Exhibit 99.2

| Q4 2007 Financial Results Investor Conference Call October 16, 2007 Robbins & Myers, Inc. |

| In addition to historical information, this release contains certain statements that constitute "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995. These forward- looking statements include, but are not limited to, all statements regarding the intent, belief or current expectations regarding the matters discussed or incorporated by reference in this document (including statements as to "beliefs," "expectations," "anticipations," "intentions" or similar words) and all statements which are not statements of historical fact. Such forward-looking statements, together with other statements that are not historical, are based on management's current expectations and involve known and unknown risks, uncertainties, contingencies and other factors that could cause results, performance or achievements to differ materially from those stated. The most significant of these risks and uncertainties are described in the Company's Form 10-K, and Form 10-Q reports filed with the Securities and Exchange Commission and include, but are not limited to: a significant decline in capital expenditures in the specialty chemical and pharmaceutical industries; a major decline in oil and natural gas prices; changes in international economic and political conditions and currency fluctuations between the U.S. dollar and other currencies; work stoppages related to union negotiations; customer order cancellations; business disruptions caused by the implementation of business computer systems; the ability of the Company to comply with the financial covenants and other provisions of its financing arrangements; events or circumstances which result in an impairment of assets, including but not limited to, goodwill; the potential impact of U.S. and foreign legislation, government regulations, and other government action, including those relating to export and import of products and materials, and changes in the interpretation and application of such laws and regulations; the outcome of audit, compliance, administrative or investigatory reviews; and general economic conditions that can affect demand in the process industries. Should one or more of these risks or uncertainties materialize or should underlying assumptions prove incorrect, the Company's actual results, performance or achievements could differ materially from those expressed in, or implied by, such forward-looking statements. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. Except as otherwise required by law, the Company does not undertake any obligation to publicly release any revisions to these forward-looking statements to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events. This presentation refers to various non-GAAP measures. The Company believes these measures are helpful to investors in assessing the Company's ongoing performance of its underlying businesses before the impact of special items on its financial performance. In addition, these non-GAAP measures provide a comparison to our previously announced earnings guidance, which excluded these special items. These non-GAAP measures are reconciled to GAAP measures in this document. Cautionary Statement Concerning Forward- Looking and Other Information |

| Quarter & Year Ended August 31, 2007 2007 Year in Review Fourth Quarter 2007 Review 2008 Objectives and Guidance Q4 and Full Year 2007 Financial Highlights |

| 2007 Year in Review Management / Talent Upgraded Business Simplified Lean Implemented; Continuous Improvement Romaco Restructuring Completed; Profitable PSG Exited Year With > 10% Operating Margins Customer-Facing Initiatives Launched Creating a Performance Culture...Creating Our Future |

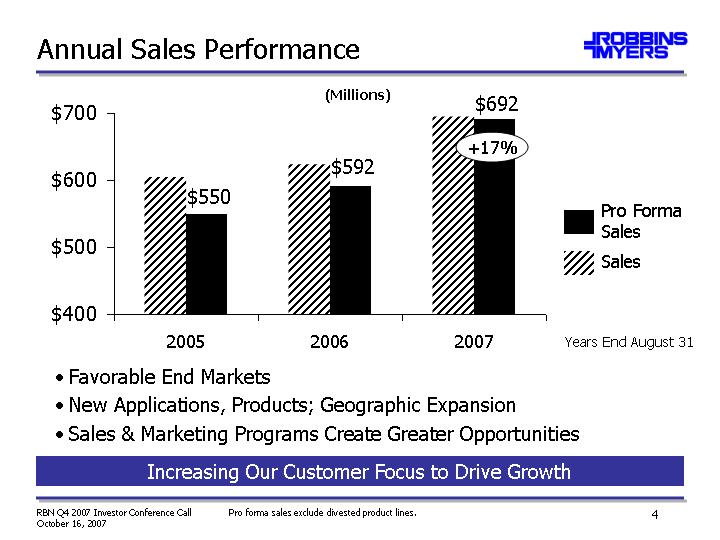

| Annual Sales Performance 2005 2006 2007 Sales 605 625 695 Pro Forma Sales 550 592 692 Favorable End Markets New Applications, Products; Geographic Expansion Sales & Marketing Programs Create Greater Opportunities Increasing Our Customer Focus to Drive Growth Sales Pro Forma Sales $592 $692 $550 (Millions) +17% Pro forma sales exclude divested product lines. Years End August 31 |

