UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-5851

MFS INTERMARKET INCOME TRUST I

(Exact name of registrant as specified in charter)

500 Boylston Street, Boston, Massachusetts 02116

(Address of principal executive offices) (Zip code)

Susan S. Newton

Massachusetts Financial Services Company

500 Boylston Street

Boston, Massachusetts 02116

(Name and address of agents for service)

Registrant’s telephone number, including area code: (617) 954-5000

Date of fiscal year end: November 30

Date of reporting period: May 31, 2012

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

MFS® InterMarket

Income Trust I

SEMIANNUAL REPORT

May 31, 2012

CMK-SEM

MFS® INTERMARKET INCOME TRUST I

New York Stock Exchange Symbol: CMK

NOT FDIC INSURED Ÿ MAY LOSE VALUE Ÿ NO BANK GUARANTEE

LETTER FROM THE CHAIRMAN AND CEO

Dear Shareholders:

World financial markets remain a venue of uncertainty. The focus has shifted most recently to the eurozone, where policymakers are attempting to develop a plan that will help debt-laden countries and prevent their woes from spreading across the region. Volatility is likely to continue as investors test the resolve of European officials to make the tough decisions needed to solve the crisis.

The U.S. economy is experiencing a period of growth. However, markets have been jittery in reaction to events in Europe and ahead of the U.S. presidential election. Voters in the United States are watching the economy closely and waiting to see if Congress agrees to cut the budget and extend the Bush administration tax cuts. Failure to do so could ultimately send the U.S. economy back into recession.

Amid this global uncertainty, managing risk becomes a top priority for investors and their advisors. At MFS® our global research platform is designed to ensure the smooth functioning

of our investment process in all business climates. Through this integrated approach, our investment staff shares ideas and evaluates opportunities across geographies, across both fundamental and quantitative disciplines, and across companies’ entire capital structure. We employ this uniquely collaborative approach to build better insights for our clients.

Additionally, we have a team of quantitative analysts that measures and assesses the risk profiles of our portfolios and securities on an ongoing basis. The chief investment risk officer, who oversees the team, reports directly to the firm’s president and chief investment officer so that the risk associated with each portfolio can be assessed objectively and independently of the portfolio management team.

We, like our investors, are mindful of the many economic challenges faced at the local, national, and international levels. It is in times such as these that we want to emphasize the merits of maintaining a long-term view, adhering to basic investing principles such as asset allocation and diversification, and working closely with investment advisors to research and identify appropriate investment opportunities.

Respectfully,

Robert J. Manning

Chairman and Chief Executive Officer

MFS Investment Management®

July 17, 2012

The opinions expressed in this letter are subject to change, may not be relied upon for investment advice, and no forecasts can be guaranteed.

1

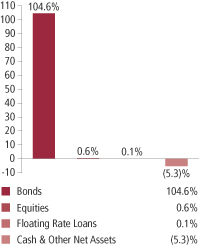

PORTFOLIO COMPOSITION

Portfolio structure (i)

| | | | |

| Fixed income sectors (i) | | | | |

| High Grade Corporates | | | 59.1% | |

| High Yield Corporates | | | 31.0% | |

| Non-U.S. Government Bonds | | | 12.8% | |

| Emerging Markets Bonds | | | 4.1% | |

| Mortgage-Backed Securities | | | 2.0% | |

| Asset-Backed Securities | | | 0.7% | |

| Collateralized Debt Obligations | | | 0.5% | |

| Floating Rate Loans | | | 0.1% | |

| U.S. Government Agencies (o) | | | 0.0% | |

| U.S. Treasury Securities | | | (5.6)% | |

| | | | |

| Composition including fixed income credit quality (a)(i) | | | | |

| AAA | | | 6.4% | |

| AA | | | 4.2% | |

| A | | | 26.2% | |

| BBB | | | 38.6% | |

| BB | | | 13.0% | |

| B | | | 15.4% | |

| CCC | | | 4.3% | |

| CC | | | 0.1% | |

| C | | | 0.1% | |

| Federal Agencies | | | 2.0% | |

| Not Rated | | | (5.6)% | |

| Non-Fixed Income | | | 0.6% | |

| Cash & Other | | | (5.3)% | |

| |

| Portfolio facts (i) | | | | |

| Average Duration (d) | | | 5.0 | |

| Average Effective Maturity (m) | | | 6.9 yrs. | |

| |

| Issuer country weightings (i)(x) | | | | |

| United States | | | 62.3% | |

| United Kingdom | | | 6.6% | |

| Netherlands | | | 3.6% | |

| Japan | | | 2.9% | |

| France | | | 2.5% | |

| Canada | | | 2.3% | |

| Italy | | | 2.2% | |

| Spain | | | 2.1% | |

| Germany | | | 1.7% | |

| Other Countries | | | 13.8% | |

2

Portfolio Composition – continued

| (a) | For all securities other than those specifically described below, ratings are assigned to underlying securities utilizing ratings from Moody’s, Fitch, and Standard & Poor’s rating agencies and applying the following hierarchy: If all three agencies provide a rating, the middle rating (after dropping the highest and lowest ratings) is assigned; if two of the three agencies rate a security, the lower of the two is assigned. Ratings are shown in the S&P and Fitch scale (e.g., AAA). All ratings are subject to change. Federal Agencies includes rated and unrated U.S. Agency fixed-income securities, U.S. Agency mortgage-backed securities, and collateralized mortgage obligations of U.S. Agency mortgage-backed securities. Not Rated includes fixed income securities, including fixed income futures, which have not been rated by any rating agency. Non-Fixed Income includes equity securities (including convertible bonds and equity derivatives) and commodities. Cash & Other includes cash, other assets less liabilities, offsets to derivative positions, and short-term securities. The fund may not hold all of these instruments. The fund is not rated by these agencies. |

| (d) | Duration is a measure of how much a bond’s price is likely to fluctuate with general changes in interest rates, e.g., if rates rise 1.00%, a bond with a 5-year duration is likely to lose about 5.00% of its value due to the interest rate move. |

| (i) | For purposes of this presentation, the components include the market value of securities, and reflect the impact of the equivalent exposure of derivative positions, if any. These amounts may be negative from time to time. The bond component will include any accrued interest amounts. Equivalent exposure is a calculated amount that translates the derivative position into a reasonable approximation of the amount of the underlying asset that the portfolio would have to hold at a given point in time to have the same price sensitivity that results from the portfolio’s ownership of the derivative contract. When dealing with derivatives, equivalent exposure is a more representative measure of the potential impact of a position on portfolio performance than market value. Where the fund holds convertible bonds, these are treated as part of the equity portion of the portfolio. |

| (m) | In determining an instrument’s effective maturity for purposes of calculating the fund’s dollar-weighted average effective maturity, MFS uses the instrument’s stated maturity or, if applicable, an earlier date on which MFS believes it is probable that a maturity-shortening device (such as a put, pre-refunding or prepayment) will cause the instrument to be repaid. Such an earlier date can be substantially shorter than the instrument’s stated maturity. |

| (x) | Represents the portfolio’s exposure to issuer countries as a percentage of a portfolio’s total net assets. |

From time to time “Cash & Other Net Assets” may be negative due to borrowings for leverage transactions, timing of cash receipts, and/or equivalent exposure from any derivative holdings.

Percentages are based on net assets as of 5/31/12.

The portfolio is actively managed and current holdings may be different.

3

PORTFOLIO MANAGERS’ PROFILES

| | | | |

| William Adams | | — | | Investment Officer of MFS; employed in the investment management area of MFS since 2009. Portfolio manager of the fund since May 2011. |

| | |

| Ward Brown | | — | | Investment Officer of MFS; employed in the investment management area of MFS since 2008. Portfolio Manager of the fund since February 2012. |

| | |

| James Calmas | | — | | Investment Officer of MFS; employed in the investment management area of MFS since 1988. Portfolio manager of the fund since June 2007. |

| | |

| David Cole | | — | | Investment Officer of MFS; employed in the investment management area of MFS since 2004. Portfolio Manager of the fund since December 2011. |

| | |

| Matthew Ryan | | — | | Investment Officer of MFS; employed in the investment management area of MFS since 1997. Portfolio Manager of the fund since February 2012. |

Note to Shareholders: Effective December 30, 2011, David Cole became a co-manager of the fund. Effective February 3, 2012, Ward Brown and Matthew Ryan became co-managers of the fund.

OTHER NOTES

The fund’s shares may trade at a discount or premium to net asset value. Shareholders do not have the right to cause the fund to repurchase their shares at net asset value. When fund shares trade at a premium, buyers pay more than the net asset value of underlying fund shares, and shares purchased at a premium would receive less than the amount paid for them in the event of the fund’s liquidation. As a result, the total return that is calculated based on the net asset value and New York Stock Exchange price can be different.

The fund’s monthly distributions may include a return of capital to shareholders to the extent that distributions are in excess of the fund’s net investment income and net capital gains, determined in accordance with federal income tax regulations. Distributions that are treated for federal income tax purposes as a return of capital will reduce each shareholder’s basis in his or her shares and, to the extent the return of capital exceeds such basis, will be treated as gain to the shareholder from a sale of shares. Returns of shareholder capital have the effect of reducing the fund’s assets and increasing the fund’s expense ratio.

In accordance with Section 23(c) of the Investment Company Act of 1940, the fund hereby gives notice that it may from time to time repurchase shares of the fund in the open market at the option of the Board of Trustees and on such terms as the Trustees shall determine.

4

PORTFOLIO OF INVESTMENTS

5/31/12 (unaudited)

The Portfolio of Investments is a complete list of all securities owned by your fund. It is categorized by broad-based asset classes.

| | | | | | | | |

| Bonds - 108.3% | | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Aerospace - 0.8% | | | | | | | | |

| BE Aerospace, Inc., 8.5%, 2018 | | $ | 90,000 | | | $ | 98,055 | |

| Bombardier, Inc., 7.5%, 2018 (n) | | | 260,000 | | | | 283,400 | |

| Bombardier, Inc., 7.75%, 2020 (n) | | | 55,000 | | | | 60,363 | |

| CPI International, Inc., 8%, 2018 | | | 105,000 | | | | 93,975 | |

| Huntington Ingalls Industries, Inc., 7.125%, 2021 | | | 190,000 | | | | 197,125 | |

| Kratos Defense & Security Solutions, Inc., 10%, 2017 | | | 85,000 | | | | 90,100 | |

| | | | | | | | |

| | | | | | | $ | 823,018 | |

| Airlines - 0.5% | | | | | | | | |

| Continental Airlines, Inc., FRN, 0.834%, 2013 | | $ | 474,329 | | | $ | 458,913 | |

| | |

| Apparel Manufacturers - 0.5% | | | | | | | | |

| Hanesbrands, Inc., 8%, 2016 | | $ | 50,000 | | | $ | 54,813 | |

| Hanesbrands, Inc., 6.375%, 2020 | | | 55,000 | | | | 56,169 | |

| Hanesbrands, Inc., FRN, 4.145%, 2014 | | | 45,000 | | | | 45,000 | |

| Jones Group, Inc., 6.875%, 2019 | | | 60,000 | | | | 57,675 | |

| Levi Strauss & Co., 6.875%, 2022 (n) | | | 15,000 | | | | 14,888 | |

| Phillips-Van Heusen Corp., 7.375%, 2020 | | | 205,000 | | | | 223,963 | |

| | | | | | | | |

| | | | | | | $ | 452,508 | |

| Asset-Backed & Securitized - 1.2% | | | | | | | | |

| Anthracite Ltd., “A”, CDO, FRN, 0.599%, 2019 (z) | | $ | 141,109 | | | $ | 121,354 | |

| Capital Trust Realty Ltd., CDO, 5.16%, 2035 (n) | | | 206,275 | | | | 207,822 | |

| Crest Ltd., “A1” CDO, FRN, 0.952%, 2018 (z) | | | 208,501 | | | | 187,651 | |

| Equity One ABS, Inc., FRN, 4.205%, 2034 | | | 247,399 | | | | 245,813 | |

| GMAC Mortgage Corp. Loan Trust, FRN, 5.865%, 2034 | | | 169,562 | | | | 127,273 | |

| Hertz Global Holdings, Inc., 4.26%, 2014 (n) | | | 270,000 | | | | 275,411 | |

| | | | | | | | |

| | | | | | | $ | 1,165,324 | |

| Automotive - 2.6% | | | | | | | | |

| Accuride Corp., 9.5%, 2018 | | $ | 185,000 | | | $ | 193,325 | |

| Allison Transmission, Inc., 7.125%, 2019 (n) | | | 145,000 | | | | 151,525 | |

| Daimler Finance North America LLC, FRN, 1.673%, 2013 (n) | | | 320,000 | | | | 322,088 | |

| Ford Motor Co., 7.45%, 2031 | | | 35,000 | | | | 45,588 | |

| Ford Motor Credit Co. LLC, 12%, 2015 | | | 595,000 | | | | 751,188 | |

| General Motors Financial Co., Inc., 6.75%, 2018 | | | 155,000 | | | | 166,404 | |

| Goodyear Tire & Rubber Co., 7%, 2022 | | | 40,000 | | | | 39,200 | |

| Harley-Davidson Financial Services, 3.875%, 2016 (n) | | | 450,000 | | | | 475,325 | |

