UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number :811-06113

The Caldwell & Orkin Funds, Inc.

(Exact name of registrant as specified in charter)

100 S. Ashley Drive, Suite 895

Tampa, Florida 33602

(Address of principal executive offices) (Zip code)

Derek Pilecki

100 S. Ashley Drive, Suite 895

Tampa, Florida 33602

(Name and address of agent for service)

Copies to:

Benjamin Mollozzi

Ultimus Fund Solutions, LLC

225 Pictoria Drive, Suite 450

Cincinnati, OH 45256

Registrant’s telephone number, including area code:1-813-282-7870

Date of fiscal year end:April 30

Date of reporting period:April 30, 2019

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Fund’s shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports from the Fund or from your financial intermediary such as a broker-dealer or bank. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Fund electronically by contacting the Fund at (800) 467-7903 or, if you own these shares through a financial intermediary, you may contact your financial intermediary.

You may elect to receive all future reports in paper free of charge. You can inform the Fund that you wish to continue receiving paper copies of your shareholder reports by contacting the Fund at (800) 467-7903 If you own shares through a financial intermediary, you may contact your financial intermediary or follow instructions included with this disclosure to elect to continue to receive paper copies of your shareholder reports. Your election to receive reports in paper will apply to all funds held with the fund complex or at your financial intermediary.

Table of Contents | Caldwell & Orkin -

Gator Capital Long/Short Fund |

April 30, 2019 (Unaudited) | |

Management’s Discussion of Fund Performance | 2 |

Investment Results | 7 |

Fund Holdings | 9 |

Schedule of Investments | 10 |

Schedule of Securities Sold Short | 15 |

Statement of Assets and Liabilities | 18 |

Statement of Operations | 19 |

Statements of Changes in Net Assets | 20 |

Financial Highlights | 21 |

Notes to Financial Statements | 22 |

Report of Independent Registered Public Accounting Firm | 29 |

Disclosure of Fund Expenses | 31 |

Additional Information | 32 |

Privacy Policy Disclosure | 35 |

Caldwell & Orkin -

Gator Capital Long/Short Fund | Management’s Discussion

of Fund Performance |

| | April 30, 2019 (Unaudited) |

Dear Fellow Shareholder:

The Caldwell & Orkin – Gator Capital Long/Short Fund (the “Fund”) gained 6.16% over the six month period ended on April 30, 2019. The S&P 500 Total Return Index (“S&P 500”) gained 9.76% during the same period. For the 12 month period ended April 30, 2019, the Fund gained 1.21% while the S&P 500 increased by 13.49%.

Management Discussion and Analysis

The Fund rebounded strongly to end the 2019 fiscal year. We benefitted from staying with our positions through the market decline in December. Our positions were strong performers during the January rally. We attribute the ability to maintain our positions to our research process. Our research process allows us to have a high level of conviction in our positions.

The top five contributors during the 2019 fiscal year were Etsy (long), Carvana (long), Celestica (short), KKR & Co. (long), and Blackstone (long).

The top five detractors during the 2018 fiscal year were AIG (long), Invesco (long), Realogy (long), BBX Corp. (long), and Cardtronics (short).

We ended the 2019 fiscal year with gross long exposure of 90% and gross short exposure of 51% for a total gross exposure of 141% and a net exposure of 49%.

Outlook

The equity markets have had a strong rebound in early 2019 recovering from the sharp decline at the end of 2018. We are finding many attractively priced stocks and believe the stock market will eventually recognize the value we see.

We believe the economy is strong as evidenced by robust employment metrics. While we are monitoring the trade negotiations with China, we believe the strong rhetoric is simply posturing and will not have a lasting impact on economic growth. We also think the Fed is ready to support the economy with easing monetary policy if needed.

Earlier this year, we modified the name of the Fund to include “Gator Capital”. This mirrors the changes we’ve made to the portfolio that reflect our firm’s investment style. We have also included a copy of our investment thesis on SVB Financial Group for your review.

We are working hard with our research-oriented investment approach. It is our objective to make

the Fund successful in helping you compound your wealth in the years to come.

Sincerely,

Derek S. Pilecki, CFA

Portfolio Manager

2 | 1-800-467-7903 | https://gatorcapital.com/mutual-funds/gator-capital-long-short-fund/# |

Caldwell & Orkin -

Gator Capital Long/Short Fund | Management’s Discussion

of Fund Performance |

| | April 30, 2019 (Unaudited) |

SVB Financial Group (NASDAQ: SIVB)

We started a position in SVB Financial early in 2019. SIVB is the bank holding company for Silicon Valley Bank, which has a strong franchise providing commercial banking to venture capital firms and their venture-backed investment companies. Over the past 20 years, SIVB’s stock returned 17.3% annually compared to the S&P 500 returning 5.9% and the bank index returning 2.6%. These returns are a testament to the bank’s strong franchise.

Despite SIVB’s strong franchise and great long-term track record, SIVB’s stock has underperformed since the market’s highs last September. Here are some of the concerns that we’ve heard from other investors.

| | 1. | SIVB is the most asset-sensitive bank, so with the Fed further pausing interest rate increases and potentially cutting rates, SIVB is the most exposed bank to lower rates; |

| | 2. | The venture investing community has been on fire for the past few years and valuations for late stage venture companies are high so SIVB will experience a much tougher environment when the current venture capital environment reverses; |

| | 3. | SIVB will have less warrant income in Q1 due to the delayed IPO calendar created by the federal government shutdown in January; |

| | 4. | During its Investor Day in early December 2018, SIVB’s management guided forecasts for deposit balances to decline for Q4 due to expected distributions by Venture Capital funds to their limited partners; and, |

| | 5. | SIVB has periodically guided to higher expense growth than Wall Street has expected so they can continue to invest in and expand their franchise. |

We think these five concerns have pushed SIVB’s stock down to a level that is compelling. While these concerns are valid, we believe each is temporary and will not diminish the long-term franchise value of SIVB.

In addition to the recent underperformance of SIVB stock, here is what we find attractive about SIVB.

| | 1. | Extremely attractive deposit base – SIVB has one of the best deposit franchises in the country.SIVB has had a long-term focus on the venture capital community.The bank has built strong relationships with venture capitalists.They bank the venture firms and their funds, they bank the venture portfolio companies, and they bank the executives at the venture portfolio companies.When a portfolio company gets funding from a venture firm, they receive cash and deposit it at a bank.SIVB estimates it has a 60% market share among venture-backed portfolio companies.SIVB is also different from other banks in that it has moved excess deposits off of its balance sheet into money market funds and other similar short-term deposit replacement products.These off-balance sheet client assets generate fee income for SIVB and do not require equity capital support like an on-balance sheet deposit would.A few other metrics that demonstrate the quality of SIVB’s deposit franchise are the 56% loan-to-deposit |

Annual Report | April 30, 2019 | 3 |

Caldwell & Orkin -

Gator Capital Long/Short Fund | Management’s Discussion

of Fund Performance |

| | April 30, 2019 (Unaudited) |

ratio and the total cost of funds of 0.20%. For comparison, Bank of America, which is arguably regarded as the best national deposit franchise, has a loan-to-deposit ratio of 69% and a cost of funds of 1.12%.

| | 2. | Consistent double-digit loan and deposit growth – Since 1999, SIVB has grown loans per share and deposits per share at 15% and 13%, respectively.By looking at these metrics on a per share basis, we are adjusting for acquisitions, stock buybacks, and equity issuances, and get something close to the organic growth rates.The growth rates of loans and deposits have been strong for 20 years. |

| | 3. | Earnings estimates are too low – We believe the earnings estimates are too low for SIVB.We have noticed that the sell-side is mostly conservative on SIVB’s estimates because of the volatility of their warrant income.We believe the sell-side’s estimates for 2019 are even more conservative because they don’t factor the December 2018 Fed rate hike that already occurred.And we believe the messaging from SIVB management about conservative deposit growth at its Investors Day in December 2018 has caused the sell-side to lower its forecast of deposit growth too far.We’ve already seen evidence that SIVB management was too conservative on their deposit guidance in December 2018 and beat that guidance when they reported earnings in January 2019. |

| | 4. | SIVB’s positioning within Venture community is a true franchise – Over the past 30 years, SIVB has built strong relationships with the venture and private equity communities.These relationships have extended to the portfolio companies of these investment firms and the principals of both the investment firms and portfolio companies.We believe the network of relationships gives SIVB a banking franchise where firms and executives are less price sensitive on their loans and deposits in exchange for access to the SIVB network. |

| | 5. | High return on equity – With Fed Funds between 2.00% and 2.25%, SIVB reported a 20% return on tangible equity (“ROTE”).This ROTE is in the top 5% of banks and should lead to higher growth rates and a premium valuation. |

| | 6. | Reinvestment opportunities – SIVB’s high organic growth rate and high return on equity allows the bank to reinvest more of the capital it generates.This is different from most banks who may generate high returns on equity but do not have the same reinvestment opportunities.For example, U.S. Bancorp generates a +20% return on equity, but it has only grown loans and deposits per share at 5% and 9%. |

| | 7. | SIVB is a beneficiary of an easing regulatory environment – One of the major regulatory rollbacks Congress passed was the raising of bank asset levels from $50 billion to $250 billion before major regulatory programs are implemented.SIVB is about to cross the $50 billion asset level, so it will not have to deal with major regulatory issues such as the CCAR stress testing process, resolution planning, Liquidity Coverage Ratio (LCR), and Risk Management. |

| | 8. | SIVB will regain its premium valuation – SIVB is trading for 11x 2019 earnings per share estimates (“EPS”).For the previous 10 years, SIVB has usually traded between 15x and 22x EPS.We think it will regain a premium valuation as current fears fade. |

