SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2003

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number: 1-10110

BANCO BILBAO VIZCAYA ARGENTARIA, S.A.

(Exact name of Registrant as specified in its charter)

BANK BILBAO VIZCAYA ARGENTARIA, S.A.

(Translation of Registrant’s name into English)

Kingdom of Spain

(Jurisdiction of incorporation)

Plaza de San Nicolás 4

48005 Bilbao

Spain

(Address of principal executive offices)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

| | |

Title of Each Class

| | Name of Each Exchange on which Registered

|

American Depositary Shares, each representing the right to receive one ordinary share, par value €0.49 per share | | New York Stock Exchange |

| Ordinary shares, par value €0.49 per share | | New York Stock Exchange* |

Non-Cumulative Guaranteed Preference Shares, nominal value $25 each, of BBVA Preferred Capital Ltd. | | New York Stock Exchange |

Guarantee of Non-Cumulative Guaranteed Preference Shares, nominal value $25 each, of BBVA Preferred Capital Ltd. | | New York Stock Exchange** |

Non-Cumulative Guaranteed Preference Shares, Series D, nominal value $0.01 each, of BBVA Privanza International (Gibraltar) Ltd. | | New York Stock Exchange |

Guarantee of Non-Cumulative Guaranteed Preference Shares, Series D, nominal value $0.01 each, of BBVA Privanza International (Gibraltar) Ltd. | | New York Stock Exchange*** |

| * | The ordinary shares are not listed for trading, but are listed only in connection with the registration of the American Depositary Shares, pursuant to requirements of the New York Stock Exchange. |

| ** | The guarantee is not listed for trading, but is listed only in connection with the registration of the corresponding Non-Cumulative Guaranteed Preference Shares of BBVA Preferred Capital Ltd. (a wholly-owned subsidiary of Banco Bilbao Vizcaya Argentaria, S.A.) |

| *** | The guarantee is not listed for trading, but is listed only in connection with the registration of the corresponding Non-Cumulative Guaranteed Preference Shares of BBVA Privanza International (Gibraltar) Ltd. (an indirect wholly-owned subsidiary of Banco Bilbao Vizcaya Argentaria, S.A.) |

Securities registered or to be registered pursuant to Section 12(g) of the Act.

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

None

The number of outstanding shares of each class of stock of the Registrant at December 31, 2003 was:

Ordinary shares, par value €0.49 per share—3,195,852,043

Non-Cumulative Guaranteed Preference Shares, nominal value $25 each, of BBVA Preferred Capital Ltd.—9,600,000

Non-Cumulative Guaranteed Preference Shares, Series D, nominal value $0.01 each, of BBVA Privanza International (Gibraltar) Ltd.—70

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark which financial statement item the registrant has elected to follow. Item 17 ¨ Item 18 x

BANCO BILBAO VIZCAYA ARGENTARIA, S.A.

TABLE OF CONTENTS

i

ii

GLOSSARY

The terms below are used as follows throughout this Annual Report:

| | • | “Argentaria” means Argentaria, Caja Postal y Banco Hipotecario, S.A. and its consolidated subsidiaries, unless otherwise indicated or the context otherwise requires. |

| | • | “BBV” means Banco Bilbao Vizcaya, S.A. and its consolidated subsidiaries, unless otherwise indicated or the context otherwise requires. |

| | • | “BBVA”, “Bank” or “Group” means Banco Bilbao Vizcaya Argentaria, S.A. and its consolidated subsidiaries unless otherwise indicated or the context otherwise requires. BBVA was formed by the merger of BBV and Argentaria, which was approved by the shareholders of each institution on December 18, 1999. |

| | • | “Consolidated Financial Statements” means BBVA’s audited consolidated balance sheets as of December 31, 2003, 2002 and 2001 and BBVA’s audited consolidated statements of income for the years ended December 31, 2003, 2002 and 2001 included in this Annual Report. |

FORWARD-LOOKING STATEMENTS

This Annual Report contains statements that constitute “forward-looking statements” within the meaning of the U.S. Private Securities Litigation Reform Act of 1995. Forward-looking statements may include words such as “believe”, “expect”, “estimate”, “project”, “anticipate”, “should”, “intend”, “probability”, “risk”, “VaR”, “target”, “goal”, “objective” and similar expressions or variations on such expressions. Forward-looking statements are not guarantees of future performance and involve risks and uncertainties, and actual results may differ materially from those in the forward-looking statements as a result of various factors. The accompanying information in this Annual Report, including, without limitation, the information under

| | • | “Item 3. Key Information—Risk Factors”; |

| | • | “Item 4. Information on the Company”; |

| | • | “Item 5. Operating and Financial Review and Prospects”; and |

| | • | “Item 11. Quantitative and Qualitative Disclosures About Market Risk” |

identifies important factors that could cause such differences. Readers are cautioned not to place undue reliance on those forward-looking statements, which speak only as of the date hereof. BBVA undertakes no obligation to release publicly the result of any revisions to these forward-looking statements which may be made to reflect events or circumstances after the date hereof, including, without limitation, changes in its business or acquisition strategy or planned capital expenditures, or to reflect the occurrence of unanticipated events.

CERTAIN TERMS AND CONVENTIONS

First person personal pronouns used in this report, such as “we”, “us”, or “our”, mean BBVA.

In this report, “$”, “U.S. dollars”, and “dollars” refer to United States Dollars, “€” and “euro” refer to Euro and “ARP” refers to Argentinean Pesos.

PRESENTATION OF FINANCIAL INFORMATION

Accounting Principles

The merger of BBV and Argentaria approved by the shareholders of each institution on December 18, 1999, was effected through a merger by absorption of Argentaria with and into BBV and was accounted for under the purchase method of accounting under generally accepted accounting principles in the United States (“U.S. GAAP”) and under the method of “pooling of interests” under generally accepted accounting principles for banks in Spain, which include the accounting requirements established by the Bank of Spain (“Spanish GAAP”).

1

Unless otherwise indicated, the financial information contained in this Annual Report has been derived from financial statements that have been prepared in accordance with Spanish GAAP. See Note 32.2 to the Consolidated Financial Statements for a discussion of some respects in which Spanish GAAP differs from U.S. GAAP.

The Consolidated Financial Statements have been presented in the same format as that used in the consolidated financial statements included in BBVA’s annual and interim reports to shareholders. This format differs from that required by the United States Securities and Exchange Commission (the “SEC” or “Commission”) for the consolidated financial statements of bank holding companies. Consolidated balance sheets and summary statements of income that reflect the reclassifications required by the Commission are included in Note 32.2 to the Consolidated Financial Statements.

We manage our business along four segmental lines which are discussed in “Item 4. Information on the Company” and whose operating results are described in “Item 5. Operating and Financial Review and Prospects”. In addition, due to the special conditions that have continued to affect our operations in Argentina in 2003, we have elected to provide additional disclosure, as we did in our Annual Report on Form 20-F for 2002, on our Argentinean operations and discuss these operations as if they comprised a separate segment, “Argentina”, and not part of the “Banking in America” business segment, where they were included in our Annual Report on Form 20-F for 2001 and prior years.

Certain numerical information in this Annual Report may not sum due to rounding.