5

Portfolio of Investments (unaudited) – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Bonds - continued | | | | | | | | |

| Automotive - continued | | | | | | | | |

| Jaguar Land Rover PLC, 8.125%, 2021 (n) | | $ | 150,000 | | | $ | 151,500 | |

| Lear Corp., 8.125%, 2020 | | | 65,000 | | | | 72,800 | |

| RCI Banque S.A., 4.6%, 2016 (n) | | | 238,000 | | | | 237,987 | |

| | | | | | | | |

| | | | | | | $ | 2,606,930 | |

| Basic Industry - 0.1% | | | | | | | | |

| Trimas Corp., 9.75%, 2017 | | $ | 76,000 | | | $ | 83,030 | |

| | |

| Broadcasting - 3.9% | | | | | | | | |

| Allbritton Communications Co., 8%, 2018 | | $ | 50,000 | | | $ | 51,750 | |

| AMC Networks, Inc., 7.75%, 2021 (n) | | | 64,000 | | | | 71,040 | |

| CBS Corp., 5.75%, 2020 | | | 110,000 | | | | 128,356 | |

| CBS Corp., 3.375%, 2022 | | | 536,000 | | | | 533,558 | |

| Clear Channel Communications, Inc., 9%, 2021 | | | 103,000 | | | | 88,580 | |

| Clear Channel Worldwide Holdings, Inc., 7.625%, 2020 (n) | | | 50,000 | | | | 47,750 | |

| Clear Channel Worldwide Holdings, Inc., “A”, 7.625%, 2020 (n) | | | 5,000 | | | | 4,700 | |

| Hughes Network Systems LLC, 7.625%, 2021 | | | 60,000 | | | | 62,100 | |

| Inmarsat Finance PLC, 7.375%, 2017 (n) | | | 130,000 | | | | 138,450 | |

| Intelsat Bermuda Ltd., 11.25%, 2017 | | | 180,000 | | | | 176,850 | |

| Intelsat Bermuda Ltd., 11.5%, 2017 (p) | | | 235,000 | | | | 230,888 | |

| Intelsat Jackson Holdings Ltd., 11.25%, 2016 | | | 29,000 | | | | 30,269 | |

| LBI Media, Inc., 8.5%, 2017 (z) | | | 60,000 | | | | 12,000 | |

| Liberty Media Corp., 8.5%, 2029 | | | 90,000 | | | | 91,350 | |

| Liberty Media Corp., 8.25%, 2030 | | | 50,000 | | | | 50,875 | |

| LIN Television Corp., 8.375%, 2018 | | | 30,000 | | | | 30,750 | |

| Local TV Finance LLC, 9.25%, 2015 (p)(z) | | | 121,767 | | | | 124,050 | |

| NBCUniversal Media LLC, 5.95%, 2041 | | | 367,000 | | | | 437,224 | |

| Newport Television LLC, 13%, 2017 (n)(p) | | | 50,602 | | | | 52,120 | |

| Nexstar Broadcasting Group, Inc., 8.875%, 2017 | | | 45,000 | | | | 47,025 | |

| Sinclair Broadcast Group, Inc., 9.25%, 2017 (n) | | | 50,000 | | | | 55,000 | |

| Sinclair Broadcast Group, Inc., 8.375%, 2018 | | | 15,000 | | | | 16,088 | |

| SIRIUS XM Radio, Inc., 13%, 2013 (n) | | | 30,000 | | | | 33,675 | |

| SIRIUS XM Radio, Inc., 8.75%, 2015 (n) | | | 60,000 | | | | 67,650 | |

| SIRIUS XM Radio, Inc., 7.625%, 2018 (n) | | | 175,000 | | | | 187,250 | |

| Townsquare Radio LLC, 9%, 2019 (z) | | | 40,000 | | | | 41,000 | |

| Univision Communications, Inc., 6.875%, 2019 (n) | | | 125,000 | | | | 121,875 | |

| Univision Communications, Inc., 7.875%, 2020 (n) | | | 145,000 | | | | 148,263 | |

| Univision Communications, Inc., 8.5%, 2021 (n) | | | 75,000 | | | | 72,375 | |

| Vivendi S.A., 4.75%, 2022 (n) | | | 330,000 | | | | 322,635 | |

| WPP Finance, 8%, 2014 | | | 400,000 | | | | 454,161 | |

| | | | | | | | |

| | | | | | | $ | 3,929,657 | |

6

Portfolio of Investments (unaudited) – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Bonds - continued | | | | | | | | |

| Brokerage & Asset Managers - 0.8% | | | | | | | | |

| BlackRock, Inc., 3.375%, 2022 | | $ | 148,000 | | | $ | 149,818 | |

| E*TRADE Financial Corp., 7.875%, 2015 | | | 75,000 | | | | 76,125 | |

| E*TRADE Financial Corp., 12.5%, 2017 | | | 180,000 | | | | 206,550 | |

| TD AMERITRADE Holding Corp., 5.6%, 2019 | | | 350,000 | | | | 396,574 | |

| | | | | | | | |

| | | | | | | $ | 829,067 | |

| Building - 0.9% | | | | | | | | |

| Building Materials Holding Corp., 6.875%, 2018 (n) | | $ | 45,000 | | | $ | 46,463 | |

| Building Materials Holding Corp., 7%, 2020 (n) | | | 200,000 | | | | 210,000 | |

| Building Materials Holding Corp., 6.75%, 2021 (n) | | | 40,000 | | | | 40,900 | |

| CRH PLC, 8.125%, 2018 | | | 210,000 | | | | 251,255 | |

| HD Supply, Inc., 8.125%, 2019 (n) | | | 35,000 | | | | 36,488 | |

| Masonite International Corp., 8.25%, 2021 (n) | | | 95,000 | | | | 96,663 | |

| Nortek, Inc., 10%, 2018 | | | 25,000 | | | | 26,375 | |

| Nortek, Inc., 8.5%, 2021 | | | 150,000 | | | | 145,500 | |

| Roofing Supply Group LLC/Roofing Supply Finance, Inc., 10%, 2020 (z) | | | 30,000 | | | | 30,300 | |

| USG Corp., 7.875%, 2020 (n) | | | 45,000 | | | | 46,013 | |

| | | | | | | | |

| | | | | | | $ | 929,957 | |

| Business Services - 0.7% | | | | | | | | |

| Ceridian Corp., 12.25%, 2015 (p) | | $ | 65,000 | | | $ | 59,475 | |

| Fidelity National Information Services, Inc., 7.625%, 2017 | | | 45,000 | | | | 48,994 | |

| Fidelity National Information Services, Inc., 5%, 2022 (n) | | | 40,000 | | | | 38,850 | |

| iGate Corp., 9%, 2016 | | | 190,000 | | | | 201,400 | |

| Iron Mountain, Inc., 8.375%, 2021 | | | 115,000 | | | | 122,763 | |

| SunGard Data Systems, Inc., 10.25%, 2015 | | | 60,000 | | | | 61,650 | |

| SunGard Data Systems, Inc., 7.375%, 2018 | | | 140,000 | | | | 142,450 | |

| | | | | | | | |

| | | | | | | $ | 675,582 | |

| Cable TV - 2.5% | | | | | | | | |

| Bresnan Broadband Holdings LLC, 8%, 2018 (n) | | $ | 25,000 | | | $ | 25,438 | |

| CCH II LLC, 13.5%, 2016 | | | 105,000 | | | | 117,600 | |

| CCO Holdings LLC, 7.875%, 2018 | | | 160,000 | | | | 171,600 | |

| CCO Holdings LLC, 8.125%, 2020 | | | 105,000 | | | | 115,500 | |

| Cequel Communications Holdings, 8.625%, 2017 (n) | | | 150,000 | | | | 158,063 | |

| CSC Holdings LLC, 8.5%, 2014 | | | 60,000 | | | | 66,075 | |

| DIRECTV Holdings LLC, 5.875%, 2019 | | | 160,000 | | | | 184,573 | |

| DIRECTV Holdings LLC, 3.8%, 2022 | | | 410,000 | | | | 410,977 | |

| DISH DBS Corp., 6.75%, 2021 | | | 55,000 | | | | 56,788 | |

| EchoStar Corp., 7.125%, 2016 | | | 55,000 | | | | 58,850 | |

| Time Warner Cable, Inc., 5.4%, 2012 | | | 330,000 | | | | 331,086 | |

| Time Warner Cable, Inc., 8.25%, 2019 | | | 110,000 | | | | 143,560 | |

| Time Warner Cable, Inc., 4%, 2021 | | | 170,000 | | | | 177,199 | |

7

Portfolio of Investments (unaudited) – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Bonds - continued | | | | | | | | |

| Cable TV - continued | | | | | | | | |

| UPC Holding B.V., 9.875%, 2018 (n) | | $ | 100,000 | | | $ | 108,000 | |

| UPCB Finance III Ltd., 6.625%, 2020 (n) | | | 150,000 | | | | 147,750 | |

| Videotron Ltee, 5%, 2022 (n) | | | 50,000 | | | | 48,750 | |

| Virgin Media Finance PLC, 9.5%, 2016 | | | 42,000 | | | | 46,515 | |

| Ziggo Bond Co. B.V., 8%, 2018 (n) | | EUR | 100,000 | | | | 132,306 | |

| | | | | | | | |

| | | | | | | $ | 2,500,630 | |

| Chemicals - 1.6% | | | | | | | | |

| Celanese U.S. Holdings LLC, 6.625%, 2018 | | $ | 165,000 | | | $ | 174,488 | |

| Dow Chemical Co., 8.55%, 2019 | | | 540,000 | | | | 714,254 | |

| Hexion U.S. Finance Corp./Hexion Nova Scotia Finance, 8.875%, 2018 | | | 150,000 | | | | 149,250 | |

| Hexion U.S. Finance Corp./Hexion Nova Scotia Finance, 9%, 2020 | | | 25,000 | | | | 21,813 | |

| Huntsman International LLC, 8.625%, 2021 | | | 75,000 | | | | 84,000 | |

| Momentive Performance Materials, Inc., 12.5%, 2014 | | | 144,000 | | | | 150,840 | |

| Momentive Performance Materials, Inc., 11.5%, 2016 | | | 83,000 | | | | 62,250 | |

| Polypore International, Inc., 7.5%, 2017 | | | 95,000 | | | | 99,275 | |

| Sociedad Quimica y Minera de Chile S.A., 5.5%, 2020 (n) | | | 140,000 | | | | 154,064 | |

| | | | | | | | |

| | | | | | | $ | 1,610,234 | |

| Computer Software - 0.6% | | | | | | | | |

| Lawson Software, Inc., 11.5%, 2018 (n) | | $ | 110,000 | | | $ | 120,725 | |

| Lawson Software, Inc., 9.375%, 2019 (n) | | | 10,000 | | | | 10,300 | |

| Oracle Corp., 5.375%, 2040 | | | 244,000 | | | | 297,158 | |

| Syniverse Holdings, Inc., 9.125%, 2019 | | | 125,000 | | | | 134,063 | |

| TransUnion Holding Co., Inc., 9.625%, 2018 (n)(p) | | | 30,000 | | | | 31,650 | |

