UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| | |

| Investment Company Act file number | | 811-05642 |

Nuveen Multi-Market Income Fund

(Exact name of registrant as specified in charter)

Nuveen Investments

333 West Wacker Drive, Chicago, IL 60606

(Address of principal executive offices) (Zip code)

Mark L. Winget

Nuveen Investments

333 West Wacker Drive, Chicago, IL 60606

(Name and address of agent for service)

Registrant’s telephone number, including area code: (312) 917-7700

Date of fiscal year end: June 30

Date of reporting period: December 31, 2020

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policy making roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss.3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

Closed-End Funds

31 December 2020

Nuveen Closed-End Funds

| | |

| JMM | | Nuveen Multi-Market Income Fund |

As permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Fund’s annual and semi-annual shareholder reports will not be sent to you by mail unless you specifically request paper copies of the reports. Instead, the reports will be made available on the Fund’s website (www.nuveen.com), and you will be notified by mail each time a report is posted and provided with a website link to access the report.

You may elect to receive shareholder reports and other communications from the Fund electronically at any time by contacting the financial intermediary (such as a broker-dealer or bank) through which you hold your Fund shares or, if you are a direct investor, by enrolling at www.nuveen.com/e-reports.

You may elect to receive all future shareholder reports in paper free of charge at any time by contacting your financial intermediary or, if you are a direct investor, by calling 800-257-8787 and selecting option #2 or (ii) by logging into your Investor Center account at www.computershare.com/investor and clicking on “Communication Preferences”. Your election to receive reports in paper will apply to all funds held in your account with your financial intermediary or, if you are a direct investor, to all your directly held Nuveen Funds and any other directly held funds within the same group of related investment companies.

Semiannual Report

Life is Complex.

Nuveen makes things e-simple.

It only takes a minute to sign up for e-Reports. Once enrolled, you’ll receive an e-mail as soon as your Nuveen Fund information is ready—no more waiting for delivery by regular mail. Just click on the link within the e-mail to see the report and save it on your computer if you wish.

Free e-Reports right to your e-mail!

www.investordelivery.com

If you receive your Nuveen Fund dividends and statements from your financial professional or brokerage account.

or

www.nuveen.com/client-access

If you receive your Nuveen Fund dividends and statements directly from Nuveen.

NOT FDIC INSURED MAY LOSE VALUE NO BANK GUARANTEE

Table of Contents

3

Chair’s Letter to Shareholders

Dear Shareholders,

The rollout of COVID-19 vaccines has kindled the promise of a more normal economy in 2021. Until then, the economic shortfall is expected to be bridged by a combination of fiscal relief measures and easier financial conditions aimed at supporting individuals, businesses and state and local governments. The measures taken to date have already helped the U.S. economy make a significant, although incomplete, turnaround from the depths of a historic recession. In late December 2020, the U.S. government enacted another $900 billion in aid to individuals and businesses, extending some of the programs enacted earlier in the COVID-19 crisis, and more stimulus is anticipated. The U.S. Federal Reserve, along with other central banks around the world, have pledged to keep monetary conditions accommodative for as long as necessary.

While the markets’ longer-term outlook has brightened, we expect intermittent bouts of volatility to continue. COVID-19 cases are still alarmingly high in some regions, and recent economic indicators have shown the dampening effect of renewed restrictions on social and business activity in the latter months of 2020. The pandemic’s course can still be unpredictable, and achieving sufficient inoculation of the population depends on many variables, including logistics, public confidence, real-world efficacy and the emergence of variant virus strains. Additionally, the Biden administration’s full policy agenda and the potential for Congressional gridlock remain to be seen, which could cause investment outlooks to shift. Nevertheless, short-term market fluctuations can provide opportunities to invest in new ideas as well as upgrade existing positioning, within our goal of providing long-term value for our shareholders. For more than 120 years, the careful consideration of risk and reward has guided Nuveen’s focus on delivering long-term results to our shareholders.

The beginning of the year can be an opportune time to assess your portfolio’s resilience and readiness for what may come next. We encourage you to review your time horizon, risk tolerance and investment goals with your financial professional. On behalf of the other members of the Nuveen Fund Board, we look forward to continuing to earn your trust in the months and years ahead.

Sincerely,

Terence J. Toth

Chair of the Board

February 22, 2021

4

Portfolio Managers’ Comments

Nuveen Multi-Market Income Fund (JMM)

Nuveen Multi-Market Income Fund (JMM) features portfolio management by Nuveen Asset Management, LLC (NAM), an affiliate of Nuveen Fund Advisers, LLC, the Fund’s investment adviser. The Fund’s portfolio managers are Jason J. O’Brien, CFA, and Peter L. Agrimson, CFA.

Here the Fund’s portfolio management team discusses key investment strategies and the Fund’s performance for the six-month reporting period December 31, 2020.

An Update on COVID-19 Coronavirus and its Impact on the Securities Markets

The start of vaccinations across Western countries has been encouraging for the markets, although the discovery of new variants of the COVID-19 coronavirus could cause expectations to be reassessed. The vaccine rollouts have also been slower than expected in some regions. Nevertheless, there are more vaccines still in development, some of which have announced positive trial results, and governments are looking to adjust rollout plans to speed distribution.

The economic recovery moderated in late 2020, as a resurgence of infections triggered another tightening in restrictions. The slower pace is expected to persist into 2021, prompting pledges from central banks and governments to sustain the recovery with policy support. In late December 2020, the U.S. government approved a $900 billion relief package, and more stimulus is anticipated from the Biden administration in 2021.

Markets rallied on optimism for normalization in daily life and in the economy, furthering the recovery from the March 2020 sell-off. Although the detection of the virus in China was made public in December 2019, markets did not start to fully acknowledge the risks and potential economic impact until the latter portion of February 2020, when outbreaks outside of China were first reported. Global stock markets sold off severely, with the S&P 500® Index reaching a bear market (a 20% drop from the previous high) within three weeks, the fastest bear market decline in history. Even certain parts of the bond market suffered; below investment grade municipal and corporate bonds generally dropped the furthest, mostly out of concerns for the continued financial stability of lower quality issuers. Demand for safe-haven assets, along with mounting recession fears, drove the yield on the 10-year U.S. Treasury note to 0.5% in March 2020, an all-time low. Additionally, oil prices collapsed to an 18-year low on supply glut concerns, as shut-downs across the global economy sharply reduced oil demand, although oil prices have recovered to well above those lows.

While most markets have recovered the majority of their losses, volatility will likely remain elevated until the health crisis itself is under control (via fewer new cases, lower infection rates and/or wider immunity across populations). The situation remains fluid, given production and logistical challenges with rolling out the vaccine as well as public trust in it, and the potential for more harmful variants of the virus. The distribution of phase 3-tested vaccines has narrowed the range of outcomes for the course of the pandemic itself and the global economy, but there is still uncertainty in the timing of a full recovery.

Nuveen Fund Advisors, LLC, and their portfolio management teams are monitoring the situation carefully and continuously refining their views and approaches to managing their funds to best pursue investment objectives while mitigating risks through all market environments.

What key strategies were used to manage the Fund during the six-month reporting period ended December 31, 2020?

The Fund’s investment objective is to achieve high monthly income consistent with prudent risk to capital. The portfolio management team invests the Fund’s assets primarily in debt securities, including, but not limited to, U.S. agency and privately issued mortgage-backed securities, corporate debt securities, and asset-backed securities. At least 65% of the

5

Portfolio Managers’ Comments (continued)

Fund’s total assets must be invested in securities that, at the time of purchase, are rated investment grade or of comparable quality. The Fund may utilize derivatives. The Fund uses leverage.

How did the Fund perform during the six-month reporting period ended December 31, 2020?

The table in the Performance Overview and Holding Summaries section of this report provides total returns at net asset value (NAV) for the period ended December 31, 2020. The Fund’s total return at NAV is compared with the performance of a corresponding market index.

For the six-month reporting period ended December 31, 2020, the Fund outperformed both the Bloomberg Barclays U.S. Government/Mortgage Bond Index and its Blended Benchmark, which is composed of 75% Bloomberg Barclays U.S. Government/Mortgage Index and 25% Bloomberg Barclays U.S. Corporate High-Yield Index, each of which are further described in the Glossary of Terms Used in This Report.

Economic growth rebounded strongly during the reporting period, although it slowed near the end relative to the dramatic post-COVID-19 crisis lockdown surge seen earlier in 2020. Unemployment continued to fall, industrial activity expanded and consumer spending held up well even amid continued concerns about the spread of COVID-19. Despite the severity of renewed outbreaks in many countries, lockdowns were significantly less restrictive than earlier in the reporting period, allowing economic activity to maintain its momentum. Surprisingly positive vaccine trial results later in the reporting period further boosted sentiment.

As expected, Federal Reserve (Fed) policymakers left rates unchanged throughout the reporting period as the U.S. economy continued to recover from its deepest recession in history. In September 2020, the Fed indicated its intent to leave the Federal Funds rate at the current level through at least 2023. Policymakers also announced a more flexible approach to targeting an average inflation rate of 2% over time, which will allow inflation to run hotter before the central bank feels compelled to increase rates. At the December 2020 meeting, Fed policymakers issued a fresh set of economic projections, increasing 2020’s gross domestic product (GDP) growth forecast to -2.4%. The Fed also slightly increased GDP and inflation forecasts for the next two years and lowered the unemployment outlook as the economy recovered. In addition, the central bank continued its quantitative easing (QE) program, buying roughly $80 billion of Treasury securities a month across the yield curve. Despite the Fed’s QE buying operations, the combination of economic expansion and greater vaccine certainty pushed longer maturity Treasury yields higher. Meanwhile, rates at the front end remained firmly anchored by the Fed’s commitment to remain on hold, allowing the yield curve to steepen modestly. The 10-year Treasury yield rose 27 basis points over the six-month reporting period to end at 0.93%.

The ongoing and unprecedented fiscal and monetary stimulus continued to boost the credit markets, which enjoyed strong performance. Specifically, the Fed’s support through the Primary and Secondary Market Corporate Credit Facilities was a key driver in the recovery of corporate bond prices. Also, with yields low and volatility suppressed, investors gained confidence in moving down the credit spectrum. Investment grade corporations issued $1.8 trillion worth of bonds in 2020 (60% above 2019’s issuance level), which was easily absorbed by the market. Corporate issuers took advantage of low yields and strong investor appetite to improve balance sheet liquidity and extend the duration profile of their liabilities. Investment grade credit spreads tightened and the segment outperformed Treasuries driven by these strong technical dynamics, improved corporate earnings, reduced election uncertainty, positive vaccine developments and the signing of a $900 billion fiscal package at the end of the reporting period.

