UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: | 811-06094 |

| |

Exact name of registrant as specified in charter: | Aberdeen Latin America Equity Fund, Inc. |

| |

Address of principal executive offices: | 1735 Market Street, 32nd Floor |

| Philadelphia, PA 19103 |

| |

Name and address of agent for service: | Ms. Andrea Melia |

| Aberdeen Asset Management Inc. |

| 1735 Market Street 32nd Floor |

| Philadelphia, PA 19103 |

| |

Registrant’s telephone number, including area code: | 866-839-5205 |

| |

Date of fiscal year end: | December 31 |

| |

Date of reporting period: | December 31, 2013 |

Item 1. Reports to Stockholders. –

Aberdeen’s Investor Relations Services

We invite you to enroll today.

As part of Aberdeen’s commitment to shareholders, we invite you to visit the Fund on the web at www.aberdeenlaq.com. From this page, you can view monthly fact sheets, portfolio manager commentary, distribution and performance information, updated daily fact sheets courtesy of Morningstar®, portfolio charting, and other timely data.

Enroll today

Did you know you can be among the first to receive information from your Fund?

Enroll in our e-mail services and be among the first to recieve information regarding your investments. Complete the enclosed card and return in the postage-paid envelope or sign-up today online.

Please take a look at Aberdeen’s award-winning Closed-End Fund Talk Channel, where a series of fund manager webcasts and short films are posted. Visit Aberdeen’s Closed-End Fund Talk Channel at www.aberdeen-asset.us/aam.nsf/usClosed/aberdeentv.

Contact us:

1. Enroll in Investor Relations services at:

http://www.aberdeen-asset.us/aam.nsf/usclosed/email

2. Call us toll free at 1-866-839-5205 in the U.S., or

3. Email us at InvestorRelations@aberdeen-asset.com

4. Visit www.aberdeen-asset.us/cef

Stop the paper

Did you know that you can receive your shareholder reports online?

By enrolling in this convenient service, you will receive electronic versions of important Fund documents including annual reports, semi-annual reports, prospectuses, and proxy statements.

There’s never been a faster, simple or more environmentally-friendly way to receive your investment information.

To enroll in electronic delivery, follow these simple steps:

1. Go to http://www.aberdeen-asset.us/cef

2. Click on the link for “Email Services” which takes you here

http://www.aberdeen-asset.us/aam.nsf/usclosed/email

3. Click “Sign-up”

Please note that Aberdeen does not share our shareholder information with any other organizations. You can return to this site at any time to change your email address or edit your preferences.

Letter to Shareholders (unaudited)

December 31, 2013

Dear Shareholder,

We present this Annual Report which covers the activities of Aberdeen Latin America Equity Fund, Inc. (the “Fund”) for the twelve-month period ended December 31, 2013. The Fund’s principal investment objective is to seek long-term capital appreciation by investing primarily in Latin American equity securities.

Total Return Performance

For the year ended December 31, 2013, the total return to shareholders of the Fund net of fees, based on the net asset value (“NAV”) of the Fund, was (13.2%), assuming reinvestment of dividends and distributions, versus a return of (13.4%) for the Fund’s benchmark, the MSCI Emerging Markets Latin America Index (“MSCI EM Latin America Index”). The Fund’s total return for the year ended December 31, 2013 is based on the reported NAV at period end.

Share Price and NAV

For the year ended December 31, 2013, based on market price, the Fund’s total return was (13.4%), assuming reinvestment of dividends and distributions. The Fund’s share price decreased (22.6%) over the twelve months, from $36.24 on December 31, 2012 to $28.05 on December 31, 2013. The Fund’s share price on December 31, 2013 represented a discount of 10.2% to the NAV per share of $31.22 on that date, compared with a discount of 9.9% to the NAV per share of $40.23 on December 31, 2012.

Open Market Repurchase Program

The Fund’s policy is generally to buy back Fund shares on the open market when the Fund trades at certain discounts to NAV. During the fiscal year ended December 31, 2013 and fiscal year ended December 31, 2012, the Fund did not repurchase any shares.

Portfolio Holdings Disclosure

The Fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. The Fund’s Forms N-Q are available on the SEC’s website at http://www.sec.gov and may be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C. Information about the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330. The information on Form N-Q is also available to shareholders on the Fund’s website or upon request and without charge by calling Investor Relations toll-free at 1-866-839-5205.

Proxy Voting

A description of the policies and procedures that the Fund uses to determine how to vote proxies relating to portfolio securities, and information regarding how the Fund voted proxies relating to portfolio

securities during the most recent twelve months ended June 30 is available by August 30 of the relevant year: (i) upon request and without charge by calling Investor Relations toll-free at 1-866-839-5205; and (ii) on the SEC’s website at http://www.sec.gov.

Investor Relations Information

As part of our ongoing commitment to provide information to our shareholders, I invite you to visit the Fund on the web at www.aberdeenlaq.com. From this page, you can view monthly fact sheets, portfolio manager commentary, distribution and performance information, updated daily fact sheets courtesy of Morningstar®, conduct portfolio charting and other timely data.

Please take a look at Aberdeen’s award-winning Closed-End Fund Talk Channel, where you can watch fund manager web casts and view our latest short films. For replays of recent broadcasts or to register for upcoming events, please visit Aberdeen’s Closed-End Fund Talk Channel at www.aberdeen-asset.us/aam.nsf/usClosed/aberdeentv.

Please ensure that you are enrolled in our email services, which feature timely news from Aberdeen portfolio managers located around the world. Enroll today at www.aberdeen-asset.us/aam.nsf/usclosed/email and be among the first to receive the latest closed-end fund news, announcements of upcoming fund manager web casts, films and other information. Please note that Aberdeen does not share our shareholder information with any other organizations.

Please contact Aberdeen Asset Management Inc. by:

· Calling toll free at 1-866-839-5205 in the United States;

· Emailing InvestorRelations@aberdeen-asset.com;

· Visiting Aberdeen Closed-End Fund Center at

http://www.aberdeen-asset.us/aam.nsf/usclosed/home;

· Visiting www.aberdeenlaq.com.

Yours sincerely,

Christian Pittard

President

All amounts are U.S. Dollars unless otherwise stated.

| Aberdeen Latin America Equity Fund, Inc. | 1 |

Report of the Investment Adviser (unaudited)

December 31, 2013

Market/Economic Review

Latin American stock markets fell during the 2013 calendar year, underperforming the broader emerging markets asset class amid a period of significant volatility. Markets began the year on a positive note, buoyed by an improving global economic backdrop. In May 2013, however, the U.S. Federal Reserve’s (Fed) indication that it might begin scaling back its asset purchase program sparked a sell-off. In addition, fears of a slowdown in the Chinese economy weighed on Latin American exporters that rely on Chinese demand. Towards the end of the year, market sentiment improved following a U.S. debt deal and positive economic data from China. However, gains were reversed as improving U.S. data led the Fed to announce that it would start trimming its bond purchases in January 2014, which triggered fears of increased fund outflows from Latin America. Currency weakness and lackluster commodity prices put further pressure on Latin American stock markets.

Fund Performance Review

With about 70% of the Fund in Brazilian Real-denominated assets, the significant depreciation of the Real versus most major global currencies was the key driver of the Fund’s absolute performance for the 12-month period ended December 31, 2013.

At the stock level, weakness in the Fund’s Brazilian holdings was counterbalanced by good stock selection in Mexico, Chile and Argentina. In Brazil, consumer-focused holdings, including retailers Arezzo Industria e Comercio S.A. and Lojas Renner S.A., shopping mall operator Multiplan Emreendimento Imobiliarious S.A. and cosmetics maker Natura Cosmeticos S.A., were among the main detractors from performance, reflecting the muted consumer spending environment. The lack of exposure to Mexico’s America Movil also had a negative impact. Shares in the telecommunications company rose after its attempt to take over Dutch firm KPN was blocked by the latter’s shareholders.

Conversely, the Fund’s holdings in airport operators OMA and Asur performed well, thanks to robust passenger traffic growth and investor optimism about Mexico’s prospects. Brazilian lender Banco Bradesco also outperformed versus the overall market on the back of improving asset quality and good loan growth. Shares of the Fund’s sole Argentine holding, steel-pipe manufacturer Tenaris S.A., were buoyed by investor confidence in the U.S. economic recovery and hopes that Mexican energy sector reforms would boost demand for its products.

Asset allocation during the annual period had a positive impact on Fund performance, aided by the exposure to Argentina, which is not represented in the benchmark MSCI Emerging Markets (EM) Latin America Index, as well as the lack of exposure to Peru, which was the worst-performing Latin American market.

