Wells Fargo Commercial Mortgage Securities

Filed: 29 Mar 17, 12:00am

| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-206677-15 | ||

Free Writing Prospectus

Structural and Collateral Term Sheet

$1,008,188,843

(Approximate Initial Pool Balance)

$826,084,000

(Approximate Aggregate Certificate Balance of Offered Certificates)

BANK 2017-BNK4

as Issuing Entity

Wells Fargo Commercial Mortgage Securities, Inc.

as Depositor

Bank of America, National Association

Morgan Stanley Mortgage Capital Holdings LLC

Wells Fargo Bank, National Association

as Sponsors and Mortgage Loan Sellers

Commercial Mortgage Pass-Through Certificates

Series 2017-BNK4

March 28, 2017

| WELLS FARGO SECURITIES | BofA MERRILL | MORGAN |

Co-Lead Manager and | Co-Lead Manager and | Co-Lead Manager and |

Academy Securities

|

STATEMENT REGARDING THIS FREE WRITING PROSPECTUS

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (‘‘SEC’’) (SEC File No. 333-206677) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC Web site at www.sec.gov. Alternatively, the depositor, any underwriter, or any dealer participating in the offering will arrange to send you the prospectus after filing if you request it by calling toll free 1-800-745-2063 (8 a.m. – 5 p.m. EST) or by emailing wfs.cmbs@wellsfargo.com.

Nothing in this document constitutes an offer of securities for sale in any jurisdiction where the offer or sale is not permitted. The information contained herein is preliminary as of the date hereof, supersedes any such information previously delivered to you and will be superseded by any such information subsequently delivered and ultimately by the final prospectus relating to the securities. These materials are subject to change, completion, supplement or amendment from time to time.

This free writing prospectus has been prepared by the underwriters for information purposes only and does not constitute, in whole or in part, a prospectus for the purposes of Directive 2003/71/EC (as amended) and/or Part VI of the Financial Services and Markets Act 2000, as amended, or other offering document.

STATEMENT REGARDING ASSUMPTIONS AS TO SECURITIES, PRICING ESTIMATES AND OTHER INFORMATION

The attached information contains certain tables and other statistical analyses (the “Computational Materials”) which have been prepared in reliance upon information furnished by the Mortgage Loan Sellers. Numerous assumptions were used in preparing the Computational Materials, which may or may not be reflected herein. As such, no assurance can be given as to the Computational Materials’ accuracy, appropriateness or completeness in any particular context; or as to whether the Computational Materials and/or the assumptions upon which they are based reflect present market conditions or future market performance. The Computational Materials should not be construed as either projections or predictions or as legal, tax, financial or accounting advice. You should consult your own counsel, accountant and other advisors as to the legal, tax, business, financial and related aspects of a purchase of these securities. Any weighted average lives, yields and principal payment periods shown in the Computational Materials are based on prepayment and/or loss assumptions, and changes in such prepayment and/or loss assumptions may dramatically affect such weighted average lives, yields and principal payment periods. In addition, it is possible that prepayments or losses on the underlying assets will occur at rates higher or lower than the rates shown in the attached Computational Materials. The specific characteristics of the securities may differ from those shown in the Computational Materials due to differences between the final underlying assets and the preliminary underlying assets used in preparing the Computational Materials. The principal amount and designation of any security described in the Computational Materials are subject to change prior to issuance. None of Wells Fargo Securities, LLC, Merrill Lynch, Pierce, Fenner & Smith Incorporated, Morgan Stanley & Co. LLC, Academy Securities, Inc., or any of their respective affiliates, make any representation or warranty as to the actual rate or timing of payments or losses on any of the underlying assets or the payments or yield on the securities. The information in this presentation is based upon management forecasts and reflects prevailing conditions and management’s views as of this date, all of which are subject to change. In preparing this presentation, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us by or on behalf of the Mortgage Loan Sellers or which was otherwise reviewed by us.

This free writing prospectus contains certain forward-looking statements. If and when included in this free writing prospectus, the words “expects”, “intends”, “anticipates”, “estimates” and analogous expressions and all statements that are not historical facts, including statements about our beliefs or expectations, are intended to identify forward-looking statements. Any forward-looking statements are made subject to risks and uncertainties which could cause actual results to differ materially from those stated. Those risks and uncertainties include, among other things, declines in general economic and business conditions, increased competition, changes in demographics, changes in political and social conditions, regulatory initiatives and changes in customer preferences, many of which are beyond our control and the control of any other person or entity related to this offering. The forward-looking statements made in this free writing prospectus are made as of the date stated on the cover. We have no obligation to update or revise any forward-looking statement.

Wells Fargo Securities is the trade name for the capital markets and investment banking services of Wells Fargo & Company and its subsidiaries, including but not limited to Wells Fargo Securities, LLC, a member of NYSE, FINRA, NFA and SIPC, Wells Fargo Prime Services, LLC, a member of FINRA, NFA and SIPC, and Wells Fargo Bank, N.A. Wells Fargo Securities, LLC and Wells Fargo Prime Services, LLC are distinct entities from affiliated banks and thrifts.

IMPORTANT NOTICE REGARDING THE OFFERED CERTIFICATES

The information herein is preliminary and may be supplemented or amended prior to the time of sale. In addition, the Offered Certificates referred to in these materials and the asset pool backing them are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis.

The underwriters described in these materials may from time to time perform investment banking services for, or solicit investment banking business from, any company named in these materials. The underwriters and/or their affiliates or respective employees may from time to time have a long or short position in any security or contract discussed in these materials.

The information contained herein supersedes any previous such information delivered to any prospective investor and will be superseded by information delivered to such prospective investor prior to the time of sale.

IMPORTANT NOTICE RELATING TO AUTOMATICALLY-GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of any email communication to which this free writing prospectus is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) any representation that these materials are accurate or complete and may not be updated or (3) these materials possibly being confidential, are not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 2 |

| BANK 2017-BNK4 | Certificate Structure |

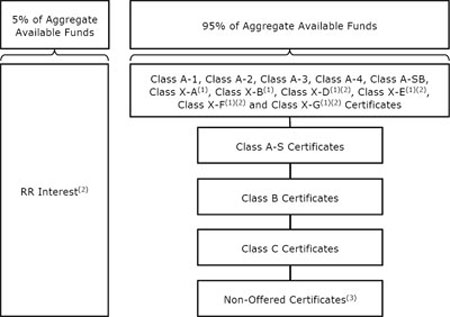

I. Certificate Structure

| Class | Expected Ratings (Fitch/KBRA/Moody’s)(1) | Approximate Initial Certificate Balance or Notional Amount(2) | Approx. Initial Credit Support(3) | Pass-Through Rate Description | Weighted Average Life (Years)(4) | Expected Principal Window(4) | Certificate Principal to Value Ratio(5) | Certificate Principal U/W NOI Debt Yield(6) | ||||||||

| Offered Certificates | ||||||||||||||||

| A-1 | AAAsf/AAA(sf)/Aaa(sf) | $33,805,000 | 30.000% | (7) | 2.68 | 05/17 – 02/22 | 41.4% | 16.1% | ||||||||

| A-2 | AAAsf/AAA(sf)/Aaa(sf) | $88,384,000 | 30.000% | (7) | 4.82 | 02/22 – 02/22 | 41.4% | 16.1% | ||||||||

| A-3 | AAAsf/AAA(sf)/Aaa(sf) | $235,000,000 | 30.000% | (7) | 9.74 | 10/26 – 02/27 | 41.4% | 16.1% | ||||||||

| A-4 | AAAsf/AAA(sf)/Aaa(sf) | $268,432,000 | 30.000% | (7) | 9.85 | 02/27 – 03/27 | 41.4% | 16.1% | ||||||||

| A-SB | AAAsf/AAA(sf)/Aaa(sf) | $44,824,000 | 30.000% | (7) | 7.24 | 02/22 – 10/26 | 41.4% | 16.1% | ||||||||

| A-S | AAAsf/AAA(sf)/Aa3(sf) | $67,045,000 | 23.000% | (7) | 9.91 | 03/27 – 03/27 | 45.5% | 14.7% | ||||||||

| X-A | AAAsf/AAA(sf)/Aaa(sf) | $670,445,000(8) | N/A | Variable(9) | N/A | N/A | N/A | N/A | ||||||||

| X-B | A-sf/AAA(sf)/NR | $155,639,000(10) | N/A | Variable(11) | N/A | N/A | N/A | N/A | ||||||||

| B | AA-sf/AA-(sf)/NR | $43,100,000 | 18.500% | (7) | 9.91 | 03/27 – 03/27 | 48.1% | 13.9% | ||||||||

| C | A-sf/A-(sf)/NR | $45,494,000 | 13.750% | (7) | 9.91 | 03/27 – 03/27 | 51.0% | 13.1% | ||||||||

| Non-Offered Certificates | ||||||||||||||||

| X-D | BBB-sf/BBB-(sf)/NR | $56,270,000(12) | N/A | Variable(13) | N/A | N/A | N/A | N/A | ||||||||

| X-E | BB-sf/BB-(sf)/NR | $21,550,000(14) | N/A | Variable(15) | N/A | N/A | N/A | N/A | ||||||||

| X-F | B-sf/B-(sf)/NR | $10,775,000(16) | N/A | Variable(17) | N/A | N/A | N/A | N/A | ||||||||

| X-G | NR/NR/NR | $43,100,400(18) | N/A | Variable(19) | N/A | N/A | N/A | N/A | ||||||||

| D | BBB-sf/BBB-(sf)/NR | $56,270,000 | 7.875% | (7) | 9.92 | 03/27 – 04/27 | 54.4% | 12.3% | ||||||||

| E | BB-sf/BB-(sf)/NR | $21,550,000 | 5.625% | (7) | 9.99 | 04/27 – 04/27 | 55.8% | 12.0% | ||||||||

| F | B-sf/B-(sf)/NR | $10,775,000 | 4.500% | (7) | 9.99 | 04/27 – 04/27 | 56.4% | 11.8% | ||||||||

| G | NR/NR/NR | $43,100,400 | 0.000% | (7) | 9.99 | 04/27 – 04/27 | 59.1% | 11.3% | ||||||||

| Non-Offered Eligible Vertical Interest | ||||||||||||||||

| RR Interest | NR/NR/NR | $50,409,442.16 | N/A | WAC(20) | 9.01 | 05/17 – 04/27 | N/A | N/A | ||||||||

| Notes: | |

| (1) | The expected ratings presented are those of Fitch Ratings, Inc. (“Fitch”), Kroll Bond Rating Agency, Inc. (“KBRA”) and Moody’s Investors Service, Inc. (“Moody’s”), which the depositor hired to rate the Offered Certificates. One or more other nationally recognized statistical rating organizations that were not hired by the depositor may use information they receive pursuant to Rule 17g-5 under the Securities Exchange Act of 1934, as amended (the “Exchange Act”) or otherwise, to rate or provide market reports and/or published commentary related to the Offered Certificates. We cannot assure you as to what ratings a non-hired nationally recognized statistical rating organization would assign or that its reports will not express differing, possibly negative, views of the mortgage loans and/or the Offered Certificates. The ratings of each Class of Offered Certificates address the likelihood of the timely distribution of interest and, except in the case of the Class X-A and X-B Certificates, the ultimate distribution of principal due on those Classes on or before the Rated Final Distribution Date. See “Risk Factors—Other Risks Relating to the Certificates—Nationally Recognized Statistical Rating Organizations May Assign Different Ratings to the Certificates; Ratings of the Certificates Reflect Only the Views of the Applicable Rating Agencies as of the Dates Such Ratings Were Issued; Ratings May Affect ERISA Eligibility; Ratings May Be Downgraded” and “Ratings” in the Preliminary Prospectus, expected to be dated March 28, 2017 (the “Preliminary Prospectus”). Fitch, KBRA and Moody’s have informed us that the “sf” designation in their ratings represents an identifier for structured finance product ratings. |

| (2) | The certificate balances and notional amounts set forth in the table are approximate. The actual initial certificate balances and notional amounts may be larger or smaller depending on the initial pool balance of the mortgage loans definitively included in the pool of mortgage loans, which aggregate cut-off date balance may be as much as 5% larger or smaller than the amount presented in the Preliminary Prospectus. |

| (3) | The approximate initial credit support with respect to the Class A-1, A-2, A-3, A-4 and A-SB Certificates represents the approximate credit enhancement for the Class A-1, A-2, A-3, A-4 and A-SB Certificates in the aggregate. The RR Interest only provides credit support to the limited extent that losses incurred on the underlying mortgage loans are allocated to it, on the one hand, and to the Offered Certificates and the Non-Offered Certificates, on the other hand,pro rata, in accordance with their respective Percentage Allocation Entitlements. |

| (4) | Weighted Average Lives and Expected Principal Windows are calculated based on an assumed prepayment rate of 0% CPR and the “Structuring Assumptions” described under “Yield and Maturity Considerations—Weighted Average Life” in the Preliminary Prospectus. |

| (5) | The Certificate Principal to Value Ratio for each Class of Certificates (other than the Class A-1, A-2, A-3, A-4 and A-SB Certificates) is calculated as the product of (a) the weighted average Cut-off Date LTV Ratio for the mortgage loans and (b) a fraction, the numerator of which is the total initial Certificate Balance of such Class of Certificates and all Classes of Principal Balance Certificates senior to such Class of Certificates and the denominator of which is the total initial Certificate Balance of all of the Principal Balance Certificates (other than the RR Interest). The Certificate Principal to Value Ratio for each of the Class A-1, A-2, A-3, A-4 and A-SB Certificates is calculated in the aggregate for those Classes as if they were a single Class and is calculated as the product of (a) the weighted average Cut-off Date LTV Ratio for the mortgage loans and (b) a fraction, the numerator of which is the total initial aggregate Certificate Balances of such Classes of Certificates and the denominator of which is the total initial Certificate Balance of all of the Principal Balance Certificates (other than the RR Interest). In any event, however, excess mortgaged property value associated with a mortgage loan will not be available to offset losses on any other mortgage loan. |

