| As filed with the Securities and Exchange | Registration No. 333- |

| Commission on November 21, 2014 | |

| UNITED STATES SECURITIES AND EXCHANGE COMMISSION | |

| Washington, D.C. 20549 | |

| FORM S-3 | |

| REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 | |

| VOYA RETIREMENT INSURANCE AND ANNUITY COMPANY | |

| (Exact name of registrant as specified in its charter) | |

| Connecticut | |

| (State or jurisdiction of incorporation or organization) | |

| 71-0294708 | |

| (I.R.S. Employer Identification Number) | |

| One Orange Way, C2N, Windsor, Connecticut 06095-4774, 1-800-262-3862 | |

| (Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices) | |

| J. Neil McMurdie, Senior Counsel | |

| Voya Retirement Insurance and Annuity Company | |

| One Orange Way, C2N, Windsor, Connecticut 06095-4774 | |

| (860) 580-2824 | |

| As soon as practical after the effective date of this registration statement. It is proposed | |

| that this filing become effective December 15, 2014. A request for acceleration is included | |

| with this filing. | |

| (Approximate date of commencement of proposed sale to the public) | |

| If the only securities being registered on this Form are being offered pursuant to dividend or | |

| interest reinvestment plans, please check the following box: [ ] | |

| If any of the securities being registered on this Form are to be offered on a delayed or continuous | |

| basis pursuant to Rule 415 under the Securities Act of 1933, other than securities offered only in | |

| connection with dividend or interest reinvestment plans, check the following box: [ ] | |

| If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under | |

| the Securities Act, please check the following box and list the Securities Act registration | |

| statement number of the earlier effective registration statement for the same offering. [ X ] | |

| 333-180532 | |

| If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, | |

| check the following box and list the Securities Act registration statement number of the earlier | |

| effective registration statement for the same offering. [ ] | |

| If this Form is a registration statement pursuant to General Instruction I.D. or a post-effective | ||||

| amendment thereto that shall become effective upon filing with the Commission pursuant to | ||||

| Rule 462(e) under the Securities Act, check the following box. [ ] | ||||

| If this Form is a post-effective amendment to a registration statement filed pursuant to General | ||||

| Instruction I.D. filed to register additional securities or additional classes of securities pursuant to | ||||

| Rule 413(b) under the Securities Act, check the following box. [ ] | ||||

| Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a | ||||

| non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated | ||||

| filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. | ||||

| (Check one): | ||||

| Large accelerated filer ¨ | Accelerated filer | ¨ | ||

| Non-accelerated filer x | Smaller reporting company ¨ | |||

| (Do not check if a smaller reporting company) | ||||

| Calculation of Registration Fee | ||||

| Title of Each | Proposed | Proposed | ||

| Class of | Maximum | Maximum | ||

| Securities to be | Amount to be | Offering Price | Aggregate | Amount of |

| Registered | Registered | Per Unit | Offering Price | Registration Fee |

| Guaranteed | * | * | $27,710,810 | $3,220.00** |

| Accumulation | ||||

| Account Interests | ||||

| *The proposed maximum aggregate offering price is estimated solely for the purpose of | ||||

| determining the registration fee. The amount to be registered and the proposed maximum | ||||

| offering price per unit are not applicable since these securities are not issued in predetermined | ||||

| amounts or units. | ||||

| **Pursuant to Rule 457(p) under the Securities Act of 1933 (the “1933 Act”), the Amount of | ||||

| Registration Fee is offset by $3,220.00 fee paid in a previous registration statement (333- | ||||

| 199032) submitted to the SEC on September 30, 2014 (Accession No. 0000837010-14-000145), | ||||

| and later withdrawn on October 20, 2014 (Accession No. 0000837010-14-000147). | ||||

| Pursuant to Rule 429(b) of the 1933 Act, unsold securities previously registered under | ||||

| Registration Statement No. 333-180532 are being carried forward to this Registration Statement. | ||||

| As of October 31, 2014, the amount of such unsold securities was $49,115,000. | ||||

| PART I |

| INFORMATION REQUIRED IN PROSPECTUS |

| Voya Retirement Insurance and Annuity Company | |

| Guaranteed Accumulation Account Prospectus – December 15, 2014 | |

| Introduction | |

| The Guaranteed Accumulation Account (“GAA”) is a fixed interest option available during the accumulation | |

| phase of certain variable annuity contracts issued by Voya Retirement Insurance and Annuity Company (the | |

| “Company,” “we,” “us,” “our”). Read this prospectus carefully before investing in GAA and save it for future | |

| reference. | |

| General Description | |

| GAA offers investors the opportunity to earn specified guaranteed rates of interest for specified periods of time, | |

| called guaranteed terms. We generally offer several guaranteed terms at any one time for those considering investing | |

| in GAA. Each guaranteed term offers a guaranteed interest rate for investments that remain in GAA for the duration | |

| of the specific guaranteed term. The guaranteed term establishes both the length of time for which we agree to credit | |

| a guaranteed interest rate and how long your investment must remain in GAA in order to receive the guaranteed | |

| interest rate. | |

| We guarantee both principal and interest if, and only if, your investment remains invested for the full | |

| guaranteed term. Charges related to the contract, such as a maintenance fee or early withdrawal charge, may still | |

| apply even if you do not withdraw until the end of a guaranteed term.Investments taken out of GAA prior to the | |

| end of a guaranteed term may be subject to a market value adjustment, which may result in an investment | |

| gain or loss. See “Market Value Adjustment,” page 11. | |

| This prospectus will explain: | |

| · | Guaranteed interest rates and guaranteed terms; |

| · | Contributions to GAA; |

| · | Types of guaranteed terms available, and how they are classified; |

| · | How rates are offered; |

| · | How there can be an investment risk, and how we calculate gain or loss; |

| · | Contract charges that can affect your account value in GAA; |

| · | Taking investments out of GAA; and |

| · | How to reinvest or withdraw at maturity. |

| Additional Disclosure Information | |

| Neither the Securities and Exchange Commission (“SEC”) nor any state securities commission has approved or | |

| disapproved of these securities or passed on the accuracy or adequacy of this prospectus. Any representation to the | |

| contrary is a criminal offense. We do not intend for this prospectus to be an offer to sell or a solicitation of an offer | |

| to buy these securities in any state or jurisdiction that does not permit their sale. We have not authorized anyone to | |

| provide you with information that is different than that contained in this prospectus. | |

| Our Home Office: | |

| Voya Retirement Insurance and Annuity Company | |

| One Orange Way | |

| Windsor, Connecticut 06095-4774 | |

| 1-800-262-3862 | |

| PRO.GAA-14 | |

| Table of Contents | ||

| Summary | 3 | |

| Description of the Guaranteed Accumulation Account | 6 | |

| General, Contributions to GAA, Deposit Period, Guaranteed Terms, Guaranteed Term Classifications, | ||

| Guaranteed Interest Rates, Interest Rate Lock, Maturity of a Guaranteed Term, Maturity Value Transfer | ||

| Provision | ||

| Transfers | 9 | |

| Transfers from GAA, Transfers Between Guaranteed Term Classifications | ||

| Withdrawals | 10 | |

| Deferral of Payments, Reinvestment Privilege | ||

| Market Value Adjustment (“MVA”) | 11 | |

| Calculation of the MVA, MVA Formula | ||

| Contract Charges | 13 | |

| Other Topics | 13 | |

| Anti-Money Laundering, The Company, Income Phase, Contract Loans, Investments, Distribution of | ||

| Contracts, Taxation, Experts, Legal Matters, Further Information, Incorporation of Certain Documents by | ||

| Reference, Inquiries | ||

| Appendix I - Examples of Market Value Adjustment Calculations | 18 | |

| Appendix II - Examples of Market Value Adjustment at Various Yields | 22 | |

| PRO.GAA-14 | 2 | |

| Summary | ||||

| GAA is a fixed interest option that may be available during the accumulation | Questions: Contacting | |||

| phase of your annuity contract. The following is a summary of certain facts | the Company.To answer | |||

| about GAA. | your questions, contact your | |||

| local representative or write or | ||||

| In General.Amounts that you invest in GAA will earn a guaranteed interest | call our Home Office at: | |||

| rate if left in GAA for a specified period of time (the guaranteed term). You | ||||

| must invest amounts in GAA for the full guaranteed term in order to receive | Customer Service | |||

| the quoted guaranteed interest rate. If you withdraw or transfer those amounts | Defined Contribution | |||

| before the end of the guaranteed term, we may apply a “market value | Administration | |||

| adjustment,” which may be positive or negative. | P.O. Box 990063 | |||

| Hartford, CT 06199-0063 | ||||

| Deposit Periods.A deposit period is the time during which we offer a | 1-800-262-3862 | |||

| specific guaranteed interest rate if you deposit dollars for a specific | ||||

| guaranteed term. For a particular guaranteed interest rate and guaranteed term | ||||