Agency mortgage-backed securities (MBS) generated excess returns over Treasuries, but significantly lagged other major fixed income asset classes. Fed bond buying remained significant and supportive of the sector, which offers an attractive spread compared to Treasuries. Spreads for credit risk transfer (CRT) and non-agency MBS tightened versus Treasuries as investors sought excess yields outside of corporate bond alternatives.

Commercial mortgage-backed securities (CMBS) and asset-backed securities (ABS) generated excess returns versus Treasuries. The CMBS market saw a significant rally in spreads even as supply came to the market, which was primarily

6

the result of a “catch-up” trade to other non-securitized asset classes that had previously recovered to pre-COVID-19 levels. As the reporting period progressed, investors gained confidence that significant downside risk was unlikely in the CMBS market due to a sustained flattening of default rates. The ABS market shifted into a higher gear later in the reporting period, mostly driven by news of multiple COVID-19 vaccines. Spreads tightened in COVID-19 sensitive sectors such as aircraft ABS and almost any other securities offering attractive yields.

High yield credit outpaced the rest of the fixed income market as spreads tightened by more than 264 basis points overall versus Treasuries, led by the lower quality tiers as investors moved down the rating spectrum to pick up additional yield. The segment experienced significant inflows during the reporting period, which helped support the ongoing and robust new issue market. For the reporting period, domestic high yield new issuance totaled a record-breaking $450 billion on a gross basis, although approximately two-thirds was related to refinancings. The refinancing trend allowed companies to extend maturity profiles and essentially buy time, which benefited the fundamental backdrop within high yield. Refinancings also supported the technical backdrop by mitigating the amount of net new supply the market needed to absorb.

The Fund outperformed during the reporting period in large part due to its asset allocation breakdown. Markets continued to recover during the second half of the reporting period and all spread sectors posted positive excess returns over Treasuries. Specifically, the Fund’s overweight positions in ABS, CMBS, non-agency MBS and investment grade credit all benefited performance, mainly driven by the CMBS and ABS sectors. Esoteric ABS and lower rated investment grade CMBS performed well late in the reporting period as these segments recovered some of their underperformance from the first half of 2020. The Fund’s investment grade credit overweight also contributed favorably to performance. In addition, the Fund’s underweight to securities at the long end of yield curve proved beneficial to results as the curve steepened and prices for these longer maturity securities fell more.

Offsetting some of the positive effect from yield curve positioning, the Fund’s modestly longer duration stance versus its benchmark detracted from performance because interest rates rose during the reporting period. Also, an underweight position in the high yield sector early in the reporting period, as well as security selection within the segment, were modest drags on performance relative to the benchmark. Finally, the Fund’s up-in-quality bias among its high yield holdings detracted because lower quality credits outperformed during the reporting period.

We continued to manage the Fund with many of the same overarching investment themes, focusing on bottom-up security selection and sector positioning as the most significant drivers of performance. Our goal is to generate income through broad exposure to the securitized and corporate sectors of the bond market. From a positioning standpoint, the Fund maintained overweights to ABS, CMBS and MBS and remained focused on bottom-up security selection to generate income and price returns in those sectors. The ABS and CMBS sectors lagged during 2020’s initial recovery due to less direct benefit from Fed buying, but the spread gap for these segments compressed during this reporting period. Given this narrowing, the ABS and CMBS sectors ended the reporting period more fairly valued relative to corporates, which will continue to drive our focus on bottom-up analysis. Also, later in the reporting period, the Fund continued to rotate into high yield credit while selling investment grade credit because some of these securities reached their spread targets.

The Fund used U.S. Treasury futures as part of an overall portfolio construction strategy to manage portfolio duration and yield curve exposure. These future positions had a negligible impact on performance during the reporting period. The Fund also used interest rate swaps as part of an overall portfolio construction strategy to manage duration and overall portfolio yield curve exposure. The swap positions had a negative impact on performance during the reporting period.

The Fund may also purchase securities on a when-issued or forward commitment (delayed delivery) basis. Delivery and payment for securities that have been purchased in this manner can take place a month or more after the transaction date. Such securities do not earn interest, are subject to market fluctuation and may increase or decrease in value prior to their delivery. The purchase of securities on a when-issued or forward commitment basis may increase the volatility of the Fund’s net asset value if the Fund makes such purchases while remaining substantially fully invested.

7

Fund Leverage

IMPACT OF THE FUND’S LEVERAGE STRATEGY ON PERFORMANCE

One important factor impacting the returns of the Fund’s common shares relative to its comparative benchmarks was the Fund’s use of leverage through reverse repurchase agreements and mortgage dollar rolls. The Fund uses leverage because our research has shown that, over time, leveraging provides opportunities for additional income. The opportunity arises when short-term rates that the Fund pays on its leveraging instruments are lower than the interest the Fund earns on its portfolio securities that it has bought with the proceeds of that leverage. This has been particularly true in the recent market environment where short-term rates have been low by historical standards.

However, use of leverage can expose Fund common shares to additional price volatility. When the Fund uses leverage, the Fund’s common shares will experience a greater increase in their net asset value if the securities acquired through the use of leverage increase in value, but will also experience a correspondingly larger decline in their net asset value if the securities acquired through leverage decline in value. All this will make the shares’ total return performance more variable over time.

In addition, common share income in levered funds will typically decrease in comparison to unlevered funds when short-term interest rates increase and increase when short-term interest rates decrease. In recent quarters, fund leverage expenses have generally tracked the overall movement of short-term interest rates. While fund leverage expenses are somewhat higher than their recent lows, leverage nevertheless continues to provide the opportunity for incremental common share income, particularly over longer-term periods.

The Fund’s use of leverage had a positive impact on total return performance during this reporting period.

As of December 31, 2020, the Fund’s percentages of leverage are shown in the accompanying table.

| | | | |

| | | JMM | |

Effective Leverage* | | | 23.10 | % |

Regulatory Leverage* | | | 0.00 | % |

| * | Effective leverage is a Fund’s effective economic leverage, and includes both regulatory leverage and the leverage effects of reverse repurchase agreements, certain derivative and other investments in the Fund’s portfolio that increase the Fund’s investment exposure. Regulatory leverage consists of preferred shares issued or borrowings of a Fund. Both of these are part of a Fund’s capital structure. The Fund, however, may from time to time borrow on a typically transient basis in connection with its day-to-day operations, primarily in connection with the need to settle portfolio trades. Such incidental borrowings are excluded from the calculation of the Fund’s effective leverage ratio. Regulatory leverage is subject to asset coverage limits set forth in the Investment Company Act of 1940. |

THE FUND’S LEVERAGE

Reverse Repurchase Agreements

As noted above, the Fund utilized reverse repurchase agreements in which, the Fund sells to a counterparty a security that it holds with a contemporaneous agreement to repurchase the same security at an agreed-upon price and date. The Fund’s transactions in reverse repurchase agreements are as shown in the accompanying table.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Current Reporting Period | | | | | | Subsequent to the Close of

the Reporting Period | |

| July1, 2020 | | | Sales | | | Purchases | | | December 31, 2020 | | | Average Balance Outstanding | | | | | | Sales | | | Purchases | | | February 25, 2021 | |

| | $24,776,000 | | | | $1,471,763 | | | | $(4,035,691) | | | | $22,212,071 | | | | $(23,046,388) | | | | | | | | $3,019,218 | | | | $(1,611,289) | | | | $23,620,000 | |

Refer to Notes to Financial Statements, Note 8 – Fund Leverage for further details.

8

Common Share Information

COMMON SHARE DISTRIBUTION INFORMATION

The following information regarding the Fund’s distributions is current as of December 31, 2020. The Fund’s distribution levels may vary over time based on the Fund’s investment activity and portfolio investment value changes.

During the current reporting period, the Fund’s distributions to common shareholders were as shown in the accompanying table.

| | | | |

| Monthly Distributions (Ex-Dividend Date) | | Per

Common

Share

Amounts | |

July 2020 | | $ | 0.0270 | |

August | | | 0.0270 | |

September | | | 0.0270 | |

October | | | 0.0245 | |

November | | | 0.0245 | |

December 2020 | | | 0.0245 | |

Total Distributions from Net Investment Income | | $ | 0.1545 | |

| | | | |

Current Distribution Rate* | | | 4.09 | % |

| * | Current distribution rate is based on the Fund’s current annualized monthly distribution divided by the Fund’s current market price. The Fund’s monthly distributions to its shareholders may be comprised of ordinary income, net realized capital gains and, if at the end of the fiscal year the Fund’s cumulative net ordinary income and net realized gains are less than the amount of the Fund’s distributions, a return of capital for tax purposes. |

The Fund seeks to pay regular monthly dividends out of its net investment income at a rate that reflects its past and projected net income performance. To permit the Fund to maintain a more stable monthly dividend, the Fund may pay dividends at a rate that may be more or less than the amount of net income actually earned by the Fund during the period. Distributions to shareholders are determined on a tax basis, which may differ from amounts recorded in the accounting records. In instances where the monthly dividend exceeds the earned net investment income, the Fund would report a negative undistributed net ordinary income. Refer to Note 6 – Income Tax Information for additional information regarding the amounts of undistributed net ordinary income and undistributed net long-term capital gains and the character of the actual distributions paid by the Fund during its most recent tax year end.

All monthly dividends paid by the Fund during the current reporting period were paid from net investment income. If a portion of the Fund’s monthly distributions is sourced from or comprised of elements other than net investment income, including capital gains and/or a return of capital, shareholders will be notified of those sources. For financial reporting purposes, per share amounts of the Fund’s distributions for the reporting period are presented in this report’s Financial Highlights. For income tax purposes, distribution information for the Fund as of its most recent tax year end is presented in Note 6 – Income Tax Information within the Notes to Financial Statements of this report.

ANNOUNCEMENT OF LEVEL DISTRIBUTION POLICY

On February 25, 2021 (subsequent to the close of this reporting period), the Fund announced that its Board of Trustees approved the adoption of a level distribution policy. The level distribution policy is intended to provide shareholders with stable, but not guaranteed, cash flow, independent of the amount or timing of income earned or capital gains realized by the Fund. The Fund intends to distribute all or substantially all of its net investment income through its regular monthly distribution and to distribute realized capital gains at least annually. In addition, in any monthly period, in order to maintain its level distribution amount, the Fund may pay out more or less than its net investment income

9

Common Share Information (continued)

during the period. As a result, distribution sources may include net investment income, realized gains and return of capital. [If the Fund’s distribution includes anything other than net investment income, the Fund will provide a notice of its best estimate of the distribution sources at that time, which may be viewed at www.nuveen.com/CEFdistributions. These estimates may not match the final tax characterization (for the full year’s distributions) contained in shareholders’ 1099-DIV forms delivered after the end of the calendar year.] The level distribution policy will become effective with the Fund’s March distribution.

