Back to Contents

This report (“Annual Report”) comprises the annual report of Cable and Wireless plc in accordance with United Kingdom requirements. and, in substantial part, the Company’s Annual Report on Form 20-F in accordance with the requirements of the United States Securities and Exchange Commission (“SEC”). The 2005 Annual Review is published as a separate document.

It should be noted that the Company restated its 2004 Form 20-F filing to include amendments to certain figures included in the US GAAP Reconciliation of its Form 20-F originally filed on 21 June 2004. As such, only the amended 2004 form 20-F filed on 28 July 2005 will include figures for 2004 that are completely consistent with the historic figures shown in the US GAAP Reconciliation in this 2005 filing.

Unless otherwise stated in this Annual Report the terms “Cable & Wireless”, the “Group”, “it”, “we”, “us” and “our” refer to Cable and Wireless plc and its subsidaries, collectively. The term “Company” refers to Cable and Wireless plc.

Cable & Wireless prepares its financial information in accordance with UK Generally Accepted Accounting Principles (“UK GAAP”). Unless otherwise indicated, any reference in this report to Financial Statements is to the Financial Statements of Cable & Wireless (including the Notes to the financial statements) included in this report. UK GAAP differs from generally accepted accounting principles in the United States (“US GAAP”). The material differences between UK GAAP and US GAAP relevant to Cable & Wireless are explained on pages 144 to 152.

Cable & Wireless publishes its Financial Statements in pounds sterling (“£”). On 31 March 2005, the noon buying rate in New York City for cable transfers in pounds sterling as certified for customs purposes by the Federal Reserve Bank of New York was US$1.89 = £1. On 26 August 2005 the noon buying rate was US$1.81 = £1. For additional information on exchange rates between pounds sterling and the US dollar see exchange rates on page 156.

References to a year in this report are, unless otherwise indicated, references to the Company’s financial year ending 31 March of such year. In this report, financial and statistical information is, unless otherwise indicated, stated on the basis of the Group’s financial year.

This document is dated 20 September 2005 including the Legal proceedings section at pages 93 to 95. Note 33 to the Financial statements for the year ended 31 March 2005 discusses legal proceedings also but has not been updated to reflect most recent developments given that the Financial statements are dated 3 June 2005.

This document includes terms which may be specific to the industry, the Group or UK GAAP. A Glossary of terms is included on pages 162 to 165 to explain and define such terms or to give the US GAAP equivalent, as appropriate.

2 2005 Annual Report

Back to Contents

| | | |

| | | |

| | | Profile |

| | | | | |

| | | | | |

| | | 4 | | About us and highlights |

| | | 5 | | Chairman’s statement |

| | | 7 | | Chief Executive’s review |

| | | | | |

| | | Business overview |

| | | | | |

| | | 11 | | Introduction |

| | | 12 | | Geographic operations |

| | | 18 | | Services |

| | | 20 | | Regulatory framework |

| | | 23 | | History and development |

| | | | | of Cable & Wireless |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

| | | | | |

Back to Contents

About usand highlights

About us

Cable & Wireless is the leading telecoms operator in the majority of countries in which it operates. It is the second largest fixed network telecoms operator in the UK.

Its principal operations are in the UK, the Caribbean, Panama, Macau and Monaco. It provides voice, data, broadband, internet protocol (“IP”) and mobile services to business and residential customers, fixed and mobile telecoms carriers, mobile operators and content, application and internet providers.

Its extensive international network conveys traffic between these operations and provides a platform from which to offer telecommunication services to other carriers.

Highlights

Cable & Wireless completed the second year of its turnaround programme with a robust financial performance and further progress in reshaping the Group. Key developments included:

| – | restructuring of UK operations around customer segments; |

| – | acquisition of Bulldog Communications and a controlling interest in Monaco Telecom; |

| – | expansion of National Telcos’ broadband and mobile activities; |

| – | completion of US exit for £220 million and withdrawal from Japanese domestic market; and |

We achieved further cost savings in the traditional legacy voice and data sectors. Led by a strengthened management team, we accelerated investment to position the Group for profitable growth in new services. Shortly after the year end, we announced a three-year plan to develop an IP-based Next Generation Network in the UK and confirmed that Bulldog had completed the first phase of its local loop unbundling programme ahead of schedule. In National Telcos, we have continued to invest in our broadband and mobile infrastructure.

| | Profit before tax and exceptionals

(continuing operations):a |

| | – | up 13 per cent to £361 million |

| | | |

| | Earnings per share (total Group): |

| | – | 13.0 pence per share |

| | | |

| | Full year dividend: |

| | – | up 21 per cent to 3.8 pence |

| | | |

| | a | This is a non-UK GAAP financial measure which is used by management as a key performance measure. A reconciliation is set out on page 87. |

Back to Contents

Chairman’s statement

Richard Lapthorne Chairman |

| | | |

| | – | Turnaround programme on track |

| | | |

| | – | Revenue from continuing operations stable at constant currency |

| | | |

| | – | Initiated £190 million investment in Next Generation Networks |

| | | |

| | – | Targeted National Telcos investment in broadband, IP and mobile |

The past 12 months have been a time of transition as Cable & Wireless entered a new phase in the three-year programme to revive the Group. By the end of the year, the Chief Executive and his new team were no longer preoccupied with the Group’s past, and had turned confidently to face the future.

A year of transition

Over the past year, management has delivered on the promises it made in June 2003. We completed our exit from the US market at considerably lower cost than originally expected. This allowed the Chief Executive to concentrate on the restructuring of our UK business and on defining a path to a sustainable position in this market. An enormous amount of work has gone into improving operations and tightening cost controls in the legacy businesses. Customer focus has been central to our new structures.

We are also seeing some excellent groundwork in network development. A prime example is our investment in Bulldog, the UK broadband operator we acquired last May. Bulldog gives us network access across the “last mile” to the customer, enabling us to offer an end-to-end service in competition with BT. Building our customer base in this way is an important goal as we embark upon investment of £190 million over three years in our UK IP-based Next Generation Network. This new technology offers network economies that will benefit our customers and improve our margins. In this context, we welcome Ofcom’s vision of a UK telecommunications market based on realistic and sustainable competition among players willing to invest in future technological strength.

Our financial disciplines and continued cost reduction have created a stable framework so that Cable & Wireless can move forward. Since November, a corporate reorganisation has refocused our activities on the key customer segments at the heart of our business. We are now well-placed to exploit rising global demand for broadband, IP and mobile services across the whole market, from large multinational corporations to residential users.

Outside the UK, our National Telcos have become more aggressive in dealing with competition. Co-operation and communication have also improved between our operations, so that these businesses can benefit from each others’ experiences of the rapidly liberalising telecom landscape. We are successfully capitalising on the controlling stake in Monaco Telecom acquired a year ago, and will take opportunities to expand our footprint into new geographies as appropriate.

The exit from the US and disposal of our Japanese business kept our cash intact, which allowed us, in November 2004, to launch a £250 million share buyback. As at March 2005 we had bought back 60.5 million shares, at an average price of 124.4 pence.

