Use these links to rapidly review the document

TABLE OF CONTENTS

Item 9. Changes in and Disagreements With Accountants on Accounting and Financial Disclosure

Table of Contents

United States

Securities and Exchange Commission

Washington, DC 20549

FORM 10-K

ý Annual Report Pursuant to Section 13 or 15(d) of the Securities

Exchange Act of 1934, as amended (the "Exchange Act")

For the fiscal year ended December 31, 2014

or

o Transition Report Pursuant to Section 13 or 15(d) of the Exchange Act

For the transition period from to

Commission File Number 001-08029

THE RYLAND GROUP, INC.

(Exact name of registrant as specified in its charter)

| | |

| Maryland | | 52-0849948 |

(State or other jurisdiction

of incorporation or organization) | | (I.R.S. employer identification no.) |

3011 Townsgate Road, Suite 200, Westlake Village, California 91361

(Address of principal executive offices)

Registrant's telephone number, including area code: (805) 367-3800

Securities registered pursuant to Section 12(b) of the Act:

| | |

| Title of each class | | Name of each exchange on which registered

|

| Common stock, par value $1.00 per share | | New York Stock Exchange |

| Preferred stock purchase rights | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yesý Noo

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yeso Noý

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yesý Noo

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yesý Noo

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| | | | | | |

| Large accelerated filer ý | | Accelerated filer o | | Non-accelerated filer o

(Do not check if a smaller

reporting company) | | Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

Yeso Noý

The aggregate market value of the common stock of The Ryland Group, Inc. held by nonaffiliates of the registrant (45,712,911 shares) at June 30, 2014, was $1,802,917,210. The number of shares of common stock of The Ryland Group, Inc. outstanding on February 23, 2015, was 46,681,044.

Table of Contents

DOCUMENT INCORPORATED BY REFERENCE

| | |

Name of Document | | Location in Report |

Proxy Statement for the 2015 Annual Meeting of Stockholders | | Part III |

2

Table of Contents

THE RYLAND GROUP, INC.

FORM 10-K

INDEX

3

Table of Contents

PART I

Item 1. Business

With headquarters in Southern California, The Ryland Group, Inc., a Maryland corporation (the "Company"), is one of the nation's largest homebuilders and a mortgage-finance company. The Company is traded on the New York Stock Exchange ("NYSE") under the symbol "RYL." Founded in 1967, the Company has built more than 315,000 homes. In addition, RMC Mortgage Corporation and its subsidiaries ("RMCMC") and Ryland Mortgage Company (collectively referred to as "RMC") have provided mortgage financing and related services for more than 255,000 homebuyers.

The Company consists of six reportable segments: four geographically determined homebuilding regions; financial services; and corporate. All of the Company's business is conducted and located in the United States, and its operations span all significant aspects of the homebuying process—from design, construction and sale to mortgage origination, title and escrow services. The homebuilding operations are, by far, the most substantial part of its business, comprising approximately 98 percent of consolidated revenues in 2014. The homebuilding segments generate nearly all of their revenues from sales of completed homes, with a lesser amount from sales of land and lots. In addition to building single-family detached homes, the homebuilding segments also build attached homes, such as townhomes and condominiums that share common walls and roofs. The Company generally builds homes for entry-level buyers and first- and second-time move-up buyers. Its prices generally range from $160,000 to more than $650,000, with the average price of a home closed during 2014 being $333,000. The financial services segment provides mortgage-related products and services, as well as title and escrow services, to its homebuyers.

The Company has traditionally concentrated on expanding its operations by investing its available capital in both existing and new markets. New and existing communities are evaluated based on returns, profitability and cash flow, and both senior and local management are incentivized based on the achievement of such returns. Management monitors the land acquisition process, sales revenues, margins and returns achieved in each of the Company's markets as part of its capital allocation process. (See "Part I, Item 1A, Risk Factors.")

The Company, which is diversified throughout the United States, believes diversification not only reduces its exposure to economic and market fluctuations, but also enhances its growth potential. Capital is strategically allocated to avoid concentration in any given geographic area and to reduce the risk associated with excessive dependence on local market anomalies. Subject to macroeconomic and local market conditions, the Company generally tries to either manage its exposure or expand its presence in its existing markets in an effort to be among the largest builders in each of those markets. In managing its exposure, the Company may decide to reduce its inventory position in a market because of current factors or conditions, or it may exit a market that is no longer viable for the achievement of its strategic goals. It may seek diversification by expanding within existing divisions or by selectively entering new markets, primarily through establishing start-up or satellite operations, or by acquiring local builders.

The Company's national scale has provided opportunities for the negotiation of volume discounts and rebates from material suppliers. Its scale, as well as the strength and transparency of its balance sheet and its relationship with the banking industry, has provided the Company with a lower cost of capital, compared to smaller and more localized competitors. The Company believes that economies of scale and diversification may contribute to improvements in its operating margins during periods of growth and mitigate its overall risk.

Committed to product innovation, the Company conducts ongoing research into consumer preferences and trends. It is constantly adapting and improving its floor plans, design features and customized options. The Company strives to offer value, quality, location and selection to all of its homebuyers.

The Company is dedicated to building quality homes and customer relationships. With customer satisfaction as a major priority, it continues to make innovative enhancements designed to attract homebuyers. The Company continually improves its methods of collecting customer feedback by using

4

Table of Contents

systems for tracking requests, processing issues and promoting customer interaction. In addition, it uses a third party to analyze customer feedback in order to better serve its homebuyers' needs.

The Company enters into land development joint ventures, from time to time, for the purpose of building lot positions, reducing its risk profile and enhancing its return on capital. It periodically partners with developers, other homebuilders or financial investors to develop finished lots for sale to the joint ventures' members or to other third parties.

Recent Trends

As a result of its strategic initiatives, strong balance sheet, liquidity, broad geographic presence and experienced personnel, the Company was able to capitalize on attractive land acquisition opportunities in markets with improving affordability statistics, demographics and household creation trends from 2012 to 2014. The Company began to expand more aggressively through accelerated land acquisitions in most markets, as well as through its acquisitions of homebuilders with operations in the Charlotte, Phoenix and Raleigh markets during 2012 and, during 2013, in the Dallas market and in the Delaware, New Jersey and Pennsylvania tri-state area. As a result, the Company was able to increase community count, improve operating leverage and return to higher profitability. The Company believes that continued revenue growth and improved financial performance will most likely come from a greater presence in its established markets, should economic progress continue, and that it is well positioned to take advantage of such opportunities, especially in markets that are showing employment growth and a healthy demographic outlook.

Homebuilding

General

The Company's homes are built on-site and marketed in four major geographic regions, or segments: North, Southeast, Texas and West. Within each of those segments, the Company operated in the following metropolitan areas at December 31, 2014:

| | |

| North | | Baltimore, Chicago, Delaware, Indianapolis, Metro Washington, D.C., Minneapolis/St. Paul, New Jersey, Northern Virginia and Philadelphia |

| Southeast | | Atlanta, Charleston, Charlotte, Myrtle Beach, Orlando, Raleigh/Durham and Tampa |

| Texas | | Austin, Dallas/Fort Worth, Houston and San Antonio |

| West | | Denver, Las Vegas, Phoenix and Southern California |

The Company has decentralized operations to capitalize on the expertise of its local division presidents and management teams. Each of its homebuilding divisions across the country generally consists of a division president; a controller; management personnel focused on land acquisition, entitlement and development, sales, construction, product development, customer service and purchasing; and accounting and administrative personnel. The Company's operations in each of its homebuilding markets may differ due to a number of market-specific factors, including regional economic conditions and job growth; land availability and development requirements; consumer preferences; competition from other homebuilders; and resale home activity. The Company not only considers each of these factors upon entering into new markets, but also in determining the extent of its operations and the allocation of its capital in existing markets. Market experience of local management teams is critical to the decision-making process regarding the Company's operations.

