UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-05984

|

| The New Ireland Fund, Inc. |

| (Exact name of registrant as specified in charter) |

|

| BNY Mellon Investment Servicing (US) Inc. |

| One Boston Place, 34th Floor |

| Boston, MA 02108 |

| (Address of principal executive offices) (Zip code) |

|

| BNY Mellon Investment Servicing (US) Inc. |

| One Boston Place, 34th Floor |

| Boston, MA 02108 |

| (Name and address of agent for service) |

Registrant’s telephone number, including area code: 508 871 8500

Date of fiscal year end: October 31

Date of reporting period: October 31, 2012

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

| Item 1. | Reports to Stockholders. |

The Report to Shareholders is attached herewith.

Annual Report

October 31, 2012

Cover photograph - St. Andrew’s Church, Dublin City

Provided courtesy of Tourism Ireland

Letter to Shareholders

Dear Shareholder,

Introduction

Although Europe continues to have its economic problems, particularly in Greece, Spain and Portugal, Ireland has made significant progress in improving its economic position and earlier this month a budget was introduced for the coming year, which is expected to further improve its performance. Advances have been made in some of the key areas of the economy, particularly the property and banking sectors, as overseas investors acquired holdings indicating their belief that the country will continue to make progress over the coming years, which in turn should allow them to achieve worthwhile returns on their investments. This, together with the continued growth in exports and the forecast of a stronger growth in GDP for 2013, is helping the overall level of confidence both from within the country and from outside of it. This has also been reflected in the number of companies, particularly from the U.S., who during the past 12 months have been setting up operations in Ireland, which will help employment, particularly in the services sector, and will also benefit exports. As the New Ireland Fund, Inc. (the “Fund”) has to invest at least 80% of its assets in Irish Securities, this should continue to help the performance of the Fund.

While there has been some improvement in the unemployment statistics, the number of unemployed continues to remain high and is expected to stay around the current level for the foreseeable future.

As shown below, the performance of the Fund during the fiscal year ended October 31, 2012 has been good with the Fund’s Net Asset Value (“NAV”) increasing by 13.9% over the 12 months as compared to the increase of 12.9% of the Irish Stock Market Index (“ISEQ”), in U.S. dollar terms*. Over the most recent fiscal quarter, the increase in NAV was 12.9% as compared to the increase of 8.4% of the ISEQ.

The Fund’s Investment Advisor, Kleinwort Benson Investors International Ltd, (“KBII”), who have just completed their first full fiscal year of management of the Fund were recently awarded the prestigious Investment Manager of the Year award for Ireland by World Finance magazine and this is seen as very positive for the Fund, going forward.

As has been previously announced, in June the Fund conducted a tender offer under which 15% of the Fund’s outstanding shares were repurchased. A second tender offer, for another 5% of stock, was conditional on more than 50% of shares being tendered but, as this figure was not reached in the June tender, the second tender will not be going ahead. Mainly as a result of the costs related to the June tender offer, there was no net income for the fiscal year and because of this, as well as net capital gains being offset by loss carry forwards, no distributions will be made for the fiscal year ended October 31, 2012.

| * | All returns are quoted in U.S. Dollars unless otherwise stated |

1

The Board continues to review its Discount Management Program and, while it did not undertake the second tender offer mentioned above, subject to regular Board review, the Fund will continue to operate its share repurchase program with the intention of repurchasing Fund shares whenever the discount is above 10%.

Performance

As previously mentioned, for the fiscal year, the Fund’s NAV increased by 13.9% as compared to the ISEQ, which returned an increase of 12.9% over the same period. In the final fiscal quarter of the year the NAV increased by 12.9%, as compared to the increase of 8.4% in the ISEQ over the same period.

When compared to the broad European benchmark index, the Euro Stoxx 50, the Irish ISEQ index trailed by 5.4% for the past quarter but has significantly outperformed it by almost 10% over the last 12 month period. The U.S. dollar weakened by over 5% versus the euro, over the last three months, thereby boosting investor returns in U.S. dollar terms but it strengthened by almost 9%, versus the euro, over the full fiscal year. On a like for like comparison, in local currency terms, the Irish equity market has beaten the S&P 500 by over 6% over the past 12 months.

While developments in the euro zone fiscal crisis were again significant, the quarter proved to be a strong one for most asset classes. European leaders agreed in principle to sever the link between sovereigns and their banks, and a little while after that the European Central Bank (“ECB”) indicated that it was willing to buy peripheral economy bonds, on strict conditions. These developments, combined with further U.S. Federal Reserve easing, led to a reduction in perceived risk in financial markets, and helped equities to make good gains. Euro zone bond markets also rose strongly as bonds in peripheral markets performed well which, in turn, helped peripheral equity markets such as Ireland.

The more positive market was reflected in the strong stock performance from many of the Fund’s preferred quality cyclical stocks such as Smurfit Kappa, Irish Continental Group and Kingspan. Their performance contributed strongly to Fund performance over the quarter.

During fiscal 2012, we continued to implement the Share Repurchase Program and over the 12 months, the Fund repurchased and retired 316,714 shares at a cost of $2.4 million. In addition, under the tender offer completed in June 2012, 924,000 shares were repurchased at a cost of almost $7.5 million. Overall, these repurchases represent a reduction of 19.4% of the shares outstanding at October 31, 2011, and they positively impacted the Fund’s NAV by 9 cents per share.

Irish Economic Review

GDP statistics released during the period were moderately disappointing, showing a flat economy in the second quarter of 2012. Over the last four quarters for which data is available, growth was positive in two of the quarters, and negative in two, indicating an approximately flat pace of growth.

2

Matching the mixed tone of the historic data, forecasts have generally been stable. The Central Bank of Ireland (CBI) cut its 2012 GDP growth forecast from 0.7% to 0.5%, while the private-sector consensus has fallen from 0.7% to 0.6%. For 2013, the Central Bank is forecasting stronger growth of 1.7%, while the private sector consensus is for a fairly similar rate of 1.6%. The export sector is the driver behind the forecasted growth and the CBI estimates that the export sector will show growth of 3% to 4% in 2012 and 2013, respectively.

Worries about the labor market and the government debt situation weigh on the Irish consumer, and retail sales were poor in 2011 and continued to be poor in 2012, falling by 1.7% in volume terms for the period to the end of September, relative to the same period of 2011. Few, if any, forecasters expect the recovery to be led by the consumer sector, which remains under severe pressure from high debt levels, high unemployment, and fiscal tightening. However, it is interesting to note that there was an upward trend in retail sales during Q3, with sales rising 1.1%, 0.4% and 0.9% in July, August and September, respectively.

Consumer confidence remains volatile and picked up considerably in recent months reaching its highest level, since October 2007, in August of this year, but this was followed by a sharp drop in September and has to be viewed in the context of the high volatility of the index itself.

Business confidence, as measured by the Purchasing Managers Index (PMI) for the manufacturing sector, has held up very well in recent months, and has been above the breakeven 50% level for seven consecutive months. The same indicator was far weaker in almost all other Eurozone economies over the seven month period. This suggests that the manufacturing sector is expanding in Ireland, although at a moderate pace.

There has been a steady, but mild, trend downwards in unemployment, as measured by the “live register”. The number of unemployed on this measure has fallen from a peak of 449,000 in August of 2011 to 435,000 in July of this year. Broadly speaking, the unemployment rate still stands at a very high level of 14.8%. As would be expected, unemployment is a key driver of mortgage delinquencies, and so is also a closely watched indicator for those analyzing the condition of the banking sector.

The Irish Headline rate of inflation has been trending downwards in recent months. In September (the last available data point) the rate had fallen to 1.6%, year on year. The Harmonized Index of Consumer Prices (“HICP”) - the common measure of inflation used by all EU countries, which among other things excludes the impact of mortgage interest rates - is higher, at 2.4%. The Central Bank is forecasting 1.8% for Headline inflation for the whole of 2012, while the private sector consensus is slightly higher, at 1.9%. The domestic economy is generating very little upwards price pressure, with inflation generally arising from imported goods and services.

Demand for credit from businesses and households continues to remain depressed. The annual rate of loans to households dropped by 3.7% in September, identical to the rate observed in March and June. Lending for house

3

purchases was 2% lower on an annual basis, in September, - a fractional improvement - whereas lending to the non-financial corporate sector declined by 4.2% over the same period, marking a continuing deterioration which has been in place for some months now. As the Irish economy is growing at only a very moderate pace, and financial institutions continue to shrink their balance sheets, private sector credit growth is likely to continue to be weak in the near term.

