Exhibit 99.5

Public

Accounts

Ministry of Finance

Office of the

Comptroller General

For the Fiscal Year Ended

March 31, 2015

National Library of Canada Cataloguing in Publication Data

British Columbia. Office of the Comptroller General.

Public accounts for the year ended…— 2000/2001—

Annual.

Report year ends Mar. 31.

Continues: British Columbia. Ministry of Finance.

Public accounts. ISSN 1187—8657.

ISSN 1499—1659 = Public accounts—British Columbia.

Office of the Comptroller General

1. British Columbia—Appropriations and

expenditures—Periodicals. 2. Revenue—British

Columbia—Periodicals.

3. Finance, Public—British Columbia—Periodicals. 1.

British Columbia. Ministry of Finance. 2. Title.

HJ13.B74 352.4’09711’05 C2001—960204—9

July 15, 2015

Victoria, British Columbia

Lieutenant Governor of the Province of British Columbia

MAY IT PLEASE YOUR HONOUR:

The undersigned has the honour to present the Public Accounts of the Government of the Province of British Columbia for the fiscal year ended March 31, 2015.

| MICHAEL DE JONG |

| Minister of Finance |

Ministry of Finance

Victoria, British Columbia

Honourable Michael de Jong

Minister of Finance

I have the honour to submit herewith the Public Accounts of the Government of the Province of British Columbia for the fiscal year ended March 31, 2015.

Respectfully submitted,

| STUART NEWTON |

| Comptroller General |

British Columbia’s Public Accounts

The Public Accounts include the Summary Financial Statements of the provincial Government Reporting Entity, which includes the financial results of all ministries and Crown agencies presented on a consolidated basis. The supporting notes and schedules define the accounting policies followed in preparing the province’s financial statements and form an integral part of the overall financial picture of the province’s financial activities in fiscal year 2014/15.

Responsibility for the preparation of the government’s financial statements rests with the Office of the Comptroller General. Although accounting policies are based in Public Sector Accounting Standards (PSAS), the application of standards to specific programs and transactions is the responsibility of the preparer who must use professional judgement to determine the treatment that is most representative of the underlying economic substance and best serves the information requirements of the users of government financial statements. To ensure due diligence in the application of accounting policies, decisions are based on comprehensive understanding of the substance of transactions, reference to existing and emerging accounting standards, and consultation with standard setters, other jurisdictions and the audit community.

We are fortunate in British Columbia to have had a review of the budget and reporting process. The Budget Process Review Panel report set out some very clear principles for financial reporting based on user needs. At that time PSAS were determined to best meet the needs identified in the report. This has guided our principles—based financial reporting since then. Currently, much of the challenge faced by changing accounting standards relates to PSAS moving away from some of the principles included in the Budget Process Review Panel report. These principles have been used by government as the basis for budgeting annual expenditures and relied upon by users of the financial statements in establishing the government’s accountability for financial management and ensuring consistency in presentation.

Despite the growing complexity of the reporting process, British Columbia remains committed to timely delivery of the Public Accounts each year and continues to focus on consistency in budgeting and financial reporting based on the comparability of its Estimates and Public Accounts, and the focus on “one bottom line”; that is, the Summary Financial Statements of the province.

Throughout the year, we work with the Office of the Auditor General to implement changes in accounting standards, address audit findings and recommendations, and improve the transparency of financial reporting. In doing so, we are mindful of the need to maintain consistency in the fundamental principles of accounting, and the comparability of financial information over a long period of time. This continuity allows the users of financial information to compare government’s financial performance against their fiscal plan, and to understand the province’s financial performance over longer periods of time. These objectives help to demonstrate accountability for financial performance to the public, both in the current year and over the longer term.

One qualification regarding government transfers remains: how to account for the government transfers is the subject of much debate nationally and internationally among both preparers and auditors. In the absence of a clear consensus on the application of the standard, it would be imprudent to make such a significant change only to have to change back at a later date. Therefore, until the situation is resolved, I have chosen to maintain our current position to ensure the long term comparability of financial information from year to year. We will continue to work with standard setters, other jurisdictions, the accounting community, and the Auditor General’s Office towards a consistent application of the transfer standard.

I would like to thank the Select Standing Committee on Public Accounts of the Legislative Assembly, government ministries, Crown corporations and agencies, and the Auditor General and her staff for their cooperation and support in preparing the 2014/15 Public Accounts.

Comments or questions regarding the Public Accounts document are encouraged and much appreciated. Please direct your comments or questions to me by mail at PO Box 9413 STN PROV GOVT, Victoria BC V8W 9V1; e—mail at: Stuart.Newton@gov.bc.ca; by telephone at 250—387—6692, or by fax at 250—356—2001.

Further information on the government’s financial performance is also provided through the Consolidated Revenue Fund Extracts (available on the Internet — website http://www.fin.gov.bc.ca/ocg.htm). These extracts compare actual to planned spending of ministries on an appropriation basis, fulfilling ministries’ accountability back to the Legislative Assembly.

| STUART NEWTON |

| Comptroller General |

PROVINCE OF BRITISH COLUMBIA

PUBLIC ACCOUNTS 2014/15

Contents

Overview (Unaudited) | |

Public Accounts Content | 9 |

Legislative Compliance and Accounting Policy Report | 10 |

Financial Statement Discussion and Analysis Report | 11 |

Highlights | 11 |

Discussion and Analysis | 13 |

Economic Highlights | 28 |

| |

Summary Financial Statements | |

Statement of Responsibility for the Summary Financial Statements of the Government of the Province of British Columbia | 33 |

Report of the Auditor General of British Columbia | 35 |

Consolidated Statement of Financial Position | 41 |

Consolidated Statement of Operations | 42 |

Consolidated Statement of Change in Net Liabilities | 43 |

Consolidated Statement of Cash Flow | 44 |

Notes to Consolidated Summary Financial Statements | 46 |

Reporting Entity | 83 |

Consolidated Statement of Financial Position by Sector | 86 |

Consolidated Statement of Operations by Sector | 90 |

Statement of Financial Position for Self—supported Crown Corporations and Agencies | 94 |

Summary of Results of Operations and Statement of Equity for Self—supported Crown Corporations and Agencies | 96 |

Consolidated Statement of Tangible Capital Assets | 98 |

Consolidated Statement of Guaranteed Debt | 99 |

| |

Supplementary Information (Unaudited) | |

Adjusted Net Income of Crown Corporations, Agencies and the SUCH Sector | 103 |

SUCH Statement of Financial Position | 106 |

SUCH Statement of Operations | 108 |

Consolidated Staff Utilization | 109 |

| |

Consolidated Revenue Fund Extracts (Unaudited) | |

Statement of Financial Position | 113 |

Statement of Operations | 115 |

Statement of Cash Flow | 116 |

Schedule of Net Revenue by Source | 118 |

Schedule of Comparison of Estimated Expenses to Actual Expenses | 120 |

Schedule of Financing Transaction Disbursements | 122 |

Schedule of Write—offs, Extinguishments and Remissions | 123 |

| |

Provincial Debt Summary | |

Overview of Provincial Debt (Unaudited) | 127 |

Provincial Debt (Unaudited) | 128 |

Change in Provincial Debt (Unaudited) | 129 |

Reconciliation of Summary Financial Statements’ Deficit (Surplus) to Change in Taxpayer—supported Debt and Total Debt (Unaudited) | 130 |

Reconciliation of Total Debt to Summary Financial Statements’ Debt (Unaudited) | 130 |

Change in Provincial Debt, Comparison to Budget (Unaudited) | 131 |

Interprovincial Comparison of Taxpayer—supported Debt as a Percentage of Gross Domestic Product (Unaudited) | 132 |

Interprovincial Comparison of Taxpayer—supported Debt Service Costs as a Percentage of Revenue (Unaudited) | 133 |

Report of the Auditor General of British Columbia on the Summary of Provincial Debt, Key Indicators of Provincial Debt, and Summary of Performance Measures | 135 |

Summary of Provincial Debt | 137 |

Key Indicators of Provincial Debt | 139 |

Summary of Performance Measures | 140 |

| |

Definitions (Unaudited) | 141 |

| |

Acronyms (Unaudited) | 144 |

PROVINCE OF BRITISH COLUMBIA

PUBLIC ACCOUNTS 2014/15

Public Accounts Content

Financial Statement Discussion and Analysis (Unaudited)—this section provides a written commentary on the Summary Financial Statements plus additional information on the financial performance of the provincial government.

Summary Financial Statements—these audited statements have been prepared to disclose the financial impact of the government’s activities. They aggregate the Consolidated Revenue Fund (CRF), the taxpayer—supported Crown corporations and agencies (government organizations), the self—supported Crown corporations and agencies (government business enterprises) and the school districts, universities, colleges, institutes and health organizations (SUCH) sector.

Supplementary Information (Unaudited)—this section provides supplementary schedules containing detailed information on the results of those Crown corporations and agencies that are part of the government reporting entity and the impact of the SUCH sector on the province’s financial statements.

Consolidated Revenue Fund Extracts (Unaudited)— the CRF reflects the core operations of the province as represented by the operations of government ministries and legislative offices. Its statements are included in an abridged form. The CRF Extracts include a summary of the CRF Statement of Financial Position, the CRF Statement of Operating Results, the CRF Statement of Cash Flow, a CRF Schedule of Net Revenue by Source, a CRF Schedule of Expenses, a CRF Schedule of Financing Transactions, and a CRF Schedule of Write—offs, Extinguishments and Remissions, as required by statute.