| to apply to your account dollars, you must invest them during the deposit | ||||

| period in which that rate and term are offered. | ||||

| Guaranteed Terms.A guaranteed term is the period of time account dollars must be left in GAA in order to earn | ||||

| the guaranteed interest rate specified for that guaranteed term. We may offer different guaranteed terms at different | ||||

| times. Check with your representative or the Company to learn the details about the guaranteed term(s) currently | ||||

| offered. We reserve the right to limit the number of guaranteed terms or the availability of certain guaranteed terms. | ||||

| In addition, under certain contracts, we reserve the right to discontinue offering GAA, or to limit the availability of | ||||

| GAA guaranteed term classifications. | ||||

| Some annuity contracts that offer GAA distinguish between short- and long-term classifications of GAA. Under | ||||

| those contracts, we make the following distinction: | ||||

| · | Short-term classification—three years or less; and | |||

| · | Long-term classification—between three and ten years. | |||

| Guaranteed Interest Rates.We guarantee different interest rates, depending upon when account dollars are | ||||

| invested in GAA. The interest rate we guarantee is an annual effective yield; that means that the rate reflects a full | ||||

| year’s interest. We credit interest at a rate that will provide the guaranteed annual effective yield over one year. The | ||||

| guaranteed interest rate(s) is guaranteed for that deposit period and for the length of the guaranteed term. | ||||

| The guaranteed interest rates we offer will always meet or exceed the minimum interest rates agreed to in the | ||||

| contract, if any. Not all contracts provide for minimum interest rates for the GAA. Apart from meeting the | ||||

| contractual minimum interest rates, if any, we can in no way guarantee any aspect of future offerings. | ||||

| Interest Rate Lock.Certain contracts may provide a 45 day interest rate lock in connection with external transfers | ||||

| into GAA, which you must elect at the time you initiate the external transfer. Under this rate lock provision, if | ||||

| applicable, we will deposit external transfers to the deposit period offering the greater of (a) and (b) where: | ||||

| (a) | Is the guaranteed interest rate for the deposit period in effect at the time we receive the rate lock | |||

| election; and | ||||

| (b) | Is the guaranteed interest rate for the deposit period in effect at the time we receive an external transfer | |||

| from your prior provider. | ||||

| If applicable, this rate lock will be available to all external transfers received for 45 days from the date we receive a | ||||

| rate lock election. In the event we receive an external transfer after this 45 day time period, it will be deposited to | ||||

| the deposit period in effect at the time we receive the external transfer, and will earn the guaranteed interest rate for | ||||

| that guaranteed term. Only one rate lock may be in effect at one time per contract – once a rate lock has been | ||||

| elected, that rate lock will apply to all external transfers received during that 45 day period, and you may not elect to | ||||

| begin a new rate lock period during that 45 day period. | ||||

| PRO.GAA-14 | 3 | |||

| Amounts subject to the rate lock will not be deposited until the external transfer has been received, and will not be | ||

| credited interest until deposited. This could result in the deposit being credited interest for a shorter term than if a | ||

| rate lock had not been elected. The cost of providing a rate lock may be a factor we consider when determining the | ||

| guaranteed interest rate for a deposit period, which impacts the guaranteed interest rate for all investors in that | ||

| guaranteed term. | ||

| Fees and Other Deductions.We do not make deductions from amounts in GAA to cover mortality and expense | ||

| risks. Rather, we consider these risks when determining the credited rate. The following other types of charges may | ||

| be deducted from amounts held in, withdrawn or transferred from GAA: | ||

| · | Market Value Adjustment (“MVA”). An MVA may be applied to amounts transferred or withdrawn prior to | |

| the end of a guaranteed term, which reflects changes in interest rates since the deposit period. The MVA may | ||

| be positive or negative, and therefore may increase or decrease the amount withdrawn to satisfy a transfer or | ||

| withdrawal request. See“Market Value Adjustment.” | ||

| · | Tax Penalties and/or Tax Withholding. Amounts withdrawn may be subject to withholding for federal income | |

| taxes, as well as a 10% penalty tax for amounts withdrawn prior to your having attained age 59½. See | ||

| “Taxation”; see also the“Tax Considerations”section of the contract prospectus. | ||

| · | Early Withdrawal Charge. An early withdrawal charge, which is a deferred sales charge, may apply to amounts | |

| withdrawn from the contract, in order to reimburse us for some of the sales and administrative expenses | ||

| associated with the contract. See“Contract Charges”; see also the“Fees”section of the contract prospectus. | ||

| · | Maintenance Fee. An annual maintenance fee of up to $50 may be deducted pro rata from all funding options | |

| including GAA. See“Contract Charges”; see also the“Fees”section of the contract prospectus. | ||

| · | Transfer Fees. Under some contracts transfer fees of up to $10 per transfer may be deducted from amounts held | |

| in or transferred from GAA during the accumulation phase. See“Contract Charges”; see also the“Fees” | ||

| section of the contract prospectus. | ||

| · | Premium Taxes. We may deduct a charge for premium taxes of up to 4% from amounts in GAA. See | |

| “Contract Charges”;see also the“Fees”section of the contract prospectus. | ||

| · | Front End Sales Charges. Under some contracts, we may deduct front end sales charges of up to 6%. See | |

| “Contract Charges”; see also the“Fees”section of the contract prospectus. | ||

| Market Value Adjustment (“MVA”).If you withdraw or transfer all or part of your account value from GAA | ||

| before the guaranteed term is complete, an MVA may apply. The MVA reflects the change in the value of the | ||

| investment due to changes in interest rates since the date of deposit. The MVA may be positive or negative | ||

| depending upon interest rate activity at the time of withdrawal or transfer. | ||

| Any MVA applied to a withdrawal or transfer from GAA will be calculated as an “aggregate MVA,” which is | ||

| the sum of all MVAs applicable due to the withdrawal. See the sidebar on page 11 for an example of the calculation | ||

| of the aggregate MVA. The following withdrawals will be subject to an aggregate MVA only if it is positive: | ||

| · | Withdrawals due to the election of a lifetime income option; and | |

| · | Withdrawals due to the death of the participant (if paid within the first six months following death). For certain | |

| contracts issued in the state of New York, this provision also applies in the event of disability, as defined in the | ||

| contract. | ||

| All other withdrawals will be subject to an aggregate MVA, regardless of whether it is positive or negative, | ||

| including: | ||

| · | Withdrawals due to the election of a nonlifetime income option; | |

| · | Payments due to the death of the participant, if paid more than six months following death (or disability, if | |

| applicable); and | ||

| · | Full or partial withdrawals during the accumulation phase (except for withdrawals at the end of a guaranteed | |

| term or pursuant to the maturity value transfer provision - see“Maturity of a Guaranteed Term”and | ||

| “Maturity Value Transfer Provision”). | ||

| Under certain contracts that guarantee a death benefit equal to the greater of the “adjusted purchase total” or the | ||

| current account value (excluding loans), the calculation of the current account value will include the aggregate MVA | ||

| only if it is positive, regardless of whether the death benefit is paid within six months following death. See the | ||

| “Death Benefit”section of the contract prospectus. Under some of these contracts, an election to defer payment of | ||

| the death benefit will result in the application of the aggregate MVA, whether positive or negative, when the | ||

| beneficiary elects to begin distribution of the death benefit. | ||

| See“Description of the Guaranteed Accumulation Account”and“Market Value Adjustment.” | ||

| PRO.GAA-14 | 4 | |

| Maturity of a Guaranteed Term.On or before the end of a guaranteed term, the contract holder or you, if | ||

| applicable, may instruct us to: | ||

| · | Transfer the matured amount to one or more new guaranteed terms available under the current deposit period; | |

| · | Transfer the matured amount to other available investment options; or | |

| · | Withdraw the matured amount. | |

| Amounts withdrawn may be subject to an early withdrawal charge, maintenance fee, tax withholding, and tax | ||

| penalties. See“Contract Charges”; see also the“Fees”and“Tax Considerations”sections of the contract | ||

| prospectus. When a guaranteed term ends, if we have not received instructions, we will automatically reinvest the | ||

| maturing investment into a guaranteed term available in the current deposit period. See“Maturity Value Transfer | ||

| Provision.”For contracts that distinguish between short- and long-term classifications, we will generally transfer | ||

| the maturing investment to the available deposit period for the guaranteed term having the shortest maturity within | ||

| the same classification. For other contracts, we will generally transfer the maturing investment in the following | ||

| manner based upon availability: | ||

| · | To a guaranteed term of the same duration, if available; | |

| · | To a guaranteed term with the next shortest duration, if available; or | |

| · | To a guaranteed term with the next longest duration. | |

| If you do not provide instructions concerning the maturing amount on or before the end of a guaranteed term, and | ||

| this amount is automatically reinvested as noted above, the maturity value transfer provision will apply. | ||

