Exhibit 99.10

This page intentionally left blank

2024

British Columbia

Financial and Economic

Review

84th Edition

(August 2024)

This page intentionally left blank

Table of Contents

| 2024 Financial and Economic Review – August 2024 |

This page intentionally left blank

Table of Contents

| Part 1 — Economic Review | 1 | |

| 2023 Overview | 3 | |

| British Columbia Economy | 4 | |

| External Trade and Commodity Prices | 5 | |

| Population | 8 | |

| Labour Market | 8 | |

| Consumer Spending, Inflation and Wages | 9 | |

| Housing | 10 | |

| Tourism | 12 | |

| Global Economy | 12 | |

| United States | 13 | |

| Canada | 14 | |

| Asia | 15 | |

| Europe | 15 | |

| Financial Markets | 15 | |

| Charts | ||

| 1.1 | Provincial Economic Growth | 3 |

| 1.2 | British Columbia Real GDP Growth by Industry | 4 |

| 1.3 | Composition of British Columbia GDP by Industry | 5 |

| 1.4 | International Export Shares by Market | 6 |

| 1.5 | Lumber and Natural Gas Prices | 7 |

| 1.6 | Housing Starts | 11 |

| 1.7 | Home Sales and Price | 11 |

| 1.8 | Visitor Entries to British Columbia | 12 |

| 1.9 | Global Economic Growth | 13 |

| 1.10 | Canadian Dollar | 16 |

| Map | ||

| 1.1 | Net Interprovincial and International Migration in B.C., 2023 | 8 |

| Tables | ||

| 1.1 | British Columbia Population and Labour Market Statistics | 9 |

| 1.2 | British Columbia Price and Earnings Indicators | 10 |

| Topic Box | ||

| Historical Data Volatility | 17 | |

| Part 2 — Financial Review | 19 | |

| 2023/24 Overview | 20 | |

| Revenue | 22 | |

| Expense | 33 | |

| Provincial Capital Spending | 37 | |

| Provincial Debt | 48 | |

| Pension Plans | 52 | |

| Contractual Rights | 53 | |

| Contractual Obligations | 54 | |

| 2023/24 Public Accounts Audit Qualification | 55 | |

| 2024 Financial and Economic Review – August 2024 | | i |

Table of Contents

| Charts | ||

| 2.1 | 2023/24 Deficit - Major Changes from Budget 2023 | 21 |

| 2.2 | Revenue Changes from Budget 2023 | 22 |

| 2.3 | Expense Changes from Budget 2023 | 33 |

| 2.4 | Total Capital Spending by Sector | 37 |

| 2.5 | Capital Spending Changes from Budget 2023 | 39 |

| 2.6 | Financing Taxpayer-Supported Capital Spending | 42 |

| 2.7 | Total Provincial Debt by Sector | 49 |

| 2.8 | Change in Ending Debt Level from Budget 2023 | 49 |

| 2.9 | Reconciliation of Surplus/Deficit to Change in Debt | 50 |

| Tables | ||

| 2.1 | 2023/24 Fiscal Summary | 20 |

| 2.2.1 | Personal Income Tax Revenue Changes from Budget 2023 | 22 |

| 2.2.2 | Corporate Income Tax Revenue Changes from Budget 2023 | 23 |

| 2.2.3 | Consumption Tax Revenue Changes from Budget 2023 | 23 |

| 2.2.4 | Property Tax Revenue Changes from Budget 2023 | 24 |

| 2.2.5 | Other Tax Revenue Changes from Budget 2023 | 24 |

| 2.2.6 | Energy and Mineral Revenue Changes from Budget 2023 | 25 |

| 2.2.7 | Forest Revenue Changes from Budget 2023 | 26 |

| 2.2.8 | Other Revenue Changes from Budget 2023 | 27 |

| 2.2.9 | Federal Government Transfer Changes from Budget 2023 | 27 |

| 2.3 | Revenue by Source | 30 |

| 2.4 | Expense by Ministry, Program and Agency | 31 |

| 2.5 | 2023/24 Operating Results by Quarter | 32 |

| 2.6 | Capital Spending | 38 |

| 2.7 | Capital Expenditure Projects Greater Than $50 Million | 43 |

| 2.8 | Provincial Debt Summary | 48 |

| 2.9 | Key Debt Indicators | 51 |

| 2.10 | Interprovincial Comparison of Credit Ratings, July 2024 | 52 |

| 2.11 | Pension Plan Balances | 53 |

| 2.12 | Taxpayer-Supported Contractual Obligations | 55 |

| Part 3 — Supplementary Information | 57 | |

| General Description of the Province | 59 | |

| Constitutional Framework | 60 | |

| Provincial Government | 61 | |

| Annual Financial Cycle | 63 | |

| Government’s Financial Statements | 65 | |

| Charts | ||

| 3.1 | Financial Planning and Reporting Cycle Overview | 64 |

| Tables | ||

| 3.1 | Provincial Taxes (as of July 2024) | 67 |

| 3.2 | Interprovincial Comparisons of Tax Rates - 2024 | 73 |

| ii | | 2024 Financial and Economic Review – August 2024 |

Table of Contents

| Appendix 1 - Economic Review Supplementary Tables | 75 | |

| Tables | ||

| A1.1A | Aggregate and Labour Market Indicators | 76 |

| A1.1B | Prices, Earnings and Financial Indicators | 78 |

| A1.1C | Other Indicators | 80 |

| A1.1D | Commodity Production Indicators | 82 |

| A1.2 | British Columbia Real GDP at Market Prices, Expenditure Based | 84 |

| A1.3 | British Columbia GDP at Basic Prices, by Industry | 86 |

| A1.4 | British Columbia GDP, Income Based | 88 |

| A1.5 | Employment by Industry in British Columbia | 90 |

| A1.6 | Capital Investment by Industry | 91 |

| A1.7 | British Columbia International Goods Exports by Major Market and Selected Commodities, 2023 | 92 |

| A1.8 | British Columbia International Goods Exports by Market Area | 93 |

| A1.9 | Historical Commodity Prices (in US Dollars) | 94 |

| A1.10 | British Columbia Forest Sector Economic Activity Indicators | 95 |

| A1.11 | Historical Value of Mineral, Petroleum and Natural Gas Shipments | 96 |

| A1.12 | Petroleum and Natural Gas Activity Indicators | 97 |

| A1.13 | Supply and Consumption of Electrical Energy in British Columbia | 98 |

| A1.14 | Components of British Columbia Population Change | 99 |

| Appendix 2 - Financial Review Supplementary Tables | 101 | |

| Tables | ||

| A2.1 | Operating Statement - 2012/13 to 2023/24 | 103 |

| A2.2 | Statement of Financial Position - 2012/13 to 2023/24 | 104 |

| A2.3 | Changes in Financial Position - 2012/13 to 2023/24 | 105 |

| A2.4 | Revenue by Source - 2012/13 to 2023/24 | 106 |

| A2.5 | Revenue by Source Supplementary Information - 2012/13 to 2023/24 | 107 |

| A2.6 | Expense by Function - 2012/13 to 2023/24 | 108 |

| A2.7 | Expense by Function Supplementary Information - 2012/13 to 2023/24 | 109 |

| A2.8 | Full-Time Equivalents (FTEs) - 2012/13 to 2023/24 | 110 |

| A2.9 | Capital Spending - 2012/13 to 2023/24 | 111 |

| A2.10 | Provincial Debt - 2012/13 to 2023/24 | 112 |

| A2.11 | Provincial Debt Supplementary Information - 2012/13 to 2023/24 | 113 |

| A2.12 | Key Provincial Debt Indicators - 2012/13 to 2023/24 | 114 |

| A2.13 | Historical Operating Statement Surplus (Deficit) | 115 |

| A2.14 | Historical Provincial Debt Summary | 116 |

| 2024 Financial and Economic Review – August 2024 | | iii |

This page intentionally left blank

Part 1

Economic Review1

1 Reflects information available as of June 27, 2024.

| 2024 Financial and Economic Review – August 2024 |

This page intentionally left blank

Part 1 – Economic Review

2023 Overview

Following two years of strong growth, economic activity in British Columbia, like other provinces, expanded at a slower pace in 2023. Last year the B.C. economy faced the continued impact of high interest rates and inflationary pressures, slowing domestic and global demand, as well as climate-related disruptions.

Statistics Canada published 2023 real dollar GDP by industry at basic prices in the preliminary release of its Provincial Economic Accounts in May 2024. The following analysis refers to these real GDP figures, as opposed to the commonly reported income and expenditure market prices data released late in the year.2

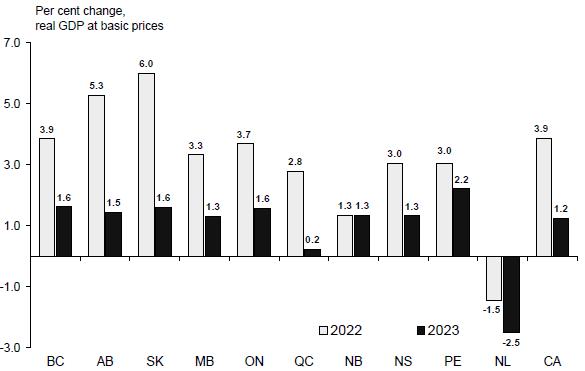

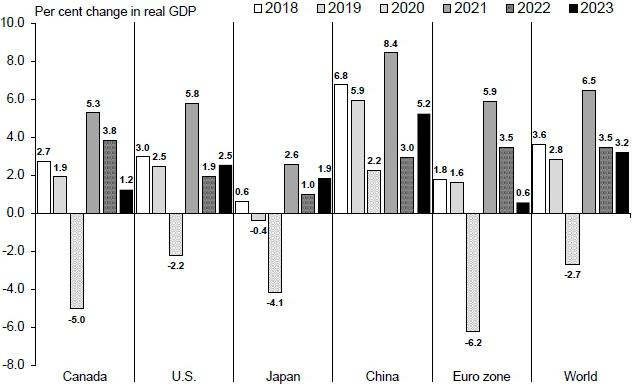

In 2023, B.C.’s real GDP growth of 1.6 per cent ranked second highest among provinces (tied with Saskatchewan and Ontario) and outperformed the national average. B.C.’s economy expanded at a slower pace last year than the 3.9 per cent gain in 2022, which was supported by the pandemic recovery.

