UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number 811-05823

DOMINI INVESTMENT TRUST

(Exact Name of Registrant as Specified in Charter)

532 Broadway, 9th Floor, New York, New York 10012

(Address of Principal Executive Offices)

Carole M. Laible

Domini Impact Investments LLC

532 Broadway, 9th Floor

New York, New York 10012

(Name and Address of Agent for Service)

Registrant’s Telephone Number, including Area Code: 212-217-1100

Date of Fiscal Year End: July 31

Date of Reporting Period: July 31, 2017

| Item 1. | Reports to Stockholders. |

A copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 follows.

| KEEP IN TOUCH WITH DOMINI |

A report like this comes twice a year, but your dollars work for change all year long. Stay connected with us on Facebook and Twitter:

|

facebook.com/dominifunds

facebook.com/dominifunds twitter.com/dominifunds

twitter.com/dominifunds

| SIGN UP FOR E-DELIVERY |

If you invest directly with Domini, you can avoid an annual fee of $15 by signing up for paperless E-Delivery of your statements, reports and tax forms — just log into your account, go to “Account Options,” and select “E-Delivery Option.”

If you invest through a financial advisor, brokerage firm, or employer-sponsored retirement plan, why not ask your advisor or plan sponsor how to receive your documents electronically? It can reduce your carbon footprint, save trees, and unclutter your life, all with just a few strokes of your keyboard! |

THE WAY YOU INVEST MATTERS®

Dear Fellow Shareholders:

The past few years have been extraordinary. Reviewing the headlines, one sees a broad range of issues that continue to develop: The Syrian refugee crisis, the scandalous revelation of sham accounts at one of our nation’s leading banks — along with the resignation of the CEO, the Panama Papers and the zika virus. The Department of Labor withdrew two legal bulletins that discouraged fiduciaries from considering the social and environmental impacts of their investments, and there were concerted efforts to avoid a point of no return on climate change. Meanwhile, the globe’s population continued to grow. Then came November, and the Presidential election, the sweep of the Senate, and a whole new approach to stewardship of this great American experiment.

For those of us interested in tracking social and environmental progress, the news has not been encouraging. We have had further affirmation that climate change is real and is manmade. We have had continuing acts of terror. Meanwhile, corporations have taken increasingly open positions that seem to refute the Administration’s stated policies, whether relating to immigration, gender-identity, climate, or race relations.

To say that global markets have shrugged off the tumult would be an understatement. Markets have been rising with extremely low volatility, in an almost eerily calm fashion. While on the one hand it makes sense — corporate earnings continue to rise and that is good for stocks — on the other hand one is left wondering how we can possibly see companies growing their earnings amidst all the uncertainty in the world.

There are some reasons for the market’s continued rise. Going forward, investors anticipate a potentially lower corporate tax rate in the U.S., making their ownership more valuable still. Interest rates, while rising, are nowhere near high enough to offer competition to stocks for investable dollars. The financial case still exists for equities. Higher earnings, less pesky government interest in how the profits are made, little competition from other potential investments, and that potential ability to keep more of the profits, by paying lower taxes, provide a formidable backdrop. This has all been good for stocks in the short term. However, as investors for the long haul, and as citizens of this planet, we have many concerns.

2

THE WAY YOU INVEST MATTERS®

One of the most exciting developments of the past year has been the rapid acceptance of the United Nations Sustainable Development Goals (SDGs). This 17-point program was adopted in 2015 and lays out the issues, from Zero Hunger to Decent Work and Economic Growth, to Life Below Water, that the world’s nations have committed to address, in partnership with the private sector. Strongly supportive of Peace, Justice and Strong Institutions, the goals focus on cross-cutting issues such as gender equality and North-South economic cooperation. They even include a nod to corporate sustainability reporting, a provision Domini Impact Investments urged UN delegates and ambassadors to include, in meetings we attended back in 2012 and 2013.

The SDGs present an ambitious vision for the future, recognizing that societal and environmental challenges are intertwined. According to the UN Development Programme Administrator, Helen Clark, “We are advocating for countries to have access to the funding they need to improve the lives of all their peoples and to be able to do that in ways which safeguard the integrity of vital ecosystems.” At Domini Impact Investments, “universal human dignity and ecological sustainability” have long been our guiding principles. We were delighted to see the close alignment between our approach and the SDGs, as a more holistic vision for the future has taken hold globally.

As your mutual fund manager, we have undertaken an initiative to more deliberately track our efforts on your behalf and to consider how they support the SDGs. The essay in this annual report is a part of that initiative. In it we study one aspect of Life Below Water, sustainable seafood. As with all the goals, the hurdles are enormous and progress slow. Nonetheless, noteworthy actions have been taken. We hope you enjoy reading about these efforts.

On social and ecological levels, the past twelve months have documented for us the continuing need to have the voice of investors at the table as citizens of the planet. Investors stand at the junction between one of the strongest, most organized and universal forces on the planet — finance — and the very real impact that finance has, for good or bad. The role of the socially responsible investor has never been more important.

Thank you for your investment and for your continuing support of responsible investing.

Sincerely,

Amy Domini Chair

|

Carole Laible President |

3

THE WAY YOU INVEST MATTERS®

Michael Kors Adopts Protections for Migrant Workers

No worker should ever have to pay for their job. Once they are employed, they must be able to understand the terms of their employment and be free to leave at any time. These are basic principles that most of us take for granted, but for millions of migrant workers around the world, they are very far from the norm. Many workers are placed in conditions of bonded labor, indebted to unscrupulous recruitment agencies, sometimes without access to their passports. We have been working with other investors and companies in our portfolios to change that.

We reached agreement to withdraw our shareholder proposal with Michael Kors, after constructive conversations with the company’s General Counsel. Michael Kors improved its labor requirements for its suppliers, and updated its public reporting describing the actions it is taking to address modern slavery. Among the company’s new commitments, the company will ensure that no worker in its global supply chain pays for employment, and that any recruitment fees found will be “promptly” reimbursed. Michael Kors will also require all new suppliers to disclose information about the recruitment agencies they use, prior to onboarding these suppliers into its supply chain. In addition, the company strengthened its non-discrimination policies and its protections for younger workers. We look forward to continuing our conversation with the company about implementation of these strong commitments.

Visit domini.com to read our paper, Protecting Migrant Workers.

Defending our Right to Submit Shareholder Proposals

Domini has submitted more than 280 shareholder proposals to more than 100 companies since 1994, because the shareholder proposal has proven to be a highly effective corporate accountability tool. The Financial CHOICE Act, pending before the U.S. Senate, includes a provision that would effectively eliminate our ability to submit shareholder proposals by raising the bar so high to submit a proposal that only a handful of the largest institutional investors in the world could do so. We are actively coordinating with other investors to defeat this legislation.

We published two articles on the topic, in Responsible Investor and on the Harvard Law School Forum on Corporate Governance and Financial Regulation (available at domini.com). In mid-July, we joined other investors in meetings with Senate Banking Committee staff. Our articles were used by the investor coalition to help educate Senate staff about the importance of the shareholder proposal rule.

Visit domini.com to learn more about our work on your behalf to engage corporations and policy makers on social and environmental issues, and read our quarterly Social Impact Updates.

4

THE WAY YOU INVEST MATTERS®

The Impact of How We Eat

The oceans cover more than 70% of the Earth’s surface, representing 99% of the living space on our planet, by volume. More than three billion people depend on marine and coastal biodiversity for their livelihoods, and their primary source of protein.

Today, however, the oceans are under severe threat from climate change, toxic pollution and unsustainable fishing practices. These factors threaten both the continued availability of fish for consumption as well as the healthiness of the fish we consume.

The idea that the supply of fish in the ocean is limitless has contributed to all of us taking it for granted. It is estimated that two-thirds of the world’s fish stocks are either fished at their limit or overfished, and Greenpeace reports that fish at the top of the food chain, such as tuna, are disappearing quickly. Additionally, the World Bank estimates that the economic losses due to overfishing are approximately $50 billion per year.

Seafood differs substantially from other animal-based industrial agriculture. While it is easy to track and manage livestock, there isn’t a single scientific authority that can conclusively answer the question of how many fish are in the sea, or even how many species of life the oceans support. According to the United Nations, our oceans contain nearly 200,000 species, but actual numbers may lie in the millions.

Companies that depend on the seafood supply chain have a host of issues to manage, including overfishing, destructive fishing practices, and labor rights abuses. The field of sustainable seafood is complex, with a bewildering array of acronyms, certification systems and open questions to consider. We hope that this essay will help to clear up some of that confusion and give you a good sense of what some companies in our portfolios are doing to address these key challenges. We also provide some resources that you, as a consumer, can use to make smarter seafood choices.

The Cost of Modern Fishing

Seafood is the last major food source that is still caught in the wild, but the oceans cannot replenish fish at the rate we are pulling them out. Currently, about half of the world’s seafood is wild-caught and, as discussed below, farmed fish depend heavily on wild-caught feed. Modern fishing fleets are capable of catching larger quantities of fish at a time, but do not always efficiently target their nets to ensure they avoid accidentally catching other species (these non-target species are known as “bycatch”). According to Greenpeace, 100 million sharks, 300,000 whales and dolphins and 100,000 albatrosses are inadvertently caught and killed

5

THE WAY YOU INVEST MATTERS®

every year in nets or on fishing lines. In addition, some fishing practices — like bottom trawling — destroy habitats, including coral formations.

