadian Dollar

Sell

4/15/15

2,434,593

2,502,771

68,178

Chilean Peso

Buy

4/15/15

1,298

23,009

(21,711)

Euro

Sell

6/17/15

999,189

1,122,328

123,139

Hungarian Forint

Buy

6/17/15

1,483,188

1,518,740

(35,552)

Israeli Shekel

Buy

4/15/15

3,062,484

3,132,181

(69,697)

Israeli Shekel

Sell

4/15/15

3,062,484

3,054,593

(7,891)

Japanese Yen

Sell

5/20/15

750,561

765,875

15,314

Malaysian Ringgit

Buy

5/20/15

37,859

32,545

5,314

New Zealand Dollar

Buy

4/15/15

859,325

841,879

17,446

Norwegian Krone

Buy

6/17/15

26,501

27,685

(1,184)

Singapore Dollar

Sell

5/20/15

1,587,156

1,616,717

29,561

Swedish Krona

Sell

6/17/15

735,507

757,997

22,490

Swiss Franc

Sell

6/17/15

259,090

263,542

4,452

Turkish Lira

Sell

6/17/15

226,089

170,881

(55,208)

UBS AG

Australian Dollar

Sell

4/15/15

236,614

291,997

55,383

British Pound

Buy

6/17/15

473,701

492,362

(18,661)

Canadian Dollar

Sell

4/15/15

1,687,637

1,774,041

86,404

Chilean Peso

Buy

4/15/15

1,890

24,056

(22,166)

Euro

Sell

6/17/15

1,498,731

1,655,226

156,495

Japanese Yen

Sell

5/20/15

438,569

447,743

9,174

New Taiwan Dollar

Sell

5/20/15

1,560,210

1,537,787

(22,423)

New Zealand Dollar

Buy

4/15/15

2,219,803

2,228,893

(9,090)

Norwegian Krone

Buy

6/17/15

1,503,497

1,490,890

12,607

Master Intermediate Income Trust 53

FORWARD CURRENCY CONTRACTS at 3/31/15 (aggregate face value $126,528,888) (Unaudited) cont.

Counterparty

Currency

Contract type

Delivery date

Value

Aggregate face value

Unrealized appreciation/ (depreciation)

UBS AG cont.

Norwegian Krone

Sell

6/17/15

$1,484,616

$1,534,352

$49,736

Swedish Krona

Buy

6/17/15

13,578

64,000

(50,422)

WestPac Banking Corp.

Australian Dollar

Sell

4/15/15

639,217

673,856

34,639

Canadian Dollar

Sell

4/15/15

747,035

830,623

83,588

Euro

Sell

6/17/15

1,912,163

2,012,031

99,868

New Zealand Dollar

Buy

4/15/15

1,477,630

1,508,701

(31,071)

South Korean Won

Buy

5/20/15

47,171

48,003

(832)

Total

$1,785,486

FUTURES CONTRACTS OUTSTANDING at 3/31/15 (Unaudited)

Number of contracts

Value

Expiration date

Unrealized appreciation/ (depreciation)

Euro-Bobl 5 yr (Long)

29

$4,035,920

Jun-15

$11,148

Euro-Bund 10 yr (Long)

9

1,536,361

Jun-15

21,750

Euro-Buxl 30 yr (Short)

10

1,894,161

Jun-15

(127,553)

U.S. Treasury Bond 30 yr (Short)

1

163,875

Jun-15

(408)

U.S. Treasury Bond Ultra 30 yr (Long)

24

4,077,000

Jun-15

(17,829)

U.S. Treasury Note 2 yr (Short)

84

18,409,125

Jun-15

(38,230)

U.S. Treasury Note 5 yr (Short)

152

18,272,063

Jun-15

(69,974)

U.S. Treasury Note 10 yr (Short)

79

10,183,594

Jun-15

(95,993)

Total

$(317,089)

WRITTEN SWAP OPTIONS OUTSTANDING at 3/31/15 (premiums $3,638,025) (Unaudited)

Counterparty Fixed Obligation % to receive or (pay)/ Floating rate index/Maturity date

Expiration date/strike

Contract amount

Value

Bank of America N.A.