Chart 1.1 Provincial Economic Growth

Sources: Statistics Canada (Tables 36-10-0402-01 and 36-10-0434-03 – May 2024 Preliminary Industry Accounts)

In 2023, B.C. employment increased by 1.6 per cent, supported by high immigration, while wages and salaries rose by 7.1 per cent. Home construction reached a record high in 2023 despite high interest rates and construction costs and labour shortages. At the same time, home sales fell by 9.2 per cent and the average home sale price decreased by 2.6 per cent as markets adjusted to high mortgage rates.

| 2 | Provincial and national real GDP by industry estimates are based on Statistics Canada’s preliminary industry accounts, released in May 2024. Further information on British Columbia’s economic performance is expected to be available in November 2024, when Statistics Canada releases revised GDP by industry data for 2023 and previous years, together with the full income and expenditure accounts for 2023. |

| 2024 Financial and Economic Review – August 2024 | | 3 |

Part 1 – Economic Review

Consumer spending on goods edged down 0.1 per cent in 2023, while supplementary data showed that consumer spending on services continued to recover. Price pressures in B.C. moderated across a broad range of goods and services but remained elevated in 2023. Overall, B.C.’s inflation rate averaged 3.9 per cent last year, down from 6.9 per cent in 2022. Meanwhile, weaker demand and lower commodity prices led to a 13.5 per cent decline in B.C.’s goods exports relative to 2022.

British Columbia Economy

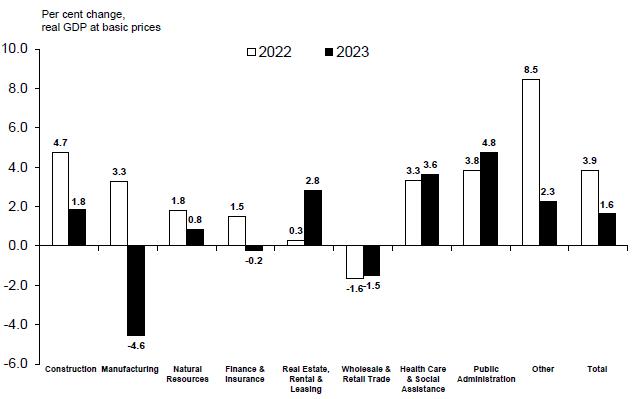

B.C.’s real GDP grew by 1.6 per cent in 2023, driven by B.C.’s service-producing industries while activity in goods-producing industries decreased compared to the previous year.

Service-producing industries grew by 2.4 per cent in 2023, supported by strong population growth. The service sector experienced broad-based annual gains, led by real estate, rental and leasing (+2.8 per cent) and professional, scientific and technical services (+4.7 per cent). The transportation and warehousing (+5.7 per cent), public administration (+4.8 per cent), and health care and social assistance (+3.6 per cent) sectors also contributed to overall growth, while the largest decline occurred in wholesale and retail trade (-1.5 per cent). Service-producing industries that were heavily affected by COVID-19 related disruptions continued to recover in 2023, with all major sectors surpassing pre-pandemic levels except for accommodation and food services, and transportation and warehousing.

B.C.’s goods-producing industries decreased by 0.8 per cent in 2023, following two years of solid growth. In 2023, activity declined in B.C.’s manufacturing (-4.6 per cent); utilities (-9.2 per cent); and agriculture, forestry, fishing and hunting (-6.5 per cent) sectors. Meanwhile, mining, quarrying and oil and gas extraction (+4.7 per cent) and construction (+1.8 per cent) activities contributed to annual economic growth.

Chart 1.2 British Columbia Real GDP Growth by Industry

Source: Statistics Canada (Table 36-10-0402-01 – May 2024 Preliminary Industry Accounts)

Note: Other includes industries such as transportation and warehousing, educational services, and professional, scientific and technical services

| 4 | | 2024 Financial and Economic Review – August 2024 |

Part 1 – Economic Review

In 2023, service-producing industries accounted for 76.2 per cent of B.C.’s economy and goods-producing industries represented 23.8 per cent. The real estate and rental and leasing sector formed the largest share of the service-producing industries, followed by wholesale and retail trade. The construction industry continued to make up the largest share of the goods-producing industries, followed by the manufacturing sector.

Chart 1.3 Composition of British Columbia GDP by Industry

Source: Statistics Canada (Table 36-10-0400-01 – May 2024 Preliminary Industry Accounts)

(numbers may not add to 100 per cent due to rounding)

External Trade and Commodity Prices

Exports by destination:

Lower prices for key commodities in 2023 contributed to a decline in B.C. merchandise exports. In addition, exports leaving B.C. ports were affected by a labour relations dispute in July 2023. B.C. merchandise exports to the U.S. and China (B.C.’s two largest international trading partners) declined in 2023, while exports to Japan and the European Union saw moderate increases. Overall, B.C. goods exports declined by 13.5 per cent last year compared to 2022.

B.C.’s merchandise exports to the U.S. fell by 18.3 per cent in 2023 compared to 2022, following two years of strong growth. The annual decline largely reflected a 32.4 per cent decrease in energy products (primarily natural gas) as well as a 32.0 per cent decrease in wood products (primarily softwood lumber). Meanwhile, exports of machinery and equipment to the U.S. increased for a third consecutive year, up 15.2 per cent in 2023 compared to 2022.

| 2024 Financial and Economic Review – August 2024 | | 5 |

Part 1 – Economic Review

B.C.’s goods exports to China decreased by 6.5 per cent in 2023, largely due to declines in exports of energy products (-14.0 per cent) and pulp and paper products (-11.3 per cent). Meanwhile, B.C.’s goods exports to Japan increased by 3.5 per cent in 2023, following two years of double-digit growth. In 2023, gains in goods exports to Japan were concentrated in energy products (+31.4 per cent), while exports of wood products declined by 30.8 per cent.

Appendix Tables A1.7 and A1.8 provide further detail on exports by major market and commodity groups.

In 2023, the share of B.C.’s international merchandise exports destined to the U.S. averaged 54.3 per cent, down from 57.5 per cent in 2022. Exports to China accounted for 14.1 per cent in 2023, up from 13.1 per cent in 2022, while exports to Japan represented 11.1 per cent, up from 9.3 per cent in 2022.

Chart 1.4 International Export Shares by Market

Source: BC Stats – accessed June 2024

Note: Other Asia includes Hong Kong, Taiwan, South Korea and India

(numbers may not add to 100 per cent due to rounding)

Exports by commodity and prices:

In 2023, the decline in B.C. merchandise exports largely reflected an 18.9 per cent decrease in exports of energy products (primarily natural gas and coal) as well as a 31.1 per cent decrease in wood products exports (primarily softwood lumber). Meanwhile, exports of machinery and equipment increased by 9.5 per cent in 2023 compared to 2022.

Energy prices eased in 2023 from the elevated levels seen in 2022 following Russia’s invasion of Ukraine. In addition, tight monetary policy and global recession concerns weighed on oil prices in 2023. The West Texas Intermediate (WTI) price averaged $77.6 US/barrel in 2023, down 18.1 per cent from 2022. Meanwhile, the plant inlet price of natural gas averaged $1.77 C/GJ in 2023, down 56.9 per cent from 2022, reflecting higher supply, slowing global economic activity and weaker demand due to mild winter weather in North America. Similarly, the annual average price for metallurgical coal fell by 19.9 per cent in 2023 compared to 2022.

| 6 | | 2024 Financial and Economic Review – August 2024 |

Part 1 – Economic Review

High interest rates also weighed on U.S. construction activity, reducing demand for B.C. lumber in 2023. The price of Western spruce-pine-fir (SPF) 2x4 averaged $398 US/000 board feet in 2023, which was 51.1 per cent below the elevated levels observed in 2022.

The effects of slower global economic activity on industrial metal and mineral prices were mixed. In 2023, molybdenum, gold, and silver experienced strong price growth compared to the previous year. Meanwhile, prices for copper and zinc were lower compared to 2022 and the price for lead was relatively unchanged.

Chart 1.5 Lumber and Natural Gas Prices

Sources: Ministry of Forests; Ministry of Energy, Mines and Low Carbon Innovation.

Exports of services:

Supplementary tourism data for 2023 suggested that B.C.’s nominal international exports of services continued to recover from a sharp decline in 2020. At the national level, Canadian exports of services experienced strong growth in 2023.

Manufacturing shipments:

Like merchandise exports, B.C.’s manufacturing sector was affected by lower commodity prices and the port labour relations dispute, with disruptions to the supply of raw materials as well as transportation. Overall in 2023, the nominal value of B.C.’s manufacturing shipments fell by 5.4 per cent compared to 2022, largely due to a sharp decline in shipments of wood products (-26.8 per cent), which outweighed relatively broad-based gains across other industries.

| 2024 Financial and Economic Review – August 2024 | | 7 |

Part 1 – Economic Review

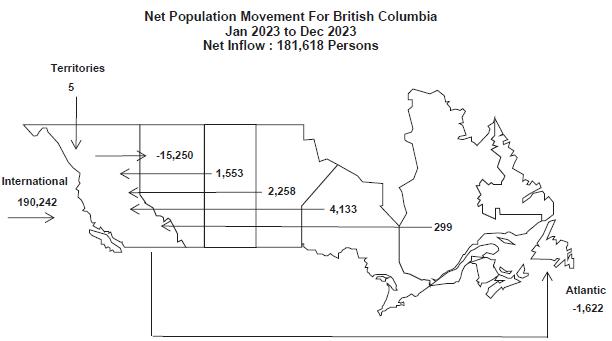

Population

B.C. saw strong population growth in 2023 due to a record level of international migration. B.C.’s population on July 1, 2023 was 5.519 million people, an increase of 3.0 per cent from the same date in 2022 and the fastest growth rate since 1994. In 2023, net international migration rose by 190,242 persons, reflecting higher immigration targets for permanent residents introduced by the federal government and an expansion of federal immigration programs for temporary residents. Meanwhile, net interprovincial migration to B.C. declined (-8,624 persons) for the first time since 2012, largely due to out-migration to Alberta. Overall, B.C. welcomed a total of 181,618 net migrants in 2023, surpassing 2022’s previous record-setting year. At the same time, B.C. saw a small natural decline (total births minus deaths) in 2023, which subtracted from the province’s population count for a third consecutive year.