The Company markets attached and detached single-family homes, which are generally targeted to entry-level and first- and second-time move-up buyers. Its diverse product lines are tailored to the local styles and preferences found in each of its geographic markets. The product line offered in a particular community is determined in conjunction with the land acquisition process and is dependent upon a number of factors, including consumer preferences, competitive product offerings, and construction and development costs.

The Company generally offers several different floor plans within its communities, each with unique architectural styles. Exteriors may be further distinguished by the use of stone, stucco, brick or siding. Some home designs may be used in multiple communities across several divisions within the Company,

5

Table of Contents

with modifications to suit local trends. Additionally, new designs are continuously being developed to replace or augment existing ones in order to ensure that homes reflect current consumer preferences. The Company relies on its own architectural staff and also engages unaffiliated architectural firms to develop new designs.

Homebuyers are able to customize certain features of their homes by selecting from numerous options and upgrades displayed in the Company's model homes and design centers. These design centers, which are conveniently located in most of the Company's markets, feature state-of-the-art technology and showcase upgrades that represent sources of additional revenue and profit for the Company. The Company typically offers a variety of potential options and upgrades for an additional charge, such as different choices of flooring, countertops and appliances. It designs its base house and option packages to meet the needs of its customers. Options and upgrades contributed 14.0 percent of homebuilding revenues in 2014 and resulted in significantly higher margins in comparison to base homes.

Land Acquisition and Development

The Company's long-term objective is to control a portfolio of building lots sufficient to meet its anticipated homebuilding requirements for a period of approximately four to five years. The Company acquires land only after completing due diligence and feasibility studies. The land acquisition process is controlled by a corporate land approval committee to help ensure that transactions meet the Company's standards for financial performance and risk. In the ordinary course of its homebuilding business, the Company utilizes both direct acquisition and lot option purchase contracts to acquire and control lot inventory for use in the sale and construction of homes. The Company's land acquisition activities include the purchase of finished lots from developers and the purchase of undeveloped entitled land from third parties. The Company generally does not purchase unentitled or unzoned land.

Although control of lot inventory through the use of option contracts minimizes the Company's investment, such a strategy is not viable in certain markets due to the absence of third-party land developers. In other markets, competitive conditions may prevent the Company from controlling quality lots solely through the use of option contracts. In such situations, the Company may acquire undeveloped entitled land and/or finished lots on a bulk basis. The Company utilizes the selective development of land to gain access to prime locations, increase margins and position itself as a leader in the area through its influence over a community's character, layout and amenities. After determining the size, style, price range, density, layout and overall design of a community, the Company obtains governmental and other approvals necessary to begin the development process. Land is then graded; roads, utilities and other infrastructure are installed; and individual homesites are created.

Materials Costs

Substantially all materials used in construction are available from a number of sources, and prices may fluctuate due to various factors. To increase purchasing efficiencies, the Company not only standardizes certain building materials and products, but also acquires such products through national and regional supply contracts. The Company has, on occasion, experienced shortages of certain materials. If shortages were to occur in the future, it could result in longer construction times and higher costs than those experienced in the past.

Construction

Substantially all on-site construction is performed for a fixed price by independent subcontractors selected on a competitive-bid basis. The Company generally obtains a minimum of three competitive bids for each phase of construction. Construction activities are supervised by the Company's production team, which coordinates subcontractor work; monitors quality; and ensures compliance with local zoning and building codes. The construction time for homes depends on the weather, availability of labor or subcontractors, materials, home size, geological conditions, as well as on other factors. The duration of the home construction process is generally between three and six months. The Company has an integrated financial and homebuilding management system that assists in scheduling production and controlling costs. Through this system, the Company monitors construction status and job costs incurred for each home during each phase of construction. The system provides for detailed budgeting and allows the Company to track and control actual costs, versus construction bids, for each community and subcontractor. The Company has, on occasion, experienced shortages of skilled labor in certain markets. If shortages were to

6

Table of Contents

occur in the future, it could result in longer construction times and higher costs than those experienced in the past.

The Company, its subcontractors and its suppliers maintain insurance, subject to deductibles and self-insured amounts, to protect against various risks associated with homebuilding activities, including, among others, general liability, "all-risk" property, workers' compensation, automobile and employee fidelity. The Company accrues for expected costs associated with deductibles and self-insured amounts, when appropriate.

Sales and Marketing

The Company generally markets its homes to entry-level and first- and second-time move-up buyers through targeted product offerings in each of the communities in which it operates. The Company's marketing strategy is determined during the land acquisition and feasibility stages of a community and may be updated based on observed trends after the community opens. Employees and independent real estate brokers sell the Company's homes generally by showing furnished models. A new order is reported when a sales contract has been signed by the homebuyer, approved by the Company and secured by a deposit, subject to cancellation. The Company normally starts construction of a home when a customer has selected a lot, chosen a floor plan and received preliminary mortgage approval. Construction may begin prior to this, however, in order to satisfy market demand for completed homes and to facilitate construction scheduling and/or cost savings. Homebuilding revenues are recognized when home sales are closed, title and possession are transferred to the buyer, and there is no significant continuing involvement from the homebuilder.

The Company advertises directly to potential homebuyers through the Internet and in newspapers and trade publications, as well as with marketing brochures and newsletters. It also uses billboards; radio and television advertising; and its Website to market the location, price range and availability of its homes. The Company attempts to operate in conspicuously located communities that permit it to take advantage of local traffic patterns. Model homes play a significant role in the Company's marketing efforts by creating an attractive atmosphere, in which to showcase its floor plans, options and upgrades.

The Company's sales contracts require an earnest money deposit. The amount of earnest money received varies between markets and communities. Buyers are generally required to pay additional deposits when they select options or upgrades for their homes. Most of the Company's sales contracts stipulate that when homebuyers cancel their contracts with the Company, it has the right to retain their earnest money and option deposits. Its operating divisions may, however, refund a portion of such deposits. The Company's sales contracts may also include contingencies that permit homebuyers to cancel and receive a refund of their deposits if they cannot obtain mortgage financing at prevailing or specified interest rates within a specified time period, or if they cannot sell an existing home. The length of time between the signing of a sales contract for a home and delivery of the home to the buyer may vary, depending on customer preferences, lot availability, permit approval and construction cycles.

Customer Service and Warranties

The Company's operating divisions are responsible for conducting pre-closing quality control inspections and responding to homebuyers' post-closing needs. The Company believes that prompt and courteous acknowledgment of its homebuyers' needs during and after construction reduces post-closing repair costs; enhances its reputation for quality and service; and ultimately leads to repeat and referral business.

The Company provides each homeowner with product warranties covering workmanship and materials for one year, certain mechanical systems for two years and structural systems for ten years from the time of closing. The Company believes its warranty program meets or exceeds terms customarily offered in the homebuilding industry. The subcontractors who perform the construction services also provide warranties on workmanship.

Seasonality

The Company experiences seasonal variations in its quarterly operating results and capital requirements. Historically, new order activity is higher during the spring and summer months. As a result, in the third and fourth quarters of its fiscal year, the Company typically has more homes under construction, closes

7

Table of Contents

more homes, and has greater revenues, which may contribute to additional selling, general and administrative and gross profit leverage resulting in greater operating income. In addition to the overall volume of homes the Company sells and delivers, its results in a given period are significantly affected by the geographic mix of markets in which it operates; the number and characteristics of the communities the Company has open for sales in those markets; and the products it sells from those communities during the period. Historical results are not necessarily indicative of current or future homebuilding activities.