Exchequer returns for the first ten months of the year have been mildly encouraging with tax revenues coming in slightly ahead of target. At this stage, the government’s fiscal targets could be missed in either direction, but should be reasonably close to target either way.

On broader fiscal issues, the announcement by the ECB that it would introduce “Outright Monetary Transactions”, or OMTs, was seen as highly significant. In essence the ECB has said that it will buy unlimited amounts of government bonds of a country that gets into financial difficulties, with certain conditions, which include that the country in question must request assistance, must agree to fiscal and reform measures, and must have financial market access. Given that Ireland is meeting its fiscal targets and has been having some access to the bond markets in recent times, the ECB program could be seen as a ‘backstop’ financing measure in case of difficulties in the financial markets, and is a significant step forward.

Equity Market Review

During the fourth quarter, World stock markets posted positive returns in local currency terms. Over the 12 months, with the exception of Japan, markets delivered positive returns in local currencies, however they were weaker in U.S. dollar terms given the strength of the dollar over the year.

| | | | | | | | | | | | | | | | | | | | |

| | | Quarter Ended

October 31, 2012 | | 12 Months Ended

October 31, 2012 |

| | | | |

| | | Local

Currency | | U.S. $ | | Local

Currency | | U.S. $ |

Irish Equities (ISEQ) | | | | 3.0% | | | | | 8.4% | | | | | 21.6% | | | | | 12.9% | |

| | | | |

U.S. equities (S&P 500) | | | | 3.0% | | | | | 3.0% | | | | | 15.2% | | | | | 15.2% | |

U.S. Equities (NASDAQ) | | | | 1.6% | | | | | 1.6% | | | | | 12.2% | | | | | 12.2% | |

U.K. Equities (FTSE 100) | | | | 3.7% | | | | | 6.6% | | | | | 8.5% | | | | | 8.3% | |

Japanese Equities(Topix) | | | | 1.9% | | | | | -0.5% | | | | | -0.5% | | | | | -2.9% | |

| | | | |

Dow Jones Eurostoxx 50 | | | | 8.2% | | | | | 13.8% | | | | | 10.7% | | | | | 2.8% | |

German Equities (DAX) | | | | 7.2% | | | | | 12.8% | | | | | 18.2% | | | | | 9.8% | |

French Equities (CAC 40) | | | | 4.7% | | | | | 10.2% | | | | | 10.7% | | | | | 2.9% | |

Dutch Equities (AEX) | | | | 1.9% | | | | | 7.3% | | | | | 11.9% | | | | | 4.0% | |

Note-Indices are total return

4

Highlights regarding some of the significant contributors to the Fund’s performance are detailed below:

Smurfit Kappa Group PLC: Smurfit Kappa continues to deliver strong operational results as well as demonstrating meaningful management of the balance sheet through debt restructuring and pay down. Private equity stakes were also reduced further over the period thus increasing liquidity and interest in the stock.

FBD Holdings PLC: FBD had strong results and raised guidance over the period. In particular, strong underwriting results were delivered by the company. Also in recent months, they announced a significant increase in the dividend and hinted at the potential for further dividend growth.

Irish Continental Group PLC: Strong management delivered operational performance in line with market expectations. An attractive and growing dividend continues to support the stock. Over recent months, the stock has been particularly strong on the back of a forthcoming tender offer to buy back stock at a premium.

United Drug PLC: Having lagged for some time, the stock performed strongly on the back of upgrades to its earnings forecasts and the announcement of a number of meaningful acquisitions that will add to their business. The company also recently announced that it intends to move its listing to the London stock exchange.

Kingspan Group PLC: Kingspan is a quality cyclically exposed stock, which delivered solid earnings growth and continues to give positive guidance. Over recent months, the company announced a significant acquisition of a specialty materials business from ThyssenKrupp in Germany, news which was positively received by the market.

Market Outlook

Against a fragile global background in which Western economies are collectively de-leveraging from past excesses, Ireland continues to move forward. Ireland is building on its position as the “poster boy” within the European Union for its radical reform, related to restructuring and the implementation of austerity programs. This was also reflected in the Irish Prime Minister being featured recently on the front page of Time magazine under the banner headline “Celtic Comeback”. A further small but newsworthy point was the recent upgrade by Fitch, the rating agency, of Ireland’s rating from negative to stable BBB+.

A continued slow but steady improvement is forecast for the Irish economy over the next few years. As highlighted above, there will be a continued growth divergence between that of the subdued domestic economy versus the more positive export exposed side of the economy. The export economy is doing very well, not least because unit labor costs have come down by around 25% since 2009, relative to most of Europe. Furthermore, Ireland still has strong trade linkages to the U.S. and the U.K. which, in relative terms, have held up better than other economies. Export dependence does of course leave the economy

5

exposed to the continued demand of other countries, but it is hoped that this does not occur to any great extent.

The Irish stock market has performed fairly strongly, and consistently, since its lows in 2009 and as this recovery is expected to continue, it is believed that it currently lends itself to active stock picking opportunities. On a frequent basis, the Fund’s Investment Advisor continues to meet with the management of companies that the Fund is invested in, and this allows them to maintain a high quality focus looking for strong balance sheets, cash flow and management. The Advisor focuses on stocks with positive earnings momentum and dividend paying ability when possible. To date, they have been avoiding low quality and deep value stocks, as they don’t believe the recovery to be strong enough, at this point in time, to benefit the more “fragile” stocks.

Sincerely

| | |

| |

|

Peter J. Hooper | | Sean Hawkshaw |

Chairman | | President |

December 20, 2012 | | December 20, 2012 |

6

Investment Summary (unaudited)

Total Return (%)

| | | | | | | | | | | | | | | | | | | | |

| | | Market Value (a) | | Net Asset Value (a) |

| | | Cumulative | | Average

Annual | | Cumulative | | Average

Annual |

One Year | | | | 16.50 | | | | | 16.50 | | | | | 13.94 | | | | | 13.94 | |

Three Year | | | | 26.12 | | | | | 8.04 | | | | | 18.43 | | | | | 5.80 | |

Five Year | | | | -38.79 | | | | | -9.35 | | | | | -37.81 | | | | | -9.06 | |

Ten Year | | | | 143.34 | | | | | 9.30 | | | | | 107.53 | | | | | 7.57 | |

Per Share Information and Returns

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | 2003 | | 2004 | | 2005 | | 2006 | | 2007 | | 2008 | | 2009 | | 2010 | | 2011 | | 2012 |

Net Asset

Value ($) | | | | 16.29 | | | | | 20.74 | | | | | 24.36 | | | | | 32.55 | | | | | 30.95 | | | | | 10.18 | | | | | 8.20 | | | | | 7.70 | | | | | 8.45 | | | | | 9.59 | |

Income

Dividends ($) | | | | — | | | | | (0.09 | ) | | | | (0.03 | ) | | | | (0.16 | ) | | | | (0.24 | ) | | | | (0.36 | ) | | | | (0.33 | ) | | | | — | | | | | (0.06 | ) | | | | (0.02 | ) |

Capital Gains | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Other

Distributions ($) | | | | — | | | | | — | | | | | — | | | | | (1.77 | ) | | | | (2.40 | ) | | | | (4.86 | ) | | | | (2.76 | ) | | | | — | | | | | — | | | | | — | |

Total Net Asset Value Return (%) (a) | | | | 47.55 | | | | | 28.14 | | | | | 17.51 | | | | | 45.97 | | | | | 2.88 | | | | | -58.62 | | | | | 26.91 | | | | | -6.10 | | | | | 10.69 | | | | | 13.94 | |

Notes

| (a) | Total Market Value returns reflect changes in share market prices and assume reinvestment of dividends and capital gain distributions, if any, at the price obtained under the Dividend Reinvestment and Cash Purchase Plan (“the Plan”). Total Net Asset Value returns reflect changes in share net asset value and assume reinvestment of dividends and capital gain distributions, if any, at the price obtained under the Plan. For more information with regard to the Plan, see page 23. |

Past results are not necessarily indicative of future performance of the Fund.