Map 1.1 Net Interprovincial and International Migration in B.C., 2023

Source: BC Stats

Labour Market

B.C.’s labour market experienced moderate gains in 2023, following two years of strong job growth. Employment grew by 43,900 jobs (+1.6 per cent) in 2023, with most of the expansion observed in the second half of the year. The composition of jobs improved, with 49,500 net new full-time jobs offsetting a decline of 5,600 part-time jobs. The annual increase in net new-full time jobs showed continued employment growth among women, who accounted for 56.6 per cent of those jobs. The number of jobs created was balanced between the public sector (+26,100 jobs) and self-employment (+24,000 jobs) while private sector employment declined (-6,300 jobs).

Employment gains in 2023 were mainly driven by growth in the services-producing sector (+53,200 jobs), led by educational services (+16,600 jobs); finance, insurance, real estate, rental and leasing (+11,600 jobs) and accommodation and food services (+9,200 jobs). Meanwhile, employment in the goods sector was lower than the previous year (-9,200 jobs), largely reflecting a decline in manufacturing (-12,300 jobs).

| 8 | | 2024 Financial and Economic Review – August 2024 |

Part 1 – Economic Review

Despite continued employment growth overall, the recovery from the pandemic has been uneven across industries. December 2023 data showed that employment remained below pre-pandemic (February 2020) levels in business, building, and other support services (-34,100 jobs); construction (-32,200 jobs); accommodation and food services (-19,500 jobs); and agriculture (-1,100 jobs).

B.C.’s labour force expanded by 2.2 per cent in 2023, up from 1.0 per cent growth in 2022. Labour force expansion was driven by more landed immigrants looking for jobs last year (+2.5 per cent), which exceeded growth among those born in Canada (+0.5 per cent). B.C.’s labour force participation rate edged up to 65.2 per cent in 2023 from 65.1 per cent in 2022. While the labour force participation rate for the prime-age group has surpassed its pre-pandemic five-year average, the labour force participation rate among the 55+ years age group has declined. An aging workforce poses challenges for labour markets in B.C. and across the country.

B.C.’s unemployment rate has risen from the historical lows observed in 2022, with labour force expansion outpacing job gains in 2023. B.C.’s unemployment rate averaged 5.2 per cent in 2023, up from 4.6 per cent in 2022. Meanwhile, job vacancies in the province have been easing. The province’s job vacancy rate reached 4.4 per cent in December 2023, down from its peak of 7.2 per cent in December 2021.

Appendix Table A1.5 provides more details on employment by sector and subsectors.

Table 1.1 British Columbia Population and Labour Market Statistics

| Units | 2019 | 2020 | 2021 | 2022 | 2023 | |||||||||||||

| Population (as of July 1) | (thousands) | 5,111 | 5,176 | 5,227 | 5,356 | 5,519 | ||||||||||||

| (% change) | 1.8 | 1.3 | 1.0 | 2.5 | 3.0 | |||||||||||||

| Net Migration | ||||||||||||||||||

| International | (persons) | 70,859 | (3,155 | ) | 73,863 | 142,231 | 190,242 | |||||||||||

| Interprovincial | (persons) | 14,265 | 19,310 | 31,047 | 6,515 | (8,624 | ) | |||||||||||

| Labour Force | (thousands) | 2,813 | 2,761 | 2,852 | 2,881 | 2,944 | ||||||||||||

| (% change) | 2.9 | (1.9 | ) | 3.3 | 1.0 | 2.2 | ||||||||||||

| Employment | (thousands) | 2,678 | 2,509 | 2,664 | 2,748 | 2,792 | ||||||||||||

| (% change) | 2.7 | (6.3 | ) | 6.2 | 3.2 | 1.6 | ||||||||||||

| Unemployment Rate | (%) | 4.8 | 9.1 | 6.6 | 4.6 | 5.2 | ||||||||||||

Sources: Statistics Canada (Tables 17-10-0005-01, 17-10-0040-01, 17-10-0020-01, 14-10-0023-01 - accessed June 2024)

Consumer Spending, Inflation and Wages

Consumer spending on goods edged down 0.1 per cent in 2023, following 3.1 per cent growth in 2022. Further, Statistics Canada reported that the port labour relations dispute in B.C. impacted retailers through the summer of 2023. The pull back in nominal retail trade coupled with elevated inflation indicates that the volume of retail trade also declined last year as higher interest rates reduced consumer’s purchasing power. In 2023, lower retail sales were concentrated in four of nine subsectors including gasoline stations (-9.2 per cent); building material and garden equipment and supplies dealers (-14.5 per cent); sporting goods, hobby, book and music retailers (-10.9 per cent) and furniture, home furnishing, electronics and appliances stores (-5.4 per cent). Meanwhile, annual sales growth was led by health and personal care stores (+11.4 per cent), clothing and accessories stores (+10.4 per cent), and general merchandise retailers (+5.7 per cent).

| 2024 Financial and Economic Review – August 2024 | | 9 |

Part 1 – Economic Review

While retail trade data offers detailed information on consumer spending on goods, there is a lack of timely comprehensive data for consumer spending on services at the provincial level. National data shows that household spending on services grew by 2.7 per cent on a real basis and by 6.9 per cent on a nominal basis in 2023. In B.C., nominal sales at food services and drinking places, a component of the service sector, continued to improve in 2023, up 10.4 per cent compared to 2022, partly reflecting higher prices.

In 2023, price pressures in B.C. moderated among a broad number of goods and services but remained elevated. B.C.’s Consumer Price Index (CPI) inflation rate averaged 3.9 per cent in 2023, down from 6.9 per cent in 2022, partly due to lower gasoline prices. Annual price growth was led by shelter (+5.7 per cent) and food (+7.1 per cent). Higher shelter prices reflected faster growth for mortgage costs as financing was initiated or renewed at higher borrowing rates, while strong immigration and rising homeownership costs for potential homebuyers added upward pressure on rental demand. At the same time, grocery price growth (+7.5 per cent) eased somewhat compared to 2022 but remained elevated and prices for food purchased from restaurants rose at the fastest pace since 1991.

Wages in B.C. continued to rise in 2023 as employers faced labour shortages despite some improvement in job vacancies across most sectors compared to the previous year. Employee compensation (aggregate wages, salaries, and employers’ social contributions) increased by 7.2 per cent in 2023 following 9.7 per cent growth in 2022, reflecting gains in both jobs and wages. The average weekly wage rate increased by 6.2 per cent in 2023 compared to 2022, rising faster than the consumer price index for B.C.

Table 1.2 British Columbia Price and Earnings Indicators

| Units | 2019 | 2020 | 2021 | 2022 | 2023 | |||||||||||||

| Consumer Price Index | (2002=100) | 131.4 | 132.4 | 136.1 | 145.5 | 151.2 | ||||||||||||

| (% change) | 2.3 | 0.8 | 2.8 | 6.9 | 3.9 | |||||||||||||

| Average Weekly Wage Rate | ($) | 1,021 | 1,094 | 1,137 | 1,191 | 1,265 | ||||||||||||

| (% change) | 2.0 | 7.1 | 3.9 | 4.8 | 6.2 | |||||||||||||

| Compensation of Employees 1, 2 | ($ millions) | 152,568 | 152,704 | 172,036 | 188,707 | 202,207 | ||||||||||||

| (% change) | 5.6 | 0.1 | 12.7 | 9.7 | 7.2 | |||||||||||||

| Primary Household Income 1 | ($ millions) | 218,490 | 218,224 | 240,702 | 262,498 | n/a | ||||||||||||

| (% change) | 7.0 | (0.1 | ) | 10.3 | 9.1 | n/a | ||||||||||||

| Net Operating Surplus (Corporations) 1 | ($ millions) | 29,607 | 36,139 | 48,809 | 53,368 | n/a | ||||||||||||

| (% change) | (13.3 | ) | 22.1 | 35.1 | 9.3 | n/a |

| 1 | As of November 2023 Provincial Economic Accounts |

| 2 | Component of income-based GDP, including wages, salaries and employers’ social contributions earned in B.C. by residents and non-residents of the province. 2023 value for compensation of employees is from Statistics Canada Table 36-10-0205-01. Sources: Statistics Canada (Tables 18-10-0005-01, 14-10-0064-01, 36-10-0221-01, 36-10-0205-01, 36-10-0224-01 - accessed June 2024) |

Sources: Statistics Canada (Tables 18-10-0005-01, 14-10-0064-01, 36-10-0221-01, 36-10-0205-01, 36-10-0224-01 – accessed June 2024)

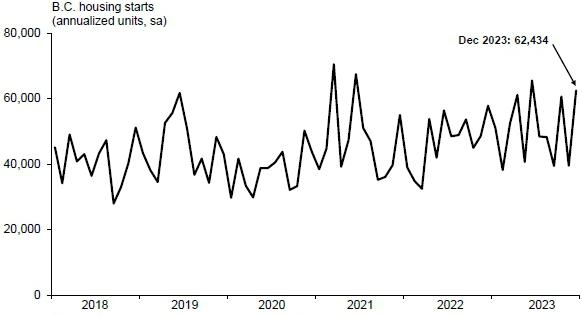

Housing

B.C. home construction activity strengthened in 2023. Housing starts totaled 50,490 units in 2023, the province’s highest annual pace on record and up 8.1 per cent compared to 2022. Among segments, multi-family housing starts rose by 18.2 per cent and single-family housing starts declined by 29.7 per cent. All major Census Metropolitan Areas (CMA) in B.C. saw growth in homes under construction in 2023. However, home completions were mixed, with large annual gains reported in Victoria and Abbotsford while declines occurred in the Vancouver and Kelowna CMAs compared to 2022.

| 10 | | 2024 Financial and Economic Review – August 2024 |

Part 1 – Economic Review

Meanwhile, the value of B.C. residential building permits (a leading indicator of potential new housing activity) decreased by 11.1 per cent compared to 2022, following strong growth in the previous two years.

Chart 1.6 Housing Starts

Sources: Canada Mortgage and Housing Corporation; Haver Analytics

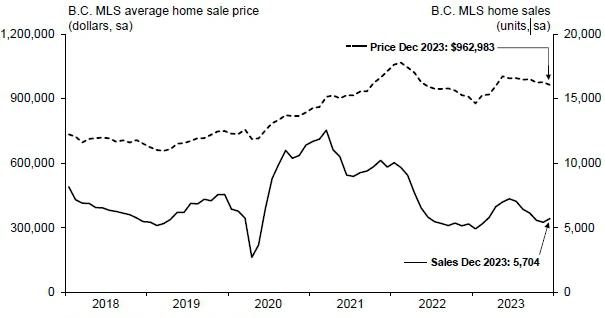

High interest rates continued to weigh on home sales activity last year, which saw MLS home sales in B.C. fall to the lowest level in a decade. In 2023, MLS home sales declined by 9.2 per cent compared to 2022 while the MLS average home sale price was 2.6 per cent lower than 2022. Sales activity decreased in nearly every region in 2023, including large markets such as Greater Vancouver (-10.0 per cent), Okanagan Mainline (-16.0 per cent), Fraser Valley (-4.1 per cent) and Victoria (-8.7 per cent). In 2023, weaker home sales contributed to declines in MLS composite benchmark house prices (which incorporate benchmark attributes by dwelling type) across regional markets including the Fraser Valley (-9.8 per cent), Vancouver Island (-6.2 per cent), Victoria (-6.3 per cent), Okanagan Valley (-4.4 per cent) and Greater Vancouver (-2.7 per cent).