Outlook

After a difficult 2013, we think that market sentiment may remain cautious going into 2014. The pace of Fed tapering of its monetary easing policy is likely to continue to affect investor sentiment, in our opinion, despite the positive economic implications of a U.S. recovery. We believe that Mexico’s energy reform bodes well for growth in the medium term, but higher taxes under the fiscal reform could drag on consumption growth in the near term. With elections scheduled for October 2014, we feel that the Brazilian government could maintain its focus on combating stubborn inflation, which may prove challenging in an environment of subdued growth. In Chile, the policy initiatives of the newly-elected president, Michelle Bachelet, likely will be closely watched, as she has pledged to raise corporate taxes to fund social spending. Despite the uncertainty, we think that Latin American economies may continue to be buoyed by an expanding consumer class, still-healthy foreign direct investment and relatively low levels of government debt. We believe that the companies that the Fund holds are positioned to do well, even in leaner times.

Aberdeen Asset Managers Limited

Dividend Reinvestment and Cash Purchase Plan (unaudited)

Computershare Trust Company, N.A., the Fund’s transfer agent, sponsors and administers a Dividend Reinvestment and Direct Stock Purchase Plan (the “Plan”), which is available to shareholders.

The Plan allows registered shareholders and first time investors to buy and sell shares and automatically reinvest dividends and capital gains through the transfer agent. This may be a cost-effective way to invest in the Fund.

Please note that for both purchases and reinvestment purposes, shares will be purchased in the open market at the current share price and cannot be issued directly by the Fund.

For more information about the Plan and a brochure that includes the terms and conditions of the Plan, please call Computershare at 1-800-647-0584 or visit www.computershare.com/buyaberdeen.

2 | Aberdeen Latin America Equity Fund, Inc. | |

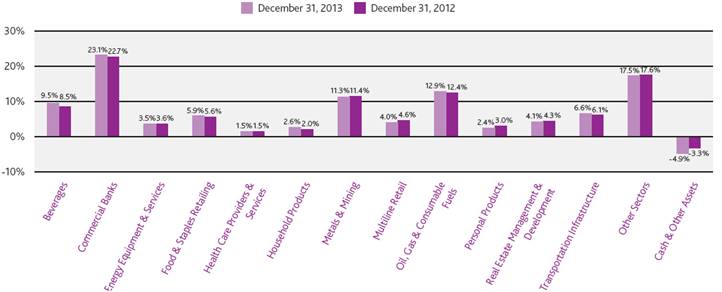

Portfolio Summary (unaudited)

December 31, 2013

The following chart summarizes the composition of the Fund’s portfolio, in Standard & Poor’s Industry Classification Standard (“GICS”) sectors, expressed as a percentage of net assets. An industry classification standard sector can include more than one industry group. As of December 31, 2013, the Fund did not have more than 25% of its assets invested in any industry group. The sectors, as classified by S&P’s Global Industry Classification Standard sectors, are comprised of several industry groups.

Asset Allocation by Sector

Top 10 Holdings (unaudited)

December 31, 2013

| | Holding | | Sector | | Country | | Percent of Net Assets |

1. | | Banco Bradesco S.A. | | Commercial Banks | | Brazil | | 8.7% |

2. | | Vale S.A., ADR | | Metals & Mining | | Brazil | | 8.4% |

3. | | Petroleo Brasileiro S.A., SPON ADR | | Oil, Gas & Consumable Fuels | | Brazil | | 7.7% |

4. | | Grupo Financiero Banorte S.A.B. de C.V. | | Commercial Banks | | Mexico | | 5.8% |

5. | | Itau Unibanco Holding S.A., PN, ADR | | Commercial Banks | | Brazil | | 5.6% |

6. | | Fomento Economico

Mexicano S.A.B. de C.V., ADR | | Beverages | | Mexico | | 4.4% |

7. | | Ultrapar Participacoes S.A. | | Oil, Gas & Consumable Fuels | | Brazil | | 4.4% |

8. | | AMBEV S.A. | | Beverages | | Brazil | | 4.0% |

9. | | Lojas Renner S.A. | | Multiline Retail | | Brazil | | 3.7% |

10. | | Multiplan Empreendimentos

Imobiliarios S.A. | | Real Estate Management & Development | | Brazil | | 3.6% |

| Aberdeen Latin America Equity Fund, Inc. | 3 |

Total Investment Returns (unaudited)

December 31, 2013

The following table summarizes Fund performance compared to the MSCI EM Latin America index, the Fund’s benchmark, for the 1-year, 3-year, 5-year and 10-year periods annualized ended December 31, 2013.

| | 1 Year | | 3 Years | | 5 Years | | 10 Years | |

Net Asset Value (NAV) | | (13.15)% | | (2.67)% | | 18.81% | | 17.75% | |

Market Value | | (13.38)% | | (3.54)% | | 19.85% | | 18.26% | |

MSCI EM Latin America Index | | (13.36)% | | (8.76)% | | 12.15% | | 14.53% | |

Aberdeen Asset Managers Limited has entered into a written contract with the Fund to waive fees, without which performance would be lower. See Note 3 in the Notes to Financial Statements. This contract aligns with the term of the advisory agreement and may not be terminated prior to the next annual consideration of the advisory agreement. Returns represent past performance. Total investment return at net asset value is based on changes in the net asset value of Fund shares and assumes reinvestment of dividends and distributions, if any, at market prices pursuant to the dividend reinvestment program sponsored by the Fund’s transfer agent. Total investment return at market value is based on changes in the market price at which the shares traded on the NYSE MKT during the period and assumes reinvestment of dividends and distributions, if any, at market prices pursuant to the dividend reinvestment program sponsored by the Fund’s transfer agent. The Fund’s total return is based on the reported NAV on each annual period. Because the Fund’s shares trade in the stock market based on investor demand, the Fund may trade at a price higher or lower than its NAV. Therefore, returns are calculated based on both market price and NAV. Past performance is no guarantee of future results. The performance information provided does not reflect the deduction of taxes that a shareholder would pay on distributions received from the Fund. The current performance of the Fund may be lower or higher than the figures shown. The Fund’s yield, return, market price and NAV will fluctuate. Performance information current to the most recent month-end is available by calling 866-839-5205.

The gross expense ratio is 1.14%. The net expense ratio after fee waivers is 1.12%.

4 | Aberdeen Latin America Equity Fund, Inc. | |

Portfolio of Investments

December 31, 2013

No. of

Shares | | Description | | Value | |

LONG-TERM EQUITY SECURITIES—104.9% | | | |

ARGENTINA—3.5% | | | |

ENERGY EQUIPMENT & SERVICES—3.5% | | | |

188,000 | | Tenaris S.A., ADR (cost $6,616,597) | | $ 8,213,720 | |

BRAZIL—69.1% | | | |

BEVERAGES—4.0% | | | |

1,276,830 | | AMBEV S.A. | | 9,373,613 | |

COMMERCIAL BANKS—14.5% | | | |

1,493,970 | | Banco Bradesco S.A. | | 20,231,998 | |

36,930 | | Banco Itaú Holding Financeira S.A., PN | | 490,730 | |

966,114 | | Itau Unibanco Holding S.A., PN, ADR | | 13,110,167 | |

| | | | 33,832,895 | |

COMMERCIAL SERVICES & SUPPLIES—0.9% | | | |

154,200 | | Valid Solucoes e Servicos de Seguranca em Meios de Pagamento e Identificacao S.A. | | 2,104,584 | |

DIVERSIFIED FINANCIAL SERVICES—1.5% | | | |

757,563 | | BM&F Bovespa S.A. | | 3,551,403 | |

FOOD PRODUCTS—1.7% | | | |

191,368 | | BRF S.A. | | 3,994,860 | |

HEALTH CARE PROVIDERS & SERVICES—1.5% | | | |

831,000 | | Odontoprev S.A. | | 3,462,427 | |

MACHINERY—1.2% | | | |

204,844 | | WEG S.A. | | 2,705,495 | |

METALS & MINING—11.3% | | | |

307,800 | | Bradespar S.A., PN | | 3,272,067 | |

1,277,359 | | Vale S.A., ADR | | 19,479,725 | |

251,117 | | Vale S.A., PN, ADR | | 3,518,149 | |

| | | | 26,269,941 | |

MULTILINE RETAIL—3.7% | | | |

333,096 | | Lojas Renner S.A. | | 8,612,422 | |

OIL, GAS & CONSUMABLE FUELS—12.4% | | | |

46,000 | | Petroleo Brasileiro S.A., ADR | | 633,880 | |

1,221,433 | | Petroleo Brasileiro S.A., SPON ADR | | 17,942,851 | |

431,000 | | Ultrapar Participacoes S.A., ADR | | 10,193,149 | |

| | | | 28,769,880 | |

PERSONAL PRODUCTS—2.4% | | | |

319,000 | | Natura Cosmeticos S.A. | | 5,593,739 | |

REAL ESTATE MANAGEMENT & DEVELOPMENT—3.6% | | | |

393,334 | | Multiplan Empreendimentos Imobiliarios S.A. | | 8,319,325 | |

ROAD & RAIL—1.7% | | | |

274,050 | | Localiza Rent a Car S.A. | | 3,865,798 | |

See Note to Financial Statements.