7

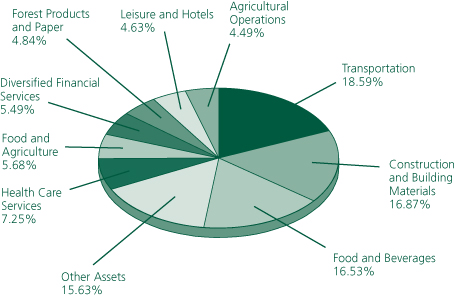

Portfolio by Market Sector as of October 31, 2012

(Percentage of Net Assets)

Top 10 Holdings by Issuer as of October 31, 2012

| | | | | | |

Holding | | Sector | | % of

Net Assets | |

CRH PLC | | Construction and Building Materials | | | 11.30% | |

Kerry Group PLC, Series A | | Food and Beverages | | | 10.88% | |

Ryanair Holdings PLC | | Transportation | | | 10.68% | |

Aryzta AG | | Food and Agriculture | | | 5.68% | |

Smurfit Kappa Group PLC | | Forest Products and Paper | | | 4.84% | |

Irish Continental Group PLC | | Transportation | | | 4.69% | |

Paddy Power PLC | | Leisure and Hotels | | | 4.63% | |

Origin Enterprises PLC | | Agricultural Operations | | | 4.49% | |

Kingspan Group PLC | | Construction and Building Materials | | | 4.49% | |

Dragon Oil PLC | | Energy | | | 4.19% | |

8

The New Ireland Fund, Inc.

Portfolio Holdings

| | | | | | | | |

| | |

| October 31, 2012 | | Shares | | | Value (U.S.)

(Note A) | |

| | | | | | | | |

COMMON STOCKS (99.52%) | | | | | | | | |

COMMON STOCKS OF IRISH COMPANIES (96.91%) | | | | | | | | |

| | |

Agricultural Operations (4.49%) | | | | | | | | |

Origin Enterprises PLC | | | 402,529 | | | $ | 2,222,016 | |

| | | | | | | | |

| | |

Business Services (1.11%) | | | | | | | | |

DCC PLC | | | 19,286 | | | | 550,925 | |

| | | | | | | | |

| | |

Business Support Services (2.43%) | | | | | | | | |

CPL Resources PLC | | | 285,169 | | | | 1,200,953 | |

| | | | | | | | |

| | |

Construction and Building Materials (16.87%) | | | | | | | | |

CRH PLC | | | 300,432 | | | | 5,590,375 | |

Grafton Group PLC-UTS | | | 121,708 | | | | 531,798 | |

Kingspan Group PLC | | | 212,741 | | | | 2,221,911 | |

| | | | | | | | |

| | | | | | | 8,344,084 | |

| | | | | | | | |

| | |

Diversified Financial Services (5.49%) | | | | | | | | |

FBD Holdings PLC | | | 129,854 | | | | 1,623,764 | |

IFG Group PLC | | | 130,393 | | | | 236,550 | |

TVC Holdings PLC* | | | 815,973 | | | | 856,448 | |

| | | | | | | | |

| | | | | | | 2,716,762 | |

| | | | | | | | |

| | |

Energy (4.19%) | | | | | | | | |

Dragon Oil PLC | | | 232,276 | | | | 2,073,786 | |

| | | | | | | | |

| | |

Financial (1.46%) | | | | | | | | |

Bank of Ireland (The)* | | | 6,101,796 | | | | 719,514 | |

| | | | | | | | |

| | |

Food and Agriculture (5.68%) | | | | | | | | |

Aryzta AG | | | 57,835 | | | | 2,810,362 | |

| | | | | | | | |

| | |

Food and Beverages (16.53%) | | | | | | | | |

C&C Group PLC | | | 269,779 | | | | 1,291,354 | |

Glanbia PLC | | | 121,774 | | | | 1,155,064 | |

Kerry Group PLC, Series A | | | 102,898 | | | | 5,382,772 | |

Total Produce PLC | | | 552,258 | | | | 347,076 | |

| | | | | | | | |

| | | | | | | 8,176,266 | |

| | | | | | | | |

| | |

Forest Products and Paper (4.84%) | | | | | | | | |

Smurfit Kappa Group PLC | | | 217,273 | | | | 2,393,123 | |

| | | | | | | | |

See Notes to Financial Statements.

9

The New Ireland Fund, Inc.

Portfolio Holdings (continued)

| | | | | | | | |

| | |

| October 31, 2012 | | Shares | | | Value (U.S.)

(Note A) | |

| | | | | | | | |

COMMON STOCKS (continued) | | | | | | | | |

| | |

Health Care Services (7.25%) | | | | | | | | |

Elan Corp. PLC-Sponsored ADR* | | | 152,261 | | | $ | 1,644,419 | |

ICON PLC-Sponsored ADR* | | | 25,173 | | | | 592,573 | |

United Drug PLC | | | 370,124 | | | | 1,347,618 | |

| | | | | | | | |

| | | | | | | 3,584,610 | |

| | | | | | | | |

| | |

Leisure and Hotels (4.63%) | | | | | | | | |

Paddy Power PLC | | | 31,048 | | | | 2,290,822 | |

| | | | | | | | |

| | |

Mining (3.35%) | | | | | | | | |

Kenmare Resources PLC* | | | 2,627,445 | | | | 1,658,070 | |

| | | | | | | | |

| | |

Transportation (18.59%) | | | | | | | | |

Aer Lingus Group PLC* | | | 213,852 | | | | 285,424 | |

Irish Continental Group PLC | | | 95,317 | | | | 2,322,034 | |

Ryanair Holdings PLC* | | | 911,868 | | | | 5,281,774 | |

Ryanair Holdings PLC-Sponsored ADR* | | | 40,511 | | | | 1,306,480 | |

| | | | | | | | |

| | | | | | | 9,195,712 | |

| | | | | | | | |

TOTAL COMMON STOCKS OF IRISH COMPANIES

(Cost $38,388,407) | | | | | | | 47,937,005 | |

| | | | | | | | |

COMMON STOCKS OF GERMAN COMPANIES (2.61%) | | | | | | | | |

| | |

Information Technology (2.61%) | | | | | | | | |

SAP AG | | | 17,752 | | | | 1,292,778 | |

| | | | | | | | |

TOTAL COMMON STOCKS OF GERMAN COMPANIES (Cost $1,057,809) | | | | | | | 1,292,778 | |

| | | | | | | | |

TOTAL COMMON STOCKS BEFORE FOREIGN CURRENCY ON DEPOSIT

(Cost $39,446,216) | | | | | | $ | 49,229,783 | |

| | | | | | | | |

See Notes to Financial Statements.

10

The New Ireland Fund, Inc.

Portfolio Holdings (continued)

| | | | | | | | |

| | |

| October 31, 2012 | | Face Value | | | Value (U.S.)

(Note A) | |

| | | | | | | | |

FOREIGN CURRENCY ON DEPOSIT (0.44%)

Euro | | | €167,097 | | | $ | 216,526 | |

| | | | | | | | |

TOTAL FOREIGN CURRENCY ON DEPOSIT

(Cost $216,526)** | | | | | | | 216,526 | |

| | | | | | | | |

TOTAL INVESTMENTS (99.96%)

(Cost $39,662,742) | | | | | | | 49,446,309 | |

OTHER ASSETS AND LIABILITIES (0.04%) | | | | | | | 21,884 | |

| | | | | | | | |

NET ASSETS (100.00%) | | | | | | $ | 49,468,193 | |

| | | | | | | | |

| | | | |

| * | | | | Non-income producing security. |

| ** | | | | Foreign currency held on deposit at JPMorgan Chase & Co. |

| ADR | | – | | American Depositary Receipt traded in U.S. dollars. |

| UTS | | – | | Units |

The Inputs of methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. Transfers in and out of levels are recognized at market value at the end of the period. The summary of inputs used to value the Fund’s net assets as of October 31, 2012 is as follows (See Note A – Security Valuation in the Notes to Financial Statements):

| | | | | | | | | | | | | | | | |

| | | Total

Value at

10/31/12 | | | Level 1

Quoted

Price | | | Level 2

Significant

Observable

Input | | | Level 3

Significant

Unobservable

Input | |

Investments in Securities † | | | | | | | | | | | | | | | | |

Common Stocks* | | | | | | | | | | | | | | | | |

Agricultural Operations | | $ | 2,222,016 | | | $ | 2,222,016 | | | $ | — | | | $ | — | |

Business Services | | | 550,925 | | | | 550,925 | | | | — | | | | — | |

Business Support Services | | | 1,200,953 | | | | 1,200,953 | | | | — | | | | — | |

Construction and Building Materials | | | 8,344,084 | | | | 8,344,084 | | | | — | | | | — | |

Diversified Financial Services | | | 2,716,762 | | | | 1,860,314 | | | | 856,448 | | | | — | |

Energy | | | 2,073,786 | | | | 2,073,786 | | | | — | | | | — | |

Financial | | | 719,514 | | | | 719,514 | | | | — | | | | — | |

Food and Agriculture | | | 2,810,362 | | | | 2,810,362 | | | | — | | | | — | |

Food and Beverages | | | 8,176,266 | | | | 8,176,266 | | | | — | | | | — | |

Forest Products & Paper | | | 2,393,123 | | | | 2,393,123 | | | | — | | | | — | |

Health Care Services | | | 3,584,610 | | | | 3,584,610 | | | | — | | | | — | |

Information Technology | | | 1,292,778 | | | | 1,292,778 | | | | — | | | | — | |

Leisure and Hotels | | | 2,290,822 | | | | 2,290,822 | | | | — | | | | — | |

Mining | | | 1,658,070 | | | | 1,658,070 | | | | — | | | | — | |

Transportation | | | 9,195,712 | | | | 9,195,712 | | | | — | | | | — | |

| | | | | | | | | | | | | | | | |

Total Common Stocks | | $ | 49,229,783 | | | $ | 48,373,335 | | | $ | 856,448 | | | $ | — | |

| | | | | | | | | | | | | | | | |

| † | Total Investments exclude Foreign Currency on Deposit and Other Assets. |

| * | See Portfolio Holdings detail for country breakout. |

The Fund did not have any significant transfers in and out of Level 1 and Level 2 during the period.