Accelerated Amortization of Goodwill

The Consolidated Financial Statements are based on the Spanish statutorily approved financial statements included in BBVA’s reports to shareholders. The auditors’ reports for the years ended December 31, 1999 and 2000 were qualified with respect to the early amortization of goodwill arising mainly from the acquisition of our Latin American subsidiaries. In accordance with Spanish GAAP, this goodwill should have been capitalized and amortized over 10 years. U.S. securities regulations do not currently allow the use in filings with the Commission of financial statements on which the auditors’ report is qualified with respect to a material departure from generally accepted accounting principles. The financial statements included herein reflect adjustments of the Spanish statutorily approved financial statements solely for purposes of complying with U.S. securities regulations. The adjustments consist of the reversal of the early amortization of goodwill and the amortization of such goodwill over a period of five years, the estimated period of the associated assets’ useful life. The following table reflects these adjustments for the periods presented. This adjustment does not affect the year ended December 31, 2002 and 2003.

| | |

| | | Year ended December 31,

2001

|

| | | (in millions of euro) |

Net attributable profit as reported in BBVA’s Annual Report to shareholders | | 2,363 |

Net attributable profit reflecting reversal of early amortization of goodwill | | 1,843 |

Statistical and Financial Information

The following principles should be noted in reviewing the statistical and financial information contained herein:

| | • | Average balances, when used, are based on the beginning and the month-end balances during each year. We do not believe that such monthly averages present trends that are materially different from those that would be presented by daily averages. |

| | • | The book value of BBVA’s ordinary shares held by its consolidated subsidiaries has been deducted from stockholders’ equity. |

| | • | Unless otherwise stated, any reference to loans refers to both loans and leases. |

2

| | • | Interest income figures include interest income on non-accruing loans to the extent that cash payments have been received in the period in which they are due. |

| | • | Financial information with respect to subsidiaries may not reflect consolidation adjustments. |

Disclosures in this Annual Report with respect to the amount of “substandard loans” at any date reflect Bank of Spain classifications at such date. See “Item 4. Information on the Company—Selected Statistical Information—Assets—Loan Loss Reserve”, “—Substandard Loans” and “—Foreign Country Outstandings”. These classifications differ from the classifications applied by U.S. banks in reporting loans as non-accrual, past due, restructured and as potential problem loans. One of the most important differences is that under Bank of Spain classifications, in the case of loans which are classified as substandard because any payment of principal or interest is 90 days or more past due, initially only past due payments of principal or interest (to the extent accruing at the time that the relevant loan is classified as substandard) are treated as substandard. If any payment on a loan is past due for more than one year, or if, regardless of the time past due, the aggregate amount of past due principal and interest exceeds 25% of the principal amount of the loan, then the entire principal amount of the loan is required to be classified as substandard.

Translation into Euro Currency

The Consolidated Financial Statements are stated in euro. Financial data as of and for periods prior to December 31, 2001 included elsewhere in this Annual Report have been restated from pesetas into euro using the exchange rate in effect as of January 1, 1999 of Ptas.166.386 = €1.00. Data in pesetas converted to euro at such exchange rates show the same trends as would have been presented if the data had been presented in pesetas.

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not Applicable.

Not Applicable.

Not Applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

3

ITEM 3. KEY INFORMATION

A. Selected Financial Data

Spanish GAAP Data

The historical financial information set forth below has been selected from, and should be read together with, the Consolidated Financial Statements included herein. For information concerning the preparation and presentation of financial information contained herein, see “Presentation of Financial Information”. Also see Note 32.2 of the Consolidated Financial Statements for a presentation of our balance sheet and income statement reconciled to U.S. GAAP.

| | | | | | | | | | | | | | | |

| | | Year ended December 31,

| |

Consolidated statement of income data

| | 2003

| | | 2002

| | | 2001

| | | 2000

| | | 1999(1)

| |

| | | (in millions of euro, except per share/ADS data (in euro) and percentages) | |

Net interest income | | 6,741 | | | 7,808 | | | 8,824 | | | 6,995 | | | 4,370 | |

Net fee income | | 3,263 | | | 3,668 | | | 4,038 | | | 3,369 | | | 2,077 | |

| | |

|

| |

|

| |

|

| |

|

| |

|

|

Basic margin | | 10,004 | | | 11,476 | | | 12,862 | | | 10,364 | | | 6,447 | |

Market operations | | 652 | | | 765 | | | 490 | | | 779 | | | 497 | |

| | |

|

| |

|

| |

|

| |

|

| |

|

|

Ordinary revenue | | 10,656 | | | 12,241 | | | 13,352 | | | 11,143 | | | 6,944 | |

General administrative expenses | | (5,031 | ) | | (5,772 | ) | | (6,725 | ) | | (5,937 | ) | | (3,834 | ) |

Depreciation and amortization | | (511 | ) | | (631 | ) | | (742 | ) | | (653 | ) | | (388 | ) |

Other operating revenues and expenses, net | | (219 | ) | | (261 | ) | | (286 | ) | | (177 | ) | | (143 | ) |

| | |

|

| |

|

| |

|

| |

|

| |

|

|

Net operating income | | 4,895 | | | 5,577 | | | 5,599 | | | 4,376 | | | 2,579 | |

Net income from companies accounted for by the equity method | | 383 | | | 33 | | | 393 | | | 589 | | | 200 | |

Amortization of consolidation goodwill(2) | | (639 | ) | | (679 | ) | | (1,143 | ) | | (923 | ) | | (482 | ) |

Net income on Group transactions | | 553 | | | 361 | | | 954 | | | 1,307 | | | 1,038 | |

Net loan loss provisions | | (1,277 | ) | | (1,743 | ) | | (1,919 | ) | | (973 | ) | | (694 | ) |

Net securities write-downs | | — | | | 3 | | | (43 | ) | | (7 | ) | | (18 | ) |

Extraordinary items, net | | (103 | ) | | (433 | ) | | (727 | ) | | (751 | ) | | (357 | ) |

| | |

|

| |

|

| |

|

| |

|

| |

|

|

Pre-tax profit(2) | | 3,812 | | | 3,119 | | | 3,114 | | | 3,618 | | | 2,266 | |

Corporate income tax and other taxes | | (915 | ) | | (653 | ) | | (625 | ) | | (962 | ) | | (488 | ) |

| | |

|

| |

|

| |

|

| |

|

| |

|

|

Income before minority interests(2) | | 2,897 | | | 2,466 | | | 2,489 | | | 2,656 | | | 1,778 | |

Minority interests | | (670 | ) | | (747 | ) | | (646 | ) | | (682 | ) | | (342 | ) |

| | |

|

| |

|

| |

|

| |

|

| |

|

|

Net attributable profit(2) | | 2,227 | | | 1,719 | | | 1,843 | | | 1,974 | | | 1,436 | |

| | |

|

| |

|

| |

|

| |

|

| |

|

|

Per Share/ADS(3) data | | | | | | | | | | | | | | | |

Operating income(4) | | 1.53 | | | 1.75 | | | 1.75 | | | 1.44 | | | 1.24 | |

Number of shares | | 3,195,852,043 | | | 3,195,852,043 | | | 3,195,852,043 | | | 3,195,852,043 | | | 2,133,235,006 | |

Net attributable profit(4) | | 0.70 | | | 0.54 | | | 0.58 | | | 0.65 | | | 0.69 | |

Dividends(4)(5) | | 0.38 | | | 0.35 | | | 0.38 | | | 0.36 | | | 0.28 | |

4

| | | | | | | | | | | | | | | |

| | | At December 31,

| |

Consolidated balance sheet data

| | 2003

| | | 2002

| | | 2001

| | | 2000

| | | 1999(1)

| |

| | | (in millions of euro, except per share/ADS data (in euro)

and percentages) | |

Total assets(2) | | 287,150 | | | 279,542 | | | 309,062 | | | 296,345 | | | 157,545 | |

Loans and leases, net | | 148,827 | | | 141,315 | | | 150,220 | | | 137,467 | | | 68,494 | |

Deposits | | 141,049 | | | 146,560 | | | 166,499 | | | 154,146 | | | 79,155 | |

Marketable debt securities and subordinated debt | | 41,782 | | | 34,010 | | | 32,986 | | | 31,571 | | | 16,071 | |

Minority interests | | 5,426 | | | 5,674 | | | 6,394 | | | 6,304 | | | 4,379 | |

Capital and reserves(2) | | 11,473 | | | 11,842 | | | 12,770 | | | 13,047 | | | 5,516 | |

| | | | | |

Consolidated ratios | | | | | | | | | | | | | | | |

Profitability ratios: | | | | | | | | | | | | | | | |

Net interest margin(6) | | 2.4 | % | | 2.70 | % | | 2.92 | % | | 2.58 | % | | 3.33 | % |

Return on average total assets(7) | | 1.04 | % | | 0.85 | % | | 0.82 | % | | 0.98 | % | | 1.24 | % |

Return on average capital and reserves(8) | | 12.45 | % | | 13.07 | % | | 13.96 | % | | 18.68 | % | | 26.12 | % |

| | | | | |

Credit quality data | | | | | | | | | | | | | | | |

Loan loss reserve | | 4,736 | | | 5,346 | | | 6,320 | | | 8,155 | | | 2,277 | |

Loan loss reserve as a percentage of total loans and leases | | 3.09 | % | | 3.65 | % | | 4.05 | % | | 5.71 | % | | 3.23 | % |

Substandard loans(9) | | 3,126 | | | 3,531 | | | 2,743 | | | 2,862 | | | 1,365 | |

