| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-257991-02 | ||

|  |  |

Free Writing Prospectus

Structural and Collateral Term Sheet

$764,418,400

(Approximate Initial Pool Balance)

$639,244,000

(Approximate Aggregate Certificate Balance of Offered Certificates)

Wells Fargo Commercial Mortgage Trust 2021-C61

as Issuing Entity

Wells Fargo Commercial Mortgage Securities, Inc.

as Depositor

LMF Commercial, LLC

Wells Fargo Bank, National Association

Ladder Capital Finance LLC

Column Financial, Inc.

UBS AG

BSPRT CMBS Finance, LLC

Oceanview Commercial Mortgage Finance, LLC

as Sponsors and Mortgage Loan Sellers

Commercial Mortgage Pass-Through Certificates

Series 2021-C61

November 15, 2021

WELLS FARGO SECURITIES

Co-Lead Manager and Joint Bookrunner | CREDIT SUISSE

Co-Lead Manager and Joint Bookrunner | UBS SECURITIES LLC

Co-Lead Manager and Joint Bookrunner |

Academy Securities Co-Manager

| Drexel Hamilton Co-Manager

| Siebert Williams Shank Co-Manager

|

STATEMENT REGARDING THIS FREE WRITING PROSPECTUS

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-257991) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC Web site at www.sec.gov. Alternatively, the depositor, any underwriter, or any dealer participating in the offering will arrange to send you the prospectus after filing if you request it by calling toll free 1-800-745-2063 (8 a.m. – 5 p.m. EST) or by emailing wfs.cmbs@wellsfargo.com.

Nothing in this document constitutes an offer of securities for sale in any jurisdiction where the offer or sale is not permitted. The information contained herein is preliminary as of the date hereof, supersedes any such information previously delivered to you and will be superseded by any such information subsequently delivered and ultimately by the final prospectus relating to the securities. These materials are subject to change, completion, supplement or amendment from time to time.

This free writing prospectus has been prepared by the underwriters for information purposes only and does not constitute, in whole or in part, a prospectus for the purposes of (i) Regulation (EU) 2017/1129 (as amended), (ii) such Regulation as it forms part of UK domestic law, or (iii) Part VI of the UK Financial Services and Markets Act 2000, as amended; and does not constitute an offering document for any other purpose.

STATEMENT REGARDING ASSUMPTIONS AS TO SECURITIES, PRICING ESTIMATES AND OTHER INFORMATION

The attached information contains certain tables and other statistical analyses (the “Computational Materials”) which have been prepared in reliance upon information furnished by the Mortgage Loan Sellers. Numerous assumptions were used in preparing the Computational Materials, which may or may not be reflected herein. As such, no assurance can be given as to the Computational Materials’ accuracy, appropriateness or completeness in any particular context; or as to whether the Computational Materials and/or the assumptions upon which they are based reflect present market conditions or future market performance. The Computational Materials should not be construed as either projections or predictions or as legal, tax, financial or accounting advice. You should consult your own counsel, accountant and other advisors as to the legal, tax, business, financial and related aspects of a purchase of these securities. Any weighted average lives, yields and principal payment periods shown in the Computational Materials are based on prepayment and/or loss assumptions, and changes in such prepayment and/or loss assumptions may dramatically affect such weighted average lives, yields and principal payment periods. In addition, it is possible that prepayments or losses on the underlying assets will occur at rates higher or lower than the rates shown in the attached Computational Materials. The specific characteristics of the securities may differ from those shown in the Computational Materials due to differences between the final underlying assets and the preliminary underlying assets used in preparing the Computational Materials. The principal amount and designation of any security described in the Computational Materials are subject to change prior to issuance. None of Wells Fargo Securities, LLC, UBS Securities LLC, Credit Suisse Securities (USA) LLC, Academy Securities, Inc., Drexel Hamilton, LLC, Siebert Williams Shank & Co., LLC or any of their respective affiliates, make any representation or warranty as to the actual rate or timing of payments or losses on any of the underlying assets or the payments or yield on the securities. The information in this presentation is based upon management forecasts and reflects prevailing conditions and management’s views as of this date, all of which are subject to change. In preparing this presentation, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us by or on behalf of the Mortgage Loan Sellers or which was otherwise reviewed by us.

This free writing prospectus contains certain forward-looking statements. If and when included in this free writing prospectus, the words “expects”, “intends”, “anticipates”, “estimates” and analogous expressions and all statements that are not historical facts, including statements about our beliefs or expectations, are intended to identify forward-looking statements. Any forward-looking statements are made subject to risks and uncertainties which could cause actual results to differ materially from those stated. Those risks and uncertainties include, among other things, declines in general economic and business conditions, increased competition, changes in demographics, changes in political and social conditions, regulatory initiatives and changes in customer preferences, many of which are beyond our control and the control of any other person or entity related to this offering. The forward-looking statements made in this free writing prospectus are made as of the date stated on the cover. We have no obligation to update or revise any forward-looking statement.

Wells Fargo Securities is the trade name for the capital markets and investment banking services of Wells Fargo & Company and its subsidiaries, including but not limited to Wells Fargo Securities, LLC, a member of NYSE, FINRA, NFA and SIPC, Wells Fargo Prime Services, LLC, a member of FINRA, NFA and SIPC, and Wells Fargo Bank, N.A. Wells Fargo Securities, LLC and Wells Fargo Prime Services, LLC are distinct entities from affiliated banks and thrifts.

IMPORTANT NOTICE REGARDING THE OFFERED CERTIFICATES

The information herein is preliminary and may be supplemented or amended prior to the time of sale. In addition, the Offered Certificates referred to in these materials and the asset pool backing them are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis.

The underwriters described in these materials may from time to time perform investment banking services for, or solicit investment banking business from, any company named in these materials. The underwriters and/or their affiliates or respective employees may from time to time have a long or short position in any security or contract discussed in these materials.

The information contained herein supersedes any previous such information delivered to any prospective investor and will be superseded by information delivered to such prospective investor prior to the time of sale.

IMPORTANT NOTICE RELATING TO AUTOMATICALLY-GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of any email communication to which this free writing prospectus is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) any representation that these materials are accurate or complete and may not be updated or (3) these materials possibly being confidential, are not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

1

| Wells Fargo Commercial Mortgage Trust 2021-C61 | Certificate Structure |

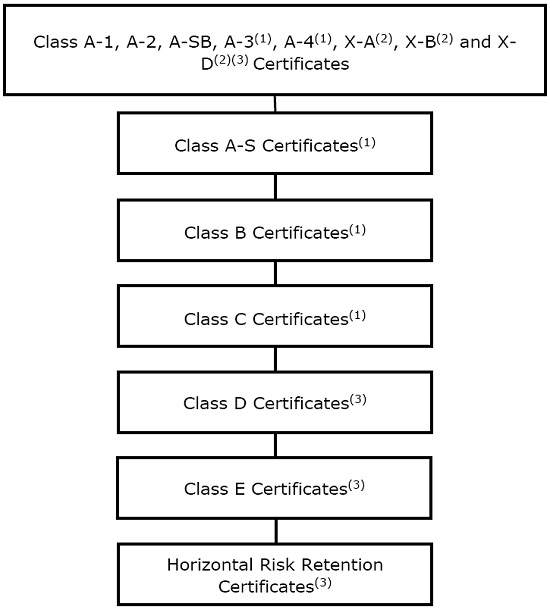

I. Certificate Structure

| Class | Expected Ratings (Fitch/ KBRA / Moody’s)(1) | Approximate Initial Certificate Balance or Notional Amount(2) | Approx. Initial Credit | Pass-Through Rate Description | Weighted Average Life (Years)(4) | Expected Principal Window(4) | Certificate Principal to Value Ratio(5) | Certificate Principal U/W NOI Debt Yield(6) | ||

| Offered Certificates | ||||||||||

| A-1 | AAAsf/AAA(sf)/Aaa(sf) | $18,512,000 | 30.000% | (7) | 2.48 | 1/22 – 5/26 | 42.0% | 14.9% | ||

| A-2 | AAAsf/AAA(sf)/Aaa(sf) | $108,135,000 | 30.000% | (7) | 4.68 | 5/26 – 12/26 | 42.0% | 14.9% | ||

| A-SB | AAAsf/AAA(sf)/Aaa(sf) | $28,529,000 | 30.000% | (7) | 7.28 | 12/26 – 7/31 | 42.0% | 14.9% | ||

| A-3(8) | AAAsf/AAA(sf)/Aaa(sf) | (8)(9) | 30.000% | (7) | (9) | (9) | 42.0% | 14.9% | ||

| A-4(8) | AAAsf/AAA(sf)/Aaa(sf) | (8)(9) | 30.000% | (7) | (9) | (9) | 42.0% | 14.9% | ||

| X-A | AAAsf/AAA(sf)/Aaa(sf) | $535,092,000(10) | N/A | Variable(11) | N/A | N/A | N/A | N/A | ||

| X-B | A-sf/AAA(sf)/NR | $104,152,000(12) | N/A | Variable(13) | N/A | N/A | N/A | N/A | ||

| A-S(8) | AAAsf/AAA(sf)/Aa2(sf) | $24,844,000(8) | 26.750% | (7) | 9.94 | 11/31 – 11/31 | 43.9% | 14.2% | ||

| B(8) | AA-sf/AA+(sf)/NR | $38,221,000(8) | 21.750% | (7) | 9.94 | 11/31 – 11/31 | 46.9% | 13.3% | ||

| C(8) | A-sf/A+(sf)/NR | $41,087,000(8) | 16.375% | (7) | 9.94 | 11/31 – 11/31 | 50.1% | 12.5% | ||

| Non-Offered Certificates | ||||||||||

| X-D(14) | BBB-sf/BBB(sf)/NR | $36,528,000(15) | N/A | Variable(16) | N/A | N/A | N/A | N/A | ||

| D | BBBsf/BBB+(sf)/NR | $27,711,000 | 12.750% | (7) | 9.96 | 11/31 – 12/31 | 52.3% | 11.9% | ||

| E(14) | BBB-sf/BBB(sf)/NR | $8,817,000 | 11.597% | (7) | 10.03 | 12/31 – 12/31 | 53.0% | 11.8% | ||

| Risk Retention Certificates | ||||||||||

| F-RR(14) | BBB-sf/BBB(sf)/NR | $11,249,000 | 10.125% | (7) | 10.03 | 12/31 – 12/31 | 53.9% | 11.6% | ||

| G-RR | BB+sf/BBB-(sf)/NR | $12,421,000 | 8.500% | (7) | 10.03 | 12/31 – 12/31 | 54.9% | 11.4% | ||

| H-RR | BB-sf/BB(sf)/NR | $10,511,000 | 7.125% | (7) | 10.03 | 12/31 – 12/31 | 55.7% | 11.2% | ||

| J-RR | B-sf/B+(sf)/NR | $10,511,000 | 5.750% | (7) | 10.03 | 12/31 – 12/31 | 56.5% | 11.0% | ||

| K-RR | NR/B-(sf)/NR | $7,644,000 | 4.750% | (7) | 10.03 | 12/31 – 12/31 | 57.1% | 10.9% | ||

| L-RR | NR/NR/NR | $36,310,400 | 0.000% | (7) | 10.03 | 12/31 – 12/31 | 59.9% | 10.4% | ||

Notes:

| (1) | The expected ratings presented are those of Kroll Bond Rating Agency, LLC (“KBRA”), Fitch Ratings, Inc. (“Fitch”), and Moody’s Investors Service, Inc. (“Moody’s”), which the depositor hired to rate the Offered Certificates. One or more other nationally recognized statistical rating organizations that were not hired by the depositor may use information they receive pursuant to Rule 17g-5 under the Securities Exchange Act of 1934, as amended (the “Exchange Act”) or otherwise, to rate or provide market reports and/or published commentary related to the Offered Certificates. We cannot assure you as to what ratings a non-hired nationally recognized statistical rating organization would assign or that its reports will not express differing, possibly negative, views of the mortgage loans and/or the Offered Certificates. The ratings of each Class of Offered Certificates address the likelihood of the timely distribution of interest and, except in the case of the Class X-A and X-B Certificates, the ultimate distribution of principal due on those Classes on or before the Rated Final Distribution Date. See “Risk Factors—Other Risks Relating to the Certificates—Nationally Recognized Statistical Rating Organizations May Assign Different Ratings to the Certificates; Ratings of the Certificates Reflect Only the Views of the Applicable Rating Agencies as of the Dates Such Ratings Were Issued; Ratings May Affect ERISA Eligibility; Ratings May Be Downgraded” and “Ratings” in the Preliminary Prospectus, expected to be dated November 15, 2021 (the “Preliminary Prospectus”). KBRA, Fitch and Moody’s have informed us that the “sf” designation in their ratings represents an identifier for structured finance product ratings. |