Provincial Debt Summary—this section presents unaudited schedules and unaudited statements that provide further details on provincial debt and reconcile the Summary Financial Statements debt to the province’s total debt. Also included are the audited Summary of Provincial Debt, Key Indicators of Provincial Debt and Summary of Performance Measures.

This publication is available on the Internet at: www.fin.gov.bc.ca

Additional Information Available (Unaudited)

The following information is available only on the Internet at: www.fin.gov.bc.ca

Consolidated Revenue Fund Supplementary Schedules —this section contains schedules that provide details of financial activities of the CRF, including details of expenses by ministerial appropriations, an analysis of statutory appropriations, Special Accounts and Special Fund balances and operating statements, and financing transactions.

Consolidated Revenue Fund Detailed Schedules of Payments—this section contains detailed schedules of salaries, wages, travel expenses, grants and other payments.

Financial Statements of Government Organizations and Enterprises—this section contains links to the audited financial statements of those Crown corporations, agencies and SUCH sector entities that are included in the government reporting entity.

9

PROVINCE OF BRITISH COLUMBIA

PUBLIC ACCOUNTS 2014/15

Legislative Compliance and Accounting Policy Report

The focus of the province’s financial reporting is the Summary Financial Statements, which consolidate the operating and financial results of the province’s Crown corporations, agencies, school districts, universities, colleges, institutes and health organizations with the Consolidated Revenue Fund. These are general—purpose statements designed to meet, to the extent possible, the information needs of a variety of users.

The Public Accounts are prepared in accordance with the Financial Administration Act and the Budget Transparency and Accountability Act (BTAA).

The BTAA was amended in 2001 with the passing of Bill 5. Under section 20 of that Bill, the government has mandated that “all accounting policies and practices applicable to documents required to be made public under this Act for the government reporting entity must conform to generally accepted accounting principles.”

For senior governments, generally accepted accounting principles (GAAP) is generally considered to be the recommendations and guidelines of the Canadian Public Sector Accounting Board.

Section 4.1 of the BTAA established an Accounting Policy Advisory Committee (APAC) to advise Treasury Board on the implementation of GAAP for the government reporting entity (GRE). With the government’s transition to full GAAP for the 2004/05 year, the role of APAC changed to include the provision of advice on evolving developments in accounting standards by the accounting profession, as well as emerging issues within government.

10

PROVINCE OF BRITISH COLUMBIA

PUBLIC ACCOUNTS 2014/15

Financial Statement Discussion and Analysis Report

Highlights

The highlights section provides a summary of the key events affecting the financial statements based on information taken from the Summary Financial Statements and Provincial Debt Summary included in the Public Accounts. The budget figures are from pages 122, 124, 127, 130 and 132 of the Budget and Fiscal Plan 2014/15—2016/17.

Budget and Actual Results 2014/15

| | In Millions | | Variance | |

| | | | 2014/15 | | | | | | 2014/15 | | 2014/15 | |

| | 2014/15 | | Updated | | 2014/15 | | 2013/14 | | Actual to | | vs | |

| | Budget | | Forecast | | Actual | | Actual | | Budget | | 2013/14 | |

| | $ | | $ | | $ | | $ | | $ | | $ | |

Revenue | | 44,800 | | 45,772 | | 46,122 | | 43,728 | | 1,322 | | 2,394 | |

Expense | | (44,416 | ) | (44,793 | ) | (44,439 | ) | (43,401 | ) | (23 | ) | (1,038 | ) |

Surplus(deficit) before forecast allowance | | 384 | | 979 | | 1,683 | | 327 | | 1,299 | | 1,356 | |

Forecast allowance | | (200 | ) | (100 | ) | | | | | 200 | | | |

Surplus (deficit) for the year | | 184 | | 879 | | 1,683 | | 327 | | 1,499 | | 1,356 | |

| | | | | | | | | | | | | |

Capital spending: | | | | | | | | | | | | | |

Taxpayer—supported capital spending | | 4,030 | | 3,637 | | 3,407 | | 3,151 | | (623 | ) | 256 | |

Self—supported capital spending | | 2,590 | | 2,604 | | 2,491 | | 2,519 | | (99 | ) | (28 | ) |

Total capital spending | | 6,620 | | 6,241 | | 5,898 | | 5,670 | | (722 | ) | 228 | |

| | | | | | | | | | | | | |

Provincial debt: | | | | | | | | | | | | | |

Taxpayer—supported | | 43,075 | | 42,302 | | 41,880 | | 41,068 | | (1,195 | ) | 812 | |

Self—supported | | 21,463 | | 21,428 | | 21,040 | | 19,625 | | (423 | ) | 1,415 | |

Total provincial debt | | 64,538 | | 63,730 | | 62,920 | | 60,693 | | (1,618 | ) | 2,227 | |

Taxpayer—supported debt to GDP ratio | | 18.4 | % | 17.7 | % | 17.5 | % | 18.2 | % | (0.9 | ) | (0.7 | ) |

Summary Accounts Surplus (Deficit)

The province ended the year with a surplus of $1,683 million, which was $1,499 million higher than the surplus forecast in the Budget and Fiscal Plan 2014/15—2016/17. The 2014/15 surplus of $1,683 million was $1,356 million greater than the surplus of $327 million in fiscal year 2013/14.

Revenue increased by 5.5% in 2014/15 compared to expected average annual growth of 2.6%, while expenses increased by 2.4% compared to expected average annual growth of 2.2% over the fiscal plan period.

11

PROVINCE OF BRITISH COLUMBIA

PUBLIC ACCOUNTS 2014/15

Financial Statement Discussion and Analysis Report

Capital Spending

Taxpayer—supported infrastructure spending on hospitals, schools, post—secondary facilities, transit, and roads totaled $3,407 million in 2014/15. Self—supported infrastructure spending on electrical generation, transmission and distribution projects, the Port Mann Bridge and other capital assets totaled $2,491 million in 2014/15.

Provincial Debt

Taxpayer—supported debt increased by $812 million in 2014/15 while self—supported debt increased by $1,415 million. The increase in total debt of $2,227 million was $1,618 million less than the budgeted increase in total debt of $3,845 million. The key measure of taxpayer—supported debt to GDP ended the year at 17.5%, less than the 18.4% forecast in the budget.

12

PROVINCE OF BRITISH COLUMBIA

PUBLIC ACCOUNTS 2014/15

Financial Statement Discussion and Analysis Report

Discussion and Analysis

The detailed analysis section provides an overview of significant trends relating to the Statement of Operations, Statement of Financial Position and Provincial Debt.

Revenue Analysis

Revenue analysis helps users understand the government’s finances in terms of its revenue sources and allows them to evaluate the revenue producing capacity of the government.

Revenue by Source

Revenue by source provides an outline of the primary sources of provincial revenue and how results change between those sources over time. Revenues are broken down into separate components of taxation, contributions from the federal government, natural resources and other sources, which include fees and licenses, contributions from self—supported Crown corporations, and investment income.

| | In Millions | |

| | 2010/11 | | 2011/12 | | 2012/13 | | 2013/14 | | 2014/15 | |

| | Actual | | Actual | | Actual | | Actual | | Actual | |

| | $ | | $ | | $ | | $ | | $ | |

Taxation | | 19,031 | | 20,145 | | 21,050 | | 20,930 | | 23,056 | |

Contributions from federal government | | 8,009 | | 7,718 | | 7,044 | | 7,502 | | 7,326 | |

Fees and licences | | 4,440 | | 4,735 | | 4,907 | | 5,210 | | 5,425 | |

Natural resources | | 2,729 | | 2,812 | | 2,473 | | 2,955 | | 2,937 | |

Miscellaneous | | 2,687 | | 2,673 | | 2,613 | | 3,194 | | 2,804 | |

Net earnings of self—supported Crown corporations | | 2,940 | | 2,691 | | 2,776 | | 2,701 | | 3,371 | |

Investment income | | 843 | | 1,022 | | 1,173 | | 1,236 | | 1,203 | |

Total revenue | | 40,679 | | 41,796 | | 42,036 | | 43,728 | | 46,122 | |

Provincial revenues increased by $2,394 million in 2014/15. The improvement in provincial revenue was primarily due to significant increases in taxation revenue of $2,126 million. The net earnings of self—supported Crown corporations increased by $670 million, and fees and licences revenue increased by $215 million. Increases in these significant sources of revenue were offset by decreases in contributions from the federal government and other sources of revenue totaling $617 million.

In 2014/15, tax revenue increased by $2,126 million (10.2%). Personal income tax revenue increased by $1,214 million (17.7%) and corporate income tax revenue increased by $208 million (8.6%). Provincial sales tax increased by $322 million (5.8%), property transfer tax revenue increased by $128 million (13.7%), and tobacco tax revenue increased by $28 million (3.9%) in 2014/15. All other tax revenues increased by $226 million over the same period.

The net earnings of self—supported Crown corporations including BC Hydro, ICBC, BC Lottery Corp and the Liquor Distribution Branch increased by $670 million in 2014/15.

Contributions from the federal government were $176 million lower than contributions received in 2013/14. This decrease was mainly the result of annual adjustment to the province’s share of Canada Health and Social transfers.