| TransUnion LLC/TransUnion Financing Corp., 11.375%, 2018 | | | 15,000 | | | | 17,569 | |

| | | | | | | | |

| | | | | | | $ | 611,465 | |

| Computer Software - Systems - 0.5% | | | | | | | | |

| Audatex North America, Inc., 6.75%, 2018 (n) | | $ | 45,000 | | | $ | 46,350 | |

| CDW LLC/CDW Finance Corp., 12.535%, 2017 | | | 30,000 | | | | 32,100 | |

| CDW LLC/CDW Finance Corp., 8.5%, 2019 | | | 135,000 | | | | 138,713 | |

| CDW LLC/CDW Finance Corp., 8.5%, 2019 (n) | | | 25,000 | | | | 25,688 | |

| DuPont Fabros Technology, Inc., REIT, 8.5%, 2017 | | | 195,000 | | | | 212,550 | |

| | | | | | | | |

| | | | | | | $ | 455,401 | |

| Conglomerates - 1.3% | | | | | | | | |

| Amsted Industries, Inc., 8.125%, 2018 (n) | | $ | 175,000 | | | $ | 185,500 | |

| Dynacast International LLC, 9.25%, 2019 (z) | | | 70,000 | | | | 72,100 | |

| Griffon Corp., 7.125%, 2018 | | | 140,000 | | | | 140,700 | |

| Ingersoll-Rand Global Holding Co. Ltd., 6%, 2013 | | | 290,000 | | | | 307,111 | |

| Ingersoll-Rand Global Holding Co. Ltd., 9.5%, 2014 | | | 350,000 | | | | 399,889 | |

| Tomkins LLC/Tomkins, Inc., 9%, 2018 | | | 153,000 | | | | 168,109 | |

| | | | | | | | |

| | | | | | | $ | 1,273,409 | |

8

Portfolio of Investments (unaudited) – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Bonds - continued | | | | | | | | |

| Consumer Products - 1.0% | | | | | | | | |

| ACCO Brands Corp., 6.75%, 2020 | | $ | 15,000 | | | $ | 15,413 | |

| Easton-Bell Sports, Inc., 9.75%, 2016 | | | 80,000 | | | | 87,400 | |

| Elizabeth Arden, Inc., 7.375%, 2021 | | | 90,000 | | | | 98,213 | |

| FGI Operating Co./FGI Finance, Inc., 7.875%, 2020 (z) | | | 5,000 | | | | 5,138 | |

| Jarden Corp., 7.5%, 2020 | | | 100,000 | | | | 108,250 | |

| Libbey Glass, Inc., 10%, 2015 | | | 8,000 | | | | 8,520 | |

| Libbey Glass, Inc., 6.875%, 2020 (z) | | | 30,000 | | | | 30,075 | |

| Mattel, Inc., 5.45%, 2041 | | | 219,000 | | | | 246,048 | |

| Newell Rubbermaid, Inc., 5.5%, 2013 | | | 360,000 | | | | 373,641 | |

| | | | | | | | |

| | | | | | | $ | 972,698 | |

| Consumer Services - 0.8% | | | | | | | | |

| Realogy Corp., 11.5%, 2017 | | $ | 95,000 | | | $ | 84,075 | |

| Service Corp. International, 6.75%, 2015 | | | 10,000 | | | | 10,800 | |

| Service Corp. International, 7%, 2017 | | | 335,000 | | | | 372,688 | |

| Western Union Co., FRN, 1.054%, 2013 | | | 340,000 | | | | 341,535 | |

| | | | | | | | |

| | | | | | | $ | 809,098 | |

| Containers - 0.3% | | | | | | | | |

| Ball Corp., 5%, 2022 | | $ | 52,000 | | | $ | 52,520 | |

| Reynolds Group, 7.125%, 2019 (n) | | | 200,000 | | | | 205,500 | |

| Sealed Air Corp., 8.125%, 2019 (n) | | | 15,000 | | | | 16,275 | |

| Sealed Air Corp., 8.375%, 2021 (n) | | | 15,000 | | | | 16,500 | |

| Tekni-Plex, Inc., 9.75%, 2019 (z) | | | 15,000 | | | | 14,888 | |

| | | | | | | | |

| | | | | | | $ | 305,683 | |

| Defense Electronics - 0.3% | | | | | | | | |

| BAE Systems Holdings, Inc., 6.375%, 2019 (n) | | $ | 150,000 | | | $ | 176,735 | |

| ManTech International Corp., 7.25%, 2018 | | | 80,000 | | | | 84,400 | |

| | | | | | | | |

| | | | | | | $ | 261,135 | |

| Electrical Equipment - 0.4% | | | | | | | | |

| Avaya, Inc., 9.75%, 2015 | | $ | 70,000 | | | $ | 57,750 | |

| Avaya, Inc., 7%, 2019 (z) | | | 25,000 | | | | 22,375 | |

| Ericsson, Inc., 4.125%, 2022 | | | 298,000 | | | | 300,778 | |

| | | | | | | | |

| | | | | | | $ | 380,903 | |

| Electronics - 1.1% | | | | | | | | |

| Freescale Semiconductor, Inc., 9.25%, 2018 (n) | | $ | 100,000 | | | $ | 105,250 | |

| Freescale Semiconductor, Inc., 8.05%, 2020 | | | 45,000 | | | | 42,750 | |

| Nokia Corp., 5.375%, 2019 | | | 35,000 | | | | 28,566 | |

| Sensata Technologies B.V., 6.5%, 2019 (n) | | | 260,000 | | | | 260,650 | |

| Tyco Electronics Group S.A., 3.5%, 2022 | | | 126,000 | | | | 126,923 | |

9

Portfolio of Investments (unaudited) – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Bonds - continued | | | | | | | | |

| Electronics - continued | | | | | | | | |

| Tyco Electronics Ltd., 6%, 2012 | | $ | 500,000 | | | $ | 508,579 | |

| | | | | | | | |

| | | | | | | $ | 1,072,718 | |

| Emerging Market Quasi-Sovereign - 1.9% | | | | | | | | |

| Comision Federal de Electricidad, 5.75%, 2042 (n) | | $ | 202,000 | | | $ | 205,030 | |

| Development Bank of Kazakhstan, 5.5%, 2015 (n) | | | 282,000 | | | | 289,755 | |

| Gaz Capital S.A., 5.999%, 2021 (n) | | | 342,000 | | | | 357,219 | |

| Petrobras International Finance Co., 7.875%, 2019 | | | 163,000 | | | | 197,144 | |

| Petrobras International Finance Co., 6.75%, 2041 | | | 167,000 | | | | 192,460 | |

| Petroleos Mexicanos, 5.5%, 2021 | | | 178,000 | | | | 195,800 | |

| Petroleos Mexicanos, 4.875%, 2022 (n) | | | 110,000 | | | | 115,500 | |

| Petroleos Mexicanos, 6.5%, 2041 (n) | | | 127,000 | | | | 142,558 | |

| Ras Laffan Liquefied Natural Gas Co. Ltd., 5.832%, 2016 (n) | | | 188,442 | | | | 201,915 | |

| | | | | | | | |

| | | | | | | $ | 1,897,381 | |

| Emerging Market Sovereign - 0.5% | | | | | | | | |

| Republic of Philippines, 6.375%, 2034 | | $ | 126,000 | | | $ | 154,980 | |

| Republic of Slovakia, 4.375%, 2022 (z) | | | 200,000 | | | | 191,000 | |

| Republic of South Africa, 6.25%, 2041 | | | 107,000 | | | | 125,859 | |

| | | | | | | | |

| | | | | | | $ | 471,839 | |

| Energy - Independent - 3.7% | | | | | | | | |

| ATP Oil & Gas Corp., 11.875%, 2015 | | $ | 65,000 | | | $ | 34,613 | |

| BreitBurn Energy Partners LP, 8.625%, 2020 | | | 45,000 | | | | 46,688 | |

| BreitBurn Energy Partners LP, 7.875%, 2022 (n) | | | 55,000 | | | | 53,900 | |

| Carrizo Oil & Gas, Inc., 8.625%, 2018 | | | 40,000 | | | | 41,800 | |

| Chaparral Energy, Inc., 7.625%, 2022 (n) | | | 115,000 | | | | 117,588 | |

| Chesapeake Energy Corp., 6.875%, 2020 | | | 55,000 | | | | 52,113 | |

| Concho Resources, Inc., 8.625%, 2017 | | | 60,000 | | | | 65,400 | |

| Concho Resources, Inc., 6.5%, 2022 | | | 115,000 | | | | 120,175 | |

| Continental Resources, Inc., 8.25%, 2019 | | | 90,000 | | | | 99,900 | |

| Denbury Resources, Inc., 8.25%, 2020 | | | 125,000 | | | | 135,000 | |

| Energy XXI Gulf Coast, Inc., 9.25%, 2017 | | | 155,000 | | | | 166,625 | |

| EQT Corp., 4.875%, 2021 | | | 198,000 | | | | 204,272 | |

Everest Acquisition LLC/Everest Acquisition Finance, Inc.,

9.375%, 2020 (n) | | | 200,000 | | | | 205,000 | |

| EXCO Resources, Inc., 7.5%, 2018 | | | 140,000 | | | | 118,300 | |

| Harvest Operations Corp., 6.875%, 2017 (n) | | | 155,000 | | | | 162,363 | |

| Hilcorp Energy I/Hilcorp Finance Co., 8%, 2020 (n) | | | 35,000 | | | | 37,275 | |

| Laredo Petroleum, Inc., 9.5%, 2019 | | | 65,000 | | | | 72,150 | |

| Laredo Petroleum, Inc., 7.375%, 2022 (n) | | | 15,000 | | | | 15,338 | |

| LINN Energy LLC, 6.5%, 2019 (n) | | | 35,000 | | | | 33,950 | |

| LINN Energy LLC, 8.625%, 2020 | | | 55,000 | | | | 58,300 | |

10

Portfolio of Investments (unaudited) – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Bonds - continued | | | | | | | | |

| Energy - Independent - continued | | | | | | | | |

| LINN Energy LLC, 7.75%, 2021 | | $ | 72,000 | | | $ | 73,620 | |

| Newfield Exploration Co., 6.625%, 2016 | | | 95,000 | | | | 97,138 | |

| Newfield Exploration Co., 6.875%, 2020 | | | 115,000 | | | | 121,900 | |

| OGX Petroleo e Gas Participacoes S.A., 8.5%, 2018 (n) | | | 293,000 | | | | 282,013 | |

| Pioneer Natural Resources Co., 7.5%, 2020 | | | 190,000 | | | | 234,942 | |

| Plains Exploration & Production Co., 8.625%, 2019 | | | 70,000 | | | | 75,950 | |

| QEP Resources, Inc., 6.875%, 2021 | | | 180,000 | | | | 194,850 | |

| Range Resources Corp., 8%, 2019 | | | 65,000 | | | | 70,850 | |

| SandRidge Energy, Inc., 8%, 2018 (n) | | | 165,000 | | | | 165,000 | |

| SM Energy Co., 6.5%, 2021 | | | 90,000 | | | | 92,025 | |

| Southwestern Energy Co., 4.1%, 2022 (n) | | | 256,000 | | | | 259,489 | |

| Swift Energy Co., 7.875%, 2022 | | | 40,000 | | | | 40,400 | |

| Talisman Energy, Inc., 7.75%, 2019 | | | 50,000 | | | | 62,440 | |

| Whiting Petroleum Corp., 6.5%, 2018 | | | 55,000 | | | | 57,475 | |

| | | | | | | | |

| | | | | | | $ | 3,668,842 | |

| Energy - Integrated - 1.4% | | | | | | | | |

| BP Capital Markets PLC, 4.5%, 2020 | | $ | 106,000 | | | $ | 118,457 | |

| BP Capital Markets PLC, 4.742%, 2021 | | | 240,000 | | | | 273,000 | |

| Cenovus Energy, Inc., 4.5%, 2014 | | | 140,000 | | | | 149,902 | |

| Hess Corp., 8.125%, 2019 | | | 120,000 | | | | 155,940 | |

| Pacific Rubiales Energy Corp., 7.25%, 2021 (n) | | | 142,000 | | | | 151,940 | |

