UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM N-CSRS

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-06135

Templeton Institutional Funds

(Exact name of registrant as specified in charter)

300 S.E. 2nd Street, Fort Lauderdale, FL 33301-1923

(Address of principal executive offices) (Zip code)

Craig S. Tyle, One Franklin Parkway, San Mateo, CA 94403-1906

(Name and address of agent for service)

Registrant’s telephone number, including area code: (954) 527-7500

Date of fiscal year end: 12/31

Date of reporting period: 6/30/17

| Item 1. | Reports to Stockholders. |

| | |

| | Semiannual Report June 30, 2017 |

Templeton Institutional Funds

Emerging Markets Series

Foreign Smaller Companies Series

Global Equity Series

International Equity Series

Franklin Templeton Investments

Gain From Our Perspective®

At Franklin Templeton Investments, we’re dedicated to one goal: delivering exceptional asset management for our clients. By bringing together multiple, world-class investment teams in a single firm, we’re able to offer specialized expertise across styles and asset classes, all supported by the strength and resources of one of the world’s largest asset managers. This has helped us to become a trusted partner to individual and institutional investors across the globe.

Contents

Semiannual Report

Visit ftinstitutional.com for fund updates, to access your account, or to find investment insights.

|

| Not FDIC Insured | May Lose Value | No Bank Guarantee |

| | | | | | |

| | | |

| ftinstitutional.com | | Not part of the semiannual report | | | 1 | |

Semiannual Report

Economic and Market Overview

The global economy generally expanded during the period under review. In this environment, global developed and emerging market stocks rose, as measured by the MSCI All Country World Index. Global markets were aided by improved industrial commodity prices at certain points during the period, generally upbeat economic data across regions, investor optimism about pro-growth and pro-business policies in the U.S., hopes of tax reforms under the Trump administration, Emmanuel Macron’s election as France’s president and encouraging corporate earnings reports.

However, investors expressed concerns about the timing and economic effects of the U.K.’s exit from the European Union (also known as “Brexit”) and the U.S. executive order banning entry from some Muslim-majority countries. Other headwinds included the health of European banks, concerns about political uncertainty in the U.S. and European Union, geopolitical tensions in certain regions, worries about global oversupply in oil production despite a pact to extend cuts, and hawkish comments from key central bankers around the world toward period-end.

U.S. economic growth decelerated in 2017’s first quarter, largely due to slower growth in consumer spending and declines in private inventory investment and government spending. However, growth accelerated in the second quarter due to increases in consumer spending, business investment and federal government spending. The unemployment rate decreased from 4.7% in December 2016 to 4.4% at period-end.1 Annual inflation, as measured by the Consumer Price Index, decreased from 2.1% to 1.6% during the period. After increasing its benchmark interest rate in March, the U.S. Federal Reserve (Fed), at its June meeting, made the widely anticipated increase to its target range for the federal funds rate from 0.75%–1.00% to 1.00%–1.25%, amid signs of a growing U.S. economy, a strengthening labor market and an improvement in business spending.

In Europe, the U.K.’s economy grew at a slower rate in 2017’s first quarter over the previous quarter, largely due to slower growth in household spending. The eurozone’s growth increased in the first quarter over the previous quarter. The bloc’s annual inflation rate fluctuated during the reporting period and ended slightly higher from where it began. During the period, the European Central Bank kept its key policy rates unchanged.

In Asia, Japan’s quarterly gross domestic product (GDP) remained unchanged in 2017’s first quarter compared to 2016’s fourth quarter. In April 2017, the Bank of Japan (BOJ) slightly increased its GDP forecasts for the 2017–2018 fiscal year. However, the BOJ lowered its inflation forecast.

In emerging markets, Brazil’s quarterly GDP grew for the first time in two years, as its first-quarter 2017 GDP grew compared to the previous quarter. The country’s central bank cut its benchmark interest rate four times between January and June 2017 to spur economic growth. Russia’s GDP grew in 2017’s first quarter compared to the prior-year period. The Bank of Russia reduced its key interest rate in March, April and June 2017 to try to revive its economy. China’s economy grew faster in the first half of 2017 compared to the first half of 2016, driven by solid growth in industrial production, services, fixed-asset investment, retail sales, and imports and exports. The People’s Bank of China left its benchmark interest rate unchanged during the period. Overall, emerging market stocks, as measured by the MSCI Emerging Markets Index, rose during the period.

The foregoing information reflects our analysis and opinions as of June 30, 2017. The information is not a complete analysis of every aspect of any market, country, industry, security or fund. Statements of fact are from sources considered reliable.

1. Source: Bureau of Labor Statistics.

| | | | |

| | | |

| 2 | | Semiannual Report | | ftinstitutional.com |

Emerging Markets Series

We are pleased to bring you Emerging Markets Series’ (Fund’s) semiannual report for the period ended June 30, 2017.

Your Fund’s Goal and Main Investments

The Fund seeks long-term capital growth. Under normal market conditions, the Fund invests at least 80% of its net assets in securities issued by “emerging market companies,” as defined in the Fund’s prospectus.

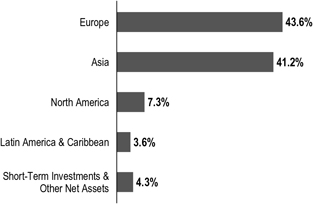

Geographic Composition

Based on Total Net Assets as of 6/30/17

Performance Overview

The Fund delivered a +22.66% cumulative total return for the six months under review. In comparison, the Standard & Poor’s®/International Finance Corporation Investable Composite Index generated a +18.74% total return, and the MSCI Emerging Markets (EM) Index posted a total return of +18.60% during the same period.1 The indexes measure global emerging market stock performance. Please note, index performance information is provided for reference and we do not attempt to track an index but rather undertake investments on the basis of fundamental research. The Fund’s return reflects the effect of fees and expenses for professional management, while an index does not have such costs. In addition, an index is not subject to investment flows while the Fund is subject to purchases and redemptions that could impact performance. You can find the Fund’s long-term performance data in the Performance Summary beginning on page 7.

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. For most recent month-end performance, go to ftinstitutional.com or call a Franklin Templeton Institutional Services representative at (800) 321-8563.

Investment Strategy

Our investment strategy employs a fundamental research, value-oriented, long-term approach. We focus on the market price of a company’s securities relative to our evaluation of the company’s long-term earnings, asset value and cash flow potential. We also consider a company’s profit and loss outlook, balance sheet strength, cash flow trends and asset value in relation to the current price. Our analysis considers the company’s corporate governance behavior as well as its position in its sector, the economic framework and political environment.

Manager’s Discussion

During the six months under review, key contributors to the Fund’s absolute performance included investments in Samsung Electronics, Tencent Holdings and Brilliance China Automotive Holdings.

Samsung Electronics is a major South Korea-based manufacturer of consumer electronics. It is one of the world’s largest manufacturers of mobile phones, smartphones, tablets and televisions. The company is also a leading supplier of memory chips for high-end phones and is a key provider of organic light-emitting diodes (OLED) displays. Key drivers of the stock price included strong first-quarter 2017 corporate results, robust second-quarter earnings guidance, proposed share buybacks and announcement of a cancelation of all existing Treasury shares. Strong demand for Samsung’s new high-end smartphone, the Galaxy S8, which was released in March 2017, also supported sentiment.

Tencent is one of the world’s largest and most widely used Internet service portals. The company provides value-added Internet, mobile and telecommunication services and online advertising under the strategic goal of providing users with “one-stop online lifestyle services.” Over the last decade,

1. Source: Morningstar.

The indexes are unmanaged and include reinvestment of any income or distributions. They do not reflect any fees, expenses or sales charges. One cannot invest directly in an index, and an index is not representative of the Fund’s portfolio.

