November 22, 2010

Ms. Linda Cvrkel

Branch Chief

Securities and Exchange Commission

Division of Corporation Finance

100 F Street, N.E.

Washington, DC 20549

Dear Ms. Cvrkel:

This letter is in response to the comment letter of the staff of the United States Securities and Exchange Commission (the “Commission”) dated November 9, 2010 (the “Comment Letter”), related to the Annual Report on Form 10-K of Denny’s Corporation (the “Company”) for the fiscal year ended December 30, 2009. We have set forth below the text of the comments contained in the Comment Letter in italics, followed by the Company’s response.

Form 10-K for the year ended December 30, 2009

Item 1A. Risk Factors, page 3

SEC Comment:

| 1. | In future filings, please revise the last sentence of the first paragraph of this section to clarify that you have discussed all known material risks. Your risk factors section should only reference material risks known to you and not those that you do not anticipate or do not consider significant. |

Registrant’s Response:

The Company acknowledges the Staff’s comment and confirms that future filings will be revised to clarify that all known material risks have been discussed.

Management’s Discussion and Analysis

- Liquidity and Capital Resources, page 21

SEC Comment:

| 2. | Please revise future filings to include the estimated amount of capital expenditures for the upcoming fiscal year. |

Registrant’s Response:

The Company acknowledges the Staff’s comment and confirms that future filings will be revised to include the estimated amount of capital expenditures for the upcoming fiscal year.

Notes to the Financial Statements

Note 2. Summary of Significant Accounting Policies

- Gift Cards, page F-9

SEC Comment:

| 3. | We note your disclosure that you recognize breakage on gift cards when, among other things, sufficient gift card history is available to estimate your potential breakage. Please tell us whether you have recognized any amounts related to breakage in your historical financial statements. If so, please tell us and expand your footnote in future filings to disclose in greater detail the method for which you recognize breakage, including the period over which breakage is recognized and why you believe your methodology is appropriate. |

Registrant’s Response:

The Company began selling gift cards in the fourth quarter of 2006. Prior to 2007, we sold gift certificates. At December 30, 2009, the outstanding liabilities for gift cards and gift certificates were approximately $4.1 million and $0.3 million, respectively.

We recognized $0.2 million and $0.1 million in breakage on gift cards and gift certificates combined for the years ended December 30, 2009 and December 26, 2007, respectively. No breakage was recognized during fiscal 2008. Of these amounts, approximately $123,000 of the breakage recognized during 2009 related to gift cards. All remaining amounts recognized relate to gift certificates.

We evaluate breakage related to gift cards and gift certificates separately, but generally under the same methodology. Based on our historical analysis, we recognize breakage two years following the sale date of the gift card or gift certificate. Our historical data shows that after two years approximately 91% of gift cards or gift certificates sold have been redeemed and that future redemptions are insignificant. We maintain a liability for future redemptions based on a year-by-year analysis of gift cards and gift certificates outstanding, which represents approximately 5% of gift cards or gift certificates sold. We believe that the amounts recognized for breakage have been and will continue to be insignificant.

The Company acknowledges the Staff’s comment and confirms that future filings will be revised to include expanded disclosure regarding our breakage methodology.

- Adjustments to Previously Issued Financial Statements, page F-10

SEC Comment:

| 4. | We note from your disclosure in Note 2 that during fiscal 2009 you recorded immaterial adjustments to correct errors in income tax accounting for the deductions of expired income tax credits and the related release of the valuation allowance established in connection with fresh start reporting on January 7, 1998. In light of the fact that these adjustments reduce net income by approximately 13% in 2008, it would appear that these adjustments have a material effect on the statement of income for that fiscal year. In this regard, please provide us more details as to the nature of these adjustments and why you believe the adjustments are immaterial. Also, please explain to us why you believe it is appropriate to correct these errors in the Form 10-K for fiscal 2009 rather than file an amendment to the Form 10-K for fiscal 2008. Additionally, considering the existence of these material errors, please reconsider your conclusion that disclosure controls and procedures were effective as of December 30, 2009 or explain to us why you believe that your conclusion on disclosure controls and procedures is appropriate. |

Registrant’s Response:

Please find attached our memorandum that describes 1) the nature of the adjustments, 2) our consideration of and conclusions with regard to SEC Staff Accounting Bulletin No. 99, “Materiality,” 3) our accounting treatment of the related income tax adjustments and 4) our conclusions regarding the effectiveness of disclosure controls and procedures related to the adjustments.

