EXHIBIT (c)(ii)

Consolidated Financial Statements of the Co-registrant

2006 – 07 Report on

State Finances

of the Queensland Government – 30 June 2007

| | |

Incorporating the Outcomes Report and the Consolidated Financial Statements | |

|

Contents

| | |

| | | Page |

| |

| Message from the Treasurer | | 2 |

| |

| Scope of the Report | | 3 |

| |

| Outcomes Report - Uniform Presentation Framework | | |

| |

Overview and Analysis | | 4-01 |

| |

Operating Statement by Sector | | 4-08 |

| |

Balance Sheet by Sector | | 4-09 |

| |

Cash Flow Statement by Sector | | 4-10 |

| |

General Government Sector Expenses by Function | | 4-11 |

| |

General Government Sector Purchases of Non-financial Assets by Function | | 4-12 |

| |

Loan Council Allocation | | 4-12 |

| |

Certification of Outcomes Report | | 4-13 |

| |

| Audited Consolidated Financial Statements | | |

| |

Overview and Analysis | | 5-01 |

| |

Income Statement | | 5-07 |

| |

Balance Sheet | | 5-08 |

| |

Statement of Changes in Equity | | 5-10 |

| |

Cash Flow Statement | | 5-11 |

| |

Notes to the Financial Statements | | 5-12 |

| |

Certification of Consolidated Financial Statements | | 5-80 |

| |

Independent Audit Report to the Treasurer of Queensland | | 5-81 |

| |

| Attachment A: Reconciliation of UPF and AAS Operating Result | | 6-01 |

| | |

| Report on State Finances 2006-07 - Government of Queensland | | 1 |

Message from the Treasurer

As outlined in the Charter of Social and Fiscal Responsibility, the Government is committed to fiscal transparency and accountability. A key objective of this report is to facilitate a meaningful assessment of the State’s financial performance over the 2006-07 financial year and its net worth at balance date.

This report provides details of the State’s financial operations and position on both a Government Finance Statistics (Outcomes Report) and Australian Accounting Standards (Consolidated Financial Statements) basis.

In endorsing this report, I place on record my appreciation of the professionalism and co-operation extended to Queensland Treasury by agency personnel and of the Treasury staff involved in its preparation.

ANDREW FRASER MP

TREASURER

| | |

| Report on State Finances 2006-07 - Government of Queensland | | 2 |

Scope of the Report

The Report on State Finances, incorporating the Outcomes Report and Consolidated Financial Statements, provides a comprehensive analysis of Government finances for the 2006-07 financial year.

These reports are prepared using different methodologies, each giving a view of government finances. The Outcomes Report outlines the operations of the Queensland Government excluding valuation adjustments to reflect costs more appropriately related to the underlying operations of government. The Consolidated Financial Statements include valuation adjustments on assets and liabilities.

The Outcomes Report

The Outcomes Report contains financial statements that are prepared and presented on a Government Finance Statistics (GFS) basis and in accordance with the Uniform Presentation Framework (UPF) agreed to at the 1991 Premiers’ Conference. The primary objective of the UPF is to provide uniform and comparable reporting of Commonwealth, State and Territory governments’ financial information.

Queensland’s annual Budget is prepared in accordance with the UPF, and the Outcomes Report compares achieved financial results with revised forecasts.

The UPF presentation is primarily structured on a sectoral basis with a focus on the General Government and Public Non-financial Corporations sectors.

One of the Government’s key fiscal principles is the maintenance of a General Government operating surplus as measured in GFS terms.

The Consolidated Financial Statements

The Consolidated Financial Statements outline the operations of the Queensland Government on an accrual basis in accordance with Australian Accounting Standard AAS 31 Financial Reporting by Governments and other applicable standards. The statements present the income statement, balance sheet and cash flows of the Queensland Total State sector on a consolidated basis.

Financial statements for the General Government, Public Non-financial Corporations and Public Financial Corporations sectors are disclosed in the disaggregated information note to the financial statements (Note 2).

Refer Note 51 for a full list of consolidated entities.

Where applicable, comparatives have been restated to agree with changes in presentation in the financial statements for the current reporting period and to correct timing differences and/or errors from prior periods.

Related Publications

This report comprises one of a number of key publications relating to the financial performance of the Queensland Public Sector including:

| | - | the annual Budget papers |

| | - | the Treasurer’s Consolidated Fund Financial Report |

| | - | the annual reports of the various departments, statutory bodies, Government-owned corporations and other entities that comprise the Queensland Government. |

| | |

| Report on State Finances 2006-07 - Government of Queensland | | 3 |

2006 – 07

Outcomes Report

Uniform Presentation Framework of the

Queensland Government – 30 June 2007

Outcomes Report - Overview and Analysis

Overview

The General Government GFS operating result for 2006-07 was a surplus of $1.856 billion, or $537 million lower than forecast at the time of the 2007-08 Budget. The decrease in the surplus primarily reflects a technical adjustment deeming the tax arising on the gain on the sale of Energex’s electricity and gas retail businesses, the Allgas distribution network and the competitive parts of Ergon Energy’s electricity retail business to be a return of capital.

A GFS cash surplus of $2.304 billion was recorded for 2006-07 in the General Government sector. This is $582 million higher than the estimated actual of $1.722 billion, due to increased receipts from taxes and grants and marginally lower expenditure.

The General Government’s net worth increased to $117.831 billion as at 30 June 2007, an improvement of $3.365 billion over the estimated actual forecast of $114.466 billion, mainly as a result of revaluations of non-financial assets.

Capital purchases in the General Government sector exceeded the estimated actual forecast by $281 million, and occurred over a range of agencies.

No net borrowings were required in the General Government sector due to the utilisation of existing cash balances.

The Government has met all of its fiscal commitments under the Charter of Social and Fiscal Responsibility—see page 4-02.

Summary of Key GFS Financial Aggregates

Outlined in the table below are the GFS aggregates, by sector.

| | | | | | | | | | | | | | | | | | |

| | | General Government

Sector | | | Public Non-financial

Corporations Sector | | | Non-financial Public

Sector | |

| | Est. Actual

$ million | | | Outcome

$ million | | | Est. Actual

$ million | | | Outcome

$ million | | | Est. Actual

$ million | | | Outcome

$ million | |

Revenue | | 32,557 | | | 31,981 | | | 9,412 | | | 11,796 | | | 38,057 | | | 40,977 | |

Expenses | | 30,164 | | | 30,125 | | | 10,015 | | | 10,972 | | | 36,267 | | | 38,298 | |

Net operating balance | | 2,393 | | | 1,856 | | | (604 | ) | | 824 | | | 1,790 | | | 2,679 | |

Cash surplus/(deficit) | | 1,722 | | | 2,304 | | | (4,924 | ) | | (3,704 | ) | | (3,202 | ) | | (1,399 | ) |

Capital purchases | | 4,137 | | | 4,418 | | | 7,436 | | | 6,363 | | | 11,573 | | | 10,635 | |

Net worth | | 114,466 | | | 117,831 | | | 21,516 | | | 20,648 | | | 114,466 | | | 117,930 | |

Net debt | | (26,423 | ) | | (26,686 | ) | | 15,774 | | | 16,969 | | | (10,650 | ) | | (9,718 | ) |

Net Borrowing | | 743 | | | (262 | ) | | 3,761 | | | 3,792 | | | 4,505 | | | 3,529 | |

| | |

| Outcomes Report 2006-07 - Government of Queensland | | 4-01 |

Outcomes Report - Overview and Analysis

Meeting the Government’s Fiscal Commitments

The Government has met all of its fiscal commitments under the Charter of Social and Fiscal Responsibility:

| | | | |

Achievement of Fiscal Principles of the Queensland Government |

Principle | | Achievement | | Indicator |

| | |

Competitive tax environment The Government will ensure that State taxes and charges remain competitive with the other states and territories in order to maintain a competitive tax environment for business development and jobs growth. | | ü | | Taxation revenue per capita: Qld: $2,053/capita Other States: $2,421/capita. |

| | |

Affordable service provision The Government will ensure that its level of service provision is sustainable by maintaining an overall General Government operating surplus, as measured in Government Finance Statistics terms. | | ü | | GFS operating surplus of $1.856 billion. |

| | |

Sustainable borrowings for capital investment Borrowings or other financial arrangements will only be undertaken for capital investments and only where these can be serviced within the operating surplus, consistent with maintaining a AAA credit rating. | | ü | | GG total purchases of non-financial assets $4.418 billion; no new borrowings. AAA credit rating confirmed by Moody’s and Standard & Poor’s (highest rating available). |

| | |

Prudent management of financial risk The Government will ensure that the State’s financial assets cover all accruing and expected future liabilities of the General Government sector. | | ü | | GG net financial worth: $24.133 billion. |

| | |

Building the State’s net worth The Government will maintain and seek to increase Total State net worth. | | ü | | GG net worth increased by $13.385 billion to $117.831 billion during 2006-07. |

Net Operating Balance

The GFS operating result for 2006-07 in the General Government Sector is a surplus of $1.856 billion. The surplus reflects the continuing strength of the economy flowing through to taxation and related revenues and investment returns.

With approximately $27 billion in funds invested in a portfolio of equities, property, cash and fixed interest, the performance of domestic and international financial markets have a major influence on the actual result. Investment returns on these assets were 14.1%, slightly higher than expected at the time of the 2007-08 Budget.

