| |

| |

UNITED STATES |

SECURITIES AND EXCHANGE COMMISSION |

Washington, D.C. 20549 |

| |

FORM 10-Q |

| |

(Mark One) |

[X] | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE |

SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended June 30, 2005 |

OR |

[ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE |

SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from | | to |

Commission File Number: 1-9916 |

| |

|

| |

Freeport-McMoRan Copper & Gold Inc. |

| (Exact name of registrant as specified in its charter) |

Delaware | 74-2480931 |

(State or other jurisdiction of incorporation or organization) | (IRS Employer Identification No.) |

| | |

1615 Poydras Street | |

New Orleans, Louisiana | 70112 |

| (Address of principal executive offices) | (Zip Code) |

| |

| |

(504) 582-4000 |

| (Registrant's telephone number, including area code) |

| |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes X No __

Indicate by check mark whether the registrant is an accelerated filer (as defined in Rule 12b-2 of the Securities Exchange Act of 1934). Yes X No __

On June 30, 2005, there were issued and outstanding 177,342,552 shares of the registrant’s Class B Common Stock, par value $0.10 per share.

FREEPORT-McMoRan COPPER & GOLD INC.

| | |

| | Page |

| 3 |

| | |

| |

| | |

| 3 |

| | |

| 4 |

| | |

| 5 |

| | |

| 6 |

| | |

| 11 |

| | |

| 12 |

| | |

| |

| 13 |

| | |

| 36 |

| | |

| 36 |

| | |

| 36 |

| | |

| 36 |

| | |

| 37 |

| | |

| 37 |

| | |

| 37 |

| | |

| 38 |

| | |

| E-1 |

| | |

FREEPORT-McMoRan COPPER & GOLD INC.

FREEPORT-McMoRan COPPER & GOLD INC.

| | | June 30, | | | December 31, | |

| | | 2005 | | | 2004 | |

| | | (In Thousands) | |

| ASSETS | | | | | | | | |

| Current assets: | | | | | | | | |

| Cash and cash equivalents | | $ | 585,434 | | | $ | 551,450 | |

| Restricted cash | | | 500 | | | | 500 | |

| Accounts receivable | | | 302,184 | | | | 435,062 | |

| Inventories | | | 435,248 | | | | 466,712 | |

| Prepaid expenses and other | | | 9,975 | | | | 6,223 | |

| Total current assets | | | 1,333,341 | | | | 1,459,947 | |

| Property, plant, equipment and development costs, net | | | 3,146,065 | | | | 3,199,292 | |

| Deferred mining costs | | | 273,225 | | | | 220,415 | |

| Other assets | | | 152,697 | | | | 159,539 | |

| Investment in PT Smelting | | | 52,936 | | | | 47,802 | |

| Total assets | | $ | 4,958,264 | | | $ | 5,086,995 | |

| | | | | | | | | |

| LIABILITIES AND STOCKHOLDERS’ EQUITY | | | | | | | | |

| Current liabilities: | | | | | | | | |

| Accounts payable and accrued liabilities | | $ | 346,862 | | | $ | 386,590 | |

| Current portion of long-term debt and short-term borrowings | | | 193,706 | | | | 78,214 | |

| Accrued income taxes | | | 110,165 | | | | 92,346 | |

| Rio Tinto share of joint venture cash flows | | | 59,890 | | | | 60,224 | |

| Unearned customer receipts | | | 52,981 | | | | 33,021 | |

| Accrued interest payable | | | 46,981 | | | | 47,167 | |

| Total current liabilities | | | 810,585 | | | | 697,562 | |

| Long-term debt, less current portion: | | | | | | | | |

| Senior notes | | | 900,386 | | | | 911,336 | |

| Convertible senior notes | | | 575,000 | | | | 575,000 | |

| Equipment and other loans | | | 61,303 | | | | 67,624 | |

| Atlantic Copper debt | | | 39,210 | | | | 4,426 | |

| Redeemable preferred stock | | | 12,501 | | | | 179,880 | |

| PT Puncakjaya Power bank debt | | | - | | | | 135,426 | |

| Total long-term debt, less current portion | | | 1,588,400 | | | | 1,873,692 | |

| Accrued postretirement benefits and other liabilities | | | 203,949 | | | | 200,228 | |

| Deferred income taxes | | | 938,210 | | | | 932,416 | |

| Minority interests | | | 196,134 | | | | 219,448 | |

| Stockholders' equity: | | | | | | | | |

| Convertible perpetual preferred stock | | | 1,100,000 | | | | 1,100,000 | |

| Class B common stock | | | 28,621 | | | | 28,496 | |

| Capital in excess of par value of common stock | | | 1,886,486 | | | | 1,852,816 | |

| Retained earnings | | | 730,528 | | | | 604,680 | |

| Accumulated other comprehensive income | | | 9,588 | | | | 11,342 | |

| Common stock held in treasury | | | (2,534,237 | ) | | | (2,433,685 | ) |

| Total stockholders’ equity | | | 1,220,986 | | | | 1,163,649 | |

| Total liabilities and stockholders’ equity | | $ | 4,958,264 | | | $ | 5,086,995 | |

The accompanying notes are an integral part of these financial statements.

FREEPORT-McMoRan COPPER & GOLD INC.

| | | Three Months Ended | | | Six Months Ended | |

| | | June 30, | | | June 30, | |

| | | 2005 | | | 2004 | | | 2005 | | | 2004 | |

| | | (In Thousands, Except Per Share Amounts) | |

| Revenues | $ | 902,909 | | $ | 486,334 | | $ | 1,705,974 | | $ | 846,519 | |

| Cost of sales: | | | | | | | | | | | | |

| Production and delivery | | 390,586 | | | 371,679 | | | 755,592 | | | 647,291 | |

| Depreciation and amortization | | 54,159 | | | 42,590 | | | 111,085 | | | 68,000 | |

| Total cost of sales | | 444,745 | | | 414,269 | | | 866,677 | | | 715,291 | |

| Exploration expenses | | 2,342 | | | 2,787 | | | 4,262 | | | 5,014 | |

| General and administrative expenses | | 25,379 | | | 22,576 | | | 46,993 | | | 38,136 | |

| Total costs and expenses | | 472,466 | | | 439,632 | | | 917,932 | | | 758,441 | |

| Operating income | | 430,443 | | | 46,702 | | | 788,042 | | | 88,078 | |

| Equity in PT Smelting earnings (losses) | | 2,562 | | | (2,548 | ) | | 5,158 | | | (2,906 | ) |

| Interest expense, net | | (35,292 | ) | | (39,339 | ) | | (72,840 | ) | | (72,729 | ) |

| Gains (losses) on early extinguishment and | | | | | | | | | | | | |

| conversion of debt | | - | | | 643 | | | 37 | | | (14,000 | ) |

| Other income (expense), net | | 8,143 | | | (368 | ) | | 16,095 | | | 3,174 | |

| Income before income taxes and minority | | | | | | | | | | | | |

| interests | | 405,856 | | | 5,090 | | | 736,492 | | | 1,617 | |

| Provision for income taxes | | (188,684 | ) | | (38,210 | ) | | (352,712 | ) | | (56,551 | ) |

| Minority interests in net income of | | | | | | | | | | | | |

| consolidated subsidiaries | | (26,800 | ) | | (5,118 | ) | | (47,888 | ) | | (2,687 | ) |

| Net income (loss) | | 190,372 | | | (38,238 | ) | | 335,892 | | | (57,621 | ) |

| Preferred dividends | | (15,125 | ) | | (15,073 | ) | | (30,250 | ) | | (15,241 | ) |

| Net income (loss) applicable to common stock | $ | 175,247 | | $ | (53,311 | ) | $ | 305,642 | | $ | (72,862 | ) |

| | | | | | | | | | | | | |

| Net income (loss) per share of common stock: | | | | | | | | | | | | |

| Basic | | $0.98 | | | $(0.30 | ) | | $1.71 | | | $(0.39 | ) |

| Diluted | | $0.91 | | | $(0.30 | ) | | $1.62 | | | $(0.39 | ) |

| Average common shares outstanding: | | | | | | | | | | | | |

| Basic | | 178,324 | | | 175,202 | | | 178,822 | | | 186,570 | |

| Diluted | | 219,990 | | | 175,202 | | | 220,516 | | | 186,570 | |

| | | | | | | | | | | | | |

| Dividends paid per share of common stock | | $0.25 | | | $0.20 | | | $1.00 | | | $0.40 | |

The accompanying notes are an integral part of these financial statements.

FREEPORT-McMoRan COPPER & GOLD INC.

