Cable & Wireless Public Limited (CWP) Inactive

Filed: 28 Jul 05, 12:00am

As filed with the Securities and Exchange Commission on June 21, 2004

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F/A

(amendment No. 1)

| (Mark One) | |

| REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

| OR | |

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| OR | |

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from N/A to N/A |

Commission file number: 1-10309

CABLE AND WIRELESS PUBLIC LIMITED COMPANY

(Exact name of Registrant as specified in its charter)

ENGLAND AND WALES

(Jurisdiction of incorporation or organization)

124 Theobalds Road, London WC1X 8RX, United Kingdom

(Address of principal executive offices)

Securities registered or to be registered pursuant to Section 12(b) of the Act

| Title of each class | Name of each exchange on which registered |

| American Depositary Shares | New York Stock Exchange |

| Ordinary Shares of nominal value 25 pence each | New York Stock Exchange* |

Securities registered or to be registered pursuant to Section 12(g) of the Act.

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

None

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital

or common stock as of the close of the period covered by the annual report.

2,385,467,990 Ordinary Shares of nominal value 25p each

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ![]() No

No ![]()

Indicate by check mark which financial statement item the registrant has elected to follow:

Item 17 ![]() Item 18

Item 18 ![]()

C&W regularly evaluates the effectiveness of its internal controls over financial reporting and disclosure controls and procedures, including in connection with the filing of, and certification with respect to, its annual report and Form 20-F. Through an ongoing programme of review, C&W identified certain corrections to the reported US GAAP reconciliation of its 2004 and 2003 financial results. Although the Company believes that these adjustments are not material to the 2004 results, the Company has nevertheless determined that it would be appropriate to take account of these corrections in connection with re-filing the 2004 20-F. The adjustments, and changes in respect of clarification of disclosures, made in the US GAAP reconciliation footnote to the financial statements are the only changes made to the amended Form 20-F filed on January 18, 2005. Since filing its annual report on Form 20-F on June 21, 2004, Cable and Wireless plc has filed additional information about the Company and its more recent results of operations on Form 6-K.

C&W has already taken measures in connection with its internal controls and disclosure controls and procedures as it has deemed appropriate to enhance its controls and to address any deficiencies and weaknesses that have been identified. Among other things, C&W has enhanced its controls by including additional US GAAP resources in the preparation of its US GAAP reconciliation, in both the Group’s business units and also in the central external financial reporting team. Management believes that these improvements help to enhance controls over financial reporting and disclosure.

This report (“Annual Report”) comprises the annual report of Cable and Wireless plc in accordance with United Kingdom requirements and, in substantial part, its annual report on Form 20-F in accordance with the requirements of the United States Securities and Exchange Commission (“SEC”). The Annual Review 2004 is published as a separate document.

In this report references to the ‘Company’ are to Cable and Wireless plc, and references to the ‘Group’, ‘Cable & Wireless Group’ and ‘Cable & Wireless’ are to the Company, its consolidated subsidiaries and associated companies and joint ventures unless the context otherwise requires. References to ‘Cable & Wireless Group Companies’ are to any companies within the Cable & Wireless Group.

Cable & Wireless prepares its financial information in accordance with UK Generally Accepted Accounting Principles (“UK GAAP”). Unless otherwise indicated, any reference in this report to Financial Statements is to the Financial Statements of Cable & Wireless (including the Notes to the Financial Statements) included in this report. UK GAAP differs from generally accepted accounting principles in the United States (“US GAAP”). The material differences between UK GAAP and US GAAP relevant to Cable & Wireless are explained on pages 141 to 149.

Cable & Wireless publishes its Financial Statements in pounds sterling (“£”). On 31 March 2004, the noon buying rate in New York City for cable transfers in pounds sterling as certified for customs purposes by the Federal Reserve Bank of New York was US $1.84 = £1. On 1 June 2004 the noon buying rate was US$1.84 = £1. For additional information on exchange rates between pounds sterling and the US dollar see exchange rates on page 152.

References to a year in this report are, unless otherwise indicated, references to the Company’s financial year ending 31 March of such year. In this report, financial and statistical information is, unless otherwise indicated, stated on the basis of the Company’s financial year.

This document is dated 21 June 2004 including the Legal Proceedings section at pages 18 to 21. Note 30 to the Financial Statements for the year ended 31 March 2004 discusses legal proceedings also but has not been updated to reflect most recent developments given that the Financial Statements are dated 1 June 2004.

cautionary statement regarding forward-looking statements

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report contains certain forward-looking statements with respect to the financial condition, results of operation and business of Cable & Wireless.

Statements that are not historical facts, including statements about Cable & Wireless’ beliefs and expectations, are forward-looking statements. Words such as ‘believes’, ‘anticipates’, ‘expects’, ‘intends’ and ‘plans’ and similar expressions are intended to identify forward- looking statements, but are not the exclusive means of identifying such statements. These statements are based on current plans, estimates and projections and, therefore, undue reliance should not be placed on them. Forward-looking statements speak only as of the date they are made, and you should not assume that they have been revised or updated in the light of new information or future events.

Written and/or oral forward-looking statements may also be made in, amongst others, the periodic reports to the Securities and Exchange Commission on Forms 6-K, summary financial statements to shareholders, proxy statements, offering circulars and prospectuses, press releases and other written materials and in oral statements made by Cable & Wireless’ Directors, officers or employees to third parties, including financial analysts.

Forward-looking statements involve inherent risks and uncertainties. Cable & Wireless cautions investors that a number of factors could cause actual results to differ, in some instances materially, from those anticipated or implied in any forward-looking statement. These factors include:

Risks specific to Cable & Wireless’ business |

| • | failure to improve the performance and financial position of the Group successfully or to adapt as needed to changing market conditions could adversely affect the Group’s business, results of operations and potential for growth; |

| • | transformation initiatives can lead to execution risk; |

| • | US exit; |

| • | the Group may not be able to adapt adequately to technological changes in communication and information technology; |

| • | the Group’s results depend on the introduction of appropriate new products and services as the industry undergoes rapid changes; |

| • | network failure may expose the Group to potential liability or loss of customers; |

| • | dependency on key personnel and skills; |

| • | the Group is reliant on third parties for certain activities under outsourcing contracts; failure of those third parties to provide the contracted services may expose the Group to additional cost and liability; |

| • | the Group is dependent on a number of critical IT systems to be able to conduct its business and process financial information; |

Regulatory risk |

| • | Cable & Wireless’ business may be materially adversely affected by changes in regulation and government policy in the countries in which it operates; |

| • | exposure to other telecommunications operators and the behaviour of other market participants may have a detrimental effect on the Group’s operations; |

| • | the Group may lose revenue if unlicensed operators are able to gain access to the Group’s network; |

Risks specific to the telecommunications industry |

| • | the Group’s business may be affected by a business downturn; |

| • | generally unfavourable telecommunications market conditions may adversely affect the Group’s financial condition and results of operations; |

| • | the Group’s operations could suffer from adverse effects of competition and price pressures on the demand for products and services; |

| • | competitors of Cable & Wireless may gain competitive advantage by successfully completing a restructuring or bankruptcy reorganisation process; |

| • | continued overcapacity and other factors could lead to lower prices for the Group’s products and services; |

Legal and other |

| • | the Group may not have or be unable to obtain sufficient insurance to cover all foreseeable risks; |

| • | the historic activities of the Group’s insurance subsidiary may result in material claims; |

| • | volatility in the financial markets may require the Group to provide further cash funding to its pension funds; |

| • | fluctuations in currency exchange rates may adversely affect the Group’s reported results and financial condition; |

| • | class actions may adversely impact the Group’s financial condition; and |

| • | mobile communications devices may pose health risks. |

Trends and factors that are expected to particularly affect Cable & Wireless’ results are discussed in more detail elsewhere in this Annual Report, including, without limitation, in the Business Description and the Operating and Financial Review.