| Aberdeen Latin America Equity Fund, Inc. | 5 |

Portfolio of Investments (continued)

December 31, 2013

No. of

Shares | | Description | | Value | |

LONG-TERM EQUITY SECURITIES (continued) | | | |

BRAZIL (continued) | | | |

SOFTWARE—1.1% | | | |

156,000 | | Totvs S.A. | | $ 2,443,895 | |

SPECIALTY RETAIL—2.2% | | | |

397,000 | | Cia Hering | | 5,031,387 | |

TEXTILES, APPAREL & LUXURY GOODS—2.3% | | | |

432,277 | | Arezzo Industria e Comercio S.A. | | 5,450,987 | |

TOBACCO—1.5% | | | |

338,000 | | Souza Cruz S.A. | | 3,454,140 | |

TRANSPORTATION INFRASTRUCTURE—1.6% | | | |

289,400 | | Wilson Sons Limited, BDR | | 3,792,836 | |

| | Total Brazil (cost $146,329,031) | | 160,629,627 | |

CHILE—6.9% | | | |

AIRLINES—0.2% | | | |

23,143 | | Latam Airlines Group S.A. | | 362,483 | |

BEVERAGES—1.1% | | | |

318,000 | | Embotelladora Andina S.A., PNB | | 1,458,521 | |

540,000 | | Viña Concha y Toro S.A. | | 1,007,137 | |

| | | | 2,465,658 | |

CHEMICALS—0.2% | | | |

18,800 | | Sociedad Química y Minera de Chile S.A., PNB | | 478,721 | |

COMMERCIAL BANKS—1.3% | | | |

11,653,724 | | Banco de Chile | | 1,685,792 | |

25,113,969 | | Banco Santander Chile | | 1,452,973 | |

| | | | 3,138,765 | |

ELECTRIC UTILITIES—0.5% | | | |

3,780,000 | | Enersis S.A. | | 1,133,029 | |

INDUSTRIAL CONGLOMERATES—0.1% | | | |

18,518 | | Antarchile S.A. | | 249,515 | |

IT SERVICES—0.6% | | | |

592,000 | | Sonda S.A. | | 1,419,583 | |

MULTILINE RETAIL—0.3% | | | |

77,000 | | S.A.C.I. Falabella | | 691,674 | |

OIL, GAS & CONSUMABLE FUELS—0.6% | | | |

98,000 | | Empresas COPEC S.A. | | 1,313,008 | |

PAPER & FOREST PRODUCTS—0.3% | | | |

298,570 | | Empresas CMPC S.A. | | 727,376 | |

REAL ESTATE MANAGEMENT & DEVELOPMENT—0.5% | | | |

692,000 | | Parque Arauco S.A. | | 1,277,457 | |

See Note to Financial Statements.

6 | Aberdeen Latin America Equity Fund, Inc. | |

Portfolio of Investments (continued)

December 31, 2013

No. of

Shares | | Description | | Value | |

LONG-TERM EQUITY SECURITIES (continued) | | | |

CHILE (continued) | | | |

WATER UTILITIES—1.2% | | | |

84,144 | | Inversiones Aguas Metropolitanas S.A., ADR(a)(b)(c) | | $ 2,857,648 | |

| | Total Chile (cost $11,630,400) | | 16,114,917 | |

COLOMBIA—3.0% | | | |

COMMERCIAL BANKS—1.4% | | | |

268,000 | | Bancolombia S.A. | | 3,307,648 | |

FOOD & STAPLES RETAILING—1.6% | | | |

233,901 | | Almacenes Exito S.A. | | 3,635,767 | |

| | Total Colombia (cost $6,902,376) | | 6,943,415 | |

MEXICO—22.1% | | | |

BEVERAGES—4.4% | | | |

104,402 | | Fomento Economico Mexicano S.A.B. de C.V., ADR | | 10,217,824 | |

COMMERCIAL BANKS—5.8% | | | |

1,937,097 | | Grupo Financiero Banorte S.A.B. de C.V. | | 13,551,445 | |

FOOD & STAPLES RETAILING—4.4% | | | |

1,339,000 | | Organización Soriana S.A.B. de C.V.(d) | | 4,820,051 | |

2,048,000 | | Wal-Mart de México S.A.B. de C.V., Series V | | 5,377,049 | |

| | | | 10,197,100 | |

HOUSEHOLD PRODUCTS—2.6% | | | |

2,119,700 | | Kimberly-Clark de Mexico S.A.B. de C.V. | | 6,027,991 | |

TRANSPORTATION INFRASTRUCTURE—4.9% | | | |

190,000 | | Grupo Aeroportuario del Centro Norte S.A.B. de C.V., ADR(d) | | 5,073,000 | |

51,134 | | Grupo Aeroportuario del Sureste S.A.B. de C.V., ADR | | 6,372,830 | |

| | | | 11,445,830 | |

| | Total Mexico (cost $24,546,828) | | 51,440,190 | |

PERU—0.2% | | | |

CONSTRUCTION & ENGINEERING—0.2% | | | |

20,384 | | Grana y Montero S.A., ADR (cost $416,510)(d) | | 432,752 | |

GLOBAL—0.1% | | | |

VENTURE CAPITAL—0.1% | | | |

2,237,292 | (e) | Emerging Markets Ventures l, L.P. (cost $785,672)(b)(c)(d)(f)(g) | | 95,465 | |

| | Total Long-Term Equity Securities (cost $197,227,414) | | 243,870,086 | |

See Note to Financial Statements.

| Aberdeen Latin America Equity Fund, Inc. | 7 |

Portfolio of Investments (concluded)

December 31, 2013

Principal Amount (000’s) | | Description | | Value | |

SHORT-TERM INVESTMENT—1.2% | | | |

UNITED KINGDOM—1.2% | | | |

$2,765 | | Citibank London, overnight deposit, 0.03%, 01/02/14 (cost $2,765,000) | | $ 2,765,000 | |

| | Total Investments—106.1% (cost $199,992,414) | | 246,635,086 | |

| | Liabilities in Excess of Cash and Other Assets—(6.1)% | | (14,104,374 | ) |

| | Net Assets—100.0% | | $ 232,530,712 | |

(a) SEC Rule 144A security. Such securities are traded only among “qualified institutional buyers.”

(b) Fair Valued Security. Fair Values are determined pursuant to procedures approved by the Board of Directors. See Note (2).

(c) Illiquid Security.

(d) Non-income producing security.

(e) Represents contributed capital.

(f) Restricted security, not readily marketable. (See Note 6).

(g) As of December 31, 2013, the aggregate amount of open commitments for the Fund is $262,708. (See Note 6).

ADR American Depositary Receipts.

BDR Brazilian Depositary Receipts.

PN Preferred Shares.

PNB Preferred Shares, Class B.

See Notes to Financial Statements.

