0000831001 srt:NorthAmericaMember us-gaap:ConsumerPortfolioSegmentMember 2019-04-01 2019-06-30 0000831001 us-gaap:CommercialPortfolioSegmentMember c:LeaseFinancingMember c:FinancingReceivables30to89DaysPastDueMember 2018-12-31 0000831001 us-gaap:ForeignGovernmentDebtSecuritiesMember us-gaap:FairValueInputsLevel1Member us-gaap:FairValueMeasurementsRecurringMember 2018-12-31 0000831001 srt:WeightedAverageMember us-gaap:FairValueInputsLevel3Member us-gaap:InterestRateContractMember c:MeasurementInputMeanReversionMember c:ValuationTechniqueModelbasedMember 2019-06-30

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

(Mark One)

|

| |

| ☒ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended June 30, 2019

OR

|

| |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 1-9924

Citigroup Inc.

(Exact name of registrant as specified in its charter)

|

| | | | |

| Delaware | | 52-1568099 |

| (State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

| 388 Greenwich Street, | New York | NY | | 10013 |

(Address of principal executive offices)

| | (Zip code) |

(212) 559-1000

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Securities Exchange Act of 1934 formatted in Inline XBRL: See Exhibit 99.01

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company" and “emerging growth company” in Rule 12b-2 of the Exchange Act. |

| | | | | | | |

| Large accelerated filer | ☒ | Accelerated filer | ☐ | Non-accelerated filer | ☐ | Smaller reporting company | ☐ |

| | | | | | | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. Yes ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

Number of shares of Citigroup Inc. common stock outstanding on June 30, 2019: 2,259,056,466

Available on the web at www.citigroup.com

CITIGROUP’S SECOND QUARTER 2019—FORM 10-Q

|

| |

| OVERVIEW | |

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | |

| Executive Summary | |

| Summary of Selected Financial Data | |

SEGMENT AND BUSINESS—INCOME (LOSS) AND REVENUES | |

| SEGMENT BALANCE SHEET | |

| Global Consumer Banking (GCB) | |

| North America GCB | |

| Latin America GCB | |

| Asia GCB | |

| Institutional Clients Group | |

| Corporate/Other | |

OFF-BALANCE SHEET ARRANGEMENTS | |

| CAPITAL RESOURCES | |

MANAGING GLOBAL RISK TABLE OF CONTENTS | |

| MANAGING GLOBAL RISK | |

| INCOME TAXES | |

FUTURE APPLICATION OF ACCOUNTING STANDARDS | |

DISCLOSURE CONTROLS AND PROCEDURES | |

DISCLOSURE PURSUANT TO SECTION 219 OF THE IRAN THREAT REDUCTION AND SYRIA HUMAN RIGHTS ACT | |

| FORWARD-LOOKING STATEMENTS | |

FINANCIAL STATEMENTS AND NOTES TABLE OF CONTENTS | |

| CONSOLIDATED FINANCIAL STATEMENTS | |

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED) | |

UNREGISTERED SALES OF EQUITY SECURITIES, PURCHASES OF EQUITY SECURITIES AND DIVIDENDS | |

OVERVIEW

This Quarterly Report on Form 10-Q should be read in conjunction with Citigroup’s Annual Report on Form 10-K for the year ended December 31, 2018 (2018 Annual Report on Form 10-K) and Citigroup’s Quarterly Report on Form 10-Q for the quarter ended March 31, 2019 (First Quarter of 2019 Form 10-Q).

Additional information about Citigroup is available on Citi’s website at www.citigroup.com. Citigroup’s annual reports on Form 10-K, quarterly reports on Form 10-Q and proxy statements, as well as other filings with the U.S. Securities and Exchange Commission (SEC), are available free of charge through Citi’s website by clicking on the “Investors” page and selecting “All SEC Filings.” The SEC’s website also contains current reports on Form 8-K, and other information regarding Citi at www.sec.gov.

Certain reclassifications, including a realignment of certain businesses, have been made to the prior periods’ financial statements and disclosures to conform to the current period’s presentation. For additional information on certain recent reclassifications, see Notes 1 and 3 to the Consolidated Financial Statements below and Notes 1 and 3 to the Consolidated Financial Statements in Citi’s 2018 Annual Report on Form 10-K.

Throughout this report, “Citigroup,” “Citi” and “the Company” refer to Citigroup Inc. and its consolidated subsidiaries.

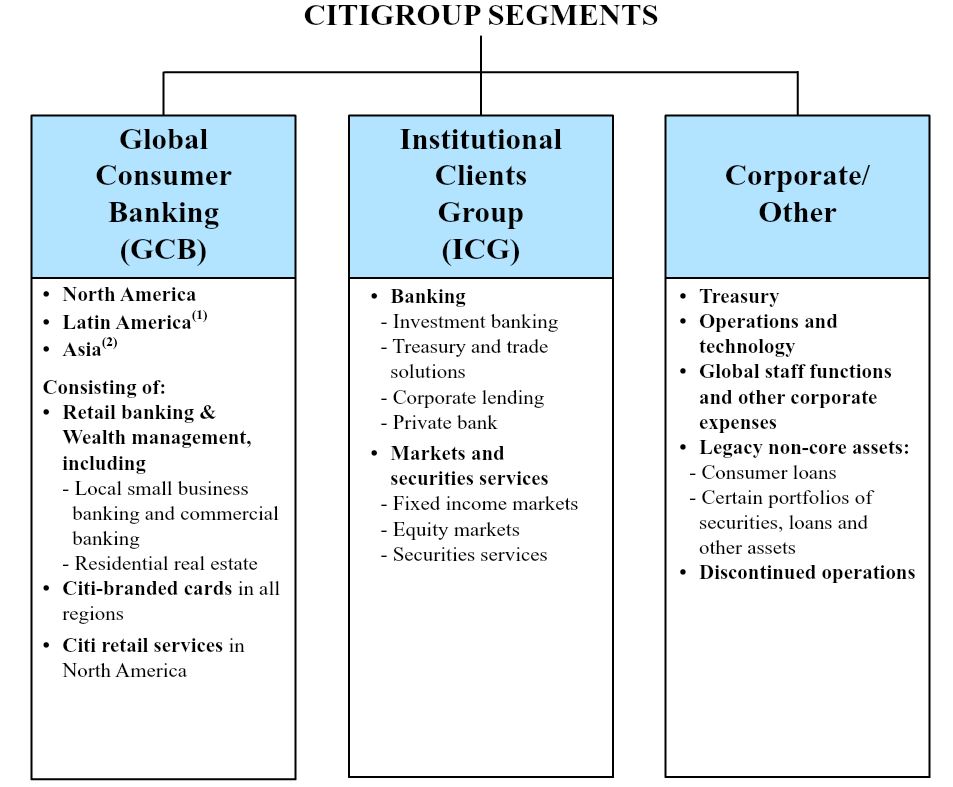

Citigroup is managed pursuant to two business segments: Global Consumer Banking and Institutional Clients Group, with the remaining operations in Corporate/Other.

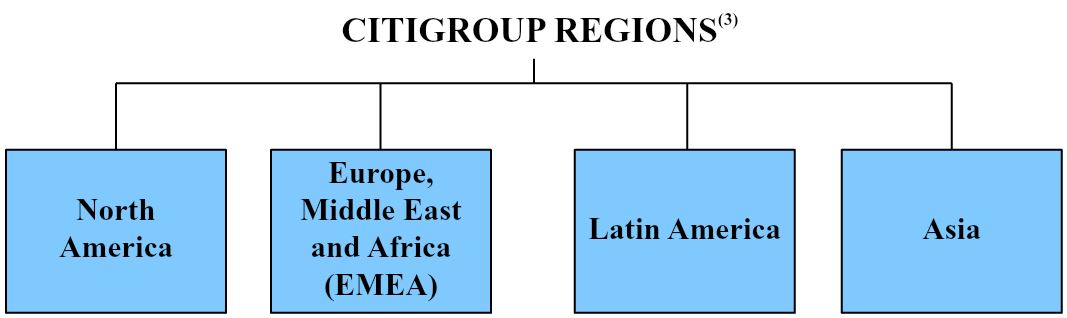

The following are the four regions in which Citigroup operates. The regional results are fully reflected in the segment results above.

| |

| (1) | Latin America GCB consists of Citi’s consumer banking business in Mexico. |

| |

| (2) | Asia GCB includes the results of operations of GCB activities in certain EMEA countries for all periods presented. |

| |

| (3) | North America includes the U.S., Canada and Puerto Rico, Latin America includes Mexico and Asia includes Japan. |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION

AND RESULTS OF OPERATIONS

EXECUTIVE SUMMARY

Second Quarter of 2019—Results Demonstrated Continued Progress

As described further throughout this Executive Summary, during the second quarter of 2019, Citi continued to demonstrate steady progress toward improving its profitability and returns, despite an uncertain environment. During the quarter, Citi had revenue growth and positive operating leverage in every region in Global Consumer Banking (GCB), excluding the impact of foreign currency translation into U.S. dollars for reporting purposes (FX translation). (Citi’s results of operations excluding the impact of FX translation are non-GAAP financial measures.)

Citi also showed continued momentum across treasury and trade solutions, securities services and the private bank in the Institutional Clients Group (ICG), while investment banking and fixed income and equity markets revenues were impacted by a challenging market environment. Citi’s results in the quarter also included a pretax gain of approximately $350 million (approximately $270 million after-tax) on Citi’s investment in Tradeweb (an electronic trading platform), recorded in fixed income markets within ICG.

Citi continued to demonstrate strong expense discipline, resulting in the eleventh consecutive quarter of positive operating leverage. Citi also had deposit and loan growth in both GCB and ICG, while credit quality remained broadly stable.

In the quarter, Citi continued to return capital to its shareholders, including $4.6 billion in the form of common stock repurchases and dividends. Citi repurchased approximately 54 million common shares, contributing to a 10% reduction in average outstanding common shares from the prior-year period. Despite progress in returning capital to shareholders, Citi’s key regulatory capital metrics remained strong (see “Capital” below).