corporate overview

CONTENTS

| 4 | ||

| 6 | ||

| 8 | ||

| 14 | ||

| 17 | ||

| 18 | ||

| 22 | ||

| 24 | ||

| 32 | ||

| 38 | ||

| 41 | ||

| 41 | ||

| 43 | ||

| 44 | ||

| 46 | ||

| 47 | ||

| 53 | ||

| 57 | ||

| 59 | ||

| 66 | ||

| 81 | ||

| 82 | ||

| 84 | ||

| 87 | ||

| 88 | ||

| 89 | ||

| 90 | ||

| 91 | ||

| 92 | ||

| 97 | ||

| 150 | ||

| 151 | ||

| 152 | ||

| 152 | ||

| 153 | ||

| 155 | ||

| 155 | ||

| 156 | ||

| 158 | ||

| Inside back cover | ||

| – Registrar | ||

| – Scrip dividend scheme/dividend reinvestment plan | ||

| – Financial calendar | ||

| – ShareGIFT | ||

| – Company Secretary and registered office | ||

| – American Depositary Receipts | ||

| – Global Invest Direct facility | ||

| – Investor relations |

corporate overview

The telecommunications industry continues to face challenging market conditions. Revenues from traditional voice services continue their gradual decline in favour of a variety of mobile and IP services. Trends indicate that increased volumes of voice and data traffic will be carried over IP networks and, while traditional voice will continue to be important, reduced demand will keep margins under pressure. As the telecommunications landscape evolves it will be those providers that can address the needs of customers in their migration to new low-cost, more flexible IP based solutions that will prosper.

In the past year, significant restructuring has been initiated in line with the priorities set by management in June 2003. The first step in this process was to re-organise the Group on a geographic basis, enabling management to examine the market dynamics and regulatory environment faced by each business unit. The objective was to begin to stabilise operations by introducing new management, reducing costs, controlling cash and, most importantly, addressing customer needs.

National Telcos |

Liberalisation progressed in most markets in which the Group operates, leading to greater competitive pressure for most National Telco businesses. In response, the Group is developing operating priorities to limit margin erosion and maximise cash flow. In the Caribbean, where liberalisation is advanced, senior management have increased their involvement in the businesses to ensure better co-ordination and accountability. The regional management structure was delayered and a local Head of Operations for the Caribbean was appointed. Initiatives were also undertaken to address the growth in demand for mobile services through an accelerated roll out of the GSM network and a refocusing of sales and marketing programmes to serve the most attractive customer segments. Across all National Telcos, common metrics are being introduced to measure and drive performance and to facilitate the transfer of skills and experience between business units.

In June 2004, Cable & Wireless acquired a controlling stake in Monaco Telecom from Vivendi Universal. Monaco Telecom has the exclusive licence to provide fixed line, mobile, internet access and cable services in Monaco until at least 2014.

UK Business |

In June 2003, management outlined a three-year transformation plan for the UK business. The objective in year one was to stabilise operations by reducing capital expenditure and operating costs, introducing new skills and

redesigning systems and processes. The benefits of the initiatives taken in these areas are reflected in the financial performance of the UK business this year. The business achieved stable revenues after several years of decline and tightened control of capital expenditure, which together have led to the generation of a pre- exceptional operating profit and of break-even cash flow.

The UK business has been restructured around three customer segments, Enterprise, Business and Carrier Services. Enterprise customers are estimated to comprise the top 550 businesses and institutions that together represent 50 per cent of the UK’s annual telecommunications business market. Products and services based on internet protocol (IP) are increasingly critical to this segment.

In the UK the majority of data traffic has yet to migrate to IP and this presents an important opportunity. Cable & Wireless has an established position in this segment. Its strength in voice services, its IP backbone, skills and experience enable it to partner Enterprise customers beginning their migration to new IP services.

An estimated 400,000 Business customers represent the remaining 50 per cent of the annual telecommunications business revenue in the UK. Cable & Wireless serves between 10 and 15 per cent of these customers and has renewed its focus on this segment. Business customers require cost effective voice services and, until recently, made limited use of data. However, the acceleration of broadband penetration in the UK has the potential to change the economics of access for Business customers, providing high-quality, low-cost voice and data applications on a single platform. Cable & Wireless’ acquisition of Bulldog Communications in May 2004 strengthens its opportunities to meet the growing demand for broadband access. In addition, the changes to the regulation of local loop unbundling have the potential to reduce the cost of access and increase penetration.

The Carrier Services segment, which generates close to 50 per cent of revenues in the UK business, was also important to the stabilisation of the UK business during the year as it enabled the business to utilise available network capacity for short-term wholesale contracts. Continued opportunities in this segment are offered by new entrants to consumer telecommunications using carrier pre-select services, the growth in demand for mobile services and the increasing demand for IP and broadband.

Europe and Japan |

In continental Europe, the Group primarily provides services to other licensed telecommunications operators and to

corporate overview

multinational corporations some of which are headquartered in the UK.

Cable & Wireless IDC provides international voice and data services to companies in Japan and South East Asia. The markets in which it operates are dominated by Nippon Telegraph and Telephone Corporation.

Both operations have achieved significant cost reductions during the year and cost containment will continue to be an area of focus.

The Group continues to face challenges in implementing its strategic initiatives including those linked to the rapid changes in the telecommunications industry, global economic conditions and the markets in which the Group operates. The Group remains committed to capitalising on its core skills and its key customers. Please see ‘Risk Factors’ for further commentary on certain of the challenges facing the Group.

business description

BUSINESS DESCRIPTION

This section contains:

| SUMMARY |

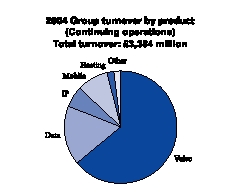

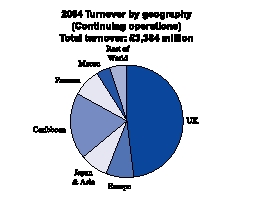

Cable & Wireless is an international telecommunications business with annual revenue of £3.7 billion in the year to 31 March 2004, of which £3.4 billion related to continuing operations, and customers in some 80 countries. Headquartered in London, Cable & Wireless’ principal operations are in the United Kingdom, Europe, the Caribbean, Panama, Macau and Japan. Cable & Wireless provides voice, data and IP services to business and residential customers and wholesale services to carriers, mobile operators and content, application and internet providers.

History

For over 120 years, Cable & Wireless has provided telecommunications services, networks and equipment to business and residential customers around the world. Except for some 30 years as a state-owned company after the Second World War, Cable & Wireless has been a publicly owned limited company since its earliest days.

In the United Kingdom, Cable & Wireless, through Mercury Communications, was an early competitor in the liberalised telecommunications market. In April 1997, Cable & Wireless Communications plc (“CWC”) was formed by the merger of Mercury Communications with Nynex CableComms, Bell Cablemedia and Videotron.

In September 1998, Cable & Wireless acquired MCI Telecommunication Corporation’s internet business in the United States and worldwide. In June 1999, Cable & Wireless acquired International Digital Communications Inc. (now re-named Cable & Wireless IDC Inc.), one of Japan’s international telecommunications carriers.

In October 1999, Cable & Wireless completed the sale of its interest in One2One, its UK mobile phone business, to Deutsche Telekom. One2One was a joint venture with MediaOne Group Inc and the joint venture partners received £6.9 billion in cash.

In May 2000, Cable & Wireless took full ownership of the corporate, business, IP and wholesale operations of CWC (CWC DataCo), while the consumer telephone, internet and cable TV operations (CWC ConsumerCo) were acquired by ntl Incorporated.

In August 2000, Cable & Wireless disposed of its interest in Cable & Wireless HKT Limited (based in Hong Kong) to a subsidiary of PCCW Limited. Cable & Wireless received cash and shares in PCCW equivalent to an interest of approximately 20 per cent in the enlarged company. The PCCW shares were subsequently sold by Cable & Wireless in September 2000 and June 2003 for a total consideration of approximately £1,160 million.