8 | Aberdeen Latin America Equity Fund, Inc. | |

| | |

Statement of Assets and Liabilities | | | |

| | | |

As of December 31, 2013 | | | |

| | | |

Assets | | | |

| | | |

Investments, at value (Cost $199,992,414) | | $ | 246,635,086 | |

Cash (including $936,036 of foreign currencies with a cost of $1,078,248) | | 936,126 | |

Dividends receivable | | 587,424 | |

Prepaid expenses and other assets | | 42,053 | |

Total assets | | | 248,200,689 | |

| | | |

Liabilities | | | |

Dividends and Distributions (Note 2) | | 14,704,862 | |

Investment advisory fees payable (Note 3) | | 519,444 | |

Administration fees payable (Note 3) | | 52,472 | |

Investor relations fees payable (Note 3) | | 20,922 | |

Directors’ fees payable | | 8,275 | |

Chilean repatriation taxes (Note 2) | | 202,159 | |

Accrued expenses and other liabilities | | 161,843 | |

Total liabilities | | 15,669,977 | |

| | | |

Net Assets | | $ | 232,530,712 | |

| | | |

Net Assets consist of | | | |

Capital stock, $0.001 par value (Note 5) | | $ | 7,449 | |

Paid-in capital | | 185,585,048 | |

Distributions in excess of net investment income | | (483,826 | ) |

Accumulated net realized gain on investments and foreign currency related transactions | | 783,918 | |

Net unrealized appreciation on investments and foreign currency translation | | 46,638,123 | |

Net Assets applicable to shares outstanding | | $ | 232,530,712 | |

Net asset value per share, based on 7,448,517 shares issued and outstanding | | $ | 31.22 | |

| | | |

| | | |

See Notes to Financial Statements. | | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| Aberdeen Latin America Equity Fund, Inc. | 9 |

| | | |

| | | |

| | | | | | |

| | |

Statement of Operations | | | |

| | | |

For the Year Ended December 31, 2013 | | | |

| | | |

Investment Income | | | |

| | | |

Income: | | | |

Dividends and other income | | $ 8,507,758 | |

Less: Foreign taxes withheld | | (575,938 | ) |

Total investment income | | 7,931,820 | |

| | | |

Expenses: | | | |

Investment advisory fees (Note 3) | | 2,272,154 | |

Custodian’s fees and expenses | | 208,850 | |

Directors’ fees and expenses | | 186,331 | |

Administration fees (Note 3) | | 167,307 | |

Investor relations fees and expenses (Note 3) | | 76,170 | |

Independent auditor’s fees and expenses | | 63,480 | |

Insurance expense | | 60,583 | |

Reports to shareholders and proxy solicitation | | 58,650 | |

Transfer agent’s fees and expenses | | 23,546 | |

Legal fees and expenses | | 11,330 | |

Miscellaneous | | 27,284 | |

Chilean repatriation taxes (Note 2) | | 20,554 | |

Total expenses | | 3,176,239 | |

Less: Fee waivers (Note 3) | | (51,808 | ) |

Net expenses | | 3,124,431 | |

| | | |

Net investment income | | 4,807,389 | |

| | | |

Net Realized and Unrealized Gain/(Loss) on Investments and Foreign Currency Related Transactions | | | |

Net realized gain/(loss) on: | | | |

Investment transactions* | | 11,494,135 | |

Foreign currency transactions | | (175,276 | ) |

Net change in unrealized depreciation of investments and foreign currency translation (Note 2) | | (58,063,042 | ) |

Net realized and unrealized loss on investments and foreign currency transactions | | (46,744,183 | ) |

Net Decrease in Net Assets Resulting from Operations | | $ (41,936,794 | ) |

| | | |

* Includes realized gain distributions from underlying venture capital investments of $64,591. | | | |

| | | |

| | | |

See Notes to Financial Statements. | | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

10 | Aberdeen Latin America Equity Fund, Inc. | |

| | | |

| | | |

| | | | | |

| | |

Statements of Changes in Net Assets | | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | For the | | | For the | |

| | | Year Ended

December 31, 2013 | | | Year Ended

December 31, 2012 | |

| | | | | | | |

Increase/(Decrease) in Net Assets | | | | | | | |

| | | | | | | |

Operations: | | | | | |

Net investment income | | | $ | 4,807,389 | | | $ | 4,122,294 | |

Net realized gain on investments and foreign currency related transactions | | | 11,318,859 | | | 19,475,147 | |

Net change in unrealized appreciation/(depreciation) on investments and foreign currency translations | | | (58,063,042 | ) | | 40,491,565 | |

Net increase/(decrease) in net assets resulting from operations | | | (41,936,794 | ) | | 64,089,006 | |

| | | | | | | |

Dividends and distributions to shareholders from: | | | | | | | |

Net investment income | | | (2,950,879 | ) | | (3,045,103 | ) |

Net realized gain on investments | | | (22,156,582 | ) | | (8,973,824 | ) |

Total dividends and distributions to shareholders | | | (25,107,461 | ) | | (12,018,927 | ) |

Total increase/(decrease) in net assets resulting from operations | | | (67,044,255 | ) | | 52,070,079 | |

| | | | | | | |

Net Assets | | | | | | | |

Beginning of year | | | 299,574,967 | | | 247,504,888 | |

End of year* | | | $ | 232,530,712 | | | $ | 299,574,967 | |

| | | | |

* Includes distributions in excess of net investment income of $(483,826) and $(1,863,736), respectively. | |

| | | | | | | |

| | | | | | | |

See Notes to Financial Statements. | | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| Aberdeen Latin America Equity Fund, Inc. | 11 |

| | | | | | | |

| | | | | | | |

| | | | | | | | | | | | | |

Financial Highlights

| | For the Fiscal Years Ended December 31, | |

| | 2013 | | 2012 | | 2011 | | 2010 | | 2009 | |

PER SHARE OPERATING PERFORMANCE(a) | | | | | | | | | | | |

Net asset value, beginning of year | | $40.22 | | $33.23 | | $41.95 | | $43.41 | | $21.26 | |

Net investment income | | 0.65 | | 0.55 | | 0.71 | | 0.44 | | 0.58 | |

Net realized and unrealized gain/(loss) on investments and foreign currency related transactions | | (6.28 | ) | 8.05 | | (7.44 | ) | 8.19 | | 22.54 | |

Net increase/(decrease) in net assets resulting from operations | | (5.63 | ) | 8.60 | | (6.73 | ) | 8.63 | | 23.12 | |

Dividends and distributions to shareholders: | | | | | | | | | | | |

Net investment income | | (0.40 | ) | (0.41 | ) | (0.65 | ) | (0.47 | ) | (1.00 | ) |

Net realized gain | | (2.97 | ) | (1.20 | ) | (1.34 | ) | (9.62 | ) | – | |

Total dividends and distributions to shareholders | | (3.37 | ) | (1.61 | ) | (1.99 | ) | (10.09 | ) | (1.00 | ) |

Anti-dilutive impact due to capital shares tendered | | – | | – | | – | | – | | 0.03 | |

Net asset value, end of year | | $31.22 | | $40.22 | | $33.23 | | $41.95 | | $43.41 | |

Market value, end of year | | $28.05 | | $36.24 | | $30.10 | | $38.72 | | $39.42 | |

Total Investment Return Based on:(b) | | | | | | | | | | | |

Market value | | (13.38% | ) | 25.53% | | (17.47% | ) | 24.75% | | 120.93% | |

Net asset value | | (13.13% | )(d) | 26.20% | (d) | (15.90% | ) | 22.74% | | 109.30% | |

Ratio/Supplementary Data | | | | | | | | | | | |

Net assets, end of year (000 omitted) | | $232,531 | | $299,575 | | $247,505 | | $312,472 | | $265,101 | |

Average net assets (000 omitted) | | $278,822 | | $277,904 | | $291,612 | | $268,440 | | $194,682 | |

Ratio of expenses to average net assets, net of fee waivers(c) | | 1.12% | | 1.16% | | 1.18% | | 1.35% | | 1.28% | |

Ratio of expenses to average net assets, excluding fee waivers(c) | | 1.14% | | 1.18% | | 1.18% | | 1.35% | | 1.28% | |

Ratio of expenses to average net assets, excluding fees waivers and taxes | | 1.11% | | 1.14% | | 1.16% | | 1.27% | | 1.21% | |

Ratio of net investment income to average net assets | | 1.72% | | 1.48% | | 1.82% | | 1.03% | | 1.84% | |

Portfolio turnover rate | | 14.36% | | 16.47% | | 11.93% | | 7.52% | | 75.70% | |

(a) Based on average shares outstanding.

(b) Total investment return is calculated assuming a purchase of common stock on the first day and a sale on the last day of each reporting period. Dividends and distributions, if any, are assumed, for purposes of this calculation to be reinvested at prices obtained under the Fund’s dividend reinvestment plan. Total investment return does not reflect brokerage commissions.

(c) Ratios include the effect of Chilean taxes.

(d) The total return shown above includes the impact of financial statement rounding of the NAV per share.

See Notes to Financial Statements.

12 | Aberdeen Latin America Equity Fund, Inc. | |

Notes to Financial Statements

December 31, 2013

1. Organization

Aberdeen Latin America Equity Fund, Inc. (the “Fund”) was incorporated in Maryland on April 17, 1990 and commenced investment operations on October 30, 1991. The Fund is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as a non-diversified closed-end, management investment company. The Fund trades on the NYSE MKT under the ticker symbol “LAQ”.

