UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number 811-05823

DOMINI SOCIAL INVESTMENT TRUST

(Exact Name of Registrant as Specified in Charter)

532 Broadway, 9th Floor, New York, New York 10012

(Address of Principal Executive Offices)

Amy Domini Thornton

Domini Social Investments LLC

532 Broadway, 9th Floor

New York, New York 10012

(Name and Address of Agent for Service)

Registrant’s Telephone Number, including Area Code: 212-217-1100

Date of Fiscal Year End: July 31

Date of Reporting Period: July 31, 2014

| Item 1. | Reports to Stockholders. |

A copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 follows.

| ANNUAL REPORT 2014 | | JULY 31, 2014 | |

DOMINI SOCIAL EQUITY FUND®

INVESTOR SHARES, CLASS A SHARES, INSTITUTIONAL SHARES & CLASS R SHARES

DOMINI INTERNATIONAL SOCIAL EQUITY FUNDSM

INVESTOR SHARES, CLASS A SHARES & INSTITUTIONAL SHARES

DOMINI SOCIAL BOND FUND®

INVESTOR SHARES & INSTITUTIONAL SHARES

| KEEP IN TOUCH WITH DOMINI |

A report like this comes twice a year, but your dollars work for change all year long. Stay connected with us on Facebook and Twitter:

|

| SIGN UP FOR E-DELIVERY |

If you invest directly with Domini, you can also avoid an annual fee of $15 by signing up for paperless E-Delivery of your statements, reports and tax forms — just log into your account, go to “Account Options,” and select “E-Delivery Option.”

If you invest through a financial advisor, brokerage firm, or employer-sponsored retirement plan, why not ask your advisor or plan sponsor how to receive your documents electronically? It can reduce your carbon footprint, save trees, and unclutter your life, all with just a few strokes of your keyboard! |

THE WAY YOU INVEST MATTERS®

Dear Fellow Shareholders:

The year ended July 31, 2014 was a particularly good one for the Domini Social Equity Fund, which outperformed the S&P 500 by 3 percent. Our international fund also posted strong returns, although not as strong as its benchmark index, the MSCI EAFE.

Responsible investing means committing oneself to continuously reviewing the standards used to make our investment decisions, and staying current as industries change. One area that has seen tremendous change is food production. There are many factors driving these changes, and our responses to them: the obesity epidemic, indications that food additives or storage containers may affect human health, changes in the chemistry of soil, rivers and lakes as pesticides flow downstream and the alarming dangers to farm workers exposed to chemicals. These are but a few of the reasons that we now must ask harder questions of the companies we invest in, and expect better answers.

The transformation of our food production systems began decades ago. Over fifty years ago, I can recall the first artificial product, served in a plastic container, that my mother put on the table. I’ll never forget my father’s reaction. He grabbed the container, asking, “What’s this?” My mother laughed and told him to settle down, but he persisted, staring at the ingredients before declaring, “This is soap! You are feeding our children soap!” Now my father was not a radical man, but he was an Italian immigrant and brought with him a love of all things fresh. He won the argument that day. At the time, none of us considered that there might be far larger implications to consider and that massive transformations were under way. In fact, the very definition of food was being expanded to include untested ingredients, including those that might be harmful to humans.

Today, responsible investors see many opportunities in the current counter-revolution in food production. The growth of demand for organics alone has spurred a range of positive impacts. The local family farm can convert a small operation into one that specializes in a product that can command a price that makes farming an economically viable option. The niche restaurant can pull in a wider clientele that is seeking local, organic products. The large purchasers begin to feel the demand but cannot source only locally, so they contract for thousands of acres of organic produce, often making it necessary for a large supplier to become organic. This in turn improves the health and safety of the workforce on the farm and the water system in the area.

2

THE WAY YOU INVEST MATTERS®

We see in the field of sustainable agriculture many of the hard choices that exist in other fields. People want healthier, higher quality products, which, in many cases, drives up prices. Still, as we witnessed in the evolution of cellular telephones, sometimes the wealthy create sufficient demand to spur the kind of healthy competition that drives prices down while quality continues to improve. Certainly, there are trade-offs as small-scale organic farming is brought to the mainstream, but the entry of so many conventional mega-stores such as Walmart and Target into the organic food sales area surely demonstrates that dramatic changes are once again underway.

The issues are complicated. As more of the human population moves off of subsistence living to a market-based economy, the demand for proteins, frequently in the form of meat, rises. Meat production creates a whole host of issues ranging from animal welfare to climate change considerations. Even when the demand is for a simple grain, it can cause discouraging results. We saw this in the growth of popularity of quinoa. As world demand grew, this staple for the Bolivian poor became too expensive for many. There was no cheaper grain to turn to and the poor suffered great hardship, even starvation.

At Domini Social Investments, the research we conduct to understand these changes to our food systems is core to the investment process. Whether it is expressed in the avoidance of many manufacturers of agricultural chemicals, in the search for systems that provide safer food for all, or in the proxy votes we cast or the hard questions we ask of corporate managers, we view our social and environmental standards as key to the process of helping both the public and corporations understand what is at stake.

Agriculture is a complicated business, but the results are simple. I began with a story of my father, and I’ll end with one. He was growing eggplants. One day he turned to me and asked if I had tried vinegar as an insect deterrent. I said I had tried it mixed with soap and water and that it seemed to work pretty well. I asked, “What got you so interested in organic farming?” He looked at me with disappointment. “This is food,” he said. “People eat it.”

Very truly yours,

Amy Domini

amy@domini.com

3

THE WAY YOU INVEST MATTERS®

Expanding Our Influence

Every year, we see numerous opportunities to engage the broader community of institutional investors on questions of corporate and investor responsibility. This past year, we participated in events convened by Ernst & Young to discuss recent trends in corporate governance and the SEC’s review of financial reporting requirements. At each, we shared the table with corporate executives and some of the world’s largest institutional investors. We were also pleased to join a panel at this year’s Millstein Governance Forum at Columbia Law School to speak about corporate social responsibility.

We are particularly interested in influencing initiatives to improve corporate reporting. We participated in roundtable discussions about Integrated Reporting, an emerging approach to corporate reporting that integrates financial and sustainability considerations, and met with Mary Jo White, the Chair of the Securities and Exchange Commission, to advocate for mandatory corporate political contributions reporting. Our General Counsel continues to serve as a member of the SEC’s Investor Advisory Committee, and is a member of the Human Rights and Reporting Assurance Framework’s Eminent Persons Group, helping to guide the development of a reporting format to communicate corporate compliance with the UN Guiding Principles on Business and Human Rights. In September, we met with UN Ambassadors representing Hungary, New Zealand, Denmark and Canada to encourage the inclusion of corporate sustainability reporting in the UN’s Sustainable Development Goals.

Steve Lydenberg’s Dilemmas in Responsible Investment Published in China

“Ultimately, responsible investment implies a redefinition of what is called ‘success’ in investment, from a one-dimensional, purely financial approach to a multi-dimensional approach…. In other words, responsible investment implies a paradigm change.”

- Steven Lydenberg and Céline Louche, Dilemmas in Responsible Investment (2011)

Steve Lydenberg, a founder of the Domini Social Equity Fund currently in charge of Domini’s strategic vision, spent a week in China lecturing and celebrating the translation of his book, Dilemmas in Responsible Investment (coauthored with Céline Louche), into Chinese. Steve is a founder of the Initiative for Responsible Investment at the Harvard Kennedy School, where he is an adjunct lecturer in public policy. A student of Steve’s corporate social responsibility course facilitated his invitation to Nankai University in Tiajing, where he participated in several roundtable discussions with faculty, students and the China Social Investment Forum. He then delivered a formal presentation on the book and socially responsible investing at the School of Economics.

4

THE WAY YOU INVEST MATTERS®

Sustainability is a journey, and no company is perfect. We are therefore willing to work with those companies that face significant challenges but demonstrate a commitment to improve. Here are a few highlights of our corporate engagement work over the past twelve months.

Following a Domini-authored letter on behalf of institutional investors managing more than $490 billion, and further conversations with us, Amazon.com agreed to remove several categories of semi-automatic weapons accessories from its website and to amend its prohibited weapons policy.

For more than ten years, we have asked companies to disclose their political contributions and lobbying positions. We withdrew our shareholder proposal to JetBlue Airways when the company agreed to begin publishing its political contributions, including contributions to trade associations. In 2008, we helped convince the company to begin sustainability reporting.

When corporations don’t pay their fair share of taxes, somebody else must pick up the tab. Countries around the world are losing billions in tax revenues, all in the name of shareholder value. Google is one of several companies at the center of a global debate about aggressive corporate strategies to avoid paying taxes, generally through the use of offshore tax havens. Our first of its kind shareholder proposal, asking Google to adopt a set of ethical principles to guide its tax strategies, helped to raise awareness of this critical issue and opened dialogue with the company. We also raised these issues with Microsoft, Merck, Coca-Cola and Apple.

Other highlights included meetings with the CEO and senior management of PNC Financial Services* regarding its investments in the Pennsylvania coal industry and its impact on climate change, and a meeting with The Walt Disney Company’s Chief Financial Officer regarding a range of sustainability issues. Domini has been in dialogue with Disney for more than 15 years, and played a role in the development of the company’s international labor standards program.

Visit www.domini.com for more stories, a list of all shareholder proposals we’ve filed on your behalf, and to read our quarterly Social Impact Updates.

*We are serving a supporting role in this engagement.

5

THE WAY YOU INVEST MATTERS®

INVESTING IN BETTER FOOD PRODUCTION

The complexity of our food production systems is astounding, as are its staggering impacts on climate change and human rights. Any given meal or afternoon snack can touch on issues as far-ranging as the survival of the orangutan or a land rights dispute in Africa. Climate change, water scarcity, nutritional content, marketing to children, animal welfare and labor rights are all on the table.