The dollar value, number of shares or principal amount, and names of all portfolio holdings are listed in the Fund’s Statement of Investments (SOI). The SOI begins on page 33.

| | | | | | |

| | | |

| ftinstitutional.com | | Semiannual Report | | | 3 | |

EMERGING MARKETS SERIES

Tencent has maintained steady growth under its user-oriented operating strategies. Internet stocks in China rebounded in the first half of 2017 following pressure in the fourth quarter of 2016. Tencent’s shares further benefited from a better-than-expected double-digit increase in first-quarter revenues, driven by the online gaming, online advertising and social networking segments.

| | | | |

| Top 10 Countries | | | |

| 6/30/17 | | | |

| | | % of Total

Net Assets | |

| China | | | 18.1% | |

| South Korea | | | 17.8% | |

| Taiwan | | | 13.3% | |

| India | | | 7.9% | |

| South Africa | | | 7.4% | |

| Russia | | | 6.0% | |

| Brazil | | | 4.5% | |

| Indonesia | | | 4.0% | |

| Thailand | | | 3.7% | |

| U.K. | | | 3.3% | |

Brilliance China Automotive manufactures and sells automobiles to the Chinese domestic market, predominantly through its joint venture with German luxury car manufacturer BMW. The company announced an in-line set of figures for 2016, and better-than-expected first-quarter 2017 earnings growth driven by strong sales growth. Expectations for a continuation of strong sales momentum in the second half of 2017, supported by resilient luxury car demand and the continued rise of China’s upper middle class, also drove share price performance over the period. An encouraging outlook based upon new vehicle launches, increased financing revenues, a supportive macroeconomic environment and attractive valuations further supported investor sentiment in the stock.

In contrast, key detractors included positions in IMAX, LUKOIL and Glenmark Pharmaceuticals.

IMAX is one of the world’s leading entertainment technology companies, specializing in immersive motion picture technologies. The company combines proprietary software, theater architecture and equipment to create high-quality motion picture experiences. Its systems are used globally, including a notable market position in China. Gross profit margin for first-quarter 2017 was down from first-quarter 2016, when box-office figures were helped by a stronger movie slate. In June, the company announced a cost-cutting program and proposed further share buybacks.

| | | | |

| Top 10 Holdings | | | |

6/30/17 | | | |

Company Sector/Industry, Country | | % of Total

Net Assets | |

| Samsung Electronics Co. Ltd. | | | 7.5% | |

Technology Hardware, Storage & Peripherals, South Korea | | | | |

Brilliance China Automotive Holdings Ltd.

Automobiles, China | | | 6.8% | |

Taiwan Semiconductor Manufacturing Co. Ltd.

Semiconductors & Semiconductor Equipment, Taiwan | | | 6.6% | |

Naspers Ltd.

Media, South Africa | | | 6.2% | |

Unilever PLC

Personal Products, U.K. | | | 3.3% | |

Hon Hai Precision Industry Co. Ltd.

Electronic Equipment, Instruments & Components, Taiwan | | | 3.3% | |

Tencent Holdings Ltd.

Internet Software & Services, China | | | 3.0% | |

ICICI Bank Ltd.

Banks, India | | | 2.5% | |

Astra International Tbk PT

Automobiles, Indonesia | | | 2.3% | |

Alibaba Group Holding Ltd.

Internet Software & Services, China | | | 1.9% | |

LUKOIL is a Russia-based energy company primarily involved in the exploration, production, marketing and refining of oil and oil-related products. The company is one of the world’s largest oil companies in terms of reserves. Although the company delivered first-quarter 2017 results that beat expectations, its shares underperformed due to weak investor sentiment in the Russian market in general and a decline in crude oil prices. After surging 55.93% in U.S. dollar terms in 2016, the Russian market gave back some of those gains in the first half of 2017, with the MSCI Russia Index declining 13.96%.1 Key reasons for the correction were a decline in oil prices and geopolitical worries, including additional U.S. sanctions.

Glenmark Pharmaceuticals is an Indian manufacturer of generic drugs and pharmaceutical ingredients. Glenmark produces formulation products in areas such as oncology, respiratory and cardiac. It also researches and develops its own chemical and biological entities. In addition to India, the U.S. is its main market. Its share price declined significantly in May as the company announced weaker-than-expected first-quarter 2017 operating performance with disappointing revenue growth. Sales in India were impacted by the government’s demonetization program to recall large-denominated currency

| | | | |

| | | |

| 4 | | Semiannual Report | | ftinstitutional.com |

EMERGING MARKETS SERIES

notes, while price declines and lower sales for a cholesterol-lowering drug pressured sales in the U.S.

It is important to recognize the effect of currency movements on the Fund’s performance. In general, if the value of the U.S. dollar goes up compared with a foreign currency, an investment traded in that foreign currency will go down in value because it will be worth fewer U.S. dollars. This can have a negative effect on Fund performance. Conversely, when the U.S. dollar weakens in relation to a foreign currency, an investment traded in that foreign currency will increase in value, which can contribute to Fund performance. For the six months ended June 30, 2017, the U.S. dollar declined in value relative to most currencies. As a result, the Fund’s performance was positively affected by the portfolio’s investment predominantly in securities with non-U.S. currency exposure. However, one cannot expect the same result in future periods.

During the past six months, we increased the Fund’s holdings in Russia, South Korea, Peru and the Czech Republic as we continued to invest in opportunities we considered to be attractive. In sector terms, we added to the Fund’s holdings in financials and materials and made some purchases in health care.2 Key purchases included new positions in Sberbank of Russia, the country’s leading bank, and POSCO in South Korea, one of the world’s largest steel producers. We also increased the Fund’s holding in Alibaba Group Holding, China’s largest e-commerce company.

Conversely, we reduced the Fund’s investments in China, Hong Kong, South Africa and the U.K. to focus on stocks we considered to be more attractively valued within our investment universe. In sector terms, we reduced holdings in industrials and consumer discretionary and conducted some sales in information technology (IT).3 Key sales included reducing holdings in the aforementioned Tencent and in Brazilian financial conglomerate Itau Unibanco Holding. We also closed the Fund’s position in Remgro, a South African holding company with interests in food, finance and health care.

Thank you for your continued participation in Emerging Markets Series. We look forward to serving your future investment needs.

| | |

| |

Chetan Sehgal, CFA Portfolio Manager |

The foregoing information reflects our analysis, opinions and portfolio holdings as of June 30, 2017, the end of the reporting period. The way we implement our main investment strategies and the resulting portfolio holdings may change depending on factors such as market and economic conditions. These opinions may not be relied upon as investment advice or an offer for a particular security. The information is not a complete analysis of every aspect of any market, country, industry, security or the Fund. Statements of fact are from sources considered reliable, but the investment manager makes no representation or warranty as to their completeness or accuracy. Although historical performance is no guarantee of future results, these insights may help you understand our investment management philosophy.

CFA® is a trademark owned by CFA Institute.

2. The financials sector comprises banks, capital markets, diversified financial services and insurance in the SOI. The materials sector comprises chemicals, construction materials, and metals and mining in the SOI. The health care sector comprises biotechnology and pharmaceuticals in the SOI.