| | | Six Months Ended June 30, | |

| | | 2005 | | | 2004 | |

| | | (In Thousands) | |

| Cash flow from operating activities: | | | | | | | | |

| Net income (loss) | | $ | 335,892 | | | $ | (57,621 | ) |

| Adjustments to reconcile net income (loss) to net cash provided by | | | |

| (used in) operating activities: | | | | | | | | |

| Depreciation and amortization | | | 111,085 | | | | 68,000 | |

| (Gains) losses on early extinguishment and conversion of debt | | | (37 | ) | | | 14,000 | |

| Deferred income taxes | | | 5,327 | | | | 69,564 | |

| Equity in PT Smelting (earnings) losses | | | (5,158 | ) | | | 2,906 | |

| Minority interests' share of net income | | | 47,888 | | | | 2,687 | |

| Increase in deferred mining costs | | | (52,810 | ) | | | (57,707 | ) |

| Amortization of deferred financing costs | | | 4,010 | | | | 4,460 | |

| Currency translation gains | | | (6,252 | ) | | | (1,847 | ) |

| Elimination of profit on PT Freeport Indonesia sales to | | | | | | | | |

| PT Smelting | | | 25 | | | | 1,956 | |

| Provision for inventory obsolescence | | | 3,000 | | | | 4,025 | |

| Other | | | 14,937 | | | | 5,986 | |

| (Increases) decreases in working capital: | | | | | | | | |

| Accounts receivable | | | 123,278 | | | | (47,949 | ) |

| Inventories | | | 25,155 | | | | (33,007 | ) |

| Prepaid expenses and other | | | (2,406 | ) | | | (63,766 | ) |

| Accounts payable and accrued liabilities | | | (8,100 | ) | | | (28,286 | ) |

| Rio Tinto share of joint venture cash flows | | | (334 | ) | | | (30,484 | ) |

| Accrued income taxes | | | 25,011 | | | | (41,868 | ) |

| (Increase) decrease in working capital | | | 162,604 | | | | (245,360 | ) |

| Net cash provided by (used in) operating activities | | | 620,511 | | | | (188,951 | ) |

| Cash flow from investing activities: | | | | | | | | |

| PT Freeport Indonesia capital expenditures | | | (53,428 | ) | | | (59,583 | ) |

| Atlantic Copper capital expenditures | | | (5,863 | ) | | | (15,257 | ) |

| Proceeds from insurance settlement | | | 2,016 | | | | - | |

| Investment in PT Smelting and other | | | 131 | | | | (1,219 | ) |

| Sale of restricted investments | | | - | | | | 19,346 | |

| Decrease in Atlantic Copper restricted cash | | | - | | | | 11,000 | |

| Net cash used in investing activities | | | (57,144 | ) | | | (45,713 | ) |

| Cash flow from financing activities: | | | | | | | | |

| Net proceeds from sale of senior notes | | | - | | | | 344,354 | |

| Proceeds from other debt | | | 65,647 | | | | 57,708 | |

| Repayments of debt | | | (235,249 | ) | | | (337,184 | ) |

| Redemption of preferred stock | | | (215 | ) | | | (1,110 | ) |

| Net proceeds from sale of convertible perpetual preferred stock | | | - | | | | 1,067,000 | |

| Purchase of FCX common shares from Rio Tinto | | | - | | | | (881,868 | ) |

| Purchases of FCX common shares | | | (80,227 | ) | | | (99,477 | ) |

| Cash dividends paid: | | | | | | | | |

| Common stock | | | (179,658 | ) | | | (74,655 | ) |

| Preferred stock | | | (30,251 | ) | | | (5,219 | ) |

| Minority interests | | | (71,425 | ) | | | (929 | ) |

| Net proceeds from exercised stock options | | | 2,016 | | | | 4,030 | |

| Bank credit facilities fees and other | | | (21 | ) | | | (1,886 | ) |

| Net cash (used in) provided by financing activities | | | (529,383 | ) | | | 70,764 | |

| Net increase (decrease) in cash and cash equivalents | | | 33,984 | | | | (163,900 | ) |

| Cash and cash equivalents at beginning of year | | | 551,450 | | | | 463,652 | |

| Cash and cash equivalents at end of period | | $ | 585,434 | | | $ | 299,752 | |

The accompanying notes are an integral part of these financial statements.

FREEPORT-McMoRan COPPER & GOLD INC.

| 1. | NEW ACCOUNTING STANDARDS |

Deferred Mining Costs. In the mining industry, the costs of removing overburden and waste material to access mineral deposits are referred to as “stripping costs.” Currently, Freeport-McMoRan Copper & Gold Inc. (FCX) applies the deferred mining cost method in accounting for its post-production stripping costs, which FCX refers to as overburden removal costs. The deferred mining cost method is used by some companies in the metals mining industry; however, industry practice varies. The deferred mining cost method matches the cost of production with the sale of the related metal from the open pit by assigning each metric ton of ore removed an equivalent amount of overburden tonnage, thereby averaging overburden removal costs over the life of the mine. The mining cost capitalized in inventory and the amounts charged to cost of goods sold do not represent the actual costs incurred to mine the ore in any given period. The application of the deferred mining cost method has resulted in an asset on FCX’s balance sheets (“Deferred Mining Costs”) totaling $273.2 million at June 30, 2005, and $220.4 million at December 31, 2004. For further information, see Note 1 in FCX’s 2004 Annual Report on Form 10-K.

In March 2005, the Financial Accounting Standards Board (FASB) ratified Emerging Issues Task Force (EITF) Issue No. 04-6, “Accounting for Stripping Costs Incurred during Production in the Mining Industry,” which requires that stripping costs be considered costs of the extracted minerals and recognized as a component of inventory to be recognized in cost of sales in the same period as the revenue from the sale of inventory. As a result, capitalization of stripping costs is appropriate only to the extent product inventory exists at the end of a reporting period. The guidance in EITF Issue No. 04-6 is effective for financial statements issued for fiscal years beginning after December 15, 2005, with early adoption permitted. Companies may apply this guidance either by recognition of a cumulative effect adjustment to beginning retained earnings in the period of adoption or by restating prior period financial statements. FCX expects to adopt the guidance on January 1, 2006, with the most significant impacts of adoption being the deferred mining costs asset on FCX’s balance sheet on that date will be charged, net of taxes and minority interest share, as a cumulative effect adjustment to beginning retained earnings and future stripping costs will effectively be charged to cost of sales as incurred. Adoption of the new guidance will have no impact on FCX’s cash flows. The pro forma impact of applying EITF Issue No. 04-6 to the periods reported in this quarterly report on Form 10-Q would be to reduce net income by $12.1 million or $0.06 per diluted share for the second quarter of 2005 and $28.1 million or $0.13 per diluted share for the 2005 six-month period, and to increase net losses by $12.8 million or $0.07 per share for the second quarter of 2004 and $28.0 million or $0.15 per share for the 2004 six-month period.

Stock-Based Payments. Refer to Note 1 in FCX’s 2004 Annual Report on Form 10-K for FCX’s accounting for share-based payments, including stock options. Through June 30, 2005, FCX has accounted for grants of employee stock options under the recognition principles of Accounting Principles Board (APB) Opinion No. 25, “Accounting for Stock Issued to Employees,” and related interpretations, which require compensation costs for stock-based employee compensation plans to be recognized based on the difference on the date of grant, if any, between the quoted market price of the stock and the amount an employee must pay to acquire the stock. If FCX had applied the fair value recognition provisions of Statement of Financial Accounting Standards (SFAS) No. 123, “Accounting for Stock-Based Compensation,” which requires stock-based compensation to be recognized based on the use of a fair value method, FCX’s net income would have been reduced by $3.4 million, $0.02 per diluted share, for the second quarter of 2005 and $6.3 million, $0.06 per diluted share, for the first six months of 2005. In 2004, FCX’s net loss would have been increased by $1.1 million, $0.01 per diluted share, for the second quarter of 2004 and $2.2 million, $0.01 per diluted share, for the first six months of 2004.

In December 2004, the FASB issued SFAS No. 123 (revised 2004), “Share-Based Payment” (SFAS No. 123R). SFAS No. 123R requires all share-based payments to employees, including grants of employee stock options, to be recognized in the financial statements based on their fair values. SFAS No. 123R’s effective date is interim periods beginning after June 15, 2005. However, in April 2005 the Securities and Exchange Commission provided for a deferral of the effective date to fiscal periods beginning after June 15, 2005. FCX is still reviewing the provisions of SFAS No. 123R and has not yet determined if it will adopt SFAS No. 123R before January 1, 2006. Based on currently outstanding employee stock options, FCX estimates the pro forma charge to earnings before taxes and minority interest sharing for the full year 2005 would total approximately $22 million, and the pro forma reduction in net income would be approximately $13 million, $0.07 per share using average basic shares outstanding for the second quarter of 2005.

FCX basic net income (loss) per share of common stock was calculated by dividing net income (loss) applicable to common stock by the weighted average number of common shares outstanding during the period. The following is a reconciliation of net income (loss) and weighted average common shares outstanding for purposes of calculating diluted net income (loss) per share (in thousands, except per share amounts):

| | | Three Months Ended | | Six Months Ended | |

| | | June 30, | | June 30, | |

| | | 2005 | | 2004 | | 2005 | | 2004 | |

| Net income (loss) before preferred dividends | | $ | 190,372 | | $ | (38,238 | ) | $ | 335,892 | | $ | (57,621 | ) |

| Preferred dividends | | | (15,125 | ) | | (15,073 | ) | | (30,250 | ) | | (15,241 | ) |

| Net income (loss) applicable to common stock | | | 175,247 | | | (53,311 | ) | | 305,642 | | | (72,862 | ) |

| Plus income impact of assumed conversion of: | | | | | | | | | | | | | |

| 5½% Convertible Perpetual Preferred Stock | | | 15,125 | | | - | | | 30,250 | | | - | |

| 7% Convertible Senior Notes | | | 10,287 | | | - | | | 20,609 | | | - | |

| Diluted net income (loss) applicable to common stock | | $ | 200,659 | | $ | (53,311 | ) | $ | 356,501 | | $ | (72,862 | ) |

| | | | | | | | | | | | | | |

| Weighted average common shares outstanding | | | 178,324 | | | 175,202 | | | 178,822 | | | 186,570 | |