Chart 1.7 Home Sales and Price

Sources: Canadian Real Estate Association; Haver Analytics

| 2024 Financial and Economic Review – August 2024 | | 11 |

Part 1 – Economic Review

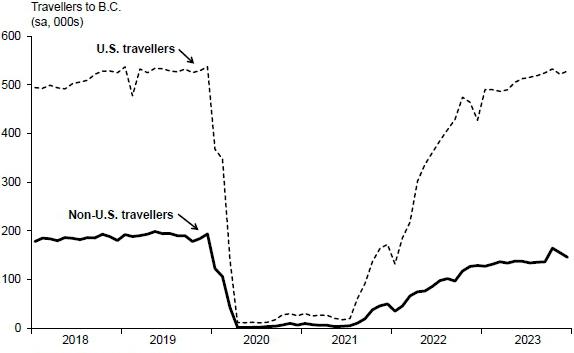

Tourism

B.C.’s tourism sector continued to expand in 2023. The number of international non-resident travellers visiting B.C. gradually increased throughout the year. Overall, the number of international travellers rose by 50.4 per cent compared to 2022. In 2023, the number of U.S. travellers increased by 48.3 per cent and the number of non-U.S. travellers increased by 58.6 per cent compared to the previous year. The ongoing recovery in visitor numbers has brought the level of international travellers entering B.C. closer to pre-pandemic levels.

Chart 1.8 Visitor Entries to British Columbia

Sources: Statistics Canada; Haver Analytics

Global Economy

The global economy eased in 2023, partly due to the cooling effects of high interest rates on demand. The International Monetary Fund estimates that global real GDP advanced by 3.2 per cent in 2023, down from 3.5 per cent growth in the previous year. By the second half of 2023, the rate of inflation had decreased significantly in many countries due to rising interest rates, falling energy prices, and improved supply chains compared to 2022. This deceleration led several central banks, including the Bank of Canada, the Federal Reserve, and the European Central Bank, to pause interest rate increases.

In 2023, the U.S. economy strengthened despite weaker global demand, driven by robust consumer and government spending. U.S. real GDP grew by 2.5 per cent last year, up from 1.9 per cent growth in 2022. Conversely, Canadian economic growth eased to 1.2 per cent in 2023, down from 3.8 per cent in 2022.

Overseas, China reported economic growth of 5.2 per cent last year, up from 3.0 per cent growth in 2022 but still below the pace of economic output observed prior to the onset of the pandemic. Japan’s economy grew by 1.9 per cent last year, up from 1.0 per cent growth in 2022. Meanwhile, euro zone real GDP growth slowed to 0.6 per cent in 2023 from 3.5 per cent growth in 2022.

| 12 | | 2024 Financial and Economic Review – August 2024 |

Part 1 – Economic Review

Chart 1.9 Global Economic Growth

Sources: International Monetary Fund (April 2024); Haver Analytics

United States

The U.S. economy steadily expanded throughout 2023. Nearly all major components of real GDP saw gains, supported by higher consumption of services and government spending. Export activity picked up in the second half of 2023 while business investment slowed amid tighter financial conditions. Overall, U.S. real GDP increased by 2.5 per cent in 2023, up from 1.9 per cent growth in 2022.

The U.S. labour market continued to grow in 2023, although at a slower pace than the prior year. U.S. employment was 2.3 per cent higher in 2023 compared to 2022 and the unemployment rate averaged 3.6 per cent, down from 3.7 per cent. Meanwhile, the annual labour force participation rate increased by 0.4 percentage points in 2023, with 62.6 per cent of Americans eligible to work participating in the labour market last year.

High interest rates continued to weigh on U.S. housing market activity in 2023. New housing construction fell for a second consecutive year, down 8.5 per cent compared to 2022, and totalled 1.42 million units for the year. Sales of existing homes fell by 18.7 per cent in 2023 compared to 2022, while sales of new single-family homes rose by 3.9 per cent. Last year the median sales price for existing homes increased by 1.0 per cent and the median sales price for new single-family homes decreased by 1.4 per cent compared to 2022.

The U.S. current account deficit (the combined balances of trade in goods and services income, and net unilateral current transfers) decreased to $US 905.4 billion in 2023 from $US 1,012.1 billion in 2022. As a share of nominal U.S. GDP, the current account deficit averaged -3.3 per cent in 2023.

| 2024 Financial and Economic Review – August 2024 | | 13 |

Part 1 – Economic Review

Canada

The Canadian economy expanded by 1.2 per cent in 2023, following growth of 3.8 per cent in 2022. The increase in Canadian real GDP was led by gains in exports of goods and services, household consumption (primarily services), and government spending. Gains were partly offset by a decline in inventories, continued weakness in business investment (primarily residential investment), and higher imports of services.

The Canadian labour market continued to grow throughout 2023, supported by strong population growth. Employment rose by 2.4 per cent last year, adding 477,900 jobs compared to 2022. However, employment in accommodation and food services; business, building and other support services; and the agriculture sector had not yet returned to pre-pandemic levels by the end of 2023. Meanwhile, the national unemployment rate averaged 5.4 per cent in 2023, up 0.1 percentage points from the previous year’s record annual low.

High interest rates continued to slow Canadian housing market activity last year. In 2023, Canadian total MLS home sales experienced double-digit declines for a second consecutive year, down by 11.2 per cent compared to 2022. Reduced demand led to a 3.6 per cent decrease in the national average home sale price in 2023, the first annual decline since 2018. Meanwhile, Canadian housing starts fell by 8.2 per cent last year following a 3.4 per cent decline in 2022, reflecting lower single-family and multi-family unit construction. In addition, the value of residential building permits fell by 7.9 per cent compared to 2022, following annual growth of 2.6 per cent in the previous year.

Consumer price inflation in Canada eased in 2023, partly due to lower energy prices, but remained above the Bank of Canada’s target range. On an annual basis, Canadian consumer prices rose by 3.9 per cent in 2023, down from 6.8 per cent growth in 2022. Slower inflation contributed to weaker nominal retail sales growth of 1.9 per cent in 2023 following 8.3 per cent annual sales growth in 2022 amid high inflation. In 2023, sales at motor vehicles and parts dealers (+7.7 per cent), food and beverage stores (+3.7 per cent), and health and personal care retailers (+8.7 per cent) were the primary contributors to annual growth. The largest decline occurred in sales at gas stations (-12.3 per cent), partly reflecting slower price growth compared to 2022.

Canadian nominal goods exports fell last year amid lower global commodity prices. In 2023, nominal goods exports decreased by 2.2 per cent compared to 2022, mainly due to declines in exports of energy products and forestry products and building and packaging materials. In contrast, exports of services experienced strong growth, rising by 13.8 per cent compared to 2022, driven by higher exports of travel services and commercial services.

Canada’s current account deficit increased to $21.0 billion in 2023, up $10.7 billion compared with 2022, largely due to the trade in goods balance shifting from a surplus to a deficit. As a share of nominal Canadian GDP, the current account deficit averaged -0.7 per cent in 2023 compared to an average of -0.4 per cent in 2022.

| 14 | | 2024 Financial and Economic Review – August 2024 |

Part 1 – Economic Review

Asia

China’s economy experienced mixed results in 2023 reflecting the ongoing downturn in the property sector and muted consumer spending. Efforts by the government to revive the property sector included measures to reduce mortgage rates and increase infrastructure investments. However, housing investment, home sales and prices remained weak last year. In contrast, growth in industrial production, particularly in manufacturing and mining, strengthened in the second half of 2023. Overall, China’s real GDP increased by 5.2 per cent in 2023, following growth of 3.0 per cent in 2022, which was the slowest growth observed in nearly 50 years excluding the pandemic.

In Japan, pandemic-related restrictions were lifted at the beginning of 2023, resulting in a temporary rebound in consumer spending in the first half of the year. While increased demand in the service sector led to higher profits for businesses, Japan experienced negative net exports of goods in 2023 amid weaker foreign demand. Overall, Japan’s real GDP increased by 1.9 per cent in 2023, up from 1.0 per cent growth in the previous year.

Europe

Slowing global demand, energy market volatility and geopolitical tensions weighed on economic momentum in the euro zone last year. In addition, high interest rates reduced private consumption and corporate investment. The partial withdrawal of fiscal support also weighed on economic growth. Overall, the euro zone economy increased by 0.6 per cent in 2023 compared to 2022, down from 3.5 per cent growth in the previous year. In 2023, euro zone economic growth was led by Spain, France and Italy, while Germany, the euro zone’s largest economy, reported a slight contraction.

Financial Markets

The Federal Reserve (the Fed) and the Bank of Canada (BoC) along with other central banks, continued to raise interest rates last year to address persistent elevated global inflation, although at a slower pace than in 2022.

The target range for the U.S. federal funds rate started 2023 at 4.25 to 4.50 per cent, well above the 0.00 to 0.25 per cent range at the beginning of 2022. The Fed introduced a series of 0.25 percentage point (pp) increases in its first three meetings in 2023, to reach a target range of 5.00 to 5.25 per cent in May. After pausing in June, the Fed increased rates by another 0.25 pp in July, bringing the target range up to 5.25 to 5.50 per cent, where it remained for the balance of 2023. At the same time, the Fed continued its commitment to reducing its holdings of Treasury securities, and agency debt and mortgage-backed securities.

