UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-05876

LORD ABBETT SERIES FUND, INC.

(Exact name of Registrant as specified in charter)

90 Hudson Street, Jersey City, NJ 07302

(Address of principal executive offices) (Zip code)

John T. Fitzgerald, Esq., Vice President & Assistant Secretary

90 Hudson Street, Jersey City, NJ 07302

(Name and address of agent for service)

Registrant’s telephone number, including area code: (888) 522-2388

Date of fiscal year end: 12/31

Date of reporting period: 12/31/2020

| Item 1: | | Report(s) to Shareholders. |

LORD ABBETT

ANNUAL REPORT

Lord Abbett

Series Fund—Bond Debenture Portfolio

For the fiscal year ended December 31, 2020

Table of Contents

Lord Abbett Series Fund — Bond Debenture Portfolio

Annual Report

For the fiscal year ended December 31, 2020

From left to right: James L.L. Tullis, Independent Chairman of the Lord Abbett Funds and Douglas B. Sieg, Director, President, and Chief Executive Officer of the Lord Abbett Funds. | | Dear Shareholders: We are pleased to provide you with this overview of the performance of Lord Abbett Series Fund – Bond Debenture Portfolio for the fiscal year ended December 31, 2020. On this page and the following pages, we discuss the major factors that influenced fiscal year performance. For additional information about the Fund, please visit our website at www.lordabbett.com, where you also can access the quarterly commentaries that provide updates on the Fund’s performance and other portfolio related updates. Thank you for investing in Lord Abbett mutual funds. We value the trust that you place in us and look forward to serving your investment needs in the years to come. Best regards,

Douglas B. Sieg

Director, President, and Chief Executive Officer |

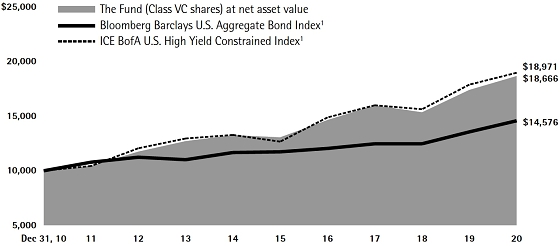

For the fiscal year ended December 31, 2020, the Fund returned 7.30%, reflecting performance at the net asset value (NAV) of Class VC shares with all distributions reinvested, compared to its benchmark, the Bloomberg Barclays U.S. Aggregate Bond Index,1 which returned 7.51% over the same period.

The trailing twelve-month period was characterized by several market-moving events. After trade tensions continued to ebb and flow in the final months of 2019, U.S. President Donald Trump signed a “phase one” trade deal with China on the 15th of January 2020 and markets priced in a likelihood of two more interest rate cuts in 2020. The tide turned abruptly in February and March 2020, as the outbreak of the COVID-19 pandemic and the expected economic damage resulting from a sudden slowdown in corporate spending, individual spending, consumer confidence, and thus recessionary and deflationary pressures, triggered a severe sell-off. As the COVID-19 pandemic fueled fears of slowing global growth, oil prices fell precipitously, with the primary U.S. oil contract closing in negative territory for the first time in history, although it has since rebounded. During the month of March, the S&P 500

1

Index2 experienced its fastest bear market since 1987 and the longest U.S. economic expansion in history ended at 128 months.

The U.S. Federal Reserve (Fed) responded to the COVID-19 outbreak with a breadth of policy measures which lifted investors’ confidence in the markets. The Fed launched a $700 billion quantitative easing program, decreased the reserve requirements to zero for thousands of banks, and cut the federal funds rate to the current target range of 0–0.25%. Next, the Fed announced additional stimulus programs, including open-ended asset purchases, purchases of corporate debt, and a commitment to a new small business lending program. Additionally, the central bank announced $2.3 trillion of credit support by expanding the Primary Market Corporate Credit Facility (PMCCF), the Secondary Market Corporate Credit Facility (SMCCF), and the Term Asset-Backed Securities Loan Facility (TALF). Most notably, the expanded measures included the purchase of select fallen angels.

Risk assets began to stage a recovery in April and May 2020 on the back of progress with respect to COVID-19 treatments and vaccines, commentary from several corporations that indicated stabilization in April and May, and massive monetary and fiscal policy globally. Positive market sentiment continued into the third quarter of 2020 as well. In addition to the factors listed above, tailwinds for the continued rally in risk assets included a rebound in earnings revisions and further progress in COVID-19 treatments, as evidenced by

multiple drugs reaching Phase III trials. In September, however, market sentiment soured amid political volatility related to the U.S. Supreme Court vacancy, increased COVID-19 concerns in Europe as global deaths topped one million, heightened uncertainty leading up to the U.S. Presidential election, and worries about stalled fiscal stimulus talks in Washington.

Despite the volatility in the fall, the markets rallied in the month of November with the Dow Jones Industrial Average having its best month since 1987. The rally was largely attributed to the conclusion of the U.S. Presidential election and positive vaccine news. Specifically, Former U.S. Vice President Biden defeated U.S. President Trump in the U.S. Presidential election, while the Republican Party narrowed the Democratic majority in the House. Soon after, Pfizer/BioNTech, Moderna, and AstraZeneca each announced a COVID-19 vaccine with greater than 90% efficacy rate. In December, as expected, the Food and Drug Administration (FDA) granted emergency use authorization for the Pfizer/BioNTech and Moderna vaccines. Monetary and fiscal policy remained largely supportive, as the Fed maintained interest rates near zero in its December meeting and noted that it would continue its monthly pace of at least $120 billion of asset purchases until “substantial further progress has been made toward the Committee’s maximum employment and price stability goals”. Additionally, Congress passed a fifth COVID-19 relief package, worth roughly

2

$900 billion, with approximately $325 billion in small business relief.

The Fund takes a flexible, multi-sector approach, which emphasizes credit sensitive sectors of the market, compared to its benchmark, which is largely comprised of U.S. Treasuries and government-related securities. The Fund benefited from an allocation to equity during the period, specifically equity-related securities tied to innovative companies in the information technology and health care sectors. The asset class’s return profile was advantageous during the market recovery, which began in late-March. Additionally, the Fund’s underweight allocation to mortgage backed securities (MBS) contributed to relative performance, as MBS underperformed the Bloomberg Barclays U.S. Aggregate Bond Index during the period. The allocation to high yield bonds contributed meaningfully to relative performance as the Fund had exposure to many high-performing investments throughout the year, particularly in the energy and communications industries.

The Fund’s modest allocations to bank loans and collateralized loan obligations (CLOs) detracted from relative performance during the period. The asset classes faced pronounced outflows and a negative technical backdrop. The Fund’s modest allocation to sovereign bonds was also a relative detractor during the year.

The Fund’s portfolio is actively managed and, therefore, its holdings and the weightings of a particular issuer or

particular sector as a percentage of portfolio assets are subject to change. Sectors may include many industries.

1 The Bloomberg Barclays U.S. Aggregate Bond Index is an index of U.S dollar-denominated, investment-grade U.S. government and corporate securities, and mortgage pass-through securities, and asset-backed securities. Indexes are unmanaged, do not reflect the deduction of fees or expenses, and an investor cannot invest directly in an index.

2 The S&P 500® Index is widely regarded as the standard for measuring large cap U.S. stock market performance and includes a representative sample of leading companies in leading industries.

Unless otherwise specified, indexes reflect total return, with all dividends reinvested. Indexes are unmanaged, do not reflect the deduction of fees or expenses, and are not available for direct investment.

Important Performance and Other Information

Performance data quoted in the following pages reflect past performance and are no guarantee of future results. Current performance may be higher or lower than the performance quoted. The investment return and principal value of an investment in the Fund will fluctuate so that shares, on any given day or when redeemed, may be worth more or less than their original cost. You can obtain performance data current to the most recent month end by calling Lord Abbett at 888-522-2388 or referring to www.lordabbett.com.

During certain periods shown, expense waivers and reimbursements were in place. Without such expense waivers and reimbursements, the Fund’s returns would have been lower.

The annual commentary above discusses the views of the Fund’s management and various portfolio holdings of the Fund as of December 31, 2020. These views and portfolio holdings may have changed after this date. Information provided in the commentary is not a recommendation to buy or sell securities. Because the Fund’s portfolio is actively managed and may change significantly, the Fund may no longer own the securities described above or may have otherwise changed its position in the securities. For more recent information about the Fund’s portfolio holdings, please visit www.lordabbett.com.

3

A Note about Risk: See Notes to Financial Statements for a discussion of investment risks. For a more detailed discussion of the risks associated with the Fund, please see the Fund’s prospectus.

Mutual funds are not insured by the FDIC, are not deposits or other obligations of, or guaranteed by, banks, and are subject to investment risks including possible loss of principal amount invested.

The Fund serves as an underlying investment vehicle for variable annuity contracts and variable life insurance policies.

4

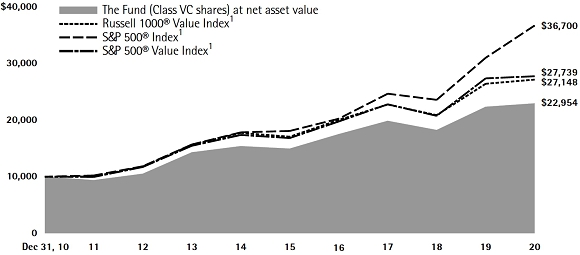

Investment Comparison

Below is a comparison of a $10,000 investment in Class VC shares with the same investment in the Bloomberg Barclays U.S. Aggregate Bond Index and the ICE BofA U.S. High Yield Constrained Index, assuming reinvestment of all dividends and distributions. The Fund’s shares are sold only to insurance company separate accounts that fund certain variable annuity and variable life contracts. This line graph comparison does not reflect the sales charges or other expenses of these contracts. If those sales charges and expenses were reflected, returns would be lower. The graph and performance table below do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. During certain periods, expenses of the Fund have been waived or reimbursed by Lord Abbett; without such waiver or reimbursement of expenses, the Fund’s returns would have been lower. Past performance is no guarantee of future results.

Average Annual Total Returns for the

Periods Ended December 31, 2020 |

| | | 1 Year | | 5 Years | | 10 Years | |

| Class VC | | 7.30% | | 7.41% | | 6.44% | |

| 1 | Performance for each unmanaged index does not reflect any fees or expenses. The performance of each index is not necessarily representative of the Fund’s performance. |

5

Expense Example

As a shareholder of the Fund, you incur ongoing costs, including management fees; expenses related to the Fund’s services arrangements with certain insurance companies; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (July 1, 2020 through December 31, 2020).

The Example reflects only expenses that are deducted from the assets of the Fund. Fees and expenses, including sales charges applicable to the various insurance products that invest in the Fund, are not reflected in this Example. If such fees and expenses were reflected in the Example, the total expenses shown would be higher. Fees and expenses regarding such variable insurance products are separately described in the prospectus related to those products.