Back to Contents

Chairman’s statement

| Results and dividend | |

| The 2005 financial performance demonstrates our progress. Profit before taxation and exceptional items for continuing operations, for the year ended 31 March 2005, was £361 million. Revenue from continuing operations at £3,023 million, was stable at constant currency compared to 2004. | |

| | |

| The Board has recommended a full year dividend of 3.8 pence per share, after paying 1.16 pence per share at the interim stage. This represents a 21 per cent increase in the total dividend, indicating our confidence in the Group. | |

| | |

| The Board | |

| The Board was strengthened during the year. In July, George Battersby joined the executive team as Group Human Resources Director and in December, Harris Jones was appointed as Executive Director, International Businesses. We also appointed three new Non-executive Directors, Kate Nealon, Agnès Touraine and Clive Butler. Their combined experience has significantly broadened the skills of our Board as we undertake the next stage of the Group’s transformation. Kevin Loosemore resigned from the Board on 1 December 2004 and left Cable & Wireless at the end of the financial year, we would like to thank him for his contributions. Dr Janet Morgan retired from the Board in July 2004 having served 16 years during which time her contribution has been considerable, and for which we thank her. | |

| | |

| On page 36, our senior Non-executive Director reports on the four key aspects of good corporate governance. I am pleased to report that Cable & Wireless continues to operate governance to high standards. | |

| | |

| Our team | |

| Cost-cutting and corporate reorganisation has inevitably been unsettling for staff, and I want to thank our management and employees for meeting the challenges so far with resilience and determination. Their contribution has enabled us to strengthen our business for the future. | |

| | |

| Looking ahead | |

| Our markets continue to suffer from excess capacity and severe price competition. Performance improvement will come from efficiencies and cost-cutting, and a shift in our sales mix towards broadband, IP and mobile. We are in a unique position to help our customers embrace these new technologies and I look forward with confidence to the year ahead. | |

| | |

| Richard Lapthorne | |

| Chairman | |

Back to Contents

Chief Executive’s review

Francesco Caio Chief Executive Officer |

| | | |

| | | Focusing on margin |

| | | and investing in profitable growth |

| | | |

| | | |

| | | |

| | | |

| | | |

| We have defined a clear path for our business based around key trends in customer demand and the rapid shift in technology. It is key to our success to manage margins in traditional services and to be able to invest for profitable growth in new services. |

| | |

| In 2005 we made solid progress in strengthening Cable & Wireless’ competitive position: |

| | |

| – | we have focused the Group on markets where we have a relevant presence and can develop and maintain a sustainable position; |

| | |

| – | we completed the US exit and the sale of our domestic business in Japan; |

| | |

| – | we committed to invest £190 million over three years in a UK Next Generation Network to increase competitiveness and enhance financial performance; |

| | |

| – | we focused National Telcos to compete in the growth areas of mobile and broadband and continue to reduce costs; |

| | |

| – | we reshaped our UK business into four customer-focused segments, Enterprise, Business, Carrier Services and Bulldog, each led by experienced telecom professionals; and |

| | |

| – | in May 2005 we completed the first phase of Bulldog’s unbundling programme to cover 30 per cent of UK households, just a year after acquisition. |

| | |

| We streamlined central management and relocated our head office to Bracknell, reflecting our reduced cost base and a culture where the centre drives performance across the Group. Worldwide we are a leaner organisation, in line with our aim to be the lowest cost provider in all our markets. |

| | |

| Industry context |

| The telecoms industry is experiencing profound structural changes. There are common challenges and opportunities across the Group that have shaped our strategic priorities. Revenues from traditional services continue to decline, so we must protect margins by further forcing down costs. At the same time, we are pursuing growth. As new broadband, IP and mobile services replace legacy services we are investing to win customers in these highly competitive growth areas. |

| | |

| UK Group |

| Our UK operations are focused around the customer segments of Enterprise, Business and Carrier Services. At present, 67 per cent of our revenues in the UK are generated by switched voice services, however, we have adopted targeted strategies for each customer segment as they migrate to new technologies. These customers are also supported by our operations in Europe, Asia, and the US. |

Back to Contents

Chief Executive’s review

Enterprise

Enterprise provides integrated telecommunication services to large corporations and central government departments. The convergence of voice, data and internet access on IP-based services is reshaping the way many businesses operate. Migrating to IP offers lower costs and more sophisticated services, such as video-streaming, multi-party conferencing and remote access into corporate IT systems.

Enterprise won a number of new contracts with major customers. Although our current revenue is still generated primarily by traditional services – which are subject to continued decline – we have made solid gains in winning IP business, which now accounts for 13 per cent of Enterprise turnover.

Cable & Wireless has the network and the capabilities to support our biggest customers as they make the transition to new generation, IP-based technologies.

Business

Business addresses a market that includes a wide range of customers. In the last year we have focused on the top end of the segment and saw new business wins with Damovo, easyJet, Lothian Health Board and Littlewoods. Overall, however, revenue was reduced by severe competition. Pressure on revenues in legacy services has been higher than in Enterprise reflecting the fact that, as many customers only buy switched voice, they have higher price sensitivity and propensity to switch.

Take-up of IP is growing among our small business customers. We are developing a new portfolio of packaged and bundled products such as Intelligent Voice and Straight Talk. The services, including IP, are being designed for ease of implementation and use.

Carrier Services

Cable & Wireless has worldwide coverage across 200 countries and is one of the world’s largest carriers of international voice and data. Carrier Services generates 45 per cent of UK revenue and operates in a highly competitive market that continues to suffer from over-capacity and declining margins, although these have been partially offset by increased volumes. Our innovative customer solutions have won notable contracts. We now enable the Post Office to provide a fixed phone line service, and won an international termination deal with Skype, the Voice over IP (“VoIP”) operator for which we now transport around 100 million minutes a year. This year we will expand our services to international customers by offering wholesale VoIP. By taking a Group-wide view of network assets, Carrier Services aims to improve utilisation of our international network.

| | We continue to develop new services for mobile carriers and launched MMX, a platform to exchange pictures and multimedia messages developed with Vodafone. We operate one of the largest Global 3G roaming exchanges and support email roaming for a third of the world’s mobile networks. We also launched our Global Carrier multi-protocol label switching (“MPLS”) service, which can transmit any type of traffic in IP format, including time-sensitive and business-critical information and we have already signed up eight significant carriers.

Revenue declined following a fall in mobile termination rates, imposed on all carriers in the UK by Ofcom, but had no impact on profits. In Europe we downsized and refocused on the demands of a customer base of fewer, larger clients.

Bulldog

The acquisition in May 2004 of Bulldog, the broadband operator, was an important step in advancing our UK access strategy. Local loop unbundling (“LLU”) strengthens our presence in the valuable access network, while Bulldog’s appeal to the residential and small/home office market (the so-called SoHos) broadens our UK customer base. This additional traffic increases use of the existing core network and can, in future, migrate very simply to our Next Generation Network.

Through LLU, Bulldog puts its own equipment inside BT’s local exchanges to take control of the “last mile” copper link (the “local loop”) into the customer’s home or office. Access to this last mile improves our end-to-end control of the network resulting in lower outpayments to BT and, hence, higher gross margins. It also allows us to innovate, differentiate and control the end-to-end quality of our services to business and residential customers.

LLU enables Cable & Wireless to redefine its position in the telecom industry away from the alternative network model. We have the capability, the core network, and the funding to exploit unbundling. LLU enables us to make the most of these advantages to differentiate our business from our competitors.

Our unbundling programme has made rapid progress. We reached our initial target of 400 exchanges in May 2005, seven months ahead of the original timetable. The Bulldog team, under its new Chief Executive, is now progressing with plans to extend its UK coverage and intends to unbundle an additional 200 exchanges by March 2006 and a further 200 exchanges in the first half of 2006/07 bringing the total number of exchanges unbundled to 800. This will increase planned investment and start-up losses in 2005/06. |

Back to Contents

Bulldog’s dual super-fast 4Mbps broadband and voice telephony offer attracted early customer enthusiasm in the residential and SoHo markets and we quickly followed this with the release of 8Mbps across all 400 exchanges. As the roll-out progresses we have supported it with a broader commercial marketing programme. With the largest non-incumbent telecom network in the UK, our new end-to-end infrastructure has offered customers a real choice of total fixed voice and broadband provider for the first time.

