UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-05876

LORD ABBETT SERIES FUND, INC.

(Exact name of Registrant as specified in charter)

90 Hudson Street, Jersey City, New Jersey 07302-3973

(Address of principal executive offices) (Zip code)

Lawrence B. Stoller, Esq.

Vice President, Secretary, and Chief Legal Officer

90 Hudson Street, Jersey City, New Jersey 07302-3973

(Name and address of agent for service)

Registrant’s telephone number, including area code: (888) 522-2388

Date of fiscal year end: 12/31

Date of reporting period: 12/31/2022

| Item 1: | Report(s) to Shareholders. |

LORD ABBETT

ANNUAL REPORT

Lord Abbett

Series Fund—Bond Debenture Portfolio

For the fiscal year ended December 31, 2022

Table of Contents

Lord Abbett Series Fund — Bond Debenture Portfolio

Annual Report

For the fiscal year ended December 31, 2022

From left to right: James L.L. Tullis, Independent Chair of the Lord Abbett Funds and Douglas B. Sieg, Director, President, and Chief Executive Officer of the Lord Abbett Funds. | | Dear Shareholders: We are pleased to provide you with this overview of the performance of Lord Abbett Series Fund – Bond Debenture Portfolio for the fiscal year ended December 31, 2022. On this page and the following pages, we discuss the major factors that influenced fiscal year performance. For detailed and timely information about the Fund, please visit our website at www.lordabbett.com, where you can also access the quarterly commentaries that provide updates on the Fund’s performance and other portfolio related updates. Thank you for investing in Lord Abbett mutual funds. We value the trust that you place in us and look forward to serving your investment needs in the years to come. Best regards,

Douglas B. Sieg Director, President and Chief Executive Officer |

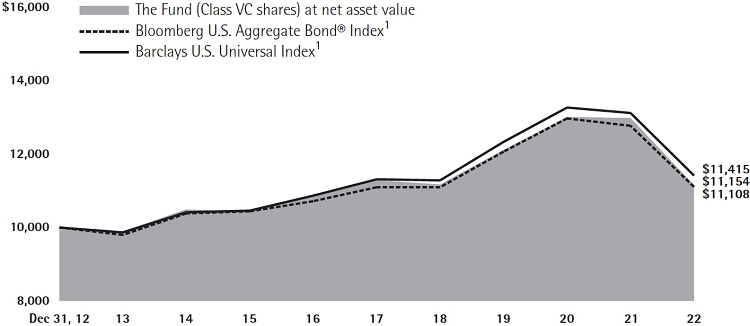

For the fiscal year ended December 31, 2022, the Fund returned -12.80%, reflecting performance at the net asset value (NAV) of Class VC shares with all distributions reinvested, compared to its benchmark, the Bloomberg U.S. Aggregate Bond Index,1 which returned -13.01% over the same period.

The twelve-month period ending December 31, 2022 introduced meaningful headwinds for U.S. markets that led to selloffs in virtually all asset classes. The major risks over the period were inflationary pressures, which reached multi-decade highs, and the most rapid pace of interest rate hikes implemented in history by the U.S. Federal Reserve (Fed). Rates spiked across

the U.S. yield curve as a result, with U.S. Treasury yields at almost all maturities reaching their highest levels in years. Other notable challenges for markets included supply chain dislocations and labor shortages influenced in part by the Omicron variant of COVID-19, as well as escalating geopolitical tensions headlined by Russia’s invasion of Ukraine.

The surge in interest rates over the year caused softness in both major fixed income and equity indices. Equities fared the worst amid the sell-off, with the S&P 500 Index2 returning -18.11% over the period and experiencing its worst year since the Global Financial Crisis (GFC) of 2008. The tech-heavy NASDAQ3 also logged its worst year since

1

2008, declining -32.54% over the period as growth-related stocks in semiconductor and software sectors suffered in the face of inflationary pressures. Within fixed income, higher rates caused underperformance in longer duration bonds. These included U.S. Treasuries4 and investment grade bonds5 which returned -12.46% and -15.76% over the period, respectively. However, high yield bond6 and leveraged loan7 indexes outperformed the investment grade index for the period because of their lower duration profiles. Notably, high yield bonds and leveraged loans returned -11.21% and -1.06%, respectively, outperforming higher quality bonds despite recessionary fears in the U.S. economy contributing to wider spreads. Leveraged loans in particular were able to significantly outperform relative to other assets given their insulation from interest rate volatility due to their floating-rate coupons.

Inflationary concerns began to take focus towards the end of 2021 before becoming a dominant storyline in 2022. Headline consumer price index (CPI) readings had hovered a little above 5% year-over-year for most of 2021, which led investors to question whether this period of rising prices would be more persistent than originally thought. This debate intensified in the beginning of the year as inflation readings continued as climb throughout the first half of 2022, with CPI peaking at 9.1% year-over-year in June. The surge in prices was due primarily to an imbalance between supply and demand dynamics across multiple industries, including energy, food, and used cars.

Inflationary pressures throughout the period were most evident in energy costs, which rose more than 30% year-over-year

by the end of June. The energy sector, which had been subject to rising consumer demand as global economies reopened from lockdowns induced by COVID-19, faced added friction with Russia’s invasion of Ukraine as Russia had been a large exporter of oil and certain minerals. Various sanctions were instilled on Russia from Western nations in response to their aggression towards Ukraine, which contributed to surging prices. Crude oil specifically reached over $100 per barrel, the highest value since 2014.

The Fed pivoted towards a much more hawkish stance on monetary policy during the period given the surge in inflation. After remaining mostly consistent in its messaging around expectations that price pressures would be transitory, elevated and more persistent inflation pressures caused the Fed to move the target federal funds rate into more restrictive territory. This resulted in a 25-basis point (bps) hike in the federal funds rate at the March Federal Open Market Committee (FOMC) meeting, the first hike in more than three years. Six additional rate hikes followed in the succeeding months, one of 50 bps, and four consecutive hikes of 75 bps and an additional one of 50 bps as inflation prints continued to come mostly in hotter than expected, resulting in a federal funds rate at a range of 4.25%-4.50% by the end of 2022. Bond yields shot up amid this aggressive policy, leading to a bearish curve flattening and ultimately periods of significant yield curve inversion, with the spread between the 2-year and 10-year Treasury yields hitting its most negative level in more than 40 years.

Key macroeconomic indicators trended lower throughout the period. Most notably, the U.S. reported real GDP decline of -1.6%

2

in the first quarter of 2022 and -0.9% in the second quarter before returning to growth in the third quarter. Worries of an impending recession resulted in consumer sentiment dropping to levels worse than during the height of the COVID-19 pandemic and the GFC of 2008, according to the U.S. Consumer Confidence Index.

Despite rising recessionary signs, select bright spots in the U.S. economy supported the idea that a potential recession would be shallow. One of the most positive developments seemed to be the traction behind the peak inflation narrative, which gained momentum in the fourth quarter from lower-than-expected CPI prints in both October and November. In addition, energy prices retracted from their multi-year highs, rent prices began to stabilize, and wage growth showed signs of softening. Job growth also remained strong in the period, and the U.S. national unemployment rate continued to hover around pre-COVID lows. Companies also cited relatively stable demand in both second and third quarter earnings seasons as consumers remained resilient despite higher prices. Separately, labor shortages eased, and supply chain frictions moderated, providing added benefits for companies managing generally higher input costs.

The Fund takes a flexible, multi-sector approach, which emphasizes credit sensitive sectors of the market, compared to its benchmark, which is largely comprised of U.S. Treasuries and government-related securities. Notably, the Fund’s allocation to lower rated, but shorter duration securities ultimately contributed to relative performance as government securities, which have lower

carry and longer duration profiles, underperformed. The Fund’s sub-investment grade allocation was primarily comprised of U.S. high yield corporate bonds, which outperformed the index. Many of these investments were within the Energy and Basic Industry sectors, which were broadly supported by a positive relationship to resilient commodity prices, leading to better returns relative to other sectors such as Media and Telecommunications. The Fund also had a modest allocation to bank loans that provided a boost to relative performance. Specifically, loans were one of the strongest performing asset classes for the period, as loan returns were more insulated from interest rate volatility given their floating rate nature. Separately, strong security selection within structured products, including collateralized loan obligations (CLOs) and commercial mortgage-backed securities (CMBS) was a positive contributor to relative performance. In addition to being higher rated investments with more muted spread widening, many of these securities are also floating rate instruments and exhibited similar protection against rising interest rates as bank loans throughout the year.

Several allocations detracted from relative performance over the period, one of which was U.S. equities. Stocks came under pressure throughout the year, underperforming bonds amid rising interest rates and heightened inflationary pressures. Strikingly, this was the worst performance for U.S. equity markets since the Global Financial Crisis of 2008. The Fund’s equity exposure was significantly lowered over the period in consideration of these headwinds and finished the year

3

close to historic lows of the Fund’s allocation. The Fund’s relative performance was also affected by modest exposure to Emerging Market (EM) bonds. EM bonds underperformed U.S. high yield bonds due to a combination of factors, including sensitivity to interest rate hikes from global central banks, as well as an appreciating

U.S. dollar that can pressure EM issuers with dollar-denominated liabilities.

The Fund’s portfolio is actively managed and, therefore, its holdings and the weightings of a particular issuer or particular sector as a percentage of portfolio assets are subject to change. Sectors may include many industries.

1 The Bloomberg U.S. Aggregate Bond Index is an index of U.S dollar-denominated, investment-grade U.S. government and corporate securities, and mortgage pass-through securities, and asset-backed securities.

2 The S&P 500® Index is widely regarded as the standard for measuring large cap U.S. stock market performance and includes a representative sample of leading companies in leading industries.

3 The Nasdaq Composite Index is the market capitalization-weighted index of over 2,500 common equities listed on the Nasdaq stock exchange.

4 As represented by the U.S. Treasury component of the Bloomberg U.S. Government Index as of 12/31/2022.

5 As represented by the Bloomberg US Corp Investment Grade Index as of 12/31/2022.

6 As represented by the ICE BofA U.S. High Yield Constrained Index as of 12/31/2022.

7 As represented by the Credit Suisse Leveraged Loan Index as of 12/31/2022.

Unless otherwise specified, indexes reflect total return, with all dividends reinvested. Indexes are unmanaged, do not reflect the deduction of fees or expenses, and are not available for direct investment.

Important Performance and Other Information

Performance data quoted in the following pages reflect past performance and are no guarantee of future results. Current performance may be higher or lower than the performance quoted. The investment return and principal value of an investment in the Fund will fluctuate so that shares, on any given day or when redeemed, may

be worth more or less than their original cost. You can obtain performance data current to the most recent month end by calling Lord Abbett at 888-522-2388 or referring to www.lordabbett.com.

During certain periods shown, expense waivers and reimbursements were in place. Without such expense waivers and reimbursements, the Fund’s returns would have been lower.

The annual commentary above discusses the views of the Fund’s management and various portfolio holdings of the Fund as of December 31, 2022. These views and portfolio holdings may have changed after this date. Information provided in the commentary is not a recommendation to buy or sell securities. Because the Fund’s portfolio is actively managed and may change significantly, the Fund may no longer own the securities described above or may have otherwise changed its position in the securities. For more recent information about the Fund’s portfolio holdings, please visit www.lordabbett.com.

A Note about Risk: See Notes to Financial Statements for a discussion of investment risks. For a more detailed discussion of the risks associated with the Fund, please see the Fund’s prospectus.

Mutual funds are not insured by the FDIC, are not deposits or other obligations of, or guaranteed by, banks, and are subject to investment risks including possible loss of principal amount invested.

The Fund serves as an underlying investment vehicle for variable annuity contracts and variable life insurance policies.