NUVEEN CLOSED-END FUND DISTRIBUTION AMOUNTS

The Nuveen Closed-End Funds’ monthly and quarterly periodic distributions to shareholders are posted on www.nuveen.com and can be found on Nuveen’s enhanced closed-end fund resource page, which is at https://www.nuveen.com/resource-center-closed-end-funds, along with other Nuveen closed-end fund product updates. To ensure timely access to the latest information, shareholders may use a subscribe function, which can be activated at this web page (https://www.nuveen.com/subscriptions).

COMMON SHARE REPURCHASES

During August 2020, the Fund’s Board of Trustees reauthorized an open-market common share repurchase program, allowing the Fund to repurchase an aggregate of up to approximately 10% of its outstanding common shares.

As of December 31, 2020, and since the inception of the Fund’s repurchase program, the Fund has cumulatively repurchased and retired its outstanding common shares as shown in the accompanying table.

| | | | |

| | | JMM | |

Common shares cummulatively repurchased and retired | | | 1,800 | |

Common shares authorized for repurchase | | | 945,000 | |

During the current reporting period, the Fund did not repurchase any of its outstanding common shares.

OTHER SHARE INFORMATION

As of December 31, 2020, and during the current reporting period, the Fund’s common share price was trading at premium/(discount) to its NAV as shown in the accompanying table.

| | | | |

Common share NAV | | $ | 7.82 | |

Common share price | | $ | 7.19 | |

Premium/(Discount) to NAV | | | (8.06 | )% |

6-Month average premium/(discount) to NAV | | | (8.97 | )% |

10

| | |

| JMM | | Nuveen Multi-Market Income Fund Performance Overview and Holding Summaries as of December 31, 2020 |

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section.

Average Annual Total Returns as of December 31, 2020

| | | | | | | | | | | | | | | | |

| | | Cumulative | | | Average Annual | |

| | | 6-Month | | | 1-Year | | | 5-Year | | | 10-Year | |

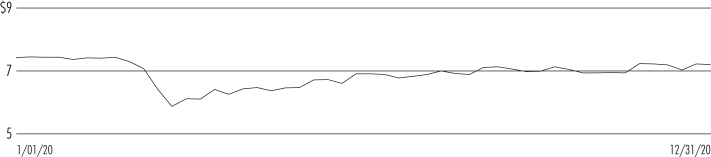

| JMM at Common Share NAV | | | 6.67% | | | | 1.86% | | | | 4.48% | | | | 4.95% | |

| JMM at Common Share Price | | | 6.50% | | | | 1.77% | | | | 5.71% | | | | 4.65% | |

| Bloomberg Barclays U.S. Government/Mortgage Bond Index | | | (0.22)% | | | | 6.36% | | | | 3.49% | | | | 3.16% | |

| Blended Benchmark1 | | | 2.57% | | | | 6.69% | | | | 4.79% | | | | 4.09% | |

Past performance is not predictive of future results. Current performance may be higher or lower than the data shown. Returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the sale of Fund shares. Returns at NAV are net of Fund expenses, and assume reinvestment of distributions. Comparative index return information is provided for the Fund’s shares at NAV only. Indexes are not available for direct investment.

Common Share Price Performance — Weekly Closing Price

| 1. | The Blended Benchmark consists of: 1) 25% of the Bloomberg Barclays U.S. Corporate High-Yield Index and 2) 75% of the Bloomberg Barclays U.S. Government/Mortgage Index. |

11

This data relates to the securities held in the Fund’s portfolio of investments as of the end of the reporting period. It should not be construed as a measure of performance for the Fund itself. Holdings are subject to change.

For financial reporting purposes, the ratings disclosed are the highest rating given by one of the following national rating agencies: Standard & Poor’s Group, Moody’s Investors Service, Inc. or Fitch, Inc. This treatment of split-rated securities may differ from that used for other purposes, such as for Fund investment policies. Credit ratings are subject to change. AAA, AA, A and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below-investment grade ratings. Holdings designated N/R are not rated by these national rating agencies.

Fund Allocation

(% of net assets)

| | | | |

| Asset-Backed and Mortgage-Backed Securities | | | 98.5% | |

| Corporate Bonds | | | 30.8% | |

| Sovereign Debt | | | 1.7% | |

| Contingent Capital Securities | | | 0.9% | |

| Municipal Bonds | | | 0.7% | |

| Common Stock | | | 0.2% | |

| Repurchase Agreements | | | 2.0% | |

| Other Assets Less Liabilities | | | (4.8)% | |

Net Assets Plus Reverse Repurchase Agreements | | | 130.0% | |

| Reverse Repurchase Agreements | | | (30.0)% | |

Net Assets | | | 100% | |

Portfolio Composition

(% of total investments)

| | | | |

| Asset-Backed and Mortgage-Backed Securities | | | 73.1% | |

| Oil, Gas & Consumable Fuels | | | 2.3% | |

| Equity Real Estate Investment Trust | | | 1.8% | |

| Media | | | 1.5% | |

| Chemicals | | | 1.5% | |

| Diversified Telecommunication Services | | | 1.4% | |

| Diversified Financial Services | | | 1.4% | |

| Metals & Mining | | | 1.0% | |

| Other | | | 14.5% | |

| Repurchase Agreements | | | 1.5% | |

Total | | | 100% | |

Portfolio Credit Quality

(% of total long-term

investments)

| | | | |

| AAA | | | 3.8% | |

| AA | | | 3.1% | |

| A | | | 7.2% | |

| BBB | | | 24.2% | |

| BB or Lower | | | 23.9% | |

| U.S. Treasury/Agency | |

| 28.8%

|

|

| N/R | | | 8.8% | |

| N/A | | | 0.2% | |

Total | | | 100% | |

12

| | |

| JMM | | Nuveen Multi-Market Income Fund Portfolio of Investments December 31, 2020 |

| | | (Unaudited) |

| | | | | | | | | | | | | | | | | | | | | | |

Principal

Amount (000) | | | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | |

| | | | | | LONG-TERM INVESTMENTS – 132.8% (98.5% of Total Investments) | |

| | |

| | | | | | ASSET-BACKED AND MORTGAGE-BACKED SECURITIES – 98.5% ( 73.1% of Total Investments) | |

| | | | | | |

| $ | 207 | | | | | 321 Henderson Receivables VI LLC, Series 2010-1A, 144A | | | 9.310% | | | | 7/15/61 | | | | Aaa | | | $ | 247,474 | |

| | 250 | | | | | ACE Securities Corp Manufactured Housing Trust, Series 2003-MH1, 144A | | | 6.500% | | | | 8/15/30 | | | | A+ | | | | 264,116 | |

| | 500 | | | | | Adams Outdoor Advertising LP, Series 2018-1B,144A | | | 5.653% | | | | 11/15/48 | | | | BBB | | | | 528,852 | |

| | 61 | | | | | Alternative Loan Trust, Series 2003-J3 | | | 5.250% | | | | 11/25/33 | | | | Aaa | | | | 63,022 | |

| | 96 | | | | | Alternative Loan Trust, Series 2004-J2 | | | 6.500% | | | | 3/25/34 | | | | AA+ | | | | 98,227 | |

| | 1,658 | | | | | American Homes 4 Rent Trust, Series 2015-SFR2 Trust, (I/O), 144A | | | 0.000% | �� | | | 10/17/52 | | | | N/R | | | | 17 | |

| | 175 | | | | | AMSR 2019-SFR1 Trust, 144A | | | 3.247% | | | | 1/19/39 | | | | Baa2 | | | | 180,728 | |

| | 241 | | | | | Bayview Financial Mortgage Pass-Through Trust, Series 2005-D | | | 5.500% | | | | 12/28/35 | | | | Aa3 | | | | 239,684 | |

| | 33 | | | | | Bayview Financial Mortgage Pass-Through Trust, Series 2006-C | | | 6.352% | | | | 11/28/36 | | | | Caa3 | | | | 33,352 | |

| | 418 | | | | | BX Commercial Mortgage Trust 2019-XL, 144A, (1-Month LIBOR reference rate + 1.800% spread), (3) | | | 1.959% | | | | 10/15/36 | | | | N/R | | | | 414,549 | |

| | 500 | | | | | CARS-DB4 LP, Series 2020-1A, 144A | | | 4.520% | | | | 2/15/50 | | | | BBB | | | | 523,041 | |

| | 954 | | | | | CF Hippolyta LLC, Series 2020-1 B2, 144A | | | 2.600% | | | | 7/15/60 | | | | A- | | | | 963,502 | |

| | 94 | | | | | Chase Funding Trust, Series 2003-3 | | | 5.160% | | | | 3/25/33 | | | | Ba1 | | | | 97,133 | |

| | 500 | | | | | CHL GMSR Issuer Trust, Series 2018-GT1, 144A, (1-Month LIBOR reference rate + 2.750% spread), (3) | | | 2.898% | | | | 5/25/23 | | | | N/R | | | | 492,606 | |

| | 425 | | | | | Citigroup Commercial Mortgage Trust 2015-GC29 | | | 4.151% | | | | 4/10/48 | | | | A- | | | | 434,603 | |

| | 600 | | | | | Citigroup Commercial Mortgage Trust 2016-P5, 144A | | | 3.000% | | | | 10/10/49 | | | | BBB- | | | | 442,445 | |

| | 450 | | | | | Citigroup Commercial Mortgage Trust 2018-TBR, 144A, (1-Month LIBOR reference rate + 1.800% spread), (3) | | | 1.959% | | | | 12/15/36 | | | | BBB- | | | | 412,631 | |

| | 92 | | | | | Citigroup Global Markets Mortgage Securities VII Inc, Series 2003-1, 144A | | | 6.000% | | | | 9/25/33 | | | | BB | | | | 91,685 | |

| | 500 | | | | | COMM 2013-LC13 Mortgage Trust, 144A | | | 5.287% | | | | 8/10/46 | | | | BB- | | | | 446,326 | |

| | 775 | | | | | COMM 2015-CCRE22 Mortgage Trust | | | 4.106% | | | | 3/10/48 | | | | A- | | | | 818,725 | |

| | 450 | | | | | COMM 2015-CCRE25 Mortgage Trust | | | 4.538% | | | | 8/10/48 | | | | A- | | | | 465,289 | |

| | 500 | | | | | COMM 2015-CCRE26 Mortgage Trust | | | 4.480% | | | | 10/10/48 | | | | A- | | | | 529,161 | |

| | 69 | | | | | Commonbond Student Loan Trust, Series 2017-B-GS, 144A | | | 4.440% | | | | 9/25/42 | | | | Aa3 | | | | 72,475 | |