Behind each familiar brand lies a complex set of relationships stretching across the globe. We view these relationships as opportunities for positive impact. As investors, we can create the incentives for companies to simultaneously be more transparent and to dig deeper to ensure their businesses are operating responsibly. Through your investment in the Domini Funds, your money is working to help catalyze this process of transformation.

For this report, we focus on a handful of issues that lie beneath the surface, hidden from the consumer’s view. We discuss a few actions we have taken and provide some brief examples of companies that are making efforts to reduce their footprint and have a more positive impact.

Pesticides and Pollinators

It is imperative that we pay attention to the overall resiliency of our food systems. It is said that a chain is only as strong as its weakest link, and the lowly honeybee is in peril.

Honeybees are the most economically important pollinators globally and contribute more than $24 billion to the U.S. economy each year. According to the US Department of Agriculture, “[a]bout one mouthful in three in our diet directly or indirectly benefits from honeybee pollination.” Crops dependent upon honeybees include almonds, blueberries, apples, lemons and zucchini. Since 2006, however, commercial honeybee colony loss rates have averaged 30 percent each winter, compared to historical losses of 10 to 15 percent. “Colony Collapse Disorder” is a global syndrome that produces the sudden catastrophic loss of a hive. The USDA warns that if losses continue at current levels, “it could threaten the economic viability of the bee pollination industry.”

Scientists believe a series of contributing factors are to blame, including loss of natural forage areas due to land-use changes, inadequate diets, mite infestations, diseases, loss of genetic diversity and certain commercial beekeeping practices. Although a single cause may never be found, an independent four-year scientific analysis of 800 peer-reviewed studies recently concluded that neonicotinoid pesticides (“neonics”) are a “key factor in the decline of bees” and their widespread use poses a threat to the infrastructure that enables food production. Neonics are a “systemic”

6

THE WAY YOU INVEST MATTERS®

pesticide used on more than 140 different crops in 120 countries, and are the most widely used group of insecticides globally. They are used to pre-coat seeds, where they are then taken up by the entire plant, and are also sprayed. The European Union has taken steps to ban certain neonics, and the EPA has required that warning labels be put on certain products containing neonics.

While scientists and policymakers continue to study pollinator declines, there are a few things that we can do as investors and consumers. First, we can make our own determination about the social and economic value of the pesticide industry. The Domini Funds do not invest in companies that derive significant revenues from the manufacture of pesticides, such as Bayer, Monsanto, The Dow Chemical Co., DuPont and Syngenta.

As investors, we can engage with the companies that sell pesticides, or utilize them in their supply chains. For example, we spoke with Campbell Soup Company about its approach to pesticide use in its supply chain. Pesticide control is an area of focus within the company’s sustainable agriculture programs. The company seeks to use pesticides only optimally, and as a last resort.

Working with other concerned investors, we sent letters to food producers and retailers and home improvement companies that sell pesticides and pesticide-treated plants to alert them to the severe risks to bees and the potential economic implications. The Home Depot has taken a lead on this issue by announcing that it will require its suppliers to label all plants pretreated with neonics, and that it will work with suppliers to eliminate neonics in plant production. The company is also providing its customers with a list of neonic-free alternatives for home application. We are in active dialogue with Lowe’s about the science, encouraging that company to follow Home Depot’s lead and to ultimately take these products off the shelf. Your backyard garden may be an important refuge for bees. Let your garden supplier know that you need to ensure that it is a safe one.

Genetically Modified Organisms (GMOs)

We have received a number of questions from Domini Funds shareholders about genetically modified organisms (GMOs). Our concerns about the widespread use of genetic engineering in food production relate to human health as well as broader ecological impacts, including increased use of pesticides on crops that have been engineered to resist their application. It is important to recognize, however, that GMOs have been part of the U.S. food system for 20 years, and are pervasive.

We do recognize companies that have made special commitments to either avoid GMOs or label their products so that their consumers can make more informed decisions. As of 2014, 94 percent of American-grown soybeans are genetically engineered. WhiteWave Foods, however, the

7

THE WAY YOU INVEST MATTERS®

owner of the Silk, Land O Lakes and Horizon Organic brands, uses non-genetically modified soybeans in the production of most of its soy products.

Lindt & Sprüngli, the Swiss chocolate company, reports that it will not use any raw materials that have been genetically modified or that are derived from genetically modified organisms, as long as non-modified raw materials are available. The company tests its products for more than 200 types of pesticides and has participated in Sustainable Tree Crops, a program in West/Central Africa to promote the minimization of agricultural chemical use by farmers. Lindt also monitors its supply chain for human rights violations, which have been a persistent systemic problem in worldwide cocoa production.

Nissin Foods Holdings (Japan), known for its Cup Noodles brand, has a policy and monitoring system to ensure it uses only non-GMO corn and soy in addition to extensive screening systems to test for more than 700 chemicals and substances in its food products including heavy metals, animal feed additives and agricultural chemicals. The company does not use artificial food additives, including coloring. Nissin has a history of donating its instant food products for disaster relief efforts and recently announced it will start selling low-priced, nutrition enhanced cup noodles in Bangladesh.

Chipotle Mexican Grill has been making waves in its industry for high-profile commercials challenging traditional farming techniques and promoting a more natural approach. The company provides explicit and detailed GMO labeling on its website and strives to purchase its produce from local sources. We commend the company for these efforts, but would like to see more comprehensive data to enable us to evaluate progress. We therefore joined another investor in submitting a shareholder proposal this year requesting a sustainability report. More than 31 percent of shares were voted in favor of our proposal, and we look forward to continuing our dialogue with the company.

In October, we joined other investors in asking companies to refrain from using corporate funds to oppose GMO labeling legislation, citing risks to corporate reputation if consumers learned that their favorite brands opposed their right to know what is in their foods. In 2012, Proposition 37, a California measure to introduce GMO labeling, was defeated after intense lobbying, including opposition from Unilever, Campbell Soup Company, Monsanto, Kraft Foods Group, The Hershey Company and PepsiCo. These persistent contradictions between corporate political activity, corporate sustainability policies and the public interest are a regular aspect of our corporate dialogues.

8

THE WAY YOU INVEST MATTERS®

Choosing Local and Organic

The most responsible alternative to pesticides and genetic engineering, of course, is organic agriculture. It is not possible to speak about the dramatic growth of the market for organic foods without mentioning Whole Foods Market, reportedly the largest seller of organic produce in the country. The company also has a notable commitment to local food producers. The company reports that in 2013 approximately 25 percent of its produce came from local farms and that it disbursed $10 million in loans to 147 local producers. The company also has a strong commitment to GMO labeling and has received consistently high marks for its seafood practices from Greenpeace.

United Natural Foods, an important supplier to Whole Foods, reports that it is the largest wholesale trader of organic foods in the U.S., and the nation’s leading distributor of organic fresh produce and perishable items. The company supports GMO labeling and helped to launch the Non-GMO Project, which maintains a GMO verification and labeling program.

Casino Guichard-Perrachon (France) operates more than 11,000 supermarkets and convenience stores in France, Latin America and Southeast Asia. Founded in 1898, the company has made impressive commitments to the environment, to local farmers and to consumers, through budget-conscious private label products and improved nutritional content. It has also been steadily increasing its organic product offerings. The company maintains a consistent “no-GMO” policy and eliminated palm oil from 73 percent of its Casino-branded products by 2012. It has also launched a number of commitments to local sourcing, and has developed various partnerships with local small-scale farmers, including providing funding in times of financial stress. In Colombia, as of 2010, the company’s local subsidiary procured 88 percent of its products from local small and medium-sized enterprises.

Deforestation

Deforestation is one of the principal drivers of climate change, accounting for 17 percent of greenhouse gas emissions. The Consumer Goods Forum, an industry association, has acknowledged that “the consumer goods industry, through its growing use of soya, palm oil, beef, paper and board, creates many of the economic incentives which drive deforestation.” The Forum has committed to mobilize resources to achieve “zero net deforestation,” and although the term “net” deforestation is cause for concern because it implies that one forest is interchangeable for another, the industry’s acknowledgment of its impact is a hopeful sign. All 400 members of the Forum, representing all the world’s major consumer goods manufacturers, retailers and service providers, have committed to zero net deforestation by 2020.

9

THE WAY YOU INVEST MATTERS®

Corporations like Mondelēz International and PepsiCo purchase significant quantities of these commodities through supply chains that may begin in a rainforest in Indonesia or a farm in Brazil. Climate change impacts from deforestation and poor forest management can be reduced through increased use of recycled materials, independent third party certification schemes, and monitoring of supply chains.

The shareholder proposal is an effective tool for encouraging corporate management to come to the table to discuss our concerns. We developed a proposal that we have submitted to several of the largest food companies, asking for public reports assessing each company’s impact on deforestation and its plans to mitigate these risks. We’ve asked these companies to report on their impact by commodity, as each carries its own set of risks and possible solutions. Among these commodities, palm oil has received the most attention because its production is responsible for large-scale forest conversion in the tropics and extensive carbon emissions.

In January, Mondelēz International (Oreo, Nutter Butter and Ritz Crackers) updated its website to address deforestation in its supply chain — a direct response to our shareholder proposal. These new disclosures were followed by the publication of an action plan to ensure that all palm oil is produced on legally held land without the use of forced or child labor. We are currently in dialogue on these policies, encouraging the company to provide more robust data to its investors.

Our shareholder proposal also brought PepsiCo to the table. Although best known for its iconic namesake, Pepsi now offers a diversified line of brands including Frito-Lay, Quaker Oats, Tropicana, Izze, and Sabra hummus. In May, after we withdrew our shareholder proposal and in the face of a continuing campaign led by Rainforest Action Network, the company adopted forestry and palm oil policies, including a number of notable commitments. We will continue to work with Pepsi to discuss how these commitments will be implemented and publicly reported.

