Exhibit 99.4

2012

British Columbia

Financial and Economic

Review

72nd Edition

(July 2012)

| Ministry of Finance |

2012 Financial and Economic Review — July 2012

Table of Contents

Chapter One — Economic Review | 1 |

2011 Overview | 3 |

British Columbia Economy | 3 |

External Trade and Commodity Prices | 4 |

Population | 6 |

Labour and Income Developments | 7 |

Inflation | 7 |

Consumer Expenditure and Housing | 8 |

Tourism | 9 |

External Environment | 9 |

United States Economy | 9 |

Canadian Economy | 10 |

International Economy | 10 |

Financial Markets | 11 |

Conclusion | 12 |

| |

Charts | |

1.1 | Provincial economic growth | 3 |

1.2 | British Columbia real GDP by industry | 4 |

1.3 | Export shares by market | 5 |

1.4 | Lumber and natural gas prices | 6 |

1.5 | Retail sales | 8 |

1.6 | Visitor entries to British Columbia | 9 |

1.7 | External economic growth | 11 |

1.8 | Canadian dollar | 12 |

Map 1.1 Net interprovincial and international migration in BC, 2011 | 6 |

| | |

Tables | |

1.1 | British Columbia Population and Labour Market Statistics | 7 |

1.2 | Price and Earnings Indices | 8 |

| | |

Appendix 1 — Economic Review | 13 |

| | |

Tables | |

A1.1A | Aggregate and Labour Market Indicators | 14 |

A1.1B | Prices, Earnings and Financial Indicators | 15 |

A1.1C | Other Indicators | 16 |

A1.1D | Commodity Production Indicators | 17 |

A1.2 | British Columbia Real GDP at Market Prices, Expenditure Based | 18 |

A1.3 | British Columbia GDP at Basic Prices, by Industry | 19 |

A1.4 | British Columbia GDP, Income Based | 20 |

A1.5 | Employment by Industry in British Columbia | 21 |

A1.6 | Capital Investment by Industry | 22 |

A1.7 | British Columbia International Goods Exports by Major Market and Selected Commodities, 2011 | 23 |

A1.8 | British Columbia International Goods Exports by Market Area | 24 |

A1.9 | Historical Commodity Prices (in U.S. Dollars) | 25 |

A1.10 | British Columbia Forest Sector Economic Activity Indicators | 26 |

A1.11 | Historical Value of Mineral, Petroleum and Natural Gas Shipments | 27 |

A1.12 | Petroleum and Natural Gas Activity Indicators | 27 |

2012 Financial and Economic Review — July 2012

i

Table of Contents

A1.13 | Supply and Consumption of Electrical Energy in British Columbia | 28 |

A1.14 | Components of British Columbia Population Change | 29 |

| |

Chapter Two — Financial Review | 31 |

2011/12 Overview | 33 |

Revenue | 34 |

Expense | 40 |

Provincial Capital Spending | 42 |

Taxpayer-supported Capital Spending | 43 |

Self-supported Capital Spending | 46 |

Financing Capital Spending | 46 |

Provincial Debt | 47 |

Taxpayer-supported Debt | 48 |

Self-supported Debt | 49 |

Debt Indicators | 50 |

Credit Rating | 51 |

Statement of Financial Position | 51 |

Unfunded Pension Liabilities | 53 |

| |

Topic Box | |

Review of the Province’s Financial Condition | 55 |

| |

Charts | |

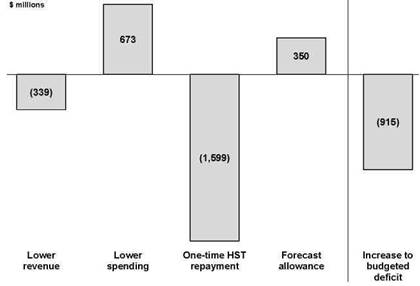

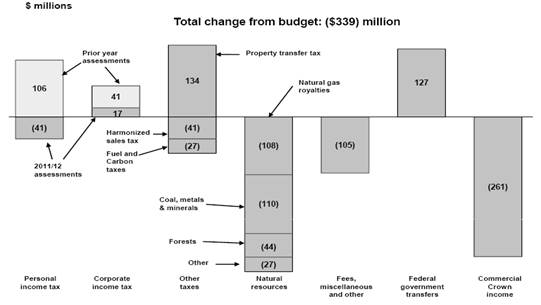

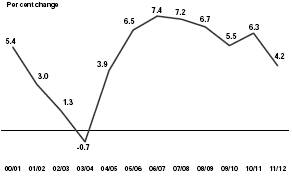

2.1 | 2011/12 deficit — major changes from Budget 2011 | 34 |

2.2 | Revenue changes from Budget 2011 | 34 |

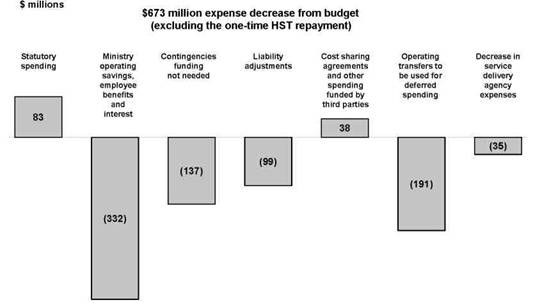

2.3 | Expense changes from Budget 2011 | 40 |

2.4 | Capital spending, 2011/12 | 42 |

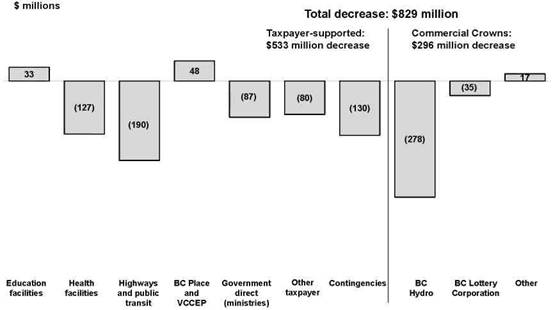

2.5 | Capital spending changes from Budget 2011 | 42 |

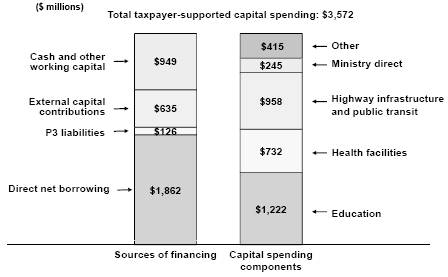

2.6 | Financing taxpayer-supported capital spending | 47 |

2.7 | Provincial debt components | 47 |

2.8 | Debt changes from Budget 2011 | 48 |

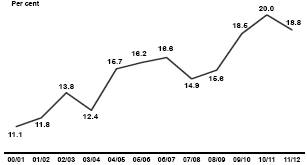

2.9 | Taxpayer-supported debt to GDP ratio | 48 |

2.10 | 2011/12 changes in financial position | 52 |

| |

Tables | |

2.1 | Operating Statement | 33 |

2.2 | Consumption and Other Tax Revenues Change from Budget 2011 | 35 |

2.3 | Energy and Mineral Revenues Change from Budget 2011 | 36 |

2.4 | Forest Revenues Change from Budget 2011 | 36 |

2.5 | Other Revenue Change from Budget 2011 | 36 |

2.6 | Revenue by Source | 38 |

2.7 | Expense by Ministry, Program and Agency | 39 |

2.8 | Capital Spending | 43 |

2.9 | Capital Expenditure Projects Greater Than $50 Million | 44 |

2.10 | Provincial Debt Summary | 49 |

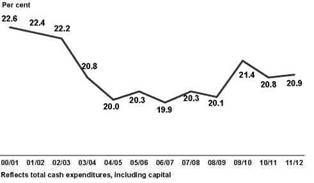

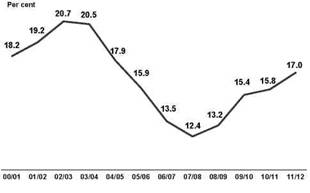

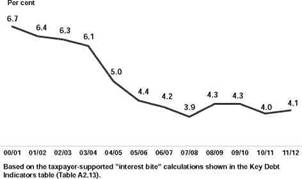

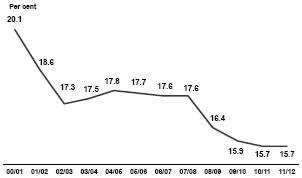

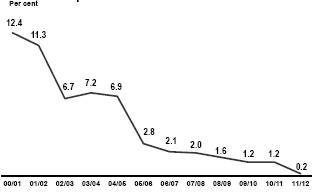

2.11 | Key Debt Indicators — 2007/08 to 2011/12 | 50 |

2.12 | Interprovincial Comparison of Credit Ratings, July 2012 | 51 |

2.13 | Net Liabilities and Accumulated Surplus | 51 |

2.14 | Pension Plan Balances | 53 |

2012 Financial and Economic Review — July 2012

ii

Table of Contents

Appendix 2 — Financial Review | 61 |

| |

Government’s Financial Statements | 63 |

Government Reporting Entity | 63 |

Compliance with GAAP | 63 |

2011/12 Public Accounts Audit Qualification | 64 |

| |

Supplementary Schedules | 65 |

| |

Tables | |

A2.1 | 2011/12 Forecasts – Year in Review | 66 |

A2.2 | Operating Statement – 2000/01 to 2011/12 | 67 |

A2.3 | Statement of Financial Position – 2000/01 to 2011/12 | 68 |

A2.4 | Changes in Financial Position – 2001/02 to 2011/12 | 69 |

A2.5 | Revenue by Source – 2000/01 to 2011/12 | 70 |

A2.6 | Revenue by Source Supplementary Information – 2000/01 to 2011/12 | 71 |

A2.7 | Expense by Function – 2000/01 to 2011/12 | 72 |

A2.8 | Expense by Function Supplementary Information – 2000/01 to 2011/12 | 73 |

A2.9 | Full-Time Equivalents (FTEs) – 2000/01 to 2011/12 | 74 |

A2.10 | Capital Spending – 2000/01 to 2011/12 | 75 |

A2.11 | Provincial Debt – 2000/01 to 2011/12 | 76 |

A2.12 | Provincial Debt Supplementary Information – 2000/01 to 2011/12 | 77 |

A2.13 | Key Provincial Debt Indicators – 2000/01 to 2011/12 | 78 |

A2.14 | Historical Operating Statement Surplus (Deficit) | 79 |

A2.15 | Historical Provincial Debt Summary | 80 |

| | |

Chapter Three — Commercial Crown Corporations Review | 81 |

| |

Introduction | 83 |

| |

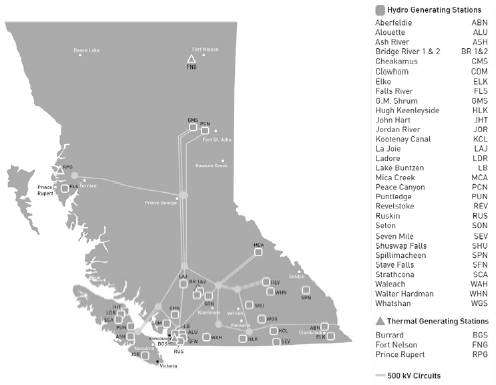

BC Hydro and Power Authority | 83 |

| |

BC Liquor Distribution Branch | 87 |

| |

BC Lottery Corporation | 89 |

| |

Insurance Corporation of BC | 92 |

| |

Columbia Power Corporation | 95 |

| |

Transportation Investment Corporation | 97 |

| |

BC Railway Company | 98 |

| |

Charts | |

3.1 | Domestic electricity supply versus demand | 85 |

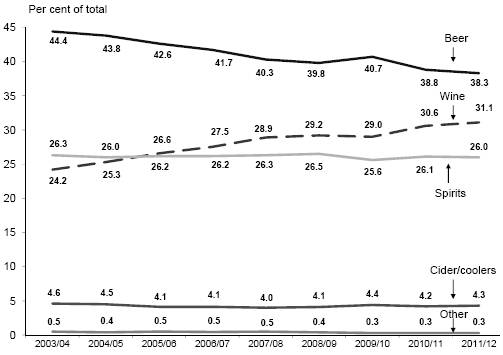

3.2 | Liquor sales by category | 88 |

3.3 | Interprovincial gaming comparisons | 91 |

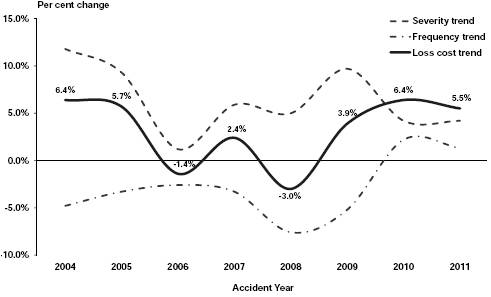

3.4 | ICBC bodily injury claims loss cost trend | 94 |

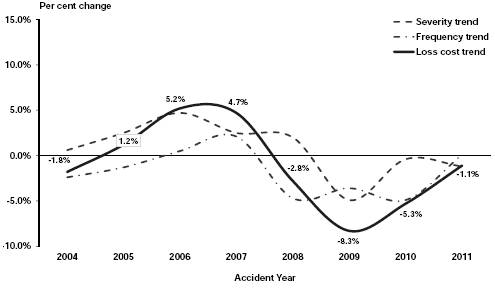

3.5 | ICBC collision claims loss cost trend | 95 |

Map 3.1 500 kV transmission system and major generating stations | 84 |

| |

Tables | |

3.1 | British Columbia Hydro and Power Authority Five-Year Income Statement | 86 |

3.2 | Liquor Distribution Branch Five-Year Income Statement | 87 |

3.3 | British Columbia Lottery Corporation Five-Year Income Statement | 90 |

3.4 | Insurance Corporation of British Columbia Five-Year Income Statement | 93 |

2012 Financial and Economic Review — July 2012

iii

Table of Contents

3.5 | Columbia Power Corporation Five-Year Income Statement | 96 |

3.6 | Transportation Investment Corporation Five-Year Income Statement | 97 |

3.7 | British Columbia Railway Company Five-Year Income Statement | 98 |

| |

Chapter 4 — Supplementary Information | 101 |

| |

General Description of the Province | 102 |

Geography | 102 |

Physiography | 102 |

Climate and Vegetation | 102 |

Population | 103 |

| |

Constitutional Framework | 103 |

| |

Provincial Government | 104 |

| |

Legislature | 104 |

Executive | 104 |

Judiciary | 105 |

Provincial Government Jurisdiction | 105 |

| |

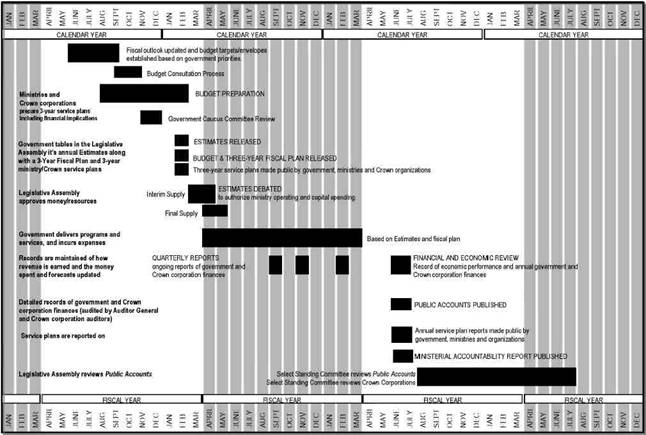

The Annual Financial Cycle | 106 |

Planning and Budget Preparation | 107 |

Implementation and Reporting | 107 |

Evaluation | 107 |

Accountability | 107 |

| |

Summary of Tax Changes Announced in 2012 | 108 |

| |

Charts | |

4.1 | Financial Planning and Reporting Cycle Overview | 106 |

| | |

Tables | |

4.1 | Provincial Taxes (as of July 2012) | 115 |

4.2 | Interprovincial Comparisons of Tax Rates — 2012 | 120 |

2012 Financial and Economic Review — July 2012

iv

| Chapter One |

| |

| Economic Review (1) |

(1) Reflects information available at July 9, 2012

2012 Financial and Economic Review — July 2012

Chapter 1 — Economic Review

2011 Overview

In 2011, British Columbia’s economy performed well relative to most other Canadian provinces, with gains over 2010 in several major indicators.