4 | 1-800-467-7903 | https://gatorcapital.com/mutual-funds/gator-capital-long-short-fund/# |

Caldwell & Orkin -

Gator Capital Long/Short Fund | Management’s Discussion

of Fund Performance |

| | April 30, 2019 (Unaudited) |

| | 9. | SIVB is generating excess capital, and management has started buying back stock – With rising interest rates, SIVB’s return on equity is above 20% and greater than its organic growth rate, so the bank is generating more capital than it can reinvest.Since SIVB doesn’t pay a dividend, management has started to use the excess capital to repurchase stock. |

Bear Case:

Although we think the bullish investment thesis for SIVB is compelling, we always consider the bear case. Here are the main bearish points as we understand them and our reasons that we can still own the stock despite these points:

| | 1. | SIVB faces interest rate headwinds if rates decline - SIVB is one of the most asset-sensitive banks, so with the Fed becoming dovish, SIVB’s earnings are at risk due to lower rates.A bank is asset-sensitive when its earnings increase due to higher short-term rates.SIVB is the most asset-sensitive bank because its assets are mostly floating rate loans and it has the lowest cost deposit base in the country. |

| | | We note that the bank’s management has said that they are layering in interest rate hedges to reduce the asset sensitivity. We don’t love interest rate hedging of this kind because we think it is costly, and if it works, the stock’s valuation will not reflect the value of the hedges. |

| | | In our view, we think the Fed is in more of a pausing rates phase than an actual cutting rates phase, so we don’t think SIVB’s earnings will go down. If the Fed does cut rates, we believe SIVB’s long-term growth rate will be unaffected. In fact, the bank’s loan growth may mitigate the earnings impact of lower rates. We believe the low valuation is already pricing in several rate cuts by the Fed. |

| | 2. | Technology start-up valuations and velocity may be unsustainable - We are reaching cyclically high levels of venture capital investing.SIVB’s earnings could decline in multiple ways in a venture investing downturn.The last VC downturn took close to 20 years to recover prior peak levels. |

| | | We may be near a peak in venture investing, but what if the peak is 4-5 years away? We haven’t seen a runaway IPO market for tech IPOs, yet. Yes, some tech unicorns have had down rounds and lost value, but there continues to be significant innovation in the venture community. |

| | 3. | SIVB’s technology lending is vulnerable to recession - SIVB’s technology lending is actually high-risk but is currently disguised by low current losses.SIVB’s technology lending has also expanded significantly since the Internet Boom/Bust. |

| | 4. | SIVB may have been growing Capital Call loans too fast- SIVB fastest growing loan category is Capital Call loans to private equity funds.These loans are facing increasing competition from many banks because they have experienced almost no credit charge-offs in their history.This category of loans has grown substantially since the Great Financial Crisis and is relatively untested in a recession. |

Annual Report | April 30, 2019 | 5 |

Caldwell & Orkin -

Gator Capital Long/Short Fund | Management’s Discussion

of Fund Performance |

| | April 30, 2019 (Unaudited) |

| | | We note this is a valid criticism. The growth rate that SIVB has experienced may slow and spreads may tighten due to competition. SIVB management would say they have the best customer franchise with the private equity funds, so they expect to be able to maintain or grow their market share. In our experience, private equity fund managers are economic players and would be willing to move business to another bank for a better rate. We are less concerned about the credit performance of these loans because we think there is low likelihood of default by private equity funds, and SIVB will have multiple avenues to recover on any defaults. |

| | 5. | SIVB’s gains from warrants may be unsustainable - As part of its lending business, SIVB typically receives warrants in the borrower.Since SIVB has a large portfolio of lending clients, it also has a large portfolio of warrants.Each quarter, a small portion of these companies have liquidity events, which allows SIVB to book warrant gains.Some critics claim that the warrant income will dry up when the venture investing cycling dries up.We think investors already discount warrant income, so SIVB’s stock does not have a lot of embedded premium in its stock price due to potential warrant income. |

| | 6. | SIVB is taking another shot at investment banking - SIVB recently announced the acquisition of Leerink Partners, an investment bank focused on the healthcare and life sciences sector.The theory is SVB will be able to capture the investment banking business of their biotech clients who are now just commercial banking clients.The secondary plan is to expand the investment bank to other sectors such as technology.The two criticisms of this deal are the high price ($280 million cash) and the fact that SIVB had an investment bank 15 years ago (SVB Alliant) that they had to close. |

The performance data quoted represents past performance. Past performance is no guarantee of future results. The investment returns and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Please call800-467-7903or visit www.CaldwellOrkin.com for current month-end performance.

6 | 1-800-467-7903 | https://gatorcapital.com/mutual-funds/gator-capital-long-short-fund/# |

Caldwell & Orkin -

Gator Capital Long/Short Fund | Investment Results |

| | April 30, 2019 (Unaudited) |

Average Annual Total Returns(a) as of April 30, 2019 |

| | One Year | Three Year | Five Year | Ten Year |

Caldwell & Orkin - Gator Capital Long/Short Fund | 1.21% | -1.11% | 1.26% | 0.78% |

S&P 500 Total Return Index(b) | 13.49% | 14.87% | 11.63% | 15.32% |

Eurekahedge Long Short Equities Hedge Fund Index(c) | -0.19% | 6.05% | 4.65% | 7.06% |

| | | | | |

Total annualized Fund operating expenses for the Fund is 2.54% as described in the Prospectus, dated August 28, 2018. This amount includes Acquired Fund Fees and Expenses, as well as interest and dividend expenses related to short sales, which if excluded would result in an annual operating expense rate of 1.85%. Additional information about the Fund’s current fees and expenses for the fiscal year ended April 30, 2019 is contained in the Financial Highlights. |

(a) | Return figures reflect any change in price per share and assume the reinvestment of all distributions. The Fund’s returns reflect any fee reductions during the applicable period. If such fee reductions had not occurred, the quoted performance would have been lower.The table does not reflect the deduction of taxes. The Fund’s returns represent past performance and do not guarantee future results. |

(b) | Investors should expect that the Fund’s performance may fluctuate independently of stock market indices, such as the S&P 500 Total Return Index. The S&P 500 Total Return Index is a widely recognized unmanaged index of 500 common stock prices adjusted to reflect the reinvestment of dividends and distributions. You may not invest directly in an index. |

(c) | The Eurekahedge Long Short Equities Hedge Fund Index is an unmanaged index comprised of long/short equity hedge funds. According to its sponsor, Eurekahedge Pte. Ltd., the Eurekahedge Index is an equally weighted index of 1028 constituent funds designed to provide a broad measure of the performance of underlying hedge fund managers. The returns of the Eurekahedge Index do not include sales charges or fees, which would lower performance. You may not invest directly in an index. |

You should consider the Fund’s investment objectives, risks, charges and expenses carefully before you invest. The Fund’s prospectus contain important information about the Fund’s investment objectives, potential risks, management fees, charges and expenses, and other information and should be read carefully before investing. You may obtain a current copy of the Fund’s prospectus or performance data current to the most recent month by calling 1-800-467-7903.

The Fund is distributed by Ultimus Fund Distributors, LLC, member FINRA/SIPC.