| (6) | The Certificate Principal U/W NOI Debt Yield for each Class of Certificates (other than the Class A-1, A-2, A-3, A-4 and A-SB Certificates) is calculated as the product of (a) the weighted average U/W NOI Debt Yield for the mortgage loans and (b) a fraction, the numerator of which is the total initial Certificate Balance of all of the Classes of Principal Balance Certificates (other than the RR Interest) and the denominator of which is the total initial Certificate Balance for such Class of Certificates and all Classes of Principal Balance Certificates senior to such Class of Certificates. The Certificate Principal U/W NOI Debt Yield for each of the Class A-1, A-2, A-3, A-4 and A-SB Certificates is calculated in the aggregate for those Classes as if they were a single Class and is calculated as the product of (a) the weighted average U/W NOI Debt Yield for the mortgage loans and (b) a fraction, the numerator of which is the total initial Certificate Balance of all of the Classes of Principal Balance Certificates (other than the RR Interest) and the denominator of which is the total aggregate initial Certificate Balances for the Class A-1, A-2, A-3, A-4 and A-SB Certificates. In any event, however, cash flow from each mortgaged property supports only the related mortgage loan and will not be available to support any other mortgage loan. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 3 |

| BANK 2017-BNK4 | Certificate Structure |

| (7) | The pass-through rates for the Class A-1, A-2, A-3, A-4, A-SB, A-S, B, C, D, E, F and G Certificates in each case will be one of the following: (i) a fixed rateper annum, (ii) a variable rate per annum equal to the weighted average of the net mortgage interest rates on the mortgage loans for the related distribution date, (iii) a variable rateper annum equal to the lesser of (a) a fixed rate and (b) the weighted average of the net mortgage interest rates on the mortgage loans for the related distribution date or (iv) a variable rateper annum equal to the weighted average of the net mortgage interest rates on the mortgage loans for the related distribution date minus a specified percentage. For purposes of the calculation of the weighted average of the net mortgage interest rates on the mortgage loans for each distribution date, the mortgage interest rates will be adjusted as necessary to a 30/360 basis. |

| (8) | The Class X-A Certificates are notional amount certificates. The Notional Amount of the Class X-A Certificates will be equal to the aggregate Certificate Balance of the Class A-1, A-2, A-3, A-4 and A-SB Certificates outstanding from time to time. The Class X-A Certificates will not be entitled to distributions of principal. |

| (9) | The pass-through rate for the Class X-A Certificates for any distribution date will be aper annum rate equal to the excess, if any, of (a) the weighted average of the net mortgage interest rates on the mortgage loans for the related distribution date, over (b) the weighted average of the pass-through rates on the Class A-1, A-2, A-3, A-4 and A-SB Certificates for the related distribution date, weighted on the basis of their respective Certificate Balances outstanding immediately prior to that distribution date. For purposes of the calculation of the weighted average of the net mortgage interest rates on the mortgage loans for each distribution date, the mortgage interest rates will be adjusted as necessary to a 30/360 basis. |

| (10) | The Class X-B Certificates are notional amount certificates. The Notional Amount of the Class X-B Certificates will be equal to the aggregate Certificate Balance of the Class A-S, B and C Certificates outstanding from time to time. The Class X-B Certificates will not be entitled to distributions of principal. |

| (11) | The pass-through rate for the Class X-B Certificates for any distribution date will be aper annum rate equal to the excess, if any, of (a) the weighted average of the net mortgage interest rates on the mortgage loans for the related distribution date, over (b) the weighted average of the pass-through rates on the Class A-S, B and C Certificates for the related distribution date, weighted on the basis of their respective Certificate Balances outstanding immediately prior to that distribution date. For purposes of the calculation of the weighted average of the net mortgage interest rates on the mortgage loans for each distribution date, the mortgage interest rates will be adjusted as necessary to a 30/360 basis. |

| (12) | The Class X-D Certificates are notional amount certificates. The Notional Amount of the Class X-D Certificates will be equal to the Certificate Balance of the Class D Certificates outstanding from time to time. The Class X-D Certificates will not be entitled to distributions of principal. |

| (13) | The pass-through rate for the Class X-D Certificates for any distribution date will be aper annum rate equal to the excess, if any, of (a) the weighted average of the net mortgage interest rates on the mortgage loans for the related distribution date, over (b) the pass-through rate on the Class D Certificates for the related distribution date. For purposes of the calculation of the weighted average of the net mortgage interest rates on the mortgage loans for each distribution date, the mortgage interest rates will be adjusted as necessary to a 30/360 basis. |

| (14) | The Class X-E Certificates are notional amount certificates. The Notional Amount of the Class X-E Certificates will be equal to the Certificate Balance of the Class E Certificates outstanding from time to time. The Class X-E Certificates will not be entitled to distributions of principal. |

| (15) | The pass-through rate for the Class X-E Certificates for any distribution date will be aper annum rate equal to the excess, if any, of (a) the weighted average of the net mortgage interest rates on the mortgage loans for the related distribution date, over (b) the pass-through rate on the Class E Certificates for the related distribution date. For purposes of the calculation of the weighted average of the net mortgage interest rates on the mortgage loans for each distribution date, the mortgage interest rates will be adjusted as necessary to a 30/360 basis. |

| (16) | The Class X-F Certificates are notional amount certificates. The Notional Amount of the Class X-F Certificates will be equal to the Certificate Balance of the Class F Certificates outstanding from time to time. The Class X-F Certificates will not be entitled to distributions of principal. |

| (17) | The pass-through rate for the Class X-F Certificates for any distribution date will be aper annum rate equal to the excess, if any, of (a) the weighted average of the net mortgage interest rates on the mortgage loans for the related distribution date, over (b) the pass-through rate on the Class F Certificates for the related distribution date. For purposes of the calculation of the weighted average of the net mortgage interest rates on the mortgage loans for each distribution date, the mortgage interest rates will be adjusted as necessary to a 30/360 basis. |

| (18) | The Class X-G Certificates are notional amount certificates. The Notional Amount of the Class X-G Certificates will be equal to the Certificate Balance of the Class G Certificates outstanding from time to time. The Class X-G Certificates will not be entitled to distributions of principal. |

| (19) | The pass-through rate for the Class X-G Certificates for any distribution date will be aper annum rate equal to the excess, if any, of (a) the weighted average of the net mortgage interest rates on the mortgage loans for the related distribution date, over (b) the pass-through rate on the Class G Certificates for the related distribution date. For purposes of the calculation of the weighted average of the net mortgage interest rates on the mortgage loans for each distribution date, the mortgage interest rates will be adjusted as necessary to a 30/360 basis. |

| (20) | The effective interest rate for the RR Interest will be the weighted average of the net mortgage interest rates on the mortgage loans for the related distribution date, the mortgage interest rates will be adjusted as necessary to a 30/360 basis. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 4 |

| BANK 2017-BNK4 | Transaction Highlights |

II. Transaction Highlights

Mortgage Loan Sellers:

| Mortgage Loan Seller | Number of Mortgage Loans | Number of Mortgaged Properties | Aggregate Cut-off Date Balance | % of Initial Pool Balance | |||||

| Bank of America, National Association(1) | 17 | 20 | $427,856,282 | 42.4 | % | ||||

| Morgan Stanley Mortgage Capital Holdings LLC(2) | 17 | 28 | 296,069,149 | 29.4 | |||||

| Wells Fargo Bank, National Association(3) | 14 | 16 | 284,263,413 | 28.2 | |||||

| Total | 48 | 64 | $1,008,188,843 | 100.0 | % | ||||

| (1) | The mortgage loan secured by the mortgaged property identified on Annex A-1 to the Preliminary Prospectus as The Summit Birmingham, representing approximately 6.1% of the aggregate principal balance of the pool of mortgage loans as of the cut-off date, is part of a whole loan that was co-originated by Barclays Bank PLC (“Barclays”) and BANA. The mortgage loan secured by the mortgaged property identified on Annex A-1 to the Preliminary Prospectus as Key Center Cleveland, representing approximately 4.0% of the aggregate principal balance of the pool of mortgage loans as of the cut-off date, is part of a whole loan that was co-originated by Citi Real Estate Funding Inc. (“Citi”), Deutsche Bank AG, New York Branch (“DB”) and BANA. |

| (2) | The mortgage loan secured by the mortgaged property identified on Annex A-1 to the Preliminary Prospectus as Pentagon Center, representing approximately 5.5% of the aggregate principal balance of the pool of mortgage loans as of the cut-off date, is part of a whole loan that was co-originated by Goldman Sachs Mortgage Company (“GSMC”) and Morgan Stanley Bank, N.A. (“MSBNA”). The mortgage loan, consisting of Note A-4, Note A-5 and Note A-6, is expected to be acquired by MSMCH prior to the closing date, and will be sold by MSMCH into the BANK 2017-BNK4 securitization. The mortgage loan secured by the mortgaged property identified on Annex A-1 to the Preliminary Prospectus as Merrill Lynch Drive, representing approximately 4.1% of the aggregate principal balance of the pool of mortgage loans as of the cut-off date, is part of a whole loan that was co-originated by Barclays and MSBNA. The mortgage loan, consisting of Note A-3, is expected to be acquired by MSMCH prior to the closing date, and will be sold by MSMCH into the BANK 2017-BNK4 securitization. |

| (3) | The mortgage loan secured by the mortgaged property identified on Annex A-1 to the Preliminary Prospectus as One West 34th Street, representing approximately 6.0% of the aggregate principal balance of the pool of mortgage loans as of the cut-off date, is part of a whole loan that was co-originated by GSMC and WFB. |

Loan Pool:

| Initial Pool Balance: | $1,008,188,843 |

| Number of Mortgage Loans: | 48 |

| Average Cut-off Date Balance per Mortgage Loan: | $21,003,934 |

| Number of Mortgaged Properties: | 64 |

| Average Cut-off Date Balance per Mortgaged Property(1): | $15,752,951 |

| Weighted Average Mortgage Interest Rate: | 4.848% |

| Ten Largest Mortgage Loans as % of Initial Pool Balance: | 52.5% |

| Weighted Average Original Term to Maturity or ARD (months): | 114 |

| Weighted Average Remaining Term to Maturity or ARD (months): | 113 |

| Weighted Average Original Amortization Term (months)(2): | 336 |

| Weighted Average Remaining Amortization Term (months)(2): | 335 |

| Weighted Average Seasoning (months): | 2 |

| (1) | Information regarding mortgage loans secured by multiple properties is based on an allocation according to relative appraised values or the allocated loan amounts or property-specific release prices set forth in the related loan documents or such other allocation as the related mortgage loan seller deemed appropriate. |

| (2) | Excludes any mortgage loan that does not amortize. |

Credit Statistics:

| Weighted Average U/W Net Cash Flow DSCR(1): | 1.83x |

| Weighted Average U/W Net Operating Income Debt Yield(1): | 11.3% |

| Weighted Average Cut-off Date Loan-to-Value Ratio(1): | 59.1% |

| Weighted Average Balloon or ARD Loan-to-Value Ratio(1): | 53.8% |

| % of Mortgage Loans with Additional Subordinate Debt(2): | 21.5% |

| % of Mortgage Loans with Single Tenants(3): | 19.4% |

| (1) | With respect to any mortgage loan that is part of a whole loan, loan-to-value ratio, debt service coverage ratio and debt yield calculations include the relatedpari passucompanion loan(s) but exclude any related subordinate secured loan(s) (unless otherwise stated). The debt service coverage ratio, debt yield and loan-to-value ratio information do not take into account any subordinate debt (whether or not secured by the related mortgaged property), that currently exists or is allowed under the terms of any mortgage loan. The information for each mortgaged property that relates to a mortgage loan that is cross-collateralized or cross-defaulted with one or more other mortgage loans is based upon the principal balance of that mortgage loan, except that the applicable loan-to-value ratio, debt service coverage ratio, and debt yield for each such mortgage loan is based upon the ratio or yield (as applicable) for the aggregate indebtedness evidenced by all loans in the group (without regard to any limitation on the amount of indebtedness secured by any mortgaged property in such cross-collateralized group). On an individual basis, without regard to the cross-collateralization feature, any mortgage loan that is part of a cross-collateralized group of mortgage loans may have a higher loan-to-value ratio, lower debt service coverage ratio and/or lower debt yield than is presented herein. With respect to the mortgage loan secured by the mortgaged property identified on Annex A-1 to the Preliminary Prospectus as D.C. Office Portfolio, all loan-to-value and debt yield calculations are net of the $5,000,000 earnout reserve. See “Description of the Mortgage Pool—Mortgage Pool Characteristics” in the Preliminary Prospectus and Annex A-1 to the Preliminary Prospectus. |

| (2) | The percentage figure expressed as “% of Mortgage Loans with Additional Subordinate Debt” is determined as a percentage of the initial pool balance and does not take into account any future subordinate debt (whether or not secured by the mortgaged property), if any, that may be permitted under the terms of any mortgage loan or the pooling and servicing agreement. See “Description of the Mortgage Pool—Additional Indebtedness—Other Unsecured Indebtedness” in the Preliminary Prospectus. |

| (3) | Excludes mortgage loans that are secured by multiple single tenant properties. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 5 |

| BANK 2017-BNK4 | Transaction Highlights |

Loan Structural Features:

Amortization:Based on the Initial Pool Balance, 51.3% of the mortgage pool (35 mortgage loans) has scheduled amortization, as follows:

32.1% (22 mortgage loans) requires amortization during the entire loan term; and

19.2% (13 mortgage loans) provides for an interest-only period followed by an amortization period.