See Notes to Financial Statements.

11

The New Ireland Fund, Inc.

Statement of Assets and Liabilities

October 31, 2012

| | | | | | | | |

ASSETS: | | | | | | | | |

Investments at value (Cost $39,446,216)

See accompanying schedule | | | U.S. | | | $ | 49,229,783 | |

Cash | | | | | | | 170,210 | |

Foreign currency (Cost $216,526) | | | | | | | 216,526 | |

Dividends receivable | | | | | | | 53,858 | |

Receivable for Fund shares sold | | | | | | | 4,379 | |

Prepaid expenses | | | | | | | 8,290 | |

| | | | | | | | |

Total Assets | | | | | | | 49,683,046 | |

| | | | | | | | |

| | |

LIABILITIES: | | | | | | | | |

Payable for Fund shares redeemed | | | | | | | 6,420 | |

Printing fees payable | | | | | | | 53,807 | |

Accrued legal fees payable | | | | | | | 32,995 | |

Investment advisory fee payable (Note B) | | | | | | | 27,542 | |

Accrued audit fees payable | | | | | | | 40,300 | |

Custodian fees payable (Note B) | | | | | | | 14,214 | |

Administration fee payable (Note B) | | | | | | | 10,591 | |

Directors’ fees and expenses | | | | | | | 23,245 | |

Accrued expenses and other payables | | | | | | | 5,739 | |

| | | | | | | | |

Total Liabilities | | | | | | | 214,853 | |

| | | | | | | | |

NET ASSETS | | | U.S. | | | $ | 49,468,193 | |

| | | | | | | | |

| | |

AT OCTOBER 31, 2012 NET ASSETS CONSISTED OF: | | | | | | | | |

Common Stock, U.S. $.01 Par Value -

Authorized 20,000,000 Shares

Issued and Outstanding 5,156,348 Shares | | | U.S. | | | $ | 51,563 | |

Additional Paid-in Capital | | | | | | | 53,053,566 | |

Accumulated Net Investment Loss | | | | | | | (327,818 | ) |

Accumulated Net Realized Loss | | | | | | | (13,093,244 | ) |

Net Unrealized Appreciation of Securities,

Foreign Currency and Net Other Assets | | | | | | | 9,784,126 | |

| | | | | | | | |

TOTAL NET ASSETS | | | U.S. | | | $ | 49,468,193 | |

| | | | | | | | |

| | |

NET ASSET VALUE PER SHARE

(Applicable to 5,156,348 outstanding shares)

(authorized 20,000,000 shares) | | | | | | | | |

(U.S. $49,468,193 ÷ 5,156,348) | | | U.S. | | | $ | 9.59 | |

| | | | | | | | |

See Notes to Financial Statements.

12

The New Ireland Fund, Inc.

Statement of Operations

| | | | | | | | | | | | |

| | | | | | For the Year Ended

October 31, 2012 | |

| | | |

INVESTMENT INCOME | | | | | | | | | | | | |

Dividends | | | | | | | U.S. | | | $ | 1,179,401 | |

Less: foreign taxes withheld | | | | | | | | | | | (18,536 | ) |

| | | | | | | | | | | | |

| | | |

TOTAL INVESTMENT INCOME | | | | | | | | | | | 1,160,865 | |

| | | | | | | | | | | | |

| | | |

EXPENSES | | | | | | | | | | | | |

Investment advisory fee (Note B) | | $ | 331,126 | | | | | | | | | |

Directors’ fees | | | 255,588 | | | | | | | | | |

Legal fees | | | 224,185 | | | | | | | | | |

Administration fee (Note B) | | | 106,924 | | | | | | | | | |

Printing and mailing expenses | | | 100,797 | | | | | | | | | |

Compliance fees | | | 68,238 | | | | | | | | | |

Insurance premiums | | | 54,560 | | | | | | | | | |

Audit fees | | | 40,300 | | | | | | | | | |

Custodian fees (Note B) | | | 23,942 | | | | | | | | | |

Other | | | 153,253 | | | | | | | | | |

| | | | | | | | | | | | |

| | | |

TOTAL EXPENSES | | | | | | | | | | | 1,358,913 | |

| | | | | | | | | | | | |

| | | |

NET INVESTMENT LOSS | | | | | | | U.S. | | | $ | (198,048 | ) |

| | | | | | | | | | | | |

| | |

REALIZED AND UNREALIZED GAIN ON INVESTMENTS

AND FOREIGN CURRENCY | | | | | | | | | |

Realized gain/(loss) on: | | | | | | | | | | | | |

Securities transactions | | | 2,979,569 | | | | | | | | | |

Foreign currency transactions | | | (152,185 | ) | | | | | | | | |

| | | | | | | | | | | | |

Net realized gain on investments and foreign currency during the year | | | | | | | | | | | 2,827,384 | |

| | | | | | | | | | | | |

Net change in unrealized appreciation of: | | | | | | | | | | | | |

Securities | | | 2,772,683 | | | | | | | | | |

Foreign currency and net other assets | | | 43,650 | | | | | | | | | |

| | | | | | | | | | | | |

Net unrealized appreciation of investments and foreign currency during the year | | | | | | | | | | | 2,816,333 | |

| | | | | | | | | | | | |

| | |

NET REALIZED AND UNREALIZED GAIN ON INVESTMENTS AND FOREIGN CURRENCY | | | | | | | | 5,643,717 | |

| | | | | | | | | | | | |

| | | |

NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | | | | | | | U.S. | | | $ | 5,445,669 | |

| | | | | | | | | | | | |

See Notes to Financial Statements.

13

The New Ireland Fund, Inc.

Statements of Changes in Net Assets

| | | | | | | | | | | | | | | | |

| | | Year Ended October 31, 2012 | | | Year Ended October 31, 2011 | |

| | | | |

Net investment income/(loss) | | | U.S. | | | $ | (198,048 | ) | | | U.S. | | | $ | 84,933 | |

Net realized gain on investments and foreign currency transactions | | | | | | | 2,827,384 | | | | | | | | 437,926 | |

Net unrealized appreciation of investments, foreign currency holdings and net other assets | | | | | | | 2,816,333 | | | | | | | | 4,703,321 | |

| | | | | | | | | | | | | | | | |

Net increase in net assets resulting from operations | | | | | | | 5,445,669 | | | | | | | | 5,226,180 | |

| | | | | | | | | | | | | | | | |

| | | |

DISTRIBUTIONS TO SHAREHOLDERS FROM: | | | | | | | | | | | | | |

Net investment income | | | | | | | (127,802 | ) | | | | | | | (400,589 | ) |

| | | | | | | | | | | | | | | | |

Total distributions | | | | | | | (127,802 | ) | | | | | | | (400,589 | ) |

| | | | | | | | | | | | | | | | |

| | | | |

CAPITAL SHARE TRANSACTIONS: | | | | | | | | | | | | | | | | |

Value of 316,714 and 280,053 shares repurchased, respectively (Note F) | | | | | | | (2,444,590 | ) | | | | | | | (2,187,501 | ) |

Value of 924,000 and 0 shares, respectively, in connection with a Tender Offer (Note F) | | | | | | | (7,475,160 | ) | | | | | | | — | |

Value of 631 and 0 shares issued, respectively, to shareholders in connection with a stock distribution (Note E) | | | | | | | 4,379 | | | | | | | | — | |

| | | | | | | | | | | | | | | | |

| | | |

NET DECREASE IN NET ASSETS RESULTING FROM CAPITAL SHARE TRANSACTIONS | | | | (9,915,371 | ) | | | | | | | (2,187,501 | ) |

| | | | | | | | | | | | | | | | |

Total Increase/(decrease) in net assets | | | | | | | (4,597,504 | ) | | | | | | | 2,638,090 | |

| | | | | | | | | | | | | | | | |

| | | |

NET ASSETS | | | | | | | | | | | | | |

Beginning of year | | | | | | | 54,065,697 | | | | | | | | 51,427,607 | |

| | | | | | | | | | | | | | | | |

End of year (Including accumulated/undistributed net investment income/(loss) of $(327,818) and $115,616, respectively) | | | U.S. | | | $ | 49,468,193 | | | | U.S. | | | $ | 54,065,697 | |

| | | | | | | | | | | | | | | | |

See Notes to Financial Statements.