| (2) | The Certificate Balances and Notional Amounts set forth in the table are approximate. The actual initial Certificate Balances and Notional Amounts may be larger or smaller depending on the initial pool balance of the mortgage loans definitively included in the pool of mortgage loans, which aggregate cut-off date balance may be as much as 5% larger or smaller than the amount presented in the Preliminary Prospectus. In addition, the Notional Amounts of the Class X-A or X-B Certificates may vary depending upon the final pricing of the Classes of Principal Balance Certificates (as defined below) or trust components whose Certificate Balances comprise such Notional Amounts, and, if, as a result of such pricing, the pass-through rate of the Class X-A or X-B Certificates, as applicable, would be equal to zero at all times, such Class of Certificates may not be issued on the closing date of this securitization. |

| (3) | The approximate initial credit support with respect to the Class A-1, A-2, A-SB, A-3 and A-4 Certificates represents the approximate credit enhancement for the Class A-1, A-2, A-SB, A-3 and A-4 Certificates in the aggregate, taking into account the Certificate Balances of the Class A-3 and Class A-4 trust components. The approximate initial credit support set forth for the Class A-S certificates represents the approximate initial credit enhancement for the underlying Class A-S trust component. The approximate initial credit support set forth for the Class B certificates represents the approximate initial credit enhancement for the underlying Class B trust component. The approximate initial credit support set forth for the Class C certificates represents the approximate initial credit enhancement for the underlying Class C trust component. |

| (4) | Weighted Average Lives and Expected Principal Windows are calculated based on an assumed prepayment rate of 0% CPR and the “Structuring Assumptions” described under “Yield and Maturity Considerations—Weighted Average Life” in the Preliminary Prospectus. |

| (5) | The Certificate Principal to Value Ratio for each Class of Certificates (other than the Class A-1, A-2, A-SB, A-3 and A-4 Certificates) is calculated as the product of (a) the weighted average Cut-off Date LTV Ratio for the mortgage loans and (b) a fraction, the numerator of which is the total initial Certificate Balance of such Class of Certificates and all Classes of Principal Balance Certificates (or, with respect to the Class A-3, A-4, A-S, B or C Certificates, the trust component with the same alphanumeric designation) senior to such Class of Certificates and the denominator of which is the total initial Certificate Balance of all of the Classes of Principal Balance Certificates (or, with respect to the Class A-3, A-4, A-S, B or C Certificates, the trust component with the same alphanumeric designation). The Certificate Principal to Value Ratio for each of the Class A-1, A-2, A-SB, A-3 and A-4 Certificates is calculated in the aggregate for those Classes as if they were a single Class and is calculated as the product of (a) the weighted average Cut-off Date LTV Ratio for the mortgage loans and (b) a fraction, the numerator of which is the total initial Certificate Balance of such Classes of Certificates (or, with respect to the Class A-3 or A-4 Certificates, the trust component with the same alphanumeric designation) and the denominator of which is the total initial Certificate Balance of all of the Classes of Principal Balance Certificates (or, with respect to the Class A-3, A-4, A-S, B or C Certificates, the trust component with the same alphanumeric designation). In any event, however, excess mortgaged property value associated with a mortgage loan will not be available to offset losses on any other mortgage loan. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

3

| Wells Fargo Commercial Mortgage Trust 2021-C61 | Certificate Structure |

| (6) | The Certificate Principal U/W NOI Debt Yield for each Class of Certificates (other than the Class A-1, A-2, A-SB, A-3 and A-4 Certificates) is calculated as the product of (a) the weighted average U/W NOI Debt Yield for the mortgage loans and (b) a fraction, the numerator of which is the total initial Certificate Balance of all of the Classes of Principal Balance Certificates (or, with respect to the Class A-3, A-4, A-S, B or C Certificates, the trust component with the same alphanumeric designation) and the denominator of which is the total initial Certificate Balance of such Class of Certificates and all Classes of Principal Balance Certificates (or, with respect to the Class A-3, A-4, A-S, B or C Certificates, the trust component with the same alphanumeric designation) senior to such Class of Certificates. The Certificate Principal U/W NOI Debt Yield for each of the Class A-1, A-2, A-SB, A-3 and A-4 Certificates is calculated in the aggregate for those Classes as if they were a single Class and is calculated as the product of (a) the weighted average U/W NOI Debt Yield for the mortgage loans and (b) a fraction, the numerator of which is the total initial Certificate Balance of all of the Classes of Principal Balance Certificates (or, with respect to the Class A-3, A-4, A-S, B or C Certificates, the trust component with the same alphanumeric designation) and the denominator of which is the total initial Certificate Balance of such Classes of Certificates (or, with respect to the Class A-3 and Class A-4 Certificates, the trust component with the same alphanumeric designation). In any event, however, cash flow from each mortgaged property supports only the related mortgage loan and will not be available to support any other mortgage loan. | |

| (7) | The pass-through rates for the Class A-1, A-2, A-SB, A-3, A-4, A-S, B, C, D, E, F-RR, G-RR, H-RR, J-RR, K-RR and L-RR Certificates in each case for any distribution date will be one of the following: (i) a fixed rate per annum, (ii) a variable rate per annum equal to the weighted average of the net mortgage interest rates on the mortgage loans for the related distribution date, (iii) a variable rate per annum equal to the lesser of (a) a fixed rate and (b) the weighted average of the net mortgage interest rates on the mortgage loans for the related distribution date or (iv) a variable rate per annum equal to the weighted average of the net mortgage interest rates on the mortgage loans for the related distribution date minus a specified percentage. For purposes of the calculation of the weighted average of the net mortgage interest rates on the mortgage loans for each distribution date, the mortgage interest rates will be adjusted as necessary to a 30/360 basis. | |

| (8) | The Class A-3-1, A-3-2, A-3-X1, A-3-X2, A-4-1, A-4-2, A-4-X1, A-4-X2, A-S-1, A-S-2, A-S-X1, A-S-X2, B-1, B-2, B-X1, B-X2, C-1, C-2, C-X1 and C-X2 Certificates are also offered certificates. Such Classes of Certificates, together with the Class A-3, A-4, A-S, B and C Certificates, constitute the “Exchangeable Certificates”. The Class A-1, A-2, A-SB, D, E, F-RR, G-RR, H-RR, J-RR, K-RR and L-RR Certificates, together with the Exchangeable Certificates with a Certificate Balance, are referred to as the “Principal Balance Certificates”. Each class of Exchangeable Certificates will have the Certificate Balance or Notional Amount and pass-through rate described below under “Exchangeable Certificates”.

| |

| (9) | The exact initial Certificate Balances or Notional Amounts of the Class A-3, A-3-X1, A-3-X2, A-4, A-4-X1 and A-4-X2 trust components (and consequently, the exact initial Certificate Balances or Notional Amounts of the Exchangeable Certificates with an “A-3” or “A-4” designation) are unknown and will be determined based on the final pricing of the Certificates. However, the initial Certificate Balances, weighted average lives and principal windows of the Class A-3 and Class A-4 trust components are expected to be within the applicable ranges reflected in the following chart. The aggregate initial Certificate Balance of the Class A-3 and Class A-4 trust components is expected to be approximately $379,916,000, subject to a variance of plus or minus 5%. The Class A-3-X1 and A-3-X2 trust components will have initial Notional Amounts equal to the initial Certificate Balance of the Class A-3 trust component. The Class A-4-X1 and A-4-X2 trust components will have initial Notional Amounts equal to the initial Certificate Balance of the Class A-4 trust component. In the event that the Class A-4 Certificates are issued at $379,916,000, the Class A-3 Certificates will not be issued. | |

Trust Components | Expected Range of Approximate Initial | Expected Range of Weighted Average Life (Years) | Expected Range of Principal Window |

| Class A-3 | $0 – $175,000,000 | NAP – 9.41 | NAP / 12/29 – 10/31 |

| Class A-4 | $204,916,000 – $379,916,000 | 9.68 – 9.90 | 12/29 – 11/31 / 10/31 – 11/31 |

| (10) | The Class X-A Certificates are notional amount certificates. The Notional Amount of the Class X-A Certificates will be equal to the aggregate Certificate Balance of the Class A-1, A-2 and A-SB Certificates and the Class A-3 and A-4 trust components outstanding from time to time. The Class X-A Certificates will not be entitled to distributions of principal. |

| (11) | The pass-through rate for the Class X-A Certificates for any distribution date will be a per annum rate equal to the excess, if any, of (a) the weighted average of the net mortgage interest rates on the mortgage loans for the related distribution date, over (b) the weighted average of the pass-through rates on the Class A-1, A-2 and A-SB Certificates and the Class A-3, A-3-X1, A-3-X2, A-4, A-4-X1 and A-4-X2 trust components for the related distribution date, weighted on the basis of their respective Certificate Balances or Notional Amounts outstanding immediately prior to that distribution date (but excluding trust components with a Notional Amount in the denominator of such weighted average calculation). For purposes of the calculation of the weighted average of the net mortgage interest rates on the mortgage loans for each distribution date, the mortgage interest rates will be adjusted as necessary to a 30/360 basis. |

| (12) | The Class X-B Certificates are notional amount certificates. The Notional Amount of the Class X-B Certificates will be equal to the aggregate Certificate Balance of the Class A-S, B and C trust components outstanding from time to time. The Class X-B Certificates will not be entitled to distributions of principal. |

| (13) | The pass-through rate for the Class X-B Certificates for any distribution date will be a per annum rate equal to the excess, if any, of (a) the weighted average of the net mortgage interest rates on the mortgage loans for the related distribution date, over (b) the weighted average of the pass-through rates on the Class A-S, A-S-X1, A-S-X2, B, B-X1, B-X2, C, C-X1 and C-X2 trust components for the related distribution date, weighted on the basis of their respective Certificate Balances or Notional Amounts outstanding immediately prior to that distribution date (but excluding trust components with a Notional Amount in the denominator of such weighted average calculation). For purposes of the calculation of the weighted average of the net mortgage interest rates on the mortgage loans for each distribution date, the mortgage interest rates will be adjusted as necessary to a 30/360 basis. |

| (14) | The initial Notional Amount of the Class X-D Certificates and the initial Certificate Balance of each of the Class E and F-RR Certificates are subject to change based on final pricing of all Certificates and the final determination of the horizontal risk retention certificates that will be retained by the retaining sponsor through a third party purchaser as part of the U.S. risk retention requirements. For more information regarding the methodology and key inputs and assumptions used to determine the sizing of the horizontal risk retention certificates, see “Credit Risk Retention” in the Preliminary Prospectus. |

| (15) | The Class X-D Certificates are notional amount certificates. The Notional Amount of the Class X-D Certificates will be equal to the aggregate Certificate Balance of the Class D and E Certificates outstanding from time to time. The Class X-D Certificates will not be entitled to distributions of principal. |

| (16) | The pass-through rate for the Class X-D Certificates for any distribution date will be a per annum rate equal to the excess, if any, of (a) the weighted average of the net mortgage interest rates on the mortgage loans for the related distribution date, over (b) the weighted average of the pass-through rates on the Class D and E Certificates for the related distribution date, weighted on the basis of their respective Certificate Balances outstanding immediately prior to that distribution date. For purposes of the calculation of the weighted average of the net mortgage interest rates on the mortgage loans for each distribution date, the mortgage interest rates will be adjusted as necessary to a 30/360 basis.

|

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

4

| Wells Fargo Commercial Mortgage Trust 2021-C61 | Transaction Highlights |

II. Transaction Highlights

Mortgage Loan Sellers:

| Mortgage Loan Seller | Number of Mortgage Loans | Number of Mortgaged Properties | Aggregate Cut-off Date Balance | % of Initial Pool Balance | ||||||||

| LMF Commercial, LLC | 20 | 41 | $189,149,596 | 24.7 | % | |||||||

| Wells Fargo Bank, National Association | 10 | 39 | 185,688,995 | 24.3 | ||||||||

| Ladder Capital Finance LLC | 6 | 6 | 117,415,492 | 15.4 | ||||||||

| Column Financial, Inc. | 7 | 16 | 99,917,428 | 13.1 | ||||||||

| UBS AG | 10 | 55 | 70,029,223 | 9.2 | ||||||||

| BSPRT CMBS Finance, LLC | 6 | 6 | 65,102,232 | 8.5 | ||||||||

| Oceanview Commercial Mortgage Finance, LLC | 2 | 2 | 37,115,435 | 4.9 | ||||||||

