Wells Fargo Commercial Mortgage Securities

Filed: 28 Feb 18, 12:00am

| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-206677-23 | ||

|  |

Free Writing Prospectus

Collateral Term Sheet

$733,448,985

(Approximate Aggregate Cut-off Date Balance of Mortgage Pool)

Wells Fargo Commercial Mortgage Trust 2018-C43

as Issuing Entity

Wells Fargo Commercial Mortgage Securities, Inc.

as Depositor

Barclays Bank PLC

Wells Fargo Bank, National Association

BSPRT Finance, LLC

C-III Commercial Mortgage LLC

Rialto Mortgage Finance, LLC

as Sponsors and Mortgage Loan Sellers

Commercial Mortgage Pass-Through Certificates

Series 2018-C43

February 27, 2018

WELLS FARGO SECURITIES Co-Lead Manager and Joint Bookrunner | BARCLAYS Co-Lead Manager and Joint Bookrunner | |

Academy Securities Co-Manager |

STATEMENT REGARDING THIS FREE WRITING PROSPECTUS

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (‘‘SEC’’) (SEC File No. 333-206677) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC Web site at www.sec.gov. Alternatively, the depositor, any underwriter, or any dealer participating in the offering will arrange to send you the prospectus after filing if you request it by calling toll free 1-800-745-2063 (8 a.m. – 5 p.m. EST) or by emailing wfs.cmbs@wellsfargo.com.

Nothing in this document constitutes an offer of securities for sale in any jurisdiction where the offer or sale is not permitted. The information contained herein is preliminary as of the date hereof, supersedes any such information previously delivered to you and will be superseded by any such information subsequently delivered and ultimately by the final prospectus relating to the securities. These materials are subject to change, completion, supplement or amendment from time to time.

This free writing prospectus has been prepared by the underwriters for information purposes only and does not constitute, in whole or in part, a prospectus for the purposes of Directive 2003/71/EC (as amended) and/or Part VI of the Financial Services and Markets Act 2000, as amended, or other offering document.

STATEMENT REGARDING ASSUMPTIONS AS TO SECURITIES, PRICING ESTIMATES AND OTHER INFORMATION

The attached information contains certain tables and other statistical analyses (the “Computational Materials”) which have been prepared in reliance upon information furnished by the Mortgage Loan Sellers. Numerous assumptions were used in preparing the Computational Materials, which may or may not be reflected herein. As such, no assurance can be given as to the Computational Materials’ accuracy, appropriateness or completeness in any particular context; or as to whether the Computational Materials and/or the assumptions upon which they are based reflect present market conditions or future market performance. The Computational Materials should not be construed as either projections or predictions or as legal, tax, financial or accounting advice. You should consult your own counsel, accountant and other advisors as to the legal, tax, business, financial and related aspects of a purchase of these securities. Any weighted average lives, yields and principal payment periods shown in the Computational Materials are based on prepayment and/or loss assumptions, and changes in such prepayment and/or loss assumptions may dramatically affect such weighted average lives, yields and principal payment periods. In addition, it is possible that prepayments or losses on the underlying assets will occur at rates higher or lower than the rates shown in the attached Computational Materials. The specific characteristics of the securities may differ from those shown in the Computational Materials due to differences between the final underlying assets and the preliminary underlying assets used in preparing the Computational Materials. The principal amount and designation of any security described in the Computational Materials are subject to change prior to issuance. None of Wells Fargo Securities, LLC, Barclays Capital Inc., Academy Securities, Inc., or any of their respective affiliates, make any representation or warranty as to the actual rate or timing of payments or losses on any of the underlying assets or the payments or yield on the securities. The information in this presentation is based upon management forecasts and reflects prevailing conditions and management’s views as of this date, all of which are subject to change. In preparing this presentation, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us by or on behalf of the Mortgage Loan Sellers or which was otherwise reviewed by us.

This free writing prospectus contains certain forward-looking statements. If and when included in this free writing prospectus, the words “expects”, “intends”, “anticipates”, “estimates” and analogous expressions and all statements that are not historical facts, including statements about our beliefs or expectations, are intended to identify forward-looking statements. Any forward-looking statements are made subject to risks and uncertainties which could cause actual results to differ materially from those stated. Those risks and uncertainties include, among other things, declines in general economic and business conditions, increased competition, changes in demographics, changes in political and social conditions, regulatory initiatives and changes in customer preferences, many of which are beyond our control and the control of any other person or entity related to this offering. The forward-looking statements made in this free writing prospectus are made as of the date stated on the cover. We have no obligation to update or revise any forward-looking statement.

Wells Fargo Securities is the trade name for the capital markets and investment banking services of Wells Fargo & Company and its subsidiaries, including but not limited to Wells Fargo Securities, LLC, a member of NYSE, FINRA, NFA and SIPC, Wells Fargo Prime Services, LLC, a member of FINRA, NFA and SIPC, and Wells Fargo Bank, N.A. Wells Fargo Securities, LLC and Wells Fargo Prime Services, LLC are distinct entities from affiliated banks and thrifts.

IMPORTANT NOTICE REGARDING THE OFFERED CERTIFICATES

The information herein is preliminary and may be supplemented or amended prior to the time of sale. In addition, the Offered Certificates referred to in these materials and the asset pool backing them are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis.

The underwriters described in these materials may from time to time perform investment banking services for, or solicit investment banking business from, any company named in these materials. The underwriters and/or their affiliates or respective employees may from time to time have a long or short position in any security or contract discussed in these materials.

The information contained herein supersedes any previous such information delivered to any prospective investor and will be superseded by information delivered to such prospective investor prior to the time of sale.

IMPORTANT NOTICE RELATING TO AUTOMATICALLY-GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of any email communication to which this free writing prospectus is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) any representation that these materials are accurate or complete and may not be updated or (3) these materials possibly being confidential, are not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 2 |

A. Transaction Highlights

Mortgage Loan Sellers:

| Mortgage Loan Seller | Number of Mortgage Loans | Number of Mortgaged Properties | Aggregate Cut-off Date Balance | % of Initial Pool Balance | ||||

| Barclays Bank PLC | 11 | 55 | $274,101,121 | 37.4% | ||||

| Wells Fargo Bank, National Association | 17 | 20 | 226,917,078 | 30.9 | ||||

| BSPRT Finance, LLC | 6 | 14 | 79,333,178 | 10.8 | ||||

| C-III Commercial Mortgage LLC | 22 | 30 | 79,065,982 | 10.8 | ||||

| Rialto Mortgage Finance, LLC | 7 | 13 | 74,031,625 | 10.1 | ||||

Total | 63 | 132 | $733,448,985 | 100.0% |

Loan Pool:

| Initial Pool Balance: | $733,448,985 |

| Number of Mortgage Loans: | 63 |

| Average Cut-off Date Balance per Mortgage Loan: | $11,642,047 |

| Number of Mortgaged Properties: | 132 |

| Average Cut-off Date Balance per Mortgaged Property(1): | $5,556,432 |

| Weighted Average Mortgage Interest Rate: | 4.634% |

| Ten Largest Mortgage Loans as % of Initial Pool Balance: | 50.1% |

| Weighted Average Original Term to Maturity or ARD (months): | 119 |

| Weighted Average Remaining Term to Maturity or ARD (months): | 118 |

| Weighted Average Original Amortization Term (months)(2): | 355 |

| Weighted Average Remaining Amortization Term (months)(2): | 355 |

| Weighted Average Seasoning (months): | 1 |

| (1) | Information regarding mortgage loans secured by multiple properties is based on an allocation according to relative appraised values or the allocated loan amounts or property-specific release prices set forth in the related loan documents or such other allocation as the related mortgage loan seller deemed appropriate. |

| (2) | Excludes any mortgage loan that does not amortize. |

Credit Statistics:

| Weighted Average U/W Net Cash Flow DSCR(1): | 1.89x |

| Weighted Average U/W Net Operating Income Debt Yield(1): | 11.1% |

| Weighted Average Cut-off Date Loan-to-Value Ratio(1): | 60.7% |

| Weighted Average Balloon or ARD Loan-to-Value Ratio(1): | 54.6% |

| % of Mortgage Loans with Additional Subordinate Debt(2): | 19.8% |

| % of Mortgage Loans with Single Tenants(3): | 28.3% |

| (1) | With respect to any mortgage loan that is part of a whole loan, loan-to-value ratio, debt service coverage ratio and debt yield calculations include the relatedpari passucompanion loan(s) but exclude any related subordinate debt (unless otherwise stated). The debt service coverage ratio, debt yield and loan-to-value ratio information do not take into account any subordinate debt (whether or not secured by the related mortgaged property), that currently exists or is allowed under the terms of any mortgage loan. See “Description of the Mortgage Pool—Mortgage Pool Characteristics” in the Preliminary Prospectus and Annex A-1 to the Preliminary Prospectus. |

| (2) | The percentage figure expressed as “% of Mortgage Loans with Additional Subordinate Debt” is determined as a percentage of the initial pool balance and does not take into account any future subordinate debt (whether or not secured by the mortgaged property), if any, that may be permitted under the terms of any mortgage loan or the pooling and servicing agreement. See “Description of the Mortgage Pool—Additional Indebtedness—Other Unsecured Indebtedness” in the Preliminary Prospectus. |

| (3) | Excludes mortgage loans that are secured by multiple single tenant properties. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 3 |

| Wells Fargo Commercial Mortgage Trust 2018-C43 | Certain Loan Information |

| B. Summary of the Whole Loans |

| Property Name | Mortgage Loan Seller in WFCM 2018-C43 | Note(s)(1) | Original Balance | Holder of Note(1) | Lead Servicer for Whole Loan | Master Servicer Under Lead Securitization Servicing Agreement | Special Servicer Under Lead Securitization Servicing Agreement |

| Moffett Towers II - Building 2 | Barclays | A-1 | $65,000,000 | WFCM 2018-C43 | Yes | Wells Fargo Bank, National Association | Midland Loan Services, a Division of PNC Bank, National Association |