In September 2001, Cable & Wireless disposed of its interest in Cable & Wireless Optus Limited (based in Australia) to a subsidiary of Singapore Telecommunications Limited (SingTel). Cable & Wireless received cash and SingTel shares and bonds, which were subsequently sold.

The web services and hosting businesses, Digital Island, Inc. and selected assets and the majority of business activities of EXDS, Inc (formerly Exodus Communications, Inc) were acquired in 2002.

Recent acquisitions and disposals |

In June 2003, Cable & Wireless announced that it planned to withdraw from the US domestic market. On 8 December 2003, Cable & Wireless USA, Inc. and Cable & Wireless Internet Services, Inc. (together, with certain of their affiliates, referred to as “Cable & Wireless America” or “CWA”) entered into an agreement with an affiliate of Gores Technologies LLC (“Gores”) to sell substantially all of the assets of CWA for a sum of US$125 million, subject to higher and better offers pursuant to a court-supervised competitive auction conducted under Section 363 of the US Bankruptcy Code. On that date, and at the request of Gores, CWA filed for Chapter 11 bankruptcy protection under the US Bankruptcy Code.

As a result of the subsequent auction process, on 23 January 2004, SAVVIS Communications Corporation (“SAVVIS”) entered into an agreement with CWA for SAVVIS to acquire substantially all of the assets of CWA for a sum of US$155 million in cash and approximately US$12.4 million of assumed liabilities. The contract contained certain conditions of a standard nature, including regulatory approvals. All of the conditions to the sale were satisfied and completion of the sale was announced on 8 March 2004.

Page 6

business description

Cable & Wireless understands that the proceeds of the sale will be applied to satisfy outstanding liabilities of CWA and the remaining assets of CWA will be wound down by the CWA estate.

The CWA estate is responsible for dealing with creditors and related aspects of the Chapter 11 process. The CWA estate has filed a Plan of Liquidation and associated documents with the US Bankruptcy Court. The Plan, which is supported by the CWA Creditors’ Committee and by Cable and Wireless plc, is subject to approval by relevant classes of creditors and the US Bankruptcy Court in due course. Copies of the Plan are publicly available. If the Plan is approved, among other things:

| • | certain classes of creditors will receive a monetary return from the estate; |

| • | any claims which creditors have against the estate will be released; |

| • | claims of Cable and Wireless plc and its non-bankrupt affiliates against the CWA estate will be settled and potential claims of the CWA estate against Cable and Wireless plc and such affiliates will be released; and |

| • | all shares held in CWA (including those held by Cable & Wireless affiliates) will be cancelled. |

As of 8 December 2003 the CWA entities were deconsolidated from the Group. These entities have separate boards and are no longer subject to Cable & Wireless Group operating requirements. CWA is subject to the jurisdiction of the US Bankruptcy Court. Accordingly, apart from certain financial discussions, references to CWA in this document are limited.

In order to provide US connectivity for data and IP services to Cable & Wireless’ multinational customers based in the United Kingdom and other regions, Cable & Wireless continues to operate in the United States.

The licences held by TeleYemen, Cable & Wireless’ subsidiary in Yemen, expired on 31 December 2003 and the Group ceased operations in Yemen from that date.

In addition, during 2004 the Group disposed of certain domestic businesses in Sweden, Belgium, the Netherlands, Italy, Switzerland, France and Germany and the domestic data business in Russia.

On 28 May 2004, Cable & Wireless announced the purchase of the share capital of Bulldog Communications Limited (“Bulldog”), a UK company specialising in the provision of broadband services, for a sum of £18.6 million. Bulldog offers a wide range of high-speed broadband services using digital subscriber line technology, both on the basis of BT

wholesale tariffs and, increasingly, as a principal, having installed its own equipment in 38 BT exchanges in central London under Local Loop Unbundling regulation.

On 2 June 2004 Cable and Wireless announced the purchase of a 55 per cent stake in Monaco Telecom S.A (“Monaco Telecom”) from Vivendi Universal for a total consideration of Euro 162 million, through the acquisition of 100 per cent of the issued share capital of Compagnie Monegasque de Communication.

The transaction was completed on 18 June 2004.

On completion, Cable & Wireless transferred a 6 per cent stake in Monaco Telecom to Compagnie Monégasque de Banque S.A.M (“CMB”) for consideration of Euro 18 million. CMB is Cable & Wireless’ financial partner in Monaco Telecom and its 6 per cent stake is subject to certain put and call agreements with Cable & Wireless. Cable & Wireless has full management control of Monaco Telecom.

Cable & Wireless has entered into a shareholders’ agreement with the Principality, which contains, among other provisions, a prohibition on either Cable & Wireless or the Principality (subject to certain limited exceptions) selling their shares in Monaco Telecom for 5 years, mutual pre-emption rights on the transfer of shares and certain other limited rights in favour of the Principality. The Principality also has a put option entitling it to put its 45 per cent shareholding in Monaco Telecom at certain times after 1 January 2008. The exercise price under the put option is fair market value, taking into account the nature of the minority stake in Monaco Telecom.

Monaco Telecom is an integrated telecommunications operator created in 1997 following the privatisation of the Principality’s incumbent public telecommunications operator. Monaco Telecom has a licence to provide public telecommunications services throughout Monaco, with exclusive rights to provide fixed line, mobile, internet access, and cable services in Monaco until at least 2014. Internationally, Monaco Telecom has operated a mobile network in Kosovo since 2000, under a management contract and at the beginning of 2003 it was awarded the second GSM licence in Afghanistan as the strategic partner in a consortium 51 per cent owned by the Aga Khan Fund for Economic Development.

For the year ended 31 December 2003, Monaco Telecom reported consolidated turnover of Euro 172 million, net profit of Euro 18 million, and had Euro 74 million of net assets at that date which included Euro 73 million of cash.

Page 7

business description

Capital expenditure |

Capital expenditure on plant, equipment and property totalled £0.3 billion in 2004 compared with £0.8 billion in 2003 and £1.9 billion in 2002.

Cable & Wireless’ capital expenditure in 2004 included the following third party investments:

| • | network build, totalling £70 million, mainly relating to international and pan-regional capacity as well as the UK network; |

| • | the continued rollout out of the GSM mobile network primarily in the Caribbean and Panama and upgrades to existing networks, totalling £120 million; |

| • | information technology (“IT”), totalling £79 million, including expenditure on billing systems, network management systems, and IT support for capital projects; and |

| • | network terminating equipment and customer premises equipment totalling £72 million. |

The above numbers include working capital allocations.

| BUSINESS OVERVIEW |

Products and services |

Cable & Wireless provides a variety of services including voice, data, IP and mobile to its customers through its national and international operations.

Voice |

Cable & Wireless offers domestic and international voice services via switched and dedicated facilities to residential, business, corporate and multinational customers.

Through its Carrier Services operations, Cable & Wireless provides wholesale services and interconnect to mobile operators and carriers with customers including incumbent former monopolies, mobile operators and regional telecommunications companies and service providers.

Cable & Wireless offers mobile voice and messaging services, principally using GSM (Global System for Mobile Communications) and TDMA (Time Division Multiple Access) technology. As at 31 March 2004, Cable & Wireless subsidiaries, branches and associates provided mobile telecommunications services to 3.1 million customers around the world, of which some one million relates to associate companies.

In countries where Cable & Wireless is the local incumbent operator, such as the Caribbean, Panama and Macau, customers are typically served through Cable & Wireless’

own fixed line and mobile network facilities. In other regions, customers are primarily connected to the Cable & Wireless network via third party local loops and leased line facilities or directly via fibre or microwave links.

Data |

Cable & Wireless has a portfolio of data services including traditional data transport services (frame relay) and national and international switched and dedicated services based on ATM (Asynchronous Transfer Mode, a high speed digital transmission technology).