Interest-Only:Based on the Initial Pool Balance, 48.7% of the mortgage pool (13 mortgage loans) provides for interest-only payments during the entire loan term. The weighted average Cut-off Date Loan-to-Value Ratio and weighted average U/W Net Cash Flow DSCR for those mortgage loans are 56.7% and 2.00x, respectively.

Hard Lockboxes: Based on the Initial Pool Balance, 69.9% of the mortgage pool (22 mortgage loans) has hard lockboxes in place.

Reserves:The mortgage loans require amounts to be escrowed monthly as follows (excluding any mortgage loans with springing provisions):

| Real Estate Taxes: | 68.8% of the pool |

| Insurance: | 40.9% of the pool |

| Capital Replacements: | 61.4% of the pool |

| TI/LC: | 60.3% of the pool(1) |

| (1) | The percentage of Initial Pool Balance for mortgage loans with TI/LC reserves is based on the aggregate principal balance allocable to loans that include office, retail, industrial and mixed-use properties. |

Call Protection/Defeasance: Based on the Initial Pool Balance, the mortgage pool has the following call protection and defeasance features:

91.0% of the mortgage pool (44 mortgage loans) features a lockout period, then defeasance only until an open period;

4.9% of the mortgage pool (three mortgage loans) features a lockout period, then the greater of a prepayment premium or yield maintenance until an open period; and

4.1% of the mortgage pool (one mortgage loan) features no lockout period, but requires the greater of a prepayment premium or yield maintenance until an open period.

Prepayment restrictions for each mortgage loan reflect the entire life of the mortgage loan. Please refer to Annex A-1 to the Preliminary Prospectus and the footnotes related thereto for further information regarding individual loan call protection applicable to each mortgage loan.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 6 |

| BANK 2017-BNK4 | Issue Characteristics |

| III. | Issue Characteristics |

| Securities Offered: | $826,084,000 approximate monthly pay, multi-class, commercial mortgage REMIC pass-through certificates consisting of ten classes (Classes A-1, A-2, A-3, A-4, A-SB, A-S, B, C, X-A and X-B), which are offered pursuant to a registration statement filed with the SEC (such classes of certificates, the “Offered Certificates”). |

| Mortgage Loan Sellers: | Bank of America, National Association (“BANA”) Morgan Stanley Mortgage Capital Holdings LLC (“MSMCH”) and Wells Fargo Bank, National Association (“WFB”). |

| Joint Bookrunners and Co-Lead Managers: | Wells Fargo Securities, LLC, Merrill Lynch, Pierce, Fenner & Smith Incorporated and Morgan Stanley & Co. LLC |

| Co-Manager: | Academy Securities Inc. |

| Rating Agencies: | Fitch Ratings, Inc., Kroll Bond Rating Agency, Inc. and Moody’s Investors Service, Inc. |

| Master Servicer: | Wells Fargo Bank, National Association |

| Special Servicer: | Rialto Capital Advisors, LLC |

| Certificate Administrator: | Wells Fargo Bank, National Association |

| Trustee: | Wilmington Trust, National Association |

| Operating Advisor: | Pentalpha Surveillance LLC |

| Asset Representations Reviewer: | Pentalpha Surveillance LLC |

| U.S. Credit Risk Retention: | For a discussion of the manner in which the U.S. credit risk retention requirements are being addressed by Wells Fargo Bank, National Association, as the retaining sponsor, see “Credit Risk Retention” in the Preliminary Prospectus. |

| EU Risk Retention: | For a discussion of the manner in which each of Bank of America, National Association, Morgan Stanley Bank, N.A. and Wells Fargo Bank, National Association will covenant and represent to each other, the issuing entity and the trustee to retain a material net economic interest in the securitization for the purpose of the EU risk retention requirements and due diligence requirements, see “EU Securitization Risk Retention Requirements” in the Preliminary Prospectus. |

| Risk Retention Consultation Party: | Wells Fargo Bank, National Association |

| Initial Majority Controlling Class Certificateholder: | RREF III Debt AIV, LP or another affiliate of Rialto Capital Advisors, LLC. |

| Cut-off Date: | The Cut-off Date with respect to each mortgage loan is the due date for the monthly debt service payment that is due in April 2017 (or, in the case of any mortgage loan that has its first due date in May 2017, the date that would have been its due date in April 2017 under the terms of that mortgage loan if a monthly debt service payment were scheduled to be due in that month). |

| Expected Closing Date: | On or about April 19, 2017. |

| Determination Dates: | The 11th day of each month (or if that day is not a business day, the next succeeding business day), commencing in May 2017. |

| Distribution Dates: | The fourth business day following the Determination Date in each month, commencing in May 2017. |

| Rated Final Distribution Date: | The Distribution Date in May 2050. |

| Interest Accrual Period: | With respect to any Distribution Date, the calendar month immediately preceding the month in which such Distribution Date occurs. |

| Day Count: | The Offered Certificates will accrue interest on a 30/360 basis. |

| Minimum Denominations: | $10,000 for each Class of Offered Certificates (other than the Class X-A and X-B Certificates) and $1,000,000 for the Class X-A and X-B Certificates. Investments may also be made in any whole dollar denomination in excess of the applicable minimum denomination. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 7 |

| BANK 2017-BNK4 | Issue Characteristics |

| Clean-up Call: | 1.0% |

| Delivery: | DTC, Euroclear and Clearstream Banking |

| ERISA/SMMEA Status: | Each Class of Offered Certificates is expected to be eligible for exemptive relief under ERISA. No Class of Offered Certificates will be SMMEA eligible. |

| Risk Factors: | THE CERTIFICATES INVOLVE CERTAIN RISKS AND MAY NOT BE SUITABLE FOR ALL INVESTORS. SEE THE “RISK FACTORS” SECTION OF THE PRELIMINARY PROSPECTUS. |

| Bond Analytics Information: | The Certificate Administrator will be authorized to make distribution date statements, CREFC® reports and certain supplemental reports (other than confidential information) available to certain financial modeling and data provision services, including Bloomberg, L.P., Trepp, LLC, Intex Solutions, Inc., Markit Group Limited, Interactive Data Corp., BlackRock Financial Management, Inc., CMBS.com, Inc., Moody’s Analytics and Thomson Reuters Corporation. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 8 |

| BANK 2017-BNK4 | Characteristics of the Mortgage Pool |

| IV. | Characteristics of the Mortgage Pool(1) |

| A. | Ten Largest Mortgage Loans |

| Mortgage Loan Seller | Mortgage Loan Name | City | State | Number of Mortgage Loans / Mortgaged Properties | Mortgage Loan Cut-off Date Balance ($) | % of Initial Pool Balance (%) | Property Type | Number of SF/Rooms | Cut-off Date Balance Per SF/Room | Cut-off Date LTV Ratio (%)(2)(3) | Balloon or ARD LTV Ratio (%)(2)(3) | U/W NCF DSCR (x) | U/W NOI Debt Yield (%)(2) | |||||||||||

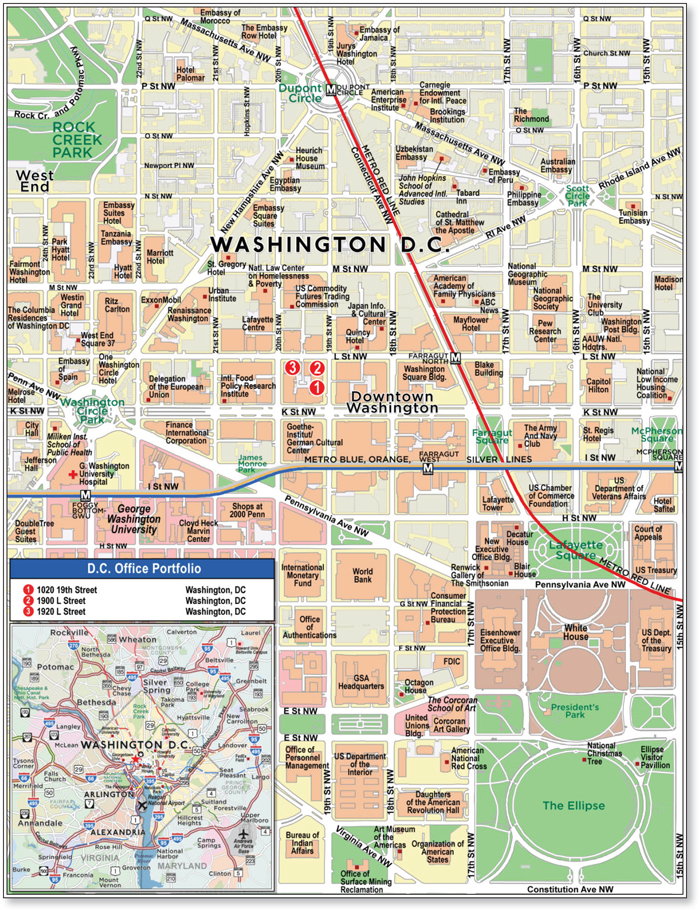

| BANA | D.C. Office Portfolio | Washington | DC | 1 / 3 | $70,000,000 | 6.9 | % | Office | 328,319 | $320 | 53.5 | % | 53.5 | % | 1.71 | x | 9.3 | % | ||||||

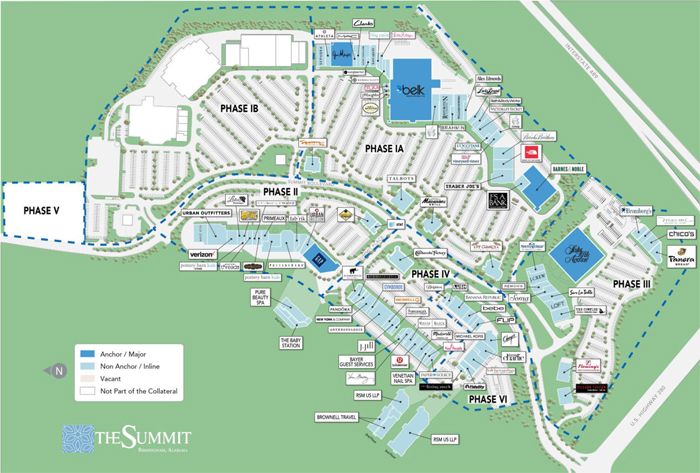

| BANA | The Summit Birmingham | Birmingham | AL | 1 / 1 | 61,875,000 | 6.1 | Retail | 681,245 | 305 | 54.3 | 54.3 | 1.68 | 8.7 | |||||||||||

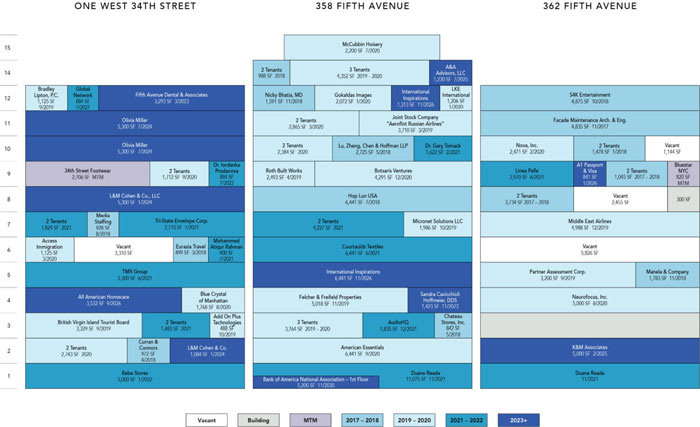

| WFB | One West 34th Street | New York | NY | 1 / 1 | 60,000,000 | 6.0 | Office | 210,338 | 713 | 53.6 | 53.6 | 1.63 | 7.6 | |||||||||||

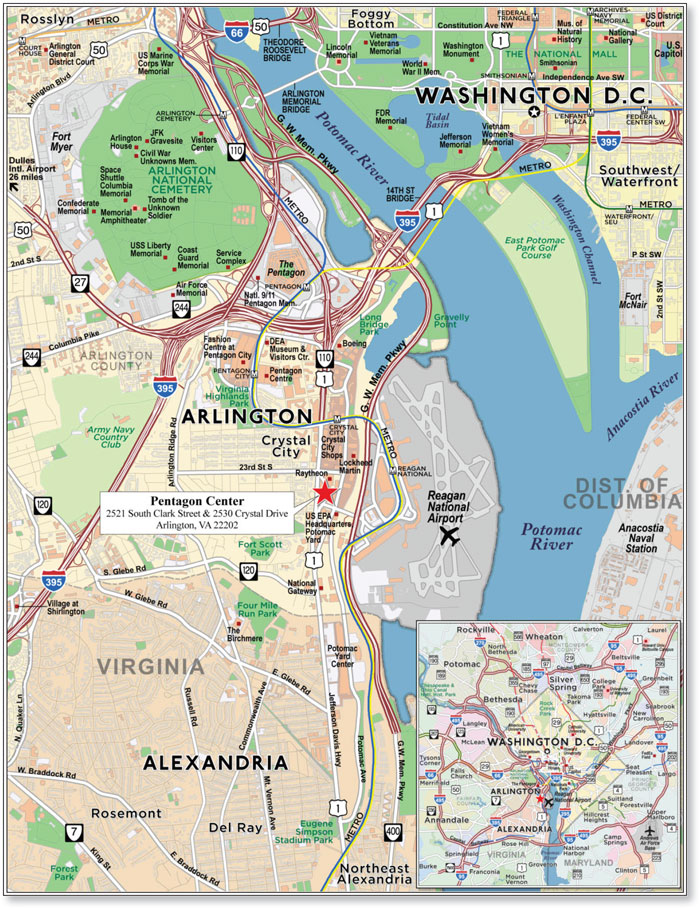

| MSMCH | Pentagon Center | Arlington | VA | 1 / 1 | 55,000,000 | 5.5 | Office | 911,818 | 230 | 55.3 | 55.3 | 2.75 | 12.1 | |||||||||||