| A-2 | $18,750,000 | Barclays Bank PLC | No | ||||

| A-3 | $40,000,000 | WFCM 2017-C42 | No | ||||

| A-4 | $41,250,000 | BANK 2018-BNK10 | No | ||||

| Airport Business Center | WFB(2) | A-1 | $60,000,000 | WFB | Yes(2) | Wells Fargo Bank, National Association(2) | Midland Loan Services, LLC(2) |

| A-2 | $50,000,000 | WFCM 2018-C43 | No | ||||

| A-3 | $40,000,000 | WFB | No | ||||

| SoCal Portfolio | Barclays(3) | A-1-1 | $50,000,000 | Citi Real Estate Funding Inc. | Yes(3) | TBD(3) | TBD(3) |

| A-1-2 | $35,000,000 | Citi Real Estate Funding Inc. | No | ||||

| A-1-3 | $15,000,000 | Citi Real Estate Funding Inc. | No | ||||

| A-1-4 | $37,580,000 | Citi Real Estate Funding Inc. | No | ||||

| A-2-1 | $45,000,000 | WFCM 2018-C43 | No | ||||

| A-2-2 | $46,720,000 | Barclays Bank PLC | No | ||||

| Houston Distribution Center | Barclays | A-1 | $35,000,000 | UBS 2018-C8 | Yes | Midland Loan Services, a Division of PNC Bank, National Association | Midland Loan Services, a Division of PNC Bank, National Association |

| A-2 | $14,000,000 | UBS 2018-C8 | No | ||||

| A-3 | $35,000,000 | WFCM 2018-C43 | No | ||||

| Apple Campus 3 | WFB | A-1 | $80,000,000 | WFB | No | Wells Fargo Bank, National Association

| Torchlight Loan Services, LLC |

| A-2 | $30,000,000 | WFCM 2018-C43 | No | ||||

| A-3 | $94,000,000 | BANK 2018-BNK10 | Yes | ||||

| A-4 | $68,000,000 | BMARK 2018-B2 | No | ||||

| A-5 | $68,000,000 | Goldman Sachs Mortgage Company | No |

| (1) | Unless otherwise indicated, each note not currently held by a securitization trust is expected to be contributed to a future securitization. No assurance can be provided that any such note will not be split further. |

| (2) | The related whole loan is expected to initially be serviced under the WFCM 2018-C43 pooling and servicing agreement until the securitization of the related “lead” pari passu note (namely, the related pari passu note marked “Yes” in the column entitled “Lead Servicer for Whole Loan”), after which the related whole loan will be serviced under the pooling and servicing agreement governing such securitization of the related “lead” pari passu note. The master servicer and special servicer for such securitization will be identified in a notice, report or statement to holders of the WFCM 2018-C43 certificates after the closing of such securitization. |

| (3) | The related “lead” pari passu note (namely, the related pari passu note marked “Yes” in the column entitled “Lead Servicer for Whole Loan”), is expected to be contributed to a securitization which is expected to close prior to the Closing Date. The related whole loan is expected to be serviced under the pooling and servicing agreement governing such securitization of the related “lead” pari passu note. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 4 |

| Wells Fargo Commercial Mortgage Trust 2018-C43 |

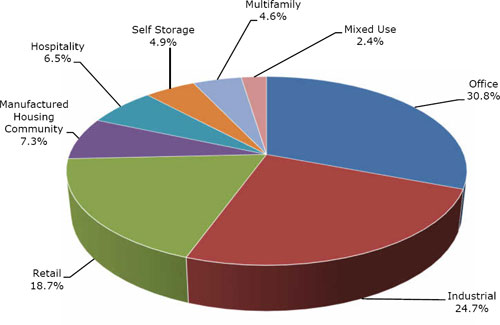

C. Property Type Distribution

| Property Type | Number of Mortgaged Properties | Aggregate Balance ($) | % of Initial Pool Balance (%) | Weighted Average Cut-off Date LTV Ratio (%) | Weighted Average Balloon or ARD LTV Ratio (%) | Weighted Average U/W NCF DSCR (x) | Weighted Average U/W NOI Debt Yield (%) | Weighted Average U/W NCF Debt Yield (%) | Weighted Average Mortgage Rate (%) |

| Office | 20 | $225,952,294 | 30.8% | 57.9% | 52.2% | 2.18x | 12.0% | 11.1% | 4.141% |

| Suburban | 16 | 212,604,294 | 29.0 | 57.8 | 51.9 | 2.20 | 12.1 | 11.2 | 4.108 |

| Medical | 4 | 13,348,000 | 1.8 | 59.8 | 56.7 | 1.89 | 9.9 | 9.4 | 4.677 |

| Industrial | 17 | 181,296,184 | 24.7 | 59.8 | 55.8 | 1.81 | 10.8 | 9.8 | 4.794 |

| Flex | 7 | 81,819,657 | 11.2 | 59.1 | 58.0 | 2.02 | 10.5 | 9.7 | 4.593 |

| Warehouse Distribution | 3 | 45,346,527 | 6.2 | 59.0 | 49.8 | 1.48 | 10.9 | 9.6 | 5.082 |

| Warehouse | 2 | 31,600,000 | 4.3 | 60.2 | 57.4 | 1.79 | 10.4 | 9.7 | 4.863 |

| Manufacturing | 4 | 13,330,000 | 1.8 | 64.1 | 59.0 | 1.73 | 12.2 | 10.9 | 4.820 |

| Manufacturing/Warehouse | 1 | 9,200,000 | 1.3 | 62.6 | 55.3 | 1.69 | 12.4 | 10.8 | 4.880 |

| Retail | 41 | 137,431,128 | 18.7 | 62.9 | 58.3 | 1.81 | 9.8 | 9.3 | 4.640 |

| Single Tenant | 21 | 59,276,084 | 8.1 | 61.3 | 61.0 | 2.06 | 9.0 | 8.9 | 4.250 |

| Unanchored | 11 | 38,136,972 | 5.2 | 63.6 | 55.0 | 1.38 | 9.8 | 9.0 | 5.142 |

| Anchored | 7 | 36,245,786 | 4.9 | 64.5 | 57.7 | 1.91 | 11.1 | 10.3 | 4.721 |

| Shadow Anchored | 2 | 3,772,285 | 0.5 | 67.0 | 56.3 | 1.42 | 10.1 | 9.2 | 4.939 |

| Manufactured Housing Community | 27 | 53,215,127 | 7.3 | 64.0 | 54.3 | 1.53 | 10.5 | 10.3 | 5.289 |

| Manufactured Housing Community | 27 | 53,215,127 | 7.3 | 64.0 | 54.3 | 1.53 | 10.5 | 10.3 | 5.289 |

| Hospitality | 7 | 48,027,533 | 6.5 | 60.7 | 47.3 | 1.91 | 15.0 | 13.3 | 5.152 |

| Limited Service | 7 | 48,027,533 | 6.5 | 60.7 | 47.3 | 1.91 | 15.0 | 13.3 | 5.152 |

| Self Storage | 10 | 35,762,082 | 4.9 | 63.6 | 54.5 | 1.41 | 9.5 | 9.3 | 5.140 |

| Self Storage | 10 | 35,762,082 | 4.9 | 63.6 | 54.5 | 1.41 | 9.5 | 9.3 | 5.140 |

| Multifamily | 6 | 34,046,625 | 4.6 | 64.8 | 58.8 | 1.96 | 10.5 | 10.0 | 4.672 |

| Garden | 6 | 34,046,625 | 4.6 | 64.8 | 58.8 | 1.96 | 10.5 | 10.0 | 4.672 |

| Mixed Use | 4 | 17,718,012 | 2.4 | 62.6 | 55.8 | 1.50 | 10.2 | 9.4 | 4.760 |

| Office/Industrial | 1 | 7,930,000 | 1.1 | 66.6 | 57.1 | 1.53 | 10.1 | 9.4 | 4.600 |

| Office/Retail | 2 | 6,598,958 | 0.9 | 59.4 | 54.7 | 1.48 | 10.2 | 9.4 | 4.890 |

| Retail/Education | 1 | 3,189,054 | 0.4 | 59.4 | 54.7 | 1.48 | 10.2 | 9.4 | 4.890 |

| Total/Weighted Average: | 132 | $733,448,985 | 100.0% | 60.7% | 54.6% | 1.89x | 11.1% | 10.3% | 4.634% |

| (1) | Because this table presents information relating to the mortgaged properties and not the mortgage loans, the information for mortgage loans secured by more than one mortgaged property is based on allocated amounts (allocating the principal balance of the mortgage loan to each of those properties according to the relative appraised values of the mortgaged properties or the allocated loan amounts or property-specific release prices set forth in the related mortgage loan documents or such other allocation as the related mortgage loan seller deemed appropriate). With respect to any mortgage loan that is part of a whole loan, the loan-to-value ratio, debt service coverage ratio and debt yield calculations include the relatedpari passu companion loan(s) but exclude any related subordinate debt (unless otherwise stated). With respect to each mortgage loan, debt service coverage ratio, debt yield and loan-to-value ratio information do not take into account any subordinate debt (whether or not secured by the related mortgaged property) that currently exists or is allowed under the terms of such mortgage loan. See Annex A-1 to the Preliminary Prospectus. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 5 |

(THIS PAGE INTENTIONALLY LEFT BLANK)