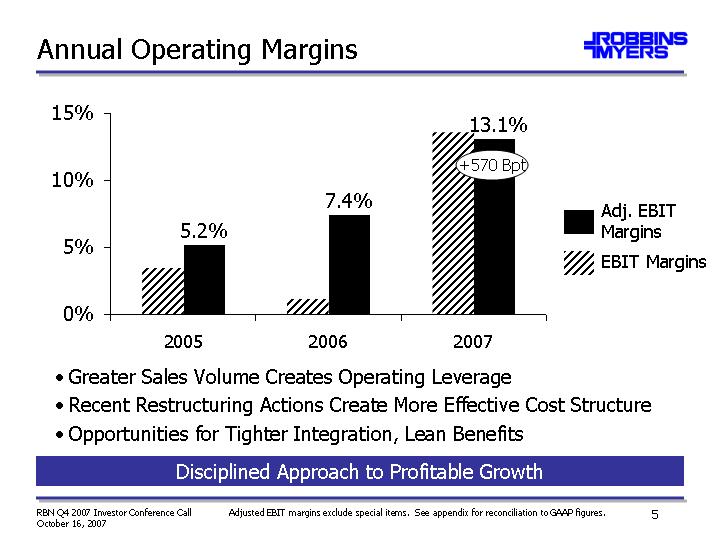

| Annual Operating Margins 2005 2006 2007 EBIT Margins 0.035 0.012 0.136 Adjusted EBIT Margins 0.052 0.074 0.131 Greater Sales Volume Creates Operating Leverage Recent Restructuring Actions Create More Effective Cost Structure Opportunities for Tighter Integration, Lean Benefits Disciplined Approach to Profitable Growth EBIT Margins Adj. EBIT Margins 7.4% 13.1% 5.2% +570 Bpt Adjusted EBIT margins exclude special items. See appendix for reconciliation to GAAP figures. |

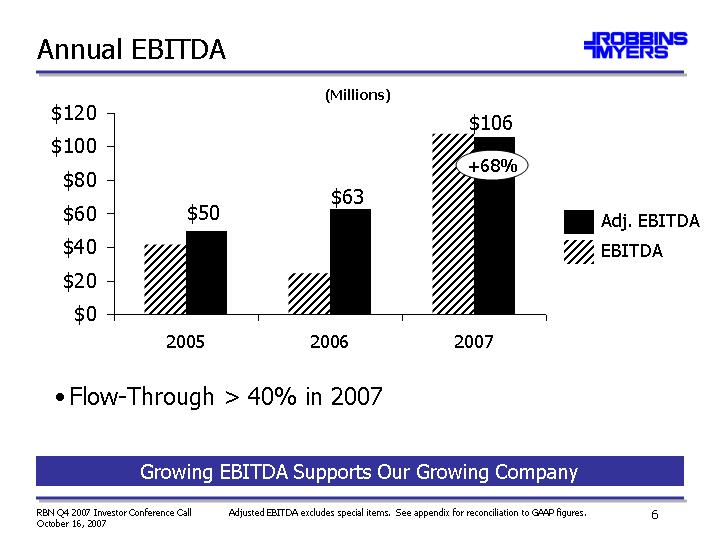

| Annual EBITDA 2005 2006 2007 EBITDA 42 25 108 Adjusted EBITDA 50 63 106 Flow-Through > 40% in 2007 Growing EBITDA Supports Our Growing Company EBITDA Adj. EBITDA $63 $106 $50 (Millions) +68% Adjusted EBITDA excludes special items. See appendix for reconciliation to GAAP figures. |