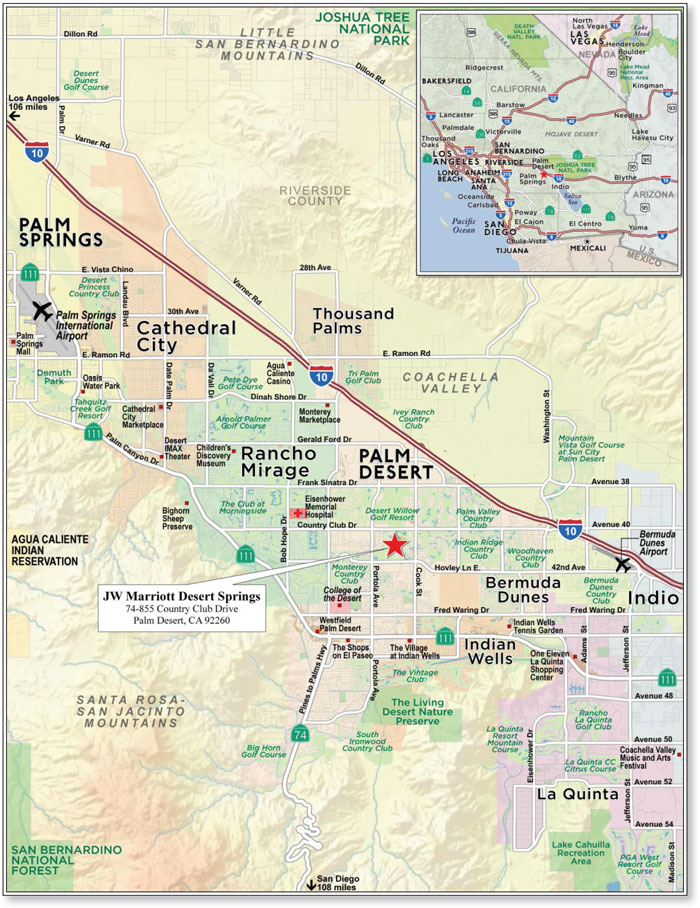

| MSMCH | JW Marriott Desert Springs | Palm Desert | CA | 1 / 1 | 54,863,232 | 5.4 | Hospitality | 884 | 129,767 | 71.3 | 66.0 | 2.31 | 20.3 | |||||||||||

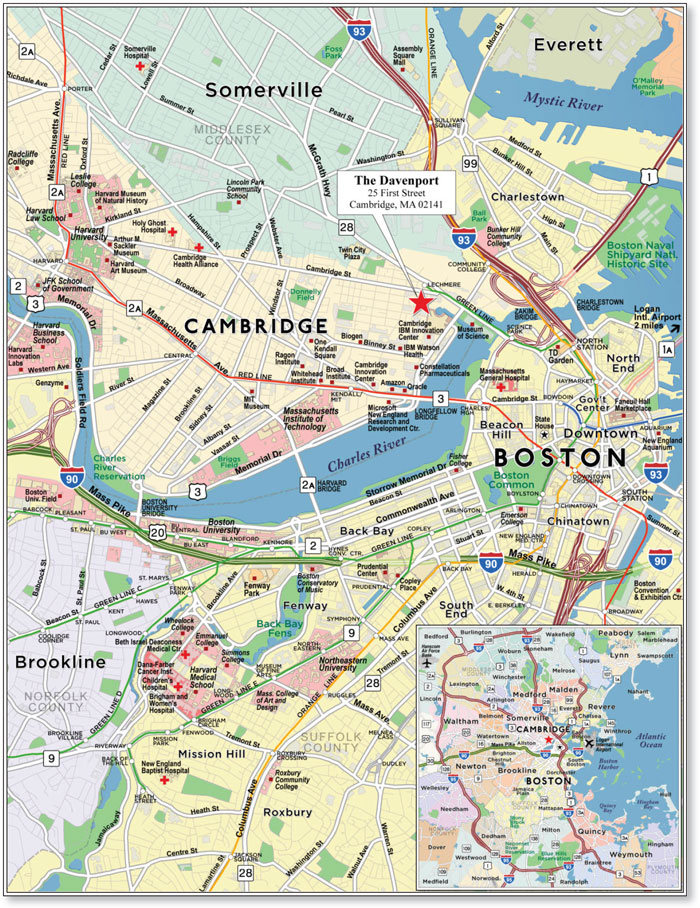

| WFB | The Davenport | Cambridge | MA | 1 / 1 | 50,000,000 | 5.0 | Office | 230,864 | 455 | 49.1 | 49.1 | 1.86 | 8.6 | |||||||||||

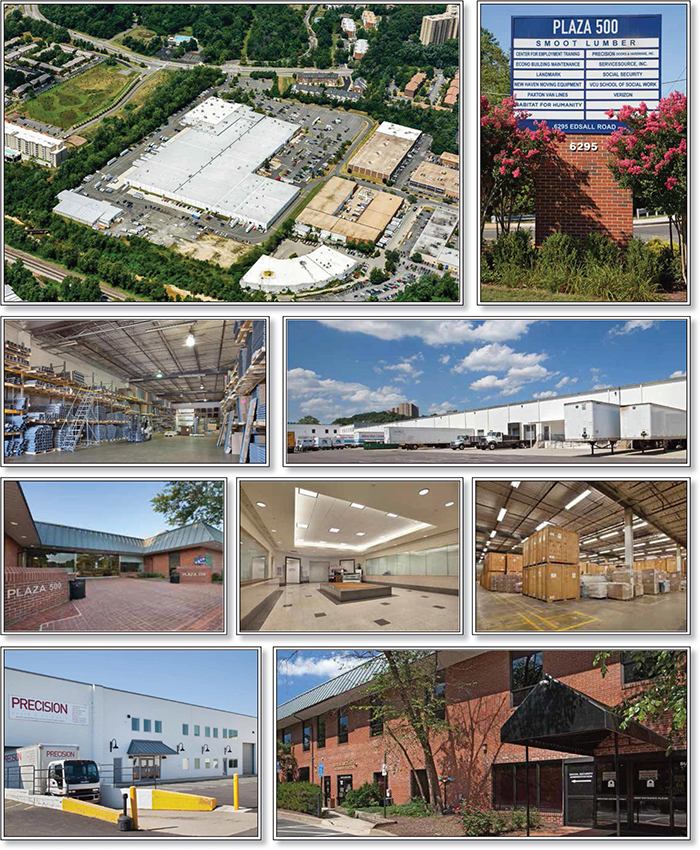

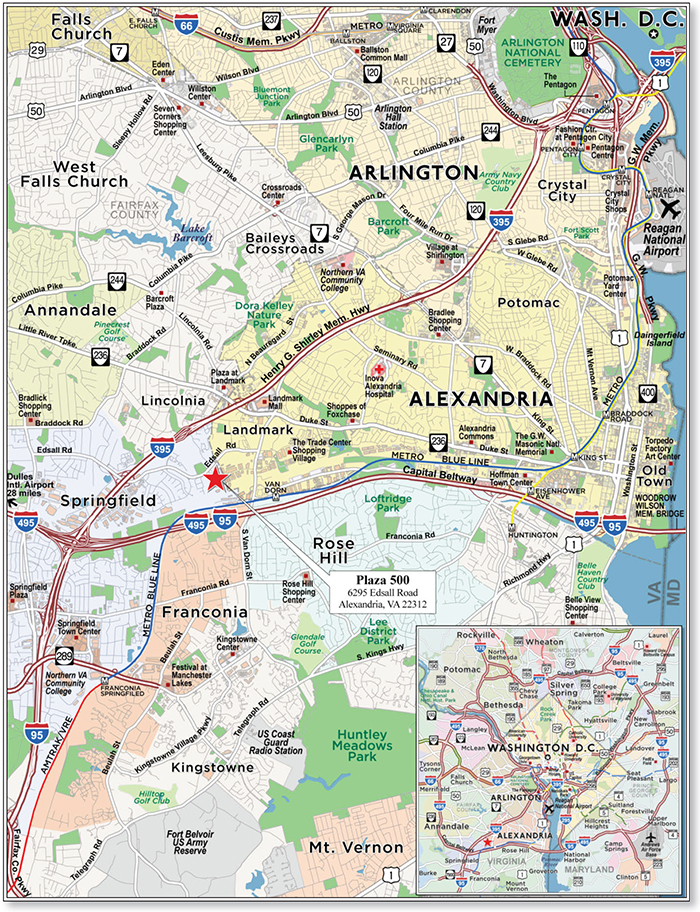

| BANA | Plaza 500 | Alexandria | VA | 1 / 1 | 48,750,000 | 4.8 | Industrial | 502,807 | 97 | 65.0 | 65.0 | 1.79 | 8.7 | |||||||||||

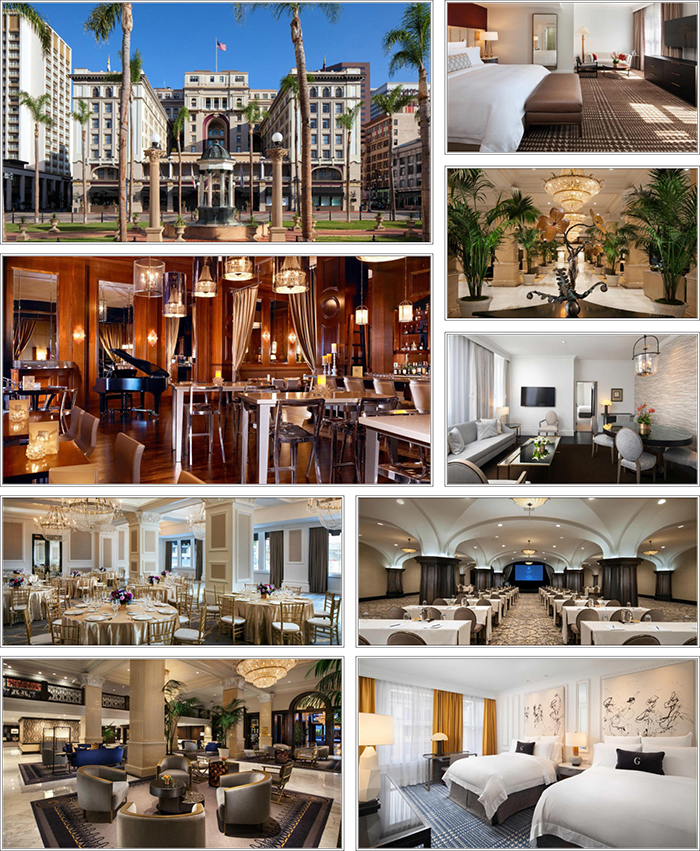

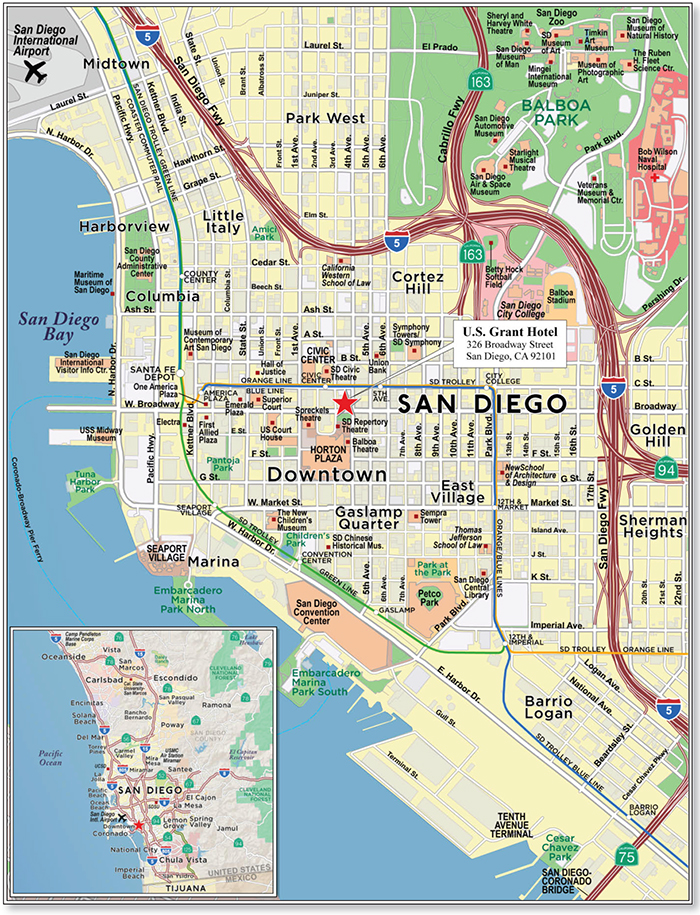

| BANA | U.S. Grant Hotel | San Diego | CA | 1 / 1 | 47,000,000 | 4.7 | Hospitality | 270 | 174,074 | 47.9 | 42.0 | 1.66 | 14.0 | |||||||||||