Actual Expenses

The first line of the table on the following page provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading titled “Expenses Paid During Period 7/1/20 – 12/31/20” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table on the following page provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

6

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | Beginning

Account

Value | | Ending

Account

Value | | Expenses

Paid During

Period† | |

| | | 7/1/20 | | 12/31/20 | | 7/1/20 -

12/31/20 | |

| Class VC | | | | | | | | | | | | |

| Actual | | $ | 1,000.00 | | | $ | 1,109.80 | | | $ | 4.83 | |

| Hypothetical (5% Return Before Expenses) | | $ | 1,000.00 | | | $ | 1,020.56 | | | $ | 4.62 | |

| † | Net expenses are equal to the Fund’s annualized expense ratio of 0.91%, multiplied by the average account value over the period, multiplied by 184/366 (to reflect one-half year period). |

Portfolio Holdings Presented by Sector

December 31, 2020

| Sector* | %** |

| Agency | 0.17 | % |

| Asset Backed | 2.55 | % |

| Automotive | 3.88 | % |

| Banking | 5.84 | % |

| Basic Industry | 5.29 | % |

| Capital Goods | 4.47 | % |

| Consumer Goods | 5.36 | % |

| Energy | 8.55 | % |

| Financial Services | 2.49 | % |

| Foreign Government | 2.60 | % |

| Health Care | 7.24 | % |

| Insurance | 2.30 | % |

| Leisure | 6.43 | % |

| Media | 4.84 | % |

| Mortgage Backed | 3.51 | % |

| Municipal | 2.63 | % |

| Real Estate | 1.28 | % |

| Retail | 5.27 | % |

| Services | 2.36 | % |

| Technology & Electronics | 8.64 | % |

| Telecommunications | 3.74 | % |

| Transportation | 4.08 | % |

| Utilities | 6.09 | % |

| Repurchase Agreement | 0.20 | % |

| Money Market Fund(a) | 0.17 | % |

| Time Deposit(a) | 0.02 | % |

| Total | 100.00 | % |

| * | | A sector may comprise several industries. |

| ** | | Represents percent of total investments. |

| (a) | | Securities were purchased with the cash collateral from loaned securities. |

7

Schedule of Investments

December 31, 2020

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount

(000) | | | Fair

Value | |

| LONG-TERM INVESTMENTS 98.89% | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| ASSET-BACKED SECURITIES 3.28% | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| Automobiles 0.02% | | | | | | | | | | | | |

| ACC Trust 2018-1 C† | | 6.81% | | 2/21/2023 | | $ | 244 | | | $ | 245,150 | |

| TCF Auto Receivables Owner Trust 2016-1A B† | | 2.32% | | 6/15/2022 | | | 67 | | | | 66,565 | |

| Total | | | | | | | | | | | 311,715 | |

| | | | | | | | | | | | | |

| Credit Cards 0.11% | | | | | | | | | | | | |

| Perimeter Master Note Business Trust 2019-2A A† | | 4.23% | | 5/15/2024 | | | 1,235 | | | | 1,279,680 | |

| | | | | | | | | | | | | |

| Other 3.15% | | | | | | | | | | | | |

| AMMC CLO XII Ltd. 2013-12A DR† | | 2.906%

(3 Mo. LIBOR + 2.70% | )# | 11/10/2030 | | | 391 | | | | 363,191 | |

| Apex Credit CLO LLC 2017-2A B† | | 2.089%

(3 Mo. LIBOR + 1.85% | )# | 9/20/2029 | | | 522 | | | | 522,937 | |

| Battalion CLO XV Ltd. 2019-16A B† | | 2.218%

(3 Mo. LIBOR + 2.00% | )# | 12/19/2032 | | | 1,714 | | | | 1,714,182 | |

| Benefit Street Partners CLO XIX Ltd. 2019-19A B† | | 2.237%

(3 Mo. LIBOR + 2.00% | )# | 1/15/2033 | | | 578 | | | | 579,175 | |

| Carlyle US CLO Ltd. 2019-4A B† | | 2.937%

(3 Mo. LIBOR + 2.70% | )# | 1/15/2033 | | | 1,141 | | | | 1,147,207 | |

| Cedar Funding VI CLO Ltd. 2016-6A DR† | | 3.218%

(3 Mo. LIBOR + 3.00% | )# | 10/20/2028 | | | 657 | | | | 643,359 | |

| Greywolf CLO III Ltd. 2020-3RA A1R† | | 1.506%

(3 Mo. LIBOR + 1.29% | )# | 4/15/2033 | | | 1,399 | | | | 1,403,419 | |

| Halcyon Loan Advisors Funding Ltd. 2015-2A CR† | | 2.365%

(3 Mo. LIBOR + 2.15% | )# | 7/25/2027 | | | 465 | | | | 463,666 | |

| Halcyon Loan Advisors Funding Ltd. 2017-2A A2† | | 1.918%

(3 Mo. LIBOR + 1.70% | )# | 1/17/2030 | | | 680 | | | | 681,714 | |

| Hardee’s Funding LLC 2018-1A A2II† | | 4.959% | | 6/20/2048 | | | 1,310 | | | | 1,404,704 | |

| Jamestown CLO VII Ltd. 2015-7A BR† | | 1.865%

(3 Mo. LIBOR + 1.65% | )# | 7/25/2027 | | | 1,202 | | | | 1,179,385 | |

| Kayne CLO 5 Ltd. 2019-5A A† | | 1.565%

(3 Mo. LIBOR + 1.35% | )# | 7/24/2032 | | | 2,300 | | | | 2,303,125 | |

| Kayne CLO 7 Ltd. 2020-7A A1† | | 1.418%

(3 Mo. LIBOR + 1.20% | )# | 4/17/2033 | | | 3,316 | | | | 3,308,200 | |

| KKR CLO 9 Ltd. 9 B1R† | | 1.987 (3 Mo. LIBOR + 1.75% | )# | 7/15/2030 | | | 500 | | | | 500,072 | |

| KVK CLO Ltd. 2013-A BR† | | 1.679% (3 Mo. LIBOR + 1.45% | )# | 1/14/2028 | | | 268 | | | | 265,719 | |

| Marble Point CLO XVII Ltd. 2020-1A A† | | 1.518%

(3 Mo. LIBOR + 1.30% | )# | 4/20/2033 | | | 2,050 | | | | 2,049,289 | |

| Marble Point CLO XVII Ltd. 2020-1A B† | | 1.988%

(3 Mo. LIBOR + 1.77% | )# | 4/20/2033 | | | 652 | | | | 653,440 | |

| 8 | See Notes to Financial Statements. |

Schedule of Investments (continued)

December 31, 2020

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount

(000) | | | Fair

Value | |

| Other (continued) | | | | | | | | | | | | |

| Mariner CLO Ltd. 2017-4A D† | | 3.265%

(3 Mo. LIBOR + 3.05% | )# | 10/26/2029 | | $ | 694 | | | $ | 683,167 | |

| Mountain View CLO 2017-1A BR† | | 1.98%

(3 Mo. LIBOR + 1.75% | )# | 10/16/2029 | | | 762 | | | | 762,955 | |

| Mountain View CLO X Ltd. 2015-10A BR† | | 1.574%

(3 Mo. LIBOR + 1.35% | )# | 10/13/2027 | | | 1,336 | | | | 1,316,656 | |

| Neuberger Berman Loan Advisers CLO Ltd. 2019-35A A1† | | 1.558% (3 Mo. LIBOR + 1.34% | )# | 1/19/2033 | | | 750 | | | | 752,345 | |

| Northwoods Capital 20 Ltd. 2019-20A C† | | 3.015%

(3 Mo. LIBOR + 2.80% | )# | 1/25/2030 | | | 1,099 | | | | 1,099,642 | |

| Octagon Investment Partners 29 Ltd. 2016-1A AR† | | 1.395%

(3 Mo. LIBOR + 1.18% | )# | 1/24/2033 | | | 1,250 | | | | 1,246,922 | |

| Octagon Investment Partners 48 Ltd. 2020-3A A† | | 1.732%

(3 Mo. LIBOR + 1.50% | )# | 10/20/2031 | | | 2,000 | | | | 2,007,358 | |

| OZLM Funding III Ltd. 2013-3A A2AR† | | 2.166%

(3 Mo. LIBOR + 1.95% | )# | 1/22/2029 | | | 1,200 | | | | 1,201,466 | |

| Palmer Square Loan Funding Ltd. 2018-1A A2† | | 1.287%

(3 Mo. LIBOR + 1.05% | )# | 4/15/2026 | | | 884 | | | | 874,575 | |

| Palmer Square Loan Funding Ltd. 2018-1A B† | | 1.637%

(3 Mo. LIBOR + 1.40% | )# | 4/15/2026 | | | 670 | | | | 656,899 | |

| Planet Fitness Master Issuer LLC 2018-1A A2I† | | 4.262% | | 9/5/2048 | | | 1,520 | | | | 1,523,301 | |

| Planet Fitness Master Issuer LLC 2018-1A A2II† | | 4.666% | | 9/5/2048 | | | 1,900 | | | | 1,901,775 | |

| Planet Fitness Master Issuer LLC 2019-1A A2† | | 3.858% | | 12/5/2049 | | | 857 | | | | 811,749 | |

| Regatta VI Funding Ltd. 2016-1A DR† | | 2.918%

(3 Mo. LIBOR + 2.70% | )# | 7/20/2028 | | | 250 | | | | 242,347 | |

| Regatta XVI Funding Ltd. 2019-2A B† | | 2.287%

(3 Mo. LIBOR + 2.05% | )# | 1/15/2033 | | | 2,300 | | | | 2,303,093 | |

| West CLO Ltd. 2014-2A BR† | | 1.98% (3 Mo. LIBOR + 1.75% | )# | 1/16/2027 | | | 459 | | | | 458,201 | |

| Total | | | | | | | | | | | 37,025,235 | |

| Total Asset-Backed Securities (cost $38,593,700) | | | | | | | | | | | 38,616,630 | |

| | | | | | | | | | | | | |

| | | | | | | Shares

(000) | | | | | |

| | | | | | | | | | | | | |

| COMMON STOCKS 10.74% | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| Advertising 0.30% | | | | | | | | | | | | |

| Snap, Inc. Class A* | | | | | | | 71 | | | | 3,537,195 | |

| | | | | | | | | | | | | |

| Air Transportation 0.37% | | | | | | | | | | | | |

| Hawaiian Holdings, Inc. | | | | | | | 109 | | | | 1,931,442 | |

| JetBlue Airways Corp.* | | | | | | | 166 | | | | 2,411,415 | |

| Total | | | | | | | | | | | 4,342,857 | |

| | See Notes to Financial Statements. | 9 |

Schedule of Investments (continued)

December 31, 2020

| Investments | | Shares

(000) | | | Fair

Value | |

| Auto Parts & Equipment 0.04% | | | | | | |

| Chassix Holdings, Inc. | | | 59 | | | $ | 505,537 | |

| | | | | | | | | |

| Automakers 0.47% | | | | | | | | |

| Ferrari NV (Italy)(a) | | | 14 | | | | 3,117,340 | |

| Harley-Davidson, Inc. | | | 66 | | | | 2,406,309 | |

| Total | | | | | | | 5,523,649 | |

| | | | | | | | | |

| Banking 0.62% | | | | | | | | |

| East West Bancorp, Inc. | | | 29 | | | | 1,458,521 | |

| South State Corp. | | | 27 | | | | 1,980,803 | |

| SVB Financial Group* | | | 10 | | | | 3,869,768 | |

| Total | | | | | | | 7,309,092 | |

| | | | | | | | | |

| Beverages 0.27% | | | | | | | | |

| Boston Beer Co., Inc. (The) Class A* | | | 2 | | | | 1,746,968 | |

| Brown-Forman Corp. Class B | | | 18 | | | | 1,416,634 | |

| Total | | | | | | | 3,163,602 | |

| | | | | | | | | |

| Diversified Capital Goods 0.59% | | | | | | | | |

| Enphase Energy, Inc.* | | | 30 | | | | 5,274,453 | |

| Trane Technologies plc (Ireland)(a) | | | 9 | | | | 1,336,488 | |

| UTEX Industries, Inc. | | | 8 | | | | 298,457 | |

| Total | | | | | | | 6,909,398 | |

| | | | | | | | | |

| Electronics 1.03% | | | | | | | | |

| Advanced Micro Devices, Inc.* | | | 43 | | | | 3,946,832 | |

| Amphenol Corp. Class A | | | 14 | | | | 1,852,357 | |

| Roku, Inc.* | | | 13 | | | | 4,218,646 | |

| Trimble, Inc.* | | | 31 | | | | 2,074,210 | |

| Total | | | | | | | 12,092,045 | |

| | | | | | | | | |

| Energy: Exploration & Production 0.17% | | | | | | | | |

| Continental Resources, Inc.(b) | | | 74 | | | | 1,200,560 | |

| Oasis Petroleum, Inc.* | | | 21 | | | | 779,854 | |

| Total | | | | | | | 1,980,414 | |

| | | | | | | | | |

| Food: Wholesale 0.10% | | | | | | | | |

| Performance Food Group Co.* | | | 24 | | | | 1,165,493 | |

| | | | | | | | | |

| Gaming 0.15% | | | | | | | | |

| Wynn Resorts Ltd. | | | 16 | | | | 1,762,292 | |

| 10 | See Notes to Financial Statements. |

Schedule of Investments (continued)