Bulldog has similar characteristics to a start-up in the early days of mobile; it is marketing led, innovative, and offers customers a fast, convenient, good value service. For clarity of management and transparency, we are therefore reporting the results of Bulldog separately in our segmental analysis.

Next Generation Networks and Operations

In all our markets, we are an infrastructure-based competitor. Control of our own network is a key source of competitive advantage through which we can provide high-quality, cost-effective innovative services. The creation last year of an integrated management structure for network systems and operations has enabled us to enhance quality of service, identify investment priorities, reduce hand-offs and target cost reductions.

We have carried out a review of our existing UK network, and launched a programme to address operating costs, interconnection costs and loading. The first phase of this programme will cut costs by £50 million in 2006 enabling us to mitigate, to some extent, the continuing effects of price pressure.

The network review also demonstrated the significant benefits of moving to an IP-based Next Generation Network architecture, and the associated IT systems and processes. In April we announced investment of £190 million over three years to transform our core UK network into a single integrated IP platform, carrying voice, data and internet services.

This decision was driven by the shift in demand in all customer segments towards IP-based products, and the rapid advance in IP technologies. The development of new services will be supported by Bulldog’s expanding broadband access network, which will feed traffic into the IP core. We expect our new IP architecture to be in place by the end of 2008.

A large proportion of the anticipated £190 million capital expenditure on our Next Generation Network will replace expenditure that would otherwise have been needed to maintain our legacy system, leaving a net increase in planned investment over the three years of £35 million.

| | Over the next three years UK voice and data traffic will continue to migrate to IP. Cable & Wireless has the scale to lead this transformation. Our infrastructure size, combined with the efficiency of putting all traffic onto a single IP-based core network, will deliver significant economies. Our Next Generation Network will offer customers greater functionality and customised solutions, at an attractive price. The benefit for Cable & Wireless will be lower operating and maintenance costs, and a more flexible network that can accommodate significant growth in traffic at a much lower capital cost, offering the potential to achieve a higher margin.

Ofcom

The regulatory framework is fundamental to our business and our investment decisions. The strategic review by Ofcom, the telecom and media regulator, provides an opportunity to create a more transparent and effective regulatory regime in areas where BT still controls access to customers. The promised level playing field must become a reality. Establishing the appropriate structure and processes to obtain equality of access to BT’s local loop assets will enable the market to take the lead in setting prices for products and services where there is already competition.

We are encouraged by Ofcom’s emphasis on infrastructure-based competition. We are also pleased that the regulator has adopted the principle of equivalence as the tool to deliver parity in the market. Successfully implemented, this would require BT to offer regulated products to competitors at exactly the same price and quality of service as it does to BT’s own businesses. There should be no discrimination between non-BT customers and BT’s own operations when purchasing products such as wholesale broadband capacity and call origination. Our recent experience has shown considerable room for improvement in, for example, BT’s co-operation over local loop unbundling.

It is critical that equivalence is designed into BT’s planned 21st Century Network so that new barriers to entry are not created by BT’s migration to next generation systems. Fair infrastructure-based competition must be at the heart of the UK telecoms market if customers are to benefit from the variety of services that new technologies can offer and the UK is to recapture its pre-eminent position as a business location. |

Back to Contents

Chief Executive’s review

National Telcos

Cable & Wireless is the market leader in integrated fixed, broadband and mobile services in 34 countries. Our National Telcos have delivered solid results in the context of an increasingly liberalised environment. As at 31 March 2005 88 per cent of our National Telco revenues were generated by companies operating in liberalised markets although not all of these are yet fully competitive. Revenues increased by 10 per cent due to good performances in Panama and Rest of the World and the acquisition of Monaco Telecom. Mobile revenues grew by 26 per cent and data and IP revenues grew by 13 per cent year on year. (All revenue changes are expressed at constant currency.)

Our new leadership team aims to take advantage of the National Telcos’ breadth of operations. We believe that this increased cross-business co-operation, and sharing of knowledge and expertise across our geographies, will continue to sharpen performance.

Our National Telcos’ markets are at different stages of liberalisation. Each has its own customer profile but the competitive challenges they face are similar, and so must be the response:

| | |

| – | reducing the costs of legacy services, where margins are under pressure; |

| | |

| – | investing further in the key growth services of broadband, IP and mobile; and |

| | |

| – | developing sales and marketing skills to stay ahead of the competition. |

In broadband and IP we are leaders in most of our markets and are investing to meet growing demand. Many of the countries in which we operate still have relatively low take-up of broadband and IP services, and we are well positioned to offer services that assist customers in the transition. We have started to invest in IP backbones in countries where traffic volumes justify the expenditure, including in the Caribbean where hurricane damage has accelerated infrastructure replacement. Upgrades are underway in Monaco, Macau, the Cayman Islands and Grenada.

Across all the National Telcos, we have established tight financial discipline and control over investment. This has sharpened our focus on initiatives that produce results. We intend to expand broadband and mobile services and this strategy will determine our investment decisions. The future

Over the last two years we have created a more focused and streamlined platform, better equipped to face the challenges and opportunities from the rapidly transforming telecommunications industry.

Our markets will remain very challenging, but I believe that we can build on our early achievements. In the UK, our reorganisation will sharpen our customer focus and strengthen our competitive position. The investment in Bulldog and our Next Generation Network will further distinguish us from other UK operators. In our overseas businesses, we will strive to maintain profitable market leadership.

Francesco Caio

Chief Executive Officer

Back to Contents

Business overview

Introduction

Cable & Wireless is a leading international telecommunications company with principal operations in the United Kingdom, the Caribbean, Panama, Macau and Monaco. Cable & Wireless provides voice, data, internet protocol (“IP”) and mobile services to business and residential customers as well as to fixed and mobile telecommunications operators and content, application and internet providers.

Business overview

Cable & Wireless’ strategy is to exploit growing demand for broadband, IP and mobile services in markets where it can achieve significant scale. As a result, Cable & Wireless intends to be the number one or two operator in the principal markets in which it operates. To continue to achieve this as the telecommunications industry faces unprecedented changes in customer behaviour, technology and market structure, the Group must protect margins by reducing costs whilst accelerating investment to position itself for profitable growth in new services.

During the past two years, Cable & Wireless has pursued this strategy, exiting markets where it did not have a relevant position, reshaping its operations, investing for growth and streamlining the central office.

Exit from US and Japan

In 2005, the Group completed its exit from the United States and Japan, two markets where it did not have sufficient scale to sustain a competitive position. To exit the US, the Group agreed, at the request of the purchaser, to sell its business through a Chapter 11 process under the United States Bankruptcy Code. In Japan, the Group conducted a competitive auction process culminating in the sale of the Group’s Japanese subsidiary.