Illegal, unreported and unregulated fishing is also a substantial problem, accounting for an estimated 19% of the global catch. One-third of all fish sold in the United States is believed to be caught illegally. Not only do poachers ignore catch quotas established by governments, they also use outlawed equipment, including nets stretching 15 miles or more that scoop up everything in their path. The Wall Street Journal reports that “the most critical area for poaching is off the coast of West Africa, where illegal, unauthorized and unregulated fishing accounts for an estimated 40% of fish caught.” Illegal fishing threatens marine ecosystems and food security in some of the world’s poorest countries.

The Hope for Sustainable Aquaculture

The other half of the world’s seafood is produced via aquaculture, or fish farming, a practice that dates back thousands of years. Today, the vast majority of aquaculture production comes from Asia, with China alone accounting for 60% of the global aquaculture output. Aquaculture has grown in response to rising consumer demand and declining stocks of wild fish. According to experts, farmed fish production may surpass wild catches by 2019.

As the production of farmed fish increases, so do its side effects. The most common type of aquaculture consists of farming in net pens or cages anchored to the sea floor in the ocean or near the coast. As with many other types of farming practices, aquaculture presents challenges. In some fish farms, densely packed pens can lead to high disease rates, which producers try to avoid with the liberal use of antibiotics. Infectious diseases among farmed fish can also spread to native populations, introducing non-native diseases into the environment or facilitating disease through unsanitary conditions. When farmed fish escape their pens, they pose a threat to wild fish populations.

Another issue with farmed fish is their feed. Fish species like salmon and tuna are carnivorous and require a diet high in fat. To feed and sustain these kinds of farmed fish, other fish species, such as sardines or mackerel, must be harvested from the ocean. Producers use fish meal, which combines fish oil, wheat products, and chemicals into pellets which are then fed to cultivated fish. The National Oceanic and Atmospheric Administration (NOAA), a U.S. government agency, reports that one pound of farmed salmon uses the fish oil from about five pounds of wild fish and fish meal from 1.3 pounds of fish. If we accept that large scale aquaculture is here to stay, we must ensure that it is done sustainably.

Open ocean aquaculture can be part of the solution, but it should only be used to cultivate species that are native in open water systems. Open

6

THE WAY YOU INVEST MATTERS®

ocean aquaculture entails moving pens into the open ocean where the water is pristine and currents are strong enough to continually flush the farms of fish waste and pests. The open ocean also provides fish with more consistent salinity and temperature. That means the fish are less stressed and vulnerable to disease, which promotes better growth and minimizes the need for antibiotics or vaccines.

For the cultivation of non-native species, land-based tank systems can be used. Due to the high costs of operation, however, tank-based systems currently represent just half a percent of total industry production. The best land-based closed systems are capable of recycling 99% of their water. In addition, the water can be monitored continuously, which lessens the risk of disease and the need for antibiotics.

Plant-based feeds may also be a sustainable option for fish farms. Efforts to replace proteins from fish meal with grains and oilseeds started many years ago. Today, entrepreneurs are working on alternative feeds like algae and large corporations like Cargill (not currently approved for the Domini Funds) are investing in genetically modified oilseeds. In addition, researchers are trying to determine whether popular carnivorous fish like trout, yellowtail, walleye, and Atlantic salmon can survive on vegetarian and fish-free diets. If so, fish farmers would be able to drastically reduce their use of fish meal.

Currently, there are no publicly traded aquaculture companies that meet Domini’s standards for investment. Farmed fish, however, is part of the supply chain of many companies in the food industry, including food manufacturers, distributors, and retailers that meet Domini’s standards for investment.

Labor Rights in The Seafood Supply Chain

Labor rights are a major concern throughout the seafood supply chain, whether it’s wild-caught or farmed. In “Protecting Migrant Workers,” an essay in the Domini Funds’ most recent Semi-Annual Report, we described how our research department identified the enslavement of migrant workers as a high risk in the seafood supply chain. Costco, Sysco, William Morrisons and other major companies have joined the Seafood Task Force (www.seafoodtaskforce.global), a multi-stakeholder alliance that aims to tackle forced labor and human trafficking in seafood production. Domini continues to work with other investors and companies on these and other challenges facing migrant workers.

Certifications and Traceability

Companies depend upon global supply chains that can be complex, multi-tiered and opaque. However, we cannot hope to ensure that our seafood is truly sustainably sourced without end-to-end traceability, meaning that each unit of seafood sold to a consumer can be traced all the way back to

7

THE WAY YOU INVEST MATTERS®

its point of harvest at sea or on a farm. Traceability of supply chains also supports compliance with restrictions on illegal, unreported and unregulated fishing. Traceability is a daunting logistical task, but rapid advances are being made in the development of affordable tracking systems. Companies are increasingly using a variety of certifications, as well as joining multi-stakeholder task forces and industry associations, to advance the dialogue on sustainable seafood sourcing practices.

The Marine Stewardship Council (MSC), originally formed out of a collaboration between the World Wildlife Fund (WWF) and Unilever (at the time, one of the world’s largest producers of frozen seafood), offers one of the most widely used sustainable seafood certification systems for wild-catch fisheries. The MSC Fisheries Standard is based on three pillars: sustainable fish stocks, minimizing environmental impact, and effective management. It is important to view MSC as a process, rather than a “seal of approval.” Many MSC-certified fisheries have significant room to improve. If a fishery meets the standard for certification, the fishery then must submit an action plan on how it will improve its performance and must undergo surveillance audits on an annual basis. The certification must be renewed every five years. MSC also offers a Chain of Custody standard, which ensures that seafood is traceable to an MSC-certified fishery.

The Aquaculture Stewardship Council (ASC) standards were developed by NGOs, marine scientists and the salmon industry. ASC certifies twelve species of farm-raised seafood against standards that focus on both the environmental and social impacts of farming.

Two other initiatives we are watching closely include the Ocean Disclosure Project and Fish Tracker. The Ocean Disclosure Project, launched by the Sustainable Fisheries Partnership (SFP), prompts companies to publicly disclose extensive information about the wild-caught seafood they buy. William Morrison Supermarket (UK) was one of the five initial signatories when it launched in 2015 and remains the project’s only publicly traded participant. We are also optimistic about the launch of Fish Tracker, an initiative by Investor Watch, to align capital markets with sustainable fisheries management. Though these initiatives are in their early stages, Domini values these resources to further our research and engagement activities.

Finally, the Monterey Bay Aquarium’s Seafood Watch program has developed science-based standards for fisheries and aquaculture to help distinguish between which species are sustainable options and which seafood would be best to avoid (“red-rated”) due to concerns with overfishing or destructive fishing or farming practices. Similarly, Greenpeace maintains its own “Red List” which highlights species of

8

THE WAY YOU INVEST MATTERS®

seafood the organization believes should not be made commercially available due to various risks such as overfishing or illegal fishing practices.

The Corporate Response

Corporate sustainable seafood policies generally rely upon a mix of certification standards, including MSC, ASC and others, as well as, species-specific policies. As you will see from the brief profiles below, among our Funds’ current holdings with exposure to seafood, there are a range of policies and approaches to the difficult issues companies face.

In the United States, Whole Foods was the first retailer to sell MSC-certified products back in 2000. For three consecutive years, Whole Foods has received the top ranking in Greenpeace’s “Carting Away the Oceans” report, which annually ranks supermarket chains on their approach to seafood sourcing. Whole Foods prohibits the sale of red-rated seafood, and states that it will not sell seafood that is overfished, poorly managed, or caught in ways that cause harm to habitats or other wildlife. In March 2017, the company announced that it was establishing sustainability and traceability requirements for canned tuna. Whole Foods also requires suppliers to track each lot of tuna from the boat to the cannery. In addition, the company requires that farm-raised seafood be third-party verified to meet its Responsibly Farmed Standards, which prohibits the use of antibiotics. In August, Amazon.com acquired Whole Foods. We will be watching closely to see whether Amazon maintains Whole Foods’ long-term commitment to sustainable seafood.

Sainsbury’s, the second largest British supermarket chain, has also been sourcing MSC-certified fish since 2000 and, according to MSC, is considered a global leader in sustainable seafood. In 2016, 76% of its wild-caught seafood was MSC-certified and the company is working towards having all fish it sells certified sustainable by 2020.

Unlike Whole Foods, which will not carry “red-rated” species under any circumstances, Costco’s seafood sourcing policy states that it will not sell certain wild species that have been identified as at great risk, unless sources are certified by the MSC. Rather than simply avoid fish from fisheries that fail to meet MSC standards, the company is working with a group of WWF sponsored Fishery Improvement Projects (FIP) designed to bring fisheries up to MSC standards. Costco’s major canned tuna suppliers are participants in the International Seafood Sustainability Foundation, which is undertaking “science-based initiatives for the long-term conservation and sustainable use of tuna stocks, reducing bycatch and promoting ecosystem health.” The company works to source farmed fish from suppliers that are ASC-certified and has participated in the implementation of ASC dialogues that include salmon, shrimp, tilapia,

9

THE WAY YOU INVEST MATTERS®

and pangasius. Domini has been in dialogue with Costco on seafood issues since 2010, most recently around its involvement in addressing human rights issues in the supply of shrimp from Thailand.

U.S. supermarket chain Kroger reports that 69% of its total seafood volume came from MSC-certified fisheries. The company states that traceability and the removal of illegally sourced seafood is a critical component of a comprehensive sustainable seafood policy and commitment. Since 2009, Kroger has reportedly supported 23 FIPs through sourcing, letters to stakeholders, and/or direct funding.

Metro AG is the third-largest retailer in Germany and one of Europe’s leading fish wholesalers. Metro has a sustainable fish selection that includes a wide range of MSC and ASC-certified products. By 2020, Metro is seeking to offer 80% of its twelve best-selling types of fish and seafood from sustainably certified sources. Currently, Metro reports that 90% of its aquaculture seafood is certified. The company also works with small-scale fishermen in support of more sustainable practices. To address the substantial pressure on fish stocks in Japan, Metro’s subsidiary Metro Cash & Carry Japan is working with a local university to raise fish from fertilized fish eggs to ensure a fully traceable and sustainable aquaculture process.

