Exhibit 17(c)

Annual Report to Shareholders

December 31, 2009

Western Asset Funds, Inc.

Western Asset Absolute Return Portfolio

Western Asset High Yield Portfolio

Western Asset Inflation Indexed Plus Bond Portfolio

Western Asset Intermediate Bond Portfolio

Western Asset Intermediate Plus Bond Portfolio

Western Asset Limited Duration Bond Portfolio

Western Asset Non-U.S. Opportunity Bond Portfolio

Contents

For more information, visit us on the web

at www.westernassetfunds.com.

Annual Report to Shareholders

Investment Commentary

Western Asset Funds, Inc.

Financial Market Overview

While 2008 was characterized by upheaval in the financial markets, periods of extreme volatility, illiquidity and heightened risk aversion, 2009 was largely a return to more normal conditions and increased investor risk appetite.

Looking back at the tail end of 2008, investors fled fixed-income securities that were seen as being risky and flocked to the relative safety of short-term Treasuries, driving the latter’s prices higher and their yields to historically low levels. In contrast, non-Treasury spreads widened to historically wide levels in some cases, as the market priced in worst-case scenarios. This caused nearly every spread sector to lag equal-durationi Treasuries during the year. While this trend continued in early 2009, some encouraging economic data and a thawing of the once frozen credit markets helped bolster investor confidence.

In a stunning turnaround, by the end of the first quarter of 2009, risk aversion had been replaced by robust demand for riskier, and higher-yielding, fixed-income securities. Despite some temporary setbacks, riskier assets continued to perform well during the remainder of the year. Looking at 2009 as a whole, every spread sector outperformed equal-duration Treasuries.

While economic news often surprised on the upside during 2009, incoming economic data did not suggest a dramatic rebound in growth in 2010. As such, the Federal Reserve Board (“Fed”)ii continued its accommodative monetary policy during 2009. The Fed met eight times in 2009 and, on each occasion, kept the federal funds rateiii in a range of 0 to 1/4 percent. This trend continued at the Fed’s meeting in January 2010. At that time, the Fed said that it “will maintain the target range for the federal funds rate at 0 to 1/4 percent and continues to anticipate that economic conditions, including low rates of resource utilization, subdued inflation trends, and stable inflation expectations, are likely to warrant exceptionally low levels of the federal funds rate for an extended period.”

Economic Review

While the U.S. economy was weak during the first half of the twelve-month reporting period ended December 31, 2009, the lengthiest recession since the Great Depression finally appeared to have ended during the second half of the year.

Looking back, the U.S. Department of Commerce reported that first quarter 2009 U.S. gross domestic product (“GDP”)iv contracted 6.4%. The economic environment then started to get relatively better during the second quarter, as GDP fell 0.7%. The economy’s more modest contraction was due, in part, to smaller declines in both exports and business spending. After contracting four consecutive quarters, the Commerce Department reported that third quarter 2009 GDP growth was 2.2%. A variety of factors helped the economy to expand, including the government’s $787 billion stimulus program, its “Cash for Clunkers” car rebate program, which helped spur an increase in car sales, and tax credits for first-time home buyers. Economic growth then accelerated during the fourth quarter of 2009, as the advance estimate for GDP growth was 5.7%. The Commerce Department cited a slower drawdown in business inventories and consumer spending as contributing factors spurring the economy’s higher growth rate.

Even before GDP advanced in the third quarter, there were signs that the economy was starting to regain its footing. The manufacturing sector, as measured by the Institute for Supply Management’s PMIv, rose to 52.9 in August 2009, the first time it surpassed 50 since January 2008 (a reading below 50 indicates a contraction, whereas a reading above 50 indicates an expansion). PMI data subsequently showed that manufacturing expanded from September through December as well. In addition, December’s PMI reading of 55.9 was the highest since April 2006.

There were some mixed signals from the housing market toward the end of the reporting period. According to its most recent data, the S&P/Case-Shiller Home Price Indexvi indicated that month-over-month home prices rose for the sixth straight month in November. However, according to the National Association of Realtors, while existing home sales rose 7.4% in November, sales fell by nearly 17% in December.

One area that remained weak—and could hamper the magnitude of economic recovery—was the labor market. While monthly job losses have moderated compared to earlier in the year, the unemployment rate remained elevated during the reporting period. After reaching a twenty-six-year high of 10.1% in October 2009, the unemployment rate fell to 10.0% in November and remained unchanged the following month. Since December 2007, the unemployment rate has more than doubled and the number of unemployed workers has risen by more than eight million.

ii

Annual Report to Shareholders

Market Review

Both short- and long-term Treasury yields fluctuated during the reporting period. When the period began, Treasury yields were extremely low, given numerous “flights to quality” that were triggered by the fallout from the financial crisis in 2008. After starting the period at 0.76% and 2.25%, respectively, two- and ten-year Treasury yields then generally moved higher (and their prices lower) until early June. Two- and ten-year yields peaked at 1.42% and 3.98%, respectively, before falling and ending the reporting period at 1.14% and 3.85%, respectively. Over the twelve months ended December 31, 2009, longer-term yields moved higher than their shorter-term counterparts as economic data improved and there were concerns regarding future inflation given the government’s massive stimulus program. In a reversal from 2008, investor risk aversion faded during the twelve-month reporting period, driving spread sector (non-Treasury) prices higher. For the twelve months ended December 31, 2009, the Barclays Capital U.S. Aggregate Indexvii returned 5.93%.

During the reporting period, there was a shift in terms of expectations for inflation. Fears of inflation had increased in mid-2008 (before the reporting period began). This was, in part, due to sharply rising oil prices, which peaked at $145 a barrel in July 2008. Fears of inflation were then replaced with fears of deflation, as global economic conditions weakened and the financial crisis took hold in the fall of 2008. By the end of 2008, oil prices had fallen to $45 a barrel as demand waned and oil reserves moved higher. While inflation, as measured by the Consumer Price Index for All Urban Consumers (“CPI-U”)viii, was 2.7% during the twelve-month period ended December 31, 2009, there were fears of higher inflation in the future. This was due to central banks’ accommodative monetary policies, signs that the global economy was recovering and rising oil prices, which hit $79 a barrel in December 2009. Inflation expectations led to increased demand for U.S. Treasury Inflation-Protected Securities (“TIPS”)ix, and the Barclays Capital Global Real Index: U.S. TIPSx gained 11.41% during the twelve months ended December 31, 2009.

The investment grade bond market generated solid results during the reporting period. Spreads on these securities had moved to extremely wide levels in late 2008, as the weakening economy and credit crunch triggered fears of escalating default rates. Investment grade bond spreads then significantly narrowed in 2009, as the economic environment improved and corporate profits were often better than expected. All told, the investment grade bond asset class, as measured by the Barclays Capital U.S. Credit Indexxi, returned 16.04% during the twelve-month period ended December 31, 2009.

In the mortgage-backed securities market, both agency and non-agency issues did well during the year. Agencies were supported by the government’s purchase programs of these securities as they sought to keep long-term interest rates low in an attempt to revive the housing market. The non-agency sector improved, particularly later in the year, as housing data stabilized and there was positive sentiment surrounding the launch of the Public-Private Investment Program (“PPIP”).

The high-yield bond market produced very strong results during the twelve months ended December 31, 2009. In sharp contrast to its poor results in 2008, the asset class posted positive returns during eleven of the twelve months of the reporting period. This strong rally was due to a variety of factors, including the unfreezing of the credit markets, improving economic data and strong investor demand. All told, the Barclays Capital U.S. Corporate High Yield 2% Issuer Cap Indexxii returned 58.76% for the twelve months ended December 31, 2009.

Emerging market debt prices rallied sharply—posting positive returns during every month but February of 2009. This rally was triggered by rising commodity prices, optimism that the worst of the global recession was over and increased investor risk appetite. Over the twelve months ended December 31, 2009, the JPMorgan Emerging Markets Bond Index Global (“EMBI Global”)xiii returned 28.18%.

Market Outlook

Some economists have floated the notion of a double-dip economic recession because of the expiration of various fiscal and monetary stimulus programs. However, we believe this economic phenomenon seems unlikely. As long as the Fed maintains the current low rate environment, which we believe it will, access to credit should remain sufficient. Given the elevated levels of unemployment, the recent dip in jobless claims is a positive sign that the labor market is stabilizing. The financial market is focused on consumer spending, but we believe more sustained gains in capital expenditures and exports will be key to the U.S. recovery.

We believe that the Fed is likely to keep the federal funds rate anchored at 0 to 1/4 percent in the near future. A large concern the Fed now faces is excess bank reserves. Government support from the Troubled Asset Relief Program (“TARP”) and the Fed’s various special liquidity programs helped banks restore their balance sheets, but banks then held on to reserves in

iii

Annual Report to Shareholders

excess of their capital requirements. As the recovery accelerates, banks may quickly reduce these excess reserves by extending credit. We believe increased lending should stimulate economic activity but, in doing so, might also contribute to inflationary pressures. Therefore, as the Fed manages the level of bank reserves, in our opinion, it must be careful not to inhibit economic growth and increase inflation. As long as the economic recovery is still in its infancy, we believe the Fed should continue its current policies.

Although the labor market is stabilizing, the declining trend in jobless claims reflects a drop-off in layoffs rather than an increase in hires. For unemployment to truly decline, we will need to see specific types of job growth. We believe the source of new job growth will probably have to come from the service sector, as the housing market remains weak and is unlikely to contribute significant new jobs any time soon. The recent increase in industrial production and capacity utilization indicates that factory-related jobs could increase in the coming year.

Despite an uptick in consumer spending in November, most likely due to the holidays, we think consumers will likely continue to demonstrate a more conservative mindset with increased savings and less consumption. Businesses, especially those that are export-oriented, should benefit from a lower U.S. dollar and increased future spending. Corporate profits in the fourth quarter of 2009 showed improvement, leading to a better outlook for the business sector compared to a year ago. Therefore, we think that businesses, rather than consumers, are likely to be the primary contributors to future economic growth. Considering current Fed policies, the likelihood of moderate inflation in the months ahead, a stabilizing labor market and an improved business climate, we find fears of a double-dip recession to be exaggerated.

Western Asset Management Company

January 29, 2010

iv

Annual Report to Shareholders

The views expressed in this commentary reflect those solely of Western Asset Management Company (“Western Asset”) as of the date of the commentary and may differ from those of Legg Mason, Inc. or its affiliates. Any such views are subject to change at any time based on market or other conditions, and Western Asset and Legg Mason Investor Services, LLC disclaim any responsibility to update such views. These views are not intended to be a forecast of future events, a guarantee of future results or investment advice. Forecasts are inherently limited and should not be relied upon as an indication of actual or future performance. Because investment decisions for the Funds are based on numerous factors, these views may not be relied upon as an indication of trading intent on behalf of the Funds or any Legg Mason fund. The information contained herein has been prepared from sources believed to be reliable, but is not guaranteed by Western Asset or Legg Mason Investor Services, LLC as to its accuracy or completeness.