IP |

Cable & Wireless focuses on three IP product sets: IP communications that enable customers to migrate from traditional telecommunications services to IP services with improved functionality; access solutions; and transit to IP networks and the internet. Access solutions include value-added security services such as managed firewalls, intrusion detection and response, scanning and analysis (such as email virus protection) and authentication and encryption services.

Cable & Wireless’ IP-VPN QoS solution delivers these products through a multi protocol switching based IP solution which creates virtual private networks and allows customers to prioritise traffic to best fit their business needs. IP-VPN QoS delivers a secure intranet environment over which voice, video, data and other traffic can flow and can incorporate business partners and remote workers as well as the customers’ own sites.

In the Caribbean, Panama, Macau and Rest of the World, Cable & Wireless also provides residential and business customers with dial-up IP and other internet services, including broadband ADSL (Asymmetrical Digital Subscriber Line) solutions.

Page 8

business description

Geographic operations |

Cable & Wireless’ principal operations are in the United Kingdom, Europe, the Caribbean, Japan, Panama and Macau. Rest of the World comprises the Group’s operations in Guernsey, Bahrain and the Maldives, together with smaller operations in the Seychelles, Bermuda, Sakhalin in Russia, Diego Garcia, Falkland Islands, Fiji, Ascension, St Helena, Vanuatu and the Solomon Islands.

Cable & Wireless provides voice, data and IP services to large corporate customers, business and residential customers. In addition, the United Kingdom, the Caribbean, Panama and Macau provide specialist wholesale services to carriers, mobile operators and content, application and internet providers.

For a discussion of Cable & Wireless’ revenue by geographic market for the past three years, see Operating and Financial Review – Group Turnover.

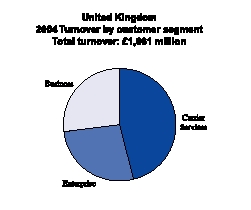

United Kingdom |

Overview |

The UK telecommunications market is mature with a considerable number of competitors, significant network capacity and competitive pricing. In the United Kingdom, Cable & Wireless is the largest fixed line telecommunications services provider after BT.

The UK business provides a full range of services to businesses, from international and domestic voice, data and IP services to complex web hosting solutions and professional services.

Significant progress has been made in transforming the UK business with the exit or sale of 34 properties, the insourcing of some IT activities and an overall headcount reduction of approximately 1,280, net of recruitment activities to enhance the skill mix of the business. With the cash position of the business stabilised and the asset base realigned, future capital expenditure will be focused on the delivery of new capabilities and system improvements.

Enterprise (Revenue £453 million) |

Enterprise generates approximately 27 per cent of the UK business’ revenues. This segment comprises large national and international businesses which purchase telecommunications services in the business’ territories. In the UK market, Enterprise customers represent 50 per cent of the telecommunications market spend from businesses with more than five employees. Companies in this segment buy telecommunications services from a variety of suppliers, although many have a longer-term relationship with a primary supplier.

The UK business has a number two position in the enterprise segment in the UK market. For approximately 50 enterprises, Cable & Wireless UK supplies over half of their requirements and is the main partner in developing and managing their telecommunication networks. For other enterprise customers in the UK market, Cable & Wireless is typically the second provider of voice based services.

Cable & Wireless’ objective in the enterprise market is to become the partner of choice for more companies as they transition from legacy voice to IP. Cable & Wireless believes that this will lead to a gradual shift in the revenue mix away from switched voice. However, switched voice will continue to generate the majority of revenues in the shorter term.

A key step in achieving this objective was the creation of a separate professional services division in April 2004. Cable & Wireless’ professional services offering includes consultancy, project management and a portfolio of managed services for a broad range of customers which builds on component products such as Home and Remote Working, Customer Interaction Management Services (Call Centres), Business Continuity and Security Services.

The professional services division includes the UK Infrastructure services group which provides a single source for hardware installation and the maintenance of voice, data and cabling systems, together with systems development and

Page 9

business description

integration services for information and communications technologies.

Business (Revenue £445 million) |

Services to Business customers generated some 27 per cent of the UK revenues. Cable & Wireless provides both voice and data services to the business segment, with voice representing over 80 per cent of total Business revenues. However, customers are increasingly beginning to purchase voice and data as a bundled service to simplify the purchasing process. There is rapid growth in demand for new services including:

| • | the replacement of leased lines with ADSL and symmetric digital subscriber lines; |

| • | combination of voice and data on a single network; and |

| • | increased bandwidth. |

Carrier Services (Revenue £763 million) |

Carrier Services generate approximately half of Cable & Wireless UK business’ revenue. This market is highly competitive.

The UK Carrier Services’ operations serve customers in three main segments:

| • | large international telecommunications companies, mainly focused on long distance international voice; |

| • | national mobile operators, buying international voice and transport/backbone services, which are one of the fastest growing sectors in the United Kingdom; there is also small but increasing demand from the mobile operators for new data services such as Roaming for data, GSM, short messaging services (“SMS”) and multimedia messaging services; and |

| • | regional and domestic operators, including resellers and ISPs. |

Carrier Services also provide carrier pre-select services (a method of indirect voice access) to UK providers who resell telecommunication services under their own brands to residential customers. This enables UK residential consumers to select an alternative operator to BT for their voice calls in advance, without having to dial additional codes or programming on-site equipment.

US network |

Cable & Wireless continues to operate in the US market through a small, predominantly international network. The business provides US connectivity for data and IP services to Cable & Wireless’ multinational customers based in other regions; primarily those served by the United Kingdom and Japan.

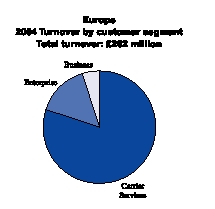

Europe |

The principal operations in continental Europe are in Germany, France, Spain and Italy, together with smaller operations in Russia, Belgium, the Netherlands, Switzerland and Sweden.

The continental European telecommunications market comprises EU countries which are mature and fully liberalised; mature and competitive non-EU markets; and the liberalising markets of Eastern Europe.

During the last 12 months the continental European operations have been refocused on Enterprise customers and the existing wholesale business. Cable & Wireless Europe has withdrawn from the provision of IP and data connectivity services to small and medium sized business customers. In Spain, Cable & Wireless has retained its network integration business, which operates across all segments of the Spanish market.

The continental European reorganisation has resulted in a reduction in the European network coverage, a reduction in work force from 1,136 to 519 employees and a reduction in customers from 29,000 to fewer than 1,000.

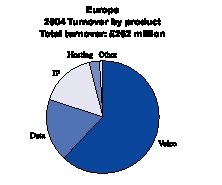

Carrier Services (Revenue £208 million) |

Carrier Services’ revenues represent over three-quarters of revenue in continental Europe. The main Carrier Services’ customers are mobile operators and telecommunications operators.

Page 10

business description

Caribbean |

![]()

Cable & Wireless operates in 16 Caribbean countries. The following statements apply to these countries unless otherwise stated. The principal businesses are in Jamaica (82 per cent owned), Barbados (81 per cent owned), the Cayman Islands (100 per cent owned) and Trinidad and Tobago (49 per cent owned).

In nearly all of the Caribbean countries in which it operates, Cable & Wireless is the incumbent, fixed and mobile operator providing some or all of the domestic and international telecommunications services.

In the Caribbean countries where Cable & Wireless’ subsidiaries and branches provide domestic telephone services, the number of telephone lines in service totalled approximately 830,000 at 31 March 2004, an overall decrease of approximately 30,000 in the year. During the same period, Cable & Wireless’ mobile subscribers of these territories increased from 943,000 to 1,141,000.

Cable & Wireless has mobile licenses in all of its Caribbean countries with the exception of the British Virgin Islands, Guadaloupe and Martinique. The Caribbean operations provide a range of mobile services, including pre- and post-paid services, SMS and international inbound and outbound roaming.