Total | 61 | 165 | $764,418,400 | 100.0 | % | |||||||

Loan Pool:

| Initial Pool Balance: | $764,418,400 |

| Number of Mortgage Loans: | 61 |

| Average Cut-off Date Balance per Mortgage Loan: | $12,531,449 |

| Number of Mortgaged Properties: | 165 |

| Average Cut-off Date Balance per Mortgaged Property(1): | $4,632,839 |

| Weighted Average Mortgage Interest Rate: | 3.9099% |

| Ten Largest Mortgage Loans as % of Initial Pool Balance: | 45.5% |

| Weighted Average Original Term to Maturity or ARD (months): | 112 |

| Weighted Average Remaining Term to Maturity or ARD (months): | 108 |

| Weighted Average Original Amortization Term (months)(2): | 354 |

| Weighted Average Remaining Amortization Term (months)(2): | 351 |

| Weighted Average Seasoning (months): | 3 |

| (1) | Information regarding mortgage loans secured by multiple properties is based on an allocation according to relative appraised values or the allocated loan amounts or property-specific release prices set forth in the related loan documents or such other allocation as the related mortgage loan seller deemed appropriate. |

| (2) | Excludes any mortgage loan that does not amortize. |

Credit Statistics:

| Weighted Average U/W Net Cash Flow DSCR(1)(2): | 2.15x |

| Weighted Average U/W Net Operating Income Debt Yield(1)(2): | 10.4% |

| Weighted Average Cut-off Date Loan-to-Value Ratio(1)(2): | 59.9% |

| Weighted Average Balloon or ARD Loan-to-Value Ratio(1)(2): | 55.7% |

| % of Mortgage Loans with Additional Subordinate Debt(3): | 5.8% |

| % of Mortgage Loans with Single Tenants(4): | 21.7% |

| (1) | With respect to any mortgage loan that is part of a whole loan, loan-to-value ratio, debt service coverage ratio and debt yield calculations include the related pari passu companion loan(s) but exclude any related subordinate companion loan(s) (unless otherwise stated). The debt service coverage ratio, debt yield and loan-to-value ratio information do not take into account any subordinate debt (whether or not secured by the related mortgaged property), that currently exists or is allowed under the terms of any mortgage loan. The information for each mortgaged property that relates to a mortgage loan that is cross-collateralized or cross-defaulted with one or more other mortgage loans is based upon the principal balance of that mortgage loan, except that the applicable loan-to-value ratio, debt service coverage ratio, and debt yield for each such mortgage loan is based upon the ratio or yield (as applicable) for the aggregate indebtedness evidenced by all loans in the group (without regard to any limitation on the amount of indebtedness secured by any mortgaged property in such cross-collateralized group). See “Description of the Mortgage Pool—Mortgage Pool Characteristics” in the Preliminary Prospectus and Annex A-1 to the Preliminary Prospectus. |

| (2) | For certain of the mortgage loans, underwritten net cash flow, underwritten net operating income and appraised values of the related mortgaged properties were determined, or were calculated based on information as of a date, prior to the emergence of the novel coronavirus pandemic and the economic disruption resulting from measures to combat the pandemic, and the loan-to-value, debt service coverage and debt yield metrics presented in this term sheet may not reflect current market conditions. |

| (3) | The percentage figure expressed as “% of Mortgage Loans with Additional Subordinate Debt” is determined as a percentage of the initial pool balance and does not take into account any future subordinate debt (whether or not secured by the mortgaged property), if any, that may be permitted under the terms of any mortgage loan or the pooling and servicing agreement. See “Description of the Mortgage Pool—Additional Indebtedness” in the Preliminary Prospectus. |

| (4) | Excludes mortgage loans that are secured by multiple single tenant properties. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

5

| Wells Fargo Commercial Mortgage Trust 2021-C61 | Transaction Highlights |

Loan Structural Features:

Amortization: Based on the Initial Pool Balance, 43.0% of the mortgage pool (32 mortgage loans) has scheduled amortization, as follows:

23.4% (17 mortgage loans) requires amortization during the entire loan term; and

19.6% (15 mortgage loans) provides for an interest-only period followed by an amortization period.

Interest-Only: Based on the Initial Pool Balance, 57.0% of the mortgage pool (29 mortgage loans) provides for interest-only payments during the entire loan term through maturity or ARD. The Weighted Average Cut-off Date Loan-to-Value Ratio and Weighted Average U/W Net Cash Flow DSCR for those mortgage loans are 58.4% and 2.39x, respectively.

Hard Lockboxes: Based on the Initial Pool Balance, 47.1% of the mortgage pool (17 mortgage loans) have hard lockboxes in place.

Reserves: The mortgage loans require amounts to be escrowed monthly as follows (excluding any mortgage loans with springing provisions):

| Real Estate Taxes: | 71.9% of the pool |

| Insurance: | 58.5% of the pool |

| Capital Replacements: | 74.0% of the pool |

| TI/LC: | 52.1% of the pool(1) |

| (1) The percentage of Initial Pool Balance for mortgage loans with TI/LC reserves is based on the aggregate principal balance allocable to loans that include office, retail, mixed use and industrial properties. | |

Call Protection/Defeasance: Based on the Initial Pool Balance, the mortgage pool has the following call protection and defeasance features:

81.1% of the mortgage pool (48 mortgage loans) features a lockout period, then defeasance only until an open period;

8.9% of the mortgage pool (7 mortgage loans) features a lockout period, then the greater of a prepayment premium (1.0%) or yield maintenance until an open period;

3.3% of the mortgage pool (1 mortgage loans) features the greater of a prepayment premium (0.5%) or yield maintenance then an open period;

2.8% of the mortgage pool (2 mortgage loans) features a lockout period, then the greater of a prepayment premium (2.0%) or yield maintenance until an open period;

1.8% of the mortgage pool (1 mortgage loans) features a lockout period, then the greater of a prepayment premium (1.0%) or yield maintenance then defeasance until an open period;

1.5% of the mortgage pool (1 mortgage loans) features a lockout period, then the greater of a prepayment premium (3.0%) or yield maintenance then defeasance until an open period;

0.7% of the mortgage pool (1 mortgage loans) features the greater of a prepayment premium (1.0%) or yield maintenance then an open period;

Prepayment restrictions for each mortgage loan reflect the entire life of the mortgage loan. Please refer to Annex A-1 to the Preliminary Prospectus and the footnotes related thereto for further information regarding individual loan call protection.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

6

| Wells Fargo Commercial Mortgage Trust 2021-C61 | Transaction Highlights |

III. COVID-19 Update

The following table contains information regarding the status of the mortgage loans and mortgaged properties provided by the respective borrowers as of the date set forth in the “Information As Of Date” column. The information from the borrowers has not been independently verified by the Mortgage Loan Sellers, the Underwriters or any other party, and there can be no assurance that the status of the Mortgage Loans and of the related Mortgaged Properties has not changed since the date in the “Information As-Of Date” column. The cumulative effects of the COVID-19 emergency on the global economy may cause tenants to be unable to pay their rent and borrowers to be unable to pay debt service under the mortgage loans. As a result, we cannot assure you that the information in the following table is indicative of future performance or that tenants or borrowers will not seek rent or debt service relief (including forbearance arrangements) or other lease or loan modifications in the future. Such actions may lead to shortfalls and losses on the certificates. Any information in the following table will be superseded by the information contained under the heading “Description of the Mortgage Pool—COVID-19 Considerations” in the Preliminary Prospectus.

Mortgage Loan Seller | Information As Of Date | Origination Date | Mortgaged Property Name | Mortgaged Property Type | August Debt Service Payment Received (Y/N) | September Debt Service Payment Received (Y/N) | October Debt Service Payment Received (Y/N) | Forbearance or Other Debt Service Relief Requested (Y/N) | Other Loan Modification Requested (Y/N) | Lease Modification or Rent Relief Requested (Y/N) | Total SF or Unit Count Making Full September Rent Payment (%) | UW September Base Rent Paid (%) | Total SF or Unit Count Making Full October Rent Payment (%) | UW October Base Rent Paid (%) |

| LMF | 11/1/2021 | 12/18/2019 | Martin Village | Retail | Y | Y | Y | Y(1) | N(2) | Y(1) | 100.0% | 100.0% | 100.0% | 100.0% |

| UBS AG | 11/4/2021 | 12/30/2019 | Cabela’s - Mitchell | Retail | Y | Y | Y | N | N | Y(3) | 100.0% | 100.0% | 100.0% | 100.0% |

| LCF | 11/3/2021 | 3/6/2020 | Shoppes on University | Retail | Y | Y | Y | N | Y(4) | Y(5) | 97.0% | 97.0% | 97.0% | 97.0% |

| UBS AG | 11/4/2021 | 11/27/2019 | Wyndham National Hotel Portfolio(6) | Hospitality | Y | Y | Y | N | N | N | NAP | NAP | NAP | NAP |

| LCF | 10/29/2021 | 2/28/2020 | Willow Plaza | Retail | Y | Y | Y | N | Y(7) | N | 92.0% | 92.0% | 99.0% | 99.0% |

| (1) | With respect to the Martin Village Mortgage Loan, the largest tenant, Regal Cinemas (“Regal”), representing 65.3% of net rentable area and 77.6% of underwritten base rent, announced it would close all of its theaters in the United States in March 2020 and subsequently reopened its theater at the Martin Village property on August 21, 2020. On October 5, 2020 Regal announced it would again temporally close all theaters in the United States due to a lack of theatrical releases. Regal reopened its theater at the Martin Village property for a second time on May 7, 2021 and the theater continued to be open and operational as of November 12, 2021. Regal paid reduced rent for the periods from April 2020 through July 2020 and November 2020 through June 2021, resulting in approximately $1.37 million in past due rent. While the borrower and Regal have not yet come to an agreement on repayment terms for the approximate $1.37 million in past due rent, Regal has been paying its full contractual rent since July 2021. |

On May 27, 2020 the second largest tenant, Mor Furniture, representing 27.3% of net rentable area and 13.4% of underwritten base rent, entered into a lease modification with the borrower, allowing the tenant to defer a total of $67,500 of rent between April 1, 2020 and June 30, 2020 ($22,500 gross per month). The tenant was required to repay $22,500 of the deferred rent by December 31, 2020, which amount was repaid in full. The remaining $45,000 is required to be repaid in twelve equal monthly payments of $3,750 starting January 1, 2021, which amount has been paid as agreed. Additionally, the lease term has been extended for 12 months.

| (2) | With respect to the Martin Village Mortgage Loan, on June 2, 2020, the lender and the borrower agreed to a loan modification, allowing funds to be drawn from the $1,200,000 Regal Cinema TI Reserve (“Regal Reserve”) to pay shortfalls in operating expenses, debt service and monthly reserves. A total of $91,727 was drawn from the Regal Reserve in June 2020 and such amount was fully repaid in July 2020. On December 29, 2020, the loan modification was reinstated to extend the borrower’s ability to use the Regal Reserve to pay monthly shortfalls. A total of $257,392 was drawn from the Regal Reserve from January 2021 through May 2021, and the total amount drawn was repaid to the Regal Reserve from May 2021 through October 2021. As of November 1, 2021, the Regal Reserve was fully-funded with $1,200,000 and an additional $203,545 had been swept into a separate critical tenant reserve as a result of an ongoing critical tenant cash sweep. |

On July 3, 2020 the third largest tenant, The Rock Pizza, representing 4.2% of net rentable area and 7.1% of underwritten base rent, agreed to a lease modification with the borrower, allowing base rent for April 2020 through September 2020 to be deferred by 50%. The deferred base rent ($34,830) is required to be repaid in 12 equal monthly payments of $2,903 starting January 2021, which amount has been paid as agreed. Additionally, the lease term has been extended for 12 months.

| (3) | The mortgage loan seller approved a lease amendment that allowed the sole tenant, Bass Pro Shop/Cabela’s, to defer May rent totaling $108,333, which was required to be repaid in three equal monthly installments in January, February, and March 2021. As of February 28, 2021, the tenant had repaid the deferred rent in full. The tenant resumed its full rent payments in June 2020 and there has been no interruption in debt service payments since origination in December 2019, as the borrower paid May debt service out-of-pocket. |

| (4) | In 2020, the Shoppes on University Mortgage Loan was modified in a manner that, notwithstanding the occurrence of a debt service coverage-related cash management trigger event, deferred the related borrower’s obligation under the related loan agreement to establish a clearing account and the declaration of such cash management trigger event until, at the lender’s option, the monthly payment date on September 6, 2020. Such modification also provided for, among other things, monthly debt service payments through the September 2020 payment each being paid a month early. |

| (5) | With respect to the Shoppes on University Mortgage Loan, the second largest tenant, Planet Fitness, representing approximately 22.6% of the net rentable area and 18.8% of underwritten base rent at the related Mortgaged Property, was temporarily closed for business during 2020 due to the COVID-19 pandemic and, as such, entered a lease modification whereby the tenant would, commencing April 1, 2020, pay 50% of base rent through the first day of the second month after the tenant would be permitted, by public authority, to re-open to the public, would continue to pay its full share of operating costs during such period and would make the landlord whole on unpaid rent (such deferred rent to be paid in six equal monthly installments commencing on the first day of the second month after the tenant would be permitted, by public authority, to re-open to the public). Planet Fitness officially reopened on May 29, 2020 and was required to begin paying unpaid rent on August 1, 2020. As of February 1, 2021, Planet Fitness has paid all unpaid rent. In addition, tenants Check Mart of Florida and Menchie’s received relief on common area maintenance and tax due in June 2020, and tenant Check Mart of Florida received relief on common area maintenance and tax due in July 2020. |

| (6) | With respect to the Wyndham National Hotel Portfolio Properties, please see Annex A-1 for information relating to occupancy, ADR and RevPAR. |

| (7) | The related borrower requested a modification related to certain debt service coverage ratio tests and the funding of certain reserves in the related loan documents but was not granted the request. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