Annual Report | April 30, 2019 | 7 |

Caldwell & Orkin -

Gator Capital Long/Short Fund | Investment Results |

| | April 30, 2019 (Unaudited) |

Comparison of the Growth of a $10,000 Investment in the Caldwell & Orkin - Gator Capital Long/Short Fund,the S&P 500® Total Return Index and the Eurekahedge Long Short Equities Hedge Fund Index

The chart above assumes an initial investment of $10,000 made on April 30, 2009 and held through April 30, 2019. The S&P 500®Total Return Index is a widely recognized unmanaged index of equity prices and is representative of a broader market and range of securities than is found in the Fund’s portfolio.The Eurekahedge Long Short Equities Hedge Fund Index is an unmanaged index comprised of long/short equity hedge funds. Individuals cannot invest directly in an index; however, an individual can invest in exchange-traded funds or other investment vehicles that attempt to track the performance of a benchmark index.THE FUND’S RETURNS REPRESENT PAST PERFORMANCE AND DO NOT GUARANTEE FUTURE RESULTS. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment returns and principal values will fluctuate so that your shares, when redeemed, may be worth more or less than their original purchase price.

Current performance may be lower or higher than the performance data quoted. For more information on the Fund, and to obtain performance data current to the most recent month-end, or to request a prospectus, please call 1-800-467-7903. You should carefully consider the investment objectives, potential risks, management fees, and charges and expenses of the Fund before investing. The Fund’s prospectus contains this and other information about the Fund, and should be read carefully before investing.

The Fund is distributed by Ultimus Fund Distributors, LLC, member FINRA/SIPC.

8 | 1-800-467-7903 | https://gatorcapital.com/mutual-funds/gator-capital-long-short-fund/# |

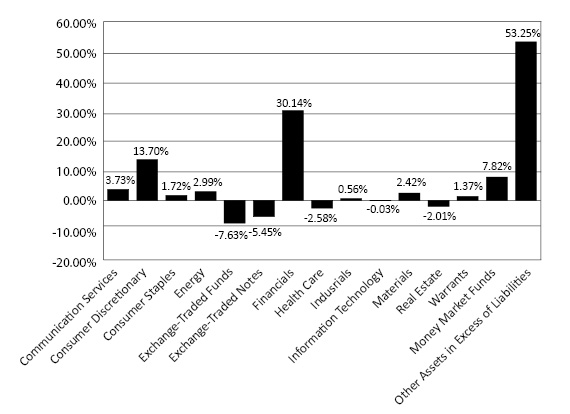

Caldwell & Orkin -

Gator Capital Long/Short Fund | Fund Holdings |

| | April 30, 2019 (Unaudited) |

Net Sector Exposure

April 30, 2019*

* | Sector weightings are calculated as a percentage of net assets and include short positions. Portfolio holdings are subject to change. |

The Caldwell & Orkin - Gator Capital Long/Short Fund’s (the “Fund”) investment objective is to provide long-term capital growth with a short-term focus on capital preservation.

Availability of Portfolio Schedule – (Unaudited)

The Fund files a complete schedule of portfolio holdings with the Securities and Exchange Commission (“SEC”) for the first and third quarters of each fiscal year within sixty days after the end of the period. The Fund’s portfolio holdings are available on the SEC’s website at www.sec.gov.

Annual Report | April 30, 2019 | 9 |

Caldwell & Orkin -

Gator Capital Long/Short Fund | Schedule of Investments |

| | April 30, 2019 |

| | Shares | | | Fair Value | |

COMMON STOCKS — LONG — 88.91% | | | | | | | | |

Asset Management & Custody Banks — 12.36% | | | | | | | | |

Ameriprise Financial, Inc. | | | 2,500 | | | $ | 366,925 | |

Blackstone Group LP (The) | | | 15,900 | | | | 627,413 | |

BrightSphere Investment Group plc | | | 15,900 | | | | 233,094 | |

KKR & Company, Inc., Class A | | | 23,000 | | | | 562,350 | |

Legg Mason, Inc. | | | 16,000 | | | | 535,200 | |

Victory Capital Holdings, Inc.(a) | | | 23,300 | | | | 384,217 | |

Waddell & Reed Financial, Inc., Class A | | | 9,000 | | | | 168,570 | |

| | | | | | | | 2,877,769 | |

Automobile Manufacturers — 1.13% | | | | | | | | |

General Motors Company | | | 6,750 | | | | 262,912 | |

| | | | | | | | | |

Automotive Retail — 1.89% | | | | | | | | |

Carvana Company(a) | | | 3,900 | | | | 279,084 | |

Sonic Automotive, Inc., Class A | | | 8,000 | | | | 161,840 | |

| | | | | | | | 440,924 | |

Broadcasting — 0.95% | | | | | | | | |

Entercom Communications Corporation, Class A | | | 32,000 | | | | 220,160 | |

| | | | | | | | | |

Casinos & Gaming — 7.83% | | | | | | | | |

Caesars Entertainment Corporation(a) | | | 55,500 | | | | 519,481 | |

Las Vegas Sands Corporation | | | 6,000 | | | | 402,300 | |

Melco Resorts & Entertainment Ltd. - ADR | | | 20,000 | | | | 502,000 | |

MGM Resorts International | | | 15,000 | | | | 399,450 | |

| | | | | | | | 1,823,231 | |

Communications Equipment — 0.60% | | | | | | | | |

Juniper Networks, Inc. | | | 5,000 | | | | 138,850 | |

| | | | | | | | | |

Consumer Finance — 8.49% | | | | | | | | |

Ally Financial, Inc. | | | 3,000 | | | | 89,130 | |

Capital One Financial Corporation | | | 4,700 | | | | 436,301 | |

Navient Corporation | | | 15,000 | | | | 202,650 | |

OneMain Holdings, Inc. | | | 16,500 | | | | 560,505 | |

SLM Corporation | | | 42,000 | | | | 426,720 | |

Synchrony Financial | | | 7,500 | | | | 260,025 | |

| | | | | | | | 1,975,331 | |

Diversified Banks — 5.68% | | | | | | | | |

Barclays PLC, Sponsored - ADR | | | 59,000 | | | | 505,040 | |

See accompanying notes which are an integral part of these financial statements.

10 | 1-800-467-7903 | https://gatorcapital.com/mutual-funds/gator-capital-long-short-fund/# |

Caldwell & Orkin -

Gator Capital Long/Short Fund |

Schedule of Investments

|

| | April 30, 2019 |

| | Shares | | | Fair Value | |

Diversified Banks — 5.68% - continued | | | | | | | | |

JPMorgan Chase & Company | | | 3,800 | | | $ | 440,990 | |

Wells Fargo & Company | | | 7,800 | | | | 377,598 | |

| | | | | | | | 1,323,628 | |

Diversified Capital Markets — 4.67% | | | | | | | | |

Credit Suisse Group AG - ADR | | | 42,000 | | | | 558,600 | |

Deutsche Bank AG | | | 30,000 | | | | 248,400 | |

UBS Group AG | | | 20,729 | | | | 278,598 | |

| | | | | | | | 1,085,598 | |

Food Retail — 0.89% | | | | | | | | |

Kroger Company (The) | | | 8,000 | | | | 206,240 | |

| | | | | | | | | |

Homebuilding — 2.19% | | | | | | | | |

Lennar Corporation, Class A | | | 9,800 | | | | 509,894 | |

| | | | | | | | | |

Hotels Resorts & Cruise Lines — 1.63% | | | | | | | | |

BBX Capital Corporation | | | 68,595 | | | | 380,016 | |

| | | | | | | | | |

Internet Software & Services — 2.41% | | | | | | | | |

IAC/InterActiveCorp(a) | | | 2,500 | | | | 562,100 | |

| | | | | | | | | |

Investment Banking & Brokerage — 4.51% | | | | | | | | |

Charles Schwab Corporation (The) | | | 11,250 | | | | 515,025 | |

E*TRADE Financial Corporation | | | 6,600 | | | | 334,356 | |

Interactive Brokers Group, Inc., Class A | | | 600 | | | | 32,544 | |

Stifel Financial Corporation | | | 1,200 | | | | 71,604 | |

TD Ameritrade Holding Corporation | | | 1,800 | | | | 94,644 | |

| | | | | | | | 1,048,173 | |

Life & Health Insurance — 1.26% | | | | | | | | |

Lincoln National Corporation | | | 4,400 | | | | 293,568 | |

| | | | | | | | | |

Movies & Entertainment — 0.37% | | | | | | | | |

Viacom, Inc., Class B | | | 3,000 | | | | 86,730 | |

| | | | | | | | | |

Multi-Sector Holdings — 3.36% | | | | | | | | |

Berkshire Hathaway, Inc., Class B(a) | | | 1,900 | | | | 411,749 | |

Jefferies Financial Group, Inc. | | | 18,000 | | | | 370,260 | |

| | | | | | | | 782,009 | |

See accompanying notes which are an integral part of these financial statements.