Reshaping the UK business

Following its review in 2004 of the dynamics of the UK market, the Group restructured its United Kingdom operations and in April 2005 announced a three-year plan to develop an IP-based Next Generation Network. In addition, the Group acquired Bulldog Communications Ltd (“Bulldog”) in May 2004, a UK-based broadband provider specialising in local loop unbundling (“LLU”). Through Bulldog and its investment in a Next Generation Network, Cable & Wireless is in the process of redefining its position in the UK telecom industry, moving away from the alternative network model. To effect this move, the UK is now structured around the following key customer segments:

| – | the Enterprise segment comprising businesses and institutions with the biggest telecoms spend in the UK. Cable & Wireless’ objective in Enterprise is to be the partner of choice in transitioning customers to new generation, IP-based technologies; |

| | |

| – | the Business segment, comprising small and medium-sized companies. Cable & Wireless aims to be a credible, strong supplier to small and medium-sized customers through targeted sales of bundled products, including IP services; |

| – | the Carrier Services segment comprising large telecoms companies that provide long distance international voice services; mobile operators buying international voice and transport services; and operators, including resellers and ISPs. Cable & Wireless’ objective in Carrier Services is to leverage the depth of its intercontinental network and advanced services to position the Group as the backbone of choice for mobile and other operators. In November 2004, management commenced a restructuring of its European operations to focus principally on Carrier Services; |

| | |

| – | the SoHo/consumer segment which Cable & Wireless addresses through Bulldog. Bulldog provides high speed data and voice services in the UK via LLU. |

The Group’s remaining operations in the United States, Europe and Asia provide international services to UK-based Enterprise and Carrier Services customers.

Relocation of Group Head Office

Consistent with the steps taken to reshape and re-focus Cable & Wireless, the Group has relocated its head office from central London. This move has combined corporate and UK functions and has resulted in a shift towards a more customer oriented, responsive culture.

National Telcos

Almost all the 34 national markets in which the National Telcos operate are now fully or partially liberalised and present very similar competitive challenges. For this reason Cable & Wireless’ strategy across the National Telcos is based on three principles: invest in key growth services of broadband, IP and mobile; lower costs on legacy services where margins are under pressure and develop sales and marketing skills.

In line with these principles, Cable & Wireless acquired Monaco Telecom in June 2004. Monaco Telecom is a fully integrated telecommunications company.

In addition, the Group completed the roll out of its GSM network across the National Telcos, improving coverage and services to residential and business customers across 22 businesses. The Group also launched proactive marketing initiatives to increase broadband penetration across the National Telcos.

Going forward, the Group aims to take advantage of the National Telcos’ breadth of operations, increasing cross-business cooperation and sharing knowledge and expertise across the National Telcos geographies to continue to improve performance.

Back to Contents

Business overview

Geographic operations

Cable & Wireless Group

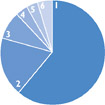

Cable & Wireless 2005 Turnover by geography

(Continuing operations)

Total turnover: £3,023 million

|

1. United Kingdom

2. Caribbean

3. Panama

4. Macau

5. Monaco

6. Rest of the World |

Cable & Wireless has principal operations in the United Kingdom, the Caribbean, Panama, Macau and Monaco. The Group’s operations are managed and reported on a country-based structure.

The Caribbean, Panama, Macau, Monaco and Rest of the World are collectively referred to as the National Telcos. For a discussion of Cable & Wireless’ turnover by geographic operation for the past three years, see Operating and financial review – Group turnover.

United Kingdom

United Kingdom 2005 Turnover by customer segment

Total turnover: £1,602 million

|

1. Enterprise

2. Business

3. Carrier services |

Cable & Wireless is the largest fixed voice telecommunications service provider in the United Kingdom after BT, the incumbent telecom operator.

The UK operation is structured around three key customer segments known as Enterprise, Business and Carrier Services. Additionally, the SoHo/Consumer customer segment is served through Bulldog. The UK sells voice and data services over fixed line networks using legacy and IP platforms.

The UK uses the United States (“CWAO”), Europe and Asia to provide services to UK-based Enterprise and Carrier Services customers with international service requirements. For this reason, the United States, Europe and Asia operations are managed from the UK and organised around the three relevant customer segments. This section discusses the customer segments in the UK and

provides an outline of the operations that support the UK, the United States, Europe and Asia. For a discussion on Bulldog and on the United States, Europe and Asia see page 13.

UK Enterprise (2005 Turnover: £475 million)

Cable & Wireless defines Enterprise customers as large national and international organisations where significant customisation of their telecommunications services is required. Enterprise customers purchase voice and data telecommunications services.

Enterprise customers typically buy telecommunications services from a variety of suppliers, although many have a longer-term relationship with a primary supplier. Enterprise customers often require interconnection between multiple sites, so deep network reach is important. As a result, Cable & Wireless generally competes against other operators with large networks. Price pressure continues to be significant in this market.

Cable & Wireless’ objective in the Enterprise market is to become the partner of choice for companies as they transition from voice and data services delivered over legacy platforms to new voice, data and integrated services delivered over IP-based platforms. Currently, fixed voice represents 54 per cent of total turnover for Enterprise customers in the UK.

Cable & Wireless addresses the needs of its UK-based Enterprise customers for international services through its presence in the United States, Europe and Asia.

UK Business (2005 Turnover: £394 million)

Cable & Wireless defines business customers as mid-sized companies who purchase voice and data services over legacy and IP-based platforms through direct or indirect sales channels. Often, Business customers are regional entities with one or a small number of sites. Cable & Wireless aims to serve these customers through standardised service offerings. This market attracts competition from operators with both large and relatively small networks.

Currently, fixed voice represents 39 per cent of total turnover for Business customers in the UK. Customers in the Business market are more easily able to switch providers, resulting in significant price pressure and high levels of churn across all services delivered over legacy platforms, particularly fixed voice services. The key area of growth in this market is voice, data and integrated services delivered over IP-based platforms. These platforms allow customers to access enhanced features such as voice, video and data provided through a single cost-effective platform.

UK Carrier Services (2005 Turnover: £733 million)

Cable & Wireless defines Carrier Services customers as large national and international telecommunications operators or resellers who purchase wholesale services mainly focusing on voice and data services delivered over legacy platforms.

Back to Contents

Carrier Services provide fixed voice and data services to the following types of customers:

| – | large international telecommunications operators, who buy fixed long distance and international fixed voice services; |

| | |

| – | national mobile operators, who buy both international voice and data transport/backbone services to allow them to connect their radio networks via the fixed infrastructure. To serve mobile operators in their migration to new “3G” networks, we have launched services that support international data roaming; |

| | |

| – | regional and domestic telecommunications operators to whom we sell fixed voice and data services; |

| | |

| – | virtual telecommunications operators and resellers, who purchase voice services using Carrier Pre-Select (“CPS”). CPS allows consumer calls to be automatically connected from the incumbent operator network to the network of a competing operator. Virtual operators purchase CPS services from Cable & Wireless and re-sell them under their own brands to residential customers; and |

| | |

| – | Internet Service Providers (“ISP”), who buy data and internet transport services. |

Currently, fixed voice represents 91 per cent of total UK Carrier Services turnover. The Carrier Services market is highly competitive and price sensitive. As a result, significant price declines have been seen in all key service areas.

Driven by the requirements of its Carrier Services customers, Cable & Wireless leverages its presence in the United States, Europe and Asia as well as the National Telcos to provide voice and data services internationally.

SoHo/Consumer (Bulldog)

2005 Total turnover: £11 million

In May 2004 Cable & Wireless acquired 100 per cent of Bulldog in order to capture the growth opportunity in broadband, leverage the Cable & Wireless backbone network and expand the Group’s IP network.

Bulldog provides IP services by way of broadband internet access to SoHo and residential customers. Bulldog uses full LLU to connect directly to customers, providing voice telephony and high speed internet access services independent of the incumbent operator.

