UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549

FORM N-CSR CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811- 57347 John Hancock Financial Trends Fund, Inc. (Exact name of registrant as specified in charter) 601 Congress Street, Boston, Massachusetts 02210 (Address of principal executive offices) (Zip code)

Alfred P. Ouellette Senior Attorney and Assistant Secretary

601 Congress Street Boston, Massachusetts 02210 (Name and address of agent for service)

Registrant's telephone number, including area code: 617-663-4324

Date of fiscal year end: December 31

Date of reporting period: December 31, 2005

ITEM 1. REPORT TO SHAREHOLDERS.

Table of contents

Your fund at a glance

page 1

Managers’ report

page 2

Fund’s investments

page 6

Financial statements

page 10

Directors & officers

page 28

For more information

page 33

Dear Fellow Shareholders,

After a year spent mostly in the red, the stock market managed to eke out modest gains in 2005 on the strength of rallies in the summer and late fall. During the year, investors worried about rising interest rates, spiking oil prices and hurricane disasters, all of which had the potential to derail the economy and corporate earnings growth. They both remained in good shape, however, and the broad market managed to finish the year in the black, as measured by the Standard & Poor’s 500 Index’s 4.91% return, including reinvested dividends.

Financial stocks outpaced the market, with the Standard & Poor’s 500 Financial Index returning 6.50% . Leading the way were capital market-sensitive companies such as investment bankers, asset managers and trust and custody banks. Regional banks and thrifts mostly brought up the rear in this rising interest rate environment, which put a crimp on their net interest margins.

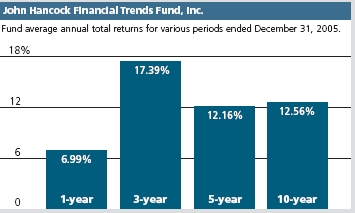

We are again pleased to report that the Fund outperformed both the broad market and financial stocks as a group, returning 6.99% at net asset value. That return also topped the 6.57% return of the average open-end financial services fund, according to Lipper, Inc. As Jim Schmidt reports on the following pages, the biggest contributors to the Fund’s outperformance were its holdings in capital market-related companies and excellent stock selection which helped offset the Fund’s overweight in lagging regional banks and thrifts.

The Fund’s result this year is a confirmation of the strength of the Fund’s management team, which has produced the Fund’s superb long-term net asset value returns shown on the next page. It also underscores the importance of asking shareholders several years ago for permission to broaden the Fund’s scope to allow it to invest in financial stocks beyond banks located in the Southeast. We are gratified that we did and that you agreed.

As we enter 2006, we remain confident in the portfolio management team’s ability to work hard in their quest to provide shareholders with the best possible results. As always, I want to assure you that your Board of Directors is also working on your behalf, putting your interests above all else.

Sincerely,

Franklin C. Golden, Chairman of John Hancock Financial Trends Fund, Inc.

This commentary reflects the chairman’s views as of December 31, 2005. They are subject to change at any time.

YOUR FUND AT A GLANCE

The Fund seeks long-term capital appreciation with current income as a secondary objective by investing at least 80% of its assets in stocks of U.S. and foreign financial services companies of any size.

Over the last twelve months

* The stock market made modest gains in 2005 as it grappled with historic high oil prices, rising interest rates and major hurricanes.

* Financial stocks outperformed the overall market, on the strength of the capital markets-related groups.

* The Fund’s holdings in capital-market names were the biggest contributors, along with strong stock selection.

The total returns for the Fund are at net asset value and include the reinvestment of all distributions. The performance data contained within this material represents past performance, which does not guarantee future results.

Top 10 holdings

3.0%

Wachovia Corp.

3.0%

Citigroup, Inc.

2.8%

Wells Fargo & Co.

2.7%

Prudential Financial, Inc.

2.6%

U.S. Bancorp.

2.6%

Zions Bancorp.

2.5%

Bank of America Corp.

2.5%

Pinnacle Financial Partners, Inc.

2.5%

JPMorgan Chase & Co.

2.5%

SunTrust Banks, Inc.

As a percentage of net assets on December 31, 2005.

1

BY JAMES K. SCHMIDT, CFA, LISA A. WELCH AND THOMAS M. FINUCANE, PORTFOLIO MANAGERS, SOVEREIGN ASSET MANAGEMENT LLC

MANAGERS’ REPORT

JOHN HANCOCK Financial Trends Fund, Inc.

Effective December 31, 2005, the investment management teams of John Hancock Advisers were reorganized into Sovereign Asset Management LLC, a wholly owned subsidiary of John Hancock Life Insurance Company. The restructuring did not have any impact on your fund, which continues to be managed by the same team, using the same investment philosophy and process.

The stock market advanced in a choppy fashion and produced modest returns over the last 12 months. Throughout the year, investors struggled with concerns that rising short-term interest rates, record-high oil prices and fallout from two major Gulf Coast hurricanes would stall economic growth, hurt corporate profits and even spark inflation. Brief rallies in the summer and again in late fall helped the market move into the black. For the year ending December 31, 2005, the Standard & Poor’s 500 Index returned 4.91%, including reinvested dividends.

Financial stocks outperformed the broader market on the strength of capital markets-related companies, such as investment bankers, asset managers and trust and custody banks. They ben efited from the resilient markets that were fertile ground for increased merger and acquisitions activity and debt and equity issuance. For the year, the Standard & Poor’s 500 Financial Index returned 6.50% including reinvested dividends. Banks were the laggards in an interest rate environment that saw short-term rates rise at the hands of the Federal Reserve, which was intent on preventing inflation. At the same time, longer-term rates, in uncharacteristic fashion, did not move up as much, making for a progressively flatter yield curve by the year’s end. That put pressure on bank margins, as the difference between what banks pay depositors and what they collect from loans shrunk. Life and health insurance companies did

“The stock market advanced in a choppy fashion and produced modest returns over the last 12 months.”

2

well all year as they turned in good results and were viewed as safe havens that had little taint of scandal or negative news headlines.

Fund performance

For the year ended December 31, 2005, John Hancock Financial Trends Fund, Inc. posted a total return of 6.99% at net asset value and 0.21% at market value. The difference in the Fund’s net asset value (NAV) performance and its market performance stems from the fact that the market share price is subject to the dynamics of secondary market trading, which could cause it to trade at a discount or premium to the Fund’s NAV share price at any time. The Fund’s NAV return exceeded the Fund’s benchmark Standard & Poor’s 500 Financial Index and the 6.57% return of the average open-end financial services fund, according to Lipper, Inc.

Fund positioning produces results

While a large part of our holdings remains in regional banks and thrifts, we did make some modest adjustments to the portfolio during the year to benefit from better capital-markets activity. Our strategy paid off as these capital-market companies were some of our biggest contributors to performance.

Capital-markets winners

Several of our better performers were investment bankers Lehman Brothers Holdings, Inc., Goldman Sachs Group, Inc. and Raymond James Financial, Inc. They benefited from a resurgence in merger and acquisitions activity that began late last year, and an unexpected surge in equity and debt issuance. That boosted earnings at Goldman Sachs. Lehman Brothers, always known for its fixed-income trading, has fleshed out its investment banking business, leading to better underwriting and market recognition of both its fundamentals and valuation.

“Our strategy paid off as these capital-market companies were some of our biggest contributors to performance.”

With asset managers, our overweight and stock selection also served us well. Some of the top contributors to performance were Legg Mason, Inc., Franklin Resources, Inc. and Affiliated Managers Group, Inc., all of which continued to grow their asset base with strong inflows into their mutual funds. Legg Mason’s good performance also

3

Industry

distribution1

Regional

banks -- 42%

Diversified

banks -- 11%

Investment banking

& brokerage -- 10%

Asset management &

custody banks -- 7%

Thrifts & mortgage

finance -- 7%

Other diversified

financial

services -- 6%

Life & health

insurance -- 6%

Multi-line

insurance -- 4%

Reinsurance -- 2%

Consumer

finance -- 2%

Property & casualty

insurance -- 2%

Specialized

finance -- 1%

stemmed from its deal with Citigroup, Inc. whereby it gave Citigroup its brokerage arm in exchange for Citigroup’s asset management group, virtually doubling Legg Mason’s assets under management. Custody bank State Street Corp. was another contributor that was lifted by better market activity and tighter expense controls.