Annual Report | April 30, 2019 | 11 |

Caldwell & Orkin -

Gator Capital Long/Short Fund |

Schedule of Investments

|

| | April 30, 2019 |

| | Shares | | | Fair Value | |

Office Services & Supplies — 0.56% | | | | | | | | |

Knoll, Inc. | | | 6,000 | | | $ | 131,040 | |

| | | | | | | | | |

Oil & Gas Storage & Transportation — 2.99% | | | | | | | | |

EnLink Midstream, LLC | | | 23,000 | | | | 268,870 | |

SemGroup Corporation, Class A | | | 20,000 | | | | 261,200 | |

Teekay Corporation | | | 40,000 | | | | 166,400 | |

| | | | | | | | 696,470 | |

Packaged Foods & Meats — 0.83% | | | | | | | | |

B&G Foods, Inc. | | | 5,250 | | | | 136,500 | |

Dean Foods Company | | | 34,000 | | | | 57,800 | |

| | | | | | | | 194,300 | |

Property & Casualty Insurance — 2.17% | | | | | | | | |

Ambac Financial Group, Inc.(a) | | | 27,000 | | | | 504,900 | |

| | | | | | | | | |

Real Estate Services — 1.51% | | | | | | | | |

Realogy Holdings Corporation | | | 27,000 | | | | 351,540 | |

| | | | | | | | | |

Regional Banks — 15.57% | | | | | | | | |

Ameris Bancorp | | | 2,250 | | | | 82,035 | |

BankUnited, Inc. | | | 12,000 | | | | 438,960 | |

Citizens Financial Group, Inc. | | | 17,000 | | | | 615,401 | |

ConnectOne Bancorp, Inc. | | | 15,000 | | | | 327,450 | |

FNB Corporation | | | 20,000 | | | | 242,600 | |

Simmons First National Corporation, Class A | | | 3,000 | | | | 76,170 | |

Sterling Bancorp | | | 21,000 | | | | 449,820 | |

SunTrust Banks, Inc. | | | 8,600 | | | | 563,128 | |

SVB Financial Group(a) | | | 1,500 | | | | 377,580 | |

Synovus Financial Corporation | | | 2,625 | | | | 96,757 | |

Western Alliance Bancorporation(a) | | | 7,300 | | | | 348,794 | |

| | | | | | | | 3,618,695 | |

Specialized Consumer Services — 0.35% | | | | | | | | |

H&R Block, Inc. | | | 3,000 | | | | 81,630 | |

| | | | | | | | | |

Specialty Chemicals — 1.16% | | | | | | | | |

Axalta Coating Systems Ltd.(a) | | | 10,000 | | | | 269,800 | |

| | | | | | | | | |

Steel — 1.26% | | | | | | | | |

SunCoke Energy, Inc.(a) | | | 34,000 | | | | 292,740 | |

See accompanying notes which are an integral part of these financial statements.

12 | 1-800-467-7903 | https://gatorcapital.com/mutual-funds/gator-capital-long-short-fund/# |

Caldwell & Orkin -

Gator Capital Long/Short Fund |

Schedule of Investments

|

| | April 30, 2019 |

| | Shares | | | Fair Value | |

Systems Software — 1.10% | | | | | | | | |

BlackBerry Ltd.(a) | | | 28,000 | | | $ | 257,040 | |

| | | | | | | | | |

Technology Hardware Storage & Peripherals — 0.51% | | | | | | | | |

Hewlett Packard Enterprise Company | | | 7,500 | | | | 118,575 | |

| | | | | | | | | |

Thrifts & Mortgage Finance — 0.68% | | | | | | | | |

MGIC Investment Corporation(a) | | | 2,000 | | | | 29,280 | |

Radian Group, Inc. | | | 5,440 | | | | 127,405 | |

| | | | | | | | 156,685 | |

| | | | | | | | | |

Total Common Stocks — Long

(Cost $20,040,947) | | | | | | | 20,690,548 | |

PREFERRED STOCKS — LONG — 0.31% | | | | | | | | |

Financials — 0.31% | | | | | | | | |

Federal National Mortgage Association, Series R, 7.63%(a) | | | 7,441 | | | | 72,327 | |

| | | | | | | | | |

Total Preferred Stocks — Long (Cost $46,995) | | | | | | | 72,327 | |

WARRANTS — LONG — 1.37% | | | | | | | | |

American International Group, Inc.,

Expires 01/19/21, Strike Price $44 | | | 37,500 | | | | 301,500 | |

Zions Bancorp NA,

Expires 05/22/20, Strike Price $35 | | | 1,100 | | | | 18,436 | |

| | | | | | | | | |

Total Warrants — Long (Cost $551,855) | | | | | | | 319,936 | |

See accompanying notes which are an integral part of these financial statements.

Annual Report | April 30, 2019 | 13 |

Caldwell & Orkin -

Gator Capital Long/Short Fund |

Schedule of Investments

|

| | April 30, 2019 |

| | Shares | | | Fair Value | |

MONEY MARKET FUNDS — 7.82% | | | | | | | | |

First American Treasury Obligations Fund - Class X, 2.36%(b) | | | 1,820,130 | | | $ | 1,820,130 | |

| | | | | | | | | |

Total Money Market Funds

(Cost $1,820,130) | | | | | | | 1,820,130 | |

Total Investments — 98.41% (Cost $22,459,927) | | | | 22,902,941 | |

| | | | | | | | | |

Other Assets in Excess of Liabilities — 1.59% | | | | | | | 368,964 | |

NET ASSETS — 100.00% | | | | | | $ | 23,271,905 | |

(a) | Non-income producing security. |

(b) | Rate disclosed is the seven day effective yield as of April 30, 2019. |

ADR - American Depositary Receipt.

The sub-industries shown on the schedule of investments are based on the Global Industry Classification Standard, or GICS® (“GICS”). The GICS was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC (“S&P”). GICS is a service mark of MSCI, Inc. and S&P and has been licensed for use by Ultimus Fund Solutions, LLC.

See accompanying notes which are an integral part of these financial statements.

14 | 1-800-467-7903 | https://gatorcapital.com/mutual-funds/gator-capital-long-short-fund/# |

Caldwell & Orkin -

Gator Capital Long/Short Fund | Schedule of Securities Sold Short |

| | April 30, 2019 |

| | Shares | | | Fair Value | |

COMMON STOCKS — SHORT — (38.56)% | | | | | | | | |

Asset Management & Custody Banks — (0.94)% | | | | | | | | |

Hamilton Lane, Inc., Class A | | | (4,500 | ) | | $ | (219,870 | ) |

| | | | | | | | | |

Automobile Manufacturers — (1.33)% | | | | | | | | |

Tesla, Inc.(a) | | | (1,300 | ) | | | (310,298 | ) |

| | | | | | | | | |

Biotechnology — (1.51)% | | | | | | | | |

China Biologic Products Holdings, Inc.(a) | | | (3,500 | ) | | | (350,910 | ) |

| | | | | | | | | |

Consumer Finance — (0.79)% | | | | | | | | |

LendingClub Corporation(a) | | | (58,000 | ) | | | (184,440 | ) |

| | | | | | | | | |

Data Processing & Outsourced Services — (1.01)% | | | | | | | | |

Western Union Company (The) | | | (12,100 | ) | | | (235,224 | ) |

| | | | | | | | | |

Electronic Manufacturing Services — (1.23)% | | | | | | | | |

Celestica, Inc.(a) | | | (40,000 | ) | | | (285,200 | ) |

| | | | | | | | | |

Health Care Distributors — (1.07)% | | | | | | | | |

Patterson Companies, Inc. | | | (11,400 | ) | | | (248,976 | ) |

| | | | | | | | | |

Industrial REITs — (1.00)% | | | | | | | | |

Duke Realty Corporation | | | (7,500 | ) | | | (233,400 | ) |

| | | | | | | | | |

Life & Health Insurance — (0.76)% | | | | | | | | |

Athene Holding Ltd., Class A(a) | | | (3,900 | ) | | | (176,124 | ) |

| | | | | | | | | |

Regional Banks — (18.09)% | | | | | | | | |

Berkshire Hills Bancorp, Inc. | | | (7,500 | ) | | | (224,925 | ) |

Columbia Banking System, Inc. | | | (6,375 | ) | | | (239,318 | ) |

Commerce Bancshares, Inc. | | | (3,900 | ) | | | (235,677 | ) |

Community Bank System, Inc. | | | (5,400 | ) | | | (358,884 | ) |

CVB Financial Corporation | | | (8,000 | ) | | | (173,600 | ) |

First Republic Bank | | | (2,800 | ) | | | (295,736 | ) |

Fulton Financial Corporation | | | (18,000 | ) | | | (310,500 | ) |

Glacier Bancorp, Inc. | | | (5,625 | ) | | | (239,569 | ) |

Heritage Financial Corporation | | | (5,250 | ) | | | (158,917 | ) |

NBT Bancorp, Inc. | | | (6,000 | ) | | | (228,120 | ) |

See accompanying notes which are an integral part of these financial statements.