4

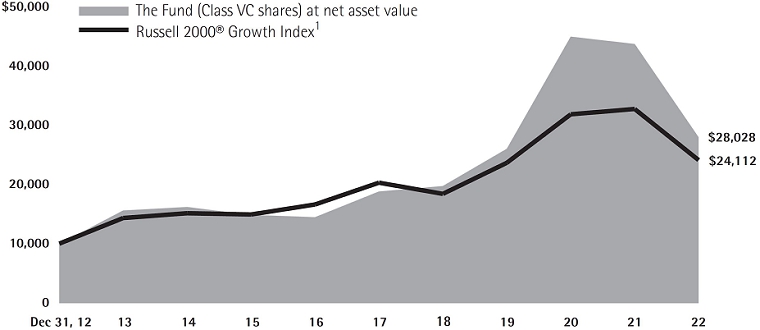

Investment Comparison

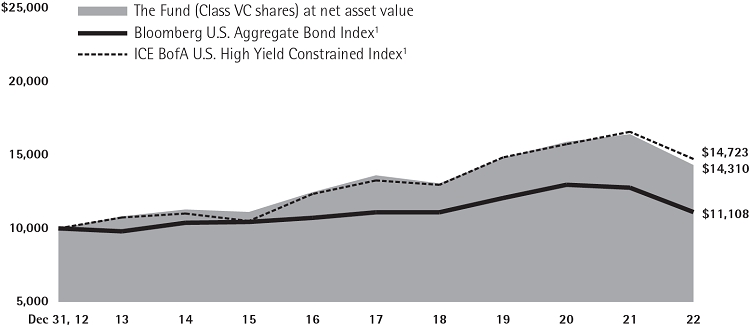

Below is a comparison of a $10,000 investment in Class VC shares with the same investment in the Bloomberg U.S. Aggregate Bond Index and the ICE BofA U.S. High Yield Constrained Index, assuming reinvestment of all dividends and distributions. The Fund’s shares are sold only to insurance company separate accounts that fund certain variable annuity and variable life contracts. This line graph comparison does not reflect the sales charges or other expenses of these contracts. If those sales charges and expenses were reflected, returns would be lower. The graph and performance table below do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. During certain periods, expenses of the Fund have been waived or reimbursed by Lord Abbett; without such waiver or reimbursement of expenses, the Fund’s returns would have been lower. Past performance is no guarantee of future results.

Average Annual Total Returns for the

Periods Ended December 31, 2022

| | | 1 Year | | 5 Years | | 10 Years | |

| Class VC | | | –12.80% | | | 1.01% | | | 3.65% | |

1 Performance for each unmanaged index does not reflect any fees or expenses. The performance of each index is not necessarily representative of the Fund’s performance.

5

Expense Example

As a shareholder of the Fund, you incur ongoing costs, including management fees; expenses related to the Fund’s services arrangements with certain insurance companies; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (July 1, 2022 through December 31, 2022).

The Example reflects only expenses that are deducted from the assets of the Fund. Fees and expenses, including sales charges applicable to the various insurance products that invest in the Fund, are not reflected in this Example. If such fees and expenses were reflected in the Example, the total expenses shown would be higher. Fees and expenses regarding such variable insurance products are separately described in the prospectus related to those products.

Actual Expenses

The first line of the table on the following page provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading titled “Expenses Paid During Period 7/1/22 – 12/31/22” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table on the following page provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

6

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | Beginning

Account

Value | | Ending

Account

Value | | Expenses

Paid During

Period† | |

| | | 7/1/22 | | 12/31/22 | | 7/1/22 -

12/31/22 | |

| Class VC | | | | | | | |

| Actual | | $1,000.00 | | $1,007.10 | | $4.50 | |

| Hypothetical (5% Return Before Expenses) | | $1,000.00 | | $1,020.72 | | $4.53 | |

| | |

| † | Net expenses are equal to the Fund’s annualized expense ratio of 0.89%, multiplied by the average account value over the period, multiplied by 184/365 (to reflect one-half year period). |

Portfolio Holdings Presented by Sector

December 31, 2022

| Sector* | %** |

| Asset Backed Securities | 5.28 | % |

| Basic Materials | 4.20 | % |

| Communications | 7.13 | % |

| Consumer, Cyclical | 10.10 | % |

| Consumer, Non-cyclical | 12.25 | % |

| Energy | 16.32 | % |

| Financials | 8.99 | % |

| Foreign Government | 2.71 | % |

| Industrial | 5.05 | % |

| Mortgage-Backed Securities | 3.63 | % |

| Municipal | 2.62 | % |

| Technology | 4.32 | % |

| U.S. Government | 8.24 | % |

| Utilities | 6.31 | % |

| Time Deposits(a) | 0.01 | % |

| Money Market Funds(a) | 0.09 | % |

| Repurchase Agreements | 2.75 | % |

| Total | 100.00 | % |

| | | |

| * | | A sector may comprise several industries. |

| ** | | Represents percent of total investments, which excludes derivatives. |

| (a) | | Securities were purchased with the cash collateral from loaned securities. |

7

Schedule of Investments

December 31, 2022

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount | | | Fair

Value | |

| LONG-TERM INVESTMENTS 100.79% | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| ASSET-BACKED SECURITIES 5.47% | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| Automobiles 0.95% | | | | | | | | | | | | |

| Carvana Auto Receivables Trust NP1 2020-N1A E† | | 5.20% | | 7/15/2027 | | $ | 1,250,000 | | | $ | 1,152,529 | |

| Drive Auto Receivables Trust 2021-3 A3 | | 0.79% | | 10/15/2025 | | | 1,410,350 | | | | 1,400,482 | |

| Mercedes-Benz Auto Receivables Trust 2022-1 A3 | | 5.21% | | 8/16/2027 | | | 3,815,000 | | | | 3,850,608 | |

| Santander Drive Auto Receivables Trust 2022-3 B | | 4.13% | | 8/16/2027 | | | 1,120,000 | | | | 1,093,414 | |

| Westlake Automobile Receivables Trust 2021-1A F† | | 3.91% | | 9/15/2027 | | | 3,118,000 | | | | 2,823,096 | |

| Total | | | | | | | | | | | 10,320,129 | |

| | | | | | | | | | | | | |

| Credit Card 0.97% | | | | | | | | | | | | |

| American Express Credit Account Master Trust 2021-1 A | | 0.90% | | 11/15/2026 | | | 3,677,000 | | | | 3,414,045 | |

| American Express Credit Account Master Trust 2022-2 A | | 3.39% | | 5/15/2027 | | | 1,604,000 | | | | 1,558,152 | |

| American Express Credit Account Master Trust 2022-3 A | | 3.75% | | 8/15/2027 | | | 1,207,000 | | | | 1,180,907 | |

| Capital One Multi-Asset Execution Trust 2022-A2 A | | 3.49% | | 5/15/2027 | | | 865,000 | | | | 841,833 | |

| Genesis Sales Finance Master Trust 2021-AA A† | | 1.20% | | 12/21/2026 | | | 1,298,000 | | | | 1,216,239 | |

| Perimeter Master Note Business Trust 2019-2A A† | | 4.23% | | 5/15/2024 | | | 2,330,255 | | | | 2,306,118 | |

| Total | | | | | | | | | | | 10,517,294 | |

| | | | | | | | | | | | | |

| Other 3.55% | | | | | | | | | | | | |

| AMMC CLO Ltd. 2021-24A C† | | 6.443%

(3 Mo. LIBOR + 2.20% | )# | 1/20/2035 | | | 820,000 | | | | 768,799 | |

| Arbor Realty Commercial Real Estate Notes Ltd. 2022-FL2 A† | | 6.186%

(1 Mo. Term SOFR + 1.85% | )# | 5/15/2037 | | | 1,410,000 | | | | 1,375,483 | |

| Avant Loans Funding Trust 2021-REV1 A† | | 1.21% | | 7/15/2030 | | | 1,367,000 | | | | 1,302,621 | |

| Ballyrock CLO Ltd. 2019-1A A1R† | | 5.109%

(3 Mo. LIBOR + 1.03% | )# | 7/15/2032 | | | 450,000 | | | | 440,769 | |

| Benefit Street Partners CLO XIX Ltd. 2019-19A B† | | 6.079%

(3 Mo. LIBOR + 2.00% | )# | 1/15/2033 | | | 578,133 | | | | 561,808 | |

| Dryden Senior Loan Fund 2022-113A A1† | | 6.518%

(3 Mo. Term SOFR + 2.00% | )# | 10/20/2035 | | | 1,200,000 | | | | 1,198,283 | |

| Elmwood CLO Ltd. 2022-8A A1† | | 6.816% | | 11/20/2035 | | | 2,000,000 | | | | 1,994,968 | |

| Flatiron CLO 18 Ltd. 2018-1A A† | | 5.075%

(3 Mo. Term SOFR + 2.00% | )# | 4/17/2031 | | | 2,500,000 | | | | 2,465,985 | |

| Greywolf CLO III Ltd. 2020-3RA A1R† | | 5.588%

(3 Mo. Term SOFR + 1.55% | )# | 4/15/2033 | | | 1,398,603 | | | | 1,378,688 | |

| 8 | See Notes to Financial Statements. |

Schedule of Investments (continued)

December 31, 2022

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount | | | Fair

Value | |

| Other (continued) | | | | | | | | | | | | |

| Halcyon Loan Advisors Funding Ltd. 2015-2A CR† | | 6.508%

(3 Mo. LIBOR + 2.15% | )# | 7/25/2027 | | $ | 465,000 | | | $ | 459,076 | |

| Halcyon Loan Advisors Funding Ltd. 2017-2A A2† | | 5.779%

(3 Mo. LIBOR + 1.70% | )# | 1/17/2030 | | | 679,855 | | | | 666,603 | |

| Hardee’s Funding LLC 2018-1A A2II† | | 4.959% | | 6/20/2048 | | | 567,998 | | | | 535,312 | |

| Madison Park Funding XIII Ltd. 2014-13A AR2† | | 5.177%

(3 Mo. LIBOR + .95% | )# | 4/19/2030 | | | 773,869 | | | | 765,769 | |

| Marble Point CLO XVII Ltd. 2020-1A A† | | 5.543%

(3 Mo. LIBOR + 1.30% | )# | 4/20/2033 | | | 2,050,466 | | | | 2,014,583 | |

| Marble Point CLO XVII Ltd. 2020-1A B† | | 6.013%

(3 Mo. LIBOR + 1.77% | )# | 4/20/2033 | | | 651,646 | | | | 625,438 | |

| MF1 LLC 2022-FL9 A† | | 6.471%

(1 Mo. Term SOFR + 2.15% | )# | 6/19/2037 | | | 2,620,000 | | | | 2,597,487 | |

| Neuberger Berman Loan Advisers CLO Ltd. 2020-37A AR† | | 5.213%

(3 Mo. LIBOR + .97% | )# | 7/20/2031 | | | 670,000 | | | | 656,666 | |

| Oaktree CLO Ltd. 2019-4 BR† | | 5.943%

(3 Mo. LIBOR + 1.70% | )# | 10/20/2032 | | | 1,460,000 | | | | 1,404,798 | |

| OCP CLO Ltd. 2016-12A AR2† | | 5.199%

(3 Mo. Term SOFR + 1.27% | )# | 4/18/2033 | | | 2,400,000 | | | | 2,330,090 | |

| OCP CLO Ltd. 2021-21A C† | | 6.143%

(3 Mo. LIBOR + 1.90% | )# | 7/20/2034 | | | 620,000 | | | | 568,507 | |

| OCP CLO Ltd. 2021-22A B1† | | 5.943%

(3 Mo. LIBOR + 1.70% | )# | 12/2/2034 | | | 1,860,000 | | | | 1,782,470 | |

| OneMain Financial Issuance Trust 2020-2A A† | | 1.75% | | 9/14/2035 | | | 1,300,000 | | | | 1,137,659 | |

| Palmer Square CLO Ltd. 2022-5A A† | | 5.658%

(3 Mo. Term SOFR + 2.00% | )# | 10/20/2035 | | | 1,414,000 | | | | 1,414,595 | |

| PFS Financing Corp. 2022-C A† | | 3.89% | | 5/15/2027 | | | 3,432,000 | | | | 3,289,230 | |

| Rad CLO Ltd. 2020-7A A1† | | 5.279%

(3 Mo. LIBOR + 1.20% | )# | 4/17/2033 | | | 316,336 | | | | 310,116 | |

| Regata XII Funding Ltd. 2019-1A CR† | | 6.079%

(3 Mo. LIBOR + 2.00% | )# | 10/15/2032 | | | 560,000 | | | | 525,402 | |

| Regatta XVIII Funding Ltd. 2021-1A B† | | 5.529%

(3 Mo. LIBOR + 1.45% | )# | 1/15/2034 | | | 1,060,000 | | | | 1,007,972 | |

| SEB Funding LLC 2021-1A A2† | | 4.969% | | 1/30/2052 | | | 1,858,343 | | | | 1,578,198 | |

| Signal Peak CLO Ltd. 2021-10A B† | | 6.075%

(3 Mo. LIBOR + 1.75% | )# | 1/24/2035 | | | 1,180,000 | | | | 1,117,910 | |

| Sunrun Demeter Issuer 2021-2A A† | | 2.27% | | 1/30/2057 | | | 1,377,758 | | | | 1,078,085 | |

| Voya CLO Ltd. 2022-3A A1† | | 6.012%

(3 Mo. Term SOFR + 2.00% | )# | 10/20/2034 | | | 1,150,000 | | | | 1,145,885 | |

| Total | | | | | | | | | | | 38,499,255 | |

| Total Asset-Backed Securities (cost $61,306,412) | | | | | | | | | 59,336,678 | |

| | See Notes to Financial Statements. | 9 |

Schedule of Investments (continued)