During the quarter, the Federal Reserve Board advised Citi that it did not object to the capital plan submitted as part of Citi’s 2019 Comprehensive Capital Analysis and Review (CCAR). Accordingly, Citi intends to return $21.5 billion of capital to its common shareholders over the next four quarters, beginning in the third quarter of 2019 (for additional information, see “Equity Security Repurchases” and “Dividends” below).

While global growth has continued, economic forecasts for 2019 have been lowered and various economic, political and other risks and uncertainties could create a more volatile operating environment and impact Citi’s businesses and future results. For a discussion of the risks and uncertainties that could impact Citi’s businesses, results of operations and financial condition during the remainder of 2019, see each respective business’s results of operations and “Forward-Looking Statements” below, as well as each respective business’s results of operations and the “Managing Global Risk” and “Risk Factors” sections in Citi’s 2018 Annual Report on Form 10-K.

Second Quarter of 2019 Results Summary

Citigroup

Citigroup reported net income of $4.8 billion, or $1.95 per share, compared to net income of $4.5 billion, or $1.63 per share, in the prior-year period. Net income increased 7% from the prior-year period, primarily driven by higher revenues, lower expenses and a lower effective tax rate, partially offset by higher cost of credit. Earnings per share increased 20%, including the Tradeweb gain. Excluding the Tradeweb gain, earnings per share of $1.83 increased 12%, primarily reflecting the 10% reduction in average shares outstanding, driven by the common stock repurchases as well as the lower effective tax rate. (Citi’s results of operations excluding gains are non-GAAP financial measures.)

Citigroup revenues of $18.8 billion in the second quarter of 2019 increased 2% from the prior-year period, reflecting the Tradeweb gain and higher revenues across GCB, partially offset by declines in investment banking and fixed income and equity markets revenues, as well as mark-to-market losses on loan hedges in ICG.

Citigroup’s end-of-period loans increased 3% to $689 billion versus the prior-year period. Excluding the impact of FX translation, Citigroup’s end-of-period loans also grew 3%, as 4% aggregate growth in GCB and ICG was partially offset by the continued wind-down of legacy assets in Corporate/Other. Citigroup’s end-of-period deposits increased 5% to $1.0 trillion versus the prior-year period. Excluding the impact of FX translation, Citigroup’s deposits also increased 5%, primarily driven by 6% growth in ICG deposits as well as 3% growth in GCB.

Expenses

Citigroup operating expenses of $10.5 billion decreased 2% versus the prior-year period, as efficiency savings and the wind-down of legacy assets were partially offset by continued investments and volume-driven growth. Year-over-year, ICG operating expenses were down 2% and Corporate/Other operating expenses decreased 20%, while GCB operating expenses were largely unchanged.

Cost of Credit

Citi’s total provisions for credit losses and for benefits and claims of $2.1 billion increased 16% from the prior-year period. The increase was primarily driven by higher net credit losses in both Citi-branded cards and Citi retail services in North America GCB as well as normalization in credit trends in ICG.

Net credit losses of $2.0 billion increased 15% versus the prior-year period. Consumer net credit losses of $1.9 billion increased 11% from the prior-year period, primarily reflecting volume growth and seasoning in the North America cards portfolios. Corporate net credit losses increased to $70 million from a net recovery of $2 million in the prior-year period, reflecting credit normalization in ICG. For additional

information on Citi’s consumer and corporate credit costs and allowance for loan losses, see each respective business’s results of operations and “Credit Risk” below.

Capital

Citigroup’s Common Equity Tier 1 (CET1) Capital and Tier 1 Capital ratios were 11.9% and 13.4% as of June 30, 2019, respectively, compared to 12.1% and 13.8% as of June 30, 2018, both based on the Basel III Standardized Approach for determining risk-weighted assets. The decline in regulatory capital ratios primarily reflected the return of capital to common shareholders, partially offset by net income. Citigroup’s Supplementary Leverage ratio as of June 30, 2019 was 6.4%, compared to 6.6% as of June 30, 2018. For additional information on Citi’s capital ratios and related components, see “Capital Resources” below.

Global Consumer Banking

GCB net income of $1.4 billion increased 11%. Excluding the impact of FX translation, net income also increased 11%, driven primarily by higher revenues and a lower effective tax rate, partially offset by higher expenses and cost of credit. GCB operating expenses of $4.7 billion were largely unchanged versus the prior-year period. Excluding the impact of FX translation, expenses increased 1%, as continued investments and volume-driven expenses were largely offset by efficiency savings.

GCB revenues of $8.5 billion increased 3% versus the prior-year period. Excluding the impact of FX translation, revenues increased 4%, driven by growth in all three regions. North America GCB revenues of $5.2 billion increased 3%, primarily driven by growth in Citi-branded cards and Citi retail services, as retail banking revenues were largely unchanged. In North America GCB, Citi-branded cards revenues of $2.2 billion increased 7%, primarily driven by growth in interest-earning balances. Citi retail services revenues of $1.6 billion increased 1% versus the prior-year period, primarily reflecting loan growth, partially offset by higher contractual partner payments. Retail banking revenues of $1.4 billion were largely unchanged versus the prior-year period. Excluding mortgage revenues, retail banking revenues of $1.2 billion increased 1% from the prior-year period, as improved growth in deposit volumes was partially offset by lower deposit spreads in commercial banking.

North America GCB average deposits of $183 billion increased 2% year-over-year, average retail banking loans of $58 billion increased 4% year-over-year and assets under management of $68 billion grew 12%. Average Citi-branded card loans of $88 billion increased 2%, while Citi-branded card purchase sales of $93 billion increased 8% versus the prior-year period. Average Citi retail services loans of $49 billion increased 5% versus the prior-year period, while Citi retail services purchase sales of $23 billion increased 4%. For additional information on the results of operations of North America GCB for the second quarter of 2019, see “Global Consumer Banking—North America GCB” below.

International GCB revenues (consisting of Latin America GCB and Asia GCB (which includes the results of operations in certain EMEA countries)) of $3.3 billion increased 3%

versus the prior-year period. Excluding the impact of FX translation, international GCB revenues increased 4% versus the prior-year period. On this basis, Latin America GCB revenues increased 3% versus the prior-year period, including the impact of the revenues associated with an asset management business in Mexico sold in the third quarter of 2018. Excluding this impact, Latin America GCB revenues increased 5%, primarily driven by an increase in cards revenues and improved deposit spreads. Asia GCB revenues increased 5%, including a gain from a building sale. Excluding this gain, revenues increased 3%, primarily driven by higher deposit revenues as well as a recovery in investment revenues. For additional information on the results of operations of Latin America GCB and Asia GCB for the second quarter of 2019, including the impact of FX translation, see “Global Consumer Banking—Latin America GCB” and “Global Consumer Banking—Asia GCB” below.

Year-over-year, international GCB average deposits of $130 billion increased 5%, average retail banking loans of $90 billion increased 2%, assets under management of $108 billion increased 5%, average card loans of $25 billion increased 4% and card purchase sales of $26 billion increased 6%, all excluding the impact of FX translation.

Institutional Clients Group

ICG net income of $3.3 billion increased 3%, primarily driven by a decrease in expenses and a lower effective tax rate, partially offset by higher cost of credit. ICG operating expenses decreased 2% to $5.4 billion, as efficiency savings more than offset investments and volume-related expenses.

ICG revenues of $9.7 billion were largely unchanged in the second quarter of 2019, as the Tradeweb gain was offset by a 3% decrease in Banking revenues and a 4% decrease in Markets and securities services revenues. The decrease in Banking revenues included the impact of $75 million of losses on loan hedges within corporate lending, compared to gains of $23 million in the prior-year period.

Banking revenues of $5.1 billion (excluding the impact of gains (losses) on loan hedges within corporate lending) decreased 1%, as growth in treasury and trade solutions and the private bank was more than offset by lower revenues in investment banking and corporate lending. Investment banking revenues of $1.3 billion decreased 10%, but outperformed the market wallet. Advisory revenues decreased 36% to $232 million, equity underwriting revenues decreased 6% to $314 million and debt underwriting revenues increased 2% to $737 million, all versus the prior-year period.

Treasury and trade solutions revenues of $2.4 billion increased 4% versus the prior-year period, and 7% excluding the impact of FX translation, reflecting continued strong client engagement, with growth in deposits and transaction volumes as well as improved trade spreads. Private bank revenues increased 2% to $866 million versus the prior-year period, reflecting growth with new and existing clients, which drove higher lending and deposit volumes as well as growth in assets under management, partially offset by spread compression. Corporate lending revenues decreased 24% to $463 million. Excluding the impact of gains (losses) on loan hedges,

corporate lending revenues decreased 9% versus the prior-year period, reflecting lower spreads and higher hedging costs.

Markets and securities services revenues of $4.7 billion increased 4% from the prior-year period, including the Tradeweb gain. Excluding the Tradeweb gain, Markets and securities services revenues decreased 4% from the prior-year period, as higher revenues in securities services were more than offset by lower fixed income and equity markets revenues. Fixed income markets revenues of $3.3 billion increased 8% from the prior-year period, including the Tradeweb gain. Excluding the Tradeweb gain, fixed income markets revenues decreased 4%, reflecting the challenging market environment, particularly in rates. Equity markets revenues of $790 million decreased 9%, primarily reflecting lower client activity in cash equities and prime finance, partially offset by strong corporate client activity in derivatives. Securities services revenues of $682 million increased 3% versus the prior-year period, and 7% excluding the impact of FX translation, reflecting higher rates as well as an increase in client activity. For additional information on the results of operations of ICG for the second quarter of 2019, see “Institutional Clients Group” below.

Corporate/Other

Corporate/Other net income was $54 million in the second quarter of 2019, compared to a net loss of $14 million in the prior-year period. Operating expenses of $481 million declined 20% from the prior-year period, largely reflecting the wind-down of legacy assets. Corporate/Other revenues of $532 million increased 1% from the prior-year period, as higher treasury revenues and gains were largely offset by the continued wind-down of legacy assets. For additional information on the results of operations of Corporate/Other for the second quarter of 2019, see “Corporate/Other” below.