December 31, 2020

| Investments | | Shares

(000) | | | Fair

Value | |

| Hotels 0.11% | | | | | | |

| Hilton Worldwide Holdings, Inc. | | | 11 | | | $ | 1,256,793 | |

| | | | | | | | | |

| Investments & Miscellaneous Financial Services 0.11% | | | | | | | | |

| MarketAxess Holdings, Inc. | | | 2 | | | | 1,262,649 | |

| | | | | | | | | |

| Machinery 0.42% | | | | | | | | |

| Generac Holdings, Inc.* | | | 10 | | | | 2,313,215 | |

| Graco, Inc. | | | 18 | | | �� | 1,288,843 | |

| Toro Co. (The) | | | 14 | | | | 1,313,913 | |

| Total | | | | | | | 4,915,971 | |

| | | | | | | | | |

| Managed Care 0.09% | | | | | | | | |

| BioNTech SE ADR*(b) | | | 14 | | | | 1,114,460 | |

| | | | | | | | | |

| Media: Diversified 0.26% | | | | | | | | |

| Walt Disney Co. (The)* | | | 17 | | | | 3,094,736 | |

| | | | | | | | | |

| Medical Products 0.56% | | | | | | | | |

| Align Technology, Inc.* | | | 6 | | | | 2,970,618 | |

| IDEXX Laboratories, Inc.* | | | 7 | | | | 3,619,559 | |

| Total | | | | | | | 6,590,177 | |

| | | | | | | | | |

| Metals/Mining (Excluding Steel) 0.16% | | | | | | | | |

| Freeport-McMoRan, Inc. | | | 73 | | | | 1,897,587 | |

| | | | | | | | | |

| Personal & Household Products 0.20% | | | | | | | | |

| Gibson Brands, Inc. | | | 9 | | | | 1,110,258 | (c) |

| Pola Orbis Holdings, Inc.(d) | | JPY | 60 | | | | 1,218,392 | |

| Remington Outdoor Co., Inc. | | | 16 | | | | – | (e) |

| Revlon, Inc. Class A | | | 149 | | | | 32,450 | |

| Total | | | | | | | 2,361,100 | |

| | | | | | | | | |

| Pharmaceuticals 0.43% | | | | | | | | |

| Acceleron Pharma, Inc.* | | | 22 | | | | 2,830,545 | |

| Mirati Therapeutics, Inc.* | | | 10 | | | | 2,256,801 | |

| Total | | | | | | | 5,087,346 | |

| | | | | | | | | |

| Real Estate Development & Management 0.40% | | | | | | | | |

| CoStar Group, Inc.* | | | 3 | | | | 2,985,424 | |

| Innovative Industrial Properties, Inc. | | | 9 | | | | 1,704,574 | |

| Total | | | | | | | 4,689,998 | |

| | See Notes to Financial Statements. | 11 |

Schedule of Investments (continued)

December 31, 2020

| Investments | | Shares

(000) | | | Fair

Value | |

| Real Estate Investment Trusts 0.10% | | | | | | |

| CBRE Group, Inc. Class A* | | | 18 | | | $ | 1,153,860 | |

| | | | | | | | | |

| Recreation & Travel 0.25% | | | | | | | | |

| Vail Resorts, Inc. | | | 11 | | | | 2,961,439 | |

| | | | | | | | | |

| Restaurants 0.51% | | | | | | | | |

| Shake Shack, Inc. Class A* | | | 70 | | | | 5,966,053 | |

| | | | | | | | | |

| Software/Services 1.95% | | | | | | | | |

| Airbnb, Inc.* | | | – | (f) | | | 20,552 | |

| DocuSign, Inc.* | | | 7 | | | | 1,574,551 | |

| Five9, Inc.* | | | 20 | | | | 3,414,752 | |

| Match Group, Inc.* | | | 9 | | | | 1,366,758 | |

| MongoDB, Inc.* | | | 5 | | | | 1,645,480 | |

| Pinduoduo, Inc. ADR* | | | 13 | | | | 2,303,492 | |

| Pinterest, Inc. Class A* | | | 85 | | | | 5,596,228 | |

| RingCentral, Inc. Class A* | | | 4 | | | | 1,692,859 | |

| Spotify Technology SA (Sweden)*(a) | | | 4 | | | | 1,157,319 | |

| Take-Two Interactive Software, Inc.* | | | 6 | | | | 1,275,623 | |

| Trade Desk, Inc. (The) Class A* | | | 1 | | | | 1,149,435 | |

| Veeva Systems, Inc. Class A* | | | 6 | | | | 1,720,075 | |

| Total | | | | | | | 22,917,124 | |

| | | | | | | | | |

| Specialty Retail 0.13% | | | | | | | | |

| Claires Holdings LLC | | | 1 | | | | 233,456 | |

| SiteOne Landscape Supply, Inc.* | | | 8 | | | | 1,323,767 | |

| Total | | | | | | | 1,557,223 | |

| | | | | | | | | |

| Support: Services 0.45% | | | | | | | | |

| Bright Horizons Family Solutions, Inc.* | | | 7 | | | | 1,241,722 | |

| TopBuild Corp.* | | | 7 | | | | 1,209,406 | |

| Uber Technologies, Inc.* | | | 55 | | | | 2,824,176 | |

| Total | | | | | | | 5,275,304 | |

| | | | | | | | | |

| Telecommunications: Wireless 0.26% | | | | | | | | |

| QUALCOMM, Inc. | | | 20 | | | | 3,103,013 | |

| | | | | | | | | |

| Theaters & Entertainment 0.11% | | | | | | | | |

| Live Nation Entertainment, Inc.* | | | 18 | | | | 1,315,439 | |

| | | | | | | | | |

| Transportation: Infrastructure/Services 0.01% | | | | | | | | |

| ACBL Holdings Corp. | | | 4 | | | | 73,680 | (c) |

| 12 | See Notes to Financial Statements. |

Schedule of Investments (continued)

December 31, 2020

| Investments | | | | | | Shares

(000) | | | Fair

Value | |

| Trucking & Delivery 0.12% | | | | | | | | | | |

| AMERCO | | | | | | | 3 | | | $ | 1,407,276 | |

| Total Common Stocks (cost $106,768,926) | | | | | | | | | | | 126,292,802 | |

| | | | | | | | | | | | | |

| | | Interest

Rate | | Maturity

Date | | Principal

Amount

(000) | | | | | |

| | | | | | | | | | | | | |

| CONVERTIBLE BOND 0.27% | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| Automakers | | | | | | | | | | | | |

| Tesla, Inc. | | | | | | | | | | | | |

| (cost $2,121,143) | | 2.00% | | 5/15/2024 | | $ | 280 | | | $ | 3,184,132 | |

| | | | | | | | | | | | | |

| FLOATING RATE LOANS(g) 4.71% | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| Aerospace/Defense 0.09% | | | | | | | | | | | | |

| Alloy Finco Limited 2020 USD Term Loan B2 (Jersey)(a) | | 8.50% (1 Mo. LIBOR + 6.50%) | | 3/6/2024 | | | 656 | | | | 618,494 | |

| Alloy Finco Limited USD Holdco PIK Term Loan PIK 13.50% (Jersey)(a) | | 0.50% | | 3/6/2025 | | | 999 | | | | 417,924 | |

| Total | | | | | | | | | | | 1,036,418 | |

| | | | | | | | | | | | | |

| Air Transportation 0.30% | | | | | | | | | | | | |

| American Airlines, Inc. 2017 Incremental Term Loan | | 2.158%

(1 Mo. LIBOR + 2.00%) | | 12/15/2023 | | | 1,999 | | | | 1,806,954 | |

| American Airlines, Inc. Repriced TL B due 2023 | | – | (h) | 4/28/2023 | | | 669 | | | | 606,547 | |

| JetBlue Airways Corporation Term Loan | | 6.25%

(3 Mo. LIBOR + 5.25%) | | 6/17/2024 | | | 1,094 | | | | 1,127,639 | |

| Total | | | | | | | | | | | 3,541,140 | |

| | | | | | | | | | | | | |

| Cable & Satellite Television 0.05% | | | | | | | | | | | | |

| Cablevision Lightpath LLC Term Loan B | | 3.75%

(3 Mo. LIBOR +3.25%) | | 1/24/2028 | | | 595 | | | | 594,803 | |

| | | | | | | | | | | | | |

| Chemicals 0.19% | | | | | | | | | | | | |

| Illuminate Buyer, LLC Term Loan | | 4.147%

(1 Mo. LIBOR + 4.00%) | | 6/30/2027 | | | 1,124 | | | | 1,125,922 | |

| Starfruit Finco B.V 2018 USD Term Loan B (Netherlands)(a) | | 3.153% (1 Mo. LIBOR + 3.00%) | | 10/1/2025 | | | 1,105 | | | | 1,095,921 | |

| Total | | | | | | | | | | | 2,221,843 | |

| | | | | | | | | | | | | |

| Diversified Capital Goods 0.01% | | | | | | | | | | | | |

| UTEX Industries Inc. 2020 First Out Exit Term Loan A | | 8.50%

(3 Mo. LIBOR + 7.00%) | | 11/1/2024 | | | 108 | | | | 108,878 | |

| | See Notes to Financial Statements. | 13 |

Schedule of Investments (continued)

December 31, 2020

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount

(000) | | | Fair

Value | |

| Diversified Capital Goods (continued) | | | | | | | | | | |

| UTEX Industries Inc. 2020 Second Out Term Loan | | 11.00%

(1 Mo. LIBOR + 9.50%) | | 12/3/2025 | | $ | 52 | | | $ | 51,403 | |

| Total | | | | | | | | | | | 160,281 | |

| | | | | | | | | | | | | |

| Electric: Generation 0.12% | | | | | | | | | | | | |

| EFS Cogen Holdings I LLC 2020 Term Loan B | | 4.50%

(3 Mo. LIBOR + 3.50%) | | 10/1/2027 | | | 1,122 | | | | 1,118,799 | |

| Frontera Generation Holdings LLC 2018 Term Loan B | | 5.25%

(3 Mo. LIBOR + 4.25%) | | 5/2/2025 | | | 1,386 | | | | 367,288 | |

| Total | | | | | | | | | | | 1,486,087 | |

| | | | | | | | | | | | | |

| Electric: Integrated 0.13% | | | | | | | | | | | | |

| Astoria Energy LLC 2020 Term Loan B | | 4.50%

(3 Mo. LIBOR +3.50%) | | 12/10/2027 | | | 1,518 | | | | 1,511,410 | |

| | | | | | | | | | | | | |

| Food: Wholesale 0.13% | | | | | | | | | | | | |

| Chobani, LLC 2020 Term Loan B | | 4.50%

(1 Mo. LIBOR + 3.50%) | | 10/20/2027 | | | 652 | | | | 652,278 | |

| JBS USA Lux S.A. 2019 Term Loan B (Luxembourg)(a) | | 2.147% (1 Mo. LIBOR + 2.00%) | | 5/1/2026 | | | 870 | | | | 864,401 | |

| Total | | | | | | | | | | | 1,516,679 | |

| | | | | | | | | | | | | |

| Gaming 0.39% | | | | | | | | | | | | |

| Mohegan Tribal Gaming Authority 2016 Term Loan B | | 6.375% (3 Mo. LIBOR + 5.38%) | | 10/13/2023 | | | 1,472 | | | | 1,417,575 | |

| Penn National Gaming, Inc. 2018 1st Lien Term Loan B | | 3.00% (1 Mo. LIBOR + 2.25%) | | 10/15/2025 | | | 947 | | | | 937,272 | |

| Playtika Holding Corp Term Loan B | | 7.00%

(3 Mo. LIBOR + 6.00%) | | 12/10/2024 | | | 2,242 | | | | 2,259,662 | |

| Total | | | | | | | | | | | 4,614,509 | |

| | | | | | | | | | | | | |

| Health Services 0.50% | | | | | | | | | | | | |

| Global Medical Response, Inc. 2020 Term Loan B | | 5.75%

(3 Mo. LIBOR + 4.75%) | | 10/2/2025 | | | 1,860 | | | | 1,851,420 | |

| National Mentor Holdings, Inc. 2019 Term Loan B | | 4.397%

(1 Mo. LIBOR + 4.25%) | | 3/9/2026 | | | 666 | | | | 666,258 | |

| National Mentor Holdings, Inc. 2019 Term Loan C | | 4.51%

(3 Mo. LIBOR + 4.25%) | | 3/9/2026 | | | 30 | | | | 30,490 | |

| Parexel International Corporation Term Loan B | | 2.897%

(1 Mo. LIBOR + 2.75%) | | 9/27/2024 | | | 1,200 | | | | 1,182,364 | |

| RegionalCare Hospital Partners Holdings, Inc. 2018 Term Loan B | 3.897% (1 Mo. LIBOR + 3.75%) | | 11/16/2025 | | | 971 | | | | 970,506 | |

| U.S. Renal Care, Inc. 2019 Term Loan B | | 5.147%

(1 Mo. LIBOR + 5.00%) | | 6/26/2026 | | | 1,181 | | | | 1,177,175 | |

| Total | | | | | | | | | | | 5,878,213 | |

| 14 | See Notes to Financial Statements. |

Schedule of Investments (continued)