7

| Wells Fargo Commercial Mortgage Trust 2021-C61 | Issue Characteristics |

IV. Issue Characteristics

| Securities Offered: | $639,244,000 approximate monthly pay, multi-class, commercial mortgage REMIC pass-through certificates consisting of thirty classes (Classes A-1, A-2, A-SB, A-3, A-3-1, A-3-2, A-3-X1, A-3-X2, A-4, A-4-1, A-4-2, A-4-X1, A-4-X2, A-S, A-S-1, A-S-2, A-S-X1, A-S-X2, B, B-1, B-2, B-X1, B-X2, C, C-1, C-2, C-X1, C-X2, X-A and X-B), which are offered pursuant to a registration statement filed with the SEC (such classes of certificates, the “Offered Certificates”). |

| Mortgage Loan Sellers: | LMF Commercial, LLC (“LMF”), Wells Fargo Bank, National Association (“WFB”), Ladder Capital Finance LLC (“LCF”), Column Financial, Inc. (“Column”), UBS AG, by and through its branch office at 1285 Avenue of the Americas, New York, New York (“UBS”), BSPRT CMBS Finance, LLC (“BSPRT”) and Oceanview Commercial Mortgage Finance, LLC (“Oceanview”) |

| Joint Bookrunners and Co-Lead Managers: | Wells Fargo Securities, LLC, UBS Securities LLC and Credit Suisse Securities (USA) LLC |

| Co-Managers: | Academy Securities, Inc., Drexel Hamilton, LLC and Siebert Williams Shank & Co., LLC |

| Rating Agencies: | Kroll Bond Rating Agency, LLC, Fitch Ratings, Inc., and Moody’s Investors Service, Inc. |

| Master Servicer: | Wells Fargo Bank, National Association |

| Special Servicer: | CWCapital Asset Management LLC |

| Certificate Administrator: | Computershare Trust Company, N.A. |

| Trustee: | Wilmington Trust, National Association |

| Operating Advisor: | Pentalpha Surveillance LLC |

| Asset Representations Reviewer: | Pentalpha Surveillance LLC |

| Initial Majority Controlling Class Certificateholder: | LD III Sub IV LLC |

| U.S. Credit Risk Retention: | For a discussion on the manner in which the U.S. credit risk retention requirements will be satisfied by Wells Fargo Bank, National Association, as the retaining sponsor, see “Credit Risk Retention” in the Preliminary Prospectus.

This transaction is being structured with a “third party purchaser” that will acquire an “eligible horizontal residual interest”, which will be comprised of the Class F-RR, G-RR, H-RR, J-RR, K-RR and L-RR Certificates (the “horizontal risk retention certificates”). LD III Sub IV LLC (in satisfaction of the retention obligations of Wells Fargo Bank, National Association, as the retaining sponsor) will be contractually obligated to retain (or to cause its “majority-owned affiliate” to retain) the horizontal risk retention certificates for a minimum of five years after the closing date, subject to certain permitted exceptions provided for under the risk retention rules. During this time, LD III Sub IV LLC will agree to comply with hedging, transfer and financing restrictions that are applicable to third party purchasers under the credit risk retention rules. For additional information, see “Credit Risk Retention” in the Preliminary Prospectus.

|

| EU/UK Credit Risk Retention | None of the sponsors, the depositor, the underwriters, or their respective affiliates, or any other party to the transaction intends to retain a material net economic interest in the securitization constituted by the issue of the Certificates, or take any other action in respect of such securitization, in a manner prescribed or contemplated by (i) Regulation (EU) 2017/2402, or (ii) such Regulation as it forms part of UK domestic law. In particular, no such person undertakes to take any action which may be required by any investor for the purposes of its compliance with any applicable requirement under either such Regulation. Furthermore, the arrangements described under “Credit Risk Retention” in the Preliminary Prospectus have not been structured with the objective of ensuring compliance by any person with any requirements of either such Regulation. See “Risk Factors—Other Risks Relating to the Certificates—EU Securitization Regulation and UK Securitization Regulation Due Diligence Requirements” in the Preliminary Prospectus.

|

| Cut-off Date: | The Cut-off Date with respect to each mortgage loan is the payment due date for the monthly debt service payment that is due in December 2021 (or, in the case of any mortgage loan that has its first payment due date in January 2022, the date that would have been its payment due date in December 2021 under the terms of that mortgage loan if a monthly debt service payment were scheduled to be due in that month). |

| Expected Closing Date: | On or about December 6, 2021. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

8

| Wells Fargo Commercial Mortgage Trust 2021-C61 | Issue Characteristics |

| Determination Dates: | The 11th day of each month (or if that day is not a business day, the next succeeding business day), commencing in January 2022. |

| Distribution Dates: | The 4th business day following the Determination Date in each month, commencing in January 2022. |

| Rated Final Distribution Date: | The Distribution Date in November 2054. |

| Interest Accrual Period: | With respect to any Distribution Date, the calendar month immediately preceding the month in which such Distribution Date occurs. |

| Day Count: | The Offered Certificates will accrue interest on a 30/360 basis. |

| Minimum Denominations: | $10,000 for each Class of Offered Certificates (other than the Class X-A and X-B Certificates) and $1,000,000 for the Class X-A and X-B Certificates. Investments may also be made in any whole dollar denomination in excess of the applicable minimum denomination. |

| Clean-up Call: | 1.0% |

| Delivery: | DTC, Euroclear and Clearstream Banking |

| ERISA/SMMEA Status: | Each Class of Offered Certificates is expected to be eligible for exemptive relief under ERISA. No Class of Offered Certificates will be SMMEA eligible. |

| Risk Factors: | THE CERTIFICATES INVOLVE CERTAIN RISKS AND MAY NOT BE SUITABLE FOR ALL INVESTORS. SEE THE “RISK FACTORS” SECTION OF THE PRELIMINARY PROSPECTUS. |

| Bond Analytics Information: | The Certificate Administrator will be authorized to make distribution date statements, CREFC® reports and certain supplemental reports (other than confidential information) available to certain financial modeling and data provision services, including Bloomberg, L.P., Trepp, LLC, Intex Solutions, Inc., Interactive Data Corp., Markit Group Limited, BlackRock Financial Management, Inc., CMBS.com, Inc., Moody’s Analytics, Inc., Morningstar Credit Information & Analytics, LLC, KBRA Analytics, LLC, MBS Data, LLC, Thomson Reuters Corporation and RealINSIGHT. |

| Tax Treatment | For U.S. federal income tax purposes, the issuing entity will consist of two or more REMICs arranged in a tiered structure and a trust (the “grantor trust”). The upper-most REMIC will issue REMIC regular interests some of which will be held by the grantor trust (such grantor trust-held REMIC regular interests, the “trust components”). The Offered Certificates (other than the Exchangeable Certificates) will represent REMIC regular interests (other than the trust components). The Exchangeable Certificates will represent beneficial ownership of one or more of the trust components held by the grantor trust. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

9

| Wells Fargo Commercial Mortgage Trust 2021-C61 | Characteristics of the Mortgage Pool |

V. Characteristics of the Mortgage Pool

A. Ten Largest Mortgage Loans(1)

| Mortgage Loan Seller | Mortgage Loan Name | City | State | Number of Mortgage Loans / Mortgaged Properties | Mortgage Loan Cut-off Date Balance ($) | % of Initial Pool Balance (%) | Property Type | Number of SF/ Units/Pad | Cut-off Unit/Pad | Cut-off Date LTV Ratio (%) | Balloon or ARD LTV Ratio (%) | U/W NCF DSCR (x) | U/W NOI Debt Yield (%) |

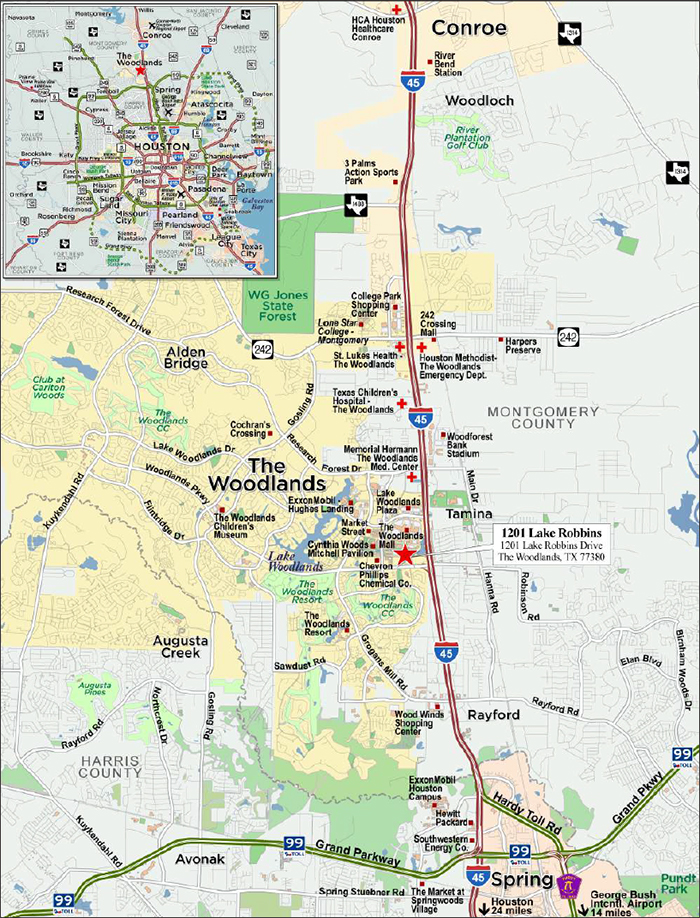

| WFB | 1201 Lake Robbins | The Woodlands | TX | 1 / 1 | $70,000,000 | 9.2% | Office | 807,586 | $310 | 55.3% | 55.3% | 2.26x | 9.2% |

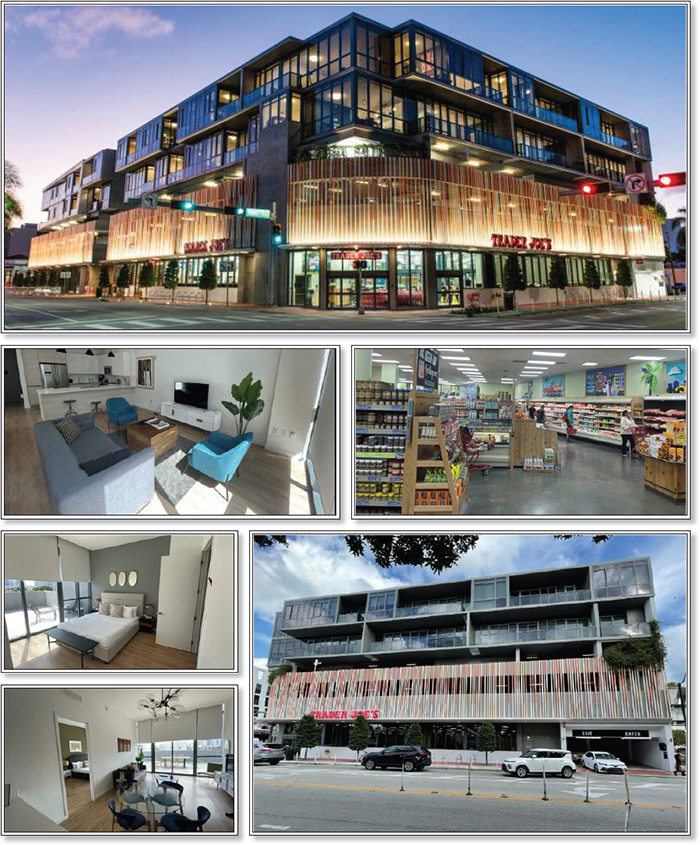

| LCF | 17 West Miami | Miami Beach | FL | 1 / 1 | 55,000,000 | 7.2 | Mixed Use | 63,146 | 871 | 65.9 | 65.9 | 1.90 | 7.5 |