RESULTS OF OPERATIONS

SUMMARY OF SELECTED FINANCIAL DATA—PAGE 1

Citigroup Inc. and Consolidated Subsidiaries

|

| | | | | | | | | | | | | | | | |

| | Second Quarter | | Six Months | |

| In millions of dollars, except per share amounts and ratios | 2019 | 2018 | % Change | 2019 | 2018 | % Change |

| Net interest revenue | $ | 11,950 |

| $ | 11,665 |

| 2 | % | $ | 23,709 |

| $ | 22,837 |

| 4 | % |

| Non-interest revenue | 6,808 |

| 6,804 |

| — |

| 13,625 |

| 14,504 |

| (6 | ) |

| Revenues, net of interest expense | $ | 18,758 |

| $ | 18,469 |

| 2 | % | $ | 37,334 |

| $ | 37,341 |

| — | % |

| Operating expenses | 10,500 |

| 10,712 |

| (2 | ) | 21,084 |

| 21,637 |

| (3 | ) |

| Provisions for credit losses and for benefits and claims | 2,093 |

| 1,812 |

| 16 |

| 4,073 |

| 3,669 |

| 11 |

|

| Income from continuing operations before income taxes | $ | 6,165 |

| $ | 5,945 |

| 4 | % | $ | 12,177 |

| $ | 12,035 |

| 1 | % |

| Income taxes | 1,373 |

| 1,444 |

| (5 | ) | 2,648 |

| 2,885 |

| (8 | ) |

| Income from continuing operations | $ | 4,792 |

| $ | 4,501 |

| 6 | % | $ | 9,529 |

| $ | 9,150 |

| 4 | % |

Income from discontinued operations, net of taxes(1) | 17 |

| 15 |

| 13 |

| 15 |

| 8 |

| 88 |

|

Net income before attribution of noncontrolling interests | $ | 4,809 |

| $ | 4,516 |

| 6 | % | $ | 9,544 |

| $ | 9,158 |

| 4 | % |

| Net income attributable to noncontrolling interests | 10 |

| 26 |

| (62 | ) | 35 |

| 48 |

| (27 | ) |

| Citigroup’s net income | $ | 4,799 |

| $ | 4,490 |

| 7 | % | $ | 9,509 |

| $ | 9,110 |

| 4 | % |

| Less: | | |

|

| | | |

| Preferred dividends—Basic | $ | 296 |

| $ | 318 |

| (7 | )% | $ | 558 |

| $ | 590 |

| (5 | )% |

| Dividends and undistributed earnings allocated to employee restricted and deferred shares that contain nonforfeitable rights to dividends, applicable to basic EPS | 50 |

| 49 |

| 2 |

| 109 |

| 90 |

| 21 |

|

Income allocated to unrestricted common shareholders for basic and diluted EPS | $ | 4,453 |

| $ | 4,123 |

| 8 | % | $ | 8,842 |

| $ | 8,430 |

| 5 | % |

| Earnings per share | | |

|

| | |

| |

| Basic | | |

|

| | |

| |

| Income from continuing operations | $ | 1.94 |

| $ | 1.62 |

| 20 | % | $ | 3.81 |

| $ | 3.30 |

| 15 | % |

| Net income | 1.95 |

| 1.63 |

| 20 |

| 3.82 |

| 3.31 |

| 15 |

|

| Diluted | | |

|

| | | |

| Income from continuing operations | $ | 1.94 |

| $ | 1.62 |

| 20 | % | $ | 3.81 |

| $ | 3.30 |

| 15 | % |

| Net income | 1.95 |

| 1.63 |

| 20 |

| 3.82 |

| 3.31 |

| 15 |

|

| Dividends declared per common share | 0.45 |

| 0.32 |

| 41 |

| 0.90 |

| 0.64 |

| 41 |

|

Table continues on the next page, including footnotes.

SUMMARY OF SELECTED FINANCIAL DATA—PAGE 2

Citigroup Inc. and Consolidated Subsidiaries

|

| | | | | | | | | | | | | |

| | Second Quarter | | Six Months | |

| In millions of dollars, except per share amounts, ratios and direct staff | 2019 | 2018 | % Change | 2019 | 2018 | % Change |

| At June 30: | | | | | | |

| Total assets | $ | 1,988,226 |

| $ | 1,912,334 |

| 4 | % | | | |

| Total deposits | 1,045,607 |

| 996,730 |

| 5 |

| | | |

| Long-term debt | 252,189 |

| 236,822 |

| 6 |

| | | |

| Citigroup common stockholders’ equity | 179,379 |

| 181,059 |

| (1 | ) | | | |

| Total Citigroup stockholders’ equity | 197,359 |

| 200,094 |

| (1 | ) | | | |

Direct staff (in thousands) | 200 |

| 205 |

| (2 | ) | | | |

| Performance metrics | | |

|

| | | |

| Return on average assets | 0.97 | % | 0.94 | % |

|

| 0.98 | % | 0.96 | % | |

Return on average common stockholders’ equity(2) | 10.1 |

| 9.2 |

|

|

| 10.2 |

| 9.5 |

| |

Return on average total stockholders’ equity(2) | 9.8 |

| 9.0 |

|

|

| 9.8 |

| 9.2 |

| |

| Efficiency ratio (total operating expenses/total revenues) | 56.0 |

| 58.0 |

|

|

| 56.5 |

| 57.9 |

| |

| Basel III ratios | | | | | | |

Common Equity Tier 1 Capital(3) | 11.89 | % | 12.14 | % | | | | |

Tier 1 Capital(3) | 13.43 |

| 13.77 |

| | | | |

Total Capital(3) | 16.36 |

| 16.31 |

| | | | |

| Supplementary Leverage ratio | 6.38 |

| 6.60 |

| | | | |

| Citigroup common stockholders’ equity to assets | 9.02 | % | 9.47 | % | |

|

| | |

| Total Citigroup stockholders’ equity to assets | 9.93 |

| 10.46 |

| |

|

| | |

Dividend payout ratio(4) | 23.1 |

| 19.6 |

| | 23.6 | % | 19.3 | % | |

Total payout ratio(5) | 102.5 |

| 74.9 |

| | 108.9 |

| 73.1 |

| |

| Book value per common share | $ | 79.40 |

| $ | 71.95 |

| 10 | % |

|

| | |

Tangible book value (TBV) per share(6) | 67.64 |

| 61.29 |

| 10 |

| | | |

| |

| (1) | See Note 2 to the Consolidated Financial Statements in Citi’s 2018 Annual Report on Form 10-K for additional information on Citi’s discontinued operations. |

| |

| (2) | The return on average common stockholders’ equity is calculated using net income less preferred stock dividends divided by average common stockholders’ equity. The return on average total Citigroup stockholders’ equity is calculated using net income divided by average Citigroup stockholders’ equity. |

| |

| (3) | Citi’s reportable Common Equity Tier 1 (CET1) Capital and Tier 1 Capital ratios were the lower derived under the U.S. Basel III Standardized Approach, whereas the reportable Total Capital ratio was the lower derived under the U.S. Basel III Advanced Approaches framework. This reflects the U.S. Basel III requirement to report the lower of risk-based capital ratios under both the Standardized Approach and Advanced Approaches in accordance with the Collins Amendment of the Dodd-Frank Act. |

| |

| (4) | Dividends declared per common share as a percentage of net income per diluted share. |

| |

| (5) | Total common dividends declared plus common stock repurchases as a percentage of net income available to common shareholders. See “Consolidated Statement of Changes in Stockholders’ Equity,” Note 9 to the Consolidated Financial Statements and “Equity Security Repurchases” below for the component details. |

| |

| (6) | For information on TBV, see “Capital Resources—Tangible Common Equity, Book Value Per Share, Tangible Book Value Per Share and Returns on Equity” below. |

SEGMENT AND BUSINESS—INCOME (LOSS) AND REVENUES

CITIGROUP INCOME

|

| | | | | | | | | | | | | | | | |

| | Second Quarter | | Six Months | |

| In millions of dollars | 2019 | 2018 | % Change | 2019 | 2018 | % Change |

| Income from continuing operations | | | | | | |

| Global Consumer Banking | | | | | | |

| North America | $ | 721 |

| $ | 719 |

| — | % | $ | 1,490 |

| $ | 1,557 |

| (4 | )% |

| Latin America | 262 |

| 197 |

| 33 |

| 514 |

| 376 |

| 37 |

|

Asia(1) | 430 |

| 360 |

| 19 |

| 846 |

| 733 |

| 15 |

|

| Total | $ | 1,413 |

| $ | 1,276 |

| 11 | % | $ | 2,850 |

| $ | 2,666 |

| 7 | % |

| Institutional Clients Group |

|

| |

|

|

|

| |

|

|

| North America | $ | 1,022 |

| $ | 1,030 |

| (1 | )% | $ | 1,736 |

| $ | 1,888 |

| (8 | )% |

| EMEA | 1,005 |

| 986 |

| 2 |

| 2,130 |

| 2,099 |

| 1 |

|

| Latin America | 491 |

| 517 |

| (5 | ) | 994 |

| 1,011 |

| (2 | ) |

| Asia | 825 |

| 708 |

| 17 |

| 1,805 |

| 1,577 |

| 14 |

|

| Total | $ | 3,343 |

| $ | 3,241 |

| 3 | % | $ | 6,665 |

| $ | 6,575 |

| 1 | % |

| Corporate/Other | 36 |

| (16 | ) | NM |

| 14 |

| (91 | ) | NM |

|

| Income from continuing operations | $ | 4,792 |

| $ | 4,501 |

| 6 | % | $ | 9,529 |

| $ | 9,150 |

| 4 | % |

| Discontinued operations | $ | 17 |

| $ | 15 |

| 13 | % | $ | 15 |

| $ | 8 |

| 88 | % |

| Less: Net income attributable to noncontrolling interests | 10 |

| 26 |

| (62 | ) | 35 |

| 48 |

| (27 | ) |

| Citigroup’s net income | $ | 4,799 |

| $ | 4,490 |

| 7 | % | $ | 9,509 |

| $ | 9,110 |

| 4 | % |

| |

| (1) | Asia GCB includes the results of operations of GCB activities in certain EMEA countries for all periods presented. |