In comparison, the Bank of Canada started the year by increasing its target for the overnight interest rate by 0.25 pp to reach 4.50 per cent in January 2023. The BoC held the overnight rate steady at subsequent meetings held in March and April, while emphasizing the importance of assessing the impact of previous interest rate increases on inflation given the lagged effect of monetary policy. Persistent price pressures and robust consumer spending prompted further rate hikes of 0.25 pp in June and July, bringing the overnight rate to 5.00 per cent before pausing for the remainder of 2023 amid diminishing excess demand, a slowdown in economic activity, and some easing of inflationary pressures.

| 2024 Financial and Economic Review – August 2024 | | 15 |

Part 1 – Economic Review

The Canadian dollar’s exchange rate versus the US dollar was relatively stable in 2023, primarily guided by the interest rate and economic activity differentials between the two countries. This trend marked a shift from the volatility experienced in recent years when investors sought safe haven assets such as the US dollar amid the onset of evolving geopolitical tensions and uncertainty around global inflationary pressures. While the loonie strengthened towards the end of last year, it averaged 74.1 US cents in 2023 overall, down from 76.8 US cents in 2022.

Chart 1.10 Canadian Dollar

Source: Bank of Canada – accessed April 2024.

| 16 | | 2024 Financial and Economic Review – August 2024 |

Part 1 – Economic Review

Historical Data Volatility

Individual economic variables have unique characteristics. An important characteristic from a budgeting and planning perspective is the historical data volatility of a variable. Typically, variables that are more volatile over history are more difficult to forecast than variables that are more stable. This topic box summarizes the volatility of historical data from 1981 to 2022. Economic variables were relatively more volatile in 2020 and 2021, reflecting the impact of the COVID-19 pandemic.

One of the most common measurements of data volatility is the standard deviation, which is frequently reported by agencies such as Statistics Canada and the Bank of Canada. Generally, the standard deviation of a variable measures how far the individual data points are from the average (mean) of all the data points in the series on an absolute basis (that is, without regard to whether each data point is above or below the average).

If a variable’s data points are generally close to the average, then the standard deviation will be relatively low (meaning that the variable is relatively stable). An example of a relatively stable variable is presented in Chart 1, which displays the annual growth rate of B.C.’s population.

Chart 1 – An Example of Historical Data Stability

Conversely, if a variable’s data points are generally spread out from the average, then the variable will have a relatively high standard deviation (meaning that the variable is relatively volatile). The annual growth rate of the natural gas price in Chart 2 is an example of a relatively volatile variable.

Chart 2 – An Example of Historical Data Volatility

The standard deviations and averages of selected key economic variables’ growth rates over different time periods are presented in Table 1. For instance, B.C. real GDP growth had a standard deviation of 2.5 percentage points and an average of 2.8 per cent from 2013 to 2022. This means that growth rates between 0.3 and 5.3 per cent are within one standard deviation of the average annual real GDP growth rate of 2.8 per cent over this period.

Standard deviations can vary widely across indicators and time. Variables such as the natural gas price and net operating surplus of corporations were relatively volatile from 2013 to 2022, while variables such as population and the consumer price index were relatively stable (see Chart 3). Meanwhile, some variables like the price of natural gas have become more volatile over time, whereas other variables like population have become more stable (see Table 1).

Chart 3 – Recent Data Volatility

The Ministry of Finance manages the uncertainty associated with data volatility by incorporating prudence in the Province’s budget and fiscal plan.

| 2024 Financial and Economic Review – August 2024 | | 17 |

Part 1 – Economic Review

Table 1 – Data Volatility

Standard deviations and averages of growth rates of selected B.C. economic variables and prices

| 1982-2022 | 2003-2022 | 2013-2022 | ||||||||||||||||||||||

| Standard | Standard | Standard | ||||||||||||||||||||||

| Deviation | Deviation | Deviation | ||||||||||||||||||||||

| All figures are based on the annual per cent | Average2 | (percentage | Average2 | (percentage | Average2 | (percentage | ||||||||||||||||||

| change of calendar year data1 | (%) | points) | (%) | points) | (%) | points) | ||||||||||||||||||

| Real GDP | 2.6 | 2.5 | 2.7 | 2.3 | 2.8 | 2.5 | ||||||||||||||||||

| Nominal GDP | 5.4 | 3.5 | 5.3 | 4.1 | 6.0 | 4.6 | ||||||||||||||||||

| Nominal consumption | 5.5 | 2.4 | 4.9 | 2.7 | 5.0 | 3.5 | ||||||||||||||||||

| Nominal business investment | 5.6 | 9.2 | 7.5 | 7.6 | 7.3 | 6.5 | ||||||||||||||||||

| Nominal residential home sales | 11.8 | 24.1 | 9.8 | 23.4 | 12.0 | 27.8 | ||||||||||||||||||

| Nominal household income | 5.3 | 2.5 | 4.9 | 2.1 | 5.2 | 1.3 | ||||||||||||||||||

| Nominal compensation of employees | 5.0 | 3.0 | 4.9 | 3.3 | 5.6 | 3.5 | ||||||||||||||||||

| Nominal net operating surplus of corporations | 11.3 | 29.9 | 8.1 | 16.8 | 9.6 | 15.5 | ||||||||||||||||||

| Consumer price index | 2.6 | 2.0 | 1.9 | 1.4 | 2.2 | 1.9 | ||||||||||||||||||

| Exchange rate | -0.1 | 5.4 | 1.1 | 6.5 | -2.5 | 5.4 | ||||||||||||||||||

| Copper price | 6.4 | 24.5 | 12.3 | 29.0 | 2.7 | 21.2 | ||||||||||||||||||

| Natural gas price | 9.7 | 40.8 | 11.5 | 49.8 | 24.6 | 59.0 | ||||||||||||||||||

| Pulp price | 3.9 | 21.2 | 6.2 | 18.7 | 5.3 | 20.7 | ||||||||||||||||||

| SPF 2x4 price | 5.8 | 22.5 | 9.2 | 25.8 | 13.7 | 28.1 | ||||||||||||||||||

| Housing starts | 3.2 | 23.1 | 6.6 | 22.8 | 6.3 | 14.7 | ||||||||||||||||||

| Population | 1.6 | 0.7 | 1.3 | 0.5 | 1.6 | 0.4 | ||||||||||||||||||

1 Calendar and fiscal year data yield similar data volatility results

2 Measured as the mean

Sources: Statistics Canada; Haver Analytics; Ministry of Energy, Mines & Low Carbon Innovation; Ministry of Forests; The Canadian Real Estate Association;

Canada Mortgage and Housing Corporation; Ministry of Finance calculations

| 18 | | 2024 Financial and Economic Review – August 2024 |

PART 2

FINANCIAL REVIEW

| 2024 Financial and Economic Review – August 2024 |

Part 2 – Financial Review

2023/24 Overview

Table 2.1 2023/24 Fiscal Summary

| 2023/24 | Actual | |||||||||||||||

| ($ millions) | Budget | Actual | Variance | 2022/23 1 | ||||||||||||

| Revenue | 77,690 | 79,623 | 1,933 | 81,790 | ||||||||||||

| Expense | (80,206 | ) | (84,060 | ) | (3,854 | ) | (79,344 | ) | ||||||||

| Pandemic Recovery Contingencies | (1,000 | ) | (598 | ) | 402 | (1,490 | ) | |||||||||

| Forecast allowance | (700 | ) | - | 700 | - | |||||||||||

| Surplus (Deficit) | (4,216 | ) | (5,035 | ) | (819 | ) | 956 | |||||||||

| Capital spending: | ||||||||||||||||

| Taxpayer-supported capital spending | 11,813 | 8,772 | (3,041 | ) | 6,755 | |||||||||||

| Self-supported capital spending | 4,027 | 4,584 | 557 | 4,165 | ||||||||||||

| Total capital spending | 15,840 | 13,356 | (2,484 | ) | 10,920 | |||||||||||

| Provincial Debt: | ||||||||||||||||

| Taxpayer-supported debt | 75,617 | 75,402 | (215 | ) | 59,888 | |||||||||||

| Self-supported debt | 31,607 | 32,060 | 453 | 29,492 | ||||||||||||

| Total debt (including forecast allowance) | 107,924 | 107,462 | (462 | ) | 89,380 | |||||||||||

| Key debt affordability metrics: | ||||||||||||||||

| Taxpayer-supported debt-to-GDP ratio | 18.9 | % | 18.5 | % | -0.4 | % | 15.2 | % | ||||||||

| Taxpayer-supported debt-to-revenue ratio | 100.1 | % | 97.9 | % | -2.2 | % | 74.3 | % | ||||||||

| 1 | Figures have been restated to reflect government accounting policies in effect at March 31, 2024, and the impact of Statistics Canada’s historical data revisions of economic growth. |

The provincial government ended the 2023/24 fiscal year with a deficit of $5.0 billion, $819 million higher than Budget 2023. (See Table 2.5 for detailed quarterly changes to the forecast.)

Revenue totalled $79.6 billion in 2023/24, $1.9 billion higher than the Budget 2023 projection. Higher revenues were recorded in taxation, investment earnings, miscellaneous sources and commercial Crown corporations’ net incomes, partly offset by lower natural resources revenues and federal government transfers. (See Revenue section for further details.)

Total government expenses were $3.4 billion higher than Budget 2023 due mainly to fire and emergency management costs, compensation increases under the Shared Recovery Mandate, and funding for various housing and shelter initiatives using statutory spending authorization. (See Expense section for further details.)

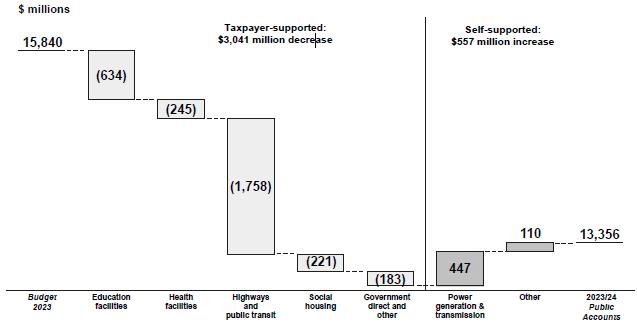

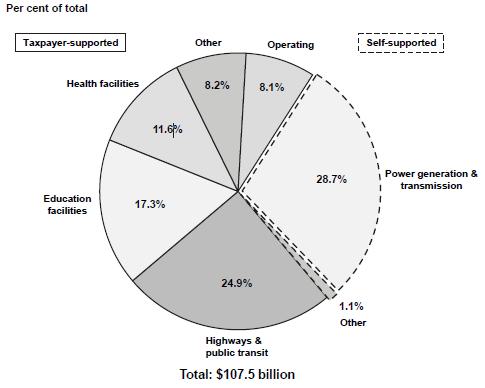

Taxpayer-supported capital spending on hospitals, schools, post-secondary institutions, transportation infrastructure, social housing and other projects totalled $8.8 billion, $3 billion less than Budget 2023 due to changes in the timing of projects across the sectors.