- New Accounting Standards, page F-11

SEC Comment:

| 5. | We note your disclosure that the adoption of FASB ASC 805-10 resulted in a $2 million reduction to both your deferred tax asset and valuation allowance since you reversed only the valuation allowance related to the deferred tax asset recognized during 2009. You also note that in the prior year, you would have recognized $2 million as income tax expense with a corresponding reduction to goodwill. In light of your disclosure that subsequent to the effective date, the FASB ASC requires additional reversal of deferred tax asset valuation allowance to be recorded as a component of income tax expense, please explain to us why you did not recognize $2 million in income tax expense in 2009. |

Registrant’s Response:

The adoption of FASB ASC 805-10 resulted in a benefit to income tax expense versus a decrease in goodwill for the reduction in valuation allowances established in connection with fresh start reporting. The reduction in the deferred tax asset resulted in $2 million of income tax expense. The reduction in the valuation allowance resulted in a $2 million benefit to income tax expense. These adjustments offset each other within income tax expense.

Also, in our disclosure we stated, “in the prior year, we would have recognized $2 million as income tax expense with a corresponding reduction to goodwill.” This comment was intended to explain how the 2009 accounting for deferred tax assets would have impacted 2008 if the new accounting standard had been in effect during the prior year. This comment was not intended to suggest that an adjustment should have been recorded in 2008. Additionally, this comment did not relate to the adjustment referred to in Comment 4. We do not expect that this comment will be included in future filings.

Note 5. Goodwill and Other Intangible Assets, page F-14

SEC Comment:

| 6. | Please revise your footnote in future filings to include all disclosures required by ASC 350-20-50-1 regarding the changes in the carrying amount of goodwill for each period for which a balance sheet is presented. |

Registrant’s Response:

The Company acknowledges the Staff’s comment and confirms that future filings will be revised to include all disclosures required by ASC 350-20-50-1 regarding changes in the carrying amount of goodwill for each period for which a balance sheet is presented.

SEC Comment:

| 7. | Also, please revise your footnote to disclose your accounting policy relating to your treatment of costs incurred to renew or extend the term of recognized intangible assets pursuant to ASC 350-30-50-2(c). |

Registrant’s Response:

The Company acknowledges the Staff’s comment and confirms that future filings will be revised to include our accounting policy relating to the treatment of costs incurred to renew or extend the term of recognized intangible assets pursuant to ASC 350-30—50-2(c).

Note 9. Fair Value of Financial Instruments, page F-17

SEC Comment:

| 8. | We note from your disclosures in Note 2 and Note 15 that you have cash-settled restricted stock and performance units which are both classified as liabilities on the balance sheet and adjusted to fair value at each balance sheet date. As these are liabilities measured at fair value on a recurring basis, they appear to be included in the scope of SFAS 157. Please revise the notes to the financial statements in future filings to include the disclosure requirements on paragraph 32 of SFAS No. 157 as it relates to these liabilities. |

Registrant’s Response:

The Company acknowledges the Staff’s comment; however we do not believe the cash-settled restricted stock and performance units are included in the scope of SFAS 157. SFAS 157 paragraph 2 states that “This Statement does not apply under accounting pronouncements that address share-based payment transactions: FASB Statement 123 (revised 2004), Share-Based Payment, and its related interpretive accounting pronouncements that address share-based payment transactions. ASC 820-10-15-2 provides guidance on Subtopics not within scope and states that the “guidance in the Fair Value Measurements and Disclosures Topic does not apply as follows: a. Under accounting principles that address share-based payment transactions (see Topic 718 and Subtopic 5 05-50).”

Note 14. Income Taxes, page F-24

SEC Comment:

| 9. | We note that in fiscal 2009 the statutory provision rate was significantly reduced by a portion of net operating losses, capital losses and unused income tax credits resulting from the establishment or reduction in the valuation allowance. Please provide us details of this amount and explain to us why you believe this adjustment is appropriate. |

Registrant’s Response:

During 2009, the statutory provision rate included a 35% reduction principally related to the reversal of valuation allowances associated with the utilization of net operating losses, temporary differences and alternative minimum tax credits during the year. Specifically, the Company recorded a $6.6 million, or 15%, reduction related to net operating losses, an $8.2 million, or 19%, reduction related to temporary differences and a $0.9 million, or 1%, reduction related to alternative minimum taxes. These adjustments to the statutory provision are required under the provisions of ASC 740.