NM Not meaningful

CITIGROUP REVENUES |

| | | | | | | | | | | | | | | | |

| | Second Quarter | | Six Months | |

| In millions of dollars | 2019 | 2018 | % Change | 2019 | 2018 | % Change |

| Global Consumer Banking | | | | | | |

| North America | $ | 5,158 |

| $ | 5,004 |

| 3 | % | $ | 10,343 |

| $ | 10,161 |

| 2 | % |

| Latin America | 1,432 |

| 1,375 |

| 4 |

| 2,813 |

| 2,715 |

| 4 |

|

Asia(1) | 1,915 |

| 1,865 |

| 3 |

| 3,800 |

| 3,794 |

| — |

|

| Total | $ | 8,505 |

| $ | 8,244 |

| 3 | % | $ | 16,956 |

| $ | 16,670 |

| 2 | % |

| Institutional Clients Group |

|

| |

|

| | |

|

|

| North America | $ | 3,478 |

| $ | 3,511 |

| (1 | )% | $ | 6,597 |

| $ | 6,777 |

| (3 | )% |

| EMEA | 2,960 |

| 3,043 |

| (3 | ) | 6,130 |

| 6,210 |

| (1 | ) |

| Latin America | 1,195 |

| 1,168 |

| 2 |

| 2,355 |

| 2,384 |

| (1 | ) |

| Asia | 2,088 |

| 1,975 |

| 6 |

| 4,333 |

| 4,181 |

| 4 |

|

| Total | $ | 9,721 |

| $ | 9,697 |

| — | % | $ | 19,415 |

| $ | 19,552 |

| (1 | )% |

| Corporate/Other | 532 |

| 528 |

| 1 |

| 963 |

| 1,119 |

| (14 | ) |

| Total Citigroup net revenues | $ | 18,758 |

| $ | 18,469 |

| 2 | % | $ | 37,334 |

| $ | 37,341 |

| — | % |

| |

| (1) | Asia GCB includes the results of operations of GCB activities in certain EMEA countries for all periods presented. |

SEGMENT BALANCE SHEET(1)

|

| | | | | | | | | | | | | | | |

| In millions of dollars | Global Consumer Banking | Institutional Clients Group | Corporate/Other and consolidating eliminations(2) | Citigroup parent company- issued long-term debt and stockholders’ equity(3) | Total Citigroup consolidated |

| Assets | | | | | |

| Cash and deposits with banks | $ | 9,323 |

| $ | 71,804 |

| $ | 122,116 |

| $ | — |

| $ | 203,243 |

|

| Securities borrowed and purchased under agreements to resell | 175 |

| 259,341 |

| 253 |

| — |

| 259,769 |

|

| Trading account assets | 1,041 |

| 295,151 |

| 10,639 |

| — |

| 306,831 |

|

| Investments | 1,064 |

| 117,471 |

| 231,167 |

| — |

| 349,702 |

|

Loans, net of unearned income and allowance for loan losses

| 304,569 |

| 360,298 |

| 11,337 |

| — |

| 676,204 |

|

| Other assets | 38,943 |

| 110,571 |

| 42,963 |

| — |

| 192,477 |

|

Net inter-segment liquid assets(4) | 81,471 |

| 239,509 |

| (320,980 | ) | — |

| — |

|

| Total assets | $ | 436,586 |

| $ | 1,454,145 |

| $ | 97,495 |

| $ | — |

| $ | 1,988,226 |

|

| Liabilities and equity | | | | | |

| Total deposits | $ | 315,923 |

| $ | 714,759 |

| $ | 14,925 |

| $ | — |

| $ | 1,045,607 |

|

Securities loaned and sold under agreements to repurchase | 4,255 |

| 176,844 |

| 34 |

| — |

| 181,133 |

|

| Trading account liabilities | 411 |

| 135,394 |

| 489 |

| — |

| 136,294 |

|

| Short-term borrowings | 370 |

| 26,646 |

| 15,426 |

| — |

| 42,442 |

|

Long-term debt(3) | 1,752 |

| 53,783 |

| 44,513 |

| 152,141 |

| 252,189 |

|

| Other liabilities | 21,023 |

| 92,664 |

| 18,764 |

| — |

| 132,451 |

|

Net inter-segment funding (lending)(3) | 92,852 |

| 254,055 |

| 2,593 |

| (349,500 | ) | — |

|

| Total liabilities | $ | 436,586 |

| $ | 1,454,145 |

| $ | 96,744 |

| $ | (197,359 | ) | $ | 1,790,116 |

|

Total stockholders’ equity(5) | — |

| — |

| 751 |

| 197,359 |

| 198,110 |

|

| Total liabilities and equity | $ | 436,586 |

| $ | 1,454,145 |

| $ | 97,495 |

| $ | — |

| $ | 1,988,226 |

|

| |

| (1) | The supplemental information presented in the table above reflects Citigroup’s consolidated GAAP balance sheet by reporting segment as of June 30, 2019. The respective segment information depicts the assets and liabilities managed by each segment as of such date. |

| |

| (2) | Consolidating eliminations for total Citigroup and Citigroup parent company assets and liabilities are recorded within Corporate/Other. |

| |

| (3) | The total stockholders’ equity and the majority of long-term debt of Citigroup reside in the Citigroup parent company balance sheet. Citigroup allocates stockholders’ equity and long-term debt to its businesses through inter-segment allocations as shown above. |

| |

| (4) | Represents the attribution of Citigroup’s liquid assets (primarily consisting of cash, marketable equity securities and available-for-sale debt securities) to the various businesses based on Liquidity Coverage Ratio (LCR) assumptions. |

| |

| (5) | Corporate/Other equity represents noncontrolling interests. |

GLOBAL CONSUMER BANKING

Global Consumer Banking (GCB) consists of consumer banking businesses in North America, Latin America (consisting of Citi’s consumer banking business in Mexico) and Asia. GCB provides traditional banking services to retail customers through retail banking, including commercial banking, and Citi-branded cards and Citi retail services (for additional information on these businesses, see “Citigroup Segments” above). GCB is focused on its priority markets in the U.S., Mexico and Asia with 2,399 branches in 19 countries and jurisdictions as of June 30, 2019. At June 30, 2019, GCB had approximately $437 billion in assets and $316 billion in deposits.

GCB’s overall strategy is to leverage Citi’s global footprint and be the pre-eminent bank for the affluent and emerging affluent consumers in large urban centers. In credit cards and in certain retail markets (including commercial banking), Citi serves customers in a somewhat broader set of segments and geographies.

|

| | | | | | | | | | | | | | | | |

| | Second Quarter | | Six Months | |

| In millions of dollars, except as otherwise noted | 2019 | 2018 | % Change | 2019 | 2018 | % Change |

| Net interest revenue | $ | 7,272 |

| $ | 7,019 |

| 4 | % | $ | 14,525 |

| $ | 13,999 |

| 4 | % |

| Non-interest revenue | 1,233 |

| 1,225 |

| 1 |

| 2,431 |

| 2,671 |

| (9 | ) |

| Total revenues, net of interest expense | $ | 8,505 |

| $ | 8,244 |

| 3 | % | $ | 16,956 |

| $ | 16,670 |

| 2 | % |

| Total operating expenses | $ | 4,663 |

| $ | 4,652 |

| — | % | $ | 9,271 |

| $ | 9,329 |

| (1 | )% |

| Net credit losses | $ | 1,889 |

| $ | 1,726 |

| 9 | % | $ | 3,780 |

| $ | 3,462 |

| 9 | % |

| Credit reserve build (release) | 99 |

| 154 |

| (36 | ) | 175 |

| 298 |

| (41 | ) |

| Provision (release) for unfunded lending commitments | 5 |

| 3 |

| 67 | % | 10 |

| 2 |

| NM |

|

| Provision for benefits and claims | 19 |

| 22 |

| (14 | ) | 31 |

| 48 |

| (35 | ) |

| Provisions for credit losses and for benefits and claims (LLR & PBC) | $ | 2,012 |

| $ | 1,905 |

| 6 | % | $ | 3,996 |

| $ | 3,810 |

| 5 | % |

| Income from continuing operations before taxes | $ | 1,830 |

| $ | 1,687 |

| 8 | % | $ | 3,689 |

| $ | 3,531 |

| 4 | % |

| Income taxes | 417 |

| 411 |

| 1 |

| 839 |

| 865 |

| (3 | ) |

| Income from continuing operations | $ | 1,413 |

| $ | 1,276 |

| 11 | % | $ | 2,850 |

| $ | 2,666 |

| 7 | % |

| Noncontrolling interests | 1 |

| 1 |

| — |

| 1 |

| 3 |

| (67 | ) |

| Net income | $ | 1,412 |

| $ | 1,275 |

| 11 | % | $ | 2,849 |

| $ | 2,663 |

| 7 | % |

Balance Sheet data and ratios (in billions of dollars) |

|

| |

|

| | |

|

|

| Total EOP assets | $ | 437 |

| $ | 422 |

| 4 | % | | |

|

|

| Average assets | 431 |

| 417 |

| 3 |

| $ | 429 |

| $ | 420 |

| 2 | % |

| Return on average assets | 1.31 | % | 1.23 | % |

|

| 1.34 | % | 1.28 | % |

|

|

| Efficiency ratio | 55 |

| 56 |

|

|

| 55 |

| 56 |

|

|

|

| Average deposits | $ | 313 |

| $ | 306 |

| 2 |

| $ | 312 |

| $ | 307 |

| 2 |

|

| Net credit losses as a percentage of average loans | 2.45 | % | 2.28 | % |

|

| 2.46 | % | 2.29 | % |

|

|

| Revenue by business |

|

| |

|

| | |

|

|

| Retail banking | $ | 3,574 |

| $ | 3,483 |

| 3 | % | $ | 7,041 |

| $ | 6,947 |

| 1 | % |

Cards(1) | 4,931 |

| 4,761 |

| 4 |

| 9,915 |

| 9,723 |

| 2 |

|

| Total | $ | 8,505 |

| $ | 8,244 |

| 3 | % | $ | 16,956 |

| $ | 16,670 |

| 2 | % |

| Income from continuing operations by business |

|

| |

|

| | |

|

|

| Retail banking | $ | 629 |

| $ | 577 |

| 9 | % | $ | 1,155 |

| $ | 1,097 |

| 5 | % |

Cards(1) | 784 |

| 699 |

| 12 |

| 1,695 |

| 1,569 |

| 8 |

|

| Total | $ | 1,413 |

| $ | 1,276 |

| 11 | % | $ | 2,850 |

| $ | 2,666 |

| 7 | % |

Table continues on the next page, including footnotes.