Inflation

The Company may be adversely affected during periods of inflation because of higher land, construction and personnel costs. Additionally, inflation may cause an increase in interest rates resulting not only in higher costs to finance the Company's operations but also in higher mortgage interest rates, affecting the affordability of its products to prospective buyers. While the Company generally attempts to pass on increases in its costs to its customers through increased sales prices, market conditions may limit the Company's ability to do so. During periods when we are unable to raise sales prices at rates to compensate for these higher costs, or if mortgage rates increase significantly, the Company's revenues, gross profit margins and net income could be adversely affected.

Financial Services

The Company's financial services segment provides mortgage-related products and services, as well as title and escrow services, to its homebuyers. The Company's financial services segment includes RMC, RH Insurance Company, Inc. ("RHIC"), Columbia National Risk Retention Group, Inc. ("CNRRG") and Ryland Insurance Services ("RIS"). By aligning its operations with the Company's homebuilding segments, the financial services segment leverages this relationship to offer its lending services to homebuyers. Providing mortgage financing and other services to its customers helps the Company monitor its backlog and closing process. The mortgage capture rate represents the percentage of homes closed and available to capture by the Company that were financed with mortgage loans obtained from RMC. Substantially all of the loans the Company originates are sold to third party investors within a short period of time in the secondary mortgage market on a servicing-released basis. The third-party investor then services and manages the loans.

Loan Origination

In 2014, RMC's mortgage operations consisted primarily of loans originated in connection with sales of the Company's homes. During the year, RMC originated 3,914 loans totaling $1.1 billion. The vast majority of that amount was used for purchasing homes built by the Company, while the remainder was used for purchasing homes built by others, purchasing existing homes or refinancing existing mortgage loans.

RMC arranges various types of mortgage financing, including conventional, Federal Housing Administration ("FHA") and Veterans Administration ("VA") mortgages, with various fixed- and adjustable-rate features. RMC is approved to originate loans that conform to guidelines established by the Federal Home Loan Mortgage Corporation ("Freddie Mac") and the Federal National Mortgage Association ("Fannie Mae").

Title and Escrow Services

Cornerstone Title Company, doing business as Ryland Title Company, is a 100 percent-owned subsidiary of RMCMC that provides escrow and title services and acts as a title insurance agent primarily for the Company's homebuyers. At December 31, 2014, it provided title services in Arizona, Colorado, Delaware, Florida, Illinois, Indiana, Maryland, Minnesota, Nevada, New Jersey, Pennsylvania, Texas and Virginia. Additionally, the Company provides title services through joint ventures in Georgia and South Carolina.

Insurance Services

RIS, a 100 percent-owned subsidiary of RMCMC, previously provided insurance services to the Company's homebuyers. Effective December 2013, RIS ceased writing new policies. During 2013, RIS provided insurance services to 38.1 percent of the Company's homebuyers.

RHIC, a 100 percent-owned subsidiary of the Company, provided insurance services to the homebuilding segments' subcontractors in certain markets. Effective June 1, 2008, RHIC ceased writing new policies. Registered and licensed under Section 431, Article 19 of the Hawaii Revised Statutes, RHIC is required to

8

Table of Contents

meet certain minimum capital and surplus requirements. Additionally, no dividends may be paid without prior approval of the Hawaii Insurance Commissioner.

CNRRG, a 100 percent-owned subsidiary of the Company and some of its affiliates, was established to directly offer structural warranty coverage to protect homeowners against liability risks arising in connection with the homebuilding business of the Company and its affiliates.

Corporate

Corporate is a non-operating reportable segment with the sole purpose of supporting operations. Corporate implements strategic initiatives; monitors and allocates capital; establishes operational policies and internal control standards; and provides financial, human resource, information technology, insurance, legal and tax compliance services. In addition, it performs administrative functions associated with a publicly traded entity.

Real Estate and Economic Conditions

The Company is significantly affected by fluctuations in national and local economic conditions such as unemployment rates, interest rates and levels of consumer confidence. The effects of these fluctuations can differ among the various geographic markets in which the Company operates. During 2014, mortgage availability headwinds and slow household formation growth impacted the Company's ability to attract homebuyers.

Inventory risk can be substantial for homebuilders. The market value of land, lots and housing inventories fluctuates as a result of changing market and economic conditions. The Company must continuously locate and acquire land not only for expansion into new markets, but also for replacement and expansion of land inventory within current markets. The Company employs various measures designed to control inventory risk, including a corporate land approval process and a continuous review of operational metrics by senior management. It cannot, however, assure that these measures will avoid or eliminate this risk. The Company has experienced substantial losses from inventory and other valuation adjustments and write-offs in prior years.

Competition

The Company competes for homebuyers, properties, raw materials, skilled labor, employees and management talent with a large number of national, regional and local homebuilding companies in each of its markets. The strong presence of national homebuilders, plus the viability of regional and local homebuilders, impacts the level of competition in many markets. The Company also competes with other housing alternatives, including existing homes and rental properties. Principal competitive factors in the homebuilding industry include price; design; quality; reputation; relationships with developers; accessibility of subcontractors; availability and location of lots; and availability of customer financing. The Company's financial services segment competes with other mortgage companies to arrange financing for homebuyers. Principal competitive factors include interest rates, fees and other mortgage loan product features available to the consumer.

Employees

At December 31, 2014, the Company had 1,502 employees. The Company considers its employee relations to be good. No employees are represented by a collective bargaining agreement.

Website Access to Reports

The Company files annual, quarterly and special reports; proxy statements; and other information with the U.S. Securities and Exchange Commission ("SEC") under the Exchange Act and the Securities Act of 1933, as amended (the "Securities Act"). The Company files information electronically with the SEC, and its filings are available on the SEC's Website atwww.sec.gov. The Company's Website address iswww.ryland.com. Information on the Company's Website is not part of this report. The Company makes its Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, XBRL filings, Current Reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act available on its Website as soon as possible after it electronically files such material with or furnishes it to the SEC. To retrieve any of this information, visitwww.ryland.com, select "Investor Relations," scroll down the page to "Financial Information" and select "SEC Filings." Through its Website, the Company shares information about itself with the securities marketplace.

9

Table of Contents

Item 1A. Risk Factors

The homebuilding industry is cyclical in nature and has experienced downturns, which have in the past and may in the future cause the Company to incur losses in financial and operating results.

The Company is affected by the cyclical nature of the homebuilding industry, which is sensitive to many factors, including fluctuations in general and local economic conditions; interest rates; housing demand; employment levels; levels of new and existing homes for sale; demographic trends; availability of homeowner financing; and consumer confidence. In recent years, the markets served by the Company, and the U.S. homebuilding industry as a whole, experienced a prolonged decrease in demand for new homes, as well as an oversupply of new and existing homes available-for-sale. In addition, an oversupply of alternatives to new homes, such as rental properties and existing homes, can depress prices and reduce margins.

Demand for new homes is sensitive to economic conditions over which the Company has no control, such as the availability of mortgage financing and the level of employment.