Add: Shares issuable upon conversion of: | | | | | | | | | | | | | |

| 5½% Convertible Perpetual Preferred Stock | | | 21,152 | | | - | | | 21,034 | | | - | |

| 7% Convertible Senior Notes | | | 18,625 | | | - | | | 18,625 | | | - | |

| Dilutive stock options | | | 1,408 | | | - | | | 1,555 | | | - | |

| Restricted stock | | | 481 | | | - | | | 480 | | | - | |

| Weighted average common shares outstanding for | | | | | | | | | | | | | |

| purposes of calculating diluted net income (loss) | | | | | | | | | | | | | |

| per share | | | 219,990 | | | 175,202 | | | 220,516 | | | 186,570 | |

| | | | | | | | | | | | | | |

| Diluted net income (loss) per share of common stock | | $ | 0.91 | | $ | (0.30 | ) | $ | 1.62 | | $ | (0.39 | ) |

| | | | | | | | | | | | | | |

Outstanding stock options with exercise prices greater than the average market price of the common stock during the period are excluded from the computation of diluted net income per share of common stock. FCX’s convertible instruments are also excluded when including the conversion of these instruments increases reported diluted net income per share or when FCX reports a net loss for the period. A recap of the excluded amounts follows (in thousands, except exercise prices):

| | Three Months Ended | | Six Months Ended | |

| | June 30, | | June 30, | |

| | 2005 | | 2004 | | 2005 | | 2004 | |

| Weighted average outstanding options | 5,463 | | 2,346 | | 2,732 | | - | |

| Weighted average exercise price | $36.98 | | $36.13 | | $36.98 | | - | |

| | | | | | | | | |

| Dividends on 5½% Convertible Perpetual Preferred Stock | - | | $15,125 | | - | | $15,293 | a |

| Weighted average shares issuable upon conversion | - | | 20,682 | | - | | 10,563 | a |

| | | | | | | | | |

| Interest on 7% Convertible Senior Notes | - | | $10,357 | b | - | | $20,715 | b |

| Weighted average shares issuable upon conversion | - | | 18,625 | | - | | 18,625 | |

| | | | | | | | | |

| Interest on 8¼% Convertible Senior Notes | N/A | | $1,399 | b | N/A | | $3,363 | b |

| Weighted average shares issuable upon conversion | N/A | | 4,653 | | N/A | | 5,464 | |

| | | | | | | | | |

| a. | FCX’s 5½% Convertible Perpetual Preferred Stock was issued on March 30, 2004. |

| b. | Amounts are net of the effective United States federal alternative minimum tax rate of two percent. |

Stock-Based Compensation Plans. As of June 30, 2005, FCX has four stock-based employee compensation plans and two stock-based director compensation plans, which are more fully described in Note 7 of FCX’s 2004 Annual Report on Form 10-K. FCX accounts for options granted under all of its plans using the recognition and measurement principles of APB Opinion No. 25 and related interpretations, which require compensation cost for stock-based employee compensation plans to be recognized based on the difference on the date of grant, if any, between the quoted market price of the stock and the amount an employee must pay to acquire the stock. Because all the plans require that the option exercise price be at least the market price on the date of grant, FCX recognizes no compensation expense on the grant or exercise of its employees’ options. The following table illustrates the effect on net income and earnings per share if FCX had applied the fair value recognition provisions of SFAS No. 123 which requires compensation cost for all stock-based employee compensation plans to be recognized based on a fair value method (in thousands, except per share amounts).

| | | Three Months Ended | | Six Months Ended | |

| | | June 30, | | June 30, | |

| | | 2005 | | 2004 | | 2005 | | 2004 | |

| Net income (loss) applicable to common stock, as reported | | $ | 175,247 | | $ | (53,311 | ) | $ | 305,642 | | $ | (72,862 | ) |

| Add: Stock-based employee compensation expense | | | | | | | | | | | | | |

| included in reported net income (loss) for stock option | | | | | | | | | | | | | |

| conversions, stock appreciation rights (SARs) and | | | | | | | | | | | | | |

| restricted stock units, net of taxes and minority interests | | | 1,898 | | | (16 | ) | | 4,457 | | | 374 | |

| Deduct: Total stock-based employee compensation | | | | | | | | | | | | | |

| expense determined under fair value-based method for | | | | | | | | | | | | | |

| all awards, net of taxes and minority interests | | | (5,339 | ) | | (1,041 | ) | | (10,754 | ) | | (2,583 | ) |

| Pro forma net income (loss) applicable to common stock | | $ | 171,806 | | $ | (54,368 | ) | $ | 299,345 | | $ | (75,071 | ) |

| | | | | | | | | | | | | | |

| Earnings (loss) per share: | | | | | | | | | | | | | |

| Basic - as reported | | $ | 0.98 | | $ | (0.30 | ) | $ | 1.71 | | $ | (0.39 | ) |

| Basic - pro forma | | $ | 0.96 | | $ | (0.31 | ) | $ | 1.67 | | $ | (0.40 | ) |

| | | | | | | | | | | | | | |

| Diluted - as reported | | $ | 0.91 | | $ | (0.30 | ) | $ | 1.62 | | $ | (0.39 | ) |

| Diluted - pro forma | | $ | 0.89 | | $ | (0.31 | ) | $ | 1.56 | | $ | (0.40 | ) |

| | | | | | | | | | | | | | |

For the pro forma computations, the values of option grants were calculated on the dates of grant using the Black-Scholes option pricing model. No other discounts or restrictions related to vesting or the likelihood of vesting of stock options were applied. The following table summarizes the calculated average fair values and weighted-average assumptions used to determine the fair value of FCX’s stock option grants under SFAS No. 123 during the periods presented.

| | Three Months Ended | | Six Months Ended | |

| | June 30, | | June 30, | |

| | 2005 | | 2004 | | 2005 | | 2004 | |

| Fair value per stock option | $ | 12.90 | | $ | 13.73 | | $ | 13.97 | | $ | 15.00 | |

| Risk-free interest rate | | 3.7 | % | | 4.3 | % | | 3.9 | % | | 3.7 | % |

| Expected volatility rate | | 45 | % | | 48 | % | | 46 | % | | 49 | % |

| Expected life of options (in years) | | 6 | | | 6 | | | 6 | | | 6 | |

| Assumed annual dividend | $ | 1.00 | | $ | 0.80 | | $ | 1.00 | | $ | 0.80 | |

See Note 1 above and Note 1 in FCX’s Annual Report on Form 10-K for a discussion of the requirements of SFAS No. 123R.

FCX has two operating segments: “mining and exploration” and “smelting and refining.” The mining and exploration segment consists of FCX’s Indonesian activities including PT Freeport Indonesia’s copper and gold mining operations, PT Puncakjaya Power’s power-generating operations (after eliminations with PT Freeport Indonesia) and FCX’s Indonesian exploration activities. The smelting and refining segment includes Atlantic Copper’s operations in Spain and PT Freeport Indonesia’s equity investment in PT Smelting in Gresik, Indonesia. The segment data presented below were prepared on the same basis as FCX’s consolidated financial statements.

| | | Mining and Exploration | | Smelting and Refining | | Eliminations and Other | | FCX Total | |

| | | (In Thousands) | |

| Three months ended June 30, 2005: | | | | | | | | | | | | | |

| Revenues | | $ | 678,386 | a | $ | 331,897 | | $ | (107,374 | ) | $ | 902,909 | |

| Production and delivery | | | 223,355 | | | 321,909 | | | (154,678 | )b | | 390,586 | |

| Depreciation and amortization | | | 44,217 | | | 7,141 | | | 2,801 | | | 54,159 | |

| Exploration expenses | | | 2,272 | | | - | | | 70 | | | 2,342 | |

| General and administrative expenses | | | 18,425 | c | | 2,901 | | | 4,053 | c | | 25,379 | |

| Operating income (loss) | | $ | 390,117 | | $ | (54 | ) | $ | 40,380 | | $ | 430,443 | |

| Equity in PT Smelting earnings | | $ | - | | $ | 2,562 | | $ | - | | $ | 2,562 | |

| Interest expense, net | | $ | 5,897 | | $ | 4,387 | | $ | 25,008 | | $ | 35,292 | |

| Provision for income taxes | | $ | 138,007 | | $ | - | | $ | 50,677 | | $ | 188,684 | |

| Capital expenditures | | $ | 29,939 | | $ | 3,139 | | $ | (33 | ) | $ | 33,045 | |

| Total assets | | $ | 3,870,969 | d | $ | 717,707 | e | $ | 369,588 | | $ | 4,958,264 | |

| | | | | | | | | | | | | | |

| Three months ended June 30, 2004: | | | | | | | | | | | | | |

| Revenues | | $ | 330,841 | a | $ | 171,736 | | $ | (16,243 | ) | $ | 486,334 | |

| Production and delivery | | | 175,243 | | | 201,542 | | | (5,106 | )b | | 371,679 | |

| Depreciation and amortization | | | 33,417 | | | 7,028 | | | 2,145 | | | 42,590 | |

| Exploration expenses | | | 2,679 | | | - | | | 108 | | | 2,787 | |

| General and administrative expenses | | | 16,339 | c | | 3,114 | | | 3,123 | c | | 22,576 | |

| Operating income (loss) | | $ | 103,163 | | $ | (39,948 | ) | $ | (16,513 | ) | $ | 46,702 | |

| Equity in PT Smelting losses | | $ | - | | $ | 2,548 | | $ | - | | $ | 2,548 | |

| Interest expense, net | | $ | 5,494 | | $ | 2,919 | | $ | 30,926 | | $ | 39,339 | |

| Provision for income taxes | | $ | 37,522 | | $ | - | | $ | 688 | | $ | 38,210 | |

| Capital expenditures | | $ | 34,002 | | $ | 6,491 | | $ | 6 | | $ | 40,499 | |

| Total assets | | $ | 3,561,840 | d | $ | 681,039 | e | $ | 482,635 | | $ | 4,725,514 | |

| | | | | | | | | | | | | | |

| Six months ended June 30, 2005: | | | | | | | | | | | | | |

| Revenues | | $ | 1,365,784 | a | $ | 604,013 | | $ | (263,823 | ) | $ | 1,705,974 | |

| Production and delivery | | | 417,233 | | | 585,486 | | | (247,127 | ) | | 755,592 | |

| Depreciation and amortization | | | 91,142 | | | 14,230 | | | 5,713 | | | 111,085 | |

| Exploration expenses | | | 4,164 | | | - | | | 98 | | | 4,262 | |

| General and administrative expenses | | | 51,607 | c | | 5,905 | | | (10,519 | )c | | 46,993 | |

| Operating income (loss) | | $ | 801,638 | | $ | (1,608 | ) | $ | (11,988 | ) | $ | 788,042 | |

| Equity in PT Smelting earnings | | $ | - | | $ | 5,158 | | $ | - | | $ | 5,158 | |

| Interest expense, net | | $ | 11,624 | | $ | 8,192 | | $ | 53,024 | | $ | 72,840 | |

| Provision for income taxes | | $ | 283,326 | | $ | - | | $ | 69,386 | | $ | 352,712 | |

| Capital expenditures | | $ | 53,508 | | $ | 5,863 | | $ | (80 | ) | $ | 59,291 | |