The Fund seeks long-term capital appreciation by investing primarily in Latin American equity securities.

2. Summary of Significant Accounting Policies

The following is a summary of significant accounting policies followed by the Fund in the preparation of its financial statements. The policies conform to accounting principles generally accepted in the United States of America (“GAAP”). The preparation of financial statements requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, disclosure of contingent assets and liabilities at the date of the financial statements, and the reported amounts of income and expenses for the period. Actual results could differ from those estimates. The accounting records of the Fund are maintained in U.S. Dollars.

(a) Security Valuation:

The Fund is required to value its securities at fair market value, which is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

Equity securities that are traded on an exchange are valued at the last quoted sale price on the principal exchange on which the security is traded at the “Valuation Time” subject to application, when appropriate, of the valuation factors described in the paragraph below. The Valuation Time is as of the close of regular trading on the New York Stock Exchange (usually 4:00 p.m. Eastern Time). In the absence of a sale price, the security is valued at the mean of the bid/ask price quoted at the close on the principal exchange on which the security is traded. Securities traded on NASDAQ are valued at the NASDAQ official closing price. Closed-end funds and exchange-traded funds (“ETFs”) are valued at the market price of the security at the Valuation Time. A security using any of these pricing methodologies is determined to be a Level 1 investment.

Foreign equity securities that are traded on foreign exchanges that close prior to the Valuation Time are valued by applying valuation factors to the last sale price or the mean price as noted above. Valuation factors are provided by an independent pricing service provider. These valuation factors are used when pricing the Fund’s portfolio holdings to estimate market movements between the time foreign markets close and the time the Fund values such foreign securities. These

valuation factors are based on inputs such as depositary receipts, indices, futures, sector indices/ETFs, exchange rates, and local exchange opening and closing prices of each security. When prices with the application of valuation factors are utilized, the value assigned to the foreign securities may not be the same as quoted or published prices of the securities on their primary markets. A security that applies a valuation factor is determined to be a Level 2 investment because the exchange-traded price has been adjusted. Valuation factors are not utilized if the independent pricing service provider is unable to provide a valuation factor or if the valuation falls below a predetermined threshold; in such case, the security is determined to be a Level 1 investment.

In the event that a security’s market quotation is not readily available or is deemed unreliable (for reasons other than because the foreign exchange on which they trade closed prior to the Valuation Time), the security is valued at fair value as determined by the Fund’s Pricing Committee (which is appointed by the Board of Directors), taking into account the relevant factors and surrounding circumstances using valuation policies and procedures approved by the Board. A security that has been fair valued by the Pricing Committee may be classified as Level 2 or 3 depending on the nature of the inputs.

The Fund also invests in a venture capital private placement security, which represented 0.04% of the net assets of the Fund as of December 31, 2013. The capital private placement security is deemed to be a restricted security. In the absence of readily ascertainable market values this security is valued at fair value as determined in good faith by, or under the direction of the Board, under procedures established by the Board. The Fund’s estimate of fair value assumes a willing buyer and a willing seller neither of whom are acting under the compulsion to buy or sell. Although this security may be resold in privately negotiated transactions, the price realized on such sales could differ from the price originally paid by the Fund or the current carrying values, and the difference could be material. This security is categorized as Level 3 investment. Level 3 investments have significant unobservable inputs, as they trade infrequently. In determining the fair value of these investments, management uses the market approach which includes as the primary input the capital balance reported; however, adjustments to the reported capital balance may be made based on various factors, including, but not limited to, the attributes of the interest held, including the rights and obligations, and any restrictions or illiquidity of such interests, and the fair value of these venture capital investments.

In accordance with the authoritative guidance on fair value measurements and disclosures under GAAP, the Fund discloses the fair value of its investments using a three level hierarchy that classifies the inputs to valuation techniques used to measure the fair value. The

| Aberdeen Latin America Equity Fund, Inc. | 13 |

Notes to Financial Statements (continued)

December 31, 2013

hierarchy assigns Level 1 measurements to valuations based upon unadjusted quoted prices in active markets for identical assets, Level 2 measurements to valuations based upon other significant observable input, including adjusted quoted prices in active markets for identical assets and Level 3 measurements to valuations based upon unobservable inputs that are significant to the valuation. Observable inputs are inputs that reflect the assumptions market participants would use in pricing the asset or liability, which are based on market data obtained from sources independent of the reporting entity. Unobservable inputs are inputs that reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing the asset or liability developed based on the best information

available in the circumstances. The three-tier hierarchy of inputs is summarized below:

Level 1 – quoted prices in active markets for identical investments;

Level 2 – other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc); or

Level 3 – significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments).

A financial instrument’s level within the fair value hierarchy is based upon the lowest level of any input that is significant to the fair value measurement.

The following is a summary of the inputs used as of December 31, 2013 in valuing the Fund’s investments carried at fair value. The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. Refer to the Portfolio of Investments for a detailed breakout of the security types:

Investments, at value | | Level 1 | | Level 2 | | Level 3 | | Balance as of

12/31/2013 | |

Long-Term Investments | | | | | | | | | |

Venture Capital | | $– | | $– | | $95,465 | | $95,465 | |

Water Utilities | | – | | 2,857,648 | | – | | 2,857,648 | |

Other | | 240,916,973 | | – | | – | | 240,916,973 | |

Short-Term Investments | | – | | 2,765,000 | | – | | 2,765,000 | |

Total | | $240,916,973 | | $5,622,648 | | $95,465 | | $246,635,086 | |

Amounts listed as “–” are $0 or round to $0.

For movements between the levels within the fair value hierarchy, the Fund has adopted a policy of recognizing transfers at the end of each period. For the year ended December 31, 2013, there have been no transfers between levels and no significant changes to the fair valuation methodologies.

The significant unobservable inputs used in the fair value measurement of the Fund’s venture capital holdings are audited financial statements, expenses incurred from the partnership, interim financial statements, capital calls, and distributions. These unobservable inputs are used by taking the most recent quarterly valuation statements and adjusting the value using the unobservable inputs mentioned above. Significant increases (decreases) in any of those inputs in isolation would result in a significantly lower (higher) fair value measurement.

| | Fair Value

at 12/31/13 | | Valuation Technique | | Unobservable Inputs | | Range |

Venture Capital | | $95,465 | | Partner Capital Value/Net Asset Value | | Capital Calls & Distributions | | $0 – ($47,865) |

The following is a reconciliation of investments in which significant unobservable inputs (Level 3) were used in determining value:

Investments, at value | | Balance as of 12/31/2012 | | Accrued discounts/ premiums | | Realized gain/(loss) | | Change in unrealized appreciation/ (depreciation) | | Capital Contributed | | Distributions/ Sales | | Transfers into Level 3 | | Transfers out of Level 3 | | Balance as of 12/31/2013 | |

Venture Capital | | $185,775 | | $– | | $(871,918) | | $810,437 | | $58,182 | | $(87,011) | | $– | | $– | | $95,465 | |

Total | | $185,775 | | $– | | $(871,918) | | $810,437 | | $58,182 | | $(87,011) | | $– | | $– | | $95,465 | |

Change in unrealized appreciation/depreciation relating to Level 3 investments still held at December 31, 2013 is $(3,621).

14 | Aberdeen Latin America Equity Fund, Inc. | |

Notes to Financial Statements (continued)

December 31, 2013

(b) Short-Term Investment:

The Fund sweeps available cash into a short-term time deposit available through Brown Brothers Harriman & Co. (“BBH & Co.”), the Fund’s custodian. The short-term time deposit is a variable rate account classified as a short-term investment.

(c) Foreign Currency Translations:

Foreign securities, currencies, and other assets and liabilities denominated in foreign currencies are translated into U.S. Dollars at the exchange rate of said currencies against the U.S. Dollar, as of the Valuation Time, as provided by an independent pricing service approved by the Board.

Foreign currency amounts are translated into U.S. Dollars on the following basis:

(I) market value of investment securities, other assets and liabilities at the rate of exchange at the Valuation Time; and

(II) purchases and sales of investment securities, income and expenses at the relevant rates of exchange prevailing on the respective dates of such transactions.

The Fund does not isolate that portion of gains and losses on investments in equity securities which is due to changes in the foreign exchange rates from that which is due to changes in market prices of equity securities. Accordingly, realized and unrealized foreign currency gains and losses with respect to such securities are included in the reported net realized and unrealized gains and losses on investment transactions balances.