Investment market volatility impacts more on the Queensland outcomes in GFS terms than it does for other states. This is in part due to differences in the way Queensland’s public sector superannuation arrangements are structured. If Queensland’s superannuation arrangements were structured on the same basis as generally applied in other states, the General Government sector underlying operating balance for 2006-07 would be a surplus of $746 million, as outlined below:

| | |

Calculation of underlying operating balance | | 2006-07

Outcome

$ million |

GFS net operating balance | | 1,856 |

Less investment earnings in excess of long term rate | | 1,110 |

Underlying Balance | | 746 |

| | |

| Outcomes Report 2006-07 - Government of Queensland | | 4-02 |

Outcomes Report - Overview and Analysis

| | | | |

Revenue | | 2006-07

Est. Actual

$ million | | 2006-07

Outcome

$ million |

Taxation revenue | | 8,375 | | 8,484 |

Current grants and subsidies | | 13,384 | | 13,536 |

Capital grants | | 811 | | 820 |

Sales of goods and services | | 2,937 | | 2,889 |

Interest income | | 3,268 | | 3,348 |

Other | | 3,781 | | 2,905 |

| | |

Total Revenue | | 32,557 | | 31,981 |

Total revenue decreased by $576 million over the 2006-07 estimated actual. This was largely due to the change in tax treatment of the retail energy asset sales transactions during the year, included in the table above as Other revenue.

Other variations include:

| - | An increase in taxation revenue from higher than expected transfer duty and payroll tax collections. |

| - | An increase in current grants and subsidies from slightly higher GST revenue grants from the Commonwealth Government and higher payments for natural disaster relief measures. |

| - | Marginally higher interest income than forecast at the time of the Budget. |

| | | | |

Expenses | | 2006-07

Est. Actual

$ million | | 2006-07

Outcome

$ million |

Gross operating expenses | | | | |

Employee expenses | | 13,229 | | 13,239 |

Other operating expenses | | 6,239 | | 6,115 |

Depreciation | | 1,780 | | 1,880 |

Superannuation interest expense | | 1,064 | | 1,154 |

Other interest expense | | 218 | | 179 |

Current transfers | | 6,477 | | 6,344 |

Capital transfers | | 1,157 | | 1,215 |

| | |

Total Expenses | | 30,164 | | 30,125 |

Total expenses were largely in line with that forecast at the time of the 2007-08 Budget. Major variances include:

| - | higher depreciation expenses for the Department of Main Roads |

| - | an increase in superannuation interest expense, following the actuarial review |

| - | an increase in capital grants, primarily to local governments |

| - | lower current transfers, including grants and subsidies to the community and community service obligation (CSO) payments to QR. Expenditure on these items is largely demand driven. |

| | |

| Outcomes Report 2006-07 - Government of Queensland | | 4-03 |

Outcomes Report - Overview and Analysis

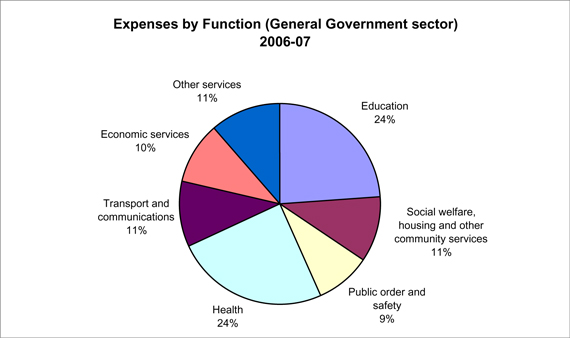

General Government expenditure is focussed on the delivery of core services to the community. As shown in the chart below, Education and Health account for the largest share of expenses.

Cash Surplus

A cash surplus of $2.304 billion was recorded for the 2006-07 financial year in the General Government sector, an increase of $582 million over the 2006-07 estimated actual. Net cash flows from operating activities were $728 million higher than estimated.

The General Government sector recorded net cash inflows from operating activities for the 2006-07 financial year of $33.154 billion reflecting the continued effect of the property market activity on transfer duty as well as employment and wage growth on payroll tax revenue and strong returns on investments.

The increased cash generated from operating activities in 2006-07 has been utilised to fund higher investments in capital (property, plant and equipment) with outlays of $4.418 billion. In addition, interest earnings on long-term investments held to meet future employee entitlements ($3.026 billion) were re-invested during 2006-07.

Receipts from operating activities were $551 million higher than forecast, due to higher than expected revenue from taxes, grants, interest and royalties.

Payments for operating activities were $177 million lower than forecast primarily due to lower grants and subsidies expenditure, mainly CSO payments to Queensland Rail.

Capital Purchases and Borrowings

Purchases of non-financial assets (i.e. capital expenditure) totalled $4.418 billion, exceeding forecasts by $281 million. This record level of expenditure for the sector was mainly in the areas of health, education and transport. The expenditure has been funded mainly from operating cash flows and the utilisation of existing cash balances.

The outflow of borrowings of $262 million in the cash flow statement is mainly lending to the Public Non-Financial Corporations sector.

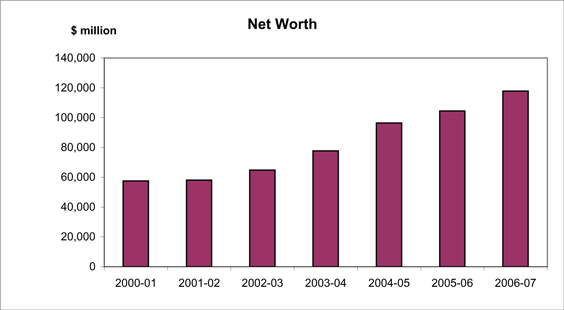

Net Worth

The General Government sector’s net worth increased to $117.831 billion as at 30 June 2007. This is $3.365 billion higher than the forecast of $114.466 billion. This growth reflects the impact of the Government’s operating surplus in 2006-07 and increases as part of the State’s asset revaluation cycle.

Upward revaluations of non-financial assets by the departments of Natural Resources and Water ($3.11 billion), Main Roads ($2.711 billion), Education, Training and the Arts ($1.508 billion), Housing ($813 million), Public Works ($ 435 million) and Health ($422 million) contributed to the improved net worth recorded by the State.

| | |

| Outcomes Report 2006-07 - Government of Queensland | | 4-04 |

Outcomes Report - Overview and Analysis

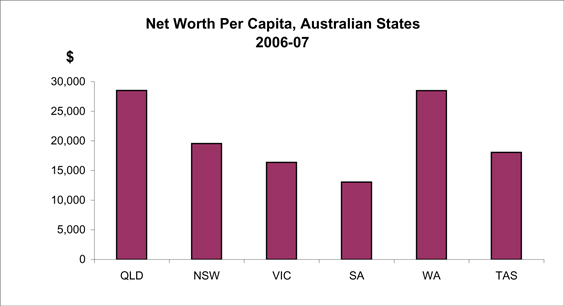

The chart below shows Queensland’s strong net worth compared with the other states.

Note:

| 1. | Western Australia values land under roads as part of its overall asset base. This has been adjusted to allow comparison with other jurisdictions which do not value land under roads. |

Source: Victoria and Western Australia Outcome Results; New South Wales, South Australia and Tasmania 2007-08 Budget Papers. Population data from ABS 3101.0.

| | |

| Outcomes Report 2006-07 - Government of Queensland | | 4-05 |

Outcomes Report - Overview and Analysis

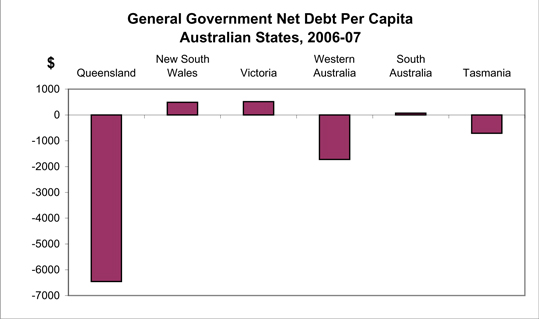

Net Debt

Net debt is the most common measure used to judge the overall strength of a jurisdiction’s fiscal position. High levels of net debt impose a call on future revenue flows to service that debt and can limit government flexibility to adjust outlays.

In 2006-07 there has been a further strengthening of the General Government sector’s already strong net debt position, from an estimated negative $26.423 billion to a negative $26.686 billion.

Queensland’s negative net debt of $6,458 per capita compares to the average net debt of $191 per capita of the other states.

Source: Victoria and Western Australia Outcome Results; New South Wales, South Australia and Tasmania 2007-08 Budget Papers. Population data from ABS 3101.0.

| | |

| Outcomes Report 2006-07 - Government of Queensland | | 4-06 |

Outcomes Report - Overview and Analysis

Public Non-Financial Corporations (PNFC) Sector

The Public Non-Financial Corporations sector comprises bodies such as Government-owned corporations that provide goods and services that are market, non-regulatory and non-financial in nature. PNFCs are financed through sales to consumers of their goods and services and may be supplemented by explicit government payments to fund community service obligations.

| - | The PNFC sector recorded a net operating surplus of $824 million which was $1.428 billion higher than forecast. The increase is due to a technical adjustment deeming the tax on the gain on the sale of Energex’s electricity and gas retail businesses, the Allgas distribution network and the competitive parts of Ergon Energy’s electricity retail business to be a return of capital. Higher than estimated electricity pool prices have driven increased sales of goods and services and operating expenses. |

| - | The cash deficit of $3.704 billion is less than forecast due to lower capital expenditure. |

| - | The net worth of the PNFC sector has declined due to the effect of high current pool prices on hedging positions. |

State Financial Sector (Total State)

The Total State sector includes all State Government departments and statutory authorities, public non-financial corporations, public financial corporations and their controlled entities. All material inter-entity and intra-entity transactions and balances have been eliminated to the extent practicable.

| - | A net operating surplus of $2.785 billion was recorded in 2006-07, reflecting the strong performance of the General Government Sector. |

| - | A total State cash deficit of $1.349 billion was achieved in 2006-07 after allowing for purchases of non-financial assets of $10.647 billion. |

| - | In 2006-07, the Total State’s net debt position is negative $13.296 billion. |

| | |

| Outcomes Report 2006-07 - Government of Queensland | | 4-07 |

Operating Statement by Sector

Operating Statement 2006-07 ($million) - by sector(a)