13

PROVINCE OF BRITISH COLUMBIA

PUBLIC ACCOUNTS 2014/15

Financial Statement Discussion and Analysis Report

Natural resource revenues decreased by $18 million (0.6%) in 2014/15. Petroleum, natural gas and mineral royalties increased $21 million (1.3%), forest revenues increased by $35 million (4.9%) and other sources of natural resource revenue decreased by $74 million (11.2%).

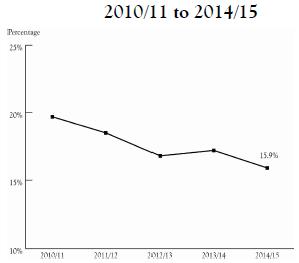

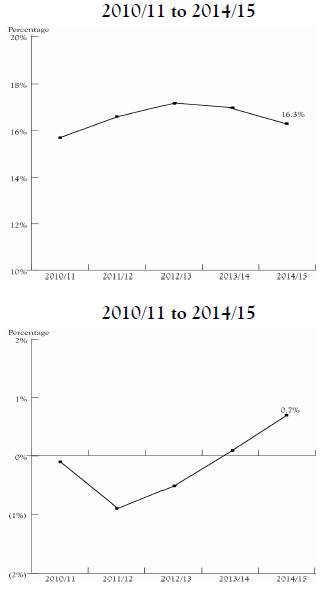

Own—source Revenue to GDP

The ratio of own—source revenue to GDP represents the amount of revenue the provincial government is taking from the provincial economy in the form of taxation, natural resource revenue, earnings of self—supported Crown corporations and user fees and licences (own—source revenue is all revenue except for federal transfers).

Own—source revenue to GDP has increased marginally in 2014/15 ending the year at 16.3%.

Percentage Change in Revenue

Trend analysis of revenue provides users with information about significant changes in revenue over time and between sources. This enables users to evaluate past performance and assess potential implications for the future.

Over the five years since 2010/11 total revenue has increased in line with the increase in GDP. While fees and licences revenue and taxation revenue have exceeded the growth in GDP, natural resource revenues trail the change in GDP slightly. Only contributions from the federal government have decreased over the past five years to 91.9% of the amount received in 2010/11.

14

PROVINCE OF BRITISH COLUMBIA

PUBLIC ACCOUNTS 2014/15

Financial Statement Discussion and Analysis Report

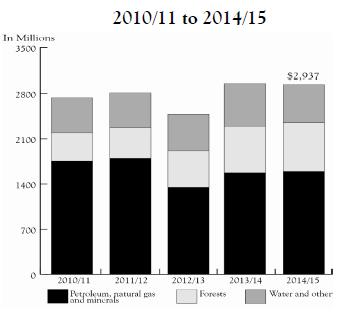

Natural Resource Revenue

The chart of natural resource revenue by source explains past trends of natural resource revenue in total and by major category.

Petroleum, natural gas and mineral revenues increased by $21 million from 2013/14. These categories of natural resource revenue account for 54.3% of natural resource revenue compared to 53.2% in 2013/14.

Forestry revenue increased by $35 million in 2014/15. The proportion of natural resource revenue derived from forestry increased to 25.6% in 2014/15 from 24.4% in 2013/14.

Water and other resource revenues decreased by $74 million in the year. They comprise 20.1% of provincial natural resource revenue.

Government—to—Government Transfers to Total Revenue

The ratio of government—to—government transfers to total revenue is an indicator of how dependent the province is on transfers from the Federal government. An increasing trend shows more reliance and a decreasing trend shows less.

Federal transfers decreased by $176 million in 2014/15. This decrease was mainly the result of annual adjustment to the province’s share of Canada Health and Social transfers.

15

PROVINCE OF BRITISH COLUMBIA

PUBLIC ACCOUNTS 2014/15

Financial Statement Discussion and Analysis Report

Expense Analysis

The following analysis helps users understand the impact of the government’s spending on the economy, the government’s allocation and use of resources, and the cost of government programs.

Expense by Function

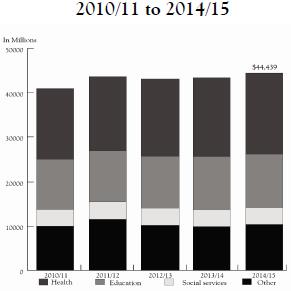

Expense by function provides a summary of the major areas of government spending, and changes in spending over time. Functions, which indicate the purpose of expenditures, are defined by Statistics Canada’s Financial Management System of Government Statistics. The province uses the following functions: health, education, social services, interest, natural resources and economic development, transportation, other, protection of persons and property, and general government. The health, education and social services functions account for approximately three quarters of the province’s total operating costs.

| | In Millions | |

| | 2010/11 | | 2011/12 | | 2012/13 | | 2013/14 | | 2014/15 | |

| | Actual | | Actual | | Actual | | Actual | | Actual | |

| | $ | | $ | | $ | | $ | | $ | |

Health | | 15,992 | | 16,917 | | 17,502 | | 17,862 | | 18,370 | |

Education | | 11,165 | | 11,227 | | 11,528 | | 11,827 | | 11,827 | |

Social services | | 3,786 | | 3,940 | | 3,990 | | 3,805 | | 3,847 | |

Interest | | 2,252 | | 2,383 | | 2,390 | | 2,482 | | 2,498 | |

Natural resources and economic development | | 2,349 | | 1,873 | | 2,092 | | 1,755 | | 2,191 | |

Transportation | | 1,580 | | 1,545 | | 1,555 | | 1,580 | | 1,608 | |

Other | | 1,208 | | 1,415 | | 1,346 | | 1,184 | | 1,288 | |

Protection of persons and property | | 1,448 | | 1,512 | | 1,539 | | 1,520 | | 1,451 | |

General government | | 1,146 | | 2,834 | | 1,262 | | 1,386 | | 1,359 | |

Total expense | | 40,926 | | 43,646 | | 43,204 | | 43,401 | | 44,439 | |

Government program spending increased by $1,038 million in 2014/15.

The province increased spending on health by $508 million (2.8%), natural resource and economic development sector by $436 million (24.8%), and the social services sector by $42 million (1.1%). Spending in all other sectors increased by $52 million over 2013/14.

16

PROVINCE OF BRITISH COLUMBIA

PUBLIC ACCOUNTS 2014/15

Financial Statement Discussion and Analysis Report

In 2014/15, provincial operating expenses were $44,439 million, a $1,038 million (2.4%) increase from 2013/14. Program spending has increased by $3,513 million (8.6%) since 2010/11. This is compared to increases in GDP of 15.9% over the same period.

Expense to GDP

The ratio of expense to GDP represents the amount of government spending in relation to the overall provincial economy.

Government spending as a percentage of GDP decreased from 18.9% to 18.6% in 2014/15, indicating that government spending continues to increase at a rate below economic growth as represented by GDP.

17

PROVINCE OF BRITISH COLUMBIA

PUBLIC ACCOUNTS 2014/15

Financial Statement Discussion and Analysis Report

Changes in Actual Results from 2013/14 to 2014/15

| | In Millions | |

| | Revenue | | Expense | | Surplus | |

| | $ | | $ | | $ | |

2013/14 Surplus | | 43,728 | | 43,401 | | 327 | |

Increase in taxation revenue | | 2,126 | | | | 2,126 | |

Increase in earnings from self—supported Crown corporations | | 670 | | | | 670 | |

Increase in fees and licences revenue | | 215 | | | | 215 | |

Decrease in other revenue | | (617 | ) | | | (617 | ) |

Increase in health spending | | | | 508 | | (508 | ) |

Increase in natural resource and economic development | | | | 436 | | (436 | ) |

Increase in social services spending | | | | 42 | | (42 | ) |

Increase in other expenses | | | | 52 | | (52 | ) |

Subtotal of changes in actual results | | 2,394 | | 1,038 | | 1,356 | |

| | 46,122 | | 44,439 | | | |

2014/15 Surplus | | | | | | 1,683 | |

| | | | | | | |

2013/14 Accumulated Surplus | | | | | | 1,346 | |

2014/15 Accumulated Surplus before Accumulated Other Comprehensive income | | | | | | 3,029 | |

Accumulated other comprehensive income from self—supported Crown corporations and agencies | | | | | | 223 | |

2014/15 Accumulated Surplus | | | | | | 3,252 | |

The year over year increase in total revenue of $2,394 million, offset by the increase in total expense of $1,038 million, resulted in a surplus that was $1,356 million higher than 2013/14. Accumulated surplus increased from $1,346 million in 2013/14 to $3,252 million at the end of 2014/15.

18

PROVINCE OF BRITISH COLUMBIA

PUBLIC ACCOUNTS 2014/15

Financial Statement Discussion and Analysis Report

Changes from 2014/15 Budget

| | In Millions | |

| | | | | | Forecast | | | |

| | Revenue | | Expense | | Allowance | | Surplus | |

| | $ | | $ | | $ | | $ | |

Surplus per Budget March 2014 | | 44,800 | | 44,416 | | (200 | ) | 184 | |

Increased taxation revenue | | 899 | | | | | | 899 | |

Increased self—supported Crown corporations earnings | | 486 | | | | | | 486 | |

Increased fees and licences | | 89 | | | | | | 89 | |

Increased investment earnings | | 112 | | | | | | 112 | |

Decreased other revenues | | (264 | ) | | | | | (264 | ) |

Increased social services spending | | | | 144 | | | | (144 | ) |

Increased natural resources and economic development spending | | | | 434 | | | | (434 | ) |

Decreased health spending | | | | (313 | ) | | | 313 | |

Decreased other program spending | | | | (242 | ) | | | 242 | |

Forecast allowance | | | | | | 200 | | 200 | |

Subtotal of changes in actual results compared to budget | | 1,322 | | 23 | | 200 | | 1,499 | |

Actual Results | | 46,122 | | 44,439 | | 0 | | 1,683 | |

Revenue was $1,322 million (3.0%) higher than the budgeted amount of $44,800 million and expenses increased marginally by $23 million.