Similar to last year, Statistics Canada only published real dollar industry-side GDP data in the preliminary release of its Provincial Economic Accounts in April 2012. As a result, the following analysis refers to real GDP figures at basic prices, as opposed to the usual market price definition.

BC’s economy grew by 2.9 per cent in 2011 (third highest among provinces), slightly lower than the 3.2 per cent growth observed in 2010. Despite some slowing in the latter part of the year, most indicators of economic performance through 2011 showed improvement relative to the previous year.

Chart 1.1 Provincial Economic Growth

Source: Statistics Canada, April 2012 Preliminary Industry Accounts

Externally, BC’s international merchandise exports fared well in 2011, increasing by 14.0 per cent over 2010. Shipments of manufactured goods also made strong gains in 2011, growing by 6.5 per cent on the year.

Domestically, BC housing starts fell slightly in 2011, dropping 0.3 per cent to average 26,400 annualized units for the year. Retail sales, however, climbed by 3.1 per cent, despite a drop in confidence among consumers.

British Columbia Economy(2)

BC’s real GDP grew by 2.9 per cent in 2011, after expanding by 3.2 per cent in 2010.

The improvement in 2011 reflects the BC economy’s continued recovery from the 2008/2009 recession, with annual gains in both the service-producing as well as goods-producing industries. Output in the province’s service-producing sectors increased by 2.0 per cent in 2011, down slightly from the 2.2 per cent rise recorded in 2010.

(2) Provincial and National real GDP estimates are based on Statistics Canada’s preliminary industry accounts, released in April 2012. Further information on British Columbia’s economic performance will be available in November 2012, when Statistics Canada releases revised GDP data for 2011 and previous years for the full income and expenditure accounts, including nominal data.

2012 Financial and Economic Review — July 2012

3

Chapter 1 — Economic Review

On the services side, notable real GDP growth was recorded in the transportation and warehousing sector (+4.1 per cent), finance, insurance and real estate sector (+3.2 per cent) and health care and social assistance sector (+1.9 per cent). At the same time, growth in BC’s goods-producing industries jumped 5.6 per cent in 2011, following a 6.8 per cent increase during the previous year. Major gains in 2011 were observed in construction (+6.7 per cent), mining, oil and gas extraction (+6.0 per cent) and manufacturing (+3.1 per cent).

Chart 1.2 British Columbia real GDP by industry

Source: Statistics Canada, April 2012 Preliminary Industry Accounts

External Trade and Commodity Prices

Exports by destination:

BC’s merchandise exports climbed 14.0 per cent in 2011, an even higher rate of growth than the 13.8 per cent recorded in 2010. The continued strength in exports was achieved despite ongoing weakness in the US economy. However, China continued to boost BC exports in 2011 with its steady appetite for BC lumber, as well as pulp, coal and copper.

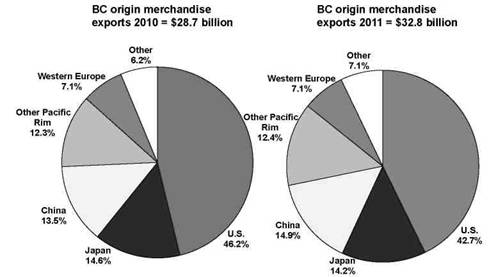

Exports of BC goods to the US improved by 5.4 per cent in 2011, which was stronger than the 2.8 per cent increase in 2010. Despite annual gains in each of the last two years, the value of BC merchandise exports to the US in 2011 continued to hover around the low levels observed during the mid-1990s.

In contrast, China’s booming economy continued to demand a rapidly increasing amount of BC’s exports, as the total value of BC merchandise exports to China grew by 25.4 per cent in 2011. This annual gain was driven by exports of wood products (+75.7 per cent), pulp and paper products (+31.4 per cent) and metallic mineral products (+8.3 per cent). Appendix Tables A1.7 and A1.8 provide further detail on exports by major market and commodity groups.

2012 Financial and Economic Review — July 2012

4

Chapter 1 — Economic Review

The strong Canadian dollar and ongoing slow US economic recovery continued to hamper US demand for goods from BC, as just 42.7 per cent of BC’s total international goods exports went to the US in 2011 (the lowest share since 1990), and was down from 46.2 per cent in the previous year. Most of this market share was absorbed by Asian countries, particularly China and South Korea.

Chart 1.3 Export shares by market

Source: BC Stats

Commodity exports and prices:

BC saw strong export growth in 2011 for most major commodity groups, led by energy products, which increased 24.9 per cent compared to 2010. Significant annual gains were also observed in exports of wood products (+11.7 per cent), metallic minerals (+11.6 per cent), machinery and equipment (+6.6 per cent) and pulp and paper products (+6.0 per cent).

The price of natural gas remained at a low level throughout 2011, with the Plant Inlet price averaging $2.47 C/GJ during 2011. This is down from $2.94 C/GJ in 2010 — a much lower level than the prices observed in recent years.

The price of oil fluctuated through 2011, but rose on average compared to 2010. The West Texas Intermediate daily oil price averaged $94.88 US/barrel on the year, representing a lofty 19.4 per cent increase from the $79.48 US/barrel recorded in 2010.

Prices for SPF lumber remained fairly flat in 2011, falling by just 0.3 per cent for the year after climbing 40.4 per cent in 2010. The price of pulp rose slightly in 2011, up 3.3 per cent, while the price of newsprint saw a 9.5 per cent gain over 2010.

· Lumber prices averaged $254 US per thousand board feet in 2011, inching down from $255 US in the previous year;

· Pulp prices averaged $961 US per tonne, up from $930 US in 2010; and

· Newsprint prices climbed to $625 US per tonne from $571 US per tonne in 2010.

2012 Financial and Economic Review — July 2012

5

Chapter 1 — Economic Review

Chart 1.4 Lumber and natural gas prices

Source: Madison’s Lumber Reporter and Ministry of Energy and Mines

Population

BC’s population grew by 1.0 per cent as of July 1, 2011. During the 2011 calendar year, BC experienced an increase of 46,177 persons. Most of this growth was attributable to the 35,882 persons BC welcomed via net international migration. In 2011, interprovincial migration in BC was negative for the first time since 2002, as a net total of 1,920 persons left BC for other provinces. A natural increase of 12,215 persons also added to the total population of the province for 2011.

Map 1.1 Net interprovincial and international migration in BC, 2011

Net Population Movement For British Columbia

Jan 2011 to Dec 2011

Net Inflow : 33,962 Persons

Source: BC Stats

2012 Financial and Economic Review — July 2012

6

Chapter 1 — Economic Review

Labour and Income Developments

Employment growth in BC was slow in 2011, increasing by just 0.8 per cent (or 18,200 jobs) compared to 2010. Full-time employment rose by 0.5 per cent (or 9,300 jobs), while part-time employment increased by 1.7 per cent (or 8,800 jobs). BC’s unemployment rate edged down 0.1 percentage points to average 7.5 per cent in 2011, slightly higher than the national average of 7.4 per cent. Meanwhile, BC’s labour force expanded by 0.6 per cent in 2011, following an increase of 1.7 per cent in 2010.

Employment in BC’s goods-producing industries rose by 1.1 per cent (or 4,700 jobs) in 2011 after growing 0.9 per cent in the previous year. Annual job gains in the construction sector (+14,100 jobs) more than offset losses in the primary industries sector (-6,200 jobs), manufacturing sector (-1,900 jobs) and utilities sector (-1,200 jobs).

BC’s services sector saw employment grow by 0.7 per cent in 2011, adding 13,400 jobs compared to the previous year. Major job gains were observed in accommodation and food services (+19,500 jobs), professional, scientific and technical services (+7,800 jobs), transportation and warehousing (+5,500 jobs) and services to business management (+3,200 jobs) — see Appendix Table A1.5 for more details.

Table 1.1 British Columbia Population and Labour Market Statistics

| | Units | | 2007 | | 2008 | | 2009 | | 2010 | | 2011 | |

Population (as of July 1) | | (thousands) | | 4,310 | | 4,384 | | 4,460 | | 4,530 | | 4,573 | |

| | (% change) | | 1.6 | | 1.7 | | 1.7 | | 1.6 | | 1.0 | |

Net Migration | | | | | | | | | | | | | |

International | | (persons) | | 42,333 | | 54,052 | | 50,306 | | 37,349 | | 35,882 | |

Interprovincial | | (persons) | | 16,776 | | 10,849 | | 9,672 | | 4,678 | | -1,920 | |

Labour Force | | (thousands) | | 2,322 | | 2,376 | | 2,403 | | 2,443 | | 2,458 | |

| | (% change) | | 3.0 | | 2.4 | | 1.1 | | 1.7 | | 0.6 | |

Employment | | (thousands) | | 2,223 | | 2,266 | | 2,218 | | 2,257 | | 2,275 | |

| | (% change) | | 3.5 | | 2.0 | | (2.1 | ) | 1.7 | | 0.8 | |

Unemployment Rate | | (%) | | 4.3 | | 4.6 | | 7.7 | | 7.6 | | 7.5 | |

Source: Statistics Canada

Inflation

Consumer price inflation in BC rose by 2.4 per cent in 2011 compared to 2010, as increases in the inflation of non-durables and services more than offset price deflation in durable and semi-durable goods. Rising fuel, electricity and food prices pushed up prices for non-durables, while higher prices for restaurants and education provided upward inflationary pressure on the services side. Prices for durables eased in response to lower prices for home entertainment, furniture and household appliances. At the same time, lower prices for items such as clothing, footwear and household textiles led to the overall decline in the semi-durable component.

2012 Financial and Economic Review — July 2012

7

Chapter 1 — Economic Review

Table 1.2 Price and Earnings Indices

| | Units | | 2007 | | 2008 | | 2009 | | 2010 | | 2011 | |

Consumer Price Index | | (2002=100) | | 110.0 | | 112.3 | | 112.3 | | 113.8 | | 116.5 | |

(British Columbia) | | (% change) | | 1.8 | | 2.1 | | — | | 1.3 | | 2.4 | |

| | | | | | | | | | | | | |

Average weekly earnings | | ($) | | 747.1 | | 777.9 | | 797.9 | | 822.8 | | 837.4 | |

| | (% change) | | 2.9 | | 4.1 | | 2.6 | | 3.1 | | 1.8 | |

| | | | | | | | | | | | | |

Labour income (1) | | ($millions) | | 98,573 | | 102,468 | | 100,629 | | 104,630 | | n/a | |

| | (% change) | | 4.9 | | 4.0 | | (1.8 | ) | 4.0 | | n/a | |

| | | | | | | | | | | | | |

Personal income (1) | | ($millions) | | 151,620 | | 158,061 | | 157,668 | | 163,953 | | n/a | |

| | (% change) | | 6.3 | | 4.2 | | (0.2 | ) | 4.0 | | n/a | |

| | | | | | | | | | | | | |

Corporate profits (pre-tax) (1) | | ($millions) | | 21,951 | | 24,892 | | 17,778 | | 21,608 | | n/a | |

| | (% change) | | (2.0 | ) | 13.4 | | (28.6 | ) | 21.5 | | n/a | |

(1) | As of November 2011 Provincial Economic Accounts |

| Source: Statistics Canada |

Consumer Expenditure and Housing

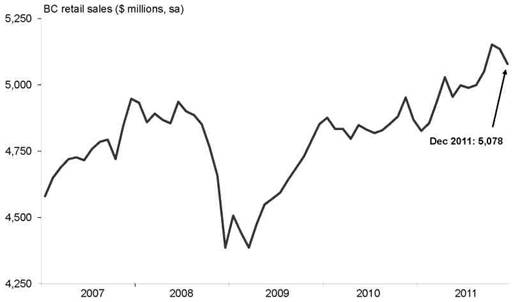

Retail sales in BC advanced by 3.1 per cent in 2011, a slower rate than the 5.4 per cent growth observed in 2010. Notable gains were achieved at gas stations, clothing stores and motor vehicle and parts dealers. Although retail activity improved in 2011, BC placed second last among provinces in retail sales growth on the year.

Following a sizable increase in 2010, BC housing starts remained fairly flat in 2011, falling just 0.3 per cent to reach 26,400 units. An annual decline of 22.6 per cent in single unit starts offset a gain of 16.8 per cent in multiple unit starts. At the same time, residential building permits (a leading indicator of potential new housing activity) dropped by 8.8 per cent in 2011 compared to 2010.