December 31, 2020

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount

(000) | | | Fair

Value | |

| Insurance Brokerage 0.10% | | | | | | | | | | |

| Hub International Limited 2018 Term Loan B | | 2.965%

(3 Mo. LIBOR + 2.75%) | | 4/25/2025 | | $ | 1,164 | | | $ | 1,144,485 | |

| | | | | | | | | | | | | |

| Machinery 0.12% | | | | | | | | | | | | |

| Vertical Midco GmbH USD Term Loan B (Germany)(a) | | 4.57% (6 Mo. LIBOR + 4.25%) | | 7/30/2027 | | | 1,433 | | | | 1,446,211 | |

| | | | | | | | | | | | | |

| Personal & Household Products 0.21% | | | | | | | | | | | | |

| FGI Operating Company, LLC Exit Term Loan | | 10.254%

(3 Mo. LIBOR + 10.00%) | | 5/16/2022 | | | 106 | | | | 23,215 | (i) |

| Revlon Consumer Products Corporation 2020 Term Loan B2 | | 4.25% (3 Mo. LIBOR + 3.50%) | | 6/30/2025 | | | 2,110 | | | | 1,239,572 | |

| TGP Holdings III, LLC 2018 1st Lien Term Loan | | 5.00%

(3 Mo. LIBOR + 4.00%) | | 9/25/2024 | | | 1,199 | | | | 1,197,204 | |

| Total | | | | | | | | | | | 2,459,991 | |

| | | | | | | | | | | | | |

| Rail 0.15% | | | | | | | | | | | | |

| Genesee & Wyoming Inc. (New) Term Loan | | 2.254%

(3 Mo. LIBOR + 2.00%) | | 12/30/2026 | | | 1,727 | | | | 1,725,989 | |

| | | | | | | | | | | | | |

| Recreation & Travel 0.33% | | | | | | | | | | | | |

| Alterra Mountain Company Term Loan B1 | | 2.897%

(1 Mo . LIBOR + 2.75%) | | 7/31/2024 | | $ | 1,127 | | | $ | 1,114,341 | |

| Delta 2 (LUX) S.a.r.l. 2018 USD Term Loan (Luxembourg)(a) | | 3.50% (1 Mo . LIBOR + 2.50%) | | 2/1/2024 | | | 1,198 | | | | 1,189,272 | |

| Motion Finco Sarl Delayed Draw Term Loan B2 (Luxembourg)(a) | – | (h) | 11/12/2026 | | | 186 | | | | 179,686 | |

| Motion Finco Sarl USD Term Loan B1 (Luxembourg)(a) | | – | (h) | 11/12/2026 | | | 1,403 | | | | 1,357,447 | |

| Total | | | | | | | | | | | 3,840,746 | |

| | | | | | | | | | | | | |

| Restaurants 0.35% | | | | | | | | | | | | |

| IRB Holding Corp 2020 Term Loan B | | 3.75%

(6 Mo. LIBOR +2.75%) | | 2/5/2025 | | | 1,767 | | | | 1,755,541 | |

| Panera Bread Co. Term Loan A | | 2.438%

(1 Mo . LIBOR + 2.25%) | | 7/18/2022 | | | 1,758 | | | | 1,687,352 | |

| Zaxby’s Operating Company LLC 1st Lien Term Loan | | – | (h) | 12/10/2027 | | | 684 | | | | 686,068 | |

| Total | | | | | | | | | | | 4,128,961 | |

| | | | | | | | | | | | | |

| Software/Services 0.65% | | | | | | | | | | | | |

| Cornerstone OnDemand, Inc. Term Loan B | | 4.394%

(1 Mo . LIBOR + 4.25%) | | 4/22/2027 | | | 1,068 | | | | 1,074,352 | |

| LogMeIn, Inc. Term Loan B | | 4.903%

(1 Mo . LIBOR + 4.75%) | | 8/31/2027 | | | 3,153 | | | | 3,148,838 | |

| | See Notes to Financial Statements. | 15 |

Schedule of Investments (continued)

December 31, 2020

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount

(000) | | | Fair

Value | |

| Software/Services (continued) | | | | | | | | | | | | |

| Omnitracs, Inc. 2020 Incremental Term Loan | | 4.403%

(1 Mo . LIBOR + 4.25%) | | 3/23/2025 | | $ | 1,107 | | | $ | 1,113,629 | |

| Tibco Software Inc. 2020 Term Loan B3 | | 3.90%

(1 Mo . LIBOR + 3.75%) | | 6/30/2026 | | | 1,140 | | | | 1,121,355 | |

| Ultimate Software Group Inc. (The) Term Loan B | | 3.897%

(1 Mo . LIBOR + 3.75%) | | 5/4/2026 | | | 1,204 | | | | 1,204,828 | |

| Total | | | | | | | | | | | 7,663,002 | |

| | | | | | | | | | | | | |

| Specialty Retail 0.30% | | | | | | | | | | | | |

| BJ’s Wholesale Club, Inc. 2017 1st Lien Term Loan | | 2.154%

(1 Mo . LIBOR + 2.00%) | | 2/3/2024 | | | 1,038 | | | | 1,038,363 | |

| Claire’s Stores, Inc. 2019 Term Loan B | | 6.647%

(1 Mo . LIBOR + 6.50%) | | 12/18/2026 | | | 680 | | | | 574,852 | |

| Harbor Freight Tools USA, Inc. 2020 Term Loan B | | 4.00%

(1 Mo . LIBOR + 3.25%) | | 10/19/2027 | | | 913 | | | | 914,979 | |

| PetSmart, Inc. Consenting Term Loan | | 4.50%

(6 Mo. LIBOR + 3.50%) | | 3/11/2022 | | | 1,008 | | | | 1,010,325 | |

| Total | | | | | | | | | | | 3,538,519 | |

| | | | | | | | | | | | | |

| Support: Services 0.47% | | | | | | | | | | | | |

| Drive Chassis HoldCo, LLC 2019 2nd Lien Term Loan | | 8.474%

(3 Mo. LIBOR + 8.25%) | | 4/10/2026 | | | 1,300 | | | | 1,297,159 | |

| NEP/NCP Holdco, Inc. 2018 1st Lien Term Loan | | 3.395%

(1 Mo . LIBOR + 3.25%) | | 10/20/2025 | | | 1,949 | | | | 1,855,257 | |

| Pike Corporation 2020 Term Loan B | | 4.12%

(1 Mo . LIBOR + 3.00%) | | 7/24/2026 | | | 588 | | | | 588,468 | |

| Sabre GLBL Inc. 2020 Term Loan B | | – | (h) | 12/10/2027 | | | 723 | | | | 726,045 | |

| Trans Union, LLC 2019 Term Loan B5 | | 1.898%

(1 Mo . LIBOR + 1.75%) | | 11/16/2026 | | | 1,032 | | | | 1,030,110 | |

| Total | | | | | | | | | | | 5,497,039 | |

| | | | | | | | | | | | | |

| Technology Hardware & Equipment 0.12% | | | | | | | | | | | | |

| Delta Topco, Inc. 2020 Term Loan B | | 4.50%

(6 Mo. LIBOR +3.75%) | | 12/1/2027 | | | 1,453 | | | | 1,455,535 | |

| Total Floating Rate Loans (cost $56,100,098) | | | | | | | | | | | 55,461,861 | |

| | | | | | | | | | | | | |

| FOREIGN GOVERNMENT OBLIGATIONS 2.78% | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| Argentina 0.30% | | | | | | | | | | | | |

| Ciudad Autonoma De Buenos Aires†(a) | | 7.50% | | 6/1/2027 | | | 1,503 | | | | 1,255,020 | |

| Province of Santa Fe†(a) | | 6.90% | | 11/1/2027 | | | 2,051 | | | | 1,415,211 | |

| Provincia de Mendoza Argentina†(a) | | 2.75% | | 3/19/2029 | | | 1,317 | | | | 895,560 | |

| Total | | | | | | | | | | | 3,565,791 | |

| 16 | See Notes to Financial Statements. |

Schedule of Investments (continued)

December 31, 2020

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount

(000) | | | Fair

Value | |

| Bermuda 0.15% | | | | | | | | | | | | |

| Bermuda Government International Bond† | | 2.375% | | 8/20/2030 | | $ | 896 | | | $ | 941,920 | |

| Bermuda Government International Bond† | | 3.375% | | 8/20/2050 | | | 794 | | | | 858,513 | |

| Total | | | | | | | | | | | 1,800,433 | |

| | | | | | | | | | | | | |

| China 0.12% | | | | | | | | | | | | |

| China Government International Bond†(a) | | 2.25% | | 10/21/2050 | | | 1,410 | | | | 1,400,763 | |

| | | | | | | | | | | | | |

| Egypt 0.24% | | | | | | | | | | | | |

| Arab Republic of Egypt†(a) | | 5.577% | | 2/21/2023 | | | 2,626 | | | | 2,779,243 | |

| | | | | | | | | | | | | |

| Ghana 0.09% | | | | | | | | | | | | |

| Republic of Ghana†(a) | | 6.375% | | 2/11/2027 | | | 1,073 | | | | 1,117,727 | |

| | | | | | | | | | | | | |

| Honduras 0.11% | | | | | | | | | | | | |

| Honduras Government†(a) | | 5.625% | | 6/24/2030 | | | 1,087 | | | | 1,247,333 | |

| | | | | | | | | | | | | |

| Ivory Coast 0.12% | | | | | | | | | | | | |

| Ivory Coast Government International Bond†(d) | | 5.875% | | 10/17/2031 | | EUR | 1,090 | | | | 1,475,765 | |

| | | | | | | | | | | | | |

| Kenya 0.37% | | | | | | | | | | | | |

| Republic of Kenya†(a) | | 7.25% | | 2/28/2028 | | $ | 1,918 | | | | 2,156,622 | |

| Republic of Kenya†(a) | | 8.25% | | 2/28/2048 | | | 1,924 | | | | 2,209,041 | |

| Total | | | | | | | | | | | 4,365,663 | |

| | | | | | | | | | | | | |

| Morocco 0.10% | | | | | | | | | | | | |

| Morocco Government International Bond†(a) | | 3.00% | | 12/15/2032 | | | 1,168 | | | | 1,189,036 | |

| | | | | | | | | | | | | |

| Mongolia 0.31% | | | | | | | | | | | | |

| Development Bank of Mongolia LLC†(a) | | 7.25% | | 10/23/2023 | | | 2,254 | | | | 2,419,870 | |

| Mongolia Government International Bond†(a) | | 5.125% | | 4/7/2026 | | | 1,145 | | | | 1,230,952 | |

| Total | | | | | | | | | | | 3,650,822 | |

| | | | | | | | | | | | | |

| Nigeria 0.06% | | | | | | | | | | | | |

| Republic of Nigeria†(a) | | 6.50% | | 11/28/2027 | | | 644 | | | | 695,536 | |

| | | | | | | | | | | | | |

| Peru 0.17% | | | | | | | | | | | | |

| Peruvian Government International Bond(a) | | 2.392% | | 1/23/2026 | | | 630 | | | | 673,161 | |

| Peruvian Government International Bond(a) | | 2.78% | | 12/1/2060 | | | 1,289 | | | | 1,303,179 | |

| Total | | | | | | | | | | | 1,976,340 | |

| | | | | | | | | | | | | |

| Sri Lanka 0.07% | | | | | | | | | | | | |

| Republic of Sri Lanka†(a) | | 5.875% | | 7/25/2022 | | | 1,203 | | | | 838,274 | |

| | | | | | | | | | | | | |

| Ukraine 0.32% | | | | | | | | | | | | |

| Ukraine Government†(a) | | 7.375% | | 9/25/2032 | | | 3,394 | | | | 3,739,764 | |

| | See Notes to Financial Statements. | 17 |

Schedule of Investments (continued)