Annual Report | April 30, 2019 | 15 |

Caldwell & Orkin -

Gator Capital Long/Short Fund |

Schedule of Securities Sold Short

|

| | April 30, 2019 |

| | Shares | | | Fair Value | |

Regional Banks — (18.09)% - continued | | | | | | | | |

Old National Bancorp | | | (7,500 | ) | | $ | (128,100 | ) |

People’s United Financial, Inc. | | | (12,600 | ) | | | (217,854 | ) |

South State Corporation | | | (4,200 | ) | | | (317,772 | ) |

Southside Bancshares, Inc. | | | (6,800 | ) | | | (238,884 | ) |

Trustmark Corporation | | | (7,125 | ) | | | (256,215 | ) |

UMB Financial Corporation | | | (4,600 | ) | | | (321,356 | ) |

United Bankshares, Inc. | | | (6,750 | ) | | | (264,870 | ) |

| | | | | | | | (4,210,297 | ) |

Residential REITs — (2.52)% | | | | | | | | |

American Homes 4 Rent, Class A | | | (12,750 | ) | | | (305,745 | ) |

Invitation Homes, Inc. | | | (11,250 | ) | | | (279,675 | ) |

| | | | | | | | (585,420 | ) |

Thrifts & Mortgage Finance — (8.31)% | | | | | | | | |

Capitol Federal Financial, Inc. | | | (17,000 | ) | | | (234,600 | ) |

Meridian Bancorp, Inc. | | | (21,000 | ) | | | (361,620 | ) |

Northfield Bancorp, Inc. | | | (15,000 | ) | | | (225,000 | ) |

Northwest Bancshares, Inc. | | | (18,000 | ) | | | (313,740 | ) |

Oritani Financial Corporation | | | (12,750 | ) | | | (221,212 | ) |

Provident Financial Services, Inc. | | | (9,500 | ) | | | (251,940 | ) |

Territorial Bancorp, Inc. | | | (938 | ) | | | (27,155 | ) |

Washington Federal, Inc. | | | (9,000 | ) | | | (298,260 | ) |

| | | | | | | | (1,933,527 | ) |

Total Common Stocks — Short (Proceeds Received $8,948,082) | | | | | | | (8,973,686 | ) |

EXCHANGE-TRADED FUNDS — SHORT — (7.63)% | | | | | | | | |

Direxion Daily FTSE China Bear 3X Shares | | | (3,705 | ) | | | (160,241 | ) |

Direxion Daily FTSE China Bull 3X Shares | | | (7,975 | ) | | | (193,713 | ) |

Direxion Daily Gold Miners Bear 3X Shares | | | (15,000 | ) | | | (329,699 | ) |

Direxion Daily Gold Miners Bull 3X Shares | | | (13,575 | ) | | | (213,128 | ) |

Direxion Daily Junior Gold Minors Index Bear 3X Shares | | | (7,361 | ) | | | (354,948 | ) |

Direxion Daily Junior Gold Minors Index Bull 3X Shares | | | (23,063 | ) | | | (174,356 | ) |

Direxion Daily S&P Oil & Gas Exp. & Prod. Bear 3X Shares | | | (24,900 | ) | | | (229,329 | ) |

Direxion Daily S&P Oil & Gas Exp. & Prod. Bull 3x Shares | | | (10,872 | ) | | | (120,136 | ) |

| | | | | | | | | |

Total Exchange-Traded Funds — Short (Proceeds Received $2,380,534) | | | | | | | (1,775,550 | ) |

See accompanying notes which are an integral part of these financial statements.

16 | 1-800-467-7903 | https://gatorcapital.com/mutual-funds/gator-capital-long-short-fund/# |

Caldwell & Orkin -

Gator Capital Long/Short Fund |

Schedule of Securities Sold Short

|

| | April 30, 2019 |

| | Shares | | | Fair Value | |

EXCHANGE-TRADED NOTES — SHORT — (5.45)% | | | | | | | | |

VelocityShares 3x Inverse Crude Oil ETN | | | (30,261 | ) | | $ | (165,528 | ) |

VelocityShares 3x Inverse Natural Gas ETN | | | (1,650 | ) | | | (202,785 | ) |

VelocityShares 3x Inverse Silver ETN | | | (12,290 | ) | | | (383,079 | ) |

VelocityShares 3x Long Crude Oil ETN | | | (5,410 | ) | | | (115,882 | ) |

VelocityShares 3x Long Natural Gas ETN | | | (5,700 | ) | | | (140,220 | ) |

VelocityShares 3x Long Silver ETN | | | (4,170 | ) | | | (261,709 | ) |

| | | | | | | | | |

Total Exchange-Traded Notes — Short (Proceeds Received $1,836,690) | | | | | | | (1,269,203 | ) |

TOTAL SECURITIES SOLD SHORT — (51.64)% (Proceeds Received $13,165,306) | | | | | | | (12,018,439 | ) |

(a) | Non-income producing security. |

(b) | Rate disclosed is the seven day effective yield as of April 30, 2019. |

ADR - American Depositary Receipt

REIT - Real Estate Investment Trust

The sub-industries shown on the schedule of investments are based on the Global Industry Classification Standard, or GICS® (“GICS”). The GICS was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC (“S&P”). GICS is a service mark of MSCI, Inc. and S&P and has been licensed for use by Ultimus Fund Solutions, LLC.

See accompanying notes which are an integral part of these financial statements.

Annual Report | April 30, 2019 | 17 |

Caldwell & Orkin -

Gator Capital Long/Short Fund | Statement of Assets and Liabilities |

| | April 30, 2019 |

Assets | | | | |

Investments is securities at fair value (cost $22,459,927) | | $ | 22,902,941 | |

Deposit held by broker for securities sold short | | | 12,255,173 | |

Receivable for fund shares sold | | | 260 | |

Receivable for investments sold | | | 419,097 | |

Dividends and interest receivable | | | 25,980 | |

Tax reclaims receivable | | | 2,017 | |

Prepaid expenses | | | 21,113 | |

Total Assets | | | 35,626,581 | |

| | | | | |

Liabilities | | | | |

Securities sold short, at value (proceeds received $13,165,306) | | | 12,018,439 | |

Payable for fund shares redeemed | | | 239,933 | |

Payable for investments purchased | | | 44,423 | |

Payable for dividends declared on short sales | | | 2,976 | |

Payable to Adviser | | | 1,507 | |

Payable to Administrator | | | 8,267 | |

Other accrued expenses | | | 39,131 | |

Total Liabilities | | | 12,354,676 | |

| | | | | |

Net Assets | | $ | 23,271,905 | |

| | | | | |

Net Assets consist of: | | | | |

Paid-in capital | | | 26,805,639 | |

Accumulated deficit | | | (3,533,734 | ) |

Net Assets | | $ | 23,271,905 | |

| | | | | |

Shares outstanding, par value $0.10 per share (30,000,000 authorized shares) | | | 1,115,657 | |

| | | | | |

Net asset value, offering price and redemption price per share(a) | | $ | 20.86 | |

(a) | Redemption price may differ from net asset value if redemption fee is applied. |

See accompanying notes which are an integral part of these financial statements.

18 | 1-800-467-7903 | https://gatorcapital.com/mutual-funds/gator-capital-long-short-fund/# |

Caldwell & Orkin -

Gator Capital Long/Short Fund | Statement of Operations |

| | For the Year Ended April 30, 2019 |

Investment Income | | | | |

Dividend income (net of foreign taxes withheld of $234) | | $ | 639,913 | |

Interest income | | | 138,754 | |

Total investment income | | | 778,667 | |

| | | | | |

Expenses | | | | |

Investment Advisory | | | 343,280 | |

Legal | | | 107,626 | |

Directors | | | 37,611 | |

Registration | | | 33,854 | |

Fund accounting | | | 32,195 | |

Administration | | | 30,000 | |

Custodian | | | 21,834 | |

Audit | | | 21,000 | |

Compliance Services | | | 20,000 | |

Transfer agent | | | 19,711 | |

Report printing | | | 15,356 | |

Sub transfer agent | | | 9,218 | |

Insurance | | | 5,971 | |

Pricing | | | 4,530 | |

Miscellaneous | | | 22,861 | |

Interest | | | 272,835 | |

Dividend expense on securities sold short | | | 136,233 | |

Total expenses | | | 1,134,115 | |

Fees contractually waived by Adviser | | | (39,325 | ) |

Net Expenses | | | 1,094,790 | |

Net investment loss | | | (316,123 | ) |

| | | | | |

Net Realized and Change in Unrealized Gain (Loss) on Investments | | | | |

Net realized gain (loss) from: | | | | |

Investments | | | 1,689,129 | |

Securities sold short | | | (1,263,947 | ) |

Foreign currency transactions | | | 2 | |

Change in unrealized depreciation on: | | | | |

Investments | | | (1,586,093 | ) |

Securities sold short | | | 683,437 | |

Foreign currency translations | | | (18 | ) |

Net realized and unrealized gain (loss) on investments and securities sold short | | | (477,490 | ) |

Net decrease in net assets resulting from operations | | $ | (793,613 | ) |

See accompanying notes which are an integral part of these financial statements.