All investments are subject to risk including the loss of principal. All index performance reflects no deduction for fees, expenses or taxes. Please note that an investor cannot invest directly in an index.

| i | | Duration is the measure of the price sensitivity of a fixed-income security to an interest rate change of 100 basis points. Calculation is based on the weighted average of the present values for all cash flows. |

| ii | | The Federal Reserve Board (“Fed”) is responsible for the formulation of policies designed to promote economic growth, full employment, stable prices and a sustainable pattern of international trade and payments. |

| iii | | The federal funds rate is the rate charged by one depository institution on an overnight sale of immediately available funds (balances at the Federal Reserve) to another depository institution; the rate may vary from depository institution to depository institution and from day to day. |

| iv | | Gross domestic product (“GDP”) is the market value of all final goods and services produced within a country in a given period of time. |

| v | | The Institute for Supply Management’s PMI is based on a survey of purchasing executives who buy the raw materials for manufacturing at more than 350 companies. It offers an early reading on the health of the manufacturing sector. |

| vi | | The S&P/Case-Shiller Home Price Index measures the residential housing market, tracking changes in the value of the residential real estate market in twenty metropolitan regions across the United States. |

| vii | | The Barclays Capital U.S. Aggregate Index is a broad-based bond index comprised of government, corporate, mortgage- and asset-backed issues, rated investment grade or higher, and having at least one year to maturity. |

| viii | | The Consumer Price Index for All Urban Consumers (“CPI-U”) is a measure of the average change in prices over time of goods and services purchased by households, which covers approximately 87% of the total population and includes, in addition to wage earners and clerical worker households, groups such as professional, managerial and technical workers, the self-employed, short-term workers, the unemployed and retirees and others not in the labor force. |

| ix | | U.S. Treasury Inflation-Protected Securities (“TIPS”) are inflation-indexed securities issued by the U.S. Treasury in five-year, ten-year and twenty-year maturities. The principal is adjusted to the Consumer Price Index, the commonly used measure of inflation. The coupon rate is constant, but generates a different amount of interest when multiplied by the inflation-adjusted principal. |

| x | | The Barclays Capital Global Real Index: U.S. TIPS represents an unmanaged market index made up of U.S. Treasury Inflation-Linked Index securities. |

| xi | | The Barclays Capital U.S. Credit Index is an index composed of corporate and non-corporate debt issues that are investment grade (rated Baa3/BBB- or higher). |

| xii | | The Barclays Capital U.S. Corporate High Yield 2% Issuer Cap Index is an index of the 2% Issuer Cap component of the Barclays Capital U.S. Corporate High Yield Index, which covers the U.S. dollar-denominated, non-investment grade, fixed-rate, taxable corporate bond market. |

| xiii | | The JPMorgan Emerging Markets Bond Index Global (“EMBI Global”) tracks total returns for U.S. dollar-denominated debt instruments issued by emerging market sovereign and quasi-sovereign entities: Brady bonds, loans, Eurobonds and local market instruments. |

v

Annual Report to Shareholders

Management’s Discussion of Fund Performance

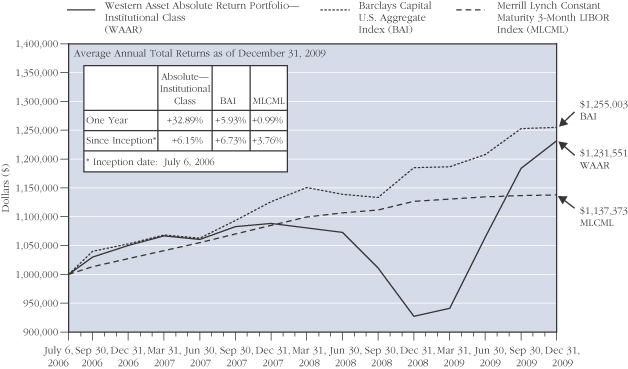

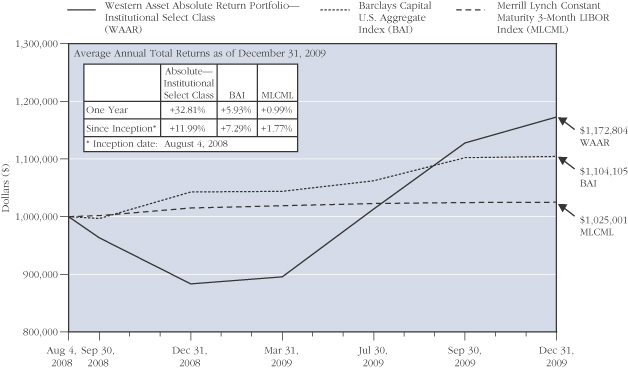

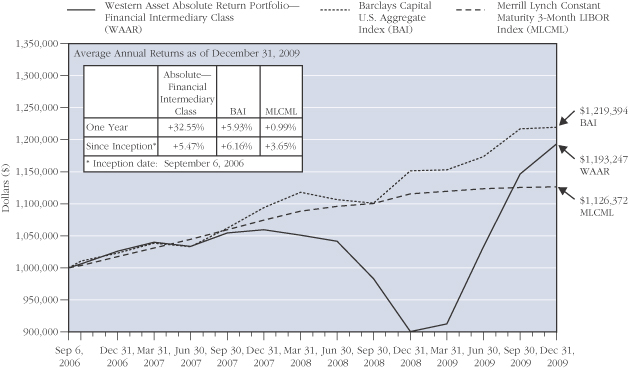

Western Asset Absolute Return Portfolio

Performance Review

For the twelve months ended December 31, 2009, Institutional Class shares of Western Asset Absolute Return Portfolio returned 32.89%. The Fund’s unmanaged benchmarks, the Barclays Capital U.S. Aggregate Indexi and the Merrill Lynch Constant Maturity 3-Month LIBOR Indexii, returned 5.93% and 0.99%, respectively, for the same period. The Lipper Flexible Income Funds Category Average1 returned 30.34% over the same time frame.

PERFORMANCE SNAPSHOT as of December 31, 2009 (unaudited)

| | | | |

| | | 6 MONTHS | | 12 MONTHS |

Western Asset Absolute Return Portfolio: | | | | |

Institutional Class | | 15.70% | | 32.89% |

Financial Intermediary Class | | 15.59% | | 32.55% |

Institutional Select Class | | 15.73% | | 32.81% |

Barclays Capital U.S. Aggregate Index | | 3.95% | | 5.93% |

Merrill Lynch Constant Maturity 3-Month LIBOR Index | | 0.26% | | 0.99% |

Lipper Flexible Income Funds Category Average1 | | 15.11% | | 30.34% |

The performance shown represents past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown above. Principal value, investment returns and yields will fluctuate and investors’ shares, when redeemed, may be worth more or less than their original cost. To obtain performance data current to the most recent month-end, please visit our website at www.leggmason.com/individualinvestors.

All share class returns assume the reinvestment of all distributions, including returns of capital, if any, at net asset value and the deduction of all Fund expenses. Returns have not been adjusted to include the deduction of taxes that a shareholder would pay on Fund distributions. Performance figures for periods shorter than one year represent cumulative figures and are not annualized.

Performance figures reflect expense reimbursements and/or fee waivers, without which the performance would have been lower.

The 30-Day SEC Yields for the period ended December 31, 2009 for Institutional, Financial Intermediary and Institutional Select Class shares were 4.42%, 4.18% and 4.42%, respectively. Absent current expense reimbursements and/or fee waivers, the 30-Day SEC Yields for Institutional, Financial Intermediary and Institutional Select Class shares would have been 4.42%, 4.06% and 4.39%, respectively. The 30-Day SEC Yield is the average annualized net investment income per share for the 30-day period indicated and is subject to change.

TOTAL ANNUAL OPERATING EXPENSES (unaudited)

As of the Fund’s most current prospectus dated July 1, 2009, the gross total operating expense ratios for Institutional, Financial Intermediary and Institutional Select Class shares were 0.83%, 1.38% and 0.85%, respectively.

Actual expenses may be higher. For example, expenses may be higher than those shown if average net assets decrease. Net assets are more likely to decrease and Fund expense ratios are more likely to increase when markets are volatile.

As a result of contractual expense limitations, the ratio of expenses, other than interest, brokerage, taxes, deferred organizational expenses and extraordinary expenses, to average net assets will not exceed 0.80% for Institutional Class shares, 1.05% for Financial Intermediary Class shares and 0.80% for Institutional Select Class shares until April 30, 2010.

| 1 | | Lipper, Inc., a wholly-owned subsidiary of Reuters, provides independent insight on global collective investments. Returns are based on the period ended December 31, 2009, including the reinvestment of all distributions, including returns of capital, if any, calculated among the 14 funds for the six-month period and among the 14 funds for the twelve-month period in the Fund’s Lipper category. |

1

Annual Report to Shareholders

In 2009, the financial markets largely stabilized, economic conditions improved and investor risk aversion abated. Collectively, this helped the spread sectors (non-Treasuries) to generate strong returns. Against this backdrop, the Fund generated very strong performance for the period and significantly outperformed its benchmarks.

The largest contributors to relative performance for the period were the portfolio’s exposures to the high-yield sector and bank loans. Within the high-yield sector, our Industrials holdings were the strongest performers. Among our high-yield holdings, Ford Motor Credit Co. and SandRidge Energy Inc. were significant contributors as, in both cases, their spreads tightened from their elevated levels in 2008 and early 2009. Among our bank loan holdings, SunGard Data Systems Inc. was a standout. Our overweight to investment grade bonds was another meaningful contributor to results, particularly within the Industrials and Financials sectors. Within the investment grade bond space, Wachovia Corp., Morgan Stanley, United Health Group Inc. and Continental Airlines Inc. were strong performers. Our exposure to non-agency mortgage-backed securities (“MBS”) was also a large contributor to performance. The asset class generated strong results as housing data improved and there was positive sentiment surrounding the launch of the Public-Private Investment Program (“PPIP”). Elsewhere, our asset-backed securities, emerging market debt and non-dollar investments also contributed to results, albeit to a lesser extent. While the Fund significantly outperformed its benchmarks during the reporting period, its cash position was a detractor from relative results given the extremely low yields available from short-term money market instruments.

We made several adjustments to the portfolio during the twelve-month reporting period. We significantly reduced our exposure to agency MBS, finding them less attractive as their spreads had narrowed given the government’s direct purchase of these securities. With the government set to phase out its purchasing program, we determined that more attractive opportunities could be found in other areas of the market. We also pared our exposure to high-yield bonds given their strong performance during the fiscal year. In contrast, the portfolio’s cash position increased as we looked for compelling opportunities in the marketplace.

During the reporting period, we utilized Eurodollar futures/options and Treasury futures/options to manage the portfolio’s durationiii and yield curveiv exposure. Interest rate swaps were utilized to manage our interest rate exposure throughout the yield curve. We also used credit default swaps and index credit default swaps to manage the portfolio’s exposure to the corporate market. Overall, the use of these instruments positively contributed to performance.

Western Asset Management Company

January 19, 2010

2

Annual Report to Shareholders

The information provided is not intended to be a forecast of future events, a guarantee of future results or investment advice. Views expressed may differ from those of the firm as a whole.

Portfolio holdings and breakdowns are as of December 31, 2009 and are subject to change and may not be representative of the portfolio managers’ current or future investments. Please refer to pages 12 through 30 for a list and percentage breakdown of the Fund’s holdings.

The mention of sector breakdowns is for informational purposes only and should not be construed as a recommendation to purchase or sell any securities. The information provided regarding such sectors is not a sufficient basis upon which to make an investment decision. Investors seeking financial advice regarding the appropriateness of investing in any securities or investment strategies discussed should consult their financial professional. The Fund’s top five sector holdings (as a percentage of net assets) as of December 31, 2009 were: Corporate Bonds and Notes (41.0%), Mortgage-Backed Securities (12.3%), U.S. Government and Agency Obligations (11.5%), Loan Participations and Assignments (7.7%) and Asset-Backed Securities (6.0%). The Fund’s portfolio composition is subject to change at any time.

RISKS: All investments are subject to risk including the loss of principal. Fixed-income securities involve interest rate, credit, inflation and reinvestment risks. As interest rates rise, the value of fixed-income securities falls. High-yield securities include greater price volatility, illiquidity and possibility of default. International investments are subject to special risks including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets. The use of leverage may increase volatility and possibility of loss. Potential active and frequent trading may result in higher transaction costs and increased investor liability. Asset-backed, mortgage-backed or mortgage-related securities are subject to prepayment and extension risks. Derivatives, such as options, futures and swaps, can be illiquid, may disproportionately increase losses, and have a potentially large impact on Fund performance. Please see the Fund’s prospectus for more information on these and other risks.

All index performance reflects no deduction for fees, expenses or taxes. Please note that an investor cannot invest directly in an index.

| i | | The Barclays Capital U.S. Aggregate Index is a broad-based bond index comprised of government, corporate, mortgage- and asset-backed issues, rated investment grade or higher, and having at least one year to maturity. |

| ii | | The Merrill Lynch Constant Maturity 3-Month LIBOR Index is based on the assumed purchase of a synthetic instrument having three months to maturity and with a coupon equal to the closing quote for three-month LIBOR. That issue is sold the following day (priced at a yield equal to the current day closing three-month LIBOR rate) and is rolled into a new three-month instrument. The Index, therefore, will always have a constant maturity equal to exactly three months. |

| iii | | Duration is the measure of the price sensitivity of a fixed-income security to an interest rate change of 100 basis points. Calculation is based on the weighted average of the present values for all cash flows. |

| iv | | The yield curve is the graphical depiction of the relationship between the yield on bonds of the same credit quality but different maturities. |

3

Annual Report to Shareholders

Special Shareholder Notice

Western Asset Absolute Return Portfolio

Effective August 20, 2009, the Fund is managed by a team of portfolio managers, sector specialists and other investment professionals. S. Kenneth Leech, Stephen A. Walsh, Michael C. Buchanan and Keith J. Gardner serve as co-leaders of this team and are responsible for the day-to-day strategic oversight of the Fund’s investments and for supervising the day-to-day operations of the various sector specialist teams dedicated to the specific asset classes in which the Fund invests. Messrs. Leech, Walsh, Buchanan and Gardner are employed by Western Asset Management Company. As portfolio managers, their focus is on portfolio structure, including sector allocation, duration i weighting and term structure decisions. Each portfolio manager has been responsible for the Fund since its inception.

| i | | Duration is the measure of the price sensitivity of a fixed-income security to an interest rate change of 100 basis points. Calculation is based on the weighted average of the present values for all cash flows. |

4

Annual Report to Shareholders

Expense Example (Unaudited)

Western Asset Absolute Return Portfolio

As a shareholder of the Fund, you may incur two types of costs; (1) transaction cost and (2) ongoing costs including management fees, distribution (12b-1) fees on Financial Intermediary Class shares, and other Fund expenses. These examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The examples are based on an investment of $1,000 invested on July 1, 2009 and held through December 31, 2009. The ending values assume dividends were reinvested at the time they were paid.