Chart 1.5 Retail sales

Source: Statistics Canada

2012 Financial and Economic Review — July 2012

8

Chapter 1 — Economic Review

Home sales in BC improved by 2.8 per cent in 2011 compared to the previous year, following a drop of 12.2 per cent in 2010. At the same time, home prices in BC continued to rise, with the average price reaching $561,000 — an increase of 11.1 per cent over 2010.

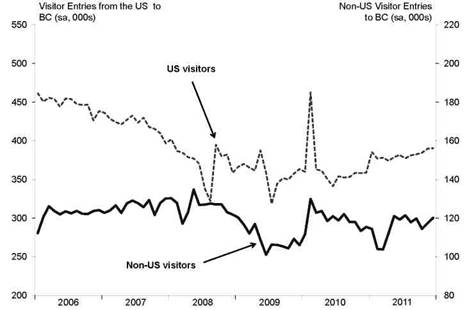

Tourism

In 2011, the number of international travelers to BC fell by 4.3 per cent compared to the previous year, after climbing 3.5 per cent in 2010. Non-US visitors declined by 3.3 per cent in 2011, while travelers from the US fell by 4.7 per cent on the year. The number of travelers to BC has fallen in six of the past seven years (except for the gain in 2010), and currently resides at levels observed in the early 1990s.

Chart 1.6 Visitor entries to British Columbia

Source: Statistics Canada

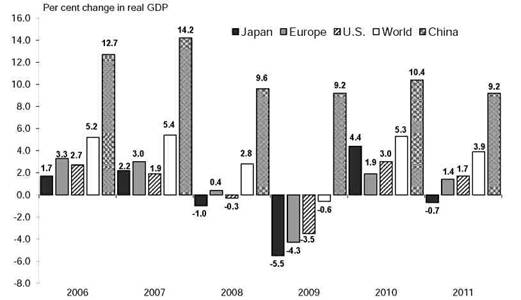

External Environment

Economic uncertainty reverberated throughout the world in 2011, as the global economy continued its long recovery following the 2008/2009 recession. Overall, world economic growth advanced by 3.9 per cent in 2011, down slightly from the 5.3 per cent gain recorded in 2010. The Japanese economy contracted in 2011 after returning to growth in 2010, while the Euro area economies grew by just 1.4 per cent compared to the previous year. Meanwhile, China surged again, recording 9.2 per cent annual growth in 2011, after a gain of 10.4 per cent in 2010.

United States Economy

The US economy is currently experiencing a period of sluggish economic activity as it continues its slow recovery from the housing collapse and ensuing financial crisis that began in late 2008. US real GDP expanded by 1.7 per cent in 2011, a significant slowdown from the 3.0 per cent growth observed in 2010.

2012 Financial and Economic Review — July 2012

9

Chapter 1 — Economic Review

The US employment situation remained bleak in 2011, with 5.8 million American workers having lost their jobs since the January 2008 peak. The unemployment rate fell to 9.0 per cent from 9.6 per cent in 2010, but remained high relative to historical levels. Although about 150,000 new jobs were created on average each month in 2011, it would take about three years at this rate to regain all the jobs lost since early 2008.

The US housing market also continued to struggle in 2011, as housing starts averaged just 606,900 units on the year. Although this represents a 3.4 per cent increase from 2010, starts remained at historically low levels throughout the year.

The US current account deficit (the combined balances on trade in goods and services income, and net unilateral current transfers) widened in 2011, to reach –$466 billion from –$442 billion recorded for the previous year.

Canadian Economy

The Canadian economy grew by 2.6 per cent in 2011 following a 3.4 per cent increase in 2010, as real GDP advanced in every province on the year. Canada’s goods-producing industries improved by 3.6 per cent in 2011, which was slower than the 6.1 per cent growth recorded in 2010. At the same time, growth in the country’s service industries rose by 2.3 per cent in 2011, down from 2.7 per cent in 2010.

Canada’s current account deficit narrowed slightly in 2011 to reach –$48.4 billion after recording a balance of –$50.9 billion in 2010. The value of Canadian merchandise exports rose 12.0 per cent in 2011, posting another strong year after rising by 11.9 per cent in 2010. Meanwhile, shipments of manufactured goods also increased on the year, as the total value of Canadian shipments rose 7.8 per cent in 2011 following a gain of 8.9 per cent in 2010.

Canada’s labour market continued its steady gains in 2011, as the number of jobs improved by 265,200 jobs (or 1.6 per cent) over the previous year. At the same time, the national unemployment rate averaged 7.4 per cent in 2011, down from the 8.0 per cent observed in 2010.

Canadian housing starts also increased, climbing by 2.1 per cent to average 194,000 units, after a 27.4 per cent gain in 2010. Residential building permits grew by 2.3 per cent in 2011, following a sizeable jump of 25.2 per cent during the previous year. Further, national home sales rebounded in 2011, as sales were up by 2.4 per cent after declining by 3.9 per cent in 2010.

Canadian retail sales improved by 4.1 per cent in 2011 compared to the previous year, after a 5.6 per cent annual gain in 2010. Stronger employment gains likely aided retail sales growth, which moved upward despite a decline in consumer confidence during 2011.

International Economy

In 2011, the European sovereign debt crisis continued to shroud the global economy in uncertainty. Widespread concern over debt struggles in several nations — especially Greece, Spain, Portugal and Italy — sent domestic bond yields in these countries soaring and dampened the value of the euro currency. Overall, however, Europe’s economy expanded by 1.4 per cent in 2011 after a 1.9 per cent increase in 2010.

2012 Financial and Economic Review — July 2012

10

Chapter 1 — Economic Review

Chart 1.7 External economic growth

Source: International Monetary Fund, April 2012

Japan’s economy contracted 0.7 per cent in 2011, after a healthy gain of 4.4 per cent in the previous year. The drop in 2011 marks the third year in the past four in which Japanese real GDP has recorded an annual contraction.

Meanwhile, the International Monetary Fund estimates that global real GDP grew by 3.9 per cent in 2011, bolstered by sustained strength in emerging and developing economies. In particular, the Chinese economy continued its rapid growth in 2011, expanding by 9.2 per cent on the year.

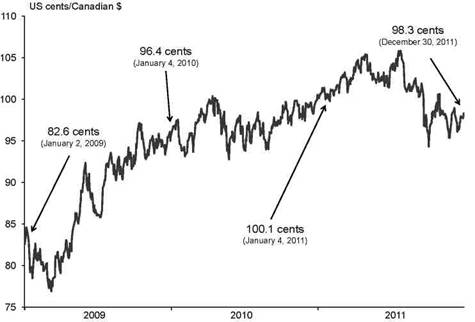

Financial Markets

The Bank of Canada continued to hold the overnight target rate at 1.00 per cent in 2011, where it has remained since September 2010. On several occasions throughout the year, Bank officials cited uncertainty in the global economic outlook (brought on largely by the European debt crisis) as a central reason for its decision to remain at 1.00 per cent.

The slower than expected US economic recovery, including weakness in the labour market and stagnant housing activity, pushed the US Federal Reserve to hold its intended federal funds rate in the 0.00 to 0.25 per cent range throughout all of 2011. Reserve officials have held the rate in this highly accommodative range since December 2008.

After beginning 2011 at 100.1 US cents, the value of the Canadian dollar remained close to parity throughout the year. The loonie averaged 101.1 US cents in 2011, as the dollar’s high value was attributed to a still weak US dollar as well as strong commodity prices.

2012 Financial and Economic Review — July 2012

11

Chapter 1 — Economic Review

Chart 1.8 Canadian dollar

Source: Bank of Canada

Conclusion

BC’s economy slowed slightly in 2011, expanding by 2.9 per cent after growing by 3.2 per cent in 2010. The recovery was broadly based, with both the goods and services sectors experiencing gains. BC’s economic growth in 2011 fared well relative to other Canadian jurisdictions, placing third among provinces and above the national average for the year.

Domestically, employment in BC rose 0.8 per cent in 2011, an increase of 18,200 jobs, with gains in both full-time and part-time employment. Meanwhile, BC’s annual unemployment rate edged down 0.1 percentage points to average 7.5 per cent on the year, slightly higher than the national average. Following a very strong 2010, BC housing starts held fairly steady in 2011, reaching 26,400 units (a slight drop of 0.3 per cent over the previous year). BC retail sales also increased in 2011, climbing 3.1 per cent over the year.

Internationally, BC merchandise exports continued to surge in 2011, rising 14.0 per cent over the previous year, supported by strong Asian demand for resource-based commodities such as BC lumber, pulp, coal and copper. Shipments of manufactured goods also made strong gains in 2011, growing by 6.5 per cent on the year.

2012 Financial and Economic Review — July 2012

12

| Appendix 1 |

| |

| Economic Review |

2012 Financial and Economic Review — July 2012

Appendix 1 — Economic Review

Table A1.1A Aggregate and Labour Market Indicators

| | | | | | Real GDP | | Personal | | Capital | | Business | | | | | | Unemployment | |

| | Population (1) | | Nominal GDP | | (chained) | | income | | investment | | incorporations | | Labour force | | Employment | | rate | |

| | (thousands) | | ($ millions) | | ($2002 millions) | | ($ millions) | | ($ millions) | | (number) | | (thousands) | | (thousands) | | (per cent) | |

1982 | | 2,877 | | 45,024 | | 79,324 | | 40,425 | | | | | | 1,427 | | 1,253 | | 12.1 | |

1983 | | 2,908 | | 47,477 | | 79,824 | | 41,634 | | | | | | 1,446 | | 1,245 | | 13.9 | |

1984 | | 2,947 | | 49,840 | | 80,440 | | 43,734 | | | | | | 1,465 | | 1,245 | | 15.0 | |

1985 | | 2,975 | | 53,540 | | 86,026 | | 46,588 | | | | | | 1,493 | | 1,280 | | 14.3 | |

1986 | | 3,004 | | 56,547 | | 86,187 | | 48,911 | | | | | | 1,526 | | 1,332 | | 12.7 | |

1987 | | 3,049 | | 62,515 | | 91,503 | | 52,903 | | | | | | 1,567 | | 1,378 | | 12.1 | |

1988 | | 3,115 | | 69,408 | | 96,824 | | 58,298 | | | | | | 1,599 | | 1,435 | | 10.3 | |

1989 | | 3,197 | | 75,582 | | 100,007 | | 65,009 | | | | | | 1,659 | | 1,508 | | 9.1 | |

1990 | | 3,292 | | 79,350 | | 101,408 | | 72,038 | | | | | | 1,703 | | 1,560 | | 8.4 | |

1991 | | 3,374 | | 81,849 | | 101,593 | | 75,336 | | 17,370 | | | | 1,751 | | 1,578 | | 9.9 | |

1992 | | 3,469 | | 87,242 | | 104,216 | | 78,610 | | 17,979 | | | | 1,800 | | 1,617 | | 10.1 | |

1993 | | 3,568 | | 94,077 | | 108,874 | | 81,914 | | 18,875 | | | | 1,848 | | 1,668 | | 9.7 | |

1994 | | 3,676 | | 100,512 | | 111,945 | | 85,703 | | 21,353 | | | | 1,918 | | 1,743 | | 9.1 | |

1995 | | 3,777 | | 105,670 | | 114,620 | | 90,056 | | 20,591 | | | | 1,951 | | 1,786 | | 8.5 | |

1996 | | 3,874 | | 108,865 | | 117,442 | | 92,661 | | 19,408 | | 23,237 | | 1,986 | | 1,813 | | 8.7 | |

1997 | | 3,949 | | 114,383 | | 121,177 | | 95,925 | | 22,552 | | 22,958 | | 2,032 | | 1,860 | | 8.5 | |

1998 | | 3,983 | | 115,641 | | 122,766 | | 98,135 | | 20,819 | | 20,759 | | 2,038 | | 1,858 | | 8.8 | |

1999 | | 4,011 | | 120,921 | | 126,708 | | 101,465 | | 21,152 | | 21,009 | | 2,064 | | 1,894 | | 8.3 | |

2000 | | 4,039 | | 131,333 | | 132,578 | | 107,624 | | 21,799 | | 21,388 | | 2,080 | | 1,931 | | 7.2 | |

2001 | | 4,076 | | 133,514 | | 133,403 | | 110,369 | | 23,414 | | 19,474 | | 2,081 | | 1,920 | | 7.7 | |

2002 | | 4,098 | | 138,193 | | 138,193 | | 113,451 | | 23,732 | | 20,987 | | 2,134 | | 1,953 | | 8.5 | |

2003 | | 4,122 | | 145,642 | | 141,435 | | 117,126 | | 25,434 | | 22,531 | | 2,172 | | 1,998 | | 8.0 | |

2004 | | 4,155 | | 157,675 | | 146,541 | | 124,263 | | 29,665 | | 24,703 | | 2,190 | | 2,033 | | 7.2 | |

2005 | | 4,197 | | 169,664 | | 153,489 | | 131,408 | | 33,254 | | 30,937 | | 2,221 | | 2,092 | | 5.8 | |

2006 | | 4,244 | | 182,251 | | 159,729 | | 142,696 | | 39,912 | | 33,273 | | 2,255 | | 2,147 | | 4.8 | |

2007 | | 4,310 | | 192,117 | | 164,496 | | 151,620 | | 42,670 | | 34,036 | | 2,322 | | 2,223 | | 4.3 | |

2008 | | 4,384 | | 199,441 | | 165,641 | | 158,061 | | 46,936 | | 30,085 | | 2,376 | | 2,266 | | 4.6 | |

2009 | | 4,460 | | 191,863 | | 162,225 | | 157,668 | | 39,001 | | 26,431 | | 2,403 | | 2,218 | | 7.7 | |

2010 | | 4,530 | | 203,147 | | 167,140 | | 163,953 | | 42,534 | | 30,305 | | 2,443 | | 2,257 | | 7.6 | |

2011 | | 4,573 | | n/a | | n/a | | n/a | | 46,109 | | 30,847 | | 2,458 | | 2,275 | | 7.5 | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | Personal | | Capital | | Business | | | | | | Unemployment | |

| | Population (1) | | Nominal GDP | | Real GDP | | income | | investment | | incorporations | | Labour force | | Employment | | rate | |

| | (% change) | | (% change) | | (% change) | | (% change) | | (% change) | | (% change) | | (% change) | | (% change) | | (change) | |