Sysco, a food distribution company that supplies restaurants, hotels, hospitals and schools, reports that as of 2015, 9 of its top 10 Sysco Brand seafood products came from certified fisheries or fisheries engaged in a comprehensive FIP. Sysco is also collaborating with WWF to improve its seafood procurement practices.

The seafood supply chain does not only affect food for human consumption. The Canadian retailer, Loblaw, for example, offers MSC-certified dog and cat food products across over 1,000 supermarkets.

Tiger Brands, South Africa’s largest food and consumer healthcare company, has a 42% ownership in Oceana Group Ltd, which is the only direct exposure to a fishery in the Domini Funds’ portfolios. Oceana, a black-owned company, publishes reports on its environmental and social impact and has partnered with WWF to advance ecosystem-focused fisheries management practices.

10

THE WAY YOU INVEST MATTERS®

Looking Ahead

On September 25, 2015, the United Nations announced its new global sustainability agenda, in the form of seventeen Sustainable Development Goals (SDGs). SDG 14 is to “Conserve and sustainably use the oceans, seas and marine resources.” Each goal is accompanied by a set of targets.

We believe that it is critical for the private sector, including corporations, investors and consumers, to play an active role in promoting the SDGs and delivering on their ambitious targets. This is an imperative if we are to serve the needs of a rapidly growing human population while respecting planetary limits.

Human civilization cannot survive without healthy ecosystems. Financial returns, of course, are also at stake, as corporations depend upon dwindling natural resources to deliver value to shareholders. You’ll be hearing more from Domini on how our work aligns with the SDGs and how we intend to strengthen those efforts, including efforts to improve the sustainability of seafood.

With the exception of Cargill, which is not currently approved for investment, the holdings discussed above can be found in the portfolios of the Domini Funds, included herein. The composition of the Funds’ portfolios is subject to change.

The Domini Funds are not insured and are subject to market risks. Investment return, principal value, and yield may fluctuate. An investor’s shares when redeemed may be worth more or less than their original cost. You may lose money.

This report is not authorized for distribution to prospective investors of the Domini Funds referenced herein unless preceded or accompanied by a current prospectus for the relevant Fund. Nothing herein contained is to be considered a recommendation concerning the merits of any noted company, or an offer of sale or a solicitation of an offer to buy shares of any Fund or company referenced in this report. Such offering is only made by prospectus, which includes details as to the offering price and other material information. Please read the prospectus carefully before investing. The Domini Funds are distributed by DSIL Investment Services LLC (DSILD), Member FINRA. Domini Impact Investments LLC (Domini) is the Funds’ investment manager. The Funds are subadvised by Wellington Management Company LLP. DSILD and Domini are not affiliated with Wellington Management Company LLP 9/17

11

Don’t underestimate your effectiveness as a consumer — you have the power to change entire industries with your choices and collective voice. Here are some fish-buying tips and resources:

| • | Diversify the species of seafood you consume. Shrimp, salmon, tuna, tilapia, and pollock are among the most widely consumed seafood in the United States. Environmental organizations warn that the overconsumption of certain species can lead to various risks for consumers and the environment. |

NRDC: The Smart Seafood Buying Guide (www.nrdc.org/stories/smart-seafood-buying-guide) helps consumers diversify the types of seafood they eat, avoid species high in mercury, buy seafood sourced from countries with strong regulations and support local community fisheries.

| • | Be picky about where you shop. You can choose to shop at retailers that have made a concerted effort to offer more certified and sustainable seafood. You can request to talk to the manager of the seafood department or reach out to the corporate office to inquire about what it would take for the store to support more sustainable seafood options. If you notice that your local grocery store is doing a poor job communicating their policies or consistently performing low in reports such as Greenpeace’s annual Carting Away the Oceans, don’t be afraid to speak up. |

Greenpeace: Carting Away the Oceans (cato.greenpeaceusa.org) provides annual rankings of food retailers that can help consumers make educated decisions on where to shop for seafood. See also Greenpeace’s Sustainable Seafood Consumer Hub at http://seafood.greenpeaceusa.org/

| • | Choose your fish wisely. Take advantage of available consumer resources and guides — they exist to help empower consumers to make sustainable seafood choices, whether you are shopping at your local grocery store or if you are out to dinner. |

Monterey Bay Aquarium: Seafood Watch (www.seafoodwatch.org) highlights which species of fish are “Best Choices” (green), “Good Alternatives” (yellow), or ones to “Avoid” (red). The aquarium also offers national, regional and state guides on their website and as a smartphone app.

NOAA: FishWatch: (www.fishwatch.gov) The National Oceanic and Atmospheric Administration publishes FishWatch U.S. Seafood Facts, a comprehensive online resource where you can view profiles of over 100 species of U.S. farmed or U.S. wild-caught species of seafood that include information on population, fishing rates, habitat impacts, as well as health and nutrition facts.

12

Performance Commentary (Unaudited)

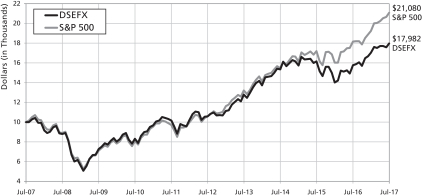

For the year ended July 31, 2017, the Domini Impact Equity Fund Investor shares returned 14.07%, lagging the S&P 500 Index, which returned 16.04%.

The Fund is managed through a two-step process designed to capitalize on the strengths of Domini Impact Investments LLC (“Domini”) and Wellington Management Company LLP (“Wellington Management”). Domini creates an approved list of companies based on its social, environmental and governance analysis, and Wellington then utilizes a disciplined and systematic process to manage the portfolio. Wellington Management’s philosophy relies on systematically exploiting sources of excess returns, stemming from both common behavioral, market structure, and risk premia inefficiencies in the market and the belief that certain factors are strongly associated with stock outperformance.

Security selection was the primary detractor from the Fund’s performance relative to the S&P 500 Index, driven by weak selection in the consumer discretionary, information technology, and health care sectors. Within consumer discretionary, underperformance was driven primarily by positions in retailers, particularly Foot Locker and Ross Stores. Relative underperformance in information technology was driven by our overweight position in IBM, and our underweight positions of strong-performing Apple and Facebook during the period. In health care, our overweight position in Edwards Lifesciences detracted most during the period. Both the Foot Locker and Edwards Lifesciences positions were eliminated by the end of the period.

The Fund’s sector allocations partially offset the negative results from security selection, primarily driven by an underweight allocation to the poor performing energy sector and an overweight allocation to the strong performing information technology sector. Additionally, security selection in the industrials, financials, and energy sectors aided relative performance.

From a market capitalization standpoint, the portfolio’s strong security selection within mid-cap securities ($2 to $10 billion) and large-cap ($20 to $50 billion) compared to the S&P 500 Index were primary contributors to relative performance. However, weak security selection in mega-cap (>$50 billion) securities partially offset these strong returns. The portfolio benefited from an overweight allocation to small-cap (<$2 billion) securities.

Over the last year, the Fund’s positive relative exposure to Wellington’s valuation and quality themes added to returns compared to the benchmark. Valuation did particularly well in the second half of 2016 at the expense of momentum. These trends have reversed in 2017, with the market becoming more singularly focused on momentum.

13

Top detractors from relative performance, compared to the S&P 500 Index, included Foot Locker (consumer discretionary), Ross Stores (consumer discretionary), and Verizon (telecommunication services). Top contributors to relative performance included Prudential Financial (financials), Applied Materials (information technology), and Unum Group (financials).

During the period Wellington Management deployed refinements to its portfolio construction process, to reduce trading costs and market impact by making better use of available liquidity. These refinements are designed to augment Wellington’s historically strong management of trading costs.

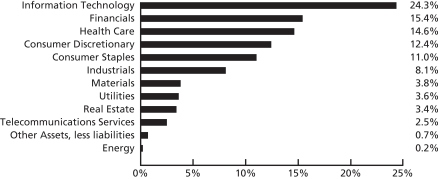

TEN LARGEST HOLDING (Unaudited)

| SECURITY DESCRIPTION | % NET ASSETS | SECURITY DESCRIPTION | % NET ASSETS | |||||||

| Apple Inc. | 3.7% | Consolidated Edison Inc. | 2.8% | |||||||

| Alphabet Inc. Class A | 3.3% | Gilead Sciences Inc. | 2.7% | |||||||

| PepsiCo Inc. | 3.1% | Cummins Inc. | 2.6% | |||||||

| Prudential Financial Inc. | 3.0% | International Business Machines Corp |

| 2.5% |

| |||||

| Amazon.com Inc. | 2.9% | |||||||||

| Unum Group | 2.4% | |||||||||

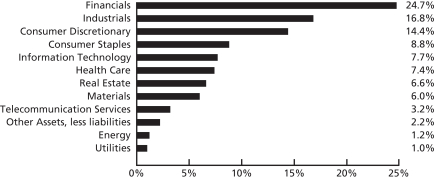

PORTFOLIO HOLDINGS BY INDUSTRY SECTOR (% OF NET ASSETS) (Unaudited)

The Fund is subject to market, sector concentration, style and foreign investing risks. Investing internationally involves special risks, such as currency fluctuations, social and economic instability, differing security regulations and accounting standards limited public information possible changes in taxation, and periods of illiquidity.