Actual Expense

The first line for each class in the table below provides information about actual account values and actual expenses for each class. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During the Period” to estimate the expenses you paid on your account if your shares were held through the entire period.

Hypothetical Examples for Comparison Purposes

The second line for each class in the table below provides information about hypothetical account values and hypothetical expenses based on the relevant class’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the class’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare these 5% hypothetical examples with the 5% hypothetical examples for the relevant classes that appear in the shareholder reports of other funds. Because each example is intended to be comparable to the examples provided by other funds, it is based on a hypothetical investment of $1,000 invested on July 1, 2009 and held through December 31, 2009. The ending values assume dividends were reinvested at the time they were paid.

| | | | | | | | | |

| | | Beginning Account Value

7/1/09 | | Ending Account Value

12/31/09 | | Expenses Paid A During the Period 7/1/09 to 12/31/09 |

Institutional Class: | | | | | | | | | |

Actual | | $ | 1,000.00 | | $ | 1,157.00 | | $ | 4.35 |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | 1,021.17 | | | 4.08 |

Institutional Select Class: | | | | | | | | | |

Actual | | $ | 1,000.00 | | $ | 1,157.30 | | $ | 4.35 |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | 1,021.17 | | | 4.08 |

Financial Intermediary Class: | | | | | | | | | |

Actual | | $ | 1,000.00 | | $ | 1,155.90 | | $ | 5.71 |

Hypothetical (5% return before expenses) | | | 1,000.00 | | | 1,019.91 | | | 5.35 |

| A | | These calculations are based on expenses incurred from July 1, 2009 to December 31, 2009. The dollar amounts shown as “Expenses Paid” are equal to the annualized expense ratios of 0.80%, 0.80% and 1.05% for the Institutional Class, Institutional Select Class and the Financial Intermediary Class, respectively, multiplied by the average values over the period, multiplied by the number of days in the most recent fiscal half-year then divided by 365. |

5

Annual Report to Shareholders

Performance Information (Unaudited)

Western Asset Absolute Return Portfolio

The graphs compare the Fund’s total returns to that of two broad-based securities market indexes. The graphs illustrate the cumulative total return of an initial $1,000,000 investment in each of the Institutional Class, Institutional Select Class and Financial Intermediary Class of the Fund, for the periods indicated. The lines for the Fund represent the total return after deducting all Fund investment management and other administrative expenses and the transaction costs of buying and selling securities. The lines representing the securities market indexes do not include any transaction costs associated with buying and selling securities in the indexes or other investment management or administrative expenses.

Total return measures investment performance in terms of appreciation or depreciation in the Fund’s net asset value per share, plus dividends and any capital gain distributions. It assumes that dividends and distributions were reinvested at the time they were paid. Returns (and the graphs and tables found below) do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Average annual returns tend to smooth out variations in a fund’s return, so that they differ from actual year-to-year results.

Bonds are subject to a variety of risks, including interest rate, credit and inflation risk. Non-U.S. investments are subject to currency fluctuations, social, economic and political risk.

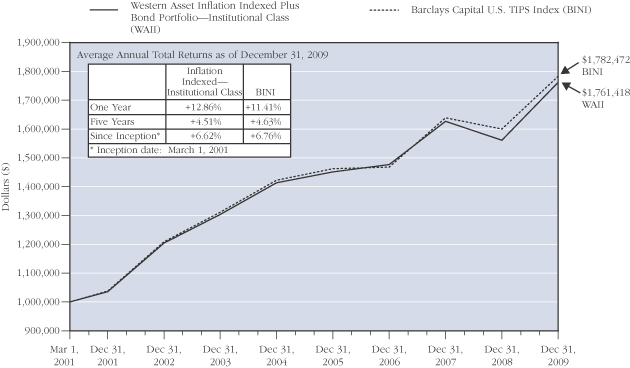

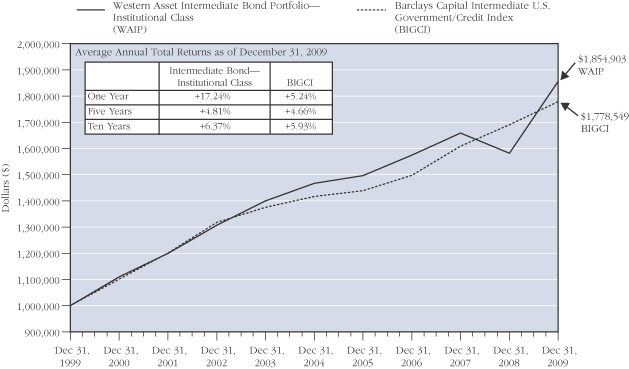

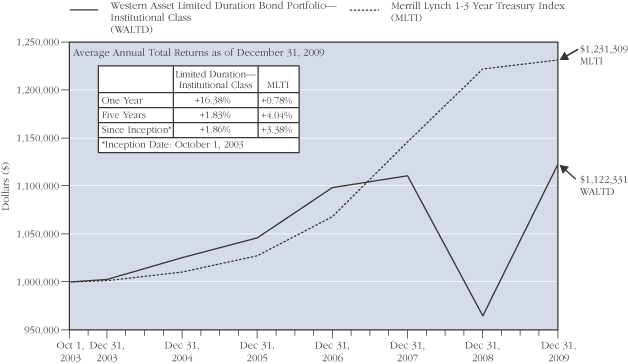

Growth of a $1,000,000 Investment—Institutional Class

The performance data quoted represent past performance and do not guarantee future results. Current performance may be lower or higher than the performance data quoted. To obtain the most recent month-end performance information, please visit www.westernassetfunds.com. The investment return and principal value of the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. Calculations assume reinvestment of all distributions, including returns of capital, if any, at net asset value and the deduction of all Fund expenses. Performance would have been lower if fees had not been waived in various periods.

6

Annual Report to Shareholders

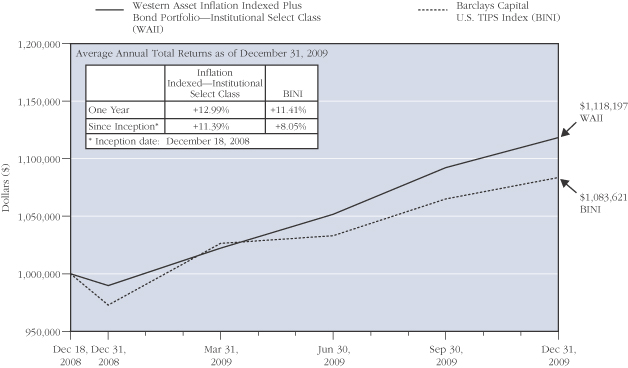

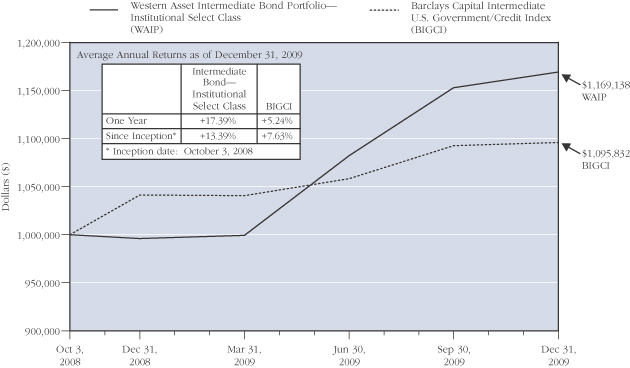

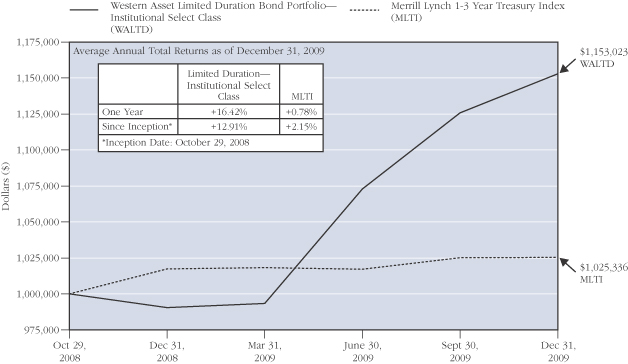

Growth of a $1,000,000 Investment—Institutional Select Class (Unaudited)

The performance data quoted represent past performance and do not guarantee future results. Current performance may be lower or higher than the performance data quoted. To obtain the most recent month-end performance information, please visit www.westernassetfunds.com. The investment return and principal value of the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. Calculations assume reinvestment of all distributions, including returns of capital, if any, at net asset value and the deduction of all Fund expenses. Performance would have been lower if fees had not been waived in various periods.

7

Annual Report to Shareholders

Performance Information—(Unaudited) Continued

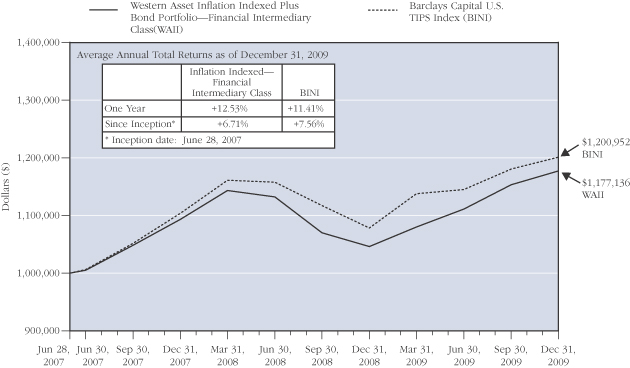

Growth of a $1,000,000 Investment—Financial Intermediary Class

The performance data quoted represent past performance and do not guarantee future results. Current performance may be lower or higher than the performance data quoted. To obtain the most recent month-end performance information, please visit www.westernassetfunds.com. The investment return and principal value of the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. Calculations assume reinvestment of all distributions, including returns of capital, if any, at net asset value and the deduction of all Fund expenses. Performance would have been lower if fees had not been waived in various periods.

8

Annual Report to Shareholders

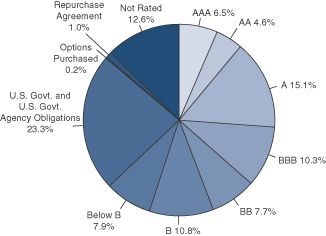

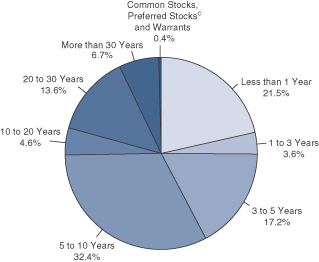

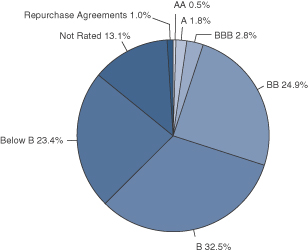

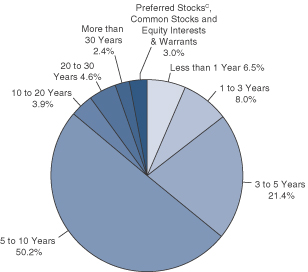

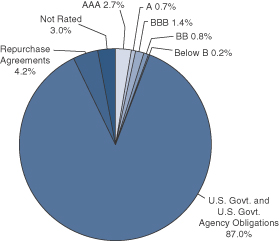

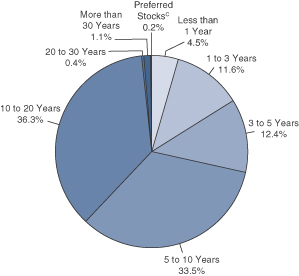

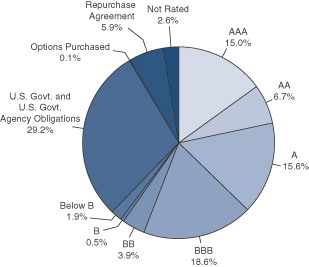

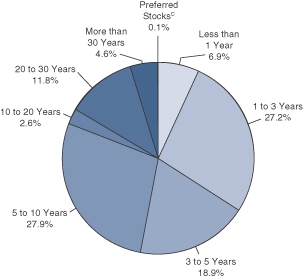

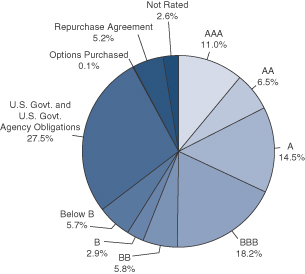

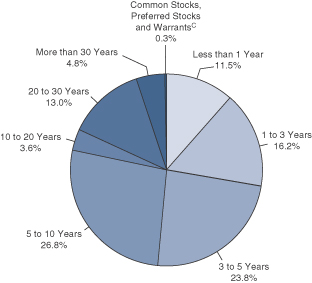

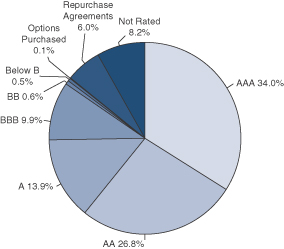

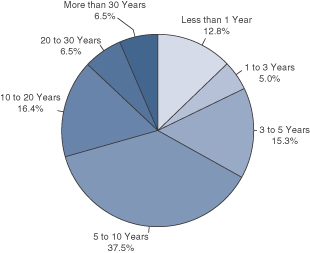

Portfolio Composition (Unaudited) (as of December 31, 2009)A

Standard & Poor’s Debt RatingsB

(as a percentage of the portfolio)