3. The industrials sector comprises construction and engineering, trading companies and distributors, and transportation infrastructure in the SOI. The consumer discretionary sector comprises auto components; automobiles; Internet and direct marketing retail; media; hotels, restaurants and leisure; and textiles, apparel and luxury goods in the SOI. The IT sector comprises electronic equipment, instruments and components; Internet software and services; IT services; semiconductors and semiconductor equipment; software; and technology hardware, storage and peripherals in the SOI.

| | | | | | |

| | | |

| ftinstitutional.com | | Semiannual Report | | | 5 | |

EMERGING MARKETS SERIES

|

Chetan Sehgal is an executive vice president and the Director of Global Emerging Markets/Small Cap Strategies for the Templeton Emerging Markets Group. In this capacity, he is responsible for strengthening the overall Global Emerging Markets and Small Cap strategies, providing guidance and thought leadership, coordinating appropriate resources and coverage, and leveraging the group’s expertise to add value across products within the strategies. Prior to joining Franklin Templeton in 1995, Mr. Sehgal was a senior ratings analyst for the Credit Rating Information Services of India, Ltd. Mr. Sehgal earned a B.E. mechanical (honors) from the University of Bombay and a post-graduate diploma in management from the Indian Institute of Management in Bangalore, where he specialized in finance and business policy and graduated as an institute scholar. Mr. Sehgal speaks English and Hindi and is a Chartered Financial Analyst (CFA) charterholder. |

| | | | |

| | | |

| 6 | | Semiannual Report | | ftinstitutional.com |

EMERGING MARKETS SERIES

Performance Summary as of June 30, 2017

The performance table does not reflect any taxes that a shareholder would pay on Fund dividends, capital gain distributions, if any, or any realized gains on the sale of Fund shares. Total return reflects reinvestment of the Fund’s dividends and capital gain distributions, if any, and any unrealized gains or losses. Your dividend income will vary depending on dividends or interest paid by securities in the Fund’s portfolio, adjusted for operating expenses. Capital gain distributions are net profits realized from the sale of portfolio securities.

Performance as of 6/30/171

| | | | | | | | |

| | | Cumulative

Total Return2 | | | Average Annual

Total Return3 | |

6-Month | | | +22.66% | | | | +22.66% | |

1-Year | | | +31.73% | | | | +31.73% | |

5-Year | | | +25.81% | | | | +4.70% | |

10-Year | | | +19.90% | | | | +1.83% | |

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. For most recent month-end performance, go to ftinstitutional.com or call a Franklin Templeton Institutional Services representative at (800) 321-8563.

See page 8 for Performance Summary footnotes.

| | | | | | |

| | | |

| ftinstitutional.com | | Semiannual Report | | | 7 | |

EMERGING MARKETS SERIES

PERFORMANCE SUMMARY

Total Annual Operating Expenses4

| | | | |

| | | With Waiver | | Without Waiver |

| | | 1.31% | | 1.44% |

All investments involve risks, including possible loss of principal. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. The Fund’s ability to invest in smaller company securities that may have limited liquidity involves additional risks, such as relatively small revenues, limited product lines and small market share. Historically, these stocks have exhibited greater price volatility than larger company stocks, especially over the short term. The Fund is actively managed but there is no guarantee that the manager’s investment decisions will produce the desired results. The Fund’s prospectus also includes a description of the main investment risks.

1. The Fund has an expense reduction contractually guaranteed through 4/30/18. Fund investment results reflect the expense reduction; without this reduction, the results would have been lower.

2. Cumulative total return represents the change in value of an investment over the periods indicated.

3. Average annual total return represents the average annual change in value of an investment over the periods indicated. Return for less than one year, if any, has not been annualized.

4. Figures are as stated in the Fund’s current prospectus and may differ from the expense ratios disclosed in the Your Fund’s Expenses and Financial Highlights sections in this report. In periods of market volatility, assets may decline significantly, causing total annual Fund operating expenses to become higher than the figures shown.

| | | | |

| | | |

| 8 | | Semiannual Report | | ftinstitutional.com |

EMERGING MARKETS SERIES

Your Fund’s Expenses

As a Fund shareholder, you can incur two types of costs: (1) transaction costs, including sales charges (loads) on Fund purchases and redemptions, if applicable; and (2) ongoing Fund costs, including management fees, distribution and service (12b-1) fees, if applicable, and other Fund expenses. All mutual funds have ongoing costs, sometimes referred to as operating expenses. The table below shows ongoing costs of investing in the Fund and can help you understand these costs and compare them with those of other mutual funds. The table assumes a $1,000 investment held for the six months indicated.

Actual Fund Expenses

The table below provides information about actual account values and actual expenses in the columns under the heading “Actual.” In these columns the Fund’s actual return, which includes the effect of Fund expenses, is used to calculate the “Ending Account Value.” You can estimate the expenses you paid during the period by following these steps (of course, your account value and expenses will differ from those in this illustration): Divide your account value by $1,000 (if your account had an $8,600 value, then $8,600 ÷ $1,000 = 8.6). Then multiply the result by the number in the row for your class of shares under the headings “Actual” and “Expenses Paid During Period” (if Actual Expenses Paid During Period were $7.50, then 8.6 x $7.50 = $64.50). In this illustration, the actual expenses paid this period are $64.50.

Hypothetical Example for Comparison with Other Funds

Under the heading “Hypothetical” in the table, information is provided about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. This information may not be used to estimate the actual ending account balance or expenses you paid for the period, but it can help you compare ongoing costs of investing in the Fund with those of other funds. To do so, compare this 5% hypothetical example for the class of shares you hold with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that expenses shown in the table are meant to highlight ongoing costs and do not reflect any transactional costs. Therefore, information under the heading “Hypothetical” is useful in comparing ongoing costs only, and will not help you compare total costs of owning different funds. In addition, if transactional costs were included, your total costs would have been higher.

| | | | | | | | | | | | | | | | |

| | | | | Actual (actual return after expenses) | | | | Hypothetical (5% annual return before expenses) | | | | |

Beginning

Account

Value 1/1/17 | | | | Ending

Account

Value 6/30/17 | | Expenses

Paid During

Period

1/1/17–6/30/171,2 | | | | Ending

Account

Value 6/30/17 | | Expenses

Paid During

Period

1/1/17–6/30/171,2 | | | | Net

Annualized

Expense

Ratio2 |

| $1,000 | | | | $1,226.60 | | $7.40 | | | | $1,018.15 | | $6.71 | | | | 1.34% |

1. Expenses are equal to the annualized expense ratio for the six-month period as indicated above—in the far right column—multiplied by the simple average account value over the period indicated, and then multiplied by 181/365 to reflect the one-half year period.

2. Reflects expenses after fee waivers and expense reimbursements.

| | | | | | |

| | | |

| ftinstitutional.com | | Semiannual Report | | | 9 | |

Foreign Smaller Companies Series

We are pleased to bring you Foreign Smaller Companies Series’ (Fund’s) semiannual report for the period ended June 30, 2017. Effective at the market close on December 10, 2013, the Fund closed to new investors. Existing shareholders may add to their accounts. We believe this closure will help us manage the inflow of assets and allow us to effectively manage our current level of assets.

Your Fund’s Goal and Main Investments

The Fund seeks long-term capital growth. Under normal market conditions, the Fund invests at least 80% of its net assets in investments of smaller companies located outside the U.S., including emerging markets.

Performance Overview

The Fund delivered a +20.12% cumulative total return for the six months under review. In comparison, the MSCI All Country World Index ex USA Small Cap Index, which measures performance of global developed and emerging market small-cap equities, excluding the U.S., posted a +15.83% total return.1 Please note, index performance information is provided for reference and we do not attempt to track the index but rather undertake investments on the basis of fundamental research. You can find the Fund’s long-term performance data in the Performance Summary beginning on page 13.

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. For most recent month-end performance, go to ftinstitutional.com or call a Franklin Templeton Institutional Services representative at (800) 321-8563.

Investment Strategy

When choosing equity investments, we apply a bottom-up, value-oriented, long-term approach, focusing on the market price of a company’s securities relative to our evaluation of the company’s long-term earnings, asset value and cash flow potential. We also consider a company’s price/earnings ratio, profit margins and liquidation value.