Note 20. Quarterly Data (Unaudited), page F-30

SEC Comment:

| 10. | We note that your table of quarterly financial information for fiscal 2008 includes a note that net income in the first, second and third quarters has been adjusted from amounts previously reported to reflect certain adjustments discussed in Note 2. Please note that when amounts included in this disclosure vary from the amounts previously reported on the Form 10-Q filed for any quarter, Item 302(A)(2) of Regulation S-K requires you to reconcile the amounts given with those previously reported and describe the reason for the difference. We believe that you should separately show the amounts previously reported and the adjusted amounts in addition to explaining reason for each difference. Please revise in future filings, as applicable. |

Registrant’s Response:

The Company acknowledges the Staff’s comment and confirms that future filings will be revised, as applicable, to include a reconciliation of the previously reported quarterly financial information in accordance with Item 302(A)(2) of Regulation S-K.

Definitive Proxy Statement on Schedule 14A

Annual Cash Incentives, page 22

SEC Comment:

| 11. | We note that your compensation committee reviews competitive compensation market analysis of published surveys to determine the compensation levels of your named executive officers. In future filings, to the extent the compensation committee is benchmarking compensation against surveys and such benchmarking is a material consideration to the committee’s determination of compensation levels, please identify the component companies. Please confirm that you will comply with this comment in future filings. |

Registrant’s Response:

Our Compensation Committee typically benchmarks compensation of Company executive officers against a restaurant industry peer group (which we identify). The Compensation Committee does also review survey data, but only as a general market check. The Company acknowledges the Staff’s comment and confirms that to the extent the Compensation Committee benchmarks against any of the component companies in survey data, it will, in future filings, identify such companies.

On behalf of the Company, the Company acknowledges that (i) it is responsible for the adequacy and accuracy of the disclosure in the filing; (ii) staff comments or changes to disclosure in response to staff comments do not foreclose the Commission from taking any action with respect to the filing; and (iii) the Company may not assert staff comments as a defense in any proceeding initiated by the Commission or any person under the federal securities laws of the United States.

We believe the details discussed in this response to your letter sufficiently address the comments raised. However, we are available to discuss this matter further.

| Respectfully, | |||

| /s/ F. Mark Wolfinger | |||

| F. Mark Wolfinger | |||

| Executive Vice President | |||

| Chief Administrative Officer and | |||

| Chief Financial Officer | |||

Exhibit 1

Denny’s Corporation

SAB 99 Analysis – Income Tax Issue

November 2009

Updated November 2010

Purpose

To document the Company’s SAB 99 analysis of the income tax/goodwill adjustment identified in the fourth quarter of 2009.

Background

On January 7, 1998, the Company emerged from Chapter 11 bankruptcy. As part of the fresh start accounting, we recorded a full valuation allowance against certain deferred tax assets including Work Opportunity Tax Credits (WOTC) generated between 1989 and 1994. The WOTC expires after 15 years; however, current tax law allows us to take a deduction for the expired credits in the year subsequent to expiration. As the WOTC started to expire in 2004, we began to take the allowed deduction in the subsequent year. Accordingly, we took deductions in 2005, 2006, 2007 and 2008.

As noted in FASB ASC 852-10-45-20 (prior authoritative literature: paragraph 38 of SOP 90-7, Financial Reporting by Entities in Reorganization under the Bankruptcy Code), the income tax benefit from the release of a valuation allowance established at the date of reorganization for deferred tax assets of pre-reorganization deductible temporary differences and carryforwards should be recognized as follows:

| · | First, reduce to zero reorganization value in excess of amounts allocable to identifiable assets, |

| · | Second, reduce to zero other intangible assets, |

| · | Third, increase additional paid-in capital. |

However, the elimination of a valuation allowance related to an acquired tax benefit as a result of the elimination of the deferred tax asset should not be recorded as an adjustment to goodwill (pre-Codification SFAS 109, Accounting for Income Taxes, paragraph 30). For example, an acquired operating loss carryforward may expire subsequent to an acquisition. If a valuation allowance had been recognized for the related deferred tax asset in the acquisition accounting, both the deferred tax asset and the related valuation allowance would be eliminated upon expiration of the carryforward with no adjustment to goodwill.