1983 | | 1.1 | | 5.4 | | 0.6 | | 3.0 | | — | | — | | 1.3 | | (0.7 | ) | 1.8 | |

1984 | | 1.4 | | 5.0 | | 0.8 | | 5.0 | | — | | — | | 1.3 | | 0.0 | | 1.1 | |

1985 | | 0.9 | | 7.4 | | 6.9 | | 6.5 | | — | | — | | 1.9 | | 2.8 | | (0.7 | ) |

1986 | | 1.0 | | 5.6 | | 0.2 | | 5.0 | | — | | — | | 2.2 | | 4.1 | | (1.6 | ) |

1987 | | 1.5 | | 10.6 | | 6.2 | | 8.2 | | — | | — | | 2.7 | | 3.4 | | (0.6 | ) |

1988 | | 2.2 | | 11.0 | | 5.8 | | 10.2 | | — | | — | | 2.0 | | 4.1 | | (1.8 | ) |

1989 | | 2.6 | | 8.9 | | 3.3 | | 11.5 | | — | | — | | 3.8 | | 5.1 | | (1.2 | ) |

1990 | | 3.0 | | 5.0 | | 1.4 | | 10.8 | | — | | — | | 2.6 | | 3.4 | | (0.7 | ) |

1991 | | 2.5 | | 3.1 | | 0.2 | | 4.6 | | — | | — | | 2.8 | | 1.1 | | 1.5 | |

1992 | | 2.8 | | 6.6 | | 2.6 | | 4.3 | | 3.5 | | — | | 2.8 | | 2.5 | | 0.2 | |

1993 | | 2.9 | | 7.8 | | 4.5 | | 4.2 | | 5.0 | | — | | 2.7 | | 3.1 | | (0.4 | ) |

1994 | | 3.0 | | 6.8 | | 2.8 | | 4.6 | | 13.1 | | — | | 3.8 | | 4.5 | | (0.6 | ) |

1995 | | 2.8 | | 5.1 | | 2.4 | | 5.1 | | (3.6 | ) | — | | 1.7 | | 2.4 | | (0.6 | ) |

1996 | | 2.6 | | 3.0 | | 2.5 | | 2.9 | | (5.7 | ) | — | | 1.8 | | 1.6 | | 0.2 | |

1997 | | 1.9 | | 5.1 | | 3.2 | | 3.5 | | 16.2 | | (1.2 | ) | 2.3 | | 2.6 | | (0.2 | ) |

1998 | | 0.9 | | 1.1 | | 1.3 | | 2.3 | | (7.7 | ) | (9.6 | ) | 0.3 | | (0.1 | ) | 0.3 | |

1999 | | 0.7 | | 4.6 | | 3.2 | | 3.4 | | 1.6 | | 1.2 | | 1.3 | | 1.9 | | (0.5 | ) |

2000 | | 0.7 | | 8.6 | | 4.6 | | 6.1 | | 3.1 | | 1.8 | | 0.8 | | 2.0 | | (1.1 | ) |

2001 | | 0.9 | | 1.7 | | 0.6 | | 2.6 | | 7.4 | | (8.9 | ) | 0.0 | | (0.6 | ) | 0.5 | |

2002 | | 0.5 | | 3.5 | | 3.6 | | 2.8 | | 1.4 | | 7.8 | | 2.6 | | 1.7 | | 0.8 | |

2003 | | 0.6 | | 5.4 | | 2.3 | | 3.2 | | 7.2 | | 7.4 | | 1.8 | | 2.3 | | (0.5 | ) |

2004 | | 0.8 | | 8.3 | | 3.6 | | 6.1 | | 16.6 | | 9.6 | | 0.8 | | 1.7 | | (0.8 | ) |

2005 | | 1.0 | | 7.6 | | 4.7 | | 5.7 | | 12.1 | | 25.2 | | 1.5 | | 2.9 | | (1.4 | ) |

2006 | | 1.1 | | 7.4 | | 4.1 | | 8.6 | | 20.0 | | 7.6 | | 1.5 | | 2.6 | | (1.0 | ) |

2007 | | 1.6 | | 5.4 | | 3.0 | | 6.3 | | 6.9 | | 2.3 | | 3.0 | | 3.5 | | (0.5 | ) |

2008 | | 1.7 | | 3.8 | | 0.7 | | 4.2 | | 10.0 | | (11.6 | ) | 2.4 | | 2.0 | | 0.3 | |

2009 | | 1.7 | | (3.8 | ) | (2.1 | ) | (0.2 | ) | (16.9 | ) | (12.1 | ) | 1.1 | | (2.1 | ) | 3.1 | |

2010 | | 1.6 | | 5.9 | | 3.0 | | 4.0 | | 9.1 | | 14.7 | | 1.7 | | 1.7 | | (0.1 | ) |

2011 | | 1.0 | | n/a | | n/a | | n/a | | 8.4 | | 1.8 | | 0.6 | | 0.8 | | (0.1 | ) |

(1) As at July 1. Data take into account adjustments made for net census undercount in 1996, 2001 and 2006, and non-permanent residents.

Sources: Statistics Canada and BC Stats, Ministry of Finance, based on federal, provincial and industry data.

2012 Financial and Economic Review — July 2012

14

Appendix 1 — Economic Review

Table A1.1B Prices, Earnings and Financial Indicators

| | | | | | | | | | | | Personal | | | | | | | |

| | | | | | Average | | | | | | Disposable | | | | | | Conventional | |

| | BC | | Vancouver | | weekly | | Labour | | Personal income | | Income | | Prime | | Can/US | | (5 year) | |

| | CPI | | CPI | | wage rate(1) | | income | | per capita | | per capita | | rate | | exchange rate | | mortgage rate | |

| | (2002=100) | | (2002=100) | | ($) | | ($ millions) | | (dollars) | | (dollars) | | (per cent) | | (US cents) | | (per cent) | |

1982 | | 57.3 | | 56.6 | | — | | 26,497 | | 14,053 | | 11,468 | | 15.8 | | 81.1 | | 18.0 | |

1983 | | 60.4 | | 59.7 | | — | | 27,018 | | 14,320 | | 11,580 | | 11.2 | | 81.1 | | 13.2 | |

1984 | | 62.8 | | 62.1 | | — | | 27,811 | | 14,839 | | 12,134 | | 12.1 | | 77.2 | | 13.6 | |

1985 | | 64.8 | | 64.0 | | — | | 29,100 | | 15,659 | | 12,777 | | 10.6 | | 73.2 | | 12.1 | |

1986 | | 66.7 | | 66.2 | | — | | 30,339 | | 16,284 | | 13,135 | | 10.5 | | 72.0 | | 11.2 | |

1987 | | 68.7 | | 68.2 | | — | | 32,837 | | 17,353 | | 13,860 | | 9.5 | | 75.4 | | 11.2 | |

1988 | | 71.2 | | 70.6 | | — | | 36,110 | | 18,717 | | 14,846 | | 10.8 | | 81.3 | | 11.6 | |

1989 | | 74.4 | | 73.8 | | — | | 40,295 | | 20,336 | | 16,156 | | 13.3 | | 84.5 | | 12.1 | |

1990 | | 78.4 | | 77.8 | | — | | 44,216 | | 21,882 | | 17,003 | | 14.1 | | 85.7 | | 13.4 | |

1991 | | 82.6 | | 81.9 | | — | | 46,296 | | 22,330 | | 17,309 | | 9.9 | | 87.3 | | 11.1 | |

1992 | | 84.8 | | 84.3 | | — | | 48,924 | | 22,662 | | 17,454 | | 7.5 | | 82.7 | | 9.5 | |

1993 | | 87.8 | | 87.3 | | — | | 51,312 | | 22,959 | | 17,802 | | 5.9 | | 77.5 | | 8.8 | |

1994 | | 89.5 | | 89.1 | | — | | 53,972 | | 23,314 | | 17,968 | | 6.9 | | 73.2 | | 9.5 | |

1995 | | 91.6 | | 91.3 | | — | | 56,768 | | 23,841 | | 18,300 | | 8.6 | | 72.9 | | 9.2 | |

1996 | | 92.4 | | 92.1 | | — | | 58,517 | | 23,917 | | 18,221 | | 6.1 | | 73.3 | | 7.9 | |

1997 | | 93.1 | | 92.6 | | 612.55 | | 60,681 | | 24,294 | | 18,484 | | 5.0 | | 72.2 | | 7.1 | |

1998 | | 93.4 | | 93.0 | | 620.99 | | 61,965 | | 24,638 | | 18,676 | | 6.6 | | 67.4 | | 6.9 | |

1999 | | 94.4 | | 93.9 | | 628.12 | | 64,045 | | 25,294 | | 19,298 | | 6.4 | | 67.3 | | 7.6 | |

2000 | | 96.1 | | 96.0 | | 639.18 | | 68,369 | | 26,645 | | 20,276 | | 7.3 | | 67.3 | | 8.4 | |

2001 | | 97.7 | | 97.8 | | 648.31 | | 70,044 | | 27,076 | | 20,934 | | 5.8 | | 64.6 | | 7.4 | |

2002 | | 100.0 | | 100.0 | | 668.75 | | 72,900 | | 27,683 | | 21,618 | | 4.2 | | 63.7 | | 7.0 | |

2003 | | 102.2 | | 102.0 | | 684.22 | | 75,605 | | 28,412 | | 22,197 | | 4.7 | | 71.4 | | 6.4 | |

2004 | | 104.2 | | 104.0 | | 687.15 | | 80,599 | | 29,906 | | 23,321 | | 4.0 | | 76.8 | | 6.2 | |

2005 | | 106.3 | | 106.0 | | 704.71 | | 85,805 | | 31,312 | | 24,214 | | 4.4 | | 82.5 | | 6.0 | |

2006 | | 108.1 | | 108.0 | | 725.80 | | 93,963 | | 33,626 | | 26,109 | | 5.8 | | 88.2 | | 6.7 | |

2007 | | 110.0 | | 110.2 | | 747.06 | | 98,573 | | 35,182 | | 27,287 | | 6.1 | | 93.1 | | 7.1 | |

2008 | | 112.3 | | 112.8 | | 777.88 | | 102,468 | | 36,054 | | 28,480 | | 4.7 | | 93.7 | | 7.1 | |

2009 | | 112.3 | | 112.9 | | 797.85 | | 100,629 | | 35,352 | | 28,279 | | 2.4 | | 87.6 | | 5.6 | |

2010 | | 113.8 | | 114.9 | | 822.81 | | 104,630 | | 36,195 | | 29,175 | | 2.6 | | 97.1 | | 5.6 | |

2011 | | 116.5 | | 117.5 | | 837.37 | | n/a | | n/a | | n/a | | 3.0 | | 101.1 | | 5.4 | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | Personal | | | | | | | |

| | | | | | Average | | | | | | Disposable | | | | | | Conventional | |

| | BC | | Vancouver | | weekly | | Labour | | Personal income | | Income | | Prime | | Can/US | | (5 year) | |

| | CPI | | CPI | | wage rate(1) | | income | | per capita | | per capita | | rate | | exchange rate | | mortgage rate | |

| | (% change) | | (% change) | | (% change) | | (% change) | | (% change) | | (% change) | | (change) | | (change) | | (change) | |

1983 | | 5.4 | | 5.5 | | — | | 2.0 | | 1.9 | | 1.0 | | (4.6 | ) | 0.1 | | (4.8 | ) |

1984 | | 4.0 | | 4.0 | | — | | 2.9 | | 3.6 | | 4.8 | | 0.9 | | (3.9 | ) | 0.4 | |

1985 | | 3.2 | | 3.1 | | — | | 4.6 | | 5.5 | | 5.3 | | (1.5 | ) | (4.0 | ) | (1.5 | ) |

1986 | | 2.9 | | 3.4 | | — | | 4.3 | | 4.0 | | 2.8 | | (0.1 | ) | (1.3 | ) | (0.9 | ) |

1987 | | 3.0 | | 3.0 | | — | | 8.2 | | 6.6 | | 5.5 | | (1.0 | ) | 3.4 | | (0.0 | ) |

1988 | | 3.6 | | 3.5 | | — | | 10.0 | | 7.9 | | 7.1 | | 1.3 | | 5.8 | | 0.5 | |

1989 | | 4.5 | | 4.5 | | — | | 11.6 | | 8.6 | | 8.8 | | 2.5 | | 3.2 | | 0.4 | |

1990 | | 5.4 | | 5.4 | | — | | 9.7 | | 7.6 | | 5.2 | | 0.7 | | 1.2 | | 1.3 | |

1991 | | 5.4 | | 5.3 | | — | | 4.7 | | 2.0 | | 1.8 | | (4.1 | ) | 1.6 | | (2.2 | ) |

1992 | | 2.7 | | 2.9 | | — | | 5.7 | | 1.5 | | 0.8 | | (2.5 | ) | (4.5 | ) | (1.6 | ) |

1993 | | 3.5 | | 3.6 | | — | | 4.9 | | 1.3 | | 2.0 | | (1.5 | ) | (5.2 | ) | (0.7 | ) |

1994 | | 1.9 | | 2.1 | | — | | 5.2 | | 1.5 | | 0.9 | | 0.9 | | (4.3 | ) | 0.8 | |

1995 | | 2.3 | | 2.5 | | — | | 5.2 | | 2.3 | | 1.8 | | 1.8 | | (0.4 | ) | (0.4 | ) |

1996 | | 0.9 | | 0.9 | | — | | 3.1 | | 0.3 | | (0.4 | ) | (2.6 | ) | 0.5 | | (1.2 | ) |

1997 | | 0.8 | | 0.5 | | — | | 3.7 | | 1.6 | | 1.4 | | (1.1 | ) | (1.1 | ) | (0.9 | ) |

1998 | | 0.3 | | 0.4 | | 1.4 | | 2.1 | | 1.4 | | 1.0 | | 1.6 | | (4.8 | ) | (0.1 | ) |

1999 | | 1.1 | | 1.0 | | 1.1 | | 3.4 | | 2.7 | | 3.3 | | (0.2 | ) | (0.1 | ) | 0.6 | |

2000 | | 1.8 | | 2.2 | | 1.8 | | 6.8 | | 5.3 | | 5.1 | | 0.8 | | 0.0 | | 0.8 | |

2001 | | 1.7 | | 1.9 | | 1.4 | | 2.4 | | 1.6 | | 3.2 | | (1.5 | ) | (2.8 | ) | (0.9 | ) |

2002 | | 2.4 | | 2.2 | | 3.2 | | 4.1 | | 2.2 | | 3.3 | | (1.6 | ) | (0.9 | ) | (0.4 | ) |

2003 | | 2.2 | | 2.0 | | 2.3 | | 3.7 | | 2.6 | | 2.7 | | 0.5 | | 7.7 | | (0.6 | ) |

2004 | | 2.0 | | 2.0 | | 0.4 | | 6.6 | | 5.3 | | 5.1 | | (0.7 | ) | 5.5 | | (0.2 | ) |

2005 | | 2.0 | | 1.9 | | 2.6 | | 6.5 | | 4.7 | | 3.8 | | 0.4 | | 5.7 | | (0.2 | ) |

2006 | | 1.7 | | 1.9 | | 3.0 | | 9.5 | | 7.4 | | 7.8 | | 1.4 | | 5.6 | | 0.7 | |

2007 | | 1.8 | | 2.0 | | 2.9 | | 4.9 | | 4.6 | | 4.5 | | 0.3 | | 4.9 | | 0.4 | |

2008 | | 2.1 | | 2.4 | | 4.1 | | 4.0 | | 2.5 | | 4.4 | | (1.4 | ) | 0.6 | | (0.0 | ) |

2009 | | — | | 0.1 | | 2.6 | | (1.8 | ) | (1.9 | ) | (0.7 | ) | (2.3 | ) | (6.1 | ) | (1.4 | ) |

2010 | | 1.3 | | 1.8 | | 3.1 | | 4.0 | | 2.4 | | 3.2 | | 0.2 | | 9.5 | | (0.0 | ) |

2011 | | 2.4 | | 2.3 | | 1.8 | | n/a | | n/a | | n/a | | 0.4 | | 4.0 | | (0.2 | ) |

(1) Data prior to 1997 are not available.