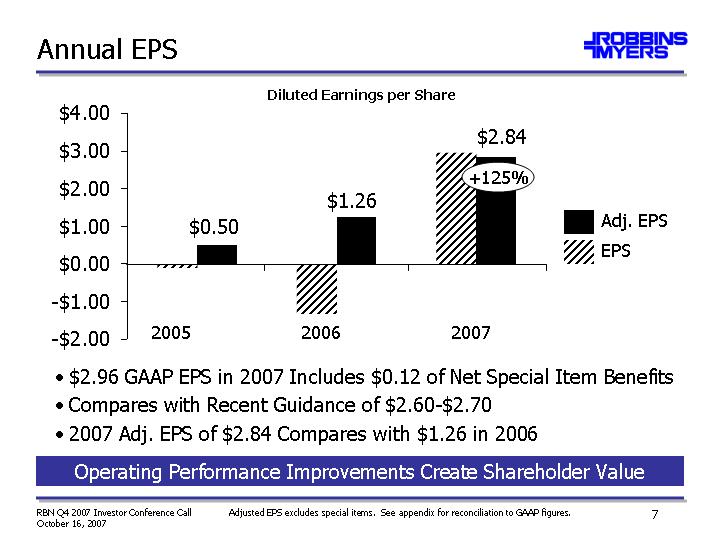

| Annual EPS 2005 2006 2007 EPS -0.1 -1.31 2.96 Adjusted EPS 0.5 1.26 2.84 Real 2005 EPS number -0.02 $2.96 GAAP EPS in 2007 Includes $0.12 of Net Special Item Benefits Compares with Recent Guidance of $2.60-$2.70 2007 Adj. EPS of $2.84 Compares with $1.26 in 2006 Operating Performance Improvements Create Shareholder Value EPS Adj. EPS $1.26 $2.84 $0.50 2005 2006 2007 +125% Adjusted EPS excludes special items. See appendix for reconciliation to GAAP figures. Diluted Earnings per Share |

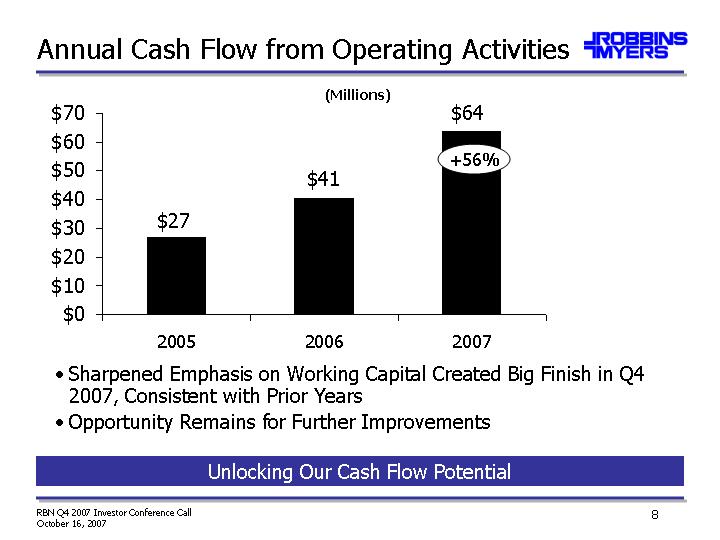

| Annual Cash Flow from Operating Activities 2005 2006 2007 EBITDA 0 0 0 Adjusted EBITDA 26.8 40.5 63.9 Sharpened Emphasis on Working Capital Created Big Finish in Q4 2007, Consistent with Prior Years Opportunity Remains for Further Improvements Unlocking Our Cash Flow Potential $41 $64 $27 (Millions) +56% |

| Q4 2007 Overview Operating / Strategic Actions Hired New Leaders for HR, China Positioned to Implement ERP Projects Throughout FY '08 Sold Previously-Used Romaco UK Facility Financial Results Significant Sales Growth Consistent Margin Gains Strong Cash Flow Expanding Capabilities, Improving Financial Results |

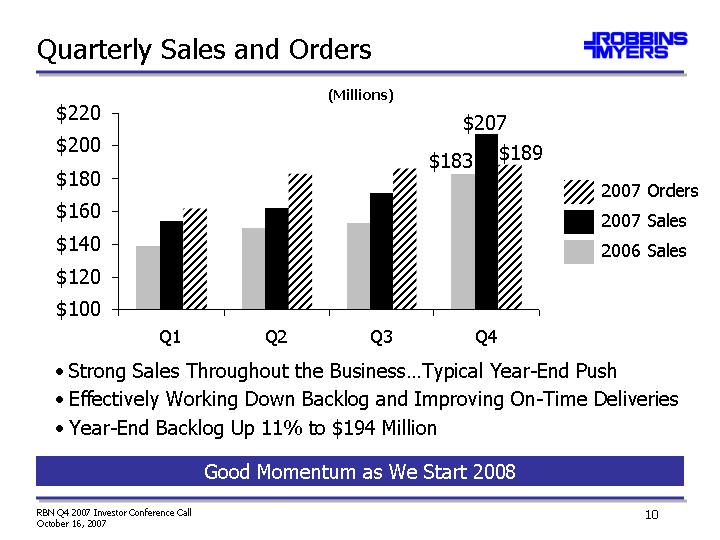

| Quarterly Sales and Orders Q1 Q2 Q3 Q4 Good Momentum as We Start 2008 Strong Sales Throughout the Business...Typical Year-End Push Effectively Working Down Backlog and Improving On-Time Deliveries Year-End Backlog Up 11% to $194 Million 2006 Sales 2007 Sales 2007 Orders $189 $207 $183 (Millions) |