Demand for new homes is sensitive to changes in economic conditions such as the level of employment, consumer confidence, consumer income, the availability of financing and interest rate levels. During the last few years, the mortgage lending industry has experienced significant instability. As a result of increased default rates, particularly (but not entirely) with regard to subprime and other nonconforming loans, many lenders have reduced their willingness to make residential mortgage loans and have tightened their credit requirements with regard to them. Fewer loan products, stricter loan qualification standards and higher down payments have made it more difficult for some borrowers to finance home purchases. Although the Company's financial services segment offers mortgage loans to potential buyers, the Company may no longer be able to offer financing terms that are attractive to those buyers. Lack of available mortgage financing at acceptable rates reduces demand for the homes the Company builds and, in some instances, causes potential buyers to cancel contracts they have signed.

Because most of the Company's homebuyers finance the purchase of their homes, the terms and availability of mortgage financing can affect the demand for and the ability to complete the purchase of a home, as well as the Company's future operating and financial results.

The Company's business and earnings depend on the ability of its homebuyers to obtain financing for the purchase of their homes. Many of the Company's homebuyers must sell their existing homes in order to buy a home from the Company. In recent years, the mortgage lending industry as a whole experienced significant instability due to, among other things, defaults on subprime and other loans, resulting in the declining market value of such loans. In light of these developments, lenders, investors, regulators and other third parties questioned the adequacy of lending standards and other credit requirements for several loan programs made available to borrowers in recent years. This has led to tightened credit requirements and an increase in indemnity claims for mortgages that were originated and sold by the Company. Deterioration in credit quality among subprime and other nonconforming loans has caused most lenders to eliminate subprime mortgages and most other loan products that do not conform to Fannie Mae, Freddie Mac, FHA or VA standards. Fewer loan products and tighter loan qualifications, in turn, make it more difficult for a borrower to finance the purchase of a new home or the purchase of an existing home from a potential move-up buyer who wishes to purchase one of the Company's homes. If the Company's potential homebuyers or the buyers of the homebuyers' existing homes cannot obtain suitable financing, or if increased indemnity claims are made for mortgages that are originated and sold, the result will have an adverse effect on the Company's operating and financial results and performance.

Rising interest rates; decreased availability of mortgage financing or of certain mortgage programs; higher down payment requirements; or increased monthly mortgage costs, as discussed above, may lead to reduced demand for the Company's homes and mortgage loan services. Increased interest rates can also hinder the Company's ability to realize its backlog because its home purchase contracts provide customers with a financing contingency. Financing contingencies allow customers to cancel their home purchase contracts in the event that they cannot arrange for adequate financing. As a result, rising interest rates can decrease the Company's home sales and mortgage originations. Any of these factors could have an adverse impact on the Company's financial condition and results of operations.

10

Table of Contents

As a result of turbulence in the credit markets and mortgage finance industry in 2008 and 2009, the federal government has taken on a significant role in supporting mortgage lending through its conservatorship of Fannie Mae and Freddie Mac, both of which purchase home mortgages and mortgage-backed securities originated by mortgage lenders, and its insurance of mortgages originated by lenders through the FHA and VA. FHA backing of mortgages has recently been particularly important to the mortgage finance industry and to the Company's business. In 2014, 31.3 percent of the Company's homebuyers who chose to finance with RMC purchased a home using an FHA- or VA-backed loan. In addition, the Federal Reserve has purchased a sizable amount of mortgage-backed securities in an effort to stabilize mortgage interest rates and to support the market for mortgage-backed securities. The availability and affordability of mortgage loans, including consumer interest rates for such loans, could be adversely affected by a curtailment or ceasing of the federal government's mortgage-related programs or policies. The FHA may continue to impose stricter loan qualification standards, raise minimum down payment requirements, impose higher mortgage insurance premiums and other costs, and/or limit the number of mortgages it insures. Due to growing federal budget deficits, the U.S. Treasury may not be able to continue supporting the mortgage-related activities of Fannie Mae, Freddie Mac, the FHA and the VA at present levels, or it may significantly revise the federal government's participation in and support of the residential mortgage market. In this regard, the Federal Reserve has announced reductions in its monthly bond purchase stimulus program.

Since the availability of Fannie Mae, Freddie Mac, FHA- and VA-backed mortgage financing is an important factor in marketing and selling many of the Company's homes, any limitations, restrictions or changes in the availability of such government-backed financing could reduce its home sales and adversely affect the Company's results of operations, including its income from RMC.

The Company may be subject to indemnification claims on mortgages sold to third parties.

Substantially all of the loans the Company originates are sold within a short period of time in the secondary mortgage market on a servicing-released basis. The mortgage industry has experienced substantial increases in delinquencies, foreclosures and foreclosures-in-process. All mortgages are generally sold, and under certain limited circumstances RMC is required to indemnify loan investors for losses incurred on sold loans. Reserves are created to address repurchase and indemnity claims made by these third-party investors or purchasers. These reserves are based on pending claims received that are associated with previously sold mortgage loans, industry foreclosure data, the Company's portfolio delinquency and foreclosure rates on sold loans made available by investors, as well as on historical loss payment patterns used to develop ultimate loss projections. Estimating loss has been made more difficult by the recent processing delays related to foreclosure losses affecting agencies and financial institutions. Because of the uncertainties inherent in estimating these matters, the Company cannot provide assurance that the amounts reserved will be adequate or that any potential inadequacies will not have an adverse effect on its results of operations.

Tax law changes could make home ownership more expensive or less attractive.

Significant expenses of owning a home, including mortgage interest expense and real estate taxes, generally are deductible expenses for the purpose of calculating an individual's federal and, in some cases, state taxable income, subject to various limitations under current tax law and policy. If federal or state governments change income tax laws by eliminating or substantially reducing these income tax benefits, as some policymakers have discussed, the after-tax cost of owning a new home will increase significantly. This could adversely impact both demand for and/or sales prices of new homes.

The Company is subject to inventory risk for its land, options for land, building lots and housing inventory.

The market value of the Company's land, building lots and housing inventories fluctuates as a result of changing market and economic conditions. In addition, inventory carrying costs can result in losses in poorly performing projects or markets. Changes in economic and market conditions have caused the Company to dispose of land and options for land and housing inventories on a basis that has resulted in loss and required it to write down or reduce the carrying value of its inventory. During the year ended December 31, 2014, the Company decided not to pursue development and construction in certain areas where it held land or made option deposits, which resulted in $2.5 million in recorded write-offs of option deposits and preacquisition feasibility costs. The Company can provide no assurance that it will not need to record additional write-offs in the future.

11

Table of Contents

In the course of its business, the Company makes land acquisitions. Although it employs various measures, including its land approval process and continued review by senior management, designed to manage inventory risk, the Company cannot assure that these measures will enable it to avoid or eliminate its inventory risk.

Construction costs can fluctuate and impact the Company's margins.

The homebuilding industry has, from time to time, experienced significant difficulties, including shortages of qualified tradespeople; reliance on local subcontractors who may be inadequately capitalized; shortages of materials; and volatile increases in the cost of materials, particularly increases in the prices of lumber, drywall and cement, which are significant components of home construction costs. The Company may not be able to recapture increased costs by raising prices because of either market conditions or because it fixes its prices at the time home sales contracts are signed.

Supply shortages and other risks related to demand for building materials and/or skilled labor could increase costs and delay deliveries.

There is a high level of competition in the homebuilding industry for skilled labor and building materials. Rising costs or shortages in building materials or skilled labor could cause increases in construction costs and construction delays. The Company is generally unable to pass on increases in construction costs to homebuyers who have already entered into purchase contracts. A purchase contract generally fixes the price of the home at the time the contract is signed, and this may occur well in advance of when construction commences. Further, the Company may not be able to pass on rising construction costs because of market conditions. Sustained increases in construction costs due to competition for materials and skilled labor, as well as higher commodity prices (including prices for lumber, metals and other building material inputs), among other things, may decrease the Company's margins over time.