Full LLU refers to the process by which providers, such as Bulldog install their own Digital Subscriber Line (“DSL”) equipment in rented space within an incumbent operator’s local exchanges. DSL technology allows Bulldog to deliver broadband capabilities to customers over ordinary copper telephone lines.

The ability to deliver IP services using its own network provides Bulldog with technological advantages over competitors reselling the incumbent’s products. This allows Bulldog to differentiate its service offerings, maintain full bandwidth control and own the customer from end-to-end.

In September 2004, Cable & Wireless announced the initial LLU plan for Bulldog including the target to unbundle 400 exchanges by December 2005. Bulldog had completed LLU on 252 exchanges as at 31 March 2005 and completed LLU on 400 exchanges in May 2005.

Cable & Wireless believes LLU is more than an opportunity to offer fast internet access. LLU can also provide a cost effective platform from which Cable & Wireless can launch a wide range of new and existing telecom services from voice to video.

United States (“CWAO”)

2005 Total turnover: £16 million

Cable & Wireless operates in the United States through its subsidiary Cable & Wireless Americas Operations, Inc. (“CWAO”).

CWAO operates a small, efficient and predominantly international network. The business provides US connectivity for data and IP services to Enterprise customers principally those based in the UK.

Europe

2005 Total turnover: £186 million

Cable & Wireless’ operations in continental Europe are in Germany, France, Spain and Italy, together with smaller operations in Russia, Belgium, The Netherlands, Switzerland and Sweden.

The continental European operations are focused on Carrier Services, and also support UK Enterprise customers. Carrier Services represents over 80 per cent of turnover in continental Europe. The main Carrier Services customers are mobile operators and other telecommunications operators.

Asia

2005 Total turnover: £39 million

Cable & Wireless’ operations in Asia span Australia, China, Hong Kong, India, Japan and Singapore and focus on Carrier Services and Enterprise segments. The Group’s network of 33 nodes in 13 countries provides a footprint across the entire region.

Following the disposal of the Group’s domestic business in Japan in February 2005, the Asia operations have been focused on serving Enterprise customers that require IP and managed data services to and from Asia (principally those based in the UK) and Carrier Services customers in Asia that require voice, IP and data services to the rest of the world.

Back to Contents

Business overview

Geographic operations

National Telcos

National Telcos 2005 Turnover by service

Total turnover: £1,191 million

|

1. International Voice

2. Domestic Voice

3. Data

4. IP

5. Mobile

6. Other |

In the National Telcos, Cable & Wireless typically operates the domestic fixed line telecom network and associated international interconnect facilities. Its fixed and mobile voice, data and IP services meet the needs of corporate and residential customers, including the fast-growing demand for internet access through dial-up IP and broadband ADSL connections.

Almost all the 34 markets in which Cable & Wireless operates are fully or partially liberalised. The principal exception is Monaco Telecom which has an exclusive concession to operate international, domestic, data and mobile services until 2023. As competition has intensified across the National Telcos, Cable & Wireless has transformed its organisation, taking on its new competition by investing in innovation, such as GSM networks, managing and reducing costs, and marketing proactively.

Caribbean

Caribbean 2005 Turnover by service

Total turnover: £550 million

|

1. International Voice

2. Domestic Voice

3. Data

4. IP

5. Mobile

6. Other |

Overview

Cable & Wireless operates in 16 Caribbean countries providing domestic and international voice, data and IP services to residential and business customers. The Caribbean’s principal businesses are subsidiary operations in Jamaica, Barbados, and the Cayman Islands and an equity holding in Trinidad and Tobago.

In nearly all the Caribbean countries in which it operates, Cable & Wireless is the incumbent operator, providing domestic and international fixed and mobile voice and data services and IP

services. Liberalisation is at an advanced stage across the Caribbean with nearly all markets either fully liberalised or in transition to competitive markets. Further discussion on liberalisation is in Regulatory framework.

In response to growing competition and to customer demand, Cable & Wireless is increasingly focused on developing and enhancing its mobile and IP service offerings, whilst retaining its position in fixed voice services.

In order to develop and enhance mobile services in the Caribbean, Cable & Wireless continued its expansion of GSM mobile services to reach all 13 of the countries in which Cable & Wireless holds mobile licences. Cable & Wireless continues to enhance network coverage, capacity and roaming capabilities, enabling the launch of new products and services, including mobile email, prepaid pan-Caribbean roaming and mobile messaging services (“MMS”).

At 31 March 2005, there were over 900 GSM equipped sites in the Caribbean with land mass coverage on most islands between 65 per cent and 99 per cent. During the year, Cable & Wireless total mobile subscribers in these countries increased from 1,141,000 to 1,367,000.

During 2005, Cable & Wireless expanded its broadband capabilities across the Caribbean. Sales and marketing activities have been focused on the rebranding of broadband services. Investment has been focused on increasing the number of fixed lines enabled to deliver broadband service, average prices have been reduced and line speeds increased. DSL customers at 31 March 2005 were approximately 38,000, an increase of over 125 per cent from 31 March 2004.

In the Caribbean countries where Cable & Wireless provides domestic voice services, customers at 31 March 2005 totalled 735,000, an overall decrease of approximately 12 per cent in the year. This reduction is a result of customers substituting mobile services for fixed line services.

Jamaica

Cable & Wireless Jamaica Limited (“Cable & Wireless Jamaica”), a subsidiary of Cable & Wireless, is the incumbent operator and is the largest of Cable & Wireless’ Caribbean operations (by turnover) generating 37 per cent of the Caribbean’s turnover in 2005. Cable & Wireless Jamaica is the largest telecommunications company in Jamaica.

Cable & Wireless Jamaica provides domestic and international fixed and mobile voice and data services and IP services to residential and business customers.

The Jamaican market has been liberalising since March 2000. In addition to Cable & Wireless Jamaica, there are currently two active competitors in the mobile sector, 10 active ISPs (out of a total of 76 licensed parties), 32 licensed data service providers and two competitors in the domestic voice sector. The international carrier

Back to Contents

market has been liberalised since March 2003 and now comprises 68 licensed carriers, of which six are active and interconnect with Cable & Wireless Jamaica. Nine ISPs offer internet services to end customers over Cable & Wireless’ network.

Barbados

Cable & Wireless (Barbados) Limited (“Cable & Wireless Barbados”), a subsidiary of Cable & Wireless, is the incumbent operator and provides domestic and international fixed and mobile voice and data services and IP services to residential and business customers. Cable & Wireless Barbados generated 18 per cent of the Caribbean’s turnover in 2005. Cable & Wireless Barbados is the largest telecommunications company in Barbados.

The Barbados domestic fixed and mobile voice markets have been liberalising since August 2003, while liberalisation in the data and IP market has been longstanding. The domestic voice telecommunications market is now fully liberalised with three licensed operators, none of which were active at 31 March 2005. International services were liberalised in February 2005 with two licences issued and both operators active in the market using their own international facilities. Three mobile licences have been issued to competitors in Barbados and two are currently active in the market. Seven ISPs offer internet services to end customers over Cable & Wireless’ network.

Cayman Islands

Cable and Wireless (Cayman Islands) Limited (“Cable & Wireless Cayman Islands”), a wholly owned subsidiary of Cable & Wireless, is the incumbent operator and provides domestic and international fixed and mobile voice and data services and IP services to residential and business customers in the Cayman Islands. Cable & Wireless Cayman Islands generated 11 per cent of the Caribbean’s turnover in 2005. Cable & Wireless Cayman Islands is the largest telecommunications company in the Cayman Islands.