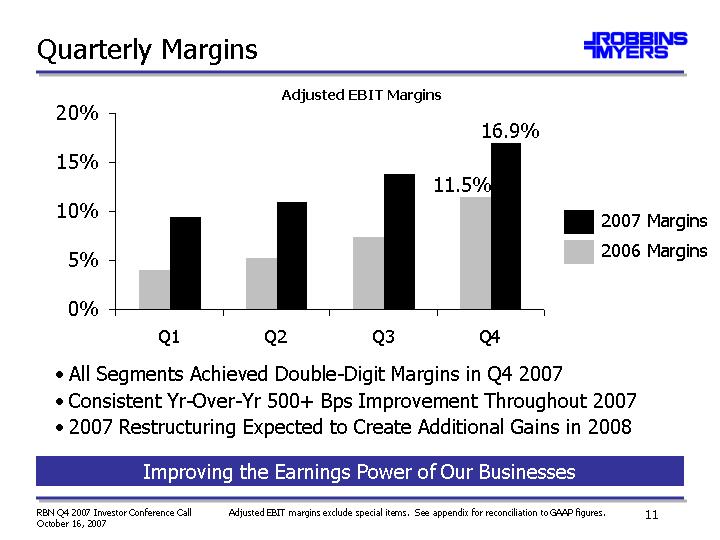

| Quarterly Margins Q1 Q2 Q3 Q4 Last Year's Margins 0.04 0.053 0.074 0.115 Margins 0.095 0.109 0.138 0.169 All Segments Achieved Double-Digit Margins in Q4 2007 Consistent Yr-Over-Yr 500+ Bps Improvement Throughout 2007 2007 Restructuring Expected to Create Additional Gains in 2008 Improving the Earnings Power of Our Businesses 16.9% 11.5% Adjusted EBIT Margins 2006 Margins 2007 Margins Adjusted EBIT margins exclude special items. See appendix for reconciliation to GAAP figures. |

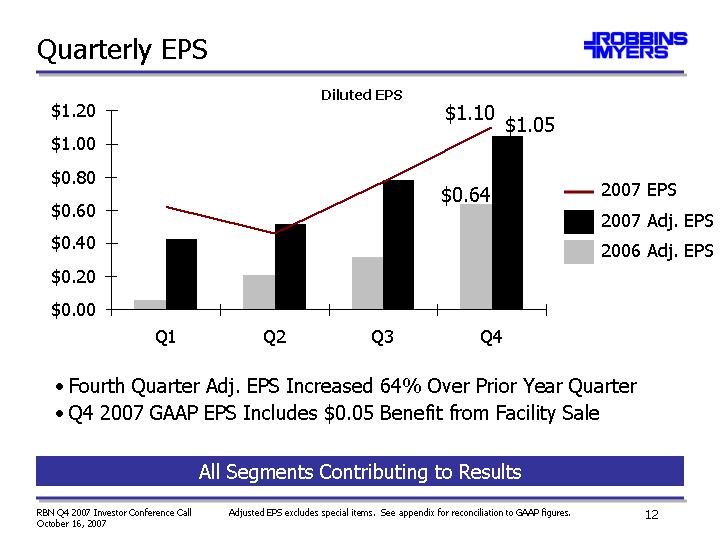

| Quarterly EPS Q1 Q2 Q3 Q4 2006 DEPS -2.02 0.08 -0.01 0.56 2007 DEPS 0.62 0.46 0.77 1.1 2006 Adj DEPS 0.06 0.21 0.32 0.64 2007 Adj DEPS 0.43 0.52 0.78 1.05 2006 Adj. EPS 2007 Adj. EPS $1.05 $0.64 2007 EPS $1.10 All Segments Contributing to Results Fourth Quarter Adj. EPS Increased 64% Over Prior Year Quarter Q4 2007 GAAP EPS Includes $0.05 Benefit from Facility Sale Adjusted EPS excludes special items. See appendix for reconciliation to GAAP figures. Diluted EPS |

| Fluid Management Group (FMG) Q4 Results Yr-Yr Orders Increased 4% Energy Markets Remain Supportive Esp. Outside of North America Good FY '08 Start in September Yr-Yr Sales Grew 15% Lean Initiatives Improve Through- Put EBIT Margins Expanded 170 Bps to 28.5% Capitalizing on Re-Alignment of Business Platform Leveraging Fixed Cost As Volume Increases Focused on Capturing Market Opportunities Q4 2006 Q4 2007 East 73.2 84 Q4 2006 Q4 2007 East 19.6 24 Sales EBIT |