Shortages in the availability of subcontract labor may delay construction schedules and increase the Company's costs.

The Company conducts its construction operations as a general contractor with construction and development work performed by unaffiliated third-party subcontractors. As a consequence, the Company depends on the continued availability of and satisfactory performance by these subcontractors for the design and construction of its homes. The Company cannot make assurances that there will be sufficient availability of and satisfactory performance by these unaffiliated third-party subcontractors. In addition, inadequate subcontractor resources could delay the Company's construction schedules and have a material adverse effect on its business.

Because the homebuilding industry is competitive, the business practices of other homebuilders can have an impact on the Company's financial results and cause these results to decline.

The residential homebuilding industry is highly competitive. The Company competes with a large number of national, regional and local homebuilding companies in each of its markets. This competition could cause the Company to adjust selling prices in response to competitive conditions in the markets in which it operates and could require it to increase the use of sales incentives. The Company cannot predict whether these measures will be successful or if additional incentives will be made in the future. It also competes with other housing alternatives, including existing homes and rental housing. The homebuilding industry's principal competitive factors are home price, availability of customer financing, design, quality, reputation, relationships with developers, accessibility of subcontractors, and availability and location of homesites. Any of the foregoing factors could have an adverse impact on the Company's financial performance and results of operations.

The Company's financial services segment competes with other mortgage bankers to arrange financing for homebuyers. The principal competitive factors for the financial services segment include interest rates, fees and other features of mortgage loan products available to the consumer.

Homebuilding is subject to warranty claims in the ordinary course of business that can be subject to uncertainty.

As a homebuilder, the Company is subject to warranty claims arising in the ordinary course of business. The Company records warranty and other reserves for the homes it sells to cover expected costs of materials and outside labor during warranty periods based on historical experience in the Company's

12

Table of Contents

markets and on the judgment of the qualitative risks associated with the types of homes built by the Company, including analyses of historical claims. Because of the uncertainties inherent to these matters, the Company cannot provide assurance that the amounts reserved for warranty claims will be adequate or that any potential inadequacies will not have an adverse effect on its results of operations.

Because the Company's business is subject to various regulatory and environmental limitations, it may not be able to conduct its business as planned.

The Company's homebuilding segments are subject to various local, state and federal laws, statutes, ordinances, rules and regulations concerning zoning, building design, construction, stormwater permitting and discharge, and similar matters, as well as open spaces, wetlands and environmentally protected areas. These include local regulations that impose restrictive zoning and density requirements in order to limit the number of homes that can be built within the boundaries of a particular area, as well as other municipal or city land planning restrictions, requirements or limitations. The Company may also experience periodic delays in homebuilding projects due to regulatory compliance, municipal appeals and other governmental planning processes in any of the markets in which it operates. These factors could result in delays or increased operational costs.

With respect to originating, processing, selling and servicing mortgage loans, the Company's financial services segment is subject to the rules and regulations of FHA, Freddie Mac, Fannie Mae, VA and the U.S. Department of Housing and Urban Development ("HUD"). Mortgage origination activities are further subject to the Equal Credit Opportunity Act, Federal Truth-in-Lending Act and the Real Estate Settlement Procedures Act, and their associated regulations. These and other federal and state statutes and regulations prohibit discrimination and establish underwriting guidelines that include provisions for audits, inspections and appraisals; require credit reports on prospective borrowers; fix maximum loan amounts; and require the disclosure of certain information concerning credit and settlement costs. The Company is required to submit audited financial statements annually, and each agency or other entity has its own financial requirements. The Company's affairs are also subject to examination by these entities at all times to assure compliance with applicable regulations, policies and procedures.

The Company's ability to grow its business and operations depends, to a significant degree, upon its ability to access capital on favorable terms.

The ability to access capital on favorable terms is an important factor in growing the Company's business and operations in a profitable manner. In 2007, Moody's lowered the Company's debt rating to non-investment grade, and Standard & Poor's ("S&P") also reduced the Company's investment-grade rating to non-investment grade in 2008. The Company received additional downgrades in 2008 and 2011. At December 31, 2014, Moody's reported the Company's rating outlook as stable and S&P reported its rating outlook as positive. The loss of an investment-grade rating affects the cost, availability and terms of credit available to the Company, making it more difficult and costly to access the debt capital markets for funds that may be required to implement its business plans.

Natural disasters may have a significant impact on the Company's business.

The climates and geology of many of the states in which the Company operates present increased risks of natural disasters. To the extent that hurricanes, severe storms, tornadoes, earthquakes, droughts, floods, wildfires or other natural disasters or similar events occur, its business and financial condition may be adversely affected.

Information technology failures and data security breaches could harm the Company's business.

The Company's information technology systems are dependent upon global communications providers, Web browsers, telephone systems and other aspects of the Internet infrastructure that have experienced significant systems failures and electrical outages in the past. While it takes measures to ensure its major systems have redundant capabilities, the Company's systems are susceptible to outages from fire, floods, power loss, telecommunications failures, break-ins, cyber attacks and similar events. Despite the Company's implementation of network security measures, its servers are vulnerable to computer viruses, break-ins and similar disruptions resulting from unauthorized tampering with its computer systems. The occurrence of any of these events could disrupt or damage the Company's information technology systems and hamper its internal operations, its ability to provide services to its customers and the ability of its customers to access the Company's information technology systems. In addition, the Company's business

13

Table of Contents

requires the collection and retention of large volumes of internal and customer data. The Company also maintains personally identifiable information about its employees. The integrity and protection of customer, employee and company data is critical to the Company. A material network breach in the security of the Company's information technology systems could include the theft of customer or employee data or its intellectual property or trade secrets. To the extent that any disruption or security breach results in a loss or damage to the Company's data, or in the inappropriate disclosure of confidential information, it could cause significant damage to its reputation, affect relationships with its customers, reduce demand for the Company's services, lead to claims against the Company and ultimately harm its business. In addition, the Company may be required to incur significant costs to protect against damage caused by these disruptions or security breaches in the future.

The Company's short-term investments and marketable securities are subject to certain risks which could materially and adversely affect its overall financial condition.

The Company invests a portion of its available cash and cash equivalent balances by purchasing marketable securities with maturities in excess of three months in a managed portfolio. The primary objectives of these investments are the preservation of capital and the maintenance of a high degree of liquidity, with a secondary objective being the attainment of yields higher than those earned on the Company's cash and cash equivalent balances. Should any of the Company's short-term investments or marketable securities lose value or have their liquidity impaired, it could materially and adversely affect the Company's overall financial condition by limiting its ability to fund operations.

Item 1B. Unresolved Staff Comments

None.

Item 2. Properties

The Company leases office space for its corporate headquarters in Westlake Village, California, and for its IT Department and RMC's operations center in Scottsdale, Arizona. In addition, the Company leases office space in the various markets in which it operates. The Company believes that its existing facilities are adequate for the Company's current and planned levels of operation. Because of the nature of the Company's homebuilding operations, significant amounts of property are held as inventory in the ordinary course of its homebuilding business. See Item 1. "Business" for a discussion of the Company's homebuilding operations.

Item 3. Legal Proceedings

Contingent liabilities may arise from obligations incurred in the ordinary course of business or from the usual obligations of on-site housing producers for the completion of contracts.