Cable & Wireless has accelerated its investment in a new GSM network in the Caribbean. At 31 March 2004 GSM services had been launched commercially in Jamaica, Barbados, the Cayman Islands, St Lucia, Grenada, Dominica and St Vincent.

At 31 March 2004, there were over 500 base stations with land mass coverage typically ranging from 60 per cent to 90 per cent. GSM technology provides higher transmission speeds enabling Cable & Wireless to offer new mobile services including internet access, multimedia messaging and E-banking.

The Caribbean operations also provide a full range of internet services to customers, including dial-up, directconnect, web hosting, web-site design and ADSL services which provide broadband access.

As at 31 March 2004 a significant proportion of Caribbean revenues were exposed to competition with most markets in which Cable & Wireless operates fully liberalised. Others are in transition from monopoly environments to competitive markets. Cable & Wireless is engaged in dialogue with those host governments to provide for an orderly liberalisation.

The table below shows the dates of market liberalisation for the principal Caribbean operations.

Country | National | International | Mobile | Data & Internet | |||||||||

| Jamaica | Sep-01 | Mar-03 | Mar-00 | Mar-00 | |||||||||

| Barbados | Nov-03 | See Note 1 | Aug-03 | Long standing | |||||||||

| Trinidad and Tobago | See Note 2 | See Note 2 | See Note 2 | Long standing | |||||||||

| Cayman | July-03 | April-04 | Feb-04 | Nov-03 | |||||||||

| Note 1: Under discussion with the Government of Barbados and the Government of Barbados has expressed its intention to introduce competition in international services in July 2004. |

| Note 2: In Trinidad and Tobago the Government is in the process of finalising the passage of the Telecommunications Act 2001. Thereafter, management believes that the mobile market will be liberalised within one year, with national and international market sectors to follow, although no timetable has yet been announced. |

Jamaica |

Jamaica is the largest of the Caribbean operations generating 38 per cent of the Caribbean’s revenue in 2004. Cable & Wireless holds an 82 per cent interest in Cable & Wireless Jamaica Limited, the largest provider of telecommunications services in Jamaica.

Cable & Wireless Jamaica provides domestic and international fixed line, internet, data and mobile telecommunication services to residential and business customers. In additon to Cable & Wireless Jamaica, there are currently two active competitors in the mobile sector (with a third licence recently announced), ten active “ISPs” (out of a total of 64 licensed parties), 27 licensed data service providers and one competitor in the domestic fixed line sector, as well as a number of resellers. The international carrier market has been liberalised since March 2003 and now comprises 59 licensed carriers, of which 14 are active and interconnect with Cable & Wireless Jamaica.

Barbados |

Cable & Wireless (Barbados) Limited is 81 per cent owned by Cable & Wireless and provides domestic and international fixed line, internet, data and mobile telecommunications services to residential and business customers.

Page 11

business description

Three mobile licences have been issued to competitors in Barbados and two of these competitors launched services in February 2004. Four ISPs offer internet services to end customers over Cable & Wireless’ network. The domestic telecommunications market is now fully liberalised. The introduction of competition in international services is currently under discussion with the Government which has expressed its intention to introduce such competition in July 2004.

Cayman Islands |

Cable and Wireless (Cayman Islands) Limited provides domestic, international, internet, data and mobile services to residential and business customers in the Cayman Islands. In July 2003, the Government of the Cayman Islands and Cable & Wireless agreed terms under which Cable & Wireless would surrender its exclusivity. The market is now fully liberalised. At 31 March 2004, 20 new entrants had been licensed in various telecommunications, broadcasting and other communication market sectors.

Trinidad and Tobago |

In Trinidad and Tobago Cable & Wireless operates through its 49 per cent owned joint venture, Telecommunications Services of Trinidad and Tobago Limited (“TSTT”). The controlling 51 per cent shareholding is owned by National Enterprises Limited, a public company with majority state ownership. TSTT provides domestic and international fixed line, internet, data and mobile telecommunications services to residential and business customers. TSTT contributed 21 per cent of the Caribbean’s operating profit in 2004.

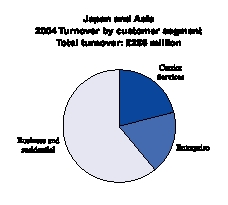

Japan and Asia |

Overview |

The Japan division comprises Cable & Wireless’ operations in Japan and Asia, excluding Macau. Japan accounts for over 88 per cent of the division’s revenue.

Business and residential (Revenue £174 million) |

Cable & Wireless IDC Inc. sells voice, data, IP and hosting products to the small and medium sized business market in Japan through its own sales force and also through a variety of agents and partners. Smaller business customers and residential customers are served mainly through indirect channels and resellers. Cable & Wireless IDC Inc. had 75,000 residential and 22,000 business customers as at

31 March 2004.

Carrier Services (Revenue £60 million) |

Cable & Wireless’ operations in Japan and Asia sell voice, IP and data products to other operators and ISPs.

Enterprise (Revenue £52 million) |

Cable & Wireless IDC Inc., together with operations in Hong Kong, Singapore, Australia and India provide corporate enterprises with international networking services. In addition, these operations offer full design and management services for a variety of IP based solutions.

Page 12

business description

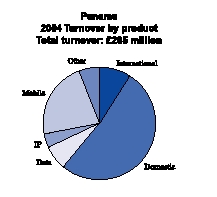

Panama |

Cable & Wireless owns a 49 per cent interest in, has management control of and consequently consolidates, the largest telecommunications company in Panama, Cable & Wireless Panama S.A. The Panamanian Government holds 49 per cent of the shares while the remaining two per cent are held by the company’s employees through a trust fund.

As at 31 March 2004, some 50 competitors had over 100 licences to offer basic voice telephony services. Cable & Wireless Panama is in the process of negotiating interconnection agreements with several of these operators. At 31 March 2004, competition in fixed line services was largely confined to international and national long-distance services.

Cable & Wireless has one direct mobile competitor in Panama. Current regulations provide for a duopoly within mobile until 2007.

Cable & Wireless Panama provides a full range of internet services to customers, including dial-up, web hosting, web-site design and broadband access. The internet sector has been competitive for many years and at 31 March 2004 there were some 13 internet access providers and 130 internet/web related service competitors in the sector.

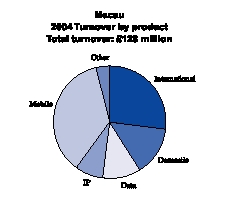

Macau |

In Macau, Cable & Wireless’ subsidiary is Companhia de Telecomunicações de Macau S.A.R.L. (“CTM”). CTM is managed and 51 per cent owned by Cable & Wireless. The other shareholders of CTM are Portugal Telecom Group, 28 per cent, CITIC Pacific Limited, 20 per cent, and Direcção dos Serviços de Correios de Macau, one per cent.

In Macau, CTM is the domestic incumbent offering a full range of international and domestic, fixed, internet, data and mobile services.

CTM owns and operates fully digital domestic fixed line networks and international interconnect facilities via microwave, satellite systems and international submarine and land cables. CTM has exclusive rights to operate local and international fixed telecommunications services within, to and from Macau until the end of 2011 when the asset may revert to the Macau Government at zero value. The exclusivity is to be reviewed by the Macau Government and CTM in 2006 and its conditions may be changed subject to agreement. The Macau Government has the right to redeem the concession in 2006 with one year prior notice subject to compensation as set out in the relevant Concession Agreement. In 2003, the government enacted the External Facilities Act, which provides for competition in leased lines and transit services. As at 1 June 2004, no licence had been issued under the Act.

CTM operates a GSM mobile network. The mobile market was liberalised in 2001 and two competitors launched services in August 2001. CTM has two main competitors. CTM retains a significant market share. In the Macau telecommunications market, mobiles outnumber fixed lines. The government is considering the issue of Third Generation Wireless (“3G”) and Code Division Multiple Access licences. As at 1 June 2004 no tender arrangements had been announced.

CTM also operates a data centre offering a wide selection of web-based and hosting services and an ATM network for broadband ADSL access.