|

| | | | | | | | | | | | | | | | |

| Foreign currency (FX) translation impact | | |

|

| | | |

| Total revenue—as reported | $ | 8,505 |

| $ | 8,244 |

| 3 | % | $ | 16,956 |

| $ | 16,670 |

| 2 | % |

Impact of FX translation(2) | — |

| (29 | ) |

|

| — |

| (142 | ) |

|

|

Total revenues—ex-FX(3) | $ | 8,505 |

| $ | 8,215 |

| 4 | % | $ | 16,956 |

| $ | 16,528 |

| 3 | % |

| Total operating expenses—as reported | $ | 4,663 |

| $ | 4,652 |

| — | % | $ | 9,271 |

| $ | 9,329 |

| (1 | )% |

Impact of FX translation(2) | — |

| (23 | ) |

|

| — |

| (93 | ) |

|

|

Total operating expenses—ex-FX(3) | $ | 4,663 |

| $ | 4,629 |

| 1 | % | $ | 9,271 |

| $ | 9,236 |

| — | % |

| Total provisions for LLR & PBC—as reported | $ | 2,012 |

| $ | 1,905 |

| 6 | % | $ | 3,996 |

| $ | 3,810 |

| 5 | % |

Impact of FX translation(2) | — |

| (2 | ) |

|

| — |

| (22 | ) |

|

|

Total provisions for LLR & PBC—ex-FX(3) | $ | 2,012 |

| $ | 1,903 |

| 6 | % | $ | 3,996 |

| $ | 3,788 |

| 5 | % |

| Net income—as reported | $ | 1,412 |

| $ | 1,275 |

| 11 | % | $ | 2,849 |

| $ | 2,663 |

| 7 | % |

Impact of FX translation(2) | — |

| (4 | ) |

|

| — |

| (19 | ) |

|

|

Net income—ex-FX(3) | $ | 1,412 |

| $ | 1,271 |

| 11 | % | $ | 2,849 |

| $ | 2,644 |

| 8 | % |

| |

| (1) | Includes both Citi-branded cards and Citi retail services. |

| |

| (2) | Reflects the impact of FX translation into U.S. dollars at the second quarter of 2019 and year-to-date 2019 average exchange rates for all periods presented. |

| |

| (3) | Presentation of this metric excluding FX translation is a non-GAAP financial measure. |

NM Not meaningful

NORTH AMERICA GCB

North America GCB provides traditional retail banking, including commercial banking, and its Citi-branded cards and Citi retail services card products to retail customers and small to mid-size businesses, as applicable, in the U.S. North America GCB’s U.S. cards product portfolio includes its proprietary portfolio (including the Citi Double Cash, Thank You and Value cards) and co-branded cards (including, among others, American Airlines and Costco) within Citi-branded cards as well as its co-brand and private label relationships (including, among others, Sears, The Home Depot, Best Buy and Macy’s) within Citi retail services.

As of June 30, 2019, North America GCB had 688 retail bank branches concentrated in the six key metropolitan areas of New York, Chicago, Miami, Washington, D.C., Los Angeles and San Francisco. Also as of June 30, 2019, North America GCB had approximately 9.1 million retail banking customer accounts, $58.3 billion in retail banking loans and $184.0 billion in deposits. In addition, North America GCB had approximately 118.9 million Citi-branded and Citi retail services credit card accounts with $140.2 billion in outstanding card loan balances.

|

| | | | | | | | | | | | | | | | |

| | Second Quarter | | Six Months | |

| In millions of dollars, except as otherwise noted | 2019 | 2018 | % Change | 2019 | 2018 | % Change |

| Net interest revenue | $ | 5,030 |

| $ | 4,780 |

| 5 | % | $ | 10,088 |

| $ | 9,530 |

| 6 | % |

| Non-interest revenue | 128 |

| 224 |

| (43 | ) | 255 |

| 631 |

| (60 | ) |

| Total revenues, net of interest expense | $ | 5,158 |

| $ | 5,004 |

| 3 | % | $ | 10,343 |

| $ | 10,161 |

| 2 | % |

| Total operating expenses | $ | 2,720 |

| $ | 2,666 |

| 2 | % | $ | 5,389 |

| $ | 5,311 |

| 1 | % |

| Net credit losses | $ | 1,428 |

| $ | 1,278 |

| 12 | % | $ | 2,857 |

| $ | 2,574 |

| 11 | % |

| Credit reserve build (release) | 82 |

| 115 |

| (29 | ) | 180 |

| 238 |

| (24 | ) |

| Provision (release) for unfunded lending commitments | 6 |

| 2 |

| NM |

| 11 |

| (2 | ) | NM |

|

| Provision for benefits and claims | 6 |

| 5 |

| 20 |

| 12 |

| 11 |

| 9 |

|

| Provisions for credit losses and for benefits and claims | $ | 1,522 |

| $ | 1,400 |

| 9 | % | $ | 3,060 |

| $ | 2,821 |

| 8 | % |

| Income from continuing operations before taxes | $ | 916 |

| $ | 938 |

| (2 | )% | $ | 1,894 |

| $ | 2,029 |

| (7 | )% |

| Income taxes | 195 |

| 219 |

| (11 | ) | 404 |

| 472 |

| (14 | ) |

| Income from continuing operations | $ | 721 |

| $ | 719 |

| — | % | $ | 1,490 |

| $ | 1,557 |

| (4 | )% |

| Noncontrolling interests | — |

| — |

| — |

| — |

| — |

| — |

|

| Net income | $ | 721 |

| $ | 719 |

| — | % | $ | 1,490 |

| $ | 1,557 |

| (4 | )% |

Balance Sheet data and ratios (in billions of dollars) |

|

| |

|

| |

| |

|

|

|

| Average assets | $ | 253 |

| $ | 244 |

| 4 | % | $ | 252 |

| $ | 246 |

| 2 | % |

| Return on average assets | 1.14 | % | 1.18 | % |

|

| 1.19 | % | 1.28 | % |

|

|

| Efficiency ratio | 53 |

| 53 |

|

|

| 52 |

| 52 |

|

|

|

| Average deposits | $ | 183.0 |

| $ | 179.9 |

| 2 |

| $ | 182.7 |

| $ | 180.4 |

| 1 |

|

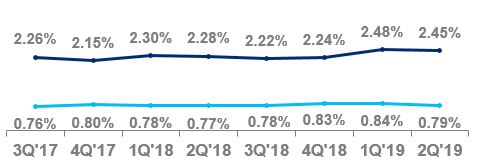

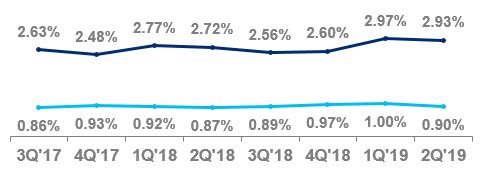

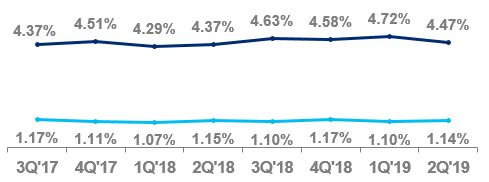

| Net credit losses as a percentage of average loans | 2.93 | % | 2.72 | % |

|

| 2.95 | % | 2.74 | % |

|

|

| Revenue by business |

|

| |

|

| |

| |

|

|

|

| Retail banking | $ | 1,351 |

| $ | 1,348 |

| — | % | $ | 2,667 |

| $ | 2,655 |

| — | % |

| Citi-branded cards | 2,197 |

| 2,062 |

| 7 |

| 4,392 |

| 4,294 |

| 2 |

|

| Citi retail services | 1,610 |

| 1,594 |

| 1 |

| 3,284 |

| 3,212 |

| 2 |

|

| Total | $ | 5,158 |

| $ | 5,004 |

| 3 | % | $ | 10,343 |

| $ | 10,161 |

| 2 | % |

| Income from continuing operations by business |

|

| |

|

| |

| |

|

|

|

| Retail banking | $ | 114 |

| $ | 161 |

| (29 | )% | $ | 197 |

| $ | 301 |

| (35 | )% |

| Citi-branded cards | 364 |

| 309 |

| 18 |

| 746 |

| 734 |

| 2 |

|

| Citi retail services | 243 |

| 249 |

| (2 | ) | 547 |

| 522 |

| 5 |

|

| Total | $ | 721 |

| $ | 719 |

| — | % | $ | 1,490 |

| $ | 1,557 |

| (4 | )% |

NM Not meaningful

2Q19 vs. 2Q18

Net income was largely unchanged, as higher revenues and a lower effective tax rate were offset by higher cost of credit and higher expenses.

Revenues increased 3%, reflecting growth in Citi-branded cards and Citi retail services.

Retail banking revenues were largely unchanged. Excluding mortgage revenues (decline of 9%), revenues were up 1%, as growth in deposit volumes was partially offset by lower deposit spreads in commercial banking. Average deposits increased 2% and assets under management increased 12%. The decline in mortgage revenues was driven by spread compression, partially offset by higher volumes.

Cards revenues increased 4%. In Citi-branded cards, revenues increased 7%, primarily driven by continued growth in interest-earning balances. Average loans increased 2% and purchase sales increased 8%.

Citi retail services revenues increased 1%, primarily driven by organic loan growth and the benefit of the L.L.Bean portfolio acquisition, partially offset by higher contractual partner payments. Average loans increased 5% and purchase sales increased 4%.

Expenses increased 2%, as higher volume-related expenses and investments were largely offset by efficiency savings.