December 31, 2020

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount

(000) | | | Fair

Value | |

| United Arab Emirates 0.25% | | | | | | | | | | |

| Abu Dhabi Government International†(a) | | 3.125% | | 5/3/2026 | | $ | 2,607 | | | $ | 2,898,006 | |

| Total Foreign Government Obligations (cost $30,839,525) | | | | | | | | | | | 32,740,496 | |

| | | | | | | | | | | | | |

| HIGH YIELD CORPORATE BONDS 70.37% | | | | | | | | | | | | |

| | | | | | | | | | | | | |

| Advertising 0.15% | | | | | | | | | | | | |

| Clear Channel Worldwide Holdings, Inc.† | | 5.125% | | 8/15/2027 | | | 1,148 | | | | 1,160,915 | |

| Clear Channel Worldwide Holdings, Inc. | | 9.25% | | 2/15/2024 | | | 576 | | | | 584,700 | |

| Total | | | | | | | | | | | 1,745,615 | |

| | | | | | | | | | | | | |

| Aerospace/Defense 1.50% | | | | | | | | | | | | |

| Carrier Global Corp. | | 2.70% | | 2/15/2031 | | | 1,608 | | | | 1,729,676 | |

| Huntington Ingalls Industries, Inc. | | 3.844% | | 5/1/2025 | | | 714 | | | | 795,678 | |

| Leidos, Inc.† | | 3.625% | | 5/15/2025 | | | 1,212 | | | | 1,356,640 | |

| Raytheon Technologies Corp. | | 4.125% | | 11/16/2028 | | | 1,625 | | | | 1,937,698 | |

| Signature Aviation US Holdings, Inc.† | | 4.00% | | 3/1/2028 | | | 3,272 | | | | 3,299,027 | |

| Signature Aviation US Holdings, Inc.† | | 5.375% | | 5/1/2026 | | | 27 | | | | 27,742 | |

| TransDigm, Inc. | | 5.50% | | 11/15/2027 | | | 5,757 | | | | 6,060,970 | |

| TransDigm, Inc.† | | 6.25% | | 3/15/2026 | | | 1,048 | | | | 1,117,435 | |

| TransDigm, Inc. | | 6.375% | | 6/15/2026 | | | 1,282 | | | | 1,329,274 | |

| Total | | | | | | | | | | | 17,654,140 | |

| | | | | | | | | | | | | |

| Agency 0.17% | | | | | | | | | | | | |

| Temasek Financial I Ltd. (Singapore)†(a) | | 2.50% | | 10/6/2070 | | | 1,980 | | | | 1,995,567 | |

| | | | | | | | | | | | | |

| Air Transportation 1.46% | | | | | | | | | | | | |

| Alaska Airlines 2020-1 Class A Pass Through Trust† | | 4.80% | | 2/15/2029 | | | 1,597 | | | | 1,764,062 | |

| Azul Investments LLP† | | 5.875% | | 10/26/2024 | | | 2,821 | | | | 2,643,305 | |

| British Airways 2020-1 Class A Pass Through Trust (United Kingdom)†(a) | | 4.25% | | 5/15/2034 | | | 603 | | | | 647,094 | |

| Delta Air Lines 2019-1 Class AA Pass Through Trust | | 3.204% | | 4/25/2024 | | | 1,949 | | | | 2,006,752 | |

| Delta Air Lines, Inc.† | | 7.00% | | 5/1/2025 | | | 2,118 | | | | 2,446,748 | |

| Delta Air Lines, Inc./SkyMiles IP Ltd.† | | 4.50% | | 10/20/2025 | | | 1,317 | | | | 1,408,143 | |

| Delta Air Lines, Inc./SkyMiles IP Ltd.† | | 4.75% | | 10/20/2028 | | | 1,773 | | | | 1,936,689 | |

| JetBlue 2019-1 Class A Pass Through Trust | | 2.95% | | 11/15/2029 | | | 975 | | | | 903,369 | |

| Mileage Plus Holdings LLC/Mileage Plus Intellectual Property Assets Ltd.† | | 6.50% | | 6/20/2027 | | | 1,989 | | | | 2,141,904 | |

| United Airlines 2020-1 Class A Pass Through Trust | | 5.875% | | 4/15/2029 | | | 1,172 | | | | 1,269,530 | |

| Total | | | | | | | | | | | 17,167,596 | |

| 18 | See Notes to Financial Statements. |

Schedule of Investments (continued)

December 31, 2020

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount

(000) | | | Fair

Value | |

| Auto Loans 0.35% | | | | | | | | | | |

| Ford Motor Credit Co. LLC | | 4.00% | | 11/13/2030 | | $ | 927 | | | $ | 976,298 | |

| General Motors Financial Co., Inc. | | 5.25% | | 3/1/2026 | | | 1,632 | | | | 1,925,247 | |

| Mclaren Finance plc(d) | | 5.00% | | 8/1/2022 | | GBP | 900 | | | | 1,198,444 | |

| Total | | | | | | | | | | | 4,099,989 | |

| | | | | | | | | | | | | |

| Auto Parts & Equipment 0.84% | | | | | | | | | | | | |

| Adient Global Holdings Ltd.† | | 4.875% | | 8/15/2026 | | $ | 1,158 | | | | 1,191,292 | |

| Adient US LLC† | | 7.00% | | 5/15/2026 | | | 994 | | | | 1,082,814 | |

| Allison Transmission, Inc.† | | 3.75% | | 1/30/2031 | | | 914 | | | | 936,850 | |

| Antofagasta plc (Chile)†(a) | | 2.375% | | 10/14/2030 | | | 1,164 | | | | 1,169,820 | |

| Clarios Global LP / Clarios US Finance Co.† | | 8.50% | | 5/15/2027 | | | 1,643 | | | | 1,787,682 | |

| Lear Corp. | | 3.80% | | 9/15/2027 | | | 938 | | | | 1,052,779 | |

| Lear Corp. | | 4.25% | | 5/15/2029 | | | 1,100 | | | | 1,258,569 | |

| Magna International, Inc. (Canada)(a) | | 2.45% | | 6/15/2030 | | | 875 | | | | 941,875 | |

| Tenneco, Inc.† | | 7.875% | | 1/15/2029 | | | 403 | | | | 453,228 | |

| Total | | | | | | | | | | | 9,874,909 | |

| | | | | | | | | | | | | |

| Automakers 1.92% | | | | | | | | | | | | |

| BMW US Capital LLC† | | 4.15% | | 4/9/2030 | | | 2,241 | | | | 2,712,217 | |

| Ford Motor Co. | | 9.00% | | 4/22/2025 | | | 5,024 | | | | 6,180,198 | |

| Ford Motor Co. | | 9.625% | | 4/22/2030 | | | 1,510 | | | | 2,133,411 | |

| General Motors Co. | | 6.125% | | 10/1/2025 | | | 1,043 | | | | 1,265,924 | |

| Mclaren Finance plc. (United Kingdom)†(a) | | 5.75% | | 8/1/2022 | | | 657 | | | | 640,575 | |

| Tesla, Inc.† | | 5.30% | | 8/15/2025 | | | 6,185 | | | | 6,455,594 | |

| Volkswagen Group of America Finance LLC† | | 3.35% | | 5/13/2025 | | | 1,693 | | | | 1,862,362 | |

| Volkswagen Group of America Finance LLC† | | 3.75% | | 5/13/2030 | | | 1,177 | | | | 1,359,799 | |

| Total | | | | | | | | | | | 22,610,080 | |

| | | | | | | | | | | | | |

| Banking 4.97% | | | | | | | | | | | | |

| ABN AMRO Bank NV (Netherlands)†(a) | | 4.75% | | 7/28/2025 | | | 1,705 | | | | 1,966,079 | |

| AIB Group plc (Ireland)†(a) | | 4.263%

(3 Mo. LIBOR + 1.87% | )# | 4/10/2025 | | | 1,203 | | | | 1,316,339 | |

| Australia & New Zealand Banking Group Ltd. (United Kingdom)†(a) | 6.75% (USD Swap + 5.17% | )# | – | (j) | | 1,026 | | | | 1,198,353 | |

| Banco Latinoamericano de Comercio Exterior SA (Panama)†(a) | | 2.375% | | 9/14/2025 | | | 1,307 | | | | 1,339,688 | |

| Banco Nacional de Panama (Panama)†(a) | | 2.50% | | 8/11/2030 | | | 305 | | | | 305,762 | |

| Bangkok Bank pcl (Hong Kong)†(a) | | 5.00%

(5 Yr Treasury CMT + 4.73% | )# | – | (j) | | 2,106 | | | | 2,207,194 | |

| Bank of America Corp. | | 4.45% | | 3/3/2026 | | | 1,137 | | | | 1,325,662 | |

| Bank of Ireland Group plc (Ireland)†(a) | | 4.50% | | 11/25/2023 | | | 1,942 | | | | 2,129,999 | |

| | See Notes to Financial Statements. | 19 |

Schedule of Investments (continued)