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 6 |

| Wells Fargo Commercial Mortgage Trust 2018-C43 |

D. Large Loan Summaries

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 7 |

| MOFFETT TOWERS II – BUILDING 2 |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 8 |

| MOFFETT TOWERS II – BUILDING 2 |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 9 |

| No. 1 – Moffett Towers II - Building 2 | ||||||||

| Loan Information | Property Information | |||||||

| Mortgage Loan Seller: | Barclays Bank PLC | Single Asset/Portfolio: | Single Asset | |||||

| Credit Assessment | Property Type: | Office | ||||||

| (DBRS/Fitch/Moody’s): | BBB/BBB-/NR | Specific Property Type: | Suburban | |||||

| Original Principal Balance(1): | $65,000,000 | Location: | Sunnyvale, CA | |||||

| Cut-off Date Balance(1): | $65,000,000 | Size(5): | 362,563 SF | |||||

| % of Initial Pool Balance: | 8.9% | Cut-off Date Balance Per SF(1)(5): | $455.09 | |||||

| Loan Purpose: | Refinance | Year Built/Renovated: | 2017/NAP | |||||

| Borrower Name: | MT2 B2 LLC | Title Vesting: | Fee | |||||

| Borrower Sponsor: | The Jay Paul Company | Property Manager: | Self-managed | |||||

| Mortgage Rate: | 3.6189% | 4thMost Recent Occupancy (As of)(6): | NAP | |||||

| Note Date: | November 16, 2017 | 3rdMost Recent Occupancy (As of)(6): | NAP | |||||

| Anticipated Repayment Date: | NAP | 2ndMost Recent Occupancy (As of)(6): | NAP | |||||

| Maturity Date: | December 6, 2027 | Most Recent Occupancy (As of)(6): | NAP | |||||

| IO Period: | 60 months | Current Occupancy (As of): | 100.0% (12/1/2017) | |||||

| Loan Term (Original): | 120 months | |||||||

| Seasoning: | 3 months | |||||||

| Amortization Term (Original): | 360 months | Underwriting and Financial Information: | ||||||

| Loan Amortization Type: | Interest-only, Amortizing Balloon | 4thMost Recent NOI (As of)(6): | NAP | |||||

| Interest Accrual Method: | Actual/360 | 3rdMost Recent NOI (As of)(6): | NAP | |||||

| Call Protection(2): | L(27),D(86),O(7) | 2ndMost Recent NOI (As of)(6): | NAP | |||||

| Lockbox Type: | Hard/Upfront Cash Management | Most Recent NOI (As of)(6): | NAP | |||||

| Additional Debt(1): | Yes | |||||||

| Additional Debt Type(1)(3): | Pari Passu; Mezzanine | |||||||

| U/W Revenues: | $22,525,092 | |||||||

| U/W Expenses: | $2,840,101 | |||||||

| U/W NOI: | $19,684,992 | |||||||

| Escrows and Reserves(4): | U/W NCF: | $18,805,659 | ||||||

| U/W NOI DSCR(1): | 2.18x | |||||||

| Type: | Initial | Monthly(4) | Cap (If Any) | U/W NCF DSCR(1): | 2.08x | |||

| Taxes | $0 | $111,859 | NAP | U/W NOI Debt Yield(1): | 11.9% | |||

| Insurance | $0 | Springing | NAP | U/W NCF Debt Yield(1): | 11.4% | |||

| Rent Concessions Reserve | $8,332,337 | $0 | NAP | As-Is Appraised Value: | $351,000,000 | |||

| TI/LC Reserve | $19,433,495 | $0 | NAP | As-Is Appraisal Valuation Date: | October 18, 2017 | |||

| Debt Service Reserve | $1,000,000 | Springing | NAP | Cut-off Date LTV Ratio(1): | 47.0% | |||

| Parking Abatement Reserve | $2,700,000 | Springing | NAP | LTV Ratio at Maturity or ARD(1): | 42.4% | |||

| Amenities Rent Reserve | $286,310 | Springing | NAP | |||||

| (1) | See “The Mortgage Loan” section. All statistical information related to balance per square foot, loan-to-value ratios, debt service coverage ratios and debt yields are based on the Moffett Towers II - Building 2 Whole Loan (as defined below). The Cut-off Date LTV Ratio, LTV Ratio at Maturity or ARD, U/W NCF DSCR and U/W NOI Debt Yield based on the Moffett Towers II - Building 2 Whole Loan and the Moffett Towers II - Building 2 Mezzanine Loan (as defined below) (together, the “Moffett Towers II - Building 2 Total Debt”), are 76.9%, 72.3%, 1.23x and 7.3%, respectively. |

| (2) | The lockout period will be at least 27 payments, beginning with and including the first payment date of January 6, 2018. Defeasance of the Moffett Towers II - Building 2 Mortgage Loan (as defined below) is permitted at any time after the earlier to occur of (i) two years after the closing date of the securitization that includes the last note to be securitized or (ii) November 16, 2020. The assumed lockout period of 27 payments is based on the expected WFCM 2018-C43 securitization trust closing date in March 2018. |

| (3) | See “Subordinate and Mezzanine Indebtedness” section. |

| (4) | Certain springing Escrows and Reserves are required on a one-time basis. See “Escrows” section. |

| (5) | Size of 362,563 square feet is comprised of 350,633 square feet of office space in the Moffett Towers II - Building 2 Property (as defined below) along with 11,930 square feet of space allocated to the Moffett Towers II - Building 2 Property in a 59,650 square foot fitness/amenities building, based on a specified to-be 20.0% share in the common elements of the Moffett Towers II Campus (as defined below). See “Amenities and Common Areas” section. |

| (6) | Historical occupancy, operating and financial information is unavailable as the Moffett Towers II - Building 2 Property (as defined below) was built in 2017. |

The Mortgage Loan.The mortgage loan (the “Moffett Towers II - Building 2 Mortgage Loan”) is part of a whole loan (the “Moffett Towers II - Building 2 Whole Loan”) evidenced by fourpari passu notes secured by a first mortgage encumbering the fee simple interest in a Class A office building fully leased to a wholly-owned subsidiary of Amazon.com, Inc. (“Amazon”) located in Sunnyvale, California (the “Moffett Towers II - Building 2 Property”). The Moffett Towers II - Building 2 Whole Loan was co-originated on November 16, 2017 by Barclays Bank PLC and Morgan Stanley Bank, N.A. The Moffett Towers II - Building 2 Whole Loan had an original principal balance of $165,000,000, has an outstanding principal balance as of the Cut-off Date of $165,000,000 and accrues interest at an interest rate of 3.6189%per annum. The Moffett Towers II - Building 2 Whole Loan had an initial term of 120 months, has a remaining term of 117 months as of the Cut-off Date and requires interest-only payments for the first 60 payment periods followed by payments of principal and interest based on a 30-year amortization schedule. The Moffett Towers II - Building 2 Whole Loan matures on December 6, 2027.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 10 |

| MOFFETT TOWERS II – BUILDING 2 |

Note A-1, which will be contributed to the WFCM 2018-C43 securitization trust, had an original principal balance of $65,000,000, has an outstanding principal balance as of the Cut-off Date of $65,000,000 and represents the controlling interest in the Moffett Towers II – Building 2 Whole Loan. The non-controlling Note A-3, had an original principal balance of $40,000,000, has an outstanding principal balance as of the Cut-off Date of $40,000,000 and was contributed to the WFCM 2017-C42 securitization trust. The non-controlling Note A-4, had an original principal balance of $41,250,000, has an outstanding principal balance as of the Cut-off Date of $41,250,000 and was contributed to the BANK 2018-BNK10 securitization trust. The non-controlling Note A-2 is expected to be contributed to a future securitization trust or trusts (Note A-2, Note A-3 and Note A-4, collectively, the “Moffett Towers II – Building 2 Companion Loans”). The lender provides no assurances that any non-securitized notes will not be split further. See“Description of the Mortgage Pool—The Whole Loans—The Serviced Pari Passu Whole Loans”in the Preliminary Prospectus.

Note Summary

| Notes | Original Balance | Note Holder | Controlling Interest | |

| A-1 | $65,000,000 | WFCM 2018-C43 | Yes | |

| A-2 | $18,750,000 | Barclays Bank PLC | No | |

| A-3 | $40,000,000 | WFCM 2017-C42 | No | |

| A-4 | $41,250,000 | BANK 2018-BNK10 | No | |

| Total | $165,000,000 |

Following the lockout period, on any date before June 6, 2027, the borrower has the right to defease the Moffett Towers II - Building 2 Whole Loan in whole, but not in part. The lockout period will expire on the earlier to occur of (i) two years after the closing date of the securitization that includes the last note to be securitized or (ii) November 16, 2020. The Moffett Towers II - Building 2 Whole Loan is prepayable without penalty on or after June 6, 2027.

Sources and Uses

| Sources | Uses | |||||||

| Original whole loan amount | $165,000,000 | 61.1% | Loan payoff | $207,408,056 | 76.8% | |||

| Mezzanine loan | 105,000,000 | 38.9 | Reserves | 31,752,142 | 11.8 | |||

| Return of equity | 20,183,519 | 7.5 | ||||||

| Closing costs | 10,656,282 | 3.9 | ||||||

| Total Sources | $270,000,000 | 100.0% | Total Uses | $270,000,000 | 100.0% |

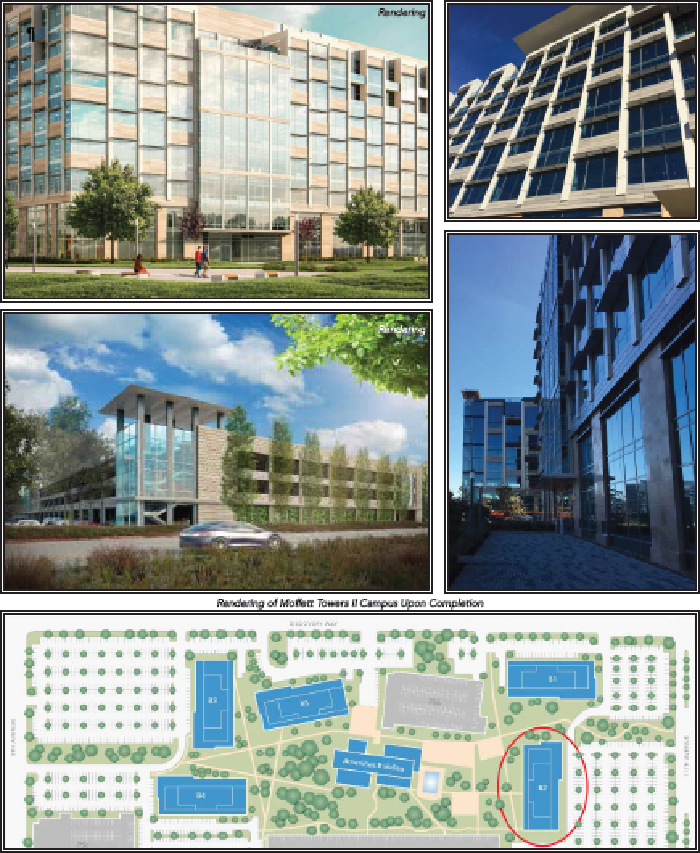

The Property.The Moffett Towers II - Building 2 Property is a newly-constructed, eight-story, Class A office building totaling 350,633 square feet in Sunnyvale, California. As of December 1, 2017, the Moffett Towers II – Building 2 Property was 100.0% leased to a wholly-owned subsidiary of Amazon on a triple-net basis through April 2028, with two, seven-year extension options and no early termination options. Amazon serves as guarantor of the lease and, as of the origination date, has taken possession of the Moffett Towers II - Building 2 Property and commenced the build out of its space. Outstanding rent concessions and tenant improvement allowances related to the Amazon lease were deposited into escrow by the borrower on the origination date (See “Escrows” section).