December 31, 2022

| Investments | | Shares | | | Fair

Value | |

| COMMON STOCKS 5.39% | | | | | | |

| | | | | | | | | |

| Aerospace & Defense 0.15% | | | | | | | | |

| Huntington Ingalls Industries, Inc. | | | 6,922 | | | $ | 1,596,767 | |

| | | | | | | | | |

| Auto Components 0.10% | | | | | | | | |

| Chassix Holdings, Inc. | | | 59,475 | | | | 1,040,812 | |

| | | | | | | | | |

| Automobiles 0.11% | | | | | | | | |

| Tesla, Inc.* | | | 9,788 | | | | 1,205,686 | |

| | | | | | | | | |

| Beverages 0.21% | | | | | | | | |

| Brown-Forman Corp. Class B | | | 17,038 | | | | 1,119,056 | |

| Treasury Wine Estates Ltd. (Australia)(a) | | | 125,760 | | | | 1,161,823 | |

| Total | | | | | | | 2,280,879 | |

| | | | | | | | | |

| Biotechnology 0.40% | | | | | | | | |

| Alnylam Pharmaceuticals, Inc.* | | | 9,198 | | | | 2,185,905 | |

| Amgen, Inc. | | | 4,145 | | | | 1,088,643 | |

| Genmab A/S ADR* | | | 26,212 | | | | 1,110,864 | |

| Total | | | | | | | 4,385,412 | |

| | | | | | | | | |

| Capital Markets 0.10% | | | | | | | | |

| MarketAxess Holdings, Inc. | | | 3,946 | | | | 1,100,500 | |

| | | | | | | | | |

| Commercial Services & Supplies 0.10% | | | | | | | | |

| Tetra Tech, Inc. | | | 7,300 | | | | 1,059,887 | |

| | | | | | | | | |

| Electric: Utilities 0.11% | | | | | | | | |

| PG&E Corp.* | | | 71,127 | | | | 1,156,525 | |

| | | | | | | | | |

| Electric-Generation 0.00% | | | | | | | | |

| Frontera Generation Holdings LLC | | | 9,472 | | | | 142 | |

| | | | | | | | | |

| Entertainment 0.27% | | | | | | | | |

| Bilibili, Inc. ADR*(b) | | | 71,653 | | | | 1,697,459 | |

| Genting Singapore Ltd. (Singapore)(a) | | | 1,750,862 | | | | 1,249,516 | |

| Total | | | | | | | 2,946,975 | |

| | | | | | | | | |

| Food Products 0.51% | | | | | | | | |

| Archer-Daniels-Midland Co. | | | 13,260 | | | | 1,231,191 | |

| Campbell Soup Co. | | | 19,415 | | | | 1,101,801 | |

| General Mills, Inc. | | | 19,063 | | | | 1,598,433 | |

| Hershey Co. (The) | | | 7,007 | | | | 1,622,611 | |

| Total | | | | | | | 5,554,036 | |

| 10 | See Notes to Financial Statements. |

Schedule of Investments (continued)

December 31, 2022

| Investments | | Shares | | | Fair

Value | |

| Health Care Providers & Services 0.10% | | | | | | | | |

| Medpace Holdings, Inc.* | | | 5,298 | | | $ | 1,125,348 | |

| | | | | | | | | |

| Hotels, Restaurants & Leisure 0.32% | | | | | | | | |

| McDonald’s Corp. | | | 4,111 | | | | 1,083,372 | |

| Starbucks Corp. | | | 11,431 | | | | 1,133,955 | |

| Wynn Resorts Ltd.* | | | 14,621 | | | | 1,205,794 | |

| Total | | | | | | | 3,423,121 | |

| | | | | | | | | |

| Household Durables 0.12% | | | | | | | | |

| DR Horton, Inc. | | | 14,614 | | | | 1,302,692 | |

| | | | | | | | | |

| Insurance 0.42% | | | | | | | | |

| Kinsale Capital Group, Inc. | | | 4,172 | | | | 1,091,062 | |

| Markel Corp.* | | | 868 | | | | 1,143,581 | |

| Progressive Corp. (The) | | | 8,736 | | | | 1,133,147 | |

| W R Berkley Corp. | | | 15,527 | | | | 1,126,794 | |

| Total | | | | | | | 4,494,584 | |

| | | | | | | | | |

| Interactive Media & Services 0.12% | | | | | | | | |

| Pinterest, Inc. Class A* | | | 53,968 | | | | 1,310,343 | |

| | | | | | | | | |

| Internet & Catalog Retail 0.20% | | | | | | | | |

| Alibaba Group Holding Ltd. ADR* | | | 24,880 | | | | 2,191,679 | |

| | | | | | | | | |

| Machinery 0.11% | | | | | | | | |

| Deere & Co. | | | 2,745 | | | | 1,176,946 | |

| | | | | | | | | |

| Metals & Mining 0.44% | | | | | | | | |

| Freeport-McMoRan, Inc. | | | 28,383 | | | | 1,078,554 | |

| Newmont Corp. | | | 45,612 | | | | 2,152,887 | |

| Nucor Corp. | | | 12,030 | | | | 1,585,674 | |

| Total | | | | | | | 4,817,115 | |

| | | | | | | | | |

| Miscellaneous Financials 0.05% | | | | | | | | |

| UTEX Industries, Inc. | | | 8,205 | | | | 551,786 | |

| | | | | | | | | |

| Personal Products 0.21% | | | | | | | | |

| Gibson Brands Private Equity | | | 9,449 | | | | 1,110,258 | |

| Kose Corp. (Japan)(a) | | | 10,464 | | | | 1,136,947 | |

| Total | | | | | | | 2,247,205 | |

| | See Notes to Financial Statements. | 11 |

Schedule of Investments (continued)

December 31, 2022

| Investments | | | | | | Shares | | | Fair

Value | |

| Pharmaceuticals 0.52% | | | | | | | | | | | | |

| Cardinal Health, Inc. | | | | | | | 19,730 | | | $ | 1,516,645 | |

| Cigna Corp. | | | | | | | 3,401 | | | | 1,126,887 | |

| Daiichi Sankyo Co. Ltd. (Japan)(a) | | | | | | | 56,895 | | | | 1,831,262 | |

| Madrigal Pharmaceuticals, Inc.* | | | | | | | 3,956 | | | | 1,148,229 | |

| Total | | | | | | | | | | | 5,623,023 | |

| | | | | | | | | | | | | |

| Professional Services 0.09% | | | | | | | | | | | | |

| Booz Allen Hamilton Holding Corp. | | | | | | | 9,703 | | | | 1,014,158 | |

| | | | | | | | | | | | | |

| Specialty Retail 0.25% | | | | | | | | | | | | |

| Claires Holdings LLC | | | | | | | 1,067 | | | | 426,891 | (c) |

| Five Below, Inc.* | | | | | | | 7,024 | | | | 1,242,335 | |

| Genuine Parts Co. | | | | | | | 6,089 | | | | 1,056,502 | |

| Total | | | | | | | | | | | 2,725,728 | |

| | | | | | | | | | | | | |

| Textiles, Apparel & Luxury Goods 0.27% | | | | | | | | | | | | |

| Cie Financiere Richemont SA Class A (Switzerland)(a) | | | | | | | 13,344 | | | | 1,730,182 | |

| Hermes International (France)(a) | | | | | | | 755 | | | | 1,168,628 | |

| Total | | | | | | | | | | | 2,898,810 | |

| | | | | | | | | | | | | |

| Transportation Infrastructure 0.11% | | | | | | | | | | | | |

| ACBL Holdings Corp. | | | | | | | 3,684 | | | | 145,518 | |

| Canadian Pacific Railway Ltd. (Canada)(a) | | | | | | | 14,461 | | | | 1,078,646 | |

| Total | | | | | | | | | | | 1,224,164 | |

| Total Common Stocks (cost $58,249,646) | | | | | | | | | | | 58,454,323 | |

| | | | | | | | | | | | | |

| | | Interest

Rate | | Maturity

Date | | | Principal

Amount | | | | | |

| CORPORATE BONDS 70.96% | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| Aerospace/Defense 1.11% | | | | | | | | | | | | |

| Bombardier, Inc. (Canada)†(a) | | 6.00% | | 2/15/2028 | | $ | 1,052,000 | | | | 974,089 | |

| Bombardier, Inc. (Canada)†(a) | | 7.125% | | 6/15/2026 | | | 1,828,000 | | | | 1,776,879 | |

| Lockheed Martin Corp. | | 5.10% | | 11/15/2027 | | | 1,155,000 | | | | 1,182,532 | |

| Raytheon Technologies Corp. | | 4.125% | | 11/16/2028 | | | 1,625,000 | | | | 1,558,634 | |

| TransDigm, Inc. | | 4.625% | | 1/15/2029 | | | 2,531,000 | | | | 2,229,874 | |

| TransDigm, Inc. | | 5.50% | | 11/15/2027 | | | 4,532,000 | | | | 4,264,974 | |

| Total | | | | | | | | | | | 11,986,982 | |

| 12 | See Notes to Financial Statements. |

Schedule of Investments (continued)

December 31, 2022

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount | | | Fair

Value | |

| Agriculture 0.96% | | | | | | | | | | | | |

| BAT Capital Corp. | | 7.75% | | 10/19/2032 | | $ | 1,051,000 | | | $ | 1,133,643 | |

| Cargill, Inc.† | | 4.875% | | 10/10/2025 | | | 1,378,000 | | | | 1,373,945 | |

| Darling Ingredients, Inc.† | | 6.00% | | 6/15/2030 | | | 1,091,000 | | | | 1,067,925 | |

| Imperial Brands Finance plc (United Kingdom)†(a) | | 6.125% | | 7/27/2027 | | | 1,436,000 | | | | 1,431,402 | |

| JT International Financial Services BV (Netherlands)†(a) | | 6.875% | | 10/24/2032 | | | 1,573,000 | | | | 1,673,197 | |

| Viterra Finance BV (Netherlands)†(a) | | 2.00% | | 4/21/2026 | | | 1,707,000 | | | | 1,482,224 | |

| Viterra Finance BV (Netherlands)†(a) | | 3.20% | | 4/21/2031 | | | 1,518,000 | | | | 1,150,268 | |

| Viterra Finance BV (Netherlands)†(a) | | 5.25% | | 4/21/2032 | | | 1,306,000 | | | | 1,150,686 | |

| Total | | | | | | | | | | | 10,463,290 | |

| | | | | | | | | | | | | |

| Airlines 1.94% | | | | | | | | | | | | |

| Air Canada (Canada)†(a) | | 3.875% | | 8/15/2026 | | | 1,815,000 | | | | 1,610,690 | |

| Alaska Airlines 2020-1 Class A Pass Through Trust† | | 4.80% | | 2/15/2029 | | | 1,676,328 | | | | 1,598,461 | |

| American Airlines, Inc./AAdvantage Loyalty IP Ltd.† | | 5.75% | | 4/20/2029 | | | 4,588,000 | | | | 4,201,511 | |