Insurance helps

Life and health insurance companies produced some of the financial sector’s best results, and our strong stock selections in this group were beneficial. Prudential Financial, Inc., one of our top contributors, was recognized for its cost cutting and product rationalization efforts in the United States and its revenue growth overseas, particularly in Asia. Another, Hartford Financial Services Group, Inc., benefited from being tilted toward life and annuity products -- market-sensitive assets that helped boost company earnings in the period. One of the Fund’s biggest detractors was property and casualty company RenaissanceRe Holdings Ltd., which was hurt by both losses from Katrina and accounting irregularities that resulted in a change in top management.

Laggards: banks/mortgage companies

Having a significant overweight in regional banks was a drawback for the Fund, as they were the sector’s laggards, struggling with margin compression and tougher spread-revenue growth. What’s more, bank merger activity slowed down, with many fewer deals done in 2005 than in the prior year. Nevertheless, the Fund had one bank takeout in 2005, when Amegy Bancorp., Inc. was taken over by Zions Bancorp. during the summer. Several of the Fund’s detractors were banks that reported sizeable shortfalls in interest revenues and

4

missed their targets for quarterly earnings, such as Fifth Third Bancorp, TCF Financial Corp. and First Horizon National Corp. Another laggard was mortgage giant Freddie Mac, whose accounting woes kept it in the headlines. Although the bank sector overweight held us back, some of the bank sector loss was offset by superior stock picking. Several of the Fund’s better performers were banks perceived to be asset sensitive -- that is, improving spread revenue as interest rates rise. These included Zions Bancorp., Colonial BancGroup, Inc. and Commerce Bancshares, Inc.

“...financial services stocks typically start a period of outperformance a few months prior to when the Fed stops raising rates...”

Outlook

We continue to be cautiously optimistic about the prospects for financial stocks. Because of the flat yield-curve environment, continued high energy costs and fears that credit quality will deteriorate, we recently made a few minor adjustments to position the Fund more defensively. We pared back somewhat our exposure to capital market-sensitive names whose valuations have reached levels somewhat ahead of underlying fundamentals. Looking forward, financial services stocks typically start a period of outperformance a few months prior to when the Fed stops raising rates, which could happen in the first half of 2006. As for banks, although merger activity was slow this year, we still believe it will remain as a long-term theme, especially among some of the smaller banks in the southeast.

This commentary reflects the views of the portfolio managers through the end of the Fund’s period discussed in this report. The managers’ statements reflect their own opinions. As such, they are in no way guarantees of future events and are not intended to be used as investment advice or a recommendation regarding any specific security. They are also subject to change at any time as market and other conditions warrant.

Sector investing is subject to greater risks than the market as a whole.

1 As a percentage of net assets on December 31, 2005.

5

F I N A N C I A L S TAT E M E N T S

FUND’S INVESTMENTS

Securities owned by the Fund on December 31, 2005

This schedule is divided into two main categories: common stocks and short-term investments. Common stocks are further broken down by industry group. Short-term investments, which represent the Fund’s cash position, are listed last.

Issuer

Shares

Value

Common stocks 99.76%

$77,500,366

(Cost $40,306,654)

Asset Management & Custody Banks 7.27%

5,648,980

Affiliated Managers Group, Inc. (I)(L)

22,700

1,821,675

Bank of New York Co., Inc. (The)

26,000

828,100

Eaton Vance Corp.

15,000

410,400

Franklin Resources, Inc.

6,500

611,065

Northern Trust Corp.

5,000

259,100

State Street Corp.

31,000

1,718,640

Consumer Finance 2.35%

1,824,480

MBNA Corp.

67,200

1,824,480

Diversified Banks 10.96%

8,519,099

Bank of America Corp.

42,848

1,977,435

U.S. Bancorp.

68,000

2,032,520

Wachovia Corp.

44,653

2,360,358

Wells Fargo & Co.

34,200

2,148,786

Investment Banking & Brokerage 10.31%

8,010,981

Ameritrade Holding Corp. (I)

10,300

247,200

Goldman Sachs Group, Inc. (The)

4,550

581,080

Legg Mason, Inc.

15,650

1,873,149

Lehman Brothers Holdings, Inc.

11,500

1,473,955

Merrill Lynch & Co., Inc.

27,500

1,862,575

Morgan Stanley

8,250

468,105

Raymond James Financial, Inc.

39,950

1,504,917

Life & Health Insurance 5.83%

4,533,227

AFLAC, Inc.

21,500

998,030

Prudential Financial, Inc.

28,510

2,086,647

StanCorp Financial Group, Inc.

29,000

1,448,550

See notes to financial statements.

6

F I N A N C I A L S TAT E M E N T S

Issuer

Shares

Value

Multi-Line Insurance 4.15%

$3,222,546

American International Group, Inc.

16,000

1,091,680

Genworth Financial, Inc.

15,050

520,429

Hartford Financial Services Group, Inc. (The)

18,750

1,610,437

Other Diversified Financial Services 5.90%

4,580,636

Citigroup, Inc.

47,600

2,310,028

JPMorgan Chase & Co.

48,960

1,943,222

National Financial Partners Corp.

6,230

327,386

Property & Casualty Insurance 1.85%

1,434,744

Ambac Financial Group, Inc.

7,500

577,950

ProAssurance Corp. (I)

17,615

856,794

Regional Banks 41.45%

32,203,243

Alabama National Bancorp.

9,000

582,840

Ameris Bancorp.

21,480

426,163

BancorpSouth, Inc.

38,167

842,346

BB&T Corp. (L)

38,382

1,608,590

BOK Financial Corp.

26,776

1,216,434

Capital City Bank Group, Inc.

26,327

902,753

City National Corp.

17,500

1,267,700

Colonial BancGroup, Inc. (The)

38,112

907,828

Commerce Bancshares, Inc.

19,847

1,034,426

Commercial Bankshares, Inc.

35,551

1,257,439

Community Bancorp. (I)

880

27,817

Compass Bancshares, Inc.

26,025

1,256,747

Fifth Third Bancorp.

21,500

810,980

First Bancorp. of North Carolina

18,532

373,605

First Charter Corp.

28,500

674,310

First Horizon National Corp.

21,080

810,315

Hancock Holding Co.

15,000

567,150

LSB Bancshares, Inc.

56,512

999,584

M&T Bank Corp.

10,000

1,090,500

Marshall & Ilsley Corp.

19,250

828,520

National City Corp.

18,000

604,260

North Fork Bancorp., Inc.

25,000

684,000

Peoples BancTrust Co., Inc. (The)

52,800

1,028,016

Pinnacle Financial Partners, Inc. (I)

78,000

1,948,440

PNC Financial Services Group, Inc.

23,000

1,422,090

Provident Bankshares Corp.

20,156

680,668

Seacoast Banking Corp. of Florida

69,520

1,595,484

See notes to financial statements.

7

F I N A N C I A L S TAT E M E N T S

Issuer

Shares

Value

Regional Banks (continued)

Summit Bancshares, Inc.

18,600

$334,428

SunTrust Banks, Inc.

26,556

1,932,215

TCF Financial Corp.

42,000

1,139,880

Trustmark Corp.

32,000

879,040

Western Alliance Bancorp. (I)

1,730

51,675

Whitney Holding Corp.

14,300

394,108

Zions Bancorp.