Maturity Schedule

(as a percentage of the portfolio)

| A | | The pie charts above represent the composition of the Fund’s portfolio as of December 31, 2009 and do not include derivatives such as Futures Contracts, Options Written, and Swaps. The Fund is actively managed. As a result, the composition of the portfolio holdings and sectors are subject to change at any time. |

| B | | Standard & Poor’s Ratings Service provides capital markets with credit ratings for the evaluation and assessment of credit risk. These ratings are the opinions of S&P and not absolute measures of quality or guarantees of performance. |

| C | | Common Stocks, Preferred Stocks and Warrants do not have defined maturity dates. |

9

Annual Report to Shareholders

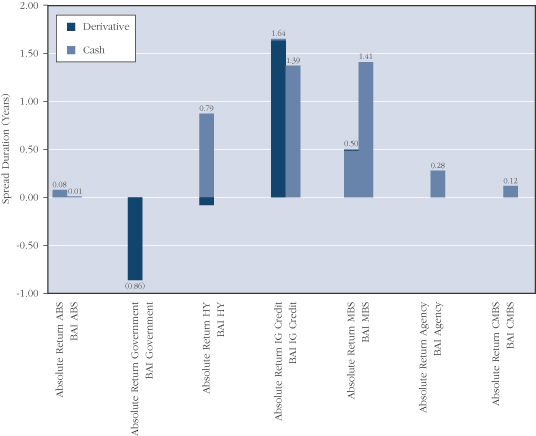

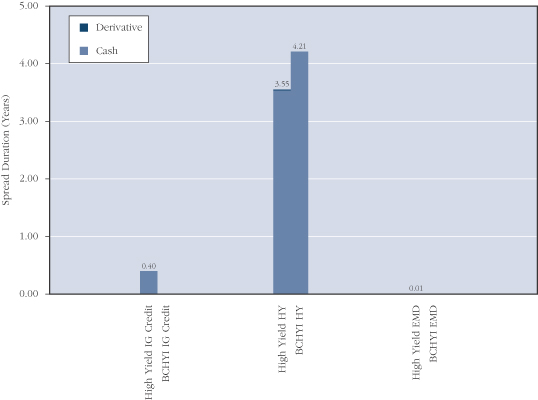

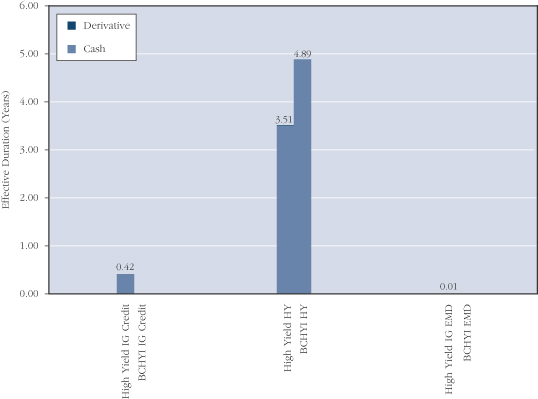

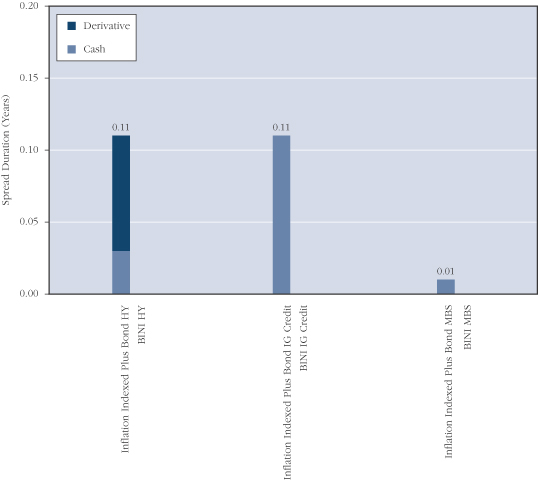

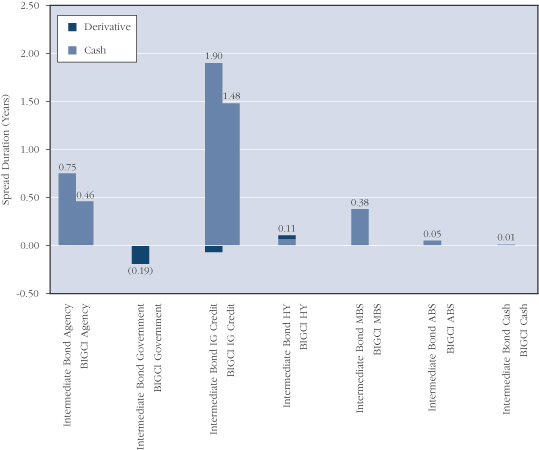

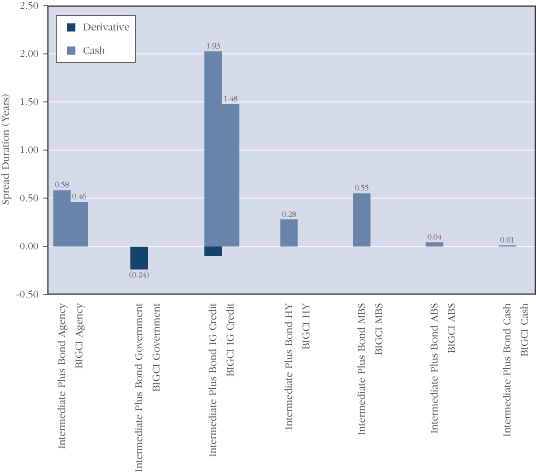

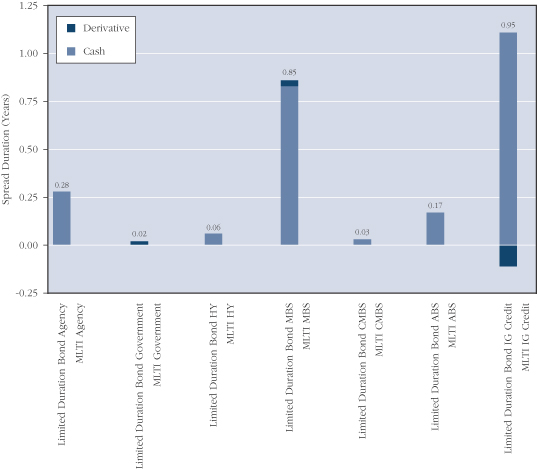

Spread Duration

Western Asset Absolute Return Portfolio

December 31, 2009 (Unaudited)

Economic Exposure

Spread duration is defined as the change in value for a 100 basis point change in the spread relative to Treasuries. The spread over Treasuries is the annual risk-premium demanded by investors to hold non-Treasury securities. This chart highlights the market sector exposure of the Fund’s portfolio and the exposure relative to the selected benchmarks as of the end of the reporting period.

| | | | |

| ABS | | — | | Asset Backed Securities |

| BAI | | — | | Barclays Capital U.S. Aggregate Index |

| CMBS | | — | | Commercial Mortgage Backed Securities |

| HY | | — | | High Yield |

| IG Credit | | — | | Investment Grade Credit |

| MBS | | — | | Mortgage Backed Securities |

10

Annual Report to Shareholders

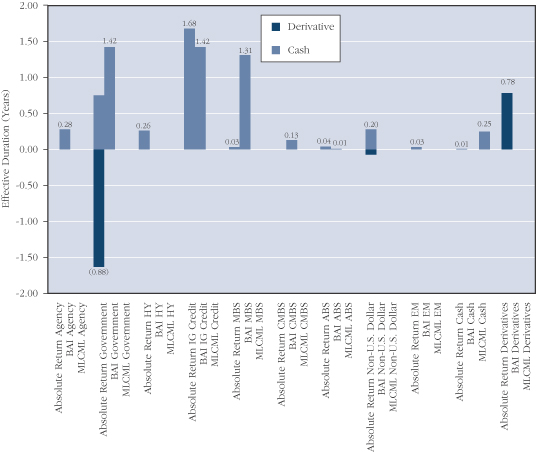

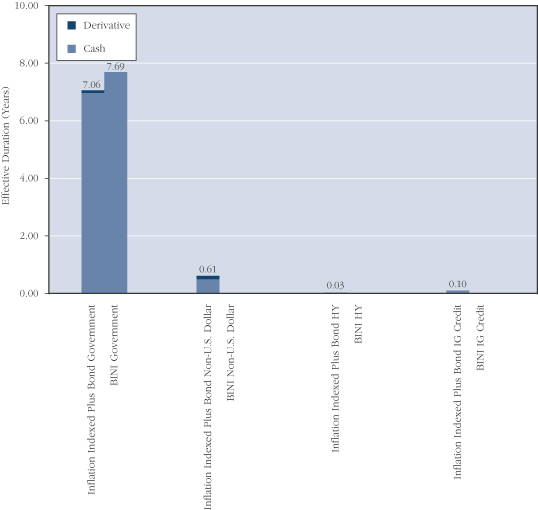

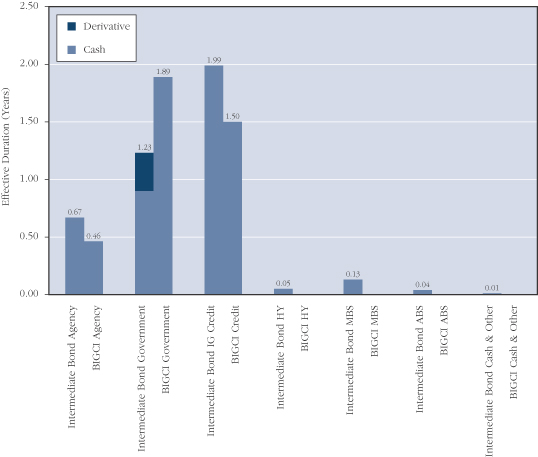

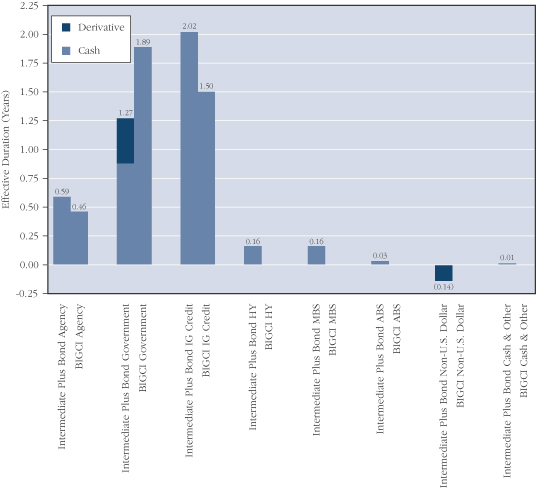

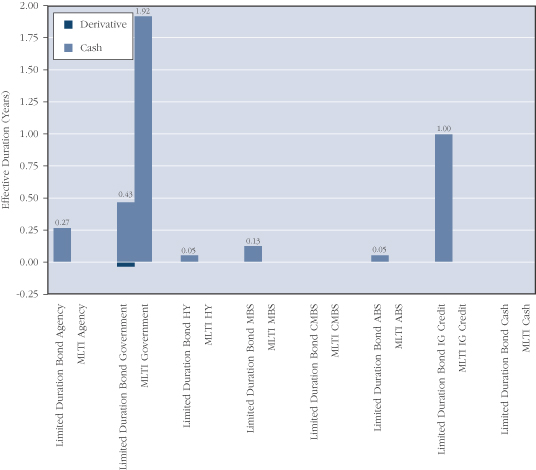

Effective Duration

Western Asset Absolute Return Portfolio

December 31, 2009 (Unaudited)

Interest Rate Exposure

Effective duration is defined as the change in value for a 100 basis point change in Treasury yields. This chart highlights the interest rate exposure of the Fund’s portfolio relative to the selected benchmarks as of the end of the reporting period.