The Moffett Towers II - Building 2 Property comprises a portion of the first phase (“Phase I”) of the planned approximately 1.8 million square foot, five-building Moffett Towers II office campus (the “Moffett Towers II Campus”) located on 47.3 acres in Sunnyvale, California. Phase I of the Moffett Towers II Campus development includes the Moffett Towers II - Building 2 Property and an adjacent surface parking lot (completed in 2017) as well as the 350,633 square foot Moffett Towers II - Building 1 (April 2018 expected completion), an enclosed parking structure (April 2018 expected completion) and a 59,650 square foot fitness/amenities building (July 2018 expected completion). The Moffett Towers II - Building 2 Property will feature access to the fitness/amenities building and the enclosed parking structure once completed pursuant to a declaration of covenants, conditions, restrictions and easement and charges agreement (see “Amenities and Common Areas” section). Inclusive of the future enclosed parking structure (of which 361 spaces are dedicated to Amazon pursuant to its lease) and the completed surface parking lot (of which 707 spaces are dedicated to Amazon pursuant to its lease), the Moffett Towers II - Building 2 Property has a parking ratio of 3.3 spaces per 1,000 square feet. On the origination date, the Moffett Towers II - Building 2 Guarantor (as defined below) executed a separate guaranty for the completion and delivery of the fitness/amenities building and the enclosed parking structure (see “Completion Guaranty” section). Additionally, the Moffett Towers II - Building 2 Whole Loan documents require upfront and springing reserves related to the completion and delivery of the fitness/amenities building and the enclosed parking structure (see “Escrows” section). Subsequent phases of the Moffett Towers II Campus development are expected to include the construction of three additional 350,633 square foot Class A office buildings as well as two separate enclosed parking structures.

Amazon (NASDAQ: AMZN) is an American e-commerce company headquartered in Seattle, Washington. Founded in 1994, Amazon is now one of the largest online retailers in the world selling a wide range of products, services and entertainment to consumers. Amazon has reported that it increased net income from an approximately $241.0 million loss in 2014 to an approximately $2.4 billion profit in 2016 with total net sales of approximately $136.0 billion in 2016. Most recently, net sales increased to $43.7 billion in the third quarter of 2017, up approximately 34.0% from one year earlier. Amazon employed approximately 341,400 employees as of December 31, 2016.

The Moffett Towers II - Building 2 Property is expected to house Amazon’s Lab126, a research and development subsidiary that designs and engineers high-profile consumer electronics. Lab126 began in 2004, originally creating the Kindle family of products and has since produced numerous devices such as Amazon’s Fire tablets, Fire TV and Amazon Echo. Lab126 is headquartered in the nearby Moffett Towers I property, which is located approximately 0.5 miles from the Moffett Towers II - Building 2 Property.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 11 |

| MOFFETT TOWERS II – BUILDING 2 |

The following table presents certain information relating to the tenancy at the Moffett Towers II - Building 2 Property:

Major Tenants

| Tenant Name | Credit Rating (Fitch/Moody’s/S&P)(1) | Tenant NRSF(2) | % of NRSF(2) | Annual U/W Base Rent PSF(2)(3)(4)(5) | Annual U/W Base Rent(3)(4)(5) | % of Total Annual U/W Base Rent | Lease Expiration Date |

| Major Tenant | |||||||

| Amazon | NR/Baa1/AA- | 362,563 | 100.0% | $55.81 | $20,233,410 | 100.0% | 4/30/2028(6) |

| Total Major Tenant | 362,563 | 100.0% | $55.81 | $20,233,410 | 100.0% | ||

| Vacant Space | 0 | 0.0% | |||||

| Collateral Total | 362,563 | 100.0% | |||||

| (1) | Certain ratings are those of the parent company whether or not the parent company guarantees the lease. |

| (2) | Tenant NRSF of 362,563 square feet is comprised of 350,633 square feet of office space in the Moffett Towers II - Building 2 Property along with 11,930 square feet of space allocated to the Moffett Towers II - Building 2 Property in a 59,650 square foot fitness/amenities building, based on a specified to-be 20.0% share in the common elements of the Moffett Towers II Campus. See “Amenities and Common Areas” section. |

| (3) | Annual U/W Base Rent PSF and Annual U/W Base Rent include $2,830,405 of straight-line rent through the maturity date of the Moffett Towers II - Building 2 Whole Loan. |

| (4) | Amazon has five months of free rent and eight months of waived fitness/amenities use fees remaining, all of which were deposited into escrow on the origination date. The borrower also deposited $286,310 into escrow on the origination date for an amenities rent reserve, which represents six months of use fees due for the fitness/amenities building commencing on the targeted completion and delivery date (July 31, 2018) of such fitness/amenities building to Amazon in accordance with the Amazon lease (see “Escrows” section). |

| (5) | Amazon is entitled to a base rent abatement in the amount of $15,000 per day for each day elapsing beyond the targeted completion and delivery date (April 15, 2018) of the 361-spaces allocated to Amazon within the enclosed parking structure in accordance with the Amazon lease. An amount equal to 180 days of base rent abatements ($2,700,000) was deposited into escrow on the origination date (see “Escrows” section). |

| (6) | Amazon has two, seven-year lease renewal options. |

The following table presents certain information relating to the lease rollover schedule at the Moffett Towers II - Building 2 Property:

Lease Expiration Schedule(1)

| Year Ending December 31, | No. of Leases Expiring | Expiring NRSF | % of Total NRSF | Cumulative Expiring NRSF | Cumulative % of Total NRSF | Annual U/W Base Rent(2) | % of Annual U/W Base Rent(2) | Annual U/W Base Rent PSF(2) |

| MTM | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2018 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2019 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2020 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2021 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2022 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2023 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2024 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2025 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2026 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2027 | 0 | 0 | 0.0% | 0 | 0.0% | $0 | 0.0% | $0.00 |

| 2028 | 1 | 362,563 | 100.0% | 362,563 | 100.0% | $20,233,410 | 100.0% | $55.81 |

| Thereafter | 0 | 0 | 0.0% | 362,563 | 100.0% | $0 | 0.0% | $0.00 |

| Vacant | 0 | 0 | 0.0% | 362,563 | 100.0% | $0 | 0.0% | $0.00 |

| Total/Weighted Average | 1 | 362,563 | 100.0% | $20,233,410 | 100.0% | $55.81 |

| (1) | Information obtained from the underwritten rent roll. |

| (2) | Annual U/W Base Rent, % of Annual U/W Base Rent and Annual U/W Base Rent PSF include $2,830,405 of straight-line rent through the maturity date of the Moffett Towers II - Building 2 Whole Loan. |

The following table presents historical occupancy percentages at the Moffett Towers II - Building 2 Property:

Historical Occupancy

12/31/2013(1) | 12/31/2014(1) | 12/31/2015(1) | 12/31/2016(1) | 12/1/2017(2) | ||||

| NAP | NAP | NAP | NAP | 100.0% |

| (1) | Historical Occupancy prior to 12/6/2017 is not applicable as the Moffett Towers II - Building 2 Property was built in 2017. |

| (2) | Information obtained from the underwritten rent roll. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 12 |

| MOFFETT TOWERS II – BUILDING 2 |

Underwritten Net Cash Flow. The following table presents certain information relating to the underwritten net cash flow at the Moffett Towers II - Building 2 Property:

Cash Flow Analysis(1)

| U/W | % of U/W Effective Gross Income | U/W $ per SF | |||

| Base Rent(2) | $20,233,410 | 89.8% | $55.81 | ||

| Grossed Up Vacant Space | 0 | 0.0 | 0.00 | ||

| Total Reimbursables | 2,751,378 | 12.2 | 7.59 | ||

| Less Vacancy & Credit Loss(3) | (459,696) | (2.0) | (1.27) | ||

| Effective Gross Income | $22,525,092 | 100.0% | $62.13 | ||

| Total Operating Expenses | $2,840,101 | 12.6% | $7.83 | ||

| Net Operating Income | $19,684,992 | 87.4% | $54.29 | ||

| TI/LC | 806,820 | 3.6 | 2.23 | ||

| Capital Expenditures | 72,513 | 0.3 | 0.20 | ||

| Net Cash Flow | $18,805,659 | 83.5% | $51.87 | ||

| NOI DSCR(4) | 2.18x | ||||

| NCF DSCR(4) | 2.08x | ||||

| NOI DY(4) | 11.9% | ||||

| NCF DY(4) | 11.4% |

| (1) | Historical Cash Flows are not available as the Moffett Towers II - Building 2 Property was built in 2017. |

| (2) | U/W Base Rent includes $2,830,405 of straight-line rent through the maturity date of the Moffett Towers II - Building 2 Whole Loan. |

| (3) | The underwritten economic vacancy is 2.0%. The Moffett Towers II - Building 2 Property was 100.0% occupied as of December 1, 2017. |

| (4) | Debt service coverage ratios and debt yields are based on the Moffett Towers II - Building 2 Whole Loan. |

Appraisal.As of the appraisal valuation date of October 18, 2017 the Moffett Towers II - Building 2 Property had an “as-is” appraised value of $351,000,000. The appraiser also concluded to a “hypothetical go dark” appraised value of $246,600,000.