Annual Report | April 30, 2019 | 19 |

Caldwell & Orkin -

Gator Capital Long/Short Fund | Statements of Changes in Net Assets |

| | |

| | | For the Year Ended

April 30, 2019 | | | For the Year Ended

April 30, 2018(a) | |

Increase (Decrease) in Net Assets due to: | | | | | | | | |

Operations | | | | | | | | |

Net investment loss | | $ | (316,123 | ) | | $ | (991,128 | ) |

Net realized gain on investments, securities sold short and foreign currency translations | | | 425,184 | | | | 2,239,013 | |

Net change in unrealized depreciation of investments and securities sold short | | | (902,674 | ) | | | (2,283,128 | ) |

Net decrease in net assets resulting from operations | | | (793,613 | ) | | | (1,035,243 | ) |

| | | | | | | | | |

Capital Transactions | | | | | | | | |

Proceeds from shares sold | | | 975,619 | | | | 5,866,467 | |

Amount paid for shares redeemed | | | (26,695,781 | ) | | | (71,669,354 | ) |

Proceeds from redemption fees (Note 2) | | | 1,013 | | | | 12,923 | |

Net decrease in net assets resulting from capital transactions | | | (25,719,149 | ) | | | (65,789,964 | ) |

Total Decrease in Net Assets | | | (26,512,762 | ) | | | (66,825,207 | ) |

| | | | | | | | | |

Net Assets | | | | | | | | |

Beginning of year | | | 49,784,667 | | | | 116,609,874 | |

End of year | | $ | 23,271,905 | | | $ | 49,784,667 | |

| | | | | | | | | |

Share Transactions | | | | | | | | |

Shares sold | | | 47,546 | | | | 286,524 | |

Shares redeemed | | | (1,347,903 | ) | | | (3,497,522 | ) |

Net decrease in shares outstanding | | | (1,300,357 | ) | | | (3,210,998 | ) |

(a) | As of April 30, 2018, accumulated net investment loss was $(286,589). |

See accompanying notes which are an integral part of these financial statements.

20 | 1-800-467-7903 | https://gatorcapital.com/mutual-funds/gator-capital-long-short-fund/# |

Caldwell & Orkin -

Gator Capital Long/Short Fund | Financial Highlights |

| | |

For a share outstanding during each year.

| | For the

Year

Ended

April 30,

2019 | | | For the

Year

Ended

April 30,

2018 | | | For the

Year

Ended

April 30,

2017 | | | For the

Year

Ended

April 30,

2016 | | | For the

Year

Ended

April 30,

2015 | |

Selected Per Share Data | | | | | | | | | | | | | | | | | | | | |

Net asset value, beginning of year | | $ | 20.61 | | | $ | 20.72 | | | $ | 21.57 | | | $ | 22.94 | | | $ | 20.88 | |

Investment operations: | | | | | | | | | | | | | | | | | | | | |

Net investment income (loss) | | | (0.19 | )(a) | | | (0.24 | )(a) | | | (0.25 | ) | | | (0.36 | ) | | | (0.49 | ) |

Net realized and unrealized gain (loss)

on investments | | | 0.44 | (b) | | | 0.13 | (b) | | | (0.60 | ) | | | 0.30 | | | | 2.71 | |

Total from investment operations | | | 0.25 | | | | (0.11 | ) | | | (0.85 | ) | | | (0.06 | ) | | | 2.22 | |

| | | | | | | | | | | | | | | | | | | | | |

Less distributions to shareholders from: | | | | | | | | | | | | | | | | | | | | |

Net realized gains | | | — | | | | — | | | | — | | | | (1.32 | ) | | | (0.17 | ) |

Total distributions | | | — | | | | — | | | | — | | | | (1.32 | ) | | | (0.17 | ) |

| | | | | | | | | | | | | | | | | | | | | |

Paid in capital from redemption fees | | | — | (c) | | | — | (c) | | | — | (c) | | | 0.01 | | | | 0.01 | |

Net asset value, end of year | | $ | 20.86 | | | $ | 20.61 | | | $ | 20.72 | | | $ | 21.57 | | | $ | 22.94 | |

| | | | | | | | | | | | | | | | | | | | | |

Total Return(d) | | | 1.21 | % | | | (0.53 | )% | | | (3.94 | )% | | | (0.56 | )% | | | 10.68 | % |

| | | | | | | | | | | | | | | | | | | | | |

Ratios and Supplemental Data: | | | | | | | | | | | | | | | | | | | | |

Net assets, end of year (000 omitted) | | $ | 23,272 | | | $ | 49,785 | | | $ | 116,610 | | | $ | 208,328 | | | $ | 128,935 | |

Ratios to Average Net Assets: | | | | | | | | | | | | | | | | | | | | |

Ratio of net expenses to average net assets(e) | | | 3.19 | % | | | 2.41 | % | | | 2.00 | % | | | 2.95 | % | | | 2.64 | % |

Ratio of expenses to average net assets before waiver by Adviser | | | 3.31 | % | | | 2.41 | % | | | 2.00 | % | | | 2.95 | % | | | 2.64 | % |

Ratio of net investment income (loss) to average net assets | | | (0.92 | )% | | | (1.19 | )% | | | (1.18 | )% | | | (2.06 | )% | | | (1.80 | )% |

Portfolio Turnover Rate | | | 240 | % | | | 531 | % | | | 500 | % | | | 415 | % | | | 434 | % |

(a) | Calculated using average shares outstanding. |

(b) | The amount shown for a share outstanding throughout the period does not accord with the change in aggregate gains and losses in the portfolio of securities during the period because of timing of sales and purchases of fund shares in relation to fluctuating market values during the period. |

(c) | Rounds to less than $0.005 per share. |

(d) | Total return in the above table represents the rate that the investor would have earned or lost on an investment in the Fund, assuming reinvestment of distributions. |

(e) | Excluding dividend and interest expense, the ratios of net expenses to average net assets were 2.00%, 1.85%, 1.40%, 1.37% and 1.44% for the fiscal years ended April 30, 2019, 2018, 2017, 2016 and 2015, respectively. |

See accompanying notes which are an integral part of these financial statements.

Annual Report | April 30, 2019 | 21 |

Caldwell & Orkin -

Gator Capital Long/Short Fund | Notes to Financial Statements |

| | April 30, 2019 |

1. ORGANIZATION

The Caldwell & Orkin - Gator Capital Long/Short Fund (the “Fund”), formerly the Caldwell & Orkin Market Opportunity Fund, is the only investment portfolio of The Caldwell & Orkin Funds, Inc. (the “Company”), an open-end, diversified management investment company registered under the Investment Company Act of 1940, as amended (the “1940 Act”), and incorporated under the laws of the State of Maryland on August 15, 1989. The Fund’s investment objective is to provide long-term capital growth with a short-term focus on capital preservation. Gator Capital Management, LLC (the “Adviser”), the Fund’s investment adviser, uses a fundamental-driven, multi-dimensional investment process focusing on active allocation, security selection and surveillance to achieve the Fund’s investment objective.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The Fund is an investment company and follows accounting and reporting guidance under Financial Accounting Standards Board Accounting Standards Codification (“ASC”) Topic 946, “Financial Services-Investment Companies”. The following is a summary of significant accounting policies consistently followed by the Fund in the preparation of its financial statements. The policies are in conformity with accounting principles generally accepted in the United States of America (“GAAP”).

Use of Estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Securities Valuation

Securities are stated at the closing price on the date at which the net asset value (“NAV”) is being determined. If the date of determination is not a trading date, or the closing price is not otherwise available, the last bid price is used for a fair value instead. Debt securities are valued at the price provided by an independent pricing service. Any assets or securities for which market quotations are not readily available are valued at fair value as determined in good faith by or under the direction of the Fund’s Board of Directors (the “Board”) in accordance with the Fund’s Fair Value Pricing Policy.