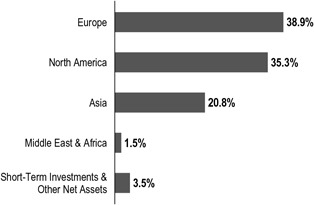

Geographic Composition

Based on Total Net Assets as of 6/30/17

Manager’s Discussion

Several holdings performed well during the six months under review. Italy-based Interpump Group manufactures piston pumps and hydraulic products. Historically, about two-thirds of earnings growth has been driven by mergers and acquisitions (M&A) done at what we considered attractive valuation multiples and with related synergies. After doubling its revenues over the last five years, we feel Interpump’s M&A engine has remained well in place, with several options under scrutiny. Exposure to end markets such as trucks, agriculture and construction equipment and earth-moving machines, particularly in the U.S. (a geographical market that accounts for a significant portion of the group’s revenues), also helped drive growth.

Italy-based Technogym is the world’s second-largest gym equipment manufacturer. The company has a solid global market share, and recent efforts to expand revenue in the U.S. looked promising to us. Technogym’s shares were supported by the company’s advanced technology and recently announced partnership with IBM Watson (not a Fund holding).

India-based Dewan Housing Finance benefited from its low valuation, a positive shift in investor sentiment and growth opportunities in the mortgage finance industry. Despite the recent share price appreciation, Dewan has continued to trade at a sizable discount to many of its peers. This is partially due to Dewan’s relatively low return on equity, a measure of profitability that is mainly a function of the company’s

1. Source: Morningstar.

The index is unmanaged and includes reinvestment of any income or distributions. It does not reflect any fees, expenses or sales charges. One cannot invest directly in an index, and an index is not representative of the Fund’s portfolio.

See www.franklintempletondatasources.com for additional data provider information.

The dollar value, number of shares or principal amount, and names of all portfolio holdings are listed in the Fund’s Statement of Investments (SOI). The SOI begins on page 38.

| | | | |

| | | |

| 10 | | Semiannual Report | | ftinstitutional.com |

FOREIGN SMALLER COMPANIES SERIES

extensive branch network relative to other firms. Over time, we believe Dewan could see the benefits of its branch network, including higher asset density and better operating leverage.

| | | | |

| Portfolio Composition | | | |

| 6/30/17 | | | |

| Sector/Industry | | % of Total

Net Assets | |

Machinery | | | 11.5% | |

Leisure Products | | | 7.4% | |

Capital Markets | | | 6.3% | |

Electronic Equipment, Instruments & Components | | | 6.1% | |

Textiles, Apparel & Luxury Goods | | | 6.0% | |

Banks | | | 4.0% | |

Household Durables | | | 3.7% | |

Real Estate Management & Development | | | 3.4% | |

Specialty Retail | | | 3.0% | |

Pharmaceuticals | | | 2.7% | |

Construction & Engineering | | | 2.6% | |

Thrifts & Mortgage Finance | | | 2.6% | |

Professional Services | | | 2.5% | |

Personal Products | | | 2.4% | |

Food Products | | | 2.4% | |

Containers & Packaging | | | 2.4% | |

Life Sciences Tools & Services | | | 2.2% | |

Auto Components | | | 2.1% | |

Other | | | 22.4% | |

Short-Term Investments & Other Net Assets | | | 4.3% | |

In contrast, the Fund had some underperformers during the six months under review. Mullen Group is a Canadian oil services company that owns a network of independently operated businesses. Weakness in energy markets impacted its share price during the period. However, Mullen has a diversified business mix and a strong track record for generating attractive returns on capital. The company’s strategy is to be the dominant player in select niche markets with favorable competitive dynamics, such as better pricing power and higher barriers to entry. Mullen typically navigates through business cycles strategically, which includes maintaining a balance sheet that allows for making opportunistic acquisitions. We believe the company is in good shape to capitalize on a recovery in energy markets.

Shares of Badger Daylighting, North America’s largest operator of specialized hydro-excavation trucks for the utility and petroleum sectors, fell after the Canada-based company announced disappointing quarterly results. In our longer-term perspective, we believe Badger’s key technology, the Badger Hydrovac excavator used primarily for digging trenches in

| | | | |

| Top 10 Holdings | | | |

6/30/17 | | | |

Company Sector/Industry, Country | | % of Total

Net Assets | |

Tsumura & Co.

Pharmaceuticals, Japan | | | 2.0% | |

Dewan Housing Finance Corp. Ltd.

Thrifts & Mortgage Finance, India | | | 1.9% | |

Kobayashi Pharmaceutical Co. Ltd.

Personal Products, Japan | | | 1.9% | |

Bucher Industries AG

Machinery, Switzerland | | | 1.9% | |

Techtronic Industries Co. Ltd.

Household Durables, Hong Kong | | | 1.9% | |

Interpump Group SpA

Machinery, Italy | | | 1.8% | |

The Thule Group AB

Leisure Products, Sweden | | | 1.8% | |

Rational AG

Machinery, Germany | | | 1.7% | |

Huhtamaki OYJ

Containers & Packaging, Finland | | | 1.7% | |

Gerresheimer AG

Life Sciences Tools & Services, Germany | | | 1.6% | |

congested grounds, will continue to provide the company with a competitive edge.

Despite its shares’ short-term underperformance, we have still seen substantial further potential for Japan-based sportswear exporter Asics to expand its sales channels and take full advantage of its untapped brand value. The global popularity of fitness and running and a growing recognition of Asics products’ high performance should, in our view, also remain a growth driver for the company.

It is important to recognize the effect of currency movements on the Fund’s performance. In general, if the value of the U.S. dollar goes up compared with a foreign currency, an investment traded in that foreign currency will go down in value because it will be worth fewer U.S. dollars. This can have a negative effect on Fund performance. Conversely, when the U.S. dollar weakens in relation to a foreign currency, an investment traded in that foreign currency will increase in value, which can contribute to Fund performance. For the six months ended June 30, 2017, the U.S. dollar declined in value relative to most currencies. As a result, the Fund’s performance was positively affected by the portfolio’s investment predominantly in securities with non-U.S. currency exposure. However, one cannot expect the same result in future periods.

| | | | | | |

| | | |

| ftinstitutional.com | | Semiannual Report | | | 11 | |

FOREIGN SMALLER COMPANIES SERIES

Thank you for your continued participation in Foreign Smaller Companies Series. We look forward to serving your future investment needs.

| | |

| |

Harlan B. Hodes, CPA Portfolio Manager |

The foregoing information reflects our analysis, opinions and portfolio holdings as of June 30, 2017, the end of the reporting period. The way we implement our main investment strategies and the resulting portfolio holdings may change depending on factors such as market and economic conditions. These opinions may not be relied upon as investment advice or an offer for a particular security. The information is not a complete analysis of every aspect of any market, country, industry, security or the Fund. Statements of fact are from sources considered reliable, but the investment manager makes no representation or warranty as to their completeness or accuracy. Although historical performance is no guarantee of future results, these insights may help you understand our investment management philosophy.

| | | | |

| | | |

| 12 | | Semiannual Report | | ftinstitutional.com |

FOREIGN SMALLER COMPANIES SERIES

Performance Summary as of June 30, 2017

The performance table does not reflect any taxes that a shareholder would pay on Fund dividends, capital gain distributions, if any, or any realized gains on the sale of Fund shares. Total return reflects reinvestment of the Fund’s dividends and capital gain distributions, if any, and any unrealized gains or losses. Your dividend income will vary depending on dividends or interest paid by securities in the Fund’s portfolio, adjusted for operating expenses. Capital gain distributions are net profits realized from the sale of portfolio securities.

Performance as of 6/30/171

| | | | | | | | |

| | | Cumulative

Total Return2 | | | Average Annual

Total Return3 | |

| | |

6-Month | | | +20.12% | | | | +20.12% | |

| | |

1-Year | | | +25.08% | | | | +25.08% | |

| | |

5-Year | | | +62.34% | | | | +10.18% | |

| | |

10-Year | | | +59.91% | | | | +4.81% | |

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. For most recent month-end performance, go to ftinstitutional.com or call a Franklin Templeton Institutional Services representative at (800) 321-8563.