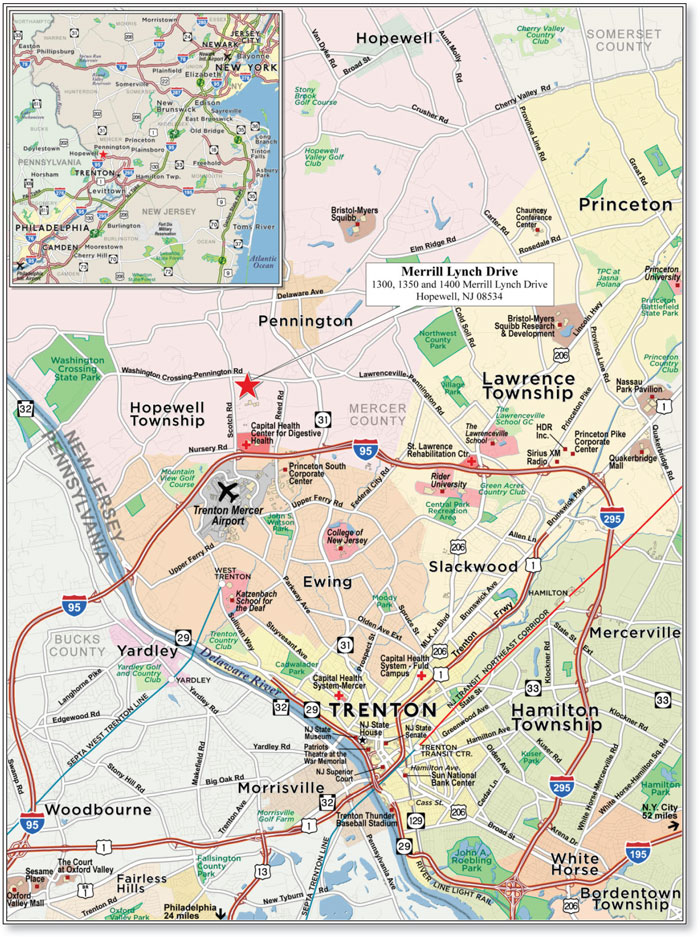

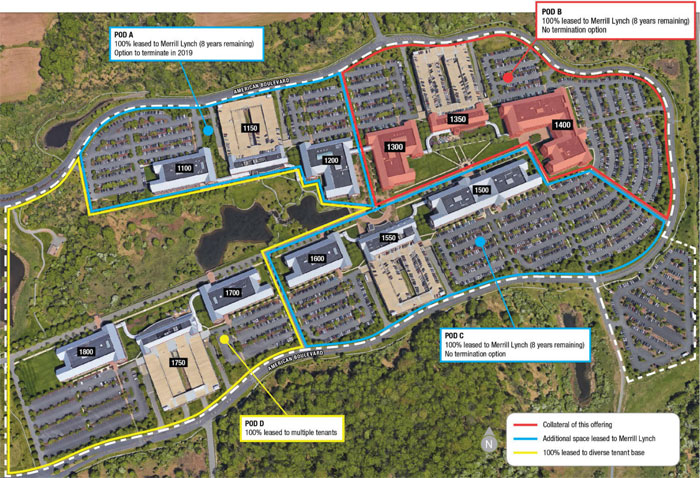

| MSMCH | Merrill Lynch Drive | Hopewell | NJ | 1 / 1 | 41,440,000 | 4.1 | Office | 553,841 | 187 | 67.7 | 67.7 | 2.95 | 11.8 | |||||||||||

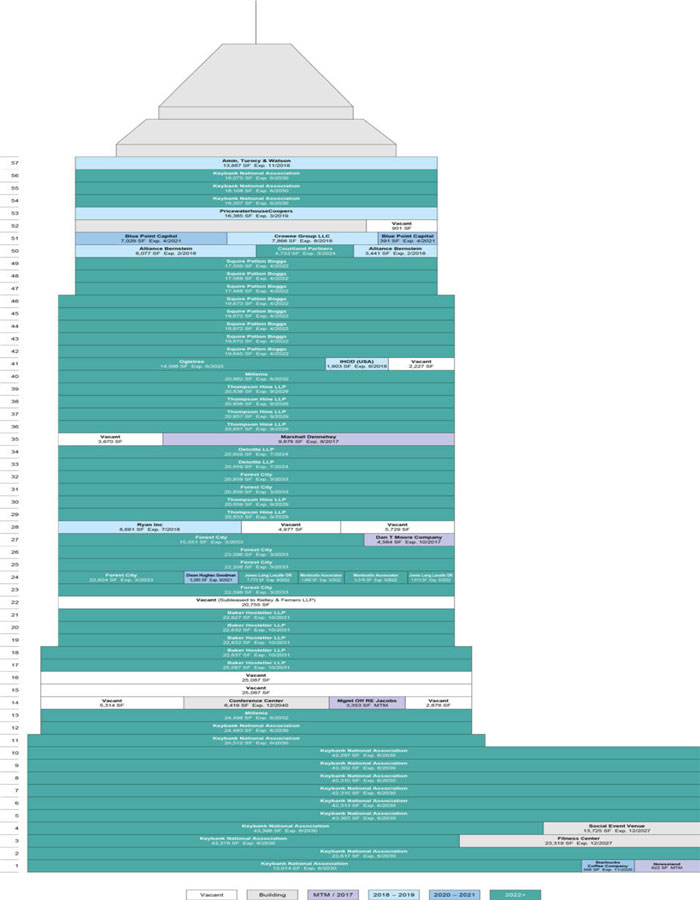

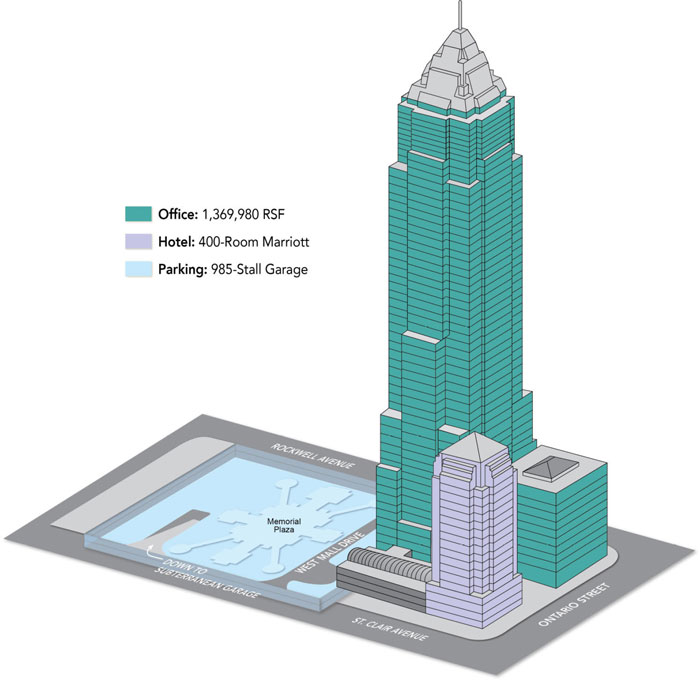

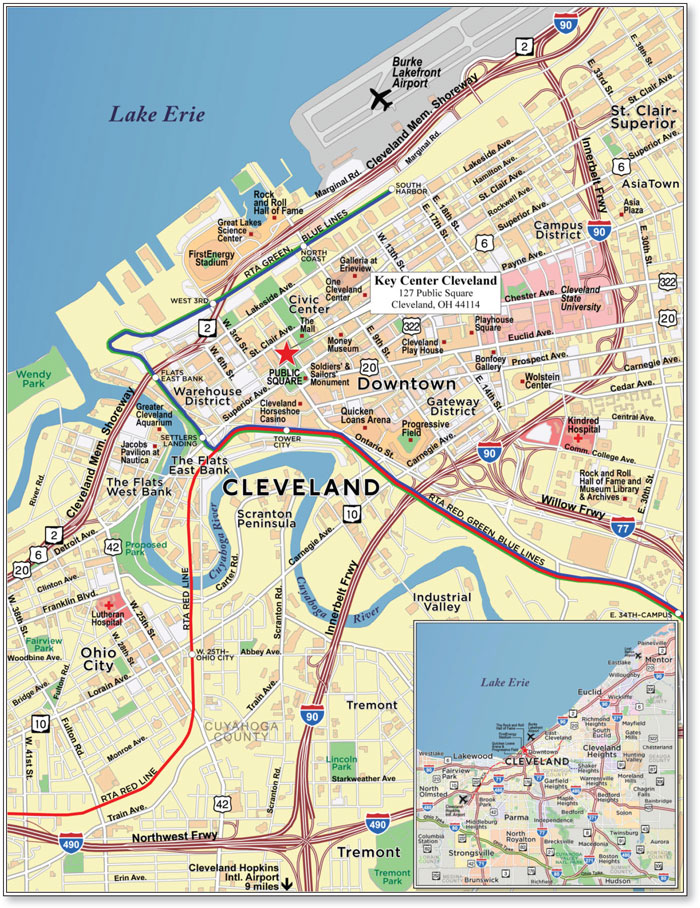

| BANA | Key Center Cleveland | Cleveland | OH | 1 / 1 | 40,000,000 | 4.0 | Mixed Use | 1,369,980 | 161 | 60.8 | 49.6 | 1.59 | 12.3 | |||||||||||

| Top Three Total/Weighted Average | 3 / 5 | $191,875,000 | 19.0 | % | 53.8 | % | 53.8 | % | 1.68 | x | 8.6 | % | ||||||||||||

| Top Five Total/Weighted Average | 5 / 7 | $301,738,232 | 29.9 | % | 57.2 | % | 56.3 | % | 1.99 | x | 11.3 | % | ||||||||||||

| Top Ten Total/Weighted Average | 10 / 12 | $528,928,232 | 52.5 | % | 57.4 | % | 55.5 | % | 1.97 | x | 11.2 | % | ||||||||||||

| Non-Top Ten Total/Weighted Average | 38 / 52 | $479,260,611 | 47.5 | % | 60.9 | % | 52.0 | % | 1.68 | x | 11.4 | % | ||||||||||||

| (1) | With respect to any mortgage loan that is part of a whole loan, Cut-off Date Balance Per SF/Room, loan-to-value ratio, debt service coverage ratio and debt yield calculations include the relatedpari passu companion loan(s) but exclude any related subordinate secured loan(s) (unless otherwise stated). With respect to each mortgage loan, debt service coverage ratio, debt yield and loan-to-value ratio information do not take into account subordinate debt (whether or not secured by the related mortgaged property), if any, that currently exists or is allowed under the terms of such mortgage loan. |

| (2) | With respect to the mortgage loan secured by the mortgaged property identified on Annex A-1 to the Preliminary Prospectus as D.C. Office Portfolio, all loan-to-value and debt yield calculations are net of the $5,000,000 earnout reserve. |

| (3) | With respect to the mortgage loans secured by the mortgaged properties identified on Annex A-1 to the Preliminary Prospectus as The Davenport and Key Center Cleveland, all loan-to-value calculations are based off as-stabilized appraised values. The Cut-off Date LTV Ratio and the Balloon or ARD LTV Ratio based on the as-is appraised values are 51.5% and 51.5%, and 72.3% and 59.0%, respectively for The Davenport and Key Center Cleveland, respectively. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 9 |

| BANK 2017-BNK4 | Characteristics of the Mortgage Pool |

| B. | Summary of the Whole Loans |

| Property Name(1) | Note(s) | Related Notes in Loan Group (Original Balance) | Holder of Note / Anticipated Securitization | Lead Servicer for | Current Master Servicer Under Related Securitization Servicing Agreement | Current Special Servicer Under Related Securitization Servicing Agreement |

| D.C. Office Portfolio | A-1 | $70,000,000 | BANK 2017-BNK4 | Yes | Wells Fargo Bank, National Association | Rialto Capital Advisors, LLC |

| A-2 | $35,000,000 | BANA(2) | No | TBD | TBD | |

| The Summit Birmingham | A-1 | $61,875,000 | BANK 2017-BNK4 | No | Wells Fargo Bank, National Association | Rialto Capital Advisors, LLC |

| A-2 | $73,325,000 | BACM 2017-BNK3 | Yes | Wells Fargo Bank, National Association | Midland Loan Services, a Division of PNC Bank, National Association | |

| A-3 | $50,000,000 | BBCMS 2017-C1 | No | Wells Fargo Bank, National Association | Rialto Capital Advisors, LLC | |

| A-4 | $22,800,000 | WFCM 2017-RB1(3) | No | Wells Fargo Bank, National Association | C-III Asset Management LLC | |

| One West 34th Street | A-1 | $60,000,000 | BANK 2017-BNK4 | Yes | Wells Fargo Bank, National Association | Rialto Capital Advisors, LLC |

| A-2 | $30,000,000 | WFB(4) | No | TBD | TBD | |

| A-3 | $60,000,000 | GSMC(5) | No | TBD | TBD | |

| Pentagon Center | A-1 | $25,000,000 | GSMS 2017-GS5 | (6) | Midland Loan Services, a Division of PNC Bank, National Association | Rialto Capital Advisors, LLC |

| A-2 | $80,000,000 | GSMC(7) | (6) | TBD | TBD | |

| A-3 | $50,000,000 | MSBNA(8) | No | TBD | TBD | |

| A-4, A-5 & A-6 | $55,000,000 | BANK 2017-BNK4 | No | Wells Fargo Bank, National Association | Rialto Capital Advisors, LLC | |