| | | | | | | | | | | | | | |

| Six months ended June 30, 2004: | | | | | | | | | | | | | |

| Revenues | | $ | 518,025 | a | $ | 382,953 | | $ | (54,459 | ) | $ | 846,519 | |

| Production and delivery | | | 326,515 | | | 413,658 | | | (92,882 | )b | | 647,291 | |

| Depreciation and amortization | | | 50,603 | | | 14,095 | | | 3,302 | | | 68,000 | |

| Exploration expenses | | | 4,868 | | | - | | | 146 | | | 5,014 | |

| General and administrative expenses | | | 93,351 | c | | 6,096 | | | (61,311 | )c | | 38,136 | |

| Operating income (loss) | | $ | 42,688 | | $ | (50,896 | ) | $ | 96,286 | | $ | 88,078 | |

| Equity in PT Smelting losses | | $ | - | | $ | 2,906 | | $ | - | | $ | 2,906 | |

| Interest expense, net | | $ | 11,213 | | $ | 6,771 | | $ | 54,745 | | $ | 72,729 | |

| Provision for income taxes | | $ | 17,943 | | $ | - | | $ | 38,608 | | $ | 56,551 | |

| Capital expenditures | | $ | 59,703 | | $ | 15,257 | | $ | (120 | ) | $ | 74,840 | |

| a. | Includes PT Freeport Indonesia’s sales to PT Smelting totaling $194.9 million in the 2005 quarter, $166.2 million in the 2004 quarter, $429.0 million in the 2005 six-month period and $293.2 million in the 2004 six-month period. |

| b. | Includes deferral (recognition) of intercompany profits on 25 percent of PT Freeport Indonesia’s sales to PT Smelting, for which the final sale to third parties must occur for profit recognition, totaling $(2.6) million in the 2005 quarter, $10.3 million in the 2004 quarter and $2.0 million in the 2004 six-month period. |

| c. | Includes charges to the mining and exploration segment for FCX stock option exercises which are eliminated in consolidation totaling $0.7 million in the 2005 quarter, $2.2 million in the 2004 quarter, $17.4 million in the 2005 six-month period and $66.8 million in the 2004 six-month period. |

| d. | Includes PT Freeport Indonesia’s trade receivables with PT Smelting totaling $71.9 million at June 30, 2005, and $71.8 million at June 30, 2004. |

| e. | Includes PT Freeport Indonesia’s equity investment in PT Smelting totaling $52.9 million at June 30, 2005, and $54.4 million at June 30, 2004. |

The components of inventories follow (in thousands):

| | | | June 30, | | December 31, | |

| | | | 2005 | | 2004 | |

| PT Freeport Indonesia: | Concentrates - Average cost | | $ | 9,501 | | $ | 11,830 | |

| Atlantic Copper: | Concentrates - First in, first out (FIFO) | | | 70,442 | | | 148,246 | |

| | Work in process - FIFO | | | 120,337 | | | 86,710 | |

| | Finished goods - FIFO | | | 1,051 | | | 6,479 | |

| Total product inventories | | | 201,331 | | | 253,265 | |

| Total materials and supplies, net | | | 233,917 | | | 213,447 | |

| Total inventories | | $ | 435,248 | | $ | 466,712 | |

The average cost method was used to determine the cost of essentially all materials and supplies inventory. Materials and supplies inventory is net of obsolescence reserves totaling $17.1 million at June 30, 2005 and December 31, 2004.

The components of net periodic pension benefit cost for the three months ended June 30, 2005 and 2004 follow (in thousands):

| | FCX | | PT Freeport Indonesia | | Atlantic Copper | |

| | 2005 | | 2004 | | 2005 | | 2004 | | 2005 | | 2004 | |

| Service cost | $ | 165 | | $ | 213 | | $ | 900 | | $ | 821 | | $ | - | | $ | - | |

| Interest cost | | 596 | | | 610 | | | 940 | | | 824 | | | 1,239 | | | 1,248 | |

| Expected return on plan assets | | (234 | ) | | 253 | | | (353 | ) | | (448 | ) | | - | | | - | |

| Amortization of prior service cost | | 1,019 | | | 944 | | | 225 | | | 237 | | | - | | | - | |

| Amortization of net actuarial loss | | - | | | - | | | 178 | | | 70 | | | 231 | | | 219 | |

| Net periodic benefit cost | $ | 1,546 | | $ | 2,020 | | $ | 1,890 | | $ | 1,504 | | $ | 1,470 | | $ | 1,467 | |

The components of net periodic pension benefit cost for the six months ended June 30, 2005 and 2004 follow (in thousands):

| | FCX | | PT Freeport Indonesia | | Atlantic Copper | |

| | 2005 | | 2004 | | 2005 | | 2004 | | 2005 | | 2004 | |

| Service cost | $ | 344 | | $ | 284 | | $ | 1,831 | | $ | 1,702 | | $ | - | | $ | - | |

| Interest cost | | 1,114 | | | 993 | | | 1,912 | | | 1,707 | | | 2,528 | | | 2,543 | |

| Expected return on plan assets | | (256 | ) | | (69 | ) | | (718 | ) | | (928 | ) | | - | | | - | |

| Amortization of prior service cost | | 1,963 | | | 1,888 | | | 457 | | | 491 | | | - | | | - | |

| Amortization of net actuarial loss | | - | | | - | | | 362 | | | 146 | | | 472 | | | 449 | |

| Net periodic benefit cost | $ | 3,165 | | $ | 3,096 | | $ | 3,844 | | $ | 3,118 | | $ | 3,000 | | $ | 2,992 | |

Interest expense excludes capitalized interest of $1.0 million in the second quarter of 2005, $0.7 million in the second quarter of 2004, $1.9 million in the first six months of 2005 and $1.1 million in the first six months of 2004.

A summary of FCX’s comprehensive income is shown below (in thousands).

| | | Three Months Ended | | Six Months Ended | |

| | | June 30, | | June 30, | |

| | | 2005 | | 2004 | | 2005 | | 2004 | |

| Net income (loss) | | $ | 190,372 | | $ | (38,238 | ) | $ | 335,892 | | $ | (57,621 | ) |

| Other comprehensive income (loss): | | | | | | | | | | | | | |

| Change in unrealized derivatives’ fair value, net of taxes | | | | | | | | | | | | | |

| of $0.8 million for the three months ended | | | | | | | | | | | | | |

| June 30, 2005, $1.0 million for the six months ended | | | | | | | | | | | | | |

| June 30, 2005 and $0.1 million for the 2004 periods | | | (1,047 | ) | | 32 | | | (1,345 | ) | | (114 | ) |

| Reclass to earnings, net of taxes of $0.1 million | | | | | | | | | | | | | |

| for the 2005 periods and none for the 2004 periods | | | (192 | ) | | 476 | | | (95 | ) | | 982 | |

| Total comprehensive income (loss) | | $ | 189,133 | | $ | (37,730 | ) | $ | 334,452 | | $ | (56,753 | ) |

| | | | | | | | | | | | | | |

| 8. | RATIO OF EARNINGS TO FIXED CHARGES |

The ratio of earnings to fixed charges for the first six months of 2005 and 2004 was 10.7 to 1 and 1.0 to 1, respectively. For this calculation, earnings consist of income from continuing operations before income taxes, minority interests and fixed charges. Fixed charges include interest and that portion of rent deemed representative of interest.

----------------------

The information furnished herein should be read in conjunction with FCX's financial statements contained in its 2004 Annual Report on Form 10-K. The information furnished herein reflects all adjustments which are, in the opinion of management, necessary for a fair statement of the results for the periods. All such adjustments are, in the opinion of management, of a normal recurring nature.

TO THE BOARD OF DIRECTORS AND STOCKHOLDERS OF

FREEPORT-McMoRan COPPER & GOLD INC.

We have reviewed the condensed consolidated balance sheet of Freeport-McMoRan Copper & Gold Inc. (a Delaware Corporation) and subsidiaries as of June 30, 2005 and the related consolidated statements of operations for the three-month and six-month periods ended June 30, 2005 and 2004, and the consolidated statements of cash flows for the six-month periods ended June 30, 2005 and 2004. These financial statements are the responsibility of the Company’s management.

We conducted our review in accordance with the standards of the Public Company Accounting Oversight Board (United States). A review of interim financial information consists principally of applying analytical procedures to financial data, and making inquiries of persons responsible for financial and accounting matters. It is substantially less in scope than an audit conducted in accordance with the standards of the Public Company Accounting Oversight Board (United States), the objective of which is the expression of an opinion regarding the financial statements taken as a whole. Accordingly, we do not express such an opinion.

Based on our review, we are not aware of any material modifications that should be made to the condensed consolidated financial statements referred to above for them to be in conformity with United States generally accepted accounting principles.

We have previously audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States), the consolidated balance sheet of Freeport-McMoRan Copper & Gold Inc. as of December 31, 2004, and the related consolidated statements of income, stockholder’s equity, and cash flows for the year then ended (not presented herein), and in our report dated March 9, 2005, we expressed an unqualified opinion on those consolidated financial statements. In our opinion, the information set forth in the accompanying condensed consolidated balance sheet as of December 31, 2004, is fairly stated, in all material respects, in relation to the consolidated balance sheet from which it has been derived.

ERNST & YOUNG LLP

New Orleans, Louisiana

July 25, 2005

OVERVIEW

In management’s discussion and analysis, “we,”“us” and “our” refer to Freeport-McMoRan Copper & Gold Inc. (FCX) and its consolidated subsidiaries. References to “aggregate” amounts mean the total of our share and Rio Tinto plc’s share as our joint venture partner. You should read this discussion in conjunction with our financial statements, the related discussion and analysis of financial condition and results of operations and the discussion of our “Business and Properties” in our Form 10-K for the year ended December 31, 2004, filed with the Securities and Exchange Commission. The results of operations reported and summarized below are not necessarily indicative of future operating results.