See page 14 for Performance Summary footnotes.

| | | | | | |

| | | |

| ftinstitutional.com | | Semiannual Report | | | 13 | |

FOREIGN SMALLER COMPANIES SERIES

PERFORMANCE SUMMARY

Total Annual Operating Expenses4

| | | | |

| | | With Waiver | | Without Waiver |

| | | 0.98% | | 0.99% |

All investments involve risks, including possible loss of principal. The Fund invests in foreign securities, which can involve exposure to currency volatility and political, economic and regulatory uncertainty. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. The Fund’s investments in smaller company stocks carry special risks as such stocks have historically exhibited greater price volatility than large company stocks, particularly over the short term. Additionally, smaller companies often have relatively small revenues, limited product lines and small market share. The Fund is actively managed but there is no guarantee that the manager’s investment decisions will produce the desired results. The Fund’s prospectus also includes a description of the main investment risks.

1. The Fund has a fee waiver associated with any investment it makes in a Franklin Templeton money fund and/or other Franklin Templeton fund, contractually guaranteed through 4/30/18. Fund investment results reflect the fee waiver; without this waiver, the results would have been lower.

2. Cumulative total return represents the change in value of an investment over the periods indicated.

3. Average annual total return represents the average annual change in value of an investment over the periods indicated. Return for less than one year, if any, has not been annualized.

4. Figures are as stated in the Fund’s current prospectus and may differ from the expense ratios disclosed in the Your Fund’s Expenses and Financial Highlights sections in this report. In periods of market volatility, assets may decline significantly, causing total annual Fund operating expenses to become higher than the figures shown.

| | | | |

| | | |

| 14 | | Semiannual Report | | ftinstitutional.com |

FOREIGN SMALLER COMPANIES SERIES

Your Fund’s Expenses

As a Fund shareholder, you can incur two types of costs: (1) transaction costs, including sales charges (loads) on Fund purchases and redemptions, if applicable; and (2) ongoing Fund costs, including management fees, distribution and service (12b-1) fees, if applicable, and other Fund expenses. All mutual funds have ongoing costs, sometimes referred to as operating expenses. The table below shows ongoing costs of investing in the Fund and can help you understand these costs and compare them with those of other mutual funds. The table assumes a $1,000 investment held for the six months indicated.

Actual Fund Expenses

The table below provides information about actual account values and actual expenses in the columns under the heading “Actual.” In these columns the Fund’s actual return, which includes the effect of Fund expenses, is used to calculate the “Ending Account Value.” You can estimate the expenses you paid during the period by following these steps (of course, your account value and expenses will differ from those in this illustration): Divide your account value by $1,000 (if your account had an $8,600 value, then $8,600 ÷ $1,000 = 8.6). Then multiply the result by the number in the row for your class of shares under the headings “Actual” and “Expenses Paid During Period” (if Actual Expenses Paid During Period were $7.50, then 8.6 x $7.50 = $64.50). In this illustration, the actual expenses paid this period are $64.50.

Hypothetical Example for Comparison with Other Funds

Under the heading “Hypothetical” in the table, information is provided about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. This information may not be used to estimate the actual ending account balance or expenses you paid for the period, but it can help you compare ongoing costs of investing in the Fund with those of other funds. To do so, compare this 5% hypothetical example for the class of shares you hold with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that expenses shown in the table are meant to highlight ongoing costs and do not reflect any transactional costs. Therefore, information under the heading “Hypothetical” is useful in comparing ongoing costs only, and will not help you compare total costs of owning different funds. In addition, if transactional costs were included, your total costs would have been higher.

| | | | | | | | | | | | | | | | |

| | | | | Actual (actual return after expenses) | | | | Hypothetical (5% annual return before

expenses) | | | | |

Beginning

Account

Value 1/1/17 | | | | Ending

Account

Value 6/30/17 | | Expenses

Paid During

Period

1/1/17–6/30/171,2 | | | | Ending

Account

Value 6/30/17 | | Expenses

Paid During

Period

1/1/17–6/30/171,2 | | | | Net

Annualized

Expense

Ratio2 |

| $1,000 | | | | $1,201.20 | | $5.29 | | | | $1,019.98 | | $4.86 | | | | 0.97% |

1. Expenses are equal to the annualized expense ratio for the six-month period as indicated above—in the far right column—multiplied by the simple average account value over the period indicated, and then multiplied by 181/365 to reflect the one-half year period.

2. Reflects expenses after fee waivers and expense reimbursements.

| | | | | | |

| | | |

| ftinstitutional.com | | Semiannual Report | | | 15 | |

Global Equity Series

This semiannual report for Global Equity Series (Fund) covers the period ended June 30, 2017.

Your Fund’s Goal and Main Investments

The Fund seeks long-term capital growth. Under normal market conditions, the Fund invests at least 80% of its net assets in equity securities of companies located anywhere in the world, including developing markets.

Performance Overview

The Fund delivered a +11.40% cumulative total return for the six months under review. For comparison, the Fund’s benchmark, the MSCI All Country World Index (ACWI), which measures stock market performance in global developed and emerging markets, generated a +11.82% total return.1 Please note, index performance information is provided for reference and we do not attempt to track an index but rather undertake investments on the basis of fundamental research. You can find the Fund’s long-term performance data in the Performance Summary beginning on page 21.

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. For most recent month-end performance, go to ftinstitutional.com or call a Franklin Templeton Institutional Services representative at (800) 321-8563.

Investment Strategy

We employ a bottom-up, value-oriented, long-term investment strategy. Our in-depth fundamental research evaluates a company’s potential to grow earnings, asset value and/or cash flow. We also consider a company’s price/earnings ratio, profit margins and liquidation value.

Manager’s Discussion

The Fund delivered double-digit absolute gains, but slightly trailed its benchmark, the MSCI ACWI, during the reporting period. In general, stock selection buoyed Fund performance, but was largely offset by unfavorable sector allocations during the period. Although stocks sustained upward momentum through the bulk of the period, market leadership transitioned

Geographic Composition

Based on Total Net Assets as of 6/30/17

from cyclical, value-oriented stocks back to defensive, growth-oriented issues as the period progressed. The market’s increasingly defensive posture was consistent with mixed global economic and political newsflow. Growth slowed in the world’s two largest economies (the U.S. and China), major central banks incrementally tightened policy and political tensions in key markets such as the U.S., Japan and the U.K remained elevated. Yet, investors focused more on positive factors: continued corporate earnings strength, still abundant liquidity and a favorable election outcome in France, which creates a window of opportunity for structural change and further European reform and integration. We, too, have been encouraged by positive political and economic developments in Europe, which rewarded our long-standing overweighted allocation to the region.

At the sector level, energy holdings were largely responsible for the modest relative underperformance.2 Although the Fund actually benefited from stock selection in the sector, our significant overweighting proved challenging during a period when oil fell briefly into bear market territory amid the worst start to a year since 1997. Yet, we believe consensus pessimism in oil markets is misplaced, and we believe concerns about rising North American supply are overblown as global stockpiles paint a tighter overall inventory picture. There are even nascent signs of improvement in the U.S., where the last week of June had one of the largest inventory drawdowns on record. As inventories slowly turn, we could begin to see production come under pressure if persistently low prices

1. Source: Morningstar.

The index is unmanaged and includes reinvestment of any income or distributions. It does not reflect any fees, expenses or sales charges. One cannot invest directly in an index, and an index is not representative of the Fund’s portfolio.