Sources: Statistics Canada and BC Stats, Ministry of Finance, based on federal, provincial and industry data.

2012 Financial and Economic Review — July 2012

15

Appendix 1 — Economic Review

Table A1.1C Other Indicators

| | Manufacturing | | | | Housing | | Non-residential | | Tourism | | High-tech | | BC product | |

| | shipments | | Retail sales(1) | | starts | | building permits | | GDP(2) | | GDP(2) | | exports | |

| | ($ millions) | | ($ millions) | | (number) | | ($ millions) | | ($ millions) | | ($ millions) | | ($ millions) | |

1982 | | — | | — | | 19,807 | | 1,026 | | — | | — | | 12,353 | |

1983 | | — | | — | | 22,607 | | 775 | | — | | — | | 13,244 | |

1984 | | — | | — | | 16,169 | | 827 | | — | | — | | 15,748 | |

1985 | | — | | — | | 17,969 | | 812 | | — | | — | | 13,591 | |

1986 | | — | | — | | 20,687 | | 912 | | — | | — | | 13,033 | |

1987 | | — | | — | | 28,944 | | 999 | | — | | — | | 15,883 | |

1988 | | — | | — | | 30,487 | | 1,647 | | — | | — | | 17,822 | |

1989 | | — | | — | | 38,894 | | 1,812 | | — | | — | | 18,307 | |

1990 | | — | | — | | 36,720 | | 1,833 | | — | | — | | 16,605 | |

1991 | | — | | 25,022 | | 31,875 | | 1,803 | | — | | — | | 15,253 | |

1992 | | 24,398 | | 26,194 | | 40,621 | | 2,082 | | — | | — | | 16,336 | |

1993 | | 26,583 | | 28,463 | | 42,807 | | 1,944 | | — | | — | | 19,033 | |

1994 | | 30,333 | | 31,770 | | 39,408 | | 1,772 | | — | | — | | 22,856 | |

1995 | | 34,207 | | 34,219 | | 27,057 | | 1,966 | | — | | — | | 26,873 | |

1996 | | 32,932 | | 34,775 | | 27,641 | | 1,957 | | — | | — | | 25,717 | |

1997 | | 33,496 | | 36,591 | | 29,351 | | 1,960 | | 4,482 | | 5,193 | | 26,699 | |

1998 | | 31,757 | | 35,762 | | 19,931 | | 2,022 | | 5,668 | | 5,528 | | 25,942 | |

1999 | | 36,679 | | 36,373 | | 16,309 | | 2,104 | | 4,807 | | 5,632 | | 29,044 | |

2000 | | 40,699 | | 38,435 | | 14,418 | | 2,089 | | 5,048 | | 6,367 | | 33,639 | |

2001 | | 38,303 | | 40,719 | | 17,234 | | 2,125 | | 5,191 | | 6,388 | | 31,680 | |

2002 | | 38,610 | | 43,265 | | 21,625 | | 1,771 | | 5,238 | | 6,875 | | 28,828 | |

2003 | | 39,772 | | 44,421 | | 26,174 | | 1,880 | | 5,233 | | 7,499 | | 28,264 | |

2004 | | 41,607 | | 47,219 | | 32,925 | | 2,070 | | 5,692 | | 7,988 | | 31,008 | |

2005 | | 42,883 | | 49,379 | | 34,667 | | 3,212 | | 6,150 | | 8,568 | | 34,167 | |

2006 | | 44,480 | | 53,133 | | 36,443 | | 3,921 | | 6,510 | | 9,047 | | 33,466 | |

2007 | | 42,418 | | 56,930 | | 39,195 | | 3,933 | | 6,881 | | 10,342 | | 31,524 | |

2008 | | 39,435 | | 57,783 | | 34,321 | | 3,678 | | 7,068 | | 10,508 | | 33,124 | |

2009 | | 32,798 | | 55,222 | | 16,077 | | 3,139 | | 6,744 | | 10,461 | | 25,240 | |

2010 | | 35,542 | | 58,220 | | 26,479 | | 3,018 | | 7,197 | | n/a | | 28,721 | |

2011 | | 37,854 | | 60,005 | | 26,400 | | 3,136 | | n/a | | n/a | | 32,752 | |

| | | | | | | | | | | | | | | |

| | Manufacturing | | | | Housing | | Non-residential | | Tourism | | High-tech | | BC product | |

| | shipments | | Retail sales(1) | | starts | | building permits | | GDP(2) | | GDP(2) | | exports | |

| | (% change) | | (% change) | | (% change) | | (% change) | | (% change) | | (% change) | | (% change) | |

1983 | | — | | — | | 14.1 | | (24.5 | ) | — | | — | | 7.2 | |

1984 | | — | | — | | (28.5 | ) | 6.7 | | — | | — | | 18.9 | |

1985 | | — | | — | | 11.1 | | (1.7 | ) | — | | — | | (13.7 | ) |

1986 | | — | | — | | 15.1 | | 12.3 | | — | | — | | (4.1 | ) |

1987 | | — | | — | | 39.9 | | 9.6 | | — | | — | | 21.9 | |

1988 | | — | | — | | 5.3 | | 64.9 | | — | | — | | 12.2 | |

1989 | | — | | — | | 27.6 | | 10.0 | | — | | — | | 2.7 | |

1990 | | — | | — | | (5.6 | ) | 1.2 | | — | | — | | (9.3 | ) |

1991 | | — | | — | | (13.2 | ) | (1.6 | ) | — | | — | | (8.1 | ) |

1992 | | — | | 4.7 | | 27.4 | | 15.5 | | — | | — | | 7.1 | |

1993 | | 9.0 | | 8.7 | | 5.4 | | (6.7 | ) | — | | — | | 16.5 | |

1994 | | 14.1 | | 11.6 | | (7.9 | ) | (8.9 | ) | — | | — | | 20.1 | |

1995 | | 12.8 | | 7.7 | | (31.3 | ) | 11.0 | | — | | — | | 17.6 | |

1996 | | (3.7 | ) | 1.6 | | 2.2 | | (0.4 | ) | — | | — | | (4.3 | ) |

1997 | | 1.7 | | 5.2 | | 6.2 | | 0.1 | | — | | — | | 3.8 | |

1998 | | (5.2 | ) | (2.3 | ) | (32.1 | ) | 3.2 | | 26.5 | | 6.5 | | (2.8 | ) |

1999 | | 15.5 | | 1.7 | | (18.2 | ) | 4.0 | | (15.2 | ) | 1.9 | | 12.0 | |

2000 | | 11.0 | | 5.7 | | (11.6 | ) | (0.7 | ) | 5.0 | | 13.1 | | 15.8 | |

2001 | | (5.9 | ) | 5.9 | | 19.5 | | 1.7 | | 2.8 | | 0.3 | | (5.8 | ) |

2002 | | 0.8 | | 6.3 | | 25.5 | | (16.6 | ) | 0.9 | | 7.6 | | (9.0 | ) |

2003 | | 3.0 | | 2.7 | | 21.0 | | 6.1 | | (0.1 | ) | 9.1 | | (2.0 | ) |

2004 | | 4.6 | | 6.3 | | 25.8 | | 10.1 | | 8.8 | | 6.5 | | 9.7 | |

2005 | | 3.1 | | 4.6 | | 5.3 | | 55.2 | | 8.0 | | 7.3 | | 10.2 | |

2006 | | 3.7 | | 7.6 | | 5.1 | | 22.1 | | 5.9 | | 5.6 | | (2.1 | ) |

2007 | | (4.6 | ) | 7.1 | | 7.6 | | 0.3 | | 5.7 | | 14.3 | | (5.8 | ) |

2008 | | (7.0 | ) | 1.5 | | (12.4 | ) | (6.5 | ) | 2.7 | | 1.6 | | 5.1 | |

2009 | | (16.8 | ) | (4.4 | ) | (53.2 | ) | (14.7 | ) | (4.6 | ) | (0.4 | ) | (23.8 | ) |

2010 | | 8.4 | | 5.4 | | 64.7 | | (3.9 | ) | 6.7 | | n/a | | 13.8 | |

2011 | | 6.5 | | 3.1 | | (0.3 | ) | 3.9 | | n/a | | n/a | | 14.0 | |

(1) Retail sales data have been revised from 1991 to 2006 and are now classified under the North American Industry Classification System (NAICS 2002).

(2) Data prior to 1997 are not available.

Sources: Statistics Canada and BC Stats, Ministry of Finance, based on federal, provincial and industry data.

2012 Financial and Economic Review — July 2012

16

Appendix 1 — Economic Review

Table A1.1D Commodity Production Indicators

| | Lumber | | Timber scale | | Pulp | | Newsprint, etc | | Oil & natural | | Coal | | Solid mineral | | Electric pwr | | Farm cash | | Landed value of | |

| | production | | data | | shipments | | production | | gas production | | production | | shipments | | generated | | receipts | | seafood products | |

| | (thousand m3) | | (thousand m3) | | (000 tonnes) | | (000 tonnes) | | ($ millions) | | (000 tonnes) | | ($ millions) | | (GW.h) | | ($ millions) | | ($ millions) | |

1982 | | 23,855 | | — | | 2,662 | | 1,862 | | — | | 11,769 | | — | | 48,238 | | 962 | | 241 | |

1983 | | 30,773 | | — | | 3,221 | | 2,120 | | — | | 11,717 | | — | | 47,213 | | 917 | | 210 | |

1984 | | 30,884 | | — | | 2,836 | | 2,082 | | — | | 20,771 | | — | | 52,369 | | 1,005 | | 243 | |

1985 | | 32,994 | | — | | 3,298 | | 2,481 | | — | | 22,993 | | 2,524 | | 59,126 | | 1,061 | | 378 | |

1986 | | 31,468 | | — | | 3,628 | | 2,629 | | — | | 20,361 | | 2,512 | | 50,759 | | 1,106 | | 405 | |

1987 | | 37,336 | | — | | 4,136 | | 2,762 | | — | | 21,990 | | 2,896 | | 63,066 | | 1,122 | | 455 | |

1988 | | 36,736 | | — | | 4,141 | | 2,845 | | — | | 24,942 | | 3,325 | | 60,943 | | 1,206 | | 573 | |

1989 | | 35,952 | | — | | 4,189 | | 2,834 | | — | | 24,800 | | 3,344 | | 57,655 | | 1,255 | | 513 | |

1990 | | 33,514 | | — | | 3,547 | | 2,992 | | — | | 24,557 | | 3,092 | | 60,662 | | 1,299 | | 559 | |

1991 | | 31,406 | | — | | 4,014 | | 2,667 | | 858 | | 24,965 | | 2,950 | | 62,981 | | 1,342 | | 492 | |

1992 | | 33,396 | | — | | 3,825 | | 2,708 | | 890 | | 17,173 | | 2,577 | | 64,058 | | 1,404 | | 533 | |

1993 | | 33,935 | | — | | 4,040 | | 3,110 | | 1,089 | | 20,633 | | 2,415 | | 58,774 | | 1,446 | | 605 | |

1994 | | 33,671 | | — | | 4,763 | | 2,983 | | 1,270 | | 22,583 | | 2,632 | | 61,015 | | 1,538 | | 728 | |

1995 | | 32,611 | | 75,430 | | 4,572 | | 2,833 | | 1,040 | | 24,350 | | 3,438 | | 58,006 | | 1,586 | | 604 | |

1996 | | 32,671 | | 73,099 | | 4,390 | | 2,801 | | 1,333 | | 25,422 | | 3,004 | | 71,765 | | 1,706 | | 590 | |

1997 | | 31,562 | | 69,155 | | 4,532 | | 2,649 | | 1,588 | | 27,876 | | 3,047 | | 66,961 | | 1,738 | | 604 | |

1998 | | 30,238 | | 65,451 | | 4,462 | | 2,567 | | 1,574 | | 24,868 | | 2,893 | | 67,710 | | 1,780 | | 547 | |

1999 | | 32,397 | | 75,878 | | 4,995 | | 3,016 | | 2,091 | | 24,845 | | 2,445 | | 68,045 | | 1,885 | | 613 | |

2000 | | 34,346 | | 76,009 | | 5,152 | | 3,126 | | 4,783 | | 25,682 | | 2,891 | | 68,241 | | 2,024 | | 667 | |

2001 | | 32,606 | | 69,796 | | 4,710 | | 2,879 | | 5,666 | | 27,006 | | 2,867 | | 57,332 | | 2,201 | | 647 | |

2002 | | 35,501 | | 75,208 | | 4,477 | | 2,900 | | 4,251 | | 24,397 | | 2,864 | | 64,945 | | 2,174 | | 664 | |