14

| AVERAGE ANNUAL TOTAL RETURNS (Unaudited) | Investor shares | S&P 500 | ||||

| As of 7/31/17 | 1 Year | 14.07% | 16.04% | |||

| 5 Year | 11.19% | 14.78% | ||||

| 10 Year | 6.04% | 7.74% | ||||

| Since Inception (6/3/91) | 8.33% | 9.53% | ||||

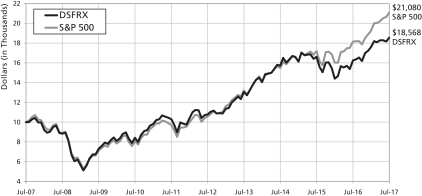

COMPARISON OF $10,000 INVESTMENT IN THE DOMINI IMPACT EQUITY FUND INVESTOR SHARES AND S&P 500 (Unaudited)

Past performance is no guarantee of future results. The Fund’s returns quoted above represent past performance after all expenses. The returns reflect any applicable expense waivers in effect during the periods shown. Without such waivers, Fund performance would be lower. Investment return, principal value, and yield will fluctuate. Your shares, when redeemed, may be worth more or less than their original cost. Call 1-800-582-6757 or visit www.domini.com for performance information current to the most recent month-end, which may be lower or higher. A 2.00% fee applies on sales/exchanges made less than 30 days after purchase/exchange, with certain exceptions. Quoted performance data does not reflect the deduction of this fee, which would reduce the performance quoted. See the Fund’s prospectus for further information.

On November 30, 2006, the Fund changed from a passive to active management strategy. Performance from Fund inception through November 29, 2006, reflects the former passive investment strategy.

Per the prospectus supplement dated May 1, 2017, the Fund’s gross and net annual operating expenses totaled 1.08% of net assets. Until 11/30/17, the Fund’s Manager has contractually agreed to limit certain ordinary Investor share expenses to 1.25% of its average daily net assets per annum, absent an earlier modification by the Fund’s Board.

The table and the graph do not reflect the deduction of fees and taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Total return for the Domini Impact Equity Fund is based on the Fund’s net asset values and assumes all dividend and capital gains were reinvested. An investment in the Fund is not a bank deposit and is not insured. You may lose money.

The Standard & Poor’s 500 Index (S&P 500) is an unmanaged index of common stocks. Investors cannot invest directly in the S&P 500.

15

| AVERAGE ANNUAL TOTAL RETURNS (Unaudited) | ||||||||

| Class A shares (with 4.75% maximum Sales Charge) | Class A shares (without Sales Charge) | S&P 500 | ||||||

| As of 7/31/17 | 1 Year | 8.55% | 13.97% | 16.04% | ||||

| 5 Year | 10.10% | 11.17% | 14.78% | |||||

| 10 Year* | 5.53% | 6.04% | 7.74% | |||||

| Since Inception (6/3/91)* | 8.12% | 8.33% | 9.53% | |||||

COMPARISON OF $10,000 INVESTMENT IN THE DOMINI IMPACT EQUITY FUND CLASS A SHARES AND S&P 500 (WITH 4.75% MAXIMUM SALES CHARGE)* (Unaudited)

Past performance is no guarantee of future results. The Fund’s returns quoted above represent past performance after all expenses. The returns reflect any applicable expense waivers in effect during the periods shown. Without such waivers, Fund performance would be lower. Investment return, principal value, and yield will fluctuate. Your shares, when redeemed, may be worth more or less than their original cost. Call 1-800-498-1351 or visit www.domini.com for performance information current to the most recent month-end, which may be lower or higher. A 2.00% fee applies on sales/exchanges made less than 30 days after purchase/exchange, with certain exceptions. Quoted performance data does not reflect the deduction of this fee, which would reduce the performance quoted. See the Fund’s prospectus for further information.

On November 30, 2006, the Fund changed from a passive to active management strategy. Performance from Fund inception through November 29, 2006, reflects the former passive investment strategy.

Per the prospectus supplement dated May 1, 2017, the Fund’s gross and net annual operating expenses totaled 1.35% and 1.12% of net assets, respectively. Until 11/30/17, the Fund’s Manager has contractually agreed to limit certain ordinary Class A share expenses to 1.18% of its average daily net assets per annum absent an earlier modification by the Fund’s Board. The Fund’s total return would have been lower without this limit.

The table and the graph do not reflect the deduction of fees and taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Total return for the Domini Impact Equity Fund is based on the Fund’s net asset values and assumes all dividend and capital gains were reinvested. An investment in the Fund is not a bank deposit and is not insured. You may lose money.

The Standard & Poor’s 500 Index (S&P 500) is an unmanaged index of common stocks. Investors cannot invest directly in the S&P 500.

*Class A shares were not offered prior to November 28, 2008. All performance information for time periods beginning prior to November 28, 2008 is the performance of the Investor shares. This performance has not been adjusted to reflect the expenses of the Class A shares, but does, where noted, reflect an adjustment for the maximum applicable sales charge of 4.75%.

16

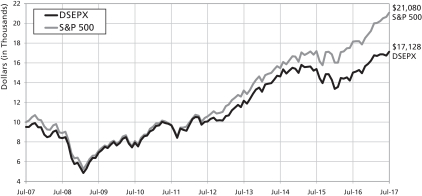

| AVERAGE ANNUAL TOTAL RETURNS (Unaudited) | Institutional shares | S&P 500 | ||||

| As of 7/31/17 | 1 Year | 14.51% | 16.04% | |||

| 5 Year | 11.61% | 14.78% | ||||

| 10 Year* | 6.04% | 7.74% | ||||

| Since Inception (6/3/91)* | 8.33% | 9.53% | ||||

COMPARISON OF $500,000 INVESTMENT IN THE DOMINI IMPACT EQUITY FUND INSTITUTIONAL SHARES AND S&P 500* (Unaudited)

Past performance is no guarantee of future results. The Fund’s returns quoted above represent past performance after all expenses. The returns reflect any applicable expense waivers in effect during the periods shown. Without such waivers, Fund performance would be lower. Investment return, principal value, and yield will fluctuate. Your shares, when redeemed, may be worth more or less than their original cost. Call 1-800-498-1351 or visit www.domini.com for performance information current to the most recent month-end, which may be lower or higher. A 2.00% fee applies on sales/exchanges made less than 30 days after purchase/exchange, with certain exceptions. Quoted performance data does not reflect the deduction of this fee, which would reduce the performance quoted. See the Fund’s prospectus for further information.

On November 30, 2006, the Fund changed from a passive to active management strategy. Performance from Fund inception through November 29, 2006, reflects the former passive investment strategy.

Per the prospectus supplement dated May 1, 2017, the Fund’s gross and net annual operating expenses totaled 0.75% and 0.74% of net assets, respectively. Until 11/30/17, the Fund’s Manager has contractually agreed to limit certain ordinary Institutional share expenses to 0.80% of its average daily net assets per annum absent an earlier modification by the Fund’s Board.

The table and the graph do not reflect the deduction of fees and taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Total return for the Domini Impact Equity Fund is based on the Fund’s net asset values and assumes all dividend and capital gains were reinvested. An investment in the Fund is not a bank deposit and is not insured. You may lose money.

The Standard & Poor’s 500 Index (S&P 500) is an unmanaged index of common stocks. Investors cannot invest directly in the S&P 500.

*Institutional shares were not offered prior to November 28, 2008. All performance information for time periods beginning prior to November 28, 2008 is the performance of the Investor shares. This performance has not been adjusted to reflect the expenses of the Institutional shares.

17

| AVERAGE ANNUAL TOTAL RETURNS (Unaudited) | Class R shares | S&P 500 | ||||

| As of 7/31/17 | 1 Year | 14.20% | 16.04% | |||

| 5 Year | 11.52% | 14.78% | ||||

| 10 Year | 6.38% | 7.74% | ||||

| Since Inception (6/3/91)* | 8.50% | 9.53% | ||||

COMPARISON OF $10,000 INVESTMENT IN THE DOMINI IMPACT EQUITY FUND CLASS R SHARES AND S&P 500* (Unaudited)

Past performance is no guarantee of future results. The Fund’s returns quoted above represent past performance after all expenses. The returns reflect any applicable expense waivers in effect during the periods shown. Without such waivers, Fund performance would be lower. Investment return, principal value, and yield will fluctuate. Your shares, when redeemed, may be worth more or less than their original cost. Call 1-800-498-1351 or visit www.domini.com for performance information current to the most recent month-end, which may be lower or higher. A 2.00% fee applies on sales/exchanges made less than 30 days after purchase/exchange, with certain exceptions. Quoted performance data does not reflect the deduction of this fee, which would reduce the performance quoted. See the Fund’s prospectus for further information.

On November 30, 2006, the Fund changed from a passive to active management strategy. Performance from Fund inception through November 29, 2006, reflects the former passive investment strategy.

Per the prospectus supplement dated May 1, 2017, the Fund’s gross and net annual operating expenses totaled 0.76% of net assets. Until 11/30/17, the Fund’s Manager has contractually agreed to limit certain ordinary Class R share expenses to 0.90% of its average daily net assets per annum absent an earlier modification by the Fund’s Board.

The table and the graph do not reflect the deduction of fees and taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Total return for the Domini Impact Equity Fund is based on the Fund’s net asset values and assumes all dividend and capital gains were reinvested. An investment in the Fund is not a bank deposit and is not insured. You may lose money.

The Standard & Poor’s 500 Index (S&P 500) is an unmanaged index of common stocks. Investors cannot invest directly in the S&P 500.

*Class R shares were not offered prior to November 28, 2003. All performance information for the portion of the period prior to November 28, 2003 is the performance of the Investor shares and has not been adjusted to reflect the expenses of the Class R shares.

