OMB APPROVAL

OMB Number: 3235-0570

Expires: January 31, 2014

Estimated average burden hours per response: 20.6

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-05773

ING Balanced Portfolio, Inc.

(Exact name of registrant as specified in charter)

7337 E. Doubletree Ranch Rd., Scottsdale, AZ | | 85258 |

(Address of principal executive offices) | | (Zip code) |

The Corporation Trust Incorporated, 300 E. Lombard Street, Baltimore, MD 21201

(Name and address of agent for service)

Registrant’s telephone number, including area code: 1-800-992-0180

Date of fiscal year end: | December 31 |

| |

Date of reporting period: | January 1, 2012 to December 31, 2012 |

ITEM 1. REPORTS TO STOCKHOLDERS.

The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Act (17 CFR 270.30e-1):

Annual Report

December 31, 2012

Classes ADV, I, S and S2

ING Variable Product Funds

n ING Balanced Portfolio

n ING BlackRock Science and Technology Opportunities Portfolio

n ING Growth and Income Portfolio

n ING Intermediate Bond Portfolio

n ING Money Market Portfolio

n ING Small Company Portfolio

E-Delivery Sign-up – details inside

E-Delivery Sign-up – details inside

This report is submitted for general information to shareholders of the ING Funds. It is not authorized for distribution to prospective shareholders unless accompanied or preceded by a prospectus which includes details regarding the funds' investment objectives, risks, charges, expenses and other information. This information should be read carefully.

President's Letter | | | 1 | | |

Market Perspective | | | 2 | | |

Portfolio Managers' Reports | | | 4 | | |

Shareholder Expense Examples | | | 15 | | |

Report of Independent Registered Public Accounting Firm | | | 17 | | |

Statements of Assets and Liabilities | | | 18 | | |

Statements of Operations | | | 21 | | |

Statements of Changes in Net Assets | | | 23 | | |

Financial Highlights | | | 26 | | |

Notes to Financial Statements | | | 29 | | |

| Summary Portfolios of Investments | | | 49 | | |

Tax Information | | | 95 | | |

Director/Trustee and Officer Information | | | 96 | | |

Advisory Contract Approval Discussion | | | 101 | | |

PROXY VOTING INFORMATION

A description of the policies and procedures that the Portfolios use to determine how to vote proxies related to portfolio securities is available: (1) without charge, upon request, by calling Shareholder Services toll-free at (800) 992-0180; (2) on the ING Funds' website at www.inginvestment.com; and (3) on the U.S. Securities and Exchange Commission's ("SEC's") website at www.sec.gov. Information regarding how the Portfolios voted proxies related to portfolio securities during the most recent 12-month period ended June 30 is available without charge on the ING Funds' website at www.inginvestment.com and on the SEC's website at www.sec.gov.

QUARTERLY PORTFOLIO HOLDINGS

The Portfolios file their complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. This report contains a summary portfolio of investments for certain Portfolios. The Portfolios' Forms N-Q are available on the SEC's website at www.sec.gov. The Portfolios' Forms N-Q may be reviewed and copied at the SEC's Public Reference Room in Washington, DC, and information on the operation of the Public Reference Room may be obtained by calling (800) SEC-0330. The Portfolios' Forms N-Q, as well as a complete portfolio of investments, are available without charge upon request from the Portfolios by calling Shareholder Services toll-free at (800) 992-0180.

Looking forward

Dear Shareholder,

Normally I end my letters by exhorting clients to keep their portfolios focused on long-term goals and well diversified in terms of assets and geography, and to discuss thoroughly any proposed investment changes with their financial advisors before taking action. This month, the reminders are up front to emphasize their importance as we conclude an eventful year and take a look forward.

A central theme over the past few years has been the impact government and central bank policymaking has had on economic and market outcomes. Private-sector forces, which tend to restore equilibrium in normal times, have not done enough to allow policymakers to scale back their involvement. An important reason for this is that the framework within which private-sector decisions are made requires substantial overhaul; economic and monetary ties in the euro zone need to be strengthened, the U.S. must make some difficult fiscal decisions and the success of a number of economies depends on the introduction of structural reforms.

Since the world economy is still sluggish, supportive public policies will remain critical in 2013 and beyond. However, what might we anticipate over the long term? For insight into this question, I turned to a recent report published by the National Intelligence Council — a U.S. government agency that serves as a bridge between the U.S. intelligence and policy communities — entitled "Global Trends 2030: Alternative Worlds." The report identifies four "megatrends" that the Council considers likely to emerge over the next 20 years or so. Among these are two that potentially carry implications for future investment themes. Individual empowerment will accelerate owing to growth of the global middle class, says the Council, potentially leading to a virtuous cycle of global economic expansion and creating dynamic markets for new products and technologies. Meanwhile, emerging nations will wield greater regional influence, and the health of the global economy increasingly will be linked to how well the developing world fares. This suggests that a portfolio of securities that provide exposure to developed and emerging market economies — such as ING Funds seeks to provide — may offer attractive potential for some time to come.

It's important to remember that these are projections and subject to change, but they point to the value of keeping one's portfolio well diversified to meet the challenges and take advantage of the opportunities that lie ahead.

All of us at ING Funds extend our best wishes for a happy and prosperous new year. We appreciate your continued confidence in us, and we look forward to serving your investment needs in the future.

Sincerely,

Shaun Mathews

President and Chief Executive Officer

ING Funds

January 4, 2013

The views expressed in the President's Letter reflect those of the President as of the date of the letter. Any such views are subject to change at any time based upon market or other conditions and ING Funds disclaims any responsibility to update such views. These views may not be relied on as investment advice and because investment decisions for an ING Fund are based on numerous factors, may not be relied on as an indication of investment intent on behalf of any ING Fund. Reference to specific company securities should not be construed as recommendations or investment advice.

International investing poses special risks including currency fluctuation, economic and political risks not found in investments that are solely domestic.

1

MARKET PERSPECTIVE: YEAR ENDED DECEMBER 31, 2012

In the early part of our fiscal year, global equities in the form of the MSCI World IndexSM measured in local currencies including net reinvested dividends, enjoyed the best first quarter rally since 1998. But in the two months from early April the MSCI World IndexSM slumped 11% as, for the third consecutive year, the basis of earlier optimism was undermined by events. The recovery from there was dramatic and the MSCI World IndexSM ended up 15.71% for the whole year, despite slow, patchy improvement in economic data, and investors' frustration at the futile efforts of global leaders to resolve key problems. It came because central banks, by their actions, made risky assets much more attractive. (The MSCI World IndexSM returned 15.83% for the one year ended December 31, 2012, measured in U.S. dollars.)

Much of the early upbeat sentiment rested on a sharp improvement in the employment situation, probably the most important driver of economic activity. But the improvement faded fast: the three-month average of 245,000 new jobs reported in March slumped to only 94,000 in September, before rebounding less than one third of the way to 139,000 by December. The unemployment rate was still uncomfortably high at 7.7%.

By December, other economic data, from average hourly earnings growth to consumer confidence to retail sales were mostly inconclusive. Final third quarter gross domestic product ("GDP") growth was revised up to 3.1%, but it didn't feel like it and the next few quarters were expected to show growth at about half of this level.

The housing market however, seemed clearly to be on the mend. The final S&P/Case-Shiller 20-City Composite Home Price Index showed a 4.3% year-over-year gain, while new home sales in November were the highest since April 2010.

Also in the relative doldrums was China, responsible for much of global GDP growth in recent years. GDP increased by 7.4% in the third quarter of 2012 over the same quarter in 2011, the lowest rise in three years.

And yet despite the shortage of good news, the MSCI World IndexSM ended December 16% above the low point in early June. How could this be? One reason was a growing sense that the euro zone's enduring sovereign debt crisis might at last be approaching the end-game. Another was a third round of quantitative easing launched by the Federal Reserve.