26,772

2,022,892

Reinsurance 2.35%

1,825,262

Assured Guaranty Ltd. (Bermuda)

23,650

600,473

Axis Capital Holdings Ltd. (Bermuda)

12,000

375,360

Max Re Capital Ltd. (Bermuda)

13,600

353,192

RenaissanceRe Holdings Ltd. (Bermuda)

11,250

496,237

Specialized Finance 0.45%

345,890

CIT Group, Inc.

6,680

345,890

Thrifts & Mortgage Finance6.89%

5,351,278

Countrywide Financial Corp.

18,000

615,420

First Financial Holdings, Inc.

40,500

1,244,160

Freddie Mac

23,000

1,503,050

Hudson City Bancorp., Inc.

34,150

413,898

South Street Financial Corp.

95,000

878,750

Washington Mutual, Inc.

16,000

696,000

Interest

Par value

Issuer, description, maturity date

rate

(000)

Value

Short-term investments 3.93%

$3,055,460

(Cost $3,055,460)

Certificates of Deposit 0.03%

27,468

Deposits in mutual banks

$27

27,468

Joint Repurchase Agreement 0.20%

153,000

Investment in a joint repurchase agreement transaction

with Morgan Stanley -- Dated 12-30-05 due 1-03-06

(Secured by U.S. Treasury Inflation Indexed Note 3.375%

due 1-15-12)

3.500%

153

153,000

See notes to financial statements.

8

F I N A N C I A L S TAT E M E N T S

Issuer

Shares

Value

Cash Equivalents 3.70%

$2,874,992

AIM Cash Investment Trust (T)

2,874,992

2,874,992

Total investments 103.69%

$80,555,826

Other assets and liabilities, net (3.69%)

($2,866,901)

Total net assets 100.00%

$77,688,925

(I) Non-income-producing security.

(L) All or a portion of this security is on loan as of December 31, 2005.

(T) Represents investment of securities lending collateral.

Parenthetical disclosure of a foreign country in the security description represents country of a foreign issuer.

The percentage shown for each investment category is the total value of that category as a percentage of the net assets of the Fund.

See notes to financial statements.

9

F I N A N C I A L S TAT E M E N T S

ASSETS AND LIABILITIES

December 31, 2005

This Statement of Assets and Liabilities is the Fund’s balance sheet. It shows the value of what the Fund owns, is due and owes. You’ll also find the net asset value for each common share.

Assets

Investments at value (cost $43,362,114)

including $2,818,620 of securities loaned

$80,555,826

Cash

159

Dividends and interest receivable

135,516

Total assets

80,691,501

Liabilities

Payable upon return of securities loaned

2,874,992

Payable to affiliates

Management fees

50,386

Other

11,994

Other payables and accrued expenses

65,204

Total liabilities

3,002,576

Net assets

Capital paid-in

40,212,716

Accumulated net realized gain on investments

222,191

Net unrealized appreciation of investments

37,193,712

Accumulated net investment income

60,306

Net assets

$77,688,925

Net asset value per share

Based on 3,993,124 shares outstanding --

50 million shares authorized with par value

of $0.001 per share

$19.46

See notes to financial statements.

10

F I N A N C I A L S TAT E M E N T S

OPERATIONS

For the year ended December 31, 2005

This Statement of Operations summarizes the Fund’s investment income earned and expenses incurred in operating the Fund. It also shows net gains (losses) for the period stated.

Investment income

Dividends

$1,751,612

Interest

34,538

Securities lending

1,075

Total investment income

1,787,225

Expenses

Investment management fees

485,848

Directors’ fees

130,941

Administration fees

112,119

Professional fees

53,885

Miscellaneous

32,771

Printing

24,511

Custodian fees

22,776

Transfer agent fees

17,941

Compliance fees

1,826

Securities lending fees

47

Total expenses

882,665

Net investment income

904,560

Realized and unrealized gain

Net realized gain on investments

1,433,399

Change in net unrealized appreciation

(depreciation) of investments

2,412,459

Net realized and unrealized gain

3,845,858

Increase in net assets from operations

$4,750,418

See notes to financial statements.

11

F I N A N C I A L S TAT E M E N T S

CHANGES IN NET ASSETS

These Statements of Changes in Net Assets show how the value of the Fund’s net assets has changed during the last two periods. The difference reflects earnings less expenses, any investment gains and losses and distributions, if any, paid to shareholders.

Year

Year

ended

ended

12-31-041

12-31-05

Increase (decrease) in net assets

From operations

Net investment income

$759,889

$904,560

Net realized gain

4,746,268

1,433,399

Change in net unrealized

appreciation (depreciation)

4,972,340

2,412,459

Increase in net assets resulting

from operations

10,478,497

4,750,418

Distributions to common shareholders

From net investment income

(798,624)

(878,487)

From net realized gain

(3,858,676)

(2,411,048)

(4,657,300)

(3,289,535)

Net assets

Beginning of period

70,406,845

76,228,042

End of period2

$76,228,042

$77,688,925

1 Audited by previous auditor.

2 Includes accumulated net investment income of $34,233 and $60,306, respectively.

See notes to financial statements.

12

F I N A N C I A L H I G H L I G H T S

FINANCIAL HIGHLIGHTS

COMMON SHARES The Financial Highlights show how the Fund’s net asset value for a share has changed since the end of the previous period.

Period ended

12-31-011

12-31-021

12-31-031

12-31-041

12-31-05

Per share operating performance

Net asset value,

beginning of period

$16.58

$15.67

$14.39

$17.63

$19.09

Net investment income2

0.22

0.16

0.17

0.19

0.23

Net realized and unrealized

gain (loss) on investments

1.49

(0.66)

3.813

2.44

0.96

Total from

investment operations

1.71

(0.50)

3.98

2.63

1.19

Less distributions

From net investment income

(0.24)

(0.16)

(0.16)

(0.20)

(0.22)

From net realized gain

(2.38)

(0.62)

(0.58)

(0.97)

(0.60)

(2.62)

(0.78)

(0.74)

(1.17)

(0.82)

Net asset value, end of period

$15.67

$14.39

$17.63

$19.09

$19.46

Per share market value,

end of period

$13.17

$12.36

$18.40

$17.47

$16.68

Total return at market value4 (%)

14.41

(0.25)

58.66

1.54

0.21

Ratios and supplemental data

Net assets, end of period

(in millions)

$62

$57

$70

$76

$78

Ratio of expenses

to average net assets (%)

1.23

1.16

1.20

1.22

1.18

Ratio of net investment income

to average net assets (%)

1.23

1.04

1.04

1.04

1.21

Portfolio turnover (%)

53

42

26

10

4

1 Audited by previous auditor.

2 Based on the average of the shares outstanding.

3 Net of federal income taxes of $0.39 per share for the year ended 12-31-03, on net long-term capital gains retained by the Fund.

4 Assumes dividend reinvestment.

See notes to financial statements.

13

NOTES TO STATEMENTS

Note A Accounting policies

John Hancock Financial Trends Fund, Inc. (the “Fund”) is a diver-sified closed-end management investment company registered under the Investment Company Act of 1940.

Significant accounting policies of the Fund are as follows:

Valuation of investments

Securities in the Fund’s portfolio are valued on the basis of market quotations, valuations provided by independent pricing services or, if quotations are not readily available, or the value has been materially affected by events occurring after the closing of a foreign market, at fair value as determined in good faith in accordance with procedures approved by the Directors. Short-term debt investments which have a remaining maturity of 60 days or less may be valued at amortized cost, which approximates market value. Investments in AIM Cash Investment Trust are valued at their net asset value each business day.

Joint repurchase agreement

Pursuant to an exemptive order issued by the Securities and Exchange Commission, the Fund, along with other registered investment companies having a management contract with John Hancock Advisers, LLC (the “Adviser”), a wholly owned subsidiary of John Hancock Financial Services, Inc., may participate in a joint repurchase agreement transaction. Aggregate cash balances are invested in one or more large repurchase agreements, whose underlying securities are obligations of the U.S. government and/or its agencies. The Fund’s custodian bank receives delivery of the underlying securities for the joint account on the Fund’s behalf. The Adviser is responsible for ensuring that the agreement is fully collateralized at all times.