18

DOMINI IMPACT EQUITY FUND

PORTFOLIOOF INVESTMENTS

July 31, 2017

| SECURITY | SHARES | VALUE | ||||||

| Common Stocks – 99.3% | ||||||||

| Consumer Discretionary – 12.4% | ||||||||

Amazon.com Inc (a) | 25,312 | $ | 25,002,687 | |||||

Best Buy Co Inc | 866 | 50,522 | ||||||

Burlington Stores Inc (a) | 38,047 | 3,311,230 | ||||||

Chipotle Mexican Grill Inc (a) | 29,124 | 10,011,957 | ||||||

Coach Inc | 348 | 16,405 | ||||||

Comcast Corp Cl A | 444,504 | 17,980,187 | ||||||

Gap Inc/The | 445 | 10,604 | ||||||

Home Depot Inc/The | 218 | 32,613 | ||||||

JC Penney Co Inc (a) | 1,546 | 8,364 | ||||||

Kohl’s Corp | 212 | 8,766 | ||||||

L Brands Inc | 219 | 10,159 | ||||||

Lear Corp | 36,990 | 5,481,548 | ||||||

Lowe’s Cos Inc | 364 | 28,174 | ||||||

Marriott International Inc/MD Cl A | 146 | 15,212 | ||||||

Michael Kors Holdings Ltd (a) | 235 | 8,563 | ||||||

NIKE Inc Cl B | 376 | 22,203 | ||||||

Ralph Lauren Corp | 82 | 6,203 | ||||||

Ross Stores Inc | 316,193 | 17,491,797 | ||||||

Scripps Networks Interactive Inc Cl A | 145,764 | 12,741,231 | ||||||

Staples Inc | 666 | 6,760 | ||||||

Starbucks Corp | 414 | 22,348 | ||||||

Target Corp | 181 | 10,257 | ||||||

TJX Cos Inc/The | 205,050 | 14,417,066 | ||||||

Walt Disney Co/The | 242 | 26,603 | ||||||

|

| |||||||

| 106,721,459 | ||||||||

|

| |||||||

| Consumer Staples – 11.0% | ||||||||

Avon Products Inc (a) | 2,873 | 10,458 | ||||||

Campbell Soup Co | 80,865 | 4,272,098 | ||||||

Coca Cola Co/The | 292 | 13,385 | ||||||

Colgate-Palmolive Co | 218,787 | 15,796,421 | ||||||

Costco Wholesale Corp | 73,364 | 11,628,928 | ||||||

Estee Lauder Cos Inc/The Cl A | 120 | 11,879 | ||||||

General Mills Inc | 175 | 9,741 | ||||||

Kimberly-Clark Corp | 141 | 17,366 | ||||||

Kraft Heinz Co/The | 223 | 19,504 | ||||||

Kroger Co/The | 860 | 21,087 | ||||||

Loblaw Companies LTD | 79,972 | 4,342,168 | ||||||

Mondelez International Inc Cl A | 265 | 11,665 | ||||||

National Beverage Corp | 28,556 | 2,916,139 | ||||||

PepsiCo Inc | 228,424 | 26,636,523 | ||||||

Procter + Gamble Co/The | 155 | 14,077 | ||||||

Sysco Corp | 178,211 | 9,377,463 | ||||||

Walgreens Boots Alliance Inc | 244,345 | 19,711,311 | ||||||

Whole Foods Market Inc | 248 | 10,356 | ||||||

|

| |||||||

| 94,820,569 | ||||||||

|

| |||||||

19

DOMINI IMPACT EQUITY FUND

PORTFOLIOOF INVESTMENTS (continued)

July 31, 2017

| SECURITY | SHARES | VALUE | ||||||

| Energy – 0.2% | ||||||||

Subsea 7 SA ADR | 134,203 | $ | 1,987,546 | |||||

|

| |||||||

| 1,987,546 | ||||||||

|

| |||||||

| Financials – 15.4% | ||||||||

AGNC Investment Corp | 109,628 | 2,321,921 | ||||||

American Express Co | 191 | 16,279 | ||||||

Banco Santander Brasil SA | 211,722 | 1,721,300 | ||||||

Bank of America Corp | 120,524 | 2,907,039 | ||||||

Bank of Montreal | 34,100 | 2,587,167 | ||||||

Bank of Nova Scotia/The | 37,616 | 2,343,853 | ||||||

Canadian Imperial Bank of Commerce | 53,003 | 4,602,781 | ||||||

DBS Group Holdings Ltd ADR | 106,738 | 6,847,243 | ||||||

Hartford Financial Services Group Inc/The | 96,599 | 5,312,945 | ||||||

Intercontinental Exchange Inc | 195 | 13,008 | ||||||

Invesco Mortgage Capital Inc | 125,474 | 2,086,633 | ||||||

Lincoln National Corp | 53,106 | 3,879,924 | ||||||

Loews Corp | 56,499 | 2,750,371 | ||||||

MetLife Inc | 264,764 | 14,562,020 | ||||||

MFA Financial Inc | 815,843 | 6,926,507 | ||||||

MGIC Investment Corp (a) | 191,235 | 2,231,712 | ||||||

Morgan Stanley | 292 | 13,695 | ||||||

National Bank Of Canada | 85,343 | 3,831,922 | ||||||

ORIX Corp ADR (a) | 27,030 | 2,238,895 | ||||||

PNC Financial Services Group Inc/The | 190 | 24,472 | ||||||

Popular Inc | 122,024 | 5,142,091 | ||||||

Prudential Financial Inc | 228,412 | 25,863,091 | ||||||

Radian Group Inc | 245,438 | 4,275,530 | ||||||

Regions Financial Corp | 273,143 | 3,987,888 | ||||||

Two Harbors Investment Corp | 538,798 | 5,328,712 | ||||||

Unum Group | 414,409 | 20,774,323 | ||||||

US Bancorp | 346 | 18,262 | ||||||

|

| |||||||

| 132,609,584 | ||||||||

|

| |||||||

| Health Care – 14.6% | ||||||||

Baxter International Inc | 47,532 | 2,874,735 | ||||||

Biogen Inc | 42,139 | 12,203,033 | ||||||

Bruker Corp | 50,108 | 1,437,097 | ||||||

Celgene Corp (a) | 47,243 | 6,397,175 | ||||||

Cooper Cos Inc/The | 19,705 | 4,805,458 | ||||||

Gilead Sciences Inc | 305,710 | 23,261,474 | ||||||

IDEXX Laboratories Inc (a) | 105,948 | 17,636,104 | ||||||

Intuitive Surgical Inc (a) | 899 | 843,496 | ||||||

Masimo Corp (a) | 41,257 | 3,902,912 | ||||||

Merck & Co Inc | 307,178 | 19,622,531 | ||||||

Quest Diagnostics Inc | 184,128 | 19,942,904 | ||||||

Sanofi ADR | 205,652 | 9,739,679 | ||||||

Taro Pharmaceutical Industries Ltd (a) | 13,198 | 1,508,927 | ||||||

Waters Corp (a) | 11,202 | 1,942,875 | ||||||

|

| |||||||

| 126,118,400 | ||||||||

|

| |||||||

20

DOMINI IMPACT EQUITY FUND

PORTFOLIOOF INVESTMENTS (continued)

July 31, 2017

| SECURITY | SHARES | VALUE | ||||||

| Industrials – 8.1% | ||||||||

3m Co | 115 | $ | 23,135 | |||||

Alaska Air Group Inc | 55,468 | 4,727,538 | ||||||

Applied Industrial Technologies Inc | 12,610 | 712,465 | ||||||

Cummins Inc | 132,390 | 22,228,280 | ||||||

Herman Miller Inc | 64,000 | 2,155,200 | ||||||

JetBlue Airways Corp (a) | 1,688 | 37,018 | ||||||

LSC Communications Inc | 409 | 8,744 | ||||||

ManpowerGroup Inc | 44,202 | 4,736,244 | ||||||

PACCAR Inc | 200,455 | 13,721,145 | ||||||

Robert Half International Inc | 246,711 | 11,163,673 | ||||||

RR Donnelley & Sons Co | 569 | 7,033 | ||||||

Toro Co/The | 60,485 | 4,299,879 | ||||||

United Parcel Service Inc Cl B | 131 | 14,448 | ||||||

United Rentals Inc (a) | 52,783 | 6,279,066 | ||||||

|

| |||||||

| 70,113,868 | ||||||||

|

| |||||||

| Information Technology – 24.3% | ||||||||

Advanced Micro Devices Inc (a) | 3,150 | 42,872 | ||||||

Alphabet Inc Cl A (a) | 29,894 | 28,264,777 | ||||||

Apple Inc | 212,755 | 31,643,051 | ||||||

Applied Materials Inc | 446,074 | 19,765,539 | ||||||

Cisco Systems Inc | 504 | 15,851 | ||||||

Citrix Systems Inc | 85,208 | 6,729,728 | ||||||

Electronic Arts Inc (a) | 73,961 | 8,634,207 | ||||||

Euronet Worldwide Inc (a) | 7,138 | 689,602 | ||||||

F5 Networks Inc (a) | 121,545 | 14,676,559 | ||||||

Facebook Inc Cl A (a) | 40,097 | 6,786,417 | ||||||

First Solar Inc (a) | 358 | 17,653 | ||||||

FUJIFILM Holdings Corp ADR (a) | 27,239 | 998,718 | ||||||

HP Inc | 145,662 | 2,782,144 | ||||||

Intel Corp | 563,339 | 19,981,634 | ||||||

International Business Machines Corp | 146,839 | 21,243,198 | ||||||

Lam Research Corp | 100,243 | 15,984,749 | ||||||

Mastercard Inc Cl A | 38,492 | 4,919,278 | ||||||

Microsoft Corp | 88,514 | 6,434,968 | ||||||

Motorola Solutions Inc | 201 | 18,227 | ||||||

Synopsys Inc (a) | 202,264 | 15,487,354 | ||||||

VMware Inc Cl A (a) | 43,116 | 3,997,284 | ||||||

|

| |||||||

| 209,113,810 | ||||||||

|

| |||||||

| Materials – 3.8% | ||||||||

Domtar Corp | 227,700 | 8,893,962 | ||||||

Louisiana-Pacific Corp (a) | 122,001 | 3,063,445 | ||||||

Nucor Corp | 230 | 13,264 | ||||||

Sherwin-Williams Co/The | 26,961 | 9,093,136 | ||||||

Steel Dynamics Inc | 332,713 | 11,781,367 | ||||||

WestRock Co | 256 | 14,700 | ||||||

|

| |||||||

| 32,859,874 | ||||||||

|

| |||||||

21

DOMINI IMPACT EQUITY FUND

PORTFOLIOOF INVESTMENTS (continued)