In the euro zone, amid ongoing protests against fiscal austerity, a €100 billion recapitalization bailout for Spain's shaky banks was tortuously agreed upon in June. Attention returned to Greece in July where the continuation of the country's bailout rested on the outcome of an examination by creditors of its parlous fiscal state. With prospects for the euro looking increasingly tenuous, European Central Bank ("ECB") President Draghi came out on July 26 with a statement unprecedented in its explicitness, that the ECB was "ready to do whatever it takes to preserve the euro." Under certain conditions, the ECB would buy without limitation the 1-3 year bonds of a country in difficulties.

In September, Federal Reserve Chairman Bernanke announced a third round of quantitative easing: an additional $40 billion of agency mortgage-backed securities would be purchased monthly. Then in December, "Operation Twist" was replaced by $45 billion in monthly Treasury purchases. Exceptionally low policy interest rates would remain at least until the unemployment rate fell to 6.5%.

So the year ended with central bankers sounding increasingly determined to underpin the euro and the prices of risky assets. This was enough to drive those prices higher despite dark political clouds. In Europe, inter-governmental squabbling dangerously held back agreement on Greece's next bailout tranche until November 27. In the U.S., the newly-elected Congress looked rather like the old one, and an ominous year-end cocktail of deflationary tax increases and spending cuts was forestalled by an eleventh-hour agreement on tax increases alone which postponed an even bigger conflict on spending and the debt ceiling until March.

In U.S. fixed income markets the Barclays Capital U.S. Aggregate Bond Index ("BCAB") of investment grade bonds rose 4.22% in 2012. The Barclays Capital U.S. Treasury Index, a sub-index of the BCAB, returned only 1.99% as risk appetite recovered. By contrast the Barclays Capital U.S. Corporate Investment Grade Bond Index, also a sub-index of the BCAB, rose 9.82%, while the Barclays Capital High-Yield Bond — 2% Issuer Constrained Composite Index (not part of the BCAB index) gained 15.78%.

U.S. equities, represented by the S&P 500® Index including dividends, advanced 16.00% in the fiscal year. By sector, financials led the way with a return of 28.82%, followed by consumer discretionary with a return of 23.92%. No sector incurred a loss, but defensive utilities' slim 1.29% gain reflected improved risk appetite. Operating earnings per share for S&P 500® companies set a new record in the second quarter of 2012, and barely slipped in the third.

In currency markets, the dollar fell 1.76% against the euro, which rebounded after Draghi's July pronouncements, and 4.38% against the pound, which moved in sympathy with the euro, reflecting close trade ties. But the dollar gained 12.79% over the yen in 2012, as Japan's parliamentary opposition won a landslide in December elections and promised unlimited monetary easing.

In international markets, the MSCI Japan® Index soared 21.57%, due mainly to the monetary stimulus referred to above. This was despite the effect on Japan's export focused economy of the euro zone crisis, the slowdown in China and a return to recession. The MSCI Europe ex UK® Index rose 18.78% due to central bank initiatives, in the face of economic news that was unremittingly bad, also including a return to recession and record unemployment at 11.7%. The MSCI UK® Index added 10.19%, boosted by financials but held back by large, lagging energy and materials. The U.K. GDP grew 1% in the third quarter, but this was largely due to one-time statistical anomalies.

Parentheses denote a negative number.

All indices are unmanaged and investors cannot invest directly in an index. Past performance does not guarantee future results. The performance quoted represents past performance. Investment return and principal value of an investment will fluctuate, and shares, when redeemed, may be worth more or less than their original cost. The Portfolios' performance is subject to change since the period's end and may be lower or higher than the performance data shown. Please call (800) 992-0180 or log on to www.inginvestment.com to obtain performance data current to the most recent month end.

Market Perspective reflects the views of ING's Chief Investment Risk Officer only through the end of the period, and is subject to change based on market and other conditions.

2

Index | | Description | |

Barclays Capital High Yield Bond — 2% Issuer Constrained Composite Index | | An unmanaged index that includes all fixed-income securities having a maximum quality rating of Ba1, a minimum amount outstanding of $150 million, and at least one year to maturity. | |

Barclays Capital U.S. Aggregate Bond Index | | An unmanaged index of publicly issued investment grade U.S. Government, mortgage-backed, asset-backed and corporate debt securities. | |

Barclays Capital U.S. Corporate Investment Grade Bond Index | | An unmanaged index consisting of publicly issued, fixed rate, nonconvertible, investment grade debt securities. | |

Barclays Capital U.S. Treasury Index | | An unmanaged index that includes public obligations of the U.S. Treasury. Treasury bills, certain special issues, such as state and local government series bonds (SLGs), as well as U.S. Treasury TIPS and STRIPS, are excluded. | |

MSCI EAFE® Index | | An unmanaged index that measures the performance of securities listed on exchanges in Europe, Australasia and the Far East. It includes the reinvestment of dividends net of withholding taxes, but does not reflect fees, brokerage commissions or other expenses of investing. | |

MSCI Europe ex UK® Index | | A free float-adjusted market capitalization index that is designed to measure developed market equity performance in Europe, excluding the UK. | |

MSCI Japan® Index | | A free float-adjusted market capitalization index that is designed to measuredeveloped market equity performance in Japan. | |

MSCI UK® Index | | A free float-adjusted market capitalization index that is designed to measure developed market equity performance in the UK. | |

MSCI World IndexSM | | An unmanaged index that measures the performance of over 1,400 securities listed on exchanges in the U.S., Europe, Canada, Australia, New Zealand and the Far East. | |

NYSE Arca Tech 100 Index | | A multi-industry technology index measuring the performance of companies using technology innovation across a broad spectrum of industries. It is comprised of 100 listed and over-the-counter stocks from 14 different subsectors including computer hardware, software, semiconductors, telecommunications, data storage and processing, electronics and biotechnology. | |

Russell 2000® Index | | An unmanaged index that measures the performance of securities of small U.S. companies.

iMoneyNet First Tier Retail Index An unmanaged index that includes the most broadly based money market funds. | |

Russell 3000® Index | | An unmanaged index that measures the performance of the largest 3000 U.S. companies representing approximately 98% of the investable U.S. equity market. | |

S&P 500® Index | | An unmanaged index that measures the performance of securities of approximately 500 large-capitalization companies whose securities are traded on major U.S. stock markets. | |

S&P/Case-Shiller 20-City Composite Home Price Index | | A composite index of the home price index for the top 20 Metropolitan Statistical Areas in the United States. The index is published monthly by Standard & Poor's. | |

S&P Target Risk Growth Index | | Seeks to provide increased exposure to equities, while also using some fixed-income exposure to dampen risk. | |

3

PORTFOLIO MANAGERS' REPORT

ING Balanced Portfolio (the "Portfolio") seeks total return consisting of capital appreciation (both realized and unrealized) and current income; the secondary investment objective is long-term capital appreciation. The Portfolio is managed by Christopher F. Corapi, Christine Hurtsellers, CFA, Heather Hackett, CFA, and Paul Zemsky, CFA, Portfolio Managers, of ING Investment Management Co. LLC — the Sub-Adviser.

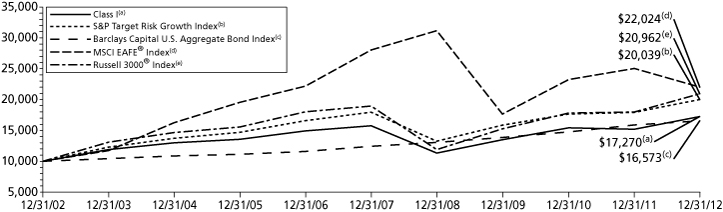

Performance: For the year ended December 31, 2012, the Portfolio's Class I shares provided a total return of 13.64% compared to the S&P Target Risk Growth Index, Barclays Capital U.S. Aggregate Bond Index, MSCI EAFE® Index and Russell 3000® Index, which returned 11.72%, 4.21%, 17.32% and 16.42%, respectively, for the same period.