Provisions increased 9% from the prior-year period, primarily driven by higher net credit losses, partially offset by a lower net loan loss reserve build. Net credit losses increased 12%, primarily driven by higher net credit losses in Citi-branded cards (up 10% to $723 million) and Citi retail services (up 11% to $654 million). The increase in net credit losses primarily reflected volume growth and seasoning in both cards portfolios.

The net loan loss reserve build in the current quarter was $88 million, reflecting volume growth and seasoning in both cards portfolios (compared to a build of $117 million in the prior-year period).

For additional information on North America GCB’s retail banking, including commercial banking, and its Citi-branded cards and Citi retail services portfolios, see “Credit Risk—Consumer Credit” below.

For additional information on Citi retail services’ co-brand and private label credit card products with Sears, see “Forward-Looking Statements” below and “North America GCB” and “Risk Factors—Strategic Risks” in Citi’s 2018 Annual Report on Form 10-K.

2019 YTD vs. 2018 YTD

Year-to-date, North America GCB experienced similar trends to those described above. Net income decreased 4%, as higher cost of credit and higher expenses were partially offset by a lower effective tax rate and higher revenues.

Revenues increased 2%. Excluding the impact of the $150 million gain on the Hilton portfolio sale in the prior-year period, revenues increased 3%, reflecting higher revenues in Citi-branded cards and Citi retail services. Retail banking revenues were largely unchanged. Excluding mortgage revenues (decline of 11%), retail banking revenues increased 2%, driven by the same factors described above. Cards revenues increased 2% (4% excluding the Hilton gain). In Citi-branded cards, revenues increased 2% (6% excluding the Hilton gain), driven by the same factors described above. Citi retail services revenues increased 2%, driven by the same factors described above.

Expenses increased 1%, driven by the same factors described above.

Provisions increased 8%. Net credit losses increased 11%, driven by volume growth and seasoning in both cards portfolios. This increase was partially offset by a 19% decline in the net loan loss reserve build.

LATIN AMERICA GCB

Latin America GCB provides traditional retail banking, including commercial banking, and its Citi-branded card products to retail customers and small to mid-size businesses in Mexico through Citibanamex, one of Mexico’s largest banks.

At June 30, 2019, Latin America GCB had 1,459 retail branches in Mexico, with approximately 30.3 million retail banking customer accounts, $20.1 billion in retail banking loans and $29.2 billion in deposits. In addition, the business had approximately 5.4 million Citi-branded card accounts with $5.7 billion in outstanding card loan balances.

|

| | | | | | | | | | | | | | | | |

| | Second Quarter | | Six Months | % Change |

| In millions of dollars, except as otherwise noted | 2019 | 2018 | % Change | 2019 | 2018 |

| Net interest revenue | $ | 1,017 |

| $ | 1,013 |

| — | % | $ | 1,992 |

| $ | 2,010 |

| (1 | )% |

| Non-interest revenue | 415 |

| 362 |

| 15 |

| 821 |

| 705 |

| 16 |

|

| Total revenues, net of interest expense | $ | 1,432 |

| $ | 1,375 |

| 4 | % | $ | 2,813 |

| $ | 2,715 |

| 4 | % |

| Total operating expenses | $ | 765 |

| $ | 779 |

| (2 | )% | $ | 1,500 |

| $ | 1,534 |

| (2 | )% |

| Net credit losses | $ | 285 |

| $ | 278 |

| 3 | % | $ | 583 |

| $ | 556 |

| 5 | % |

| Credit reserve build | 10 |

| 33 |

| (70 | ) | 3 |

| 75 |

| (96 | ) |

| Provision (release) for unfunded lending commitments | (1 | ) | — |

| — |

| (1 | ) | 1 |

| NM |

|

| Provision for benefits and claims | 13 |

| 17 |

| (24 | ) | 19 |

| 37 |

| (49 | ) |

| Provisions for credit losses and for benefits and claims (LLR & PBC) | $ | 307 |

| $ | 328 |

| (6 | )% | $ | 604 |

| $ | 669 |

| (10 | )% |

| Income from continuing operations before taxes | $ | 360 |

| $ | 268 |

| 34 | % | $ | 709 |

| $ | 512 |

| 38 | % |

| Income taxes | 98 |

| 71 |

| 38 |

| 195 |

| 136 |

| 43 |

|

| Income from continuing operations | $ | 262 |

| $ | 197 |

| 33 | % | $ | 514 |

| $ | 376 |

| 37 | % |

| Net income | $ | 262 |

| $ | 197 |

| 33 | % | $ | 514 |

| $ | 376 |

| 37 | % |

Balance Sheet data and ratios (in billions of dollars) |

|

| |

|

| |

| |

|

|

|

| Average assets | $ | 45 |

| $ | 43 |

| 5 | % | $ | 45 |

| $ | 44 |

| 2 | % |

| Return on average assets | 2.34 | % | 1.84 | % |

|

| 2.30 | % | 1.72 | % |

|

|

| Efficiency ratio | 53 |

| 57 |

|

|

| 53 |

| 57 |

|

|

|

| Average deposits | $ | 29.2 |

| $ | 28.3 |

| 3 |

| $ | 28.9 |

| $ | 28.6 |

| 1 |

|

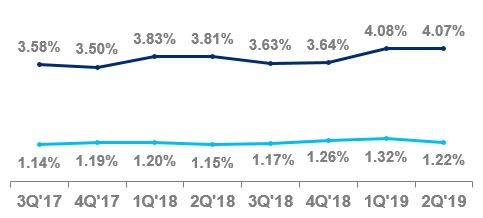

| Net credit losses as a percentage of average loans | 4.47 | % | 4.37 | % |

|

| 4.57 | % | 4.33 | % |

|

|

| Revenue by business |

|

| |

|

| | |

|

|

| Retail banking | $ | 1,015 |

| $ | 993 |

| 2 | % | $ | 2,023 |

| $ | 1,952 |

| 4 | % |

| Citi-branded cards | 417 |

| 382 |

| 9 |

| 790 |

| 763 |

| 4 |

|

| Total | $ | 1,432 |

| $ | 1,375 |

| 4 | % | $ | 2,813 |

| $ | 2,715 |

| 4 | % |

| Income from continuing operations by business |

|

| |

|

| |

| |

|

|

|

| Retail banking | $ | 192 |

| $ | 152 |

| 26 | % | $ | 389 |

| $ | 286 |

| 36 | % |

| Citi-branded cards | 70 |

| 45 |

| 56 |

| 125 |

| 90 |

| 39 |

|

| Total | $ | 262 |

| $ | 197 |

| 33 | % | $ | 514 |

| $ | 376 |

| 37 | % |

| FX translation impact |

|

| |

|

| | |

|

|

|

| Total revenues—as reported | $ | 1,432 |

| $ | 1,375 |

| 4 | % | $ | 2,813 |

| $ | 2,715 |

| 4 | % |

Impact of FX translation(1) | — |

| 13 |

|

|

| — |

| (31 | ) |

|

|

Total revenues—ex-FX(2) | $ | 1,432 |

| $ | 1,388 |

| 3 | % | $ | 2,813 |

| $ | 2,684 |

| 5 | % |

| Total operating expenses—as reported | $ | 765 |

| $ | 779 |

| (2 | )% | $ | 1,500 |

| $ | 1,534 |

| (2 | )% |

Impact of FX translation(1) | — |

| 6 |

|

|

| — |

| (16 | ) |

|

|

Total operating expenses—ex-FX(2) | $ | 765 |

| $ | 785 |

| (3 | )% | $ | 1,500 |

| $ | 1,518 |

| (1 | )% |

| Provisions for LLR & PBC—as reported | $ | 307 |

| $ | 328 |

| (6 | )% | $ | 604 |

| $ | 669 |

| (10 | )% |

Impact of FX translation(1) | — |

| 3 |

|

|

| — |

| (9 | ) |

|

|

Provisions for LLR & PBC—ex-FX(2) | $ | 307 |

| $ | 331 |

| (7 | )% | $ | 604 |

| $ | 660 |

| (8 | )% |

| Net income—as reported | $ | 262 |

| $ | 197 |

| 33 | % | $ | 514 |

| $ | 376 |

| 37 | % |

Impact of FX translation(1) | — |

| 2 |

|

|

| — |

| (5 | ) |

|

|

Net income—ex-FX(2) | $ | 262 |

| $ | 199 |

| 32 | % | $ | 514 |

| $ | 371 |

| 39 | % |

| |

| (1) | Reflects the impact of FX translation into U.S. dollars at the second quarter of 2019 and year-to-date 2019 average exchange rates for all periods presented. |

| |

| (2) | Presentation of this metric excluding FX translation is a non-GAAP financial measure. |

NM Not meaningful

The discussion of the results of operations for Latin America GCB below excludes the impact of FX translation for all periods presented. Presentations of the results of operations, excluding the impact of FX translation, are non-GAAP financial measures. For a reconciliation of certain of these metrics to the reported results, see the table above.

2Q19 vs. 2Q18

Net income increased 32%, reflecting higher revenues, lower expenses and lower cost of credit.

Revenues increased 3% from the prior year. Excluding revenues associated with the sale of an asset management business in Mexico in the third quarter of 2018, revenues increased 5%, primarily driven by an increase in cards revenues and improved deposit spreads.

Retail banking revenues increased 1% compared to the prior-year period. Excluding the revenues associated with the asset management business, retail banking revenues increased 3%, as modest deposit growth (average deposits up 2%) and improved deposit spreads were partially offset by lower average loans (down 2%), reflecting the ongoing slowdown in overall economic growth and industry volumes in Mexico. Cards revenues increased 8%, primarily driven by continued volume growth, reflecting higher purchase sales (up 7%) and full-rate revolving loans, as well as higher rates. Average cards loans grew 2%.

Expenses decreased 3%, as efficiency savings more than offset ongoing investment spending and volume-driven growth.

Provisions decreased 7%, primarily driven by a lower net loan loss reserve build, reflecting lower volumes.

For additional information on Latin America GCB’s retail banking, including commercial banking, and its Citi-branded cards portfolios, see “Credit Risk—Consumer Credit” below.

2019 YTD vs. 2018 YTD

Year-to-date, Latin America GCB experienced similar trends to those described above. Net income increased 39%, driven by the same factors described above.