Non-Performing loans as a percentage of total loans and leases | | 1.74 | % | | 2.37 | % | | 1.75 | % | | 2.00 | % | | 1.93 | % |

Loan loss reserve as a percentage of substandard loans | | 151.5 | % | | 151.42 | % | | 230.40 | % | | 284.94 | % | | 166.81 | % |

| (2) | In our Spanish statutory financial statements for the years ended December 31, 2000 and 1999, we amortized goodwill on an accelerated basis. See “Presentation of Financial Information”. |

| (3) | Each American Depositary Share (“ADS”) represents the right to receive one ordinary share. |

| (4) | Calculated on the basis of the weighted average number of BBVA’s ordinary shares outstanding during the relevant period. |

| (5) | Calculated based on total dividends paid in respect of each period indicated. |

| (6) | Represents net interest income as a percentage of average total assets. |

| (7) | Represents income before minority interests as a percentage of average total assets. |

| (8) | Represents net attributable profit as a percentage of average capital and reserves. |

| (9) | Only past due payments, and not outstanding principal, are included in the balance of substandard loans unless and until the entire principal amount is classified as substandard under applicable Bank of Spain rules. |

5

U.S. GAAP Information

| | | | | | | | | | | | | | | |

| | | Year ended December 31,

|

| | | 2003

| | 2002

| | 2001

| | Restated

2000(1)

| | | 2000

| | Restated (*)

1999(1)

| | 1999(1)

|

| | | (in millions of euro, except per share/ADS data (in euro) or as otherwise indicated) |

Consolidated statement of income data | | | | | | | | | | | | | | | |

| | | | | | | |

Net income(2) | | 1,906 | | 1,846 | | 680 | | 1,413 | | | 1,544 | | 1,056 | | 1,038 |

Basic earnings per share/ADS(3)(4) | | 0.60 | | 0.58 | | 0.21 | | 0.47 | | | 0.51 | | 0.51 | | 0.50 |

Diluted earnings per share/ADS(3)(4) | | 0.60 | | 0.58 | | 0.21 | | 0.46 | | | 0.50 | | 0.50 | | 0.49 |

Dividends per share/ADS (in dollars)(4)(5) | | 0.34 | | 0.33 | | 0.34 | | 0.39 | | | 0.39 | | 0.27 | | 0.27 |

| | | | | | | |

Consolidated balance sheet data as at December 31 | | | | | | | | | | | | | | | |

| | | | | | | |

Total assets(6) | | 287,912 | | 290,430 | | 322,612 | | 308,644 | (7) | | 313,120 | | 165,431 | | 165,300 |

Stockholders’ equity(6) | | 19,583 | | 18,908 | | 21,226 | | 22,579 | | | 22,579 | | 10,070 | | 9,939 |

Basic stockholders’ equity per share/ADS(4) | | 6.13 | | 5.92 | | 6.64 | | 7.43 | | | 7.43 | | 4.82 | | 4.76 |

Diluted stockholders’ equity per share/ADS(4) | | 6.13 | | 5.91 | | 6.63 | | 7.33 | | | 7.33 | | 4.77 | | 4.71 |

| (1) | The restated amounts are calculated according to the guidance of paragraphs 36-37 of APB 20 “correction of an error”, which is described in Note 32.2.B.15 to our consolidated financial statements included in our Annual Report on Form 20-F for 2002, in order to reflect the actual timing and substance of all transactions associated with the “unreported funds” described under “Item 8—Financial Information—Legal Proceedings”. |

| (2) | We generally refer to our income after taxes and minority interests as “net attributable profit”. In the case of the U.S. GAAP information provided above, the term “net income” is used for consistency with Note 32.2 to our Consolidated Financial Statements, which includes additional U.S. GAAP information and generally refers to “net income” in cases in which we would otherwise use the term “net attributable profit”. |

| (3) | Calculated on the basis of the weighted average number of BBVA’s ordinary shares outstanding during the relevant period. |

| (4) | Each ADS represents the right to receive one ordinary share. |

| (5) | Dividends per share/ADS are translated into dollars for 2003 through 1999, at an average exchange rate for each year, calculated based on the average of the noon buying rates for euro from the Federal Reserve Bank of New York on the last date of each month during the relevant period, expressed in dollars per €1.00. |

| (6) | At the end of the reported period. |

| (7) | Total assets were restated for 2000 from €313,120 million to €308,612 million due to a reclassification of certain assets of Bancomer, as reported in our Annual Report on Form 20-F for 2001. |

Exchange Rates

On January 1, 1999, the euro was introduced as a new currency in the following 11 European Union (“EU”) member states, forming the European Monetary and Economic Union at such date: Austria, Belgium, Finland, France, Germany, Ireland, Italy, Luxembourg, the Netherlands, Portugal and Spain. As of January 2001, the euro was also introduced as the new currency in Greece. The currencies of the participating member states were nondecimal subdivisions of the euro until January 1, 2002 and for up to six months thereafter. The exchange rate at which the peseta has been irrevocably fixed against the euro is Ptas.166.386 = €1.00. Beginning January 1, 2002, the participating member states issued new euro-denominated bills and coins for use in cash transactions. By July 1, 2002, the participating member states withdrew from circulation the bills and coins denominated in their respective currencies, and they are no longer legal tender for any transactions.

The following table sets forth, for the years indicated, the average exchange rate for each year, which reflects the average of the noon buying rates for euro from the Federal Reserve Bank of New York on the last date of each month during the relevant period, for the years ended December 31, 1999 through 2003, and for the year ended December 31, 2004 (through June 30), expressed in dollars per €1.00.

| | |

Year ended December 31,

| | Average

|

1999 | | 1.0588 |

2000 | | 0.9207 |

2001 | | 0.8909 |

2002 | | 0.9495 |

2003 | | 1.1411 |

2004 (through June 25) | | 1.2275 |

6

The following table describes, for the periods and dates indicated, information concerning the noon buying rate for euro from the Federal Reserve Bank of New York, expressed in dollars per €1.00.

| | | | |

Month ended

| | High

| | Low

|

December 31, 2003 | | 1.2597 | | 1.1956 |

January 31, 2004 | | 1.2853 | | 1.2389 |

February 28, 2004 | | 1.2848 | | 1.2426 |

March 31, 2004 | | 1.2431 | | 1.2088 |

April 30, 2004 | | 1.2358 | | 1.1802 |

May 31, 2004 | | 1.2274 | | 1.1801 |

June 30, 2004 (through June 25) | | 1.2320 | | 1.2006 |

The noon buying rate for euro from the Federal Reserve Bank of New York, expressed in dollars per €1.00, on June 25, 2004, was $1.2145. Unless otherwise indicated, amounts that have been converted to euro in this Annual Report have been done so at the corresponding exchange rate published by the European Central Bank on December 31 of the relevant year.

At December 31, 2003, approximately 30.8% of our assets and approximately 33.2% of our liabilities were denominated in currencies other than euro (principally dollars).

For a discussion of our foreign currency exposure, please see “Item 11. Quantitative and Qualitative Disclosures About Market Risk—Market Risk Management—Market risk in 2003—Structural Exchange Rate Risk”.

| B. | Capitalization and Indebtedness |

Not applicable.

| C. | Reasons for the Offer and Use of Proceeds |

Not applicable.

Risks Relating to us

Since our loan portfolio is highly concentrated in Spain, adverse changes affecting the Spanish economy could have a material adverse effect on our financial condition.

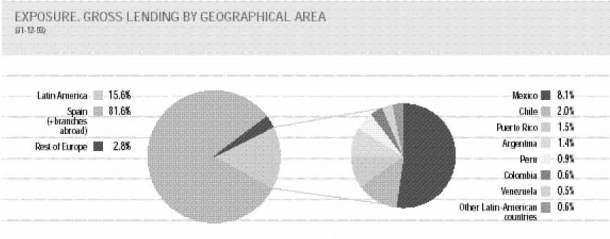

We historically have developed our lending business in Spain, which continues to be our main place of business. As of December 31, 2003, business activity in Spain accounted for 76.25% of our loan portfolio. See “Item 4. Information on the Company—Selected Statistical Information—Loans by Geographic Area”. Any adverse changes affecting the Spanish economy are likely to have a significant adverse impact on our loan portfolio and, as a result, on our financial condition and results of operations.