Portfolio Specifics: Performance of our tactical asset allocation strategies was additive over the year. During May, we initiated an overweight to large-cap core, with a corresponding underweight to emerging markets, which we held until the middle of September. Over this time, domestic equity outperformed international equity and, therefore, this position was additive to performance. Toward the end of the year, we initiated a large-cap value overweight with a large-cap growth underweight, which was slightly beneficial. Certain valuation metrics supported this position. Specifically, growth stocks outperformed for four years in a period of slow growth and deleveraging in the United States.

We believe private sector deleveraging to be complete and anticipate a continued U.S. cyclical recovery, which would aid value stocks. We also believe value's overweight to financials to be supported by continued quantitative easing from the U.S. Federal Reserve (the "Fed"), strength in recovering U.S. housing and expectations of gradual improvement in European financial stocks. We believe the continued negative earnings momentum in technology, overweighted in growth, could reward our underweight growth position.

At the beginning of December, anticipating that fiscal support would be stronger in non-U.S. countries than in the U.S., where fiscal cliff-driven austerity measures were just beginning, we initiated an overweight to non-U.S. equity. This included MSCI EAFE® and emerging market equities, with a corresponding underweight to large-cap core domestic equity. We increased this position slightly toward the end of the year. We also initiated a modest high yield overweight, with a corresponding U.S. core fixed income underweight toward the end of 2012. With the "search for yield" a key investment theme; and with additional quantitative easing, continued low rates and diminished economic fears, these factors provided strong support for an overweight to high yield bonds relative to core bonds. At the beginning of May, we increased our strategic allocation to U.S. equities. We also initiated a strategic allocation to the ING Mid Cap Value sleeve, as well as the ING High Yield Bond sleeve. At the same time, we decreased our strategic allocation to international stocks and increased our allocation to emerging markets. We also decreased our allocation to U.S. domestic bonds.

The Portfolio beat its S&P Target Risk benchmark due partially to outperformance of the underlying funds as well as the Index holding a significant allocation to underperforming short term Treasuries. The Portfolio held a higher weighting to equities which was beneficial to performance. Among the underlying equity funds, the Large Cap Growth, International Equity and Emerging Markets Equity sleeves outperformed their individual benchmarks, while Growth and Income Portfolio, Large Cap Value, Mid Cap Value and Mid Cap Opportunities underperformed. The Portfolios underlying fixed income funds were additive to performance with the ING Intermediate Bond sleeve and the ING Global Bond sleeve outperforming over the period.

Current Strategy and Outlook: Despite the thirteenth-hour compromise on the fiscal cliff, risks remain for 2013, but we continue to be optimistic. Global financial markets are currently indicating low levels of stress and turbulence. In addition, we anticipate that monetary and fiscal policies will be more expansionary outside the U.S. than within going forward. With many central banks expected to keep stimulating their economies, we could see further equity gains in 2013. We believe both European and Japanese valuations are more attractive than those in the United States, but there are still questions about 2013-14 economic growth in both regions. Chinese economic developments continue to support a recovery in the equity market, and China should be expected to continue to be a catalyst for emerging markets.

Looking ahead, we also believe that large cap value has relatively attractive valuations. It has a concentration in financials, which stand to benefit from improvements in U.S. housing and a continuation of open-ended quantitative easing from the Fed. Our current positioning reflects these views, with an overweight to value over growth, an overweight to non-U.S. equity, as well as an overweight to high yield bonds. Fundamentals in the high yield asset class are currently attractive, with low default rates. We expect returns for high yield bonds to come from the higher coupon rather than broad price movement going forward.

Investment Type Allocation

as of December 31, 2012

(as a percentage of net assets)

Common Stock | | | 61.9 | % | |

Corporate Bonds/Notes | | | 10.0 | % | |

U.S. Government Agency Obligations | | | 6.8 | % | |

Exchange-Traded Funds | | | 6.2 | % | |

Collateralized Mortgage Obligations | | | 4.1 | % | |

Foreign Government Bonds | | | 4.0 | % | |

U.S. Treasury Obligations | | | 2.3 | % | |

Asset-Backed Securities | | | 1.1 | % | |

Preferred Stock | | | 0.1 | % | |

Purchased Options | | | 0.1 | % | |

Assets in Excess of Other Liabilities* | | | 3.4 | % | |

Net Assets | | | 100.0 | % | |

* Includes short-term investments and purchased options.

Portfolio holdings are subject to change daily.

Top Ten Holdings

as of December 31, 2012*

(as a percentage of net assets)

iShares iBoxx $ High Yield Corporate Bond Fund | | | 3.4 | % | |

SPDR Barclays Capital High Yield Bond ETF | | | 2.6 | % | |

ExxonMobil Corp. | | | 1.4 | % | |

Apple, Inc. | | | 1.2 | % | |

Brazil Notas do Tesouro Nacional Series F,

10.000%, 01/01/23 | | | 1.2 | % | |

Fannie Mae, 3.000%, 11/25/42 | | | 0.9 | % | |

Pfizer, Inc. | | | 0.8 | % | |

Google, Inc. — Class A | | | 0.8 | % | |

Coca-Cola Enterprises, Inc. | | | 0.8 | % | |

United States Treasury Bond, 2.750%, 08/15/42 | | | 0.7 | % | |

* Excludes short-term investments.

Portfolio holdings are subject to change daily.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Portfolio may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

4

PORTFOLIO MANAGERS' REPORT

Average Annual Total Returns for the Periods Ended December 31, 2012 | |

| | 1 Year | | 5 Year | | 10 Year | | Since Inception

of Class S

May 29, 2003 | |

Class I | | | 13.64 | % | | | 1.87 | % | | | 5.62 | % | | | — | | |

Class S | | | 13.49 | % | | | 1.63 | % | | | — | | | | 4.81 | % | |

S&P Target Risk Growth Index | | | 11.72 | % | | | 2.21 | % | | | 7.20 | % | | | 6.73 | %(1) | |

Barclays Capital U.S. Aggregate Bond Index | | | 4.21 | % | | | 5.95 | % | | | 5.18 | % | | | 4.97 | %(1) | |

MSCI EAFE® Index | | | 17.32 | % | | | (3.69 | )% | | | 8.21 | % | | | 7.83 | %(1) | |

Russell 3000® Index | | | 16.42 | % | | | 2.04 | % | | | 7.68 | % | | | 6.83 | %(1) | |

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING Balanced Portfolio against the indices indicated. An index has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Portfolio's performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on portfolio distributions or the redemption of portfolio shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

The performance update illustrates performance for a variable investment option available through a variable contract. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns

and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. Please log on to www.inginvestment.com or call (800) 992-0180 to get performance through the most recent month end.

This report contains statements that may be "forward-looking" statements. Actual results may differ materially from those projected in the "forward-looking" statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers' views are subject to change at any time based on market and other conditions.

Portfolio holdings are subject to change daily.

(1) Since inception performance for the indices is shown from June 1, 2003.

Effective March 1, 2002, ING Investments, LLC began serving as investment adviser and ING Investment Management Co. LLC, the former investment adviser, began serving as sub-adviser to the Portfolio.

5

ING BLACKROCK SCIENCE AND TECHNOLOGY OPPORTUNITIES PORTFOLIO

PORTFOLIO MANAGERS' REPORT

ING BlackRock Science and Technology Opportunities Portfolio (the "Portfolio") seeks long-term capital appreciation. The Portfolio is managed by Thomas P. Callan, CFA, Managing Director and Senior Portfolio Manager, Erin Xie, PhD, Managing Director and Portfolio Manager and Jean M. Rosenbaum, CFA, Managing Director and Portfolio Manager of BlackRock Advisors, LLC — the Sub-Adviser.*

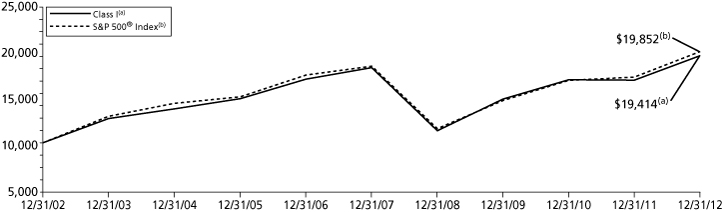

Performance: For the year ended December 31, 2012, the Portfolio's Class I shares provided a total return of 7.89% compared to the S&P 500® Index and the NYSE Arca Tech 100 IndexSM, which returned 16.00% and 21.40%, respectively, for the same period.