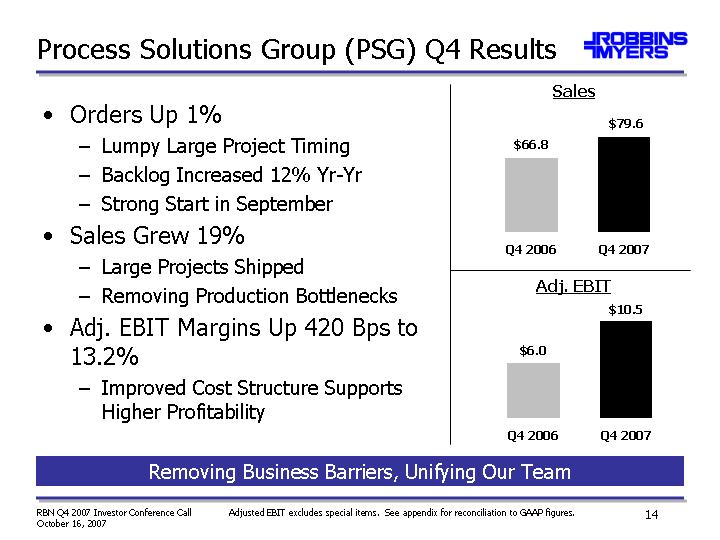

| Process Solutions Group (PSG) Q4 Results Orders Up 1% Lumpy Large Project Timing Backlog Increased 12% Yr-Yr Strong Start in September Sales Grew 19% Large Projects Shipped Removing Production Bottlenecks Adj. EBIT Margins Up 420 Bps to 13.2% Improved Cost Structure Supports Higher Profitability Removing Business Barriers, Unifying Our Team Q4 2006 Q4 2007 PSG 66.8 79.6 Q4 2006 Q4 2007 East 6 10.5 Sales Adj. EBIT Adjusted EBIT excludes special items. See appendix for reconciliation to GAAP figures. |

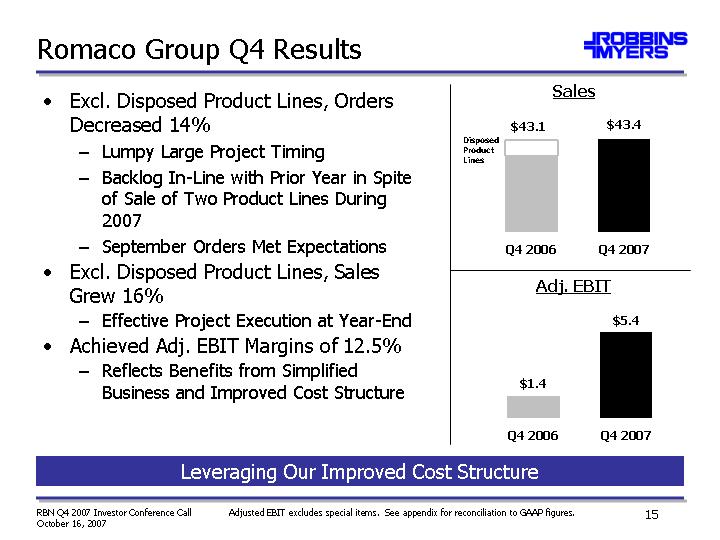

| Romaco Group Q4 Results Excl. Disposed Product Lines, Orders Decreased 14% Lumpy Large Project Timing Backlog In-Line with Prior Year in Spite of Sale of Two Product Lines During 2007 September Orders Met Expectations Excl. Disposed Product Lines, Sales Grew 16% Effective Project Execution at Year-End Achieved Adj. EBIT Margins of 12.5% Reflects Benefits from Simplified Business and Improved Cost Structure Leveraging Our Improved Cost Structure Q4 2006 Q4 2007 Romaco 37.4 43.4 Divested 5.7 Sales $43.1 $43.4 Disposed Product Lines Adj. EBIT Q4 2006 Q4 2007 East 1.4 5.4 Adjusted EBIT excludes special items. See appendix for reconciliation to GAAP figures. |

| 2008 Objectives Expand Key Account Management, Sales Training Increase Asian Presence Simplify and Integrate Operations Launch Management Development Programs Embed Lean Throughout the Company Hitting Our Stride |