| | 828 | | | | | Connecticut Avenue Securities Trust, Series 2019-R07, 144A, (1-Month LIBOR reference rate + 2.100% spread), (3) | | | 2.248% | | | | 10/25/39 | | | | B | | | | 825,733 | |

| | 600 | | | | | Connecticut Avenue Securities Trust, Series 2020-R02, 144A, (1-Month LIBOR reference rate + 2.000% spread), (3) | | | 2.148% | | | | 1/25/40 | | | | B | | | | 595,772 | |

| | 250 | | | | | CPT MORTGAGE TRUST, Series 2019-CPT, 144A | | | 2.997% | | | | 11/13/39 | | | | N/R | | | | 244,476 | |

| | 340 | | | | | Credit Suisse First Boston Mortgage Securities Corp, Series 2003-8 | | | 6.183% | | | | 4/25/33 | | | | AAA | | | | 343,610 | |

| | 82 | | | | | Credit Suisse First Boston Mortgage Securities Corp, Series 2005-11 | | | 6.000% | | | | 12/25/35 | | | | D | | | | 8,601 | |

| | 500 | | | | | Credit Suisse Mortgage Capital Certificates 2019-ICE4, 144A, (1-Month LIBOR reference rate + 1.600% spread), (3) | | | 1.759% | | | | 5/15/36 | | | | Baa3 | | | | 494,983 | |

| | 219 | | | | | Credit-Based Asset Servicing and Securitization LLC, Series 2007-SP1, 144A | | | 5.021% | | | | 12/25/37 | | | | Aaa | | | | 224,395 | |

| | 250 | | | | | CSMC 2014-USA OA LLC, 144A | | | 4.373% | | | | 9/15/37 | | | | B- | | | | 183,050 | |

| | 120 | | | | | CSMC Mortgage-Backed Trust 2006-7 | | | 6.000% | | | | 8/25/36 | | | | Caa3 | | | | 77,362 | |

| | 56 | | | | | CWABS Asset-Backed Certificates Trust, Series 2004-13 | | | 5.603% | | | | 5/25/35 | | | | Aaa | | | | 56,539 | |

| | 1,167 | | | | | DB Master Finance LLC, Series 2017-1A, 144A | | | 4.030% | | | | 11/20/47 | | | | BBB | | | | 1,239,261 | |

| | 1,149 | | | | | Domino’s Pizza Master Issuer LLC, Series 2015-1A, 144A | | | 4.474% | | | | 10/25/45 | | | | BBB+ | | | | 1,214,252 | |

| | 121 | | | | | Domino’s Pizza Master Issuer LLC, Series 2017-1A, 144A | | | 3.082% | | | | 7/25/47 | | | | BBB+ | | | | 121,897 | |

| | 604 | | | | | Driven Brands Funding LLC, Series 2018-1A, 144A | | | 4.739% | | | | 4/20/48 | | | | BBB- | | | | 640,571 | |

| | 1,449 | | | | | Driven Brands Funding LLC, Series 2019-1A, 144A | | | 4.641% | | | | 4/20/49 | | | | BBB- | | | | 1,540,588 | |

| | 1,500 | | | | | Fannie Mae TBA, (MDR), (WI/DD) | | | 2.000% | | | | TBA | | | | Aaa | | | | 1,557,947 | |

| | 2,000 | | | | | Fannie Mae TBA, (MDR), (WI/DD) | | | 3.000% | | | | TBA | | | | Aaa | | | | 2,097,020 | |

| | 12 | | | | | Fannie Mae Mortgage Pool FN 709700, (4) | | | 5.500% | | | | 6/01/33 | | | | N/R | | | | 14,297 | |

| | — | | | (12) | | Fannie Mae Mortgage Pool FN 745279, (4) | | | 5.000% | | | | 2/01/21 | | | | N/R | | | | 6 | |

| | 66 | | | | | Fannie Mae Mortgage Pool FN 745324, (4) | | | 6.000% | | | | 3/01/34 | | | | Aaa | | | | 72,917 | |

| | 28 | | | | | Fannie Mae Mortgage Pool FN 763687, (4) | | | 6.000% | | | | 1/01/34 | | | | N/R | | | | 31,285 | |

| | 66 | | | | | Fannie Mae Mortgage Pool FN 766070, (4) | | | 5.500% | | | | 2/01/34 | | | | N/R | | | | 75,263 | |

| | 24 | | | | | Fannie Mae Mortgage Pool FN 828346, (4) | | | 5.000% | | | | 7/01/35 | | | | N/R | | | | 27,520 | |

| | 12 | | | | | Fannie Mae Mortgage Pool FN 878059, (4) | | | 5.500% | | | | 3/01/36 | | | | N/R | | | | 13,886 | |

| | 13 | | | | | Fannie Mae Mortgage Pool FN 882685, (4) | | | 6.000% | | | | 6/01/36 | | | | N/R | | | | 14,103 | |

| | 42 | | | | | Fannie Mae Mortgage Pool FN 995018, (4) | | | 5.500% | | | | 6/01/38 | | | | N/R | | | | 49,540 | |

| | 943 | | | | | Fannie Mae Mortgage Pool FN AS8583, (4) | | | 3.500% | | | | 1/01/47 | | | | Aaa | | | | 1,004,775 | |

| | 722 | | | | | Fannie Mae Mortgage Pool FN AW4182, (4) | | | 3.500% | | | | 2/01/44 | | | | N/R | | | | 775,364 | |

13

| | |

| |

| JMM | | Nuveen Multi-Market Income Fund (continued) |

| | Portfolio of Investments December 31, 2020 |

| | (Unaudited) |

| | | | | | | | | | | | | | | | | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| |

| | | | ASSET-BACKED AND MORTGAGE-BACKED SECURITIES (continued) | |

| $ | 69 | | | Fannie Mae Mortgage Pool FN BH4019, (4) | | | 4.000% | | | | 9/01/47 | | | | N/R | | | $ | 74,533 | |

| | 1,331 | | | Fannie Mae Mortgage Pool FN BM5126, (4) | | | 3.500% | | | | 1/01/48 | | | | N/R | | | | 1,454,250 | |

| | 351 | | | Fannie Mae Mortgage Pool FN BM5839, (4) | | | 3.500% | | | | 11/01/47 | | | | Aaa | | | | 383,001 | |

| | 405 | | | Fannie Mae Mortgage Pool FN BM6038, (4) | | | 4.000% | | | | 1/01/45 | | | | Aaa | | | | 443,406 | |

| | 1,399 | | | Fannie Mae Mortgage Pool FN MA3305, (4) | | | 3.500% | | | | 3/01/48 | | | | N/R | | | | 1,482,720 | |

| | 91 | | | Fannie Mae Mortgage Pool FN MA3332, (4) | | | 3.500% | | | | 4/01/48 | | | | Aaa | | | | 96,120 | |

| | 1,178 | | | Fannie Mae Mortgage Pool FN MA3333, (4) | | | 4.000% | | | | 4/01/48 | | | | Aaa | | | | 1,260,842 | |

| | 2,476 | | | Fannie Mae Mortgage Pool FN MA4159, (4) | | | 2.500% | | | | 10/01/50 | | | | N/R | | | | 2,612,061 | |

| | 73 | | | Fannie Mae REMIC Trust 2002-W1 | | | 5.501% | | | | 2/25/42 | | | | Aaa | | | | 81,542 | |

| | 363 | | | Fannie Mae REMIC Trust 2003-W1 | | | 3.174% | | | | 12/25/42 | | | | AAA | | | | 131,523 | |

| | 155 | | | Fannie Mae REMIC Trust 2018-81, (I/O) | | | 3.000% | | | | 11/25/48 | | | | Aaa | | | | 17,939 | |

| | 155 | | | Fannie Mae REMIC Trust 2018-81 | | | 0.000% | | | | 11/25/48 | | | | N/R | | | | 141,784 | |

| | 300 | | | Four Seas LP, 144A | | | 4.950% | | | | 8/28/27 | | | | N/R | | | | 292,559 | |

| | 15 | | | Freddie Mac Gold Pool FG C00676, (4) | | | 6.500% | | | | 11/01/28 | | | | N/R | | | | 16,534 | |

| | 1,906 | | | Freddie Mac Gold Pool FG G08528, (4) | | | 3.000% | | | | 4/01/43 | | | | Aaa | | | | 2,027,188 | |

| | 644 | | | Freddie Mac Gold Pool FG G08566, (4) | | | 3.500% | | | | 1/01/44 | | | | N/R | | | | 692,101 | |

| | 1,519 | | | Freddie Mac Gold Pool FG G08747, (4) | | | 3.000% | | | | 2/01/47 | | | | Aaa | | | | 1,606,612 | |

| | 982 | | | Freddie Mac Gold Pool FG G18497, (4) | | | 3.000% | | | | 1/01/29 | | | | N/R | | | | 1,032,451 | |

| | 1,170 | | | Freddie Mac Gold Pool FG G60138, (4) | | | 3.500% | | | | 8/01/45 | | | | Aaa | | | | 1,285,903 | |

| | 624 | | | Freddie Mac Gold Pool FG G60238, (4) | | | 3.500% | | | | 10/01/45 | | | | Aaa | | | | 681,910 | |

| | 993 | | | Freddie Mac Gold Pool FG Q40718, (4) | | | 3.500% | | | | 5/01/46 | | | | N/R | | | | 1,061,122 | |

| | 1,428 | | | Freddie Mac Gold Pool FG Q40841, (4) | | | 3.000% | | | | 6/01/46 | | | | N/R | | | | 1,501,558 | |

| | 1,909 | | | Freddie Mac Pool FR ZT0541, (4) | | | 4.000% | | | | 6/01/48 | | | | N/R | | | | 2,082,322 | |

| | 511 | | | Freddie Mac Pool FR ZT0542, (4) | | | 4.000% | | | | 7/01/48 | | | | N/R | | | | 561,540 | |

| | 724 | | | Freddie Mac Structured Agency Credit Risk Debt Notes, Series STARC 2019-HQA1, 144A, (1-Month LIBOR reference rate + 2.350% spread), (3) | | | 2.498% | | | | 2/25/49 | | | | BB- | | | | 722,075 | |

| | 446 | | | Freddie Mac Structured Agency Credit Risk Debt Notes, Series STARC 2019-HQA4, 144A, (1-Month LIBOR reference rate + 2.050% spread), (3) | | | 2.198% | | | | 11/25/49 | | | | B+ | | | | 444,977 | |

| | 500 | | | FREMF 2017-K724 Mortgage Trust, 144A | | | 3.484% | | | | 11/25/23 | | | | BBB- | | | | 518,147 | |

| | 138 | | | Ginnie Mae I Pool GN 604567, (4) | | | 5.500% | | | | 8/15/33 | | | | N/R | | | | 162,201 | |