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | General Government

Sector | | | Public Non-financial

Corporations Sector | | | Non-financial Public

Sector | | | Public

Financial

Corporations

Sector | | | State

Financial

Sector | |

| | | | | Est. Actual | | | Actual | | | Est. Actual | | | Actual | | | Est. Actual | | | Actual | | | Actual (b) | | | Actual (b) | |

| | GFS Revenue | | | | | | | | | | | | | | | | | | | | | | | | |

| | Taxation revenue | | 8,375 | | | 8,484 | | | — | | | — | | | 8,034 | | | 8,116 | | | — | | | 8,111 | |

| | Current grants and subsidies | | 13,384 | | | 13,536 | | | 1,487 | | | 1,315 | | | 13,356 | | | 13,493 | | | — | | | 13,493 | |

| | Capital grants | | 811 | | | 820 | | | 9 | | | 12 | | | 808 | | | 822 | | | — | | | 822 | |

| | Sales of goods and services | | 2,937 | | | 2,889 | | | 7,341 | | | 9,842 | | | 10,069 | | | 12,503 | | | 966 | | | 13,294 | |

| | Interest income | | 3,268 | | | 3,348 | | | 140 | | | 192 | | | 3,409 | | | 3,540 | | | 2,562 | | | 4,836 | |

| | Other | | 3,781 | | | 2,905 | | | 433 | | | 434 | | | 2,381 | | | 2,503 | | | 32 | | | 2,495 | |

| | Total Revenue | | 32,557 | | | 31,981 | | | 9,412 | | | 11,796 | | | 38,057 | | | 40,977 | | | 3,560 | | | 43,051 | |

| | | | | | | | | |

less | | GFS Expenses | | | | | | | | | | | | | | | | | | | | | | | | |

| | Gross operating expenses | | | | | | | | | | | | | | | | | | | | | | | | |

| | Employee expenses | | 13,229 | | | 13,239 | | | 2,275 | | | 1,888 | | | 15,504 | | | 15,127 | | | 163 | | | 15,167 | |

| | Other operating expenses | | 6,239 | | | 6,115 | | | 3,269 | | | 5,637 | | | 8,955 | | | 11,145 | | | 1,141 | | | 12,226 | |

| | Depreciation | | 1,780 | | | 1,880 | | | 1,597 | | | 1,564 | | | 3,377 | | | 3,444 | | | 20 | | | 3,464 | |

| | Superannuation interest expense | | 1,064 | | | 1,154 | | | — | | | — | | | 1,064 | | | 1,154 | | | — | | | 1,154 | |

| | Other interest expense | | 218 | | | 179 | | | 964 | | | 991 | | | 1,182 | | | 1,171 | | | 2,091 | | | 1,999 | |

| | Other property expenses | | — | | | — | | | 1,831 | | | 825 | | | — | | | — | | | 39 | | | — | |

| | Current transfers | | 6,477 | | | 6,344 | | | 51 | | | 67 | | | 5,010 | | | 5,057 | | | — | | | 5,057 | |

| | Capital transfers | | 1,157 | | | 1,215 | | | 28 | | | — | | | 1,175 | | | 1,201 | | | — | | | 1,201 | |

| | Total Expenses | | 30,164 | | | 30,125 | | | 10,015 | | | 10,972 | | | 36,267 | | | 38,298 | | | 3,454 | | | 40,266 | |

| | | | | | | | | |

equals | | GFS net operating balance | | 2,393 | | | 1,856 | | | (604 | ) | | 824 | | | 1,790 | | | 2,679 | | | 105 | | | 2,785 | |

| | | | | | | | | |

less | | Net acquisition of non-financial assets | | | | | | | | | | | | | | | | | | | | | | | | |

| | Purchases of non-financial assets | | 4,137 | | | 4,418 | | | 7,436 | | | 6,363 | | | 11,573 | | | 10,635 | | | 11 | | | 10,647 | |

| | Sales of non-financial assets | | (290 | ) | | (471 | ) | | (191 | ) | | (127 | ) | | (481 | ) | | (452 | ) | | (1 | ) | | (454 | ) |

| | less Depreciation | | 1,780 | | | 1,880 | | | 1,597 | | | 1,564 | | | 3,377 | | | 3,444 | | | 20 | | | 3,464 | |

| | plus Change in inventories | | 23 | | | 13 | | | 23 | | | 65 | | | 46 | | | 78 | | | — | | | 78 | |

| | plus Other movements in non-financial assets | | (95 | ) | | (13 | ) | | (28 | ) | | 7 | | | (123 | ) | | (6 | ) | | — | | | (6 | ) |

| | equals Total net acquisition of non-financial assets | | 1,996 | | | 2,067 | | | 5,643 | | | 4,745 | | | 7,639 | | | 6,811 | | | (10 | ) | | 6,802 | |

| | | | | | | | | |

equals | | GFS Net lending/(borrowing) (Fiscal balance) | | 397 | | | (211 | ) | | (6,246 | ) | | (3,921 | ) | | (5,849 | ) | | (4,132 | ) | | 115 | | | (4,017 | ) |

| (a) | Numbers may not add due to rounding. |

| (b) | In accordance with UPF requirements, estimates for Public Financial Corporations and State Financial sectors are not included in Budget documentation. |

| | |

| Outcomes Report 2006-07 - Government of Queensland | | 4-08 |

Balance Sheet by Sector

Balance Sheet 2006-07 ($million) - by sector(a)

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | General Government

Sector | | | Public Non-financial

Corporations Sector | | | Non-financial Public

Sector | | | Public Financial

Corporations

Sector | | | State

Financial

Sector | |

| | | Est. Actual | | | Actual | | | Est. Actual | | | Actual | | | Est. Actual | | | Actual | | | Actual (b) | | | Actual (b) | |

Assets | | | | | | | | | | | | | | | | | | | | | | | | |

Financial assets | | | | | | | | | | | | | | | | | | | | | | | | |

Cash and deposits | | 1,873 | | | 1,049 | | | 2,435 | | | 3,481 | | | 4,308 | | | 4,530 | | | 49 | | | 1,162 | |

Advances paid | | 887 | | | 908 | | | 335 | | | 326 | | | 851 | | | 882 | | | — | | | 882 | |

Investments, loans and placements | | 27,404 | | | 27,501 | | | 1,141 | | | 1,353 | | | 28,545 | | | 28,853 | | | 42,636 | | | 51,312 | |

Other non-equity assets | | 3,394 | | | 3,048 | | | 1,351 | | | 2,762 | | | 3,001 | | | 4,830 | | | 156 | | | 4,945 | |

Equity | | 23,514 | | | 22,525 | | | 185 | | | 706 | | | 2,215 | | | 2,716 | | | 1 | | | 783 | |

| | | | | | | | |

Total financial assets | | 57,072 | | | 55,029 | | | 5,447 | | | 8,628 | | | 38,920 | | | 41,811 | | | 42,842 | | | 59,085 | |

| | | | | | | | |

Non-financial assets | | 87,592 | | | 93,698 | | | 39,974 | | | 39,311 | | | 127,532 | | | 132,974 | | | 115 | | | 133,089 | |

| | | | | | | | |

Total assets | | 144,665 | | | 148,727 | | | 45,421 | | | 47,938 | | | 166,452 | | | 174,785 | | | 42,957 | | | 192,173 | |

| | | | | | | | |

Liabilities | | | | | | | | | | | | | | | | | | | | | | | | |

Deposits held | | 1 | | | — | | | 68 | | | 35 | | | 68 | | | 35 | | | 6,734 | | | 3,032 | |

Advances received | | 459 | | | 505 | | | 1 | | | — | | | 460 | | | 505 | | | — | | | 505 | |

Borrowing | | 3,282 | | | 2,266 | | | 19,616 | | | 22,094 | | | 22,527 | | | 24,008 | | | 32,372 | | | 36,523 | |

Superannuation liability | | 18,823 | | | 20,177 | | | — | | | — | | | 18,823 | | | 20,177 | | | — | | | 20,177 | |

Other employee entitlements and provisions | | 4,216 | | | 4,368 | | | 1,210 | | | 1,132 | | | 5,394 | | | 5,484 | | | 1,724 | | | 7,208 | |

Other non-equity liabilities | | 3,418 | | | 3,580 | | | 3,010 | | | 4,029 | | | 4,715 | | | 6,646 | | | 194 | | | 6,799 | |

| | | | | | | | |

Total liabilities | | 30,198 | | | 30,896 | | | 23,905 | | | 27,290 | | | 51,986 | | | 56,855 | | | 41,023 | | | 74,243 | |

| | | | | | | | |

Net Worth | | 114,466 | | | 117,831 | | | 21,516 | | | 20,648 | | | 114,466 | | | 117,930 | | | 1,934 | | | 117,930 | |

| | | | | | | | |

Net financial worth | | 26,874 | | | 24,133 | | | (18,458 | ) | | (18,662 | ) | | (13,066 | ) | | (15,044 | ) | | 1,819 | | | (15,159 | ) |

Net debt | | (26,423 | ) | | (26,686 | ) | | 15,774 | | | 16,969 | | | (10,650 | ) | | (9,718 | ) | | (3,580 | ) | | (13,296 | ) |

| (a) | Numbers may not add due to rounding. |

| (b) | In accordance with UPF requirements, estimates for Public Financial Corporations and State Financial sectors are not included in Budget documentation. |

| (c) | Estimated Actuals have been restated where subsequent changes in classification have occurred, to ensure comparability with estimates. |

| | |

| Outcomes Report 2006-07 - Government of Queensland | | 4-09 |

Cash Flow Statement by Sector

Cash Flow Statement 2006-07 ($million) - by sector(a)