| Petro-Canada, 6.05%, 2018 | | | 500,000 | | | | 591,111 | |

| | | | | | | | |

| | | | | | | $ | 1,440,350 | |

| Engineering - Construction - 0.1% | | | | | | | | |

| B-Corp. Merger Sub, Inc., 8.25%, 2019 (n) | | $ | 75,000 | | | $ | 75,000 | |

| | |

| Entertainment - 0.5% | | | | | | | | |

| AMC Entertainment, Inc., 8.75%, 2019 | | $ | 155,000 | | | $ | 165,850 | |

| AMC Entertainment, Inc., 9.75%, 2020 | | | 95,000 | | | | 102,125 | |

| Cedar Fair LP, 9.125%, 2018 | | | 60,000 | | | | 66,450 | |

| Cinemark USA, Inc., 8.625%, 2019 | | | 135,000 | | | | 146,813 | |

| | | | | | | | |

| | | | | | | $ | 481,238 | |

| Financial Institutions - 2.5% | | | | | | | | |

| Ally Financial, Inc., 5.5%, 2017 | | $ | 190,000 | | | $ | 190,171 | |

| CIT Group, Inc., 5.25%, 2014 (n) | | | 135,000 | | | | 137,363 | |

| CIT Group, Inc., 5.25%, 2018 | | | 70,000 | | | | 68,950 | |

| CIT Group, Inc., 6.625%, 2018 (n) | | | 207,000 | | | | 214,763 | |

| CIT Group, Inc., 5.5%, 2019 (n) | | | 110,000 | | | | 106,975 | |

| General Electric Capital Corp., 6%, 2019 | | | 130,000 | | | | 152,610 | |

| General Electric Capital Corp., 5.5%, 2020 | | | 250,000 | | | | 286,119 | |

11

Portfolio of Investments (unaudited) – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Bonds - continued | | | | | | | | |

| Financial Institutions - continued | | | | | | | | |

| General Electric Capital Corp., FRN, 1.319%, 2014 | | $ | 300,000 | | | $ | 301,041 | |

| GMAC, Inc., 8%, 2031 | | | 20,000 | | | | 22,500 | |

| Icahn Enterprises LP, 8%, 2018 | | | 45,000 | | | | 47,644 | |

| International Lease Finance Corp., 4.875%, 2015 | | | 45,000 | | | | 44,343 | |

| International Lease Finance Corp., 8.625%, 2015 | | | 45,000 | | | | 49,050 | |

| International Lease Finance Corp., 8.75%, 2017 | | | 80,000 | | | | 88,800 | |

| International Lease Finance Corp., 7.125%, 2018 (n) | | | 152,000 | | | | 167,200 | |

| Nationstar Mortgage LLC/Capital Corp., 10.875%, 2015 | | | 155,000 | | | | 167,400 | |

| Nationstar Mortgage LLC/Capital Corp., 9.625%, 2019 (n) | | | 35,000 | | | | 36,400 | |

| PHH Corp., 9.25%, 2016 | | | 85,000 | | | | 88,400 | |

| SLM Corp., 8.45%, 2018 | | | 145,000 | | | | 152,975 | |

| SLM Corp., 8%, 2020 | | | 195,000 | | | | 199,587 | |

| SLM Corp., 7.25%, 2022 | | | 15,000 | | | | 14,682 | |

| | | | | | | | |

| | | | | | | $ | 2,536,973 | |

| Food & Beverages - 3.8% | | | | | | | | |

| Anheuser-Busch InBev S.A., 7.75%, 2019 | | $ | 370,000 | | | $ | 489,535 | |

| ARAMARK Corp., 8.5%, 2015 | | | 300,000 | | | | 307,128 | |

| B&G Foods, Inc., 7.625%, 2018 | | | 155,000 | | | | 165,850 | |

| Conagra Foods, Inc., 5.875%, 2014 | | | 500,000 | | | | 542,247 | |

| Del Monte Foods Co., 7.625%, 2019 | | | 15,000 | | | | 14,550 | |

| JBS USA LLC/JBS USA Finance, 8.25%, 2020 (n) | | | 50,000 | | | | 47,750 | |

| Kraft Foods, Inc., 6.75%, 2014 | | | 150,000 | | | | 163,913 | |

| Kraft Foods, Inc., 6.125%, 2018 | | | 130,000 | | | | 156,805 | |

| Kraft Foods, Inc., 3.5%, 2022 (z) | | | 528,000 | | | | 539,648 | |

| Miller Brewing Co., 5.5%, 2013 (n) | | | 380,000 | | | | 398,633 | |

| Pernod Ricard S.A., 5.75%, 2021 (n) | | | 156,000 | | | | 176,148 | |

| Pernod-Ricard S.A., 4.45%, 2022 (n) | | | 151,000 | | | | 157,598 | |

| Pinnacle Foods Finance LLC, 9.25%, 2015 | | | 125,000 | | | | 127,500 | |

| Pinnacle Foods Finance LLC, 8.25%, 2017 | | | 25,000 | | | | 26,125 | |

| SABMiller Holdings, Inc., 3.75%, 2022 (n) | | | 414,000 | | | | 438,684 | |

| TreeHouse Foods, Inc., 7.75%, 2018 | | | 80,000 | | | | 86,400 | |

| | | | | | | | |

| | | | | | | $ | 3,838,514 | |

| Food & Drug Stores - 0.6% | | | | | | | | |

| CVS Caremark Corp., 3.25%, 2015 | | $ | 180,000 | | | $ | 190,237 | |

| CVS Caremark Corp., 5.75%, 2041 | | | 350,000 | | | | 415,482 | |

| | | | | | | | |

| | | | | | | $ | 605,719 | |

| Forest & Paper Products - 0.5% | | | | | | | | |

| Boise, Inc., 8%, 2020 | | $ | 95,000 | | | $ | 104,025 | |

| Cascades, Inc., 7.75%, 2017 | | | 65,000 | | | | 64,675 | |

| Georgia-Pacific Corp., 8%, 2024 | | | 60,000 | | | | 79,730 | |

12

Portfolio of Investments (unaudited) – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Bonds - continued | | | | | | | | |

| Forest & Paper Products - continued | | | | | | | | |

| Graphic Packaging Holding Co., 7.875%, 2018 | | $ | 60,000 | | | $ | 66,150 | |

| Smurfit Kappa Group PLC, 7.75%, 2019 (n) | | EUR | 100,000 | | | | 129,833 | |

| Tembec Industries, Inc., 11.25%, 2018 (n) | | $ | 40,000 | | | | 39,700 | |

| | | | | | | | |

| | | | | | | $ | 484,113 | |

| Gaming & Lodging - 2.0% | | | | | | | | |

| Boyd Gaming Corp., 7.125%, 2016 | | $ | 65,000 | | | $ | 62,075 | |

| Caesars Operating Escrow LLC, 8.5%, 2020 (n) | | | 125,000 | | | | 124,531 | |

| Fontainebleau Las Vegas Holdings LLC, 10.25%, 2015 (a)(d)(n) | | | 115,000 | | | | 72 | |

| GWR Operating Partnership LLP, 10.875%, 2017 | | | 50,000 | | | | 56,500 | |

| Harrah’s Operating Co., Inc., 11.25%, 2017 | | | 195,000 | | | | 207,188 | |

| Harrah’s Operating Co., Inc., 10%, 2018 | | | 4,000 | | | | 2,640 | |

| Harrah’s Operating Co., Inc., 10%, 2018 | | | 81,000 | | | | 54,675 | |

| Marriott International, Inc., 5.625%, 2013 | | | 230,000 | | | | 237,232 | |

| MGM Mirage, 10.375%, 2014 | | | 15,000 | | | | 16,875 | |

| MGM Mirage, 6.625%, 2015 | | | 35,000 | | | | 35,941 | |

| MGM Mirage, 7.5%, 2016 | | | 20,000 | | | | 20,450 | |

| MGM Resorts International, 11.375%, 2018 | | | 105,000 | | | | 121,013 | |

| MGM Resorts International, 9%, 2020 | | | 185,000 | | | | 202,575 | |

| Penn National Gaming, Inc., 8.75%, 2019 | | | 145,000 | | | | 159,863 | |

| Pinnacle Entertainment, Inc., 8.75%, 2020 | | | 70,000 | | | | 76,125 | |

| Pinnacle Entertainment, Inc., 7.75%, 2022 | | | 30,000 | | | | 31,650 | |

Rivers Pittsburgh Borrower LP/Rivers Pittsburgh Finance Corp.,

9.5%, 2019 (z) | | | 15,000 | | | | 15,338 | |

| Seven Seas Cruises S. de R.L., 9.125%, 2019 (n) | | | 115,000 | | | | 118,450 | |

| Wyndham Worldwide Corp., 6%, 2016 | | | 1,000 | | | | 1,126 | |

| Wyndham Worldwide Corp., 5.75%, 2018 | | | 250,000 | | | | 280,394 | |

| Wyndham Worldwide Corp., 7.375%, 2020 | | | 55,000 | | | | 66,877 | |

| Wynn Las Vegas LLC, 7.75%, 2020 | | | 115,000 | | | | 124,919 | |

| | | | | | | | |

| | | | | | | $ | 2,016,509 | |

| Industrial - 1.3% | | | | | | | | |

| Altra Holdings, Inc., 8.125%, 2016 | | $ | 65,000 | | | $ | 69,388 | |

| Cornell University, 4.35%, 2014 | | | 240,000 | | | | 254,597 | |

| Johns Hopkins University, 5.25%, 2019 | | | 470,000 | | | | 572,338 | |

| Mueller Water Products, Inc., 8.75%, 2020 | | | 71,000 | | | | 78,455 | |

| Princeton University, 4.95%, 2019 | | | 310,000 | | | | 375,202 | |

| | | | | | | | |

| | | | | | | $ | 1,349,980 | |

| Insurance - 1.9% | | | | | | | | |

| American International Group, Inc., 8.25%, 2018 | | $ | 100,000 | | | $ | 120,246 | |

| American International Group, Inc., 8.175% to 2038, FRN to 2068 | | | 140,000 | | | | 145,425 | |

| Metropolitan Life Global Funding I, 5.125%, 2014 (n) | | | 180,000 | | | | 193,769 | |