7

A substantial percentage of our customer base is particularly sensitive to adverse developments in the economy, which renders our lending activities relatively riskier than if we lent primarily to higher-income customer segments.

Medium- and small-size companies and middle and lower middle income individuals typically have less financial strength than large companies and high-income individuals and accordingly can be expected to be more negatively affected by adverse developments in the economy. As a result, it is generally accepted that lending to these segments of our existing and targeted customer base represents a relatively higher degree of risk than lending to other groups.

A substantial portion of our loan portfolio consists of residential mortgages and consumer loans to middle and lower middle income customers and commercial loans to medium and small companies. Consequently, during periods of slowdown in economic activity we may experience higher levels of past due amounts which could result in higher levels of allowance for loan losses. We cannot assure you that we will not suffer substantial adverse effects on our base portfolio to these customer segments in the event of adverse developments in the economy.

Increased exposure to real estate in Spain makes us more vulnerable to developments in this market.

The decrease in interest rates in Spain has caused an increase in the demand of mortgage loans in the last few years. This has had repercussions in housing prices, which have also risen significantly. As residential mortgages are one of our main assets, comprising 30%, 40% and 42% of our loan portfolio at December 31, 2001, 2002 and 2003, respectively, we are currently highly exposed to developments in real estate markets. A strong increase in interest rates in Spain might have a significant negative impact in mortgage payment delinquency rates. An increase in such delinquency rates could have an adverse effect on our business, financial condition and results of operations.

Highly-indebted households and corporations could endanger our asset quality and future revenues.

Spanish households and firms have reached, in recent years, a high indebtedness level, which represents increased risk for the Spanish banking system. The increase of loans referenced to variable rates make debt service on such loans more vulnerable to changes in interest rates than in the past. The increase in households’ and firms’ indebtedness also limits their ability to incur additional debt, decreasing the number of new products we may otherwise be able to sell them.

A sudden shortage of funds could cause an increase in our costs of funding and an adverse effect on our operating revenues.

Historically, one of our principal sources of funds has been savings and demand deposits. Time deposits represented 36.2%, 35.0% and 31.1% of our total funding at December 31, 2001, 2002 and 2003 respectively. Large-denomination time deposits may, under some circumstances, such as during periods of significant changes in market interest rates for these types of deposit products and resulting increased competition for such funds, be a less stable source of deposits than savings and demand deposits. In addition, since we rely heavily on short-term deposits for our funding, we cannot assure you that, in the event of a sudden or unexpected shortage of funds in the banking systems or money markets in which we operate, we will be able to maintain our current levels of funding without incurring higher funding costs or having to liquidate certain of our assets.

We face increasing competition in our business lines.

The markets in which we operate are highly competitive. Financial sector reforms in the markets in which we operate have increased competition among both local and foreign financial institutions, and we believe that this trend will continue. For example, the adoption of the euro as the common currency throughout the EU is making it easier for European banks to compete against us in Spain. In addition, the trend towards consolidation in the banking industry has created larger and stronger banks with which we must now compete.

We also face competition from non-bank competitors, such as:

| | • | department stores (for some credit products); |

8

We cannot assure you that this competition will not adversely affect our business, financial condition and results of operations.

Our business is particularly vulnerable to volatility in interest rates.

Our results of operations are substantially dependent upon the level of our net interest income, which is the difference between interest income from interest-earning assets and interest expense on interest-bearing liabilities. Interest rates are highly sensitive to many factors beyond our control, including deregulation of the financial sectors in the markets in which we operate, monetary policies pursued by national governments, domestic and international economic and political conditions and other factors.

Changes in market interest rates could affect the spread between interest rates charged on interest-earning assets and interest rates paid on interest-bearing liabilities and thereby negatively affect our results of operations. For example, an increase in interest rates could cause our interest expense on deposits to increase more significantly and quickly than our interest income from loans, resulting in a reduction in our net interest income.

In addition, income from treasury operations is particularly vulnerable to interest rate volatility. Since 64.30% of our portfolio consists of variable interest rate loans maturing in more than one year, rising interest rates may also bring about an increase in the non-performing loan portfolio.

Our financial statements and periodic disclosure under securities laws may not give you the same information as financial statements prepared under U.S. accounting rules and periodic disclosures provided by domestic U.S. issuers.

Publicly available information about public companies in Spain is generally less detailed and not as frequently updated as the information that is regularly published by or about listed companies in the United States. In addition, although we are subject to the periodic reporting requirements of the United States Securities Exchange Act of 1934 (the “Exchange Act”), the periodic disclosure required of foreign issuers under the Exchange Act is more limited than the periodic disclosure required of U.S. issuers. Finally, we maintain our financial accounts and records and prepare our financial statements in conformity with Spanish GAAP, which differs in certain respects from U.S. GAAP, the financial reporting standard to which many investors in the United States may be better accustomed.

Risks Relating to Latin America

The devaluation of the Argentinean peso, the adverse macroeconomic conditions prevailing in Argentina and emergency measures adopted by the Argentinean government have had, and may continue to have, a material adverse effect on our business, financial condition and results of operations.

Argentina’s economic situation deteriorated sharply in late 2001. The beginning of 2002 was marked by the continued movement of capital out of Argentina, the end of convertibility of the peso, devaluation, and the return of inflation. The crisis had a strong impact on the financial system and jeopardized the solvency and liquidity of banks. In 2003, macroeconomic conditions in Latin America and Argentina improved, but significant uncertainty regarding the scope and pace of the recovery remained.

As a result of the measures described in “Item 4. Information on the Company––Business Overview—Business Areas—Argentina”, we have written off our entire investment in Argentina to date. However, despite our provisions and write-downs, the situation in Argentina may continue to have a material adverse effect on our business, financial condition and results of operations.

We cannot assure you that the laws and regulations currently governing the Argentinean economy will not change in the future, or that any changes which may occur will not adversely affect our business, financial condition or results of our operations in the country, or the business which we transact with counterparties located in the country.

Risks relating to our investments in Argentina in light of the current social and political crises include the potential for: (i) civil unrest, rioting, looting, nationwide protests, widespread social unrest and strikes, (ii) expropriation, nationalization and forced renegotiation or modification of existing contracts, (iii) additional restrictions on repatriation of investments and transfer of funds abroad, (iv) adverse changes to taxation policies, including retroactive tax claims and (v) further changes in laws and policies of Argentina affecting foreign trade and investment.

9

Our Latin American subsidiaries’ growth, asset quality and profitability may be affected by volatile macroeconomic conditions, including government default on public debt, in the Latin American countries where they operate.

The Latin American countries where we operate have experienced significant economic volatility in recent decades, characterized by slow growth, declining investment and significant inflation. This volatility has resulted in fluctuations in the levels of deposits and in the relative economic strength of various segments of the economies to which we lend. Negative and fluctuating economic conditions, such as a changing interest rate environment, also affect our profitability by causing lending margins to decrease and leading to decreased demand for higher-margin products and services.

Negative and fluctuating economic conditions in some Latin American countries could result in government defaults on public debt. This could affect us in two ways: directly, through portfolio losses, and indirectly, through instabilities that a default in public debt could cause to the banking system as a whole, particularly since commercial banks’ exposure to government debt is generally high in several Latin American countries in which we operate.

While we seek to mitigate these risks through the conservative risk policies described in “Item 11. Quantitative and Qualitative Disclosures About Market Risk”, no assurance can be given that our Latin American subsidiaries’ growth, asset quality and profitability will not be affected by volatile macroeconomic conditions in the Latin American countries in which we operate.

Latin American economies can be directly and negatively affected by adverse developments in other countries.

Financial and securities markets in Latin American countries in which we operate, are to varying degrees, influenced by economic and market conditions in other countries in Latin America and beyond. Negative developments in the economy or securities markets in one country, particularly in an emerging market, may have a negative impact on other emerging market economies. These developments may adversely affect the business, financial condition and operating results of our subsidiaries in Latin America.

We are exposed to foreign exchange and, in some instances, political risks as well as other risks in the Latin American countries in which we operate, which could cause an adverse impact on our business, financial condition and results of operations.