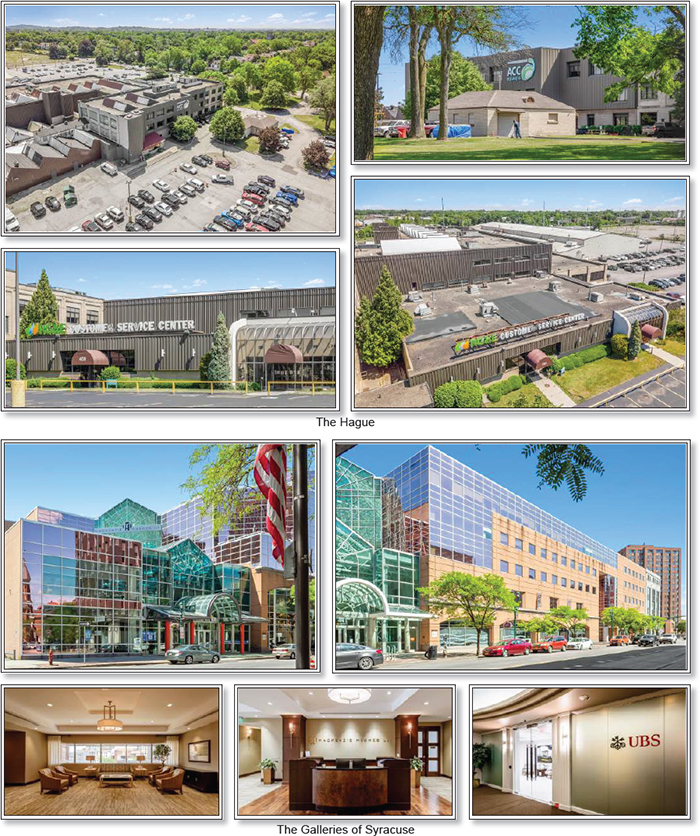

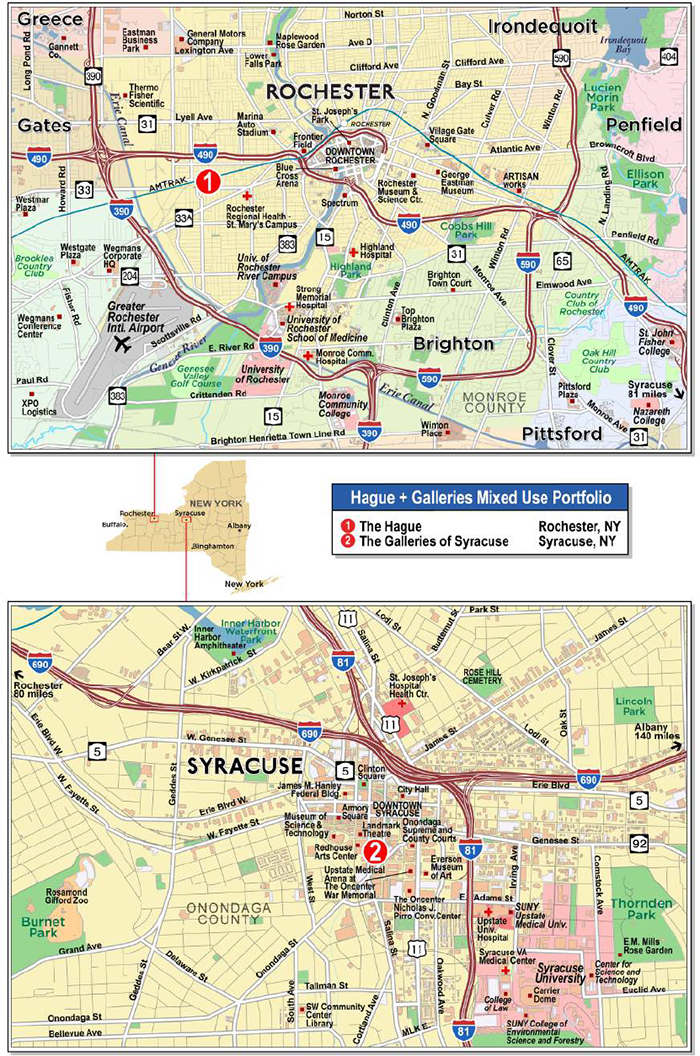

| LMF | Hague + Galleries Mixed Use Portfolio | Various | NY | 1 / 2 | 37,000,000 | 4.8 | Various | 485,248 | 76 | 58.7 | 58.7 | 1.89 | 11.3 |

| LMF | TLR Portfolio | Various | FL | 1 / 3 | 35,000,000 | 4.6 | Multifamily | 688 | 120,640 | 65.4 | 65.4 | 1.78 | 7.4 |

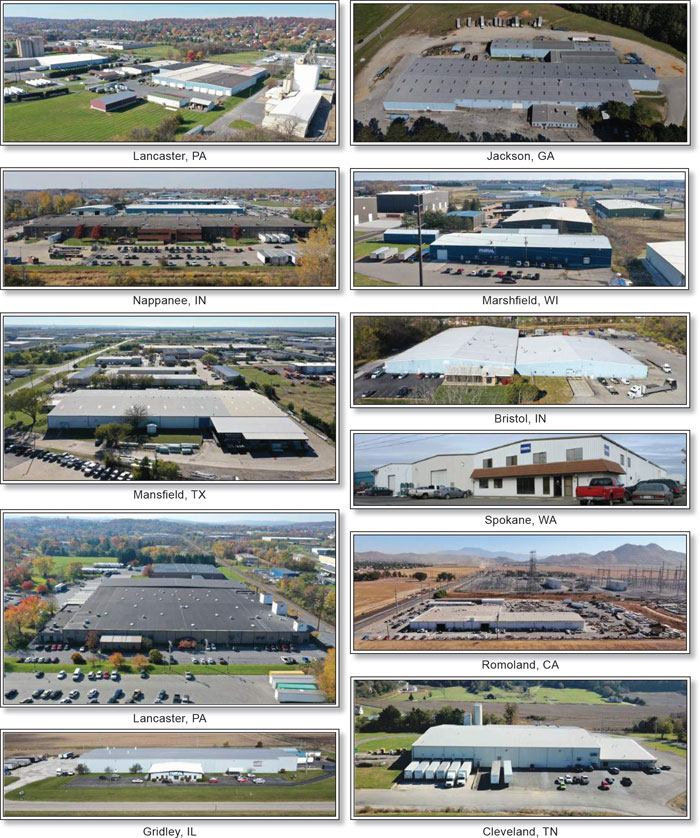

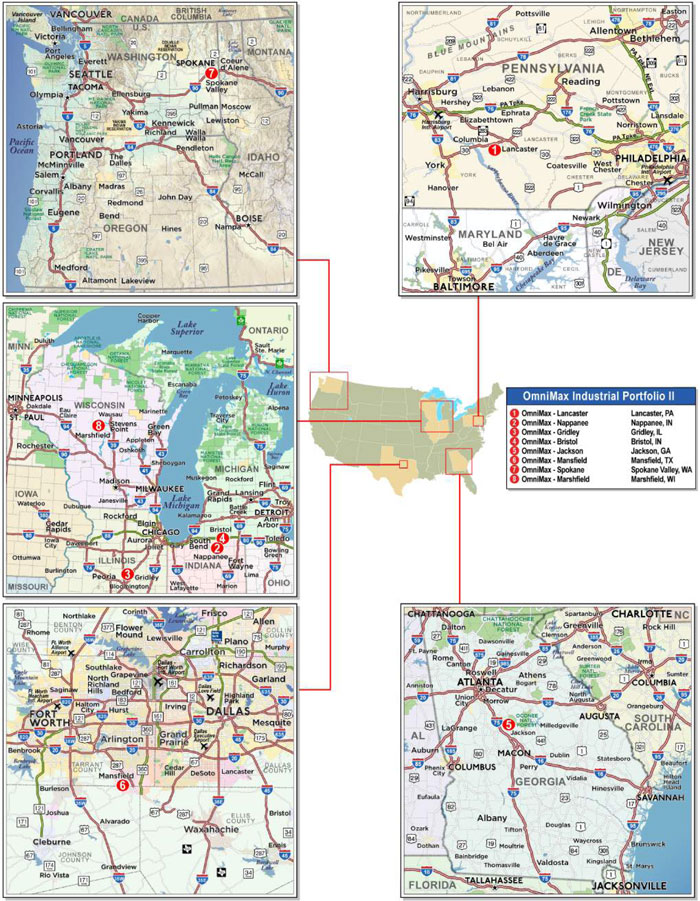

| Column | OmniMax Industrial Portfolio II | Various | Various | 1 / 8 | 33,313,851 | 4.4 | Industrial | 683,992 | 49 | 66.6 | 66.6 | 2.26 | 8.7 |

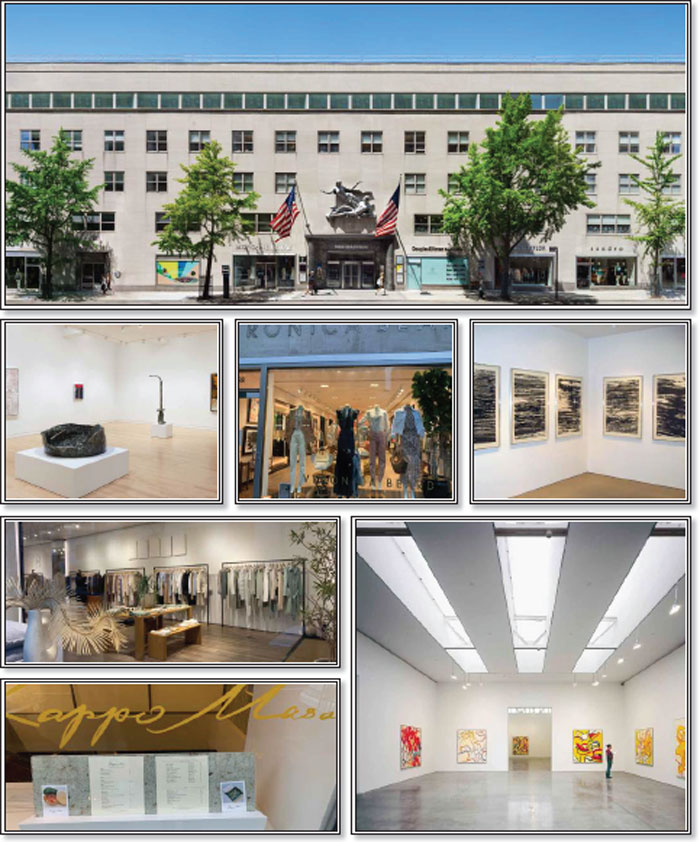

| Column | 980 Madison | New York | NY | 1 / 1 | 25,000,000 | 3.3 | Mixed Use | 134,843 | 716 | 27.6 | 27.6 | 4.08 | 15.2 |

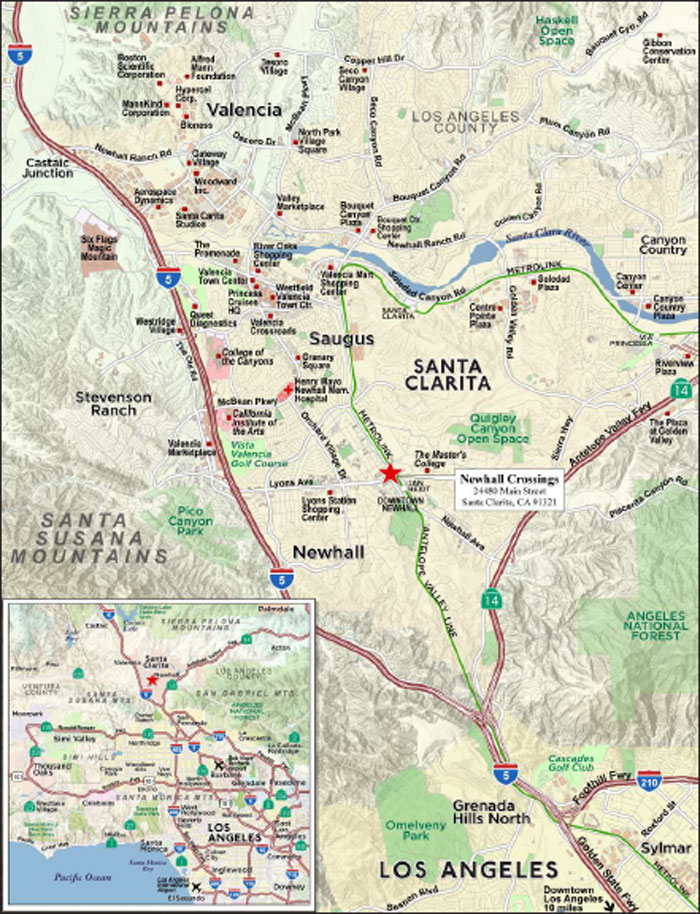

| LCF | Newhall Crossings | Santa Clarita | CA | 1 / 1 | 25,000,000 | 3.3 | Mixed Use | 77,227 | 324 | 61.7 | 61.7 | 1.90 | 7.5 |