| Azul Investments LLP† | | 5.875% | | 10/26/2024 | | | 2,396,000 | | | | 1,931,568 | |

| British Airways Pass Through Trust 2019-1A (United Kingdom)†(a) | | 3.30% | | 6/15/2034 | | | 685,744 | | | | 583,624 | |

| British Airways Pass-Through Trust A (United Kingdom)†(a) | | 4.25% | | 5/15/2034 | | | 499,060 | | | | 447,840 | |

| Delta Air Lines, Inc.† | | 7.00% | | 5/1/2025 | | | 2,203,000 | | | | 2,253,335 | |

| Delta Air Lines, Inc./SkyMiles IP Ltd.† | | 4.75% | | 10/20/2028 | | | 1,723,000 | | | | 1,622,221 | |

| Hawaiian Brand Intellectual Property Ltd./HawaiianMiles Loyalty Ltd.† | | 5.75% | | 1/20/2026 | | | 1,695,347 | | | | 1,537,510 | |

| JetBlue 2019-1 Class A Pass Through Trust | | 2.95% | | 11/15/2029 | | | 876,269 | | | | 729,364 | |

| Mileage Plus Holdings LLC/Mileage Plus Intellectual Property Assets Ltd.† | | 6.50% | | 6/20/2027 | | | 1,350,000 | | | | 1,345,143 | |

| United Airlines 2020-1 Class A Pass Through Trust | | 5.875% | | 4/15/2029 | | | 2,194,104 | | | | 2,166,303 | |

| United Airlines, Inc.† | | 4.625% | | 4/15/2029 | | | 1,197,000 | | | | 1,044,324 | |

| Total | | | | | | | | | | | 21,071,894 | |

| | | | | | | | | | | | | |

| Apparel 0.14% | | | | | | | | | | | | |

| Levi Strauss & Co.† | | 3.50% | | 3/1/2031 | | | 1,907,000 | | | | 1,516,046 | |

| | | | | | | | | | | | | |

| Auto Manufacturers 1.20% | | | | | | | | | | | | |

| Allison Transmission, Inc.† | | 3.75% | | 1/30/2031 | | | 1,355,000 | | | | 1,116,181 | |

| BMW US Capital LLC† | | 4.15% | | 4/9/2030 | | | 1,500,000 | | | | 1,427,693 | |

| Ford Motor Co. | | 3.25% | | 2/12/2032 | | | 5,013,000 | | | | 3,768,381 | |

| Ford Motor Co. | | 6.10% | | 8/19/2032 | | | 2,144,000 | | | | 1,983,806 | |

| Ford Motor Credit Co. LLC | | 2.90% | | 2/10/2029 | | | 1,452,000 | | | | 1,161,651 | |

| Ford Motor Credit Co. LLC | | 4.00% | | 11/13/2030 | | | 2,916,000 | | | | 2,399,299 | |

| Ford Motor Credit Co. LLC | | 7.35% | | 11/4/2027 | | | 1,096,000 | | | | 1,125,811 | |

| Total | | | | | | | | | | | 12,982,822 | |

| | See Notes to Financial Statements. | 13 |

Schedule of Investments (continued)

December 31, 2022

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount | | | Fair

Value | |

| Banks 3.43% | | | | | | | | | | | | |

| ABN AMRO Bank NV (Netherlands)†(a) | | 3.324%

(5 Yr. Treasury CMT + 1.90% | )# | 3/13/2037 | | $ | 1,200,000 | | | $ | 870,229 | |

| Alfa Bank AO Via Alfa Bond Issuance PLC (Ireland)(a) | | 5.50%

(5 Yr. Treasury CMT + 4.55% | ) | 10/26/2031 | | | 2,645,000 | | | | – | (d)(e) |

| Australia & New Zealand Banking Group Ltd. (Australia)†(a) | | 6.742% | | 12/8/2032 | | | 2,525,000 | | | | 2,557,871 | |

| Bank of America Corp. | | 3.384%

(SOFR + 1.33% | )# | 4/2/2026 | | | 2,839,000 | | | | 2,713,757 | |

| Bank of Ireland Group plc (Ireland)†(a) | | 2.029%

(1 Yr. Treasury CMT + 1.10% | )# | 9/30/2027 | | | 1,201,000 | | | | 1,015,645 | |

| Bank of Ireland Group PLC (Ireland)†(a) | | 6.253%

(1 Yr. Treasury CMT + 2.65% | )# | 9/16/2026 | | | 1,666,000 | | | | 1,653,769 | |

| Bank OZK | | 2.75%

(3 Mo. Term SOFR + 2.09% | )# | 10/1/2031 | | | 2,069,000 | | | | 1,767,211 | |

| BankUnited, Inc. | | 4.875% | | 11/17/2025 | | | 1,178,000 | | | | 1,160,928 | |

| Danske Bank A/S (Denmark)†(a) | | 4.298%

(1 Yr. Treasury CMT + 1.75% | )# | 4/1/2028 | | | 584,000 | | | | 537,851 | |

| First-Citizens Bank & Trust Co. | | 6.125% | | 3/9/2028 | | | 2,793,000 | | | | 2,844,353 | |

| Home BancShares, Inc. | | 3.125%

(3 Mo. Term SOFR + 1.82% | )# | 1/30/2032 | | | 1,058,000 | | | | 889,391 | |

| HSBC Holdings plc (United Kingdom)(a) | | 2.999%

(SOFR + 1.43% | )# | 3/10/2026 | | | 5,768,000 | | | | 5,425,882 | |

| JPMorgan Chase & Co. | | 3.54%

(3 Mo. LIBOR + 1.38% | )# | 5/1/2028 | | | 4,306,000 | | | | 3,968,947 | |

| Morgan Stanley | | 4.679%

(SOFR + 1.65% | )# | 7/17/2026 | | | 1,379,000 | | | | 1,356,693 | |

| NatWest Group PLC (United Kingdom)(a) | | 7.472%

(5 Yr. Treasury CMT + 2.85% | )# | 11/10/2026 | | | 1,602,000 | | | | 1,668,818 | |

| Oesterreichische Kontrollbank AG (Austria)(a) | | 4.625% | | 11/3/2025 | | | 1,851,000 | | | | 1,861,242 | |

| Standard Chartered PLC (United Kingdom)†(a) | | 7.767%

(5 Yr. Treasury CMT + 3.45% | )# | 11/16/2028 | | | 1,621,000 | | | | 1,720,193 | |

| SVB Financial Group | | 4.25%

(5 Yr. Treasury CMT + 3.07% | )# | 11/15/2026 | | | 1,115,000 | | | | 733,585 | |

| United Overseas Bank Ltd. (Singapore)†(a) | | 2.00%

(5 Yr. Treasury CMT + 1.23% | )# | 10/14/2031 | | | 1,420,000 | | | | 1,241,121 | |

| US Bancorp | | 3.00% | | 7/30/2029 | | | 1,090,000 | | | | 959,321 | |

| Webster Financial Corp. | | 4.10% | | 3/25/2029 | | | 1,622,000 | | | | 1,474,320 | |

| Western Alliance Bancorp | | 3.00%

(3 Mo. Term SOFR + 2.25% | )# | 6/15/2031 | | | 893,000 | | | | 754,669 | |

| Total | | | | | | | | | | | 37,175,796 | |

| 14 | See Notes to Financial Statements. |

Schedule of Investments (continued)

December 31, 2022

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount | | | Fair

Value | |

| Beverages 0.83% | | | | | | | | | | | | |

| Bacardi Ltd.† | | 2.75% | | 7/15/2026 | | $ | 1,749,000 | | | $ | 1,582,734 | |

| Bacardi Ltd.† | | 4.70% | | 5/15/2028 | | | 1,500,000 | | | | 1,434,920 | |

| Becle SAB de CV (Mexico)†(a) | | 2.50% | | 10/14/2031 | | | 1,270,000 | | | | 988,625 | |

| Brown-Forman Corp. | | 4.50% | | 7/15/2045 | | | 1,192,000 | | | | 1,095,642 | |

| Central American Bottling Corp./CBC Bottling Holdco SL/Beliv Holdco SL (Guatemala)†(a) | | 5.25% | | 4/27/2029 | | | 1,196,000 | | | | 1,117,345 | |

| PepsiCo, Inc. | | 3.00% | | 10/15/2027 | | | 1,839,000 | | | | 1,727,685 | |

| PepsiCo, Inc. | | 4.20% | | 7/18/2052 | | | 1,116,000 | | | | 1,022,884 | |

| Total | | | | | | | | | | | 8,969,835 | |

| | | | | | | | | | | | | |

| Biotechnology 0.44% | | | | | | | | | | | | |

| Amgen, Inc. | | 4.20% | | 2/22/2052 | | | 2,655,000 | | | | 2,118,741 | |

| Regeneron Pharmaceuticals, Inc. | | 2.80% | | 9/15/2050 | | | 4,216,000 | | | | 2,632,816 | |

| Total | | | | | | | | | | | 4,751,557 | |

| | | | | | | | | | | | | |

| Building Materials 0.32% | | | | | | | | | | | | |

| Builders FirstSource, Inc.† | | 4.25% | | 2/1/2032 | | | 1,153,000 | | | | 936,793 | |

| Lennox International, Inc. | | 1.70% | | 8/1/2027 | | | 885,000 | | | | 760,121 | |

| Smyrna Ready Mix Concrete LLC† | | 6.00% | | 11/1/2028 | | | 889,000 | | | | 797,246 | |

| Vulcan Materials Co. | | 4.50% | | 6/15/2047 | | | 1,186,000 | | | | 990,792 | |

| Total | | | | | | | | | | | 3,484,952 | |

| | | | | | | | | | | | | |

| Chemicals 1.98% | | | | | | | | | | | | |

| Albemarle Corp. | | 4.65% | | 6/1/2027 | | | 1,332,000 | | | | 1,301,066 | |

| Ashland LLC† | | 3.375% | | 9/1/2031 | | | 1,306,000 | | | | 1,045,545 | |

| Cabot Corp. | | 5.00% | | 6/30/2032 | | | 1,342,000 | | | | 1,244,751 | |

| Celanese US Holdings LLC | | 6.165% | | 7/15/2027 | | | 3,391,000 | | | | 3,350,073 | |

| CF Industries, Inc.† | | 4.50% | | 12/1/2026 | | | 1,047,000 | | | | 1,014,898 | |

| FMC Corp. | | 3.45% | | 10/1/2029 | | | 893,000 | | | | 789,147 | |

| Ingevity Corp.† | | 3.875% | | 11/1/2028 | | | 1,275,000 | | | | 1,098,591 | |

| NOVA Chemicals Corp. (Canada)†(a) | | 4.25% | | 5/15/2029 | | | 1,305,000 | | | | 1,068,756 | |

| OCP SA (Morocco)†(a) | | 3.75% | | 6/23/2031 | | | 2,847,000 | | | | 2,394,925 | |

| Olin Corp. | | 5.00% | | 2/1/2030 | | | 1,347,000 | | | | 1,231,528 | |

| Olin Corp. | | 5.125% | | 9/15/2027 | | | 1,304,000 | | | | 1,234,523 | |

| SCIH Salt Holdings, Inc.† | | 4.875% | | 5/1/2028 | | | 2,328,000 | | | | 2,001,951 | |

| SCIH Salt Holdings, Inc.† | | 6.625% | | 5/1/2029 | | | 1,462,000 | | | | 1,179,512 | |

| SK Invictus Intermediate II Sarl (Luxembourg)†(a) | | 5.00% | | 10/30/2029 | | | 1,402,000 | | | | 1,151,463 | |

| Sociedad Quimica y Minera de Chile SA (Chile)†(a) | | 3.50% | | 9/10/2051 | | | 1,789,000 | | | | 1,319,177 | |

| Total | | | | | | | | | | | 21,425,906 | |

| | See Notes to Financial Statements. | 15 |

Schedule of Investments (continued)