We operate commercial banks in 10 Latin American countries and our overall success as a global business depends, in part, upon our ability to succeed in differing economic, social and political conditions. We are confronted with different legal and regulatory requirements in many of the jurisdictions in which we operate. These include, but are not limited to, different tax regimes and laws relating to the repatriation of funds or nationalization of assets. Our international operations may also expose us to risks and challenges which our local competitors may not be required to face, such as exchange rate risk, difficulty in managing a local entity from abroad, and political risk which may be particular to foreign investors. Our expansion in these markets requires us to respond to rapid changes in market conditions in these countries. We cannot assure you that we will continue to succeed in developing and implementing policies and strategies that are effective in each country in which we operate or that any of the foregoing factors will not have a material adverse effect on our business, financial condition and results of operations.

Regulatory changes in Latin America that are beyond our control may have a material effect on our business, financial condition and results of operations.

A number of banking regulations designed to maintain the safety and soundness of banks and limit their exposure to risk are applicable in certain Latin American countries in which we operate. Local regulations differ in a number of material respects from equivalent regulations in Spain and the United States.

Changes in regulations that are beyond our control may have a material effect on our business and operations. In addition, since some of the banking laws and regulations have been recently adopted, the manner in which those laws and related regulations are applied to the operations of financial institutions is still evolving. No assurance can be given that laws or regulations will be enforced or interpreted in a manner that will not have a material adverse effect on our business, financial condition and results of operations.

ITEM 4. INFORMATION ON THE COMPANY

A. History and Development of the Company

BBVA’s predecessor bank, BBV, was incorporated as a limited liability company (asociedad anónima or “S.A.”) under the Spanish Corporations Law on October 1, 1988. BBVA was formed as the result of a merger by absorption of Argentaria into BBV that was approved by the shareholders of each institution on December 18, 1999 and registered on January 28, 2000. It conducts its

10

business under the commercial name “BBVA”. BBVA is registered with the Commercial Registry of Vizcaya (Spain). It has its registered office at Plaza de San Nicolás 4, Bilbao, Spain, 48005, telephone number 34-94-420-3001. BBVA’s agent in the U.S. for U.S. federal securities law purposes is Raúl Santoro de Mattos Almeida (BBVA New York, 1345 Avenue of the Americas, 45th floor, NY, New York, 10105). BBVA is incorporated for an unlimited term.

Capital Expenditures

Our principal capital expenditures from 2001 to the date of this Annual Report were the following:

2004

Grupo Financiero BBVA Bancomer, S.A. de C.V (“Bancomer”). On January 30, 2004, our Board of Directors adopted a resolution to launch a tender offer for the approximated 40.6% of the shares of Bancomer, our Mexican affiliate, which were not already owned by BBVA. The tender offer was launched on February 19, 2004 and expired on March 19, 2004. As a result of the successful completion of the tender offer and subsequent purchases amounting to 0.56% of Bancomer’s capital stock, at March 31, 2004, we owned 99.44% of Bancomer’s outstanding shares. On February 5, 2004, to strengthen our capital ratios and finance a portion of the cost of the Bancomer tender offer, we sold 195,000,000 of our newly-issued ordinary shares to institutional investors in Spain and outside of Spain at the offer price of €10.25 per share.

BBVA Banco Francés, S.A. (“Banco Francés”). On March 18, 2004, the Board of Directors of Banco Francés, our Argentine affiliate, resolved to implement a plan intended to improve Banco Frances’s adjusted stockholders’ equity and enable Banco Frances to comply with new minimum capital requirements established by the Argentine Central Bank. The plan provides for:

| a) | a capital increase of up to ARP 385 million (approximately US$132.2 million (€108 million as of March 31, 2004)), which will be submitted for approval at an ordinary and extraordinary stockholders meeting and to the appropriate local authorities and |

| b) | the sale of Banco Francés’s entire interest in Banco Francés (Cayman) Limited, which has been approved by regulatory authorities of the Cayman Islands. |

BBVA, as Banco Francés’s largest shareholder, intends to participate in this plan by:

| (1) | capitalizing a loan granted by BBVA to Banco Francés in an amount up to US$77.7 million (€63.6 million as of March 31, 2004) and |

| (2) | subscribing to a capital increase in an amount up to US$40 million (€32.7 million as of March 31, 2004). |

Furthermore, BBVA will acquire from Banco Francés its entire interest in Banco Francés (Cayman) Limited for a purchase price of US$238.5 million (€195 million as of March 31, 2004), which is based on the independent valuation of Banco Francés (Cayman) Limited by two independent valuation experts.

The two transactions involving Banco Frances described above will not affect BBVA’s consolidated operating results because (i) in the case of the loan capitalization, BBVA had previously fully provisioned the loan, and (ii) in the case of the purchase of Banco Frances (Cayman) Limited, this entity was already fully consolidated by BBVA.

2003

During 2003, BBVA acquired 0.176% of the capital stock of Gas Natural S.D.G, S.A. (“Gas Natural”) for €12.7 million, raising its interest in Gas Natural to 3.241%.

During 2003, BBVA purchased 4.76% of the capital stock of Bancomer for a total of €304 million, raising its interest to 59.43% as of December 31, 2003.

2002

On May 14, 2002, Banco Francés sold its interest in BBVA Uruguay (60.88%) to BBVA for $55 million, after obtaining authorization from the Central Bank of Uruguay. As a result of this transaction, BBVA’s ownership interest in BBVA Uruguay increased from 80.66% to 100%.

On May 15, 2002, Terra Networks, S.A. (“Terra Networks”) and BBVA entered into a preliminary agreement for the integration of Uno-e Bank, S.A. and the individual consumer financing business of Finanzia Banco de Crédito, S.A. (“Finanzia”), BBVA’s wholly-owned subsidiary, whereby Terra Networks’ holding in Uno-e Bank would decrease to 33%. This integration transaction and the percentage of ownership held by Terra Networks were subject to the formalization of final contracts, which were

11

executed on January 10, 2003, and approved at extraordinary shareholders’ meetings of Finanzia and Uno-e Bank held on April 23, 2003. In connection with the integration transaction, Terra Networks was granted a put option over its shares in the resulting combined entity giving it the right to require BBVA to purchase such shares. For more information relating to this transaction, see “Item 5. Operating and Financial Review and Prospects—Liquidity and Capital Resources—Agreement with Terra Networks” and “Item 7. Major Shareholders and Related Party Transactions—Related Party Transactions—Uno-e Bank Agreement”.

On June 8, 2004, the European Commission approved plans by BBVA and Banca Nazionale del Lavore (“BNL”) to form a consumer-finance 50-50 joint venture in Italy. The new company will provide consumer credit products, such as credit cards, personal loans and salary advances.

In two transactions in June and November 2002, BBVA purchased from the Mexican government its 3% and 2.5% interests in Bancomer for approximately €240 million and €175 million, respectively. As a result of these transactions, BBVA’s ownership interest in Bancomer increased to 54.67% as of December 31, 2002.

2001

In January 2001, BBVA acquired 200 million shares of Bancomer from the Bank of Montreal, representing approximately 2.2% of Bancomer’s capital stock, for approximately $125 million. On April 4, 2001, BBVA reached an agreement with Bank of Montreal to purchase in two tranches 812 million shares of Bancomer for a total of $558 million. The first tranche, consisting of 500 million shares, was acquired in April 2001, and the second tranche, consisting of 312 million shares, in May 2001, raising BBVA’s holding in Bancomer to 48%. Additional purchases of shares of Bancomer amounting to $140 million were made in October and November 2001, increasing BBVA’s stake in Bancomer to 49% as of December 31, 2001.

BBVA acquired in the first and last quarters of 2001 a 4.87% interest in BNL for approximately €398 million, increasing its holding in BNL to 14.8% as of December 31, 2001. BBVA increased its holding to 14.9% as of January 31, 2002.

Capital Divestitures

Our principal capital divestitures from 2001 to the date of this Annual Report were the following:

2004

On June 18, 2004 BBVA sold its 5.01% interest in Acerinox, S.A. for €146.6 million, giving rise to a capital gain of €35 million.

In January 2004, BBVA sold 2.2% of the capital stock of Gas Natural. At the time the transaction closed, BBVA had not completed preparation of its 2003 Consolidated Financial Statements and therefore, in accordance with Spanish GAAP, reflected the amortization of €70 million of consolidation goodwill which resulted from the transaction in such financial statements rather than in its 2004 Consolidated Financial Statements.