July 31, 2017

| SECURITY | SHARES | VALUE | ||||||

| Real Estate – 3.4% | ||||||||

CBRE Group Inc Cl A (a) | 60,382 | $ | 2,293,912 | |||||

Equity Commonwealth (a) | 32,842 | 1,037,150 | ||||||

Host Hotels & Resorts Inc | 408,710 | 7,626,529 | ||||||

Mack Cali Realty Corp | 289,321 | 7,591,783 | ||||||

Mid-America Apartment Communities Inc | 39,229 | 4,061,378 | ||||||

Omega Healthcare Investors Inc | 135,542 | 4,281,772 | ||||||

Weingarten Realty Investors | 70,548 | 2,289,988 | ||||||

|

| |||||||

| 29,182,512 | ||||||||

|

| |||||||

| Telecommunication Services – 2.5% | ||||||||

AT&T Inc | 44,897 | 1,750,983 | ||||||

BCE Inc | 85,976 | 4,034,854 | ||||||

Rogers Communications Inc Cl B | 31,553 | 1,640,756 | ||||||

Telephone & Data Systems Inc | 182,230 | 5,180,799 | ||||||

Telus Corporation | 72,044 | 2,594,172 | ||||||

Verizon Communications Inc | 127,078 | 6,150,575 | ||||||

|

| |||||||

| 21,352,139 | ||||||||

|

| |||||||

| Utilities – 3.6% | ||||||||

Avangrid Inc | 119,649 | 5,434,458 | ||||||

Consolidated Edison Inc | 293,201 | 24,294,635 | ||||||

Eversource Energy | 17,833 | 1,084,068 | ||||||

|

| |||||||

| 30,813,161 | ||||||||

|

| |||||||

| Total Investments – 99.3% (Cost $719,142,026) (b) | 855,692,922 | |||||||

| Other Assets, less liabilities – 0.7% | 6,004,646 | |||||||

|

| |||||||

| Net Assets – 100.0% | $861,697,568 | |||||||

|

| |||||||

(a) Non-income producing security.

(b) The aggregate cost for federal income tax purposes is $719,503,911. The aggregate gross unrealized appreciation is $151,371,159 and the aggregate gross unrealized depreciation is $15,182,148, resulting in net unrealized appreciation of $136,189,011.

ADR — American Depository Receipt

SEE NOTES TO FINANCIAL STATEMENTS

22

DOMINI IMPACT INTERNATIONAL EQUITY FUND

Performance Commentary (Unaudited)

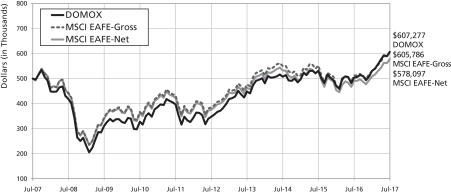

For the year ended July 31, 2017, the Domini Impact International Equity Fund Investor shares returned 20.61%, outperforming the MSCI EAFE Index, which returned 18.32% (gross) and 17.77% (net) during the period.

The Fund is managed through a two-step process designed to capitalize on the strengths of Domini Impact Investments LLC (“Domini”) and Wellington Management Company LLP (“Wellington Management”). Domini creates an approved list of companies based on its social, environmental and governance analysis, and Wellington then utilizes a disciplined and systematic process to manage the portfolio. Wellington Management’s philosophy relies on systematically exploiting sources of excess returns, stemming from both common behavioral, market structure, and risk premia inefficiencies in the market and the belief that certain factors are strongly associated with stock outperformance.

During the period, security selection was the primary driver of outperformance relative to the MSCI EAFE Index. Strong security selection within the materials, consumer staples, and information technology sectors aided relative results. Within materials, our positions in Norsk Hydro, Mitsubishi Gas and Sims Metal Management were particularly additive to EAFE-relative results. Partially offsetting these positive results was weak security selection within the telecommunication services and energy sectors.

Overall, top contributors to relative performance included Norsk Hydro (materials), ING Groep (financials), and STMicroelectronics (information technology). Top detractors included TPG Telecom (telecommunication services), Central Japan Railway Company (industrials) and Royal Mail (industrials). TPG Telecom was eliminated from the portfolio prior to the end of the period.

Typically, the Fund’s sector exposures generally fall within +/- 3% of the benchmark, but occasionally fall outside that range. From an allocation perspective, sector positioning relative to the MSCI EAFE Index contributed to relative results during the period. An underweight allocation to the underperforming health care sector and an overweight allocation to the strong performing information technology sector aided relative performance.

From a regional perspective, the portfolio’s strong security selection within Europe, Japan, and the Middle East contributed to relative results. This positive relative performance was partially offset by negative selection within North America and Asia (ex-Japan). The Fund benefited from an overweight position in European banks and household durables stocks. Our exposure to emerging market stocks, which represent a relatively small portion of the portfolio’s investments (under 10%), also provided a return tailwind. This helped to partially offset an underweight model exposure to European and Japanese equities.

23

From a market capitalization standpoint, the portfolio’s strong security selection within mid-cap securities (US$2 to US$10 billion) and large-cap (US$10 to US$20 billion) compared to the MSCI EAFE Index were primary contributors to relative performance, partially offset by weak security selection in the $20 to $50 billion market cap range. The portfolio also benefited from an underweight allocation to mega-cap (>US$50 billion) securities.

TEN LARGEST HOLDINGS (Unaudited)

| SECURITY DESCRIPTION | % NET ASSETS | SECURITY DESCRIPTION | % NET ASSETS | |||||||

| Sanofi | 2.9% | Allianz SE | 1.8% | |||||||

| Unilever PLC | 2.3% | Cie de Saint-Gobain | 1.7% | |||||||

| Nissan Motor Company Ltd. | 2.1% | Siemens AG | 1.7% | |||||||

| Adecco Group AG | 1.9% | DBS Group Holdings Ltd. | 1.6% | |||||||

| Kering | 1.8% | Sandvik AB | 1.6% | |||||||

PORTFOLIO HOLDINGS BY INDUSTRY SECTOR (% OF NET ASSETS) (Unaudited)

24

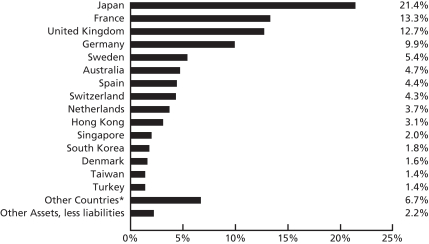

PORTFOLIO HOLDINGS BY COUNTRY (% OF NET ASSETS) (Unaudited)

An investment in the Domini Impact International Equity Fund is not a bank deposit and is not insured. You may lose money. The Fund is subject to market, sector concentration, foreign investing and style risks. Investing internationally involves special risks, such as currency fluctuations, social and economic instability, differing securities regulations and accounting standards, limited public information, possible changes in taxation, and periods of illiquidity. These risks are magnified in emerging markets.

*Other countries include Norway (1.2%), China (0.8%), South Africa (0.8%), United States (0.6%), Belgium (0.5%), Indonesia (0.5%), Panama (0.5%), Brazil (0.4%), Hungary (0.4%), Italy (0.3%), Mexico (0.3%), Finland (0.2%), Israel (0.1%), Thailand (0.1%), and Ireland (0.0%).

25

| AVERAGE ANNUAL TOTAL RETURNS (Unaudited) | ||||||||

| Investor shares | MSCI EAFE (gross) | MSCI EAFE (net) | ||||||

| As of 7/31/17 | 1 Year | 20.61% | 18.32% | 17.77% | ||||

| 5 Year | 11.86% | 9.55% | 9.06% | |||||

| 10 Year | 1.96% | 1.94% | 1.46% | |||||

| Since Inception (12/27/06) | 2.21% | 2.80% | 2.52% | |||||

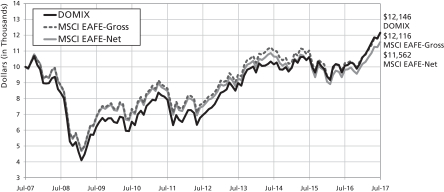

COMPARISON OF $10,000 INVESTMENT IN THE DOMINI IMPACT INTERNATIONAL EQUITY FUND INVESTOR SHARES AND MSCI EAFE (GROSS)/(NET) (Unaudited)

Past performance is no guarantee of future results. The Fund’s returns quoted above represent past performance after all expenses. The returns reflect any applicable expense waivers in effect during the periods shown. Without such waivers, Fund performance would be lower. Investment return, principal value, and yield will fluctuate. Your shares, when redeemed, may be worth more or less than their original cost. Call 1-800-582-6757 or visit www.domini.com for performance information current to the most recent month-end, which may be lower or higher. A 2.00% fee applies on sales/exchanges made less than 30 days after purchase/exchange, with certain exceptions. Quoted performance data does not reflect the deduction of this fee, which would reduce the performance quoted. See the Fund’s prospectus for further information.