December 31, 2022

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount | | | Fair

Value | |

| Coal 0.34% | | | | | | | | | | | | |

| SunCoke Energy, Inc.† | | 4.875% | | 6/30/2029 | | $ | 1,212,000 | | | $ | 1,041,941 | |

| Warrior Met Coal, Inc.† | | 7.875% | | 12/1/2028 | | | 2,683,000 | | | | 2,648,370 | |

| Total | | | | | | | | | | | 3,690,311 | |

| | | | | | | | | | | | | |

| Commercial Services 1.25% | | | | | | | | | | | | |

| Adani Ports & Special Economic Zone Ltd. (India)†(a) | | 3.828% | | 2/2/2032 | | | 1,007,000 | | | | 762,731 | |

| Adani Ports & Special Economic Zone Ltd. (India)†(a) | | 4.375% | | 7/3/2029 | | | 2,280,000 | | | | 1,917,710 | |

| AMN Healthcare, Inc.† | | 4.625% | | 10/1/2027 | | | 882,000 | | | | 814,783 | |

| Ashtead Capital, Inc.† | | 5.50% | | 8/11/2032 | | | 1,155,000 | | | | 1,108,101 | |

| Block, Inc. | | 3.50% | | 6/1/2031 | | | 1,196,000 | | | | 955,843 | |

| Cleveland Clinic Foundation (The) | | 4.858% | | 1/1/2114 | | | 700,000 | | | | 599,221 | |

| Georgetown University (The) | | 2.943% | | 4/1/2050 | | | 1,246,000 | | | | 792,984 | |

| Global Payments, Inc. | | 2.90% | | 5/15/2030 | | | 1,538,000 | | | | 1,263,561 | |

| Hertz Corp. (The)† | | 5.50% | | 10/15/2024 | | | 987,000 | | | | 37,012 | |

| Hertz Corp. (The)† | | 6.00% | | 1/15/2028 | | | 1,887,000 | | | | 169,830 | |

| ITR Concession Co. LLC† | | 5.183% | | 7/15/2035 | | | 785,000 | | | | 733,485 | |

| Johns Hopkins University | | 2.813% | | 1/1/2060 | | | 692,000 | | | | 435,437 | |

| Metropolitan Museum of Art (The) | | 3.40% | | 7/1/2045 | | | 1,975,000 | | | | 1,557,504 | |

| Movida Europe SA (Luxembourg)†(a) | | 5.25% | | 2/8/2031 | | | 1,088,000 | | | | 817,190 | |

| United Rentals North America, Inc. | | 4.875% | | 1/15/2028 | | | 789,000 | | | | 749,436 | |

| University of Miami | | 4.063% | | 4/1/2052 | | | 992,000 | | | | 813,538 | |

| Total | | | | | | | | | | | 13,528,366 | |

| | | | | | | | | | | | | |

| Computers 1.24% | | | | | | | | | | | | |

| Apple, Inc. | | 2.90% | | 9/12/2027 | | | 1,600,000 | | | | 1,494,101 | |

| Apple, Inc. | | 3.20% | | 5/11/2027 | | | 3,601,000 | | | | 3,418,511 | |

| Booz Allen Hamilton, Inc.† | | 3.875% | | 9/1/2028 | | | 976,000 | | | | 866,427 | |

| Booz Allen Hamilton, Inc.† | | 4.00% | | 7/1/2029 | | | 827,000 | | | | 729,074 | |

| Condor Merger Sub, Inc.† | | 7.375% | | 2/15/2030 | | | 291,000 | | | | 234,492 | |

| Crowdstrike Holdings, Inc. | | 3.00% | | 2/15/2029 | | | 6,407,000 | | | | 5,414,171 | |

| Teledyne FLIR LLC | | 2.50% | | 8/1/2030 | | | 1,603,000 | | | | 1,297,414 | |

| Total | | | | | | | | | | | 13,454,190 | |

| | | | | | | | | | | | | |

| Cosmetics/Personal Care 0.19% | | | | | | | | | | | | |

| GSK Consumer Healthcare Capital U.S. LLC | | 3.625% | | 3/24/2032 | | | 2,389,000 | | | | 2,103,929 | |

| | | | | | | | | | | | | |

| Distribution/Wholesale 0.30% | | | | | | | | | | | | |

| Ferguson Finance plc (United Kingdom)†(a) | | 3.25% | | 6/2/2030 | | | 2,229,000 | | | | 1,895,300 | |

| H&E Equipment Services, Inc.† | | 3.875% | | 12/15/2028 | | | 1,563,000 | | | | 1,334,091 | |

| Total | | | | | | | | | | | 3,229,391 | |

| 16 | See Notes to Financial Statements. |

Schedule of Investments (continued)

December 31, 2022

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount | | | Fair

Value | |

| Diversified Financial Services 1.55% | | | | | | | | | | | | |

| AG Issuer LLC† | | 6.25% | | 3/1/2028 | | $ | 1,220,000 | | | $ | 1,123,053 | |

| Blackstone Holdings Finance Co. LLC† | | 2.00% | | 1/30/2032 | | | 1,609,000 | | | | 1,185,926 | |

| CDP Financial, Inc. (Canada)(a) | | 1.00% | | 5/26/2026 | | | 4,582,000 | | | | 4,078,641 | |

| CPPIB Capital, Inc. (Canada)†(a) | | 4.125% | | 10/21/2024 | | | 1,699,000 | | | | 1,679,552 | |

| CPPIB Capital, Inc. (Canada)†(a) | | 4.818%

(SOFR Index + 1.25% | )# | 4/4/2025 | | | 4,056,000 | | | | 4,131,651 | |

| Intercontinental Exchange, Inc. | | 4.00% | | 9/15/2027 | | | 1,839,000 | | | | 1,778,579 | |

| Jane Street Group/JSG Finance, Inc.† | | 4.50% | | 11/15/2029 | | | 896,000 | | | | 771,855 | |

| Neuberger Berman Group LLC/Neuberger Berman Finance Corp.† | | 4.875% | | 4/15/2045 | | | 1,377,000 | | | | 1,117,370 | |

| USAA Capital Corp.† | | 2.125% | | 5/1/2030 | | | 1,129,000 | | | | 927,928 | |

| Total | | | | | | | | | | | 16,794,555 | |

| | | | | | | | | | | | | |

| Electric 5.75% | | | | | | | | | | | | |

| AES Corp. (The) | | 2.45% | | 1/15/2031 | | | 2,495,000 | | | | 1,990,664 | |

| Atlantic City Electric Co. | | 4.00% | | 10/15/2028 | | | 1,149,000 | | | | 1,096,154 | |

| Ausgrid Finance Pty Ltd. (Australia)†(a) | | 4.35% | | 8/1/2028 | | | 1,217,000 | | | | 1,130,632 | |

| Black Hills Corp. | | 4.35% | | 5/1/2033 | | | 1,166,000 | | | | 1,029,374 | |

| Calpine Corp.† | | 3.75% | | 3/1/2031 | | | 1,352,000 | | | | 1,090,328 | |

| Calpine Corp.† | | 4.50% | | 2/15/2028 | | | 1,198,000 | | | | 1,071,231 | |

| Calpine Corp.† | | 4.625% | | 2/1/2029 | | | 3,814,000 | | | | 3,278,739 | |

| Calpine Corp.† | | 5.00% | | 2/1/2031 | | | 2,841,000 | | | | 2,387,886 | |

| Calpine Corp.† | | 5.125% | | 3/15/2028 | | | 1,328,000 | | | | 1,187,667 | |

| Clearway Energy Operating LLC† | | 4.75% | | 3/15/2028 | | | 1,731,000 | | | | 1,600,302 | |

| Cleveland Electric Illuminating Co.† | | 3.50% | | 4/1/2028 | | | 1,118,000 | | | | 1,020,689 | |

| Constellation Energy Generation LLC | | 5.60% | | 6/15/2042 | | | 1,171,000 | | | | 1,133,760 | |

| Constellation Energy Generation LLC | | 6.25% | | 10/1/2039 | | | 2,067,000 | | | | 2,117,503 | |

| Duke Energy Corp. | | 4.30% | | 3/15/2028 | | | 1,839,000 | | | | 1,772,921 | |

| EDP Finance BV (Netherlands)† | | 6.30% | | 10/11/2027 | | | 2,264,000 | | | | 2,332,677 | |

| El Paso Electric Co. | | 5.00% | | 12/1/2044 | | | 1,203,000 | | | | 1,057,697 | |

| Electricite de France SA (France)†(a) | | 3.625% | | 10/13/2025 | | | 1,000,000 | | | | 964,914 | |

| Electricite de France SA (France)†(a) | | 4.50% | | 9/21/2028 | | | 1,250,000 | | | | 1,185,597 | |

| Empresa de Transmision Electrica SA (Panama)†(a) | | 5.125% | | 5/2/2049 | | | 1,205,000 | | | | 977,333 | |

| Enel Finance International NV (Netherlands)†(a) | | 3.50% | | 4/6/2028 | | | 1,329,000 | | | | 1,165,030 | |

| Entergy Arkansas LLC | | 4.95% | | 12/15/2044 | | | 1,109,000 | | | | 967,977 | |

| FirstEnergy Corp. | | 4.40% | | 7/15/2027 | | | 2,518,000 | | | | 2,347,905 | |

| FirstEnergy Corp. | | 5.35% | | 7/15/2047 | | | 1,420,000 | | | | 1,270,280 | |

| FirstEnergy Transmission LLC† | | 2.866% | | 9/15/2028 | | | 1,356,000 | | | | 1,185,696 | |

| FirstEnergy Transmission LLC† | | 4.55% | | 4/1/2049 | | | 1,271,000 | | | | 1,034,428 | |

| | See Notes to Financial Statements. | 17 |

Schedule of Investments (continued)

December 31, 2022

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount | | | Fair

Value | |

| Electric (continued) | | | | | | | | | | | | |

| Indianapolis Power & Light Co.† | | 4.05% | | 5/1/2046 | | $ | 1,608,000 | | | $ | 1,298,396 | |

| Indianapolis Power & Light Co.† | | 5.65% | | 12/1/2032 | | | 969,000 | | | | 996,886 | |

| ITC Holdings Corp.† | | 4.95% | | 9/22/2027 | | | 1,129,000 | | | | 1,115,324 | |

| Louisville Gas & Electric Co. | | 4.375% | | 10/1/2045 | | | 1,017,000 | | | | 845,607 | |

| Minejesa Capital BV (Netherlands)†(a) | | 4.625% | | 8/10/2030 | | | 1,354,000 | | | | 1,191,791 | |

| Monongahela Power Co.† | | 3.55% | | 5/15/2027 | | | 1,188,000 | | | | 1,118,408 | |

| NextEra Energy Operating Partners LP† | | 3.875% | | 10/15/2026 | | | 2,267,000 | | | | 2,078,827 | |

| NextEra Energy Operating Partners LP† | | 4.50% | | 9/15/2027 | | | 1,774,000 | | | | 1,630,284 | |

| NRG Energy, Inc.† | | 3.875% | | 2/15/2032 | | | 2,781,000 | | | | 2,094,023 | |

| NSG Holdings LLC/NSG Holdings, Inc.† | | 7.75% | | 12/15/2025 | | | 496,892 | | | | 483,500 | |

| Ohio Edison Co.† | | 5.50% | | 1/15/2033 | | | 909,000 | | | | 903,572 | |

| Pacific Gas and Electric Co. | | 3.50% | | 8/1/2050 | | | 1,806,000 | | | | 1,128,593 | |

| Pacific Gas and Electric Co. | | 4.95% | | 7/1/2050 | | | 1,580,000 | | | | 1,231,023 | |

| Pattern Energy Operations LP/Pattern Energy Operations, Inc.† | | 4.50% | | 8/15/2028 | | | 1,173,000 | | | | 1,053,828 | |

| PG&E Corp. | | 5.00% | | 7/1/2028 | | | 1,547,000 | | | | 1,414,681 | |

| Puget Energy, Inc. | | 4.10% | | 6/15/2030 | | | 1,000,000 | | | | 895,291 | |

| Union Electric Co. | | 2.625% | | 3/15/2051 | | | 1,655,000 | | | | 1,050,334 | |

| Vistra Operations Co. LLC† | | 4.375% | | 5/1/2029 | | | 2,555,000 | | | | 2,206,580 | |