Environmental Matters. According to a Phase I environmental site assessment (“ESA”) dated October 19, 2017, a recognized environmental condition (“REC”) was determined to exist at the Moffett Towers II - Building 2 Property. The Moffett Towers II - Building 2 Property was part of a larger campus historically used by Lockheed Martin for aerospace manufacturing, research and development that covered approximately 660 acres, known as the Lockheed Martin Plant One Campus. The Lockheed Martin Plant One Campus is included in a Site Cleanup Requirements Order issued by the Regional Water Quality Control Board (“RWQCB”) which applies to a large portion of the Lockheed Martin Plant One Campus. No significant sources of soil or groundwater pollution have been identified on the Moffett Towers II - Building 2 Property during historical or more recent investigations of the Plant One Campus. The responsible party associated with this release has been identified by state and Federal regulatory agencies as Lockheed Martin, and Lockheed Martin is currently conducting response actions under state and Federal oversight. Although there is an active regulatory status, the ESA concluded, given the absence of impact, that no further action is warranted and the REC will not prevent or impede the use of the Moffett Towers II - Building 2 Property. The REC is further described under “Description of the Mortgage Pool—Mortgage Pool Characteristics–Environmental Considerations” in the Preliminary Prospectus.

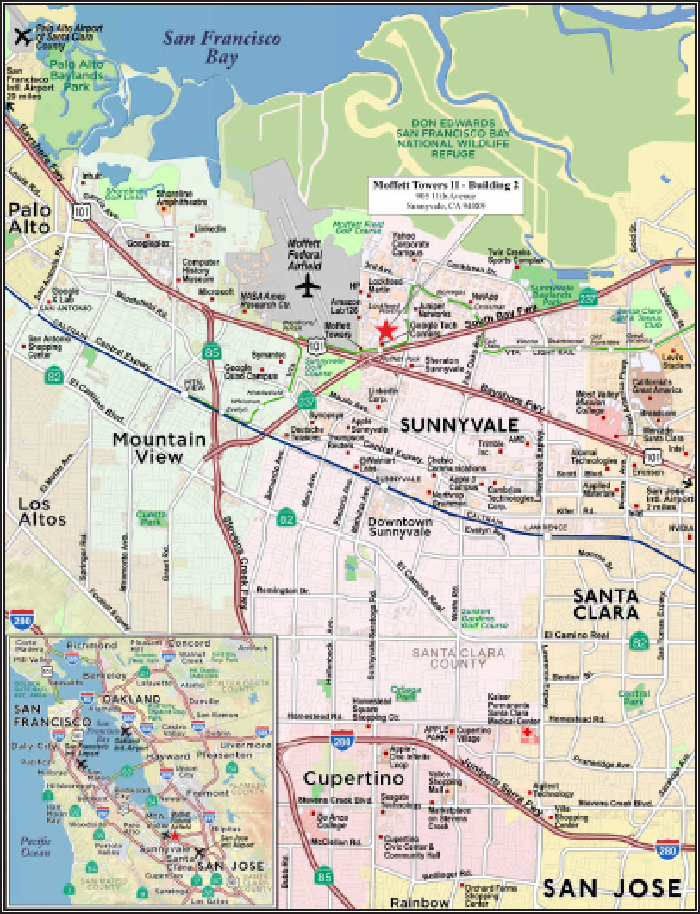

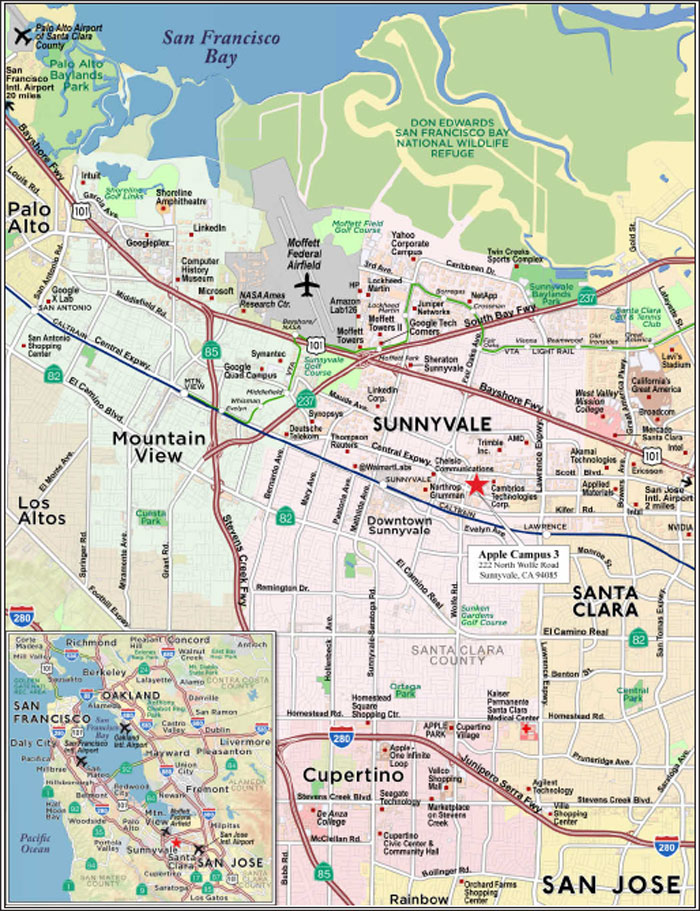

Market Overview and Competition.The Moffett Towers II - Building 2 Property is located in Moffett Park, in the northern portion of the Sunnyvale submarket within Silicon Valley. Moffett Park is a 519-acre area comprised of recently developed office spaces and research and development buildings. Notable high technology firms currently in Moffett Park include Google Inc., Hewlett Packard, Juniper Networks, Lab 126 (an Amazon subsidiary), Lockheed-Martin, Microsoft, Motorola, NetApp and Rambus. The Moffett Towers II - Building 2 Property is just north of State Highway 237, which forms the southern border of the Moffett Park area and provides access from Interstate 680 and Interstate 280 to the northeast and U.S. Highway 101 in Sunnyvale to the southwest. U.S. Highway 101 runs northward through San Francisco and southward through San Jose, terminating in the city of Los Angeles. The Santa Clara County Transit System provides bus service county-wide with stops near the Moffett Towers II - Building 2 Property. In addition, a Santa Clara Light Rail System station is located directly across the street from the Moffett Towers II - Building 2 Property and services the surrounding residential communities.

According to the appraisal, overall vacancy in Silicon Valley and the Sunnyvale submarket was 11.1% and 2.4%, respectively, as of the second quarter of 2017. In the first half of 2017, 315,272 square feet of office space was delivered to the Sunnyvale submarket, with 426,404 square feet of absorption. According to the appraisal, as of the second quarter of 2017, new supply under construction in Silicon Valley stood at approximately 2.8 million square feet, which consisted of approximately 0.7 million square feet of build-to-suit construction and 2.1 million square feet of speculative construction. As of the second quarter of 2017, the total office average asking rent for the Sunnyvale submarket was $52.20 per square foot (fully-serviced), which is in-line with the Silicon Valley total office average asking rent of $53.40 per square foot (fully-serviced). Within the Sunnyvale submarket, the average asking rent for Class A office properties is $58.20 per square foot (fully-serviced).

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 13 |

| MOFFETT TOWERS II – BUILDING 2 |

The following table presents certain information relating to comparable leases to the Moffett Towers II - Building 2 Property:

Comparable Leases(1)

| Property Name/Location | Year Built | Class | Stories | Total GLA (SF) | Tenant Name | Lease Date/Term | Lease Area (SF) | Annual Base Rent PSF | Lease Type |

Towers at Great America Santa Clara, CA | 2002 | A | 6 | 374,214 | Macom Connectivity | May 2017 / 1 Yr | 55,393 | $42.00 | NNN |

Santa Clara Square Ph. II Bldg. 4 Santa Clara, CA | 2016 | A | 6 | 220,156 | AMD | Aug. 2016 / 10 Yrs | 220,156 | $42.60 | NNN |

Moffett Gateway Santa Clara, CA | 2016 | A | 7 | 612,796 | Google, Inc. | July 2016 / 11 Yrs | 612,796 | $44.40 | NNN |

Santa Clara Square Ph. II Bldg. 5 Santa Clara, CA | 2016 | A | 6 | 220,156 | Cambridge Industries | May 2016 / 7 Yrs | 74,376 | $43.80 | NNN |

Central & Wolfe Campus Sunnyvale, CA | 2018 (Est.) | A | 4 | 871,214 | Apple, Inc. | Sep. 2015 / 13 Yrs | 871,214 | $40.08 | NNN |

599 Castro Mountain View, CA | 2017 | A | 4 | 94,918 | Pure Storage | Aug. 2017 / 7 Yrs | 45,000 | $90.00 | NNN |

| (1) | Information obtained from the appraisal. |

The Borrower.The borrower for the Moffett Towers II - Building 2 Whole Loan is MT2 B2 LLC, a Delaware limited liability company and a special purpose entity with two independent directors (the “Moffett Towers II - Building 2 Borrower”). Legal counsel to the Moffett Towers II Building 2 Borrower delivered a non-consolidation opinion in connection with the origination of the Moffett Towers II - Building 2 Whole Loan. Paul Guarantor LLC, a Delaware limited liability company, (the “Moffett Towers II - Building 2 Guarantor”) is the guarantor of certain nonrecourse carveouts under the Moffett Towers II - Building 2 Whole Loan. Paul Guarantor LLC is wholly owned by the Jay Paul Revocable Living Trust, of which Jay Paul is trustee and grantor. The Moffett Towers II – Building 2 Guarantor will be required to maintain a minimum net worth, excluding its interest in the Moffett Towers II - Building 2 Property, of $225,000,000 and liquidity of at least $10,000,000.