2003 | | 36,031 | | 74,899 | | 4,762 | | 2,919 | | 6,230 | | 23,073 | | 2,887 | | 63,051 | | 2,248 | | 645 | |

2004 | | 39,879 | | 81,690 | | 4,724 | | 2,976 | | 6,784 | | 27,313 | | 3,740 | | 60,496 | | 2,360 | | 635 | |

2005 | | 41,013 | | 83,590 | | 4,932 | | 2,953 | | 8,967 | | 26,718 | | 5,384 | | 67,811 | | 2,388 | | 706 | |

2006 | | 41,051 | | 80,350 | | 4,736 | | 3,019 | | 7,148 | | 23,161 | | 5,991 | | 62,021 | | 2,346 | | 788 | |

2007 | | 36,677 | | 72,675 | | 4,717 | | 2,763 | | 6,912 | | 25,941 | | 5,611 | | 72,217 | | 2,391 | | 723 | |

2008 | | 28,192 | | 61,137 | | 4,021 | | 2,514 | | 9,240 | | 26,163 | | 7,403 | | 65,854 | | 2,523 | | 718 | |

2009 | | 22,975 | | 48,835 | | 3,708 | | 2,021 | | 4,129 | | 21,193 | | 5,622 | | 62,201 | | 2,532 | | 696 | |

2010 | | 27,095 | | 63,315 | | 4,277 | | 1,677 | | 4,433 | | 26,040 | | 7,166 | | 59,477 | | 2,534 | | 864 | |

2011 | | 29,137 | | 69,384 | | 4,491 | | 1,539 | | 4,835 | | 27,431 | | 8,592p | | 66,395 | | 2,636 | | n/a | |

| | | | | | | | | | | | | | | | | | | | | |

| | Lumber | | Timber scale | | Pulp | | Newsprint, etc | | Oil & natural | | Coal | | Solid mineral | | Electric pwr | | Farm cash | | Value of | |

| | production | | data | | shipments | | production | | gas production | | production | | shipments | | generated | | receipts | | seafood products | |

| | (% change) | | (% change) | | (% change) | | (% change) | | (% change) | | (% change) | | (% change) | | (% change) | | (% change) | | (% change) | |

1983 | | 29.0 | | — | | 21.0 | | 13.9 | | — | | (0.4 | ) | — | | (2.1 | ) | (4.7 | ) | (12.9 | ) |

1984 | | 0.4 | | — | | (12.0 | ) | (1.8 | ) | — | | 77.3 | | — | | 10.9 | | 9.6 | | 15.7 | |

1985 | | 6.8 | | — | | 16.3 | | 19.2 | | — | | 10.7 | | — | | 12.9 | | 5.7 | | 55.6 | |

1986 | | (4.6 | ) | — | | 10.0 | | 6.0 | | — | | (11.4 | ) | (0.5 | ) | (14.2 | ) | 4.2 | | 7.1 | |

1987 | | 18.6 | | — | | 14.0 | | 5.1 | | — | | 8.0 | | 15.3 | | 24.2 | | 1.4 | | 12.3 | |

1988 | | (1.6 | ) | — | | 0.1 | | 3.0 | | — | | 13.4 | | 14.8 | | (3.4 | ) | 7.6 | | 25.9 | |

1989 | | (2.1 | ) | — | | 1.2 | | (0.4 | ) | — | | (0.6 | ) | 0.6 | | (5.4 | ) | 4.0 | | (10.5 | ) |

1990 | | (6.8 | ) | — | | (15.3 | ) | 5.5 | | — | | (1.0 | ) | (7.5 | ) | 5.2 | | 3.5 | | 9.0 | |

1991 | | (6.3 | ) | — | | 13.2 | | (10.8 | ) | — | | 1.7 | | (4.6 | ) | 3.8 | | 3.3 | | (12.0 | ) |

1992 | | 6.3 | | — | | (4.7 | ) | 1.5 | | 3.7 | | (31.2 | ) | (12.6 | ) | 1.7 | | 4.7 | | 8.3 | |

1993 | | 1.6 | | — | | 5.6 | | 14.8 | | 22.4 | | 20.1 | | (6.3 | ) | (8.2 | ) | 3.0 | | 13.5 | |

1994 | | (0.8 | ) | — | | 17.9 | | (4.1 | ) | 16.6 | | 9.5 | | 9.0 | | 3.8 | | 6.4 | | 20.3 | |

1995 | | (3.1 | ) | — | | (4.0 | ) | (5.0 | ) | (18.1 | ) | 7.8 | | 30.6 | | (4.9 | ) | 3.1 | | (17.0 | ) |

1996 | | 0.2 | | (3.1 | ) | (4.0 | ) | (1.1 | ) | 28.2 | | 4.4 | | (12.6 | ) | 23.7 | | 7.6 | | (2.3 | ) |

1997 | | (3.4 | ) | (5.4 | ) | 3.2 | | (5.4 | ) | 19.1 | | 9.7 | | 1.4 | | (6.7 | ) | 1.9 | | 2.4 | |

1998 | | (4.2 | ) | (5.4 | ) | (1.5 | ) | (3.1 | ) | (0.9 | ) | (10.8 | ) | (5.1 | ) | 1.1 | | 2.4 | | (9.4 | ) |

1999 | | 7.1 | | 15.9 | | 11.9 | | 17.5 | | 32.8 | | (0.1 | ) | (15.5 | ) | 0.5 | | 5.9 | | 12.1 | |

2000 | | 6.0 | | 0.2 | | 3.1 | | 3.6 | | 128.7 | | 3.4 | | 18.2 | | 0.3 | | 7.4 | | 8.8 | |

2001 | | (5.1 | ) | (8.2 | ) | (8.6 | ) | (7.9 | ) | 18.5 | | 5.2 | | (0.8 | ) | (16.0 | ) | 8.7 | | (3.0 | ) |

2002 | | 8.9 | | 7.8 | | (4.9 | ) | 0.7 | | (25.0 | ) | (9.7 | ) | (0.1 | ) | 13.3 | | (1.2 | ) | 2.6 | |

2003 | | 1.5 | | (0.4 | ) | 6.4 | | 0.7 | | 46.6 | | (5.4 | ) | 0.8 | | (2.9 | ) | 3.4 | | (2.9 | ) |

2004 | | 10.7 | | 9.1 | | (0.8 | ) | 2.0 | | 8.9 | | 18.4 | | 29.5 | | (4.1 | ) | 5.0 | | (1.6 | ) |

2005 | | 2.8 | | 2.3 | | 4.4 | | (0.8 | ) | 32.2 | | (2.2 | ) | 44.0 | | 12.1 | | 1.2 | | 11.2 | |

2006 | | 0.1 | | (3.9 | ) | (4.0 | ) | 2.2 | | (20.3 | ) | (13.3 | ) | 11.3 | | (8.5 | ) | (1.7 | ) | 11.6 | |

2007 | | (10.7 | ) | (9.6 | ) | (0.4 | ) | (8.5 | ) | (3.3 | ) | 12.0 | | (6.3 | ) | 16.4 | | 1.9 | | (8.2 | ) |

2008 | | (23.1 | ) | (15.9 | ) | (14.8 | ) | (9.0 | ) | 33.7 | | 0.9 | | 31.9 | | (8.8 | ) | 5.5 | | (0.7 | ) |

2009 | | (18.5 | ) | (20.1 | ) | (7.8 | ) | (19.6 | ) | (55.3 | ) | (19.0 | ) | (24.1 | ) | (5.5 | ) | 0.3 | | (3.1 | ) |

2010 | | 17.9 | | 29.7 | | 15.3 | | (17.0 | ) | 7.4 | | 22.9 | | 25.8 | | (4.4 | ) | 0.1 | | 24.1 | |

2011 | | 7.5 | | 9.6 | | 5.0 | | (8.2 | ) | 9.1 | | 5.3 | | 25.8 | | 11.6 | | 4.0 | | n/a | |

Sources: Statistics Canada and BC Stats, Ministry of Finance, based on federal, provincial and industry data.

2012 Financial and Economic Review — July 2012

17

Appendix 1 — Economic Review

Table A1.2 British Columbia Real GDP at Market Prices, Expenditure Based

| | | | | | | | | | Machinery and | | | | | | | | | |

| | Consumer | | Government | | Residential | | Non-Residential | | Equipment | | Business | | | | | | | |

| | Expenditure | | Expenditure | | Investment | | Investment | | Investment | | Investment | | Exports | | Imports | | Real GDP | |

| | (millions of 2002 $, chained) | |

1988 | | 57,649 | | 20,887 | | 6,647 | | 4,846 | | 4,453 | | 15,844 | | 41,153 | | 40,168 | | 96,824 | |

1989 | | 61,216 | | 21,259 | | 7,651 | | 5,370 | | 5,295 | | 18,245 | | 40,426 | | 43,926 | | 100,007 | |

1990 | | 63,788 | | 22,152 | | 7,790 | | 5,325 | | 5,330 | | 18,379 | | 40,078 | | 45,889 | | 101,408 | |

1991 | | 63,972 | | 23,548 | | 7,368 | | 5,593 | | 5,254 | | 18,119 | | 40,825 | | 46,431 | | 101,593 | |

1992 | | 66,034 | | 24,415 | | 9,056 | | 4,388 | | 5,138 | | 18,674 | | 42,286 | | 48,547 | | 104,216 | |

1993 | | 68,115 | | 24,775 | | 9,289 | | 4,186 | | 5,150 | | 18,760 | | 44,034 | | 48,195 | | 108,874 | |

1994 | | 70,986 | | 24,868 | | 9,342 | | 5,388 | | 5,888 | | 20,605 | | 46,727 | | 55,624 | | 111,945 | |

1995 | | 72,960 | | 24,487 | | 8,224 | | 5,421 | | 5,972 | | 19,541 | | 49,407 | | 56,261 | | 114,620 | |

1996 | | 75,660 | | 25,144 | | 8,350 | | 4,859 | | 5,792 | | 18,981 | | 49,936 | | 55,930 | | 117,442 | |

1997 | | 78,443 | | 25,057 | | 8,783 | | 6,277 | | 6,781 | | 21,757 | | 51,917 | | 59,953 | | 121,177 | |

1998 | | 79,749 | | 25,743 | | 7,601 | | 5,099 | | 7,321 | | 20,013 | | 53,381 | | 59,318 | | 122,766 | |

1999 | | 81,984 | | 25,614 | | 7,016 | | 5,420 | | 7,652 | | 20,093 | | 58,065 | | 62,938 | | 126,708 | |

2000 | | 84,482 | | 26,672 | | 7,090 | | 5,423 | | 8,188 | | 20,713 | | 63,050 | | 67,745 | | 132,578 | |

2001 | | 86,296 | | 27,952 | | 7,752 | | 6,343 | | 8,284 | | 22,389 | | 61,927 | | 67,912 | | 133,403 | |

2002 | | 89,238 | | 28,260 | | 8,982 | | 5,890 | | 8,021 | | 22,893 | | 62,706 | | 68,144 | | 138,193 | |

2003 | | 92,250 | | 28,357 | | 9,969 | | 6,620 | | 8,133 | | 24,747 | | 63,918 | | 71,816 | | 141,435 | |

2004 | | 96,187 | | 28,346 | | 11,459 | | 7,222 | | 8,841 | | 27,587 | | 67,013 | | 77,380 | | 146,541 | |

2005 | | 100,180 | | 28,606 | | 12,184 | | 7,539 | | 10,577 | | 30,166 | | 70,162 | | 82,051 | | 153,489 | |

2006 | | 106,222 | | 29,127 | | 13,049 | | 8,861 | | 11,943 | | 33,637 | | 72,341 | | 88,328 | | 159,729 | |

2007 | | 111,787 | | 30,338 | | 13,266 | | 8,791 | | 12,983 | | 34,564 | | 74,546 | | 93,626 | �� | 164,496 | |

2008 | | 114,489 | | 31,865 | | 12,713 | | 10,019 | | 13,138 | | 35,383 | | 72,110 | | 94,602 | | 165,641 | |

2009 | | 114,834 | | 32,901 | | 11,304 | | 8,519 | | 9,553 | | 29,531 | | 66,392 | | 86,257 | | 162,225 | |

2010 | | 119,193 | | 33,433 | | 11,853 | | 10,831 | | 10,694 | | 33,631 | | 70,364 | | 94,754 | | 167,140 | |

2011 | | n/a | | n/a | | n/a | | n/a | | n/a | | n/a | | n/a | | n/a | | n/a | |

| | (annual percentage change) | |

1988 | | 5.0 | | 6.4 | | 11.4 | | 21.2 | | 30.1 | | 20.0 | | 5.8 | | 8.3 | | 5.8 | |

1989 | | 6.2 | | 1.8 | | 15.1 | | 10.8 | | 18.9 | | 15.2 | | (1.8 | ) | 9.4 | | 3.3 | |

1990 | | 4.2 | | 4.2 | | 1.8 | | (0.8 | ) | 0.7 | | 0.7 | | (0.9 | ) | 4.5 | | 1.4 | |

1991 | | 0.3 | | 6.3 | | (5.4 | ) | 5.0 | | (1.4 | ) | (1.4 | ) | 1.9 | | 1.2 | | 0.2 | |

1992 | | 3.2 | | 3.7 | | 22.9 | | (21.5 | ) | (2.2 | ) | 3.1 | | 3.6 | | 4.6 | | 2.6 | |

1993 | | 3.2 | | 1.5 | | 2.6 | | (4.6 | ) | 0.2 | | 0.5 | | 4.1 | | (0.7 | ) | 4.5 | |

1994 | | 4.2 | | 0.4 | | 0.6 | | 28.7 | | 14.3 | | 9.8 | | 6.1 | | 15.4 | | 2.8 | |

1995 | | 2.8 | | (1.5 | ) | (12.0 | ) | 0.6 | | 1.4 | | (5.2 | ) | 5.7 | | 1.1 | | 2.4 | |

1996 | | 3.7 | | 2.7 | | 1.5 | | (10.4 | ) | (3.0 | ) | (2.9 | ) | 1.1 | | (0.6 | ) | 2.5 | |

1997 | | 3.7 | | (0.3 | ) | 5.2 | | 29.2 | | 17.1 | | 14.6 | | 4.0 | | 7.2 | | 3.2 | |

1998 | | 1.7 | | 2.7 | | (13.5 | ) | (18.8 | ) | 8.0 | | (8.0 | ) | 2.8 | | (1.1 | ) | 1.3 | |