14

The New Ireland Fund, Inc.

Financial Highlights (For a Fund share outstanding throughout each period)

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Year Ended October 31, | |

| | | | | | 2012 | | | 2011 | | | 2010 | | | 2009 | | | 2008 | |

| | | | | | |

Operating Performance: | | | | | | | | | | | | | | | | | | | | | | | | |

Net Asset Value, Beginning of Year | | | U.S. | | | | $8.45 | | | | $7.70 | | | | $8.20 | | | | $10.18 | | | | $30.95 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Net Investment Income/(Loss) | | | | | | | (0.04 | ) | | | 0.01 | | | | 0.05 | | | | (0.06 | ) | | | 0.34 | |

Net Realized and Unrealized Gain/(Loss) on Investments | | | | | | | 1.11 | | | | 0.76 | | | | (0.61 | ) | | | 1.23 | | | | (15.77 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Net Increase/(Decrease) in Net Assets Resulting from Investment Operations | | | | | | | 1.07 | | | | 0.77 | | | | (0.56 | ) | | | 1.17 | | | | (15.43 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Distributions to Shareholders from: | | | | | | | | | | | | | | | | | | | | | | | | |

Net Investment Income | | | | | | | (0.02 | ) | | | (0.06 | ) | | | — | | | | (0.33 | ) | | | (0.36 | ) |

Net Realized Gains | | | | | | | — | | | | — | | | | — | | | | (2.76 | ) | | | (4.86 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total from Distributions | | | | | | | (0.02 | ) | | | (0.06 | ) | | | — | | | | (3.09 | ) | | | (5.22 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Anti-Dilutive/(Dilutive) Impact of Capital Share Transactions | | | | | | | 0.09 | ††††† | | | 0.04 | †††† | | | 0.06 | ††† | | | (0.06 | )†† | | | (0.12 | )† |

| | | | | | | | | | | | | | | | | | | | | | | | |

Net Asset Value, End of Period | | | U.S. | | | | $9.59 | | | | $8.45 | | | | $7.70 | | | | $8.20 | | | | $10.18 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Share Price, End of Period | | | U.S. | | | | $8.84 | | | | $7.61 | | | | $6.51 | | | | $7.09 | | | | $8.95 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total NAV Investment Return (a) | | | | | | | 13.82% | | | | 10.69% | | | | (6.10)% | | | | 26.91% | | | | (58.62)% | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total Market Investment Return (b) | | | | | | | 16.50% | | | | 17.91% | | | | (8.18)% | | | | 25.06% | | | | (61.20)% | |

| | | | | | | | | | | | | | | | | | | | | | | | |

|

RATIOS TO AVERAGE NET ASSETS/SUPPLEMENTAL DATA: | |

Net Assets,

End of Period (000’s) | | | U.S. | | | | $49,468 | | | | $54,066 | | | | $51,428 | | | | $57,786 | | | | $50,896 | |

Ratio of Net Investment

Income/(Loss) to

Average Net Assets | | | | | | | (0.39)% | | | | 0.15% | | | | 0.69% | | | | (0.87)% | | | | 1.67% | |

Ratio of Operating Expenses

to Average Net Assets | | | | | | | 2.66% | | | | 2.22% | | | | 2.02% | | | | 2.65% | | | | 1.56% | |

Portfolio Turnover Rate | | | | | | | 21% | | | | 23% | | | | 11% | | | | 16% | | | | 21% | |

| (a) | | Based on share net asset value and reinvestment of distribution at the price obtained under the Dividend Reinvestment and Cash Purchase Plan. |

| (b) | | Based on share market price and reinvestment of distributions at the price obtained under the Dividend Reinvestment and Cash Purchase Plan. |

| † | | Amount represents $0.13 per share impact for shares repurchased by the Fund under the Share Repurchase Program and $0.25 per share impact for the new shares issued as Capital Gain Stock Distribution. |

| †† | | Amount represents $0.08 per share impact for shares repurchased by the Fund under the Share Repurchase Program and $0.14 per share impact for the new shares issued as Capital Gain Stock Distribution. |

| ††† | | Amount represents $0.06 per share impact for shares repurchased by the Fund under the Share Repurchase Program. |

| †††† | | Amount represents $0.04 per share impact for the shares repurchased by the Fund under the Share Repurchase Program. |

| ††††† | | Amount represents $0.09 per share impact for shares repurchased by the Fund. $0.09 per share impact represents $0.06 for shares repurchased under the Share Repurchase Program and $0.03 per share impact related to the Tender Offer, which was completed in June, 2012. |

See Notes to Financial Statements.

15

The New Ireland Fund, Inc.

Notes to Financial Statements

The New Ireland Fund, Inc. (the “Fund”) was incorporated under the laws of the State of Maryland on December 14, 1989 and is registered as a non-diversified, closed-end management investment company under the Investment Company Act of 1940, as amended (the “1940 Act”). The Fund’s investment objective is long-term capital appreciation through investment primarily in equity securities of Irish Companies. The Fund is designed for U.S. and other investors who wish to participate in the Irish securities markets. In order to take advantage of significant changes that have occurred in the Irish economy and to advance the Fund’s investment objective, the investment strategy now has a bias towards Ireland’s growth companies.

Under normal circumstances, the Fund will invest at least 80% of its total assets in equity and fixed income securities of Irish companies. To the extent that the balance of the Fund’s assets is not so invested, it will have the flexibility to invest the remaining assets in non-Irish companies that are listed on a recognized stock exchange. The Fund may invest up to 25% of its assets in equity securities that are not listed on any securities exchange.

A. Significant Accounting Policies:

The following is a summary of significant accounting policies consistently followed by the Fund in the preparation of its financial statements.

Security Valuation: Securities listed on a stock exchange for which market quotations are readily available are valued at the closing prices on the date of valuation, or if no such closing prices are available, at the last bid price quoted on such day. If there are no such quotations available for the date of valuation, the last available closing price will be used. The value of securities and other assets for which no market quotations are readily available, or whose values have been materially affected by events occurring before the Fund’s pricing time but after the close of the securities’ primary markets, are valued by methods deemed by the Board of Directors to represent fair value. Short-term securities that mature in 60 days or less are valued at amortized cost.

Fair Value Measurements: As described above, the Fund utilizes various methods to measure the fair value of most of its investments on a recurring basis. U.S. Generally Accepted Accounting Principals (“GAAP”) establishes a hierarchy that prioritizes inputs to valuation methods. The three levels of inputs are:

Level 1 – unadjusted quoted prices in active markets for identical assets or liabilities that the Fund has the ability to access.

Level 2 – observable inputs other than quoted prices included in level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument on an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data.

Level 3 – unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available, representing the Fund’s own assumptions about the assumptions a market participant would use in valuing the asset or liability, and would be based on the best information available.

16

The New Ireland Fund, Inc.

Notes to Financial Statements (continued)

The availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including, for example, the type of security, whether the security is new and not yet established in the marketplace, the liquidity of markets, and other characteristics particular to the security. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value is greatest for instruments categorized in level 3.

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety, is determined based on the lowest level input that is significant to the fair value measurement in its entirety. A summary of the levels of the Fund’s investments as of October 31, 2012 is included with the Fund’s Portfolio of Investments.

At the end of each calendar quarter, management evaluates the Level 2 and Level 3 assets and liabilities, if any, for changes in liquidity, including but not limited to: whether a broker is willing to execute at the quoted price, the depth and consistency of prices from third party services, and the existence of contemporaneous, observable trades in the market. Additionally, management evaluates the Level 1 and Level 2 assets and liabilities on a quarterly basis for changes in listings or delistings on national exchanges.

Dividends and Distributions to Stockholders: Distributions are determined on a tax basis and may differ from net investment income and realized capital gains for financial reporting purposes. Differences may be permanent or temporary. Permanent differences are reclassified among capital accounts in the financial statements to reflect their tax character. Temporary differences arise when certain items of income, expense, gain or loss are recognized in different periods for financial statement and tax purposes; these differences will reverse at some point in the future. Differences in classification may also result from the treatment of short-term gain as ordinary income for tax purposes.