13

Portfolio of Investments (unaudited) – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Bonds - continued | | | | | | | | |

| Insurance - continued | | | | | | | | |

| Principal Financial Group, Inc., 8.875%, 2019 | | $ | 250,000 | | | $ | 327,152 | |

| Prudential Financial, Inc., 3.625%, 2012 | | | 230,000 | | | | 231,796 | |

| Prudential Financial, Inc., 6.2%, 2015 | | | 450,000 | | | | 494,806 | |

| Unum Group, 7.125%, 2016 | | | 370,000 | | | | 424,589 | |

| | | | | | | | |

| | | | | | | $ | 1,937,783 | |

| Insurance - Health - 0.4% | | | | | | | | |

| AMERIGROUP Corp., 7.5%, 2019 | | $ | 80,000 | | | $ | 85,600 | |

| WellPoint, Inc., 6.8%, 2012 | | | 320,000 | | | | 323,019 | |

| | | | | | | | |

| | | | | | | $ | 408,619 | |

| Insurance - Property & Casualty - 2.3% | | | | | | | | |

| Aon Corp., 3.5%, 2015 | | $ | 350,000 | | | $ | 365,843 | |

| CNA Financial Corp., 5.875%, 2020 | | | 390,000 | | | | 426,943 | |

| Liberty Mutual Group, Inc., 4.95%, 2022 (n) | | | 299,000 | | | | 298,294 | |

| Liberty Mutual Group, Inc., 10.75% to 2038, FRN to 2088 (n) | | | 150,000 | | | | 207,000 | |

| PartnerRe Ltd., 5.5%, 2020 | | | 257,000 | | | | 274,441 | |

| QBE Capital Funding III Ltd., FRN, 7.25%, 2041 (n) | | | 310,000 | | | | 283,650 | |

| ZFS Finance USA Trust V, 6.5% to 2017, FRN to 2067 (n) | | | 500,000 | | | | 481,250 | |

| | | | | | | | |

| | | | | | | $ | 2,337,421 | |

| International Market Quasi-Sovereign - 2.5% | | | | | | | | |

| EDF Energies Nouvelles S.A., 6.5%, 2019 (n) | | $ | 450,000 | | | $ | 531,409 | |

| ING Bank N.V., 3.9%, 2014 (n) | | | 530,000 | | | | 556,732 | |

| Irish Life & Permanent PLC, 3.6%, 2013 (e)(n) | | | 700,000 | | | | 674,904 | |

| Israel Electric Corp. Ltd., 6.7%, 2017 (n) | | | 236,000 | | | | 245,626 | |

| Vestjysk Bank A/S, FRN, 1.023%, 2013 (n) | | | 240,000 | | | | 240,796 | |

| Westpac Banking Corp., 3.45%, 2014 (n) | | | 220,000 | | | | 232,181 | |

| | | | | | | | |

| | | | | | | $ | 2,481,648 | |

| International Market Sovereign - 10.2% | | | | | | | | |

| Commonwealth of Australia, 5.75%, 2021 | | AUD | 80,000 | | | $ | 95,836 | |

| Federal Republic of Germany, 3.75%, 2015 | | EUR | 512,000 | | | | 693,683 | |

| Federal Republic of Germany, 4.25%, 2018 | | EUR | 207,000 | | | | 312,095 | |

| Federal Republic of Germany, 6.25%, 2030 | | EUR | 173,000 | | | | 355,525 | |

| Government of Bermuda, 5.603%, 2020 (n) | | $ | 115,000 | | | | 131,675 | |

| Government of Canada, 4.5%, 2015 | | CAD | 171,000 | | | | 181,796 | |

| Government of Canada, 4.25%, 2018 | | CAD | 90,000 | | | | 101,336 | |

| Government of Canada, 5.75%, 2033 | | CAD | 31,000 | | | | 47,344 | |

| Government of Japan, 1.7%, 2017 | | JPY | 71,000,000 | | | | 970,389 | |

| Government of Japan, 1.1%, 2020 | | JPY | 37,000,000 | | | | 490,871 | |

| Government of Japan, 2.1%, 2024 | | JPY | 17,000,000 | | | | 242,092 | |

| Government of Japan, 2.2%, 2027 | | JPY | 39,000,000 | | | | 554,669 | |

14

Portfolio of Investments (unaudited) – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Bonds - continued | | | | | | | | |

| International Market Sovereign - continued | | | | | | | | |

| Government of Japan, 2.4%, 2037 | | JPY | 41,000,000 | | | $ | 592,222 | |

| Kingdom of Belgium, 5.5%, 2017 | | EUR | 229,000 | | | | 331,474 | |

| Kingdom of Denmark, 3%, 2021 | | DKK | 467,000 | | | | 91,272 | |

| Kingdom of Spain, 4.6%, 2019 | | EUR | 357,000 | | | | 399,539 | |

| Kingdom of Sweden, 5%, 2020 | | SEK | 335,000 | | | | 60,134 | |

| Kingdom of the Netherlands, 3.75%, 2014 | | EUR | 400,000 | | | | 530,607 | |

| Kingdom of the Netherlands, 5.5%, 2028 | | EUR | 46,000 | | | | 83,891 | |

| Republic of Austria, 4.65%, 2018 | | EUR | 166,000 | | | | 240,112 | |

| Republic of Finland, 3.875%, 2017 | | EUR | 46,000 | | | | 65,752 | |

| Republic of France, 6%, 2025 | | EUR | 114,000 | | | | 191,961 | |

| Republic of France, 4.75%, 2035 | | EUR | 242,000 | | | | 381,833 | |

| Republic of Iceland, 4.875%, 2016 (n) | | $ | 166,000 | | | | 167,887 | |

| Republic of Italy, 4.25%, 2015 | | EUR | 190,000 | | | | 232,361 | |

| Republic of Italy, 5.25%, 2017 | | EUR | 572,000 | | | | 700,194 | |

| Republic of Italy, 3.75%, 2021 | | EUR | 217,000 | | | | 233,679 | |

| State of Israel, 4%, 2022 | | $ | 504,000 | | | | 517,130 | |

| United Kingdom Treasury, 8%, 2015 | | GBP | 228,000 | | | | 445,876 | |

| United Kingdom Treasury, 8%, 2021 | | GBP | 169,000 | | | | 406,822 | |

| United Kingdom Treasury, 4.25%, 2036 | | GBP | 157,000 | | | | 302,146 | |

| | | | | | | | |

| | | | | | | $ | 10,152,203 | |

| Local Authorities - 0.3% | | | | | | | | |

Louisiana Gas & Fuels Tax Rev. (Build America Bonds), FRN,

3%, 2043 | | $ | 310,000 | | | $ | 312,992 | |

| | |

| Machinery & Tools - 0.7% | | | | | | | | |

| Case Corp., 7.25%, 2016 | | $ | 50,000 | | | $ | 54,625 | |

| Case New Holland, Inc., 7.875%, 2017 | | | 350,000 | | | | 399,000 | |

| NESCO LLC/NESCO Holdings Corp., 11.75%, 2017 (z) | | | 50,000 | | | | 50,500 | |

| RSC Equipment Rental, Inc., 8.25%, 2021 | | | 115,000 | | | | 121,613 | |

| UR Financing Escrow Corp., 5.75%, 2018 (n) | | | 45,000 | | | | 45,788 | |

| UR Financing Escrow Corp., 7.625%, 2022 (n) | | | 45,000 | | | | 46,013 | |

| | | | | | | | |

| | | | | | | $ | 717,539 | |

| Major Banks - 9.6% | | | | | | | | |

| ABN AMRO Bank N.V., 3%, 2014 (n) | | $ | 400,000 | | | $ | 401,107 | |

| ABN AMRO Bank N.V., 4.25%, 2017 (n) | | | 400,000 | | | | 401,072 | |

| Bank of America Corp., 7.375%, 2014 | | | 280,000 | | | | 302,103 | |

| Bank of America Corp., 6.5%, 2016 | | | 430,000 | | | | 465,619 | |

| Barclays Bank PLC, 5.125%, 2020 | | | 340,000 | | | | 364,589 | |

| Barclays Bank PLC, FRN, 1.508%, 2014 | | | 190,000 | | | | 190,060 | |

| Commonwealth Bank of Australia, 5%, 2019 (n) | | | 320,000 | | | | 354,822 | |

| Credit Suisse New York, 5.5%, 2014 | | | 490,000 | | | | 520,703 | |

15

Portfolio of Investments (unaudited) – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Bonds - continued | | | | | | | | |

| Major Banks - continued | | | | | | | | |

| Credit Suisse New York, FRN, 1.426%, 2014 | | $ | 250,000 | | | $ | 250,040 | |

| DBS Bank Ltd., 2.35%, 2017 (n) | | | 400,000 | | | | 398,748 | |

| Goldman Sachs Group, Inc., 6%, 2014 | | | 700,000 | | | | 735,585 | |

| Goldman Sachs Group, Inc., 5.75%, 2022 | | | 409,000 | | | | 419,614 | |

| HSBC USA, Inc., 4.875%, 2020 | | | 360,000 | | | | 369,415 | |

| ING Bank N.V., 3.75%, 2017 (n) | | | 407,000 | | | | 400,163 | |

| ING Bank N.V., FRN, 1.523%, 2013 (n) | | | 380,000 | | | | 379,807 | |

| Intesa Sanpaolo S.p.A., FRN, 2.866%, 2014 (n) | | | 200,000 | | | | 187,217 | |

| JPMorgan Chase & Co., 4.625%, 2021 | | | 360,000 | | | | 381,465 | |

| JPMorgan Chase & Co., FRN, 1.223%, 2014 | | | 380,000 | | | | 378,049 | |

| JPMorgan Chase Capital XXII, 6.45%, 2087 | | | 261,000 | | | | 257,741 | |

| JPMorgan Chase Capital XXVII, 7%, 2039 | | | 69,000 | | | | 69,061 | |

| Macquarie Bank Ltd., 5%, 2017 (n) | | | 167,000 | | | | 170,216 | |

| Macquarie Group Ltd., 6%, 2020 (n) | | | 230,000 | | | | 230,388 | |

| Merrill Lynch & Co., Inc., 6.4%, 2017 | | | 40,000 | | | | 42,508 | |

| Morgan Stanley, 6%, 2014 | | | 160,000 | | | | 162,780 | |

| Morgan Stanley, 7.3%, 2019 | | | 110,000 | | | | 114,040 | |

| Morgan Stanley, 5.625%, 2019 | | | 180,000 | | | | 171,744 | |

| Morgan Stanley, FRN, 2.065%, 2014 | | | 260,000 | | | | 250,239 | |

| Royal Bank of Scotland Group PLC, 7.648% to 2031, FRN to 2049 | | | 150,000 | | | | 114,375 | |

| Royal Bank of Scotland PLC, 6.125%, 2021 | | | 200,000 | | | | 213,400 | |

| Standard Chartered PLC, 3.85%, 2015 (n) | | | 290,000 | | | | 302,620 | |

| Wells Fargo & Co., 4.375%, 2013 | | | 410,000 | | | | 419,706 | |

| Wells Fargo & Co., 7.98% to 2018, FRN to 2049 | | | 141,000 | | | | 153,338 | |

| | | | | | | | |

| | | | | | | $ | 9,572,334 | |

| Medical & Health Technology & Services - 2.8% | | | | | | | | |

| Aristotle Holding, Inc., 3.9%, 2022 (n) | | $ | 200,000 | | | $ | 207,521 | |

| Biomet, Inc., 10%, 2017 | | | 60,000 | | | | 63,825 | |

| Biomet, Inc., 10.375%, 2017 (p) | | | 45,000 | | | | 47,897 | |

| Biomet, Inc., 11.625%, 2017 | | | 65,000 | | | | 68,900 | |

| Cardinal Health, Inc., 5.8%, 2016 | | | 279,000 | | | | 324,454 | |

| Davita, Inc., 6.375%, 2018 | | | 160,000 | | | | 162,000 | |

| Davita, Inc., 6.625%, 2020 | | | 95,000 | | | | 96,188 | |

| Fresenius Medical Care AG & Co. KGaA, 9%, 2015 (n) | | | 65,000 | | | | 74,263 | |

| Fresenius Medical Care Capital Trust III, 5.625%, 2019 (n) | | | 30,000 | | | | 29,775 | |

| HCA, Inc., 8.5%, 2019 | | | 205,000 | | | | 226,269 | |

| HCA, Inc., 7.5%, 2022 | | | 110,000 | | | | 115,294 | |

| HCA, Inc., 5.875%, 2022 | | | 45,000 | | | | 44,663 | |

| HealthSouth Corp., 8.125%, 2020 | | | 305,000 | | | | 325,588 | |

| Hospira, Inc., 6.05%, 2017 | | | 130,000 | | | | 146,853 | |

| IASIS Healthcare LLC/IASIS Capital Corp., 8.375%, 2019 | | | 65,000 | | | | 61,100 | |

| McKesson Corp., 3.25%, 2016 | | | 340,000 | | | | 366,442 | |

16

Portfolio of Investments (unaudited) – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Bonds - continued | | | | | | | | |

| Medical & Health Technology & Services - continued | | | | | | | | |

| Physio-Control International, Inc., 9.875%, 2019 (z) | | $ | 55,000 | | | $ | 58,300 | |

| Tenet Healthcare Corp., 9.25%, 2015 | | | 65,000 | | | | 71,744 | |

| Truven Health Analytics, Inc., 10.625%, 2020 (z) | | | 25,000 | | | | 25,125 | |