| | 79 | | | Ginnie Mae I Pool GN 631574, (4) | | | 6.000% | | | | 7/15/34 | | | | N/R | | | | 91,409 | |

| | 500 | | | GS Mortgage Securities Corp Trust, Series 2018-TWR, 144A, (1-Month LIBOR reference rate + 0.900% spread), (3) | | | 1.059% | | | | 7/15/31 | | | | AAA | | | | 495,808 | |

| | 67 | | | GSMPS Mortgage Loan Trust, Series 2001-2, 144A | | | 7.500% | | | | 6/19/32 | | | | N/R | | | | 66,796 | |

| | 382 | | | GSMPS Mortgage Loan Trust, Series 2003-3, 144A | | | 7.000% | | | | 6/25/43 | | | | N/R | | | | 434,158 | |

| | 359 | | | GSMPS Mortgage Loan Trust, Series 2005-RP1, 144A | | | 8.500% | | | | 1/25/35 | | | | B2 | | | | 412,423 | |

| | 495 | | | GSMPS Mortgage Loan Trust, Series 2005-RP2, 144A | | | 7.500% | | | | 3/25/35 | | | | AAA | | | | 517,412 | |

| | 476 | | | GSMPS Mortgage Loan Trust, Series 2005-RP3, 144A | | | 7.500% | | | | 9/25/35 | | | | AAA | | | | 496,655 | |

| | 310 | | | GSMPS Mortgage Loan Trust, Series 2005-RP3, 144A | | | 8.000% | | | | 9/25/35 | | | | Caa1 | | | | 334,368 | |

| | 500 | | | Hardee’s Funding LLC, Series 2020-1A A2, 144A | | | 3.981% | | | | 12/20/50 | | | | BBB | | | | 512,535 | |

| | 478 | | | Horizon Aircraft Finance II Ltd, Series 2019-1, 144A | | | 4.703% | | | | 7/15/39 | | | | BBB | | | | 409,538 | |

| | 244 | | | Horizon Aircraft Finance III Ltd, Series 2019-2, 144A | | | 4.458% | | | | 11/15/39 | | | | BBB | | | | 209,216 | |

| | 212 | | | Impac Secured Assets CMN Owner Trust, Series 2000-3 | | | 8.000% | | | | 10/25/30 | | | | CC | | | | 207,516 | |

| | 494 | | | JG Wentworth XXXVII LLC, Series 2016-1A, 144A | | | 5.190% | | | | 6/17/69 | | | | Baa2 | | | | 575,258 | |

| | 823 | | | JGWPT XXV LLC, Series 2012-1A, 144A | | | 7.140% | | | | 2/15/67 | | | | Aa3 | | | | 1,052,910 | |

| | 353 | | | JGWPT XXVI LLC, Series 2012-2A, 144A | | | 6.770% | | | | 10/17/61 | | | | A1 | | | | 441,358 | |

| | 241 | | | JP Morgan Alternative Loan Trust, Series 2006-S1 | | | 6.500% | | | | 3/25/36 | | | | D | | | | 192,763 | |

| | 500 | | | JP Morgan Chase Commercial Mortgage Securities Trust, Series 2016-JP4, 144A | | | 3.421% | | | | 12/15/49 | | | | BBB- | | | | 403,239 | |

| | 500 | | | JP Morgan Chase Commercial Mortgage Securities Trust, Series 2018-BCON, 144A | | | 3.756% | | | | 1/05/31 | | | | BBB- | | | | 496,107 | |

| | 500 | | | JPMDB Commercial Mortgage Securities Trust, Series 2017-C7, 144A | | | 3.000% | | | | 10/15/50 | | | | BBB- | | | | 439,828 | |

| | 400 | | | Manhattan West, Series 2020-1MW, 144A | | | 2.335% | | | | 9/10/39 | | | | Baa3 | | | | 401,227 | |

| | 267 | | | MASTR Alternative Loan Trust, Series 2004-1 | | | 7.000% | | | | 1/25/34 | | | | Aaa | | | | 287,836 | |

| | 190 | | | MASTR Alternative Loan Trust, Series 2004-5 | | | 7.000% | | | | 6/25/34 | | | | AA+ | | | | 198,484 | |

| | 167 | | | MASTR Asset Securitization Trust, Series 2003-11 | | | 5.250% | | | | 12/25/33 | | | | A | | | | 171,466 | |

| | 288 | | | MASTR Reperforming Loan Trust, Series 2005-1, 144A | | | 7.500% | | | | 8/25/34 | | | | N/R | | | | 262,088 | |

| | 635 | | | Mid-State Capital Corp 2004-1 Trust | | | 6.005% | | | | 8/15/37 | | | | AA+ | | | | 676,105 | |

| | 43 | | | Mid-State Capital Corp 2004-1 Trust | | | 8.900% | | | | 8/15/37 | | | | A1 | | | | 47,906 | |

| | 621 | | | Mid-State Capital Corp 2005-1 Trust | | | 5.745% | | | | 1/15/40 | | | | AA | | | | 669,884 | |

| | 240 | | | Mid-State Capital Trust, Series 2010-1, 144A | | | 5.250% | | | | 12/15/45 | | | | AAA | | | | 246,856 | |

| | 205 | | | Mid-State Capital Trust, Series 2010-1, 144A | | | 7.000% | | | | 12/15/45 | | | | AAA | | | | 213,462 | |

| | 196 | | | Mid-State Trust XI | | | 5.598% | | | | 7/15/38 | | | | Baa3 | | | | 209,438 | |

| | 500 | | | Morgan Stanley Bank of America Merrill Lynch Trust, Series 2016-C28 | | | 4.628% | | | | 1/15/49 | | | | A3 | | | | 486,441 | |

14

| | | | | | | | | | | | | | | | | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| |

| | | | ASSET-BACKED AND MORTGAGE-BACKED SECURITIES (continued) | |

| $ | 67 | | | Morgan Stanley Mortgage Loan Trust, Series 2006-2 | | | 5.750% | | | | 2/25/36 | | | | N/R | | | $ | 65,866 | |

| | 500 | | | MSCG Trust 2015-ALDR, 144A | | | 3.462% | | | | 6/07/35 | | | | BBB- | | | | 386,661 | |

| | 316 | | | MVW Owner Trust, Series 2017-1, 144A | | | 2.420% | | | | 12/20/34 | | | | AAA | | | | 323,735 | |

| | 1,000 | | | Natixis Commercial Mortgage Securities Trust, Series 2019-MILE, 144A, 1-Month LIBOR reference rate + 2.750% spread), (3) | | | 2.909% | | | | 7/15/36 | | | | N/R | | | | 967,810 | |

| | 272 | | | New Residential Mortgage LLC, Series 2018-FNT2, 144A | | | 4.920% | | | | 7/25/54 | | | | N/R | | | | 271,842 | |

| | 412 | | | New Residential Mortgage Loan Trust, Series 2014-1, 144A | | | 6.047% | | | | 1/25/54 | | | | BBB | | | | 446,643 | |

| | 714 | | | New Residential Mortgage Loan Trust, Series 2015-2, 144A | | | 5.524% | | | | 8/25/55 | | | | Baa1 | | | | 770,493 | |

| | 262 | | | NRZ Excess Spread-Collateralized Notes, Series 2018-FNT1 144A | | | 4.690% | | | | 5/25/23 | | | | N/R | | | | 261,308 | |

| | 489 | | | Planet Fitness Master Issuer LLC, Series 2018-FT1, 144A | | | 4.666% | | | | 9/05/48 | | | | BBB- | | | | 487,127 | |

| | 500 | | | PNMAC FMSR ISSUER TRUST, Series 2018-FT1, 144A, (1-Month LIBOR reference rate + 2.350% spread), (3) | | | 2.498% | | | | 4/25/23 | | | | N/R | | | | 483,627 | |

| | 500 | | | PNMAC GMSR ISSUER TRUST, Series 2018-GT1, 144A, (1-Month LIBOR reference rate + 2.850% spread), (3) | | | 2.998% | | | | 2/25/23 | | | | N/R | | | | 491,547 | |

| | 500 | | | PNMAC GMSR ISSUER TRUST, Series 2018-GT2, 144A, (1-Month LIBOR reference rate + 2.650% spread), (3) | | | 2.798% | | | | 8/25/25 | | | | N/R | | | | 482,750 | |

| | 307 | | | RALI Series 2005-QS12 Trust | | | 5.500% | | | | 8/25/35 | | | | Caa2 | | | | 306,362 | |

| | 485 | | | RBS Commercial Funding Inc 2013-SMV Trust, 144A | | | 3.584% | | | | 3/11/31 | | | | BBB- | | | | 449,720 | |

| | 276 | | | Sesac Finance LLC, Series 2019-1,144A | | | 5.216% | | | | 7/25/49 | | | | N/R | | | | 292,935 | |

| | 344 | | | Sierra Timeshare 2019-3 Receivables Funding LLC, 144A | | | 4.180% | | | | 8/20/36 | | | | BB | | | | 337,825 | |

| | 490 | | | Sonic Capital LLC, Series 2018-1A, 144A | | | 4.026% | | | | 2/20/48 | | | | BBB | | | | 503,448 | |

| | 382 | | | Sonic Capital LLC, Series 2020-1A, 144A | | | 3.845% | | | | 1/20/50 | | | | BBB | | | | 407,364 | |

| | 500 | | | Stack Infrastructure Issuer LLC, Series 2020-1A A2, 144A | | | 1.893% | | | | 8/25/45 | | | | A- | | | | 505,277 | |

| | 750 | | | STACR Trust, Series 2018-HRP2, 144A, (1-Month LIBOR reference rate + 2.400% spread), (3) | | | 2.548% | | | | 2/25/47 | | | | BBB- | | | | 750,953 | |

| | 330 | | | START Ireland, Series 2019-1, 144A | | | 5.095% | | | | 3/15/44 | | | | BB | | | | 280,637 | |

| | 361 | | | Start Ltd/Bermuda, Series 2018-1, 144A | | | 4.089% | | | | 5/15/43 | | | | BBB+ | | | | 351,070 | |

| | 183 | | | Structured Receivables Finance, Series 2010-A LLC, 144A | | | 5.218% | | | | 1/16/46 | | | | AAA | | | | 196,276 | |

| | 482 | | | Taco Bell Funding LLC, Series 2016-1A, 144A | | | 4.377% | | | | 5/25/46 | | | | BBB | | | | 485,231 | |

| | 603 | | | Taco Bell Funding LLC, Series 2016-1A, 144A | | | 4.970% | | | | 5/25/46 | | | | BBB | | | | 650,470 | |

| | 312 | | | Thunderbolt Aircraft Lease Ltd, Series 2017-A, 144A | | | 4.212% | | | | 5/17/32 | | | | A | | | | 300,722 | |