For tax purposes at October, 31, 2012 and October 31, 2011, the Fund distributed $127,802 and $400,589, respectively, of ordinary income. The Fund did not have any net long-term capital gains for years ended October 31, 2012 and October 31, 2011.

Permanent differences between book and tax basis reporting for the year ended October 31, 2012 have been identified and appropriately reclassified to reflect an increase in accumulated net investment loss of $117,584, a decrease in accumulated net realized loss of $152,185 and a decrease in paid-in-capital of $34,601. These adjustments were related to Section 988 gain (loss) reclasses and net operation losses. Net assets were not affected by this reclassification.

U.S. Federal Income Taxes: It is the Fund’s intention to continue to qualify as a regulated investment company under Subchapter M of the Internal Revenue Code of 1986, as amended, and distribute all of its taxable income within the prescribed time. It is also the intention of the Fund to make distributions in sufficient amounts to avoid Fund excise tax. Accordingly, no provision for U.S. Federal income taxes is required.

Management has analyzed the Fund’s tax positions taken on Federal income tax returns for all open tax years (October 31, 2012, 2011, 2010 and 2009), and has concluded that no provision for federal income tax is required in the Fund’s financial statements. The Fund’s federal and state income and federal excise tax returns for tax

17

The New Ireland Fund, Inc.

Notes to Financial Statements (continued)

years for which the applicable statutes of limitations have not expired are subject to examination by the Internal Revenue Service and state departments of revenue.

Currency Translation: The books and records of the Fund are maintained in U.S. dollars. Foreign currency amounts are translated into U.S. dollars at the spot rate of such currencies against U.S. dollars by obtaining from FT-Interactive Data Corp. (“FT-IDC”) each day the current 4:00pm London time spot rate and future rate (the future rates are quoted in 30-day increments) on foreign currency contracts. Net realized foreign currency gains and losses resulting from changes in exchange rates include foreign currency gains and losses between trade date and settlement date on investment securities transactions, foreign currency transactions and the difference between the amounts of interest and dividends recorded on the books of the Fund and the amount actually received. The portion of foreign currency gains and losses related to fluctuation in exchange rates between the initial purchase trade date and subsequent sale trade date is included in realized gains and losses on security transactions.

Forward Foreign Currency Contracts: The Fund may enter into forward foreign currency contracts for non-trading purposes in order to protect investment securities and related receivables and payables against future changes in foreign currency exchange rates. Fluctuations in the value of such contracts are recorded as unrealized gains or losses; realized gains or losses include net gains or losses on contracts which have been terminated by settlements or by entering into offsetting commitments. Risks associated with such contracts include movement in the value of the foreign currency relative to the U.S. dollar and the ability of the counterparty to perform. There were no such contracts open in the Fund as of October 31, 2012.

Securities Transactions and Investment Income: Securities transactions are recorded based on their trade date. Realized gains and losses from securities sold are recorded on the identified cost basis. Dividend income is recorded on the ex-dividend date except that certain dividends from foreign securities are recorded as soon as the Fund is informed of the ex-dividend date. Withholding taxes on foreign dividends have been provided for in accordance with the Fund’s understanding of the applicable country’s tax rules and rates. Non-cash dividends, if any, are recorded at the fair market value of the securities received. Interest income is recorded on the accrual basis.

Use of Estimates: The preparation of financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

B. Management Services:

The Fund has entered into an investment advisory agreement (the “Investment Advisory Agreement”) with Kleinwort Benson Investors International Ltd. (“KBII”). Effective July 21, 2011, under the Investment Advisory Agreement, the Fund paid a monthly fee at an annualized rate equal to 0.65% of the value of the average daily net assets of the Fund up to the first $50 million, 0.60% of the value of the average daily net assets of the Fund over $50 million and up to and including $100 million and 0.50% of the value of the average daily net assets of the Fund on amounts in excess of $100 million. In addition, KBII provides investor services to existing and potential shareholders.

18

The New Ireland Fund, Inc.

Notes to Financial Statements (continued)

The Fund has entered into an administration agreement (the “Administration Agreement”) with BNY Mellon Investment Servicing (US) Inc. (“BNY Mellon”). The Fund pays BNY Mellon an annual fee payable monthly. During the year ended October 31, 2012, the Fund incurred expenses of U.S. $106,924 in administration fees to BNY Mellon.

The Fund has entered into an agreement with JPMorgan Chase & Co. to serve as custodian of the Fund’s assets. During the year ended October 31, 2012, the Fund incurred expenses for JPMorgan Chase & Co. of U.S. $23,942.

C. Purchases and Sales of Securities:

The cost of purchases and proceeds from sales of securities for the year ended October 31, 2012 excluding U.S. government and short-term investments, aggregated U.S. $10,391,996 and U.S. $18,087,166, respectively.

D. Components of Distributable Earnings:

At October 31, 2012, the components of distributable earnings on a tax basis were as follows:

| | | | | | | | | | | | | | | | | | |

Capital Loss Carryforward | | | Qualified

Late Year

Losses Deferred | | | Undistributed Ordinary Income | | | Undistributed Long-Term Gains | | | Net Unrealized Appreciation | |

| $ | (10,912,824 | ) | | $ | (327,818 | ) | | $ | — | | | $ | — | | | $ | 7,603,706 | |

As of October 31, 2012, the Fund had a capital loss carryforward of $10,912,824, which will expire on October 31, 2018. During the year ended October 31, 2012 $2,851,085 of capital loss carryforward was utilized.

On December 22, 2010, the Regulated Investment Company Modernization Act of 2010 was enacted to modernize several of the federal income and excise tax provisions related to regulated investment companies. Under pre-enactment law, capital losses could be carried forward for eight years, and carried forward as short-term capital losses, irrespective of the character of the original loss. New net capital losses (those earned in taxable years beginning after December 22, 2010) may be carried forward indefinitely and must retain the character of the original loss. Such new net capital losses generally must be used by a regulated investment company before it uses any net capital losses incurred in taxable years beginning on or before December 22, 2010. This increases the likelihood that net capital losses incurred in taxable years beginning on or before December 22, 2010 will expire unused.

Under current laws, certain ordinary losses after January 1st may be deferred and treated as occurring on the first day of the following fiscal year. For the fiscal year ended October 31, 2012, the Fund elected to defer the following losses incurred from January 2012 through October 31, 2012:

| | |

Late Year Ordinary Losses Deferral | |

| $ | 327,818 | |

19

The New Ireland Fund, Inc.

Notes to Financial Statements (continued)

The aggregate cost of investments and the composition of unrealized appreciation and depreciation on investments and appreciation on assets and liabilities in foreign currencies on a tax basis as of October 31, 2012 were as follows:

| | | | | | | | | | | | | | | | | | | | |

Total Cost of Investments | | Gross Unrealized Appreciation on Investments | | | Gross Unrealized Depreciation on Investments | | | Net Unrealized Appreciation on Investments | | | Gross Unrealized Appreciation on Foreign Currency | | | Net Unrealized Appreciation | |

$41,626,636 | | $ | 12,427,338 | | | $ | (4,824,191 | ) | | $ | 7,603,147 | | | $ | 559 | | | $ | 7,603,706 | |

E. Common Stock:

For the year ended October 31, 2012, the Fund issued 631 shares in connection with stock distribution in the amount of $4,379. For the year ended October 31, 2011, the Fund issued no shares in connection with stock distribution.

F. Share Repurchase Program:

In accordance with Section 23(c) of the Investment Company Act of 1940, as amended, the Fund hereby gives notice that it may from time to time repurchase shares of the Fund in the open market at the option of the Board of Directors and upon such terms as the Directors shall determine.

For the year ended October 31, 2012, the Fund repurchased 316,714 (4.95% of the shares outstanding at October 31, 2011) of its shares for a total cost of $2,444,590, at an average discount of 12.52% of net asset value. In addition the Fund had a tender offer of 924,000 (14.4% of the shares outstanding at October 31, 2011) of its shares for a total cost of $7,475,160, at an average discount of 2.06% of net asset value.

For the year ended October 31, 2011, the Fund repurchased 280,053 (4.19% of the shares outstanding at October 31, 2010 year end) of its shares for a total cost of $2,187,501, at an average discount of 11.86% of net asset value.

G. Market Concentration:

Because the Fund concentrates its investments in securities issued by corporations in Ireland, its portfolio may be subject to special risks and considerations typically not associated with investing in a broader range of domestic securities. In addition, the Fund is more susceptible to factors adversely affecting the Irish economy than a comparable fund not concentrated in these issuers to the same extent.