Unilever, the owner of numerous brands, including Ben & Jerry’s and Lipton tea, is among the world’s largest consumers of palm oil, using 1.5 million tons a year to make products such as Dove soap, Magnum ice cream and Vaseline lotion, representing about 3 percent of global production. The company has set a target of buying all of its palm oil from traceable sources by 2020, meaning that the company will be able to track all of the oil it buys back to the plantation on which it was grown. Traceability is a key concern in this area and a number of companies have made similar commitments.

Like many companies of Unilever’s size, we see numerous causes for both praise and concern. In September 2013, Domini publicly endorsed Oxfam International’s “Behind the Brands” campaign, an assessment of the ten

10

THE WAY YOU INVEST MATTERS®

largest food companies on a range of issues, including climate change and the rights of farmers and women. In Oxfam’s latest report from February 2014, Unilever ranked second out of the ten food companies scored, with an overall rating of “fair.” Unilever was the first company to be awarded a “good” score for its impact on farmers. According to Oxfam, “Farmers are likely to get a better deal with Unilever than with many companies. The company understands farmers’ issues and is addressing them. More could be done to ensure suppliers’ are treating farmers fairly, however.” Oxfam also noted actions taken on climate change and water usage, and new commitments on land rights supporting women.

The big news in the palm oil industry this year was the adoption of forestry and human rights policies by Wilmar International, Golden Agri-Resources and Cargill, three of the largest palm oil traders. Although none of these companies are currently approved for the Domini Funds’ portfolios, we remain cautiously optimistic that these policies will bring meaningful change to the palm oil industry, a $44 billion industry that currently presents severe risks to forests and human rights. Much credit is due to the persistent work of committed activists, including Rainforest Action Network, Greenpeace and Oxfam, as well as concerned social investors.

* * *

Consider this report to be a work in progress. None of the companies cited here are without controversy and few of these problems will be solved overnight. In addition, the issues discussed here just scratch the surface. As diversified investors, however, we must wrestle with all of these issues — from risks to critical ecosystems to labor rights.

The issues presented by global food production are serious, but there has never been such a bright spotlight shining on them, giving us hope for continued progress. In the meantime, we will continue to monitor corporate behavior and use our influence when we see an opportunity to ensure that your concerns are addressed.

The holdings discussed above can be found in the portfolios of the Domini Funds, included herein. Bayer, Dow Chemical, DuPont, Golden Agri-Resources, Hershey, Monsanto, Syngenta, Walmart and Wilmar International are not currently approved for, or held by, any of the Domini Funds. Cargill is privately held and is therefore ineligible for investment. As of July 31, 2014, Campbell’s, Lindt & Sprüngli, Nissin Foods, United Natural Foods and WhiteWave Foods were not held by any of the Domini Funds. The composition of the Funds’ portfolios is subject to change.

An investment in the Domini Social Equity Fund and the Domini International Social Equity Fund is subject to market risks such as sector concentration and style risk. Investing internationally involves special risks, such as currency fluctuations, social and economic instability, differing securities regulations and accounting standards, limited public information, possible changes in taxation, and periods of illiquidity. You may lose money.

The preceding profiles should not be deemed an offer to sell or a solicitation of an offer to buy the stock or bonds of any of the companies noted, or a recommendation concerning the merits of any of these companies as an investment.

This material must be preceded or accompanied by a current prospectus. DSIL Investment Services LLC, Distributor. 09/14

11

Performance Commentary (Unaudited)

For the year ended July 31, 2014, the Fund’s Investor shares gained 20.07%, outperforming the S&P 500 Index, which returned 16.94%.

The Fund is managed through a two-step process designed to capitalize on the strengths of Domini Social Investments and Wellington Management. Domini creates an approved list of companies based on its social, environmental and governance analysis, and Wellington then utilizes a systematic and disciplined process to manage the portfolio.

The environment over the past year was especially conducive for the Fund’s approach, which seeks to identify stocks that we believe will outperform based on defined quantitative factors, such as valuation, quality and momentum. In this period, these factors were very effective and contributed to the relative outperformance, aided by improving macroeconomic conditions in the United States. A modest number of ADR (American depository receipt) positions in European and Asian companies, such as Shire PLC, also boosted relative results.

Individual stock selection, as opposed to our exposure to specific industries, drove the fiscal year’s relative outperformance. Stock selection within the health care, industrials, information technology and telecommunications sectors was particularly beneficial to performance.

Top contributors to performance relative to the S&P 500 included: Southwest Airlines, a passenger airline that saw its shares rise after the company posted impressive fourth quarter 2013 results driven by higher unit revenue growth, lower total unit costs and more capacity; Shire, an Irish specialty pharmaceutical company that beat expectations in the first quarter of 2014 due to a combination of strong product sales and cost discipline, along with speculation of a proposed acquisition by AbbVie that valued the company at a large premium to its pre-announcement market price; and Mylan, a global pharmaceutical company that saw its shares rise as the company performed above expectations after its Agila acquisition and the FDA’s new guidance on generic drug Advair, which the company believes will support its development program. Due to these factors, we eliminated our position in Mylan during the period.

The top detractors from relative performance during the period included: Coach, an international accessory retailer that saw its shares fall as declining market share, weak online revenues and margin compression in the North American handbag segment lowered future sales expectations; J.M. Smucker, a manufacturer and marketer of branded food products that saw profits fall as lower coffee prices weighed on sales; and AGCO, an agricultural equipment manufacturer that saw its shares fall as a result of a decline in earnings and falling commodity prices reducing demand for agricultural equipment.

12

TEN LARGEST HOLDING (Unaudited)

| SECURITY DESCRIPTION | % NET ASSETS | SECURITY DESCRIPTION | % NET ASSETS | |||||||

| Microsoft Corporation | 4.2% | Kroger Co/The | 2.7% | |||||||

| Intel Corp | 3.3% | National Oilwell Varco Inc | 2.5% | |||||||

| Apache Corp | 3.1% | Celgene Corp | 2.5% | |||||||

| Eli Lilly & Co | 3.1% | Consolidated Edison Inc | 2.4% | |||||||

| Apple Inc | 3.1% | Southwest Airlines Co | 2.4% | |||||||

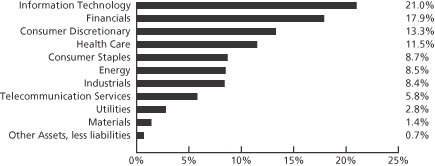

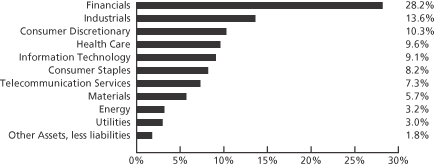

PORTFOLIO HOLDINGS BY INDUSTRY SECTOR (% OF NET ASSETS) (Unaudited)

13

| AVERAGE ANNUAL TOTAL RETURNS (Unaudited) | Investor shares | S&P 500 | ||||

| As of 7/31/14 | 1 Year | 20.07% | 16.94% | |||

| 5 Year | 16.13% | 16.79% | ||||

| 10 Year | 7.02% | 8.00% | ||||

| Since Inception (6/3/91) | 8.71% | 9.36% | ||||

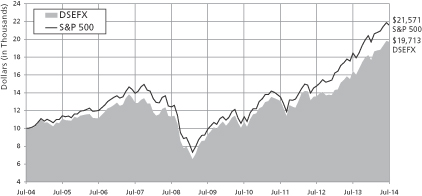

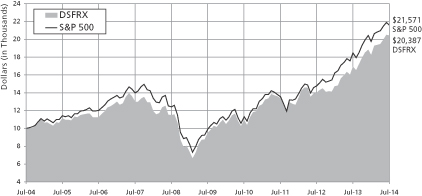

COMPARISON OF $10,000 INVESTMENT IN THE DOMINI SOCIAL EQUITY FUND INVESTOR SHARES AND S&P 500 (Unaudited)

Past performance is no guarantee of future results. The Fund’s returns quoted above represent past performance after all expenses. Investment return, principal value, and yield will fluctuate. Your shares, when redeemed, may be worth more or less than their original cost. Call 1-800-582-6757 or visit www.domini.com for performance information current to the most recent month-end, which may be lower or higher. A 2.00% fee applies on sales/exchanges made less than 30 days after purchase/exchange, with certain exceptions. Quoted performance data does not reflect the deduction of this fee, which would reduce the performance quoted. See the Fund’s prospectus for further information.

The Fund’s gross annual operating expenses totaled 1.20% of net assets as of 7/31/14. Until 11/30/14, the Fund’s Manager has contractually agreed to limit certain ordinary Investor share expenses to 1.25% of its average daily net assets per annum, absent an earlier modification by the Fund’s Board.

The table and the graph do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The graph illustrates the growth of a hypothetical $10,000 initial investment. Total return for the Domini Social Equity Fund is based on the Fund’s net asset values and assumes all dividend and capital gains were reinvested. An investment in the Fund is not a bank deposit and is not insured. The Fund is subject to market risks such as sector concentration and style risk. You may lose money.

The Standard & Poor’s 500 Index (S&P 500) is an unmanaged index of common stocks. Investors cannot invest directly in the S&P 500.