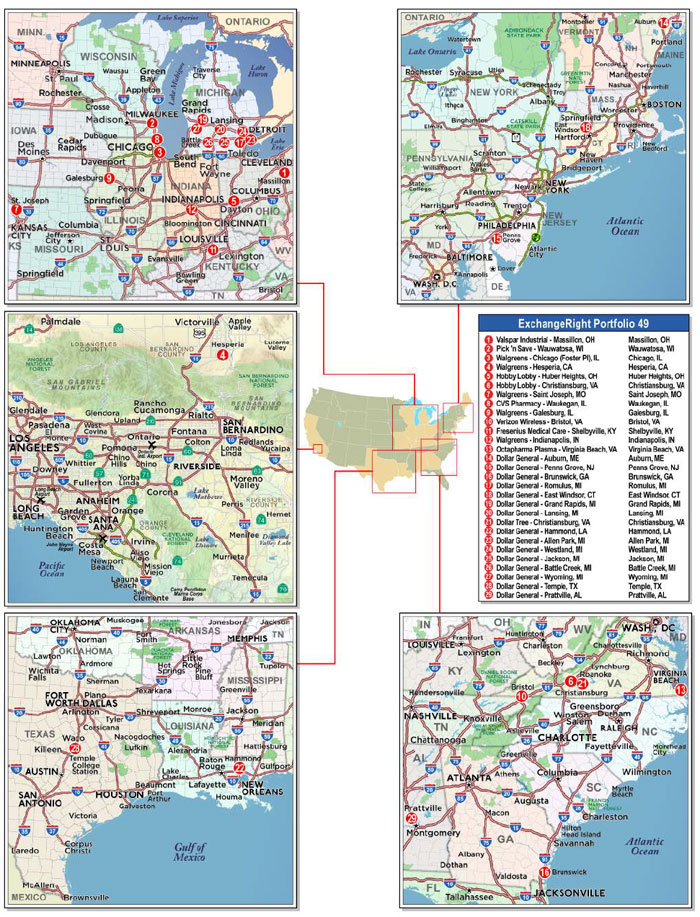

| WFB | ExchangeRight 49 | Various | Various | 1 / 29 | 23,800,000 | 3.1 | Various | 621,901 | 111 | 61.5 | 61.5 | 2.56 | 9.4 |

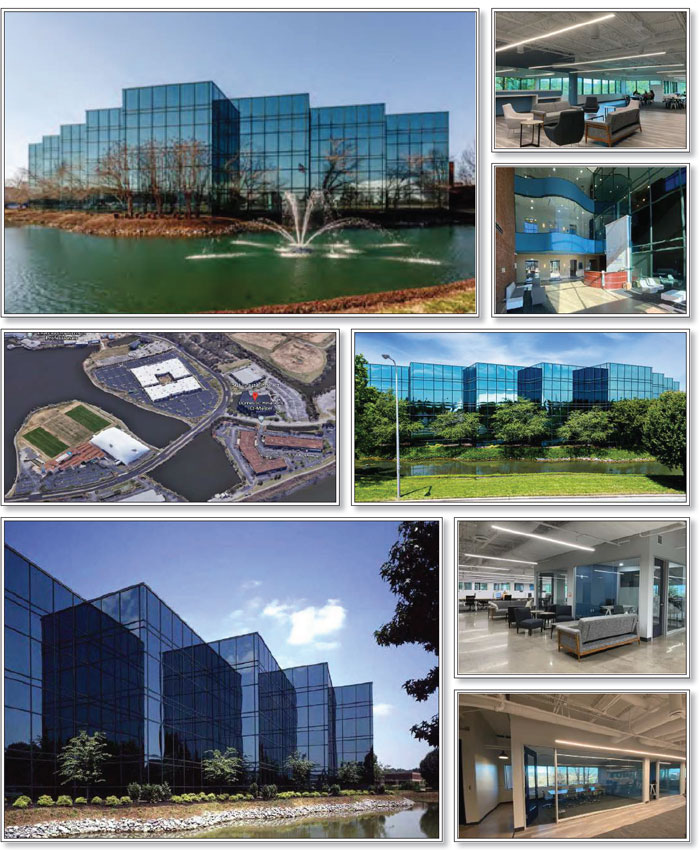

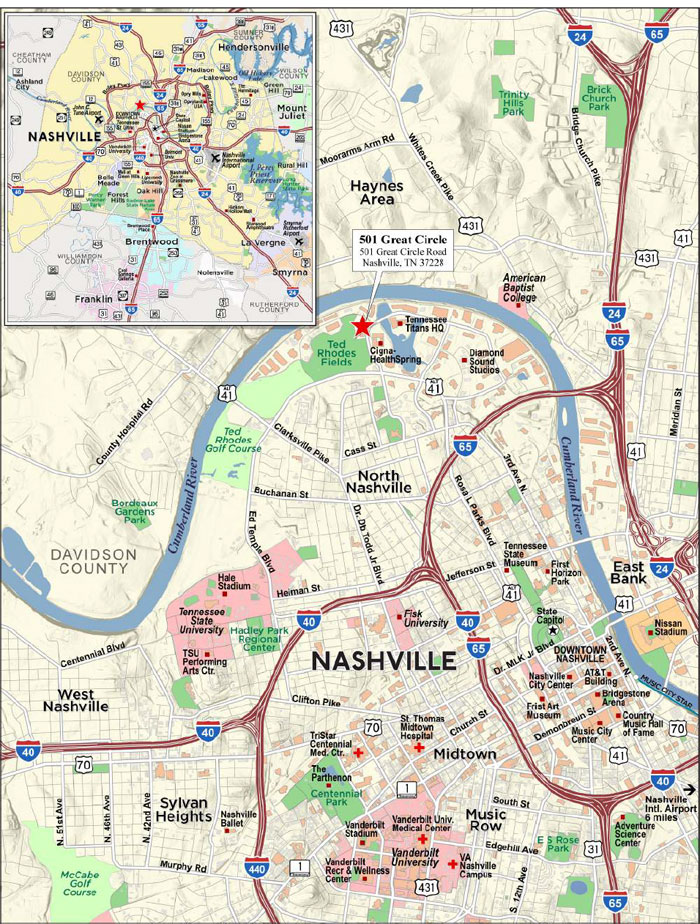

| Oceanview | 501 Great Circle | Nashville | TN | 1 / 1 | 23,365,435 | 3.1 | Office | 109,295 | 214 | 63.5 | 50.4 | 1.67 | 10.0 |

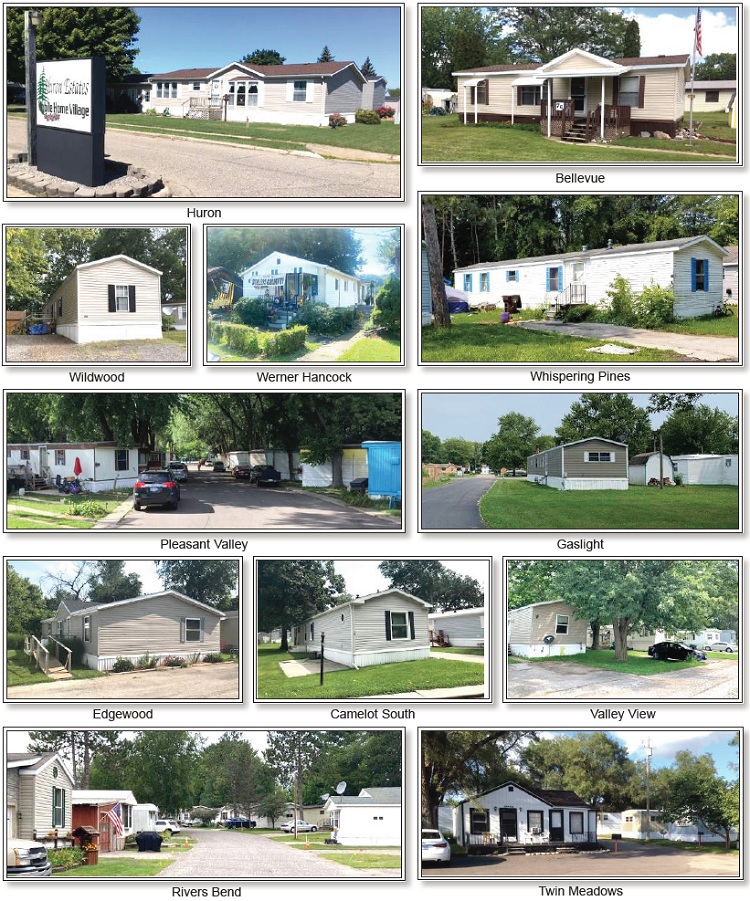

| LMF | SSA Midwest MHC Portfolio | Various | Various | 1 / 12 | 20,700,000 | 2.7 | Manufactured Housing | 971 | 21,318 | 72.2 | 62.5 | 1.57 | 9.3 |

| Top Three Total/Weighted Average | 3 / 4 | $162,000,000 | 21.2% | 59.7% | 59.7% | 2.05x | 9.1% | ||||||

| Top Five Total/Weighted Average | 5 / 15 | $230,313,851 | 30.1% | 61.5% | 61.5% | 2.04x | 8.8% | ||||||

| Top Ten Total/Weighted Average | 10 / 59 | $348,179,286 | 45.5% | 59.9% | 58.4% | 2.16x | 9.3% | ||||||

| Non-Top Ten Total/Weighted Average | 51 / 106 | $416,239,114 | 54.5% | 60.0% | 53.3% | 2.14x | 11.3% | ||||||

| (1) | With respect to any mortgage loan that is part of a whole loan, Cut-off Date Balance Per SF/Unit/Pad, loan-to-value ratio, debt service coverage ratio and debt yield calculations include the related pari passu companion loan(s) (unless otherwise stated). With respect to each mortgage loan, debt service coverage ratio, debt yield and loan-to-value ratio information do not take into account subordinate debt (whether or not secured by the related mortgaged property), if any, that currently exists or is allowed under the terms of such mortgage loan. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

10

| Wells Fargo Commercial Mortgage Trust 2021-C61 | Characteristics of the Mortgage Pool |

B. Summary of the Whole Loans

| No. | Loan Name | Mortgage Loan Seller in WFCM 2020-C61 | Trust Cut-off Date Balance | Aggregate Pari Passu Companion Loan Cut-off Date Balance(1) | Controlling Pooling/Trust & Servicing Agreement | Master Servicer | Special Servicer | Related Pari Passu Companion Loan(s) Securitizations | Related Pari Passu Companion Loan(s) Original Balance |

| 1 | 1201 Lake Robbins | WFB | $70,000,000 | $250,000,000 | BANK 2021-BNK37(2) | Wells Fargo Bank, N.A. | CWCapital Asset Management LLC | BANK 2021-BNK37 Future Securitization | $180,000,000 |

| 4 | TLR Portfolio | LMF | 35,000,000 | 83,000,000 | WFCM 2021-C61(3) | Wells Fargo Bank, N.A.(3) | CWCapital Asset Management LLC(3) | Future Securitization | 48,000,000 |

| 6 | 980 Madison | Column | 25,000,000 | 96,500,000 | CSMC 2021-980M(4) | KeyBank National Association | Argentic Services Company LP | CSMC 2021-980M | 71,500,000 |

| 8 | ExchangeRight 49 | WFB | 23,800,000 | 68,800,000 | BANK 2021-BNK37(2) | Wells Fargo Bank, N.A. | CWCapital Asset Management LLC | BANK 2021-BNK37 | 45,000,000 |

| 11 | Meadowood Mall | WFB | 19,000,000 | 80,000,000 | WFCM 2021-C61(3) | Wells Fargo Bank, N.A.(3) | CWCapital Asset Management LLC(3) | Future Securitization | 61,000,000 |

| 28 | Wyndham National Hotel Portfolio | UBS AG | 9,499,623 | 137,744,535 | UBS 2019-C18 | Wells Fargo Bank, N.A. | Wells Fargo Bank, N.A. | BBCMS 2021-C10 BBCMS 2021-C11 Future Securitization | 128,244,912 |

| (1) | The Aggregate Pari Passu Companion Loan Cut-off Date Balance excludes any related Subordinate Companion Loans. |

| (2) | The BANK 2021-BNK37 transaction is expected to close on or about November 22, 2021. |

| (3) | The related whole loan is expected to initially be serviced under the WFCM 2021-C61 securitization pooling and servicing agreement until the securitization of the related “lead” pari passu note, after which the related whole loan will be serviced under the pooling and servicing agreement governing such securitization of the related “lead” pari passu note. The master servicer and special servicer for such securitization will be identified in a notice, report or statement to holders of the WFCM 2021-C61 certificates after the closing of such securitization. Control rights with respect to the related whole loan will be exercised by the holder of the “lead” pari passu note or, in the case of the Meadowood Mall Whole Loan, the holder of the subordinate companion note. |

| (4) | Control rights are currently exercised by the holder of the related Subordinate Companion Loan until the occurrence and during the continuation of a control appraisal period for the related whole loan, as described under “Description of the Mortgage Pool—The Whole Loans—The Non-Serviced AB Whole Loan—The 980 Madison Whole Loan in the Preliminary Prospectus. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