Investment transactions

Investment transactions are recorded as of the date of purchase, sale or maturity. Net realized gains and losses on sales of investments are determined on the identified cost basis.

Securities lending

The Fund may lend securities to certain qualified brokers who pay the Fund negotiated lender fees. The loans are collateralized at all times with cash or securities with a market value at least equal to the market value of the securities on loan. As with other extensions of credit, the Fund may bear the risk of delay of the loaned securities in recovery or even loss of rights in the collateral, should the borrower of the securities fail financially. On December 31, 2005, the Fund loaned securities having a market value of $2,818,620 collateralized by cash in the amount of $2,874,992. The cash collateral was invested in a short-term instrument. Securities lending expenses are paid by the Fund to the Adviser.

14

Federal income taxes

The Fund qualifies as a “regulated investment company” by complying with the applicable provisions of the Internal Revenue Code and will not be subject to federal income tax on taxable income that is distributed to shareholders. Therefore, no federal income tax provision is required.

Dividends, interest and distributions

Dividend income on investment securities is recorded on the ex-dividend date or, in the case of some foreign securities, on the date thereafter when the Fund identifies the dividend. Interest income on investment securities is recorded on the accrual basis. Foreign income may be subject to foreign withholding taxes, which are accrued as applicable.

The Fund records distributions to shareholders from net investment income and net realized gains, if any, on the ex-dividend date. During the year ended December 31, 2004, the tax character of distributions paid was as follows: ordinary income $1,605,955 and long-term capital gain $3,051,345. During the year ended December 31, 2005, the tax character of distributions paid was as follows: ordinary income $991,732 and long-term capital gain $2,297,803.

As of December 31, 2005, the components of distributable earnings on a tax basis included $89,600 of undistributed ordinary income and $198,085 of undistributed long-term gain.

Such distributions and distributable earnings, on a tax basis, are determined in conformity with income tax regulations, which may differ from accounting principles generally accepted in the United States of America. Distributions in excess of tax basis earnings and profits, if any, are reported in the Fund’s financial statements as a return of capital.

Use of estimates

The preparation of these financial statements, in accordance with accounting principles generally accepted in the United States of America, incorporates estimates made by management in determining the reported amount of assets, liabilities, revenues and expenses of the Fund. Actual results could differ from these estimates.

Note B Management and administration fees and transactions with affiliates and others

The Fund has an investment management contract with the Adviser, under which the Adviser furnishes office space, furnishings and equipment and provides the services of persons to manage the investment of the Fund’s assets and to continually review, supervise and administer the Fund’s investment program. Under the investment management agreement the Fund pays a monthly management fee to the Adviser at an annual rate of 0.65% of the Fund’s average weekly net asset value, or a flat annual fee of $50,000, whichever is higher. If total Fund expenses exceed 2% of the Fund’s average weekly net asset value in any one year, the Fund may require the Adviser to reimburse the Fund for such excess, subject to a minimum fee of $50,000.

Effective December 31, 2005, the investment management teams of the Adviser were reorganized into Sovereign Asset Management LLC (“Sovereign”), a wholly owned subsidiary of John Hancock Life Insurance Company (“JHLICo”). The Adviser remains the principal advisor on the Fund and Sovereign acts as subadviser under the supervision of the Adviser. The restructuring did not have an impact on the Fund, which continues to be managed using the same investment philosophy and process. The Fund is not responsible for payment of the subadvisory fees.

15

The Fund has an administration agreement with the Adviser under which the Adviser provides certain administrative services required by the Fund. The Fund pays a monthly administration fee to the Adviser at an annual rate of 0.15% of the Fund’s average weekly net assets value, or a flat annual fee of $22,000, whichever is higher. The compensation for the year amounted to $112,119. The Fund also reimbursed JHLICo for certain compliance costs, included in the Fund’s Statement of Operations.

The Fund does not pay remuneration to its Officers. Certain Officers of the Fund are Officers of the Adviser.

Note C Fund share transactions

The Fund had no share transactions during the last two years.

One shareholder beneficially owned approximately 18% of the Fund’s shares at December 31, 2005.

The Fund from time-to-time may, but is not required to, make open market repurchases of its shares in order to attempt to reduce or eliminate the amount of any market value discount or to increase the net asset value of its shares, or both. In addition, the Board currently intends each quarter during periods when the Fund’s shares are trading at a discount from the net asset value to consider the making of tender offers. The Board may at any time, however, decide that the Fund should not make share repurchases or tender offers.

Note D Investment transactions

Purchases and proceeds from sales or maturities of securities, other than short-term securities and obligations of the U.S. government, during the year ended December 31, 2005, aggregated $3,129,032 and $5,397,291, respectively.

The cost of investments owned on December 31, 2005, including short-term investments, for federal income tax purposes, was $43,367,302. Gross unrealized appreciation and depreciation of investments aggregated $37,594,233 and $405,709, respectively, resulting in net unrealized appreciation of $37,188,524 The difference between book basis and tax basis net unrealized appreciation of investments is attributable primarily to the tax deferral of losses on certain sales of securities.

Change in independent auditor (unaudited)

Based on the recommendation of the Audit Committee of the Fund, the Board of Directors has determined not to retain Deloitte & Touche LLP as the Fund’s Independent Registered Public Accounting Firm and voted to appoint PricewaterhouseCoopers LLP for the fiscal year ended December 31, 2005. During the two most recent fiscal years, Deloitte & Touche LLP’s audit reports contained no adverse opinion or disclaimer of opinion; nor were their reports qualified as to uncertainty, audit scope or accounting principles. Further, there were no disagreements between the Fund and Deloitte & Touche LLP on accounting principles, finan-cial statements disclosure or audit scope, which, if not resolved to the satisfaction of Deloitte & Touche LLP, would have caused them to make reference to the disagreement in their reports.

16

AUDITORS’ REPORT

Report of Independent Registered Public Accounting Firm

To the Board of Trustees and Shareholders of John Hancock Financial Trends Fund, Inc.,

In our opinion, the accompanying statement of assets and liabilities, including the schedule of investments, and the related statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of John Hancock Financial Trends Fund, Inc. (the “Fund”) at December 31, 2005, the results of its operations, the changes in its net assets and the financial highlights for the periods indicated, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fund’s management; our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audit, which included confirmation of securities at December 31, 2005 by correspondence with the custodian and brokers, provide a reasonable basis for our opinion. The statement of changes in net assets of the Fund for the year ended December 31, 2004, and the financial highlights for each of the four years ended on or before December 31, 2004 were audited by another independent registered public accounting firm, whose report dated February 18, 2005 expressed an unqualified opinion thereon.

PricewaterhouseCoopers LLP Boston, Massachusetts February 15, 2006

17

TAX INFORMATION

Unaudited

For federal income tax purposes, the following information is furnished with respect to the distributions of the Fund, if any, paid during its taxable year ended December 31, 2005.

This Fund has designated distributions of $2,297,803 to shareholders as a long-term capital gain dividend.

With respect to the ordinary dividends paid by the Fund for the fiscal year ended December 31, 2005, 100% of the dividends qualify for the corporate dividends-received deduction.

The Fund hereby designates the maximum amount allowable of its net taxable income as qualified dividend income as provided in the Jobs and Growth Tax Relief Reconciliation Act of 2003. This amount will be reflected on Form 1099-DIV for the calendar year 2005.

Shareholders were mailed a 2005 U.S. Treasury Department Form 1099-DIV in January 2006. This will reflect the total of all distributions that are taxable for calendar year 2005.