14

| AVERAGE ANNUAL TOTAL RETURNS (Unaudited) | ||||||||

| Class A shares (with 4.75% maximum Sales Charge) | Class A shares (without Sales Charge) | S&P 500 | ||||||

| As of 7/31/14 | 1 Year | 14.46% | 20.17% | 16.94% | ||||

| 5 Year | 15.05% | 16.18% | 16.79% | |||||

| 10 Year* | 6.50% | 7.02% | 8.00% | |||||

| Since Inception (6/3/91)* | 8.48% | 8.71% | 9.36% | |||||

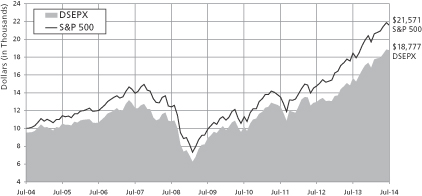

COMPARISON OF $10,000 INVESTMENT IN THE DOMINI SOCIAL EQUITY FUND CLASS A SHARES AND S&P 500 (WITH 4.75% MAXIMUM SALES CHARGE)* (Unaudited)

Past performance is no guarantee of future results. The Fund’s returns quoted above represent past performance after all expenses. Investment return, principal value, and yield will fluctuate. Your shares, when redeemed, may be worth more or less than their original cost. Call 1-800-498-1351 or visit www.domini.com for performance information current to the most recent month-end, which may be lower or higher. A 2.00% fee applies on sales/exchanges made less than 30 days after purchase/exchange, with certain exceptions. Quoted performance data does not reflect the deduction of this fee, which would reduce the performance quoted. See the Fund’s prospectus for further information.

The Fund’s gross annual operating expenses totaled 1.54% of net assets as of 7/31/14. Until 11/30/14, the Fund’s Manager has contractually agreed to limit certain ordinary A share expenses to 1.18% of its average daily net assets per annum absent an earlier modification by the Fund’s Board. The Fund’s total return would have been lower without this limit.

The table and the graph do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The graph illustrates the growth of a hypothetical $10,000 initial investment. Total return for the Domini Social Equity Fund is based on the Fund’s net asset values and assumes all dividend and capital gains were reinvested. An investment in the Fund is not a bank deposit and is not insured. The Fund is subject to market risks such as sector concentration and style risk. You may lose money.

The Standard & Poor’s 500 Index (S&P 500) is an unmanaged index of common stocks. Investors cannot invest directly in the S&P 500.

*Class A shares were not offered prior to November 28, 2008. All performance information for time periods beginning prior to November 28, 2008 is the performance of the Investor shares. This performance has not been adjusted to reflect the lower expenses of the Class A shares, but does, where noted, reflect an adjustment for the maximum applicable sales charge of 4.75%.

15

| AVERAGE ANNUAL TOTAL RETURNS (Unaudited) | Institutional shares | S&P 500 | ||||

| As of 7/31/14 | 1 Year | 20.59% | 16.94% | |||

| 5 Year | 16.65% | 16.79% | ||||

| 10 Year* | 7.02% | 8.00% | ||||

| Since Inception (6/3/91)* | 8.71% | 9.36% | ||||

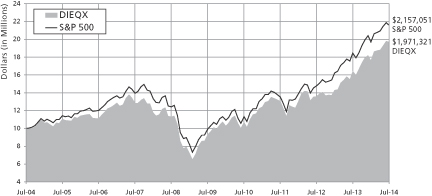

COMPARISON OF $1 MILLION INVESTMENT IN THE DOMINI SOCIAL EQUITY FUND INSTITUTIONAL SHARES AND S&P 500* (Unaudited)

Past performance is no guarantee of future results. The Fund’s returns quoted above represent past performance after all expenses. Investment return, principal value, and yield will fluctuate. Your shares, when redeemed, may be worth more or less than their original cost. Call 1-800-498-1351 or visit www.domini.com for performance information current to the most recent month-end, which may be lower or higher. A 2.00% fee applies on sales/exchanges made less than 30 days after purchase/exchange, with certain exceptions. Quoted performance data does not reflect the deduction of this fee, which would reduce the performance quoted. See the Fund’s prospectus for further information.

The Fund’s gross annual operating expenses totaled 0.81% of net assets as of 7/31/14. Until 11/30/14, the Fund’s Manager has contractually agreed to limit certain ordinary Institutional share expenses to 0.80% of its average daily net assets per annum absent an earlier modification by the Fund’s Board. The Fund’s total return would have been lower without this limit.

The table and the graph do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The graph illustrates the growth of a hypothetical $1,000,000 initial investment. Total return for the Domini Social Equity Fund is based on the Fund’s net asset values and assumes all dividend and capital gains were reinvested. An investment in the Fund is not a bank deposit and is not insured. The Fund is subject to market risks such as sector concentration and style risk. You may lose money.

The Standard & Poor’s 500 Index (S&P 500) is an unmanaged index of common stocks. Investors cannot invest directly in the S&P 500.

*Institutional shares were not offered prior to November 28, 2008. All performance information for time periods beginning prior to November 28, 2008 is the performance of the Investor shares. This performance has not been adjusted to reflect the lower expenses of the Institutional shares.

16

| AVERAGE ANNUAL TOTAL RETURNS (Unaudited) | Class R shares | S&P 500 | ||||

| As of 7/31/14 | 1 Year | 20.52% | 16.94% | |||

| 5 Year | 16.54% | 16.79% | ||||

| 10 Year | 7.38% | 8.00% | ||||

| Since Inception (6/3/91)* | 8.87% | 9.36% | ||||

COMPARISON OF $10,000 INVESTMENT IN THE DOMINI SOCIAL EQUITY FUND CLASS R SHARES AND S&P 500*(Unaudited)

Past performance is no guarantee of future results. The Fund’s returns quoted above represent past performance after all expenses. Investment return, principal value, and yield will fluctuate. Your shares, when redeemed, may be worth more or less than their original cost. Call 1-800-498-1351 or visit www.domini.com for performance information current to the most recent month-end, which may be lower or higher. A 2.00% fee applies on sales/exchanges made less than 30 days after purchase/exchange, with certain exceptions. Quoted performance data does not reflect the deduction of this fee, which would reduce the performance quoted. See the Fund’s prospectus for further information.

The Fund’s gross annual operating expenses totaled 0.90% of net assets as of 7/31/14. Until 11/30/14, the Fund’s Manager has contractually agreed to limit certain ordinary R share expenses to 0.90% of its average daily net assets per annum absent an earlier modification by the Fund’s Board.

The table and the graph do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The graph illustrates the growth of a hypothetical $10,000 initial investment. Total return for the Domini Social Equity Fund is based on the Fund’s net asset values and assumes all dividend and capital gains were reinvested. An investment in the Fund is not a bank deposit and is not insured. The Fund is subject to market risks such as sector concentration and style risk. You may lose money.

The Standard & Poor’s 500 Index (S&P 500) is an unmanaged index of common stocks. Investors cannot invest directly in the S&P 500.

*Class R shares were not offered prior to November 28, 2003. All performance information for time periods beginning prior to November 28, 2003 is the performance of the Investor shares. This performance has not been adjusted to reflect the lower expenses of the Class R shares.