Net Liabilities and Accumulated Surplus

In accordance with Canadian generally accepted accounting principles, the government’s Consolidated Statement of Financial Position is presented on a net liabilities basis. Net liabilities represent net future cash outflows resulting from past transactions and events. An analysis of net liabilities and accumulated surplus helps users to assess the government’s overall financial position and the future revenue required to pay for past transactions and events.

| | In Millions | | Variance | |

| | | | | | | | 2014/15 | | 2014/15 | |

| | 2014/15 | | 2014/15 | | 2013/14 | | Budget | | vs | |

| | Budget | | Actual | | Actual | | to Actual | | 2013/14 | |

| | $ | | $ | | $ | | $ | | $ | |

Financial assets | | 41,588 | | 42,377 | | 39,733 | | 789 | | 2,644 | |

Less: liabilities | | (82,674 | ) | (81,279 | ) | (78,818 | ) | 1,395 | | (2,461 | ) |

Net Liabilities | | (41,086 | ) | (38,902 | ) | (39,085 | ) | 2,184 | | 183 | |

Less: non—financial assets | | 42,843 | | 42,154 | | 40,912 | | (689 | ) | 1,242 | |

Accumulated surplus | | 1,757 | | 3,252 | | 1,827 | | 1,495 | | 1,425 | |

19

PROVINCE OF BRITISH COLUMBIA

PUBLIC ACCOUNTS 2014/15

Financial Statement Discussion and Analysis Report

The accumulated surplus represents the sum of the current and prior years’ operating results, and accumulated changes in other comprehensive income. At March 31, 2015, the accumulated surplus was $3,252 million, $1,495 million higher than budget.

Financial assets were $2,644 million higher than 2013/14 as the result of increases in cash, cash equivalents, and temporary investments of $874 million, equity in self—supported Crown corporations and agencies of $432 million, and loans for the purchase of assets, recoverable from agencies of $1,396 million. These increases were offset by decreases of $58 million in other financial assets.

Liabilities increased by $2,461 million from 2013/14. Self—supported debt increased by $1,424 million and taxpayer—supported debt increased by $932 million to fund infrastructure programs, provide capital financing to self—supported Crown corporations and agencies, and support working capital requirements. Other liabilities, including accounts payable and deferred revenue, increased by $105 million from 2013/14.

Non—financial assets typically represent resources, such as tangible capital assets, that the government can use in the future to provide services. Non—financial assets increased by $1,242 million over 2013/14 as government invested in infrastructure spending.

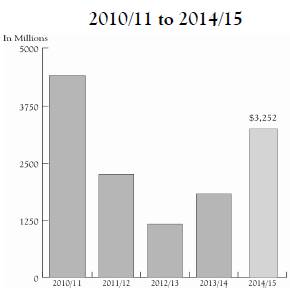

Accumulated Surplus

The accumulated surplus represents current and all prior years’ operating results. In 2014/15, the province had an accumulated surplus of $3,252 million, $1,425 million higher than in 2013/14. The positive operating results of prior years and the current year provide the flexibility to sustain core public services.

20

PROVINCE OF BRITISH COLUMBIA

PUBLIC ACCOUNTS 2014/15

Financial Statement Discussion and Analysis Report

Components of Net Liabilities

Financial Assets

Trend analysis of financial assets provides users with information regarding the amount of resources available to the government that can be converted to cash to meet obligations or fund operations.

| | In Millions | |

| | 2010/11 | | 2011/12 | | 2012/13 | | 2013/14 | | 2014/15 | |

| | Actual | | Actual | | Actual | | Actual | | Actual | |

| | $ | | $ | | $ | | $ | | $ | |

Cash, cash equivalents, temporary investments and warehouse investments | | 3,060 | | 3,235 | | 3,174 | | 2,802 | | 3,676 | |

Accounts receivable | | 2,342 | | 2,408 | | 2,456 | | 3,449 | | 3,489 | |

Equity in self—supported Crown corporations and agencies | | 7,093 | | 6,998 | | 7,541 | | 7,839 | | 8,271 | |

Loans for the purchase of assets, recoverable from agencies | | 12,947 | | 14,846 | | 16,907 | | 18,921 | | 20,317 | |

Other financial assets | | 7,057 | | 7,021 | | 7,508 | | 6,722 | | 6,624 | |

Total financial assets | | 32,499 | | 34,508 | | 37,586 | | 39,733 | | 42,377 | |

In 2014/15, financial assets increased by $2,644 million primarily due to an increase in capital loans to Crown agencies. Recoverable capital loans increased by $1,396 million as the province provided funding to Crown agencies for capital projects, equity in self—supported Crown corporations increased by $432 million, and all other financial assets increased by $816 million.

Liabilities

Trend analysis of liabilities provides users with information to understand and assess the demands on financial assets and the revenue raising capacity of government.

| | In Millions | |

| | 2010/11 | | 2011/12 | | 2012/13 | | 2013/14 | | 2014/15 | |

| | Actual | | Actual | | Actual | | Actual | | Actual | |

| | $ | | $ | | $ | | $ | | $ | |

Taxpayer—supported debt | | 33,079 | | 36,012 | | 39,828 | | 41,761 | | 42,693 | |

Self—supported debt | | 13,030 | | 14,942 | | 17,011 | | 19,041 | | 20,465 | |

Total financial statement debt | | 46,109 | | 50,954 | | 56,839 | | 60,802 | | 63,158 | |

Accounts payable and other liabilities | | 7,919 | | 9,119 | | 9,149 | | 8,298 | | 8,312 | |

Deferred revenue | | 10,750 | | 10,459 | | 9,896 | | 9,718 | | 9,809 | |

Total liabilities | | 64,778 | | 70,532 | | 75,884 | | 78,818 | | 81,279 | |

In 2014/15, total liabilities increased by $2,461 million. Liabilities are obligations that must be settled at a future date by the transfer or use of assets. Taxpayer—supported debt increased in 2014/15 by $932 million, while self—supported debt increased by $1,424 million. Information relating to the government’s debt management can be found in more detail in the analysis of the total provincial debt on page 25. Deferred revenue increased by $91 million while accounts payable and other liabilities increased by $14 million.

21

PROVINCE OF BRITISH COLUMBIA

PUBLIC ACCOUNTS 2014/15

Financial Statement Discussion and Analysis Report

Non—financial Assets

Trend analysis of non—financial assets provides users with information to assess the management of a government’s infrastructure and long—term non—financial assets.

| | In Millions | |

| | 2010/11 | | 2011/12 | | 2012/13 | | 2013/14 | | 2014/15 | |

| | Actual | | Actual | | Actual | | Actual | | Actual | |

| | $ | | $ | | $ | | $ | | $ | |

Tangible capital assets | | 34,278 | | 35,692 | | 36,762 | | 37,778 | | 39,028 | |

Other non—financial assets | | 2,398 | | 2,592 | | 2,709 | | 3,134 | | 3,126 | |

Total non—financial assets | | 36,676 | | 38,284 | | 39,471 | | 40,912 | | 42,154 | |

Management of non—financial assets has a direct impact on the level and quality of services a government is able to provide to its constituents. Non—financial assets typically represent resources that government can use in the future to provide services. At March 31, 2015, non—financial assets were $42,154 million which was $1,242 million higher than 2013/14 and $5,478 million higher than 2010/11. The majority of the province’s non—financial assets represent capital expenditures for tangible capital assets net of amortization. The government has increased its investment in infrastructure spending by $1,250 million in 2014/15, to ensure service potential is available to deliver programs and services in future periods. Capital expenditures are not included on the Consolidated Statement of Operations and have no effect on the current surplus. They reduce future surpluses in the form of amortization expense as the service potential of assets is used to deliver programs and services.

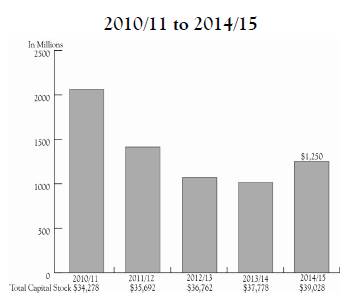

Change in Capital Stock

This measure shows the impact of net changes to the government’s stock of physical capital. Positive amounts demonstrate an investment in infrastructure to replace existing capital and provide service potential in future periods.

The net annual investment in capital was $1,250 million in 2014/15, and $6,809 million since 2010/11. Total capital stock has also increased steadily over that period which indicates that capital infrastructure is available to continue providing programs and services in future periods.