Securities Transactions and Related Investment Income

The Fund follows industry practice and records securities transactions on trade date for financial reporting purposes. Dividend income is recorded on the ex-dividend date. Realized gains and losses from investment transactions are determined using the specific identification method. Interest income which includes amortization of premium and accretion of discount, is accrued as earned.

22 | 1-800-467-7903 | https://gatorcapital.com/mutual-funds/gator-capital-long-short-fund/# |

Caldwell & Orkin -

Gator Capital Long/Short Fund | Notes to Financial Statements |

| | April 30, 2019 |

Fair Value Measurements

A three-tier hierarchy has been established to classify fair value measurements for disclosure purposes. Inputs refer broadly to the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk. Inputs may be observable or unobservable. Observable inputs are inputs that reflect the assumptions market participants would use in pricing the asset or liability that are developed based on market data obtained from sources independent of the reporting entity. Unobservable inputs are inputs that reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing the asset or liability that are developed based on the best information available.

Various inputs are used in determining the value of the Fund’s investments as of the reporting period end. These inputs are categorized in the following hierarchy under applicable financial accounting standards:

Level 1 – | Unadjusted quoted prices in active markets for identical investments and/or registered investment companies where the value per share is determined and published and is the basis for current transactions for identical assets or liabilities at the valuation date. |

Level 2 – | Quoted prices which are not active quoted prices for similar assets or liabilities in active markets or inputs other than quoted process that are observable (either directly or indirectly) for substantially the full term of the asset of liability. |

Level 3 – | Significant unobservable prices or inputs (including the Fund’s own assumptions in determining the fair value of investments) where there is little or no market for the asset or liability at the measurement date. |

The following is a summary of the inputs used as of April 30, 2019 in valuing the Fund’s investments carried at value:

Investments in Securities* | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

Assets | | | | | | | | | | | | | | | | |

Common Stocks | | $ | 20,690,548 | | | $ | — | | | $ | — | | | $ | 20,690,548 | |

Preferred Stock | | | 72,327 | | | | — | | | | — | | | | 72,327 | |

Warrants | | | 319,936 | | | | — | | | | — | | | | 319,936 | |

Money Market Funds | | | 1,820,130 | | | | — | | | | — | | | | 1,820,130 | |

Total | | $ | 22,902,941 | | | $ | — | | | $ | — | | | $ | 22,902,941 | |

Liabilities | | | | | | | | | | | | | | | | |

Securities Sold Short | | | | | | | | | | | | | | | | |

Common Stocks | | $ | (8,973,686 | ) | | $ | — | | | $ | — | | | $ | (8,973,686 | ) |

Exchange-Traded Funds | | $ | (1,775,550 | ) | | | | | | | | | | $ | (1,775,550 | ) |

Exchange-Traded Notes | | $ | (1,269,203 | ) | | $ | — | | | $ | — | | | $ | (1,269,203 | ) |

Total | | $ | (12,018,439 | ) | | $ | — | | | $ | — | | | $ | (12,018,439 | ) |

* | For detailed industry descriptions, see the accompanying Schedule of Investments. |

Annual Report | April 30, 2019 | 23 |

Caldwell & Orkin -

Gator Capital Long/Short Fund |

Notes to Financial Statements

|

| | April 30, 2019 |

The Fund did not hold any assets at any time during the reporting period in which significant unobservable inputs were used in determining fair value; therefore, no reconciliation of Level 3 securities is included for this reporting period.

Share Valuation

The NAV per share of the Fund is calculated by dividing the sum of the value of the securities held by the Fund, plus cash or other assets, minus all liabilities (including estimated accrued expenses) by the total number of shares outstanding for the Fund, rounded to the nearest cent. The Fund’s shares will not be priced on the days on which the New York Stock Exchange is closed for trading. The offering and redemption price per share for the Fund is equal to the Fund’s NAV per share.

The Fund charges a 2.00% redemption fee on shares held less than 90 days. These fees are deducted from the redemption proceeds otherwise payable to the shareholder. The Fund will retain the fee charged as paid-in capital and such fees become part of the Fund’s daily NAV calculation. For the fiscal year ended April 30, 2019, the Fund recorded $1,013 in redemption fee proceeds.

Federal Income Taxes

The Fund makes no provision for federal income tax or excise tax. The Fund has qualified and intends to qualify each year as a regulated investment company (“RIC”) under subchapter M of the Internal Revenue Code of 1986, as amended, by complying with the requirements applicable to RICs and by distributing substantially all of its taxable income. The Fund also intends to distribute sufficient net investment income and net capital gains, if any, so that it will not be subject to excise tax on undistributed income and gains. If the required amount of net investment income or gains is not distributed, the Fund could incur a tax expense.

The Fund may be subject to taxes imposed by countries in which it invests. Such taxes are generally based on income and/or capital gains earned or repatriated. Taxes are accrued and applied to net investment income, net realized gains and unrealized appreciation as such income and/or gains are earned.

The Fund recognizes tax benefits or expenses of uncertain tax positions only when the position is “more likely than not” to be sustained assuming examination by tax authorities. Management of the Fund has reviewed tax positions taken in tax years that remain subject to examination by all major tax jurisdictions, including federal (i.e., the previous three tax year ends and the interim tax period since then, as applicable) and has concluded that no provision for unrecognized tax benefits or expenses is required in these financial statements and does not expect this to change over the next twelve months. The Fund recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the Statement of Operations. During the year, the Fund did not incur any interest or penalties.

24 | 1-800-467-7903 | https://gatorcapital.com/mutual-funds/gator-capital-long-short-fund/# |

Caldwell & Orkin -

Gator Capital Long/Short Fund |

Notes to Financial Statements

|

| | April 30, 2019 |

3. FEES AND OTHER TRANSACTIONS WITH AFFILIATES AND OTHER SERVICE PROVIDERS

The Fund has entered into a management agreement (the “Management Agreement”) with the Adviser pursuant to which the Adviser provides space, facilities, equipment and personnel necessary to perform administrative and investment management services for the Fund. The Management Agreement provides that the Adviser is responsible for the management of the Fund’s portfolio. For such services and expenses assumed by the Adviser, the Fund pays a monthly advisory fee at incremental annual rates as follows:

Advisory Fee | Average Daily Net Assets |

1.00% | Up to $250 million |

0.90% | In excess of $250 million but not greater than $500 million |

0.80% | In excess of $500 million |

The Adviser has agreed to reimburse the Fund to the extent necessary to prevent the Fund’s annual ordinary operating expenses (excluding taxes, expenses related to the execution of portfolio transactions and the investment activities of the Fund such as, for example, interest, dividend expenses on securities sold short, brokerage commissions and fees and expenses charged to the Fund by any investment company in which the Fund invests and extraordinary charges such as litigation costs) from exceeding 2.00% of the Fund’s average net assets. For the fiscal year ended April 30, 2019, the Adviser waived fees and reimbursed expenses in the amount of $39,325 for the Fund. During the fiscal year ended April 30, 2019, the Adviser earned $343,280 from the Fund, before the waiver described above.

Ultimus Fund Solutions, LLC (the “Administrator”) provides fund accounting, fund administration and transfer agency services under a Master Services Agreement to the Fund. The Fund pays the Administrator fees for its fund accounting, fund administration, and transfer agency services under the Master Services Agreement. In addition, the Fund pays out-of-pocket expenses including, but not limited to postage, supplies and costs of pricing the Fund’s securities. For the fiscal year ended April 30, 2019, the Administrator earned fees of $30,000 for administration services, $32,195 for fund accounting services and $19,711 for transfer agent services.

Under a Compliance Consulting Agreement with the Fund, the Administrator provides the Fund with a Chief Compliance Officer along with support services. The Fund pays the Administrator an annual fee to provide these services. For the fiscal year ended April 30, 2019, the Administrator earned fees of $20,000 for compliance services.

Ultimus Fund Distributors, LLC (the “Distributor”) serves as distributor to the Fund. The Fund does not pay the Distributor for these services. The Distributor is a wholly-owned subsidiary of the Administrator.

Certain officers of the Fund are also officers of the Administrator and the Distributor.

Annual Report | April 30, 2019 | 25 |

Caldwell & Orkin -

Gator Capital Long/Short Fund |

Notes to Financial Statements

|

| | April 30, 2019 |

4. DIRECTOR COMPENSATION

The Fund pays each Director, in cash, an annual fee of $8,000 per year, plus $1,500 for each in-person meeting attended and $1,000 for each telephonic meeting attended. The Fund also reimburses Directors’ actual out-of-pocket expenses relating to attendance at meetings. Prior to November 11, 2017, each Director received an annual fee of $15,000 per year, plus $3,500 for each in-person meeting attended and $1,500 for each telephonic meeting attended. Until May 18, 2018, the Directors received their compensation entirely in shares of the Fund (i.e., Directors received shares of the Fund with a value equal to the cash compensation they would have otherwise received).