The Borrower Sponsor.The borrower sponsor is the Jay Paul Company, a privately held, opportunity-driven real estate firm based in San Francisco, California. Founded in 1975, Jay Paul Company concentrates on the acquisition, development, and management of commercial properties throughout California. Jay Paul Company has developed over 11.0 million square feet of institutional quality space. Jay Paul Company’s portfolio includes other properties in Moffett Park, including Moffett Gateway, Moffett Towers and Moffett Towers II. Jay Paul Company is currently redeveloping over 55 acres in Moffett Park, including Moffett Place, a new, Class A office development, which is expected to contain approximately 1.9 million square feet of net rentable building area, in six, eight-story buildings.

Escrows.The Moffett Towers II - Building 2 Whole Loan documents provide for upfront reserves in the amount of $19,433,495 for outstanding tenant improvements relating to the Amazon space and $8,332,337 for outstanding rent concessions due under the Amazon lease.

The Moffett Towers II - Building 2 Whole Loan documents also provide for upfront reserves in the amount of $2,700,000 for a parking rent abatement reserve and $286,310 for an amenities rent reserve related to the completion and delivery of the enclosed parking structure and the fitness/amenities building, respectively, which amounts were deposited into a lender-controlled account (the “Parking and Amenities Building Account”). The parking rent abatement reserve represents 180 days of base rent abatements ($15,000 per day) due to Amazon for each day elapsing beyond the targeted completion and delivery date (April 15, 2018) of the 361 spaces allocated to Amazon within the enclosed parking structure, in accordance with the Amazon lease. The amenities rent reserve represents six months of use fees due for the fitness/amenities building, pursuant to the Amazon lease, commencing on the targeted completion and delivery date (July 31, 2018) of such fitness/amenities building to Amazon in accordance with the Amazon lease (use fees that would be due for the fitness/amenities building following the origination date through July 31, 2018 are included in the $8,332,337 upfront reserve for outstanding rent concessions due under the Amazon lease). If the terms of the Required Parking Spaces Satisfaction (as defined below) have not been satisfied on or prior to September 15, 2018, the Moffett Towers II - Building 2 Borrower will be required to deposit an additional $2,700,000 into the Parking and Amenities Building Account. If the terms of the Amenities Building Satisfaction (as defined below) have not been satisfied on or prior to January 31, 2019, the Moffett Towers II - Building 2 Borrower will be required to deposit an additional $286,310 (the “Additional Amenities Rent Amount”) into the Parking and Amenities Building Account. Amounts on deposit in the Parking and Amenities Building Account will be held by the lender as additional collateral for the Moffett Towers II - Building 2 Whole Loan. Provided no event of default under the Moffett Towers II - Building 2 Whole Loan is continuing, the amounts deposited into the Parking and Amenities Building Account will be released to the Moffett Towers II - Building 2 Borrower upon the occurrence of the related Required Parking Spaces Satisfaction or Amenities Building Satisfaction, as applicable.

A “Required Parking Spaces Satisfaction” will occur on the date that (i) the Moffett Towers II - Building 2 Borrower delivers evidence reasonably acceptable to the lender that the Moffett Towers II - Building 2 Borrower has delivered 361 additional spaces to Amazon pursuant to its lease and (ii) Amazon has delivered written confirmation that (a) the Moffett Towers II - Building 2 Borrower has delivered 361 additional spaces to Amazon pursuant to its lease and (b) Amazon is no longer entitled to base rent abatement related to the delivery of the enclosed parking structure pursuant to its lease.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 14 |

| MOFFETT TOWERS II – BUILDING 2 |

An “Amenities Building Satisfaction” will occur on the date that (i) the Moffett Towers II - Building 2 Borrower delivers evidence reasonably acceptable to the lender that the amenities building has been completed in conformance with all applicable requirements and (ii) Amazon has delivered written confirmation that the amenities building is useable and has commenced the payment of the use fees applicable to the amenities building pursuant to the Amazon lease.

Additionally, the Moffett Towers II - Building 2 Whole Loan documents provide for an upfront reserve in the amount of $1,000,000 for a debt service reserve which amount was deposited into a lender-controlled account (the “Debt Service Reserve Account”). If the Required Parking Spaces Satisfaction has not occurred on or prior to September 15, 2018, the Moffett Towers II - Building 2 Borrower will be required to deposit an additional $1,000,000 into the Debt Service Reserve Account. Provided no event of default under the Moffett Towers II - Building 2 Whole Loan is continuing, amounts remaining in the Debt Service Reserve Account will be released to the Moffett Towers II - Building 2 Borrower upon the occurrence of the Required Parking Spaces Satisfaction.

The Moffett Towers II - Building 2 Whole Loan documents require monthly reserve deposits for real estate taxes in an amount equal to one-twelfth of the real estate taxes that the lender estimates will be payable during the next twelve months, initially $111,859. The Moffett Towers II - Building 2 Whole Loan documents do not require ongoing monthly escrows for insurance premiums as long as the Moffett Towers II - Building 2 Borrower provides the lender with evidence that the Moffett Towers II - Building 2 Property is insured via an acceptable blanket insurance policy and such policy is in full force and effect. The Moffett Towers II - Building 2 Whole Loan documents do not provide for monthly reserve deposits for capital expenditures at origination, but provide for the lender to reassess the amount necessary for capital expenditures at the Moffett Towers II - Building 2 Property and may require monthly capital expenditures reserve deposits if necessary to maintain proper operation of the Moffett Towers II - Building 2 Property.

Lockbox and Cash Management.The Moffett Towers II - Building 2 Whole Loan is structured with a hard lockbox and an in-place cash management. The Moffett Towers II - Building 2 Borrower was required at origination to deliver letters to all tenants at the Moffett Towers II - Building 2 Property directing them to pay all rents directly into a lender-controlled lockbox account. All funds received by the Moffett Towers II - Building 2 Borrower or the manager are required to be deposited in the lockbox account within one business day following receipt. Funds on deposit in the lockbox account are required to be swept on each business day into a lender-controlled cash management account and applied on each payment date to the payment of debt service, the funding of required reserves, budgeted monthly operating expenses, common charges under various reciprocal easement agreements, including the CCR (as defined below), approved extraordinary operating expenses, debt service on the Moffett Towers II - Building 2 Mezzanine Loan (as defined below) and, during a Lease Sweep Period (as defined below), to the payment of an amount equal to $438,291 to fund a lease sweep reserve account (the “Lease Sweep Reserve Account”) until the aggregate funds swept in the Lease Sweep Reserve Account during such lease sweep equals the Lease Sweep Reserve Threshold (as defined below) and then to the Debt Service Reserve Account until the aggregate funds transferred to the Lease Sweep Reserve Account and the Debt Service Reserve Account during such lease sweep equals the Lease Sweep and Debt Service Reserve Cap (as defined below). Provided no Trigger Period (as defined below) is continuing, excess cash in the deposit account will be disbursed to the Moffett Towers II - Building 2 Borrower in accordance with the Moffett Towers II - Building 2 Whole Loan documents. If a Trigger Period is continuing (other than a Trigger Period due to a Lease Sweep Period), excess cash in the deposit account will be transferred to an account (the “Cash Collateral Account”) held by the lender as additional collateral for the Moffett Towers II - Building 2 Whole Loan.

A “Trigger Period” will commence upon the earlier of the following:

| (i) | an event of default under the Moffett Towers II - Building 2 Whole Loan; |

| (ii) | if, as of the last day of any calendar quarter during the term of the Moffett Towers II - Building 2 Whole Loan (a) the credit rating of a Lease Sweep Tenant Party (as defined below) under a Lease Sweep Lease (as defined below) by Fitch, Moody’s or S&P is less than “BBB-”, “Baa3” or “BBB-”, respectively and (b) the debt service coverage ratio falls below 1.50x based on the Moffett Towers II - Building 2 Whole Loan or 1.10x based on the Moffett Towers II - Building 2 Total Debt (a “Low Debt Service Period”); |

| (iii) | the commencement of a Lease Sweep Period; or |

| (iv) | an event of default under the Moffett Towers II - Building 2 Mezzanine Loan |

A Trigger Period will end:

| (a) | with regard to clause (i) and (iv) above, upon the cure of such event of default; |

| (b) | with regard to clause (ii) above, upon the earlier to occur of (1) the date that the debt service coverage ratio is at least 1.50x based on the Moffett Towers II - Building 2 Whole Loan and 1.10x based on the Moffett Towers II - Building 2 Total Debt for two consecutive calendar quarters and (2) the balance of funds on deposit in the Cash Collateral Account is equal to $17,531,650 ($50.00 per square foot); and |

| (c) | with regard to clause (iii) above, upon the ending of such Lease Sweep Period. |

A “Lease Sweep Period” will commence following the earliest to occur of any of the following (each a “Lease Sweep Event”):

| (i) | with respect to the Amazon lease, Amazon fails to renew or extend such lease on or prior to December 6, 2025; |

| (ii) | the date on which, with respect to any Lease Sweep Lease, (a) a Lease Sweep Tenant Party cancels or terminates its Lease Sweep Lease with respect to all or a Material Termination Portion (as defined below) of the Lease Sweep Space (as defined below) subject to such Lease Sweep Lease prior to the then current expiration date under such Lease Sweep Lease, or (b) a Lease Sweep Tenant Party delivers to the Moffett Towers II - Building 2 Borrower notice that it is |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 15 |

| MOFFETT TOWERS II – BUILDING 2 |

canceling or terminating its Lease Sweep Lease with respect to all or a Material Termination Portion of the Lease Sweep Space subject to such Lease Sweep Lease (the affected space being the “Terminated Space”); provided, however, no Lease Sweep Period will commence pursuant to this clause (ii) if, in connection with such termination or cancellation (or delivery of notice of termination or cancellation), the Moffett Towers II - Building 2 Borrower simultaneously enters into a replacement lease with an entity or a wholly-owned subsidiary of an entity rated “BBB-” or equivalent by at least two of Fitch, Moody’s and S&P (an “Investment Grade Entity”) covering the Terminated Space, provided that such replacement lease is a qualified lease and the occupancy conditions, as specified in the Moffett Towers II - Building 2 Whole Loan documents, are satisfied with respect to such replacement lease on or prior to the date of such termination or cancellation (or delivery of notice of termination or cancellation);

| (iii) | the date on which, with respect to any Lease Sweep Lease, a Lease Sweep Tenant Party ceases operating its business (i.e., “goes dark”) at 20.0% or more of its Lease Sweep Space on a rentable square foot basis (a “Dark Period Event” and the affected space, the “Dark Space”), provided, however, that if the Lease Sweep Tenant Party either (a) is an Investment Grade Entity or (b) has subleased the Dark Space portion of its premises to an Investment Grade Entity who has accepted delivery thereof (i.e., the lease has commenced) and is paying unabated rent at a contract rate no less than the contract rate required under the Lease Sweep Lease, such Lease Sweep Tenant Party will not be deemed to have “gone dark” for purposes of this clause (iii) and no Lease Sweep Period will commence pursuant to this clause (iii); |

| (iv) | upon an event of default under a Lease Sweep Lease by the tenant thereunder that continues beyond any applicable notice and cure period; |

| (v) | upon a Lease Sweep Tenant Party being subject to an insolvency proceeding; or |

| (vi) | the date on which Amazon is no longer an Investment Grade Entity (an “Amazon Downgrade Event”). |