22

PROVINCE OF BRITISH COLUMBIA

PUBLIC ACCOUNTS 2014/15

Financial Statement Discussion and Analysis Report

Net Liabilities and Accumulated Surplus

| | In Millions | |

| | 2010/11 | | 2011/12 | | 2012/13 | | 2013/14 | | 2014/15 | |

| | Actual | | Actual | | Actual | | Actual | | Actual | |

| | $ | | $ | | $ | | $ | | $ | |

Financial assets | | 32,499 | | 34,508 | | 37,586 | | 39,733 | | 42,377 | |

Less: liabilities | | (64,778 | ) | (70,532 | ) | (75,884 | ) | (78,818 | ) | (81,279 | ) |

Net liabilities | | (32,279 | ) | (36,024 | ) | (38,298 | ) | (39,085 | ) | (38,902 | ) |

Less: non—financial assets | | 36,676 | | 38,284 | | 39,471 | | 40,912 | | 42,154 | |

Accumulated surplus | | 4,397 | | 2,260 | | 1,173 | | 1,827 | | 3,252 | |

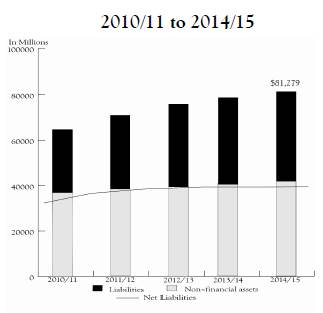

Net liabilities decreased by $183 million in 2014/15, due to increased investment in infrastructure. The liabilities include deferred revenue of $9,809 million which represents unearned revenues and restricted contributions that will be recognized as revenue in future periods.

The financial measure of net liabilities has remained stable while investments in infrastructure have increased resulting in an increase in accumulated surplus. The accumulated surplus of the province was $3,252 million at the end of 2014/15, indicating that the cumulative result of all past annual surpluses and deficits is positive, or that the province remains in a positive net financial position.

Non—financial Assets as a Portion of Liabilities

The chart provides an indication of what proportion of liabilities are used to fund capital infrastructure as opposed to funding working capital requirements including accounts payable and other operating liabilities, as well as revenue deferred to future periods. Over the past five years, non—financial assets have increased while the measure of net liabilities has remained stable.

23

PROVINCE OF BRITISH COLUMBIA

PUBLIC ACCOUNTS 2014/15

Financial Statement Discussion and Analysis Report

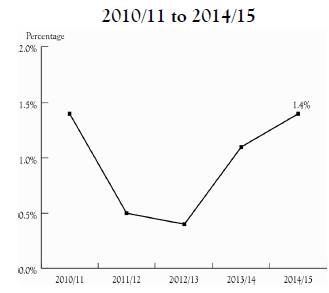

Net Liabilities to GDP

The net liabilities to GDP ratio provides an indication of the province’s ability to maintain existing programs and meet existing creditor requirements without increasing the debt burden on the economy as a whole.

The decrease in net liabilities to GDP is the result of net liabilities remaining below the increase in economic growth as represented by GDP in 2014/15. Net liabilities include deferred revenue that will be recognized as revenue in future periods, and obligations to outside parties including accounts payable and debt.

Surplus (Deficit) to GDP

The surplus (deficit) to GDP ratio is an indicator of sustainability that compares the province’s financial results to the overall results of the economy.

Results in the positive range of the chart indicate that the economy is growing faster than net government spending.

24

PROVINCE OF BRITISH COLUMBIA

PUBLIC ACCOUNTS 2014/15

Financial Statement Discussion and Analysis Report

Total Provincial Debt

Analysis of total provincial debt helps users to assess the extent of long—term liabilities and the government’s ability to meet future debt obligations.

| | In Millions | |

| | 2010/11 | | 2011/12 | | 2012/13 | | 2013/14 | | 2014/15 | |

| | Actual | | Actual | | Actual | | Actual | | Actual | |

| | $ | | $ | | $ | | $ | | $ | |

Gross debt | | 46,109 | | 50,954 | | 56,839 | | 60,802 | | 63,158 | |

Less: sinking fund assets | | (1,410 | ) | (1,491 | ) | (1,778 | ) | (835 | ) | (977 | ) |

Third party guarantees and non—guaranteed debt | | 455 | | 730 | | 755 | | 726 | | 739 | |

Total provincial debt | | 45,154 | | 50,193 | | 55,816 | | 60,693 | | 62,920 | |

When reporting to rating agencies, the province adds to its financial statement debt, all debt guarantees and the debt directly incurred by self—supported Crown corporations, reduced by sinking fund assets. This balance is referred to as the total provincial debt.

Total provincial debt is $238 million lower than the amounts reported in the province’s financial statements after deducting sinking funds held to pay down the debt, and including guaranteed debt and the debt of self—supported Crown corporations. Overall, total provincial debt increased by $2,227 million in 2014/15 because the government borrowed to fund capital projects and working capital requirements.

The largest increases in the debt of self—supported Crown agencies were the debt of the British Columbia Hydro and Power Authority which increased by $985 million and the debt of Transportation Investment Corporation which increased by $126 million. Taxpayer—supported debt increased due to BC Transportation Financing Authority debt increasing by $516 million; health sector debt increasing by $484 million; education sector debt increasing by $487 million; and other increases in taxpayer—supported debt of $268 million.

Provincial government direct operating debt decreased by $943 million compared to 2013/14.

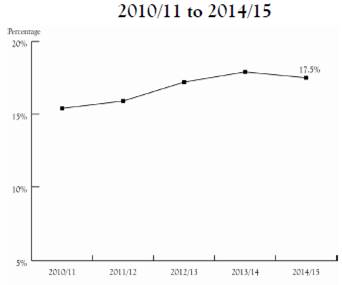

Taxpayer—supported debt to GDP

The ratio of taxpayer—supported debt to GDP is a key measure used by financial analysts and investors to assess a province’s ability to repay debt and is a key measure monitored by the bond rating agencies. An increasing ratio means that debt is growing faster than the growth of the economy as measured by GDP.

At the end of 2014/15 taxpayer—supported debt to GDP was 17.5% which was, lower than the budgeted level of 18.4%.

25

PROVINCE OF BRITISH COLUMBIA

PUBLIC ACCOUNTS 2014/15

Financial Statement Discussion and Analysis Report

Strong Credit Rating

Reflecting the province’s fiscal performance, British Columbia has maintained a strong and stable credit rating with all three credit rating agencies. In 2014/15, Moody’s Investors Service Inc. gave the province an Aaa credit rating (2014: Aaa); Standard and Poor’s gave the province an AAA credit rating (2014: AAA); and Dominion Bond Rating Service gave the province an AA(high) credit rating (2014: AA (high)).

Credit Ratings May 2015

| | Rating Agency1 | | | |

| | Moody’s Investors | | | | Dominion Bond | |

Jurisdiction | | Service Inc. | | Standard and Poor’s | | Rating Service | |

British Columbia | | Aaa | | AAA | | AA (high) | |

Alberta | | Aaa | | AAA | | AAA | |

Saskatchewan | | Aaa | | AAA | | AA | |

Manitoba | | Aa1 | | AA | | A (high) | |

Ontario | | Aa2 | | AA– | | AA (low) | |

Quebec | | Aa2 | | A+ | | A (high) | |

New Brunswick | | Aa2 | | A+ | | A (high) | |

Nova Scotia | | Aa2 | | A+ | | A (high) | |

Prince Edward Island | | Aa2 | | A | | A (low) | |

Newfoundland | | Aa2 | | A+ | | A | |

Canada | | Aaa | | AAA | | AAA | |

1 The rating agencies assign letter ratings to borrowers. The major categories, in descending order of credit quality, are: AAA/Aaa; AA/Aa; A; BBB/Baa; BB/Ba; and B. The “1”, “2”, “3”, “high”, “low”, “–”, and “+” modifiers show relative standing within the major categories. For example, AA+ exceeds AA.

A more comprehensive overview of provincial debt, including key debt indicators is located on pages 127—140.

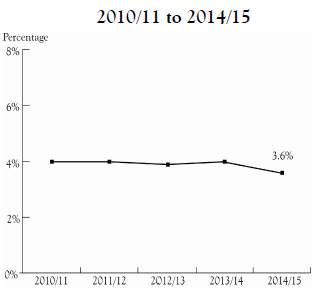

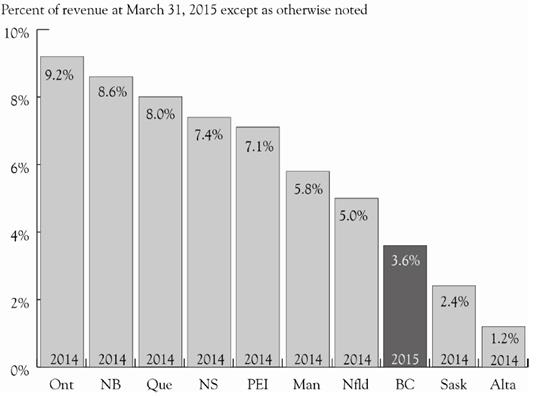

Public Debt Charges to Revenue (the Interest Bite)

The public debt charges to revenue indicator is often referred to as the “interest bite”. This provides users with the percentage of the province’s revenue used to pay interest on debt. The ratio is sensitive to the cost of debt arising from either increasing interest rates or increasing debt, as well as decreases in revenue.

If an increasing proportion of provincial revenue is required to pay interest on provincial debt, less money is left to provide core public services. The interest bite has decreased over the last five years from 4.0% in 2010/11. In 2014/15, the province spent 3.6 cents of each revenue dollar on interest on the provincial debt.

26

PROVINCE OF BRITISH COLUMBIA

PUBLIC ACCOUNTS 2014/15

Financial Statement Discussion and Analysis Report

Non—Hedged Foreign Currency Debt to Total Provincial Debt

The ratio of non—hedged foreign currency debt to total provincial debt shows the degree of vulnerability of a government’s public debt position to swings in exchange rates.