17

DOMINI SOCIAL EQUITY FUND

PORTFOLIOOF INVESTMENTS

July 31, 2014

| SECURITY | SHARES | VALUE | ||||||

Common Stocks – 99.3% |

| |||||||

Consumer Discretionary – 13.3% |

| |||||||

Amazon.com Inc (a) | 29 | $ | 9,077 | |||||

AutoZone Inc (a) | 7,500 | 3,877,725 | ||||||

Bed Bath & Beyond Inc (a) | 256,100 | 16,208,569 | ||||||

Best Buy Co Inc | 866 | 25,746 | ||||||

Brinker International Inc | 51,300 | 2,300,292 | ||||||

Buckle Inc/The | 43,100 | 1,917,950 | ||||||

Chipotle Mexican Grill Inc (a) | 11,635 | 7,824,538 | ||||||

Coach Inc | 133 | 4,596 | ||||||

DIRECTV (a) | 233,300 | 20,075,465 | ||||||

Expedia Inc | 66,100 | 5,249,662 | ||||||

FUJIFILM Holdings Corp ADR | 92,900 | 2,648,579 | ||||||

Fossil Group Inc (a) | 58,800 | 5,762,400 | ||||||

Gap Inc/The | 255,545 | 10,249,910 | ||||||

Harman International Industries Inc | 23,100 | 2,507,505 | ||||||

Home Depot Inc/The | 218 | 17,625 | ||||||

JC Penney Co Inc (a) | 1,546 | 14,501 | ||||||

Johnson Controls Inc | 283 | 13,369 | ||||||

Kohl’s Corp | 405,600 | 21,715,824 | ||||||

L Brands Inc | 219 | 12,695 | ||||||

Lowe’s Cos Inc | 364 | 17,417 | ||||||

Macy’s Inc | 78,100 | 4,513,399 | ||||||

McDonald’s Corp | 101 | 9,551 | ||||||

Michael Kors Holdings Ltd (a) | 88,600 | 7,219,128 | ||||||

NIKE Inc Cl B | 188 | 14,500 | ||||||

PetSmart Inc | 63,800 | 4,347,332 | ||||||

Priceline Group Inc/The (a) | 5,800 | 7,206,210 | ||||||

Scholastic Corp | 316 | 11,193 | ||||||

Staples Inc | 666 | 7,719 | ||||||

Starbucks Corp | 207 | 16,080 | ||||||

TJX Cos Inc/The | 37,500 | 1,998,375 | ||||||

Target Corp | 181 | 10,786 | ||||||

Tiffany & Co | 152 | 14,837 | ||||||

TripAdvisor Inc (a) | 28,200 | 2,674,488 | ||||||

Viacom Inc Cl B | 23,900 | 1,975,813 | ||||||

Walt Disney Co/The | 56,742 | 4,873,003 | ||||||

|

| |||||||

| 135,345,859 | ||||||||

|

| |||||||

| SECURITY | SHARES | VALUE | ||||||

Consumer Staples – 8.7% |

| |||||||

Avon Products Inc | 374 | $ | 4,937 | |||||

Coca-Cola Co/The | 292 | 11,473 | ||||||

Costco Wholesale Corp | 120 | 14,105 | ||||||

Delhaize Group SA ADR | 226,400 | 3,674,472 | ||||||

Estee Lauder Cos Inc/The Cl A | 63,600 | 4,672,056 | ||||||

JM Smucker Co/The | 195,400 | 19,469,656 | ||||||

Kellogg Co | 85,800 | 5,133,414 | ||||||

Keurig Green Mountain Inc | 44,400 | 5,296,032 | ||||||

Kimberly-Clark Corp | 21,241 | 2,206,303 | ||||||

Koninklijke Ahold NV ADR | 586,800 | 10,251,396 | ||||||

Kraft Foods Group Inc | 223 | 11,949 | ||||||

Kroger Co/The | 555,430 | 27,204,961 | ||||||

Mondelez International Inc Cl A | 265 | 9,540 | ||||||

PepsiCo Inc | 161 | 14,184 | ||||||

Procter & Gamble Co/The | 155 | 11,985 | ||||||

Sysco Corp | 293,100 | 10,460,739 | ||||||

Whole Foods Market Inc | 248 | 9,479 | ||||||

|

| |||||||

| 88,456,681 | ||||||||

|

| |||||||

Energy – 8.5% | ||||||||

ARC Resources Ltd | 380 | 10,486 | ||||||

Apache Corp | 309,591 | 31,782,612 | ||||||

Concho Resources Inc (a) | 100 | 14,080 | ||||||

National Oilwell Varco Inc | 316,120 | 25,618,365 | ||||||

Newfield Exploration Co (a) | 58,300 | 2,349,490 | ||||||

Noble Energy Inc | 170 | 11,303 | ||||||

Oil States International Inc (a) | 158,100 | 9,689,949 | ||||||

Penn West Petroleum Ltd | 915 | 7,073 | ||||||

Pioneer Natural Resources Co | 88 | 19,488 | ||||||

18

DOMINI SOCIAL EQUITY FUND

PORTFOLIOOF INVESTMENTS (continued)

July 31, 2014

| SECURITY | SHARES | VALUE | ||||||

Energy (Continued) |

| |||||||

Southwestern Energy Co (a) | 424,237 | $ | 17,215,537 | |||||

|

| |||||||

| 86,718,383 | ||||||||

|

| |||||||

Financials – 17.9% |

| |||||||

American Capital Agency Corp | 110,000 | 2,543,200 | ||||||

American Express Co | 191 | 16,808 | ||||||

Apollo Investment Corp | 1,851,500 | 15,719,235 | ||||||

Brandywine Realty Trust | 164,600 | 2,559,530 | ||||||

E*TRADE Financial Corp (a) | 153,600 | 3,228,672 | ||||||

Generac Holdings Inc (a) | 82,360 | 3,574,424 | ||||||

Genworth Financial Inc Cl A (a) | 173,000 | 2,266,300 | ||||||

Hartford Financial Services Group Inc/The | 596,600 | 20,379,856 | ||||||

Hatteras Financial Corp | 315,100 | 6,034,165 | ||||||

ING Groep NV ADR (a) | 196,800 | 2,552,496 | ||||||

Invesco Mortgage Capital Inc | 153,900 | 2,613,222 | ||||||

KeyCorp | 333,200 | 4,511,528 | ||||||

Kimco Realty Corp | 453,200 | 10,142,616 | ||||||

Lincoln National Corp | 162,300 | 8,502,897 | ||||||

MFA Financial Inc | 927,600 | 7,550,664 | ||||||

MetLife Inc | 107,900 | 5,675,540 | ||||||

PNC Financial Services Group Inc/The | 195,490 | 16,139,654 | ||||||

Piedmont Office Realty Trust Inc Cl A | 792,200 | 15,408,290 | ||||||

Prudential Financial Inc | 202,800 | 17,637,516 | ||||||

Retail Properties of America Inc Cl A | 282,600 | 4,253,130 | ||||||

Symetra Financial Corp | 145,300 | 3,312,840 | ||||||

Two Harbors Investment Corp | 722,600 | 7,392,198 | ||||||

| SECURITY | SHARES | VALUE | ||||||

Financials (Continued) |

| |||||||

US Bancorp/MN | 346 | $ | 14,542 | |||||

Unum Group | 556,700 | 19,111,511 | ||||||

|

| |||||||

| 181,140,834 | ||||||||

|

| |||||||

Health Care – 11.5% |

| |||||||

Alexion Pharmaceuticals Inc (a) | 40,900 | 6,502,691 | ||||||

Becton Dickinson and Co | 128 | 14,879 | ||||||

CR Bard Inc | 18,000 | 2,686,140 | ||||||

CareFusion Corp (a) | 94,200 | 4,125,018 | ||||||

Celgene Corp (a) | 292,600 | 25,500,090 | ||||||

Edwards Lifesciences Corp (a) | 30,000 | 2,707,500 | ||||||

Eli Lilly & Co | 513,200 | 31,335,992 | ||||||

Gilead Sciences Inc (a) | 216,700 | 19,838,885 | ||||||

Hospira Inc (a) | 57,800 | 3,206,166 | ||||||

Novartis AG ADR | 161,000 | 13,997,340 | ||||||

Novo Nordisk A/S ADR | 67,200 | 3,094,560 | ||||||

Owens & Minor Inc | 110,100 | 3,643,209 | ||||||

|

| |||||||

| 116,652,470 | ||||||||

|

| |||||||

Industrials – 8.4% | ||||||||

3M Co | 115 | 16,202 | ||||||

AGCO Corp | 340,500 | 16,585,755 | ||||||

Cummins Inc | 83 | 11,569 | ||||||

Deere & Co | 162,800 | 13,855,908 | ||||||

Emerson Electric Co | 38,400 | 2,444,160 | ||||||

First Solar Inc (a) | 358 | 22,593 | ||||||

Herman Miller Inc | 422 | 12,339 | ||||||

Interface Inc | 692 | 10,968 | ||||||

JetBlue Airways Corp (a) | 1,688 | 18,095 | ||||||

Pitney Bowes Inc | 549,300 | 14,864,058 | ||||||

RR Donnelley & Sons Co | 739,829 | 12,843,431 | ||||||

Southwest Airlines Co | 856,754 | 24,229,003 | ||||||

United Parcel Service Inc Cl B | 131 | 12,719 | ||||||

|

| |||||||

| 84,926,800 | ||||||||

|

| |||||||

19

DOMINI SOCIAL EQUITY FUND

PORTFOLIOOF INVESTMENTS (continued)

July 31, 2014

| SECURITY | SHARES | VALUE | ||||||

Information Technology – 21.0% |

| |||||||

Advanced Micro Devices Inc (a) | 3,150 | $ | 12,317 | |||||

Apple Inc | 324,630 | 31,024,889 | ||||||

Applied Materials Inc | 762 | 15,972 | ||||||

Cisco Systems Inc | 504 | 12,716 | ||||||

EMC Corp/MA | 373 | 10,929 | ||||||

F5 Networks Inc (a) | 66,300 | 7,464,717 | ||||||

Facebook Inc Cl A (a) | 71,500 | 5,194,475 | ||||||

Google Inc Cl A (a) | 2,016 | 1,168,373 | ||||||

Google Inc Cl C (a) | 3,016 | 1,723,946 | ||||||

Intel Corp | 985,541 | 33,399,984 | ||||||

International Business Machines Corp | 72,452 | 13,886,875 | ||||||

MasterCard Inc Cl A | 173,800 | 12,887,270 | ||||||

Microsoft Corp | 983,339 | 42,440,911 | ||||||

Motorola Solutions Inc | 201 | 12,800 | ||||||

NVIDIA Corp | 645,500 | 11,296,250 | ||||||

Oracle Corp | 423,600 | 17,109,204 | ||||||

Power Integrations Inc | 260 | 13,996 | ||||||

QUALCOMM Inc | 134,700 | 9,927,390 | ||||||

SanDisk Corp | 76,400 | 7,006,644 | ||||||

SunPower Corp (a) | 1,124 | 41,285 | ||||||

Symantec Corp | 141,700 | 3,352,622 | ||||||

Texas Instruments Inc | 300 | 13,875 | ||||||

United Microelectronics Corp ADR | 1,786,000 | 3,911,340 | ||||||

Western Digital Corp | 112,400 | 11,220,892 | ||||||

| SECURITY | SHARES | VALUE | ||||||

Information Technology (Continued) |

| |||||||

Xerox Corp | 1,209 | $ | 16,031 | |||||

Yahoo! Inc (a) | 649 | 23,241 | ||||||

|

| |||||||

| 213,188,944 | ||||||||

|

| |||||||

Materials – 1.4% |

| |||||||

Domtar Corp | 395,200 | 14,195,584 | ||||||

MeadWestvaco Corp | 329 | 13,752 | ||||||

Nucor Corp | 230 | 11,551 | ||||||

|

| |||||||

| 14,220,887 | ||||||||

|

| |||||||

Telecommunication Services – 5.8% |

| |||||||

AT&T Inc | 63,535 | 2,261,211 | ||||||

CenturyLink Inc | 594,900 | 23,343,876 | ||||||

Frontier Communications Corp | 2,767,000 | 18,123,850 | ||||||

KT Corp ADR | 576,500 | 9,258,590 | ||||||

Spark New Zealand Ltd ADR | 321,100 | 3,838,751 | ||||||

TELUS Corp | 63,700 | 2,223,130 | ||||||

Verizon Communications Inc | 263 | 13,260 | ||||||

|

| |||||||

| 59,062,668 | ||||||||

|

| |||||||

Utilities – 2.8% | ||||||||

Cia Paranaense de Energia ADR | 208,300 | 3,236,982 | ||||||

Consolidated Edison Inc | 441,900 | 24,786,171 | ||||||

Energen Corp | 187 | 15,265 | ||||||

|

| |||||||

| 28,038,418 | ||||||||

|

| |||||||

Total Common Stocks – 99.3% |

| 1,007,751,944 | ||||||

Other Assets, less liabilities – 0.7% |

| 7,285,791 | ||||||

|

| |||||||

Net Assets – 100.0% |

| $ | 1,015,037,735 | |||||

|

| |||||||

(a) Non-income producing security.