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | General Government

Sector | | | Public Non-financial

Corporations Sector | | | Non-financial Public

Sector | | | Public Financial

Corporations

Sector | | | State

Financial

Sector | |

| | | Est. Actual | | | Actual | | | Est. Actual | | | Actual | | | Est. Actual | | | Actual | | | Actual (b) | | | Actual (b) | |

Receipts from operating activities | | | | | | | | | | | | | | | | | | | | | | | | |

Taxes received | | 8,374 | | | 8,430 | | | — | | | — | | | 8,034 | | | 8,046 | | | — | | | 8,040 | |

Grants and subsidies received | | 14,171 | | | 14,288 | | | 1,624 | | | 1,906 | | | 14,267 | | | 14,787 | | | — | | | 14,787 | |

Sales of goods and services | | 3,238 | | | 3,088 | | | 8,768 | | | 9,532 | | | 11,797 | | | 12,376 | | | 1,068 | | | 13,247 | |

Other receipts | | 6,820 | | | 7,348 | | | 1,061 | | | 1,003 | | | 6,959 | | | 7,570 | | | 2,675 | | | 8,691 | |

Total | | 32,603 | | | 33,154 | | | 11,454 | | | 12,441 | | | 41,056 | | | 42,779 | | | 3,742 | | | 44,765 | |

Payments for operating activities | | | | | | | | | | | | | | | | | | | | | | | | |

Payments for goods and services | | (18,710 | ) | | (18,796 | ) | | (5,990 | ) | | (6,909 | ) | | (24,514 | ) | | (25,485 | ) | | (194 | ) | | (25,507 | ) |

Grants and subsidies | | (7,352 | ) | | (7,023 | ) | | (51 | ) | | (87 | ) | | (5,875 | ) | | (5,703 | ) | | — | | | (5,703 | ) |

Interest | | (218 | ) | | (179 | ) | | (909 | ) | | (804 | ) | | (1,127 | ) | | (983 | ) | | (2,213 | ) | | (1,950 | ) |

Other payments | | (755 | ) | | (859 | ) | | (1,254 | ) | | (1,321 | ) | | (1,650 | ) | | (1,774 | ) | | (963 | ) | | (2,712 | ) |

Total | | (27,034 | ) | | (26,857 | ) | | (8,203 | ) | | (9,122 | ) | | (33,166 | ) | | (33,945 | ) | | (3,370 | ) | | (35,872 | ) |

| | | | | | | | |

Net cash inflows from operating activities | | 5,569 | | | 6,297 | | | 3,251 | | | 3,319 | | | 7,890 | | | 8,833 | | | 372 | | | 8,893 | |

| | | | | | | | |

Payments for investments in non-financial assets | | | | | | | | | | | | | | | | | | | | | | | | |

Purchases of non-financial assets | | (4,137 | ) | | (4,418 | ) | | (7,436 | ) | | (6,363 | ) | | (11,573 | ) | | (10,635 | ) | | (11 | ) | | (10,647 | ) |

Sales of non-financial assets | | 290 | | | 471 | | | 191 | | | 127 | | | 481 | | | 452 | | | 1 | | | 454 | |

Total | | (3,847 | ) | | (3,947 | ) | | (7,245 | ) | | (6,236 | ) | | (11,092 | ) | | (10,183 | ) | | (10 | ) | | (10,193 | ) |

| | | | | | | | |

Payments for investments in financial assets for policy purposes | | 1,409 | | | 1,572 | | | 2,982 | | | 3,027 | | | 3,223 | | | 3,434 | | | — | | | 3,434 | |

| | | | | | | | |

Payments for investments in financial assets for liquidity purposes | | (3,617 | ) | | (4,275 | ) | | 187 | | | 79 | | | (3,430 | ) | | (4,196 | ) | | (3,279 | ) | | (7,225 | ) |

| | | | | | | | |

Receipts from financing activities | | | | | | | | | | | | | | | | | | | | | | | | |

Advances received (net) | | (15 | ) | | 33 | | | — | | | (1 | ) | | (15 | ) | | 32 | | | — | | | 32 | |

Borrowing (net) | | 743 | | | (262 | ) | | 3,761 | | | 3,792 | | | 4,505 | | | 3,529 | | | (3,874 | ) | | (739 | ) |

Deposits received (net) | | — | | | (1 | ) | | 20 | | | (145 | ) | | 21 | | | (145 | ) | | 1,304 | | | (228 | ) |

Distributions paid | | — | | | — | | | (929 | ) | | (784 | ) | | — | | | — | | | (292 | ) | | — | |

Other financing (net) | | — | | | — | | | (1,086 | ) | | (1,065 | ) | | 82 | | | 100 | | | 5,799 | | | 6,384 | |

Total | | 729 | | | (230 | ) | | 1,766 | | | 1,797 | | | 4,592 | | | 3,515 | | | 2,936 | | | 5,449 | |

| | | | | | | | |

Net increase/(decrease) in cash held | | 242 | | | (583 | ) | | 940 | | | 1,986 | | | 1,183 | | | 1,404 | | | 20 | | | 357 | |

| | | | | | | | |

Net cash from operating activities and investments in non-financial assets | | 1,722 | | | 2,350 | | | (3,995 | ) | | (2,917 | ) | | (3,202 | ) | | (1,350 | ) | | 362 | | | (1,300 | ) |

Finance leases and similar arrangements | | — | | | 46 | | | — | | | 3 | | | — | | | 49 | | | — | | | 49 | |

Distributions paid | | — | | | — | | | (929 | ) | | (784 | ) | | — | | | — | | | (292 | ) | | — | |

GFS Surplus/(deficit) | | 1,722 | | | 2,304 | | | (4,924 | ) | | (3,704 | ) | | (3,202 | ) | | (1,399 | ) | | 70 | | | (1,349 | ) |

| (a) | Numbers may not add due to rounding. |

| (b) | In accordance with UPF requirements, estimates for Public Financial Corporations and State Financial sectors are not included in Budget documentation. |

| | |

| Outcomes Report 2006-07 - Government of Queensland | | 4-10 |

General Government Sector Expenses by Function

| | |

| | | Actual

2006-07

$ million |

General Public Services | | 1,331 |

Other general public services | | 1,331 |

| |

Public Order and Safety | | 2,688 |

Police and fire protection services | | 1,605 |

Law courts and legal services | | 566 |

Prisons and corrective services | | 448 |

Other public order and safety | | 69 |

| |

Education | | 7,219 |

Primary and secondary education | | 5,595 |

Tertiary education | | 667 |

Pre-school education and education not definable by level | | 684 |

Transportation of students | | 153 |

Education n.e.c. | | 121 |

| |

Health | | 7,378 |

Acute care institutions | | 4,937 |

Mental health institutions | | 211 |

Nursing homes for the aged | | 179 |

Community health services | | 1,632 |

Public health services | | 227 |

Health research | | 95 |

Health administration n.e.c. | | 97 |

| |

Social Security and Welfare | | 1,474 |

Welfare services | | 1,447 |

Social security and welfare n.e.c. | | 28 |

| |

Housing and Community Amenities | | 1,010 |

Housing and community development | | 755 |

Water supply | | 169 |

Sanitation and protection of the environment | | 86 |

| |

Recreation and Culture | | 696 |

Recreation facilities and services | | 465 |

Cultural facilities and services | | 225 |

Recreation and culture n.e.c. | | 6 |

| |

Fuel and Energy | | 942 |

Fuel affairs and services | | 553 |

Electricity and other energy | | 390 |

| |

Agriculture, Forestry, Fishing and Hunting | | 1,117 |

Agriculture | | 1,002 |

Forestry, fishing and hunting | | 115 |

| |

Mining, manufacturing and construction | | 168 |

Mining and mineral resources other than fuels | | 83 |

Construction | | 85 |

| |

Transport and Communications | | 3,224 |

Road transport | | 1,608 |

Water transport | | 90 |

Rail transport | | 534 |

Air transport | | 12 |

Other transport | | 958 |

Communications | | 22 |

| |

Other Economic Affairs | | 786 |

Tourism and area promotion | | 84 |

Labour and employment affairs | | 445 |

Other economic affairs | | 258 |

| |

Other Purposes | | 2,090 |

Nominal superannuation interest | | 1,154 |

Public debt transactions | | 181 |

General purpose inter-government transactions | | 562 |

Natural disaster relief | | 190 |

Other purposes n.e.c. | | 4 |

| | |

Total | | 30,125 |

| | |

| | |

| Outcomes Report 2006-07 - Government of Queensland | | 4-11 |

General Government Sector Purchases of Non-financial Assets by

Function and Loan Council Allocation

General Government Sector

Purchases of Non-financial Assets by Function

| | |

| | | 2006-07

Outcome

$ million |

General public services | | 375 |

Public order and safety | | 371 |

Education | | 429 |

Health | | 574 |

Social security and welfare | | 79 |

Housing and community amenities | | 387 |

Recreation and culture | | 150 |

Agriculture, forestry, fishing and hunting | | 137 |

Mining, manufacturing and construction | | 9 |

Transport and communications | | 1,882 |

Other economic affairs | | 25 |

| |

Total | | 4,418 |

Loan Council Allocation

The Australian Loan Council requires all jurisdictions to advise the Loan Council Allocations (LCA) outcome for the last financial year as part of the annual Outcomes Report. The LCA represents each government’s call on financial markets for a given financial year. A tolerance limit of two percent of non-financial public sector receipts applies between the LCA budget update and the outcome. The LCA outcome exceeds the Budget estimate by more than this.