The Fund reports certain foreign currency related transactions and foreign taxes withheld on security transactions as components of realized gains for financial reporting purposes, whereas such foreign currency related transactions are treated as ordinary income for U.S. federal income tax purposes.

Net unrealized currency gains or losses from valuing foreign currency denominated assets and liabilities at period end exchange rates are reflected as a component of net unrealized appreciation/depreciation in value of investments, and translation of other assets and liabilities denominated in foreign currencies.

Net realized foreign exchange gains or losses represent foreign exchange gains and losses from transactions in foreign currencies and forward foreign currency contracts, exchange gains or losses realized between the trade date and settlement date on security transactions, and the difference between the amounts of interest and dividends recorded on the Fund’s books and the U.S. dollar equivalent of the amounts actually received.

Foreign security and currency transactions may involve certain considerations and risks not typically associated with those of domestic

origin, including unanticipated movements in the value of the foreign currency relative to the U.S. Dollar. When the U.S. Dollar rises in value against foreign currency, the Fund’s investments denominated in that currency will lose value because its currency is worth fewer U.S. Dollars; the opposite effect occurs if the U.S. Dollar falls in relative value.

(d) Security Transactions and Investment Income:

Security transactions are recorded on the trade date. Realized and unrealized gains/(losses) from security and currency transactions are calculated on the identified cost basis. Dividend income is recorded on the ex-dividend date except for certain dividends on foreign securities, which are recorded as soon as the Fund is informed after the ex-dividend date. Interest income and expenses are recorded on an accrual basis.

(e) Distributions:

On an annual basis, the Fund intends to distribute its net realized capital gains, if any, by way of a final distribution to be declared during the calendar quarter ending December 31. Dividends and distributions to shareholders are recorded on the ex-dividend date.

Dividends and distributions to shareholders are determined in accordance with federal income tax regulations, which may differ from GAAP. These differences are primarily due to differing treatments for passive foreign investment companies, wash sales, foreign taxes passed through to shareholders, investments in partnerships, and foreign currencies.

(f) Federal Income Taxes and Foreign Taxes:

The Fund intends to continue to qualify as a “regulated investment company” by complying with the provisions available to certain investment companies, as defined in Subchapter M of the Internal Revenue Code of 1986, as amended, and to make distributions of net investment income and net realized capital gains sufficient to relieve the Fund from all, or substantially all, federal income taxes. Therefore, no federal income tax provision is required.

Income received by the Fund from sources within certain Latin America countries may be subject to withholding and other taxes imposed by such countries. Also, certain Latin American countries impose taxes on funds remitted or repatriated from such countries.

The Fund incurs foreign Chilean taxes on income and realized gains generated from Chilean securities with no Chilean market presence. For the year ended December 31, 2013, the Fund incurred $20,554 of such expenses. The Fund also accrues foreign Chilean taxes on securities with little to no Chilean market presence in an amount equal to what the Fund would owe if the securities were sold and the proceeds repatriated on the valuation date as a liability and reduction of unrealized gains. As of December 31, 2013 there was no accrual necessary.

| Aberdeen Latin America Equity Fund, Inc. | 15 |

Notes to Financial Statements (continued)

December 31, 2013

The Fund recognizes the tax benefits of uncertain tax positions only where the position is “more likely than not” to be sustained assuming examination by tax authorities. Management of the Fund has concluded that there are no significant uncertain tax positions that would require recognition in the financial statements. Since tax authorities can examine previously filed tax returns, the Fund’s U.S. federal and state tax returns for each of the four years up to the year ended December 31, 2013 are subject to such review.

(g) Partnership Accounting Policy:

The Fund records its pro-rata share of the income/(loss) and capital gains/(losses) allocated from the underlying partnerships and adjusts the cost of the underlying partnerships accordingly. These amounts are included in the Fund’s Statement of Operations.

3. Agreements and Transactions with Affiliates and Other Service Providers

(a) Investment Adviser:

Aberdeen Asset Managers Limited (“AAML”) serves as the Fund’s investment adviser with respect to all investments. AAML is a direct wholly-owned subsidiary of Aberdeen Asset Management PLC. AAML receives, as compensation for its advisory services from the Fund, an annual fee, calculated weekly and paid quarterly, equal to 1.00% of the first $100 million of the Fund’s average weekly market value or net assets (whichever is lower), 0.90% of the next $50 million and 0.80% of amounts above $150 million. Effective March 6, 2013, AAML has agreed to contractually waive a portion of its advisory fee. Prior to March 6, 2013, AAML voluntarily waived an equal portion of its advisory fee. For the year ended December 31, 2013, AAML earned $2,272,154 for advisory services, of which AAML waived $51,808.

(b) Fund Administration:

BBH & Co. is the U.S. Administrator for the Fund and certain other funds advised by AAML and its affiliates (collectively the “Funds”). The Funds pay BBH & Co. a monthly administration and fund accounting service fee at an annual rate of 0.02% of the Funds’ aggregate assets up to $250 million, 0.015% for the next $250 million and 0.01% in excess of $500 million.

The Fund pays its pro rata portion of the fee based on its level of assets with a monthly minimum of $2,500. For the year ended December 31, 2013, BBH & Co. earned $41,191 from the Fund for administrative and fund accounting services.

BTG Pactual Chile S.A. Administradora de Fondos de Inversien de Capital Extranjero (formerly, Celfin Capital S.A. Administradora de Fondos de Capital Extranjero) (“BTG Pactual Chile”) serves as the Fund’s Chilean administrator. For its services, BTG Pactual Chile is paid an annual fee by the Fund equal to the greater of 2,000 Unidad de Fomentos (“U.F.s”) or 0.10% of the Fund’s average weekly market value

or net assets invested in Chile (whichever is lower) and an annual reimbursement of out-of pocket expenses not to exceed 500 U.F.s. In addition, an accounting fee is also paid to BTG Pactual Chile. For the year ended December 31, 2013, the administration fees and accounting fees earned by BTG Pactual Chile from the Fund amounted to $116,503 and $9,613, respectively.

Please see Note 11, “Subsequent Events” for more information.

(c) Investor Relations:

Under the terms of an Investor Relations Services Agreement, Aberdeen Asset Management Inc. (“AAMI”), an affiliate of AAML, serves as the Fund’s investor relations services provider.

Pursuant to the terms of the Investor Relations Services Agreement, AAMI provides, among other things, objective and timely information to shareholders based on publicly-available information; provides information efficiently through the use of technology while offering shareholders immediate access to knowledgeable investor relations representatives; develops and maintains effective communications with investment professionals from a wide variety of firms; creates and maintains investor relations communication materials such as fund manager interviews, films and webcasts, published white papers, magazine and articles and other relevant materials discussing the Fund’s investment results, portfolio positioning and outlook; develops and maintains effective communications with large institutional shareholders; responds to specific shareholder questions; and reports activities and results to the Board and management detailing insight into general shareholder sentiment.

For the year ended December 31, 2013, the Fund incurred fees of approximately $74,424 for investor relations services. Investor relations fees and expenses in the Statement of Operations include certain out-of-pocket expenses.

(d) Director Purchase Plan:

Fifty percent (50%) of the annual retainer of the Independent Directors is invested in Fund shares and, at the option of each Independent Director, 100% of the annual retainer can be invested in shares of the Fund. During the year ended December 31, 2013, 1,688 shares were purchased pursuant to the Directors compensation plan. As of December 31, 2013, the Directors as a group owned less than 1% of the Fund’s outstanding shares.

4. Investment Transactions

For the year ended December 31, 2013, Fund purchases and sales of securities, other than short-term investments, were $39,580,916 and $58,455,174, respectively.

16 | Aberdeen Latin America Equity Fund, Inc. | |

Notes to Financial Statements (continued)

December 31, 2013

5. Capital

The authorized capital stock of the Fund is 100,000,000 shares of common stock, $0.001 par value. As of December 31, 2013 there were 7,448,517 common shares issued and outstanding.

6. Restricted Securities

Certain of the Fund’s investments are restricted as to resale and are valued at fair value as determined in good faith by, or under the direction of, the Board under procedures established by the Board in the absence of readily ascertainable market values.

Security | | Acquisition Date(s) | | Cost | | Fair Value

at 12/31/13 | | Percent of

Net Assets | | Distributions

Received | | Open

Commitments | |

Emerging Markets Ventures l, L.P. | | 01/22/98 – 01/10/06 | | $785,672 | | $95,465 | | 0.04 | | $2,558,766 | | $262,708 | |

Total | | | | $785,672 | | $95,465 | | 0.04 | | $2,558,766 | | $262,708 | |

The Fund may incur certain costs in connection with the disposition of the above securities.