| Vistra Operations Co. LLC† | | 5.125% | | 5/13/2025 | | | 2,220,000 | | | | 2,174,901 | |

| Wisconsin Electric Power Co. | | 4.75% | | 9/30/2032 | | | 1,103,000 | | | | 1,084,241 | |

| Total | | | | | | | | | | | 62,393,474 | |

| | | | | | | | | | | | | |

| Electronics 0.34% | | | | | | | | | | | | |

| Amphenol Corp. | | 2.80% | | 2/15/2030 | | | 1,875,000 | | | | 1,604,629 | |

| Honeywell International, Inc.(f) | | 4.125% | | 11/2/2034 | | EUR | 1,284,000 | | | | 1,361,771 | |

| Imola Merger Corp.† | | 4.75% | | 5/15/2029 | | $ | 886,000 | | | | 770,491 | |

| Total | | | | | | | | | | | 3,736,891 | |

| | | | | | | | | | | | | |

| Energy-Alternate Sources 0.56% | | | | | | | | | | | | |

| Sweihan PV Power Co. PJSC (United Arab Emirates)†(a) | | 3.625% | | 1/31/2049 | | | 1,668,593 | | | | 1,345,486 | |

| TerraForm Power Operating LLC† | | 4.75% | | 1/15/2030 | | | 1,484,000 | | | | 1,293,712 | |

| TerraForm Power Operating LLC† | | 5.00% | | 1/31/2028 | | | 1,000,000 | | | | 901,710 | |

| Topaz Solar Farms LLC† | | 5.75% | | 9/30/2039 | | | 2,634,410 | | | | 2,504,112 | |

| Total | | | | | | | | | | | 6,045,020 | |

| | | | | | | | | | | | | |

| Engineering & Construction 0.42% | | | | | | | | | | | | |

| Aeropuerto Internacional de Tocumen SA (Panama)†(a) | | 5.125% | | 8/11/2061 | | | 2,907,000 | | | | 2,389,138 | |

| Fluor Corp. | | 4.25% | | 9/15/2028 | | | 2,391,000 | | | | 2,156,139 | |

| Total | | | | | | | | | | | 4,545,277 | |

| 18 | See Notes to Financial Statements. |

Schedule of Investments (continued)

December 31, 2022

| | | Interest | | Maturity | | Principal | | | Fair | |

| Investments | | Rate | | Date | | Amount | | | Value | |

| Entertainment 1.67% | | | | | | | | | | | | |

| Churchill Downs, Inc.† | | 4.75% | | 1/15/2028 | | $ | 1,787,000 | | | $ | 1,601,902 | |

| Churchill Downs, Inc.† | | 5.50% | | 4/1/2027 | | | 2,671,000 | | | | 2,535,060 | |

| Live Nation Entertainment, Inc.† | | 3.75% | | 1/15/2028 | | | 2,128,000 | | | | 1,818,541 | |

| Merlin Entertainments Ltd. (United Kingdom)†(a) | | 5.75% | | 6/15/2026 | | | 1,360,000 | | | | 1,275,432 | |

| Midwest Gaming Borrower LLC/Midwest Gaming Finance Corp† | | 4.875% | | 5/1/2029 | | | 1,984,000 | | | | 1,690,694 | |

| Mohegan Gaming & Entertainment† | | 8.00% | | 2/1/2026 | | | 2,032,000 | | | | 1,904,024 | |

| Resorts World Las Vegas LLC/RWLV Capital, Inc.† | | 4.625% | | 4/16/2029 | | | 2,000,000 | | | | 1,421,463 | |

| SeaWorld Parks & Entertainment, Inc.† | | 5.25% | | 8/15/2029 | | | 1,820,000 | | | | 1,587,038 | |

| Warnermedia Holdings, Inc.† | | 5.141% | | 3/15/2052 | | | 1,970,000 | | | | 1,439,730 | |

| WMG Acquisition Corp.† | | 3.00% | | 2/15/2031 | | | 1,417,000 | | | | 1,134,585 | |

| WMG Acquisition Corp.† | | 3.75% | | 12/1/2029 | | | 1,919,000 | | | | 1,652,835 | |

| Total | | | | | | | | | | | 18,061,304 | |

| | | | | | | | | | | | | |

| Environmental Control 0.32% | | | | | | | | | | | | |

| Madison IAQ LLC† | | 4.125% | | 6/30/2028 | | | 1,677,000 | | | | 1,404,487 | |

| Madison IAQ LLC† | | 5.875% | | 6/30/2029 | | | 1,372,000 | | | | 942,947 | |

| Republic Services, Inc. | | 2.375% | | 3/15/2033 | | | 1,433,000 | | | | 1,146,999 | |

| Total | | | | | | | | | | | 3,494,433 | |

| | | | | | | | | | | | | |

| Food 1.59% | | | | | | | | | | | | |

| Bellis Acquisition Co. PLC(f) | | 3.25% | | 2/16/2026 | | GBP | 1,350,000 | | | | 1,334,023 | |

| Campbell Soup Co. | | 2.375% | | 4/24/2030 | | $ | 952,000 | | | | 794,385 | |

| Hershey Co. (The) | | 2.65% | | 6/1/2050 | | | 1,008,000 | | | | 659,389 | |

| Kraft Heinz Foods Co. | | 4.375% | | 6/1/2046 | | | 4,002,000 | | | | 3,270,399 | |

| Kraft Heinz Foods Co. | | 4.875% | | 10/1/2049 | | | 3,623,000 | | | | 3,163,313 | |

| Lamb Weston Holdings, Inc.† | | 4.125% | | 1/31/2030 | | | 1,243,000 | | | | 1,099,496 | |

| McCormick & Co., Inc. | | 2.50% | | 4/15/2030 | | | 2,046,000 | | | | 1,710,943 | |

| Post Holdings, Inc.† | | 4.50% | | 9/15/2031 | | | 1,666,000 | | | | 1,403,614 | |

| Post Holdings, Inc.† | | 4.625% | | 4/15/2030 | | | 2,303,000 | | | | 1,991,692 | |

| Smithfield Foods, Inc.† | | 5.20% | | 4/1/2029 | | | 2,021,000 | | | | 1,850,464 | |

| Total | | | | | | | | | | | 17,277,718 | |

| | | | | | | | | | | | | |

| Gas 0.22% | | | | | | | | | | | | |

| Brooklyn Union Gas Co. (The)† | | 3.407% | | 3/10/2026 | | | 1,368,000 | | | | 1,283,861 | |

| Southwest Gas Corp. | | 4.05% | | 3/15/2032 | | | 1,247,000 | | | | 1,098,356 | |

| Total | | | | | | | | | | | 2,382,217 | |

| | | | | | | | | | | | | |

| Health Care-Products 0.60% | | | | | | | | | | | | |

| Alcon Finance Corp.† | | 2.60% | | 5/27/2030 | | | 1,552,000 | | | | 1,322,030 | |

| Boston Scientific Corp. | | 6.75% | | 11/15/2035 | | | 1,597,000 | | | | 1,759,471 | |

| | | |

| | See Notes to Financial Statements. | 19 |

Schedule of Investments (continued)

December 31, 2022

| | | Interest | | Maturity | | Principal | | | Fair | |

| Investments | | Rate | | Date | | Amount | | | Value | |

| Health Care-Products (continued) | | | | | | | | | | | | |

| Edwards Lifesciences Corp. | | 4.30% | | 6/15/2028 | | $ | 1,411,000 | | | $ | 1,351,614 | |

| GE HealthCare Technologies, Inc.† | | 6.377% | | 11/22/2052 | | | 687,000 | | | | 733,848 | |

| Medline Borrower LP† | | 3.875% | | 4/1/2029 | | | 1,682,000 | | | | 1,358,627 | |

| Total | | | | | | | | | | | 6,525,590 | |

| | | | | | | | | | | | | |

| Health Care-Services 3.56% | | | | | | | | | | | | |

| Catalent Pharma Solutions, Inc.† | | 3.125% | | 2/15/2029 | | | 1,365,000 | | | | 1,088,588 | |

| Centene Corp. | | 2.50% | | 3/1/2031 | | | 1,513,000 | | | | 1,186,794 | |

| Centene Corp. | | 3.00% | | 10/15/2030 | | | 1,327,000 | | | | 1,090,800 | |

| Centene Corp. | | 3.375% | | 2/15/2030 | | | 3,631,000 | | | | 3,077,726 | |

| Centene Corp. | | 4.625% | | 12/15/2029 | | | 1,807,000 | | | | 1,655,376 | |

| Charles River Laboratories International, Inc.† | | 3.75% | | 3/15/2029 | | | 1,304,000 | | | | 1,155,142 | |

| Elevance Health, Inc. | | 2.25% | | 5/15/2030 | | | 1,299,000 | | | | 1,077,553 | |

| Hadrian Merger Sub, Inc.† | | 8.50% | | 5/1/2026 | | | 1,187,000 | | | | 1,050,738 | |

| HCA, Inc. | | 3.50% | | 9/1/2030 | | | 2,358,000 | | | | 2,039,259 | |

| HCA, Inc. | | 7.69% | | 6/15/2025 | | | 640,000 | | | | 671,453 | |

| Kaiser Foundation Hospitals | | 4.15% | | 5/1/2047 | | | 873,000 | | | | 744,064 | |

| Memorial Sloan-Kettering Cancer Center | | 4.20% | | 7/1/2055 | | | 1,478,000 | | | | 1,214,782 | |

| ModivCare Escrow Issuer, Inc.† | | 5.00% | | 10/1/2029 | | | 1,864,000 | | | | 1,574,335 | |

| Molina Healthcare, Inc.† | | 3.875% | | 11/15/2030 | | | 1,553,000 | | | | 1,318,380 | |

| Molina Healthcare, Inc.† | | 3.875% | | 5/15/2032 | | | 2,065,000 | | | | 1,717,841 | |

| Montefiore Obligated Group | | 5.246% | | 11/1/2048 | | | 1,553,000 | | | | 1,167,051 | |

| Mount Sinai Hospitals Group, Inc. | | 3.737% | | 7/1/2049 | | | 1,566,000 | | | | 1,162,307 | |

| New York & Presbyterian Hospital (The) | | 4.063% | | 8/1/2056 | | | 1,020,000 | | | | 808,274 | |

| NYU Langone Hospitals | | 4.368% | | 7/1/2047 | | | 1,191,000 | | | | 994,608 | |

| Providence St. Joseph Health Obligated Group | | 2.532% | | 10/1/2029 | | | 1,160,000 | | | | 984,111 | |

| Rede D’or Finance Sarl (Luxembourg)†(a) | | 4.95% | | 1/17/2028 | | | 912,000 | | | | 843,801 | |

| Roche Holdings, Inc.† | | 2.314% | | 3/10/2027 | | | 1,268,000 | | | | 1,157,020 | |

| Seattle Children’s Hospital | | 2.719% | | 10/1/2050 | | | 1,672,000 | | | | 1,060,881 | |

| Tenet Healthcare Corp.† | | 4.375% | | 1/15/2030 | | | 1,319,000 | | | | 1,143,995 | |

| Tenet Healthcare Corp.† | | 4.875% | | 1/1/2026 | | | 1,154,000 | | | | 1,093,614 | |

| Tenet Healthcare Corp.† | | 6.125% | | 10/1/2028 | | | 2,221,000 | | | | 1,993,192 | |

| Tenet Healthcare Corp.† | | 6.125% | | 6/15/2030 | | | 1,770,000 | | | | 1,689,562 | |

| UnitedHealth Group, Inc. | | 2.95% | | 10/15/2027 | | | 686,000 | | | | 636,238 | |

| UnitedHealth Group, Inc. | | 4.20% | | 5/15/2032 | | | 1,630,000 | | | | 1,552,224 | |

| UnitedHealth Group, Inc. | | 5.875% | | 2/15/2053 | | | 1,542,000 | | | | 1,675,140 | |

| Total | | | | | | | | | | | 38,624,849 | |

| | | |

| 20 | See Notes to Financial Statements. | |

Schedule of Investments (continued)