Portfolio Specifics: Portfolio returns were positive for the one year ended December 2012. The Portfolio's performance trailed both its Morningstar Technology peer group average, which returned 13.10%, and the NYSE Arca Tech 100 IndexSM.

The positive absolute performance of the Portfolio in 2012 was led primarily by positioning in three sub-industries; application software, data processing & outsources services and computer hardware. The stocks owned in these particular groups are benefiting from a number of factors including multi-year service trends in cloud-based computing, migration from cash-based to electronic-based payment transactions and a wealthier emerging market consumer. On a single names basis, Apple Inc. was the largest contributor as it rose nearly 33% and was held at an average portfolio weight of 10%, which was in-line with most Tech fund peers throughout the year. We have since reduced exposure to Apple given its strong run and evidence of growing competition in the smart-phone arena.

In a relative sense, underperformance came from stock selection in the communications equipment, internet software & services, semiconductors and systems software sub-industries. Additionally, the Portfolio's overweight to semiconductors and underweight to biotechnology were relative detractors from an allocation standpoint. In communications equipment, stocks such as F5 Networks and Ciena Corp came under significant pressure prior to their disposal from the Portfolio. Enterprise IT spending slowed during the second half of the year as companies took a more cautious view of the economic outlook. As a result, earnings estimates were trimmed for 2012 and 2013, disappointing investors. For the internet software space, we had positioned ourselves overweight to begin the year only to pull back exposure in the second half given concerns about the US 'fiscal cliff', declines in European growth and a deceleration in China. We still like the group, but rather than mining for smaller-caps with unproven business models, we have been drawn to more established players where cash flow metrics look most attractive, such as Google and eBay. Lastly, stock-specific performance volatility in the semiconductors and systems software sub-industry further hampered relative results.

Current Strategy and Outlook: At period end, there are two things the investment team believes will continue to shape the Portfolio's positioning. The first is that the world economy will continue to muddle along, just above stall speed, continuing to test investors' convictions. Secondly, macro-uncertainty and financial repression (i.e. low real yields) will continue to cause investors to crowd into higher quality shares on the margin, despite valuation spreads for this cohort of stocks that are at the high end of historical ranges. As a result, the Portfolio continues to have only a very modest bet on continued growth in the world economy, as the team maintains a careful balance of defensive and cyclical exposures.

Within the context of maintaining balance, an overweight to semiconductors is one area we are constructive on in the near-to-medium term. Inventory levels in the channel are well controlled as the industry has been under-shipping demand for a while. The share values did not reflect a cyclical upturn, which we believe is possible as the macroeconomic and political issues begin to be worked through. We believe the U.S. housing market is beginning to recover and should help drive a broader industrial recovery. This outlook coupled with reasonable valuations keeps us optimistic on the shares of analog semiconductor companies in particular given their greater exposure to the industrial end market.

Industry Diversification

as of December 31, 2012

(as a percentage of net assets)

Semiconductors & Semiconductor Equipment | | | 19.9 | % | |

Information Technology | | | 16.3 | % | |

IT Services | | | 16.3 | % | |

Communications Equipment | | | 13.4 | % | |

Internet Software & Services | | | 10.4 | % | |

Computers & Peripherals | | | 10.0 | % | |

Internet & Catalog Retail | | | 4.9 | % | |

Software | | | 2.6 | % | |

Electronic Equipment, Instruments & Components | | | 2.2 | % | |

Health Care | | | 1.3 | % | |

Assets in Excess of Other Liabilities* | | | 2.7 | % | |

Net Assets | | | 100.0 | % | |

* Includes short-term investments.

Portfolio holdings are subject to change daily.

Top Ten Holdings

as of December 31, 2012*

(as a percentage of net assets)

Apple, Inc. | | | 8.4 | % | |

Cisco Systems, Inc. | | | 5.4 | % | |

Google, Inc. — Class A | | | 5.1 | % | |

Qualcomm, Inc. | | | 4.9 | % | |

Visa, Inc. | | | 3.9 | % | |

Salesforce.com, Inc. | | | 3.4 | % | |

eBay, Inc. | | | 3.0 | % | |

Oracle Corp. | | | 2.6 | % | |

International Business Machines Corp. | | | 2.5 | % | |

Xilinx, Inc. | | | 2.4 | % | |

* Excludes short-term investments.

Portfolio holdings are subject to change daily.

* Effective September 25, 2012, Paul Ma was removed as a co-portfolio manager for the Portfolio. On December 12, 2012, the Board of Directors of the Portfolio approved a proposal to reorganize the Portfolio with and into ING MidCap Opportunities Portfolio, which is not included in this report. The proposed reorganization is subject to approval by shareholders of the Portfolio at a shareholder meeting scheduled to be held on or about March 12, 2013. The Portfolio will notify its shareholders if shareholder approval of the proposed reorganization is not obtained. If shareholder approval of the proposed reorganization is obtained, it is expected that the reorganization will take place on or about March 23, 2013.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Portfolio may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

6

ING BLACKROCK SCIENCE AND TECHNOLOGY OPPORTUNITIES PORTFOLIO

PORTFOLIO MANAGERS' REPORT

Average Annual Total Returns for the Periods Ended December 31, 2012 | |

| | 1 Year | | 5 Year | | 10 Year | | Since Inception

of Class ADV

December 16, 2008 | | Since Inception

of Class S2

February 27, 2009 | |

Class ADV | | | 7.30 | % | | | — | | | | — | | | | 13.97 | % | | | — | | |

Class I | | | 7.89 | % | | | 1.04 | % | | | 7.99 | % | | | — | | | | — | | |

Class S(1) | | | 7.63 | % | | | 0.80 | % | | | 2.15 | % | | | — | | | | — | | |

Class S2 | | | 7.41 | % | | | — | | | | — | | | | — | | | | 17.60 | % | |

S&P 500® Index | | | 16.00 | % | | | 1.66 | % | | | 7.10 | % | | | 14.58 | %(2) | | | 21.42 | %(3) | |

NYSE Arca Tech 100 IndexSM | | | 21.40 | % | | | 7.63 | % | | | 11.68 | % | | | 21.85 | %(2) | | | 25.55 | %(3) | |

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING BlackRock Science and Technology Opportunities Portfolio against the indices indicated. An index has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Portfolio's performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on portfolio distributions or the redemption of portfolio shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

The performance update illustrates performance for a variable investment option available through a variable contract. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. Please call (800) 992-0180 to get performance through the most recent month end.

This report contains statements that may be "forward-looking" statements. Actual results may differ materially from those projected in the "forward-looking" statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers' views are subject to change at any time based on market and other conditions.

Portfolio holdings are subject to change daily.

(1) On December 16, 2003, all outstanding shares of Class S were fully redeemed. On July 20, 2005, Class S recommenced operations. The returns for Class S include the performance for Class I, adjusted to reflect the higher expenses of Class S, for the period December 17, 2003 to July 19, 2005.

(2) Since inception performance for the indices is shown from January 1, 2009.

(3) Since inception performance for the indices is shown from March 1, 2009.

Effective March 1, 2002, ING Investments, LLC began serving as investment adviser. Formerly, ING Investment Management Co. LLC served as the investment adviser. Prior to January 1, 2004, the Portfolio was sub-advised by a different sub-adviser.

7

ING GROWTH AND INCOME PORTFOLIO

PORTFOLIO MANAGERS' REPORT

ING Growth and Income Portfolio (the "Portfolio") seeks to maximize total return through investments in a diversified portfolio of common stocks and securities convertible into common stock. It is anticipated that capital appreciation and investment income will both be major factors in achieving total return. The Portfolio is managed by Christopher F. Corapi and Michael Pytosh, Portfolio Managers of ING Investment Management Co. LLC — the Sub-Adviser.