18

Investment objective and policy

The Fund’s primary investment objective is long-term capital appreciation. Its secondary investment objective is current income. The Fund will seek to achieve its primary investment objective of long-term capital appreciation by investing at least 80% (65% prior to January 25, 2002) of its assets in stocks of U.S. and foreign financial services companies of any size. These companies include banks, thrifts, finance companies, brokerage and advisory firms, real estate-related firms, insurance companies and financial holding companies. These companies are usually regulated by governmental or quasi-governmental entities, and as a result, are subject to the risk that regulatory developments will adversely affect them. With respect to the Fund’s investment policy of investing at least 80% of “assets” in equity securities, “assets” is defined as net assets plus the amount of any borrowings for investment purposes. The Fund will notify shareholders at least 60 days prior to any change in this policy. In abnormal market conditions, the Fund may take temporary defensive positions. As such, the Fund may temporarily invest all of its assets in investment-grade, short-term securities. In such circumstances, the Fund may not achieve its objective. The Fund’s current investment restriction, relating to industry concentration, has been modified to remove the reference to the banking and savings industry so that it reads as follows: “Except for temporary defensive purposes, the Fund may not invest more than 25% of its total assets in any one industry or group of related industries except that the Fund will invest more than 25% of its assets in the financial services sector.”

Repurchase agreement

A repurchase agreement is a contract under which the Fund would acquire a security for a relatively short period (usually not more than seven days) subject to the obligation of the seller to repurchase and the Fund to resell such security at a fixed time and price (representing the Fund’s cost plus interest). The Fund will enter into repurchase agreements only with member banks of the Federal Reserve System and with “primary dealers” in U.S. government securities. The Adviser will continuously monitor the creditworthiness of the parties with whom the Fund enters into repurchase agreements.

Repurchase transactions must be fully collateralized at all times, but they involve some credit risk to the Fund if the other party defaults on its obligations and the Fund is delayed or prevented from liquidating the collateral. The Fund has established a procedure providing that the securities serving as collateral for each repurchase agreement must be delivered to the Fund’s custodian either physically or in book-entry form and that the collateral must be marked to market daily to ensure that each repurchase agreement is fully collateralized at all times. In the event of bankruptcy or other default by a seller on a repurchase agreement, the Fund could experience delays in liquidating the underlying securities and could experience losses, including the possible decline in the value of the underlying securities during the period while the Fund seeks to enforce its rights thereto, possible subnormal levels of income, lack of access to income during this period and the expense of enforcing its rights.

By-laws

In January 2003, the Board of Directors adopted several amendments to the Fund’s by-laws, including provisions relating to the calling of a special meeting and requiring advance notice of shareholder proposals or nominees for Director. The advance notice provisions in the by-laws require shareholders to notify the Fund in writing of any proposal that they intend to present at an annual meeting of shareholders, including any

19

nominations for Director, between 90 and 120 days prior to the first anniversary of the mailing date of the notice from the prior year’s annual meeting of shareholders. The notification must be in the form prescribed by the by-laws. The advance notice provisions provide the Fund and its Directors with the opportunity to thoughtfully consider and address the matters proposed before the Fund prepares and mails its proxy statement to shareholders. Other amendments set forth the procedures that must be followed in order for a shareholder to call a special meeting of shareholders. The Fund is presently listed on NASDAQ and per a grandfathering provision it is not required to hold annual shareholder meetings. The Board approved the above amendment to the Fund’s by-laws to provide a defined structure for the submission of shareholder proposals should the circumstances change and an annual meeting be required. Please contact the Secretary of the Fund for additional information about the advance notice requirements or the other amendments to the by-laws.

In November 2005, the Fund’s Board of Directors adopted several amendments to the Fund’s by-laws regarding the Chairman of the Board position: The Chairman of the Board shall at all times be a director who is not an interested person of the Fund as that term is defined by the Investment Company Act of 1940. The scope of the Chairman’s responsibilities and fidu-ciary obligations were further defined. Lastly, disclosure regarding the election, resignation and removal of the Chairman as well as the filling of a vacancy was added.

At a quarterly meeting of the Fund’s Board of Directors held February 13, 2006, the Board amended Article II Section 2 of the Fund’s ByLaws to state that a special meeting of the stockholders, unless otherwise provided by law or by the Articles of Incorporation, may be called for any purpose or purposes by a majority of the Board of Directors, the President, or, subject to Section 2(c), by the Secretary of the Corporation upon the written request of stockholders entitled to cast at least 35% of all votes entitles to be cast at the meeting.

Dividends and distributions

During the year ended December 31, 2005, dividends from net investment income totaling $0.220 per share and capital gain distributions totaling $0.604 per share were paid to shareholders. The dates of payments and the amounts per share are as follows:

INCOME

PAYMENT DATE

DIVIDEND

August 11, 2005

$0.110

December 30, 2005

0.110

CAPITAL

GAIN

PAYMENT DATE

DISTRIBUTION

August 11, 2005

$0.302

December 30, 2005

0.302

Dividend reinvestment plan

The Fund offers its registered shareholders an automatic Dividend Reinvestment Plan (the “Plan”), which enables each participating shareholder to have all dividends (including income dividends and/or capital gains distributions) payable in cash, reinvested by Mellon Investor Services (the “Plan Agent”) in shares of the Fund’s common stock. However, shareholders may elect not to enter into, or may terminate at any time without penalty, their participation in the Plan by notifying the Plan Agent in writing. Shareholders who do not participate in the Plan will receive all dividends in cash.

In the case of shareholders such as banks, brokers or nominees who hold shares for others who are the bene-ficial owners, the Plan Agent will administer the Plan on the basis of record ownership of shares. These record shareholders will receive dividends under the Plan on behalf of participating bene-ficial owners and cash on behalf of non-participating

20

beneficial owners. These recordholders will then credit the beneficial owners’ accounts with the appropriate stock or cash distribution.

Whenever the market price of the Fund’s stock equals or exceeds net asset value per share, participating shareholders will be issued stock valued at the greater of (i) net asset value per share or (ii) 95% of the market price. If the net asset value per share of the Fund’s stock exceeds the market price per share, the Plan Agent shall make open market purchases of the Fund’s stock for each participating shareholder’s account. These purchases may begin no sooner than five business days prior to the payment date for the dividend and will end up to thirty days after the payment date. If shares cannot be purchased within thirty days after the payment date, the balance of shares will be purchased from the Fund at the average price of shares purchased on the open market. Each participating shareholder will be charged a pro rata share of brokerage commissions on all open market purchases.

The shares issued to participating shareholders, including fractional shares, will be held by the Plan Agent in the name of the shareholder. The Plan Agent will confirm each acquisition made for the account of the participating shareholders as soon as practicable after the payment date of the distribution.

The reinvestment of dividends does not relieve participating shareholders of any federal, state or local income tax that may be due with respect to each dividend. Dividends reinvested in shares will be treated on your federal income tax return as though you had received a dividend in cash in an amount equal to the fair market value of the shares received, as determined by the prices for shares of the Fund on the Nasdaq National Market System as of the dividend payment date. Distributions from the Fund’s long-term capital gains will be taxable to you as long-term capital gains. The confirmation referred to above will contain all the information you will require for determining the cost basis of shares acquired and should be retained for that purpose. At year end, each account will be supplied with detailed information necessary to determine total tax liability for the calendar year.

All correspondence or additional information concerning the Plan should be directed to the Plan Agent, Mellon Bank, N.A., c/o Mellon Investor Services at P.O. Box 3338, South Hackensack, New Jersey 07606-1938 (Telephone: 1-800-852-0218).

Shareholder communication and assistance

If you have any questions concerning the Fund, we will be pleased to assist you. If you hold shares in your own name and not with a brokerage firm, please address all notices, correspondence, questions or other communications regarding the Fund to the transfer agent at:

Mellon Investor Services Newport Office Center VII 480 Washington Boulevard Jersey City, NJ 07310 Telephone: 1-800-852-0218

If your shares are held with a brokerage firm, you should contact that firm, bank or other nominee for assistance.