| Maturity Value Transfer Provision.If we automatically transfer the matured investment into the current deposit | ||

| period, the contract holder or you, if applicable, may, for a limited time, transfer or withdraw all or a portion of the | ||

| matured investment that was transferred without the application of an MVA. As described in“Fees and Other | ||

| Deductions”above, other fees, including an early withdrawal charge and a maintenance fee, may be assessed on | ||

| amounts withdrawn. See“Description of the Guaranteed Accumulation Account.” | ||

| Transfer of Account Dollars.Generally, account dollars invested in GAA may be transferred among guaranteed | ||

| terms offered through GAA, and/or to other investment options offered through the contract. However: | ||

| · | Transfers may not be made during the deposit period in which your account dollars are invested in GAA or for | |

| 90 days after the close of that deposit period; and | ||

| · | We may apply an MVA to transfers made before the end of a guaranteed term. | |

| Transfers to other investment options offered through the contract may be subject to limits on frequent or disruptive | ||

| transfers or limits imposed by the underlying funds. See the“Transfers” and “Investment Options”sections of | ||

| your contract prospectus. | ||

| Investments.Guaranteed interest rates credited during any guaranteed term do not necessarily relate to investment | ||

| performance. Deposits received into GAA will generally be invested in federal, state and municipal obligations, | ||

| corporate bonds, preferred stocks, real estate mortgages, real estate, certain other fixed income investments, and | ||

| cash or cash equivalents. All of our general assets are available to meet guarantees under GAA. | ||

| Amounts allocated to GAA are held in a nonunitized separate account established by the Company under | ||

| Connecticut law. To the extent provided for in the contract, assets of the separate account are not chargeable with | ||

| liabilities arising out of any other business that we conduct. See“Investments.” | ||

| Notification of Maturity.We will notify the contract holder or you, if applicable, at least 18 calendar days prior to | ||

| the maturity of a guaranteed term. We will include information relating to the current deposit period’s guaranteed | ||

| interest rates and the available guaranteed terms. You may obtain information concerning available deposit periods, | ||

| guaranteed interest rates, and guaranteed terms five business days prior to the maturity date by calling | ||

| 1-800-262-3862. See“Description of the Guaranteed Accumulation Account—General”and“Maturity of a | ||

| Guaranteed Term.” | ||

| PRO.GAA-14 | 5 | |

| Description of the Guaranteed Accumulation Account | ||

| General | ||

| GAA offers guaranteed interest rates for specific guaranteed terms. For a particular guaranteed interest rate and | ||

| guaranteed term to apply to your account dollars, you must invest them during the deposit period during which that | ||

| rate and term are offered. Each deposit period may offer more than one guaranteed term. Guaranteed terms may be | ||

| classified according to length of time to maturity, and each deposit period may offer various guaranteed terms within | ||

| these classifications. | ||

| Any MVA applied to a withdrawal or transfer from GAA will be calculated as an “aggregate MVA,” which is | ||

| the sum of all MVAs applicable due to the withdrawal. See the sidebar on page 11 for an example of the calculation | ||

| of the aggregate MVA. The following withdrawals will be subject to an aggregate MVA only if it is positive: | ||

| · | Withdrawals due to the election of a lifetime income option; and | |

| · | Withdrawals due to the death of the participant (under certain contracts the withdrawal must be paid within the | |

| first six months following death). For certain contracts issued in the state of New York, this provision also | ||

| applies in the event of disability, as defined in the contract. | ||

| All other withdrawals will be subject to an aggregate MVA, regardless of whether it is positive or negative, | ||

| including: | ||

| · | Withdrawals due to the election of a nonlifetime income option; | |

| · | Payments due to the death of the participant, if paid more than six months following death (or disability, if | |

| applicable); and | ||

| · | Full or partial withdrawals during the accumulation phase (except for withdrawals at the end of a guaranteed | |

| term or pursuant to the maturity value transfer provision, see“Maturity of a Guaranteed Term”and | ||

| “Maturity Value Transfer Provision”). | ||

| We maintain a toll-free telephone number for those wishing to obtain information concerning available deposit | ||

| periods, guaranteed interest rates, and guaranteed terms. The telephone number is 1-800-262-3862. At least 18 | ||

| calendar days before a guaranteed term matures, we will notify the contract holder or you, if applicable, of the | ||

| upcoming deposit period dates and the current guaranteed interest rates, guaranteed terms and projected matured | ||

| guaranteed term values. | ||

| Contributions to GAA | ||

| The contract holder or you, if applicable, may invest in the guaranteed terms available in the current deposit period | ||

| by allocating new purchase payments to GAA or by transferring a sum from other funding options available under | ||

| the contract or from other guaranteed terms. | ||

| Though we may require a minimum payment(s) to a contract, we do not require a minimum investment for a | ||

| guaranteed term. Refer to the contract prospectus for any minimum payment(s) that may apply to a contract. We | ||

| reserve the right to establish a minimum amount for transfers from other funding options. | ||

| Investments may not be transferred from a guaranteed term during the deposit period in which the investment is | ||

| applied nor during the first 90 days after the close of the deposit period. This restriction does not apply to amounts | ||

| transferred or withdrawn under the maturity value transfer provision. See“Maturity Value Transfer Provision.” | ||

| Deposit Period | ||

| The deposit period is the period of time during which the contract holder or you, if applicable, may direct | ||

| investments to a particular guaranteed term(s) and receive a stipulated guaranteed interest rate(s). Each deposit | ||

| period may be a month, a calendar quarter, or any other period of time we specify. | ||

| PRO.GAA-14 | 6 | |

| Guaranteed Terms | |||

| A guaranteed term is the time we specify during which we credit the guaranteed interest rate. Generally, we will | |||

| offer at least one guaranteed term of three years or less and one guaranteed term of more than three years in any | |||

| deposit period. However, under certain contracts we reserve the right to limit the guaranteed terms or guaranteed | |||

| term classifications offered, as well as the right to discontinue offering GAA. We offer guaranteed terms at our | |||

| discretion for various periods ranging from one to ten years. | |||

| Guaranteed Term Classifications | |||

| Some contracts distinguish between long-term and short-term guaranteed term classifications. The following are the | |||

| guaranteed term classifications: | |||

| · | Short-term—All guaranteed terms of three years or less; and | ||

| · | Long-term—All guaranteed terms of between three and ten years. | ||

| During each deposit period, we may offer more than one guaranteed term within each guaranteed term classification. | |||

| The contract holder or you, if applicable, may allocate investments to guaranteed terms within one or both | |||

| guaranteed term classifications during a deposit period. | |||

| Guaranteed Interest Rates | |||

| Guaranteed interest rates are the rates that we guarantee will be credited on amounts applied during a deposit period | |||

| for a specific guaranteed term. Guaranteed interest rates are annual effective yields, reflecting a full year’s interest. | |||

| We credit interest at a rate that will provide the guaranteed annual effective yield over one year. Guaranteed interest | |||

| rates are credited according to the length of the guaranteed term as follows: | |||

| Guaranteed Terms of One Year or Less:The guaranteed interest rate is credited from the date of deposit to the | |||

| last day of the guaranteed term. | |||

| Guaranteed Terms of Greater than One Year:Except for certain contracts issued in the state of New York, | |||

| several different guaranteed interest rates may be applicable during a guaranteed term of more than one year. The | |||

| initial guaranteed interest rate is credited from the date of deposit to the end of a specified period within the | |||

| guaranteed term. We may credit several different guaranteed interest rates for subsequent specific periods of time | |||

| within the guaranteed term. For example, for a five-year guaranteed term we may guarantee 5% for the first year, | |||

| 4.75% for the next two years, and 4.5% for the remaining two years. | |||

| We will not guarantee or credit a guaranteed interest rate below the minimum rate specified in the contract for GAA, | |||

| if any. Additionally, we will not credit interest at a rate above the guaranteed interest rate we announce prior to the | |||

| start of a deposit period. Not all contracts provide for minimum interest rates for GAA. | |||

| Our guaranteed interest rates are influenced by, but do not necessarily correspond to, interest rates available on fixed | |||

| income investments we may buy using deposits directed to GAA. See“Investments.”We consider other factors | |||

| when determining guaranteed interest rates including regulatory and tax requirements, sales commissions and | |||

| administrative expenses borne by the Company, general economic trends, competitive factors, and whether an | |||

| interest rate lock is being offered for that guaranteed term under certain contracts.We make the final | |||

| determination regarding guaranteed interest rates. We cannot predict the level of future guaranteed interest | |||

| rates. | |||

| Interest Rate Lock | |||

| Certain contracts may provide a 45 day interest rate lock in connection with external transfers into GAA, which you | |||

| must elect at the time you initiate the external transfer. Under this rate lock provision, if applicable, we will deposit | |||

| external transfers to the deposit period offering the greater of (a) and (b) where: | |||