Performance: For the year ended December 31, 2012, the Portfolio's Class I shares provided a total return of 15.78% compared to the S&P 500® Index, which returned 16.00% for the same period.

Portfolio Specifics: Despite a reporting period of fairly good investment results, the Portfolio slightly lagged its benchmark after the deduction of fees and expenses. During the period, stock selection benefited the Portfolio, notably selection within information technology and healthcare. Stock selection within financials and consumer staples detracted value.

Within information technology, an overweight in Seagate Technology Inc. was the largest contributor to performance. Shares of enterprise storage company Seagate Technology outperformed based on positive earnings revisions due to better supply-demand conditions and higher pricing, improved long-term profitability due to industry consolidation and $2 billion in dividends and share repurchases.

Our overweight position of apparel company Michael Kors outperformed the market after the company's same-store sales, licensing revenues and operating margins strongly exceeded expectations in 2012. In addition, the company raised fiscal year 2013 guidance over 100%. Furthermore, Michael Kors is rapidly gaining market share of the high-end women's handbag market.

In financials, not owning Bank of America Corp. was unfavorable to returns. In October, the company reported third quarter earnings that exceeded consensus. While the quarter was highlighted by strong commercial loan growth, capital ratio building, lower non-interest expense and margin expansion, the results also reflected weakness in consumer, banking, cards, trading, loans and brokerage. The Portfolio does not own Bank of America as we believe the firm's revenue picture remains muted despite improvements in capital structure and mortgage-related costs.

Allegheny Technologies is a specialty metals and components supplier. Its shares underperformed after disappointing earnings results for the third straight quarter. The earnings miss was driven by the impact of global economic weakness on customers' inventory management and on overall demand for the company's products.

Current Strategy and Outlook: We adhere to the investment process, and have been taking advantage of market volatility to add to existing positions during corrections or to initiate new positions. Currently the Portfolio is overweight in the energy, industrials and telecommunications sectors and underweight in financials, utilities and consumer discretionary sectors.

Sector Diversification

as of December 31, 2012

(as a percentage of net assets)

Information Technology | | | 19.1 | % | |

Financials | | | 14.4 | % | |

Energy | | | 12.1 | % | |

Health Care | | | 11.8 | % | |

Industrials | | | 11.1 | % | |

Consumer Discretionary | | | 10.8 | % | |

Consumer Staples | | | 10.1 | % | |

Telecommunication Services | | | 3.4 | % | |

Materials | | | 3.4 | % | |

Utilities | | | 1.6 | % | |

Assets in Excess of Other Liabilities* | | | 2.2 | % | |

Net Assets | | | 100.0 | % | |

* Includes short-term investments.

Portfolio holdings are subject to change daily.

Top Ten Holdings

as of December 31, 2012*

(as a percentage of net assets)

Apple, Inc. | | | 5.5 | % | |

ExxonMobil Corp. | | | 4.9 | % | |

Google, Inc. — Class A | | | 4.3 | % | |

Pfizer, Inc. | | | 3.0 | % | |

Wells Fargo & Co. | | | 2.8 | % | |

Oracle Corp. | | | 2.6 | % | |

Comcast Corp. — Class A | | | 2.5 | % | |

Verizon Communications, Inc. | | | 2.4 | % | |

JPMorgan Chase & Co. | | | 2.2 | % | |

Philip Morris International, Inc. | | | 1.9 | % | |

* Excludes short-term investments.

Portfolio holdings are subject to change daily.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Portfolio may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

8

ING GROWTH AND INCOME PORTFOLIO

PORTFOLIO MANAGERS' REPORT

Average Annual Total Returns for the Periods Ended December 31, 2012 | |

| | 1 Year | | 5 Year | | 10 Year | | Since Inception

of Class ADV

December 20, 2006 | | Since Inception

of Class S

June 11, 2003 | | Since Inception

of Class S2

February 27, 2009 | |

Class ADV | | | 15.24 | % | | | 0.89 | % | | | — | | | | 1.79 | % | | | — | | | | — | | |

Class I | | | 15.78 | % | | | 1.37 | % | | | 6.85 | % | | | — | | | | — | | | | — | | |

Class S | | | 15.47 | % | | | 1.12 | % | | | — | | | | — | | | | 5.59 | % | | | — | | |

Class S2 | | | 15.30 | % | | | — | | | | — | | | | — | | | | — | | | | 19.28 | % | |

S&P 500® Index | | | 16.00 | % | | | 1.66 | % | | | 7.10 | % | | | 2.29 | %(1) | | | 6.32 | %(2) | | | 21.42 | %(3) | |

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING Growth and Income Portfolio against the index indicated. An index has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Portfolio's performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on portfolio distributions or the redemption of portfolio shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

The performance update illustrates performance for a variable investment option available through a variable contract. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost.

Please log on to www.inginvestment.com or call (800) 992-0180 to get performance through the most recent month end.

This report contains statements that may be "forward-looking" statements. Actual results may differ materially from those projected in the "forward-looking" statements.

The views expressed in this report reflect those of the portfolio manager only through the end of the period as stated on the cover. The portfolio manager's views are subject to change at any time based on market and other conditions.

Portfolio holdings are subject to change daily.

(1) Since inception performance for the index is shown from January 1, 2007.

(2) Since inception performance for the index is shown from June 1, 2003.

(3) Since inception performance for the index is shown from March 1, 2009.

Effective March 1, 2002, ING Investments, LLC began serving as investment adviser and ING Investment Management Co. LLC, the former investment adviser, began serving as sub-adviser to the Portfolio.

9

ING INTERMEDIATE BOND PORTFOLIO

PORTFOLIO MANAGERS' REPORT

ING Intermediate Bond Portfolio (the "Portfolio") seeks to maximize total return consistent with reasonable risk. The Portfolio seeks its objective through investments in a diversified portfolio consisting primarily of debt securities. It is anticipated that capital appreciation and investment income will both be major factors in achieving total return. The Portfolio is managed by Christine Hurtsellers, CFA, Matthew Toms, CFA, and Michael Mata, Portfolio Managers of ING Investment Management Co. LLC — the Sub-Adviser.

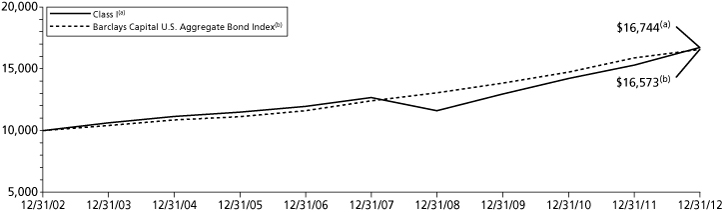

Performance: For the year ended December 31, 2012, the Portfolio's Class I shares provided a total return of 9.39% compared to the Barclays Capital U.S. Aggregate Bond Index, which returned 4.21% for the same period.

Portfolio Specifics: Fortunately, the world did not come to an end in December as the Mayans had predicted. In fact, fixed income investors continued to endorse risk assets and finished the year strongly, with most spread sectors rallying and driving up U.S. interest rates as the year ended. The Portfolio ended the year by delivering strong positive absolute returns as well as outperforming the benchmark over the period.

The Portfolio strongly outperformed the benchmark index in the first quarter of 2012 largely due to overweighting spread sector assets such as non-agency mortgage backed securities ("MBS") and high yield corporate bonds as the markets embraced risk-taking. Security selection within investment grade credit and emerging market debt helped performance.

In the second quarter, the Portfolio added back performance on a relative basis as risk aversion picked up, and the underweight exposure to U.S. Treasury assets hurt performance of the Portfolio in April and May.

The Portfolio's duration positioning was modestly short to U.S. interest rates during the second half of 2012 which, as interest rates moved higher and the U.S. yield curve steepened, had a positive impact on relative returns.