Revenues increased 5%, reflecting higher revenues in both retail banking and cards. Retail banking revenues increased 5%, driven by the same factors described above. Cards revenues increased 5%, driven by the same factors described above.

Expenses decreased 1%, driven by the same factors described above.

Provisions decreased 8%, driven by the same factors described above.

ASIA GCB

Asia GCB provides traditional retail banking, including commercial banking, and its Citi-branded card products to retail customers and small to mid-size businesses, as applicable. During the second quarter of 2019, Asia GCB’s most significant revenues in Asia were from Hong Kong, Korea, Singapore, India, Australia, Taiwan, Thailand, Philippines, Indonesia and Malaysia. Included within Asia GCB, traditional retail banking and Citi-branded card products are also provided to retail customers in certain EMEA countries, primarily Poland, Russia and the United Arab Emirates.

At June 30, 2019, on a combined basis, the businesses had 252 retail branches, approximately 16.1 million retail banking customer accounts, $70.8 billion in retail banking loans and $102.6 billion in deposits. In addition, the businesses had approximately 15.2 million Citi-branded card accounts with $19.2 billion in outstanding card loan balances.

|

| | | | | | | | | | | | | | | | |

| | Second Quarter | | Six Months | % Change |

In millions of dollars, except as otherwise noted(1) | 2019 | 2018 | % Change | 2019 | 2018 |

| Net interest revenue | $ | 1,225 |

| $ | 1,226 |

| — | % | $ | 2,445 |

| $ | 2,459 |

| (1 | )% |

| Non-interest revenue | 690 |

| 639 |

| 8 |

| 1,355 |

| 1,335 |

| 1 |

|

| Total revenues, net of interest expense | $ | 1,915 |

| $ | 1,865 |

| 3 | % | $ | 3,800 |

| $ | 3,794 |

| — | % |

| Total operating expenses | $ | 1,178 |

| $ | 1,207 |

| (2 | )% | $ | 2,382 |

| $ | 2,484 |

| (4 | )% |

| Net credit losses | $ | 176 |

| $ | 170 |

| 4 | % | $ | 340 |

| $ | 332 |

| 2 | % |

| Credit reserve build (release) | 7 |

| 6 |

| 17 |

| (8 | ) | (15 | ) | 47 |

|

| Provision (release) for unfunded lending commitments | — |

| 1 |

| (100 | ) | — |

| 3 |

| (100 | ) |

| Provisions for credit losses | $ | 183 |

| $ | 177 |

| 3 | % | $ | 332 |

| $ | 320 |

| 4 | % |

| Income from continuing operations before taxes | $ | 554 |

| $ | 481 |

| 15 | % | $ | 1,086 |

| $ | 990 |

| 10 | % |

| Income taxes | 124 |

| 121 |

| 2 |

| 240 |

| 257 |

| (7 | ) |

| Income from continuing operations | $ | 430 |

| $ | 360 |

| 19 | % | $ | 846 |

| $ | 733 |

| 15 | % |

| Noncontrolling interests | 1 |

| 1 |

| — |

| 1 |

| 3 |

| (67 | ) |

| Net income | $ | 429 |

| $ | 359 |

| 19 | % | $ | 845 |

| $ | 730 |

| 16 | % |

Balance Sheet data and ratios (in billions of dollars) |

|

|

|

|

|

| |

| |

|

|

|

| Average assets | $ | 133 |

| $ | 130 |

| 2 | % | $ | 133 |

| $ | 131 |

| 2 | % |

| Return on average assets | 1.29 | % | 1.11 | % |

|

| 1.28 | % | 1.12 | % |

|

|

| Efficiency ratio | 62 |

| 65 |

| | 63 |

| 65 |

|

|

|

| Average deposits | $ | 100.7 |

| $ | 97.6 |

| 3 |

| $ | 100.0 |

| $ | 98.4 |

| 2 |

|

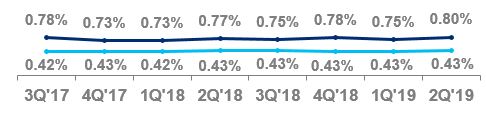

| Net credit losses as a percentage of average loans | 0.80 | % | 0.77 | % |

|

| 0.77 | % | 0.75 | % |

|

|

| Revenue by business | | | | | |

|

|

| Retail banking | $ | 1,208 |

| $ | 1,142 |

| 6 | % | $ | 2,351 |

| $ | 2,340 |

| — | % |

| Citi-branded cards | 707 |

| 723 |

| (2 | ) | 1,449 |

| 1,454 |

| — |

|

| Total | $ | 1,915 |

| $ | 1,865 |

| 3 | % | $ | 3,800 |

| $ | 3,794 |

| — | % |

| Income from continuing operations by business |

|

|

|

|

|

| | |

|

|

| Retail banking | $ | 323 |

| $ | 264 |

| 22 | % | $ | 569 |

| $ | 510 |

| 12 | % |

| Citi-branded cards | 107 |

| 96 |

| 11 |

| 277 |

| 223 |

| 24 |

|

| Total | $ | 430 |

| $ | 360 |

| 19 | % | $ | 846 |

| $ | 733 |

| 15 | % |

|

| | | | | | | | | | | | | | | | |

| FX translation impact |

|

|

| | |

|

|

| Total revenues—as reported | $ | 1,915 |

| $ | 1,865 |

| 3 | % | $ | 3,800 |

| $ | 3,794 |

| — | % |

Impact of FX translation(2) | — |

| (42 | ) |

|

| — |

| (111 | ) |

|

|

Total revenues—ex-FX(3) | $ | 1,915 |

| $ | 1,823 |

| 5 | % | $ | 3,800 |

| $ | 3,683 |

| 3 | % |

| Total operating expenses—as reported | $ | 1,178 |

| $ | 1,207 |

| (2 | )% | $ | 2,382 |

| $ | 2,484 |

| (4 | )% |

Impact of FX translation(2) | — |

| (29 | ) |

|

| — |

| (77 | ) |

|

|

Total operating expenses—ex-FX(3) | $ | 1,178 |

| $ | 1,178 |

| — | % | $ | 2,382 |

| $ | 2,407 |

| (1 | )% |

| Provisions for loan losses—as reported | $ | 183 |

| $ | 177 |

| 3 | % | $ | 332 |

| $ | 320 |

| 4 | % |

Impact of FX translation(2) | — |

| (5 | ) |

|

| — |

| (13 | ) |

|

|

Provisions for loan losses—ex-FX(3) | $ | 183 |

| $ | 172 |

| 6 | % | $ | 332 |

| $ | 307 |

| 8 | % |

| Net income—as reported | $ | 429 |

| $ | 359 |

| 19 | % | $ | 845 |

| $ | 730 |

| 16 | % |

Impact of FX translation(2) | — |

| (6 | ) |

|

| — |

| (14 | ) |

|

|

Net income—ex-FX(3) | $ | 429 |

| $ | 353 |

| 22 | % | $ | 845 |

| $ | 716 |

| 18 | % |

| |

| (1) | Asia GCB includes the results of operations of GCB activities in certain EMEA countries for all periods presented. |

| |

| (2) | Reflects the impact of FX translation into U.S. dollars at the second quarter of 2019 and year-to-date 2019 average exchange rates for all periods presented. |

| |

| (3) | Presentation of this metric excluding FX translation is a non-GAAP financial measure. |

The discussion of the results of operations for Asia GCB below excludes the impact of FX translation for all periods presented. Presentations of the results of operations, excluding the impact of FX translation, are non-GAAP financial measures. For a reconciliation of certain of these metrics to the reported results, see the table above.

2Q19 vs. 2Q18

Net income increased 22%, reflecting higher revenues and a lower effective tax rate, partially offset by higher cost of credit.

Revenues increased 5%, including a gain from a building sale. Excluding the gain, revenues increased 3%, driven by higher retail banking revenues.

Retail banking revenues increased 8% compared to the prior-year period. Excluding the gain, retail banking revenues increased 4%, primarily driven by higher deposit revenues as well as a recovery in investment revenues due to improved market sentiment. Investment sales increased 8%, while assets under management grew 10%, average deposits increased 6% and average loans increased 4%. Retail lending revenues declined 2%, as continued growth in personal loans was more than offset by lower mortgage revenues due to spread compression.

Cards revenues were largely unchanged, as continued growth in average loans (up 4%) and purchase sales (up 5%) were offset by spread compression.

Expenses were largely unchanged, as efficiency savings offset volume-driven growth and ongoing investment spending.

Provisions increased 6%, primarily driven by higher net credit losses, reflecting volume growth and seasoning. Overall credit quality continued to remain stable in the region.

For additional information on Asia GCB’s retail banking, including commercial banking, and its Citi-branded cards portfolios, see “Credit Risk—Consumer Credit” below.

2019 YTD vs. 2018 YTD

Year-to-date, Asia GCB experienced similar trends to

those described above. Net income increased 18%, due to higher revenues, lower expenses and a lower effective tax rate, partially offset by higher cost of credit.

Revenues increased 3%, driven by growth in both retail banking and cards. Retail banking revenues increased 3%, driven by growth in deposits, partially offset by lower investment and retail lending revenues. Cards revenues were up 3%, including a modest one-time gain. Excluding the gain, cards revenues were up 1%, driven by continued growth in average loans and purchase sales, partially offset by spread compression.

Expenses decreased 1%, as volume-driven growth and ongoing investment spending were more than offset by efficiency savings.

Provisions were up 8%, driven by the same factors described above.

INSTITUTIONAL CLIENTS GROUP

Institutional Clients Group (ICG) includes Banking and Markets and securities services (for additional information on these businesses, see “Citigroup Segments” above). ICG provides corporate, institutional, public sector and high-net-worth clients around the world with a full range of wholesale banking products and services, including fixed income and equity sales and trading, foreign exchange, prime brokerage, derivative services, equity and fixed income research, corporate lending, investment banking and advisory services, private banking, cash management, trade finance and securities services. ICG transacts with clients in both cash instruments and derivatives, including fixed income, foreign currency, equity and commodity products. For more information on ICG’s business activities, see “Institutional Clients Group” in Citi’s 2018 Annual Report on Form 10-K.