The Cayman Islands market was fully liberalised in early 2004. At 31 March 2005, 18 new entrants have been licensed in various telecommunications, broadcasting and other communication market sectors. Most licensees have multiple licences. In addition to Cable & Wireless Cayman Islands, there are currently two active competitors in the mobile sector (out of the six licensed); two active ISPs; three active fixed-wireless providers; and one active reseller of telephony services.

Trinidad and Tobago

Telecommunications Services of Trinidad and Tobago Limited (“TSTT”), a 49 per cent equity investment of Cable & Wireless, is the incumbent operator and provides domestic and international fixed and mobile voice and data services and IP services to residential and business customers. TSTT is the largest telecommunications company in Trinidad and Tobago.

The process of liberalisation is under way in the Trinidad and Tobago market although no additional licences have been issued. TSTT and Cable & Wireless are in negotiations with the government of

Trinidad and Tobago to ensure an orderly liberalisation.

Panama

Panama 2005 Turnover by service

Total turnover: £257 million

|

1. International Voice

2. Domestic Voice

3. Data

4. IP

5. Mobile

6. Other |

Cable & Wireless Panama S.A. (“Cable & Wireless Panama”), a subsidiary of Cable & Wireless, is the incumbent operator and provides domestic and international voice, data and IP services to residential and business customers in Panama. Cable & Wireless Panama is the largest telecommunications company in Panama.

The telecoms market in Panama has been liberalising since 2003. International and domestic fixed line services are now fully liberalised, whilst Cable & Wireless Panama operates in a duopoly in the mobile market (with Telefonica) until 2008. Competition in fixed line voice services is concentrated in international and long distance services with 56 and 32 operators licensed in each segment, respectively. IP services have been liberalised for many years with 84 licensees.

In light of the increased competition and in line with customer demand Cable & Wireless Panama continues to focus on the development of its mobile and IP capabilities as well as maintaining high standards in customer service and retaining its market leading position in fixed line services.

In the year to March 2005, Cable & Wireless Panama continued its investment in GSM services to enable an expansion of capacity in order to meet the increase in demand for its services. Total mobile customers increased to 634,000 at 31 March 2005, an increase of 25 per cent over the prior year.

Cable & Wireless Panama has also invested in DSL services in the year. This investment has enabled the launch of a range of bundled IP solutions for business as well as an increase in access for residential customers. At the 31 March 2005, DSL customer numbers were 38,000 an increase of over 123 per cent in the year.

During the year to March 2005, Cable & Wireless Panama has continued to focus on retaining its market leading position in fixed line. Activities have focused on customer service improvement and customer retention. Fixed line customers in Panama have increased from 360,000 at 31 March 2004 to 383,000 at 31 March 2005.

Back to Contents

Business overview

Geographic operations

Macau

Macau 2005 Turnover by service

Total turnover: £117 million

|

1. International Voice

2. Domestic Voice

3. Data

4. IP

5. Mobile

6. Other |

Companhia de Telecomunicações de Macau S.A.R.L. (“CTM”), a subsidiary of Cable & Wireless, is the incumbent operator in Macau offering international and domestic fixed and mobile voice and data and IP services to business and residential customers. In addition, CTM provides an international transit service through its nodes in Hong Kong and Singapore serving national and international carriers. CTM is the largest telecommunications company in Macau.

CTM is the exclusive provider of domestic fixed voice services in Macau, with the licence expiring in 2011. The remaining market segments are fully liberalised with active competition in most sectors from local and international operators.

In the mobile market Macau has issued two further licences for GSM technology and one other licence for CDMA technology.

The internet market was liberalised in October 2000. CTM is the leading provider with only one competitor in the dial-up internet access market, at present there is no active competition in the broadband DSL access market.

In response to changes in the competitive environment and customer demand, CTM continues to focus on enhancing its fixed line voice and data services whilst further developing capabilities in mobile and IP services.

The Macau government is considering the issue of a Third Generation Wireless (“3G”) licence. Licensing procedures for 3G are expected to be announced in the fourth quarter of calendar 2005.

Monaco Telecom

Monaco Telecom 2005 Turnover by service

Total turnover £100 million (9.5 months)

|

1. International Voice

2. Domestic Voice

3. Data

4. IP

5. Mobile

6. Other |

Monaco Telecom S.A.M. (“Monaco Telecom”), a subsidiary of Cable & Wireless, was acquired on 18 June 2004. Monaco Telecom was created in 1997 following the privatisation of the incumbent operator. Monaco Telecom provides fixed and mobile voice and data services as well as IP services. It holds an exclusive licence to provide domestic and international fixed and mobile voice services, internet access and cable services in Monaco until 2023.

The focus within Monaco is on the quality of service while maintaining pricing parity with neighbouring countries. Outside Monaco, it is developing its international activities in network management and satellite services.

The primary growth opportunities within Monaco are focused on mobile and DSL. Since acquisition, mobile subscribers have increased 21 per cent to 35,000. During the same period, the DSL lines have increased 17 per cent to 7,500.

Monaco Telecom is also focused on maintaining its fixed turnover contribution from fixed to mobile substitution by creating value added services, customer service improvements, and high value product bundles. In addition, Monaco Telecom intends to leverage its wide portfolio of telecommunication services in the Principality by offering convergent communication services and billing.

Outside the Principality, Monaco Telecom has provided network services to a mobile network in Kosovo under a management contract since 2000. At the beginning of 2003, Monaco Telecom was awarded the second GSM licence in Afghanistan as the strategic partner in a consortium 51 per cent owned by the Aga Khan Fund for Economic Development. These contracts are included in Other turnover for financial reporting purposes.

Back to Contents

Rest of the World

Rest of the World 2005 Turnover by service

Total turnover: £167 million

|

1. International Voice

2. Domestic Voice

3. Data

4. IP

5. Mobile

6. Other |

Overview

Rest of the World comprises Cable & Wireless’ subsidiary operations in Guernsey and the Maldives together with smaller operations in the Seychelles, Bermuda, Sakhalin in Russia, Diego Garcia, Falkland Islands, Fiji, Ascension, St Helena, Vanuatu, Solomon Islands, Jersey and the Isle of Man. Cable & Wireless also has an associate holding in Bahrain. Guernsey and the Maldives account for 60 per cent of the Rest of the World turnover.

In the geographies where Cable & Wireless operates, it is typically the incumbent operator, providing domestic and international fixed and mobile voice and data services as well as IP services. The status of liberalisation across the Rest of the World is varied. Most businesses however are currently in transition to liberalised markets. Further details on the liberalisation status of the Rest of the World can be found in the regulatory section on page 22.

Guernsey

Cable & Wireless operates in Guernsey through its wholly owned subsidiary Cable and Wireless Guernsey Ltd (“Cable & Wireless Guernsey”). Cable & Wireless Guernsey is the incumbent operator in Guernsey providing domestic and international fixed and mobile voice and data services and IP services to all residential, business and government customers.

The States of Guernsey liberalised the market in 2002.

At 31 March 2005, in addition to Cable & Wireless Guernsey, there were two competitors for domestic and international voice and one competitor for mobile.

Maldives

Cable & Wireless operates in the Maldives through its subsidiary Dhivehi Raajjeyge Gulhun Private Limited (“Dhiraagu”). Dhiraagu is the incumbent operator and provides domestic and international voice and mobile services and IP services to residential and business customers.

The Maldives began liberalisation in 2002. At 31 March 2005, in addition to Dhiraagu, there was one competitor in the IP market and one licence issued in the mobile market with competition expected to begin in the next fiscal year.