2.916/3 month USD-LIBOR-BBA/Apr-25

Apr-15/2.916

$20,151,100

$20

(1.9125)/3 month USD-LIBOR-BBA/Apr-25

Apr-15/1.9125

20,170,400

29,650

2.955/3 month USD-LIBOR-BBA/Sep-25

Sep-15/2.955

40,302,200

105,591

(2.04375)/3 month USD-LIBOR-BBA/Apr-25

Apr-15/2.04375

20,170,400

111,341

1.66/3 month USD-LIBOR-BBA/Jul-20

Jul-15/1.66

20,170,400

174,676

Barclays Bank PLC

2.3775/3 month USD-LIBOR-BBA/May-25

May-15/2.3775

20,151,100

60,252

2.265/3 month USD-LIBOR-BBA/May-25

May-15/2.265

20,151,100

105,793

Citibank, N.A.

2.902/3 month USD-LIBOR-BBA/Apr-25

Apr-15/2.902

20,151,100

101

(1.602)/3 month USD-LIBOR-BBA/Apr-25

Apr-15/1.602

20,151,100

3,023

(1.932)/3 month USD-LIBOR-BBA/Apr-25

Apr-15/1.932

10,085,200

21,179

2.28/3 month USD-LIBOR-BBA/Apr-25

Apr-15/2.28

20,151,100

21,360

2.205/3 month USD-LIBOR-BBA/Apr-25

Apr-15/2.205

20,151,100

43,325

54 Master Intermediate Income Trust

WRITTEN SWAP OPTIONS OUTSTANDING at 3/31/15 (premiums $3,638,025) (Unaudited) cont.

Counterparty Fixed Obligation % to receive or (pay)/ Floating rate index/Maturity date

Expiration date/strike

Contract amount

Value

Citibank, N.A. cont.

(2.052)/3 month USD-LIBOR-BBA/Apr-25

Apr-15/2.052

$10,085,200

$62,730

(1.481)/3 month USD-LIBOR-BBA/May-20

May-15/1.481

20,151,100

76,373

(2.223)/3 month USD-LIBOR-BBA/May-25

May-15/2.223

5,037,775

101,209

(1.509)/3 month USD-LIBOR-BBA/May-20

May-15/1.509

40,302,200

173,299

Credit Suisse International

2.895/3 month USD-LIBOR-BBA/Apr-25

Apr-15/2.895

20,202,300

20

(1.80)/3 month USD-LIBOR-BBA/Apr-25

Apr-15/1.80

20,180,000

9,081

(1.80125)/3 month USD-LIBOR-BBA/Apr-25

Apr-15/1.80125

20,180,000

9,283

(1.94)/3 month USD-LIBOR-BBA/Apr-25

Apr-15/1.94

20,180,000

45,809

(1.94125)/3 month USD-LIBOR-BBA/Apr-25

Apr-15/1.94125

20,180,000

46,414

Goldman Sachs International

(1.92)/3 month USD-LIBOR-BBA/Apr-25

Apr-15/1.92

15,113,300

56,826

(1.885)/3 month USD-LIBOR-BBA/Jan-46

Jan-16/1.885

3,681,050

83,641

(2.35)/3 month USD-LIBOR-BBA/May-45

May-15/2.35

5,037,775

111,536

(2.5025)/3 month USD-LIBOR-BBA/May-45

May-15/2.5025

5,037,775

196,876

JPMorgan Chase Bank N.A.

(6.00 Floor)/3 month USD-LIBOR-BBA/Mar-18

Mar-18/6.00

6,568,000

977,318

Total

$2,626,726

WRITTEN OPTIONS OUTSTANDING at 3/31/15 (premiums $351,484) (Unaudited)

Expiration date/strike price

Contract amount

Value

Federal National Mortgage Association 30 yr 3.0s TBA commitments (Put)

May-15/$101.57

$11,000,000

$48,598

Federal National Mortgage Association 30 yr 3.0s TBA commitments (Put)

May-15/100.57

11,000,000

19,063

Federal National Mortgage Association 30 yr 3.0s TBA commitments (Put)

Apr-15/102.07

11,000,000

23,034

Federal National Mortgage Association 30 yr 3.0s TBA commitments (Put)