On December 23, 2011, Countrywide Home Loans, Inc. ("Countrywide") filed a lawsuit against Ryland Mortgage Company alleging breach of contract related to repurchase and indemnity obligations arising out of the sale of mortgage loans associated with loan purchase agreements between Countrywide and Ryland Mortgage Company. In the third quarter of 2014, Ryland Mortgage Company settled the lawsuit and any other potential claims related to repurchase and indemnity obligations arising out of the sale of mortgage loans associated with loan purchase agreements between Countrywide and Ryland Mortgage Company. (See Note L, "Commitments and Contingencies.")

The Company is party to various other legal proceedings generally incidental to its businesses. Based on evaluation of these matters and discussions with counsel, management believes that it is not probable that liabilities arising from these matters will have a material adverse effect on the financial condition, results of operations and cash flows of the Company.

Item 4. Mine Safety Disclosures

Not applicable.

14

Table of Contents

PART II

Item 5. Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Market for Common Equity, Common Stock Prices and Dividends

The Company lists its common shares on the NYSE, trading under the symbol "RYL." The latest reported sale price of the Company's common stock on February 10, 2015, was $44.42, and there were 1,435 common stockholders of record on that date.

The following table presents high and low market prices, as well as dividend information, for the Company:

| | | | | | | | | | | | | | | | | | | | |

2014 | | |

HIGH | | |

LOW | | | DIVIDENDS

DECLARED

PER SHARE | |

2013 | | |

HIGH | | |

LOW | | | DIVIDENDS

DECLARED

PER SHARE |

| | | |

|---|

| First quarter | | $ | 46.67 | | $ | 38.07 | | $ | 0.03 | | First quarter | | $ | 43.00 | | $ | 33.50 | | $ | 0.03 |

| Second quarter | | | 42.70 | | | 35.96 | | | 0.03 | | Second quarter | | | 50.42 | | | 35.65 | | | 0.03 |

| Third quarter | | | 40.35 | | | 31.22 | | | 0.03 | | Third quarter | | | 43.70 | | | 33.04 | | | 0.03 |

| Fourth quarter | | | 39.54 | | | 30.33 | | | 0.03 | | Fourth quarter | | | 44.63 | | | 35.70 | | | 0.03 |

| |

Issuer Purchases of Equity Securities

The following table summarizes the Company's purchases of its own equity securities during the year ended December 31, 2014:

| | | | | | | | | | | | | |

PERIOD

| | |

TOTAL

NUMBER OF

SHARES

PURCHASED | | |

AVERAGE

PRICE PAID

PER SHARE | | | TOTAL NUMBER

OF SHARES

PURCHASED AS

PART OF PUBLICLY

ANNOUNCED PLANS

OR PROGRAMS | | | APPROXIMATE

DOLLAR VALUE OF

SHARES THAT MAY

YET BE PURCHASED

UNDER THE PLANS

OR PROGRAMS | |

| | |

|---|

| (in thousands, except share data) | |

|---|

August 1–31 | | | 560,000 | | $ | 34.12 | | | 560,000 | | $ | 123,198 | |

September 1–30 | | | 300,000 | | | 35.26 | | | 300,000 | | | 112,619 | |

| | | | | | | | | | | | | | |

Total | | | 860,000 | | $ | 34.52 | | | 860,000 | | | | |

| | |

On December 6, 2006, the Company announced that it had received authorization from its Board of Directors to purchase shares totaling $175.0 million. The Company repurchased 860,000 shares in accordance with this authorization during the year ended December 31, 2014. There were approximately 2.9 million shares available for purchase in accordance with this authorization, based on the Company's stock price at December 31, 2014. This authorization does not have an expiration date. The Company did not purchase any of its own equity securities during the years ended December 31, 2013 or 2012.

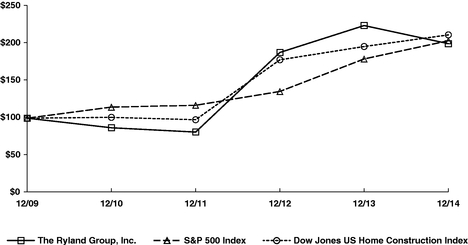

Performance Graph

The following performance graph and related information shall not be deemed "soliciting material" or be "filed" with the SEC, nor shall such information be incorporated by reference into any future filing under the Securities Act or the Exchange Act, except to the extent that the Company specifically incorporates it by reference into such filing.

15

Table of Contents

The following graph compares the Company's cumulative total stockholder return since December 31, 2009, to the S&P 500 and the Dow Jones U.S. Home Construction indices for the calendar years ended December 31:

COMPARISON OF FIVE-YEAR CUMULATIVE TOTAL RETURN1

Among The Ryland Group, Inc., The S&P 500 Index

And The Dow Jones U.S. Home Construction Index

Securities Authorized for Issuance Under Equity Compensation Plans

The Company's equity compensation plan information as of December 31, 2014, is summarized as follows:

| | | | | | |

| | NUMBER OF SECURITIES TO

BE ISSUED UPON EXERCISE

OF OUTSTANDING OPTIONS,

WARRANTS AND RIGHTS

| | WEIGHTED-AVERAGE

EXERCISE PRICE OF

OUTSTANDING OPTIONS,

WARRANTS AND RIGHTS

| | NUMBER OF SECURITIES

REMAINING AVAILABLE FOR

FUTURE ISSUANCE UNDER

EQUITY COMPENSATION

PLANS (EXCLUDING

SECURITIES REFLECTED

IN COLUMN (a))

|

|---|

PLAN CATEGORY

| | (a)

| | (b)

| | (c)

|

|---|

| |

Equity compensation plans approved by stockholders | | 1,753,581 | | $ 23.30 | | 3,633,175 |

Equity compensation plans not approved by stockholders1 | |

– | |

– | |

– |

| |

- 1

- The Company does not have any equity compensation plans that have not been approved by stockholders.

16

Table of Contents

Item 6. Selected Financial Data

| | | | | | | | | | | | | | | | |

| | YEAR ENDED DECEMBER 31, | |

(in millions, except per share data) | | | 2014 | | | 2013 | | | 2012 | | | 2011 | | | 2010 | |

| | |

ANNUAL RESULTS | | | | | | | | | | | | | | | | |

REVENUES | | | | | | | | | | | | | | | | |

Homebuilding | | $ | 2,570 | | $ | 2,089 | | $ | 1,271 | | $ | 863 | | $ | 970 | |

Financial services | | | 45 | | | 52 | | | 37 | | | 27 | | | 31 | |

| | | | |

TOTAL REVENUES | | | 2,615 | | | 2,141 | | | 1,308 | | | 890 | | | 1,001 | |

| | | | |

Cost of sales | | | 2,008 | | | 1,654 | | | 1,027 | | | 727 | | | 844 | |

Operating expenses | | | 327 | | | 294 | | | 231 | | | 199 | | | 225 | |

| | | | |

TOTAL EXPENSES | | | 2,335 | | | 1,948 | | | 1,258 | | | 926 | | | 1,069 | |

| | | | |

Other income (loss) | | | 4 | | | 3 | | | (6 | ) | | 3 | | | (13 | ) |

| | | | |

Income (loss) from continuing operations before taxes | | | 284 | | | 196 | | | 44 | | | (33 | ) | | (81 | ) |

Tax expense (benefit) | | | 108 | | | (183 | ) | | 2 | | | (3 | ) | | – | |

| | | | |

Net income (loss) from continuing operations | | | 176 | | | 379 | | | 42 | | | (30 | ) | | (81 | ) |