2. The energy sector comprises energy equipment and services and oil, gas and consumable fuels in the SOI.

The dollar value, number of shares or principal amount, and names of all portfolio holdings are listed in the Fund’s Statement of Investments (SOI). The SOI begins on page 44.

| | | | |

| | | |

| 16 | | Semiannual Report | | ftinstitutional.com |

GLOBAL EQUITY SERIES

discourage investment in future production. Financial speculation has further pressured oil, with net positioning in futures markets revealing one of the highest levels of short trades on record, a potential contrarian indicator. Finally, geopolitical relations among the world’s largest oil producers are mostly stable, compliance to the production cuts by the Organization of the Petroleum Exporting Countries is high, and firmer oil price benefits Saudi Arabia as it prepares to conduct an initial public offering of Saudi Arabian Oil Co. (commonly known as Aramco), one of the world’s largest companies. Despite such encouraging underpinnings for an eventual oil price recovery, energy stocks continue to trade near 90-year lows based on relative price-to-book value, offering a number of what we consider to be compelling bargains for long-term value investors.

At the stock level, our positions in U.K.-based oilfield services firm Petrofac3 and U.S. exploration and production company Apache were among the Fund’s biggest individual laggards. Petrofac’s shares declined sharply after the U.K.’s Serious Fraud Office (SFO) launched an investigation into bribery allegations related to the firm’s past relationship with controversial Monaco-based consultancy Unaoil. Although we had been constructive on the stock given the company’s healthy pipeline of outstanding bids, strategic refocus on core assets and prudent balance sheet deleveraging, the escalating fraud investigation seems to us a thesis changer. Over the past three years, nearly all of the SFO’s investigations have led to charges being filed. Of particular concern, the executives currently running Petrofac also ran the company when the alleged improprieties occurred. Any legal action against these individuals could materially impact Petrofac’s ability to win new business, without which we believe the company’s financial situation is tenuous. A change in circumstances requires a reassessment of the new reality, and we decided to liquidate our stake in Petrofac given the rising risk profile. Meanwhile, Apache’s shares lagged after the firm reported an unexpected loss and disappointing 2017 production guidance. We continue to like Apache’s longer term prospects, given the strong cash-flow generating capabilities of its low-cost international assets (in Egypt and the North Sea) and an attractive growth pipeline in U.S. shale, including a potential major new discovery in the Permian Basin. We initially invested in Apache on the premise that its attractive growth pipeline was deeply undervalued by a short-term-oriented

| | | | |

| Portfolio Composition | |

| 6/30/17 | | | |

| Sector/Industry | | % of Total

Net Assets | |

Banks | | | 11.8% | |

Oil, Gas & Consumable Fuels | | | 10.5% | |

Pharmaceuticals | | | 9.9% | |

Technology Hardware, Storage & Peripherals | | | 5.3% | |

Insurance | | | 4.5% | |

Software | | | 4.2% | |

Media | | | 4.0% | |

Biotechnology | | | 3.6% | |

Wireless Telecommunication Services | | | 3.2% | |

Chemicals | | | 2.9% | |

Metals & Mining | | | 2.8% | |

Internet Software & Services | | | 2.8% | |

Aerospace & Defense | | | 2.7% | |

Diversified Telecommunication Services | | | 2.6% | |

Other | | | 25.7% | |

Short-Term Investments & Other Net Assets | | | 3.5% | |

market; the market now ascribes a higher value to these assets, and while the stock is no longer an outright bargain in our view, it remains a core holding with potential for future appreciation as value materializes.

An underweighted position in consumer staples also notably detracted during a period when the defensive sector came back into favor.4 We continue to believe that the historic valuation premium commanded by consumer staples stocks is likely to limit long-term investment returns in a commoditized sector subject to extreme pricing pressure and deteriorating earnings trends. For exposure to quality stocks with defensive characteristics, we continue to prefer health care to consumer staples given, among other things, the near-record valuation gap between the two sectors.

Even-weighted information technology (IT) holdings also detracted, pressured by Japanese electronics firm Konica Minolta.5 Its shares declined after the firm reported disappointing quarterly results and projected declining earnings for its current fiscal year amid higher restructuring costs and expenditures. Although many market participants remain skeptical about the firm’s near-term product transitions and strategic initiatives, we believe the stock is attractive on a longer term horizon. We believe many investors continue to

3. No longer held by period-end.

4. The consumer staples sector comprises beverages, food and staples retailing, and personal products in the SOI.

5. The IT sector comprises communications equipment; electronic equipment, instruments and components; Internet software and services; IT services; semiconductors and semiconductor equipment; software; and technology hardware, storage and peripherals in the SOI.

| | | | | | |

| | | |

| ftinstitutional.com | | Semiannual Report | | | 17 | |

GLOBAL EQUITY SERIES

underappreciate the company’s success in gradually lowering dependency on its still-profitable office equipment business, while it is increasing focus on more attractive growth segments such as commercial printing, medical and various industrials businesses. The company’s ability to consistently return its high free cash flow to shareholders also remains undervalued, in our analysis. We continue to find selective value opportunities within the IT sector more broadly, and note that three of the Fund’s absolute contributors during the period were from the sector: South Korean semiconductor and consumer electronics manufacturer Samsung Electronics, U.S. enterprise software firm Oracle, and consumer technology giant Apple. Samsung was a significant relative contributor, benefiting from a more stable South Korean political environment, the cancelation of billions of U.S. dollars’ worth of its Treasury shares and a raft of earnings upgrades from Wall Street analysts. Although sentiment on the stock is beginning to improve as results highlight operational progress, our analysis indicates to us that the market continues to undervalue the sustainability of Samsung’s dominant, low-cost position in core markets due to excessive focus on problem areas of lesser business impact. Trading at what we considered low valuation multiples and with the company holding a large net cash position, Samsung’s improving business mix shift and increasing focus on shareholder returns remain significantly undervalued, in our analysis.

Turning to contributors, stock selection and an overweighted allocation in telecommunication services led the sector to deliver the best relative sector returns during the review period.6 Japanese mobile operator and technology conglomerate SoftBank Group led sector outperformance. Its shares rose to the highest levels in nearly two decades after the firm’s majority-owned U.S. telecommunications subsidiary, Sprint,7 reported better-than-expected sales and subscriber growth. The higher share price also reflected rising optimism that SoftBank might be able to execute a long-desired merger between Sprint and another U.S. major mobile operator, T-Mobile U.S.,7 under a new Republican administration. SoftBank Chairman Masayoshi Son recently met with President Donald Trump and pledged to invest US$50 billion and create 50,000 jobs in the U.S., an indication that SoftBank is working to curry favor with the new administration to facilitate a deal that, if executed, we believe could represent a potential share price catalyst. Elsewhere at SoftBank, the core Japanese telecommunications business is providing strong, stable free

| | | | |

| Top 10 Holdings | | | |

| 6/30/17 | | | |

Company Sector/Industry, Country | | % of Total

Net Assets | |

Samsung Electronics Co. Ltd. Technology Hardware, Storage & Peripherals, South Korea | | | 2.5% | |

Oracle Corp. Software, U.S. | | | 2.2% | |

BP PLC Oil, Gas & Consumable Fuels, U.K. | | | 2.1% | |

Microsoft Corp. Software, U.S. | | | 2.0% | |

Apple Inc. Technology Hardware, Storage & Peripherals, U.S. | | | 1.9% | |

Alphabet Inc. Internet Software & Services, U.S. | | | 1.9% | |

Citigroup Inc. Banks, U.S. | | | 1.8% | |

Comcast Corp. Media, U.S. | | | 1.7% | |

HSBC Holdings PLC Banks, U.K. | | | 1.7% | |

JPMorgan Chase & Co. Banks, U.S. | | | 1.6% | |

cash flow; Chinese technology subsidiary Alibaba Group Holding7 continues to realize outsized growth; and the newly acquired U.K. semiconductor manufacturer ARM Holdings,7 while expensive and value-destructive in the near-term, in our view, offers another exciting long-term growth driver. SoftBank’s stock remains excessively cheap on a sum-of-the-parts basis, in our analysis.