(b) The aggregate cost for federal income tax purposes is $822,604,740. The aggregate gross unrealized appreciation is $200,964,449 and the aggregate gross unrealized depreciation is $15,817,245, resulting in net unrealized appreciation of $185,147,204.

ADR — American Depository Receipt

SEE NOTES TO FINANCIAL STATEMENTS

20

DOMINI INTERNATIONAL SOCIAL EQUITY FUND

Performance Commentary (Unaudited)

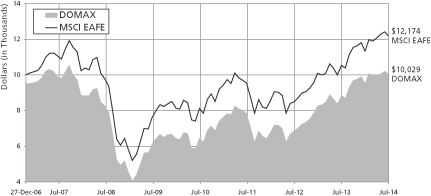

For the year ended July 31, 2014, the Fund’s Investor shares gained 13.15%, underperforming the MSCI EAFE Index, which returned 15.55%.

The Fund is managed through a two-step process designed to capitalize on the strengths of Domini Social Investments and Wellington Management. Domini creates an approved list of companies based on its social, environmental and governance analysis, and Wellington then utilizes a disciplined and systematic process to manage the portfolio.

Performance benefited over the period from a modest tilt toward cheaper, more cyclically-sensitive stocks in Europe and Japan, as investors increasingly took on additional risk following improvement in the macroeconomic conditions of both regions. An overweight to emerging market stocks was also rewarded during the period, as emerging markets rallied to break a prolonged slump. Factors detracting from performance during the period included an overweight to mid-cap stocks, which lagged the rest of the market-capitalization spectrum on a relative basis.

Individual stock selection, rather than our exposure to particular industries, was the predominant contributor to the fiscal year’s relative performance. In particular, the Fund benefited from strong stock selection within the consumer discretionary, information technology and health care sectors.

Top contributors to performance relative to MSCI EAFE included: Shire, an Irish specialty pharmaceutical company that beat expectations in the first quarter of 2014 due to a combination of strong product sales and cost discipline, along with speculation of a proposed acquisition by AbbVie that valued the company at a large premium to its pre-announcement market price; Next, a UK-based retailer that saw its shares rise after reporting strong fiscal year 2013 results highlighted by 24% earnings growth, driven primarily by lower tax charges and boosts from share buybacks; and Orange, a French multinational telecommunications provider that saw its shares rise after the company predicted a key measure of earnings would hold steady after years of decline, along with talk of a possible bid from German rival Deutsche Telekom.

The top detractors from relative performance during the period included: Arrium, an Australian-based international mining and materials company that saw its shares drop as it was impacted by an adverse exchange rate, weaker iron ore prices, delays in long-product demand from infrastructure projects and overall slowing mining activity; Fred Olsen Energy, a Norwegian offshore-drilling contractor that fell after reporting below-consensus results, partially driven by increased operating costs and an operating loss in its Engineering division; and WM Morrison Supermarkets, a UK-based food retailer that fell sharply after management announced a profit warning for the 2014 and 2015

21

fiscal years due to a strong shift in strategy implemented in response to deteriorating sales trends and strong competition from hard discounters.

TEN LARGEST HOLDINGS (Unaudited)

| SECURITY DESCRIPTION | % NET ASSETS | SECURITY DESCRIPTION | % NET ASSETS | |||||||

| Novartis AG | 2.9% | Next plc | 1.8% | |||||||

| BT Group plc | 2.1% | Continental AG | 1.7% | |||||||

| Associated British Foods plc | 2.0% | Otsuka Holdings Co Ltd | 1.7% | |||||||

| Merck KGaA | 1.9% | Dai Nippon Printing Co Ltd | 1.7% | |||||||

| Shire plc | 1.9% | FUJIFILM Holdings Corp | 1.6% | |||||||

PORTFOLIO HOLDINGS BY INDUSTRY SECTOR (% OF NET ASSETS) (Unaudited)

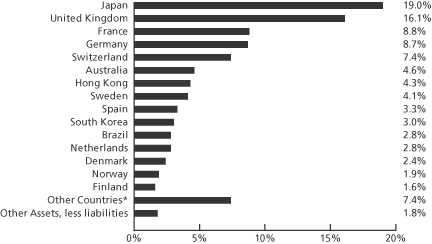

PORTFOLIO HOLDINGS BY COUNTRY (% OF NET ASSETS) (Unaudited)

*Other countries include South Africa (1.3%), New Zealand (1.3%), Austria (1.1%), United States (0.9%), China (0.7%), Belgium (0.6%), Taiwan (0.5%), Ireland (0.4%), Malaysia (0.2%), Poland (0.2%), India (0.1%) and Singapore (0.1%).

22

| AVERAGE ANNUAL TOTAL RETURNS (Unaudited) | Investor shares | MSCI EAFE | ||||

| As of 7/31/14 | 1 Year | 13.15% | 15.55% | |||

| 5 Year | 10.32% | 9.88% | ||||

| Since Inception (12/27/06) | 0.68% | 2.62% | ||||

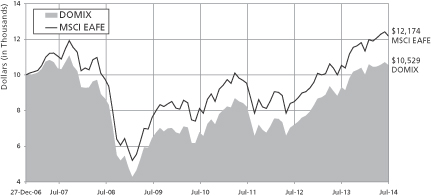

COMPARISON OF $10,000 INVESTMENT IN THE DOMINI INTERNATIONAL SOCIAL EQUITY FUND INVESTOR SHARES AND MSCI EAFE (Unaudited)

Past performance is no guarantee of future results. The Fund’s returns quoted above represent past performance after all expenses. Investment return, principal value, and yield will fluctuate. Your shares, when redeemed, may be worth more or less than their original cost. Call 1-800-582-6757 or visit www.domini.com for performance information current to the most recent month-end, which may be lower or higher. A 2.00% fee applies on sales/exchanges made less than 30 days after purchase/exchange, with certain exceptions. Quoted performance data does not reflect the deduction of this fee, which would reduce the performance quoted. See the Fund’s prospectus for further information.

The Fund’s gross annual operating expenses totaled 1.62% of net assets as of 7/31/14. Until 11/30/14, the Fund’s Manager has contractually agreed to limit certain ordinary Investor share expenses to 1.60% of its average daily net assets per annum absent an earlier modification by the Fund’s Board. The Fund’s total return would have been lower without this limit.

The table and the graph do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The graph illustrates the growth of a hypothetical $10,000 initial investment. Total return for the Domini International Social Equity Fund is based on the Fund’s net asset values and assumes all dividend and capital gains were reinvested. An investment in the Fund is not a bank deposit and is not insured. The Fund is subject to market risks such as sector concentration and style risk. You may lose money.

Investing internationally involves special risks, such as currency fluctuations, social and economic instability, differing securities regulations and accounting standards, limited public information, possible changes in taxation, and periods of illiquidity. These risks are magnified in emerging markets.

The Morgan Stanley Capital International Europe Australasia Far East (MSCI EAFE) index is an unmanaged index of common stocks. Investors cannot invest directly in an index.

23

| AVERAGE ANNUAL TOTAL RETURNS (Unaudited) | ||||||||

| Class A shares (with 4.75% maximum Sales Charge) | Class A shares (with- out Sales Charge) | MSCI EAFE | ||||||

| As of 7/31/14 | 1 Year | 7.78% | 13.16% | 15.55% | ||||

| 5 Year | 9.29% | 10.36% | 9.88% | |||||

| Since Inception (12/27/06)* | 0.04% | 0.68% | 2.62% | |||||

COMPARISON OF $10,000 INVESTMENT IN THE DOMINI INTERNATIONAL SOCIAL EQUITY FUND CLASS A SHARES AND MSCI EAFE (WITH 4.75% MAXIMUM SALES CHARGE)* (Unaudited)

Past performance is no guarantee of future results. The Fund’s returns quoted above represent past performance after all expenses. Investment return, principal value, and yield will fluctuate. Your shares, when redeemed, may be worth more or less than their original cost. Call 1-800-498-1351 or visit www.domini.com for performance information current to the most recent month-end, which may be lower or higher. A 2.00% fee applies on sales/exchanges made less than 30 days after purchase/exchange, with certain exceptions. Quoted performance data does not reflect the deduction of this fee, which would reduce the performance quoted. See the Fund’s prospectus for further information.

The Fund’s gross annual operating expenses totaled 1.82% of net assets as of 7/31/14. Until 11/30/14, the Fund’s Manager has contractually agreed to limit certain ordinary A share expenses to 1.57% of its average daily net assets per annum absent an earlier modification by the Fund’s Board. The Fund’s total return would have been lower without this limit.

The table and the graph do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The graph illustrates the growth of a hypothetical $10,000 initial investment. Total return for the Domini International Social Equity Fund is based on the Fund’s net asset values and assumes all dividend and capital gains were reinvested. An investment in the Fund is not a bank deposit and is not insured. The Fund is subject to market risks such as sector concentration and style risk. You may lose money.

Investing internationally involves special risks, such as currency fluctuations, social and economic instability, differing securities regulations and accounting standards, limited public information, possible changes in taxation, and periods of illiquidity. These risks are magnified in emerging markets.

The Morgan Stanley Capital International Europe Australasia Far East (MSCI EAFE) index is an unmanaged index of common stocks. Investors cannot invest directly in an index.