| | | | |

| ABS | | — | | Asset Backed Securities |

| BAI | | — | | Barclays Capital U.S. Aggregate Index |

| CMBS | | — | | Commercial Mortgage Backed Securities |

| EM | | — | | Emerging Markets |

| HY | | — | | High Yield |

| IG Credit | | — | | Investment Grade Credit |

| MBS | | — | | Mortgage Backed Securities |

| MLCML | | — | | Merrill Lynch Constant Maturity 3-Month LIBOR Index |

11

Annual Report to Shareholders

Portfolio of Investments

Western Asset Absolute Return Portfolio

December 31, 2009

| | | | | | | | | | | | | |

| | | % OF

NET ASSETS | | RATE | | MATURITY

DATE | | PAR/

SHARES† | | VALUE | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | |

Long-Term Securities | | 86.3% | | | | | | | | | | | |

| | | | | |

Corporate Bonds and Notes | | 41.0% | | | | | | | | | | | |

| | | | | |

Aerospace and Defense | | 0.5% | | | | | | | | | | | |

L-3 Communications Corp. | | | | 5.875% | | 1/15/15 | | $ | 130,000 | | $ | 129,837 | |

L-3 Communications Corp. | | | | 6.375% | | 10/15/15 | | | 960,000 | | | 963,600 | |

L-3 Communications Corp. | | | | 5.200% | | 10/15/19 | | | 520,000 | | | 514,351 | A |

| | | | | | | | | | | | | |

| | | | | | | | | | | | 1,607,788 | |

| | | | | | | | | | | | | |

Airlines | | 0.6% | | | | | | | | | | | |

Continental Airlines Inc. | | | | 9.250% | | 5/10/17 | | | 230,000 | | | 233,738 | |

Continental Airlines Inc. | | | | 6.820% | | 5/1/18 | | | 60,915 | | | 55,433 | |

Continental Airlines Inc. Pass-Through Certificates | | | | 7.250% | | 11/10/19 | | | 980,000 | | | 997,150 | |

Continental Airlines Inc. | | | | 6.703% | | 6/15/21 | | | 53,553 | | | 49,805 | |

United Air Lines Inc. | | | | 7.032% | | 10/1/10 | | | 12,818 | | | 12,818 | |

United Air Lines Inc. | | | | 7.186% | | 10/1/12 | | | 48,504 | | | 48,747 | |

US Airways Pass-Through Trust | | | | 6.850% | | 1/30/18 | | | 301,948 | | | 247,597 | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | 1,645,288 | |

| | | | | | | | | | | | | |

Beverages | | 0.2% | | | | | | | | | | | |

Dr. Pepper Snapple Group Inc. | | | | 6.820% | | 5/1/18 | | | 460,000 | | | 516,036 | |

| | | | | | | | | | | | | |

| | | | | |

Building Products | | N.M. | | | | | | | | | | | |

Associated Materials Inc. | | | | 11.250% | | 3/1/14 | | | 55,000 | | | 53,075 | |

Masco Corp. | | | | 7.125% | | 8/15/13 | | | 50,000 | | | 52,044 | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | 105,119 | |

| | | | | | | | | | | | | |

Capital Markets | | 3.5% | | | | | | | | | | | |

Goldman Sachs Capital II | | | | 5.793% | | 12/29/49 | | | 60,000 | | | 46,500 | B |

Lehman Brothers Holdings Capital Trust VII | | | | 5.857% | | 11/29/49 | | | 100,000 | | | 30 | B,C |

Lehman Brothers Holdings Inc. | | | | 5.625% | | 1/24/13 | | | 1,000,000 | | | 205,000 | C |

Lehman Brothers Holdings Inc. | | | | 6.200% | | 9/26/14 | | | 320,000 | | | 62,400 | C |

Lehman Brothers Holdings Inc. | | | | 6.750% | | 12/28/17 | | | 2,350,000 | | | 705 | C |

Merrill Lynch and Co. Inc. | | | | 5.450% | | 2/5/13 | | | 3,490,000 | | | 3,672,426 | |

Merrill Lynch and Co. Inc. | | | | 6.050% | | 5/16/16 | | | 1,980,000 | | | 1,997,816 | |

Morgan Stanley | | | | 6.625% | | 4/1/18 | | | 2,160,000 | | | 2,335,323 | |

The Goldman Sachs Group Inc. | | | | 6.150% | | 4/1/18 | | | 1,800,000 | | | 1,926,898 | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | 10,247,098 | |

| | | | | | | | | | | | | |

Commercial Banks | | 2.4% | | | | | | | | | | | |

Wachovia Corp. | | | | 5.625% | | 10/15/16 | | | 730,000 | | | 746,419 | |

Wachovia Corp. | | | | 5.750% | | 2/1/18 | | | 6,120,000 | | | 6,386,636 | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | 7,133,055 | |

| | | | | | | | | | | | | |

12

Annual Report to Shareholders

| | | | | | | | | | | | | |

| | | % OF

NET ASSETS | | RATE | | MATURITY

DATE | | PAR/

SHARES† | | VALUE | |

| | | | | | | | | | | | | |

Corporate Bonds and Notes—Continued | | | | | | | | | | | | | |

| | | | | |

Commercial Services and Supplies | | 0.1% | | | | | | | | | | | |

Republic Services Inc. | | | | 5.500% | | 9/15/19 | | $ | 290,000 | | $ | 294,481 | A |

| | | | | | | | | | | | | |

| | | | | |

Consumer Finance | | 6.2% | | | | | | | | | | | |

American Express Co. | | | | 6.800% | | 9/1/66 | | | 40,000 | | | 35,800 | B |

American General Finance Corp. | | | | 6.900% | | 12/15/17 | | | 1,000,000 | | | 694,354 | |

Caterpillar Financial Services Corp. | | | | 5.450% | | 4/15/18 | | | 500,000 | | | 520,788 | |

Ford Motor Credit Co. | | | | 5.700% | | 1/15/10 | | | 270,000 | | | 270,010 | |

Ford Motor Credit Co. | | | | 9.750% | | 9/15/10 | | | 2,000,000 | | | 2,063,698 | |

Ford Motor Credit Co. | | | | 7.000% | | 10/1/13 | | | 7,800,000 | | | 7,788,253 | |

Ford Motor Credit Co. | | | | 12.000% | | 5/15/15 | | | 1,610,000 | | | 1,867,001 | |

GMAC LLC | | | | 6.875% | | 9/15/11 | | | 949,000 | | | 934,765 | A |

GMAC LLC | | | | 6.000% | | 12/15/11 | | | 1,013,000 | | | 992,740 | A |

GMAC LLC | | | | 6.625% | | 5/15/12 | | | 949,000 | | | 930,020 | A |

GMAC LLC | | | | 7.500% | | 12/31/13 | | | 273,000 | | | 263,445 | A |

GMAC LLC | | | | 8.000% | | 12/31/18 | | | 185,000 | | | 162,800 | A |

GMAC LLC | | | | 8.000% | | 11/1/31 | | | 729,000 | | | 656,100 | A |

John Deere Capital Corp. | | | | 5.350% | | 4/3/18 | | | 800,000 | | | 845,474 | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | 18,025,248 | |

| | | | | | | | | | | | | |

Diversified Financial Services | | 4.2% | | | | | | | | | | | |

Air 2 US | | | | 8.027% | | 10/1/19 | | | 856,466 | | | 738,166 | A |

BAC Capital Trust XIV | | | | 5.630% | | 12/31/49 | | | 40,000 | | | 27,600 | B |

Citigroup Inc. | | | | 5.500% | | 2/15/17 | | | 5,570,000 | | | 5,271,064 | |

Citigroup Inc. | | | | 6.875% | | 3/5/38 | | | 1,380,000 | | | 1,377,265 | |

East Lane Re Ltd. | | | | 6.281% | | 5/6/11 | | | 300,000 | | | 292,500 | A,D |

El Paso Performance-Linked | | | | 7.750% | | 7/15/11 | | | 340,000 | | | 348,555 | A |

General Electric Capital Corp. | | | | 5.625% | | 5/1/18 | | | 2,800,000 | | | 2,869,275 | |

General Electric Capital Corp. | | | | 6.375% | | 11/15/67 | | | 60,000 | | | 52,050 | B |

Leucadia National Corp. | | | | 8.125% | | 9/15/15 | | | 250,000 | | | 255,000 | |

PHH Corp. | | | | 7.125% | | 3/1/13 | | | 110,000 | | | 101,750 | |

Vanguard Health Holding Co. II LLC | | | | 9.000% | | 10/1/14 | | | 330,000 | | | 341,962 | |

ZFS Finance USA Trust II | | | | 6.450% | | 12/15/65 | | | 500,000 | | | 445,000 | A,B |

| | | | | | | | | | | | | |

| | | | | | | | | | | | 12,120,187 | |

| | | | | | | | | | | | | |

Diversified Telecommunication Services | | 1.8% | | | | | | | | | | | |

AT&T Inc. | | | | 5.500% | | 2/1/18 | | | 2,930,000 | | | 3,057,209 | |

Citizens Communications Co. | | | | 7.875% | | 1/15/27 | | | 160,000 | | | 147,200 | |

Level 3 Financing Inc. | | | | 9.250% | | 11/1/14 | | | 180,000 | | | 170,100 | |

Qwest Corp. | | | | 7.500% | | 10/1/14 | | | 190,000 | | | 197,363 | |

Verizon Communications Inc. | | | | 6.100% | | 4/15/18 | | | 1,150,000 | | | 1,249,945 | |

13

Annual Report to Shareholders

Portfolio of Investments—Continued

Western Asset Absolute Return Portfolio—Continued

| | | | | | | | | | | | | |

| | | % OF

NET ASSETS | | RATE | | MATURITY

DATE | | PAR/

SHARES† | | VALUE | |

| | | | | | | | | | | | | |

Corporate Bonds and Notes—Continued | | | | | | | | | | | | | |

| | | | | |

Diversified Telecommunication Services—Continued | | | | | | | | | | | | | |

Windstream Corp. | | | | 8.625% | | 8/1/16 | | $ | 480,000 | | $ | 488,400 | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | 5,310,217 | |

| | | | | | | | | | | | | |

Electric Utilities | | 1.4% | | | | | | | | | | | |

Energy Future Holdings Corp. | | | | 10.875% | | 11/1/17 | | | 20,000 | | | 16,350 | |

Energy Future Holdings Corp. | | | | 11.250% | | 11/1/17 | | | 5,404,516 | | | 3,823,695 | E |

FirstEnergy Corp. | | | | 6.450% | | 11/15/11 | | | 83,000 | | | 88,997 | |

FirstEnergy Corp. | | | | 7.375% | | 11/15/31 | | | 100,000 | | | 108,390 | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | 4,037,432 | |

| | | | | | | | | | | | | |

Energy Equipment and Services | | 0.1% | | | | | | | | | | | |

Parker Drilling Co. | | | | 9.625% | | 10/1/13 | | | 180,000 | | | 184,950 | |

| | | | | | | | | | | | | |

| | | | | |

Food and Staples Retailing | | 1.7% | | | | | | | | | | | |

CVS Corp. | | | | 9.350% | | 1/10/23 | | | 500,000 | | | 487,205 | A,F |

CVS Corp. | | | | 5.298% | | 1/11/27 | | | 29,766 | | | 27,147 | A,G |

CVS Lease Pass-Through Trust | | | | 5.880% | | 1/10/28 | | | 42,437 | | | 39,702 | |

CVS Lease Pass-Through Trust | | | | 6.036% | | 12/10/28 | | | 114,152 | | | 108,027 | |

Safeway Inc. | | | | 7.250% | | 2/1/31 | | | 1,360,000 | | | 1,565,284 | |

The Kroger Co. | | | | 5.000% | | 4/15/13 | | | 1,620,000 | | | 1,713,174 | |

The Kroger Co. | | | | 6.150% | | 1/15/20 | | | 1,100,000 | | | 1,177,273 | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | 5,117,812 | |

| | | | | | | | | | | | | |

Food Products | | 0.1% | | | | | | | | | | | |

Sara Lee Corp. | | | | 6.250% | | 9/15/11 | | | 150,000 | | | 160,034 | |

| | | | | | | | | | | | | |

| | | | | |

Health Care Equipment and Supplies | | 0.2% | | | | | | | | | | | |

Zimmer Holdings Inc. | | | | 4.625% | | 11/30/19 | | | 660,000 | | | 654,009 | |

| | | | | | | | | | | | | |

| | | | | |

Health Care Providers and Services | | 5.1% | | | | | | | | | | | |

AmerisourceBergen Corp. | | | | 5.875% | | 9/15/15 | | | 50,000 | | | 54,491 | |

HCA Inc. | | | | 6.300% | | 10/1/12 | | | 274,000 | | | 274,000 | |

HCA Inc. | | | | 9.125% | | 11/15/14 | | | 10,000 | | | 10,550 | |

HCA Inc. | | | | 6.500% | | 2/15/16 | | | 619,000 | | | 588,050 | |

HCA Inc. | | | | 9.250% | | 11/15/16 | | | 910,000 | | | 977,113 | |

HCA Inc. | | | | 9.625% | | 11/15/16 | | | 630,000 | | | 681,975 | E |

Humana Inc. | | | | 7.200% | | 6/15/18 | | | 340,000 | | | 347,731 | H |

Tenet Healthcare Corp. | | | | 9.000% | | 5/1/15 | | | 525,000 | | | 567,000 | A |