| (a) | Is the guaranteed interest rate for the deposit period in effect at the time we receive the rate lock | ||

| election; and | |||

| (b) | Is the guaranteed interest rate for the deposit period in effect at the time we receive an external transfer | ||

| from your prior provider. | |||

| PRO.GAA-14 | 7 | ||

| If applicable, this rate lock will be available to all external transfers received for 45 days from the date we receive a | ||||

| rate lock election. In the event we receive an external transfer after this 45 day time period, it will be deposited to | ||||

| the deposit period in effect at the time we receive the external transfer, and will earn the guaranteed interest rate for | ||||

| that guaranteed term. Only one rate lock may be in effect at one time per contract – once a rate lock has been | ||||

| elected, that rate lock will apply to all external transfers received during that 45 day period, and you may not elect to | ||||

| begin a new rate lock period during that 45 day period. | ||||

| Amounts subject to the rate lock will not be deposited until the external transfer has been received, and will not be | ||||

| credited interest until deposited. This could result in the deposit being credited interest for a shorter term than if a | ||||

| rate lock had not been elected. The cost of providing a rate lock may be a factor we consider when determining the | ||||

| guaranteed interest rate for a deposit period, which impacts the guaranteed interest rate for all investors in that | ||||

| guaranteed term. | ||||

| Maturity of a Guaranteed Term | ||||

| At least 18 calendar days prior to the maturity of a guaranteed term, we will notify the contract holder or you, if | ||||

| applicable, of the upcoming deposit period, the projected value of the amount maturing at the end of the guaranteed | ||||

| term, and the guaranteed interest rate(s) and guaranteed term(s) available for the current deposit period. | ||||

| When a guaranteed term matures, the amounts in any maturing guaranteed term may be: | ||||

| · | Transferred to one or more new guaranteed terms available under the current deposit period; | |||

| · | Transferred to other available investment options; or | |||

| · | Withdrawn from the contract. | |||

| We do not apply an MVA to amounts transferred or surrendered from a guaranteed term on the date the guaranteed | ||||

| term matures. Amounts withdrawn, however, may be subject to an early withdrawal charge, a maintenance fee, | ||||

| taxation, and tax penalties. If we have not received direction from the contract holder or you, if applicable, by the | ||||

| maturity date of a guaranteed term, we will automatically transfer the matured value to one of the following: | ||||

| · | For contracts distinguishing between short- and long-term classifications, we will generally transfer the amount | |||

| maturing to the available deposit period for the guaranteed term having the shortest maturity within the same | ||||

| classification, though it may be different than the maturing term; or | ||||

| · | For contracts that do not distinguish between short- and long-term classifications, we will generally transfer the | |||

| maturing amount as follows: | ||||

| > | To a guaranteed term of the same duration, if available; | |||

| > | To a guaranteed term with the next shortest duration, if available; or | |||

| > | To a guaranteed term with the next longest duration. | |||

| The contract holder or you, if applicable, will receive a confirmation statement, plus information on the new | ||||

| guaranteed interest rate(s) and guaranteed terms. | ||||

| Maturity Value Transfer Provision | Business Day— | |||

| any day on which the | ||||

| If we automatically reinvest the proceeds from a matured guaranteed term, the | New York Stock | |||

| contract holder or you, if applicable, may transfer or withdraw from GAA the | Exchange (“NYSE”) | |||

| amount that was reinvested without an MVA. An early withdrawal charge and | is open. | |||

| maintenance fee may apply to withdrawals. If the full amount reinvested is | ||||

| transferred or withdrawn, we will include interest credited to the date of the transfer | ||||

| or withdrawal. This provision is only available until the last business day of the | ||||

| month following the maturity date of the prior guaranteed term. This provision only | ||||

| applies to the first transfer or withdrawal request received from the contract holder | ||||

| or you, if applicable, with respect to a particular matured guaranteed term value, | ||||

| regardless of the amount involved in the transaction. | ||||

| PRO.GAA-14 | 8 | |||

| Transfers | |

| We allow the contract holder or you, if applicable, to transfer all or a portion of your account value to GAA or to | |

| other investment options under the contract. We do not allow transfers from any guaranteed term to any other | |

| guaranteed term or investment option during the deposit period for that guaranteed term or for 90 days following the | |

| close of that deposit period, except for amounts transferred under the maturity value transfer provision. | |

| We do not apply an MVA to the value transferred upon maturity of a guaranteed term nor for values transferred | |

| under the maturity value transfer provision. We do not count either of these types of transfers as one of the 12 free | |

| transfers allowed per calendar year by those contracts allowing only 12 free transfers. Transfers to other investment | |

| options through the contract may be subject to limits on frequent or disruptive transfers or limits imposed by the | |

| underlying funds. See the“Transfers”and“Investment Options”sections of your contract prospectus. | |

| When the contract holder or you, if applicable, requests the transfer of a specific dollar amount, we account for any | |

| applicable MVA in determining the amount to be withdrawn from a guaranteed term(s) to fulfill the request. | |

| Therefore, the amount we actually withdraw from the guaranteed term(s) may be more or less than the requested | |

| dollar amount. See“Appendix I”for an example. For more information on transfers, see the contract prospectus. | |

| Transfers from GAA | |

| For contracts that do not distinguish between short- and long-term classifications, the contract holder or you, if | |

| applicable, may choose the guaranteed term from which funds will first be withdrawn. If there is more than one | |

| guaranteed term of the same duration, we will withdraw funds starting from the oldest guaranteed term that has not | |

| reached maturity. | |

| If we do not receive direction, we will withdraw funds pro rata from each guaranteed term in which you are | |

| invested. If there is more than one guaranteed term of the same duration, we will withdraw funds starting from the | |

| oldest guaranteed term that has not reached maturity. | |

| For contracts that distinguish between short- and long-term classifications, the contract holder or you, if applicable, | |

| may choose the guaranteed term classification from which funds will be first withdrawn. We will withdraw funds | |

| starting from the oldest guaranteed term that has not reached maturity within the classification chosen. | |

| If we do not receive direction, we will withdraw funds pro rata from the guaranteed term classifications, starting | |

| with the oldest guaranteed term that has not reached maturity, and any other investment options. | |

| We will apply an MVA to transfers made before the end of a guaranteed term. See“Market Value Adjustment.” | |

| Transfers between Guaranteed Term Classifications | |

| (For contracts that distinguish between short-term and long-term classifications only) | |

| The contract holder or you, if applicable, may transfer amounts from short-term guaranteed terms to available long- | |

| term guaranteed terms of the current deposit period, or from long-term guaranteed terms to available short-term | |

| guaranteed terms of the current deposit period. | |

| For example, funds may be transferred from a three-year guaranteed term (any time after 90 days from the close of | |

| the deposit period applicable to that three-year guaranteed term) to the open deposit period of a seven-year | |

| guaranteed term. | |

| Funds will be first transferred from the oldest deposit period for which the guaranteed term has not reached | |

| maturity and we will assess an MVA on the transferred amount. These transfers are counted toward the 12 free | |

| transfers allowed per calendar year by those contracts allowing only 12 free transfers. | |

| We do not permit the transfer of value from one guaranteed term prior to its maturity to another guaranteed term | |

| within the same classification. For example, we do not permit transfers from one-year to three-year, one-year to | |

| one-year, five-year to seven-year, or ten-year to seven-year guaranteed terms. | |

| PRO.GAA-14 | 9 |

| Withdrawals | |

| The contract allows for full or partial withdrawals from GAA at any time during the accumulation phase. To make a | |

| full or partial withdrawal, a request form (available from us) must be properly completed and submitted to our Home | |

| Office (or other designated office as provided in the contract). | |

| Partial withdrawals are made pro rata from funding options unless the contract holder or you, if applicable, request | |

| otherwise. For contracts that do not distinguish between short- and long-term classifications, each guaranteed term is | |

| considered a separate funding option for the purpose of a partial withdrawal. | |

| The contract holder or you, if applicable, may choose the guaranteed term from which funds will be withdrawn. If | |

| there is more than one guaranteed term of the same duration, we will withdraw funds starting from the oldest | |

| guaranteed term that has not reached maturity. If no guaranteed term is elected, we will withdraw funds pro rata | |

| from each guaranteed term in which you are invested. | |

| For contracts distinguishing between short- and long-term classifications, each guaranteed term classification is | |

| considered a separate funding option for the purpose of a partial withdrawal. The contract holder or you, if | |

| applicable, may elect to take a partial withdrawal from either guaranteed term classification. We will first withdraw | |

| funds from the oldest guaranteed term that has not reached maturity within the chosen classification. If no | |

| guaranteed term classification is elected, we will withdraw funds pro rata from each classification (starting with the | |

| oldest guaranteed term that has not reached maturity) and other funding options. | |

| We may apply an MVA to withdrawals made prior to the end of a guaranteed term, except for withdrawals made | |

| under the maturity value transfer provision. See“Market Value Adjustment.”We may deduct an early withdrawal | |