H. Risk Factors:

Investing in the Fund may involve certain risks including, but not limited to, those described below.

The prices of securities held by the Fund may decline in response to certain events, including those directly involving the companies whose securities are owned by the Fund; conditions affecting the general economy; overall market changes; local, regional or global political, social or economic instability; and currency, interest rate and commodity price fluctuations. The growth-oriented, equity-type securities generally purchased by the Fund may involve large price swings and potential for loss.

Investments in securities issued by entities based outside the United States may also be affected by currency controls; different accounting, auditing, financial reporting, and legal standards and practices in some countries; expropriation; changes in tax policy; greater market volatility; differing securities market structures; higher transaction costs;

20

The New Ireland Fund, Inc.

Notes to Financial Statements (continued)

and various administrative difficulties, such as delays in clearing and settling portfolio transactions or in receiving payment of dividends. These risks may be heightened in connection with investments in developing countries.

I. Subsequent Event:

Management has evaluated the impact of all subsequent events on the Fund through the date the financial statements were issued.

21

The New Ireland Fund, Inc.

Report of Independent Registered Public Accounting Firm

To the Board of Director and Shareholders of

The New Ireland Fund, Inc.

We have audited the accompanying statements of assets and liabilities of The New Ireland Fund, Inc. (the “Fund”), including the portfolio holdings, as of October 31, 2012, the related statement of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. The Fund is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of October 31, 2012, by correspondence with the custodian. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of The New Ireland Fund, Inc. as of October 31, 2012, and the results of their operations for the year then ended, and the changes in their net assets for each of the two years in the period then ended, and the financial highlights for the periods indicated thereon, in conformity with accounting principles generally accepted in the United States of America.

TAIT, WELLER & BAKER LLP

Philadelphia, Pennsylvania

December 18, 2012

22

Additional Information (unaudited)

Dividend Reinvestment and Cash Purchase Plan

The Fund will distribute to shareholders, at least annually, substantially all of its net income from dividends and interest payments and expects to distribute substantially all its net realized capital gains annually. Pursuant to the Dividend Reinvestment and Cash Purchase Plan (the “Plan”) approved by the Fund’s Board of Directors (the “Directors”), each shareholder will be deemed to have elected, unless American Stock Transfer & Trust Company (the “Plan Agent”) is instructed otherwise by the shareholder in writing, to have all distributions automatically reinvested by the Plan Agent in Fund shares pursuant to the Plan. Distributions with respect to Fund shares registered in the name of a broker-dealer or other nominee (i.e., in “street name”) will be reinvested by the broker or nominee in additional Fund shares under the Plan, unless the service is not provided by the broker or nominee or the shareholder elects to receive distributions in cash. Investors who own Fund shares registered in street names may not be able to transfer those shares to another broker-dealer and continue to participate in the Plan. These shareholders should consult their broker-dealer for details. Shareholders who do not participate in the Plan will receive all distributions in cash paid by check in U.S. dollars mailed directly to the shareholder by the Plan Agent, as paying agent. Shareholders who do not wish to have distributions automatically reinvested should notify the Fund, in care of the Plan Agent for The New Ireland Fund, Inc.

The Plan Agent will serve as agent for the shareholders in administering the Plan. If the Directors of the Fund declare an income dividend or a capital gains distribution payable either in the Fund’s common stock or in cash, as shareholders may have elected, non-participants in the Plan will receive cash and participants in the Plan will receive common stock to be issued by the Fund. If the market price per share on the valuation date equals or exceeds net asset value per share on that date, the Fund will issue new shares to participants at net asset value or, if the net asset value is less than 95% of the market price on the valuation date, then at 95% of the market price. The valuation date will be the dividend or distribution payment date or, if that date is not a trading day on the New York Stock Exchange, Inc. (“New York Stock Exchange”), the next preceding trading day. If the net asset value exceeds the market price of Fund shares at such time, participants in the Plan will be deemed to have elected to receive shares of stock from the Fund, valued at market price on the valuation date. If the Fund should declare a dividend or capital gains distribution payable only in cash, the Plan Agent as agent for the participants, will buy Fund shares in the open market, on the New York Stock Exchange or elsewhere, with the cash in respect of such dividend or distribution, for the participants’ account on, or shortly after, the payment date.

Participants in the Plan have the option of making additional cash payments to the Plan Agent, annually, in any amount from U.S. $100 to U.S. $3,000, for investment in the Fund’s common stock. The Plan Agent will use all funds received from participants (as well as any dividends and capital gain distributions received in cash) to purchase Fund shares in the open market on or about January 15 of each year. Any voluntary cash payments received more than thirty days prior to such date will be returned by the Plan Agent, and interest will not be paid on any uninvested cash payments. To avoid unnecessary cash accumulations and to allow ample time for receipt and processing by the Plan Agent, it is suggested that the participants send in voluntary cash payments to be received by the Plan Agent approximately ten days before January 15. A participant

23

Additional Information (unaudited) (continued)

may withdraw a voluntary cash payment by written notice, if the notice is received by the Plan Agent not less than forty-eight hours before such payment is to be invested.

The Plan Agent maintains all shareholder accounts in the Plan and furnishes written confirmations of all transactions in the account, including information needed by shareholders for personal and U.S. Federal tax records. Shares in the account of each Plan participant will be held by the Plan Agent in non-certificated form in the name of the participant, and each shareholder’s proxy will include those shares purchased pursuant to the Plan.

In the case of shareholders such as banks, brokers or nominees who hold shares for beneficial owners, the Plan Agent will administer the Plan on the basis of the number of shares certified from time to time by the shareholder as representing the total amount registered in the shareholder’s name and held for the account of beneficial owners who are participating in the Plan.

There is no charge to participants for reinvesting dividends or capital gains distributions. The Plan Agent’s fee for the handling of the reinvestment of dividends and distributions will be paid by the Fund. However, each participant’s account will be charged a pro rata share of brokerage commissions incurred with respect to the Plan Agent’s open market purchases in connection with the reinvestment of dividends or capital gains distributions. A participant will also pay brokerage commissions incurred in purchases in connection with the reinvestment of dividends or capital gains distributions. A participant will also pay brokerage commissions incurred in purchases from voluntary cash payments made by the participant. Brokerage charges for purchasing small amounts of stock of individual accounts through the Plan are expected to be less than the usual brokerage charges for such transactions, because the Plan Agent will be purchasing stock for all participants in blocks and prorating the lower commission thus attainable.

The automatic reinvestment of dividends and distributions will not relieve participants of any U.S. Federal income tax which may be payable on such dividends or distributions.

Experience under the Plan may indicate that changes are desirable. Accordingly, the Fund reserves the right to amend or terminate the Plan as applied to any voluntary cash payment made and any dividend or distribution paid subsequent to notice of the change sent to all shareholders at least ninety days before the record date for such dividend or distribution. The Plan also may be amended or terminated by the Plan Agent with at least ninety days written notice to all shareholders. All correspondence concerning the Plan should be directed to the Plan Agent for The New Ireland Fund, Inc. in care of American Stock Transfer & Trust Company, 59 Maiden Lane, New York, New York, 10038, telephone number (718) 921-8283.

24

Additional Information (unaudited) (continued)

Meeting of Shareholders

On June 5, 2012, the Fund held its Annual Meeting of Shareholders. The following Directors were elected by the following votes: Peter J. Hooper 4,886,543 For; 483,463 Abstaining, George G. Moore 4,937,471 For; 432,534 Abstaining. David Dempsey, Denis Kelleher and Margaret Duffy continue to serve in their capacities as Directors of the Fund.

Fund’s Privacy Policy

The New Ireland Fund, Inc. appreciates the privacy concerns and expectations of its registered shareholders and safeguarding their nonpublic personal information (“Information”) is of great importance to the Fund.

The Fund collects Information pertaining to its registered shareholders, including matters such as name, address, tax I.D. number, Social Security number and instructions regarding the Fund’s Dividend Reinvestment Plan. The Information is collected from the following sources:

| | • | | Directly from the registered shareholder through data provided on |

applications or other forms and through account inquiries by mail, telephone

or e-mail.

| | • | | From the registered shareholder’s broker as the shares are initially transferred |

into registered form.

Except as permitted by law, the Fund does not disclose any Information about its current or former registered shareholders to anyone. The disclosures made by the Fund are primarily to the Fund’s service providers as needed to maintain account records and perform other services for the Fund’s shareholders. The Fund maintains physical, electronic, and procedural safeguards to protect the shareholders’ Information in the Fund’s possession.