Tenet Healthcare Corp. | | | | 10.000% | | 5/1/18 | | | 525,000 | | | 588,000 | A |

Tenet Healthcare Corp. | | | | 8.875% | | 7/1/19 | | | 29,000 | | | 31,320 | A |

14

Annual Report to Shareholders

| | | | | | | | | | | | | |

| | | % OF

NET ASSETS | | RATE | | MATURITY

DATE | | PAR/

SHARES† | | VALUE | |

| | | | | | | | | | | | | |

Corporate Bonds and Notes—Continued | | | | | | | | | | | | | |

| | | | |

Health Care Providers and Services—Continued | | | | | | | | | | | |

U.S. Oncology Holdings Inc. | | | | 7.178% | | 3/15/12 | | $ | 382,000 | | $ | 357,170 | D,E |

UnitedHealth Group Inc. | | | | 4.875% | | 2/15/13 | | | 6,360,000 | | | 6,654,239 | |

UnitedHealth Group Inc. | | | | 4.875% | | 4/1/13 | | | 940,000 | | | 985,045 | |

UnitedHealth Group Inc. | | | | 6.000% | | 2/15/18 | | | 1,210,000 | | | 1,249,867 | |

WellPoint Inc. | | | | 5.875% | | 6/15/17 | | | 1,470,000 | | | 1,514,470 | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | 14,881,021 | |

| | | | | | | | | | | | | |

Hotels, Restaurants and Leisure | | 0.2% | | | | | | | | | | | |

Inn of the Mountain Gods Resort and Casino | | | | 12.000% | | 11/15/10 | | | 250,000 | | | 103,438 | C,F |

MGM MIRAGE | | | | 10.375% | | 5/15/14 | | | 45,000 | | | 48,825 | A |

MGM MIRAGE | | | | 6.625% | | 7/15/15 | | | 140,000 | | | 108,850 | |

MGM MIRAGE | | | | 11.125% | | 11/15/17 | | | 105,000 | | | 116,287 | A |

River Rock Entertainment Authority | | | | 9.750% | | 11/1/11 | | | 220,000 | | | 207,350 | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | 584,750 | |

| | | | | | | | | | | | | |

Household Durables | | 0.2% | | | | | | | | | | | |

Norcraft Cos. | | | | 9.000% | | 11/1/11 | | | 480,000 | | | 480,600 | F |

| | | | | | | | | | | | | |

| | | | | |

Household Products | | 0.2% | | | | | | | | | | | |

Reynolds Group DL Escrow Inc./Reynolds Group Escrow LLC | | | | 7.750% | | 10/15/16 | | | 465,000 | | | 475,462 | A |

| | | | | | | | | | | | | |

| | | | | |

Independent Power Producers and Energy Traders | | 1.8% | | | | | | | | | | | |

Calpine Corp. | | | | 8.000% | | 6/1/16 | | | 355,000 | | | 365,650 | A |

Dynegy Holdings Inc. | | | | 7.750% | | 6/1/19 | | | 30,000 | | | 26,025 | |

Edison Mission Energy | | | | 7.750% | | 6/15/16 | | | 110,000 | | | 93,500 | |

Edison Mission Energy | | | | 7.000% | | 5/15/17 | | | 80,000 | | | 63,200 | |

Edison Mission Energy | | | | 7.200% | | 5/15/19 | | | 250,000 | | | 189,375 | |

Edison Mission Energy | | | | 7.625% | | 5/15/27 | | | 90,000 | | | 60,975 | |

Mirant Mid Atlantic LLC | | | | 10.060% | | 12/30/28 | | | 915,837 | | | 966,208 | |

NRG Energy Inc. | | | | 7.375% | | 2/1/16 | | | 250,000 | | | 250,313 | |

The AES Corp. | | | | 7.750% | | 3/1/14 | | | 1,300,000 | | | 1,319,500 | |

The AES Corp. | | | | 7.750% | | 10/15/15 | | | 300,000 | | | 304,500 | |

The AES Corp. | | | | 8.000% | | 10/15/17 | | | 1,630,000 | | | 1,672,787 | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | 5,312,033 | |

| | | | | | | | | | | | | |

| | | | | |

Insurance | | 2.8% | | | | | | | | | | | |

Allstate Life Global Funding Trust | | | | 5.375% | | 4/30/13 | | | 440,000 | | | 469,689 | |

American International Group Inc. | | | | 5.850% | | 1/16/18 | | | 4,420,000 | | | 3,626,738 | |

15

Annual Report to Shareholders

Portfolio of Investments—Continued

Western Asset Absolute Return Portfolio—Continued

| | | | | | | | | | | | | |

| | | % OF

NET ASSETS | | RATE | | MATURITY

DATE | | PAR/

SHARES† | | VALUE | |

| | | | | | | | | | | | | |

Corporate Bonds and Notes—Continued | | | | | | | | | | | | | |

| | | | | |

Insurance—Continued | | | | | | | | | | | | | |

ASIF Global Financing XIX | | | | 4.900% | | 1/17/13 | | $ | 1,400,000 | | $ | 1,288,354 | A |

MetLife Inc. | | | | 6.400% | | 12/15/36 | | | 50,000 | | | 43,750 | |

Metropolitan Life Global Funding I | | | | 5.125% | | 4/10/13 | | | 1,130,000 | | | 1,197,111 | A |

Pacific Life Global Funding | | | | 5.150% | | 4/15/13 | | | 1,040,000 | | | 1,086,693 | A |

Teachers Insurance & Annuity Association of America | | | | 6.850% | | 12/16/39 | | | 220,000 | | | 227,422 | A |

The Travelers Cos. Inc. | | | | 6.250% | | 3/15/37 | | | 120,000 | | | 109,319 | B |

| | | | | | | | | | | | | |

| | | | | | | | | | | | 8,049,076 | |

| | | | | | | | | | | | | |

| | | | | |

Media | | 1.3% | | | | | | | | | | | |

Affinion Group Inc. | | | | 11.500% | | 10/15/15 | | | 430,000 | | | 450,425 | |

Charter Communications Operating LLC | | | | 10.875% | | 9/15/14 | | | 160,000 | | | 179,200 | A |

Comcast Corp. | | | | 6.500% | | 1/15/17 | | | 70,000 | | | 77,494 | |

Comcast Corp. | | | | 5.700% | | 5/15/18 | | | 2,350,000 | | | 2,470,438 | |

DISH DBS Corp. | | | | 7.875% | | 9/1/19 | | | 400,000 | | | 419,500 | |

Gannett Co. Inc. | | | | 6.375% | | 4/1/12 | | | 40,000 | | | 40,000 | |

News America Inc. | | | | 6.650% | | 11/15/37 | | | 50,000 | | | 52,815 | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | 3,689,872 | |

| | | | | | | | | | | | | |

| | | | | |

Metals and Mining | | 0.9% | | | | | | | | | | | |

Freeport-McMoRan Copper & Gold Inc. | | | | 8.375% | | 4/1/17 | | | 1,910,000 | | | 2,091,450 | |

Steel Dynamics Inc. | | | | 7.750% | | 4/15/16 | | | 410,000 | | | 426,912 | G |

| | | | | | | | | | | | | |

| | | | | | | | | | | | 2,518,362 | |

| | | | | | | | | | | | | |

| | | | | |

Multiline Retail | | 0.2% | | | | | | | | | | | |

The Neiman-Marcus Group Inc. | | | | 9.000% | | 10/15/15 | | | 505,212 | | | 493,845 | E |

| | | | | | | | | | | | | |

| | | | | |

Oil, Gas and Consumable Fuels | | 4.6% | | | | | | | | | | | |

Anadarko Petroleum Corp. | | | | 5.950% | | 9/15/16 | | | 540,000 | | | 584,116 | |

Belden and Blake Corp. | | | | 8.750% | | 7/15/12 | | | 1,060,000 | | | 991,100 | |

Chesapeake Energy Corp. | | | | 6.375% | | 6/15/15 | | | 400,000 | | | 392,000 | |

Chesapeake Energy Corp. | | | | 6.500% | | 8/15/17 | | | 100,000 | | | 98,000 | |

Chesapeake Energy Corp. | | | | 7.250% | | 12/15/18 | | | 55,000 | | | 55,413 | |

Dynegy Roseton/Danskammer Pass Through Trust | | | | 7.670% | | 11/8/16 | | | 420,000 | | | 405,300 | |

El Paso Corp. | | | | 7.000% | | 6/15/17 | | | 1,690,000 | | | 1,676,128 | |

Energy Transfer Partners LP | | | | 6.700% | | 7/1/18 | | | 3,800,000 | | | 4,068,660 | |

Kinder Morgan Energy Partners LP | | | | 6.000% | | 2/1/17 | | | 1,000,000 | | | 1,049,914 | |

Petrohawk Energy Corp. | | | | 9.125% | | 7/15/13 | | | 250,000 | | | 261,250 | |

16

Annual Report to Shareholders

| | | | | | | | | | | | | |

| | | % OF

NET ASSETS | | RATE | | MATURITY

DATE | | PAR/

SHARES† | | VALUE | |

| | | | | | | | | | | | | |

Corporate Bonds and Notes—Continued | | | | | | | | | | | | | |

| | | | | |

Oil, Gas and Consumable Fuels—Continued | | | | | | | | | | | | | |

SandRidge Energy Inc. | | | | 8.625% | | 4/1/15 | | $ | 1,000,000 | | $ | 1,000,000 | E |

Whiting Petroleum Corp. | | | | 7.250% | | 5/1/12 | | | 160,000 | | | 160,800 | |

XTO Energy Inc. | | | | 5.500% | | 6/15/18 | | | 2,508,000 | | | 2,675,201 | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | 13,417,882 | |

| | | | | | | | | | | | | |

Pharmaceuticals | | N.M. | | | | | | | | | | | |

Leiner Health Products Inc. | | | | 11.000% | | 6/1/12 | | | 250,000 | | | 25 | C,F |

| | | | | | | | | | | | | |

| | | | | |

Real Estate Investment Trusts (REITs) | | N.M. | | | | | | | | | | | |

Health Care Property Investors Inc. | | | | 6.450% | | 6/25/12 | | | 60,000 | | | 61,773 | |

| | | | | | | | | | | | | |

| | | | | |

Real Estate Management and Development | | 0.2% | | | | | | | | | | | |

Realogy Corp. | | | | 10.500% | | 4/15/14 | | | 755,000 | | | 653,075 | |

| | | | | | | | | | | | | |

| | | | | |

Tobacco | | 0.3% | | | | | | | | | | | |

Lorillard Tobacco Co. | | | | 8.125% | | 6/23/19 | | | 900,000 | | | 989,447 | |

| | | | | | | | | | | | | |

| | | | | |

Trading Companies and Distributors | | 0.1% | | | | | | | | | | | |

Ashtead Capital Inc. | | | | 9.000% | | 8/15/16 | | | 200,000 | | | 200,250 | A |

| | | | | | | | | | | | | |

| | | | | |

Wireless Telecommunication Services | | 0.1% | | | | | | | | | | | |

Cricket Communications Inc. | | | | 7.750% | | 5/15/16 | | | 315,000 | | | 314,212 | |

| | | | | | | | | | | | | |

Total Corporate Bonds and Notes

(Cost—$119,020,795) | | | | | | | | | | | | 119,280,439 | |

Asset-Backed Securities | | 6.0% | | | | | | | | | | | |

| | | | | |

Fixed Rate Securities | | 1.6% | | | | | | | | | | | |

ABSC Manufactured Housing Contract 2004-CN1 | | | | 8.400% | | 12/2/30 | | | 170,000 | | | 127,500 | A |

Associates Manufactured Housing Pass Through Certificates 1997-CLB2 | | | | 8.900% | | 6/15/28 | | | 1,798,409 | | | 1,649,861 | G |

Bombardier Capital Mortgage Securitization Corp. 2000-A A3 | | | | 7.830% | | 6/15/30 | | | 1,637,648 | | | 1,065,893 | |

Centex Home Equity 2003-B AF4 | | | | 3.735% | | 2/25/32 | | | 142,664 | | | 110,372 | |

Hertz Vehicle Financing LLC 2009-2A A2 | | | | 5.290% | | 3/25/16 | | | 510,000 | | | 508,849 | A |