We operate through our majority-owned subsidiaries, PT Freeport Indonesia and PT Puncakjaya Power (Puncakjaya Power), and through Atlantic Copper, S.A. (Atlantic Copper) and PT Irja Eastern Minerals (Eastern Minerals), our principal wholly owned subsidiaries. PT Freeport Indonesia, our principal operating subsidiary, conducts exploration, mining and production activities in a 24,700-acre area called Block A located in Papua, Indonesia. PT Freeport Indonesia also conducts exploration activities (which are currently suspended, but are under review for resumption) in an approximate 500,000-acre area called Block B in Papua. Puncakjaya Power’s sole business is to supply power to PT Freeport Indonesia’s operations. Our principal asset is the Grasberg minerals district, which contains the largest single gold reserve and the second-largest copper reserve of any mine in the world.

Atlantic Copper’s operations are in Spain and involve the smelting and refining of copper concentrates and the marketing of refined copper and precious metals in slimes. PT Freeport Indonesia owns a 25 percent interest in PT Smelting, an Indonesian company which operates a copper smelter and refinery in Gresik, Indonesia. Eastern Minerals conducts mineral exploration activities (which are currently suspended) in Papua, Indonesia.

We own 90.64 percent of PT Freeport Indonesia, of which 9.36 percent is owned through our wholly owned subsidiary, PT Indocopper Investama. The Government of Indonesia owns the remaining 9.36 percent of PT Freeport Indonesia. In July 2004, we received a request from the Indonesian Department of Energy and Mineral Resources that we offer to sell to Indonesian nationals shares in PT Indocopper Investama at fair market value. In response to this request and in view of the potential benefits of having additional Indonesian ownership in our project, we have agreed to consider a potential sale of an interest in PT Indocopper Investama at fair market value. Neither our Contract of Work nor Indonesian law requires us to divest any portion of our ownership interest in PT Freeport Indonesia or PT Indocopper Investama.

Outlook

Annual sales are expected to approximate 1.47 billion pounds of copper and 2.8 million ounces of gold in 2005, increases of nearly 50 percent for copper and nearly 100 percent for gold compared with 2004. Using estimated sales volumes for the remainder of 2005 and assuming prices of $1.40 per pound of copper and $420 per ounce of gold for the remainder of 2005, FCX estimates that it would generate operating cash flows in excess of $1.2 billion in 2005, with over $600 million in the second half of the year. Each $0.10 per pound change in copper prices in the balance of the year would affect 2005 cash flows by approximately $40 million and each $25 per ounce change in gold prices would affect cash flows by approximately $20 million.

PT Freeport Indonesia’s share of sales for 2006 are estimated to approximate 1.4 billion pounds of copper and 1.9 million ounces of gold. Average annual sales volumes over the next five years (2005 to 2009) are expected to approximate 1.35 billion pounds of copper and 2.2 million ounces of gold. Annual and quarterly sales volumes may vary from these estimates depending on the areas being mined within the Grasberg open pit. Based on these estimates of average annual sales volumes over the next five years and copper prices of approximately $1.40 per pound and gold prices of approximately $420 per ounce, the impact on our annual cash flow for each $0.10 per pound change in copper prices would approximate $69 million, including the effects of price changes on related royalty costs, and for each $25 per ounce change in gold prices would approximate $28 million.

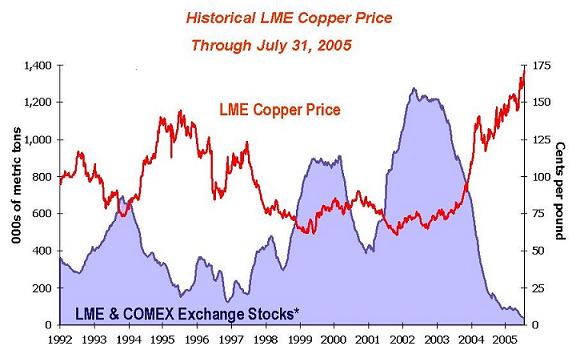

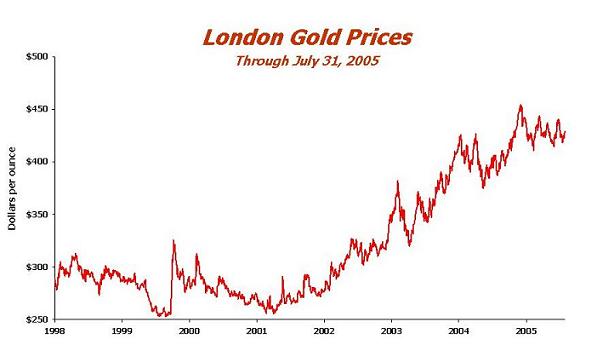

As shown in the graphs below, world metal prices for copper have fluctuated during the period from 1992 through July 2005 from a low of approximately $0.60 per pound in 2001 to a high of $1.71 per pound on July 29, 2005, and world gold prices have fluctuated during the period from 1998 through July 2005 from a low of approximately $250 per ounce in 1999 to a high of approximately $456 per ounce in 2004. Copper and gold prices are affected by numerous factors beyond our control as described further in our Form 10-K for the year ended December 31, 2004.

* Excludes Shanghai stocks, producer, consumer and merchant stocks.

The graph above presents London Metal Exchange (LME) copper prices and reported stocks of copper at the LME and New York Commodity Exchange (COMEX) through July 31, 2005. Market fundamentals for copper continued to be very positive in the first half of 2005. LME and COMEX inventories are at very low levels of less than 50,000 metric tons. Copper prices averaged $1.54 per pound in the second quarter of 2005, with prices ranging from $1.41 per pound to $1.66 per pound. The LME spot copper price closed at $1.71 per pound on July 29, 2005. As a result of continued low inventory levels, expectations of continued strong demand and limited supplies, the outlook for copper markets in 2005 is positive. Global demand in the first half of 2005 remained sufficiently strong to absorb increasing global production volumes. Most market analysts expect copper supplies to increase in the second half of 2005 as smelter capacity is projected to increase, and many project lower than current prices during the second half of 2005. Future copper prices will be determined by demand from China, economic performance in the United States (U.S.) and other industrialized countries, the timing of the development of new supplies of copper, production levels of mines and copper smelters and other factors. We consider the underlying supply and demand conditions in the global copper markets to be positive for our company.

Gold prices continue to be supported by a weak U.S. dollar, ongoing geopolitical tensions, growing investment demand for gold and actions by gold producers to reduce hedge positions. Gold prices averaged $427 per ounce in the second quarter of 2005, with prices ranging from $414 per ounce to $443 per ounce. The London gold price closed at approximately $429 per ounce on July 29, 2005.

CONSOLIDATED RESULTS

Summary comparative results for the second-quarter and six-month periods follow (in millions, except per share amounts):

| | Second Quarter | | Six Months | |

| | 2005 | | 2004 | | 2005 | | 2004 | |

| Revenues | $ | 902.9 | | $ | 486.3 | | $ | 1,706.0 | | $ | 846.5 | |

| Operating income | | 430.4 | | | 46.7 | | | 788.0 | | | 88.1 | |

| Net income (loss) applicable to common stock | | 175.2 | | | (53.3 | ) | | 305.6 | | | (72.9 | ) |

| Diluted net income (loss) per share of common stock | | 0.91 | | | (0.30 | ) | | 1.62 | | | (0.39 | ) |

Consolidated revenues include PT Freeport Indonesia’s sale of copper concentrates, which also contain significant quantities of gold and silver, and the sale by Atlantic Copper of copper anodes, copper cathodes, and gold in anodes and slimes. Consolidated revenues for the second quarter of 2005 and the first six months of 2005 were significantly higher than consolidated revenues for the 2004 periods, primarily reflecting substantially higher copper and gold sales volumes and prices than the 2004 periods. Second-quarter and six-month 2004 results were adversely affected by lower ore grades and reduced mill throughput as PT Freeport Indonesia completed its efforts to restore safe access to the higher-grade ore areas in its Grasberg open-pit mine following the fourth-quarter 2003 slippage and debris flow events. In addition, Atlantic Copper’s scheduled major maintenance turnaround adversely affected its 2004 revenues.

At June 30, 2005, we had consolidated embedded derivatives on copper sales totaling 272.5 million pounds recorded at an average price of $1.54 per pound. We expect final prices on these sales over the next several months. We estimate that a two-cent change in the average price used for these embedded derivatives and realized prices for these sales would have an approximate $5.5 million impact on our 2005 consolidated revenues and an approximate $3 million impact on our 2005 consolidated net income.

Second-quarter 2005 consolidated revenues included net additions of $12.6 million ($6.7 million to net income or $0.03 per share) primarily for final pricing of concentrates sold in prior quarters, compared with a net decrease of $5.6 million ($2.9 million to net income or $0.02 per share) to second-quarter 2004 revenues. Six-month 2005 consolidated revenues included net additions of $8.7 million ($4.6 million to net income or $0.02 per share) compared with $7.2 million ($3.7 million to net income or $0.02 per share), primarily for final pricing of concentrates sold in prior years.

Consolidated revenues and net income vary significantly with fluctuations in the market prices of copper and gold and other factors. Based on PT Freeport Indonesia’s projected share of copper sales for the remainder of 2005 (830 million pounds) and assuming an average price of $1.40 per pound of copper, each $0.01 per pound change in the average price realized in the balance of the year would have an approximate $8 million impact on our annual revenues and an approximate $4 million impact on our annual net income. A $5 per ounce change in the average price realized in the balance of the year on PT Freeport Indonesia’s projected share of gold sales for the remainder of 2005 (1.6 million ounces) would have an approximate $8 million impact on our annual revenues and an approximate $4 million impact on our annual net income.

On limited past occasions, in response to market conditions, we have entered into copper and gold price protection contracts for a portion of our expected future mine production to mitigate the risk of adverse price fluctuations. We currently have no copper or gold price protection contracts relating to our mine production. We have outstanding gold-denominated and silver-denominated preferred stock with dividends and redemption amounts determined by commodity prices.