A Lease Sweep Period (other than a Lease Sweep Period triggered by clause (v) above) will not be triggered (or, if already triggered, may be terminated) if the Moffett Towers II - Building 2 Borrower delivers to the lender an acceptable letter of credit in an amount equal to $12,272,155 ($35.00 per square foot) provided, if such Lease Sweep Period is triggered by clause (iii) or (vi) above, such acceptable letter of credit will be in an amount equal to $17,531,650 ($50.00 per square foot).

A Lease Sweep Period will end on the earliest of the applicable of the following to occur:

| (a) | with regard to clauses (i) and (ii) above, the date on which, with respect to each Lease Sweep Space (1) in the case of clause (i), the Lease Sweep Tenant Parties have exercised a renewal or an extension right under their respective Lease Sweep Lease, provided that the Lease Sweep Lease in question is a qualified lease and the occupancy conditions, as specified in the Moffett Towers II - Building 2 Whole Loan documents, are satisfied, (2) in the case of clauses (i) and (ii) above, one or more replacement tenants acceptable to the lender (in its sole but good faith discretion) execute and deliver replacement lease(s) covering the Requisite Lease Sweep Space (as defined below), provided that such replacement lease(s) are qualified leases and the occupancy conditions, as specified in the Moffett Towers II - Building 2 Whole Loan documents, are satisfied or (3) a combination of lease renewals or extensions (as described in subclause (1) of this clause (a)) and replacement lease(s) (as described in subclause (2) of this clause (a)) occurs; |

| (b) | with regard to clauses (iii) and (vi) above, the date on which either (1) one or more replacement tenants acceptable to the lender (in its sole but good faith discretion) execute and deliver replacement lease(s) covering the Requisite Lease Sweep Space, provided that such replacement tenant(s) and lease(s) are qualified leases and the occupancy conditions, as specified in the Moffett Towers II - Building 2 Whole Loan documents, are satisfied or (2) for a Dark Period Event or an Amazon Downgrade Event, Amazon is restored as an Investment Grade Entity or the entirety of the Lease Sweep Space has been sublet to an Investment Grade Entity who has accepted delivery thereof (i.e., the lease has commenced) and is paying unabated rent at a contract rate no less than the contract rate required under the Lease Sweep Lease; |

| (c) | with regard to clause (iv) above, the date on which the event of default has been cured and no other event of default under such Lease Sweep Lease occurs for a period of three consecutive months following such cure; |

| (d) | with regard to clause (v) above, the Lease Sweep Tenant Party insolvency proceeding has terminated and the applicable Lease Sweep Lease has been affirmed, assumed or assigned in a manner satisfactory to the lender; and |

| (e) | with regard to clauses (i), (ii), (iii), (iv) and (vi) above, the date on which the aggregate amount of funds transferred into the Lease Sweep Reserve Account and the Debt Service Reserve Account equals the applicable Lease Sweep And Debt Reserve Cap (as defined below) and if a Lease Sweep Period is continuing due to the occurrence of more than one Lease Sweep Event, the aggregate amount of funds required to be transferred over the course of the Lease Sweep Period will be equal to the amount of the largest Lease Sweep and Debt Service Reserve Cap applicable to all then-continuing Lease Sweep Periods, such that each Lease Sweep Period will be treated as concurrent and not duplicative or independent of another. |

The “Lease Sweep and Debt Service Reserve Cap” means (a) with respect to a Lease Sweep Period continuing solely pursuant to clause (i) and/or (iv) above, $12,272,155 ($35.00 per square foot), (b) with respect to a Lease Sweep Period continuing solely pursuant to clause (ii) above, $35.00 per square foot of the Terminated Space, (c) with respect to a Lease Sweep Period continuing pursuant to clause (iii) above, whether or not a Lease Sweep Period pursuant to clauses (i), (ii) and/or (iv) above is concurrently continuing, $50.00 per square foot of Dark Space or (d) with respect to clause (vi) above, whether or not a Lease Sweep Period pursuant to clauses (i), (ii), (iii) and/or (iv) above is concurrently continuing, $17,531,650 ($50.00 per square foot).

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 16 |

| MOFFETT TOWERS II – BUILDING 2 |

The “Lease Sweep Reserve Threshold” means (a) with respect to a Lease Sweep Period continuing solely pursuant to clauses (i), (iv) and/or (vi) above, $10,518,990 ($30.00 per square foot) or (b) with respect to a Lease Sweep Period continuing solely pursuant to clause (ii) and/or (iii) above, $30.00 per square foot of the Dark Space or Terminated Space.

The “Lease Sweep Space” means the space demised under a Lease Sweep Lease.

A “Lease Sweep Lease” is the Amazon lease or any replacement lease or leases which cover at least 75.0% of the rentable square feet demised under the Amazon lease as of November 16, 2017 (the “Requisite Lease Sweep Space”).

A “Lease Sweep Tenant Party” is a tenant under a Lease Sweep Lease or its direct or indirect parent company (if any).

A “Material Termination Portion” is, with respect to any space under a Lease Sweep Lease, if the tenant under a Lease Sweep Lease cancels or terminates its Lease Sweep Lease with respect to at least 40,000 square feet of space (or, if a full floor of space is less than 40,000 square feet, a full floor of space) but less than the entirety of the space under such Lease Sweep Lease, the portion of space under the Lease Sweep Lease affected by such cancellation or termination.

Property Management. The Moffett Towers II - Building 2 Property is managed by an affiliate of the Moffett Towers II - Building 2 Borrower.

Assumption.The Moffett Towers II - Building 2 Borrower has, at any time following the securitization of the Moffett Towers II – Building 2 Whole Loan, the right to transfer the Moffett Towers II - Building 2 Property, provided that certain conditions are satisfied, including: (i) no event of default under the Moffett Towers II – Building 2 Whole Loan documents or mezzanine loan documents has occurred and is continuing, (ii) the Moffett Towers II - Building 2 Borrower has provided the lender with 60 days’ prior written notice, (iii) the proposed transferee qualifies as a qualified transferee under the Moffett Towers II - Building 2 Whole Loan documents, (iv) the payment of a transfer fee of 0.5% of the then outstanding principal balance of the Moffett Towers II - Building 2 Whole Loan in the case of the first transfer, and 1.0% of the then outstanding principal balance of the Moffett Towers II - Building 2 Whole Loan in the case of any subsequent transfer, and (v) the lender has received rating agency confirmation that such assumption will not result in a downgrade of the respective ratings assigned to the Series 2018-C43 certificates and similar confirmations from each rating agency rating any securities backed by any of the Moffett Towers II - Building 2 Companion Loans.

Partial Release. Not permitted.

Real Estate Substitution.Not permitted.

Subordinate and Mezzanine Indebtedness.Barclays Bank PLC funded a $105,000,000 mezzanine loan (the “Moffett Towers II - Building 2 Mezzanine Loan”) to MT2 B2 MEZZ LLC (the “Moffett Towers II - Building 2 Mezzanine Borrower”), a Delaware limited liability company owning 100.0% of the borrower under the Moffett Towers II - Building 2 Whole Loan. The Moffett Towers II - Building 2 Mezzanine Loan is secured by a pledge of the Moffett Towers II - Building 2 Mezzanine Borrower’s interest in the Moffett Towers II - Building 2 Borrower under the Moffett Towers II - Building 2 Whole Loan. The Moffett Towers II - Building 2 Mezzanine Loan accrues interest at a rate of 5.900% perannumand requires interest-only payments through the maturity date of December 6, 2027. The rights of the lender of the Moffett Towers II - Building 2 Mezzanine Loan are further described under “Description of the Mortgage Pool—Additional Indebtedness—Mezzanine Indebtedness” in the Preliminary Prospectus.

Amenities and Common Areas. The Moffett Towers II - Building 2 Property will feature access to the fitness/amenities building and the enclosed parking structure (the “Common Area Spaces”) once completed. To govern access to the Common Area Spaces, the Moffett Towers II - Building 2 Borrower is subject to a declaration of covenants, conditions, restrictions and easement and charges agreement (the “CCR”) made by MT II LLC, an affiliate of the borrower sponsor and the owner of the non-collateral buildings at the Moffett Towers II Campus. The CCR grants the Moffett Towers II - Building 2 Borrower non-exclusive easement rights over the Common Area Spaces and contemplates that the Common Area Spaces that it governs will be expanded over time as the remaining portions of the Moffett Towers II Campus are completed. Ownership of the Common Area Spaces governed by the CCR is held by Moffett Towers II Association LLC (the “Association”), whose membership is comprised of the Moffett Towers II - Building 2 Borrower and MT II LLC. The Association is obligated to maintain insurance coverage over the Common Area Spaces and is also responsible for maintenance of the Common Area Spaces, subject to the terms of the Amazon leases. The CCR delineates shares of the voting interest in the Association based on the number of completed buildings at the Moffett Towers II Campus, with each completed building entitled to a proportionate share of the voting interest. As of the origination date, the Moffett Towers II - Building 2 Borrower was the sole voting member of the Association. The CCR provides that as each of the four non-collateral buildings at the Moffett Towers II Campus is completed, the respective owner of each non-collateral building will obtain a share of the voting interest in the Association proportionate to the number of then completed buildings at the Moffett Towers II Campus (both collateral and non-collateral). Provided that all five buildings are completed in accordance with the Moffett Towers II Campus development plan, each building will be entitled to a one-fifth (or 20.0%) share of the voting interest in the Association.