| Universal Health Services, Inc., 7%, 2018 | | | 70,000 | | | | 74,900 | |

| Universal Hospital Services, Inc., 8.5%, 2015 (p) | | | 145,000 | | | | 147,719 | |

| USPI Finance Corp., 9%, 2020 (n) | | | 30,000 | | | | 31,125 | |

| Vanguard Health Systems, Inc., 8%, 2018 | | | 60,000 | | | | 58,800 | |

| | | | | | | | |

| | | | | | | $ | 2,828,745 | |

| Metals & Mining - 1.8% | | | | | | | | |

| ArcelorMittal, 5.5%, 2021 | | $ | 393,000 | | | $ | 374,243 | |

| Cloud Peak Energy, Inc., 8.25%, 2017 | | | 175,000 | | | | 178,938 | |

| Cloud Peak Energy, Inc., 8.5%, 2019 | | | 125,000 | | | | 128,750 | |

| Consol Energy, Inc., 8%, 2017 | | | 165,000 | | | | 165,413 | |

| Consol Energy, Inc., 8.25%, 2020 | | | 45,000 | | | | 45,000 | |

| Fortescue Metals Group Ltd., 8.25%, 2019 (n) | | | 210,000 | | | | 216,825 | |

| Gold Fields Orogen Holding Ltd., 4.875%, 2020 (n) | | | 207,000 | | | | 195,908 | |

| Peabody Energy Corp., 6%, 2018 (n) | | | 40,000 | | | | 39,900 | |

| Peabody Energy Corp., 6.25%, 2021 (n) | | | 40,000 | | | | 39,900 | |

| Vale Overseas Ltd., 4.375%, 2022 | | | 281,000 | | | | 280,880 | |

| Vale Overseas Ltd., 6.875%, 2039 | | | 117,000 | | | | 134,746 | |

| | | | | | | | |

| | | | | | | $ | 1,800,503 | |

| Mortgage-Backed - 2.0% | | | | | | | | |

| Fannie Mae, 6.5%, 2036 (f) | | $ | 401,601 | | | $ | 456,202 | |

| Fannie Mae, 6%, 2037 | | | 279,844 | | | | 308,898 | |

| Freddie Mac, 4.224%, 2020 | | | 275,759 | | | | 313,275 | |

| Ginnie Mae, 9%, 2016 | | | 26,422 | | | | 29,467 | |

| Ginnie Mae, 11%, 2018 - 2019 | | | 1,761 | | | | 1,769 | |

| Ginnie Mae, 5.612%, 2058 | | | 461,691 | | | | 492,126 | |

| Ginnie Mae, 6.357%, 2058 | | | 396,136 | | | | 424,531 | |

| | | | | | | | |

| | | | | | | $ | 2,026,268 | |

| Natural Gas - Distribution - 0.1% | | | | | | | | |

| AmeriGas Finance LLC, 6.75%, 2020 | | $ | 45,000 | | | $ | 44,325 | |

| Ferrellgas LP/Ferrellgas Finance Corp., 6.5%, 2021 | | | 55,000 | | | | 49,225 | |

| | | | | | | | |

| | | | | | | $ | 93,550 | |

| Natural Gas - Pipeline - 3.0% | | | | | | | | |

| Atlas Pipeline Partners LP, 8.75%, 2018 | | $ | 150,000 | | | $ | 159,000 | |

| Colorado Interstate Gas Co., 6.8%, 2015 | | | 32,000 | | | | 37,202 | |

| Crosstex Energy, Inc., 8.875%, 2018 | | | 145,000 | | | | 152,250 | |

| El Paso Corp., 7%, 2017 | | | 145,000 | | | | 162,739 | |

17

Portfolio of Investments (unaudited) – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Bonds - continued | | | | | | | | |

| Natural Gas - Pipeline - continued | | | | | | | | |

| El Paso Corp., 7.75%, 2032 | | $ | 150,000 | | | $ | 171,201 | |

| Enbridge Energy Partners LP, 4.2%, 2021 | | | 400,000 | | | | 426,904 | |

| Energy Transfer Equity LP, 7.5%, 2020 | | | 125,000 | | | | 135,000 | |

| Energy Transfer Partners LP, 6.5%, 2042 | | | 348,000 | | | | 369,435 | |

| Enterprise Products Operating LP, 5.65%, 2013 | | | 500,000 | | | | 517,569 | |

| Enterprise Products Partners LP, 8.375% to 2016, FRN to 2066 | | | 59,000 | | | | 63,720 | |

| Enterprise Products Partners LP, 7.034% to 2018, FRN to 2068 | | | 38,000 | | | | 40,470 | |

| Kinder Morgan Energy Partners LP, 5.85%, 2012 | | | 271,000 | | | | 274,234 | |

| Kinder Morgan Energy Partners LP, 6.375%, 2041 | | | 360,000 | | | | 410,502 | |

| Rockies Express Pipeline LLC, 5.625%, 2020 (n) | | | 48,000 | | | | 42,480 | |

| | | | | | | | |

| | | | | | | $ | 2,962,706 | |

| Network & Telecom - 3.0% | | | | | | | | |

| AT&T, Inc., 3.875%, 2021 | | $ | 480,000 | | | $ | 524,409 | |

| British Telecommunications PLC, 5.15%, 2013 | | | 255,000 | | | | 261,547 | |

| Centurylink, Inc., 7.65%, 2042 | | | 267,000 | | | | 254,454 | |

| Cincinnati Bell, Inc., 8.25%, 2017 | | | 30,000 | | | | 30,600 | |

| Citizens Communications Co., 9%, 2031 | | | 60,000 | | | | 54,900 | |

| France Telecom, 4.375%, 2014 | | | 240,000 | | | | 253,053 | |

| Frontier Communications Corp., 8.125%, 2018 | | | 70,000 | | | | 71,225 | |

| Qwest Communications International, Inc., 7.125%, 2018 (n) | | | 95,000 | | | | 100,361 | |

| Qwest Corp., 7.5%, 2014 | | | 95,000 | | | | 106,412 | |

| Telefonica Emisiones S.A.U., 2.582%, 2013 | | | 500,000 | | | | 493,161 | |

| Verizon Communications, Inc., 8.75%, 2018 | | | 440,000 | | | | 601,510 | |

| Windstream Corp., 8.125%, 2018 | | | 15,000 | | | | 15,563 | |

| Windstream Corp., 7.75%, 2020 | | | 175,000 | | | | 175,000 | |

| Windstream Corp., 7.75%, 2021 | | | 35,000 | | | | 35,088 | |

| | | | | | | | |

| | | | | | | $ | 2,977,283 | |

| Oil Services - 0.3% | | | | | | | | |

| Chesapeake Energy Corp., 6.625%, 2019 (n) | | $ | 35,000 | | | $ | 30,275 | |

| Dresser-Rand Group, Inc., 6.5%, 2021 | | | 40,000 | | | | 40,800 | |

| Pioneer Drilling Co., 9.875%, 2018 | | | 125,000 | | | | 131,250 | |

| Pioneer Drilling Co., 9.875%, 2018 (n) | | | 10,000 | | | | 10,500 | |

| Unit Corp., 6.625%, 2021 | | | 60,000 | | | | 59,700 | |

| | | | | | | | |

| | | | | | | $ | 272,525 | |

| Oils - 0.3% | | | | | | | | |

| Phillips 66, 4.3%, 2022 (n) | | $ | 243,000 | | | $ | 253,067 | |

| | |

| Other Banks & Diversified Financials - 6.3% | | | | | | | | |

| American Express Centurion Bank, 5.5%, 2013 | | $ | 250,000 | | | $ | 259,726 | |

| Bancolombia S.A., 5.95%, 2021 | | | 102,000 | | | | 105,570 | |

18

Portfolio of Investments (unaudited) – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Bonds - continued | | | | | | | | |

| Other Banks & Diversified Financials - continued | | | | | | | | |

| BB&T Corp., 2.05%, 2014 | | $ | 300,000 | | | $ | 306,106 | |

| BBVA Senior Finance S.A. Unipersonal, FRN, 2.59%, 2014 | | | 300,000 | | | | 282,907 | |

| Capital One Financial Corp., FRN, 1.616%, 2014 | | | 370,000 | | | | 367,154 | |

| Citigroup, Inc., 6.375%, 2014 | | | 230,000 | | | | 246,668 | |

| Citigroup, Inc., 6.01%, 2015 | | | 200,000 | | | | 214,281 | |

| Citigroup, Inc., 8.5%, 2019 | | | 204,000 | | | | 249,853 | |

| Danske Bank A/S, 3.75%, 2015 (n) | | | 510,000 | | | | 503,914 | |

| Groupe BPCE S.A., 12.5% to 2019, FRN to 2049 (n) | | | 243,000 | | | | 235,717 | |

| HSBC Holdings PLC, 4%, 2022 | | | 352,000 | | | | 358,288 | |

| LBG Capital No. 1 PLC, 7.875%, 2020 (n) | | | 100,000 | | | | 87,305 | |

| Lloyds TSB Bank PLC, 5.8%, 2020 (n) | | | 205,000 | | | | 211,048 | |

| Rabobank Nederland N.V., 3.375%, 2017 | | | 242,000 | | | | 247,989 | |

| Santander Holdings USA, Inc., 4.625%, 2016 | | | 50,000 | | | | 48,676 | |

| Santander International Debt S.A., 2.991%, 2013 (n) | | | 500,000 | | | | 471,724 | |

| Santander UK PLC, 8.963% to 2030, FRN to 2049 | | | 200,000 | | | | 194,000 | |

| SunTrust Banks, Inc., 3.5%, 2017 | | | 288,000 | | | | 297,061 | |

| Svenska Handelsbanken AB, 4.875%, 2014 (n) | | | 580,000 | | | | 613,152 | |

| UBS Preferred Funding Trust V, 6.243% to 2016, FRN to 2049 | | | 349,000 | | | | 320,382 | |

| Union Bank, 3%, 2016 | | | 690,000 | | | | 725,389 | |

| | | | | | | | |

| | | | | | | $ | 6,346,910 | |

| Pharmaceuticals - 1.2% | | | | | | | | |

| Celgene Corp., 2.45%, 2015 | | $ | 130,000 | | | $ | 132,952 | |

| Celgene Corp., 3.95%, 2020 | | | 300,000 | | | | 315,932 | |

| Pfizer, Inc., 6.2%, 2019 | | | 500,000 | | | | 631,024 | |

| Valeant Pharmaceuticals International, Inc., 6.5%, 2016 (n) | | | 35,000 | | | | 35,700 | |

| Valeant Pharmaceuticals International, Inc., 7%, 2020 (n) | | | 75,000 | | | | 72,563 | |

| | | | | | | | |

| | | | | | | $ | 1,188,171 | |

| Pollution Control - 0.4% | | | | | | | | |

| Heckmann Corp., 9.875%, 2018 (z) | | $ | 60,000 | | | $ | 57,000 | |

| Republic Services, Inc., 5.25%, 2021 | | | 320,000 | | | | 368,871 | |

| | | | | | | | |

| | | | | | | $ | 425,871 | |

| Printing & Publishing - 0.4% | | | | | | | | |

| American Media, Inc., 13.5%, 2018 (z) | | $ | 9,917 | | | $ | 8,529 | |

| Nielsen Finance LLC, 11.5%, 2016 | | | 45,000 | | | | 50,850 | |

| Nielsen Finance LLC, 7.75%, 2018 | | | 85,000 | | | | 91,375 | |

| Pearson Funding Four PLC, 3.75%, 2022 (n) | | | 201,000 | | | | 203,829 | |

| | | | | | | | |

| | | | | | | $ | 354,583 | |

| Railroad & Shipping - 0.0% | | | | | | | | |

| Kansas City Southern de Mexico S.A. de C.V., 6.125%, 2021 | | $ | 40,000 | | | $ | 43,300 | |