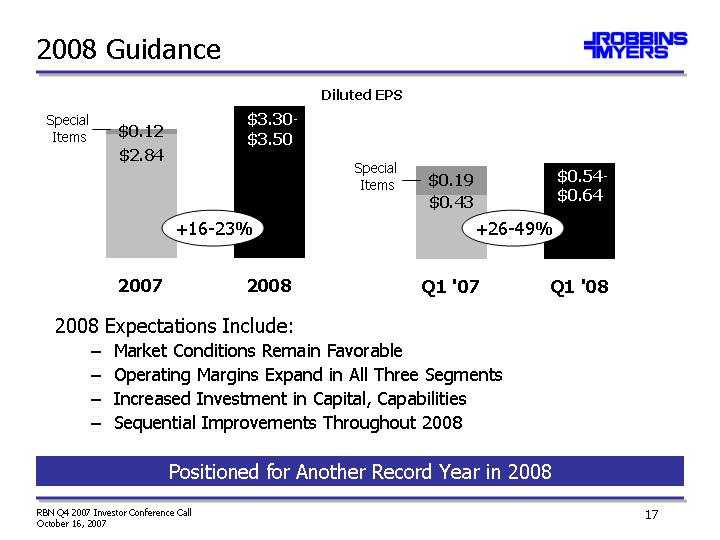

| 2008 Guidance 2007 2008 Core 2.84 3.5 Special Items 0.12 +16-23% 2008 Expectations Include: Market Conditions Remain Favorable Operating Margins Expand in All Three Segments Increased Investment in Capital, Capabilities Sequential Improvements Throughout 2008 Positioned for Another Record Year in 2008 Q1 '07 Q1 '08 Core 0.43 0.64 Special Items 0.19 +26-49% Special Items Special Items Diluted EPS |

| Summary Healthy End Markets Support Further Growth Announced Restructuring Efforts Completed More Responsive Organization Lower Cost Structure Continuous Improvement Creates Future Operational Improvements Balance Sheet Supports Both Organic and Strategic Growth Management Team Capable of Taking Business to a New Level Focused on Creating Shareholder Value |

| Q4 2007 Financial Results Investor Conference Call October 16, 2007 Financial Highlights |

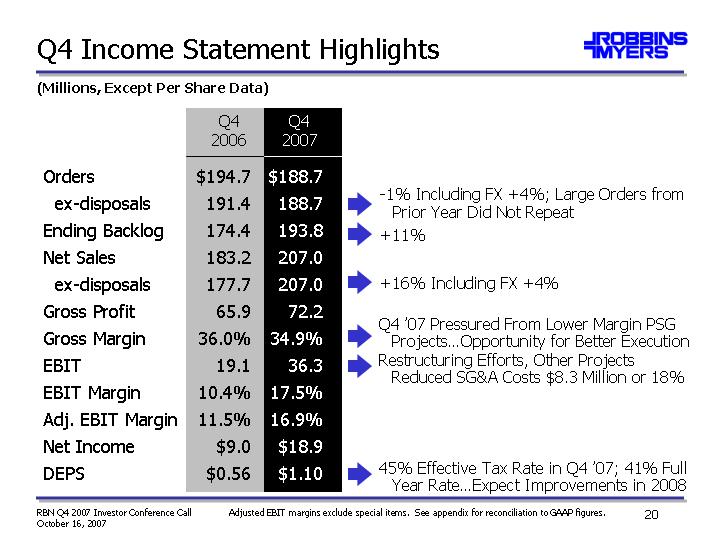

| Q4 Income Statement Highlights Orders ex-disposals Ending Backlog Net Sales ex-disposals Gross Profit Gross Margin EBIT EBIT Margin Adj. EBIT Margin Net Income DEPS (Millions, Except Per Share Data) Q4 2007 Q4 2006 $188.7 188.7 193.8 207.0 207.0 72.2 34.9% 36.3 17.5% 16.9% $18.9 $1.10 $194.7 191.4 174.4 183.2 177.7 65.9 36.0% 19.1 10.4% 11.5% $9.0 $0.56 - -1% Including FX +4%; Large Orders from Prior Year Did Not Repeat Q4 '07 Pressured From Lower Margin PSG Projects...Opportunity for Better Execution +16% Including FX +4% 45% Effective Tax Rate in Q4 '07; 41% Full Year Rate...Expect Improvements in 2008 Adjusted EBIT margins exclude special items. See appendix for reconciliation to GAAP figures. Restructuring Efforts, Other Projects Reduced SG&A Costs $8.3 Million or 18% +11% |