December 31, 2020

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount

(000) | | | Fair

Value | |

| Banking (continued) | | | | | | | | | | | | |

| BankUnited, Inc. | | 4.875% | | 11/17/2025 | | $ | 1,178 | | | $ | 1,356,376 | |

| BBVA USA | | 3.875% | | 4/10/2025 | | | 1,353 | | | | 1,517,843 | |

| BNP Paribas SA (France)†(a) | | 4.50%

(5 Yr Treasury CMT + 2.94% | )# | – | (j) | | 1,991 | | | | 2,013,210 | |

| CIT Group, Inc. | | 5.25% | | 3/7/2025 | | | 527 | | | | 599,133 | |

| CIT Group, Inc. | | 6.125% | | 3/9/2028 | | | 3,668 | | | | 4,488,018 | |

| Citigroup, Inc. | | 4.45% | | 9/29/2027 | | | 1,164 | | | | 1,373,173 | |

| Credit Suisse Group AG (Switzerland)†(a) | | 5.10%

(5 Yr Treasury CMT + 3.29% | )# | – | (j) | | 1,964 | | | | 2,047,470 | |

| Fifth Third Bancorp | | 8.25% | | 3/1/2038 | | | 377 | | | | 638,304 | |

| Global Bank Corp. (Panama)†(a) | | 5.25%

(3 Mo. LIBOR + 3.30% | )# | 4/16/2029 | | | 1,746 | | | | 1,910,779 | |

| Goldman Sachs Group, Inc. (The) | | 3.50% | | 11/16/2026 | | | 1,020 | | | | 1,145,844 | |

| Goldman Sachs Group, Inc. (The) | | 4.25% | | 10/21/2025 | | | 1,100 | | | | 1,262,190 | |

| Home BancShares, Inc. | | 5.625%

(3 Mo. LIBOR + 3.58% | )# | 4/15/2027 | | | 1,156 | | | | 1,181,919 | |

| Huntington Bancshares, Inc. | | 5.70%

(3 Mo. LIBOR + 2.88% | )# | – | (j) | | 1,217 | | | | 1,226,127 | |

| ING Groep NV (Netherlands)(a) | | 5.75%

(5 Yr Treasury CMT + 4.34% | )# | – | (j) | | 2,544 | | | | 2,767,147 | |

| Intesa Sanpaolo SpA (Italy)†(a) | | 5.71% | | 1/15/2026 | | | 4,060 | | | | 4,648,962 | |

| JPMorgan Chase & Co. | | 3.54%

(3 Mo. LIBOR + 1.38% | )# | 5/1/2028 | | | 1,306 | | | | 1,493,898 | |

| JPMorgan Chase & Co. | | 4.60%(SOFR + 3.13% | )# | – | (j) | | 875 | | | | 904,531 | |

| JPMorgan Chase & Co. | | 6.10%

(3 Mo. LIBOR + 3.33% | )# | – | (j) | | 1,088 | | | | 1,193,678 | |

| Kookmin Bank (South Korea)†(a) | | 1.75% | | 5/4/2025 | | | 1,560 | | | | 1,622,893 | |

| Macquarie Bank Ltd. (United Kingdom)†(a) | | 6.125%

(5 Yr. Swap rate + 3.70% | )# | – | (j) | | 2,136 | | | | 2,287,304 | |

| Morgan Stanley | | 3.125% | | 7/27/2026 | | | 1,144 | | | | 1,282,055 | |

| OneMain Finance Corp. | | 4.00% | | 9/15/2030 | | | 1,333 | | | | 1,384,800 | |

| Popular, Inc. | | 6.125% | | 9/14/2023 | | | 1,370 | | | | 1,484,594 | |

| SVB Financial Group | | 3.125% | | 6/5/2030 | | | 1,247 | | | | 1,406,121 | |

| Turkiye Vakiflar Bankasi TAO (Turkey)†(a) | | 6.50% | | 1/8/2026 | | | 2,340 | | | | 2,404,699 | |

| US Bancorp | | 3.00% | | 7/30/2029 | | | 1,090 | | | | 1,217,840 | |

| Washington Mutual Bank(k) | | 6.875% | | 6/15/2011 | | | 1,250 | | | | 125 | (e) |

| Webster Financial Corp. | | 4.10% | | 3/25/2029 | | | 1,622 | | | | 1,790,440 | |

| Total | | | | | | | | | | | 58,438,549 | |

| 20 | See Notes to Financial Statements. |

Schedule of Investments (continued)

December 31, 2020

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount

(000) | | | Fair

Value | |

| Beverages 0.95% | | | | | | | | | | | | |

| Bacardi Ltd.† | | 2.75% | | 7/15/2026 | | $ | 1,749 | | | $ | 1,855,239 | |

| Bacardi Ltd.† | | 4.70% | | 5/15/2028 | | | 1,843 | | | | 2,188,148 | |

| Becle SAB de CV (Mexico)†(a) | | 3.75% | | 5/13/2025 | | | 1,438 | | | | 1,570,913 | |

| Brown-Forman Corp. | | 3.50% | | 4/15/2025 | | | 797 | | | | 883,259 | |

| Brown-Forman Corp. | | 4.50% | | 7/15/2045 | | | 1,192 | | | | 1,607,599 | |

| PepsiCo, Inc. | | 3.60% | | 3/1/2024 | | | 978 | | | | 1,067,846 | |

| Suntory Holdings Ltd. (Japan)†(a) | | 2.25% | | 10/16/2024 | | | 1,913 | | | | 2,002,076 | |

| Total | | | | | | | | | | | 11,175,080 | |

| | | | | | | | | | | | | |

| Brokerage 0.21% | | | | | | | | | | | | |

| Charles Schwab Corp. (The) | | 5.375%

(5 Yr Treasury CMT + 4.97% | )# | – | (j) | | 1,591 | | | | 1,775,954 | |

| Credit Suisse Group AG (Switzerland)†(a) | | 4.50%

(5 Yr. Treasury CMT + 3.55% | )# | – | (j) | | 668 | | | | 672,943 | |

| Total | | | | | | | | | | | 2,448,897 | |

| | | | | | | | | | | | | |

| Building & Construction 1.01% | | | | | | | | | | | | |

| Beazer Homes USA, Inc. | | 7.25% | | 10/15/2029 | | | 1,164 | | | | 1,316,082 | |

| Century Communities, Inc. | | 6.75% | | 6/1/2027 | | | 856 | | | | 916,438 | |

| D.R. Horton, Inc. | | 2.60% | | 10/15/2025 | | | 697 | | | | 752,476 | |

| ITR Concession Co. LLC† | | 5.183% | | 7/15/2035 | | | 785 | | | | 932,783 | |

| NVR, Inc. | | 3.00% | | 5/15/2030 | | | 2,122 | | | | 2,323,016 | |

| PulteGroup, Inc. | | 6.375% | | 5/15/2033 | | | 2,250 | | | | 3,091,781 | |

| Toll Brothers Finance Corp. | | 4.875% | | 3/15/2027 | | | 1,084 | | | | 1,242,329 | |

| Toll Brothers Finance Corp. | | 5.625% | | 1/15/2024 | | | 1,208 | | | | 1,339,243 | |

| Total | | | | | | | | | | | 11,914,148 | |

| | | | | | | | | | | | | |

| Building Materials 1.03% | | | | | | | | | | | | |

| Allegion plc (Ireland)(a) | | 3.50% | | 10/1/2029 | | | 918 | | | | 1,019,757 | |

| Ferguson Finance plc (United Kingdom)†(a) | | 3.25% | | 6/2/2030 | | | 1,929 | | | | 2,154,202 | |

| Lennox International, Inc. | | 1.35% | | 8/1/2025 | | | 909 | | | | 930,328 | |

| Lennox International, Inc. | | 1.70% | | 8/1/2027 | | | 1,111 | | | | 1,131,171 | |

| Masonite International Corp.† | | 5.375% | | 2/1/2028 | | | 952 | | | | 1,023,819 | |

| Owens Corning, Inc. | | 4.30% | | 7/15/2047 | | | 1,670 | | | | 2,010,728 | |

| Owens Corning, Inc. | | 4.40% | | 1/30/2048 | | | 1,255 | | | | 1,513,951 | |

| Vertical Holdco GmbH†(d) | | 6.625% | | 7/15/2028 | | EUR | 667 | | | | 877,563 | |

| Vulcan Materials Co. | | 4.50% | | 6/15/2047 | | $ | 1,186 | | | | 1,471,670 | |

| Total | | | | | | | | | | | 12,133,189 | |

| | See Notes to Financial Statements. | 21 |

Schedule of Investments (continued)

December 31, 2020

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount

(000) | | | Fair

Value | |

| Cable & Satellite Television 2.10% | | | | | | | | | | | | |

| Cable One, Inc.† | | 4.00% | | 11/15/2030 | | $ | 990 | | | $ | 1,030,219 | |

| CCO Holdings LLC/CCO Holdings Capital Corp.† | | 5.125% | | 5/1/2027 | | | 2,783 | | | | 2,957,007 | |

| CCO Holdings LLC/CCO Holdings Capital Corp.† | | 5.75% | | 2/15/2026 | | | 2,946 | | | | 3,043,513 | |

| CSC Holdings LLC† | | 5.50% | | 4/15/2027 | | | 2,372 | | | | 2,516,692 | |

| CSC Holdings LLC† | | 5.75% | | 1/15/2030 | | | 1,274 | | | | 1,398,221 | |

| CSC Holdings LLC† | | 6.50% | | 2/1/2029 | | | 1,046 | | | | 1,182,948 | |

| DISH DBS Corp. | | 7.75% | | 7/1/2026 | | | 6,811 | | | | 7,633,394 | |

| LCPR Senior Secured Financing DAC (Ireland)†(a) | | 6.75% | | 10/15/2027 | | | 1,133 | | | | 1,220,808 | |

| Radiate Holdco LLC/Radiate Finance, Inc.† | | 4.50% | | 9/15/2026 | | | 635 | | | | 656,431 | |

| Radiate Holdco LLC/Radiate Finance, Inc.† | | 6.50% | | 9/15/2028 | | | 1,399 | | | | 1,471,573 | |

| Ziggo BV (Netherlands)†(a) | | 5.50% | | 1/15/2027 | | | 1,491 | | | | 1,558,982 | |

| Total | | | | | | | | | | | 24,669,788 | |

| | | | | | | | | | | | | |

| Chemicals 0.42% | | | | | | | | | | | | |

| CF Industries, Inc.† | | 4.50% | | 12/1/2026 | | | 1,047 | | | | 1,241,108 | |

| Chemours Co. (The)† | | 5.75% | | 11/15/2028 | | | 1,291 | | | | 1,319,241 | |

| FMC Corp. | | 3.45% | | 10/1/2029 | | | 1,050 | | | | 1,199,221 | |

| Ingevity Corp.† | | 3.875% | | 11/1/2028 | | | 1,123 | | | | 1,133,528 | |

| Total | | | | | | | | | | | 4,893,098 | |

| | | | | | | | | | | | | |

| Consumer/Commercial/Lease Financing 1.08% | | | | | | | | | | | | |

| Avolon Holdings Funding Ltd. (Ireland)†(a) | | 4.25% | | 4/15/2026 | | | 559 | | | | 602,676 | |

| Nationstar Mortgage Holdings, Inc.† | | 5.125% | | 12/15/2030 | | | 901 | | | | 942,869 | |

| Navient Corp. | | 6.125% | | 3/25/2024 | | | 1,728 | | | | 1,850,023 | |

| Navient Corp. | | 6.75% | | 6/25/2025 | | | 2,209 | | | | 2,405,049 | |

| Navient Corp. | | 6.75% | | 6/15/2026 | | | 872 | | | | 952,115 | |

| OneMain Finance Corp. | | 7.125% | | 3/15/2026 | | | 1,617 | | | | 1,914,132 | |

| OneMain Finance Corp. | | 5.375% | | 11/15/2029 | | | 377 | | | | 425,067 | |

| Quicken Loans LLC† | | 5.25% | | 1/15/2028 | | | 1,111 | | | | 1,188,076 | |

| Quicken Loans LLC/Quicken Loans Co-Issuer, Inc.† | | 3.625% | | 3/1/2029 | | | 852 | | | | 870,637 | |

| Quicken Loans LLC/Quicken Loans Co-Issuer, Inc.† | | 3.875% | | 3/1/2031 | | | 921 | | | | 957,840 | |

| USAA Capital Corp.† | | 2.125% | | 5/1/2030 | | | 609 | | | | 640,800 | |

| Total | | | | | | | | | | | 12,749,284 | |

| | | | | | | | | | | | | |

| Discount Stores 1.02% | | | | | | | | | | | | |

| Amazon.com, Inc. | | 4.25% | | 8/22/2057 | | | 1,325 | | | | 1,888,142 | |

| Amazon.com, Inc. | | 4.80% | | 12/5/2034 | | | 2,179 | | | | 2,990,889 | |

| Amazon.com, Inc. | | 5.20% | | 12/3/2025 | | | 3,295 | | | | 4,010,416 | |

| Costco Wholesale Corp. | | 1.75% | | 4/20/2032 | | | 1,511 | | | | 1,571,737 | |

| 22 | See Notes to Financial Statements. |

Schedule of Investments (continued)