| charge and a maintenance fee depending upon the terms of the contract. The early withdrawal charge is a deferred | |

| sales charge that may be deducted upon withdrawal to reimburse us for some of the sales and administrative | |

| expenses associated with the contract. A maintenance fee up to $50 may be deducted pro rata from each of the | |

| funding options, including GAA. Refer to the contract prospectus for a description of these fees. When a request for | |

| a partial withdrawal of a specific dollar amount is made, we will include the MVA in determining the amount to be | |

| withdrawn from the guaranteed term(s) to fulfill the request. Therefore, the amount we actually take from the | |

| guaranteed term(s) may be more or less than the dollar amount requested. See“Appendix I”for an example. | |

| Deferral of Payments | |

| Under certain emergency conditions, we may defer payment of a GAA withdrawal for up to six months. Refer to the | |

| contract prospectus for more details. | |

| Reinvestment Privilege | |

| If allowed by the contract, the contract holder or you, if applicable, may elect to reinvest all or a portion of a full | |

| withdrawal during the 30 days following such a withdrawal. We must receive amounts for reinvestment within 60 | |

| days of the withdrawal. | |

| We will apply reinvested amounts to the current deposit period. This means that the guaranteed annual interest rate | |

| and guaranteed terms available on the date of reinvestment will apply. Amounts are reinvested in the guaranteed | |

| term classifications, where applicable, in the same proportion as prior to the full withdrawal. Any negative MVA we | |

| applied to a withdrawal will not be refunded, and any taxes that were withheld may also not be refunded. Refer to | |

| the contract prospectus for further details. | |

| PRO.GAA-14 | 10 |

| Market Value Adjustment (“MVA”) | ||

| Aggregate MVAis the total of | ||

| all MVAs applied due to a | We apply an MVA to amounts transferred or withdrawn from GAA prior to | |

| transfer or withdrawal. | the end of a guaranteed term. To accommodate early withdrawals or transfers, | |

| we may need to liquidate certain assets or use cash that could otherwise be | ||

| Calculation of the Aggregate | invested at current interest rates. When we sell assets prematurely we could | |

| MVA–In order to satisfy a | realize a profit or loss depending upon market conditions. | |

| transfer or withdrawal, | ||

| amounts may be withdrawn | The MVA reflects changes in interest rates since the deposit period. When | |

| from more than one guaranteed | interest rates increase after the deposit period, the value of the investment | |

| term, with more than one | decreases and the market value adjustment amount may be negative. | |

| guaranteed interest rate. In | Conversely, when interest rates decrease after the deposit period, the value of | |

| order to determine the MVA | the investment increases and the market value adjustment amount may be | |

| applicable to such a transfer or | positive. Therefore, the application of an MVA may increase or decrease the | |

| withdrawal, the MVAs | amount withdrawn from a guaranteed term to satisfy a withdrawal or transfer | |

| applicable toeach guaranteed | request. | |

| termwill be added together, in | ||

| order to determine the | An MVA applied to a withdrawal or transfer from GAA will be calculated as | |

| “aggregate MVA.” | an “aggregate MVA,” which is the sum of all MVAs applicable due to the | |

| withdrawal. See the sidebar on this page for an example of the calculation of | ||

| Example:$1,000 withdrawal, | the | aggregate MVA. The following withdrawals will be subject to an |

| two guaranteed terms. | aggregate MVA only if it is positive: | |

| · | Withdrawals due to the election of a lifetime income option; and | |

| MVA1 = $10, MVA2 = - $30 | · | Withdrawals due to the death of the participant (if paid within the first six |

| $10 + -$30 = - $20. | months following death). For certain contracts issued in the state of New | |

| Aggregate MVA = - $20. | York, this provision also applies in the event of disability, as defined in | |

| the contract. | ||

| Example:$1,000 withdrawal, | ||

| two guaranteed terms. | All other withdrawals will be subject to an aggregate MVA, regardless of | |

| whether it is positive or negative, including: | ||

| MVA1 = $30, MVA2 = - $10 | · | Withdrawals due to the election of a nonlifetime income option; |

| $30 + - $10 = $20. | · | Payments due to the death of the participant, if paid more than six months |

| Aggregate MVA = $20. | following death (or disability, if applicable under your contract); and | |

| · | Full or partial withdrawals during the accumulation phase (except for | |

| withdrawals at the end of a guaranteed term or pursuant to the maturity | ||

| value transfer provision). See“Maturity of a Guaranteed Term”and | ||

| “Maturity Value Transfer Provision.” | ||

| Should two or more guaranteed terms have the same guaranteed interest rate and mature on the same date, we | ||

| will calculate an MVA applicable to each. | ||

| Under some contracts, election of a systematic distribution option, as described in the contract prospectus, will not | ||

| result in an MVA being applied to amounts withdrawn from GAA. | ||

| Under certain contracts that guarantee a death benefit equal to the greater of the “adjusted purchase total” or the | ||

| current account value (excluding loans), the calculation of the current account value will include the aggregate MVA | ||

| only if it is positive, regardless of whether the death benefit is paid within six months following death. See the | ||

| “Death Benefit”section of the contract prospectus. Under some of these contracts, an election to defer payment of | ||

| the death benefit will result in the application of the aggregate MVA, whether positive or negative, when the | ||

| beneficiary elects to begin distribution of the death benefit. | ||

| Calculation of the MVA | ||

| There are two methods for calculating the MVA, and the method that applies to you will be set forth in your | ||

| contract.You should check your contract to see which method of calculating the MVA applies to you. | ||

| PRO.GAA-14 | 11 | |

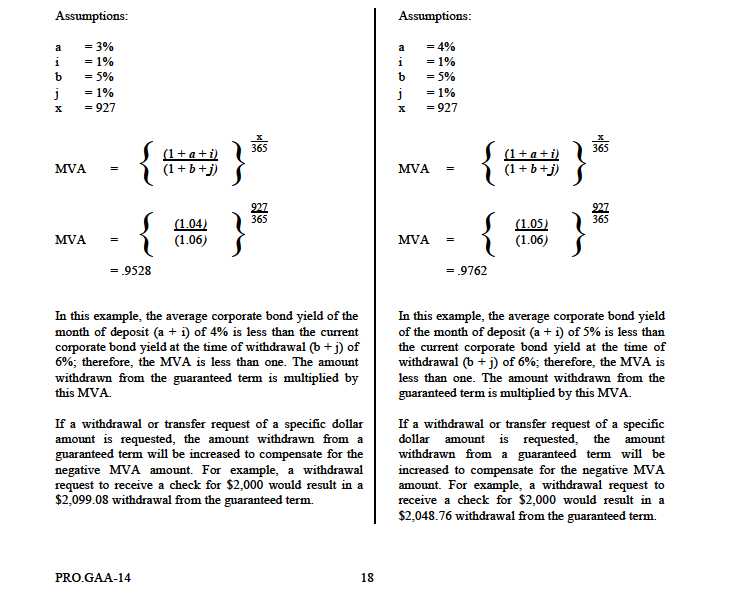

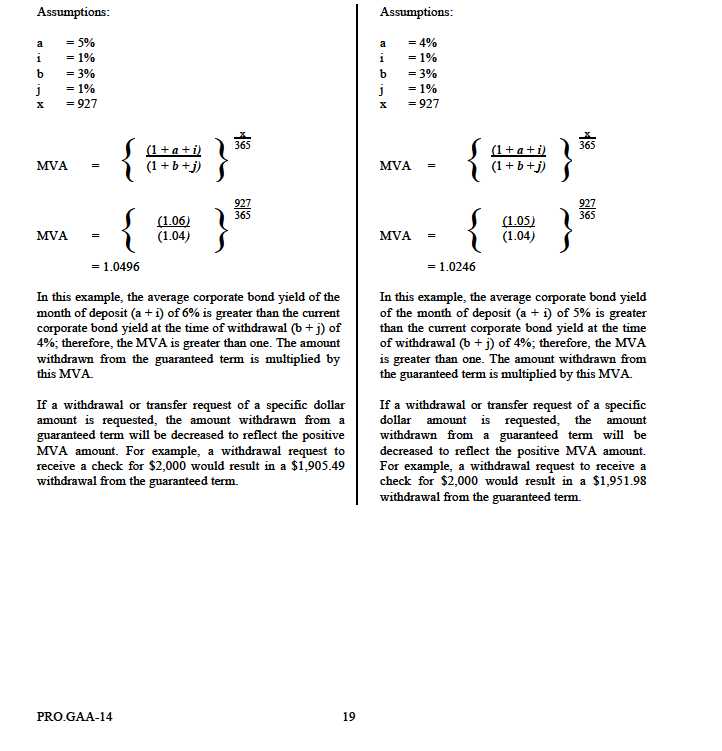

| Method One.For contracts that use Method One to calculate the MVA, the amount of the MVA depends on the | |