21

Board Consideration of and Continuation of Investment Advisory Agreement: John Hancock Financial Trends Fund, Inc.

Section 15(c) of the Investment Company Act of 1940 (the “1940 Act”) requires the Board of Directors (the “Board”) of John Hancock Financial Trends Fund, Inc. (the “Fund”), including a majority of the Directors who have no direct or indirect interest in the investment advisory agreement and are not “interested persons” of the Fund, as defined in the 1940 Act (the “Independent Directors”), annually to review and consider the continuation of the investment advisory agreement (the “Advisory Agreement”) with John Hancock Advisers, LLC (the “Adviser”) for the Fund.

At a meeting held on July 25, 2005, the Board, including the Independent Directors, considered the factors and reached the conclusions described below relating to the selection of the Adviser and the continuation of the Advisory Agreement. During such meeting, the Independent Directors also met in executive session with their independent legal counsel. In evaluating the Advisory Agreement, the Board, including the Independent Directors, reviewed a broad range of information requested for this purpose by the Independent Directors, including but not limited to the following: (i) The investment performance of the Fund and a broader universe of relevant funds (the “Universe”) selected by Lipper Inc. (“Lipper”), an independent provider of investment company data for a range of periods, (ii) advisory and other fees incurred by, and the expense ratios of, the Fund and a group of comparable funds selected by Lipper (the “Peer Group”) (iii) the advisory fees of comparable portfolios of other clients of the Adviser, (iv) the Adviser’s financial results and condition, including its and certain of its affiliates’ profitability from services performed for the Fund, (v) breakpoints in the Peer Group’s fees, (vi) the Adviser’s record of compliance with applicable laws and regulations, with the Fund’s investment policies and restrictions, and with the Fund’s Code of Ethics and the structure and responsibilities of the Adviser’s compliance department (vii) the background and experience of senior management and investment professionals, (viii) the nature, cost and character of advisory and non-investment management services provided by the Adviser and its affiliates.

The nature, extent, and quality of the services provided by the Adviser

In this regard, the Directors reviewed the services being provided by the Adviser to the Fund including, without limitation, its investment advisory and administrative services to the Fund, the terms of the Investment Advisory Agreement and the separate Administration Agreement between the Fund and the Adviser, the Adviser’s coordination of services for the Fund over the years, and its provision of officers to the Fund (including the Fund’s chief compliance officer). After reviewing the foregoing information, the Directors concluded that the quality, extent and nature of the services provided by the Advisor were satisfactory and adequate for the Fund.

The investment performance of the Fund and Adviser

In this regard, the Directors compared the performance of the Fund with the performance of comparable indexes and funds. The Directors also considered the consistency of the Adviser’s management of the Fund with the Fund’s investment objective and policies, and long-term performance of the Fund. The Directors also considered the Fund’s historical discounts/premiums from net asset value, and a Lipper comparison report

22

included in the materials provided to the Board prior to the meeting (the “Evaluation Materials”). Following further discussion, the Directors concluded that the investment performance of the Fund and Adviser was satisfactory.

The costs of the services to be provided and profits to be realized by the Adviser and its affiliates from the relationship with the Fund

In this regard, the Directors considered the Adviser’s staffing, personnel and methods of operating; the financial condition of the Adviser and the level of commitment to the Fund and the Adviser by the principals of the Adviser; the asset levels of the Fund; and the overall expenses of the Fund. The Directors then compared the fees and expenses of the Fund (including the management fee) to other funds comparable to the Fund in terms of the type of fund, the style of investment management (including, in particular, other financial services funds) and the nature of the investment strategy and markets invested in, among other factors. To assist in its review, the Directors considered the information and comparisons included in the Lipper report in the Evaluation Materials. Following this comparison and upon further consideration and discussion of the foregoing, the Directors concluded that the fees to be paid to the Adviser by the Fund were fair and reasonable.

The extent to which economies of scale would be realized as the Fund grows and whether advisory fee levels reflect these economies of scale for the benefits of the Fund’s investors

In this regard, the Directors considered the Fund’s fee arrangements with the Adviser, the Fund’s fee arrangements with other service providers, and the expense limits that are included in the Fund’s Investment Advisory Agreement. Following discussion of the Fund’s current asset levels and fee caps, the Directors determined that, while the Fund does not have fee breakpoints, the Fund’s fee arrangements with the Adviser included provisions to protect the Fund from excessive fees at lower asset levels (subject to a $50,000 management fee floor) for the benefit of shareholders.

Other factors and broader review

As discussed above, the Board reviewed detailed materials received from the Adviser as part of the annual re-approval process under Section 15(c) of the 1940 Act. The Board also regularly reviews and assesses the quality of the services that the Fund receives throughout the year. In this regard, the Board reviews reports of the Adviser at least quarterly, which include, among other things, a detailed portfolio review, detailed fund performance reports and compliance reports. In addition, the Board meets with portfolio managers and senior investment officers at various times throughout the year.

After considering the above-described factors and based on its deliberations and its evaluation of the information described above, the Board concluded that approval of the continuation of the Advisory Agreement for the Fund was the in the best interest of the Fund and its shareholders. Accordingly, the Board unanimously approved the continuation of the Advisory Agreement.

At a meeting held on November 3, 2005, the Board reviewed a Sub-Advisory Agreement among the Fund, the Adviser and Sovereign Asset Management, LLC, an affiliate of the Adviser (the “Sub-Adviser”). At that meeting, the Adviser proposed, and the Board approved, a reorganization of the Adviser’s operations and the transfer to the Sub-Adviser of all of the Adviser’s investment personnel. As a result of this restructuring, the Adviser remains the principal adviser to the Fund and the Sub-Adviser

23

acts as sub-adviser under the supervision of the Adviser. In evaluating the Sub-Adviser Agreement, the Board relied upon the review that it conducted at the July 25, 2005 meeting, its familiarity with the operations and personnel transferred to Sovereign and representations by the Adviser that the reorganization would not result in a change in the quality of services provided under the Sub-Advisory Agreement or the personnel responsible for the day-to-day management of the Fund. The Board also reviewed an analysis of the fee paid by the Adviser to the Sub-Adviser under the Sub-Advisory Agreement relative to sub-advisory fees paid by the Adviser and its affiliates to third party sub-advisers and fees paid by a peer group of unaffiliated investment companies. After considering the above-described factors and based on its deliberations and its evaluation of the information described above, the Board concluded that approval of the Sub-Advisory Agreement was the in the best interest of the Fund and its shareholders. Accordingly, the Board unanimously approved the the Sub-Advisory Agreement, which became effective on December 31, 2005,

24

Information about the portfolio managers

Management Biographies and Fund ownership Below is an alphabetical list of the portfolio managers who share joint responsibility for the day-to-day investment management of the Fund. It provides a brief summary of their business careers over the past five years and their range of beneficial share ownership in the Fund as of December 31, 2005.

Thomas M. Finucane Vice President, Sovereign Asset Management LLC (since 2005) Vice President, John Hancock Advisers, LLC (2004-2005) Senior Vice President, State Street Research & Management (2002-2004) Vice President, John Hancock Advisers, LLC (1990-2002) Began business career in 1983 Rejoined fund team in 2004 Fund ownership – None

James K. Schmidt, CFA Executive Vice President, Sovereign Asset Management LLC since 2005 Executive Vice President, John Hancock Advisers, LLC (1992-2005) Began business career in 1979 Joined fund team in 1991 Fund ownership – None

Lisa A. Welch Vice President, Sovereign Asset Management LLC since 2005 Vice President, John Hancock Advisers, LLC (1998-2005) Began business career in 1986 Joined fund team in 1998 Fund ownership – None

Other Accounts the Portfolio Managers are Managing The table below indicates for each portfolio manager information about the accounts over which the portfolio manager has day-to-day investment responsibility. All information on the number of accounts and total assets in the table is as of December 31, 2005. For purposes of the table, “Other Pooled Investment Vehicles” may include investment partnerships and group trusts, and “Other Accounts” may include separate accounts for institutions or individuals, insurance company general or separate accounts, pension funds and other similar institutional accounts.