11

| Wells Fargo Commercial Mortgage Trust 2021-C61 | Characteristics of the Mortgage Pool |

C. Mortgage Loans with Additional Secured and Mezzanine Financing

| Loan No. | Mortgage Loan Seller | Mortgage Loan Name | Mortgage Loan Cut-off Date Balance ($) | % of Initial Pool Balance (%) | Sub Debt Cut-off Date Balance ($) | Mezzanine Debt Cut-off Date Balance ($) | Total Debt Interest Rate (%)(1) | Mortgage Loan U/W NCF DSCR (x)(2) | Total Debt U/W NCF DSCR (x) | Mortgage Loan Cut-off Date U/W NOI Debt Yield (%)(2) | Total Debt Cut-off Date U/W NOI Debt Yield (%) | Mortgage Loan Cut-off Date LTV Ratio (%)(2) | Total Debt Cut-off Date LTV Ratio (%) |

| 6 | Column | 980 Madison | $25,000,000 | 3.3% | $101,100,000 | $40,000,000 | 4.6770% | 4.08x | 1.28x | 15.2% | 6.2% | 27.6% | 67.9% |

| 9 | Oceanview | 501 Great Circle | 23,365,435 | 3.1 | NAP | 2,800,000 | 4.5171 | 1.67 | 1.31 | 10.0 | 8.9 | 63.5 | 71.2 |

| 11 | WFB | Meadowood Mall | 19,000,000 | 2.5 | 28,000,000 | NAP | 5.6981 | 2.98 | 1.81 | 19.8 | 14.7 | 35.2 | 47.6 |

| Total/Weighted Average | $67,365,435 | 8.8% | $129,100,000 | $42,800,000 | 4.8601% | 2.93x | 1.44x | 14.7% | 9.5% | 42.2% | 63.3% | ||

| (1) | Total Debt Interest Rate for any specified mortgage loan reflects the weighted average of the interest rates on the respective components of the total debt. |

| (2) | With respect to any mortgage loan that is part of a whole loan, the loan-to-value ratio, debt service coverage ratio and debt yield calculations include the related pari passu companion loan(s) but excludes any related subordinate companion loan. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

12

| Wells Fargo Commercial Mortgage Trust 2021-C61 | Characteristics of the Mortgage Pool |

D. Previous Securitization History(1)

| Loan No. | Mortgage Loan Seller | Mortgage Loan or Mortgaged Property Name | City | State | Property Type | Mortgage Loan or Mortgaged Property Cut-off Date Balance ($) | % of Initial Pool Balance (%) | Previous Securitization |

| 4.01 | LMF | Bahia Apartments | Tampa | FL | Multifamily | $17,470,482 | 2.3% | FREMF 2019-KJ26 |

| 4.02 | LMF | Royal Breeze Apartments | Clearwater | FL | Multifamily | 10,466,265 | 1.4 | Fannie Mae AN2360 |

| 4.03 | LMF | Lenox Place Apartments | Tampa | FL | Multifamily | 7,063,253 | 0.9 | Fannie Mae AN2359 |

| 8.01 | WFB | Valspar Industrial - Massillon, OH | Massillon | OH | Industrial | 3,957,624 | 0.5 | WFRBS 2014-C21 |

| 8.07 | WFB | Walgreens - Saint Joseph, MO | Saint Joseph | MO | Retail | 1,095,794 | 0.1 | JPMBB 2015-C30 |

| 10.05 | LMF | Bellevue | Bellevue | MI | Manufactured Housing | 2,055,000 | 0.3 | WFCM 2018-C43 |

| 10.06 | LMF | Edgewood | Springfield | OH | Manufactured Housing | 1,185,000 | 0.2 | WFCM 2018-C43 |

| 10.10 | LMF | Camelot South | Delta | OH | Manufactured Housing | 900,000 | 0.1 | WFCM 2018-C43 |

| 10.12 | LMF | Valley View | Quincy | IL | Manufactured Housing | 844,000 | 0.1 | WFCM 2018-C43 |

| 11 | WFB | Meadowood Mall | Reno | NV | Retail | 19,000,000 | 2.5 | GSMS 2012-GC6 |

| 12 | WFB | Highland Village Plaza | Highland | CA | Retail | 18,115,000 | 2.4 | UBSBB 2013-C5 |

| 13 | BSPRT | Poplar Run | Alexandria | VA | Office | 17,955,000 | 2.3 | CMLT 2008-LS1 |

| 14 | BSPRT | Tech Ridge Office Park | Tulsa | OK | Office | 17,324,688 | 2.3 | JPMCC 2016-JP4 |

| 15 | WFB | StorQuest Thousand Oaks | Thousand Oaks | CA | Self Storage | 14,000,000 | 1.8 | COMM 2015-DC1 |

| 16.01 | Column | Cardinal Creek | Columbus | OH | Multifamily | 5,771,155 | 0.8 | FRESB 2016-SB5 |

| 16.02 | Column | Courtship Village | Lancaster | OH | Multifamily | 4,642,884 | 0.6 | FRESB 2017-SB30 |

| 16.03 | Column | Kingswood Court | Newark | OH | Multifamily | 3,564,537 | 0.5 | FRESB 2018-SB49 |

| 20 | BSPRT | Village East Shopping Center | Salem | OR | Retail | 13,000,000 | 1.7 | BSCMS 2007-PW16 |

| 27.01 | LMF | Olive Properties | Las Vegas | NV | Multifamily | 3,800,000 | 0.5 | Fannie Mae AN5011 |

| 27.02 | LMF | Fremont Gardens | Las Vegas | NV | Multifamily | 3,100,000 | 0.4 | Fannie Mae AN5010 |

| 27.03 | LMF | Casa Bonita Apartments | Las Vegas | NV | Multifamily | 3,100,000 | 0.4 | FRESB 2019-SB68 |

| 44.01 | UBS AG | Walgreens - Greenville | Greenville | MI | Retail | 3,460,000 | 0.5 | WFCM 2014-LC16 |

| 52 | WFB | Walgreens - Socorro | Socorro | TX | Retail | 3,700,000 | 0.5 | MSBAM 2012-C5 |

| Total | $175,570,682 | 23.0% |

| (1) | The table above represents the most recent securitization with respect to the mortgaged property securing the related mortgage loan, based on information provided by the related borrower or obtained through searches of a third-party database. While loans secured by the above mortgaged properties may have been securitized multiple times in prior transactions, mortgage loans in this securitization are only listed in the above chart if the mortgage loan paid off a loan in another securitization. The information has not otherwise been confirmed by the mortgage loan sellers. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

13

| Wells Fargo Commercial Mortgage Trust 2021-C61 | Characteristics of the Mortgage Pool |

E. Mortgage Loans with Scheduled Balloon Payments and Related Classes

| Class A-2(1) | ||||||||||||||||

| Loan No. | Mortgage Loan Seller | Mortgage Loan Name | State | Property Type | Mortgage Loan Cut-off Date Balance ($) | % of Initial Pool Balance (%) | Mortgage Loan Balance at Maturity or ARD($) | % of Class A-2 Certificate Principal Balance (%)(2) | SF | Loan per SF ($) | U/W NCF DSCR (x) | U/W NOI Debt Yield (%) | Cut-off Date LTV Ratio (%) | Balloon or ARD LTV Ratio (%) | Rem. IO Period (mos.) | Rem. Term to Maturity or ARD (mos.) |

| 5 | Column | OmniMax Industrial Portfolio II | Various | Industrial | $33,313,851 | 4.4% | $33,313,851 | 30.8% | 683,992 | $49 | 2.26x | 8.7% | 66.6% | 66.6% | 53 | 53 |

| 6 | Column | 980 Madison | NY | Mixed Use | 25,000,000 | 3.3 | 25,000,000 | 23.1 | 134,843 | 716 | 4.08 | 15.2 | 27.6 | 27.6 | 55 | 55 |

| 8 | WFB | ExchangeRight 49 | Various | Various | 23,800,000 | 3.1 | 23,800,000 | 22.0 | 621,901 | 111 | 2.56 | 9.4 | 61.5 | 61.5 | 57 | 57 |

| 11 | WFB | Meadowood Mall | NV | Retail | 19,000,000 | 2.5 | 16,630,360 | 15.4 | 456,841 | 175 | 2.98 | 19.8 | 35.2 | 30.8 | 0 | 60 |

| 43 | LMF | South Holland Industrial | IL | Industrial | 5,500,000 | 0.7 | 5,500,000 | 5.1 | 202,902 | 27 | 2.15 | 10.2 | 59.8 | 59.8 | 58 | 58 |

| Total/Weighted Average | $106,613,851 | 13.9% | $104,244,211 | 96.4% | 2.88x | 12.4% | 50.4% | 49.6% | 45 | 56 | ||||||

| (1) | The table above presents the mortgage loan(s) whose balloon payments would be applied to pay down the principal balance of the Class A-2 Certificates, assuming a 0% CPR and applying the “Structuring Assumptions” described in the Preliminary Prospectus, including the assumptions that (i) none of the mortgage loans in the pool experience prepayments prior to maturity, defaults or losses; (ii) there are no extensions of maturity dates of any mortgage loans in the pool; and (iii) each mortgage loan in the pool is paid in full on its stated maturity date. Each Class of Certificates evidences undivided ownership interests in the entire pool of mortgage loans. Debt service coverage ratio, debt yield and loan-to-value ratio information do not take into account subordinate debt (whether or not secured by the related mortgaged property), if any, that currently exists or is allowed under the terms of any mortgage loan. See Annex A-1 to the Preliminary Prospectus. |

| (2) | Reflects the percentage equal to the Balloon Balance divided by the initial Class A-2 Certificate Balance. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

14

| Wells Fargo Commercial Mortgage Trust 2021-C61 | Characteristics of the Mortgage Pool |

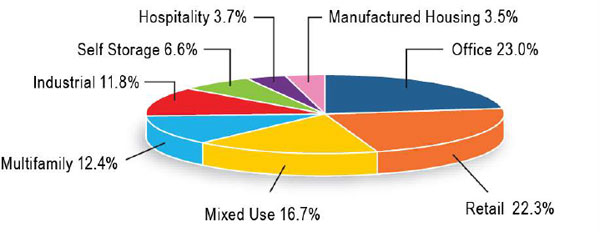

F. Property Type Distribution(1)

| Property Type | Number of Mortgaged Properties | Aggregate Cut-off Date Balance ($) | % of Initial Pool Balance (%) | Weighted Average Cut-off Date LTV Ratio (%) | Weighted Average Balloon LTV Ratio (%) | Weighted Average U/W NCF DSCR (x) | Weighted Average U/W NOI Debt Yield (%) | Weighted Average U/W NCF Debt Yield (%) | Weighted Average Mortgage Rate (%) |

| Office | 13 | $175,806,556 | 23.0% | 59.9% | 54.7% | 2.04x | 10.3% | 9.4% | 3.9849% |

| Suburban | 5 | 133,147,416 | 17.4 | 59.7 | 53.6 | 2.04 | 10.1 | 9.3 | 3.8055 |

| CBD | 1 | 18,130,000 | 2.4 | 58.7 | 58.7 | 1.89 | 11.3 | 9.7 | 5.0500 |

| Medical | 6 | 17,381,432 | 2.3 | 64.7 | 59.4 | 1.96 | 10.1 | 9.6 | 4.0920 |

| Flex | 1 | 7,147,708 | 0.9 | 53.7 | 53.7 | 2.68 | 13.1 | 11.9 | 4.3650 |

| Retail | 47 | 170,498,950 | 22.3 | 59.4 | 52.2 | 2.09 | 11.7 | 11.1 | 3.8416 |

| Anchored | 8 | 68,644,917 | 9.0 | 65.9 | 55.5 | 1.85 | 11.5 | 10.7 | 3.9442 |

| Single Tenant | 33 | 49,054,961 | 6.4 | 60.7 | 58.1 | 2.11 | 9.5 | 9.3 | 3.8079 |