*Class A shares were not offered prior to November 28, 2008. All performance information for time periods beginning prior to November 28, 2008 is the performance of the Investor shares. Unless otherwise noted, this performance has not been adjusted to reflect the lower expenses of the Class A shares, but does, where noted, reflect an adjustment for the maximum applicable sales charges of 4.75%.

24

| AVERAGE ANNUAL TOTAL RETURNS (Unaudited) | Institutional shares | MSCI EAFE | ||||

| As of 7/31/14 | 1 Year | 13.60% | 15.55% | |||

| 5 Year* | 10.32% | 9.88% | ||||

| Since Inception (12/27/06)* | 0.68% | 2.62% | ||||

COMPARISON OF $1 MILLION INVESTMENT IN THE DOMINI INTERNATIONAL SOCIAL EQUITY FUND INSTITUTIONAL SHARES AND MSCI EAFE* (Unaudited)

Past performance is no guarantee of future results. The Fund’s returns quoted above represent past performance after all expenses. Investment return, principal value, and yield will fluctuate. Your shares, when redeemed, may be worth more or less than their original cost. Call 1-800-498-1351 or visit www.domini.com for performance information current to the most recent month-end, which may be lower or higher. A 2.00% fee applies on sales/exchanges made less than 30 days after purchase/exchange, with certain exceptions. Quoted performance data does not reflect the deduction of this fee, which would reduce the performance quoted. See the Fund’s prospectus for further information.

The Fund’s gross annual operating expenses totaled 1.16% of net assets as of 7/31/14. Until 11/30/14, the Fund’s Manager has contractually agreed to limit certain ordinary Institutional share expenses to 1.27% of its average daily net assets per annum absent an earlier modification by the Fund’s Board.

The table and the graph do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The graph illustrates the growth of a hypothetical $1,000,000 initial investment. Total return for the Domini International Social Equity Fund is based on the Fund’s net asset values and assumes all dividend and capital gains were reinvested. An investment in the Fund is not a bank deposit and is not insured. The Fund is subject to market risks such as sector concentration and style risk. You may lose money.

Investing internationally involves special risks, such as currency fluctuations, social and economic instability, differing securities regulations and accounting standards, limited public information, possible changes in taxation, and periods of illiquidity. These risks are magnified in emerging markets.

The Morgan Stanley Capital International Europe Australasia Far East (MSCI EAFE) index is an unmanaged index of common stocks. Investors cannot invest directly in an index.

*Institutional shares were not offered prior to November 30, 2012. All performance information for time periods beginning prior to November 28, 2012 is the performance of the Investor shares. Unless otherwise noted, this performance has not been adjusted to reflect the lower expenses of the Institutional shares.

25

DOMINI INTERNATIONAL SOCIAL EQUITY FUND

PORTFOLIOOF INVESTMENTS

July 31, 2014

| COUNTRY/SECURITY | INDUSTRY | SHARES | VALUE | |||||||

Common Stock – 94.6% | ||||||||||

Australia – 4.6% | ||||||||||

Bank of Queensland Ltd | Banks | 186,755 | $ | 2,156,274 | ||||||

Bendigo and Adelaide Bank Ltd | Banks | 170,240 | 2,003,769 | |||||||

Dexus Property Group | Real Estate | 2,447,163 | 2,689,880 | |||||||

GPT Group/The | Real Estate | 164,311 | 618,890 | |||||||

REA Group Ltd | Media | 96,790 | 4,217,289 | |||||||

TPG Telecom Ltd | Telecommunication Services | 419,520 | 2,131,464 | |||||||

|

| |||||||||

| 13,817,566 | ||||||||||

|

| |||||||||

Austria – 1.1% | ||||||||||

EVN AG | Utilities | 73,053 | 1,010,124 | |||||||

Voestalpine AG | Materials | 49,604 | 2,181,247 | |||||||

|

| |||||||||

| 3,191,371 | ||||||||||

|

| |||||||||

Belgium – 0.6% | ||||||||||

Delhaize Group SA | Food & Staples Retailing | 29,215 | 1,904,991 | |||||||

|

| |||||||||

| 1,904,991 | ||||||||||

|

| |||||||||

China – 0.7% | ||||||||||

Beijing Capital International Airport Co Ltd Cl H | Transportation | 492,000 | 338,478 | |||||||

Byd Co Ltd Cl H | Automobiles & Components | 3,000 | 19,841 | |||||||

China Travel International Investment Hong Kong Ltd | Consumer Services | 4,776,000 | 1,137,063 | |||||||

Sino-Ocean Land Holdings Ltd | Real Estate | 1,016,401 | 593,604 | |||||||

|

| |||||||||

| 2,088,986 | ||||||||||

|

| |||||||||

Denmark – 2.4% | ||||||||||

Danske Bank A/S | Banks | 124,909 | 3,606,369 | |||||||

Pandora A/S | Consumer Durables & Apparel | 7,470 | 510,849 | |||||||

Rockwool International A/S Cl B | Capital Goods | 6,669 | 1,111,311 | |||||||

Vestas Wind Systems A/S (a) | Capital Goods | 43,046 | 1,939,570 | |||||||

|

| |||||||||

| 7,168,099 | ||||||||||

|

| |||||||||

Finland – 1.6% | ||||||||||

Neste Oil OYJ | Energy | 217,225 | 4,010,930 | |||||||

Nokia OYJ | Technology Hardware & Equipment | 115,012 | 910,454 | |||||||

|

| |||||||||

| 4,921,384 | ||||||||||

|

| |||||||||

France – 8.8% | ||||||||||

Accor SA | Consumer Services | 27,947 | 1,352,345 | |||||||

AXA SA | Insurance | 184,070 | 4,225,627 | |||||||

Cap Gemini SA | Software & Services | 39,193 | 2,839,785 | |||||||

Casino Guichard Perrachon SA | Food & Staples Retailing | 18,439 | 2,220,620 | |||||||

Cie Generale des Etablissements Michelin | Automobiles & Components | 19,817 | 2,172,211 | |||||||

CNP Assurances | Insurance | 133,651 | 2,623,717 | |||||||

26

DOMINI INTERNATIONAL SOCIAL EQUITY FUND

PORTFOLIOOF INVESTMENTS (continued)

July 31, 2014

| COUNTRY/SECURITY | INDUSTRY | SHARES | VALUE | |||||||

France (Continued) | ||||||||||

Credit Agricole SA | Banks | 272,893 | $ | 3,688,640 | ||||||

Orange SA | Telecommunication Services | 294,069 | 4,601,306 | |||||||

Sanofi | Pharma, Biotech & Life Sciences | 3,950 | 414,389 | |||||||

SCOR SE | Insurance | 52,494 | 1,687,346 | |||||||

Valeo SA | Automobiles & Components | 6,648 | 795,923 | |||||||

|

| |||||||||

| 26,621,909 | ||||||||||

|

| |||||||||

Germany – 7.9% | ||||||||||

Allianz SE | Insurance | 22,606 | 3,760,633 | |||||||

Continental AG | Automobiles & Components | 24,425 | 5,256,151 | |||||||

Deutsche Post AG | Transportation | 131,940 | 4,218,067 | |||||||

Merck KGaA | Pharma, Biotech & Life Sciences | 64,310 | 5,682,473 | |||||||

Muenchener Rueckversicherungs AG | Insurance | 19,291 | 4,089,802 | |||||||

Talanx AG | Insurance | 22,517 | 801,101 | |||||||

|

| |||||||||

| 23,808,227 | ||||||||||

|

| |||||||||

Hong Kong – 4.3% | ||||||||||

Great Eagle Holdings Ltd | Real Estate | 325,585 | 1,171,576 | |||||||

Hongkong Land Holdings Ltd | Real Estate | 507,000 | 3,465,389 | |||||||

Hysan Development Co Ltd | Real Estate | 301,000 | 1,444,679 | |||||||

Jardine Strategic Holdings Ltd | Capital Goods | 16,000 | 571,860 | |||||||

Johnson Electric Holdings Ltd | Capital Goods | 147,625 | 571,448 | |||||||

Sino Land Co Ltd | Real Estate | 1,125,045 | 1,932,664 | |||||||

Swire Pacific Ltd Cl A | Real Estate | 110,500 | 1,421,993 | |||||||

Wheelock & Co Ltd | Real Estate | 470,471 | 2,372,219 | |||||||

|

| |||||||||

| 12,951,828 | ||||||||||

|

| |||||||||

India – 0.1% | ||||||||||

Hero MotoCorp Ltd | Automobiles & Components | 9,593 | 411,737 | |||||||

|

| |||||||||

| 411,737 | ||||||||||

|

| |||||||||

Ireland – 0.4% | ||||||||||

Irish Bank Resolution Corp Ltd/Old (a) (c) | Banks | 138,674 | 0 | |||||||

Smurfit Kappa Group PLC | Materials | 60,293 | 1,307,404 | |||||||

|

| |||||||||

| 1,307,404 | ||||||||||

|

| |||||||||

Japan – 19.0% | ||||||||||

Asahi Glass Co Ltd | Capital Goods | 612,000 | 3,627,645 | |||||||

Astellas Pharma Inc | Pharma, Biotech & Life Sciences | 35,500 | 481,542 | �� | ||||||

Bandai Namco Holdings Inc | Consumer Durables & Apparel | 38,600 | 977,205 | |||||||

Calsonic Kansei Corp | Automobiles & Components | 237,000 | 1,559,188 | |||||||

Central Japan Railway Co | Transportation | 22,400 | 3,182,218 | |||||||

Dai Nippon Printing Co Ltd | Commercial & Professional Services | 487,000 | 4,997,268 | |||||||

Daiwa House Industry Co Ltd | Real Estate | 128,000 | 2,599,058 | |||||||

Fast Retailing Co Ltd | Retailing | 48 | 15,852 | |||||||

FUJIFILM Holdings Corp | Technology Hardware & Equipment | 164,823 | 4,706,380 | |||||||