The LCA Outcome surplus reflects the continuing strength of the economy flowing through to taxation and other revenues, upward revisions to GST payments from the Australian Government and investment returns above the long-term assumed rate of return. In addition, the proceeds on the sale of Energex’s electricity and gas retail businesses, the Allgas distribution network and the competitive parts of Ergon Energy’s electricity retail business contributed to the revised Loan Council Allocation.

| | | | | |

| | | 2006-07

Budget

$ million | | 2006-07

Outcome

$ million | |

General Government sector cash deficit/(surplus)1 | | 796 | | (2,304 | ) |

PNFC sector cash deficit/(surplus)1 | | 3,305 | | 3,704 | |

Non-financial Public Sector cash deficit/(surplus)1 | | 4,101 | | 1,400 | |

| | |

Net cash flows from investments in financial assets for policy purposes | | — | | (3,434 | ) |

Memorandum items2 | | 118 | | 425 | |

| | |

LOAN COUNCIL ALLOCATION | | 4,219 | | (1,609 | ) |

Notes:

| 1. | Figures in brackets represent surpluses |

| 2. | Other memorandum items include operating leases and local government borrowings |

| | |

| Outcomes Report 2006-07 - Government of Queensland | | 4-12 |

Certification of Outcomes Report

Management Certification

The foregoing Outcomes Report contains financial statements prepared and presented on a Government Finance Statistics (GFS) basis and is in accordance with the Uniform Presentation Framework (UPF) agreed to at the 1991 Premiers’ Conference. In addition, Queensland’s Loan Council Allocation and disclosure of General Government expenses by purpose are included.

The Report separately discloses outcomes for the General Government, Public Non-financial Corporations, Public Financial Corporations and State Financial sectors within Queensland. Entities excluded from this report include local governments. Queensland public sector entities consolidated for this report are listed in the Consolidated Financial Statements, taking into account intra and inter-agency eliminations.

Only those agencies considered material by virtue of their financial transactions and balances are consolidated in this report.

In our opinion, we certify that the Outcomes Report has been properly drawn up, in accordance with GFS principles and UPF requirements, to present a true and fair view of:

| (i) | the operating statement and cash flows of the Queensland State Government for the financial year; and |

| (ii) | the balance sheet of the Government at 30 June 2007. |

At the date of certification of this report, we are not aware of any material circumstances that would render any particulars included in the Outcomes Report misleading or inaccurate.

| | |

Leigh Pickering | | Gerard Bradley, CPA FCA |

Director | | Under Treasurer |

Fiscal and Taxation Policy | | Queensland Treasury |

Queensland Treasury | | |

| |

Date 11 October 2007 | | |

| | |

| Outcomes Report 2006-07 - Government of Queensland | | 4-13 |

2006 - 07

Consolidated Financial

Statements

of the Queensland Government - 30 June 2007

Consolidated Financial Statements - Overview and Analysis

The following analysis compares current year Total State performance on an accounting basis with last year’s balances, restated for changes in accounting policies, presentational and timing differences and errors.

Overview

| - | The State recorded a surplus for the year of $5.385 billion, consisting of a surplus from continuing operations of $3.456 billion (2006, $4.705 billion) and a surplus from discontinued operations of $1.929 billion (2006, $136 million). |

| - | The State’s net assets position increased to $117.930 billion at 30 June 2007, an increase of $13.484 billion over the restated 2006 net assets of $104.446 billion. |

| - | Increased cash generated from the State operating surplus in 2006-07 has been utilised to fund higher investments in capital (property, plant and equipment) with outlays of $10.635 billion compared to $7.773 billion for the previous year. Interest earnings on long-term investments (held to meet future employee entitlements) were re-invested during 2006-07. |

Summary of Key Financial Aggregates of the Consolidated Financial Statements

The table below provides aggregate information under Australian Accounting Standards:

| | | | |

Total State | | 2007 $ million | | 2006 $ million |

| Revenue from operations | | | | |

Commonwealth and other grants | | 14,473 | | 13,527 |

Sales of goods and services | | 10,478 | | 7,690 |

Taxes, fees and fines | | 9,286 | | 7,912 |

Investment income | | 4,747 | | 4,324 |

Royalties and other territorial revenue | | 1,430 | | 1,547 |

Other | | 702 | | 560 |

| | | | |

| | 41,116 | | 35,560 |

| | | | |

| Expenses from operations | | | | |

Employee expenses | | 15,978 | | 14,278 |

Supplies and services | | 9,076 | | 6,429 |

Depreciation and amortisation | | 3,461 | | 3,105 |

Grants and other contributions | | 6,008 | | 5,186 |

Finance costs | | 1,518 | | 1,096 |

Share of net losses of associates using the equity method | | 4 | | 3 |

Other | | 1,930 | | 561 |

| | | | |

| | 37,975 | | 30,658 |

| | | | |

Gains | | 1,194 | | 432 |

| | | | |

Losses | | 879 | | 629 |

| | | | |

Surplus/(Deficit) from continuing operations | | 3,456 | | 4,705 |

| | | | |

Surplus/(Deficit) from discontinued operations | | 1,929 | | 136 |

| | | | |

Net Surplus/(Deficit) | | 5,385 | | 4,841 |

| | | | |

Assets | | 192,141 | | 165,790 |

Liabilities | | 74,211 | | 61,344 |

| | | | |

Net Assets | | 117,930 | | 104,446 |

| | | | |

| | |

| State Finances Report 2006-07 - Government of Queensland | | 5-01 |

Consolidated Financial Statements - Overview and Analysis

Operating Result

The whole-of-Government operating result from continuing operations for the 2006-07 year was a surplus of $3.456 billion (2006, $4.705 billion). The surplus from discontinued operations totalled $1.929 billion (2006, $136 million) due to the disposal of State assets.

Revenue

Revenue from continuing operations for 2006-07 was $41.116 billion, an increase of $5.556 billion (15.6%) from 2005-06 ($35.56 billion).

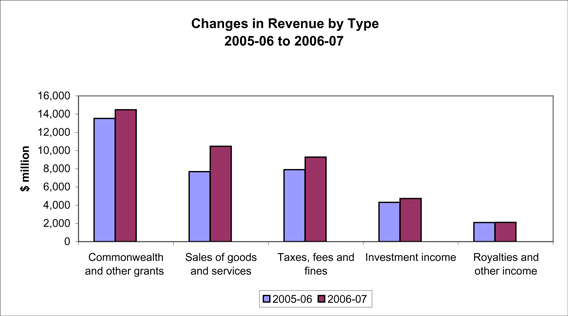

Changes in revenues by type are shown in the following chart:

Commonwealth and other grants comprised 35% of total State revenue in 2006-07 and grew from $13.527 billion in 2005-06 to $14.473 billion in 2006-07 (an increase of $946 million). The major contributor to this increase was grants from the Commonwealth for education and health ($500 million). GST revenue also increased from 2005-06 ($ 319 million), primarily reflecting stronger consumption expenditure in the economy.

Sales of goods and services increased by $2.788 billion in 2006-07 primarily due to higher electricity pool prices.

Taxes, fees and fines grew by $1.374 billion (17.4%) reflecting high levels of employment and the ongoing strength of the property sector. Transfer duty grew by $579 million and payroll tax increased by $308 million.

Investment income grew by $423 million to $4.747 billion in 2006-07, reflecting continued strong returns on funds invested with the Queensland Investment Corporation, resulting in an extra $157 million in distributions. Interest income from onlendings to bodies such as local governments also increased by $165 million.

| | |

| State Finances Report 2006-07 - Government of Queensland | | 5-02 |

Consolidated Financial Statements - Overview and Analysis

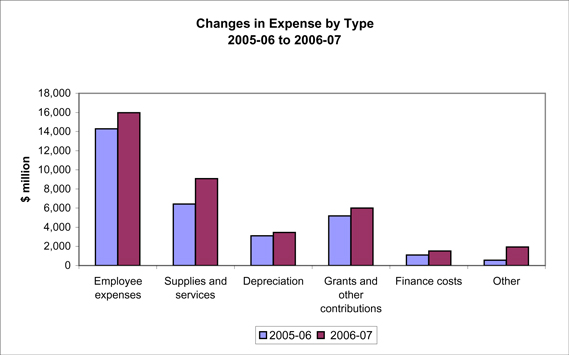

Expenses

The State’s expenses for 2006-07 in relation to continuing operations totalled $37.975 billion, an increase of $7.317 billion (23.9%) from 2005-06 ($30.658 billion).

Changes in expenses by type are shown in the following chart:

Employee expenses for 2006-07 increased $1.7 billion to $15.978 billion compared with $14.278 billion in 2005-06. This growth reflects wage increases from established enterprise bargaining agreements and additional staffing associated with service growth and enhancements, including the Health Action Plan.

Supplies and services have increased $2.647 billion to $9.076 billion in 2006-07 mainly due to higher electricity pool prices. Other increases in expenditure were in the departments of Health and Education as well as the expansion of QR’s operations.

Depreciation was $356 million higher than 2005-06 due to revaluations and purchases of additional assets during the course of 2006-07.

The increase in grants and other contributions of $822 million (15.9%) primarily represents grant payments by Education (non-state schools), Health (public hospital support services, and home, community and rural health services) and Natural Resources and Water (vegetation management framework).

Finance costs have increased from $1.096 billion to $1.518 billion, due to higher levels of borrowings by the State’s commercial entities to fund capital expansion.

Other expenses have increased in 2006-07 primarily due to WorkCover Queensland claims expenses which returned to normal levels after unusually low claims expenses in 2005-06 as a result of actuarial adjustments.

Discontinued Operations

During 2006-07 the State disposed of the retail arm of Energex’s gas and electricity businesses and Golden Casket Lottery Corporation Ltd, resulting in a gain of $1.781 billion. The gain and the results of the entities sold have been included in discontinued operations.