| relationship between: | |

| · | The average corporate bond yield (US Treasury Rate plus spread over Treasury) of the month of deposit for the |

| corresponding guaranteed term; and | |

| · | The current corporate bond yield (US Treasury Rate plus spread over Treasury) at the time of withdrawal for a |

| period equal to the remainder of the guaranteed term. | |

| If the current corporate bond yield at the time of withdrawal is less than the average corporate bond yield of the | |

| month of deposit, the MVA will decrease the amount withdrawn from a guaranteed term to satisfy a transfer or | |

| withdrawal request (the MVA will be positive). If the current corporate bond yield at the time of withdrawal is | |

| greater than the average corporate bond yield of the month of deposit, the MVA will increase the amount withdrawn | |

| from a guaranteed term (the MVA will be negative). | |

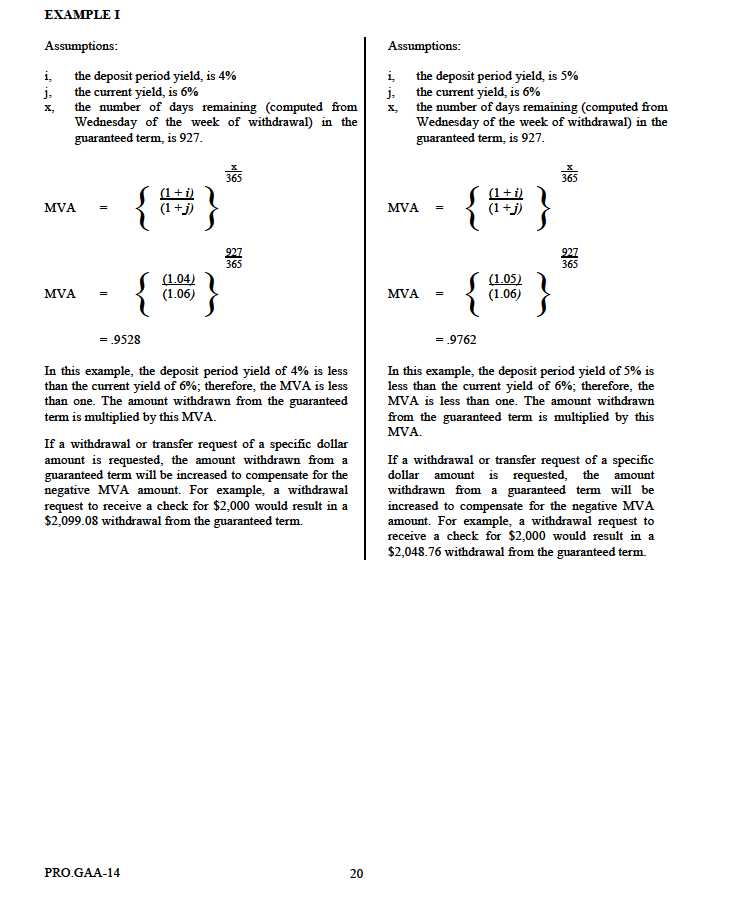

| Method Two.For contracts that do not use Method One to calculate the MVA, the amount of the MVA depends on | |

| the relationship between: | |

| · | The deposit period yield of U.S. Treasury Notes that will mature in the last quarter of the guaranteed term; and |

| · | The current yield of such U.S. Treasury Notes at the time of withdrawal. |

| If the current yield is less than the deposit period yield, the MVA will decrease the amount withdrawn from a | |

| guaranteed term to satisfy a transfer or withdrawal request (the MVA will be positive). If the current yield is greater | |

| than the deposit period yield, the MVA will increase the amount withdrawn from a guaranteed term (the MVA will | |

| be negative). | |

| Deposit Period Yield.We determine the deposit period yield used in the MVA calculation by considering | |

| interest rates prevailing during the deposit period of the guaranteed term from which the transfer or withdrawal will | |

| be made. First, we identify the Treasury Notes that mature in the last three months of the guaranteed term. Then, we | |

| determine their yield-to-maturity percentages for the last business day of each week in the deposit period. We then | |

| average the resulting percentages to determine the deposit period yield. Treasury Note information may be found | |

| each business day in publications such as the Wall Street Journal which publishes the yield-to-maturity percentages | |

| for all Treasury Notes as of the preceding business day. | |

| Current Yield.We use the same Treasury Notes identified for the deposit period yield to determine the current | |

| yield—Treasury Notes that mature in the last three months of the guaranteed term. However, we use the yield-to- | |

| maturity percentages for the last business day of the week preceding the withdrawal and average those percentages | |

| to get the current yield. | |

| MVA Formulas | |

| Method One.The mathematical formula used to determine the MVA using Method One is: | |

| Where: | |

| ais the average of the US Treasury Rate in effect on the first four Fridays of the month of deposit for the | |

| corresponding guaranteed term; | |

| bis the US Treasury Rate in effect on the withdrawal date (based on the previous Friday) for a period equal to the | |

| remainder of the guaranteed term; | |

| iis the average of the spread over Treasury on the Barclays US Corporate Investment Grade Index (if unavailable a | |

| similar service will be utilized) in effect on the first four Fridays of the month of deposit for the corresponding | |

| guaranteed term; | |

| jis the spread over Treasury on the Barclays US Corporate Investment Grade Index (if unavailable a similar service | |

| will be utilized) in effect on the withdrawal date (based on the previous Friday) for a period equal to the remainder | |

| of the guaranteed term; and | |

| xis the number of days remaining, (computed from Wednesday of the week of withdrawal) in the guaranteed term. | |

| Note that the Company may change the weekdays noted above, subject to the terms of your contract. | |

| PRO.GAA-14 | 12 |

| Where: | |

| iis the deposit period yield; | |

| jis the current yield; and | |

| xis the number of days remaining (computed from Wednesday of the week of withdrawal) in the guaranteed term. | |

| For examples of how we calculate MVA, refer toAppendix I. | |

| We make an adjustment in the formula of the MVA to reflect the period of time remaining in the guaranteed term | |

| from the Wednesday of the week of a withdrawal. | |

| Contract Charges | |

| Certain charges may be deducted directly or indirectly from the funding options available under the contract, | |

| including GAA. | |

| The contract may have a maintenance fee of up to $50 that we will deduct, on an annual basis, pro rata from all | |

| funding options including GAA. We may also deduct a maintenance fee upon full withdrawal of a contract. | |

| The contract may have an early withdrawal charge that we will deduct, if applicable, upon a full or partial | |

| withdrawal from the contract. If the withdrawal occurs prior to the maturity of a guaranteed term, both the early | |

| withdrawal charge and an MVA may be assessed. | |

| We do not deduct mortality and expense risk charges and other asset-based charges that may apply to variable | |

| funding options from GAA. These charges are only applicable to the variable funding options. | |

| We may deduct a charge for premium taxes of up to 4% from amounts in GAA, and, under some contracts, front end | |

| sales charges of up to 6%. | |

| Under certain contracts, we reserve the right to charge $10 for each transfer of accumulated value between available | |

| investment options over 12 free transfers per calendar year. | |

| Refer to the contract prospectus for further details on contract charges. | |

| Other Topics | |

| Anti-Money Laundering | |

| In order to protect against the possible misuse of our products in money laundering or terrorist financing, we have | |

| adopted an anti-money laundering program satisfying the requirements of the USA PATRIOT Act and other current | |

| anti-money laundering laws. Among other things, this program requires us, our agents and customers to comply with | |

| certain procedures and standards that will allow us to verify the identity of the sponsoring organization and that | |

| contributions and loan repayments are not derived from improper sources. | |

| Under our anti-money laundering program, we may require customers, and/or beneficiaries to provide sufficient | |

| evidence of identification, and we reserve the right to verify any information provided to us by accessing | |

| information databases maintained internally or by outside firms. | |

| PRO.GAA-14 | 13 |

| We may also refuse to accept certain forms of payments or loan repayments (traveler’s cheques, cashier's checks, | |

| bank drafts, bank checks and treasurer's checks, for example) or restrict the amount of certain forms of payments or | |

| loan repayments (money orders totaling more than $5,000, for example). In addition, we may require information as | |

| to why a particular form of payment was used (third party checks, for example) and the source of the funds of such | |

| payment in order to determine whether or not we will accept it. Use of an unacceptable form of payment may result | |

| in us returning the payment to you. | |

| Applicable laws designed to prevent terrorist financing and money laundering might, in certain | |

| circumstances, require us to block certain transactions until authorization is received from the appropriate | |

| regulator. We may also be required to provide additional information about you and your policy to | |

| government regulators. | |

| Our anti-money laundering program is subject to change without notice to take account of changes in applicable | |

| laws or regulations and our ongoing assessment of our exposure to illegal activity. | |

| The Company | |

| Voya Retirement Insurance and Annuity Company (the “Company,” “we,” “us,” our”) is a stock life insurance | |