2003

On January 13, 2003, BBVA announced its intention to sell its Brazilian affiliate, Banco Bilbao Vizcaya Argentaria Brasil, S.A. (“BBV Brasil”) to Banco Bradesco, S.A. (“Bradesco”). On June 9, 2003, upon completion of due diligence, receipt of authorizations from regulatory authorities and approval by the corresponding corporate bodies, BBVA transferred 100% of BBV Brasil to Bradesco, in consideration for which Bradesco paid 35,481,460,311 of its newly-issued ordinary shares and 34,948,501,563 of its newly-issued preferred shares, totaling 4.44% of Bradesco’s share capital, as well as 1,864 million Brazilian Reais in cash, for a total consideration of approximately 2,626 million Brazilian Reais (approximately $900 million). We were required, under Spanish GAAP, to take an extraordinary charge in 2002 relating to exchange rate differences relating to our investment in BBV Brasil accumulated up to December 31, 2002. Under the transaction agreements with Bradesco, in addition to the cash consideration and equity participation described above, we have been granted the right to nominate one member of Bradesco’s board of directors so long as we maintain, subject to exceptions relating to capital increases where shareholders are not offered preemptive rights, at least a 4.0% interest in Bradesco’s share capital. We have agreed for a period of two years from the closing date or so long as we have a right to nominate one member of Bradesco’s board of directors, whichever is longer, that we will not control and/or manage a financial institution in Brazil. See Note 32.2.D.13 to the Consolidated Financial Statements.

In March 2003, BBVA sold its 25% interest in Metrovacesa Residencial, S.A., resulting in a capital gain of €2.1 million.

On June 5, 2003, BBVA agreed to sell its holding in Crédit Lyonnais, S.A., to Crédit Agricole, S.A. in exchange for €482 million in cash, representing 67% of consideration, and 16.3 million shares of Crédit Agricole, S.A., representing the remaining 33% of consideration. BBVA immediately sold the Crédit Agricole shares to institutional investors at a price of €16.64 per share, for a total consideration of €271 million. As a result of this transaction, BBVA liquidated its participation in Crédit Lyonnais and recorded a capital gain of €342 million.

In July 2003, BBVA sold 3% of the capital stock of Gamesa, giving rise to a capital gain of €29.9 million.

12

In the last quarter of 2003, BBVA sold 2.465% of the capital stock of Repsol-YPF, giving rise to a loss of €73.3 million.

In 2003, a series of purchases and sales of shares of Telefónica de España, S.A., resulting in a 0.57% net reduction of our holding, gave rise to a capital gain of €220 million.

In 2003, a series of purchases and sales of shares of Iberdrola, S.A., resulting in a 1.02% net reduction of our holding, gave rise to a capital gain of €45.3 million.

In December 2003, BBVA sold its entire 9.9% interest in the Moroccan bank Wafabank, S.A. to Omnium Nord Africain, S.A. The total sale price was 529,505,625 dirhams (approximately €48 million) and gave rise to a capital gain of €3.5 million.

In December 2003, Banco Sabadell, S.A. launched a tender offer for the shares of Banco Atlántico, S.A. at a price of €71.79 per share. The transaction was completed in March, 2004 and BBVA sold its entire 24.37% interest in Banco Atlántico, which gave rise to a capital gain of approximately €218 million.

2002

In the first quarter of 2002, BBVA sold 3.82% of its holding in Metrovacesa, S.A., giving rise to a capital gain of €14 million. In June 2002, BAMI, S.A. Inmobiliaria de Construcciones y Terrenos agreed to purchase BBVA’s 23.9% interest in the capital stock of Metrovacesa, S.A. for €545.4 million (€36.55 per share). This transaction closed on July 17, 2002. As a result of this sale, as of December 31, 2002, BBVA had a 0.58% interest in Metrovacesa, S.A. The transaction gave rise to a capital gain of approximately €361 million.

2001

In March 2001, BBVA sold its interest in Profuturo GNP, S.A. de C.V. Administradora de Fondos de Pensiones for $190 million.

B. Business Overview

BBVA is a highly diversified international financial group, with strengths in the traditional banking businesses of retail banking, asset management, private banking and wholesale banking. We also have a portfolio of industrial holdings in some of Spain’s leading companies.

Business Areas

Reorganization in 2003

In 2003, we reorganized our business areas with a view to optimizing the earnings and value-creation of each line of business and to more closely align our organizational structure with the manner in which management has been setting business strategy and monitoring our operating results. The principal features of the reorganization were the following: (i) our Retail Banking in Spain and Portugal area now includes retail banking, and asset management and private banking, (which had been included in a separate Asset Management and Private Banking business area in 2002) in Spain and Portugal, (ii) our Banking in America area now includes all of our Latin American operations, including our Mexican operations (which had been a separate business area in 2002) and asset management and private banking in Latin America (but excluding our operations in Argentina, which is a separate business area, and in Brazil, as discussed below) and (iii) as a result of our agreement to sell our entire interest in BBV Brasil in January 2003, and the closing of such sale in June 2003, our Corporate Activities and Other business area included our interest in BBV Brasil for the period January to June 2003, accounted for under the equity method, and for 2002 and 2001, accounted under full consolidation. Due to the special conditions that have affected our operations in Argentina in 2003, we have continued to provide additional disclosure on our Argentinean operations and discuss these operations as if they comprised a separate business area, “Argentina”, and not part of the business area “Banking in America”, where they were included in our Annual Report on Form 20-F for 2001 and prior years. See “Presentation of Financial Information—Accounting Principles”.

13

The following is a description of our business areas:

| | • | Retail Banking in Spain and Portugal: formed by BBVA’s retail banking, asset management and private banking businesses in Spain and Portugal, covering the residential customer and small and medium entities (“SME”) segments in these markets. This area also includes the Finanzia / Uno-e group (which specializes in the e-banking business, consumer financing and card product distribution), BBVA Portugal, our private banking businesses (other than international private banking), and our mutual and pension fund management and insurance businesses. |

| | • | Wholesale and Investment Banking: includes BBVA’s business activities with large companies and institutions through national and international corporate banking and institutional banking. In addition, this business area includes our trading businesses located in Spain, Europe and New York, our equity distribution and origination business and security deposit and custody service business, as well as part of our real estate business. |

| | • | Banking in America: includes the operations of each of our subsidiary banks in Latin America and their investee companies, including pension management companies and insurance companies, as well as our international private banking business. As described above, this business area includes our operations in Mexico and excludes our operations in Argentina. |

| | • | Corporate Activities and Other: includes our holdings in large industrial corporations and in financial entities, as well as the activities and results of our support units, such as the Assets and Liabilities Management Committee (ALCO). In addition, this business area includes our other operations or activities that, by their nature, cannot be assigned to another business area, such as country risk provisions and amortization of goodwill (except for goodwill relating to the holdings owned by the Business and Real Estate Projects unit, which is included in the Wholesale and Investment Banking business area). As described above, this area included the operations of BBV Brasil, until the closing of its sale in June 2003. |

| | • | Argentina: includes our subsidiaries Banco Francés and Grupo Consolidar. |

The foregoing description of our business areas is consistent with our current internal organization. The financial information for our business areas for the years 2003, 2002 and 2001 presented below has been prepared on a uniform basis to reflect the reorganization of our business areas in 2003 described above. Unless otherwise indicated, the financial information provided below for each business area does not reflect the elimination of transactions between companies within one business area or between different business areas, since we consider these transactions to be an integral part of each business area’s activities. For the presentation and discussion of our consolidated operating results in “Item 5—Operating and Financial Review and Prospects” and elsewhere in this Annual Report, however, such intra- and inter-business area transactions are eliminated and the eliminations are generally reflected in the operating results of the Corporate Activities and Other business area.