Bahrain

Cable & Wireless operates in Bahrain through its associate Bahrain Telecommunications Company B.S.C. (“Batelco”). Batelco provides domestic and international fixed and mobile voice and data and IP services to residential and business customers.

In Bahrain, competition in domestic mobile, in the form of MTC Vodafone, was introduced in 2003. Internet services were liberalised on a similar timeframe. In the summer of 2004 the market for international services and facilities was liberalised. In the second half of 2004 a licence to provide national fixed line services was put up for sale but as yet no additional licences have been awarded, resulting in Batelco currently being the only licence holder for the provision of domestic fixed line services and IP.

Back to Contents

Business overview

Services

Cable & Wireless 2005 Turnover by service

(Continuing operations)

Total turnover: £3,023 million

|

1. Voice

2. Data

3. IP

4. Mobile

5. Other |

Cable & Wireless provides voice, data, and IP services to business and residential customers across the world. The Group delivers these services over fixed line and mobile networks. The majority of services are delivered over traditional legacy platforms, with a small but growing proportion being delivered over IP-based platforms.

The term legacy platform generally refers to the existing communications and transmission infrastructure that underpins most telecom operator networks across the world that were deployed up until the late 1990’s. Each family of service delivered over legacy technology generally requires a proprietary platform to deliver service, resulting in multiple overlapping telecommunication networks.

The term internet protocol (“IP”) generally refers to a set of protocols or rules that govern how interconnected devices communicate. IP-based devices share data in ‘packets,’ or discrete bundles of data. IP networks allow the delivery of voice, video and data over the same network, allowing simplification of network design and operation, and supporting the delivery of new integrated services.

Historically, in many operations, Cable & Wireless was the incumbent operator, focusing on voice and data services over fixed lines on legacy platforms. Today, most markets in which Cable & Wireless operates have liberalised. New voice and data services delivered over mobile and IP networks are growing and over time, replacing services on our fixed line networks.

New IP-based platforms allow Cable & Wireless to deliver new types of integrated service that blur the old boundaries between voice and data/fixed and mobile and deliver seamless integrated communications to end users.

Voice services

Fixed voice

Cable & Wireless offers domestic and international voice services to residential, corporate and other telecommunication companies and service providers. In the UK, Cable & Wireless also provides services to non-telecommunication companies who provide residential telephony, but do not have their own network infrastructure.

The majority of fixed voice turnover is delivered over legacy platforms, using traditional copper telephone lines and switch networks.

Cable & Wireless also offers IP-based voice services, such as voice over IP (“VoIP”). These services can provide enhanced end user functionality (for example, providing better integration between customers’ own voice and data networks) at reduced cost.

Mobile voice

Cable & Wireless offers domestic and international mobile voice services to residential and business customers outside the United Kingdom. Cable & Wireless delivers voice services to mobile handsets through wireless technologies such as GSM.

Global system for mobile communications (“GSM”) is a standard for digital mobile telephone transmissions that allows global roaming and enhanced features for data transmission as compared with time division multiple access (“TDMA”) networks. Because of the increased turnover potential associated with GSM technologies, Cable & Wireless has been expanding its GSM networks throughout the National Telcos in recent years.

Data services

Fixed data

Cable & Wireless offers data services to businesses that operate over fixed-line networks using legacy platforms, including leased line services, and networking services based on Frame Relay and asynchronous transfer mode (“ATM”) technology.

Leased line services predominantly utilise a technology known as synchronous digital hierarchy (“SDH”) to deliver data from point-to-point.

Frame Relay and ATM services provide an additional layer of intelligence and functionality beyond leased lines, allowing customers to build and manage complex networks across multiple locations and to prioritise traffic flows through their network.

Cable & Wireless also offers ‘next generation’ data services, such as IP virtual private networks (“IP-VPN”) and internet services that are delivered over IP-based networks.

IP-VPN allows customers to replace traditional private data networks with virtual private networks (“VPN”) which can reduce the expense and complexity of private networks, while providing enhanced services such as the bundling of voice, video and data.

Back to Contents

Mobile data

Cable & Wireless offers a range of data services for its mobile customers utilising SMS and MMS based technologies.

IP Services

Cable & Wireless provides customised services to many of its large corporate customers. Typically, these involve the development of integrated voice, data transmission and/or data storage solutions that are uniquely configured for individual customers.

Increasingly, these service solutions are offered using IP-based platforms and technologies and include voice services such as VoIP and data services such as IP-VPN.

IP access solutions provide security services (such as managed firewalls), intrusion detection, scanning and analysis (such as email virus protection), and authentication and encryption services to control access into customers’ networks.

IP contact centres enable our customers to manage all contact with their customers including incoming and outbound calls, emails or web contact requests.

Bulldog and the National Telcos provide broadband services that include voice and internet access as well as dial-up narrowband internet access, that allow business and residential customers to access the internet from their business or home.

Back to Contents

Business overview

Regulatory framework

Cable & Wireless, like other international telecommunication providers around the world, faces various regulatory and market access constraints in various countries resulting from laws, public policies and licensing requirements. This reflects the perception of telecommunications as a public service, a history of special or exclusive rights to provide services and often, a move towards liberalisation. Generally, specialist telecommunications regulation is administered through enforcement of conditions contained in ‘authorisations’ or in operating and service licences held by the Group and its subsidiaries.

Most of the markets in which Cable & Wireless operates are fully liberalised although some are in transition to competitive markets, and a few small geographies are expected to remain monopolies for the foreseeable future. Where countries have moved to competitive environments, Cable & Wireless has actively engaged with governments in order to facilitate an orderly transition to a fully competitive environment. The discussions involve negotiating fair regulatory arrangements that provide for equal treatment during the transitional period and beyond.

In all jurisdictions where it operates, Cable & Wireless is required to comply with regulations that affect its business. The Group believes it complies in all material respects with all material regulatory obligations and where regulatory compliance issues emerge it takes action to ensure compliance.

Licensing

Cable & Wireless provides international and domestic telecommunications services under general authorisation regimes or licences in the jurisdictions in which it operates. These licences are either held by Cable & Wireless itself or by local operating entities owned either wholly or partly, directly or indirectly, by Cable & Wireless.

The Group believes it has all licences material to the running of its business. It is possible that from time to time, as further products and services are deployed or changed, additional licences or authorisations will be required. Where the Group identifies the need for further licences or authorisations, it intends to acquire such licences. The terms of the Group’s licences vary, although most remain in effect for a fixed period of 10 to 25 years, or for an indefinite period subject to notice of termination after a specified minimum period. Licence fees are sometimes required, either as a fixed annual fee or a fee equal to a percentage of the revenue or profits arising from the licence.

In 2003 the European Union established a harmonised framework for licensing laid out under the electronic communications directives. This has been transposed into national law by most of the member states. As a result these member states will no longer issue individual telecommunications licences to companies except in exceptional circumstances such as the allocation of spectrum. Therefore, for Cable & Wireless, most of the telecommunications licences it holds in EU member states, including those in the UK, have been revoked and replaced by the relevant general authorisations under the new

regulatory regime. Cable & Wireless will continue to offer telecommunications services subject to obligations set forth in general conditions as dictated by the relevant electronic communications directive and individual member states.

Outside the European Union, Cable & Wireless operates in Guernsey, the Isle of Man, Monaco, Norway, Russia and Switzerland with relevant licences and authorisations.

Some licences provide that, upon their termination, the relevant government may purchase, or have the option to purchase, the property, plant and equipment of the licensee in that territory at a fair market value. In some cases, where the Group owns an operating company jointly with government, that government has the right to purchase, at specified times, the whole or part of the Group’s shareholding in the operating company.