Lehman XS Trust 2007-1 WF1 | | | | 7.000% | | 1/25/37 | | | 1,294,520 | | | 745,360 | |

Oakwood Mortgage Investors Inc. 1999-D A1 | | | | 7.840% | | 11/15/29 | | | 267,276 | | | 215,685 | |

Pegasus Aviation Lease Securitization 2000-1 A2 | | | | 8.370% | | 3/25/30 | | | 390,000 | | | 120,900 | A,G |

| | | | | | | | | | | | | |

| | | | | | | | | | | | 4,544,420 | |

| | | | | | | | | | | | | |

17

Annual Report to Shareholders

Portfolio of Investments—Continued

Western Asset Absolute Return Portfolio—Continued

| | | | | | | | | | | | | |

| | | % OF

NET ASSETS | | RATE | | MATURITY

DATE | | PAR/

SHARES† | | VALUE | |

| | | | | | | | | | | | | |

Asset-Backed Securities—Continued | | | | | | | | | | | | | |

| | | | | |

Indexed SecuritiesD | | 4.3% | | | | | | | | | | | |

ACE Securities Corp. 2006-GP1 A | | | | 0.361% | | 2/25/31 | | $ | 382,749 | | $ | 286,798 | |

Amortizing Residential Collateral Trust 2005-BC5 M1 | | | | 1.266% | | 7/25/32 | | | 594,682 | | | 383,675 | |

Bear Stearns Asset-Backed Securities Trust 2006-SD2 | | | | 0.431% | | 6/25/36 | | | 495,261 | | | 465,943 | |

Citigroup Mortgage Loan Trust Inc. 2006-SHL1 A1 | | | | 0.431% | | 11/25/45 | | | 141,665 | | | 103,878 | A |

Citigroup Mortgage Loan Trust Inc. 2007-SHL1 A | | | | 0.631% | | 11/25/46 | | | 439,661 | | | 208,753 | A |

Countrywide Home Equity Loan Trust 2006-B 2A | | | | 0.403% | | 5/15/36 | | | 326,054 | | | 121,841 | |

Fremont Home Loan Trust 2006-B 2A2 | | | | 0.331% | | 8/25/36 | | | 1,017,089 | | | 723,571 | |

GMAC Mortgage Corp. Loan Trust 2006-HE4 A1 | | | | 0.411% | | 12/25/36 | | | 1,819,841 | | | 729,320 | |

GSAA Home Equity Trust 2007-6 A4 | | | | 0.531% | | 5/25/47 | | | 2,090,000 | | | 1,130,968 | |

GSAMP Trust 2006-SEA1 A | | | | 0.531% | | 5/25/36 | | | 336,413 | | | 232,125 | A |

GSRPM Mortgage Loan Trust 2006-2 A2 | | | | 0.531% | | 9/25/36 | | | 480,661 | | | 290,121 | A |

HSI Asset Securitization Corp. Trust 2007-NC1 A3 | | | | 0.411% | | 4/25/37 | | | 2,740,000 | | | 946,870 | |

Indymac Seconds Asset Backed Trust A-A | | | | 0.361% | | 6/25/36 | | | 1,295,992 | | | 123,003 | |

IXIS Real Estate Capital Trust 2005-HE4 A3 | | | | 0.571% | | 2/25/36 | | | 882,158 | | | 765,025 | |

Lehman XS Trust 2006-16N A4B | | | | 0.471% | | 11/25/46 | | | 654,891 | | | 180,803 | |

Lehman XS Trust 2006-2N 1A1 | | | | 0.491% | | 2/25/46 | | | 409,850 | | | 212,947 | |

Lehman XS Trust 2006-GP3 2A2 | | | | 0.451% | | 6/25/46 | | | 652,388 | | | 109,008 | |

Lehman XS Trust 2007-2N 3A1 | | | | 0.321% | | 2/25/37 | | | 1,550,614 | | | 1,344,192 | |

MASTR Second Lien Trust 2005-1 A | | | | 0.501% | | 9/25/35 | | | 216,625 | | | 181,882 | |

MASTR Specialized Loan Trust 2006-3 A | | | | 0.491% | | 6/25/46 | | | 409,005 | | | 226,118 | A |

MASTR Specialized Loan Trust 2007-1 A | | | | 0.601% | | 1/25/37 | | | 355,415 | | | 92,408 | A |

Morgan Stanley Home Equity Loans 2007-1 A3 | | | | 0.371% | | 12/25/36 | | | 2,720,000 | | | 924,669 | |

Morgan Stanley Mortgage Loan Trust 2006-12XS | | | | 0.351% | | 10/25/36 | | | 80,886 | | | 80,936 | |

Nelnet Student Loan Trust 2008-4 A4 | | | | 1.762% | | 4/25/24 | | | 860,000 | | | 897,836 | |

Option One Mortgage Loan Trust 2005-1 A4 | | | | 0.631% | | 2/25/35 | | | 803,209 | | | 619,998 | |

RAAC 2006-RP4 A | | | | 0.521% | | 1/25/46 | | | 586,006 | | | 353,256 | A |

Structured Asset Securities Corp. 2007-BC4 A3 | | | | 0.481% | | 11/25/37 | | | 882,229 | | | 822,977 | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | 12,558,921 | |

| | | | | | | | | | | | | |

Stripped Securities | | 0.1% | | | | | | | | | | | |

First Franklin Mortgage Loan Asset-Backed Certificates 2006-FF5 2A5 | | | | 0.000% | | 4/25/36 | | | 1,050,000 | | | 263,894 | I2 |

| | | | | | | | | | | | | |

18

Annual Report to Shareholders

| | | | | | | | | | | | | |

| | | % OF

NET ASSETS | | RATE | | MATURITY

DATE | | PAR/

SHARES† | | VALUE | |

| | | | | | | | | | | | | |

Asset-Backed Securities—Continued | | | | | | | | | | | | | |

| | | | | |

Variable Rate SecuritiesJ | | N.M. | | | | | | | | | | | |

GSAMP Trust 2006-S3 A1 | | | | 6.085% | | 5/25/36 | | $ | 359,238 | | $ | 23,175 | B |

| | | | | | | | | | | | | |

Total Asset-Backed Securities

(Cost—$26,745,178) | | | | | | | | | | | | 17,390,410 | |

Mortgage-Backed Securities | | 12.3% | | | | | | | | | | | |

| | | | | |

Fixed Rate Securities | | 0.2% | | | | | | | | | | | |

Banc of America Funding Corp. 2006-8T2 A2 | | | | 5.791% | | 10/25/36 | | | 119,554 | | | 117,036 | |

BlackRock Capital Finance LP 1997-R1 | | | | 7.750% | | 3/25/37 | | | 62,490 | | | 9,530 | A,G |

Indymac Manufactured Housing Contract A2-2 | | | | 6.170% | | 12/25/11 | | | 450,724 | | | 419,316 | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | 545,882 | |

| | | | | | | | | | | | | |

Indexed SecuritiesD | | 7.5% | | | | | | | | | | | |

American Home Mortgage Assets 2006-6 A1A | | | | 0.421% | | 12/25/46 | | | 309,703 | | | 150,931 | |

American Home Mortgage Investment Trust 2005-4 5A | | | | 5.350% | | 11/25/45 | | | 729,178 | | | 532,266 | |

Banc of America Mortgage Securities 2003-F 1A1 | | | | 4.123% | | 7/25/33 | | | 29,058 | | | 26,088 | |

Banc of America Mortgage Securities 2004-A 1A1 | | | | 5.409% | | 2/25/34 | | | 64,129 | | | 53,113 | |

Bear Stearns Adjustable Rate Mortgage Trust 2005-12 23A1 | | | | 5.727% | | 2/25/36 | | | 2,686,819 | | | 1,708,864 | |

Bear Stearns Alt-A Trust 2004-10 1A1 | | | | 0.911% | | 9/25/34 | | | 169,729 | | | 124,159 | |

Bear Stearns Alt-A Trust 2004-11 1A2 | | | | 1.071% | | 11/25/34 | | | 113,886 | | | 59,117 | |

Bear Stearns Alt-A Trust 2005-2 1A1 | | | | 0.731% | | 3/25/35 | | | 52,376 | | | 32,999 | |

Bear Stearns Mortgage Funding Trust 2006-AR5 1A1 | | | | 0.391% | | 12/25/46 | | | 1,005,480 | | | 473,505 | |

Citigroup Mortgage Loan Trust Inc. 2005-9 1A1 | | | | 0.491% | | 11/25/35 | | | 505,391 | | | 267,842 | |

Countrywide Alternative Loan Trust 2005-24 4A1 | | | | 0.463% | | 7/20/35 | | | 706,838 | | | 373,478 | |

Countrywide Alternative Loan Trust 2005-51 2A1 | | | | 0.533% | | 11/20/35 | | | 433,015 | | | 231,080 | |

Countrywide Alternative Loan Trust 2005-59 1A1 | | | | 0.616% | | 11/20/35 | | | 604,306 | | | 317,188 | |

Countrywide Alternative Loan Trust 2005-76 3A1 | | | | 0.491% | | 1/25/46 | | | 462,832 | | | 252,834 | |

Countrywide Alternative Loan Trust 2005-J12 | | | | 0.501% | | 8/25/35 | | | 255,505 | | | 128,496 | |

Countrywide Alternative Loan Trust 2006-OA10 4A3 | | | | 0.501% | | 8/25/46 | | | 2,030,608 | | | 308,019 | |

19

Annual Report to Shareholders

Portfolio of Investments—Continued

Western Asset Absolute Return Portfolio—Continued

| | | | | | | | | | | | | |

| | | % OF

NET ASSETS | | RATE | | MATURITY

DATE | | PAR/

SHARES† | | VALUE | |

| | | | | | | | | | | | | |

Mortgage-Backed Securities—Continued | | | | | | | | | | | | | |

| | | | | |

Indexed Securities—Continued | | | | | | | | | | | | | |

Countrywide Alternative Loan Trust 2006-OA8 1A2 | | | | 0.461% | | 7/25/46 | | $ | 670,001 | | $ | 171,113 | |

Countrywide Home Loans 2001-HYB1 1A1 | | | | 3.666% | | 6/19/31 | | | 30,840 | | | 29,446 | |

Countrywide Home Loans 2003-60 1A1 | | | | 4.727% | | 2/25/34 | | | 449,939 | | | 387,940 | |

Countrywide Home Loans 2003-HYB1 1A1 | | | | 5.044% | | 5/19/33 | | | 32,068 | | | 29,039 | |

Countrywide Home Loans 2006-3 1A2 | | | | 0.561% | | 3/25/36 | | | 491,670 | | | 99,054 | |

Deutsche Mortgage Securities Inc. 2004-4 7AR2 | | | | 0.681% | | 6/25/34 | | | 272,210 | | | 202,491 | |

First Horizon Alternative Mortgage Securities 2005-AA12 1A1 | | | | 2.707% | | 2/25/36 | | | 497,767 | | | 274,707 | |

Greenpoint Mortgage Funding Trust 2006-AR2 1A2 | | | | 0.481% | | 4/25/36 | | | 3,257,473 | | | 1,031,886 | |

Greenpoint Mortgage Funding Trust 2006-AR3 3A1 | | | | 0.461% | | 4/25/36 | | | 627,887 | | | 264,891 | |

GSR Mortgage Loan Trust 2006-0A1 2A2 | | | | 0.491% | | 8/25/46 | | | 709,035 | | | 189,648 | |

Harborview Mortgage Loan Trust 2006-13 A | | | | 0.413% | | 11/19/46 | | | 515,122 | | | 245,571 | |

Harborview Mortgage Loan Trust 2006-14 2A1A | | | | 0.383% | | 1/25/47 | | | 1,068,314 | | | 519,345 | |

Harborview Mortgage Loan Trust 2007-7 2A1A | | | | 1.231% | | 11/25/47 | | | 1,475,100 | | | 767,159 | |

Impac CMB Trust 2004-5 1A1 | | | | 0.591% | | 10/25/34 | | | 238,572 | | | 171,929 | |

Impac CMB Trust 2004-6 1A2 | | | | 1.011% | | 10/25/34 | | | 337,015 | | | 241,009 | |

Impac CMB Trust 2005-7 A1 | | | | 0.491% | | 11/25/35 | | | 464,800 | | | 263,693 | |

Impac Secured Assets Corp. 2004-3 1A4 | | | | 1.031% | | 11/25/34 | | | 15,019 | | | 13,416 | |

Impac Secured Assets Corp. 2005-2 | | | | 0.551% | | 3/25/36 | | | 350,372 | | | 134,898 | |

Lehman XS Trust 2006-GP2 1A1A | | | | 0.301% | | 6/25/46 | | | 10,771 | | | 10,657 | |

Merit Securities Corp. 11PA B2 | | | | 1.731% | | 9/28/32 | | | 31,607 | | | 25,711 | A |