| company organized under the insurance laws of the State of Connecticut in 1976. Through a merger, our operations | |

| include the business of Aetna Variable Annuity Life Insurance Company (formerly known as Participating Annuity | |

| Life Insurance Company, an Arkansas life insurance company organized in 1954). Prior to January 1, 2002, the | |

| Company was known as Aetna Life Insurance and Annuity Company. From January 1, 2002, until August 31, 2014, | |

| the Company was known as ING Life Insurance and Annuity Company. | |

| We are an indirect, wholly owned subsidiary of Voya Financial, Inc. (“VoyaTM”), which until April 7, 2014, was | |

| known as ING U.S., Inc. In May 2013 the common stock of Voya began trading on the NYSE under the symbol | |

| "VOYA" and Voya completed its initial public offering of common stock. | |

| Voya is an affiliate of ING Groep N.V. (“ING”), a global financial institution active in the fields of insurance, | |

| banking and asset management. In 2009 ING announced the anticipated separation of its global banking and | |

| insurance businesses, including the divestiture of Voya, which together with its subsidiaries, including the | |

| Company, constitutes ING’s U.S.-based retirement, investment management and insurance operations. As of | |

| November 18, 2014, ING’s ownership of Voya was approximately 19%. Under an agreement with the European | |

| Commission, ING is required to divest itself of 100% of Voya by the end of 2016. | |

| We are engaged in the business of issuing life insurance and annuities. Our principal executive offices are located at: | |

| One Orange Way | |

| Windsor, Connecticut 06095-4774 | |

| Income Phase | |

| GAA may not be used as a funding option during the income phase. Amounts invested in guaranteed terms must be | |

| transferred to one or more of the options available to fund income payments before income payments can begin. | |

| An aggregate MVA, as previously described, may be applied to amounts transferred to fund income payments | |

| before the end of a guaranteed term. Amounts used to fund lifetime income payments will only receive an aggregate | |

| MVA to the extent it is positive; however amounts transferred to fund a nonlifetime income payment option may be | |

| subject to either a positive or negative aggregate MVA. | |

| Refer to the contract prospectus for a further discussion of the income phase. | |

| PRO.GAA-14 | 14 |

| Contract Loans | ||

| (403(b) and some 457 and 401(a) Plans Only) | ||

| The contract holder or you, if applicable, may not take a loan from amounts held in GAA, but we include amounts | ||

| invested in GAA when calculating the account value that determines the amount available for a loan. Amounts held | ||

| in GAA must be transferred to a funding option available for loans in order to be received as a loan. Refer to the | ||

| contract prospectus for more information on contract loans. We will apply an MVA to amounts transferred from | ||

| guaranteed terms due to a loan request. | ||

| Investments | ||

| Amounts applied to GAA will be deposited in a nonunitized separate account established under Connecticut law. | ||

| A nonunitized separate account is a separate account in which neither the contract holder nor you participate in the | ||

| performance of the assets through unit values or any other interest. Contract holders and participants allocating | ||

| funds to the nonunitized separate account do not receive a unit value of ownership of assets accounted for in this | ||

| separate account. The risk of investment gain or loss is borne entirely by the Company. All Company obligations | ||

| due to allocations to the nonunitized separate account are contractual guarantees of the Company and are accounted | ||

| for in the separate account. All of the general assets of the Company are available to meet our contractual | ||

| guarantees. To the extent provided for in the applicable contract, the assets of the nonunitized separate account are | ||

| not chargeable with liabilities resulting from any other business of the Company. Income, gains and losses of the | ||

| separate account are credited to or charged against the separate account without regard to other income, gains or | ||

| losses of the Company. | ||

| Types of Investments.We intend to invest primarily in investment-grade fixed income securities including: | ||

| · | Securities issued by the United States Government; | |

| · | Issues of U.S. Government agencies or instrumentalities (these issues may or may not be guaranteed by the | |

| United States Government); | ||

| · | Debt securities that have an investment grade, at the time of purchase, within the four highest grades assigned | |

| by Moody’s Investors Services, Inc. (Aaa, Aa, A or Baa), Standard & Poor’s Corporation (AAA, AA, A or | ||

| BBB) or any other nationally recognized rating service; | ||

| · | Other debt instruments, including those issued or guaranteed by banks or bank holding companies, and of | |

| corporations, which although not rated by Moody’s, Standard & Poor’s, or other nationally recognized rating | ||

| services, are deemed by the Company’s management to have an investment quality comparable to securities that | ||

| may be purchased as stated above; or | ||

| · | Commercial paper, cash or cash equivalents, and other short-term investments having a maturity of less than | |

| one year that are considered by the Company’s management to have investment quality comparable to | ||

| securities, which may be purchased as stated above. | ||

| We may invest in futures and options. We purchase financial futures, related options and options on securities solely | ||

| for non-speculative hedging purposes. Should securities prices be expected to decline, we may sell a futures contract | ||

| or purchase a put option on futures or securities to protect the value of securities held in or to be sold for the | ||

| nonunitized separate account. Similarly, if securities prices are expected to rise, we may purchase a futures contract | ||

| or a call option against anticipated positive cash flow or may purchase options on securities. | ||

| We are not obligated to invest the assets attributable to the contracts according to any particular strategy, | ||

| except as required by Connecticut and other state insurance laws. The guaranteed interest rates established | ||

| by the Company may not necessarily relate to the performance of the nonunitized separate account. | ||

| Distribution of Contracts | ||

| The Company’s subsidiary, Voya Financial Partners, LLC serves as the principal underwriter for the variable | ||

| annuity contracts that include GAA as an investment option. Voya Financial Partners, LLC, a Delaware limited | ||

| liability company, is registered as a broker-dealer with the SEC. Voya Financial Partners, LLC is also a member of | ||

| the Financial Industry Regulatory Authority (“FINRA”) and the Securities Investor Protection Corporation | ||

| (“SIPC”). Voya Financial Partners, LLC’s principal office is located at One Orange Way, Windsor, Connecticut | ||

| 06095-4774. | ||

| PRO.GAA-14 | 15 | |

| As principal underwriter, Voya Financial Partners, LLC may enter into arrangements with one or more | |

| registered broker-dealers to offer and sell the contracts. We and our affiliate(s) may also sell the contracts directly. | |

| All individuals offering and selling the contracts must be registered representatives of a broker-dealer and must be | |

| licensed as insurance agents to sell variable annuity contracts. For additional information, see the contract | |

| prospectus. | |

| Taxation | |

| You should seek advice from your tax adviser as to the application of federal (and where applicable, state and local) | |

| tax laws to amounts paid to or distributed under the contracts. Refer to the applicable contract prospectus for a | |

| further discussion of tax considerations. | |

| Taxation of the Company.We are taxed as a life insurance company under Part I of Subchapter L of the Internal | |

| Revenue Code. The Company owns all assets supporting the contract obligations of GAA. Any income earned on | |

| such assets is considered income to the Company. We do not intend to make any provision or impose a charge under | |

| the contracts with respect to any tax liability of the Company. | |

| Taxation of Payments and Distributions.For information concerning the tax treatment of payments to and | |

| distributions from the contracts, please refer to the applicable contract prospectus. | |

| Experts | |

| The consolidated financial statements of the Company on Form 10-K for the year ended December 31, 2013 | |

| (including schedules appearing therein), have been audited by Ernst & Young LLP, independent registered public | |

| accounting firm, as set forth in their reports thereon, included therein, and incorporated herein by reference. Such | |

| consolidated financial statements are incorporated herein by reference in reliance upon such reports given on the | |

| authority of such firm as experts in accounting and auditing. | |

| Legal Matters | |

| For information regarding legal matters affecting the Company or the distributor of the variable annuity contracts, | |

| please refer to the applicable contract prospectus. | |

| Further Information | |

| This prospectus does not contain all of the information contained in the registration statement of which this | |

| prospectus is a part. Portions of the registration statement have been omitted from this prospectus as allowed by the | |

| SEC. You may obtain the omitted information from the offices of the SEC, as described below. | |

| We are required by the Securities Exchange Act of 1934 (the “Exchange Act”) to file periodic reports and other | |

| information with the SEC. You may inspect or copy information concerning the Company at the Public Reference | |

| Branch of the SEC at: | |

| SEC Public Reference Branch | |

| 100 F Street, NE, Room 1580 | |

| Washington, D.C. 20549 | |

| You may also obtain copies of these materials at prescribed rates from the Public Reference Branch of the | |

| above office. You may obtain information on the operation of the Public Reference Branch by calling the SEC at | |

| either 1-800-SEC-0330 or 1-202-551-8090 or by e-mailing publicinfo@sec.gov. You may also find more | |

| information about the Company by visiting the Company’s homepage on the internet at | |

| https://voyaretirement.voyaplans.com. | |

| Our filings are available to the public on the SEC’s website at www.sec.gov. (This uniform resource locator (URL) | |