We were also encouraged by the outperformance of the Fund’s overweighted financials holdings, led by a mix of European and Asian banks.8 Conditions continue to generally improve in the European banking sector, where earnings revisions have returned to a positive trajectory, regulatory capital has been largely rebuilt and the bulk of post-crisis re-regulation efforts are now complete. As economic data have picked up and certain risky political events have been favorably resolved, demand for credit has increased. Indeed, private loan growth is steadily rising in Europe, with favorable implications for bank earnings. Yet, little of this good news has made it into the price of European bank shares, which continue to look undervalued to us based on price-to-earnings, price-to-book value and dividend yields, relative to both their own history and to their

6. The telecommunication services sector comprises diversified telecommunication services and wireless telecommunication services in the SOI.

7. Not a Fund holding.

8. The financials sector comprises banks, capital markets, consumer finance, diversified financial services, insurance, and thrifts and mortgage finance in the SOI.

| | | | |

| | | |

| 18 | | Semiannual Report | | ftinstitutional.com |

GLOBAL EQUITY SERIES

U.S. peers. In Asia, the lowly valued South Korean market has offered some of the best financials sector opportunities, in our analysis. Shares of South Korean lender Hana Financial Group finished among the Fund’s top contributors during the period, rallying amid signs that a new government in South Korea could deliver fiscal stimulus, reform the rigid corporate chaebol structure (large, mostly family-owned conglomerates) and normalize economic ties with China. Prospects for improving corporate governance and political stability have combined with rising interest rates and genuine economic growth to benefit the banking sector in emerging Asia more generally.

Stock selection also drove outperformance in the underweighted industrials sectors, led by German airline Deutsche Lufthansa.9 Its shares rose to a three-year high after the company reported solid first-quarter 2017 earnings attributable to successes at its maintenance and logistics businesses. Following a difficult several years, Lufthansa has more recently begun to report encouraging progress on a number of fronts. Pricing is improving, fuel costs remain low, the pension deficit has fallen significantly from its 2016 highs and a recent favorable accord with the pilots’ union reduces the risk of further industrial actions. Wall Street analysts, who were almost uniformly negative on Lufthansa in recent years, have issued a number of upgrades recently and the stock has appreciated and improved on a number of key valuation metrics.

Encouragingly, the Fund’s overweighted health care holdings outperformed during the period.10 Pharmaceuticals stocks have steadily rebounded in the first half of 2017 after a difficult 2016 marked by election cycle political rhetoric. We argued that the political threat to drugmakers was overdone and added to our holdings during 2016’s weakness. Recent signs from Washington suggest to us that health care reform initiatives may indeed be less punitive to pharmaceuticals earnings than initially feared. Within the sector, we continue to favor innovative companies we feel have portfolios of high-margin, long-duration products and think are facing little competition or have demonstrable advantages over existing therapies.

From a regional standpoint, all major geographic regions benefited from favorable allocations (underweighting in North America and overweightings in Europe and Asia), although stock-specific weakness in Europe offset stock-level performance. Nevertheless, we were encouraged by positive

developments in Europe during the period and continue to find what we consider attractive bottom-up bargains in the region. Although economic indicators in the U.S. are softening and the political environment remains hostile, Europe is experiencing an encouraging combination of genuine economic momentum and a political climate now conducive to structural reform. To the first point, unemployment in Europe recently hit an eight-year low, gross domestic product growth has outpaced the U.S. in 2016 for the first time since the global financial crisis, and corporate profits are solidly accelerating. Encouragingly, European equity markets attracted record weekly investment inflows during 2017’s second quarter. On the political front, Emmanuel Macron’s victory in the French presidential election (and subsequent success in parliamentary votes) creates a historic opportunity for genuine reform and closer European integration.

It is important to recognize the effect of currency movements on the Fund’s performance. In general, if the value of the U.S. dollar goes up compared with a foreign currency, an investment traded in that foreign currency will go down in value because it will be worth fewer U.S. dollars. This can have a negative effect on Fund performance. Conversely, when the U.S. dollar weakens in relation to a foreign currency, an investment traded in that foreign currency will increase in value, which can contribute to Fund performance. For the six months ended June 30, 2017, the U.S. dollar declined in value relative to most currencies. As a result, the Fund’s performance was positively affected by the portfolio’s substantial investment in securities with non-U.S. currency exposure. However, one cannot expect the same result in future periods.

More broadly, we continue to stress the value of fundamental investing, active stock picking and disciplined risk management in the current environment. Overall, we assess that equities offer selectively attractive opportunities, and should continue to generate investor interest in a lower-yield, lower-return environment in which asset owners are under pressure to meet challenging return targets. However, in our opinion, this is not the point in the cycle to buy equities indiscriminately. We believe monetary policy has never been so loose and experimental, artificially depressing the price of money and skewing the risk-free rate (and therefore the assets that are priced off of it). Global debt levels have never been so high, generating a flood of liquidity that has saturated many financial

9. The industrials sector comprises aerospace and defense, airlines, building products, industrial conglomerates and machinery in the SOI.

10. The health care sector comprises biotechnology, health care equipment and supplies, health care providers and services, life sciences tools and services, and pharmaceuticals in the SOI.

See www.franklintempletondatasources.com for additional data provider information.

| | | | | | |

| | | |

| ftinstitutional.com | | Semiannual Report | | | 19 | |

GLOBAL EQUITY SERIES

assets. Political tensions remain elevated, and policymakers may struggle to turn pro-growth campaign promises into actual legislation. Meanwhile, we believe stocks have become commoditized into “factor buckets,” and are thought of today not as ownership stakes in long-term, cash-generating businesses, but instead as high-or-low-beta, high-or-low-quality, defensive-or-aggressive, risk-on-or-off, etc. These are all unusual conditions that create additional challenges for fundamentally oriented security analysts. Yet, it is our belief that all of these trends are temporary, as price eventually converges with value over time and a healthy market needs investors with the ability to facilitate price discovery. After a long, fallow period for active value investors, we were encouraged by 2016’s value rally and, despite the more recent pull-back, we anticipate a supportive environment for value investing over our long-term horizon.

Thank you for your continued participation in Global Equity Series. We look forward to serving your future investment needs.

| | | | |

| | Peter A. Nori, CFA |

| | Antonio T. Docal, CFA |

| | Cindy L. Sweeting, CFA |

| |

| | Portfolio Management Team |

The foregoing information reflects our analysis, opinions and portfolio holdings as of June 30, 2017, the end of the reporting period. The way we implement our main investment strategies and the resulting portfolio holdings may change depending on factors such as market and economic conditions. These opinions may not be relied upon as investment advice or an offer for a particular security. The information is not a complete analysis of every aspect of any market, country, industry, security or the Fund. Statements of fact are from sources considered reliable, but the investment manager makes no representation or warranty as to their completeness or accuracy. Although historical performance is no guarantee of future results, these insights may help you understand our investment management philosophy.

| | | | |

| | | |

| 20 | | Semiannual Report | | ftinstitutional.com |

GLOBAL EQUITY SERIES

Performance Summary as of June 30, 2017

The performance table does not reflect any taxes that a shareholder would pay on Fund dividends, capital gain distributions, if any, or any realized gains on the sale of Fund shares. Total return reflects reinvestment of the Fund’s dividends and capital gain distributions, if any, and any unrealized gains or losses. Your dividend income will vary depending on dividends or interest paid by securities in the Fund’s portfolio, adjusted for operating expenses. Capital gain distributions are net profits realized from the sale of portfolio securities.