Self-supported capital spending of $4.6 billion was $557 million higher than budget mainly in power generation and transmission projects. (See Capital section for further details.)

| 20 | | 2024 Financial and Economic Review – August 2024 |

Part 2 - Financial Review

Chart 2.1 2023/24 Deficit – Major Changes from Budget 2023

Decline of $819 million

$ millions

Taxpayer-supported debt ended the year at $75.4 billion, which is $215 million lower than forecast in Budget 2023 mainly due to impacts of lower opening balance and lower capital spending. Self-supported debt was $32.1 billion, $453 million higher than budget mainly reflecting higher power generation and transmission projects. (See Provincial Debt section for further details.)

Financial information in this publication, including this chapter and Appendix 2, is sourced from the government’s 2023/24 Public Accounts.

| 2024 Financial and Economic Review – August 2024 | | 21 |

Part 2 - Financial Review

Revenue

Revenue totalled $79.6 billion in 2023/24, $1.9 billion higher than the Budget 2023 projection and down 2.6 per cent from 2022/23. Compared to budget, higher revenues were recorded in taxation, investment earnings, miscellaneous sources, federal government transfers and commercial Crown corporations’ net incomes, partly offset by lower natural resources revenues.

Changes of the major revenue components from Budget 2023 are outlined as follows.

Chart 2.2 Revenue Changes from Budget 2023

Total revenue increased by $1,933 million

$ millions

Income Tax Revenue

Personal income tax revenue was up $490 million mainly due to the effects of stronger 2022 tax assessments and improved 2023 household income compared to what was reported in 2022/23. In 2022, B.C. household income increased 6.8 per cent while total tax returns increased 3.9 per cent, mainly reflecting strong employment incomes, taxable income, and number of taxfilers offset by declines in capital gains income and relatively flat investment incomes from middle to higher income earning individuals, resulting in a one-time revenue gain of $608 million. This improvement was partially offset by $118 million decrease due to the carry-forward impacts of the lower 2022 tax returns on 2023/24 base revenue compared to budget assumptions.

Table 2.2.1 Personal Income Tax Revenue Changes from Budget 2023

| Revenue | Public | Public | ||||||||||||||||||||

| changes | Indicators | Budget | Accounts | Accounts | ||||||||||||||||||

| ($ millions) | (annual percent change) | 2023 | 2022/23 | 2023/24 | ||||||||||||||||||

| Prior year adjustment - mainly stronger 2022 tax returns compared to what was recorded in 2022/23 Public Accounts | 608 | Household income | 2022 | 7.1 | % | 7.1 | % | 6.8 | % | |||||||||||||

| 2023 | 6.1 | % | 6.1 | % | 6.9 | %1 | ||||||||||||||||

| 2024 | 4.3 | % | 4.3 | % | 4.4 | % 1 | ||||||||||||||||

| Carry-forward impacts of the lower 2022 tax returns and taxable income compared to budget assumptions | (118 | ) | B.C taxable income | 2022 | 6.2 | % | 2.5 | % | 4.3 | % | ||||||||||||

| 490 | 2023 | 6.0 | % | 5.9 | % | 6.0 | % | |||||||||||||||

| 2024 | 4.3 | % | 4.3 | % | 4.7 | % | ||||||||||||||||

| 22 | | 2024 Financial and Economic Review – August 2024 |

Part 2 – Financial Review

Corporate income tax revenue was up $147 million mainly due to higher entitlement of prior year partially offset by lower 2023 instalment payments from the federal government. The prior years’ final settlement payment relating to 2022 tax year resulted in a $1,329 million increase mainly reflecting the change in timing of revenue recognition using the preliminary 2022 tax assessment information at 2022/23 Public Accounts. In 2022, B.C. taxable income increased 3.3 per cent compared to the 9.3 per cent annual increase in the net operating surplus of B.C. corporations. This increase was partly offset by $1,182 million decrease in 2023 instalments, mainly reflecting lower federal government forecast of national corporate taxable income and corporate profits.

Table 2.2.2 Corporate Income Tax Revenue Changes from Budget 2023

| Revenue changes ($millions) | Indicators ($billions) | Budget 2023 | Public Accounts 2023/24 | |||||||||||

| Prior years’ settlement payment | ||||||||||||||

| 2022 tax year | 1,329 | Payment Share | 13.60 | % | 13.74 | % | ||||||||

| Advance instalments (2023/24) | (1,182 | ) | 2023 national corporate tax base | 547.1 | 457.3 | |||||||||

| 147 | 2022 national corporate tax base | 564.6 | 539.7 | |||||||||||

| 2022 B.C. corporate tax base | 76.8 | 73.8 | ||||||||||||

Other Tax Revenue

Sales tax revenues were $143 million higher than budget due to higher nominal expenditure on consumption of goods mainly durable and semi-durable goods. Higher reassessments and lower refunds also contributed to higher sales tax revenue.

Table 2.2.3 Consumption Tax Revenue Changes from Budget 2023

| Revenue changes ($ millions) | Indicators (annual percent change for the 2023 calendar year) | Budget 2023 | Public Accounts 1 2023/24 | |||||||||||

| Nominal consumer expenditures | ||||||||||||||

| on goods and services | 6.9 | % | 5.3 | % | ||||||||||

| on semi-durable goods | 2.3 | % | 5.2 | % | ||||||||||

| on services | 10.3 | % | 7.8 | % | ||||||||||

| Provincial sales | 143 | Nominal business investment | 1.4 | % | 8.3 | % | ||||||||

| Tobacco | (88 | ) | Consumer price index | 3.9 | % | 3.9 | % | |||||||

| Fuel | (90 | ) | Real GDP | 0.4 | % | 1.0 | % | |||||||

| Carbon | (169 | ) | Nominal GDP | 2.8 | % | 3.2 | % | |||||||

| (204 | ) | Retail sales | 1.8 | % | -0.1 | % | ||||||||

1 Budget 2024 forecast for most variables, except retail sales and consumer price index which are actuals. | ||||||||||||||

Property transfer tax revenue was $194 million higher than budget due to higher-than-expected number of transactions resulting from an improvement to mortgage rates outlook and net in-migration. Compared to 2022/23, revenue decreased $300 million (-13.1 per cent), as the average tax per residential transaction decreased 11.8 per cent, and the number of residential transactions decreased by 6.4 per cent.

Fuel tax revenue was down $90 million from budget mainly due to lower sales volumes on most fuel types.

| 2024 Financial and Economic Review – August 2024 | | 23 |

Part 2 – Financial Review

Carbon tax revenue was down $169 million from budget mainly due to higher refunds related to heavy fuel oil as well as lower than assumed natural gas, gasoline and diesel sales volumes. The 2023/24 revenue includes the carbon tax rate increase from $50 to $65 per tonne of carbon dioxide equivalent emissions on April 1, 2023.

Tobacco tax revenue was down $88 million from budget reflecting a decline in consumption volumes.

Property tax revenue was $117 million higher than budget due to higher revenues from residential, business property taxes and BC Assessment Authority property levies. The speculation and vacancy tax revenue at $87 million in 2023/24 was $3 million lower than the budget estimate, based on declarations by property owners for 2023 as well as reassessments relating to prior tax years.

Table 2.2.4 Property Tax Revenue Changes from Budget 2023

| Revenue changes ($ millions) | ||||

| Residential tax | 62 | |||

| Non-residential tax | 38 | |||

| Speculation and vacancy tax | (3 | ) | ||

| Other | 20 | |||

| Total changes | 117 | |||

Insurance premium tax revenue was $73 million higher than budget mainly due to higher activity and higher premiums charged by industry reflecting increased assessments of risks including climate change and inflationary increases, and increased prior year taxable premiums, partially offset by impacts of ICBC rebates.

Employer health tax revenue was $155 million higher than budget mainly due to increases in employer payrolls, reflecting improved compensation of employee growth as well as increased reassessments relating to prior tax years.

Table 2.2.5 Other Tax Revenue Changes from Budget 2023

| Revenue changes ($millions) | Indicators (annual percent change for the 2023 calendar year) | Budget 2023 | 2023/24 Public | |||||||||||

| Employer health | 155 | Compensation of employees | 6.3 | % | 6.7 | % | ||||||||

| Insurance premium | 73 | |||||||||||||

| 228 | ||||||||||||||

1 Budget 2024 forecast | ||||||||||||||

| 24 | | 2024 Financial and Economic Review – August 2024 |

Part 2 – Financial Review

Natural Resources Revenue

Natural gas royalties were $1,193 million lower than budget due to lower prices for natural gas and natural gas byproducts, partly offset by a corresponding decreased in utilization of credits under the royalty programs. In 2023/24 natural gas prices averaged $1.30 ($Cdn/gigajoule, plant inlet), a 57.2 per cent decrease from budget assumption. Byproducts include pentane, butane and condensate whose prices are more closely aligned to oil rather than natural gas. The Ministry of Indigenous Relations and Reconciliation recovered $106 million of natural gas royalties revenue in support of revenue sharing and other agreements with First Nations.

Table 2.2.6 Energy and Mineral Revenue Changes from Budget 2023

| Revenue changes ($ millions) | Indicators | Budget 2023 | Actual 2023/24 | |||||||||||

| Natural gas royalties | (1,193 | ) | Natural gas price ($Cdn/GJ, plant inlet) | $ | 3.04 | $ | 1.30 | |||||||

| Natural gas production (annual change) | 8.9 | % | 7.7 | % | ||||||||||

| Pentane price ($C/bbl) | $ | 93.71 | $ | 91.96 | ||||||||||

| Condensates price ($C/bbl) | $ | 86.95 | $ | 86.47 | ||||||||||

| Petroleum royalties | (9 | ) | Oil price ($US/bbl) | $ | 80.79 | $ | 78.01 | |||||||

| Coal, metals and other minerals | (90 | ) | Metallurgical coal price ($US/tonne) | $ | 252 | $ | 282 | |||||||

| Copper price ($US/lb) | $ | 3.56 | $ | 3.79 | ||||||||||

| Electricity sales under the Columbia River Treaty | (74 | ) | Electricity price ($US/Mwh) | $ | 107.84 | $ | 86.15 | |||||||

| Bonus bids and Crown land drilling licences and leases | (69 | ) | ||||||||||||

| Fees and levies collected by the BC Energy Regulator | 18 | |||||||||||||

| (1,417 | ) | |||||||||||||

Coal, metals and other minerals revenue was $90 million lower than budget mainly due to lower coal and copper production volumes, reflecting intermittent plant and project challenges as well as higher mining and capital costs, partly offset by increased commodity prices reflecting improved global demand and global supply shortage for high-quality coal raw material. Metallurgical coal prices averaged $282 (US/ tonne) in 2023/24, up 11.9 per cent from the budget assumption. Copper prices were $3.79 (US/lb) in 2023/24, up 6.5 per cent from the budget assumption. The Ministry of Indigenous Relations and Reconciliation recovered $152 million of coal, metals and other minerals revenue in support of revenue sharing and other agreements with First Nations.