| | 500 | | | Vericrest Opportunity Loan Trust, Series 2019-NPL2, 144A | | | 6.292% | | | | 2/25/49 | | | | N/R | | | | 484,457 | |

| | 150 | | | Vericrest Opportunity Loan Trust, Series 2019-NPL7, 144A | | | 3.967% | | | | 10/25/49 | | | | N/R | | | | 149,808 | |

| | 500 | | | Verus Securitization Trust, Series 2017-1, 144A | | | 5.273% | | | | 1/25/47 | | | | A | | | | 519,462 | |

| | 1,000 | | | VOLT LXXXIV LLC, Series 2019-NP10, 144A | | | 3.967% | | | | 12/27/49 | | | | N/R | | | | 999,820 | |

| | 207 | | | Washington Mutual MSC Mortgage Pass-Through Certificates Series 2003-MS4 Trust | | | 5.500% | | | | 2/25/33 | | | | N/R | | | | 209,326 | |

| | 14 | | | Washington Mutual MSC Mortgage Pass-Through Certificates Series 2004-RA3 Trust | | | 5.978% | | | | 8/25/38 | | | | Aaa | | | | 15,024 | |

| | 970 | | | Wendy’s Funding LLC, Series 2018-1A, 144A | | | 3.573% | | | | 3/15/48 | | | | BBB | | | | 999,915 | |

| | 482 | | | Wendy’s Funding LLC, Series 2019-1A, 144A | | | 3.783% | | | | 6/15/49 | | | | BBB | | | | 511,223 | |

| | 750 | | | WFRBS Commercial Mortgage Trust 2011-C3, 144A | | | 5.335% | | | | 3/15/44 | | | | A1 | | | | 738,213 | |

| | 1,000 | | | Wingstop Funding LLC, Series 2020-1A A2, 144A | | | 2.841% | | | | 12/05/50 | | | | N/R | | | | 1,020,270 | |

| $ | 72,741 | | | Total Asset-Backed and Mortgage-Backed Securities (cost $71,447,588) | | | | | | | | | | | | | | | 72,839,284 | |

| | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| |

| | | | CORPORATE BONDS – 30.8% (22.8% of Total Investments) | |

| |

| | | | Aerospace & Defense – 1.1% | |

| | | | | |

| $ | 300 | | | Boeing Co/The, (4) | | | 3.450% | | | | 11/01/28 | | | | Baa2 | | | $ | 321,746 | |

| | 100 | | | Howmet Aerospace Inc | | | 6.875% | | | | 5/01/25 | | | | BBB- | | | | 118,000 | |

| | 200 | | | Rolls-Royce PLC, 144A | | | 5.750% | | | | 10/15/27 | | | | BB- | | | | 221,500 | |

| | 150 | | | Triumph Group Inc | | | 5.250% | | | | 6/01/22 | | | | CCC- | | | | 142,875 | |

| | 750 | | | Total Aerospace & Defense | | | | | | | | | | | | | | | 804,121 | |

| | | | | |

| | | | Air Freight & Logistics – 0.1% | | | | | | | | | | | | |

| | | | | |

| | 100 | | | Cargo Aircraft Management Inc, 144A | | | 4.750% | | | | 2/01/28 | | | | Ba3 | | | | 103,125 | |

| | | | | |

| | | | Airlines – 0.2% | | | | | | | | | | | | |

| | | | | |

| | 100 | | | Delta Air Lines Inc, 144A | | | 7.000% | | | | 5/01/25 | | | | Baa2 | | | | 115,434 | |

15

| | |

| |

| JMM | | Nuveen Multi-Market Income Fund (continued) |

| | Portfolio of Investments December 31, 2020 |

| | (Unaudited) |

| | | | | | | | | | | | | | | | | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | | | | |

| | | | Auto Components – 1.1% | | | | | | | | | | | | |

| | | | | |

| $ | 250 | | | Adient Global Holdings Ltd, 144A | | | 4.875% | | | | 8/15/26 | | | | B | | | $ | 256,875 | |

| | 100 | | | Adient US LLC, 144A | | | 9.000% | | | | 4/15/25 | | | | Ba3 | | | | 111,500 | |

| | 200 | | | Clarios Global LP / Clarios US Finance Co, 144A | | | 8.500% | | | | 5/15/27 | | | | CCC+ | | | | 217,282 | |

| | 250 | | | Dana Inc | | | 5.375% | | | | 11/15/27 | | | | BB+ | | | | 265,000 | |

| | 800 | | | Total Auto Components | | | | | | | | | | | | | | | 850,657 | |

| | | | | |

| | | | Automobiles – 0.8% | | | | | | | | | | | | |

| | | | | |

| | 125 | | | Ford Motor Co | | | 8.500% | | | | 4/21/23 | | | | BB+ | | | | 140,947 | |

| | 400 | | | General Motors Financial Co Inc, (4) | | | 3.600% | | | | 6/21/30 | | | | BBB | | | | 446,277 | |

| | 525 | | | Total Automobiles | | | | | | | | | | | | | | | 587,224 | |

| | | | | |

| | | | Banks – 0.3% | | | | | | | | | | | | |

| | | | | |

| | 250 | | | Caelus Re VI Ltd, 144A, (3-Month U.S. Treasury Bill reference rate + 5.500% spread), (3) | | | 5.558% | | | | 6/07/23 | | | | N/R | | | | 254,025 | |

| | | | | |

| | | | Capital Markets – 0.4% | | | | | | | | | | | | |

| | | | | |

| | 200 | | | Donnelley Financial Solutions Inc | | | 8.250% | | | | 10/15/24 | | | | B | | | | 212,000 | |

| | 100 | | | LPL Holdings Inc, 144A | | | 4.625% | | | | 11/15/27 | | | | BB | | | | 103,500 | |

| | 300 | | | Total Capital Markets | | | | | | | | | | | | | | | 315,500 | |

| | | | | |

| | | | Chemicals – 2.0% | | | | | | | | | | | | |

| | | | | |

| | 250 | | | Calumet Specialty Products Partners LP / Calumet Finance Corp, 144A | | | 11.000% | | | | 4/15/25 | | | | B- | | | | 252,500 | |

| | 200 | | | CF Industries Inc | | | 3.450% | | | | 6/01/23 | | | | BB+ | | | | 208,500 | |

| | 50 | | | Kraton Polymers LLC / Kraton Polymers Capital Corp, 144A | | | 4.250% | | | | 12/15/25 | | | | BB- | | | | 51,005 | |

| | 375 | | | NOVA Chemicals Corp, 144A | | | 5.000% | | | | 5/01/25 | | | | BB- | | | | 392,812 | |

| | 200 | | | OCI NV, 144A | | | 4.625% | | | | 10/15/25 | | | | BB | | | | 207,500 | |

| | 50 | | | Rayonier AM Products Inc, 144A | | | 7.625% | | | | 1/15/26 | | | | B1 | | | | 52,138 | |

| | 175 | | | Tronox Inc, 144A | | | 6.500% | | | | 5/01/25 | | | | Ba3 | | | | 187,250 | |

| | 100 | | | Univar Solutions USA Inc/Washington, 144A | | | 5.125% | | | | 12/01/27 | | | | BB | | | | 105,625 | |

| | 1,400 | | | Total Chemicals | | | | | | | | | | | | | | | 1,457,330 | |

| | | | | |

| | | | Commercial Services & Supplies – 0.7% | | | | | | | | | | | | |

| | | | | |

| | 50 | | | CDW LLC / CDW Finance Corp | | | 3.250% | | | | 2/15/29 | | | | Ba2 | | | | 50,985 | |

| | 100 | | | GFL Environmental Inc, 144A | | | 4.250% | | | | 6/01/25 | | | | BB- | | | | 103,750 | |

| | 150 | | | GFL Environmental Inc, 144A | | | 3.500% | | | | 9/01/28 | | | | BB- | | | | 153,031 | |

| | 200 | | | Prime Security Services Borrower LLC / Prime Finance Inc, 144A | | | 5.750% | | | | 4/15/26 | | | | BB- | | | | 219,000 | |

| | 500 | | | Total Commercial Services & Supplies | | | | | | | | | | | | | | | 526,766 | |

| | | | | |

| | | | Communications Equipment – 0.6% | | | | | | | | | | | | |

| | | | | |

| | 100 | | | CommScope Inc, 144A | | | 8.250% | | | | 3/01/27 | | | | B3 | | | | 106,750 | |

| | 325 | | | Gray Television Inc, 144A | | | 4.750% | | | | 10/15/30 | | | | BB- | | | | 329,875 | |

| | 425 | | | Total Communications Equipment | | | | | | | | | | | | | | | 436,625 | |

| | | | | |

| | | | Consumer Finance – 0.3% | | | | | | | | | | | | |

| | | | | |

| | 200 | | | Curo Group Holdings Corp, 144A | | | 8.250% | | | | 9/01/25 | | | | B- | | | | 190,000 | |

| | | | | |

| | | | Containers & Packaging – 0.2% | | | | | | | | | | | | |

| | | | | |

| | 75 | | | Ball Corp | | | 2.875% | | | | 8/15/30 | | | | BB+ | | | | 74,813 | |

| | 100 | | | Silgan Holdings Inc | | | 4.125% | | | | 2/01/28 | | | | BB | | | | 103,875 | |

| | 175 | | | Total Containers & Packaging | | | | | | | | | | | | | | | 178,688 | |

| | | | | |

| | | | Distributors – 0.1% | | | | | | | | | | | | |

| | | | | |

| | 100 | | | H&E Equipment Services Inc, 144A | | | 3.875% | | | | 12/15/28 | | | | BB- | | | | 100,753 | |

| | | | | |

| | | | Diversified Financial Services – 1.9% | | | | | | | | | | | | |

| | | | | |

| | 500 | | | GE Capital International Funding Co Unlimited Co | | | 3.373% | | | | 11/15/25 | | | | BBB+ | | | | 556,372 | |

| | 300 | | | Jefferies Finance LLC / JFIN Co-Issuer Corp, 144A | | | 6.250% | | | | 6/03/26 | | | | BB | | | | 310,594 | |

| | 250 | | | Navient Corp | | | 0.061% | | | | 3/25/24 | | | | Ba3 | | | | 266,875 | |

| | 225 | | | Quicken Loans LLC, 144A | | | 5.250% | | | | 1/15/28 | | | | Ba1 | | | | 240,188 | |

| | 1,275 | | | Total Diversified Financial Services | | | | | | | | | | | | | | | 1,374,029 | |