Per the prospectus supplement dated May 1, 2017, the Fund’s gross and net annual operating expenses totaled 1.46% of net assets. Until 11/30/17, the Fund’s Manager has contractually agreed to limit certain ordinary Investor share expenses to 1.60% of its average daily net assets per annum absent an earlier modification by the Fund’s Board.

The table and the graph do not reflect the deduction of fees and taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Total return for the Domini Impact International Equity Fund is based on the Fund’s net asset values and assumes all dividend and capital gains were reinvested.

The Morgan Stanley Capital International Europe Australasia Far East (MSCI EAFE) index is an unmanaged index of common stocks. It is not available for direct investment. MSCI EAFE (gross) includes the reinvestment of dividends but reflects no deduction for fees, expenses or taxes. MSCI EAFE (net) includes the reinvestment of dividends net of withholding tax, but does not reflect other fees, expenses or taxes.

26

| AVERAGE ANNUAL TOTAL RETURNS (Unaudited) | ||||||||||

| Class A shares (with 4.75% maximum Sales Charge) | Class A shares (without Sales Charge) | MSCI EAFE (gross) | MSCI EAFE (net) | |||||||

| As of 7/31/17 | 1 Year | 14.72% | 20.44% | 18.32% | 17.77% | |||||

| 5 Year | 10.78% | 11.86% | 9.55% | 9.06% | ||||||

| 10 Year* | 1.47% | 1.96% | 1.94% | 1.46% | ||||||

| Since Inception (12/27/06)* | 1.74% | 2.21% | 2.80% | 2.52% | ||||||

COMPARISON OF $10,000 INVESTMENT IN THE DOMINI IMPACT INTERNATIONAL EQUITY FUND CLASS A SHARES AND MSCI EAFE (GROSS)/(NET) (WITH 4.75% MAXIMUM SALES CHARGE)* (Unaudited)

Past performance is no guarantee of future results. The Fund’s returns quoted above represent past performance after all expenses. The returns reflect any applicable expense waivers in effect during the periods shown. Without such waivers, Fund performance would be lower. Investment return, principal value, and yield will fluctuate. Your shares, when redeemed, may be worth more or less than their original cost. Call 1-800-498-1351 or visit www.domini.com for performance information current to the most recent month-end, which may be lower or higher. A 2.00% fee applies on sales/exchanges made less than 30 days after purchase/exchange, with certain exceptions. Quoted performance data does not reflect the deduction of this fee, which would reduce the performance quoted. See the Fund’s prospectus for further information.

Per the prospectus supplement dated May 1, 2017, the Fund’s gross and net annual operating expenses totaled 1.53% and 1.47% of net assets, respectively. Until 11/30/17, the Fund’s Manager has contractually agreed to limit certain ordinary Class A share expenses to 1.57% of its average daily net assets per annum absent an earlier modification by the Fund’s Board.

The table and the graph do not reflect the deduction fees and taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Total return for the Domini Impact International Equity Fund is based on the Fund’s net asset values and assumes all dividend and capital gains were reinvested.

The Morgan Stanley Capital International Europe Australasia Far East (MSCI EAFE) index is an unmanaged index of common stocks. It is not available for direct investment. MSCI EAFE (gross) includes the reinvestment of dividends but reflects no deduction for fees, expenses or taxes. MSCI EAFE (net) includes the reinvestment of dividends net of withholding tax, but does not reflect other fees, expenses or taxes.

*Class A shares were not offered prior to November 28, 2008. All performance information for time periods beginning prior to November 28, 2008 is the performance of the Investor shares. Unless otherwise noted, this performance has not been adjusted to reflect the expenses of the Class A shares, but does, where noted, reflect an adjustment for the maximum applicable sales charges of 4.75%.

27

| AVERAGE ANNUAL TOTAL RETURNS (Unaudited) | ||||||||

| Institutional shares | MSCI EAFE (gross) | MSCI EAFE (net) | ||||||

| As of 7/31/17 | 1 Year | 20.80% | 18.32% | 17.77% | ||||

| 5 Year* | 11.86% | 9.55% | 9.06% | |||||

| 10 Year* | 1.96% | 1.94% | 1.46% | |||||

| Since Inception (12/27/06)* | 2.21% | 2.80% | 2.52% | |||||

COMPARISON OF $500,000 INVESTMENT IN THE DOMINI IMPACT INTERNATIONAL EQUITY FUND INSTITUTIONAL SHARES AND MSCI EAFE (GROSS)/(NET)* (Unaudited)

Past performance is no guarantee of future results. The Fund’s returns quoted above represent past performance after all expenses. The returns reflect any applicable expense waivers in effect during the periods shown. Without such waivers, Fund performance would be lower. Investment return, principal value, and yield will fluctuate. Your shares, when redeemed, may be worth more or less than their original cost. Call 1-800-498-1351 or visit www.domini.com for performance information current to the most recent month-end, which may be lower or higher. A 2.00% fee applies on sales/exchanges made less than 30 days after purchase/exchange, with certain exceptions. Quoted performance data does not reflect the deduction of this fee, which would reduce the performance quoted. See the Fund’s prospectus for further information.

Per the prospectus supplement dated May 1, 2017, the Fund’s gross and net annual operating expenses totaled 1.04% of net assets. Until 11/30/17, the Fund’s Manager has contractually agreed to limit certain ordinary Institutional share expenses to 1.27% of its average daily net assets per annum absent an earlier modification by the Fund’s Board.

The table and the graph do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Total return for the Domini Impact International Equity Fund is based on the Fund’s net asset values and assumes all dividend and capital gains were reinvested.

The Morgan Stanley Capital International Europe Australasia Far East (MSCI EAFE) index is an unmanaged index of common stocks. It is not available for direct investment. MSCI EAFE (gross) includes the reinvestment of dividends but reflects no deduction for fees, expenses or taxes. MSCI EAFE (net) includes the reinvestment of dividends net of withholding tax, but does not reflect other fees, expenses or taxes.

*Institutional shares were not offered prior to November 30, 2012. All performance information for time periods beginning prior to November 28, 2012 is the performance of the Investor shares. Unless otherwise noted, this performance has not been adjusted to reflect the expenses of the Institutional shares.

28

DOMINI IMPACT INTERNATIONAL EQUITY FUND

PORTFOLIOOF INVESTMENTS

July 31, 2017

| COUNTRY/SECURITY | INDUSTRY | SHARES | VALUE | |||||||

| Common Stock – 97.8% | ||||||||||

Australia – 4.7% | ||||||||||

Bendigo & Adelaide Bank Ltd | Banks | 559,430 | $ | 4,966,427 | ||||||

BlueScope Steel Ltd | Materials | 171,947 | 1,809,270 | |||||||

Boral Ltd | Materials | 122,264 | 675,458 | |||||||

Challenger Ltd/Australia | Diversified Financials | 707,354 | 7,256,604 | |||||||

Dexus | Real Estate | 1,226,495 | 9,184,639 | |||||||

Flight Centre Travel Group Ltd | Consumer Services | 61,071 | 2,120,888 | |||||||

Fortescue Metals Group Ltd | Materials | 1,009,443 | 4,625,804 | |||||||

Harvey Norman Holdings Ltd | Retailing | 689,641 | 2,406,013 | |||||||

Mirvac Group | Real Estate | 6,813,568 | 11,803,962 | |||||||

Sims Metal Management Ltd | Materials | 389,690 | 4,834,636 | |||||||

Westpac Banking Corp | Banks | 1,344 | 34,143 | |||||||

|

| |||||||||

| 49,717,844 | ||||||||||

|

| |||||||||

Belgium – 0.5% | ||||||||||

UCB SA | Pharma, Biotech & Life Sciences | 69,399 | 5,036,929 | |||||||

|

| |||||||||

| 5,036,929 | ||||||||||

|

| |||||||||

Brazil – 0.4% | ||||||||||

M Dias Branco SA | Food & Beverage | 254,115 | 4,127,641 | |||||||

|

| |||||||||

| 4,127,641 | ||||||||||

|

| |||||||||

China – 0.8% | ||||||||||

Beijing Capital International Airport Co Ltd Cl H | Transportation | 680,188 | 1,071,210 | |||||||

Nine Dragons Paper Holdings Ltd | Materials | 3,783,961 | 5,639,496 | |||||||

Ping An Insurance Group Co of China Ltd Cl H | Insurance | 312,562 | 2,319,157 | |||||||

|

| |||||||||

| 9,029,863 | ||||||||||

|

| |||||||||

Denmark – 1.6% | ||||||||||

Danske Bank A/S | Banks | 47,694 | 1,924,349 | |||||||

H Lundbeck A/S | Pharma, Biotech & Life Sciences | 118,420 | 7,087,196 | |||||||

TDC A/S | Telecommunication Services | 199,762 | 1,227,205 | |||||||

Vestas Wind Systems A/S | Capital Goods | 72,222 | 7,030,242 | |||||||

|

| |||||||||

| 17,268,992 | ||||||||||

|

| |||||||||

Finland – 0.2% | ||||||||||

Orion Oyj Cl B | Pharma, Biotech & Life Sciences | 23,073 | 1,162,388 | |||||||

Valmet OYJ | Capital Goods | 64,720 | 1,175,096 | |||||||

|

| |||||||||

| 2,337,484 | ||||||||||

|

| |||||||||

29

DOMINI IMPACT INTERNATIONAL EQUITY FUND

PORTFOLIOOF INVESTMENTS (continued)