Loss from discontinued operations, net of taxes | | | – | | | – | | | (2 | ) | | (21 | ) | | (4 | ) |

| | | | |

NET INCOME (LOSS) | | $ | 176 | | $ | 379 | | $ | 40 | | $ | (51 | ) | $ | (85 | ) |

| | | | |

YEAR-END POSITION | | | | | | | | | | | | | | | | |

ASSETS | | | | | | | | | | | | | | | | |

Cash, cash equivalents and marketable securities | | $ | 580 | | $ | 631 | | $ | 615 | | $ | 563 | | $ | 739 | |

Housing inventories | | | 2,046 | | | 1,650 | | | 1,077 | | | 795 | | | 752 | |

Other assets | | | 426 | | | 499 | | | 240 | | | 186 | | | 111 | |

Assets of discontinued operations | | | – | | | – | | | 2 | | | 35 | | | 51 | |

| | | | |

TOTAL ASSETS | | | 3,052 | | | 2,780 | | | 1,934 | | | 1,579 | | | 1,653 | |

| | | | |

LIABILITIES | | | | | | | | | | | | | | | | |

Debt and financial services credit facilities | | | 1,532 | | | 1,470 | | | 1,134 | | | 874 | | | 880 | |

Other liabilities | | | 421 | | | 385 | | | 272 | | | 215 | | | 207 | |

Liabilities of discontinued operations | | | – | | | 1 | | | 2 | | | 6 | | | 4 | |

| | | | |

TOTAL LIABILITIES | | | 1,953 | | | 1,856 | | | 1,408 | | | 1,095 | | | 1,091 | |

| | | | |

NONCONTROLLING INTEREST | | | 14 | | | 16 | | | 22 | | | 34 | | | 62 | |

STOCKHOLDERS' EQUITY | | | 1,085 | | | 908 | | | 504 | | | 450 | | | 500 | |

| | | | |

TOTAL EQUITY | | $ | 1,099 | | $ | 924 | | $ | 526 | | $ | 484 | | $ | 562 | |

| | | | |

PER COMMON SHARE DATA | | | | | | | | | | | | | | | | |

NET INCOME (LOSS) | | | | | | | | | | | | | | | | |

Basic | | | | | | | | | | | | | | | | |

Continuing operations | | $ | 3.77 | | $ | 8.22 | | $ | 0.93 | | $ | (0.67 | ) | $ | (1.83 | ) |

Discontinued operations | | | 0.00 | | | 0.00 | | | (0.04 | ) | | (0.47 | ) | | (0.10 | ) |

| | | | |

Total | | | 3.77 | | | 8.22 | | | 0.89 | | | (1.14 | ) | | (1.93 | ) |

| | | | |

Diluted | | | | | | | | | | | | | | | | |

Continuing operations | | | 3.09 | | | 6.79 | | | 0.88 | | | (0.67 | ) | | (1.83 | ) |

Discontinued operations | | | 0.00 | | | 0.00 | | | (0.04 | ) | | (0.47 | ) | | (0.10 | ) |

| | | | |

Total | | $ | 3.09 | | $ | 6.79 | | $ | 0.84 | | $ | (1.14 | ) | $ | (1.93 | ) |

| | | | |

DIVIDENDS DECLARED | | $ | 0.12 | | $ | 0.12 | | $ | 0.12 | | $ | 0.12 | | $ | 0.12 | |

STOCKHOLDERS' EQUITY | | $ | 23.43 | | $ | 19.64 | | $ | 11.16 | | $ | 10.12 | | $ | 11.31 | |

| | |

17

Table of Contents

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations

The following management's discussion and analysis is intended to assist the reader in understanding the Company's business and is provided as a supplement to, and should be read in conjunction with, the Company's consolidated financial statements and accompanying notes. The Company's results of operations discussed below are presented in conformity with U.S. generally accepted accounting principles ("GAAP").

Forward-Looking Statements

Certain statements in this Annual Report may be regarded as "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995, and may qualify for the safe harbor provided for in Section 21E of the Exchange Act. These forward-looking statements represent the Company's expectations and beliefs concerning future events, and no assurance can be given that the results described in this Annual Report will be achieved. These forward-looking statements can generally be identified by the use of statements that include words such as "anticipate," "believe," "could," "estimate," "expect," "foresee," "goal," "intend," "likely," "may," "plan," "project," "should," "target," "will" or other similar words or phrases. All forward-looking statements contained herein are based upon information available to the Company on the date of this Annual Report. Except as may be required under applicable law, the Company does not undertake any obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

These forward-looking statements are subject to risks, uncertainties and other factors, many of which are outside of the Company's control that could cause actual results to differ materially from the results discussed in the forward-looking statements. The factors and assumptions upon which any forward-looking statements herein are based are subject to risks and uncertainties which include, among others:

- •

- economic changes nationally or in the Company's local markets, including volatility and increases in interest rates, the impact of, and changes in, governmental stimulus, tax and deficit reduction programs, inflation, changes in consumer demand and confidence levels and the state of the market for homes in general;

- •

- changes and developments in the mortgage lending market, including revisions to underwriting standards for borrowers and lender requirements for originating and holding mortgages, changes in government support of and participation in such market, and delays or changes in terms and conditions for the sale of mortgages originated by the Company;

- •

- the availability and cost of land and the future value of land held or under development;

- •

- increased land development costs on projects under development;

- •

- shortages of skilled labor or raw materials used in the production of homes;

- •

- increased prices for labor, land and materials used in the production of homes;

- •

- increased competition;

- •

- failure to anticipate or react to changing consumer preferences in home design;

- •

- increased costs and delays in land development or home construction resulting from adverse weather conditions or other factors;

- •

- potential delays or increased costs in obtaining necessary permits as a result of changes to laws, regulations or governmental policies (including those that affect zoning, density, building standards, the environment and the residential mortgage industry);

- •

- delays in obtaining approvals from applicable regulatory agencies and others in connection with the Company's communities and land activities;

- •

- changes in the Company's effective tax rate and assumptions and valuations related to its tax accounts;

- •

- the risk factors set forth in this Annual Report on Form 10-K; and

- •

- other factors over which the Company has little or no control.

18

Table of Contents

Results of Operations

Overview

During 2014, the Company saw continued improvement in most of the economic indicators salient to the homebuilding industry: employment rates continued to rise, consumer confidence improved and interest rates remained at historically low levels. Sales pace, however, continued to be a challenge amidst slower household formation growth and a restrictive mortgage underwriting environment. The Company believes that the housing market as a whole is likely to move forward in its recovery as affordability remains attractive and homeownership remains near historically low levels. It believes that continued improvement in employment levels; low interest rates; slow relaxation of the mortgage underwriting environment; historically low production of single-family homes; and a steady increase of potential buyers due, in part, to an expected rise in the number of household formations should eventually drive more attractive sales absorption rates that will facilitate a healthier, sustainable long-term recovery. The Company remains structurally lean and, as a result of community count growth over the last several years, expects to achieve greater leverage with comparable volume levels than in past years.

Throughout 2014, the Company's strategic homebuilding initiatives continued to generate year-over-year improvements in volume, operational efficiencies and profitability while, at the same time, maintaining a strong balance sheet. The Company made significant progress in achieving its operational goals in 2014 with a 22.2 percent increase in consolidated revenues; a 1.0 percent rise in housing gross profit margin; and a 1.0 percent decrease in the selling, general and administrative expense ratio, all of which led to an improvement in homebuilding operations profitability, compared to the same period in the prior year. The Company reported increases of 9.3 percent in closings and 5.6 percent in sales for the year ended December 31, 2014, compared to 2013. The Company believes that continued revenue growth and improved financial performance will most likely come from a greater presence in its established markets, improvements in operational leverage and a return to more traditional sales absorption rates should economic progress continue.