Consolidated production and delivery costs were higher for the 2005 periods than the 2004 periods primarily because of higher production costs at PT Freeport Indonesia and higher costs of concentrate purchases at Atlantic Copper caused by increased production volumes and higher metals prices. Consolidated depreciation and amortization expense increased to $54.2 million in the second quarter of 2005 and $111.1 million in the first six months of 2005, compared with $42.6 million in the second quarter of 2004 and $68.0 million in the first six months of 2004, primarily because of higher copper sales volumes at PT Freeport Indonesia during the 2005 periods. Exploration expenses decreased to $2.3 million in the second quarter of 2005 and $4.3 million in the first six months of 2005 from $2.8 million in the second quarter of 2004 and $5.0 million in the first six months of 2004 (see “Mining and Exploration - Exploration Activities”). Consolidated general and administrative expenses increased to $25.4 million in the second quarter of 2005 and $47.0 million in the first six months of 2005 from $22.6 million in the second quarter of 2004 and $38.1 million in the first six months of 2004 (see “Other Financial Results”).

Net interest expense decreased to $35.3 million in the second quarter of 2005 from $39.3 million in the second quarter of 2004 primarily because we reduced average debt levels. Losses on early extinguishment and conversion of debt totaled $14.0 million ($13.7 million to net income or $0.07 per share) for the first six months of 2004 resulting primarily from the early conversions of our 8¼% Convertible Senior Notes (see “Capital Resources and Liquidity - Financing Activities”).

Other income (expense) includes the impact of translating into U.S. dollars Atlantic Copper’s net euro-denominated liabilities, primarily its retiree pension obligations. Changes in the U.S. dollar/euro exchange rate require us to adjust the dollar value of our net euro-denominated liabilities and record the adjustment in earnings. The exchange rate was $1.36 per euro at December 31, 2004, $1.30 per euro at March 31, 2005 and $1.21 per euro at June 30, 2005. Exchange rate effects on our net income from euro-denominated liabilities were gains (losses) of $3.4 million in the second quarter of 2005, $(0.2) million in the second quarter of 2004, $6.3 million in the first six months of 2005 and $1.8 million in the first six months of 2004. Other income also included interest income of $3.3 million in the second quarter of 2005, $1.8 million in the second quarter of 2004, $7.0 million in the first six months of 2005 and $3.2 million in the first six months of 2004.

PT Freeport Indonesia’s Contract of Work provides for a 35 percent corporate income tax rate. PT Indocopper Investama pays a 30 percent corporate income tax on dividends it receives from its 9.36 percent ownership in PT Freeport Indonesia. In addition, the tax treaty between Indonesia and the U.S. provides for a withholding tax rate of 10 percent on dividends and interest that PT Freeport Indonesia and PT Indocopper Investama pay to their parent company, FCX. Prior to 2005, we also incurred a U.S. alternative minimum tax at an effective rate of two percent based primarily on consolidated income, net of smelting and refining results. As a result of the enactment of the American Jobs Creation Act of 2004, the 90 percent limitation on the use of foreign tax credits to offset the U.S. federal alternative minimum tax liability has been repealed effective January 1, 2005. Based on current projections, we expect that the removal of this limitation will reduce our U.S. federal taxes beginning in 2005. In 2004, our U.S. federal alternative minimum tax liability totaled $8.2 million. We currently record no income taxes at Atlantic Copper, which is subject to taxation in Spain, because it has not generated significant taxable income in recent years and has substantial tax loss carryforwards for which we have provided no financial statement benefit. We receive no consolidated tax benefit from these losses because they cannot be used to offset PT Freeport Indonesia’s profits in Indonesia.

Parent company costs consist primarily of interest, depreciation and amortization, and general and administrative expenses. We receive minimal tax benefit from these costs, including interest expense, primarily because our parent company generates no taxable income from U.S. sources. As a result, our provision for income taxes as a percentage of our consolidated income before income taxes and minority interests will vary as PT Freeport Indonesia’s income changes, absent changes in Atlantic Copper and parent company costs. Summaries of the approximate significant components of the calculation of our consolidated provision for income taxes are shown below (in thousands, except percentages).

| | Three Months Ended | | Six Months Ended | |

| | June 30, | | June 30, | |

| | 2005 | | 2004 | | 2005 | | 2004 | |

Mining and exploration segment operating incomea | $ | 390,780 | | $ | 105,399 | | $ | 819,087 | | $ | 109,531 | |

| Mining and exploration segment interest expense, net | | (5,897 | ) | | (5,494 | ) | | (11,624 | ) | | (11,213 | ) |

| Intercompany operating profit (deferred) recognized | | 48,350 | | | (9,561 | ) | | (15,220 | ) | | 38,619 | |

| Income before taxes | | 433,233 | | | 90,344 | | | 792,243 | | | 136,937 | |

| Indonesian corporate income tax rate (35%) plus U.S. | | | | | | | | | | | | |

| alternative minimum tax rate (2%) for 2004 | | 35 | % | | 37 | % | | 35 | % | | 37 | % |

| Corporate income taxes | | 151,632 | | | 33,427 | | | 277,285 | | | 50,667 | |

| | | | | | | | | | | | | |

| Approximate PT Freeport Indonesia net income | | 281,601 | | | 56,917 | | | 514,958 | | | 86,270 | |

| Withholding tax on FCX’s equity share | | 9.064 | % | | 9.064 | % | | 9.064 | % | | 9.064 | % |

| Withholding taxes | | 25,524 | | | 5,159 | | | 46,676 | | | 7,820 | |

| | | | | | | | | | | | | |

| PT Indocopper Investama corporate income tax | | 6,957 | | | - | | | 21,081 | | | - | |

| Other, net | | 4,571 | | | (376 | ) | | 7,670 | | | (1,936 | ) |

| FCX consolidated provision for income taxes | $ | 188,684 | | $ | 38,210 | | $ | 352,712 | | $ | 56,551 | |

| | | | | | | | | | | | | |

| FCX consolidated effective tax rate | | 46 | % | | b | | | 48 | % | | b | |

| | | | | | | | | | | | | |

| a. | Excludes charges for FCX stock option exercises, which are eliminated in consolidation, totaling $0.7 million for the 2005 quarter, $2.2 million for the 2004 quarter, $17.4 million for the 2005 six-month period and $66.8 million for the 2004 six-month period. |

| b. | Rates are not meaningful given the small amounts of consolidated income before taxes and minority interests for the 2004 periods. |

RESULTS OF OPERATIONS

We have two operating segments: “mining and exploration” and “smelting and refining.” The mining and exploration segment consists of our Indonesian activities including PT Freeport Indonesia’s copper and gold mining operations, Puncakjaya Power’s power generating operations (after eliminations with PT Freeport Indonesia) and our Indonesian exploration activities, including those of Eastern Minerals. The smelting and refining segment includes Atlantic Copper’s operations in Spain and PT Freeport Indonesia’s equity investment in PT Smelting. Summary comparative operating income (loss) data by segment follow (in millions):

| | Second Quarter | | Six Months | |

| | 2005 | | 2004 | | 2005 | | 2004 | |

Mining and explorationa | $ | 390.1 | | $ | 103.2 | | $ | 801.6 | | $ | 42.7 | |

| Smelting and refining | | (0.1 | ) | | (40.0 | ) | | (1.6 | ) | | (50.9 | ) |

Intercompany eliminations and othera, b | | 40.4 | | | (16.5 | ) | | (12.0 | ) | | 96.3 | |

| FCX operating income | $ | 430.4 | | $ | 46.7 | | $ | 788.0 | | $ | 88.1 | |

| | | | | | | | | | | | | |

| a. | Includes charges to the mining and exploration segment for FCX stock option exercises, which are eliminated in consolidation, totaling $0.7 million in the 2005 quarter, $2.2 million in the 2004 quarter, $17.4 million for the 2005 six-month period and $66.8 million for the 2004 six-month period. |

| b. | We defer recognizing profits on PT Freeport Indonesia’s sales to Atlantic Copper and on 25 percent of PT Freeport Indonesia’s sales to PT Smelting until their sales of final products to third parties. Changes in the amount of these deferred profits impacted operating income by $48.3 million in the second quarter of 2005, $(9.6) million in the second quarter of 2004, $(15.2) million in the first six months of 2005 and $38.6 million in the first six months of 2004. Our consolidated earnings can fluctuate materially depending on the timing and prices of these sales. At June 30, 2005, our deferred profits to be recognized in future periods’ operating income totaled $96.1 million, $50.5 million to net income, after taxes and minority interest sharing. |

MINING AND EXPLORATION

PT Freeport Indonesia Operating Results

| | | | Second Quarter | | Six Months | |

| | | | 2005 | | 2004 | | 2005 | | 2004 | |

PT Freeport Indonesia Operating Data, Net of Rio Tinto’s Interest | | | | | | |

| Copper (recoverable) | | | | | | | | | | |

| Production (000s of pounds) | | | 302,300 | | 209,300 | | 637,900 | | 316,400 | |

| Production (metric tons) | | | 137,100 | | 94,900 | | 289,300 | | 143,500 | |

| Sales (000s of pounds) | | | 313,700 | | 205,100 | | 641,800 | | 310,500 | |

| Sales (metric tons) | | | 142,300 | | 93,000 | | 291,100 | | 140,800 | |

| Average realized price per pound | | | $1.53 | | $1.22 | | $1.54 | | $1.24 | |

| Gold (recoverable ounces) | | | | | | | | | | |

| Production | | | 591,300 | | 364,900 | | 1,200,700 | | 490,200 | |

| Sales | | | 616,400 | | 351,100 | | 1,211,700 | | 474,900 | |

| Average realized price per ounce | | | $428.23 | | $389.97 | | $427.54 | | $393.80 | |

| | | | | | | | | | | |

PT Freeport Indonesia, 100% Aggregate Operating Data | | | | | | | | |

| Ore milled (metric tons per day) | | | 211,800 | | 164,200 | | 205,600 | | 158,000 | |