| JW Marriott Desert Springs | A-1 | $60,000,000 | BACM 2017-BNK3 | Yes | Wells Fargo Bank, National Association | Midland Loan Services, a Division of PNC Bank, National Association |

| A-2 & A-3 | $55,000,000 | BANK 2017-BNK4 | No | Wells Fargo Bank, National Association | Rialto Capital Advisors, LLC | |

| The Davenport | A-1 | $55,000,000 | WFCM 2017-RB1(3) | Yes | Wells Fargo Bank, National Association | C-III Asset Management LLC |

| A-2 | $50,000,000 | BANK 2017-BNK4 | No | Wells Fargo Bank, National Association | Rialto Capital Advisors, LLC | |

| Merrill Lynch Drive | A-1 | $41,500,000 | BBCMS 2017-C1 | Yes | Wells Fargo Bank, National Association | Rialto Capital Advisors, LLC |

| A-2 | $20,660,000 | WFCM 2017-RB1(3) | No | Wells Fargo Bank, National Association | C-III Asset Management LLC | |

| A-3 | $41,440,000 | BANK 2017-BNK4 | No | Wells Fargo Bank, National Association | Rialto Capital Advisors, LLC | |

| Key Center Cleveland | A-1 | $50,000,000 | CGCMT 2017-P7(9) | Yes | Wells Fargo Bank, National Association | Rialto Capital Advisors, LLC |

| A-2 | $40,000,000 | BANK 2017-BNK4 | No | Wells Fargo Bank, National Association | Rialto Capital Advisors, LLC | |

| A-3 & A-6 | $60,000,000 | JPMDB 2017-C5(10) | No | Midland Loan Services, a Division of PNC Bank, National Association | LNR Partners, LLC | |

| A-4 | $30,000,000 | Citi(11) | No | TBD | TBD | |

| A-5 | $40,000,000 | BANA(12) | No | TBD | TBD | |

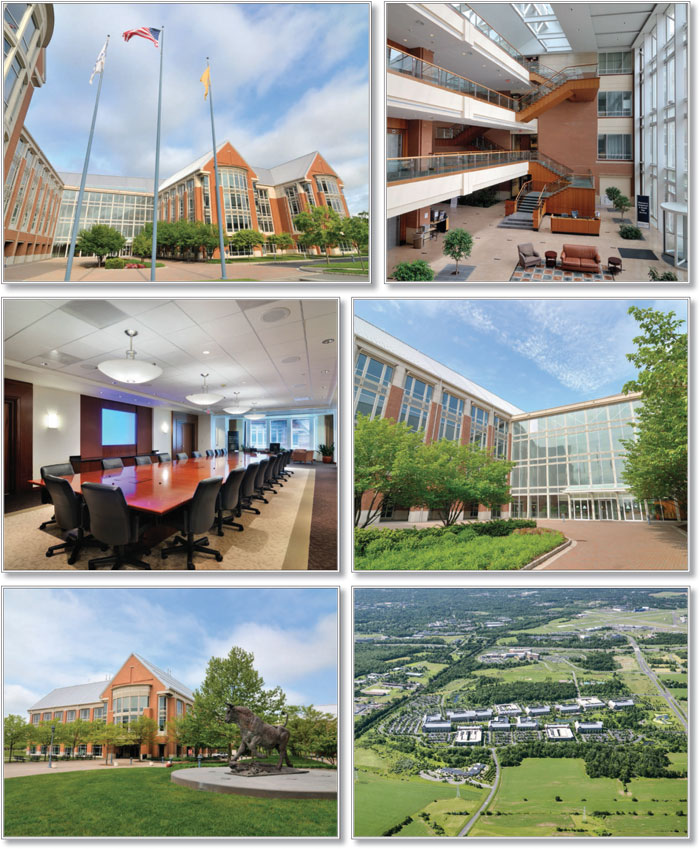

| American Greetings HQ | A-1-1 | $38,000,000 | BANK 2017-BNK4 | Yes | Wells Fargo Bank, National Association | Rialto Capital Advisors, LLC |

| A-1-2 | $27,000,000 | MSC 2016-BNK2 | No | Wells Fargo Bank, National Association | C-III Asset Management LLC | |

| A-2 | $27,000,000 | MSBAM 2016-C32 | No | Wells Fargo Bank, National Association | Midland Loan Services, a Division of PNC Bank, National Association | |

| Ralph’s Food Warehouse Portfolio | A-1 | $25,000,000 | BANK 2017-BNK4 | Yes | Wells Fargo Bank, National Association | Rialto Capital Advisors, LLC |

| A-2 | $17,000,000 | MSBNA(13) | No | Wells Fargo Bank, National Association | Rialto Capital Advisors, LLC |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 10 |

| BANK 2017-BNK4 | Characteristics of the Mortgage Pool |

| (1) | The mortgage loans secured by the mortgaged properties identified on Annex A-1 to the Preliminary Prospectus as D.C. Office Portfolio, The Summit Birmingham, Key Center Cleveland and American Greetings HQ are being contributed to the securitization by BANA. The mortgage loans secured by the mortgaged properties identified on Annex A-1 to the Preliminary Prospectus as One West 34th Street and The Davenport are being contributed to the securitization by WFB. The mortgage loans secured by the mortgaged properties identified on Annex A-1 to the Preliminary Prospectus as Pentagon Center, JW Marriott Desert Springs, Merrill Lynch Drive and Ralph’s Food Warehouse Portfolio are being contributed to the securitization by MSMCH. |

| (2) | The relatedpari passuNote A-2 is currently held by BANA and is expected to be contributed to one or more future securitizations. No assurance can be provided that Note A-2 will not be split further. |

| (3) | The WFCM 2017-RB1 securitization has not yet closed, however, based on a publicly available preliminary prospectus for such securitization, it is expected that (i) the non-controlling Note A-4 of the Summit Birmingham whole loan will be included in that securitization by Barclays, (ii) the controlling Note A-1 of The Davenport whole loan will be included in that securitization by WFB, (iii) the non-controlling Note A-2 of the Merrill Lynch Drive whole loan will be included in that securitization by Barclays and (iv) that securitization will close prior to this transaction. |

| (4) | The relatedpari passuNote A-2 is currently held by WFB and is expected to be contributed to one or more future securitizations. No assurance can be provided that Note A-2 will not be split further. |

| (5) | The relatedpari passuNote A-3 is currently held by GSMC and is expected to be contributed to one or more future securitizations. No assurance can be provided that Note A-3 will not be split further. |

| (6) | The Pentagon Center whole loan is currently being serviced under the GSMS 2017-GS5 pooling and servicing agreement, however, upon the securitization of Note A-2, servicing will shift to the servicing agreement governing the securitization of Note A-2 (the “Pentagon Center Note A-2 Securitization Servicing Agreement”). |

| (7) | The relatedpari passuNote A-2 is currently held by GSMC and is expected to be contributed to one or more future securitizations. No assurance can be provided that Note A-2 will not be split further. |

| (8) | The relatedpari passuNote A-3 is currently held by MSBNA and is expected to be contributed to one or more future securitizations. No assurance can be provided that Note A-3 will not be split further. |

| (9) | The CGCMT 2017-P7 securitization has not yet closed, however, based on a publicly available preliminary prospectus for such securitization, it is expected that (i) the controlling Note A-1 of the Key Center Cleveland whole loan will be included in that securitization by Citi and (ii) that securitization will close prior to this transaction. |

| (10) | The JPMDB 2017-C5 securitization has not yet closed, however, based on a publicly available preliminary prospectus for such securitization, it is expected that (i) the non-controlling Notes A-3 and A-6 of the Key Center Cleveland whole loan will be included in that securitization by DB and (ii) that securitization will close prior to this transaction. |

| (11) | The relatedpari passuNote A-4 is currently held by Citi and is expected to be contributed to one or more future securitizations. No assurance can be provided that Note A-4 will not be split further. |

| (12) | The relatedpari passuNote A-5 is currently held by BANA and is expected to be contributed to one or more future securitizations. No assurance can be provided that Note A-5 will not be split further. |

| (13) | The relatedpari passuNote A-2 is currently held by MSBNA and is expected to be contributed to one or more future securitizations. No assurance can be provided that Note A-2 will not be split further. |

| C. | Mortgage Loans with Additional Secured and Mezzanine Financing |

| Loan No. | Mortgage Loan Seller | Mortgage Loan Name | Mortgage Loan Cut-off Date Balance ($) | % of Initial Pool Balance (%) | Subordinate Debt Cut-off Date Balance ($) | Mezzanine Debt Cut-off Date Balance ($) | Total Debt Interest Rate (%)(1) | Mortgage Loan U/W NCF DSCR (x)(2) | Total Debt U/W NCF DSCR (x) | Mortgage Loan Cut- off Date U/W NOI Debt Yield (%)(2)(3) | Total Debt Cut-off Date U/W NOI Debt Yield (%)(3) | Mortgage Loan Cut-off Date LTV Ratio (%)(2)(3)(4) | Total Debt Cut-off Date LTV Ratio (%)(3)(4) |

| 1 | BANA | D.C. Office Portfolio | $70,000,000 | 6.9% | NAP | $25,000,000 | 5.141% | 1.71x | 1.28x | 9.3% | 7.4% | 53.5% | 66.9% |

| 5 | MSMCH | JW Marriott Desert Springs | 54,863,232 | 5.4 | NAP | 16,000,000 | 5.791 | 2.31 | 1.89 | 20.3 | 17.8 | 71.3 | 81.2 |

| 10 | BANA | Key Center Cleveland | 40,000,000 | 4.0 | NAP | 42,500,000 | 6.515 | 1.59 | 1.17 | 12.3 | 10.3 | 60.8 | 72.5 |

| 12 | BANA | American Greetings HQ(5) | $37,669,589 | 3.7 | $14,708,996 | NAP | 4.755 | 1.45 | 1.11 | 10.8 | 9.3 | 61.3 | 71.2 |

| 25 | MSMCH | Plaza at Milltown Commercial Center | 13,849,834 | 1.4 | NAP | 1,200,000 | 5.732 | 1.28 | 1.07 | 8.5 | 7.8 | 68.0 | 73.9 |

| Total/Weighted Average | $216,382,655 | 21.5% | $14,708,996 | $84,700,000 | 5.530% | 1.77x | 1.37x | 12.9% | 10.9% | 61.6% | 72.8% | ||

| (1) | Total Debt Interest Rate for any specified mortgage loan reflects the weighted average of the interest rates on the respective components of the total debt. |

| (2) | With respect to the D.C. Office Portfolio mortgage loan, The JW Marriott Desert Springs mortgage loan and the Key Center Cleveland mortgage loan, which are each part of a whole loan, the loan-to-value ratio, debt service coverage ratio and debt yield calculations include the relatedpari passu companion loan(s). |

| (3) | With respect to the D.C. Office Portfolio mortgage loan, all loan-to-value and debt yield calculations are net of the $5,000,000 earnout reserve. |

| (4) | With respect to the Key Center Cleveland mortgage loan, all loan-to-value calculations are based off the as-stabilized appraised value. The Cut-off Date LTV Ratio and the Balloon or ARD LTV Ratio percent based on the as-is appraised values are 72.3% and 59.0%, respectively. |

| (5) | For information regarding the American Greetings HQ State of Ohio Subordinate Secured Loan see the description of the American Greetings HQ mortgage loan herein and see also “Description of the Mortgage Pool—Additional Indebtedness—Other Secured Indebtedness” in the Preliminary Prospectus. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 11 |

| BANK 2017-BNK4 | Characteristics of the Mortgage Pool |

D. Previous Securitization History(1)

| Loan No. | Mortgage Loan Seller | Mortgage Loan or Mortgaged Property Name | City | State | Property Type | Mortgage Loan or Mortgaged Property Cut-off Date Balance ($) | % of Initial Pool Balance (%) | Previous Securitization | |||||||||

| 1 | BANA | D.C. Office Portfolio | Washington | DC | Office | $70,000,000 | 6.9 | % | WBCMT 2007-C31 | ||||||||

| 4 | MSMCH | Pentagon Center | Arlington | VA | Office | 55,000,000 | 5.5 | (2) | |||||||||

| 13 | WFB | The Shoppes at South Bay | Torrance | CA | Retail | 37,000,000 | 3.7 | CD 2007-CD4 | |||||||||

| 16 | WFB | Preferred Freezer Philadelphia | Philadelphia | PA | Industrial | 24,000,000 | 2.4 | CWCI 2007-C3 | |||||||||

| 19.01 | WFB | SpringHill Suites Boca Raton | Boca Raton | FL | Hospitality | 9,250,000 | 0.9 | LBUBS 2003-C8 | |||||||||

| 19.02 | WFB | TownePlace Suites Boca Raton | Boca Raton | FL | Hospitality | 5,750,000 | 0.6 | LBUBS 2003-C8 | |||||||||

| 19.03 | WFB | TownePlace Suites Ft Lauderdale West | Fort Lauderdale | FL | Hospitality | 5,000,000 | 0.5 | LBUBS 2003-C8 | |||||||||

| 24 | BANA | King Plaza Center | Daly City | CA | Retail | 16,000,000 | 1.6 | MSC 2007-T27 | |||||||||

| 25 | MSMCH | Plaza at Milltown Commercial Center | Waipahu | HI | Mixed Use | 13,849,834 | 1.4 | UBSBB 2012-C4 | |||||||||

| 27 | WFB | Hilton Garden Inn Chattanooga Downtown | Chattanooga | TN | Hospitality | 11,986,732 | 1.2 | BACM 2007-3 | |||||||||