The following table provides net attributable profit information for our business areas for the years ended December 31, 2003, 2002 and 2001.

| | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Net Attributable Profit/

(Loss)

| | | % of Subtotal

| | | % of Net Attributable

Profit/(Loss)

| |

| | | Year ended December 31,

| |

Business Area

| | 2003

| | | 2002

| | | 2001

| | | 2003

| | | 2002

| | | 2001

| | | 2003

| | | 2002

| | | 2001

| |

| | | (in millions of euro) | | | | | | | | | | | | | | | | | | | |

Retail Banking in Spain and Portugal | | 1,239 | | | 1,266 | | | 1,173 | | | 51 | % | | 53 | % | | 47 | % | | 56 | % | | 73 | % | | 63 | % |

Wholesale and Investment Banking | | 468 | | | 382 | | | 531 | | | 19 | % | | 16 | % | | 21 | % | | 21 | % | | 22 | % | | 29 | % |

Banking in America | | 715 | | | 736 | | | 807 | | | 30 | % | | 31 | % | | 32 | % | | 32 | % | | 43 | % | | 44 | % |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Subtotal | | 2,422 | | | 2,384 | | | 2,511 | | | 100 | % | | 100 | % | | 100 | % | | 109 | % | | 138 | % | | 136 | % |

| | |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

| |

|

|

Corporate Activities and Other | | (205 | ) | | (656 | ) | | (451 | ) | | | | | | | | | | | (9 | )% | | (38 | )% | | (24 | )% |

Argentina | | 10 | | | (9 | ) | | (217 | ) | | | | | | | | | | | — | | | — | | | (12 | )% |

| | |

|

| |

|

| |

|

| | | | | | | | | | |

|

| |

|

| |

|

|

Net attributable profit | | 2,227 | | | 1,719 | | | 1,843 | | | | | | | | | | | | 100 | % | | 100 | % | | 100 | % |

| | |

|

| |

|

| |

|

| | | | | | | | | | |

|

| |

|

| |

|

|

14

Retail Banking in Spain and Portugal

Lending in this business area as of December 31, 2003, was approximately €91,295 million, an increase of 13.9% from €80,152 million as of December 31, 2002, principally due to growth in mortgage lending.

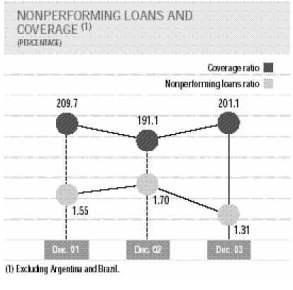

The non-performing loan (“NPL”) ratio fell to 0.88% as of December 31, 2003, from 1.00% as of December 31, 2002. The loan coverage ratio rose to 271.1% as of December 31, 2003, from 220.8% as of December 31, 2002.

Customer deposits and marketable debt securities, which were €51,894 million as of December 31, 2003, decreased by 1.3%, principally due to the cancellation of an agreement to manage certain government accounts in January 2003. Mutual and pension funds under management were €49,334 million as of December 31, 2003, an increase of 12.2%, due to the launch of new funds during 2003.

The business area’s main lines of activity focused on implementing the Financial Services Plan, including the Personal, Commercial and Special Plans described below, which are the focus of the new business model launched by BBVA at the end of 2002. Significant progress was made in 2003 in the development of the three customer approach methods devised by this business area: (i) Personal Financial Services, aimed at residential customers, (ii) Commercial Financial Services, for SMEs and businesses and (iii) Special Financial Services, which are offered through Finanzia and Uno-e Bank.

| • | Personal Financial Services: focuses on retail customers and is aimed at customers getting more value out of their relationship with us by being offered a wider range of products and services at attractive prices made available through different channels, along with solutions tailored to their specific needs. |

| | — | As part of this strategy, 450 of our most significant branches and over 6,000 employees were reoriented toward a customer sales strategy consistent with our Personal Financial Services approach. Also in 2003, 150 of our most significant branches in Spain were physically refurbished to enhance their role as sales and customer services centers and increase the efficiency of their operations and differentiation of services based on customers requirements. |

| | — | Also as part of our Personal Financial Services approach, in 2003, BBVA reorganized its private banking business by integrating it into the newly restructured Asset Management and Private Banking unit of the Retail Banking Spain and Portugal business area. |

| • | Commercial Financial Services: focuses on professionals, businesses and SMEs and implementing business models and organizational changes channeled focused on improving BBVA’s market position and taking it closer to its customers. Specifically, progress is being made in the risk, human resources, organization, technology and systems, products and channels areas to ensure that the actions required to enable BBVA to implement its new, focused approach to the segment are performed in 2004. |

| • | Special Financial Services: focuses on financings related to capital goods, vehicles and consumer goods, on-line banking and remittances. A redefinition of this approach was completed after the merger of Finanzia and Uno-e in 2003. |

The business units included in the Retail Banking in Spain and Portugal business area are:

| | • | Commercial Banking in Spain |

| | • | Small and Medium Entities (SME) Banking |

| | • | Assets Management and Private Banking |

| | • | Special Financial Services |

| | • | Insurance Business in Europe |

15

Commercial Banking in Spain

The Commercial Banking in Spain unit makes the biggest contribution to the Retail Banking Spain and Portugal business area and accounts for 73% (80% in 2002) of the business area’s ordinary revenue, 78% (85% in 2002) of customer funds and 71% (72% in 2002) of lending. The Commercial Banking in Spain unit serves the residential, commercial and small business customer segments, providing specialist mortgage banking, personal banking and private banking, among other services.

In 2003, lending by the Commercial Banking in Spain unit increased significantly to €85.2 billion, an increase of 14.2% from €74.6 billion in 2002, principally due to strong growth in mortgage products. Mortgages, increased 20.2% in 2003 to €15,734 million, due to the wide range of mortgage products we offer, which include the first 30-year fixed-rate mortgage in the Spanish market, the Hipoteca Mix Dos Tramos. This product guarantees a fixed rate for the first five years and may include an interest rate cap to protect customers against severe interest rate increases.

Our SME financing business focused in 2003 on increasing leasing activity and, in addition, a significant effort was made to increase point-of-sales (“POS”) to generate increased fee revenue—13,250 new POS terminals (for credit card payments) were installed during the year.

To increase customer funds in 2003, we endeavored to increase the breadth and attractiveness of our products. One example was the Libreta Flexible, a deposit product that combines the simplicity of a traditional passbook account with guaranteed returns. As of December 31, 2003, the Libreta Flexible’s deposit balance was €2,353 million.

We also launched several new mutual fund products designed to provide investors with favorable returns in a rising stock market, but also afford them a level of investment protection during market declines. Two versions of our Extra 5 fund, which were launched in September, attracted more than €3.4 billion as of December 31, 2003. In 2003, we also launched a set of pension plan products under the brand name BBVA Protección. These plans are tailored to each customer’s needs and risk profile and attracted more than €800 million as of December 31, 2003.

By launching several innovative products, such as theTarjeta Diez (Ten card) and theTarjeta Infinite (Infinite card), BBVA was able to issue more than 7 million new credit cards in 2003. BBVA was also active in developing new means of payment, such as BBVA VIA T, for toll road payment, or the Mobipay service, which employs mobile telephony.

BBVA continued to focus on moving customers to alternative channels to accomplish their banking transactions and in 2003 the number of transactions performed at our branches decreased by approximately 20 million with 72% of such transactions being completed through alternative channels. In addition, telephone banking users increased by approximately 15% in 2003 and internet transactions increased by 29.2% to 77.5 million. BBVA was named, for the second consecutive year, the Best Consumer Internet Bank in Europe by Global Finance magazine.

Small and Medium Entities (SME) Banking

SME Banking, the second most significant unit in the Retail Banking in Spain and Portugal business area, in terms of both business volume and contribution to net attributable profit, specializes in the management of the SME segment in Spain. As of December 31, 2003, the SME Banking unit managed a loan portfolio of €20.5 billion and approximately €7 billion of customer deposits, with year-on-year growth of 14.5% and 12.2%, respectively. In addition, in 2003, our leasing, renting and confirming businesses saw year-on-year increases of 22.3%, 30.2% and 34.3%, respectively.

In 2003, we were the leading Spanish bank in issuing SME loans funded by the Instituto de Crédito Oficial (ICO), a Spanish government agency, with a market share of 19.7%, according to ICO statistics.

Regarding customer funds managed, we launched five new mutual funds targeted at SMEs and were successful in increasing funds captured by 40.6% to €765 million as of December 31, 2003.

Consistent with our strategy to increase use of alternative channels and, in particular, the Internet, we launched a new product, SIETE net, which along with our prior Internet products, BBVA net c@sh and BBVA net office, had as users over 42,000 companies, which transacted collections and payments worth €58 billion through this electronic channel, in 2003.

Asset Management and Private Banking

The Asset Management and Private Banking business unit consists of eight subunits that can be grouped together, by business activity, in three blocks:

| | • | Pensions, Asset Management, Global Administration and Savings Investment Services, which focus mainly on product generation; |

16

| | • | Personal Banking and BBVA Patrimonios, which have responsibility for the highest-income customer segment and |

| | • | Control and Business Development, which are support subunits. |

Total funds managed by the Asset Management and Private Banking unit as of December 31, 2003, were approximately €18 billion, an increase of 11.4% over 2002.