19

Portfolio of Investments (unaudited) – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Bonds - continued | | | | | | | | |

| Real Estate - 1.5% | | | | | | | | |

| Boston Properties LP, REIT, 3.7%, 2018 | | $ | 193,000 | | | $ | 201,552 | |

| Boston Properties LP, REIT, 3.85%, 2023 | | | 377,000 | | | | 378,565 | |

| CNL Lifestyle Properties, Inc., REIT, 7.25%, 2019 | | | 45,000 | | | | 40,275 | |

| Entertainment Properties Trust, REIT, 7.75%, 2020 | | | 85,000 | | | | 92,838 | |

| HCP, Inc., REIT, 5.375%, 2021 | | | 283,000 | | | | 316,043 | |

| Kennedy Wilson, Inc., 8.75%, 2019 | | | 40,000 | | | | 41,200 | |

| Kimco Realty Corp., REIT, 6.875%, 2019 | | | 82,000 | | | | 97,633 | |

| MPT Operating Partnership LP, REIT, 6.875%, 2021 | | | 80,000 | | | | 82,400 | |

| WEA Finance LLC, REIT, 6.75%, 2019 (n) | | | 250,000 | | | | 297,508 | |

| | | | | | | | |

| | | | | | | $ | 1,548,014 | |

| Retailers - 2.5% | | | | | | | | |

| Academy Ltd., 9.25%, 2019 (n) | | $ | 65,000 | | | $ | 68,575 | |

| AutoZone, Inc., 6.5%, 2014 | | | 420,000 | | | | 456,000 | |

| AutoZone, Inc., 3.7%, 2022 | | | 78,000 | | | | 80,488 | |

| Burlington Coat Factory Warehouse Corp., 10%, 2019 | | | 95,000 | | | | 98,088 | |

| Gap, Inc., 5.95%, 2021 | | | 379,000 | | | | 391,332 | |

| J. Crew Group, Inc., 8.125%, 2019 | | | 80,000 | | | | 80,300 | |

| Limited Brands, Inc., 6.9%, 2017 | | | 70,000 | | | | 77,875 | |

| Limited Brands, Inc., 7%, 2020 | | | 35,000 | | | | 38,675 | |

| Limited Brands, Inc., 6.95%, 2033 | | | 40,000 | | | | 38,400 | |

| Macy’s, Inc., 7.875%, 2015 | | | 330,000 | | | | 388,175 | |

| Neiman Marcus Group, Inc., 10.375%, 2015 | | | 85,000 | | | | 88,932 | |

| QVC, Inc., 7.375%, 2020 (n) | | | 70,000 | | | | 76,300 | |

| Rite Aid Corp., 9.25%, 2020 (z) | | | 45,000 | | | | 43,088 | |

| Sally Beauty Holdings, Inc., 6.875%, 2019 (n) | | | 40,000 | | | | 42,600 | |

| Staples, Inc., 9.75%, 2014 | | | 260,000 | | | | 292,821 | |

| Toys “R” Us Property Co. II LLC, 8.5%, 2017 | | | 55,000 | | | | 56,581 | |

| Toys “R” Us, Inc., 10.75%, 2017 | | | 145,000 | | | | 157,688 | |

| Yankee Acquisition Corp., 8.5%, 2015 | | | 2,000 | | | | 2,050 | |

| YCC Holdings LLC/Yankee Finance, Inc., 10.25%, 2016 (p) | | | 45,000 | | | | 45,113 | |

| | | | | | | | |

| | | | | | | $ | 2,523,081 | |

| Specialty Chemicals - 0.3% | | | | | | | | |

| Ecolab, Inc., 4.35%, 2021 | | $ | 240,000 | | | $ | 262,266 | |

| Koppers, Inc., 7.875%, 2019 | | | 35,000 | | | | 37,363 | |

| | | | | | | | |

| | | | | | | $ | 299,629 | |

| Specialty Stores - 0.2% | | | | | | | | |

| Michaels Stores, Inc., 11.375%, 2016 | | $ | 70,000 | | | $ | 74,376 | |

| Michaels Stores, Inc., 7.75%, 2018 | | | 140,000 | | | | 145,950 | |

| | | | | | | | |

| | | | | | | $ | 220,326 | |

20

Portfolio of Investments (unaudited) – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Bonds - continued | | | | | | | | |

| Supermarkets - 0.7% | | | | | | | | |

| Delhaize Group, 5.875%, 2014 | | $ | 290,000 | | | $ | 306,659 | |

| Safeway, Inc., 6.25%, 2014 | | | 400,000 | | | | 430,876 | |

| | | | | | | | |

| | | | | | | $ | 737,535 | |

| Telecommunications - Wireless - 2.3% | | | | | | | | |

| American Tower Corp., 4.625%, 2015 | | $ | 180,000 | | | $ | 191,108 | |

| American Tower Corp., REIT, 4.7%, 2022 | | | 328,000 | | | | 340,486 | |

| Clearwire Corp., 12%, 2015 (n) | | | 135,000 | | | | 117,788 | |

| Cricket Communications, Inc., 7.75%, 2020 | | | 120,000 | | | | 109,800 | |

| Crown Castle International Corp., 9%, 2015 | | | 65,000 | | | | 70,688 | |

| Crown Castle International Corp., 7.125%, 2019 | | | 250,000 | | | | 268,438 | |

| Crown Castle Towers LLC, 6.113%, 2020 (n) | | | 363,000 | | | | 424,178 | |

| MetroPCS Wireless, Inc., 7.875%, 2018 | | | 50,000 | | | | 50,500 | |

| Rogers Communications, Inc., 6.8%, 2018 | | | 200,000 | | | | 246,604 | |

| Sprint Capital Corp., 6.875%, 2028 | | | 75,000 | | | | 55,688 | |

| Sprint Nextel Corp., 6%, 2016 | | | 110,000 | | | | 100,650 | |

| Sprint Nextel Corp., 8.375%, 2017 | | | 95,000 | | | | 91,200 | |

| Sprint Nextel Corp., 9%, 2018 (n) | | | 25,000 | | | | 27,063 | |

| Wind Acquisition Finance S.A., 11.75%, 2017 (n) | | | 230,000 | | | | 195,500 | |

| | | | | | | | |

| | | | | | | $ | 2,289,691 | |

| Telephone Services - 0.4% | | | | | | | | |

| Cogent Communications Group, Inc., 8.375%, 2018 (n) | | $ | 40,000 | | | $ | 42,900 | |

| Level 3 Financing, Inc., 9.375%, 2019 | | | 85,000 | | | | 90,313 | |

| Level 3 Financing, Inc., 8.625%, 2020 (n) | | | 40,000 | | | | 40,800 | |

| Oi S.A., 5.75%, 2022 (n) | | | 216,000 | | | | 211,140 | |

| | | | | | | | |

| | | | | | | $ | 385,153 | |

| Tobacco - 1.9% | | | | | | | | |

| Altria Group, Inc., 9.25%, 2019 | | $ | 410,000 | | | $ | 563,323 | |

| B.A.T. International Finance PLC, 3.25%, 2022 (z) | | | 618,000 | | | | 612,216 | |

| Lorillard Tobacco Co., 8.125%, 2019 | | | 141,000 | | | | 175,830 | |

| Lorillard Tobacco Co., 6.875%, 2020 | | | 170,000 | | | | 201,445 | |

| Reynolds American, Inc., 6.75%, 2017 | | | 300,000 | | | | 361,301 | |

| | | | | | | | |

| | | | | | | $ | 1,914,115 | |

| Transportation - 0.1% | | | | | | | | |

| Navios South American Logistics, Inc., 9.25%, 2019 | | $ | 79,000 | | | $ | 72,680 | |

| | |

| Transportation - Services - 1.3% | | | | | | | | |

| ACL I Corp., 10.625%, 2016 (n)(p) | | $ | 99,927 | | | $ | 95,455 | |

| Avis Budget Car Rental LLC, 8.25%, 2019 | | | 45,000 | | | | 46,575 | |

| Avis Budget Car Rental LLC, 8.25%, 2019 (n) | | | 20,000 | | | | 20,700 | |

21

Portfolio of Investments (unaudited) – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Bonds - continued | | | | | | | | |

| Transportation - Services - continued | | | | | | | | |

| Avis Budget Car Rental LLC, 9.75%, 2020 | | $ | 35,000 | | | $ | 38,325 | |

| CEVA Group PLC, 8.375%, 2017 (n) | | | 155,000 | | | | 150,738 | |

| Commercial Barge Line Co., 12.5%, 2017 | | | 185,000 | | | | 209,513 | |

| Erac USA Finance Co., 6.375%, 2017 (n) | | | 340,000 | | | | 397,338 | |

| Hertz Corp., 7.5%, 2018 | | | 31,000 | | | | 32,279 | |

| Navios Maritime Acquisition Corp., 8.625%, 2017 | | | 115,000 | | | | 108,100 | |

| Navios Maritime Holdings, Inc., 8.875%, 2017 | | | 50,000 | | | | 51,250 | |

| Swift Services Holdings, Inc., 10%, 2018 | | | 140,000 | | | | 150,500 | |

| | | | | | | | |

| | | | | | | $ | 1,300,773 | |

| U.S. Government Agencies and Equivalents - 0.0% | | | | | | | | |

| National Credit Union Administration Guaranteed Note, 2.9%, 2020 | | $ | 20,000 | | | $ | 21,200 | |

| | |

| Utilities - Electric Power - 6.4% | | | | | | | | |

| AES Corp., 8%, 2017 | | $ | 260,000 | | | $ | 288,600 | |

| Allegheny Energy, Inc., 5.75%, 2019 (n) | | | 340,000 | | | | 370,135 | |

| Atlantic Power Corp., 9%, 2018 (z) | | | 55,000 | | | | 55,825 | |

| Calpine Corp., 8%, 2016 (n) | | | 105,000 | | | | 112,613 | |

| Calpine Corp., 7.875%, 2020 (n) | | | 225,000 | | | | 238,500 | |

| CMS Energy Corp., 4.25%, 2015 | | | 250,000 | | | | 260,591 | |

| CMS Energy Corp., 5.05%, 2022 | | | 196,000 | | | | 203,043 | |

| Covanta Holding Corp., 7.25%, 2020 | | | 70,000 | | | | 75,987 | |

| Covanta Holding Corp., 6.375%, 2022 | | | 25,000 | | | | 25,922 | |

| Dolphin Subsidiary ll, Inc., 7.25%, 2021 (n) | | | 70,000 | | | | 76,125 | |

| Duke Energy Corp., 3.35%, 2015 | | | 380,000 | | | | 402,808 | |

| Edison Mission Energy, 7%, 2017 | | | 85,000 | | | | 45,475 | |

| EDP Finance B.V., 6%, 2018 (n) | | | 380,000 | | | | 334,544 | |

| Enel Finance International S.A., 5.7%, 2013 (n) | | | 300,000 | | | | 304,817 | |

| Enel Finance International S.A., 6.25%, 2017 (n) | | | 260,000 | | | | 264,854 | |

| Energy Future Holdings Corp., 10%, 2020 | | | 120,000 | | | | 127,500 | |

| Energy Future Holdings Corp., 10%, 2020 | | | 330,000 | | | | 355,575 | |

| Energy Future Holdings Corp., 11.75%, 2022 (n) | | | 60,000 | | | | 61,200 | |

| Exelon Generation Co. LLC, 5.2%, 2019 | | | 150,000 | | | | 168,605 | |

| GenOn Energy, Inc., 9.875%, 2020 | | | 155,000 | | | | 143,375 | |

| Georgia Power Co., 6%, 2013 | | | 150,000 | | | | 161,174 | |

| Iberdrola Finance Ireland Ltd., 3.8%, 2014 (n) | | | 440,000 | | | | 434,009 | |