| 29 | WFB | Crossroads Shopping Center- Bakersfield | Bakersfield | CA | Retail | 8,853,000 | 0.9 | CGCMT 2007-C6 | |||||||||

| 32 | BANA | Alameda Apartments | Alameda | CA | Multifamily | 7,165,372 | 0.7 | MSC 2006-IQ12 | |||||||||

| 33 | WFB | North Main Self Storage | Manteca | CA | Self Storage | 6,982,307 | 0.7 | BSCMS 2007-T26 | |||||||||

| 37 | BANA | Best Western – Hannaford, OH | Cincinnati | OH | Hospitality | 6,440,508 | 0.6 | CSMC 2007-C3 | |||||||||

| 38 | WFB | Huntsville Commons | Huntsville | AL | Retail | 6,375,000 | 0.6 | WBCMT 2007-C30 | |||||||||

| 40 | MSMCH | Kingwood Forest Apartments | Shreveport | LA | Multifamily | 5,500,000 | 0.5 | BACM 2007-2 | |||||||||

| 42 | MSMCH | Barry Plaza | Chicago | IL | Retail | 5,200,000 | 0.5 | GSMS 2012-GCJ9 | |||||||||

| 43 | WFB | 301-333 S Abbot Avenue | Milpitas | CA | Retail | 4,986,466 | 0.5 | MLCFC 2007-7 | |||||||||

| 45 | WFB | Walgreens Bluffton | Bluffton | SC | Retail | 4,054,908 | 0.4 | CWCI 2007-C2 | |||||||||

| 47 | WFB | Phenix Square | Phenix City | AL | Retail | 2,025,000 | 0.2 | CD 2007-CD4 | |||||||||

| Total | $305,419,126 | 30.3 | % | ||||||||||||||

| (1) | The table above represents the most recent securitization with respect to the mortgaged property securing the related mortgage loan, based on information provided by the related borrower or obtained through searches of a third-party database. While loans secured by the above mortgaged properties may have been securitized multiple times in prior transactions, mortgage loans in this securitization are only listed in the above chart if the mortgage loan paid off a loan in another securitization. The information has not otherwise been confirmed by the mortgage loan sellers. |

| (2) | With respect to the Pentagon Center mortgage loan, the related mortgaged property was previously securitized in the MSC 2007-IQ14, BSCMS 2007-PWR16, WBCMT 2007-C32, WBCMT 2007-C31, BACM 2007-2 and MSC 2007-HQ12 transactions. The Pentagon Center Property was previously financed as part of a 20-property office portfolio financing which was modified and extended in December 2010 by the previous lender. See “Description of the Mortgage Pool — Loan Purpose; Default History, Bankruptcy Issues and Other Proceedings” in the Preliminary Prospectus. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 12 |

| BANK 2017-BNK4 | Characteristics of the Mortgage Pool |

E. Mortgage Loans with Scheduled Balloon Payments and Related Classes

Class A-2(1)

| Loan No. | Mortgage Loan Seller | Mortgage Loan Name | State | Property Type | Mortgage Loan Cut-off Date Balance ($) | % of Initial Pool Balance (%) | Mortgage Loan Balance at Maturity ($) | % of Class A-2 Certificate Principal Balance (%)(2) | Rooms /SF | Loan Per Room / SF ($) | U/W NCF DSCR (x) | U/W NOI Debt Yield (%) | Cut-off Date LTV Ratio (%) | Balloon LTV Ratio (%) | Rem. IO Period (mos.) | Rem. Term to Maturity (mos.) | ||||||||||||||||||||||

| 5 | MSMCH | JW Marriott Desert Springs | CA | Hospitality | $54,863,232 | 5.4 | % | $50,832,722 | 57.5 | % | 884 | $129,767 | 2.31 | x | 20.3 | % | 71.3 | % | 66.0 | % | 0 | 58 | ||||||||||||||||

| 9 | MSMCH | Merrill Lynch Drive | NJ | Office | 41,440,000 | 4.1 | 41,440,000 | 46.9 | 553,841 | 187 | 2.95 | 11.8 | 67.7 | 67.7 | 58 | 58 | ||||||||||||||||||||||

| Total/Weighted Average | $96,303,232 | 9.6 | % | $92,272,722 | 104.4 | % | 2.59 | x | 16.6 | % | 69.8 | % | 66.7 | % | 25 | 58 | ||||||||||||||||||||||

| (1) | The table above presents the mortgage loan(s) whose balloon payments would be applied to pay down the principal balance of the Class A-2 Certificates, assuming a 0% CPR and applying the “Structuring Assumptions” described in the Preliminary Prospectus, including the assumptions that (i) none of the mortgage loans in the pool experience prepayments prior to maturity, defaults or losses; (ii) there are no extensions of maturity dates of any mortgage loans in the pool; and (iii) each mortgage loan in the pool is paid in full on its stated maturity date. Each Class of Certificates evidences undivided ownership interests in the entire pool of mortgage loans. Debt service coverage ratio, debt yield and loan-to-value ratio information do not take into account subordinate debt (whether or not secured by the related mortgaged property), if any, that currently exists or is allowed under the terms of any mortgage loan. See Annex A-1 to the Preliminary Prospectus. |

| (2) | Reflects the percentage equal to the Balloon Balance divided by the initial Class A-2 Certificate Balance. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 13 |

| BANK 2017-BNK4 | Characteristics of the Mortgage Pool |

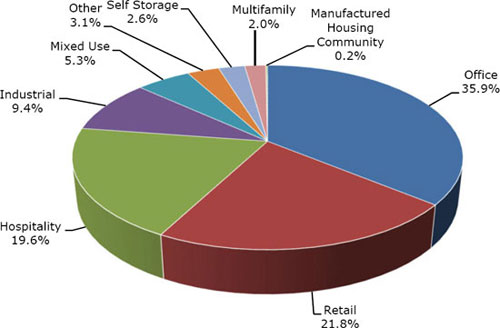

F. Property Type Distribution(1)

| Property Type | Number of Mortgaged Properties | Aggregate Cut-off Date Balance ($) | % of Initial Pool Balance (%) | Weighted Average Cut-off Date LTV Ratio (%) | Weighted Average Balloon or ARD LTV Ratio (%) | Weighted Average U/W NCF DSCR (x) | Weighted Average U/W NOI Debt Yield (%) | Weighted Average U/W NCF Debt Yield (%) | Weighted Average Mortgage Rate (%) | |||||||||||||||||

| Office | 10 | $362,109,589 | 35.9 | % | 58.0 | % | 55.2 | % | 1.96 | x | 9.9 | % | 9.4 | % | 4.498 | % | ||||||||||

| Suburban | 5 | 182,109,589 | 18.1 | 63.6 | 58.1 | 2.18 | 11.3 | 10.9 | 4.536 | |||||||||||||||||

| CBD | 5 | 180,000,000 | 17.9 | 52.3 | 52.3 | 1.73 | 8.5 | 8.0 | 4.459 | |||||||||||||||||

| Retail | 28 | 220,206,846 | 21.8 | 59.3 | 54.4 | 1.66 | 10.0 | 9.5 | 4.975 | |||||||||||||||||

| Anchored | 12 | 94,592,143 | 9.4 | 60.3 | 54.6 | 1.74 | 10.7 | 10.1 | 5.044 | |||||||||||||||||

| Lifestyle Center | 1 | 61,875,000 | 6.1 | 54.3 | 54.3 | 1.68 | 8.7 | 8.1 | 4.762 | |||||||||||||||||

| Single Tenant | 11 | 40,473,067 | 4.0 | 59.7 | 51.3 | 1.47 | 10.3 | 10.1 | 5.315 | |||||||||||||||||

| Shadow Anchored | 2 | 13,080,171 | 1.3 | 73.7 | 62.7 | 1.43 | 10.0 | 9.1 | 4.902 | |||||||||||||||||

| Unanchored | 2 | 10,186,466 | 1.0 | 59.4 | 54.4 | 1.90 | 10.2 | 9.5 | 4.380 | |||||||||||||||||

| Hospitality | 10 | 197,646,602 | 19.6 | 59.6 | 50.8 | 1.96 | 16.2 | 13.1 | 5.202 | |||||||||||||||||

| Full Service | 5 | 165,706,094 | 16.4 | 60.3 | 52.5 | 1.95 | 16.2 | 12.9 | 5.201 | |||||||||||||||||

| Limited Service | 5 | 31,940,508 | 3.2 | 55.6 | 41.9 | 1.97 | 16.1 | 14.1 | 5.203 | |||||||||||||||||

| Industrial | 6 | 94,502,199 | 9.4 | 63.8 | 61.9 | 1.77 | 9.6 | 9.0 | 4.776 | |||||||||||||||||

| Flex | 4 | 66,002,199 | 6.5 | 64.9 | 63.0 | 1.70 | 9.1 | 8.6 | 4.699 | |||||||||||||||||

| Cold Storage | 1 | 24,000,000 | 2.4 | 60.9 | 60.9 | 2.01 | 10.6 | 10.2 | 4.990 | |||||||||||||||||

| Light Industrial | 1 | 4,500,000 | 0.4 | 63.4 | 51.7 | 1.56 | 10.6 | 9.8 | 4.770 | |||||||||||||||||

| Mixed Use | 2 | 53,849,834 | 5.3 | 62.7 | 51.3 | 1.51 | 11.3 | 10.7 | 5.234 | |||||||||||||||||

| Office/Hospitality/Parking | 1 | 40,000,000 | 4.0 | 60.8 | 49.6 | 1.59 | 12.3 | 11.5 | 5.310 | |||||||||||||||||

| Retail/Office | 1 | 13,849,834 | 1.4 | 68.0 | 56.1 | 1.28 | 8.5 | 8.3 | 5.016 | |||||||||||||||||

| Other | 1 | 31,397,064 | 3.1 | 54.9 | 42.0 | 1.52 | 11.5 | 11.3 | 5.520 | |||||||||||||||||

| Parking Garage | 1 | 31,397,064 | 3.1 | 54.9 | 42.0 | 1.52 | 11.5 | 11.3 | 5.520 | |||||||||||||||||

| Self Storage | 2 | 25,982,307 | 2.6 | 54.0 | 50.9 | 2.06 | 10.0 | 9.8 | 4.538 | |||||||||||||||||

| Self Storage | 2 | 25,982,307 | 2.6 | 54.0 | 50.9 | 2.06 | 10.0 | 9.8 | 4.538 | |||||||||||||||||

| Multifamily | 4 | 20,656,902 | 2.0 | 52.5 | 43.9 | 1.63 | 10.9 | 10.4 | 4.892 | |||||||||||||||||

| Garden | 2 | 12,665,372 | 1.3 | 54.9 | 46.2 | 1.74 | 11.8 | 11.0 | 4.813 | |||||||||||||||||

| Mid Rise | 2 | 7,991,531 | 0.8 | 48.8 | 40.2 | 1.45 | 9.6 | 9.4 | 5.016 | |||||||||||||||||

| Manufactured Housing Community | 1 | 1,837,500 | 0.2 | 69.3 | 59.1 | 1.53 | 10.5 | 10.3 | 5.363 | |||||||||||||||||

| Manufactured Housing Community | 1 | 1,837,500 | 0.2 | 69.3 | 59.1 | 1.53 | 10.5 | 10.3 | 5.363 | |||||||||||||||||

| Total/Weighted Average: | 64 | $1,008,188,843 | 100.0 | % | 59.1 | % | 53.8 | % | 1.83 | x | 11.3 | % | 10.3 | % | 4.848 | % | ||||||||||

Because this table presents information relating to the mortgaged properties and not the mortgage loans, (a) the information for mortgage loans secured by more than one mortgaged property (other than through cross-collateralization with other mortgage loans) is based on allocated amounts (allocating the principal balance of the mortgage loan to each of those properties according to the relative appraised values of the mortgaged properties or the allocated loan amounts or property-specific release prices set forth in the related mortgage loan documents or such other allocation as the related mortgage loan seller deemed appropriate) and (b) the information for each mortgaged property that relates to a mortgage loan that is cross-collateralized or cross-defaulted with other mortgage loans is based upon the principal balance of that mortgage loan, except that the applicable loan-to-value ratio, debt service coverage ratio and debt yield for each such mortgage loan is based upon the ratio or yield (as applicable) for the aggregate indebtedness evidenced by all loans in the group (without regard to any limitation on the amount of indebtedness secured by any mortgaged property in such cross-collateralized group). On an individual basis, without regard to the cross-collateralization feature, any mortgage loan that is part of a cross-collateralized group of mortgage loans may have a higher loan-to-value ratio, lower debt service coverage ratio and/or lower debt yield than is presented herein. With respect to any mortgage loan that is part of a whole loan, the loan-to-value ratio, debt service coverage ratio and debt yield calculations include the relatedpari passu companion loan(s) but exclude any related subordinate secured loan(s) (unless otherwise stated). With respect to each mortgage loan, debt service coverage ratio, debt yield and loan-to-value ratio information do not take into account of any subordinate debt (whether or not secured by the related mortgaged property) that currently exists or is allowed under the terms of such mortgage loan. With respect to the mortgage loan secured by the mortgaged property identified on Annex A-1 to the Preliminary Prospectus as D.C. Office Portfolio, all loan-to-value and debt yield calculations are net of the $5,000,000 earnout reserve. See Annex A-1 to the Preliminary Prospectus.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 14 |