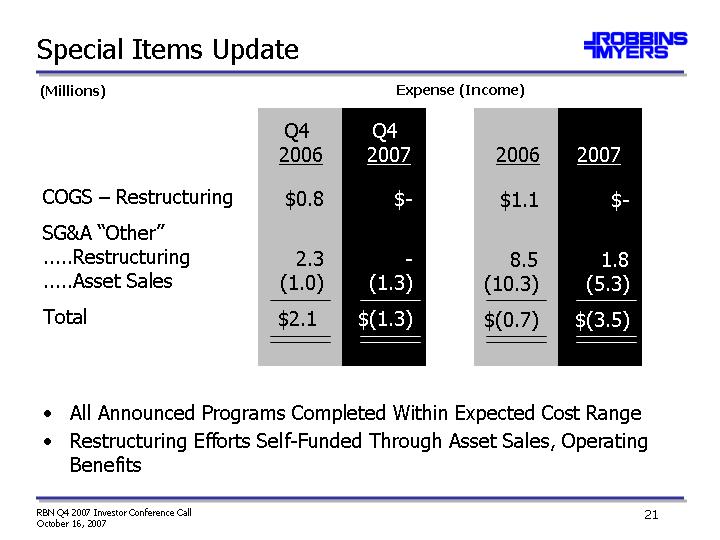

| Special Items Update Q4 2006 COGS - Restructuring SG&A "Other" ......Restructuring ......Asset Sales Total $0.8 2.3 (1.0) $2.1 $- - - (1.3) $(1.3) All Announced Programs Completed Within Expected Cost Range Restructuring Efforts Self-Funded Through Asset Sales, Operating Benefits (Millions) Expense (Income) 2006 $1.1 8.5 (10.3) $(0.7) 2007 $- 1.8 (5.3) $(3.5) Q4 2007 |

| Q4 Segment Highlights Orders Ending Backlog Net Sales FX Impact on Sales EBIT Goodwill Impairment Restructuring Costs Asset Sale (Gains) Adj. EBIT Adj. EBIT Margin Q4 2007 Q4 2006 $80.4 43.0 84.0 +1% 24.0 - - - - - - 24.0 28.5% $77.6 33.3 73.2 19.6 - - - - - - 19.6 26.8% FMG Q4 2007 Q4 2006 $71.4 98.9 79.6 +5% 10.5 - - - - - - 10.5 13.2% $70.7 88.4 66.8 6.2 - - (0.2) - - 6.0 9.0% PSG Q4 2007 Q4 2006 $36.9 52.0 43.4 +5% 6.7 - - - - (1.3) 5.4 12.5% $46.3 52.7 43.1 (0.7) - - 3.2 (1.1) 1.4 3.3% Romaco (Millions) |

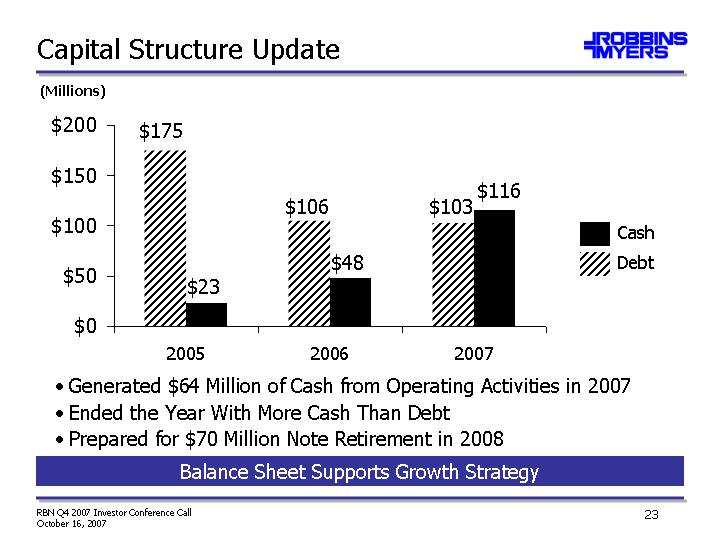

| Capital Structure Update 2005 2006 2007 Debt 175 105.5 103 Cash 23 48 116 Generated $64 Million of Cash from Operating Activities in 2007 Ended the Year With More Cash Than Debt Prepared for $70 Million Note Retirement in 2008 Balance Sheet Supports Growth Strategy $103 Debt Cash $116 $106 $48 $175 $23 (Millions) |