December 31, 2022

| | | Interest | | Maturity | | Principal | | | Fair | |

| Investments | | Rate | | Date | | Amount | | | Value | |

| Home Builders 0.29% | | | | | | | | | | | | |

| NVR, Inc. | | 3.00% | | 5/15/2030 | | $ | 1,297,000 | | | $ | 1,091,736 | |

| PulteGroup, Inc. | | 6.375% | | 5/15/2033 | | | 1,215,000 | | | | 1,215,830 | |

| Toll Brothers Finance Corp. | | 4.35% | | 2/15/2028 | | | 874,000 | | | | 795,589 | |

| Total | | | | | | | | | | | 3,103,155 | |

| | | | | | | | | | | | | |

| Home Furnishings 0.07% | | | | | | | | | | | | |

| Leggett & Platt, Inc. | | 4.40% | | 3/15/2029 | | | 828,000 | | | | 778,946 | |

| | | | | | | | | | | | | |

| Household Products/Wares 0.11% | | | | | | | | | | | | |

| SC Johnson & Son, Inc.† | | 4.75% | | 10/15/2046 | | | 1,300,000 | | | | 1,156,931 | |

| | | | | | | | | | | | | |

| Insurance 1.64% | | | | | | | | | | | | |

| AIA Group Ltd. (Hong Kong)†(a) | | 3.20% | | 9/16/2040 | | | 1,940,000 | | | | 1,388,091 | |

| AIA Group Ltd. (Hong Kong)†(a) | | 3.375% | | 4/7/2030 | | | 1,304,000 | | | | 1,148,742 | |

| Arch Capital Finance LLC | | 4.011% | | 12/15/2026 | | | 1,183,000 | | | | 1,129,780 | |

| Assurant, Inc. | | 2.65% | | 1/15/2032 | | | 1,306,000 | | | | 969,017 | |

| Assurant, Inc. | | 3.70% | | 2/22/2030 | | | 1,191,000 | | | | 1,011,227 | |

| AXIS Specialty Finance plc (United Kingdom)(a) | | 5.15% | | 4/1/2045 | | | 1,595,000 | | | | 1,367,964 | |

| Brown & Brown, Inc. | | 2.375% | | 3/15/2031 | | | 2,120,000 | | | | 1,617,789 | |

| Fidelity National Financial, Inc. | | 4.50% | | 8/15/2028 | | | 869,000 | | | | 825,850 | |

| Global Atlantic Fin Co.† | | 4.70%

(5 Yr. Treasury CMT + 3.80% | )# | 10/15/2051 | | | 1,000,000 | | | | 763,283 | |

| Northwestern Mutual Life Insurance Co. (The)† | | 3.85% | | 9/30/2047 | | | 1,456,000 | | | | 1,117,599 | |

| PartnerRe Finance B LLC | | 3.70% | | 7/2/2029 | | | 1,806,000 | | | | 1,633,117 | |

| Selective Insurance Group, Inc. | | 5.375% | | 3/1/2049 | | | 1,169,000 | | | | 1,006,878 | |

| Teachers Insurance & Annuity Association of America† | | 4.27% | | 5/15/2047 | | | 889,000 | | | | 731,155 | |

| Teachers Insurance & Annuity Association of America† | | 4.90% | | 9/15/2044 | | | 1,506,000 | | | | 1,384,130 | |

| Transatlantic Holdings, Inc. | | 8.00% | | 11/30/2039 | | | 934,000 | | | | 1,163,311 | |

| W R Berkley Corp. | | 3.15% | | 9/30/2061 | | | 900,000 | | | | 551,802 | |

| Total | | | | | | | | | | | 17,809,735 | |

| | | | | | | | | | | | | |

| Internet 2.34% | | | | | | | | | | | | |

| Alibaba Group Holding Ltd. (China)(a) | | 2.125% | | 2/9/2031 | | | 3,468,000 | | | | 2,769,446 | |

| Amazon.com, Inc. | | 3.15% | | 8/22/2027 | | | 7,000,000 | | | | 6,589,343 | |

| Gen Digital, Inc.† | | 6.75% | | 9/30/2027 | | | 1,126,000 | | | | 1,104,944 | |

| Go Daddy Operating Co. LLC/GD Finance Co., Inc.† | | 5.25% | | 12/1/2027 | | | 1,235,000 | | | | 1,171,002 | |

| Meta Platforms, Inc. | | 4.45% | | 8/15/2052 | | | 2,247,000 | | | | 1,797,245 | |

| Netflix, Inc.(f) | | 3.625% | | 5/15/2027 | | EUR | 2,500,000 | | | | 2,581,116 | |

| Netflix, Inc. | | 4.875% | | 4/15/2028 | | $ | 3,733,000 | | | | 3,612,933 | |

| | | |

| | See Notes to Financial Statements. | 21 |

Schedule of Investments (continued)

December 31, 2022

| | | Interest | | Maturity | | Principal | | | Fair | |

| Investments | | Rate | | Date | | Amount | | | Value | |

| Internet (continued) | | | | | | | | | | | | |

| Tencent Holdings Ltd. (China)†(a) | | 3.595% | | 1/19/2028 | | $ | 3,150,000 | | | $ | 2,892,546 | |

| Tencent Holdings Ltd. (China)†(a) | | 3.925% | | 1/19/2038 | | | 2,149,000 | | | | 1,716,143 | |

| VeriSign, Inc. | | 2.70% | | 6/15/2031 | | | 1,384,000 | | | | 1,130,618 | |

| Total | | | | | | | | | | | 25,365,336 | |

| | | | | | | | | | | | | |

| Investment Companies 0.08% | | | | | | | | | | | | |

| Temasek Financial I Ltd. (Singapore)†(a) | | 2.50% | | 10/6/2070 | | | 1,480,000 | | | | 869,689 | |

| | | | | | | | | | | | | |

| Iron-Steel 0.58% | | | | | | | | | | | | |

| ArcelorMittal SA (Luxembourg)(a) | | 6.55% | | 11/29/2027 | | | 1,141,000 | | | | 1,148,325 | |

| Baffinland Iron Mines Corp./Baffinland Iron Mines LP (Canada)†(a) | | 8.75% | | 7/15/2026 | | | 661,000 | | | | 627,778 | |

| Mineral Resources Ltd. (Australia)†(a) | | 8.50% | | 5/1/2030 | | | 1,798,000 | | | | 1,824,961 | |

| Steel Dynamics, Inc. | | 3.45% | | 4/15/2030 | | | 486,000 | | | | 428,449 | |

| United States Steel Corp. | | 6.875% | | 3/1/2029 | | | 1,102,000 | | | | 1,071,140 | |

| Vale Overseas Ltd. (Brazil)(a) | | 3.75% | | 7/8/2030 | | | 1,309,000 | | | | 1,148,237 | |

| Total | | | | | | | | | | | 6,248,890 | |

| | | | | | | | | | | | | |

| Leisure Time 0.19% | | | | | | | | | | | | |

| Life Time, Inc.† | | 5.75% | | 1/15/2026 | | | 895,000 | | | | 833,916 | |

| NCL Corp. Ltd.† | | 5.875% | | 2/15/2027 | | | 1,378,000 | | | | 1,195,353 | |

| Total | | | | | | | | | | | 2,029,269 | |

| | | | | | | | | | | | | |

| Lodging 1.74% | | | | | | | | | | | | |

| Boyd Gaming Corp. | | 4.75% | | 12/1/2027 | | | 1,201,000 | | | | 1,120,341 | |

| Genting New York LLC/GENNY Capital, Inc.† | | 3.30% | | 2/15/2026 | | | 1,306,000 | | | | 1,142,648 | |

| Hilton Domestic Operating Co., Inc.† | | 3.75% | | 5/1/2029 | | | 1,268,000 | | | | 1,098,519 | |

| Hilton Domestic Operating Co., Inc. | | 4.875% | | 1/15/2030 | | | 3,480,000 | | | | 3,159,457 | |

| Las Vegas Sands Corp. | | 3.50% | | 8/18/2026 | | | 1,835,000 | | | | 1,658,930 | |

| Marriott International, Inc. | | 3.50% | | 10/15/2032 | | | 1,250,000 | | | | 1,043,297 | |

| Sands China Ltd. (Macau)(a) | | 3.35% | | 3/8/2029 | | | 1,638,000 | | | | 1,340,395 | |

| Sands China Ltd. (Macau)(a) | | 4.875% | | 6/18/2030 | | | 1,640,000 | | | | 1,443,430 | |

| Sands China Ltd. (Macau)(a) | | 5.90% | | 8/8/2028 | | | 1,442,000 | | | | 1,352,110 | |

| Travel + Leisure Co. | | 6.00% | | 4/1/2027 | | | 1,439,000 | | | | 1,368,216 | |

| Wynn Las Vegas LLC/Wynn Las Vegas Capital Corp.† | | 5.25% | | 5/15/2027 | | | 2,424,000 | | | | 2,191,419 | |

| Wynn Las Vegas LLC/Wynn Las Vegas Capital Corp.† | | 5.50% | | 3/1/2025 | | | 2,000,000 | | | | 1,902,812 | |

| Total | | | | | | | | | | | 18,821,574 | |

| | | |

| 22 | See Notes to Financial Statements. | |

Schedule of Investments (continued)

December 31, 2022

| | | Interest | | Maturity | | Principal | | | Fair | |

| Investments | | Rate | | Date | | Amount | | | Value | |

| Machinery-Diversified 0.28% | | | | | | | | | | | | |

| nVent Finance Sarl (Luxembourg)(a) | | 2.75% | | 11/15/2031 | | $ | 783,000 | | | $ | 604,421 | |

| TK Elevator US Newco, Inc.† | | 5.25% | | 7/15/2027 | | | 1,240,000 | | | | 1,103,104 | |

| Westinghouse Air Brake Technologies Corp. | | 3.45% | | 11/15/2026 | | | 1,421,000 | | | | 1,321,946 | |

| Total | | | | | | | | | | | 3,029,471 | |

| | | | | | | | | | | | | |

| Media 2.00% | | | | | | | | | | | | |

| Cable One, Inc.† | | 4.00% | | 11/15/2030 | | | 2,012,000 | | | | 1,581,313 | |

| CCO Holdings LLC/CCO Holdings Capital Corp.† | | 5.00% | | 2/1/2028 | | | 1,746,000 | | | | 1,589,200 | |

| CCO Holdings LLC/CCO Holdings Capital Corp.† | | 5.375% | | 6/1/2029 | | | 1,881,000 | | | | 1,705,173 | |

| CCO Holdings LLC/CCO Holdings Capital Corp.† | | 6.375% | | 9/1/2029 | | | 1,484,000 | | | | 1,397,431 | |

| CSC Holdings LLC† | | 4.125% | | 12/1/2030 | | | 2,713,000 | | | | 1,920,899 | |

| DISH Network Corp.† | | 11.75% | | 11/15/2027 | | | 2,371,000 | | | | 2,444,857 | |

| FactSet Research Systems, Inc. | | 3.45% | | 3/1/2032 | | | 1,962,000 | | | | 1,650,161 | |

| LCPR Senior Secured Financing DAC (Ireland)†(a) | | 6.75% | | 10/15/2027 | | | 708,000 | | | | 663,623 | |

| News Corp.† | | 3.875% | | 5/15/2029 | | | 1,559,000 | | | | 1,354,514 | |

| Nexstar Media, Inc.† | | 4.75% | | 11/1/2028 | | | 1,280,000 | | | | 1,109,133 | |

| Univision Communications, Inc.† | | 4.50% | | 5/1/2029 | | | 2,508,000 | | | | 2,102,043 | |

| UPC Broadband Finco BV (Netherlands)†(a) | | 4.875% | | 7/15/2031 | | | 2,867,000 | | | | 2,390,533 | |

| VZ Secured Financing BV (Netherlands)†(a) | | 5.00% | | 1/15/2032 | | | 2,228,000 | | | | 1,814,553 | |

| Total | | | | | | | | | | | 21,723,433 | |

| | | | | | | | | | | | | |

| Metal Fabricate-Hardware 0.22% | | | | | | | | | | | | |

| Roller Bearing Co. of America, Inc.† | | 4.375% | | 10/15/2029 | | | 2,799,000 | | | | 2,423,794 | |