July 31, 2017

| COUNTRY/SECURITY | INDUSTRY | SHARES | VALUE | |||||||

France – 13.3% | ||||||||||

AXA SA | Insurance | 125,123 | $ | 3,682,101 | ||||||

BNP Paribas SA | Banks | 35,345 | 2,732,418 | |||||||

Carrefour SA | Food & Staples Retailing | 355 | 8,500 | |||||||

Casino Guichard Perrachon SA | Food & Staples Retailing | 75,094 | 4,563,139 | |||||||

Cie de Saint-Gobain | Capital Goods | 322,225 | 17,813,673 | |||||||

Cie Generale des Etablissements Michelin | Automobiles & Components | 52,292 | 7,049,940 | |||||||

CNP Assurances | Insurance | 202,651 | 4,874,083 | |||||||

Credit Agricole SA | Banks | 923,550 | 16,169,660 | |||||||

Faurecia | Automobiles & Components | 57,059 | 3,157,103 | |||||||

Kering | Consumer Durables & Apparel | 54,578 | 19,014,684 | |||||||

Orange SA | Telecommunication Services | 411,479 | 6,898,605 | |||||||

Peugeot SA | Automobiles & Components | 755,153 | 16,190,575 | |||||||

Sanofi | Pharma, Biotech & Life Sciences | 323,856 | 30,821,028 | |||||||

STMicroelectronics NV | Semiconductors & Semiconductor Equipment | 477,178 | 8,118,219 | |||||||

|

| |||||||||

| 141,093,728 | ||||||||||

|

| |||||||||

Germany – 9.9% | ||||||||||

adidas AG | Consumer Durables & Apparel | 22,962 | 5,224,937 | |||||||

Allianz SE | Insurance | 89,203 | 18,930,670 | |||||||

Bayerische Motoren Werke AG | Automobiles & Components | 116,260 | 10,651,757 | |||||||

CECONOMY AG | Retailing | 516,121 | 5,781,425 | |||||||

Deutsche Lufthansa AG | Transportation | 380,824 | 8,160,424 | |||||||

Fraport AG Frankfurt Airport Services Worldwide | Transportation | 62,571 | 6,242,523 | |||||||

Innogy SE | Utilities | 185,137 | 7,745,546 | |||||||

Merck KGaA | Pharma, Biotech & Life Sciences | 145,767 | 15,957,143 | |||||||

Metro Wholesale & Food Specialist AG (a) | Food & Staples Retailing | 157,866 | 3,176,208 | |||||||

Siemens AG | Capital Goods | 130,293 | 17,627,381 | |||||||

Suedzucker AG | Food & Beverage | 175,125 | 3,722,699 | |||||||

Vonovia SE | Real Estate | 65,722 | 2,654,292 | |||||||

|

| |||||||||

| 105,875,005 | ||||||||||

|

| |||||||||

Hong Kong – 3.1% | ||||||||||

ASM Pacific Technology Ltd | Semiconductors & Semiconductor Equipment | 539,672 | 6,992,799 | |||||||

Great Eagle Holdings Ltd | Real Estate | 189,790 | 1,041,273 | |||||||

Hongkong Land Holdings Ltd | Real Estate | 281,634 | 2,117,888 | |||||||

Hysan Development Co Ltd | Real Estate | 160,208 | 775,384 | |||||||

Kerry Properties Ltd | Real Estate | 851,179 | 2,986,153 | |||||||

Wharf Holdings Ltd/The | Real Estate | 1,372,526 | 11,677,670 | |||||||

Wheelock & Co Ltd | Real Estate | 926,838 | 6,989,720 | |||||||

Xinyi Glass Holdings Ltd | Automobiles & Components | 684,955 | 708,621 | |||||||

|

| |||||||||

| 33,289,508 | ||||||||||

|

| |||||||||

30

DOMINI IMPACT INTERNATIONAL EQUITY FUND

PORTFOLIOOF INVESTMENTS (continued)

July 31, 2017

| COUNTRY/SECURITY | INDUSTRY | SHARES | VALUE | |||||||

Hungary – 0.4% | ||||||||||

Richter Gedeon Nyrt | Pharma, Biotech & Life Sciences | 150,532 | $ | 3,834,555 | ||||||

|

| |||||||||

| 3,834,555 | ||||||||||

|

| |||||||||

Indonesia – 0.5% | ||||||||||

Telekomunikasi Indonesia Persero Tbk PT | Telecommunication Services | 14,496,126 | 5,102,584 | |||||||

|

| |||||||||

| 5,102,584 | ||||||||||

|

| |||||||||

Ireland – 0.0% | ||||||||||

Irish Bank Resolution Corp Ltd/Old (a) (b) | Banks | 138,674 | 0 | |||||||

|

| |||||||||

| 0 | ||||||||||

|

| |||||||||

Israel – 0.1% | ||||||||||

Taro Pharmaceutical Industries Ltd (a) | Pharma, Biotech & Life Sciences | 13,404 | 1,532,479 | |||||||

|

| |||||||||

| 1,532,479 | ||||||||||

|

| |||||||||

Italy – 0.3% | ||||||||||

A2A SpA | Utilities | 1,604,257 | 2,719,862 | |||||||

|

| |||||||||

| 2,719,862 | ||||||||||

|

| |||||||||

Japan – 21.4% | ||||||||||

Asahi Glass Co Ltd | Capital Goods | 281,973 | 11,866,369 | |||||||

Astellas Pharma Inc | Pharma, Biotech & Life Sciences | 439,466 | 5,599,965 | |||||||

Brother Industries Ltd | Technology Hardware & Equipment | 225,445 | 5,753,698 | |||||||

Central Japan Railway Co | Transportation | 95,110 | 15,278,542 | |||||||

Dai Nippon Printing Co Ltd | Commercial & Professional Services | 845,134 | 9,308,368 | |||||||

Daiichi Sankyo Co Ltd | Pharma, Biotech & Life Sciences | 149,961 | 3,268,076 | |||||||

Ezaki Glico Co Ltd | Food & Beverage | 56,300 | 2,955,247 | |||||||

FUJIFILM Holdings Corp | Technology Hardware & Equipment | 20,044 | 735,222 | |||||||

GungHo Online Entertainment Inc | Software & Services | 620,655 | 1,673,878 | |||||||

Ibiden Co Ltd | Technology Hardware & Equipment | 280,099 | 4,856,959 | |||||||

K’s Holdings Corp | Retailing | 255,899 | 5,132,107 | |||||||

Medipal Holdings Corp | Health Care Equipment & Services | 227,876 | 4,167,948 | |||||||

Mitsubishi Gas Chemical Co Inc | Materials | 566,503 | 13,109,626 | |||||||

Mitsui Fudosan Co Ltd | Real Estate | 519,997 | 11,927,530 | |||||||

Mixi Inc | Software & Services | 149,602 | 8,218,328 | |||||||

Morinaga & Co Ltd/Japan | Food & Beverage | 28,768 | 1,645,448 | |||||||

MS&AD Insurance Group Holdings Inc | Insurance | 433,298 | 15,183,763 | |||||||

Nintendo Co Ltd | Software & Services | 6,406 | 2,172,921 | |||||||

Nippon Electric Glass Co Ltd | Technology Hardware & Equipment | 184,160 | 6,516,726 | |||||||

31

DOMINI IMPACT INTERNATIONAL EQUITY FUND

PORTFOLIOOF INVESTMENTS (continued)

July 31, 2017

| COUNTRY/SECURITY | INDUSTRY | SHARES | VALUE | |||||||

Japan (Continued) | ||||||||||

Nissan Motor Co Ltd | Automobiles & Components | 2,294,238 | $ | 22,756,549 | ||||||

Nisshin Seifun Group Inc | Food & Beverage | 98,025 | 1,607,505 | |||||||

Nomura Holdings Inc | Diversified Financials | 2,699,273 | 16,044,912 | |||||||

Nomura Real Estate Holdings Inc | Real Estate | 104,485 | 2,068,991 | |||||||

NTN Corp | Capital Goods | 5,300 | 24,702 | |||||||

ORIX Corp | Diversified Financials | 540,841 | 8,573,085 | |||||||

Rohm Co Ltd | Semiconductors & Semiconductor Equipment | 154,502 | 11,955,221 | |||||||

Seino Holdings Co Ltd | Transportation | 247,806 | 3,332,637 | |||||||

Shimamura Co Ltd | Retailing | 47,874 | 5,944,443 | |||||||

Tokyo Electron Ltd | Semiconductors & Semiconductor Equipment | 9,783 | 1,378,978 | |||||||

Toppan Printing Co Ltd | Commercial & Professional Services | 891,626 | 9,408,896 | |||||||

Toyo Seikan Group Holdings Ltd | Materials | 184,941 | 3,027,814 | |||||||

Yamada Denki Co Ltd | Retailing | 626,436 | 3,339,253 | |||||||

Yamazaki Baking Co Ltd | Food & Beverage | 85,600 | 1,715,176 | |||||||

Zeon Corp | Materials | 584,300 | 7,313,335 | |||||||

|

| |||||||||

| 227,862,218 | ||||||||||

|

| |||||||||

Mexico – 0.3% | ||||||||||

Arca Continental SAB de CV | Food & Beverage | 390,197 | 2,893,279 | |||||||

|

| |||||||||

| 2,893,279 | ||||||||||

|

| |||||||||

Netherlands – 3.7% | ||||||||||

ABN AMRO Group NV | Banks | 355,880 | 10,032,223 | |||||||

ING Groep NV | Banks | 834,956 | 15,568,501 | |||||||