Apr-15/101.07

11,000,000

1,969

Total

$92,664

FORWARD PREMIUM SWAP OPTION CONTRACTS OUTSTANDING at 3/31/15 (Unaudited)

Counterparty Fixed right or obligation % to receive or (pay)/ Floating rate index/ Maturity date

Expiration date/strike

Contract amount

Premium receivable/ (payable)

Unrealized appreciation/ (depreciation)

Goldman Sachs International

1.955/3 month USD-LIBOR-BBA/Apr-25 (Purchased)

Apr-15/1.955

$14,105,770

$(78,992)

$(3,526)

(2.155)/3 month USD-LIBOR-BBA/Apr-25 (Purchased)

Apr-15/2.155

14,105,770

(78,992)

(4,937)

Master Intermediate Income Trust 55

FORWARD PREMIUM SWAP OPTION CONTRACTS OUTSTANDING at 3/31/15 (Unaudited) cont.

Counterparty Fixed right or obligation % to receive or (pay)/ Floating rate index/ Maturity date

Expiration date/strike

Contract amount

Premium receivable/ (payable)

Unrealized appreciation/ (depreciation)

JPMorgan Chase Bank N.A.

2.117/3 month USD-LIBOR-BBA/Feb-27 (Purchased)

Feb-17/2.117

$5,037,775

$(123,441)

$35,013

2.035/3 month USD-LIBOR-BBA/Feb-27 (Purchased)

Feb-17/2.035

5,037,775

(128,005)

13,783

(3.035)/3 month USD-LIBOR-BBA/Feb-27 (Purchased)

Feb-17/3.035

5,037,775

(134,045)

(16,071)

(3.117)/3 month USD-LIBOR-BBA/Feb-27 (Purchased)

Feb-17/3.117

5,037,775

(141,058)

(33,829)

2.655/3 month USD-LIBOR-BBA/Feb-19 (Written)

Feb-17/2.655

22,065,500

146,184

41,461

2.56/3 month USD-LIBOR-BBA/Feb-19 (Written)

Feb-17/2.56

22,065,500

141,058

25,905

(1.56)/3 month USD-LIBOR-BBA/Feb-19 (Written)

Feb-17/1.56

22,065,500

127,038

(22,507)

(1.655)/3 month USD-LIBOR-BBA/Feb-19 (Written)

Feb-17/1.655

22,065,500

125,773

(42,145)

Total

$(144,480)

$(6,853)

TBA SALE COMMITMENTS OUTSTANDING at 3/31/15 (proceeds receivable $47,935,195) (Unaudited)

Agency

Principal amount

Settlement date

Value

Federal National Mortgage Association, 5 1/2s, March 1, 2045

$1,000,000

3/12/15

$1,128,125

Federal National Mortgage Association, 4 1/2s, April 1, 2045

19,000,000

4/14/15

20,727,812

Federal National Mortgage Association, 3 1/2s, April 1, 2045

25,000,000

4/14/15

26,263,673

Total

$48,119,610

OTC INTEREST RATE SWAP CONTRACTS OUTSTANDING at 3/31/15 (Unaudited)

Swap counterparty/ Notional amount

Upfront premium received (paid)

Termination date

Payments made by fund per annum

Payments received by fund per annum

Unrealized appreciation/ (depreciation)

Bank of America N.A.

CAD

4,121,000 E

$—

6/17/20

3 month CAD-BA-CDOR

1.385%

$23,882

CAD

17,845,000 E

—

6/17/17

0.93%

3 month CAD-BA-CDOR

(11,835)

CAD

7,339,000 E

—

6/17/20

3 month CAD-BA-CDOR

1.25%

4,230

CAD

9,894,000 E

—

6/17/17

1.00%

3 month CAD-BA-CDOR

(17,420)

56 Master Intermediate Income Trust

OTC INTEREST RATE SWAP CONTRACTS OUTSTANDING at 3/31/15 (Unaudited) cont.

Swap counterparty/ Notional amount

Upfront premium received (paid)

Termination date

Payments made by fund per annum

Payments received by fund per annum

Unrealized appreciation/ (depreciation)

Citibank, N.A.

NZD

1,128,000

$—

2/17/25

3 month NZD-BBR-FRA

3.765%

$1,115

NZD

3,992,000

—

2/5/25

3.62%