Therefore, as the valuation allowance had been recognized for the WOTC in the fresh start accounting, both the deferred tax asset and the related valuation allowance related to the WOTC were eliminated upon expiration with no adjustment to goodwill. The deduction we took in the subsequent year was considered to be an event that occurred subsequent to fresh start accounting where deductions are separated from tax credits within the Internal Revenue Code. Accordingly, we did not consider it appropriate to continue to trace forward the fresh start reporting tax credit subsequent to expiration.

Effective January 1, 2009, the Company adopted ASC 805 (prior authoritative literature: SFAS 141R, Business Combinations). ASC 805 requires that any additional reversal of deferred tax asset valuation allowance established in connection with our fresh start reporting on January 7, 1998 be recorded as a component of income tax expense rather than as a reduction to the goodwill established in connection with the fresh start reporting. Accordingly, upon adoption of ASC 805, the Company has properly recorded the reversal of the valuation allowance for the WOTC deduction as a component of income tax expense.

Issue #1

Assessment of Adjustment

During the fourth quarter of 2009, the Company, along with its external auditors, reviewed its accounting treatment for the WOTC and whether or not it should record a reduction to goodwill in the year the deduction is taken. Specifically, we referred to ASC 740-10-55-37 and the related ASC Example 20 (prior authoritative literature: paragraphs 243-244 of SFAS 109, Accounting for Income Taxes), which notes that there may be situations where the use of an operating loss or tax credit carryforward does not result in the recognition of a tax benefit, because that carryforward is essentially replaced by a deductible temporary difference. Because the requirements for recognition of acquired tax benefits are the same, whether those benefits are associated with deductible tempora ry differences or carryforwards, an acquiring enterprise would need to continue to trace forward an intervening transaction reported for tax purposes that results in the replacement of an acquired carryforward (the benefit of which was not recognized at the acquisition because of the establishment of a valuation allowance) by a deductible temporary difference.

Based on our analysis of the references stated previously, we have concluded that the deductions taken in the subsequent year cannot be separated from the tax credits for which fresh start accounting applies. Accordingly, we should have recorded a write off to goodwill in the year the deduction was taken.

Guidance

In assessing materiality for the correction of an error, a company must consider the factors discussed in SEC Staff Accounting Bulletin No. 99, Materiality (SAB 99).

The Company also considered the following guidance:

| · | SEC Staff Accounting Bulletin No. 108, Considering the Effects of Prior Year Misstatement when Quantifying Misstatement in Current Year Financial Statements |

| · | ASC 250 (prior authoritative literature: SFAS No. 154, Accounting Changes and Error Corrections) |

SAB 99 Analysis

The following table summarizes the impact of the error in each affected period:

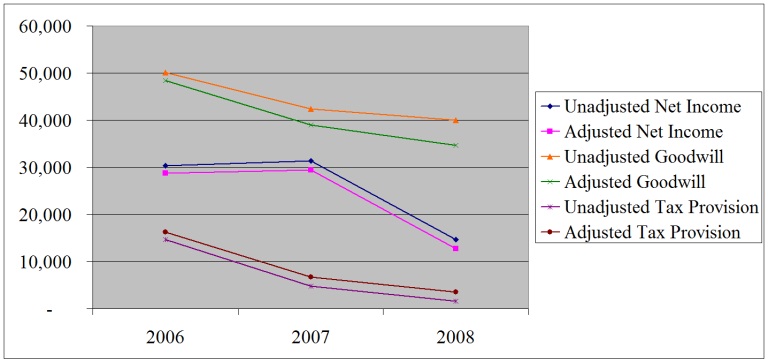

| 2006 | 2007 | 2008 | Total | |||||||||||||

| As reported: | ||||||||||||||||

| Net income before taxes | $ | 44,774 | $ | 36,159 | $ | 16,264 | ||||||||||

| Provision for income taxes | 14,668 | 4,808 | 1,602 | |||||||||||||

| Net income | $ | 30,106 | $ | 31,351 | $ | 14,662 | ||||||||||

| Basic EPS | $ | 0.31 | $ | 0.33 | $ | 0.15 | ||||||||||

| Diluted EPS | $ | 0.31 | $ | 0.32 | $ | 0.15 | ||||||||||

| Adjustment: | ||||||||||||||||

| Tax adjustment | $ | 1,610 | $ | 1,867 | $ | 1,920 | $ | 5,397 | ||||||||

| As adjusted: | ||||||||||||||||

| Net income before taxes | $ | 44,774 | $ | 36,159 | $ | 16,264 | ||||||||||

| Provision for income taxes | 16,278 | 6,675 | 3,522 | |||||||||||||

| Net income | $ | 28,496 | $ | 29,484 | $ | 12,742 | ||||||||||

| Basic EPS | $ | 0.29 | $ | 0.31 | $ | 0.13 | ||||||||||

| Diluted EPS | $ | 0.30 | $ | 0.30 | $ | 0.13 | ||||||||||

In determining the materiality of the adjustment, we considered the following factors to be of particular importance. Each of these factors is discussed in further detail below:

| · | The proposed adjustment does not affect any financial trends. |

| · | The Company has not been a tax paying entity over the previous three years; accordingly, income tax expense reported in the financial statements is not an important metric to users of the financial statements. The following statement was included in a 2006 analyst report “We do not yet believe EPS is a meaningful indicator for valuing Denny’s, as is it likely there are still several below-the-line items, including an abnormal tax rate.” |

| · | In each of Company's analyst reports, the key metrics used to calculate the company’s valuation and give estimates are Adjusted Income Before Taxes, EBITDA and Adjusted EBITDA. None of the analysts covering the Company use operating income or net income as a key metric without some level of adjustment. |

| · | Upon adoption of SFAS 141R (effective January 1, 2009), any additional reversal of deferred tax asset valuation allowance established in connection with the Company’s fresh start reporting on January 7, 1998 is recorded as a component of income tax expense rather than as a reduction to the goodwill. Accordingly, upon adoption of SFAS 141R, the Company should record the reversal of the valuation allowance for the WOTC deduction as a component of income tax expense. |

2

Below is the detailed SAB 99 analysis:

Applicable Quantitative Measures

The table below details the quantitative impact on a percentage basis of the proposed adjustments to record income tax expense and write-off goodwill.

| Fiscal Year | ||||||||||||

| 2006 | * | 2007 | 2008 | |||||||||

| Annual Impact of Error: | ||||||||||||

| Rollover | $ | 1,610 | $ | 1,867 | $ | 1,920 | ||||||

| Iron Curtain | 1,610 | 3,477 | 5,397 | |||||||||

| Impact under Rollover Method: | ||||||||||||

| Provision for Income Taxes | 11.0 | % | 38.8 | % | 119.9 | % | ||||||

| Net Income | 5.3 | % | 6.0 | % | 13.1 | % | ||||||

| Goodwill | 3.2 | % | 8.2 | % | 13.5 | % | ||||||

| Total Assets | 0.4 | % | 0.9 | % | 1.6 | % | ||||||

| Shareholders' Deficit | -0.7 | % | -1.9 | % | -3.1 | % | ||||||

| Adjusted Income before Taxes | 0.0 | % | 0.0 | % | 0.0 | % | ||||||

| Adjusted EBITDA | 0.0 | % | 0.0 | % | 0.0 | % | ||||||

| Impact under Iron Curtain: | ||||||||||||

| Goodwill | 3.2 | % | 8.2 | % | 13.5 | % | ||||||

| Total Assets | 0.4 | % | 0.9 | % | 1.6 | % | ||||||

| Shareholders' Deficit | -0.7 | % | -1.9 | % | -3.1 | % | ||||||

*NOTE: The Company took WOTC deductions of approximately $300k in 2005 (pretax); however, such amount is considered immaterial for further analysis (adjustment to beginning retained deficit would be approximately $100k). No WOTC deductions were taken prior to 2005.

Though certain items are considered quantitatively significant, we believe it is appropriate to also evaluate these items using qualitative measures.

Applicable Qualitative Measures

The following chart reflect the trends for both unadjusted and adjusted net income, goodwill and income tax expense As they show, the proposed adjustments have virtually no impact on the trends for these items.

We believe that the following metrics are key to assessing the qualitative materiality of recording the proposed adjustments:

3

Adjusted Income Before Tax, EBITDA, and Adjusted EBITDA

Similar to the GAAP metric of operating income, non-GAAP metrics such as Adjusted Income Before Taxes, EBITDA and Adjusted EBIDTA represent the financial performance of basic company operations and operating cash flows for investment and debt service. Among other items, these non-GAAP metrics exclude income tax expense. These non-GAAP metrics are a key measure by which analysts measure our performance and upon which our most significant debt covenant ratios are based.