Honda Motor Co Ltd | Automobiles & Components | 260 | 9,054 | |||||||

Ibiden Co Ltd | Technology Hardware & Equipment | 92,100 | 1,840,882 | |||||||

Kawasaki Kisen Kaisha Ltd | Transportation | 774,000 | 1,650,515 | |||||||

27

DOMINI INTERNATIONAL SOCIAL EQUITY FUND

PORTFOLIOOF INVESTMENTS (continued)

July 31, 2014

| COUNTRY/SECURITY | INDUSTRY | SHARES | VALUE | |||||||

Japan (Continued) | ||||||||||

Konica Minolta Inc | Technology Hardware & Equipment | 131,400 | $ | 1,403,223 | ||||||

MS&AD Insurance Group Holdings Inc | Insurance | 87,400 | 1,990,010 | |||||||

Nippon Electric Glass Co Ltd | Technology Hardware & Equipment | 379,000 | 2,123,956 | |||||||

Nishi-Nippon City Bank Ltd/The | Banks | 169,000 | 438,874 | |||||||

Nissan Motor Co Ltd | Automobiles & Components | 55,800 | 547,580 | |||||||

Nisshin Seifun Group Inc | Food & Beverage | 204,150 | 2,384,743 | |||||||

Nisshin Steel Co Ltd | Materials | 114,980 | 1,552,998 | |||||||

Nomura Real Estate Holdings Inc | Real Estate | 30,900 | 574,292 | |||||||

NTN Corp | Capital Goods | 5,300 | 25,550 | |||||||

ORIX Corp | Diversified Financials | 31,200 | 504,379 | |||||||

Otsuka Holdings Co Ltd | Pharma, Biotech & Life Sciences | 159,500 | 5,080,405 | |||||||

Ricoh Co Ltd | Technology Hardware & Equipment | 106,900 | 1,224,096 | |||||||

Rohm Co Ltd | Semiconductors & Semiconductor Equipment | 11,600 | 654,146 | |||||||

Seiko Epson Corp | Technology Hardware & Equipment | 23,900 | 1,023,359 | |||||||

Seino Holdings Co Ltd | Transportation | 252,693 | 2,717,547 | |||||||

T&D Holdings Inc | Insurance | 61,200 | 768,319 | |||||||

Tokyo Gas Co Ltd | Utilities | 214,000 | 1,222,873 | |||||||

Toppan Printing Co Ltd | Commercial & Professional Services | 577,451 | 4,399,945 | |||||||

Toray Industries Inc | Materials | 1,394 | 9,439 | |||||||

Toyo Seikan Group Holdings Ltd | Materials | 120,300 | 1,874,133 | |||||||

Yamada Denki Co Ltd | Retailing | 119,800 | 425,323 | |||||||

Yamazaki Baking Co Ltd | Food & Beverage | 52,000 | 658,374 | |||||||

|

| |||||||||

| 57,250,371 | ||||||||||

|

| |||||||||

Malaysia – 0.2% | ||||||||||

YTL Corp Bhd | Utilities | 1,217,900 | 597,874 | |||||||

|

| |||||||||

| 597,874 | ||||||||||

|

| |||||||||

Netherlands – 2.8% | ||||||||||

Aegon NV | Insurance | 180,942 | 1,466,228 | |||||||

Akzo Nobel NV | Materials | 40,847 | 2,939,641 | |||||||

Koninklijke Ahold NV | Food & Staples Retailing | 225,481 | 3,928,476 | |||||||

|

| |||||||||

| 8,334,345 | ||||||||||

|

| |||||||||

New Zealand – 1.3% | ||||||||||

Telecom Corp of New Zealand Ltd (d) | Telecommunication Services | 1,594,989 | 3,844,642 | |||||||

|

| |||||||||

| 3,844,642 | ||||||||||

|

| |||||||||

Norway – 1.9% | ||||||||||

DNB ASA | Banks | 92,478 | 1,635,812 | |||||||

Norsk Hydro ASA | Materials | 272,694 | 1,613,684 | |||||||

Subsea 7 SA | Energy | 144,627 | 2,409,836 | |||||||

|

| |||||||||

| 5,659,332 | ||||||||||

|

| |||||||||

28

DOMINI INTERNATIONAL SOCIAL EQUITY FUND

PORTFOLIOOF INVESTMENTS (continued)

July 31, 2014

| COUNTRY/SECURITY | INDUSTRY | SHARES | VALUE | |||||||

Poland – 0.2% | ||||||||||

Orange Polska SA | Telecommunication Services | 174,403 | $ | 575,467 | ||||||

|

| |||||||||

| 575,467 | ||||||||||

|

| |||||||||

Singapore – 0.1% | ||||||||||

Singapore Airlines Ltd | Transportation | 53,000 | 435,406 | |||||||

|

| |||||||||

| 435,406 | ||||||||||

|

| |||||||||

South Africa – 1.3% | ||||||||||

MTN Group Ltd | Telecommunication Services | 190,610 | 3,947,901 | |||||||

Sanlam Ltd | Insurance | 2,531 | 14,365 | |||||||

|

| |||||||||

| 3,962,266 | ||||||||||

|

| |||||||||

South Korea – 3.0% | ||||||||||

GS Holdings | Energy | 52,988 | 2,410,026 | |||||||

Industrial Bank of Korea | Banks | 91,435 | 1,355,684 | |||||||

KT Corp | Telecommunication Services | 75,020 | 2,419,905 | |||||||

SK Hynix Inc (a) | Semiconductors & Semiconductor Equipment | 64,420 | 2,802,886 | |||||||

|

| |||||||||

| 8,988,501 | ||||||||||

|

| |||||||||

Spain – 3.3% | ||||||||||

Acerinox SA | Materials | 177,600 | 2,953,275 | |||||||

Banco Santander SA | Banks | 44,444 | 446,192 | |||||||

Banco Santander SA Rights (a) (c) | Banks | 44,444 | 9,106 | |||||||

Gamesa Corp Tecnologica SA (a) | Capital Goods | 134,681 | 1,685,184 | |||||||

Red Electrica Corp SA | Utilities | 54,505 | 4,679,903 | |||||||

|

| |||||||||

| 9,773,660 | ||||||||||

|

| |||||||||

Sweden – 4.1% | ||||||||||

Atlas Copco AB Cl A | Capital Goods | 440 | 13,113 | |||||||

Hennes & Mauritz AB Cl B | Retailing | 277 | 11,311 | |||||||

Holmen AB Cl B | Materials | 72,009 | 2,422,374 | |||||||

Husqvarna AB Cl B | Consumer Durables & Apparel | 89,365 | 704,070 | |||||||

Investor AB Cl B | Diversified Financials | 72,380 | 2,599,065 | |||||||

Skandinaviska Enskilda Banken AB Cl A | Banks | 122,894 | 1,643,332 | |||||||

Skanska AB Cl B | Capital Goods | 209,819 | 4,354,837 | |||||||

SKF AB Cl B | Capital Goods | 385 | 9,065 | |||||||

TeliaSonera AB | Telecommunication Services | 60,364 | 451,602 | |||||||

|

| |||||||||

| 12,208,769 | ||||||||||

|

| |||||||||

Switzerland – 7.4% | ||||||||||

Aryzta AG | Food & Beverage | 25,919 | 2,342,969 | |||||||

Baloise Holding AG | Insurance | 17,225 | 2,072,725 | |||||||

Clariant AG | Materials | 21,488 | 399,798 | |||||||

Logitech International SA | Technology Hardware & Equipment | 76,076 | 1,115,121 | |||||||

Novartis AG | Pharma, Biotech & Life Sciences | 100,823 | 8,766,154 | |||||||

Swiss Life Holding AG (a) | Insurance | 13,792 | 3,187,447 | |||||||

29

DOMINI INTERNATIONAL SOCIAL EQUITY FUND

PORTFOLIOOF INVESTMENTS (continued)

July 31, 2014

| COUNTRY/SECURITY | INDUSTRY | SHARES | VALUE | |||||||

Switzerland (Continued) | ||||||||||

Swiss Re AG | Insurance | 51,704 | $ | 4,392,569 | ||||||

|

| |||||||||

| 22,276,783 | ||||||||||

|

| |||||||||

Taiwan – 0.5% | ||||||||||

Asustek Computer Inc | Technology Hardware & Equipment | 139,000 | 1,468,863 | |||||||

|

| |||||||||

| 1,468,863 | ||||||||||

|

| |||||||||

United Kingdom – 16.1% | ||||||||||

3i Group PLC | Diversified Financials | 610,898 | 3,880,099 | |||||||

Associated British Foods PLC | Food & Beverage | 131,108 | 6,137,406 | |||||||

Aviva PLC | Insurance | 409,687 | 3,467,093 | |||||||

Barratt Developments PLC | Consumer Durables & Apparel | 301,640 | 1,769,567 | |||||||

Berendsen PLC | Commercial & Professional Services | 106,439 | 1,877,267 | |||||||

BG Group PLC | Energy | 20,954 | 413,197 | |||||||

BT Group PLC | Telecommunication Services | 950,855 | 6,225,147 | |||||||

Hammerson PLC | Real Estate | 324,977 | 3,286,137 | |||||||

InterContinental Hotels Group PLC | Consumer Services | 36,140 | 1,466,227 | |||||||

Kingfisher PLC | Retailing | 87,299 | 440,936 | |||||||

Marks & Spencer Group PLC | Retailing | 1,781 | 12,892 | |||||||

Next PLC | Retailing | 48,516 | 5,537,224 | |||||||

Persimmon PLC | Consumer Durables & Apparel | 62,920 | 1,325,190 | |||||||