The international trend is for telecommunications liberalisation and the replacement of exclusive licences with non-exclusive licences alongside rules governing competition between operators. Jurisdictions that currently support monopoly provision may also decide to promote competition, and Cable & Wireless anticipates that some existing exclusive licences will not be renewed on an exclusive basis, or that governments will seek to withdraw their exclusivity before the licence expires, replacing the current operating licence with a non-exclusive licence.

The Group is committed to participating in discussions on the introduction of competition in any territory where its government wishes to do so.

There is no guarantee that an agreement to provide either a monopoly or franchised service will remain in effect for the full term of the agreement.

Regulation by jurisdiction

The regulatory institutions and policies of the jurisdictions in which the Group operates are varied.

Europe

The regulatory framework in member states of the European Union is harmonised by EU directives, though there are divergences in regulatory policy and practice between member states. Many member states have implemented, or are implementing, the directives of the European Union 2003 electronic communications package. This package seeks to harmonise telecommunications across the European Union, and involves the concept of Significant Market Power to determine which operators should have prior obligations placed on them, on the grounds that such operators might exploit that market position to the detriment of competition and therefore consumers. This speed of adoption of the electronic communications package varies significantly across the EU and this can affect the ability of the non-incumbents to compete.

Back to Contents

United Kingdom

The telecommunications market in the United Kingdom is governed by the EU communications package (described above) which has been transposed into national law by the Communications Act 2003 (“UK Comms Act”). The UK Comms Act sets the framework for the regulation of telecommunications and broadcasting markets as well as the civilian use of spectrum in the United Kingdom. Insofar as it applies to telecommunications markets, it updates the Telecommunications Act 1984 and transposes the EU electronic communications directives into UK law. It also lays out the powers and duties of the industry regulator, the Office of Communications (“Ofcom”).

Following reviews by Ofcom, BT has been designated as having Significant Market Power in a number of markets. BT is therefore required to provide cost-based interconnection for switched voice services and leased line access circuits (Partial Private Circuits) to providers of public electronic communications networks such as Cable & Wireless on non-discriminatory terms. Such services are subject to network charge controls. The network charge controls applying to BT are in the process of being reviewed. It is not yet clear what form the new controls will take given that over the likely four-year period of the next cap BT will be migrating from legacy to next generation networks.

Following the review of wholesale International Direct Dial (“IDD”) markets, Cable & Wireless has a designation of Significant Market Power on wholesale IDD routes from the United Kingdom to four destinations: Ascension, Diego Garcia, Montserrat and Turks & Caicos. The obligations associated with this designation are minimal.

In addition, in common with all other providers of fixed public voice networks in the United Kingdom, Cable & Wireless has been designated as having Significant Market Power (“SMP”) in the markets for geographic call termination on the UK network. As this designation has been applied to all operators, obligations are likely to be minimal and the Group expects that there will be little or no impact.

In early 2004, Ofcom undertook a Strategic Review of the UK Telecommunications market. This review is nearly complete, with Ofcom now consulting on its decision to accept BT’s voluntary undertakings in lieu of a reference to the Competition Commission pursuant to Section 154 of the Enterprise Act 2002.

BT’s undertakings offer to provide a number of existing regulated products on an Equivalence of Inputs (“EoI”) basis. This means that BT’s own business and other communications providers (such as Cable & Wireless) would be supplied with the same product, at the same price, using the same operational processes and systems. Where products are provided on an EoI basis, other communications providers would be in a position to compete more effectively with BT than today. The timetable for implementation of the Strategic Review recommendations is scheduled to continue to 2010.

BT has committed to provide products delivered over its Next Generation Network that are in markets where BT has been designated with SMP on an EoI basis. This is subject to some restrictions where provision of those products on an EoI basis would not be reasonably practical.

In addition, BT has committed to set up an Access Services Division under separate management, which would control and operate the local access network separately from other network assets.

BT’s undertakings, if accepted by Ofcom, would become legally binding, with breaches enforced through the High Court.

In those markets where BT has been designated with SMP and is subject to regulatory obligations, the designation and obligations will continue to remain in force subject to the standard process for removal of such obligations.

The Caribbean

Cable & Wireless has businesses in 16 countries in the Caribbean. Whilst in the past Cable & Wireless was exclusively licensed in the majority of these territories, nearly all are now either fully liberalised or are in transition to competitive markets. Cable & Wireless is engaged in ongoing dialogues with host governments and regulators to ensure that the regulatory environment is fair and consistent.

The regulatory frameworks in which the most significant Cable & Wireless Caribbean businesses operate are described in this section.

Cable & Wireless Jamaica operates in a fully liberalised market, regulated by the Office of Utilities Regulation.

Cable & Wireless Barbados is now operating in a fully liberalised market since the issuance of international licences to competitors in February 2005. The regulatory authority for fixed telecommunications in Barbados is the Fair Trading Commission. The Ministry of Industry and International Business regulates mobile telecommunications.

Cable & Wireless Cayman Islands operates in a fully liberalised market. Cable & Wireless Cayman Islands is subject to the regulation of the Information and Communications Technology Authority. Five member states of the Organisation of Eastern Caribbean States (Dominica, Grenada, St Kitts and Nevis, St Lucia, St Vincent and the Grenadines) are contracted in a single jurisdiction for telecommunications regulation with a regional regulator, the Eastern Caribbean Telecoms Authority (“ECTEL”), and are also subject to the jurisdiction of national regulators, the National Telecoms Regulatory Committees. Telecommunications markets in the ECTEL states are fully liberalised.

Japan

Following the sale of Cable & Wireless IDC Inc., Cable & Wireless UK applied for its own telecommunications registration with the Japanese Ministry of Internal Affairs and Communications. Cable & Wireless UK (Japan branch) was registered in September 2004 and

Back to Contents

Business overview

Regulatory framework

is authorised to provide certain telecommunications services in Japan including international and domestic data services, IP access and leased circuits.

The separation of telecommunication business licences between Type I (facilities) and Type II (services) was abolished in 2004. Telecommunication licences now are classified as notified or registered telecommunication licences.

United States

Cable & Wireless Americas Operations, Inc. provides international communications services to customers who require service to, from or through the United States. Under US law, the Federal Communications Commission (“FCC”) regulate interstate and international telecommunications services while state commissions regulate intrastate services. Non-dominant service providers such as CWAO are subject to a lesser degree of regulation than designated dominant service providers. CWAO also provides information services, which generally are not regulated in the United States.

The regulated telecommunications services provided by CWAO may be classified as either common carrier or private carrier services depending upon the nature of the service offering. As a general matter, US law requires that common carrier services be offered (a) upon reasonable request, (b) on rates, terms and classifications which are just and reasonable, (c) without unjust discrimination or undue preferences basis, and (d) pursuant to authorisation of the FCC. Private carriers generally are not subject to these requirements, but are required to make contributions to the federal universal service fund based on international and interstate telecommunications revenues, in the same manner as common carriers. Intrastate telecommunications services are subject to regulation by the relevant state public utility commission and may be subject to licensing requirements, tariffs, and/or subsidy mechanisms.

Other markets

Cable & Wireless Panama operates in a partially liberalised market. The regulator is Ente Regulador De Los Servicios Publicos. Cable & Wireless Panama is a full service provider across fixed line and mobile markets for business and residential customers. There has been increasing regulatory activity on the broadband front in 2005 with wholesale broadband services already being available and plans in place to introduce local loop unbundling. In the area of mobile the regulator has recently sought to introduce indirect access over mobile.