P O R T F O L I O M A N A G E R

O T H E R A C C O U N T S M A N A G E D B Y T H E P O R T F O L I O M A N A G E R S

Thomas M. Finucane

Other Investment Companies:

5 funds with assets of approximately $4.2 billion.

Other Pooled Investment Vehicles: None

Other Accounts: None

James K. Schmidt, CFA

Other Investment Companies:

6 funds with assets of approximately $5.4 billion.

Other Pooled Investment Vehicles: None

Other Accounts: None

25

Lisa A. Welch

Other Investment Companies:

6 funds with assets of approximately $5.4 billion.

Other Pooled Investment Vehicles: None

Other Accounts: None

When a portfolio manager is responsible for the management of more than one account, the potential arises for the portfolio manager to favor one account over another. For the reasons outlined below, the Fund does not believe that any material conflicts are likely to arise out of a portfolio manager’s responsibility for the management of the Fund as well as one or more other accounts. The Adviser and the Sub-Adviser have adopted procedures, overseen by the Chief Compliance Officer, that are intended to monitor compliance with the policies referred to in the following paragraphs:

* The Sub-Adviser has policies that require a portfolio manager to allocate investment opportunities in an equitable manner and generally to allocate such investments proportionately among all accounts with similar investment objectives.

* When a portfolio manager intends to trade the same security for more than one account, the policies of the Sub-Adviser generally require that such trades for the individual accounts are aggregated so each account receives the same price. Where not possible or may not result in the best possible price, the Sub-Adviser will place the order in a manner intended to result in as favorable a price as possible for such client.

* The investment performance on specific accounts is not a factor in determining the portfolio manager’s compensation. See “Compensation of Portfolio Managers” below. Neither the Adviser nor the Sub-Adviser receives a performance-based fee with respect any accounts managed by the Fund’s portfolio manager.

* The Sub-Adviser imposes certain trading restrictions and reporting requirements for accounts in which a portfolio manager or certain family members have a personal interest in order to confirm that such accounts are not favored over other accounts.

* The Sub-Adviser seeks to avoid portfolio manager assignments with potentially conflicting situations. However, where a portfolio manager is responsible for accounts with differing investment objectives and policies, it is possible that the portfolio manager will conclude that it is in the best interest of one account to sell a portfolio security while another account continues to hold or increase the holding in such security.

Compensation of Portfolio Managers

The Sub-Adviser has adopted a system of compensation for portfolio managers and others involved in the investment process that is applied consistently among investment professionals. At the Sub-Adviser, the structure of compensation of investment professionals is currently comprised of the following basic components: fixed base salary, and an annual investment bonus plan, as well as customary benefits that are offered generally to all full-time employees of the Sub-Adviser. A limited number of senior portfolio managers, who serve as officers of both the Sub-Adviser and its parent company, may also receive options or restricted stock grants of common shares of Manulife Financial.

Only investment professionals are eligible to participate in the Investment Bonus Plan on an annual basis. While the amount of any bonus is discretionary, the following factors are generally used in determining bonuses: 1) The investment performance of all accounts managed by the investment professional over one and three- year periods are considered. The pre-tax

26

performance of each account is measured relative to an appropriate peer group benchmark. 2) The profitability of the Sub-Adviser and its parent company are also considered in determining bonus awards, with greater emphasis placed upon the profitability of the Adviser. 3) The more intangible contributions of an investment professional to the Sub-Adviser’s business, including the investment professional’s support of sales activities, new fund/strategy idea generation, professional growth and development, and management, where applicable, are evaluating in determining the amount of any bonus award.

While the profitability of the Sub-Adviser and the investment performance of the accounts that the investment professionals maintain are factors in determining an investment professional’s overall compensation, the investment professional’s compensation is not linked directly to the net asset value of any fund.

27

DIRECTORS & OFFICERS

This chart provides information about the Directors and Officers who oversee your John Hancock fund. Officers elected by the Directors manage the day-to-day operations of the Fund and execute policies formulated by the Directors.

Independent Directors

Name, age

Position(s) held with Fund

Director

Principal occupation(s) and other

of Fund

directorships during past 5 years

since1

Franklin C. Golden, Born: 1950

1989

Chairman and Director

Managing Director, Wachovia Securities, Inc. (since 2001) (broker dealer); President,

James Myers and Company (full-service broker dealer) (until 2001); President, Financial Trends

Fund, Inc. (until 2001); Executive Vice President, IJL/Wachovia (until 1991); Past Director

and Chairman of the National Association of Securities Dealers (NASD) District 7 Business

Conduct Committee.

Robert G. Freedman, Born: 1938

1996

Director

Executive Vice President and Chief Investment Officer, Sovereign Asset Management and

NM Capital Management, Inc. (until 2000); Vice Chairman and Chief Investment Officer,

Assistant Vice President and Assistant Secretary, the Adviser and each of the John

Hancock funds, John Hancock Funds and The Berkeley Group.

The business address for all Directors and Officers is 601 Congress Street, Boston, Massachusetts 02210-2805.

1 Each Director serves until resignation, retirement age or until his or her successor is elected.

29

30

31

32

For more information

The Fund’s proxy voting policies, procedures and records are available without charge, upon request:

By phone

On the Fund’s Web site

On the SEC’s Web site

1-800-225-5291

www.jhfunds.com/proxy

www.sec.gov

Investment adviser

Transfer agent

Independent registered

John Hancock Advisers, LLC

and registrar

public accounting firm

601 Congress Street

Mellon Investor Services

PricewaterhouseCoopers LLP

Boston, MA 02210-2805

Newport Office Center VII

125 High Street

480 Washington Boulevard

Boston, MA 02110

Subadviser

Jersey City, NJ 07310

Sovereign Asset Management

Stock symbol

LLC

Independent directors’

Listed Nasdaq Symbol:

101 Huntington Avenue

counsel

JHFT

Boston, MA 02199

Kilpatrick Stockton LLP

For shareholder assistance

1100 Peachtree Street

Custodian

refer to page 21

Atlanta, Georgia 30309-4530

The Bank of New York

One Wall Street

Fund counsel

New York, NY 10286

Wilmer Cutler Pickering

Hale and Dorr LLP

60 State Street

Boston, MA 02109-1803

How to contact us

Internet

www.jhfunds.com

Mail

Regular mail:

Mellon Investor Services

Newport Office Center VII

480 Washington Boulevard

Jersey City, NJ 07310

Phone

Customer service representatives

1-800-852-0218

Portfolio commentary

1-800-344-7054

24-hour automated information

1-800-843-0090

TDD line

1-800-231-5469

A listing of month-end portfolio holdings is available on our Web site, www.jhfunds.com. A more detailed portfolio holdings summary is available on a quarterly basis 60 days after the fiscal quarter on our Web site or upon request by calling 1-800-225-5291, or on the Securities and Exchange Commission’s Web site, www.sec.gov.

As of the end of the period, December 31, 2005, the registrant has adopted a code of ethics, as defined in Item 2 of Form N-CSR, that applies to its Chief Executive Officer, Chief Financial Officer and Treasurer (respectively, the principal executive officer, the principal financial officer and the principal accounting officer, the “Senior Financial Officers”). A copy of the code of ethics is filed as an exhibit to this Form N-CSR.

The code of ethics was amended effective May 1, 2005 to address new Rule 204A-1 under the Investment Advisers Act of 1940 and to make other related changes.

The most significant amendments were:

(a) Broadening of the General Principles of the code to cover compliance with all federal securities laws.

(b) Eliminating the interim requirements (since the first quarter of 2004) for access persons to preclear their personal trades of John Hancock mutual funds. This was replaced by post-trade reporting and a 30 day hold requirement for all employees.