7. Open Market Repurchase Program

The Board authorized, but does not require, Fund management to make open market purchases from time to time in an amount up to 10% of the Fund’s outstanding shares, in accordance with Rule 10b-18 under the Securities Exchange Act of 1934, as amended, and other applicable federal securities laws. Such purchases may be made when, in the reasonable judgment of Fund management, such repurchases may enhance shareholder value and when the Fund’s shares are trading at a discount to net asset value of 12% or more, subject to intraday fluctuations that may result in repurchases at discounts below 12%. The Board has instructed Fund management to report repurchase activity to it regularly, and to post the number of shares repurchased on the Fund’s website on a monthly basis. For the year ended December 31, 2013, the Fund did not repurchase shares through this program.

8. Portfolio Investment Risks

(a) Risks Associated with Foreign Securities and Currencies:

Investments in securities of foreign issuers carry certain risks not ordinarily associated with investments in securities of U.S. issuers. These risks include, among others, future political and economic developments, and the possible imposition of exchange controls or other foreign governmental laws and restrictions. In addition, with respect to certain countries, there is the possibility of expropriation of assets, confiscatory taxation, political or social instability or diplomatic developments, which could adversely affect investments in those countries.

Certain countries may also impose substantial restrictions on investments in their capital markets by foreign entities, including restrictions on investments in issuers of industries deemed sensitive to relevant national interests. These factors may limit the investment opportunities available and result in a lack of liquidity and high price volatility with respect to securities of issuers from developing countries.

(b) Risks Associated with Latin American Markets:

The Latin American securities markets are substantially smaller, less liquid and more volatile than the major securities markets in the United States. A high proportion of the securities of many companies in Latin American countries may be held by a limited number of persons, which may limit the number of securities available for investment by the Fund. The limited liquidity of Latin American country securities markets may also affect the Fund’s ability to acquire or dispose of securities at the price and time it wishes to do so.

(c) Risks of concentrating investments in Brazil:

The Fund’s performance will be influenced by political, social and economic factors affecting Brazil. Special risks include exposure to currency fluctuations, less liquidity, less developed or efficient trading markets, lack of comprehensive company information, political instability and differing accounting and legal standards. Because the Fund’s investments are concentrated in Brazil, the Fund’s performance could be more volatile than that of more geographically diversified funds.

As an emerging market, the Brazilian market tends to be more volatile than the markets of more mature economies, and generally has a less diverse and less mature economic structure and a less stable political system than those of developed countries. Certain political, economic, legal and currency risks have contributed to a high level of price volatility in the Brazilian equity and currency markets and could adversely affect investments in the Fund. Brazil has historically experienced high rates of inflation and may continue to do so. Inflationary pressures may slow the rate of growth of the Brazilian economy and may lead to further government intervention in the economy, which could adversely affect the fund’s investments. Brazil continues to suffer from chronic structural public sector deficits. Unanticipated political or social developments may result in increased volatility in the Fund’s share price and sudden and significant investment losses.

| Aberdeen Latin America Equity Fund, Inc. | 17 |

Notes to Financial Statements (continued)

December 31, 2013

(d) Risks Associated with Restricted Securities:

The Fund, subject to local investment limitations, may invest up to 10% of its assets (at the time of commitment) in illiquid equity securities, including securities of venture capital funds (whether in corporate or partnership form) that invest primarily in emerging markets. When investing through another investment fund, the Fund will bear its proportionate share of the expenses incurred by that underlying fund, including management fees. Such securities are expected to be illiquid which may involve a high degree of business and financial risk and may result in substantial losses. Because of the current absence of any liquid trading market for these investments, the venture capital funds may take longer to liquidate than would be the case for publicly traded securities. Although these securities may be resold in privately negotiated transactions, the prices realized on such sales could be substantially less than those originally paid by the Fund or the current carrying values and these differences could be material. Further, companies whose securities are not publicly traded may not be subject

to the disclosures and other investor protection requirements applicable to companies whose securities are publicly traded.

9. Contingencies

In the normal course of business, the Fund may provide general indemnifications pursuant to certain contracts and organizational documents. The Fund's maximum exposure under these arrangements is dependent on future claims that may be made against the Fund and, therefore, cannot be estimated; however, based on experience, the risk of loss from such claims is considered remote.

10. Tax Information

The U.S. federal income tax basis of the Fund's investments and the net unrealized appreciation as of December 31, 2013 were as follows:

Tax Basis of

Investments | | Appreciation | | Depreciation | | Net

Unrealized

Appreciation | |

$200,126,460 | | $74,861,494 | | $(28,352,868) | | $46,508,626 | |

Income and capital gain distributions are determined in accordance with federal income tax regulations, which may differ from GAAP.

The tax character of distributions paid during the fiscal years ended December 31, 2013 and December 31, 2012 was as follows:

| | December 31, 2013 | | December 31, 2012 | |

Distributions paid from: | | | | | |

Ordinary income | | $3,559,088 | | $3,079,217 | |

Long-term capital gains | | $21,548,373 | | $8,939,710 | |

Total tax character of distributions | | $25,107,461 | | $12,018,927 | |

At December 31, 2013, the components of accumulated earnings on a tax basis, for the Fund were as follows:

Undistributed ordinary income | | 434,137 | |

Other book/tax differences | | (134,046 | ) |

Unrealized appreciation | | $46,638,123 | |

Total accumulated earnings | | $46,938,214 | |

During the year ended December 31, 2013, the Fund did not have any and, therefore, did not utilize any capital loss carryforwards. Under the Regulated Investment Company Modernization Act of 2010, the Fund is permitted to carry forward capital losses incurred in taxable years beginning after December 22, 2010 for an unlimited period. However, any losses incurred during those future taxable years will be required to be utilized prior to the losses incurred in pre-enactment taxable years. As a result of this ordering rule, pre-enactment capital loss carryforwards may be more likely to expire unused. Additionally, post-enactment capital losses that are carried forward will retain their character as either short-term or long-term capital losses rather than being considered all short-term as under previous law.

GAAP requires that certain components of net assets be adjusted to reflect permanent differences between financial and tax reporting. Accordingly, during the year ended December 31, 2013, $476,600 has been reclassified from undistributed net investment income and $476,600 to accumulated net realized gain on investments and foreign currency related transactions as a result of permanent differences primarily attributable to partnership investments, foreign currencies, and dividend redesignations. These reclassifications have no effect on net assets or net asset values per share.

11. Subsequent Events

Management has evaluated the need for disclosures and/or adjustments resulting from subsequent events through the date the

18 | Aberdeen Latin America Equity Fund, Inc. | |

Notes to Financial Statements (concluded)

December 31, 2013

financials statements were issued. Based on this evaluation, no adjustments were required to the financial statements as of December 31, 2013.

On December 10, 2013, the Board of Directors approved a transition of services from BBH & Co., the Fund's administrator and custodian, to AAMI and State Street Bank and Trust Company ("State Street"). AAMI was approved as the Fund's administrator pursuant to an Administration Agreement between the Fund and AAMI, under which

the Fund will pay AAMI 0.08% of the Fund's average net monthly assets, computed monthly. State Street will serve as the Fund's sub-administrator pursuant to a Sub-Administration Agreement between AAMI and State Street, under which AAMI will pay State Street a sub-administration fee. The Board approved State Street as the Fund's custodian, to serve pursuant to a Custodian Agreement between the Fund and State Street. Management anticipates that the transition of services from BBH & Co. to AAMI and State Street will be complete as of April 1, 2014.

| Aberdeen Latin America Equity Fund, Inc. | 19 |

Report of Independent Registered Public Accounting Firm

To the Board of Directors and Shareholders of

Aberdeen Latin America Equity Fund, Inc.:

In our opinion, the accompanying statement of assets and liabilities, including the portfolio of investments, and the related statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of Aberdeen Latin America Equity Fund, Inc. (the "Fund") at December 31, 2013, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as "financial statements") are the responsibility of the Fund's management; our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities at December 31, 2013 by correspondence with the custodian and venture capital issuers, provide a reasonable basis for our opinion.