In each analyst report, the key metrics used to calculate the Company’s valuation and give estimates are EBITDA and Adjusted EBITDA. In addition, some analysts use adjusted EPS. None of the analysts covering the Company use operating income or net income as a key metric without some level of adjustment. The following analyst report excerpts provided the most direct comments to the use of these non-GAAP metrics:

| · | April 2006 - “We do not yet believe EPS is a meaningful indicator for valuing Denny’s, as is it likely there are still several below-the-line items, including an abnormal tax rate.” He also states, “given the turnaround nature of Denny’s story, we believe it is appropriate for investors to focus on 2007 EBITDA as a basis for valuation.” |

| · | February 2008 - “We adjusted our results for all one-time and noncash charges including restructurings, exit costs, asset sales and stock-based compensation.” |

Net income and EPS

Net income and EPS are the GAAP measures by which companies are ultimately compared. However, for the Company, these have not been a significant measure over the past several years due to:

| 1. | Significant amortization and depreciation of intangibles and fixed assets due to the emergence from bankruptcy in 1998. |

| 2. | Significant interest expense resulting from being a highly leveraged company. |

| 3. | Variability resulting from timing and amounts of assets sales. These asset sales include the sale of real estate for company-owned, franchisee-operating units and the sale of company-owned restaurants to franchisees. Asset sales are valued by management and investors based on the cash they provide to pay down debt rather than the gain they provide to net income. |

| 4. | Significant non-recurring items such as gain/loss on the interest rate swap and the write-off of deferred financing costs. |

| 5. | We have maintained a full valuation allowance which has resulted in an abnormal tax rate. |

Investor Reaction

Management believes that investors are currently reactive to several specific items as they relate to Denny’s:

| 1. | Sales growth |

| 2. | Debt reduction |

| 3. | Adjusted income before taxes and Adjusted EBITDA performance |

| 4. | Company and franchise operating margin |

| 5. | Cash flows available to repay debt |

None of these items are affected by these adjustments.

Other Applicable Qualitative Measures

We have addressed several qualitative measures above as part of our quantitative analysis. This section will specifically address the points noted in SAB 99 that may not have been addressed above.

| 1. | Does the misstatement arise from an item capable of precise measurement or does it arise from an estimate and, if so, the degree of imprecision inherent in the estimate? |

Response: The proposed adjustment relates to an unusual and complex fact pattern; however, the amount of the adjustment can be definitively quantified.

| 2. | Does the misstatement mask a change in earnings or other trends? |

Response: No. See charts above.

| 3. | Does the misstatement hide a failure to meet analysts' consensus expectations for the enterprise? |

Response: No. Income tax expense is excluded by analysts when evaluating the performance of the company. No guidance is given to analysts for any measure that includes income tax expense. The guidance we provide includes same-store sales, new restaurant openings, adjusted EBITDA, adjusted income before taxes, cash interest expense and capital expenditures.

4

| 4. | Does the misstatement change a loss into income or vice versa? |

Response: No.

| 5. | Does the misstatement concern a segment or other portion of the registrant's business that has been identified as playing a significant role in the registrant's operations or profitability? |

Response: No. The Company has only one segment.

| 6. | Does the misstatement affect the registrant's compliance with regulatory requirements? |

Response: No. There are no regulatory requirements.

| 7. | Does the misstatement affect the registrant's compliance with loan covenants or other contractual requirements? |

Response: No. There are no covenants that include income tax expense.

| 8. | Does the misstatement have the effect of increasing management's compensation – for example, by satisfying requirements for the award of bonuses or other forms of incentive compensation? |

Response: No. Management bonuses are not based on any measure impacted by income tax expense.

| 9. | Does the misstatement involve concealment of an unlawful transaction? |

Response: No. The potential adjustment results from a misinterpretation of applicable accounting literature.

Conclusion #1

Based on the procedures performed, we concluded that the misstatement is immaterial to the prior period financial statements and that in our judgment the users of the financial statements would not have been influenced by the inclusion or correction of the error.

After reviewing the twelve months financial results for fiscal year 2009, management concluded that it would be prudent to correct the error as an immaterial error correction and not correct it (prospectively) as an out of period adjustment. Accordingly, management concluded that the prior year financial statements should be corrected, even though such revision previously was and continues to be immaterial to the prior year financial statements. As correcting prior year financial statements for immaterial errors would not require previously filed reports to be amended under SAB 108, we will correct the error to the prior year financial statements in the Form 10-K for fiscal year 2009. Our external auditors also agree with this accounting treatment.