The second half of the year was more like the first quarter, where our overweights to investment grade and high yield credit, commercial mortgage-backed securities ("CMBS") and non-agency mortgages all helped relative returns as those spread sectors outperformed over the period. Overweighting agency mortgages and asset-backed securities were just a slight drag on relative performance as these underperformed. Underweighting U.S. Treasuries to fund other spread sector overweight positions helped as Treasuries underperformed. Lastly, security selection with investment grade corporates, agency mortgages and CMBS were all contributors to relative returns, while security selection in U.S. Treasuries was a drag on relative returns over the period.

Throughout the year, Treasury futures and swaps were used to manage duration. These holdings along with cash bonds led our duration and curve management to a net modest contribution over the period. Currency forwards were used for currency risk management which along with cash bonds added to the slight underperformance versus the benchmark as they were a net detractor. These together added slightly to outperformance versus the benchmark. Credit default swaps were used for both sector management and issue selection, which when combined with cash bonds were the largest contributors to excess returns for the year.

Current Strategy and Outlook: The New Year's celebrations are behind us, a fresh start is on the books for 2013, and it seems that a majority of the headwinds from 2012 have dissipated. However, we believe global imbalances are here to stay with minimal European growth being a drag on the global economy for the foreseeable future. In contrast, private sector growth in the U.S. appears to be sustainable against the backstop of highly accommodative monetary policy (substantial bond buying by the Federal Reserve). The stimulus cycle across emerging markets that featured broad rate cuts in 2012 is now paying dividends to investors. Despite the presence of political uncertainty and volatility likely induced at times by these global imbalances, our forecast is for sustained positive macro momentum and modest global growth in 2013.

Spread sectors for 2013 will largely be a different game than in 2012 given our base-case scenario of moderate economic growth, abundant financial liquidity, and good credit quality. Yields in the highest quality segments like U.S. Treasuries, agencies, agency mortgages and asset-backed securities look far less attractive relative to credit sensitive sectors like investment grade corporates, non-agency MBS, high yield corporates and emerging market sovereigns and corporates. The fixed income landscape has richened with valuations further stretched by capital flows from investors hungry for sources of sustainable yield and income. As such, we are maintaining constructive on these spread sensitive areas: investment grade and high yield credit, non-agency MBS and emerging market debt. These look to be areas better positioned to perform coming into 2013.

Investment Type Allocation

as of December 31, 2012

(as a percentage of net assets)

Corporate Bonds/Notes | | | 31.0 | % | |

U.S. Government Agency Obligations | | | 29.2 | % | |

Collateralized Mortgage Obligations | | | 16.6 | % | |

Affiliated Mutual Funds | | | 11.3 | % | |

U.S. Treasury Obligations | | | 10.7 | % | |

Asset-Backed Securities | | | 4.9 | % | |

Foreign Government Bonds | | | 2.3 | % | |

Preferred Stock | | | 1.0 | % | |

Purchased Options | | | 0.2 | % | |

Liabilities in Excess of Other Assets* | | | (7.2 | )% | |

Net Assets | | | 100.0 | % | |

* Includes short-term investments and purchased options.

Portfolio holdings are subject to change daily.

Top Ten Holdings

as of December 31, 2012

(as a percentage of net assets)

ING Emerging Markets Hard Currency Sovereign

Debt Fund Class P | | | 4.7 | % | |

ING Emerging Markets Local Currency Debt Fund | | | |

Class P | | | 3.7 | % | |

Ginnie Mae, 3.500%, 05/15/41 | | | 3.2 | % | |

ING Emerging Markets Corporate Debt Fund Class P | | | 2.9 | % | |

United States Treasury Note, 0.250%, 11/30/14 | | | 2.9 | % | |

United States Treasury Bond, 2.750%, 08/15/42 | | | 2.4 | % | |

Brazil Notas do Tesouro Nacional Series F,

10.000%, 01/01/23 | | | 2.3 | % | |

United States Treasury Bond, 1.625%, 11/15/22 | | | 2.1 | % | |

Ginnie Mae, 3.000%, 08/15/42 | | | 1.6 | % | |

Fannie Mae, 3.500%, 06/25/42 | | | 1.5 | % | |

Portfolio holdings are subject to change daily.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Portfolio may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

10

ING INTERMEDIATE BOND PORTFOLIO

PORTFOLIO MANAGERS' REPORT

Average Annual Total Returns for the Periods Ended December 31, 2012 | |

| | 1 Year | | 5 Year | | 10 Year | | Since Inception

of Class ADV

December 20, 2006 | | Since Inception

of Class S2

February 27, 2009 | |

Class ADV | | | 8.85 | % | | | 5.09 | % | | | — | | | | 5.09 | % | | | — | | |

Class I | | | 9.39 | % | | | 5.72 | % | | | 5.29 | % | | | — | | | | — | | |

Class S | | | 9.08 | % | | | 5.44 | % | | | 5.02 | % | | | — | | | | — | | |

Class S2 | | | 8.93 | % | | | — | | | | — | | | | — | | | | 10.40 | % | |

Barclays Capital U.S. Aggregate Bond Index | | | 4.21 | % | | | 5.95 | % | | | 5.18 | % | | | 6.12 | %(1) | | | 6.74 | %(2) | |

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING Intermediate Bond Portfolio against the index indicated. An index has has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Portfolio's performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on portfolio distributions or the redemption of portfolio shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

The performance update illustrates performance for a variable investment option available through a variable contract. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost.

Please log on to www.inginvestment.com or call (800) 992-0180 to get performance through the most recent month end.

This report contains statements that may be "forward-looking" statements. Actual results may differ materially from those projected in the "forward-looking" statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers' views are subject to change at any time based on market and other conditions.

Portfolio holdings are subject to change daily.

(1) Since inception performance for the the index is shown from January 1, 2007.

(2) Since inception performance for the index is shown from March 1, 2009.

Effective March 1, 2002, ING Investments, LLC began serving as investment adviser and ING Investment Management Co. LLC, the former investment adviser, began serving as sub-adviser to the Portfolio.

11

ING MONEY MARKET PORTFOLIO

PORTFOLIO MANAGERS' REPORT

ING Money Market Portfolio (the "Portfolio") seeks to provide high current return, consistent with preservation of capital and liquidity, through investment in high-quality money market instruments, while maintaining a stable share price of $1.00 per share. The Portfolio is managed by David S. Yealy, Portfolio Manager of ING Investment Management Co. LLC — the Sub-Adviser.

Performance: For the year ended December 31, 2012, the Portfolio's Class I shares provided a total return of 0.03% compared to the iMoneyNet First Tier Retail Index, which returned 0.02% for the same period.

Portfolio Specifics: Preservation of capital, limiting credit risk and keeping an excess liquidity cushion due to the still elevated risks in the market remain our primary objectives for the Portfolio. Maximizing the yield and return of the Portfolio remains a secondary objective in light of the current market conditions and risks and the low absolute level of rates. The Portfolio's Adviser and Distributor continue to waive fees to the extent necessary to maintain a 0.00% net yield, as do most of our competitors due to the historically low level of rates on money market securities.

The first quarter of 2012 was highlighted by a modestly improving U.S. economy, including job creation, and a market-perceived reduction in risk from the European sovereign credit crisis due to new measures implemented by the various central banks and the European Central Bank ("ECB"). The most important action by the ECB was the introduction of the three-year Long Term Refinancing Operations during the fourth quarter of 2011, followed by a second round of funding in February 2012. This reduced the short-term funding needs for the European banks which struggled to maintain adequate low cost short-term funding, a large portion of which is normally supplied by U.S. money market funds. The Federal Reserve Board (the "Fed"), in attempt to increase transparency, announced new disclosure that included a summary of predictions of the next anticipated move in the federal funds rate. The initial disclosure was for the next anticipated move to come late in 2014. Short-term money market rates remained anchored in their historical low range due to the expectations for rates to remain at current levels for the foreseeable future.