The sale of Ergon’s Powerdirect business has not been treated as discontinued because it has retained part of its retail business.

| | |

| State Finances Report 2006-07 - Government of Queensland | | 5-03 |

Consolidated Financial Statements - Overview and Analysis

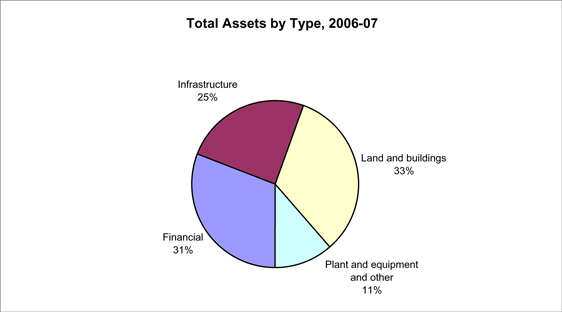

Assets

Assets controlled by the Government at 30 June 2007 totalled $192.141 billion (2006, $165.79 billion). The increase of $26.351 billion in assets is a result of:

| - | Higher property, plant and equipment balances of $16.868 billion reflecting, investment in water, roads and transport, (including QR) and upward revaluations of non-financial assets by the departments of Natural Resources and Water ($3.11 billion), Main Roads ($2.711 billion), Education, Training and the Arts ($1.508 billion), Housing ($ 813 million), Public Works ($435 million) and Health ($422 million). |

| - | Increased holdings of financial assets, up $9.481 billion. This increase primarily represents the reinvestment of earnings on the State’s financial assets set aside to meet future employee entitlements, and the investment of borrowings undertaken in advance of requirements. |

The main types of assets owned by the State are detailed in the following chart:

| | |

| State Finances Report 2006-07 - Government of Queensland | | 5-04 |

Consolidated Financial Statements - Overview and Analysis

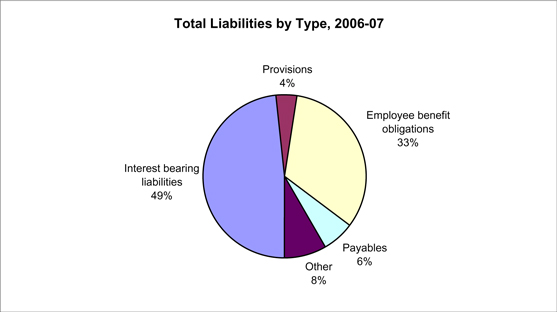

Liabilities

The total liabilities of the Queensland Government at 30 June 2007 were $74.211 billion, an increase of $12.9 billion (21%) over 2005-06 ($61.344 billion). The increase is largely due to:

| - | An increase in interest bearing liabilities ($5.041 billion) reflecting increased borrowing by the State’s commercial entities to expand their capital base. |

| - | Employee entitlement obligations such as superannuation and long service leave increasing by $2.826 billion. |

| - | Other liabilities increasing by $4.303 billion mainly due to the current value of derivatives in the electricity sector. |

The components of State liabilities are shown in the following chart:

Maintenance of Credit Ratings

Queensland’s strong credit rating position is illustrated in the following table:

| | | | |

| | | Moody’s

Investors

Service | | Standard

& Poor’s |

| | |

Long-term local currency rating | | Aaa | | AAA |

Short-term rating | | P-1 | | A-1+ |

Long-term foreign currency rating | | Aaa | | AAA |

These ratings are the highest available.

Because of these strong ratings, the Queensland Treasury Corporation continues to be in a position to borrow at advantageous rates.

Queensland’s debt ratio (total liabilities to total assets) at 30 June 2007 was 38.7 percent (2006, 37 percent).

The State’s gearing ratio (interest bearing liabilities to net assets) was 23.39 percent at 30 June 2007 (2006, 22.83 percent).

It is anticipated these ratios will increase over time as the State increases its borrowings to fund the capital program.

| | |

| State Finances Report 2006-07 - Government of Queensland | | 5-05 |

Consolidated Financial Statements - Overview and Analysis

Cash Flow Statement

The Cash Flow Statement is split between the Non-financial Public sector on page 5-11 and the Public Financial Corporations sector (refer Note 39 (b)).

The Non-financial Public sector recorded net cash flows from operating activities for the 2006-07 financial year of $8.833 billion, slightly lower than the 2005-06 net cash inflows of $9.133 billion.

Capital purchases were $10.635 billion, up $2.862 billion from 2005-06 mainly due to outlays by the State’s commercial entities on water, ports and rail projects. In addition, earnings on investments set aside for employee benefits were reinvested and reflected as a net acquisition of investments during 2006-07.

An increase in net borrowings for the State of $3.567 billion was undertaken in 2006-07 to partially fund growth in capital outlays by the State’s commercial entities. This is up from $1.518 billion in 2005-06.

| | |

| State Finances Report 2006-07 - Government of Queensland | | 5-06 |

| | |

| 2006 - 07 | |  |

| Audited Information | |

Consolidated Financial Statements of the Queensland Government 30 June 2007 | |

| |

Income Statement

for the year ended 30 June 2007

| | | | | | |

| | | Notes | | 2007 | | 2006 |

| | | | | $M | | $M |

Revenue from Continuing Operations | | | | | | |

| | | |

Commonwealth and other grants | | 3 | | 14,473 | | 13,527 |

Sales of goods and services | | 4 | | 10,478 | | 7,690 |

Taxes, fees and fines | | 5 | | 9,286 | | 7,912 |

Investment income | | 6 | | 4,747 | | 4,324 |

Royalties and other territorial revenue | | 7 | | 1,430 | | 1,547 |

Other | | 8 | | 702 | | 560 |

| | | | | | |

| | | | 41,116 | | 35,560 |

| | | | | | |

Expenses from Continuing Operations | | | | | | |

| | | |

Employee expenses | | 9 | | 15,978 | | 14,278 |

Supplies and services | | | | 9,076 | | 6,429 |

Depreciation and amortisation | | 10 | | 3,461 | | 3,105 |

Grants and other contributions | | | | 6,008 | | 5,186 |

Finance costs | | 11 | | 1,518 | | 1,096 |

Share of net losses of associates using the equity method | | 40 | | 4 | | 3 |

Other | | 12 | | 1,930 | | 561 |

| | | | | | |

| | | | 37,975 | | 30,658 |

| | | | | | |

Gains | | | | | | |

Gains on sale of assets | | 13 | | 1,047 | | 41 |

Revaluation increments and impairment reversals | | 14 | | 147 | | 391 |

| | | | | | |

| | | | 1,194 | | 432 |

Losses | | | | | | |

Loss on sale of assets | | 15 | | — | | 2 |

Loss on revaluation of assets | | 16 | | 418 | | 205 |

Impairment losses | | 17 | | 20 | | 75 |

Other losses | | 18 | | 441 | | 347 |

| | | | | | |

| | | | 879 | | 629 |

| | | |

Surplus/(Deficit) before Income Tax Expense | | | | 3,456 | | 4,705 |

| | | |

Income tax credit/(expense) | | 2 | | — | | — |

| | | | | | |

Surplus/(Deficit) from continuing operations | | | | 3,456 | | 4,705 |

| | | |

Surplus/(Deficit) from discontinued operations | | 53 | | 1,929 | | 136 |

| | | | | | |

Net Surplus/(Deficit) | | | | 5,385 | | 4,841 |

| | | | | | |

This Income Statement should be read in conjunction with the accompanying notes.

Note 2 provides disaggregated information in relation to the components of the net surplus/(deficit).

| | |

| Audited Consolidated Financial Statements 2006-07 - Government of Queensland | | 5-07 |

Balance Sheet

as at 30 June 2007

| | | | | | |

| | | Notes | | 2007 | | 2006 |

| | | | | $M | | $M |

Assets | | | | | | |

Current Assets | | | | | | |

Cash and cash equivalents | | 19 | | 1,162 | | 644 |

Receivables and loans | | 20 | | 4,038 | | 3,563 |

Financial assets at fair value through profit or loss | | 21 | | 13,445 | | 9,902 |

Other investments | | 22 | | 679 | | 237 |

Derivative financial instruments | | 23 | | 812 | | 440 |

Inventories | | 24 | | 911 | | 880 |

Other | | 27 | | 426 | | 455 |

| | | | | | |

| | | | 21,473 | | 16,121 |

| | | |

Non-current assets classified as held for sale | | 28 | | 101 | | 107 |

Assets of disposal group | | 53 | | 318 | | 628 |

| | | | | | |

| | | | 21,892 | | 16,856 |

| | | | | | |

Non-Current Assets | | | | | | |

Receivables and loans | | 20 | | 4,611 | | 4,209 |

Financial assets at fair value through profit or loss | | 21 | | 32,824 | | 29,475 |

Other investments | | 22 | | 84 | | 39 |

Derivative financial instruments | | 23 | | 523 | | 129 |

Investments accounted for using the equity method | | 40 | | 67 | | 64 |

Investment properties | | 25 | | 992 | | 839 |

Biological assets | | 26 | | 1,092 | | 1,147 |

Property, plant and equipment | | 29 | | 128,714 | | 111,827 |

Intangibles | | 30 | | 979 | | 993 |

Other | | 27 | | 363 | | 212 |

| | | | | | |

| | | | 170,249 | | 148,934 |

| | | | | | |

Total Assets | | | | 192,141 | | 165,790 |

| | | | | | |

Liabilities | | | | | | |

| | | |

Current Liabilities | | | | | | |

Payables | | 32 | | 4,366 | | 3,703 |

Employee benefit obligations | | 33 | | 2,618 | | 2,459 |

Financial liabilities held at fair value through profit or loss | | 34 | | 8,532 | | 3,769 |

Financial liabilities held at amortised cost | | 35 | | 220 | | 184 |

Derivative financial instruments | | 23 | | 2,717 | | 344 |

Provisions | | 36 | | 1,069 | | 964 |

Other | | 37 | | 843 | | 749 |

| | | | | | |

| | | | 20,365 | | 12,172 |

| | | |

Liabilities associated with assets of disposal group | | 53 | | 86 | | 178 |

| | | | | | |

| | | | 20,451 | | 12,350 |

| | | | | | |

| | |

| Audited Consolidated Financial Statements 2006-07 - Government of Queensland | | 5-08 |

Balance Sheet

as at 30 June 2007

| | | | | | |

| | | Notes | | 2007 | | 2006 |

| | | | | $M | | $M |

Non-Current Liabilities | | | | | | |

Payables | | 32 | | 381 | | 338 |

Employee benefit obligations | | 33 | | 21,697 | | 19,026 |

Financial liabilities held at fair value through profit or loss | | 34 | | 26,600 | | 26,393 |

Financial liabilities held at amortised cost | | 35 | | 594 | | 558 |

Derivative financial instruments | | 23 | | 1,393 | | 126 |

Provisions | | 36 | | 2,001 | | 1,975 |

Other | | 37 | | 1,094 | | 578 |

| | | | | | |

| | | | 53,760 | | 48,994 |

| | | | | | |

Total Liabilities | | | | 74,211 | | 61,344 |

| | | | | | |

Net Assets | | | | 117,930 | | 104,446 |

| | | | | | |

Equity | | | | | | |

Accumulated surplus | | 38 | | 57,306 | | 52,154 |

Reserves | | 38 | | 60,525 | | 52,292 |

| | | | | | |

State interest | | | | 117,831 | | 104,446 |

| | | | | | |

Minority interest | | | | 99 | | — |

| | | | | | |

Total Equity | | | | 117,930 | | 104,446 |

| | | | | | |

This Balance Sheet should be read in conjunction with the accompanying notes.