Completion Guaranty. On the origination date, the Moffett Towers II - Building 2 Guarantor executed a separate guaranty for the completion and delivery of the fitness/amenities building and the enclosed parking structure. Among other things, the completion guaranty provides that in the event that neither the Moffett Towers II - Building 2 Borrower nor MT II LLC (an affiliate of the borrower sponsor and the owner of the non-collateral buildings at the Moffett Towers II Campus) is able to complete and deliver the fitness/amenities building and the enclosed parking structure (or otherwise achieve the Required Parking Spaces Satisfaction) on or prior to the one year anniversary of the respective targeted completion date of each (i.e., July 31, 2019 in the case of the fitness/amenities building; April 15, 2019 in the case of the enclosed parking structure or Required Parking Spaces Satisfaction), the Moffett Towers II - Building 2 Guarantor is required to pay any costs, expenses or liabilities incurred by the lender to effectuate the completion and delivery of such fitness/amenities building and enclosed parking structure (or otherwise achieve the Required Parking Spaces Satisfaction).

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 17 |

| MOFFETT TOWERS II – BUILDING 2 |

Ground Lease.None.

Terrorism Insurance.The Moffett Towers II - Building 2 Whole Loan documents require that the “all risk” insurance policy required to be maintained by the Moffett Towers II - Building 2 Borrower provide coverage for terrorism in an amount equal to the full replacement cost of the Moffett Towers II - Building 2 Property, or that if the Terrorism Risk Insurance Program Reauthorization Act is no longer in effect and such policies contain an exclusion for acts of terrorism, the Moffett Towers II - Building 2 Borrower will obtain, to the extent available, a stand-alone policy that provides the same coverage as the policies would have if such exclusion did not exist.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 18 |

(THIS PAGE INTENTIONALLY LEFT BLANK)

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 19 |

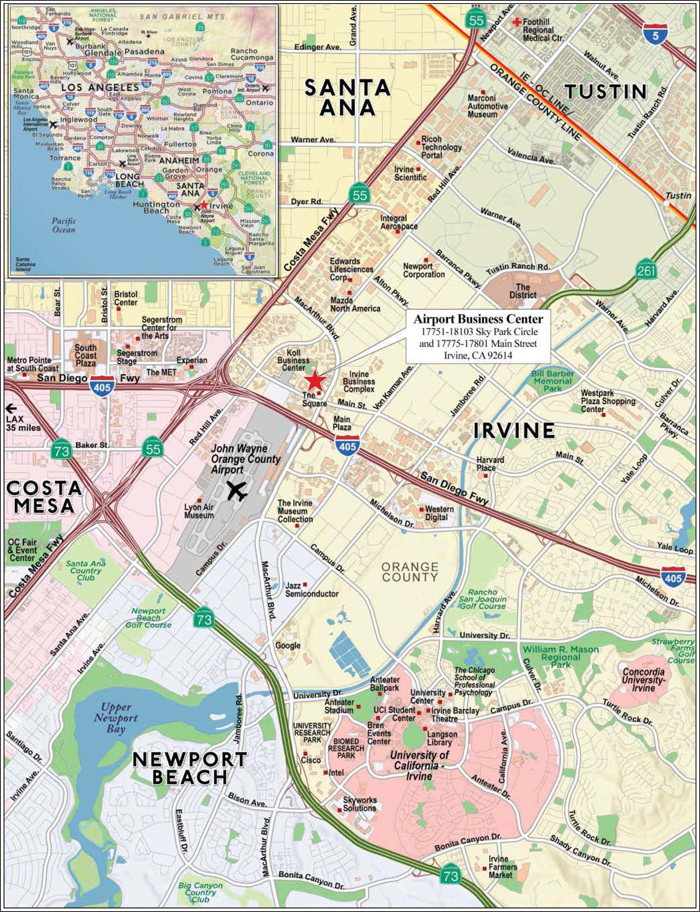

| AIRPORT BUSINESS CENTER |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 20 |

| AIRPORT BUSINESS CENTER |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| 21 |

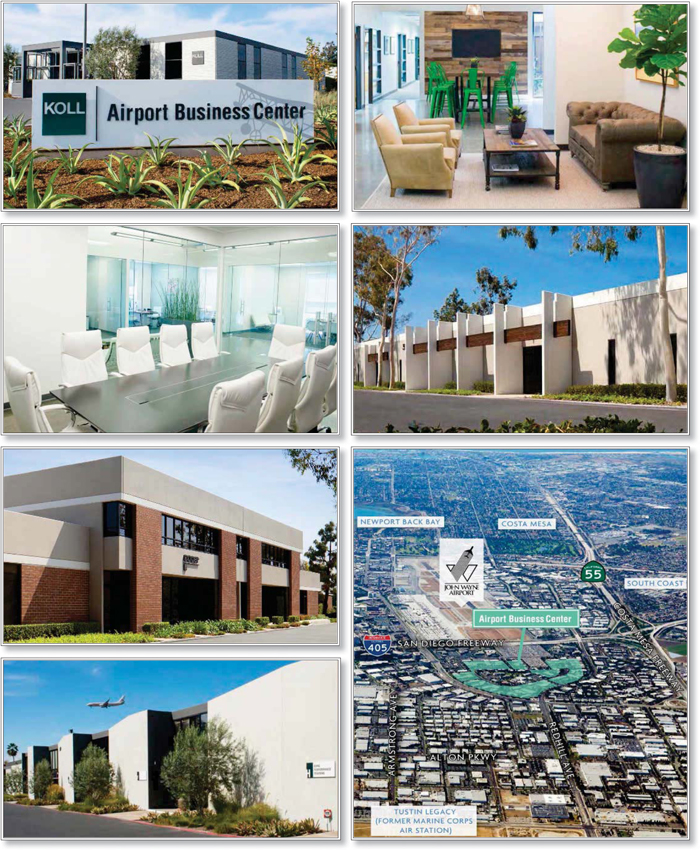

| No. 2 – Airport Business Center | ||||||

| Loan Information | Property Information | |||||

| Mortgage Loan Seller: | Wells Fargo Bank, National Association | Single Asset/Portfolio: | Single Asset | |||

| Credit Assessment (DBRS/Fitch/Moody’s): | NR/NR/NR | Property Type: | Industrial | |||

| Original Principal Balance(1): | $50,000,000 | Specific Property Type: | Flex | |||

| Cut-off Date Balance(1): | $50,000,000 | Location: | Irvine, CA | |||

| % of Initial Pool Balance: | 6.8% | Size: | 1,170,571 SF | |||

| Loan Purpose: | Refinance | Cut-off Date Balance Per SF(1): | $128.14 | |||

| Borrower Name: | AIC Owner, LLC | Year Built/Renovated: | 1969/2005 | |||

| Sponsors: | DK Properties, L.P. | Title Vesting: | Fee | |||

| Mortgage Rate: | 4.375% | Property Manager: | Self-managed | |||

| Note Date: | January 24, 2018 | 4thMost Recent Occupancy (As of): | 91.0% (12/31/2013) | |||

| Anticipated Repayment Date: | NAP | 3rdMost Recent Occupancy (As of): | 93.0% (12/31/2014) | |||

| Maturity Date: | February 7, 2028 | 2rdMost Recent Occupancy (As of): | 96.0% (12/31/2015) | |||

| IO Period: | 120 months | Most Recent Occupancy (As of): | 97.0% (12/31/2016) | |||

| Loan Term (Original): | 120 months | Current Occupancy (As of): | 96.8% (1/31/2018) | |||

| Seasoning: | 1 month | |||||

| Amortization Term (Original): | NAP | Underwriting and Financial Information: | ||||

| Loan Amortization Type: | Interest-only, Balloon | |||||

| Interest Accrual Method: | Actual/360 | 4thMost Recent NOI (As of): | $11,321,411 (12/31/2014) | |||

| Call Protection: | L(25),D(91),O(4) | 3rdMost Recent NOI (As of): | $12,153,147 (12/31/2015) | |||

| Lockbox Type: | Hard/Upfront Cash Management | 2ndMost Recent NOI (As of): | $12,904,375 (12/31/2016) | |||

| Additional Debt(1)(2): | Yes | Most Recent NOI (As of): | $13,635,662 (TTM 10/31/17) | |||

| Additional Debt Type(1)(2): | Pari Passu;Mezzanine | |||||

| U/W Revenues: | $18,889,349 | |||||

| U/W Expenses: | $4,222,532 | |||||

| U/W NOI: | $14,666,817 | |||||

| U/W NCF: | $14,116,649 | |||||

| U/W NOI DSCR(1)(2): | 2.20x | |||||

| Escrows and Reserves(3): | U/W NCF DSCR(1)(2): | 2.12x | ||||

| U/W NOI Debt Yield(1)(2): | 9.8% | |||||

| Type: | Initial | Monthly | Cap (If Any) | U/W NCF Debt Yield(1)(2): | 9.4% | |

| Taxes | $52,146 | $52,144 | NAP | As-Is Appraised Value: | $244,600,000 | |

| Insurance | $31,883 | $17,474 | NAP | As-Is Appraisal Valuation Date: | December 13, 2017 | |

| Replacement Reserves | $0 | $21,418 | $525,000 | Cut-off Date LTV Ratio(1)(2): | 61.3% | |

| TI/LC Reserves | $0 | $73,015 | NAP | LTV Ratio at Maturity(1)(2): | 61.3% | |