| Average ore grade | | | | | | | | | | |

| Copper (percent) | | | .98 | | .82 | | 1.06 | | .67 | |

| Gold (grams per metric ton) | | | 1.43 | | .95 | | 1.52 | | .69 | |

| Recovery rates (percent) | | | | | | | | | | |

| Copper | | | 87.4 | | 88.2 | | 88.5 | | 86.6 | |

| Gold | | | 83.8 | | 84.6 | | 83.3 | | 81.5 | |

| Copper (recoverable) | | | | | | | | | | |

| Production (000s of pounds) | | | 349,200 | | 229,000 | | 739,500 | | 347,900 | |

| Production (metric tons) | | | 158,400 | | 103,900 | | 335,400 | | 157,800 | |

| Sales (000s of pounds) | | | 362,500 | | 224,100 | | 743,900 | | 340,900 | |

| Sales (metric tons) | | | 164,400 | | 101,600 | | 337,400 | | 154,600 | |

| Gold (recoverable ounces) | | | | | | | | | | |

| Production | | | 727,400 | | 383,600 | | 1,491,300 | | 514,900 | |

| Sales | | | 758,600 | | 369,600 | | 1,501,800 | | 499,700 | |

Mill throughput, which varies depending on ore types being processed, averaged 211,800 metric tons of ore per day in the second quarter of 2005, 164,200 metric tons of ore in the second quarter of 2004, 205,600 metric tons of ore in the first six months of 2005 and 158,000 metric tons of ore in the first six months of 2004. Mill rates in the second quarter of 2005 were impacted by unplanned downtime for mill maintenance activities during late June and the processing of hard ore. Mill rates are projected to average in excess of 220,000 metric tons of ore per day during the remainder of 2005. Approximate average daily throughput processed at our mill facilities from each of our producing mines follows (metric tons of ore per day):

| | Second Quarter | | Six Months | |

| | 2005 | | 2004 | | 2005 | | 2004 | |

| Grasberg open pit | 169,500 | | 118,700 | | 163,400 | | 112,600 | |

| Deep Ore Zone underground mine | 42,300 | | 45,500 | | 42,200 | | 45,400 | |

| Total mill throughput | 211,800 | | 164,200 | | 205,600 | | 158,000 | |

| | | | | | | | | |

Second-quarter 2005 copper ore grades averaged 0.98 percent, compared with 0.82 percent for the second quarter of 2004. Second-quarter copper recovery rates were 87.4 percent, compared with 88.2 percent for the second quarter of 2004. For the second quarter of 2005, gold ore grades averaged 1.43 grams per metric ton (g/t), compared with 0.95 g/t for the second quarter of 2004. Gold recovery rates averaged 83.8 percent for the second quarter of 2005, compared with 84.6 percent for the second quarter of 2004. The 2005 grades reflect the return to normal mining operations at Grasberg, including accessing higher grade material.

Production from the Deep Ore Zone (DOZ) underground mine averaged 42,300 metric tons of ore per day in the second quarter of 2005, representing 20 percent of mill throughput as it continued to perform above design capacity of 35,000 metric tons of ore per day. PT Freeport Indonesia is expanding the capacity of the DOZ underground operation to a sustained rate of 50,000 metric tons per day with the installation of a second crusher and additional ventilation, which are expected to be completed by 2007. PT Freeport Indonesia’s share of capital expenditures for the DOZ expansion totaled $5.5 million in the first half of 2005 and are expected to approximate $37 million through the projected 2007 ramp-up, with approximately $12 million estimated for the remainder of 2005. The DOZ mine, a block cave operation, is one of the world’s largest underground mines.

In 2004, PT Freeport Indonesia commenced its “Common Infrastructure” project, which will provide access to its large undeveloped underground ore bodies located in the Grasberg minerals district through a tunnel system located approximately 400 meters deeper than its existing underground tunnel system. PT Freeport Indonesia’s share of capital expenditures for its Common Infrastructure project totaled $8.9 million in the first half of 2005 and is estimated to total approximately $8 million for the remainder of 2005. The Common Infrastructure project is progressing according to plan.

PT Freeport Indonesia is also proceeding with plans to develop Big Gossan, a high-grade deposit located near the existing milling complex. Our Board of Directors has approved this project and aggregate capital expenditures from 2006 to 2009 for Big Gossan are expected to total approximately $225 million ($195 million net to PT Freeport Indonesia, with approximately $50 million in 2006). Production is expected to ramp up to 7,000 metric tons per day by 2010 (average annual aggregate incremental production of 135 million pounds of copper and 65,000 ounces of gold, with PT Freeport Indonesia receiving 60 percent of these amounts). The Big Gossan mine is expected to be an open-stope mine with cemented backfill, which is a higher-cost mining method than the block-cave method used at the DOZ mine.

PT Freeport Indonesia Revenues

A summary of changes in PT Freeport Indonesia revenues between the periods follows (in millions):

| | Second | | Six | |

| | Quarter | | Months | |

| PT Freeport Indonesia revenues - prior year period | $ | 330.8 | | $ | 518.0 | |

| Sales volumes: | | | | | | |

| Copper | | 132.5 | | | 409.5 | |

| Gold | | 103.5 | | | 290.2 | |

| Price realizations: | | | | | | |

| Copper | | 98.5 | | | 196.4 | |

| Gold | | 23.6 | | | 40.9 | |

| Adjustments, primarily for copper pricing on prior period open sales | | 22.7 | | | (1.4 | ) |

| Treatment charges, royalties and other | | (33.2 | ) | | (87.8 | ) |

| PT Freeport Indonesia revenues - current year period | $ | 678.4 | | $ | 1,365.8 | |

| | | | | | | |

PT Freeport Indonesia achieved significantly higher production and sales in the 2005 periods compared with the 2004 periods, reflecting higher ore grades and milling rates than the 2004 periods. Copper sales volumes totaled 313.7 million pounds in the second quarter of 2005, 53 percent higher than the 205.1 million pounds reported in the second quarter of 2004. Second-quarter 2005 copper price realizations of $1.53 per pound were $0.31 per pound higher than the second-quarter 2004 realizations of $1.22 per pound. Gold sales volumes totaled 616,400 ounces in the second quarter of 2005, 76 percent higher than the 351,100 ounces reported in the second quarter of 2004. Gold price realizations of $428.23 per ounce in the second quarter of 2005 were over $38 an ounce higher than second-quarter 2004 realizations of $389.97 per ounce. For the six-month periods, copper sales volumes totaled 641.8 million pounds in 2005, more than double the 310.5 million pounds in 2004, and gold sales volumes totaled 1,211,700 ounces, more than two and one half times higher than the 474,900 ounces in 2004. Copper price realizations of $1.54 per pound in the first six months of 2005 were $0.30 per pound higher than the 2004 period realizations of $1.24 per pound. Gold price realizations of $427.54 per ounce in the first six months of 2005 were almost $34 an ounce higher than 2004 period realizations of $393.80 per ounce.

Treatment charges vary with the volume of metals sold and the price of copper, and royalties vary with the volume of metals sold and the prices of copper and gold. In addition, treatment charges vary based on PT Freeport Indonesia’s customer mix as sales to PT Smelting are subject to a minimum rate (see below). Market rates for treatment and refining charge rates began to increase significantly in late 2004; however, PT Freeport Indonesia expects its 2005 rates to approximate its 2004 rates because of its customer mix.

Royalties totaled $17.7 million in the second quarter of 2005 and $36.5 million in the first six months of 2005 compared with $7.9 million in the second quarter of 2004 and $12.7 million in the first six months of 2004, reflecting higher sales volumes and metal prices.

Substantially all of PT Freeport Indonesia’s concentrate sales contracts provide final copper pricing in a specified future period based on prices quoted on the LME. PT Freeport Indonesia records revenues and invoices its customers based on LME prices at the time of shipment. Under accounting rules, these terms create an “embedded derivative” in our concentrate sales contracts which must be adjusted to fair value through earnings each period until the date of final copper pricing. PT Freeport Indonesia’s second-quarter 2005 revenues include net additions of $13.7 million for adjustments to the fair value of embedded copper derivatives in concentrate sales contracts, compared with net reductions of $15.8 million in the second quarter of 2004. PT Freeport Indonesia’s six-month 2005 revenues included net additions of $22.2 million for adjustments to the fair value of embedded derivatives in concentrate sales contracts, compared with net reductions of $0.8 million in the 2004 period.

PT Freeport Indonesia has revised its mine plans to incorporate second-quarter results and to reflect updated sequencing plans in the Grasberg open pit. PT Freeport Indonesia expects its share of sales to approximate 1.47 billion pounds of copper and 2.8 million ounces of gold for 2005. At the Grasberg mine, the sequencing in mining areas with varying ore grades causes fluctuations in the timing of ore production, which impacts sales volumes, particularly for gold. Second-half 2005 sales volumes are expected to be 29 percent higher for copper and 32 percent higher for gold than during the first half of the year. PT Freeport Indonesia expects its sales for the third quarter of 2005 to approximate 380 million pounds of copper and 575 thousand ounces of gold, with sales of 450 million pounds of copper and 1,025 thousand ounces of gold for the fourth quarter of 2005. PT Freeport Indonesia estimates its share of sales for 2006 to approximate 1.4 billion pounds of copper and 1.9 million ounces of gold, and average annual sales for the period 2005 - 2009 to approximate 1.35 billion pounds of copper and 2.2 million ounces of gold.

PT Freeport Indonesia has long-term contracts to provide approximately 60 percent of Atlantic Copper’s copper concentrate requirements at market prices and nearly all of PT Smelting’s copper concentrate requirements. Under the PT Smelting contract, for the first 15 years of PT Smelting’s operations beginning December 1998, the treatment and refining charges on the majority of the concentrate PT Freeport Indonesia provides will not fall below specified minimum rates, subject to renegotiation in 2008. The rate was $0.23 per pound during the period from the commencement of PT Smelting’s operations in 1998 until April 2004, when it declined to a minimum of $0.21 per pound. Market rates for 2005, excluding price participation, under long-term contracts settled in late 2004 approximate $0.21 per pound. Including price participation at current copper prices of approximately $1.70 per pound, PT Smelting’s rates exceed the minimum $0.21 per pound. Taking into account taxes and minority interest, an equivalent change in smelting and refining charge rates would essentially offset in our consolidated operating results.