Note 2 provides disaggregated information in relation to the components of the net assets.

| | |

| Audited Consolidated Financial Statements 2006-07 - Government of Queensland | | 5-09 |

Statement of Changes in Equity

for the year ended 30 June 2007

| | | | | | |

| | | 2007 | | | 2006 | |

| | | $M | | | $M | |

Total equity at the beginning of the financial year before accounting policy changes and error corrections | | 104,446 | | | 92,014 | |

| | |

Effect of error correction/timing adjustments in opening balances on: | | | | | | |

Accumulated surplus (refer Note 38) | | — | | | (26 | ) |

| | | | | | |

Total adjusted equity at the beginning of the financial year | | 104,446 | | | 91,988 | |

| | |

Revaluation increment/(decrement) and impairment of non-current assets | | 10,439 | | | 7,584 | |

Revaluation of financial instruments | | (2,157 | ) | | 116 | |

Actuarial gain/(loss) on superannuation | | (282 | ) | | (90 | ) |

Other | | — | | | (7 | ) |

| | | | | | |

Net income recognised directly in equity | | 8,000 | | | 7,603 | |

| | |

Net surplus/(deficit) | | 5,385 | | | 4,841 | |

| | |

Total recognised income and expense for the period | | 13,385 | | | 12,444 | |

| | |

Transactions with owners as owners | | | | | | |

Net assets of entities not previously consolidated | | — | | | 14 | |

| | |

Minority interest increase | | 99 | | | — | |

| | | | | | |

Total equity at the end of the financial year | | 117,930 | | | 104,446 | |

| | | | | | |

| | |

| Audited Consolidated Financial Statements 2006-07 - Government of Queensland | | 5-10 |

Cash Flow Statement

for the year ended 30 June 2007

| | | | | | | | |

| | | Notes | | 2007 $M | | | 2006 $M | |

Cash Flows from Operating Activities | | | | | | | | |

Receipts | | | | | | | | |

Grants and subsidies received | | | | 14,787 | | | 13,965 | |

Sales of goods and services | | | | 11,241 | | | 10,225 | |

Taxes, fees and fines | | | | 9,181 | | | 7,842 | |

Interest received | | | | 3,541 | | | 3,494 | |

Royalties and other territorial receipts | | | | 1,866 | | | 1,510 | |

Dividends received | | | | 51 | | | 33 | |

GST input tax credits received | | | | 1,663 | | | 1,600 | |

Other | | | | 448 | | | 488 | |

| | | |

Payments | | | | | | | | |

Employee expenses | | | | (13,920 | ) | | (12,498 | ) |

Supplies and services | | | | (11,576 | ) | | (10,091 | ) |

Grants and subsidies paid | | | | (5,893 | ) | | (5,285 | ) |

Borrowing costs paid | | | | (1,115 | ) | | (1,048 | ) |

GST remitted to the ATO | | | | (707 | ) | | (988 | ) |

Other | | | | (734 | ) | | (114 | ) |

| | | | | | | | |

Net Cash Inflow from Operating Activities | | 39(a) | | 8,833 | | | 9,133 | |

| | | | | | | | |

Cash Flows from Investing Activities | | | | | | | | |

Receipts | | | | | | | | |

Proceeds from sale of property, plant and equipment | | | | 452 | | | 486 | |

Proceeds from sale of subsidiaries | | | | 3,436 | | | — | |

Proceeds from sale of investments | | | | 1,869 | | | 541 | |

Loans and advances redeemed | | | | 105 | | | 119 | |

| | | |

Payments | | | | | | | | |

Acquisition of property, plant and equipment | | | | (10,635 | ) | | (7,773 | ) |

Acquisition of investments | | | | (6,065 | ) | | (4,287 | ) |

Loans and advances made | | | | (257 | ) | | (158 | ) |

| | | | | | | | |

Net Cash Outflow from Investing Activities | | | | (11,095 | ) | | (11,072 | ) |

| | | | | | | | |

Cash Flows from Financing Activities | | | | | | | | |

Receipts | | | | | | | | |

Proceeds from borrowings | | | | 5,547 | | | 3,596 | |

Capital issue - Minority interest | | | | 99 | | | — | |

| | | |

Payments | | | | | | | | |

Repayment of borrowings | | | | (1,980 | ) | | (2,078 | ) |

| | | | | | | | |

Net Cash from Financing Activities | | | | 3,666 | | | 1,518 | |

| | | | | | | | |

Net Cash Flows from Public Financial Corporations (PFC) | | 39(b) | | 20 | | | 2 | |

| | | | | | | | |

Net Increase/(Decrease) in Cash | | | | 1,424 | | | (419 | ) |

Net Increase/(Decrease) in non-eliminated Cash Balances with PFC | | | | (1,067 | ) | | 689 | |

Cash at the Beginning of the Financial Year | | | | 805 | | | 535 | |

| | | | | | | | |

Cash Held at End of Year | | 19 | | 1,162 | | | 805 | |

| | | | | | | | |

This Cash Flow Statement should be read in conjunction with the accompanying notes.

| | |

| Audited Consolidated Financial Statements 2006-07 - Government of Queensland | | 5-11 |

Notes to the Financial Statements

| 1. | Significant Accounting Policies |

The following summary presents the significant accounting policies that have been adopted in preparing and presenting the consolidated financial statements of the Government of Queensland.

These consolidated financial statements have been prepared in accordance with the Financial Administration and Audit Act 1977, applicable Australian Accounting Standards and Concepts, Urgent Issues Group Consensus Views and other authoritative pronouncements.

This financial report is a general purpose financial report.

New accounting standards and interpretations which have been published and are not mandatory for 30 June 2007 reporting periods are set out below:

AASB 1: First-time Adoption of Australian Equivalents to International Financial Reporting Standards

AASB 4: Insurance Contracts

AASB 7: Financial Instruments: Disclosures

AASB 101: Presentation of Financial Statements

AASB 117: Leases

AASB 118: Revenue

AASB 120: Accounting for Government Grants and Disclosure of Government Assistance

AASB 121: The Effects of Changes in Foreign Exchange Rates

AASB 127: Consolidated and Separate Financial Statements

AASB 131: Interests in Joint Ventures

AASB 132: Financial Instruments: Presentation

AASB 139: Financial Instruments: Recognition and Measurement

AASB 1048: Interpretation and Application of Standards

AASB 1049: Financial Reporting of General Government Sectors by Governments

AASB 2007-1: Amendments to Australian Accounting Standards arising from AASB Interpretation 11 [AASB 2]

AASB 2007-2: Amendments to Australian Accounting Standards arising from AASB Interpretation 12 [AASB 1, AASB 117, AASB 118, AASB 120, AASB 127, AASB 131 & AASB 1038]

AASB 2007-3: Amendments to Australian Accounting Standards arising from AASB 8 [AASB 5, AASB 6, AASB 102, AASB 107, AASB 119, AASB 127, AASB 134, AASB 136, AASB 1023 & AASB 1038]

AASB 2007-4: Amendments to Australian Accounting Standards arising from ED 151 and Other Amendments [AASB 1, 2, 3, 4, 5, 6, 7, 102, 107, 108, 110, 112, 114, 116, 117, 118, 119, 120, 121, 127, 128, 129, 130, 131, 132, 133, 134, 136, 137, 138, 139, 141, 1023 & 1038]

AASB 2007-5: Amendments to Australian Accounting Standard – Inventories Held for Distribution by Not-for-Profit Entities [AASB 102]

AASB 2007-6: Amendments to Australian Accounting Standards arising from AASB 123 [AASB 1, AASB 101, AASB 107, AASB 111, AASB 116 & AASB 138 and Interpretations 1 & 12]

Interpretation 4: Determining whether an Arrangement contains a Lease [revised]

Interpretation 10: Interim Financial reporting and Impairment

Interpretation 11: AASB 2 - Group and Treasury Share Transactions

Interpretation 12: Service Concession Arrangements

Interpretation 129: Disclosure - Service Concession Arrangements [revised]

The State has not adopted these standards and interpretations early. Application of these standards will not affect any of the amounts recognised in the financial statements, but will impact the type of information disclosed.

The statements have been prepared on an accrual basis that recognises the financial effects of transactions and events when they occur.

| | |

| Audited Consolidated Financial Statements 2006-07 - Government of Queensland | | 5-12 |

Notes to the Financial Statements

| 1. | Significant Accounting Policies continued |

| (b) | The Government Reporting Entity |

In accordance with AASB 127 Consolidated and Separate Financial Statements , these consolidated financial statements include the values of all material assets, liabilities, equities, revenues and expenses controlled by the Government of Queensland.