Revenue from bonus bids and rents on drilling licences and leases was $69 million lower than budget due to lower bonus bid revenue ($61 million), reflecting the impact of updated accounting standards, and lower fee and rental revenue ($8 million). Effective 2023/24 bonus bid revenue is recognized in full at the time an authorization for the sale of a Crown land tenure is awarded. Previously bonus bid revenue recognition reflected a ten-year deferral of cash receipts from the sale of Crown land tenures.

| 2024 Financial and Economic Review – August 2024 | | 25 |

Part 2 – Financial Review

Revenue from other energy sources was $65 million lower than budget mainly due to the effects of lower Mid-Columbia (Mid-C) electricity and petroleum prices, partly offset by higher fees and levies collected by BC Energy Regulator. In 2023/24, petroleum prices averaged $78.01 ($US per barrel), down 3.4 per cent from budget ($80.79) and Mid-C electricity prices averaged $86.15 ($US per mega-watt hour), down 20.1 per cent from the budget assumption ($107.84). Average Mid-C electricity prices reflect mitigated market concerns regarding natural gas production and hydro generation constraints, as well as peak capacity shortages. The Ministry of Indigenous Relations and Reconciliation recovered $67 million of Columbia River Treaty electricity sales revenue in support of revenue sharing and other agreements with First Nations.

Forests revenue was $189 million lower than budget mainly due to lower than expected stumpage and logging tax revenues, reflecting lower Crown harvest volumes as well as decreased average stumpage rate and lumber prices. Logging tax revenue was $88 million lower than budget. The total Crown harvest volumes for 2023/24 were 32.1 million cubic metres, 15.5 per cent lower than budget. The reduction in harvest reflects the impact of logging deferrals in old growth forests and reduced fibre supply due in part to pest epidemics and wildfires. Lumber prices for spruce, pine and fir (SPF) 2x4 averaged $398 ($US/1000 bf) in 2023, slightly lower than the budget assumption ($400). The Ministry of Indigenous Relations and Reconciliation recovered $170 million of stumpage revenue in support of an interim enhancement to the Forest Consultation and Revenue Sharing Agreements with First Nations.

Table 2.2.7 Forest Revenue Changes from Budget 2023

| Revenue changes ($ millions) | Indicators | Budget 2023 | Actual 2023/24 | |||||||||||

| Stumpage from timber tenures | (70 | ) | SPF 2x4 | |||||||||||

| ($US/1000 bf, calendar year) | $ | 400 | $ | 398 | ||||||||||

| BC Timber Sales | (73 | ) | Total stumpage rate ($/m3 ) | $ | 18.07 | $ | 17.88 | |||||||

| Logging Tax | (88 | ) | Harvest volumes (million m3) | 38.0 | 32.1 | |||||||||

| Recoveries relating to revenue sharing payments to First Nations | 27 | |||||||||||||

| Other receipts | 15 | |||||||||||||

| (189 | ) | |||||||||||||

Other natural resource revenues, comprised of revenue from water rentals and hunting and fishing licenses, were $15 million lower than budget mainly due to lower water rentals revenue.

Other Taxpayer-Supported Sources

Revenue from fees, investment earnings and other miscellaneous sources totalled $12 billion, up $1.5 billion from budget.

Fee revenue totalled $5.3 billion, up $85 million from budget mainly due to higher revenues reported by post-secondary institutions, health authorities and other fees partly offset by lower revenues from K-12 school districts and recoveries related to nominal rent tenures.

Revenue from investment earnings was $1.7 billion, up $369 million from budget due to higher overall investment returns reflecting higher interest rates, partly offset by lower recoveries through the fiscal agency loan program. Lower vote recovery funding was equally offset by lower expenses.

| 26 | | 2024 Financial and Economic Review – August 2024 |

Part 2 – Financial Review

Table 2.2.8 Other Revenue Changes from Budget 2023

| Revenue changes ($ millions) | ||||||

| Fees | 85 | Higher revenues from post-secondary institutions, health authorities and other fees partly offset by lower revenues from K-12 school districts and recoveries related to nominal rent tenures. | ||||

| Miscellaneous sources | 999 | Higher revenues in taxpayer-supported SUCH sector agencies, higher PharmaCare and other vote recoveries | ||||

| Investment earnings | 369 | Higher overall investment returns partly offset by lower recoveries through the fiscal agency loan program | ||||

| 1,453 | ||||||

Miscellaneous revenue totalled $5 billion, up $999 million from budget mainly due to higher revenues from SUCH1 sector agencies and higher vote recoveries related to the Pharma Care and other health spending programs. The higher vote recovery funding had an equal and offsetting expense increase.

Federal Government Transfers

Contributions from the federal government totalled $13.7 billion, $141 million above budget.

Canada Health Transfer and Canada Social Transfer entitlements were up $420 million mainly due to one-time funding of $273 million to strengthen public health care, higher than assumed B.C. share of the national population (13.76 per cent compared to 13.62 per cent forecast at budget) and reimbursement of Canada Health Act deductions.

Table 2.2.9 Federal Government Transfer Changes from Budget 2023

| Revenue changes ($ millions) | ||||||

| B.C. health and social transfers revenue | 147 | Higher than assumed B.C. share of the national population and reimbursement of Canada Health Act deductions | ||||

| One-time B.C. health funding | 273 | One-time additional health transfer to strengthen public health care | ||||

| Disaster Financial Assistance Arrangements | (748 | ) | Mainly timing changes in recovery projects from past Disaster Financial Assistance Arrangements (DFAA) events now reprofiled to future years | |||

| Vote recoveries | 364 | Mainly higher labour market & skills training, transportation, child care, home care and mental health funding partly offset by lower local government transfers | ||||

| SUCH sector | 38 | Higher transfers to taxpayer-supported SUCH sector agencies (mainly post-secondary institutions) | ||||

| Crown corporations and agencies | 14 | Higher transfers to taxpayer supported Crown entities mainly BC Housing | ||||

| Other receipts | 53 | Mainly higher receipts from B.C.’s share of federal cannabis excise tax entitlement | ||||

| 141 | ||||||

1 SUCH: School districts, universities, colleges and institutes, and health organizations.

| 2024 Financial and Economic Review – August 2024 | | 27 |

Part 2 – Financial Review

Other federal government contributions were down $279 million from budget. The decrease mainly reflects an $748 million decrease in transfers under the Disaster Financial Assistance Arrangements (DFAA), partly offset by higher vote recoveries. The decrease in revenue reflects timing changes in recovery projects from past DFAA events now reprofiled to future years. Ministries received $364 million higher vote recovery mainly due to increased funding in support of labour market and skills training, transportation, child care, home care and mental health programs, partly offset by lower local government transfers. The higher revenues reported as vote recoveries have an equal and offsetting expense increase. Other ministry receipts were $53 million higher than budget mainly due to B.C.’s share of federal cannabis excise tax reflecting increased varieties of cannabis products, consumption and number of licensed cannabis retailers. SUCH sector entities (mainly post-secondary institutions) received $38 million higher contributions. Taxpayer-supported Crown corporations received $14 million higher contributions, mainly by BC Housing.

Commercial Crown Corporations

The net income of commercial Crown corporations (government business enterprises) was $4.5 billion in 2023/24, $1.0 billion higher than Budget 2023, and $1.1 billion higher than 2022/23. The variance from budget in overall earnings is mainly due to an improvement in operating results of ICBC.

British Columbia Hydro and Power Authority

BC Hydro’s net income was $323 million, $389 million lower than the forecast in Budget 2023 primarily due to the B.C. Electricity Affordability Credits issued to customers. Many variances, including those related to revenues, cost of energy, amortization, finance charges and others are deferred to regulatory accounts, as approved by the British Columbia Utilities Commission, and do not impact net income.

British Columbia Liquor Distribution Branch

BC Liquor Distribution Branch’s net income of $1.1 billion was $2 million lower than the forecast in Budget 2023 and $51 million lower than 2022/23 due to lower sales volumes over the year.

British Columbia Lottery Corporation

BC Lottery Corporation’s net income of $1.4 billion2 was $155 million lower than the prior year and $27 million lower than Budget 2023. The decrease in net income was primarily due to lower revenues attributed to reduced discretionary spending by patrons.

| 2 | Net of payments to the federal government and payments to the BC First Nations Gaming Revenue Sharing Limited Partnership in accordance with section 14.3 of the Gaming Control Act (B.C.). |

| 28 | | 2024 Financial and Economic Review – August 2024 |

Part 2 – Financial Review

Insurance Corporation of British Columbia

The Insurance Corporation of British Columbia’s reported net income was $1.4 billion, compared to $nil net income projected in Budget 2023, and $1.3 billion higher than the previous year. The improvement was mainly due to unanticipated higher investment earnings and lower claims activity compared to plan, and net of the rebate payments to customers.