Page 13

business description

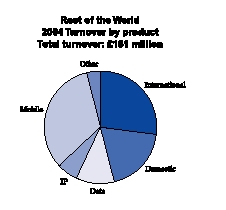

Rest of the World |

Rest of the World comprises Cable & Wireless’ businesses in Guernsey, Bahrain and the Maldives, together with smaller operations in the Seychelles, Bermuda, Sakhalin in Russia, Diego Garcia, Falkland Islands, Fiji, Ascension, St Helena, Vanuatu and Solomon Islands. Guernsey and the Maldives account for 54 per cent of the Rest of the World revenue.

Guernsey |

Cable & Wireless owns 100 per cent of Cable and Wireless Guernsey Ltd (“C&W Guernsey”). C&W Guernsey is the incumbent operator in Guernsey providing fixed and mobile voice and data services to all segments of the market, including residential, businesses and government. Another provider is planning to launch 3G mobile services in summer 2004 in line with the States of Guernsey’s liberalisation policy.

Maldives |

Cable & Wireless has a 45 per cent interest in, and management control of, Dhivehi Raajjeyge Gulhun Private Limited (“Dhiraagu”). The remaining 55 per cent are held by the government of the Maldives. Dhiraagu provides exclusive domestic and international fixed and mobile telecommunication services to residential and business customers. The government has announced its intention to license a second mobile operator and has invited bids to

undertake a feasibility study. Internet services were liberalised in January 2003.

Bahrain |

Cable & Wireless owns 20 per cent of its associate Bahrain Telecommunications Company (“Batelco”). Batelco provides domestic and international fixed line and mobile telecommunication, data and internet services to residential and business customers. The Government of Bahrain has announced its intention to sell its equity holding in Batelco. The Government has a holding of 36.67 per cent. The telecommunications market in Bahrain has begun to be liberalised, with MTC Vodafone launching a mobile service in December 2003.

Infrastructure |

In the Caribbean, Panama, Macau and Rest of the World, Cable & Wireless typically operates as the domestic incumbent, owning and operating the domestic fixed line networks and associated international interconnect facilities. Cable & Wireless also has international and domestic network facilities in the United Kingdom, Japan, continental Europe and the United States.

Cable & Wireless operates significant international submarine cable and satellite systems. Many of Cable & Wireless’ subsidiaries and associates also own and operate mobile networks. Examples include Jamaica (GSM and TDMA) and Trinidad and Tobago (GSM and TDMA) in the Caribbean as well as Panama (GSM and TDMA), Macau (GSM), the Maldives (GSM) and Bahrain (GSM).

Cable & Wireless continues to expand its GSM network in the Caribbean and has rolled out GSM networks in Jamaica, Barbados, Cayman, St Lucia, Dominica, Grenada and St Vincent with further GSM launches planned across the Caribbean during 2004.

Cable & Wireless companies also operate some 20 data centres within its national and international operations offering a wide selection of web-based and hosting services.

| REGULATORY FRAMEWORK |

Cable & Wireless, like other international telecommunication providers, faces regulatory and market access constraints in various countries resulting from laws, public policies and licensing requirements. This reflects the perception of telecommunications as a public service, a history of special or exclusive rights to provide services and, often, a structured move towards liberalisation and the introduction of competition. Generally, specialist telecommunications

regulation is administered through enforcement of conditions contained in operating and service licences held by the Group and its subsidiaries.

Many of the markets in which Cable & Wireless operates are in transition from monopoly environments to competitive markets. With the global trend towards liberalisation, Cable & Wireless is engaged with host governments, who want to

Page 14

business description

modify exclusive licences, in order to facilitate an orderly transition to a fully competitive environment. The discussions involve negotiating revised regulatory arrangements which provide for equal treatment and opportunity during the transitional period.

In all jurisdictions where it operates, Cable & Wireless is required to comply with regulations which affect its business. The Group believes it complies in all material respects with all material regulatory obligations and where regulatory compliance issues emerge it takes action to ensure compliance.

Licensing |

Cable & Wireless provides international and domestic telecommunications services under exclusive and non-exclusive licences in the jurisdictions in which it operates. These licences are either held by Cable & Wireless itself or by local operating entities owned either wholly or partly, directly or indirectly, by Cable & Wireless.

The Group believes it has all licences material to the running of its business. It is possible that from time to time, as further products and services are deployed or changed, additional licences or authorisations will be required. Where the Group identifies the need for further licences or authorisations, it intends to acquire such licences. The terms of the Group’s licences vary, although most remain in effect for a fixed period of 10 to 25 years, or for an indefinite period subject to notice of termination after a specified minimum period. Licence fees are sometimes required, either as a fixed annual fee or a fee equal to a percentage of the revenue or profits arising from the licence.

Following the implementation of the European Union electronic communications directive, which was intended to be transposed into national law by member states by 25 July 2003, member states of the European Union will no longer issue individual telecommunications licences to companies except in exceptional circumstances such as the allocation of spectrum. Therefore, Cable & Wireless expects that substantially all telecommunications licences it holds in EU member states will be revoked. Cable & Wireless will continue to offer telecommunications services subject to obligations set forth in general conditions as dictated by the electronic communications directive and individual member states.

Some licences provide that, upon their termination, the relevant government may purchase, or have the option to purchase, the property, plant and equipment of the licensee in that territory at a fair market value. In some cases, where the Group owns an operating company jointly with government, that government has the right to purchase, at

specified times, the whole or part of the Group’s shareholding in the operating company.

The international trend is for telecommunications liberalisation and the replacement of exclusive licences with non-exclusive licences alongside rules governing competition between operators. Jurisdictions that currently support monopoly provision may also decide to promote competition, and Cable & Wireless anticipates that some existing exclusive licences will not be renewed on an exclusive basis or that governments will seek to withdraw their exclusivity before the licence expires.

The Group is committed to participating in discussions on the introduction of competition in any territory where its government wishes to do so.

There is no guarantee that an agreement to provide either a monopoly or franchised service will remain in effect for the full term of the agreement.

Regulation by jurisdiction |

The regulatory institutions and policies of the jurisdictions in which the Group operates are varied.

Europe |

Following the transposition of the EU electronic communications directives into national laws, member states will no longer require market entrants to hold an individual licence. Instead, providers of electronic communications networks and services are regulated through general authorisations. Accordingly the individual licences that Cable & Wireless holds in EU member states have been or will be revoked in the near future. Outside the European Union, Cable & Wireless operates in Guernsey, the Isle of Man, Norway, Russia and Switzerland with relevant licences and authorisations.

The regulatory framework in member states of the European Union is harmonised by EU directives though there are divergences in regulatory policy and practice between member states. The directives of the European Union 2003 electronic communications package were adopted by the European Union in February 2002 and seek to harmonise telecommunications across the European Union. Member states were required to implement the directives by 25 July 2003, although many have not met this requirement. The legislative package involves the concept of significant market power to determine which operators should have prior obligations placed on them, on the grounds that such operators might exploit that market position to the detriment of competition and therefore consumers.

Page 15

business description

United Kingdom |

The telecommunications market in the United Kingdom is regulated primarily under the Communications Act 2003 (“UK Comms Act”). The UK Comms Act sets the framework for the regulation of telecommunications broadcasting markets as well as the civilian use of spectrum in the United Kingdom. Insofar as it applies to telecommunications markets, it updates the Telecommunications Act 1984 and transposes the EU electronic communications directives into UK law. It also lays out the powers and duties of the industry regulator, the Office of Communications (“Ofcom”).

Following reviews by Ofcom, BT has been designated as having Significant Market Power in a number of markets. BT is therefore required to provide cost-based interconnection for switched voice services and leased line access circuits (Partial Private Circuits) to providers of public electronic communications networks such as Cable & Wireless on non-discriminatory terms. Such services are subject to network charge controls.