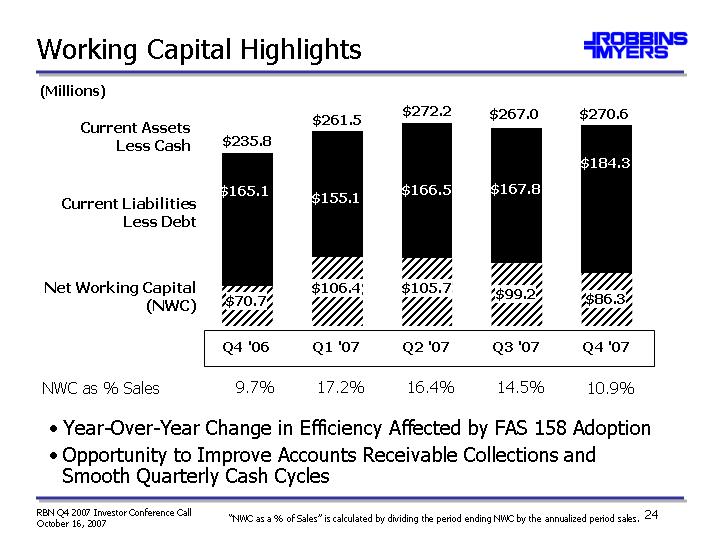

| Working Capital Highlights Q4 2005 Q1 2006 Q2 2006 Q3 2006 Q4 '06 Q1 '07 Q2 '07 Q3 '07 Q4 '07 Net Working Capital 84.4 90.2 98.1 89 70.7 106.4 105.7 99.2 86.3 Net Current Liab 164.3 155.9 148.8 148.7 165.1 155.1 166.5 167.8 184.3 % of Sales 0.162 0.164 0.145 0.096 0.172 0.163 0.145 0.104 Net Current Assets 248.7 246.1 246.9 237.7 235.8 261.5 271.2 267 270.6 Current Assets Less Cash $235.8 $261.5 Current Liabilities Less Debt Net Working Capital (NWC) NWC as % Sales "NWC as a % of Sales" is calculated by dividing the period ending NWC by the annualized period sales. 9.7% 17.2% 16.4% 14.5% $272.2 $267.0 10.9% $270.6 Year-Over-Year Change in Efficiency Affected by FAS 158 Adoption Opportunity to Improve Accounts Receivable Collections and Smooth Quarterly Cash Cycles (Millions) |

| Q4 2007 Financial Results Investor Conference Call October 16, 2007 Questions? |

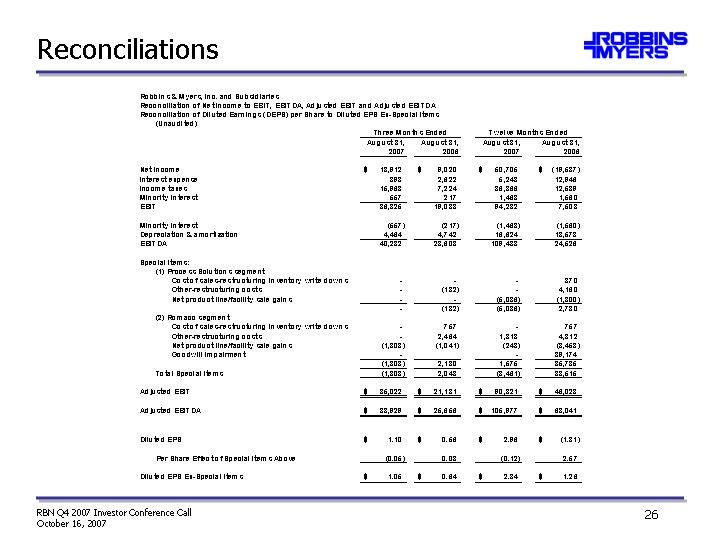

| Reconciliations |