More information about commercial Crown corporations’ financial results and performance measures is provided in each corporation’s Annual Service Plan Report available at its respective website.

| 2024 Financial and Economic Review – August 2024 | | 29 |

Part 2 – Financial Review

| Table 2.3 Revenue by Source | |||||||||

| ($ millions) | Budget 2023 | Actual 2023/24 | Actual 2022/23 | ||||||

| Taxation | |||||||||

| Personal income | 15,953 | 16,443 | 17,268 | ||||||

| Corporate income | 5,938 | 6,085 | 9,156 | ||||||

| Employer health | 2,731 | 2,886 | 2,720 | ||||||

| Sales 1 | 10,187 | 10,330 | 9,818 | ||||||

| Fuel | 1,072 | 982 | 1,021 | ||||||

| Carbon | 2,811 | 2,642 | 2,161 | ||||||

| Tobacco | 565 | 477 | 531 | ||||||

| Property | 3,488 | 3,605 | 3,253 | ||||||

| Property transfer | 1,799 | 1,993 | 2,293 | ||||||

| Insurance premium | 780 | 853 | 804 | ||||||

| 45,324 | 46,296 | 49,025 | |||||||

| Natural resources | |||||||||

| Natural gas royalties | 2,016 | 823 | 2,255 | ||||||

| Forests | 846 | 657 | 1,887 | ||||||

| Other natural resources 2 | 1,902 | 1,663 | 1,975 | ||||||

| 4,764 | 3,143 | 6,117 | |||||||

| Other revenue | |||||||||

| Post-secondary education fees | 2,770 | 2,840 | 2,651 | ||||||

| Other fees and licences 3 | 2,412 | 2,427 | 2,285 | ||||||

| Investment earnings | 1,349 | 1,718 | 1,314 | ||||||

| Miscellaneous 4 | 3,989 | 4,988 | 4,445 | ||||||

| 10,520 | 11,973 | 10,695 | |||||||

| Contributions from the federal government | |||||||||

| Health and social transfers | 8,970 | 9,390 | 8,606 | ||||||

| Other federal contributions 5 | 4,623 | 4,344 | 3,921 | ||||||

| 13,593 | 13,734 | 12,527 | |||||||

| Commercial Crown corporation net income | |||||||||

| BC Hydro | 712 | 323 | 360 | ||||||

| Liquor Distribution Branch | 1,150 | 1,148 | 1,199 | ||||||

| BC Lottery Corporation 6 | 1,456 | 1,429 | 1,584 | ||||||

| ICBC 7 | - | 1,399 | 131 | ||||||

| Other 8 | 171 | 178 | 152 | ||||||

| 3,489 | 4,477 | 3,426 | |||||||

| Total revenue | 77,690 | 79,623 | 81,790 |

| 1 | Includes provincial sales tax and HST/PST housing transition tax related to prior years. |

| 2 | Columbia River Treaty, Crown land tenures, other energy and minerals, water rental and other resources. |

| 3 | Healthcare-related, motor vehicle, and other fees. |

| 4 | Includes reimbursements for health care and other services provided to external agencies, and other recoveries. |

| 5 | Includes contributions for health, education, community development, housing and social service programs, and transportation projects. |

| 6 | Net of payments to the federal government and payments to the BC First Nations Gaming Revenue Sharing Limited Partnership in accordance with section 14.3 of the Gaming Control Act (B.C.) |

| 7 | Does not include non-controlling interest. |

| 8 | Includes Columbia Power Corporation, BC Railway Company, Columbia Basin power projects, and post-secondary institutions’ self-supported subsidiaries. |

| 30 | | 2024 Financial and Economic Review – August 2024 |

Part 2 – Financial Review

Table 2.4 Expense by Ministry, Program and Agency

| ($ millions) | Budget 2023 1 | Contin- gencies allocation | Pandemic & Recovery Contingencies | Statutory author- ization 2 | Total author- izations | Actual 2023/24 | Actual 2022/23 1 | ||||||||||||||

| Office of the Premier | 16 | - | - | - | 16 | 16 | 14 | ||||||||||||||

| Agriculture and Food | 112 | 102 | - | 46 | 260 | 259 | 292 | ||||||||||||||

| Attorney General | 773 | 90 | - | 207 | 1,070 | 1,069 | 809 | ||||||||||||||

| Children and Family Development | 1,912 | 240 | - | - | 2,152 | 2,152 | 1,742 | ||||||||||||||

| Citizens’ Services | 683 | 51 | - | - | 734 | 733 | 768 | ||||||||||||||

| Education and Child Care | 8,874 | 298 | - | 1 | 9,173 | 9,172 | 8,233 | ||||||||||||||

| Emergency Management and Climate Readiness | 101 | 91 | - | 401 | 593 | 593 | 821 | ||||||||||||||

| Energy, Mines and Low Carbon Innovation | 129 | 221 | - | 5 | 355 | 350 | 399 | ||||||||||||||

| Environment and Climate Change Strategy | 255 | 518 | - | 12 | 785 | 785 | 578 | ||||||||||||||

| Finance | 1,578 | 69 | - | 1,504 | 3,151 | 3,151 | 4,059 | ||||||||||||||

| Forests | 846 | 80 | - | 891 | 1,817 | 1,750 | 1,075 | ||||||||||||||

| Health | 28,674 | 1,249 | 581 | - | 30,504 | 30,504 | 26,385 | ||||||||||||||

| Housing | 897 | 18 | - | - | 915 | 915 | 901 | ||||||||||||||

| Indigenous Relations and Reconciliation | 188 | 185 | - | - | 373 | 372 | 770 | ||||||||||||||

| Jobs, Economic Development and Innovation | 113 | 97 | - | - | 210 | 209 | 225 | ||||||||||||||

| Labour | 21 | 25 | - | - | 46 | 46 | 34 | ||||||||||||||

| Mental Health and Addictions | 27 | 62 | - | - | 89 | 88 | 198 | ||||||||||||||

| Municipal Affairs | 269 | 42 | - | - | 311 | 310 | 1,923 | ||||||||||||||

| Post-Secondary Education and Future Skills | 2,770 | 552 | - | - | 3,322 | 3,322 | 2,692 | ||||||||||||||

| Public Safety and Solicitor General | 1,028 | 62 | - | - | 1,090 | 1,089 | 1,124 | ||||||||||||||

| Social Development and Poverty Reduction | 4,745 | - | - | - | 4,745 | 4,745 | 4,684 | ||||||||||||||

| Tourism, Arts, Culture and Sport | 182 | 54 | 17 | - | 253 | 252 | 427 | ||||||||||||||

| Transportation and Infrastructure | 1,021 | 53 | - | - | 1,074 | 1,074 | 2,044 | ||||||||||||||

| Water, Land and Resource Stewardship | 203 | 235 | - | - | 438 | 438 | 583 | ||||||||||||||

| Total ministries and Office of the Premier | 55,417 | 4,394 | 598 | 3,067 | 63,476 | 63,394 | 60,780 | ||||||||||||||

| Management of public funds and debt | 1,309 | - | - | 280 | 1,589 | 1,588 | 1,314 | ||||||||||||||

| Contingencies Vote 3 | 5,500 | (4,397 | ) | (598 | ) | - | 505 | 11 | 1 | ||||||||||||

| Funding for capital expenditures | 4,540 | - | - | - | 4,540 | 3,551 | 2,248 | ||||||||||||||

| Refundable tax credit transfers | 3,159 | - | - | - | 3,159 | 2,885 | 3,920 | ||||||||||||||

| Legislative Assembly and other appropriations | 214 | 3 | - | - | 217 | 215 | 181 | ||||||||||||||

| Total appropriations | 70,139 | - | - | 3,347 | 73,486 | 71,644 | 68,444 | ||||||||||||||

| Elimination of transactions between appropriations 4 | (32 | ) | - | - | (7 | ) | (39 | ) | (32 | ) | (24 | ) | |||||||||

| Prior year liability adjustments | - | - | - | - | - | (75 | ) | (98 | ) | ||||||||||||

| Consolidated revenue fund expense | 70,107 | - | - | 3,340 | 73,447 | 71,537 | 68,322 | ||||||||||||||

| Expenses recovered from external entities | 4,909 | - | - | - | 4,909 | 5,819 | 4,919 | ||||||||||||||

| Funding provided to service delivery agencies | (41,212 | ) | - | - | - | (41,212 | ) | (44,172 | ) | (38,236 | ) | ||||||||||

| Total direct program spending | 33,804 | - | - | 3,340 | 37,144 | 33,184 | 35,005 | ||||||||||||||

| Service delivery agency expense | |||||||||||||||||||||

| School districts | 8,356 | - | - | - | 8,356 | 8,659 | 7,933 | ||||||||||||||

| Universities | 6,369 | - | - | - | 6,369 | 6,630 | 6,053 | ||||||||||||||

| Colleges and institutes | 1,574 | - | - | - | 1,574 | 1,792 | 1,591 | ||||||||||||||

| Health authorities and hospital societies | 22,645 | - | - | - | 22,645 | 26,272 | 22,814 | ||||||||||||||

| Other service delivery agencies | 8,458 | - | - | - | 8,458 | 8,121 | 7,438 | ||||||||||||||

| Total service delivery agency expense | 47,402 | - | - | - | 47,402 | 51,474 | 45,829 | ||||||||||||||

| Total expense | 81,206 | - | - | 3,340 | 84,546 | 84,658 | 80,834 |

| 1 | Figures have been restated to reflect government’s organization and accounting policies in effect at March 31, 2024. |

| 2 | Statutory authorizations are appropriations permitted by an Act other than a Supply Act. |

| 3 | Budget 2023 includes the following spending allocations: $1.0 billion for Pandemic Recovery and $4.5 billion for General Programs and CleanBC. |

| 4 | Reflects payments made under an agreement where an expense from a voted appropriation is recorded as revenue by a special account (Housing Endowment Fund and British Columbia Training and Education Savings Program). |

| 2024 Financial and Economic Review – August 2024 | | 31 |

Part 2 – Financial Review

Table 2.5 2023/24 Operating Results by Quarter

| ($ millions) | |||||||||||||||

| 2023/24 deficit at Budget 2023 (February 28, 2023) | (4,216 | ) | (4,216 | ) | |||||||||||

| 2023/24 deficit at the First Quarterly Report (September 27, 2023) | (6,674 | ) | |||||||||||||

| 2023/24 deficit at the Second Quarterly Report (November 28, 2023) | (5,557 | ) | |||||||||||||

| 2023/24 deficit at the Third Quarterly Report (February 22, 2024) | (5,914 | ) | |||||||||||||

| Q1 | Q2 | Q3 | Q4 | Total | |||||||||||

| Update | Update | Update | Update | Changes | |||||||||||

| Revenue1 changes: | |||||||||||||||

| Personal income tax – changes based on 2022 tax assessment and improvement in household income | (522 | ) | 551 | 460 | 1 | 490 | |||||||||

| Corporate income tax – changes in prior-year settlement payment and in instalments, reflecting final 2022 tax assessment and revised outlook of 2023 & 2024 national corporate taxable income | 99 | 579 | (531 | ) | - | 147 | |||||||||

| Provincial sales tax – higher 2022/23 carry forward and year-to-date sales activity | 175 | - | - | (32 | ) | 143 | |||||||||

| Property transfer tax – due to higher than expected sales results | 151 | - | - | 43 | 194 | ||||||||||

| Carbon tax – lower sales volume in most fuel types reflecting prior year and year-to-date results | (111 | ) | (50 | ) | - | (8 | ) | (169 | ) | ||||||