December 31, 2020

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount

(000) | | | Fair

Value | |

| Discount Stores (continued) | | | | | | | | | | | | |

| Dollar General Corp. | | 3.50% | | 4/3/2030 | | $ | 1,350 | | | $ | 1,551,382 | |

| Total | | | | | | | | | | | 12,012,566 | |

| | | | | | | | | | | | | |

| Diversified Capital Goods 0.65% | | | | | | | | | | | | |

| Dover Corp. | | 2.95% | | 11/4/2029 | | | 1,320 | | | | 1,446,080 | |

| Hillman Group, Inc. (The)† | | 6.375% | | 7/15/2022 | | | 1,311 | | | | 1,305,776 | |

| Leggett & Platt, Inc. | | 4.40% | | 3/15/2029 | | | 974 | | | | 1,115,245 | |

| Siemens Financieringsmaatschappij NV (Netherlands)†(a) | | 3.25% | | 5/27/2025 | | | 1,235 | | | | 1,372,036 | |

| Westinghouse Air Brake Technologies Corp. | | 3.45% | | 11/15/2026 | | | 1,338 | | | | 1,469,962 | |

| Westinghouse Air Brake Technologies Corp. | | 4.95% | | 9/15/2028 | | | 794 | | | | 942,820 | |

| Total | | | | | | | | | | | 7,651,919 | |

| | | | | | | | | | | | | |

| Electric: Distribution/Transportation 0.59% | | | | | | | | | | | | |

| Adani Transmission Ltd. (India)†(a) | | 4.25% | | 5/21/2036 | | | 965 | | | | 1,025,089 | |

| Atlantic City Electric Co. | | 4.00% | | 10/15/2028 | | | 1,149 | | | | 1,350,264 | |

| Empresa de Transmision Electrica SA (Panama)†(a) | | 5.125% | | 5/2/2049 | | | 1,205 | | | | 1,504,087 | |

| Empresas Publicas de Medellin ESP (Colombia)†(a) | | 4.25% | | 7/18/2029 | | | 1,689 | | | | 1,818,969 | |

| Monongahela Power Co.† | | 3.55% | | 5/15/2027 | | | 1,188 | | | | 1,286,358 | |

| Total | | | | | | | | | | | 6,984,767 | |

| | | | | | | | | | | | | |

| Electric: Generation 2.61% | | | | | | | | | | | | |

| Adani Renewable Energy RJ Ltd./Kodangal Solar | | | | | | | | | | | | |

| Parks Pvt Ltd/Wardha Solar Maharash (India)†(a) | | 4.625% | | 10/15/2039 | | | 1,429 | | | | 1,484,965 | |

| Calpine Corp.† | | 3.75% | | 3/1/2031 | | | 1,350 | | | | 1,339,477 | |

| Calpine Corp.† | | 4.625% | | 2/1/2029 | | | 1,513 | | | | 1,558,057 | |

| Calpine Corp.† | | 5.00% | | 2/1/2031 | | | 1,101 | | | | 1,152,196 | |

| Calpine Corp.† | | 5.125% | | 3/15/2028 | | | 963 | | | | 1,014,410 | |

| Clearway Energy Operating LLC† | | 4.75% | | 3/15/2028 | | | 656 | | | | 704,177 | |

| Clearway Energy Operating LLC | | 5.75% | | 10/15/2025 | | | 844 | | | | 889,892 | |

| Dayton Power & Light Co. (The) | | 3.95% | | 6/15/2049 | | | 898 | | | | 1,045,294 | |

| DPL, Inc. | | 4.35% | | 4/15/2029 | | | 1,363 | | | | 1,530,901 | |

| Greenko Solar Mauritius Ltd. (Mauritius)†(a) | | 5.95% | | 7/29/2026 | | | 909 | | | | 986,339 | |

| NextEra Energy Operating Partners LP† | | 3.875% | | 10/15/2026 | | | 2,442 | | | | 2,611,414 | |

| NextEra Energy Operating Partners LP† | | 4.50% | | 9/15/2027 | | | 1,709 | | | | 1,917,105 | |

| NRG Energy, Inc.† | | 3.75% | | 6/15/2024 | | | 1,802 | | | | 1,973,644 | |

| NRG Energy, Inc.† | | 4.45% | | 6/15/2029 | | | 518 | | | | 601,574 | |

| NRG Energy, Inc.† | | 5.25% | | 6/15/2029 | | | 697 | | | | 768,314 | |

| NRG Energy, Inc. | | 5.75% | | 1/15/2028 | | | 3,273 | | | | 3,581,889 | |

| NSG Holdings LLC/NSG Holdings, Inc.† | | 7.75% | | 12/15/2025 | | | 1,204 | | | | 1,281,110 | |

| | See Notes to Financial Statements. | 23 |

Schedule of Investments (continued)

December 31, 2020

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount

(000) | | | Fair

Value | |

| Electric: Generation (continued) | | | | | | | | | | | | |

| Pattern Energy Operations LP/Pattern Energy | | | | | | | | | | | | |

| Operations, Inc.† | | 4.50% | | 8/15/2028 | | $ | 673 | | | $ | 711,277 | |

| TerraForm Power Operating LLC† | | 4.75% | | 1/15/2030 | | | 1,484 | | | | 1,591,160 | |

| TerraForm Power Operating LLC† | | 5.00% | | 1/31/2028 | | | 561 | | | | 631,420 | |

| Topaz Solar Farms LLC† | | 5.75% | | 9/30/2039 | | | 2,934 | | | | 3,371,963 | |

| Total | | | | | | | | | | | 30,746,578 | |

| | | | | | | | | | | | | |

| Electric: Integrated 2.33% | | | | | | | | | | | | |

| Arizona Public Service Co. | | 2.95% | | 9/15/2027 | | | 1,333 | | | | 1,465,562 | |

| Ausgrid Finance Pty Ltd. (Australia)†(a) | | 4.35% | | 8/1/2028 | | | 1,217 | | | | 1,413,027 | |

| Black Hills Corp. | | 4.35% | | 5/1/2033 | | | 1,155 | | | | 1,400,428 | |

| El Paso Electric Co. | | 5.00% | | 12/1/2044 | | | 1,203 | | | | 1,430,918 | |

| Electricite de France SA (France)†(a) | | 3.625% | | 10/13/2025 | | | 1,044 | | | | 1,171,331 | |

| Enel Finance International NV (Netherlands)†(a) | | 2.65% | | 9/10/2024 | | | 1,493 | | | | 1,591,492 | |

| Enel Finance International NV (Netherlands)†(a) | | 3.50% | | 4/6/2028 | | | 1,829 | | | | 2,084,846 | |

| Entergy Arkansas LLC | | 4.00% | | 6/1/2028 | | | 1,589 | | | | 1,862,054 | |

| Entergy Arkansas LLC | | 4.95% | | 12/15/2044 | | | 1,109 | | | | 1,208,859 | |

| FirstEnergy Corp. | | 3.90% | | 7/15/2027 | | | 2,118 | | | | 2,336,411 | |

| Florida Power & Light Co. | | 2.85% | | 4/1/2025 | | | 1,098 | | | | 1,196,561 | |

| HAT Holdings I LLC/HAT Holdings II LLC† | | 6.00% | | 4/15/2025 | | | 808 | | | | 865,570 | |

| Indianapolis Power & Light Co.† | | 4.05% | | 5/1/2046 | | | 1,608 | | | | 1,967,042 | |

| Louisville Gas & Electric Co. | | 4.375% | | 10/1/2045 | | | 1,017 | | | | 1,285,394 | |

| Ohio Power Co. | | 4.15% | | 4/1/2048 | | | 1,223 | | | | 1,551,805 | |

| Puget Energy, Inc. | | 4.10% | | 6/15/2030 | | | 1,733 | | | | 1,962,345 | |

| Puget Sound Energy, Inc. | | 4.223% | | 6/15/2048 | | | 1,174 | | | | 1,502,283 | |

| Union Electric Co. | | 2.625% | | 3/15/2051 | | | 1,064 | | | | 1,115,328 | |

| Total | | | | | | | | | | | 27,411,256 | |

| | | | | | | | | | | | | |

| Electronics 1.42% | | | | | | | | | | | | |

| Amphenol Corp. | | 2.05% | | 3/1/2025 | | | 936 | | | | 989,382 | |

| Amphenol Corp. | | 2.80% | | 2/15/2030 | | | 1,875 | | | | 2,069,595 | |

| Flex Ltd. | | 4.875% | | 5/12/2030 | | | 1,277 | | | | 1,537,527 | |

| FLIR Systems, Inc. | | 2.50% | | 8/1/2030 | | | 1,137 | | | | 1,194,240 | |

| KLA Corp. | | 4.10% | | 3/15/2029 | | | 776 | | | | 931,133 | |

| Lam Research Corp. | | 4.875% | | 3/15/2049 | | | 808 | | | | 1,167,986 | |

| Micron Technology, Inc. | | 5.327% | | 2/6/2029 | | | 1,763 | | | | 2,207,146 | |

| NVIDIA Corp. | | 3.20% | | 9/16/2026 | | | 1,872 | | | | 2,121,725 | |

| NXP BV/NXP Funding LLC/NXP USA, Inc. (Netherlands)†(a) | | 3.40% | | 5/1/2030 | | | 1,117 | | | | 1,268,532 | |

| Trimble, Inc. | | 4.75% | | 12/1/2024 | | | 1,455 | | | | 1,664,161 | |

| 24 | See Notes to Financial Statements. |

Schedule of Investments (continued)

December 31, 2020

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount

(000) | | | Fair

Value | |

| Electronics (continued) | | | | | | | | | | | | |

| Xilinx, Inc. | | 2.95% | | 6/1/2024 | | $ | 1,445 | | | $ | 1,555,102 | |

| Total | | | | | | | | | | | 16,706,529 | |

| | | | | | | | | | | | | |

| Energy: Exploration & Production 4.28% | | | | | | | | | | | | |

| Apache Corp. | | 4.25% | | 1/15/2030 | | | 1,920 | | | | 2,019,600 | |

| Apache Corp. | | 4.75% | | 4/15/2043 | | | 698 | | | | 725,041 | |

| Apache Corp. | | 5.10% | | 9/1/2040 | | | 3,118 | | | | 3,349,901 | |

| Centennial Resource Production LLC† | | 5.375% | | 1/15/2026 | | | 2,211 | | | | 1,547,700 | |

| Centennial Resource Production LLC† | | 6.875% | | 4/1/2027 | | | 2,838 | | | | 2,044,509 | |

| Continental Resources, Inc. | | 4.375% | | 1/15/2028 | | | 2,148 | | | | 2,194,805 | |

| Continental Resources, Inc.† | | 5.75% | | 1/15/2031 | | | 1,569 | | | | 1,744,500 | |

| Diamondback Energy, Inc. | | 3.50% | | 12/1/2029 | | | 1,267 | | | | 1,354,909 | |

| Diamondback Energy, Inc. | | 4.75% | | 5/31/2025 | | | 515 | | | | 580,243 | |

| Endeavor Energy Resources LP/EER Finance, Inc.† | | 5.50% | | 1/30/2026 | | | 1,131 | | | | 1,162,696 | |

| Endeavor Energy Resources LP/EER Finance, Inc.† | | 5.75% | | 1/30/2028 | | | 1,114 | | | | 1,203,343 | |

| EQT Corp. | | 7.875% | | 2/1/2025 | | | 1,604 | | | | 1,828,793 | |

| Hilcorp Energy I LP/Hilcorp Finance Co.† | | 5.00% | | 12/1/2024 | | | 1,670 | | | | 1,663,562 | |

| Hilcorp Energy I LP/Hilcorp Finance Co.† | | 5.75% | | 10/1/2025 | | | 340 | | | | 345,064 | |

| Hilcorp Energy I LP/Hilcorp Finance Co.† | | 6.25% | | 11/1/2028 | | | 1,174 | | | | 1,204,477 | |

| Indigo Natural Resources LLC† | | 6.875% | | 2/15/2026 | | | 2,018 | | | | 2,068,450 | |

| Jagged Peak Energy LLC | | 5.875% | | 5/1/2026 | | | 753 | | | | 781,588 | |

| Laredo Petroleum, Inc. | | 10.125% | | 1/15/2028 | | | 2,341 | | | | 1,994,532 | |