27

PROVINCE OF BRITISH COLUMBIA

PUBLIC ACCOUNTS 2014/15

Financial Statement Discussion and Analysis Report

Economic Highlights

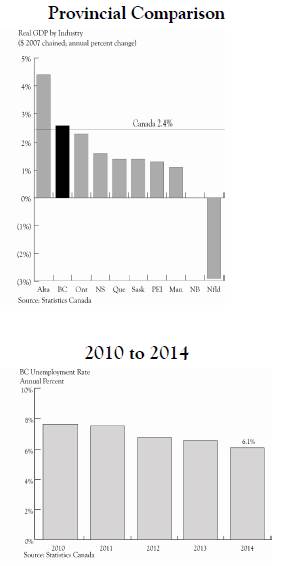

British Columbia’s economy grew by an estimated 2.6% in the 2014 calendar year, the second highest rate among provinces and above the national average of 2.4%, according to preliminary GDP by industry data from Statistics Canada. The estimated 2.6% growth for British Columbia in 2014 is higher than the government’s Budget 2015 estimate of 2.2%.

Real Gross Domestic Product in Calendar Year 2014

Growth was observed across most major industries in 2014 with the exception of educational services (down 4.0%), agriculture, forestry, fishing and hunting (down 3.7%), utilities (down 1.4%), and information and cultural industries (down 0.2%). The strongest gains among industries in 2014 were observed in mining, quarrying and oil and gas extraction (up 4.6%), retail trade (up 4.6%) and real estate, rental and leasing services (up 3.9%). Construction, manufacturing, as well as transportation and warehousing, also saw steady gains in 2014.

Retail sales, an indicator of consumer spending, increased by 5.6% in 2014. Also, the value of merchandise exports from British Columbia increased by 7.1% in 2014 despite unbalanced external demand for BC products.

Unemployment Rate in Calendar Year 2014

British Columbia saw a decline in its annual unemployment rate in 2014, falling to 6.1% from the 6.6% rate observed in 2013. The unemployment rate in BC in 2014 was lower than the national average of 6.9%. The average level of employment in 2014 was higher than the pre—recession level observed in 2008 (by about 36,500 jobs).

28

PROVINCE OF BRITISH COLUMBIA

PUBLIC ACCOUNTS 2014/15

Financial Statement Discussion and Analysis Report

Risks and Uncertainties

The government’s main exposure to risks and uncertainties arises from variables which the government does not directly control. These include:

· assumptions underlying revenue and Crown corporation forecasts such as economic factors, commodity prices and weather conditions;

· the outcome of litigation, arbitration, and negotiations with third parties;

· potential changes to federal transfer allocations, cost—sharing agreements with the federal government and impacts on the provincial income tax bases arising from federal tax policy and budget changes;

· utilization rates for government services such as health care, children and family services, and income assistance;

· exposure to interest rate fluctuations, foreign exchange rates and credit risk; and

· changes in Canadian generally accepted accounting principles.

The following are the approximate effect of changes in some of the key variables on the surplus:

Key Fiscal Sensitivities

| | | | Annual Fiscal Impact | |

Variable | | Increase Of | | ($ millions) | |

Nominal GDP | | 1% | | $150 to $250 | |

Lumber prices (US$/thousand board feet) | | $50 | | $75 to $1001 | |

Natural gas prices (Cdn$/gigajoule) | | 50 cents | | $1402 | |

US exchange rate (US cents/Cdn$) | | 1 cent | | $(25) to $(50) | |

Interest rate | | 1 percentage point | | $(91) | |

Debt | | $500 million | | $(16) | |

1Sensitivity relates to stumpage revenue only. Depending on market conditions, changes in stumpage revenue may be offset by changes in border tax revenue.

2Sensitivities can vary significantly, especially at lower prices.

Although the government is unable to directly control these variables, strategies have been implemented to mitigate these risks and uncertainties. The development of taxation, financial and corporate regulatory policy to reinforce British Columbia’s position as an attractive place to invest and create jobs will help offset the increase in competition for investment as a result of globalization of economic and financial markets. As in previous years, the government applied a forecast allowance in the budget to account for risks to revenue, expenditure, Crown corporations’, school districts’, universities’, colleges’, institutes’, and health organizations’ (SUCH sector) forecasts. The use of forecast allowances recognizes the uncertainties in predicting future economic developments.

Risk management in relation to debt is discussed in Note 20 on page 68 of the Notes to the Consolidated Summary Financial Statements.

29

Summary Financial Statements

Province of British Columbia

For the Fiscal Year Ended

March 31, 2015

Statement of Responsibility

for the Summary Financial Statements

of the Government of the Province of British Columbia

Responsibility for the integrity and objectivity of the Summary Financial Statements for the Government of the Province of British Columbia rests with the government. The Comptroller General prepares these financial statements in accordance with the Budget Transparency and Accountability Act (BTAA), which requires generally accepted accounting principles (GAAP) for senior governments in Canada, supported by regulations of Treasury Board under the BTAA. The fiscal year of the government is from April 1 to March 31 of the following year.

To fulfill its accounting and reporting responsibilities, the government maintains financial management and internal control systems. These systems give due consideration to costs, benefits and risks, and are designed to provide reasonable assurance that transactions are properly authorized by the Legislative Assembly, are executed in accordance with prescribed regulations and are properly recorded. This is done to maintain accountability of public money and safeguard the assets and properties of the Province of British Columbia under government administration. The Comptroller General of British Columbia maintains the accounts of British Columbia, a centralized record of the government’s financial transactions, and obtains additional information as required from ministries, Crown corporations, agencies, school districts, universities, colleges, institutes and health organizations to meet accounting and reporting requirements.

The Auditor General of British Columbia provides an independent opinion on the financial statements prepared by the government. The duties of the Auditor General in that respect are contained in section 11 of the Auditor General Act.

Annually, the financial statements are tabled in the legislature as part of the Public Accounts, and are referred to the Select Standing Committee on Public Accounts of the Legislative Assembly. The Select Standing Committee on Public Accounts reports to the Legislative Assembly with the results of its examination and any recommendations it may have with respect to the financial statements and accompanying audit opinions.

Approved on behalf of the Government of the Province of British Columbia:

| /s/ MICHAEL DE JONG |

| MICHAEL DE JONG |

| Chair, Treasury Board |

INDEPENDENT AUDITOR’S REPORT

To the Legislative Assembly of the Province of British Columbia

Report on the Summary Financial Statements

I have audited the accompanying summary financial statements of the Government of the Province of British Columbia (“the Government”), which comprise the consolidated statement of financial position as at March 31, 2015, and the consolidated statements of operations, change in net liabilities and cash flow for the year then ended, and a summary of significant accounting policies and other explanatory information.

Government’s Responsibility for the Summary Financial Statements

Government is responsible for the preparation and fair presentation of these summary financial statements in accordance with the Budget Transparency and Accountability Act as set out in note 1(a) to the summary financial statements, and for such internal control as it determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditor General’s Responsibility

My responsibility is to express an opinion on these summary financial statements based on my audit. I conducted my audit in accordance with Canadian generally accepted auditing standards. Those standards require that I comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the summary financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the summary financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the summary financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the summary financial statements.

I believe that the audit evidence I have obtained is sufficient and appropriate to provide a basis for my qualified audit opinion.

MINISTRY OF FINANCE

Independent Auditor’s Report - Summary Financial Statements

Basis for Qualified Opinion

Inappropriate deferral of revenues

Government’s accounting treatment for funds received from other governments and for externally restricted funds received from non-government sources is to initially record them as deferred revenue (a liability) and then recognize revenue in the statement of operations either on the same basis as the related expenditures occur or, in the case of funds for the purchase or construction of capital assets, to recognize revenue on the same basis as the related assets are amortized.

In this respect, the summary financial statements are not in accordance with Canadian public sector accounting standards which require that (i) transfers from other governments be recorded as revenues, except when the transfer meets the definition of a liability for the recipient government, and (h) externally restricted funds received from non-government sources be recorded as revenue in the period in which the funds are used for the purpose(s) specified.

Had government made an adjustment, when this was first brought to its attention, for those funds received that in my opinion do not meet the definition of a liability or which have already been used for the purpose(s) specified, liabilities as at March 31, 2015, would have been less by $4,241 million, the accumulated surplus at the beginning of the year would have been greater by $4,050 million and current year revenue would have been greater by $191 million.

Qualified Opinion

In my opinion, except for the effects of the matters described in the Basis for Qualified Opinion paragraphs, the summary financial statements present fairly, in all material respects, the financial position of the Government of the Province of British Columbia as at March 31, 2015, and the results of its operations, change in its net liabilities, and its cash flows for the year then ended in accordance with the Budget Transparency and Accountability Act as set out in note 1(a) to the summary financial statements, which conform with Canadian public sector accounting standards.