ICG’s international presence is supported by trading floors in approximately 80 countries and a proprietary network in 98 countries and jurisdictions. At June 30, 2019, ICG had approximately $1.5 trillion in assets and $715 billion in deposits, while two of its businesses—securities services and issuer services—managed approximately $19.0 trillion in assets under custody compared to $17.8 trillion at the end of the prior-year period.

|

| | | | | | | | | | | | | | | | |

| | Second Quarter | | Six Months | % Change |

| In millions of dollars, except as otherwise noted | 2019 | 2018 | % Change | 2019 | 2018 |

| Commissions and fees | $ | 1,046 |

| $ | 1,127 |

| (7 | )% | $ | 2,167 |

| $ | 2,340 |

| (7 | )% |

| Administration and other fiduciary fees | 696 |

| 713 |

| (2 | ) | 1,366 |

| 1,407 |

| (3 | ) |

| Investment banking | 1,100 |

| 1,246 |

| (12 | ) | 2,212 |

| 2,231 |

| (1 | ) |

| Principal transactions | 1,930 |

| 2,339 |

| (17 | ) | 4,562 |

| 5,183 |

| (12 | ) |

Other(1) | 716 |

| 179 |

| NM |

| 1,000 |

| 644 |

| 55 |

|

| Total non-interest revenue | $ | 5,488 |

| $ | 5,604 |

| (2 | )% | $ | 11,307 |

| $ | 11,805 |

| (4 | )% |

| Net interest revenue (including dividends) | 4,233 |

| 4,093 |

| 3 |

| 8,108 |

| 7,747 |

| 5 |

|

| Total revenues, net of interest expense | $ | 9,721 |

| $ | 9,697 |

| — | % | $ | 19,415 |

| $ | 19,552 |

| (1 | )% |

| Total operating expenses | $ | 5,356 |

| $ | 5,460 |

| (2 | )% | $ | 10,783 |

| $ | 10,966 |

| (2 | )% |

| Net credit losses | $ | 72 |

| $ | (1 | ) | NM |

| $ | 127 |

| $ | 104 |

| 22 | % |

| Credit reserve build (release) | 47 |

| 32 |

| 47 |

| (7 | ) | (143 | ) | 95 |

|

| Provision (release) for unfunded lending commitments | (16 | ) | (6 | ) | NM |

| 4 |

| 23 |

| (83 | ) |

| Provisions for credit losses | $ | 103 |

| $ | 25 |

| NM |

| $ | 124 |

| $ | (16 | ) | NM |

|

| Income from continuing operations before taxes | $ | 4,262 |

| $ | 4,212 |

| 1 | % | $ | 8,508 |

| $ | 8,602 |

| (1 | )% |

| Income taxes | 919 |

| 971 |

| (5 | ) | 1,843 |

| 2,027 |

| (9 | ) |

| Income from continuing operations | $ | 3,343 |

| $ | 3,241 |

| 3 | % | $ | 6,665 |

| $ | 6,575 |

| 1 | % |

| Noncontrolling interests | 10 |

| 12 |

| (17 | ) | 21 |

| 27 |

| (22 | ) |

| Net income | $ | 3,333 |

| $ | 3,229 |

| 3 | % | $ | 6,644 |

| $ | 6,548 |

| 1 | % |

EOP assets (in billions of dollars) | $ | 1,454 |

| $ | 1,397 |

| 4 | % | | | |

Average assets (in billions of dollars) | 1,450 |

| 1,406 |

| 3 |

| $ | 1,432 |

| $ | 1,397 |

| 3 | % |

| Return on average assets | 0.92 | % | 0.92 | % |

|

| 0.94 | % | 0.95 | % |

|

|

| Efficiency ratio | 55 |

| 56 |

|

|

| 56 |

| 56 |

|

|

|

| Revenues by region | | |

|

| | |

|

|

| North America | $ | 3,478 |

| $ | 3,511 |

| (1 | )% | $ | 6,597 |

| $ | 6,777 |

| (3 | )% |

| EMEA | 2,960 |

| 3,043 |

| (3 | ) | 6,130 |

| 6,210 |

| (1 | ) |

| Latin America | 1,195 |

| 1,168 |

| 2 |

| 2,355 |

| 2,384 |

| (1 | ) |

| Asia | 2,088 |

| 1,975 |

| 6 |

| 4,333 |

| 4,181 |

| 4 |

|

| Total | $ | 9,721 |

| $ | 9,697 |

| — | % | $ | 19,415 |

| $ | 19,552 |

| (1 | )% |

| Income from continuing operations by region | | |

|

| | |

|

|

|

| North America | $ | 1,022 |

| $ | 1,030 |

| (1 | )% | $ | 1,736 |

| $ | 1,888 |

| (8 | )% |

| EMEA | 1,005 |

| 986 |

| 2 |

| 2,130 |

| 2,099 |

| 1 |

|

| Latin America | 491 |

| 517 |

| (5 | ) | 994 |

| 1,011 |

| (2 | ) |

| Asia | 825 |

| 708 |

| 17 |

| 1,805 |

| 1,577 |

| 14 |

|

| Total | $ | 3,343 |

| $ | 3,241 |

| 3 | % | $ | 6,665 |

| $ | 6,575 |

| 1 | % |

|

| | | | | | | | | | | | | | | | |

Average loans by region (in billions of dollars) | | |

|

| | |

|

|

|

| North America | $ | 178 |

| $ | 165 |

| 8 | % | $ | 176 |

| $ | 162 |

| 9 | % |

| EMEA | 85 |

| 80 |

| 6 |

| 85 |

| 79 |

| 8 |

|

| Latin America | 33 |

| 33 |

| — |

| 34 |

| 34 |

| — |

|

| Asia | 63 |

| 68 |

| (7 | ) | 63 |

| 68 |

| (7 | ) |

| Total | $ | 359 |

| $ | 346 |

| 4 | % | $ | 358 |

| $ | 343 |

| 4 | % |

EOP deposits by business (in billions of dollars) | | | | | |

|

|

| Treasury and trade solutions | $ | 488 |

| $ | 459 |

| 6 | % | | |

|

|

All other ICG businesses | 227 |

| 217 |

| 5 |

|

|

|

|

|

|

|

| Total | $ | 715 |

| $ | 676 |

| 6 | % |

|

|

|

|

|

|

(1) The second quarter of 2019 includes an approximate $350 million gain on Citi's investment in Tradeweb.

NM Not meaningful

ICG Revenue Details

|

| | | | | | | | | | | | | | | | |

| | Second Quarter | | Six Months | % Change |

| In millions of dollars | 2019 | 2018 | % Change | 2019 | 2018 |

Investment banking revenue details | | | | | | |

| Advisory | $ | 232 |

| $ | 361 |

| (36 | )% | $ | 610 |

| $ | 576 |

| 6 | % |

| Equity underwriting | 314 |

| 335 |

| (6 | ) | 486 |

| 551 |

| (12 | ) |

| Debt underwriting | 737 |

| 726 |

| 2 |

| 1,541 |

| 1,425 |

| 8 |

|

| Total investment banking | $ | 1,283 |

| $ | 1,422 |

| (10 | )% | $ | 2,637 |

| $ | 2,552 |

| 3 | % |

| Treasury and trade solutions | 2,441 |

| 2,336 |

| 4 |

| 4,836 |

| 4,604 |

| 5 |

|

Corporate lending—excluding gains (losses) on loan hedges(1) | 538 |

| 589 |

| (9 | ) | 1,107 |

| 1,110 |

| — |

|

| Private bank | 866 |

| 848 |

| 2 |

| 1,746 |

| 1,752 |

| — |

|

| Total banking revenues (ex-gains (losses) on loan hedges) | $ | 5,128 |

| $ | 5,195 |

| (1 | )% | $ | 10,326 |

| $ | 10,018 |

| 3 | % |

Corporate lending—gains (losses) on loan hedges(1) | $ | (75 | ) | $ | 23 |

| NM |

| $ | (306 | ) | $ | 46 |

| NM |

|

| Total banking revenues (including gains (losses) on loan hedges), net of interest expense | $ | 5,053 |

| $ | 5,218 |

| (3 | )% | $ | 10,020 |

| $ | 10,064 |

| — | % |

Fixed income markets(2) | $ | 3,323 |

| $ | 3,082 |

| 8 | % | $ | 6,775 |

| $ | 6,507 |

| 4 | % |

| Equity markets | 790 |

| 864 |

| (9 | ) | 1,632 |

| 1,967 |

| (17 | ) |

| Securities services | 682 |

| 665 |

| 3 |

| 1,320 |

| 1,306 |

| 1 |

|

| Other | (127 | ) | (132 | ) | 4 |

| (332 | ) | (292 | ) | (14 | ) |

| Total markets and securities services revenues, net of interest expense | $ | 4,668 |

| $ | 4,479 |

| 4 | % | $ | 9,395 |

| $ | 9,488 |

| (1 | )% |

| Total revenues, net of interest expense | $ | 9,721 |

| $ | 9,697 |

| — | % | $ | 19,415 |

| $ | 19,552 |

| (1 | )% |

| Commissions and fees | $ | 198 |

| $ | 182 |

| 9 | % | $ | 372 |

| $ | 357 |

| 4 | % |

Principal transactions(3) | 1,870 |

| 2,114 |

| (12 | ) | 4,247 |

| 4,306 |

| (1 | ) |

Other(2) | 533 |

| 28 |

| NM |

| 683 |

| 303 |

| NM |

|

| Total non-interest revenue | $ | 2,601 |

| $ | 2,324 |

| 12 | % | $ | 5,302 |

| $ | 4,966 |

| 7 | % |

| Net interest revenue | 722 |

| 758 |

| (5 | ) | 1,473 |

| 1,541 |

| (4 | ) |

| Total fixed income markets | $ | 3,323 |

| $ | 3,082 |

| 8 | % | $ | 6,775 |

| $ | 6,507 |

| 4 | % |

| Rates and currencies | $ | 2,118 |

| $ | 2,241 |

| (5 | )% | $ | 4,520 |

| $ | 4,718 |

| (4 | )% |