Following the review of wholesale International Direct Dial (“IDD”) markets, Cable & Wireless has a designation of Significant Market Power on wholesale IDD routes from the United Kingdom to four destinations: Ascension, Diego Garcia, Montserrat and Turks & Caicos. The obligations associated with this designation are minimal.

In addition, in common with all other providers of fixed public voice networks in the United Kingdom, Cable & Wireless has been designated as having Significant Market Power in the markets for geographic call termination on the UK network. As this designation has been applied to all operators, obligations are likely to be minimal and the Group expects that there will be little or no impact.

Ofcom has launched a review of the UK telecommunications regulatory framework which Cable & Wireless understands is scheduled to be completed by end of calendar year 2004.

The Caribbean |

Cable & Wireless has businesses in 16 countries in the Caribbean. Cable & Wireless is, or has been, exclusively licensed in the majority of these territories which are now either fully liberalised or are in transition. Cable & Wireless is engaged in ongoing dialogues with host governments to facilitate an orderly transition to liberalisation.

The regulatory frameworks in which the most significant Cable & Wireless Caribbean businesses operate are described in this section.

Cable & Wireless Jamaica operates in a fully liberalised market, regulated by the Office of Utilities Regulation.

Cable & Wireless Barbados operates in fully liberalised fixed line and mobile domestic markets. The international market is scheduled to be liberalised later in 2004. The regulatory authority for fixed telecommunications in Barbados is the Fair Trading Commission. Mobile telecommunications are regulated by the Ministry of Industry and International Business.

Cable & Wireless Cayman Islands operates in a fully liberalised market. Cable & Wireless Cayman Islands is subject to the regulation of the Information and Communications Technology Authority.

Five member states of the Organisation of Eastern Caribbean States (Dominica, Grenada, St Kitts and Nevis, St Lucia, St Vincent and the Grenadines) are contracted in a single jurisdiction for telecommunications regulation with a regional regulator, the Eastern Caribbean Telecoms Authority (“ECTEL”), and are also subject to the jurisdiction of national regulators, the National Telecoms Regulatory Committees. Telecommunications markets in the ECTEL states are fully liberalised.

Japan |

Cable & Wireless IDC is a registered telecommunications business and is approved by the Ministry of Public Management, Home Affairs, Posts and Telecommunications. Among the services Cable & Wireless IDC provides in Japan are web hosting, international and domestic voice and data services, IP access, managed corporate services, and wholesale services to other carriers in the Asian region.

Substantial revisions to the Telecommunication Business Law came into effect as of 1 April 2004. Under these revisions, the separation of telecommunication business licences between Type I (facilities) and Type II (services) was abolished. Telecommunication licences now are classified as notified or registered telecommunication licences. The revisions also introduced a significant degree of tariff deregulation, relieving non-dominant operators of the need to file tariffs.

Interconnection charges for origination and termination of traffic on the networks of Nippon Telegraph and Telephone (“NTT”) East Corporation and NTT West Corporation impact the profitability of Cable & Wireless IDC’s voice business. The Ministry of Public Management, Home Affairs, Posts and Telecommunications regulates these interconnection charges. Certain interconnection charges used by Cable & Wireless IDC’s voice services were retroactively adjusted to reflect actual traffic trends resulting in an increase of approximately 10 per cent from 1 April 2003 compared to the prior year. There is the possibility of further retrospective increases later in 2004.

business description

United States |

As discussed more fully at the beginning of this section, on 23 January 2004, Cable & Wireless Internet Services, Inc. and Cable & Wireless USA, Inc. together with certain of their affiliates referred to as “CWA” entered into an agreement with SAVVIS Communications Corporation (“SAVVIS”) for SAVVIS to acquire substantially all of the assets of CWA. This followed the sale process under Chapter 11, Section 363 of the US Bankruptcy Code. All of the conditions to the sale were satisfied and the completion of the sale was announced on 8 March 2004.

In order to provide US connectivity for data and IP services to Cable & Wireless’ multinational customers based in other regions, Cable & Wireless continues to operate in the United States through its subsidiary Cable & Wireless Americas Operations, Inc. (“CWAO”). CWAO provides international, interstate and intrastate communications services to customers who require service to, from or through the United States. Under US law, interstate and international telecommunications services are regulated by the Federal Communications Commission (“FCC”) while intrastate services are regulated by state commissions. Non-dominant service providers such as CWAO are subject to a lesser degree of regulation than designated dominant service providers. CWAO also provides information services which generally are not regulated in the United States.

The regulated telecommunications services provided by CWAO may be classified as either common carrier or private carrier services depending upon the nature of the service offering. As a general matter, US law requires that common carrier services be offered (a) upon reasonable request, (b) on rates, terms and classifications which are just and reasonable, (c) without unjust discrimination or undue preferences basis, and (d) pursuant to authorisation of the FCC. Private carriers generally are not subject to these requirements, but are required to make contributions to the federal universal

service fund based on international and interstate telecommunications revenues, in the same manner as common carriers. Intrastate telecommunications services are subject to regulation by the relevant state public utility commission and may be subject to licensing requirements, tariffs, and/or subsidy mechanisms.

Other markets |

Cable & Wireless Panama operates in a fully liberalised market. The regulator is Ente Regulador De Los Servicios Publicos.

CTM Macau has an exclusive concession agreement to provide fixed national and international services until 2011 (subject to review in 2006). Mobile and IP services were liberalised in 2001. CTM Macau is subject to the regulation of the Office for the Development of Telecommunications and Information Technology.

Batelco, a Cable & Wireless associate company in which Cable & Wireless has a holding of 20 per cent, operates in Bahrain where the market is in the process of liberalisation. Currently there is competition in domestic mobile and internet services with the remainder of services liberalising in July 2004. Batelco is regulated by the Telecommunications Regulatory Authority.

The licence TeleYemen held for operating the international carrier in Yemen expired at the end of 2003. As a consequence Cable & Wireless has now exited that market.

Cable & Wireless has smaller operations and interests in other countries, which are at varying stages of liberalisation.

| PROPERTY |

As at 31 March 2004, Cable & Wireless and its subsidiaries lease or own in excess of 2,000 properties. The majority of sites are located in the United Kingdom, Panama and the Caribbean although the spread of properties extends across continental Europe, Asia, and islands in the Atlantic and Indian Oceans. Numerically, the bulk of properties are small technical sites, which house equipment necessary to support Cable & Wireless’ operations. In general, Cable & Wireless’ technical properties enjoy the protection of telecommunications legislation, which has the aim of ensuring the continuity of Cable & Wireless’ networks.

The size of Cable & Wireless’ property portfolio has reduced significantly over the last financial year primarily as a consequence of the disposal of the US domestic business together with other smaller operations in and around Europe. Additionally, a continuing rationalisation programme is being carried out, generally focusing on reducing office space, to match Cable & Wireless’ reduced headcount and ongoing operational requirements. Acquisition of both office and technical sites occurs where required.

business description

LEGAL PROCEEDINGS |

Class action litigation against Cable and Wireless plc |

Between December 2002 and February 2003, 10 shareholder class action lawsuits were filed in the United States District Court for the Eastern District of Virginia naming Cable and Wireless plc and several of its officers and directors as defendants.

In March 2003, the Court consolidated all of the cases into one action, styled as In re Cable and Wireless plc Securities Litigation, Civil Action No. 02-1860-A.

In May 2003, the lead plaintiffs filed a consolidated complaint that alleged violations of certain sections of the Securities and Exchange Act of 1934 and the rules promulgated thereunder. A central allegation was that the defendants made false and misleading statements about the Company’s financial condition by failing to disclose on a timely basis the existence of a tax indemnity and a ratings trigger to place money in escrow until any liability which the Company may have had under the tax indemnity was finally determined. The indemnity and ratings trigger appeared in an agreement reached in 1999 between the Company and Deutsche Telekom for the sale of the Company’s interest in the mobile telephone company that operated under the name One2One.