The Fund’s privacy policy applies only to its individual registered shareholders. If you own shares of the Fund through a third party broker, bank or other financial institution, that institution’s privacy policies will apply to you and the Fund’s privacy policy will not.

Portfolio Information

The Fund files its complete schedule of portfolio holdings with the Securities and Exchange Commission (“SEC”) for the first and third quarters of each fiscal year on Form N-Q. The Fund’s Form N-Q is available (1) by calling 1-800-468-6475; (2) on the Fund’s website located at http://www.newirelandfund.com; (3) on the SEC’s website at http://www.sec.gov; or (4) for review and copying at the SEC’s Public Reference Room (“PRR”) in Washington, DC. Information regarding the operation of the PRR may be obtained by calling 1-800-SEC-0330.

Proxy Voting Information

A description of the policies and procedures that the Fund uses to determine how to vote proxies relating to portfolio securities held by the Fund is available, without charge and upon request, by calling 1-800-468-6475. This information is also available from the EDGAR database or the SEC’s website at http://www.sec.gov. Information regarding how the Fund voted proxies relating to portfolio securities during the most recent twelve-month period ended June 30 is available at http://www.sec.gov.

25

Additional Information (unaudited) (continued)

Amended and Restated Bylaws

In November 2012, the Fund’s Board of Directors amended and restated the Bylaws of the Fund in their entirety for general updating purposes and to make other changes. These changes include, among other things, (i) adding an advance notice provision, which sets forth the time within which stockholders must submit nominations and other business to be properly brought before the Fund’s annual meetings; (ii) permitting a Board vacancy to be filled by remaining Directors for the full term of the class in which the vacancy occurred; (iii) permitting Directors to be removed only by a two-thirds vote of stockholders; (iv) providing procedures for the calling of special meetings of stockholders; and (v) permitting notice by electronic transmission.

Certifications

The Fund’s president has certified to the New York Stock Exchange (“NYSE”) that,as of June 27, 2012, he was not aware of any violation by the Fund of applicable NYSE corporate governance listing standards. The Fund’s reports to the SEC on Forms N-CSR and N-CSRS contain certifications by the Fund’s principal executive officer and principal financial officer that relate to the Fund’s disclosure in such reports and that are required by rule 30a2(a) under the Investment Company Act.

Tax Information

For non-corporate shareholders 90.46%, or the maximum amount allowable under the Jobs and Growth Tax Relief Reconciliation Act of 2003, of income earned by the Fund for the period November 1, 2011 to October 31, 2012 may represent qualified dividend income.

For the fiscal year ended October 31, 2012, the Fund had no designated long-term capital gains.

26

Board of Directors/Officers (unaudited)

| | | | | | | | | | | |

Name Address, and Age | | Position(s)

Held with

the Fund | | Term of

Office and

Length of

Time

Served* | | Principal Occupation(s) and Other Directorships During Past Five Years | | Number of

Portfolios in

Fund Complex

Overseen by

Director |

INDEPENDENT DIRECTORS: | | | | | | | | | |

| | | | |

Peter J. Hooper, 72 Westchester Financial Center, Suite 1000 50 Main Street White Plains, NY 10606 | | Director and Chairman of the Board | | Since 1990 Current term expires in 2015 | | President, Hooper Associates – Consultants (1994 to present); Director, The Ireland United States Council for Commerce and Industry (1984 to present). | | | | 1 | |

| | | | |

David Dempsey, 63 Bentley Associates L.P. 250 Park Avenue –

Suite 1101 New York, NY 10177 | | Director | | Since 2007 Current Term expires in 2013 | | Managing Director, Bentley Associates L.P., (1992 to present). | | | | 1 | |

| | | | |

Margaret Duffy, 69 164 East 72 Street, Suite 7B New York, NY 10021 | | Director | | Since 2006 Current Term expires in 2014 | | Retired Partner Arthur Andersen LLP and currently a Financial Consultant; Director, The Dyson-Kissner-Moran Corporation (2000 to 2010). | | | | 1 | |

| | | | |

Denis P. Kelleher, 73 17 Battery Place New York, NY 10004 | | Director | | Since 1991 Current Term expires in 2013 | | Chairman and Chief Executive Officer, Wall Street Access-Financial Services (1981 to present). | | | | 1 | |

| | | | |

George G. Moore, 61 9411 Cornwell Farm Great Falls, VA 22066 | | Director | | Since 2004 Current term expires in 2015 | | Managing Partner, Ravensdale Capital (2011 to present); Advisor, Neustar Corporation (2011 to 2012); Chairman & CEO, TARGUS Information (1993 to 2012); Chairman, Erne Heritage Holdings (1990 to Present); Chairman, Virginia Distillery Company (2011 to present). | | | | 1 | |

| | * | Each Director shall serve until the expiration of his or her current term and until his or her successor is elected and qualified. |

27

Board of Directors/Officers (unaudited) (continued)

| | | | | | |

Name Address, and Age | | Position(s)

Held with

the

Fund | | Term of

Office and

Length of

Time

Served* | | Principal Occupation(s) and Other Directorships During Past Five Years |

OFFICERS**: | | |

| | | |

Sean Hawkshaw, 48 Kleinwort Benson Investors International Ltd One Rockefeller Plaza, 32nd Floor New York, NY 10020 | | President | | Since 2011 | | Chief Executive Officer & Director, Kleinwort Benson Investors International Ltd (2002 to Present); Director, Kleinwort Benson Investors Dublin Limited (1994 to Present); Director, Kleinwort Benson Fund Managers Limited (2002 to Present); Director, Kleinwort Bensons Investors Institutional Funds PLC (2004 to Present); Director Kleinwort Benson/Lothbury Qualifying Investor Public Limited Company (2006 to Present); Director, Irish Auditing and Accounting Supervisory Authority (2006 to Present); Director KBC Asset Management (U.K.) Ltd (2002 to 2010); Director KBC Life Fund Management Ireland Ltd (2003 to 2009); Director Fusion Alternative Investments PLC (2008 to Present); Director, Irish Association of Investment Managers (2003 to Present). |

| | | |

Lelia Long, 50 BNY Mellon Center One Boston Place 201 Washington Street, 34th Floor Boston, Massachusetts 02109 | | Treasurer | | Since 2002 | | Investment Management Consultant (2009 to present); Compliance Director, Vigilant Compliance Services, (2009 to present); Chief Compliance Officer, Simple Alternatives LLC (2010 to Present); Chief Compliance Officer, Pemberwick Investment Advisors, LLC (2010 to Present); Senior Vice President, Bank of Ireland Asset Management (U.S.) Limited (2000 to 2008). |

| | | |

Salvatore Faia, 49 BNY Mellon Center One Boston Place 201 Washington Street, 34th Floor Boston, Massachusetts 02109 | | Chief Compliance Officer | | Since 2005 | | President, Vigilant Compliance Services, (2004 to present); Director, EIP Growth and Income Fund (2005 to present). |

| | | |

Colleen Cummings, 41 4400 Computer Drive Westborough, MA 01580 | | Assistant Treasurer | | Since 2006 | | Vice President and Director, BNY Mellon Investment Servicing (US) Inc. (2004 to present). |

| | | |

Vincenzo A. Scarduzio, 40 301 Bellevue Parkway, 2nd Floor Wilmington, DE 19809 | | Secretary | | Since 2005 | | Vice President and Assistant Counsel, BNY Mellon Investment Servicing (US) Inc. (2010 to present); Assistant Vice President, BNY Mellon Investment Servicing (US) Inc. (2006 to 2010). |

| | * | Each Director shall serve until the expiration of his or her current term and until his or her successor is elected and qualified. |

| | ** | Each Officer of the Fund will hold office until a successor has been elected by the Board of Directors. |

28

This page left blank intentionally.

The New Ireland Fund, Inc.

Directors and Officers

| | |

Peter J. Hooper | | – Chairman of the Board |

Sean Hawkshaw | | – President |

David Dempsey | | – Director |

Margaret Duffy | | – Director |

Denis P. Kelleher | | – Director |

George G. Moore | | – Director |

Lelia Long | | – Treasurer |

Colleen Cummings | | – Assistant Treasurer |

Vincenzo Scarduzio | | – Secretary |

Salvatore Faia | | – Chief Compliance Officer |

Principal Investment Adviser

Kleinwort Benson Investors

International Ltd.

One Rockefeller Plaza - 32nd Floor

New York, NY 10020

Administrator

BNY Mellon Investment Servicing (US) Inc.

4400 Computer Drive

Westborough, Massachusetts 01581

Custodian

JPMorgan Chase & Co.

North America Investment Services