Report on Other Legal and Regulatory Requirements

As required by section 11(2) of the Auditor General Act, I report that, except for the effects of the matters described in the Basis for Qualified Opinion paragraphs, the summary financial statements are presented fairly in accordance with Canadian public sector accounting standards, which is one of the financial reporting frameworks included in Canadian generally accepted accounting principles.

| /s/ Carol Bellringer |

Victoria, British Columbia | Carol Bellringer, CPA, FCA |

July 8, 2015 | Auditor General |

PROVINCE OF BRITISH COLUMBIA

PUBLIC ACCOUNTS 2014/15

Summary Financial Statements

Consolidated Statement of Financial Position

as at March 31, 2015

| | | | In Millions | |

| | Note | | 2015 | | 2014 | |

| | | | $ | | $ | |

Financial Assets | | | | | | | |

Cash and cash equivalents | | | | 3,237 | | 2,382 | |

Temporary investments | | | | 439 | | 420 | |

Accounts receivable | | 3 | | 3,489 | | 3,449 | |

Inventories for resale | | 4 | | 85 | | 75 | |

Due from other governments | | 5 | | 896 | | 790 | |

Due from self—supported Crown corporations and agencies | | 6 | | 633 | | 848 | |

Equity in self—supported Crown corporations and agencies | | 7 | | 8,271 | | 7,839 | |

Loans, advances and mortgages receivable | | 8 | | 1,902 | | 1,824 | |

Other investments | | 9 | | 2,131 | | 2,350 | |

Sinking fund investments | | 10 | | 977 | | 835 | |

Loans for purchase of assets, recoverable from agencies | | 11 | | 20,317 | | 18,921 | |

| | | | 42,377 | | 39,733 | |

Liabilities | | | | | | | |

Accounts payable and accrued liabilities | | 12 | | 5,369 | | 5,134 | |

Employee future benefits | | 13 | | 1,921 | | 1,870 | |

Due to other governments | | 14 | | 711 | | 1,042 | |

Due to Crown corporations, agencies and trust funds | | 15 | | 50 | | 38 | |

Deferred revenue | | 16 | | 9,809 | | 9,718 | |

Employee pension plans | | 17 | | 261 | | 214 | |

Taxpayer—supported debt | | 18 | | 42,693 | | 41,761 | |

Self—supported debt | | 19 | | 20,465 | | 19,041 | |

| | | | 81,279 | | 78,818 | |

Net assets (liabilities) | | 21 | | (38,902 | ) | (39,085 | ) |

| | | | | | | |

Non—financial Assets | | | | | | | |

Tangible capital assets | | 22 | | 39,028 | | 37,778 | |

Restricted assets | | 23 | | 1,553 | | 1,493 | |

Prepaid program costs | | 24 | | 866 | | 775 | |

Other assets | | 25 | | 707 | | 866 | |

| | | | 42,154 | | 40,912 | |

Accumulated surplus (deficit) | | 26 | | 3,252 | | 1,827 | |

| | | | | | | |

Measurement uncertainty | | 2 | | | | | |

Contingencies and contractual obligations | | 27 | | | | | |

The accompanying notes and supplementary statements are an integral part of these financial statements.

Prepared in accordance with Canadian generally accepted accounting principles.

| /s/ STUART NEWTON | |

| STUART NEWTON | |

| Comptroller General | |

41

PROVINCE OF BRITISH COLUMBIA

PUBLIC ACCOUNTS 2014/15

Summary Financial Statements

Consolidated Statement of Operations

for the Fiscal Year Ended March 31, 2015

| | In Millions | |

| | 2015 | | 2014 | |

| | Estimates | | | | | |

| | (Note 33) | | Actual | | Actual | |

| | $ | | $ | | $ | |

Revenue | | | | | | | |

| | | | | | | |

Taxation (Note 28) | | 22,157 | | 23,056 | | 20,930 | |

Contributions from the federal government | | 7,363 | | 7,326 | | 7,502 | |

Fees and licenses | | 5,336 | | 5,425 | | 5,210 | |

Natural resources (Note 29) | | 3,010 | | 2,937 | | 2,955 | |

Miscellaneous | | 2,958 | | 2,804 | | 3,194 | |

Net earnings of self—supported Crown corporations and agencies (Note 7) | | 2,885 | | 3,371 | | 2,701 | |

Investment income | | 1,091 | | 1,203 | | 1,236 | |

| | 44,800 | | 46,122 | | 43,728 | |

Expense (Note 30) | | | | | | | |

| | | | | | | |

Health | | 18,683 | | 18,370 | | 17,862 | |

Education | | 11,899 | | 11,827 | | 11,827 | |

Social services | | 3,703 | | 3,847 | | 3,805 | |

Interest | | 2,578 | | 2,498 | | 2,482 | |

Natural resources and economic development | | 1,757 | | 2,191 | | 1,755 | |

Transportation | | 1,629 | | 1,608 | | 1,580 | |

Other | | 1,594 | | 1,288 | | 1,184 | |

Protection of persons and property | | 1,393 | | 1,451 | | 1,520 | |

General government | | 1,180 | | 1,359 | | 1,386 | |

| | 44,416 | | 44,439 | | 43,401 | |

Surplus (deficit) for the year before unusual items | | 384 | | 1,683 | | 327 | |

Forecast allowance | | (200 | ) | | | | |

| | | | | | | |

Surplus (deficit) for the year | | 184 | | 1,683 | | 327 | |

| | | | | | | |

Accumulated surplus (deficit)—beginning of year as restated (Note 26) | | | | 1,346 | | 1,019 | |

Accumulated surplus (deficit)—before other comprehensive income | | | | 3,029 | | 1,346 | |

Accumulated other comprehensive income from self—supported Crown corporations and agencies (see page 97)—beginning of year | | | | 481 | | 154 | |

Other comprehensive income from self—supported Crown corporations and agencies (see page 97) | | | | (258 | ) | 327 | |

Accumulated other comprehensive income from self—supported Crown corporations and agencies (see page 97)—end of year | | | | 223 | | 481 | |

Accumulated surplus (deficit)—end of year | | | | 3,252 | | 1,827 | |

The accompanying notes and supplementary statements are an integral part of these financial statements.

42

PROVINCE OF BRITISH COLUMBIA

PUBLIC ACCOUNTS 2014/15

Summary Financial Statements

Consolidated Statement of Change in Net Liabilities

for the Fiscal Year Ended March 31, 2015

| | In Millions | |

| | 2015 | | 2014 | |

| | Estimates | | Actual | | Actual | |

| | $ | | $ | | $ | |

| | | | | | | |

Surplus (deficit) for the year | | 184 | | 1,683 | | 327 | |

Effect of change in tangible capital assets: | | | | | | | |

Acquisition of tangible capital assets | | (4,030 | ) | (3,407 | ) | (3,151 | ) |

(Gain) or loss on sale of tangible capital assets | | (168 | ) | (135 | ) | (601 | ) |

Amortization of tangible capital assets | | 2,147 | | 2,080 | | 2,071 | |

Disposals and valuation adjustments | | 226 | | 212 | | 665 | |

| | (1,825 | ) | (1,250 | ) | (1,016 | ) |

Effect of change in: | | | | | | | |

Restricted assets | | (53 | ) | (60 | ) | (51 | ) |

Prepaid program costs | | (1 | ) | (91 | ) | (85 | ) |

Other assets | | 4 | | 159 | | (289 | ) |

| | (50 | ) | 8 | | (425 | ) |

Effect of self—supported Crown corporations’ and agencies’ other comprehensive income | | (175 | ) | (258 | ) | 327 | |

Decrease (increase) in net liabilities | | (1,866 | ) | 183 | | (787 | ) |

Net (liabilities)—beginning of year | | (39,220 | ) | (39,085 | ) | (38,298 | ) |

Net (liabilities)—end of year (Note 21) | | (41,086 | ) | (38,902 | ) | (39,085 | ) |

The accompanying notes and supplementary statements are an integral part of these financial statements.

43

PROVINCE OF BRITISH COLUMBIA

PUBLIC ACCOUNTS 2014/15

Summary Financial Statements

Consolidated Statement of Cash Flow

for the Fiscal Year Ended March 31, 2015

| | In Millions | |

| | 2015 | | 2014 | |

| | Receipts | | Disbursements | | Net | | Net | |

| | $ | | $ | | $ | | $ | |

Operating Transactions | | | | | | | | | |

| | | | | | | | | |

Surplus (deficit) for the year1 | | | | | | 1,683 | | 327 | |

Non—cash items included in surplus (deficit): | | | | | | | | | |

Amortization of tangible capital asset | | | | | | 2,080 | | 2,071 | |

Amortization of public debt deferred revenue and deferred charges | | | | | | (356 | ) | (365 | ) |

Concessionary loan adjustments (decrease) | | | | | | (12 | ) | (3 | ) |

(Gain) or loss on sale of tangible capital assets | | | | | | (135 | ) | (601 | ) |

Valuation adjustment | | | | | | 204 | | 224 | |

Net earnings of self—supported Crown corporations and agencies | | | | | | (3,371 | ) | (2,701 | ) |

Temporary investments (increase) decrease | | | | | | (19 | ) | 545 | |

Accounts receivable (increase) | | | | | | (210 | ) | (1,172 | ) |

Due from other governments (increase) decrease | | | | | | (106 | ) | 136 | |

Due from self—supported Crown corporations and agencies decrease (increase) | | | | | | 215 | | (426 | ) |

Accounts payable and accrued liabilities increase (decrease) | | | | | | 235 | | (11 | ) |

Employee future benefits increase | | | | | | 51 | | 77 | |

Due to other governments (decrease) | | | | | | (331 | ) | (965 | ) |

Due to Crown corporations, agencies and funds increase (decrease) | | | | | | 12 | | (1 | ) |