1999 | | 2.8 | | (0.5 | ) | (7.7 | ) | 6.3 | | 4.5 | | 0.4 | | 8.8 | | 6.1 | | 3.2 | |

2000 | | 3.0 | | 4.1 | | 1.1 | | 0.1 | | 7.0 | | 3.1 | | 8.6 | | 7.6 | | 4.6 | |

2001 | | 2.1 | | 4.8 | | 9.3 | | 17.0 | | 1.2 | | 8.1 | | (1.8 | ) | 0.2 | | 0.6 | |

2002 | | 3.4 | | 1.1 | | 15.9 | | (7.1 | ) | (3.2 | ) | 2.3 | | 1.3 | | 0.3 | | 3.6 | |

2003 | | 3.4 | | 0.3 | | 11.0 | | 12.4 | | 1.4 | | 8.1 | | 1.9 | | 5.4 | | 2.3 | |

2004 | | 4.3 | | (0.0 | ) | 14.9 | | 9.1 | | 8.7 | | 11.5 | | 4.8 | | 7.7 | | 3.6 | |

2005 | | 4.2 | | 0.9 | | 6.3 | | 4.4 | | 19.6 | | 9.3 | | 4.7 | | 6.0 | | 4.7 | |

2006 | | 6.0 | | 1.8 | | 7.1 | | 17.5 | | 12.9 | | 11.5 | | 3.1 | | 7.7 | | 4.1 | |

2007 | | 5.2 | | 4.2 | | 1.7 | | (0.8 | ) | 8.7 | | 2.8 | | 3.0 | | 6.0 | | 3.0 | |

2008 | | 2.4 | | 5.0 | | (4.2 | ) | 14.0 | | 1.2 | | 2.4 | | (3.3 | ) | 1.0 | | 0.7 | |

2009 | | 0.3 | | 3.3 | | (11.1 | ) | (15.0 | ) | (27.3 | ) | (16.5 | ) | (7.9 | ) | (8.8 | ) | (2.1 | ) |

2010 | | 3.8 | | 1.6 | | 4.9 | | 27.1 | | 11.9 | | 13.9 | | 6.0 | | 9.9 | | 3.0 | |

2011 | | n/a | | n/a | | n/a | | n/a | | n/a | | n/a | | n/a | | n/a | | n/a | |

Source: Statistics Canada

2012 Financial and Economic Review — July 2012

18

Appendix 1 — Economic Review

Table A1.3 British Columbia GDP at Basic Prices, by Industry

| | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Crop and | | Fishing, | | Forestry | | Mining, | | | | | | | | Transportation | | Wholesale | | Finance, | | | | | | Real GDP | |

| | Animal | | Hunting and | | and | | Oil and Gas | | | | | | | | and | | and Retail | | Insurance and | | Other | | Public | | at Basic | |

| | Production | | Trapping | | Logging | | Extraction | | Manufacturing | | Construction | | Utilities | | Warehousing | | Trade | | Real Estate | | Services | | Administration | | Prices | |

| | (millions of 2002 $, chained) | |

1998 | | 909 | | 153 | | 2,952 | | 3,324 | | 11,255 | | 6,101 | | 2,991 | | 7,273 | | 11,977 | | 25,076 | | 34,223 | | 6,339 | | 112,913 | |

1999 | | 979 | | 118 | | 2,789 | | 3,329 | | 12,840 | | 5,881 | | 3,040 | | 7,575 | | 12,158 | | 25,838 | | 34,762 | | 6,588 | | 116,307 | |

2000 | | 975 | | 135 | | 2,638 | | 3,344 | | 14,990 | | 5,795 | | 3,058 | | 8,122 | | 12,689 | | 26,284 | | 36,157 | | 6,790 | | 121,546 | |

2001 | | 1,141 | | 111 | | 2,647 | | 4,252 | | 13,667 | | 6,021 | | 2,389 | | 7,997 | | 13,055 | | 27,019 | | 37,079 | | 6,919 | | 122,848 | |

2002 | | 1,058 | | 134 | | 2,713 | | 4,383 | | 13,687 | | 6,328 | | 2,837 | | 8,072 | | 13,566 | | 28,078 | | 38,253 | | 7,128 | | 126,761 | |

2003 | | 1,053 | | 130 | | 2,761 | | 4,298 | | 13,884 | | 6,927 | | 2,844 | | 8,135 | | 14,114 | | 28,884 | | 39,272 | | 7,188 | | 130,026 | |

2004 | | 1,057 | | 150 | | 3,129 | | 4,270 | | 14,723 | | 7,675 | | 2,819 | | 8,447 | | 14,710 | | 30,503 | | 39,955 | | 7,202 | | 135,021 | |

2005 | | 1,061 | | 146 | | 3,102 | | 4,643 | | 15,435 | | 8,115 | | 3,236 | | 9,208 | | 15,436 | | 31,834 | | 41,266 | | 7,268 | | 141,339 | |

2006 | | 1,078 | | 164 | | 3,022 | | 4,645 | | 15,904 | | 8,936 | | 2,882 | | 9,390 | | 16,464 | | 33,290 | | 42,945 | | 7,506 | | 146,762 | |

2007 | | 1,134 | | 128 | | 2,855 | | 4,422 | | 15,885 | | 9,097 | | 3,268 | | 9,412 | | 17,469 | | 34,698 | | 44,533 | | 7,772 | | 150,874 | |

2008 | | 1,147 | | 107 | | 2,463 | | 4,598 | | 14,546 | | 9,501 | | 3,185 | | 9,207 | | 17,209 | | 35,201 | | 45,689 | | 8,090 | | 151,695 | |

2009 | | 1,157 | | 108 | | 2,168 | | 4,293 | | 12,657 | | 8,617 | | 3,057 | | 8,977 | | 16,360 | | 36,603 | | 45,394 | | 8,261 | | 148,300 | |

2010 | | 1,156 | | 98 | | 2,514 | | 4,595 | | 13,156 | | 9,673 | | 2,945 | | 9,234 | | 16,833 | | 37,636 | | 46,011 | | 8,409 | | 153,085 | |

2011 | | 1,128 | | 105 | | 2,797 | | 4,873 | | 13,562 | | 10,323 | | 3,219 | | 9,615 | | 17,070 | | 38,851 | | 46,505 | | 8,509 | | 157,525 | |

| | (annual percentage change) | |

1998 | | (4.8 | ) | (35.1 | ) | 0.6 | | 6.0 | | (2.2 | ) | (7.8 | ) | 2.6 | | 1.4 | | 5.2 | | 1.3 | | 2.9 | | 1.0 | | 1.2 | |

1999 | | 7.7 | | (23.0 | ) | (5.5 | ) | 0.2 | | 14.1 | | (3.6 | ) | 1.7 | | 4.1 | | 1.5 | | 3.0 | | 1.6 | | 3.9 | | 3.0 | |

2000 | | (0.4 | ) | 14.6 | | (5.4 | ) | 0.5 | | 16.7 | | (1.5 | ) | 0.6 | | 7.2 | | 4.4 | | 1.7 | | 4.0 | | 3.1 | | 4.5 | |

2001 | | 17.0 | | (17.5 | ) | 0.3 | | 27.1 | | (8.8 | ) | 3.9 | | (21.9 | ) | (1.5 | ) | 2.9 | | 2.8 | | 2.6 | | 1.9 | | 1.1 | |

2002 | | (7.3 | ) | 21.0 | | 2.5 | | 3.1 | | 0.1 | | 5.1 | | 18.7 | | 0.9 | | 3.9 | | 3.9 | | 3.2 | | 3.0 | | 3.2 | |

2003 | | (0.4 | ) | (3.0 | ) | 1.8 | | (1.9 | ) | 1.4 | | 9.5 | | 0.3 | | 0.8 | | 4.0 | | 2.9 | | 2.7 | | 0.8 | | 2.6 | |

2004 | | 0.4 | | 15.3 | | 13.3 | | (0.7 | ) | 6.0 | | 10.8 | | (0.9 | ) | 3.8 | | 4.2 | | 5.6 | | 1.7 | | 0.2 | | 3.8 | |

2005 | | 0.4 | | (2.5 | ) | (0.9 | ) | 8.7 | | 4.8 | | 5.7 | | 14.8 | | 9.0 | | 4.9 | | 4.4 | | 3.3 | | 0.9 | | 4.7 | |

2006 | | 1.6 | | 12.2 | | (2.6 | ) | 0.0 | | 3.0 | | 10.1 | | (10.9 | ) | 2.0 | | 6.7 | | 4.6 | | 4.1 | | 3.3 | | 3.8 | |

2007 | | 5.2 | | (22.2 | ) | (5.5 | ) | (4.8 | ) | (0.1 | ) | 1.8 | | 13.4 | | 0.2 | | 6.1 | | 4.2 | | 3.7 | | 3.5 | | 2.8 | |

2008 | | 1.2 | | (16.5 | ) | (13.7 | ) | 4.0 | | (8.4 | ) | 4.5 | | (2.6 | ) | (2.2 | ) | (1.5 | ) | 1.5 | | 2.6 | | 4.1 | | 0.5 | |

2009 | | 0.9 | | 1.4 | | (12.0 | ) | (6.6 | ) | (13.0 | ) | (9.3 | ) | (4.0 | ) | (2.5 | ) | (4.9 | ) | 4.0 | | (0.6 | ) | 2.1 | | (2.2 | ) |

2010 | | (0.1 | ) | (10.0 | ) | 16.0 | | 7.0 | | 3.9 | | 12.3 | | (3.7 | ) | 2.9 | | 2.9 | | 2.8 | | 1.4 | | 1.8 | | 3.2 | |

2011 | | (2.4 | ) | 7.4 | | 11.2 | | 6.0 | | 3.1 | | 6.7 | | 9.3 | | 4.1 | | 1.4 | | 3.2 | | 1.1 | | 1.2 | | 2.9 | |

Source: Statistics Canada

2012 Financial and Economic Review — July 2012

19

Appendix 1 — Economic Review

Table A1.4 British Columbia GDP, Income Based

| | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | Interest and | | Accrued Net | | Net Income of | | | | | | Indirect | | Capital Cons. | | | | | | | |

| | | | Corporation | | Miscellaneous | | Income of | | Non-farm | | Inventory | | Net Domestic | | Taxes | | Allowances and | | | | GDP | | GDP at | |

| | Labour | | Profits before | | Investment | | Farm | | unincorporated | | Valuation | | Product at | | less | | Misc. Valuation | | Statistical | | at Market | | Basic | |

| | Income | | Taxes | | Income | | Operators | | Business | | Adjustment | | Basic Prices | | Subsidies | | Adjustments | | Discrepency | | Prices | | Prices | |

| | ($ millions) | |

1986 | | 30,339 | | 4,213 | | 4,893 | | 113 | | 3,745 | | (212 | ) | 45,603 | | 6,098 | | 7,337 | | 21 | | 56,547 | | 52,961 | |

1987 | | 32,837 | | 6,430 | | 5,085 | | 115 | | 3,954 | | (324 | ) | 50,679 | | 6,696 | | 7,517 | | 205 | | 62,515 | | 58,401 | |

1988 | | 36,110 | | 7,250 | | 5,820 | | 154 | | 4,283 | | (285 | ) | 56,076 | | 7,486 | | 8,044 | | 546 | | 69,408 | | 64,666 | |

1989 | | 40,295 | | 5,925 | | 7,183 | | 72 | | 4,580 | | (195 | ) | 60,769 | | 8,765 | | 8,748 | | 209 | | 75,582 | | 69,726 | |

1990 | | 44,216 | | 3,670 | | 7,887 | | 73 | | 4,796 | | 120 | | 63,803 | | 9,007 | | 9,590 | | (9 | ) | 79,350 | | 73,384 | |

1991 | | 46,296 | | 2,926 | | 7,650 | | 106 | | 5,067 | | (107 | ) | 64,888 | | 9,715 | | 10,016 | | 180 | | 81,849 | | 75,084 | |

1992 | | 48,924 | | 3,321 | | 7,586 | | 80 | | 5,563 | | (616 | ) | 68,325 | | 11,092 | | 10,601 | | 691 | | 87,242 | | 79,617 | |

1993 | | 51,312 | | 4,328 | | 8,035 | | 83 | | 6,034 | | (843 | ) | 72,905 | | 12,440 | | 11,258 | | 1,430 | | 94,077 | | 85,593 | |

1994 | | 53,972 | | 6,756 | | 8,649 | | 63 | | 6,665 | | (660 | ) | 79,662 | | 13,164 | | 12,043 | | (140 | ) | 100,512 | | 91,565 | |

1995 | | 56,768 | | 7,419 | | 8,808 | | 87 | | 6,758 | | (167 | ) | 83,942 | | 13,522 | | 12,882 | | (407 | ) | 105,670 | | 96,417 | |

1996 | | 58,517 | | 7,246 | | 8,731 | | 59 | | 7,173 | | (231 | ) | 85,950 | | 14,014 | | 13,494 | | (138 | ) | 108,865 | | 99,306 | |

1997 | | 60,681 | | 8,286 | | 8,444 | | 89 | | 7,780 | | 101 | | 90,040 | | 14,480 | | 14,526 | | (4 | ) | 114,383 | | 104,562 | |

1998 | | 61,965 | | 7,335 | | 8,355 | | 166 | | 8,285 | | (24 | ) | 90,860 | | 14,515 | | 15,050 | | (6 | ) | 115,641 | | 105,904 | |

1999 | | 64,045 | | 9,309 | | 8,365 | | 199 | | 8,723 | | (373 | ) | 95,125 | | 14,972 | | 15,659 | | 22 | | 120,921 | | 110,806 | |

2000 | | 68,369 | | 11,596 | | 10,184 | | 54 | | 9,078 | | (80 | ) | 104,232 | | 15,608 | | 16,526 | | (2 | ) | 131,333 | | 120,756 | |

2001 | | 70,044 | | 11,392 | | 8,834 | | 141 | | 9,637 | | 47 | | 105,163 | | 15,810 | | 17,539 | | 70 | | 133,514 | | 122,772 | |

2002 | | 72,900 | | 11,389 | | 8,828 | | 53 | | 10,591 | | (369 | ) | 108,406 | | 16,443 | | 18,341 | | 17 | | 138,193 | | 126,764 | |