16

| | | | | | | | | | | | | | | | | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | | | | |

| | | | Diversified Telecommunication Services – 1.9% | | | | | | | | | | | | |

| | | | | |

| $ | 300 | | | AT&T Inc, (4) | | | 4.300% | | | | 2/15/30 | | | | A- | | | $ | 358,356 | |

| | 100 | | | Avaya Inc, 144A | | | 6.125% | | | | 9/15/28 | | | | BB- | | | | 106,826 | |

| | 500 | | | Qwest Corp | | | 6.750% | | | | 12/01/21 | | | | BBB- | | | | 523,075 | |

| | 50 | | | Switch Ltd, 144A | | | 3.750% | | | | 9/15/28 | | | | BB | | | | 50,750 | |

| | 200 | | | Telenet Finance Luxembourg Notes Sarl, 144A | | | 5.500% | | | | 3/01/28 | | | | BB+ | | | | 213,294 | |

| | 175 | | | Zayo Group Holdings Inc, 144A | | | 4.000% | | | | 3/01/27 | | | | B1 | | | | 175,438 | |

| | 1,325 | | | Total Diversified Telecommunication Services | | | | | | | | | | | | | | | 1,427,739 | |

| | | | | |

| | | | Electric Utilities – 0.3% | | | | | | | | | | | | |

| | | | | |

| | 50 | | | NRG Energy Inc, 144A | | | 3.375% | | | | 2/15/29 | | | | BB+ | | | | 51,190 | |

| | 200 | | | Talen Energy Supply LLC | | | 6.500% | | | | 6/01/25 | | | | B | | | | 163,000 | |

| | 250 | | | Total Electric Utilities | | | | | | | | | | | | | | | 214,190 | |

| | | | | |

| | | | Energy Equipment & Services – 0.4% | | | | | | | | | | | | |

| | | | | |

| | 250 | | | Archrock Partners LP / Archrock Partners Finance Corp, 144A | | | 6.875% | | | | 4/01/27 | | | | B+ | | | | 269,063 | |

| | | | | |

| | | | Entertainment – 0.1% | | | | | | | | | | | | |

| | | | | |

| | 100 | | | Cinemark USA Inc, 144A | | | 8.750% | | | | 5/01/25 | | | | BB+ | | | | 108,000 | |

| | | | | |

| | | | Equity Real Estate Investment Trust – 2.4% | | | | | | | | | | | | |

| | | | | |

| | 150 | | | GLP Capital LP / GLP Financing II Inc | | | 4.000% | | | | 1/15/31 | | | | BBB- | | | | 163,683 | |

| | 250 | | | Iron Mountain Inc, 144A | | | 5.250% | | | | 3/15/28 | | | | BB- | | | | 263,822 | |

| | 75 | | | Iron Mountain Inc, 144A | | | 4.500% | | | | 2/15/31 | | | | BB- | | | | 78,563 | |

| | 150 | | | MPH Acquisition Holdings LLC, 144A | | | 5.750% | | | | 11/01/28 | | | | B- | | | | 146,625 | |

| | 325 | | | MPT Operating Partnership LP / MPT Finance Corp | | | 3.500% | | | | 3/15/31 | | | | BBB- | | | | 335,562 | |

| | 500 | | | Regency Centers LP, (4) | | | 2.950% | | | | 9/15/29 | | | | BBB+ | | | | 534,157 | |

| | 250 | | | SITE Centers Corp | | | 4.250% | | | | 2/01/26 | | | | BBB | | | | 269,870 | |

| | 1,700 | | | Total Equity Real Estate Investment Trust | | | | | | | | | | | | | | | 1,792,282 | |

| | | | | |

| | | | Food & Staples Retailing – 0.9% | | | | | | | | | | | | |

| | | | | |

| | 250 | | | Albertsons Cos Inc / Safeway Inc / New Albertsons LP / Albertsons LLC, 144A | | | 7.500% | | | | 3/15/26 | | | | BB- | | | | 279,762 | |

| | 250 | | | Chobani LLC / Chobani Finance Corp Inc, 144A | | | 4.625% | | | | 11/15/28 | | | | B1 | | | | 253,750 | |

| | 150 | | | Del Monte Foods Inc, 144A | | | 11.875% | | | | 5/15/25 | | | | CCC+ | | | | 170,250 | |

| | 650 | | | Total Food & Staples Retailing | | | | | | | | | | | | | | | 703,762 | |

| | | | | |

| | | | Gas Utilities – 0.3% | | | | | | | | | | | | |

| | | | | |

| | 200 | | | Suburban Propane Partners LP/Suburban Energy Finance Corp | | | 5.875% | | | | 3/01/27 | | | | BB- | | | | 209,000 | |

| | | | | |

| | | | Health Care Equipment & Supplies – 0.1% | | | | | | | | | | | | |

| | | | | |

| | 50 | | | RP Escrow Issuer LLC, 144A | | | 5.250% | | | | 12/15/25 | | | | B- | | | | 52,296 | |

| | | | | |

| | | | Health Care Providers & Services – 1.2% | | | | | | | | | | | | |

| | | | | |

| | 100 | | | Centene Corp | | | 4.250% | | | | 12/15/27 | | | | BBB- | | | | 106,000 | |

| | 100 | | | Centene Corp | | | 4.625% | | | | 12/15/29 | | | | BBB- | | | | 111,021 | |

| | 50 | | | CHS/Community Health Systems Inc, 144A | | | 5.625% | | | | 3/15/27 | | | | B | | | | 53,762 | |

| | 50 | | | CHS/Community Health Systems Inc, 144A | | | 6.000% | | | | 1/15/29 | | | | B | | | | 54,013 | |

| | 100 | | | DaVita Inc, 144A | | | 4.625% | | | | 6/01/30 | | | | Ba3 | | | | 106,000 | |

| | 50 | | | Encompass Health Corp | | | 4.625% | | | | 4/01/31 | | | | B+ | | | | 53,500 | |

| | 250 | | | Global Medical Response Inc, 144A | | | 6.500% | | | | 10/01/25 | | | | B | | | | 261,250 | |

| | 100 | | | Molina Healthcare Inc, 144A | | | 4.375% | | | | 6/15/28 | | | | BB- | | | | 105,250 | |

| | 50 | | | Tenet Healthcare Corp, 144A | | | 4.625% | | | | 6/15/28 | | | | BB- | | | | 52,375 | |

| | 850 | | | Total Health Care Providers & Services | | | | | | | | | | | | | | | 903,171 | |

| | | | | |

| | | | Hotels, Restaurants & Leisure – 0.7% | | | | | | | | | | | | |

| | | | | |

| | 100 | | | Cedar Fair LP / Canada’s Wonderland Co / Magnum Management Corp / Millennium Op, 144A | | | 5.500% | | | | 5/01/25 | | | | Ba2 | | | | 104,250 | |

| | 50 | | | MGM Growth Properties Operating Partnership LP / MGP Finance Co-Issuer Inc, 144A | | | 4.625% | | | | 6/15/25 | | | | BB+ | | | | 53,550 | |

| | 250 | | | Scientific Games International Inc, 144A | | | 8.625% | | | | 7/01/25 | | | | B- | | | | 273,750 | |

17

| | |

| |

| JMM | | Nuveen Multi-Market Income Fund (continued) |

| | Portfolio of Investments December 31, 2020 |

| | (Unaudited) |

| | | | | | | | | | | | | | | | | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | | | | |

| | | | Hotels, Restaurants & Leisure (continued) | | | | | | | | | | | | |

| $ | 100 | | | Yum! Brands Inc, 144A | | | 7.750% | | | | 4/01/25 | | | | B+ | | | $ | 110,750 | |

| | 500 | | | Total Hotels, Restaurants & Leisure | | | | | | | | | | | | | | | 542,300 | |

| | | | | |

| | | | Household Durables – 0.4% | | | | | | | | | | | | |

| | | | | |

| | 50 | | | Kronos Acquisition Holdings Inc / KIK Custom Products Inc, 144A | | | 5.000% | | | | 12/31/26 | | | | B2 | | | | 52,125 | |

| | 250 | | | M/I Homes Inc | | | 5.625% | | | | 8/01/25 | | | | BB- | | | | 260,000 | |

| | 300 | | | Total Household Durables | | | | | | | | | | | | | | | 312,125 | |

| | | | | |

| | | | Independent Power & Renewable Electricity Producers – 0.3% | | | | | | | | | | | | |

| | | | | |

| | 200 | | | Calpine Corp, 144A | | | 3.750% | | | | 3/01/31 | | | | BB+ | | | | 198,066 | |

| | | | | |

| | | | Interactive Media & Services – 0.1% | | | | | | | | | | | | |

| | | | | |

| | 50 | | | Arches Buyer Inc, 144A | | | 4.250% | | | | 6/01/28 | | | | B1 | | | | 50,635 | |

| | | | | |

| | | | Internet Software & Services – 0.5% | | | | | | | | | | | | |

| | | | | |

| | 175 | | | J2 Global Inc, 144A | | | 4.625% | | | | 10/15/30 | | | | BB | | | | 184,625 | |

| | 200 | | | Rackspace Technology Global Inc, 144A | | | 5.375% | | | | 12/01/28 | | | | B- | | | | 209,540 | |

| | 375 | | | Total Internet Software & Services | | | | | | | | | | | | | | | 394,165 | |

| | | | | |

| | | | IT Services – 0.4% | | | | | | | | | | | | |

| | | | | |

| | 50 | | | Austin BidCo Inc, 144A | | | 7.125% | | | | 12/15/28 | | | | CCC+ | | | | 52,188 | |

| | 50 | | | Booz Allen Hamilton Inc, 144A | | | 3.875% | | | | 9/01/28 | | | | Ba2 | | | | 51,500 | |

| | 200 | | | Unisys Corp, 144A | | | 6.875% | | | | 11/01/27 | | | | BB- | | | | 218,500 | |

| | 300 | | | Total IT Services | | | | | | | | | | | | | | | 322,188 | |

| | | | | |

| | | | Leisure Products – 0.4% | | | | | | | | | | | | |

| | | | | |

| | 250 | | | Mattel Inc, 144A | | | 6.750% | | | | 12/31/25 | | | | BB- | | | | 263,868 | |

| | | | | |

| | | | Life Sciences Tools & Services – 0.1% | | | | | | | | | | | | |

| | | | | |

| | 75 | | | Avantor Funding Inc, 144A | | | 4.625% | | | | 7/15/28 | | | | BB | | | | 79,313 | |

| | | | | |

| | | | Machinery – 0.5% | | | | | | | | | | | | |

| | | | | |

| | 200 | | | Mueller Water Products Inc, 144A | | | 5.500% | | | | 6/15/26 | | | | BB | | | | 207,250 | |

| | 150 | | | Navistar International Corp, 144A | | | 6.625% | | | | 11/01/25 | | | | B3 | | | | 157,147 | |