The Pension subunit’s assets under management as of December 31, 2003 were €12.2 billion, an increase of 10.7% over 2002, for more than 1,280,000 participants. More than €6.4 billion of such funds relate to individual pension plans and approximately €5.8 billion to corporate pension and similar plans.

With respect to private banking in Spain, the BBVA Patrimonios and Personal Banking subunits manage total funds of €12,105 million. BBVA Patrimonios focuses on high-net worth individuals (with financial assets of over €2 million) and manages funds of €6,315 million belonging to more than 1,000 customers. Personal Banking provides customized advisory services to our medium-to-high income customers. This subunit has more than 70,000 customers and total funds under management of €5,790 million as of December 31, 2003.

BBVA Portugal

In 2003, the BBVA Portugal unit’s customer loans increased by 7.6%, boosted by a 32.8% increase in mortgage lending, while the non-performing loan ratio fell to 0.65% as of December 31, 2003, from 0.91% as of December 31, 2002.

The BBVA Portugal unit’s funds under management increased by 3.9% in 2003 principally due to strong growth in mutual funds assets, which increased by 19.8% over 2002. In 2003, we launched three new mutual funds, including the first guaranteed fund to be marketed in Portugal, Extra 5 BBVA. Seven new types of structured deposit products were also launched in 2003.

Special Financial Services

The Special Financial Services unit is comprised of Finanzia, our on-line bank Uno-e Bank and Dinero Express. In June 2003, Uno-e Bank was acquired by the consumer finance division of our subsidiary Finanzia. As a result of this transaction, we increased our ownership in Uno-e Bank to 67%.

- Finanzia manages collaboration agreements with distributors, manufacturers and importers in order to finance their sales. Total net lending amounted to €2,169 million at December 31, 2003.

- Uno-e Bank had funds under management of €1,101 million as of December 31, 2003, principally due to growth in mutual funds assets, from €15 million to €52 million.

- Dinero Express provides fast remittance services for immigrants to send money from Spain to their home countries of Ecuador, Colombia, Peru, the Dominican Republic and Argentina, where it has more than 1,000 payment points.

Insurance Business in Europe

This unit engages in direct insurance and reinsurance and insurance broking in Spain and Portugal and markets its products mainly through BBVA’s branches. In January 2004, BBVA entered into an agreement to sell to AXA Aurora Iberica, S.A. de Seguros y Reaseguros its 50% holding in Hilo Direct, S.A. de Seguros y Reaseguros, although BBVA’s products will still be distributed through the BBVA network until mid 2007.

Wholesale and Investment Banking

The Wholesale and Investment Banking business area focuses on large corporate, governmental, non-governmental organizations and institutional investor clients.

The business units included in this business area are:

| | • | Global Corporate Banking; |

17

| | • | Global Markets and Distribution |

| | • | Business and Real Estate Projects and |

| | • | Global Transaction Services. |

Global Corporate Banking

The Global Corporate Banking unit was created in 2003 to strengthen BBVA’s relationship with its large Spanish and multi-national customers and take advantage of this customer segment’s high growth potential. The Global Corporate Banking unit is further subdivided into the following four subunits to manage its corporate banking activities: Corporate Banking Iberia, Corporate Banking Europe and Asia, Corporate Banking America and Global and Investment Banking. The Global Corporate Banking unit has branches in New York, London, Paris, Milan and Hong Kong.

Global Corporate Banking also includes the Capital Markets subunit which handles the unit’s syndicated loan and structured finance transaction activities. In 2003, the Capital Markets subunit was particularly active in designing and structuring leveraged finance transactions and project financings. Also in 2003, the Capital Markets subunit, in conjunction with the Global Markets and Distribution unit, acted as joint book runner in more than ten public offerings of fixed-income securities, including a €5 billion offering by the Kingdom of Spain and a €1 billion offering by Repsol, S.A. The Capital Markets subunit also participated in public offerings by John Deere, Altadis, Caminhos de Ferro and Enersis and private placement offerings for Ford Motor Credit, HSH Nordbank and Dexia, as well as over 20 euro medium term note program offerings, including for Volvo, Cadbury Schweppes, Portugal Telecom, Valeo and L’Oréal, for which BBVA acted as one of the dealers.

Global Corporate Banking’s Corporate Finance subunit is responsible for advising on mergers and acquisitions and providing general corporate advisory services.

Institutional Banking

The Institutional Banking unit focuses on governmental and institutional clients, including the Spanish government and the governments of Spain’s autonomous communities and private organizations, associations, foundations and insurance companies. This unit has a network of 42 branches in Spain, Portugal and Belgium.

In 2003, the Institutional Banking unit submitted bids for over 38 public contracts offered by the Spanish government. Among the new contracts awarded to the Institutional Banking unit were management of the Spanish Ministry of Defense’s treasury and payments departments, management of the payrolls of the Spanish Ministries of Justice, Finance and Public Authorities, the National Statistics Institute (INE) and of the National Employment Institute (INEM).

The Institutional Banking unit operates in these markets under the BBVA brand name and through Banco de Crédito Local (BCL), a BBVA subsidiary that specializes in long-term financing. To finance its lending activities, BCL has a euro commercial paper program for up to €1.5 billion and a euro medium-term note program and a fixed-income security program for €4 billion each. In 2003, BCL carried out the first-ever issue of public covered bonds in the euro market with the sale of €1.5 billion aggregate principal amount of fixed-income securities guaranteed by loans and credits granted by the issuer to the public sector.

Global Markets and Distribution

The Global Markets and Distribution unit focuses on a wide range of securities market-oriented activities. This business unit engages in both treasury operations on behalf of BBVA and transactions for third-parties, which, as of December 31, 2003, accounted for approximately 60% of the Global Markets and Distribution unit’s net attributable profit. In 2003, BBVA’s securities brokerage affiliate, BBVA Bolsa, S.A., was merged into the Global Markets and Distribution unit, broadening the range of products available to offer BBVA’s clients through this business unit.

In 2003, weak securities markets encouraged investors to purchase fixed-income and government debt securities. The Global Markets and Distribution unit also experienced strong activity in the securities lending business, foreign exchange transactions and interest rate-related products. In addition, the Global Markets and Distribution unit participates actively in the cross-selling of products and services with other BBVA business areas and units. For example, the Global Markets and Distribution unit has made fixed-income and equity security products, as well as mutual funds, available for marketing and sale through BBVA’s retail banking branch network.

18

The Global Markets and Distribution is particularly active in a number of securities and trading markets, including the AIAF fixed-income market, the Spanish stock market, the Spanish foreign exchange market for euro/U.S. dollar transactions and the Spanish government debt securities market.

Business and Real Estate Projects

The Business and Real Estate Projects unit manages a portfolio of 127 investments with a book value as of December 31, 2003 of €992 million and unrealized gains amounting to €749 million, which is an increase of €200 million compared to total unrealized gains as of December 31, 2002. Its investment portfolio is diversified among the real estate, capital goods and services sectors.

Divestitures from this investment portfolio in 2003 amounted to approximately €230 million, giving rise to capital gains of €100 million. The most significant disposition related to the sale by Corporación IBV, which is 50%-owned by BBVA, of its 6% interest in the capital stock of Gamesa Corporación Tecnológica, giving rise to a capital gain of €30 million. Following this transaction, Corporación IBV’s interest in Gamesa decreased to 31.8%.

In 2003, the Business and Real Estate Projects unit made investments totaling €140 million in 10 real estate development projects with approximately 700,000 m2 of buildable land and sold mature real estate projects with a total of 550,000 m2 of buildable land, giving rise to capital gains of approximately €70 million. As of December 31, 2003, the Business and Real Estate Projects unit’s real estate development portfolio consisted of 2.5 million m2 of buildable land and 4,000 dwellings under management, distributed among 44 projects.

Global Transaction Services

The Global Transaction Services unit was created in 2003 to manage BBVA’s corporate and institutional transaction business, which is global in scope and offers a wide range of products and services, including domestic and international collections and payments, loans, trade bill discounting, factoring, confirming, credit cards, foreign trade, electronic banking, correspondent banking and cash pooling systems services.

Banking in America