2003 | | 75,605 | | 12,364 | | 9,151 | | 83 | | 11,312 | | 637 | | 114,303 | | 17,580 | | 18,956 | | (46 | ) | 145,642 | | 133,213 | |

2004 | | 80,599 | | 16,764 | | 9,708 | | 118 | | 12,256 | | (66 | ) | 124,831 | | 18,664 | | 19,720 | | (88 | ) | 157,675 | | 144,463 | |

2005 | | 85,805 | | 19,631 | | 10,418 | | 9 | | 13,061 | | 147 | | 134,821 | | 19,881 | | 20,773 | | (61 | ) | 169,664 | | 155,533 | |

2006 | | 93,963 | | 22,408 | | 9,910 | | (31 | ) | 13,702 | | (409 | ) | 145,566 | | 20,899 | | 21,895 | | (86 | ) | 182,251 | | 167,375 | |

2007 | | 98,573 | | 21,951 | | 11,128 | | (55 | ) | 14,411 | | 475 | | 152,915 | | 22,250 | | 23,346 | | 38 | | 192,117 | | 176,299 | |

2008 | | 102,468 | | 24,892 | | 12,018 | | (118 | ) | 14,507 | | (1,022 | ) | 159,496 | | 21,634 | | 25,054 | | 8 | | 199,441 | | 184,558 | |

2009 | | 100,629 | | 17,778 | | 8,784 | | (46 | ) | 16,151 | | 754 | | 150,979 | | 21,699 | | 26,007 | | 107 | | 191,863 | | 177,093 | |

2010 | | 104,630 | | 21,608 | | 8,894 | | (38 | ) | 17,609 | | 548 | | 160,401 | | 22,787 | | 27,214 | | (105 | ) | 203,147 | | 187,510 | |

2011 | | n/a | | n/a | | n/a | | n/a | | n/a | | n/a | | n/a | | n/a | | n/a | | n/a | | n/a | | n/a | |

| | (annual percentage change) | |

1986 | | 4.3 | | 21.5 | | (0.9 | ) | — | | 9.1 | | — | | 5.2 | | 3.7 | | 6.1 | | — | | 5.6 | | 5.5 | |

1987 | | 8.2 | | 52.6 | | 3.9 | | — | | 5.6 | | — | | 11.1 | | 9.8 | | 2.5 | | — | | 10.6 | | 10.3 | |

1988 | | 10.0 | | 12.8 | | 14.5 | | — | | 8.3 | | — | | 10.6 | | 11.8 | | 7.0 | | — | | 11.0 | | 10.7 | |

1989 | | 11.6 | | (18.3 | ) | 23.4 | | — | | 6.9 | | — | | 8.4 | | 17.1 | | 8.8 | | — | | 8.9 | | 7.8 | |

1990 | | 9.7 | | (38.1 | ) | 9.8 | | — | | 4.7 | | — | | 5.0 | | 2.8 | | 9.6 | | — | | 5.0 | | 5.2 | |

1991 | | 4.7 | | (20.3 | ) | (3.0 | ) | — | | 5.7 | | — | | 1.7 | | 7.9 | | 4.4 | | — | | 3.1 | | 2.3 | |

1992 | | 5.7 | | 13.5 | | (0.8 | ) | — | | 9.8 | | — | | 5.3 | | 14.2 | | 5.8 | | — | | 6.6 | | 6.0 | |

1993 | | 4.9 | | 30.3 | | 5.9 | | — | | 8.5 | | — | | 6.7 | | 12.2 | | 6.2 | | — | | 7.8 | | 7.5 | |

1994 | | 5.2 | | 56.1 | | 7.6 | | — | | 10.5 | | — | | 9.3 | | 5.8 | | 7.0 | | — | | 6.8 | | 7.0 | |

1995 | | 5.2 | | 9.8 | | 1.8 | | — | | 1.4 | | — | | 5.4 | | 2.7 | | 7.0 | | — | | 5.1 | | 5.3 | |

1996 | | 3.1 | | (2.3 | ) | (0.9 | ) | — | | 6.1 | | — | | 2.4 | | 3.6 | | 4.8 | | — | | 3.0 | | 3.0 | |

1997 | | 3.7 | | 14.4 | | (3.3 | ) | — | | 8.5 | | — | | 4.8 | | 3.3 | | 7.6 | | — | | 5.1 | | 5.3 | |

1998 | | 2.1 | | (11.5 | ) | (1.1 | ) | — | | 6.5 | | — | | 0.9 | | 0.2 | | 3.6 | | — | | 1.1 | | 1.3 | |

1999 | | 3.4 | | 26.9 | | 0.1 | | — | | 5.3 | | — | | 4.7 | | 3.1 | | 4.0 | | — | | 4.6 | | 4.6 | |

2000 | | 6.8 | | 24.6 | | 21.7 | | — | | 4.1 | | — | | 9.6 | | 4.2 | | 5.5 | | — | | 8.6 | | 9.0 | |

2001 | | 2.4 | | (1.8 | ) | (13.3 | ) | — | | 6.2 | | — | | 0.9 | | 1.3 | | 6.1 | | — | | 1.7 | | 1.7 | |

2002 | | 4.1 | | (0.0 | ) | (0.1 | ) | — | | 9.9 | | — | | 3.1 | | 4.0 | | 4.6 | | — | | 3.5 | | 3.3 | |

2003 | | 3.7 | | 8.6 | | 3.7 | | — | | 6.8 | | — | | 5.4 | | 6.9 | | 3.4 | | — | | 5.4 | | 5.1 | |

2004 | | 6.6 | | 35.6 | | 6.1 | | — | | 8.3 | | — | | 9.2 | | 6.2 | | 4.0 | | — | | 8.3 | | 8.4 | |

2005 | | 6.5 | | 17.1 | | 7.3 | | — | | 6.6 | | — | | 8.0 | | 6.5 | | 5.3 | | — | | 7.6 | | 7.7 | |

2006 | | 9.5 | | 14.1 | | (4.9 | ) | — | | 4.9 | | — | | 8.0 | | 5.1 | | 5.4 | | — | | 7.4 | | 7.6 | |

2007 | | 4.9 | | (2.0 | ) | 12.3 | | — | | 5.2 | | — | | 5.0 | | 6.5 | | 6.6 | | — | | 5.4 | | 5.3 | |

2008 | | 4.0 | | 13.4 | | 8.0 | | — | | 0.7 | | — | | 4.3 | | (2.8 | ) | 7.3 | | — | | 3.8 | | 4.7 | |

2009 | | (1.8 | ) | (28.6 | ) | (26.9 | ) | — | | 11.3 | | — | | (5.3 | ) | 0.3 | | 3.8 | | — | | (3.8 | ) | (4.0 | ) |

2010 | | 4.0 | | 21.5 | | 1.3 | | — | | 9.0 | | — | | 6.2 | | 5.0 | | 4.6 | | — | | 5.9 | | 5.9 | |

2011 | | n/a | | n/a | | n/a | | n/a | | n/a | | n/a | | n/a | | n/a | | n/a | | n/a | | n/a | | n/a | |

Source: Statistics Canada

2012 Financial and Economic Review — July 2012

20

Appendix 1 — Economic Review

Table A1.5 Employment by Industry in British Columbia

| | 2001 | | 2002 | | 2003 | | 2004 | | 2005 | | 2006 | | 2007 | | 2008 | | 2009 | | 2010 | | 2011 | |

| | (thousands) | |

Total — all industries | | 1,920 | | 1,953 | | 1,998 | | 2,033 | | 2,092 | | 2,147 | | 2,223 | | 2,266 | | 2,218 | | 2,257 | | 2,275 | |

| | | | | | | | | | | | | | | | | | | | | | | |

Primary industries | | 66 | | 67 | | 78 | | 72 | | 76 | | 78 | | 83 | | 78 | | 73 | | 73 | | 66 | |

Agriculture | | 25 | | 30 | | 33 | | 37 | | 39 | | 35 | | 36 | | 33 | | 33 | | 32 | | 26 | |

Forestry, logging & support activities | | 25 | | 25 | | 27 | | 21 | | 21 | | 21 | | 24 | | 17 | | 14 | | 16 | | 14 | |

Fishing, hunting and trapping | | 5 | | 3 | | 4 | | 3 | | 2 | | 3 | | 3 | | 2 | | 2 | | 2 | | — | |

Mining and oil & gas extraction | | 11 | | 9 | | 13 | | 11 | | 14 | | 19 | | 20 | | 25 | | 24 | | 23 | | 25 | |

| | | | | | | | | | | | | | | | | | | | | | | |

Manufacturing | | 194 | | 194 | | 203 | | 206 | | 195 | | 193 | | 199 | | 185 | | 161 | | 166 | | 164 | |

Food, beverages & tobacco | | 26 | | 27 | | 31 | | 31 | | 31 | | 24 | | 28 | | 30 | | 29 | | 27 | | 30 | |

Wood products | | 49 | | 44 | | 48 | | 46 | | 45 | | 44 | | 44 | | 34 | | 27 | | 29 | | 30 | |

Paper | | 15 | | 17 | | 14 | | 12 | | 12 | | 15 | | 15 | | 13 | | 11 | | 10 | | 9 | |

Printing & related support activities | | 9 | | 8 | | 8 | | 8 | | 8 | | 8 | | 6 | | 9 | | 8 | | 7 | | 8 | |

Primary metals | | 8 | | 6 | | 9 | | 7 | | 7 | | 7 | | 6 | | 5 | | 5 | | 7 | | 6 | |

Metal fabrication | | 13 | | 13 | | 14 | | 14 | | 18 | | 15 | | 15 | | 16 | | 13 | | 13 | | 11 | |

Transportation equipment | | 10 | | 13 | | 12 | | 11 | | 9 | | 10 | | 12 | | 10 | | 10 | | 9 | | 9 | |

Machinery manufacturing | | 7 | | 10 | | 9 | | 9 | | 10 | | 9 | | 9 | | 6 | | 6 | | 8 | | 9 | |

Other manufacturing | | 57 | | 57 | | 59 | | 67 | | 55 | | 62 | | 65 | | 59 | | 50 | | 57 | | 51 | |

| | | | | | | | | | | | | | | | | | | | | | | |

Construction | | 111 | | 117 | | 117 | | 142 | | 163 | | 174 | | 192 | | 215 | | 193 | | 191 | | 205 | |

General contractors | | 40 | | 41 | | 46 | | 50 | | 64 | | 64 | | 65 | | 83 | | 73 | | 75 | | 83 | |

Special trade contractors | | 71 | | 75 | | 71 | | 91 | | 99 | | 110 | | 127 | | 132 | | 120 | | 115 | | 122 | |

| | | | | | | | | | | | | | | | | | | | | | | |

Utilities | | 11 | | 11 | | 11 | | 9 | | 10 | | 8 | | 10 | | 13 | | 12 | | 14 | | 13 | |

| | | | | | | | | | | | | | | | | | | | | | | |

Transportation and warehousing | | 113 | | 111 | | 117 | | 117 | | 119 | | 117 | | 124 | | 124 | | 113 | | 119 | | 124 | |

Transportation | | 109 | | 106 | | 111 | | 112 | | 115 | | 110 | | 117 | | 118 | | 107 | | 112 | | 116 | |

Warehousing and storage | | 4 | | 5 | | 6 | | 5 | | 5 | | 6 | | 7 | | 6 | | 6 | | 7 | | 8 | |

| | | | | | | | | | | | | | | | | | | | | | | |

Trade | | 303 | | 320 | | 326 | | 311 | | 326 | | 343 | | 359 | | 349 | | 362 | | 370 | | 355 | |

Wholesale trade | | 67 | | 72 | | 76 | | 65 | | 78 | | 80 | | 80 | | 86 | | 86 | | 82 | | 78 | |

Retail trade | | 236 | | 247 | | 250 | | 246 | | 248 | | 263 | | 279 | | 263 | | 275 | | 288 | | 277 | |

| | | | | | | | | | | | | | | | | | | | | | | |

Finance, Insurance, Real Estate & Leasing | | 121 | | 125 | | 126 | | 129 | | 132 | | 133 | | 142 | | 143 | | 139 | | 142 | | 139 | |

Finance | | 56 | | 57 | | 60 | | 56 | | 59 | | 59 | | 67 | | 63 | | 59 | | 67 | | 54 | |

Insurance | | 25 | | 24 | | 21 | | 27 | | 26 | | 26 | | 29 | | 30 | | 28 | | 28 | | 32 | |

Real estate | | 28 | | 33 | | 34 | | 35 | | 35 | | 38 | | 37 | | 40 | | 42 | | 38 | | 44 | |

Leasing | | 12 | | 11 | | 11 | | 11 | | 13 | | 10 | | 10 | | 11 | | 10 | | 9 | | 10 | |

| | | | | | | | | | | | | | | | | | | | | | | |

Public administration | | 91 | | 90 | | 95 | | 98 | | 94 | | 90 | | 93 | | 100 | | 105 | | 111 | | 109 | |

Federal administration | | 31 | | 33 | | 37 | | 34 | | 33 | | 34 | | 34 | | 37 | | 39 | | 46 | | 44 | |

Provincial administration | | 33 | | 27 | | 29 | | 29 | | 30 | | 27 | | 26 | | 26 | | 27 | | 28 | | 25 | |

Local administration | | 27 | | 29 | | 29 | | 34 | | 32 | | 29 | | 33 | | 37 | | 40 | | 37 | | 40 | |

| | | | | | | | | | | | | | | | | | | | | | | |

Other service industries | | 910 | | 918 | | 925 | | 950 | | 977 | | 1,011 | | 1,021 | | 1,060 | | 1,060 | | 1,072 | | 1,100 | |

Education & related services | | 136 | | 136 | | 137 | | 132 | | 143 | | 152 | | 154 | | 157 | | 161 | | 167 | | 167 | |

Health & welfare services | | 196 | | 211 | | 214 | | 218 | | 212 | | 230 | | 234 | | 241 | | 257 | | 264 | | 261 | |

Professional, scientific & technical | | 139 | | 134 | | 138 | | 142 | | 159 | | 165 | | 164 | | 169 | | 164 | | 174 | | 182 | |

Information, culture & recreation | | 105 | | 106 | | 106 | | 110 | | 110 | | 111 | | 115 | | 116 | | 114 | | 108 | | 109 | |

Services to business management | | 71 | | 72 | | 79 | | 82 | | 91 | | 96 | | 96 | | 99 | | 94 | | 91 | | 94 | |