Merrill Lynch Mortgage Investors Trust 2004-A3 4A3 | | | | 5.055% | | 5/25/34 | | | 963,198 | | | 915,962 | |

Residential Accredit Loans Inc. 2007-Q01 A1 | | | | 0.381% | | 2/25/47 | | | 3,044,336 | | | 1,573,938 | |

Structured Adjustable Rate Mortgage Loan Trust 2004-7 A1 | | | | 0.636% | | 6/25/34 | | | 21,077 | | | 14,593 | |

Structured Adjustable Rate Mortgage Loan Trust 2005-19XS | | | | 0.551% | | 10/25/35 | | | 1,509,538 | | | 908,378 | |

Structured Asset Mortgage Investments Inc. 2003-AR2 A1 | | | | 0.603% | | 12/19/33 | | | 109,654 | | | 89,394 | |

Structured Asset Mortgage Investments Inc. 2006-AR6 | | | | 0.421% | | 7/25/46 | | | 1,929,220 | | | 963,563 | |

Structured Asset Mortgage Investments Inc. 2007-AR4 A1 | | | | 0.431% | | 9/25/47 | | | 1,128,962 | | | 1,052,530 | |

20

Annual Report to Shareholders

| | | | | | | | | | | | | |

| | | % OF

NET ASSETS | | RATE | | MATURITY

DATE | | PAR/

SHARES† | | VALUE | |

| | | | | | | | | | | | | |

Mortgage-Backed Securities—Continued | | | | | | | | | | | | | |

| | | | | |

Indexed Securities—Continued | | | | | | | | | | | | | |

Structured Asset Securities Corp. 2002-08A 7A1 | | | | 3.123% | | 5/25/32 | | $ | 101,035 | | $ | 88,169 | |

Structured Asset Securities Corp. 2002-11A 1A1 | | | | 3.242% | | 6/25/32 | | | 26,268 | | | 22,527 | |

Structured Asset Securities Corp. 2002-16A 1A1 | | | | 4.320% | | 8/25/32 | | | 239,808 | | | 239,507 | |

Structured Asset Securities Corp. 2002-18A 1A1 | | | | 4.226% | | 9/25/32 | | | 16,220 | | | 13,357 | |

Structured Asset Securities Corp. 2004-NP1 A | | | | 0.631% | | 9/25/33 | | | 218,944 | | | 185,008 | A,F |

Thornburg Mortgage Securities Trust 2004-1 I2A | | | | 0.681% | | 3/25/44 | | | 37,651 | | | 35,283 | |

WaMu Mortgage Pass-Through Certificates 2006-AR2 A1A | | | | 1.484% | | 4/25/46 | | | 4,143,643 | | | 2,038,485 | |

WaMu Mortgage Pass-Through Certificates 2006-AR3 A1A | | | | 1.514% | | 5/25/46 | | | 3,368,978 | | | 1,653,608 | |

WaMu Mortgage Pass-Through Certificates 2006-AR4 DA | | | | 1.514% | | 6/25/46 | | | 1,803,344 | | | 718,749 | |

WaMu Mortgage Pass-Through Certificates 2006-AR6 2A | | | | 1.504% | | 8/25/46 | | | 2,466,622 | | | 1,303,161 | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | 21,929,794 | |

| | | | | | | | | | | | | |

| | | | | |

Variable Rate SecuritiesJ | | 4.6% | | | | | | | | | | | |

Adjustable Rate Mortgage Trust 2004-1 4A1 | | | | 5.552% | | 1/25/35 | | | 3,791,451 | | | 3,534,985 | |

Banc of America Funding Corp. 2006-D 6A1 | | | | 5.851% | | 5/20/36 | | | 1,291,439 | | | 795,940 | |

Bear Stearns Adjustable Rate Mortgage Trust 2004-12 1A1 | | | | 4.804% | | 2/25/35 | | | 123,374 | | | 101,449 | |

Bear Stearns Alt-A Trust 2003-5 2A1 | | | | 3.080% | | 12/25/33 | | | 592,703 | | | 521,209 | |

Bear Stearns Alt-A Trust 2005 -10 21A1 | | | | 3.820% | | 1/25/36 | | | 451,903 | | | 249,200 | |

BlackRock Capital Finance LP 1996-R1 | | | | 9.580% | | 9/25/26 | | | 261,329 | | | 71,866 | G |

MASTR Adjustable Rate Mortgages Trust 2003-3 3A4 | | | | 3.194% | | 9/25/33 | | | 1,797,705 | | | 1,491,043 | |

Morgan Stanley Mortgage Loan Trust 2004-6AR | | | | 3.929% | | 8/25/34 | | | 104,491 | | | 77,627 | |

Morgan Stanley Mortgage Loan Trust 2006-3AR 2A3 | | | | 5.187% | | 3/25/36 | | | 536,281 | | | 329,918 | |

Nomura Asset Acceptance Corp. 2006-AF2 4A | | | | 6.573% | | 8/25/36 | | | 575,398 | | | 258,330 | |

Sequoia Mortgage Trust 2007-4 4A1 | | | | 5.965% | | 7/20/47 | | | 1,547,103 | | | 1,068,430 | |

Structured Adjustable Rate Mortgage Loan Trust 2004-17 A1 | | | | 1.752% | | 11/25/34 | | | 59,243 | | | 44,953 | |

21

Annual Report to Shareholders

Portfolio of Investments—Continued

Western Asset Absolute Return Portfolio—Continued

| | | | | | | | | | | | |

| | | % OF

NET ASSETS | | RATE | | MATURITY

DATE | | PAR/

SHARES† | | VALUE |

| | | | | | | | | | | | |

Mortgage-Backed Securities—Continued | | | | | | | | | | |

| | | | | |

Variable Rate Securities—Continued | | | | | | | | | | | | |

Structured Adjustable Rate Mortgage Loan Trust 2004-4 3A2 | | | | 3.262% | | 4/25/34 | | $ | 988,130 | | $ | 805,837 |

Structured Adjustable Rate Mortgage Loan Trust 2005-20 4A1 | | | | 5.912% | | 10/25/35 | | | 2,014,390 | | | 1,402,066 |

Thornburg Mortgage Securities Trust 2007-4 2A1 | | | | 6.200% | | 9/25/37 | | | 1,368,282 | | | 1,092,969 |

Thornburg Mortgage Securities Trust 2007-4 3A1 | | | | 6.198% | | 9/25/37 | | | 1,375,790 | | | 1,099,421 |

Wells Fargo Mortgage-Backed Securities Trust 2005-AR9 4A1 | | | | 3.685% | | 5/25/35 | | | 452,017 | | | 406,081 |

| | | | | | | | | | | | |

| | | | | | | | | | | | 13,351,324 |

| | | | | | | | | | | | |

Total Mortgage-Backed Securities

(Cost—$57,552,078) | | | | | | | | | | | | 35,827,000 |

Loan Participations and AssignmentsD | | 7.7% | | | | | | | | | | |

| | | | | |

Aerospace and Defense | | 0.2% | | | | | | | | | | |

Dubai Aerospace Enterprise, Term Loan, Tranche B1 | | | | 4.040% | | 1/29/10 | | | 287,234 | | | 262,819 |

Dubai Aerospace Enterprise, Term Loan, Tranche B2 | | | | 4.010% | | 1/29/10 | | | 280,287 | | | 256,463 |

| | | | | | | | | | | | |

| | | | | | | | | | | | 519,282 |

| | | | | | | | | | | | |

Auto Components | | 0.3% | | | | | | | | | | |

Allison Transmission Inc., Term Loan, Tranche B | | | | 2.990% to 3.040% | | 2/10/10 | | | 956,866 | | | 875,771 |

| | | | | | | | | | | | |

| | | | | |

Automobiles | | 0.3% | | | | | | | | | | |

Chrysler Financial Services NA LLC, First Lien Term Loan | | | | 4.240% | | 1/15/10 | | | 977,500 | | | 951,433 |

| | | | | | | | | | | | |

| | | | | |

Containers and Packaging | | 0.6% | | | | | | | | | | |

Amscan Holdings Inc., Term Loan, Tranche B | | | | 2.501% | | 3/25/10 | | | 972,500 | | | 875,250 |

Graham Packaging Company LP, Term Loan C | | | | 6.750% | | 3/31/10 | | | 873,303 | | | 877,306 |

| | | | | | | | | | | | |

| | | | | | | | | | | | 1,752,556 |

| | | | | | | | | | | | |

22

Annual Report to Shareholders

| | | | | | | | | | | | | |

| | | % OF

NET ASSETS | | RATE | | MATURITY

DATE | | PAR/

SHARES† | | VALUE | |

| | | | | | | | | | | | | |

Loan Participations and Assignments—Continued | | | | | | | | | | | | | |

| | | | | |

Distributors | | 0.2% | | | | | | | | | | | |

Keystone Automotive Industries Inc., Term Loan, Tranche B | | | | 3.741% to 5.750% | | 3/31/10 | | $ | 941,200 | | $ | 592,956 | |

| | | | | | | | | | | | | |

| | | | | |

Electric Utilities | | 0.4% | | | | | | | | | | | |

TXU, Term Loan, Tranche B2 | | | | 3.735% to 3.751% | | 3/31/10 | | | 1,221,875 | | | 992,774 | |

| | | | | | | | | | | | | |

| | | | | |

Energy Equipment and Services | | 0.3% | | | | | | | | | | | |

Brand Energy, Term Loan, Tranche B | | | | 3.563% | | 2/26/10 | | | 977,500 | | | 905,409 | |

| | | | | | | | | | | | | |

| | | | | |

Hotels, Restaurants and Leisure | | 0.6% | | | | | | | | | | | |

Harrah’s Entertainment Inc., Term Loan B | | | | 3.282% | | 1/26/10 | | | 806,853 | | | 651,366 | |

Las Vegas Sands LLC, Delayed Term Loan | | | | 2.010% | | 3/31/10 | | | 197,000 | | | 171,988 | |

Las Vegas Sands LLC, Term Loan, Tranche B | | | | 2.010% | | 3/31/10 | | | 780,000 | | | 680,968 | |

Wimar Opco LLC, Term Loan, Tranche B | | | | 3.250% | | 3/31/10 | | | 947,645 | | | 285,478 | C |

| | | | | | | | | | | | | |

| | | | | | | | | | | | 1,789,800 | |

| | | | | | | | | | | | | |

IT Services | | 0.6% | | | | | | | | | | | |

First Data Corp., Term Loan B2 | | | | 2.999% to 3.001% | | 3/31/10 | | | 989,873 | | | 879,255 | |

SunGard Data Systems Inc., Term Loan, Tranche A | | | | 1.985% | | 1/11/10 | | | 28,206 | | | 26,588 | |

SunGard Data Systems Inc., Term Loan, Tranche B | | | | 3.869% to 3.900% | | 2/9/10 | | | 932,103 | | | 895,013 | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | 1,800,856 | |

| | | | | | | | | | | | | |

Media | | 2.4% | | | | | | | | | | | |

Cedar Fair LP, Term Loan, Tranche B | | | | 2.231% to 4.231% | | 1/29/10 | | | 923,652 | | | 911,337 | |

Charter Communications Operating LLC, Term Loan | | | | 2.260% | | 2/26/10 | | | 980,000 | | | 917,525 | |

Citadel Communication Group, Term Loan, Tranche B | | | | 1.990% | | 1/29/10 | | | 996,220 | | | 735,127 | C |

Idearc Inc., Term Loan | | | | 10.250% | | 3/31/10 | | | 385,750 | | | 379,000 | |

Insight Midwest Holdings LLC, Term Loan, Tranche B | | | | 2.290% | | 1/4/10 | | | 675,000 | | | 641,250 | |

23

Annual Report to Shareholders

Portfolio of Investments—Continued

Western Asset Absolute Return Portfolio—Continued

| | | | | | | | | | | | |

| | | % OF

NET ASSETS | | RATE | | MATURITY

DATE | | PAR/

SHARES† | | VALUE |

| | | | | | | | | | | | |

Loan Participations and Assignments—Continued | | | | | | | | | | | | |

| | | | | |

Media—Continued | | | | | | | | | | | | |

Lodgenet Entertainment Corp., Term Loan, Tranche B | | | | 2.260% | | 3/31/10 | | $ | 795,225 | | $ | 719,679 |

Univision Communications, Term Loan, Tranche B | | | | 2.501% | | 3/31/10 | | | 1,000,000 | | | 867,000 |

UPC Broadband Holding, Term Loan, Tranche N1 | | | | 1.985% | | 1/4/10 | | | 1,296,576 | | | 1,211,218 |

UPC, Term Loan | | | | 3.735% | | 1/4/10 | | | 703,424 | | | 681,970 |

| | | | | | | | | | | | |

| | | | | | | | | | | | 7,064,106 |

| | | | | | | | | | | | |

Metals and Mining | | 0.3% | | | | | | | | | | |