The major themes during the second and third quarters were modest economic growth in the United States, a poor but improving job market in the U.S. and slowing growth in the euro zone. In addition, there continued to be elevated market risk from the euro zone due to Greece, Spain, Italy and other countries experiencing very difficult economic conditions and funding issues. While various central banks and the ECB addressed the euro zone problems, they continued to struggle to find a permanent solution. The Fed continued to view the U.S. economic recovery as slow and at risk without additional policy accommodation. At its September 13 meeting, the Fed extended the outlook for the federal funds rate to be kept in the 0% to 0.25% range until the middle of 2015, from 2014 previously.

The fourth quarter saw the unemployment rate hold steady at an elevated 7.8% and inflation remained below the Fed's longer-run objective. The housing market continued to improve as distressed sales as a percentage of overall sales dropped. At the Fed's final meeting of the year in December it announced it would continue with its quantitative easing by extending the purchase of securities beyond year-end. The political debates over the fiscal cliff issues and the raising of the debt ceiling became the hot topic once we got past the Presidential election in November. We believe that these issues, along with the need to reduce the U.S. debt, will be the primary drivers of the markets in the near-term. The rates for short-term money market securities traded in a narrow range at historically low levels throughout 2012, due in part to the Fed keeping the federal funds rate anchored between 0% to 0.25%.

During the reporting period, the Portfolio followed the strategy of taking on a limited amount of interest rate risk while maintaining reduced longer-term credit exposure. The Portfolio ended the period with a 45 day weighted average maturity ("WAM"). This was slightly shorter than the peer average of 47 days for the iMoneyNet First Tier Retail category, but did have a higher WAM for the majority of the period.

The Portfolio maintained limited exposure to European banks during the reporting period by investing in those issuers that we had the highest confidence of being able to weather the deteriorating credit conditions in the euro zone, as well as a possible default by one or more countries such as Greece, Spain, Italy and other weak members of the European Union. We invested in short-term U.S. government securities from time to time and maintained a higher repurchase agreement exposure on a daily basis at a slight yield concession to the higher yielding bank debt in order to further reduce credit risk.

Outlook and Current Strategy: Our current strategy for the Portfolio will continue to focus on maintaining an extended WAM posture with limited credit risk. We will look to extend our WAM during any backup in rates to levels that offer enough yield pickup relative to the increased risk, as these backups would be expected to be temporary in nature in light of the Fed's position. Exposure to European banks is expected to remain low or be reduced further until we see resolution to the European sovereign debt crisis and funding issues.

Preservation of capital and liquidity remain our top objectives. We plan on maintaining reasonable daily and short-term liquidity to give the Portfolio flexibility to take advantage of any periods of temporary increases in yields. That being said, liquidity will not be as high as it was in the past, given the drag in yields from the low rates on repurchase agreements and other lower risk short-term liquidity securities, including U.S. government securities.

Principal Risk Factors: Although the Portfolio seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in the Portfolio.

Investment Type Allocation

as of December 31, 2012

(as a percentage of net assets)

Asset Backed Commercial Paper | | | 29.6 | % | |

Other Note | | | 27.0 | % | |

Treasury Debt | | | 14.1 | % | |

Government Agency Repurchase Agreement | | | 8.8 | % | |

Financial Company Commercial Paper | | | 7.8 | % | |

Certificate of Deposit | | | 5.6 | % | |

Other Instrument | | | 4.7 | % | |

Government Agency Debt | | | 2.7 | % | |

Other Commercial Paper | | | 0.7 | % | |

Liabilities in Excess of Other Assets | | | (1.0 | )% | |

Net Assets | | | 100.0 | % | |

Portfolio holdings are subject to change daily.

Top Ten Holdings

as of December 31, 2012

(as a percentage of net assets)

Goldman Sachs Repurchase Agreement

dated 12/31/12, 0.200%, due 01/02/13,

$50,000,556 to be received upon repurchase

(Collateralized by $50,990,000, FHLB,

0.170%-0.300%, Market Value plus accrued

interest $51,004,531 due 12/09/13-12/20/13) | | | 5.1 | % | |

Treasury Bill, 0.030%, 01/17/13 | | | 5.0 | % | |

BlackRock Liquidity Funds, TempFund, Institutional

Class, 0.144%, 01/02/13 | | | 4.7 | % | |

Treasury Bill, 0.050%, 01/10/13 | | | 3.9 | % | |

Deutsche Bank Repurchase Agreement

dated 12/31/12, 0.200%, due 01/02/13,

$35,835,398 to be received upon repurchase

(Collateralized by $26,212,263, FMNT and FNNT,

0.625%-6.090%, Market Value plus accrued

interest $36,551,700 due 12/29/14-09/27/27) | | | 3.7 | % | |

Treasury Bill, 0.060%, 01/03/13 | | | 3.4 | % | |

Wells Fargo Bank NA, 0.380%, 03/22/13 | | | 3.2 | % | |

Old Line Funding LLC, 0.321%, 04/22/13 | | | 3.1 | % | |

Barton Capital LLC, 0.187%, 01/03/13 | | | 3.0 | % | |

Concord Minutemen Capital Co., 0.652%, 04/02/13 | | | 2.9 | % | |

Portfolio holdings are subject to change daily.

* Please see Note 5 for more information regarding the contractual waiver in place to reimburse certain expenses of the Portfolio to the extent necessary to assist the Portfolio in maintaining a net yield of not less than 0.00%.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Portfolio may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

12

ING SMALL COMPANY PORTFOLIO

PORTFOLIO MANAGERS' REPORT

ING Small Company Portfolio (the "Portfolio") seeks growth of capital primarily through investment in a diversified portfolio of common stocks of companies with smaller market capitalizations. The Portfolio is managed by Joseph Basset, CFA, Steve Salopek and James Hasso, Portfolio Managers of ING Investment Management Co. LLC — the Sub Adviser.*

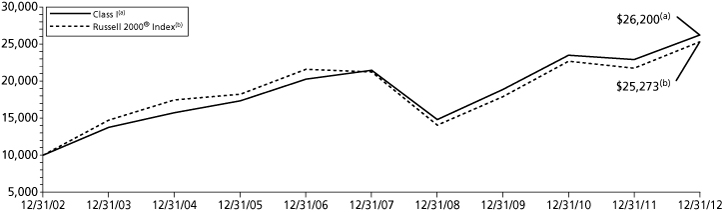

Performance: For the year ended December 31, 2012, the Portfolio's Class I shares provided a total return of 14.52% compared to the Russell 2000® Index, which returned 16.35% for the same period.

Portfolio Specifics: Benchmark returns were strongest in the first quarter as the Russell 2000® Index advanced by 12.44%. The markets experienced a pullback in the second quarter, however, and the index declined by 3.47%. Positive performance followed in the third and fourth quarters, with returns of 5.25% and 1.85% respectively. Small-caps underperformed mid-caps and large-caps, which returned 17.28% and 16.42% as measured by the Russell Mid Cap and Russell 1000® indices, respectively. Stocks with higher returns on equity held up better during the period and stocks that were less sensitive to market risk (lower beta) outperformed higher beta stocks. For the Russell 2000® Index, the consumer durables and real estate sectors were the strongest performers for the year returning 49.20% and 25.75%% respectively. Insurance and industrial materials also had strong performance, with returns of 24.12% and 23.99% respectively. The only sector posting a negative return for the period was energy which declined by 3.69%.

Stock selection within consumer services was the largest contributor to returns for the period. The Portfolio's overweight allocation to banks and capital goods also added to performance. Stock selection within energy and diversified financials detracted most from performance for the period.

The main individual contributors to performance were Nationstar Mortgage Holdings Inc. and Ariba Inc. The Portfolio's position in Nationstar Mortgage Holdings Inc. was the largest contributor to returns for the period. The company is a non-bank residential mortgage servicer with a range of services across the residential mortgage product spectrum. Strong earnings and several accretive acquisitions contributed to the stock's outperformance during the period. The stock also benefited as banks jettisoned hundreds of billions of dollars of loans, to raise capital and cut costs as housing modestly rebounded. Ariba is a provider of collaborative business commerce solutions for buying and selling goods and services in the United States and internationally. The company agreed to be acquired by SAP for approximately $4.3 billion on May 22, which was a 19% premium to the prior day's close. SAP said the acquisition will establish it as the leading business network provider, adding business-to-business collaboration to its existing solutions. The deal is also anticipated to boost SAP's cloud application portfolio with the addition of Ariba's cloud-based procurement solutions.