Employee pension plan increase | | | | | | 47 | | 49 | |

Items applicable to future operations increase (decrease) | | | | | | 104 | | (611 | ) |

Contributions from self—supported Crown corporations and agencies | | | | | | 2,651 | | 2,516 | |

Cash derived from (used for) operations | | | | | | 2,742 | | (911 | ) |

| | | | | | | | | |

Capital Transactions | | | | | | | | | |

Tangible capital assets dispositions (acquisitions) | | 211 | | (3,407 | ) | (3,196 | ) | (2,489 | ) |

Cash (used for) capital | | 211 | | (3,407 | ) | (3,196 | ) | (2,489 | ) |

| | | | | | | | | |

Investment Transactions | | | | | | | | | |

Investment in self—supported Crown corporations and agencies | | 30 | | | | 30 | | 214 | |

Loans, advances and mortgages receivable (issues) | | 227 | | (325 | ) | (98 | ) | (181 | ) |

Other investments—net decrease | | 218 | | | | 218 | | 291 | |

Restricted assets—net (increase) | | | | (60 | ) | (60 | ) | (51 | ) |

Sinking fund investments—net (increase) decrease | | 558 | | (700 | ) | (142 | ) | 943 | |

Cash (used for) derived from investments | | 1,033 | | (1,085 | ) | (52 | ) | 1,216 | |

Sub—total cash (requirements) | | | | | | (506 | ) | (2,184 | ) |

44

PROVINCE OF BRITISH COLUMBIA

PUBLIC ACCOUNTS 2014/15

Summary Financial Statements

Consolidated Statement of Cash Flow—Continued

for the Fiscal Year Ended March 31, 2015

| | In Millions | |

| | 2015 | | 2014 | |

| | Receipts | | Disbursements | | Net | | Net | |

| | $ | | $ | | $ | | $ | |

| | | | | | | | | |

Sub—total cash (requirements) carried forward from previous page | | | | | | (506 | ) | (2,184 | ) |

| | | | | | | | | |

Financing Transactions2 | | | | | | | | | |

Public debt increases | | 31,105 | | (28,347 | ) | 2,758 | | 4,372 | |

(Used for) purchase of assets, recoverable from agencies | | 12,069 | | (13,466 | ) | (1,397 | ) | (2,015 | ) |

Cash derived from financing | | 43,174 | | (41,813 | ) | 1,361 | | 2,357 | |

Increase in cash and cash equivalents | | | | | | 855 | | 173 | |

Cash and cash equivalents—beginning of year | | | | | | 2,382 | | 2,209 | |

Cash and cash equivalents—end of year | | | | | | 3,237 | | 2,382 | |

| | | | | | | | | |

Cash and cash equivalents are made up of: | | | | | | | | | |

Cash | | | | | | 2,499 | | 1,143 | |

Cash equivalents | | | | | | 738 | | 1,239 | |

| | | | | | 3,237 | | 2,382 | |

1Interest received during the year was $1,190 million (2014: $1,236 million). Interest paid during the year was $2,489 million (2014: $2,483 million). Interest received is made up of interest income from the Statement of Operations in the amount of $1,203 million (2014: $1,236 million) plus the change in accrued interest receivable in the amount of $(13) million (2014: nil). Interest paid is made up of interest expense from the Statement of Operations in the amount of $2,498 million (2014: $2,482 million) plus the change in accrued interest payable in the amount of $(9) million (2014: $1 million).

2Financing transaction receipts are from debt issues and disbursements are for debt repayments.

The accompanying notes and supplementary statements are an integral part of these financial statements.

45

PROVINCE OF BRITISH COLUMBIA

PUBLIC ACCOUNTS 2014/15

Notes to Consolidated Summary Financial Statements

for the Fiscal Year Ended March 31, 2015

1. Significant Accounting Policies

(a) BASIS OF ACCOUNTING

The government’s Summary Financial Statements are prepared in accordance with the Budget Transparency and Accountability Act (BTAA), which requires generally accepted accounting principles (GAAP) for senior governments in Canada, supported by regulations of Treasury Board under the BTAA.

(b) REPORTING ENTITY

These financial statements include the accounts of organizations that meet the criteria of control (by the province) as established under Canadian Public Sector Accounting Standards. The reporting entity also includes government partnerships.

A list of organizations included in these consolidated financial statements may be found on pages 83. Trusts administered by government or government organizations are excluded from the reporting entity.

(c) PRINCIPLES OF CONSOLIDATION

Taxpayer—supported Crown corporations, agencies, and the school districts, universities, colleges, institutes, health organizations (SUCH) and the Consolidated Revenue Fund (CRF) are consolidated using the full consolidation method. The government’s interests in government partnerships are recorded on a proportional consolidation basis. Self—supported Crown corporations, agencies, entities and government business partnerships are consolidated using the modified equity basis of consolidation.

Organizations are reviewed annually to determine whether they can be expected to meet the definition of self—supported over their normal course of operations. In determining whether organizations will be able to maintain their operations and meet their liabilities from revenues received from sources outside of the government reporting entity, the following factors are considered as they apply:

i) The organization’s history of maintaining its operations and meeting its liabilities;

ii) Whether the organization would continue to maintain its operations and meet its liabilities without relying on sales to, or subsidies in cash or kind from, the government reporting entity;

iii) Past, present and future economic conditions within which the organization operates; and

iv) Whether the organization has realistic and specific plans that show how it expects to be able to maintain its operations and meet its liabilities in the future.

The status of self—supported organizations is not changed in response to financial results which are reasonably expected to be temporary in nature. Organizations are classified as self—supported on establishment and during a start up period if they are reasonably expected to meet the definition of self—supported in their normal course of operations.

The definitions of these consolidation methods can be found on page 141.

Adjustments are made for Crown corporations, agencies and entities whose fiscal year ends are different from the government’s fiscal year end of March 31. These Crown corporations, agencies and entities consist of the British Columbia Assessment Authority (December 31), the British Columbia Public School Employers’ Association (June 30), the Insurance Corporation of British Columbia (December 31), and all school districts (June 30).

46

PROVINCE OF BRITISH COLUMBIA

PUBLIC ACCOUNTS 2014/15

1. Significant Accounting Policies—Continued

Statistics Canada’s Financial Management System for Government Statistics provides the guidance for establishing segment disclosure and function reporting. The Consolidated Statement of Financial Position by Sector and the Consolidated Statement of Operations by Sector are found on pages 86 — 93. These statements include the operations of the CRF, taxpayer—supported Crown corporations and agencies, and SUCH sector organizations. Each taxpayer—supported Crown corporation, agency and SUCH sector organization is assigned to a sector based on its major activity. Sectors are identified using functions. The nature of each function is described in greater detail under Note 1(d) Classification by Sector.

(d) SPECIFIC ACCOUNTING POLICIES

Classification by Sector

The province uses the following sectors: health, education, social services, natural resources and economic development, protection of persons and property, transportation, general government, debt servicing and other.

The health sector includes the provincial health care system. It includes providing medical, hospital and preventive care, and other health—related services such as laboratories and diagnostic facilities.

The education sector includes education services. It includes elementary, secondary, and post—secondary schools. It also includes other education services such as programs to upgrade the skills of individuals and to provide apprenticeship training.

The social services sector includes outlays that the province made to help disadvantaged individuals and families overcome obstacles and circumstances which threaten their well—being. It includes counselling and rehabilitation services, transfer payments to individuals who are unable to lead a normal life due to a physical or mental disability, and services and goods provided by the province to the elderly.

The natural resources and economic development sector includes the promotion and development of industries, as well as the development and conservation of the natural resources on which these industries depend. It includes regulating the various industrial activities that are carried on in the province, as well as research related to resource conservation.

The protection of persons and property sector includes the protection of persons and property from negligence, abuse and crime. It includes policing, operating and maintaining courts of law and correctional facilities. It includes services related to new immigrants. It also includes negotiations to resolve land, resources, governance and jurisdictional issues with First Nations.

The transportation sector includes the operation and maintenance of transportation systems. This includes highway infrastructure, other road systems and public transit.

The general government sector is composed of three sub—categories. These are general administration, executive and legislature, and other general government services. General administration includes central accounting, budgeting, tax administration and collection, and other centralized administrative services. Executive and legislature includes the political, law enactment and constitutional activities of the province.

The debt servicing sector represents the financial impacts of activities related to management of public debt.

The other sector consists of activities, such as housing and culture, which cannot be allocated to any of the specifically described sector classifications.

Revenue

All revenue is recorded on an accrual basis. For corporate income tax, the cash received from the federal government is used as the basis for estimating the tax revenue. Annual tax revenues also include adjustments between the estimated revenues of previous years and actual amounts, as well as revenues from reassessments relating to prior years. Revenues do not include estimates of unreported taxes, or the impact of future reassessments that cannot be reliably determined.

Personal income tax revenue is accrued in the year earned based on estimates of household and taxable income. The revenue reported in the fiscal year is based on a proration of the calendar year estimates.

47

PROVINCE OF BRITISH COLUMBIA

PUBLIC ACCOUNTS 2014/15

Notes to Consolidated Summary Financial Statements

for the Fiscal Year Ended March 31, 2015—Continued

1. Significant Accounting Policies—Continued

Direct taxes, such as sales, fuel, carbon, property transfer and tobacco, are recorded during the period in which the taxable event occurs and when authorized by legislation. Property tax revenues are recorded based on a pro—ration of actual property tax billings for each of the calendar years that comprise the fiscal year.