| NRG Energy, Inc., 7.375%, 2017 | | | 60,000 | | | | 61,950 | |

| NRG Energy, Inc., 8.25%, 2020 | | | 235,000 | | | | 231,475 | |

| Oncor Electric Delivery Co., 5.95%, 2013 | | | 430,000 | | | | 457,538 | |

| Oncor Electric Delivery Co., 4.1%, 2022 (n) | | | 302,000 | | | | 306,698 | |

| PPL WEM Holdings PLC, 3.9%, 2016 (n) | | | 370,000 | | | | 389,847 | |

| Progress Energy, Inc., 3.15%, 2022 | | | 452,000 | | | | 456,557 | |

22

Portfolio of Investments (unaudited) – continued

| | | | | | | | |

| Issuer | | Shares/Par | | | Value ($) | |

| | | | | | | | |

| Bonds - continued | | | | | | | | |

| Utilities - Electric Power - continued | | | | | | | | |

| Texas Competitive Electric Holdings Co. LLC, 11.5%, 2020 (n) | | $ | 45,000 | | | $ | 30,150 | |

| | | | | | | | |

| | | | | | | $ | 6,445,492 | |

| Total Bonds (Identified Cost, $103,713,738) | | | | | | $ | 108,325,528 | |

| | |

| Preferred Stocks - 0.2% | | | | | | | | |

| Other Banks & Diversified Financials - 0.2% | | | | | | | | |

| Ally Financial, Inc., 7% (z) | | | 50 | | | $ | 42,872 | |

| Ally Financial, Inc., “A”, 8.5% | | | 4,301 | | | | 93,762 | |

| GMAC Capital Trust I, 8.125% | | | 3,075 | | | | 70,479 | |

| Total Preferred Stocks (Identified Cost, $238,342) | | | | | | $ | 207,113 | |

| | |

| Convertible Bonds - 0.1% | | | | | | | | |

| Network & Telecom - 0.1% | | | | | | | | |

| Nortel Networks Corp., 2.125%, 2014 (a)(d) (Identified Cost, $93,781) | | $ | 95,000 | | | $ | 94,050 | |

| | |

| Floating Rate Loans (g)(r) - 0.1% | | | | | | | | |

| Broadcasting - 0.0% | | | | | | | | |

| Gray Television, Inc., Term Loan B, 3.74%, 2014 | | $ | 39,277 | | | $ | 38,884 | |

| | |

| Financial Institutions - 0.1% | | | | | | | | |

| Springleaf Finance Corp., Term Loan, 5.5%, 2017 | | $ | 43,780 | | | $ | 40,186 | |

| Total Floating Rate Loans (Identified Cost, $70,935) | | | | | | $ | 79,070 | |

| | |

| Common Stocks - 0.1% | | | | | | | | |

| Automotive - 0.0% | | | | | | | | |

| Accuride Corp. (a) | | | 2,303 | | | $ | 13,634 | |

| | |

| Broadcasting - 0.1% | | | | | | | | |

| New Young Broadcasting Holding Co., Inc. (a) | | | 10 | | | $ | 29,250 | |

| | |

| Printing & Publishing - 0.0% | | | | | | | | |

| American Media Operations, Inc. (a) | | | 2,541 | | | $ | 14,103 | |

| | |

| Special Products & Services - 0.0% | | | | | | | | |

| Mark IV Industries LLC, Common Units, “A” (a) | | | 275 | | | $ | 9,625 | |

| Total Common Stocks (Identified Cost, $145,999) | | | | | | $ | 66,612 | |

| | |

| Convertible Preferred Stocks - 0.1% | | | | | | | | |

| Automotive - 0.1% | | | | | | | | |

| General Motors Co., 4.75% (Identified Cost, $78,500) | | | 1,570 | | | $ | 57,650 | |

23

Portfolio of Investments (unaudited) – continued

| | | | | | | | | | | | | | | | |

| Warrants - 0.1% | | | | | | | | | | | | | | | | |

| Issuer | | Strike Price | | | First Exercise | | | Shares/Par | | | Value ($) | |

| | | | | | | | | | | | | | | | |

| Broadcasting - 0.1% | | | | | | | | | | | | | | | | |

| New Young Broadcasting Holding Co., Inc. (1 share for 1 warrant) (a) (Identified Cost, $40,124) | | $ | 0.01 | | | | 7/14/10 | | | | 21 | | | $ | 61,425 | |

| | | | |

| Money Market Funds - 4.6% | | | | | | | | | | | | | | | | |

| MFS Institutional Money Market Portfolio, 0.13%, at Cost and Net Asset Value (v) | | | | | | | | 4,653,454 | | | $ | 4,653,454 | |

| Total Investments (Identified Cost, $109,034,873) | | | | | | | $ | 113,544,902 | |

| | |

| Other Assets, Less Liabilities - (13.6)% | | | | | | | | (13,552,161 | ) |

| Net Assets - 100.0% | | | | | | | | | | | | | | $ | 99,992,741 | |

| (a) | Non-income producing security. |

| (d) | In default. Interest and/or scheduled principal payment(s) have been missed. |

| (e) | Guaranteed by Minister for Finance of Ireland. |

| (f) | All or a portion of the security has been segregated as collateral for open futures contracts. |

| (g) | The rate shown represents a weighted average coupon rate on settled positions at period end, unless otherwise indicated. |

| (n) | Securities exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be sold in the ordinary course of business in transactions exempt from registration, normally to qualified institutional buyers. At period end, the aggregate value of these securities was $27,560,957, representing 27.56% of net assets. |

| (p) | Payment-in-kind security. |

| (r) | Remaining maturities of floating rate loans may be less than stated maturities shown as a result of contractual or optional prepayments by the borrower. Such prepayments cannot be predicted with certainty. These loans may be subject to restrictions on resale. Floating rate loans generally have rates of interest which are determined periodically by reference to a base lending rate plus a premium. |

| (v) | Underlying affiliated fund that is available only to investment companies managed by MFS. The rate quoted for the MFS Institutional Money Market Portfolio is the annualized seven-day yield of the fund at period end. |

| (z) | Restricted securities are not registered under the Securities Act of 1933 and are subject to legal restrictions on resale. These securities generally may be resold in transactions exempt from registration or to the public if the securities are subsequently registered. Disposal of these securities may involve time-consuming negotiations and prompt sale at an acceptable price may be difficult. The fund holds the following restricted securities: |

| | | | | | | | | | |

| Restricted Securities | | Acquisition

Date | | Cost | | | Value | |

| Ally Financial, Inc., 7% (Preferred Stock) | | 4/13/11-4/14/11 | | | $46,875 | | | | $42,872 | |

| American Media, Inc., 13.5%, 2018 | | 12/22/10 | | | 10,056 | | | | 8,529 | |

| Anthracite Ltd., “A”, CDO, FRN, 0.599%, 2019 | | 1/28/10 | | | 107,982 | | | | 121,354 | |

| Atlantic Power Corp., 9%, 2018 | | 10/26/11-3/02/12 | | | 54,723 | | | | 55,825 | |

| Avaya, Inc., 7%, 2019 | | 5/24/12 | | | 22,876 | | | | 22,375 | |

| B.A.T. International Finance PLC, 3.25%, 2022 | | 5/31/12 | | | 612,216 | | | | 612,216 | |

24

Portfolio of Investments (unaudited) – continued

| | | | | | | | | | | | |

| Restricted Securities - continued | | Acquisition

Date | | | Cost | | | Value | |

| Crest Ltd., “A1” CDO, FRN, 0.952%, 2018 | | | 1/21/10 | | | | $165,399 | | | | $187,651 | |

| Dynacast International LLC, 9.25%, 2019 | | | 7/12/11-7/15/11 | | | | 70,703 | | | | 72,100 | |

FGI Operating Co./FGI Finance, Inc.,

7.875%, 2020 | | | 4/12/12 | | | | 5,000 | | | | 5,138 | |

| Heckmann Corp., 9.875%, 2018 | | | 4/04/12 | | | | 59,671 | | | | 57,000 | |

| Kraft Foods, Inc., 3.5%, 2022 | | | 5/30/12 | | | | 523,248 | | | | 539,648 | |

| LBI Media, Inc., 8.5%, 2017 | | | 7/18/07 | | | | 59,386 | | | | 12,000 | |

| Libbey Glass, Inc., 6.875%, 2020 | | | 5/11/12 | | | | 30,000 | | | | 30,075 | |

| Local TV Finance LLC, 9.25%, 2015 | | | 5/02/07-11/30/10 | | | | 122,401 | | | | 124,050 | |

| NESCO LLC/NESCO Holdings Corp., 11.75%, 2017 | | | 4/05/12 | | | | 49,101 | | | | 50,500 | |

| Physio-Control International, Inc., 9.875%, 2019 | | | 1/13/12-1/30/12 | | | | 55,894 | | | | 58,300 | |

| Republic of Slovakia, 4.375%, 2022 | | | 5/10/12 | | | | 198,168 | | | | 191,000 | |

| Rite Aid Corp., 9.25%, 2020 | | | 5/03/12-5/21/12 | | | | 44,613 | | | | 43,088 | |

| Rivers Pittsburgh Borrower LP/Rivers Pittsburgh Finance Corp., 9.5%, 2019 | | | 5/30/12 | | | | 15,000 | | | | 15,338 | |

| Roofing Supply Group LLC/Roofing Supply Finance, Inc., 10%, 2020 | | | 5/24/12 | | | | 30,000 | | | | 30,300 | |

| Tekni-Plex, Inc., 9.75%, 2019 | | | 5/10/12 | | | | 14,814 | | | | 14,888 | |

| Townsquare Radio LLC, 9%, 2019 | | | 3/30/12 | | | | 39,607 | | | | 41,000 | |

| Truven Health Analytics, Inc., 10.625%, 2020 | | | 5/24/12-5/25/12 | | | | 25,010 | | | | 25,125 | |

| Total Restricted Securities | | | | | | | | | | | $2,360,372 | |

| % of Net Assets | | | | | | | | | | | 2.4% | |

The following abbreviations are used in this report and are defined:

| CDO | | Collateralized Debt Obligation |

| FRN | | Floating Rate Note. Interest rate resets periodically and may not be the rate reported at period end. |

| PLC | | Public Limited Company |

| REIT | | Real Estate Investment Trust |

Abbreviations indicate amounts shown in currencies other than the U.S. dollar. All amounts are stated in U.S. dollars unless otherwise indicated. A list of abbreviations is shown below:

25

Portfolio of Investments (unaudited) – continued

Derivative Contracts at 5/31/12

Forward Foreign Currency Exchange Contracts at 5/31/12

| | | | | | | | | | | | | | | | | | | | | | |

| Type | | Currency | | Counterparty | | Contracts to

Deliver/

Receive | | | Settlement

Date Range | | In

Exchange

For | | | Contracts at

Value | | | Net

Unrealized

Appreciation

(Depreciation) | |

| Asset Derivatives | | | | | | | | | | | | |

| SELL | | AUD | | Westpac Banking Corp. | | | 91,435 | | | 7/13/12 | | $ | 93,135 | | | $ | 88,753 | | | $ | 4,382 | |

| SELL | | CAD | | Merrill Lynch International Bank | | | 331,015 | | | 7/13/12 | | | 330,206 | | | | 320,193 | | | | 10,013 | |

| SELL | | DKK | | Goldman Sachs International | | | 518,529 | | | 7/13/12 | | | 91,138 | | | | 86,340 | | | | 4,798 | |

| SELL | | EUR | | JPMorgan Chase Bank N.A. | | | 754,537 | | | 7/13/12 | | | 986,542 | | | | 933,181 | | | | 53,361 | |

| SELL | | GBP | | Barclays Bank PLC | | | 348,521 | | | 7/13/12 | | | 552,393 | | | | 537,047 | | | | 15,346 | |

| SELL | | GBP | | Deutsche Bank AG | | | 348,521 | | | 7/13/12 | | | 552,291 | | | | 537,047 | | | | 15,244 | |

| SELL | | IDR | | JPMorgan Chase Bank N.A. | | | 1,361,190,000 | | | 6/04/12 | | | 146,129 | | | | 144,807 | | | | 1,322 | |

| BUY | | JPY | | Credit Suisse Group | | | 62,995,955 | | | 7/13/12 | | | 779,055 | | | | 804,256 | | | | 25,201 | |

| SELL | | SEK | | Credit Suisse Group | | | 410,578 | | | 7/13/12 | | | 60,144 | | | | 56,435 | | | | 3,709 | |

| | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | $ | 133,376 | |

| | | | | | | | | | | | | | | | | | | | | | |