Key detractors from performance were Bill Barrett Corp. and Thompson Creek Metals Co. Inc. Bill Barrett Corp., an independent exploration and production company focused on gas and oil, was the largest detractor from performance during the period. The stock experienced a large decline in the first half of the year for two main reasons. One, natural gas prices were under pressure due to oversupply of the commodity. Two, the company engaged in a large spending program to diversify its business and increase its exposure to oil and gas liquids. Investors displayed skepticism regarding the company's efforts and the markets became impatient with the speed of the transitions and the additional capital expenditures they required.

Thompson Creek Metals Co., Inc. operates two molybdenum mines in North America along with roasting facilities to further process the output. The company benefited from better than expected molybdenum pricing; however, the key driver to performance has been the construction of the Mt. Milligan copper mining project, which is now fully funded. As a result, investor concerns have moved away from the risks associated with capital expenditure budgeting to operational risks, which are less pronounced. We remain holders of the stock, and in fact have been aggressive buyers as we think current prices imbed significant negative value for the new copper mine. Mt. Milligan should be completed by the end of 2013. Once more tangible progress is apparent on such things as the mill facility or the tailings pond, we believe investors will shift their attention away from recent management missteps and begin assessing the value of a functional copper mine in a safe jurisdiction, with output expected in a year.

Current Strategy and Outlook: We are cautious about the global macroeconomic landscape and continue to assess the potential impact that it may have on the performance of companies and valuations. The Portfolio's positioning has not changed significantly. We seek to remain nimble and continue to focus on what we believe are quality companies, i.e., companies that have strong managements, strong balance sheets and good cash flow generation capabilities. Even among cyclical companies our primary focus is on management quality, cash flows and the strength of the balance sheet. We believe the Portfolio is well positioned going forward, as we think that investors will continue to focus on companies' fundamentals due to increased economic uncertainty.

Sector Diversification

as of December 31, 2012

(as a percentage of net assets)

Financials | | | 23.0 | % | |

Industrials | | | 18.1 | % | |

Information Technology | | | 15.5 | % | |

Consumer Discretionary | | | 13.9 | % | |

Health Care | | | 10.8 | % | |

Materials | | | 5.9 | % | |

Energy | | | 5.6 | % | |

Utilities | | | 2.7 | % | |

Consumer Staples | | | 1.7 | % | |

Exchange-Traded Funds | | | 1.2 | % | |

Assets in Excess of Other Liabilities* | | | 1.6 | % | |

Net Assets | | | 100.0 | % | |

* Includes short-term investments.

Portfolio holdings are subject to change daily.

Top Ten Holdings

as of December 31, 2012*

(as a percentage of net assets)

Acuity Brands, Inc. | | | 1.2 | % | |

iShares Russell 2000 Index Fund | | | 1.2 | % | |

Brady Corp. | | | 1.1 | % | |

HB Fuller Co. | | | 1.1 | % | |

Watts Water Technologies, Inc. | | | 1.0 | % | |

Starwood Property Trust, Inc. | | | 1.0 | % | |

Actuant Corp. | | | 1.0 | % | |

Waste Connections, Inc. | | | 1.0 | % | |

Unit Corp. | | | 1.0 | % | |

Worthington Industries | | | 1.0 | % | |

* Excludes short-term investments.

Portfolio holdings are subject to change daily.

* Effective April 30, 2012, James Hasso has been added as a portfolio manager to the Portfolio.

Portfolio holdings and characteristics are subject to change and may not be representative of current holdings and characteristics. The outlook for this Portfolio may differ from that presented for other ING Funds. Performance for the different classes of shares will vary based on differences in fees associated with each class.

13

ING SMALL COMPANY PORTFOLIO

PORTFOLIO MANAGERS' REPORT

Average Annual Total Returns for the Periods Ended December 31, 2012 | |

| | 1 Year | | 5 Year | | 10 Year | | Since Inception

of Class ADV

December 16, 2008 | | Since Inception

of Class S2

February 27, 2009 | |

Class ADV | | | 14.01 | % | | | — | | | | — | | | | 15.79 | % | | | — | | |

Class I | | | 14.52 | % | | | 4.08 | % | | | 10.11 | % | | | — | | | | |

Class S | | | 14.26 | % | | | 3.83 | % | | | 9.85 | % | | | — | | | | — | | |

Class S2 | | | 14.08 | % | | | — | | | | — | | | | — | | | | 22.51 | % | |

Russell 2000® Index | | | 16.35 | % | | | 3.56 | % | | | 9.72 | % | | | 15.81 | %(1) | | | 24.29 | %(2) | |

Based on a $10,000 initial investment, the graph and table above illustrate the total return of ING Small Company Portfolio against the index indicated. An index has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Portfolio's performance is shown without the imposition of any expenses or charges which are, or may be, imposed under your annuity contract. Total returns would have been lower if such expenses or charges were included.

The performance graph and table do not reflect the deduction of taxes that a shareholder will pay on portfolio distributions or the redemption of portfolio shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

The performance update illustrates performance for a variable investment option available through a variable contract. The performance shown indicates past performance and is not a projection or prediction of future results. Actual investment returns

and principal value will fluctuate so that shares and/or units, at redemption, may be worth more or less than their original cost. Please log on to www.inginvestment.com or call (800) 992-0180 to get performance through the most recent month end.

This report contains statements that may be "forward-looking" statements. Actual results may differ materially from those projected in the "forward-looking" statements.

The views expressed in this report reflect those of the portfolio manager, only through the end of the period as stated on the cover. The portfolio manager's views are subject to change at any time based on market and other conditions.

Portfolio holdings are subject to change daily.

(1) Since inception performance for the index is January 1, 2009.

(2) Since inception performance for the index is March 1, 2009.

Effective March 1, 2002, ING Investments, LLC began serving as investment adviser and ING Investment Management Co. LLC, the former investment adviser, began serving as sub-adviser to the Portfolio.

14

SHAREHOLDER EXPENSE EXAMPLES (UNAUDITED)

As a shareholder of a Portfolio, you incur two types of costs: (1) transaction costs, including redemption fees and exchange fees; and (2) ongoing costs, including management fees, distribution and/or service (12b-1) fees, and other Portfolio expenses. These Examples are intended to help you understand your ongoing costs (in dollars) of investing in a Portfolio and to compare these costs with the ongoing costs of investing in other mutual funds.

The Examples are based on an investment of $1,000 invested at the beginning of the period and held for the entire period from July 1, 2012 to December 31, 2012. The Portfolios' expenses are shown without the imposition of any charges which are, or may be, imposed under your annuity contract. Expenses would have been higher if such charges were included.

Actual Expenses

The left section of the table shown below, "Actual Portfolio Return," provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section under the heading entitled "Expenses Paid During the Period" to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The right section of the table shown below, "Hypothetical (5% return before expenses)," provides information about hypothetical account values and hypothetical expenses based on a Portfolio's actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not a Portfolio's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in a Portfolio and other mutual funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other mutual funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as redemption fees or exchange fees. Therefore, the hypothetical lines of the table are useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different mutual funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | Actual Portfolio Return | | Hypothetical (5% return before expenses) | |

ING Balanced Portfolio | | Beginning

Account

Value

July 1,

2012 | | Ending

Account

Value

December 31,

2012 | | Annualized

Expense

Ratio | | Expenses Paid

During the

Period Ended

December 31,

2012* | | Beginning

Account

Value

July 1,

2012 | | Ending

Account

Value

December 31,

2012 | | Annualized

Expense

Ratio | | Expenses Paid

During the

Period Ended

December 31,

2012* | |