Management communicated the findings and the resolution to the Audit Committee in the January 26, 2010 Audit Committee meeting.

Issue #2

Evaluation of Control Deficiency

The errors noted above arose from a misapplication of GAAP, specifically ASC 740. As a result, our policies and procedures (i.e. controls) for recording the release of valuation allowance established at the date of reorganization related to WOTC were not effective at preventing or detecting errors for fiscal year 2006, 2007 and 2008. We had properly accounted for the release of valuation allowance established at the date of reorganization for deferred tax assets other than the WOTC during these years. Given the existence of known errors for the WOTC, we believe the likelihood of errors occurring is at least at the reasonably possible level for these years. To assess the likelihood of errors occurring that could be material, we considered the factors described in the following paragraphs.

In our SAB 99 analysis above, we concluded that the actual misstatements arising from the ineffective policies and procedures for recording the release of valuation allowance established at the date of reorganization for WOTC were immaterial to the prior period financial statements and that in our judgment the users of the financial statements would not have been influenced by the inclusion or correction of the error. We noted that the potential magnitude of the error is the same as the actual error that occurred in 2006, 2007 and 2008 (i.e. because the ineffective control resulted in error occurred on each transaction).

Based on the foregoing, we concluded that it is not reasonably possible that the ineffective policies and procedures for recording the release of valuation allowance established at the date of reorganization would result in errors that are material to the company’s financial reporting. Thus, we determined that this error was the result of a significant deficiency, but did not rise to the level of a material weakness.

We also evaluated the potential magnitude of errors arising from the control deficiency in future periods (i.e., 2009) to determine whether or not it was reasonably possible such errors would be material. We concluded that since the Company should record the reversal of valuation allowance for the WOTC as a component of income tax expense upon adoption of SFAS 141R (effective January 1, 2009) no control deficiency exists during the 2009 fiscal year (we properly accounted for such transactions).

5

Additional evaluation of deficiency

This error also gives rise to questions about whether the Company personnel involved in internal controls over financial reporting are sufficiently competent in applying US GAAP. It is our belief that our accounting department is competent in relation to US GAAP and this deficiency is not indicative of its inability to select and implement accounting policies that comply with US GAAP. We note that our tax department informed our external auditors of the WOTC deductions in 2006 and asked them for input on the accounting. We believe our accounting staff demonstrates an adequate level of competence and expertise in the application of GAAP for management to have effective internal control over financial reporting. Key observations about our management and accounting staff include:

| · | The VP of Tax has prior Big 4 experience and has demonstrated on an ongoing basis his ability to appropriately apply FAS 109. |

| · | The CAO and Mgr of External Reporting have prior Big 4 experience and have demonstrated on an ongoing basis their ability of keeping abreast of new accounting standards. |

| · | The VP of Tax, the CAO and Mgr of External Reporting are aware of their strengths and weaknesses and seek the advice from our external auditors with technical accounting questions that are outside their respective area of expertise. |

| · | The accounting staff is proactive in identifying potential issues, whether it stems from new accounting standards or significant transactions. Frequently the staff will draft position papers on the issue and solicit auditor feedback where necessary. |

| · | The accounting staff has not ignored or been negligent in timely researching and addressing the accounting implications for unusual or infrequent transactions. |

| · | The accounting staff meets at least quarterly with our external auditors to talk about the upcoming quarter/year end. In these meetings, the account staff prepares an agenda listing out all key accounting issues/considerations and the meetings are very open and candid as we cover the agenda or other issues/concerns that arise. |

| · | The accounting staff takes its responsibility seriously to research GAAP and does not treat our external auditors as part of its control system to identify issues. |

| · | The Disclosure Committee meets on a quarterly basis to discuss current accounting polices/transactions (the Disclosure Committee includes members from different departments to make sure that all transactions are properly reflected and accounted for in the Company’s financial statements). |

Overall, we believe that our internal control system over financial reporting will ensure that information about new, non routine, subjective transactions (including tax transactions) are routed to the appropriate individuals and that our financial reporting personnel have adequate US GAAP expertise to make sure that an appropriate accounting policy is selected and properly applied.

Conclusion #2

We believe that the error was not the result of a control deficiency that constitutes a material weakness as of December 31, 2006, 2007 or 2008. In addition, any control deficiency related to this issue was remediated prior to December 30, 2009, our fiscal 2009 year-end.

6