| BANK 2017-BNK4 | Characteristics of the Mortgage Pool |

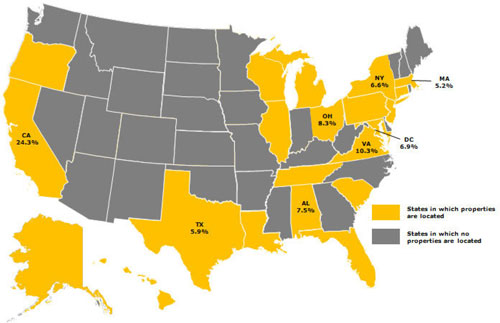

G. Geographic Distribution(1)(2)

| Location | Number of Mortgaged Properties | Aggregate Cut-off Date Balance ($) | % of Initial Pool Balance (%) | Weighted Average Cut-off Date LTV Ratio (%) | Weighted Average Balloon or ARD LTV Ratio (%) | Weighted Average U/W NCF DSCR (x) | Weighted Average U/W NOI Debt Yield (%) | Weighted Average U/W NCF Debt Yield (%) | Weighted Average Mortgage Rate (%) | |||||||||||||||||

| California | 13 | $244,616,906 | 24.3 | % | 59.8 | % | 55.0 | % | 1.83 | x | 12.8 | % | 10.9 | % | 4.989 | % | ||||||||||

| Southern | 6 | 182,491,232 | 18.1 | 62.3 | 57.3 | 1.79 | 13.8 | 11.2 | 5.118 | |||||||||||||||||

| Northern | 7 | 62,125,674 | 6.2 | 52.5 | 48.3 | 1.92 | 10.2 | 9.8 | 4.610 | |||||||||||||||||

| Virginia | 2 | 103,750,000 | 10.3 | 59.9 | 59.9 | 2.30 | 10.5 | 10.3 | 4.438 | |||||||||||||||||

| Ohio | 3 | 84,110,097 | 8.3 | 61.4 | 47.9 | 1.55 | 11.8 | 11.0 | 5.039 | |||||||||||||||||

| Alabama | 4 | 75,750,000 | 7.5 | 56.9 | 55.4 | 1.62 | 8.9 | 8.3 | 4.830 | |||||||||||||||||

| District of Columbia | 3 | 70,000,000 | 6.9 | 53.5 | 53.5 | 1.71 | 9.3 | 8.7 | 4.758 | |||||||||||||||||

| New York | 2 | 66,825,000 | 6.6 | 54.8 | 54.3 | 1.59 | 7.6 | 7.2 | 4.410 | |||||||||||||||||

| Texas | 6 | 59,441,478 | 5.9 | 62.0 | 51.6 | 1.80 | 13.4 | 11.7 | 5.056 | |||||||||||||||||

| Massachusetts | 2 | 52,295,000 | 5.2 | 49.1 | 49.1 | 1.88 | 8.7 | 8.2 | 4.243 | |||||||||||||||||

| Other(3) | 29 | 251,400,362 | 24.9 | 62.0 | 53.2 | 1.90 | 12.2 | 11.5 | 5.040 | |||||||||||||||||

| Total/Weighted Average | 64 | $1,008,188,843 | 100.0 | % | 59.1 | % | 53.8 | % | 1.83 | x | 11.3 | % | 10.3 | % | 4.848 | % | ||||||||||

| (1) | The mortgaged properties are located in 21 states, the District of Columbia and Puerto Rico. |

| (2) | Because this table presents information relating to the mortgaged properties and not the mortgage loans, (a) the information for mortgage loans secured by more than one mortgaged property (other than through cross-collateralization with other mortgage loans) is based on allocated amounts (allocating the principal balance of the mortgage loan to each of those properties according to the relative appraised values of the mortgaged properties or the allocated loan amounts or property-specific release prices set forth in the related mortgage loan documents or such other allocation as the related mortgage loan seller deemed appropriate), and (b) the information for each mortgaged property that relates to a mortgage loan that is cross-collateralized or cross-defaulted with other mortgage loans is based upon the principal balance of that mortgage loan, except that the applicable loan-to-value ratio, debt service coverage ratio and debt yield for each such mortgage loan is based upon the ratio or yield (as applicable) for the aggregate indebtedness evidenced by all loans in the group (without regard to any limitation on the amount of indebtedness secured by any mortgaged property in such cross-collateralized group). On an individual basis, without regard to the cross-collateralization feature, any mortgage loan that is part of a cross-collateralized group of mortgage loans may have a higher loan-to-value ratio, lower debt service coverage ratio and/or lower debt yield than is presented herein. With respect to any mortgage loan that is part of a whole loan, the loan-to-value ratio, debt service coverage ratio and debt yield calculations include the relatedpari passucompanion loan(s) but exclude any related subordinate secured loan(s) (unless otherwise stated). With respect to each mortgage loan, debt service coverage ratio, debt yield and loan-to-value ratio information do not take into account of any subordinate debt (whether or not secured by the related mortgaged property) that currently exists or is allowed under the terms of such mortgage loan. With respect to the mortgage loan secured by the mortgaged property identified on Annex A-1 to the Preliminary Prospectus as D.C. Office Portfolio, all loan-to-value and debt yield calculations are net of the $5,000,000 earnout reserve. See Annex A-1 to the Preliminary Prospectus. |

| (3) | Includes 14 other states and Puerto Rico. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 15 |

| BANK 2017-BNK4 | Characteristics of the Mortgage Pool |

| H. | Characteristics of the Mortgage Pool(1) |

| CUT-OFF DATE BALANCE | |||||||||

| Range of Cut-off Date Balances ($) | Number of Mortgage Loans | Aggregate Cut- off Date Balance | % of Initial Pool Balance | ||||||

| 1,837,500 - 2,000,000 | 1 | $1,837,500 | 0.2 | % | |||||

| 2,000,001 - 3,000,000 | 2 | 4,320,000 | 0.4 | ||||||

| 3,000,001 - 5,000,000 | 3 | 13,541,374 | 1.3 | ||||||

| 5,000,001 - 6,000,000 | 5 | 27,035,000 | 2.7 | ||||||

| 6,000,001 - 7,000,000 | 7 | 46,670,380 | 4.6 | ||||||

| 7,000,001 - 8,000,000 | 4 | 30,578,254 | 3.0 | ||||||

| 8,000,001 - 9,000,000 | 1 | 8,853,000 | 0.9 | ||||||

| 9,000,001 - 15,000,000 | 4 | 49,566,114 | 4.9 | ||||||

| 15,000,001 - 20,000,000 | 3 | 55,000,000 | 5.5 | ||||||

| 20,000,001 - 30,000,000 | 4 | 96,890,754 | 9.6 | ||||||

| 30,000,001 - 50,000,000 | 9 | 372,158,236 | 36.9 | ||||||

| 50,000,001 - 70,000,000 | 5 | 301,738,232 | 29.9 | ||||||

| Total: | 48 | $1,008,188,843 | 100.0 | % | |||||

| Average: | $21,003,934 | ||||||||

| UNDERWRITTEN NOI DEBT SERVICE COVERAGE RATIO | |||||||||

| Range of U/W NOI DSCRs (x) | Number of Mortgage Loans | Aggregate Cut- off Date Balance | % of Initial Pool Balance | ||||||

| 1.21 - 1.30 | 4 | $23,904,908 | 2.4 | % | |||||

| 1.31 - 1.40 | 3 | 31,607,141 | 3.1 | ||||||

| 1.41 - 1.50 | 1 | 7,991,531 | 0.8 | ||||||

| 1.51 - 1.60 | 7 | 114,134,695 | 11.3 | ||||||

| 1.61 - 1.70 | 6 | 88,714,466 | 8.8 | ||||||

| 1.71 - 1.80 | 6 | 193,662,105 | 19.2 | ||||||

| 1.81 - 1.90 | 3 | 125,227,199 | 12.4 | ||||||

| 1.91 - 2.00 | 2 | 19,819,744 | 2.0 | ||||||

| 2.01 - 2.50 | 13 | 251,823,823 | 25.0 | ||||||

| 2.51 - 3.00 | 2 | 96,440,000 | 9.6 | ||||||

| 3.01 - 3.10 | 1 | 54,863,232 | 5.4 | ||||||

| Total: | 48 | $1,008,188,843 | 100.0 | % | |||||

| Weighted Average: | 2.00x | ||||||||

| UNDERWRITTEN NCF DEBT SERVICE COVERAGE RATIO | |||||||||

| Range of U/W NCF DSCRs (x) | Number of Mortgage Loans | Aggregate Cut- off Date Balance | % of Initial Pool Balance | ||||||

| 1.20 | 3 | $19,850,000 | 2.0 | % | |||||

| 1.21 - 1.30 | 3 | 28,679,742 | 2.8 | ||||||

| 1.31 - 1.40 | 2 | 30,982,307 | 3.1 | ||||||

| 1.41 - 1.50 | 8 | 97,291,662 | 9.7 | ||||||

| 1.51 - 1.60 | 7 | 99,445,381 | 9.9 | ||||||

| 1.61 - 1.70 | 7 | 250,197,500 | 24.8 | ||||||

| 1.71 - 1.80 | 2 | 118,750,000 | 11.8 | ||||||

| 1.81 - 1.90 | 4 | 102,207,287 | 10.1 | ||||||

| 1.91 - 2.00 | 1 | 20,000,000 | 2.0 | ||||||

| 2.01 - 2.50 | 9 | 144,344,964 | 14.3 | ||||||

| 2.51 - 2.95 | 2 | 96,440,000 | 9.6 | ||||||

| Total: | 48 | $1,008,188,843 | 100.0 | % | |||||

| Weighted Average: | 1.83x | ||||||||

| LOAN PURPOSE | |||||||||

| Loan Purpose | Number of Mortgage Loans | Aggregate Cut- off Date Balance | % of Initial Pool Balance | ||||||

| Refinance | 27 | $489,628,965 | 48.6 | % | |||||

| Acquisition | 20 | 471,559,878 | 46.8 | ||||||

| Recapitalization | 1 | 47,000,000 | 4.7 | ||||||

| Total: | 48 | $1,008,188,843 | 100.0 | % | |||||

| MORTGAGE RATE | |||||||||

| Range of Mortgage Rates (%) | Number of Mortgage Loans | Aggregate Cut- off Date Balance | % of Initial Pool Balance | ||||||

| 3.930 - 4.000 | 1 | $41,440,000 | 4.1 | % | |||||

| 4.001 - 4.250 | 2 | 55,200,000 | 5.5 | ||||||

| 4.251 - 4.500 | 4 | 150,000,000 | 14.9 | ||||||

| 4.501 - 4.750 | 7 | 143,066,251 | 14.2 | ||||||

| 4.751 - 5.000 | 11 | 233,331,626 | 23.1 | ||||||

| 5.001 - 5.250 | 11 | 183,290,648 | 18.2 | ||||||

| 5.251 - 5.500 | 9 | 98,572,500 | 9.8 | ||||||

| 5.501 - 5.750 | 2 | 78,397,064 | 7.8 | ||||||

| 6.251 - 6.290 | 1 | 24,890,754 | 2.5 | ||||||

| Total: | 48 | $1,008,188,843 | 100.0 | % | |||||

| Weighted Average: | 4.848% | ||||||||

| UNDERWRITTEN NOI DEBT YIELD | |||||||||

| Range of U/W NOI Debt Yields (%) | Number of Mortgage Loans | Aggregate Cut- off Date Balance | % of Initial Pool Balance | ||||||

| 7.6 - 8.0 | 4 | $79,850,000 | 7.9 | % | |||||

| 8.1 - 9.0 | 8 | 233,287,049 | 23.1 | ||||||

| 9.1 - 10.0 | 5 | 113,896,701 | 11.3 | ||||||

| 10.1 - 11.0 | 11 | 135,746,927 | 13.5 | ||||||

| 11.1 - 12.0 | 5 | 107,003,415 | 10.6 | ||||||

| 12.1 - 13.0 | 5 | 110,367,395 | 10.9 | ||||||

| 13.1 - 14.0 | 3 | 65,454,548 | 6.5 | ||||||

| 14.1 - 15.0 | 2 | 50,888,315 | 5.0 | ||||||

| 15.1 - 16.0 | 2 | 31,331,262 | 3.1 | ||||||

| 16.1 - 17.0 | 1 | 20,000,000 | 2.0 | ||||||

| 17.1 - 18.0 | 1 | 5,500,000 | 0.5 | ||||||

| 20.1 - 20.3 | 1 | 54,863,232 | 5.4 | ||||||

| Total: | 48 | $1,008,188,843 | 100.0 | % | |||||

| Weighted Average: | 11.3% | ||||||||

| UNDERWRITTEN NCF DEBT YIELD | |||||||||

| Range of U/W NCF Debt Yields (%) | Number of Mortgage Loans | Aggregate Cut- off Date Balance | % of Initial Pool Balance | ||||||

| 7.1 - 8.0 | 7 | $170,904,908 | 17.0 | % | |||||

| 8.1 - 9.0 | 7 | 236,232,141 | 23.4 | ||||||

| 9.1 - 10.0 | 12 | 134,806,128 | 13.4 | ||||||

| 10.1 - 11.0 | 5 | 54,733,851 | 5.4 | ||||||

| 11.1 - 12.0 | 8 | 188,429,006 | 18.7 | ||||||

| 12.1 - 13.0 | 3 | 99,401,583 | 9.9 | ||||||

| 13.1 - 14.0 | 3 | 38,427,240 | 3.8 | ||||||

| 14.1 - 15.0 | 1 | 24,890,754 | 2.5 | ||||||

| 15.1 - 15.4 | 2 | 60,363,232 | 6.0 | ||||||

| Total: | 48 | $1,008,188,843 | 100.0 | % | |||||

| Weighted Average: | 10.3% | ||||||||