| | 350 | | | Total Machinery | | | | | | | | | | | | | | | 364,397 | |

| | | | | |

| | | | Media – 2.0% | | | | | | | | | | | | |

| | | | | |

| | 500 | | | Altice France SA/France, 144A | | | 7.375% | | | | 5/01/26 | | | | B | | | | 526,250 | |

| | 200 | | | Cablevision Lightpath LLC, 144A | | | 3.875% | | | | 9/15/27 | | | | B+ | | | | 201,250 | |

| | 200 | | | DISH DBS Corp | | | 5.875% | | | | 11/15/24 | | | | B2 | | | | 209,707 | |

| | 250 | | | Entercom Media Corp, 144A | | | 7.250% | | | | 11/01/24 | | | | CCC+ | | | | 249,375 | |

| | 90 | | | Nielsen Finance LLC / Nielsen Finance Co, 144A | | | 5.000% | | | | 4/15/22 | | | | BB- | | | | 90,237 | |

| | 200 | | | Radiate Holdco LLC / Radiate Finance Inc, 144A | | | 4.500% | | | | 9/15/26 | | | | B1 | | | | 206,250 | |

| | 1,440 | | | Total Media | | | | | | | | | | | | | | | 1,483,069 | |

| | | | | |

| | | | Metals & Mining – 1.3% | | | | | | | | | | | | |

| | | | | |

| | 250 | | | Alcoa Nederland Holding BV, 144A | | | 6.125% | | | | 5/15/28 | | | | BB+ | | | | 273,125 | |

| | 250 | | | First Quantum Minerals Ltd, 144A | | | 6.875% | | | | 10/15/27 | | | | B- | | | | 271,250 | |

| | 150 | | | Freeport-McMoRan Inc | | | 3.875% | | | | 3/15/23 | | | | Ba1 | | | | 156,495 | |

| | 100 | | | Freeport-McMoRan Inc | | | 5.250% | | | | 9/01/29 | | | | Ba1 | | | | 111,250 | |

| | 50 | | | Hudbay Minerals Inc, 144A | | | 6.125% | | | | 4/01/29 | | | | B+ | | | | 53,875 | |

| | 85 | | | Joseph T Ryerson & Son Inc, 144A | | | 8.500% | | | | 8/01/28 | | | | B | | | | 96,262 | |

| | 885 | | | Total Metals & Mining | | | | | | | | | | | | | | | 962,257 | |

| | | | | |

| | | | Mortgage Real Estate Investment Trust – 0.2% | | | | | | | | | | | | |

| | | | | |

| | 125 | | | HAT Holdings I LLC / HAT Holdings II LLC, 144A | | | 6.000% | | | | 4/15/25 | | | | BB+ | | | | 133,750 | |

18

| | | | | | | | | | | | | | | | | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | | | | |

| | | | Oil, Gas & Consumable Fuels – 3.0% | | | | | | | | | | | | |

| | | | | |

| $ | 250 | | | Enable Midstream Partners LP, (4) | | | 4.400% | | | | 3/15/27 | | | | BBB- | | | $ | 252,191 | |

| | 100 | | | EnLink Midstream LLC | | | 5.375% | | | | 6/01/29 | | | | BB+ | | | | 97,250 | |

| | 200 | | | Genesis Energy LP / Genesis Energy Finance Corp | | | 5.625% | | | | 6/15/24 | | | | B+ | | | | 194,500 | |

| | 500 | | | MPLX LP, (4) | | | 4.800% | | | | 2/15/29 | | | | BBB | | | | 603,988 | |

| | 100 | | | NuStar Logistics LP | | | 5.750% | | | | 10/01/25 | | | | BB- | | | | 106,500 | |

| | 200 | | | Occidental Petroleum Corp | | | 5.875% | | | | 9/01/25 | | | | Ba2 | | | | 213,000 | |

| | 50 | | | Occidental Petroleum Corp | | | 5.500% | | | | 12/01/25 | | | | Ba2 | | | | 52,131 | |

| | 275 | | | PBF Holding Co LLC / PBF Finance Corp | | | 7.250% | | | | 6/15/25 | | | | B+ | | | | 178,265 | |

| | 200 | | | Southwestern Energy Co | | | 7.500% | | | | 4/01/26 | | | | BB | | | | 209,800 | |

| | 250 | | | Western Midstream Operating LP | | | 5.050% | | | | 2/01/30 | | | | BB | | | | 278,125 | |

| | 2,125 | | | Total Oil, Gas & Consumable Fuels | | | | | | | | | | | | | | | 2,185,750 | |

| | | | | |

| | | | Pharmaceuticals – 0.8% | | | | | | | | | | | | |

| | | | | |

| | 100 | | | Bausch Health Cos Inc, 144A | | | 5.000% | | | | 1/30/28 | | | | B | | | | 103,054 | |

| | 225 | | | Endo Dac / Endo Finance LLC / Endo Finco Inc, 144A | | | 5.875% | | | | 10/15/24 | | | | B+ | | | | 227,812 | |

| | 220 | | | Teva Pharmaceutical Finance Netherlands III BV | | | 6.750% | | | | 3/01/28 | | | | Ba2 | | | | 248,875 | |

| | 545 | | | Total Pharmaceuticals | | | | | | | | | | | | | | | 579,741 | |

| | | | | |

| | | | Professional Services – 0.3% | | | | | | | | | | | | |

| | | | | |

| | 200 | | | Dun & Bradstreet Corp/The, 144A | | | 6.875% | | | | 8/15/26 | | | | BB+ | | | | 215,000 | |

| | | | | |

| | | | Real Estate Management & Development – 0.3% | | | | | | | | | | | | |

| | | | | |

| | 250 | | | Hunt Cos Inc, 144A | | | 6.250% | | | | 2/15/26 | | | | BB- | | | | 256,250 | |

| | | | | |

| | | | Road & Rail – 0.4% | | | | | | | | | | | | |

| | | | | |

| | 250 | | | United Rentals North America Inc | | | 4.875% | | | | 1/15/28 | | | | BB- | | | | 266,250 | |

| | | | | |

| | | | Software – 0.1% | | | | | | | | | | | | |

| | | | | |

| | 50 | | | Black Knight InfoServ LLC, 144A | | | 3.625% | | | | 9/01/28 | | | | Ba3 | | | | 51,188 | |

| | | | | |

| | | | Specialty Retail – 0.6% | | | | | | | | | | | | |

| | | | | |

| | 50 | | | L Brands Inc, 144A | | | 6.875% | | | | 7/01/25 | | | | BB | | | | 54,289 | |

| | 50 | | | L Brands Inc, 144A | | | 6.625% | | | | 10/01/30 | | | | B+ | | | | 55,625 | |

| | 100 | | | Lithia Motors Inc, 144A | | | 4.375% | | | | 1/15/31 | | | | BB | | | | 107,250 | |

| | 200 | | | Staples Inc, 144A | | | 10.750% | | | | 4/15/27 | | | | B3 | | | | 199,000 | |

| | 400 | | | Total Specialty Retail | | | | | | | | | | | | | | | 416,164 | |

| | | | | |

| | | | Trading Companies & Distributors – 0.6% | | | | | | | | | | | | |

| | | | | |

| | 300 | | | Air Lease Corp, (4) | | | 3.875% | | | | 7/03/23 | | | | BBB | | | | 320,313 | |

| | 50 | | | WESCO Distribution Inc, 144A | | | 7.125% | | | | 6/15/25 | | | | BB- | | | | 54,992 | |

| | 50 | | | WESCO Distribution Inc, 144A | | | 7.250% | | | | 6/15/28 | | | | BB- | | | | 56,864 | |

| | 400 | | | Total Trading Companies & Distributors | | | | | | | | | | | | | | | 432,169 | |

| | | | | |

| | | | Wireless Telecommunication Services – 0.4% | | | | | | | | | | | | |

| | | | | |

| | 250 | | | Hughes Satellite Systems Corp | | | 6.625% | | | | 8/01/26 | | | | BB | | | | 282,868 | |

| $ | 21,595 | | | Total Corporate Bonds (cost $21,935,204) | | | | | | | | | | | | | | | 22,765,293 | |

| | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | | | | |

| | | | SOVEREIGN DEBT – 1.7% (1.2% of Total Investments) | | | | | | | | | | | | |

| | | | | |

| | | | Bahrain – 0.4% | | | | | | | | | | | | |

| | | | | |

| $ | 250 | | | Bahrain Government International Bond, 144A | | | 7.000% | | | | 10/12/28 | | | | B+ | | | $ | 289,202 | |

| | | | | |

| | | | Egypt – 0.6% | | | | | | | | | | | | |

| | | | | |

| | 400 | | | Egypt Government International Bond, 144A | | | 5.875% | | | | 6/11/25 | | | | B+ | | | | 433,851 | |

| | | | | |

| | | | El Salvador – 0.1% | | | | | | | | | | | | |

| | | | | |

| | 100 | | | El Salvador Government International Bond, 144A | | | 5.875% | | | | 1/30/25 | | | | B+ | | | | 94,500 | |

19

| | |

| |

| JMM | | Nuveen Multi-Market Income Fund (continued) |

| | Portfolio of Investments December 31, 2020 |

| | (Unaudited) |

| | | | | | | | | | | | | | | | | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | | | | |

| | | | Sri Lanka – 0.2% | | | | | | | | | | | | |

| | | | | |

| $ | 250 | | | Sri Lanka Government International Bond, 144A | | | 6.125% | | | | 6/03/25 | | | | CCC+ | | | $ | 148,200 | |

| | | | | |

| | | | Turkey – 0.4% | | | | | | | | | | | | |

| | | | | |

| | 250 | | | Turkey Government International Bond | | | 5.950% | | | | 1/15/31 | | | | B2 | | | | 260,625 | |

| $ | 1,250 | | | Total Sovereign Debt (cost $1,245,107) | | | | | | | | | | | | | | | 1,226,378 | |

| | | | | |

Principal

(000) | | | Description (1), (5) | | Coupon | | | Maturity | | | Ratings (2) | | | Value | |

| | |

| | | | CONTINGENT CAPITAL SECURITIES – 0.9% (0.7% of Total Investments) | | | | |

| | | | | |

| | | | Banks – 0.6% | | | | | | | | | | | | |

| | | | | |

| $ | 200 | | | Banco Bilbao Vizcaya Argentaria SA | | | 6.500% | | | | N/A (6) | | | | Ba2 | | | $ | 213,124 | |

| | 200 | | | Societe Generale SA, 144A | | | 6.750% | | | | N/A (6) | | | | BB | | | | 224,074 | |

| | 400 | | | Total Banks | | | | | | | | | | | | | | | 437,198 | |

| | | | | |

| | | | Capital Markets – 0.3% | | | | | | | | | | | | |

| | | | | |