Performance as of 6/30/17

| | | | | | | | |

| | | Cumulative

Total Return1 | | | Average Annual

Total Return2 | |

6-Month | | | +11.40% | | | | +11.40% | |

1-Year | | | +25.20% | | | | +25.20% | |

5-Year | | | +68.09% | | | | +10.94% | |

Since Inception (3/31/08) | | | +52.77% | | | | +4.69% | |

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. For most recent month-end performance, go to ftinstitutional.com or call a Franklin Templeton Institutional Services representative at (800) 321-8563.

See page 22 for Performance Summary footnotes.

| | | | | | |

| | | |

| ftinstitutional.com | | Semiannual Report | | | 21 | |

GLOBAL EQUITY SERIES

PERFORMANCE SUMMARY

Total Annual Operating Expenses3

All investments involve risks, including possible loss of principal. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments; investments in emerging markets involve heightened risks related to the same factors. To the extent the Fund focuses on particular countries, regions, industries, sectors or types of investment from time to time, it may be subject to greater risks of adverse developments in such areas of focus than a fund that invests in a wider variety of countries, regions, industries, sectors or investments. The Fund is actively managed but there is no guarantee that the manager’s investment decisions will produce the desired results. The Fund’s prospectus also includes a description of the main investment risks.

1. Cumulative total return represents the change in value of an investment over the periods indicated.

2. Average annual total return represents the average annual change in value of an investment over the periods indicated. Return for less than one year, if any, has not been annualized.

3. Figures are as stated in the Fund’s current prospectus and may differ from the expense ratios disclosed in the Your Fund’s Expenses and Financial Highlights sections in this report. In periods of market volatility, assets may decline significantly, causing total annual Fund operating expenses to become higher than the figures shown.

| | | | |

| | | |

| 22 | | Semiannual Report | | ftinstitutional.com |

GLOBAL EQUITY SERIES

Your Fund’s Expenses

As a Fund shareholder, you can incur two types of costs: (1) transaction costs, including sales charges (loads) on Fund purchases and redemptions, if applicable; and (2) ongoing Fund costs, including management fees, distribution and service (12b-1) fees, if applicable, and other Fund expenses. All mutual funds have ongoing costs, sometimes referred to as operating expenses. The table below shows ongoing costs of investing in the Fund and can help you understand these costs and compare them with those of other mutual funds. The table assumes a $1,000 investment held for the six months indicated.

Actual Fund Expenses

The table below provides information about actual account values and actual expenses in the columns under the heading “Actual.” In these columns the Fund’s actual return, which includes the effect of Fund expenses, is used to calculate the “Ending Account Value.” You can estimate the expenses you paid during the period by following these steps (of course, your account value and expenses will differ from those in this illustration): Divide your account value by $1,000 (if your account had an $8,600 value, then $8,600 ÷ $1,000 = 8.6). Then multiply the result by the number in the row for your class of shares under the headings “Actual” and “Expenses Paid During Period” (if Actual Expenses Paid During Period were $7.50, then 8.6 x $7.50 = $64.50). In this illustration, the actual expenses paid this period are $64.50.

Hypothetical Example for Comparison with Other Funds

Under the heading “Hypothetical” in the table, information is provided about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. This information may not be used to estimate the actual ending account balance or expenses you paid for the period, but it can help you compare ongoing costs of investing in the Fund with those of other funds. To do so, compare this 5% hypothetical example for the class of shares you hold with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that expenses shown in the table are meant to highlight ongoing costs and do not reflect any transactional costs. Therefore, information under the heading “Hypothetical” is useful in comparing ongoing costs only, and will not help you compare total costs of owning different funds. In addition, if transactional costs were included, your total costs would have been higher.

| | | | | | | | | | | | | | | | |

| | | | | Actual (actual return after expenses) | | | | Hypothetical (5% annual return before expenses) | | | | |

Beginning

Account

Value 1/1/17 | | | | Ending

Account

Value 6/30/17 | | Expenses

Paid During

Period

1/1/17–6/30/171 | | | | Ending

Account

Value 6/30/17 | | Expenses

Paid During

Period

1/1/17–6/30/171 | | | | Annualized

Expense

Ratio |

| $1,000 | | | | $1,114.00 | | $4.30 | | | | $1,020.73 | | $4.11 | | | | 0.82% |

1. Expenses are equal to the annualized expense ratio for the six-month period as indicated above—in the far right column—multiplied by the simple average account value over the period indicated, and then multiplied by 181/365 to reflect the one-half year period.

| | | | | | |

| | | |

| ftinstitutional.com | | Semiannual Report | | | 23 | |

International Equity Series

This semiannual report for International Equity Series (Fund) covers the period ended June 30, 2017.

Your Fund’s Goal and Main Investments

The Fund seeks long-term capital growth. Under normal market conditions, the Fund invests at least 80% of its net assets in foreign (non-U.S.) equity securities.

Performance Overview

The Fund’s Primary shares delivered a +13.24% cumulative total return for the six months under review. For comparison, the Fund’s benchmark, the MSCI All Country World Index (ACWI) ex USA Index, which measures stock market performance in global developed and emerging markets excluding the U.S., generated a +14.45% total return for the period under review.1 The Fund’s other benchmark, the MSCI Europe, Australasia, Far East Index, which measures stock market performance in global developed markets excluding the U.S. and Canada, posted a +14.23% total return.1 Please note, index performance information is provided for reference and we do not attempt to track an index but rather undertake investments on the basis of fundamental research. You can find the Fund’s long-term performance data in the Performance Summary beginning on page 29.

Performance data represent past performance, which does not guarantee future results. Investment return and principal value will fluctuate, and you may have a gain or loss when you sell your shares. Current performance may differ from figures shown. For most recent month-end performance, go to ftinstitutional.com or call a Franklin Templeton Institutional Services representative at (800) 321-8563.

Investment Strategy

We employ a bottom-up, value-oriented, long-term investment strategy. We focus on the market price of a company’s securities relative to our evaluation of the company’s long-term earnings, asset value and cash flow potential. We also consider a company’s price/earnings ratio, profit margins and liquidation value.

Geographic Composition

Based on Total Net Assets as of 6/30/17

Manager’s Discussion

The Fund delivered double-digit absolute gains, but slightly trailed its benchmark, the MSCI ACWI ex USA Index, during the reporting period. In general, stock selection buoyed Fund performance, but was largely offset by unfavorable sector allocations during the period. Although stocks sustained upward momentum through the bulk of the period, market leadership transitioned from cyclical, value-oriented stocks back to defensive, growth-oriented issues as the period progressed. The market’s increasingly defensive posture was consistent with mixed global economic and political newsflow. Growth slowed in the world’s two largest economies (the U.S. and China), major central banks incrementally tightened policy and political tensions in key markets such as the U.S., Japan and the U.K remained elevated. Yet, investors focused more on positive factors: continued corporate earnings strength, still-abundant liquidity and a favorable election outcome in France, which creates a window of opportunity for structural change and further European reform and integration. We, too, have been encouraged by positive political and economic developments in Europe, which rewarded our long-standing overweighted allocation to the region.

At the sector level, energy holdings were largely responsible for the modest relative underperformance.2 Our significant overweighting proved challenging during a period when oil fell

1. Source: Morningstar.

The indexes are unmanaged and include reinvested dividends. They do not reflect any fees, expenses or sales charges. One cannot invest directly in an index, and an index is not representative of the Fund’s portfolio.

2. The energy sector comprises energy equipment and services and oil, gas and consumable fuels in the SOI.

The dollar value, number of shares or principal amount, and names of all portfolio holdings are listed in the Fund’s Statement of Investments (SOI). The SOI begins on page 50.

| | | | |

| | | |

| 24 | | Semiannual Report | | ftinstitutional.com |

INTERNATIONAL EQUITY SERIES