| Matador Resources Co. | | 5.875% | | 9/15/2026 | | | 838 | | | | 822,288 | |

| MEG Energy Corp. (Canada)†(a) | | 7.00% | | 3/31/2024 | | | 1,504 | | | | 1,522,800 | |

| MEG Energy Corp. (Canada)†(a) | | 7.125% | | 2/1/2027 | | | 3,299 | | | | 3,414,465 | |

| Murphy Oil Corp. | | 5.75% | | 8/15/2025 | | | 1,165 | | | | 1,162,210 | |

| Murphy Oil Corp. | | 6.875% | | 8/15/2024 | | | 849 | | | | 865,089 | |

| Parsley Energy LLC/Parsley Finance Corp.† | | 5.625% | | 10/15/2027 | | | 802 | | | | 878,992 | |

| PDC Energy, Inc. | | 5.75% | | 5/15/2026 | | | 2,368 | | | | 2,449,400 | |

| Range Resources Corp. | | 5.00% | | 3/15/2023 | | | 911 | | | | 889,933 | |

| Seven Generations Energy Ltd. (Canada)†(a) | | 5.375% | | 9/30/2025 | | | 1,272 | | | | 1,298,222 | |

| SM Energy Co. | | 6.125% | | 11/15/2022 | | | 755 | | | | 735,004 | |

| SM Energy Co. | | 6.625% | | 1/15/2027 | | | 314 | | | | 251,985 | |

| SM Energy Co. | | 6.75% | | 9/15/2026 | | | 2,051 | | | | 1,666,438 | |

| Southwestern Energy Co. | | 6.45% | | 1/23/2025 | | | 1,106 | | | | 1,149,549 | |

| Southwestern Energy Co. | | 7.75% | | 10/1/2027 | | | 1,120 | | | | 1,211,364 | |

| Southwestern Energy Co. | | 8.375% | | 9/15/2028 | | | 1,608 | | | | 1,747,695 | |

| Tengizchevroil Finance Co. International Ltd. (Kazakhstan)†(a) | | 3.25% | | 8/15/2030 | | | 1,185 | | | | 1,257,254 | |

| | See Notes to Financial Statements. | 25 |

Schedule of Investments (continued)

December 31, 2020

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount

(000) | | | Fair

Value | |

| Energy: Exploration & Production (continued) | | | | | | | | | | | | |

| Texaco Capital, Inc. | | 8.625% | | 11/15/2031 | | $ | 722 | | | $ | 1,162,921 | |

| Total | | | | | | | | | | | 50,299,322 | |

| | | | | | | | | | | | | |

| Environmental 0.10% | | | | | | | | | | | | |

| Waste Pro USA, Inc.† | | 5.50% | | 2/15/2026 | | | 1,143 | | | | 1,172,038 | |

| | | | | | | | | | | | | |

| Food & Drug Retailers 0.43% | | | | | | | | | | | | |

| Albertsons Cos, Inc./Safeway, Inc./New Albertsons LP/Albertsons LLC† | 4.625% | | 1/15/2027 | | | 712 | | | | 758,141 | |

| Albertsons Cos, Inc./Safeway, Inc./New Albertsons LP/Albertsons LLC† | 4.875% | | 2/15/2030 | | | 1,224 | | | | 1,349,925 | |

| Rite Aid Corp. | | 7.70% | | 2/15/2027 | | | 1,318 | | | | 1,265,820 | |

| Rite Aid Corp.† | | 8.00% | | 11/15/2026 | | | 1,549 | | | | 1,658,654 | |

| Total | | | | | | | | | | | 5,032,540 | |

| | | | | | | | | | | | | |

| Food: Wholesale 2.01% | | | | | | | | | | | | |

| Arcor SAIC (Argentina)†(a) | | 6.00% | | 7/6/2023 | | | 1,380 | | | | 1,360,349 | |

| BRF SA (Brazil)†(a) | | 4.875% | | 1/24/2030 | | | 1,086 | | | | 1,180,357 | |

| Campbell Soup Co. | | 3.125% | | 4/24/2050 | | | 2,821 | | | | 2,985,385 | |

| Chobani LLC/Chobani Finance Corp., Inc.† | | 7.50% | | 4/15/2025 | | | 1,312 | | | | 1,379,850 | |

| FAGE International SA/FAGE USA Dairy Industry, Inc. (Luxembourg)†(a) | 5.625% | | 8/15/2026 | | | 1,241 | | | | 1,276,443 | |

| JBS USA LUX SA/JBS USA Finance, Inc.† | | 6.75% | | 2/15/2028 | | | 3,083 | | | | 3,467,666 | |

| Kraft Heinz Foods Co. | | 4.375% | | 6/1/2046 | | | 1,277 | | | | 1,381,700 | |

| Kraft Heinz Foods Co.† | | 4.875% | | 10/1/2049 | | | 580 | | | | 676,670 | |

| Kraft Heinz Foods Co. | | 5.00% | | 6/4/2042 | | | 1,219 | | | | 1,430,272 | |

| Kraft Heinz Foods Co. | | 5.20% | | 7/15/2045 | | | 869 | | | | 1,033,328 | |

| Lamb Weston Holdings, Inc.† | | 4.625% | | 11/1/2024 | | | 633 | | | | 661,485 | |

| McCormick & Co., Inc. | | 2.50% | | 4/15/2030 | | | 1,046 | | | | 1,121,322 | |

| McCormick & Co., Inc. | | 4.20% | | 8/15/2047 | | | 1,393 | | | | 1,771,948 | |

| Smithfield Foods, Inc.† | | 5.20% | | 4/1/2029 | | | 2,168 | | | | 2,582,387 | |

| Sysco Corp. | | 2.40% | | 2/15/2030 | | | 1,250 | | | | 1,302,614 | |

| Total | | | | | | | | | | | 23,611,776 | |

| | | | | | | | | | | | | |

| Forestry/Paper 0.29% | | | | | | | | | | | | |

| Norbord, Inc. (Canada)†(a) | | 6.25% | | 4/15/2023 | | | 1,060 | | | | 1,153,964 | |

| Suzano Austria GmbH (Brazil)(a) | | 3.75% | | 1/15/2031 | | | 1,147 | | | | 1,218,401 | |

| Weyerhaeuser Co. | | 7.375% | | 3/15/2032 | | | 716 | | | | 1,074,463 | |

| Total | | | | | | | | | | | 3,446,828 | |

| 26 | See Notes to Financial Statements. |

Schedule of Investments (continued)

December 31, 2020

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount

(000) | | | Fair

Value | |

| Gaming 2.57% | | | | | | | | | | | | |

| Boyd Gaming Corp. | | 4.75% | | 12/1/2027 | | $ | 1,201 | | | $ | 1,250,013 | |

| Boyd Gaming Corp. | | 6.00% | | 8/15/2026 | | | 715 | | | | 743,600 | |

| Caesars Entertainment, Inc.† | | 8.125% | | 7/1/2027 | | | 3,047 | | | | 3,377,074 | |

| Caesars Resort Collection LLC/CRC Finco, Inc.† | | 5.25% | | 10/15/2025 | | | 1,593 | | | | 1,611,965 | |

| Caesars Resort Collection LLC/CRC Finco, Inc.† | | 5.75% | | 7/1/2025 | | | 619 | | | | 656,652 | |

| Churchill Downs, Inc.† | | 4.75% | | 1/15/2028 | | | 399 | | | | 420,871 | |

| Churchill Downs, Inc.† | | 5.50% | | 4/1/2027 | | | 671 | | | | 711,975 | |

| GLP Capital LP/GLP Financing II, Inc. | | 4.00% | | 1/15/2031 | | | 1,278 | | | | 1,396,975 | |

| GLP Capital LP/GLP Financing II, Inc. | | 5.75% | | 6/1/2028 | | | 1,666 | | | | 1,978,150 | |

| Las Vegas Sands Corp. | | 3.50% | | 8/18/2026 | | | 2,000 | | | | 2,141,273 | |

| Las Vegas Sands Corp. | | 3.90% | | 8/8/2029 | | | 1,226 | | | | 1,318,808 | |

| Melco Resorts Finance Ltd. (Hong Kong)†(a) | | 5.75% | | 7/21/2028 | | | 1,262 | | | | 1,346,238 | |

| MGM Growth Properties Operating Partnership LP/MGP Finance Co-Issuer, Inc.† | | 4.625% | | 6/15/2025 | | | 889 | | | | 953,008 | |

| Mohegan Gaming & Entertainment† | | 7.875% | | 10/15/2024 | | | 1,250 | | | | 1,307,812 | |

| Penn National Gaming, Inc.† | | 5.625% | | 1/15/2027 | | | 2,251 | | | | 2,352,520 | |

| Scientific Games International, Inc.† | | 7.00% | | 5/15/2028 | | | 1,136 | | | | 1,223,358 | |

| Scientific Games International, Inc.† | | 7.25% | | 11/15/2029 | | | 1,145 | | | | 1,258,573 | |

| Stars Group Holdings BV/Stars Group US Co-Borrower LLC (Netherlands)†(a) | | 7.00% | | 7/15/2026 | | | 1,147 | | | | 1,209,368 | |

| Wynn Macau Ltd. (Macau)†(a) | | 5.125% | | 12/15/2029 | | | 1,194 | | | | 1,221,492 | |

| Wynn Macau Ltd. (Macau)†(a) | | 5.50% | | 10/1/2027 | | | 2,772 | | | | 2,882,326 | |

| Wynn Macau Ltd. (Macau)†(a) | | 5.625% | | 8/26/2028 | | | 763 | | | | 801,097 | |

| Total | | | | | | | | | | | 30,163,148 | |

| | | | | | | | | | | | | |

| Gas Distribution 1.96% | | | | | | | | | | | | |

| AI Candelaria Spain SLU (Spain)†(a) | | 7.50% | | 12/15/2028 | | | 1,300 | | | | 1,517,763 | |

| Buckeye Partners LP | | 6.375%

(3 Mo. LIBOR + 4.02% | )# | 1/22/2078 | | | 3,170 | | | | 2,391,115 | |

| Colonial Enterprises, Inc.† | | 3.25% | | 5/15/2030 | | | 748 | | | | 846,578 | |

| Dominion Energy Gas Holdings LLC | | 3.60% | | 12/15/2024 | | | 1,175 | | | | 1,300,368 | |

| ENN Energy Holdings Ltd. (China)†(a) | | 2.625% | | 9/17/2030 | | | 1,242 | | | | 1,249,848 | |

| Florida Gas Transmission Co. LLC† | | 4.35% | | 7/15/2025 | | | 1,145 | | | | 1,301,336 | |

| National Fuel Gas Co. | | 5.50% | | 1/15/2026 | | | 2,268 | | | | 2,618,323 | |

| NGPL PipeCo LLC† | | 4.875% | | 8/15/2027 | | | 2,012 | | | | 2,279,917 | |

| Northern Natural Gas Co.† | | 4.30% | | 1/15/2049 | | | 811 | | | | 987,293 | |

| ONE Gas, Inc. | | 4.50% | | 11/1/2048 | | | 1,149 | | | | 1,539,520 | |

| Sabal Trail Transmission LLC† | | 4.246% | | 5/1/2028 | | | 1,125 | | | | 1,291,943 | |

| Sabine Pass Liquefaction LLC† | | 4.50% | | 5/15/2030 | | | 909 | | | | 1,078,089 | |

| | See Notes to Financial Statements. | 27 |

Schedule of Investments (continued)

December 31, 2020

| Investments | | Interest

Rate | | Maturity

Date | | Principal

Amount

(000) | | | Fair

Value | |

| Gas Distribution (continued) | | | | | | | | | | | | |

| Transportadora de Gas Internacional SA ESP (Colombia)†(a) | | 5.55% | | 11/1/2028 | | $ | 2,056 | | | $ | 2,431,240 | |

| Western Midstream Operating LP | | 5.05% | | 2/1/2030 | | | 2,002 | | | | 2,229,898 | |

| Total | | | | | | | | | | | 23,063,231 | |

| | | | | | | | | | | | | |