| | | | | | | | | | | | | |

| Mining 1.36% | | | | | | | | | | | | |

| Anglo American Capital plc (United Kingdom)†(a) | | 5.625% | | 4/1/2030 | | | 1,100,000 | | | | 1,094,693 | |

| FMG Resources August 2006 Pty Ltd. (Australia)†(a) | | 4.375% | | 4/1/2031 | | | 4,005,000 | | | | 3,338,602 | |

| FMG Resources August Pty. Ltd. (Australia)†(a) | | 6.125% | | 4/15/2032 | | | 1,346,000 | | | | 1,257,225 | |

| Fresnillo PLC (Mexico)(a) | | 4.25% | | 10/2/2050 | | | 274,000 | | | | 216,198 | |

| Glencore Funding LLC† | | 2.50% | | 9/1/2030 | | | 2,300,000 | | | | 1,872,150 | |

| Hecla Mining Co. | | 7.25% | | 2/15/2028 | | | 1,194,000 | | | | 1,177,500 | |

| Kaiser Aluminum Corp.† | | 4.50% | | 6/1/2031 | | | 1,528,000 | | | | 1,230,116 | |

| Mirabela Nickel Ltd. | | 1.00% | | 9/10/2044 | | | 15,172 | | | | 1 | (d) |

| Newmont Corp. | | 2.25% | | 10/1/2030 | | | 1,318,000 | | | | 1,062,376 | |

| Novelis Corp.† | | 4.75% | | 1/30/2030 | | | 2,071,000 | | | | 1,840,746 | |

| Teck Resources Ltd. (Canada)(a) | | 3.90% | | 7/15/2030 | | | 1,913,000 | | | | 1,715,309 | |

| Total | | | | | | | | | | | 14,804,916 | |

| | | |

| | See Notes to Financial Statements. | 23 |

Schedule of Investments (continued)

December 31, 2022

| | | Interest | | Maturity | | Principal | | | Fair | |

| Investments | | Rate | | Date | | Amount | | | Value | |

| Miscellaneous Manufacturing 0.21% | | | | | | | | | | | | |

| Eaton Corp. | | 4.15% | | 3/15/2033 | | $ | 1,342,000 | | | $ | 1,251,792 | |

| Hillenbrand, Inc. | | 3.75% | | 3/1/2031 | | | 1,275,000 | | | | 1,047,158 | |

| Total | | | | | | | | | | | 2,298,950 | |

| | | | | | | | | | | | | |

| Multi-National 0.35% | | | | | | | | | | | | |

| Asian Development Bank (Philippines)(a) | | 4.597%

(SOFR Index + 1.00% | )# | 4/6/2027 | | | 3,683,000 | | | | 3,765,033 | |

| | | | | | | | | | | | | |

| Office/Business Equipment 0.10% | | | | | | | | | | | | |

| CDW LLC/CDW Finance Corp. | | 3.569% | | 12/1/2031 | | | 1,287,000 | | | | 1,062,948 | |

| | | | | | | | | | | | | |

| Oil & Gas 12.10% | | | | | | | | | | | | |

| Antero Resources Corp.† | | 5.375% | | 3/1/2030 | | | 4,893,000 | | | | 4,542,955 | |

| Apache Corp. | | 4.25% | | 1/15/2030 | | | 2,793,000 | | | | 2,476,502 | |

| Apache Corp. | | 4.75% | | 4/15/2043 | | | 1,641,000 | | | | 1,241,047 | |

| Apache Corp. | | 5.10% | | 9/1/2040 | | | 3,580,000 | | | | 2,974,864 | |

| California Resources Corp.† | | 7.125% | | 2/1/2026 | | | 2,160,000 | | | | 2,078,395 | |

| Callon Petroleum Co. | | 6.375% | | 7/1/2026 | | | 2,011,000 | | | | 1,877,521 | |

| Callon Petroleum Co.† | | 8.00% | | 8/1/2028 | | | 1,951,000 | | | | 1,862,383 | |

| Cenovus Energy, Inc. (Canada)(a) | | 2.65% | | 1/15/2032 | | | 1,364,000 | | | | 1,092,576 | |

| Cenovus Energy, Inc. (Canada)(a) | | 3.75% | | 2/15/2052 | | | 2,668,000 | | | | 1,885,429 | |

| Cenovus Energy, Inc. (Canada)(a) | | 5.40% | | 6/15/2047 | | | 3,846,000 | | | | 3,458,504 | |

| Chesapeake Energy Corp.† | | 6.75% | | 4/15/2029 | | | 2,643,000 | | | | 2,576,793 | |

| CITGO Petroleum Corp.† | | 7.00% | | 6/15/2025 | | | 1,160,000 | | | | 1,134,109 | |

| CNX Resources Corp.† | | 7.25% | | 3/14/2027 | | | 1,068,000 | | | | 1,061,827 | |

| Comstock Resources, Inc.† | | 5.875% | | 1/15/2030 | | | 1,615,000 | | | | 1,390,515 | |

| Comstock Resources, Inc.† | | 6.75% | | 3/1/2029 | | | 1,713,000 | | | | 1,549,083 | |

| Continental Resources, Inc. | | 4.375% | | 1/15/2028 | | | 4,075,000 | | | | 3,740,402 | |

| Continental Resources, Inc.† | | 5.75% | | 1/15/2031 | | | 1,644,000 | | | | 1,533,565 | |

| Crescent Energy Finance LLC† | | 7.25% | | 5/1/2026 | | | 1,716,000 | | | | 1,619,243 | |

| CrownRock LP/CrownRock Finance, Inc.† | | 5.00% | | 5/1/2029 | | | 1,840,000 | | | | 1,663,076 | |

| Diamondback Energy, Inc. | | 3.50% | | 12/1/2029 | | | 2,292,000 | | | | 2,015,840 | |

| Diamondback Energy, Inc. | | 4.25% | | 3/15/2052 | | | 2,616,000 | | | | 1,925,627 | |

| Diamondback Energy, Inc. | | 4.40% | | 3/24/2051 | | | 2,777,000 | | | | 2,128,083 | |

| Encino Acquisition Partners Holdings LLC† | | 8.50% | | 5/1/2028 | | | 1,734,000 | | | | 1,587,104 | |

| Endeavor Energy Resources LP/EER Finance, Inc.† | | 5.75% | | 1/30/2028 | | | 2,818,000 | | | | 2,702,885 | |

| Exxon Mobil Corp. | | 3.043% | | 3/1/2026 | | | 823,000 | | | | 785,920 | |

| Geopark Ltd. (Colombia)†(a) | | 5.50% | | 1/17/2027 | | | 418,000 | | | | 360,034 | |

| Helmerich & Payne, Inc. | | 2.90% | | 9/29/2031 | | | 2,358,000 | | | | 1,919,779 | |

| Hess Corp. | | 5.60% | | 2/15/2041 | | | 1,617,000 | | | | 1,535,587 | |

| | | |

| 24 | See Notes to Financial Statements. | |

Schedule of Investments (continued)

December 31, 2022

| | | Interest | | Maturity | | Principal | | | Fair | |

| Investments | | Rate | | Date | | Amount | | | Value | |

| Oil & Gas (continued) | | | | | | | | | | | | |

| Hess Corp. | | 5.80% | | 4/1/2047 | | $ | 693,000 | | | $ | 665,092 | |

| Kosmos Energy Ltd.† | | 7.125% | | 4/4/2026 | | | 467,000 | | | | 398,855 | |

| Kosmos Energy Ltd.† | | 7.75% | | 5/1/2027 | | | 2,079,000 | | | | 1,738,762 | |

| Laredo Petroleum, Inc.† | | 7.75% | | 7/31/2029 | | | 2,617,000 | | | | 2,358,922 | |

| Laredo Petroleum, Inc. | | 10.125% | | 1/15/2028 | | | 3,500,000 | | | | 3,418,570 | |

| Matador Resources Co. | | 5.875% | | 9/15/2026 | | | 1,088,000 | | | | 1,047,656 | |

| MC Brazil Downstream Trading Sarl (Luxembourg)†(a) | | 7.25% | | 6/30/2031 | | | 1,536,000 | | | | 1,269,593 | |

| MEG Energy Corp. (Canada)†(a) | | 5.875% | | 2/1/2029 | | | 2,312,000 | | | | 2,183,222 | |

| MEG Energy Corp. (Canada)†(a) | | 7.125% | | 2/1/2027 | | | 2,420,000 | | | | 2,471,732 | |

| Murphy Oil Corp. | | 5.875% | | 12/1/2027 | | | 2,000,000 | | | | 1,928,020 | |

| Murphy Oil Corp. | | 6.375% | | 7/15/2028 | | | 1,241,000 | | | | 1,196,299 | |

| Nabors Industries, Inc.† | | 7.375% | | 5/15/2027 | | | 1,083,000 | | | | 1,050,347 | |

| Occidental Petroleum Corp. | | 6.125% | | 1/1/2031 | | | 3,933,000 | | | | 3,976,714 | |

| Occidental Petroleum Corp. | | 6.625% | | 9/1/2030 | | | 837,000 | | | | 866,826 | |

| Occidental Petroleum Corp. | | 7.50% | | 5/1/2031 | | | 1,013,000 | | | | 1,084,062 | |

| OQ SAOC (Oman)†(a) | | 5.125% | | 5/6/2028 | | | 1,782,000 | | | | 1,694,128 | |

| Ovintiv, Inc. | | 6.50% | | 2/1/2038 | | | 1,948,000 | | | | 1,937,638 | |

| Patterson-UTI Energy, Inc. | | 3.95% | | 2/1/2028 | | | 1,394,000 | | | | 1,230,723 | |

| Patterson-UTI Energy, Inc. | | 5.15% | | 11/15/2029 | | | 1,562,000 | | | | 1,403,253 | |

| PDC Energy, Inc. | | 5.75% | | 5/15/2026 | | | 2,868,000 | | | | 2,742,382 | |

| Permian Resources Operating LLC† | | 5.375% | | 1/15/2026 | | | 1,659,000 | | | | 1,512,783 | |

| Permian Resources Operating LLC† | | 6.875% | | 4/1/2027 | | | 3,588,000 | | | | 3,390,294 | |

| Pioneer Natural Resources Co. | | 2.15% | | 1/15/2031 | | | 1,344,000 | | | | 1,065,467 | |

| Precision Drilling Corp. (Canada)†(a) | | 6.875% | | 1/15/2029 | | | 1,295,000 | | | | 1,207,337 | |

| QatarEnergy Trading LLC (Qatar)†(a) | | 3.30% | | 7/12/2051 | | | 5,399,000 | | | | 3,999,579 | |

| Range Resources Corp.† | | 4.75% | | 2/15/2030 | | | 2,643,000 | | | | 2,332,586 | |

| Range Resources Corp. | | 8.25% | | 1/15/2029 | | | 2,791,000 | | | | 2,879,726 | |

| Rockcliff Energy II LLC† | | 5.50% | | 10/15/2029 | | | 1,194,000 | | | | 1,093,973 | |

| Saudi Arabian Oil Co. (Saudi Arabia)(a) | | 2.875% | | 4/16/2024 | | | 1,600,000 | | | | 1,553,021 | |

| Saudi Arabian Oil Co. (Saudi Arabia)†(a) | | 4.375% | | 4/16/2049 | | | 2,895,000 | | | | 2,499,844 | |

| Shell International Finance BV (Netherlands)(a) | | 2.875% | | 5/10/2026 | | | 914,000 | | | | 861,843 | |

| Shell International Finance BV (Netherlands)(a) | | 6.375% | | 12/15/2038 | | | 1,473,000 | | | | 1,626,460 | |

| SM Energy Co. | | 6.625% | | 1/15/2027 | | | 4,388,000 | | | | 4,233,542 | |

| SM Energy Co. | | 6.75% | | 9/15/2026 | | | 1,112,000 | | | | 1,081,337 | |

| Southwestern Energy Co. | | 4.75% | | 2/1/2032 | | | 1,212,000 | | | | 1,038,096 | |

| Southwestern Energy Co. | | 5.375% | | 2/1/2029 | | | 2,333,000 | | | | 2,166,202 | |