5. INVESTMENT PORTFOLIO TRANSACTIONS

During the fiscal year ended April 30, 2019, the Fund purchased $54,335,466 and sold $66,250,240 of securities, excluding securities sold short and short-term investments.

Short Sales and Segregated Cash

Short sales are transactions in which the Fund sells a security it does not own, in anticipation of a decline in the market value of that security. To initiate such a transaction, the Fund must borrow the security to deliver to the buyer upon the short sale; the Fund is then obligated to replace the security borrowed by purchasing it in the open market at some later date, completing the transaction.

The Fund will incur a loss if the market price of the security increases between the date of the short sale and the date on which the Fund replaces the borrowed security. The Fund will realize a gain if the security declines in value between those dates.

All short sales must be fully collateralized. The Fund maintains the collateral in segregated accounts consisting of cash and/or U.S. Government securities sufficient to collateralize the market value of its short positions. Typically, the segregated cash with brokers and other financial institutions exceeds the minimum required. Deposits with brokers for securities sold short are invested in money market instruments. Segregated cash is held at the custodian in the name of the broker per a tri-party agreement between the Fund, the custodian, and the broker.

The Fund may also sell short “against the box”, i.e., the Fund enters into a short sale as described above, while holding an offsetting long position in the same security which it sold short. If the Fund enters into a short sale against the box, it will segregate an equivalent amount of securities owned by the Fund as collateral while the short sale is outstanding.

The Fund limits the value of its short positions (excluding short sales “against the box”) to 60% of the Fund’s total net assets. At April 30, 2019, the Fund had approximately 52% of its total net assets in short positions.

For the year ended April 30, 2019, the cost of investments purchased to cover short sales and the proceeds from investments sold short were $21,378,347 and $18,870,394, respectively.

26 | 1-800-467-7903 | https://gatorcapital.com/mutual-funds/gator-capital-long-short-fund/# |

Caldwell & Orkin -

Gator Capital Long/Short Fund |

Notes to Financial Statements

|

| | April 30, 2019 |

6. FEDERAL TAX INFORMATION

As of April 30, 2019, the net unrealized appreciation (depreciation) of investments, including short securities, for tax purposes was as follows:

Gross unrealized appreciation | | $ | 2,454,743 | |

Gross unrealized depreciation | | | (1,940,727 | ) |

Net unrealized appreciation | | $ | 514,016 | |

At April 30, 2019, the aggregate cost of securities for federal income tax purposes was $10,370,486 for the Fund.

At April 30, 2019, the components of distributable earnings (accumulated losses) on a tax basis was as follows:

Accumulated capital and other losses | | $ | (4,047,732 | ) |

Unrealized appreciation | | | 513,998 | |

| | | $ | (3,533,734 | ) |

The difference between book basis and tax basis unrealized appreciation is attributable primarily to the tax deferral of wash losses and investments in partnerships and certain other investments.

Certain capital losses incurred after October 31, and within the current taxable year, are deemed to arise on the first business day of the Fund’s following taxable year. Late year Ordinary Losses incurred after December 31 are deemed to arise on the first business day of the Fund’s following taxable year. For the tax year ended April 30, 2019, the Fund deferred $239,944 in Qualified Late Year Ordinary Losses.

As of April 30, 2019, the Fund has available for tax purposes an unused capital loss carryforward of $3,807,788 of short-term capital losses with no expiration, which is available to offset against future taxable net capital gains.

GAAP requires that certain components of net assets relating to permanent differences be reclassified between financial and tax reporting. These reclassifications have no effect on net assets or net asset value per share. For the year ended April 30, 2019, the Fund increased accumulated earnings by $494,167 and decreased paid-in capital by $494,167. These reclassifications are due to investments in partnerships, commodities, nondeductible dividend expenses and certain other temporary and permanent book and tax reclassifications

7. COMMITMENTS AND CONTINGENCIES

Under the Fund’s organizational documents, its officers and directors are indemnified against certain liability arising out of the performance of their duties to the Fund. Additionally, in the normal course of business, the Fund enters into contracts with service providers that may

Annual Report | April 30, 2019 | 27 |

Caldwell & Orkin -

Gator Capital Long/Short Fund |

Notes to Financial Statements

|

| | April 30, 2019 |

contain general indemnification clauses, which may permit indemnification to the extent permissible under applicable law. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred.

8. SUBSEQUENT EVENTS

Management of the Fund has evaluated the need for disclosures and/or adjustments resulting from subsequent events through the date these financial statements were issued. Based upon this evaluation, management has determined there were no additional items requiring adjustment of the financial statements or additional disclosure.

28 | 1-800-467-7903 | https://gatorcapital.com/mutual-funds/gator-capital-long-short-fund/# |

Caldwell & Orkin -

Gator Capital Long/Short Fund | Report of Independent Registered

Public Accounting Firm |

| | April 30, 2019 |

To the Shareholders and Board of Directors

of Caldwell & Orkin - Gator Capital Long/Short Fund

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities of Caldwell & Orkin - Gator Capital Long/Short Fund (formerly known as Caldwell & Orkin Market Opportunity Fund) (the “Fund”), a series of shares of The Caldwell & Orkin Funds, Inc., including the schedule of investments, as of April 30, 2019, the related statement of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, financial highlights for each of the five years in the period then ended, and the related notes (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund as of April 30, 2019, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America.

Basis for Opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB. We have served as the Fund’s auditor since 1998.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Fund is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audits we are required to obtain an understanding of internal control over financial reporting, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. Our procedures included

Annual Report | April 30, 2019 | 29 |

Caldwell & Orkin -

Gator Capital Long/Short Fund | Report of Independent Registered

Public Accounting Firm |

| | April 30, 2019 |

confirmation of securities owned as of April 30, 2019 by correspondence with the custodian and brokers; when replies were not received from brokers, we performed other auditing procedures. We believe that our audits provide a reasonable basis for our opinion.

TAIT, WELLER & BAKER LLP

Philadelphia, Pennsylvania

June21, 2019

30 | 1-800-467-7903 | https://gatorcapital.com/mutual-funds/gator-capital-long-short-fund/# |

Caldwell & Orkin -

Gator Capital Long/Short Fund | Disclosure of Fund Expenses |

| | April 30, 2019 (Unaudited) |

We believe it is important for you to understand the impact of fees and expenses on your investment in the Fund. As a shareholder of the Fund, you incur two types of costs: (1) transaction costs related to the purchase and redemption of Fund shares, including redemption fees and brokerage commissions (if applicable); and (2) ongoing costs, including management fees, administrative expenses, portfolio transaction costs and other Fund expenses. A mutual fund’s ongoing costs are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The following example is intended to help you understand your ongoing costs (in dollars and cents) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The below example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period indicated, November 1, 2018 through April 30, 2019. The table below illustrates the Fund’s expenses in two ways:

Based on Actual Fund Returns

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Based on a Hypothetical 5% Return for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as redemption fees or brokerage commissions. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | Beginning

Account Value

November 1, 2018 | Ending

Account Value

April 30, 2019 | Expenses

Paid During

Period(a) | Annualized

Expense

Ratio |

Actual | $1,000.00 | $1,061.60 | $19.62 | 3.84% |

Hypothetical(b) | $1,000.00 | $1,005.76 | $19.09 | 3.84% |

(a) | Expenses are equal to the Fund’s annualized expense ratios, multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period). |

(b) | Hypothetical assumes 5% annual return before expenses. |

Annual Report | April 30, 2019 | 31 |

Caldwell & Orkin -

Gator Capital Long/Short Fund | Additional Information |

| | April 30, 2019(Unaudited) |

Caldwell & Orkin Board of Directors and Officers (as of April 30, 2019)

Name, Position(s) Held with Fund,

and Age | Term of

Office and

Length of

Time

Served | Principal Occupation(s) During Past Five Years | Number of

Funds in

Fund

Complex

Overseen

by Director | Other

Directorships

Held by

Director During the Past 5 Years |

DISINTERESTED DIRECTORS | | | |

Frederick T. Blumer Director and Chairman of the Board Year of Birth: 1958 | Indefinite Term, Director Since 1990, Chairman Since 2004 | Mr. Blumer is the Chairman & CEO of Mile Auto, Inc. (since March 2017) and Chairman of Vehcon, Inc. (since 2012), and was CEO of Vehcon, Inc. (from 2012-2017). | One | None |

Rhett E. Ingerick Director and Chairman of the Audit Committee Year of Birth: 1974 | Indefinite Term,