In addition to the allegations relating to the tax indemnity, the consolidated complaint also alleged that the defendants made false and misleading statements by: (1) failing to disclose certain lease liability commitments and (2) improperly recognising revenue received from sales of capacity to other carriers.

The plaintiffs sought unspecified money damages in their complaints.

The Company (and related individuals) filed motions to dismiss the class action complaint, which were heard on 31 October 2003. In March 2004, the Court issued orders in respect of the motions to dismiss.

The Court orders state in summary that:

| • | the defendants’ motions (including Cable and Wireless plc) to dismiss the consolidated class action complaint are granted; |

| • | the motion of Sir Ralph Robins, the Company’s former chairman, to dismiss the claims against him for lack of personal jurisdiction is granted; and |

| • | the defendants’ alternative motions to dismiss the claims of foreign (non-US) purchasers for lack of subject matter jurisdiction are denied. |

On 5 May 2004, the Court issued a Memorandum of Opinion, which dealt with the motion of Sir Ralph Robins to dismiss. The Opinion held that the Court has neither specific nor general jurisdiction over Sir Ralph Robins because his contacts with the United States were minimal.

In addition, on 15 June 2004, the Court issued a Memorandum of Opinion and Orders relating to the previous orders issued in March 2004. The Court stated that it would not grant leave to amend the complaint and ordered that judgement be entered against the plaintiffs. The Court found that the complaint, which alleged violations of US securities laws, failed to state a claim. The Memorandum of Opinion and Orders issued on 15 June 2004 disposed of all remaining claims in the case against Cable and Wireless plc, subject to appeal.

Resolution of dispute with IBM UK Limited |

Disputes between (1) Cable and Wireless plc and IBM United Kingdom Limited, (2) Cable & Wireless USA, Inc. and International Business Machines Corporation and (3) IBM Japan Limited and Cable & Wireless IDC Incorporated (collectively “Cable & Wireless” and “IBM” respectively) arose out of a Global Framework Agreement (“GFA”) dated 20 December 2000, and related agreements, pursuant to which IBM agreed to supply to Cable & Wireless information technology services.

On 8 September 2003, an amicable resolution of the matters in dispute was agreed upon by Cable & Wireless and IBM – the terms of which are confidential – following which, by consent, Cable & Wireless and IBM entered a Tomlin Order at the High Court of England and Wales. The effect of that order was to stay the legal proceedings, which existed between Cable & Wireless and IBM in relation to the disputes. On 31 December 2003, the terms of the GFA expired (Cable & Wireless having given notice to terminate the same in June 2003) and in January 2004, all services previously provided by IBM under the terms of the GFA were insourced back to Cable & Wireless.

Class action securities litigation against Digital Island, Inc., Cable & Wireless and others |

Digital Island Inc. (“Digital Island”), Cable and Wireless plc, Dali Acquisition Corp. (“Dali”) (a former subsidiary of Cable & Wireless which subsequently merged with Digital Island to form Cable & Wireless Internet Services, Inc.), and certain of the then present and former directors of Digital Island, were named as defendants in six separate putative class action lawsuits alleging various claims arising out of Cable & Wireless’ acquisition of Digital Island in August 2001. Three of the lawsuits were filed in the US District

business description

Court for the District of Delaware and three were filed in the Delaware Court of Chancery. The three federal lawsuits were consolidated into a single case.

The federal suit alleged that the defendants violated federal securities laws by failing to disclose on a timely basis that Digital Island had entered into certain business agreements with Bloomberg, L.P., and Major League Baseball. It further alleged that compensation agreements with certain officers and/or directors of the company violated the federal securities ‘all-holders’ rule. One state lawsuit alleged violations of Delaware law based upon similar allegations.

The other two state lawsuits alleged various violations of Delaware law against the same corporate defendants and the present and former Digital Island directors, including that they failed to disclose all material facts relating to Digital Island’s relationship with Microsoft, and that they failed to obtain a fair price for Digital Island shares.

On 10 September 2002, a federal District Court granted the defendants’ motion to dismiss the federal lawsuits with prejudice. Plaintiffs appealed the decision to the US Circuit Court of Appeals for the Third Circuit. On 6 February 2004, the US Circuit Court of Appeals for the Third Circuit upheld the decision of the federal District Court that the lawsuits be dismissed. This decision is final as to Cable and Wireless plc.

Litigation with Cibertec Internacional, S.A. and Inversiones Kamasu, S.A. |

Cibertec Internacional, S.A. and Inversiones Kamasu, S.A. initiated proceedings against Cable & Wireless Panama, S.A. and Cable and Wireless (CALA Management Services) Limited in Panama on 29 October 1999. The claim was for approximately US$125 million and alleged breach of contract. On 18 December 2002, the Civil Circuit Judge of the First Judicial Circuit of Panama handed down a decision against Cable & Wireless Panama, S.A. awarding damages of US$67,255,000, including moral damages and costs. The judge dismissed the complaint against Cable and Wireless (CALA Management Services) Limited.

Cable & Wireless Panama, S.A. subsequently appealed the judgment on 3 December 2002 and the parties settled the case on 28 October 2003. The settlement was approved by the First Superior Court of Panama on 6 November 2003. Under the terms of the settlement, Cable & Wireless Panama, S.A. did not accept or recognise any liability to the plaintiffs but voluntarily agreed to make a payment of US$14.5 million to the plaintiffs. The plaintiffs have waived all claims in this matter against Cable & Wireless Panama, S.A. and Cable and Wireless (CALA Management Services) Limited.

Claim against the Minister of Finance and Economy, Panama |

On 16 December 2002, a complaint was filed by two Panamanian lawyers exercising a public action at the Third Chamber of the Supreme Court of Justice of Panama questioning the law governing and rules of Public Bid No. 06 96 won by INTEL, S.A. (now Cable & Wireless Panama, S.A.). Complaints filed at the Third Chamber of the Supreme Court of Justice must be filed against the public officer who enacted the relevant regulation of act. This complaint was filed against the Minister of Finance and Economy in Panama specifically alleging that the Operating Agreement executed between Cable and Wireless (CALA Management Services) Limited and INTEL, S.A. (now Cable & Wireless Panama, S.A.) as part of the privatisation agreements was null and void ab initio, on the grounds that it had not been published in the Official Gazette in Panama.

The Operating Agreement enables Cable & Wireless Panama, S.A. to use the technical and management know-how of Cable and Wireless (CALA Management Services) Limited to more effectively fulfil its obligations under the concession granted to it by the Government of Panama to install, operate and exploit telecommunication services in Panama. Cable & Wireless Panama, S.A., due to its close interest in the outcome of the complaint requested recognition by the Court and permission to participate in the proceedings. The Court agreed to this.

On 21 March 2003, the Court permitted the claim to proceed. Cable & Wireless Panama, S.A. filed an appeal against the admission of the claim to proceed, however the Court confirmed its decision to permit the claim to proceed on 17 March 2004.

As required by Panamanian law, the Administrations General Attorney has provided an opinion to the Court in defence of the law or regulation which is the subject of the complaint. The Administrations General Attorney has opined that the Operating Agreement complied with all the requirements established by the law and by the rules of Public Bid No. 06 96 and was countersigned by the General Comptroller acting with due authorisation.

The proceedings are on-going.

Panamanian counsel consider this claim to be without merit and none of Cable and Wireless plc, Cable & Wireless Panama, S.A. or Cable and Wireless (CALA Management Services) Limited is party to the complaint. However, if the complaint were to be successful, the concession under which Cable & Wireless Panama, S.A. operates will not be affected, however the Operating Agreement could be declared null and void and then the complainants could file a complaint against Cable and Wireless (CALA Management

business description

Services) Limited requiring the return of all management fees collected under the agreement since its execution on 20 May 1997. This would amount to approximately £60 million. In the event that this complaint is successful, Cable & Wireless and its subsidiaries intend to vigorously pursue any legal recourse available to them.

Claim by Caribtel (Caribbean) Limited |