The Company continues to maintain a geographically diverse footprint in order to manage risk and believes that it is well positioned to take advantage of favorable trends and opportunities in all of its markets. The number of active communities rose 21.0 percent to 351 active communities at December 31, 2014, from 290 active communities at December 31, 2013. Significant ongoing land acquisitions in its existing markets should enhance the Company's ability to establish additional market penetration and create a platform for future growth. Investments in new communities increased consolidated inventory owned by $397.5 million, or 24.3 percent, at December 31, 2014, compared to December 31, 2013.

The Company's net income from continuing operations totaled $175.8 million, or $3.09 per diluted share, for the year ended December 31, 2014, compared to $379.1 million, or $6.79 per diluted share, for 2013 and $42.4 million, or $0.88 per diluted share, for 2012. The decrease in net income for 2014, compared to 2013, was primarily due to a $258.9 million tax benefit related to the reversal of the Company's deferred tax valuation allowance in 2013, which also restored income tax expense in 2014. The increase in net income for 2013, compared to 2012, was primarily due to a reversal of the Company's deferred tax asset valuation allowance; a rise in closing volume; higher housing gross profit margin, including lower inventory valuation adjustments and write-offs; a reduced selling, general and administrative expense ratio; pretax charges related to early retirement of debt in 2012; and a decline in interest expense. Pretax charges related to inventory and other valuation adjustments and write-offs totaled $2.4 million, $2.0 million and $6.3 million for the years ended December 31, 2014, 2013 and 2012, respectively.

The Company's consolidated revenues rose 22.2 percent to $2.6 billion for the year ended December 31, 2014, from $2.1 billion for 2013. This increase was primarily attributable to a 9.3 percent rise in closings and to a 12.5 percent higher average closing price. The increase in average closing price was due to a change in the product and geographic mix of homes delivered, as well as to a more accommodating price environment during 2014, versus 2013. The Company's consolidated revenues rose 63.6 percent to $2.1 billion for the year ended December 31, 2013, from $1.3 billion for the same period in the prior year. This increase was primarily attributable to a 46.1 percent rise in closings and to a 12.5 percent higher average closing price. The increase in average closing price was due to price increases in existing communities, as well as to a change in the product and geographic mix of homes delivered during 2013,

19

Table of Contents

versus 2012. Revenues for the homebuilding and financial services segments totaled $2.6 billion and $45.2 million in 2014, compared to $2.1 billion and $51.4 million in 2013 and $1.3 billion and $37.6 million in 2012, respectively.

The Company reported a rise in closing volume for the year ended December 31, 2014, compared to 2013, primarily due to higher backlog at the beginning of the year, as well as to an increase in sales. New orders rose 5.6 percent to 7,668 units for the year ended December 31, 2014, from 7,262 units for 2013 primarily due to an increase in the number of active communities, partially offset by lower sales absorption rates. New order dollars increased 15.2 percent for the year ended December 31, 2014, compared to 2013. The Company's average monthly sales absorption rate was 2.0 homes per community for the year ended December 31, 2014, versus 2.3 homes per community for 2013. The Company's average monthly sales absorption rate is calculated as the net new orders in the period divided by the average number of active communities during the period divided by the number of months in that period.

Selling, general and administrative expense totaled 11.2 percent of homebuilding revenues for the year ended December 31, 2014, compared to 12.2 percent and 15.0 percent for the same periods in 2013 and 2012, respectively. The year-over-year decreases were primarily attributable to higher leverage that resulted from increased revenues.

The financial services segment reported pretax earnings of $7.4 million, $20.1 million and $13.1 million for the years ended December 31, 2014, 2013 and 2012, respectively. The decrease in pretax earnings for 2014, compared to 2013, was primarily attributable to a decrease in locked loan pipeline volume, which was due, in part, to the reversal of the accelerated timing of loan locks during 2013; an increase in litigation expense; and higher expense related to a change in estimate of ultimate insurance loss liability. The rise in pretax earnings for 2013, compared to 2012, was primarily due to increases in locked loan pipeline and origination volumes, as well as to a rise in title income, partially offset by increased personnel costs and by higher expense related to estimates of ultimate insurance loss liability.

The Company maintained a strong balance sheet, ending the year with $580.0 million in cash, cash equivalents and marketable securities. After the maturity of the $126.5 million of 5.4 percent senior notes in January 2015, which were paid after year end with existing cash, the Company's earliest senior debt maturity is in 2017. Its net debt-to-capital ratio, including marketable securities, was 43.1 percent at December 31, 2014, compared to 45.8 percent at December 31, 2013. Stockholders' equity per share rose 19.3 percent to $23.43 at December 31, 2014, compared to $19.64 at December 31, 2013.

The net debt-to-capital ratio, including marketable securities, is a non-GAAP financial measure that is calculated as debt, net of cash, cash equivalents and marketable securities, divided by the sum of debt and total stockholders' equity, net of cash, cash equivalents and marketable securities. The Company believes that the net debt-to-capital ratio, including marketable securities, is useful in understanding the leverage employed in its operations and in comparing it with other homebuilders.

Homebuilding Overview

The combined homebuilding operations reported pretax earnings from continuing operations of $303.5 million, $201.8 million and $62.6 million for 2014, 2013 and 2012, respectively. Homebuilding results in 2014 improved from those in 2013 primarily due to a rise in revenues; higher housing gross profit margin; a reduced selling, general and administrative expense ratio; and a decline in interest expense. Homebuilding results in 2013 improved from those in 2012 primarily due to a rise in closing volume; higher housing gross profit margin, including lower inventory and other valuation adjustments and write-offs; a decline in interest expense; and a reduced selling, general and administrative expense ratio.

20

Table of Contents

STATEMENTS OF EARNINGS

| | | | | | | | | | |

| | YEAR ENDED DECEMBER 31, | |

(in thousands, except units) | | | 2014 | | | 2013 | | | 2012 | |

| | |

REVENUES | | | | | | | | | | |

Housing | | $ | 2,555,967 | | $ | 2,082,838 | | $ | 1,263,120 | |

Land and other | | | 13,934 | | | 6,537 | | | 7,727 | |

| | | | |

TOTAL REVENUES | | | 2,569,901 | | | 2,089,375 | | | 1,270,847 | |

EXPENSES | | | | | | | | | | |

Housing cost of sales | | | | | | | | | | |

Cost of sales | | | 1,998,379 | | | 1,649,223 | | | 1,017,124 | |

Valuation adjustments and write-offs | | | (77 | ) | | 146 | | | 5,166 | |

| | | | |

Total housing cost of sales | | | 1,998,302 | | | 1,649,369 | | | 1,022,290 | |

Land and other cost of sales | | | 9,342 | | | 4,827 | | | 5,182 | |

| | | | |

Total cost of sales | | | 2,007,644 | | | 1,654,196 | | | 1,027,472 | |

Selling, general and administrative | | | 258,781 | | | 224,995 | | | 164,688 | |

Interest | | | – | | | 8,358 | | | 16,118 | |

| | | | |

TOTAL EXPENSES | | | 2,266,425 | | | 1,887,549 | | | 1,208,278 | |

| | | | |

PRETAX EARNINGS | | $ | 303,476 | | $ | 201,826 | | $ | 62,569 | |

| | |

Closings (units) | | | 7,677 | | | 7,027 | | | 4,809 | |

Housing gross profit margin | | | 21.8 | % | | 20.8 | % | | 19.1 | % |

Selling, general and administrative ratio | | | 10.1 | % | | 10.8 | % | | 13.0 | % |

| | |