PT Freeport Indonesia Costs

Gross profit per pound of copper (¢)/per ounce of gold and silver ($): | | | | |

Three Months Ended June 30, 2005 | | | | | | | | | | | | |

| Pounds of copper sold (000s) | | 313,700 | | | 313,700 | | | | | | | |

| Ounces of gold sold | | | | | | | | 616,400 | | | | |

| Ounces of silver sold | | | | | | | | | | | 1,057,700 | |

| | | | | | | | | | | | | |

| | | By-Product | | | Co-Product Method | |

| | | Method | | | Copper | | | Gold | | | Silver | |

| Revenues, after adjustments shown below | | 153.4 | ¢ | | 153.4 | ¢ | | $428.23 | | | $7.04 | |

| | | | | | | | | | | | | |

| Site production and delivery, before net non- | | | | | | | | | | | | |

| cash and nonrecurring costs shown below | | 70.5 | a | | 45.0 | b | | 126.01 | b | | 2.06 | b |

| Gold and silver credits | | (86.5 | ) | | - | | | - | | | - | |

| Treatment charges | | 21.6 | | | 13.8 | | | 38.68 | | | 0.63 | |

| Royalty on metals | | 5.7 | | | 3.6 | | | 10.11 | | | 0.17 | |

Unit net cash costsc | | 11.3 | | | 62.4 | | | 174.80 | | | 2.86 | |

| Depreciation and amortization | | 14.1 | | | 9.0 | | | 25.20 | | | 0.41 | |

| Noncash and nonrecurring costs, net | | 0.7 | | | 0.5 | | | 1.30 | | | 0.02 | |

| Total unit costs | | 26.1 | | | 71.9 | | | 201.30 | | | 3.29 | |

| Revenue adjustments, primarily for pricing | | | | | | | | | | | | |

| on prior period open sales | | 3.7 | | | 3.6 | | | 0.12 | | | (0.03 | ) |

| PT Smelting intercompany profit elimination | | 0.8 | | | 0.5 | | | 1.45 | | | 0.02 | |

| Gross profit per pound/ounce | | 131.8 | ¢ | | 85.6 | ¢ | | $228.50 | | | $3.74 | |

| | | | | | | | | | | | | |

Three Months Ended June 30, 2004 | | | | | | | | | | | | |

| Pounds of copper sold (000s) | | 205,100 | | | 205,100 | | | | | | | |

| Ounces of gold sold | | | | | | | | 351,100 | | | | |

| Ounces of silver sold | | | | | | | | | | | 824,900 | |

| | | | | | | | | | | | | |

| | | By-Product | | | Co-Product Method | |

| | | Method | | | Copper | | | Gold | | | Silver | |

| Revenues, after adjustments shown below | | 122.0 | ¢ | | 122.0 | ¢ | | $389.97 | | | $6.15 | |

| | | | | | | | | | | | | |

| Site production and delivery, before net non- | | | | | | | | | | | | |

| cash and nonrecurring costs shown below | | 84.0 | d | | 53.8 | e | | 170.37 | e | | 2.64 | e |

| Gold and silver credits | | (68.8 | ) | | - | | | - | | | - | |

| Treatment charges | | 21.2 | | | 13.6 | | | 42.90 | | | 0.66 | |

| Royalty on metals | | 3.8 | | | 2.5 | | | 7.78 | | | 0.12 | |

Unit net cash costsc | | 40.2 | | | 69.9 | | | 221.05 | | | 3.42 | |

| Depreciation and amortization | | 16.3 | | | 10.4 | | | 33.03 | | | 0.51 | |

| Noncash and nonrecurring costs, net | | 1.4 | | | 0.9 | | | 2.84 | | | 0.04 | |

| Total unit costs | | 57.9 | | | 81.2 | | | 256.92 | | | 3.97 | |

| Revenue adjustments, primarily for pricing | | | | | | | | | | | | |

| on prior period open sales | | (4.5 | ) | | (4.4 | ) | | (2.29 | ) | | (0.15 | ) |

| PT Smelting intercompany profit elimination | | (5.0 | ) | | (3.2 | ) | | (10.15 | ) | | (0.16 | ) |

| Gross profit per pound/ounce | | 54.6 | ¢ | | 33.2 | ¢ | | $120.61 | | | $1.87 | |

| | | | | | | | | | | | | |

| a. | Net of deferred mining costs totaling $20.6 million or 6.6¢ per pound. Upon adoption of Emerging Issues Task Force (EITF) Issue No. 04-6 (see Note 1 of Notes to Consolidated Financial Statements), mining costs will no longer be deferred. |

| b. | Net of deferred mining costs totaling $13.2 million or 4.2¢ per pound for copper, $7.2 million or $11.74 per ounce for gold and $0.2 million or $0.19 per ounce for silver. See Note a above. |

| c. | For a reconciliation of unit net cash costs to production and delivery costs applicable to sales reported in FCX’s consolidated financial statements refer to “Product Revenues and Production Costs” below. |

| d. | Net of deferred mining costs totaling $31.5 million or 15.4¢ per pound. See Note a above. |

| e. | Net of deferred mining costs totaling $20.2 million or 9.8¢ per pound for copper, $10.9 million or $31.14 per ounce for gold and $0.4 million or $0.48 per ounce for silver. See Note a above. |

Gross profit per pound of copper (¢)/per ounce of gold and silver ($): | | | | |

Six Months Ended June 30, 2005 | | | | | | | | | | | | |

| Pounds of copper sold (000s) | | 641,800 | | | 641,800 | | | | | | | |

| Ounces of gold sold | | | | | | | | 1,211,700 | | | | |

| Ounces of silver sold | | | | | | | | | | | 2,328,000 | |

| | | | | | | | | | | | | |

| | | By-Product | | | Co-Product Method | |

| | | Method | | | Copper | | | Gold | | | Silver | |

| Revenues, after adjustments shown below | | 154.2 | ¢ | | 154.2 | ¢ | | $427.54 | | | $7.02 | |

| | | | | | | | | | | | | |

| Site production and delivery, before net non- | | | | | | | | | | | | |

| cash and nonrecurring costs shown below | | 64.6 | a | | 42.1 | b | | 115.39 | b | | 1.92 | b |

| Gold and silver credits | | (82.8 | ) | | - | | | - | | | - | |

| Treatment charges | | 21.7 | | | 14.2 | | | 38.80 | | | 0.65 | |

| Royalty on metals | | 5.7 | | | 3.7 | | | 10.17 | | | 0.17 | |

Unit net cash costsc | | 9.2 | | | 60.0 | | | 164.36 | | | 2.74 | |

| Depreciation and amortization | | 14.2 | | | 9.3 | | | 25.38 | | | 0.42 | |

| Noncash and nonrecurring costs, net | | 0.4 | | | 0.3 | | | 0.78 | | | 0.01 | |

| Total unit costs | | 23.8 | | | 69.6 | | | 190.52 | | | 3.17 | |

| Revenue adjustments, primarily for pricing | | | | | | | | | | | | |

| on prior period open sales | | 3.2 | | | 3.3 | | | (2.47 | ) | | 0.06 | |

| PT Smelting intercompany profit elimination | | - | | | - | | | (0.01 | ) | | - | |

| Gross profit per pound/ounce | | 133.6 | ¢ | | 87.9 | ¢ | | $234.54 | | | $3.91 | |

| | | | | | | | | | | | | |

Six Months Ended June 30, 2004 | | | | | | | | | | | | |

| Pounds of copper sold (000s) | | 310,500 | | | 310,500 | | | | | | | |

| Ounces of gold sold | | | | | | | | 474,900 | | | | |

| Ounces of silver sold | | | | | | | | | | | 1,378,200 | |

| | | | | | | | | | | | | |

| | | By-Product | | | Co-Product Method | |

| | | Method | | | Copper | | | Gold | | | Silver | |

| Revenues, after adjustments shown below | | 123.6 | ¢ | | 123.6 | ¢ | | $393.80 | | | $6.14 | |

| | | | | | | | | | | | | |

| Site production and delivery, before net non- | | | | | | | | | | | | |

| cash and nonrecurring costs shown below | | 104.2 | d | | 69.3 | e | | 218.23 | e | | 3.51 | e |

| Gold and silver credits | | (63.1 | ) | | - | | | - | | | - | |

| Treatment charges | | 21.7 | | | 14.4 | | | 45.46 | | | 0.73 | |

| Royalty on metals | | 4.1 | | | 2.7 | | | 8.58 | | | 0.14 | |

Unit net cash costsc | | 66.9 | | | 86.4 | | | 272.27 | | | 4.38 | |

| Depreciation and amortization | | 16.3 | | | 10.8 | | | 34.13 | | | 0.55 | |

| Noncash and nonrecurring costs, net | | 1.0 | | | 0.6 | | | 2.00 | | | 0.03 | |

| Total unit costs | | 84.2 | | | 97.8 | | | 308.40 | | | 4.96 | |

| Revenue adjustments, primarily for pricing | | | | | | | | | | | | |

| on prior period open sales | | 6.0 | | | 5.8 | | | 0.62 | | | 0.20 | |

| PT Smelting intercompany profit elimination | | (0.6 | ) | | (0.4 | ) | | (1.32 | ) | | (0.02 | ) |

| Gross profit per pound/ounce | | 44.8 | ¢ | | 31.2 | ¢ | | $84.70 | | | $1.36 | |

| | | | | | | | | | | | | |

| a. | Net of deferred mining costs totaling $52.8 million or 8.2¢ per pound. Upon adoption of EITF Issue No. 04-6 (see Note 1 of Notes to Consolidated Financial Statements), mining costs will no longer be deferred. |

| b. | Net of deferred mining costs totaling $34.4 million or 5.4¢ per pound for copper, $17.8 million or $14.70 per ounce for gold and $0.6 million or $0.25 per ounce for silver. See Note a above. |