PricewaterhouseCoopers LLP

February 27, 2014

20 | Aberdeen Latin America Equity Fund, Inc. | |

Tax Information (unaudited)

The following information is provided with respect to the distributions paid by The Latin America Equity Fund, Inc. during the fiscal year ended December 31, 2013:

Payable

Date | | Total Cash

Distribution | | Long-Term

Capital

Gain | | Net

Ordinary

Dividends | | Foreign

Taxes

Paid(1) | | Gross

Ordinary

Dividend | | Qualified

Dividends(2) | | Foreign

Source

Income | |

10/18/13 | | 1.396600 | | 1.3682 | | 0.02840 | | 0.038661 | | 0.067061 | | 0.031679 | | 100% | |

01/17/14 | | 1.974200 | | 1.56608 | | 0.40812 | | 0.038661 | | 0.446781 | | 0.211059 | | 100% | |

| | | | | | | | | | | | | | | |

(1) | The foreign taxes paid represent taxes incurred by the Fund on interest received from foreign sources. Foreign taxes paid may be included in taxable income with an offsetting deduction from gross income or may be taken as a credit for taxes paid to foreign governments. You should consult your tax advisor regarding the appropriate treatment of foreign taxes paid. |

(2) | The Fund hereby designates the amount indicated above or the maximum amount allowable by law. |

| Aberdeen Latin America Equity Fund, Inc. | 21 |

Supplemental Information (unaudited)

Board Approval of Investment Advisory Agreement

The Investment Company Act of 1940 (the "1940 Act") and the terms of the investment advisory agreement (the "Advisory Agreement") between the Aberdeen Latin America Equity Fund, Inc. (the "Fund") and Aberdeen Asset Managers Limited (the "Adviser") require that, the Advisory Agreement be approved annually at an in-person meeting by the Board of Directors (the "Board"), including a majority of the Directors who have no direct or indirect interest in the Advisory Agreement and are not "interested persons" of the Fund, as defined in the Investment Company Act (the "Independent Directors").

At its in-person meeting on December 10, 2013, the Board voted unanimously to renew the Advisory Agreement between the Fund and the Adviser. In considering whether to approve the renewal of the Fund's Advisory Agreement, the Board members received and considered a variety of information provided by the Adviser relating to the Fund, the Advisory Agreement and the Adviser, including comparative performance, fee and expense information of a peer group of funds selected by Strategic Insight Mutual Fund Research and Consulting, LLC ("SI"), an independent third-party provider of investment company data, performance information for relevant benchmark indices and other information regarding the nature, extent and quality of services provided by the Adviser under the Advisory Agreement. The Board's materials also included: (i) information on the investment performance of the Fund and the performance of a peer group of funds and the Fund's performance benchmark; (ii) information on the Fund's advisory fees and other expenses, including information comparing the Fund's expenses to those of a peer group of funds and information about any applicable expense limitations and fee "breakpoints"; (iii) information about the profitability of the Advisory Agreement to the Adviser; (iv) a report prepared by the Adviser in response to a request submitted by the Independent Directors' independent legal counsel on behalf of such Directors; and (v) a memorandum from the Independent Directors' independent legal counsel on the responsibilities of the Board of Directors in considering approval of the investment advisory arrangement under the 1940 Act and Maryland law.

The Board also considered other matters such as: (i) the Adviser's financial results and financial condition, (ii) each Fund's investment objective and strategies, (iii) the Adviser's investment personnel and operations, (iv) the procedures employed to determine the value of the Fund's assets, (v) the allocation of the Fund's brokerage, and the use, if any, of "soft" commission dollars to pay the Fund's expenses and to pay for research and other similar services, (vi) the resources devoted to, and the record of compliance with, the Fund's investment policies and restrictions, policies on personal securities transactions and other compliance policies, and (vii) possible conflicts of interest. Throughout the process, the Board members were afforded the opportunity to ask questions of and request additional information from management.

The Independent Directors were advised by separate independent legal counsel throughout the process. The Independent Directors also consulted in executive sessions with counsel to the Independent Directors regarding consideration of the renewal of the Advisory Agreement. In considering whether to approve the continuation of the Advisory Agreement, the Board, including the Independent Directors, did not identify any single factor as determinative. Individual Directors may have evaluated the information presented differently from one another, giving different weights to various factors. Matters considered by the Board, including the Independent Directors, in connection with its approval of the continuation of the Advisory Agreement included the factors listed below.

In addition to the materials requested by the Board in connection with their consideration of the renewal of the Advisory Agreement, it was noted that the Board received materials in advance of each regular quarterly meeting that provided information relating to the services provided by the Adviser.

As part of their deliberations, the Board members considered the following:

The nature, extent and quality of the services provided to the Fund under the Agreement. The Board considered the nature, extent and quality of the services provided by the Adviser to the Fund and the resources dedicated to the Fund by the Adviser and its affiliates. The Boards reviewed, among other things, the Advisers' investment experience. The Board received information regarding the Adviser's compliance with applicable laws and SEC and other regulatory inquiries or audits of the Fund and the Adviser. The Board also considered the background and experience of the Adviser's senior management personnel and the qualifications, background and responsibilities of the portfolio managers primarily responsible for the day-to-day portfolio management services for the Fund. In addition, the Board considered the financial condition of the Adviser and ability to provide a high level and quality of service to the Fund. The Board also considered information received from the Fund's Chief Compliance Officer regarding the Adviser's compliance policies and procedures. The Board also took into account the Adviser's risk management processes. The Board considered the Adviser' brokerage policies and practices. Management reported to the Board on, among other things, its business plans and organizational changes. The Board also took into account their knowledge of management and the quality of the performance of management's duties through Board meetings, discussion and reports during the preceding year.

22 | Aberdeen Latin America Equity Fund, Inc. | |

Supplemental Information (unaudited) (continued)

Investment performance of the Fund and the Adviser. The Board received and reviewed with management, among other performance data, information compiled by SI as to the Fund's total return, as compared to the funds in the Fund's Morningstar category (the "Morningstar Group"). Additionally, because of the limited number of funds in the Fund's Morningstar Group, the Fund's performance was also compared against a peer group consisting of other comparable closed-end funds (the "Peer Group").

The Board received and considered: information for the Fund's total return on a gross and net basis and relative to the Fund's benchmark; the Fund's share performance and premium/discount information; and the impact of foreign currency movements on the Fund's performance. The Board also received and reviewed information as to the Fund's total return against its Morningstar Group average and other comparable Aberdeen-managed funds and segregated accounts. The Board considered management's discussion of the factors contributing to differences in performance, including differences in the investment strategies of each of these other funds and accounts. The Board also reviewed information as to the Fund's discount/premium ranking relative to its Morningstar Group. The Board took into account management's discussion of the Fund's performance, including that the Fund's annualized net total return was at the median of the Funds in the Fund's Morningstar Group and below the median of the peers in the Fund's Peer Group for the one- and three- year periods ended September 30, 2013. The Fund's annualized total return was above the median of the Fund's Morningstar Group and above the median of the Fund's Peer Group for the five- and ten- year periods ended September 30, 2013. The Board also noted that the Fund's annualized net total returns for the one-, three-, five- and 10-year periods ended September 30, 2013 were above those of the Fund's benchmark, the MSCI EM Latin America Index.

The costs of the services provided and profits realized by the Adviser and its affiliates from their relationships with the Fund.The Board reviewed with management the effective annual management fee rate paid by the Fund to the Adviser for investment management services. Additionally, the Board received and considered information compiled at the request of the Fund by SI, comparing the Fund's effective annual management fee rate with the fees paid by the Peer Group. The Board also took into account the management fee structure, including that management fees for the Fund were based on the Fund's total managed assets. Management noted that due to the unique strategy and structure of the Fund, Aberdeen currently does not have any closed-end funds that are directly comparable to the Fund. Management provided to the Board the annual fee schedules, payable monthly, for each US closed-end, country-specific equity fund managed by AAMAL. Although there were no other substantially similar Aberdeen-advised US vehicles against which to compare advisory fees, the Adviser provided information for other Aberdeen products with similar investment strategies to those of the Fund where available. In evaluating the Fund's advisory fees, the Board took into account the demands, complexity and quality of the investment management of the Fund.

In addition to the foregoing, the Board considered the Fund's fees and expenses as compared to its Peer Group, consisting of closed-end funds in the Fund's Morningstar expense category as compiled by SI, which indicated that the Fund's effective management fee rate (computed based on average managed assets for the six months ended June 30, 2013, and which reflects both the advisory fee and the current administration fee) was below the median expense ratio of its Peer Group; and, the Fund's annualized net total expense ratio based on average net assets for the six months ended June 30, 2013 was below the median of the Peer Group.