| is an inactive textual reference only and is not intended to incorporate the SEC website into this prospectus.) When | |

| looking for more information about the contract, you may find it useful to use the number assigned to the | |

| registration statement under the Securities Act of 1933. This number is 333-_________. | |

| PRO.GAA-14 | 16 |

| You can also find this prospectus and other information the Company files electronically with the SEC on the SEC’s | ||

| web site at http://www.sec.gov. | ||

| Incorporation of Certain Documents by Reference | ||

| The SEC allows us to “incorporate by reference” information that we file with the SEC into this prospectus, | ||

| which means that incorporated documents are considered part of this prospectus. We can disclose important | ||

| information to you by referring you to those documents. This prospectus incorporates by reference the: | ||

| · | Annual Report on Form 10-K for the year ended December 31, 2013; and | |

| · | Quarterly Report on Form 10-Q for the period ended September 30, 2014. | |

| Form 10-K contains additional information about the Company and includes certified financial statements as of | ||

| December 31, 2013 and 2012, and for each of the three years in the period ended December 31, 2013. We were not | ||

| required to file any other reports pursuant to Sections 13(a) or 15(d) of the Exchange Act since September 30, 2014. | ||

| All documents subsequently filed by the Company pursuant to Sections 13(a), 13(c), 14 or 15(d) of the Exchange | ||

| Act, prior to the termination of the offering shall be deemed to be incorporated by reference into this prospectus. | ||

| You may request a free copy of any documents incorporated by reference in this prospectus (including any exhibits | ||

| that are specifically incorporated by reference in them). Please direct your request to: | ||

| Voya Retirement Insurance and Annuity Company | ||

| Customer Service | ||

| One Orange Way | ||

| Windsor, CT 06095-4774 | ||

| 1-800-262-3862 | ||

| Inquiries | ||

| You may contact us directly by writing or calling to us at the address or phone number shown above. | ||

| PRO.GAA-14 | 17 | |

| Appendix I |

| Examples of Market Value Adjustment Calculations |

| The following are examples of market value adjustment ("MVA”) calculations using several hypothetical |

| yields, applicable to contracts that use Method One to calculate the MVA.These examples do not include the |

| effect of any early withdrawal charge or other fees that may be assessed under the contract upon withdrawal. |

| EXAMPLE I |

| ais the average of the US Treasury Rate in effect on the first four Fridays of the month of deposit for the |

| corresponding guaranteed term; |

| bis the US Treasury Rate in effect on the withdrawal date (based on the previous Friday) for a period equal to the |

| remainder of the guaranteed term; |

| iis the average of the spread over Treasury on the Barclays US Corporate Investment Grade Index (if unavailable a |

| similar service will be utilized) in effect on the first four Fridays of the month of deposit for the corresponding |

| guaranteed term; |

| jis the spread over Treasury on the Barclays US Corporate Investment Grade Index (if unavailable a similar service |

| will be utilized) in effect on the withdrawal date (based on the previous Friday) for a period equal to the remainder |

| of the guaranteed term; and |

| xis the number of days remaining, (computed from Wednesday of the week of withdrawal) in the guaranteed term. |

| Note that the Company may change the weekdays noted above, subject to the terms of your contract. |

| EXAMPLE II |

| ais the average of the US Treasury Rate in effect on the first four Fridays of the month of deposit for the |

| corresponding guaranteed term; |

| bis the US Treasury Rate in effect on the withdrawal date (based on the previous Friday) for a period equal to the |

| remainder of the guaranteed term; |

| iis the average of the spread over Treasury on the Barclays US Corporate Investment Grade Index (if unavailable a |

| similar service will be utilized) in effect on the first four Fridays of the month of deposit for the corresponding |

| guaranteed term; |

| jis the spread over Treasury on the Barclays US Corporate Investment Grade Index (if unavailable a similar service |

| will be utilized) in effect on the withdrawal date (based on the previous Friday) for a period equal to the remainder |

| of the guaranteed term; and |

| xis the number of days remaining, (computed from Wednesday of the week of withdrawal) in the guaranteed term. |

| Note that the Company may change the weekdays noted above, subject to the terms of your contract. |

| The following are examples of market value adjustment ("MVA") calculations using several hypothetical |

| deposit period yields and current yields, applicable to contracts that use Method Two to calculate the MVA. |

| These examples do not include the effect of any early withdrawal charge or other fees that may be assessed under |

| the contract upon withdrawal. |

| EXAMPLE II | |||

| Assumptions: | Assumptions: | ||

| i, | the deposit period yield, is 6% | i, | the deposit period yield, is 5% |

| j, | the current yield, is 4% | j, | the current yield, is 4% |

| x, | the number of days remaining (computed from | x, | the number of days remaining (computed from |

| Wednesday of the week of withdrawal) in the | Wednesday of the week of withdrawal) in the | ||

| guaranteed term, is 927. | guaranteed term, is 927. | ||

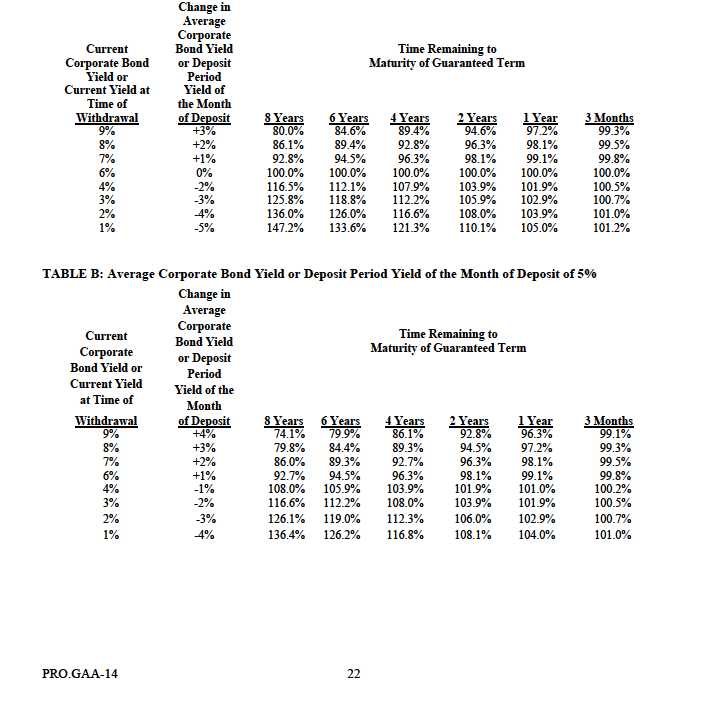

| Appendix II | |

| Examples of Market Value Adjustment at Various Yields | |

| The following hypothetical examples show the market value adjustment (“MVA”) at time of withdrawal for various | |

| times remaining in the guaranteed term, based on: | |

| · | Method One, which uses the current and average corporate bond yields (US Treasury Rate plus spread over |

| Treasury) in the MVA calculations; and | |

| · | Method Two, which uses the current and deposit period yields in the MVA calculations. |

| Table A illustrates the application of the MVA based on an average corporate bond yield or deposit period yield of | |

| the month of deposit of 6%; Table B illustrates the application of the MVA based on an average corporate bond | |

| yield or deposit period yield of the month of deposit of 5%. The MVA will have either a positive or negative | |

| influence on the amount withdrawn from or remaining in a guaranteed term. Also, the amount of the MVA generally | |

| decreases as the end of the guaranteed term approaches. | |

| TABLE A: Average Corporate Bond Yield or Deposit Period Yield of the Month of Deposit of 6% | |

| PART II |

| INFORMATION NOT REQUIRED IN PROSPECTUS |

| Item 14. Other Expenses of Issuance and Distribution |

| Not Applicable |

| Item 15. Indemnification of Directors and Officers |

| Section 33-779 of the Connecticut General Statutes (“CGS”) provides that a corporation may |

| provide indemnification of or advance expenses to a director, officer, employee or agent only as |

| permitted by Sections 33-770 to 33-778, inclusive, of the CGS. Reference is hereby made to |

| Section 33-771(e) of the CGS regarding indemnification of directors and Section 33-776(d) of |

| CGS regarding indemnification of officers, employees and agents of Connecticut corporations. |

| These statutes provide in general that Connecticut corporations incorporated prior to January 1, |

| 1997 shall, except to the extent that their certificate of incorporation expressly provides |

| otherwise, indemnify their directors, officers, employees and agents against “liability” (defined |

| as the obligation to pay a judgment, settlement, penalty, fine, including an excise tax assessed |

| with respect to an employee benefit plan, or reasonable expenses incurred with respect to a |

| proceeding) when (1) a determination is made pursuant to Section 33-775 that the party seeking |

| indemnification has met the standard of conduct set forth in Section 33-771 or (2) a court has |

| determined that indemnification is appropriate pursuant to Section 33-774. Under Section 33- |