(c) A new requirement for “heightened preclearance” with investment supervisors by any access person trading in a personal position worth $100,000 or more.

ITEM 3. AUDIT COMMITTEE FINANCIAL EXPERT.

Russell L. Page is the audit committee financial expert and is “independent”, pursuant to general instructions on Form N-CSR Item 3.

ITEM 4. PRINCIPAL ACCOUNTANT FEES AND SERVICES.

(a) Audit Fees

The aggregate fees billed for professional services rendered by the principal accountant(s) for the audit of the registrant’s annual financial statements or services that are normally provided by the accountant(s) in connection with statutory and regulatory filings or engagements amounted to $36,200 for the fiscal year ended December 31, 2004 and $24,300 for the fiscal year ended December 31, 2005. These fees were billed to the registrant and were approved by the registrant’s audit committee.

(b) Audit-Related Services

There were no audit-related fees during the fiscal year ended December 31, 2004 and fiscal year ended December 31, 2005 billed to the registrant or to the registrant's investment adviser (not including any sub-adviser whose role is primarily portfolio management and is subcontracted with or overseen by another investment adviser), and any entity controlling, controlled by, or under common control with the adviser that provides ongoing services to the registrant ("control affiliates").

(c) Tax Fees

The aggregate fees billed for professional services rendered by the principal accountant(s) for the tax compliance, tax advice and tax planning (“tax fees”) amounted to $2,250 for the fiscal year ended December 31, 2004 and $2,500 for the fiscal year ended December 31, 2005. The nature of the services comprising the tax fees was the review of the registrant’s income tax returns and tax distribution requirements. These fees were billed to the registrant and were approved by the registrant’s audit committee. There were no tax fees billed to the control affiliates.

(d) All Other Fees

There were no other fees during the fiscal year ended December 31, 2004 and fiscal year ended December 31, 2005 billed to the registrant or to the control affiliates.

(e)(1) See attachment "Approval of Audit, Audit-related, Tax and Other Services", with the audit committee pre-approval policies and procedures.

(e)(2) There were no fees that were approved by the audit committee pursuant to the de minimis exception for the fiscal years ended December 31, 2004 and December 31, 2005 on behalf of the registrant or on behalf of the control affiliates that relate directly to the operations and financial reporting of the registrant.

(f) According to the registrant’s principal accountant, for the fiscal year ended December 31, 2005, the percentage of hours spent on the audit of the registrant's financial statements for the most recent fiscal year that were attributed to work performed by persons who were not full-time, permanent employees of principal accountant was less than 50%.

(g) The aggregate non-audit fees billed by the registrant's accountant(s) for services rendered to the registrant and rendered to the registrant's control affiliates for each of the last two fiscal years of the registrant were $67,250 for the fiscal year ended December 31, 2004, and $99,700 for the fiscal year ended December 31, 2005.

(h) The audit committee of the registrant has considered the non-audit services provided by the registrant’s principal accountant(s) to the control affiliates and has determined that the services that were not pre-approved are compatible with maintaining the principal accountant(s)' independence.

ITEM 5. AUDIT COMMITTEE OF LISTED REGISTRANTS.

Not applicable at this time.

ITEM 6. SCHEDULE OF INVESTMENTS.

Not applicable.

ITEM 7. DISCLOSURE OF PROXY VOTING POLICIES AND PROCEDURES FOR CLOSED-END MANAGEMENT INVESTMENT COMPANIES.

See attached Exhibit “Proxy Voting Policies and Procedures”.

ITEM 8. PORTFOLIO MANAGERS OF CLOSED-END MANAGEMENT INVESTMENT COMPANIES.

(a) Management Biographies and Fund ownership

Below is an alphabetical list of the portfolio managers who share joint responsibility for the day-today investment management of the Fund. It provides a brief summary of their business careers over the past five years and their range of beneficial share ownership in the Fund as of December 31, 2005.

Thomas M. Finucane Vice President, Sovereign Asset Management LLC (since 2005) Vice President, John Hancock Advisers, LLC (2004-2005) Senior Vice President, State Street Research & Management (2002-2004) Vice President, John Hancock Advisers, LLC (1990-2002) Began business career in 1983

Rejoined fund team in 2004 Fund ownership - None

James K. Schmidt, CFA Executive Vice President, Sovereign Asset Management LLC since 2005 Executive Vice President, John Hancock Advisers, LLC (1992-2005) Began business career in 1979 Joined fund team in 1991 Fund ownership - None

Lisa A. Welch Vice President, Sovereign Asset Management LLC since 2005 Vice President, John Hancock Advisers, LLC (1998-2005) Began business career in 1986 Joined fund team in 1998 Fund ownership - None

(b) Other Accounts the Portfolio Managers are Managing

The table below indicates for each portfolio manager information about the accounts over which the portfolio manager has day-to-day investment responsibility. All information on the number of accounts and total assets in the table is as of December 31, 2005. For purposes of the table, “Other Pooled Investment Vehicles” may include investment partnerships and group trusts, and “Other Accounts” may include separate accounts for institutions or individuals, insurance company general or separate accounts, pension funds and other similar institutional accounts.

PORTFOLIO MANAGER

OTHER ACCOUNTS MANAGED BY THE PORTFOLIO

MANAGERS

Thomas M. Finucane

Other Investment Companies:

5 funds with assets of approximately $4.2 billion.

Other Pooled Investment Vehicles: None

Other Accounts: None

James K. Schmidt, CFA

Other Investment Companies:

6 funds with assets of approximately $5.4 billion.

Other Pooled Investment Vehicles: None

Other Accounts: None

Lisa A. Welch

Other Investment Companies:

6 funds with assets of approximately $5.4 billion.

Other Pooled Investment Vehicles: None

Other Accounts: None

(c) When a portfolio manager is responsible for the management of more than one account, the potential arises for the portfolio manager to favor one account over another. For the reasons outlined below, the Fund does not believe that any material conflicts are likely to arise out of a portfolio manager’s responsibility for the management of the Fund as well as one or more other accounts. The Adviser and the Sub-Adviser have adopted procedures, overseen by the Chief Compliance Officer, that are intended to monitor compliance with the policies referred to in the following paragraphs:

* The Sub-Adviser has policies that require a portfolio manager to allocate investment opportunities in an equitable manner and generally to allocate such investments proportionately among all accounts with similar investment objectives.

* When a portfolio manager intends to trade the same security for more than one account, the policies of the Sub-Adviser generally require that such trades for the individual accounts are aggregated so each account receives the same price. Where not possible or may not result in the best possible price, the Sub-Adviser will place the order in a manner intended to result in as favorable a price as possible for such client.

* The investment performance on specific accounts is not a factor in determining the portfolio manager’s compensation. See “Compensation of Portfolio Managers” below. Neither the Adviser nor the Sub-Adviser receives a performance-based fee with respect any accounts managed by the Fund’s portfolio manager.

* The Sub-Adviser imposes certain trading restrictions and reporting requirements for accounts in which a portfolio manager or certain family members have a personal interest in order to confirm that such accounts are not favored over other accounts.

* The Sub-Adviser seeks to avoid portfolio manager assignments with potentially conflicting situations. However, where a portfolio manager is responsible for accounts with differing investment objectives and policies, it is possible that the portfolio manager will conclude that it is in the best interest of one account to sell a portfolio security while another account continues to hold or increase the holding in such security.

(d) Compensation of Portfolio Managers

The Sub-Adviser has adopted a system of compensation for portfolio managers and others involved in the investment process that is applied consistently among investment professionals. At the Sub-Adviser, the structure of compensation of investment professionals is currently comprised of the following basic components: fixed base salary, and an annual investment bonus plan, as well as customary benefits that are offered generally to all full-time employees of the Sub-Adviser. A limited number of senior portfolio managers, who serve as officers of both the Sub-Adviser and its parent company, may also receive options or restricted stock grants of common shares of Manulife Financial.