Only those agencies considered material by virtue of the size of their financial transactions and/or resources managed are consolidated for the purposes of this report.

Where control of an entity is obtained during the financial year, its results are included in the Income Statement from the date control commences. Where control of an entity ceases during a financial year, its results are included for that part of the year during which control existed.

The Queensland Government economic entity includes all State Government departments, Public

Non-financial Corporations, Public Financial Corporations and their controlled entities. Refer Note 51 for a full list of entities included in each sector.

In the process of reporting the Government of Queensland as a single economic entity, all material inter-entity and intra-entity transactions and balances have been eliminated to the extent practicable.

Assets, liabilities, revenues and expenses that are attributed reliably to each sector of the Queensland Government economic entity are disclosed in Note 2. For disclosure purposes, transactions and balances between sectors have not been eliminated, but those between entities within each sector have been eliminated. The financial impact of inter-sector transactions and balances is disclosed in Note 2, under the heading of Consolidation Adjustments.

A brief description of each broad sector of the Government’s activities, determined in accordance with the Government Financial Statistics Standards, (Australian Bureau of Statistics), follows:

General Government Sector

The primary function of General Government sector agencies is to provide public services that:

| | - | are non-trading in nature and that are for the collective benefit of the community; |

| | - | are largely financed by way of taxes, fees and other compulsory charges; and |

| | - | involve the transfer or redistribution of income. |

Public Non-financial Corporations Sector

The primary function of enterprises in the Public Non-financial Corporations sector is to provide goods and services that:

| | - | are trading, non-regulatory or non-financial in nature; and |

| | - | are financed by way of sales of goods and services to consumers. |

| | | | |

| Audited Consolidated Financial Statements 2006-07 - Government of Queensland | | 5-13 |

Notes to the Financial Statements

| 1. | Significant Accounting Policies continued |

Public Financial Corporations Sector

The Public Financial Corporations sector comprises publicly owned institutions which provide financial services usually on a commercial basis.

Functions they perform may include:

| | - | accepting on-call, term or savings deposits; |

| | - | investment fund management; |

| | - | having the authority to incur liabilities and acquire financial assets in the market on their own account; or |

| | - | providing insurance services. |

The reporting period of the consolidated entity is the year ended 30 June 2007.

The consolidated financial statements adopt the following valuation methodologies:

| | - | superannuation, WorkCover, motor vehicle accident liabilities, Queensland Government Insurance Fund and the Queensland Government Long Service Leave Central Scheme provisions are based on actuarial valuations; |

| | - | investments and other financial assets are recorded at market value; |

| | - | borrowings and other financial liabilities are recorded at market value; |

| | - | power purchase agreements are valued at fair value; |

| | - | land, buildings, infrastructure, major plant and equipment, heritage and cultural assets are valued at fair value and other classes of assets are valued at cost; |

| | - | inventories (other than those held for distribution) are valued at the lower of cost and net realisable value under AASB 102 Inventories. |

Historical cost accounting principles are otherwise employed.

Unless otherwise stated, the accounting policies adopted for the reporting period are consistent with those of the previous reporting period. In accordance with AASB 101 Presentation of Financial Statements and AASB 108 Accounting Policies, Changes in Accounting Estimates and Errors, changes to accounting policies are applied retrospectively unless specific transitional provisions apply.

All amounts in the consolidated financial statements have been rounded to the nearest $1 million or where the amount is less than $500,000 to zero, unless otherwise indicated.

| (g) | Comparative Information |

Where applicable, comparatives have been restated to agree with changes in presentation in the financial statement for the current reporting period.

AASB 108 requires that material prior period errors be corrected retrospectively by either restating comparative amounts if the error occurred in the prior year; or restating the opening balances of assets, liabilities and equity of the prior year where the error occurred before the prior year.

| | | | |

| Audited Consolidated Financial Statements 2006-07 - Government of Queensland | | 5-14 |

Notes to the Financial Statements

| 1. | Significant Accounting Policies continued |

Business combinations are recognised in accordance with AASB 3 Business Combinations and accounted for using the purchase method, regardless of whether equity instruments or other assets and liabilities are acquired.

Cost is measured as the fair value of the assets given, or liabilities incurred or assumed at the date of exchange plus costs directly attributable to the acquisition.

Identifiable assets acquired and liabilities and contingent liabilities assumed in a business combination are measured initially at their fair value at the acquisition date, irrespective of the extent of any minority interest. The excess of cost of acquisition over the fair value of the State’s share of the identifiable net assets acquired is recorded as goodwill. If the cost of acquisition is less than the State’s share of the fair value of the identifiable net assets of the subsidiary acquired, the difference is recognised directly in the Income Statement, but only after a reassessment of the identification and measurement of the net assets acquired.

Where settlement of any part of the cash consideration is deferred, the amounts payable in the future are discounted to their present value as at the date of the exchange. The discount rate used is the borrowing rate applicable to similar borrowing from independent financiers under comparable terms and conditions.

Associates are those entities over which the economic entity has significant influence but not control. Such entities are accounted for using the equity method of accounting. The State’s share of its associates’ post-acquisition profits or losses is recognised in the Income Statement and its share of post-acquisition movements in reserves is recognised in the reserves. The cumulative post-acquisition movements are recognised against the carrying amount of the investment.

Commonwealth and other grants are normally recognised as revenue when the recipient entity obtains control over the grant, usually upon receipt. Where the grant is of a reciprocal nature, revenue is recognised as and when the obligation is fulfilled. When revenue, including grants, has been received in advance for services or work still to be completed at balance date, this revenue is considered to be unearned and is reported in other liabilities. Refer Note 37.

Assets received at below fair value, including those received free of charge and that can be measured reliably are recognised at their fair value as revenue when control over the assets is obtained, normally either on receipt of the assets or on notification that the assets have been secured.

Contributions of services are recognised only if the services would have been purchased if they had not been donated and their fair value can be reliably measured. Where this is the case, an equal amount is recognised as a revenue and an expense.

Non-repayable developer or customer contributions are recognised as revenue and as assets in accordance with Urgent Issues Group 1017 Developer and Customer Contributions for Connection to a Price Regulated Network.

To the extent practicable, revenues from the sale of goods and services (including gas and electricity), fines and regulatory fees are recognised when the transaction or event giving rise to the revenue occurs.

State taxation is recognised as revenue upon the earlier of receipt by the responsible agency of a taxpayer’s self-assessment, or at the time the taxpayer’s obligation to pay arises pursuant to the issue of an assessment. Taxation also includes interest and penalties.

| | | | |

| Audited Consolidated Financial Statements 2006-07 - Government of Queensland | | 5-15 |

Notes to the Financial Statements

| 1. | Significant Accounting Policies continued |

| (k) | Revenue Recognition continued |

The main types of taxation and fee revenues raised by the State Government are:

| | - | transfer and other duties; |

| | - | various gaming and lottery taxes. |

Investment income includes interest, dividends and other income earned during the financial year. Interest is recognised on an accrual basis and dividends when declared. Net realised gains from the sale of investments and unrealised gains from the revaluation of certain investments also form part of investment income.

Net increments in the market values of biological assets are recognised as revenues.

Borrowing costs are recognised as expenses in the period in which they are incurred.

The Government is exempt from Commonwealth taxation except for Fringe Benefits Tax and Goods and Services Tax (GST).

Revenues, expenses and assets are recognised net of GST, except where the amount of GST incurred is not recoverable from the Australian Taxation Office (ATO). In these circumstances the GST is recognised as part of the acquisition cost of the asset or as part of the item of expense.

Receivables and payables are stated with the amount of GST included. The amounts of GST receivable from, or payable to, the ATO are included as a current asset or liability in the Balance Sheet.

Cash flows are included in the Cash Flow Statement on a gross basis. The GST components of cash flows arising from investing and financing activities which are recoverable from, or payable to, the ATO are classified as operating cash flows.

‘Cash’ includes cash on hand and at bank and deposits at call which are readily convertible to cash on hand and are subject to an insignificant risk of changes in value, net of outstanding bank overdrafts.

Trade debtors are recognised at the nominal amount due. Receivables are assessed periodically for impairment.

Settlement by finance lease debtors is within the terms of the lease, ranging from 2 to 99 years. Title is passed to the purchaser on full repayment. Refer Note 20.

Credit Risk Exposure and Management

Credit or liquidity risk represents the extent of credit related losses that the State may be subject to on amounts to be exchanged under loans, accounts receivable and other financial assets. The maximum credit risk at balance date in relation to each class of recognised financial assets is the carrying amount of those assets net of any provisions for impairment. The credit risk in relation to receivables is managed in the following manner:

| | | | |

| Audited Consolidated Financial Statements 2006-07 - Government of Queensland | | 5-16 |

Notes to the Financial Statements

| 1. | Significant Accounting Policies continued |

| | - | trading terms require payment within a specified period after the goods and services are applied; |

| | - | outstanding accounts are assessed for impairment at each reporting date based on objective evidence of impairment; |

| | - | bad debts are written off as they are incurred; and |

| | - | impairment losses are recognised in the Income Statement. |

Inventories (other than those held for distribution) are carried at the lower of cost and net realisable value under AASB 102. For most agencies, cost is determined on either a first-in-first-out or average cost basis and includes expenditure incurred in acquiring the inventories and bringing them to their existing condition and location, except for training costs which are expensed as incurred. Where inventories are acquired for no or nominal consideration, the cost is the current replacement cost as at the date of acquisition.

Inventories held for distribution are those inventories which the State distributes for no or nominal consideration. These are measured at the lower of cost and current replacement cost.

All inventories are classified as current assets.