| Unanchored | 4 | 30,488,995 | 4.0 | 57.3 | 48.7 | 2.02 | 10.6 | 10.1 | 3.6112 |

| Regional Mall | 1 | 19,000,000 | 2.5 | 35.2 | 30.8 | 2.98 | 19.8 | 18.7 | 3.9300 |

| Shadow Anchored | 1 | 3,310,077 | 0.4 | 62.5 | 49.5 | 2.00 | 12.5 | 11.2 | 3.8300 |

| Mixed Use | 5 | 127,840,000 | 16.7 | 56.5 | 56.5 | 2.31 | 9.6 | 9.2 | 3.9764 |

| Multifamily/Retail | 3 | 83,970,000 | 11.0 | 64.7 | 64.7 | 1.88 | 7.5 | 7.4 | 3.8474 |

| Office/Retail | 1 | 25,000,000 | 3.3 | 27.6 | 27.6 | 4.08 | 15.2 | 14.9 | 3.5995 |

| Industrial/Office | 1 | 18,870,000 | 2.5 | 58.7 | 58.7 | 1.89 | 11.3 | 9.7 | 5.0500 |

| Multifamily | 14 | 94,603,577 | 12.4 | 61.9 | 59.3 | 2.07 | 9.0 | 8.7 | 3.7618 |

| Garden | 12 | 78,453,577 | 10.3 | 60.8 | 58.6 | 2.20 | 9.2 | 8.8 | 3.7233 |

| Townhome | 1 | 12,350,000 | 1.6 | 67.1 | 60.9 | 1.42 | 8.1 | 8.0 | 3.8500 |

| Low Rise | 1 | 3,800,000 | 0.5 | 66.7 | 66.7 | 1.62 | 7.1 | 7.0 | 4.2700 |

| Industrial | 16 | 89,830,234 | 11.8 | 60.3 | 58.0 | 2.23 | 9.9 | 9.4 | 3.8496 |

| Flex | 5 | 42,443,759 | 5.6 | 55.1 | 50.3 | 2.17 | 10.8 | 10.1 | 3.9252 |

| Warehouse | 6 | 28,962,802 | 3.8 | 65.3 | 65.3 | 2.24 | 9.0 | 8.7 | 3.8334 |

| Manufacturing | 4 | 13,808,673 | 1.8 | 65.1 | 65.1 | 2.35 | 8.9 | 8.7 | 3.6544 |

| Warehouse Distribution | 1 | 4,615,000 | 0.6 | 62.4 | 62.4 | 2.46 | 10.5 | 9.6 | 3.8400 |

| Self Storage | 8 | 50,480,000 | 6.6 | 60.8 | 59.6 | 2.69 | 9.8 | 9.7 | 3.5306 |

| Self Storage | 8 | 50,480,000 | 6.6 | 60.8 | 59.6 | 2.69 | 9.8 | 9.7 | 3.5306 |

| Hospitality | 46 | 28,475,790 | 3.7 | 64.4 | 51.0 | 2.00 | 14.8 | 13.3 | 4.8305 |

| Limited Service | 46 | 28,475,790 | 3.7 | 64.4 | 51.0 | 2.00 | 14.8 | 13.3 | 4.8305 |

| Manufactured Housing | 16 | 26,883,294 | 3.5 | 66.1 | 56.5 | 1.68 | 10.0 | 9.7 | 3.9960 |

| Manufactured Housing | 16 | 26,883,294 | 3.5 | 66.1 | 56.5 | 1.68 | 10.0 | 9.7 | 3.9960 |

| Total | 165 | 764,418,400 | 100.0% | 59.9% | 55.7% | 2.15x | 10.4% | 9.8% | 3.9099% |

| (1) | Because this table presents information relating to the mortgaged properties and not the mortgage loans, (a) the information for mortgage loans secured by more than one mortgaged property (other than through cross-collateralization with other mortgage loans) is based on allocated loan amounts (allocating the principal balance of the mortgage loan to each of those properties according to the relative appraised values of the mortgaged properties or the allocated loan amounts or property-specific release prices set forth in the related mortgage loan documents or such other allocation as the related mortgage loan seller deemed appropriate) and (b) the information for each mortgaged property that relates to a mortgage loan that is cross-collateralized or cross-defaulted with other mortgage loans is based upon the principal balance of that mortgage loan, except that the applicable loan-to-value ratio, debt service coverage ratio and debt yield for each such mortgage loan is based upon the ratio or yield (as applicable) for the aggregate indebtedness evidenced by all loans in the group (without regard to any limitation on the amount of indebtedness secured by any mortgaged property in such cross-collateralized group). On an individual basis, without regard to the cross-collateralization feature, any mortgage loan that is part of a cross-collateralized group of mortgage loans may have a higher loan-to-value ratio, lower debt service coverage ratio and/or lower debt yield than is presented herein. With respect to any mortgage loan that is part of a whole loan, the loan-to-value ratio, debt service coverage ratio and debt yield calculations include the related pari passu companion loan(s) but exclude any related subordinate secured loan(s) (unless otherwise stated). With respect to each mortgage loan, debt service coverage ratio, debt yield and loan-to-value ratio information do not take into account any subordinate debt (whether or not secured by the related mortgaged property) that currently exists or is allowed under the terms of such mortgage loan. See Annex A-1 to the Preliminary Prospectus. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

15

| Wells Fargo Commercial Mortgage Trust 2021-C61 | Characteristics of the Mortgage Pool |

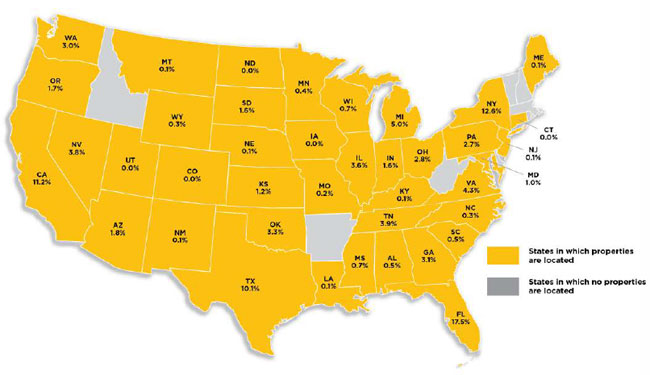

G. Geographic Distribution(1)(2)

| Location | Number of Mortgaged Properties | Aggregate Cut-off Date Balance ($) | % of Initial Pool Balance (%) | Weighted Average Cut-off Date LTV Ratio (%) | Weighted Average Balloon or ARD LTV Ratio (%) | Weighted Average U/W NCF DSCR (x) | Weighted Average U/W NOI Debt Yield (%) | Weighted Average U/W NCF Debt Yield (%) | Weighted Average Mortgage Rate (%) |

| Florida | 11 | $133,892,467 | 17.5% | 63.9% | 62.5% | 2.09x | 9.2% | 8.8% | 3.8868% |

| New York | 8 | 95,953,743 | 12.6 | 52.1 | 50.6 | 2.28 | 11.1 | 10.3 | 4.3777 |

| California | 10 | 85,836,339 | 11.2 | 59.2 | 55.6 | 2.21 | 9.4 | 9.1 | 3.6551 |

| Texas | 7 | 77,334,331 | 10.1 | 56.2 | 56.1 | 2.25 | 9.2 | 8.8 | 3.8395 |

| Michigan | 21 | 37,863,310 | 5.0 | 63.8 | 58.3 | 1.98 | 9.7 | 9.4 | 3.7800 |

| Other(3) | 108 | 333,538,212 | 43.6 | 61.3 | 54.0 | 2.12 | 11.3 | 10.6 | 3.8813 |

| Total/Weighted Average | 165 | $764,418,400 | 100.0% | 59.9% | 55.7% | 2.15x | 10.4% | 9.8% | 3.9099% |

| (1) | The mortgaged properties are located in 40 states. |

| (2) | Because this table presents information relating to the mortgaged properties and not the mortgage loans, (a) the information for mortgage loans secured by more than one mortgaged property (other than through cross-collateralization with other mortgage loans) is based on allocated amounts (allocating the principal balance of the mortgage loan to each of those properties according to the relative appraised values of the mortgaged properties or the allocated loan amounts or property-specific release prices set forth in the related mortgage loan documents or such other allocation as the related mortgage loan seller deemed appropriate) and (b) the information for each mortgaged property that relates to a mortgage loan that is cross-collateralized or cross-defaulted with other mortgage loans is based upon the principal balance of that mortgage loan, except that the applicable loan-to-value ratio, debt service coverage ratio and debt yield for each such mortgage loan is based upon the ratio or yield (as applicable) for the aggregate indebtedness evidenced by all loans in the group (without regard to any limitation on the amount of indebtedness secured by any mortgaged property in such cross-collateralized group). On an individual basis, without regard to the cross-collateralization feature, any mortgage loan that is part of a cross-collateralized group of mortgage loans may have a higher loan-to-value ratio, lower debt service coverage ratio and/or lower debt yield than is presented herein. With respect to any mortgage loan that is part of a whole loan, the loan-to-value ratio, debt service coverage ratio and debt yield calculations include the related pari passu companion loan(s) but exclude any related subordinate secured loan(s) (unless otherwise stated). With respect to each mortgage loan, debt service coverage ratio, debt yield and loan-to-value ratio information do not take into account any subordinate debt (whether or not secured by the related mortgaged property) that currently exists or is allowed under the terms of such mortgage loan. See Annex A-1 to the Preliminary Prospectus. |

| (3) | Includes 35 other states. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

16

| Wells Fargo Commercial Mortgage Trust 2021-C61 | Characteristics of the Mortgage Pool |

H. Characteristics of the Mortgage Pool(1)

| CUT-OFF DATE BALANCE | |||

| Range of Cut-off Date Balances ($) | Number of Mortgage Loans | Aggregate Cut-off Date Balance | Percent by Aggregate Cut-off Date Pool Balance (%) |

| 1,910,000 - 2,000,000 | 1 | $1,910,000 | 0.2% |

| 2,000,001 - 3,000,000 | 2 | 4,975,000 | 0.7 |

| 3,000,001 - 4,000,000 | 10 | 35,214,495 | 4.6 |

| 4,000,001 - 5,000,000 | 3 | 13,651,054 | 1.8 |

| 5,000,001 - 6,000,000 | 4 | 21,150,000 | 2.8 |

| 6,000,001 - 7,000,000 | 4 | 25,783,294 | 3.4 |

| 7,000,001 - 8,000,000 | 4 | 30,435,492 | 4.0 |

| 8,000,001 - 9,000,000 | 5 | 41,661,462 | 5.5 |

| 9,000,001 - 10,000,000 | 2 | 19,499,623 | 2.6 |

| 10,000,001 - 15,000,000 | 12 | 149,564,007 | 19.6 |

| 15,000,001 - 20,000,000 | 4 | 72,394,688 | 9.5 |

| 20,000,001 - 30,000,000 | 5 | 117,865,435 | 15.4 |

| 30,000,001 - 50,000,000 | 3 | 105,313,851 | 13.8 |

| 50,000,001 - 70,000,000 | 2 | 125,000,000 | 16.4 |

| Total: | 61 | $764,418,400 | 100.0% |

| Average | $12,531,449 |

| |

| UNDERWRITTEN NOI DEBT SERVICE COVERAGE RATIO | |||

| Range of U/W NOI DSCRs (x) | Number of Mortgage Loans | Aggregate Cut-off Date Balance | Percent by Aggregate Cut-off Date Pool Balance (%) |

| 1.31 - 1.50 | 4 | $40,500,000 | 5.3% |

| 1.51 - 2.00 | 23 | 287,652,263 | 37.6 |

| 2.01 - 2.50 | 19 | 273,176,376 | 35.7 |

| 2.51 - 3.00 | 8 | 78,564,761 | 10.3 |

| 3.01 - 3.50 | 3 | 34,525,000 | 4.5 |

| 3.51 - 4.00 | 1 | 13,000,000 | 1.7 |

| 4.01 - 4.50 | 2 | 29,000,000 | 3.8 |

| 4.51 - 5.07 | 1 | 8,000,000 | 1.0 |

| Total: | 61 | $764,418,400 | 100.0% |

| Weighted Average | 2.27x | ||

| UNDERWRITTEN NCF DEBT SERVICE COVERAGE RATIO | |||

Range of U/W NCF DSCRs (x) | Number of Mortgage Loans | Aggregate Cut-off Date Balance | Percent by Aggregate Cut-off Date Pool Balance (%) |

| 1.26 - 1.50 | 4 | $40,500,000 | 5.3% |

| 1.51 - 2.00 | 30 | $386,072,918 | 50.5 |

| 2.01 - 2.50 | 13 | $179,370,721 | 23.5 |